Cost and profit efficiency of conventional and Islamic banks in GCC countries

18

Cost and profit efficiency of conventional and Islamic banks in GCC countries Samir Abderrazek Srairi Published online: 28 November 2009 Ó Springer Science+Business Media, LLC 2009 Abstract Using stochastic frontier approach, this paper investigates the cost and profit efficiency levels of 71 commercial banks in Gulf cooperation council countries over the period 1999–2007. This study also conducts a comparative analysis of the efficiency across countries and between conventional and Islamic banks. Moreover, we examine the bank-specific variables that may explain the sources of inefficiency. The empirical results indicate that banks in the Gulf region are relatively more efficient at generating profits than at controlling costs. We also find that in terms of both cost and profit efficiency levels, the conventional banks on average are more efficient than Islamic banks. Furthermore, we observe a positive corre- lation of cost and profit efficiency with bank capitalization and profitability, and a negative one with operation cost. Higher loan activity increases the profit efficiency of banks, but it has a negative impact on cost efficiency. Keywords Banking Cost efficiency Profit efficiency Islamic banks Stochastic frontier approach GCC countries JEL classification C30 G21 1 Introduction The banking industry around the world has undergone profound and extensive changes over the last two decades. The globalization of financial markets and institutions which has been accompanied by government deregulation, financial innovations, information revolution and advanced application in communication and technology, has created a competitive banking environment and modified the tech- nology of bank production. Due to these developments and changes in the modern banking field, banks are trying to operate more efficiently in terms of cost and profit in order to stay competitive (Karim and Gee 2007). Moreover, to assist banks in confronting these challenges, financial authorities in both developed and developing countries have implemented various measures to restructure their financial sectors and to promote a deregulated banking environment. Consistent with the transformation of the banking sec- tors throughout the world, the literature related to the performance and the efficiency of banks is proliferating, and the majority of these studies cover the US and Euro- pean countries. However, a little empirical work has been undertaken to investigate efficiency in Arabian banking, and especially in Gulf countries despite the importance of this region on political and economic levels. To fill this gap and to contribute to the existing litera- ture, the main objective of this study is to provide more information on the efficiency of the banking industry in the six Gulf cooperation council (GCC) countries (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates). Thus, we analyze the cost and profit efficiency of GCC banking employing a parametric approach, and using a panel data of 71 commercial banks over a recent period 1999–2007. This paper has extended the literature in two directions. First, to our knowledge, this is the first empirical study that has analyzed profit efficiency of commercial banks in the Gulf region. Second, cost and profit efficiency levels are compared between conventional and Islamic banks in this region. S. A. Srairi (&) Riyadh Community College, King Saud University, Kingdom of Saudi Arabia, P.O. Box 28095, Riyadh 11437, Kingdom of Saudi Arabia e-mail: [email protected]; [email protected] 123 J Prod Anal (2010) 34:45–62 DOI 10.1007/s11123-009-0161-7

Transcript of Cost and profit efficiency of conventional and Islamic banks in GCC countries

Cost and profit efficiency of conventional and Islamic banksin GCC countries

Samir Abderrazek Srairi

Published online: 28 November 2009

� Springer Science+Business Media, LLC 2009

Abstract Using stochastic frontier approach, this paper

investigates the cost and profit efficiency levels of 71

commercial banks in Gulf cooperation council countries

over the period 1999–2007. This study also conducts a

comparative analysis of the efficiency across countries and

between conventional and Islamic banks. Moreover, we

examine the bank-specific variables that may explain the

sources of inefficiency. The empirical results indicate that

banks in the Gulf region are relatively more efficient at

generating profits than at controlling costs. We also find

that in terms of both cost and profit efficiency levels, the

conventional banks on average are more efficient than

Islamic banks. Furthermore, we observe a positive corre-

lation of cost and profit efficiency with bank capitalization

and profitability, and a negative one with operation cost.

Higher loan activity increases the profit efficiency of banks,

but it has a negative impact on cost efficiency.

Keywords Banking � Cost efficiency � Profit efficiency �Islamic banks � Stochastic frontier approach �GCC countries

JEL classification C30 � G21

1 Introduction

The banking industry around the world has undergone

profound and extensive changes over the last two decades.

The globalization of financial markets and institutions

which has been accompanied by government deregulation,

financial innovations, information revolution and advanced

application in communication and technology, has created a

competitive banking environment and modified the tech-

nology of bank production. Due to these developments and

changes in the modern banking field, banks are trying to

operate more efficiently in terms of cost and profit in order

to stay competitive (Karim and Gee 2007). Moreover, to

assist banks in confronting these challenges, financial

authorities in both developed and developing countries have

implemented various measures to restructure their financial

sectors and to promote a deregulated banking environment.

Consistent with the transformation of the banking sec-

tors throughout the world, the literature related to the

performance and the efficiency of banks is proliferating,

and the majority of these studies cover the US and Euro-

pean countries. However, a little empirical work has been

undertaken to investigate efficiency in Arabian banking,

and especially in Gulf countries despite the importance of

this region on political and economic levels.

To fill this gap and to contribute to the existing litera-

ture, the main objective of this study is to provide more

information on the efficiency of the banking industry in the

six Gulf cooperation council (GCC) countries (Bahrain,

Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab

Emirates). Thus, we analyze the cost and profit efficiency

of GCC banking employing a parametric approach, and

using a panel data of 71 commercial banks over a recent

period 1999–2007. This paper has extended the literature in

two directions. First, to our knowledge, this is the first

empirical study that has analyzed profit efficiency of

commercial banks in the Gulf region. Second, cost and

profit efficiency levels are compared between conventional

and Islamic banks in this region.

S. A. Srairi (&)

Riyadh Community College, King Saud University,

Kingdom of Saudi Arabia, P.O. Box 28095, Riyadh 11437,

Kingdom of Saudi Arabia

e-mail: [email protected]; [email protected]

123

J Prod Anal (2010) 34:45–62

DOI 10.1007/s11123-009-0161-7

Founded in May 1981, the GCC countries produce about

23% of the world’s oil and control more than 40% of the

world’s oil reserves. On average, oil represents more than

80% of export receipts and budget revenues, respectively.1

Over the last 6 years, the GCC incomes grew substantially

as a result of the increase in oil prices. In consequence, the

economies of these countries show growth rates much

above the world average, and are in a relatively strong

position as compared to 10 years ago. In 2001, the GCC

states decided to establish a common market by 2007, and

a monetary union, and to have a single currency before

2010. These goals are likely to promote policy coordina-

tion, reduce transaction cost, and provide a more stable

environment for business and facilitate investment deci-

sions. To reach these objectives and in response to the

globalization of financial markets, the financial and mon-

etary authorities in GCC countries, during the last decade,

have adopted financial sector liberalization programs to

free their economies. These measures included liberalizing

trade, encouraging foreign direct investment (FDI), interest

rates liberalization, allowing entry of new private banks

both domestic and foreign, strengthening the central bank’s

supervisory capacity, and implementing regulations that

helped in progressively moving the Gulf states toward

market-based economies (Elton 2003; Al-Obaidan 2008).

The GCC countries have a fairly high number of banks

with an extensive network of branches. But Gulf banks are

still small compared to the big international banks. Most

banks are family-owned with modest government equity

and a large number of specialized banks are fully owned by

the government (Elton 2003). Banks in these countries are

financially strong, well capitalized and have adopted

modern banking services (Srairi 2009). Their operations

can be characterized by satisfactory asset quality, adequate

liquidity and high levels of profitability (Islam 2003a).

Local banks follow international account standards (IAS)

and the central monetary authorities of Gulf countries have

strengthened the prudential norms in recent years (Islam

2003b). Furthermore, one important group of banking

services that have experienced rapid growth in GCC

countries is the Islamic financial services. In 2007, Gulf

States capture about 35% ($178 billion) of the total assets

of Islamic banks. These are mainly concentrated in Bah-

rain, Kuwait and the UAE. During the last 10 years, the

concept of Islamic banking has likewise developed to cover

activities of other types of financial institutions including

insurance, investment and fund management companies.

Moreover, to take advantage of Islamic financial instru-

ments, many conventional banks in GCC countries have

added Islamic banking services to their regular banking

operations.

Despite the very favourable economic environment in

GCC countries and the robust growth of both conventional

and Islamic commercial banks, the Gulf banking industry is

facing many challenges especially in view of the pressures

of globalization and the changes in the world economy and

the impact of the latest financial crises on GCC economy.

These changes have a direct impact on the banks’ main

activities, and on their performance and ability to develop

and expand their international competitive activities. Due

to these changes and the new competition from foreign

banks and non-financial companies, banks in GCC coun-

tries were induced to improve their productive perfor-

mances by reducing their costs, controlling the price of

funds and improving the pricing and mix of their outputs.

This study, using the bank-scope database, focuses on

the analysis of cost and profit efficiency of the commercial

banks in GCC countries in order to provide some inter-

esting insights on the efficiency of the Gulf banking sys-

tems that could be used by managers and policy makers

operating in these countries. Thus, the purpose of this paper

is threefold. First, we estimate a stochastic cost and profit

frontiers using a specific functional form (standard translog

function). To follow Perera et al. (2007) and Mamatzakis

et al. (2008), country-level variables are incorporated in the

common cost and profit frontiers to account for variation in

banking technologies that may be related to macro-eco-

nomics conditions and to structural and institutional fea-

tures of a country. In this research, we use the maximum

likelihood procedure of Battese and Coelli (1995) that

permits in a single step to estimate the parameters of the

cost and profit frontiers and to investigate the determinants

of bank efficiency. As a second step in the analysis, we

calculate and compare the cost and alternative profit effi-

ciency scores between country and type of banks. The

study of the differences in efficiency among GCC countries

will explain the competitive starting position of each

country, which may also shed light on the capacity to

respond to the new changing environment. Level of bank

efficiency is also compared between conventional and

Islamic commercial banks in order to provide information

on comparative managerial performance. This comparison

is related to a controversial question about the impact of

type of banks on efficiency in the banking industry (Hasan

2004). Measuring the cost efficiency of 34 commercial

banks in Malaysia, Majid et al. (2003) show that the effi-

ciency of Islamic banks is not statistically different from

the conventional banks. However, other studies (Saaid

et al. 2003; Kabir Hassan 2005) conclude that Islamic

banking industry is relatively less efficient compared to

their conventional counterparts. Finally, yet not less

importantly, we also explore the impact of certain factors

that may be correlated with bank’s efficiency. Indeed, we

include in the cost and profit functions (inefficiency term) a1 Statistics of Global Investment House (2007).

46 J Prod Anal (2010) 34:45–62

123

bank-specific variables such as size, capital adequacy,

profitability, operation cost and credit risk.

The paper is structured as follows: in the next section,

we discuss the studies on efficiency especially in the Gulf

banking industry. Section 3 presents the methodology and

the econometric model used to estimate the common cost

and profit frontiers. The data and variables concerning

outputs, input prices, country-level and bank specific are

described in Sect. 4. Section 5 explains the empirical

results of the cost and profit efficiency of commercial

banks in GCC countries, while the final section summarizes

and concludes this study.

2 Literature review

Over the last decades, there has been an extensive literature

on the cost and profit efficiency of financial institutions in

the competitive banking markets of Western Europe and

North America2 (e.g., Dietsch and Lozano-Vivas 2000;

Berger and Mester 1997; Altunbas et al. 2001; Weill 2004;

Pasiouras 2008). More recently, there have been some

studies on countries in transition (e.g., Fries and Taci 2005;

Bonin et al. 2005; Kasman and Yildirim 2006; Mat-

matzakis et al. 2008). However, empirical research on bank

efficiency in Arabic countries appears relatively scarce

(e.g., Bouchaddakh and Salah 2005 in Tunisia; Al-Fayoumi

and AlKour 2008 in Jordan). A few studies using single

country (Limam 2001; Darrat et al. 2003) or cross-country

comparison (Grigorian and Manole 2005; Ariss et al. 2007;

Ramanathan 2007) have been done on GCC countries.

Our aim in this section is to survey key studies on

efficiency in Gulf banking and summarize the most sig-

nificant results.

In a study of cost and technology efficiency in Kuwait,

Darrat et al. (2003) employed the data envelopment anal-

ysis (DEA) to estimate a number of efficiency indices for

banks over a period between 1994 and 1997. They find that

cost efficiency of Kuwaiti banks averages about 68% and

that the sources of the inefficiency are a combination of

allocative (regulatory) and technical (managerial) ineffi-

ciency. The results also indicate that larger banks are less

efficient than smaller ones, and that profitability is posi-

tively related to efficiency indices.

For the same country, Limam (2001) estimates the tech-

nical efficiency of eight Kuwaiti banks from 1994 to 1999,

using the stochastic cost frontier approach. The author fol-

lows the intermediation approach and finds that the average

cost efficiency is 91% for all banks. He also finds that banks

produce earning assets at constant returns to scale and hence

have less to gain from increasing scale of production,

through merging with other banks, than from reducing

notably their technical inefficiency. Finally, the results show

that larger bank size, higher share of equity capital in assets

and greater profitability are associated with better efficiency.

In addition to the single-country studies of cost effi-

ciency in Gulf banking, there have been three recent cross-

country studies, Grigorian and Manole (2005), Ariss et al.

(2007), and Ramanathan (2007).

Griogorian and Manole (2005) compare the efficiency

indicators of banks for the period 1997–2002 with that

of their counterparts in Kuwait, Qatar, the United Arab

Emirates, and Singapore, obtained by using DEA approach.

The results of this study show that, on average, banks in

Bahrain are more technical efficient compared to other

GCC countries, but they still lag behind their Singaporean

counterparts. The paper also finds that in terms of scale

efficiency, banks in Bahrain operate at the same level as

banks in Singapore. In addition, the findings of these

authors reveal that the inefficiencies seem to be largely

caused by pure technical inefficiency and to a lesser extent

by scale inefficiency.

The most recent study by Ariss et al. (2007) uses a non-

parametric frontier approach (DEA with constant return to

scale (CRS) assumption) to compare cost efficiency and

Malmquist productivity index (MPI) of 45 banks operating in

the six GCC countries during the period 1999–2004. They find

an average overall efficiency scores of about 78% for all banks

in GCC countries. They also find that there is a decline in the

overall efficiency index from 1999 to 2004. This decline is

caused by the decrease in allocative rather than technical

efficiency (and its component of pure technical rather than

scale efficiency). The results of country specific efficiency

indices indicate that banks in Oman on average have been the

most efficient among GCC countries followed narrowly by

banks from Bahrain and Kuwait, with Saudi Arabia being the

least efficient. Finally, the findings of the MPI show that

between 1999 and 2004, GCC banks on average have expe-

rienced a decline in the productivity of their banking system

albeit with different degree. The decline in productivity of

banking in Kuwait, Oman, and Qatar was due to both tech-

nological regress and decline in overall technological effi-

ciency. However, for Bahrain, Saudi Arabia and UAE, the

decline in MPI was the net results of technological regress and

improvement in overall technical efficiency.

To assess the efficiency of banks in GCC countries,

Ramanathan (2007) examines nearly the same sample

(over 9 banks), the same period (2000–2004), and uses the

same approach (MPI and DEA: CRS and VRS3) as that

2 See the survey article by Berger and Humphrey (1997).

3 DEA can run under either CRS or VRS. The main difference

between these two models is the treatment of returns to scale. The

VRS model ensures that a bank is compared only with banks of a

similar size, while the CRS assumption is only justifiable when all

banks are operating at an optimal scale.

J Prod Anal (2010) 34:45–62 47

123

adopted by Ariss et al. (2007). He finds, under CRS

assumption, that, for the year 2004, all six GCC countries

have at least one CRS efficient bank, and all the countries

have registered their CRS efficiencies reasonably close the

GCC average (90.1%). When the variable return to scale

(VRS) assumption is implemented in DEA, all GCC

countries have at least two VRS efficient bank, and the

average VRS efficiencies (94.2%) is larger than the cor-

responding average CRS efficiencies. The study also

reveals that all GCC countries have registered reductions in

productivity in terms of technology change (a similar result

was reached by Ariss et al. 2007). However, banks in four

of the six GCC countries (Bahrain, Kuwait, Saudi Arabia,

and the UAE) registered progress in terms of MPI during

2000–2004. The highest improvement in MPI (1.009) is

registered by the selected banks in Bahrain, while the

selected banks in Qatar have presented the highest reduc-

tions in productivity during the same period.

Our study differs from the existing literature on banking

efficiency in GCC countries on several points: First, we use

a larger number of banks (71). Second, we cover a wider

range of bank types: conventional and Islamic, and for a

longer period of time (9 years). Third, it is the first study of

Gulf banking efficiency to consider both cost and profit

efficiency using a parametric method (SFA). Fourth, to

estimate cost and profit frontier functions, we have intro-

duced country-specific variables to account for variation in

banking technologies that may be related to macroeco-

nomic conditions and to the structure of the banking sector

of a particular country.4 Fifth, our paper compares cost and

profit efficiencies scores between country and type of banks

(conventional and Islamic banks). Finally, this study tries

to identify the possible factors explaining the observed

differences of cost and profit efficiency between banks in

GCC countries.

3 Methodology

In this study, we examine cost and profit efficiency rather

than technical efficiency.5 According to Pasiouras et al.

(2008), cost efficiency is a wider concept than technical

efficiency, since it refers to both technical and allocative

efficiency. Likewise, the profit efficiency is also a wider

concept as it combines both costs and revenues in the

measurement of efficiency.

The definitions of cost and profit efficiency correspond,

respectively, to two important economic objectives: cost

minimization and profit maximization. Isik and Hassan

(2002) defined cost efficiency as a measure of how far bank’s

cost is from the best practice bank’s cost if both were to

produce the same output under the same environmental

conditions. It is measured as the ratio between the minimum

cost at which it is possible to attain a given volume of pro-

duction and the observed costs for firm. A cost efficiency

score of 0.85 would mean that the bank is using 85% of its

resources efficiently or alternatively wastes 15% of its costs

relative to a best-practice bank. Profit efficiency is a broader

concept than cost efficiency since it takes into account the

effect of the choice of vector of production on both cost and

revenues (Ariff and Can 2008). It is defined as the ratio

between the actual profit of a bank and the maximum level

that could be achieved by the most efficient bank (Maudos

et al. 2002). In other words, the number represents the per-

cent of the maximum profits that a bank is earning. Thus,

profit efficiency level equal to 0.75 means that a bank is

losing 25% in terms of profit fund. Two different versions of

the profit efficiency concept can be distinguished depending

on whether or not market power or output a price is taken

into account (Berger and Mester 1997). The standard profit

efficiency (SPE) estimates how close a bank is to producing

the maximum possible profit given a particular level of input

prices and output prices. In this case, the profit function

assumes that markets for outputs and inputs are perfectly

competitive. In contrast, the alternative profit efficiency

(APE) developed by Humphrey and Pulley (1997) assumes

the existence of imperfect competition or firms that have

market power in setting output prices. In this approach,

banks take as given the quantity of outputs and the price of

inputs and maximize profits by adjusting the price of outputs

and the quantity of inputs, unlike the standard profit effi-

ciency concept. Since our sample includes several countries

with different levels of competition, it seems more appro-

priate to use alternative profit efficiency than standard profit

efficiency. Moreover, the latter concept requires information

on output prices which is not available.

To examine the efficiency of banks using frontier

approaches, there are two models. Parametric technique,

such as stochastic frontier analysis (SFA), thick frontier

approach (TFA) and distribution free approach (DFA), uses

econometric tools and specifies the function form for the

cost or profit function. On the contrary, the non-parametric

approaches (such as DEA) and free disposable hull analysis

(FDHA) do not make an assumption concerning the func-

tional form of frontier and use a linear program to calculate

efficiency level. In the present study, we use the SFA, as

developed by Aigner et al. (1977), to estimate cost and

profit efficiency frontier. The main advantage of SFA over

DEA is that it allows us to distinguish between inefficiency

and other stochastic shocks in the estimation of efficiency

levels. In addition, by using this model, it would be easier

to add control variables, such as country-level variables, in

4 These variables will be explained in detail in Sect. 4.2.2.5 Technical efficiency is the ability to produce the maximum output

for a given bundle of inputs.

48 J Prod Anal (2010) 34:45–62

123

the equation of this model than in non-parametric tech-

niques. Hence, this approach allows us to compare effi-

ciency between country, and the efficiency of conventional

and Islamic banks.6 We illustrate the methodology using

cost efficiency first and discuss its application to the profit

function later.

In line with the recent developments in the literature

(Fries and Taci 2005; Perera et al. 2007; Mamatzakis et al.

2008) and in order to capture heterogeneity across coun-

tries, the cost function in this study is extended to

accommodate country-specific variables and thus appears

as follows:

TCijt ¼ f Pijt;Yijt;Eijt

� �þ eijt and eijt ¼ vijt þ uijt ð1Þ

where TC is total cost including both interest expenses and

operating costs, P is the vector of outputs (loans and

investment), Y is a vector of input prices (price of labor

and funds), and E is a vector of country-specific variables.

The detailed definitions of these variables are presented,

along with those of other variables used in Eq. 2 in

Table 2. This approach assumes that total cost deviates

from the optimal cost by a random disturbance vijt and an

inefficiency term uijt. vijt corresponds to random fluctua-

tions, it is a two-sided classical statistical error term that

incorporates the effect of errors of measurement of the

explanatory variables. vijt is assumed i.i.d. with [vijt * N

(0, rv2)]. The second error term uijt captures inefficiency

effects, and is assumed to follow an asymmetric half nor-

mal distribution in which both the mean u and variance ru2

may vary. The general procedure adopted in this study is to

estimate coefficients and e of Eq. 1, and to calculate effi-

ciency score for each bank in the sample. The cost frontier

can be estimated by maximum likelihood, and efficiency

levels are estimated using the regression error. In the

estimation, the terms ru2 and rv

2 are reparameterized by

r2 = ru2 ? rv

2 and c = ru2/r2. The parameter, c, lies

between 0 and 1. If it is close to zero, little inefficiency

exists and the model can be consistently estimated using

ordinary least squares. But a large value of c suggests a

deterministic frontier (Coelli 1996).

The measure of cost efficiency for any bank at time t is

calculated from the estimated frontier as CEit = 1/exp (uit).

This measure takes a value between 0 and 1. Banks with

scores closer to one are more efficient.

In order to identify factors that are correlated with bank

inefficiency, we use the model of Battese and Coelli (1995)

which permits in a single–step to calculate individual bank

efficiency score (Eq. 1) and to investigate the determinants

of inefficiency (Eq. 2). Specifically, u is assumed to be a

function of a set of bank-specific characteristics. In order to

model inefficiency, we use the following auxiliary model:

uijt ¼ oZijt þ wijt ð2Þ

where Z is a vector of explanatory bank-specific variables,

w represents a random variable which has a truncated

normal distribution (wijt * N (0, rw2 ), and q is a vector of

unknown parameters to be estimated.

For our cost function, we choose the translog specifi-

cation.7 According to Greene (1980), this function is the

most frequently selected model to measure bank efficiency,

because it presents the well-known advantage of being a

flexible functional form. Moreover, it includes, as a par-

ticular case, the Cobb-Douglas specification (Carvallo and

Kasman 2005).

The translog stochastic cost takes the following form:

ln TCijt ¼ a0 þX2

m¼1

am ln Ym;ijt þX2

s¼1

bs ln Ps;ijt þ l1T

þX8

l¼1

ql ln Ejt þ 1=2

"X2

m¼1

X2

n¼1

am;n ln Ym;ijt

� ln Yn;ijt þX2

s¼1

X2

r¼1

bs;r ln Ps;ijt � ln Pr;ijt þ l2T2

#

þX2

m¼1

X2

s¼1

um;s ln Ym;ijt � ln Ps;ijt

þX2

m¼1

kmT ln Ym;ijt þX2

s¼1

WsT ln Ps;ijt þ e ð3Þ

where subscripts i denote banks, j countries and t time

horizon and lnTC the natural log of total costs, ln Ym the

natural log of input prices, ln Ps, the natural log of output

values, while E is a vector of country-level variables in

natural log. T is the time trend variable used to capture

technical change; a, b, l, q, A, k, and w are the parameters

to be estimated, and e the composite error term. To ensure

that the estimated cost frontier is well behaved (Fries and

Taci 2005), we impose constraints on symmetry:

am;n ¼ an;m 8m; n; and bs;r ¼ br;s 8s; r

Homogeneity in pricesP2

m¼1

am ¼ 1;Pn

mam;n ¼

Ps

mum;s ¼

P2

mkm ¼ 0:

Moreover, the linear homogeneity conditions are

imposed by normalizing TC and Ym (the price of labor and

the price of funds) by the price of physical capital before

the log transformation.

6 The thick frontier approach (TFA) only provides average efficiency

scores for the whole sample.

7 Berger and Mester (1997) have compared the translog to the

alternative fourrier flexible form. They find negligible difference

between both methods.

J Prod Anal (2010) 34:45–62 49

123

In this study we also employ the profit efficiency con-

cept that implies that managers should not only pay

attention to reducing a marginal dollar of costs, but also to

raising a marginal dollar of revenue. Our approach follows

Pulley and Humphrey (1993) and Berger et al. (1996) by

assuming that firms have some market power in output

markets. Hence we choose alternative profit function

(APE) which takes output quantities as given instead of

taking output prices as given. This approach incorporates

differences across banks in market power and their ability

to exploit it (Dietsch and Weill 1999). For the APF, we use

the same translog form of the cost function, except that

total costs in Eq. 3 are replaced by total profits before tax.

To avoid a log of negative number, we transform the profit

variable as follows: ln (p ?h ?1), where h indicates the

absolute value of the minimum value of profit (p) over all

banks in sample. Thus for the bank with the lowest profit

value for the year, the dependent variable of profit function

will be equal to ln (1) = 0. Also for measuring efficiency

score under the profit function the composite error is

e = vi-ui.

The measure of profit efficiency is defined as PEit = exp

(-uit). In this case efficiency scores take a value between 0

and 1 with values closer to one indicating a fully efficient

bank.

The stochastic frontiers for cost and profit are estimated

using Frontier version 4.1 program developed by Coelli’s

(1996). The software estimates in a single–step the cost or

profit model using maximum likelihood estimation tech-

nique, and identifies potential correlates of the cost and

profit efficiency scores.

4 Data and definition of variables

4.1 Data

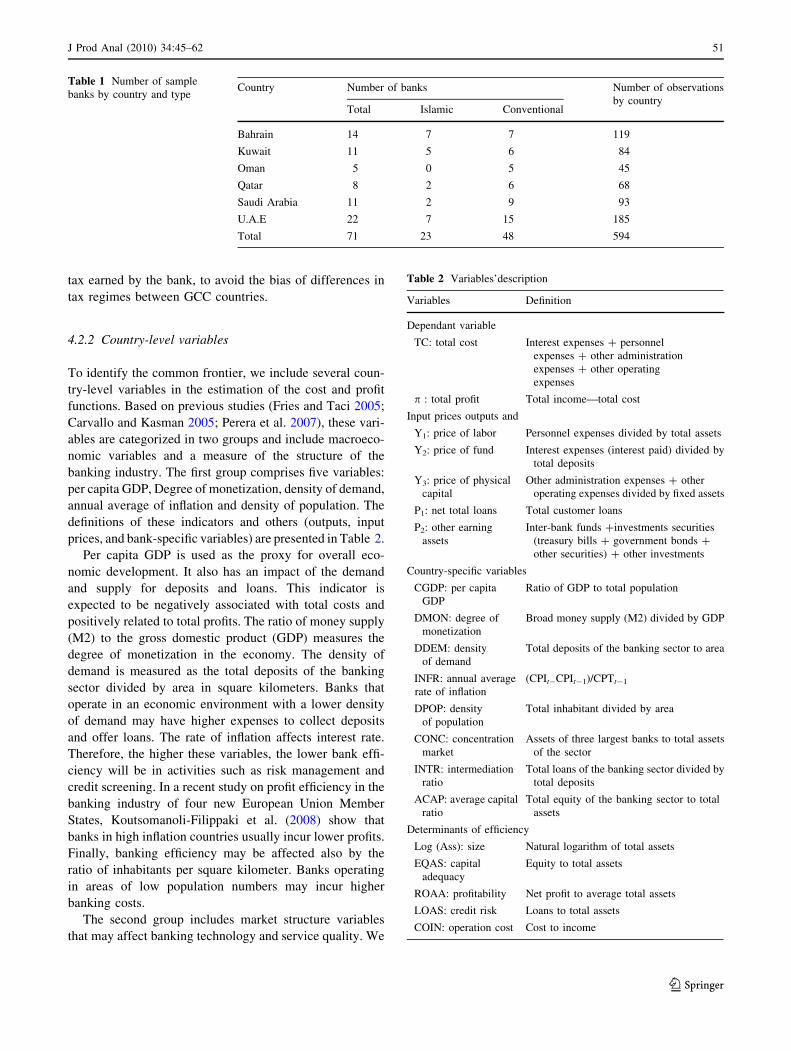

Our sample is an unbalanced panel data of 71 commercial

banks (48 conventional and 23 Islamic) from six GCC

countries: 14 banks in Bahrain, 11 banks in Kuwait, 5

banks in Oman, 8 banks in Qatar, 11 banks in Saudi Arabia,

and 22 banks in the United Arab Emirates. Altogether the

final data set contains 594 observations over the period

1999–2007 (see Table 1). All data on the bank’s balance

sheets and income statements are obtained mainly from

bankscope database of BVD-IBCA (June 2008) which

provides homogenous classification of banks and infor-

mation. In the case of missing information, we use annual

reports provided by individual banks via their websites.

The sources of macroeconomic data and the structure of

banking industry for the GCC countries are the central

banks annual reports of the respective countries and the

international financial statistics (IFS).

Since all countries have different currencies, all the

annual financial values are converted in US dollar using

appropriate average exchange rates for each year. Also, to

ensure comparability of data across countries, all values are

deflated to the year 1999 using each country’s consumer

price index (CPI).

4.2 Variables definition for estimation of cost

and profit efficiency functions

4.2.1 Outputs, input prices, total cost, and total profit

In the present study, and following the most recent studies

in the field, we adopt the intermediation approach to define

bank outputs and inputs in both cost and profit models.

According to Bos and Kool (2006), this approach is

appropriate when the banks in the sample operate as inde-

pendent entities. In this method, banks are viewed as

financial intermediates that collect purchased funds and use

labor and capital to transform these funds into loans and

other earning assets. In the alternative production approach,

banks are assumed to produce deposits, loans and invest-

ments services, using labor, physical capital and financial

capital as inputs. Bank branch efficiency studies frequently

use this method. Berger and Humphrey (1997) argue that

the intermediation approach is superior because the

majority of banks’ expenses are interest related.

In the cost and profit models, we consider two outputs8:

net total loans (total customer loans) and other earning

assets which include in the IBCA terminology investment

securities, inter-bank funds and other investments. The

input prices are: the price of capital, measured by the ratio

of non-interest expenses (operating cost net of personnel

expenses) to total fixed asset, the price of funds, computed

by dividing interest expenses9 to total deposits, and the

price of labor. Due to the lack of information about the

number of employees,10 we follow Altunbas et al. (2000),

and use a proxy measure of labor price by using the ratio of

personnel expenses divided by total assets. For the

dependent variable, total cost is defined as interest and non-

interest costs in cost efficiency function. In the case of

profit function, total profit is measured by net profit before

8 For Islamic banks, loans = Islamic operations = Murabaha receiv-

able ? Mudaraba investments ? Musharaka investments ? loans

without interest (Qard hasan) ? loans with service charge (Ju-

ala) ? other short operations (e.g., investment in Ijara assets:

leasing); other earning assets = equity investments ? investment in

associates ? investment securities (Islamic bond: Sukuk). For details

of Islamic financing contracts see (e.g., Archer et al. 1998; Zahar and

Hassan 2001; Rosly 2005).9 In case of Islamic banks, interest expenses represent profits

distributed to depositors.10 Bankscope database does not provide information on the number

of employees for each bank.

50 J Prod Anal (2010) 34:45–62

123

tax earned by the bank, to avoid the bias of differences in

tax regimes between GCC countries.

4.2.2 Country-level variables

To identify the common frontier, we include several coun-

try-level variables in the estimation of the cost and profit

functions. Based on previous studies (Fries and Taci 2005;

Carvallo and Kasman 2005; Perera et al. 2007), these vari-

ables are categorized in two groups and include macroeco-

nomic variables and a measure of the structure of the

banking industry. The first group comprises five variables:

per capita GDP, Degree of monetization, density of demand,

annual average of inflation and density of population. The

definitions of these indicators and others (outputs, input

prices, and bank-specific variables) are presented in Table 2.

Per capita GDP is used as the proxy for overall eco-

nomic development. It also has an impact of the demand

and supply for deposits and loans. This indicator is

expected to be negatively associated with total costs and

positively related to total profits. The ratio of money supply

(M2) to the gross domestic product (GDP) measures the

degree of monetization in the economy. The density of

demand is measured as the total deposits of the banking

sector divided by area in square kilometers. Banks that

operate in an economic environment with a lower density

of demand may have higher expenses to collect deposits

and offer loans. The rate of inflation affects interest rate.

Therefore, the higher these variables, the lower bank effi-

ciency will be in activities such as risk management and

credit screening. In a recent study on profit efficiency in the

banking industry of four new European Union Member

States, Koutsomanoli-Filippaki et al. (2008) show that

banks in high inflation countries usually incur lower profits.

Finally, banking efficiency may be affected also by the

ratio of inhabitants per square kilometer. Banks operating

in areas of low population numbers may incur higher

banking costs.

The second group includes market structure variables

that may affect banking technology and service quality. We

Table 1 Number of sample

banks by country and typeCountry Number of banks Number of observations

by countryTotal Islamic Conventional

Bahrain 14 7 7 119

Kuwait 11 5 6 84

Oman 5 0 5 45

Qatar 8 2 6 68

Saudi Arabia 11 2 9 93

U.A.E 22 7 15 185

Total 71 23 48 594

Table 2 Variables’description

Variables Definition

Dependant variable

TC: total cost Interest expenses ? personnel

expenses ? other administration

expenses ? other operating

expenses

p : total profit Total income—total cost

Input prices outputs and

Y1: price of labor Personnel expenses divided by total assets

Y2: price of fund Interest expenses (interest paid) divided by

total deposits

Y3: price of physical

capital

Other administration expenses ? other

operating expenses divided by fixed assets

P1: net total loans Total customer loans

P2: other earning

assets

Inter-bank funds ?investments securities

(treasury bills ? government bonds ?

other securities) ? other investments

Country-specific variables

CGDP: per capita

GDP

Ratio of GDP to total population

DMON: degree of

monetization

Broad money supply (M2) divided by GDP

DDEM: density

of demand

Total deposits of the banking sector to area

INFR: annual average

rate of inflation

(CPIt-CPIt-1)/CPTt-1

DPOP: density

of population

Total inhabitant divided by area

CONC: concentration

market

Assets of three largest banks to total assets

of the sector

INTR: intermediation

ratio

Total loans of the banking sector divided by

total deposits

ACAP: average capital

ratio

Total equity of the banking sector to total

assets

Determinants of efficiency

Log (Ass): size Natural logarithm of total assets

EQAS: capital

adequacy

Equity to total assets

ROAA: profitability Net profit to average total assets

LOAS: credit risk Loans to total assets

COIN: operation cost Cost to income

J Prod Anal (2010) 34:45–62 51

123

selected three indicators: concentration ratio, intermedia-

tion ratio and average capital ratio. Concentration ratio is

calculated as the assets of the three largest banks divided

by the total assets of the sector. If higher concentration

reflects market power for some banks, total cost is

increased through slack and inefficiency. However, if

concentration is the result of superior management and

market selection of such banks, market concentration

would be associated with lower costs because markets

remain contestable (Dietsch and Lozano-Vivas 2000; Fries

and Taci 2005; Lensink et al. 2008). The intermediation

ratio is measured by total loans to total deposits. This

variable is included in the cost and profit functions to

capture differences among the banking sectors in terms of

their capacity to convert deposits into loans. According to

Carvallo and Kasman (2005), we expect an inverse rela-

tionship between this ratio and bank costs and a positive

association with profits. As a proxy for the difference in the

regulatory conditions among countries, we use the average

capital ratio. It is measured by equity over total assets and a

negative association with total costs is expected because

less equity implies higher risk taken at greater leverage.

4.3 Determinants of efficiency

Once the cost and profit efficiency scores are calculated,

we examine internal factors that may explain the differ-

ences in efficiency across banks. For this objective, we

follow previous studies (Weill 2004; Ariff and Can 2008;

Pasiouras 2008), and we include in Eq. (2) five bank-spe-

cific variables: size, capital adequacy, profitability, opera-

tion cost and credit risk.

The natural logarithm of total assets is used as the proxy

for bank size. An overview of research shows ambiguous

results. According to Perera et al. (2007), but also Berger

et al. (1993) and Miller and Noulas (1996), larger banks are

more cost efficient than smaller banks, because large size

allows wider penetration of markets and increase in reve-

nue at a relatively less cost. However, some recent studies

(Girardone et al. 2004; Dacanay 2007) report a significant

negative relationship between bank size and efficiency.

Capital adequacy is measured as equity divided by total

assets. For many (e.g., Casu and Girardone 2004; Pasiouras

2008), this variable is positively related to efficiency.

Banks with higher ratio of equity to total assets have lower

cost and profit inefficiency. A third variable, return on

average assets, is included as a proxy for profitability. This

ratio should be positively correlated with efficiency. Gen-

erally, highly profitable banks are less cost and profit

inefficient. The credit risk or loan quality is generally

defined in the most banking efficiency studies (Mester

1996; Fries and Taci 2005; Das and Ghosh 2006) by the

ratio of non-performing loans to total loans. However, lack

of data on non-performing loans especially in Islamic

banks prevents us from utilising this ratio. Thus, this data

limitation constrains us to proxy credit risk by another

ratio: loans to total assets which has been utilized in some

recent studies (Isik and Hassan 2002; Havrylchyk 2006;

Pasiouras 2008) as a measure of risk and of bank’s loans

intensity. Banks which provide more loans are expected to

be more efficient in profit as they take more risks (Maudos

et al. 2002). However, in the case of Chinese banks, Ariff

and Can (2008) find an inverse relationship between this

variable and efficiency. They argue that banks which have

a higher ratio of loan to total assets incur higher credit risk,

and thus higher loan-loss provision, and are less efficient.

Moreover, these banks provide a large proportion of loans

to some inefficient state owned firms. The final variable

includes the operation cost indicator. It is measured as cost

to income, and is expected to be negatively related to

efficiency.

5 Empirical results

The discussion of the results on the cost and profit effi-

ciency of banks in GCC countries is organized into four

parts. First, we describe the variables used in this paper by

country and type of bank. Next, we analyze the parameters

of cost and profit frontier obtained by the stochastic frontier

approach. Third, we discuss and compare the cost and

profit efficiency scores of banks by year, country and type

of banks. Finally, we investigate the determinants of

efficiency.

5.1 Summary descriptive statistics of the data

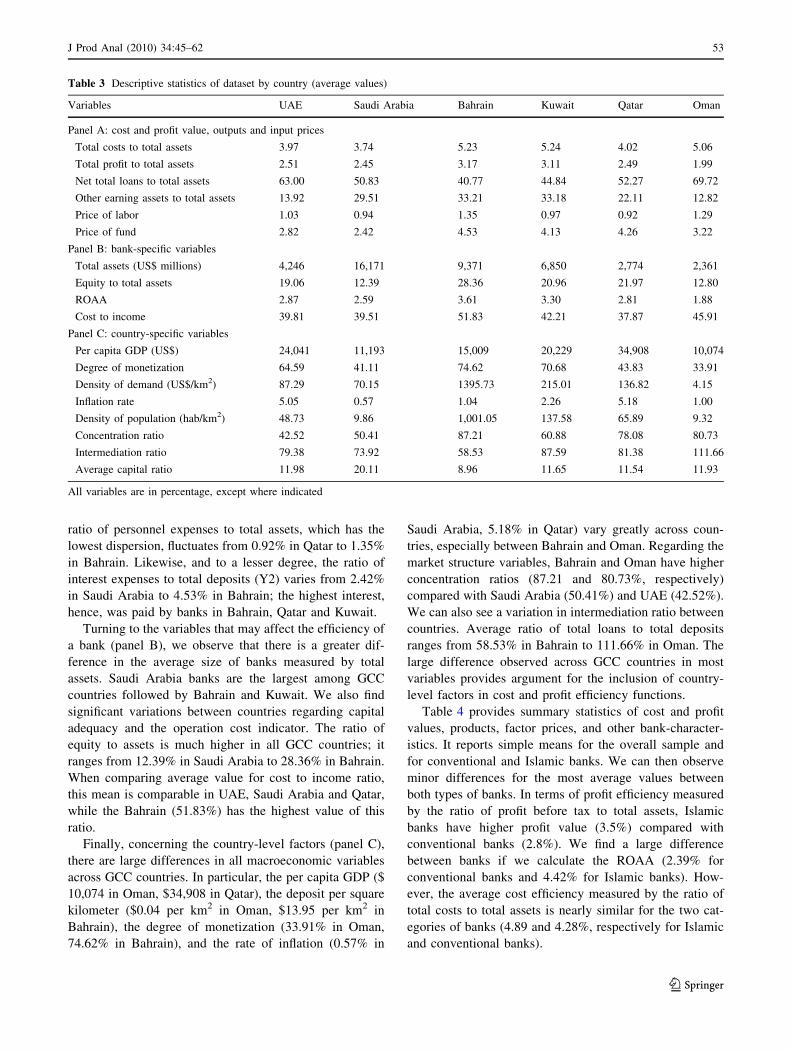

Table 3 displays some descriptive statistics by country for

the variables used in the study. Comparing the average

values across countries, we can then observe some differ-

ences regarding total cost and profit values, outputs, input

prices and other bank-specific (panels A and B). The

average cost to asset ratio is nearly similar in GCC coun-

tries; it ranges from 3.74% in Saudi Arabia to 5.24% in

Kuwait. The same report is observed for the average profit

efficiency measured by the ratio of profit before tax to total

assets of banks. This variable varies from 2% in Oman to

3.17% in Bahrain. Regarding the levels of output, differ-

ences in average value are significant, especially in the

ratio of net total loans to total assets which fluctuates from

40.77% in Bahrain to 69.72% in Oman. The difference is

also greater when we see the ratio of other earning assets to

total assets, which ranges between 12.82% in Oman to

33.21% in Bahrain. However, the average prices of labor

and funds seem to be show closer similarity between GCC

countries. Indeed, the price of labor (Y1) measured by the

52 J Prod Anal (2010) 34:45–62

123

ratio of personnel expenses to total assets, which has the

lowest dispersion, fluctuates from 0.92% in Qatar to 1.35%

in Bahrain. Likewise, and to a lesser degree, the ratio of

interest expenses to total deposits (Y2) varies from 2.42%

in Saudi Arabia to 4.53% in Bahrain; the highest interest,

hence, was paid by banks in Bahrain, Qatar and Kuwait.

Turning to the variables that may affect the efficiency of

a bank (panel B), we observe that there is a greater dif-

ference in the average size of banks measured by total

assets. Saudi Arabia banks are the largest among GCC

countries followed by Bahrain and Kuwait. We also find

significant variations between countries regarding capital

adequacy and the operation cost indicator. The ratio of

equity to assets is much higher in all GCC countries; it

ranges from 12.39% in Saudi Arabia to 28.36% in Bahrain.

When comparing average value for cost to income ratio,

this mean is comparable in UAE, Saudi Arabia and Qatar,

while the Bahrain (51.83%) has the highest value of this

ratio.

Finally, concerning the country-level factors (panel C),

there are large differences in all macroeconomic variables

across GCC countries. In particular, the per capita GDP ($

10,074 in Oman, $34,908 in Qatar), the deposit per square

kilometer ($0.04 per km2 in Oman, $13.95 per km2 in

Bahrain), the degree of monetization (33.91% in Oman,

74.62% in Bahrain), and the rate of inflation (0.57% in

Saudi Arabia, 5.18% in Qatar) vary greatly across coun-

tries, especially between Bahrain and Oman. Regarding the

market structure variables, Bahrain and Oman have higher

concentration ratios (87.21 and 80.73%, respectively)

compared with Saudi Arabia (50.41%) and UAE (42.52%).

We can also see a variation in intermediation ratio between

countries. Average ratio of total loans to total deposits

ranges from 58.53% in Bahrain to 111.66% in Oman. The

large difference observed across GCC countries in most

variables provides argument for the inclusion of country-

level factors in cost and profit efficiency functions.

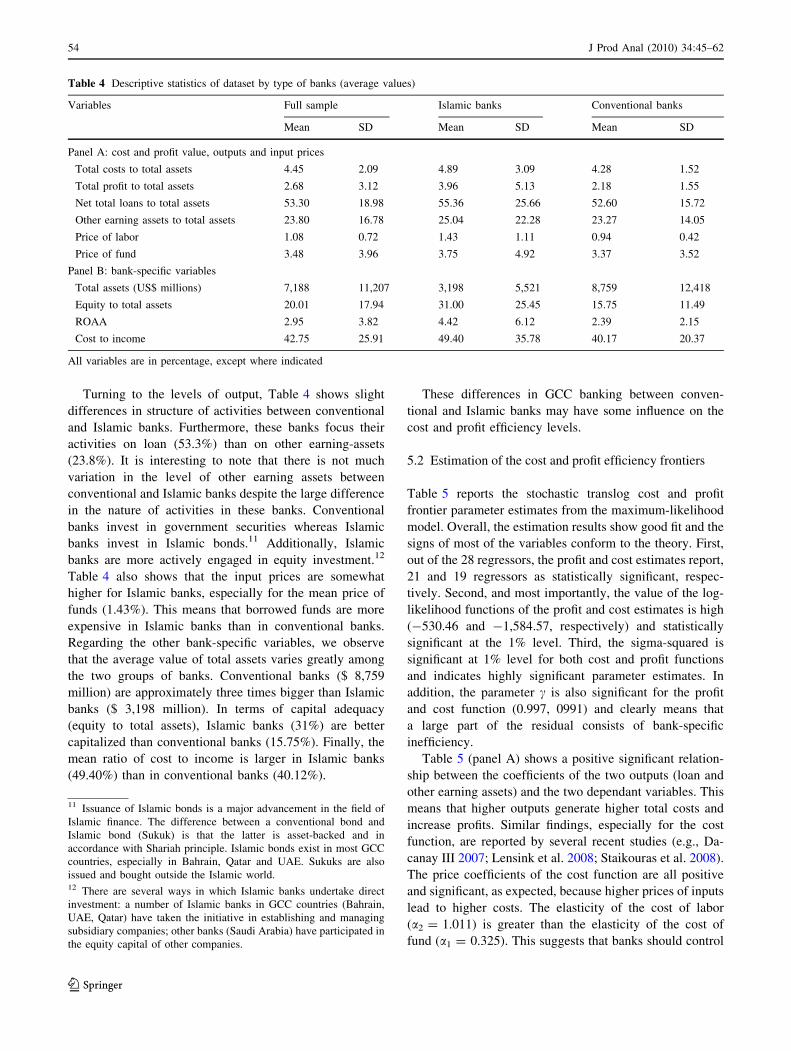

Table 4 provides summary statistics of cost and profit

values, products, factor prices, and other bank-character-

istics. It reports simple means for the overall sample and

for conventional and Islamic banks. We can then observe

minor differences for the most average values between

both types of banks. In terms of profit efficiency measured

by the ratio of profit before tax to total assets, Islamic

banks have higher profit value (3.5%) compared with

conventional banks (2.8%). We find a large difference

between banks if we calculate the ROAA (2.39% for

conventional banks and 4.42% for Islamic banks). How-

ever, the average cost efficiency measured by the ratio of

total costs to total assets is nearly similar for the two cat-

egories of banks (4.89 and 4.28%, respectively for Islamic

and conventional banks).

Table 3 Descriptive statistics of dataset by country (average values)

Variables UAE Saudi Arabia Bahrain Kuwait Qatar Oman

Panel A: cost and profit value, outputs and input prices

Total costs to total assets 3.97 3.74 5.23 5.24 4.02 5.06

Total profit to total assets 2.51 2.45 3.17 3.11 2.49 1.99

Net total loans to total assets 63.00 50.83 40.77 44.84 52.27 69.72

Other earning assets to total assets 13.92 29.51 33.21 33.18 22.11 12.82

Price of labor 1.03 0.94 1.35 0.97 0.92 1.29

Price of fund 2.82 2.42 4.53 4.13 4.26 3.22

Panel B: bank-specific variables

Total assets (US$ millions) 4,246 16,171 9,371 6,850 2,774 2,361

Equity to total assets 19.06 12.39 28.36 20.96 21.97 12.80

ROAA 2.87 2.59 3.61 3.30 2.81 1.88

Cost to income 39.81 39.51 51.83 42.21 37.87 45.91

Panel C: country-specific variables

Per capita GDP (US$) 24,041 11,193 15,009 20,229 34,908 10,074

Degree of monetization 64.59 41.11 74.62 70.68 43.83 33.91

Density of demand (US$/km2) 87.29 70.15 1395.73 215.01 136.82 4.15

Inflation rate 5.05 0.57 1.04 2.26 5.18 1.00

Density of population (hab/km2) 48.73 9.86 1,001.05 137.58 65.89 9.32

Concentration ratio 42.52 50.41 87.21 60.88 78.08 80.73

Intermediation ratio 79.38 73.92 58.53 87.59 81.38 111.66

Average capital ratio 11.98 20.11 8.96 11.65 11.54 11.93

All variables are in percentage, except where indicated

J Prod Anal (2010) 34:45–62 53

123

Turning to the levels of output, Table 4 shows slight

differences in structure of activities between conventional

and Islamic banks. Furthermore, these banks focus their

activities on loan (53.3%) than on other earning-assets

(23.8%). It is interesting to note that there is not much

variation in the level of other earning assets between

conventional and Islamic banks despite the large difference

in the nature of activities in these banks. Conventional

banks invest in government securities whereas Islamic

banks invest in Islamic bonds.11 Additionally, Islamic

banks are more actively engaged in equity investment.12

Table 4 also shows that the input prices are somewhat

higher for Islamic banks, especially for the mean price of

funds (1.43%). This means that borrowed funds are more

expensive in Islamic banks than in conventional banks.

Regarding the other bank-specific variables, we observe

that the average value of total assets varies greatly among

the two groups of banks. Conventional banks ($ 8,759

million) are approximately three times bigger than Islamic

banks ($ 3,198 million). In terms of capital adequacy

(equity to total assets), Islamic banks (31%) are better

capitalized than conventional banks (15.75%). Finally, the

mean ratio of cost to income is larger in Islamic banks

(49.40%) than in conventional banks (40.12%).

These differences in GCC banking between conven-

tional and Islamic banks may have some influence on the

cost and profit efficiency levels.

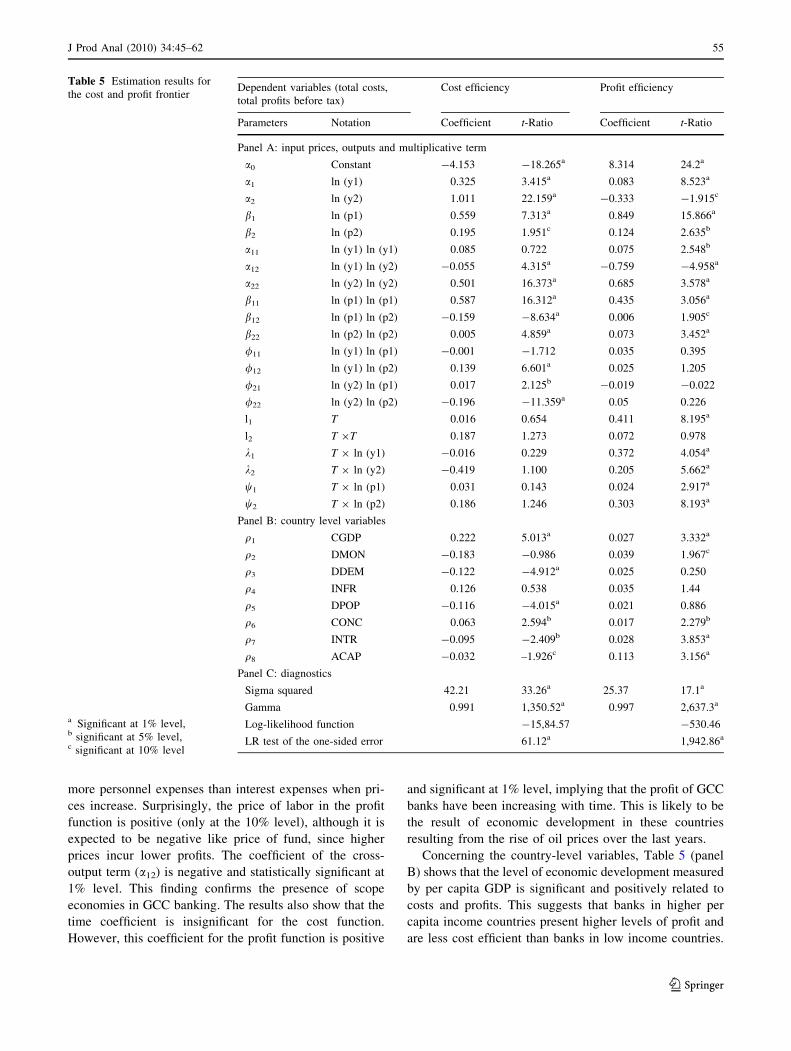

5.2 Estimation of the cost and profit efficiency frontiers

Table 5 reports the stochastic translog cost and profit

frontier parameter estimates from the maximum-likelihood

model. Overall, the estimation results show good fit and the

signs of most of the variables conform to the theory. First,

out of the 28 regressors, the profit and cost estimates report,

21 and 19 regressors as statistically significant, respec-

tively. Second, and most importantly, the value of the log-

likelihood functions of the profit and cost estimates is high

(-530.46 and -1,584.57, respectively) and statistically

significant at the 1% level. Third, the sigma-squared is

significant at 1% level for both cost and profit functions

and indicates highly significant parameter estimates. In

addition, the parameter c is also significant for the profit

and cost function (0.997, 0991) and clearly means that

a large part of the residual consists of bank-specific

inefficiency.

Table 5 (panel A) shows a positive significant relation-

ship between the coefficients of the two outputs (loan and

other earning assets) and the two dependant variables. This

means that higher outputs generate higher total costs and

increase profits. Similar findings, especially for the cost

function, are reported by several recent studies (e.g., Da-

canay III 2007; Lensink et al. 2008; Staikouras et al. 2008).

The price coefficients of the cost function are all positive

and significant, as expected, because higher prices of inputs

lead to higher costs. The elasticity of the cost of labor

(a2 = 1.011) is greater than the elasticity of the cost of

fund (a1 = 0.325). This suggests that banks should control

Table 4 Descriptive statistics of dataset by type of banks (average values)

Variables Full sample Islamic banks Conventional banks

Mean SD Mean SD Mean SD

Panel A: cost and profit value, outputs and input prices

Total costs to total assets 4.45 2.09 4.89 3.09 4.28 1.52

Total profit to total assets 2.68 3.12 3.96 5.13 2.18 1.55

Net total loans to total assets 53.30 18.98 55.36 25.66 52.60 15.72

Other earning assets to total assets 23.80 16.78 25.04 22.28 23.27 14.05

Price of labor 1.08 0.72 1.43 1.11 0.94 0.42

Price of fund 3.48 3.96 3.75 4.92 3.37 3.52

Panel B: bank-specific variables

Total assets (US$ millions) 7,188 11,207 3,198 5,521 8,759 12,418

Equity to total assets 20.01 17.94 31.00 25.45 15.75 11.49

ROAA 2.95 3.82 4.42 6.12 2.39 2.15

Cost to income 42.75 25.91 49.40 35.78 40.17 20.37

All variables are in percentage, except where indicated

11 Issuance of Islamic bonds is a major advancement in the field of

Islamic finance. The difference between a conventional bond and

Islamic bond (Sukuk) is that the latter is asset-backed and in

accordance with Shariah principle. Islamic bonds exist in most GCC

countries, especially in Bahrain, Qatar and UAE. Sukuks are also

issued and bought outside the Islamic world.12 There are several ways in which Islamic banks undertake direct

investment: a number of Islamic banks in GCC countries (Bahrain,

UAE, Qatar) have taken the initiative in establishing and managing

subsidiary companies; other banks (Saudi Arabia) have participated in

the equity capital of other companies.

54 J Prod Anal (2010) 34:45–62

123

more personnel expenses than interest expenses when pri-

ces increase. Surprisingly, the price of labor in the profit

function is positive (only at the 10% level), although it is

expected to be negative like price of fund, since higher

prices incur lower profits. The coefficient of the cross-

output term (a12) is negative and statistically significant at

1% level. This finding confirms the presence of scope

economies in GCC banking. The results also show that the

time coefficient is insignificant for the cost function.

However, this coefficient for the profit function is positive

and significant at 1% level, implying that the profit of GCC

banks have been increasing with time. This is likely to be

the result of economic development in these countries

resulting from the rise of oil prices over the last years.

Concerning the country-level variables, Table 5 (panel

B) shows that the level of economic development measured

by per capita GDP is significant and positively related to

costs and profits. This suggests that banks in higher per

capita income countries present higher levels of profit and

are less cost efficient than banks in low income countries.

Table 5 Estimation results for

the cost and profit frontier

a Significant at 1% level,b significant at 5% level,c significant at 10% level

Dependent variables (total costs,

total profits before tax)

Cost efficiency Profit efficiency

Parameters Notation Coefficient t-Ratio Coefficient t-Ratio

Panel A: input prices, outputs and multiplicative term

a0 Constant -4.153 -18.265a 8.314 24.2a

a1 ln (y1) 0.325 3.415a 0.083 8.523a

a2 ln (y2) 1.011 22.159a -0.333 -1.915c

b1 ln (p1) 0.559 7.313a 0.849 15.866a

b2 ln (p2) 0.195 1.951c 0.124 2.635b

a11 ln (y1) ln (y1) 0.085 0.722 0.075 2.548b

a12 ln (y1) ln (y2) -0.055 4.315a -0.759 -4.958a

a22 ln (y2) ln (y2) 0.501 16.373a 0.685 3.578a

b11 ln (p1) ln (p1) 0.587 16.312a 0.435 3.056a

b12 ln (p1) ln (p2) -0.159 -8.634a 0.006 1.905c

b22 ln (p2) ln (p2) 0.005 4.859a 0.073 3.452a

/11 ln (y1) ln (p1) -0.001 -1.712 0.035 0.395

/12 ln (y1) ln (p2) 0.139 6.601a 0.025 1.205

/21 ln (y2) ln (p1) 0.017 2.125b -0.019 -0.022

/22 ln (y2) ln (p2) -0.196 -11.359a 0.05 0.226

l1 T 0.016 0.654 0.411 8.195a

l2 T 9T 0.187 1.273 0.072 0.978

k1 T 9 ln (y1) -0.016 0.229 0.372 4.054a

k2 T 9 ln (y2) -0.419 1.100 0.205 5.662a

w1 T 9 ln (p1) 0.031 0.143 0.024 2.917a

w2 T 9 ln (p2) 0.186 1.246 0.303 8.193a

Panel B: country level variables

q1 CGDP 0.222 5.013a 0.027 3.332a

q2 DMON -0.183 -0.986 0.039 1.967c

q3 DDEM -0.122 -4.912a 0.025 0.250

q4 INFR 0.126 0.538 0.035 1.44

q5 DPOP -0.116 -4.015a 0.021 0.886

q6 CONC 0.063 2.594b 0.017 2.279b

q7 INTR -0.095 -2.409b 0.028 3.853a

q8 ACAP -0.032 –1.926c 0.113 3.156a

Panel C: diagnostics

Sigma squared 42.21 33.26a 25.37 17.1a

Gamma 0.991 1,350.52a 0.997 2,637.3a

Log-likelihood function -15,84.57 -530.46

LR test of the one-sided error 61.12a 1,942.86a

J Prod Anal (2010) 34:45–62 55

123

These results conform with those of Koutsomanoli-Flip-

paki et al. (2008) and Carvallo and Kasman (2005).

However, Lensink et al. (2008), found a negative rela-

tionship between GDP per capita and total costs, indicating

that an increase in GDP lowers costs. The degree of

monetization is positively associated with profits and is not

significantly related to costs. This finding differs signifi-

cantly from the study of Perera et al. (2007) which found a

significant positive relationship between the ratio of broad

money supply to GDP and total costs. Regarding other

elements of macroeconomic variables, our findings on the

effect of the density of demand is consistent with those of

Carvallo and Kasman (2005) who report a negative impact

of this variable on total costs. However, we find that the

inflation rate is neither associated with cost nor with profit.

This is because inflation during the period 1999–2007 was

largely moderate in the GCC countries. The results also

show, as expected, that the sign of the population density

variable is negative in cost function.

Turning to the market structure variables, we find that

the degree of the concentration has a positive influence on

both total costs and total profits. This is consistent with the

findings of Staikouras et al. (2008) and Perera et al. (2007).

The positive association between market concentration and

banks costs may indicate that banks that operate in less

competitive markets can charge higher prices and are under

less pressure to control their costs (Maudos et al. 2002).

The results also indicate that financial depth (loans to

deposits) decreases banking costs and increases profits.

Similar findings are reported by several studies (e.g., Fries

and Taci 2005; Carvallo and Kasman 2005; Perera et al.

2007). Finally, banking systems with a higher capital ratio

have significant higher profits and lower costs. Most

studies found that well capitalized banks are more efficient

(Berger and Mester 1997; Perera et al. 2007).

5.3 Average banks efficiencies by year, country

and type of banks

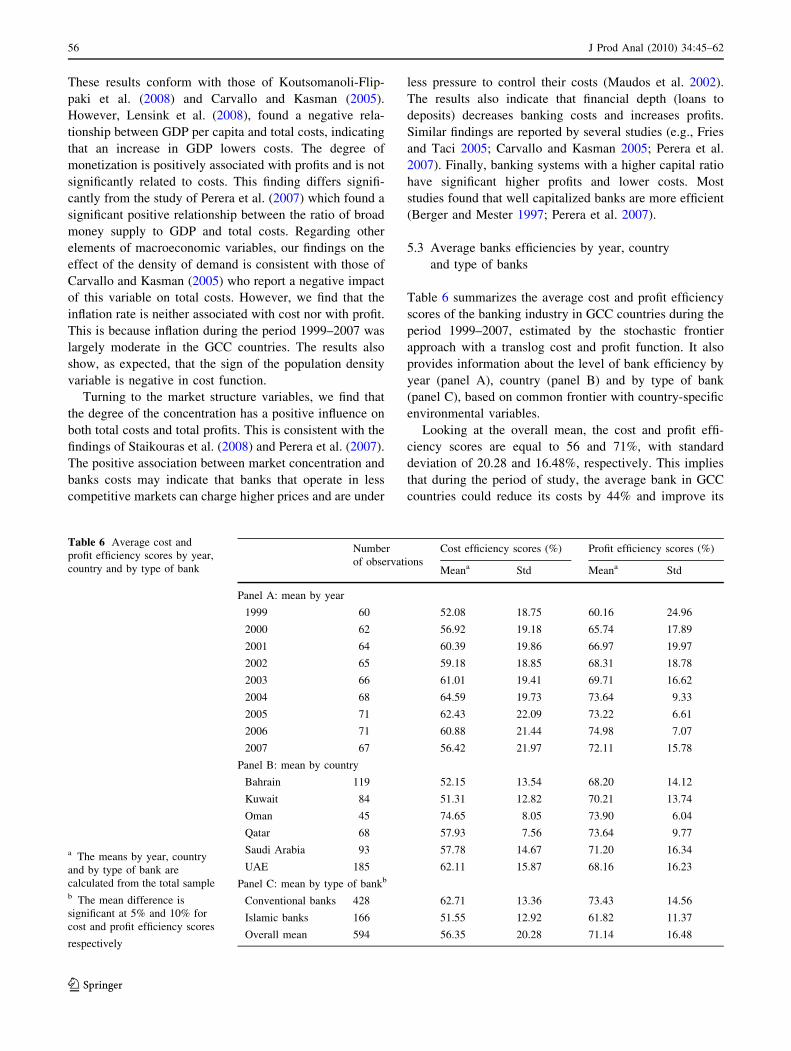

Table 6 summarizes the average cost and profit efficiency

scores of the banking industry in GCC countries during the

period 1999–2007, estimated by the stochastic frontier

approach with a translog cost and profit function. It also

provides information about the level of bank efficiency by

year (panel A), country (panel B) and by type of bank

(panel C), based on common frontier with country-specific

environmental variables.

Looking at the overall mean, the cost and profit effi-

ciency scores are equal to 56 and 71%, with standard

deviation of 20.28 and 16.48%, respectively. This implies

that during the period of study, the average bank in GCC

countries could reduce its costs by 44% and improve its

Table 6 Average cost and

profit efficiency scores by year,

country and by type of bank

a The means by year, country

and by type of bank are

calculated from the total sampleb The mean difference is

significant at 5% and 10% for

cost and profit efficiency scores

respectively

Number

of observations

Cost efficiency scores (%) Profit efficiency scores (%)

Meana Std Meana Std

Panel A: mean by year

1999 60 52.08 18.75 60.16 24.96

2000 62 56.92 19.18 65.74 17.89

2001 64 60.39 19.86 66.97 19.97

2002 65 59.18 18.85 68.31 18.78

2003 66 61.01 19.41 69.71 16.62

2004 68 64.59 19.73 73.64 9.33

2005 71 62.43 22.09 73.22 6.61

2006 71 60.88 21.44 74.98 7.07

2007 67 56.42 21.97 72.11 15.78

Panel B: mean by country

Bahrain 119 52.15 13.54 68.20 14.12

Kuwait 84 51.31 12.82 70.21 13.74

Oman 45 74.65 8.05 73.90 6.04

Qatar 68 57.93 7.56 73.64 9.77

Saudi Arabia 93 57.78 14.67 71.20 16.34

UAE 185 62.11 15.87 68.16 16.23

Panel C: mean by type of bankb

Conventional banks 428 62.71 13.36 73.43 14.56

Islamic banks 166 51.55 12.92 61.82 11.37

Overall mean 594 56.35 20.28 71.14 16.48

56 J Prod Anal (2010) 34:45–62

123

profit by 29% to match its performance with the best-

practice bank. The first result to note is the existence of

lower level of cost efficiency rather than of profit effi-

ciency. Therefore, it seems that Arab Gulf banks are more

efficient at generating profits than controlling costs. Our

findings are different from those obtained in the most

studies carried out in developed countries (e.g., Maudos

et al. 2002; Bos and Kool 2006; Ariff and Can 2008;

Staikouras et al. 2008). According to the hypothesis of

Berger and Mester (1999), the increase of profit efficiency

and the decrease of cost efficiency are the consequences of

an increasing quality of banking services which led to an

improvement of revenues. We can also explain the result

by the imperfect competition hypothesis. Indeed, due to the

dominant position of banks in GCC countries and the high

demand of financial services, these banks may have gained

higher monopoly power resulting in higher profit efficiency

and, in consequence, face less pressure to decrease costs

and to restructure their activities.

The inter-temporal comparison of the scores (panel A)

suggests that the average cost efficiency ranges between

52.08% (1999) and 56.42% (2007), while the correspond-

ing values for the average profit efficiency are 60.16%

(1999) and 72.91% (2007), respectively. Hence, along the

9 years of our sample, the profit efficiency levels (12%)

have increased more than the cost efficiency scores (4%).

However the observed improvement in efficiency is not

continuous over the period of study. Indeed, both cost and

profit efficiency scores witnessed a growth of 12% between

1999 and 2004.13 But during the period 2004–2007, the

average cost efficiency level declined from 64.59% in 2004

to 56.42% in 2007, while the average profit efficiency

scores were practically stable in the same period. The

decrease of efficiency can be explained by the increase of

competition among banks due to liberalization and open-

ness measures adopted recently in the countries, especially

in Kuwait, Qatar, Saudi Arabia and in the UAE.14

The comparison of the cost and profit efficiency scores

by country (panel B) reveals that cost efficiency varies

considerably across countries. Table 5 indicates that

Omani banks (74.65%) are the most efficient, followed by

the UAE (62.11%) and Qatari (58%) banks. The Kuwaiti

banks are the least cost efficient in the sample with a score

of 51.31%. However, profit efficiency levels show less

variation across countries. The average profit efficiency

ranges from 68.16% in the UAE to 73.90% in Oman.

Banks in Kuwait (70.21%) and in Bahrain (68.26%)

present profit efficiency scores below the average for all

GCC countries (71.14%). Except for Oman, the cost effi-

ciency scores of each country are always lower than profit

efficiency, the extreme cases being of about 15–18 per-

centage point in Bahrain, Kuwait, Qatar and Saudi Arabia.

On the other hand, in the UAE the difference between

profit and cost efficiency scores is about 6%. We can also

observe that the most profit efficient banks are not neces-

sarily the most cost efficient ones and vice versa. For

example, banks in Kuwait ranked fourth in terms of profit

efficiency, but they are the least cost efficient in the sam-

ple. Likewise, the UAE’s banks are the most cost efficient

(second place) among banks in GCC countries, while they

ranked last in terms of profit efficiency. This observation is

in line with many studies achieved in developed countries

(e.g., Berger and Mester 1997 and Rogers 1998 in USA

banks, Guevera and Maudos 2002 in EU 15 countries). If

we compare our findings concerning the classification of

country in terms of efficiency with those of the study of

Ariss et al. (2007), we find some differences. For example,

in our study banks in Bahrain are the least efficient, while

they occupied the second place in the study of Ariss et al.

(2007). Likewise, banks in Saudi Arabia are the least

efficient in the later study, but their ranks are the third and

the fourth in terms of profit and cost efficiency in our study.

We think that these differences are due to several reasons.

First, our sample contains an important number of Islamic

banks which are absent in the study of Ariss et al. (2007),

and that has probably an effect of the efficiency of banks,

especially in Bahrain, Kuwait and in the UAE.15 Second, in

our model we have introduced country-specific variables

which are omitted in the study of Ariss et al. (2007).

Finally, it seems that the choice of approach (Ariss et al.

2007 have employed non-parametric technique) and vari-

ables probably had an impact on results.

We now turn to the efficiency of conventional banks as

opposed to the efficiency of Islamic banks (panel C). As

concerns cost efficiency, comparison of the two groups of

banks shows that the conventional banks are more efficient,

on average, than Islamic banks. The mean cost efficiency

score is 62.71% for conventional banks while it is equal at

51.55% for Islamic banks. The Analysis of the dispersion

of efficiency levels shows insignificant differences between

Islamic and conventional banks (12.92 and 13.36%,

respectively). In terms of alternative profit efficiency, we

reached the same result. From Table 5, we also see that

conventional banks (73.43%), again, on average, prove to

be the most efficient than Islamic banks (61.82%).

Our findings are in line with the studies of Rosly and

Abu Baker (2003) and Yudistira (2003) which find that

Islamic banks are less efficient than conventional banks.

13 For the same period, Ariss et al. (2007) find that there is a decline

in efficiency in GCC countries due to the decrease in allocative

efficiency.14 New licenses to Islamic and foreign banks, new financial free

zones in Qatar, Dubai, and Ras Al Kaima (UAE). 15 An important number of Islamic banks exist in these countries.

J Prod Anal (2010) 34:45–62 57

123

A recent study performed by Kamaruddin et al. (2008)

reveals that Islamic banks in Malaysia during the period

1998–2004 are twice as inefficient (cost inefficiency is

equal at 28%) as typical conventional banks in the world.

This inefficiency can be explained by the lack of econo-

mies of scale due to smaller size of Islamic banks. In

addition, According to Olson and Zoubi (2008), the inef-

ficiency of Islamic banks may be due to the fact that their

customers are pre-disposed to Islamic products regardless

of cost. In the case of Islamic banks in Malaysia, Kama-

ruddin et al. (2008) explain the lower cost efficiency scores

of these banks compared to the conventional banks in

Western countries, essentially, by the high level of cost to

income ratio due to the increase of staff costs and over-

heads. Moreover, In order to have greater marketing and

promotional activities and higher investment in technology,

Islamic banks in Malaysia have incurred higher costs.

To examine whether the bank type implies different

scores of efficiency, we perform a t parametric test.16 The

result confirms significant difference in cost and profit

efficiency levels between conventional and Islamic banks.

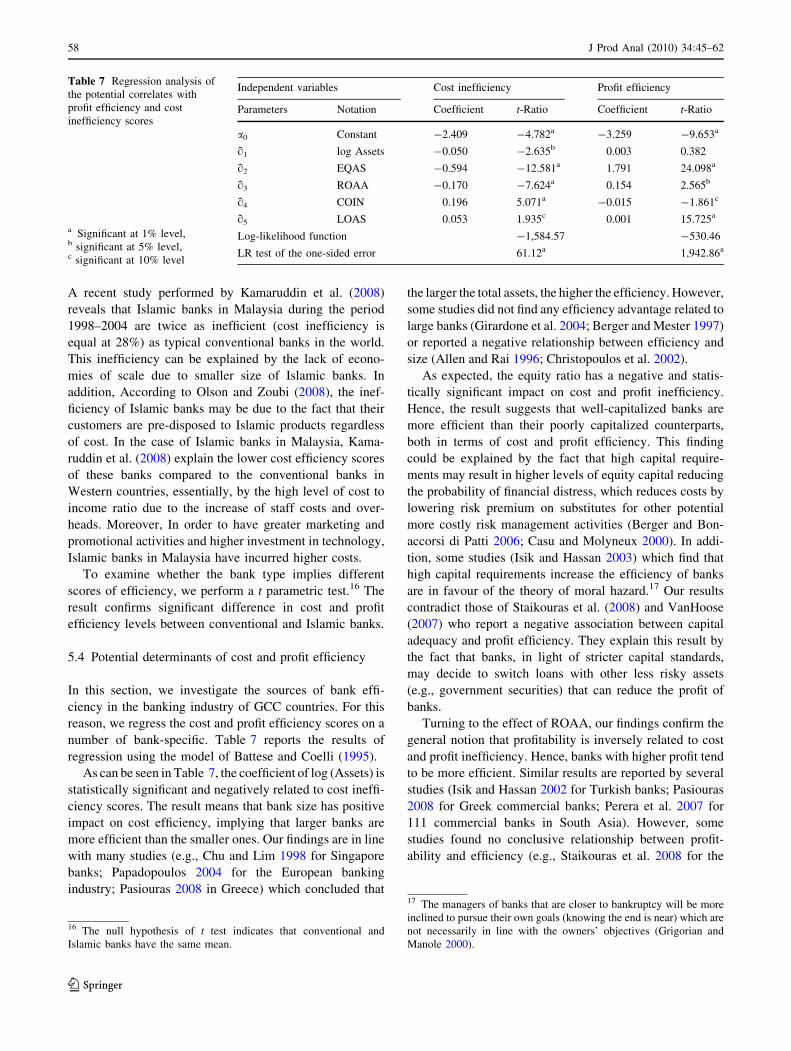

5.4 Potential determinants of cost and profit efficiency

In this section, we investigate the sources of bank effi-

ciency in the banking industry of GCC countries. For this

reason, we regress the cost and profit efficiency scores on a

number of bank-specific. Table 7 reports the results of

regression using the model of Battese and Coelli (1995).

As can be seen in Table 7, the coefficient of log (Assets) is

statistically significant and negatively related to cost ineffi-

ciency scores. The result means that bank size has positive

impact on cost efficiency, implying that larger banks are

more efficient than the smaller ones. Our findings are in line

with many studies (e.g., Chu and Lim 1998 for Singapore

banks; Papadopoulos 2004 for the European banking

industry; Pasiouras 2008 in Greece) which concluded that

the larger the total assets, the higher the efficiency. However,

some studies did not find any efficiency advantage related to

large banks (Girardone et al. 2004; Berger and Mester 1997)

or reported a negative relationship between efficiency and

size (Allen and Rai 1996; Christopoulos et al. 2002).

As expected, the equity ratio has a negative and statis-

tically significant impact on cost and profit inefficiency.

Hence, the result suggests that well-capitalized banks are

more efficient than their poorly capitalized counterparts,

both in terms of cost and profit efficiency. This finding

could be explained by the fact that high capital require-

ments may result in higher levels of equity capital reducing

the probability of financial distress, which reduces costs by

lowering risk premium on substitutes for other potential

more costly risk management activities (Berger and Bon-

accorsi di Patti 2006; Casu and Molyneux 2000). In addi-

tion, some studies (Isik and Hassan 2003) which find that

high capital requirements increase the efficiency of banks

are in favour of the theory of moral hazard.17 Our results

contradict those of Staikouras et al. (2008) and VanHoose

(2007) who report a negative association between capital

adequacy and profit efficiency. They explain this result by

the fact that banks, in light of stricter capital standards,

may decide to switch loans with other less risky assets

(e.g., government securities) that can reduce the profit of

banks.

Turning to the effect of ROAA, our findings confirm the

general notion that profitability is inversely related to cost

and profit inefficiency. Hence, banks with higher profit tend

to be more efficient. Similar results are reported by several

studies (Isik and Hassan 2002 for Turkish banks; Pasiouras

2008 for Greek commercial banks; Perera et al. 2007 for

111 commercial banks in South Asia). However, some

studies found no conclusive relationship between profit-

ability and efficiency (e.g., Staikouras et al. 2008 for the

Table 7 Regression analysis of

the potential correlates with

profit efficiency and cost

inefficiency scores

a Significant at 1% level,b significant at 5% level,c significant at 10% level

Independent variables Cost inefficiency Profit efficiency

Parameters Notation Coefficient t-Ratio Coefficient t-Ratio

a0 Constant -2.409 -4.782a -3.259 -9.653a

q1 log Assets -0.050 -2.635b 0.003 0.382

q2 EQAS -0.594 -12.581a 1.791 24.098a

q3 ROAA -0.170 -7.624a 0.154 2.565b

q4 COIN 0.196 5.071a -0.015 -1.861c

q5 LOAS 0.053 1.935c 0.001 15.725a

Log-likelihood function -1,584.57 -530.46

LR test of the one-sided error 61.12a 1,942.86a

16 The null hypothesis of t test indicates that conventional and

Islamic banks have the same mean.

17 The managers of banks that are closer to bankruptcy will be more

inclined to pursue their own goals (knowing the end is near) which are

not necessarily in line with the owners’ objectives (Grigorian and

Manole 2000).

58 J Prod Anal (2010) 34:45–62

123

banking sector of 6 South Eastern European countries) or

reported a negative association (Casu and Girarrdone 2004

for Italian banks).

Regarding the sign of coefficient on cost to income, we

observe, as expected, that this variable is positively cor-