Does Technology Lead to Better Financial Performance? A Study of Indian Commercial Banks

1

GENERAL INTRODUCTION

0.1 Background of the study

In the world today’s, business environment is characterized by

increased competition, rapid changing technology economic

liberalization and customer awareness to market. In financial

institutions, automated teller machine (ATM) was introduced in

order to perform financial transactions without the need for

cashier or bank teller In Rwanda the development of money followed

the same path as elsewhere in world; the cash based system in

Rwanda is now gradually being replaced by the card –based system.

The first ATM was invented and patented in 1939. (By Luther

simjian). The government of Rwanda is putting as tool to achieve

its vision 2020. It is in this perspective that the modernization

of national payment system became prerequisite (essential). This

model was unsuccessful prototype, but it led the way to the first

Modern ATM created by James Good fellow in 1966. Because the

ability to connect to the bank via computer was not yet available,

access to these machines was only given to a select few bank

customers. The first ATM s to use a card with a magnetic strip was

patented in 1977.

Despite the fact that the machine existed this early; it was not

until the end of the 1980s that ATMs became common place in modern

banking these modern movels of technology were well received by

consumers because they made it possible for them to access money

from their credit card or debit card 24/7 hours per day with a

1

2

quick and simple system. Also they could access money anywhere in

the world with the help of the ATM.

For all that ATM made certain aspect of life safer; it did make it

easier for counterfeiters and thieves to take advantage of

undoubtful consumers. After all, it only took having the card and a

PIN (personal identification number) to access all of somebody’s

funds. For this reason visa soon introduced the visa Risk

identification service, this computer –based program was capable of

identifying suspicious transaction and putting an end to them if

there was reason to suspect it was fraudulent. This type of system

is still in use today; with individual banks having their own

unique type of system is still today, with individual banks having

their own unique system to help keep you safe. In addition, many

countries are putting other protective barriers in place to ensure

the transaction placed on credit cards and debit cards are truly

authorized by the owner.

(www.ukfinancialoptions.co.uk,accessed,on10/07/2014) or

(www.google.en, accessed on 10/07/2014)

1. CHOICE AND INTEREST OF THE STUDY

There is three dimension or categories such as:

Personal interest

Social interest

Academic and scientific interest

2

3

1.1Personal interest

By carrying out this study, with to improve my knowledge about the

benefits for using ATM services. This work is for us an important

intellectual exercise, practice and training that compare the

knowledge; we had on the research methodology and reality of field

research.

1.2 Social interest

On the social hand, this work has an incomparable utility because

it would be one guide of Rwandan people and the clientele of BK on

new technology that is the electronic banking secured. BK is going

to be to measure its performance as compare to the other banks

performance in areas advertisement

1.3 Academic interestThe Kigali independent university culture

requires that each and every student may conduct a field research

and write final report and present it in front of the panel. This

allows him/her to get bachelor’s degree. The study will enable me

to contribute scientifically to the development of science in the

Kigali independent university especially Gisenyi campus a copy of

the final report will remain the property of the ULK library and

will be used as documentation by future researchers interested in

the same domain and will serve for reference of student who will

engaged in studied on growth commercial bank through ATM service

/good service like this one

2. DELIMITATION OF THE STUDY

3

4

This current research will be delimitated in time, in area and

field

2.1 In time: The work focuses on the period from 2008-2013, which

is five years. I think that period is sufficient /enough to verify

the research hypotheses.

2.2 In space: In space, this research will be carried out in Rubavu

district (Gisenyi) western province in BK

2.3 In domain

The study is in the domain of marketing

3. PROBLEM STATEMENT

Globalization and information and communication technology (ICT)

took the world by storm and this has posed great challenges to the

banking industry Aruba (2008). Information and communication

technology (ICT) has changed not just the business world but also

the world we live in. it has changed the way things are done that

today no matter what you plan to do, whether you will work with

people or money, with words or numbers, with technological

breakthrough and advances in telecommunications, speed of equipment

and the use of computers, bankers can now use these some links to

transmit data.

This gave rise to electronic banking which is simply the

application of information technology (telecommunications and

computers) to transmit data from one point to another. The

4

5

electronic delivery of banking services has grown rapidly in

popularity that every bank now realizes that electronic banking has

become a basic element of today’s financial services delivery. The

banks have also deployed the ATMs to other locations such as

supermarkets, tertiary institutions, hospitals, hotels restaurant

and so on. There is no doubt that the introduction of ATMs by

banks is to reduce operation costs and to ensure that the customers

are better served. But the ATM is not without challenges because

there are always people out there who would want to reap where they

did not sow The infrastructures that support the machines are

susceptible to abuse, misuse and failure in many ways, resulting in

financial loss as a result of fraud, unauthorized use of customers

personal identification number and loss of customers confidence.

ATM fraud has taken an alarming proportion and most customers are

now afraid to use their ATM cards. There is no doubt that there

must be collusion between some bank staff and fraudsters for such

fraud to succeed. This is one of the reasons customers are fret

about the security of on-line transactions. While on the hand, some

customers have not helped matters because of their carelessness or

fraudulent nature. All these have given rise to ATM challenges in

the banking industry. (www.netplaced.accessed,0n 14/7/2013

Electronic banking was found to be the relevant system needed to

solve those problems faced by non-electronic banking system(to

spend time on line s before being tendered the service robbery done

in doing transactions, the need to have cash in hands for every

5

6

service needed and language shortfalls found from some of the

bank employees and customer which do not authorize them to

communicate effectively and efficiently (BNR,2003:52)

All these importance of electronic banking system its challenges as

new need of the researcher to determine the degree of

understanding, reliability and uses of this system as well as its

potentiality to drive payment and receipts from cash to cards have

motivated the researcher to conduct his research on ‘’ THE

CONTRIBUTION OF ATM SERVICE ON GROWTH IN COMMERCIAL BANKS’’

regarding to use of ATM card, a case study of BK

Face to those problems meet in various banks of Rwanda it push to

ask the following questions.

1. What is the level of customer satisfaction for using of ATM at

BK?

2. What is the contribution of ATM service on the growth in BK?

4. RESEACH HYPOTHESES

4.1 DEFINITION

The hypothesis is defined as “the response proposed to the

questions asked upon the topic. It is formulated in clear terms

such that a response might be provided through observation and

analysis. Even more or less accurate, it helps to select the

observed facts, interpret them as well as verify them according to

the written theory ( GRAWIRTZ M.2001:35)

6

7

The following hypotheses try to give answer to the question asked;

The level of customer satisfaction of using ATM is higher to

the BK/Rubavu.

The use of ATM card contributes positively to the growth of

BK/Rubavu branch.

5. RESEACH OBJECTIVES

The work that is scientific must be supported by certain number of

objective s to which it can valorized such as aspect of the work

that is why is why the research have put our work under global

objective and specific objective

5.1 GLOBAL OBJECTIVES

The global objectives of this study are to develop a case study

with a view to describe and understanding the contribution of ATM

card service on growth of bank of Kigali.

5.2 SPECIFIC OBJECTIVES

To determine the level of customer satisfaction of the use of

ATM at BK.

To determine the contribution of ATM service impact on

growth of bank

To provide some suggestions and recommendation based on the

findings

6. METHODOLOGY

7

8

The methodology is defined as the study of good users of methods

and technique in given research to verify the hypothesis of

research and achieve at the objectives assigned on in my research,

I will use different techniques and methods as follows;

6.1 TECHNIQUEs

The technique is the way of carrying out a particular task,

especial the execution or performance of an artistic work or

scientific procedure through skills or ability in a particular

field or efficient way of doing or achieving

Something, These technique can attach on data collection and

information that allow the research to put together the base

materials (Rwigamba, 2004).

6.1.1 THE INTERVIEW TECHNIQUE

An interview is an oral questionnaire where the investigator

gathers data through direct verbal interaction with participants.

Instead of written responses, the subject gives the needed

information verbally in face to face relationship where ideas are

exchanged. KOTTAR (1990:97) defines interview as: << a method of

collecting data that involves presentation of oral verbal stimuli

reply in terms of oral verbal responses. This methods can be used

Through personal interview and if possible through telephone

interview>> this method enables me to collect completive data to

those collected with the questionnaire.

8

9

6.1.2 QUESTIONNAIRE TECHNIQUE

The questionnaire technique is a carefully designed instrument for

collecting data in accordance with the specifications of the

research questions and hypotheses. It consists of a set questions

to which the subject responds in writing. A questionnaire

therefore is a form consisting of interrelated questions prepared

by the researcher about the research problem under investigation,

based on the objectives of the study. The questionnaire was

administrated to each of the sample population

6.1.3 SAMPLING TECHNIQUE

GRINNEL and WILLIAM (1990:132) defined sampling as the process of

selecting people or case to take in a research study. LAURENCE

(1990:7), in the some context, adds that a sample is a group of

people representing only a portion of population one behalf of the

entire customer of BK Rubavu branch. A few of them will be selected

because it is difficult to find everybody and interview all of

them.

6.1.4 THE DOCUMENTARY TECHNIQUE

This technique brought me satisfactory information through reading

different document such as: The dissertation, report, reviews,

newspaper, discussion, conference and other document technique

enables us to find much information by using different document s

concerning the topic.

6.2 METHODS

9

10

A method is intellectual operation through which a discipline seeks

to attain a certain end, that is , discovery or evidence of a truth

or is a set of intellectual operations which enable to analyze ,to

understand and to explain the analyzed reality or else to structure

the research (GRAWITZ,2001) following methods were used:

comparative method. Historic method, analytical method.

6.2.1 COMPARATIVE METHOD

The comparative method is used almost in all sciences in order to

find out similarities and differences among element .it also

enabled researchers to detect other relent causes between factors

that generate similarities or between other things.

6.2.2 DIACHRONIC (historical method)

This method very important because it is facilitate to explain the

fact in start up to current situation of BK bank Gisenyi branch

and it seeks to understand the past by reading documents, relics

and interviews. Data collected is analyzed and interpreted.

6.2.3 ANALYTICAL METHOD : This method enables a systematic analysis

of information and giving more details on a case situations of data

collected on ATM cards service; this method will enable me to

analyze data from field.

7. WORK SUBDIVISION

My work is organized into three chapters it has to start with

introduction presenting significance of the study, delimitation,

10

11

statement of the problem as hypothesis ,objectives of the study,

methods and techniques used and organization of the study.

Chapter 1. Entitled “conceptual and theoretical framework or

literature review”, deals with the definition of key concepts and

presents the theories related to the study.

Chapter 2.entitled” Deals with the level of customer satisfaction

of the BK for using the ATM card service. It verifies the first

hypothesis.

Chapter 3. Deals with “assesses the contribution of ATM service on

the growth in commercial bank from BK “

CHAPTER ONE: CONCEPTUAL FRAMEWORK AND LITERATURE REVIEW

This part contains the definition of key concepts of this work, the

literature, the historical and theory on bank credits.

1.1 Definition of key concepts

This part includes the etymology and origin of used words in this

work from books, internet, library and other useful resources.

1.1.1 Service

In economic, a service is an intangible commodity, More

specifically, services area intangible equivalent of economic

goods.

11

12

Service provision is often an economic activity where the buyer

does not generally, except by exclusive contract, obtain exclusive

ownership of the thing purchased. The benefits of such a service,

if priced, are held to be self-evident in the buyer’s willingness

to pay for it. Public services are those society as a whole pays

for through taxes and other means (Valerie zeithaml,A Parasumaran,

Leonhard berry, 20000). By composing and orchestrating the

appropriate level of resources, skill, ingenuity, and experience

for effecting specific benefits for service consumers, service

providers participate in an economy without the restrictions of

carrying inventory(stock) or the need to concern themselves with

bulky raw materials. On the other hand, their investment in

expertise does require consistent service marketing and upgrade in

the face of completion which has equally few physical restrictions.

Many so-called services, however, require large physical structures

and equipment, and consume large amounts of resource, such as

transportation services and military (Valerie zenithal, a.

parasumaran, Leonhard berry, 2000).

1.1.2 GROWTH

Growth refers to an increase in some quantity over time. The

quantity can be:

Physical (e.g. , growth In height, growth in an amount of

money)

Abstract (e.g. , a system becoming more complex, an organism

becoming more mature).

12

13

It can also refer to the mode of growth, i.e. numeric models for

describing how much a particular quantity grows over time

(reinhart&rogoff, 2009).

1.1.3 COMMERCIAL BANK

The term used for a normal bank to distinguish it, from an

investment bank. After the Great Depression, the U.S. congress

required that banks only engage in banking activities, whereas

investment banks were limited to capital market activities. Since

the two no longer have to be under separate ownership, some use the

term ‘’ commercial bank’’ to refer to a bank or a division of a

bank that mostly deals with deposits and loans from corporation or

large businesses (KEVIN B.2007).

1.1.4 BANK

The name of bank derives from the Italian word ban co.<<

desk/bench>>, used during the renaissance by Florentine bankers,

who used to make their transactions above a desk covered by a green

tablecloth .however, they are traces of banking activity even in

ancient times.

In fact, the word traces its origins back to the ancient Roman

Empire where money lenders would set up their stalls in the middle

of enclosed courtyards called Marcella on a long bench a bancu,

from which the words ban co and bank are derived. As a money

changer, the merchant at the <<Banka<< did not so much invest money

as merely convert the foreign currency into the only legal tender

in Rome (www. Wikipedia.org/bank).

13

14

A bank is a financial institution licensed by a government; its

primary activities include borrowing and lending money. For example

banks are important players in financial markets and offer

financial services such as investment funds. In some countries such

as Germany, banks have historically owned major stakes in

industrial corporations while in other countries such as the United

States, banks are prohibited from owning non-financial companies.

The level of government regulation of the banking industry varies

widely, with countries such as Iceland, the united kingdom and

united states having relatively heavier regulation of the banking

sector , and countries such as china having relatively heavier

regulation ( includingstrictregulationsregarding the level of

reserves)(www.wikipedia.org/bank.

1.2 THEORETICAL FRAMEWORK

1.2.1 ORIGIN OF ATM

ATM card (visa and credit cards) came into existence in 1976 as a

replacement of what was known as bank America card. And in 1986ATM

card (e.g. visa card) began an affirmation with ATMs (automatic

teller machine) some known as DAB an gab which allows the card

holder to withdraw cash at any given time.

This operation system is dedicated to serve its members both

cardholders and merchants by facilitating public payment 24hours a

day 7days a week at customer’s dispositions. By using a pos system

( point of sale0 which is installed in a place of business where

the merchant is supposed to have an account in the bank. This

14

15

terminal card enables the card to purchase and pay the card with at

least a maximum of 200.000 frws per day (KANFAN, 2009

1.2.1 TYPES OF ATMs

ATMs broadly fall into two categories. They are briefly explained

below:

1. Lobby ATMs

These are the ATM that are installed in branch lobbies of the

concerned bank.

2. Through-the-wall- ATMs

These are the ATMs that are installed in wide range of locations

spread over the country and sometimes overseas too. They are

located not only in bank branches but also in shopping malls,

alongside departmental stores and supermarkets, and in small .mini-

branches which are frequented by more and more people. They are

found in place ranging from railway stations to shopping malls,

airports, and even on broad ship, with link between the ATM and

host computer being maintained by radiotelephone.

3. ATMs mechanism

Anyone who is desirous of using the ATM facility is to go through

the following steps:

Customer of a bank making application for the ATM card;

Manager of the bank-branch issuing the ATM CARD, fixing the

maximum cash withdrawals limits etc;15

16

Customer to gain access to the ATM by swiping the card through

a card-swipe located outside

Verification of the card opening of the lobby door, the

entrance lobbies are particularly useful for security reason

as they let the customer complete the transaction without any

potential mugger or thief being in the immediate vanity.

Customer to insert the ATM card in the insertion point of the

ATM

Customer to type the confidential PIN the process of ATM

The ATM to depict the list of function waiting to be carried

out for the customer, such as cash withdrawals etc

Customer to selects the relevant operation to be perfumed in

the ATM

The ATMs carrying out the relevant operation as selected by

the customer.

1.2.3 ATM FUNCTIONS

The major functions performed by the ATM worldwide are of two types

as described below:

1. Basic functions

Basic functions are:

A) Cash withdrawal

B) Balance enquiry(whether displayed on screen or

printed out),

16

17

C) statement ordering facility;

2. Additional functions

Additional functions are:

a) Cheque book request facility;

b) Deposit, the facility being confined to customers of the

financial institutions running the ATM in question which is

not usually available via a share ATM network

c) Funds transfer facility ,which usually involves a

customer –initiated transfer of funds to prearranged

destination, such a utilities company account to pay a bill or

to another customer account;

d) PIN change facility;

e) Passbook up date facility;

f) Dispensing traveler’s cheque, although a fairly uncommon

facility, available at international airports.

In additional to the above ATM can also be used to provide for more

function than are currently available on them. For example, they

could be used for a wide range of communication purposes as

emergency measure to alter policy, ambulance or fire services.

Similarly, sharing of ATMs might be possible in future among banks

and other service providers too such a airlines to given the

proliferation in the use of smart cards which would links up all

participating parties and growth of the virtual banking

revolution(www.banking.about.com. Accessed on, 1/6/2013)

17

18

1.2.4 INTERNATIONAL ATM

International ATM great facilitate and ease the travel plans by

making it possible for a traveling customer to withdraw funds in

dozens of countries in local currency, given that his account back

home will stand the transactions. Thus, international ATMs sharing

have made a significant contribution towards mobility around the

world. ATMs have made funds withdrawals possible internationally.

Traditionally travelers around the world used to carry traveler’s

cheques obtained from their banks by making payment of money in

their currencies. Traveler’s cheques have always been among the

more unsatisfactory financial instruments. Obtaining travelers

cheques requires payment of commission charge to buy them.

Moreover, they are not safe as anyone can forge the signature and

obtain payment since it is not required that the customer should

show the passport.

Internationally ATM sharing does away with an idea of exchanging

it, or losing the money while on travel, the advantage offered by

ATM is simply excellent. Internationally cash machine and the money

can be withdrawn whenever needed.

1.2.5. ATM around the word

ATMs have established a dominating presence in the world’s banking

industry and also in the social infransturess of towns and cities.

With the growth in the shared ATM the facility of mobile banking is

expected to catch up by leaps and bounds as such a mechanism will

result in overall cost saving to benefit the consumer . All the

18

19

shopping malls may have the shared ATM installed in their premises,

which can be accessed be cardholders of all banks .worldwide

highest concentrations of ATM occur in countries where the payment

culture is primarily cash-based. This is especially true of the Far

East, and it is therefore not surprising that japans has such ATMs

are located inside the bank premises and therefore are often

inaccessible outside banking hours.

1.2.6. BENEFIT OF ATM CARD TO THE merchant ( BK )

1. Time saving

It speed up the transactions and daily operations that include

compensation set-up between a client and his or her bank or

between the banks that share the same host which would cost them a

long time to settle those settlements using the manual cheques

system. This is because all transactions and set offs takes only

twenty four hours and this is done through a clearing house which

is the national bank of Rwanda (BNR) however the operation is

somehow manual because all the above operations are nor

automatically done because it takes twenty four hours to settle

different bank operation.

2 .Increase of customer

The use of ATM cards has increased the level of customers to BK

because it has created double attraction for instance it links both

businessmen and client to client to work together through the use

of ATM cards and both parties must be users of such ATM cards as

19

20

visa and among others in order to facilitate them to withdraw an

settlement of their transaction

3. Safety to the bank

Many banks BPR inclusive have been facing a problem of fraudulent

actions practiced by their client or sometimes by their staff like

poor entries, and inappropriate transactions. Consequently leading

to a loss to the bank, but Through using ATM cards payment system,

this has created security as result of using sophisticated

controllable machines such as automatic teller machine ( ATM) and

point of sale (pos).

4. Segmentation benefits

ATM cards for instance visa and credits being a segmented product

only to those who possess an account in a particular bank it has

enabled the bank to benefit from such services as opening up a new

profitable market for the bank exploiting existing infrastructures,

and automating administration. Similarly, processing a transaction

at POS is such less expensive than processing either cash or a

paper (cheque) lower cash holdings, opportunities and also enables

and also enables and speeds up bank commercial activities as

customers and businessmen can burden logs and bugs of cash paper

money. (www.simtel.org.domestic. ATM cards transaction flow,

accessed on 2/6/2013)

1.2.7 DEVELOPMENT OF BANK’S ATMs

20

21

The development of banking ATM( automatic teller machine) industry

has received much attention in recent years, mainly due to growing

ATM network. Recent scholarship has studied whether its growth has

maximized consumer welfare .The concern is rooted in the network

effects that depend on total number of users or customers

patronizing banking ATMs. Because the form of banking ATMs can be

regarded as network effects. The deposit-holding consumers of one

bank may potentially use their ATM cards at ATMs of competitor’s

institutions. ATM cards and ATMs form a system of complementary

components which produce account transactions. There are two type

of fees when a card-holder of one banks conducts a transaction

using an ATM owned by another ,one of which is a surcharge levied

by the banks owned the ATM , the other of which is a foreign fee

levied by the card-holder own bank. This involves the partial

incompatibility in that the foreign ATM use for account –holder is

imposing A TM fees from transaction despite the compatible

technologies (knittel and sting, 2008, 124)

1.2.8 AUTOMATED TELLER MACHINE:

ATM cards are the most convenient form of withdrawing money. It is

a magnetic card having a secret PIN (Personal Identification

Number) which is kept to be confidential by the user to prevent it

from misuse. One Can easily get money withdrawal by simply

inserting ATM cards into ATM with confidential pin code. These

Cards are also known as ATM- CUM DEBIT card. Nowadays ATM is serving

more than just withdrawing Machines. A minimum balance of Rs.1000

21

22

is compulsory to withdraw. ATM card of any bank can be access In

any bank’s ATM

s1. ATM CARD ATM Machine

Figure 1.

2. How to Avail ATM Facility

This facility is for everyone who has Savings, Current or

Cash Credit account.

To get ATM Facility on your account you have to fill up

form provided by bank.

ATM card holder has to maintain minimum balance of Rs.1000

No any additional charges for this facility.

3. How ATM Works a. Swipe Card: The card reader in the

machine reads and stores the bank account information

Recorded on the magnetic strip of the card.

b. Enter Pin: The machine converts PIN into an encryption and

sends it to the host processor compares The PIN with the recorded

information for verification. /

22

23

c. Request Amount: ATM sends the request to the host processor

which forwards it to the networks (Visa/Master Cards) for approval.

d. Account Check: The network asks the bank to authorize

withdrawal which is done after checking .The customer’s account.

e. Saying Yes: An electronic fund transfer takes place from the

bank to the host processor account. The host sends an approval code

to the bank.

f. Bill Count: An electronic eye counts out bills from cash

cartridges located either at the bottom or behind the computer

screen and pushes it out of the cash slots.

4. Other Uses of ATM Card:

24 hours Service

Cash withdrawals

Changing ATM PIN

To know about available balance

Paying routine bills, fees (utilities, phone bills, etc)

Mini bank statement (last 10 transactions)

One can deposit cheque

s5. Protecting Your Card

23

24

i. Keep your card in a safe place to avoid damage.

ii. Memorize your Personal Identification Number (PIN). Never

write the PIN down on anything in our wallet or on the card

itself. Never tell your PIN to any other person, whether to

family member, office staff.

iii. When selecting a PIN, avoid numbers and letters that relate to

your personal information. For example, don’t use your

initials, birthday, telephone or vehicle number, if you have

such a number, contact your bank and get a new PIN issued. In

most of ATM, you can change your ATM pin yourself.

iv. Immediately report a lost or stolen card to your financial

institution.

v. To help guard against fraud, keep your ATM receipts until you

check them against your monthly statement.

5. Safety Tips at the Time of Withdrawal

i. Observe your surroundings before using an ATM. If the machine

is obstructed from view or poorly lit, visit another ATM.

ii. Take a friend with you - especially at night.

iii. Have your card out and ready to use.

24

25

iv. Shield the screen and keyboard so anyone waiting to use the

ATM cannot see you enter your PIN or transaction amount.

v. Put your cash, card and receipt away immediately, Count your

money later, and always keep your receipt.

vi. If you see anyone or anything suspicious, cancel your

transaction and leave immediately. If anyone follows you after

making a transaction, go to a Crowded, well-lit area and call

the police.

vii. When using an enclosed ATM that requires your card to open the

door, avoid letting strangers Follow you inside.

viii. Check with your financial institution to determine what the

daily limit of funds that can be withdrawn from your account

is.

ix. Use swap ATM machine, Machine which take ATM card inside are

risky and some time they ate your ATM card, due to input of

wrong ATM pin, withdrawal amount given is more than balance

and for other reason.

x. Use your own Bank machine, where ever possible, the reason is

that if there is a problem in transaction then problem can be

solved by your bank directly but if other bank’s ATM is used

then to solve dispute you have to contact two bank branches.

xi. If your card jammed in ATM, report this immediately to the

bank

1.2.9 Thinks you need to know about ATM card

Do not store you ATM card with your PIN, memorize the pin and

destroy it.

25

26

The ATM card must be inserting in the right way. If the card

is not positioned right, it will not get into the card slot on

the machine. Most ATM have on arrow that point the directions

as to how to insert the plastic

The ATM card must be valid and current the ATM cards have an

expiry date on the face of them when the card is expired; it

will be ejected when you attempt to use it.

Does not use an ATM when there is a person too close to you

they may be able to see your account balances and follow you.

Do not trust your pin number to another person protect your

ATM card at all costs

Where you have a joint account, each of the account signatories

should be issued with their own card to access the cash machine

1.3. BANKING SERVICES

The simplest definition of banking services would seem to be a wide

range of financial services, including;

Payment services

Deposit and lending services

Investment, pension and insurance services

E- banking (Barbara; 2006:55) ,national consumer

council;2012:264)

Performance

Performance is one of the key terms organization”” performance””

from a process view , performance means the transformation of

inputs for achieving certain outcomes. The company inform about the

26

27

relationship between minimal and effective cost, between effective

cost and realized output (efficiency) and between output and

achieved outcome (effectiveness) of certain activities. (Richard ET

al.2009)

1.4 ATM

An unattended electronic machine in a public place, connected to a

data system and related equipment and activates by a bank customer to

obtain cash withdrawals and other banking services. Also called automatic

teller machine, cash machine, also called money machine.

An automated teller machine or automatic teller machine (ATM) is an

electronic computerized telecommunications to access their bank

accounts, order or make cash withdrawals( or cash advances using a

credit card 0 and check their account balances without the need for a

human bank teller (or cashier in the UK). Many ATMs also allow people

to deposit cash or cheques, transfer money between their bank account,

top up their prepaid accounts or even buy postage stamps.

On most modern ATMs, the customer identifies him or herself by

inserting a plastic card with a magnetic stripe or a plastic smart

card with a chip that contains his or her account number. The customer

then verifies their identity by entering a pass code, often referred

to as a PIN (Personal identification Number) of four or more digits.

Upon successful entry of the PIN, the customer may perform a

transaction. If the number is entered incorrectly several times in a

row (usually three attempts per card insertion). Some ATMs will

attempts retain the card as a security precaution to prevent

27

28

unauthorized user from discovering the PIN by guesswork. Captured

cards are often destroyed if the ATM owner is not the card issuing

bank, as non-customer’s identities cannot be reliably confirmed.

ATM: is automatic teller machine, the most visible and perhaps most

revolutionary, element of virtual banking revolution is the cash

machine as it more popularly known. The use of ATMs has greatly

changed the lives of modern men and women. the introduction of ATMs

service has come to change the entire gamut of the way the banking and

financial services are operated in the world ATM are known for their

speed and convenience giving 24 Hours access to the bank customers to

operate their bank account in the physical environment with the help

of machines. ATMs have given an edge to the banks and financial

institutions in efficiently carrying out their operations. ATMs

provide the advantage of accessing the account of customers any time

anywhere an automated teller machine is a computerized devise that

provides the customers of a financial institution with the ability to

perform financial transaction without the need for a human cleck or

bank teller(mike fenton,2009)

1.4.1 DEBIT CARD

Debit card are also known as check cards. Debit card look credit cards

or ATM cards but operate like cash or a personal check. Debit cards

are different from credit cards. While a credit is a way to ‘’pay

later’’ a debit card is way to ‘’pay now’’ when you use a debit card,

your money is quickly deducted from your checking or saving account

Debit cards are accepted at many locations, including grocery stores,

28

29

retail stores, gasoline stations, and restaurants.. You can use your

card anywhere merchants display your card’s brand name or logo. They

offer an alternative checkbook or cash.

1.4.2 ADVANTAGES OF ATM card

To the customers

ATMs provide 24hours, 7days a week and 365 days a year service

Service is quick and efficient

Privacy in transaction

Free from errors

On networking,carholder can access cash and service at any

location regardless of where he maintains account

Wider flexibility in withdrawals

Fund transfer across the branches / bank

Anywhere banking facility To the banks:

Alternative to extend banking hours

Alternative to new branches and to reduce operating expenses.

ATMs can be located in any convenient location in the city

Relieves bank employees to focus on more analytical and

innovative work

Increased market penetration.

1. The BK VISA Classic Credit Card Advantages:

• Worldwide acceptance at over 22 million merchant outlets and over

2

Million ATM locations all over the world.

29

30

• Emergency cash from VISA ATMs located worldwide including over

250 locations in Rwanda.

• Prestige as a VISA cardholder and build up of a recognized credit

history

• Free credit period up to 55 days.

• Convenient option to pay up to as low as 25% of total outstanding

balance.

• Automatic credit enhancement on renewal, subject to satisfactory

usage.

• Supplementary cards for spouse and (or) family members,

2 .The BK VISA Classic Credit Card Benefits:

A. BK Visa Classic Credit Card Pay: Especially in-built financing

feature to

Enable you to make large purchases through your Classic card.

B. BK Visa Classic Credit Card Buy: Specially arranged discounts at

carefully

Selected merchant outlets make your spending francs go further.

Periodically, BK VISA CLASSIC CREDIT Cardholders will enjoy

discounts and enhanced utilities by special arrangements with

certain merchants and

Shops. So to choose a card that is well worth your go, please call

4455

Or email [email protected] to find out more on how to get a BK Visa Classic

Credit

1.4.3 DISADVANTAGES OF ATM card

30

31

1. Cash withdrawals are restricted to certain amount as fixed by

the bank and notified to ATM cash holder

2. Cash dispensation is restricted to certain denomination of

currency notes usually 50/100/500

3.ATM could perform only particular function for other functions,

the customer has to visit the branch or direct one’s enquiries to

the concerned call centre (rajesh;2009;313).

Lack of human help to resolve problems

Higher cost due to ATM fees

Lack of security due to lighting

Limits on withdrawals all kinds of banking transactions

Ease of account access with stolen card/stolen information

Lowered opportunities to build customer relationships.

(cohen;2005;483).

Like of robbery when you leave the ATM

The ATM can break down or run out of cash

Fees charged to use ATMs of other banks can be expensive

1.4.4 Functions of Commercial Banks

1. Accepting Deposits:

Accepting deposits is one of major function of commercial bank; It

is the business of bank to accept. Deposits so that he can lend it

to other and earn interest. Basically, the money is accepted as

deposit for safe Keeping Banks also pay interest on these deposits.

31

32

To attract depositors banks maintain different types of Accounts.

These are as following.

a) Fixed Deposit Accounts: The account which is opened for fixed

period by depositing amount is

Known as fixed deposit account. The money deposited in this account

cannot be withdrawn before Expiry of period. A high rate of

interest is paid on fixed deposits.

b) Current Deposit Account: Current deposit accounts are mostly

opened by businessmen and Traders who withdraw money number of

times a day. Banks does not pay interest on these types of Account.

The bank collects certain charges from depositors for services

rendered by it.

c) Saving Account:

Saving account is most suited for those people who want to save

money for Future needs. These types of account can be opened with a

minimum initial deposit. A minimum balance has to be maintained in

account as prescribed by bank. Some restrictions are imposed on

Depositor regarding number of deposit withdrawal and amount to be

withdrawn in given period.

d) Recurring Deposit Account:

The purpose of these accounts is to encourage public for regular

saving, particularly by fixed income group. Fixed amount is deposit

is deposited at regular intervals for a fixed term and repaid on

maturity.

2. Grant of Loans and Advances

32

33

Besides accepting deposit, the second most important function of

commercial bank is advancing of loan to the public. After keeping

certain part of deposits received by bank as reserve and the rest

of balance given as loan. The different types of loan and advances

are given by bank as follow.

a) Call Money: There are generally short term credits that range

from one day to fort night. There are even one nigh call money

advances made available to bank with the help of this market. The

rate of Interest depends upon the conditions prevailing in money

market.

b) Overdraft:

In over draft, a customer can withdraw money from his current

account and available Balance below zero. When the amount withdrawn

is within the authorized limit then rate of interest Charged at

agreed rate. Overdraft is allowed normally against the security of

negotiable Instrument and credit worthy customers without security.

c) Cash Credit:

In cash credit, Bank advance loan against the customer current

asset or personal Guarantee. The borrower has option to withdraw

the funds as and when required to extent of his Needs but he cannot

exceed the credit limit allowed to him. The cash credit limit

depends on the Debtor’s needs and as agreed with the bank. The bank

charges interest only on money withdrawn from by them.

d) Discounting of Bills:

Under this type of lending, Bank pay amount before due date of bill

after

33

34

Deducting certain rate of discount or commission, the holder of

bill get money immediately without Waiting for the date of

maturity, If bill of exchange dishonored on due date the bank can

recover the Amount from the customer.

e) Direct Loan: A loans granted for a fixed maturity period more

than one year. Loans are usually secured against some collateral

security; the borrower can withdraw entire money through cheques.

The interest is charged on entire amount of loan. Repayment of loan

either in installments or in lump Sum.

3. Credit Creation

Credit creation is also an important function of commercial Bank.

The process of credit creation automatically Performed when bank

accept deposits and provide loans Prof Sayers says, “Banks are not

merely supply of money but in an important sense, they are

manufacturers of money”. In this process, customers deposit their

money in bank. Bank keeps certain amount of deposit as cash reserve

and rest of balance given as loan and advances. Banks not required

keeping the entire deposits in cash. The amount of loan does not

give directly to borrower. The borrower opens account and then bank

deposit money in that account. Here, bank’s lends money and process

of credit creation starts. The current cash reserve ratio is 6% in

2011.

4. Secondary Functions:- These are as follow:-

a. Growth Sale and Purchased of Securities:

34

35

On the behalf of customer, commercial bank sale and purchase Of

the securities of private companies as well as government

securities.

B.Transfer of Funds

Commercial Bank also provide facilities to transfer funds from one

place to

Another place in form Bank draft, cheques, mail transfer etc.

c. Collection and Payment of Credit Instrument:

Commercial Bank collect and make payment on behalf of their

customers Commercial Bank collect and pay negotiable instruments

and also pay rent, income tax fees, insurance premium etc.

d. Locker Facility:

Commercial Banks provides locker facility to their customers. We

can keep Gold, silver and important documents in locker.

e. Letter of Credit:

Letter of credit certified the credit worthiness of their

customers which issued by commercial banks.

f. Collection of Information: Commercial Banks also collect the

information relating to Industry, Trade, commerce which made

available to their customers.

g. Traveler’s Cheque ad Credit Card: Commercial Banks issue

traveler’s cheques and credit cards to their customers. They can

travel without fear of theft and loss of money. Credit card is used

to make payment for purchases so that individual does not have to

carry cash.

35

36

h. Foreign Exchange: Commercial banks provide facility to their

customers dealing in foreign Exchange; Commercial Banks are

authorized dealers in India.

I. Educational Loans: Commercial Banks also provide educational

loan to student for higher studies at reasonable rate of interest.

j. Consumer Finance: Commercial Banks provide consumer finance

facility for purchase consumer durables like televisions,

refrigerators etc.

k. Automated Teller Machine: Now days with the help of ATM, we can

deposit or withdraw money from our account any time.

1.5 CUSTOMER

A person’s company or other entity which buys good and service

produced by

anotherperson,companyorotherentity( www.investorwords.com/5877/custo

mers.htm . accessed, on28/04/2013) there are so many definition of

customer and the following are some of them : SANDRA(2009) defines

a customer as ,, the most important person ever this office in

person or by mail,, A customer is a person’s organization that buys

something ( service or goods) from a shop or business. Customer is

also a person who brings us his wants and needs, and it is our job

to handle them profitably to him and ourselves,, ( PHILIPH

HOTLER,1998) then, there are two types of customers: internal and

external customers.

1.5.1 CUSTOMER SATISFACTIONS

36

37

Is a term frequently used in marketing? It is a measure of how

products and services supplied by a company meet or surpass

customer expectation. Customer satisfaction is defined as "the

number of customers, or percentage of total customers, whose

reported experience with a firm, its products, or its services

(ratings) exceeds specified satisfaction goals. It is seen as a key

performance indicator within business and is often part of a

Balanced Scorecard. In a competitive marketplace where businesses

compete for customers, customer satisfaction is seen as a key

differentiator and increasingly has become a key element of

business strategy. Within organizations, customer satisfaction

ratings can have powerful effects. They focus employees on the

importance of fulfilling customers' expectations. Furthermore, when

these ratings dip, they warn of problems that can affect sales and

profitability.... These metrics quantify an important dynamic. When

a brand has loyal customers, it gains positive word-of-mouth

marketing, which is both free and highly effective.

Therefore, it is essential for businesses to effectively manage

customer satisfaction. To be able do this, firms need reliable and

representative measures of satisfaction. In researching

satisfaction, firms generally ask customers whether their product

or service has met or exceeded expectations. Thus, expectations are

a key factor behind satisfaction. When customers have high

expectations and the reality falls short, they will be disappointed

and will likely rate their experience as less than satisfying. For

this reason, a luxury resort, for example, might receive a lower

37

38

satisfaction rating than a budget motel—even though its facilities

and service would be deemed superior in 'absolute' terms." The

importance of customer satisfaction diminishes when a firm has

increased bargaining power. For example, cell phone plan providers,

such as AT&T and Verizon, participate in an industry that is an

oligopoly, where only a few suppliers of a certain product or

service exist. As such, many cell phone plan contracts have a lot

of fine print with provisions that they would never get away if

there were, say, 100 cell phone plan providers, because customer

satisfaction would be far too low, and customers would easily have

the option of leaving for a better contract offer. There is a

substantial body of empirical literature that establishes the

benefits of customer satisfaction for firms. This literature is

summarized by Mittel and Freneau (2010). They summarize the

outcomes in terms of customer behaviors, immediate financial

outcomes such as sales and revenues, and long-term outcomes based

on the stock market www.freemarket Wikipedia.org

1.6 HOW TO WITHDRAWALS MONEY FROM AN ATM

38

39

Insert your ATM card

Enter your PIN

Select ‘’withdrawals’’

Several amount will be displayed on the screen or enter theamount you want by pressing the numbered buttons.

Choose the account you want to withdrawals if asked

Take your cash,,,Take your card,,,,,Take your withdrawals slip

39

40

PARTIAL CONCLUSION

As conclusion of first chapter, we have been use different types of

documentation which treat about ATM banking service and clarify key

concepts in general and in particular in Rwanda where the bank of

Kigali. Rendered service quick to its customers in orders to

improve the customers satisfaction through quick services and

reliable.

40

41

CHAPTER TWO: THE LEVEL OF CUSTOMER SATISFACTION FOR USING ATM AT

BANK OF KIGALI

2. INTRODUCTION

This chapter aims to present, and analyze and discuss data

collected from the field. The data related to the use of ATM

service on growth in bank of Kigali and the challenges facing by

customers these electronic devices. The current data verify the

first hypothesis formulated as follows: the level of the use ATM

at BK bank performance by using the ATMs card service. The chapter

begins by short presentation of BK, demographic profile of

respondents, data presentation and interpretation and finally the

work ends.

2.1. PRESENTATION OF BANK OF KIGALI (RWANDA)

2.1.1 HISTORY

The Bank of Kigali was started in 1966 to provide commercial

banking services to individuals, small businesses, and large

corporations. The bank was 50 percent owned by Banque Belgolaise

before the Government of Rwanda purchased that shareholding in

2007. Subsequently, the government sold minority shareholding to

other corporate entities, including the Social Security Fund of

Rwanda and the National Post Office of Rwanda. In 2011, there were

41

42

plans for the government to divest more of its ownership in the

bank by floating 25 percent shareholding on the Rwanda Stock

Exchange (RSE). On 21 June 2011, the Rwandan Capital Market

Advisory Council approved plans for the bank to float 45 percent of

its shares on the RSE and list its shares on the RSE. Trading in

the shares of the bank started on 30 June 2011.

In December 2012, regional media reports indicated that the bank

was in the middle of an expansion into neighboring Uganda. In

February 2013, the bank received regulatory approval to open an

office in Kenya.

The Bank of Kigali is the largest commercial bank in Rwanda by

assets. As of December 2014, its total assets were approximately

US$704.54 million (RWF: 482.62 billion). The shareholders' equity

stood at approximately US$130.73 million (RWF: 89.55 billion). In

2010, the bank was ranked among the top fifteen commercial banks in

East Africa. The move will make BK the second local company to be

privatized through an IPO after government successfully sold, to

the public, 25 of 30 percent of the shares it owned in Bralirwa,

the country's largest brewery.

2.1.2 BACKGROUND OF BANK OF KIGALI RWANDA

1. Geographical location of BK/Rubavu

BK/Rubavu branch is located at Gisenyi city in western province,

Rubavu district, Gisenyi sector, Nengo cell, nearest kivu beach

before WASAC office /Rubavu

42

43

Source: http://www.BK.rw,visited on 12/08/2013

BK /Rubavu branch started its activity in 1978 in the main

objective of collecting deposit and providing won to their clients.

2. Ownership

As of December 2013, the ownership of the bank's stock stood as

depicted in the table below:

Table 1: ownership of BK (Rwanda)

Ranj2k Name of Owner Percentage Ownership

1 Government of Rwanda 29.6%

43

44

2 Social Security Fund ofRwanda 25.1%

3 Internationalinstitutionalinvestors 16.4%

4 Retail investors 12.2%

5 Local institutional investors8.8%

6 Regionalinstitutionalinvestors 6.2%

7 Employees and directors 1.6%

8 Other state-owned entities 0.10%

Total 100.00%

Source: Result of our survey (August 2015)

2.2 OBJECTIVE OF BK RWANDA

2.2.1 Mission, vision and values of BK Rwanda ltd /Rubavu branch

2.2.1 Mission Our mission is to be leader in creating value for our

stakeholders by providing the best financial services to businesses

and individual customers, through motivated and professional staff.

2.2.1.1 Vision

44

45

Bank of Kigali aspires to be the leading provider of the most

innovative financial solutions in the region.

2.2.2 Values

Customer focus

Integrity

Quality

excellence

2.3 METHODOLOGICAL APPROACH

In the following pages the researcher is going to give up details

on the methodology used to collect data based on the questionnaire,

the responses and their analysis are indicated below by the use of

tables

2.3.1 PERIOD OF SURVEY

The survey was conduct in August 2015. The questionnaires were

administered to a sample of BK customers chosen at random. The

total number of the respondents has been fixed to 95 persons. To

find a sample, we used the determinative table of the professor

ALIN BOUCHARD. Does this table stipulate that when the universe is

infinite that is so say 10,000 people one takes a sample of 96

people considering a margin of mistake of 10% (bouchard,A )

Since in our research, the universe is finished of 15,500 customers

from, we will apply this formula for the corrected size.

45

46

NC¿ N∗nN+n

nc= corrected sample,

N= population

n= size of corresponding sample to 96 While apply this formula

for our case, we find the following

NC=15,500∗9615,500+96

=148800015596

=95

This size of the sample that we investigated was classified into

parts which are followed:

We had sample size for customer which are 95

We have sample of 26 staff equally to 26

Total sample size was 121 people. Regarding to respondents was show

in form of statistical table and percentages.

2.4 IDENTIFICATION OF RESPONDENT

The identification of the respondent is done considering the

following aspects: age, sex, and educational level.

2.4.1 IDENTIFICATION OF RESPONDENTS BY AGE

The variable “age” has a great importance because it can influence

a person’s opinion on the service he receives. Thus, an adult does

not appreciate things the same way than a person who is still young

with no much experience as banking customer. This variable allowed

46

47

me to know the age group of the groups of the respondent as we can

see in the table below

Table 1.1 Distribution of respondents by age

Age Number %

18-30 25 27.5

30-40 50 52.7

40-50 12 13.3

Over 50 8 6.5

Total 95 100

Source: Result of our survey 2015

Regarding to age , the above table shows that 27.5% of the

respondents are between 18 and 30 years old ,52.7% are between 30

and 40 years old , 13.3% are between 40 and 50 years old and 6.5%

are over 50 years old. And 95% these were card holders all of them

2.4.2 Gender of respondents

The variable gender allowed identifying the number of men and women

who participated to this survey .their details are summarized in

the table below:

Table 1.2 Distribution of card holders by gender

Gender Number %

Male 70 73.8

47

48

Female 25 26.2

Total 95 100.0

Source: Result of survey, 2015

On the graphic, we have the following presentation:

Figure 1. Distribution of respondents by Gender

male female010203040506070

Gender

Gender

Source: table 1.2

From this table, we find that the majority of respondents were

male73.8% against 26.2% for women, During the survey, male are into

business than female and therefore more are into business than

female and therefore more are into business than female and

48

49

therefore more male seem to believe in the venture of the new

technology in modern banking.

2.4.3 Educational level

The educational of respondents was selected and is reflected in

summary form in the following table:

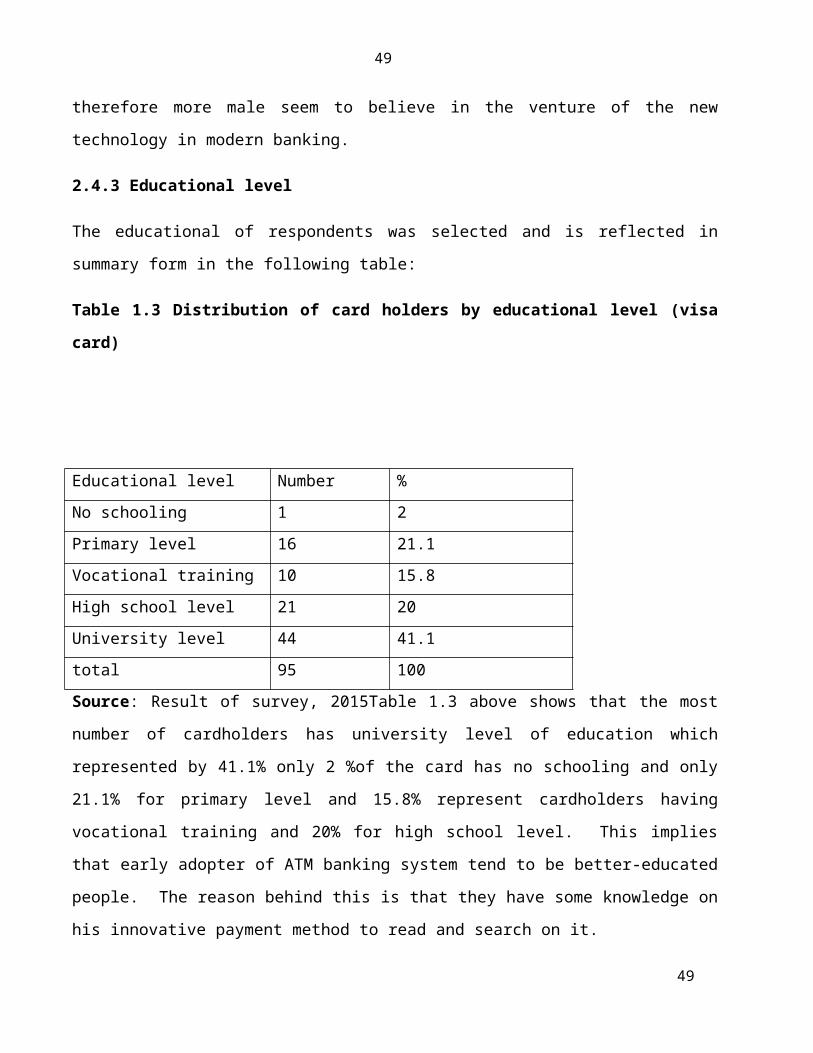

Table 1.3 Distribution of card holders by educational level (visa

card)

Educational level Number %No schooling 1 2Primary level 16 21.1Vocational training 10 15.8High school level 21 20University level 44 41.1total 95 100Source: Result of survey, 2015Table 1.3 above shows that the most

number of cardholders has university level of education which

represented by 41.1% only 2 %of the card has no schooling and only

21.1% for primary level and 15.8% represent cardholders having

vocational training and 20% for high school level. This implies

that early adopter of ATM banking system tend to be better-educated

people. The reason behind this is that they have some knowledge on

his innovative payment method to read and search on it.

49

50

Figure 2. Distributions of respondents by educational level

no schooling

primary level

vocational training

high school level

university level

010203040

Educational level

Educational level

Source: 1.3 above shows that the most number of cardholders has

university level of education which represented by 41.1% only 2 %of

the card has no schooling and only 21.1% for primary level and

15.8% represent cardholders having vocational training and 20% for

high school level This implies that early adopter of ATM banking

system tend to be better-educated people. The reason behind this

is that they have some knowledge on his innovative payment method

to read and search on it.

2.5 Type of cards mostly used by the cardholder

Table 1.4 Types of cards mostly used by the card holder

Type of banking

system

Number of

respondent

%

Master cards 5 5.2Visa horizon cards 95 94.7

50

51

Any other 0 0Total 95 100Source: Result of our survey, 2015

The table above shows that the cards is mostly used visa horizon

card as it is seen that all cardholders from different location

responded that they use visa horizon card. In addition , this is

shown by the fact that all 90 respondents that they use visa

horizon card, which is represented by 94.7% where as master and

others the research through the cardholders might be using are

represented by 5%,which is represent by 5,2%

Figure 3. Types of cards mostly used by the card holder

Master cards

Visa horizon cards

Any other0

20406080

100

Most usedcards

most usedcards

Source: from table 1.4

That shows the cards is mostly used visa horizon card as it is seen

that all cardholders from different location responded that they

use visa horizon card. In addition, this is shown by the fact that

all 90 respondents that they use visa horizon card, which is

51

52

represented by 94.7% where as master and others the research

through the cardholders might be using are represented by 5,2%

2.6 Interview of bank Kigali/ Rubavu branch employees

This is the analysis of responses provided by 26 staff of the bank

exactly in consumer banking department from the sample, the

responses and their analysis are shown here shown here under the

use of table and graphics.

2.6.1 Type of cards mostly issued by banks

Table 1.6 Type of cards mostly issued by banks

Types Number of

respondent

%

Visa card 26 100

Master card 0 0

Any other 0 0

Total 26 100

Source: Result of our survey, 2015

The table above shows the type of cards issued by BK and it shows

that it is only visa card that it issued as all the sample of 26

employees indicated visa card which represents 100% of the total

sample of the cards. So the master card or any other cards that the

research through could be issued by bank are represented by 0%.

Figure 4. Of type of cards mostly issued by bk

52

53

Type of cards mostry issued by banks

Visa cardMaster cardAny other

Source: table 1.6 shows the type of cards issued by BK and it shows

that it is only visa card that it issued as all the sample of 26

employees indicated visa card which represents 100% of the total

sample of the cards. So the master card or any other cards that the

research through could be issued by bank are represented by 0%.

2.7 Level of acceptance of this card in relation to others

Table 1.7 level of acceptance of this card in relation to others

frequency Number of respondent%

Less than 20% 0 0

21%-30% 0 0

31%-40% 1 3.8

41%-50% 12 45.8

above 13 50.5

Total 6 100

Source : our survey,2015

53

54

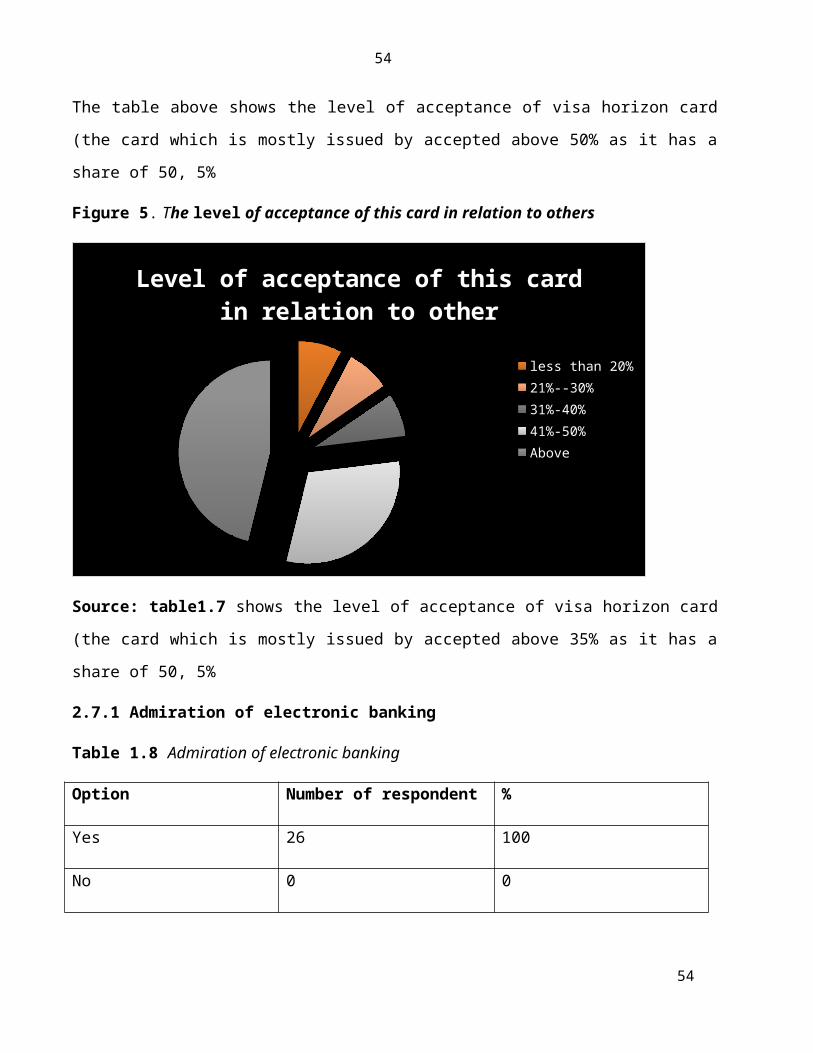

The table above shows the level of acceptance of visa horizon card

(the card which is mostly issued by accepted above 50% as it has a

share of 50, 5%

Figure 5. The level of acceptance of this card in relation to others

Level of acceptance of this card in relation to other

less than 20%21%--30%31%-40%41%-50%Above

Source: table1.7 shows the level of acceptance of visa horizon card

(the card which is mostly issued by accepted above 35% as it has a

share of 50, 5%

2.7.1 Admiration of electronic banking

Table 1.8 Admiration of electronic banking

Option Number of respondent %

Yes 26 100

No 0 0

54

55

Total 26 100

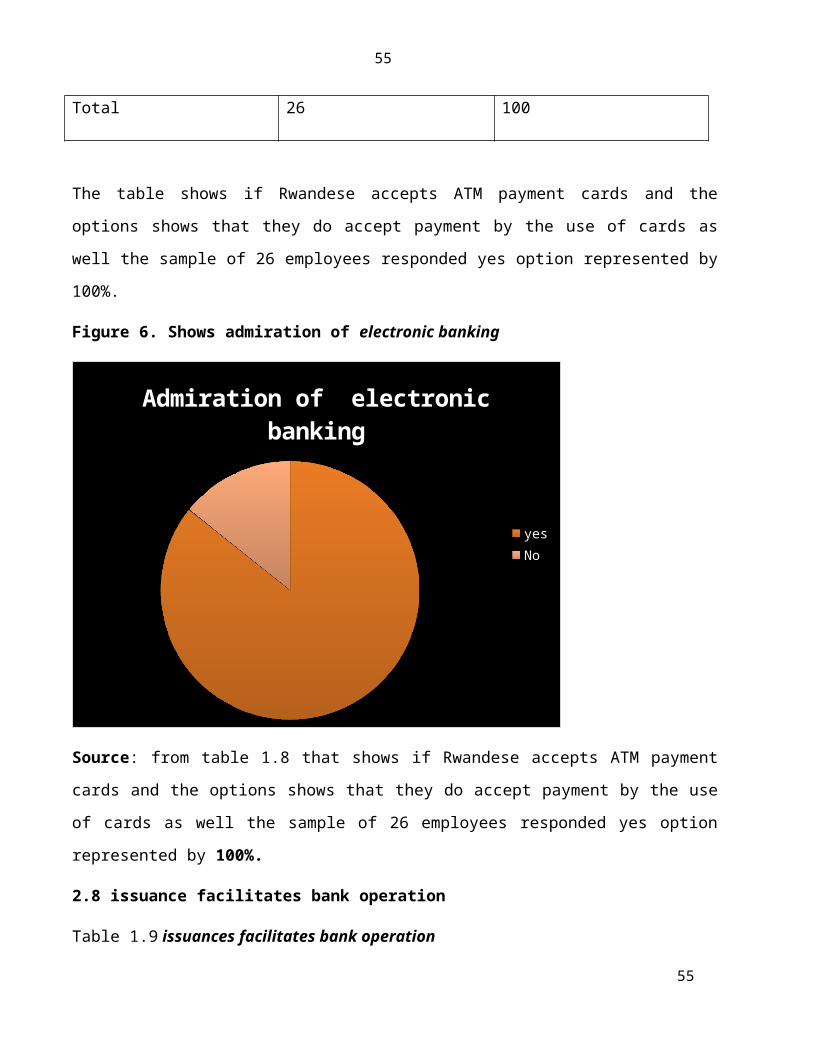

The table shows if Rwandese accepts ATM payment cards and the

options shows that they do accept payment by the use of cards as

well the sample of 26 employees responded yes option represented by

100%.

Figure 6. Shows admiration of electronic banking

Admiration of electronic banking

yesNo

Source: from table 1.8 that shows if Rwandese accepts ATM payment

cards and the options shows that they do accept payment by the use

of cards as well the sample of 26 employees responded yes option

represented by 100%.

2.8 issuance facilitates bank operation

Table 1.9 issuances facilitates bank operation

55

56

Option Number of respondents %

No 0 0

Yes 26 100

Total 26 100

Source; Result of our survey, 2015

It seem that electronic cards facilitate banking operations as all

6 respondent accepted yes option, which is represented by 100%.

When the researcher wanted to know why respondents are saying that,

they respondent that the electronic banking makes banking halls

less crowded and the workers can spend more time or energy doing

core-banking dues.

Figure 7. Issuances of cards facilitate bank operation

Yes No0

1

2

3

4

5

6

7

Issuances of facilitates bank operations

If issuances of cards facilitate bank operations

Source: table1.9

56

57

this line It seem that electronic cards facilitate banking

operations as all 6 respondent accepted yes option, which is

represented by 100%. When the researcher wanted to know why

respondents are saying that, they respondent that the electronic

banking makes banking halls less crowded and the workers can

spend more time or energy doing core-banking dues

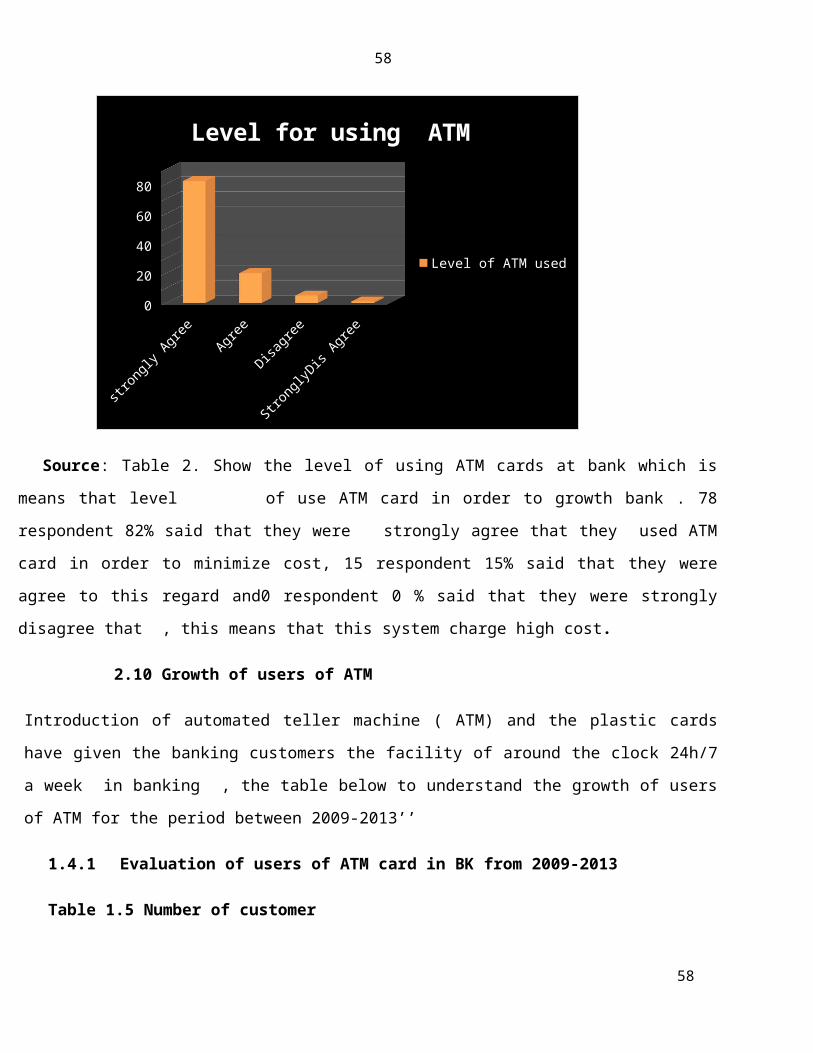

Table 2.9 Level of using ATM card at bank

Question: The level of using ATM cards?

convenience Strongly

agree

agree disagree Strongly

disagree

Total

Frequency 78 15 2 0 95% 82.1 15.7 2.1 0 100

Source: Result of our survey, 2015

The above table shows the respondent how level of use ATM card in order

to growth bank. 78 respondent 82% said that they were strongly

agree that they used ATM card in order to minimize cost, 15 respondent

15% said that they were agree to this regard and0 respondent 0 % said

that they were strongly disagree that , this means that this system

charge high cost.

Figure8. Show the level of using ATM cards at bank

57

58

strongly Agree

Agree

Disagree

StronglyDis Agree

0

20

40

60

80

Level for using ATM

Level of ATM used

Source: Table 2. Show the level of using ATM cards at bank which is

means that level of use ATM card in order to growth bank . 78

respondent 82% said that they were strongly agree that they used ATM

card in order to minimize cost, 15 respondent 15% said that they were

agree to this regard and0 respondent 0 % said that they were strongly

disagree that , this means that this system charge high cost.

2.10 Growth of users of ATM

Introduction of automated teller machine ( ATM) and the plastic cards

have given the banking customers the facility of around the clock 24h/7

a week in banking , the table below to understand the growth of users

of ATM for the period between 2009-2013’’

1.4.1 Evaluation of users of ATM card in BK from 2009-2013

Table 1.5 Number of customer

58

59

Period 2009 2010 2011 2012 2013Number of

customers

2071 2371 3092 4793 8135

Evaluation

Of customer%

14% 23% 55% 69%

Source: Result of survey, 2015. According to the table above shows

that the users of ATM cards are increasing year to years based on

being up dated to the important of using ATM card which means that in

2009 the number of customer was 2071. In the following year arrive to

2371 of users of ATM card and in 201the number of customers was 8135

of users. Regarding to the result shown above describes how the

customer of BK knows the important of using ATM card on their daily

activities.

2.11 Level of customer satisfaction with ATM banking system

Table1.5.1 Level of customer satisfaction with ATM banking system

Level of

satisfaction

Number of

respondent

%

Very satisfied 24 25,2

satisfied 60 63,1

neutral 6 6,3

dissatisfied 3 3,1

Very dissatisfied 2 2,1

Total 95 100

Source: Result of survey, 2015

59

60

From the table above 63,1% of the respondents were satisfied were

satisfied with ATM banking services, where 25,2% of respondents

were very satisfied with ATM banking services,6,3% of respondents

were neutral(not satisfied, not dissatisfied) with ATM banking

services,2,1% of respondents were very dissatisfied with electronic

banking services and 3,1% were dissatisfied with electronic banking

services.

Graphic 6. Level of customer satisfaction with ATM banking system

very satisfied

satisfied

neutral

dissatisfied

very dissatisfied

0102030405060

Level of customer satisfaction

level of stisfaction with ATM bk

Source: table 1.5.1 the level of satisfaction with ATM banking system these

graphic shows that above 63% of the respondents were satisfied were

satisfied with ATM banking services, where 12% of respondents were

very satisfied with ATM banking services, 9% of respondents were

neutral (not satisfied, not dissatisfied) with ATM banking

services, 8% of respondents were very dissatisfied with electronic

60

61

banking services and 7% were dissatisfied with electronic banking

services.

The majority says that customer satisfaction is higher because to

use withdraw by ATM easily and quick services it help bank in their

activities task rather than waiting on the outlet/ teller and

reducing queue. Let is to look forward level of customer

satisfaction instantly

Level one of customer Satisfaction “A level one customer is a

customer who is not satisfied with the company. In this case the

customer satisfaction is at minimum. The customer is likely to

leave the company and never return. He can also badmouth the

company. There are several reasons in which a customer might be

converted to a level one customer such as the deliveries not

happening on time, the service is not proper, or over commitment

being given by the sales force. Lack of features in the product

generally does not result in a level one customer satisfaction.

This is because if the features were lacking, the customer would

not buy the product at all. Thus when there are a high number of

level one customers, you can understand that the problem is from

within the company and not from outside.

Level 2 to Level 4 of customer satisfaction” Most of the companies

fall in this level. This is because this is the average level of

customer satisfaction. In this case the customer might be happy

with the brand but there is no guarantee that he will stick back

with the brand. The customer does not badmouth the company but at

61

62

the same time he does not also spread a positive word about the

product. The customer would not be brand loyal but he would be

ready to switch brands whenever there is a new offering the market.

Thus these are not the customers on whom you can rely for a long

term. Obviously each and every company will have at least 60% of

the customers who fall in this level of customer satisfaction.

Level five of customer Satisfaction“Level five of the customer

satisfaction level represents a group of customers who are highly

satisfied customers. They are unlikely to shift the brand or the

product and they have a high emotional bond with the brand. Take

shoes such as Adidas, Nike or Reebok. These are companies which try

to increase the number of highly satisfied customers as much as

possible. This is because the highly satisfied customer is likely

to spread a positive word of mouth. After that looking these level

of customer satisfaction means that the level of customer

satisfaction at BK has in level five which means that are highly

satisfied customers from that services of bank like ATM services.

PARTIAL CONCLUSION

In this chapter, we are examining the first hypothesis which says

that the level of customer satisfaction by using ATM at bank of

Kigali/Rubavu we have observed that the use of ATM is one of the

Greatest recent improvement in the bank services.ATM services it

62

63

has increased the accessibility to money as long as the client

has his/her card can go to the ATM irrespective of time, it has

supported reduces queues in the banks which speed up also

transaction speed It has greatly increased security of people

walking with money because one can move with a card that has

millions in it without any problem but you can’t walk with liquid

money more security, like one that has an electronic.

By the way, the level customer satisfaction o of bank it shows

that there are positive perceptions of customers towards the ATM

service card in bank of Kigali to growth the bank comes from it

is easy and it simples their transaction. According to customers

ATM provide full access to services and when they don’t waste

time queuing for cash at bank branch faster than writing a cheque

Otherwise ATM has positively improvement growth at bank

performance supported operation 24 hours (around clock) 7 days a

week fulfill the principle of any time and everywhere banking as

to day’s world. Time is the most valuable asset a person has and

the common saying that time is money nowadays. the majority says

that customer satisfaction is high because to use withdraw by ATM

it was easily and quick services rather waiting on the

outlet/teller and reducing queue

63

64

CHAPTER 3. THE CONTRIBUTION OF ATM SERVICE ON THE GROWTH IN

COMMERCIAL BANK’’

Introduction

In this chapter aims at verifying the second hypothesis of the

study, the researcher is going to assess the contribution of the use

of ATM on the growth of BK/Rubavu branch.

3.1. Growth of savings

‘’BK RWANDA LTD’’ RUBAVU branch offers to its customers several

options to save their money, to this end, deposit have

experience change as follows;

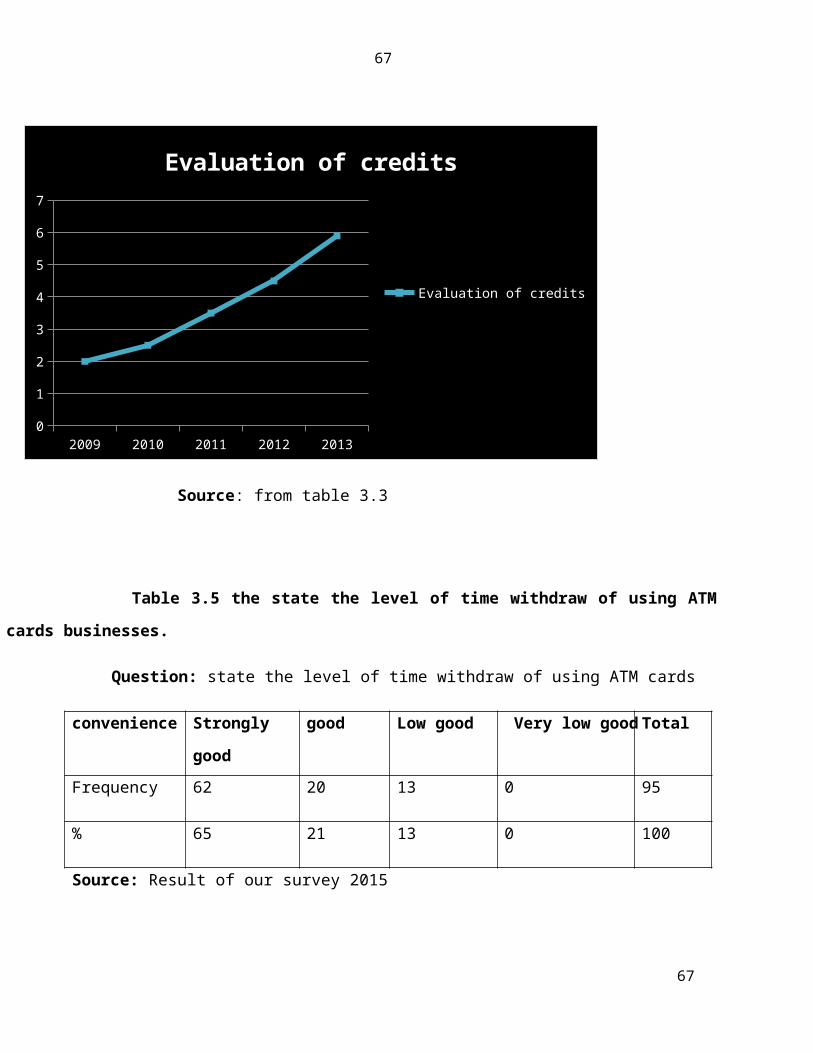

Table 3.1 Evaluation of saving ATM from 2009 to 2013 in RWf

2009 2010 2011 2012 2013

Ordinary saving 479635491 672910980 788173060 978989987 979768992

Saving performed

using

BK based service

152657850 354786254 476658698 589878856 765890889

Total saving 632293341 102769723 126483175 156886884 174565988Variation in % 30,4 56,6 40,2 44Contribution of

ATM at

30,8% 31,2% 33% 33,8% 46,40%

64

65

BK in GrowthSource: financial statement of BK /Rubavu branch from 2009 to 2013