ML19262C206.pdf - Nuclear Regulatory Commission

179

4 AMENDMENT 35 INSERTION INSTR _UCTIONS FOR REVISION TO THE LICENSE APPLICATION The following text, tables, and exhibits are to be inserted in the License Application-Operating License Stage. These pages are either replacement pages or new pages as indicated below. All replacement pages which differ from ex1. ting pages are identified with the amendment number and date in .he ' wer right hand corner. Bars located in the margin of a parcicular page indicate material which is new in the admendment indicated at the bottom of the page. Remove Old (Pages) Insert New (Pages) - LILCO letter SNRC-459 in front of Tab LICENSE APPLICATION Title page August 28, 1975 Title page Amended January 14, 1980 Amended License Applica- Amended License Applica- tion (6 pages) tion (6 Pages) Affidavit Andrew W. Wofford Affidavit Joseph P. Novarro 1972 Annual Report 1975 Annual Report 1973 Annual Report 1976 Annual heport 1974 Annual Report 1977 Annual Report - 1978 Annual Report Exhibit B (3 pages) Exhibit B (6 pages) - Tab EXHIBIT C C-1 through C-13 - LILOO Prospectus dated - October 30, 1979 with Supplement C-14 through C-20 - Attachment A to Question - 4.C - Testimony of Raymond J. Forrer pages -1- and 12 through 20 Exhibit No. 13 (2 pages) - Exhibit No. 14 (Schedule 1 - and Schedule 2) Exhibit No. 15 (Schedule 1 - and Schedule 2) Exhibit No. 16 (Schedule 1 - and Schedule 2) Exhibit No. 17 and Exhibit - = No. 18 r.s . , ,:r - ~ ' 1945 052 - 1 Amendment 35 - January 1980 60 0 2 07 0 Clj${}

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of ML19262C206.pdf - Nuclear Regulatory Commission

4

AMENDMENT 35

INSERTION INSTR _UCTIONS

FOR REVISION TO THE LICENSE APPLICATION

The following text, tables, and exhibits are to be inserted inthe License Application-Operating License Stage. These pages areeither replacement pages or new pages as indicated below.

All replacement pages which differ from ex1. ting pages areidentified with the amendment number and date in .he ' wer righthand corner. Bars located in the margin of a parcicular pageindicate material which is new in the admendment indicated at thebottom of the page.

Remove Old (Pages) Insert New (Pages)

- LILCO letter SNRC-459in front of Tab LICENSEAPPLICATION

Title page August 28, 1975 Title page Amended January14, 1980

Amended License Applica- Amended License Applica-tion (6 pages) tion (6 Pages)

Affidavit Andrew W. Wofford Affidavit Joseph P. Novarro1972 Annual Report 1975 Annual Report1973 Annual Report 1976 Annual heport1974 Annual Report 1977 Annual Report

- 1978 Annual ReportExhibit B (3 pages) Exhibit B (6 pages)

- Tab EXHIBIT CC-1 through C-13-

LILOO Prospectus dated-

October 30, 1979 withSupplementC-14 through C-20-

Attachment A to Question-

4.C - Testimony of RaymondJ. Forrer pages -1- and 12through 20

Exhibit No. 13 (2 pages)-

Exhibit No. 14 (Schedule 1-

and Schedule 2)Exhibit No. 15 (Schedule 1-

and Schedule 2)Exhibit No. 16 (Schedule 1-

and Schedule 2)Exhibit No. 17 and Exhibit

-

= No. 18r.s . ,

,:r -~ '

1945 052-

1 Amendment 35 - January 198060 0 2 07 0 Clj${}

Remove Old (Pages) Insert New (Paqqs)

Attachment B to Question-

4.C - Te_'timony of ZviBenderly (21 pages)

- Exhibit No. 56 andSchedule 1Schedule 2 and Technical-

Appendix page 1 of 4Technical Appendix page 2-

of 4 through page 4 of 4- Attachment C to Question

4.C - Opinion No. 79-14(52 pages)

- Appendix A Schedule 1 andAppendix A Schedule 2page 1

Appendix A Schedule 2-

page 2 through page 7Appendix A Schedule 3-

(6 pages)Appendix B Schedule 1 and-

Appendix B Schedule 2 page 1Appendix B Schedule 2-

page 2 through page 5Appendix B Schedule 3-

page 1 and page 2- Appendix B Schedule 3 ||

page 3 and Appendix Ctitle pageState of New York Public-

Service Commission Case27374 (3 pages) throughState of New York PublicService CommissionCases 27374 and 2737b(4 pages)

C-21 through C-23-

THESE INSTRUCTIONS ARE TO BE FILED IN FRONT OF TAB - LICENSEAPPLICATION.

066 *.

2 Amendment 35 - January 1980

BEFORE THE

UNITED STATES NUCLEAR REGULATORY COMMISSION

DOCKET NO. 50-322

IN THE MATTER OF

LONG ISLAND LIGHTING COMPANY

AMENDED

LICENSE APPLICATION

UNDER THE ATOMIC ENERGY ACT OF 1954

AS AMENDED

FOR

SHOREHAM NUCLEAR POWER STATION

UNIT 1

August 28, 1975

Amended: January 14, 1980 |

|945 054Amcndment 35 - January 1980

BEFORE THE

UNITED STATES NUCLEAR REGULATORY COMMISSION

DOCKET NO. 50-322

IN THE MATTER OF

LONG ISLAND LIGHTING COMPANY

AMENDED

LICENSE APPLICATION

Pursuant to the Atomic Energy Act of 1954, as amended,and its implementing regulations, Long Island Lighting Company(Applicant or LILCO) submits this Amended Application for theclass 103 facility operating license, as well as the byproduct,source, and special nuclear material licenses, necessary forLILCO to own and operate a nuclear electric generating unitlocated in the Town of Brookhaven, Suffolk County, New York,known as Shoreham Nuclear Power Station Unit 1 (the facility).The facility will be an integral part of LILCO's total operatingsystem.

A description of the facility and a discussion of thetechnical qualifications of LILCO and its principal contractorsare contained in the Final Safety Analysis Report submittedherewith.

I. INFORMATION INCLUDED

This Amended Application consists of: (1) the informationrequired by 10 C.F.R. g 50.33 which is set out below; (2) thetechnical information and safety analysis . report required by10 C.F.R. 8 50.34(b) which is set out in a separate documententitled " Final Safety Analysis Report, Shoreham Nuclear PowerStation Unit 1, Long Island Lighting Company," forwarded herewithand made a part hereof; (3) the environmental data required by10 C.F.R. 8 50.30(f) which is set out in a separate documententitled " Environmental Report - Operating License Stage, ShorehamNuclear Power Station Unit 1, Long Island Lighting Company,"forwarded herewith and made a part hereof; and (4) the PhysicalSecurity Plan required by 10 C.F.R. g 50.34 (c) , forwarded here-with and made a part hereof.

Amendment 35 - January 1980

1945 055

-2-

OII. INFORMATION REQUIRED BY 10 C.F.R. 0 50.33

(a) Name of Applicant

Long Island I.ighting Company

(b) Address and Principal Office of Applicant

250 Old Country RoadMineola, New York 11501

(c) Description of Business

LILCO supplies electricity ana gas in Nassauand Suffolk Counties and the Fifth Ward of the Borough of Queens,New York City, all of which are on Iong Island in the State ofNew York, except that electric energy is not supplied in theIncorporated Villages of Freeport and Rockville Centre in NassauCounty and in the Incorporated Village of Greenport in SuffolkCounty. LILCO's service area consists of 1,230 square miles

| with an estimated population of 2,884,601 persons as of January 1,1979.

The proposed nuclear generating facilit*f is a necessarypart of LILCO's continuing construction of facilities to provideelectric energy to meet increasing demand and to offset increasingdifficulties in obtaining fossil fuel.

The business of LILCO is further described in the annualreports attached as Exhibit A below.

(d) (1) Not applicable.

(d) (2) Not applicable.

(d) (3) (i) State of Incorporation

LILCO is a public utility corporation organized under theTransportation Corporation Law of the State of New York.

(d) (3) (ii) Directors and Principal Officers

All principal officers and directors of LILCO are citizensof the United States of America. Their names and resident addressesare stated in Exhibit B to this Application.

(d) (3) (iii) Absence of Foreign Control

LILCO is not owned, controlled, or dominated by an alien,a foreign corporation or a foreign government.

1945 056

Amendment 35 - January 1980,

-3-

(d) (4) Absence of Agency

LILCO is filing this Application solely for its ownpurpose and is not acting as an agent or representative ofanother person.

(e) Licenses Sought

LILCO is hereby applying for such licenses as may benecessary to the ownership, possession, use and operation ofShorehan Nuclear Power Station Unit 1 as decc.ibed in thisApplication, which facility is to be used as a part of LILCO'selectric utility plant for the generation of electric energy,including the following licenses:

Class 103 Facility Operating License

A construction permit (No. CPPR-95) for a class 103facility was issued to LILCO for the Shoreham Nuclear PowerStation Unit 1 on April 14, 1973, and was amended en May 14, |1979. This amended construction permit provides for a latestdate of completion of the facility by December 31, 1980.Pursuant to 10 C.F.R. EE 50.51 and 50.56, LILCO requeststhat upon substantial completion of construction of ShorehamNuclear Power Station Unit 1, a class 103 facility operatinglicense be issued for the facility. This license is requestedto be issued for a period of 40 years.

Byproduct, Source, and Special Nuclear Material Licenses

Pursuant to 10 C.F.R. Parts 30, 40 and 70, LILCO willneed such byproduct, source, and special nuclear materiallicenses as are necessary to authorize it to acquire, deliver,receive, possess, use and transfer such materials (and withrespect to byproduct materials, also produce and own suchmaterial) in connection with the operation of Shoreham NuclearPower Station Unit 1. It is requested that these licenses begranted for a term consistent with the class 103 facilityoperating license requested above.

LILCO has combined its applications for these licenses inthis single Application as permitted by 10 C.F.R. 8 50.31.

1945 057v,,

Amendment 35 - January 1980

-4-

(f) Financial Qualifications

Facility Costs

The estimated cost of the comple',ed facility is $1,581,000,000.The associated cost for the transmission facilities is $23,571,000.

The estimated cost of plant operation for the first five years isas follows:

(7/Mos)

Year 1 2 3 4 5 6

(Thousands of Dollars)

Fuel 16,182 27,600 29,106 32,998 37,922 43,705

Operations & 10,127 29,224 27,755 29,508 33,820 33,820Maintenance

The estimated cost of shutting down the facility and main-taining it in a safe shutdown condition involves a $9,000,000(1975 dollars) one-time cost and a $30,000 per year annual costbased on the entombment concept as described in Section 5.9 ofthe Shoreham Environmental Report-Operating License Stage.

The Applicant is financing these costs in the ordinarycourse of its business. It is anticipated that the necessaryfunda will be provided from internal sources, principally

I depreciation accruals.

The Applicant is financially qualified to engage in theproposed activities as shown by its last four consecutive AnnualReports, submitted as Exhibit A to this Application. Additionalfinancial information is presented in Exhibit C.

Insurance Program

LILCO is carrying the maximum property damage insurancepresently available for the facility through the American NuclearInsurors (ANI) and the Mutual Atomic Energy Reinsurance Pool (MAERP) .In addition to the coverage available through ANI and MAERP, it isLILCO's intent to seek from other available insurance markets anyadditional amounts of coverage necessary to protect its investment.

LILCO also will purchase nuclear liability insurance| coverage from ANI, the Mutual Atomic Energy Liability Undensriters

(MAELU), or any other acceptable insurer, in such form and in suchamount as will meet the requirements of 10 C.F.R. Part 140. Thisinsurance will be i:. effect at least as of the date of shipment ofthe first fuel bundles from the seller's facilities to the Shoreham

'

"i'*'1945 058'

Amendment 35 - January 1980

-5-

Pursuant to the terms of 10 C.F.R. E 140.20, LILCO willalso execute with the Nuclear Regulatory Commission an indemnityagreement as required by S 170 of the Atomic Energy Act of 1954,as amended.

(h) Scheduled Completion Dates

The facility is scheduled to be operational by the Springof 1981. The latest date for completion of the facility isDecember 31, 1980, as stated in CPPR-95, as amended on May 14, 1979.

(i) Regulatory Agencies and News Publications

Regulatory agencies with jurisdiction over the rates andservices incident to the proposed generation, sale and distributionof the facility's electric energy are:

New York Public Service CommissionEmpire State PlazaAlbany, New York 12223

Federal Energy Regulatory Commission |825 North Capitol Street, NEWashington, D. C. 20426

The following is a list of trade and news publicationswhich circulate the area where Shoreham Nuclear Power Station |Unit 1 will operate and which are considered appropriate to givereasonable notice of this Application to those municipalities,private utilities, public bodies and cooperatives, which mighthave a potential interest in the facility:

Newsday The New Haven Register550 Stewart Avenue Register Publishing CompanyGarden City, N. Y. 11530 367 Orange Street(516) 737-4444 New Haven, Conn. 06503

(203) 562-1121The Daily News (L.I. Edition)220 E. 42nd Street The DayNew York, N. Y. 10017 47 Eugene O'Neill Drive(212) 949-3602 New London, Conn. 06320

(203) 443-2882Bridgeport Post & Telegram410 State StreetBridgeport, Conn. 06602(203) 333-0161

|

1945 059

Amendment 35 - January 1980

-6-

(j) Restricted Data

No Restricted Data or other classified defense informationis involved in this Application, and it is not expected that anywill become involved. Nonetheless, pursuant to 10 C.F.R. @ 50.37,LILCO hereby agrees that it will not permit any individual to haveaccess to Restricted Data until the Civil Service Commission shallhave made an investigation and report to the Commission on thecharacter, associations, and loyalty of such individual and theCommission shall have determined that permitting such person tohave access to Restricted Data will not endanger the common defenseand security.

III. INFORMATION REQUIRED BY 10 C.F.R. @ 50.33a

The pertinent antitrust information was filed April 14, 1971.

IV. COMMUNICATIONS

All communications to LILCO pertaining to this Applicationshould be sent to:

Andrew W. Wofford, Vice PresidentLong Island Lighting Company175 East Old Country RoadHicksville, New York 11801

cc: Edward M. Barratt, Esq.General CounselLong Island Lighting Company250 Old Country RoadMineola, New York 11501

Edward J. Walsh, Esq.General AttorneyLong Island Lighting Company250 Old Country RoadMineola, New York 11501

1945 060Original Dated: August 28, 1975

Amended: January 14, 1980 Respectfully submitted,

LONG ISLAND LIGHTING COMPANY

r1*

') ')'

''h.e yj) . ' " - /.'? , tat o'

JO PH P. NOyARRO

i/Amendment 35 - January 1980

AFFIDAVIT

STATE OF NEW YORK): ss: Shoreham

COUNTY OF SUFFOLK)

JOSEPH P. NOVARRO, being duly sworn, states that he

is Project Manager of the Shoreham Project within Long Island

Lighting Company; that he is authorized on the part of said

Company to sign and file with the Nuclear Regulatory Commission

the foregoing Amendment No. 35 to the License Application,

Shoreham Nuclear Power Station, Docket No. 50-322, consisting

of an amended License Application and accompanying exhibits;

that Amendment No. 35 was prepared under his supervision and

direction; and that as of this date, the statements contained

therein are true and correct to the best of his knowledge,

information and belief.

k ( (Y?ALD21f/ / JOSEPH P. NOVARRO

V /(

Sworn to before me this.

14th day of January, 1980

a- }+4'"P" 1945 9g;, f-Q1X1JNE A. DirIRlCII,

' JAC.w.rv nJJic, si..e, .I New Yo&No. EW)I Yn. Sulla County,

Term lipires J/3 O/c* O

i. - .i e i -- a w w -- - m e , e, .,e i = , y u p4yy um v'9W P T" *W m'7 PTFTW '

.

,

;

F

fI

f,

i

1

i!

!

-

.

L

D

.

i

I4

)

i

'i

.'

5

m,r ,--pg-n . AJW .e63-7+V4+''^

cT Sh % / Nf I *'N% _* 'J# ## T.'$''I .' ' - ' #-'# -

1: '

'

t . ')_tr : a ., -):t , . , .

'2'

a:t'

k W, - ,

-

.

l

;

1

)-

_y4

4

$! , ,,.gu,.. . . -, .. :+:2 s a e -m.- 83- + w h - -e-,

"'" MM A hmm---mm --mumm----- i--

. .

DIRECTORS and OFFICERS

ODIRECTORS

EDWARD C. DUFFY ROBERT G. OLMSTEDRetired Vice Chairman of the Board President. Island Capital Corp.Long Island Lighting Company Investments

"^ ~

DOUGALL C. FRASER PresidentPresident. Abingdon Investment Corp- Long Island Lighting CompanyInvestments

EBEN W. PYNENATHANIEL M. GIFFEN Senior Vice PresidentChairman of the Board and First National City BankChief Executive OfficerSuffolk County Federal Savings and E. CLINTON TOWLLoan Association Member of the Board of Directors

Grumman Corp.ManufacturingLIONEL M. GOLDBERG

Vice President. Alexander & Alexander,Inc. JOHN J. TUOHY'"*#*"#* Chairman of the Board

Long Island Lighting CompanyJOHN D. 'MXWELLVice-Cha',-ma. and Director, Kollmorgen Corp.; PHYLLIS S. VINEYARDVice President, Powers Chemco. Inc. President, Suffolk Community CouncilManufacturing Voluntary Non. profit Planning Agency

OFFICERS

JOHN J. TUOHY CHARLES R. PIERCEChairman of the Board Presidentand Chief Executive Officer

J AMES W. DYE, JR. JOHN J. RUSSELLSenior Vice President - Operations, Vice President - Customer RelationsTransmission - Distribution and Purchasing

ANDREW W. WOFFORDFRANK C. MACKAY Vice President - Project ManagementSenior Vice President - Commercial Operations

EDWARD W. EACKER***"'''

THOMAS H. O'BRIENSenior Vice President - Finance MICHAEL CZUMAK

ControllerWILFRED O. UHLSenior Vice President RAYMOND J. FORREREngineering and Project Management Assocaste Controller

JOSEPH G. ACKER JOHN J. KEARNEY, JR.

Vice President -Transmission - Distribution and SecretaryService Operations

KATHLEEN M. BROWN#** ' *"I 8* * '* **7GRANT BROWN

Vice President - Employee Relations

CHARLES J. DAVISVice President - Engineering EDWARD M. BARRETT

General Counsel

IRA L. FREILICHER EDWARD J. WALSH, JR.Vice President - Public Affairs General Attorney

JOHN R. GUMMERSALL, JR. FRANCIS M. WALSHVice President - Operations and Construction General Claims Attorney

1945 063

* - - - -m 4 # ,

-, , -

.. .

...

,

, ,

. - . .%z.ue-vm.,s-d=x-,..m..-7_.- - . - -. - - - - - - - - - - - - - - -

' - ^ ' ' - ' " '--

.

.

.

4:

|,.:. .

,.

4'f.

.

f*

= .c?

's

;.

s ;.. '3

..

3g

-!.

. ,i

- ' . + : r.

.

7.y *

~ '| .g**

:.K: - . f.t ,e * w . h

e-

,

A (

m n. . u..

";. ;,

. ; -- . ~. . - ,-., ;-

_.*

,'

s. - - . n -

.', , M * * .r. . .

. ''w a, _ . . . , . . .'

-

,. ; .+ -s .g ,w . .- $; ,, a

. ..y.. ; - u ,. -.

~~ % ~, '' '.. >

$'};%a ' % , "Q, . ; _ <;~ ? :|\ F-

.g'4 ~. . g . 9 - 7 ,.y . J.Q~ ; ~ _ .; *. . v**g. - -c .

.

--:

,QQQ ^' ~'

; L R_.ia ' _ ^.%.,

.

. . .W: :. & } -. %* ,L . - Q~ f f .. ; - d.

,

F* ?.

.

_

a-

. . ,-

y..? - c n .' - y _ _ .g". m ,_ - - -, , , a

.%. .,x6 ' wy-_s- - - u-

-9. .|. . g0 . +> - s , ~ .m ,.: , ? .4-

-

-

-.

..* ;-' . , . " . * . . - g. .y W+ g ' ' . .. '*n',*, , . . y

. 4 . : .m . .. g .- *

, y ., eo: ;,,

, , . q&, b, ; * . . ..,. 1--

. .. r .a 4 _ . yQ g.. ;,-,- , ,

.:+,

* %( ; .g. q -: a w .

,. ,

* - ,. i

g&.a,,. a ,. .'. e;e.c n . - xv ".__

at-

%t * *s.,;g y ', y ,y. a

- - .gg ;;~ .;3e: .

y , n #. .:. . . :, y40%.m.p:' x , ' - + - , ..

t * aV M,y ,.g ,4 ,.

,

o..i- . . ,.ep. gg- ; , . - . - ,,. - - . > -

;

.-

4 ; -. :. : a .- - - s.. ,, .

-..a '' ' o %, g ~.

' . .; , .;,:m- ,

.

. _.

* ' , y.{ t ., . ,<4 wk, . * '_. '

2

j. ,w g,. , ,- g

4 . j - ,-.

. ,. y s .- ,,a, A. .

*. . .

s

m -. . , ,

t,

.

, ..

..'

,

.,3 >3n w::.. ::- n . .'. .. .

, s yy:. %-

* ..,.Q.''s ;

. ' + . .y ; ,whg-, .

.

. sg .c -,'

" . - .r .. ~ c. 1 v.*.-A u 4 ; . .. ,.

', 3 4 u_ |y.,D.;. .- . - ..- ,

- -a

.. ~ D U .g: T -

' Q; j,. a ; + }, w[ .. . . ; s

'i - -' . -,

t % '; ?Q;Qq . - ,'L yr , -a.

+ . i.~ .n r. .e. .

S. . h ,' ;,. .

, .g . * 'th g-l Q*'? 4(*- "' ''' . # '

.-"b-'- ', ' .'a-.' . .. , s

," , ett t s. -

>

. < .g j , 4. 7 _ f * '- ? ' ; ."( , #

y -=..

.

; ,, ..

, f fjl* 3 - -

, g j' x g - v% : g' ;J (1

' ', y,.=

,' s ? y. .[* [[ _ _ .._

-

.~. . . .. , .

t, .. m.4 . ..' .

- .-.- . n . -- , '.x ..* .. %w. :. m y- . r , -

- %

g . 2 -Q ..-

- .;' . 3. g . - ps .4'9 t, r,p Q. . . .~ ~. - . . . g..u y._ .

. .. _- . ..

: .. L yb_- 'w.f. p. Q Q. .fN ,: ,

~~-

> ; . ::-:- . .< , .: .e . . .. .

_.,; - : , .

*A, $ e ., >_ 1 4:. -

.

-'-

. . > - .' < .., ,,_

"h .- ' ..'l 'l, g= ',@ d'' '<d g ,' , . - Ja. . g

- ~ u., w :.i n d:..r.' ' ''..' f [h | [ ;, . ; z . . ,

' JMNW !* . " ' - D*~ '

v. ,-

.+~ *

,

,. 7 ..-.. . . .,.

7 . y . , s . , .

-- - - - - - - - - - - -

,~-~ ' "

,

-*'

_. ..;; _- . . , ; .

- ,p .;'

,

.{4 7.'. - .;<, |.. g, , , ;*.y DUPLICATE DOCUMENT'

.

,

0hk,

; .. ; :.3 . - n. . y --

,..- ;'

) .; . [. [ ,k [I$.(1'

'

Entire document previously*

,I*,

! u [, fr 11 .

F entered into system under:i 1 a :] '~. . "?. '

y 4,

Y''

'

.a-

_, _

i n.; of pages: 1[3-

,,I ' i,'- [z__ h k.,. k.D d ) f No.- . - - - - -

_ _ _ _ -,

-

q'- 's.

) ,35

; - --kjt. -^

> '' j .j .. 3 -a., _ _. 7 r._s v_e <. .. - .

| 9__

: ,.y- +- . .m.

'. %, rh. ' " * #4 ;

*-.- 3 ,

O

p .The search for and attainment of a

6 richer and more fulfillinglifeis adriving forcein allhumanexistence. Walt Whitman, a native-

Long Islander, expressed in hispoetry this wonder of humanity,and the glorious diversity andvariety reflected in people

e everywhere.

Celebrated as the poet ofdemocracy, Whitman told us thatin the most common of humanactivities are found the essentialelements of the meaning of life. Wehave tried to show in this year'sAnnual Report, through thepeople and places of Long Island,together with Whitman's words,how men and women, freed byenergy from the drudgery ofsurvival, better their lives inmyriad ways: by a quiet walk onthe seashore, through theconfident satisfaction of a job I Iperformed well, through theexhilaration of physical movement,

1945 0t'S or bv the c "te=v'atio" ^"denjoyment of beauty.

1.

"? c s,g*% r *

gg:=||%qq'. <

@% hpuy.. ,$ ' .

b W. ,, R,'| . : } '' <sy.,

," 4<,

1 >k %as .g - , ,

s . t [, , <s- 4 )) qQ ., . 3 ., _ JTjj { ' *

, p.

p:1 g - ,,

* *'

*k, f /=7 ( 2' '.' '' /I-

,

. M k., I f' # k;h9.; ,',

*-

fc.,. 43 ..* 4 - t, 2a

'^& '. , 5 ;. , . .~4 * : s .y*

y. .+ m., ,,g4.? , A. .L .-%

.. g p*..ea 74 4.x 4 ,m w.:y~

,.3N'-

-M,4. a,* '

-

,pLyn m ,-,

W,jj, ~. L?:54, w;, %f;-

W% + , .. md' .cw * .c;.

[lp 3 ', > -

v.4J;: .4 : p >

-

. .:s<

i d::. '.

< '

sc<;u.,

,

,

k;e; . ,

1 ~ g.: -.

+ % . ,..%:$.% , s

m %,.4. .

, ..

WW4 ~$.m .p;;y. w, . s*

.. ,

. +.

.

O,,.4.'g', Cf;;ky..

m' $| r* .y

u. 9 s 9'

. -| ' |'

D -..

sr J

:x _ ;f. g.

e l;.s . ,,

,. .. m 1,

:, ? '

*>

.?.+'e-

,. . ,f. gM5!ijl$i$m . .pigwmg:; ., .&o.

w . < 4& < w :- c.' r.m ' . mg.,y .; s . .

",

,,9 ,

1 sq .

,

rA r ,;, . , w: r.

-

. N [,~5 -. m 1 -m. '|r . ; .Y #f * $ + (, ' i$

;s gg e . 2. ,f, '.> ,' -(

'~, *f

*

*< It.!' n. "l',s' %.:"w.s' ? e ;., - 9. e< q : ;, <3,p"l. ,d, '' - ,%v

,- i' .P S

. . ps 4 p*P 4x : .

f p+ psp;7 s-'

. jA g&,q($;Qig;%.; . o J%. s% f-- .'&f,9[ ' r ,QQo r.

-

2.

.

V,w ..

'. y. e

Qb |{M$hi - W6W ^ %W 3.j.h"

. : 4 + v& y .w wf, . k. i ., y- a'3 v> y;- .p >. <t -r w ..w. a~r .. 2;

'

, , j f.; y ; , ;;,c C@ ' ,%#i;"Qb, ,tr.u r.

- ,-no +'

3:s ,,

t#f h ) / ,Pd. y *[',, +, ,4a , m '>. , ;.'-

. . , <, o<v, ,e v.- t . % f> c

y...f,. _1 v% P 'c.e r

. % 3,x , a,

Y#A [a *# r t "4 aan # , . g,

L

4, , .-

4 :.

sw, -* w W V,<. .nyg m , , . . .

A re >* ekwy;;w%n ~~ G<.'

,. ,a'

,x ,w . , ,

<pF.a _.yy' 5. .A*'3 9N.-

Jj,# b- $. ea..4)- y

.c. . . , , ~ * -3

.,.. . - .

.

'

-

t

3- . DUPLICATE DOCUMENT# *

?... f Entire document previouslyE

[T l entered into eystem under:"'

i

ANO. .

No. of Pages:~,

c ,,u . .orr

, , ..

,

- ,.

'* u , . .. a. - o. . .-, -..g.y' y

. ' .

c

].

-j>'

ai

f O)

't.

ha!} k s,.4'

-t

ta,

f

2

I

i

1 (m

$N ,DhLy 2$p

%|{Q'C,YMM4i.___W$6;&,

i.. _2 er~_ J

I:nergy, the ntwt Essential

Thia year, in additht to the discussionof LII.CO's opera:ians, our Annual Ra- hport lecles at examplas of leadership p'Sca Lcng Ishud, from the past aa tin 9% psent. g

Ocr coverilkstrates the dangers of ,

whalisj, a major Long W.and indnetry 9 dwhJoh m:pplied gwwbg America with '

wh n13 cil forlighting t=til the hteWh. L" CGnt''rt, tWO of the McStp;oaliig ew;2 gy u,wces availabler.cw c ad (ct the ktn:3 are shownd-no; nuclear power and solar+ miri. A traspoon citu2n!u.m fuel, '

niMm cd here in McDowcake" form,een nMimately yield as rauch energya J ) gc1kna cf oil or 356 poundaef . &

"a ; narch for energy souces .le In more than Irr'J,000 years ano,viu 2 ann dlwovered wood could beS >&i Water's force was harnessedne> t foUowed by the capture of

1

ernTf in windmilla. Coal was the fuel yth?I fued the ir.dustrial Revolution, {b+eoslag the primari resource b-1^00. Pay years later, en and naturalgu hd replaced coal as the snajorsources of the world's energy. Like theence- Abundant whale, now a pro-tected species, fossil fuels were longregexdad es L:axhaustible.

A ann ~e new way to use these -fueIs was c rm-S Siwith Edison's in.verdien of the electriclight balbinW9. Our reliance en eles-tricity willincreare fu the years ahead, as thisform of energyis used to meet a widerrrnge cf needs. By the year 2000, elec- -tricity may acccunt for as much as50% of total United States energy use.P.s production will rely to a great ex-

1945 067tent en new sources of fual, su,'ple-tienting diminishing ter4 plies of oilattd natural gas.

w 4.,, 4 n 1 1 g % .,a./- I " **q , ' -. .g s

'g f' , *W, f

* *.

,

:-

* e'

. hee ,$

~~* A " "-4 J %

f ,$ . a. -

g * ' ' '

$ *

+ $.4

3j

,. ,- . .. s ,n ,

. . .

* *.= e , * , * ,

..

.5 "d . ** i*s

.

J,.* { g, + ,.. .. . ., y .- , i . , w ;;i. y

# " ' '

*[ - -s <

* ''

ps . , , - f;f _ .m> ,s

=| h kgs a '

( u ;+ >c .

,. 4 .

> ..-

:.

.| ,,| {'r . -

,

.. .

g .. % e '['

g

, , - . : *

:y, - '-

. m, , .),

*. . .

-

,- y* '-

. + - ... ,

*

.

y ''. . . . _ . , 7) * " '

s **'<

*,

-

,-- y 4,, f g a. . u,.

. .-

*=g, y .4, 6,, . , . , , . ,4

-

,-, g '

,

'

,p .. n y.

- - .

,.

. .

,,& V, [ * jy' x ' ,' ' :* #., g 4

;~

% ''% '},'

'~ T( g g '., * .. , , . , . -; s l' #, .,.

% ' 'n : *x w,.

[. ,

g - . , f ..; ' .; , - ,$ .w '* '

#-i * *

|~

'U. }. . , .

- e- [,. 'I '

g .: z ., 6 .[ "h ,1

. .* '

$; * 4 # . . ^ ; t. s v ,,.3

-

m. g ~- ,, .f ^ u.}'

<f ,g-

. - 3 , --

y

*''%|~. "g.x

,? e ..'

*'%.| 4t g. ^

' #{ ;:

y :- -. .m: .a ,

- - ; , ,,

^ ,E-

r' ' '

,;'

y ,3:_ \| ~. [T .[ Nh ' :' r

~

4$ ,

' N ',* fY } 7 ,

; 4' . T{ ; , % '4;

, ,.

, 'w- , . .. ., x . . 3 2,. p j,.. , , , ,

-.. , . .

,

$ . ..j.e , a

,k 4" /'

Q . ki^q

, y . - i ' e < n , ,% ,.:.

%

_ y,

? ] | _g * |" ? , [' ~

,, w

~

.;, , ,,

gj.y, 4 -| y **\/ .

/ -d ==

7 j, ,A q'ri.'

> w,~

.

*' '

~

?? A 9 'f. .,..

,

- m

Y * *' , 5.,., % .m 2. '

, j , e. ;% , i,_ _ , _ . _ . . -

d'_ _ [ .'d,e

" ','_

, . .+

n .. . . wf fg ,f ;i*

'.,

.$* 5 ., - y .

* '' '

e

y [. [; y ~

|+ -

. .,

~. . . .-

-

.- , , , . , . y

- f |,_ , p..'

A ,,

- s .' +"'.. .. g.' 4 '

,_

, * .- e, ,,.. A;4 . 9. , ,

_ f .,+ ;--- ~ ,

.

. :

_ *;-

,

1.- , '

>{ .: , , , * .,

'.'s... , .. j!. .

*. -y , - . = ~ . - -,

"

' - ^ t-; _. . _ . .

7 ... , . . . . . .- - - - - ~ - - - - :, ,.

, . F, . .,

|' . ._,

_'4 . -

~ .; ?. . . . . . , . ' , . ^' f ._ ~ [ ' '',N' N

' ''~

.' ,3'~c

[f...~.....t .........-.-.-,...._iY.... T.--.,

y'* +, , . :.

?,._. s . . . .. ..e.._m

(# , '.

- - -- - - - - m . = ~m w m m .wrws,w n m g y n y g g x y y y p'a %

k

& ,

(% ;y''

1 a- V"y

$ t ,, ~ '

,A , b3 *

''l*

-' r

i> , ' ,'

..~.' '

, 'N ,

. ,.( ; ,~].'. ! " ,"-'}

; ._.., , r{

~ ~ Mt-

,x - '

.

:s,

-_ _ , m. -N-2

.

, ,-

<

~ ~ r. . y.9 7t_; - 1 . - ' , <

-,;f ~ > - . '_ ~ c)I s'

- , ,

'

,

'

:s:_- ( ~ ap - % !' * * ' ',i

~;4 ,g .

,

j ,' ,'' * ')|

r*Q;,

s , ,n ;4 - q e m

, . . . . . m ,< .d+

-4''

.- '7 , . .-. , . ,, <..

''

q f. .

"

- , . ,- ;" ; .),f

.a'

3 ,_' ,.' 'N

'' * gy.- .. P -'

.> ' .; _ q i :. A, s ~ ' . .) . v [r _*

h] ^,r _' '_ . , ,

- [' \ .Z,; fl .I a m ..-;; - r,,.

'

' fi./' -'f_ * g d'; .. ( p , jva .'- e > y Q.

,,

~ ]M N#MA ;.''

fig.|9. I.~NW. n.; u

y. , : * :: . y--a,c"

"

;~'

:g. . . (y. r ;;. 4 .t ~_. ', q;.,

r %N4*e,< . ,;--

: ,,

.4 'g .

Tihg- g,. .,r

M, . % < -- wew

,

- .jc s t_ .

. o zL

W d--

- h>

| s :m ~ , ;'-g , ,

, -~ g; . '% ;?)i . pa,-

- %

*

.. , .~~ ' '.* i d'- .[:. .,

g ' / S-/79', ,' ,..' ' '_^ ''

~ f-

, # -v. . .. , .

's _ ' . - ,A.

:..9 c: n.7

- ~ p %e. m .~

g y ,-w _

y ,3.

.c . ny3 3' y y ,3 : . . -- 9

s,

r.,;. %-- -

~ _g f 4,

.

-O*.M .t 1 y, .-

g,-

* ~_. , wyp. .,

-,

y ,, ' c s- p7a:, ,

9 49. nn w . . .

c- ~, ,~yp ,p d-

^

, w.m#. - ', < , .g , ' ','

.. >V-'," '

q %

-

s, _

_

m -+,)1=

,s

, - .- M: % ,_ ,

,.

,! gr- .<; 47_ ,~

_ , .u

, . k' :" . ?s

y ?. /*

| 2-

1 ,'

-~ ~. '

. 9s..'-

' f. $4,].

| iw i.mt #-. 4'

g', , &{ ..my ,;.g:f

*y . 6, ,

i y@?|;Q .% ;;'

+mu . , ;^. ,

w;ww.g . : ~ ^ ,*'

.

'

- -, - V;cn;e ur ets5[ - [?..3 ?]

~ ,;..., :->,

s - < _ , i,. 4.?j ,

-- e C' ^

g, f.s. ~ : ()1- ~ wr,. ,-ef * ~ , - , s_ - .e

i., s

? - .: . & ~ * f fL<p;,| j- y ; -. 3f|g'w 4* '

L. . W-

.J, ) .3 _ _

r ,, ,

,

g 9m :c ~ ~ ,

1, x _ % _ ;1:-

~ .: w ' ., y+ ^ 'g

. }. 3, - -

; , _, s,, ,

-r.

".t. y'j.,

- - --

, _x1 1, ,

.3- .,,

2 0.

Y f'

y n v,

^

'T._ *

t - --

,m __m j, , 31

3-_ y

".~ * .. , ' . -1-

- 1 - 4: i t: . , - ;

, ::),

-

ypp y

,j..

~> ; .;.! a ?' 3

my' . ._

% (_

s -

,

3.

. .-

%,

-

,

~.4+!

_-

' +; :

s''h-' '+ ~'''

s , , y_

w +

w

. .b.,j_a',

, ) h .

. .y- I

. ,- 4 J * - , .

- .,*?

- 3 f* . . . -

g . i

k .

.f)^);-~ '

<*' *

% '

y*

,m ; ;

34

- 3 , p,..

> n-

s _. m-

mm-3-.,_..______._, _.. , . . . . . . . . . . . . . . _..-__2-.

EXHIBIT B

LONG ISLAND LIGHTING COMPANY

BOARD OF DIRECTORS

William J. Casey

Business Address: * Rogers & Wells200 Park AvenueNew York, New York 10017212-972-7089

Residence: Glenwood RoadRoslyn Harbor, N. Y. 11576516-621-9332

Wi lliam J. Catacosinos

Business Address: * Chairman and Chicf Executive OfficerApplied Digital Data Systems, Inc.100 Marcus BoulevardHauppauge, N. Y. 11787516-231-5400

Secretary: Ms. Marion Grant

Residence: Mill Neck, N. Y. 11765516-922-4630

Edward C. Duffy

Residence: *133 Marshall Avenue !

6- 52 050b'

|

Summer Residence: Mason Drive, RD #1 Box SOACutchogue, N. Y. 11935516-734-6300

Winter Residence: 6140 Midnight Pass RoadSarasota, FL 33581813-349-5180

|945 070-

* Denotes mailing address |

Amendment 35 - January 1980

-2-

Winfield E. Fromm

Business Address: * Group Vice PresidentInstruments and Systems GroupCutler-Hammer, Inc.One Huntington Quadrangle - Suite 3S12Melville, N. Y. 11747516-293-8901

Secretary: Mrs. Edie Corl516-293-8902

Resi.lence: Laurel CourtRFD #3Lloyd Harbor, N. Y. 11743516-427-4821

Nathaniel M. Giffen

Business Address: * Chairman of the Board andChief Executive OfficerSuffolk County Federal Savingsand Loan Association2100 Middle Country RoadCentereach, N. Y. 11720516-585-6300

Secretary: Mrs. Nancy Schechter

Residence: Levon LaneMiller Place, N. Y. 11764

| 516-473-6019

Lionel M. Goldberg

Business Address: *Vice PresidentAlexander & Alexander, Inc.One Huntington QuadrangleMelville, N. Y. 11747516-249-1500Mrs. Loretta Roth

Residence: 32 Pearsall Avenue $ \Glen Cove, N. Y. 11542 Sb

| 516-676-1221 )%N

| * Denotes mailing address

Amer' ent 35 - January 1980

-3-

John D. Maxwell

Business Address: ChairmanKollmorgen Corporation31 Sea Cliff AvenueGlen Cove, N. Y. 11542516-448-1001

Secretary: Mrs. Sandra Flynn

Residence: *High Farms RoadGlen Head, N. Y. 11545

!516-448-1002

Charles R. Pierce

Business Address: * Chairman of the Board andChief Executive OfficerLong Island Lighting Company250 Old Country RoadMineola, N. Y. 11501516-228-2026

Secretary: Mrs. Hazel Morel

Residence: 21 Wayside LaneLloyd Harbor, N. Y. 11743516-423-2709 |

Eben W. Pyne

Business Address: * Senior Vice PresidentCitibank, N.A.One Citicorp Center153 East 53rd StreetNew York, N. Y. 10022212-559-9528

Secretary: Miss Eileen Vandenberg

Residence: Willets RoadOld Westbury, N. Y. 11568516-333-2084

Apartment: 200 East 66th StreetNew York, N. Y.212-688-1978

1945 072 !* Den. tes mailing addresso

Amendment 35 - January 1980

-4-

I Wilfred O. Uhl

Business Address: * PresidentLong Island Lighting Company250 Old Country RoadMineola, N. Y. 11501516-228-2100

Secretary: Miss Ann Dunn

Residence: 28 Elmwood CourtPlainview, N. Y. 11803516-681-0229

Phyllis S. Vineyard

Residence: *10 South Brewster LaneBellport, N. Y. 11713

| 516-AT6-0269

| January 31, 1979

| * Denotes mailing address

~

1945 073 O

Amendment 35 - January 1980

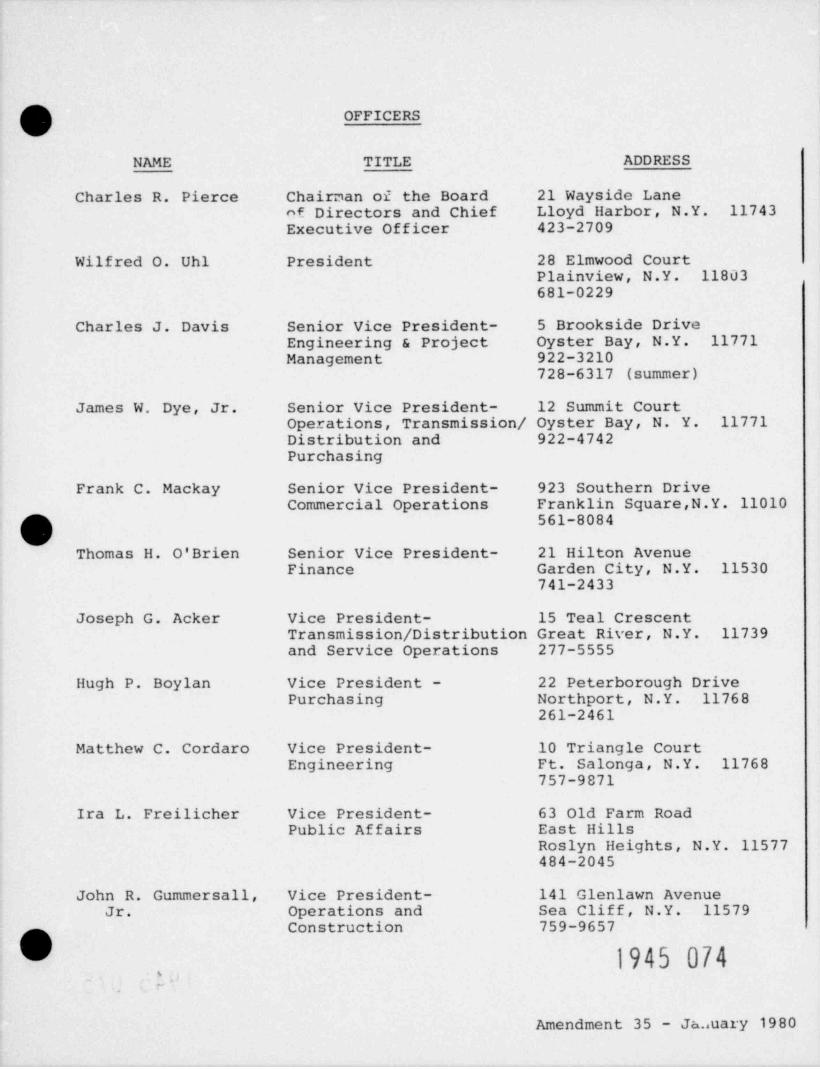

OFFICERS

NAME TITLE ADDRESS

Charles R. Pierce Chairman of the Board 21 Wayside Laneof Directors and Chief Lloyd Harbor, N.Y. 11743Executive Officer 423-2709

Wilfred O. Uhl President 28 Elmwood CourtPlainview, N.Y. 11803681-0229

Charles J. Davis Senior Vice President- 5 Brookside DriveEngineering & Project Oyster Bay, N.Y. 11771Management 922-3210

728-6317 (summer)

James W. Dye, Jr. Senior Vice President- 12 Summit CourtOperations, Transmission / Oyster Bay, N. Y. 11771Distribution and 922-4742Purchasing

Frank C. Mackay Senior Vice President- 923 Southern DriveCommercial Operations Franklin Square,N.Y. 11010

561-8084

Thomas H. O'Brien Senior Vice President- 21 Hilton AvenueFinance Garden City, N.Y. 11530

741-2433

Joseph G. Acker Vice President- 15 Teal CrescentTransmission / Distribution Great River, N.Y. 11739and Service Operations 277-5555

Hugh P. Boylan Vice President - 22 Peterborough DrivePurchasing Northport, N.Y. 11768

261-2461

Matthew C. Cordaro Vice President- 10 Triangle CourtEngineering Ft. Salonga, N.Y. 11768

757-9871

Ira L. Freilicher Vice President- 63 Old Farm RoadPublic Affairs East Hills

Roslyn Heights, N.Y. 11577484-2045

John R. Gummersall, Vice President- 141 Glenlawn AvenueJr. Operations and Sea Cliff, N.Y. 11579

Construction 759-9657

1945 074,

-

Amendment 35 - Ja..uary 1980

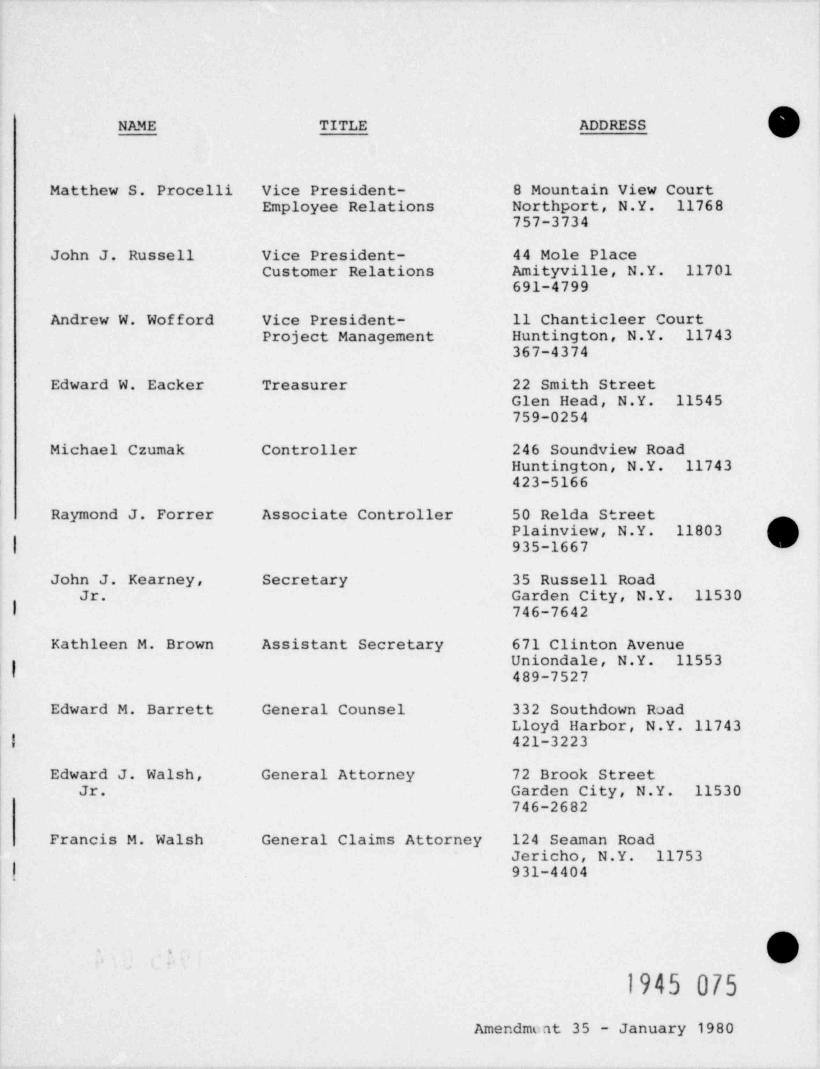

hNAME TITLE ADDRESS

Matthew S. Procelli Vice President- 8 Mountain View CourtEmployee Relations Northport, N.Y. 11768

757-3734

John J. Russell Vice President- 44 Mole PlaceCustomer Relations Amityville, N.Y. 11701

691-4799

Andrew W. Wofford Vice President- 11 Chanticleer CourtProject Management Huntington, N.Y. 11743

367-4374

Edward W. Eacker Treasurer 22 Smith StreetGlen Head, N.Y. 11545759-0254

Michael Czumak Controller 246 Soundview RoadHuntington, N.Y. 11743423-5166

Raymond J. Forrer Associate Controller 50 Relda StreetPlainview, N.Y. 11803

| 935-1667

John J. Kearney, Secretary 35 Russell RoadJr. Garden City, N.Y. 11530

| 746-7642

Kathleen M. Brown Assistant Secretary 671 Clinton Avenuei Uniondale, N.Y. 11553I 489-7527

Edward M. Barrett General Counsel 332 Southdown RoadLloyd Harbor, N.Y. 11743

| 421-3223

Edward J. Walsh, General Attorney 72 Brook StreetJr. Garden City, N.Y. 11530

746-2682

Francis M. Walsh General Claims Attorney 124 Seaman RoadJericho, N.Y. 11753

| 931-4404

|||-

1945 075Amendment 35 - January 1980

. J

-

Ecn&O

,

e

,

m

9

0

=

1945 076

'

.

) i

EXHIBIT C

ADDITIONAL FINANCIAL INFORMATION

Long Island Lighting Company forwarded to the NRC Staff via

its letters SNRC-378, dated April 19, 1979 and SNRC-453 dated

January 4, 1980, the additional financial information requested

in the January 23, 1979 NRC letter from Mr. S. A. Varga to

Mr. A. W. Wofford. That additional financial information has

been reproduced herein as Exhibit C cxcept in the case of

certain bulky testimony and exhibits from New York Public

Service Commission Cases 27374 (electric) and 27375 (gas),

which is incorporated by reference to SNRC-378 and SNRC-453.

1945 077s ,

.

C-1 Amendment 35 - January 1980

QUESTION 1.a.

Indicate the estimated annual cost by year to operate the subjectfacility for the first five full years of commercial operation.The types of costs included in the estimates should be indicatedand include (but not necessarily be limited to) operation andmaintenance expense (with fuel costs shown separately), depre-ciation, taxes and a reasonable return on investment. (Enclosedis a form which should be used for each year of the five yearperiod). Indicate the projected plant capacity of the unit foreach of the above years.

RESPONSE

See the attached forms for the response to question 1.a. foreach of the five years beginning 1981.

O

1945 078

OC-2 Amendment 35 - January 1980

ATTACHMENT FOR ITEM NO. 1_a_

ESTIMATED ANNUAL COST OF OPERATING NUCLEAR GENERATINGUNIT: SHOREHAM NUCLEAR POWER STATION, UNIT NO. 1

FOR THE CALENDAR YEAR 19_8_1

(thousands of dollars)

Operation and maintenance expensesNuclear power generation

Nuclear fuel expense (plant factor 66%). $ 16182. . . . . . .

Other operating expenses 5896. . . . . . . . . . . ....

Maintenance expenses _4231. . . . . . . . .. . . . ....

Total nuclear power generation 26309. . . ....

Transmission expenses 100. . . . . . . . . . . . . . ....

Administra+ive and general expenses

Property and liability insurance . 3100. . . . . . . . . . .

1620Other A.&G. expenses . . . . . . . . . . . . . ....4720Total A.&G. expenses . . . . . . . . . . . . . . .

TOTAL O&M EXPENSES 31129. . . . . . . . . . . ....

Depreciation expense 32300. . . . . . . . . . . . . . . ....

Taxes other than income taxes15800Property taxes . . . . . . . . . . . ... . . . . . . . .11053Other . . . . . . . . . . . . . . . . . . . . . ....

Total taxes other than income taxes 26853. ....

Income taxes - Federal 2427. . . . . . . . . . . . . . ....

Income taxes - other -. . . . . . . . . . . . . . . ....

Deferred income taxes - net 19520. . . . . . . . . . . . ....

Investment tax credit adjustments - net (2000). . . . . . ....

Return (rate of return: 10.20 %) . . . 155978. . . . . . . . . . .

TOTAL ANNUAL COST OF OPERATION $266207

1945 079.

C-3 Amendment 35 - January 1980

ATTACHMENT FOR ITEM NO. 1.a.

ESTIMATED ANNUAL COST OF OPERATING NUCLEAR GEtiSRATINGUNIT: SHOREHAM NUCLEAR POWER STATION, UNIT NO. 1

FOR THE CALENDAR YEAR 19_8_2

(thousands of dollars)

Operation and maintenance expensesNuclear power gencration

Nuclear fuel expense (plant f actor 66 %) . . . . $ 27600. . . .

16442Other operating expenses . . . . . . . . . . . . . . .12782Maintenance expenses . . . . . . . . . . . . . . . . .

Total nuclear power generation 56824. . . . . . .

107Transmission expenses . . . . . . . . . . . . . . . . . .

Administrative and general expenses

3250Property ar.d liability insurance . . . . . . . . . . . .4676Other A.&G. expenses . . . . . . . . . . . . . . . . .792TTotal A.&G. expenses . . . . . . . . . . . . . . .

64857TOTAL O&M EXPENSES O. . . . . . . . . . . . . . .

55300Depreciation expense . . . . . . . . . . . . . . . . . . .

Taxes other than income taxes28900Property taxes . . . . . . . . . . . . . . . . . . . . .14824Other . . . . . . . . . . . . . . . . . . . . . . . . .

Total taxes other than income taxes I372I. . . . .

Income taxes - Federal '. 2628. . . . . . . . . . . . . . . . .

-

Income taxes - other . . . . . . . . . . . . . . . . . . .

Deferred income taxes - net 29534. . . . . . . . . . . . . . . .

Investment tax credit adjustments - net (2000). . . . . . . . . .

Return (rate of return: 10.20 g) 147329, , , , , , , , , , , , , ,

TOTAL ANNUAL COST OF OPERATION $341372

~u

1945 080

C-4 Amendment 35 - January 1980

ATTACHMENT FOR ITEM NO. 1.a.

ESTIMATED ANNUAL COST OF OPERATING NUCLEAR GENERATINGUNIT: SHOREHAM NUCLEAR POWER STATION, UNIT NO. 1

FOR THE CALENDAR YEAR 1983

(thousands of dollars)

Operation and maintenance expensesNuclear pcwer generation

Nuclear fuel expense (plant factor 71%) $ 29106. . . . . . . .

Other operating expenses 15941. . . . . . . . . . . . . . .

Maintenance expenses 11814. . . . . . . . . . . . . . . . .Total nuclear power generation 56861. . . . . . .

Transmission expenses 114. . . . . . . . . . . . . . . . . .

Administrative and genera' expenses

Property and liability insurance . 3400. . . . . . . . . . .4441Other A.&G. expenses . . . . . . . . . . . . . . . . .7841Total A.&G. expenses . . . . . . . . . . . . . . .

TOTAL O&M EXPENSES 64816. . . . . . . . . . . . . . .

55300Depreciation expense . . . . . . . . . . . . . . . . . . .

Taxes other than income taxesProperty taxes .' 30900

. . . . . . . . . . . . . . . . . . . .14667Other . . . . . . . . . . . . . . . . . . . . . . . . .

Total taxes other than income taxes 45567. . . . .

3262Income taxes - Federal . . . . . . . . . . . . . . . . . .

Income taxes - other -

. . . . . . . . . . . . . . . . . . .

Deferred income taxes - net 33734. . . . . . . . . . . . . . . .

Investment tax credit adjustments - net (2000). . . . . . . . . .

Return (rate of return: 10. 2' % ) 138251. . . . . . . . . . . . . .

TOTAL ANNUAL COST OF OPERATION $338930

,

1945 081C-5 Amendment 35 - January 1980

ATTACHMENT FOR ITEM NO. 1.a.

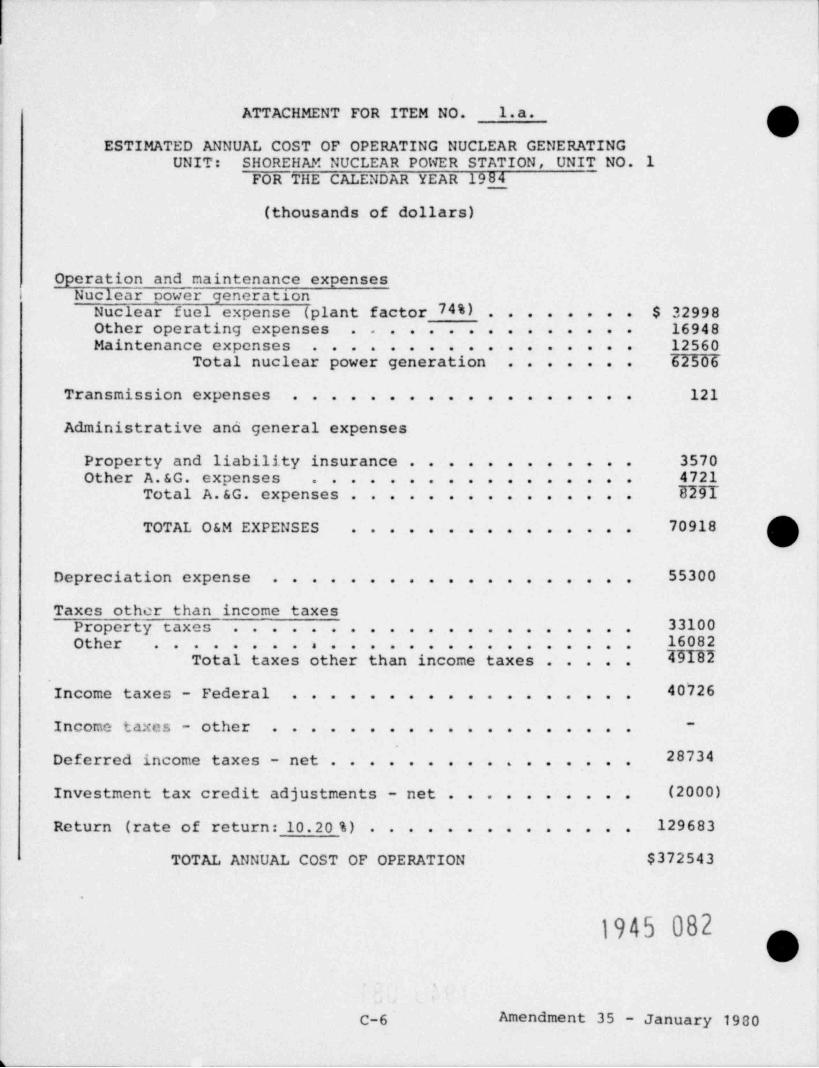

ESTIMATED ANNUAL COST OF OPERATING NUCLEAR GENERATINGUNIT: SHOREHAM NUCLEAR PONER STATION, UNIT NO. 1

FOR THE CALENDAR YEAR 1984

(thousands of dollars)

Operation and maintenance expensesNuclear power generation

Nuclear fuel expense (plant factor 74%) . . $ 32998. . . . . .

Other operating expenses 16948. . . . . . . . . . . . . . .

Maintenance expenses 12560. . . . . . . . . . . . . . . . .

Total nuclear power generation 62506. . . . . ..

Transmission expenses 121. . . . . . . . . . . . . . . . ..

Administrative and general expenses

Property and liability insurance . 3570. . . . . . . . . . .

Other A.&G. expenses 4721. . . . . . . . . . . . . . . ..

Total A.&G. expenses . 577T. . . . . . . . . . . . ..

TOTAL O&M EXPENSES 70918. . . . . . . . . . . . . ..

Depreciation expense 55300. . . . . . . . . . . . . . . . . ..

Taxes other than income taxesProperty taxes 33100. . . . . . . . . . . . . . . . . . . ..

Other 16082. . . . . . . . . . . . . . . . . . . . . . . ..Total taxes other than income taxes 47132. . . ..

Income taxes - Federal 40'726. . . . . . . . . . . . . . . . ..

Income taxes - other -. . . . . . . . . . . . . . . . . ..

Deferred income taxes - net 28734. . . . . . . . . . . . . . ..

Investment tax credit adjustments - net (2000). . . . . . . . ..

Return (rate of return: 10.20 %) 129683. . . . . . . . . . . . ..

TOTAL ANNUAL COST OF OPERATION $372543

1945 082 O

C-6 Amendment 35 - January 1980

ATTACHMENT FOR ITEM NO. 1.a.

ESTIMATED ANNUAL COST OF OPERATING NUCLEAR GENERATINGUNIT: SHOREHAM NUCLEAR POWER STATI'1N , C'!IT NO. 1

FOR THE CALENDAR YEAR 1985

(thousands of dollars)

Operation and maintenance expensesNuclear power generation

Nuclear fuel expense (plant factor 78%) $ 37922. . . . . . . .19399Other operating expenses . . . . . ..........14421Maintenance expenses . . . . . . . ..........71742Total nuclear power generation . . . . . . .

136Transmission expenses . . . . . . . . ..........

Administrative and general expenses

3750Property and liability insurance . . ..........4922Other A.&G. expenses . . . . . . . .......... EI77Total A.&G. expenses . . . . . ..........

80550TOTAL O&M EXPENSES . . . . . ..........

55300Depreciation expense . . . . . . . . . ..........

Taxes other than income taxes 35400Property taxes . . . . . . . . . . . .......... 16631Other . . . . . . . . . . . . . . . ..........

Total taxes other than income taxes 52031. . . . .

59985Income taxes - Federal . . . . . . . . ..........

-

Income taxes - other . . . . . . . . . ..........

16834Deferred income taxes - net . . . . . . ..........

(2000)Investment tax credit adjustments - net ..........

122329Return (rate of return: 10.20 %) . . . . ..........

$385029TOTAL ANNUAL COST OF OPERATION

.

''- 1945 083

C-7~ Amendment 35 - January 1980

ATTACHMENT FOR ITEM NO. 1.a.

ESTIMATED ANNUAL COST OF OPERATING NUCLEAR GENERATINGUNIT: SI*C?.EHAM NUCLEAR PGt SU STATION, UNIT NO. 1

FCR THE CALENDAR YEAR 19_86_

(thousands of dollars)

Operation and maintenar.ce expensesNuclear power generation

Nuclear fuel expe..se (plant factor 78%) . . $ 43705. . . . . .19399Other operating c:-:penses . . . . . . . . . . . . . . .14421Maintenance expenses . . . . . . . . . . . . . . . . .

Total nuclear power generation 77373'. . . . . . .

136Transmission expenses . . . . . . . . . . . . . . . . . .

Administrative and general expenses

3949Property and liability insurance . . . . . . . . . . . .5411Other A.&G. expenses . . . . . . . . . . . . . . . . . 933170tal'A.&G. e::penses . . . . . . . . . . . . . . .

87012TOTAL O&M EXPENSES O. . . . . . . . . . . . . . .

55300Depreciation expense . . . . . . . . . . . . . . . . . . .

Taxes other than income taxes 37900Property taxes . . . . . . . . . . . . . . . . . . . . . 12079Other . . . . . . . . . . . . . . . . . . . . . . . . 5IY75Total taxes other than income taxes . . . . .

66054Income taxes - Federal . . . . . . . . . . . . . . . . . .

-

Income taxes - other . . . . . . . . . . . . . . . . . . .

16834Dcferred income taxes - net . . . . . . . . . . . . . . . .

(2000)Investment tax credit adjustments - net . . . . . . . . . .

114974Return (rate of return: 10.20 %) . . . . . . . . . . . . . .

$393153TOTAL ANNUAL COST OF OPERATION

1945 084-

OC-8 Amendment 35 - January 1980

QUESTION 1.b.

Indicate the unit price per KWh experienced by each applicanton system-wide sales of electric power to all consumers forthe most recent twelve month period.

RESPONSE

For the twelve (12) months ending January 31, 1979, the KWhunit price experienced by each applicant on the LILCO systemwas 5.8 cents.

1945 085.

'

.

C-9 Amendment 35 - January 1980

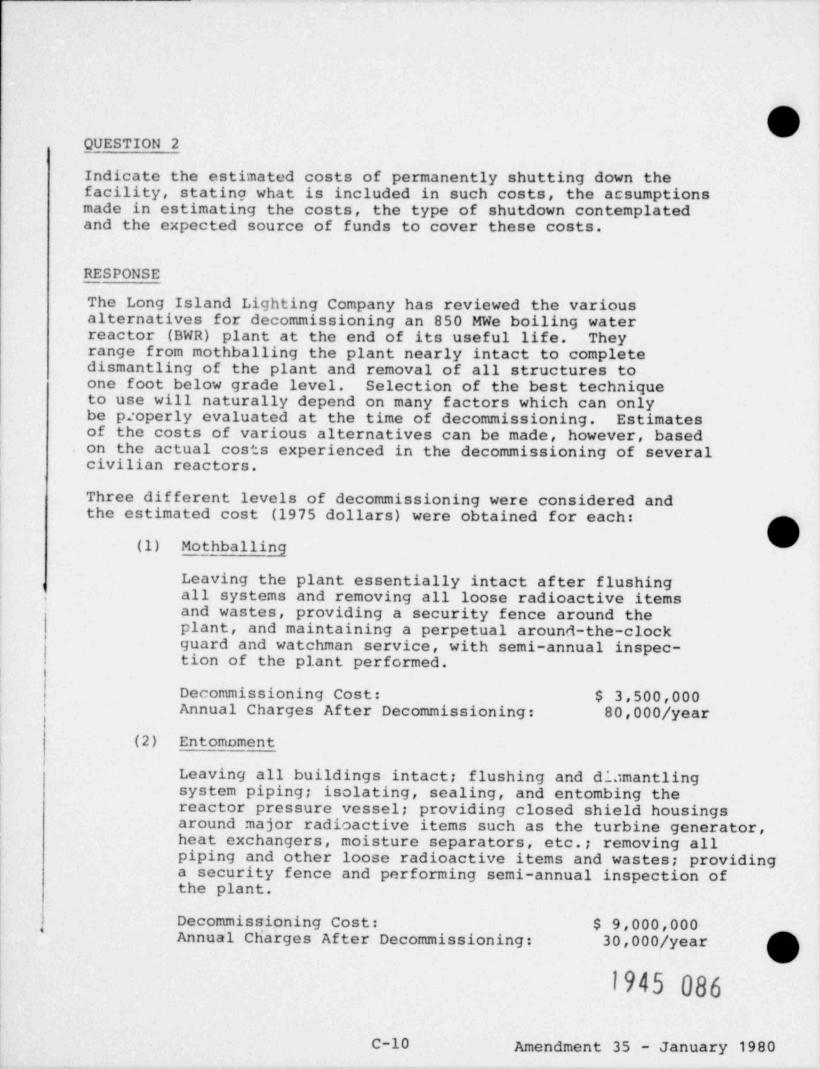

QUESTION 2

Indicate the estimated costs of permanently shutting down thefacility, statino what is included in such costs, the acsumptionsmade in estimating the costs, the type of shutdown contemplatedand the expected source of funds to cover these costs.

RESPONSE

The Long Island Lighting Company has reviewed the variousalternatives for decommissioning an 850 MWe boiling waterreactor (BWR) plant at the end of its useful life. Theyrange from mothballing the plant nearly intact to completedismantling of the plant and removal of all structures toone foot below grade level. Selection of the best techniqueto use will naturally depend on many factors which can onlybe properly evaluated at the time of decommissioning. Estimatesof the costs of various alternatives can be made, however, basedon the actual costs experienced in the decommissioning of severalcivilian reactors.

Three different levels of decommissioning were considered andthe estimated cost (1975 dollars) were obtained for each:

(1) Mothballing

Leaving the plant essentially intact after flushing,

all systems and removing all loose radioactive items,

and wastes, providing a security fence around theplant, and maintaining a perpetual around-the-clockguard and watchman service, with semi-annual inspec-tion of the plant performed.

Decommissioning Cost: $ 3,500,000' Annual Charges After Decommissioning: 80,000/ yearI

(2) Entomoment

Leaving all buildings intact; flushing and diamantlingsystem piping; isolating, sealing, and entombing thereactor pressure vessel; providing closed shield housingsaround major radioactive items such as the turbine generator,heat exchangers, moisture separators, etc.; removing allpiping and other loose radioactive items and wastes; providinga security fence and performing semi-annual inspection ofthe plant.

Decommissioning Cost: $ 9,000,000,

'

Annual Charges After Decommissioning: 30,000/ year g

1945 086

C-10 Amendment 35 - January 1980

(3) Complete Dismantling

Removal of the plant down to one foot below gradelevel, leaving the subgrade foundations essentiallyintact, backfilling to grade level, and restorationof landscaping to the approximate original condition.

Decommissioning Cost: $54,000,000

These numbers snow the range of decommissioning costs for theShoreham Unit. A 1977 Atomic Industrial Forum report, AIF/NESP-009SR, "An Engineering Evaluation of Nuclear Power ReactorDecommissioning Alternatives" indicated that the cost ofdecommissioning could be reduced if the plant were first moth-balled or entombed, and then left in that condition for a periodof time before dismantling. This approach to dismantling appearspreferable to LILCO at this time. The Applicant will continueto monitor industry developments and, at an appropriate time, adetailed decommissioning plan will be submitted to the NRC.

The source of funds will come from internal cash generation plusexternal financing as required.

1945 087

'

,

C-11 Amendment 35 - January 1980

QUESTION 3

Provide an estimate of the annual cost to maintain the shutdownof the facility in a safe condition. Indicate what is includedin the estimate, assumptions made in estimating cost and theexpected source of funds to cover these costs.

RESPONSE

Annual costs to maintain the shutdown of the facility in a safecondition, a description of what is included in the estimate,and assumptions made in estimating costs are included in responseto Question 2.

The source of funds will come from internally generated cashplus external financing as required.

O

.

I945 088 qC-12 Amendment 35 - January 1980

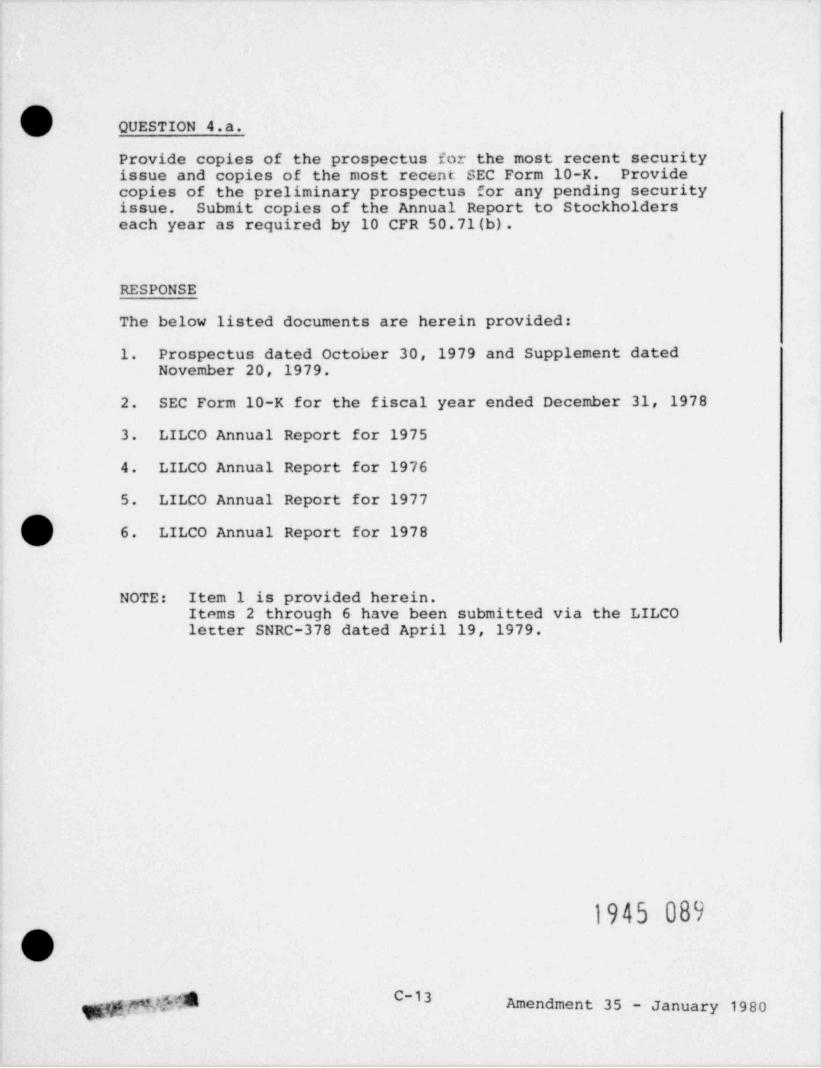

QUESTION 4.a.

Provide copies of the prospectus for the most recent securityissue and copies of the most recent SEC Form 10-K. Providecopies of the preliminary prospectus for any pending securityissue. Submit copies of the Annual Report to Stockholderseach year as required by 10 CFR 50.71(b).

RESPONSE

The below listed documents are herein provided:

1. Prospectus dated October 30, 1979 and Supplement datedNovember 20, 1979.

2. SEC Form 10-K for the fiscal year ended December 31, 1978

3. LILCO Annual Report for 1975

4. LILCO Annual Report for 1976

5. LILCO Annual Report for 1977

6. LILCO Annual Report for 1978

NOTE: Item 1 is provided herein.Items 2 through 6 have been submitted via the LILCOletter SNRC-378 dated April 19, 1979.

1945 089

gy;.{-rAVIr@ Amendment 35 - January 1980-3

QUESTION 4.b.

Describe aspects of the applicant's regulatory environmentincluding, but not necessarily limited to, the following:prescribed treatment of allowance for funds used duringconstruction and construction work in progress; form of ratebase (original cost, fair value, other) ; accounting fordeferred income taxes and investment tax credits; fueladjustment clauses in effect or proposed; historical;partially projected, or fully projected test year.

RESPONSE

The following describes various aspects of LILCO's regulatoryenvironment:

1. The test year now utilized for rate making purposes inNew York State is the 12 month period at the end of acalendar quarter no earlier in time than 150 days beforethe date of filing. This test year is to be fully adjustedto show the operating results for the first 12 months duringwhich the proposed rates will be in effect. There havebeen no restrictions placed on the types of adjustmentwhich may be made to the test year to make it representthe future period.

2. There are certain items included in construction work inprogress (CWIP) on which allowance for funds used duringconstruction (AFC) is not calculated, since they are eithertoo small or are of too short a duration in time. Theseitems are often referred to as "non-interest bearing" CWIP.Currently the average balance for these items is $45 millionon the electric side of the business and $4 million on thegas side of the business. AFC generally would be calculatedon the remainder of CWIP unless the Commission decides topermit some of it to be included in rate base. (Suchpermission is normally only granted to enable a utilitycompany to continue its financing program). The Companyis presently allowed to include $300 million of electricand $4 million of gas CWIP in its rate base.

3. In New York, the rate base is normally the average plant inservice at original cost, less the accumulated depreciationreserve, less the deferred taxes on plant-related items, plusan allowance for. working capital and any CWIP which theCommission has'Illowed to be included.

1945 091

C-14 Amendment 35 - January 1980

O4. The Commission permits deferred tax treatment on some of

the differences between book and tax depreciation whichproduces something which can be described as between flow-through accounting and normalized accounting. There is alsodeferred income tax treatment for the investment tax creditin excess of the first 4%. The Company also capitalizes aportion of its AFC net of income taxes.

5. The Commission permits both electric and gas fuel adjustmentclauses. The electric fuel adjustment clause includes thecost of fuel, excluding the cost of fuel used to make salesfor resale, plus the cost of economy purchases and the costof fuel included in non-economy purchases. The Commissionalso permits deferred fuel accounting so that fuel expensesand fuel revenues may be more closely in phase with eachother.

O

@sb%.

N

O

C-15 Amendment 35 - January 1980

QUESTION 4.c.

Describe the nature and amount of the applicant's mcqt recent raterelief action (s). In addition, indicate the nature and amount of anypending rate relief action (s). Use the attached form to provide thisinformation. Provide copies of the submitted financially-relatedtestimony and exhibits of the staff and company in the most recentrate relief action or pending action. Furnish copies of the hearingexaminer's report and recommendation, and final opinion last issuedwith respect to each participant, including all financial exhibitsreferred therein.

RESPONSE

4.c. Rate Developments

Granted Electric GasTest year utilized 12/31/77 (a) 12/31/77(a)Annual amount of revenue increase

requested-test year basis (000's) $ 147,100 $23,900Date petition filed 5/31/78 5/31/78Annual amount of revenue increase

allowed-test year basis (000's) $ 26,000 16,580Percent increase in revenues allowed 3.3% 9.1%Date of final order 4/27/79 4/27/79Effective Date 5/04/79 5/04/79Rate base finding (000's) $1,558,728 238,761Construction work in progress included

in rate base (000's) S 300,000 4,120Rate of return on rate base authorized 10.26% 10.26%Rate of return on common equityauthorized 13.7% 13.7%

Revenue Effect (000's)Amount received in year granted $ 15,300 7,200Amount received in subsequent year $ 25,700 16,900

Pending Requests Electric Gas.

Test Year 6/30/79(b)

Amount $25.6 million None

Percent 2.5%

Date filed 9/21/79

Date by which decision must jg4} 093be issued 8/80

C-16 Amendment 35 - January 1980

O4c. Rate Developments

Pending Requests (Cont.) Electric Gas

Rate of Return on Rate BaseRequested 10.49%

Rate of Return on Common EquityRequested 13.7%

Amount of Rate Base Requested $1,684,859

Amount of CWIP included inRate Base $300 million

NOTES:

(a) The Public Service Commission of the State of New York(PSC) in making its final determination recognized certainmajor adjustments to the 12/13/77 test year and concludedthat such adjustments created a new test year, calledthe rate year, the 12 months ended 4/30/80.

(b) The test year of 6/30/79 has been adjusted to a rateyear of 4/30/81.

%%

Sbb

%)%

N

O4

.

C-17 Amendment 35 - January 1980

The following financially-related testimony and exhibits of Staffand Company witnesses in rate cases 2737? (electric) and 27375 (gas)have been previously submitted via LILCO letter SNRC-378 datedApril 19, 1979 except for items C.1 and D which are provided herein:

Financially-related testimony and exhibits of Staff and Companywitnesses in rate case 27374 (electric) and 27375 (gas) willconsist of:

A. Prepared testimony and prepared exhibit #196 ofVincent A. Macri, Chief Utility Financial Analyst,Utility Finance Section, Office of Accounting andUtility Finance, N.Y. State Public Service Commission,Empire State Plaza, Albany, N.Y. 12223, datedOctober 1978 for the Staff:

Exhibit #196 contains the following:

1. LILCO - Cash Funds Requirements Excluding the Trustsfor the years 1979 and 1980

2. LILCO - Capital Structure - June 30, 1978 - Pro Forma3. LILCO - Average Capital Structure for the Rated Year4. LILCO - Moody's Utility Common Stocks - Average Long

Term Debt Positions5. LILCO - Moody's Utility Common Stocks - Average

Preferred Stock Positions6. LILCO - Moody's Utility Common Stocks - Average

Common Equity Positions7. LILCO - Cost of Long Term Debt - June 30, 1978 - Pro

Forma8. LILCO - Cost of Preferred Stock - June 30, 19789. LILCO - Financial Statistics

10. LILCO - 1978 Yields for Long Island Lighting11. LILCO - Moody's Utility Common Stocks - Financial

Statistics12. LILCO - Moody's Utility Common Stocks - Financial

Statistics - 197613. LILCO - Moody's Utility Common Stocks - Financial

Statistics - 197714. LILCO - Moody's Utility Common Stocks - Financial

Statistics - Current15. LILCO - Flowthrough Electric Utilities - Financial

Statistics for 197616. LILCO - Flowthrough Electric Utilities - Financial

Statistics for 197717. LILCO - Flowthrough Electric Utilities - Financial

Statistics - Current18. LILCO - Standard & Poor's 400 Industrials - Financial

Statistics19. LILCO - Moody's Utility Common Stocks - AFC as a

Percentage of Earnings

.

C-18 Amendment 35 - January 1980

O20. LILCO - Flowthrough Electric Utilities AFC as a

Percentage of Earnings21. LILCO - Common St ock Issuances 1976 - $20,000,000

or more22. LILCO - Common Stock Issuances 1977 - $20,000,000

or more23. LILCO - Common Stock Issuance in 1078 - $20,000,000

or more24. LILCO - Derivation of Formula for Converting Investors

Expected Return to Required Return on Equity25. LILCO - Divisors Necessary to Convert Total Return

to Required Return on Equity at Given Market to BookRatios * (* Assume 66% payout ratio)

26. LILCO - Average Capital Structure and '. c c t Rates forthe Rate Year

27. LILCO - Pre-Tax Rate of Return28. LILCO - Pro Forma Pre-Tax Coverage for the Rate Year29. LILCO - Pre-Tax Coverage Based on the 10% Limitation

of Other Income30. LILCO - Moody's Utility Common Stocks Pre-Tax Coverage

for the Twelve Months Ended December 31, 197731. LILCO - Flowthrough Utilities Pre-Tax Coverage for the

Twelve Months Ended December 31, 197732. LILCO - Moody's Utility Common Stocks Pre-Tax Coverage |h

for the Twelve Months Ended June 30, 197833. LILCO - Flowthrough Utilities Pre-Tax Coverage for the

Twelve Months Ended June 30, 197834. LILCO - AFC as a Percentage of Earnings for the Rate

Year

B. Financially-related testimony and exhibits of company witnessesin rate cases 27374 (Electric) and 27375 (Gas) :

1. Thomas H. O'Brien2. Raymond J. Forrer3. Roger F. Murray the 2nd4. Zvi Bendry (testimony and exhibit #64 which contains

Schedules 1 and 2 and a Technical Appendix)

C. The Hearing Examiner's report and recommendations, and finalopinion last issued with respect to each participant, includingall financial exhibits referred therein consists of thefollowing:

1. Recommended Decision by Administrative Law Judge DavidSchechte Issued 2/13/79 - Case 27374 and 27375

2. Opinion and Order Determining Increased RevenueRequirements - Issued 4/27/79, Case 27374 (ElectricRates) and 27375 (Gas Rates). (Attachment C to question4C provided with this submittal)

1945 096C-19 Amendment 35 - January 1980

D. Financially-related testimony and exhibits of Companywitnesses in support of the pending rate case:

1. Raymond J. Forrer (pages 1 and 12 through 20 andExhibits 13 through 18.

2. Zvi Benderly (testimony and exhibit 56 which containsschedules 1 and 2 and a technical appendix).

1945 097

C-20 Amendment 35 - January 1980

ATTACHMENT A TO QUESTION 4.C

TESTIMONY OFRAYMOND J. FORRER

1 Q. Please state your name and business address.

2 A. Raymond J. Forrer, 250 Old Country Road, Mineola, New York

3

4 Q. What is your position with Long Island Lighting Company?

5 A. I am Associate Controller, a position I have held since 1974.

6

7 Q. Have you testified in other proceedings before this Commission?

8 A. Yes. I have testified in several of the Company's rate proceedings

9 including its last electric and gas rate Cases 27374 and 27375,

10 in Case 27136, in Case 80003 "Jamesport Siting Application", and

11 in case 26798 " Empire State Power Resources. Inc."

12-

13 Q. Hr. Forter, I show you a two page document entit. led "Long Island

14 Lighting Company - Balance Sheet." Was this document prepared

15 under your direction?

16 A. Yes..

17

18 Q. I that this document be marked for identification as it

19 No. 1. Mr. rer, would you please explai t Exhibit No.

20 1 shows?

21 A. It shows the Balance She the ny as of December 31, in each.

22 of the years , 1976, 1977 and 1978 and as une 30, 1979

23 ex med from the book: of the Company by PSC prime accu..

24

1945 098'

'

NOTE: Pages 2 through 11 inclusive have been omitted intentionally.

-1- Amendment 35 - January 1980

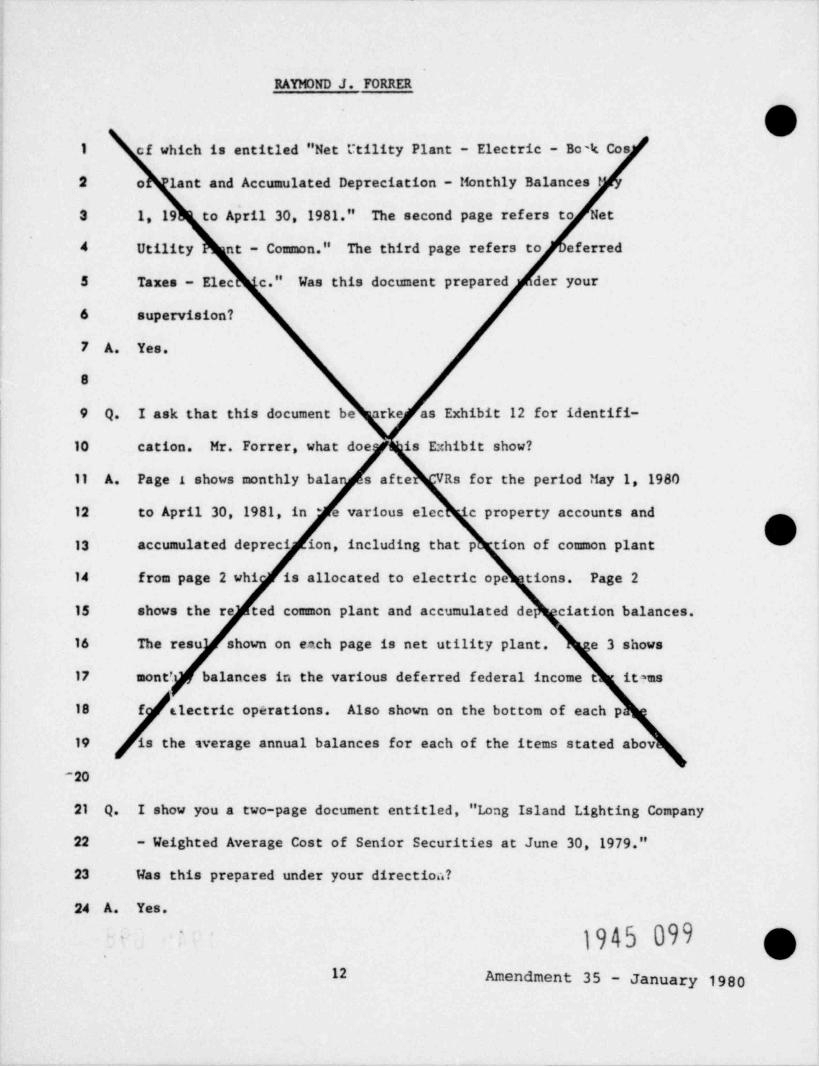

RAYMOND J. FORRER

O1 cf which is entitled " Net Utility Plant - Electric - Bo'k Cos

2 o lant and Accumulated Depreciation - Monthly Balances !

3 1, 19 to April 30, 1981." The second page refers to Net

4 Utility nt - Common." The third page refers to eferred

5 Taxes - Elec c." Was this document prepared der your

6 supervision?

7 A. Yes.

8

9 Q. I ask that this document be arke as Exhibit 12 for identifi-

10 cation. Mr. Forrer, what doe is Exhibit show?

11 A. Page I shows monthly bala s after Rs for the period May 1, 1980

12 to April 30, 1981, in ' e various elec ic property accounts and

O13 accumulated depreci ion, including that p tion of common plant

14 from page 2 whi is allocated to electric ope ations. Page 2

15 shows the re ted common plant and accumulated de ciation balances.

16 The resu shown on es.ch page is net utility plant. e 3 shows

17 mont'. balances in the various deferred federal income t it=ms

18 f electric oparations. Also shown on the bottom of each p

19 is the sverage annual balances for each of the items stated abov

~20

21 Q. I show you a two-page document entitled, "Long Island Lighting Company

22 - Weighted Average Cost of Senior Securities at June 30, 1979."

23 Was this prepared under your directica?

24 A. Yes.

1945 099 g--

12 Amendment 35 - January 1980

RAYMOND J. FORRER

1 Q. I ask that this document be marked as Exhibit 13 for identification.

2 Would you please explain this Exhibit?

3 A. Exhibit 13 shows that at cf June 30, 1979, the weighted average

4 cost of long-term debt was 7.86% and the weighted average cost

5 of preferred stock was 8.02%.

6

7 Q. I show you a two-page document entitled, "Long Island Lighting

8 Company - Estimated Cost of Senior Securities, Capital Structure,

9 and Rate of Return." W' s this prepared under your direction?a

10 A. Yes.

11

12 Q. I ask that this document be marked as Exhi'ait 14 for identification.

13 Would you please explain this Exhibit?

14 A. Exhibit 14, Schedule 1 of 2 shows that the estimated changes in the

15 senior securities during the period of July 1,1979, and April 30,

16 1981, and the cost of those changes. It reflects the pending sale

17 in October 1979 of $14.4 million of authority financing notes and a

18 proposed sale in May,1980 of $85 million of General and Refunding

19 Bonds at a cost of 10%. Also, an expected sale in December,1980 of

20 $70 million of General and Refunding Bonds at an estimated interest

21 rate of 10%. The schedule also indicates a refunding of the

22 Series A ist Mortgage Bonds of $20 million at a 3% rate in

23 September, 1980. The resulting weighted aversge cost of debt at

24 April 30, 1981, is 8.16%. The Exhibit further reflects (a) the

13 Amendment 35 - January 1980..

1945 100

RAYMOND J. FORRER

1 recent issuance of Preferred Series S $75 million, with proceeds

2 to the Company of $73,715,000 at a cost of 9.97% and (b) an

3 adjustment for the Series Q Preferred Stock Amortization of

4 the redemption premium as per Case 27236. The Preferred Stock

5 has been reduced for the sinking fund requirements relating to

6 the Series L stock in July, 1979; Series Q in June, 1980; Series

7 L in July, 1980; and Series M in November, 1980. The weighted

8 average cost of Preferred Stock at April 30, 1981 is 8.56%.

9

10 Schedule 2 of 2 reflects the estimated capital structure, cost

11 rate, and the return components for long-term debt, Preferred

12- Stock, Common Equity and customer deposits as estimated for the

13 rate year ending April 30, 1981. In addition to the additional

14 bonds and preferred stock noted on Schedule 1, this schedule

15 reflects (a) a planned issue of $120 million offering of

16 common stock in November 1979, (b) a proposed $88.8 million

?7 offering of common stock in November, 1980, (c) proceeds of

18 $2 million from the sale of shares of common stock under the

19 Employee Stock Purchase Plan and (d) proceeds of $16 million

20 from the sale of shares of common stock under the Automatic

21 Dividend Reinvestment Plan during the rate year. Finally,

22 it reflects additional retained earnings of $58.7 million

23 and the estimated changes of $0.2 million to the capital stock

24 expense.

14 Amendment 35 - January 1980

1945 101.

,

RAYMOND J. FORRER

1 Q. What else does Exhibit 14 show?

2 A. It shows the capitalization ratios of the capital structure and

3 the cost rates for each of the senior securities, 9% for customer

4 deposits and 13.7% for common equity. It also shows the resultant

S return components yielding a total required rate of rr. turn of 10.49%.

6

7 Q. Mr. Forrer, would you comment or. the apparently high common

8 equity in the Company's capital structure?

9 A. Although the common equity ratio in the Company's capital structure

10 seems high, two factors must be considered. First, in acccrdance

11 with past rate case treatment, the Resources and Construction Trust

12 have been excluded from the capital structure for rate purposes.

13 Second, theoretically, the Company could decrease the amount of

14 common equity by selling more long-term debt. But as shall be

15 demonstrated later on in my testimony, bond indenture coverage is

16 below acce . table levels, even with the full rate relief requested.

17 Therefore, the sale of additional bonds to reduce the common equity

18 might not be feasible. Other possibilities of reducing the common

19 equity ratio are to increase use of the Trusts as a financing vehicle

20 and to sell more Preferred Stock. With respect to the Trusts,

21 these were created to finance nuclear fuel and the construction

22 of the Company's share of Nine Mile Point 2 nuclear unit. It is

23 possible for the Company to borrow from the Trusts for "Other

24 Corporate Purposes" but this is merely another temporary expediency

Amendment 35-da9dhykb15

.' '

RAYMOND J. FORRER

O1 for financing and does not have a material effect on our

2 financing program. As far as Preferred Stock is concerned, the

3 preferred stock ratios are near maximum levels. In addition,

4 without rate relief the amount of Preferred Stock that could

5 be issued may be limited by the Certificate of Incorporation

6 coverage test. For the recently issued Series S 9.8% preferred,

7 the coverage was 1.51 times. The minimum required is 1.50 times.

8

9 Q. I show you a two-page document entitled, "Long Island Lighting

10 Company - Fund Requirements and Financing." Was this prepared

11 under your direction?

12 A. Yes.

13

14 Q. I ask that this document be marked as Exhibit 15 for identification.

15 Would you plear; explain this Exhibit?

16 A. Schedule 1 of the Exhibit shows the fund requirements, internal

17 cash generation, and financing for the calendar years 1979, 1980

18 and for the twelve months ended April 30, 1981. The Exhibit

19 shows the funds required for our construction program and nuclear

20 fuct and Nine Mile Point #2 expenditures to be financed through

21 the resources and constraction trusts. Also, the funds required

22 for sinking funds and bond redemption. Funds derived from internal

23 sources are shown without rate increases requested in this case.

24 The financing program including resources and construction trust

O.' 16 Amendment 35 - January 19803-

l945 103

RAYMOND J. FORRER

1 financing is shown in the section headed " Funds Provided."

2 Schedule 2 of the exhibit is similar to Schedule 1 except

3 that I have assumed the rate increase requested in this

4 filing to be effective May 1,1980.

5

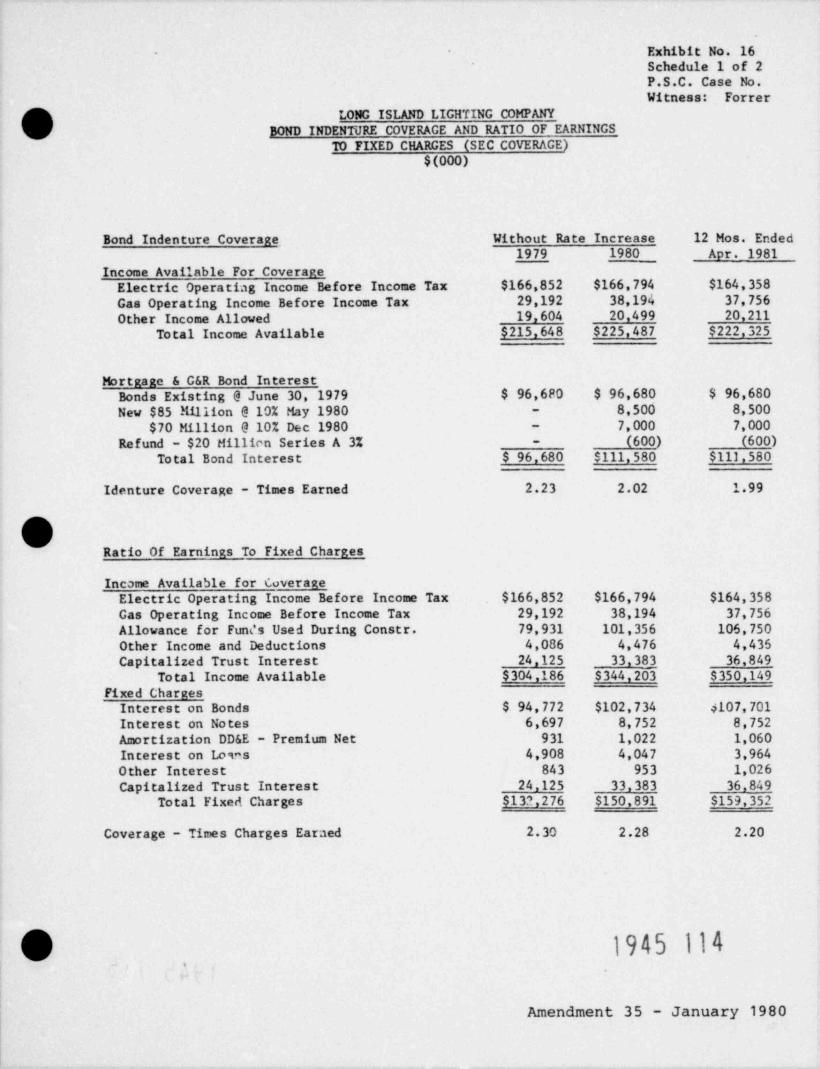

G Q. I show you a two-page document entitled, "Long Island Lighting

7 Company - Bond Indenture Coverage and Ratio of Earnings to Fixed

8 Charges (SEC Coverage)." Was this prepared under your di-ection?

9 A. Yes.

10

11 Q. I ask that this document be marked as Exhibit 16 for identification.

12 Would you please explain this Exhibit?

13 A. Schedule 1 of the Exhibit reflects the computation of the bond

14 indenture coverages and ratios of earnings to fixed charges at

15 December 31, 1979, December 31, 1980, and April 30, 1981. The

16 coverages are based on available income stated in the Schedule

17 and proposed bond financings. Schedule 1 is tabulated with-

18 out rate increases while Schedule 2 reflects the requested

19 rate increase effective on May 1,1980.

20

21 Q. Mr. Forrer, on Exhibit 16 you show the forecasted G&R bond

22 indenture coverage for the years 1979, 1980 and the rate year

23 respectively as 2.23 times, 2.02 times and 1.99 times without

24 rate relief and 2.23 times, 2.17 times and 2.22 times wi_th

17 Amendment 35 - January 1980*

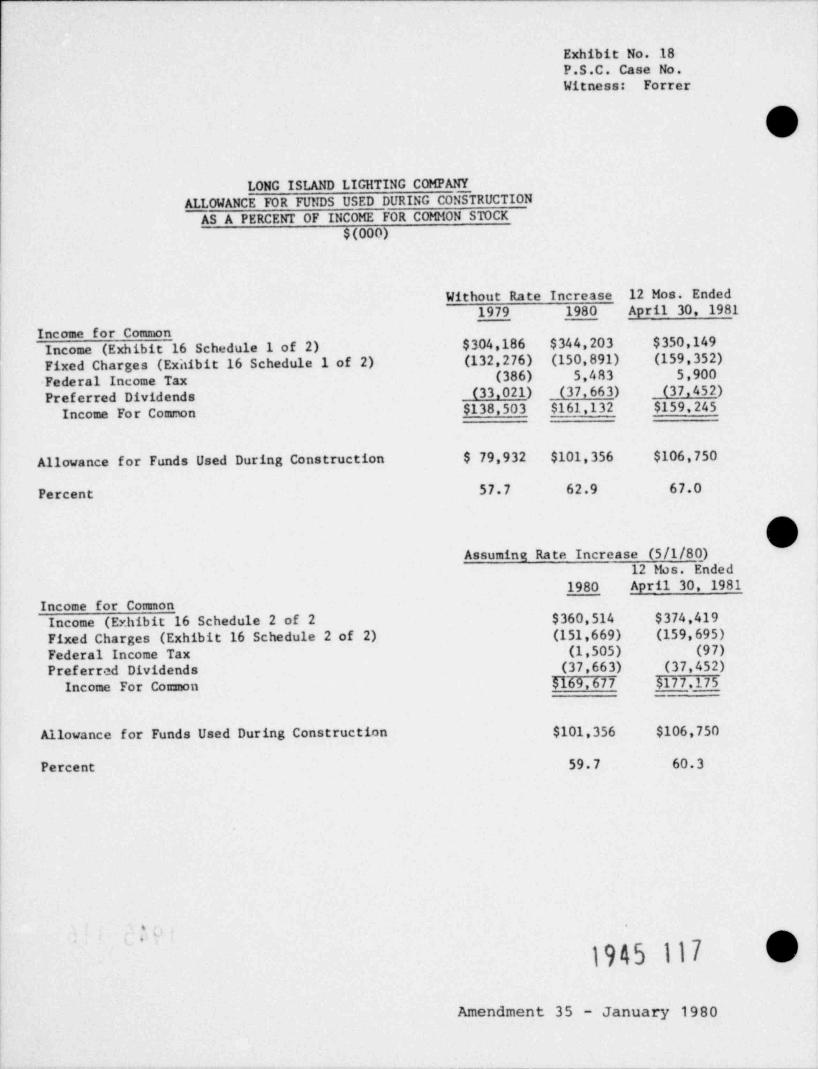

.

~ .

1945 104

RAYMOND J. FORRER

O1 rate relief. Do any of these calculations include bond sales

2 that will take place subseque st to the particular 12 months

3 period?

4 A. No. All calculations include only the annualized interest on

5 all bonds outstanding at the conclusion of the particular 12

6 month period. For example, the coverages for the year 1979

7 do not reflect any interest on bonds to be issued in 1980. If

8 I were to include the interest on the first bond issue in the

9 spring of 1980 in the 1979 calculation, the resultant coverage

10 would be 2.05 times. In Opinion 78-1, the Commission, in

11 establishing rate levels for the Company utilized as its criteria

12 a coverage of 2.3 times for the rate year including the first

13 issue of bonds to be sold after the rate year. It is clear that

14 the Company will not meet this standard at any time. Further-

15 more, the bond indenture coverage throughout the entire period

16 is approximately at the levels which the Commission has con-

17 sidered appropriate for granting interim rate relief. This

18 coverage situation will be exacerbated by the fact that egenses

19 in this presentation are based upon the levels found appropriate

20 by the Commission in the Company's most recent rate decision,

21 Opinion 79-14, issued April 29, 1979 in order to reduce the

22 controversial issues. As Associate Controller, I am familiar

23 with the Company's proposed 1980 budget and I can state that,

24 despite the strictest controls possible, it appears most likely

918 Amendment 35 - January 1980

1945 105. ,

~. .-

'

RAYMOND J. M RRER.

I that actual expenditures for operation and maintenance for the

2 year 1980 and at least the first four months of 1961 will anceed