Muhamet Aliu, Arbana Sahiti, Arben Sahiti - Banking Risk Management of Kosovo’s Commercial Banks

Upload

khangminh22Category

view

2download

0

0

ROLE OF COMMERCIAL BANKS IN DEVELOPMENT

FINANCING IN TANZANIA:

A CASE OF CONSTRUCTION SECTOR

By

Rahim Saadan

A Dissertation Submitted in Partial Fulfilment of the Requirements of

the Degree of Masters of Business Administration (Cooperate

Management) of the Mzumbe University

2013

i

CERTIFICATION

We, the undersigned, certify that we have read and hereby recommend for acceptance by

the Indian Institute of Foreign Trade, a dissertation entitled Role of Commercial Banks

in Development Financing in Tanzania: A Case of Construction Sector, in partial

fulfillment of the requirements for award of the degree of Master of Business

Administration-Corporate Management (MBA-CM) of the Mzumbe University.

Mzee Saburi

Major Supervisor

___________________

Internal Examiner

Accepted for the Board of …………………………..

__________________________________________________________

DEAN/DIRECTOR, FACULTY/DIRECTORATE/SCHOOL/BOARD

ii

DECLARATION

I, RAHIM SAADAN, declare that this dissertation is my own original work and that it

has not been presented and will not be presented to any other University for a similar or

any other degree award.

Signature____________________________

Date 07/11/2013

iii

COPYRIGHT

©

This dissertation is copyright material protected under the Berne Convention, the

Copyright Act of 1999 and other international and national enactments, in that behalf, on

intellectual property. It may not be reproduced by any means, in full or in part, except for

short extracts in fair dealings, for research or private study, critical scholarly review or

discourse with an acknowledgement, without written permission of the Mzumbe

University, on behalf of the author.

iv

ACKNOWLEDGEMENT

First and foremost, would like to thank the Almighty God for giving me strength and

health in pursuing my studies for two years.

My sincere thanks are due to my Supervisor Mzee Saburi whose guidance enabled me

properly writing this research report. Again, my thanks are due to all lectures of the

Mzumber University who gave me knowledge concerning business administration. Also

I would like to thank all respondents in the study especially staff of the Instutitions under

study;- CBs, TBA, BoT, ERB and the Ministry of Woks for their encouragement and

information support.

Moreover, would like to thank my colleagues in the MBA program that assisted me in one

way or another. Special thanks are due to Hatibu Simba and Flavia Joseph who

encouraged as well as supported me during my studies at the Institute. Their contributions

played a big role in my studies.

Likewise, my special thanks are extended to my father and mother for their untiring love,

support as well as encouragement they gave me throughout my years at the Institute and

for always being there for me. However, I can not go without thanking all who were

always there when I needed them, my friends and everybody whom in one way or another

supported and encouraged me as well as for love they showed to me.

God bless you all

v

DEDICATION

This dissertation is dedicated to my Father Dr Hamis Saadan and my mother Yusta

Kidawa

vi

ACRONYMS

ATM Automated Teller Machines

BOA Bank of Africa

BOB Bank of Baroda

BOI Bank of India

BOT Bank of Tanzania

CB Commercial Banks

CS Construction Sector

DRT Dar es Salaam Rapid Transit

ERB Engeneers Registration Board

FI Financial Institutions

LCB Local Competitive Bid

NBC National Bank of Commerce

NMB National Microfinance Bank

NPL Non-Performing Loans

PPP Public Private Pertnership

ROA Return on Assets

ROE Return on Equity

SHA Shareholders Agreement

SPA Special Purpose Company

TBA Tanzania Bankers Association

vii

ABSTRACT

The interest of the study focused on role of commercial banks in development

financing in Tanzania, the case of costruction sector. Objectively, the study aimed to

evaluate financing modalities on construction sector at pre-project, to evaluate

financing modalities on construction sector at post-project, to analyse correlation

between growth of the commercial banking industry and construction sector and to

expound financing options to the construction sector.

The study’s methodology encompassed of the survey research design that was carried out

at 6 different Institutions namely; 5 CBs, Tanzania Bankers Association (TBA), Bank of

Tanzania (BoT), 19 Construction Projects, Engineering Registration Board (ERB) and the

Ministry of Works (MoWs) in Dar es Salaam. The study deployed a sample size of 55

respondents, thus attained 92 percent response rate. Purposive and snowball sampling

procedures were applied in the study.

Results of the study showed that 97 percent of respondents identified over draft facility as

one of the Commercial Banks’ financing option, other options include term loan, finance

leasing and bid bond or guarantee as identified by 87 percent of resondents. Moreove, the

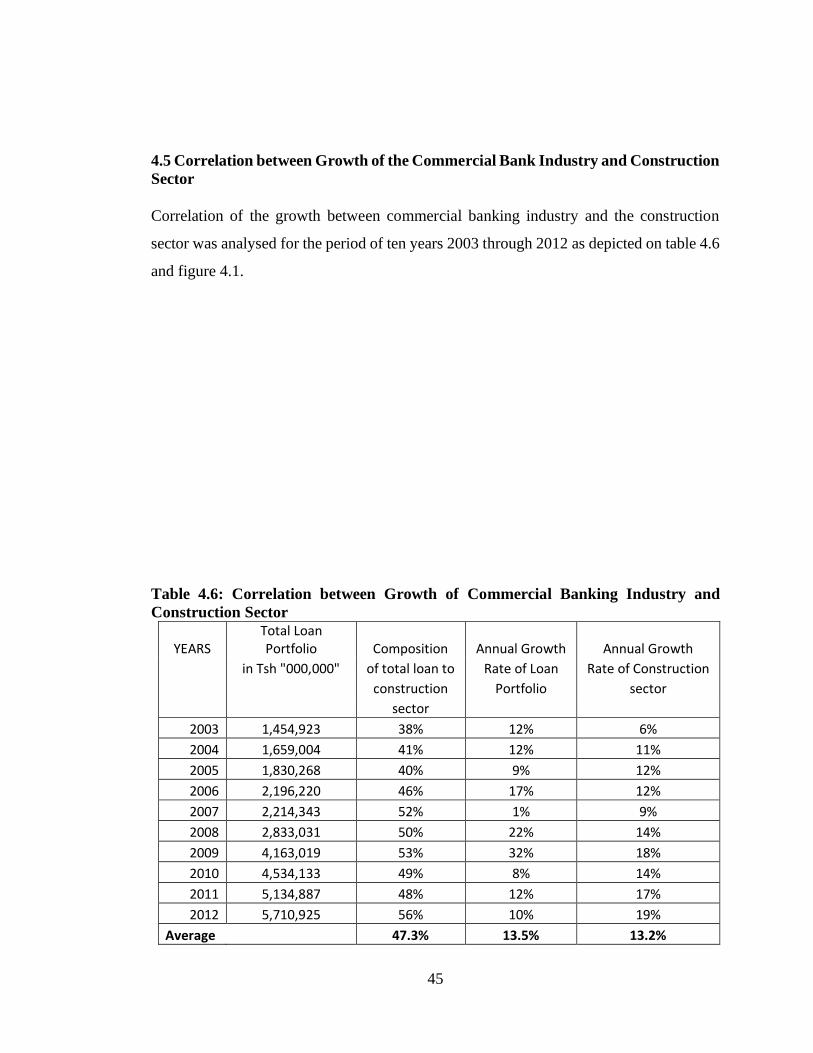

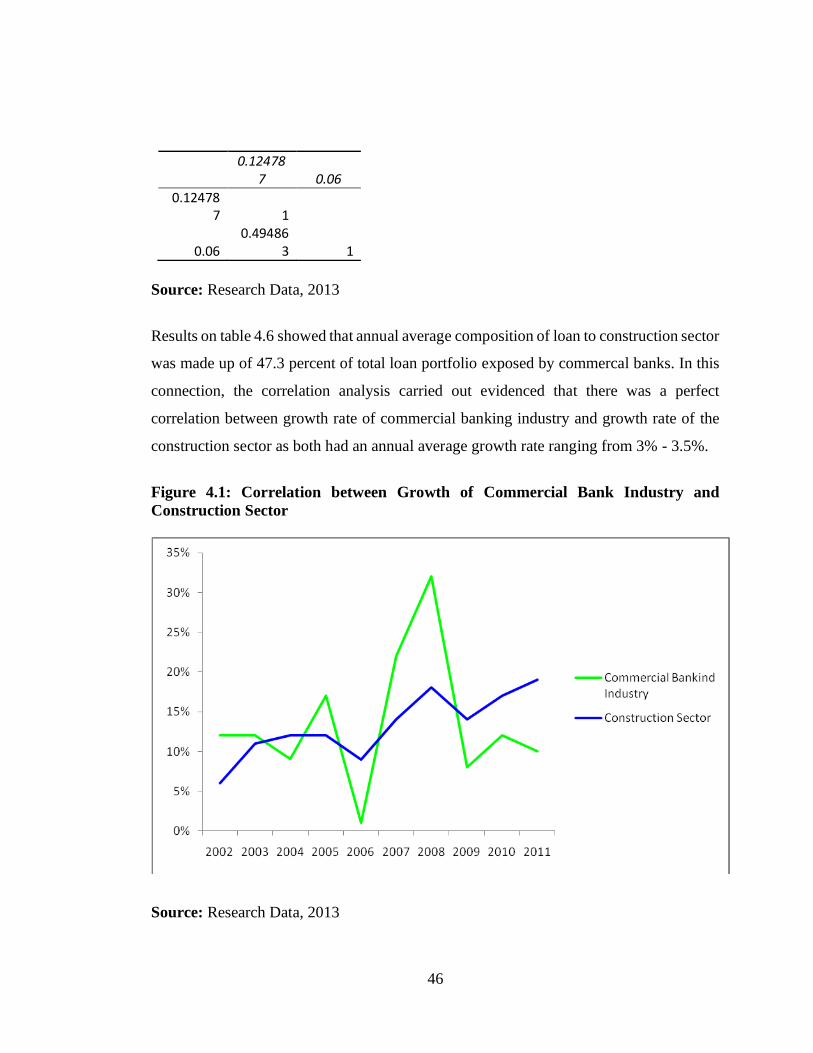

study revealed further that there was a perfect correlation between growth rate of

commercial banking industry and growth rate of the construction sector as both had an

annual average growth rate ranging from 3% - 3.5%.

The study recommended 77 percent of commercial banks found not offering credit for

finance leasing to venture it given the newly regulation of 2011 for the same permits.

However, analysis of cost of fund exposed to the construction sector and critical risk

assessment on financing the construction sector were suggested as areas for future studies.

viii

TABLE OF CONTENTS

CERTIFICATION ............................................................................................................ i

DECLARATION ..............................................................................................................ii

COPYRIGHT ................................................................................................................. iii

ACKNOWLEDGEMENT .............................................................................................. iv

DEDICATION .................................................................................................................. v

ACRONYMS ................................................................................................................... vi

ABSTRACT ....................................................................................................................vii

TABLE OF CONTENTS ............................................................................................. viii

LIST OF TABLES .......................................................................................................... xi

LIST OF FIGURES .......................................................................................................xii

CHAPTER ONE .............................................................................................................. 1

BACKGROUND TO THE PROBLEM ......................................................................... 1

1.1 Introduction ............................................................................................................... 1

1.2 Background of the Problem ...................................................................................... 1

1.3 Statement of the Research Problem .......................................................................... 4

1.4 Research Objectives .................................................................................................. 5

1.5 Research Questions ................................................................................................... 5

1.6 Significance of the Study .......................................................................................... 6

1.7 Scope and Limitations of the Study .......................................................................... 6

1.8 Delimitations of the Study ........................................................................................ 7

CHAPTER TWO ............................................................................................................. 8

LITERATURE REVIEW ................................................................................................ 8

2.1 Introduction ............................................................................................................... 8

2.2 Theoretical Literature Review .................................................................................. 8

2.3 Emperical Literature Review .................................................................................. 22

2.4 Conceptual Framework ........................................................................................... 29

ix

CHAPTER THREE ....................................................................................................... 30

RESEARCH METHODOLOGY ................................................................................. 30

3.1 Introduction ............................................................................................................. 30

3.2 Research design ...................................................................................................... 31

3.3 The study area ......................................................................................................... 31

3.4 Population .......................................................................................................... 31

3.5 Sample Size ............................................................................................................ 32

3.6 Sampling Technique ......................................................................................... 32

3.7 Sources of Data ....................................................................................................... 33

3.8 Data Analysis Plan ............................................................................................ 35

CHAPTER FOUR .......................................................................................................... 36

PRESENTATION OF RESEARCH FINDINGS, ANALYSIS AND DISCUSSION

.......................................................................................................................................... 36

4.1 Introduction ............................................................................................................. 36

4.2 Demographics Characteristics of Respondents....................................................... 37

4.3 Financing Modalities on Construction Sector at Pre-Project.................................. 39

4.4 Post-Project Financing Modality for Construction Sector...................................... 42

4.5 Correlation between Growth of the Commercial Bank Industry and Construction

Sector ............................................................................................................................ 45

4.6 Financing Options to the Construction Sector ........................................................ 47

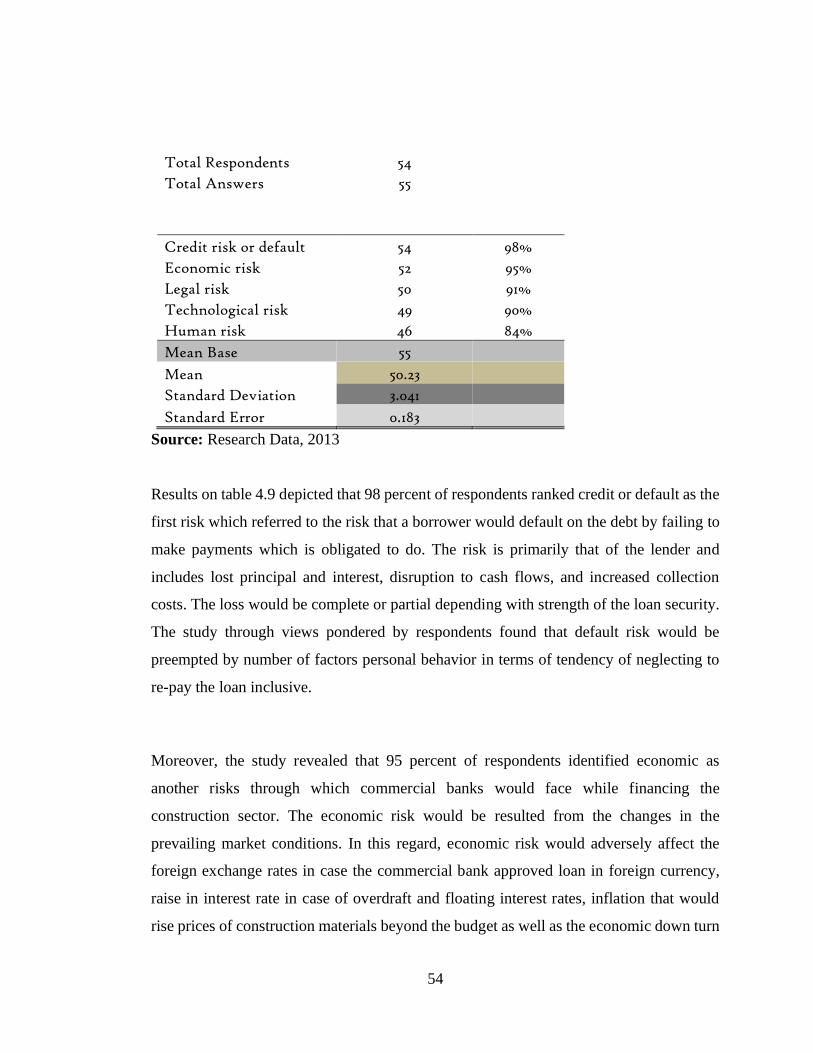

4.7 Risk Analysis Pertaining Financing Construction Sector ....................................... 53

4.8 Challenges Pertaining to Construction Sector Financing ....................................... 56

4.9 Measures taken to Overcome Construction Sector Financing ................................ 58

CHAPTER FIVE ............................................................................................................ 60

CONCLUSIONS AND RECOMMENDATIONS ....................................................... 60

5.1 Introduction ............................................................................................................. 60

x

5.2 Conclussion ............................................................................................................. 61

5.3 Recommendations ................................................................................................... 62

5.4 Area for Future Studies ........................................................................................... 63

REFERENCES ............................................................................................................... 64

APPENDIX I .................................................................................................................. 66

QUESTIONNAIRES ..................................................................................................... 66

xi

LIST OF TABLES

Table 3.1: Sample Size ................................................................................................. 32

Table 4.1: Gender and Age ........................................................................................... 38

Table 4.2: Working Experience .................................................................................... 38

Table 4.3: Level of Education....................................................................................... 39

Table 4.4: Pre-Project Financing Modalitieis ............................................................... 40

Table 4.5: Post-Project Financing Modalities .............................................................. 43

Table 4.6: Correlation between Growth of Commercial Banking Industry and

Construction Sector ...................................................................................................... 45

Table 4.7: Financing and Priority given by Commercial Banks on Construction Sector

...................................................................................................................................... 47

Table 4.8: CBs’ Financing Modalities to Construction Sector ..................................... 49

Table 4.9: Risks Pertaining to Financing the Construction Sector ............................... 53

Table 4.10: Challenges Partaining to Construction Sector Financing .......................... 56

xii

LIST OF FIGURES

Figure 2.1: Conceptual Framework .............................................................................. 29

Figure 4.1: Correlation between Growth of Commercial Bank Industry and Construction

Sector ............................................................................................................................ 46

Figure 4.2: Commercial Banks with Overdraft Facility ............................................... 49

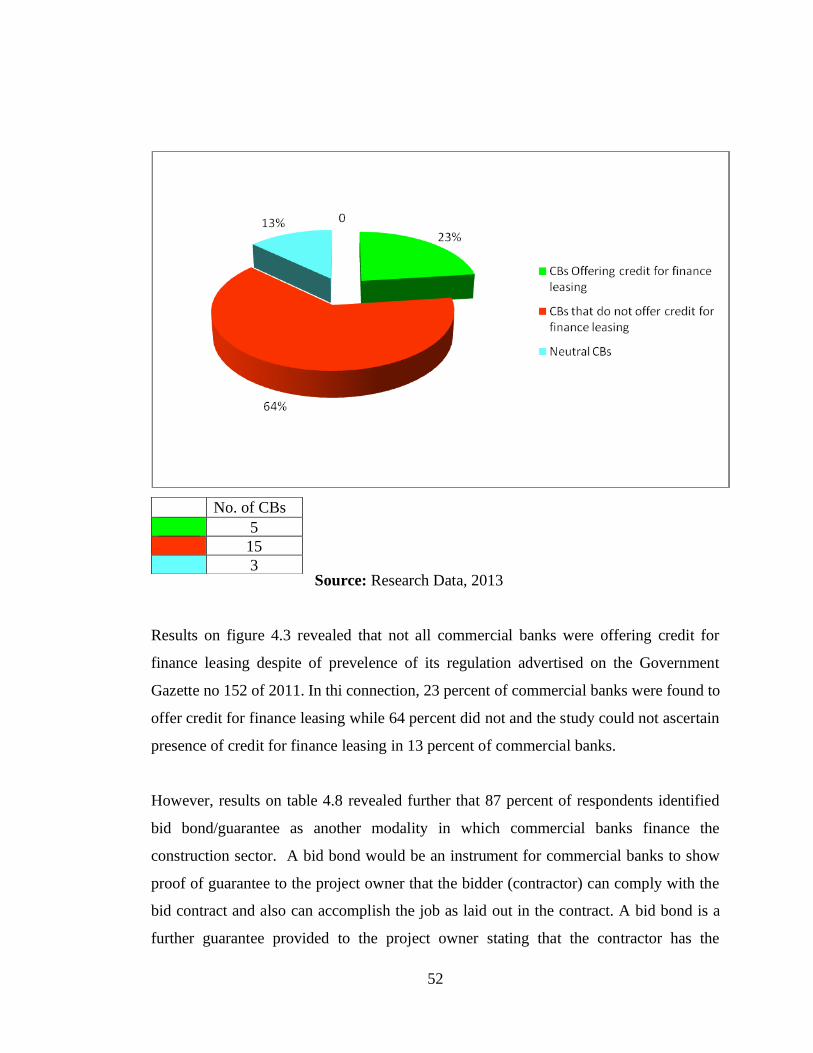

Figure 4.3: Commercial Banks offering Credit for Finance Leasing ........................... 51

1

CHAPTER ONE

BACKGROUND TO THE PROBLEM

1.1 Introduction

This chapter presents the background and statement of the research problem, also, research

objectives and research questions are enumerated in this chapter. However, the chapter

explains the significant of the study, scope and limitations as well delimiations and

organization of the proposal is stated.

1.2 Background of the Problem

A construction industry is a service providing and implementing industry whose

responsibility is to convert plans and specifications into a finished product. It also plays a

leading role in the national economy. It employs over 10 percent of the work forces and

covers about 15 percent of the government’s capital budget in the developed world. The

figures correspond to about 20 percent and 30 percent respectively, in the developing

countries (Broombridge, 2009).

The construction sector performance has a marked effect both on the economy and on

social conditions. This is especially true in developing countries, where much of these

infrastructures and service giving industries are lacking. For the development and capacity

building of the sector, the role of banks is very crucial. With the availability of funds from

international financers and allocation of budget from the government (either Central or

Local Government) both need involvement of commercial banks for financial aspects

(Basel, 2010).

Presently, Tanzania has relatively an extensive program of infrastructure development and

it is growing faster. The construction of new roads linking all regions of Tanzania

2

Mainland, high rising buildings in cities like Dar es Salaam, Arusha, Mwanza and Mbeya,

hydroelectric power generating plants, water work projects, Airfields like extension of the

Mwalimu J.K Nyerere International Airport, rapid bus transit and highways constructions

in Dar es Salaam are among the major construction activities in the country. In

consideration of quality and standards of the design and construction, commercial banks

play a significant role in the successful accomplishment of these investments. When the

quality and time of completion of construction works taken into account, the financial

capacity of the construction firms involved come into picture in developing countries

(Chijoriga, 2012).

According to Mwakyembe (2011) the general state of the construction sector of Tanzania

is characterized by low capacity, which could not handle large-scale construction demands

in the infrastructure development of the country. The government has taken a number of

measures to stimulate the performance of the domestic construction sector. Some of these

were

• Encouraging local investors to establish construction firms and participate in all

areas of construction activities,

• Reorganizing the state owned construction companies as independent

enterprises and preparing them for subsequent privatization,

• Decentralizing the rural road construction and maintenance responsibilities to

local governments,

• Assisting the local contractors by awarding various infrastructure development

projects.

The contractor of a certain project must obtain the capital resources to finance the costs of

construction. A project cannot proceed smoothly without adequate financing, and the cost

of providing adequate financing can be quite large. For these reasons, attention to project

3

financing is an important aspect of project management. In this regard, the involvement

of commercial banks to the construction sector is very important. The most prominent

constraint contractors face in the construction sector is the difficulty to find appropriate

financing for the smoothly undergoing and on time completion of the project activities

(Siku, 2010).

Tanzania embarked on economic reforms in 2000s whereby various legislations were

reviewed, enacted and some amended, among others the Tanzania investment policy

(1997) was reviewed in 2004 and the Tanzania Banking act of 1984 was repealed to the

newly prevailing Banking and Financial Institutions Act (BAFIA) of 2006. Since then

Tanzania experiences rapid growth in the financial sector and specifically commercial

banks. According to Bank of Tanzania (BoT) (2013) there are 50 Financial Institutions

comprising of 27 Commercial Banks, 10 Financial Institutions Banks and 13 Community

Banks. Again, the industry for commercial banks grew from 3 commercial banks in 1980

to 27 commercial banks in 2013.

Despite of the need for financial institutions basically commercial banks to construction

activities, the banks will generally not allow construction loans and other facilities simply

for construction firms by setting different pre-established conditions; these include

collateral and the firm's track record at the bank (Fanuel, 2010). In this connection,

construction firms working in different infrastructure development projects would infer

having limited access to formal financial services given the fact that interest rate ceilings

and collateral requirements for loan generate a gap between contractors and banks; hence,

the the situation pose for a challenge in the mutual interrelationship of the two parts where

the study would be nurtured.

4

1.3 Statement of the Research Problem

Over a decade Tanzania has been experiencing rapid growth in development financing

that would be quantified by the fact that in most of commercial banks’ financial

statements the largest component of loan portfolio is development loans in terms of

construction (Lauwo, 2012). Likewise, construction activities in terms of purchasing

land and improvements including existing buildings, grading and street improvements,

utilities, parking lots and landscaping, construction of new facilities, modernizing,

renovating or converting existing facilities and purchasing long-term machinery and

equipments had significantly grew (Mnenwa, 2011). Therefore, the aforesaid

circumstances would infer great relationship between growth of the commercial

banking industry and construction activities.

In consideration of the empirical literature review, studies related to the role of

commercial banks in support of development financing focusing on construction sector

were mostly from abroad studied in Ethiopia, Nepal, Mauritius, Peru and Singapole just

to mention a few. On contrary some studies conducted in Tanzania were mostly focusing

on issues like bank performance, credit risk management and factors causing non-

peorforming loans in commercial banks and strategies for corporate financing (Jafari,

2012).

Despite of the aforesaid remarkable growth in both commercial banks and construction

activities, various stakeholders had been experiencing difficulties on access to finance

for various development activities, and on the other hand quality of such construction

projects had been questioned. Therefore, this triggered the researcher’s interest to

conduct a thorough study on the role of commercial banks in development financing

in order to instill business growth and sustainability of both commercial banks and

their financed construction activities.

5

1.4 Research Objectives

The study aims at attainined the following general and specific objectives.

1.4.1 General Objective

The study analysed the role of commercial banks in support of Tanzania construction

sector.

1.4.2 Specific Objectives

The study specifically attained the following objectives.

(i) To evaluate financing modalities on construction sector at pre-project,

(ii) To evaluate financing modalities on construction sector at post project,

(iii) To analyse correlation between growth of the commercial banking industry

and construction sector, and

(iv) To expound financing options and policies to the construction sector.

1.5 Research Questions

1.5.1 General Research Question

The general question of the study was what is the role of commercial banks in support of

Tanzania construction sector?

1.5.2 Specific Research Question

The study answered the followng specific research qeustions.

(i) What are financing modalities on construction sector at pre-project?

(ii) How would the construction sector be financed at post project?

(iii) What is the correlation between growth of the commercial banking industry

and construction sector?, and

(iv) What would be considered as financing options to the construction sector?

6

1.6 Significance of the Study

Development financing as a field of study is very new in Tanzania context, therefore, this

study had numerous importances as enumerated hereforth.

1.6.1 Practictioners

This research would provide a foundation work to the bankers such that they know how

effective thier lending modalities to construction sectors are and how to waive risk

associated with the same.

Likewsie, through this study, options for construction financing identified and

secchallenges partaining to the construction sector revealed where the same would know

measures to take in overcoming such challenges.

1.6.2 Policy Makers

The analytical facts of the research results is expected to act as bench mark to the policy

makers (Bank of Tanzania, Institute of Bankers, construction partners, etc) to come up

with financing fit policies that enable banks increase their lending mechanism to the

constructin sector which is turning to be a backborn of Tanzania economy.

1.6.3 Academicians

The results of this study would add to the bandle of already existing knowledge regarding

the link role of commercial banks in support of development financing in focus of

construction sector. Furthermore, the study would be useful as a basis for literatures of

future research as well source for research topics as will be prescribed on the forthcoming

research report.

1.7 Scope and Limitations of the Study

The study was aware of varieties of stakeholers who finance the construction sector that

included investment banks and government guarantees just to mention a few. Given

7

variance of business motives among commercial banks (Profit) and other stakeholders

(Development) and difference financing modalities of the same, the study decided to

confine itself on commercial banks as one of the construction sector financiers to examine

the role of the same in financing the construction sector given its big number in the

industry that if giving adequate financing to the construction sector would bring about

significant impact to the sector and economy of the country at large.

Likewise, the study was carried out at the commercial banks and construction projects

where confidentiality of some information needed by the study was not exposed to due to

security and ethical reasons. Also the study experienced uncooperative attitude among

respondents that could be associated with ignoring or being busy. In this accord, the study

could not attain 100 percent response rate from its planned sample, insteady attained 92

percent.

1.8 Delimitations of the Study

Throughout this study, the limitations were overcome through a well designed research

methodology as stipulated in chapter three. Time constraint overcame through strictly

adhering to research time table, financial constraint as well overcame through use of

convenient sampling procedure that enabled the researcher to collect information from

respondents whom she was sure and convenient to get the same. On the other hand,

uncooperative attitude of respondents overcame through providing advance notice thus

avoided last minute lash.

8

CHAPTER TWO

LITERATURE REVIEW

2.1 Introduction

The chapter seeks to present literature review in form of theoretical review, empirical

review and conceptual framework. However, this chapter tries to link the objectives of the

study and related literatures carried out in and outside Tanzania.

2.2 Theoretical Literature Review

2.2.1 Definition of Key Terms

Construction sector: is one of the most booming industries in the whole world. This

industry is mainly an urban based one which is concerned with preparation as well as

construction of real estate properties. The repairing of any existing building or making

certain alterations in the same also comes under Construction Industry. This industry can

be categorized into three basic categories namely :-

-Construction involving heavy and civil engineering, the construction of large projects

such as bridge, road, etc comes under this category.

-General construction, the construction works that involve building of real estate ones

such as residential or commercial real estate assets.

-Construction projects involving specialty trades, construction works that involve building

up of specialized items namely, electric related works, works on woods.

It is generally being observed in the all round the globe in the construction sector that the

contractor individual or organization involved in the construction process specialize in

any one of the above mentioned categories. A contractor who is involved in building real

estate do not generally go for specialized trade or heavy engineering works. The same is

also true for other kind of contractors. Construction sector is a booming industry and

remain so with the continuation of the development process especially in the developing

countries. With the process of development, the migration of people takes place from the

rural to urban areas. This phenomenon is most significantly observed in the "Asian Tiger"

9

countries, China and India. Thus, the construction Industry is also on a rise in such

countries.

Commercial bank: is a financial institution that provides services, such as accepting

deposits, giving business loans and auto loans, mortgage lending, and basic investment

products like savings accounts and certificates of deposit. The traditional commercial bank

is a brick and mortar institution with tellers, safe deposit boxes, vaults and ATMs.

However, some commercial banks do not have any physical branches and require

consumers to complete all transactions by phone or Internet. In exchange, they generally

pay higher interest rates on investments and deposits, and charge lower fees.

Likiweise, commercial banking activities are different than those of investment banking,

which include underwriting, acting as an intermediary between an issuer of securities and

the investing public, facilitating mergers and other corporate reorganizations, and also

acting as a broker for institutional clients. Some commercial banks, such as Citibank and

JPMorgan Chase, also have investment banking divisions, while others, such as Ally,

operate strictly on the commercial side of the business.

However, according to Auronen (2003) commercial bank is an institution which accepts

deposits, makes business loans, and offers related services. Commercial banks also allow

for a variety of deposit accounts, such as checking, savings, and time deposit. These

institutions are run to make a profit and owned by a group of individuals, yet some may

be members of the Federal Reserve System. While commercial banks offer services to

individuals, they are primarily concerned with receiving deposits and lending to

businesses construction activities inclusive.

Development Financing: development financing created according to Broombridge

(2009) must be comprised of property that is one or more of the following: Blighted,

deteriorated, deteriorating, undeveloped, or inappropriately developed from the standpoint

10

of sound community development and growth, appropriate for rehabilitation or

conservation activities and appropriate for the economic development of the community.

The total land area within development financing in a unit, including development

financing created may not exceed five percent (5%) of the total land area of the unit. For

the purposes of this, land created by a county that subsequently becomes part of a city,

town, or incorporated village does not count against the five-percent (5%) limit for the

city, town, or incorporated village unless the city, town, or incorporated village and the

county have entered into an agreement.

Development Financing: include all of the following: a description of the boundaries of

the development financing, a description of the proposed development, both public and

private, costs of the proposed public activities, sources and amounts of funds to pay for

the proposed public activities, base valuation of the development financing, projected

incremental valuation of the development financing, estimated duration of the

development financing. Others are description of how the proposed development, both

public and private, will benefit the residents and business owners of the area in terms of

jobs, affordable housing, or services, description of the appropriate ameliorative activities

which will be undertaken if the proposed projects have a negative impact on residents or

business owners of the area in terms of jobs, affordable housing, services, or displacement

and requirement that the initial users of any new manufacturing facilities that will be

located in the area and that are included in the plan will comply with the wage

requirements.

2.2.2 Theories and Concepts

According to Bester (2009) the most prominent constraint the developing countries

construction industry face is the difficulty to find appropriate financing for the smoothly

undergoing and on time completion of project activities; i.e cash flow problem.

11

2.2.2.1 Role of Banks for a Construction Industry

Choosing an appropriate financial option and implementing a comprehensive project

management plan are vital for the successful completion of any construction project.

Banks contribute a vital role for a construction industry by providing; construction Loans

Including Overdraft Facilities, equipment financing and bonds and guarantees

Construction Loans and Overdraft Facilities

A loan is the purchase of the present use of money with the promise to repay the amount

in the future according to a pre-arranged schedule and at a specified rate of interest. In

banking and finance, loan contracts formally spell out the terms and obligations between

the lender and borrower. In all construction activities costs occur earlier than payments.

Hence, contractors in least developed countries often obtain the capital resources to

finance the costs of construction. Due to their low capacity, they are in difficulty to cover

earlier costs. Hence, to cover the costs that are related to mobilization and commencement

of a project, the project owners will facilitate advance payment for the contractors at the

early period of the project (Rajaraman and Vasishtha, (2010).

A project cannot proceed without adequate financing, and the contractor should incur

costs for adequate financing for its projects. For this reason, attention to project finance is

an important aspect of project management. Project financing mainly comprise the

different types of loans based on their time to maturity. The different term loans with their

time of maturity in the domestic commercial banks are; short term loan: Up to 1 Yr,

Mmedium term loan: 1 Yr to 5 Yrs and long term toans- more than 5 Yrs.

In essence, project finance problem is to obtain funds to bridge the time between making

expenditures and obtaining revenues (payments). Based on the conceptual plan, the cost

estimate and the construction plan, the cash flow of costs and receipts for a project can be

estimated. Normally, this cash flow will involve expenditures in early periods. Covering

12

this negative cash balance in the most beneficial or cost effective fashion is the project

finance problem.

Normally banks will not give loans with out securing the repayment of the loan. Assets

pledged as security against loan loss are called collateral. An asset purchased by the loan

or assets owned before the loan may serve as collateral. In other cases, the borrower puts

other assets, including cash to be collected, additionally that can be considered as

collateral. Credit backed by collateral is thus known as secured debt, while unsecured debt

relies on the earning power of the borrower. Most Governments survey figures suggest

that around 40 percent of all commercial and industrial loans are secured debt with

collateral (Ross, 2011).

As put by Abebe 92009) the options for borrowing by contractors to bridge their

expenditures and receipts during construction are relatively limited. For small or medium

size projects, overdrafts from bank accounts are the most common form of construction

financing. Usually a maximum limit is imposed on an overdraft account by the bank on

the basis of expected expenditures and receipts for the duration of construction.

Contractors who are engaged in large projects often own substantial assets and can make

use of other forms of financing which have lower interest charges than over drafting. This

can help in reducing the working capital problem of contractors in least developed

countries. In general, commercial banks in developing countries are reluctant to lend to

small contractors for a set of various reasons; the contractors are often first-time borrowers

without any track records at the bank, they are unable to full-fill the collateral requirements

of the bank, they can not present their last years’ financial statements to the bank and they

are unable to finance 20-50% of the investment from their own resources as required by

the bank.

Banks often require collateral or third party guarantees as compensation for the perceived

higher risk involved in lending to contractors. In some situations project owner can

13

facilitate contractor’s access to bank finance by providing them with guarantees. Banks

also can provide loans and guarantees for trustworthy contractors without securing the

repayment of loans with collateral or third party guarantee only considering the

contractor’s track record at the bank (Zemek, 2009). For a contracting agency there are

three different possible ways to stand guarantee for a contractor to get loan from banks;

guaranteeing work, guaranteeing work payments and uaranteeing loans.

Guaranteeing Work

The simplest solution from the perspective of the project owner is to prepare a letter

guaranteeing the contractor a certain amount of work. By showing this letter to the bank

the contractor will access some amount of credit. In most instances a document

guaranteeing work by itself will not be sufficient for contractors to access credit. A project

owner can only guarantee work for a certain period, not for the duration of the whole

program.

Guaranteeing Work Payments

In cases where banks consider letters of guarantee as described above as insufficient, the

project owner could agree to make payments to the contractors through the bank, allowing

the bank to withhold parts of the payments in case of bad loan repayment by the contractor.

However, the bank is legally not allowed to withhold such payments and in all instances

the consent of the contractor has to be sought. Any contract, signed by the three parties,

would have to state clearly the conditions under which the bank can withhold payments

(Gould, 2000).

The contract should have to state clearly which sums the bank would be allowed to

withhold at what moments; the amount of repayment, penalty interest, outstanding

principal and legal expenses etc. Care should be taken in using this method even in

countries where the legal framework supports it. The advantage of the method is that the

14

contractors are backed in their efforts to establish contacts with a formal financial

institution at no additional costs and collateral requirement.

This method has been developed and started in Tanzania by Commercial Bank it is known

as “Tri-Partite Agreement”. This has been intended in order to build the capacity of local

construction firms and to facilitate a good working capital for their projects. The bank

developed this method if and only if project owners / Employers are government

organization duly organized under the laws of Tanzania. In this agreement the local

construction firm should authorize the employer to channel all the payments of works

executed directly to a special proceeds account that has been opened in one of the bank’s

branches. The bank will service the loan repayment according to the terms of repayment

of the loan contract out of the special proceeds account and the bank will transfer the

remaining amount, if any, to the contractor’s account up on receipt of his application

(Elisante, 2011).

Guaranteeing Loans

A third possible way to facilitate contractor’s access to bank finance is to guarantee the

loans that the contractor taken from a bank; this is commonly known as third party

guarantee. In practice this means that the project owner would set up a guarantee fund on

the basis of which it can provide the contractors with letters of guarantee. In a letter of

guarantee the project owner agrees to share the loan risk with the bank. In case the

contractor fails to repay the loan, the project owner pays part of the outstanding debt

instead.

Banks Lending Procedure

The current procedure for lending in most domestic banks includes; a n inquiry stage,

application stage, site visit, preparation of an appraisal note, evaluation by the board /

committee, issuance of letter of intent, preparation of a legal agreement for lending for

suitable project and ending the approved amount. At each stage of the application for a

15

loan, a company is required to provide any relevant information which is required by the

banks.

Equipment Financing

Most contractors in developing countries are unable to use their own funds and savings to

invest in equipment. In situations where the contractors have insufficient capital to

purchase new equipment, they will look for second hand trucks and machines on the local

as well as foreign markets. This is seen in local construction firms clearly nowadays.

Guiding Principles to Support Contractors Finance

Scarcity of construction equipments of contractors can pose serious threats to the quality

of the works performed and to the time for completion of the construction project. The

owner of a project either pre-finances equipment by giving advance payments or by giving

guarantee for bank loans or sets up a leasing scheme in order to build the capacity of the

contracting firm with regard to equipment capability for a better quality & on time

completion of a project (Waweru and Kalani, 2009). The different possibilities of

financing equipment for construction firms are; outright purchase, truck/ equipment loan,

leasing schemes, hire purchase scheme, pre-payment (advance payment) of equipments

by the project owner and suppliers credit/ credit Sales.

Outright Purchase

In outright purchase the company immediately owns the plant/ Equipment and has title to

it. The plant is an asset, which will appear in the company books. The company has full

control over the plant/ Equipment and can use it as and where it wishes, sell it etc.

However, outright purchase requires a large initial capital outflow. This is not easy for

construction firms in least developed countries.

Truck/ Equipment Loan

16

Truck/ equipment loan is a loan facility provided for construction firms in order to

purchase the required equipments for their construction projects by securing the

repayment of the loan by the equipment that is to be purchased. The contractor has full

ownership over the equipment.

Leasing scheme

One of the possibilities for contractors to finance their equipment is to look for a leasing

arrangement. Leasing is a common way for small and medium sized enterprises around

the world to finance trucks and equipments. Financial leasing is a contractual arrangement

that allows one party (the lessee) to use an asset owned by the leasing company (the lessor)

in exchange for specified periodic payments. During the lease period legal ownership of

the asset is retained by the lessor. Most leasing contracts will include the option for the

lessee to purchase the asset at the end of the lease term for a nominal price.

The great advantage of lease finance for contractors is the absence of collateral

requirements. A leasing arrangement can be concluded quicker and simpler than a bank

loan. Rather than looking into the credit history and the asset structure of the client, leasing

companies will focus on the clients’ ability to generate sufficient cash through the

investment financed in the leasing arrangement. Leasing may be attractive to a company

which has no adequate working capital; because it enables him to keep his financial

resources as working capital for the payment of salaries and construction materials.

Another advantage of leasing over hiring of equipment is the incentive that contractors

have to properly maintain the equipment (Greuning and Bratanovic, 2006).

Leasing companies offer different options for the client at the end of the lease term; the

equipment can be purchased at residual value. The residual value is estimated at the

beginning of the lease term, based on the likely market value at the end of the period, the

client can renew the lease at a significantly reduced rental rate. Rentals during a secondary

period are lower than in the primary period and the client receives a share in the profits of

17

the equipment sale. At the end of the lease, the equipment will be sold to a third party and

the client will be allowed to share in the benefit of the sale proceeds according to a

distribution of proceeds defined in the lease contract.

According to Gorter and Bloem (2009) the end-of-lease option is an important part of the

lease contract. A pre-set purchase price stated in the contract enables the contractor to

foresee how much funds he needs for the final purchase. Contractors who have the

intention to buy the asset at the end of the lease term have an incentive to maintain the

equipment properly. The lessor is usually a financial institution (Finance Lease) or a

manufacturer/supplier (Operator Lease). In a finance lease, the lessor has no interest

whatsoever in the plant only in the financial payments that he is to receive under the lease,

and possibly the resale or scrap value of the plant at the end of the lease. However, where

a manufacturer or supplier provides plant on a lease, he may be responsible for the

operator, maintenance, spare parts.

Hire Purchase

The company pays a regular hire charge and after a predetermined time pays a nominal

sum and actually acquires the plant. There is almost normally a fairly large initial deposit.

The company may have effective control but does not have total control over the plant

until the end of the predetermined time. There may also be other restrictions on the use

and location of the plant since it technically belongs to the hiring company until the end

of the predetermined time. The plant cannot therefore be included as one of the

construction company’s assets. Normally the interest charges on the hire purchase contract

are likely to be higher than those available to the company through its normal overdraft

facilities, so that an outright purchase or credit sale is likely to be cheaper (Bofondi and

Gobbi, 2010).

Pre-Payment of Equipments by the Project

18

In many construction contracts, the equipment required for the work is purchased and pre-

financed by the project. From the point of view of preparing contractors to sustain

operations in real life situations, the option of pre-financing equipment is most important.

The contractors are not faced with the procedures and realities of financial institutions and

do not build up track records with the bank. However, for the sake of simplicity

prefinancing equipment seems a viable option for construction projects. In most schemes

the client of a project becomes the defacto owner of the equipment (Barth, Caprio and

Levine, 2010).

At the moment the equipment is handed over to the contractor, a loan agreement is signed

between the owner of the project and the contractor. The agreement allows the contracting

firms to deduct loan repayments from the work payments. In case of exclusion of a

contractor from the work for whatever reason, the client will attempt to repossess the

equipment and hand it over to new contractors entering the projects. Pre-payment

arrangements and loan contracts with the client can run into problems as soon as the client

becomes unable to either provide work or to pay contractors in time. More complications

arise when delays in payment are due to bad or slow performance of the contractors or to

circumstances beyond the control of both parties. A loan contract should have to stipulate

clearly in which circumstances the contractors are allowed to suspend their repayment

schedule.

Suppliers Credit

As propounded by Allan and Olomi (2009) supplier credit seems to be the most common

source of external financing of contractors’ equipments. A construction company

immediately owns the plant/ Equipment, but the purchase price is paid in installments,

usually with a fairly large deposit. Full control is with the purchasing company. The

installments include the purchasing price and the financing costs. Competition on the

suppliers market defines whether equipment vendors sell on credit and what they charge

in terms of down payment and interest. In many developing countries however, equipment

19

firms only provide supplier credit to larger and very well known firms. The facility is

restricted to trust worthy clients that have an established relation with the firm. For

example in Tanzania, Mantruck, dealer for folk lift and Trucks, is arranging such kind of

credit sell for the known construction firms that are trust worthy customer.

Administration of the Schemes By A Financial Institution

In some cases the project owner as well as the suppliers opts to subcontract a financial

institution for the administration of the leasing, hire purchase or suppliers’ credit scheme.

The involvement of a financial institution would ensure efficient financial management

and administration of the credit scheme. The cost of hiring the services of a financial

institution though can be high; however, it will give relief for the project owner or the

suppliers in relation to the payment collection for the equipment financing schemes.

Bonds and Guarantees

A bond is a legally enforceable financial guarantee given by a third party (the guarantor)

to a project owner (client) to guarantee the obligations of a contractor under a contract.

The guarantor agrees to pay the client a sum of money if the contractor fails to perform

his obligation under the contract. The purpose of requiring a bond is to help the client

meet the extra expenses to remedy the default and /or complete the contract. Bonds are

generally provided by the financial market, either by a bank or a surety company. The

contractor and the guarantor will seek to establish the terms and conditions under which

the bond can be called. Clients, for their part want to know that the guarantor issuing the

bond is a sound, reliable and responsible corporate body and be satisfied that if there is

need to call the bond for payment the guarantor will comply promptly (Tundu, 2012).

Mostly in Tanzania, bonds and guarantees are provided for domestic construction firms

by both local and foreign commercial banks and insurance companies. Commissions for

bonds and guarantees requested by the banks are relatively expensive than that of

insurance companies. However, some project owners may oblige the contractors to

20

provide bonds and / or guarantees only from banks. Generally, the cost of a bond is

relatively small in comparison with the price of the contract. This will depend to some

extent on the terms and conditions the client requires and the degree of risk the guarantor

attaches to the ability of the contractor to give a counter indemnity and to reply any sum

that is called (Osoki, 2011).

A guiding principle of procurement best practice is that normally a contract should not be

placed with a contractor for guarantee/ bond if there are reasonable doubts about the

contractor’s ability to meet the terms and conditions of the contract satisfactorily. Such

doubts may arise in relation to the adequacy of the contractor’s management and technical

resources to deliver on time and to the required quality standard, or where information

available suggests the contractor may have inadequate financial resources with consequent

risk.

Bonds are not always necessary and are not substitute for considered judgments about the

risks of a particular contract and the capabilities and financial resources of the available

contractors. A decision to require a bond must be part of an overall approach to risk

management and should take account of available measures to reduce the risk of default,

including a proper prequalification of tenderers. Basically there are different types of

bonds which are adopted in a construction activity. The main are; bid bond / bid security,

performance bond, advance payment guarantee / bank guarantee and retention money

guarantee.

Bid Bond / Bid Security

Bid bond / Bid Security is a bond furnished by a bidder/ contractor, as part of its bid for

the amount labeled in the bid document from a legally registered bank. In most tenders

the bid security amount is about 1% of the contract amount. The maximum limit set in

most local competitive bids (LCB) is Tanzania shillings 1,000,000.00/=. The terms and

conditions of a bid bond determine the circumstances and mechanisms by which the bond

21

can be called. The bank undertakes to pay the employer of a project up to the amount

specified in the bid bond. The conditions of the bid bond obligation are; if the bidder

withdraws its bid during the period of tender validity specified in the tender document, if

the bidder refuses to accept the correction of errors in his tender. For example: Error in

unit prices, arithmetic errors and if the bidder having been notified of the acceptance of

his tender by the employer during the period of bid validity and,refuses to sign the contract

agreement or rails to furnish the performance security.

Performance Bond

A performance bond is usually provided after contract award, for an agreed percentage of

the total contract value (normally 10 percent). The guarantor/ bank will agree to guarantee

the due performance of the contract according to the terms and conditions of the contract

agreement. The guarantor agrees with the employer in such a way that, if the contractor

in any respect fail to execute and complete the contract or commit any breach of his

obligations there under, then the guarantor will indemnify and pay the employer the sum

of amount of guarantee, such sum being payable in the types and proportions of currencies

in which the contract price is payable. If the contract amount increases, or the duration of

the contract extends, then the bond may need to be amended accordingly. A performance

bond will not by itself ensure that contracts are carried out efficiently and to time, but it

will be one of a number of pressures on the contractor to perform well (Auronen, 2009).

Advance Payment Bonds/ Bank Guarantees

This bond allows advance payments under an awarded contract to enable initial purchase

of essential materials required to perform the work. This provides significant cash flow

benefits to the contractor in order to start the new project according to the stipulated time.

Retention Bonds / Maintenance Bonds

These bonds provide the project owner with a guarantee to the value of the bond that the

contractor will fulfill its defects or maintenance obligations as stated in the contract to

release the retention money that should has been deducted from the contractor’s interim

22

payments. As works of a project are completed, the contractor is paid fully for the executed

works without any deduction. The client of a project is protected against default at the end

of the defects liability or guaranteed maintenance period up to the amount of the bond.

These bonds are still rare in use in Tanzania. However, their use should have to be

increased in order to relieve the cash flow problem of the domestic construction firms to

some extent.

The traditional retention system is to withhold a percentage from interim payments made

during the course of the contract to accumulate a fund that is available to the client if the

contractor fails to rectify defects in accordance with the contract. According to Besel

(2011) the retention money that has to be hold is 5 percent of the value of the contractor’s

work up to certified completion, reducing to 2.5% up to final acceptance of the project

works. Retention bonds give access to contractors full payment of the project at all stages

without deduction of retention money. This will create access for the contractor to use the

retention money to relieve the cash flow problem.

2.3 Emperical Literature Review

2.3.1 Tanzania Context

The study conducted by Allan and Olomi (2009) on challenges facing the Tanzania

banking sector while dealing with construction sector using a sample size of 12 banks and

15 construction projects found that the perennial complaint about the inaccessibility of

financial products to the productive sector was among the serious challenge. Results of

the study indicated that only 6% of Tanzanians (both retail and corporate) have bank

accounts. On the other hand credit was available to only 3% of the population construction

sector inclusive. Therefore, given such results created financing gap, businesses including

contractors have resorted to other but expensive financing sources.

As propounded earlier, Tanzania banking business is governed by the Banking and

Financial Institutions Act, 2006, Bank of Tanzania Act, 2006 and regulations made there

under. One of the regulatory requirements when financing construction sector is that banks

23

must demand security to cover for their advances or commitments (e.g., guarantees). The

prudential threshold is that security must have value that cover 125% of the exposure. The

25% is intended to cater for interest that will accrue and legal costs at large.

According to Mina (2010) the regulations further provide for clean lending (up to 5% of

the core capital) and partially secured lending (up to 10% of the core capital). There is

also an aggregate ceiling to unsecured and partially secured facilities. Security is required

as part of risk management. In other words, banks do not lend against security but on the

soundness of the business to repay the loan i.e., cash flow lending. Security/collateral

merely is a fall back position. Again, realization of security being a costly legal process is

not favoured by bankers.

Likewise, the study by Mweyo (2010) on corporate financing in Tanzania revealed that

47% contractors seeking financial accommodation from banks find themselves

disqualified due to lack of or inadequate collateral. As a result, collateral requirement has

now become one of the complaints leveled against banks. The typical security offered by

contractors is landed property and plant and machinery. Landed property is charged

through the creation of a mortgage whilst plant and machinery is charged by a debenture

or chattel mortgage. There was a slightly decrease in the level of loan loss with time,

however, the loss remain 25 percent and above. This situation caused CBs in Tanzania to

be very risk averse and maintain a high liquidity level despite the fact that they could lend

up to a maximum of 80 percent of total deposits. This situation implied that CBs did not

perform their key intended role and in turn they retarded investments like construction

projects and economic growth.

2.3.2 Abroad Case

According to Guillaumont (2010) who studied financing system to small and medium

constructers in Singapore using a sample size of 230 construction companies revealed P-

value of 0.03 at t-stat of 68% that inferred demand for security to the small and medium

size constructors was more pronounced than say to a first class international constructor.

24

Whether a company should be granted unsecured or partially secured loan (even the type

of collateral to be accepted) would depend of the financial and reputation standing of the

company. For instance, a first class international contractor would view reputation damage

as a very serious matter. Here it would be relevant to mention that there were a number of

cases where banks found themselves holding forged/duplicate registration cards of trucks

and earth moving machinery owned by local contractors. Typically, it would be common

to find that the equipment involved has been offered as security to more than one bank.

The underlying point here is that reputation damage was not held in high esteem by certain

local constructors.

Petit (2011) analysed efficience of commercial banks when dealing with construction

sector in Luanda found in 1998 commercial banks were 97.0 percent scale efficient and

they operated under increasing returns to scale environment. That was a minimum overall

average efficiency score recorded during the period and there were improvements to reach

an exciting average score of 99.9 percent in 2011 showing that there was convergence to

the full efficiency line over time. Under constant returns to scale, a restrictive version of

DEA model, the overall average technical efficiency was 96.1 percent while that of

variable returns to scale model was 97.3 percent, implying inefficiency divergences of 3.9

percent and 2.7 percent, respectively. These rates tell us the extent to which banks could

reduce inputs and yet produce the same amount of outputs in both cases. It was further

observable from the summary of input slacks that technical inefficiency arose more from

inefficient use of labour, fixed assets and equipment rather than underutilisation of deposit

input in the intermediation process.

Barth, Caprio and Levine (2010) studied efficiency score among local small and large

banks compared to international banks in processing loans to construction activities. The

study revealed that small banks had higher technical efficiency scores than that of large

domestic banks but lower than the scores of international banks. During the period, small

banks had average technical efficiency rates of 96.0 percent and 96.6 percent in CRS and

25

VRS models, respectively. Inefficiency divergences from the frontier were 4.0 percent

and 3.4 percent for the two models. From the Malmquist indices, the group of construction

project involved indicated a positive development in both technical and scale and

efficiency, however, by a diminutive rate of 0.2 percent. Construction projects under study

were operating on the rising part of the average cost curve, and as for all other groups,

technical inefficiency emanated from underutilisation of labour, fixed assets and

equipment.

Fernandez, Jorge and Saurina (2007) conducted a study at 10 commercial banks in Dubai

to analysing effectiveness of loan extended to construction sector, their Return on Equity

(ROE) and rate on Non-Performing Loans (NPL) components. Therefore, results of ROE

and NPL/TL show that non-performing loan of the construction sector component was

significantly negatively related to profitability the bank gained. That was, 1 percent

increase in non-performing loans decreases profitability (ROE) by 1.506 percent. The

parameter value showed further that 1 percent increase in non-performing loans decreased

profitability (ROA) by 0. 4168 percent. The results verified the hypothesis that better

credit risk management resulted in better bank performance. It was aware that profitability

was an endogenous variable meant that it influenced the magnitude of non-performing

loans extended to construction projects, since better profitability afforded the projects to

write off more bad loans. But the study was focused to analysis one side relations to NPLs

on profitability from commercial bank loans exposed to the Dubai construction sector.

On the study by Nishimura, Kazuhito and Yukiko (2009) the collected data showed that

about 57% of the class I construction firms have projects at hand with a total cost more

than One Billion Ethiopian Birr and annual turnover greater than One Hundred Million

Ethiopian Birr. According to the data obtained from the distributed questionnaires, all of

the responding construction firms disclosed that finance was very important and major

resource in construction projects. Like the finance 67% of the respondents considered

26

manpower capacity as a very important tool in their organization. The value given for the

different resources by the requested construction firms.

Again, Cornett and Cornell (2008) studied on financial resources and construction

equipments in Mongolia where their findings revealed that all of the constructors have

financial as well as equipment deficiency to run and complete their projects smoothly with

the required time, cost and /or quality. About 50% of the responding construction firms

disclosed that there was skilled manpower incapability in their organization and 67% of

them have managerial incapability to manage their projects and organizations properly.

Similarly about 42% of them lacked work experience in constructions of large

infrastructure development projects.

The study by Uyemura (2008) conducted in Ethiopia found that all the construction firms

that have been involved in the study had identical argument on the obstacles for the

development and capacity building of domestic construction firms and they indicated that

obstacles had high to extreme significance on the industry’s development. It was very

clear that the private construction firms in Ethiopia were very young. For the development

and capacity building of the firms, it was observed again that construction firsms should

have strong financial partner. According to this study, about 83% of the selected

construction firms disclosed that they prefered the private banks for the different facilities

and bank services. The main reason that they pointed out for their preference was fast and

efficient services relative to the government banks.

Furthermore, the study described that financial institutions contributed a vital role for a

construction industry by providing different services and facilities. According to the study

survey, all the banks provided the following services and facilities for the domestic

construction firms; construction loans, bonds and guarantees, overdraft facilities and

truck/ equipment loans. Therefore, the research survey clearly indicated that all of the

domestic construction firms were getting short term loans from the local banks. 58% of

27

them were taking medium and 17% long term loans. For the services and facilities that

they had provided, banks took a certain percentage of commission from their customers.

The banks’ benefits (commissions) differ from one bank to another.

On the other hand the study by Minrednard (2010) done in Legos found that banks would

not give loans without securing the repayment of the loan. The study furhter indicated that

65 percent of resondents confirmed that all of the banks requested the construction firms

to provide collateral as compensation for the perceived risks involved in lending money

to the firms. All of the local banks would request the domestic construction firms to

provide owned assets and an asset that is going to be purchased by the loan (in truck/

equipment loan) as collateral. Also, in some situations project owners can facilitate

contractor’s access to bank finance by providing them with guarantees. However, only 3

of the domestic banks indicated that they were allowed third party guarantee to secure

loans and only 1 of the banks provided loan for a construction firm if a client of a project

guarantees work payments to pass through such a bank.

In the same study, nevertheless any of the domestic construction firms didn’t get a client

who guarantee work as well as work payments to get loan from the banks. The project

owners also responded that they could not guarantee work and / or work payments for

their projects' contracting firms to get loan from banks. The other possibility that could be

used by the banks to provide loans and guarantees for construction firms was by

considering the firm's healthy relation with the banks. Three of the banks indicated that

there was a possibility in their bank to provide loans and guarantees for domestic

construction firms without securing the repayment by collateral or by any other guarantee

considering only the firms' track record in the bank (if they are proved to be credit worthy

in the bank), their experience in the business and their financial strength. It was ideal to

get such kind of domestic construction firm due to their low capacity.

28

Onother thing observed in this study was the safety margin set by the domestic banks for

collaterals secured for Bank guarantees and construction loans. The banks assumed a

safety margin up to 50% of the book value of an asset that was secured for loan repayment.

This was very high and the domestic construction firms were unable to provide the

required amount of fixed assets due to their low capacity. If the construction firm able to

provide a building as collateral, then the safety margin would be lower than the one found.

2.3.2.1 Role of Banks in Equipment Financing

Zemek (2009) study in Peru uisng 50 construction firms and 8 banks found that

construction equipments play a major role for any infrastructure development activities.

Scarcity of the required equipments would pose a serious problem on the quality of the

works to be performed and on the time for completion of the projects. It was observed that

out of the surveyed construction firms, the building contractors and firms which had

relatively strong capacity were not enjoying truck /equipment loan from their banks. One

thing that had been understood from this was that the firms in the first category were not

enjoying this facility since they won't require that much large number of equipments as

the General Contractors require and the firms in the second category can used outright

purchase of equipments from their reserved capital.

The same study found that about 83% of the responding construction firms used outright

purchase to finance their equipments. This was mainly due to unavailability of other

equipment financing schemes (leasing, hire purchase etc.). On the other hand the same

percentage of the respondents indicated that they used the projects' mobilization advance

payment that they have taken from their projects employers for trucks and equipments

purchase. This was greatly affected the projects' activities. 14 % of the responding

construction firms found using equipments leasing and hire purchase schemes. These

schemes were not provided with legally registered leasing companies in the country; they

were merely individuals who owned construction equipments.

29

2.4 Conceptual Framework

According to Besel (2009) the interconection between commercial banks and

construction sector is based on the role banks play in extending loan to the counterpart

sector. Commercial banks as the intemediator between depositors and lending persons

stand on two positions to financing the construction sector; one part position being pre-

project financning and the other post project financing.

Figure 2.1: Conceptual Framework

Source: Besel, 2009

Pre-project financing would include enabling the construction firm to acquire the job, thus

activities performed would encompass tendering, guaranteeing and bonding. On the other

hand, post project financing would include finishing and handling over of the project plus

management of the project in its lifetime.

Commercial Banks (CB)

Financing to the

Construction Sector

Pre-Project Financing

Modalities

Post-Project Financing

Modalities

Effectiveness of CB

Financing to

Constrution Sector

Inffective Effective

30

However, the financing modalities employed by commercial banks while transacting with

construction firms or projects result into the status of financing that would be supported

by the influence of other stakeholders like investment banks and the Government if all

credit risks and challenges analysed are at minimal or negligible and the firm or project

qualifies for financing. On contrary, the status of the financing would be ineffective if

some risks and challenges analysed are at red or higher than recommendable threshold.

CHAPTER THREE

RESEARCH METHODOLOGY

3.1 Introduction

31

This chapter presents the research methodology which was employed by the researcher.

It provides the research design, sample selection and size, and data collection and

administration procedures, data measurement and analysis techniques.

3.2 Research design

Research design would be referred as a set of advance decisions that make up the master

plan specifying the methods and procedures for collecting and analyzing the needed

information. In this regard, there are three major types of research design which are case

study, survey and laboratory experiment. Therefore, this study deployed a survey research

design given large scope of the study to various Institutions such as CBs, TBA, BoT,

ERB, the Ministry of Works and at 19 Construction projects. Likewise, the survey design

employed due to its easiness to administer compared to other designs like case study and

experiments. It provided an intensive and integrated investigation of a definitive search

for comprehensive information. The study however was empirical in nature, based on

mainly primary data collected by the researcher through interview and structured

questionnaires.

3.3 The study area

The study was carried out in Dar es Salaam City given the fact that about 98 percent of

head quarters for commercial bank’s are located (Bank of Tanzania, 2012) and more than

72 percent of construction activities took place (ERB, 2011). Therefore, doing the same

in Dar es Salaam, information for banking industry and construction sector were easily

obtained. In this regard, the study specifically got information from the Tanzania Bankers

Association (TBA) and Bank of Tanzaia for information related to banking issues and at

the Engeneering Registration Board (ERB), construction projects and at head quarters of

the Ministry of Works for information related to the construction sector at large.

3.4 Population

32

The population of the study included employees of Tanzania Commercial Banks and

regitemate persons working with construction sector.

3.5 Sample Size

The sample size of the study comprised of 18 respondents from five commercial banks, 4

respondents from TBA, 5 from BoT, 19 each from the identified 19 construction projects

in Dar es Salaam, 5 respondents from ERB and 4 respondents from the Mininstry of

Works. Generally 60 respondents were highligheted buth in due course of data collection

55 informants responded effectively, thus made a 92 percent response rate (Table 3.1).

Table 3.1: Sample Size

Sample Unit Planned

Sample Size

Actual

Sample Size

Percentage

Commercial Banks (CBs) 20 18 90%

Tanzania Bankers Association

(TBA)

5 4 80%

Bank of Tanzania (BoT) 5 5 100%

Construction Projects (CPs) 20 19 95%

Engeneers Registration Board

(ERB)

5 5 100%

Ministry of Works (MoWs) 5 4 80%

Total 60 55 92%

Source: Research Data, 2013

3.6 Sampling Technique

The purposive and snow ball techniques were applied to select the units of inquiry.