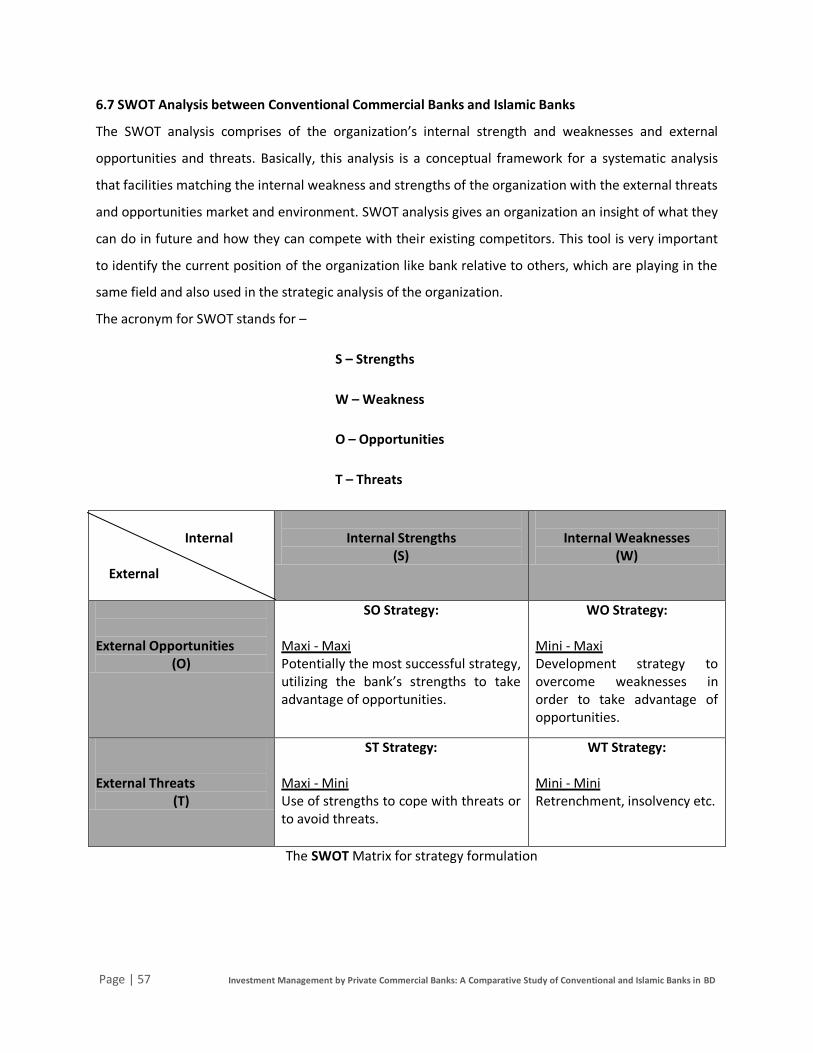

Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic...

65

Page | 1 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD CHAPTER ONE INTRODUCTION

-

Upload

independent -

Category

Documents

-

view

3 -

download

0

Transcript of Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic...

Page | 1 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

CHAPTER ONE INTRODUCTION

Page | 2 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

1.1 Preamble:

Banks are financial institutions engaged in boosting national savings and capital formation as well as

constitutes infrastructure through financing of various development projects. In performing multi-

dimensional activities like borrowing and lending of money, drawing, collecting and discounting bills,

transferring fund, safe deposit, vault/locker service, foreign exchange transaction etc. The world of

banking is undergoing a transformation. Banking today has evolved into a highly competitive and

sophisticated business in which technology increasingly provides the edge. Today’s customers want

service and information to be provided at all times and places.

After 1983, in our country, there were two types of banks: nationalized and private banks. With the

passage of time, second generation and third generation private banks were established. In the last

decade, promoters tried to upgrade the banking system mainly from the manual system with the

technology-based system. As Bangladesh is one of the largest Muslim countries in the world, the people

of this country are deeply committed to Islamic way of life as enshrined in the Holy Qur'an and the

Sunnah. Naturally, it remains a deep cry in their hearts to fashion and design their economic lives in

accordance with the precepts of Islam.

1.2 Origin of the Report:

Each professional degree needs practical knowledge of the respective field of discipline to be fruitful.

The BBA program in University of Dhaka (DU) also has an internship program so that the students can

apply their theoretical knowledge into real life’s practical situation.

This internship report has been prepared towards the execution of the partial requirement of the BBA

program as authorized by the Department of Banking and Insurance, University of Dhaka. This proposed

report has been done for Comparative investment analysis between conventional commercial banks and

Islamic Bank of Bangladesh In addition, the report would be submitted to Mr. M. Muzahidul Islam,

Supervisor, Professor, Department of Banking and Insurance, University of Dhaka. In this report I have

tried to see the things what are being done in the foreign exchange department of the assigned branch.

I have also tried to present my personal observations from each department of this branch. I had an

opportunity to be acquainted with the practical banking prevailing in Dhanmondi branch of southeast

Bank Limited. The knowledge, which has been acquired in my Internship Period, I have tried my level

best to show in this report.

Page | 3 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

1.3 Objective:

The general objective of the report was to complete the internship, as per requirement of BBA program

of University of Dhaka, one student need to work in a business organization for three months to acquire

practical knowledge about real business operation.

1.3.1 The broad objectives:

To appraise the investment activities of Dhanmondi branch of southeast Bank Limited.

Comparative analysis investment activities between the conventional commercial banks and

Islamic Banks of Bangladesh.

1.3.2 The specific objectives:

To identify the investment operation.

To evaluate the area investment of conventional commercial banks.

To evaluate the area investment of Islamic Banks.

Basic differences of investment modes between these two type of investment.

To analyze the data of previous five years.

To assess the position of the different banks

To gather the practical experience

To know the present investment portfolio of the commercial banks and Islamic Banks

To explore the strength and weakness of the commercial banks and Islamic Banks

To explore the default probability of different banks

To find out problems that faced by the banks in making investment in a more effective

manner

To suggest some common probable solution of problems those are faced by the banks

1.4 Methodology of the report:

For smooth and accurate study everyone has to follow some rules & regulations to collect for

developing the methodology of the report. In my report, I have gathered information by working with

the employees of Southeast Bank Ltd as an intern for three months. I will also manage to gather

information of other Banks’ through Internet and different journals of Bangladesh bank.

Page | 4 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

1.5 Sources of data collection:

For preparing the report I have collected data both from primary and secondary sources of data. And

both data source are equally important for research purpose and preparation of the report.

1.5.1 Primary sources:

Practical desk work

Face to face conversation with the officer

Direct observations

1.5.2 Secondary sources :

Annual reports of related banks.

Files & Folders

Memos & Circulars

Various publications on Banks,

Different circulars sent by Head Office and Bangladesh Bank

Website of the banks

Different news paper, journals and magazines

1.6 Methods of Data Analysis

Both qualitative and quantitative approaches have been used to analyze data. The techniques used to

analyzed data are as follows –

Tabular Analysis

Graphical Analysis

Trend Analysis

Index Analysis

Comparisons

Multiple Regression Analysis

SWOT Analysis

Page | 5 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

1.7 Scope of the Report:

The report covers comparative the investment operation of conventional commercial banks and Islamic

Banks of Bangladesh. The information has been collected from the personnel contact with different

designated officials who are very helpful and gracious as well as sincere that they helped me in all

working arena and from different journals of Bangladesh Bank. The area of concentration of this report

is about the analysis of the investment of the banks and tries to present theoretical analysis and

graphical analysis. In this topic there is a huge opportunity of using important tools of statistics to

evaluate the current scenario and the future prospects of investments for conventional private

commercial banks and Islamic Banks of Bangladesh. The most important one is that my honorable

teachers have increased their gracious helping hand to me to prepare this report.

1.8 Limitations:

The main limitation here is as an internee I could not share all the information every time for the

organization internal security. There are some other limitations these limitations are as follows:

The study was limited only to the investment activities of the banks.

Another Problem was time constraints. The duration of my internship Program was only three

months. But this allocated time is not enough for a complete and fruitful study.

The Bank was a busy one having heavy rush of people, whom officers need to deal with. So

allocation of time for an internee is very much difficult for the officers of the bank.

I was not assigned for a specific task in each day. So I was not able to understand banking

activities deeply.

Bank is a sophisticate business sector. So bank do not interested to provide me confidential

data. As a result in my report there is a confidential data limitation.

A data insufficiency limitation is the main constraint in the development of the report.

Page | 6 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

1.9 Activity Schedule:

Week

1

Week

2

Week

3

Week

4

Week

5

Week

6

Week

7

Week

8

Selection &

Acceptance Of

Internship

Orientation Of

The Program

Training For

Internship

Collection Of

Data

Compiling &

Analysis Of

Data

Submission Of

Final Report

Page | 7 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

CHAPTER TWO

ECONOMIC OVERVIEW OF BANGLADESH

Page | 8 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

2.1 Present Scenario of Bangladesh Economy

Bangladesh is a developing and emerging country. Now our country has created a very strong and

important position in the map of world in case of economy, democracy, culture, education, sports and

other achievement after a long critical time passed. But at the very starting time the country were not in

such position. At this time the country flew the socialism as the economic ideology with a dominant role

for the public sector. But, gradually the country tends to go through the open market economy system

and privatization in case of several industries excepting some critical and important sectors. Since the

mid-seventies, it undertook a major restructuring towards establishing a market economy with

emphasis on private sector-led economic growth. Since the 1990, the country has been achieving a great

progress to stabilize in economics and political situation that has reduced inflation as well as fiscal and

current account deficits and established a healthy foreign exchange reserve position with little current

liability. In every sectors Bangladesh makes a better development. Especially the large progress has been

occurred in health, education and poverty reduction sectors.

Bangladesh is now focusing on industrial economy so a lot of new jobs are constantly being created.

Many women are finding employment within the textiles market making clothing. In the Bangladesh

economy, textiles are the number one export. Textile mills create knit clothing and ready-made items

that are worn across the globe.

Today Bangladesh is the second highest producer and exporter of readymade garments manufacturing

products in the world. Bangladesh gains the most of the foreign currency from this sector. And it is a

very hopeful matter that there is a great possibility to take the top position within a few years. Many

new jobs mostly for women have been created by the country's dynamic private ready-made garment

industry, which grew at double-digit rates through most of the 1990s. By the late 1990s, about 1.5

million people, mostly women, were employed in the garments sector as well as Leather products

specially Footwear (Shoe manufacturing unit). During 2001-2002, export earnings from ready-made

garments reached $3,125 million, representing 52% of Bangladesh's total exports. Bangladesh has

overtaken India in apparel exports in 2009, its exports stood at 2.66 billion US dollar, ahead of India's

2.27 billion US dollar. Bangladesh's textile industry, which includes knitwear and ready-made garments

along with specialized textile products, is the nation's number one export earner, accounting for 80% of

Bangladesh's exports of $15.56 billion in 2009. Bangladesh is 2nd in world textile exports behind China

which exported $120.1 billion worth of textiles in 2009. The industry employs nearly 3.5 million workers.

Page | 9 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

Other industries which have shown very strong growth include the Chemical industry, steel industry,

mining industry and the paper and pulp industry.

Bangladesh is the top producer and exporter of jute and jute manufacturing products in the world.

Country gets a very large amount of foreign currency by exporting several items of jute products.

The Bangladesh economy also focuses strongly on agriculture in order to feed an ever-growing

population. A majority of the residents of the country have agricultural jobs. Sustenance farming is not

uncommon among the lower economic classes. The primary crops are jute and rice. In fact, the country

is one of the top four rice producers in the world. Grain is also being successfully produced in

Bangladesh. Now Bangladesh is self-sufficient in producing rice which is necessary to meet our national

demand although more than half of GDP is generated through the service sectors, nearly two thirds of

Bangladeshis are employed in the agriculture sector, with rice as the single most important product. And

in case of medicine industry Bangladesh has created a very strong position in the world. Now

Bangladesh earns huge foreign currency by exporting medicines more than 60 countries. Tea, leather

and handicraft are also major exportable commodities of Bangladesh. Another source of earning foreign

currency is frozen food which is exported in different countries in the world.

That is why the economy of Bangladesh has grown 5% - 6.5% per year despite some problems such as

political instability, poor infrastructure, corruption, insufficient power supplies and slow implantation of

economic reforms. Bangladesh’s growth was resilient during the 2008-2009 global financial crises and

recession less than other developed countries in the world.

GDP data 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12

GDP (tk) 4,724.77 5,458.22 6,147.95 6,943.20 7875.00 9147.84

GNI (tk) 5,077.52 5,942.12 6,706.96 7,589.28 8528.22 10047.23

Per capita GDP (tk) 33607 38330 42628 47536 53236 60350

Per capita GNI (tk) 36116 41728 46504 51959 57652 66283

Per capita GDP (in US$)

487 559 620 687 755 772

Per capita GNI (in US$) 523 608 676 751 818 848

Table –1: Present Scenario of Bangladesh economy

Page | 10 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

Table -2: GDP of BD

Table -3: Economic Trend

2.2 Structure of the Financial System in Bangladesh

The present structure of the financial system in Bangladesh comprises various types of banks, insurance

companies and non bank financial institutions in the formal sector. There are many financial institution

which are meeting financial needs by providing necessary money and advises to every classes of people

by a number of branches though the country and also in abroad. In Bangladesh banking sector is a very

emerging sector in financial industry. Banks are establishing many numbers of branches at increasing

rate in every corner of the country. We also inherited some financial institutions from the birth of our

country. These are non-formal financial structure comprising money lenders, merchants’ bullion traders

and indigenous bankers engaged in rudimentary forms of banking. They are still an important

component of the financial of our country. Now in our Bangladesh there are 47 banks and many

insurance and nonfinancial institutions, most of these are city concentrated.

In addition to these modern and old institutions many new types of financial institutions have also been

added during the last three decades. As a result, the financial structure as we find today is to an extent

different from those of the past. A fair idea about the financial structure may be formed if we classify

the financial institutions in the formal sector. But such classification is beset with problems because rigid

classification often becomes unrealistic. Generally financial institutions in Bangladesh may broadly be

classified as under:

year 2007 2008 2009 2010 2011

GDP 6.2% 5.8% 5.7% 6.7% 6.9%

Fiscal Year Total Export

(in Billion)

Total Import

(in Billion)

Foreign Remittance

Earnings

(in Billion)

2007-2008 $ 14.11 $ 25.205 $ 8.90

2008-2009 $ 15.56 $ 22.00 $ 9.68

2009-2010 $ 17.6 $ 23.74 $ 10.87

2010-2011 $18.81 $25.31 $11.91

Page | 11 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

2.3 Types of Financial Institutions

Among the eight types of financial institutions which are following except bank, all other 7 types of

companies are nonbanking financial institutions (NBFIs). These are governed and operated under a

special and separate law, rules and regulations. But among these banks are the leaders to supply money

in the economy. They act heart of financial system of Bangladesh. To control and regulate the banking

system there is a separate banking company act 1991in Bangladesh. However, among all of them, banks

are by far the largest components of the financial structure of the country.

1. Banks

2. Insurance Companies

3. Investment and Finance Companies

4. Leasing Companies

5. Merchant Banking Companies

6. Co-operative Banks

7. House Building Finance Companies

8. Stock Exchanges

2.4 Banking History of Bangladesh

Bangladesh inherited its banking structure from the British regime and had 49 banks and other financial

institutions before the Partition of India in 1947. But Pakistanis owned most of these banks. In the

beginning of 1971, there were 1130 branches of 12 banks in operation in Bangladesh. The foundation of

independent banking system in Bangladesh was laid through the establishment of the Bangladesh Bank

in 1972 by the Presidential Order No. 127of 1972 (which took effect on 16th December, 1971). Through

the Order, the eastern branch of the former State Bank of Pakistan at Dhaka was renamed as the

Bangladesh Bank as a full-fledged office of the central bank of Bangladesh and the entire undertaking of

the State Bank of Pakistan in, and in relation to Bangladesh has been delivered to the Bank. Bangladesh

Bank has been entrusted with all of the traditional central banking functions including the sole

responsibilities of issuing currency, Keeping the reserves, formulating and managing the monetary and

credit policy, regulating the banking system, stabilizing domestic and external monetary value,

Page | 12 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

preserving the par value of Bangladesh Taka, fostering economic growth and development and the

development of the country’s market. The Bangladesh Banks (Nationalization) Order enacted in 1972

nationalized all banks except foreign ones. Six nationalized banks were formed through merging the

existing banks of the period. The rate of growth and development of banking sector in the country was

extremely slow until 1982 when the government allowed to establish private banks and started

denationalization process: initially, the Uttara Bank in the same year and thereafter, the Pubali Bank,

and the Rupali Bank in 1986. Economic history shows that development has started everywhere with the

banking system and its contribution towards financial development of a country is the highest in the

initial stage. Modern banking system plays a vital role for a nation’s economic development. Over the

last few years the banking world has been undergoing a lot of changes due to deregulation,

technological innovations, globalization etc. These changes in the banking system also brought

revolutionary changes in a country’s economy. Present world is changing rapidly to face the challenge of

competitive free market economy. It is well recognized that there is an urgent need for better, qualified

management and better-trained staff in the dynamic global financial market.

2.5 Current Banking Scenario in Bangladesh

Table -4: Total banks in BD

Nationalized Commercial Banks (NCBs)

1. Sonali Bank

2. Janata Bank

3. Agrani Bank

4. Rupali Bank

Total number of Scheduled banks 47 Banks

State-owned Commercial Banks 4 Banks

Local private commercial banks 30 Banks

Foreign banks 9 Banks

Specialized Banks 4 Banks

Page | 13 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

Foreign Banks

1.HSBC 6.Woori Bank

2.Standard Chartered Bank 7.Bank of Alfala

3.City Bank NA 8. National Bank of Pakistan

4. Bank of Cylon 9.State Bank of India

5.Habib Bank

Local Private Commercial Banks (PCBs)

A. Conventional Private commercial Banks

1. Pubali Bank 2. Mercantile Bank

3. Uttara Bank 4. Dutch Bangla Bank

5. National Bank 6. Dhaka Bank

7. City Bank 8. 0ne Bank

9. united Commercial Bank 10. Standard Bank

11. Arab Bangladesh Bank 12. Bangladesh Commerce Bank Ltd.

13. IFIC Bank 14. Mutual Trust Bank

15. Al Baraka Bank 16. EXIM Bank

17. Trust Bank 18. Social Investment Bank

19. Eastern Bank 20. Premier Bank

21. National Credit & Commerce Bank ltd. 22. Bank Asia

23. Prime Bank 24. Southeast Bank

B. Islamic Banks

1. Islamic Bank Bangladesh Ltd. 2. Social Islami Bank Ltd.

3. ICB Islami Bank Ltd. 4. Shahjalal Islami Bank Ltd.

5. Al – Arafah Islami Bank Ltd. 6. First Security Islami Bank Ltd

Page | 14 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

Development Banks

1.Bangladesh Krishi Bank

2.Rajshahi Krishi Unnayan Bank

3.BDBL

4.BASIC Bank

Without these new more banks are up coming in market to operate the activities. In very soon they will

start their functions. Already they have their registration and license to introduce their functions. We

hope that they will help and contribute in growth the national economy. My topic is concerned with

investment analysis of 30 commercial Banks and 6 Islamic Banks.

Page | 15 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

CHAPTER THREE

CONVENTIONAL BANKS Vs. ISLAMIC BANKS

Page | 16 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

3.1 Differences between a conventional commercial bank and a Islamic Bank:

Many still do not understand the differences between the products and services offered by Islamic banking and conventional banking. Many are still saying that Islamic products and services are just conventional products that have been window dressed. Some even claim that Islamic banking only changes the terms such as ‘interest’ into profit rate, ‘Ujr or wage cost, and other Arabic terms are viewed by critics as tricks. These general statements should not be made without knowing exactly how an Islamic bank operates, as such statements will inhibit the revival and development of the Islamic banking industry. We do acknowledge that there are problems in the implementation process and other problems in Islamic banking. However, in my opinion, it is normal to experience difficulty before achieving success.

All parties, whether Syariah scholars, lawyers, judges, customers or the Islamic bank administration, are still in the learning process. It is undeniable that mistakes will occur here and there throughout this process. Islamic banking is still in the process of maturity and achieving perfection. Thus, deficiencies will occur throughout this journey. Yet, these deficiencies do not make Islamic banking haram and invalid. Just like a new Muslim who has yet to perform the five daily solah (prayers) as he is in the process of learning and understanding it, this falls under the forgivable category. What really matters is that the process is heading forward (i.e. improving) and not falling backwards.

Some of the deficiencies are due to lack of knowledge amongst the administration. Consequently, people may get an inaccurate perception of Islamic banking. The Syariah strength and observance of an Islamic bank depend strongly on the hard work of various parties, inside and outside the bank. The people who determine that Syariah compliancy is adhered to are the Chief Executive Officer (CEO), the Product Development Department, the Syariah Advisor and the Syariah Department of the bank. They are responsible for Syariah compliancy within the bank.

Without hard work and wisdom, an Islamic bank or Islamic banking will take the easy route and just copy the products and systems of conventional banking, without observing the implementation aspect of the Sariah. Society should clearly understand that the Islamic banking system has revolutionized the relationship between the customer/saver and the bank. The relationship between the customer and a conventional bank is through the loan contract that entails interest on the principal. The borrower must pay the bank within the stipulated period.

Islamic banks have changed the borrowing relationship to various concepts that are acknowledged in Islam such as partnership (Musharakahor Mudharabah), or seller (bank) and buyer/renter (customer). Changes in the relationship are not only with the ‘aqad or contract, even asset ownership has changed and is accepted by Malaysian law. This means, from the legal point of view, the trading or renting process does take place. However, many customers of Islamic banks do not recognise the efforts of Islamic banks in making changes as they do not read the contracts they sign.

The partnership principle in the finance products also offers customers profit sharing with the bank. However, if the customer faces a loss, the Islamic bank will bear part of it based on this contract. A banking system devoid of riba fulfills the needs of both customers and the general public. Islamic

Page | 17 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

banking, through the introduction of Islamic concepts, has successfully generated large profits in the business it participates.

Nevertheless, the main concern of Islamic banking is to ensure that every bit of its business process is Sariah compliant and this is more meaningful than reaping more profit. This main concern is a commitment, responsibility and preservation of the trust granted by Allah s.w.t. to human beings, which emphasizes the principle of cooperation amongst humans in fulfilling each respective need. Everyone should resist from comparing the application and productsof an Islamic bank and that of a conventional bank. The “apple to apple” comparison is not fair in this case; it is like comparing the rules and discipline of soccer and hockey. Although both games are played on the field, they have completely different concepts and disciplines.

The differences are as follows :

Conventional Banking

Differences Islamic Banking

Its functions and operations

are based fully on man-made

principles.

FUNCTIONS & OPERATIONS

Its functions and operations follow the Qur’an and the Sunnah as much as possible.

In its investment product, the

investor is promised a fixed

rate. In reality, it is a riba based

loan activity.

INVESTMENT PRODUCTS

In its investment product, an Islamic bank promotes the sharing of risk and

profit between investor and investment fund manager. There is no fixed profit

promised. Division of profit is based on real profit.

Aiming for profit without

religious or moral boundaries.

AIM Aiming for profit that adheres to Islamic discipline that is limited to that which benefit society.

Ignores zakat. ZAKAT Pays zakat as it is a social responsibility fulfilled by Islamic banks.

Page | 18 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

The retail loan product applies the system of giving out loans with multiplied interest.

RETAIL LOAN Its retail product utilizes the trading or renting of an asset, and not the loan contract.

Charging a compounding penalty on a loan if there is late payment.

PENALTY Charges compensation for any late payment, but it does not go toward the bank’s earnings .Instead, it is channeled directly to charity.

The main priority is to protect the bank’s interest; no priority is given to ensure equity development.

PRIORITY Emphasize projects that benefit society. The main aim is to ensure equity development.

Loans given by conventional banks are simple, no asset required. Their concept is “money breeds money.”

REQUIREMENT OF ASSET

Money is not generated through loans. Thus, any loan should have an underlying asset.

Evaluation stresses on the ability of the borrower to pay off the loan. Not much attention is given to the progress of the customer’s project.

EVALUATION Evaluation also stresses on the potential or viability, performance and prospect of the project that is being financed.

Earn revenue from fixed interest charged to the customer.

REVENUE EARNED Profit according to the concept of sharing profit-loss; the bank gives more attention on investing in project development.

The bank-customer relationship: loan lender and borrower.

RELATIONSHIP The bank-customer relationship: seller, buyer or partner.

3.2 A brief history and evaluation of Modern Islamic bank:

An Islamic Bank is a Financial Institution whose statutes, rules, and regulations expressly state its

commitments to the Principles of Islamic Sariah and to the banning of the receipt and payment of

interest on any of its operation.

The concept of Islamic banking is several decades old. The first attempt to establish on Islamic financial

institution took place in Pakistan in the late 1950 with the establishment of a local Islamic bank in a rural

area. Some pious landlords who deposited funds at no interest as then loaned to small landowner for

agricultural development initiated the experiment.

The second pioneering experiment of putting the principles of Islamic bank and finance into practice was

conducted in Egypt from 1963 to 1967 through the establishment of the Mitghamr saving bank in a rural

area of the Nile Delta. The experiment soon become successful more branches were opened in different

Page | 19 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

parts of the country. Although the project made a good start and initial results were more than

encouraging it suffered setback owing to changes in the political atmosphere.

Other kinds of Islamic banking for the pilgrims of Malaysia were established in 1963, which was later on

incorporated into the pilgrims Management fund Board (Tabung Hajji) in 1969.

The 1974 OIC summit in Lahore, Pakistan voted to create the inter-governmental Islami Development

Bank (IDB). The bank was created in 1975 with aim to serve as the World Bank and IMF for the member

Muslim countries. The Dubai Islamic Bank established in 1975 is considered to be the first modern

Islamic bank in the private sector. Then various Islamic banks established all over the world.

At present Islamic banks are strong position in all over the world in Pakistan, Iran, Sudan and as well as

in Bangladesh.

At last four phenomena indicate the convergence of the two financial systems.

First, A growing number of conventional banks in the Islamic world are opening Islamic subsidiaries

and or Islamic windows.

Second, Financial institutions of non Islamic world have also started offering Islamic windows and

products citigroup, ANZ Grind lays, Merrill lynch ABN anomy HSBC are some of to name among

them.

Third, Many Islamic banks are aiming their products at the non-Muslim markets.

Fourth, Some Islamic banks have bear established by initiative outside the Islamic world. The

Russian Board Bank is an example. And the fifth much of the new ijtihad is conducted in

cooperation between conventional and Islamic institution.

In August 1974, Bangladesh signed the charter of Islamic Development Bank and committed itself to

reorganize its economic and financial system as per Islamic Shariah. For the favorable attitude of the

government of the people’s republic of Bangladesh, at present six Islamic Banks operate in Bangladesh

Financial market. These are :

Page | 20 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

1. Islamic Bank Bangladesh Ltd.

2. ICB Islami Bank Ltd.

3. Al – Arafah Islami Bank Ltd.

4. Social Islami Bank Ltd.

5. Shahjalal Islami Bank Ltd.

6. First Security Islami Bank Ltd

Besides Prime Bank, Dhaka Bank, South East Bank, the premier Bank, the Jamuna Bank, HSBC Bank, And

Standard Chartered Bank also have opened Islamic banking branches .

3.3 Investment Activities of Islamic Banks:

Almighty creature said in his holy Quran that “ Ahallahul baia and harramahu Riba” that means Allah permitted trading and forbidden interest” Islamic bank is a financial institution whose statutes rules and procedures expressly state its commitment to the principles of islamic shariah and to the banning of the receipts and payment of interest in on any of its operations.

So islami bank always avoids interest and emphasizes on profit business. Islami bank financing product is Murabaha, Bai-Muazzal, Ijara, Salam, and Istisna, Out of these various debt based financing products. The most popular are Murabaha and Bai-Muazzal.

Common investment activities of an Islamic Banks are discussed as below:

Disabused financed to the business firms and persons: The most important function of an Islamic bank is disbursed finance to industries and business firm or persons.

Disbursed leased finance to various industries: Islamic banks disbursed leased finance to various industries. Lease finance may be two types operating lease and financial lease.

Issue bank Guarantee: AIBL issue bank guarantee on behalf of its clients. In this way banks helps a business firm to run their business smoothly.

Page | 21 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

3.4 Distinguishing features of Islamic Bank

The distinguishing features of Islamic Banks are:

All activities are conducted on interest-free system according to Islamic Shariah principles.

Investment is made through different modes as per Islamic Shariah.

Investment-income of the Bank is shared with Mudaraba depositors according to an agreed

upon ratio, ensuring a reasonably fair of return on their deposits.

Aims to introduce a welfare-oriented banking system and also establish equity and justice in the

field of all economic operations.

Extend socio-economic and financial services to individuals of all economic backgrounds with

strong commitment in rural enlistment.

Plays a vital role in human resources development and employment–generation, particularly

among the unemployed youths.

Portfolio of investment and investment policy have been specially tailored to achieve balanced

growth & equitable development through diversified investment operations particularly in the

priority sectors and in the less developed areas of the national and international economy.

Regular and effective guidance of powerful and highly esteemed Shariah Council consisting of

appropriate number of members representing Shariah Scholars.

3.5 Modes of Investment of Islamic Banks:

The most important objective of Islamic banking system to establish equity and justice in arena of

business and ensure equitable distribution of wealth and income. The sources of fund of the Islamic

Bank include paid up capital and deposits. Deposits mobilized by the Islamic Bank may be categorized

into three: Current deposits, ordinary savings deposits and investment term deposits (Chakma, Islami

and Karmker, 1995). Like conventional banking no return is payable on current deposits while ordinary

savings deposit holders are entitled to profit earned according to the return realized by the Bank on

investment / use of proceeds of such deposits (chakma, Islami and Karmker, 1995). Investment on term

deposit holders are entitled to proceeds from investment on the basis of signed agreement.

Islamic Bank’s modes of financing can be broadly classified into equity and debt instruments. While

equity instruments are Mudarabah and Musharakah, debt-instruments arise from sale transactions.

These fixed income instruments include Murabahah (cost-plus or mark-up sale), Bai-muajjal (price-

Page | 22 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

deffered sale), Istisna / Salam (object deffered sale or prepaid sale) and Ijarah (leasing ) (khan, 1991,

Khalf and Khan, 1992, Ahmed, 2004 and Usmani, 1999). We outline the basic concepts and properties

of these mode of investment below:

Musharakah: Sharikah is a partnership between parties in which financial capital and / or labor

act as shared inputs and profit is distributed according to the capital share of the partners or in

some agreed upon ratio. The loss, however, is distributed according to the share of the capital.

Though there can be different kinds of partnerships based on money, labor, and reputation, one

case of Sharikah is participation financing or Musharakah in which partners share both in capital

and management of the business enterprise. Thus partners in Musharakah have both control

right and claims to the profit.

Mudarabah (or qirad or muqadarah) : Mudarabah is similar to the concept of silent partnership

in which financial capital is provided by one or more partner(s) (Rabul mal) and the work is

carried out by the other partner(s) Mudarib. The funds are used in some activity for a fixed

period of time (Siddiqi, 1987). The financiers and the managers of the project share the profits in

an agreed upon ratio. The loss, however, is borne by the financiers according to their share in

the capital. The manager’s loss is not getting any reward for his services, as the ‘Rabul mal’ is

sleeping partner, he/she has a claim on profit without any say in the management of the firm.

Murabahah / Bai Muajjal : Murabahah is a sale contract at a mark-up. The seller adds a profit

component (mark-up) to the cost of the item being sold. When the purchase is on credit and the

payment for a good / asset is delayed, the contract is called Bai-muajjal. A variant would be a

sale where the payments are made in installments. These contracts create debt that can have

both short and long –term tenors. In these debt contracts, the supplier of the good has claims

on a fixed amount that must be paid before arriving at profits.

Salam / Istisna : ‘Salam sale’ is an advance purchase or product-deferred sale of a generic

goods . In a Salam contract, the buyer of a product pays in advance for a goods that is produced

and delivered later. The contract applies mainly for agricultural goods. Istisna contract is similar

to the Salam contract with the difference that in Istisna the goods is produced according to the

specifications given by the buyer. This applies mainly to manufactured goods and real estate.

Furthermore, in Istisna the payments can be made in installments over time with the

progression of the production.

Page | 23 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

Ijarah : Ijarah is a lease contract in which the lessee pays rent to the lessor for use of asset

(usufruct). In Ijarah the ownership and the right to use an asset (usufruct) are separated. It falls

under a sale-based contract as it involves the sale of asset( usufructs). A lease contract that

results in the transfer of an asset to the lessee at the end of the contract is called

o ‘Ijarah wa iqtina’ or ‘Ijarah muntahia bittamleek’.‘Ijarah wa iqtina’ combine sale and

leasing contracts and use the hire-purchase or rent-sharing principles. The ownership of

the asset is transferred to the lessee as payments for the asset are also made along with

the rent.

o After the contract period is over, the lessee assumes the ownership of the asset. Note

that in a simple Ijarah, the rental payments made are captured in the current liabilities

in the iqtinah’, however, the leased item would be in the form of a debt during the

period of lease

Page | 24 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

CHAPTER FOUR

COMMON FACTORS OF BANK INVESTMENT

Page | 25 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

4.1 Bank Investment

Investment and loan are two strategies of utilization of bank fund. Although both sources earn profit but

they have many dissimilarities also.

Investment is the use of money for the purpose of making more money to gain income, profit or

increase in capital or both. The term investment is also used to include those funds both public and

private, for relatively long period of time with the objective of earning income. Investment is mainly

made for the purpose of generation income. To meet up the liquidity requirement is one of the major

purposes of investment. So, bank’s investment means the part of bank’s loanable funds which are

employed in money market or capital market by purchasing securities for the purpose of earning profit.

4.2 Objectives of Bank Investment

Loans activities are the traditional techniques of profit earning of banks. There are some purposes,

which recently gained popularity for non-loan bank investment. There are as follows:

Maximization of wealth of shareholder: The main purpose of each activity of bank is to

maximize the wealth of the shareholders by earning appropriate profit. So, banks make

investment by part of their loan able funds to earn profit and maximize the wealth of

shareholders with minimal risk.

Diversification of risk: Banks should not use the fund to provide the loan only. Banks also invest

in the debt instruments issued by the well known companies to reduce the risk of the use of

funds.

Supporting income: Interest receipts, commissions, charges, fees are the main sources of bank

income. On the other hand, dividend / income from purchasing securities, bonus share and

capital appreciation are considered as supporting income received from investment, which

along with the conventional incomes, contributes a lot to strengthen the financial position of a

bank.

Page | 26 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

Source of supplementary liquidity: Primary reserve and secondary reserve are the conventional

sources of banks liquidity. But if the primary and secondary reserves are not enough to meet the

liquidity requirement, liquidity crisis may occur.

Reducing tax liability: Earnings from loans are always taxable. Rate of tax varies with varying

level of income. In this situation, banks can invest in different types of shares, bonds and

debentures that are tax free or tax exempted and thereby banks can enjoy reduced amount of

tax.

4.3 Characteristics of Bank Investment

Loan and investment are two major profit making activities for banks. But bank investments have

different aspects in comparison to loans. Some distinguishing and important features bank investments

are as follows:

Nature of fund

Third line of defense

Creditor status of bank

Initiative of transactions

Volume of investment relative to the size of bank

Personal vs. impersonal transactions

Secondary reserve asset vs. investment asset

Fluctuation of market price

Negotiation

Knowledge of use of fund by the provider of funds

Termination

Nature of Fund: Banks make investment with residual funds after meeting the reserve and loan

requirements. Banks have instance to utilize funds only for loan purpose without making any

investment. But there are no instances of using the excess funds to make only investment and giving no

loans. So bank investment means utilization of residual funds profitability after meeting loan

requirement.

Third Line of Defense: Bank loan is called illiquid asset. Based on liquidity, primary reserve and

secondary reserves act as the first and second line of defense respectively. Bank loan is such asset of a

Page | 27 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

bank, which cannot be used un the time of liquidity crisis. In that sanitation, bank’s investment in

securities can be used as the third line of defenses.

Creditor Status of Bank: In case of loan or investment, bank the position of creditors. In case of loan

bank is one of the few big creditors of the borrowers. But in case of investment, bank is one of many

creditors to the issuers of investment

Initiatives of Transactions: Incase of loan, the initiative of loan transactions comes from borrowers. But

in case of investment, the initiative come s from the part of the bank.

Volume of Investment Relative to the Size of Bank: Banks provide loan to creditworthy borrowers and

make profit. On the other hand, small banks make investment of different maturities through financial

market for the purpose of meeting liquidity and profitability. It indicates that the small banks make

investment by one-thirds of fund available for the purpose of making profit. But large size bank make

investment by not more than of 20% of their funds.

Personal vs. Impersonal Transaction: In case of bank’s loan activities, there is a personal transaction

between the bankers and the borrowers. But in case of investment, there are no direct transactions

between the main issuers of securities and the banks.

Secondary Reserve Asset vs. Investment Asset: Short – securities are used as secondary reserve asset

and investment assets. But in case of investment, medium and long term financial instruments should

be used.

Fluctuation of market Price: Financial instruments are affected by fluctuation of market price. But, loan

amount is accumulated and increased by nonpayment of loan installments.

Negotiation: Borrowers may bargain with the banks about loan amount, installment, security and

interest rate. But there is no such provision for debentures purchasing banks as condition are pre-fixed.

Knowledge of Use of Fund by the providers of Funds: Banks know what the borrowers will do with the

loan amount. But in case of investment fund, they have no knowledge about what the issuers of

financial securities are going to do with that fund.

Termination: incase of loan, successful termination depends on the willingness and the ability of the

borrowers rather than the bank. But the holders of debt instruments may terminate the same at their

will.

Page | 28 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

4.4 Investments Tools:

a. Government Securities I. Treasury bonds

II. Prize bonds b. Non-government Securities

c. Loans and advances

4.5 Investment Pricing

The pricing of investment products shall be judiciously and appropriately made taking in view the Bank

Rate, cost of fund, risk factor involved, current investment prices of the banking sector, demand/ supply

interaction of the investment products, socio-economic impact of investment products and national

priority. Flexibility and competitiveness shall also be taken into consideration to ensure that the pricing

is appropriate and competitive for easy marketing of the products, to yield fair rate of return on

investments as well as uphold the social welfare objectives of the Special Investment Schemes. The

pricing shall be reviewed and evaluated from time to time and be adjusted as per prevailing situation

and experience.

Investment Administration Department will be comprised of four unit or cell:

I. Disbursement

II. Custodian Cell

III. Monitoring/ Recovery Cell

IV. Compliance Cell

The Branch manager will act as coordinator of total investment procedures. He will look after works of

the relationship management department as well as investment administration department of the

branch.

Page | 29 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

4.6 Basel II Implementation and Risk Management

The banking sector in Bangladesh is undergoing significant changes. Basel II Accord, which is,

implemented from 2010 places heavy reliance on the internal risk assessment and management

techniques for the purpose of quantifying and allocating capital for credit, market and operational risks.

Continued success of a bank depends on its ability to prepare for unexpected and potentially much less

favorable, events and outcomes. To deal with risks proactively, banks are gradually shifting towards

Enterprise Wise Risk Management (EWRM) structure. EWRM framework will address the following

issues:

Strategy: Alignment of risk management activities with strategic and shareholders' value objectives;

Processes: Establishment of formal and informal risk management processes to identify, analyze,

manage, monitor and report risk knowledge and information;

Structure: Determining needs to enable the organization to execute risk management strategy and

processes.

Implementation: Delivery of this capability to the organization to enable a sustainable and valuable

risk management strategy. As part of a robust risk management process, the Bank has a Credit Risk

Management Policy document which addresses the following issues:

Establishing a credit risk environment

Setting up a sound credit approval process

Maintaining an appropriate credit administration and monitoring process and

ensuring adequate control credit risks

4.7 Five-core risks in investment

Credit Risk

Asset & Liability / Balance Sheet Risk

Foreign Exchange Risk

Internal Control & Compliance Risk

Money Laundering Risk

Page | 30 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

CHAPTER FIVE

COMPARATIVE ANALYSIS OF INVESTMENT

Page | 31 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

Investment comparison between Conventional Commercial Banks and Islamic Banks

Investment is the main source of bank’s income. Most of the earnings come from bank’s investment.

Conventional commercial banks earn from the interest of the advances provided by them as well as they

reduce their risks by diversifying their investment in the share of different companies. They make

portfolio of different types of shares, government bonds, private bonds and debentures and other

bonds. Islamic Banks of Bangladesh invest based on Islamic Sariah.The investment modes are Bai

Murabaha, Bai-Muajjal,Hire Purchase under Shirkatul Milk, Mudaraba, Musharaka, Bai-as-Sarf etc. There

are 28 conventional commercial banks (24 private commercial Banks + 4 Nationalized commercial

Banks) and 6 Islamic banks in Bangladesh.

5.1 Total Investment:

Total investment of conventional commercial Banks and Islamic Banks of previous five years is given

below:

Year Total Investment of Private

Cmmercial Banks

(in lacs)

Total Investment of Islamic Banks (in lacs)

2007 6666990 2527802

2008 8787429 3273607

2009 10569660 4427473

2010 13715680 5631193

2011 16437937 6889523

Table-5: Investment Amounts of Islamic Banks and Conventional Banks of BD

Chart- 1: Comparative investment amount between conventional Banks and Islamic Banks.

66669908787429

1056966013715680

16437937

2527802 3273607 4427473 5631193 6889523

0

5000000

10000000

15000000

20000000

2007 2008 2009 2010 2011

Conventional Commercial Banks Islamic Banks

Page | 32 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

From the above graph we can see that the investment amount has increased from year to year and in an

impressive amount for both Conventional commercial banks and Islamic banks. Though the investment

amount is very large in comparison with Islamic banks but it is natural as we are analyzing with twenty

four conventional private commercial banks and only six Islamic banks.

5.2 Percentage Change in Investment:

Year Conventional Banks Islamic Banks

Total Investment

(in lacs)

Percentage

Change

in Investment

Total Investment

(in lacs)

Percentage

Change

in Investment

2007 6666990 23.38% 2527802 21.01%

2008 8787429 31.80% 3273607 29.50%

2009 10569660 20.28% 4427473 35.24%

2010 13715680 29.76% 5631193 27.18%

2011 16437937 19.84% 6889523 22.34%

Table- 6: Percentage Change in Investment from year to year

Chart -2: Percentage Change in Investment from year to year

From the above graph we can see that like the amount of investment in Islamic banks,growth is also is

lower than that of Conventional Commercial banks in first two years but the growth rate of investment

of Islamic banks is high in 2009 which is huge and also in 2011. In 2010 which has decreased in a small

percentage. The difference was much higher in 2009 and conventional banks recovered it well in 2010

which can be a result of comparative lower growth of investment than the previous years. The

percentage change of investment was increasing in first 3 years of our observations but then it declined

in next 2 years which is not a positive sign. The investment of conventional banks fluctuated in every

23.38%

31.80%

20.28%

29.76%

19.84%21.01%

29.50%

35.24%

27.18%22.34%

0.00%

10.00%

20.00%

30.00%

40.00%

2007 2008 2009 2010 2011

Conventional Commercial Banks Islamic Banks

Page | 33 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

year of this observation which does not show consistency. The percentage change for Islamic banks was

highest in 2009 which is 35.24% and lowest in 2007 which is 12.54%. For conventional banks highest in

2009 is 31.80% and lowest is 19.84% in 2011. The percentage change was almost equal in 2010.

5.3 Growth in Deposits:

Year Conventional Commercial Banks Islamic Banks

Total Deposits

(in lacs)

Growth in deposits Total Deposits

(in lacs)

Growth in deposits

2007 8377132 19.40% 2819125 20.25%

2008 10626631 26.85% 3525129 25.04%

2009 13309538 25.24% 4736128 34.35%

2010 16489951 23.89% 5944304 25.50%

2011 20057788 21.63% 7402875 24.53%

Table-7: Comparative growth of deposits

Chart3: Comparative amount of deposits.

Here we can see deposit amounts increased year to year for both conventional banks and Islamic banks.

It shows consistency of both conventional banks and Islamic banks and also a positive sign to our

economy.

837713210626631

1330953816489951

20057788

2819125 3525129 4736128 59443047402875

0

5000000

10000000

15000000

20000000

25000000

2007 2008 2009 2010 2011

Conventional Commercial Banks Islamic Banks

Page | 34 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

Chart-4: Comparative growth rate of deposits

Here we can see growth rate of deposits of Islamic banks is higher than Conventional Commercial Banks

in every year except 2008 like percentage change in investment and we can assume an interrelation

between deposits and investment. The growth rate of deposits was highest 34.35% for Islamic banks in

2009 and 26.85% for conventional banks in 2008 .and the lowest growth rate for Islamic bank was

20.25% and for conventional banks 19.40% both of which took place in 2007 and showed the rising rate

of deposits in last 5 years.The closest difference between these two was in 2010 which was less than 2%.

5.4 Comparative Index Analysis:

Year Conventional Banks Islamic Banks

Total Investment

(in lacs)

Percentage

Change from base

year (2007)

Total Investment

(in lacs)

Percentage

Change from base

year (2007)

2007 6666990 ----- 2527802 -----

2008 8787429 31.80% 3273607 29.50%

2009 10569660 58.53% 4427473 75.15%

2010 13715680 105.72% 5631193 122.77%

2011 16437937 146.55% 6889523 172.54%

Table-8 : Comparative Index Analysis of Investment

19.40%

26.85% 25.24% 23.89%21.63%20.25%

25.04%

34.35%

25.50% 24.53%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

2007 2008 2009 2010 2011

Conventional Commercial Banks Islamic Banks

Page | 35 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

Chart-5: Comparative Index Analysis of Investment

Index analysis is the percentage change of investment from the base year. That means how much more

investment is increased in every from a fixed or base year. Index Analysis is done from 2007 to 2011. The

base year is 2007. From the above figure it can be said that in every year investment is increased in

amount than that of previous year. In 2008, 31.80% investment increases than the base year for

conventional banks and 29.50% increases for Islamic banks. In 2011 the investment increased to

146.55% for conventional banks and 172.54% for Islamic banks. So it can be concluded that after 5 years

the investment of Islamic banks has been increased more than the conventional banks.

5.5 Investment Analysis per branch:

Year Conventional Banks Islamic Banks

Total

Investment

(in lacs)

Total number of Branches

Average investment per Branch (in lacs)

Total

Investment

(in lacs)

Total number of Branches

Average investment per Branch (in lacs)

2007 6666990 1595 4179.931 2527802 312 8101.929

2008 8787429 1761 4990.022 3273607 367 8919.910

2009 10569660 1986 5322.085 4427473 457 9688.125

2010 13715680 2216 6189.386 5631193 533 10565.09

2011 16437937 2356 6977.053 6889523 563 12237.16

Table-9: Comparative investment analysis per branch

31.80%

58.53%

105.72%

146.55%

29.50%

75.15%

122.77%

172.54%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

140.00%

160.00%

180.00%

200.00%

2008 2009 2010 2011

Conventional Commercial Banks Islamic Banks

Page | 36 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

Chart-6: Comparative investment analysis per branch

From the above graph it is observed that the investment amount is many more times per branch in

Islamic banks than conventional banks. Positive sign for both conventional and Islamic banks is the

increasing amount of investment per employee year to year. It shows the skill of the bank to handle

investment. Islamic banks are conducting comparatively more investment activities per branch than

conventional banks. In 2007 where investment was only 4179.93 and 8101.929, it increased to 6977.05

and 12237.16 for conventional banks and Islamic banks respectively.

5.6 Investment Analysis per employee:

Year Conventional Banks Islamic Banks

Total

Investment

(in lacs)

Total number of employees

Average investment per employee (in lacs)

Total

Investment

(in lacs)

Total number of employees

Average investment per employee (in lacs)

2007 6666990 37163 179.3986 2527802 11566 218.5546

2008 8787429 40725 215.7748 3273607 13378 244.7008

2009 10569660 45083 234.4489 4427473 14856 298.0259

2010 13715680 51034 268.7557 5631193 16685 337.5003

2011 16437937 56085 293.0897 6889523 17997 382.8151

Table-10: Comparative investment analysis per employee.

4179.9310344990.022147 5322.084592

6189.3862826977.053056

8101.9298919.91

9688.12510565.09

12237.16

0

2000

4000

6000

8000

10000

12000

14000

2007 2008 2009 2010 2011

Conventional Commercial Banks Islamic Banks

Page | 37 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

Chart-7: Comparative investment analysis per employee

The above chart also shows superior performance of Islamic banks. In 2007 where conventional banks

invest only 1179.3985 lacs per employee, Islamic banks invest 218.5546 lacs per employee. After that

investment of both the conventional banks and Islamic banks increased gradually. In 2010 conventional

banks invest 268.7557 lacs per employee, Islamic banks invest 382.8151lacs per employee and in 2011

investment was 293.0897 and 382.8151 respectively. It can be said it shows better skill of the employees

of Islamic banks.

179.3985954215.7748066 234.4489054

268.7557315293.089721

218.5546244.7008

298.0259337.5003

382.8151

0

50

100

150

200

250

300

350

400

450

2007 2008 2009 2010 2011

Conventional Commercial Banks Islamic Banks

Page | 38 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

5.7 Investment classified by Economic Purposes:

Bangladesh Bank has classified total investment by banks into 9 different sectors which are given below:

1. Agriculture, Fishing, Forestry

2. Industry (other than capital financing)

3. Working Capital financing

4. Construction

5. Water works and Sanitary Services

6. Transport and Communication

7. Storage

8. Trade

9. Miscellaneous

The above mentioned sectors include different areas. Some of them are as follows:

Agriculture, Fishing, Forestry:

Cultivation of crops

Plantation

Agricultural machineries

Fertilizers

Livestock

Fishing

Forestry etc.

Industry (other than capital financing):

Large and medium scale industries

Jute, cotton &wearing

Beverage & Tobacco industries

Leather & leather products

Manufacturing of papers etc.

Working Capital financing:

Large and medium scale industries

Small scale & cottage industries

Service industries

Construction:

Urban housing

Rural housing

Road construction etc.

Page | 39 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

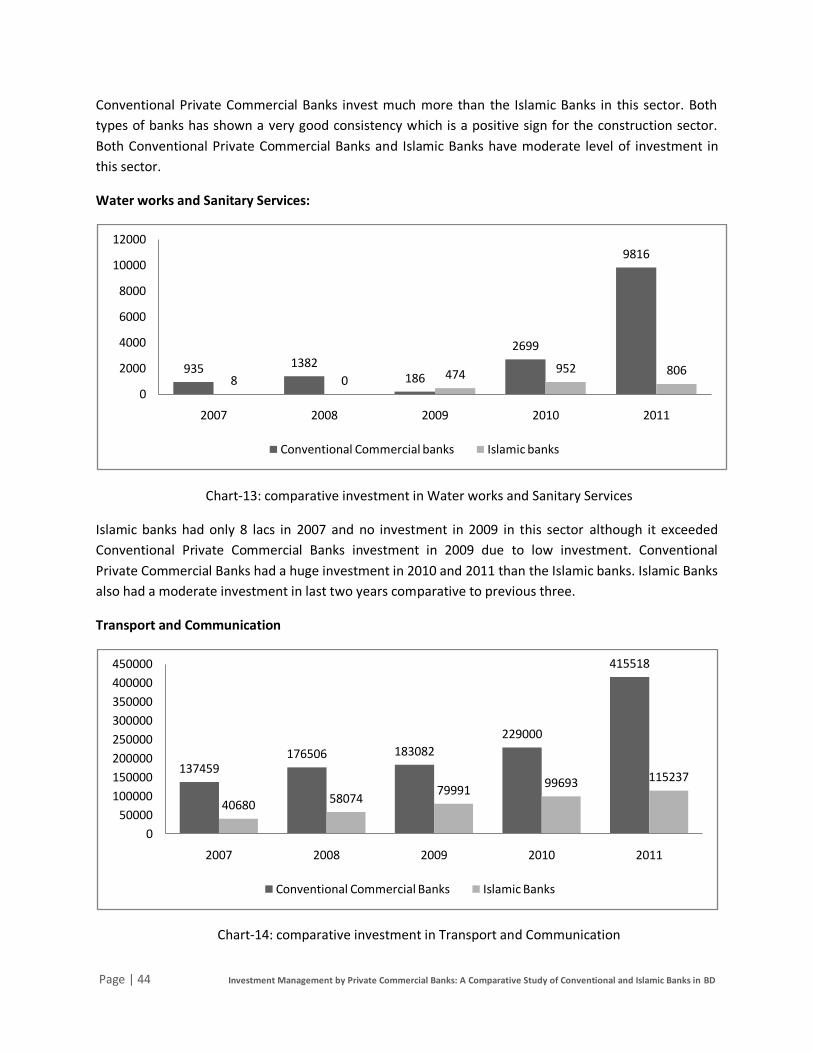

Water works and Sanitary Services:

Water works

Sanitary services etc.

Transport and Communication:

Road transport

Water transport

Air transport etc.

Storage:

Water housing

Cold storage etc.

Trade:

Wholesale & retail trade

Procurement by government

Export financing

Import financing

Leasing etc.

Miscellaneous:

Private welfare and development activities

Special credit program

Poverty alleviation

Consumer goods

Educational expense

Land purchase etc.

Page | 40 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

The comparative investment between Conventional Commercial Banks and Islamic Banks is given below:

Conventional Commercial banks(in lacs) Islamic Banks(in lacs)

2007 2008 2009 2010 2011 2007 2008 2009 2010 2011

Agriculture, Fishing, Forestry

41684 76445 65234 123502 169603 19143 39983 45975 99033 163615

Industry (other than capital financing)

1275431 1758015 2180229 2787703 3232005 582602 799367 984235 1189368 1536129

Working Capital financing

960442 1258608 1486480 1927366 2404205 557671 730171 863273 880654 870919

Construction

522333 674201 812020 1194206 1618617 157226 196156 293036 298978 563301

Water works and Sanitary Services

935 1382 186 2699 9816 8 0 474 952 806

Transport

137459 176506 183082 229000 415518 40680 58074 79991 99693 115237

Storage

5154 8861 9003 17585 31379 2517 1524 2189 8149 15491

Trade

3011909 3721276 4460221 5784888 6597591 925044 1135233 1778585 2325557 2901882

Miscellaneous

705643 1112139 1353205 1666112 1959199 242911 313099 379715 729409 722143

Table-11: Year to year Investment in different sectors by Conventional Banks and Islamic Banks

Page | 41 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

We can show the above investment information by the following chart:

Chart-8: Year to year comparative investment by conventional commercial banks and Islamic banks

From the above chart we can see that investment in trade takes the major portion of total investment

by banks and maximum investment was in 2011 in trade by conventional commercial banks. Water

works and sanitary service has the lowest portion among all the sectors. Industry sector also gets a

remarkable concentration by both the conventional banks and Islamic banks. Working capital financing,

agriculture and construction have moderate level of investment. Islamic banks have lower investment in

every sector and this is very natural as number of Islamic Banks is low. But the growth of investment by

Islamic Banks is very lucrative which is evidenced by the above graph. Investment is rising every year in

every section without some exceptional cases (i.e. water works and sanitary services in 2008 and 2009)

for both types of banks which is a good sign for the overall growth of the economy. As this chart does

not show clear picture of every sector, sector wise analysis between Conventional Private Commercial

Banks is given below:

0

1000000

2000000

3000000

4000000

5000000

6000000

7000000

Agr

icu

ltu

re, F

ish

ing,

Fo

rest

ry

Ind

ust

ry (o

ther

th

an c

apit

al fi

nan

cin

g)

Wo

rkin

g C

apit

al f

inan

cin

g

Co

nst

ruct

ion

Wat

er w

ork

s an

d S

anit

ary

Serv

ices

Tran

spo

rt

Sto

rage

Trad

e

Mis

cella

neo

us

Conventional Commercial banks(in Lacs) 2007

Conventional Commercial banks(in Lacs) 2008

Conventional Commercial banks(in Lacs) 2009

Conventional Commercial banks(in Lacs) 2010

Conventional Commercial banks(in Lacs) 2011

Islamic Banks(in Lacs) 2007

Islamic Banks(in Lacs) 2008

Islamic Banks(in Lacs) 2009

Islamic Banks(in Lacs) 2010

Islamic Banks(in Lacs) 2011

Page | 42 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

Agriculture, Fishing, Forestry:

Chart-9: comparative investment in Agriculture, Fishing, Forestry

It is usual that investment from Islamic banks will be lower than Conventional Private Commercial Banks

but as the chart shows investment in Agriculture, Fishing, Forestry is increasing more in Islamic Banks.

Where there was a huge difference in 2007 but in 2011 Islamic Banks has recovered well and the

difference is very low which shows better growth rate of Islamic banks than Conventional Private

Commercial Banks. Conventional Private Commercial Banks had a decreasing rate in 2009 but Islamic

banks had shown a good consistency in this sector.

Industry (other than capital financing):

Chart-10: comparative investment in Industry (other than capital financing)

41684

7644565234

123502

169603

19143

39983 45975

99033

163615

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

2007 2008 2009 2010 2011

Private Commercial Banks Islamic Banks

1275431

1758015

2180229

2787703

3232005

582602799367

9842351189368

1536129

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

2007 2008 2009 2010 2011

Private Commercial Banks Islamic Banks

Page | 43 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

Both types of banks have moderate level of investment in this sector and also there is a good

consistency for both types of banks. Investment from Conventional Private Commercial Banks is higher

as usual because of huge number.

Working Capital financing:

Chart-11: comparative investment in Working Capital financing

Conventional Private Commercial Banks showed a good consistency in working capital financing whereas

investment from Islamic banks slowed down from 2008 to 2011. The above chart proves Islamic banks of

Bangladesh do not emphasize much in this sector.

Construction:

Chart-12: comparative investment in Construction

9604421258608

1486480

1927366

2404205

557671730171

863273 880654 870919

0

500000

1000000

1500000

2000000

2500000

3000000

2007 2008 2009 2010 2011

Conventional Commercial Banks Islamic Banks

522333674201

812020

1194206

1618617

157226 196156293036 298978

563301

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

1800000

2007 2008 2009 2010 2011

Conventional Commercial Banks Islamic Banks

Page | 44 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

Conventional Private Commercial Banks invest much more than the Islamic Banks in this sector. Both

types of banks has shown a very good consistency which is a positive sign for the construction sector.

Both Conventional Private Commercial Banks and Islamic Banks have moderate level of investment in

this sector.

Water works and Sanitary Services:

Chart-13: comparative investment in Water works and Sanitary Services

Islamic banks had only 8 lacs in 2007 and no investment in 2009 in this sector although it exceeded

Conventional Private Commercial Banks investment in 2009 due to low investment. Conventional

Private Commercial Banks had a huge investment in 2010 and 2011 than the Islamic banks. Islamic Banks

also had a moderate investment in last two years comparative to previous three.

Transport and Communication

Chart-14: comparative investment in Transport and Communication

935 1382186

2699

9816

8 0 474 952 806

0

2000

4000

6000

8000

10000

12000

2007 2008 2009 2010 2011

Conventional Commercial banks Islamic banks

137459176506 183082

229000

415518

40680 5807479991

99693 115237

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

2007 2008 2009 2010 2011

Conventional Commercial Banks Islamic Banks

Page | 45 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

Both Conventional Private Commercial Banks and Islamic banks showed consistency in this sector.

Although difference was low in 2010 but it became large in 2011 due to huge investment from

Conventional Private Commercial Banks. The total investment from Conventional Private Commercial

Banks is more because of number of banks.

Storage:

Chart-15: comparative investment in storage

Investment in storage has increased in a large amount for both Conventional Private Commercial Banks

and Islamic banks in last two years. It decrease in 2008 than the 2007 for Conventional Private

Commercial Banks and Islamic Banks are consistent enough in this case. Although investment is

increasing but investment in this sector is minimum from the total investment.

Trade:

Chart-16: comparative investment in Trade

5154

8861 9003

17585

31379

2517 1524 2189

8149

15491

0

5000

10000

15000

20000

25000

30000

35000

2007 2008 2009 2010 2011

Conventional Commercial Banks Islamic Banks

30119093721276

4460221

5784888

6597591

925044 11352331778585

23255572901882

0

1000000

2000000

3000000

4000000

5000000

6000000

7000000

2007 2008 2009 2010 2011

Conventional Commercial Banks Islamic Banks

Page | 46 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

Both Conventional Private Commercial Banks and Islamic Banks invested maximum amount in this

sector in last 5 years and that proves the importance of this sector. Investment from Conventional

Private Commercial Banks is more as usual but both types of banks showed impressive growth rate.

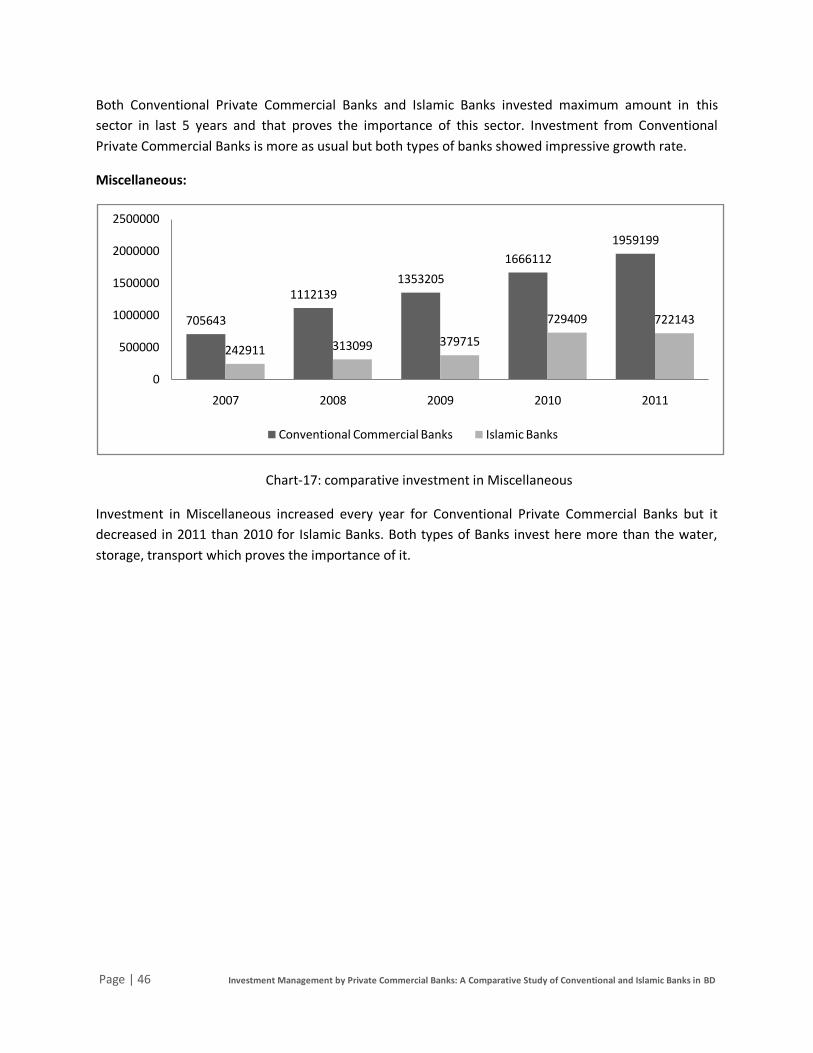

Miscellaneous:

Chart-17: comparative investment in Miscellaneous

Investment in Miscellaneous increased every year for Conventional Private Commercial Banks but it

decreased in 2011 than 2010 for Islamic Banks. Both types of Banks invest here more than the water,

storage, transport which proves the importance of it.

705643

11121391353205

1666112

1959199

242911 313099 379715

729409 722143

0

500000

1000000

1500000

2000000

2500000

2007 2008 2009 2010 2011

Conventional Commercial Banks Islamic Banks

Page | 47 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

CHAPTER SIX

REGRESSION ANALYSIS & SWOT ANALYSIS

Page | 48 Investment Management by Private Commercial Banks: A Comparative Study of Conventional and Islamic Banks in BD

6.1 Multiple Regression Analysis

Multiple regression analysis is the study of how a dependent variable related to two or more

independent variables. So to make a regression analyses there are necessary a dependent variable and

two or more independent variables.

Regression Equation: Ŷ = a + b1 X1 + b2 X2

6.2 Requirement Factors

I. Dependent Variable: Total Investment (Y)

II. Independent Variables: a. Total Deposits (X1)

b. Total Branches of Banks (X2)

Dependent Variable: The variable which is dependent on other variables or whose value depends on the

value of other independent values. To predict the value of this dependent variable it is needed to make

an equation. In the regression analysis Total Investment has taken as Dependent Variable (Y).

Independent Variable: The variable whose value does not depend on other factors, but being used to

predict or explain the dependent variable is called the independent variable. In this analysis Total

Deposits (X1) and Total number of branches (X2) are the two independent variables respectively.

6.3 Analytical Requirements:

Some key terms which are arrived from the SPSS Program, needed to arrive a regression line are as