Financial and Non-Financial Business Risk Perspectives: Empirical Evidence from Commercial Banks

22

Financial and Non-Financial Business Risk Perspectives: Empirical Evidence from Commercial Banks Ayesha Naeem Master in Business Administration Department of Management Sciences University of Gujrat, Gujrat, Pakistan E-mail: [email protected] Abstract Purpose: The purpose of this paper is to have an empirical examination regarding financial and non-financial risks because of the changing environment of banking sector. Design/methodology/approach: The paper adopts two regression models for the “controllable” variables in the data set to identify significant correlations. Size, Gearing ratio, and liquid assets found to have significantly affecting the financial risk while Size and operating efficiency established significant relationship with the non-financial risk faced by the Commercial banks. Originality/Value: This study has successfully identified the factors that are significantly affecting financial and non-financial risk faced by the banks. Findings: Results proposed that banking system in all over the world is well diversified. 1

-

Upload

universityofgujrat -

Category

Documents

-

view

4 -

download

0

Transcript of Financial and Non-Financial Business Risk Perspectives: Empirical Evidence from Commercial Banks

Financial and Non-Financial Business RiskPerspectives: Empirical Evidence from

Commercial Banks

Ayesha NaeemMaster in Business AdministrationDepartment of Management Sciences

University of Gujrat, Gujrat, PakistanE-mail: [email protected]

Abstract

Purpose: The purpose of this paper is to have an empirical examination regarding financial and non-financial risks because of the changing environment of banking sector.Design/methodology/approach: The paper adopts two regression models for the “controllable” variables in the dataset to identify significant correlations. Size, Gearing ratio,and liquid assets found to have significantly affecting the financial risk while Size and operating efficiency establishedsignificant relationship with the non-financial risk faced by the Commercial banks.Originality/Value: This study has successfully identified the factors that are significantly affecting financial and non-financial risk faced by the banks.Findings: Results proposed that banking system in all over the world is well diversified.

1

Key words: Business Risk, Financial Risk, Non-Financial Risk,Credit Risk, Operational Risk, Commercial Banks.

Paper type: research paper

1.Introduction:

A bank is a financial institution and a financialintermediary that accepts deposits and utilize those depositsinto lending activities, either by loaning directly orindirectly through capital markets. A bank is the connectionbetween customers that have customers with capital deficitsand capital surplus.

Financial intermediaries perform key financial functions ineconomies; provided for payment mechanism, match supply anddemand in financial markets, deal with complex financialinstruments and markets, provide markets transparency, performrisk transfer and risk management functions. The efficiency offinancial intermediation also can affect economic growth.Besides, banks insolvencies can result in systemic crisis.Economies that have a profitable banking sector are betterable to survive with negative shocks and contribute to thestability of the financial system Athanasoglou, Brissimis andDelis, (2005). Therefore, it is important to successfulsupervise the risks and their forecast ought to help in lessenfailures and losses.

In 21st century business environment is added complex andintricate than ever. The majority of businesses have to treatwith uncertainties and doubts in every dimension of theiroperations. Banks face a number of risks in order to conducttheir business, and how well these risks are managed andunderstood is a key driver behind profitability, and howmuch capital required by a bank to hold. Some of the mainrisks faced by banks include: CR (credit risk) risk in whichborrower fails to make the payment at promising date. LR(liquidity risk) is a type of risk that the value of a

2

portfolio, either an investment portfolio or a tradingportfolio, will decrease due to the change in value of themarket risk factors.OPR (operating risk) mostly arises duringimplementation of a company’s business functions. RR (relativerisk) is a type of risk related to the reliability ofbusiness. MER (microeconomic risk) concern with the aggregateeconomy the business is operating. IRR (internal rate of risk)is the possibility that the bank will become unprofitable, ifrising interest rates force it to pay relatively more on itsdeposits than it receives on its loans.

Without a doubt, in the present-day’s unpredictable andexplosive atmosphere all banks are in front of hefty risks.The risks that are faced by businesses can be categorized intofinancial and non-financial risks. Both of these types ofrisks are very vital in order to safely run any business. Thisstudy will scrutinize credit risk having its financial natureand operational risk with its non-financial natureIn financial risk Credit risk is extensively documented andfamiliar as the most significant and mandatory in naturesurrounded by loads of financial risk in front of banksSackett & Shaffer, (2006). The escalating variety in the kindsof counterparties i.e. from individuals to governments, andthe always mounting diversity in the outlines of commitmenti.e. from auto advances to multifaceted derivatives contacts,has supposed that management of credit risk has bound to thefront position of risk management strategies carried out byfinancial services businesses Fatemi & Fooladi, (2006). Thesupervision and directive of credit risk is now fusty infinancial businesses, where upholding is essential to be donein order to minimize possible losses from non-payment onloans. Despite the fact that in the finance pitch, supervision andmanagement of risks has always been a primary face of thebusiness distinctively upbringings in services, operationalrisk has been for the most part ignored. Until the term‘operations risk’ have officially invented in 1991 by the COSO

3

report COSO, (1991) 1. Operational risk differs from othertypes of risks as it deals with recognized processes ratherthan managing the unknown circumstances Frame, (2003).Thedepth and supervision of operational risk is fairly opposingfrom other kinds of banks financial risks. The assorted natureof operational risk from inner or outer interference tobusiness activities makes difficult methodical and logicalmeasurement parameters Jobst, (2007).Non-business risk occursfrom failures in business policies and process, businessstrategies and failure in governances. Figure 1.0 reports the financial and non-financial riskperspective that is under consideration in this study.

Figure 1: Business Risk

Risk management is a keystone of tactful banking practice.More appropriately today, banking is a business of risk. Forthis foundation well-organized and competent risk managementis utterly requisites. This study will examine the variableshaving significant affect on credit and operational risk onCommercial banks all over the world.

4

Business Risk

Non-Financial

risk

FinancialRisk

Operational Risk

CreditRisk

2. Literature review:The factors identify the empirical examination regardingfinancial and non-financial risks because of the changingenvironment of banking sector. It is the most important topicfor research because it creates interest in researchers in thebanking field. Successful supervision of risks and theirforecast ought to help in lessen failures and losses.In the literature, Al-Tamimi and Al-Mazrooei (2007); Hassan(2009); found credit risk and operational risk among mostvital risk that the banks are facing while study UAE banks.

Although, a lot of work has been carried out for the evolutionof commercial and Islamic banks efficiency in the world butvery little work has been carried out on the banking sector ofPakistan. Basher (2000) analyse the factors of Islamic bank’sperformance across eight Middle Eastern countries for (1993-1998) periods. A various number of internal and externaldeterminants were used to forecast the operational risks.Controlling for macroeconomic environment, financial marketsituation and taxation, credit activities, the consequencesshow that higher influence and large loans to assets ratios,lead to higher profitability and improve the operationalefficiency. He also reported that foreign-owned banks are moreprofitable that the domestic one. There is also evidence thatthe taxation and interest rates negatively impact the bankingsector in Pakistan.

The Jarrow-Turnbull model was establishing the studies thathad openly arbitrary interest rates at its centre. Barry Bakerand Sanint (1981) found that impulsiveness in fundaccessibility from rural banks added to prominent creditrisks.Deakins and Hussain(1994) emphasized on investing in bothresources and time during risk assessment process, which inturn makes possible for bank to not only overcome unfair

5

selection but also shows the way to beneficial customerrelationship.Barnhill, Papapanagiotou, & Schumacher, (2002) found thatthere is a sky-scraping risk of malfunction right through thephase of financial stress of banks with elevated credit riskand exact portfolios. Moreover the study found credit value ofbank’s portfolio the most significant risk factor. Brown andWang (2002) stated that blend of credit spread option andhedging significantly lessen credit risk of sub-investmentbond portfolio.

In Colombian case, Barajas et al. (1999) examines the effectsof financial liberalization on banks’ interest margin. Afterliberalization, is found that loan quality increased andoverall spread has not declined the relevance of the differentfactors behind the bank spreads are affected by such measures.

Muhammad Ashraf (2012) stated that banks with larger assetssize and with efficient management lead to greater return onassets. Their paper shows that management efficiency regardingoperating expenses positively and significantly affects thebanks’ profitability. Bank level data is used and this studyexamines the alternative measures ROA and ROE as a bank-specific function and macro-economic determinants. Peter andPeter (2006) found significant impact of negative equity riskand loan-to-value ratio as drivers of default credit riskwhile study Australian State housing authorities with main aimto approximate the likelihood of credit default risk.

Likewise Fatemi & Fooladi, (2006) while studying practicesadopted for credit risk management by large US based financialinstitutions found single most vital underlying principle ofcredit risk models it to recognize default risk ofcounterparty. The pragmatic results points that superiorcapital adequacy ratio (CAR) appears to lessen the level ofproblem of non-performing loans. Kosmidou (2008) discuss thepositive relationship of operating efficiency with banksperformance because if the operating efficiency is high then

6

it gives the assurance of increment in profitability. Ramlall(2009) stated that there are two variables like operating riskand credit risk that effects business performance. Sayilgan &Yildirim, (2009) stated that high debtor turnover period andhigh real interest rates and rate of return on assets forbanks aggravate the banks to liquidate.

Abreu and Mendes (2002) evaluated the determinants of bank’sinterest margins and profitability for some Europeancountries. They find that well capitalized banks face lowerexpected bankruptcy costs and this benefit interprets intobetter profitability. Although with a negative mark in allregressions, the unemployment rate is relevant in explanationof bank’s profitability.

The term ‘operations risk’ have formally invented in 1991 bythe COSO report COSO, (1991).Wiseman and Catanach (1997)stated that organizations need to assemble agency and prospecttheories for modelling risk, and found them as both directlyassociated with choice of risk.Ray and Cashman (1999) reported that operational riskinfluence decision making in numerous ways, additionally riskassessment is considered necessary from both marketparticipant perspective and system perspective.While studying improvement of operation risk in British retailbanks Blacker, (2000) specified that mitigation of operationalrisk holds comprehensive sequences of connections amongprocess, technology and people. The study reportedresponsibility for operation risk alleviation lies withbusiness unit management, as restrictions were rested uponbusiness unit, which convinced them litigation of operationalrisk. Elliott et al. (2000) found operational risk as a constructionof organization and the scaffold in which operational riskoperates. Cornalba and Giudici (2004) found that banks arelooking to fuse both quantitative and qualitative datarequirements of advance measurement approach to measureoperational risk.

7

Power (2005) portrayed notice to the paradox and challenges ofoperational risk plan, as being part to broaden ‘enforcedself-regulation’ into the operations of banking. The studyestablished that Basel II banking regulations has successfullyinstitutionalized the type of operational risk and pressure inthree areas; i.e. data collection, definitional issues andextents of quantification, that represent the importance ofoperational risk. In addition, Flores, Ponte & Rodrıguez,(2006) emphasized on the use of information system (IS) andcondensed capacity to take up new methods and policies forconniving and scheming operational risk.Adward and altman (2001) a new approach built around amortality risk framework to measuring the risk and returns onloans and bonds is presented. This model is shown to offersome promise in analyzing the risk-return structures ofportfolios of credit-risk exposed debt instruments. JeremyBerkowitz James O’Brien (2002) evaluates the performance ofbanks trading models by examining the statistical accuracy ofVaR (Value-at-Risk) forecast model.Laviada (2007) stated that well-ordered structure ofoperational risk management will underpin and reinforceorganization’s internal controls. His study also emphasized tolabel internal audit for whole method of completion &executionfor organizing operational risk.

This study follows the previous studies, completes and differsfrom them in many aspects: First, this study seeks, as well tostudy the determinant factors of commercial banks to examinewhether the determinants differ in terms of statisticalsignificance. Second, this study differs from the previousstudies in terms of the time of the study and the variablesthat have been used in the study model and the studypopulation as it is.

3. Research Methodology:

8

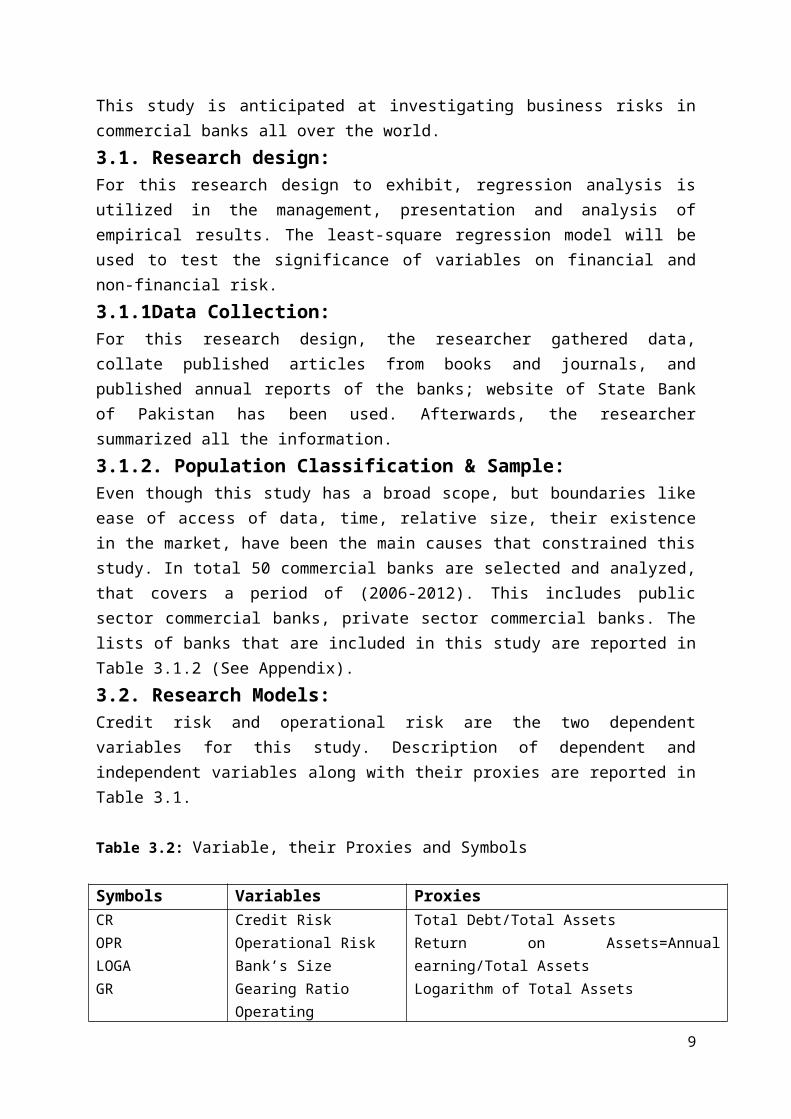

This study is anticipated at investigating business risks incommercial banks all over the world.3.1. Research design:For this research design to exhibit, regression analysis isutilized in the management, presentation and analysis ofempirical results. The least-square regression model will beused to test the significance of variables on financial andnon-financial risk.3.1.1Data Collection:For this research design, the researcher gathered data,collate published articles from books and journals, andpublished annual reports of the banks; website of State Bankof Pakistan has been used. Afterwards, the researchersummarized all the information.3.1.2. Population Classification & Sample:Even though this study has a broad scope, but boundaries likeease of access of data, time, relative size, their existencein the market, have been the main causes that constrained thisstudy. In total 50 commercial banks are selected and analyzed,that covers a period of (2006-2012). This includes publicsector commercial banks, private sector commercial banks. Thelists of banks that are included in this study are reported inTable 3.1.2 (See Appendix).3.2. Research Models:Credit risk and operational risk are the two dependentvariables for this study. Description of dependent andindependent variables along with their proxies are reported inTable 3.1.

Table 3.2: Variable, their Proxies and Symbols

Symbols Variables ProxiesCROPRLOGAGR

Credit RiskOperational RiskBank’s SizeGearing RatioOperating

Total Debt/Total AssetsReturn on Assets=Annualearning/Total AssetsLogarithm of Total Assets

9

OPELA

EfficiencyLiquid Assets

Total Debts/EquityTotal Operating Expenses/TotalAssetsTotal Loans/Total Deposits

Model (A): Financial RiskCR=β°+β1LOGA+β2GR+β3OE+β4LA+β5ℇ

Model (B): Non-Financial RiskOPR=β°+β1LOGA+β2GR+β3OE+β4LA+β5ℇ

3.3. Explanation of Variables:3.3.1. Credit RiskThis study will use debt-to-asset ratio as a proxy forevaluating credit risk as conferred by Athanasoglou, Brissimisand Delis (2008). This ratio explains how much the companyrelies on debt to finance its assets. This will be calculatedas debt capital by total assets. Barnhill, Papapanagiotou andSchumacher (2002) used debt to value ratio as root forassigning credit ratings. Bauer and Ryser (2004) stated debtratio as a significant boundary that strengthens bank’shedging options. 3.3.2. Operational RiskIn order to measure non-financial risk aspects, return onassets (ROA) will be employed as proxy for valuatingoperational risk. This ratio gives a scheme as to how well-organized organization is at using its assets to makeearnings. This will be designed by dividing a company's annualearnings by its total assets. Return on Assets (ROA) revealstangible operating presentation and recognized to havesignificant affect on operational losses. Bokpin and Isshaq(2009) used return on asset (ROA) as a proxy for measuringoverall’s firm’s earning ability. Gillet, Hubner and Plunus

10

(2010); Sensarma and Jayadev (2009); Siddiqui (2008) Finerreturn on asset (ROA) ratio will tell better skills totransform asset into net earnings which lead the way toenhanced risk management.3.3.3. Gearing RatioGearing ratio is a vital variable for the credit position.This will be measure by Debt to equity ratio, explains thecredit quality of an institution Barnhill, Papapanagiotou, &Schumacher, (2002). This variable will assign what portion ofequity and debt the banks are utilizing for its assetsfinancing.3.3.4. Bank SizeSize of the bank can be a momentous determinant of bank’sposition for the fact that it affects both the easily accessto liquidity and costs. This study will use Bank size asexplanatory variable and will use natural logarithm of totalassets as proxy for measuring bank size as used by Wiseman &Catanach;(1997)3.3.5. Operating EfficiencyThis study will measure operating efficiency of banks asindependent variable. Total operating expenses divided bytotal assets is used as proxy for measuring operatingefficiency Alexiou & Sofoklis, Sufian & Habiullah, Ramlall,(2009). This variable will explain how well a bank workout itsassets and liabilities internally in order to successfullymanage their risk dimensions.3.3.6. Liquid AssetsIn financial risk the element of liquidity of the banksconsidered most important factor of risk. In banks financialpractices, lending to other banks, institutions, individualsandCompanies from the deposits of assets side is routine practiceof banking operations. The banks earns major portion of theirincome from lending in the foam of interest. The empiricalevidence used this variable to measure the liquidity of banksby using ratio total loans to total deposits Spathis,Koasmidou, & Doumpos, (2002) ; Al-Tamimi, (2005).

11

4. Empirical Results:4.1. Descriptive & Correlation Statistics:Descriptive statistics are reported in table 4.1, which showsthe value of mean and standard deviation of all variableincluded in this study. Mean values give the idea about thecentral tendency of the values of the variables included inthis study, whereas values for standard deviation measure, putin the picture about the deviation or dispersion of the datain the sample. The first two variables i.e. credit risk andoperational risk is considered as dependent variables, whilethe rest of them are independent variables.Table: I Descriptive Statistics

Mean Std.DevCR 2.635

14.280 OPR 0.305 1.6156

LOGA 6.8011.4258

GR 35.500171.18

OPE 0.0910.4112

LA 1.7185.1731

On average, banks in our sample have a mean and standarddeviation of credit risk as 2.63 and 14.280 respectively. Andthe operational risk as 0.30 and 1.61 respectively. The credit

12

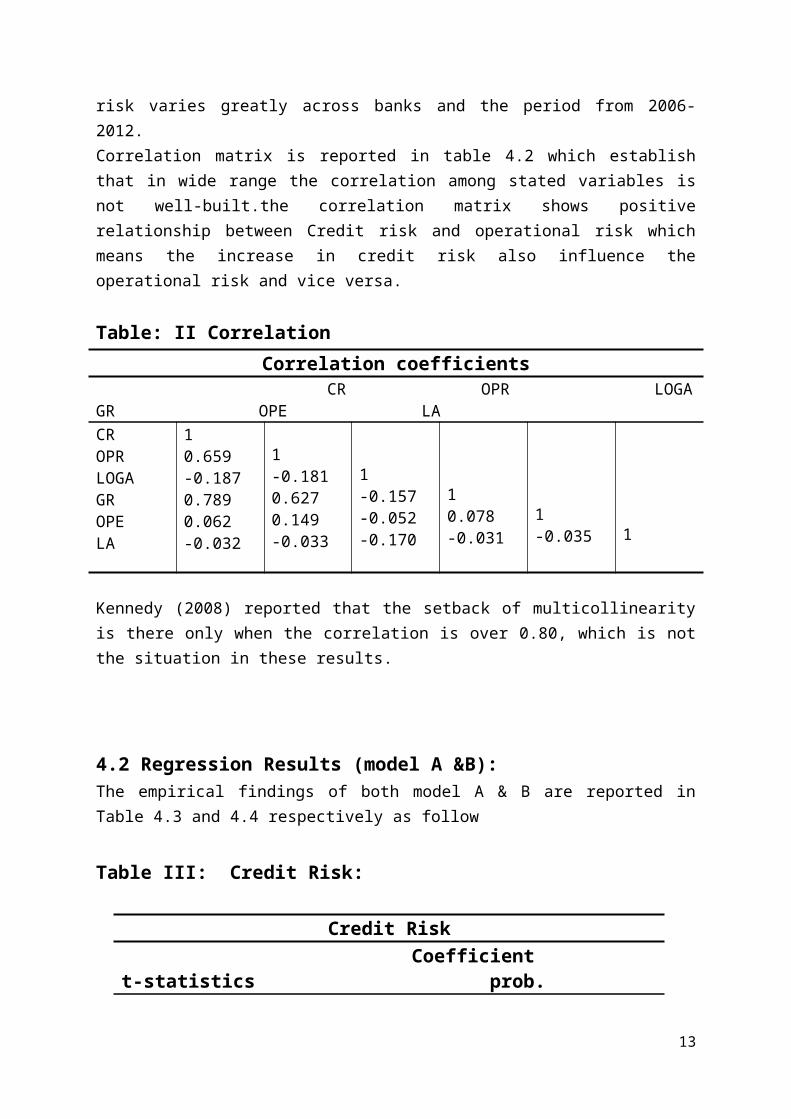

risk varies greatly across banks and the period from 2006-2012.Correlation matrix is reported in table 4.2 which establishthat in wide range the correlation among stated variables isnot well-built.the correlation matrix shows positiverelationship between Credit risk and operational risk whichmeans the increase in credit risk also influence theoperational risk and vice versa.

Table: II CorrelationCorrelation coefficients

CR OPR LOGAGR OPE LACROPRLOGAGROPELA

10.659-0.1870.7890.062-0.032

1-0.1810.6270.149-0.033

1-0.157-0.052-0.170

10.078-0.031

1-0.035 1

Kennedy (2008) reported that the setback of multicollinearityis there only when the correlation is over 0.80, which is notthe situation in these results.

4.2 Regression Results (model A &B):The empirical findings of both model A & B are reported inTable 4.3 and 4.4 respectively as follow

Table III: Credit Risk:

Credit Risk Coefficient t-statistics prob.

13

Constant 2.1483.802 0.0002 LOGA 0.3424.330 0.000GR 0.082126.47 0.000OPE -0.575-2.153 0.032LA -0.021-0.973 0.331R-squared 0.9797F-statistics 4177.152probability 0.0000

Table IV: Operational Risk:

Dependent variable: Operational Risk Coefficient t-statistics Prob. Constant 0.7362.132 0.036LOGA 0.0951.983 0.048GR 0.00514.419 0.000OPE 0.3792.328 0.020LA -0.007-0.583 0.560R-squared 0.411F-statistics 60.14Probability 0.000

The major financial risk of a banking business is credit riskSackett & Shaffer, (2006). The banks specific factors canenhance probability of credit risk at higher side. The centralnon-financial risk in a banking business is operational riskwhich measures the effective implementation of internal

14

control systems. The bank size influences the credit risk andoperational risk positively. These findings cannot besupported with the findings of (Wiseman & Catanach, (1997);Esty, (1998); How, Karim & Verhoeven, (2005); Jacobson, Linde& Roszbach, (2006); Demirovic & Thomas, (2007); Ashraf,Altunbas & Goddard, (2007); Dinger, (2009); Akhtar, Ali, &Sadaqat, (2011); Ali, Akhtar, & Ahmed, (2011)). Because largerbanks enjoy a higher return that’s the reason their risk wouldbe higher.

In debt financing it is important for banks to maintain theirgearing ratios at sufficient level. But their futurerequirements would be changed accordingly to the financialneeds of the time. The gearing ratio found to be significantpositive relationship with credit risk and operational riskaccordingly as suggested by Sensarma & jayadey, (2009). Theoperating efficiency basically measures the minimumutilization of resources which gives the maximum returns. Therelationship of operating efficiency with credit risk isnegative and operating risk is positive. The liquidity is adistinct perspective of risk management, but its effect onfinancial and non-financial risks measured in form of liquidassets. The liquid assets founds o be a negative relationshipwith credit risk and operating risk, whereas it affects theboth business risks significantly and in significantly.Spathis, Koasmidou and Doumpos (2002) stated the positiverelationship the ratio of total loans over total depositregarding the profitability of banks which means that thebanks whose credit worthiness is greater, are more liquid butit can also affect insignificantly.

5. Summary and concluding remarks:The importance of study to overcome the slit of empiricalevidence on business risk practices in banking sector ofPakistan. This study implied the financial and non-financialrisk practices for all commercial banks all over the world.This study covered the period of (2006-2012). The financial

15

risk is measured with the credit worthiness of the banks andthe nonfinancial risk is measure with the efficiency andeffectiveness of banks’ operational activities. This study hassuccessfully identified the factors that are significantlyaffecting financial and non-financial risk faced by the banks.

The relationship of bank size is found to have positive andsignificant relation with financialand non-financial risk. The operating efficiency establishedthe negative and significant relationship with credit risk.This can be explained with the fact that the extraordinarylending of loans and constant expenses is found to be themajor portion of non financial risk faced by the banks. Liquidasset is found to have a negative relationship with bothfinancial and non-financial risk, whereas its affect on creditand operational risk is significant and insignificantrespectively. The gearing ratio insignificantly affected bythe credit risk. The high geared ratio is attributed with thefact that the banks rely on the borrowing because their majorsource of finance contains debt financing with the combinationof equity finance. Finally, this study does not establish theaffect of other risk that is faced by the banking industrysuch as foreign exchange risk and market risk. This remains anaim of future research.

References:1. Akhtar, M. F., Ali, K., & Sadaqat, S. (2011). "Liquidity

Risk Management: A comparative study between Conventionaland Islamic Banks of Pakistan", Interdisciplinary Journal ofResearch in Business, 1 (1), 35-44. 158 Middle Eastern Financeand Economics - Issue 11 (2011)

2. Ali, K., Akhtar, M. F., & Ahmed, P. H. (2011). "Bank-Specific and Macroeconomic Indicators”, InternationalJournal of Business and Social Science, 2 (6), 235-242.

3. Athanasoglou, P. P., Brissimis, S. N., & Delis, M. D.(2008). "Bank-specific, industry-specific and macroeconomicdeterminants of bank profitability", Journal of

16

International Financial Markets Institutions and Money, 121–136.

4. Alexiou, C., & Sofoklis, V. (2009). “Determinants of BankProfitability: Evidence from the Greek Banking Sector”,Economic Annals, LIV No. 182, 93-118.

5. Al-Tamimi, H. A. (2005). “The Determinants of the UAECommercial Banks’ Performance: A Comparison of the Nationaland Foreign Banks”, Journal of Transnational Management, 10(4), 35 — 47.

6. Al-Tamimi, H. A., & Al-Mazrooei, F. M. (2007). "Banks’ riskmanagement: a comparison study of UAE national and foreignbanks", The Journal of Risk Finance, 8 (4), 394-409.

7. Barnhill, T. M., Papapanagiotou, J. P., & Schumacher, L.(2002). "Measuring Integrated Market and Credit Risk in BankPortfolios: An Application to a Set of Hypothetical”.

8. Barry, P. J., Baker, C. B., & Sanint, L. R. (1981)."Farmers'Credit Risks and Liquidity Management", American Journal ofAgricultural Economics, 63 (2), 216-227.

9. Bauer, W., & Ryser, M. (2004). "Risk management strategiesfor banks", Journal of Banking & Finance, 28, 331–352.

10. Blacker, K. (2000)."Mitigating Operational Risk inBritish Retail Banks", Risk Management, 2 (3), 23-33.

11. Boudriga, A., Taktak, N. B., &Jellouli, S. (2009)."Banking supervision and nonperforming loans: a cross-country analysis", 1 (4), 286-318.

12. Brown, C. A., & Wang, S. (2002). “Credit risks the caseof First Interstate Bank corp.”, International Review ofFinancial Analysis, 11, 229–248.

13. Cornalba, C., & Giudici, P. (2004). "Statistical modelsfor operational risk management", Physica , A (338), 166 –172.

14. Deakins, D., & Hussain, G. (1994)."Risk Assessment withAsymmetric Information", International Journal of BankMarketing, 12 (1), 24-31.

17

15. Demirovic, A., & Thomasn, D. C. (2007)."The Relevance ofAccounting Data in the Measurement of Credit Risk", theEuropean Journal of Finance, 13 (3), 253–268.

16. Dinger, V. (2009). "Do foreign-owned banks affect bankingsystem liquidity risk?” Journal of Comparative Economics,37, 647–657.

17. Esty, B. C. (1998). "The impact of contingent liabilityon commercial bank risk taking", Journal of FinancialEconomics, 47, 189-218.

18. Elliott, D., Letza, S., McGuinness, M., & Smallman, C.(2000). "Governance, Control and Operational Risk: TheTurnbull Effect", Risk Management, 2 (3), 47-59.

19. Fatemi, A., & Fooladi, I. (2006). "Credit riskmanagement: a survey of practices", Managerial Finance, 32(3), 227-233.

20. Frame, J. D. (2003), “Managing risk in organizations: Aguide for managers”, Jossey-Bass, San Francisco.

21. Flores, F., Ponte, E. B., & Rodrıguez, T. E. (2006)."Operational risk information system: a challenge for thebanking sector", Journal of Financial Regulation andCompliance, 14 (4), 383-401.

22. Gillet, R., Hubner, G., & Plunus, S. (2010)."Operational risk and reputation in the financial industry",Journal of Banking & Finance, 34, 224–235.

23. Ashraf, D, Altunbas, Y., & Goddard, J. (2007). "WhoTransfers Credit Risk? Determinants of the Use of CreditDerivatives by Large US Banks", The European Journal ofFinance, 13 (5), 483 500. Middle Eastern Finance and Economics - Issue11 (2011) 159

24. How, J. C., Karim, M. A., & Verhoeven, P. (2005)."Islamic Financing and Bank Risks: The Case of Malaysia",Thunderbird International Business Review, 47 (1), 75–94.

25. Isshaq, Z., & Bokpin, G. A. (2009). "Corporate liquiditymanagement of listed firms in Ghana", 1 (12), 189-198.

26. Jacobson, T. J., Linde, J., & Roszbach, K. (2006)."Internal ratings systems, implied credit risk and the

18

consistency of banks’ risk classification policies”, Journalof Banking & Finance, 30, 1899–1926.

27. Jobst, A. A. (2007). "It’s all in the data – consistentoperational risk measurement and regulation", Journal ofFinancial Regulation and Compliance, 15 (4), 423-449.

28. Kahane, L. H. (2001).” Regression Basics”, New Delhi:Sage Publications India Pvt. Ltd.

29. Koutsoyiannis, A. (2003). “Theory of Econometrics NewYork: Palgrave (Second Edition)”.

30. Laviada, A. F. (2007). "Internal audit function role inoperational risk management", Journal of FinancialRegulation and Compliance, 15 (2), 143-155.

31. Peter, V., & Peter, R. (2006). "Risk Management Model:an Empirical Assessment of the Risk of Default",International Research Journal of Finance and Economics (1),42-56.

32. Power, M. (2005). "The invention of operational risk,Review of International Political Economy”, 12 (4), 577–599.

33. Ramlall, I. (2009). “Bank-Specific, Industry-Specific andMacroeconomic Determinants of Profitability in TaiwaneseBanking System: Under Panel Data Estimation”, InternationalResearch Journal of Finance and Economics (34), 160-167.

34. Ray, D., & Cashman, E. (1999). "Operational risks,bidding strategies and information policies in restructuredpower markets", Decision Support Systems, 24, 175–182.

35. Sackett, M. M., & Shaffer, S. (2006). "Substitutesversus complements among credit risk management tools",Applied Financial Economics, 16, 1007–1017.

36. Sadaqat, M. S., Akhtar, M. F., & Ali, K. (2011). "AnAnalysis on the Performance of IPO – A Study on the KarachiStock Exchange of Pakistan", International Journal ofBusiness and Social Science, 2 (6), 275-285.

37. Spathis, C., Koasmidou, K., & Doumpos, M. (2002).“Assessing Profitability Factors in the Greek BankingSystem: A multi criteria methodology”, InternationalTransactions in Operational Research, 517-530.

19

38. Sensarma, R., & Jayadev, M. (2009). "Are bank stockssensitive to risk management?" The Journal of Risk Finance,10 (1), 7-22.

39. Siddiqui, A. (2008). "Financial contracts, risk andperformance of Islamic banking Managerial Finance”, 34 (10),680-694.

40. Sufian, F. (2009). “Determinants of Bank Profitabilityin a Developing Economy: Empirical Evidence from the ChinaBanking Sector”, Journal of Asia-Pacific Business, 10, 281-307.

41. Wiseman, R. M., & Catanach, A. H. (1997). "Alongitudinal disaggregation of operational risk underchanging regulations: evidence from the savings and loanindustry", The Academy of Management Journal, 40 (4), 799-830.

42. Bashir A. (2000). “Assessing the Performance of IslamicBanks: Some Evidence from the Middle East”, Paper presentedat the ERF 8th meeting in Jordan.

43. Ramlall, I. (2009). “Bank-Specific, Industry-Specific andMacroeconomic, Determinants of Profitability in TaiwaneseBanking System: Under Panel Data Estimation”, InternationalResearch Journal of Finance and Economics, Issue 34 (2009),pp: 160-167.

44. Abreu M. and V. Mendes. (2002). “Commercial bank interestmargins and profitability: Evidence from E.U countries”,Porto Working paper 1.series. Available at:http://www.iefs.org.uk/Papers/Abreu.pdf

45. Barajas, A., Steiner, R. & Salazar, N. (1999). “InterestSpreads in Banking in Colombia 1974-96. IMF Staff Papers”.

46. Asma Idris, Fadli Asari, and Noor Taufik, (2011),“Determinant of Islamic Banking Institutions’ profitabilityin Malaysia”, Word Applied Sciences Journal 12: 01-07-2011,ISSN 1818-4952.

47. Muhammad Ashraf, (2012); “Bank-specific andmacroeconomic profitability determinants of Islamic banksThe case of different countries”, Qualitative Research inFinancial Markets; Vol. 4 No. 2/3, 2012; pp. 255-268.

20

Appendix:List of banks included in this study:

Sr.# Countries Name of Banks1 India Abu Dhabi Commercial

Bank2 Corporation Bank3 City union Bank4 Corporate bank of

India5 Dena Bank of India6 HDFC bank7 ICICI Bank8 India Overseas Bank9 Ireland Bank of Ireland10 Armenia ARM Swiss Bank11 Pakistan Allied Bank12 Habib Bank Ltd13 Al-Habib Bank14 Alfalah Bank15 Faisal Bank16 National Bank of

Pakistan17 JS Bank18 KASB Bank19 NIB Bank20 Silk Bank21 Soneri Bank22 MCB Bank23 United Bank24 Askari Bank25 Canada Bank of Montreal26 Toronto dominion Bank27 Royal Bank28 China China Merchants Bank29 U.K HSBC Bank30 Royal bank of Scotland31 Japan Post Bank32 Higo Bank 33 Joyo Bank

21

34 Germany Aareal Bank35 Commerz Bank36 Srilanka Cylon Bank37 Hatton National Bank38 Mexico Deutsch Bank39 ING Bank40 U.S Bank of America41 Citi Bank 42 City National Bank43 Sun Trust Bank44 Standard chartered

Bank45 Sweden Nordea Bank46 South

AfricaFirst national Bank

47 Newziland ABS Bank48 Russia Alfa Bank49 Bank of Moscow50 Deniz Bank

22