Effects Of Bancassurance On Financial Performance Of ...

98

Effects Of Bancassurance On Financial Performance Of Insurance Companies In Kenya: A Case Of Selected Insurance Companies In Nairobi County by Jared Oirere Orora A thesis presented to the School of Business and Economics of Daystar University Nairobi, Kenya In partial fullfllment of the requirements for the degree of MASTERS OF BUSINESS ADMINISTRATION in Finance November 2018 Daystar University Repository Library Archives Copy

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Effects Of Bancassurance On Financial Performance Of ...

Effects Of Bancassurance On Financial Performance Of Insurance Companies In

Kenya: A Case Of Selected Insurance Companies In Nairobi County

by

Jared Oirere Orora

A thesis presented to the School of Business and Economics

of

Daystar University

Nairobi, Kenya

In partial fullfllment of the requirements for the degree of

MASTERS OF BUSINESS ADMINISTRATION

in Finance

November 2018

Daystar University Repository

Library Archives Copy

APPROVAL

EFFECTS OF BANCASSURANCE ON FINANCIAL PERFORMANCE OF INSURANCE COMPANIES IN KENYA: A CASE OF SELECTED INSURANCE COMPANIES IN NAIROBI

COUNTY

by

Jared Oirere Orora

In accordance with Daystar University policies, this thesis is accepted as a partial

fulfillment of the requirements for the Master of Business Administration degree.

Date:

Joshua Okeyo, MBA,

1st

Supervisor

Richard Maswili, MBA

2nd

Supervisor

______________________________ Samuel Muriithi, PhD, HoD, Commerce

_____________________

_________________________________

Evans Amata, PhD, Dean, School of Business and Economics

_____________________

ii

Daystar University Repository

Library Archives Copy

Copyright © 2018 Jared Orora Oirere

iii

Daystar University Repository

Library Archives Copy

DECLARATION

EFFECTS OF BANCASSURANCE ON FINANCIAL PERFORMANCE OF INSURANCE COMPANIES IN KENYA: A CASE OF SELECTED INSURANCE COMPANIES IN NAIROBI

COUNTY

I declare this thesis is my original work and has not been submitted to any other college or university for academic credit.

Signed: Date: Jared Orora Oirere

13-1532

iv

Daystar University Repository

Library Archives Copy

ACKNOWLEDGEMENTS

First and foremost, I wish to thank our Almighty God for giving me the gift of life,

patience and persistence in pursuing this study. There are a number of people without

whom this research might not have been a success and I am greatly indebted to.

I would like to acknowledge my loving parents whom have always been there for me morally

and financially towards achieving my academic dreams. My sincere and profound gratitude

goes to my mentors and supervisors, Mr. Joshua Okeyo and Mr. Richard Maswili. It would

always be my pleasure reminding you of your insightful thoughts and contributions

throughout this study. God bless you abundantly for the job well done.

v

Daystar University Repository

Library Archives Copy

TABLE OF CONTENTS

APPROVAL ....................................................................................................................... ii

DECLARATION ............................................................................................................... iv

ACKNOWLEDGEMENTS ................................................................................................ v

TABLE OF CONTENTS ................................................................................................... vi

LIST OF TABLES ........................................................................................................... viii

LIST OF FIGURES ........................................................................................................... ix

LIST OF ABBREVIATIONS AND ACRONYMS ........................................................... x

ABSTRACT ....................................................................................................................... xi

DEDICATION .................................................................................................................. xii

CHAPTER ONE ................................................................................................................. 1

INTRODUCTION AND BACKGROUND OF THE STUDY .......................................... 1

Introduction ......................................................................................................................... 1 Background of the Study .................................................................................................... 2

Statement of the Problem .................................................................................................... 9

Purpose of the Study ......................................................................................................... 10

Objectives of the Study ..................................................................................................... 10

Research Questions ........................................................................................................... 10

Justification of the Study .................................................................................................. 11

Significance of the Study .................................................................................................. 11

Scope of the Study ............................................................................................................ 12

Limitations and Delimitations of the Study ...................................................................... 12

Assumptions of the Study ................................................................................................. 13

Definition of Terms........................................................................................................... 13

Summary ........................................................................................................................... 14

CHAPTER TWO .............................................................................................................. 15

LITERATURE REVIEW ................................................................................................. 15

Introduction ....................................................................................................................... 15

Theoretical Framework ..................................................................................................... 15

General Literature Review ................................................................................................ 22

Empirical Literature Review ............................................................................................. 30

Conceptual Framework ..................................................................................................... 31

Summary ........................................................................................................................... 32

CHAPTER THREE .......................................................................................................... 33

RESEARCH METHODOLOGY...................................................................................... 33

Introduction ....................................................................................................................... 33

Research Design................................................................................................................ 33 Population of the Study ..................................................................................................... 34

Target Population .............................................................................................................. 34

Sampling Size ................................................................................................................... 34

Sampling Technique ......................................................................................................... 35

Data collection Instruments. ............................................................................................. 37

Data Collection Procedures ............................................................................................... 37

Pretesting........................................................................................................................... 38

Reliability and Validity ..................................................................................................... 38

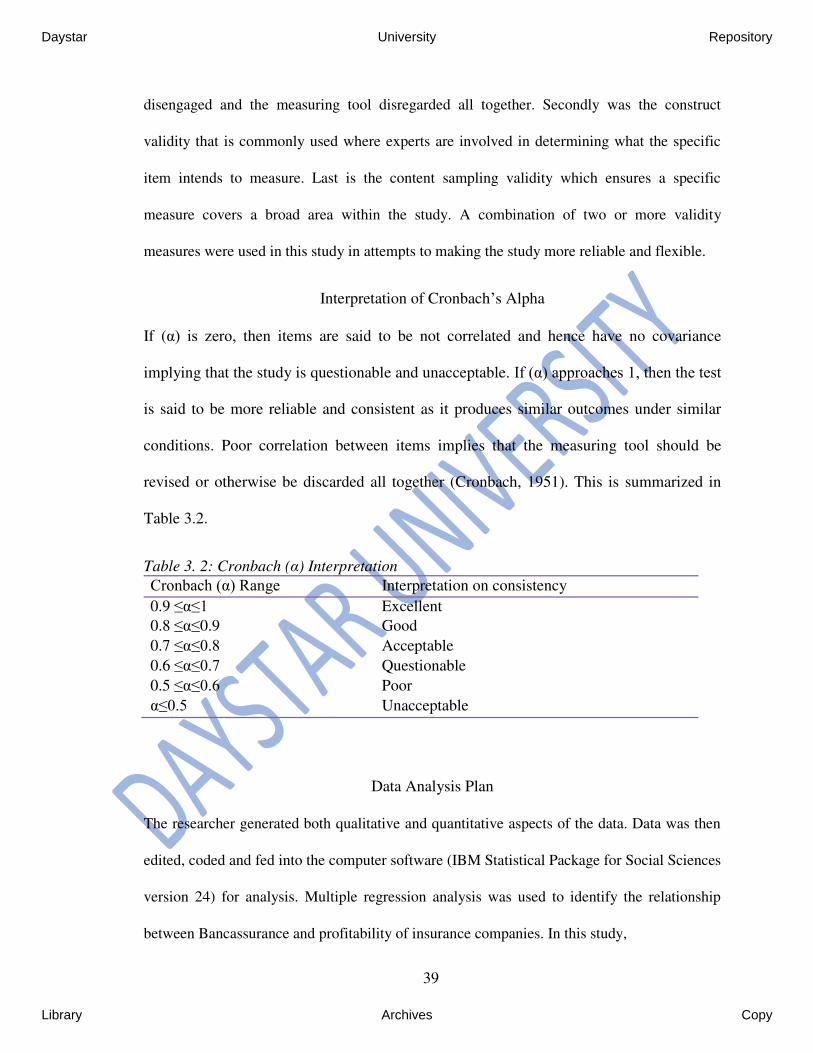

Interpretation of Cronbach’s Alpha .................................................................................. 39

Data Analysis Plan ............................................................................................................ 39

vi

Daystar University Repository

Library Archives Copy

Ethical Considerations ...................................................................................................... 40

Summary ........................................................................................................................... 41

CHAPTER FOUR ............................................................................................................. 42

DATA PRESENTATION, ANALYSIS AND INTERPRETATION .............................. 42

Introduction ....................................................................................................................... 42

Data Presentation, Analysis and Interpretation ................................................................. 42

Summary of Key Findings ................................................................................................ 57

Summary ........................................................................................................................... 58

CHAPTER FIVE .............................................................................................................. 59

DISCUSSIONS, CONCLUSIONS AND RECOMMENDATIONS ............................... 59

Introduction ....................................................................................................................... 59

Discussion of Key Findings .............................................................................................. 59

Conclusions ....................................................................................................................... 62 Recommendations ............................................................................................................. 63

Areas for Further Research ............................................................................................... 64

REFERENCES ................................................................................................................. 65

APPENDICES .................................................................................................................. 73

Appendix A: Questionnaire .............................................................................................. 73

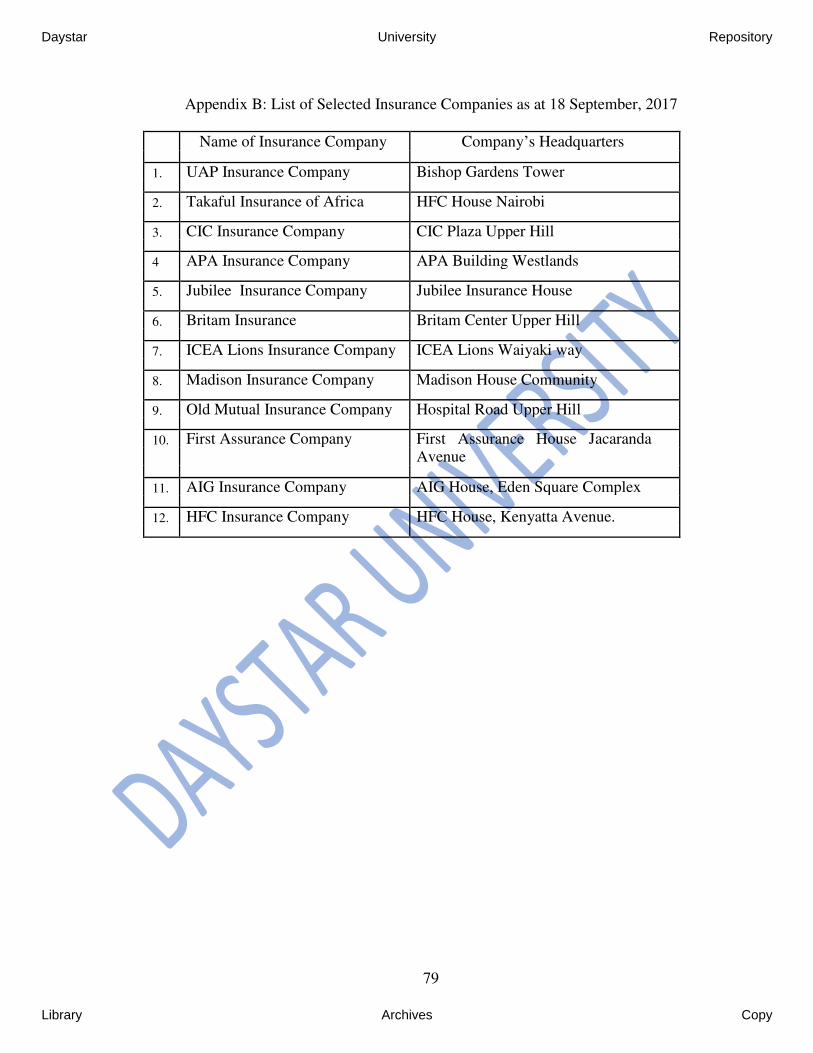

Appendix B: List of Selected Insurance Companies as at 18 September, 2017 ............... 79

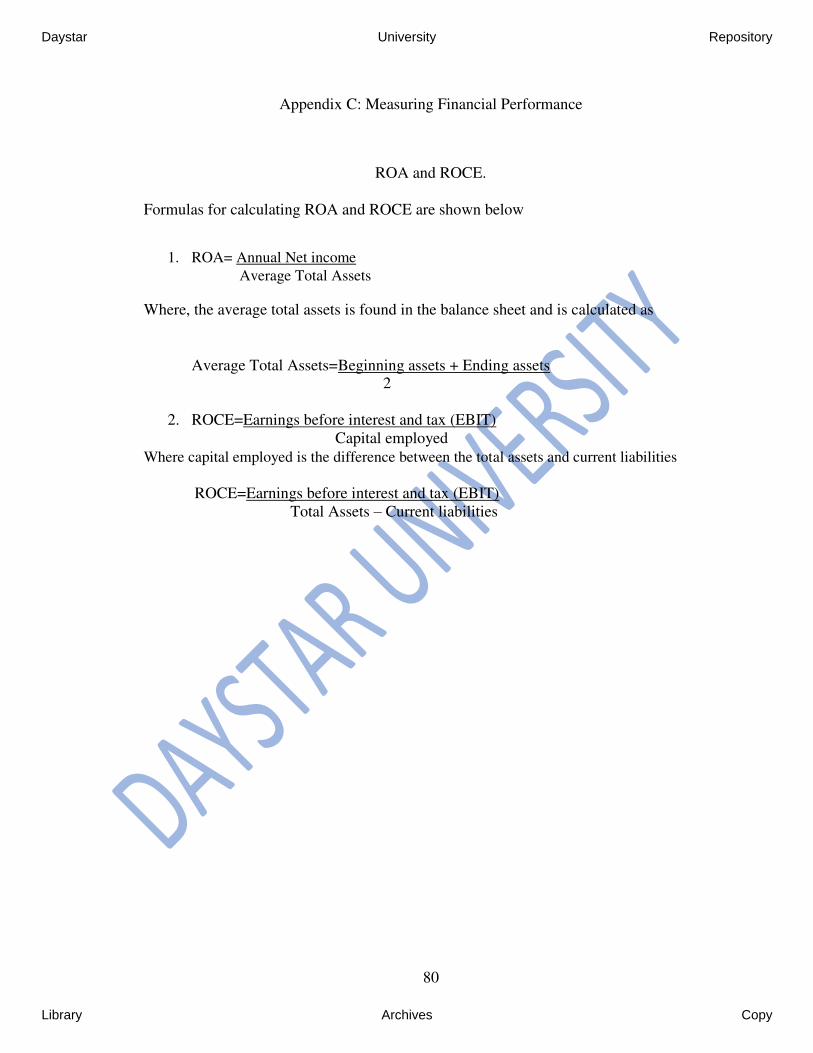

Appendix C: Measuring Financial Performance............................................................... 80

Appendix D: Results of ROA and ROCE from Selected Insurance Companies .............. 81

Appendix E: Research Permit ........................................................................................... 82

Appendix F: Anti-Plagiarism Report ................................................................................ 83

vii

Daystar University Repository

Library Archives Copy

LIST OF TABLES

Table 3. 1: Sample Size ..................................................................................................... 36

Table 3. 2: Cronbach Interpretation ................................................................................. 39

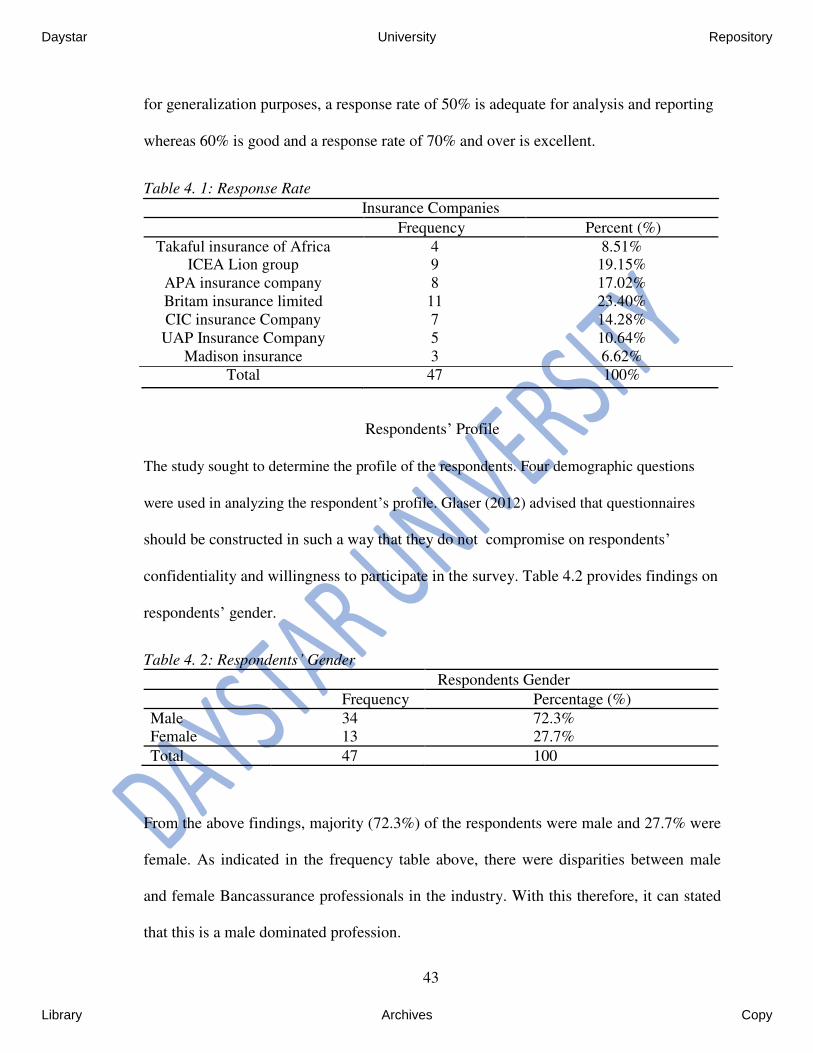

Table 4. 1: Response Rate ................................................................................................. 43

Table 4. 2: Respondents’ Gender...................................................................................... 43

Table 4. 3: Respondents Age Distribution ........................................................................ 44

Table 4. 4: Respondents’ Highest education Level ........................................................... 44

Table 4. 5: Position Held in the Organization .................................................................. 45

Table 4. 6: Bancassurance Products ................................................................................ 47

Table 4. 7: Bancassurance Models Adoptd ...................................................................... 49

Table 4. 8: Challenges Facing the Bancassurance Industry ............................................ 50 Table 4. 9: Regression Modeling ...................................................................................... 53

Table 4. 10: The ANOVA Table ........................................................................................ 54

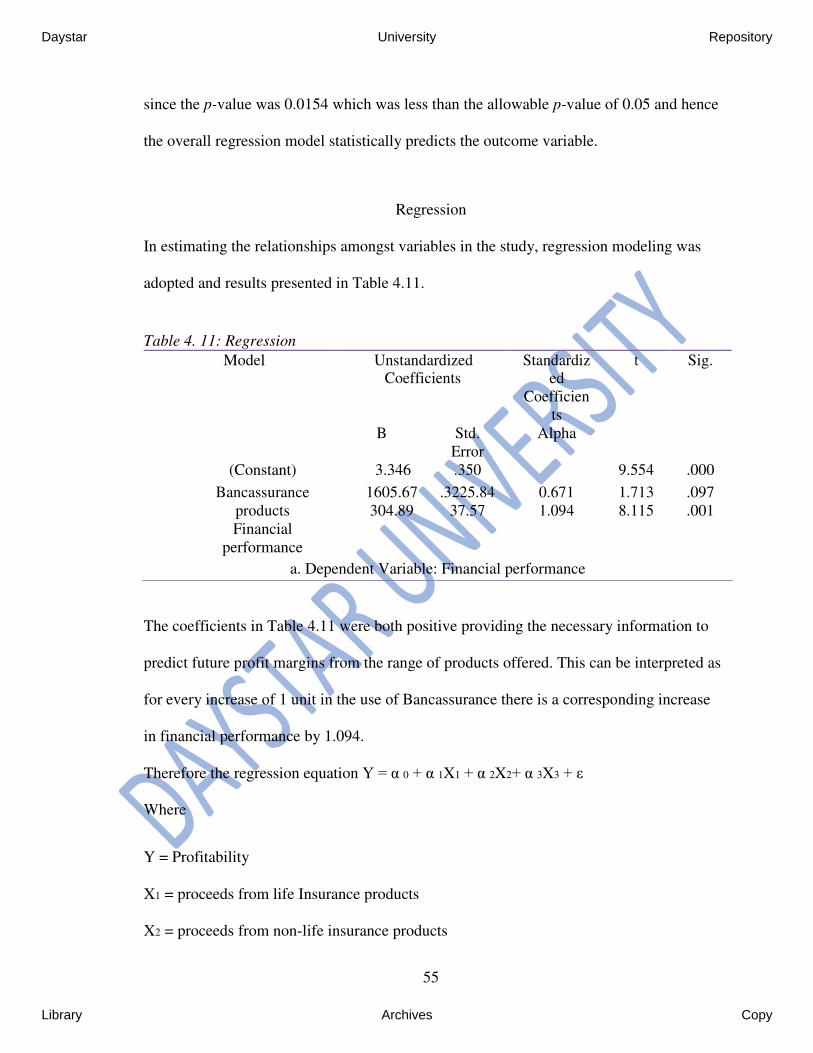

Table 4. 11: Regression .................................................................................................... 55

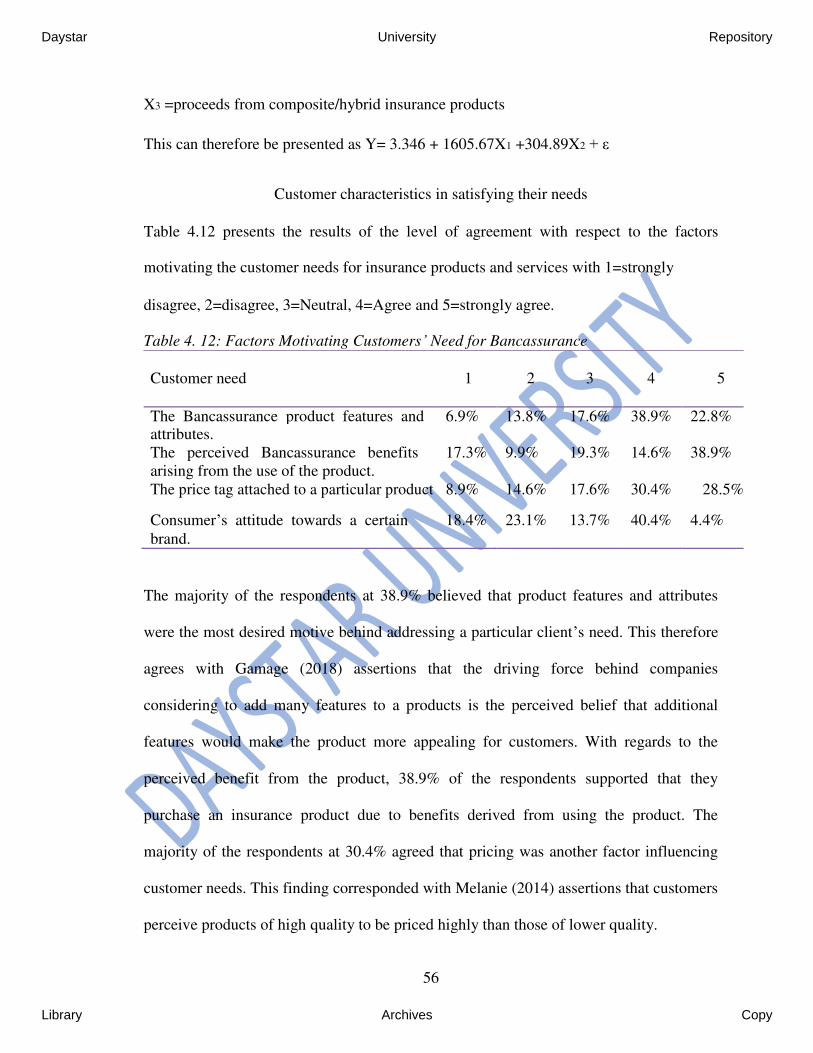

Table 4. 12: Factors Motivating Customers’ Need for Bancassurance ........................... 56

viii

Daystar University Repository

Library Archives Copy

LIST OF FIGURES

Figure 2. 1: Conceptual Framework ................................................................................ 31

Figure 4. 1: Department Worked in .................................................................................. 46

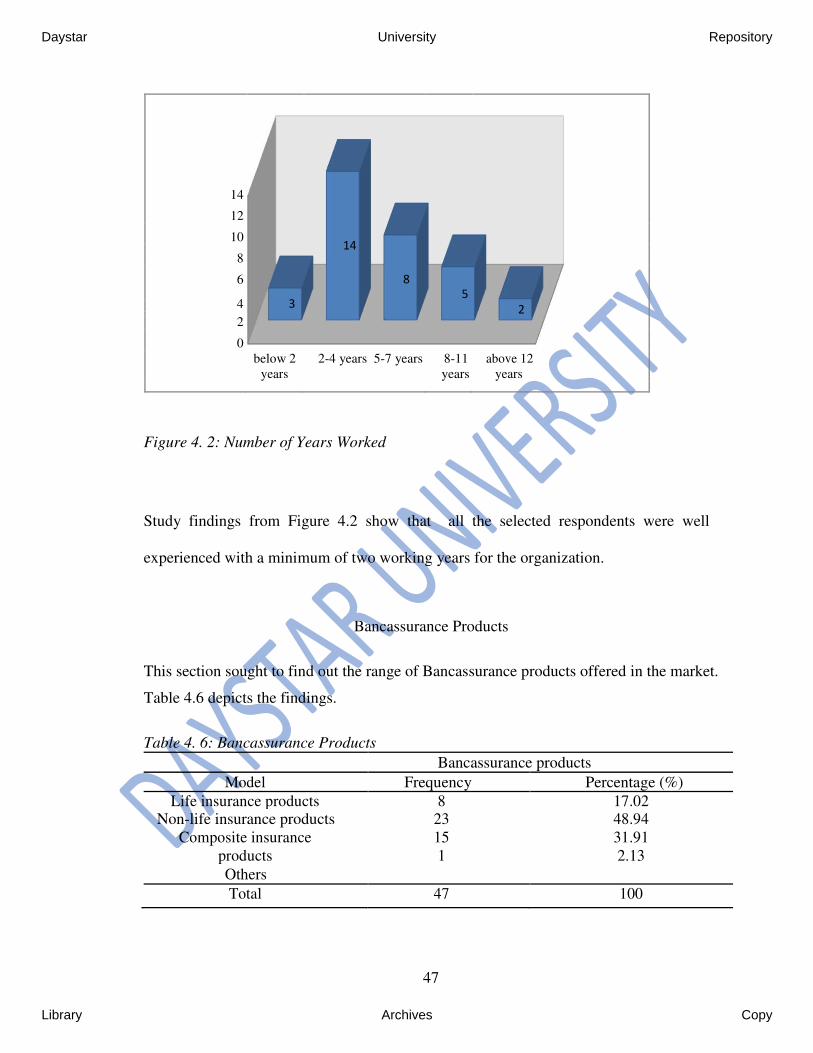

Figure 4. 2: Number of Years Worked .............................................................................. 47

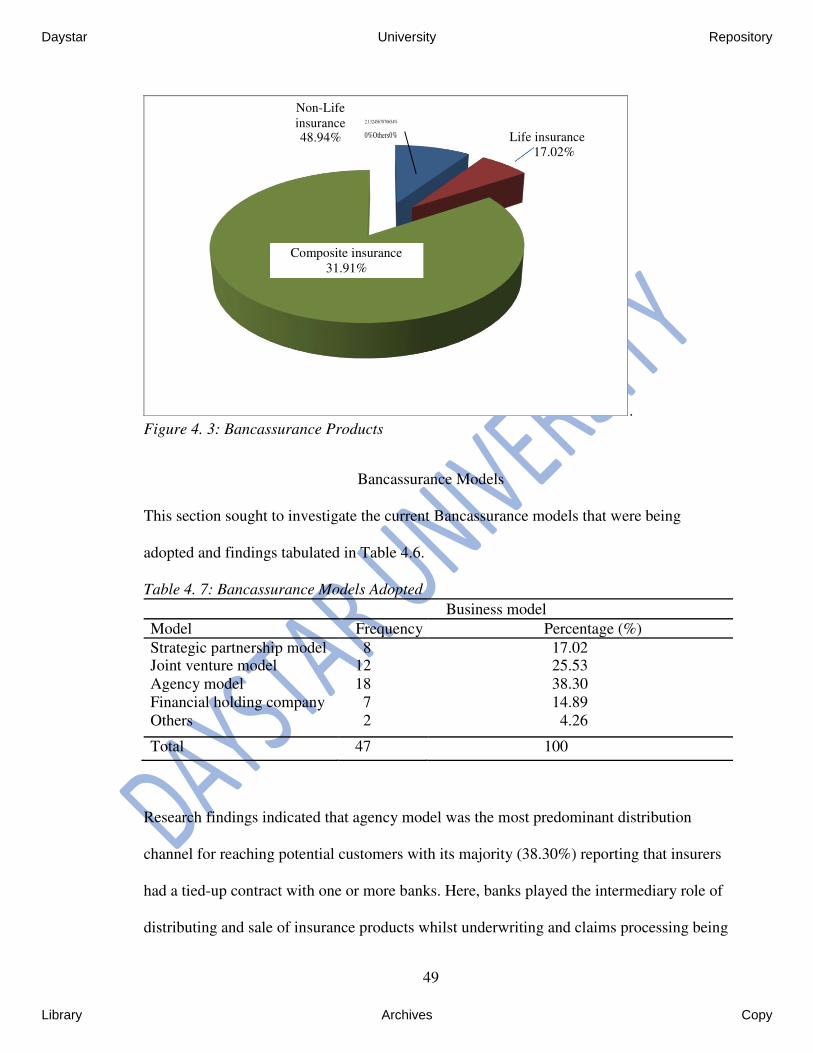

Figure 4. 3: Bancassurance Products .............................................................................. 49

ix

Daystar University Repository

Library Archives Copy

LIST OF ABBREVIATIONS AND ACRONYMS

AKI:

BIM:

BRITAM:

CBK:

CIC:

GLB Act:

HFCI:

IRA:

MIP:

NCST:

NOPAT:

OODC:

OTC:

RBI:

RGAI:

ROCE:

SEDCAR

SPSS:

WIBA:

Association of Kenya Insurers

Bank Insurance Model

British American Insurance Company

Central Bank of Kenya

The Co-operative Insurance Corporation

Gramm Leach Bliley Act

Housing Finance Corporation Insurance

Insurance Regulatory Authority

Medical Insurance Providers

National Council of Science and Technology

Net Operating Profit after Tax

Old Outdated Distribution Channel

Over the Banks Counters

Reserve Bank India

Reinsurance Group of America Incorporated

Return on Capital Employed

Standards for Education Data Collection and Reporting

Statistical Package for Social Sciences

Work Injury Benefit Act

x

Daystar University Repository

Library Archives Copy

ABSTRACT

This study aimed at assessing the effects of Bancassurance on financial performance of

insurance companies in Kenya. Its objectives were to; identify the Bancassurance models and

products, identify the challenges facing the Bancassurance industry, measure the financial

performance of the selected insurance companies and investigate how the effects of

Bancassurance had resulted to financial performances for the selected insurance companies.

The study adopted descriptive research design which gave both the quantitative and

qualitative aspects of the study. It targeted all the 12 insurance firms that had incorporated

Bancassurance business model in their business operations. Stratified random sampling

technique was used to select a sample size of 47 respondents. Data was analyzed using the

Statistical Package for Social Sciences (SPSS) version 24. Multiple regression analysis was

used to identify the relationship between Bancassurance and profitability of the insurance

companies. Study findings revealed a high preference for composite products with agency

model being best suited as the most desired distribution channel sought after by

Bancassurance firms in the Kenyan market. In addition, firms that had incorporated

Bancassurance activities in their business operations witnessed significant increase in

revenues and consequently, improved on product delivery that sought to address customer

needs. The study concluded that there was a positive and significant increase in product sales

owing to Bancassurance activities. The researcher recommended that there should be local

insights into the Bancassurance literature as a viable tool for financial performance as most of

these ideas were based on Western and Indian context. In addition, there was need for the

Bancassurance firms to engage in strong cross industry relationship-building activities that

emphasized on buyer-seller interactions which were the key ingredients that enhanced the

success of Bancassurance activities in Kenya.

xi

Daystar University Repository

Library Archives Copy

DEDICATION

I dedicate this study to my loving parents, Mr. Hobadiah Maosa Orora and Ms. Monicah

Nyamote Orora for their moral and financial support throughout this academic research.

Thank you for teaching me the core values of hard work, patience and determination

which enabled me to focus towards the successful completion of this study.

xii

Daystar University Repository

Library Archives Copy

CHAPTER ONE

INTRODUCTION AND BACKGROUND OF THE STUDY

Introduction

Bancassurance came from a combination of the two French words Banque (Bank) and

Assurance (insurance). This is basically the cross-selling of insurance products through

the banks’ platform (Voutilainen, 2005). Bancassurance therefore can be defined as a

partnership arrangement between banks and insurance companies where the insurer uses

the banks infrastructure to sell and distribute insurance products. This implies that both

the insurers and banks exploits their existing infrastructure to facilitate a transaction with

minimum investment outlay (Yasouka, 2005).

Financial performance refers to the fulfillment or accomplishment of a given task

measured against the standards of management efficiency, cost reduction and compliance.

In other words, financial performance is the degree or the process of measuring the firms

polices and operational results in monetary terms usually over a given period of time

(Juma, 2015). Jongeneel (2011) outlined five measures of financial performances; Age

and size of the firm, liquidity. Profitability (Return on Asset and Return on Capital

Employed), solvency and repayment capability of the enterprise. This study however

explored ROA and ROCE as the parameters for measuring financial performance. The

study revealed a strong evidence that Bancassurance affects financial performance in an

organization. Jongeneel (2011) found out that an increase in one unit of Bancassurance

led to an increase of 1.094 units in financial performance. However, this relationship can

be enriched by other factors such as customer needs.

1

Daystar University Repository

Library Archives Copy

Background of the Study

Global perspective of Bancassurance

France is arguably the first European country to have used the term Bancassurance in the

late 1980s and this denotes the simple distribution channel for insurance products through

banks branches. Today however, the term is used to describe all kinds of transactional

relationships between the bank and insurance companies (Ricci, 2012).

In countries like Italy, Spain, Portugal and Romania, banks still remains to be the main

distribution channel for insurance policies while countries like United Kingdom and

Germany heavily relies on traditional agents, intermediaries and brokers to sell and

distribute insurance. ‘Latin-European’ countries and Australia ranks amongst the highest

consumers of Bancassurance products while Portugal is the leading distributer of

insurance in the world with 61.8 per cent of its total insurance primarily being sold over

the bank’s counters (Jongeneel, 2011).

In India, the word Bancassurance simply means Alfinaze and is a term used to refer to

distribution of insurance products through banks whose core business is in deposit taking

mortgages and lending (Neelamegam, 2008). The Bancassurance sector opened up its

doors to practice in August, 2000 and is currently being considered as one of the most

vibrant financial sectors in the world serving over 200 million clients and a vast banking

infrastructure consisting of over 53,000 branches that run across urban and rural India

(RBI, 2006).

2

Daystar University Repository

Library Archives Copy

In the United States, Bancassurance has evolved on a full scale basis following the

enactment of the comprehensive financial modernization Act of 1999 also referred to as

Gramm-Leach-Bliley Act (GLB) which over saw Travel group insurance and Citicorp

bank merging together to offer Bancassurance products (Watson, 2010). Bancassurance

however took much longer to develop in Asian countries with its first sign noted in 2001

in Japanese markets. This was as a result of the enactment of the Financial Holding

Company Act of 2000 that permitted security firms and banks to engage in sale of

insurance products through banks. During these initial stages, insurance sales were

primarily restricted to credit life insurance and long term-fire insurance which were

closely related to banking core operations of mortgage lending. The slow pace of

Bancassurance uptake in these regions was attributed to inadequate regulatory

frameworks and guidelines governing the Bancassurance sector (Yasouka, 2005).

South Korea and Philippines whose markets were previously banned from participating in

Bancassurance are now taking a more proactive approach towards facilitating this

channel. In Singapore however, it is still a controversial issue as many critics argue that

the concept would give the banking and insurance sectors too much monopolistic control

and power over financial service markets (Gujral, 2014)

Bancassurance in Africa

Surprisingly enough, Bancassurance has not taken off with the same vigor in African soils

as compared to European markets. This has been partly attributed to stringed trust

relationships between banking and insurance institutions. Unlike lending institutions like

banks whom entrusts customers upfront with loans and hopes they will faithfully honor

3

Daystar University Repository

Library Archives Copy

their obligations, customers here have to pay first and hope that the insurer shall make

good use of their promise while paying claims whenever they are due. The concept

therefore is at its infancy stages to African mindsets with countries like Angola, Côte

d'Ivoire, Ghana, Kenya, Mozambique, Nigeria, South Africa, Tanzania, Uganda and

Zambia being well-positioned to flourish due to their appreciation in the value of

insurance and the tax incentives that comes with it (Finacord, 2014). Banks in these

regions have not only increased their size of their branch networks and deposit accounts,

but are al increasingly adopting Bancassurance as their future risk-free revenue generator.

On the other hand, insurance companies are reaping benefits as they tap-into a wider

physical spread and hence increasing their clientele-profit portfolios (Jongeneel, 2011).

In sub-Saharan regions, South Africa Bancassurance markets are by far the most

sophisticated and mature. This is mainly attributed to the presence of international and

regional banks and insurance institutions namely; Bank of Africa, Barclays, and Standard

chartered, AIG, Eco bank, Jubilee insurance, Old mutual, Sanlam and Kenyan Alliance

insurance that have dominated this markets (Florido, 2002).

Bancassurance in Kenya

Bancassurance is a relatively new concept in Kenya. In the recent past however, banking

and insurance sectors have witnessed destructive financial innovations over the last nine

years following its adoption in 2009 with Equity Bank Limited (EBL) and British

American insurance (BRITAM) taking the first initiative to facilitate this move. This was

in response to meeting the ever growing customer needs for convenience, change in

market structure and government policies (Karanja, 2011)

4

Daystar University Repository

Library Archives Copy

Currently, there are 12 insurance companies practicing Bancassurance in the country. This

includes; Takaful Insurance of Africa, ICEA Lion Group Insurance, APA Insurance

Company, CIC Insurance group, UAP Insurance Company, Madison Insurance Company,

Britam, AIG insurance, Kenindia insurance, Old Mutual insurance and the recently

launched Housing Finance Corporation Insurance (Juma, 2015). The rate of insurance

penetration currently stands at 3.5 percent and a meager 1 percent for life insurance. This

is quite low as compared to international standard rate of 6 percent for life covers while

developing counterparts like South Africa boasts a 9.94 percent insurance penetration rate

(Jaganathan, 2014).

Benefits of Bancassurance

Motives behind entry into Bancassurance vary from one set of individuals to the other.

Consumers have great accessibility to multiple financial services under one roof (both

banking and insurance products) and this has significantly enhanced customer satisfaction

and retention. Distribution costs are also reduced compared to traditional broker

distribution model with the same being passed on to consumers inform of lower premium

costs. Methods of premium payments for banking clients are also simplified as they are

debited directly from their accounts. This would not have been possible if the two

institutions worked separately.

Bank considers Bancassurance as cash cows for creating continuous revenue streams

arising from diversification strategy for business activities with minimum investment.

Banks become sort of supermarkets providing a One-Stop-Shopping facility for their

financial and insurance needs. There are endless opportunities in expanding their product

and service outreach and in-by so doing, they have improved on their customer needs 5

Daystar University Repository

Library Archives Copy

satisfaction, retention and loyalty. Besides being a one-stop-shop for financial needs,

distribution costs are significantly reduced since in most cases it’s the banks existing

employees who mobilize and advertise insurance products for a commission per each

close of sale (Carow, 2001).

Benefits to insurers are quite compelling too. They have significantly expanded their

customer base and outreach with which would rather have been difficult to access.

Moreover, insurers have the opportunity to diversify their distribution channels to avoid

over reliance on a single network. Insurers have the advantage of reducing distribution

costs compared to costs inherent to traditional agents and brokers and hence products are

offered at lower costs. Carow (2001) observed that a foreign insurer can establish its

presence quickly in a new market by using an existing network of a local bank.

Risks and Vulnerabilities Associated with Bancassurance

Entry of banks into insurance industry has intensified a long standoff between insurance

brokers and sales agents. Agents contemplate losing placements and commissions to

banks. Benoist (2002), argued that the move is not financially sound for an economy as

this shall suppress the market and give banks a near monopoly over other financial

sectors. Image and reputation risks are viewed as a detrimental factor for banks in the

event of not handling claims as they fall due. Product cannibalism is another factor that

may render Bancassurance ineffective. Alzheimer (2013) observed that there were

fundamental unethical issues by account managers and relationship officers at the bank

level whom have often resulted into misrepresentation of a product to the general public.

Lack of unified chain of command has often rendered most of its customers confused on

whom to report to in the event of a claim.

6

Daystar University Repository

Library Archives Copy

This however can be handled effectively by investing on trainings at the branch level and

the two institution working as business partners as noted by (Carow, 2001).

Financial Performance

Financial performance is a subjective measure of how well a firm can utilize its assets

from its primary mode of business to generate revenues (Doron, 2010). It is therefore a

term used in general to denote the overall financial health of an enterprise over a given

period of time. The core purpose of measuring organizational performance is to provide

researchers and managers a better understanding of the implications of selecting a

particular strategic approach.

Traditionally, the most frequently used measures of financial performance majorly

focused on stakeholders driven economy that was characterized by failure to include non-

financial factors such as products quality, employee’s morale, customer need and

satisfaction. This however led to poor predictors of financial performance (Cross, 1991).

In today’s contemporary approach however, performance measurements highlights the

intangible dimensions such as public image, customer satisfaction, employee retention

and investment in trainings. In insurance, financial performance is normally expressed in

monetary terms and this denotes the difference between revenues and expenses that can

take the form of underwriting profits, net premiums earned, return on investments, annual

turnover, and returns in equity (Chen, 2004).

Another determinant for financial performance is the level of liquidity which denotes the

ability of insurers to meet their immediate commitments and obligations to policy holders

when claims fall due (Adams, 2000).

7

Daystar University Repository

Library Archives Copy

Size and age of the insurer is another factor cited by Chaharbaghi (1999), who stressed that

large firms can exploit economies of scale and scope by becoming more efficient compared to

small firms whereas older firms benefits from brand reputation and are not prone to liability

of newness due to the experience they have enjoyed over time. On the other hand, older firms

are prone to inertia and bureaucratic ossification which may be out of touch with the changes

in technology and market conditions (Shiu, 2004). In measuring financial performance, the

study addressed customer needs and profitability (ROA and ROCE) to denote the firms

overall financial health over a period of 5 years (2013-2018).

Bancassurance and Financial Performance

Financial institutions have been grappling with decreasing interest margins due to stiff

competition, changes in technology, deregulation of financial markets and globalization

and hence the dire need for finding out new ways of carrying out financial transactions at

minimal costs (Chaharbaghi, 1999). With the modern market liberalization and cross-

listing of companies in Africa, Bancassurance has become an effective tool for easing

transactions of policies between the main insurance companies and the affiliated banks

this despite geographical distance and inter-border restrictions. Customers have an access

to one-stop-shopping at banking halls. Sigh (2010) noted that this co-operation has led the

industry to leverage on the existing infrastructures, workforce and existing customer

service relations to its full capacity.

According to Chen (2011), Bancassurance will be a norm in the near future as we have

witnessed mergers and acquisitions in the recent past. In the Kenyan context however, we

have seen Equity bank and Britam, Jubilee insurance and KCB coming together to form a

Bancassurance unit and the future of this move looks bright. The kinds of revenue streams

8

Daystar University Repository

Library Archives Copy

have been fairly steady and consistent over the past years. The study therefore sought to

investigate whether Bancassurance activities have resulted to financial performance for

the bank-insurance institutions.

Statement of the Problem

The idea of Bancassurance is a relatively new concept that has received significant

attention from European and Asian scholars with little attention of how it has influenced

financial performance of these industry players. The banking and insurance sectors plays

an integral part of the economy as they contribute heavily towards the financial

intermediation of the entire financial system. As such, their success means success to the

entire economy and consequently, their failure means failure to the economy at large

(Ansah-Adu, 2012).

Young (2013) observed that banking and insurance institutions have been witnessing

year-on-year declines in their profits and clients’ portfolios due to the rising costs of

doing businesses, new technological advancements and innovations from other sectors

players like mobile and internet banking. The industry is therefore under pressure to

change their business model to address these diverging challenges arising from

Statistics from CBK and IRA highlighted that only a handful of banks (12 out of 51 licensed

insurance companies) practiced Bancassurance, while other players are yet to explore this

option (IRA, 2014). In an effort to curb these dwindling profits and market dominance, banks

and insurers have developed the concept of Bancassurance. However, most of the

Bancassurance studies are Western based and hence the need to have such our own studies

9

Daystar University Repository

Library Archives Copy

in the Kenyan context. This study therefore sought to establish whether Bancassurance is

viable tool for financial performance of insurance industries in Kenya.

Purpose of the Study

The purpose of this study was to assess the effects of Bancassurance on financial

performance of insurance companies in Kenya.

Objectives of the Study

This study sought to address the following research objectives:

i. To identify the Bancassurance products and models in Kenya.

ii. To identify the challenges facing the Bancassurance industry in Kenya.

iii. To measure the financial performances of the selected insurance companies.

iv. To investigate the effects of Bancassurance on financial performance for the

selected insurance companies in Kenya.

Research Questions

The study sought to answer the following research questions:

i. What were the Bancassurance products and models in Kenya?

ii. What were the challenges facing the Bancassurance industry in Kenya?

iii. What was the financial performance of the selected insurance companies?

iv. What were the effects of Bancassurance and financial performance on insurance

companies in Kenya?

10

Daystar University Repository

Library Archives Copy

Justification of the Study

Financial institutions today are facing declining profit margins, intense competition,

drastic shift in customer tastes and preferences amidst fragile economic environment. In

order for these financial institutions to gain an extra coin amidst harsh economic climate,

there was the need of finding other ways of generating income and provide more value-

added services under one roof. Bancassurance therefore addressed the best possible

solution amidst these diverging challenges in the banking and insurance industry.

Significance of the Study

This study would be of great importance to several stakeholders including the insurance

sector, policy makers, researchers and the general public.

The main beneficiaries of this study would be the insurance sector that would wish to

venture into product sales through banks platforms. The study therefore provided an in-

depth insights into the Bancassurance practices as viable tools for supplementing the

banking and insurance core earnings. Through this channel, insurance companies would

be able to leverage on the banks vast customer base and marketing capabilities in entering

the untapped markets whereas banks would benefit from free based commissions from the

sale of insurance products. This therefore would adversely influence on the decision

making process on whether or not to adopt the idea of Bancassurance.

The study may benefit government agencies in reviewing their insurance and banking

policies. In by so doing, they will be expected to create a more conducive environment for

mobilizing savings and investment opportunities for its population through investing in

insurance policies.

11

Daystar University Repository

Library Archives Copy

Benefits to the general public are quite compelling too. Convenience, lower premium

rates which are passed on to the client’s due to lower distribution costs. There’s a high

likelihood that new products would be developed to suit diverging clients’ needs. This

would not have been possible if the two entities worked separately (Benoist, 2002)

To the field of academia, the study made significant contributions to the existing body of

knowledge in the field of Bancassurance and the key findings may provide information to

potential scholars in expanding the local knowledge base as they fill in the gaps arising

from the study.

Scope of the Study

The study targeted employees from insurance companies in Nairobi County. The capital

was preferred due to its near proximity to their headquarters located within the city.

Nairobi County is also metropolitan city accommodating populations of different

economic status ranging from low to high income earners and thus making the scope

more justifiable and representative of other counties.

Limitations and Delimitations of the Study

The study findings were only limited to data collected from key respondents from the

selected insurance companies in Nairobi County and therefore findings from other

counties were not captured and hence this may not be replicated to the entire country.

However, Nairobi County being metropolitan, research findings can be representative

enough to be replicated and generalized to other counties.

12

Daystar University Repository

Library Archives Copy

Assumptions of the Study

It was assumed that insurance products had gained popularity because they were being

sold over the banks counter and that Bancassurance activities were preferred to traditional

agency and broker channels of distribution. A number of reliable consultant studies were

however incorporated into the study to support this claim.

Definition of Terms

Bancassurance: is the cross-selling of insurance products using the banks distribution

networks Kumar (Kumar, 2001).

Composite/hybrid underwriter: Insurer accepting liability by guaranteeing payments in

both life and non-life business should there an event of death, loss or damage (Frinquelli,

1990).

Financial Performance: Simply means measuring the results of a firm's operations in

monetary terms as reflected in the firm's profits, return on investment and market share

(Wua & Lin, 2009).

Insurance: In financial sense, insurance is a contract in which a group of individuals (insured)

transfers their risk to another party (insurer) to provide for payment of losses from funds

contributed (premium) paid by members who transferred the risk (Ricci, 2012).

Life insurance product that guarantees a specific sum of money (sum- assured) to

beneficiaries in the event of premature death or at policy maturity (Ricci, 2012).

Premium-underwriting income which consists of earned premium after claims less

administrative expenses (Swain, 2005).

13

Daystar University Repository

Library Archives Copy

Summary

The chapter looked at the background of the study, statement of the problem, objectives

of the study and the research questions. It gave the justifications as to why the study was

conducted in Nairobi County together with their limitations and scope. The key focus area

established the background of Bancassurance across continents. The chapter also focused

in discussing what had been researched before in filling the research gap and by so doing,

developing new ideas and areas that had never been explored before.

14

Daystar University Repository

Library Archives Copy

CHAPTER TWO

LITERATURE REVIEW

Introduction

This chapter looks into the theoretical framework backed up with different Bancassurance

products and models being adopted in Kenya. It also discusses the general and empirical

literature in regard to the challenges facing the Bancassurance industry as a whole.

Finally, a conceptual framework is drawn defining the dependent and independent

variables together with the moderating variables.

Theoretical Framework

One of the most significant changes in the financial sectorial markets in Kenya has been

the development of Bancassurance which has often proved to be a profitable compliment

to the existing core businesses of the two institutions (banks and insurance). According to

Swiss Re (2008), Bancassurance has been used as a competitive strategy for achieving

increased income, reduced fixed costs and increased customer outreach.

In the late 2009, the Kenya government through the IRA felt it necessary to reform the

banking-insurance sector. This was in efforts to provide better insurance coverage to its

citizens and to increase the flow of long term financial growth. In the same year, the

regulatory body recommended opening up the sector to private players so as to improve

on service delivery and standards to a larger section of the population (Karanja, 2014).

In 2012, Britak rebranded itself to Britam implying that the brand was not restricted to

offering Kenyan products but on a global stance. This then followed with an agreement

between the insurer and Equity Bank to facilitate Bancassurance in Kenya. Jubilee

15

Daystar University Repository

Library Archives Copy

Insurance and Diamond Trust Bank, Liberty insurance and CFC Stanbic Bank followed

suit making them the three top tier Bancassurance providers in Kenya (Wairegi, 2012).

Economies of Scale Theory

Developed by Alfred Marshall in the late 1890’s, economies of scale theories can be

defined as the cost advantages that arises with the increased output or scale of operations

of a product or service (Hart, 1996). The implication here is that the greater the quantity

of a good or service is produced or delivered, the lower the per-unit fixed costs.

Therefore, economies of scale sums to the cost advantages an enterprise obtains as a result

of increased size of output or scale of operations. In a broader sense banks and insurance

companies take advantage of economies of scale arising from the law of large numbers

that focused on cost reduction through increased productivity. Marshall’s chief purpose of

creating this theory was to explain the great historical reduction in production costs

associated with increased output of the product.

Bancassurance mechanisms are thus executed by use of the bank’s branch distribution

networks. Through this insurance companies have benefited through reduced cost of

setting-up and running a new branch. Jongeneel (2011) supported this argument and

added that economies of scale was the key pivotal ingredient in the adoption of

Bancassurance practices across the continent. Therefore, the more insurance products a

bank sells, the more experience it gains along with the ultimate reduction on marginal

selling costs. That’s the reason as to why purchasing Bancassurance products over banks

counters is comparatively cheaper than those purchased from brokerage firms. This claim

is also well supported by (Kamau, 2016).

16

Daystar University Repository

Library Archives Copy

Modern Portfolio Theories

Pioneered by Harry Markowitz in 1952, the theory drew attention to constructing an

efficient frontier of optimal portfolios offering maximum possible expected return at a

given level of risk through portfolio diversification. Brealey and Myers (2003) added that

efficient portfolios consists of assets yielding high returns for a given risk. In practice a

smart investor may reduce risks of negative returns by holding different portfolios. In by

doing so he is basically attempting to remain relevant, increase earnings and maintain

feasibility in the market. Bancassurance is therefore a diversification strategy that brings

forth professional management in gaining access to the best practices of international

markets and political here say.

Bancassurance Products and Models Being Adopted in Kenya

Bancassurance products have evolved over time in response to the local market

conditions, global financial trends and the banks growing experience in insurance related

products. Therefore the feasibility, sustainability and competitiveness of bank-insurance

majorly depends on the comprehensive range of Bancassurance products offered in the

market that addressed the needs of the customer (Yasouka, 2005). Bancassurance

products can be broadly classified into three categories including; life insurance, non-life

or general insurance and composite/hybrid insurance.

Life Insurance Products

Life insurance often referred to as whole life or universal life, is a contract between the

policy holder and the insurer whereby the policy holder pays regular premiums towards

maturity of the contract and the insurer promises to pay a lump sum amount assured to the

17

Daystar University Repository

Library Archives Copy

insured’s beneficiaries in the event of premature death, disability or maturity of the

policy. Depending on the contract, events such as terminal illness and incapacitation may

trigger a payment settlement (AKI, 2016). The main features of these products are that

financial needs of the family are protected should the policy holder lose income resulting

from disability, death or critical illness.

Life insurance products are more expensive than individual products due to the presence

of multiple risks of death as well as investment returns. Products under this category

includes term assurance that provides life covers within a specified period of time with no

investments benefits. Medical insurance, travel insurance, personal accidents, retirement

packages, last expense and the recent introduction of key-man insurance are some of the

life insurance products being offered in the Kenyan market (Nyambura, 2013).

Non-Life Insurance Products

Non-life insurance also commonly referred to as general insurance provides a lump sum

amount in case of destruction to the asset insured and that of third parties. The main reason

behind insuring assets is to protect oneself against financial loses likely to occur due to fire,

theft or accidents. Non-life insurance policies includes but not limited to compulsory

motor/auto insurance which protects insured and that of third party vehicle damages

resulting from fire, burglary, explosion and accidents. Mortgages and personal loan

insurance, Home and property insurance, goods in transits insurance, fire insurance, marine

and cargo insurance constitutes to general insurance products (Nyambura, 2013).

18

Daystar University Repository

Library Archives Copy

Composite or Hybrid Insurance Products

Composite insurance often referred to as ‘co-insured’ is a contractual agreement that

combines insurance covers for several risks under one product. In essence, two or more

people are insured under one policy (Bowers, 2017). The author added that for a policy to

be composite, parties ought to have divergent/different interests where the misconduct of

one insured party will not affect another insured’s entitlement to insurance. They are

beneficial to clients in a sense that they provide multiple risks covers at affordable prices

whereas from the insurer’s perspective, they are often attractive and easily sold than

standalone products.

Bancassurance Models

The success of any business model depends on the level of integration of various

structures within the business environment. Benoist (2002) outlined four major

Bancassurance models which included; agency model, strategic partnership, joint ventures

and financial holding models as discussed here under.

Agency Model

Agency model also referred to as Pure Distribution Model is a scenario whereby banks

plays an intermediary role of distributing insurance products produced, serviced and

financed by one or more insurers. This therefore means that banks are solely responsible

for insurance sales and premium collection whilst underwriting and claims-handling

processes being operationalized by the insurer. The business assumption behind this

model is that banks are unwilling to offer such expertise internally but are willing to issue

policies at a commission (Swiss Re, 2008).

19

Daystar University Repository

Library Archives Copy

The main features of agency model is that it is quick and simple to implement with

relatively low startup costs. This is so because bank only sets up dedicated Bancassurance

units with well-trained professionals to run these departments. The model however poses

potential challenges for insurers since they have little or no control over which customers

the products are being sold to.

Strategic Alliance Model

Strategic alliance commonly referred to as Partnership agreement is a model where the

bank only sells the products of one particular insurance company. The main advantage of

this model is that insurers are able to access the banks customer base without having to

make a major financial investment while the banks are able to select the best insurer in

terms of their product offering and brand reputation.

In such agreements, both parties have a stake in the success of the business venture and its

success is determined by the level of commitment of the two entities. Potential challenges

over this model however is that, at low levels of integration both companies may end up

operating as separate entities. Adrian (2003) observed that in strong partnership, companies

engage themselves in cross holding of equity, made mutual investments and enter into a long-

term exclusive selling agreements whereas in weak partnership agreements may last for few

years with limited mutual efforts. A weak partnership arrangement provides the bank with an

advantage over the insurer since the bank acquires extensive knowledge on insurance business

and at the termination of the agreement; it may have the option of exploring their

organizational strategies with the advantage of a wider customer base.

20

Daystar University Repository

Library Archives Copy

Joint Venture Model

This is the creation of a new insurance company by an existing bank and an existing

insurance company. This therefore implies that banks and insurers establish a jointly co-

owned insurance company or a distributor. The relationship between the bank and the

insurer is reinforced by a balanced strategic share-holding. The main advantage of this

model is that there’s equal partnership and joint decision making processes. Partners

leverages on each other’s strengths while focusing on their core business. The model is

best suited for foreign insurance companies in entering new untapped markets by linking

up with domestic banks and hence allows the insurer to leverage on the banks presence in

the local market (Boyd, 1988).

Financial Conglomerate model

Also referred to as financial-holding company, financial conglomerate model is a model

where a holding company owns both the insurer and the bank. The bank staff wholly

owns the insurance sales process while the insurer acts as a product and service provider.

Potential advantage of this model is that banks had the opportunity to leverage on the

insurers existing customers, provide a one-stop-shop shopping for financial and insurance

needs. Kumar (2001), added that in this model there’s strong information flow between

the banks and insurers and thus becomes the key drivers to the success of this model.

21

Daystar University Repository

Library Archives Copy

General Literature Review

Challenges Facing the Bancassurance Industry

The Bancassurance industry has been facing several challenges since its adoption in the

Kenya. These challenges ranges from economic, social and political point of view. In

Traditional African cultural and religious practices for instance, it’ was and still a taboo to

talk or even contemplate about death as the bereaved family was well taken care of by the

extended families and ‘chamas’ with the objective of collecting monies to cater for such

diverse contingencies. Selling of Bancassurance products like funeral expense or last

expense covers to these individuals could be perceived as one is planning for their early

death (Sharma, 2005).

Macro-economic activities such as inflation and poverty is another challenge corroding

the value of Bancassurance practices in an economy. Africa’s earnings per capita is

generally low with the majority of its population living below the poverty line. There are

also instances where the sum assured paid at the end of ten or twenty years savings are not

worth the effort. Even though KRA will give the client a tax relief of 15% on annual

premiums, it may not make financial sense investing for three years only for your claim to

be delayed or rejected all together. These has therefore made the Kenya Bancassurance

practices to lag behind the rest of the world (Karanja, 2014).

Another shortfall observed by Amadeo (2016) was lack of institutional confidence in

managing Bancassurance affairs. There has been growing concern in the past that managers

only focus on developing the business and satisfying their personal interests at the expense of

22

Daystar University Repository

Library Archives Copy

the customer. Majority of them have been also implicated in money laundering schemes

and scandals while disregarding the clients’ interests.

Another drawback highlighted by Mishra (2012), was mistrust between the two institutions

where Bancassurance officers at banks have been on record in overstating claims. This is

attributed to collusions at the branch level and the information shared to the insurer may not

necessarily replicate the true picture in the ground and thus rendering the insurer to bear high

costs on claim settlements and law suits by clients through the regulator.

Theoretical Approaches to Financial Performance

The concept of performance has been extensively documented over the past decades.

Campbell (2012), believes that performance is what the organization intends to achieve

however, the author cushions readers that this should not be seen as the only determining

factor of an entity’s success.

Financial performance

Financial performance can be defined as how well an organization is performing and to

what extent it had achieved its intended outcome (Namisi, 2002). The study of Kumar,

(2014), considered age and size of the organization as the important component of

financial performance. He observed that the older the firm is, the more will be the profits

this due to the internal experience and efficiency it gains from the business lifecycle.

There are several indicators of financial performance but for the purpose of this study, the

firm’s profitability was considered and discussed.

23

Daystar University Repository

Library Archives Copy

Profitability

Profitability is the key determinant of financial performance of any sector and can be

defined as the measure of the business ability to generate revenues compared to the

amount of expenses incurred (Hofstrond, 2006). It is therefore important for the

company’s long term survival in deciding whether or not to invest into a business venture.

Profitability is measured with income and expenses whereby the income is the money

generated from business activities whereas expences are cost of resources used up or

consumed by the business activities.

Okeeno (2013) noted that there were two components of profits considered by insurance

companies. First was the premium underwriting profits which consists of earned premium

after claims less administrative expenses and the investment income that looked into the

company’s assets allocations (usually mentioned on financial statements) where majority

of these assets are invested in low risk bonds, money markets and equities. There are two

important measures of profitability namely; Return on Assets (ROA) and Return on

Capital Employed (ROCE). Their results can give the much needed information on the

financial health of the business (Swain, 2005).

Return on Asset (ROA)

Swain (2005) defined Return on asset (Return on investment) as an indicator of how

profitable a company is relative to its total assets. It’s therefore a comparative measure that

gives an idea of how efficient the management is at using its invested capital to generate

earnings. It’s therefore a performance measure that evaluates the efficiency of an investment

relative to investment costs. As a rule of the thumb, Malik (2011) suggested

that the higher the ROA, the more favorable it is for investors since it shows how efficient

24

Daystar University Repository

Library Archives Copy

the company is at managing its assets to produce greater amounts of net income. ROA

Formula is shown in appendices II. The annual net income is derived from the company’s

income statement and more adjustments are made to Net operating profit after tax

(NOPAT) to get a more accurate picture of what was actually invested into the business

(Swain, 2005).

Return on Capital Employed (ROCE)

Return on capital employed is another financial ratio that measures the company’s

profitability and the efficiency with which its capital is employed as shown in appendix II

Capital employed in general is the capital investment necessary for a business to function

which is represented as fixed asset plus the working capital. Therefore, it’s the sum of

shareholders equity and debt liabilities as provided for in appendix II.

For a company to remain in business over a long term, its ROCE should be higher than its

cost of capital otherwise continuing operations gradually reduces the earnings available

for its shareholders. It’s a better measurement of profitability since it shows how well a

company is in utilizing its equity and debt to generate returns (Bragg, 2009).

Customer Needs

Stephens (2011) defined customer needs as the motives that drives one to purchase a

particular product in many competing brands. With the increasing competitive pressures from

industry players, financial firms are constantly looking for ways of addressing diverging

customer needs through fair pricing models and products that adds value to their customers

use. Siddiqui (2010) noted that in today’s market place, customers demand more

25

Daystar University Repository

Library Archives Copy

than just competitive prices and the quality of products and services offering but are also

demanding for additional benefits that comes along with the product. In this view,

customers are willing to pay extra cash in exchange for quick and convenient services that

befits well into their lives.

One of the major goals of any enterprise is to increase production and service delivery to

its customers and understanding their expectations as a prerequisite for delivering high

standards of services for its future survival and growth. It is becoming more desirable to

develop a lasting customer centric approach in providing solutions that satisfies their

needs. Stephens (2011) believed that customers purchasing decision pattern was

influenced by product features and attributes, perceived benefits arising from the use of

the product, the products financial traits and customers attitude towards the brand.

Product Features and Attributes Satisfying Customer Needs

Product features are the basic salient characteristics of a product that distinguishes itself from

others in a competing market place (Gordon, 2014). It is therefore believed that today’s

customers make product purchases with multiple functions. This view was supported by

Gamage (2018), who argued that modern companies are producing multiple functioning

products to meet customer’s preference of greater functionality and utility. The driving force

behind considering to add many features to a product is the perceived belief that additional

features makes the product more appealing for customers. This claim was however criticized

by Siddiqui (2010), who argued that customers do not always use all the features of the

product they buy. In addition, increased new product features may increase the product

complexity and hence generating confusion in the minds of the users.

26

Daystar University Repository

Library Archives Copy

Perceived Benefits Arising from the Use of the Product

Perceived benefit is the maximum price a customer is willing to pay for the use of the

product (Stephens, 2011). This therefore is the direct benefit that a client enjoys on

purchasing a particular product. Alzheimer (2013) added that purchasing an insurance

product does not necessarily depend on price but also the value derived from using the

product, the desire to feel safe and worry nothing about your future lifestyle in the event

of an eventuality. The Bancassurance industry therefore needs to understand how their

clients perceives the value of their products and make proposals and adjustments based on

customer benefits and experience.

Products Financial Traits

These are basically the pricing strategies that sends an important message to customers.

Melanie (2014) observed that as prices increase so does the customer’s perception of the

product being sold. This is so because the spending habits of consumers is naturally

skeptical about lower prices which portrays that the product in question is of a lesser

quality. Consequently, higher prices signals that the product is exceptionally good in

quality and performance. A study by Brussels business school of economics found out

that customers are more likely to display satisfaction when the product is priced fairly.

Therefore prices that are neither too high nor too low sends a positive message that not

only the price is of a high quality but also customers are getting value for their money.

Customers Attitude towards the Product and Brand

Consumer attitude is the behavior displayed by customers in search for a product feature

from different companies in satisfying their needs. Young (2013) noted that if the

27

Daystar University Repository

Library Archives Copy

customers experience was that of dissatisfaction attributed to poor service delivery and

hence this may hinder or influence others on their future selection decision of that

particular product or brand. The Bancassurance industry therefore focuses on satisfying

these diverging customer needs should they wish to remain relevant and competitive in

the market.

Industry Regulatory Framework

Across the world, Yasouka (2005) observed that Bancassurance industry has been

adversely hampered by institutional regulatory environment which is a government body

mandated with the responsibility for rolling out best professional practices within a

country as discussed here under:-

Product Sales and Customer Protection

It has been quite a concern that many customers do not fully understand the risks and rewards

associated with the products they purchase and at the same time, internal pressures to meet

sales targets have contributed to substandard products being distributed without necessarily

addressing clients’ needs (Yasouka, 2005). One of the central questions therefore is how

much should the government intervene on Bancassurance activities? There are several

varying degrees in understanding the need or lack of government control in making economic

decisions. With this, there exists two diverging mindsets on the effects of regulation and

deregulation of financial markets. The classical liberalism theory for example argued that

markets alone should be left to regulate themselves whereas interventionist liberals supported

that government agencies should take the center stage of intervening in business activities

with the best interest of the customer. In contrast however,

28

Daystar University Repository

Library Archives Copy

Cohn (2002) noted that market operating under complete freedom focused more on

maximizing its operational efficiencies thereby promoting policies that accommodated

privatization and liberalization of financial systems. In this sense, the removal of

government control out performed regulated markets in terms of product quality and

service delivery reducing the cost of operations which resulted to high returns on

investments.

Llewellyn (2007) however believed that regulations are counterproductive in achieving

substantial economic goals. This hindered growth and development of technology and the

social goal of protecting public and private interests. Carow (2001) supported this view

adding that there were positive effects of deregulation which had significant increase in

innovations that have directly forced out incumbent market players out business. Free

market mechanisms including self-regularization by experts and professions in respective

fields yielded excellent results as depicted in developed economies.

The Kenyan insurance sector is regulated by the Insurance Regulatory Authority (IRA), a

statutory governmental body established in May 2007 through the enactment of

parliament (Insurance Act 487). The body is charged with the responsibility of regulating,

supervising and developing sound operations of all insurance companies in Kenya.

Amongst other functions, the regulator issues operating licenses, protected the interests of

the insurance policy holders, investigated and prosecuted insurance frauds, consumer

education and awareness on matters insurance (IRA, 2014).

29

Daystar University Repository

Library Archives Copy

Empirical Literature Review

Jongeneel (2011) did a study on Bancassurance entitled “Stale or staunch?” In pursuit of

exploring the present trends in Bancassurance as a feasible source of sustainable income

in the India’s insurance industry. Her findings were that Bancassurance had significantly

increased financial performance and that the concept would turn out to be a norm rather

than an exception in the near future.

Lovelin and Sreedevi (2014), did a study on the preference of Bancassurance in Taiwan.

The objective of the study was to find out the customer awareness and perception on the

role of Bancassurance and the factors influencing the buying patterns of insurance

products through the banks. Her findings were that out of the 100 respondents, 71

respondents were not even aware of the concept of Bancassurance. Further, the study

outlined customer loyalty, positive tax shelters and loan requirements as being amongst

the reasons for buying insurance products from banks.

In the recent past, a few studies have been conducted on the Kenyan insurance industry.

Notably Omondi (2013), did a study on the determinants of adoption of Bancassurance by

commercial Banks in Kenya. The results of his findings were that the adoption of the

concept was influenced by the need for new revenue streams, product diversification,

exploitation of economies of scale and the need to remain competitive in the market.

Juma (2015) did a study on the effect of Bancassurance as a penetration strategy for

insurance companies in Kenya and the findings revealed that the insurance sector had

witnessed rising sales and increased profitability. Further, the study showed that in each

product bundle, there was increased competition and overall cost reduction.

30

Daystar University Repository

Library Archives Copy

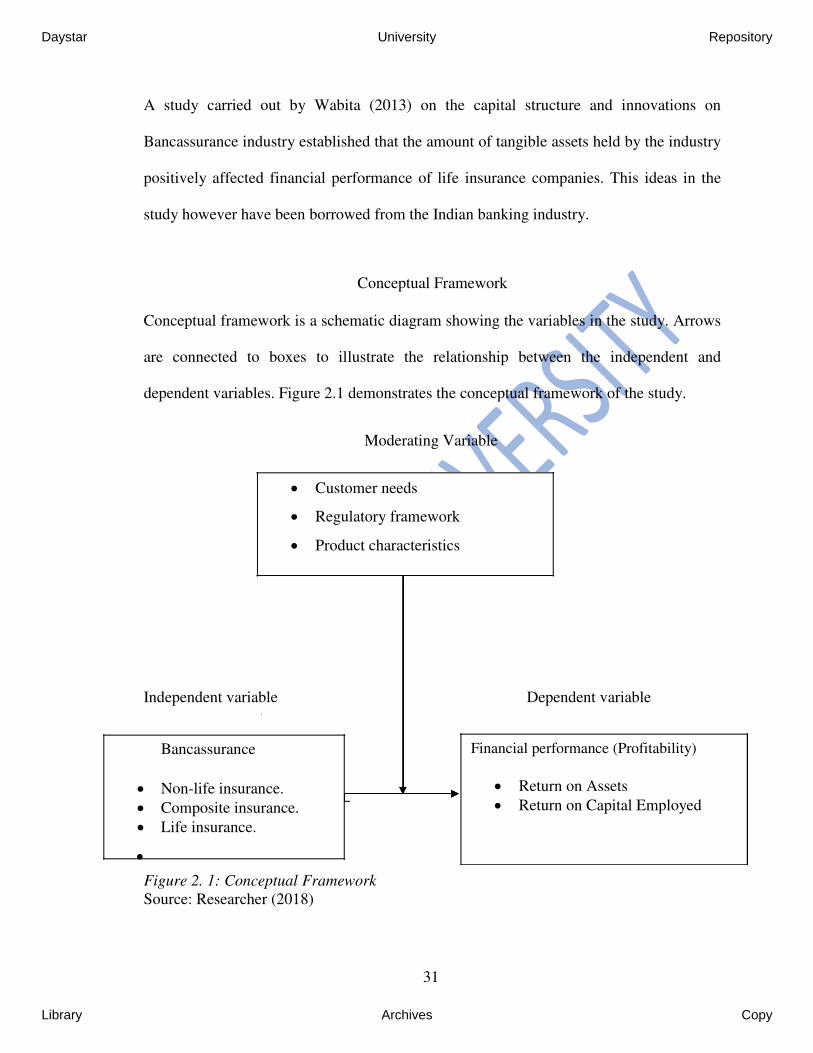

A study carried out by Wabita (2013) on the capital structure and innovations on

Bancassurance industry established that the amount of tangible assets held by the industry

positively affected financial performance of life insurance companies. This ideas in the

study however have been borrowed from the Indian banking industry.

Conceptual Framework

Conceptual framework is a schematic diagram showing the variables in the study. Arrows

are connected to boxes to illustrate the relationship between the independent and

dependent variables. Figure 2.1 demonstrates the conceptual framework of the study.

Moderating Variable

Customer needs

Regulatory framework

Product characteristics

Independent variable

Bancassurance

Non-life insurance. Composite insurance. Life insurance.

Figure 2. 1: Conceptual Framework Source: Researcher (2018)

Dependent variable

Financial performance (Profitability)

Return on Assets Return on Capital Employed

31

Daystar University Repository

Library Archives Copy

Discussion

Riggan and Sharon (2011) stated that conceptual framework is an idea model that serves

the purpose of assessing and developing realistic justifications of the study. Miles and

Huberman (1994) agreed that conceptual framework is a written or a visual product that

explains either graphically or in narrative forms of the key factors and beliefs on the

variables under study. This therefore is a system of concepts, assumptions, expectations,

beliefs and theories that supports the research.

Figure 3.1 is the proposed linkage between Bancassurance and financial performance with

the Bancassurance concept being denoted in boxes. The solid arrows show the process or

a linkage to a concept. The direction of the arrow indicated the concept being explained

by other concepts in the model. In the above framework, three variables were connected

together by arrows. The independent variable (Bancassurance products) and the

dependent variables financial performance (Profitability) where ROA and ROCE gives

the quantitative aspects used in explaining the relationships between Bancassurance and

financial performance of insurance companies in Kenya.

Summary

In examining the effects of Bancassurance on financial performance of insurance

companies, the chapter looked into literatures on Bancassurance models including the

theories and conceptual framework behind the Bancassurance practices. Bancassurance

products were discussed together with the drivers of financial performance in the

insurance industry. The chapter also presented the conceptual framework of the study

which defined the independent, dependent and intervening variables.

32

Daystar University Repository

Library Archives Copy

CHAPTER THREE

RESEARCH METHODOLOGY

Introduction

Research methodology is the systematic scientific process of conducting and solving a

research problem (Rajasekar, 2013). It is the blueprint of a structured process in which the

research is to be undertaken and thus entails data collection, measurement and analysis.

This chapter described the strategies adopted in conducting the research. The following

key areas were examined; research design, population of the study, sampling design, data

collection instruments, data collection procedures and finally data analysis.

Research Design

Research design is the roadmap or state within which a research is to be conducted. The

aim of research design is to maximize control over factors that could interfere with

consistency and validity of the findings. Research design therefore refers to the plan,

structure and strategy of the research (Kothari, 2004).

The study used descriptive research design often referred to as ex post facto which

includes all surveys, fact-finding enquiries and descriptions of the present state of affairs.

Descriptive research design was preferred as it gave both the qualitative and quantitative

aspects of the data used in reporting numerical and personal accounts on the underlying

factors under investigation (Kothari, 2004).

33

Daystar University Repository

Library Archives Copy

Population of the Study

Population is the summation of all elements of the same group which live in a particular

geographical area (Sandelowski, 2010). This is therefore a complete set of elements

(persons or objects) that possess some common characteristics established by the

researcher (Kothari, 2004). For the purpose of this study, the population constituted all the

12 Bancassurance firms in Kenya (AKI, 2010).

Target Population

Target population is the entire group of people or objects to which the researcher wishes

to generalize the study findings (Harter, 1980). The target population constituted all the

12 insurance firms that had incorporated Bancassurance business model in their business

operations (Nyambura, 2013). The 12 Bancassurance firms were conveniently chosen

since their headquarters were located in the city with majority of its population harboring

middle income earners and for this reason therefore, the results can be replicated to all

Bancassurance firms in Kenya.

Sampling Size

Sampling is the process or technique of choosing a sub-group from the population to

participate in the study. Sampling is done because it is impossible to test every single

element in the population (Mugenda & Mugenda, 2003). A sample size of 47 respondents

were conveniently selected from the 12 Bank-insurance companies.

34

Daystar University Repository

Library Archives Copy

Sampling Technique

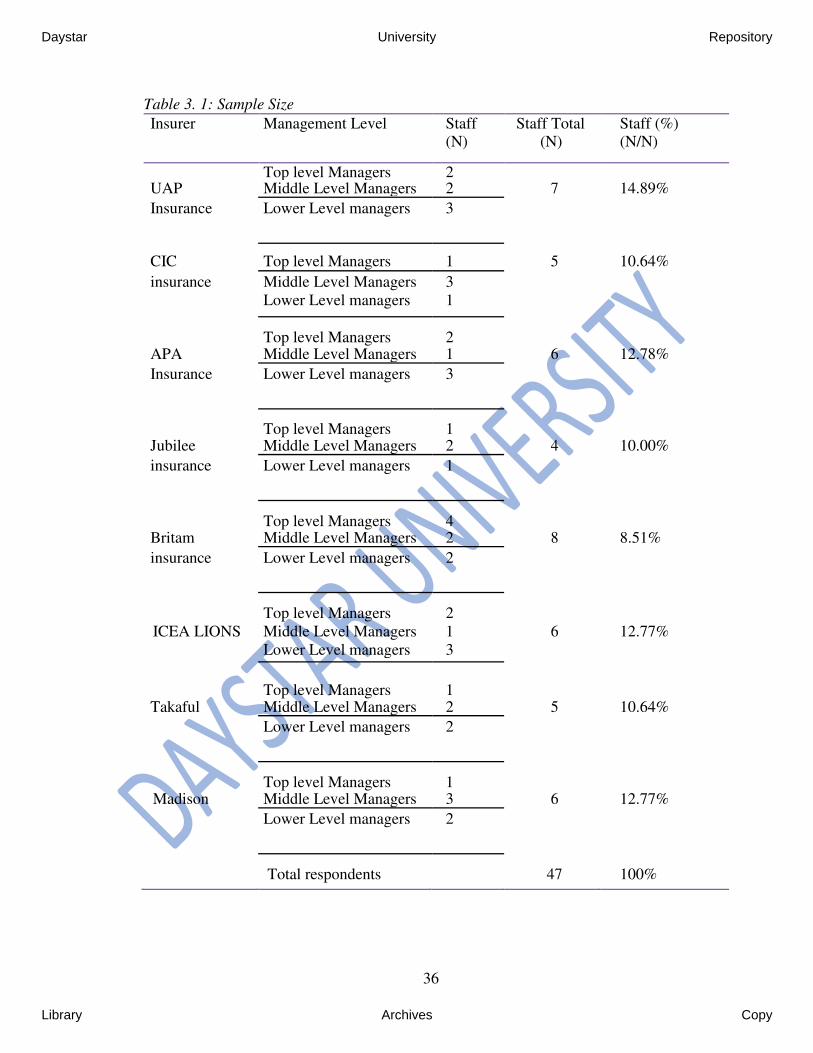

A sampling technique is a definite plan of selecting a sample before data is collected from

a given population (Alzheimer, 2013). Stratified random sampling technique was used,

where samples were divided into three strata consisting of top level managers, middle

level managers and senior officers as illustrated in Table 3.1.

35

Daystar University Repository

Library Archives Copy

Table 3. 1: Sample Size

Insurer Management Level Staff Staff Total Staff (%) (N) (N) (N/N)

Top level Managers 2 UAP Middle Level Managers 2 7 14.89%

Insurance Lower Level managers 3

CIC Top level Managers 1 5 10.64%

insurance Middle Level Managers 3

Lower Level managers 1

Top level Managers 2 APA Middle Level Managers 1 6 12.78%

Insurance Lower Level managers 3

Top level Managers 1 Jubilee Middle Level Managers 2 4 10.00%

insurance Lower Level managers 1

Top level Managers 4 Britam Middle Level Managers 2 8 8.51%

insurance Lower Level managers 2