FAC511S- Supplementary Material(1).pdf - NUST

33

1 Dear Student As you may be aware, NUST has implemented a new curriculum for the 2016 academic year for the Bachelor of Accounting degree. As a result, this has necessitated the revision of the content for Financial Accounting 101. It is in light of this, that I make available the following supplementary material to aid you in your studies. This material has to be used in conjunction with your tutorial letter and the study guide. I wish to emphasise that the study guide is not exhaustive and some of the topics presented therein may not be relevant to the revised curriculum. Where topics are not relevant, or in instances where they have not been updated, this will be pointed out within this tutorial letter and via the COLL communication channels where necessary. Furthermore, you will be required to have access to either the prescribed textbook or any other recommended accounting textbook as per the tutorial letter to ensure that you are successful in this course. I wish you the best of luck for the course. Regards Mr Mahindi

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of FAC511S- Supplementary Material(1).pdf - NUST

1

Dear Student

As you may be aware, NUST has implemented a new curriculum for the 2016 academic year for the

Bachelor of Accounting degree. As a result, this has necessitated the revision of the content for

Financial Accounting 101.

It is in light of this, that I make available the following supplementary material to aid you in your

studies.

This material has to be used in conjunction with your tutorial letter and the study guide.

I wish to emphasise that the study guide is not exhaustive and some of the topics presented therein

may not be relevant to the revised curriculum. Where topics are not relevant, or in instances where

they have not been updated, this will be pointed out within this tutorial letter and via the COLL

communication channels where necessary.

Furthermore, you will be required to have access to either the prescribed textbook or any other

recommended accounting textbook as per the tutorial letter to ensure that you are successful in this

course.

I wish you the best of luck for the course.

Regards

Mr Mahindi

2

Unit 1

• Errors and the Suspense Account Introduction In Financial Accounting 101 you are taught how to prepare a trial balance. You are also taught that the main purpose of the trial balance is to check that there are no errors in the double entry system. The fact that the two sides of a trial balance agreed does not necessarily mean that there are no errors in your entries. It only confirms that double was observed. Accountants are human beings and, as such, they are bound to make errors which may either be detected by a trial balance or not. These errors are classified into two types: errors which affect the trial balance and errors that do not affect the trial balance.

Objectives

Upon completion of this unit you will be able to:

distinguish the different types of errors

discuss errors that do not affect the trial balance

discuss the errors which affect the trial balance

correct the different types of errors using the journal

identify when to use the suspense account or not

adjust profit as given in the accounts after correction of errors

Prescribed reading

Wood, F. & Robinson, S. (2013). Bookkeeping and accounts. (8th ed.). Essex. United Kingdom. Pearson Education.

1. Errors Not Affecting Trial Balance The complete accuracy of your financial records cannot be guaranteed merely by the agreement of a trial balance. The fact that a trial balance is agreeing is only a confirmation that double was observed during the posting of transactions. A number of errors may still have occurred despite this agreement of the trial balance.

In-text question

What kind of errors can accountants and bookkeepers make during the recording of transactions in the books of accounts that will not be identified by drawing up the trial balance?

If you think about entering a wrong amount or entering in a wrong account you are right.

3

Despite their possession of high skills, accountants do make mistakes. It is the occurrence of these errors that will then require the accounting transactions to be corrected through of course the use of the journal. Before I proceed to the corrections, I want us to first identify the individual types of errors and how then they should be corrected.

The correction of any wrong accounting entry requires a clear understanding of accounting principles. For you to be able to effect any adjustment, you need to be able to say what the original entry should have been.

Once that is done the next thing that you need to do is to visual this wrong entry ask and ask yourself how to take it back to what it should have been. The answer to the in-text question is shown on the table.

Reflection

Do you still remember the effects of a debit or a credit on assets, liabilities, expenses and income?

Now let’s look at each error and discuss how they should be processed.

Error of Commssion

Error of Original entry

Error of Complete reversal

Error of principle

Compensating error

Transposition errors

Casting error

Error of Ommission

4

1.1 Error of Principle A principle is a practice that should be observed. The error of principle tells that an accounting rule has been broken. What is this accounting practice? How do you break this practice in accounting? The practice is that, for example, expenses must be debited to expense account while assets must be entered in the assets accounts. In simple terms an error of principle is therefore where a transaction has been entered in the wrong type of account.

This is best explained by example where a motor vehicle expense has been debited to a motor vehicle asset account.

For an example a payment for repairs of a motor vehicle for N$1 500 was debited to motor vehicle asset account.

The effect of such an error is that it would not disturb the agreement of a trial balance because double was observed, unfortunately incorrectly.

Date Details Dr. Cr.

01.07.2013 Motor Vehicle Expenses 1 500

Motor Vehicle Asset Account 1 500

Correction of error: Motor vehicle expenses erroneously charged to motor vehicle asset account

Let’s look at a more detailed example.

Example

On 1 July 2013, Mr Simasiku bought a vacuum cleaner by cash from Game Stores for N$3 500. The bookkeeper entered the transaction as a cleaning expense. Let’s see how you should go about correcting this error.

Solution

The transaction should have been debited to equipment and credited to the cash account. Let us look at the error as it appears in the ledgers and then correct it.

Dr Cleaning expense account Cr

Date Details Folio N$ Date Details Folio N$

01 Jul

Bank CPJ 3 500.00

01

Jul

Error: Equipment acc

c/d

3 500.00

3 500.00 3 500.00

1 Mar Balance b/d 3 500.00

5

Dr Bank expense account Cr

Date Details Folio N$ Date Details Folio N$

01 Jul 2013

Equipment c/d 3 500

Date Details Dr. Cr.

01.07.2013

Equipment 3 500

Cleaning expenses 3 500

Correction of purchase of a vacuum cleaner erroneously charged to cleaning expenses account

Dr Equipment account Cr

Date Details Folio N$ Date Details Folio N$

01 Jul Cleaning CPJ 3 500

• 1.2 Error of Omission The error of omission emanates from a situation whereby a transaction has not been completely entered in the books of accounts. This is very simple error to correct. All you need to do is to pass a journal to record the transaction for the first time. Let’s take, for example, an invoice issued to Mr J P Maliti which was not entered both in the sales account and the sales ledger.

Date Details Dr. Cr.

01.05.2013 J.P. Maliti 33 500

Sales 33 500

Credit invoice to J P Maliti completely omitted from the books

1.3 Error of Commission The error of commission involves a transaction where the amount and double entry are correct. However, the wrong personal account would have been debited or credited. This kind of an error is normally caused by similarities in the names involved. For example a credit invoice for service rendered is charged to S. Mutonguh instead of S. Mukhalabai Mutonga for say N$666.

Date Details Dr. Cr.

01.05.2013 S. Mukhalabai Mutonga 666

S. Mutonguh 666

6

Credit invoice to S. Mukhalabai Mutonga incorrectly charged to S. Mutonguh

This type of an error only involves correction of one leg of the transaction. The other leg of the transaction i.e. the credit to sales account is not adjusted.

1.4 Error of Original Entry This is very common since it the use of wrong amounts that what is on the original document. Normally this error involves using the correct digits as in the correct amount but somehow the digits are extended or the separation of dollars and cents is done wrong. Take for an example an amount of N$45.68 may be written or captured as N$456.80. In other cases a completely wrong figure is used.

What you need to remember with this kind of an accounting error is that it involves the use of correct accounts but the mistake involves a wrong figure being posted to the accounts. It therefore requires that the difference between the correct amount and the wrong amount must be calculated in order to complete the adjustments.

Let us suppose that an audit firm issued an invoice to its client for an amount of N$65 890.00 but then the bookkeeper captured the invoice amount as N$6 589.00. Now how do I correct this error within the firm’s records of accounting?

The first step is to determine the difference between the two figures.

Diff = N$65 890.00 – 6 589.00 = N$59 301.

The effect is this kind of an error will normally be an overstatement or understatement. Our journal correction would therefore be:

Date Details Dr. Cr.

01.05.2013 Accounts Receivable 59 301

Audit Fee Income 59 301

Being correction of an understatement on invoice number 3025A

1.5 Complete Reversal of Entries As the name of the error indicates, this type of error is a complete reversal of the double entry involved, with the double in reverse of what it should be on particular accounts. In simple terms, ‘correct amounts’ and ‘correct accounts’ have been used but then the amounts would be shown on the wrong side of the accounts.

That is to say where an account is supposed to have been debited, it has been credited by mistake.

Assume a cash discount has been received for N$152. The accounts clerk entered the transactions as a debit in the discount allowed account as well as a credit entry in the accounts payable.

7

Date Details Dr Cr.

01.05.2013 Accounts payable 152

Discount alloId 152

Error correction: Discount incorrectly debited to discount received account

It is very important to be able identify the accounts that need to corrected. From the given information you should be able to identify what kind of an error is involved and what the accounts that should be debited or credited.

Furthermore, you will realize where the errors do not affect the totals of the trial balance; you need to use the suspense account. This will be our next section.

1.6 Compensating Errors Compensating errors involve unrelated accounts having the same amount as an error. For example sales were over cast by N$120 while at the same Property, plant and equipment was also over casted by N$120. The adjustment would be restricted to the two accounts.

Date Details Dr Cr.

Sales 120

Property, plant and equipment 120

Correction of compensating error

1.7 Error of Transposition This error involves the wrong sequence of an amount. For example an amount of N$563.00 may be entered in the books as N$356.00. If such an error is detected the correction involves the difference between the correct amount and the wrong amount. In this case it will 563- 356 = 207.

Do the following activity to test your understanding on correcting of errors.

Activity

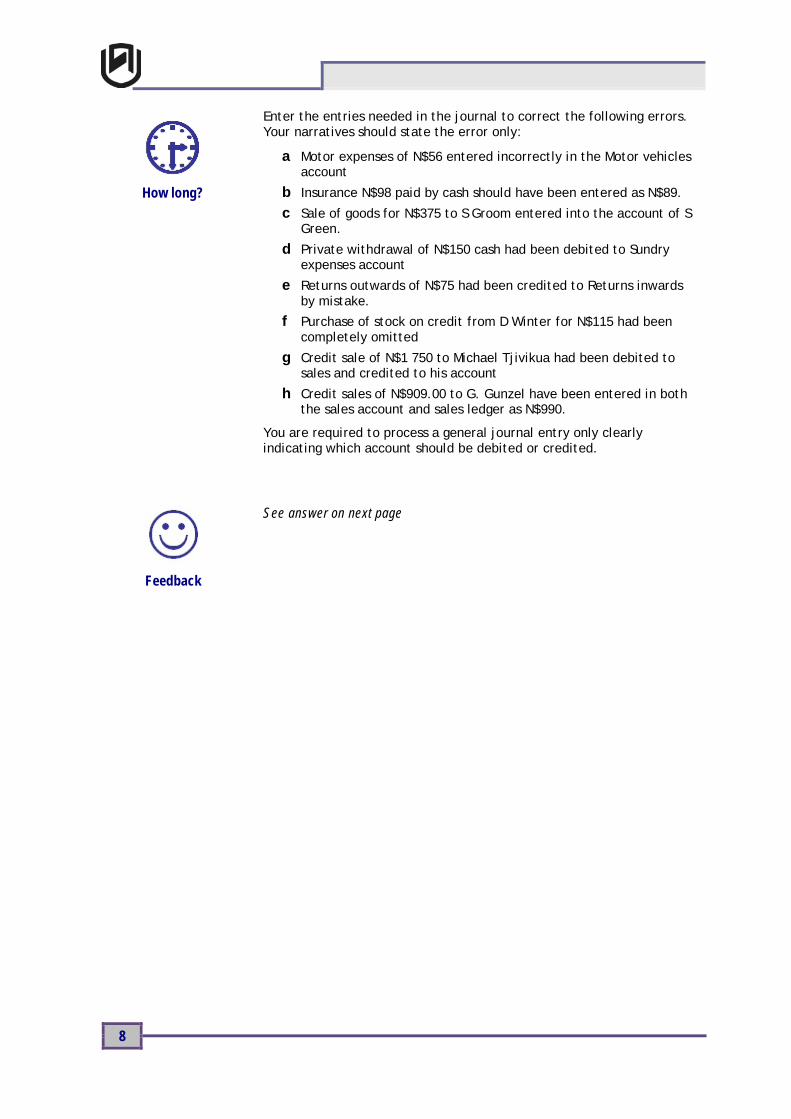

Activity 1

Time Required: You should take about 10 minutes to complete this activity.

8

How long?

Enter the entries needed in the journal to correct the following errors. Your narratives should state the error only:

a Motor expenses of N$56 entered incorrectly in the Motor vehicles account

b Insurance N$98 paid by cash should have been entered as N$89.

c Sale of goods for N$375 to S Groom entered into the account of S Green.

d Private withdrawal of N$150 cash had been debited to Sundry expenses account

e Returns outwards of N$75 had been credited to Returns inwards by mistake.

f Purchase of stock on credit from D Winter for N$115 had been completely omitted

g Credit sale of N$1 750 to Michael Tjivikua had been debited to sales and credited to his account

h Credit sales of N$909.00 to G. Gunzel have been entered in both the sales account and sales ledger as N$990.

You are required to process a general journal entry only clearly indicating which account should be debited or credited.

Feedback

See answer on next page

9

General Journal Dr Cr Motor vehicle expenses Motor Vehicles account Error of principle

56

56

Cash Insurance Error of original entry or transposition

9

9

S. Green S. Groom Error of commission

375

375

Drawings Sundry expenses Error of principle

150

150

Returns Inwards Returns outwards Error of principle

75

75

Purchases D. Winter Error of omission

115

115

Michael Tjivikua Sales account Complete reversal of entries

3 500

3 500

Sales G Gunzel Error of original entry or transposition

81

81

From the above, I hope you realized that the second last error had to be doubled up. This is how you do an error of complete reversal.

Specific errors can be corrected as follows:

Error of omission: the correct debit and credit entries must be made.

Compensating error: by adjusting the entries e.g. Reverse the overstatement

Error of principle: transferring the amount to the correct account

Error of commission: by transferring the amount to the correct account

Error of original Entry: by adjusting the entry i.e. either increase the understatement or reduce the overstatement

Complete reversal of entries: This is sometimes what more difficult to adjust. First must come the amount needed to cancel the error, and then comes the actual entry: because of this ,the correct entry is double the actual amount first recorded

2. Errors Affecting the Trial balance In the previous section, we’ve discussed accounting errors which did not affect the totals of a trial balance. However, the accounting world is not that simple. There are a number of complex errors that may require even an experienced financial accountant to take a pause and try to

10

figure out what could have gone wrong and what should done in order to correct the situations.

In-text question

What do you think may cause a trial balance not to agree?

Whenever, errors happen in accounting, the first approach is to identify the source of the error and then locate the error. The next action is the correction of the identified errors. However, the errors on a trial total may not be due to a single accounting mistake, but rather it may be as a result of several accounting mistakes that may have taken place at different times and for different amounts throughout the reporting period. It will therefore be your responsibility as an accountant to track and correct them.

Now that I have already dealt with the others I am going to deal with those that will involve the use of the suspense account.

2.1 Use of the Suspense The suspense account has two major purposes in accounting. The first is the use as a contra account when dealing with opening balances.

The second and most popular usage is that of correcting errors which normally involve a single entry. These errors involve situations in which double entry has not been observed.

Sometimes suspense account balance is not cleared by the time of preparing financial statements at the end of the year. The question that arises is how do I treat the balance? No clear guidance is given as result the treatment differs firm to firm. Some advocate that if the balance is debit it should be treated as current asset while others argue that it should be written off as expense in the statement of comprehensive income to be in line with prudence principle. If I take the latter, then credit balance should be accounted as a current liability as crediting it to profit will be in conflict with prudence principle as profit will be overstated.

Example

Assume that after preparing a trial balance there was a difference of N$2 264 on the debit side as indicated below. After some investigations it was then discovered that a credit invoice on the purchase of equipment was only credited to the supplier and no entry was made in any other account.

11

Trial Balance as at 31 December 2012 Dr Cr

Motor vehicle expenses 156

Bank 900

S. Groom 375

Drawings 150

Returns Inwards

Returns outwards

75

705

Purchases

D. Winter

1 150

115

Sales account 3 500

Suspense account 2 264

Totals 4 695 4 695

The debit side of this trial balance did not agree with the credit side by an amount of N$2 264. The balance has to be taken to the debit side of the suspense account.

Dr Suspense account Cr

Date Details Folio N$ Date Details Folio N$

31.12.12 Balance b/d 2 264 31.12.12 Plant 2 264

In terms of good accounting practices, the suspense account must be cleared at the end of each reporting period. By clearance I mean that it must be brought to a nil balance. All error posted to the suspense account must be investigated and resolved by year end. There should be no carry overs of the suspense account balances.

12

Dr Plant account Cr

Date Details Folio N$ Date Details Folio N$

31.12.12 Suspense account

2 264 31.12.12 Balance c/d 2 264

In examinations and tests you may not only be asked to correct the errors but you may frequently be required to journal entries. Now let us look at the above transaction in terms of journal entry.

General Journal of T. BrekI Dr Cr

Plant

Suspense account

2 264

2 264

Plant bought on credit not debited to Plant account but was correctly credited to James Distributers

Reflection

When do you use the suspense account and how is the suspense amount in the trial balance treated in suspense account T – Account?

We just looked at an example of error that involves a suspense account. Now let’s look at another example that involves a number of errors which affect the agreement of a trial balance.

Activity

Activity 2

Time Required: You should take about 5 minutes to complete this activity.

The trial balance of Xaco CC as at 31 December 2012 showed a difference which was posted to a suspense account. Draft financial statements for the year ended 31 December 2012 are prepared showing a net profit of N$47,240. The following errors are subsequently discovered:

Sales of N$450 to T Thomasy had been debited to Thomassony manufacturing Ltd.

A payment of N$275 for telephone charges had been entered on the debit side of the telephone account as N$375.

The sales had been undercast by N$2,000.

Repairs to a machine, amounting to N$390 had been charged to machinery account.

A cheque for N$1,500 being rent received from Atlas Ltd, had only been entered in the cash book.

How long?

13

Purchases from P. Brooks , amounting to N$765, had been received on 31 December 2000 and included in the closing stock inventory at that date, but the invoice had not been entered in the purchases journal

Required Identify the type of errors in the above transactions.

Feedback

Transaction Type of an error

Sales of N$450 to T Thomasy had been debited to Thomassony manufacturing Ltd.

Error of commission

A payment of N$275 for telephone charges had been entered on the debit side of the telephone account as N$375

Error of original entry

The sales had been under cast by N$2,000.

Casting error

Repairs to a machine, amounting to N$390 had been charged to machinery account.

Error of principle

A cheque for N$1,500 being rent received from Atlas Ltd, had only been entered in the cash book.

Posting Error

Purchases from P. Brooks , amounting to N$765, had been received on 31 December 2012 and included in the closing stock inventory at that date, but the invoice had not been entered in the purchases journal

Posting error

2.2 The Effect of Errors on Profits Some of the errors will have meant that the original profits calculated will be wrong. If the error is in one of the figures shown in the Profit or loss Statement, then the original profit will need altering.

14

Example 3

The bookkeeper of Chayos CC has extracted a trial balance on 31 March 2013 which failed to agree by N$60, a shortage on the credit side of the trial balance. A suspense account was opened for the difference.

In April 2013 the following errors made in the previous financial year Ire found:

Sales had been overcast by N$70

Insurance had been under cast by N$40

Cash received from a debtor of N$50 had been entered in the cash book only.

A purchase of N$59 had been entered in the books, debit and credit entries as N$95

Required: If the net profit had previously been calculated at N$1,600 for the year ended 31 March 2013, show the calculations of the corrected net profit.

Solution

Profit as per accounts 1,600

Add: Purchase overcast 36

1,636

Less : Sales over cast 70

Insurance under cast 40 (110)

Adjusted Profit 1,536

The approach is to look at those items which affect the profit or loss figure.

Activity

Activity 3

Time Required: You should take about 20 minutes to complete this activity.

The bookkeeping system of Turner is not computerised, and at 30 September 20X8 the bookkeeper was unable to balance the accounts. The trial balance totals are:

Debit $1,796,100 Credit $1,852,817

Nevertheless, he proceeded to prepare draft financial statements, inserting the difference as a balancing figure in the balance sheet. The draft profit and loss account showed a profit of $141,280 for the year ended 30 September 20X8.

How long?

15

He then opened a suspense account for the difference and began to check through the accounting records to find the difference. He found the following errors and omissions:

1 $8,980 - the total of the sales returns book for September 20X8 had been credited to the purchases returns account.

2 $49,600 paid for an item of plant purchased on 1 April 20X8 had been debited to plant repairs account. The entity depreciates its plant at 20% per annum on a straight line basis, with proportional depreciation in the year of purchase.

3 The cash discount totals for the month of September 20X8 had not been posted to the general ledger accounts. The figures are: Discount allowed $836 Discount received $919

4 $580 insurance prepaid at 30 September 20X7 had not been brought down as an opening balance

5 The balance of $38,260 on the telephone expense account had been omitted from the trial balance

6 A car held as a non-current asset had been sold during the year for $4,800. The proceeds of sale is entered in the cash book but had been credited to the sales account in the general ledger. The original cost of the car $12,000, and the accumulated depreciation to date $8,000, Ire included in the motor vehicles account and the accumulated depreciation account. The entity depreciates motor vehicles at 25% per annum on a straight line basis with proportionate depreciation in the year of purchase but none in the year of sale.

Required: a Draw up a statement showing the revised profit after correcting

the above errors.

b Open a suspense account for the difference between the trial balance totals. Prepare the journal entries necessary to correct the errors and eliminate the balance on the suspense account. Narratives are not required. [ADAPTED ACCA]

16

Feedback

See answer below

Profit before correction Plant Reduction in repairs

141,280.00 49,600.00

Returns 8980 x 2 Depreciation 6/12*20% *49600

17 960.00 4,960.00

Discount Allowed 836.00

Discount Received 919.00

Insurance - Opening Balance 580.00

Telephone 38,260.00

Profit on disposal of non-current asset 800.00

Disposal Proceeds - taken out of sales 4,800.00

192,599.00

67,396.00

Adjusted Profit (Loss) for the year 125,203.00

Dr Suspense account Cr

Date Details Folio N$ Date Details Folio N$

Balance b/d 56 717 Sales returns 8 980

Discount received 919 Purchases returns 8 980

Telephone acc 38 260

Discount allowed 836

Insurance 580

57 636 57 636

References

Wood, F & Robinson, S. (2013). Bookkeeping and Accounts (8th ed.). England: Pearson Education.

Wood, F. & Sangster, A. (2012). Entity Accounting (12th ed.). England: Pearson Education.

17

Keywords/Concepts

Compensating errors:

Where two errors in different accounts on different sides cancel out each other.

Complete reversal of entries:

An error where the correct amounts are posted in the correct accounts but on the wrong side of accounts

Error of commission:

An error where a correct amount is posted to a wrong personal account but observing the double entry principle

Error of omission: An error where a transaction is completely left out of the accounts.

Error of original entry:

An error where the original amount is not properly written in the books

Error of principle: An error where a correct amount is posted in the wrong type of account.

Suspense account: A special account that is used for opening balances as Ill a contra account when those errors where a single side of a transaction was not undertaken.

Transposition errors:

An error where the digits in the amount are entered in the wrong sequence.

Unit Summary

Summary

In this unit you’ve learned how to identify errors in accounting as well as how to carry out journal entries to correct those errors. You have also learned to correct a given profit figure after correcting the errors.

When dealing with errors in accounting it’s very important that you will always remember that it is the double entry principle that matters most. At the end of it you also need to recognize the effect of an error and your corrections on the accounting equation.

You will notice that it’s not always the case that all error will affect the profit. Some errors will have an indirect effect on the profit. For example where the error concerns non-current asset. Such an error will affect the amount of depreciation. Lastly, we discussed the effect of correcting any entry that affects an expense account is normally to increase or reduce an expense accounts.

Error! No text of specified style in document. Error! No text of specified style

18

Unit 4

Disposal of Non-Current Assets Introduction In this unit we’ll work through the process of derecognising or removing an item of property, plant and equipment from the books of the company. We’ll discuss the procedure of preparing the relevant journal that are required when an item of property, plant and equipment is being record and the various ways of a company may use to dispose its non-current assets.

Objectives

Upon completion of this unit you should be able to:

recognise a transaction involving a disposal of non-current asset

pass journal entries that are necessary to record the disposal transactions

calculate profit or loss on sale of non-current assets

present the gain or loss in the statement of profit and loss

Prescribed reading

Watson, A. & Kew, J. (2012). Financial Accounting An Introduction (4th ed.).Cape Town. Oxford University Press.

Wood, F & Robinson, S. (2010). Bookkeeping and Accounts (7th ed.). United Kingdom. Pearson Education.

Additional reading

Wood, F & Sangster, A. (2012). Entity Accounting (12th ed.). United Kingdom: Pearson Education.

1. De-recognition of Property, Plant and Equipment (IAS 16)

Before I deal with the mechanics of derecognition or disposal of non-current I would like to take you through the International Accounting Standard number 16.

Reflection

From your earlier studies in Financial Accounting 101 do you remember what IAS16 deals with?

Error! No text of specified style in document. Error! No text of specified style

19

The carrying amount of an item of property, plant and equipment shall be derecognised: On disposal or:

When no economic benefits are expected from its use or disposal.

The gain or loss arising from the derecognition of an item of property, plant and equipment shall be included in the profit or loss when the item is derecognised (unless IAS 17 requires on a sale or leaseback). Gains shall not be classified as revenue.

Gains on sale of non-current assets reported as other incomes while losses on sale of non-current assets are disclosed as losses in the period they occur.

However, an entity that, in the course of its ordinary activities, routinely sells items of property, plant and equipment that it has held for rental to others shall transfer such assets to inventories at their carrying amount when they cease to be rented and become held for sale.

The proceeds from the sale of such assets shall be recognised as revenue in accordance with IAS 18 Revenue. IFRS 5 does not apply when assets that are held for sale in the ordinary course of the entity are transferred to inventories.

The disposal of an item of property, plant and equipment may occur in a variety of ways (e.g. by sale, by entering into a finance lease or by donation). In determining the date of disposal of an item, an entity applies the criteria in IAS 18 for recognizing revenue from the sale of goods.

If, under the recognition principle in paragraph 7 of IAS 16, an entity recognizes in the carrying amount of an item of property, plant and equipment the cost of replacement of part of the item, then it derecognizes the amount of the replaced part regardless of whether the part had been depreciated separately. If it is not practicable for an entity to determine the carrying amount of the replace part, it may use the cost of replacement as an indication of what the cost of the replacement was at the time it was acquired or constructed.

The gain or loss arising from derecognition of an item of property, plant and equipment shall be determined as the difference between the net disposal proceeds, if any, and the carrying amount of the item.

The consideration receivable on disposal of an item of property, plant and equipment is recognized initially at its fair value. If payment for the item is deferred, the consideration received is recognized initially at the cash price equivalent. The difference between the nominal amount of the consideration and the cash price equivalent is recognized as interest revenue in accordance with IAS 18 reflecting the effective yield on the receivable.

2. Disposal of Property, Plant and Equipment There are times that an entity may voluntarily decide not to hold a non-current asset for its entire life for various reasons. The company may drop a product from its line and no longer need the equipment that was used to produce it, or managers may want to replace the machine with a more efficient one. The disposals include sales, trade-ins and retirements. When Air Namibia disposes of any old aircraft, the company may sell it to a cargo airline or regional airline. A entity may

Error! No text of specified style in document. Error! No text of specified style

20

dispose of an asset involuntarily, as the result of a casualty such as a storm, fire or accident.

Disposals of non-current assets seldom occur on the last day of the accounting period. Therefore, depreciation must be recorded to the date of disposal. The disposal of a depreciable asset usually requires two journal entries.

1 An adjusting entry to update the depreciation expense and accumulated depreciation accounts.

2 An entry to record the disposal. The cost of the asset and any accumulated depreciation at the date of disposal must be removed from the accounts. The difference between any resources received on disposal of an asset and its book value at the date of disposal is treated as a gain or loss on the disposal of the asset. This gain or loss is recorded in the Profit or loss Statement. It is not an operating revenue or expense, however, because it arises from peripheral or incidental activities rather than central operations. Gains and losses from disposal are usually shown as a separate item on the Profit or loss Statement.

Example 1

Assume that the end of year 17, Zambezia Airlines sold an aircraft that was no longer needed because of the elimination of services to a small city. The craft was sold for N$11 million cash. The original cost of the flight equipment of N$30 million was depreciated using the straight line method over 25 years with no residual value (N$1.2 million expense per year). The last accounting for depreciation was at the end of year 16; thus depreciation expense must be recorded for year 17. The computations are:

Original cost of aircraft N$30,000,000

Less: Accumulated depreciation

($1,200,000 × 17 years)

N$20,400,000

Book value at date of sale N$ 9,600,000

Cash N$11,000,000

Gain on sale of aircraft N$ 1,400,000

The above calculations show the very basic way of determining profit on sale of non-current assets.

A journal entry will be required to remove the cost and accumulated depreciation of the aircraft from the books of the company. The other journal would involve the recording of the proceeds of the sale.

Error! No text of specified style in document. Error! No text of specified style

21

Example

Journal entry

Details Dr Cr

Asset Disposal (or PPE disposal) 30,000,000

PPE (Aircraft account) 30,000,000

Bank / Cash 11,000,000

Asset Disposal 11,000,000

Aircraft – Accumulated depreciation 20,400,000

Asset Disposal 20,400,000

Asset disposal 1 400 000

Profit and loss 1 400 000

Having looked at the very basic journals that should be posted, let us also look at a basic disposal T- Account using the same information.

Dr Aircraft Disposal Account CR

N$ N$

Aircraft account 30,000,000 Aircraft Accum depreciation

20,400,000

Profit and Loss 1,400,000 Bank (proceeds) 11,000,000

31,400,000 31,400,000

The T- account is based on straight forward transaction. However, in some cases the proceeds may involve an insurance refund, staff debtors, trade in or part exchange.

2.1 Depreciation Calculation Questions dealing with disposals may require that you calculate depreciation from the day that the non-current was recognised by the entity. This may involve different methods of calculating depreciation in order to work out the accumulated depreciation to date. In some cases you may need to calculate depreciation up to the date of disposal. It will also important for you to check the depreciation policy of the entity.

Error! No text of specified style in document. Error! No text of specified style

22

The only thing that you need to master is the methods of depreciation and that it does not change the way depreciation is treated in the books of accounts. In this unit therefore calculation of depreciation using the various methods it is as assumed knowledge.

Reflection

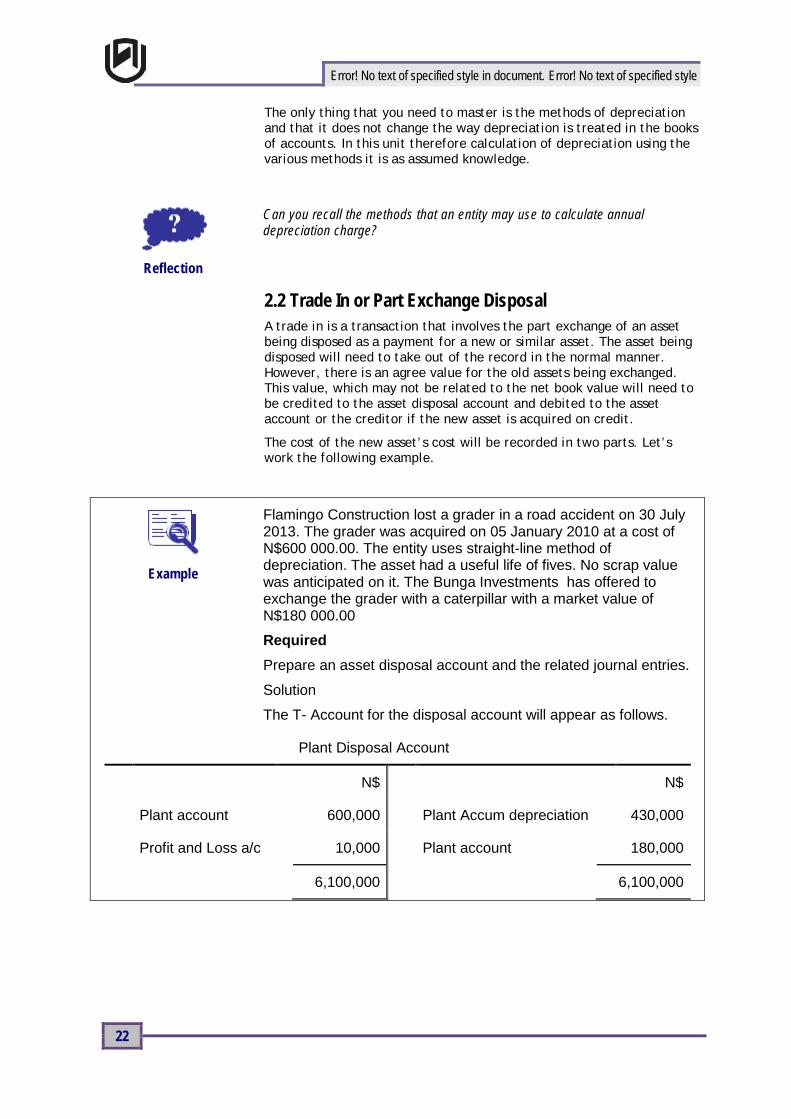

Can you recall the methods that an entity may use to calculate annual depreciation charge?

2.2 Trade In or Part Exchange Disposal A trade in is a transaction that involves the part exchange of an asset being disposed as a payment for a new or similar asset. The asset being disposed will need to take out of the record in the normal manner. However, there is an agree value for the old assets being exchanged. This value, which may not be related to the net book value will need to be credited to the asset disposal account and debited to the asset account or the creditor if the new asset is acquired on credit.

The cost of the new asset’s cost will be recorded in two parts. Let’s work the following example.

Example

Flamingo Construction lost a grader in a road accident on 30 July 2013. The grader was acquired on 05 January 2010 at a cost of N$600 000.00. The entity uses straight-line method of depreciation. The asset had a useful life of fives. No scrap value was anticipated on it. The Bunga Investments has offered to exchange the grader with a caterpillar with a market value of N$180 000.00

Required Prepare an asset disposal account and the related journal entries.

Solution

The T- Account for the disposal account will appear as follows.

Plant Disposal Account

N$ N$

Plant account 600,000 Plant Accum depreciation 430,000

Profit and Loss a/c 10,000 Plant account 180,000

6,100,000 6,100,000

Error! No text of specified style in document. Error! No text of specified style

23

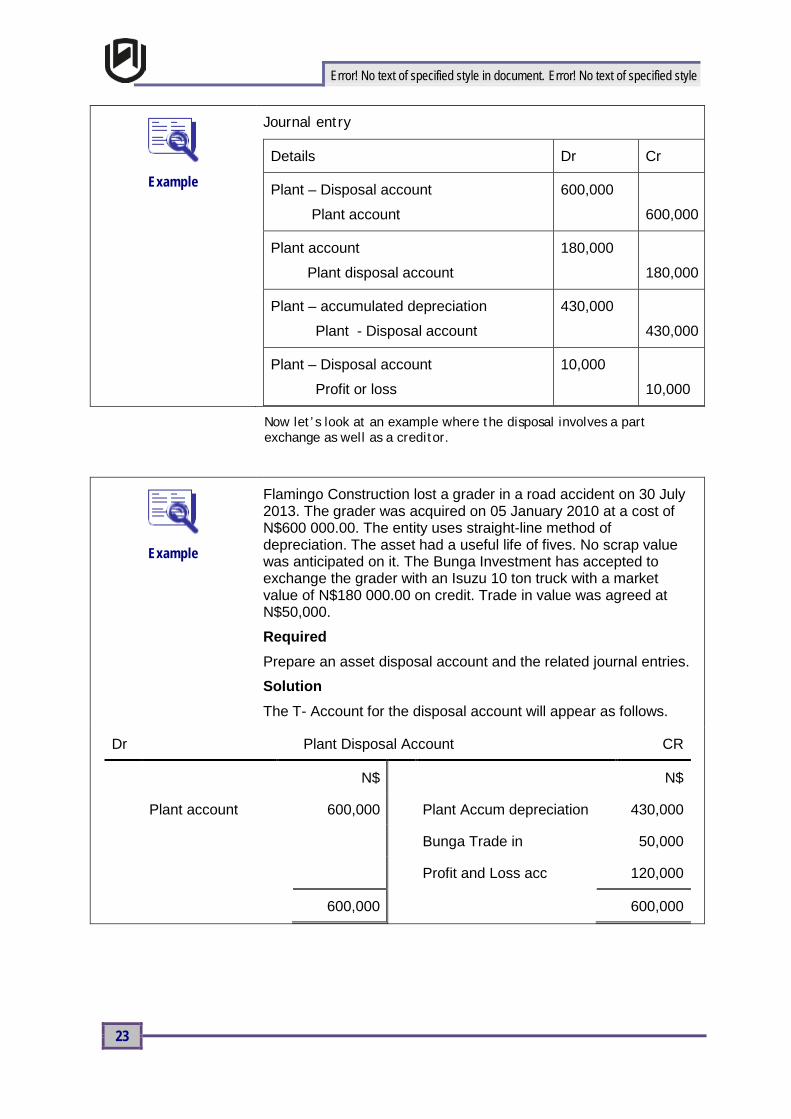

Example

Journal entry

Details Dr Cr

Plant – Disposal account

Plant account

600,000

600,000

Plant account

Plant disposal account

180,000

180,000

Plant – accumulated depreciation

Plant - Disposal account

430,000

430,000

Plant – Disposal account

Profit or loss

10,000

10,000

Now let’s look at an example where the disposal involves a part exchange as well as a creditor.

Example

Flamingo Construction lost a grader in a road accident on 30 July 2013. The grader was acquired on 05 January 2010 at a cost of N$600 000.00. The entity uses straight-line method of depreciation. The asset had a useful life of fives. No scrap value was anticipated on it. The Bunga Investment has accepted to exchange the grader with an Isuzu 10 ton truck with a market value of N$180 000.00 on credit. Trade in value was agreed at N$50,000.

Required Prepare an asset disposal account and the related journal entries.

Solution The T- Account for the disposal account will appear as follows.

Dr Plant Disposal Account CR

N$ N$

Plant account 600,000 Plant Accum depreciation 430,000

Bunga Trade in 50,000

Profit and Loss acc 120,000

600,000 600,000

Error! No text of specified style in document. Error! No text of specified style

24

Dr Bunga Investments cc CR

N$ N$

Plant disposal account

50,000 Plant account 180,000

Balance b/d 130,000

180,000 180,000

Dr Plant Equipment CR

N$ N$

Balance b/d 600,000 Plant disposal account 600,000

Bunga Investments

180,000

General Journal of Bunga Investments cc

Details Dr Cr

Plant – Disposal account

Plant account

600,000

600,000

Plant account

Bunga Investments cc

180,000

180,000

Plant – accumulated depreciation

Plant - Disposal account

430,000

430,000

Profit or loss

Plant – Disposal account

120,000

120,000

Bunga Investments cc

Plant – Disposal account

50 000

50 000

2.3 Disposals Involving Insurance Compensation This normally involves a refund from an insurance company and the item is taken out of service completely. This is normally very common with equipment and motor vehicles. The normal procedure of dealing with a disposal account would need to be followed.

The cost and the accumulated would need to be moved to the asset disposal account. Proceeds from the insurance are normally of two

Error! No text of specified style in document. Error! No text of specified style

25

types. The first is where the insurance gives the entity cash in lieu of the asset. The second scenario is where the insurance company replaces the asset completely.

Example

Flamingo Construction lost a grader in a road accident on 30 July 2013. The grader was acquired on 05 January 2010 at a cost of N$600 000.00. The entity uses straight-line method of depreciation. The asset had a useful life of fives. No scrap value was anticipated on it. The insurance has offered to settle the claim in full by a bank transfer of N$450 000.00.

Required Prepare an asset disposal account

Solution The T- Account for the disposal account will appear as follows.

Dr

Plant Disposal Account CR

N$ N$

Plant account 600,000 Plant Accum depreciation 430,000

Profit and Loss a/c 280,000 Bank insurance 450,000

880,000 880,000

Journal entry

Details Dr Cr

Plant – Disposal account

Plant account

600,000

600,000

Bank

Plant disposal account

450,000

450,000

Plant – accumulated depreciation

Plant - Disposal account

430,000

430,000

Plant – Disposal account

Profit or loss

280,000

280,000

Error! No text of specified style in document. Error! No text of specified style

26

The transaction resulted in a profit on disposal. The profit of N$280,000 will be recorded in the profit or loss statement as other incomes. Now that the asset has been taken out of the books, the cost and accumulated depreciation will also be removed from the statement of financial position.

If the credit side of the disposal account is greater than the debit, then is a profit on the sale or writing off of the assets.

Now do the following activity to test your understanding.

Activity

Activity 1 Time Required: You should take about 15 minutes to complete this activity.

Flamingo Construction lost a grader in a road accident on 30 July 2013. The grader was acquired on 05 January 2010 at a cost of N$600 000.00. The entity uses straight-line method of depreciation. The asset had a useful life of five years. No scrap value was anticipated on it. The insurance has offered to settle the claim in full by a replacing the grader with a fairly new grader previously owned by Pupup Road Makers cc with a market value of N$130,000.00 and an original cost N$230,000.00.

Required: Prepare an asset disposal account and the related journal entries.

How long?

Feedback

The T- Account for the disposal account will appear as follows.

Error! No text of specified style in document. Error! No text of specified style

27

Dr Plant Disposal Account CR

N$ N$

Plant account 600,000 Plant Accum depreciation 430,000

Plant insurance 130,000

Profit and Loss Acc 40,000

600,000 600,000

General Journal of Flamingo

Details Dr Cr

Plant – Disposal account

Plant account

600,000

600,000

Plant account

Plant disposal account

130,000

130,000

Plant – accumulated depreciation

Plant - Disposal account

430,000

430,000

Profit or loss

Plant – Disposal account

40,000

40,000

The transaction resulted in a loss on disposal. The loss of N$40,000 will be recorded in the profit or loss statement as an expense.

Now that the asset has been taken out of the books, the cost and accumulated depreciation will also be removed from the statement of financial position.

If the debit side of the disposal account is greater than the credit, then is a loss on the sale or writing off of the assets concerned.

I hope you have noticed that depreciation was calculated up to the date of disposal. It is therefore very important that you pay attention to dates especially if the depreciation policy is not given. Where specific dates are given your accumulated depreciation will be calculated on proportional basis.

Now try the following activity on your own and then compare your answer with the feedback given.

Error! No text of specified style in document. Error! No text of specified style

28

Activity

Activity 2

Time Required: You should take about 20 minutes to complete this activity.

Chineke enterprise, with financial year ending 30 June, has the following details relating to its non-current assets:

Transactions and events: 3 On 01 July 2009 bought two motor vehicles (registration no. Alfred

NA and N 57 W) at a cost of N$120 000 each, for use in its operation

4 On the same date it bought machinery at cost of N$250 000 excluding installation cost of N$25 000.

5 On 31 August 2009 bought office equipment (computers and printer/copier machine) at the total cost of N$80 000. Seventy percent of the total cost represents computers.

6 On 25 June 2011 Alfred NA overturned between Okahandja and Otjiwarongo and it was completely written off without any salvage value with 62500 km on odometer. The odometer on 30 June 2010 was 30 000km.

7 A computer which had cost N$15000 was traded in with a computer costing N$30 000 on 31 March 2011 with agreed trade in value of N$9 000. Still on the same date a printer/copier machine was sold to one of its employees for N$19 000. The proceeds are used buy a new printer/copier/fax machine on 01 April 2011 from Local computer supplier costing N$40 000 with the remaining balance to be settled over two months.

Accounting policy All assets are depreciated on straight line over their useful life

except for motor vehicles which are depreciated at units method

Computers have useful life of four years with no scrap value and printer/copier has useful life of seven years with scrap value of N$3000.

Machinery is expected to be used over 10 years with disposal value of N$25 000.

Motor vehicles are expected to travel for 200 000 kilometres each before they be sold for scrap at N$10 000 each.

Required: 8 Prepare journal entries to account for depreciation expenses for

disposed assets for the year ending 30 June 2011. Ignore closing entries

9 Prepare journal entries to derecognize assets disposed.

How long?

Error! No text of specified style in document. Error! No text of specified style

29

Feedback

See feedback below.

1

Disposal 120 000

Motor vehicles 120 000

Transfer of MV (Alfred NA) at cost to disposal account

2

Accumulated depreciation – Motor Vehicles (W4) 34 375

Disposal 34 375

Write off of accumulated depreciation of motor vehicle Alfred NA

OR 1 & 2 could be done as follows, in accordance with IAS 16 par 67 & 68

1 Accumulated depreciation- MVs (W4) 34 375

Motor vehicles 34 375

2 Disposal 85 625

Motor vehicles (carrying amount = BV) 85 625

3

Profit or loss IAS 16.68 (120000-34375) 85 625

Disposal 85 625

Loss on write of motor vehicle Alfred NA due to accident

4 Disposal 15 000

Office equipment 15 000

5

Accumulated depreciation – Office Equip (W5) 5 938

Disposal 5 938

6

Office equipment 30 000

Disposal 9 000

Creditors 21 000

Trade in of old computer for new

7 Profit or loss IAS 16.68 (15 000 – 5 938– 9000) 62

Disposal 62

Loss on disposal of computer

Error! No text of specified style in document. Error! No text of specified style

30

8 Disposal 24 000

Office equipment 24 000

9 Accumulated depreciation – Office Equip (W6) 4 750

Disposal 4 750

10 Bank (or Loan to employees) 19 000

Disposal 19 000

11 Profit or loss IAS 16.68 (24 000 – 4750 – 19000) 250

Disposal 250

We have covered all the transactions involved in derecognition of a non-currentasset. The above are not really exhaustive. What is more important is for you to remember the entry principles that should be observed in any scenario.

For example an asset may be sold to an employee on credit. All other accounts will remain only you need is to replace bank in the above with a staff debtor.

Work through the following assessment activities. I would like you to do the activities before you look at the answer.

Error! No text of specified style in document. Error! No text of specified style

31

Assessment

Activity 3 Time Required: You should take about 20 minutes to complete this activity.

Britney Spears' accounting year-end is on 31 December. On 31 December 2009 her business had the following balances:

N$

Motor vehicles 180 000 (15% VAT included)

Motor vehicles are depreciated using the straight-line method at a rate of 20 percent per annum and using the proportionate method of calculating the depreciation charge.

The following transactions occurred during 2010:

On 31 March, the business traded-in car A in part exchange for another car. The trade in amount on the car A was N$37 500 and the balance of N$82 500 was paid by cheque for the new car (car Z). Car A was originally bought on 1 April 2008 for N$100,000 (at cost).

On 1 May, the business purchased a van for N$75 000.

On 30 September, the business sold vehicle B for N$51 000. It was originally bought on 30 June 2008 for N$80 000 (at cost).

Required

10 Show the general journal entries relating to the purchase of the motor vehicles, depreciation expense and provision for depreciation and disposal accounts for 2010.

11 Show the non-current asset extract for the year ending 2010.

All the amounts are inclusive of 15% VAT. The VAT paid on the purchase of the motor vehicles is claimable from the Receiver of Revenue

Error! No text of specified style in document. Error! No text of specified style

32

Assessment

Activity 4 Time Required: You should take about 20 minutes to complete this activity.

Swakop Airlines has a financial year that ends on 30 June. The company had the following details relating to its non-current assets: Transactions and events: On 05 September 2008, Swakop Airlines acquired two helicopters (registration no. NA896 and NA777). The assets Ire acquired at N$1 300 000 and N$1 700 000 respectively for use in its operations in the tourism industry.

On 25 January 2012 helicopter NA896 had a rough landing in Katima Mulilo resulting in extensive damage to it. The helicopter was written off without any salvage value.

However, the company had an insurance policy cover for all its assets. On 15 June 2012, a cheque for N$1 050 555 was received from Sanlam Namibia as a compensation for the damaged aircraft. However, one quarter of this amount was meant to cover claims from third parties.

The company had an insurance policy cover for all its assets. On 15 June 2012, a cheque for N$1 050 555 was received from Sanlam Namibia as a compensation for the damaged aircraft. However, one quarter of this amount was meant to cover claims from third parties.

All aircrafts are depreciated using the diminishing balance method over their useful life of fifteen years with the expected residual value of N$140 000.

Required: 12 Prepare journal entries to account for depreciation expenses on

assets that Ire disposed during the year ending 30 June 2012.

13 Prepare all the necessary journal entries related to the assets that are disposed during 2012.

14 Determine whether the company made a profit or loss on disposals during the year under review.

NB: Your figures must be rounded to the nearest N$

The feedback is found in Appendix A at the end of this study guide. I urge you to try and apply your mind first to these activities before you look at the feedback.

References

IASB. (July 2011). A Guide through IFRS. Durban, South Africa: LexisNexis.

Watson, A. & Kew, J. (2012). Financial Accounting. An Introduction (4th ed.). Cape Town: Oxford University Press.

Wood, F. & Sangster. A. (2012). Entity Accounting 1. (12th ed.). United Kingdom: Pearson Education.

Wood, F. & Robinson, S. (2013). Bookkeeping and Accounts (8th ed.). United Kingdom: Pearson Education.

Error! No text of specified style in document. Error! No text of specified style

33

Keywords/Concepts

Disposal (de-recognition):

Removal of non-current asset from entity’s books by way of sale, dumping or destroying etc.

Loss or gain on disposal:

Profit or loss resulting disposing a non-current asset

Disposal account: Ledger used to record all activities relating to the disposal of a non-current asset. Also referred to as asset disposal.

Unit summary

Summary

In this unit you’ve learned how to account (by means of T ledger and general journal) for disposal of non-current asset in the books of an entity. You also learned how to account for the gains or losses resulting from disposal.