Aftermarket support and underpricing of initial public offerings

21

Journal of Financial Economics 35 (1994) 199-219. North-Holland Paul Schultz Ohio State ‘University. Columbus, OH 43210, USA Mir A. Zaman University of Northern Iowa, Cedar Falls, IA 50613, USA Received February 1993, final version received November 1993 We study the aftermarket for 72 initial public offerings (IPOs) using comprehensive trade and quote-change data from every market maker for the first three days of trading. Underwriters quote higher bid prices than other market makers for issues that commence trading at or below the offer price. Underwriters repurchase large quantities of stock in the aftermarket without risk by oversell- ing the issue by the amount of the overallotment option. If the IPO is hot, the overallotment option is exercised. If not, the short position is covered with aftermarket selling. We discuss several reasons for underwriter support. Key words: IPO; Underwriting; Stabilization JEL class$cation: G24 1. Introduction Aftermarket support of an initial public offering (IPO) is an effort by the underwriter to prop up aftermarket prices when the market price would decline without intervention. In this paper we examine aftermarket transactions from the first three days of trading, along with quotes of underwriters and other market makers, and find direct evidence that underwriters support I s in the Corresponderxe to: Paul H. Schultz, Faculty of Finance, College gf Business, Ohio State University, 1775 College Road, Columbus, OH 43210, USA. *We are grateful for the comments of William Christie, Thomas George, Michael Long, David Mayers, David Schultz, Rene Stulz, David Williams, and se at the University of Iowa and Ohio State University. Clifford Smith (the editor) refer-ee) provided suggestions that greatly improved the focus and clarity of the paper. Jeffrey Harris has provided excellent research assistance. Support of the ice Center at io State University (Schultz) and the University of Iowa (Zaman) is gratefully acknowledged. 11 tights reserved

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Aftermarket support and underpricing of initial public offerings

Journal of Financial Economics 35 (1994) 199-219. North-Holland

Paul Schultz Ohio State ‘University. Columbus, OH 43210, USA

Mir A. Zaman University of Northern Iowa, Cedar Falls, IA 50613, USA

Received February 1993, final version received November 1993

We study the aftermarket for 72 initial public offerings (IPOs) using comprehensive trade and quote-change data from every market maker for the first three days of trading. Underwriters quote higher bid prices than other market makers for issues that commence trading at or below the offer price. Underwriters repurchase large quantities of stock in the aftermarket without risk by oversell- ing the issue by the amount of the overallotment option. If the IPO is hot, the overallotment option is exercised. If not, the short position is covered with aftermarket selling. We discuss several reasons for underwriter support.

Key words: IPO; Underwriting; Stabilization JEL class$cation: G24

1. Introduction

Aftermarket support of an initial public offering (IPO) is an effort by the underwriter to prop up aftermarket prices when the market price would decline without intervention. In this paper we examine aftermarket transactions from the first three days of trading, along with quotes of underwriters and other market makers, and find direct evidence that underwriters support I s in the

Corresponderxe to: Paul H. Schultz, Faculty of Finance, College gf Business, Ohio State University, 1775 College Road, Columbus, OH 43210, USA.

*We are grateful for the comments of William Christie, Thomas George, Michael Long, David Mayers, David Schultz, Rene Stulz, David Williams, and se at the University of Iowa and Ohio State University. Clifford Smith (the editor) refer-ee) provided suggestions that greatly improved the focus and clarity of the paper. Jeffrey Harris has provided excellent research assistance. Support of the ice Center at io State University (Schultz) and the University of Iowa (Zaman) is gratefully acknowledged.

11 tights reserved

200 P.H. Schultz and M.A. Zaman, Aftermclrket support and IPO underpricing

aftermarket. This finding is important for two reasons. First, it provides indirect evidence on why IPOs are underpriced. Second, it allows a fuller characteriza- tion of the role of underwriters in initial public offerings.

Our sample consists of every trade and every quote update for the first three days of trading for 72 IPOs from March 31, 1992 through June 1, 1992. This intraday data allows us to determine how much of the volume can be attributed to buys, how much to sells, and how the trading patterns change over the first three days of trading. For the 64 sample IPOs that traded on NASDAQ in the aftermarket, we have every quote update by each of the individual market makers. These individual dealer quotes permit us to observe when underwriters and other market makers are buying or selling stock.

To compare underwriter behavior across IPOs that are likely and unlikely to be supported, we split our sample at each point in time into IPOs that trade above their offering price (henceforth hot IPOs) and IPOs that trade at or below their offering price (henceforth cold IPOs). By this definition, an IPO can change from hot to cold if the stock price drops from above the offer price to a price at or below the offer price at any time during the aftermarket; similarly, an IPO can change from cold to hot if the price rises above the offer price. Consistent with aftermarket support, we find that. underwriters spend a larger proportion of their time at the inside bid (the highest price that any dealer will pay for the stock) for cold IPOs than for hot IPOs. Other market makers spend a signifi- cantly smaller proportion of their time at the inside bid for cold IPOs than for hot IPOs. when inside quotes are recalculated after omitting underwriter quotes, we find that average inside bids are usually lower, particularly for cold IPOs. Inside ask quotes are generally the same with or without the inclusion of underwriter quotes.

We also split the sample of IPOs into those with positive initial returns (henceforth underpriced IPOs) and those with zero or negative initial returns (fully-priced IPOs) to examine the time-series behavior of IPOs and the aggre- gate buying and selling of underwriters. This analysis provides further evidence of aftermarket support. A greater proportion of aftermarket volume is from sell orders for fully-priced IPOs than for underpriced IPOs. Underwriters appear to take the opposite side of most of these trades, and, on average, repurchase large quantities of stock.

Our paper is the first to use intraday data on underwriter quotes in the aftermarket. However, other recent research provides indirect evidence of after- market support. Wanley, Kumar, and Seguin (1993) examine 1,523 firm-commit- ment I s that took place over the 1982-1987 period. They derive a model in which an investment banker’s stabilizing bid provides a put option to other dealers. n implication of their model is that th t option reduces costs to market ers an erefm-e, all being equal, abilization should have narrower spreads. their model that after adjusting for volume, nu ber of market makers, price, and volatility, spreads

P.H. Schultz and MA. Zaman, Aftermarket support and IPO underpricing 201

are narrowest for IPOs that begin trading at prices from 3% below their offtxing

price to their offering price.’ They show further that for these IPOs, spreads widen and stock prices decrease over time. In contrast, if the likelihood of trading against informed traders decreases over time, these spreads would be expected to decrease.

Hegde and Miller (1989) look at aftermarket bid-ask spreads and volume for a sample of 543 IPOs that took place m 1983 and 1984. Like anley, Kumar, and Seguin (1993), they find that spreads are narrower for recent IPOs than for other stocks. In addition, they show that volume is higher for IPOs than for other NASDAQ stocks.

Miller and Reilly (1987) study 510 IPOs that took place during 1982-1983. They too show that after adjusting for offering price, aftermarket tradmg volume, and the riskiness of the stock, bid-ask spreads are narrower for IPOs that were not underpriced. However, they find a difference in spreads on only the first day of trading.

Ruud (1993) examines initial returns of 463 IPOs from 1982 and 1983. She observes that one-fourth of the IPOs in her sample have first-day returns of zero and that the distribution of returns is right-skewed. Of the IPOs with first-day returns of zero, 69% have zero or negative returns over the following week. Ruud suggests that these results are due to delays in observing negative initial returns of IPOs caused by aftermarket support.

The remainder of the paper is organized as follows. Section 2 discusses reasons for underwriter support of IPOs in the aftermarket and discusses why it may be possible for underwriters to support stocks at prices above those at which the stock would otherwise trade. The data used in this paper are described in section 3, and the results are presented in section 4. The paper is summarized in section 5.

easons for underwriters to su s in

We view stabilization as a complement to underpricing. The reasons for maintaining an aftermarket price at or above an offer price can be the same as the reasons for originally estddishing an offer price below the initial aftermarket price. Thus, evidence of aftermarket support provides indirect evidence in favor of models of underpricing, such as those discussed telow, t at also provide motives for support. [Theories of IPO underpricing given in ock (1986) Benveniste Spindt (1989), Allen and Faulhab (1989)Y Grinblatt and (1989), and elch (1989) do not im ly afterma

‘Wealsofindt a p h t s reads are narrower for stocks that are likely to be supported. To save space, these results are omitted, but are available from the authors.

202 PH. Schultz and MA. Zaman, Aftermarket support and IPO underpricing

2.1. Why underwriters might support IPOs

Some buyers of the IPO will renege if it is overpriced. If the aftermarket price is less than the offer price, or if it appears that the underwriter is having trouble selling the issue, investors who had placed nonbinding indications of interest would rationally decline to purchase shares in the initial offering and would instead buy the shares in the aftermarket. In addition, even if an investor confirms a buy order when the offering becomes effective, they can renege without legal penalty for five business days.2 Bloomenthal (1992, pp. 8-99-8- 100) notes:

‘Although broker-dealers ordinarily do not advertise the fact, it is likely that if a customer does not pay on the settlement date (five business days from the date of the confirmation), a transaction will be canceled. Since trading will already have commenced, some customers may be influenced by the price at settlement date in determining whether or not to pay . . . .’

If aftermarket support is perceived as etrecting a permanent increase in price by reducing supply, investors will not see an advantage in waiting to purchase an IPO in the aftermarket and will be less likely to renege.

The option to cancel an indication of interest or renege on an order leads to underpricing under some circumstances. An IPO investor effectively has a put option to sell the stock back to the underwriter for the issue price by declining to take shares after placing an indication of interest or by reneging on an order. Underwriters must be compensated for the puts that they are obligated to provide, in addition to their other services. I-Iowever, state limits on underwrit- ing commissions are typically 10% to 15%, so it may be necessary to underprice IPOs to lower the implicit exercise price and minimize the value of the put written to IPO purchasers. Barry, Muscarella, and Vetsuypens (1991) observe that these limits are often a constraint on underwriters of smaller, riskier issues. In addition, the costs of reselling an issue after investors have reneged can be avoided by underpricing. If these costs are sufficiently large, it will be cheaper to reduce the value of the put and the costs of reselling the reneged shares by underpricing than to explicitly compensate the underwriter for having to write the put.

‘See Woftson, Phillips, anal Russo (1987). IIn footnote 61 (p. 4.14) they state that Federal Reserve Regulation T requires that investors pay for stock within seven days except that if the security is sold on a when-distributed basis ‘the seven days begins to run from the day the security is made available by the issuer or is distributed (i.e., the closing date)‘. Also, as discussed in th.e same footnote, the commercial codes of a number of states imply that there is no binding contract between a broker and investor prior to the distribution of certificates at the closing. In additicn, several brokers indicated to us a common belief that a binding contract does ilot exist between the broker and the purchaser of an IPO until the customer has had a chance to study the final prospectus. This document is sent out with the confirmation, after the investor has ordered the stock. However, practitioners also tell us that they will refuse to do business in the future with any customer who has reneged on an order.

P.H. Schultz and MA. Zaman, Aftermarket support and IPO underpricing 203

Aftermarket support prevents cascades. Welch (1992) argues that potential purchasers of IPOs use their ktnowledge of whether other investors are buying as well as private information to decide whether to purchase an IPO. If sales take place sequentially, a sufficiently long run of investors who decide not to pur- chase will induce all later investors with favorable information to forgo the IPO. Hence an IPO can fail even if it is fairly priced. In practice, investors who are asked to confirm indications of interest in a firm-commitment offering Fan uuaa

observe the rea.ction of previously-approached buyers through the behavior of the aftermarket price. If the aftermarket price is not above the offer price, the potential buyer can infer that previously approached buyers had negative information about the stock and can renege on their purchase. By supporting the stock in the aftermarket, the underwriter may prevent a cascade from developing if investors who are first approached to buy the I 0 pass on the issue. Similarly, the potential for cascades provides an incentive to underprice an issue to insure that a run of investors who pass on an offer does not develop in the first place.

A policy of underwriter support may also serve as an ex ante bonding mechanism. Smith (1986) discusses aftermarket support in the broader context of the underwriter’s reputation. If an underwriter pursues a policy of repurchas- ing ex post overpriced shares at a supported price, his reputation for after- market support assures that the IPOs that he underwrites in the future are perceived ex ante as less likely to be overprice, _L In addition, the implicit put option that is provided to investors makes them more willing to buy risky IPOs. This bonding mechanism may be particularly important for uninformed inves- tors who suffer from the winner’s curse of being more likely to receive shares in overpriced offers.

Finally, aftermarket support minimizes legal liability. Tinic (1988) hypothe- sizes that the possibility of legal liability under the Securities Act of 1933 provides an incentive for underpricing of IPOs as well as a reason for supporting a stock in the aftermarket. However, Drake and Vetsuypens (1992) find that purchasers of underpriced IPOs are as likely to sue as purchasers of overpriced XPOS.

2.2. How aftermarket support works

Motives for stabilization can be ascertained from the way the issue is sta lized. We distinguish between two walys of supporting an IPO in the aftermar- ket. In the first type, underwriters bring about a perma ent change in the stoc price by reducing the supply of stock. In the secon method, underwriters temporarily prop up the price of the IPO by purchasing stock for later resale.

hile investors have no reason for re i:ve

aftermarket support will lead to a permanent increase in the price, their incen- tives to renege remain if support results in only a temporary increase in the price.

204 P.H. Schultz and M.A. Zaman, Aftermarket support and IPO underpricing

We have final prospectuses for 54 of the 72 IPOs in our sample. All 54 have overallotment options that allow the underwriter to purchase additional shares from the issuer. In 48 of the 54, the overallotment option allows the purchase of 15% of the shares issued. The other six permit the underwriter to purchase an additional 7-12% of the shares issued. Underwriters are required to sell the shares purchased in this way to the public at the initial offer price, and are typically given 30 days from the effective date of the offering to exercise the option. The overallotment option gives underwriters some flexibility in the number of shares that they actually sell to the public.3 They can set the IPO price to sell the entire issue plus the 15% overallotment option. If the IPO is hot, underwriters sell the entire issue and go short by the amount of the overallot- ment option. The short position is covered by exercising the overallotment option and the entire 115% of the shares offered remains in public hands. On the other hand, if the IPO sells poorly, the 15% short position is covered by aftermarket purchases and the number of shares offered is effectively reduced.

Restricting the supply in this manner allows underwriters to effect a perma- nent change in the price of the IPO if the long-run demand curve for the stock is downward-sloping. Recent empirical work supports this conjecture. Loderer, Cooney, and Van Drunen (1991) find that announcements of primary stock offerings by regulated firms depress their stock prices. They find little evidence that th; ,!ecline is caused by revelation of adverse information. They interpret the negti,ive returns around announcements of offerings as evidence of a down- ward-sloping demand curve for stocks. Bagwell (1992) studies Dutch auction share repurchases and provides evidence that the supply curve of stock facing the repurchasing firm is upward-sloping.4

Alternatively, Hanley, Kumar, and Seguin (1993, p. 180) suggest that ‘stabiliza- tion attempts to smooth, mitigate, or avoid short-run price declines’. They observe that one implication of stabilization is that those issues most likely to be stabilized have significant price declines once stabilization is discontinued. Underwriters may be willing to purchase shares even if they expect a significant price decline to allow favored customers to return overpriced stock. Hanley, Kumar, and Seguin (1993, p. 180) also suggest that stabilization may lead the public to believe that an IPO is not overpriced. They write:

‘Moreover, if a price drop is apportioned over a number of days, the perception of overpricing may be obscured by intervening market moves, or

%tter (1987) suggest that another purpose of overallotment options is to reduce tile adverse selection problem facing uninformed investors by allowing an increase in shares sold for hot IPOs. Smith (1986) observes that the overallotment option is valuable to the underwriter only if an IPO is not overpriced, because the underwriter only gets the incremental commission revenue if the option is exercised. Mence the use of an overallotment option aligns the interests of the underwriter and IPO purchasers.

41n contrast to these studies, in which the total supply of outstanding shares is altered, t

overallotment option is sc:metimes filled with existing shareholder’s stock.

P.H. Schultz and MA. Zanlarl, Aftermarket support and IPO u~lderpr~~~~~~ 265

informational shocks, thus concealing the overprfcing from the clients (both investors and issuers).’

The two techniques of aftermarket support, stabilization and reducing the supply of shares in the aftermarket, both imply that underwriters will quote at the inside bid more often than at the inside ask, particularly if the aftermarket price of a stock is below the offering price (a cold IPO). lso, both methods suggest that there should be a disproportionate amount of selling for cold IPOs when underwriters quote bid prices that are too high to equate supply and demand. Additional key implications of the hypothesis that underwriters restrict supply in the aftermarket are that they purchase large quantities of stock when the aftermarket price is below the offer price and that they exercise overallot- ment options if the stock trades at higher prices than the offering price.

3. Data

We obtain data from the Bridge Quotation Systemon for 72 firm-commit- ment IPOs issued from March 31, 1992 through June 1, 1992. This real-time quotation service provides intraday trade and quote data for all listed and NASDAQ stocks. For each trading day, quote data for NASDAQ stocks consist of the opening inside-bid and ask quotes, opening bid and ask quotes for each market maker, and all inside-quote revisions and dealer-quote revisions throughout the day. For listed stocks, quote data consist of the opening inside-quote and all inside-quo&z revisions throughout the day. Trade data includes the transaction price, number of shares traded, and the time of the trade. Both trades and quotes are time-stamped to the minute. However, they are downloaded from different Bridge System screens, so it is not possible to determine the order of quote updates relative to trades #ithin a particular minute. Although this data is very rich, it has limitations. For example, we have no information about trades between market makers and their retail clients.

The appendix describes the sample IPOs, including their effective date, the number of shares offered, the offer price, and the price of the first trade. As shown in the third and fourth columns, one consequence of using the Bridge IPO Calendar to form the sample is that most sample IPOs are large offerings. Not including overallotment options, 32 of the 72 IPOs in our sample have proceeds in excess of $25 million. The last two columns of offer prices and first aftermarket trade prices for each I had an initial trade price above the offer price, an initial trade price equal to the offer price, and eight had an initial tra

Orders are classified as buys or sells as follo e quote wit

midpoint of the bid-ask spread are classified as buys. Transactions at pries

206 P.H. Schultz and MA. Zaman, Aftermarket support and IPO underpricing

below the midpoint of the spread are classified as sells. About 74% of the trades are classified in this way. Second, if the inside spread changes during the minute, transactions at the highest quoted ask price are classified as buys, while transac- tions at the lowest quoted bid price are categorized as sells. This classifies an additional 9% of the trades. Remaining quotes are categorized using a tick rule. f an unsigned trade occurs at a price above that of the previous price, it is

classified as a buy, and if it occurs at a price below that of the previous trade, it is classified as a sell. Trades that occur at the same price as the previous trade are classified the same way. Approximately 15% of the trades are categorized in this way. [Lee and Ready (1991) use a simple model to demonstrate that this tick test correctly classifies more than 85% of trades that occur at the midpoint of the spread.] Large interdealer transactions that are not given a price on the Bridge trade screen are omitted from comparisons of buy and sell volume.

4.1. The aftermarket behavior of initial public offeriirgs

Returns over the first trading day are shown in fig. 1. Time is measured in ten-minute increments relative to the stock’s first trade. There are 39 ten-minute intervals in the trading day, but only the initial return and the first 30 intervals are examined since some IPOs start trading well after the market opening. The initial return is measured from the offering price to the first trade price. For ten-minute intervals, returns are measured from the last trade of the previous period to the last trade of that period?

e find that all of the well-documented first-day returns of initial public offerings occur in the first ten minutes of trading. For our sample, the mean return from the offering price to the first trade is 3.9Oh, while the additional return for the first ten minutes of trading averages 3%. Our finding of a positive offer-to-open return is consistent with Barry and Jennings (1992) who report a mean offer-to-open return of 7.77% for a sample of 229 IPOs. However, their mean open-to-close return of 0.87% is much smaller than the 3% that we observe in the first ten minutes of trading. Returns over the remainder of the first day of trading and over the second and third days of trading (not shown) are not significantly different from zero.

Trading volume over ten-minute intervals of the first day of trading is shown separately in fig. 2 for the 32 underpriced and 40 fully-priced IPOs. Volume is

s. For underpriced IPOs, on average, 17% of the sive of the overallotment option) ch hands in th

s are traded

“S+e traihing starts at 930 and goes through 4:00, one minute is left over after dividing the day into tea-minute ktervals, so the last period of the day is actually an 1 l-minute interval.

P.H. Schultz and MA. Zaman, Aftermarket support and IPO underpricing 207

0.02

E 2 0.01 a

0

r

Time (I O-Minute Intervals)

Fig. 1. Average intraday aftermarket returns for the first day of trading for 72 IPOs issued between March 31 and June 1, 1992. The first return is the return earned by buying at the offer price and

selling at the price of the first trade. Other returns are measured over ten-minute intervals.

the first hour, 43% of the shares of underpriced and 21% of the shares of fully-priced IPQs trade. [Miller and Reilly (1987) also report heavy aftermarket volume for a sample of 1,106 IPOs during 1982-1983, although their average first-day turnover of 22% is much less than ours.] Trading volume of fully- priced IPOs remains consistently below that of underpriced IPOs for the first day of trading.

Practitioners have suggested to us that one possible reason for the difference in trading volume of the two types of offerings is that short-term traders, who

. ._._ ._

are most likely to trade in the aftermarket, are able to determine fully priced and avoid these issues. An alternative explaiiation Benveniste and Spindt (1989). In their model a larger fraction of offerings is allocated to regular investors in about the IPO during preselling. Presumably, be active traders.

return for revealing , these investors are

is given by underpriced information

ely to

4.2. Do underwriters support stocks in the qjhnar-ket?

or s that trade on ? underwriters ty makers. We compare the market-making behavior of unde

208 P.H. Schultz and MA. Zaman, Aftermarket support and IPO underpricing

Hours Since First Trade

I Fully-priced IPOs + Underpriced IPOs 1

Fig. 2. First-day trading volume as a proportion of shares issued for 72 IPOs issued between March 31 and June 1,1992. Intervals are ten minutes in length. An IPO is defined as underpriced if the first aftermarket trade took place at a price above the offering price, and fully-priced if the first

aftermarket trade took place at a price less than or equal to the initial offer price.

dealers using the 60 sample IPOs that traded over-the-counter after going public and that had underwriters as market makers. For each IF0 each trading day we calculate the mean percentages of time spent at the inside bid and at the inside ask, for underwriters and for other dealers, when the IPO is above its offer price (hot) and at or below the offer price (cold). As an example, to calculate the mean percentage of time spent by dealers other than the underwriter at the inside bid for IPO i when that IPO is hot, we average the percentage of time that each dealerj spends at the inside bid during periods when IPO i is hot across the J dealers other than the underwriter:

Others, Bid PCTi Hot = 9 i PCTi;g; /.J r

To get a grand mean percentage of time that other dealers bid for hot issues, we calculate a mean of the averages of the hot at some point:

IHot

C Otoyrs, Bid == Others, Bid

i, Not IffOl *

(1)

spend at the inside IH0t firms that were

(2) i= 1 I

P.H. Schultz and MA. Zaman, Aftermarket support and IPO underpricing 209

Analogous statistics are calculated for other combinations of dealer type, bid or ask quote, and hot or cold I OS. These grand means are calculated separately for each trading day and provide the basis for our statistical tests.

To test for differences in grand means between hot and cold I Os, we first estimate the standard deviation of each grand mean using the means of the I offerings. For example, the standard deviation of the percentage of time that other dealers spend at the bid for hot IPOs is

Our estimate of the standard error for the difference in the mean percent of time spent at the inside bid by other dealers for hot and cold IP

5% Diff = J I Hot

(4)

The t-statistic used to test whether other dealers sper,d more time at the inside bid for hot and cold IPOs is given by

1 =

S2 .

W.. (5)

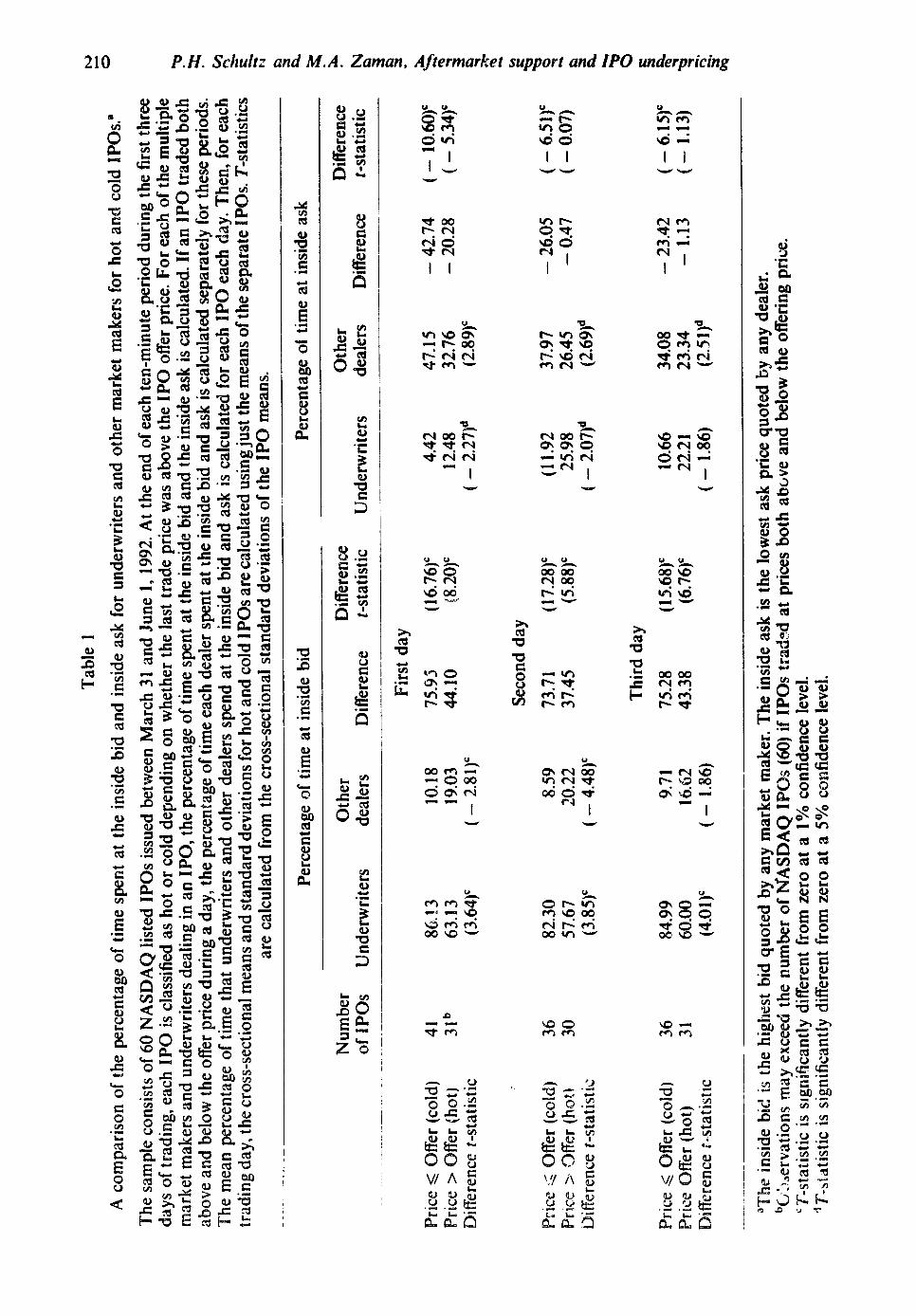

An implication of aftermarket support is that underwriters should spend more time at the inside bid for cold IPOs than for hot II%. In table 1 we test that implication. On the first day of trading, on average, underwriters spend 86.1% of their time at the inside bid for cold IPOs, but only 63.1% of their time at the inside bid for hot IPOs. A test for a difference in proportions between hot and cold IPOs yields a t-statistic of 3.64. We can reject, at a 1% confidence level, the null hypothesis that underwriters spend equal amounts of time at the inside bid for both types of IPOs. Similar results are obtained for the second and third day of trading?

Results for market makers who are not underwriters are s own in the next columns. For the first day of trading, on average, other i makers spend about 10% of their time at the insi of their time at the inside bid for hot IPOs. This difference is statistically significant, as is the difference on the second day of trading.

esults are similar when s are classifie

Tab

le

1

A

com

pari

son

of t

he p

erce

ntag

e of

tim

e sp

ent

at t

he i

nsid

e bi

d an

d in

side

ask

for

und

erw

rite

rs a

nd o

ther

mar

ket

mak

ers

for

hot

and

cold

IP

Os.

”

he s

ampl

e co

nsis

ts

of 6

0 N

ASD

AQ

lis

ted

IPO

s is

sued

bet

wee

n M

arch

3 1

and

Jun

e 1,

199

2. A

t th

e en

d of

eac

h te

n-m

inut

e pe

riod

du

ring

th

e fi

rst

thre

e s

of t

radi

ng,

each

IP

O

is c

lass

ifie

d as

hot

or

cold

dep

endi

ng

on w

heth

er t

he l

ast

trad

e pr

ice

was

abo

ve

the

IPO

of

fer

pric

e. F

or e

ach

of t

he m

ultip

le

et m

aker

s an

d un

derw

rite

rs

deal

ing

in a

n IP

O,

the

perc

enta

ge o

f ti

me

spen

t at

the

ins

ide

bid

and

the

insi

de a

sk i

s ca

lcul

ated

. If

an

IPO

tr

aded

bo

th

ve a

nd b

elow

the

off

er p

rice

dur

ing

a da

y, t

he p

erce

ntag

e of

tim

e ea

ch d

eale

r sp

ent

at t

he i

nsid

e bi

d an

d as

k is

cal

cula

ted

sepa

rate

ly

for

thes

e pe

riod

s.

perc

enta

ge

of t

ime

that

un

derw

rite

rs

and

othe

r de

aler

s sp

end

at t

he i

nsid

e bi

d an

d as

k is

cal

cula

ted

for

each

IP

O

each

cl

ay. T

hen,

fo

r ea

ch

y, th

e cr

oss-

sect

iona

l m

eans

and

sta

ndar

d de

viat

ions

for

hot

and

col

d IP

Os

are

calc

ulat

ed

usin

g ju

st t

he m

eans

of

the

sepa

rate

IP

Os.

T

-sta

tistic

s ar

e ca

lcul

ated

fr

om t

he c

ross

-sec

tiona

l st

anda

rd

devi

atio

ns

of t

he

IPO

m

eans

.

Perc

enta

ge

of t

ime

at i

nsid

e bi

d Pe

rcen

tage

of

tim

e at

ins

ide

ask

Num

ber

Oth

er

Dif

fere

nce

Oth

er

Dif

fere

nce

of I

POS

Und

erw

rite

rs

deal

ers

Dif

fere

nce

f-st

atis

tic

Und

erw

rite

rs

deal

ers

Dif

fere

nce

t-st

atis

tic

____

--__

_~-

I_._

. -_

___-

--

. . -.

-_--

Firs

t da

y

ffer

(co

ld)

ffer

(hot

) re

nce

f-st

atis

tic

41

86.1

3 10

.18

75.9

5 ( 16

.76)

’ 4.

42

47.1

5 -

42.7

4 (

- 10

.60)

31

b 63

.13

19.0

3 44

.10

(8.2

0)

12.4

8 32

.76

- 20

.28

( -

5.34

) (3

.64)

(

- 2.

81)’

(

- 2.

27id

(2

.89)

rice

< O

ffer

(co

ld)

Off

er (

hot)

fe

nce

t-st

atis

t id

36

30

82.3

0 8.

59

57.6

7 20

.22

(3.8

5)

( -

4.48

)

Seco

nd

day

73.7

1

(17.

28)

(11.

92

37.9

7 -

26.0

5 (

- 6.

51)

37.4

5 (5

.88)

25

.98

26.4

5 -

0.47

(

- 0.

07)

( -

2.07

)d

( 2.6

9)d

Thi

rd

day

rice

< O

ffer

(co

ld)

36

84.9

9 9.

71

75.2

8 (1

5.68

) 10

.66

34.0

8 -

23.4

2 (

- 6.

15)

Off

er (

hot)

31

60

.00

16.6

2 43

.38

(6.7

6)

22.2

1

23.3

4 -

1.13

(

- 1.

13)

ence

i-s

tatis

tic

(4.0

1)

I: -

1.86

) (

- 1.

86)

(2.5

1,”

-

a e

insi

de

bid

is t

he h

ighe

st b

id q

uote

d by

any

mar

ket

mak

er.

The

ins

ide

ask

is t

he l

owes

t as

k pr

ice

quot

ed

by a

ny d

eale

r.

‘CL

erva

tions

m

ay e

xcee

d th

e nu

mbe

r of

NA

SDA

Q

IPO

s (6

0) i

f IP

Os

trad

ed a

t pr

ices

bot

h ab

ove

and

belo

w t

he o

ffer

ing

pric

e.

‘T-s

tatis

tic

is s

igni

fica

ntly

di

ffer

ent

from

zer

o at

a 1

% c

onfi

denc

e le

vel.

“T-s

t&is

tic

is s

igni

fica

ntly

di

ffer

ent

from

zer

o at

a 5

% c

onfi

denc

e le

vel.

-.

P.H. Schultz and MA. Zaman, Aftermarket support and IPO underpricing 211

To test for differences between time spent at one side of the spread underwriters and other dealers, we calculate a standard deviation of the differ- ence across IPQs. For example, we estimate the standard deviation of the difference in time spent at the inside bid for hot IPOs as

d i=l _.._

I -1 .

HO?

(6)

The t-statistic used to test for differences in the percentage of time spent at the inside bid of hot IPOs for underwriters and others is

Und, Bid

t PWfO8

_ pcTO&ers,Bid

= . (7)

The next column shows the zverage, across IPOs, of the difference between the percentage of time spent at the inside bid by underwriters and the percentage of time spent at the inside bid by other dealers. For both hot and cold underwriters spend much more time at the inside bid than other dealers, but the difference is particularly strong for cold IPOs. The next column reports t-statistics calculated as in (7) that test whether the differences in time spent at the i-e; ii&e bid for underwriters and other dealers is significantly different from zero. A null hypothesis that underwriters and other market makers spend the same amount of time at the inside bid is strongly rejected for both hot and cold IPOs on all three days.

Analogous results are found for ask quotes. On average, underwriters spend only 4.4% of the first trading day at the inside ask for cold IPOs, End 12.5% of the day at the inside ask for hot IPOS. Similar results are obtained for the second and third days of trading. Conversely, other market makers spend more time at the inside ask for cold IPOs than for hot IP s on all three days. also spend significantly more time at the inside ask than do underwriters for all three days for cold IPOs.

ummarize, the results in table 1 are consistent with underwriters OS in the aftermarket.

frequently, and at the inside ask much less often, th not encumbered with investment bankin most striking for the cold

212 P.H. Schultz and M.A. Zaman, Aftermarket support and IPO unde,vpricing

I.47

1.3-

.8 1.2- &

Bid Prices

Cold <--- IPOS ---> Hot

I - With Underwriters’ -.----. Without Underwriter 1

I I

Fig. 3. Each point on the horizontal axis represents one of 60 NASDAQ-listed IPOs issued between March 31 and June 1,1992. Lines connect the inside bid and ask prices for each IPO, averaged over all ten-minute periods of the first three days of trading. The time series mean bid and ask prices for each IPO are expressed as a proportion of the initial offering price. The solid lines connect inside bid and ask prices that include underwriters; the dotted lines connect inside bid and ask prices after

underwriters are omitted.

three days of trading. The average inside bid and ask quotes are then recal- culated after omitting bid and ask quotes from underwriters. All observations are then standardized by dividing by the IPO’s offer price. Average inside bid and ask prices for individual IPOs are connected in the graph with solid lines. Average inside bid and ask prices after omitting underwriter quotes are connec- ted with dotted lines. hen the average inside bid or ask quote is the same with or without inclusion of underwriters, the overlap of the two lines is seen as a solid line.

ly one solid line (the top line) is seen for the ask price for most of his means that for almost every IPO, the aft arket inside ask me with or wit1jou.t the underwriter’s quote. n the other hand, rices without underwriter quotes are usually below the inside ask

ratio of the bid price to erwriters on the

istance fro

P.H. Schultz and MA. Zaman, Aftermarket support and IPO underpricing 213

to the inside bid with the vertical difference from the ask to the inside bid after omitting underwriters.

If the prices of supported stocks are being held above the levels that would equate supply and demand, we should observe a disproportionate number of sell orders in supported stocks. In testing this proposition, we are iderested in whether or not market makers maintain their prices over time versus lowering them to levels at which buy and sell orders are roughly offsetting. Rather than reclassifying stocks on the basis of their price relative to the offering price at each ten-minute interval, we use initial returns to split our entire sample of 72 IPOs into underpriced and fully-priced issues.

Table 2 shows the cross-sectional mean percentage of total volume from buy orders for underpriced and fully-priced IPOs for each of the first three days of trading. On the first day, 37.7% of the volume of underpriced I OS is from buy orders, while 27.8% of the volume of other IPOs is from buys. A t-statistic calculated as in (5) from the distribution of individual IPO volu:nes rejects, at a 5% confidence level, a null hypothesis that buy orders are an equal percentage of volume for both types of IPOs. For the second day of trading, buys are only a slightly larger percentage of volume for underpriced IPOs than others, and the t-statistic is insignificantly different from zero. However, for the third day of trading, buy orders are again a significantly larger portion of volume for underpriced issues than for fully-priced IPOs.

Fig. 4 shows the average percentage of volume attributed to buy orders for underpriced and fully-priced IPOs for 30-minute periods over the first day of

Table 2

Mean percent of volume from buy orders for underpriced and fully-priced IPOs over their first three days of trading.

The sample consists of 72 IPOs issued from March 31 through June 1,1992. An IPO is defined as underpriced if the first aftermarket trade took place at a price above the initial offering price. A three-part criterion is used to classify trades as buys or sells. First, if the same spread was in effect over an entire minute, trades that took place at prices above the midpoint of the bid-ask spread are categorized as buys, while trades at prices below the midpoint are classified as sells. Second, if the inside bid-ask spread changed during a miiiute, trades occurring at the lowest bid price are categorized as sells while those taking place at the highest ask price of the minute are classified as buys. Remaining trades are classified using a tick rule. Trades at prices above the previous trade are classified as buys, and trades at prices below the last trade are classified as sells. ? rades at the same

price as the previous trade receive the same classification.

First day ___-

Mean percent of volume from buy orders: Fully-priced IPOs 27.75 Underpriced IPOs 37.68

T-statistic for difference in means - 2.59”

“Significantly different from zero at the 5% confidence level.

Second Jay

- 1.1 f - -

Third day __--

28.51 39.63

--

214 P. H. Schultz and MA. Zaman. Aftermarket support and IPO underpricing

2 3 4 5 Hours Since Stock Opened

I Fuiiy-priced IPOs + Underpriced IPOs 1

Fig. 4. The proportion of volume from buy orders for half-hour intervals of the first day of trading for 72 IPOs issued between March 31 and June 1, 1992. An IPO is defined as underpriced if the first aftermarket trade took place at a price above the offering price and fully-priced if the first

aftermarket trade took place at a price less than or equal to the initia! offer price.

ecause not all IPOs started trading at the market open, the 30.minute periods depicted in this gr;>ph are measured relative to the first trade, As shown in fig. 4, during each half- hour period a larger proportion of trades are buys for underpriced IPOs than others. During the especially active first 30 minutes of trading, about 35% of the volume of underpriced IPOs is attributed to buy orders, but only 17% of the volume of fully-priced IPOs is from buy orders. For the remainder of the first day of trading, buy volume is always a greater percentage of total volume for underpriced IPOs than for fully-priced IPOs.

4.3. How do underwriters support IPOs in the aftermarket?

o under writers support OS by temporarily buying up stock for later resale ermanently reducing the supply? One implication of the writers restrict the supply of stock in the aftermarket is

exercise an overallotment option for a hot

it in our sample with

P.H. Schultz and MA. Zaman, Aftermarket support a&d IPO underpricing 215

shown) that indicates a 90.4% chance the if the stock price remains above the oflFer trading, and a 26.1% chance of exercise if during this period.

allotment option will exercised e for the entire first three days of price never exceeds

A second implication of the hypothesis that underwriters rest;ict the supply of IPO shares in the aftermarket is that they should buy large auantities of stock in the aftermarket if the stoc price is below the offer prick. “We estimate the number of shares purchased by underwriters and 0th r market makers by calculating, for each stock, the proportion of inside bi nd ask quotes given by underwriters and other market makers each minute. e then assume that buy volume is split equally among all market makers at the inside ask during a minute, and that sell volume is split equally among all market makers at the inside bid during that minute. Then, for each IPO, we sum the number of shares bought and sold by underwriters and by other market makers over the three- day period and standardize by dividing by the total number of shares issued in the IPO. This provides an approximation, not an exact count, of shares bought and sold by market participants. The assumption that all are equally likely to receive an order is probably not true. In addition, the volume does not include retail sales to the dealer’s customers.

Results are shown in table 3. Underwriters repurchase an average of 21.7% of the shares issued in fully-priced IPOs and 24.9uio of the shares issued in underpriced IPOs during the first three days of trading. I-Iowever, they resell less than 0.4% of fully-priced issues and only 3.2% of underpriced issues. On net, for

Table 3

Mean percentage of issued shares bought or sold by underwriters and other market makers in the first three days of aftermarket trading for 72 IPOs issued between March 31 and June 1, 1992. An IPO is defined as underpriced if the first aftermarket trade took place above the offer price and

fully-priced if the first trade took place at or below the offer price.

Percentage of issued shares bought in the aftermarket for Fully-priced I POs Underpriced IPOs

T-statistic for difference

Underwriters

1.68 24.93

( - 8.73)

Other dealers

7.31 21.42

( - 4.00)

Percentage of issued shares sold in the aftermarket for Fully-priced IPOs Underpriced IPOs

T-statistic for difference -

Net percentage of issued shares bought in the aftermarket for Fully-priced IPOs Underpriced IPOs

T-s?atistic for difference __- --_ -.

“Significantly di rent from zero at t

0.37 9.68 3.20 27.60

( - 3.09)” ( - 4.67)

21.32 - 2.37 21.71 - 6.22

( - 0.10) (1.27) --

216 P. H. Schulz z and M. A. Zaman, Aftermarket support and IPO underpricing

both types of issues, underwriters repurchase about 21% of the offering in the aftermarket. It seems unlikely that dealers are able to resell as many shares of fully-priced IPOs as underpriced IPOs to their retail customers. ence, pur-

chases of fully-priced shares build the underwriter’s inventory of stock. Net purchases of fully-priced shares seem to be large enough to cover short positions of the size of the overallotment option.

Dealers who are not underwriters trade much more when IPOs are under- priced than when they are fully-priced. Wowever, buy and sell orders for other market makers are roughly offsetting for both types of IPOs.

This paper examines the aftermarket for initial public offerings. We find pervasive evidence of aftermarket support by underwriters. Underwriters are almost always at the inside bid for cold IPOs. Other dealers, by contrast, are about four times as likely to be at the inside ask than the inside bid for cold IPOs. When inside bids are recalculated after omitti_;g underwriter quotes, spreads widen substantially, particularly for cold IPOs. When inside ask quotes are recalculated after omitting underwriter quotes, spreads are almost unaffected.

Volume from sell orders exceeds volume from buy orders for both hot and cold IPOs, but the imbalance is greater for cold IPOs for each of the first three days of trading. Underwriters on average repurchase over 20% of the shares issued in an IPO during the first three days of aftermarket trading. The volume of aftermarket repurchases, along with the exercise of overallotment options for hot IPOs but not cold IPOs, suggests t at stcfcks are supported in the aftermarket by permanently reducing the supply of shares.

The strong evidence of aftermarket support presents a challenge to financial theorists. Most models of IPO underpricing have no implications for the aftermarket. While it is not necessary for a model of IPO underpricing to p-edict aftermarket support, it is plausible that the same factors that make it desirable for IPO stock prices to rise above their offer prices explain the effort and expense that underwriters incur to maintain prices of IPOs above their oKer price.

Allen, Franklin and Gerald Faulhaber, 1989, Signalling by underpricing in the IPO market, Journal of Financial Economics 23, 303-323.

Bagwell, Laurie Simon, :992, Characteristics sf shareholder heterogeneity in Dutch auction stock repurchases, Journal of Finance 44, 41-105.

Barry, Christopher and Robert Jennings, 1992, The opening price performance of initial public offerings of common stock, Financial anagement 22, 54-63.

arry, Christopher, Christopher Muscarella, and Michael Vetsuypens, 1991, Underwriter warrants, underwriter compensation, and the costs of going ublic, Journal of Financial Economics 29, 113-136.

P.H. Schultz and MA. Zaman, Aftermarket s.upport and IPO urrdetpricing 217

Benveniste, Lawrence and Paul Spindt, 1989, How investment bankers determine the offer price and allocation of new issues, Journa of Financial Economics 24, 343-361.

Bloomenthal, Harold, 1992, Going public and the public corporation (Clark, Boardman, and Callaghan, Deerfield, IL).

Drake, Phillip and Michael Vetsuypens, 1992, IPO underpricing and insurance against legal liability, Financial Management 22,64-73.

Grinblatt, Mark and Chuan Yang Hwang, 1989, Signalling and the pricing of new issues, Journal of Finance 44,393-420.

Hanley, Kathleen, A. Arun Kumar, and Paul Seguin, 1993, Price stabilization in the market for new issues, Journal of Financial Economics 34, 177- 197.

Hegde, Shantaram and Robert Miller, 1989, Market-making in initial public offerings: An empirical analysis, Journal of Financial and Quantitative Analysis 24, 75-90.

Lee, Charles and Mark Ready, 1991, Inferring trade direction from intraday data, Journal of Finance 46,733-746.

Loderer, Claudio, John Cooney, and Leonard Van Drunen, 1991, The price elasticity of demand for common stock, Journal of Finance 46,621-651.

Miller, Robert and Frank Reilly, 1~87, An examination of mispricing, returns, and uncertainty for initial public offerings, Financial Management 16, 33-318.

Muscarella, Christopher, John Peavy, and Michael Vetsuypens, 1992, Optimal exercise of the over-allotment option in IPOs. Financial Analysts Journal, May/June, 76-80.

Ritter, Jay, 1987, The costs of going public, Journal of Financial Economics 19, 269-281. Ritter, Jay, 1991, The long performance of initial public offerings, Journal of Finance 46, 3-27. Rock, Kevin, 1986, Why new issues are underpriced, Joum.al of Financial Economics 15,187212. Ruud, Judith, 1993, Underwriter support and the IPO urlderpricing puzzle, Journal of Financial

Economics 34, 135- 15 1. Smith, Clifford, 1986, Raising capital: Theory and evidence,, Midland Journal of Corporate Finance

4, 6-22. Tinic, Seha, 1988, Anatomy of initial public offerings of common stock, Journal of Finance 43,

789-822. Welch, Ivo, 1989, Seasoned offerings, imitation costs, and the underpricing of initial public offerings,

Journal of Finance 44,421-449. Welch, Ivo, 1992, Sequential sales, learning, and cascades, Journal of Finance 47,695-732. Wolfson, Nicholas, Richard Phillips, and Thomas Russo, Regulation of brokers, dealers and

securities markets (Warren, Gorham, and Lamont, Boston, MA)

Appendix

Offering date, number of shares, offering price, and price of the first trade for the 72 IPOs issued between March 31 and June 1, 1992 that make up the sample:

Company Offering Shares Offering 1st tr&e

datz offered” price price

Xircom 313 l/92 Chicago Northwestern 3/3 l/92 Eskimo Pie 3/3 l/92 Longhorn Steaks 3/‘3 l/92 MWAVE 4/01/92 Seragen 4/01/92 Chipsoft 4/03/92 NCI Building 4/03/92 Pomeroy Corp 4/03/92 ERO Inc. 4/07/92 Videotelecom 4/07/92

3,5(% 8,750, 2926,089

3,297,898

$18. $20. $20.750

218 P.M. Schuitrz and b4.A. Zaman, Aftermarket support and IPO underpricing

Company Offering

date Shdres offered’

0ffering price

1st trdde price

Adesa 4/‘14/92 Affinity Biotech 4/ 14/92 Mens Wearhouse 4/14/92 Option Care 4/15/92 AGCO 4/M/92 Chromcraft Revington 4/ 16/92 Teledata 4/16/92 Worthington Foods 4/l 6/92 Clinicom 4/20/92 Steinmart 4/22/92 Sportstown O/22/92 Younkers 4/23/92 Software Etc. 4,f23/92 Morningstar 4/24/92 Qrthofix 4/24/92 Ben Franklin 4/28/92 Neozymc 4/29/92 Learning Company 4/29/92 International Family Ent 4/29/92 Premier Radio 4/29/92 Solo Serve 4/‘29/ 92 Galey and Lord 4/30/92 Intermedia Corn. 4/30/92 On the Border Cafes 4/30/92 Automotive Inds. 5/01/92 All for a Dollar 5/05,‘92 Medquist 5/05/92 Lida s/06/92 STAC Electronics 5/07/92 Lukens Medical S/07/92 Sybron 5/07/92 Valence TechncTlogy 5/07/92 Buckle Inc. 5/08/92 Dyersburg 5/l 2/92 Universal Seismic 5/l 2192 Arkansas Best 5/l 3/92 Basin Exploration 5/l 3/92 Theratech 5/l 3/92 Biocircuits 5/14/92 K rystal Company 5/14/92 Enzymatics 5/14/92 Natural Wonders 5/14/92 VMARK Software 5/14/92 Supermac Technology 5/ 15/92 Boston Scien tilic 5/l 9/92 Cardiovascular Imaging 5/l 9/92 Imperial Credit 5/19,‘i2 Kohls 5/l 9/92 National Visiofl Assoc. 5/19/92 WoIsun Burns 5/20/92 John Nuveen 5/20;92 Optical Data Systems 5/2 1 j92 Hal I Mark Electronics 5,‘22/92

2a-Q~ 2,m+(3f30 1,500,000 2,ms3t)O 4,5OO,OOO 2,5OO,ooO 3,5OO,OOO 1,750,OQO

875,uoo 3,250,OOO 1,9ofl,~ 6,170,OOfl 2,300,000 6,215,OOO 3DQ0,~ 1,!300,m

2,100,ooo 2,m,m

lO,OCtO,fKKl l,oQQ~ 2,6OQ~ 2,9@&~ 2,300,000 1,350,000 59QQ,m 2*~,~ 1 ,so0,uoO 2,5OO,OOO 3,~#00 1,375,OOO

7,250,OOO 3,6OO#OO 1,7OO,uOQ 4,600,QOO

90&m 15,7OO,OOo

2,8OO,tH0 1,250,000 2,Qt&ooo 2, ~00,octo

1,700,OOO

1,500,ooo 1 ,S00,000 2,m,oOQ

23,5OO,OOO 1,500,OOQ 2,ooo,~ 9,675,QUQ 2,500,QOO 2,2uO,O00

$11.500 % 6.OOQ $13.000 % 8.ooo $14.cKlO $11.084) $ll.OOQ $12.000 % 7.375 %13.OoO $12.uoO $12.500 %ll.oOO $1 l.OoQ $12.000 % 5.000 S35.OOO $1 l.OoQ %15.000 % 6.000 $l2.O00 %lU.OOO % 8.ooO % 8.500 $14.000 % 9.ouQ % 6.000 $11.500 $12.000 $ 6.000 $14.000 !§ 8.000 $13.500 % 9.000 $ 6.750 $14.000 S 9.500 $ 7.500 % 5.000 $12.000 % 7.000 S12.500 % 9.000 $ 9.000 S17.OuO $ 7.000 $ 8.ooo %14sIO0 $13.000 %14.000 $18. $ 9.000 $11.000

$11.500 $ 6.000 $14.500 % 8.500 $14.000 $1 l.O# $11.500 %12.OO0 % 7.375 $13.750 %13.25P %12.500 $10.500 510.750 $11.500 6 4.875 %35.0cKl %13.0OO $15.125 % 6.000 $12.500 %lQ.OMl % 8.000 $ 8.500 %14.000 % 9.500 % 6.250 $11.250 $12.375 % 6.ooO $14.000 $ 8.250 $14.500 % 8.750 % 6.750 $14.125 % 9.500 % 7.000 S 5,000 $13.000 $ 7.000 $13.000 % 9.500 $10.250 Sl7.000 $ 8.500 !§ 8.Ouo %l4.oOO $14.750 %14.OO0 $18.000 $10.000 $11.

Company Offering

date

ht. Fast Food Datawatch Carp+ Financial Federal First USA U.S. Physical Therapy Perceptive Systems Sapiens Intl. Steris carp

Shares offered”

Woes not include the shares issued if the cwerallotment option is exercised.