BEHAVIOURAL FINANCE

64

UNIVERZITY OF SARAJEVO SCHOOL OF ECONOMICS AND BUSSINES SARAJEVO MUJEZINOVIĆ AIDA BEHAVIOURAL FINANCE UNDERGRADUATE THESIS

Transcript of BEHAVIOURAL FINANCE

UNIVERZITY OF SARAJEVOSCHOOL OF ECONOMICS AND BUSSINES SARAJEVO

MUJEZINOVIĆ AIDA

BEHAVIOURAL FINANCE

UNDERGRADUATE THESIS

BEHAVIOURAL FINANCE

UNDERGRADUATE THESIS

Subject: Financial ManagementMentor: Prof. Dr. Zaimović AzraStudent: Mujezinović AidaIndex: 68770Orientation: Financial Management

CONTENT.

1. THEINTRODUCTION .................................................................................. 32. HISTORY ANDDEVELOPMENT ............................................................... 43. PROSPECTTHEORY .................................................................................... 7 3.1. The basics of prospecttheory ................................................................... 7 3.2. Certainityeffect ....................................................................................... 8 3.3. Loss aversion and the valuefunction ...................................................... 9

3.4. Mentalaccounting .................................................................................. 11 3.5. Other behavioural aspects of prospect theory........................................ 19 3.6. Conclusion on prospecttheory ............................................................... 20 4. HEURISTIC DECISIONPROCESS ............................................................ 21 4.1. Representativenessheuristic.................................................................... 21 4.2. Availibilityheuristic ............................................................................... 22 4.3. Anchoring, belief preservence and adjustmentheuristic ........................ 22 4.4. Overconfidenceheuristic ........................................................................ 23 4.5. Conclusion on heuristic decisionprocess ............................................... 245. LATEST FINANCIAL CRISIS AND BEHAVIOURALFINANCE ......... 25 5.1. The basics on financialcrisis .................................................................. 25 5.2. Behavioural and psychologicalbiases .................................................... 27 5.3. Conclusion on financialcrisis ................................................................. 30

6. PUZZLES OF FINANCE AND BEHAVIOURALFINANCE ................... 32 6.1. Over and underreaction of stockprices ................................................. 32 6.2. Hypes andpanic ..................................................................................... 33 6.3. Equity premiumpuzzle .......................................................................... 33 6.4. Winner/looserasymetry ......................................................................... 347.CONCLUSION ............................................................................................ 358.LITERATURE .............................................................................................. 369.ADDITION .................................................................................................... 38

1. THE INTRODUCTION

As I start to work, and explore on the topic of „Behaviouralfinance“, the very first thing I'd like to mention is one ofthe reasons why I had choosen this theme, specifically.

One of the major reasons is actually the latest financialcrisis that ocurred in the USA and the whole world. Main causeof that crisis was, in my and in opinion of many economicroles, psychological effect, which is the cause of almostevery finance bubble. Irrational economic behaviour offinancial institution, failure to anticipate something that wasquite obvious to happen sooner and later, as well asirrationality in the actions of the individuals.

Behavioural finance, as a theory, is part of BehaviouralEconomics which is more broad category, has evolved sharply inthe last 20-30 years. It's is actually rather controversial,still, but there are obvious evidences that it is somethingthat is in the mind of many economic analysts, investors andordinary people who have daily contact with financialinstitutions. This theory has never been more popular. Understanding the behavioural finance would help us understandthe process of decision making and its effects, as well as manyfinancial phenomenas.

After the brief introduction, I will present you the historyand development of this field, mention some important personswho brought so much to this part of finance, and show you whatthis aspect represents today. Going further, I'll introduce youwith prospect theory, as a pillar of behavioural finance, withall its main parts, goals and characteristics. After prospect theory, I'll explain, from my point of view,using the literature I found and read, heuristic decisionmaking, some major investors' biases in modern economy.Working on this part, as a method of research, includingdeductive and analytical methods, I also used interviews andquestionaires, where I wanted to prove, in practice,theoretical aspect of mental accounting, as a major part ofprospect theory. The examples of interview and questionnairecan be found as an addition to the work. I'm gonna pay special atenttion to the latest financial crisisand the explanation from behavioural finance view, as one of

the most interesting part of this work, at least to me. It wasindeed challenging to read about causes and consequences ofthis crisis in completely other light, than traditional financetalks about. To end this discussion, I decided to write about practical partof behavioural finance, concerning some major financial puzzlesof economy, somes issue we have been thought to much duringcollege, but from some other aspects, rather than this one. The work is finished with brief conclusion, as well as list ofliterature used to write about this topic.

Before I start my writting, I'd like to note that this is onevast category of finance, and it was of my decision to choosewhich topics to mention and introduce, along with selection ofscience works. This field can be explored from many views andaspects, and It was of my choice which one to present.

I hope I will successfully present the most important ones, aswell as those that are of most sigificance to modern economy.

2. HISTORY AND DEVELOPMENT

Behavioural finance is exciting new field in the finance. It isthe theory which tries to explain the psychological effects infinancial decision-making. Until 1980s the traditional finance,the principle of rationality and the utility theory mainly,were explaining (often failed to explain) many financialevents, occcuring in the markets. They found market asperfectly efficient (EMH – efficient market hypothesis)1. Mosttheories were risk-based ones. But even in the last decades ofpast century, it got quite obvious that there is not properemipirical evidence that supports this attitude, or it haslimited role in trying to explain financial puzzles. It came inminds of many that almost every investor, at some point, actsirationally and that it can affect a market as a whole. 1 Two main defintions of efficient market: „The market where the price is always right." ; „ The market where the investors are unable to gain continous excessive returns.“

It is the fact that economists tend to rely on the principle ofrationallity2 in decision making, but in real economic lifethis principle doesn't always stands. Another sore fact is thatmany people are motivated by greed and their own benefts(profits) and not social welfare, as it is suggested in manyprevious theories. The irrational human decisions are somethingthat caused the development of the behavioural finance, withthe aim of explaining the decision making issues. Thebehavioural finance developed with aim of explaing howfinancial players behave, rather than how should they behavewhich was mainly shown in traditional finance.Daniel Kahneman was the first person who started activelytalking about beahvioural finance, even in 1979 but theeconomic public wasn't even aware of his work and publicationsat that time. Daniel and his principle of „mean regression“ – which is thefact that bad performance is always followed by better one andvice versa, as well as prospect theory and literature ofinvestors biases and heuristics, which I'll explore more laterin the work, started developing this broad field of finance,behaviour and non-rationality. It was quite revolutionary, atthat time. It's often found in paperworks that „Behaviouralfinance“ is born with the Kahneman's discovery of a commonbehavioural biases, meaning mistakes, which were defined as achanges in investors' behaviour that would cause them to playagainst their own interest. That was the origination of modernbehavioural finance theory, at the beginging of 1990s.

But it's important to mention, also, that the whole storystarted much earlier, in 1896 – with the book written byGustave le Bon, „The Crowd: A study of the popular mind“ , asone of the most influential social psychology books, which ifthe prove of how much this theory was present in minds of manyones before.

In 1992, Kehman and Tversky, developed the prospect theory,naming it cumulative prospect theory. In 1995 Thaler andBenartzi offer behavioural explanation on equitiy premiumpuzzles, explaing from the behavioural aspect why sharesoutperform bonds. From that period on, many works talking about

2 The main support to EMH.

behavioural explanation of many financial events were writtenand published. 1999 was productive in the aspect of researches on thebehavioural aspects of decision making. Mental accounting, as aconcept was introduced in that years, which is a set ofcognitive operations used by individuals and householdings whendealing with daily financial activites.

2000s gave birth to two widely popular books on this field:Shleifer's „Inneficient Market: An introduction to behaviouralfinance“ and Shefrin's „Beyond Greed and Fear“ explaing thepsychology of investing. In 2001 the prospect theory was incorporated in asset pricingmodel, which was, until then, completely based on theprinciples of traditional finance: rationality and risk-basing.And in 2001 the expected utility hypothesis was definetlypronaunced dead – by Rabin and Thaler. 2002 was also extremly important year when we talk about thisfield of finance. 6 general purpose heuristics were identifiedand written about by Gilovich, Griffin and Kahneman, whichlater became as one of the most important aspects and terms inbehavioural finance. But the main reason of importance of 2002 was the Nobel prize,which was granted to Daniel Kahneman, for his work in prospecttheory, by Bank of Sweden prize in Economic Science. The mostinteresting fact is that Daniel wasn't even economist, he waspsychologist. It can be freely said that he was the man whoconnected the psychology and economy, giving birth tocompletely new science, was providing theoretical backgroundfor behavioural finance.

- PICTURE 1: Daniel Kahneman; „father“of modern behaviouralfinance theory: SOURCE:

http://en.wikipedia.org/wiki/Nobel_Memorial_Prize_in_Economic_Sciences -

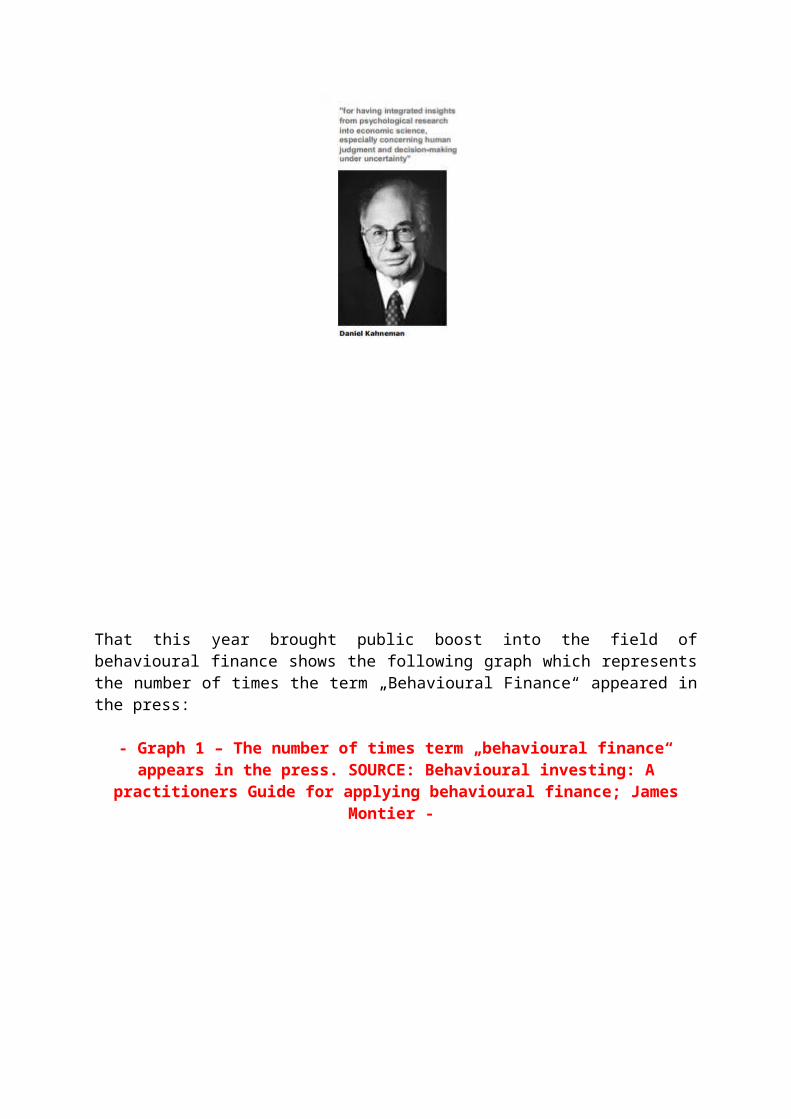

That this year brought public boost into the field ofbehavioural finance shows the following graph which representsthe number of times the term „Behavioural Finance“ appeared inthe press:

- Graph 1 – The number of times term „behavioural finance“appears in the press. SOURCE: Behavioural investing: A

practitioners Guide for applying behavioural finance; JamesMontier -

After 2002, and the Nobel prize to Daniel Kahnemen, behaviouralfinance was definetly recognized, nearly as much as traditionalfinance.Another boost and reliance on this field, started after 2008and occurance of financial crisis, when the answers and reasonswhich couldn't be found in traditional finance, started to befound in the behavioural one. That behavioural finance indeedcan provide answers to many „ How? When? Why?“– questions, willbe presented later in the work. In 2009 Shefrin described some of the behavioural biases thataffect and are done by managers of big companies, which wasquite important work at that time, during the financial crisis.He showed how one of the heuristics „overconfidence“ was one ofthe reasons of financial crisis which was completely supportedby behavioural finance.

3. PROSPECT THEORY

In almost every work I found and read, which provided mecomplete understanding of this theory, I could define it asalternative, response, objection and criticizm to the „expectedutility theory“ – the basis of traditional finance. The expected utility theory was dominant, at least untilKahneman and Tversky discovery, in understandment of decisionmaking under risky conditions. The basic difference betweenthese two theories is actually the core difference betweentraditional and behavioural finance: the expected utilitytheory is a normative theory which explains how people SHOULDbehave under risky decision-making, while the prospect theory,as an answer to the previous one, provides insight of howpeople (investors) ACTUALLY behave under the process ofdecision making, in the situation of riskiness. It can, also,be observed as a counterpoint to Von-Neumann- Morgernsterntheory on how people should make decisions. The prospect theory separates decision making process into twophases, with first one not so much researched and payedattention in the financial science :

- Editing, as a first phase of decision making process,where the editing of some decision is made, for the choiceto be easier made in a second phase

- Evaluation, as a second phase of decision making process,in which previously characterized decision is processed.

Daniel Kahneman and Tversky provided many evidence anddocuments from cognitive psychology3 experiments.

3.1. THE BASICS OF PROSPECT THEORY

The value of an edited prospect, that one that passed phase oneof decision making process, according to the prospect theory,is defined in the aspect of two terms:

3 Cognitive psychology is a subdiscipline of psychology exploring internal mental processes.

- a decision weight, which Daniel and Amos, marked with - the result that it operates on, meaning the value, v.

Each probability (p), has a decision weight, , which isconnected to it and which has the function of transforming thatvery probability.

William Forbes (2009, page 166) states that prospect theory'sis the evaulation of outcomes defined in following equation:

V (x, p, y, q) = (p)v(x) + (q)v(y)

, where as v(0)=0, (0)=0, and (1)=1, with V defined over weighted outcomes or „prospects, which are decomposed in two parts:

- a riskless, or certain, part- a risky prospect, risky part, the additional gain, or loss, which that prospect involves, relative to investor's reference point y.

3.2. CERTAINITY EFFECT

When their subjects were asked to choose between 4 lotteryoptions:

25% chance of winning 3,000 $ 20% chance of winning 4,000 $ 100% chance of winning 3,000 $ 80% of chance of winning 4000$

It is, ofcourse, quite obvious that first two and second twooptions are actually quite the same. But it is interesting thatDaniel and Tversky found that 65%, meaning more than a half, oftheir respondents decided themseleves for the options B and C.According to the expected utility theory the people should notchoose differently at all, since the choices are same. Theycalled this „certainity effect“ – that is people's preferencefor outcomes that are somewhat certain. These two psychologistsdiscovered that people tend to find events that are improbable

to happen, as almost impossible and extremly probable one asalmost certain. That explains why most of them choose options Band C. Certainity effect was first sign that people don'tbehave completely rational was it was suggested by previoustheory. People tend to have systematic irrational actions, asit was revealed with the prospect theory. Weights given to someoptions are purely of subjective manner of the one makingdecision and they often don't match with the objectiveprobability of an event. That is shown in a weight function,developed by Kahneman&Tversky:

- Graph 2: A hypothetical weighting function, according to theexpected utility and prospect theory.

SOURCE:Masami Hayashi. Financial crisis prevention: A psychological approach from behavioural finance. Taking the look at the gap that's showing between horizontaland diagonal line, the horizontal line would represent theweighting function of a prospect theory which shows that peoplehave an „euphoria“ and „dysphoria“ stage. The broken line, onthe other hand, shows that expected utility suggests that thesubjective decision weights should be equal to statedprobabilites (p(p) = P). The euphoria stage, in this case,would explain that people can sometimes perceive chances ofwinning higher then they actually are, as well as potential forloosing. People tend to fall in stage of dysephoria soon afterthey discover that there's no winning rather then gradual

depreciation, which would be rational and as predicted byexpected utility theory.

3.3. LOSS AVERSION AND THE VALUE FUNCTION Behavioural finance and those who agree with the prospecttheory found that investors are not that risk-averse, how muchthey are loss – averse, meaning that gains of equal magnitudeas losses have very different impact on people and theirdecision making. The fact is that people are more affected bylosses, and they hurt more, that the gains give pleasure, ofthe same size. Investors are ready to increase their risk, inan order to avoid even the smallest probability of loss.Nathalie Abi Saleh Dargham (2009) found that: „A $2 gain mightmake people feel better by as much as a $1 loss makes them feelworse.“People tend to feel psychological effect of losses, even twicemore that one from the gains. Person's risk is also verysubjective and it depends on human's recent history, in theaspect of losses and gains. When someone experience onefinancial loss, he becames more risk-averse, while the decreasein risk-aversion shows after several gains. Again, theinfluence of loss is much greater than one of the gains. Thisasymmetric response to financial loss and financial gainscalled disposition-effect, and that's actually what this theoryaims to capture which, on the other hand completely suspensethe principle of rationally – the basis of the expected utilitytheory, in a real enviroment.

- Graph 3: Typical value function under prospect theory

SOURCE: Masami Hayashi. Financial crisis prevention: A psychological approach from behaviouralfinance.)

The fact that value function is steeper for losses, than forgains, as it is shown in the graph is the consequnce of thedifferent psycholgical effect of losses and gains, as explainedearlier. Shefrin and Statmand (1985) found that disposition effect ofinvestors to sell good-performing shares much sooner, thatother ones, in order to catch the current gains out of it,while holding bad performing ones to save themselves out of thepain of realizing losses, again asymetric response to thesetwo. This will be explained later in much more details, underthe concept of „regret aversion“. „ Loss aversion may well explain why investors sometimes rushto make withdrawaldecisions in order to avoid losing money. As a result, smallmarket corrections have

often disintegrated into full-scale crashes, fuelled by suchpanicked investors. „ 4

Grinblatt and Han (2005) pointed out that: „Loss aversion canalso help explain momentum. Specifically, past winners haveexcess selling pressure and past losers are not shunned asquickly as they should be, and this causes underreaction topublic information. In equilibrium, past winners areundervalued and past losers are overvalued. This createsmomentum as the misvaluation reverses over time.“

3.4. MENTAL ACCOUNTING

Mental accounting is also part of the prospect theory, one ofits aspects. Defining this economic concept in its most basicform: „An economic concept established by economist RichardThaler, which contends that individuals divide their currentand future assets into separate, non-transferable portions. Thetheory supports individuals assign different levels of utilityto each asset group, which affects their consumption decisionsand other behaviors." 5

Mental accounting, as defined previously, can be viewed andunderstood from two aspects: mental accounting of households(this is where behavioural finance meets every-day actions,regardless of financial markets ) and from the aspect ofinvestors who trade on the markets on a daily basis. Even though I defined, in this work, mental accounting as apart of the prospect theory, it wouldn't be wrong if I named itas one of the two pillars of this field. The second one, asyou'd suppose is prospect theory.Mental accounting is concept defined and researched by RichardThaler.He tryied and managed to explain how people tend toseparate money on a specific accounts on some personal,subjective criteria which often depends on the loss aversion ofindividuals. Some people tend to take bigger risk and loss,

4 (Undiscovered Managers, 1999)

5 Source: investopedia.com

when it comes to some goals, while much less when it comes tosome other, in their opinion, not so important ones. Peoplecannot be viewed as simply risk-averse, risk-seeking orneutral, as it was introduced earlier in traditional finance.Investors are changeable, and this concept tries to explainthat characteristic when it comes to decision making process,which can never be explained by rational model, as it was doneuntil behavioural finance. For example, households tend to divide money (income) based onthe source of that money and intent for which is gonna be used,so many of the have account for food, for clothing,entertainment, etc.

Reading the literature I found that there are 3 parts of mentalaccounting, which receive most attention, no matter if we talkabout households or investors:

- the first component of this concept views how outcomes areperceived and evaluated by the individual, and howdecisions are made, based on those outcomes, andsubsequently checked and changed

- the second one would be that assignment of funds todifferent accounts, as I explained earlier; 90% ofindividuals tend to categorize those funds according tosource and intention for use

- the last component is the frequency with which thoseaccount are observed and choices and decisions changed.They can be balanced daily, or monthly, or even on a basisof few years.

Each of the these components of mental accounting conceptbrakes the economic principle of fungibility. „ Fungibility ofmoney is a central principle in economics. It implies that anyunit of money is substitutable for another and that thecomposition of income is irrelevant for consumption. „ 6

As a result, mental accounting influences choices, it indeedmatters in decision making process. .

Research method: questionnaires and interviews6 Source: http://ideas.repec.org/p/iza/izadps/dp3500.html

STATS:

- Hypothesis: Is mental accounting, as a psychological effect,indeed used in a every-day life of households, as it waspresented theoretically ? - Number of subjects questioned: 100 - Category of subjects: „Head“ of households ( person earning the most income)- Number of subjects interviewed: 34- Category of subjects: Private investors- Characterisrics of subject: different life styles, differentincome statements, different types of expenditures, etc. - Addition: example of questionaire; page 38. example ofinterview (note: the interview was done on Bosnian language,due to language area, but the results are, ofcourse,interpreted inEnglish) - Explaining the method: I made an online questionnaire, whichI sent, by mail, to 100 respondents. Choosing the subjects, Iwas trying to make them as random as possible, meaningdifferent life styles, income statements, marital status, age,type of expenditures etc. My goal was not to make a pattern, sothe thesis would be representatively prooved, as much as it's possible.

The very first thing I noticed when I started to analyze theresults from the data I collected, it was the fact that eachand every household answered that thex have and manage housebudget, which is the first pillar or condition for mentalaccounting existence, as a psychology effect.

GRAPH 4: The number of people that have and manage a housebudget.

SOURCE: Author's data

What was so fascinating ? It was interesting that each one ofthe separated money according to two criterias: the source ofincome from which that money came from (regular monthly salary,bonus, extra money, lottery, etc. ) and the purpose with whichis gonna be spend in the future. This decision making process,the ongoing mental-accounting process, has enormousconsequences on their everyday life, in the aspect how theyspend and how much they save, each day in the month. Mentalaccounting in behaviour to view our money differently onlybecause, in our mind, we put it aside for certain purpose, and,maybe, it came from different source they monthly income.

- GRAPH 5: Type of expenditures on which regular monthly salaryis spent on.

SOURCE: author's data

From this graph, as we can see, almost 75 subjects out of 100that were questionned said that, when they receive theirmonthly income, they separate it and first spend it on billsand food&groceries. Hardly any of the regular income is beingfirst spend on the clothing, entertainment, etc. For that typeof consumption, as it shows the following graph, is used moneythat's coming from bonuses they receive on their wages. None ofthem answered that they spend bonus on bills. For somepsychological reason, that type of expenditure is being payedout of regular wage.

GRAPH 6: Type of expenditures on which bonus money is spent on.

SOURCE: author's data

These results from data that is collected show how peopleseparate the money according to the source if income an thetype of expenditures it will be spent on. This only shows thatindividuals, in their day-to-day actions, brake the basiceconomic principle, principle of fungibility.

74% of respondents said that they separate money according tothe source of which came from, as well as on what it's gonna bespend. For some reason, individuals hardly ever spend themonthly wage on expenditures such as clothing, entertainment,etc. Rather, on those type of consumption the bonus money isspent (0% said that spend the bonus money on paying bills), ora potentional lottery winning. 42% confessed they play lottery,and they would spend that income on clothing an entertainment.

27% of respondents are owning a portfolio, and they revise itmonthly or quarterly. The gains from portfolio are mostusutally spend on reinvesting and other types of expenditures.

GRAPH 7: Type of expenditures on which portfolio gains arespent on

SOURCE: author's data

Another fact, even stronger one, was that they hardly investmoney from their salary, they rather do it from bonus money orsome other source of additional income.

The questionnaire data colleted confirmed the hypothesis thatmental accounting, as a theoretical concept, is applied withindividuals, in practice.

After I reliatively prooved the existence of mental accountingas a theoretical aspect in the practice of households, I neededto connect this concpet with capitak market, too. Because ofthe fact that capital market of our conutry is still ratherundeveloped, I didn't manage to find (it doesn't exist,

actually) public data on private investors, so I used some ofmy sources. I've done an interviews with 34 respondents, who have activeportfolios.

The first important fact I wanted to know from my respondentswas for how long do they own their portfolio, to see are theyinexperiences or rather investors with longer period ofownership. My results showed that 47,06% of them was owningportfolio for time period of 1-3 years, and 26, 47% was holdingit for 5 years and more, which was quite satisfactory resultconcerning the maturity of those portfolios.

The following graph will show you the first signs of mentalaccounting, and that is separating money according to thesource and intention to use. 70,59% of respondents said theyonly spend the money for portfolio that came out of gains ofthat same portfolio, meaning reinvesting, while only 5,88% saidthey spend the money out of regular income.

GRAPH 8: The source of income most spend on buying shares/bondsfor portfolio

Source: author's data.

To prove this even more, they next said, at least 87,88% ofthem, they would never take the part out of their regularmonthly income and spent it on portfolio purchases. The other12,12% said that the source if income doesn't have anything todo with their decision on investing.

GRAPH 9: The source of income investors would never spend onbuying shares/bonds for portfolio

SOURCE: author's data

Even though, mental accounting predicts holding of non-performing shares/bonds, due to loss and regret aversion, thatwasn't such a case with „our“ investors. Almost half of them,35,29% said they would sell that type of share/bond, in orderto avoid losses, and explit gains, while 32,35% of them saidthey would wait. The rest 26,47% of respondets said they wouldmake new purchase to compensate for losses, but wouldn't sellthe loosing share. So the aspects of loss and regret aversion,as a part of prospects theory weren't that strongly provenhere, as the concept of separating the money, according to thepreviously mentioned criteria.

The next aspects, on past loosers/winners was also ratherproven, more than a half respondets said that they rather buy

securities which had realised gains in previous period, overthose who hadn't. The rest of them said that doesn't influencetheir decision.

GRAPH 10: The preferences of investors when buying securities

SOURCE: author's data.

The euphorya states and the effects of overconfidence and self-attribution were strongly demonstarted in the fact that 44,10%of them make new purchases after they realised gains, and theother half said they mostly do that. Noone responded with no,while the opposite happens if they loose. Most of them, 79% ofsubjects interviews, said they make a pause when they loose onsome purchase/sale of securities. Also, only 5 respondets saidthey blame themselves when they make bad investment choice,while 53% of them blame the overall state on the capitalmarket, and the rest of them answered they would blame abroker, acompany, etc.

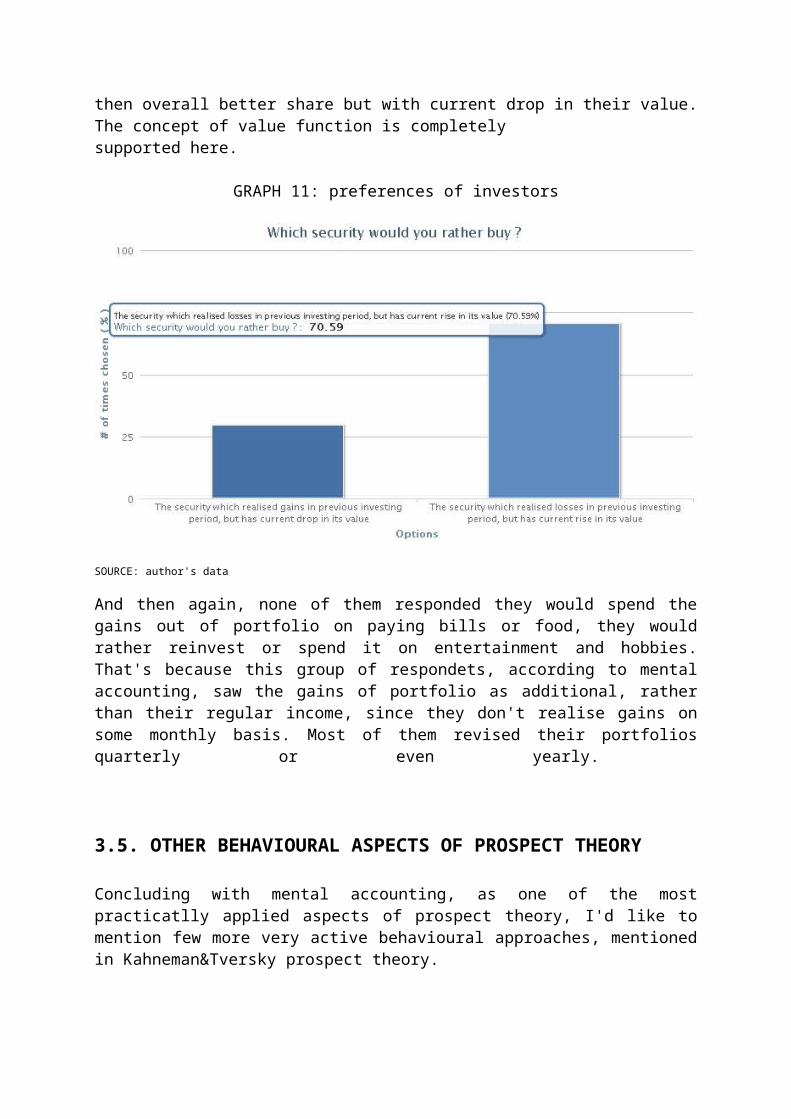

The last concept of mental accounting, and prospect theoryoverall was proven also, and that is the differentpsychological effect that losses&gains have on investors. Thatthey're more sensitive on losses then on gains, shows thefollowing graph, and the fact that 71% of them said they wouldrather buy worse share that has current rise in their value,

then overall better share but with current drop in their value.The concept of value function is completelysupported here.

GRAPH 11: preferences of investors

SOURCE: author's data

And then again, none of them responded they would spend thegains out of portfolio on paying bills or food, they wouldrather reinvest or spend it on entertainment and hobbies.That's because this group of respondets, according to mentalaccounting, saw the gains of portfolio as additional, ratherthan their regular income, since they don't realise gains onsome monthly basis. Most of them revised their portfoliosquarterly or even yearly.

3.5. OTHER BEHAVIOURAL ASPECTS OF PROSPECT THEORY

Concluding with mental accounting, as one of the mostpracticatlly applied aspects of prospect theory, I'd like tomention few more very active behavioural approaches, mentionedin Kahneman&Tversky prospect theory.

Regret aversion is pure psyhological effect that can play a keyrole in many investment decisions of individuals. It isespecially strong when we talk about pessimistic investors. Itrelates to the fact that noone likes to feel the emotion ofunsuccess, and it can be defined as a desire, as if not need,of investor to avoid the pain that could result from a badinvestment choice or decision. Investors can sometimes avoidmaking some decision, due to regret avoidance, even thoughthese decisions can be in their best interest. For example, when one investors holds in his portfolio badperforming shares, he might avoid to sell for a little while,until he's ready to admit to himself, mainly, that he made abad desicion and a lousy investment pick. This can reflectbadly on their further actions and income, for example therealized capital gains that would come from selling those non-performing shares/bonds/other type of securities can reducetaxable income. But many fail to see that advantage due to thispsychological phenomena, and rather avoid stress connected withadmitting the mistake, even though first option would be muchmore rational and beneficial.

Self-control, as a second behavioural aspect I'd like tomention, can easily be related to the concept of mentalaccouting but I decided to observe it separetely due to itsfrequent appearance in human behaviour. It is investors'tendency to set up a special accouting that are considered asoff-limits, meaning the money from those account is for someurgent and extraordinary purposes and shall not be spend on aregular basis. In that way many individuals control themselves,especially those prone to gambling. Richard Thaler, the fatherof mental accounting, notices investors find themselves toolsto improve and maintain self-control. One tool is topsychologically separate the income into non-expenditure andexpenditure one.

„Cognitive dissonance is the is a discomfort caused by holdingconflicting cognitions (e.g., ideas, beliefs, values, emotional reactions) simultaneously.“ 7 To better explain it, it is thetendency of many investors and even financial institutions, orin some cases governments to avoid the informations that areconflicting with their attitudes and previously made decisions.

7 Source: wikipedia.com

Sometimes, it is also reflected in a psychological effect tointerprete some informations wrongly, in an order to presrvethe belief in their hypothesis.

3.6. THE CONCLUSION ON PROSPECT THEORY

Prospect theory, as I could learn, defines several mentalstates that people are prone to, and which strongly affecttheir desicion making, especially when it comes to financialdesicion making. It's complete challenge, and in most waysbeats the efficient market hypothesis, theory which wasrepresentative until the 70s of the last century. The phenomena of loss-aversion explained that investors cannotbe purely classified as risk-averse and risk-seekers, as it wasdone previously. They are prone to risk in some situations,while averse in some other. This only proves that humans arenot rational beings. The prospect theory can be summed in the following definition:decision making in the situations of uncertainity. It'simportant to memorize the vaule and the weighting function, astwo key elements in this theory, the fact we, as human beings,don't value gains and losses equally. In the positive quadrantof the function (chart #3; page 9), we have positive gains, andthey never slops down, while for the losses in concave up. Thatwas the first diagram published in Econometrica, 30 years ago,by Kahneman&Tversky, and became basis for the field, todayknown as behavioural finance, or more broadly, behaviouraleconomics.

4. HEURISTIC DECISION PROCESS

Brabazon (2000) states that:„The heuristic decision process,which is the process by which the investors find things out forthemselves, usually by trial and error, leads to thedevelopment of rules of thumb. In other words, it refers torules of thumb which humans use to made decisions in complex,uncertain environments.“ The investors, when making the decision, along with theinformations they provided for themseleves from all kind ofsources, are, also, mixed with some mental and emotionalissues, meaning the factors that are subjective, and stronlyaffect the ultimate choice. Problem is that, sometimes, it'svery hard to distinguish between those two types of factors indecision making process, objective and subjective ones. According to the Kahneman&Tversky, related to the prospecttheory, the violation of economic principe of rationality inthe process od decision making should be viewed as a rule,rather than something that happens ocassionally, because theseerrors, developing even the rule of thumbs, are systematic inhuman behaviour. Thaler finds human behaviour in economic decision-making to be,systematically and substantively different from those predictedby the standard economic model. Heuristic, as a term, can be defined as some sort of littlestrategies we use, sometimes without even knowing, when tryingto make decision. Theory identified few major heuristic that affect us, duringthis desicion-making process, and they can help us make thecorrect choice, in some cases, though sometimes can lead us tocompletely wrong conclusion.

4.1. Representativeness Heuristic

Is the first behavioural element in the process od decisionmaking, defined by the Kahneman&Tversky, in early '70s of thelast century. To get more into the understanding of thisheuristic, the common bias, is to compare it to stereotypes.These are judgmental subjective statemens that people tend tohave, and that encourage them to categorize certain events,

people or subjects into different classes. It's pure relianceon steretypes. This error could bring investors to be more optimistic aboutthe stock market past winners, or past loosers. Also, it'sprone to judge some stock market as bull or bear, no matterthat almost every investors knows the fact that the excatlysame price change wont happen again. Actually, this can be also defined as a pure reliance on somepast events, especially if they're from own experience ofindividual, no matter the fact that people, as rational, mustknow that everything always has same chances for happening ornot happening again.The conclusion would be that all kind of analyses of the futureearnings and other types of forecasts are biased by thecharacteristics of stereotype decision. (Debont, 1998)

People, especially financial institutions and investors inthe stock market, are prone to overemphasize certainpatterns that they think are representative of whatthey've seen before. If they remember that exact littlething, which is 100% subjective and it depends on apersons' personality, they start to look for that samepattern again and again. And they see it too often,mentally. Adding the fact that these patterns are,objectively, very rare to happen, for example, in thestock market, it's quite obvious how the certain choice ora decision is biased.

4.2. Availibility heuristic

This type of factor in the decision making process affets thepeople's perception of likelihood of some event, or itsfrequency. It's people tendency to be biased by theinformations that are more available in the mind, meaningeasily recallable. Its most common that we're talking aboutinformations that are extremly publicly altered, visual orhappened recently. Again, the first description of this bias was given by famousKahneman&Tversky, at the same time the other heuristics areresearched and defined.

The availibitly heurisric influences people in the situation inwhich people assess the frequency of category or the probabilityof an event according to the ease with which instances oroccurrence can be brought to mind, which goes with thecharacteristics of informations previously explained. This is the most common bias, and it happens really often,therefore in almost 80% of cases leads to the wrong decision.

TABLE 1: Availability heuristic evidence in people's choice

This heuristic has commonly been documented by followingexperiment.They interviewers would ask the participants to determine thelikelihood of events that were divided into two categories, inwhich the subjects from first category were harder to recall,meaning they were older or less talked about, than those fromsecond category, even though the objective fact is thatinstance from the first category are those more often happeningin the world, even not so well publicized.

For example, Kahneman and Tversky (1973) found interestingfact. Most people think the letter R more often appears inEnglish words as the first letter than the third letter, mostprobably because the first letter provides a better cue forrecalling instances of words than does the third letter. Infact, it turns out that R appears more often as the third thanfirst letter in English words.

4.3. Anchoring, belief preservence and adjustment heuristic

Anchoring, it represents the usual human proneness to rely toomuch, or maybe is better to use the term „anchor“ – on oneaspect or piece if information, in the decision making process.Even when the new informations are available, investors tend tochange their opinion hardly, because they value system issomewhat fixed, meaning anchored by their recent opinions andobservations. For example, they could expect the earning trendto remain with historical one, which may lead to possible underreactions, or no reactions at all, to some present or futuretrend changes. Barberis and Thaler (2002) say: „At least two effects appear tobe at work. First, people are reluctant to search for evidencethat contradicts their beliefs. Second, even if they find suchevidence, they treat it with excessive skepticism.“The famous anchoring experiment again, Kahneman and Tversky,was done with wheel of fortune, like one used in the game showson TV. Kahneman&Tversky asked their participants, as one oftheir question (and they wanted the answer to be the numberbetween 1 and 100) how many nations belong to the UN – UnitedNations. But before taking the answer, they spinned the wheelin front on those subjects. Wheel showed random number,ofcouse. After that, they asked people to answer the previouslymade question. The questioned people, even though they knewthat random number in the wheel didn't had anything to do withthe potential answer, tended to answer and pick the numberwhich was close to the number on a wheel. It was 65, by theway. This, ofcourse, was completely irational. When they were askedhow come they gave the answer so close the one on the wheel,the participants said it was pure coinsidence. Statistically,they had just prove they were. Therefore, anchoring refers tothe fact that people are attracted to--they're affected bysubconscious things. It was hard for the to make logicalconnection, since they didn't had clue about potential answer.And when, in that situations, investors must come up with a

choice and a decision, they can be influenced by the mostrandom things.

4.4. Overconfidence heuristic

This heuristic is particulary interesting, because many of theanalysts of recent financial crisis relate it as one of thecauses. Investors often overestimate their ability and competence toforecast events in the financial markets, due to theyselfconfidence, and tend to risk finishing the market gamewithout any gains. (Nevins, 2004). When the failure occurs,they attribute it to the bad luck, and if they actually winthey contribute that to their competences, which leads to thenext situation and the problem of overonfidence. Daniel Kahneman used overconfidence heuristic to explain someof the patterns occuring in the stock market. He stated that:„Overconfidence about private signals causes overreaction andhence phenomena like the book/market effect and long-runreversals whereas self-attribution maintains overconfidence andallows prices to continue to overreacting, creating momentum.“

Barber and Odean conducdted the experiment among 78000investors in a brokerage firms. They divided them into fivecategories, based on their frequency of trading, and they foundthat those investors trading more heavily experienced gains 6%less, than those trading less actively. These two analystsconcluded that the reason is rather high level of trading,sometimes even on a daily basis, which is the consequence ofoverconfidence of those investors, which led to excessivetrading in the market.

Behaviourists also found positive relation between thisheuristic and overoptimism, which was reflected in thedeliberate seeking of information that would agree with yourchoice. There is also a problem of judging events by how theyappear rather than how likely they are, and human limitationsin recalling information.

Overconfidence heuristic leads to the action of agents withpositive information to be tempted to purchase some,

potentially overvalued assets, because they believe, they arethat confident, that they can sell that asset to agents witheven more extreme beliefs. With short-sale constraints,negative sentiment is sluggish to get into prices, and this canlead to asset pricing bubbles. These irrational agents, beingoverconfident, can end up bearing more of the risk and canhence earn greater expected returns in the long-run. Kyle(1997) argue that there are situations where agents are risk-neutral, overconfidence plays role of a precommitment to actaggressively, therefore causing the rational agent to slowndown with his trading activity. In equilibrium, this may causeoverconfident agents to earn greater expected profits thanrational ones. „

Yet, overconfidence can have a positive sides too. For example,Gervais and Goldstein (2004) argue that overconfidence mayactually allow and make possible better functioning oforganizations. The notion is that each team member’s marginalproductivity depends on other workers in the organization. Anoverconfident agent may overestimate his marginal productivityand work harder, therefore causing others to work harder aswell. While overconfidence causes the agent to overwork, theorganization as a whole can benefit from the positiveexternality that other players generate.Bernardo and Welch (2001) show that overconfidence in aneconomy is beneficial because increased risk taken byoverconfident agents supports the emergence of entrepreneurswho exploit new ideas

Even professional investors and economists tend to undereact onnegative, and overreact on a piece of positive informations.(could easily be related to the loss aversion, the aspect ofprospect theory).

4.5. Conclusion of heuristic decision making

Even though there are many more heuristics by which investors'decision making is biased, I decided to conclude on these four,the most common talked about, and commonly done in the process.( Many of the previous works actually are concluded out of thefirst three)

These are some another facts that put challenge on expectedutility theory, efficient market hypothesis, principle ofrationality and traditional finance, as a whole.

5. LATEST FINANCIAL CRISIS AND BEHAVIOURAL FINANCE

5.1. The basics on financial crisis

2008-2012, or according to some economics, still lasting,financial crisis, was so destructive for the worldwideeconomies that some compare it to the Great Depression,occuring in the 20s of past century. Billions and billionsdollars were lost through the failure of financialinstitutions, private companies and individuals, as well asmillion and millions of jobs.

Many of them argue, and I'll epxlain this in much more detaillater, that this crisis, as many of the other (GreatDepression, East-Asian crisis), had its roots (causes) in thebehaviour of people, meaning the causes were of psychologicalnature. Supporting this attitude, goes the fact thattraditional economicts, theories, models and traditionalfinance, as a whole, failed to anticipate, prevent, or at leastexplain what happened later on.

The behavioural finance approach reveals some of the issues,that traditional finance's theory don't admit as a facts.

After Great depression, in 1936 Keynes was first economist whohighligted the role of the psychology in the economy. Hiscauses to crisis, economic booms and busts, were ofpsychological nature, the tendency of people to be over-optimistic, in certain, and over-pessimistic in othersitutations. Minsky was another economists, who argued, decadesbefore this crisis, that financial innovation can createcurrent euphoria and growth in financial markets, but it'llinevitably, lead to crash and shake the economy from its roots.

Many argue, and it actually can be listed a a fact, that majorproblem that caused this financial crisis was housing bubble,subprime mortgages, securitization, low credit standards andcriterias. During this past decade, in the USA, people become extremlywilling to own a house. It was some sort of self-accomplishment, self-approval and admiration if you managed tobuy your own house, not to rent some. That desire was,sometimes, so strong that even those who were ompletelyuncapable to buy one, that they entered into loans, without anycollateral or other security instrument or realisticexpectation that borrower will be able to repay the same.Bankers and other financial mediators wanted to take advantageof this desire, and saw the chance for extra profits, so theycreated something that is today know as subprime mortgagesecurity.

GRAPH #8: The expansion of subprime lending in the USA, from2004-2006.

In this graph, we can see how it all started, and the sharpgrowth in home ownership, as well as in subprime lending, in2004. It was more than doubled comparing to the previous year.

The process of getting a loan at that time was going prettymuch this way. The borrower, completely inadequate to borrow inover 50% of the cases, would go to the banker and asked for aloan. In previous year, the mortgage loan was one of thehardest to get involving much of the paperwok, examination andcollateral required, but in 2004 it started to be easier to geta mortgage, than a car loan. How is that ? Well, those bankersthat approved thos subprime loans to subprime borrowers,created something know as subprime securities. After they gavethe loan, they would sell it to a special party vehicle (SPV),the institution that was specially creating for buying the

loans and other debt instruments, which would later on sell itto insitutional investors, for example mutual, hedge andpension funds. Bernanke (2010) argue that the availability of these alternativemortgage products was likely a key explanation of the housingbubble, that occured in the USA. The banker who created and sold the loan didn't care much aboutrepayment of the same, since he was only administering now thepaperwork and the servicing of the loan, he got his money forapproval for next loan. The borrower was completely blinded bythe happines he got his own house, that he didn't even thoughtabout ways of repying the excessive mortgage loan. It seemed likeeveryone were driven by greed, and the desire for extra profit,one of the greatest sins of capitalistic society. Thesecuritization process of those subprime mortgage securitiesbecame so complex, that it was almost impossible to find thesource of risk later on. Shrefrin and Statman (2011) note alsothat these aspirations for wealth and status blinded bankers tosee the risks they were taking when issuing or holding mortgagesand mortgage-related securities. Homeowners’ aspirationspropelled many into houses they could not afford. Moreover, theseaspirations evoked emotions and cognitive errors, blindinghomeowners to risk.

How come everyone neglected the rationallity ? How comeeffiecient market hypothesis failed so much, the informationsabout origination of the loan were, after some time, almostimpossible to get ? How this bubble got so huge, that, when itexploded, it lead almost whole world to the ruin ?

Behavioural finance has the answers.

Aspirations for owning a house, and the capitalistic culture of„living on the loan“, got mixed with mortgage securities andother financial innovations orginated by the banks and otherfinancial institutions, insured by another financial innovation(CDSs), and rated much above their real value by the ratingagencies, in order to maintain their clients, the failure ofgovernment to regulate properly banks, allowing them to expandtheir financial leverage much beyond desireable one, lead tounrealistic optimism of everyone and inevitably to the bubble, inthis case, housing one.Bubbles pose a major challenge to the efficient markethypothesis, and according to many, is the one to blame for

misleading so many economists in belief that markets areefficient, which inflated, in the first place, and lead to thegreatest housing bubble in history. The fact, and according tothe definition of the rational markets, which was givenpreviously in the work, the bubbles as an effect cannot exist inthe rational markets, since bubble means that prices of asssets,in this case of houses, are much different that their instristic(real) values. In the case of this crisis, we can say the bubblewas positive since the prices were much higher than theirinstristic value. ( US home prices increased 85% from 1997-2006,and again sharply rose from 2003-2006, suggesting the existenceof a bubble (Shefrim, Statman, 2011) ).

5.2. Behavioural and Psychological biases

Greed of investors and managers – according to thebehavioural finance and portfolio theory, from this pointof view, the investors are motivated by two emotions:greed and fear. The fear of decline in their currentstandard of living, moving down on the wealth scale, theytend to keep portion of their money invested in safesecurity instruments. But much stronger emotion is greed,the extreme desire to go upward on the scale of wealth,leads to acceptance of much higher risks, in theaspiration of greater satisfaction and profits. That wasmajor cause to the financial crisis. The greed of bankers,for higher profits, and the greed of individuals, forhigher standard of living. Even the greed of governmentand rating agencies, who failed to regulate financialmarket, but regulatory tools and ratings, in theaspiration of growth and, again, higher profits. AdamSzyszka (2011) claims that the greed which pushedinvestors and managers towards riskier and riskierinvestment strategies did not directly contributed to thefinancial crisis whose sources should be looked for in theglobal macroeconomic imbalance; rather, it determined itsscale, arising from the material leveraging of businessoperations and involvement in all kinds of derivatives.

Underestimation of risk - Few years before the crisisoccured, overconfidence and unrealistic optimisim ofeveryone in the market led to the underestimation of risk,involving the confirmation bias. Confirmation bias is thetendency of people to look for and admit the informations

that are only confirming something they previously adoptedin the minds, and unconsciously evade the facts that couldbe contradictory to their opinion. Specifically this bias,prevented individuals from paying atenttion and noticingthe warning signals that could erode their faith intonever-ending boom market and prosperity. During this,quite long, period of market growth, many of investorsbecame used on easy-making, and excessive prosits. Again,another bias arose, self-attribution one, which is thetendency of people to attribute their gained profits totheir own skills and abbilities, rather than overallmarket conditions. That current success in investmentdecision and choices led them to even more intenseconfidence and understimation of risks, that were iflooked rational, quite obvious, and encourage them to takeeven higher ones. During this last prosperity marketperiod, which was precedeeing the crisis, people also madeanother psychological bias. They commited andextrapolation error, which reffers to giving much weightand importance to past trends, especially short ones, andunjustifiedly extending them on future periods. In thisvery case of latest financial crisis, this error led tothe belief that the prices will continue to grow, sincethey been growing for such a long period of time, meaningthat bull period of property market will continue in thefuture. Kahneman and Tversky accounted for anotherphenomena in their prospect theory, which lead tounderesttimation of risk, and that is the tendency ofpeople to believe that some events which are unlikely tohappen, in their minds become impossible. According tothem, the overall assessment of utility of some decision-making scenario is affected by two functions that arestrongly subjective for each individual: the S-shapedvalue function and the weighting function. Kahneman andTversky (1974) argued that „ one of the properties of theweighing function is its discontinuity for the probabilityvalues close to zero and close to one. The followingfigure will show that function will give the value of zeroto the events with low probability, while those withhigher probability are assigned with complete probability,value of 1.

-Graph #9: Weighting function

SOURCE: BEHAVIOURAL ANATOMY OF THE FINANCIAL CRISIS, ADAM SZYSZKA, 2011, PAGE 8

People, at that time, simpy thought, since evidence andtheir former biases showed period of growth, is unlikely tofail, leading to the opinion that bust is almostimposssible, and they all failed to aniticpate somethingthat occured only 2-3 years later.

Imitating the others – when individuals saw who else isgetting the loans and buying the houses and increasingtheir living standards, they went in line with them. Thisis know as herding. Herding is the tendency of people toact not on basic of relevant informations, rather than ontheir observations of earlier happenings and on the basisof actions of other. All that buying lead to assetmisspricing, meaning rise and rise in the house prices.Adam Szyszka (2011) states that „each subsequent observerwill attach greater importance to the informationindicated by the behaviors of other market players than tohis own private signals.“ This behaviour causes aninformation cascade. Adam S. (2011) later on claims that„the lesser the amount and precision of the informationavailable to the decision makers, the greater their

tendency will be to ignore private signals and to copy thebehaviors of other players. „ That obviously happened withindividual investors and bankers during lastest financilcrisis. Everyone done what all else did, even though itwas completely irrational in many aspect. One of thoseindividuals who managed to pass the copying and theinformation cascade going on around in financial market,and manged to see through earned 15 $ billion in a betagainst subprime mortgage securities. The story of JohnPaulson who dug for information about mortgage securities,and his fund Paulson and Company, found privateinformations about misspricing of subprime mortgages. Buthis informations gained him profit only years later whenmean passed through copying behaviour.

Mistakes of rating agencies and government - The financialcrisis only confirmed the failure and mistakes of ratingagencies in USA. Their biggest mistake were the ratingsgiven to mortgage-based securities and the evaluation oftheir risk. According to their nature, mortgages are long-term liabilities. Despite this objective fact, the ratingagencies around the world used statistical methods forshort historical sample to evaluate the worthiness ofmortgage debt portfolios. They commited the short-serieserroe, led by the belief that since no failures ofmortgage borrowers happened at that time, they will no seefailure in the future either, during the whole lendingperiod. They were also lead by traditional opinion thatdiversification of loan portfolio could exclude thepotential insolvency of an idividual borrower. This led toassignment of high ratings to these mortgages. Anothermistake rating agency done at that time wasunderestimation of systematic risk, since they overlookedthe fact that major part of borrowers could default ontheir obligations. They thought as impossible that suchmajor events could occur and affect large number ofborrowers and shake the grounds of one economy to theroots. Rating agencies found themselves as victims of apsychological effect, demonstrated in Kahneman&Tverskyprospect theory, as tendecy to treat unlikely events ascompletely imposssible, as weighting function showed, on agraph previous given in the work. Also, there was tendencyto believe that mortgage securities were highly safe and

credible, at that time, since their opinion was thatpropery prices couldn't go down, in any way. All that,again lead to the common belief that mortgages were indeedsecure instrument and misrating kept going on.

It's interesting that government also failed to anticipatethis crash, due to their believe that financial marketshould be driven by supply and demand, and that nogovernment should intervene. After financial crisis, thestrong regulation of government and other stateinstitutions, started, manifesting in Basel III Accord.

5.2. Conclusion on financial crisis

By going through analyze of the latest financial crisis, Idemonstrated behavioural finance approach answers to causes andthe overall process of going in and through financial crisis.By relying on the psychological effects and showing theannomalies in human behaviour, it found some common mistakesdone by individual, professional, and institutional investors,that were previously hard to explain, from the aspect oftraditional finance. It shed completely new light on casues offinancial crisis. It showed how behavioural annomalies affectedalso rating agencies and government, and that no human beinginvoled is completely rational. The institutions which were specifically designed to overlookthe stability of the financial system and ensure its compliancewith regulations also failed to antcipate the importancepsychological issues will have on financial market.

Shefrin and Statman (2011) state that „ psychology is at thecenter of behavioral finance and psychology underlies much oflatest financial crisis. That psychology includes aspirations,cognition, emotions, culture, and perceptions of fairness.Aspirations propelled many renters into houses they could notafford, evoking emotions and cognitive errors that blindedhomeowners to risk. And a culture where houses are central to theAmerican Dream deepened the crisis and extended it. „

Maybe next time, as behavioural finance field develope, theeconomists will observe some of the issues overlooking thebehavioural, not only traditional finance. Because, the worlwide,not only USA, economies still feel and will feel the consequenesof financial crisis for a long time. Financial crisis left USAhouseholds and overall economy with high losses, which thefollowing graph best demonstrates.

GRAPH 10: The ratio between household debt and disposableincome in USA before, during and after the crisis.

6. PUZZLES OF FINANCE AND BEHAVIOURAL FINANCE

To conclude the story of behavioural finance, I decided to gothrough 6 major financial issues, from behavioural financepoint of view. This paragraph will try to explain these 6puzzles using the elements of prospect theory, as well asheuristic decision making.

6.1. Over and underreaction of stock prices

When we talk about stock prices, we can mention two completelyopposite effects on the prices. The first one refers tounderreaction of prices, meaning that stock market reacts onnews in two tranches: immediatly after the news is publishedand in following periods. The opposite, meaning overreactionappears if the stock prices change only after the news aboutprices is realesed, but moves differently in following periods.The concept from behavioural finance that are used in the worksaiming to explain this phenomena of under and over reaction ofthe prices are:

- coservatism and the representativness heuristic- self-attribution bias and overconfidence

According to the efficient market hypothesis and traditionalfinance, some newly published informations about should bereflected in stock market changes immediately, and changes inthe following period should be completely independent of thoseinformations released in previous days/months/quarters. To explain why this often doesn't go this way, even though itshould Barberis, Shleifer and Vishy (1998) developed a model,based on a behavioural finance approrach, in order to explainthis common phenomena by using two concepts of behaviouralfinance: conservatism and repressentativness heuristic. Theylooked on a conservatism as a reason why some informations ornew are not adequately reflected in stock prices changes in ashort time period. The fact is that an ordinary investors learnslower than it should, according to the Bayesian learning,

According to the William Forbes (Behavioural Finance, Willey)Bayes' rule stands for inferring the outcome of some event whenthe occurance of other is given. This would, according to thesethree behavioural economists, exlain the short-termunderreaction, because it's being waited for another event.Than, going forward, in the longer term the representativnessheuristic is in force, meaning investors giving to much valueto some past events, past informations, past patterns, and keepreacting on that news even in subsequent periods. Barberis,Shleifer and Vishny (1998) claim that if the investor hasobserved a series of good earning schocks, his belief thatprofits follow a trend grows. On the other hand, if he hasobserved a series of switches from positive to negativeearnings and vice versa, he may switch to the belief thatearnings are mean-reverting. Investors, simply, tend to rely onpast events and news, facts, informations even though theymight be completely irelevant for the following period,therefore creating these patterns of under and overreaction onthe stock market. Financial analysts can also overreact to some pastinformations, for example to recent earnings of a company, andon the basis of those make the forecast for the next year'sdividend per stock. Another triplet of behavioural eonomicsts tryied to explainthis phenomena by using the concepts of overonfidence bias andself-attribution, which, in my opinion better explain the wholeissue. Daniel, Hirschleifer and Subrahmanyam (1998) found thatthese over and underreaction of stock market are due totendency of investors to overestimate some privateinformations. If that informations isn't public yet, that onlygives hihger degree to their confidence, and in the case of apositive information makes the investors buy more shares thathe rationally should, and the stock market overreacts. If hisinformations appears to be true and he does a good job withbuying those share, his confidence will just go up, and he'llattribute that success completely to his skills of investing.If the opposite occurs, he'll probably blame the other.Therefore, according to Hirschleifer and Subrahmanyam (1998)overconfidence will not fade away and is likely to increase.Overconfident investors do excessive purchases and inducemomentum, by moving the prices of the shares upwards, indicatedby their private singal. Then, an initial sharp rise in stock

prices, overreaction, can be followed by moving downwards infollowing periods, if his actions appear to be unjustified, andhis information wrong. Overconfidence has a positive side too,it increases liquidity since more investors trade moreexcessively.

6.2. Hypes and panic

The empirical studies and evidence shows that investors andoverall public tend to react more strongly on a bad news,during the financial crisis, than on the good ones. Keijer andPrast (2001) found that in times of prosperity in the market,coefficient of reaction to good news is as twice as large, thanone on the bad news. This pattern supports the theory ofcognitive dissonance, the tendenvy of people, when havingfundamental opinion, they ignore or overlook the informationsthat might destroy their opinion, and pay more atenttion tothose which supports it. The first case, in the financialcrisis, creates a panic in the financial market, only worseningalready bad situtation. And the second one creates hypes.

6.3. Equity premium puzzle

Evidence show that regular investors don't conduct complextechnical analysis when wanting to invest in the securities.The major criteria on which they decided whether to invest inshares or bonds, how and when, is their investment horizon.Investors tend to hold their security portfolio as additionalsource of income, they're not interested in speculativeprofits, therefore they have lonbg planning horizon. After theycreated they portfolio, most usually out of stocks, they don'trevise it that often, usually once a year, for other needs. Butthat revision has strong psychological effect. Losses ofportfolio, even though they are not realised, since anypurchases and sales aren't made, has much stronger impact thangains, which is according to the prospect theory of Kahnemanand Tversky, and their loss aversion concept. Portfolio must,therefore, earn a return that will compensate for this emotialpain of losses on paper. Benartzi and Thaler (1995) showed thatan investor who has a 30-year planning horizon and evaluateshis portfolio once a year, requires and equity premium of about6,5% to be indifferent when choosing between stocks and bonds.

According to them, when the evaluation frequency is five years,the equity premium should be 4,65% and when we're talking aboutlonger horizon, for example ten years, that premium should be2%. Even though institutional investors don't have such astrong psychological side when evaluating their portfolio,their clients who are regular investors do, and that affectstheir position too as fund managers. Jagannathan, McGrattan,and Scherbina (2001) claim that concept of loss aversion mayalso explain pension funds, whose horizon is basicallyinfinitely long, invest relatively little in stocks.

6.4. Winner/loser asymmetry.

Shefrin and Statman (1985) state that investors are predisposedto hold their non-performing stocks for too long, and selltheir winning stocks too early. Prospect theory is used toexplain this phenomena. If the example of investor who needs acash is taken, I'll observe the case A and B. In the case Athat investor will sell share which gained him 20% of returnsince the moment he bought it and added to his portfolio, whilein the case B he'll sell share which fell for 20% from the verymoment of pruchase. First, investor sees and analyses theseshares completely isolated from one another, in term of gainsand lossed relative to the price he first payed. If he sellsthe stock B, it'll mean he must close the mental account hehas, and conclude it with loss, while selling the A one wouldaccount him with profit. Therefore, mental accounting and lossaversion make the investor want to sell the winning stock,rather than losing one. Odean (1998) found that from January toNovember, investors sold their performing stocks 1,7 times morefrequently than their loosing ones. Said in other words,winners had a 70% higher chance of being sold.This is pure psychology and behavioural annomaly of investors,even though it'd be rational to get rid of a „bad“ stock andhold on the winning one.

7.CONCLUSION

This whole behavioural finance story shed a complete new lightand answers to many events, phenomenas and annomalies in theworld of economy and finance.

Daniel Kahneman and Tversky with their prospet theory started areal revolution the field of finance, brining completely newanswers and solutions to many issues. The baheavioural financecontributed to better understanding of ordinary, as well asprofessional investors, in day day-to-day actions in verycomplex market. It completely bounded the efficient markethypothesis and traditional finance, showing that economy,especially the stock market around which everything happens,

isn't just a set of complex analysis, numbers and rationalactions of the participants. It showed the other side, thehuman being side, the psychological issues of us, as irrationalindividuals, that are mislead by all kinds of behaviouralannomalies. As a theory, prospect theory, and as a field,behavioural finance, have empirical research and studiesshowing how investors actually behave, rather than how theyshould behave accordingto sore economic models.

Fast developemnt of this field will empower the investors tobetter forecast their behaviour and it'll bring moreeffieciency to their actions. It could provide answers, andsome already did, to explain financial crisis which are doomedto occur every now and then. This fieldmight actually prevent some of the crisis, by offeringalternative insight.

Despide all these findings of behavioural finance, which canonly get broarder, especially concerning the explanation whypanics and manias happen, the practical application of thisfiled is still bit neglected. Barberis (2001) suggests thatinvestors can exploit the behavioural biases of otherinvestors. Masami Hayashi (2001) mentions the existence of atrust fund in the United States of America that is called„Undiscovered Managers“, that provides a fund section called„ Behavioural finance growth fund“, whose goal is to detectsecurities that are mispriced as a result of behavioural biasesof other players in the market. The behavioural finance, as a study must also be betteracknowledged in the colegges with the students of economy andfinance. They (we ) shouldn't just learn about traditionalfinance and the basic model which are in strength for decadesnow, despite rapid changes in the modern economy. I'm notsuggesting diminishment of traditional finance or anythingelse, but to this field, behavoural finance should definetly beadded and should be studied along with it.Separation shouldn't be made.

Behavioural finance has made two valuable innovativecontributions to traditional finance theory. In the first place,there's evidence which showed that investors and other market

players tend to make their decisions and choices, as well asevaluate the results/outcomes, based on the facts of prospecttheory, rather than expected utility one. (loss aversion, regretaversion, mental accounting, etc. ) The second contribution wouldbe the emergence of cognitive psychology in the finance, andtaking into account biases human beings always make when tryingto decide onsomething, and these are hard to overcome.

After all this reseach, I could definetly say that this field'simportance and relevance is yet to come, especially after allpaper works and studies written on the case of latest financialcrisis from the point of view of behaioural finance. Much morework, and empricial studies is needed, as well as introducingthis field into the college courses, and students ofeconomy&finance, world wide.

8. LITERATURE

1. Abi Saleh Dargham Nathalie (year uknown): The implications of behavioural finance.

2. Forbes William. (2009); Behavioural Finance. 1st edition. Willey publiciations.

3. Hayashi Masami (2001): Financial crisis prevention:A psychological approach from behavioural finance. Institute of Development Studies (IDS).

4. Kanaddhasan M., M. Phill (year uknown): Role of behavioural finance on investment decisions.

5. Montier James (2008): Behavioural Investing: A Practitioners Guide to Applying Behavioural Finance. 1st. Edition. Willey publications.

6. Naughton Tony (2002): The winner is... Behavioural finance ?. Journal of Financial services marketing.

7. Prast Henriëtte (2004): INVESTOR PSYCHOLOGY: A BEHAVIOURAL EXPLANATION OF SIX FINANCE PUZZLES.

8. Sewell Martin( 2007): Behaviural finance. University College London.

9. Shefrin H. (2000): Beyond greed and fear; Hardward Bussines School Press.

10. Shefrin Hersh, Meir Statman (2011): Behavioral Finance in the Financial Crisis: Market Efficiency, Minsky, and Keynes. Santa Clara University.

11. Subrahmanyam Avanidhar (2007): Behavioural Finance: A Review andSynthesis. Volume 14. European Financial Management.

12. Szyzka Adam (2011): Behavioural anatomy of financial crisis. Journal of Centrum Catedra.

13. Thaler Richard (1999): Mental accounting matters, Journal of behavioural decision making. 12th edition.

14. Thorsten Hens, Kremena Bachmann (2008): Behavioural finance for private banking; Willey Finance publications.

15. Tvede Lars (2002); They Psychology of finance: Understanding the behavioural dynamics of markets. Revised edition. Willey Trade publications.

16. Tversky Amos, Daniel Kahneman (1979): Prospect theory: an analysis of decision making under risk. Econometrica.

INTERNET:

17. http://www.businessinsider.com/common-behavioral-biases-2012-5?op=1

18. http://en.wikipedia.org/wiki/2007%E2%80%932012_global_financial_crisis. Entered: August 22; 11:06 a.m.

19. www.investopedia.com

20. www.wikipedia.com

21. www.behaviouralfinance.net

9.ADDITION.

AN EXAMPLE OF A QUESTIONNAIRE USED FOR DATA COLLECTING.

1. Gender.- male - female

2. Which category bellow includes your age ?- 20-30- 30-40- 40-50- 50+

3. Your marital status?- Single- Married- Divorced- Widowed

4. Number of persons currently living in your household ?- 2- 3- 4- 4+

5. Which category bellow includes your education ?- high school graduate- graduated from college- master degree- doctor degree

6. Which category bellow best describes your employment ?- working, 1-39 hours per week- working, 40+ hours per week- not working, but looking for a job- not working, and not looking for a job- retired- disabled

7. In which of the following categories your average aproximateincome is included ?- 0-1000,00 KM- 1000,00 KM – 2000,00 KM- 2000,00 KM – 30000,00 KM- 3000,00 KM+

8. How many children do you have ?- 0- 1- 2- 3- 4- 4+

9. What level of education your children, if have any, attend ?(if you don't have children, skip the question, it's not obligatory; you can choose several answers according to your needs)- elementary school- public high school- private high school- public college- private college

10. Do you receive your salary on a regular basis ?- Yes- No- Most often

11. Do you have a house budget ?- Yes- No

12. When you receive your monthly salary, on what do you spend that money first ?- Bills- Food&groceries- Clothing- Entertainment, hobbies, etc.- Other

13. Do you separate your money, according to the type of expenditures it'll be spent on ?- Yes- No- Sometimes

14. Do you receive a bonus on your salary ?- Yes- No- Sometimes

15. When you receive your bonus, on what do you spend it first ? (if you don't recieve any bonus, skip this question, it's not obligatory)- Bills- Food&groceries- Clothing- Entertainment, hobbies, etc.- Other

16. Do you play lottery ?- Yes- No

17. If you'd won lottery, on what would you spend it first ?- Bills- Food&groceries- Clothing- Entertainment, hobbies, etc.- Other 18. Do you have a portfolio ? (if no, got to the end of questionnaire)- Yes- No

19. How often do you revise your portfolio ?- Daily- Weekly- Monthly- Quarterly

- Yearly