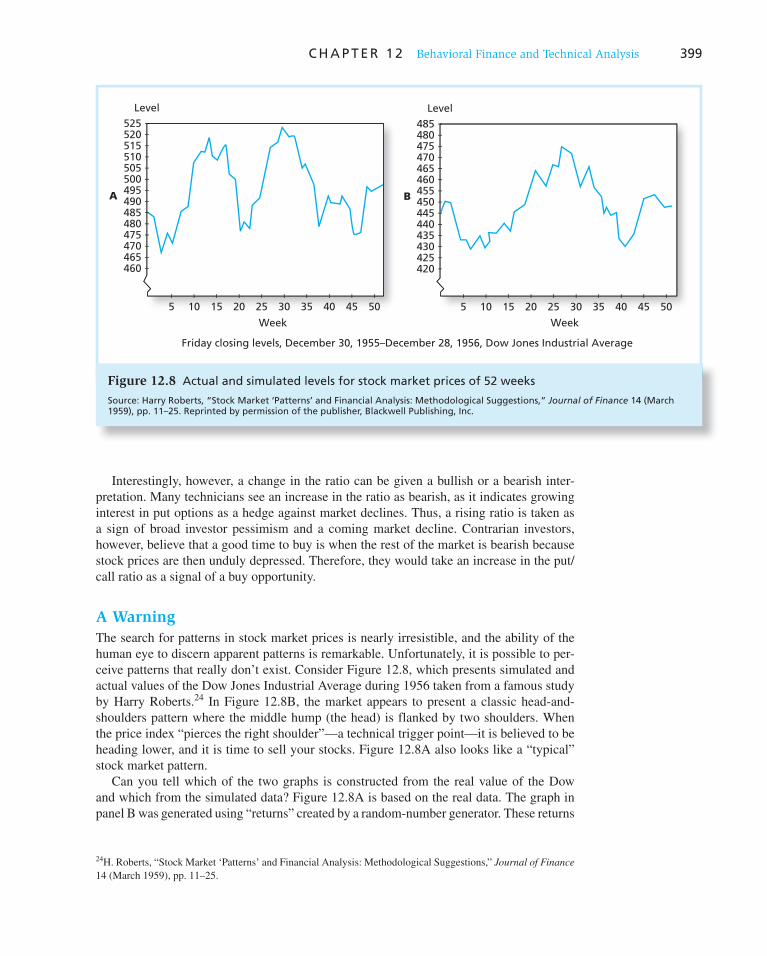

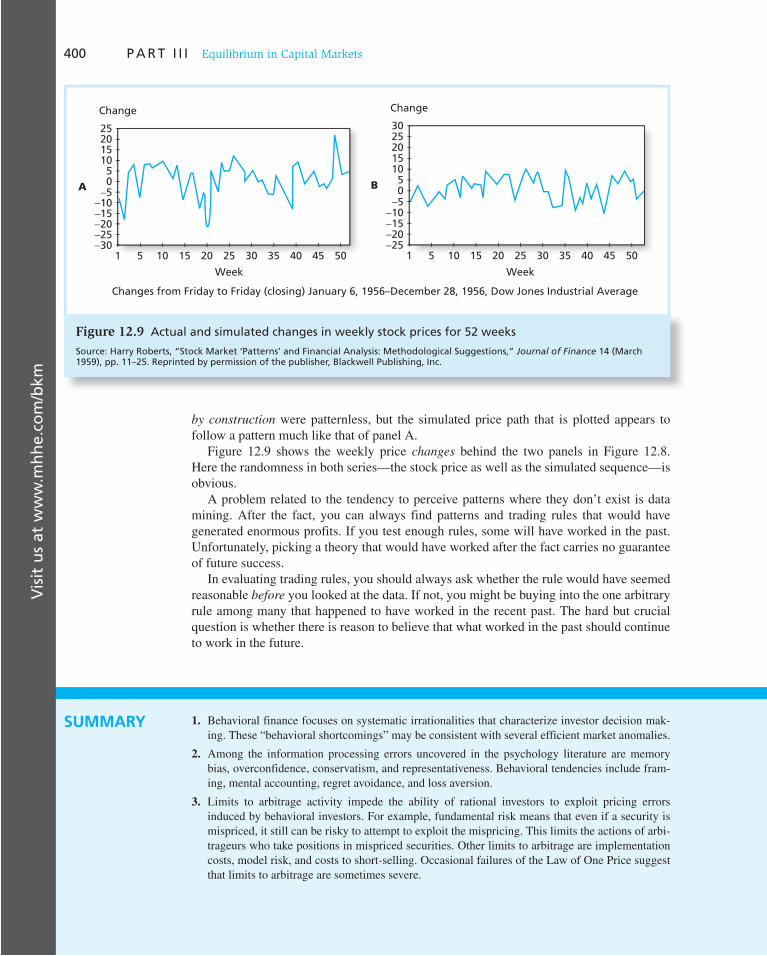

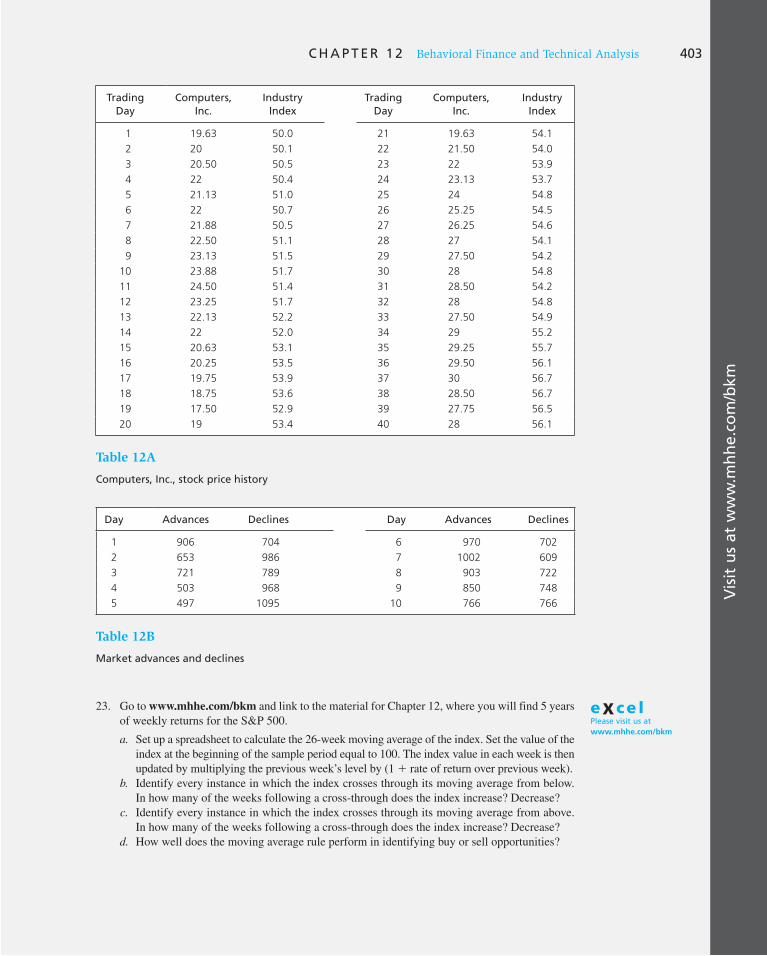

finance - WordPress.com

1065

-

Upload

khangminh22 -

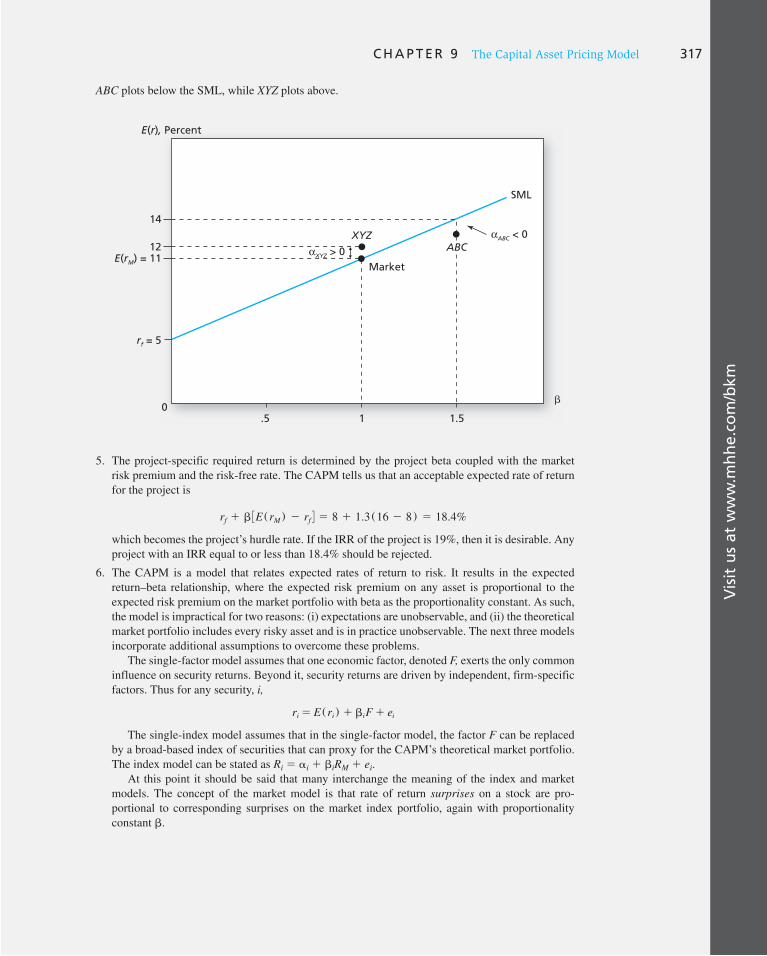

Category

Documents

-

view

0 -

download

0

Transcript of finance - WordPress.com

STUDENTS GET:

• Easy online access to homework, tests, and

quizzes assigned by your instructor.

• Immediate feedback on how you’re doing.

(No more wishing you could call your

instructor at 1 a.m.)

• Quick access to lectures, practice materials,

eBook, and more. (All the material you need

to be successful is right at your fi ngertips.)

• A Self-Quiz and Study tool that assesses

your knowledge and recommends specifi c

readings, supplemental study materials,

and additional practice work.*

*Available with select McGraw-Hill titles.

With McGraw-Hill's Connect™ Plus Finance,

Want to get better grades? (Who doesn’t?)

Prefer to do your homework online? (After all, you are online anyway…)

Need a better way to study before the big test?

(A little peace of mind is a good thing…)

STUDENTS...

finance

Less managing. More teaching. Greater learning.

INSTRUCTORS GET:

• Simple assignment management, allowing you to

spend more time teaching.

• Auto-graded assignments, quizzes, and tests.

• Detailed Visual Reporting where student and

section results can be viewed and analyzed.

• Sophisticated online testing capability.

• A fi ltering and reporting function that

allows you to easily assign and report

on materials that are correlated to

accreditation standards, learning

outcomes, and Bloom’s taxonomy.

• An easy-to-use lecture capture tool.

• The option to upload course

documents for student access.

With McGraw-Hill's Connect™ Plus Finance,

Would you like your students to show up for class more prepared? (Let’s face it, class is much more fun if everyone is engaged and prepared…)

Want an easy way to assign homework online and track student progress? (Less time grading means more time teaching…)

Want an instant view of student or class performance? (No more wondering if

students understand…)

Need to collect data and generate reports required for administration or accreditation? (Say goodbye to manually tracking student learning outcomes…)

Want to record and post your lectures for students to view online?

INSTRUCTORS...

Want an online, searchable version of your textbook?

Wish your textbook could be available online while you’re doing

your assignments?

Want to get more value from your textbook purchase?

Think learning fi nance should be a bit more interesting?

Connect™ Plus Finance eBook

If you choose to use Connect™ Plus Finance, you have an

affordable and searchable online version of your book

integrated with your other online tools.

Connect™ Plus Finance eBook offers

features like:

• Topic search

• Direct links from assignments

• Adjustable text size

• Jump to page number

• Print by section

Check out the STUDENT RESOURCES

section under the Connect™ Library tab.

Here you’ll fi nd a wealth of resources designed to help you

achieve your goals in the course. Every student has different

needs, so explore the STUDENT RESOURCES to fi nd the

materials best suited to you.

Investments

Saunders and Cornett Financial Institutions Management: A Risk

Management Approach

Seventh Edition

Saunders and Cornett Financial Markets and Institutions

Fourth Edition

International Finance

Eun and Resnick International Financial Management

Fifth Edition

Kuemmerle Case Studies in International

Entrepreneurship: Managing and Financing

Ventures in the Global Economy

First Edition

Robin International Corporate Finance

First Edition

Real Estate

Brueggeman and Fisher Real Estate Finance and Investments

Fourteenth Edition

Ling and Archer Real Estate Principles: A Value Approach

Third Edition

Financial Planning and Insurance

Allen, Melone, Rosenbloom, and Mahoney

Retirement Plans: 401(k)s, IRAs, and Other

Deferred Compensation Approaches

Tenth Edition

Altfest Personal Financial Planning

First Edition

Harrington and Niehaus Risk Management and Insurance

Second Edition

Kapoor, Dlabay, and Hughes Focus on Personal Finance: An Active

Approach to Help You Develop Successful

Financial Skills

Third Edition

Kapoor, Dlabay, and Hughes Personal Finance

Ninth Edition

Ross, Westerfield, Jaffe, and Jordan Corporate Finance: Core Principles

and Applications

Third Edition

Ross, Westerfield, and Jordan Essentials of Corporate Finance

Seventh Edition

Ross, Westerfield, and Jordan Fundamentals of Corporate Finance

Ninth Edition

Shefrin Behavioral Corporate Finance: Decisions

that Create Value

First Edition

White Financial Analysis with an Electronic

Calculator

Sixth Edition

Investments

Bodie, Kane, and Marcus Essentials of Investments

Eighth Edition

Bodie, Kane, and Marcus Investments

Ninth Edition

Hirschey and Nofsinger Investments: Analysis and Behavior

Second Edition

Hirt and Block Fundamentals of Investment Management

Ninth Edition

Jordan and Miller

Fundamentals of Investments: Valuation and

Management

Fifth Edition

Stewart, Piros, and Hiesler Running Money: Professional Portfolio

Management

First Edition

Sundaram and Das Derivatives: Principles and Practice

First Edition

Financial Institutions and Markets

Rose and Hudgins Bank Management and Financial Services

Eighth Edition

Rose and Marquis Money and Capital Markets: Financial

Institutions and Instruments in a Global

Marketplace

Eleventh Edition

Financial Management

Adair Excel Applications for Corporate Finance

First Edition

Block, Hirt, and Danielsen Foundations of Financial Management

Fourteenth Edition

Brealey, Myers, and Allen Principles of Corporate Finance

Tenth Edition

Brealey, Myers, and Allen Principles of Corporate Finance,

Concise Edition

Second Edition

Brealey, Myers, and Marcus Fundamentals of Corporate Finance

Sixth Edition

Brooks FinGame Online 5.0

Bruner Case Studies in Finance: Managing for

Corporate Value Creation

Sixth Edition

Chew The New Corporate Finance: Where Theory

Meets Practice

Third Edition

Cornett, Adair, and Nofsinger Finance: Applications and Theory

First Edition

DeMello Cases in Finance

Second Edition

Grinblatt (editor) Stephen A. Ross, Mentor: Influence through

Generations

Grinblatt and Titman Financial Markets and Corporate Strategy

Second Edition

Higgins Analysis for Financial Management

Ninth Edition

Kellison Theory of Interest

Third Edition

Kester, Ruback, and Tufano Case Problems in Finance

Twelfth Edition

Ross, Westerfield, and Jaffe Corporate Finance

Ninth Edition

Stephen A. Ross, Franco Modigliani Professor of Finance and Economics, Sloan School of Management, Massachusetts Institute of Technology, Consulting Editor

The McGraw-Hill/Irwin Series in Finance, Insurance and Real Estate

ZVI BODIE Boston University

ALEX KANE University of California, San Diego

ALAN J. MARCUS Boston College

N I N T H E D I T I O N

Investments

INVESTMENTS

Published by McGraw-Hill/Irwin, a business unit of The McGraw-Hill Companies, Inc., 1221 Avenue of the Americas, New York, NY, 10020. Copyright © 2011, 2009, 2008, 2005, 2002, 1999, 1996, 1993, 1989 by The McGraw-Hill Companies, Inc. All rights reserved. No part of this publication may be reproduced or distributed in any form or by any means, or stored in a database or retrieval system, without the prior written consent of The McGraw-Hill Companies, Inc., including, but not limited to, in any network or other electronic storage or transmission, or broadcast for distance learning.

Some ancillaries, including electronic and print components, may not be available to customers outside the United States.

This book is printed on acid-free paper. 1 2 3 4 5 6 7 8 9 0 WVR/WVR 1 0 9 8 7 6 5 4 3 2 1 0

ISBN 978-0-07-353070-3 MHID 0-07-353070-0

Vice president and editor-in-chief: Brent Gordon Publisher: Douglas Reiner Executive editor: Michele Janicek Director of development: Ann Torbert Development editor II: Karen L. Fisher Vice president and director of marketing: Robin J. Zwettler Senior marketing manager: Melissa S. Caughlin Vice president of editing, design, and production: Sesha Bolisetty Project manager: Dana M. Pauley Senior buyer: Michael R. McCormick Interior designer: Laurie J. Entringer Lead media project manager: Brian Nacik Media project manager: Joyce J. Chappetto Typeface: 10/12 Times Roman Compositor: Laserwords Private Limited Printer: Worldcolor

Library of Congress Cataloging-in-Publication Data

Bodie, Zvi. Investments / Zvi Bodie, Alex Kane, Alan J. Marcus.—9th ed. p. cm.—(The McGraw-Hill/Irwin series in finance, insurance and real estate) Includes index. ISBN-13: 978-0-07-353070-3 (alk. paper) ISBN-10: 0-07-353070-0 (alk. paper) 1. Investments. 2. Portfolio management. I. Kane, Alex. II. Marcus, Alan J. III. Title. HG4521.B564 2011332.6—dc22 2010018924

www.mhhe.com

v

ZVI BODIE Boston University

Zvi Bodie is the Norman and Adele Barron Professor of Management at Boston University. He holds a PhD from the Massachusetts Institute of Technology and has served on the finance fac-ulty at the Harvard Business School and MIT’s Sloan School of Management. Professor Bodie has published widely on pension finance and investment strategy in leading professional jour-nals. In cooperation with the Research Foundation of the CFA Institute, he has recently produced a series of Webcasts and a monograph entitled The

Future of Life Cycle Saving

and Investing.

ALEX KANE University of California, San Diego

Alex Kane is professor of finance and economics at the Graduate School of International Relations and Pacific Studies at the University of California, San Diego. He has been visit-ing professor at the Faculty of Economics, University of Tokyo; Graduate School of Business, Harvard; Kennedy School of Government, Harvard; and research asso-ciate, National Bureau of Economic Research. An author of many articles in finance and management journals, Professor Kane’s research is mainly in corpo-rate finance, portfolio man-agement, and capital markets, most recently in the measure-ment of market volatility and pricing of options.

ALAN J. MARCUS Boston College

Alan Marcus is the Mario J. Gabelli Professor of Finance in the Carroll School of Management at Boston College. He received his PhD in economics from MIT. Professor Marcus has been a visiting professor at the Athens Laboratory of Business Administration and at MIT’s Sloan School of Management and has served as a research associate at the National Bureau of Economic Research. Professor Marcus has published widely in the fields of capital markets and portfolio management. His consulting work has ranged from new-product develop-ment to provision of expert testimony in utility rate proceedings. He also spent 2 years at the Federal Home Loan Mortgage Corporation (Freddie Mac), where he developed models of mortgage pricing and credit risk. He cur-rently serves on the Research Foundation Advisory Board of the CFA Institute.

About the Authors

vi

PART III

Equilibrium in Capital Markets 280

9 The Capital Asset Pricing Model 280

10 Arbitrage Pricing Theory and Multifactor

Models of Risk and Return 318

11 The Efficient Market Hypothesis 343

12 Behavioral Finance and Technical

Analysis 381

13 Empirical Evidence on Security Returns 407

PART IV

Fixed-Income Securities 439

14 Bond Prices and Yields 439

15 The Term Structure of Interest Rates 480

16 Managing Bond Portfolios 508

Preface xvi

PART I

Introduction 1 1

The Investment Environment 1

2 Asset Classes and Financial Instruments 28

3 How Securities Are Traded 59

4 Mutual Funds and Other Investment

Companies 92

PART II

Portfolio Theory and Practice 117

5 Introduction to Risk, Return,

and the Historical Record 117

6 Risk Aversion and Capital Allocation

to Risky Assets 160

7 Optimal Risky Portfolios 196

8 Index Models 246

Brief Contents

vii

Brief Contents

PART VII

Applied Portfolio Management 819

24 Portfolio Performance Evaluation 819

25 International Diversification 863

26 Hedge Funds 903

27 The Theory of Active Portfolio

Management 926

28 Investment Policy and the Framework

of the CFA Institute 952

REFERENCES TO CFA PROBLEMS 993

GLOSSARY G-1

NAME INDEX I-1

SUBJECT INDEX I-4

PART V

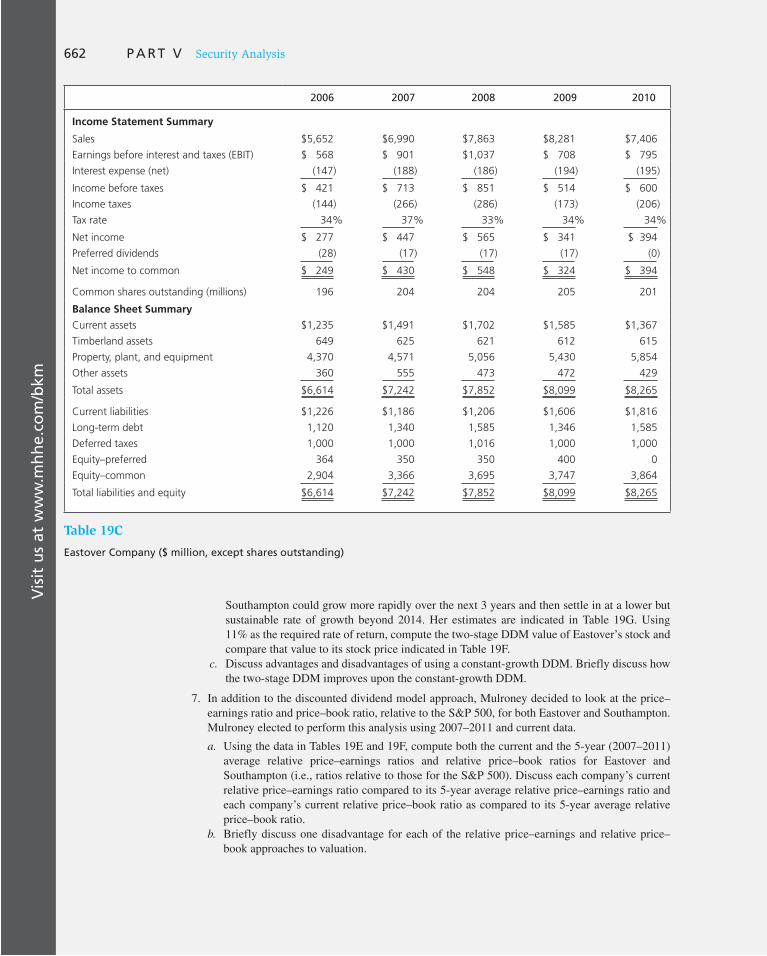

Security Analysis 548 17

Macroeconomic and Industry Analysis 548

18 Equity Valuation Models 583

19 Financial Statement Analysis 627

PART VI

Options, Futures, and Other Derivatives 667

20 Options Markets: Introduction 667

21 Option Valuation 711

22 Futures Markets 755

23 Futures, Swaps, and Risk Management 784

viii

Preface xvi

PART I

Introduction 1 Chapter 1

The Investment Environment 1

1.1 Real Assets versus Financial Assets 2

1.2 Financial Assets 4

1.3 Financial Markets and the Economy 5

The Informational Role of Financial Markets /

Consumption Timing / Allocation of Risk / Separation

of Ownership and Management / Corporate Governance

and Corporate Ethics

1.4 The Investment Process 8

1.5 Markets Are Competitive 9

The Risk–Return Trade-Off / Efficient Markets

1.6 The Players 11

Financial Intermediaries / Investment Bankers

1.7 The Financial Crisis of 2008 14

Antecedents of the Crisis / Changes in Housing Finance /

Mortgage Derivatives / Credit Default Swaps / The Rise

of Systemic Risk / The Shoe Drops / Systemic Risk and the

Real Economy

1.8 Outline of the Text 23

End of Chapter Material 24–27

Chapter 2

Asset Classes and Financial Instruments 28

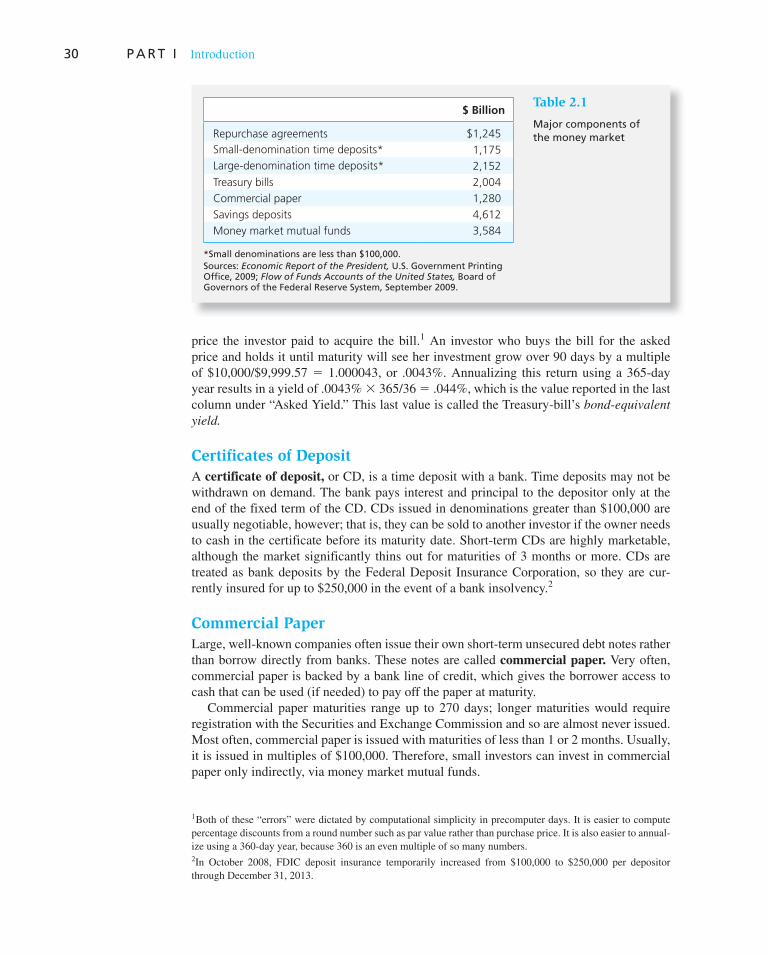

2.1 The Money Market 29

Treasury Bills / Certificates of Deposit / Commercial

Paper / Bankers’ Acceptances / Eurodollars / Repos and

Reverses / Federal Funds / Brokers’ Calls / The LIBOR

Market / Yields on Money Market Instruments

2.2 The Bond Market 34

Treasury Notes and Bonds / Inflation-Protected Treasury

Bonds / Federal Agency Debt / International Bonds /

Municipal Bonds / Corporate Bonds / Mortgages and

Mortgage-Backed Securities

2.3 Equity Securities 41

Common Stock as Ownership Shares / Characteristics of

Common Stock / Stock Market Listings / Preferred Stock /

Depository Receipts

2.4 Stock and Bond Market Indexes 44

Stock Market Indexes / Dow Jones Averages / Standard

& Poor’s Indexes / Other U.S. Market-Value Indexes /

Equally Weighted Indexes / Foreign and International

Stock Market Indexes / Bond Market Indicators

2.5 Derivative Markets 51

Options / Futures Contracts

End of Chapter Material 54–58

Chapter 3

How Securities Are Traded 59

3.1 How Firms Issue Securities 59

Investment Banking / Shelf Registration / Private

Placements / Initial Public Offerings

3.2 How Securities Are Traded 63

Types of Markets

Direct Search Markets / Brokered Markets / Dealer

Markets / Auction Markets

Types of Orders

Market Orders / Price-Contingent Orders

Trading Mechanisms

Dealer Markets / Electronic Communication

Networks (ECNs) / Specialist Markets

3.3 U.S. Securities Markets 68

NASDAQ / The New York Stock Exchange

Block Sales / Electronic Trading on the NYSE / Settlement

Electronic Communication Networks / The National

Market System / Bond Trading

Contents

ix

Contents

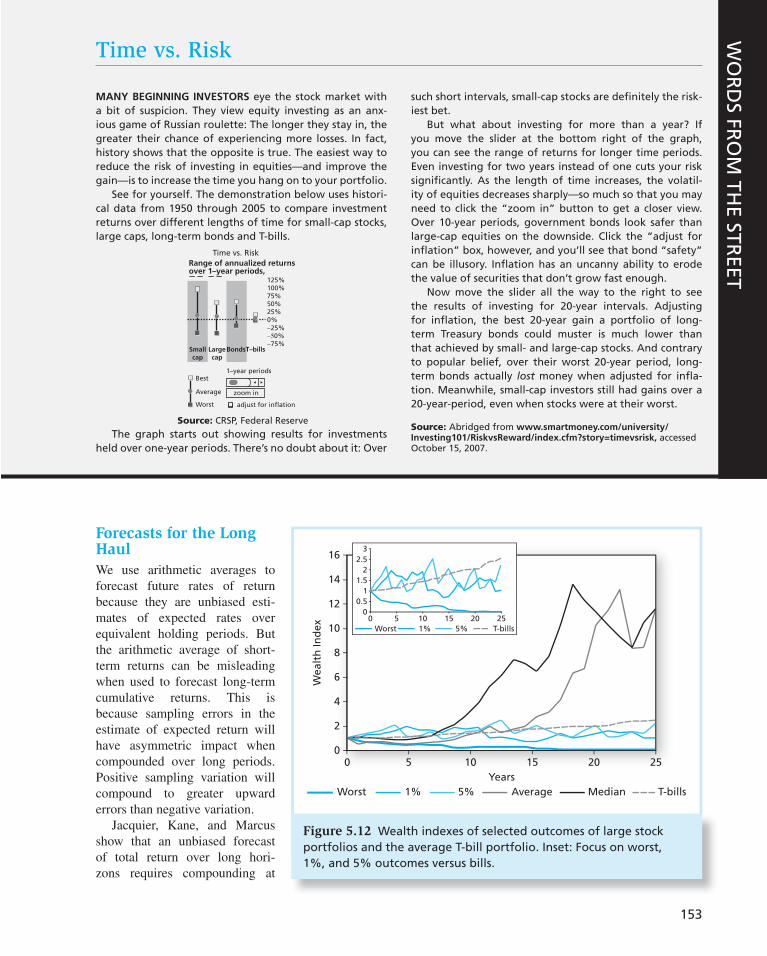

5.2 Comparing Rates of Return for Different Holding

Periods 122

Annual Percentage Rates / Continuous Compounding

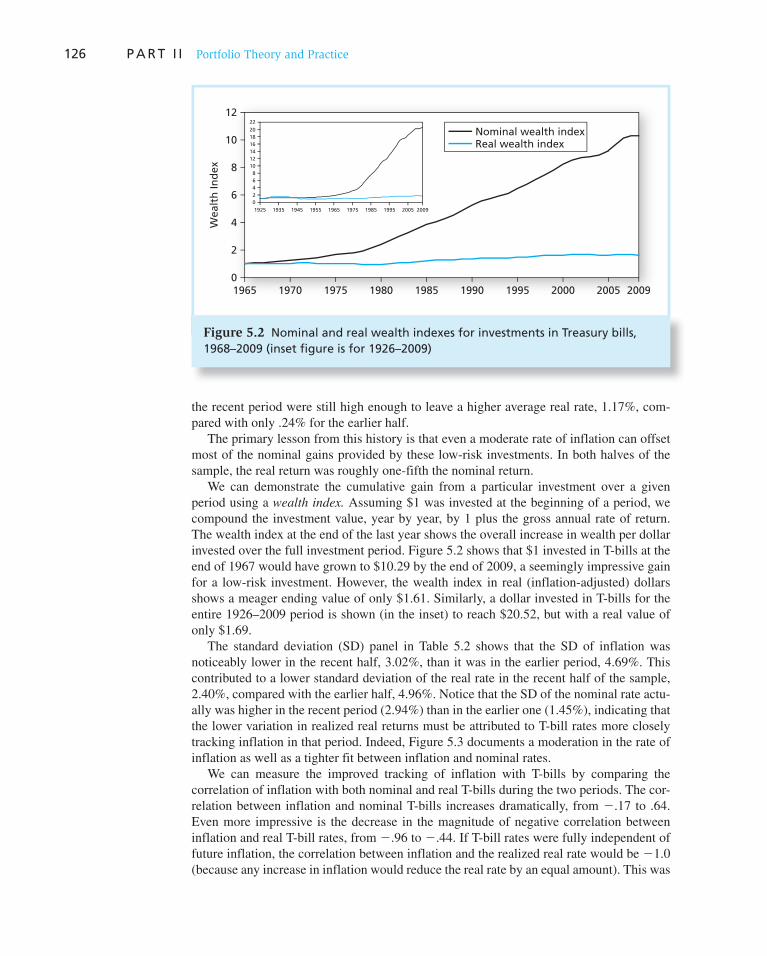

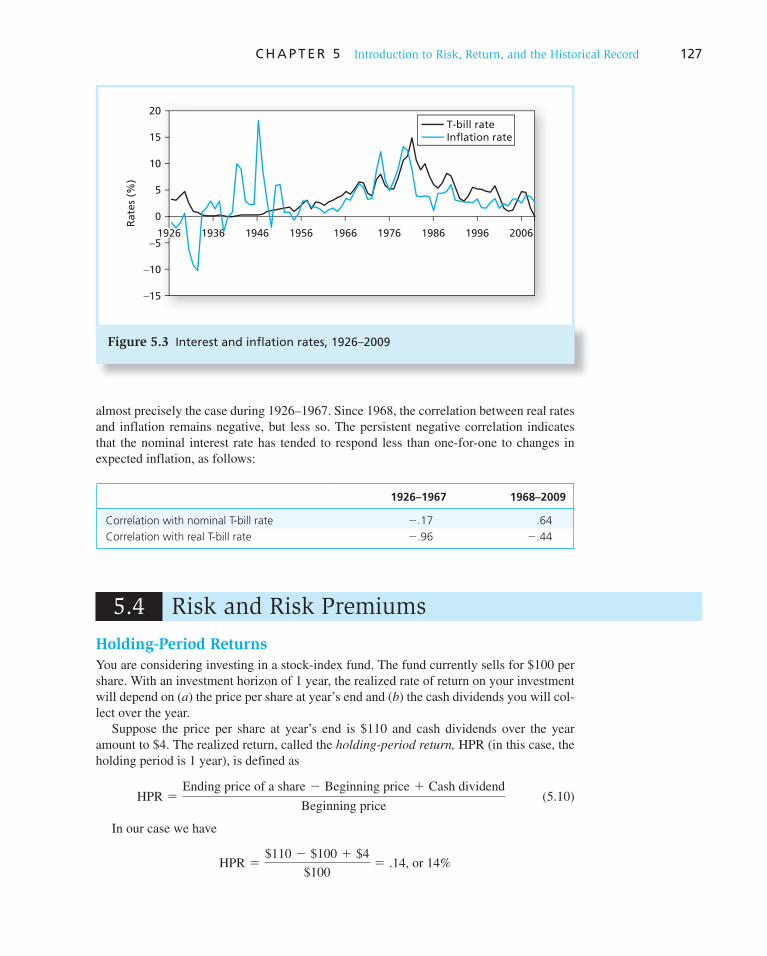

5.3 Bills and Inflation, 1926–2009 125

5.4 Risk and Risk Premiums 127

Holding-Period Returns / Expected Return and Standard

Deviation / Excess Returns and Risk Premiums

5.5 Time Series Analysis of Past Rates of Return 130

Time Series versus Scenario Analysis / Expected Returns

and the Arithmetic Average / The Geometric (Time-

Weighted) Average Return / Variance and Standard

Deviation / The Reward-to-Volatility (Sharpe) Ratio

5.6 The Normal Distribution 134

5.7 Deviations from Normality and Risk Measures 136

Value at Risk / Expected Shortfall / Lower Partial

Standard Deviation and the Sortino Ratio

5.8 Historical Returns on Risky Portfolios: Equities

and Long-Term Government Bonds 139

Total Returns / Excess Returns / Performance / A Global

View of the Historical Record

5.9 Long-Term Investments 147

Risk in the Long Run and the Lognormal Distribution /

The Sharpe Ratio Revisited / Simulation of Long-Term

Future Rates of Return / Forecasts for the Long Haul

End of Chapter Material 154–159

Chapter 6

Risk Aversion and Capital Allocation to Risky Assets 160

6.1 Risk and Risk Aversion 161

Risk, Speculation, and Gambling / Risk Aversion

and Utility Values / Estimating Risk Aversion

6.2 Capital Allocation across Risky and Risk-Free

Portfolios 167

6.3 The Risk-Free Asset 169

6.4 Portfolios of One Risky Asset and a Risk-Free

Asset 170

6.5 Risk Tolerance and Asset Allocation 174

Nonnormal Returns

6.6 Passive Strategies: The Capital Market Line 179

End of Chapter Material 182–190

Appendix A: Risk Aversion, Expected Utility, and the

St. Petersburg Paradox 191

Appendix B: Utility Functions and Equilibrium Prices

of Insurance Contracts 194

Chapter 7

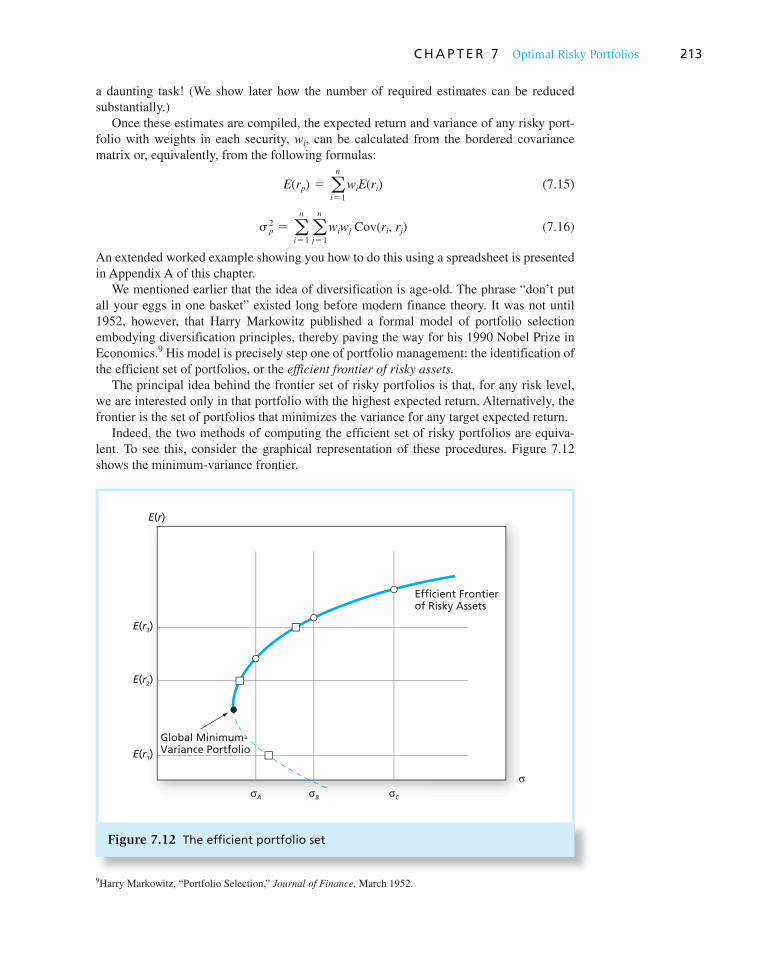

Optimal Risky Portfolios 196

7.1 Diversification and Portfolio Risk 197

7.2 Portfolios of Two Risky Assets 199

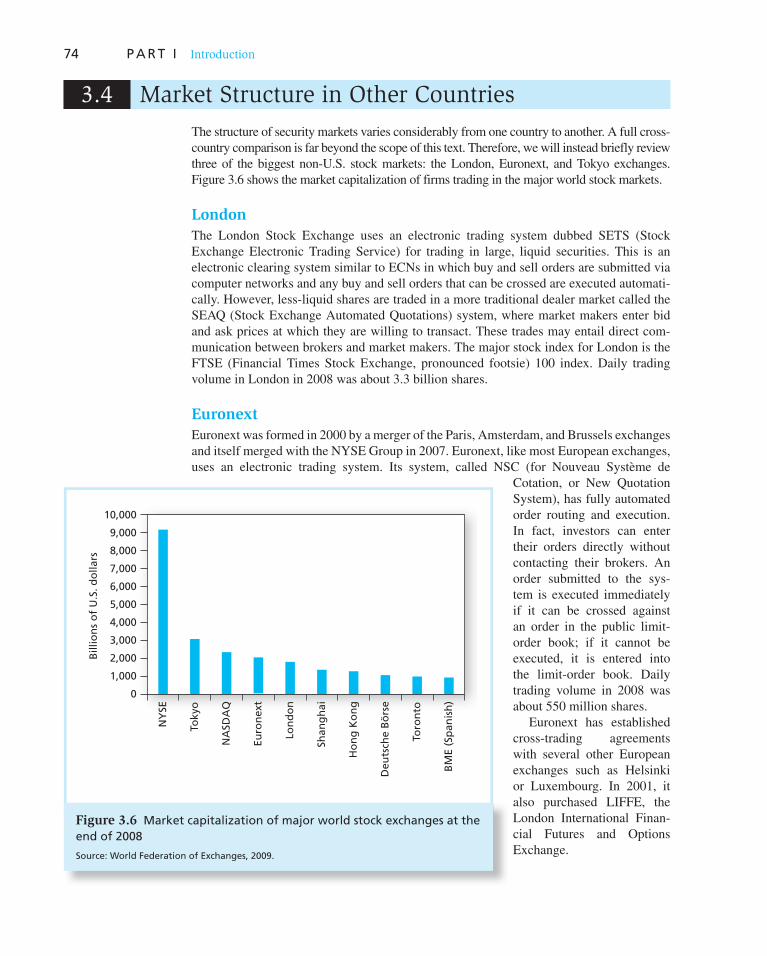

3.4 Market Structure in Other Countries 74

London / Euronext / Tokyo / Globalization

and Consolidation of Stock Markets

3.5 Trading Costs 76

3.6 Buying on Margin 76

3.7 Short Sales 79

3.8 Regulation of Securities Markets 82

Self-Regulation / The Sarbanes-Oxley Act / Insider Trading

End of Chapter Material 86–91

Chapter 4

Mutual Funds and Other Investment Companies 92

4.1 Investment Companies 92

4.2 Types of Investment Companies 93

Unit Investment Trusts / Managed Investment

Companies / Other Investment Organizations

Commingled Funds / Real Estate Investment

Trusts (REITS) / Hedge Funds

4.3 Mutual Funds 96

Investment Policies

Money Market Funds / Equity Funds / Sector Funds /

Bond Funds / International Funds / Balanced Funds /

Asset Allocation and Flexible Funds / Index Funds

How Funds Are Sold

4.4 Costs of Investing in Mutual Funds 99

Fee Structure

Operating Expenses / Front-End Load / Back-End

Load / 12b-1 Charges

Fees and Mutual Fund Returns / Late Trading

and Market Timing

4.5 Taxation of Mutual Fund Income 103

4.6 Exchange-Traded Funds 104

4.7 Mutual Fund Investment Performance:

A First Look 106

4.8 Information on Mutual Funds 109

End of Chapter Material 112–116

PART II

Portfolio Theory and Practice 117

Chapter 5

Introduction to Risk, Return, and the Historical Record 117

5.1 Determinants of the Level of Interest Rates 118

Real and Nominal Rates of Interest / The Equilibrium

Real Rate of Interest / The Equilibrium Nominal Rate

of Interest / Taxes and the Real Rate of Interest

x

Contents

PART III

Equilibrium in Capital Markets 280

Chapter 9

The Capital Asset Pricing Model 280

9.1 The Capital Asset Pricing Model 280

Why Do All Investors Hold the Market Portfolio? / The

Passive Strategy Is Efficient / The Risk Premium of

the Market Portfolio / Expected Returns on Individual

Securities / The Security Market Line

9.2 The CAPM and the Index Model 293

Actual Returns versus Expected Returns / The Index

Model and Realized Returns / The Index Model and the

Expected Return–Beta Relationship

9.3 Is the CAPM Practical? 296

Is the CAPM Testable? / The CAPM Fails Empirical

Tests / The Economy and the Validity of the CAPM / The

Investments Industry and the Validity of the CAPM

9.4 Econometrics and the Expected Return–Beta

Relationship 300

9.5 Extensions of the CAPM 301

The Zero-Beta Model / Labor Income and Nontraded

Assets / A Multiperiod Model and Hedge Portfolios /

A Consumption-Based CAPM

9.6 Liquidity and the CAPM 306

End of Chapter Material 310–317

Chapter 10

Arbitrage Pricing Theory and Multifactor Models of Risk and Return 318

10.1 Multifactor Models: An Overview 319

Factor Models of Security Returns / A Multifactor

Security Market Line

10.2 Arbitrage Pricing Theory 323

Arbitrage, Risk Arbitrage, and Equilibrium / Well-

Diversified Portfolios / Betas and Expected Returns /

The One-Factor Security Market Line

10.3 Individual Assets and the APT 330

The APT and the CAPM

10.4 A Multifactor APT 331

10.5 Where Should We Look for Factors? 333

The Fama-French (FF) Three-Factor Model

10.6 A Multifactor CAPM and the APT 336

End of Chapter Material 336–342

7.3 Asset Allocation with Stocks, Bonds, and Bills 206

The Optimal Risky Portfolio with Two Risky Assets

and a Risk-Free Asset

7.4 The Markowitz Portfolio Selection Model 211

Security Selection / Capital Allocation and the Separation

Property / The Power of Diversification / Asset Allocation

and Security Selection / Optimal Portfolios and

Nonnormal Returns

7.5 Risk Pooling, Risk Sharing, and the Risk

of Long-Term Investments 220

Risk Pooling and the Insurance Principle / Risk Pooling /

Risk Sharing / Investments for the Long Run

End of Chapter Material 224–234

Appendix A: A Spreadsheet Model for Efficient

Diversification 234

Appendix B: Review of Portfolio Statistics 239

Chapter 8

Index Models 246

8.1 A Single-Factor Security Market 247

The Input List of the Markowitz Model / Normality

of Returns and Systematic Risk

8.2 The Single-Index Model 249

The Regression Equation of the Single-Index Model /

The Expected Return–Beta Relationship / Risk and

Covariance in the Single-Index Model / The Set of

Estimates Needed for the Single-Index Model / The

Index Model and Diversification

8.3 Estimating the Single-Index Model 254

The Security Characteristic Line for Hewlett-Packard /

The Explanatory Power of the SCL for HP / Analysis

of Variance / The Estimate of Alpha / The Estimate of

Beta / Firm-Specific Risk / Correlation and Covariance

Matrix

8.4 Portfolio Construction and the Single-Index

Model 261

Alpha and Security Analysis / The Index Portfolio as an

Investment Asset / The Single-Index-Model Input List /

The Optimal Risky Portfolio of the Single-Index Model /

The Information Ratio / Summary of Optimization

Procedure / An Example

Risk Premium Forecasts / The Optimal Risky

Portfolio

8.5 Practical Aspects of Portfolio Management

with the Index Model 268

Is the Index Model Inferior to the Full-Covariance

Model? / The Industry Version of the Index Model /

Predicting Betas / Index Models and Tracking Portfolios

End of Chapter Material 274–279

xi

Contents

Bubbles and Behavioral Economics / Evaluating the

Behavioral Critique

12.2 Technical Analysis and Behavioral Finance 392

Trends and Corrections

Dow Theory / Moving Averages / Breadth

Sentiment Indicators

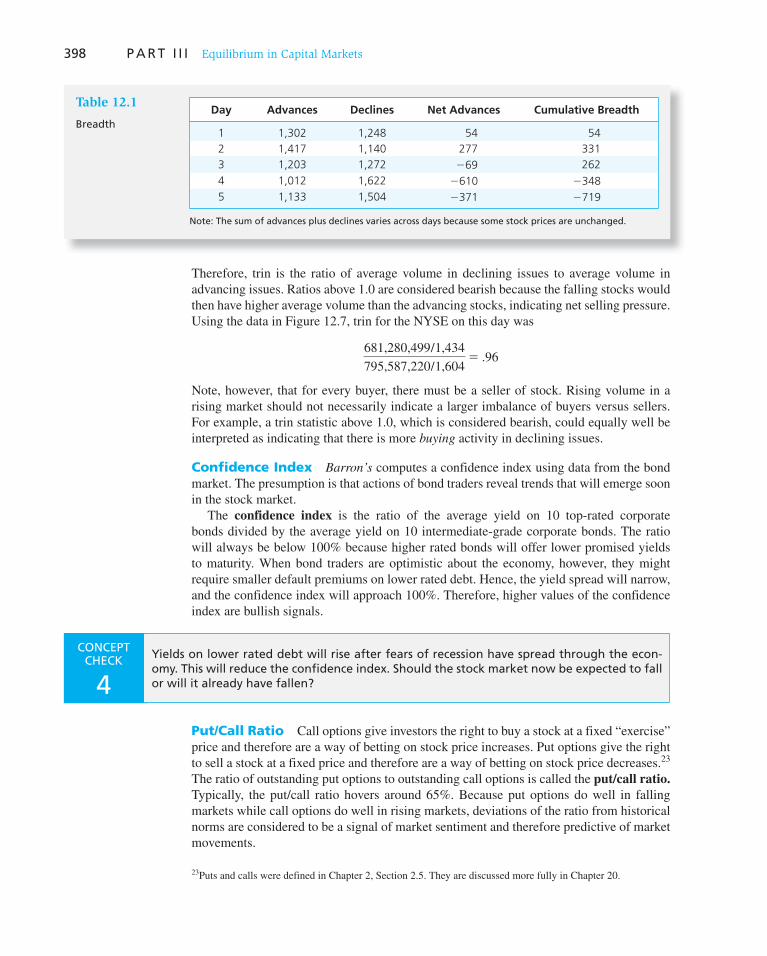

Trin Statistic / Confidence Index / Put/Call Ratio

A Warning

End of Chapter Material 400–406

Chapter 13

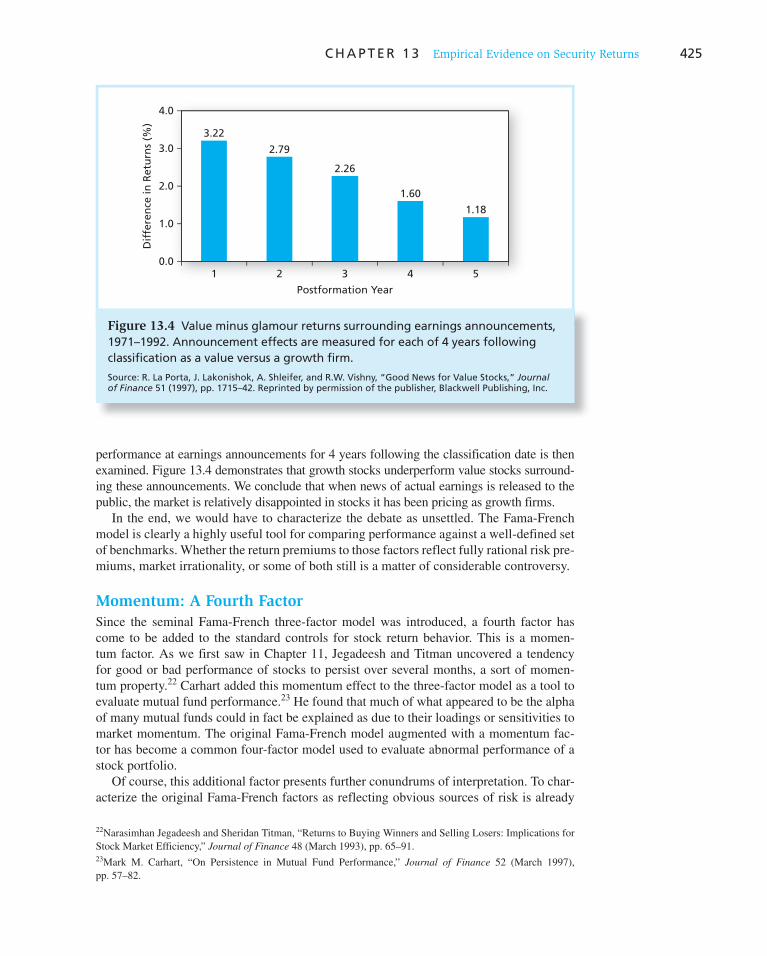

Empirical Evidence on Security Returns 407

13.1 The Index Model and the Single-Factor APT 408

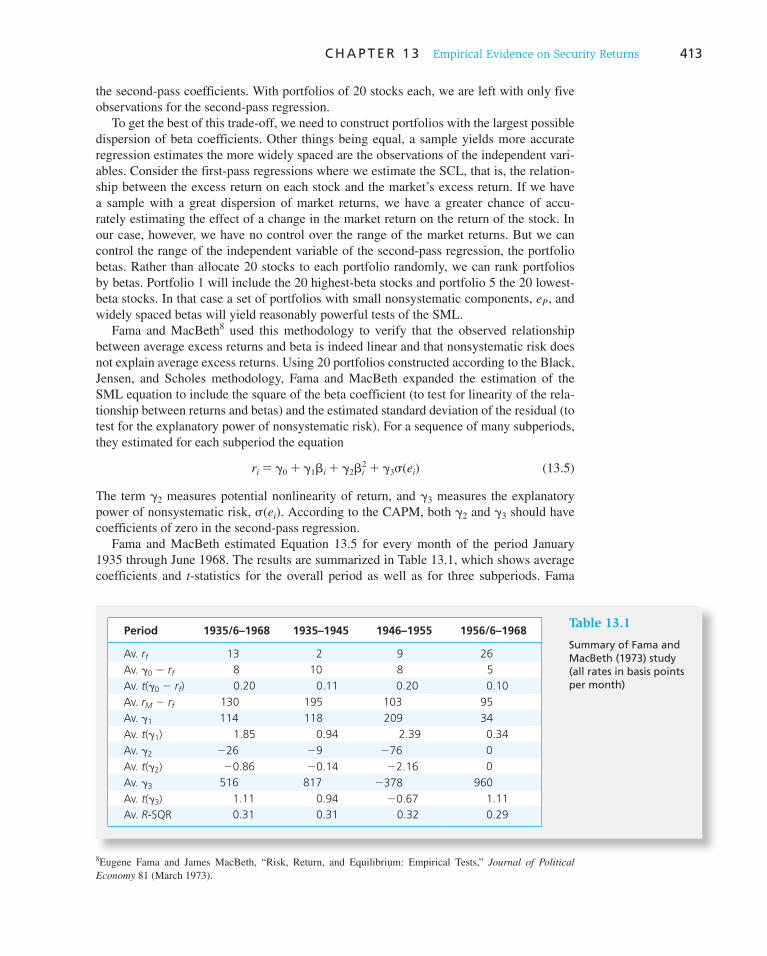

The Expected Return–Beta Relationship

Setting Up the Sample Data / Estimating the SCL /

Estimating the SML

Tests of the CAPM / The Market Index / Measurement

Error in Beta / The EMH and the CAPM / Accounting for

Human Capital and Cyclical Variations in Asset Betas /

Accounting for Nontraded Business

13.2 Tests of Multifactor CAPM and APT 417

A Macro Factor Model

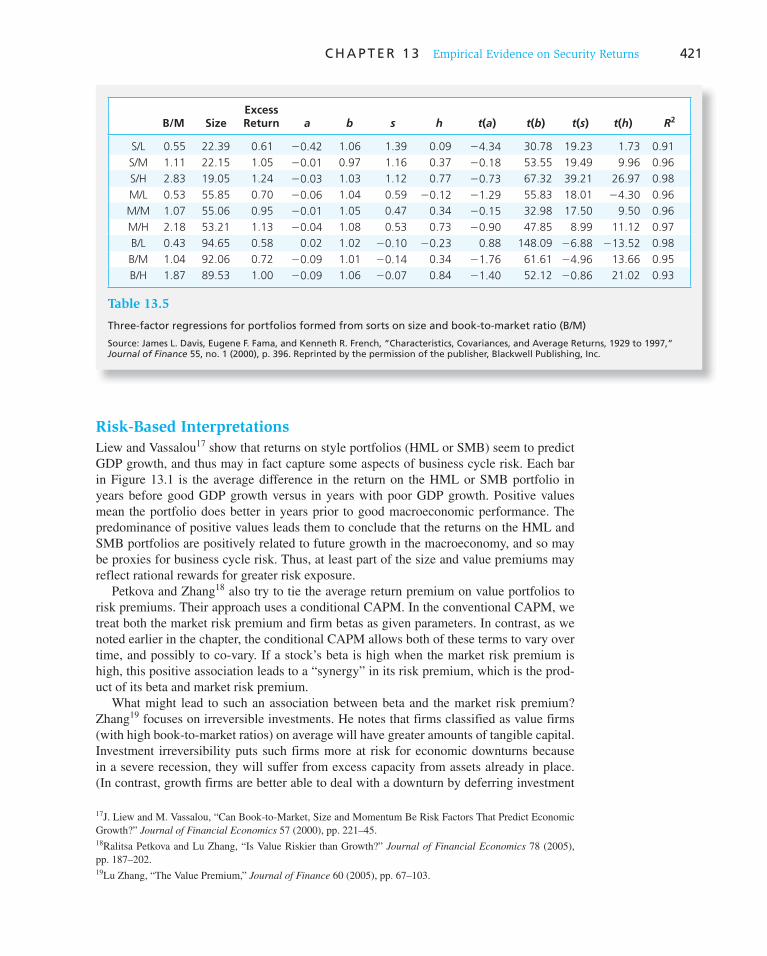

13.3 The Fama-French Three-Factor Model 419

Risk-Based Interpretations / Behavioral Explanations /

Momentum: A Fourth Factor

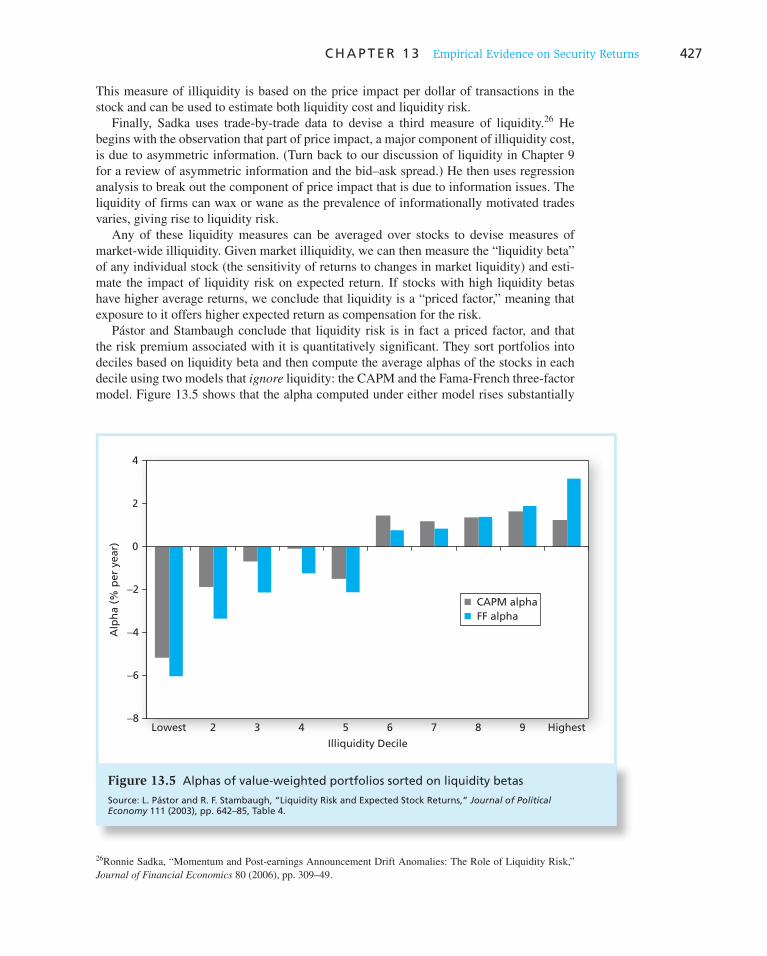

13.4 Liquidity and Asset Pricing 426

Liquidity and Efficient Market Anomalies

13.5 Consumption-Based Asset Pricing and the Equity

Premium Puzzle 428

Consumption Growth and Market Rates of Return /

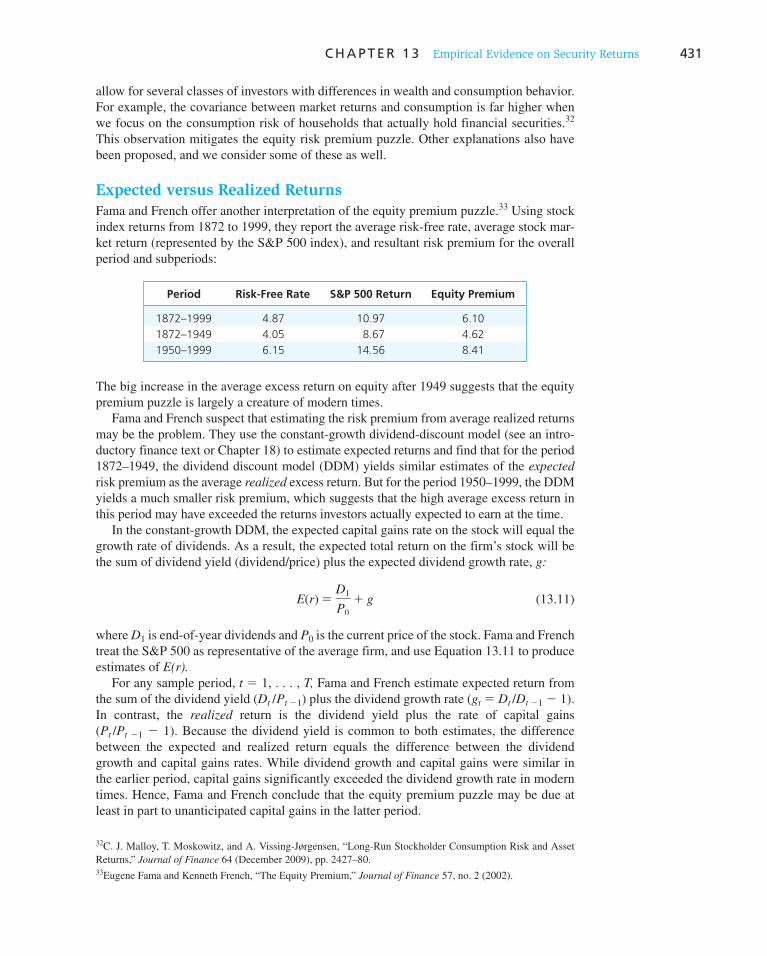

Expected versus Realized Returns / Survivorship Bias /

Extensions to the CAPM May Resolve the Equity

Premium Puzzle / Liquidity and the Equity Premium

Puzzle / Behavioral Explanations of the Equity Premium

Puzzle

End of Chapter Material 435–438

PART IV

Fixed-Income Securities 439

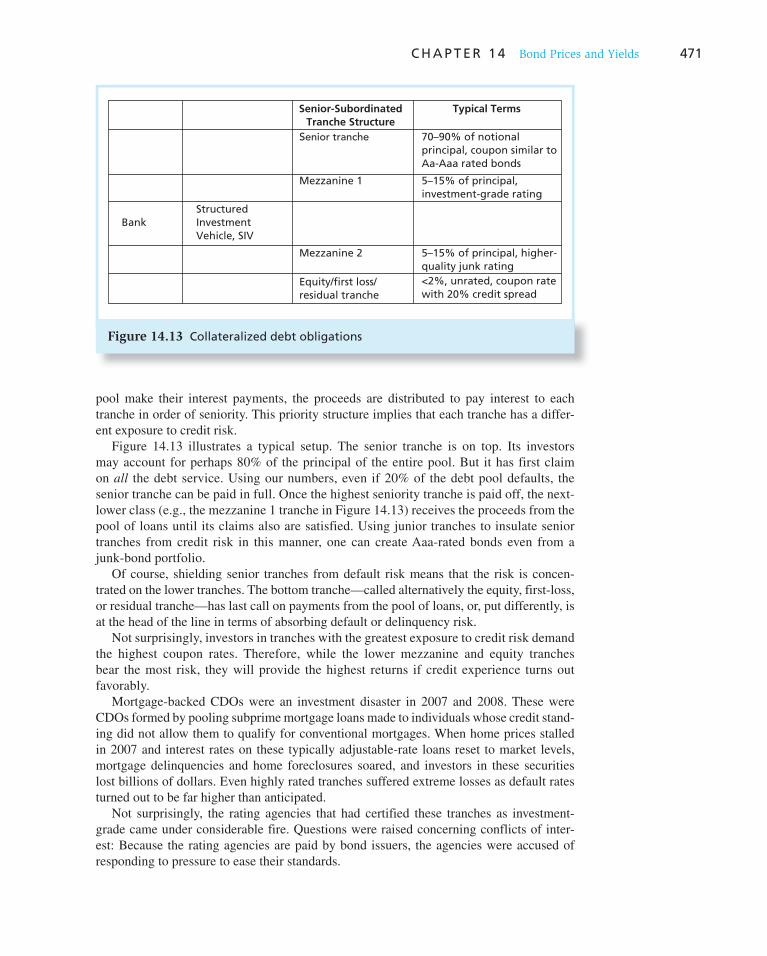

Chapter 14

Bond Prices and Yields 439

14.1 Bond Characteristics 440

Treasury Bonds and Notes

Accrued Interest and Quoted Bond Prices

Chapter 11

The Efficient Market Hypothesis 343

11.1 Random Walks and the Efficient Market

Hypothesis 344

Competition as the Source of Efficiency / Versions of the

Efficient Market Hypothesis

11.2 Implications of the EMH 348

Technical Analysis / Fundamental Analysis / Active versus

Passive Portfolio Management / The Role of Portfolio

Management in an Efficient Market / Resource Allocation

11.3 Event Studies 353

11.4 Are Markets Efficient? 356

The Issues

The Magnitude Issue / The Selection Bias Issue /

The Lucky Event Issue

Weak-Form Tests: Patterns in Stock Returns

Returns over Short Horizons / Returns over Long

Horizons

Predictors of Broad Market Returns / Semistrong Tests:

Market Anomalies

The Small-Firm-in-January Effect / The Neglected-

Firm Effect and Liquidity Effects / Book-to-Market

Ratios / Post–Earnings-Announcement Price Drift

Strong-Form Tests: Inside Information / Interpreting

the Anomalies

Risk Premiums or Inefficiencies? / Anomalies

or Data Mining?

Bubbles and Market Efficiency

11.5 Mutual Fund and Analyst Performance 368

Stock Market Analysts / Mutual Fund Managers /

So, Are Markets Efficient?

End of Chapter Material 373–380

Chapter 12

Behavioral Finance and Technical Analysis 381

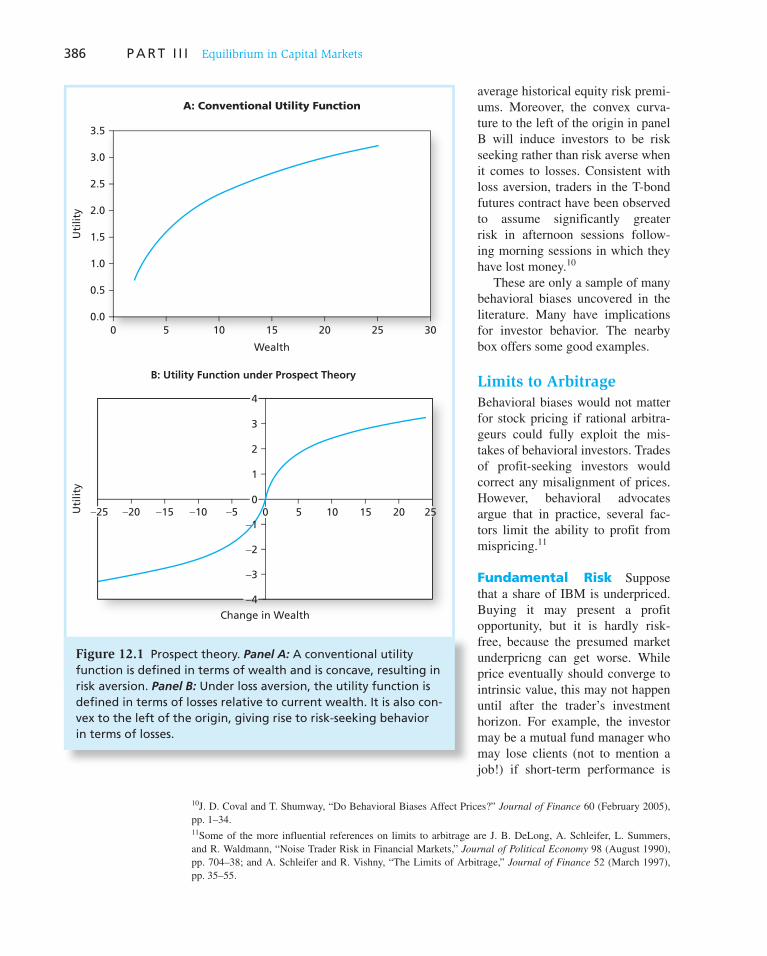

12.1 The Behavioral Critique 382

Information Processing

Forecasting Errors / Overconfidence / Conservatism /

Sample Size Neglect and Representativeness

Behavioral Biases

Framing / Mental Accounting / Regret Avoidance /

Prospect Theory

Limits to Arbitrage

Fundamental Risk / Implementation Costs / Model Risk

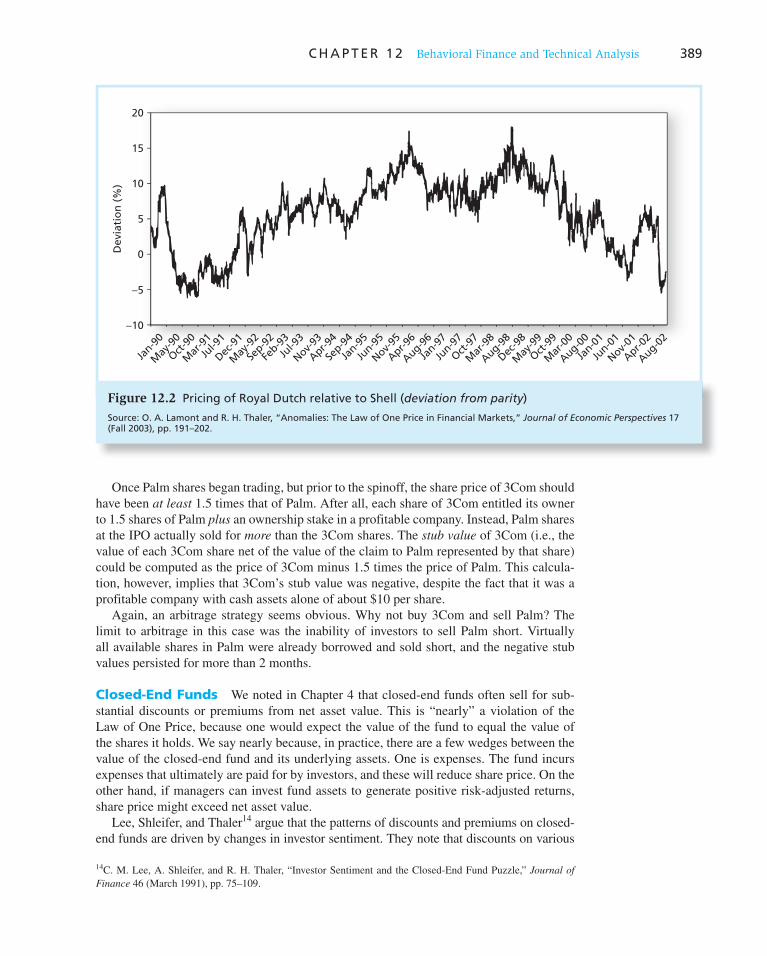

Limits to Arbitrage and the Law of One Price

“Siamese Twin” Companies / Equity Carve-Outs /

Closed-End Funds

xii

Contents

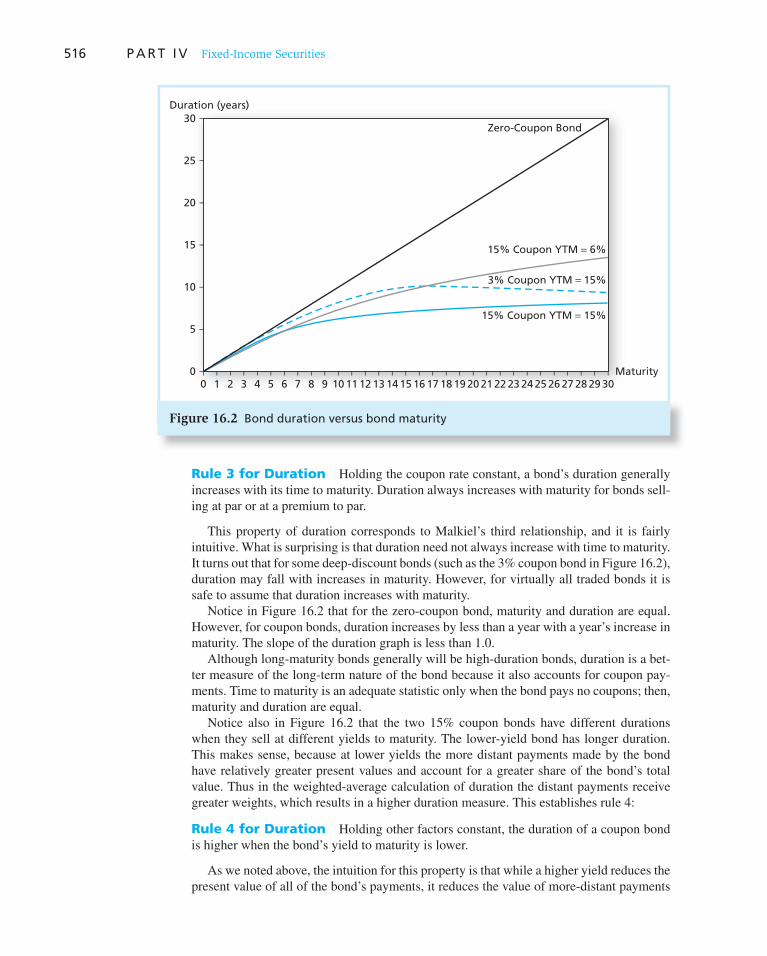

16.2 Convexity 518

Why Do Investors Like Convexity? / Duration and

Convexity of Callable Bonds / Duration and Convexity

of Mortgage-Backed Securities

16.3 Passive Bond Management 526

Bond-Index Funds / Immunization / Cash Flow Matching

and Dedication / Other Problems with Conventional

Immunization

16.4 Active Bond Management 535

Sources of Potential Profit / Horizon Analysis

End of Chapter Material 538–547

PART V

Security Analysis 548 Chapter 17

Macroeconomic and Industry Analysis 548

17.1 The Global Economy 549

17.2 The Domestic Macroeconomy 551

17.3 Demand and Supply Shocks 553

17.4 Federal Government Policy 554

Fiscal Policy / Monetary Policy / Supply-Side Policies

17.5 Business Cycles 557

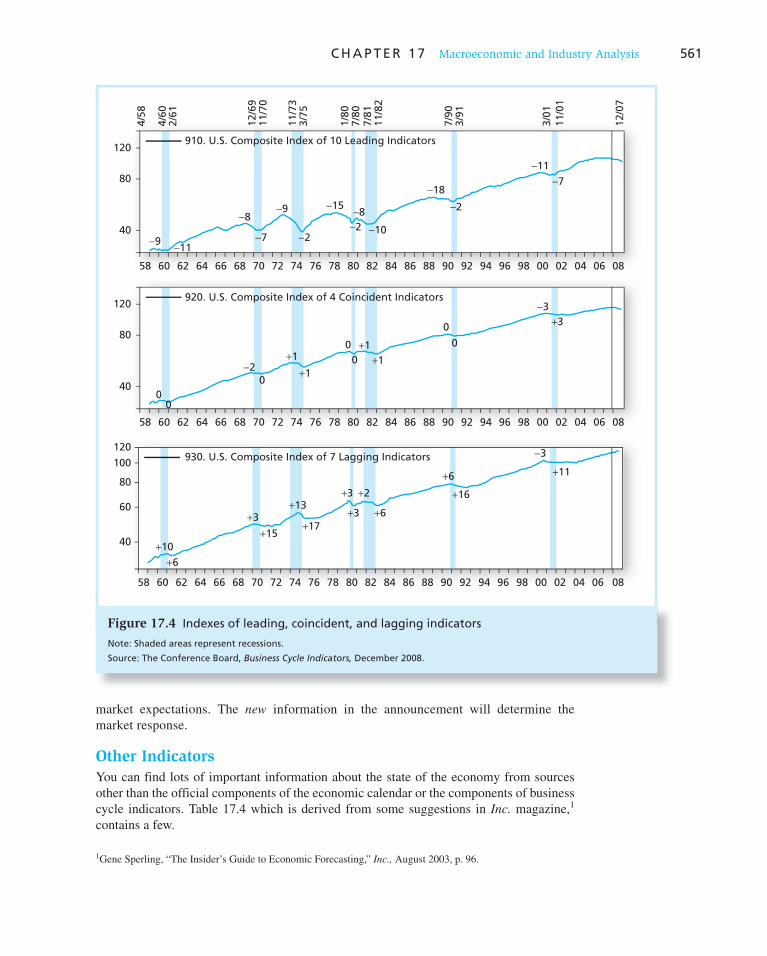

The Business Cycle / Economic Indicators / Other

Indicators

17.6 Industry Analysis 562

Defining an Industry / Sensitivity to the Business Cycle /

Sector Rotation / Industry Life Cycles

Start-Up Stage / Consolidation Stage / Maturity Stage /

Relative Decline

Industry Structure and Performance

Threat of Entry / Rivalry between Existing Competitors /

Pressure from Substitute Products / Bargaining Power of

Buyers / Bargaining Power of Suppliers

End of Chapter Material 574–582

Chapter 18

Equity Valuation Models 583

18.1 Valuation by Comparables 583

Limitations of Book Value

18.2 Intrinsic Value versus Market Price 586

18.3 Dividend Discount Models 587

The Constant-Growth DDM / Convergence of Price

to Intrinsic Value / Stock Prices and Investment

Opportunities / Life Cycles and Multistage Growth

Models / Multistage Growth Models

Corporate Bonds

Call Provisions on Corporate Bonds / Convertible

Bonds / Puttable Bonds / Floating-Rate Bonds

Preferred Stock / Other Issuers / International Bonds /

Innovation in the Bond Market

Inverse Floaters / Asset-Backed Bonds / Catastrophe

Bonds / Indexed Bonds

14.2 Bond Pricing 446

Bond Pricing between Coupon Dates

14.3 Bond Yields 451

Yield to Maturity / Yield to Call / Realized Compound

Return versus Yield to Maturity

14.4 Bond Prices over Time 456

Yield to Maturity versus Holding-Period Return / Zero-

Coupon Bonds and Treasury Strips / After-Tax Returns

14.5 Default Risk and Bond Pricing 461

Junk Bonds / Determinants of Bond Safety / Bond

Indentures

Sinking Funds / Subordination of Further Debt /

Dividend Restrictions / Collateral

Yield to Maturity and Default Risk / Credit Default Swaps /

Credit Risk and Collateralized Debt Obligations

End of Chapter Material 472–479

Chapter 15

The Term Structure of Interest Rates 480

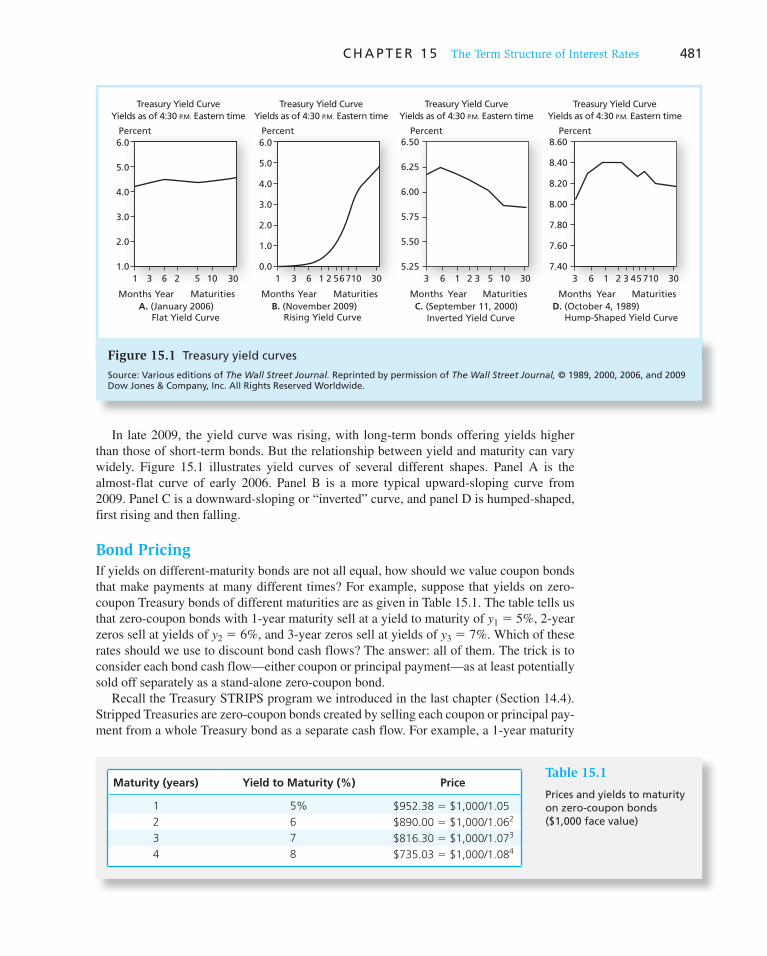

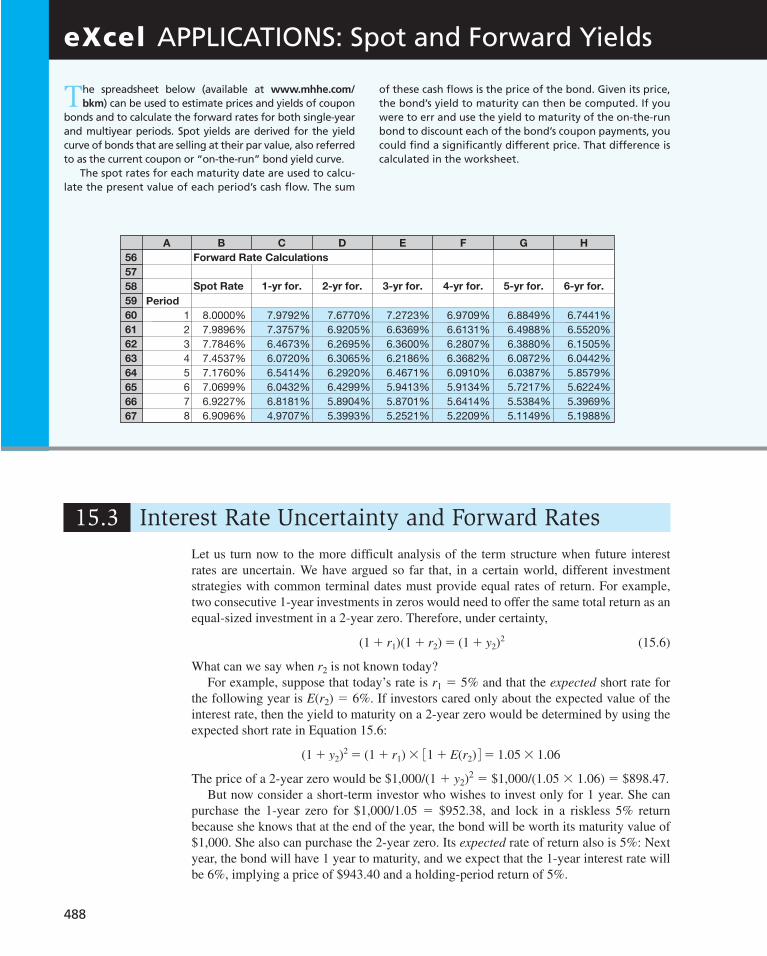

15.1 The Yield Curve 480

Bond Pricing

15.2 The Yield Curve and Future Interest Rates 483

The Yield Curve under Certainty / Holding-Period

Returns / Forward Rates

15.3 Interest Rate Uncertainty and Forward Rates 488

15.4 Theories of the Term Structure 490

The Expectations Hypothesis / Liquidity Preference

15.5 Interpreting the Term Structure 494

15.6 Forward Rates as Forward Contracts 497

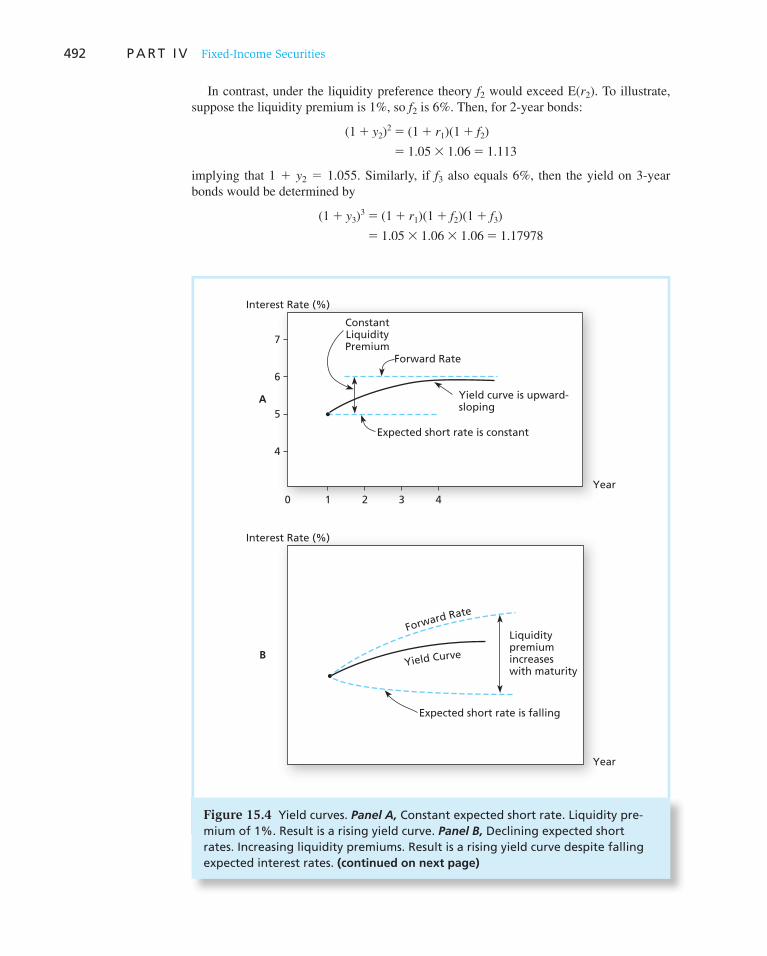

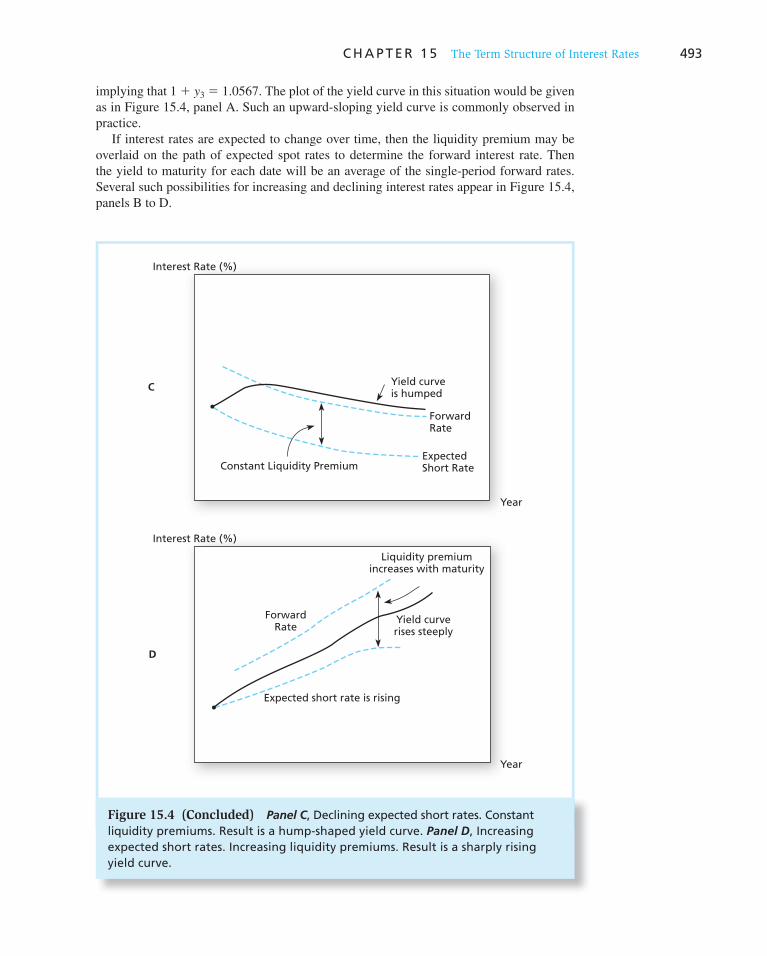

End of Chapter Material 499–507

Chapter 16

Managing Bond Portfolios 508

16.1 Interest Rate Risk 509

Interest Rate Sensitivity / Duration / What Determines

Duration?

Rule 1 for Duration / Rule 2 for Duration / Rule 3

for Duration / Rule 4 for Duration / Rule 5 for

Duration

xiii

Contents

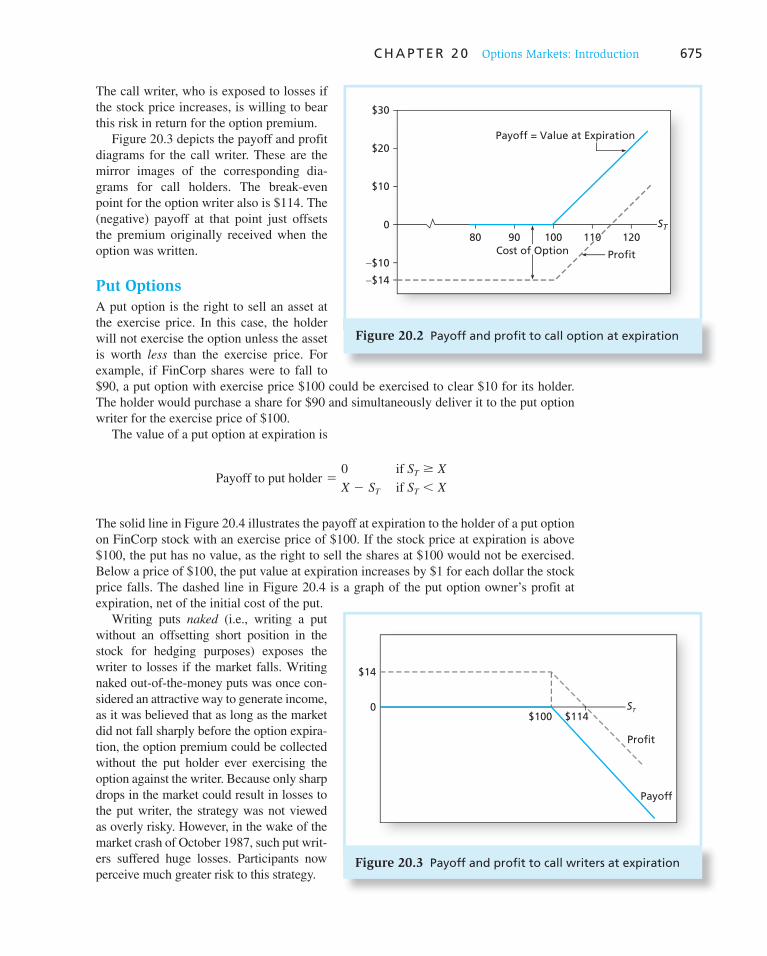

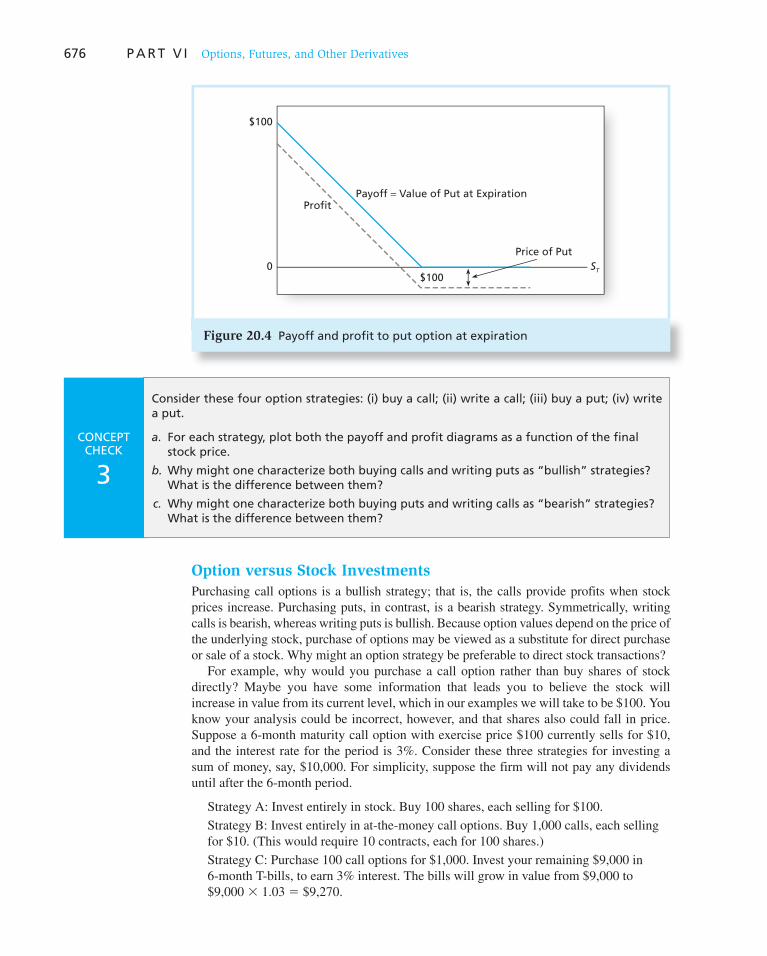

20.2 Values of Options at Expiration 674

Call Options / Put Options / Option versus Stock

Investments

20.3 Option Strategies 678

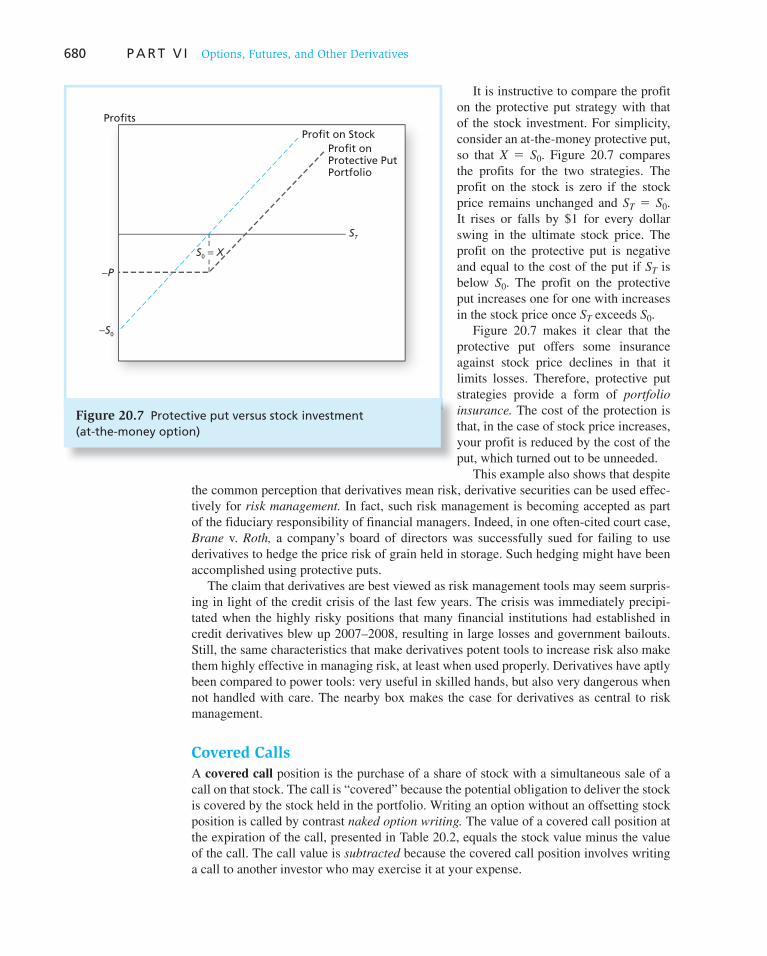

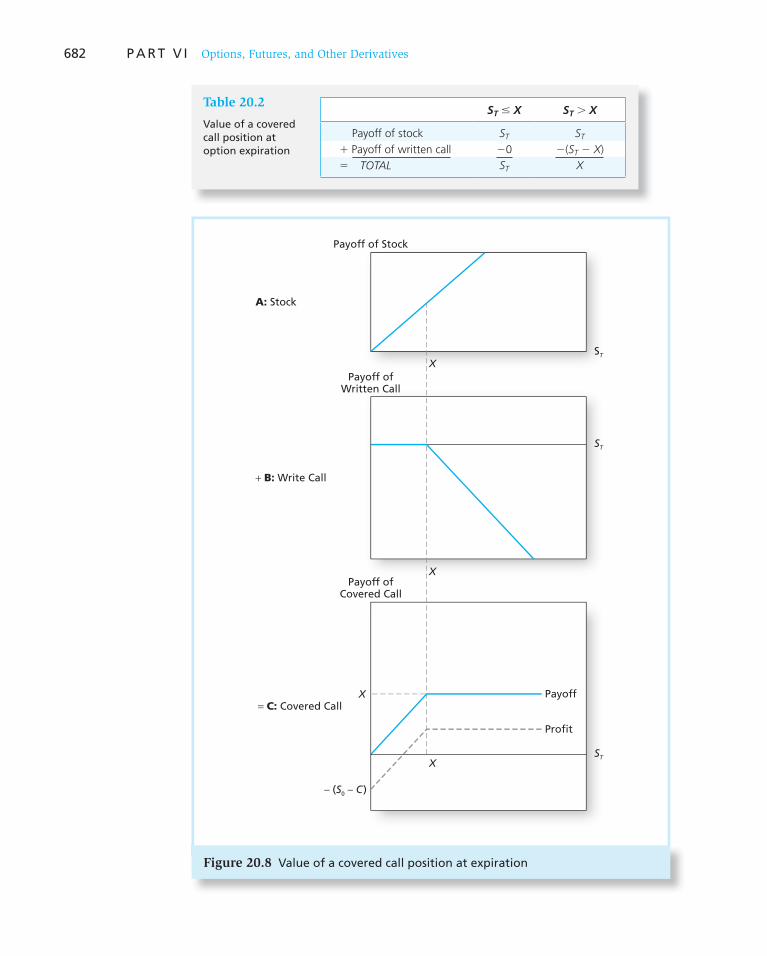

Protective Put / Covered Calls / Straddle / Spreads /

Collars

20.4 The Put-Call Parity Relationship 687

20.5 Option-like Securities 690

Callable Bonds / Convertible Securities / Warrants /

Collateralized Loans / Levered Equity and Risky Debt

20.6 Financial Engineering 696

20.7 Exotic Options 698

Asian Options / Barrier Options / Lookback Options /

Currency-Translated Options / Digital Options

End of Chapter Material 699–710

Chapter 21

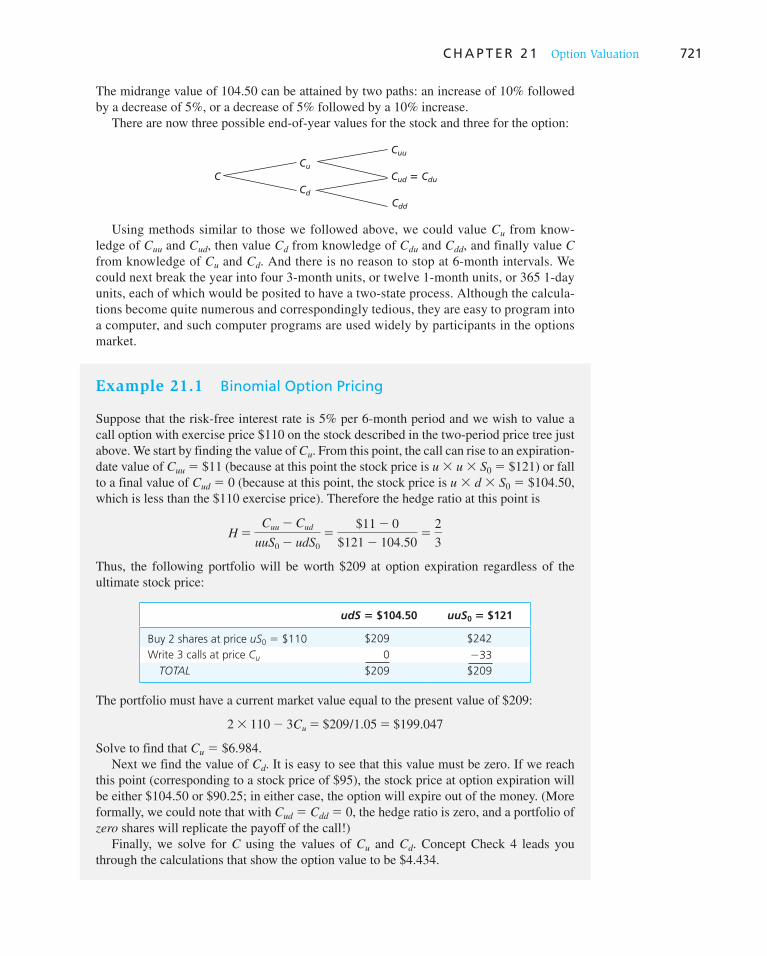

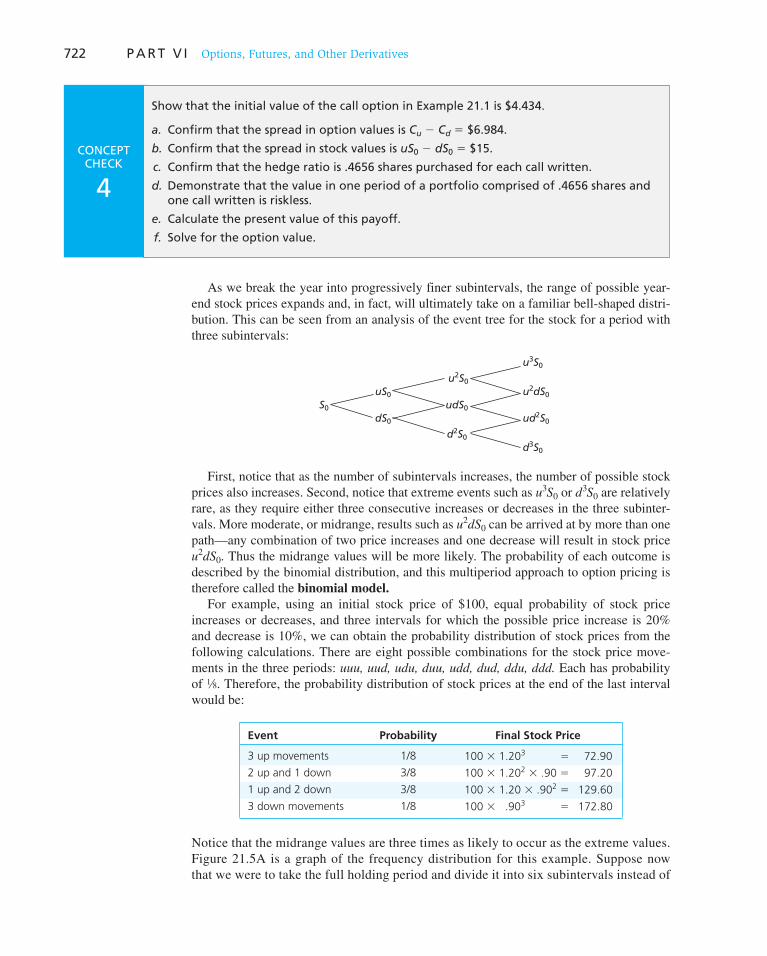

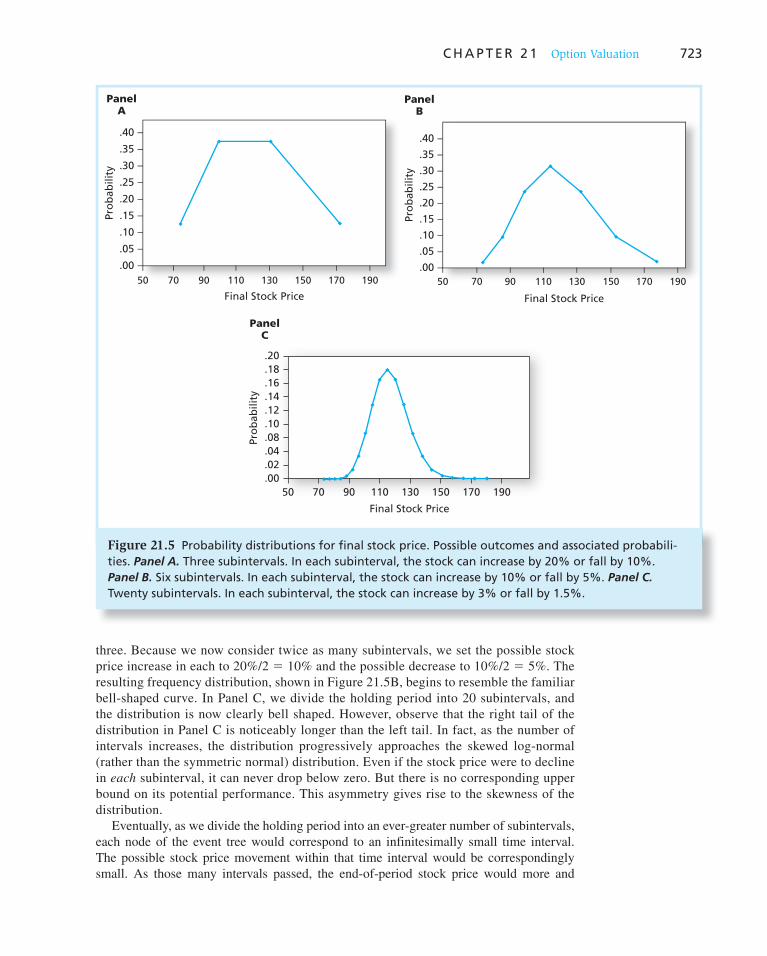

Option Valuation 711

21.1 Option Valuation: Introduction 711

Intrinsic and Time Values / Determinants of Option

Values

21.2 Restrictions on Option Values 714

Restrictions on the Value of a Call Option / Early Exercise

and Dividends / Early Exercise of American Puts

21.3 Binomial Option Pricing 718

Two-State Option Pricing / Generalizing the Two-State

Approach

21.4 Black-Scholes Option Valuation 724

The Black-Scholes Formula / Dividends and Call Option

Valuation / Put Option Valuation / Dividends and Put

Option Valuation

21.5 Using the Black-Scholes Formula 733

Hedge Ratios and the Black-Scholes Formula / Portfolio

Insurance / Hedging Bets on Mispriced Options

21.6 Empirical Evidence on Option Pricing 743

End of Chapter Material 744–754

Chapter 22

Futures Markets 755

22.1 The Futures Contract 756

The Basics of Futures Contracts / Existing Contracts

22.2 Trading Mechanics 760

The Clearinghouse and Open Interest / The Margin

Account and Marking to Market / Cash versus Actual

Delivery / Regulations / Taxation

22.3 Futures Markets Strategies 766

Hedging and Speculation / Basis Risk and Hedging

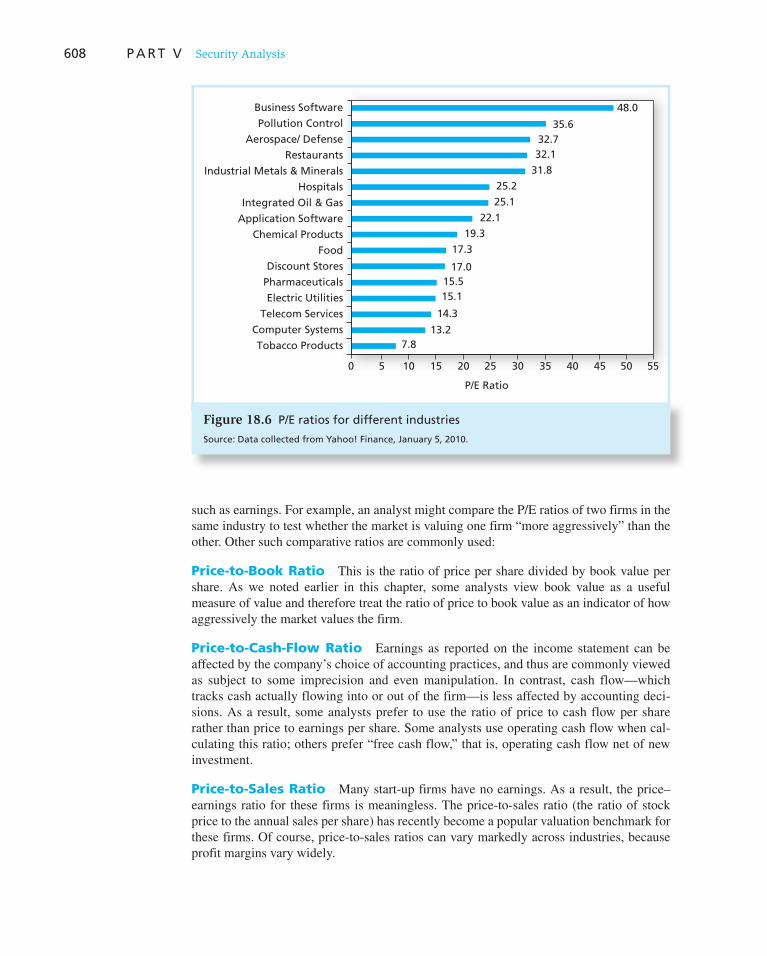

18.4 Price–Earnings Ratio 601

The Price–Earnings Ratio and Growth Opportunities /

P/E Ratios and Stock Risk / Pitfalls in P/E Analysis /

Combining P/E Analysis and the DDM / Other

Comparative Valuation Ratios

Price-to-Book Ratio / Price-to-Cash-Flow Ratio /

Price-to-Sales Ratio

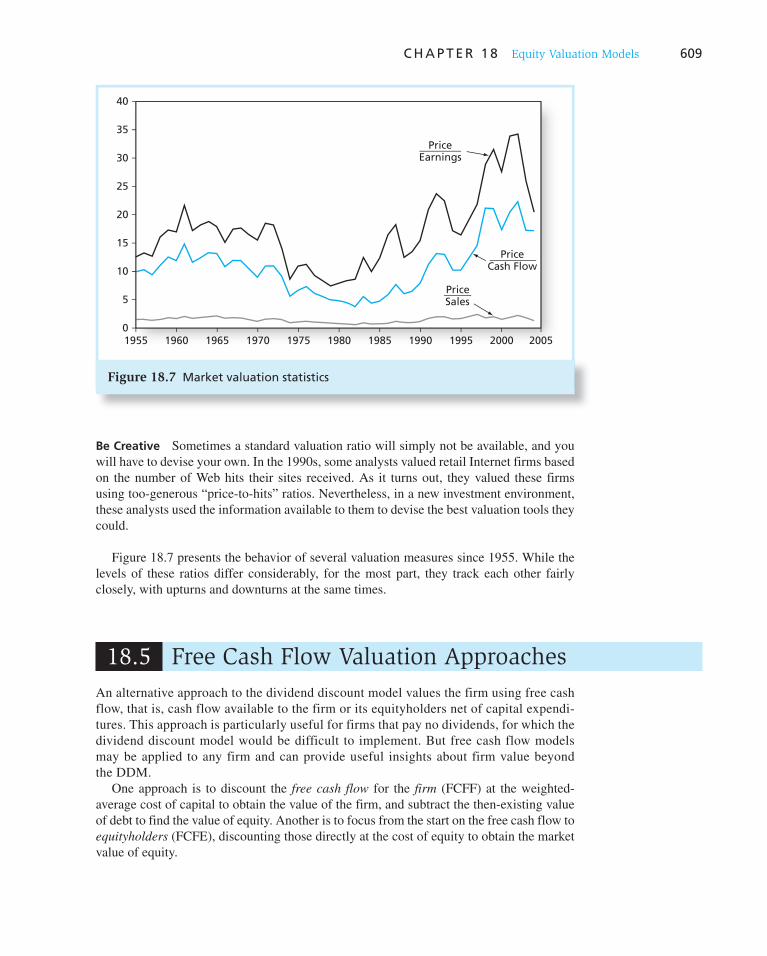

18.5 Free Cash Flow Valuation Approaches 609

Comparing the Valuation Models

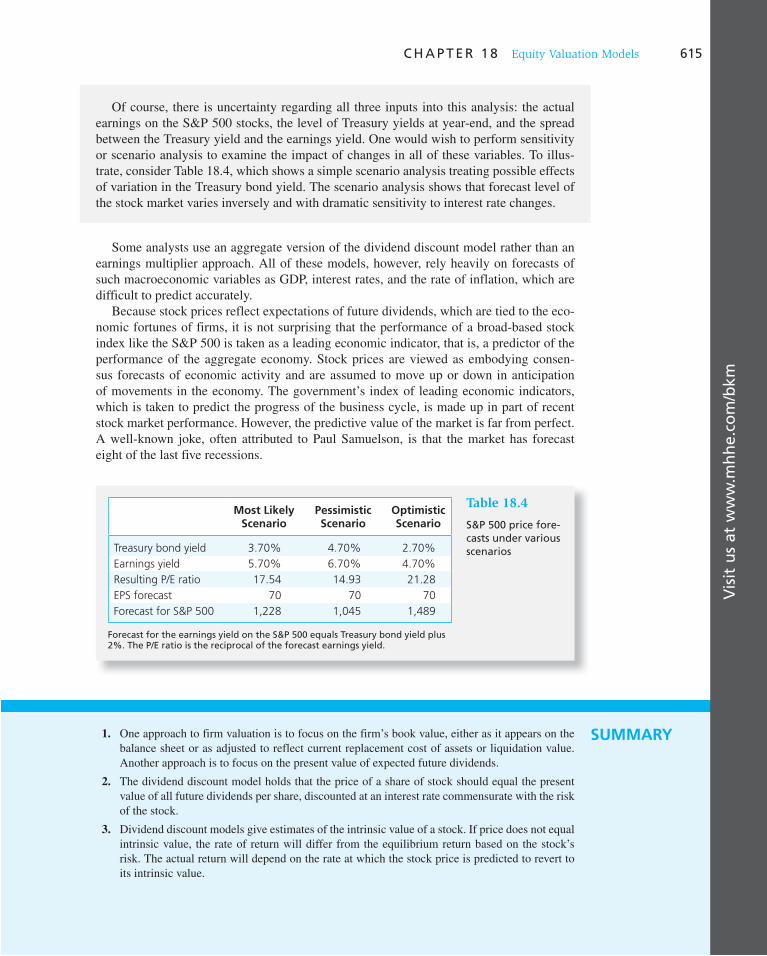

18.6 The Aggregate Stock Market 613

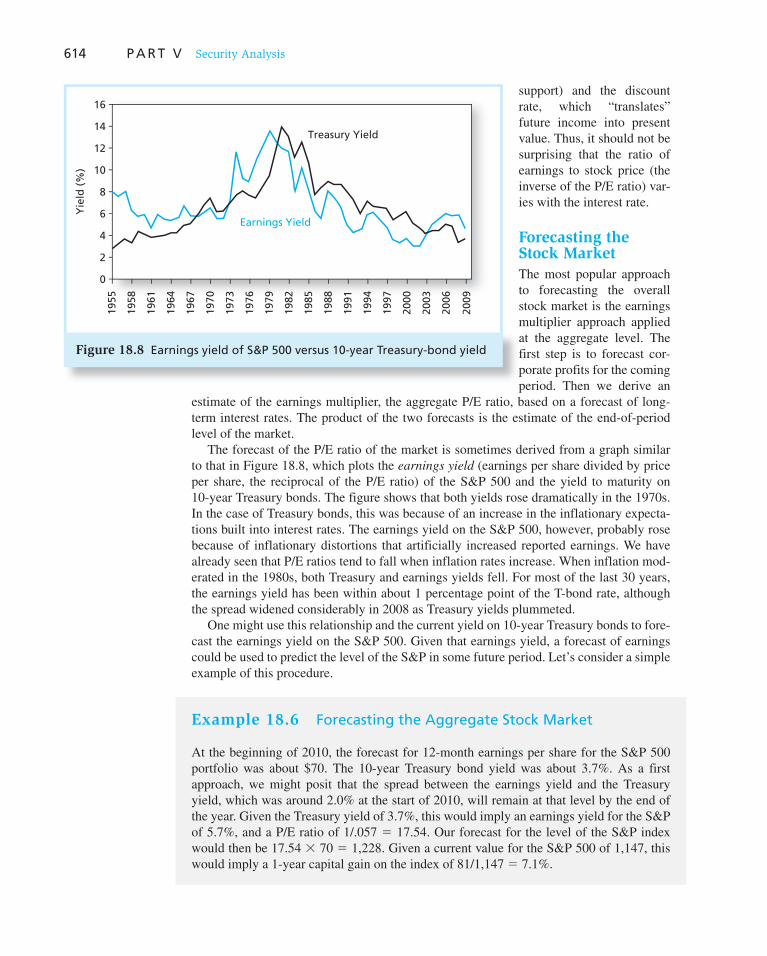

Explaining Past Behavior / Forecasting the Stock Market

End of Chapter Material 615–626

Chapter 19

Financial Statement Analysis 627

19.1 The Major Financial Statements 627

The Income Statement / The Balance Sheet /

The Statement of Cash Flows

19.2 Accounting versus Economic Earnings 632

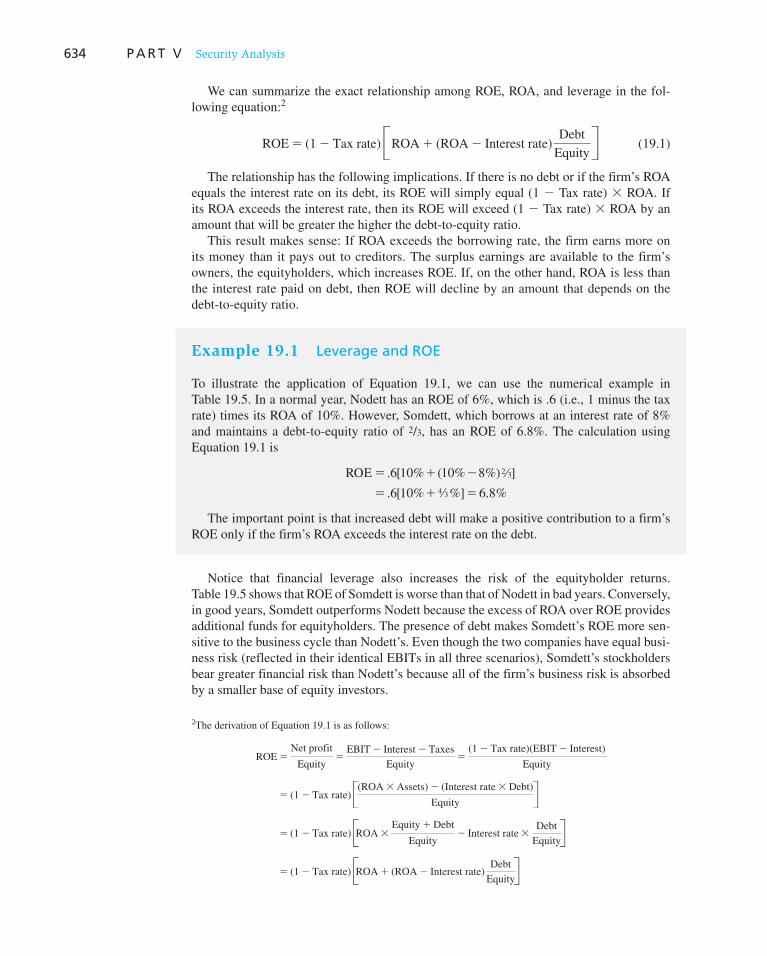

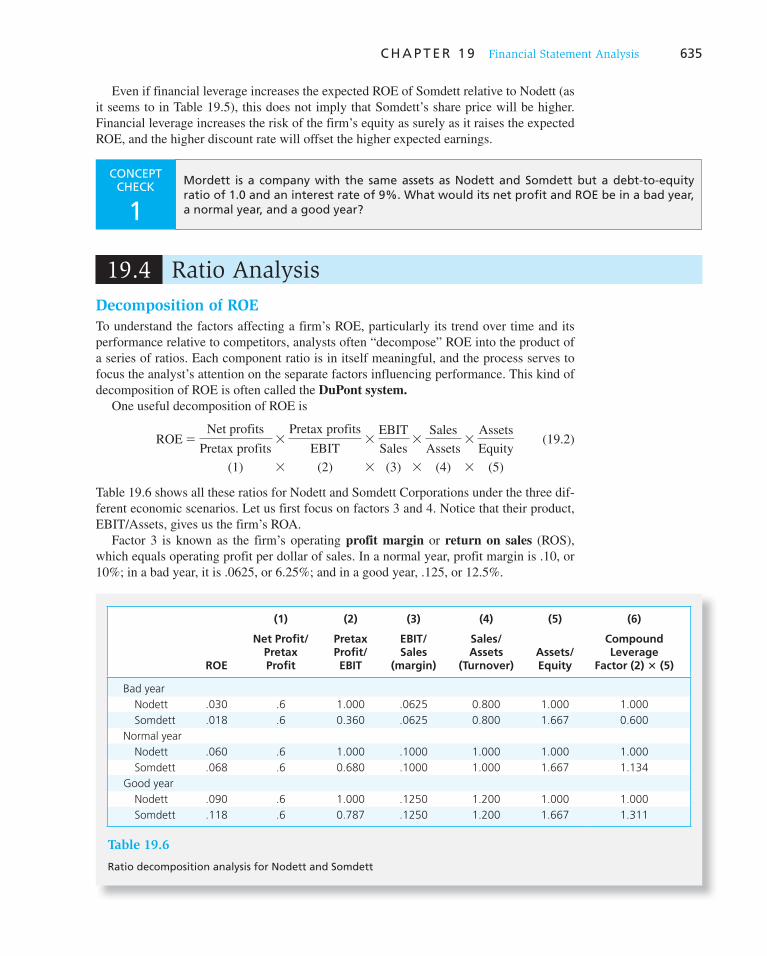

19.3 Profitability Measures 632

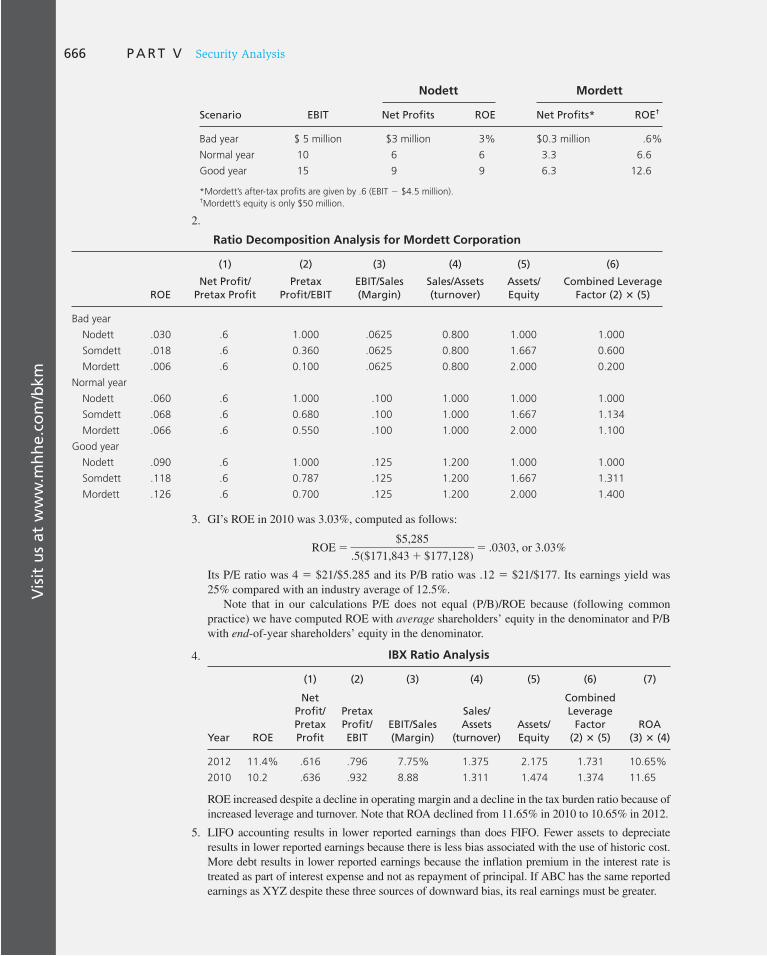

Past versus Future ROE / Financial Leverage and ROE

19.4 Ratio Analysis 635

Decomposition of ROE / Turnover and Other Asset

Utilization Ratios / Liquidity Ratios / Market Price

Ratios: Growth versus Value / Choosing a Benchmark

19.5 Economic Value Added 644

19.6 An Illustration of Financial Statement Analysis 646

19.7 Comparability Problems 648

Inventory Valuation / Depreciation / Inflation and Interest

Expense / Fair Value Accounting / Quality of Earnings /

International Accounting Conventions

19.8 Value Investing: The Graham Technique 654

End of Chapter Material 655–666

PART VI

Options, Futures, and Other Derivatives 667

Chapter 20

Options Markets: Introduction 667

20.1 The Option Contract 668

Options Trading / American and European Options /

Adjustments in Option Contract Terms / The Options

Clearing Corporation / Other Listed Options

Index Options / Futures Options / Foreign Currency

Options / Interest Rate Options

xiv

Contents

24.2 Performance Measurement for Hedge Funds 830

24.3 Performance Measurement with Changing Portfolio

Composition 833

24.4 Market Timing 834

The Potential Value of Market Timing / Valuing Market

Timing as a Call Option / The Value of Imperfect

Forecasting

24.5 Style Analysis 840

Style Analysis and Multifactor Benchmarks/Style

Analysis in Excel

24.6 Morningstar’s Risk-Adjusted Rating 844

24.7 Evaluating Performance Evaluation 845

24.8 Performance Attribution Procedures 846

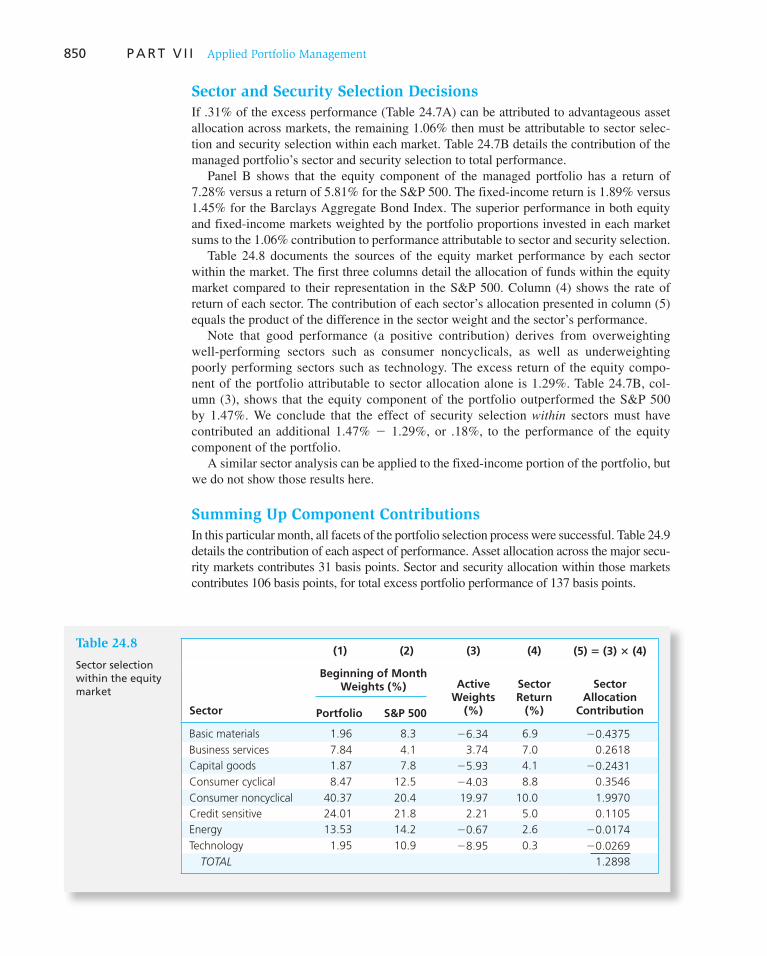

Asset Allocation Decisions / Sector and Security Selection

Decisions / Summing Up Component Contributions

End of Chapter Material 852–862

Chapter 25

International Diversification 863

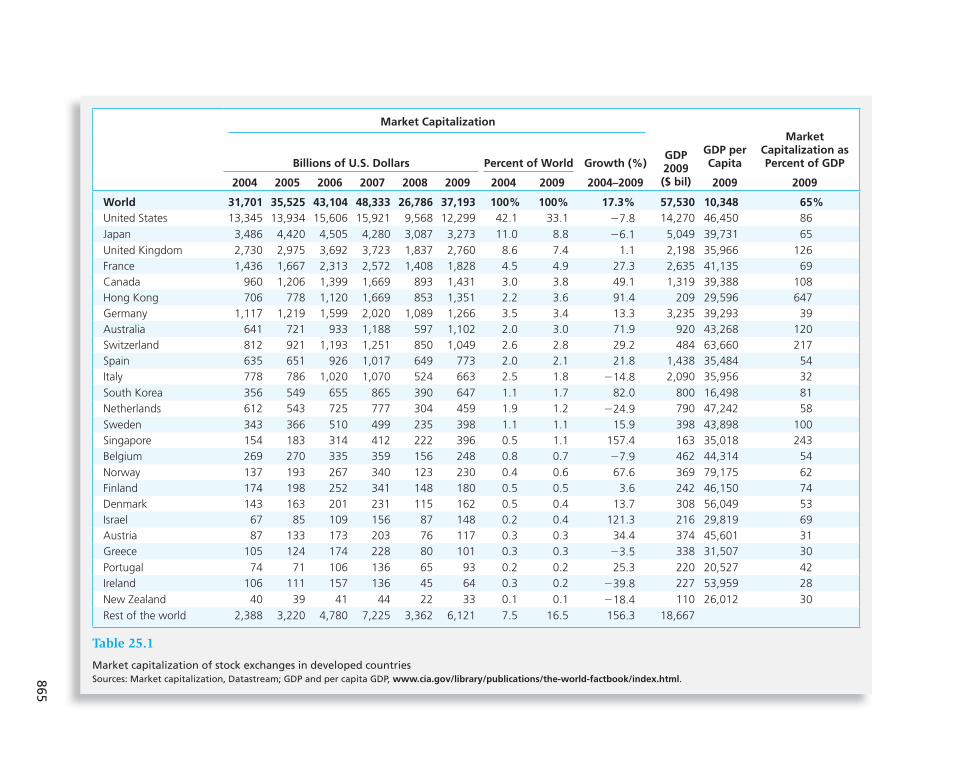

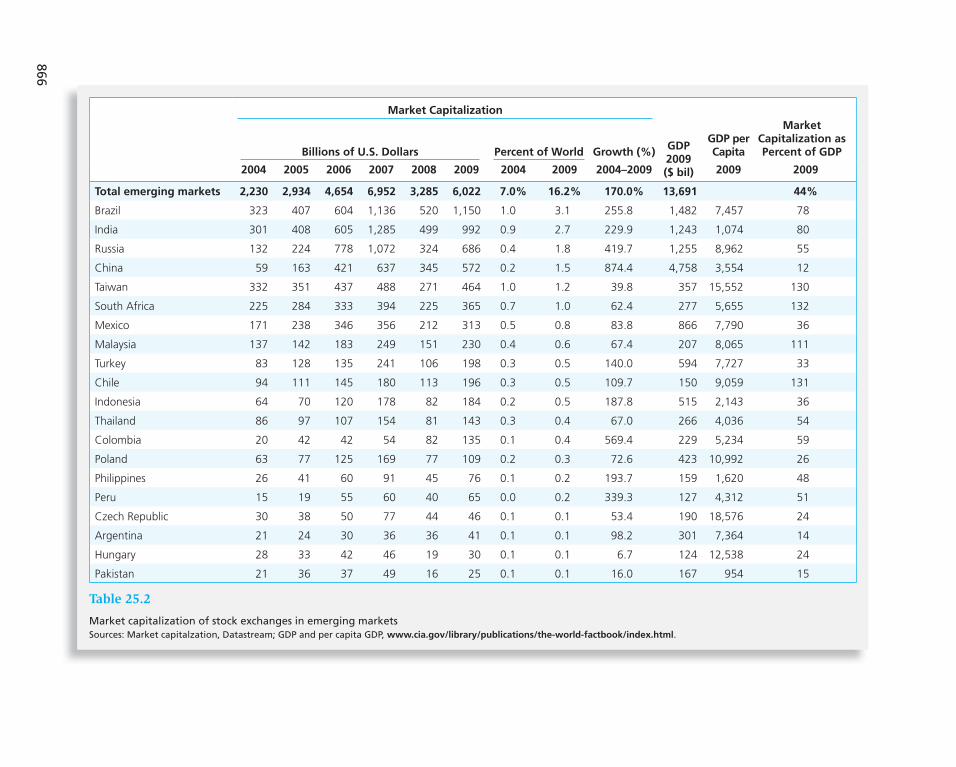

25.1 Global Markets for Equities 864

Developed Countries / Emerging Markets / Market

Capitalization and GDP / Home-Country Bias

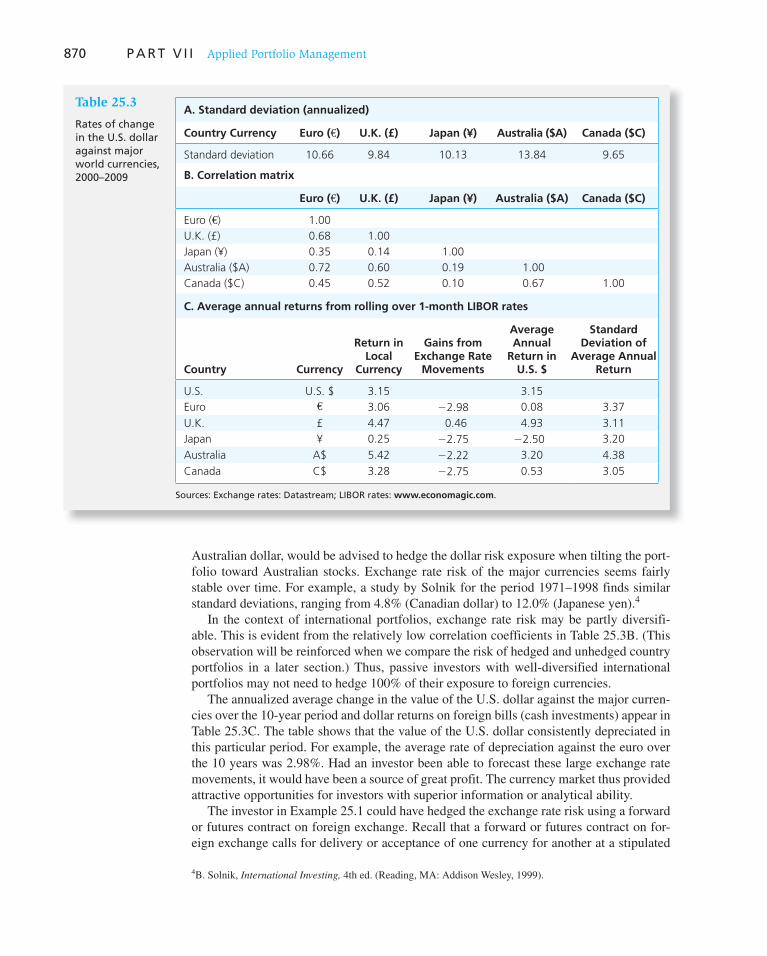

25.2 Risk Factors in International Investing 868

Exchange Rate Risk / Political Risk

25.3 International Investing: Risk, Return, and Benefits

from Diversification 875

Risk and Return: Summary Statistics / Are Investments

in Emerging Markets Riskier? / Average Country-Index

Returns and Capital Asset Pricing Theory / Benefits

from International Diversification / Misleading

Representation of Diversification Benefits / Realistic

Benefits from International Diversification / Are Benefits

from International Diversification Preserved in Bear

Markets?

25.4 Assessing the Potential of International

Diversification 888

25.5 International Investing and Performance

Attribution 893

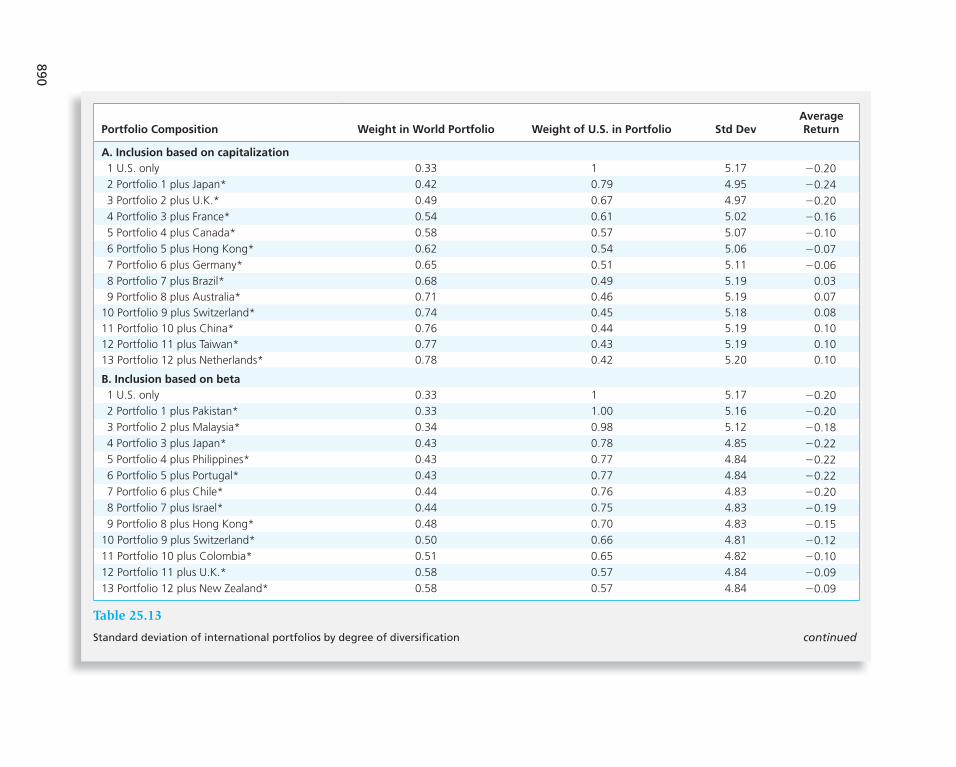

Constructing a Benchmark Portfolio of Foreign Assets /

Performance Attribution

End of Chapter Material 897–902

Chapter 26

Hedge Funds 903

26.1 Hedge Funds versus Mutual Funds 904

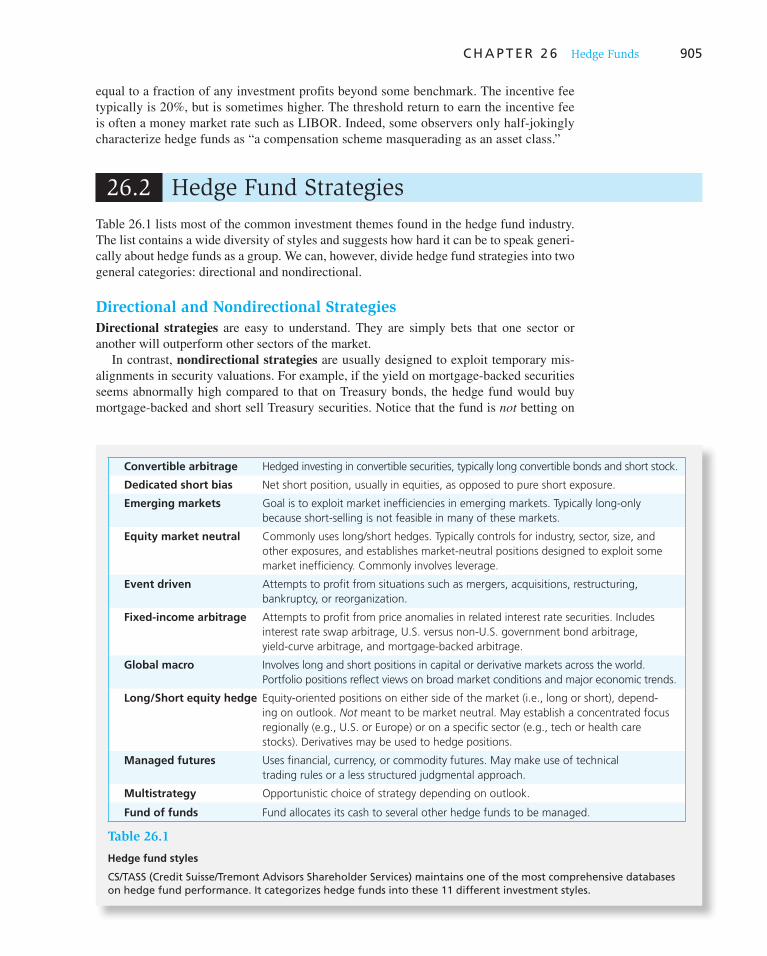

26.2 Hedge Fund Strategies 905

Directional and Nondirectional Strategies / Statistical

Arbitrage

22.4 Futures Prices 770

The Spot-Futures Parity Theorem / Spreads / Forward

versus Futures Pricing

22.5 Futures Prices versus Expected Spot Prices 776

Expectation Hypothesis / Normal Backwardation /

Contango / Modern Portfolio Theory

End of Chapter Material 778–783

Chapter 23

Futures, Swaps, and Risk Management 784

23.1 Foreign Exchange Futures 784

The Markets / Interest Rate Parity / Direct versus Indirect

Quotes / Using Futures to Manage Exchange Rate Risk

23.2 Stock-Index Futures 791

The Contracts / Creating Synthetic Stock Positions: An

Asset Allocation Tool / Index Arbitrage / Using Index

Futures to Hedge Market Risk

23.3 Interest Rate Futures 798

Hedging Interest Rate Risk

23.4 Swaps 800

Swaps and Balance Sheet Restructuring / The Swap

Dealer / Other Interest Rate Contracts / Swap Pricing /

Credit Risk in the Swap Market / Credit Default Swaps

23.5 Commodity Futures Pricing 806

Pricing with Storage Costs / Discounted Cash Flow

Analysis for Commodity Futures

End of Chapter Material 810–818

PART VII

Applied Portfolio Management 819

Chapter 24

Portfolio Performance Evaluation 819

24.1 The Conventional Theory of Performance

Evaluation 819

Average Rates of Return / Time-Weighted Returns versus

Dollar-Weighted Returns / Adjusting Returns for Risk /

The M 2 Measure of Performance / Sharpe’s Measure

as the Criterion for Overall Portfolios / Appropriate

Performance Measures in Two Scenarios

Jane’s Portfolio Represents Her Entire Risky Investment

Fund / Jane’s Choice Portfolio Is One of Many

Portfolios Combined into a Large Investment Fund

The Role of Alpha in Performance Measures / Actual

Performance Measurement: An Example / Realized

Returns versus Expected Returns

xv

Contents

Chapter 28

Investment Policy and the Framework of the CFA Institute 952

28.1 The Investment Management Process 953

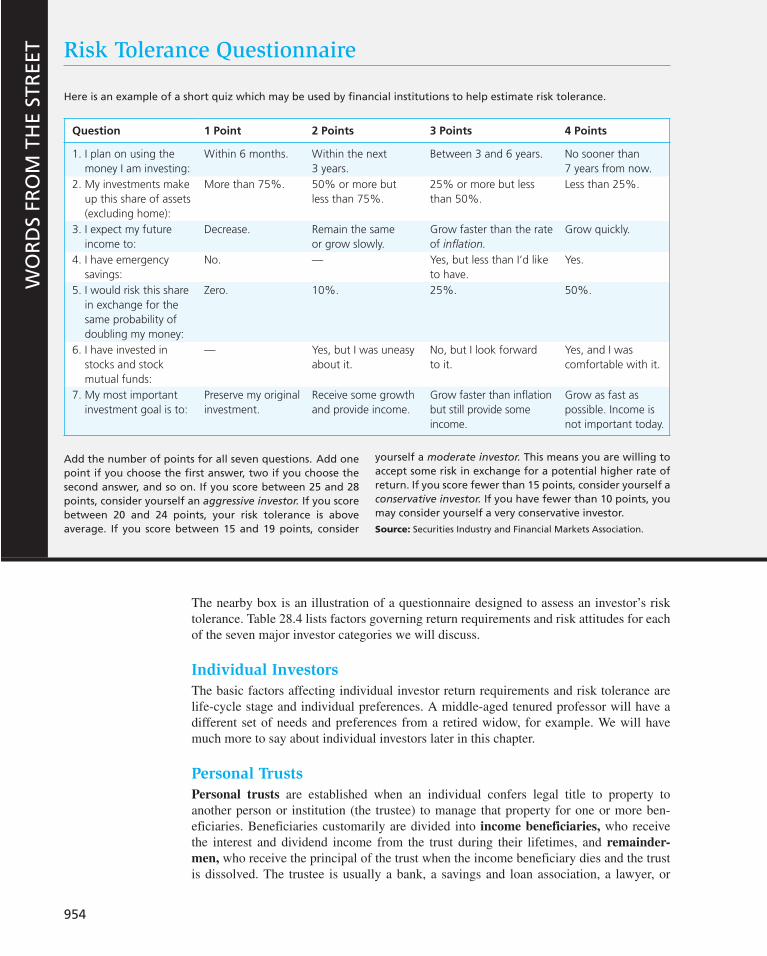

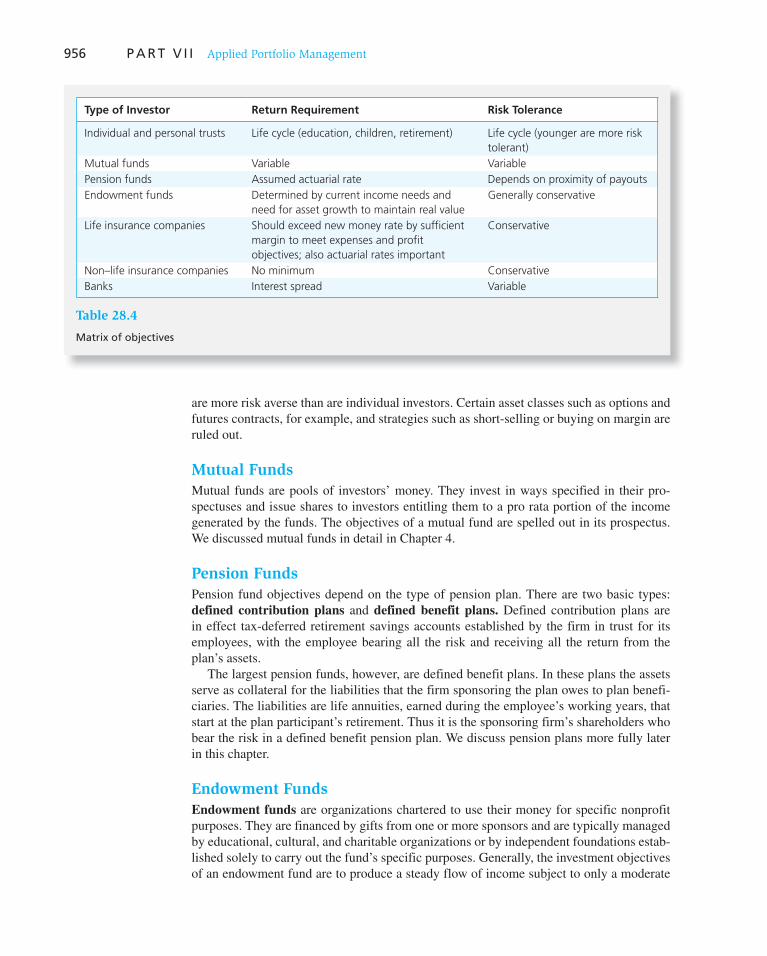

Objectives / Individual Investors / Personal Trusts /

Mutual Funds / Pension Funds / Endowment Funds / Life

Insurance Companies / Non–Life Insurance Companies /

Banks

28.2 Constraints 957

Liquidity / Investment Horizon / Regulations / Tax

Considerations / Unique Needs

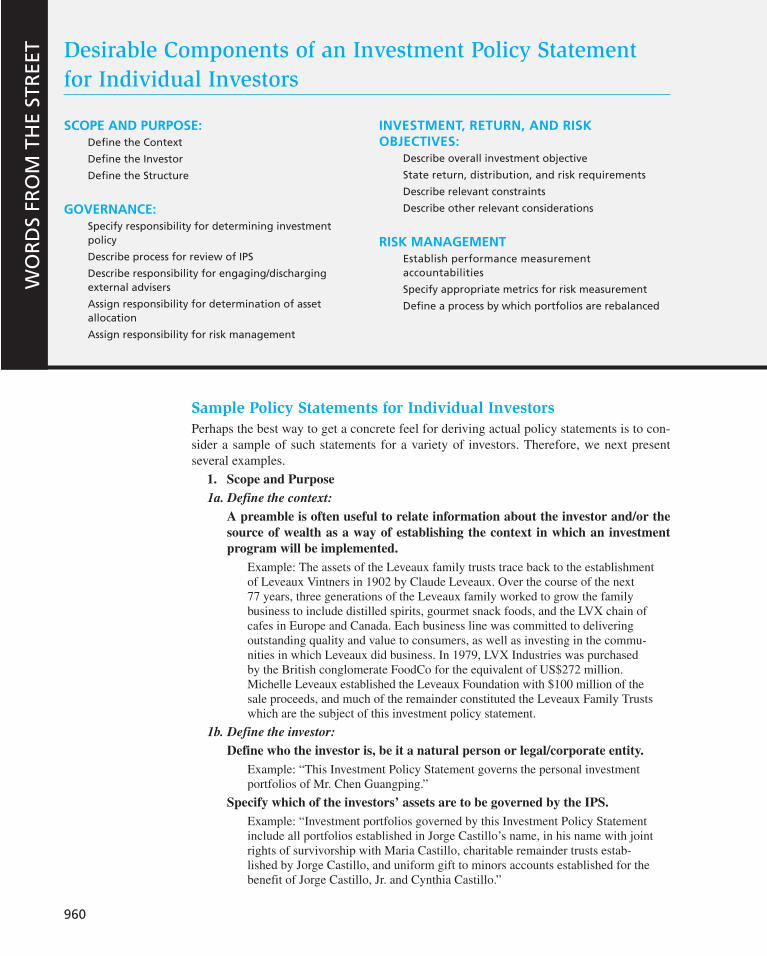

28.3 Policy Statements 959

Sample Policy Statements for Individual Investors

28.4 Asset Allocation 967

Policy Statements / Taxes and Asset Allocation

28.5 Managing Portfolios of Individual Investors 969

Human Capital and Insurance / Investment in Residence /

Saving for Retirement and the Assumption of Risk /

Retirement Planning Models / Manage Your Own

Portfolio or Rely on Others? / Tax Sheltering

The Tax-Deferral Option / Tax-Deferred Retirement

Plans / Deferred Annuities / Variable and Universal

Life Insurance

28.6 Pension Funds 975

Defined Contribution Plans / Defined Benefit Plans /

Alternative Perspectives on Defined Benefit Pension

Obligations / Pension Investment Strategies

Investing in Equities / Wrong Reasons to Invest

in Equities

28.7 Investments for the Long Run 979

Advice from the Mutual Fund Industry / Target Investing

and the Term Structure of Bonds / Making Simple

Investment Choices / Inflation Risk and Long-Term Investors

End of Chapter Material 982–992

REFERENCES TO CFA PROBLEMS 993

GLOSSARY G-1

NAME INDEX I-1

SUBJECT INDEX I-4

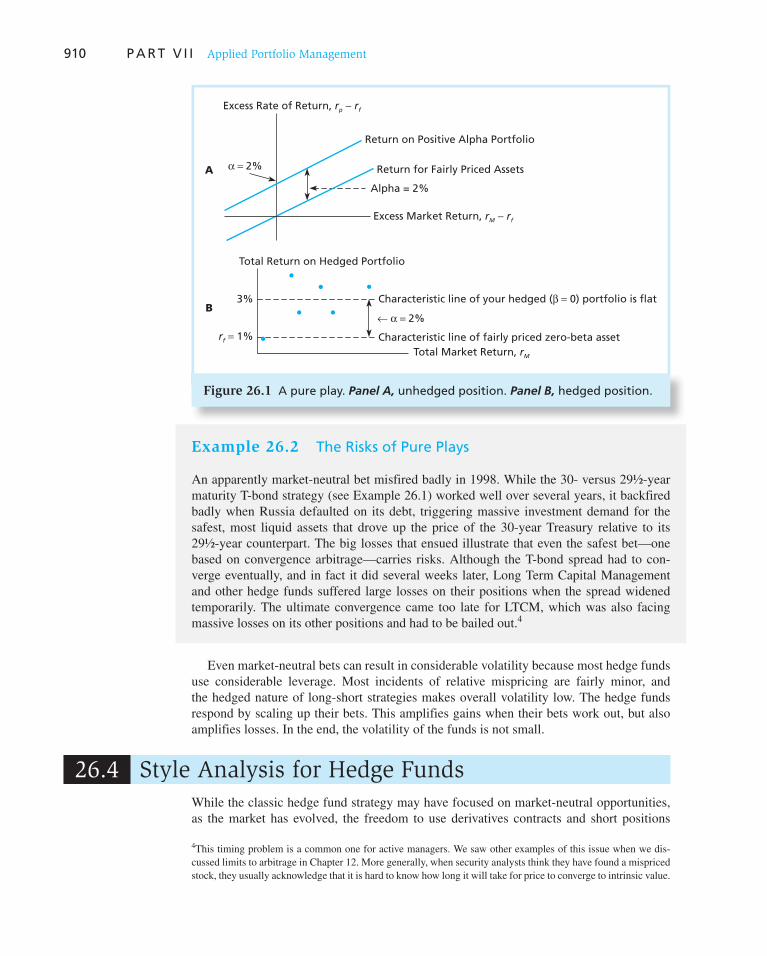

26.3 Portable Alpha 908

An Example of a Pure Play

26.4 Style Analysis for Hedge Funds 910

26.5 Performance Measurement for Hedge Funds 912

Liquidity and Hedge Fund Performance / Hedge Fund

Performance and Survivorship Bias / Hedge Fund

Performance and Changing Factor Loadings / Tail Events

and Hedge Fund Performance

26.6 Fee Structure in Hedge Funds 919

End of Chapter Material 921–925

Chapter 27

The Theory of Active Portfolio Management 926

27.1 Optimal Portfolios and Alpha Values 926

Forecasts of Alpha Values and Extreme Portfolio Weights /

Restriction of Benchmark Risk

27.2 The Treynor-Black Model and Forecast

Precision 933

Adjusting Forecasts for the Precision of Alpha /

Distribution of Alpha Values / Organizational Structure

and Performance

27.3 The Black-Litterman Model 937

A Simple Asset Allocation Decision / Step 1: The

Covariance Matrix from Historical Data / Step 2:

Determination of a Baseline Forecast / Step 3: Integrating

the Manager’s Private Views / Step 4: Revised (Posterior)

Expectations / Step 5: Portfolio Optimization

27.4 Treynor-Black versus Black-Litterman: Complements,

Not Substitutes 943

The BL Model as Icing on the TB Cake / Why Not Replace

the Entire TB Cake with the BL Icing?

27.5 The Value of Active Management 945

A Model for the Estimation of Potential Fees / Results

from the Distribution of Actual Information Ratios /

Results from Distribution of Actual Forecasts / Results

with Reasonable Forecasting Records

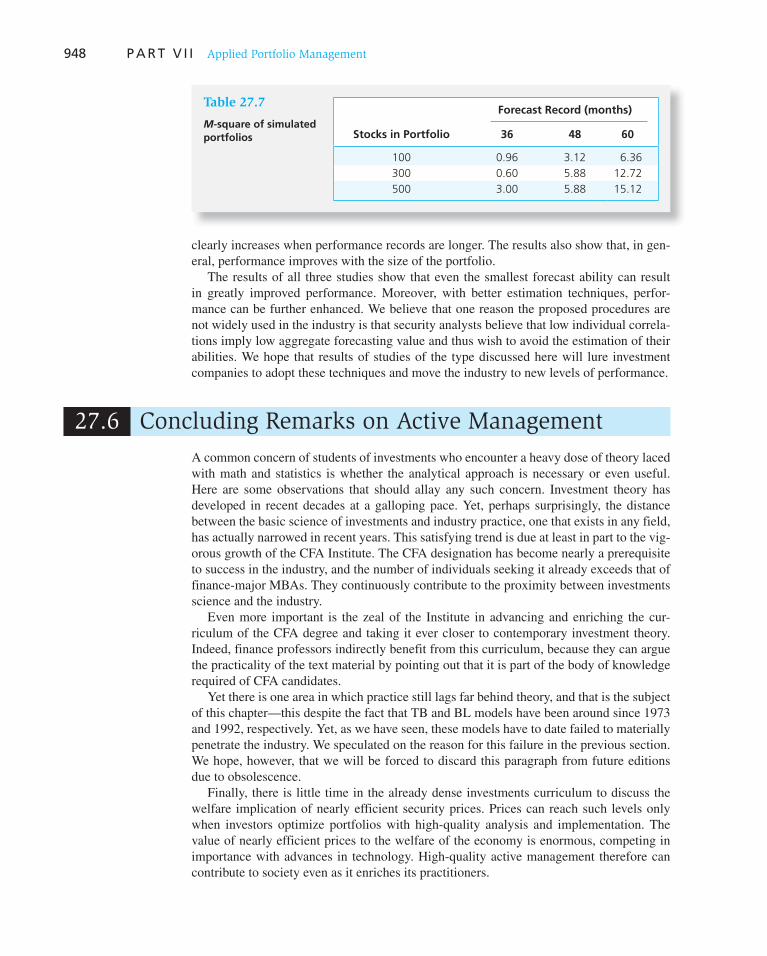

27.6 Concluding Remarks on Active Management 948

End of Chapter Material 949–951

Appendix A: Forecasts and Realizations of Alpha 950

Appendix B: The General Black-Litterman Model 950

xvi

Preface

We wrote the first edition of this textbook more

than two decades ago. The intervening years

have been a period of rapid, profound, and

ongoing change in the investments industry. This is due

in part to an abundance of newly designed securities, in

part to the creation of new trading strategies that would

have been impossible without concurrent advances in

computer technology, in part to rapid advances in the

theory of investments that have come out of the academic

community, and in part to unprecedented events in the

global securities markets. In no other field, perhaps, is the

transmission of theory to real-world practice as rapid as is

now commonplace in the financial industry. These devel-

opments place new burdens on practitioners and teachers

of investments far beyond what was required only a short

while ago. Of necessity, our text has evolved along with

financial markets and their influence on world events.

Investments, Ninth Edition, is intended primarily as a

textbook for courses in investment analysis. Our guiding

principle has been to present the material in a framework

that is organized by a central core of consistent funda-

mental principles. We make every attempt to strip away

unnecessary mathematical and technical detail, and we

have concentrated on providing the intuition that may

guide students and practitioners as they confront new

ideas and challenges in their professional lives.

This text will introduce you to major issues currently

of concern to all investors. It can give you the skills to

conduct a sophisticated assessment of watershed current

issues and debates covered by the popular media as well

as more-specialized finance journals. Whether you plan to

become an investment professional, or simply a sophisti-

cated individual investor, you will find these skills essen-

tial, especially in today’s ever-changing environment.

Our primary goal is to present material of practical

value, but all three of us are active researchers in the sci-

ence of financial economics and find virtually all of the

material in this book to be of great intellectual interest.

Fortunately, we think, there is no contradiction in the field

of investments between the pursuit of truth and the pursuit

of money. Quite the opposite. The capital asset pricing

model, the arbitrage pricing model, the efficient markets

hypothesis, the option-pricing model, and the other cen-

terpieces of modern financial research are as much intel-

lectually satisfying subjects of scientific inquiry as they

are of immense practical importance for the sophisticated

investor.

In our effort to link theory to practice, we also have

attempted to make our approach consistent with that of

the CFA Institute. In addition to fostering research in

finance, the CFA Institute administers an education and

certification program to candidates seeking the desig-

nation of Chartered Financial Analyst (CFA). The CFA

curriculum represents the consensus of a committee of

distinguished scholars and practitioners regarding the

core of knowledge required by the investment profes-

sional. This text also is used in many certification pro-

grams for the Financial Planning Association and by the

Society of Actuaries.

Many features of this text make it consistent with and

relevant to the CFA curriculum. Questions from past CFA

exams appear at the end of nearly every chapter, and, for

students who will be taking the exam, those same ques-

tions and the exam from which they’ve been taken are

listed at the end of the book. Chapter 3 includes excerpts

from the “Code of Ethics and Standards of Professional

Conduct” of the CFA Institute. Chapter 28, which dis-

cusses investors and the investment process, presents the

xvii

Preface

CFA Institute’s framework for systematically relating

investor objectives and constraints to ultimate investment

policy. End-of-chapter problems also include questions

from test-prep leader Kaplan Schweser.

In the Ninth Edition, we have continued our systematic

collection of Excel spreadsheets that give tools to explore

concepts more deeply than was previously possible.

These spreadsheets, available on the Web site for this text

( www.mhhe.com/bkm ), provide a taste of the sophisti-

cated analytic tools available to professional investors.

UNDERLYING PHILOSOPHY

In the Ninth Edition, we address many of the changes in

the investment environment, including the unprecedented

events surrounding the financial crisis.

At the same time, many basic principles remain impor-

tant. We believe that attention to these few important

principles can simplify the study of otherwise difficult

material and that fundamental principles should orga-

nize and motivate all study. These principles are crucial

to understanding the securities traded in financial markets

and in understanding new securities that will be intro-

duced in the future, as well as their effects on global mar-

kets. For this reason, we have made this book thematic,

meaning we never offer rules of thumb without reference

to the central tenets of the modern approach to finance.

The common theme unifying this book is that security

markets are nearly efficient, meaning most securities are

usually priced appropriately given their risk and return

attributes. Free lunches are rarely found in markets as

competitive as the financial market. This simple observa-

tion is, nevertheless, remarkably powerful in its implica-

tions for the design of investment strategies; as a result,

our discussions of strategy are always guided by the

implications of the efficient markets hypothesis. While

the degree of market efficiency is, and always will be, a

matter of debate (in fact we devote a full chapter to the

behavioral challenge to the efficient market hypothesis),

we hope our discussions throughout the book convey a

good dose of healthy criticism concerning much conven-

tional wisdom.

Distinctive Themes Investments is organized around several important themes:

1. The central theme is the near-informational-efficiency

of well-developed security markets, such as those

in the United States, and the general awareness that

competitive markets do not offer “free lunches” to

participants.

A second theme is the risk–return trade-off. This too

is a no-free-lunch notion, holding that in competitive

security markets, higher expected returns come only

at a price: the need to bear greater investment risk.

However, this notion leaves several questions unan-

swered. How should one measure the risk of an asset?

What should be the quantitative trade-off between

risk (properly measured) and expected return? The

approach we present to these issues is known as

modern portfolio theory, which is another organiz-

ing principle of this book. Modern portfolio theory

focuses on the techniques and implications of efficient

diversification, and we devote considerable attention

to the effect of diversification on portfolio risk as

well as the implications of efficient diversification for

the proper measurement of risk and the risk–return

relationship.

2. This text places greater emphasis on asset allocation

than most of its competitors. We prefer this emphasis

for two important reasons. First, it corresponds to

the procedure that most individuals actually follow.

Typically, you start with all of your money in a bank

account, only then considering how much to invest in

something riskier that might offer a higher expected

return. The logical step at this point is to consider

risky asset classes, such as stocks, bonds, or real

estate. This is an asset allocation decision. Second,

in most cases, the asset allocation choice is far more

important in determining overall investment perfor-

mance than is the set of security selection decisions.

Asset allocation is the primary determinant of the

risk–return profile of the investment portfolio, and so

it deserves primary attention in a study of investment

policy.

3. This text offers a much broader and deeper treatment

of futures, options, and other derivative security mar-

kets than most investments texts. These markets have

become both crucial and integral to the financial uni-

verse and are the major drivers in that universe and in

some cases, the world at large. Your only choice is to

become conversant in these markets—whether you are

to be a finance professional or simply a sophisticated

individual investor.

NEW IN THE NINTH EDITION

The following is a guide to changes in the ninth Edition.

This is not an exhaustive road map, but instead is meant to

provide an overview of substantial additions and changes

to coverage from the last edition of the text.

xviii

Preface

Chapter 19 Financial Statement Analysis We look closely at the mark-to-market accounting and

the new FASB guideline controversy in the context of the

crisis.

Chapter 20 Options Markets While much about this chapter remains constant, we

included a much-needed new box on the role of deriva-

tives in risk management.

Chapter 25 International Diversification This chapter underwent a significant revision with fully

updated results on the efficacy of international diver-

sification. It also includes an extensive discussion of an

international CAPM. Only six pages in the entire chapter

escaped any significant changes.

Chapter 26 Hedge Funds We have incorporated new treatments of style analysis

and liquidity involving hedge fund returns. We also intro-

duced the Madoff scandal and the role that hedge funds

played in the situation.

Chapter 28 Investment Policy and the Framework of the CFA Institute In this chapter, we update our discussion of investment

policy statements, with many examples derived from the

suggestions of the CFA Institute.

ORGANIZATION AND CONTENT

The text is composed of seven sections that are fairly

independent and may be studied in a variety of sequences.

Because there is enough material in the book for a two-

semester course, clearly a one-semester course will

require the instructor to decide which parts to include.

Part One is introductory and contains important insti-

tutional material focusing on the financial environment.

We discuss the major players in the financial markets,

provide an overview of the types of securities traded in

those markets, and explain how and where securities are

traded. We also discuss in depth mutual funds and other

investment companies, which have become an increas-

ingly important means of investing for individual inves-

tors. Perhaps most important, we address how financial

markets can influence all aspects of the global economy,

as in 2008.

The material presented in Part One should make it

possible for instructors to assign term projects early in

the course. These projects might require the student to

analyze in detail a particular group of securities. Many

Chapter 1 The Investment Environment This chapter has been revised extensively to include a

comprehensive section on the financial crisis of 2008 and

its causes. Background includes a timeline, and the chap-

ter addresses the now-prevalent idea of systemic risk.

Chapter 2 Asset Classes and Financial Instruments Following the financial crisis, the need to shed a bit more

light on certain classes of financial instruments became

apparent. This chapter does so by including new boxes

and other material on the strategies and failures of Fannie

Mae and Freddie Mac.

Chapter 3 How Securities Are Traded We cover the new restrictions on short selling in the wake

of the 2008 crash, and their implications for the markets.

Chapter 5 Introduction to Risk, Return, and the Historical Record Discussion of the historical record on risk and return has

been thoroughly revised, with considerable new material

on tail risk and extreme events.

Chapter 7 Optimal Risky Portfolios We added a section on stock risk in the long run and the

fallacy of “time diversification.”

Chapter 9 The Capital Asset Pricing Model We incorporated an expanded treatment of liquidity risk

and risk premia.

Chapter 11 The Efficient Market Hypothesis This chapter has been expanded to include more complete

coverage of possible security price bubbles in the wake of

the 2008 crisis.

Chapter 13 Empirical Evidence on Security Returns We revised and updated the discussion of the role of

liquidity risk in asset pricing, consistent with recent

empirical evidence.

Chapter 14 Bond Prices and Yields We added a section that discusses credit risk, focusing on

credit default swaps and their role in the 2008 crisis.

Chapter 17 Macroeconomic and Industry Analysis This chapter incorporates a new look at macro policy fol-

lowing the 2008 crisis, including global stock market dis-

persion and monetary versus fiscal policy.

xix

Preface

rationale as well as evidence that supports the hypothesis

and challenges it. Chapter 12 is devoted to the behavioral

critique of market rationality. Finally, we conclude Part

Three with Chapter 13 on empirical evidence on secu-

rity pricing. This chapter contains evidence concerning

the risk–return relationship, as well as liquidity effects on

asset pricing.

Part Four is the first of three parts on security valua-

tion. This part treats fixed-income securities—bond pric-

ing (Chapter 14), term structure relationships (Chapter 15),

and interest-rate risk management (Chapter 16). Parts

Five and Six deal with equity securities and derivative

securities. For a course emphasizing security analysis and

excluding portfolio theory, one may proceed directly from

Part One to Part Four with no loss in continuity.

Finally, Part Seven considers several topics important

for portfolio managers, including performance evalua-

tion, international diversification, active management, and

practical issues in the process of portfolio management.

This part also contains a chapter on hedge funds.

instructors like to involve their students in some sort of

investment game, and the material in these chapters will

facilitate this process.

Parts Two and Three contain the core of modern

portfolio theory. Chapter 5 is a general discussion of risk

and return, making the general point that historical returns

on broad asset classes are consistent with a risk–return

trade-off, and examining the distribution of stock returns.

We focus more closely in Chapter 6 on how to describe

investors’ risk preferences and how they bear on asset

allocation. In the next two chapters, we turn to portfolio

optimization (Chapter 7) and its implementation using

index models (Chapter 8).

After our treatment of modern portfolio theory in Part

Two, we investigate in Part Three the implications of that

theory for the equilibrium structure of expected rates of

return on risky assets. Chapter 9 treats the capital asset

pricing model and Chapter 10 covers multifactor descrip-

tions of risk and the arbitrage pricing theory. Chapter 11

covers the efficient market hypothesis, including its

A Guided Tour . . .

This book contains several features designed to make it easy for the student to understand, absorb, and apply the concepts and techniques presented.

2 2 YOU LEARNED IN Chapter 1 that the pro-

cess of building an investment portfolio usu-

ally begins by deciding how much money to

allocate to broad classes of assets, such as safe

money market securities or bank accounts,

longer term bonds, stocks, or even asset

classes like real estate or precious metals. This

process is called asset allocation. Within each

class the investor then selects specific assets

from a more detailed menu. This is called

security selection.

Each broad asset class contains many spe-

cific security types, and the many variations

on a theme can be overwhelming. Our goal

in this chapter is to introduce you to the

important features of broad classes of securi-

ties. Toward this end, we organize our tour of

financial instruments according to asset class.

Financial markets are traditionally seg-

mented into money markets and capital

markets. Money market instruments include

short-term, marketable, liquid, low-risk debt

securities. Money market instruments some-

times are called cash equivalents, or just cash

for short. Capital markets, in contrast, include

longer term and riskier securities. Securities

in the capital market are much more diverse

than those found within the money market.

For this reason, we will subdivide the capital

market into four segments: longer term bond

markets, equity markets, and the derivative

markets for options and futures.

We first describe money market instru-

ments. We then move on to debt and equity

securities. We explain the structure of various

stock market indexes in this chapter because

market benchmark portfolios play an impor-

tant role in portfolio construction and evalua-

tion. Finally, we survey the derivative security

markets for options and futures contracts.

Asset Classes and Financial Instruments

CHAPTER TWO

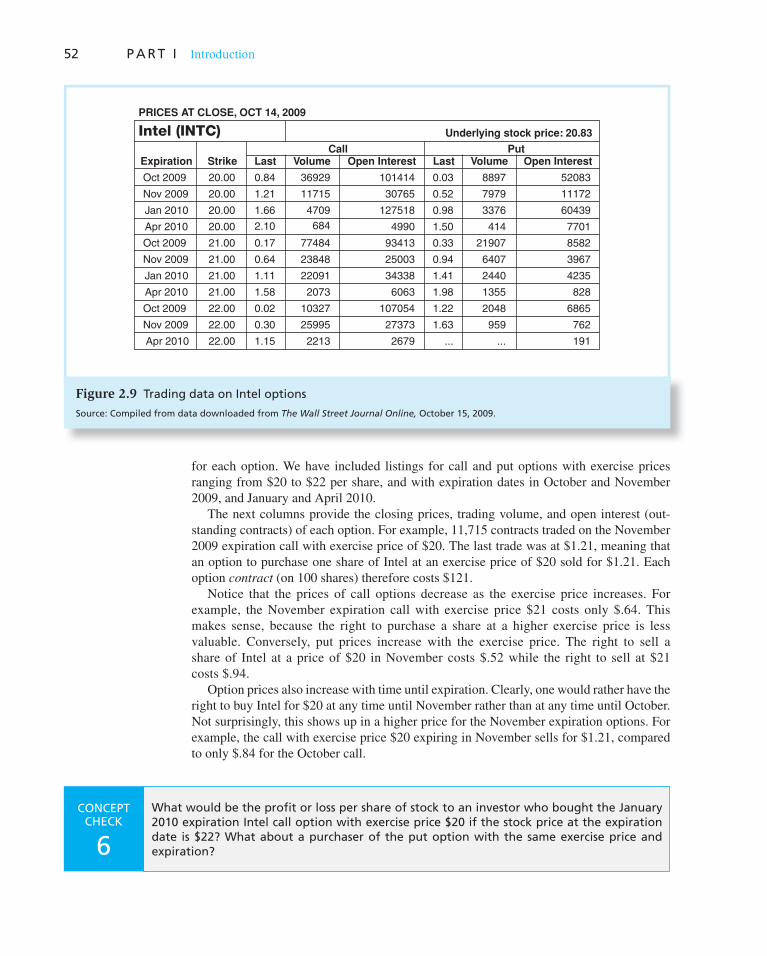

Notice that the prices of call options decrease as the exercise price increases. For example, the November expiration call with exercise price $21 costs only $.64. This makes sense, because the right to purchase a share at a higher exercise price is less valuable. Conversely, put prices increase with the exercise price. The right to sell a share of Intel at a price of $20 in November costs $.52 while the right to sell at $21 costs $.94.

Option prices also increase with time until expiration. Clearly, one would rather have the right to buy Intel for $20 at any time until November rather than at any time until October. Not surprisingly, this shows up in a higher price for the November expiration options. For example, the call with exercise price $20 expiring in November sells for $1.21, compared to only $.84 for the October call.

CONCEPT CHECK

6

What would be the profit or loss per share of stock to an investor who bought the January 2010 expiration Intel call option with exercise price $20 if the stock price at the expiration date is $22? What about a purchaser of the put option with the same exercise price and expiration?

NUMBERED EXAMPLES NUMBERED AND TITLED examples are integrated throughout chapters. Using the worked-out solutions to these examples as models, students can learn how to solve specific problems step-by-step as well as gain insight into general principles by seeing how they are applied to answer concrete questions.

Example 1.1 Carl Icahn’s Proxy Fight with Yahoo!

In February 2008, Microsoft offered to buy Yahoo! by paying its current shareholders $31 for each of their shares, a considerable premium to its closing price of $19.18 on the day before the offer. Yahoo’s management rejected that offer and a better one at $33 a share; Yahoo’s CEO Jerry Yang held out for $37 per share, a price that Yahoo! had not reached in more than 2 years. Billionaire investor Carl Icahn was outraged, arguing that management was protecting its own position at the expense of shareholder value. Icahn notified Yahoo! that he had been asked to “lead a proxy fight to attempt to remove the current board and to establish a new board which would attempt to negotiate a successful merger with Micro-soft.” To that end, he had purchased approximately 59 million shares of Yahoo! and formed a 10-person slate to stand for election against the current board. Despite this challenge, Yahoo’s management held firm in its refusal of Microsoft’s offer, and with the support of the board, Yang managed to fend off both Microsoft and Icahn. In July, Icahn agreed to end the proxy fight in return for three seats on the board to be held by his allies. But the 11-person board was still dominated by current Yahoo management. Yahoo’s share price, which had risen to $29 a share during the Microsoft negotiations, fell back to around $21 a share. Given the difficulty that a well-known billionaire faced in defeating a determined and entrenched management, it is no wonder that proxy contests are rare. Historically, about three of four proxy fights go down to defeat.

CHAPTER OPENING VIGNETTES SERVE TO OUTLINE the upcoming material in the chapter and provide students with a road map of what they will learn.

CONCEPT CHECKS A UNIQUE FEATURE of this book! These self-test questions and problems found in the body of the text enable the students to determine whether they’ve understood the preceding material. Detailed solutions are provided at the end of each chapter.

xxi

Investment bankers advise the issuing corporation on the prices it can charge for the securities issued, appropriate interest rates, and so forth. Ultimately, the investment bank-ing firm handles the marketing of the security in the primary market, where new issues of securities are offered to the public. Later, investors can trade previously issued securities among themselves in the so-called secondary market.

The End of the Stand-Alone Investment Banking Industry

Until 1999, the Glass-Steagall Act had prohibited banks in the United States from both accepting deposits and underwriting securities. In other words, it forced a separation of the investment and commercial banking industries. But when Glass-Steagall was repealed, many large commercial banks began to transform themselves into “universal banks” that could offer a full range of commercial and investment banking services. In some cases, commercial banks started their own investment banking divisions from scratch, but more frequently they expanded through merger. For example, Chase Manhattan acquired J.P. Morgan to form JPMorgan Chase. Similarly, Citigroup acquired Salomon Smith Barney to offer wealth management, brokerage, invest-ment banking, and asset management services to its cli-ents. Most of Europe had never forced the separation of commercial and investment banking, so their giant banks such as Credit Suisse, Deutsche Bank, HSBC, and UBS had long been universal banks. Until 2008, however, the stand-alone investment banking sector in the U.S. remained large and apparently vibrant, including such storied names as Goldman Sachs, Morgan-Stanley, Merrill Lynch, and Lehman Brothers.

But the industry was shaken to its core in 2008, when several investment banks were beset by enormous losses on their holdings of mortgage-backed securities. In March, on the verge of insolvency, Bear Stearns was merged into

JPMorgan Chase. On September 14, Merrill Lynch, also suffering steep mortgage-related losses, negotiated an agreement to be acquired by Bank of America. The next day, Lehman Brothers entered into the largest bankruptcy in U.S. history, having failed to find an acquirer able and willing to rescue it from its steep losses. The next week, the only two remaining major independent investment banks, Goldman Sachs and Morgan Stanley, decided to convert from investment banks to traditional bank holding companies. In doing so, they became subject to the supervision of national bank regulators such as the Federal Reserve and the far tighter rules for capital ade-quacy that govern commercial banks. 1 The firms decided that the greater stability they would enjoy as commercial banks, particularly the ability to fund their operations through bank deposits and access to emergency borrow-ing from the Fed, justified the conversion. These mergers and conversions marked the effective end of the indepen-dent investment banking industry—but not of investment banking. Those services now will be supplied by the large universal banks.

1 For example, a typical leverage ratio (total assets divided by bank capital) at commercial banks in 2008 was about 10 to 1. In contrast, leverage at investment banks reached 30 to 1. Such leverage increased profits when times were good but provided an inadequate buffer against losses and left the banks exposed to failure when their investment portfolios were shaken by large losses

WO

RD

S FR

OM

TH

E ST

REE

T

eXcel APPLICATIONS: Buying On Margin

T he Online Learning Center ( www.mhhe.com/bkm ) contains the Excel spreadsheet model below, which

makes it easy to analyze the impacts of different margin

levels and the volatility of stock prices. It also allows you to compare return on investment for a margin trade with a trade using no borrowed funds.

A B C D E F G H

Initial Equity InvestmentAmount BorrowedInitial Stock PriceShares PurchasedEnding Stock PriceCash Dividends During Hold Per.Initial Margin PercentageMaintenance Margin Percentage

Rate on Margin LoanHolding Period in Months

Return on Investment

Capital Gain on StockDividendsInterest on Margin LoanNet IncomeInitial Investment

Return on Investment

Ending

St Price

$20.0025.0030.0035.0040.0045.0050.0055.0060.0065.0070.0075.0080.00

−41.60%−121.60%−101.60%

−81.60%−61.60%−41.60%−21.60%

−1.60%18.40%38.40%58.40%78.40%98.40%

118.40%

Ending

St Price

$20.0025.0030.0035.0040.0045.0050.0055.0060.0065.0070.0075.0080.00

LEGEND:

Enter data

Value calculated

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

−18.80%−58.80%−48.80%−38.80%−28.80%−18.80%

−8.80%1.20%

11.20%21.20%31.20%41.20%51.20%

61.20%

A B C D E F HG I

Purchase Price = $100

State of theMarket ProbabilityExcellentGoodPoor

0.05

0.250.450.25

Expected Value (mean)

Standard Deviation of HPRVariance of HPR

Crash

Year-endPrice

46.00

126.50110.0089.75

2.00

4.504.003.50

−0.5600

0.27000.1000

−0.10750.3815

0.04510.00180.0273

−0.5200

0.31000.1400

−0.0675

CashDividends

T-bill Rate = 0.04

HPR

−0.6176

0.21240.0424

−0.1651

SquaredDeviationsfrom Mean

Deviationsfrom Mean

0.3815

0.04510.00180.0273

0.03800.1949

0.0976

ExcessReturns

SquaredDeviationsfrom Mean

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

SUMPRODUCT(B8:B11, E8:E11) =SUMPRODUCT(B8:B11, G8:G11) =

SQRT(G13) =

0.0576Risk PremiumStandard Deviation of Excess Return 0.1949SQRT(SUMPRODUCT(B8:B11, I8:I11)) =

SUMPRODUCT(B8:B11, H8:H11) =

Spreadsheet 5.1

Scenario analysis of holding period return of the stock-index fund

eXce lPlease visit us at www.mhhe.com/bkm

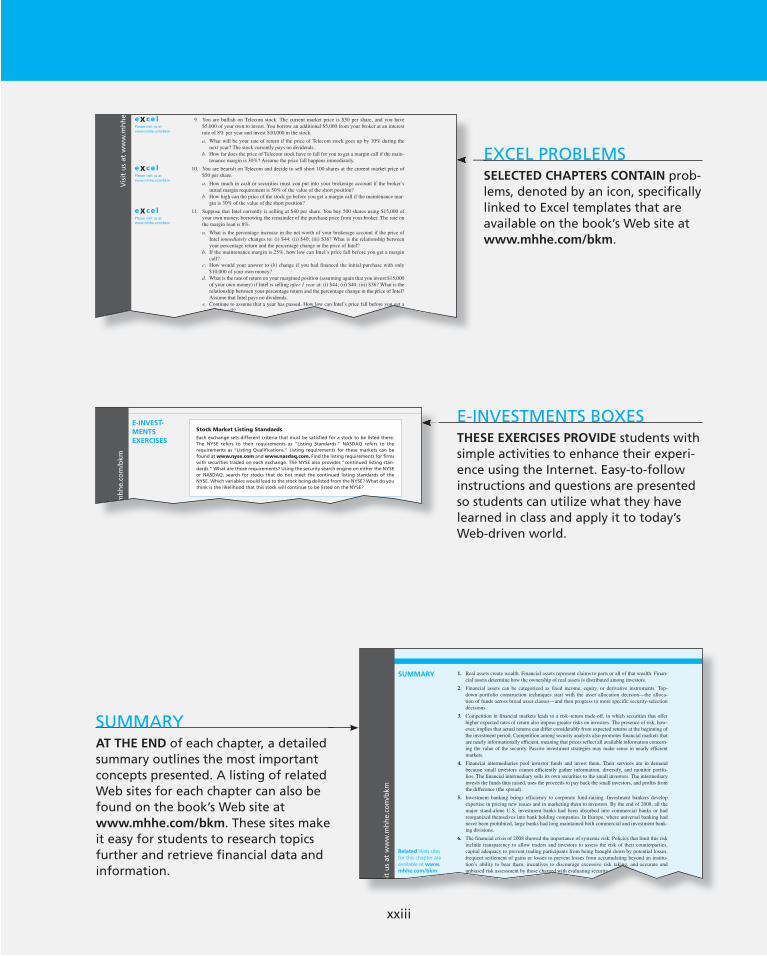

EXCEL APPLICATIONS THE NINTH EDITION features Excel Spreadsheet Applications. A sample spreadsheet is presented in the Investments text with an interactive version available on the book’s Web site at www.mhhe.com/bkm .

EXCEL EXHIBITS SELECTED EXHIBITS ARE set as Excel spreadsheets and are denoted by an icon. They are also available on the book’s Web site at www.mhhe.com/bkm .

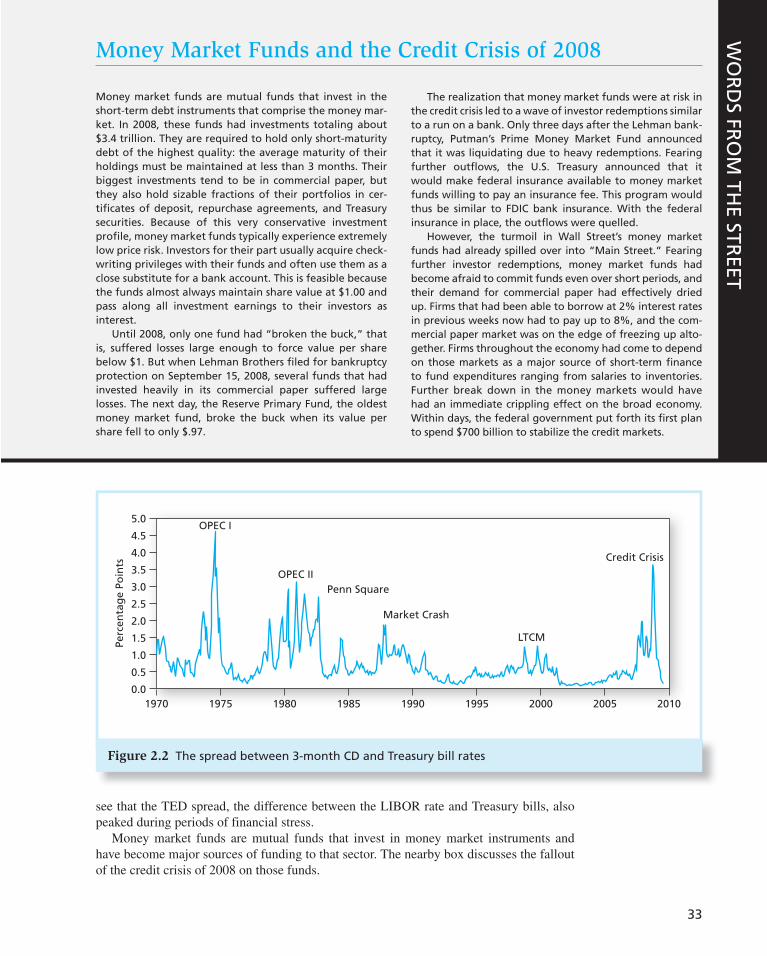

WORDS FROM THE STREET BOXES SHORT ARTICLES FROM business periodicals, such as The Wall Street

Journal, are included in boxes throughout the text. The articles are chosen for real-world relevance and clarity of presentation.

End Of Chapter Features . . .

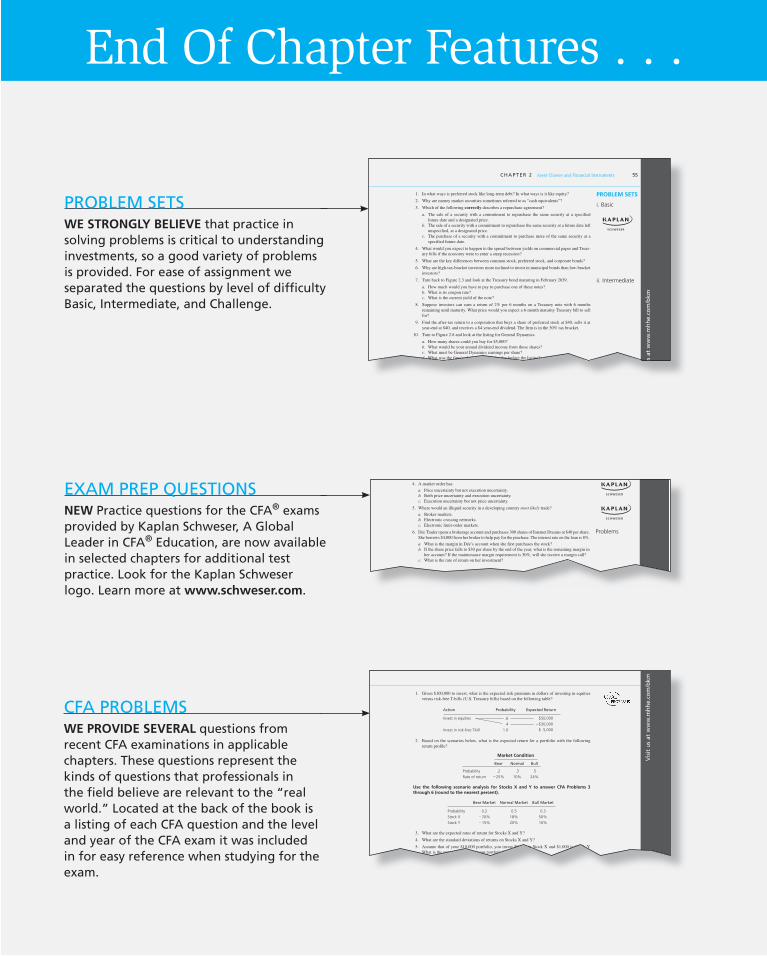

PROBLEM SETS WE STRONGLY BELIEVE that practice in solving problems is critical to understanding investments, so a good variety of problems is provided. For ease of assignment we separated the questions by level of difficulty Basic, Intermediate, and Challenge.

EXAM PREP QUESTIONS NEW Practice questions for the CFA ® exams provided by Kaplan Schweser, A Global Leader in CFA ® Education, are now available in selected chapters for additional test practice. Look for the Kaplan Schweser logo. Learn more at www.schweser.com .

CFA PROBLEMS WE PROVIDE SEVERAL questions from recent CFA examinations in applicable chapters. These questions represent the kinds of questions that professionals in the field believe are relevant to the “real world.” Located at the back of the book is a listing of each CFA question and the level and year of the CFA exam it was included in for easy reference when studying for the exam.

us

at w

ww

.mh

he.

com

/bkm

C H A P T E R 2 Asset Classes and Financial Instruments 55

1. In what ways is preferred stock like long-term debt? In what ways is it like equity?

2. Why are money market securities sometimes referred to as “cash equivalents”?

3. Which of the following correctly describes a repurchase agreement?

a. The sale of a security with a commitment to repurchase the same security at a specified future date and a designated price.

b. The sale of a security with a commitment to repurchase the same security at a future date left unspecified, at a designated price.

c. The purchase of a security with a commitment to purchase more of the same security at a specified future date.

4. What would you expect to happen to the spread between yields on commercial paper and Treas-ury bills if the economy were to enter a steep recession?

5. What are the key differences between common stock, preferred stock, and corporate bonds?

6. Why are high-tax-bracket investors more inclined to invest in municipal bonds than low-bracket investors?

7. Turn back to Figure 2.3 and look at the Treasury bond maturing in February 2039.

a. How much would you have to pay to purchase one of these notes? b. What is its coupon rate? c. What is the current yield of the note?

8. Suppose investors can earn a return of 2% per 6 months on a Treasury note with 6 months remaining until maturity. What price would you expect a 6-month maturity Treasury bill to sell for?

9. Find the after-tax return to a corporation that buys a share of preferred stock at $40, sells it at year-end at $40, and receives a $4 year-end dividend. The firm is in the 30% tax bracket.

10. Turn to Figure 2.8 and look at the listing for General Dynamics.

a. How many shares could you buy for $5,000? b. What would be your annual dividend income from those shares? c. What must be General Dynamics earnings per share? d. What was the firm’s closing price on the day before the listing?

PROBLEM SETS

i. Basic

ii. Intermediate

4. A market order has:

a. Price uncertainty but not execution uncertainty. b. Both price uncertainty and execution uncertainty. c. Execution uncertainty but not price uncertainty.

5. Where would an illiquid security in a developing country most likely trade?

a. Broker markets. b. Electronic crossing networks. c. Electronic limit-order markets.

6. Dée Trader opens a brokerage account and purchases 300 shares of Internet Dreams at $40 per share. She borrows $4,000 from her broker to help pay for the purchase. The interest rate on the loan is 8%.

a. What is the margin in Dée’s account when she first purchases the stock? b. If the share price falls to $30 per share by the end of the year, what is the remaining margin in

her account? If the maintenance margin requirement is 30%, will she receive a margin call? c. What is the rate of return on her investment?

Problems

Vis

it u

s at

ww

w.m

hh

e.co

m/b

km

1. Given $100,000 to invest, what is the expected risk premium in dollars of investing in equities versus risk-free T-bills (U.S. Treasury bills) based on the following table?

Action Probability Expected Return

Invest in equities .6 $50,000

.4 �$30,000

Invest in risk-free T-bill 1.0 $ 5,000

2. Based on the scenarios below, what is the expected return for a portfolio with the following return profile?

Market Condition

Bear Normal Bull

Probability .2 .3 .5

Rate of return �25% 10% 24%

Use the following scenario analysis for Stocks X and Y to answer CFA Problems 3 through 6 (round to the nearest percent).

Bear Market Normal Market Bull Market

Probability 0.2 0.5 0.3

Stock X �20% 18% 50%

Stock Y �15% 20% 10%

3. What are the expected rates of return for Stocks X and Y?

4. What are the standard deviations of returns on Stocks X and Y?

5. Assume that of your $10,000 portfolio, you invest $9,000 in Stock X and $1,000 in Stock Y. What is the expected return on your portfolio?

xxiii

SUMMARY AT THE END of each chapter, a detailed summary outlines the most important concepts presented. A listing of related Web sites for each chapter can also be found on the book’s Web site at www.mhhe.com/bkm . These sites make it easy for students to research topics further and retrieve financial data and information.

E-INVESTMENTS BOXES THESE EXERCISES PROVIDE students with simple activities to enhance their experi-ence using the Internet. Easy-to-follow instructions and questions are presented so students can utilize what they have learned in class and apply it to today’s Web-driven world.

EXCEL PROBLEMS SELECTED CHAPTERS CONTAIN prob-lems, denoted by an icon, specifically linked to Excel templates that are available on the book’s Web site at www.mhhe.com/bkm .

Vis

it u

s at

ww

w.m

hh

e 9. You are bullish on Telecom stock. The current market price is $50 per share, and you have

$5,000 of your own to invest. You borrow an additional $5,000 from your broker at an interest rate of 8% per year and invest $10,000 in the stock.

a. What will be your rate of return if the price of Telecom stock goes up by 10% during the next year? The stock currently pays no dividends.

b. How far does the price of Telecom stock have to fall for you to get a margin call if the main-tenance margin is 30%? Assume the price fall happens immediately.

10. You are bearish on Telecom and decide to sell short 100 shares at the current market price of $50 per share.