Strategy, Structure and Market Liberalization: Evidence from ENI (2000-06)

42

McGraw-Hill Strategy, Structure and Market Liberalization: Evidence from ENI (2000-06) Gianpaolo Abatecola, Roberto Cafferata, Sara Poggesi DSI Essays Series 7

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Strategy, Structure and Market Liberalization: Evidence from ENI (2000-06)

McGraw-Hill

Strategy, Structure and MarketLiberalization:Evidence from ENI (2000-06)

Gianpaolo Abatecola, Roberto Cafferata, Sara Poggesi

DSI Essays Series

7

cop7.qxd 3-03-2010 15:36 Pagina 1

University of Rome “Tor Vergata”Università degli Studi di Roma “Tor Vergata”

Department of Business Studies Dipartimento Studi sull’Impresa (DSI)

DSI Essays Series

Editor in ChiefRoberto Cafferata – University of Rome “Tor Vergata”, Italy[[email protected]; [email protected]]

Scientific Committee Alessandro Carretta – University of Rome “Tor Vergata”, ItalyCorrado Cerruti – University of Rome “Tor Vergata”, ItalySergio Cherubini – University of Rome “Tor Vergata”, ItalyAlessandro Gaetano – University of Rome “Tor Vergata”, ItalyClaudia Maria Golinelli – University of Rome “Tor Vergata”, ItalyHans Hinterhuber – University of Innsbruck, AustriaJoanna Ho – University of California, Irvine, U.S.A.Anne Huff – Technische Universität München, GermanyMorten Huse - Norwegian School of Management BI, NorwayMarco Meneguzzo – University of Rome “Tor Vergata”, ItalyPaola Paniccia – University of Rome “Tor Vergata”, ItalyCosetta Pepe – University of Rome “Tor Vergata”, ItalyHarald Plamper – Zeppelin University in Friedrichshafen, GermanyFrancesco Ranalli – University of Rome “Tor Vergata”, ItalySalvatore Sarcone – University of Rome “Tor Vergata”, ItalyJohn Stanworth - University of Westminster, United KingdomJonathan Williams - Bangor Business School, United Kingdom

Managing EditorsEmiliano Di Carlo – University of Rome “Tor Vergata”, Italy[[email protected]]

Sara Poggesi – University of Rome “Tor Vergata”, Italy[[email protected]]

Mario Risso – University of Rome “Tor Vergata”, Italy[[email protected]]

Guidelines for AuthorsPapers accepted by scientific conferences/symposiums/seminars, not yet published,can be sent for consideration for publication in the DSI Essays Series. The length ofeach manuscript should be maximum 40 typed pages (10.000 words) including notes,references and appendices, where appropriate. Manuscripts should be submitted inelectronic format (Word for Windows) by the author to the Editor in Chief and theManaging Editors, who will then ask two members of the Scientific Committee to sup-ply a short written review. The paper, in case revised, will be sent again by the authorto the Editor in Chief and the Managing Editors. At the end of the process, the Editor in Chief will authorize the publication of the sci-entific work. The Managing Editors will insure the loading of all the accepted papersinto the RepEc and SSRN database.

DSI Essays Series

Gianpaolo Abatecola, Roberto Cafferata, Sara Poggesi

Strategy, Structure and MarketLiberalization:Evidence from ENI (2000-06)

n. 7

McGraw-Hill

Milano • New York • San Francisco • Washington D.C. • AucklandBogotá • Lisboa • London • Madrid • Mexico City • MontrealNew Delhi • San Juan • Singapore • Sydney • Tokyo • Toronto

Copyright © 2009 The McGraw-Hill Companies, S.r.l.Publishing Group ItaliaVia Ripamonti, 89 – 20139 Milano

McGraw-HillA Division of the McGraw-Hill Companies

All rights reserved.No part of this pubblication may be reproduced or distributed in any formor by any means, or stored in a database or retrieval system, without theprior written consent of The McGraw-Hill Companies, Inc, including, butnot limited to, in any network or other electronic storage or transmission, orbroadcast for distance learning.

Production: Donatella Giuliani

ISBN 978-88-386-6704-6Printed and bound in Italy by Pronto Stampa, Fara Gera d’Adda (Bg)123456789PRSPRS109

Strategy, Structure and Market Liberalization: Evidence from ENI (2000-06)

Gianpaolo Abatecola1, Roberto Cafferata2, Sara Poggesi3

Abstract The paper explores the relationship between firm’s strategy and its structure through the case study of the Italian public utility ENI. Within the liberaliza-tion process nowadays occurring in the Italian gas market, the paper analyzes ENI’s performance in the period 2000-06 and focuses on the most relevant strategic and organizational changes of the firm and their relationship with the energy industry evolution.

The analysis is based both on public sources – such as official reports by in-ternational authorities – and on private information, such as in-depth field in-terviews with managers of the ENI’s G&P Division, ENI’s management sur-veys, historical archives and corporate governance reports. JEL Classifications: L 11, L 22, L 25, M 10, M 16 Keywords: Case study, ENI, gas market, liberalization, strategy, structure.

________________ 1 Research Fellow of Business Management, University of Rome “Tor Vergata”, Faculty of Economics, Department of Business Studies. 2 Full Professor of Management, University of Rome “Tor Vergata”, Faculty of Economics, Department of Business Studies. 3 Research Fellow of Business Management, University of Rome “Tor Vergata”, Faculty of Economics, Department of Business Studies.

Contents 1. Introduction 3 2. Theoretical background 5 3. Legislative framework 10 4. The context: ENI at the beginning of the XXI century 13 5. The analysis: ENI’s strategies in the gas market (2000-2006) 14 6. Market liberalization and ENI’s strategic reaction 16 7. Changes in the organizational structure 18 8. Discussion and conclusions 22 References 25 Tables and figures 29 Editorial notes Paper accepted for presentation at the V EIASM Workshop on “Corporate Governance, Brussels, November 15-16, 2007.

1. Introduction The paper explores the relationship between firm’s strategy and its structure through the case study of the Italian public utility ENI. Within the liberaliza-tion process nowadays occurring in the Italian gas market, the paper analyzes ENI’s performance in the period 2000-06 and focuses on the most relevant strategic and organizational changes of the firm and their relationship with the energy industry evolution.

After the Rome Treaty of 1957, the European Union (EU) settled common rules in order to defend competition (Brittain, 1991; Cozzi, Vaccà, 1992; Caf-ferata, 1994). The European Commission has recently approved several reform proposals of the current competition rules: both the Commission, and the anti-trust authorities, and the national courts alike could be applied to for making organizations and people comply to the European competition rules (Stiglitz, 1990; European Commission, 2003).

In the current phase of the European economic development and integra-tion process, one of the main problems members face is the unitary govern-ance of the European economy, which calls for important institutional changes (Muller Graff, 1996; Secchi, 1999; Maillet, 2000, 2001; Violini, 2002). The diffi-culty of achieving this goal is today linked to the absence of a strong European government, provided with all the powers necessary for example to implement and control the competition rules (Maillet, 2000; Telò, 2002). As a conse-quence, EU authorities are often involved in creating new positive tools and strengthening coordination measures to allow the European Commission to play efficiently its economic role. Indeed, the establishment of the European Central Bank and the introduction of the Euro currency were a milestone in this direction. New governance models for today’s European large State-owned companies are now part of this project.

The functions played by State-owned companies in Europe seem in conflict with the development of the globalization process, which tends to encourage privatization processes. Furthermore, everyone knows the effects of the deep crisis experienced during the 90’s by large State-owned companies. Almost every European country was involved in the process (Cafferata, 2000; Quadrio Curzio, Fortis, 2000).

In this context, some topics concerning State-owned companies, just like ENI, need to be underlined. First of all, State-owned companies and private companies must be the object of a comparative analysis starting from the dif-ferent goals and behaviours. Statutory goals are the critical element remem-bered by the top decision makers of the firm, while setting strategies with their

G. ABATECOLA, R. CAFFERATA, S. POGGESI 4

specific objectives (Simon, 1964). State-owned companies seem to have man-agement criteria, while private companies consider income the critical goal, in-fluencing both short-term and long-term strategies.

The differentiation among goals has relevant effects on risk taking and eco-nomic efficiency. Risk propensity/adversion and the ability to govern oppor-tunities and threats depend on the goal to be obtained and on the environment the firm is involved in (March, 1978; March, Shapira, 1987).

Corporate governance issues have long been studied by the scientific com-munity (Bearle, Means, 1932; Fama, 1980; Fama, Jensen, 1983). In recent years, particularly in the last decade, the analysis of these issues is a topic again. Their own statute-reforms moved State-owned companies to take into account issues which formerly belonged to privately owned stock companies. Furthermore, the same statute-reforms asked for several structural changes to cope with the general environment’s changes.

Public utilities had to face market liberalization, pressures towards privatiza-tion and the establishment of new independent agencies aimed at regulating and controlling the evolution of industries’ structures (Cafferata, 1995). Chal-lenged with these developments, they increased the use of information tech-nology and turned to new organizational models to enhance their economic performance. Creative employment of human resources, knowledge and qual-ity management are among the most relevant factors which were planned for the success of their new strategies (Bryntse, 1996; Stanley, Wisner, 2001).

This paper studies the evolution of the Italian gas market, which is nowa-days affected by the ongoing liberalization process. On the one hand, the gas market has been historically characterized by the presence of ENI itself as the incumbent player, as far as the gas supplying, warehousing and distribution are concerned; on the other hand, this market has been historically characterized by the splitting of the most relevant players involved in the gas selling.

At the end of the Nineties, several reforms were approved in order to im-plement «effective concurrency» in the European and Italian gas markets (e.g.: EU Directive n. 30/98; Italian Legislative Decree n. 164/00; EU Directive n. 55/2003; Italian Law n. 239/04). New challenges followed for the Italian pub-lic utilities.

What kind of strategic change influenced ENI’s performance in the gas business in the period 2000-06? What organizational changes affected the firm’s structure? What kind of relationship emerged between strategy and structure in the period taken into account?

Among the «strategic management» scholars, the theoretical background of the paper stands on those perspectives which, since the seminal work by Al-

Strategy, Structure and Market Liberalization: Evidence from ENI

5

fred Chandler Jr. (1962), deepened the nexus between strategy and structure. Over the years, two opposite views have been basically developed by strate-gists: on one hand, structure follows strategy (Fouraker, Stopford, 1968; Scott, 1971; Pavan, 1972; Thanheiser, 1972; Pooley-Dias, 1972; Channon, 1973; Ru-melt, 1974; Miller, 1986; Fombrun, 1989); on the other hand, strategy follows structure (Bower, 1970; Child, 1972; Galbraith, Nathanson, 1978; Hall, Saias, 1980; Donaldson, 1982, 1987; Fredrickson, 1986).

The paper has been conceived as follows. The «strategy and structure» theo-retical background is firstly highlighted. The liberalization process, nowadays affecting the Italian gas market, is then described and ENI’s strategy and struc-ture are analyzed for the period 2000-06. The firm’s growth in the gas business is also explored. ENI’s national and international competitive position is then focused on. The most relevant innovations affecting the firm’s organizational structure as a consequence of the described strategic changes are taken into ac-count.

The discussion of the main results and the implications for further research follow the analysis of the collected data.

The analysis is based both on public sources – such as official reports by in-ternational authorities (AEEG, 2007; International Energy Agency, 2007) – and on private information, such as in-depth field interviews with managers of the ENI’s G&P Division, ENI’s management surveys, historical archives and corporate governance reports. Recent works concerning the strategic change in the oil & gas industry and ENI’s privatization are also taken into account (Grant, 1993; Cafferata, 2000, 2002; Cafferata, Cibin, 1998; Cibin, Grant, 1996; Grant, Cibin, 1996; Clò, 2004).

2. Theoretical background The relationship between firm’s strategy and its structure represents one of the most discussed topics in the field of strategic management. In the years, two opposite positions have been basically developed by scholars: on one hand, structure follows strategy; on the other hand, strategy follows structure.

Chandler’s study (1962) on the evolution of the American industry is uni-versally acknowledged as the seminal work of the ongoing debate on strategy and structure. More deeply, analyzing the strategic and organizational evolution of the seventy most important American firms between 1919 and 1949, Chan-dler argued that «structure follows strategy and the most complex type of structure is the result of the correlation of several basic strategies» (p. 49).

Chandler’s thought may be summarized as follows: (pp. 50-51):

G. ABATECOLA, R. CAFFERATA, S. POGGESI 6

• «The growth of the population, the shifts from the country to the city and then to the suburbs, the stages of economic depression and prosperity, and the increasing rate of technological change; all these factors create a new demand of the goods and services provided by a society»;

• «The prospect of a new market or the threatened loss of a current one stimulated geographical expansion, vertical integration, and product diver-sification» (strategic changes follow environmental changes);

• «A new strategy required a new or at least updated organizational structure in order to let a big firm operate efficiently» (structural changes follow strategic changes);

• «The failure to develop a new internal structure and to face new external and internal opportunities and needs, was caused by the overconcentration on short-term goals by the firms’ executives; or by their inability to develop an entrepreneurial outlook, because of their past training, education or pre-sent position» (structural changes sometimes take place with a certain delay compared to strategic changes);

• «A firm’s growth without structural adjustment can lead only to economic inefficiency».

Chandler explained the abovementioned relation through a 4-phase develop-ment model which characterizes the «big industrial firm» of his time (p. 49): 1. Growth of the firm’s dimension: this leads to the creation of an administrative

office which handles one function in one local area; 2. Growth through geographical dispersion: this brings the need for a departmental

structure and some headquarters in order to manage several local field units;

3. Development of new functional areas in the firms: this calls for the creation of a central office and a multidepartmental structure;

4. Development of new lines of products or growth on a national or international scale: this brings the birth of the multidivisional structure, with the different di-visions administered by a general office.

The Chandler’s model «growth � strategy � structure» was considered as the reference pattern for the strategic management studies which followed.

Strategy, Structure and Market Liberalization: Evidence from ENI

7

Bruce Scott (1971) argued that structural changes follow strategic changes too. He applied a 3-phase development model to the «big industrial firm» (p. 5)4: I. small company with one or a few functions performed largely by one

man ager; II. growth in volume, geographic coverage and through vertical integra-

tion, multi-departmental enterprise with specialized managerial de-partments based upon functions;

III. diversification, multidivisional enterprise with divisions based largely on product-market relationships5.

Scott interpreted the strategy/structure relationship as follows: «The I, II, III sequence does appear to be a common and perhaps a dominant sequence in the United States, as suggested both by Chandler’s findings and by more recent research (Wrigley 1970). But the sequence of stages appears to be built upon two different processes. One is the tendency towards continuing proliferation of activities, and a still more different company, the other is the tendency to use more and more complex and costly equipment in a given line of endeav-our, leading towards a more integrated organization within that line of busi-ness» (p. 23).

Unlike Chandler, Scott highlighted the importance of «competitive pres-sure – the pressure of competitive marketplace», and pointed out that «the change in strategy appears to be a necessary condition for a company to change to the divisional structure. However, it is not a sufficient condition it-self. Companies that change to a strategy of diversification frequently continue ________________ 4 «Each of the stages is described in terms of nine characteristics (product line, organizational structure, product-service transactions, R&D, performance measurement, rewards, control sys-tem, strategic choice), eight of which describe the actual characteristics of the way the firm is managed, while the ninth describes the scope of strategic choice which characterizes the stra-tegic framework of the respective stage of development. The first two characteristics denote critical aspects of the relationship between the firm and its environment while the next six de-note important aspects of the part-whole relationship within the firm» (p. 6). 5 Although Scott himself acknowledged the «oversimplification» of its model, he highlighted the positive aspects of the model itself compared to the one by Chandler: «it classifies and then relates companies not by a single managerial characteristic (structure) but by eight such charac-teristics, including structure, and reduces the emphasis on geographic growth (within USA)» (p. 6). Scott points out that: «the three stages approach emphasizes that there is a cluster of mana-gerial characteristic associated with the various stages of development, a cluster which doesn’t suggest just a form of organization, but a way of managing and, to a considerable extent, a way of life within the enterprise» (p. 6).

G. ABATECOLA, R. CAFFERATA, S. POGGESI 8

to carry on with a functional structure for many years.[…] At an extreme, if there were not competition at all, any form of management structure would be adequate for operations of any degree of diversity. However, the divisional structure appears to be the most effective way to manage the strategy of diver-sification under highly competitive conditions» (Scott, 1973: 141).

Chandler’s theory was tested and endorsed by Scott’s Harvard students, for what concerns Italy (Pavan, 1972), Germany (Thanheiser, 1972), France (Poo-ley-Dias, 1972), Great Britain (Channon, 1973) and the USA (Rumelt, 1974)6. The results by Channon and Rumelt seemed to be the most interesting.

Derek Channon analyzed the one hundred most important manufacturing firms in the United Kingdom between 1950 and 1970. He confirmed Chan-dler’s statement, although with some limitations. More deeply, he argued that: «Clearly a relationship existed between diversification and structure, but the lag between the adoption of a strategy of diversification and a new structure could be long and to some degree extended by the adoption of a holding-company structure which permitted diversification to continue but without central stra-tegic control» (p. 75)7.

Richard Rumelt extended Chandler’s strategy/structure relationship to the effects of these two variables on the performance of a firm. He studied the evolution of the American large firms between 1949 and 1969 through the analysis of a random sample of about 200 companies comprised in the Fortune 500 list. Rumelt’s results generally support Chandler’s statement that strategy fol-lows structure, but also stress the thesis that structure also follows fashion8.

________________ 6 The proof of a positive correlation between the diversification strategy and the divisionalized structure concerns internationalized firms too. Fouraker and Stopford (1968: 64), for instance, argued that «the growth of foreign markets and opportunities requires diversification, reorgani-zation, and the training of many more general international managers. The organizations that have been most successful in meeting this new challenge have been those type III organiza-tions that had already developed the ability to produce general managers capable of controlling and guiding a heterogeneous, diverse enterprise». 7 Channon, more deeply, emphasized the difficulties occurring in the passage from one kind of strategy and structure to another and the importance of the transitory stage in the passage itself. «It is interesting to note that many firms underwent two structural transitions in pursuit of the strategy of diversification. Many initially adopted a holding-company structure which was ap-parently quite stable until the 1960s both among early diversifiers and many new diversifiers. However, the structure proved increasingly unstable during the latter period and was sup-ported by the widespread adoption of the multidivisional structure» (Channon, 1973: 75). 8 «The firms Chandler studied often adopted the divisionalized structure only after the old sys-tem began to collapse under the burden of diversified operations. By contrast, many corpora-tions of the 1960s, even those that were not highly diversified, split their operations into semi-

Strategy, Structure and Market Liberalization: Evidence from ENI

9

In contrast with the widely diffused Chandlerian theory, since the Seventies studies arguing that strategy follows structure have been developed. According to this kind of literature, strategy follows structure because of the limitations that the latter imposes to the firm’s decision making process.

Bower (1970: 67, 287), for instance, stated that «[…] structure may motivate or impede strategic activity […] when management chooses a particular orga-nization form, it is providing not only a framework for current operations but also the channels along which strategic information will flow […]».

In his well-known study on strategic choice, Child (1972: 49) wrote: «Internally oriented actions may involve an attempt, within the limits of resource availabil-ity and indivisibility, to establish a configuration of personnel, technologies and work organization which is both internally consistent and compatible with the scale and nature of the operations planned».

According to Hall and Saias (1980: 161): «It is necessary to recognize that in reality structure is the result of a complex play of variables other than strategy; culture, values, the past and present functioning of the organization, its history of success and failure, the psychological and sociological consequences of technological development, and so on. Structure, then, assumes a political con-tent in the same way as strategy, and there is no one reason to subordinate one to the other».

Fredrickson (1986: 294) underlined that «[…] a balanced view of the strat-egy/structure relationship must acknowledge that the strategic decision process and its outcomes can be facilitated, constrained, or simply shaped by struc-ture’s direct effects […].». Frederickson, more deeply, focused on the effects that the cognitive limitations of central decision makers may have on the global strategies of firms with highly centralized structures9.

_________________ autonomous divisions without having suffered great administrative strains. Some divisionalized because they planned to diversify, others wanted to create greater accountability for product performance, even among closely related products, and still others simply believed that the product-division structure was a better form of organization» (Rumelt, 1974: 149). 9 According to Hrebiniak e Joyce (1984: 87): «Raising the directionality question amounts to the creation of a false dichotomy of causation and a resulting irrelevant dilemma […] there is no satisfactory answer to this question because it is the question itself which is wrong». In this regard, Mintzberg (1990: 187) argued: «None take precedence, each always precedes the other and follows it [...] strategy formation is an integrated system, not an arbitrary sequence».

G. ABATECOLA, R. CAFFERATA, S. POGGESI 10

3. Legislative framework The natural gas consumption showed a marked growth all over the world be-tween 2000 and 2006, although the growth rate was lower than that between 1992 and 2000.

Among the reasons of the gas «success», the following seem the most rele-vant: • constant updating of the technologies employed in all the phases of the gas

production cycle, which allow the reduction of the distance between the gas extraction sites and the gas consumption areas;

• more possibilities of «sustainable development» as compared to other hy-drocarbons, in particular for what concerns the electric power production;

• increased gas reserves; • higher prices of oil products at international level. In Europe, Italy is the third largest market after the UK and Germany, as re-gards gas demand. In 2006, the national gas consumption was equal to 84.5 bil-lion cubic meters with a decrease of about 2% compared to 2005 (AEEG, 2007). The natural gas requirements were met by imports (76.6%) and by na-tional production (23,4%), including the gas drawn from the storage system (ENI, 2007). According to ENI’s estimates (2005a), the national gas consump-tion will be equal to 91 billion cubic metres in 2010, thus covering 36% of the national power requirements, against 33% in 2004.

The European Commission has long been committed in the development of a policy for the enhancement of competition in the energy sector through the promotion of market liberalization and the implementation of antitrust regulations.

The natural gas production cycle embraces the following activities: 1. Supply: the natural gas production and/or import. 2. Transport: the transport of natural gas from production sites or storage fields

to the distribution networks. The land transport takes place via oil pipelines and high pressure gas pipelines, the sea transport via gas tankers.

3. Storage: temporary storing of natural gas. 4. Primary distribution: activities carried out to supply raw natural gas to large

customers and gas distribution firms.

Strategy, Structure and Market Liberalization: Evidence from ENI

11

5. Secondary distribution: activities carried out to supply raw natural gas to resi-dential and commercial customers, as well as small companies operating in an urban environment.

6. Sale: gas marketing activities. In the last few years, a monopolist or oligopolistic market structure has pre-vailed in Europe. In Italy, there was a de facto vertical monopoly for almost 40 years. More deeply, the ENI group, which was established by Law 136/1953, was the incumbent player for what concerns the activities of gas acquisition, transmission and storage (through AGIP). The firm also played a dominant role in the primary distribution phase, providing gas to industrial and thermoe-lectric customers through SNAM. Moreover, ENI had almost the whole mo-nopoly for what concerns secondary distribution (through Italgas). ENI’s competitive position in the Italian gas production cycle at the end of the Eight-ies is depicted in Table 1.

The most relevant factors which pushed the EU towards the liberalization of the gas market were the following: technological innovation, the need to de-lete dominant positions and abuses which prevented the market from an effi-cient functioning and the need to enhance economic development and pro-mote growth and competition in the EU.

The gas market liberalization process was started by the Directive 98/30EC (entered into force on August 10, 1998), which established common rules for the natural gas supply, transport, distribution, supply and storage. The Direc-tive established the «rules concerning the organisation and functioning of the natural gas market, including the liquefied natural gas (LNG), the access to the market and the criteria and procedures applicable to the granting of the authorisations for supply, transport, distribution and storage of natural gas» (art. 1) . The most relevant principles of this Directive are the following: Supply: free access under non-discriminatory criteria in compliance with the Di-rective 98/22/EC. Access to the system: introduction of the Third Party Access (TPA). Under certain conditions, TPA allowed the eligible customers to access to the existing net-works infrastructures which they did not own. For what concern the organiza-tion of the access to the system, the EU member States were able to choose between «a) a negotiated procedure, in which the access to the system was made through supply contracts based on voluntary commercial agreements; b) a regulated procedure, in which the access to the system was made through

G. ABATECOLA, R. CAFFERATA, S. POGGESI 12

published tariffs and/or other terms and obligations for the use of that system; c) both these options» (art. 14-16). Eligible customers: customers that had the right to access to the gas system, such as gas facilities for the production of electric power, regardless of their con-sumption level per year, as well as other final customers consuming more than 25 million cubic metres of gas per year. Member States would have had to en-sure that the definition of eligible customers would result in an opening of the market equal to at least 20% of the total annual gas consumption of the na-tional gas market. Vertical unbundling: in order to separate activities still carried out under a mo-nopolistic system (transport, storage, distribution) from those which may be opened to competition (supply and sale), the directive envisaged the unbun-dling of accounts: «integrated natural gas firms will, in their internal account-ing, have to keep separate accounts for their natural gas transport, distribution and storage activities […]. These internal accounts will have to include a bal-ance sheet and a profit and loss account for each activity» (art.13). In Italy, the Directive 98/30/EC was implemented by the Legislative Decree 164/2000, (hereafter the Letta Decree), whose main points are the following:

Supply: from January 1, 2003 to December 31, 2010, gas firms would not have been allowed to sell to final customers more than 50% of the national con-sumption of natural gas on a yearly basis, directly or through subsidiaries or controlling companies or through subsidiaries of the same controlling firm. Moreover, from January 1, 2002 to December 31, 2010, gas firms would not have been allowed to inject, either directly or through subsidiaries, more than 75% of the gas consumed at national level into the national network. This value should have been reduced by two percentage points each year after 2002, up to a minimum value equal to 61%. These percentages, which established the so-called antitrust limits, had to be calculated net of the amount of gas directly consumed by a firm itself, or through subsidiaries or controlling companies or through subsidiaries of the same controlling firm. For what concerns the gas sales, these percentages had to be calculated net of system losses too. Access to the system: a regulated access to the system was chosen. More deeply, the natural gas transmission and dispatch were defined as public interest activi-ties. As a consequence, natural gas firms had to link to their network those us-

Strategy, Structure and Market Liberalization: Evidence from ENI

13

ers who applied for the service, if the users showed to have adequate capabili-ties and the works necessary to link the users themselves to the gas network are technically and economically feasible. This complied with the criteria estab-lished by a resolution of the Gas and Electric Energy Authority. The distribu-tion phase was considered a public service too and had to be assigned through public tenders launched by local authorities. Eligible customers: the Letta Decree established more stringent limits compared to those set by the EU. More deeply, since January 1, 2003, the gas market has been completely liberalized and all the customers, comprising the private ones, has been considered eligible. Vertical unbundling: since January 1, 2002, the natural gas transport and dispatch has been undergoing ownership unbundling from the other activities of the sector, with the exception of the storage function. The latter, however, has been undergoing accounting and management unbundling from the transport and dispatch operations, and ownership unbundling from all the other activi-ties of the sector. Moreover, since the same date, the distribution of natural gas has been undergoing ownership unbundling from the other activities of the sector. Finally, since January 1, 2002, natural gas could be sold only by firms which did not perform other activities in the same sector, except for import, export, cultivation and wholesaling.

ENI’s competitive position in the Italian gas production cycle after the lib-eralization process is depicted in Table 2. 4. The context: ENI at the beginning of the XXI

century

In 2000, ENI was a state-owned firm operating in the oil, natural gas, electric energy, petrochemical, construction and services sectors. The group was listed on the Milan and New York Stock Exchanges, was active in 69 countries all over the world and had 71,174 employees. Figure 1 shows the group’s struc-ture on December 31, 2000.

As shown in the figure, ENI carried out exploration and production activi-ties through its Exploration and Production Division (E&P), which performed exploration, production and marketing activities for what concerns oil and natural gas.

G. ABATECOLA, R. CAFFERATA, S. POGGESI 14

ENI operated through SNAM to supply, transmit, dispatch and sell natural gas, as well as to transport liquid hydrocarbons through sealines and pipelines. In the civil gas distribution sector, ENI operated trough the subsidiary Italgas.

The group operated through Agip Petroli to supply, refine and dispatch oil products. In 2000, Agip Petroli was the fifth largest firm in Europe for what concerns the overall refining capabilities. For what concerns the other activities, ENI was active in the production and sale of basic petrochemical, polymeric and elastomeric products through En-ichem; in the construction and services sector through Snamprogetti and Saipem; in the electric energy sector through EniPower (since January); in the financial sector through Enifim, Sofid and ENI International Holding Bv. 5. The analysis: ENI’s strategies in the gas market

(2000-2006) In the last 20 years, all the most relevant oil & gas firms have been developing strategies of dimensional growth to counter the increasing market turbolence (The Economist, 2005, 2006). The goal of these strategies was to achieve economies of scale in order: a) to increase the firms’ contractual power to-wards the producing countries and their national oil companies; b) to rule out any possible take-over by other energy players (Cibin, Grant, 1996; Grant, Ci-bin, 1996; Grant, 2003).

The analysis of ENI’s competitive strategies in the natural gas business be-tween 2000 and 2006 should take into account some important elements which characterized the re-organization process carried out by the firm in the ‘90s (Cafferata, 2000; Clò, 2004).

First of all, after being privatized, ENI became a listed firm focused on the maximization of the shareholders’ value. New financial tools, such as the value based management and the economic value added, were adopted to meet the new goals of the firm.

Moreover, after its reorganization process, ENI re-focused its attention on the oil & gas core business and increased its overall profitability, thanks to the strong reduction of the overhead costs through the shutting down of obsolete plants (Cafferata, Cibin, 2000). In this regard, the group’s overall debt was re-duced and the oil & gas core business grew.

In a long term business perspective, one could argue that at the beginning of the new millennium, ENI’s dimensional growth was more necessary than specifically desired, because of the threats coming from the turbulence of the oil and gas market. In this regard, Vittorio Mincato, who was the group’s Chief Executive Officer from Novem-

Strategy, Structure and Market Liberalization: Evidence from ENI

15

ber 1998 to May 2005, declared: «Once we were the largest among the small oil players […], now we are the smallest among the large players. But we will have still to grow in order to protect ourselves from any possible takeover» (Econ-omy, 2005: 18). More deeply, Mincato observed that although ENI’s capitaliza-tion in the stock exchange market raised by 70% between 1999 and 2004, an energy giant like Exxon Mobil would have needed the profits of only 4 years to buy the whole ENI group.

Before grasping ENI’s strategies in the natural gas business over the period 2000-06, the following premise has to be made. One could argue that studying ENI’s gas business without exploring its strategies in the oil business could limit the effectiveness of the analysis. In this regard, however, since its birth ENI has been focusing its activities not only in the oil business, but also in the gas one, both in Italy and in Europe. This distinctive element has been distin-guishing ENI’s strategic and organizational behaviour from that of the most relevant international players in the oil business, the so-called «seven sisters». Table 3 summarizes some data relating to the economic and financial perform-ances of the group between 2000 and 2006.

As shown in the table, ENI’s growth was relevant in the period, especially for what concerns the upstream (E&P Division) and downstream (G&P Division) phases of the gas production cycle.

In the upstream phase, the gas production and the natural gas reserves in-creased by 7.7% and 5.5% respectively in the period 2000-05, thanks to the de-velopment of internal R&D activities, significant take-overs and the re-organization of the gas portfolio, which led to a greater efficiency in the natu-ral gas production. More deeply, ENI restructured its upstream gas portfolio by effectively grouping its gas fields, investing in paying-off projects and selling, at the same time, the assets with lower profit margins.

Furthermore, the upstream growth will continue to be one of the group’s most relevant goals, as stated in the 2006-2009 strategic plan, which was illus-trated by Paolo Scaroni, ENI’s current Chief Executive Officer, on March 1, 2006 (ENI, 2006a).

Within the depicted framework, the upstream growth could have created some problems to ENI itself, because, as depicted in the regulatory back-ground of the paper, the ongoing liberalization process occurring in the Italian gas market was reducing the players possibility to sell the increased volumes of natural gas directly to It-aly..

As a consequence, ENI’s upstream growth required an effective and effi-cient strategic reaction to the gas market liberalization.

G. ABATECOLA, R. CAFFERATA, S. POGGESI 16

6. Market liberalization and ENI’s strategic reaction

ENI’s strategic reactions to the gas market liberalization process will be ana-lyzed through a focus on the supply of gas to the Italian system. In this regard, the possibility to set entry barriers in the upstream phase of the natural gas production chain seems to be one of the most important elements by which monopoly conditions in the gas market are determined.

According to AEEG’s estimates (2004) ENI’s share in the supply of gas to the Italian market was equal to 92% in 2000. The new antitrust limits imposed by the Italian legislator required ENI to reduce its share to 75% in 2002, and then by two further percentage points per year, in order to reach the minimum amount of 61%. ENI’s reaction was the following.

First of all, the firm started to sell natural gas outside Italy to players such as Edison, Plurigas and Dalmine Energie, which, importing the gas to the Italian market, were themselves ENI’s competitors in the last phase of the gas pro-duction cycle (AEEG, 2005). This because foreign sales, which AEEG and AGCM defined «innovative», were not included in the antitrust limits (AEEG, AGCM, 2004).

Second, ENI carried out a related diversification in the business of electric energy, which it produced through gas-fired plants. More deeply, through self-consumption, the firm could allocate the gas surplus which could not directly pipe into the Italian network10.

Third, ENI carried on its internationalization process. Within the EU, the group gained a lot of market shares in some target countries where the gas de-mand was increasing. ENI enlarged its activities through an increase of the gas volumes directly put on the market and through relevant investments in for-eign firms. This was also possible by ruling out territorial restrictions, called «destination clauses», from the supply contracts ENI had signed with the gas producers. More deeply, these clauses had previously limited ENI’s right to choose the specific market where to sell raw materials.

By the end of 2006, ENI’s market share, as regards gas volumes marketed in Europe, reached 18% (ENI, 2007a). The European gas demand, which was 531 Bcm in 2005, is expected to reach the threshold of about 600 Bcm in 2009

________________ 10 In 2004, ENI became the fifth producer of electric energy in Italy, reaching a 5% market share. In this regard, one could pose the following open question: will the firm develop multi-utility strategies, based on related diversification, increased intra-group demand and cost leader-ship in the gas supply sector?

Strategy, Structure and Market Liberalization: Evidence from ENI

17

(ENI, 2006b). As envisaged by the 2006-2009 strategic plan, ENI’s objective will be to further increase its market share in Europe, in order to reach a bal-ance between the gas volumes sold in Italy and Europe respectively.

For what concerns non-European countries, ENI launched a number of different projects (e.g. the exploration, production and marketing of gas; the construction of pipelines and/or LNG terminals such as Greenstream and Bluestream).

In 2004, ENI’s share in the gas supply to the national market was equal to 66% (AEEG, 2005). Notwithstanding this reduction, the group was able to keep a domi-nant market position for what concerns the gas volumes imported in Italy. In this regard, if the gas volumes sold abroad by the firm were included in its market share, the percentage of supplies controlled by the dominant operator would have reached the 84,4% in 2006, thus greatly exceeding the antitrust limits established by the legislator (AEEG, 2007).

As already pointed out, the gas transport and dispatch activities were regu-lated by the Letta decree, which offered some incentives exploited by ENI, as in the case of Snam Rete Gas. This firm implemented large investment plans yielding extra-profits, as established by the law.

For what concerns the gas sale to final customers in Italy, if one looks at the group’s reaction to the antitrust limits set by the legislator, ENI’s sales in Italy decreased by 14% approximately between 2000 and 2006, mainly because of a reduction in the sales to wholesale customers and industrial users. This reduc-tion, however, did not mean that the Italian customers were less dependent on ENI, which, thanks to its cost leadership, still maintained a competitive advan-tage compared to the other Italian gas players. Furthermore, the firm carried out a deep reorganization of its gas sale sector between 2000 and 2006.

Finally, one should take into account the different geographic areas from which ENI draws natural gas. According to the ENI’s estimates (ENI, 2006c), in 2005 ENI’s natural gas demand was mainly met by foreign suppliers (Russia 26%, Algeria 21%, the Netherlands 9%, Norway 7%) based on long-term con-tracts, while the remaining part was provided by the E&P Division.

Moreover, ENI subscribed supply contracts with take-or-pay clauses, lasting 16 years on average, which from 2008 will guarantee the supply of about 67,3 billion cubic metres of natural gas per year (Russia 28.5%, Algeria 21.5%, the Netherlands 9.8%, Norway 6%, others 3%).

Applying the well-known diversification classification system by Rumelt (1974), ENI’s geographic areas of supply did not result very diversified in 2006. More deeply, if one considers the ratio between the overall quota of gas

G. ABATECOLA, R. CAFFERATA, S. POGGESI 18

imported by ENI from Russia, Algeria and the Netherlands and the total amount of gas imported, a value of about 87% is obtained.

This evidence may support the ongoing debate on the need, for Italy, to di-versify the energy production sources and the geographic areas from which en-ergy is drawn. Moreover, this debate has become even more heated because of the tension between Russia and Ukraine in 2005.

7. Changes in the organizational structure In the period 2000-06, ENI underwent a radical reorganization because of the growth strategy and the legal requirements of the liberalization process. This change followed three directions: - changes affecting the possible configurations of the firm’s organizational

structure; - the adoption of new systems of personality in one or more functional ar-

eas, also through new personnel management methods; - the implementation of new managerial policies to change the overall cli-

mate within the firm11. Some elements which characterized ENI’s reorganization in the ‘90s should be taken into account in order to analyze the changes in the firm’s organizational structure occurring between 2000 and 2006: - the sale of those subsidiaries which were not directly related to the firm’s

core business or which were the least profitable, in line with the goals of the reorganization process; these downsizing operations impacted on the firm’s human resources management policies;

________________ 11 The reference is both to the change which started in 1992 and which transformed the firm into a joint-stock company and to the passage of power from the Chairman to the Chief Ex-ecutive Officer (CEO). With regard to the former, the first package of shares was listed in 1995, followed by another six ones which progressively reduced the State’s presence in the firm. With regard to the latter, Franco Bernabè was ENI’s CEO from 1992 to 1997; Vittorio Mincato was ENI’s CEO from 1998 to 2005. Both aimed at improving the firm’s restructuring and growth. Their policy seems to be confirmed by Paolo Scaroni, who is the current ENI’s CEO.

Strategy, Structure and Market Liberalization: Evidence from ENI

19

- a new rationalization program, which involved the simplification of the decision-making process, the delegation of responsibilities to lower level managers, the reduction of the number of the hierarchical levels and staffs […] the revision of the group’s coordination mechanisms» (Cafferata, Ci-bin, 2000: 19);

- the launch of the divisionalization process, which was considered as the best organizational option to enhance the group’s effectiveness and reac-tion capability in its growth phase12.

At the end of 2000, ENI’s group was active in the following sectors: explora-tion and production of hydrocarbons through the E&P Division; supply, transmission and distribution of natural gas through Snam and Italgas; refining and distribution of oil products through Agip Petroli; petrochemical activities through Enichem; construction and services through Snamprogetti and Saipem; production of electric energy through Eni Power. Moreover, ENI op-erated in the financial sector through Enifin, Sofid and ENI International Holding Bv, which carried out funding and insurance operations for the group’s subsidiaries.

In 2001, some firms were established in the gas business in compliance with the Letta Decree, some others were launched to support ENI’s growth strategy. In compliance with the Letta Decree, the established firms were the following (Figure 2): 1. Rete Gas Italia in November 2000, which was renamed Snam Rete Gas in

October 2001. On June 28, 2001 (effective date July 1, 2001) this new firm incorporated the Snam’s business branch «Transmission and dispatch of natural gas and LNG re-gasification»13.

2. GNL Italia in July 2001 (effective date November 1, 2001), which was to-tally controlled by Snam Rete Gas. This firm had to manage those opera-

________________ 12 In order to fully under stand the divisionalization process, one should remember that in 1992, ENI was the holding company of a series of operational subholding companies. The holding performed coordination and integration operations. Considering the huge number of organizational levels, such a model could have caused the decision making process to slow down as the growth strategy went on. As a possible result, a lack of efficiency could have been produced. The divisionalization process transformed the holding company into an integrated firm embracing three divisions: E&P, G&P and R&M. The benefits were the simplification of the governance procedures, cost reduction and a more efficient management. 13This was in compliance with the Letta Decree, which required the separation of the transport and management network from the gas selling phase in the gas production chain.

G. ABATECOLA, R. CAFFERATA, S. POGGESI 20

tions previously performed by Snam Rete Gas in the LNG re-gasification sector.

3. Stoccaggi Gas Italia in November 2001, which incorporated ENI’s and Snam’s business branches «Compression plants».

4. Italgas Più, set up by Italgas in November 2001 to carry out the gas sale and other customer management activities14.

For what concerns the growth strategy, the upstream international operations carried out by the firm were particularly relevant. In 2000, more deeply, ENI had already bought the 33.3% of Galp, which was a Portuguese firm control-ling the local gas and oil markets and the third major player in the Spanish market. In May 2000, ENI acquired the British-Borneo, which had mainly op-erated in the North Sea until 1994, had merged with Hardy Oil & Gas in 1998 and had entered the Australian, Pakistani and Timorese markets. In January 2001, ENI incorporated the British Lasmo, a firm operating in the exploration and production of hydrocarbons.

Furthermore, in 2001 ENI carried on its divisionalization process through the incorporation of Snam, whose activities were divisionalized15. As a result of this operation, the establishment of the G&P Division occurred on February 1, 2002. In this year, as a consequence, ENI’s organizational structure comprised two divisions, as depicted in Figure 316: - E&P, which was active in the exploration and production of hydrocarbons

in Italy and abroad. - G&P, which was active in the supplying, marketing and distribution of gas

and electric energy.

In 2002, the divisionalization process was carried on and, on May 30, ENI in-corporated AgipPetroli, whose activities were divisionalized. The goal was to set up a third Division, Refining & Marketing (R&M), which was established on January 1, 2003, to process and market crude oil at a national and interna-tional level.

________________ 14 More deeply, Italgas Più was born in order to comply with the Letta Decree, which required secondary distribution to be legally separated from the gas selling to final customers. 15 In this regard, one should remember that E&P Division had already been active since 1997, as a result of the incorporation of Agip and its subsidiaries into ENI. 16 In the same year, ENI acquired 30% of Albacom.

Strategy, Structure and Market Liberalization: Evidence from ENI

21

Furthermore, in the same year, ENI internationally developed its upstream and downstream activities. For what concerns the upstream operations, the firm ac-quired the Norwegian Forum Petroleum, which owned a large infrastructure for the distribution of the natural gas in the European area. For what concerns the downstream operations, ENI acquired 50% of the Spanish Union Fenosa Gas and, in joint venture with the German EnBW, the 97.81% of GVS, which was one of the most important gas transport and distribution firms in Ger-many. Saipem acquired Bouygues Offshore, a firm which was dealing with the engineering and construction of plants for the oil & gas industry and was mainly active in Europe and Africa.

In November 2002, ENI launched a voluntary and general take-over bid on Italgas shares, which ended on January 27, 2003 with the acquisition of almost all the shares of the firm. Therefore, the Italgas shares were delisted from the Milan Stock Exchange17. The most relevant implications of the Italgas opera-tion were the following (ENI G&P, 2005): - the integration of the ENI and Italgas capabilities in the group’s gas pro-

duction chain; - the establishment of a strong and integrated commercial base in the Italian

gas market; - the maximization of the value of the group’s basic assets value (Figure 4).

On June 23, 2004, ENI’s holding approved a partial spin-off of Italgas to the group and the incorporation of ItalgasPiù18. These operations allowed the di-rect access to about five million customers in Italy, the integraton of ENI’s commercial and development policies promoted by the take-over bid on Ital-gas in 2002 and the simplification of the group’s structure19. Italgas sold all its activites not directly concerning the natural gas and remained active only in the downstream operations of the Italian gas market production chain, as depicted in Figure 5.

In 2005, the minerary portfolio continued to be strenghtened: ENI acquired exploratory permits and production concessions in experienced countries such

________________ 17 Furthermore, the chemical business was dismissed. On January 1, 2002, more deeply, ENICHEM business branch named «Chemical strategic activities» was sold to Polimeri Eu-ropa. 18 The former took place on November 17, 2004; the latter occurred on December 16, 2004. 19 Furthermore, in 2004 ENI sold its stake in Albacom to British Telecom.

G. ABATECOLA, R. CAFFERATA, S. POGGESI 22

as Libia, Nigeria and Angola and in new countires with a high potential like Alaska and India, for a total area of about 67 thousand square kilometres, 44 thousand of which owned by ENI.

Furthermore, ENI enhanced its stake in the Kashagan project in Kazakh-stan from 16.67% to 18.52%. Kashagan is the biggest oil area which has been discovered in the world in the last 30 years.

In 2006, G&P Division started the reorganization of Power activities. In this regard, the selling of electric energy, which had been performed by ENIPower until 2006, would have been performed by the Division itself from 2007. This would have allowed to manage the gas and electricity portfolio in an integrated way and to develop a joint offer of gas and electricity. ENIPower would have continued to manage the production of the electic energy.

On March 27, 2006, ENI completely sold its stake in Snamprogetti to Saipem Project. An international leader in the construction and engineering sector was born from this operation.

Furthermore, in the same year, ENI continued to strengthen its competitive position acquiring assets both in experienced areas such as Northern and Western Africa, Brazil, Norway and the United States and in new areas with a high oil&gas potential such as Mali and Mozambic.

Finally, on November 14, 2006, ENI and Gazprom signed a great strategic agreement in Moscow, which foresaw an International alliance between the two firms for the development of joint projects in the upstream, midstream and downstream phases of the gas production chain. Based on a relevant tech-nological cooperation, the agreement foresaw the extension of ENI’s supply contracts from Gazprom until 2035, this strengthening furthermore ENI’s gas portfolio.

In conclusion, in the period 2000-06, as shown in this section, on one hand ENI reached the goal of rationalizing its structure by completing its division-alization process; on the other hand, the firm complied with the Italian laws concerning the liberalization of the gas business. 8. Discussion and conclusion

In the paper, the literature concerning the causal relationship between a firm’s strategy and structure has been firstly reviewed. Within the liberalization proc-ess nowadays occurring in the Italian gas market, the qualitative case study of ENI’s performance between 2000 and 2006 has been then explored. More deeply, the most relevant strategic and organizational changes regarding the firm have been highlighted.

Strategy, Structure and Market Liberalization: Evidence from ENI

23

In regard to the relationship between strategy and structure in this case study, the analysis suggests some evidence for what concerns the period taken into account.

On one hand, ENI carried on its ten-year growth strategy between 2000 and 2006 in order to counter the increasing turbulence in the energy sector. Rele-vant structural changes followed, as shown in Figure 6.

On the other hand, in 2000 the liberalization process in the natural gas mar-ket was launched in Italy. Liberalization required ENI to adopt effective «reac-tion» strategies; at the same time, ex lege organizational changes took place, as shown in Figure 7.

Combining Figures 6 and 7, a representation of the relationship between strategy and structure in the case study between 2000 and 2006 is depicted in Figure 8.

Two interconnected elements emerge from Figure 8. The first is the rela-tionship between strategy and structure, which in the «planned growth strategy structure» perspective corroborates Chandler’s thesis and is further explained by Scott’s model, which emphasizes the importance of «competitive pressure – the pressure of competitive market place» to implement strategic changes.

The second element is the influence of the liberalization process both on ENI’s organizational structure and strategy in the period taken into account.

The connections between the two perspectives are highlighted by the in-verted arrows in the figure. More deeply, the arrows link ENI’s strategies «planned during the Nineties and continuously implemented between 2000 and 2006» to those which were named as specifically «reactive» to the liberalization process.

On the left-hand side of the figure, the arrow which connects the ongoing liberalization process with ENI’s strategic planning in the Nineties means that the potential influence of the future liberalization process had already been en-visaged by the firm’s strategic planning of the period. This interpretation is corroborated by the fact that, in the period taken into account, ENI’s planned divisionalization was not influenced by those organizational changes which have been imposed by the liberalization process.

The abovementioned considerations may contribute to a more general un-derstanding of the strategy/structure relationship in the case study. If one con-siders ENI’s strategy/structure relationship since 1992, when the group was formally privatized, Figure 9 shows how these two variables have changed over time, as explained by in-depth field interviews with some managers of ENI’s G&P Division.

G. ABATECOLA, R. CAFFERATA, S. POGGESI 24

As shown in the figure, the «strategy» variable is predominant in the 1992-1996 period. There is an extensive literature analyzing the reasons leading to the group’s privatization process. This paper has summarized the most important contributions on the subject, as a precondition to better evaluate the period 2000-06 in a strategic-organizational perspective.

Unlike the previous period, the «structure» variable was predominant be-tween 1996 and 2000. For instance, some group’s subsidiaries, such as Agip and Agip Petroli, were against the organizational changes envisaged by the planning phase of the divisionalization process. This attitude impacted on ENI’s performance, with the decrease in the value of the firm’s shares between 1996 and 2000.

Thus, in a theoretical perspective, the following evidence seems relevant: al-though the existence of a transition period between the strategic changes and the structural ones does not totally account for the «strategy follows structure» theory, it at least supports the Chandlerian position that there is often a phase shift between the two variables, with possible repercussions on a firm’s per-formance. Moreover, this concept is in line with Channon’s theories [1973], as already depicted in the theoretical background section of the paper.

Finally, this paper has tried to show that in the period 2000-06, under Vit-torio Mincato’s governance, the strategic component was predominant in the firm and succeeded in complying with the structural changes imposed by the gas market liberation process in Italy. For what concerns ENI’s strat-egy/structure relationship under the current Paolo Scaroni’s governance, evi-dence suggests a macro-strategic continuity, which goes along with the ongoing organizational changes.

Strategy, Structure and Market Liberalization: Evidence from ENI

25

References AEEG (2004, 2005, 2006, 2007), Relazione annuale, Rome. AEEG, AGCM (2004), Indagine conoscitiva sullo stato della liberalizzazione del settore

del gas naturale, Rome BRITTAIN L. (1991), “Is there a Place for Industrial Policy in the Single Mar-

ket?”, University of Wales Review. Business and Economics, n. 7. BRYNTSE K. (1996), “The purchasing of public services. Exploring the pur-

chasing function in a service context”, European Journal of Purchasing and Supply Management, n. 4.

BEARLE A., MEANS G. (1932), The Modern Corporation and Private Property, New York: MacMillan.

BOWER J.L. (1970), Managing the Resource Allocation Process, Cambridge: Harvard University Press.

CAFFERATA R. (1994), “Imprese pubbliche, tutela del mercato e della concor-renza, integrazione europea”, Azienda Pubblica, n. 2.

CAFFERATA R. (1995), “Italian State-owned Holdings, Privatization and the Single Market”, The Annals of Public and Cooperative Economics, n. 4.

CAFFERATA R. (2000) (ed.), Economia e diritto nella privatizzazione delle imprese ita-liane. Il caso ENI, Turin: Giappichelli.

CAFFERATA R. (2002), “From Public to Private. The ENI Group Case”, in Schillaci C.E., Faraci R. (eds.), The Ownership & Governance in Firms in Transi-tion: The Italian Experience, Turin: Giappichelli.

CAFFERATA R., CIBIN R. (1998), “Il gruppo ENI: cambiamenti di strategia e struttura dopo la privatizzazione”, Economia Pubblica, n. 4.

CHANDLER A.D. JR. (1962), Strategy and Structure. Chapters in the History of the American Industrial Enterprise, Cambridge, MA: MIT Press.

CHANNON D.F. (1973), The Strategy and Structure of British Enterprise, New York: MacMillan.

CHILD J. (1972), “Organizational Structure, Environment and Performance: The Role of Strategic Choice”, Sociology, n. 6.

CIBIN R., GRANT R.M. (1996), “Restructuring Among the World’s Leading Oil Companies”, British Journal of Management, n. 7.

CLÒ A. (2004) (ed.), Eni 1953-2003, Bologna: Editrice Compositori. COZZI G., VACCÀ, S. (1992), “Considerazioni sulla politica industriale comuni-

taria”, Economia e politica industriale, n. 72. DONALDSON L. (1982), “Divisionalization and Diversification: A Longitudinal

Study”, Academy of Management Journal, n. 4.

G. ABATECOLA, R. CAFFERATA, S. POGGESI 26

DONALDSON L. (1987), “Strategy and Structural Adjustment to Regain Fit and Performance: In Defense of Contingency Theory”, Journal of Management Studies, n.1.

ECONOMY (2005), Le prossime mosse di Vittorio Mincato, February 17. EUROPEAN COMMISSION (2003), XXXII Relazione sulla politica di concorrenza

2002, Brussels. FAMA E.F. (1980), “Agency Problem and the Theory of the Firm”, Journal of

Political Economics, n. 2. FAMA E.F., JENSEN M. (1983), “Separation of Ownership and Control”, Journal

of Law and Economics, n. 26. FOMBRUN C.J. (1989), “Convergent Dynamics in the Production of Organiza-

tional Configurations”, Journal of Management Studies, n. 5. FOURAKER L.E., STOPFORD J.M. (1968), “Organizational Structure and the

Multinational Strategy”, Administrative Science Quarterly, n. 13. FREDRICKSON J.W. (1986), “The Strategic Decision Process and Organiza-

tional Structurex”, Academy of Management Journal, n. 11. GALBRAITH J.R., NATHANSON, D.A. (1978), Strategy Implementation: The Role of

Structure and Process, St. Paul: West Publishing. GRANT R.M. (1993), Restructuring and Strategic Change in the Oil Industry, Milan:

Franco Angeli. GRANT R.M. (2003), “Strategic Planning in a Turbulent Environment: Evi-

dence from the Oil Majors”, Strategic Management Journal, n. 24. GRANT R.M., CIBIN R. (1996), “Strategy, Structure and Market Turbulence:

The International Oil Majors, 1970-1991”, Scandinavian Journal of Manage-ment, n. 2.

HALL D.J., SAIAS M.A. (1980), “Strategy Follows Structure!”, Strategic Manage-ment Journal, n. 1.

HREBINIAK L.G., JOYCE W.F. (1984), Implementing Strategy, New York: MacMil-lan.

International Energy Agency (2007), Key World Energy Statistics, Paris. MAILLET P. (2000), “La gouvernance europèenne face aux rècents et futures

transformations èconomiques et socials”, The European Union Review, n. 2. MAILLET P. (2001), “Un modèle de gouvernance europèen favorable à

l’apparition d’une politique sociale diversifièe et coordonèe”, The European Union Review, n. 1-2.

MARCH J.G. (1978), “Bounded Rationality, Ambiguity and the Engineering of Choice”, Bell Journal of Economics, n. 9.

MARCH J.G., SHAPIRA Z. (1987), “Managerial Perspectives on Risk and Risk Taking”, Management Science, n. 11.

Strategy, Structure and Market Liberalization: Evidence from ENI

27

MILLER D. (1986), “Configurations of Strategy and Structure: Toward a Syn-thesis”, Strategic Management Journal, n. 3.

MINTZBERG H. (1990), “The Design School: Reconsidering the Basic Premises of Strategic Management”, Strategic Management Journal, n. 11.

MULLER GRAFF P.C. (1996), “Subsidiarity as a Legal Principle”, The European Union Review, n. 1.

PAVAN R.J. (1972), The Strategy and Structure of Italian Industrial Enterprise, Har-vard University, Graduate School of Business Administration: Unpublished Doctoral Dissertation.

POOLEY-DYAS G.D. (1972), The Strategy and Structure of French Industrial Enter-prise, Harvard University, Graduate School of Business Administration: Unpublished Doctoral Dissertation.

QUADRO CURZIO A., FORTIS M. (2000) (eds.), Le liberalizzazioni e le privatizza-zioni dei servizi pubblici locali, Bologna: Il Mulino.

RUMELT R.P. (1974), Strategy, Structure and Economic Performance, Cambridge: Harvard University Press.

SCOTT B.R. (1971), Stages of Corporate Development, Part. I, Cambridge: Harvard University Press.

SECCHI C. (1999), “European Economic Policy in the Post-Euro Era”, The European Union Review, n. 1.

SIMON H.A. (1964), “On the Concept of Organizational Goal”, Administrative Science Quarterly, n. 1.

STANLEY L.L. & WISNER, J.D. (2001), “The determinants of service quality: is-sues for purchasing”, European Journal of Purchasing and Supply Management, n. 8.

STIGLITZ J.E. (1990), “On the Economic Role of the State”, in Heertje, A. (ed.), The Economic Role of the State, Oxford: Basil Blackwell.

TELO M. (2002), “L’interdèpendance entre la gouvernance europèenne et la gouvernance globale”, The European Economic Review, n. 1.

THANHEISER H.T. (1972), The strategy and structure of German industrial enterprise, Harvard University, Graduate School of Business Administration: Unpub-lished Doctoral Dissertation.

THE ECONOMIST (2005), Oil in Troubled Waters, April 30. THE ECONOMIST (2006), Nervous Energy, January 7. VIOLINI L. (2002), “A la recherche d’une bonne governance”, The European Un-

ion Review, n.3.

G. ABATECOLA, R. CAFFERATA, S. POGGESI 28

Other documents ENI (2000-06), Consolidated balance sheet and income statement, Rome: Ugo Quintily. (2001-07), Corporate Governance Reports. (2005a), World Oil & Gas Review 2004, Rome: Marchesi Grafiche Editoriali. (2005b), Attività gas dell’ENI, Rome: Ugo Quintily. (2006a), Presentation of the strategic plan (2006-09), London, March 1. (2006b), Strategy and results, July 15. (2006c), Gas seminar, London, December 1. (2007), Factbook 2006, Rome, Ugo Quintily. Il Sole 24 Ore (2001-06), Dossier dell’Azionista. ENI 2000-05, Milan: Il Sole 24 Ore.

Strategy, Structure and Market Liberalization: Evidence from ENI

29

Tables and figures Table 1: ENI’s competitive position in the Italian gas production cycle before the Italian gas market liberalization.

Activity ENI’s subsidiaries Supply Agip, Snam Transport Snam Storage Agip Primary distribution Snam Secondary distribution Italgas Sale Snam, Italgas Source: adapted from ENI (2005b: 34). Table 2: ENI’s competitive position in the Italian gas production cycle after the Italian gas market liberalization.

Activity ENI’s subsidiaries Supply E&P Division, G&P Division Transport G&P Division (through Snam Rete Gas) Storage E&P Division (through Stogit) Primary Distribution G&P Division (through Snam Rete Gas) Secondary Distribution G&P Division (through Italgas) Sale G&P Division (through ItalgasPiù) Source: adapted from ENI (2005b: 34). Table 3: ENI group’s economic and financial data in millions of euros (2000-2006).

2006 2005 2004 2003 2002 2001 2000

Revenues 86,888 74,526 58,382 51,487 47,922 48,925 47,938 Operating income 19,327 16,827 12,268 9,537 8,472 10,347 10,678 Net income 9,217 8,788 7,274 5,585 4,593 7,751 5,771 Return on sales (%) 22.2 22.82 21.01 18.52 17.67 21.14 22.7 Return on equity (%) 23.83 23.84 22.93 18.94 15.66 29.51 27.9 Return on investment (%) 22.81 33.29 26.99 22.01 20.34 28.70 37.7 E&P revenues 27,173 22,531 15,346 12,746 12,877 13,960 12,308 E&P operating income 15,580 12,592 8,185 5,746 5,175 5,984 6,603 G&P revenues 28,368 22,969 17,528 16,067 15,297 16,098 14,427 G&P operating income 3,802 3,321 3,428 3,627 3,244 3,672 3,178 Source: ENI’s consolidated balance sheet and income statement, 2000-2006.

G. ABATECOLA, R. CAFFERATA, S. POGGESI 30

Figure 1: ENI on December 31, 2000.

Source: Elaboration on Il Sole 24 Ore, 2001.

Strategy, Structure and Market Liberalization: Evidence from ENI

31

Figure 2: ENI on December 31, 2001.

Source: elaboration on Il Sole 24 Ore (2002) and ENI group’s consolidated balance sheet and income statement (2002).

G. ABATECOLA, R. CAFFERATA, S. POGGESI 32

Figure 3: ENI’s on December 31, 2002.

Source: elaboration on Il Sole 24 Ore (2003) and ENI’s consolidated balance sheet and income statement (2003).

Strategy, Structure and Market Liberalization: Evidence from ENI

33

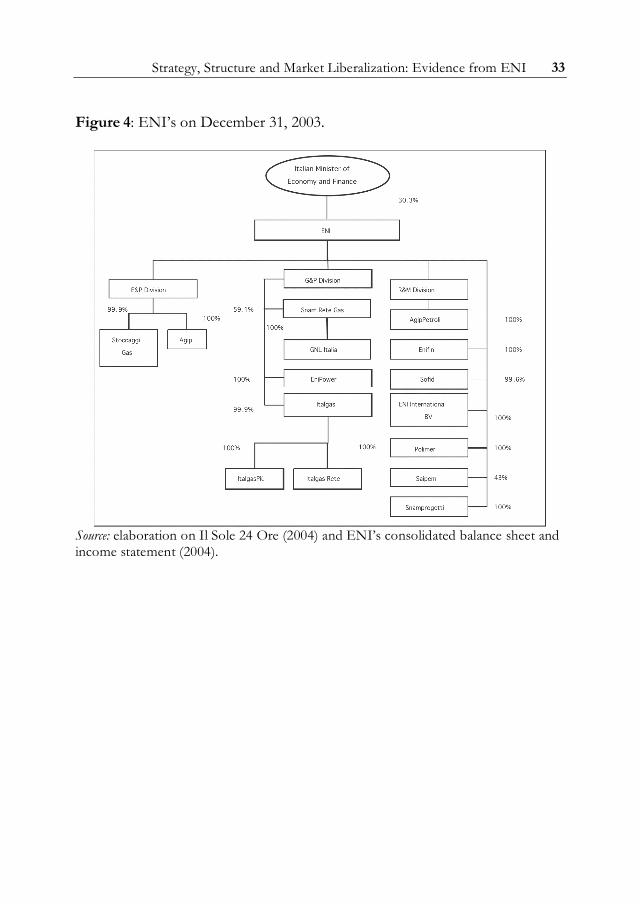

Figure 4: ENI’s on December 31, 2003.

Source: elaboration on Il Sole 24 Ore (2004) and ENI’s consolidated balance sheet and income statement (2004).

G. ABATECOLA, R. CAFFERATA, S. POGGESI 34

Figure 5: ENI on December 31, 2004.

Source: elaboration on Il Sole 24 Ore (2005) and ENI’s consolidated balance sheet and income statement (2005).

Figure 6: ENI: the influence of the growth strategy on the strategy/structure relationship (2000-06).

Growth strategy planned in the

Nineties

Strategy

(2000-2006)

Organizational

changes

Strategy, Structure and Market Liberalization: Evidence from ENI

35

Liberalization

Ex lege organi-zational changes

Growth strategy planned in the

Nineties

Strategy

(2000-2006)

Organizational

changes

Strategic «reaction»

(2000-2006)

Figure 7: ENI: the influence of the liberalization process on the strategy/structure relationship (2000-2006). Figure 8: ENI: An interpretation of the strategy/structure relationship (2000-2006).

Liberalization

Ex lege organiza-tional changes

Strategic «reaction»

(2000-2006)

G. ABATECOLA, R. CAFFERATA, S. POGGESI 36

1992-96 Strategy

1996-2000 Structure

2000-2005 Strategy

2006 Structure

Figure 9: ENI: the strategy/structure relationship since 1992.

McGraw-Hill

Strategy, Structure and MarketLiberalization:Evidence from ENI (2000-06)

Gianpaolo Abatecola, Roberto Cafferata, Sara Poggesi

DSI Essays Series

7

cop7.qxd 3-03-2010 15:36 Pagina 1