Commitment, banks and markets

30

Commitment, Banks and Markets Gaetano Antinol Department of Economics Washington University [email protected] Suraj Prasad Department of Economics Washington University [email protected] July 18, 2007 Abstract We examine how banks and nancial markets interact with one another to provide liquidity to investors. The critical assumption is that nancial markets are characterized by limited enforcement of con- tracts, and, in the event of default only a fraction of borrowersassets can be seized. Limited enforcement reduces the fraction of assets that count as collateral and thus individuals with liquidity shocks face bor- rowing constraints. We show how banks endogenously overcome these borrowing constraints by pooling resources across several depositors, and increase the liquidity provided by nancial markets. We thank Huberto Ennis, Enrique Kawamura, Todd Keister, James Peck, Jacek Suda, and Anjan Thakor for helpful conversations. We also wish to thank participants at the 2005 Midwest Economics Association Meetings, the 2005 Midwest Macroeconomics Conference, and the fall 2005 Midwest Economic Theory Conference for their helpful comments. 1

Transcript of Commitment, banks and markets

Commitment, Banks and Markets�

Gaetano Antinol�Department of EconomicsWashington [email protected]

Suraj PrasadDepartment of EconomicsWashington [email protected]

July 18, 2007

Abstract

We examine how banks and �nancial markets interact with oneanother to provide liquidity to investors. The critical assumption isthat �nancial markets are characterized by limited enforcement of con-tracts, and, in the event of default only a fraction of borrowers�assetscan be seized. Limited enforcement reduces the fraction of assets thatcount as collateral and thus individuals with liquidity shocks face bor-rowing constraints. We show how banks endogenously overcome theseborrowing constraints by pooling resources across several depositors,and increase the liquidity provided by �nancial markets.

�We thank Huberto Ennis, Enrique Kawamura, Todd Keister, James Peck, Jacek Suda,and Anjan Thakor for helpful conversations. We also wish to thank participants at the 2005Midwest Economics Association Meetings, the 2005 Midwest Macroeconomics Conference,and the fall 2005 Midwest Economic Theory Conference for their helpful comments.

1

1 Introduction

Banks engage in maturity transformation and supply liquidity with depositcontracts despite the presence of illiquid assets in their balance sheets. Thisactivity is re�ected in models of banking, which consider risk pooling as oneof the main reasons for the existence of intermediation. Mutual insuranceprovides the economic incentive to contribute to a common pool of resources,a bank, which can exploit the high return of long-term assets while in partovercoming the risk associated with idiosyncratic consumption shocks.In this paper, we study banking in a model with limited commitment

besides idiosyncratic consumption shocks. By limited commitment we meanthe inability of individuals to fully commit to repay debt.1 The signi�canceof this assumption is that it creates a role for collateral and the possibilityfor credit constraints. This allows us to consider a notion of liquidity basedon the e¢ ciency with which claims written on real assets can be traded in�nancial markets. We employ this notion in addition to the one typicallyadopted in the banking literature, which relates to the e¢ ciency with whichtechnology allows liquidation of real assets. Our main result is to showthat with limited commitment banks pool collateral, and allocate it moree¢ ciently than individuals while complementing the liquidity provided bymarket activity.To clarify, and overview some of the arguments of the paper, consider a

simple illustrative example. Imagine two individuals who may have randomliquidity needs in the future, and face the decision to allocate their wealthover two real assets, a low yielding liquid asset and a high-yielding illiquidasset. They have access to a market in which they can issue claims writtenon their real assets. If the market were to allow them to borrow against theirwealth without friction, there would be little use for the liquid asset: themarket itself would generate the liquidity they need.2 In contrast, supposethat the market does not allow individuals to borrow easily against their fu-ture returns: for example, suppose that individuals can borrow only againsta (constant) fraction of their wealth. In this case, the role of the liquid assetbecomes more important, because in the future an individual with only illiq-uid assets may be credit constrained. However, one can contemplate anotherpossibility. Suppose that the two individuals form a coalition and pool their

1This assumption is like in Kehoe and Levine (2001) and, in a di¤erent context, Azari-adis and Lambertini (2003).

2Of course, assuming that prices are aligned to eliminate arbitrage opportunities.

2

resources before undertaking investment. For simplicity, call this coalitiona bank. Pooling resources means that the bank is able to pledge a largercollateral, simply because the market allows it to borrow against a fractionof its funds, which are now the sum of the funds of the two individuals. Inas much as it will not be the case that in the future both individuals willface sudden liquidity needs, the collateral of one individual can be pledged(through the bank) to fund the liquidity needs of the other. Again, the roleof the liquid asset is diminished, this time because the bank allows betteraccess to the market. This intuition, which the example illustrated loosely,is behind an important part of our analysis, and we will model it preciselyin the following sections.The identi�cation of intermediaries as economizers of collateral also con-

tributes to a long standing debate concerning the coexistence of banks andmarkets. Diamond and Dybvig (1983) showed that deposit contracts are op-timal when individuals face uncertainty over the timing of their preferencefor consumption. In a subsequent contribution, Jacklin (1987) noted thatif individuals are allowed to issue claims on directly owned real assets uponobserving their relative patience for consumption, the presence of an interme-diary does not improve over the provision of liquidity supplied by contingentclaims markets. In the presence of markets banks�contracts have to satisfy amodi�ed incentive compatibility constraint that takes into account arbitragebetween returns on deposits and asset price movements.Diamond (1997) allows for the presence of markets by assuming restricted

participation.3 When only a fraction of the population is allowed to issueclaims on directly held real assets and trade these claims in competitive�nancial markets, banks do play a role in liquidity provision. The signi�canceof Diamond�s (1997) results is to show that as long as any fraction of thepopulation is exogenously excluded from trading in �nancial markets (but isallowed to deposit in banks), intermediaries play a role in liquidity provisionand can coexist with markets.We assume limited commitment to make market participation endoge-

nous. We show that with limited commitment the risk pooling of banks hasanother e¤ect which may allow for equilibria where the commitment problemis completely overcome, and banks and markets coexist. In addition, banks

3Wallace (1988) adopts a similar interpretation of the Diamond and Dybvig (1983)model, and considers agents as being �isolated�one from the other so that bilateral ex-change of claims is prevented.

3

�maximize� their maturity transformation role, and hold all the long termassets, while individuals directly hold only short-term assets. By poolingresources banks pool risk, but they also in e¤ect pool collateral capacity.Because not all depositors withdraw at the same time, banks can subsidizethe ability to borrow of those depositors who have high demand for liquid-ity. Thus, our result highlights the importance of banks as a commitmentmechanism in economies where enforcement of �nancial contracts is limitedor costly. Banks, therefore, can allow �nancial markets to function better,and increase the liquidity provided by them.We treat banks and individuals symmetrically in market transactions:

banks may face the same commitment problem as individuals in tradingclaims. We do assume, however, that banks are able to commit to repayingtheir depositors. The problem of the commitment of banks towards theirdepositors and its in�uence on the structure of the deposit contract hasbeen studied, for example, by Diamond and Rajan (2000). They show thatthe maturity transformation role performed by banks with deposit contractsexposes them to bankruptcy if too many depositors want to withdraw at thesame time. This vulnerability of the deposit contract constitutes an e¤ectivecommitment device for banks. Intuitively, it makes default towards theirdepositors too costly for banks. While it would not be di¢ cult to built thestructure of the model by Diamond and Rajan (2000) into our model, thereis not much additional economic insight to performing such an exercise, andwe simply invoke the additional structure of Diamond and Rajan (2000) tojustify our assumption.Following Jacklin (1987), there have been several studies that examine

the viability of banks as liquidity providers when investors have access tocompetitive �nancial markets. A paper by von Thadden (1999) considersthe presence of two assets, one with a higher short-term return but a smallerlong-term return than the other, as a way of relaxing the incentive compat-ibility constraint imposed on banks by the presence of markets. Allen andGale (2004) consider a market where banks can trade risk. Their analysishighlights the importance of limited market participation: Allen and Gale(2004) assume that banks have access to markets but individuals do not. Anexample of a di¤erent approach aimed at yielding the same results is providedby Fecht, Huang, and Martin (2004), where the population is partitioned insophisticated and unsophisticated investors who have di¤erent incentives inparticipating in direct (market) investment. Finally, an extensive discussionof the issues involved in the coexistence of banks and markets in relation to

4

liquidity provision can be found in Hellwig (1998).

2 Basic Model with Financial Markets

We begin by analyzing the model without the banking sector.

2.1 Technology and Preferences

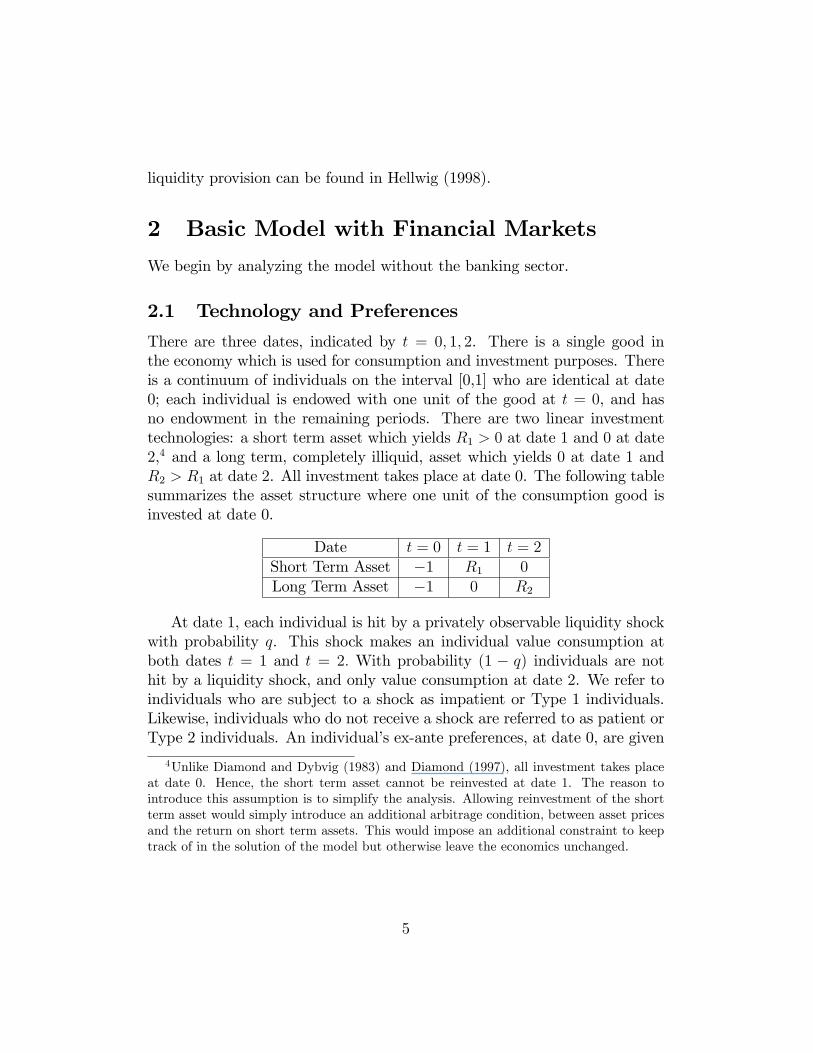

There are three dates, indicated by t = 0; 1; 2. There is a single good inthe economy which is used for consumption and investment purposes. Thereis a continuum of individuals on the interval [0,1] who are identical at date0; each individual is endowed with one unit of the good at t = 0, and hasno endowment in the remaining periods. There are two linear investmenttechnologies: a short term asset which yields R1 > 0 at date 1 and 0 at date2,4 and a long term, completely illiquid, asset which yields 0 at date 1 andR2 > R1 at date 2. All investment takes place at date 0. The following tablesummarizes the asset structure where one unit of the consumption good isinvested at date 0.

Date t = 0 t = 1 t = 2Short Term Asset �1 R1 0Long Term Asset �1 0 R2

At date 1, each individual is hit by a privately observable liquidity shockwith probability q. This shock makes an individual value consumption atboth dates t = 1 and t = 2: With probability (1 � q) individuals are nothit by a liquidity shock, and only value consumption at date 2. We refer toindividuals who are subject to a shock as impatient or Type 1 individuals.Likewise, individuals who do not receive a shock are referred to as patient orType 2 individuals. An individual�s ex-ante preferences, at date 0, are given

4Unlike Diamond and Dybvig (1983) and Diamond (1997), all investment takes placeat date 0. Hence, the short term asset cannot be reinvested at date 1. The reason tointroduce this assumption is to simplify the analysis. Allowing reinvestment of the shortterm asset would simply introduce an additional arbitrage condition, between asset pricesand the return on short term assets. This would impose an additional constraint to keeptrack of in the solution of the model but otherwise leave the economics unchanged.

5

by the utility function

U(c11; c12; c22) =

(u(c11) + �c12 with prob q

u(c22) with prob (1� q)

where cit denotes consumption by type i at date t. The function u is strictlyincreasing, twice continuously di¤erentiable, strictly concave, and satis�esthe standard Inada conditions; in addition, � > 0. The law of large numbersimplies lack of aggregate uncertainty: a fraction q of the population is hit byliquidity shocks at date 1; and the remaining fraction (1� q) derives utilityfrom date 2 consumption only. Individual preferences di¤er from those inDiamond (1997) in that individuals with liquidity shocks also get utilityout of consuming at date 2. The reason for this assumption is to createan incentive to default for individuals who become borrowers at t = 1. Inaddition, we make the following assumption:

Assumption 1: � > 0 is su¢ ciently small so that�

u0(R1q)<R1R2.

Assumption 1 states that the marginal rate of substitution between date2 consumption and date 1 consumption for the impatient type is less than themarginal rate of transformation for all technologically feasible consumptionbundles. In other words, an impatient type has preferences biased towardsdate 1 consumption. The next section characterizes optimal allocations forthe model economy.

2.2 Optimal Liquidity

Suppose that there are no informational asymmetries at date 1. Then theoptimal provision of liquidity is the solution to the following maximizationproblem.

Maxc11;c12;c22

qu(c11) + q�c12 + (1� q)u(c22)

subject to the resource constraint

qc11R1

+qc12R2

+(1� q)c22R2

= 1 (1)

and subject to the non-negativity constraint

c12 � 0:

6

The �rst order conditions to the problem are

qu0(c11) =�oq

R1; (2)

q�� �oqR2

= ��o; (3)

(1� q)u0(c22) =�o(1� q)R2

; (4)

where �o is the multiplier associated with the resource constraint and �o isthe multiplier associated with the non-negativity constraint. Let c�it denotethe optimal consumption levels for type i at date t. The following lemmacharacterizes these optimal consumption levels.5

Lemma 1 If the coe¢ cient of relative risk aversion is everywhere strictlygreater than 1 then the �rst best consumption levels must satisfy c�11 > R1,c�22 < R2 and c

�12 = 0.

In the following section we introduce �nancial markets and we examinethe e¤ect of limited enforcement on the amount of liquidity that marketsprovide. We will show that �nancial markets cannot adequately insure thosesubject to shocks relative to the case of perfect information analyzed in thissection, and that limited enforcement compounds the problem.

2.3 Financial Markets

At date 0, individuals invest a fraction of their endowment � in the shortterm asset and the remaining fraction (1 � �) in the long term asset to tryto insure themselves against the possibility of liquidity shocks. At date 1,after the shock is realized, they can buy or sell claims that pay out oneunit of the good at date 2. The price of each claim is denoted by p and ismeasured in terms of the good at date 1. At date 1, impatient types consumetheir returns from the short term asset and supply claims (borrow) against afraction of their returns from the long term asset, which is used as collateral.We denote with � the fraction of long term assets which an individual sells

5Proofs of all Lemmas and Propositions are contained in the Appendix, with the ex-ception of Lemmas 3, 4 and 5, the proofs of which can be found in Antinol� and Prasad(2007), available at http://gaetano.wustl.edu.

7

at date 1. The remaining fraction (1� �) of date 2 returns is consumed atdate 2. Patient types, on the other hand, demand claims at date 1 (lend)and consume their returns at date 2. Consumption by type i at date t, cit,is given by

c11 = �R1 + �(1� �)R2p; (5)

c12 = (1� �)(1� �)R2; (6)

c22 =�R1p+ (1� �)R2: (7)

The assumption of limited commitment is equivalent to postulating the ex-istence of an external enforcement agency that can seize a fraction � of theborrower�s assets in case he chooses to default. To prevent borrowers from de-faulting strategically, � and � must satisfy a debt incentive constraint givenby

(1� �)(1� �)R2 � (1� �)(1� �)R2:The left hand side of the constraint is what the borrower gets when he defaultson his loan at date 2, and the right hand side is what he gets if he decides topay back his creditors. When � < 1; the individual debt incentive constraintreduces to

� � �: (8)

This debt incentive constraint has a simple interpretation: only a fraction �of long term returns can be used as collateral and this therefore restricts thetotal number of claims that a borrower can supply.6

2.4 Equilibrium

An equilibrium in a �nancial market is de�ned as a triplet (p; �; �) suchthat:

1. Taking p as given, agents solve their utility maximization problem, thatis �; � 2 argmax qu(c11) + q�c12 + (1� q)u(c22) subject to (5)� (8).

2. The price p clears markets: (1� q)�R1 = qp�(1� �)R2:6As typical in these models, there will be no default in equilibrium.

8

The �rst order conditions for the individual maximization problem aregiven by the equations:

qu0(c11)(R1R2� �p)� q�(1� �) + (1� q)u0(c22)(

R1R2p

� 1) = 0 (9)

qu0(c11)(1� �)R2p� q�(1� �)R2 = �m (10)

� � � and �m � 0 with complementary slackness, (11)

where �m is the multiplier associated with the debt incentive constraint.7

The following lemma and proposition examine the e¤ect of limited en-forcement on the liquidity provided by �nancial markets.

Lemma 2 In equilibrium we haveR1R2

� p � R1R2�

and � = �. The inequali-

ties are strict if � < 1.

The lemma establishes upper and lower bounds for asset prices, and thatborrowing constraints are always binding in equilibrium. If prices of claimsare too high then all agents at t = 0 invest only in the long term asset,and markets do not clear at t = 1. If prices are too low, then all agentsat t = 0 invest in the short term asset only, and once again markets donot clear at t = 1. To understand why the debt incentive constraint binds

let us combine the inequality p � R1R2

with Assumption 1. This implies

that the quantity of date 1 consumption that an impatient agent wants inexchange for a unit of date 2 consumption is less than what the market giveshim. Therefore, impatient agents will not want to consume at all at date2. Limited enforcement of contracts, however, allows only a fraction � oflong-term returns to be used as collateral. The rest has to be consumed atdate 2.

Proposition 1 There exists a unique equilibrium with � � q and c11 �R1; c12 � 0; and c22 � R2: Inequalities are strict if and only if � < 1: More-over, � and c11 are strictly increasing in �; and c12 is strictly decreasing in�.

7The subscripts for the multipliers denote the speci�c problem that we are dealing with,in this case, markets.

9

Proposition 1 illustrates how consumption levels at date 1 of those hit byliquidity shocks are positively related to the limited enforcement parameter�.8 Therefore, �nancial markets may not be able to provide adequate insur-ance against these shocks. To gain some insight into the economics behindthis result, note that a fall in � has two contrasting e¤ects. Ex ante, beforeshocks are realized, long-term assets become less attractive for individuals,because it is more di¢ cult to borrow against them when long-term assetsprovide less collateral capacity. This e¤ect tends to increase �, the shareof endowment invested in short-term assets. However, imagine what wouldhappen with a decrease in � with investment positions unchanged: the supplyof claims would contract as individuals issuing them face higher borrowingconstraints. This e¤ect tends to drive the price of claims up until the demandfor claims equals its supply. Proposition 1 states that the general equilibriumprice e¤ect dominates. Even if a decline in � makes issuing claims againstlong-term assets more di¢ cult, the investment in long-term assets increases.Therefore, the equilibrium value of � is increasing in �: As a result, overallconsumption by impatient types at date 1 falls.9 Lemma 1 and Proposition 1allow us to endogenize the liquidity provided by a �nancial market: consump-tion levels of both types now depend on the limited enforcement parameter�. These results also indicate two potential roles that a bank can play. First,banks can improve liquidity and, second, banks can commit to repay loansby pooling collateral.

8To Pareto rank equilibria as � changes one needs to make the additional assumptionthat the marginal utility of consumption in period 2 is relatively small for impatient types.Speci�cally, a su¢ cient condition is u0 (R2) > �: When this condition holds, equilibriumallocations with higher � Pareto dominate those with lower �:

9Another way to think about what is happening is to consider that when � decreases,after preference shocks are realized, it becomes more di¢ cult to borrow, but lending is nota¤ected (it is equally easy to purchase claims, what has become harder is to sell claims).Thus, after shocks are realized only one side of the market is a¤ected; speci�cally only afraction q of the population is a¤ected. This direct e¤ect would seem to indicate that itis advantageous, ex ante, to increase �. Ex ante, however, there is another e¤ect, a pricee¤ect. Because borrowing contraints are tighter the supply of claims goes down, and theprice of claims goes up. This e¤ect involves borrowers and lenders, the entire population.Because of the di¤erent shares of population a¤ected the price e¤ect dominates, and it isactually more advantageous to invest less in the short term asset.

10

3 Banks and Financial Markets

In this section we introduce banks. Banks are modeled as depository institu-tions like in Diamond and Dybvig (1983). Competition in the banking sectorensures that banks maximize the expected utility of depositors. Taking asgiven the decisions of individuals, banks o¤er a deposit contract that paysd1 units of consumption per unit deposited to individuals who withdraw att = 1; and d2 units of consumption per unit deposited to individuals whowithdraw at t = 2. Because banks cannot observe depositor types, contractsmust be incentive compatible.Individuals at t = 0 have three choices: they can invest a fraction of their

endowment, denoted by �1; in the short term asset, another fraction, �2; inthe long term asset, and �nally deposit the remaining fraction, �3; with abank.Unlike Diamond (1997) and Allen and Gale (2004), we treat banks and

individuals symmetrically with respect market participation. Hence, the as-sumption of limited commitment applies to banks as well. Banks can defaultin markets transactions, and in this case only a fraction of the loan can berecovered. The reason for allowing for this symmetry is to understand therole of banks in overcoming debt constraints in equilibrium, without givingbanks an advantage in market transactions. We do, however, assume thatbanks can commit to repay their depositors. The role of deposit contracts ascommitment mechanisms has been studied by Diamond and Rajan (2000),and introducing their construct into our model would not provide additionalinsight into the problem we are considering.10

We prove two results. First, prices have to line up with the marginalrate of transformation. If not, then all investment is either in long or shortterm assets, and markets do not clear. Second, we prove that when thefraction of individuals with liquidity shocks is not too high relative to the loanrecovery rate, then the presence of banks allows the economy to completelyovercome the commitment problem in equilibrium. This result shows howbanks increase liquidity, and how the presence of banks allows to reducetransaction costs associated with �nancial markets.The explanation of this result, which is behind the main message of the

10Diamond and Rajan (2000) show that the failure of banks to honor their depositcontracts will result in a run, which is costly for a bank as it loses rents on its loans whenthey are liquidated ine¢ ciently. In their framework the fragility of the deposit contractallows banks to commit to repay depositors.

11

paper, is that banks pool resources across several depositors and in so doingbuild up their collateral capacity, which they can use to borrow and funddepositors who withdraw early. In other words, the same mechanism thatallows banks to subsidize the consumption of impatient depositors with theresources of patient depositors, risk pooling, also allows banks to subsidizethe borrowing capacity of impatient consumers with the collateral capacityof patient depositors, who do not need it. As long as the combined collateralis large enough to �nance early withdrawals, banks do not face any debtconstraints and can commit to repay their loans. We now formulate themaximization problems of individuals and banks.The consumption of an individual depends on the fraction of his endow-

ment deposited with a bank and his investment in long and short term assets.Consumption for type i at date t, cit, is given by

c11 = �1R1 + ��2R2p+ �3d1; (12)

c12 = (1� �)�2R2; (13)

c22 =�1R1p

+ �2R2 + �3d2: (14)

The fractions invested in all three assets have to satisfy non-negativity andfeasibility constraints:

0 � �1 � 1; (15)

0 � �2 � 1; (16)

0 � �3 � 1; (17)

�1 + �2 + �3 = 1; (18)

and the debt incentive constraint

� � �: (19)

Deposit contracts o¤ered by banks must satisfy resource constraints andincentive compatibility conditions. Let � denote the fraction of the per capitaendowment invested in the short term asset, 1 the fraction of short termreturns paid to those who make early withdrawals, and (1� 2) the fractionof long term returns paid directly to those who make late withdrawals. Theresource constraints of a bank are given by

12

d1 = � 1R1q

+ (1� �)p 2R2q

; (20)

d2 = �(1� 1)R1(1� q)p + (1� �)(1� 2)R2

(1� q) ; (21)

and incentive compatibility constraints by

u(c11) � u(�1R1 + �p�2R2 + �p�3d2) + �(1� �)�3d2; (22)

d2 �d1p: (23)

Equations (20) and (21) clearly demonstrate the e¤ects of pooling re-sources. First, notice that (1 � �)R2 is a pool of collateral against which abank can borrow to �nance the consumption of impatient types. Second, no-tice that the fraction of long term assets (1� 2) which is not used to �nanceimpatient types need not be consumed ine¢ ciently at date 2 by those hit byliquidity shocks.The fraction of assets that can be recovered by the lender in the event of

default is denoted by �B .11 As for the case of individuals, the debt incentivecompatibility constraint of banks can be written as

(1� 2)(1� �)R2 � (1� �B)(1� �)R2:

When � < 1 this reduces to 2 � �B: (24)

Finally, in solving the bank�s problem,12 it is easier to combine the resourceconstraints (20) and (21) into one resource constraint for the bank:

d2 = �(R1

(1� q)p �qd1

(1� q)p) + (1� �)(R2

(1� q) �qd1

(1� q)p): (25)

11�B may be di¤erent from �:12Details about the solution to the problem of the bank are provided in the appendix.

The strategy which we have adopted is to solve the problem of the bank subject to (25),and then verify that there exist 1 and 2 such that (20) and (21) are satis�ed.

13

3.1 Equilibrium

An equilibrium with banks and �nancial markets consists of a price p, anindividuals�portfolio (�1; �2; �3; �) a deposit contract (d1; d2); and a bank�sportfolio (�; 1; 2) such that:

1. Banks take the price p and individual portfolios (�1; �2; �3; �) as given,and choose (d1; d2) and (�; 1; 2) to maximize the expected utility ofdepositors.

2. Individuals take the price p and the actions of banks as given and choose(�1; �2; �3; �) to maximize their expected utility.

3. Financial markets clear.

The market clearing condition is given by

q�2R2�p+ �3(1� �) 2R2p = (1� q)�1R1 + �3�(1� 1)R1: (26)

Substituting �2 = 1 � �1 � �3 into the set of feasibility constraints, theindividual problem can be equivalently written as:

max�1;�3;�

q(u(c11) + �c12) + (1� q)u(c22)

subject to the constraints speci�ed in equations (12)� (14) ; (19) ; and

�1 � 0;

�3 � 0;�1 + �3 � 1:

Di¤erentiating with respect to �1; �3; and � gives the �rst order conditionsof the individuals�problem:

qu0(c11)(R1��pR2)+(1�q)u0(c22)(R1p�R2)�q�(1��)R2 = �b2��b1; (27)

qu0(c11)(d1��pR2)+(1�q)u0(c22)(d2�R2)�q�(1��)R2 = �b2��b3; (28)

14

q�2R2(u0(c11)p� �) = �b0; (29)

where �b0 is the multiplier associated with the debt incentive constraint,and �b1; �b2; and �b3 are the multipliers associates with the non-negativityconstraints for �1; �2, and �3 respectively.We focus our attention on equilibria with �3 > 0; namely equilibria in

which the banking sector is active. Equilibria with �3 = 0 would be identicalto the equilibria studied in the previous section.The bank�s problem is characterized as

maxd1;d2;�; 1; 2

q(u(c11) + �c12) + (1� q)u(c22)

subject to the constraints given by equations (12)� (24) : There is not muchimmediate insight to be gained from the �rst-order conditions to the bank�sproblem. In the appendix, we provide details about its solution as we needthem for the proofs of our results. Here, we state a series of lemmas thatsimplify our analysis and concentrate on the features of the equilibrium thatare relevant for our purposes. First, these lemmas place lower and upperbounds on asset prices. Second, they show that the non-linear incentivecompatibility constraint (22) is super�uous, which makes the problem moretractable.

Lemma 3 In equilibrium we must have p � R1R2; and hence � = � whenever

�2 > 0.

The intuition for the lemma is exactly the same as Lemma 2. If pricesof claims were too low then both types of individuals and banks would wantto invest in the short term asset and markets would never clear. Moreover,when prices of claims are high enough, individuals want to use all of theirlong term assets as collateral and hence the debt constraint binds.The following lemma shows that in solving the model we can ignore the

incentive compatibility condition for impatient agents.

Lemma 4 Suppose p � R1R2

and c11 �R1q. Then, if the incentive compat-

ibility condition for Type 2 binds, the incentive compatibility condition forType 1 is satis�ed.

15

This result allows us to simplify the equilibrium analysis and ignore theincentive compatibility condition (22). The intuition underlying this lemmais that impatient types do not bene�t from withdrawing late, because theyface debt constraints and have to ine¢ ciently consume at date 2.The following lemma and proposition provide formal statements of the

results described earlier in this section.

Lemma 5 Suppose q � �B. Then in equilibrium p =R1R2.

Intuitively, if prices di¤er from the marginal rate of transformation, thenall the investment in the economy is either only in long-term assets or onlyin short-term assets, and the market clearing condition is violated. Whenprices are below the marginal rate of transformation then all agents, includingbanks, invest in the short term assets. When prices are above the marginalrate of transformation, banks and individuals will only invest in the longterm asset and the market clearing condition again cannot hold.We now want to determine under what conditions we can �nd equilibria

such that both banks and markets coexist. In this situation, asset tradestake place between banks and individuals at prices that equal the marginalrate of transformation. We characterize the equilibrium when both banksand markets coexist and banks trade in markets in the next proposition.

Proposition 2 Let q � �B. In an equilibrium with banks and markets c11 =R1; c12 = 0; and c22 = R2: When � < 1 all long term assets are held by banksand the debt incentive constraint of banks does not bind.

Proposition 2 states two results. First banks and markets together pro-vide more liquidity relative to markets alone (higher c11 and lower c12), andconsumption allocations do not vary with �: Second, when � < 1 all longterm assets in the economy are held by banks. The reason for this is that at

prices p =R1R2

no individual will be willing to hold long term assets because

of their debt constraints. Banks, on the other hand, are indi¤erent betweenholding short and long term assets because their debt incentive constraintsdo not bind.Even though the consumption allocation in equilibrium is unique, there

are multiple portfolios that support them. We point out two important ones.In the �rst case �3 = 1; 1 = 1; 2 = 0; and � = q: In this case all of the

16

endowment is deposited in the banks and banks do not trade in markets. Inthe second case banks rely entirely on markets to �nance early withdrawalsby impatient types. This is given by � = 0; 2 = q; �1 = q; �3 = (1 � q):Banks debt constraints do not bind because of resource pooling. Poolingresources allows a bank to pool collateral and accurately predict the fractionof impatient agents (through the law of large numbers). In this case banksuse this large pool of collateral to �nance the smaller fraction of individualswho need to consume early. Even though banks and markets provide moreliquidity relative to markets alone, banks face an upper limit on the liquiditythey can provide because asset prices cannot rise above the marginal rate oftransformation.

4 Conclusion

We studied the interaction between banks and markets when the main func-tion of the �nancial system is to provide liquidity. We showed that individuallimited commitment of the type studied in Kehoe and Levine (2001) consti-tutes an additional motive for intermediation, and allows markets and banksto become complements in the supply of liquidity.The assumption of limited enforcement is a way to endogenize restricted

market participation. Limited enforcement imposes debt constraints on bor-rowers and reduces the liquidity that �nancial markets can provide. Bankscan increase liquidity if and only if enforcement is limited, and in this casemixed �nancial systems are sustained in equilibrium.The existing literature that studies banks and markets in the Diamond

and Dybvig (1983) framework imposes exogenous restrictions to market par-ticipation to allow for a mixed �nancial system. Previous literature alsotreats banks and markets asymmetrically with respect to market participa-tion. We treat individuals and banks symmetrically: both have access tomarkets in the same fashion, and, in particular, both banks and individualshave to satisfy debt incentive constraints that prevent strategic default. Weshow that in an equilibrium where banks trade in markets, the debt incen-tive constraint does not bind for the bank, but that it binds for individuals.This is because banks build collateral capacity which they can allocate moree¤ectively than individuals can, much like collecting deposits allows them toallocate risk more e¢ ciently than individuals can. Another way to expressthis idea is to note that from a social welfare perspective it is more costly

17

for banks to default than it is for an individual, as banks pool collateral andborrowing capacity.One important issue that we do not address is the analysis of bank-runs

equilibria. As noted by, for example, Diamond and Rajan (2000), there isan important relation between the possibility of bank runs and the abilityof banks to commit to repay their depositors. Bank runs, however, are alsopotentially important for the coexistence of banks and �nancial markets,because they essentially represent a (social) cost in the provision of liquidity.Therefore, an important extension of our analysis is the consideration of bankruns in a model where both banks and markets are present.

Appendix

Proof of Lemma 1: Substituting �o from (2) into (3) we have q(� �u0(c11)R1R2

) = ��O: From Assumption 1 we have �o > 0 which implies c�12 = 0.Combining (2) and (4) we have,

u0(c�22)

u0(c�11)=R1R2

(30)

From the fundamental theorem of calculus we know that

u0(R2)R2 = u

0(R1)R1 +

R2ZR1

dtu0(t)

dtdt (31)

Since the coe¢ cient of relative risk aversion is strictly above unity everywherewe know that

R2ZR1

dtu0(t)

dtdt =

R2ZR1

(tu00(t) + u0(t))dt < 0 (32)

Combining (31) and (32) we have u0(R2)R2 < u

0(R1)R1; which implies

u0(R2)

u0(R1)<R1R2

(33)

Since u is strictly concave, at the optimum we must have either c�11 > R1 orc�22 < R2: Suppose c�11 > R1; then from the resource constraint (1) it must

18

be the case that c�22 < R2: Like wise if c�22 < R2 it follows from the resource

constraint (1) that c�11 > R1: Thus at the optimum we must have c�11 > R1and c�22 < R2:�Proof of Lemma 2: Suppose p = (

R1R2

� �) in equilibrium where � > 0.

De�ne the left hand side of (9) as MU(�). Then

MU(�) = qu0(c11)

�R1R2� �

�R1R2� ���� q�(1��)+ (1� q)u0(c22)(

R1R2p

� 1)

which can be rewritten as

MU(�) = qu0(c11)R1R2(1� �)� q�(1� �) +K

where K = qu0(c11)��+ (1� q)u0(c22)(R1R2p

� 1) > 0 since u0(:) > 0:

From Assumption 1 we have qu0(c11)R1R2(1 � �) � q�(1 � �) � 0. Thus

MU(�) is strictly positive implying � = 1. Hence markets do not clear

contradicting the fact that p <R1R2

is an equilibrium price. So in equilibrium

p � R1R2:

Since we have � < 1 and p � R1R2

in equilibrium, it follows from Assump-

tion 1 that q(1� �)R2(u0(c11)p� �) = �m > 0:The complementary slackness conditions from equation (11) imply � = �.

Now suppose p = (R1R2�

+ �) in equilibrium where � > 0. Since � = � we can

write down the left hand side of equation (9) as

MU(�) = qu0(c11)

�R1R2� �

�R1R2�

+ �

���q�(1��)+(1�q)u0(c22)

��R1

(R1 + �R2�)� 1�

which is strictly negative. This implies � = 0 and markets do not clear again

resulting in a contradiction. Hence in equilibriumR1R2

� p � R1R2�

. Similar

arguments show that the inequalities are strict if � < 1:�Proof of Proposition 1: To show existence substitute the market clearingcondition into (5), (7) and (9). Since we know from Lemma 1 that � = � inequilibrium the left hand side of (9) can be de�ned in the following way

19

g(�; �) = qR1(q � �)R2q(1� �)

u0(�R1q)� q�(1� �)

+(1� q)�q�(1� �)(1� q)� � 1

�u0�(1� �)R2

�q�

(1� q) + 1��

From the inada conditions on u we have g(�; �)lim �!0

= 1 and g(�; �)lim �!1

= �1.

Since u0 is di¤erentiable it follows that g is continuous in � over [0; 1]. Hencefrom the intermediate value theorem we know that there exists � 2 (0; 1)such that g(�; �) = 0. Since p � R1

R2�in equilibrium it follows from the

market clearing condition that � � q.To show uniqueness notice that

g�(�; �) =R1R2

�u0(c11)

(q � 1)(1� �)2 +

(q � �)(1� �)u

00(c11)R1q

�+(1� q)

�u0(c22)

(�q�)(1� q)�2 �

�q�(1� �)(1� q)� � 1

�u00(c22)

�q�

(1� q) + 1�R2

�Since p � R1

R2we have

q�(1� �)(1� q)� � 1 � 0: Since u is strictly increasing and

strictly concave we have g�(�; �) < 0 for all � 2 (0; q]. Hence in equilibrium� is unique.Substitute p from the market clearing condition into equation (5). We

then have

c11 = �R1 + �(1� �)R2�(1� q)�R1q�(1� �)R2

�which can be reduced to c11 =

�R1q: Since � � q, it follows that c11 � R1.

Also since p � R1R2

we have from (7) that c22 � R2: Using Lemma 2 and

the individual consumption constraints it is possible to verify that c11 = R1;c22 = R2; and c12 = 0 if and only if � = 1:To show that � and c11 are strictly increasing in � notice that

g�(�; �) = q�+(1�q)��q�(1� �)(1� q)� � 1

�u00(c22)

(1� �)R2q(1� q) + u0(c22)

q(1� �)(1� q)�

�

20

Since u is strictly increasing and strictly concave, and sinceq�(1� �)(1� q)� �

1 � 0 it follows that g�(�; �) > 0: Using the implicit function theorem we

haved�

d�= � g�(�; �)

g�(�; �)> 0: Also

dc11d�

=R1q

d�

d�: Thus � and c11 are strictly

increasing in �: To show that c12 is strictly decreasing in � note thatdc12d�

=

� (1� �)R2 � (1� �)R2d�

d�< 0:�

Proof of Lemma 3: Let (�1; �2; �3; �); (d1; d2); ( 1; 2); �; p be an equi-librium with p < R1

R2: The proof is split into a series of claims to establish a

contradiction. The �rst claim shows that individuals do not invest anythingin the long term asset. For future reference, denote the marginal utilities inthe left hand side of (27) and (28) as MU(�1) and MU(�3) respectively.

Claim 1 �2 = 0:

To prove Claim 1 notice that when p <R1R2, from Assumption 1 we have

MU(�1) is strictly positive. This implies �b2 > 0: From the complementaryslackness conditions it follows that �2 = 0:The next claim characterizes the set of contracts that satisfy incentive

compatibility and the resource constraint.

Claim 2 d1 � R1:

To see why the above claim is true, suppose d1 > R1: Since p <R1R2

and

d1 > R1 we have

R1p=

R1(1� q)p �

R1q

(1� q)p >R1

(1� q)p �d1q

(1� q)p (34)

andR1p> R2 >

R2(1� q) �

R1q

(1� q)p >R2

(1� q) �d1q

(1� q)p (35)

Using equations (34) and (35) it follows from the resource constraint (25)that

d2 = �(R1

(1� q)p�d1q

(1� q)p)+(1��)(R2

(1� q)�d1q

(1� q)p) < �R1p+(1��)R1

p=R1p

(36)

21

This implies thatd1d2

> p which is a contradiction because the incentive

constraint (23) is violated.

Claim 3 � = 1 or �3 = 0:

To prove this claim consider two possible cases.

CASE 1: d2 �R1p:

Suppose �3 > 0 and � < 1: Consider a new deposit contract (d01; d02) with

d01 =R1q� (1� q)pd2

q, d02 = d2 and �

0 = 1: Since p <R1R2; we have

R1q� (1� q)pd2

q>R2p

q� (1� q)pd2

q(37)

which implies

d01 =R1q� (1� q)pd2

q> �(

R1q� (1� q)pd2

q)+(1��)(R2p

q� (1� q)pd2

q) = d1

(38)

Since d2 �R1pit follows from (38) that d01 � R1: The new contract (d01; d02)

satis�es the incentive constraint (23) sinced01d02

=d01d2� R1d2� p: Also since

d01 > d1 and d02 = d2 the contract satis�es the incentive constraint (22) as well.

Finally set 01 =qd01R1

and 02 = 0: Since 0 � d01 � R1 we have 0 � 01 � 1: Itcan be checked that (d01; d

02); (

01;

02); and �

0 satisfy both resource constraints(20) and (21) ; and the debt incentive constraint (24). Since �3 > 0; the newcontract increases c11 while holding c12 and c22 �xed and thus increases theexpected utility of an individual leading to a contradiction. Thus whenever

the optimal deposit contract sets d2 �R1pit must be the case that � = 1 or

�3 = 0:

CASE 2: d2 <R1p:

From Claim 2 we know that d1 � R1: Since d2 <R1pwe have MU(�1) >

MU(�3). Thus the multipliers in (27) and (28) have to satisfy �b3 > �b1 � 0which in turn implies �3 = 0:

22

Combining Claim 1 and Claim 3 it follows that markets never clear re-sulting in a contradiction. Thus in equilibrium it must be the case that p �R1R2: From (29) and Assumption 1 it follows that � = � whenever �2 > 0:�

Proof of Lemma 4: Let p � R1R2

and suppose the incentive constraint (23)

binds with d1 = d2p. De�ne c011 = �1R1 + �p�2R2 + �p�3d2. Then theincentive constraint (22) holds i¤

u(c11)� u(c011) � �(1� �)�3d2

If � = 1 then the expression above holds with equality and we are done.Now suppose � < 1:Then dividing both sides by �3d2p(1� �) we get

u(c11)� u(c011)�3d2p(1� �)

� �(1� �)�3d2�3d2p(1� �)

which reduces to�(c11 � c011)u(c11)� u(c011)

� p

Since d1 = d2p and � < 1 we have c011 < c11: Since u is strictly concaveand since c011 < c11; it follows that

�

u0(c11)>

�(c11 � c011)u(c11)� u(c011)

Since c11 <R1qit follows that

�(c11 � c011)u(c11)� u(c011)

<�

u0(c11)<R1R2

� p

Hence the incentive constraint (22) is satis�ed.�Proof of Lemma 5: The proof of Lemma 5 again is split into a seriesof claims. Figure 1 allows us to understand each step of the claim moreclearly. On the horizontal axis we have d1 and on the vertical axis we haved2. The ray through the origin given by d1 = d2p represents those pointswhere the incentive compatibility condition of type 2 binds. The two parallellines consist of all contracts that satisfy the resource constraint when � = 1and � = 0 respectively.

23

Figure 1: Graphic description of deposit contracts when p >R1R2

The proof is by contradiction. Let (�1; �2; �3; �); (d1; d2); ( 1; 2); �; p

be an equilibrium with p >R1R2:

Claim 1 d1 � R2p:

Suppose d1 > R2p: Since p >R1R2

and d1 > R2p we have

R2 >R1p>R1p(

1

(1� q) �qR2p

(1� q)R1) =

R1 � qR2p(1� q)p >

R1(1� q)p �

qd1(1� q)p

(39)and

R2 =R2

(1� q) �R2pq

(1� q)p >R2

(1� q) �d1q

(1� q)p (40)

24

Using equations (39) and (40) it follows from the resource constraint (25)that

d2 = �(R1

(1� q)p�d1q

(1� q)p)+(1��)(R2

(1� q)�d1q

(1� q)p) < �R2+(1��)R2 = R2(41)

This implies thatd1d2

> p which is a contradiction because the incentive

constraint (23) is violated.

Claim 2 Consider any (d1; d2) and � such that the incentive constraint (23)and the resource constraint (25) hold. Then there exist 1, 2 and �

0 with 0 � 1 � 1; 0 � 2 � 1 and 0 � �0 � 1 such that ( 1; 2); (d1; d2) and �0 satisfythe resource constraints (20) and (21) and the debt incentive constraint:

To prove this claim pick any (d1; d2) and any � such that the resource con-

straint (25) and the incentive constraint (23) hold. Choose 1 =qd1

(1� q)pd2 + qd1=

2. To see how 1 and 2 are chosen, draw a line through the origin thatpasses through (d1; d2): The intersection of this line with (25) when � = 1determines 1 whereas the intersection of this line with (25) when � = 0determines 2: It is clear that 1 and 2 are non negative and since theincentive constraint (23) holds it follows that d1 � (1�q)pd2+qd1 which im-plies 2 � q: Since q � �B; it follows that the banks debt incentive constraintholds.To show that the resource constraints (20) and (21) are satis�ed, pick

�0 =R2p� (qd1 + (1� q)d2p)

(R2p�R1):

Since p >R1R2

from (25) we have

d1 = �(R1q� (1� q)pd2

q) + (1� �)(R2p

q� (1� q)pd2

q) >

R1q� (1� q)pd2

q

and

d2 = �(R1

(1� q)p�d1q

(1� q)p)+(1��)(R2

(1� q)�d1q

(1� q)p) �R2

(1� q)�d1q

(1� q)p

25

which implies qd1 + (1 � q)d2p > R1 and R2p � (qd1 + (1 � q)d2p) � 0:Thus 0 � �0 � 1:To check that 1, 2, �0 and (d1; d2) satisfy (20) substitute 1, 2, �

0 in the right hand side of (20). The right hand side of (20) is givenby

qd1(1� q)pd2 + qd1

((R2p� (qd1 + (1� q)d2p))

(R2p�R1)R1q+(1�(R2p� (qd1 + (1� q)d2p))

(R2p�R1))R2p

q)

The expression above reduces to d1 and thus (20) is satis�ed. A similarexercise can be performed for (21).

Claim 3 d2 � R2: Also the deposit contract that pays R2p at date 1 and R2at date 2 has to satisfy the incentive constraint (22) :

Suppose the optimal deposit contract sets d2 < R2: Then it must be thecase that � > 0 and d1 < R2p. To see this notice that if � = 0, then d2 < R2implies

d1 =R2p

q� (1� q)pd2

q> R2p

which violates Claim 1. On the other hand if d1 � R2p then the incentiveconstraint (23) is violated.Also (23) must bind. If not banks can choose a new deposit contract

(d01; d02) and �

0 such that d2 = d02; �0 = � � � where � > 0 is su¢ ciently small,

and d01 = �0(R1q� (1� q)pd2

q) + (1� �0)(R2p

q� (1� q)pd2

q): Since p >

R1R2; it

follows that (R1q� (1� q)pd2

q) < (

R2p

q� (1� q)pd2

q) and thus

d01 = �0(R1q� (1� q)pd2

q) + (1� �0)(R2p

q� (1� q)pd2

q)

> �(R1q� (1� q)pd2

q) + (1� �)(R2p

q� (1� q)pd2

q) = d1

Since � is su¢ ciently small it follows that (23) still holds and becaused01 > d1 and d2 = d

02, the incentive constraint (22) also holds. Since d

01 < R2p

when � is su¢ ciently small, using Claim 2 we can �nd 01 and 02 such that

the resource constraints and debt incentive constraint holds. This results in

26

a contradiction. Thus when the optimal deposit contract sets d2 < R2; (23)must bind.Now to show that d2 < R2 results in a contradiction, suppose banks

choose a new contract (d001 ; d

002) with d

001 = d1 + �

0 and d002 = d2 + �

00where

�0 > 0 and �00> 0, such that

d001

d002

=d1d2= p: It can be shown that (d

001 ; d

002)

satis�es the resource constraint (25) when �0 is su¢ ciently small. Let c11 bethe equilibrium consumption level at date 1 for type 1. Since the equilibrium

consumption levels must be feasible we have c11 �R1q: Let c0011 denote the

new consumption at date 1 for the new deposit contract (d001 ; d

002). Then for �

0

su¢ ciently small it follows from Assumption 1 and the continuity of u0 that�

u0(c0011)<R1R2: Using exactly the same reasoning as in Lemma 4 it follows

that the new contract satis�es (22) : Once again from Claim 2 we know thatbanks can �nd 01 and

02 such that the resource constraints and debt incentive

constraint holds. Since the new deposit contract o¤ers a higher return forboth types it strictly dominates the old contract leading to a contradiction.Thus in equilibrium d2 � R2:Now suppose the deposit contract given by (R2p;R2) does not satisfy

(22) : From Claim 1 we know that d1 � R2p: This implies that d2 < R2 tosatisfy (22) : But this is a contradiction. Thus the deposit contract given by(R2p;R2) must satisfy (22) :

Claim 4 Banks choose � = 0:

Suppose � > 0: Then by reallocating investments across the long andshort term assets banks can choose �0 = 0, and o¤er a new contract (d01; d

02)

with

d01 =R2p

q�d2(1� q)p

q> �(

R1q�d2(1� q)p

q)+(1��)(R2p

q�d2(1� q)p

q) = d1

(42)and

d02 = d2 (43)

Since d2 � R2 it follows that d01 � R2p; and thus the new contractsatis�es (23) : Also since d01 > d1 and d02 = d2 the contract satis�es (22) as

27

well. Finally using Claim 2 we can �nd 01 and 02 such that the resource and

debt incentive constraints hold. This contradicts the fact that (d1;d2) is theoptimal contract. Thus � = 0:

Claim 5 The incentive constraint (23) binds and (d1; d2) = (R2p;R2).

To solve the banks problem when � = 0; we leave the incentive compat-ibility condition of type 1 (22) and the debt incentive constraint (24) outand check that the solution satis�es it later. We also substitute the resourceconstraints (20) and (21) with (25) and check that those two constraints holdlater. The bank�s problem is

Maxd1;d2

qu(c11) + q�c12 + (1� q)u(c22)

subject to the incentive constraint (23) and the resource constraint (25) :The �rst order conditions to the problem are given by

q�3(u0(c11)�

u0(c22)

p) = �0b

1

(1� q) ; (44)

where �0b is the multiplier associated with (23) :

Next consider the consumption constraints. We have �1R1 � �1R1pp;

�2�R2p � �2R2p; and from (23) we have �3d1 � �3d2p . Combining theseinequalities we have

�1R1 + �2�R2p+ �3d1 � �1R1pp+ �2R2p+ �3d2p (45)

which, using (12) and (14) can be rewritten as

c11c22

=�1R1 + �2�R2p+ �3d1

�1R1p+ �2R2 + �3d2

� p (46)

Since the coe¢ cient of relative risk aversion is strictly greater than 1

everywhere it follows thatu0(c22)

u0(c11)<c11c22

� p: Thus u0(c11)�u0(c22)

p> 0 which

implies �0b > 0: Thus (23) binds. Combining the binding incentive constraint(23) with the resource constraint (25) we have (d1; d2) = (R2p;R2). FromClaim 3 we know that this contract satis�es (22) : From Claim 2 we know

28

that both resource constraints (20) and (21) and the debt incentive constraint(24) are satis�ed.From the claim above it follows that MU(�3) > MU(�1) which implies

�b1 > �b3 � 0 and thus �1 = 0: Since banks choose � = 0 markets never

clear leading to a contradiction. Thus it must be the case that p =R1R2

in

equilibrium.�Proof of Proposition 2: To solve the banks problem we leave (22) and thedebt incentive constraint out and check that the solution satis�es it later. Wealso substitute (20) and (21) with (25) and check that those two constraints

hold later. When p =R1R2; the banks resource constraint becomes

d2 =R2

(1� q) �d1qR2

(1� q)R1(47)

The bank chooses (d1; d2) to maximize expected utility subject to (23)and (25). The �rst order condition to the problem is

q�3

�u0(c11)� u0(c22)

R2R1

�= �0b

�1 +

q

(1� q)

�;

where �0b is the multiplier associated with (23) :

Combining (47) withd1d2� R1R2

we have d1 � R1 and d2 � R2: From the

consumption constraints it follows that c11 � R1; whereas c22 � R2: Sincethe coe¢ cient of relative risk aversion is greater than 1 we have

u0(c22)

u0(c11)<c11c22

� R1R2

This implies that �0b > 0 which in turn implies that (23) binds. Combining(23) and (25) we have d1 = R1 and d2 = R2: Choosing � = q; 1 = 1; 2 = 0we see that (20), (21) and the debt incentive constraint are satis�ed. Alsofrom Lemma 4, (22) also holds. Now consider two possible cases. Firstsuppose � = 1: From (29) and Assumption 1 we know that � = � whenever�2 > 0: Then from the consumption constraints (12) and (14) it follows thatc11 = R1 and c22 = R2: Now consider the other case where � < 1: Then theleft-hand sides of (27) and (28) are strictly positive. Thus �2 = 0 and all longterm assets are held by banks and we again have c11 = R1 and c22 = R2.�

29

References

[1] Antinol�, G., Prasad, S., 2007. Commitment, banks and markets. Work-ing paper, Washington University in St. Louis.

[2] Allen, F., Gale, D., 2004. Financial intermediaries and markets. Econo-metrica 72(4), 1023-1061.

[3] Azariadis, C., Lambertini, L., 2003. Endogenous debt constraints in lifecycle economies. Review of Economic Studies 70, 461-487.

[4] Diamond, D., 1997. Liquidity, banks and markets. Journal of PoliticalEconomy 105, 928-956.

[5] Diamond, D., Dybvig, P., 1983. Bank runs, deposit insurance and liq-uidity. Journal of Political Economy 91, 401-419.

[6] Diamond, D., Rajan, R., 2000. A theory of bank capital. Journal ofFinance 55, 2431-2465.

[7] Fecht, F., Huang, K., Martin, A., 2004. Financial intermediaries, mar-kets and growth. Working paper, Federal Reserve Bank of New York.

[8] Hellwig, M., 1998. Banks, markets and the allocation of risks. Journalof Institutional and Theoretical Economics 154, 328-345.

[9] Jacklin, C., 1987. Demand deposits, trading restrictions and risk shar-ing. In: Prescott, E., Wallace, N. (Eds.), Contractual arrangements forintertemporal trade. University of Minnesota Press, pp. 26-47.

[10] Kehoe, T., Levine, D., 2001. Liquidity constrained markets versus debtconstrained markets. Econometrica 69, 575-598.

[11] von Thadden, E.-L., 1999. Liquidity creation through banks and mar-kets: multiple insurance and limited market access. European EconomicReview 43, 991-1006.

[12] Wallace, N., 1988. Another attempt to explain an illiquid banking sys-tem: the Diamond and Dybvig model with sequential service taken se-riously. Quarterly Review, Federal Reserve Bank of Minneapolis 12(4),3-16.

30