Chapter 5 Profit Centers

34

GROUP 2: CHARESA REIG FARRA JEAN FREOLO JUSTINE ARBOLEDA JECELLE BUERE JEY JAVIER NATHALIE OCANA CHAPTER 5: PROFIT CENTER

Transcript of Chapter 5 Profit Centers

GROUP 2:CHARESA REIG

FARRA JEAN FREOLOJUSTINE ARBOLEDAJECELLE BUEREJEY JAVIER

NATHALIE OCANA

CHAPTER 5: PROFIT CENTER

Profit Centers

-when a responsibility center’s financial performance is measured in terms of profit (I.e., by the difference between the revenues and expenses ), the center is called a profit center.

General Consideration

FUNCTIONAL ORGANIZATION

-is one in which each principal manufacturing or marketing function is performed by a separate organization unit.

DIVISIONALIZATION

When such an organization is converted to one in which major unit is responsible for both the manufacture and the marketing.

PREVALENCE OF PROFIT CENTER

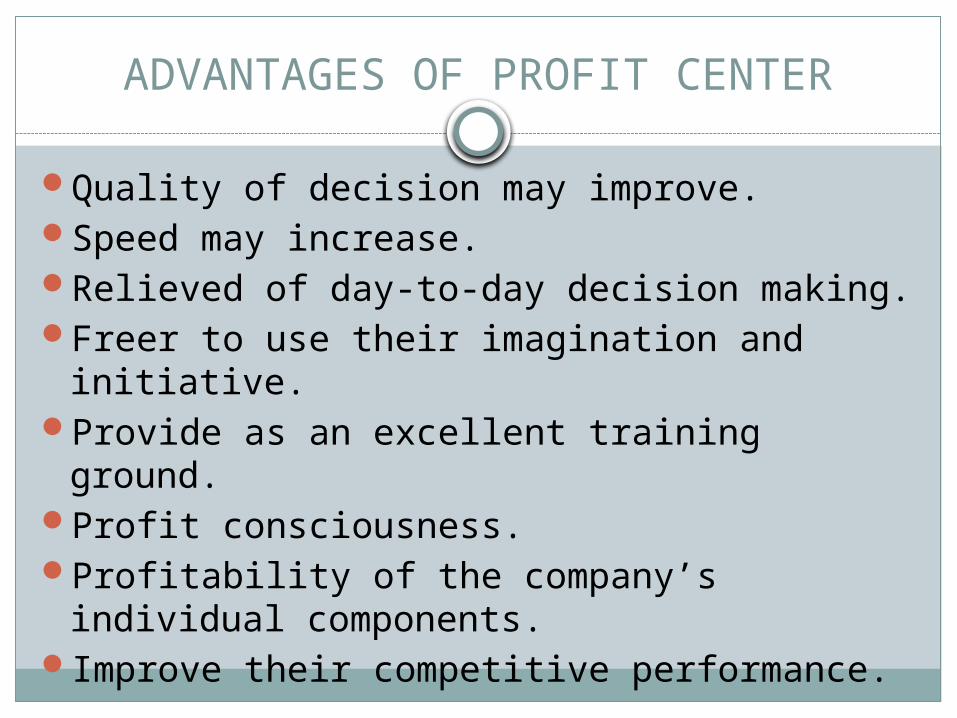

ADVANTAGES OF PROFIT CENTER

Quality of decision may improve.Speed may increase.Relieved of day-to-day decision making.Freer to use their imagination and initiative.

Provide as an excellent training ground.

Profit consciousness.Profitability of the company’s individual components.

Improve their competitive performance.

DIFFICULTIES WITH PROFIT CENTER

Loss of control.Quality of decisions may be reduced.Friction may increase.Competition may arise.May impose additional costs.Competent general managers may not exist.

Focused on short-run profitability rather than long-term.

Optimize the profits of the company as a whole.

Business Units as Profit Centers

Managers

Product Development

Manufacturing

Marketing

Constraints on Business Unit Authority

Constraints from Other Business Units

Product Decision

Marketing Decision

Procurement or Sourcing Decision

3 Types of

Decisions

If a business unit manager controls all three activities, there is usually no difficulty in assigning profit responsibility and measuring performance

The grater the degree of integration, the more difficulty becomes to assign responsibility to a single profit center for all three activities in a given product line

If these three activities are split among two or more business units, the overall success of the product may be difficult

Constraints from Corporate Management

Those resulting

from strategic

considerations

Those resulting because

uniformity is required

Those resulting from the economies

of centralizat

ion

In general, corporate constraints don not cause severe problems in a decentralized sturucture as long as they are dealt with explicity; business unit managers should understand the necessity for most constraints and should accept them with good grade

Major problems revolve around corporate service activates because they believe that they can obtain such services at less expense form outside source

OTHER PROFIT CENTERS

MEASURING PROFITABILITY

Two Types:

Management PerformanceEconomic Performance

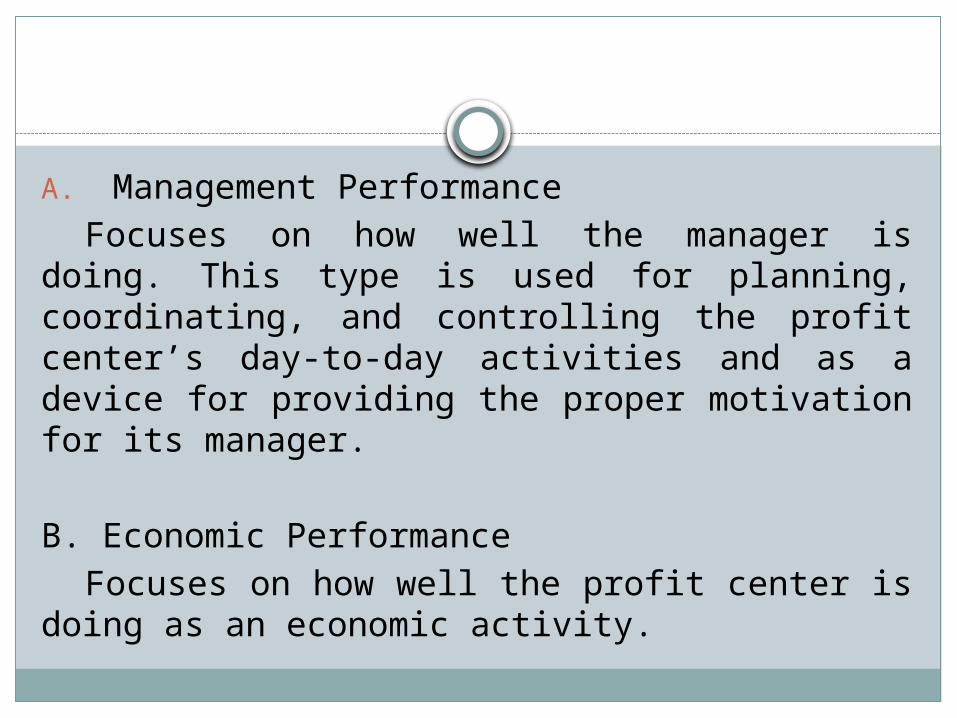

A. Management PerformanceFocuses on how well the manager is

doing. This type is used for planning, coordinating, and controlling the profit center’s day-to-day activities and as a device for providing the proper motivation for its manager.

B. Economic PerformanceFocuses on how well the profit center is

doing as an economic activity.

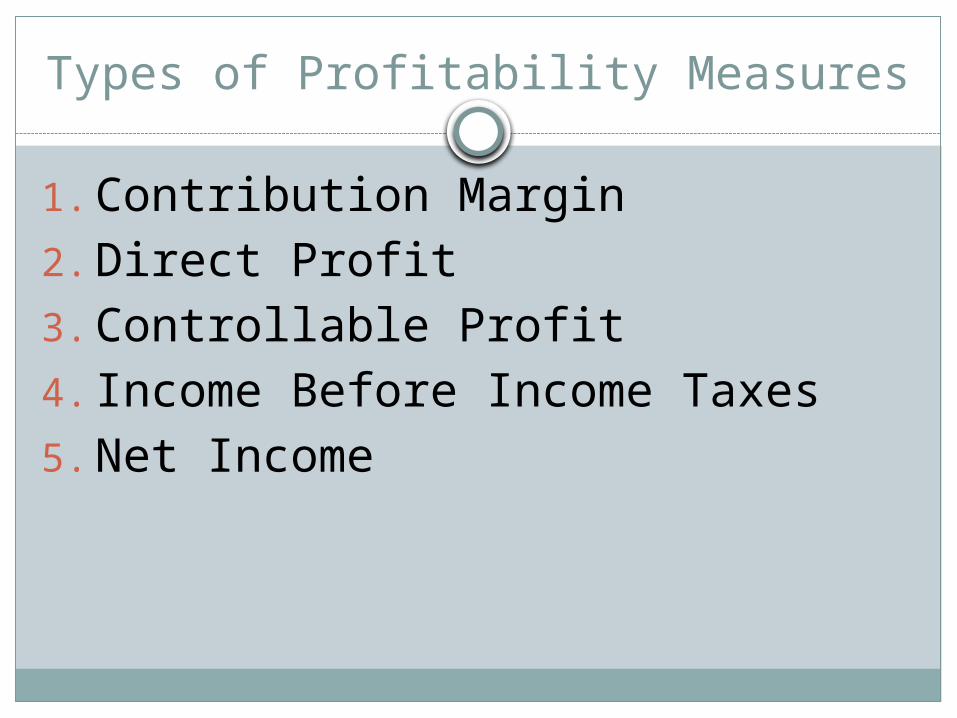

Types of Profitability Measures

1.Contribution Margin2.Direct Profit3.Controllable Profit4.Income Before Income Taxes5.Net Income

Example of a Profit Center Income Statement

Revenue Php 1000Cost of Sales 600Variable Expenses 180ContributionMargin 220Fixed Expenses incurred in the Profit Center 90Direct Profit 130Controllable Corporate Charges 10Controllable Profit 120Other Corporate Allocations 20Income Before Taxes 100 Taxes 40 Net Income Php 60

1. Contribution MarginReflects the spread between revenue

and variable expenses. The principal argument in favor of using it to measure the performance of profit center managers is that since fixed expenses are beyond their control, managers should focus their attention on maximizing contribution.

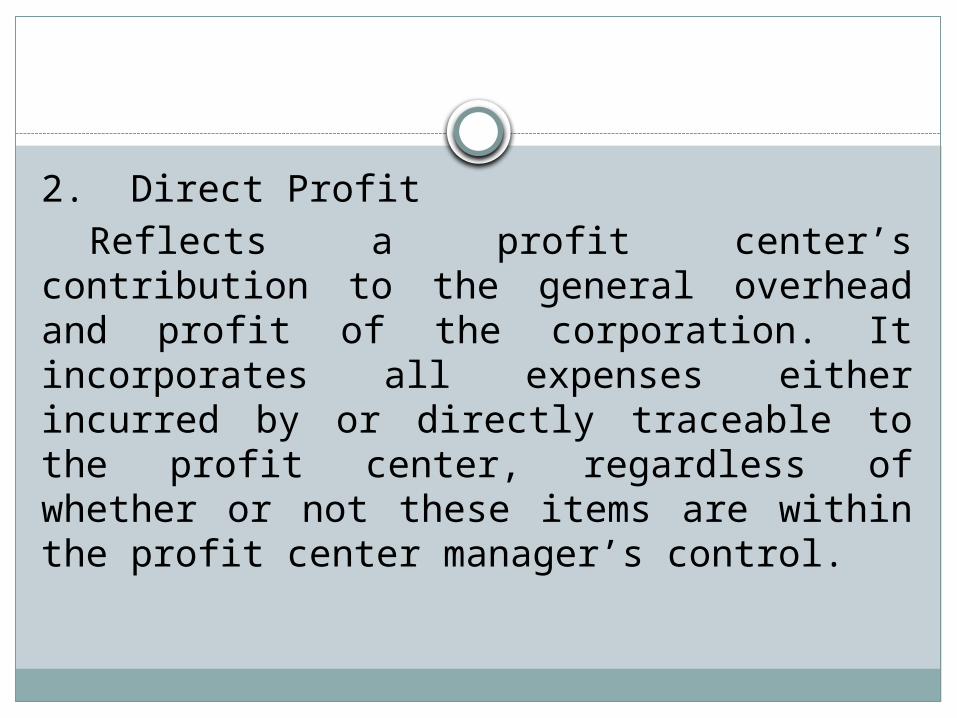

2. Direct ProfitReflects a profit center’s

contribution to the general overhead and profit of the corporation. It incorporates all expenses either incurred by or directly traceable to the profit center, regardless of whether or not these items are within the profit center manager’s control.

3. Controllable ProfitHeadquarters expenses can be

divided into two categories: controllable and non-controllable. The controllable category includes expenses that are controllable, at least to a degree, by a business unit manager.

NET INCOME BEFORE INCOME TAXES

In this measure, all corporate overhead is allocated to profit centers’ based on the relative amount of expense each profit center incurs.

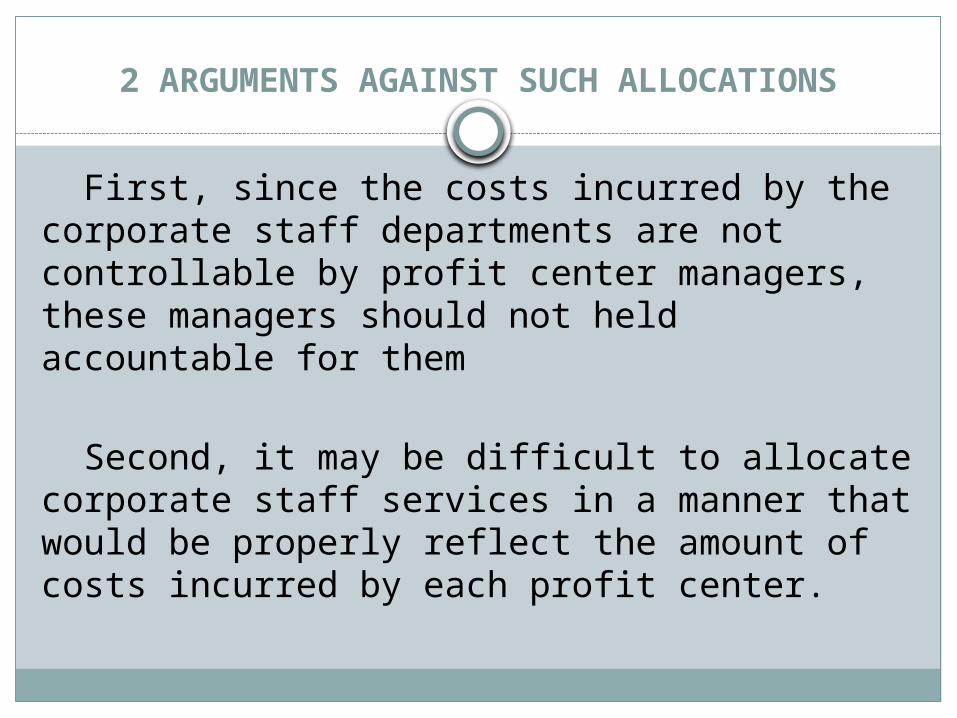

2 ARGUMENTS AGAINST SUCH ALLOCATIONS

First, since the costs incurred by the corporate staff departments are not controllable by profit center managers, these managers should not held accountable for them

Second, it may be difficult to allocate corporate staff services in a manner that would be properly reflect the amount of costs incurred by each profit center.

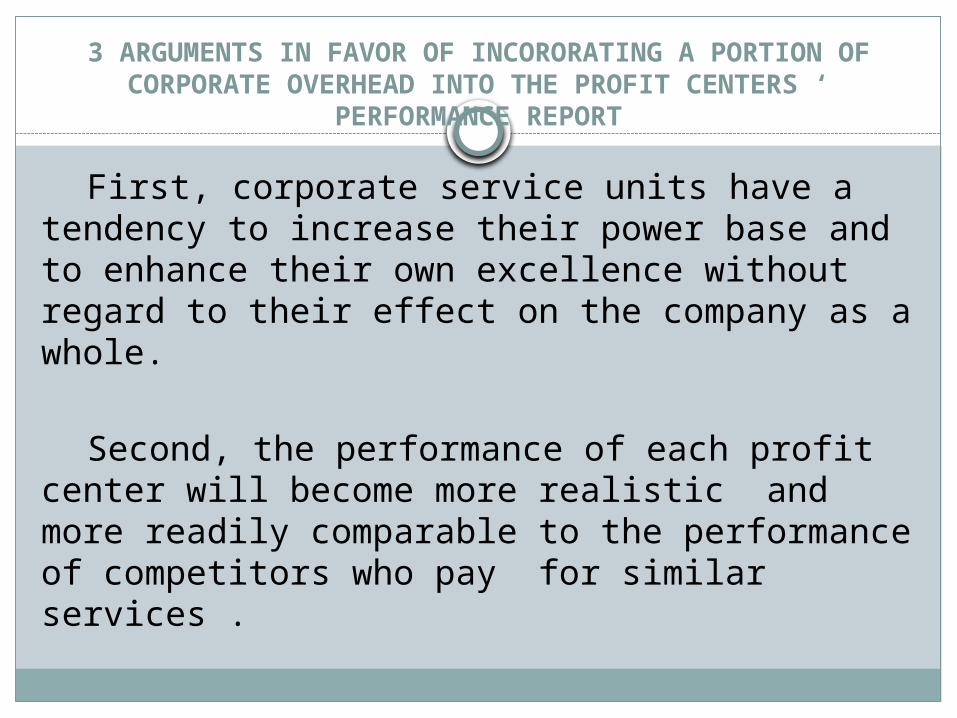

3 ARGUMENTS IN FAVOR OF INCORORATING A PORTION OF CORPORATE OVERHEAD INTO THE PROFIT CENTERS ‘

PERFORMANCE REPORT

First, corporate service units have a tendency to increase their power base and to enhance their own excellence without regard to their effect on the company as a whole.

Second, the performance of each profit center will become more realistic and more readily comparable to the performance of competitors who pay for similar services .

Finally, when managers know that their respective centers will not show a profit unless all costs, including the allocated share of corporate overhead, are recovered, they are motivated to make optimum long-term marketing decisions as to pricing, product mix, and so forth, that will ultimately benefit (and even ensure the viability of) the company as whole.

* If profit centers, are to be charged for a portion of corporate overhead this item should be calculated on the basis of budgeted, rather than actual costs in which case the “budget” and “actual” columns in the profit centers performance report will show identical amounts for this particular item.

NET INCOME

Companies measure the performance of domestic profit centers according to the bottom line, the amount of the net income after tax.

2 PRINCIPAL ARGUMENTS AGAINST USING THIS MEASURE

1. After tax income is often a constant percentage of the pretax income, in which case there would be no advantage in incorporating income taxes.

2. Since many of the decisions that affect income taxes are made at headquarters , it is not appropriate to judge profit center managers on the consequences of these decisions.

REVENUES

Choosing the appropriate method recognition is important. Should revenues be recorded when an order is made, when an order is shipped, or when cash is received?

In some situation two or more profit center may participate in a successful sales effort; ideally each center should be given appropriate credit for its part in the transaction.

MANAGEMENT CONSIDERATIONS

Most of the confusion in measuring the performance of profit center managers results from failing to separate the measurement of the manager from the economic measurement of the profit centers.

Managers should be measured on an aftertax basis only if they can influence the amount of tax their unit pays, and items that they clearly cannot influence, such as currency fluctuation, should be eliminated.

Variance analysis is always important in evaluating management performance . But even the best variance analysis system will still require the exercise of judgement, and one way to make this judgement more reliable is to eliminate all items over which the manager has no influence ( or report them in such a way that variances do not develop)