Euro Credit Pilot - UniCredit Research

110

03 2016 March 2016 Euro Credit Pilot Economics & FI/FX Research Credit Research Equity Research Cross Asset Research “ Banks take “central” stage ” EUROMONEY CREDIT RESEARCH POLL: Please participate. Click on http://www.euromoney.com/FixedIncome2016 to take part in the online survey.

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Euro Credit Pilot - UniCredit Research

03

2016

March 2016

Euro Credit Pilot

Economics & FI/FX Research

Credit Research Equity Research Cross Asset Research

“Banks take “central” stage”

EUROMONEY CREDIT RESEARCH POLL: Please participate. Click on http://www.euromoney.com/FixedIncome2016

to take part in the online survey.

March 2016 Credit Research

Euro Credit Pilot

UniCredit Research page 2 See last pages for disclaimer.

Contents 4 Top Story: credit fears return to banks due to excessive regulation

6 Credit Drivers

6 Macro: central banks to set the tone

7 Micro fundamentals: banks’ asset quality and profitability not as bad as premiums indicate

8 Debt-equity linkage: a preference for AT1

10 Credit quality trend: banks’ capitalization and asset quality holding up well

12 Corporate Hybrids: Muted new issuance activity and somewhat increased investor uncertainty

15 Valuation & Timing

16 Spread Forecast Table

17 Other Credit Markets

17 Credit Derivatives: Senior underperformance explained

19 High yield: premiums exceed inherent fundamental risk

21 Securitization: Reviving Italian NPL ABS

23 Sector allocation

24 Fundamental Credit Views

24 Telecommunications (Marketweight)

30 Media (Marketweight)

34 Technology (Marketweight)

37 Automobiles & Parts (Overweight)

43 Utilities (Overweight)

56 Oil & Gas (Overweight)

61 Industrial Goods & Services (Core) (Underweight)

65 Industrial Transportation (Marketweight)

68 Basic Resources (Overweight)

70 Chemicals (Underweight)

75 Construction & Materials (Marketweight)

77 Health Care (Marketweight)

80 Personal & Household Goods (Marketweight)

83 Food & Beverage (Marketweight)

86 Travel & Leisure (Marketweight)

87 Retail (Marketweight)

89 Banks (Overweight)

97 Financial Services (Overweight)

99 Insurance (Overweight)

Published on 4 March 2016

Cover picture © Andrey Kuzmin - fotolia.com

March 2016 Credit Research

Euro Credit Pilot

UniCredit Research page 3 See last pages for disclaimer.

In February, credit crisis fears were back with a vengeance, and this time the fears directly concerned systemic issues, namely banks. In January, the iTraxx Financials Senior index was still trading at around the 90bp area. This was already high compared to the 70bp in early December, but still around the same level as in October. However, in February, the index blew out to almost 140bp, a high not seen since 2013. This blowout in senior financials spreads was remarkable, because it takes a drastic scenario to cause a shift of such magnitude. Prior to the subprime crisis, bank credit spreads were known to be less cyclical and remained relatively calm, even in a recession. This is due to the fact that banks need to be fundamentally resilient to recession risk: otherwise, if a mild slowdown can cause a panic in bank debt, the entire financial system would be rather unstable. So what is behind this development? Are we really entering into a new financial crisis similar to that experienced after the subprime era or during the European sovereign debt crisis? In our view no, because the driver of the current development is completely different. In the present edition of the ECP, we will elaborate on these issues and will show that banks’ capitalization and asset quality are holding up well. In any case, our general recommendation remains that the sell-off is fundamentally overblown and has created a lot of attractive buying opportunities.

■ Macro Outlook: The upcoming ECB and the Fed policy decisions are likely to set the tone in markets in the coming weeks. The Bank of Japan’s decision to cut its rates deeper into negative territory at the end of January reduced expectations of a rate hike by the Fed and raised expectations of another ECB rate cut.

■ Micro Fundamentals: Elevated concerns about banks counterintuitive to higher capital and less risk exposure.

■ Debt-Equity Linkage: The February rout in AT1 (CoCo) bonds resulted in an average decline of 15%, partly reflecting market aversion in risky assets and partly mirroring regulatory factors and risks inherent in the relatively new instruments. We believe that the sell-off was overblown, and thus recommend increasing exposure to CoCo bonds, which are still trading at attractive yields.

■ Credit-Quality Trend: Concern about weak earnings, capital adequacy and credit quality have weighed heavily on European banks as of late. However, our analysis shows that European banks have become more resilient, with capital requirements on target and asset quality much improved. Many European banks currently show stable rating outlooks.

■ Corporate Hybrids: Muted new issuance activity and somewhat increased investor uncertainty

■ Valuation & Timing: We recommend positioning for a retightening in credit spreads over the coming months

■ Other Credit Markets: Credit Derivatives – Senior underperformance explained. High Yield – premiums exceed inherent fundamental risk. Securitization – Reviving Italian NPL ABS

■ Allocation: We keep our sector recommendations unchanged and overweight Automobiles, Utilities, Oil & Gas and Basic Resources.

Dr. Philip Gisdakis (UniCredit Bank) +49 89 378-13228 [email protected]

Dr. Christian Weber, CFA (UniCredit Bank) +49 89 378-12250 [email protected]

Dr. Tim Brunne (UniCredit Bank)

+49 89 378-13521 [email protected]

Holger Kapitza (UniCredit Bank) +49 89 378-28745 [email protected]

Dr. Stefan Kolek (UniCredit Bank)

+49 89 378-12495 [email protected]

Manuel Trojovsky (UniCredit Bank) +49 89 378-14145 [email protected]

March 2016 Credit Research

Euro Credit Pilot

UniCredit Research page 4 See last pages for disclaimer.

Top Story: credit fears return to banks due to excessive regulation

Remarkable blowout in financials spreads…

In February, credit crisis fears were back with a vengeance, and this time the fears directly concerned systemic issues, namely banks. In January, the iTraxx Financials Senior index was still trading at around the 90bp area. This was already high compared to the 70bp in early December, but still around the same level as in October. However, in February, the index blew out to almost 140bp, a high not seen since 2013. This blowout in senior financials spreads was remarkable, because it takes a drastic scenario to cause a shift of such magnitude. Prior to the subprime crisis, bank credit spreads were known to be less cyclical and remained relatively calm, even in a recession. This is due to the fact that banks need to be fundamentally resilient to recession risk: otherwise, if a mild slowdown can cause a panic in bank debt, the entire financial system would be rather unstable. So what is behind this development? Are we really entering into a new financial crisis similar to that experienced after the subprime era or during the European sovereign debt crisis? In our view no, because the driver of the current development is completely different. In the present edition of the ECP, we will elaborate on these issues and will show that banks’ capitalization and asset quality are holding up well. In any case, our general recommendation remains that the sell-off is fundamentally overblown and has created a lot of attractive buying opportunities.

CREDIT SPREAD DYNAMICS

iTraxx Financials Senior spread Spreads vs. stocks (in relative terms): DB, Barclays and overall

Source: iBoxx, Bloomberg, UniCredit Research

…but this time is different Looking into the rear mirror helps to put the current situation into perspective. During the subprime and the sovereign debt crises, bank asset quality was in focus, but not to a normal extent. The affected assets (mortgage debt and government bonds) usually make up a significant proportion of bank assets, and the anticipated loss severity was so high that fears emerged that several banks could collapse. This is completely different in the current environment – the concerns vary greatly from bank to bank. Some are related to potential losses from the commodity crisis. (We think that these remain limited, though). Other institutions are in focus because their business profiles are currently being restructured, which will involve considerable costs. Separately, the Italian banking system is in the spotlight because of NPL concerns and the associated strategy of the government to establish a bank asset-guarantee scheme. Of course, there are also more general concerns regarding an economic slowdown ahead, but as mentioned above, a normal cyclical downturn should not affect bank debt to the extent that we witnessed in February.

0

50

100

150

200

250

300

350

400

2010 2011 2012 2013 2014 2015 2016

iTraxx FinSen

0%

50%

100%

150%

200%

250%

300%

350%

400%

40% 50% 60% 70% 80% 90% 100% 110%

5Y C

DS

spr

ead

(inde

xed

to 1

00 fo

r 1-N

ov-2

015)

Stock price (indexed to 100 for 1-Nov-2015)

Deutsche Bank Overall Barclays

March 2016 Credit Research

Euro Credit Pilot

UniCredit Research page 5 See last pages for disclaimer.

Regulatory initiatives designed to stabilize the system can have side effects

That said, there is one common theme behind all these various issues. Although the costs involved should not threaten to bring down an institution, they may be substantial. However, with the current regulatory and market environment (negative interest rates and the overall low-yield environment), the question arises as to who should provide the funds. Due to the prevailing environment, bank profitability is low, so organic financing of new capital requirements (whatever the reason) appears to be out of the question at the moment. But, given investor expectations of persistently low profitability, the willingness to invest in bank equity and provide the necessary funds is also very limited. However, given tight capital requirements and strict rules governing how to wind down banks that cannot meet these thresholds, any larger capital requirements could escalate into credit fears quickly because of bail-in regulation. So what we are currently witnessing in the market is how regulatory initiatives that were designed to stabilize the banking system can actually destabilize it when banks get into the kind of trouble that would be otherwise be manageable.

Capital concerns can quickly translate into credit fears

The way in which equity concerns affected the debt aspect of banks’ capital structure is demonstrated in the right chart above. It shows a scatter plot of changes in 5Y CDS spreads of Deutsche Bank, Barclays and the iTraxx FinSen relative to changes in the corresponding stocks (stocks on the x-axis and spreads on the y-axis with data points indexed to 100% at 1 November 2015; the stock index is the STOXX Europe 600 Banks). Initially, the sensitivity on the spread side towards the plunge in stock prices was quite low. Stock prices dropped 25% without causing a substantial spread movement. At the beginning, it was mostly an equity story. However, once the stock price retreats beyond a certain level, spreads start to react strongly, as fears regarding potentially unsatisfiable capital requirements translate into wind-down fears.

Authorities will not push the financial system over a cliff

While we share the view that excessive regulation could trigger a banking crisis, we do not believe that the authorities will push the financial system over a cliff, causing another credit crisis. Hence, we think that the spread blowout is not justified and we recommend positioning for a retightening. Recently, ECB vice president Vitor Constâncio said that any monetary easing (if the ECB decides to take this route) must be conducted in conjunction with measures to mitigate any negative effect it will have on banks. In our economists’ view, this could result in a two-tier deposit-rate, like in Japan, among other countries. Furthermore, authorities signaled that the post-crisis trend of rising capital requirements will come to an end. ECB officials pointed out recently that they plan to reduce the central bank’s Pillar 2 requirements on individual lenders as the capital conservation buffer grows, allowing the sum of the two to remain broadly steady. The ECB expects banks to ensure they have common equity capital equivalent to about 10%, on average, of risk-weighted assets. To emphasize this, the ECB’s Daniele Nouy and Mario Draghi said that capital requirements had reached a “steady state”. In addition, authorities signaled that there may be a review in regulation that might limit banks’ ability to service coupons on AT1 bonds.

With an average yield of 10%, CoCos/AT1 appear to be the sweet spot in the capital structure at the moment

However, the sell-off not only affected senior bonds of financials, but CoCo/AT1 were also hit hard. The average price of CoCo bonds has dropped about 15 points to an average price of around 85, currently trading at around 90 on average. Moreover, the gap between dividend yields in stocks and bond yields for CoCos has opened up significantly (dividend yields rose from 4% at the start of the year to 6%, while yields of AT1s rose to 10% from 6%). Moreover, as dividend cuts further down the road are not unlikely, CoCo bonds appear to be more attractive than equity in the capital structure of banks. Moreover, in the event that banks approach the conversion point, equities are likely to underperform because of the potential dilution from a CoCo conversion. Given that the average CET1 ratio of European banks is in the area of 10-11% (for national champions even higher), the conversion triggers are fairly distant at the moment. Hence, the crucial risk factor driving markets currently is the coupon payments. If banks continue to service coupon payments, and we believe that this is the case as fundamental challenges are not that high (the above-mentioned rethinking of potential restrictions by authorities supports this view), investors will earn an attractive return.

March 2016 Credit Research

Euro Credit Pilot

UniCredit Research page 6 See last pages for disclaimer.

Credit Drivers Macro: central banks to set the tone

The upcoming ECB and the Fed policy decisions are likely to set the tone in markets in the coming weeks. The Bank of Japan’s decision to cut its rates deeper into negative territory at the end of January reduced expectations of a rate hike by the Fed and raised expectations of another ECB rate cut (see left chart). The reaction by markets to this highlighted, however, their sensitivity to negative interest rates. Reactions among Financials were notable: the iTraxx Fin Sen index surged to levels not seen since 2013. Negative interest rates – which are currently being applied by the BoJ; the ECB and the central banks of Denmark, Sweden and Switzerland – have led to flatter interest-rate curves, and coupled with regulatory overhaul, have reduced banks’ profitability in traditional (lending) margin business. The ECB and the Fed’s policy decisions will occur at a time when the global economy is witnessing weaker growth momentum, which has led to growth forecasts being lowered. At the same time, currency-regime shifts have increased volatility in foreign-exchange markets, and commodity prices have been struggling to find momentum.

Expect a package of easing measures from the ECB in March

On 9 and 10 March, the ECB is expected to implement further measures intended to boost inflation. Our economists expect the central bank to introduce a package of easing measures – which is likely to include a deposit-rate cut, probably by 10bp (as priced in by Eonia forwards) but with the risk that the cut will be larger – together with an expansion and extension of its asset purchase program. The likelihood of further easing rose after the ECB’s February CPI estimate declined to -0.2% yoy. The ECB’s ability to limit the impact of its negative rates on banks will be key for credits. Our economists estimate the direct costs of excess liquidity for banks will be EUR 5bn p.a. To put this into perspective, this represents 3% of eurozone banks’ total profits for 2014 and 5% of banks’ 2015 profits reported thus far. This amount is not negligible in the current growth environment. Thus, measures to alleviate this impact on banks’ profitability – e.g. the introduction of a two-tiered rate or the granting of larger exemptions for minimum reserves, which are strategies used, for example, by the SNB – will be important for credit spreads’ trajectories.

Expect up to three rate hikes from the Fed this year

Regarding the Fed, which decides on 16 March, comments from various FOMC members over the past few weeks suggest that they want to see evidence that the recent headwinds from the weaker global economy will not affect the US economy. Solid economic data should be supportive of global appetite for risk. The implied market probability of a rate hike in March has declined from 50% in December to below 10%. Our economists expect up to three rate hikes from the Fed this year.

FINANCIALS CREDIT SPREADS START FEELING THE IMPACT OF NEGATIVE RATES

Market implied probabilities of central banks’ actions in March 2016 iTraxx FinSen vs. 2Y Bunds

Source: Bloomberg, UniCredit Research

0

10

20

30

40

50

60

70

80

90

100

Jan-

15

Feb-

15

Mar

-15

Apr

-15

May

-15

Jun-

15

Jul-1

5

Jul-1

5

Aug

-15

Sep

-15

Oct

-15

Nov

-15

Dec

-15

Jan-

16

Feb-

16

Mar

ket i

mpl

ied

prob

abilit

y (%

)

Fed ECB

-0.8

-0.6

-0.4

-0.2

0

0.2

0.450

100

150

200

250

300

350

Jan-

12

Apr

-12

Jul-1

2

Oct

-12

Jan-

13

Apr

-13

Jul-1

3

Oct

-13

Jan-

14

Apr

-14

Jul-1

4

Oct

-14

Jan-

15

Apr

-15

Jul-1

5

Oct

-15

Jan-

16

%bp

iTraxx FinSen (reversed LS)

2Y Bunds yield (RS)

March 2016 Credit Research

Euro Credit Pilot

UniCredit Research page 7 See last pages for disclaimer.

Micro fundamentals: banks’ asset quality and profitability not as bad as premiums indicate

Elevated concerns about banks counterintuitive to higher capital and less risk exposure. Plunging stock prices and accelerating risk premiums despite fewer risk-weighted assets and more capital

Banks have been under increased pressure since the start of the year, with bank spreads 28bp wider (iBoxx Banks) and senior spreads (+20bp to 76bp) also fully reflecting rising risk aversion. As bank stocks sold off significantly (16%), valuation measures have slipped back to levels not seen since the height of the eurozone debt crisis or the financial crisis. The question is whether the current price-to-book ratio of just over 0.5x (for STOXX 600 Europe Banks, red line in the left chart) is once again the result of concerns about a potential deterioration of asset quality. During the eurozone sovereign-debt crisis, balance sheets were scrutinized because of their exposure to sovereign debt and investors were concerned whether single banks could fail along with their respective home nation’s ability to repay its public debt. In the financial crisis, the issue of asset quality was coupled with profitability as banks accumulated losses from fire sales, write-off’s and capital market turbulence. Currently, asset quality does not appear to be nearly as much at risk since banks have significantly lowered their risk-weighted assets in recent years, while at the same time increasing their capital buffers (the median Tier-1 ratio has soared from 8% to nearly 14% since 2007, black line in the left chart). With the ECB still eager to lower rates on deposits, investor concerns seem to linger on profitability rather than asset quality. Margins in the STOXX 600 Europe Banks have slipped back to late-2014 levels (4.1%, red line in the right chart), but are still positive and well above the levels seen in 2008 and 2012. Low (positive) profitability is a concern for equity investors, but less so for debtholders.

Debtholder sweet spot? Hence, concerns appear to be exaggerated, even for coupons of the debt instruments most exposed to swings in profits – CoCo notes. This is especially true with the ECB signaling it may adjust its opinion on CoCo coupon payments and ask for a change to EU banking law. The proposed change would allow supervisors the option of permitting banks to make discretionary payments to investors and staff even when a lender loses money in a given year and breaches regulatory buffers. As standing rules prohibit payments of dividends, bonuses or coupons on CoCo bonds in such a case, banks could be forced into an unpleasant situation. While not aiming to allow broad-based payments during times of stress, the ECB’s comments suggest a bank should be able to decide how to cut payouts in accordance with the firm’s business plan. The change would likely only support the implementation of a plan to conserve capital within the company, but the fact that authorities are considering such a move indicates that they do not intend to allow regulation to precipitate a crisis.

BANK EQUITY VALUATION, CAPITAL LEVEL AND PROFITABILITY

Bank’s price/book ratio vs. median T1 ratio STOXX 600 Europe Banks: profit margin and EPS (blended est.)

Source: Bloomberg, Markit, UniCredit Research

0

2

4

6

8

10

12

14

0

0.5

1

1.5

2

2.5

2001 2003 2005 2007 2009 2011 2013 2015

Med

ian

T1 R

atio

Pric

e/B

ook

Rat

io

Stoxx Europe 600 Banks (Price/Book) Median T1 Ratio

-30

-20

-10

0

10

20

30

Oct

-08

Feb-

09Ju

n-09

Oct

-09

Feb-

10Ju

n-10

Oct

-10

Feb-

11Ju

n-11

Oct

-11

Feb-

12Ju

n-12

Oct

-12

Feb-

13Ju

n-13

Oct

-13

Feb-

14Ju

n-14

Oct

-14

Feb-

15Ju

n-15

Oct

-15

Feb-

16

PROF_MARGINBEST_EPS

March 2016 Credit Research

Euro Credit Pilot

UniCredit Research page 8 See last pages for disclaimer.

Debt-equity linkage: a preference for AT1 The February rout in AT1 (CoCo) bonds resulted in an average decline of 15%, partly

reflecting market aversion in risky assets and partly mirroring regulatory factors and risks inherent in the relatively new instruments. We believe that the sell-off was overblown, and thus recommend increasing exposure to CoCo bonds, which are still trading at attractive yields. We think that CoCo bonds, rather than equities, are the sweet spot in banks’ capital structure at the moment. The sharp and broad-based drop in AT1 prices was in part triggered by the simultaneous sell-off in bank stocks and the ensuing sharp blowout in CDS spreads, which in turn was triggered by concerns about banks’ credit fundamentals. We view these concerns as unfounded, with fundamentals and credit profiles not having materially changed, but instead continuing to improve (with the usual exceptions). While the underperformance in bank shares could continue for a while given ongoing dividend cuts and limited earnings growth, the prospect for AT1s is not as negative as recent underperformance would suggest. Given attractive valuations with appealing yields of more than 10% for the universe, and more clarity regarding the likelihood of coupon payments in AT1s, we prefer these instruments to bank stocks.

Potential AT1 repricing triggers

In general, AT1s are a cheaper form of going-concern capital and can help banks buffer losses at times of stress through conversion to equity or writedown (temporary or permanent). Moreover, the fully discretionary nature of coupon payments also provides banks with financial flexibility. The negative sentiment surrounding bank fundamentals undoubtedly took its toll on AT1s. However, we also believe that part of the sell-off was technical, with few buyers willing or able to step in, creating a vicious circle in AT1 that feeds on itself. In terms of investors, the market has been in a bit of a quandary as of late: equity investors and other specialized funds were eschewing bonds – despite promising returns – due to their illiquid nature, traditional credit funds were steering clear of them due to their complexity and regulatory constraints, and many hedge funds and distressed funds have avoided them since the bonds were not cheap enough. Furthermore, there has also been substantial tiering among individual AT1 issues, particularly due to fears of potentially skipped coupon payments and concerns about insufficient available distributable items (ADI), which would also lead to coupon restrictions. Whatever the reason, AT1s dropped about 15% to an average price of around 85 points, and is currently trading at an average of around 90 points after a moderate rebound. In our opinion the sector still looks cheap, but is unlikely to cheapen further.

AT1 BONDS CONTINUE TO LOOK ATTRACTIVE AGAINST EUROPEAN BANK EQUITIES

AT1 total returns vs. STOXX Europe 600 banks and overall returns AT1 and bank equity yields

Source: iBoxx, Bloomberg, UniCredit Research

60

70

80

90

100

110

120

130

140

Dec

-13

Mar

-14

Jun-

14

Sep

-14

Dec

-14

Mar

-15

Jun-

15

Sep

-15

Dec

-15

Mar

-16

STOXX Europe 600 Banks return STOXX Europe 600 returnAT1 total return

indexed to 100 on 1 January 2014

0

2

4

6

8

10

12

Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16

Yiel

d (%

)

Yield differentialCoCo (AT1) EURDividend yield (STOXX Europe 600 Banks)

March 2016 Credit Research

Euro Credit Pilot

UniCredit Research page 9 See last pages for disclaimer.

Bank equity weakness is broad-based

On the equities side, European Bank shares are by far the largest underperformer in 2016 YTD, with the STOXX Europe 600 subindex returning -16.0% against -6.7% for the overall index. While many bank stocks have rebounded quickly, paring some of the losses suffered by mid-February, others have failed to stage a comeback, the reasons for which we outline below. A look at the index members reveals that the underperformance is broad-based, with 32 out of 47 banks having registered double-digit declines YTD. The worst-performing group with YTD returns of -20% or higher includes banks from across Europe including Germany, Greece, France, Italy, Portugal, Spain, Switzerland and the UK. This reflects the extent to which profit warnings, dividend cuts to boost capital buffers, recapitalization measures, and restructuring and litigation costs, are weighing on performance across jurisdictions. Interestingly, looking at underperformers in bank stocks, there is a substantial degree of correlation between the performance of equities and the AT1 securities of the banks in question. However, we note that recent AT1 performance also reflects factors specifically related to individual AT1s, such as the low headroom for coupon risk and strained ADIs, which vary materially among banks. A major issue potentially leading to a mandatory coupon restriction for AT1 securities is the lack of ADIs, although rating agency opinions suggest that banks have sufficient ADIs to pay their AT1 coupons. The remaining names (i.e. the outperformers) include Nordic and some Dutch and UK banks. It is no coincidence that AT1 bonds issued by these banks have fared considerably better given their higher dividends, healthier capitalization and lower AT1 coupons. Among the best performing AT1s in 2016 YTD are those issued by Swedish banks.

Dividend yields and AT1 yields As highlighted in the right chart above, the gap between dividend yields in stocks and AT1 yields diverged significantly, with the yield differential briefly hitting 500bp. However, this could reverse anytime soon. Given that dividend cuts down the road are not unlikely, AT1 bonds appear to be the more attractive spot in banks’ capital structure, as opposed to equity. If banks were to approach the conversion point, equities would likely underperform, given the dilution from a potential CoCo conversion. Perhaps equally important, while potential rights issues would not contribute to ADIs, they would weigh on banks’ equity performance to a similar extent.

Positioning for a re-tightening We continue to recommend positioning for a compression in bank senior spreads. With AT1s, we believe that a similar strategy can be implemented at a lower level of the capital structure, while avoiding the – in our view – higher risks in bank equity. Given that the average CET1 ratio of European banks is in the area of 12% (for national champions even higher), the conversion triggers are currently fairly remote. Hence the crucial risk factor driving markets at the moment is coupon restrictions. Our base case is that banks continue to honor their coupon payments, allowing investors to earn an attractive return.

March 2016 Credit Research

Euro Credit Pilot

UniCredit Research page 10 See last pages for disclaimer.

Credit quality trend: banks’ capitalization and asset quality holding up well

Concern about weak earnings, capital adequacy and credit quality have weighed heavily on European banks as of late. However, our analysis shows that European banks have become more resilient, with capital requirements on target and asset quality much improved. Many European banks currently show stable rating outlooks. However, the amount of non-performing loans (NPL) needs to be closely monitored and will likely weigh on bank’s profitability, albeit at manageable level.

Concerns about weak earnings, capital adequacy and credit quality weigh heavily on European banks

In recent weeks, investors in European banks have been worried about sluggish earnings due to weak economic growth, a prolonged period of negative interest rates and concerns about capital adequacy at some major lenders. This has put shares of banks under pressure. However, hybrid instruments like CoCos have been most heavily hit and bank credit spreads in Europe have been widening as well. For this reason, we take a closer look at banks’ capitalization and the quality of assets.

The ECB says European banks are much more resilient today, with capital requirements at target, while still-high levels of NPLs will likely be manageable

Following up on ECB’s president Mario Draghi’s hearing before the European Parliament’s Economic and Monetary Affairs committee in mid-February, at which he stated that past market turmoil appears to be more related to general factors concerning weakening economic activity, Danièle Nouy, Chair of the Supervisory Board of the ECB, also noted that the “situation in the euro area banking sector today is very different from what it was in 2012. The banking sector is much more resilient”. She continued that the quality of capital has also been substantially improved and that the sector is much more able to absorb unexpected financial or economic headwinds than a few years ago. Banks have made huge progress in meeting the fully loaded capital requirements (CRR/CRD IV) that will be in effect from 2019 onwards, she said, and the vast majority of banks meet these requirements already today. She added that there was still a subset of banks with elevated levels of NPLs but that these NPLs have been now identified, due to a harmonized definition within SREP and adequate reserves have been built, which will allow the sector to gradually lower the NPLs over the next few years.

EBA says that EU banks have continued to strengthen their capital positions and were able to improve asset quality, while NPLs will likely weigh on profitability

A recent study by the EBA (link) of 105 banks in 21 countries shows improvements in the resilience of the EU banking sector. In general, EU banks have continued to strengthen their capital positions, mainly through raising additional capital and retaining earnings. Since December 2011, the aggregate CET1 ratio has increased by 280bp to 12.6% following the efforts of banks, supervisors, and regulators to increase banks’ capital in the aftermath of the financial crisis. The improvement has been achieved more through increases in capital than reductions in RWAs. The EBA said that, between December 2013 and June 2015, lending increased, as shown by a modest increase in RWAs (the denominator of the capital ratio) by 1.3%. On a country level, CET1 ratios (fully loaded) for all banks are comfortably above the minimum, with the highest values in the Nordics (up to 22.3%), followed by the UK (12.8%), Germany (12.6%), Italy (11.1%), Spain (10%), and Portugal (9.6%). The quality of assets has also improved, albeit from a low base. Nonetheless, EU banks will need to continue addressing NPL levels, which will likely continue to weigh on banks’ profitability. Aggregate EU NPLs (of total loans), defined as 90-plus-days overdue and/or “debtor is unlikely to pay”, decreased by 50bp to 5.6% in 1H15 vs. 4Q14, while the NPL coverage ratio in EU was unchanged at 43%. As highlighted in the left chart, the ratio of NPLs not yet provisioned for (uncovered) is between 1% and 4.5%. When considering the weighted average by total assets, the ratio is about 1.9%. However, the increased level of banks’ capital and the value of collateral should be taken into account when assessing the level of additional provisions, even in the periphery, where, as a result of economic stress, NPL levels are higher. However, incentives for banks differ and banks that suffer from a high level of impaired loans coupled with a low coverage ratio may struggle to clean up their balance sheets. Low coverage ratios may result in a reluctance to resolve NPLs by disposing of them, due to material differences between the potential price and net book value, leading to losses. In contrast, high coverage ratios mean that a large share of losses has already been recognized in banks’ financial

March 2016 Credit Research

Euro Credit Pilot

UniCredit Research page 11 See last pages for disclaimer.

statements, which may encourage banks to dispose of their NPLs and achieve lower NPL ratios. The data show that smaller banks in particular report higher NPL ratios for loans, at about 18%, compared to 9% for medium-sized banks and 4% for larger banks, while smaller banks reported the lowest level of NPL coverage at 40% (compared to 40% in medium and 44% in large banks). This suggest that smaller banks may face strong market pressure to maintain their NPL coverage ratio and stick to highly provisioned loans, rather than disposing.

Basel Committee: large internationally active banks well above Basel III capital requirements

The results of the EBA study are in line with the latest Basel III monitoring exercise, published by the Basel Committee on 2 March 2016 (link). Data have been provided for a total of 230 banks, comprising 101 large internationally active banks, defined as Group 1 banks that have a Tier-1 capital of more than EUR 3bn, and 129 Group 2 banks (other). The data as of 30 June 2015, assuming full phasing-in of the Basel III requirements in 2015, show that all Group 1 banks would meet the minimum CET1 of 4.5% and the CET1 target level of 7.0% (including the capital conservation buffer) as of 2019.

European financial senior rating drift shows balanced rating actions, while a large share of European banks show stable rating outlooks

A look at rating trends in the European financial seniors universe reveals that upgrades/ downgrades are balanced amid improved capitalization and risk profile in the sector. As highlighted in the right chart, which shows rating changes in the iBoxx financial seniors universe within one year based on rating actions by Fitch, Moody’s and S&P, the pace and the severity of downgrades has moderately slowed down, while upgrades are holding up well. On 2 December 2015, S&P affirmed the ratings of most European banks after a review that followed the national introduction of bank resolution frameworks (BRRD), which requires systemic banks to have significant buffers of bail-in-able instruments for recapitalization, and the lower likelihood of extraordinary government support. In general, S&P affirmed ratings on those banks for which the removal of systemic support had been offset by better intrinsic creditworthiness and/or potential support to senior creditors from material buffers of additional loss-absorbing capacity (ALAC), and lowered ratings on those banks for which the loss of support outweighed mitigating factors.

Conclusion In conclusion, we think the recent market turmoil can be explained more by earnings-related concerns than by banks’ capitalization and asset quality. However, a prolonged environment of negative interest rates could potentially encourage some banks to try to overcome low profitability more rapidly by making loans that are more risky. Any increased competition in lending at lower credit standards may in turn subsequently trigger adverse consequences for the banking sector.

EUROPEAN BANKS HOLD UP WELL IN TERMS OF CAPITAL AND ASSET QUALITY, RESULTING IN BALANCED RATING DRIFT

Key credit metrics at a glance – major national banks iBoxx FinSen composite rating drift**

Source: Bankscope, Bloomberg*, UniCredit Research Source: rating Agencies, UniCredit Research **The left scale shows the index’s average rating actions at a given month compared to the previous year. Hence, it also takes into account the severity of the rating action. That is, a level of -1 would indicate an average deterioration of one notch per rating composite. However, we caution that since drift is limited to the IG universe, it is therefore subject to a negative bias given that it only considers bonds initially rated BBB- or higher, thus excluding rising stars while at the same time still including falling angels for at least twelve months.

DeutscheBank

BNP Paribas*

Crédit Agricole*

BPCE Group

ING Bank

HSBC

Barclays

RBSLloyds

UniCredit*

Intesa Sanpaolo*

BancoSantander BBVA

Bank of Ireland

Danske

DnBASA

Nordea

10.0

12.0

14.0

16.0

18.0

20.0

22.0

24.0

26.0

28.0

-1.0 0.0 1.0 2.0 3.0 4.0 5.0 6.0

Tota

l cap

ital r

atio

in %

Uncovered NPL ratio = Gross NPL ratio x (1 - NPL coverage) in %

- Bubble size reflects total assets

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

Upgrades (LS) Downgrades (LS) Action Rate (RS)

March 2016 Credit Research

Euro Credit Pilot

UniCredit Research page 12 See last pages for disclaimer.

Corporate Hybrids: Muted new issuance activity and somewhat increased investor uncertainty

General comment Contrary to the message the headline might convey, in a less volatile market environment, investor demand for corporate hybrids should continue to remain healthy. This has been driven by the persisting low-interest-rate environment (compared to long-term averages) on the one hand and by fair valuations of corporate hybrids relative to senior bonds on the other. Evidence of still-healthy investor demand for hybrid paper was provided by the heavily oversubscribed order books of the latest hybrid new issues from BHP, Solvay and OMV in October and November 2015. While we acknowledge that market participants have become more cautious since then, current new issue premiums would compensate investors for increased volatility. Also, when looking at overall credit quality, in terms of issue-rating distribution, we acknowledge that overall issuance quality has improved. In 2015, 77% of all issued hybrids carried an investment-grade issue rating, as opposed to 73% in 2013 and 67% in 2014.

Recap of special events in 2015 In addition to increased market volatility in the second half of 2015, corporate hybrid investors were confronted with two different potential early call events:

■ In the first half of 2015, holders of hybrids from German issuers were hit by concerns surrounding potential early calls. These concerns were triggered by a proposed change in the tax deductibility of hybrid coupons. Germany was rumored to be drafting a bill that would ban the tax deductibility of coupons of hybrid paper. While the original draft bill did not pass, Germany established a working group to assess the findings of an OECD report (published in October) and to draft a new bill that would avoid double non-taxation. We expect Germany to align a new draft bill with the final OECD report, i.e. it should not target third-party corporate hybrid paper. However, a translation into local law (also from other European countries) is still pending. According to prevalent hybrid documentation, if hybrid issuers are no longer able to claim a tax deduction on the interest paid by the notes, or if this deduction is reduced, a “tax event” will occur. This will allow the hybrid issuer to exercise an exceptional and early call right (mostly at 101).

■ In October, S&P changed its opinion regarding certain types of language describing an early call as a result of a rating event. All affected hybrids lost their equity content at S&P, and in theory, issuers would have had the right to call the bonds early due to a rating event (also mostly at 101). A few days after S&P's announcement, the first issuers unconditionally and irrevocably waived the right to call their hybrid bonds in such an event. As a result, S&P again increased the equity content on these hybrids to intermediate (50%).

■ In both cases, outstanding hybrids with cash prices trading far above their early call price dropped by several points. Although concerns of an early call proved unfounded – as issuers’ response was investor friendly – we think the two events will likely lead to different investor behavior in the medium term: In our view, investors will try to shy away from secondary market issues that are trading at cash prices far above par. Instead, they will tend to prefer hybrids with lower cash prices or switch between issues of the same issuer, where possible.

Investment performance In terms of total return, corporate hybrids started to underperform senior bonds in September 2015. Since January 2015, the total return of the iBoxx Non-financial sub index has been -6.2%, while the total return of the iBoxx Non-Fin Senior has been -0.5% (see chart below). The mixed performance of corporate hybrids, especially since the end of September, has been driven by a combination of overall-weaker market sentiment (economic growth concerns of BRIC countries, weak commodities, etc.), but also by idiosyncratic headlines. Single names that have been particularly in focus were Volkswagen, due to its emissions scandal and German utilities, driven by discussions regarding insufficient nuclear provisions. Hybrid valuations of these issuers lost several points in cash-price terms without seeing any significant investor-buying support. Later in 2015, and in early 2016, the main underperformers were commodity-related issuers like Repsol and OMV. Since January 2016, the general risk-off mode, above-average volatility and falling stock markets have negatively affected hybrid bond performance.

March 2016 Credit Research

Euro Credit Pilot

UniCredit Research page 13 See last pages for disclaimer.

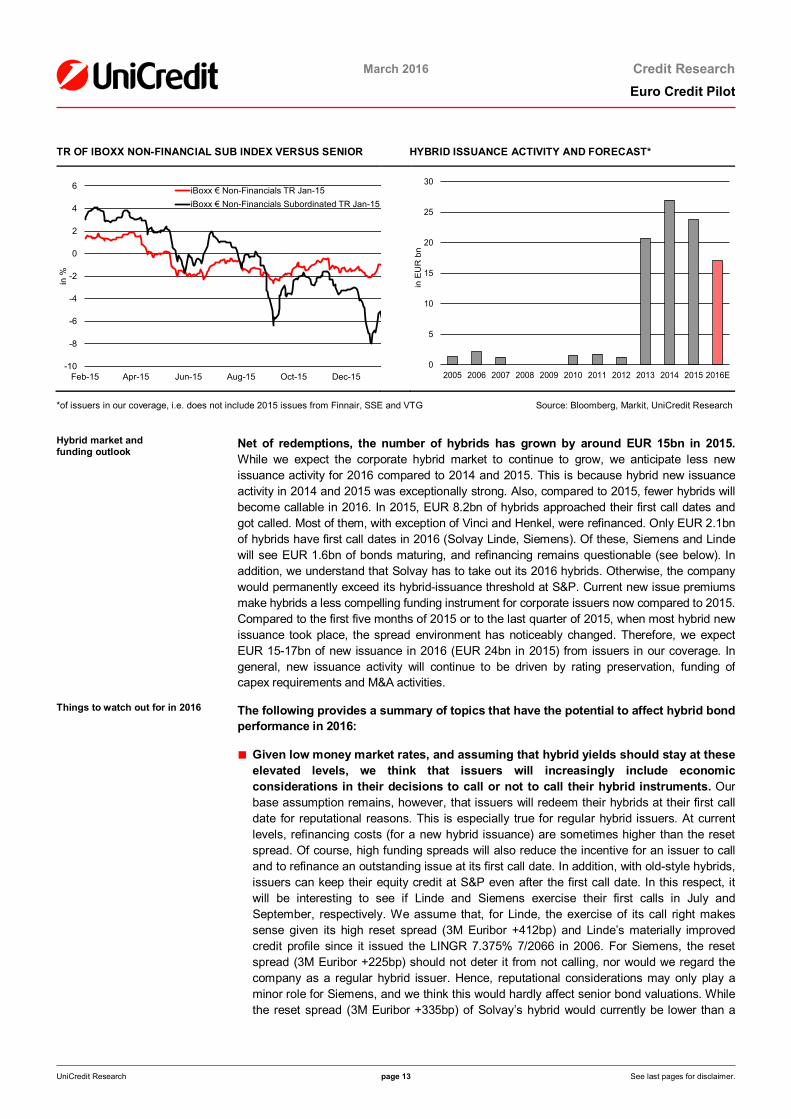

TR OF IBOXX NON-FINANCIAL SUB INDEX VERSUS SENIOR HYBRID ISSUANCE ACTIVITY AND FORECAST*

*of issuers in our coverage, i.e. does not include 2015 issues from Finnair, SSE and VTG Source: Bloomberg, Markit, UniCredit Research

Hybrid market and funding outlook

Net of redemptions, the number of hybrids has grown by around EUR 15bn in 2015. While we expect the corporate hybrid market to continue to grow, we anticipate less new issuance activity for 2016 compared to 2014 and 2015. This is because hybrid new issuance activity in 2014 and 2015 was exceptionally strong. Also, compared to 2015, fewer hybrids will become callable in 2016. In 2015, EUR 8.2bn of hybrids approached their first call dates and got called. Most of them, with exception of Vinci and Henkel, were refinanced. Only EUR 2.1bn of hybrids have first call dates in 2016 (Solvay Linde, Siemens). Of these, Siemens and Linde will see EUR 1.6bn of bonds maturing, and refinancing remains questionable (see below). In addition, we understand that Solvay has to take out its 2016 hybrids. Otherwise, the company would permanently exceed its hybrid-issuance threshold at S&P. Current new issue premiums make hybrids a less compelling funding instrument for corporate issuers now compared to 2015. Compared to the first five months of 2015 or to the last quarter of 2015, when most hybrid new issuance took place, the spread environment has noticeably changed. Therefore, we expect EUR 15-17bn of new issuance in 2016 (EUR 24bn in 2015) from issuers in our coverage. In general, new issuance activity will continue to be driven by rating preservation, funding of capex requirements and M&A activities.

Things to watch out for in 2016 The following provides a summary of topics that have the potential to affect hybrid bond performance in 2016:

■ Given low money market rates, and assuming that hybrid yields should stay at these elevated levels, we think that issuers will increasingly include economic considerations in their decisions to call or not to call their hybrid instruments. Our base assumption remains, however, that issuers will redeem their hybrids at their first call date for reputational reasons. This is especially true for regular hybrid issuers. At current levels, refinancing costs (for a new hybrid issuance) are sometimes higher than the reset spread. Of course, high funding spreads will also reduce the incentive for an issuer to call and to refinance an outstanding issue at its first call date. In addition, with old-style hybrids, issuers can keep their equity credit at S&P even after the first call date. In this respect, it will be interesting to see if Linde and Siemens exercise their first calls in July and September, respectively. We assume that, for Linde, the exercise of its call right makes sense given its high reset spread (3M Euribor +412bp) and Linde’s materially improved credit profile since it issued the LINGR 7.375% 7/2066 in 2006. For Siemens, the reset spread (3M Euribor +225bp) should not deter it from not calling, nor would we regard the company as a regular hybrid issuer. Hence, reputational considerations may only play a minor role for Siemens, and we think this would hardly affect senior bond valuations. While the reset spread (3M Euribor +335bp) of Solvay’s hybrid would currently be lower than a

-10

-8

-6

-4

-2

0

2

4

6

Feb-15 Apr-15 Jun-15 Aug-15 Oct-15 Dec-15

in %

iBoxx € Non-Financials TR Jan-15iBoxx € Non-Financials Subordinated TR Jan-15

0

5

10

15

20

25

30

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E

in E

UR

bn

March 2016 Credit Research

Euro Credit Pilot

UniCredit Research page 14 See last pages for disclaimer.

potential new issuance spread, we regard Solvay as a regular hybrid issuer (and more likely to call). In addition, we understand that the SOLBBB 6.375% 6/04 has to be redeemed, given that, otherwise, Solvay would permanently exceed its hybrid issuance threshold (≤15% of capitalization) at S&P. If one of these issuers were to consider keeping its hybrids outstanding, we would regard this as negative for the hybrid market and for sentiment in this asset class.

■ Besides the extension risk described above, we regard special event risk and, especially, methodology changes by rating agencies as key risks for corporate hybrid spreads. Unfortunately, these types of events are hardly predictable. During the course of 2015, investors faced the two special events described above and the resulting underperformance of affected hybrids. We expect the different double-non taxation initiatives from the OECD and the EU Commission to be translated into local law in 2016. We expect Germany’s draft bill to be aligned with the final results of the OECD report, i.e. not targeting third-party corporate hybrid paper. However, any EU country’s draft bill that is not aligned with the OECD report would be negative for hybrids in their respective jurisdiction. Hybrids carrying a high coupon and/or trading at a cash price significantly above their early redemption price would be particularly affected. Additionally, in the last few years, only minor methodology adjustments have been made by credit-rating agencies. In April 2013, S&P tightened its methodology in assigning 100% equity credit. In July 2013, Moody’s changed its methodology with regard to equity content for issuers downgraded to non-investment grade. Both changes led to early calls or exchange offers associated with lower bond valuations.

■ Long periods of exceptionally low interest rates, low volatility and more standardized hybrid documentation have increased investor demand for this product class. As a result, the hybrid bond market has continuously grown since 2013. Hence, we think that hybrids remain a crowded trade, as many investors are already heavily invested in corporate hybrid paper. Sometimes, investors show a preference for 1. hybrids of an issuer over its senior bonds or 2. a preference for hybrid bonds over the senior bonds of other issuers in the same rating category. In our view, this could intensify underperformance. This preference shown by investors intensified the significant underperformance of corporate hybrids, compared to seniors, at the end of September 2015. More specifically, the considerable drop in the valuation of VW hybrid paper in September (as a result of the “Dieselgate” scandal) showed that there is a lack of investor support in a sell-off – even for robust and well known credits like Volkswagen, as investors were reluctant to add additional risk. One should bear this in mind during times of increased market volatility.

March 2016 Credit Research

Euro Credit Pilot

UniCredit Research page 15 See last pages for disclaimer.

Valuation & Timing The new year kicked off with remarkable downward pressure, as global growth concerns and

plunging commodity prices kept investors nervous. However, these concerns have started to abate recently, and pressure on risky assets has receded. Equities have rebounded strongly and posted double-digit gains since mid-February (STOXX 600 Europe) as oil prices stabilized above USD 33/bbl. Although the OECD trimmed its global growth expectations (3% after 3.3%, now flat to 2015), the overall economic picture remains resilient and the expected level of growth in the eurozone over the next 12M is commensurate with spread levels that are still significantly tighter, suggesting that the upside from current levels remains appealing.

Given the substantial spread blowout that we regard as fundamentally unjustified – in Non-financials, but particularly in Financials – we recommend positioning for a retightening in credit spreads over the coming months (i.e. relatively near-term). In Non-financials, the average spread amounts to 120bp. That is only 10bp below the recent peak, which still leaves some additional short-term tightening potential, as this level compares with about 100bp at the end of last year and about 80bp prior to the VW crisis. In synthetics, spread volatility has been even higher (iTraxx Main: 80bp at the end of last year; recent peak at 125bp, current level 95bp), with additional spread tightening potential lower than in cash bonds due to the pronounced snapback in recent days. For investors wanting to place an even more aggressive bullish bet, AT1/CoCos might offer some attractive opportunities due to the recent blowout.

March 2016 Credit Research

Euro Credit Pilot

UniCredit Research page 16 See last pages for disclaimer.

Spread Forecast Table SPREAD FORECAST 2016 (BP)

Index 1-3M 3-6M A iBoxx universe + +

BBB iBoxx universe ++ +

Telecoms iBoxx universe + +

Automobiles iBoxx universe + +

Industrials iBoxx universe + +

Utilities iBoxx universe + +

Hybrids iBoxx universe ++ +

Financials Sub iBoxx universe ++ +

Financials Sub iTraxx universe ++ +

HY cash BB (ML) ++ +

HY cash B (ML) ++ +

– = negative outlook, o = neutral, + = positive outlook, ++ = very positive outlook

Source: Bloomberg, UniCredit Research

0

25

50

75

100

125

150

0

25

50

75

100

125

150

Dec-14 Jun-15 Dec-15 Jun-16 Dec-16

bp

iBoxx NFI iTraxx Mainactual forecast

0

25

50

75

100

125

150

0

25

50

75

100

125

150

Dec-14 Jun-15 Dec-15 Jun-16 Dec-16

bp

iBoxx FinSen iTraxx FinSenactual forecast

0

100

200

300

400

500

600

0

100

200

300

400

500

600

Dec-14 Jun-15 Dec-15 Jun-16 Dec-16

bp

iBoxx HY iTraxx Xoveractual forecast

March 2016 Credit Research

Euro Credit Pilot

UniCredit Research page 17 See last pages for disclaimer.

Other Credit Markets Credit Derivatives: Senior underperformance explained

Spread widening of iTraxx European spreads in the first two months of the year was accompanied by large moves in the positioning of non-dealers. We argue that demand for a cheap hedge against a systemic financial crisis has driven the sharp underperformance of the iTraxx Senior vs. the Main. This also pulled financial single-name CDS wider until mid-February.

Bank single-name spreads in the spotlight in February

Investors observed single-name CDS of financial sector entities explode in the first half of February. We think that this development was at least partly driven by investors pushing the headline spread of the iTraxx Financial Senior wider as they sought a cheap hedge against a systemic financial crisis that included buying protection on the index. While single-name stories hit the screens regarding challenges of individual banks in the first weeks of the year, these were not universally affecting the whole sector, which would be a characteristic of a systemic crisis. The surging index spread pulled single-name CDS wider across the board.

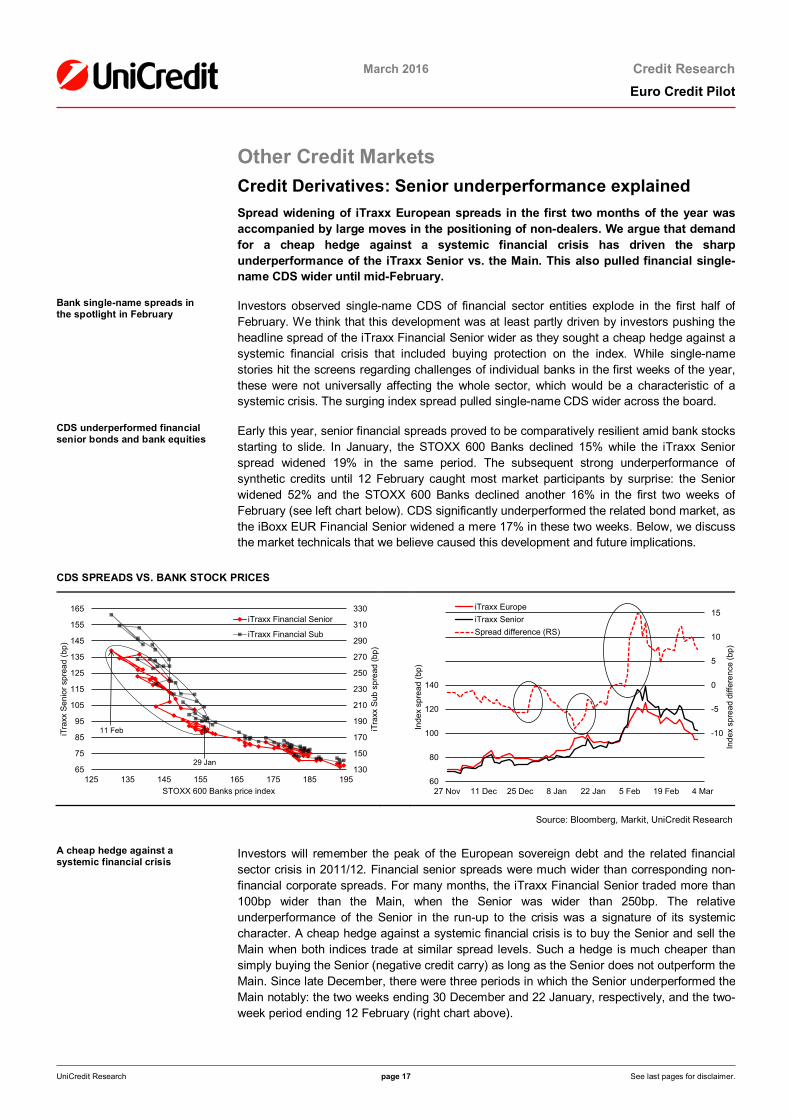

CDS underperformed financial senior bonds and bank equities

Early this year, senior financial spreads proved to be comparatively resilient amid bank stocks starting to slide. In January, the STOXX 600 Banks declined 15% while the iTraxx Senior spread widened 19% in the same period. The subsequent strong underperformance of synthetic credits until 12 February caught most market participants by surprise: the Senior widened 52% and the STOXX 600 Banks declined another 16% in the first two weeks of February (see left chart below). CDS significantly underperformed the related bond market, as the iBoxx EUR Financial Senior widened a mere 17% in these two weeks. Below, we discuss the market technicals that we believe caused this development and future implications.

CDS SPREADS VS. BANK STOCK PRICES

Source: Bloomberg, Markit, UniCredit Research

A cheap hedge against a systemic financial crisis

Investors will remember the peak of the European sovereign debt and the related financial sector crisis in 2011/12. Financial senior spreads were much wider than corresponding non-financial corporate spreads. For many months, the iTraxx Financial Senior traded more than 100bp wider than the Main, when the Senior was wider than 250bp. The relative underperformance of the Senior in the run-up to the crisis was a signature of its systemic character. A cheap hedge against a systemic financial crisis is to buy the Senior and sell the Main when both indices trade at similar spread levels. Such a hedge is much cheaper than simply buying the Senior (negative credit carry) as long as the Senior does not outperform the Main. Since late December, there were three periods in which the Senior underperformed the Main notably: the two weeks ending 30 December and 22 January, respectively, and the two-week period ending 12 February (right chart above).

130

150

170

190

210

230

250

270

290

310

330

65

75

85

95

105

115

125

135

145

155

165

125 135 145 155 165 175 185 195

iTra

xx S

ub s

prea

d (b

p)

iTra

xx S

enio

r spr

ead

(bp)

STOXX 600 Banks price index

iTraxx Financial Senior

iTraxx Financial Sub

29 Jan

11 Feb

-20

-15

-10

-5

0

5

10

15

60

80

100

120

140

160

180

200

27 Nov 11 Dec 25 Dec 8 Jan 22 Jan 5 Feb 19 Feb 4 Mar

Inde

x sp

read

diff

eren

ce (b

p)

Inde

x sp

read

(bp)

iTraxx EuropeiTraxx SeniorSpread difference (RS)

March 2016 Credit Research

Euro Credit Pilot

UniCredit Research page 18 See last pages for disclaimer.

Demand for cheap hedges underpins market fears of systemic financial crisis

In January and February, there was unusually strong demand for the cheap hedge mentioned above. We disagree that this demand was fundamentally justified, albeit the hedge was cheap to enter and rather popular. The stark demand for the trade explains the underperformance of iTraxx Senior spreads vs. the Main since mid-January. Admittedly, some investors who entered the hedge early and closed it in mid-February made a decent profit.

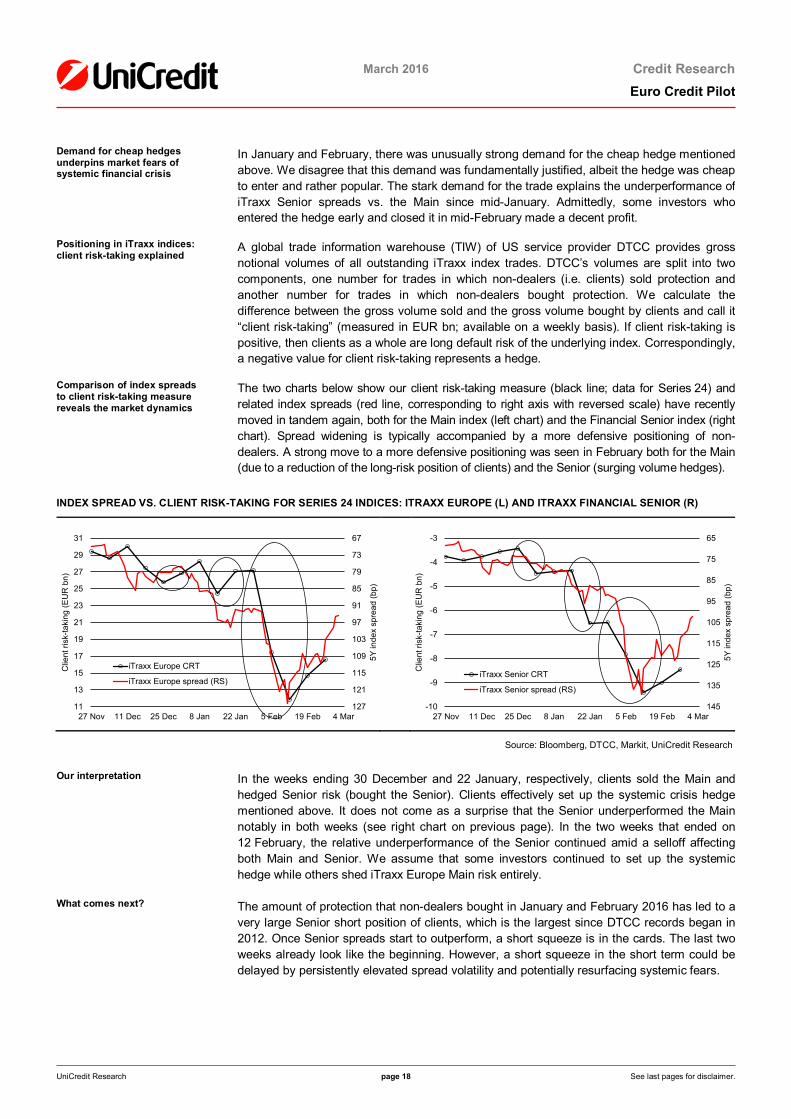

Positioning in iTraxx indices: client risk-taking explained

A global trade information warehouse (TIW) of US service provider DTCC provides gross notional volumes of all outstanding iTraxx index trades. DTCC’s volumes are split into two components, one number for trades in which non-dealers (i.e. clients) sold protection and another number for trades in which non-dealers bought protection. We calculate the difference between the gross volume sold and the gross volume bought by clients and call it “client risk-taking” (measured in EUR bn; available on a weekly basis). If client risk-taking is positive, then clients as a whole are long default risk of the underlying index. Correspondingly, a negative value for client risk-taking represents a hedge.

Comparison of index spreads to client risk-taking measure reveals the market dynamics

The two charts below show our client risk-taking measure (black line; data for Series 24) and related index spreads (red line, corresponding to right axis with reversed scale) have recently moved in tandem again, both for the Main index (left chart) and the Financial Senior index (right chart). Spread widening is typically accompanied by a more defensive positioning of non-dealers. A strong move to a more defensive positioning was seen in February both for the Main (due to a reduction of the long-risk position of clients) and the Senior (surging volume hedges).

INDEX SPREAD VS. CLIENT RISK-TAKING FOR SERIES 24 INDICES: ITRAXX EUROPE (L) AND ITRAXX FINANCIAL SENIOR (R)

Source: Bloomberg, DTCC, Markit, UniCredit Research

Our interpretation In the weeks ending 30 December and 22 January, respectively, clients sold the Main and hedged Senior risk (bought the Senior). Clients effectively set up the systemic crisis hedge mentioned above. It does not come as a surprise that the Senior underperformed the Main notably in both weeks (see right chart on previous page). In the two weeks that ended on 12 February, the relative underperformance of the Senior continued amid a selloff affecting both Main and Senior. We assume that some investors continued to set up the systemic hedge while others shed iTraxx Europe Main risk entirely.

What comes next? The amount of protection that non-dealers bought in January and February 2016 has led to a very large Senior short position of clients, which is the largest since DTCC records began in 2012. Once Senior spreads start to outperform, a short squeeze is in the cards. The last two weeks already look like the beginning. However, a short squeeze in the short term could be delayed by persistently elevated spread volatility and potentially resurfacing systemic fears.

67

73

79

85

91

97

103

109

115

121

12711

13

15

17

19

21

23

25

27

29

31

27 Nov 11 Dec 25 Dec 8 Jan 22 Jan 5 Feb 19 Feb 4 Mar

5Y in

dex

spre

ad (b

p)

Clie

nt ri

sk-ta

king

(EU

R b

n)

iTraxx Europe CRT

iTraxx Europe spread (RS)

65

75

85

95

105

115

125

135

145-10

-9

-8

-7

-6

-5

-4

-3

27 Nov 11 Dec 25 Dec 8 Jan 22 Jan 5 Feb 19 Feb 4 Mar5Y

inde

x sp

read

(bp)

Clie

nt ri

sk-ta

king

(EU

R b

n)

iTraxx Senior CRT

iTraxx Senior spread (RS)

March 2016 Credit Research

Euro Credit Pilot

UniCredit Research page 19 See last pages for disclaimer.

High yield: premiums exceed inherent fundamental risk Heightened growth concerns at the start of the year have resulted in a volatile

environment for risky assets. While the widening pressure in high-yield spreads has eased somewhat, spread-implied default rates are still overshooting credit fundamentals. As companies in the most battered sectors increase creditor-friendly measures, pronounced improvement in risk premiums has become more likely.

High-yield spreads imply a surge in default rates

Credit spreads have witnessed substantial increases in the first weeks of the year. Experiencing a setback similar to other risky assets, high-yield returns have dipped into negative territory (iBoxx EUR HY -2% YTD). The rise in non-financial high-yield spreads (iBoxx EUR HY NFI +83bp to 542bp) has been fueled by a number of concerns, particularly global growth. In the past decade, risk premiums traded significantly wider than current levels only during the financial crisis and the eurozone crisis. Spreads imply that default rates (assuming a 40% recovery rate and 2Y government yield levels of -0.5% in EUR and 0.75% in USD) could surge as high as 9% in Europe (from 3.3% in January) and 11.5% in the US (from 3.1% in January). While neither consensus growth expectations nor our economists indicate a pronounced negative turnaround in economic activity on either side of the Atlantic, there are additional reasons to assume a less drastic increase in defaults.

A spike in defaults is difficult to justify from the fundamentals side

From a micro perspective, credit fundamentals are still on a solid footing in Europe. While industrial companies exposed to demand from commodity-related sectors reported declining revenues in 4Q15, profitability across many other industrial sectors (e.g. paper, packaging, cement, toll roads) generally improved, reflecting the favorable economic path and tailwind from positive FX effects. Overall, adj. EBITDA margins for issuers in the iBoxx HY NFI have steadily climbed over the past year, reaching the highest level (17%) since 2006. While steelmakers and miners are reporting severe sales and margin declines, they have responded to rising spreads by intensifying creditor-supportive measures: e.g. ArcelorMittal with a EUR 3bn capital increase, Anglo American announcing a tender of a series of short-dated EUR and USD notes, and Glencore securing a significant credit facility. Rating agencies are taking a similar view in assuming that default rates will increase, but much more gradually and to levels well below crisis levels (12M Moody’s baseline forecast 3.4% in Europe and 4.7% in the US, left chart below). This appears reasonable as the development of leverage (net debt/EBITDA) has been very stable in European HY (median at 4x from 3.9x, black line in the right chart below).

MODERATE DEFAULT RATE INCREASE EXPECTATIONS AND HIGH RISK COMPENSATION IN EURO NON-FINANCIAL HY

US and European default rate and baseline forecast by Moody’s Leverage (net-debt [adj.] / EBITDA [adj.]) in iBoxx EUR HY NFI

Source: iBoxx, Moody’s, UniCredit Research

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Jan-

99O

ct-9

9Ju

l-00

Apr

-01

Jan-

02O

ct-0

2Ju

l-03

Apr

-04

Jan-

05O

ct-0

5Ju

l-06

Apr

-07

Jan-

08O

ct-0

8Ju

l-09

Apr

-10

Jan-

11O

ct-1

1Ju

l-12

Apr

-13

Jan-

14O

ct-1

4Ju

l-15

Apr

-16

Jan-

17

US actual Europe_ActualEurope_Baseline US_Baseline_Forecast

1.5

2

2.5

3

3.5

4

4.5

5

5.5

6

6.5

Jan-

09A

pr-0

9Ju

l-09

Oct

-09

Jan-

10A

pr-1

0Ju

l-10

Oct

-10

Jan-

11A

pr-1

1Ju

l-11

Oct

-11

Jan-

12A

pr-1

2Ju

l-12

Oct

-12

Jan-

13A

pr-1

3Ju

l-13

Oct

-13

Jan-

14A

pr-1

4Ju

l-14

Oct

-14

Jan-

15A

pr-1

5Ju

l-15

Oct

-15

Jan-

16

25% Percentile Net debt adj. / EBITDA adj. (median) 75% Percentile

March 2016 Credit Research

Euro Credit Pilot

UniCredit Research page 20 See last pages for disclaimer.

Risk compensation at elevated levels

Risk compensation has increased significantly due to spreads increasing while leverage has trended broadly sideways: the premium paid for a single unit of leverage for bonds in the iBoxx EUR HY NFI has risen to 135bp, exceeding the 10Y average (130bp) and the median (116bp). The average in 2014 was 90bp and last year 102bp. The all-time low was reached in May 2007, at 62bp, for one turn of leverage, indicating that there have clearly been worse times to add risk. Before the spread-per-unit-of-leverage ratio moves back to just the upper range of the 3Y-10Y median risk compensation band (116bp, light red shaded area in the left chart), spreads in the iBoxx EUR HY NFI could improve by 85bp, assuming stable leverage going forward. A tightening of 120bp from current levels would push risk compensation merely to the lower range of the red shaded area.

Widening pattern indicates fewer underlying growth concerns than it seems at first glance

The way the recent weakness has unfolded has added to our conviction that the excessive spread widening has been partly fueled by scarce liquidity in secondary markets. Spread performance across rating categories does not appear to reflect deeper growth concerns among credit investors. When growth is expected to dip and potentially cause trouble for weaker companies, these tend to underperform. The widening in the market turmoil has been more or less proportional, however. The ratio of BBB to A spreads in the iBoxx EUR NFI has remained stable (1.9x) and is in line with the longer-term median level (2x). Within HY, spreads across rating categories have even compressed sharply, leaving BB notes the major underperformers YTD in spread terms: spread (ASW) ratios of both CCC over BB (2.4x) and B over BB (1.5) have compressed and dipped well below their long-term median levels (2.7x and 1.8x, respectively). Interestingly, the spread ratio of BB to BBB has remained broadly stable (2.7x), and virtually flat to its long-term median (2.6x), suggesting that the widening push has been felt strongest within the more-liquid investment-grade-rated bonds. This indicates that risk aversion has risen temporarily, and that growth is still considered fairly resilient.

SOLID RISK COMPENSATION IN HIGH YIELD WITH SELL-OFF PATTERN LIQUIDITY-DRIVEN

Risk compensation iBoxx EUR HY NFI (ASW per net debt/EBITDA) iBoxx EUR HY NFI rating category spread ratios

Source: iBoxx, Bloomberg, UniCredit Research

2.5

3

3.5

4

4.5

5

5.5

0

50

100

150

200

250

300

Feb-

06

Aug

-06

Feb-

07

Aug

-07

Feb-

08

Aug

-08

Feb-

09

Aug

-09

Feb-

10

Aug

-10

Feb-

11

Aug

-11

Feb-

12

Aug

-12

Feb-

13

Aug

-13

Feb-

14

Aug

-14

Feb-

15

Aug

-15

Spread (ASW) / leverage in bp 10Y median spread/lev.3Y median spread / lev. Median net debt adj. / EBITDA (adj)

1

1.5

2

2.5

3

3.5

4

4.5

Jan-

11M

ar-1

1M

ay-1

1Ju

l-11

Sep

-11

Nov

-11

Jan-

12M

ar-1

2M

ay-1

2Ju

l-12

Sep

-12

Nov

-12

Jan-

13M

ar-1

3M

ay-1

3Ju

l-13

Sep

-13

Nov

-13

Jan-

14M

ar-1

4M

ay-1

4Ju

l-14

Sep

-14

Nov

-14

Jan-

15M

ar-1

5M

ay-1

5Ju

l-15

Sep

-15

Nov

-15

Jan-

16

CCC vs. B median CCC/BB vs. BB median B/BBCCC vs. BB median CCC/BB

March 2016 Credit Research

Euro Credit Pilot

UniCredit Research page 21 See last pages for disclaimer.

Securitization: Reviving Italian NPL ABS In a recent agreement between Italy and the EC on the way in which Italian banks might

reduce their vast stock of non-performing loans (NPLs) such that it would not be considered state aid, securitizations involving government guarantees were proposed as a solution. The plan targets the EUR 200bn of severely delinquent debt, often referred to as bad loans. The Italian government devised a guarantee mechanism that allows banks to securitize their NPLs, subject to a number of conditions. It is as yet unclear whether NPL ABS will be eligible under the ECB repo window. A number or smaller Italian banks are reportedly already exploring such deals. Despite the many concerns, caveats and complexities, we believe that the plan is a positive for Italian securitization, if only in signaling that securitization remains a viable solution. On the other hand, we do not expect the measure to materially boost investor-placed Italian securitization issuance.

Bad loans are a drag on bank balance sheets and lending capabilities

Italy’s prolonged recession and slow growth have clearly left their mark in terms of bad loans. The amount of NPLs (also referred to as “sofferenze”) potentially eligible for future securitization under the plan increased to more than EUR 200bn (about 13% of GDP) at the end of 2015, up from EUR 60bn in 2009. The elevated and growing amount of NPLs in Italy continues to weigh on the balance sheets of banks, while constraining their capital and ability to lend. As shown in the left chart below, since the onset of the financial crisis in 2008, Italian NPLs have more than tripled to 18.2% (December 2015) of total gross loans, from just 10% in 2011 and around 5% in 2007, reflecting the challenging macroeconomic backdrop and the ensuing rise in severe delinquencies. Another major roadblock for the NPL resolution has been the slow pace of write-offs resulting from the limited incentive for lenders to incur losses. Moreover, in the absence of a stronger economic recovery and without a significant pickup in write-offs and loan sales (the 2015 rate was about 8%), the bad debt ratio in Italian banks is likely to remain very high for several decades, according to IMF estimates.

NPL guarantee scheme technicalities

Under the proposed GACS mechanism, the senior tranches securitizations in question would be backed by an Italian government guarantee. The guarantee scheme specifies that senior-most ABS notes must be of IG credit quality prior to the application of the guarantee, that is, without accounting for the guarantee as such. To qualify, at least 50% of the junior and mezzanine notes (if included in the deal structure), would be placed, with the remaining junior notes being retained by the originator. Regarding the guarantee for the most senior tranche, Italy would provide it at a bank’s request, on the condition that the tranche is rated at least IG by one of the recognized credit rating agencies (please refer to our recent note for details). Importantly, the guarantee would be priced based on the average CDS spread of the previous six months for a basket of Italian issuers. Excluding the recent spread blowout in European bank senior CDS, we estimate the cost of such a guarantee to amount to 80-120bp.

ITALIAN BAD LOAN STOCKS (“SOFFERENZE”) AND LACK OF GRANULARITY IN ITALIAN NPL EXPOSURE

Banks’ NPL ratio increased to 18.2% in December 2015 Less than 25% of the bad-loan stock is of loans of EUR <250,000

Source: Bank of Italy, Bloomberg, Moody’s UniCredit Research

0

4

8

12

16

20

0

50

100

150

200

250

Dec-00 Dec-03 Dec-06 Dec-09 Dec-12 Dec-15

%EU

R b

n

Other Financial Inst. HouseholdsNFI corporations/SMEs NPL to total gross loans (RS)

0

10

20

30

40

50

60

70

0

5

10

15

20

25

30

35

Bel

ow 3

0

30 to

75

75 to

125

125

to 2

50

250

to 5

00

500

to 1

000

1000

to 2

500

2500

to 5

000

5000

to 2

5000

>250

00

# of

def

aulte

d bo

rrow

ers

(%)

Bad

loan

s (%

)

Defaulted amount buckets (EUR, thousands)

Defaulted amount (LS) Defaulted borrowers (RS)

granular "securitizable" exposure

March 2016 Credit Research

Euro Credit Pilot

UniCredit Research page 22 See last pages for disclaimer.

Breakthrough or blip? The agreement could pave the way for the re-emergence of the NPL ABS sector in Europe, which has been largely dormant since 2007. In the run-up to the financial crisis, the European ABS market saw at least 34 Italian NPL securitizations backed by assets ranging from unsecured consumer loans to residential and commercial mortgages. The introduction of a new securitization law supporting NPL transactions quickly boosted issuance in 2000. Primary activity of Italian NPL securitizations peaked in 2001, with Italian lenders making extensive use of ABS to dispose of their NPLs from past recessions. Unlike many of the granular securitizations backed by performing consumer loans and statistically predictable cash flows, NPL transactions have unique credit profiles because they mainly derive their cash flows from recoveries on distressed debt.

NPLs – from nascent to niche market