Financing Development Stage Biotechnology Companies: Reverse Mergers vs. IPOs

Upload

independentCategory

view

5download

0

ORI GINAL RESEARCH

The effects of R&D, venture capital, and technologyon the underpricing of IPOs in Taiwan

Cheng Shou Lu • Lanfeng Kao • Anlin Chen

Published online: 18 October 2011� Springer Science+Business Media, LLC 2011

Abstract Information asymmetry and value uncertainty causes high -research and

development (R&D) or high-tech Initial Public Offerings (IPOs) to become underpriced.

Venture capital can serve as a moderator to mitigate the information asymmetry and value

uncertainty to reduce IPO underpricing. High-tech industries significantly contribute to

Taiwan’s economic growth. With the unique Taiwan data, we find that venture-backed

IPOs are less underpriced. More importantly, IPO underpricing due to technology

decreases with the use of venture capital and decreases with the interaction between R&D

expenditure and technology. Technology requirement reduces the underpricing of high-

R&D IPOs. Accordingly, R&D spending reduces the underpricing of high-tech IPOs.

Keywords High-tech firms � Initial public offerings � R&D expenditure � Technology �Venture capital

JEL Classification G24

1 Introduction

R&D is important for firms to gain competitive advantages to develop new markets and to

maintain existing market share, especially for high-tech firms. R&D obviously is crucial

for firm’s future value. High-tech industries are the main engines of Taiwan’s economic

growth. In 2007, the total high-tech industries production in Taiwan is approximately 220

billion US dollars, which is about 12.3% of the GNP of Taiwan and the high-tech stocks

C. S. Lu (&)Graduate Institute of Finance, Economics, and Business Decision,National Kaohsiung University of Applied Sciences, Kaohsiung, Taiwane-mail: [email protected]

L. KaoDepartment of Finance, National University of Kaohsiung, Kaohsiung, Taiwan

A. ChenDepartment of Business Management, National Sun Yat-Sen University, Kaohsiung, Taiwan

123

Rev Quant Finan Acc (2012) 39:423–445DOI 10.1007/s11156-011-0259-7

are the most frequently traded in Taiwan Stock Exchange. Tsai and Wang (2008) suggest

that high-tech firms in Taiwan have put tremendous efforts in R&D to reduce losses and

the threat of technological competition. Consequently, Taiwan provides a good example to

examine the relation between firm value and R&D expenditure from the angle of

technology.

R&D expenditures not only reinforce corporate investments but also create information

asymmetry to outside investors. Compared with investments in tangible assets such as

factories and machinery, investments in intangible assets like R&D will cause information

asymmetry due to the restrictions of accounting assessment methods (Aboody and Lev

2000; Guo et al. 2006). In addition, from the point of view of agency theory, Jensen and

Smith (2000) show that the managers may engage in R&D investments to enhance their

own compensation. As a consequence, apart from improving a firm’s future value, R&D

also brings costs to the firms.

Reducing the uncertainty arising from R&D will be able to mitigate information

asymmetry and to reduce the related costs. Shleifer and Vishny (1997) demonstrate that

external governance mechanisms can ensure R&D beneficial to shareholders. External

monitoring mechanisms, such as venture capitalists, can effectively prevent managers’

opportunistic behaviors and ensure R&D expenditures to favor shareholders (Wright et al.

2002).

Venture capitalists provide more than just money to their portfolio companies. Firstly,

Lerner (1994b) argues that venture capitalists often take an active role in guiding the exit

decision, such as going public and that venture capital enables young firms to go public

when public market valuations are especially high. Loughran and Shive (2010) indicate

that younger firms bear the brunt of the effect of venture capital flows. Secondly, Barry

et al. (1990) and Megginson and Weiss (1991) show that venture capitalists are considered

to monitor managers and thus to certify firm value. Lerner (1995) further indicates that

venture capitalists might serve as directors when future of the venture-backed firm

becomes more uncertain. Consequently, for IPOs, where information asymmetry between

investors and issuers is extreme, monitoring and certification through venture capital are

even more important. Shu et al. (2011) confirm the reputation effect associated with

venture capital in IPOs. The venture capitalist’s reputation also helps to attract a presti-

gious underwriter for an initial public offering and ease information asymmetry leading to

less underpricing (Megginson and Weiss 1991; Lerner 1994a).

Chang and Su (2010) argue that R&D is not always beneficial. R&D induces infor-

mation asymmetry and thus raises IPO underpricing. Guo et al. (2006) indicate that an

issuer’s R&D expenditure is the main source of information asymmetry of an IPO. Chin

et al. (2006) also argue that innovation capital regulations result in accounting information

asymmetry and suggest that the greater the R&D expenditure of the issuer in Taiwan, the

greater the underpricing of its IPO.

There usually exists a high level of information asymmetry in the IPOs of high-tech

firms, which in turn leads to a relatively large amount of underpricing (Lowry and Schwert

2002). Tsai and Wang (2004) indicate that technologies and products are updated rapidly in

the dynamic competitive environment of Taiwan’s high-tech industries and that R&D can

give a significant boost to a high-tech firm’s competitive advantage.

IPOs in Taiwan are seriously underpriced (Loughran et al. 1994)1 and high-tech

industries drive the growth of Taiwan’s economy. The accumulated capitals created by

venture capitalists exceed 75 billion US dollars, which is about 19% of Taiwan GDP in

1 Loughran et al. updated the average initial returns of IPOs in 39 countries in the world in 2006.

424 C. S. Lu et al.

123

2007. Up to 2007, 49.6% of high-tech listed firms are venture-backed and 50.4% of high-

tech listed firms are non-venture-backed. Venture Capital contributes substantially to the

Taiwan economy. As a result, Taiwan IPO markets provide a good data sample to

investigate the effect of R&D on IPO underpricing through the moderating effects of

technology and venture capital. Although prior studies have ever examined the relationship

between R&D spending and IPO underpricing (Chin et al. 2006; Guo et al. 2006) or the

relationship between venture-backing and IPO underpricing (Megginson and Weiss 1991),

previous studies did not introduce the role of technology requirement nor examine the

moderating effect among R&D, venture capital, and technology on IPO underpricing. This

paper contributes to the literature by filling this gap. We investigate the effect of R&D on

IPO underpricing through the interaction effects of technology and venture capital. We

explore whether venture backing influences the relationship between R&D and IPO

underpricing and the relationship between technology and IPO underpricing. We further

investigate if the interaction between technology and R&D expenditure influences IPO

underpricing due to technology requirement or R&D spending.

Using a sample of 938 Taiwanese IPOs during 1992–2005, we find that venture capi-

talists influence the relationship between technology and IPO underpricing. The results

demonstrate that venture capital backing can signal the value of high-tech firms to

investors, which can lessen the information asymmetry due to technology. Moreover, we

show that the interaction between technology and R&D influences IPO underpricing due to

technology requirement or R&D spending. An IPO with both high technology and high

R&D spending will experience a less underpricing than an IPO only has either high R&D

spending or high technology because of the interaction between technology and R&D

spending.

The remainder of the paper is organized as follows. Section 2 describes Taiwan stock

markets. Section 3 develops hypotheses. Data source and variable measurement are

described in Sect. 4. Methodologies and results are presented in Sect. 5. Section 6 dis-

cusses the sensitivity tests. Finally, Sect. 7 concludes.

2 Taiwan stock markets

Taiwan stock markets were established in 1961. During the early period, Taiwan stock

markets were very sloppy with few stocks traded and small market capitalization. How-

ever, since 1990s numerous firms have listed on the markets each year and the transactions

and turnover have increased considerably. As of December 31st 2009, Taiwan stock

markets had 1,287 listed companies with a combined market capitalization of 764 billion

US dollars.

Unlike the stock markets in developed countries, individual investors play a significant

role in Taiwan stock markets. As of 31 December 2009, 42% of the capital of listed firms

was owned by domestic individual investors and 36% of the transactions were traded by

domestic individual investors. Investors in Taiwan are generally considered as less

informed and more sentimental.

Claessens et al. (2000) indicate that the controlling shareholders (or controlling fami-

lies) in Taiwan typically gain control by pyramid structure and cross-holding. Separation of

management from ownership control is rare. Even though there is a separation between

ownership and management, there is no separation between control and management in

Taiwan.

R&D, venture capital, and technology on IPO underpricing 425

123

IPOs in Taiwan can be offered to the market through either auction or fixed-price

method. Book-building was not allowed for IPO underwriting in Taiwan until October

2005. Even though auction method is allowed, auctions have been losing market shares in

IPO markets and are barely used. More than 90% of Taiwan IPOs are issued by the fixed-

price method. Only domestic individual investors can subscribe to fixed-priced IPO shares.

For over-subscribed IPOs, winners are determined by public lottery drawing. Allocation

winners have 7 days to decide to withdraw from their allocations or to pay for their

allocations. If a firm-commitment offering is over-subscribed and all the winners pay for

their allocations, the IPO distribution is completed. If the offering is under-subscribed or

some of the winners withdraw from their allocations, the underwriters have to purchase the

unpaid or unsubscribed shares (Lin et al. 2010).

3 Hypotheses development

Ritter (1998) and Ljungqvist and Wilhelm (2002), document that IPOs are underpriced in

many countries. Chen et al. (2002) show that Taiwan IPOs are deliberately underpriced.

IPO underpricing is generally attributed to information asymmetry. High-tech IPOs are

subject to higher underpricing since high-tech firms usually experience relatively higher

risk (Lowry and Schwert 2002). Lowry and Shu (2002) attribute the severe underpricing of

high-tech IPOs to the uncertainty concerning a high-tech firm’s future growth opportuni-

ties. Chen et al. (2007) confirm the arguments of prior studies (Lowry and Schwert 2002;

Lowry and Shu 2002) and demonstrate that IPOs of high-tech industry in Taiwan such as

electronics industry are more underpriced than those of other industries.

Venture capitalists serve as an independent governance mechanism to monitor the

management (Amit et al. 1998; Bouresli et al. 2002). Megginson and Weiss (1991) argue

that the certification role of venture capitalists enhances firm value, reduces information

asymmetry, and thus reduces IPO underpricing.

High-tech IPOs need to be more underpriced due to higher uncertainty about their

future. However, high-tech IPOs can employ the assistance of venture capitalists to reduce

the uncertainty and thereby lessen the underpricing. As a consequence, our Hypotheses 1a

and 1b are as follows:

Hypothesis 1a: High-tech IPOs are more underpriced.

Hypothesis 1b: Venture capitalists can lessen the uncertainty attached to high-tech IPOs

and thereby lessen underpricing of high-tech IPOs.

Aboody and Lev (2000) point out that R&D is a source of information asymmetry

between investors and managers. Guo et al. (2006) further argue that the R&D expendi-

tures of an IPO firm are the main source for IPO information asymmetry. Chin et al. (2006)

confirm the argument of Guo et al. (2006) with evidence from Taiwan indicating that the

accounting information asymmetry from innovation capital regulations leads to the fact

that IPOs of high R&D expenditure are more underpriced in Taiwan.

Hausman et al. (1984) and Chin et al. (2006) express a strong association between R&D

expenditures and patent counts. Patent statistics are considered as a direct measure of

R&D’s effectiveness. Chin et al. (2006) also find that pre-IPO R&D expenditures, granted

patents count, and patent citations are significantly related to IPO underpricing. Even

though R&D expenditures cause information asymmetry leading to the depreciation of firm

value, the patent creation owing to R&D expenditure raises firm value. Kortum and Lerner

426 C. S. Lu et al.

123

(2000) find that venture capital activities increase the patenting rates. Loughran and Shive

(2010) also document that high patent production firms receive venture capital money and

that venture capital can lead to innovations of new technologies or patents.

Venture capitalists can monitor R&D expenditures to favor shareholders (Wright et al.

2002). Venture capital has an important supervisory role between R&D and firm perfor-

mance (Gomez-Mejia et al. 2003; Le et al. 2006). The participation of venture capitalists

can signal the value of R&D and thus alleviate the information asymmetry caused by

R&D. We, thus, infer that venture capital has an effect on the relationship between R&D

expenditure and IPO underpricing and can reduce IPO underpricing due to R&D.

Hypotheses 2a and 2b are as follows:

Hypothesis 2a: High-R&D IPOs are more underpriced.

Hypothesis 2b: Venture capitalists can lessen the uncertainty attached to high-R&D

IPOs and thereby lessen underpricing of high-R&D IPOs.2

High-tech firms urgently need the support of R&D to create profits (Han and Chuang

2011; Wallin and Gilman 1986; Zahra 1996; Zahra and Bogner 2000). Duysters and

Hagedoorn (2000) even argue that R&D is the resource of competitive advantage in high-

tech industry. Investors generally assess higher valuation on R&D activities of high-tech

firms than those of non-tech firms (Chan et al. 1990; Zantout and Tsetsekos 1994;

Szewczyk et al. 1996). Furthermore, Tsai and Wang (2004) indicate that technologies and

products are updated rapidly in Taiwan’s high-tech industries and that R&D significantly

supports a high-tech firm’s competitive advantage. Tsai and Wang (2008) further dem-

onstrate that high-tech firms in Taiwan have put tremendous efforts in R&D to reduce

losses and the threat of technological competition.

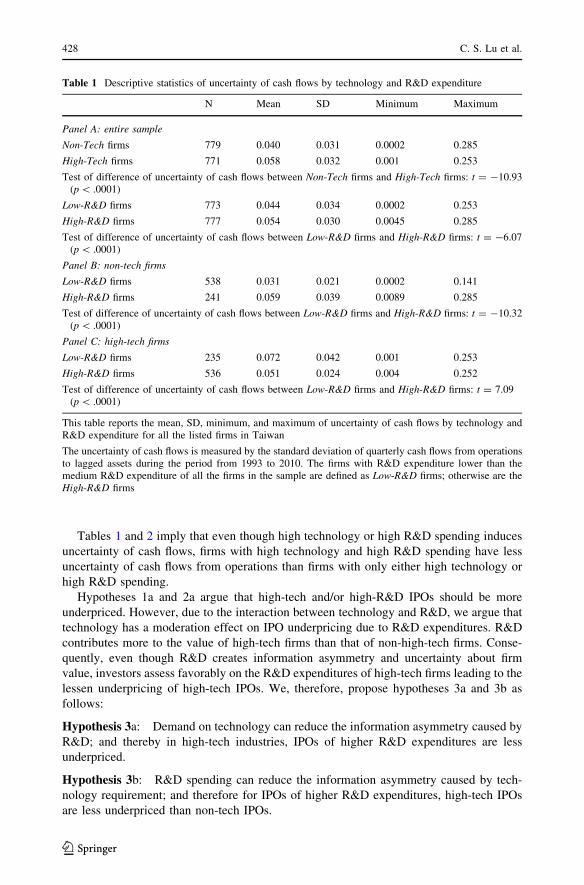

To show that a firm with high technology and high R&D spending will experience a less

information asymmetry than a firm only has either high R&D spending or high technology,

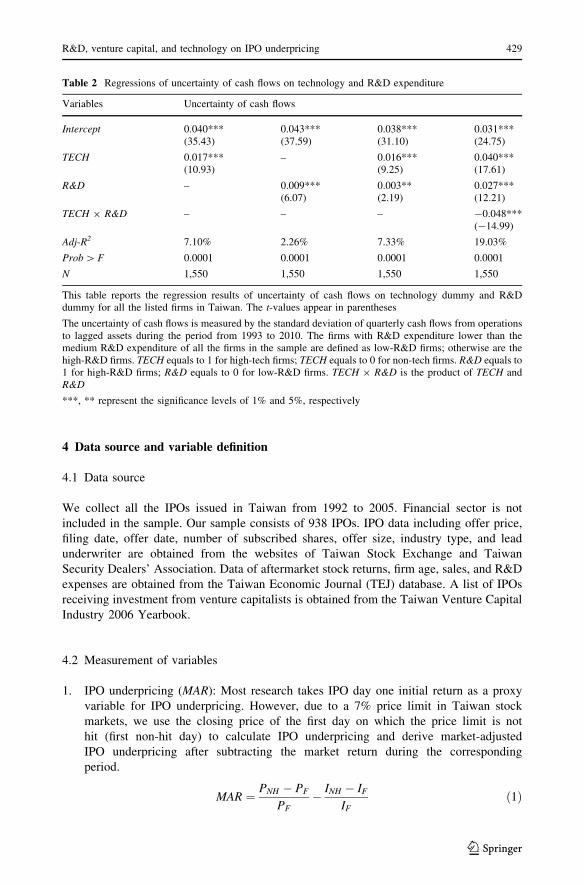

we examine the uncertainty of cash flows of firms with respect to technology and R&D

spending.3 The uncertainty of cash flows is measured by the standard deviation of quarterly

cash flows from operations to lagged assets of the listed firms in Taiwan during the period

from 1993 to 2010. Table 1 reports the descriptive statistics of the uncertainty of cash

flows of firms by technology and R&D expenditure, while Table 2 expresses the regression

results of uncertainty of cash flows on technology and R&D expenditure.

Panel A of Table 1 shows that the uncertainty of cash flows of high tech firms (high-

R&D firms) is higher than that of non-tech firms (low-R&D firms). However, Panels B and

C of Table 1 further demonstrate that the uncertainty of cash flows of firms with high-tech

and high-R&D (mean = 0.051) is lower that that of firms with high-tech and low-R&D

(mean = 0.072) and lower than that of non-tech and high-R&D (mean = 0.059). Table 2

further indicates that technology and R&D spending are both positively related to the

uncertainty of cash flows. However, the interaction of R&D spending and technology is

negatively related to the uncertainty of cash flows (coefficient = -0.048, t value =

-14.99).

2 Ideally, we should also test if patent creation can lessen the uncertainty attached to high-R&D IPOs andthereby lessen underpricing of high-R&D IPOs. However, the data of patent counts or patent citations ofIPO firm in Taiwan are not available to us. The Intellectual Property Office of Ministry of Economic Affairsin Taiwan started to report patent statistics in 2001. The patent data in the early 2000 s are not complete andnot quite reliable. How patent creation influences the underpricing of IPOs related to R&D expenditure isthus deferred to future research.3 We thank an anonymous referee for suggesting this idea to us.

R&D, venture capital, and technology on IPO underpricing 427

123

Tables 1 and 2 imply that even though high technology or high R&D spending induces

uncertainty of cash flows, firms with high technology and high R&D spending have less

uncertainty of cash flows from operations than firms with only either high technology or

high R&D spending.

Hypotheses 1a and 2a argue that high-tech and/or high-R&D IPOs should be more

underpriced. However, due to the interaction between technology and R&D, we argue that

technology has a moderation effect on IPO underpricing due to R&D expenditures. R&D

contributes more to the value of high-tech firms than that of non-high-tech firms. Conse-

quently, even though R&D creates information asymmetry and uncertainty about firm

value, investors assess favorably on the R&D expenditures of high-tech firms leading to the

lessen underpricing of high-tech IPOs. We, therefore, propose hypotheses 3a and 3b as

follows:

Hypothesis 3a: Demand on technology can reduce the information asymmetry caused by

R&D; and thereby in high-tech industries, IPOs of higher R&D expenditures are less

underpriced.

Hypothesis 3b: R&D spending can reduce the information asymmetry caused by tech-

nology requirement; and therefore for IPOs of higher R&D expenditures, high-tech IPOs

are less underpriced than non-tech IPOs.

Table 1 Descriptive statistics of uncertainty of cash flows by technology and R&D expenditure

N Mean SD Minimum Maximum

Panel A: entire sample

Non-Tech firms 779 0.040 0.031 0.0002 0.285

High-Tech firms 771 0.058 0.032 0.001 0.253

Test of difference of uncertainty of cash flows between Non-Tech firms and High-Tech firms: t = -10.93(p \ .0001)

Low-R&D firms 773 0.044 0.034 0.0002 0.253

High-R&D firms 777 0.054 0.030 0.0045 0.285

Test of difference of uncertainty of cash flows between Low-R&D firms and High-R&D firms: t = -6.07(p \ .0001)

Panel B: non-tech firms

Low-R&D firms 538 0.031 0.021 0.0002 0.141

High-R&D firms 241 0.059 0.039 0.0089 0.285

Test of difference of uncertainty of cash flows between Low-R&D firms and High-R&D firms: t = -10.32(p \ .0001)

Panel C: high-tech firms

Low-R&D firms 235 0.072 0.042 0.001 0.253

High-R&D firms 536 0.051 0.024 0.004 0.252

Test of difference of uncertainty of cash flows between Low-R&D firms and High-R&D firms: t = 7.09(p \ .0001)

This table reports the mean, SD, minimum, and maximum of uncertainty of cash flows by technology andR&D expenditure for all the listed firms in Taiwan

The uncertainty of cash flows is measured by the standard deviation of quarterly cash flows from operationsto lagged assets during the period from 1993 to 2010. The firms with R&D expenditure lower than themedium R&D expenditure of all the firms in the sample are defined as Low-R&D firms; otherwise are theHigh-R&D firms

428 C. S. Lu et al.

123

4 Data source and variable definition

4.1 Data source

We collect all the IPOs issued in Taiwan from 1992 to 2005. Financial sector is not

included in the sample. Our sample consists of 938 IPOs. IPO data including offer price,

filing date, offer date, number of subscribed shares, offer size, industry type, and lead

underwriter are obtained from the websites of Taiwan Stock Exchange and Taiwan

Security Dealers’ Association. Data of aftermarket stock returns, firm age, sales, and R&D

expenses are obtained from the Taiwan Economic Journal (TEJ) database. A list of IPOs

receiving investment from venture capitalists is obtained from the Taiwan Venture Capital

Industry 2006 Yearbook.

4.2 Measurement of variables

1. IPO underpricing (MAR): Most research takes IPO day one initial return as a proxy

variable for IPO underpricing. However, due to a 7% price limit in Taiwan stock

markets, we use the closing price of the first day on which the price limit is not

hit (first non-hit day) to calculate IPO underpricing and derive market-adjusted

IPO underpricing after subtracting the market return during the corresponding

period.

MAR ¼ PNH � PF

PF� INH � IF

IFð1Þ

Table 2 Regressions of uncertainty of cash flows on technology and R&D expenditure

Variables Uncertainty of cash flows

Intercept 0.040***(35.43)

0.043***(37.59)

0.038***(31.10)

0.031***(24.75)

TECH 0.017***(10.93)

– 0.016***(9.25)

0.040***(17.61)

R&D – 0.009***(6.07)

0.003**(2.19)

0.027***(12.21)

TECH 9 R&D – – – -0.048***(-14.99)

Adj-R2 7.10% 2.26% 7.33% 19.03%

Prob [ F 0.0001 0.0001 0.0001 0.0001

N 1,550 1,550 1,550 1,550

This table reports the regression results of uncertainty of cash flows on technology dummy and R&Ddummy for all the listed firms in Taiwan. The t-values appear in parentheses

The uncertainty of cash flows is measured by the standard deviation of quarterly cash flows from operationsto lagged assets during the period from 1993 to 2010. The firms with R&D expenditure lower than themedium R&D expenditure of all the firms in the sample are defined as low-R&D firms; otherwise are thehigh-R&D firms. TECH equals to 1 for high-tech firms; TECH equals to 0 for non-tech firms. R&D equals to1 for high-R&D firms; R&D equals to 0 for low-R&D firms. TECH 9 R&D is the product of TECH andR&D

***, ** represent the significance levels of 1% and 5%, respectively

R&D, venture capital, and technology on IPO underpricing 429

123

where PNH is the closing price of the first day on which the price limit is not hit, PF is the

offer price, and INH and IF are the market indexes of the first day on which the price limit is

not hit and the filing date, respectively.

2. Market returns prior to IPO filing date (MKT): The market condition prior to IPO filing

date can be used as public information concerning the determination of IPO offer price

(Lowry and Schwert 2002). This study uses market return 30 days prior to filing date

as an indicator of the market’s condition prior to IPO issuance:

MKT ¼ IF � IF�30

IF�30

ð2Þ

where IF is the market index on the filing date and IF-30 is the market index 30 days prior to

the filing date.

3. Subscription ratio (SUBSCRIPTION): Subscription ratio is a ratio of the number of

shares subscribed by investors to the total number of offered shares of an IPO. The

subscription ratio is used to assess the level of market demand for IPO shares.

SUBSCRIPTION is defined as follows:

SUBSCRIPTION ¼ Number of shares subscribed by investors

Number of IPO shares offered: ð3Þ

4. Offer size (PROC): To take care of information asymmetry source other than R&D

expenditure, we employ offer size, underwriter reputation, and IPO age as control

variables in our empirical design. Beatty and Ritter (1986) and Hanley (1993) use offer

size to assess IPO risk about information asymmetry and find that the larger the offer

size, the smaller the risk of information asymmetry and the less IPO underpricing. We

use the logarithm of IPO total proceeds to measure offer size.

5. Underwriter reputation (UNDR): Carter and Manaster (1990) demonstrate that

underwriter reputation can reduce the information asymmetry between the issuers

and the investors. Following Megginson and Weiss (1991), we define underwriter’s

market share as a proxy variable for underwriter reputation.

UNDR ¼ Total proceeds of IPOs underwritten by a certain underwriter

Total IPO proceeds during the sample periodð4Þ

6. Age of IPO firm (AGE): Beatty and Ritter (1986) suggest that the longer a firm has

been in existence, the better the market can gauge its business performance, which

reduces information asymmetry between the issuer and the investors. We use the

logarithm of years of an IPO from its establishment to the time of filing issuance plus

one as a proxy variable for the firm age.4

4 One is added before logging to avoid taking logarithm of zeroes.

430 C. S. Lu et al.

123

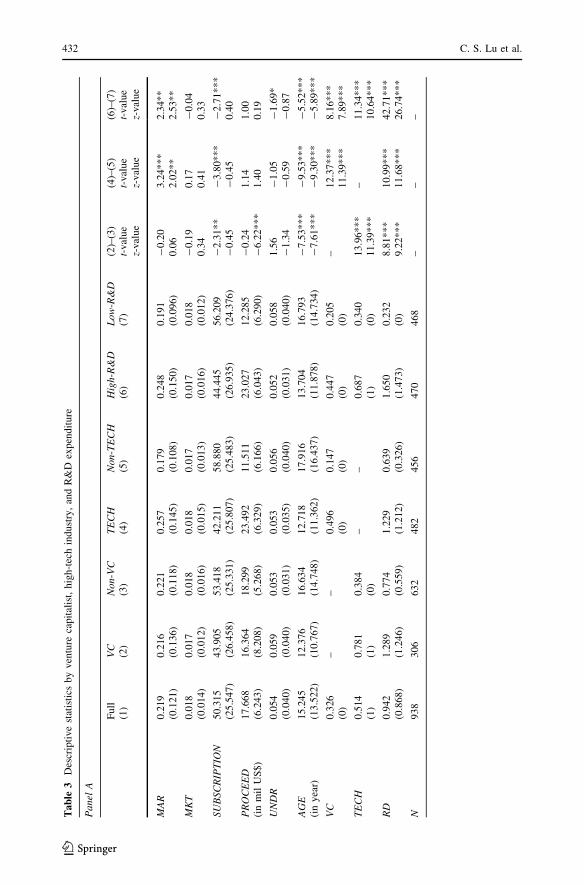

7. Venture capital (VC): VC = 1 if an IPO is venture-backed; otherwise VC = 0.

8. Demand on technology (TECH): We use a high-tech industry dummy variable as a proxy

for demand on technology. TECH = 1 if an IPO is in a high-tech industry according to

Taiwan National Science Council’s categories, i.e. pharmaceutical, OA, computer

equipment, electronics and communications, medical equipment, precision machinery,

optoelectronics equipment, or aerospace industry; otherwise TECH = 0. High-tech

IPOs are assumed to have higher demand on technology than non-high-tech IPOs.

9. R&D intensity (RD): Following Wallin and Gilman (1986) and Guo et al. (2006), we

use the ratio of R&D expenses to sales during the year prior to issuance to assess firms’

R&D; RD is defined as follows5:

RD ¼ ln 1þ RDE

SALES� 100

� �ð5Þ

where RDE and SALES are respectively R&D expenses and sales of the year prior to IPO

issuance.

5 Empirical methodologies and results

The interaction terms of variables in regression models are used to examine the moderating

effects on the relationship between the dependent and independent variables. The signif-

icant interaction terms imply moderating effects. However, the multicollinearity due to

high correlation between the main effect and its cross-product terms is often encountered

with the moderated regressions. We thus further employ the cross-product residual-cen-

tering approach suggested by Lance (1988) to avoid the multicollinearity problem in our

moderated regressions.

5.1 Descriptive statistics

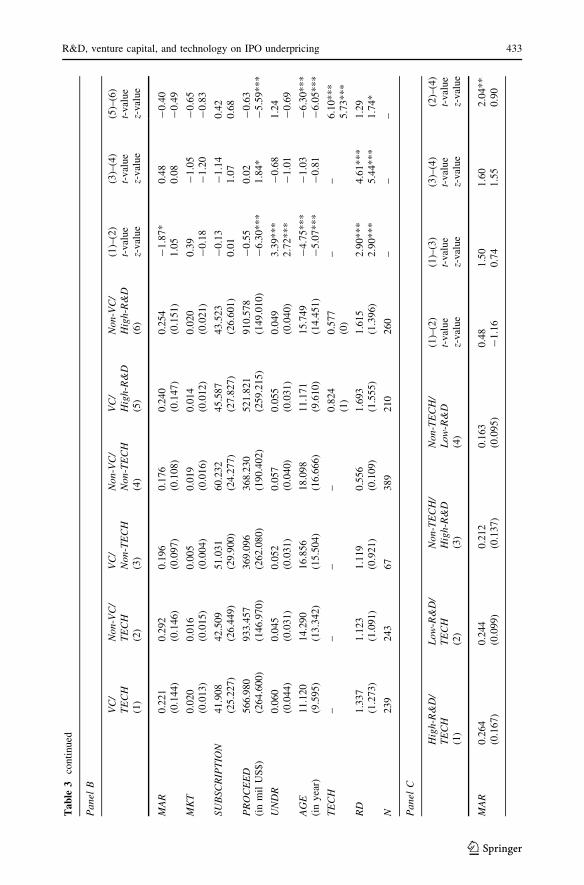

Panel A of Table 3 presents descriptive statistics for the full sample and subsamples by

venture backing, technology, and R&D spending. Panels B and C present the statistics for

the double classification between venture backing, technology, and R&D spending. Panel A

reveals that the average IPO initial return is 21.9%, which indicates that Taiwan’s IPOs are

underpriced. In addition, the average (median) underpricing levels of high-tech and high-

R&D IPOs are 25.7% (14.5%) and 24.8% (15.0%) respectively, which are higher than those

of non-high-tech and low-R&D IPOs implying that the IPOs in high-tech industries and/or

with high levels of R&D expenditure have greater information asymmetry problems.

Positive market return prior to IPO filing implies that firms tend to go public during the bull

markets. The average subscription ratio is 50.315. Note that the average subscription ratio

for non venture-backed IPOs is 53.418, while for venture-backed IPOs is a surprisingly low

at 43.905. Moreover, non-high-tech and low-R&D IPOs have subscription ratios of 58.880

and 56.209 respectively, higher than the corresponding figures for high-tech and high-R&D

IPOs indicating that investors have a greater preference for low-risk IPOs.

5 See footnote 4.

R&D, venture capital, and technology on IPO underpricing 431

123

Ta

ble

3D

escr

ipti

ve

stat

isti

csby

ven

ture

capit

alis

t,hig

h-t

ech

indust

ry,

and

R&

Dex

pen

dit

ure

Pa

nel

A

Fu

ll(1

)V

C(2

)N

on-V

C(3

)T

EC

H(4

)N

on-T

EC

H(5

)H

igh-

R&

D(6

)L

ow

-R&

D(7

)(2

)–(3

)t-

val

ue

z-val

ue

(4)–

(5)

t-val

ue

z-v

alu

e

(6)–

(7)

t-v

alu

ez-

val

ue

MA

R0

.219

(0.1

21)

0.2

16

(0.1

36

)0

.221

(0.1

18)

0.2

57

(0.1

45)

0.1

79

(0.1

08

)0

.24

8(0

.15

0)

0.1

91

(0.0

96)

-0

.20

0.0

63

.24*

**

2.0

2*

*2

.34*

*2

.53*

*

MK

T0

.018

(0.0

14)

0.0

17

(0.0

12

)0

.018

(0.0

16)

0.0

18

(0.0

15)

0.0

17

(0.0

13

)0

.01

7(0

.01

6)

0.0

18

(0.0

12)

-0

.19

0.3

40

.17

0.4

1-

0.0

40

.33

SU

BSC

RIP

TIO

N5

0.3

15

(25

.547

)4

3.9

05

(26

.45

8)

53

.41

8(2

5.3

31

)4

2.2

11

(25

.807

)5

8.8

80

(25

.48

3)

44

.44

5(2

6.9

35

)5

6.2

09

(24

.376

)-

2.3

1*

*-

0.4

5-

3.8

0*

**

-0

.45

-2

.71*

**

0.4

0

PR

OC

EE

D(i

nm

ilU

S$

)1

7.6

68

(6.2

43)

16

.36

4(8

.20

8)

18

.29

9(5

.26

8)

23

.49

2(6

.32

9)

11

.51

1(6

.16

6)

23

.02

7(6

.04

3)

12

.28

5(6

.29

0)

-0

.24

-6

.22*

**

1.1

41

.40

1.0

00

.19

UN

DR

0.0

54

(0.0

40)

0.0

59

(0.0

40

)0

.053

(0.0

31)

0.0

53

(0.0

35)

0.0

56

(0.0

40

)0

.05

2(0

.03

1)

0.0

58

(0.0

40)

1.5

6-

1.3

4-

1.0

5-

0.5

9-

1.6

9*

-0

.87

AG

E(i

ny

ear)

15

.24

5(1

3.5

22

)1

2.3

76

(10

.76

7)

16

.63

4(1

4.7

48

)1

2.7

18

(11

.362

)1

7.9

16

(16

.43

7)

13

.70

4(1

1.8

78

)1

6.7

93

(14

.734

)-

7.5

3*

**

-7

.61*

**

-9

.53*

**

-9

.30*

**

-5

.52*

**

-5

.89*

**

VC

0.3

26

(0)

––

0.4

96

(0)

0.1

47

(0)

0.4

47

(0)

0.2

05

(0)

–1

2.3

7*

**

11

.39

**

*8

.16*

**

7.8

9*

**

TE

CH

0.5

14

(1)

0.7

81

(1)

0.3

84

(0)

––

0.6

87

(1)

0.3

40

(0)

13

.96

**

*1

1.3

9*

**

–1

1.3

4*

**

10

.64

**

*

RD

0.9

42

(0.8

68)

1.2

89

(1.2

46

)0

.774

(0.5

59)

1.2

29

(1.2

12)

0.6

39

(0.3

26

)1

.65

0(1

.47

3)

0.2

32

(0)

8.8

1*

**

9.2

2*

**

10

.99

**

*1

1.6

8*

**

42

.71

**

*2

6.7

4*

**

N9

38

30

66

32

48

24

56

47

04

68

––

–

432 C. S. Lu et al.

123

Ta

ble

3co

nti

nu

ed

Pa

nel

B

VC

/T

EC

H(1

)

No

n-V

C/

TE

CH

(2)

VC

/N

on-T

EC

H(3

)

No

n-V

C/

No

n-T

EC

H(4

)

VC

/H

igh-R

&D

(5)

No

n-V

C/

Hig

h-R

&D

(6)

(1)–

(2)

t-v

alu

ez-

val

ue

(3)–

(4)

t-v

alu

ez-

val

ue

(5)–

(6)

t-v

alu

ez-

val

ue

MA

R0

.221

(0.1

44)

0.2

92

(0.1

46)

0.1

96

(0.0

97)

0.1

76

(0.1

08)

0.2

40

(0.1

47

)0

.254

(0.1

51)

-1

.87

*1

.05

0.4

80

.08

-0

.40

-0

.49

MK

T0

.020

(0.0

13)

0.0

16

(0.0

15)

0.0

05

(0.0

04)

0.0

19

(0.0

16)

0.0

14

(0.0

12

)0

.020

(0.0

21)

0.3

9-

0.1

8-

1.0

5-

1.2

0-

0.6

5-

0.8

3

SU

BSC

RIP

TIO

N4

1.9

08

(25

.227

)4

2.5

09

(26

.449

)5

1.0

31

(29

.900

)6

0.2

32

(24

.277

)4

5.5

87

(27

.82

7)

43

.52

3(2

6.6

01

)-

0.1

30

.01

-1

.14

1.0

70

.42

0.6

8

PR

OC

EE

D(i

nm

ilU

S$

)5

66

.98

0(2

64

.60

0)

93

3.4

57

(14

6.9

70

)3

69

.09

6(2

62

.08

0)

36

8.2

30

(19

0.4

02

)5

21

.82

1(2

59

.21

5)

91

0.5

78

(14

9.0

10

)-

0.5

5-

6.3

0*

**

0.0

21

.84

*-

0.6

3-

5.5

9*

**

UN

DR

0.0

60

(0.0

44)

0.0

45

(0.0

31)

0.0

52

(0.0

31)

0.0

57

(0.0

40)

0.0

55

(0.0

31

)0

.049

(0.0

40)

3.3

9*

**

2.7

2*

**

-0

.68

-1

.01

1.2

4-

0.6

9

AG

E(i

ny

ear)

11

.12

0(9

.59

5)

14

.29

0(1

3.3

42

)1

6.8

56

(15

.504

)1

8.0

98

(16

.666

)1

1.1

71

(9.6

10

)1

5.7

49

(14

.451

)-

4.7

5*

**

-5

.07

**

*-

1.0

3-

0.8

1-

6.3

0*

**

-6

.05*

**

TE

CH

––

––

0.8

24

(1)

0.5

77

(0)

––

6.1

0*

**

5.7

3*

**

RD

1.3

37

(1.2

73)

1.1

23

(1.0

91)

1.1

19

(0.9

21)

0.5

56

(0.1

09)

1.6

93

(1.5

55

)1

.615

(1.3

96)

2.9

0*

**

2.9

0*

**

4.6

1*

**

5.4

4*

**

1.2

91

.74*

N2

39

24

36

73

89

21

02

60

––

–

Pa

nel

C

Hig

h-R

&D

/T

EC

H(1

)

Lo

w-R

&D

/T

EC

H(2

)

No

n-T

EC

H/

Hig

h-R

&D

(3)

No

n-T

EC

H/

Lo

w-R

&D

(4)

(1)–

(2)

t-v

alu

ez-

val

ue

(1)–

(3)

t-val

ue

z-v

alu

e

(3)–

(4)

t-v

alu

ez-

val

ue

(2)–

(4)

t-v

alu

ez-

val

ue

MA

R0

.264

(0.1

67

)0

.244

(0.0

99)

0.2

12

(0.1

37)

0.1

63

(0.0

95

)0

.48

-1

.16

1.5

00

.74

1.6

01

.55

2.0

4*

*0

.90

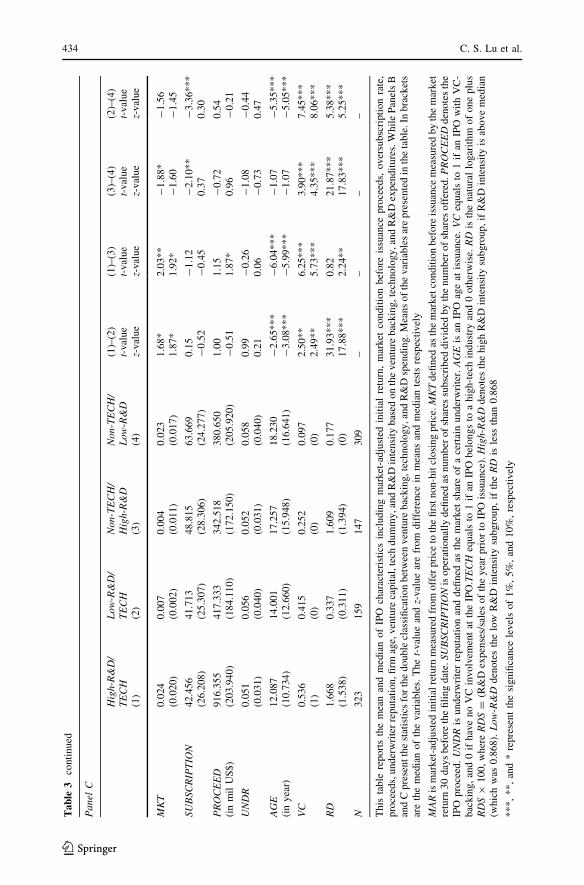

R&D, venture capital, and technology on IPO underpricing 433

123

Ta

ble

3co

nti

nu

ed

Pa

nel

C

Hig

h-R

&D

/T

EC

H(1

)

Lo

w-R

&D

/T

EC

H(2

)

No

n-T

EC

H/

Hig

h-R

&D

(3)

No

n-T

EC

H/

Lo

w-R

&D

(4)

(1)–

(2)

t-val

ue

z-v

alu

e

(1)–

(3)

t-v

alu

ez-

val

ue

(3)–

(4)

t-v

alu

ez-

val

ue

(2)–

(4)

t-v

alu

ez-

val

ue

MK

T0

.024

(0.0

20)

0.0

07

(0.0

02

)0

.004

(0.0

11)

0.0

23

(0.0

17)

1.6

8*

1.8

7*

2.0

3*

*1

.92*

-1

.88

*-

1.6

0-

1.5

6-

1.4

5

SU

BSC

RIP

TIO

N4

2.4

56

(26

.208

)4

1.7

13

(25

.30

7)

48

.81

5(2

8.3

06

)6

3.6

69

(24

.277

)0

.15

-0

.52

-1

.12

-0

.45

-2

.10

**

0.3

7-

3.3

6*

**

0.3

0

PR

OC

EE

D(i

nm

ilU

S$

)9

16

.35

5(2

03

.94

0)

41

7.3

33

(18

4.1

10

)3

42

.51

8(1

72

.15

0)

38

0.6

50

(20

5.9

20

)1

.00

-0

.51

1.1

51

.87*

-0

.72

0.9

60

.54

-0

.21

UN

DR

0.0

51

(0.0

31)

0.0

56

(0.0

40

)0

.052

(0.0

31)

0.0

58

(0.0

40)

0.9

90

.21

-0

.26

0.0

6-

1.0

8-

0.7

3-

0.4

40

.47

AG

E(i

ny

ear)

12

.08

7(1

0.7

34

)1

4.0

01

(12

.66

0)

17

.25

7(1

5.9

48

)1

8.2

30

(16

.641

)-

2.6

5*

**

-3

.08*

**

-6

.04*

**

-5

.99*

**

-1

.07

-1

.07

-5

.35

**

*-

5.0

5*

**

VC

0.5

36

(1)

0.4

15

(0)

0.2

52

(0)

0.0

97

(0)

2.5

0*

*2

.49

**

6.2

5*

**

5.7

3*

**

3.9

0*

**

4.3

5*

**

7.4

5*

**

8.0

6*

**

RD

1.6

68

(1.5

38)

0.3

37

(0.3

11

)1

.609

(1.3

94)

0.1

77

(0)

31

.93

**

*1

7.8

8*

**

0.8

22

.24*

*2

1.8

7*

**

17

.83

**

*5

.38*

**

5.2

5*

**

N3

23

15

91

47

30

9–

––

–

Th

ista

ble

rep

ort

sth

em

ean

and

med

ian

of

IPO

char

acte

rist

ics

incl

ud

ing

mar

ket

-ad

just

edin

itia

lre

turn

,m

ark

etco

nd

itio

nb

efo

reis

suan

cep

roce

eds,

ov

ersu

bsc

rip

tion

rate

,p

roce

eds,

un

der

wri

ter

repu

tati

on

,fi

rmag

e,v

entu

reca

pit

al,te

chd

um

my

,an

dR

&D

inte

nsi

tyb

ased

on

the

ven

ture

bac

kin

g,te

chno

log

y,an

dR

&D

exp

end

itu

res.

Wh

ile

Pan

els

Ban

dC

pre

sent

the

stat

isti

csfo

rth

edouble

clas

sifi

cati

on

bet

wee

nven

ture

bac

kin

g,te

chnolo

gy,an

dR

&D

spen

din

g.M

eans

of

the

var

iable

sar

epre

sente

din

the

tab

le.In

bra

cket

sar

eth

em

edia

no

fth

ev

aria

ble

s.T

he

t -v

alu

ean

dz-

val

ue

are

from

dif

fere

nce

inm

eans

and

med

ian

test

sre

spec

tiv

ely

MA

Ris

mar

ket

-ad

just

edin

itia

lre

turn

mea

sure

dfr

om

off

erp

rice

toth

efi

rst

no

n-h

itcl

osi

ng

pri

ce.M

KT

defi

ned

asth

em

ark

etco

nd

itio

nb

efo

reis

suan

cem

easu

red

by

the

mar

ket

retu

rn3

0d

ays

bef

ore

the

fili

ng

dat

e.SU

BSC

RIP

TIO

Nis

oper

atio

nal

lyd

efined

asnum

ber

of

shar

essu

bsc

ribed

div

ided

by

the

num

ber

of

shar

esoff

ered

.P

RO

CE

ED

den

ote

sth

eIP

Op

roce

ed.

UN

DR

isu

nd

erw

rite

rre

pu

tati

on

and

defi

ned

asth

em

ark

etsh

are

of

ace

rtai

nu

nd

erw

rite

r.A

GE

isan

IPO

age

atis

suan

ce.

VC

equ

als

to1

ifan

IPO

wit

hV

C-

bac

kin

g,

and

0if

hav

en

oV

Cin

vo

lvem

ent

atth

eIP

O.T

EC

Heq

ual

sto

1if

anIP

Obel

ongs

toa

hig

h-t

ech

indust

ryan

d0

oth

erw

ise.

RD

isth

en

atu

ral

logar

ith

mo

fo

ne

plu

sR

DS

91

00

,w

her

eR

DS

=(R

&D

expen

ses/

sale

sof

the

yea

rpri

or

toIP

Ois

suan

ce).

Hig

h-R

&D

den

ote

sth

eh

igh

R&

Din

ten

sity

sub

gro

up

,if

R&

Din

ten

sity

isab

ov

em

edia

n(w

hic

hw

as0

.86

8).

Lo

w-R

&D

den

ote

sth

elo

wR

&D

inte

nsi

tysu

bgro

up

,if

the

RD

isle

ssth

an0

.868

***,

**,

and

*re

pre

sent

the

signifi

cance

level

sof

1%

,5%

,an

d10%

,re

spec

tivel

y

434 C. S. Lu et al.

123

Underwriter reputation of low-R&D IPOs (UNDR = 0.058) is higher than that of for

high-R&D IPOs (UNDR = 0.052). Venture-backed, high-tech, and high-R&D IPOs are

younger. 32.6% of entire sample is venture-backed, while 49.6% of the high-tech IPOs are

venture-backed, much higher than the corresponding figure of 14.7% for non-high-tech

firms. This indicates that venture capitalists prefer to invest in high-tech firms. Moreover,

44.7% of the high-R&D IPOs are venture-backed, higher than the corresponding figure of

20.5% for low-R&D IPOs. High-tech IPOs account for more than half (51.4%) of the IPOs

in the sample. Among high-R&D IPOs, high-tech IPOs account for 68.7%, which are

higher than the 34.0% of low-R&D IPOs. Finally, the average (median) R&D intensity for

the whole sample is 0.942 (0.868), while the R&D intensity of venture-backed IPOs is

1.289 (1.246), which is much higher than that of non-venture-backed IPOs. This reveals

that venture capital backing indeed induces managers to make relatively larger investments

in R&D.

Panel B indicates that VC/TECH IPOs are less underpriced than Non-VC/TECH IPOs

(22.1% vs. 29.2%) implying that venture backing reduces the uncertainty of high-tech IPOs

and thus reduces their underpricing. The underpricing between VC/Non-TECH and Non-

VC/Non-TECH IPOs is not significantly different. Since non-tech IPOs do not experience

severe information asymmetry, they do not need the certification support from the venture

capitalists. The underprcing between VC/High-RD and Non-VC/High-RD IPOs is not

significantly different implying that the way of venture capital influencing the relation

between IPO underpricing and technology is different from that between IPO underpricing

and R&D spending. Panel C demonstrates that IPO underpricing is not significantly dif-

ferent between the double classification by technology and R&D spending. The univariate

results confirm the single classification roles but not the double classification roles of

venture capital, technology, and R&D spending in IPO underpricing. We thus further

conduct the multivariate analyses to examine the interaction among venture capital,

technology, and R&D spending on IPO underpricing.

5.2 Moderating effect of venture capital on the relationship between technology

and IPO underpricing

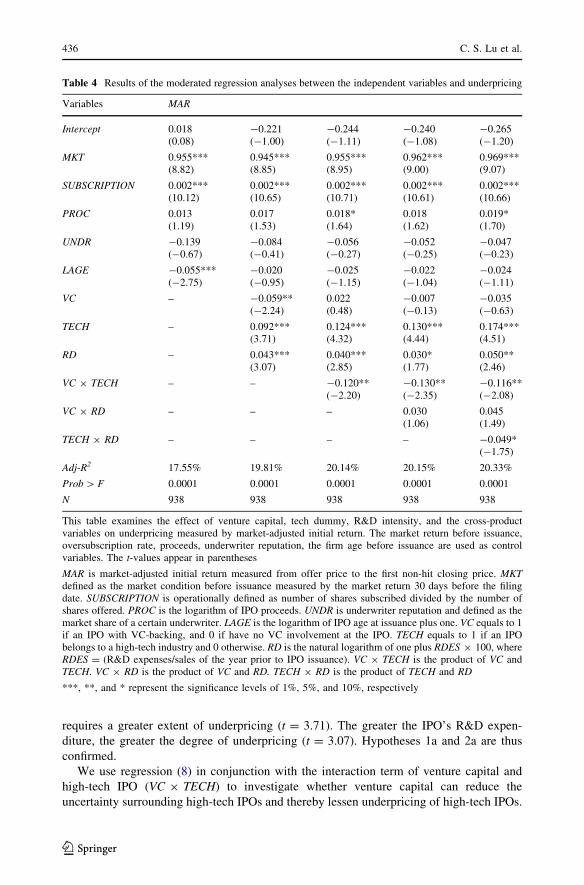

Regression (6) examines the relevant control variables related to IPO underpricing,

including market conditions prior to filing date (MKT), subscription ratio (SUBSCRIP-TION), offer size (PROC), underwrite reputation (UNDR), and age of the IPO (AGE).

MAR ¼ a0 þ a1MKT þ a2SUBSCRIPTION þ a3PROC þ a4UNDRþ a5AGE þ e ð6ÞColumn 1 of Table 4 exhibits that MKT is positively related to IPO underpricing

(t = 8.82) indicating that market condition is simply partly reflected into IPO pricing,

which is consistent with Lowry and Schwert (2002). SUBSCRIPTION is positively related

to IPO underpricing (t = 10.12) supporting the winner’s curse hypothesis, which is con-

sistent with Amihud et al. (2003).

Regression (7) includes the independent and moderating variables of R&D (RD),

venture capital backing (VC), and high-tech industry dummy (TECH).

MAR ¼b0 þ b1MKT þ b2SUBSCRIPTION þ b3PROC þ b4UNDR

þ b5AGE þ b6VC þ b7TECH þ b8RDþ mð7Þ

Column 2 of Table 4 explains that venture capital backing can effectively reduce IPO

underpricing (t = -2.24). The high-tech IPOs are relatively more risky, which ordinarily

R&D, venture capital, and technology on IPO underpricing 435

123

requires a greater extent of underpricing (t = 3.71). The greater the IPO’s R&D expen-

diture, the greater the degree of underpricing (t = 3.07). Hypotheses 1a and 2a are thus

confirmed.

We use regression (8) in conjunction with the interaction term of venture capital and

high-tech IPO (VC 9 TECH) to investigate whether venture capital can reduce the

uncertainty surrounding high-tech IPOs and thereby lessen underpricing of high-tech IPOs.

Table 4 Results of the moderated regression analyses between the independent variables and underpricing

Variables MAR

Intercept 0.018(0.08)

-0.221(-1.00)

-0.244(-1.11)

-0.240(-1.08)

-0.265(-1.20)

MKT 0.955***(8.82)

0.945***(8.85)

0.955***(8.95)

0.962***(9.00)

0.969***(9.07)

SUBSCRIPTION 0.002***(10.12)

0.002***(10.65)

0.002***(10.71)

0.002***(10.61)

0.002***(10.66)

PROC 0.013(1.19)

0.017(1.53)

0.018*(1.64)

0.018(1.62)

0.019*(1.70)

UNDR -0.139(-0.67)

-0.084(-0.41)

-0.056(-0.27)

-0.052(-0.25)

-0.047(-0.23)

LAGE -0.055***(-2.75)

-0.020(-0.95)

-0.025(-1.15)

-0.022(-1.04)

-0.024(-1.11)

VC – -0.059**(-2.24)

0.022(0.48)

-0.007(-0.13)

-0.035(-0.63)

TECH – 0.092***(3.71)

0.124***(4.32)

0.130***(4.44)

0.174***(4.51)

RD – 0.043***(3.07)

0.040***(2.85)

0.030*(1.77)

0.050**(2.46)

VC 9 TECH – – -0.120**(-2.20)

-0.130**(-2.35)

-0.116**(-2.08)

VC 9 RD – – – 0.030(1.06)

0.045(1.49)

TECH 9 RD – – – – -0.049*(-1.75)

Adj-R2 17.55% 19.81% 20.14% 20.15% 20.33%

Prob [ F 0.0001 0.0001 0.0001 0.0001 0.0001

N 938 938 938 938 938

This table examines the effect of venture capital, tech dummy, R&D intensity, and the cross-productvariables on underpricing measured by market-adjusted initial return. The market return before issuance,oversubscription rate, proceeds, underwriter reputation, the firm age before issuance are used as controlvariables. The t-values appear in parentheses

MAR is market-adjusted initial return measured from offer price to the first non-hit closing price. MKTdefined as the market condition before issuance measured by the market return 30 days before the filingdate. SUBSCRIPTION is operationally defined as number of shares subscribed divided by the number ofshares offered. PROC is the logarithm of IPO proceeds. UNDR is underwriter reputation and defined as themarket share of a certain underwriter. LAGE is the logarithm of IPO age at issuance plus one. VC equals to 1if an IPO with VC-backing, and 0 if have no VC involvement at the IPO. TECH equals to 1 if an IPObelongs to a high-tech industry and 0 otherwise. RD is the natural logarithm of one plus RDES 9 100, whereRDES = (R&D expenses/sales of the year prior to IPO issuance). VC 9 TECH is the product of VC andTECH. VC 9 RD is the product of VC and RD. TECH 9 RD is the product of TECH and RD

***, **, and * represent the significance levels of 1%, 5%, and 10%, respectively

436 C. S. Lu et al.

123

MAR ¼c0 þ c1MKT þ c2SUBSCRIPTION þ c3PROC þ c4UNDRþ c5AGE

þ c6VC þ c7TECH þ c8RDþ c9VC � TECH þ lð8Þ

Column 3 of Table 4 indicates that high-tech IPOs are more underpriced (t = 4.32). We

find that the interaction term (VC 9 TECH) is significantly negative (t = -2.20) but VC is

insignificant (t = 0.48) indicating that venture capital can thus lessen the influence of

uncertainty due to technology demand on IPO underpricing, which confirms Hypothesis

1b. Venture capital backing is a moderator and reduces the positive relationship between

technology and IPO underpricing.

5.3 The moderating effect of venture capital of the relationship between R&D and IPO

underpricing

This section employs regression (9) to investigate whether venture capital can induce

investors to assign a higher value to R&D expenditure and thereby lessen IPO

underpricing.

MAR ¼k0 þ k1MKT þ k2SUBSCRIPTION þ k3PROC þ k4UNDRþ k5AGE

þ k6VC þ k7TECH þ k8RDþ k9VC � TECH þ k10VC � RDþ tð9Þ

Column 4 of Table 4 indicates that the greater R&D the higher IPO underpricing

(t = 1.77). Moreover, the interaction term (VC 9 RD) is not significant (t = 1.06) along

with insignificant venture capital (VC) (t = -0.13), which indicates that venture capital

does not directly moderate the form of the relationship between R&D and IPO under-

pricing. This implies that venture capitalists do not directly participate in IPOs’ R&D

decisions (Le et al. 2006).

5.4 Indirect influence of venture capital on the relationship between R&D Intensity

and IPO underpricing

Column 4 of Table 4 implies that venture capital backing does not directly influence the

relationship between R&D and IPO underpricing. Thus, we further investigate if venture

capital indirectly moderates the relationship between R&D and IPO underpricing. Fol-

lowing Sharma et al. (1981) and Le et al. (2006), we divide the entire sample into two

subsets based on venture capital backing.

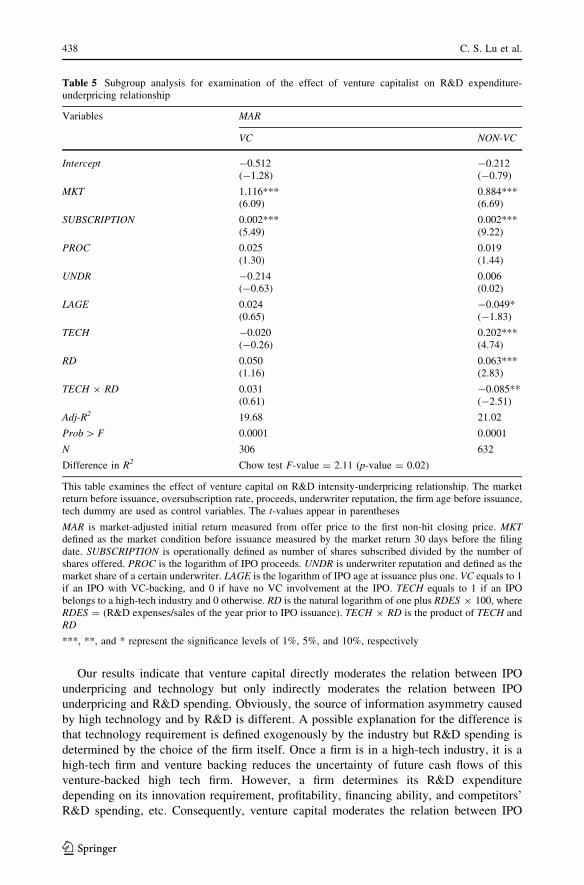

In column 1 of Table 5 for venture-backed IPOs, R&D (RD) is insignificant (t = 1.16).

In contrast, for non-venture-backed IPOs, R&D is significant with t = 2.83. The Chow test

further demonstrates that there is a significant difference in the explanatory power of the

regressions between the two sub-samples (F-value = 2.11). These results suggest that

venture capital can indirectly moderate the relationship between R&D and IPO underpricing

but not directly moderate the relationship. Venture capital is consequently a moderator

variable (homologizer) with regard to the relation between R&D and IPO underpricing

(Sharma et al. 1981; Le et al. 2006), which confirms Hypothesis 2b indirectly.6

6 We also examine the difference between VC/TECH and Non-VC/TECH, VC/Non-TECH and Non-VC/Non-TECH, VC/High-R&D and Non-VC/High-R&D, VC/Low-R&D and Non-VC/Low- R&D, TECH/High-R&D and Non-TECH/High-R&D, TECH/Low-R&D and Non-TECH/Low-R&D by running regres-sions of subsamples of VC versus non-VC, TECH versus Non-TECH, and High-R&D versus Low-R&D. Ourresults are robust to the double classifications between VC, TECH, and R&D expenditure. These results arenot reported in the paper to save space but are available from the author upon request.

R&D, venture capital, and technology on IPO underpricing 437

123

Our results indicate that venture capital directly moderates the relation between IPO

underpricing and technology but only indirectly moderates the relation between IPO

underpricing and R&D spending. Obviously, the source of information asymmetry caused

by high technology and by R&D is different. A possible explanation for the difference is

that technology requirement is defined exogenously by the industry but R&D spending is

determined by the choice of the firm itself. Once a firm is in a high-tech industry, it is a

high-tech firm and venture backing reduces the uncertainty of future cash flows of this

venture-backed high tech firm. However, a firm determines its R&D expenditure

depending on its innovation requirement, profitability, financing ability, and competitors’

R&D spending, etc. Consequently, venture capital moderates the relation between IPO

Table 5 Subgroup analysis for examination of the effect of venture capitalist on R&D expenditure-underpricing relationship

Variables MAR

VC NON-VC

Intercept -0.512(-1.28)

-0.212(-0.79)

MKT 1.116***(6.09)

0.884***(6.69)

SUBSCRIPTION 0.002***(5.49)

0.002***(9.22)

PROC 0.025(1.30)

0.019(1.44)

UNDR -0.214(-0.63)

0.006(0.02)

LAGE 0.024(0.65)

-0.049*(-1.83)

TECH -0.020(-0.26)

0.202***(4.74)

RD 0.050(1.16)

0.063***(2.83)

TECH 9 RD 0.031(0.61)

-0.085**(-2.51)

Adj-R2 19.68 21.02

Prob [ F 0.0001 0.0001

N 306 632

Difference in R2 Chow test F-value = 2.11 (p-value = 0.02)

This table examines the effect of venture capital on R&D intensity-underpricing relationship. The marketreturn before issuance, oversubscription rate, proceeds, underwriter reputation, the firm age before issuance,tech dummy are used as control variables. The t-values appear in parentheses

MAR is market-adjusted initial return measured from offer price to the first non-hit closing price. MKTdefined as the market condition before issuance measured by the market return 30 days before the filingdate. SUBSCRIPTION is operationally defined as number of shares subscribed divided by the number ofshares offered. PROC is the logarithm of IPO proceeds. UNDR is underwriter reputation and defined as themarket share of a certain underwriter. LAGE is the logarithm of IPO age at issuance plus one. VC equals to 1if an IPO with VC-backing, and 0 if have no VC involvement at the IPO. TECH equals to 1 if an IPObelongs to a high-tech industry and 0 otherwise. RD is the natural logarithm of one plus RDES 9 100, whereRDES = (R&D expenses/sales of the year prior to IPO issuance). TECH 9 RD is the product of TECH andRD

***, **, and * represent the significance levels of 1%, 5%, and 10%, respectively

438 C. S. Lu et al.

123

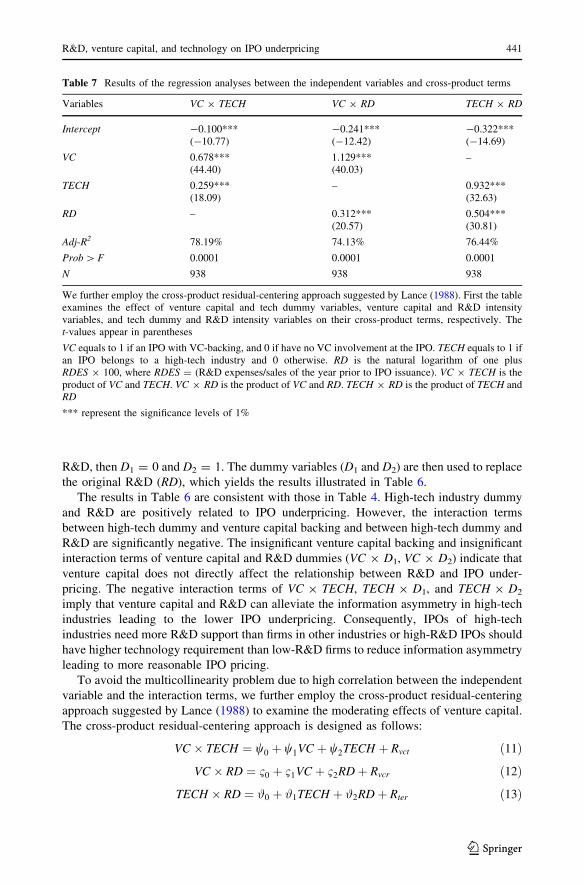

underpricing and technology and the relation between IPO underpricing and R&D

spending differently.

5.5 The interaction between technology and R&D on IPO underpricing

R&D will cause information asymmetry between the firm and investors. However,

investors can give more favorable assessment to the R&D expenditures of the firms that

have stronger demand on technology. Accordingly, technology requirement also causes

information asymmetry between the firm and investors. R&D spending supports the future

growth of high-tech firms and thus investors can assess high-tech IPOs with high R&D

spending favorably. This section investigates whether technology requirement will ease the

information asymmetry caused by its R&D and thereby lessen underpricing of high-R&D

IPOs or whether R&D spending can ease information asymmetry due to technology

requirement and thus reduce underpricing of high-tech IPOs with regression (10).

MAR ¼ h0 þ h1MKT þ h2SUBSCRIPTION þ h3PROC þ h4UNDRþ h5AGE þ h6VCþ h7TECH þ h8RDþ h9VC � TECH þ h10VC � RDþ h11TECH � RDþ x

ð10ÞColumn 5 of Table 4 exhibits that R&D is positively related to IPO underpricing

(t = 2.46). The interaction term (TECH 9 RD) is significantly negative (t = -1.75). In

addition, the significant correlation between the high-tech dummy (TECH) and IPO un-

derpricing (MAR) indicates that technology can thus reduce the uncertainty of R&D on IPO

underpricing, which confirms Hypotheses 3a and 3b. Note that for high-tech IPOs, the

R&D coefficient is only 0.001 (0.050–0.049 = 0.001, RD coefficient of 0.050 plus

TECH 9 RD coefficient of -0.049). This implies that R&D expenditure can hardly raise

underpricing of high-tech IPOs. In contrast, for non-high-tech IPOs, a 1 unit increase in

R&D will increase IPO underpricing by 0.05. This suffices to clarify that demand on

technology indeed influences investors’ assessment of R&D expenditure and can also

influence the underpricing level of IPOs or that R&D spending reduces the underpricing of

high-tech IPOs.

We demonstrate that, for non-venture-backed IPOs, R&D (RD) has relatively significant

explanatory power with regard to IPO underpricing. This implies that, for non-venture-

backed IPOs, R&D is indeed positively correlated with IPO underpricing, which explains

much of the variation in IPO underpricing. Nevertheless, there is no significant correlation

between R&D and IPO underpricing for the venture-backed IPO sample. We argue that

venture capitalists do not participate directly in R&D decision-making and thus do not

directly improve R&D quality or induce investors to appraise more favorably on the IPOs.

Rather, by providing information concerning the IPO’s R&D, venture capitalists may be

able to attract institutional investors, and thus indirectly lessen R&D-induced information

asymmetry between the issuers and investors to alleviate the effect of R&D on IPO pricing.

6 Sensitivity test

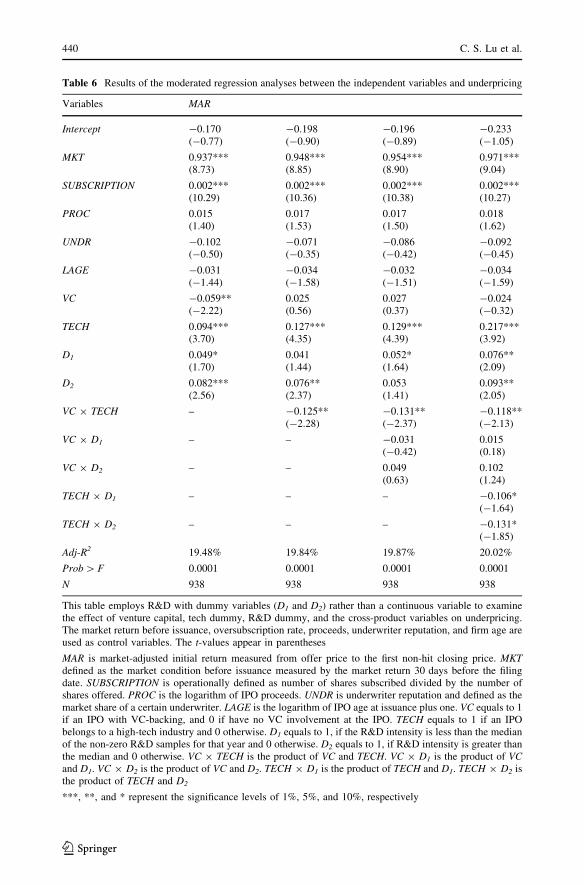

We further measure R&D with dummy variables (D1 and D2) rather than a continuous

variable to examine the role of venture capital on IPO underpricing. For IPOs with zero

R&D, D1 = 0 and D2 = 0. For IPOs with R&D less than the median of positive R&D for

that year, then D1 = 1 and D2 = 0. For IPOs with R&D greater than the median of positive

R&D, venture capital, and technology on IPO underpricing 439

123

Table 6 Results of the moderated regression analyses between the independent variables and underpricing

Variables MAR

Intercept -0.170(-0.77)

-0.198(-0.90)

-0.196(-0.89)

-0.233(-1.05)

MKT 0.937***(8.73)

0.948***(8.85)

0.954***(8.90)

0.971***(9.04)

SUBSCRIPTION 0.002***(10.29)

0.002***(10.36)

0.002***(10.38)

0.002***(10.27)

PROC 0.015(1.40)

0.017(1.53)

0.017(1.50)

0.018(1.62)

UNDR -0.102(-0.50)

-0.071(-0.35)

-0.086(-0.42)

-0.092(-0.45)

LAGE -0.031(-1.44)

-0.034(-1.58)

-0.032(-1.51)

-0.034(-1.59)

VC -0.059**(-2.22)

0.025(0.56)

0.027(0.37)

-0.024(-0.32)

TECH 0.094***(3.70)

0.127***(4.35)

0.129***(4.39)

0.217***(3.92)

D1 0.049*(1.70)

0.041(1.44)

0.052*(1.64)

0.076**(2.09)

D2 0.082***(2.56)

0.076**(2.37)

0.053(1.41)

0.093**(2.05)

VC 9 TECH – -0.125**(-2.28)

-0.131**(-2.37)

-0.118**(-2.13)

VC 9 D1 – – -0.031(-0.42)

0.015(0.18)

VC 9 D2 – – 0.049(0.63)

0.102(1.24)

TECH 9 D1 – – – -0.106*(-1.64)

TECH 9 D2 – – – -0.131*(-1.85)

Adj-R2 19.48% 19.84% 19.87% 20.02%

Prob [ F 0.0001 0.0001 0.0001 0.0001

N 938 938 938 938

This table employs R&D with dummy variables (D1 and D2) rather than a continuous variable to examinethe effect of venture capital, tech dummy, R&D dummy, and the cross-product variables on underpricing.The market return before issuance, oversubscription rate, proceeds, underwriter reputation, and firm age areused as control variables. The t-values appear in parentheses

MAR is market-adjusted initial return measured from offer price to the first non-hit closing price. MKTdefined as the market condition before issuance measured by the market return 30 days before the filingdate. SUBSCRIPTION is operationally defined as number of shares subscribed divided by the number ofshares offered. PROC is the logarithm of IPO proceeds. UNDR is underwriter reputation and defined as themarket share of a certain underwriter. LAGE is the logarithm of IPO age at issuance plus one. VC equals to 1if an IPO with VC-backing, and 0 if have no VC involvement at the IPO. TECH equals to 1 if an IPObelongs to a high-tech industry and 0 otherwise. D1 equals to 1, if the R&D intensity is less than the medianof the non-zero R&D samples for that year and 0 otherwise. D2 equals to 1, if R&D intensity is greater thanthe median and 0 otherwise. VC 9 TECH is the product of VC and TECH. VC 9 D1 is the product of VCand D1. VC 9 D2 is the product of VC and D2. TECH 9 D1 is the product of TECH and D1. TECH 9 D2 isthe product of TECH and D2

***, **, and * represent the significance levels of 1%, 5%, and 10%, respectively

440 C. S. Lu et al.

123

R&D, then D1 = 0 and D2 = 1. The dummy variables (D1 and D2) are then used to replace

the original R&D (RD), which yields the results illustrated in Table 6.

The results in Table 6 are consistent with those in Table 4. High-tech industry dummy

and R&D are positively related to IPO underpricing. However, the interaction terms

between high-tech dummy and venture capital backing and between high-tech dummy and

R&D are significantly negative. The insignificant venture capital backing and insignificant

interaction terms of venture capital and R&D dummies (VC 9 D1, VC 9 D2) indicate that

venture capital does not directly affect the relationship between R&D and IPO under-

pricing. The negative interaction terms of VC 9 TECH, TECH 9 D1, and TECH 9 D2

imply that venture capital and R&D can alleviate the information asymmetry in high-tech

industries leading to the lower IPO underpricing. Consequently, IPOs of high-tech

industries need more R&D support than firms in other industries or high-R&D IPOs should

have higher technology requirement than low-R&D firms to reduce information asymmetry

leading to more reasonable IPO pricing.

To avoid the multicollinearity problem due to high correlation between the independent

variable and the interaction terms, we further employ the cross-product residual-centering

approach suggested by Lance (1988) to examine the moderating effects of venture capital.

The cross-product residual-centering approach is designed as follows:

VC � TECH ¼ w0 þ w1VC þ w2TECH þ Rvct ð11Þ

VC � RD ¼ 10 þ 11VC þ 12RDþ Rvcr ð12Þ

TECH � RD ¼ #0 þ #1TECH þ #2RDþ Rter ð13Þ

Table 7 Results of the regression analyses between the independent variables and cross-product terms

Variables VC 9 TECH VC 9 RD TECH 9 RD

Intercept -0.100***(-10.77)

-0.241***(-12.42)

-0.322***(-14.69)

VC 0.678***(44.40)

1.129***(40.03)

–

TECH 0.259***(18.09)

– 0.932***(32.63)

RD – 0.312***(20.57)

0.504***(30.81)

Adj-R2 78.19% 74.13% 76.44%

Prob [ F 0.0001 0.0001 0.0001

N 938 938 938

We further employ the cross-product residual-centering approach suggested by Lance (1988). First the tableexamines the effect of venture capital and tech dummy variables, venture capital and R&D intensityvariables, and tech dummy and R&D intensity variables on their cross-product terms, respectively. Thet-values appear in parentheses

VC equals to 1 if an IPO with VC-backing, and 0 if have no VC involvement at the IPO. TECH equals to 1 ifan IPO belongs to a high-tech industry and 0 otherwise. RD is the natural logarithm of one plusRDES 9 100, where RDES = (R&D expenses/sales of the year prior to IPO issuance). VC 9 TECH is theproduct of VC and TECH. VC 9 RD is the product of VC and RD. TECH 9 RD is the product of TECH andRD

*** represent the significance levels of 1%

R&D, venture capital, and technology on IPO underpricing 441

123

where, Rvct, Rvcr, and Rter are the error terms of the regressions (11), (12), and (13),

respectively and results of the above regression analyses are illustrated in Table 7. The

cross-product residuals are constructed as:

Table 8 Results of the regression analyses between the cross-product residuals terms and underpricing (aresidual-centering approach)

Variables MAR

Coeff.(t-value)

VIF Coeff.(t-value)

VIF Coeff.(t-value)

VIF

Intercept -0.232(-1.05)

-0.234(-1.06)

-0.249(-1.13)

MKT 0.955***(8.95)

1.017 0.962***(9.00)

1.021 0.969***(9.07)

1.022

SUBSCRIPTION 0.002***(10.71)

1.039 0.002***(10.61)

1.044 0.002***(10.666)

1.045

PROC 0.018*(1.64)

1.105 0.018(1.62)

1.105 0.019*(1.70)

1.108

UNDR -0.056(-0.27)

1.066 -0.052(-0.25)

1.067 -0.047(-0.23)

1.067

LAGE -0.025(-1.15)

1.216 -0.022(-1.04)

1.227 -0.023(-1.11)

1.230

VC -0.060***(-2.27)

1.266 -0.060**(-2.29)

1.266 -0.062**(-2.38)

1.269

TECH 0.093***(3.74)

1.300 0.097***(3.85)

1.322 0.098***(3.98)

1.323

RD 0.040***(2.85)

1.250 0.040***(2.82)

1.250 0.040***(2.83)

1.250

Rvct -0.120**(-2.20)

1.026 -0.130**(-2.35)

1.055 -0.116**(-2.08)

1.077

Rvcr – 0.031(1.06)

1.065 0.045(1.49)

1.150

Rter – – -0.049*(-1.75)

1.134

Adj-R2 20.14% 20.15% 20.33%

Prob [ F 0.0001 0.0001 0.0001

N 938 938 938

The table examines the effect of cross-product residuals terms on underpricing. The market return beforeissuance, oversubscription rate, proceeds, underwriter reputation, the firm age before issuance are used ascontrol variables. The t-values appear in parentheses

MAR is market-adjusted initial return measured from offer price to the first non-hit closing price. MKTdefined as the market condition before issuance measured by the market return 30 days before the filingdate. SUBSCRIPTION is operationally defined as number of shares subscribed divided by the number ofshares offered. PROC is the logarithm of IPO proceeds. UNDR is underwriter reputation and defined as themarket share of a certain underwriter. LAGE is the logarithm of IPO age at issuance plus one. VC equals to 1if an IPO with VC-backing, and 0 if have no VC involvement at the IPO. TECH equals to 1 if an IPObelongs to a high-tech industry and 0 otherwise. RD is the natural logarithm of one plus RDES 9 100, where

RDES = (R&D expenses/sales of the year prior to IPO issuance). Rvct is the residual from column 1 of

Table 7. Rvcr is the residual from column 2 of Table 7. Rter is the residual from column 3 of Table 7

***, **, and * represent the significance levels of 1%, 5%, and 10%, respectively

442 C. S. Lu et al.

123

Rvct ¼ VC � TECH � w0 þ w1VC þ w2TECH� �

ð14Þ

Rvcr ¼ VC � RD� 10 þ 11VC þ 12RDð Þ ð15Þ

Rter ¼ TECH � RD� #0 þ #1TECH þ #2RD� �

ð16Þ

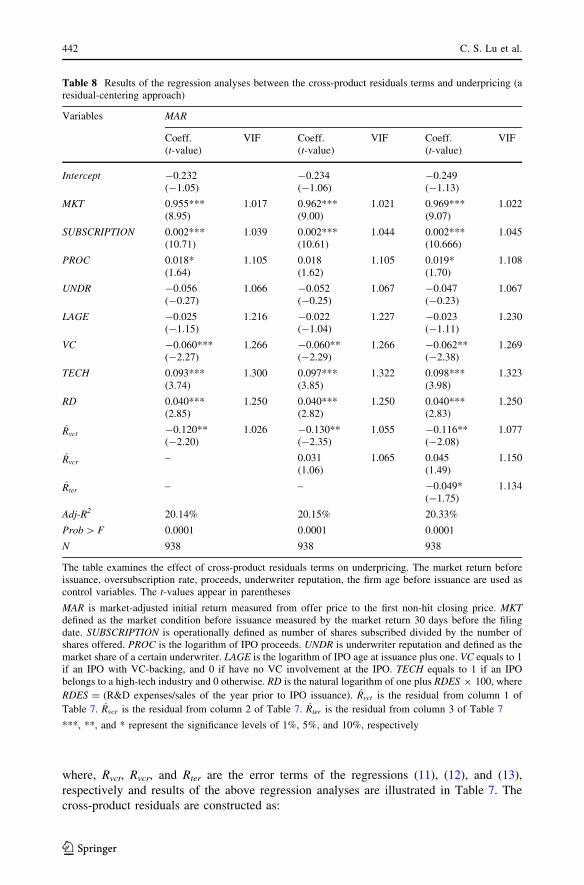

and then used to replace the interaction terms in regressions (8), (9), (10).

The cross-product residuals of Rvct in columns 1, 3, and 5 of Table 8 are significantly

negative (t = -2.20, -2.35, and -2.08) to confirms Hypothesis 1b. Furthermore, the

insignificant Rvcr in column 3 of Table 8 indicates that venture capital backing does not

directly influence the relationship between R&D and underpricing. The negative cross-

product residual terms of Rter (t = -1.75) implies that the requirement of technology can

alleviate the information asymmetry from R&D expenditures leading to the lower

underpricing or that R&D spending reduces the underpricing of high-tech IPOs. All the

variance inflation factors (VIFs) in Table 8 are smaller than 2 indicating no multicollin-

earity problems at all.

7 Conclusions

IPOs are generally underpriced which is often attributed to information asymmetry and

future value uncertainty. R&D expenditures create information asymmetry to outside

investors. Technology requirements induce the uncertainty of firms’ future value. Taiwan

is an emerging country with higher information asymmetry than developed countries

making Taiwan’s IPO data a good data set to examine the role of R&D, venture capital,

and technology on IPO underpricing.

This paper examines the effects of R&D, venture capital, and technology on the

underpricing of IPOs in Taiwan. Especially, we focus on the moderation role of venture

capital and interaction between R&D expenditure and technology. This paper reconfirms

that high-tech and/or high R&D IPOs are underpriced. More importantly, this paper

contributes to the literature by demonstrating the moderating effects of venture capital and

the interaction effect between technology and R&D on IPO underpricing. IPO underpricing

is due to technology decreases with the use of venture capital. Moreover, technology

requirement justifies the expenditures of R&D and thus, reduce the underpricing of high-

R&D IPOs. Accordingly, R&D spending supports the future growth of high-tech firms and

therefore reduces the underpricing of high-tech IPOs. IPO pricing will be more efficient by

understanding the roles among R&D expenditures, high-tech industries, and venture

capital.

Acknowledgments We appreciate the helpful comments from the seminar participants at 2010 PBFEAM,National University of Kaohsiung, and National Sun Yat-Sen University. Cheng-Shou Lu thanks NationalScience Council (Taiwan) for the financial support (Research grant: NSC98-2410-H-151-024). All theremaining errors are ours.

References

Aboody D, Lev B (2000) Information asymmetry, R&D, and insider gains. J Financ 55(6):2747–2766Amihud Y, Hauser S, Kirsh A (2003) Allocations, adverse selection, and cascades in IPOs: evidence from

the Tel Aviv stock exchange. J Financ Econ 68(1):137–158

R&D, venture capital, and technology on IPO underpricing 443

123

Amit R, Brander J, Zott C (1998) Why do venture capital firms exist? Theory and Canadian evidence. J BusVentur 13(6):441–466

Barry CB, Muscarella CJ, Peavy JW, Vetsuypens MR (1990) The role of venture capital in the creation ofpublic companies: evidence from the going-public process. J Financ Econ 27(2):447–471

Beatty RP, Ritter JR (1986) Investment banking, reputation, and the underpricing of initial public offering.J Financ Econ 15(1–2):213–232

Bouresli AK, Davidson WN III, Abdulsalam FA (2002) Role of venture capitalists in IPO corporategovernance and operating performance. Q J Bus Econ 41(3–4):71–83

Carter RB, Manaster S (1990) Initial public offerings and underwriter reputation. J Financ 45(4):1045–1068Chan SH, Martin JD, Kensinger JW (1990) Corporate research and development expenditures and share

value. J Financ Econ 26(2):255–276Chang HL, Su CW (2010) Is R&D always beneficial? Rev Pac Basin Financ Mark Policies 13(1):157–174Chen A, Hung CC, Wu CS (2002) The underpricing and excess returns of initial public offerings in Taiwan

based on noisy trading: a stochastic frontier model. Rev Quant Financ Acc 18(2):139–159Chen HC, Jhou CJ, Yeh HC (2007) Signaling by underwriter retention rate in the IPO market. Appl Econ

39(15):1973–1983Chin CL, Lee P, Kleinman G (2006) IPO anomalies and innovation capital. Rev Quant Financ Acc

27(1):67–91Claessens S, Djankov S, Lang L (2000) The separation of ownership and control in East Asian Corporations.

J Financ Econ 58(1–2):81–112Duysters G, Hagedoorn J (2000) Core competences and company performance in the world-wide computer

industry. J High Technol Manag Res 11(1):75–91Gomez-Mejia LR, Larraza-Kintana M, Makri M (2003) The determinants of executive compensation in

family-controlled public corporations. Acad Manag J 46(2):226–237Guo RJ, Lev B, Shi C (2006) Explaining the short- and long-term IPO anomalies in the US by R&D. J Bus

Financ Account 33(3):550–579Han I, Chuang CM (2011) The impacts of R&D investment on company performance: US vs. Taiwanese