Finance for Smallholders

193

Finance for Smallholders Opportunities for risk management by linking financial institutions and producer organisations CASE STUDIES REPORT Photo by ICCO Terrafina Microfinance - Fransien Wolters

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Finance for Smallholders

Finance for SmallholdersOpportunities for risk management by linking financial institutions and producer organisations

CASE STUDIES REPORT

Photo by ICCO Terrafina Microfinance - Fransien Wolters

Colophon

Funders:

Food & Business Knowledge Platform NpM, Platform for Inclusive FinanceAgriProFocus

Rural Finance working group members:

Cordaid Resi JansenFMO Frederik Jan van den BoschFMO Anton TimpersHivos Ben LeussinkHivos Leo SoldaatICCO Investments Ben NijkampICCO Terrafina Microfinance Mariel Mensink (coordinator)Oxfam Novib Bruno MolijnRabobank Foundation Albert Boogaard

Authors:

Lead consultant Joost de la Rive Box, Nedworc FoundationResearcher (Ethiopia) Shambachew Hussen, Wageningen University & Research CentreResearcher (Mali) Ibrahim Mare, Local consultantResearcher (Rwanda) Patrice Mugenzi, Wageningen University & Research CentreResearcher (Uganda) Peter Mukwana, Local consultantResearcher Marjola Trebels- Van Bolhuis, NpM, Platform for Inclusive Finance

Table of Contents

Ethiopia

Case Study E1: Lidet Savings and Credit Cooperatives Union 4

Case Study E2: Wasasa MFI 22

Case Study E3: Buusaa Gonofaa MFI 34

Case Study E4: Setit-Humera Ltd Farmers’ Cooperative Union 50

Mali

Case Study M1: Mali Biocarburant 64

Case Study M2: Soro Yiriwaso MFI 76

Case Study M3: myAgro Social Enterprise 90

Rwanda

Case Study R1: Duterimbere MFI Ltd / Nyagatare Branch 100

Case Study R2: Uniclecam Ejo Heza 112

Case Study R3: Amasezerano Community Banking Ltd 122

Case Study R4: Union des CLECAM Wisigara 128

Uganda

Case Study U1: Conservation Cotton Initiative Uganda 138

Case Study U2: Enterprise Support and Community Development Trust 150

Case Study U3: National Union of Coffee Agribusinesses and Farm Enterprises 162

Finance Fairs

Case Study Finance Fairs: Ethiopia, Uganda, Rwanda, Mali 180

4

AbstractLidet Savings and Credit Cooperatives Union operates as a financial cooperative for 111 primary cooperatives with in total 115,713 active individual household members. Lidet is not just a Savings and Credit Co-operative (SACCO) as it also includes other producer and marketing primary Co-operatives such as Multi-Purpose Co-operatives (MPCs) and Unions. Microfinance is provided both to individual farmers and to farmer groups. Apart from credit and savings, the services include microinsurance, finance training and farm-related extension. Despite the progress, a preliminary study reveals that there was a huge need for capacity building in governance and financial management issues. In line with this, ICCO Terrafina Microfinance designed a capacity building programme and trained Union staff, board members and the Union credit control committee. In a bit to improve lending procedures, training was developed for loan officers of financial cooperatives including a Cooperative Credit Assessment Matrix (CAM). This is a tool that assesses the risks of lending to a producer cooperative. Also capacity building was undertaken by ICCO Terrafina Microfinance for the staff of cooperative promotion agencies at regional, zonal and district level.

AcronymsCAM Cooperative Credit Assessment Matrix CCB Common Capacity Building DA Development Assistant ETB Ethiopian BirrMFI Microfinance InstitutionMPC Multi-Purpose CooperativeMPU Multi-Purpose UnionPO Producer OrganisationRUFIP Rural Financial Intermediation Programme, financed by IFAD (International Fund for Agricultural Development)SACCO Savings and Credit Co-operative VSLA Village Savings and Loan Association

Case Study E1

Lidet Savings and Credit Cooperatives Union

Producer Organisation (PO) /coop profile data

Type of organisationNumber of membersNumber of employeesMain crops

Cooperatives Union 111 cooperatives 26Teff barley and maize

1. Main characteristics of the case

1.1 Farmers and their organisation

Lidet Savings and Credit Cooperatives Union Ltd. is mainly serving as a second tier cooperative for more than 111 different primary cooperatives. It started its operation in March 2006 by 18 primary cooperatives of which 6 were Multi-Purpose Cooperatives (MPCs), while 12 of them were Savings and Credit Co-operatives (SACCOs). It was established with the mission of solving the socioeconomic problems and the eradication of poverty in the region, by providing reliable, convenient and quick financial services to members and customers. The Lidet secretariat aims to strengthen its member primary cooperatives, so their customers are satisfied with the financial services offered. Unlike the other regions, the Amhara Union in general and Lidet in particular do this in the sense that the member cooperatives are not just SACCOs, but also Multi-Purpose Producers and Marketing Primary Cooperatives.

“Improving financial services from Financial Cooperative Unions to Producer Marketing Cooperatives, Amhara Region, Ethiopia”

5

Kind of Producer Organisation Total numbers % of members

1 SACCO 56 50.5%

2 MPCs 38 34.2%

3 Seedling Enterprises 7 6.3%

4 Consumer Cooperatives 4 3.6%

5 Vegetable and Fruits 2 1.8%

6 Housing Development and Cooperatives 2 1.8%

7 MPUs 1 0.9%

8 Animal fattening and marketing 1 0.9%

Total 111 100%

Source: Authors computation from Lidet Union report for federal government - Update 2014-09-21

In accordance with its constitution, Lidet aims:1. To provide access to credit and financial services at an affordable interest rate to the poor

farmers, especially to women;2. To create a favourable and trusted investment climate by keeping funds of primary

cooperatives collected from members; 3. To provide training and support to primary cooperatives in the region;4. To create a better financial system for the primary cooperatives; and5. To create a platform for member cooperatives to share experience.

These functions are reflected in its organisational structure, as illustrated in the diagram below.

Currently, the services of Lidet are expanded and reach 6 districts and 140 peasant associations. There are 111 member primary cooperatives and 115,713 active individual household members under Lidet. Of this total number of individual members, about 41,894 (36%) are female. Member cooperatives are categorised into 8 different categories.

Secretary Legal office Credit management Savings office Education and

training unit Accountant

Casher

Internal Auditor

Diagram 1.1: Lidet Union’s organisational structure

Follow-up teamGeneral Assembly

Board of directors

Union Manager

6

The following table shows the progress in membership since the Union’s establishment in 2006, with respect to member primary cooperative, individual members’ gender distribution and total clients reached.

Since its establishment, Lidet has been providing a variety of services for members’ cooperatives, which include:• Provide support on practical planning preparation and other support to member primary

cooperatives and Producer Organisations (POs);• Create a culture of saving for the member cooperatives and support establishment of new

cooperative societies in the region;• Broaden and empower women and young leadership roles;• Provide quick, reliable and covenant service;• Provide training for the members’ permanent employees; • Create a better financial awareness among the member cooperatives; • Expand the financial service coverage by opening new branches; and• Establish a model for primary cooperatives.

1.2 The financial institution involved

Lidet currently has an ETB 77 million loan portfolio outstanding. The profit and loss accounts of the primary cooperatives was done for 2013/14 and profit was shared among members where the biggest profit share was ETB 50,365 and the smallest was ETB 26.-.

The Union also provides loans to Village Savings and Loan Associations (VSLAs) at a rate of 11% where the VSLA retails loans to members at 12%. Moreover, since March 2014 Lidet launched a microinsurance coverage for individual members who borrowed from the member SACCOs. The aim of this insurance is to avoid the financial burden to the remaining family members if the borrower dies before he/she paid the loan back. As a result since March, there are 828 members who joined a microinsurance service from Lidet in five months time. So far this year, only two deaths claims were filed and reimbursed according to the contract. The insurance and the VSLA servicers are very negligible compared to the core business of the Union i.e. serving the primary cooperatives.

Year Membersprimary coops

Individual members Increment

Male Female Total

06/07 18 7,698 1,221 8,919

07/08 20 9,720 1,743 11,463

08/09 23 11,740 2,357 14,097

09/10 25 14,710 3,543 18,253

10/11 30 15,107 4,320 19,427

11/12 38 15,609 4,465 20,074

12/13 80 58,127 27,619 85,726

13/14 111 73,819 41,894 115,713

Source: Lidet Union report for federal government update 2014-09-21

YearCapital

Increment in ETB

2006/07 169,464.00

2007/08 318,344.80

2008/09 572,869.30

2009/10 895,129.00

2010/11 1,194,973.00

2011/12 1,725,132.00

2012/13 4,059,878.00

2013/14 7,519,876.16

MFI profile data

Total number of active clientsNumber of employees, staff Portfolio value % of farming clients

115,71326ETB 77,027,95699% (estimated)

7

1.3 Nature of the programme

Rural SACCOs in Ethiopia are in general quite weak. Most rural SACCOs came into being after the start of the Rural Financial Intermediation Programme (RUFIP) in 2002. Ethiopia has a complex history with regard to cooperatives, as most cooperatives were politically initiated MPCs. Savings and Credit Unions and SACCOs are governed under one general cooperative law, together with marketing cooperatives and consumer cooperatives. This implies that, unlike the banking sector and microfinance sector, the supervision of financial cooperatives by the Central Bank in Ethiopia is lacking. No capital requirements, prudential norms, ratios and standard accounting practices have been defined. It was considered important to support these cooperatives since they operate in remote rural areas where microfinance institutions (MFIs) are often not operational. Since financial cooperatives need capacity building in institutional and financial management as well as on financial product development, ICCO Terrafina Microfinance is actively supporting them. Together with other concerned parties it also lobbies for development of a financial cooperative regulatory law.

The ICCO Terrafina Microfinance support to this Union started with a preliminary study by a local consultant. This study revealed a huge gap in human resources capacity, skills and knowledge in Union-boards and cooperative managers to safeguard good governance, portfolio management, financial management, accounting systems and cash management. Based on the preliminary study and the gaps identified, ICCO Terrafina Microfinance designed a capacity building programme in three phases. Beneficiaries of the programme included Union staffs (general manager, accountants and cashers); Union board members; and the Union credit control committee. They were joined by external staff from the cooperative promotion agency at regional level and three zonal level staffs namely from West Gojjam, East Gojjam and South Gonder.

The first phase of the training aimed at improving financial services from the Financial Cooperative Unions to MPCs and marketing cooperatives in Amhara region. ICCO Terrafina Microfinance designed and supported a Common Capacity Building (CCB) programme. The programme was provided for 6 financial cooperative Unions (including Lidet Union) and the cooperative promotion office at zonal and regional levels in the Amhara region. The second phase concentrated on Union product development. One element in this phase was to improve the financial services from the Unions to their primary MPC members. MPCs are the main credit recipients of the Amhara Unions. They account for 70-80% of all outstanding loans of the Unions. Most MPCs are producer/marketing cooperatives of grain staple food, mostly teff and maize. Their main activity is to buy, after harvest, the grain from the farmers for storage at the market-rate of that moment and become owner and responsible for marketing. In a bit to improve lending procedures, training was developed for loan officers of financial cooperatives using an assessment tool called “Cooperative Credit Assessment Matrix” (CAM)1, which was developed by a consultant of ICCO Terrafina Microfinance.

The objective of the training was to equip the Unions with tools to enable them to quickly analyse the key capacities and risks, and to be able to suggest proper loans to MPCs in terms of size, price and conditions. Loan demand from MPCs to Unions is usually much higher than the total value of their collateral. MPCs’ loan demand is based on estimated grain supply from members at harvest time, plus their storage and marketing facility. The CAM tool aims to facilitate increased MPC loan size beyond existing collateral possibilities, based upon investment needs and repayment capacity. In addition, ICCO Terrafina Microfinance lobbied with the regional government to have an adjustment of the requirements for SACCOs’ loan provisioning and collateral cover. Also in this product development phase of CCB, an effort was done to introduce professional solidarity lending by Union credit agents through SACCO committees and members, as well as an agri-lending product specifically for farmers, based on solidarity lending mechanisms. In line with this, trainings were given on solidarity group formation. Based on the needed assessment of the Unions, ICCO Terrafina Microfinance also provided support through funding for motorbikes for credit officers and for improvement of their salaries.

1 An excel tool with (20) concrete indicators and norms to score the institutional, financial, and marketing capacities as well as relevancy to members and credit worthiness of an MPC.

8

1.4 Other stakeholders

Cooperative Promotion Office. The Amhara Cooperative Agency is supporting the Unions at the regional, zonal and district level. At the regional level the cooperative promotion agency has a role in designing policies and rules for the way Unions should be governed. It also provides training and conducts research at the regional level. At the zonal level the agency supervises Unions on the given mandate. And at the district level, grassroots level support has been given through establishing new Unions, ensuring licensing and performing close regulatory follow-up on their operations through audit reports and inspections.

Zone/district administration office (ZAO/DAO). The agricultural services of the Government are extended starting from regional, zonal, and then district office administration and peasant association level. At the peasant association government, authorities are responsible for timely endorsement of credit clients. This is done by issuing a “Letter of Support” to Lidet - or members cooperatives - certifying that the prospective client operates in their area and that their loan requirements are assessed to be relevant and genuine.

Agricultural Development Assistants (DAs). The agricultural DA officers mainly aim to provide agricultural extension support to smallholder farmers and ensure the application and practice of good agronomic practices (GAP). At the peasant association level they are also responsible to issue the Letter of Support to Lidet Union/members’ cooperatives. They verify and certify that prospective clients’ business proposals are feasible and justified with respect to the loan size requested.

ICCO Terrafina Microfinance. ICCO Terrafina Microfinance aims to contribute to rural development and poverty alleviation through improved access to microfinance and the facilitation of expanded rural outreach by sustainable microfinance providers for rural producers and entrepreneurs in selected African countries. It was founded in January 2005 as a joint microfinance programme of ICCO, Oikocredit International and Rabobank Foundation. ICCO Terrafina Microfinance is active in supporting financial Unions and SACCOs in Ethiopia since 2007, mostly in Oromia and in southern nations. ICCO Terrafina Microfinance believes in the importance of having a diversified microfinance sector, to reduce risk and promote a multitude of best practices, adapted to the local situation and needs. Thus support has been given for institution-based MFIs and member-based financial institutions. The Rabobank Foundation consortium partner is especially interested in cooperatives, and is investigating possibilities to provide a guarantee for a loan of CBE to Lidet.

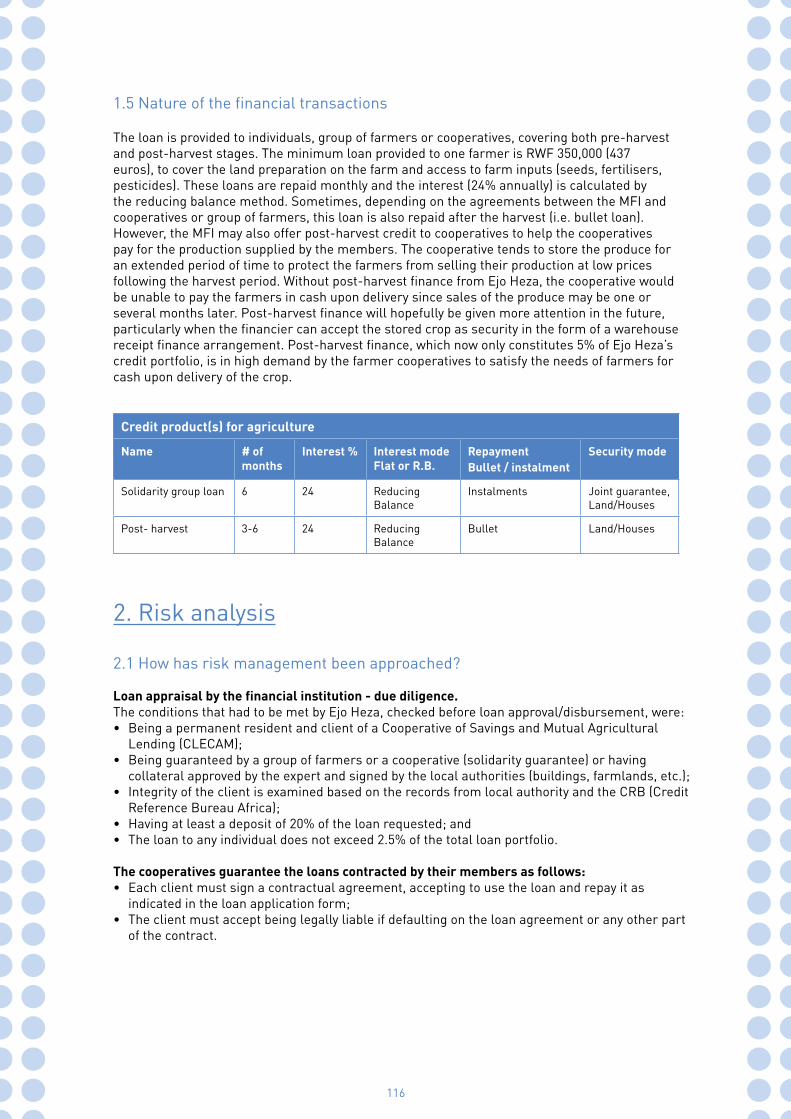

1.5 Nature of the financial transactions

Lidet Union is mainly serving as a secondary cooperative for more than 111 primary cooperatives, included as a membership umbrella. Despite these secondary cooperative activities, the Union also recently started to provide loans to VSLAs and insurance service to individual members.

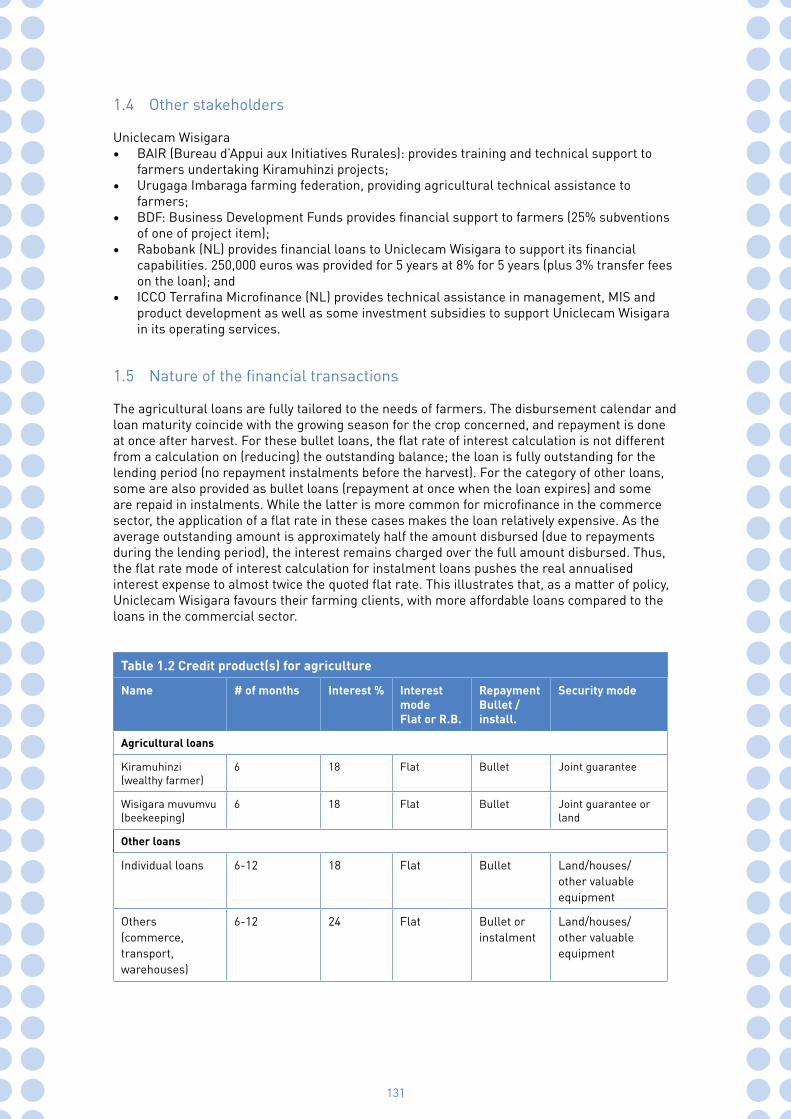

Table 1.2: Credit product(s) for agriculture

Name # of months

Interest % Interest mode Flat or R.B.

Repayment Bullet / instalment

Security mode

Member cooperative loan2

- 12% Dealing Bullet Storage, crop and collateral

VSLA - 11% Dealing Bullet Group-based

AMLD/GRD project 36 12% Dealing Bullet Land & p.guar

2 This loan is provided for member primary cooperatives, SACCOs and Multi-Purpose Unions (MPUs).

9

For member cooperatives, Unions or other producer groups, credit is approved based on the CAM-tool. The interest rate for this loan is 12% interest per annum with a bullet repayment. The purpose of the loan is dependent on the nature and activities of the cooperatives, which can differ greatly, especially in the case of MPCs which form the second largest credit-receiving category. They account for 34.2% of all outstanding membership of the Unions. Most MPCs are de-facto producer marketing cooperatives of grain staple food, mostly teff and maize. They are mainly active in buying the grain from the farmers for storage, after harvest. The loan therefore aims to have working capital and to buy the produce from their member smallholder farmers at the harvest time (i.e. post-harvest credit).

For village savings and loan associations loan is given based on a due diligence process. This loan has been provided on an 11% interest rate with a bullet repayment scheme. The loan is secured by a group security mechanism. Lidet is also administering loans provided by the AMLD/GRD project. This project is based on ETB 14 million capital, contributed by both AMLD/GRD and Lidet, where they contribute equal shares (50% / 50%). For this loan Lidet workers are directly administering the credit appraisal, disbursement and collection process. The loan is meant for animal fattening, where borrowers from the highlands invest in goat farming and farmers in the lowlands invest in sheep. The annual interest rate for this loan is 12%. The loan is given for three years with a bullet repayment and flexible interest rate charges on the amount outstanding. SACCOs are also among the primary cooperatives that take loans from the Union, with the purpose to satisfy credit demand of their members.

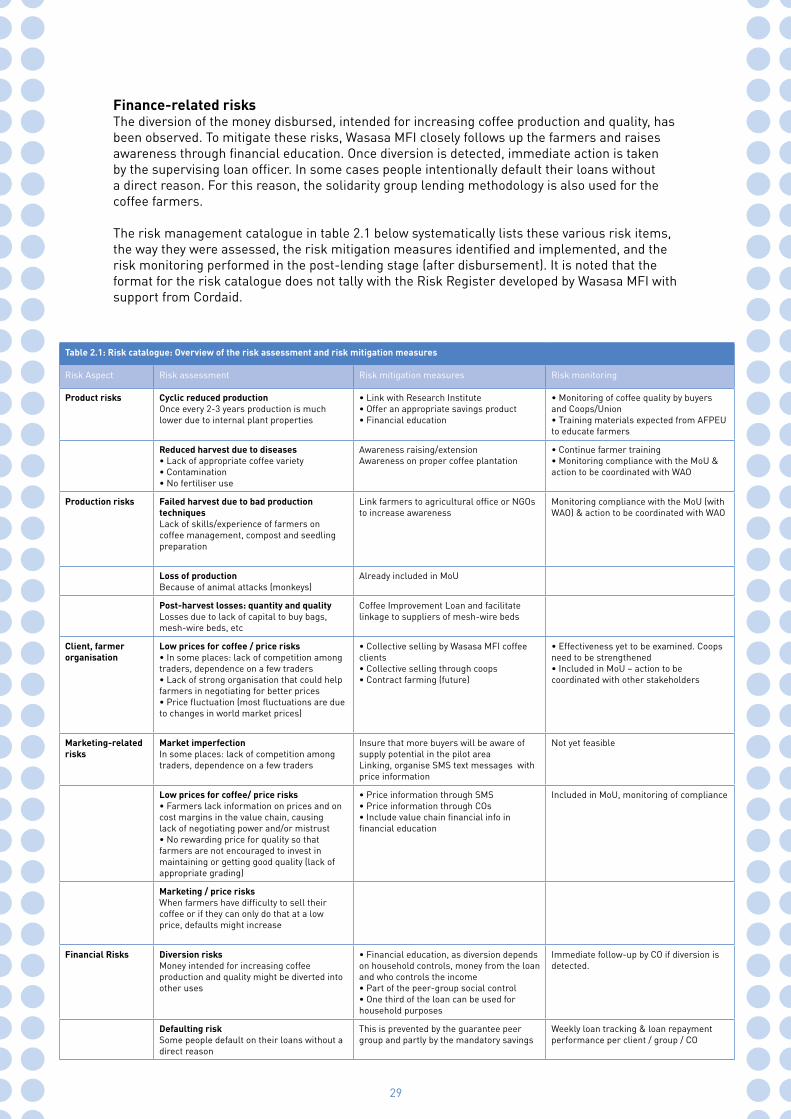

2. Risk analysis

2.1 How has risk management been approached?

Loan appraisal by the financial institution (due diligence) For each of the financial products of Lidet, a set of specific criteria is to be used in the due diligence process. Different financial products were developed for member primary cooperatives, Village Savings and Loan Associations (VSLAs) and individual AMLD/GRD project loans. The criteria and steps in the due diligence processes of each of the products are listed below.

Cooperatives and UnionsUnder this loan product only member cooperatives are eligible for loans from Lidet. The amount of credit to be granted to this member primary cooperative is based on (a) the amount of savings (mandatory and voluntary savings held at the Union); (b) storage; (c) the fixed asset ownership; (d) equivalent primary cooperative guarantee; (e) repayment history; and (f) the leadership quality of the cooperative. Based on these criteria there is a possibility to grant 25% or 35% or even 100% loan beyond the collateral requirements of the member cooperative. A remarkable change in due diligence after introduction of the Cooperative Credit Assessment Matrix (CAM) is that there is a possibility to grant loans beyond the physical collaterals that the prospective cooperative borrowers have.

Individual loans AMELD/GRD The AMELD project promoters can nominate smallholder farmers who need financial assistance under the project. In principle the nominated borrower should have fixed asset collateral such as land, be known in the village for his/her personal integrity and credit repayment history, have a permanent residence in the area of the peasant association and be able to co-sign the loan contract with his spouse. The promoters will also assist the farmers to develop a business proposal, to be submitted for the loan. The next step is confirmation and recommendation from the peasant association chairman and the agricultural extension officer, also called Development Assistant (DA). The peasant association chairman will confirm the permanent residence of the prospective borrower while the Agricultural Development officer of the peasant association will check the business proposal and will confirm and recommend it for financing

10

After all these processes and steps, Lidet will approach the prospective borrower and provide pre-loan disbursement, training and education. The training aims to create better awareness of the prospective borrower about the financial product, the terms and conditions and loan repayment discipline. Then the loan will be sanctioned and disbursed to the borrower in cash. Within 15 days’ time the borrower is expected to start the farm investments which will be checked by Lidet credit field officers as a follow-up. The borrower will be forced to repay the loan as soon as possible in case he/she did not comply with the business proposal or divert the loan to unplanned purposes.

2.2 Risk management by the stakeholders

In the design and development of the Union finance products, the lead actors have jointly assessed the risks for farmers and the primary cooperatives, and identified means to mitigate these risks. For the purpose of the case study, a distinction is made between the six crucial aspects of smallholder production, i.e. risks related to:• The specific crop: i.e. coffee;• The farming system and farm production;• The strength of the farmer organisation / Producer Organisation (PO);• The market for malt barley and food crops;• The viability of the farming system promoted; and• The financing of farmers. These risks and the way they were mitigated and managed have been tabulated in a risk catalogue (see table 2.1) and are briefly summarised below.

Product-related risksIn the Lidet Union area the main crops are teff, barley and maize. At the grassroots level, individual member farmers are exposed to the risk of having a lack of proper seed and problems with timely delivery of appropriate seeds. For the quality of the produce, the type of seeding material is essential. Poor quality seed, even if it is the right variety, may have poor germination performance, thus leading to lower yields. In order to mitigate these risks, the Union has been financing certified seedling enterprises and linking the farmers with these enterprises for easy access to seed. With respect to the individual loan given to the farmers for animal fattening, the risk of animal diseases is the main risk exposed. As a mitigation measure, close follow-up by agricultural extension offices was devised, even though it is still limited in coverage.

Production-related risksThe yield per acre for the participating farmers is still relatively low, as predominantly traditional farming systems are practiced. Yield improvement depends critically upon the availability of qualified extension officers and agronomists, methods for farmers’ education and exposure and incentives for increased production volumes. The production risk for the individual farmer refers to decisions to minimise the risk of crop failure and to maximise gross margins earned. Guidance on these issues critically depends upon the staff of the cooperatives to which the farmer belongs. A low level of financial education, weak organisational structure and human resources at both the Union and the primary cooperative levels are constraints to be addressed. With the help of ICCO Terrafina Microfinance, trainings, education, Union monitoring and a follow-up committee have been provided to the Union managers, accountants and cashers. Regional, zonal and district level cooperative agency staff were also involved in the training. The training and capacity building given is limited still and needs a continuous support at the different levels of Union operations.

Farmers’- organisation-related risksThe main risks involved at the farmers’ level are the low level of awareness about the financial services provided and about proper agricultural practices. At the cooperative and Union level there is a lack of skilled manpower at the right positions. As a mitigation measure insurance was introduced by the Union to individual members who had a loan from the cooperatives. About 828 insurance members voluntarily joined the insurance service. Further training and education about the loan were also given at the pre-disbursement and post-disbursement of loans, including application processes, steps, requirements and the details. Absence of legal experts at the Union level remains an unsolved problem.

11

Marketing-related risksThe main risk with respect to market risks under this value chain finance scheme is the lack of a good market linkage between the farmers and the POs, and the final market. In order to mitigate this, the Union tried to link the farmers and their producers’ group with the other member producers’ groups through: a) forwarding contracts; b) linking the farmers and POs to a better market such as university for animal fattening projects with respect to the AMLD/GRD project and Malt Barley Factory for malt barley producers and their respective Multi-Purpose Cooperatives (MPCs). Another resolution was to provide working capital loan to MPCs in order to facilitate them to buy and store farmers’ produce and in turn enable them to sell it at the right time. Despite all this market linking and capacity building mitigation measures, the efforts were not well organised and the coverage is very limited.

Finance-related risksThe main financial risks concern late repayment and default at both the cooperative and the final individual members’ level. To mitigate this, cooperatives were assessed with a proper due diligence process which required a proper collateral and related guarantees. Individual members were also properly assessed, trained and checked by the credit field officers. Although in a limited way, a report and audit has been conducted in order to tackle possible fraud risk at the cooperative and Union level. Field officers of the Union are mostly in the field either for proper follow-up, screening or educating the individual clients at the village level. As a result the repayment rate at the Union and cooperative level is very successful as they have a 97% repayment rate. For the risk of default as a result of death of the borrower, the Union introduced insurance and minimised the risk.

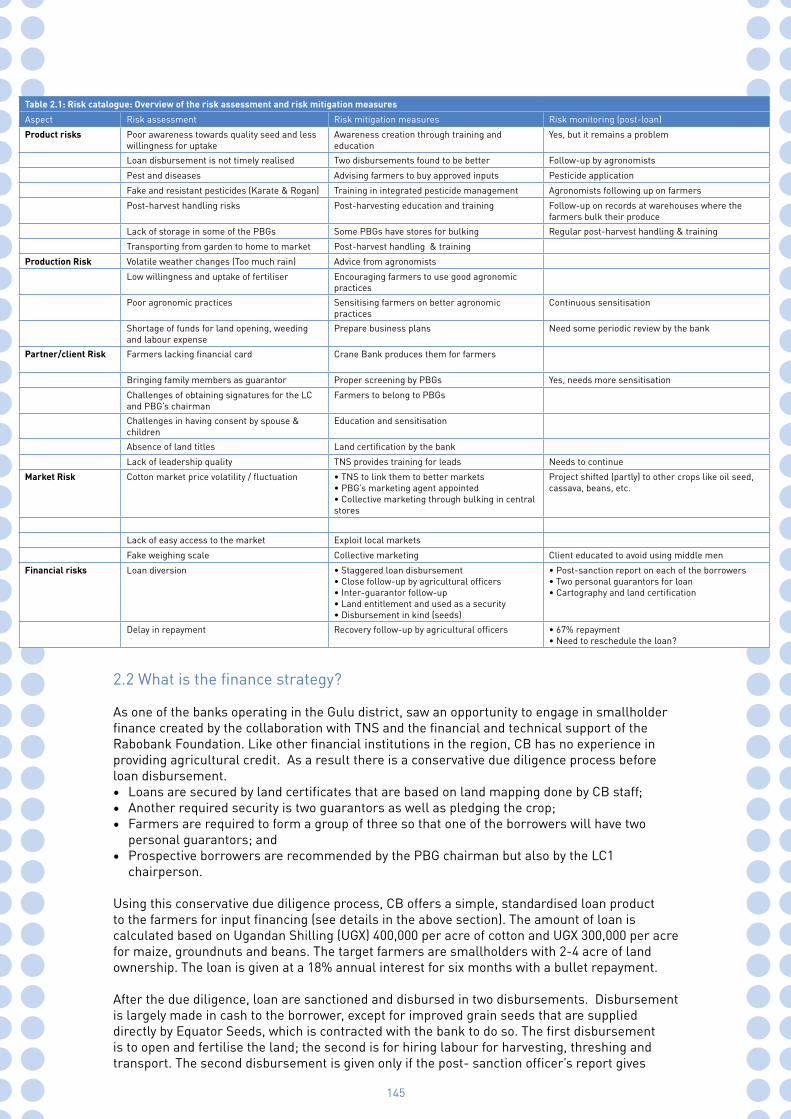

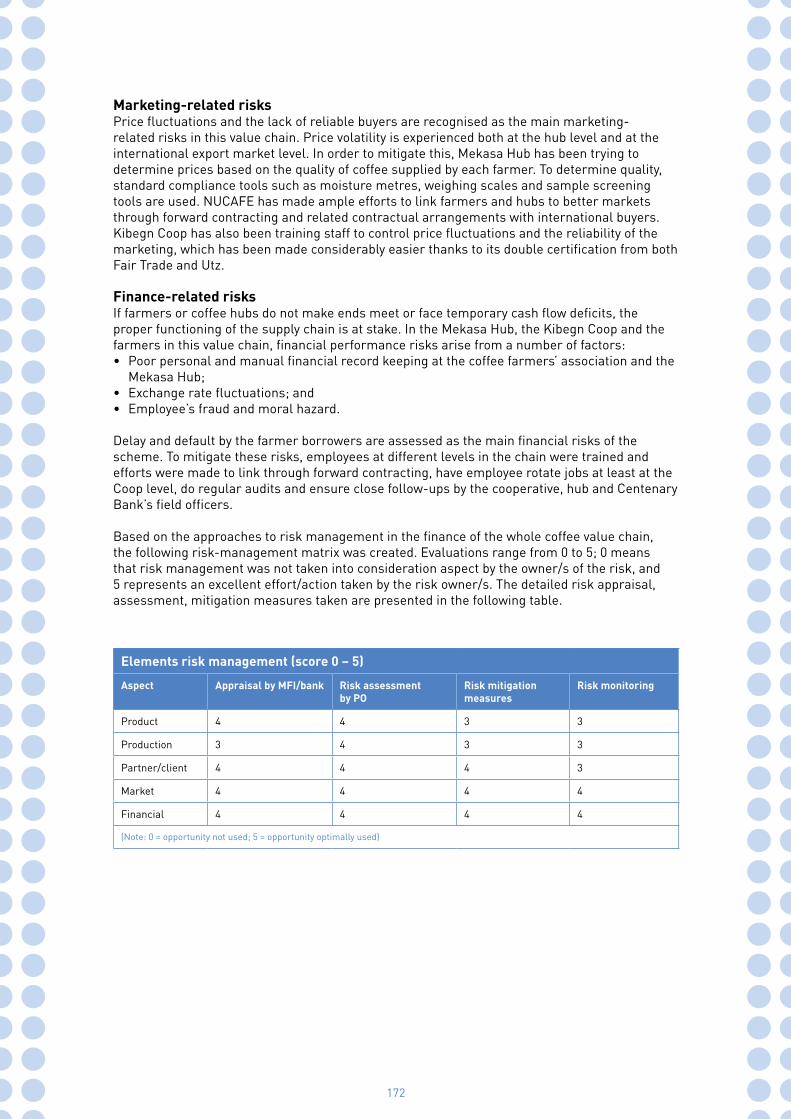

Table 2.1: Overview of main risk management items

Aspect Risk assessment the risk owner Risk mitigation measures Risk monitoring

Product risks Lack of proper seed Linking and financing seed enterprise Still there is shortage and lack of reliability

Diseases for animal Close follow-up by agricultural extension offices Limited service with limited extension offices

Poor harvesting season for crop farmers • Diversification of crops • Diversification of the type of cooperatives

• Yes, but need much more to do • There are 8 different cooperative categories

Lack of good agronomic practice Close follow-up with agri-extension officers Limited

Production Risk Members have low level of financial education Training and education Done on a limited basis

Weak organisational structure and human resources of members

Client/relationship risk Fear of premature death of borrowers Insurance So far 802 of these members are insured

Farmers have low level of awareness Training and education about the loan, application processes, steps, requirements and the details

Done. Still need much more to build the capacity of these members

Absence of legal expert in organisation

Absence of skilled human power Keeping the employee at most benefit Benefits were adjusted based on government scale

Wrong perception of borrowers towards loan Education, training, follow-up Working well

Marketing Risk Lack of good market linkage between the farmers and the POs and final market

• Forward contracts • Linking the farmers and POs to a better market such as university and Malt Barley Factory • For animal fattening university • For barley farmers Malt Barley Factory • Providing working capital loan to multi-purpose cooperatives (MPCs) to buy and store farmers’ produce

• Not yet organised• Yes, but at a limited scale

• Done, to be strengthened • Done and is promising business linkage • Is doing great based on CAM criteria

Price fluctuations Contract farming Not yet well organised

Financial risk Fraud employees Periodic review, report and audit Yearly Audit report

Early repayment • Repayment collection based on the actual interest on the repayment date • Training and education

Good and flexible enough

Lack of internal Auditor Audit is on yearly basis and done by the Coop offices. Standard is very low

Diversion of loan Close follow-up by the credit officers Immediate repayment for non-compliance

Default / moral hazard by members • Close follow-up by the credit officers• Primary cooperatives have various committees

20 days in office and good repayment progress (I.e100% repayment rate)

Risk of default by members Collaterals & equivalent cooperative as guarantor and loan based on CAM

Working well

Risk of death of the borrower Insurance coverage against death 802 insured so far

Pre-loan moral hazard (inflating demand by cooperatives)

• CAM • And due diligence process

100% repayment rate

Pre-loan moral hazard (inflating demand by individuals farmers)

Credit appraisal based on business plan recommended by PA chair and DA offices

Delay in repayment by individual borrowers • Proper examination of reasons • Close follow-up credit filed officers, primary coops credit repayment and other committees

Extension with a proof of reasonable reason

12

2.3 What is the finance strategy?

I. Financial appraisal Multiple classified criteria were applied for individual loans and loans given to the member cooperatives and VSLA. A. Individual loan AMELD/GRD

• Preparing business plan – promoters;• Having a fixed collateral asset;• Known in the village for his/ her good personality and good credit history;• Co-signing with his/her spouse; • Permanently and legally resident, approved by PA chair;• DA approves feasibility of the business plans;• Pre-disbursement education for both borrower and spouse;• Follow-up business plan implementations in 15 days; and• If not implemented the loan will be forced to be repaid.

B. For cooperatives and Unions due diligence • Membership and their mandatory and voluntary savings amount;• Taking their fixed asset as collateral;• Equivalent cooperative guarantee;• Prior credit repayment history; and• Cooperative Assessment Matrix.

Based on the CAM, a decision will be made on 25%, 35% and 100% loan. Key elements to consider while giving loans to the MPCs are the overall CAM result, credit worthiness of the borrower, like character in individual, economic evaluation/supply and demand and repayment capacity (cash flow, asset and capital position).

II. Finance Needs AssessmentBefore the application of the CAM, only tangible collaterals were considered in order to assess the demand of loan and then grant loans to cooperatives. ICCO Terrafina Microfinance provides the training about how to assess loan based on CAM. Concepts covered under the Common Capacity Building (CCB) trainings included the notion of lender and borrower and loan processing steps such as the how of loan application, appraisal, approval, signing of loan agreement and loan disbursement.

Key elements to consider while giving loans to the MPCs are the overall CAM result, credit worthiness of the borrower, like character in individual, economic evaluation/supply and demand and repayment capacity (Cash flow, asset and capital position). Credit history/character assessment, repayment capacity, balance sheet information, collateral issues, and risk management are also issues to be considered in the CAM. The following table shows the criteria and yardsticks to be considered in the CAM and appraisal norms.

S/N

CAM Results

Loan Delivery Conditions

30% Clean Loan

50% Clean Loan

Savings and Equity

Fixed Assets (67%)

Peer Guarantee

Increase Interest Rate

Reduce Loan Amount

Reject the loan

1 < 50%

2 51-65%

3 66-85%

4 > 85%

Source: SACCO Unions Capacity Building Programme in Amhara Region November 2013

Rem

arks

13

III. Financial products / Instrument The financial products are loans to member primary cooperatives, VSLAs and individual AMLD/GRD project loans. For loans to the member cooperatives, the loan is based on the CAM and there is a bullet repayment.The purpose of the loan is dependent on the nature and activities of the cooperatives. Most MPCs are de facto producer marketing cooperatives of grain staple food, mostly teff and maize. MPCs buy, after harvest, the grain from the farmers for storage at the market-rate of that moment and become owner and responsible for marketing. The loan is therefore amid to have a working capital to buy the produces from their member smallholder farmers at the harvest time.

2.4 What capacity for agri-finance has Lidet Union installed to perform these tasks?

The Union has three main leadership teams. These include a general assembly, a board of directors and monitoring, and a follow-up committee. The general assembly is composed of three appointed representatives from each of the member cooperatives/POs where at least one of them must be a female representative. The board of directors is composed of appointed leaders. Leaders are appointed based on the criteria such as a person who is known for his/her good personality and confirmed by the general assembly, for his/her admirable experience and educational background and who has no other responsibilities. Moreover, the appointee should be legally capable to be voted and should have a very good prior loan repayment history.

Currently there are about 26 permanent employees scattered over the six breaches who are responsible for 140 peasant associations. At the head quarter level everyone is committed to these financial transactions. There are monthly, quarterly, and yearly audit reports from each of the branches to the concerned regional finance offices. There are four specialised credit officers at the main branch office who are active in the field, 20 days in a month time. Moreover, the Zonal Agricultural Offices and the concerned District Agricultural Offices are closely supporting, monitoring and evaluating progresses. This clearly shows that the human resources back-up that Lidet possessed and the follow-up and monitoring activities are held accountable, with a clear assignment of operations. To conclude this section, it can be said that the Union has still not enough risk assessment capacity and systems in place. This therefore calls for a lot of support at both the Union level, at the member cooperatives’ organisational structure and from human resource capacity.

2.5 What connections were entertained by Lidet Union with other stakeholders in the sector? Who was the lead actor in orchestrating the chain?

This value chain is mostly orchestrated by the Union where they provide the loan to the member MPC, Savings and Credit Co-operatives (SACCOs), VSLAs and other marketing-related cooperatives and Unions. The main activity is done by the Union acting as a secondary cooperative where they provide loans to the member cooperatives, POs and other marketing-related cooperatives.

14

3. What makes it tick?

3.1 What are the success factors in this case? What risk mitigation measures proved effective?

Based on a microscore assessment done to all the Unions of the Amhara region, Lidet has shown an increased progress. In the first assessment report it scores 2.28 which was the lowest of all the Unions’ scores. Since then Lidet has been improving its operations and able to stand first at national level for its performance. It became highly profitable and opened branches in six districts and 140 peasant associations. It recently also started providing microinsurance products to its members. Taking into account the performances and awards in the second microscore assessment, Lidet has shown considerable progress and scored 7 out of 10, which was the biggest microscore assessment result of all Unions in the Amhara region.

Lidet is providing timely credit provision with clear requirements and procedures to be used commonly and transparently by all member cooperatives. It also provides flexible and need- based loan at a lower interest (12% Vs 18%). Trainings were given to members, member employees and leaders, and panel discussions with the concerned stakeholders were done in close collaboration with Lidet. The Union also created market linkage to farmers, Producer Organisations (POs) and consumers by providing a variety of finance products at different stages in the value chain In order to have enough funds on hand and satisfy the credit demand of the members, various bankable business proposals were developed and submitted to different lending institutions. Following the human resources rules of the Union, the employee’s interest has been addressed as much as possible.

3.2 What are the (remaining) weaknesses/threats/risks?

Shortage of the loan amount given for cooperative and Union members. It did not meet the members’ need for finance so far. There is a huge gap between the demand for and supply of loanable funds, although the Union is striving to satisfy the demand;• Member cooperatives are still not well aware of the organisation and management of

cooperatives and their operations. This needs much more capacity building in training and education and recruiting better human resources officers in the key positions;

• Lack of support from the regional and district office administration for both Lidet cooperative cash savings and credit Union and the member cooperatives and Unions. Other stakeholders’ support to the Union and its member cooperatives were very limited in various aspects; and

• Lack of well skilled human resources employees at the Union level.

3.3 Do stakeholders have a view on how to better deal with these remaining risks in the future?

• The demand for loans by member cooperative is much more than the current capacity of the Union. The Union has been (and will be) developing a bankable business plan and approach financial institutions and lenders. By doing so the Union is striving to satisfy the demand for loanable funds by the member cooperatives, Unions and enterprises;

• Member cooperatives and their respective members (mostly farmers) have a very limited level of financial education. They are insufficiently aware of the bank’s basic products, procedures and requirements. Therefore, much more effort is required for creating better awareness through trainings, education, panel and focus group discussions with farmers, farmers’ organisations and other stakeholders concerned in this financial value chain. In line with this, Lidet has been doing a good job in providing various trainings, in preparing panel discussions for members, members’ leadership staffs and other stakeholders involved in this financial service in the region where Lidet is functionally operating;

• Furthermore, the Union has been working on women training and support, in collaboration with the peasant association, district women affairs and other official bureaus;

15

• In line with the organisation’s general assembly and human resource policy, the Union is striving to secure benefits of the employees at most; and

• ICCO Terrafina Mirofinance has organised forums to discuss these challenges with the board and management of the Union and the promotion office. Attention was given to some of the points raised, like putting aside provisions for unpaid loans, diversifying guarantee systems, like introducing Solidarity groups etc. The cooperative promotion office has positively accepted the suggestion and passed directives

3.4 How can linkage between financier (Lidet Union) and Producer Organisation (PO) be strengthened?

There is a huge demand for credit by the member cooperative Unions. Despite this high demand, the supply by Lidet cooperatives’ cash savings and credit Union is way less than the demand. It therefore requires a financial source beyond the Union. One of the alternatives for the Union is to have some donations and development partner collaborations to design a bankable business proposal that may enable them to have a better credit for the Union level, which will in return be disbursed to primary cooperatives and Unions accordingly. The Linkage with Rabobank bank via ICCO Terrafina Microfinance is essential for guarantying the loan demand of Lidet.

3.5 What are the lessons learned for the industry?

• The Cooperative Credit Assessment Matrix (CAM) tool is supposed to contribute in a responsible way to increased Multi-Purpose Cooperative (MPC) loan size, beyond existing collateral possibilities. Loan demand from MPCs to Unions is usually much higher than the total value of their collateral. An MPC’s loan demand is based on estimated grain supply from members at harvest time, plus their storage and marketing facility;

• Microinsurance service can strengthen the trust between borrower and lender and create confidence to the borrower in case of premature death. It is also possible to launch the culture of having insurance even in remote rural families;

• Cooperatives can have more collective power through membership in the secondary cooperatives. This enables them to help each other in guarantee ship and share experiences from one another; and

• They need to come up with product development like organising groups within the Savings and Credit Co-operatives (SACCOs) to solve guarantee problems and at the same time mobilise more resources etc. It is a project of ICCO Terrafina Microfinance.

SourcesInterviews:1. Mr Abereham chanie Accountant (was also in charge of the Manager)2. Mr Shemeles Credit Officer 3. Mss Serkalem Zewdu Credit Officer4. Mr Salamlak Alebie Credit Officer5. Mr Abebaw Abebu Member(Tehay SACCO) General Manager 6. Miss Meseret Members member (individual client)7. Mr Belete Members member (individual client)8. Ato Dagnew ICCO Terrafina Microfinance Local Consultant

Documents: 1. ICCO Terrafina Microfinance & F&SE, 2013. SACCO Unions Capacity Building Program in

Amhara Region. Training Report on Assessment Model of Marketing Cooperatives, Addis Ababa.

2. Lidet Union 2013/14 fiscal year 4th quarterly financial repot. June 2014, Nefas Mewecha3. An Amharic version Power point document prepared by Lidet Union to federal agency for

documentary film preparation, August 16 2014. Nefas Mewecha.4. Micro Score Assessment of the six SACCOs Unions operating in Amhara, second round

assessment report. (NpM Study case documentation).5. CAM Tools and its ten dimensions ((NpM Study case documentation).

16

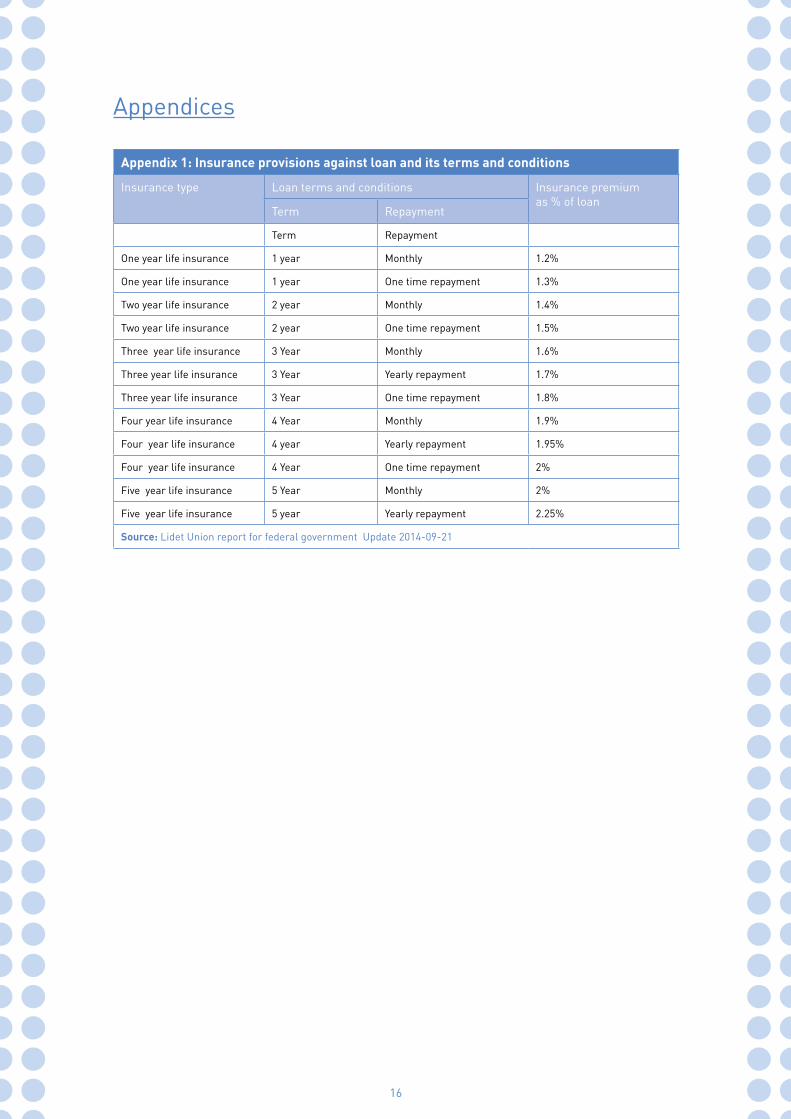

Appendices

Appendix 1: Insurance provisions against loan and its terms and conditions

Insurance type Loan terms and conditions Insurance premiumas % of loan

Term Repayment

Term Repayment

One year life insurance 1 year Monthly 1.2%

One year life insurance 1 year One time repayment 1.3%

Two year life insurance 2 year Monthly 1.4%

Two year life insurance 2 year One time repayment 1.5%

Three year life insurance 3 Year Monthly 1.6%

Three year life insurance 3 Year Yearly repayment 1.7%

Three year life insurance 3 Year One time repayment 1.8%

Four year life insurance 4 Year Monthly 1.9%

Four year life insurance 4 year Yearly repayment 1.95%

Four year life insurance 4 Year One time repayment 2%

Five year life insurance 5 Year Monthly 2%

Five year life insurance 5 year Yearly repayment 2.25%

Source: Lidet Union report for federal government Update 2014-09-21

17

Appendix 2: Microscore Assessment of the six (Savings and Credit Co-operatives (SACCOs) Unions operating in Amhara

Name of the Unions

1st assessment result

2nd assessment result

Remarks

Jabi 6.82 4.63 It failed to secure REUFIP loan and is not attentively using peach tree. It has lost rank in the completion between Unions at federal level. There seems to be a problem in its financial performance. Hence, the assessment result has lowered it to Developing category for the stated reasons.

Menkorer 2.35 3.63 It is still in the same category. It is improving a lot but its loan portfolio is still marginal, staff turnover is very high and has not won most marketing cooperatives to take loan from the Union. It has improved in outreach but some of the members are far from the centre.

Abaye Ber 6.58 5.35 Aaye Ber failed to win Rural Financial Intermediation Programme (RUFIP) loan and has lost money in the bank that should have been used as loan. The problems with Abay Ber are the increased depreciation that came from the new building. In terms of reporting and working with Marketing cooperatives it is good. Therefore it is reasonable to lower it to the emerging category.

Goh 2.89 3.89 The points for the first assessment were lower than what it deserves. The impact of the depreciation that comes from the heavy building investment has lowered its profitability. It has good relations with the marketing cooperatives. It has improved from emerging to developing category.

Ledte 2.28 7.00 Stood first at national level for its performance. It has opened branches. It is highly profitable. It is winning a lot of stakeholders to work with. It has started microinsurance. It has won RUFIP loan twice.

Tana 3.47 5.47 Tana is newly emerging and a promising one. It has won REUFIP loan and its performance is improving. The performance is encouraging in terms of profitability. The GM is new but he is catching up and the Union is fast growing.

Source: Microscore Assessment of the six SACCOs Unions operating in the Amhara region

18

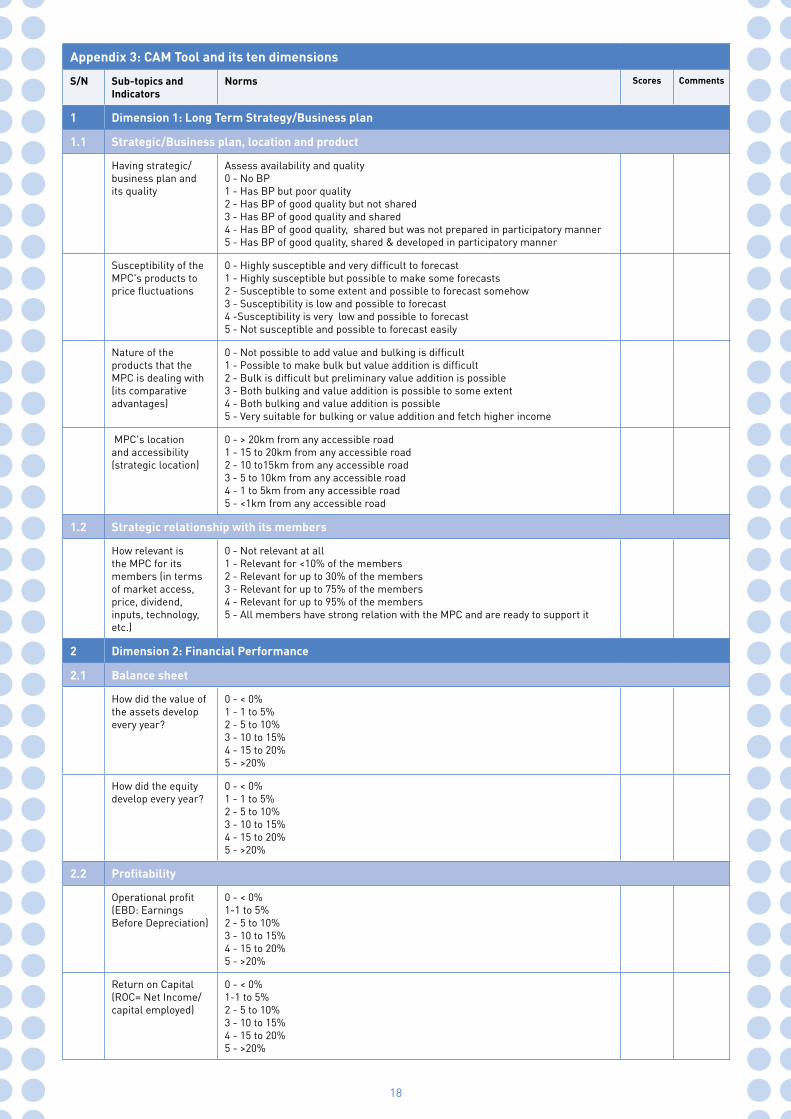

Appendix 3: CAM Tool and its ten dimensions

S/N Sub-topics and Indicators

Norms Scores Comments

1 Dimension 1: Long Term Strategy/Business plan

1.1 Strategic/Business plan, location and product

Having strategic/business plan and its quality

Assess availability and quality0 - No BP1 - Has BP but poor quality2 - Has BP of good quality but not shared3 - Has BP of good quality and shared4 - Has BP of good quality, shared but was not prepared in participatory manner5 - Has BP of good quality, shared & developed in participatory manner

Susceptibility of the MPC's products to price fluctuations

0 - Highly susceptible and very difficult to forecast 1 - Highly susceptible but possible to make some forecasts2 - Susceptible to some extent and possible to forecast somehow3 - Susceptibility is low and possible to forecast 4 -Susceptibility is very low and possible to forecast 5 - Not susceptible and possible to forecast easily

Nature of the products that the MPC is dealing with (its comparative advantages)

0 - Not possible to add value and bulking is difficult1 - Possible to make bulk but value addition is difficult 2 - Bulk is difficult but preliminary value addition is possible 3 - Both bulking and value addition is possible to some extent4 - Both bulking and value addition is possible 5 - Very suitable for bulking or value addition and fetch higher income

MPC's location and accessibility (strategic location)

0 - > 20km from any accessible road1 - 15 to 20km from any accessible road2 - 10 to15km from any accessible road3 - 5 to 10km from any accessible road4 - 1 to 5km from any accessible road5 - <1km from any accessible road

1.2 Strategic relationship with its members

How relevant is the MPC for its members (in terms of market access, price, dividend, inputs, technology, etc.)

0 - Not relevant at all1 - Relevant for <10% of the members2 - Relevant for up to 30% of the members3 - Relevant for up to 75% of the members4 - Relevant for up to 95% of the members5 - All members have strong relation with the MPC and are ready to support it

2 Dimension 2: Financial Performance

2.1 Balance sheet

How did the value of the assets develop every year?

0 - < 0% 1 - 1 to 5% 2 - 5 to 10%3 - 10 to 15%4 - 15 to 20% 5 - >20%

How did the equity develop every year?

0 - < 0% 1 - 1 to 5% 2 - 5 to 10%3 - 10 to 15%4 - 15 to 20% 5 - >20%

2.2 Profitability

Operational profit (EBD: Earnings Before Depreciation)

0 - < 0% 1-1 to 5% 2 - 5 to 10%3 - 10 to 15%4 - 15 to 20% 5 - >20%

Return on Capital (ROC= Net Income/ capital employed)

0 - < 0% 1-1 to 5% 2 - 5 to 10%3 - 10 to 15%4 - 15 to 20% 5 - >20%

19

2.3 Debt Leverage and Management

Loan truck record of the MPC over the last three years with the SACCO Union?

0 - Zero experience of taking loan 1 - Took loan one time and repayment is >50%2 - Took loan twice and repayment is 50-75%3 - Took loan three times and repayment is 75-85%4 - Took loan four times and repayment is 85-95%5 - Took loan more than four times and repayment is 100%

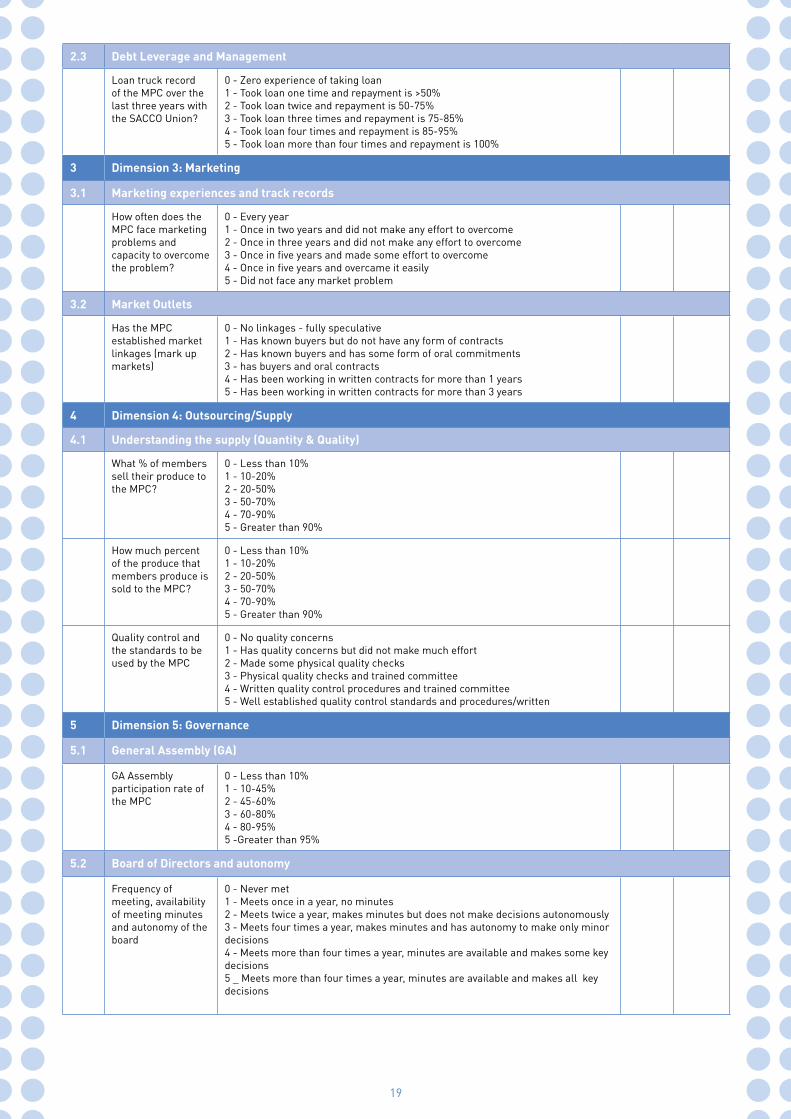

3 Dimension 3: Marketing

3.1 Marketing experiences and track records

How often does the MPC face marketing problems and capacity to overcome the problem?

0 - Every year1 - Once in two years and did not make any effort to overcome2 - Once in three years and did not make any effort to overcome3 - Once in five years and made some effort to overcome4 - Once in five years and overcame it easily5 - Did not face any market problem

3.2 Market Outlets

Has the MPC established market linkages (mark up markets)

0 - No linkages - fully speculative1 - Has known buyers but do not have any form of contracts2 - Has known buyers and has some form of oral commitments 3 - has buyers and oral contracts 4 - Has been working in written contracts for more than 1 years 5 - Has been working in written contracts for more than 3 years

4 Dimension 4: Outsourcing/Supply

4.1 Understanding the supply (Quantity & Quality)

What % of members sell their produce to the MPC?

0 - Less than 10%1 - 10-20%2 - 20-50%3 - 50-70%4 - 70-90%5 - Greater than 90%

How much percent of the produce that members produce is sold to the MPC?

0 - Less than 10%1 - 10-20%2 - 20-50%3 - 50-70%4 - 70-90%5 - Greater than 90%

Quality control and the standards to be used by the MPC

0 - No quality concerns1 - Has quality concerns but did not make much effort2 - Made some physical quality checks 3 - Physical quality checks and trained committee4 - Written quality control procedures and trained committee5 - Well established quality control standards and procedures/written

5 Dimension 5: Governance

5.1 General Assembly (GA)

GA Assembly participation rate of the MPC

0 - Less than 10%1 - 10-45%2 - 45-60%3 - 60-80%4 - 80-95%5 -Greater than 95%

5.2 Board of Directors and autonomy

Frequency of meeting, availability of meeting minutes and autonomy of the board

0 - Never met1 - Meets once in a year, no minutes2 - Meets twice a year, makes minutes but does not make decisions autonomously 3 - Meets four times a year, makes minutes and has autonomy to make only minor decisions4 - Meets more than four times a year, minutes are available and makes some key decisions 5 _ Meets more than four times a year, minutes are available and makes all key decisions

20

6 Dimension 6: Management

6.1 General Manager (GM)

Adequate delegation and responsibility of the GM

0 - Does not make any decision without consulting the board1 - Can make few decisions by consulting the board2 - Can make some operational decisions without consulting board3 - Roles are defined but cannot decide without board4 - Roles are defined but needs to inform the board5 - Roles are clearly defined and can make all decisions within that

6.2 Staffing

Sufficient and qualified staffing (Basic = GM, Accountant, Cashier; Adequate = purchaser, store keeper, security guard)

0 - Do not have any staff1 - Has only manager who is not qualified2 - Has only qualified manager3 -Has basic staff 4 - Has basic and adequate staff with some limitation on qualification5 - Has basic and adequate staff who are qualified and experienced

6.3 Incentives and benefits

The level of salaries and incentives of staff to reduce turn over

0 - Does not bother about this1 - Gives only basic salary2 - Salary revised and adjusted but not regularly3 -Salary revised and adjusted as per the labour market regularly4 - Performance evaluations made and provide basic benefits 5 - Performance evaluations made, sufficient benefits like training, bonus, credit etc.

7 Dimension 7: Administration

7.1 Bookkeeping

Availability of proper bookkeeping and financial reports (income statements, balance sheet, stock issues, etc.)

0 - Does not have any bookkeeping documents1 - Has some documents but financial reporting is not done at all2 - Has all the basic documents and reporting has been done but not regularly3 - Has all the basic documents and some financial reporting has been done regularly4 - Has all the documents and reporting has been done but has some quality limitations5 - Has all the documents and standard reporting has been done including the use of Peachtree

7.2 Auditing

Availability and quality of audits (remarks of auditor and audit qualifications)

0 - Audits never done1 - Audits done once in more than three years2 -Audits done once in more than one year3 - Audits done annually and receives strong negative comments of the auditor4 - Audits done annually and receives minor negative comments 5 - Audits done annually and receives positive comments

8 Dimension 8: Operations

8.1 Ownership, management and utilisation of assets

Ownership of assets (office, store, factory, car/trucks/motorbikes, shop, weighing machines, etc.

0 - Does not have any of these 1 - Has only few of them and the quality is very poor 2 - Has only essential ones like store and carrying capacity is small3 - Has most of them but not the required capacity and quality4 - Has most of them and the required capacity and quality5 - Has all of them and the required capacity and quality

Management and utilisation of these assets

0 - Does not have any of these assets1 - All of them are poorly managed 2 - Most of them are well managed 3 - All of them are well managed but poorly utilised 4 - All of them are well managed and utilised more than half 5 - All of them are well managed and fully utilised

21

9 Dimension 9: Enabling Environment

9.1 External Relationships and supports

Level of external relationship with enablers

0 - Does not have any external relation 1 - Relationship built by external push 2 - It builds relations but there are high interferences in its business 3 - It has built relations but there are some interferences in its business 4 - It has built relations but there are high interferences in its business 5 - It has built relations that are enabling

External support (all kinds of support) available to the MPC (NGOs, PLCs etc.)

0 - Do not have any support1 - Has one supports but with strict conditions/strings 2 - Has 2-3 supports but with some conditions/strings 3 - Has many supports without conditions/strings 4 - Has many supports but some of them hindered its growth5 - Has many supports which boosted its capacity

10 Dimension 10: Risk Assessment

10.1 Overall risk Assessment

Experiences of the MPC related to the overall risks over the last five years

0 - Risks are never discussed and managed1 - Risks are discussed by the management but never managed2 - Risks are discussed at GA level but never managed3 - Risks are discussed at GA level but only managed sometimes4 - Risks are discussed at GA level and managed most of the time 5 - Risks never happened but the MPC has the capacity and readiness to overcome

10.2 Price Risks

Experiences of the MPC related to price risks of the products it is dealing with over the last five years

0 - Happened every year 1 - Happened once in three years and the MPC was not aware2 - Happened once in five years and the MPC was not aware3 - Happened once in five year and the MPC was aware4 - Happened once in five year and the MPC was aware and mitigated 5 - Rarely happened (once in 20 years)

10.3 Production Risks

Any experience of crop failure over the last five years in the area

0 - Happened every year 1 - Happened once in three years and the MPC was not aware2 - Happened once in five years and the MPC was not aware3 - Happened once in five year and the MPC was aware4 - Happened once in five year and the MPC was aware and mitigated 5 - Rarely Happens

22

AbstractWasasa Microfinance Institution (MFI) participates in the Agricultural Finance Programme (AFPEU), which is funded by the EU and implemented by MicroSave-Cordaid. Starting from October 2012, the EU programme is working with MFIs in four countries to implement a project aiming to increase access to agricultural finance for farming households through product development. As a result of the support, Wasasa MFI has developed an inclusive financial scheme called the “Coffee Improvement Loan”. As Wasasa MFI had no previous experience in providing loans to smallholder coffee farmers, they had to start with a financial needs assessment, product development, and assessment of the risks involved in lending to smallholder coffee farmers. The programme is currently operating with 200 coffee farmers in the Chora district. The programme was supported by Cordaid. ICCO Terrafina Microfinance has also supported Wasasa MFI with guarantees for expansion of their portfolio, as well as with capacity building for MIS and product development in the malt barley value chain.

AcronymsACDI/VOCA Agricultural Cooperative Development International / Volunteers in Overseas Cooperative Assistance ACE Agricultural Cooperatives in EthiopiaACSI Amhara Credit And Savings InstitutionAFPEU Agricultural Finance Programme EuropeDA Development AssistantECX Ethiopian Commodity ExchangeETB Ethiopian BirrMFI Microfinance InstitutionMoU Memorandum Of UnderstandingOCFCU Oromia Coffee Farmers’ Cooperative UnionOSRA Oromo Self-Reliance AssociationPC Primary CooperativePO Producer OrganisationToT Training of TrainersVCD Value Chain DevelopmentWAO Woreda Agriculture OfficeWCPO Woreda Cooperatives Promotion Office

Case Study E2

Wasasa MFI

1. Main characteristics of the case

1.1 Farmers and their organisation

Chora Smallholder Coffee farmersChora is a district in the Luababora Zone of Oromia National Regional State. It is bordered on the south by Jimma Zone, on the west by Yayo, on the north by Dega and on the east by Bedele. The district has a population of 318,483 people in a predominantly rural setting (only 9,500 recorded urban households). With an area of 947 square kilometres, Chora has a population density of 125 inch/km2, which is greater than the zonal average of 72. The main economic activity of the district is agriculture.

“Coffee Value Chain Finance to Smallholder Farmers, Chora District, Ethiopia”

Producer Organisation (PO) /Coop Profile Data

Type of organisationNumber of membersMain crops Other crops

Smallholder farmers 200 farmers Coffee Khat, maize & teff

23

This includes crop farming and animal rearing. Crops grown include maize, teff, sorghum, wheat, khat, mangos, avocado and papaya. The most valued crop is coffee, followed by khat, then maize and teff. Coffee is spread over an area of over 50 square kilometres in which some 22,000 hectares of productive coffee can be found. This represents about 0.5% of the national coffee area. Some 14,500 households are involved in coffee production, giving an average of 1.5 hectare of coffee per family. This is well above the national average, yet the intensity of the production is below national average.

The Oromia Coffee Farmers’ Cooperative Union (OCFCU) Ethiopia’s Oromia Coffee Farmers’ Cooperative Union (OCFCU) aims to help small-scale coffee farmers taking advantage of the Fair Trade coffee market. The OCFCU was established in 1999 in order to help the 100,000 farmer families working in Oromia cooperatives to get through the difficult price crisis. The OCFCU comprises 34 cooperatives, cultivates 86,487 acres of land, has an average annual production of 16,507 tons and is known for its high quality coffee; all of which is heirloom, organic, and produced by smallholders. Only in its third year, the OCFCU is already starting to return 70 percent of its gross profits back to the Primary Cooperatives (PCs), in order to help cooperative members.

Part of the sales of the OCFCU’s coffee is going back to the communities to be used to build schools, which will help to address problems in the impoverished communities in an area where only about a quarter of the school-aged children attends school. Fair Trade coffee helps providing living wages to the farmers, as well as providing up to three times as much income as the average coffee producer. This income will help farmers provide for their families, increase their quality of life and allow them to continue working on their farms.

1.2 Wasasa Microfinance Institution (MFI)

Wasasa MFI S.C. was established in September 2000 by its mother NGO: the Oromo Self-Reliance Association (OSRA) to take over its microfinance activities, running since 1996. At that time it also acquired a Microfinance Business License from the National Bank of Ethiopia. Since then, the company has been working with poor communities (mainly the rural poor) by providing savings and credit services. It currently has 28 branches and 20 rural outlets operating in 34 Woreda (districts) of Oromia Regional State, with the ambition to expand every year. The Head Quarter is in Alemgena town, near to Addis Ababa. The mission of Wasasa MFI is to provide sustainable financial services to the active poor in order to employ capital for poverty alleviation.

Rural loans account for 84% of the total loan portfolio of Wasasa MFI. The large group loan product is the agricultural loan that Wasasa MFI provides through all of its branches. It accounts for a large proportion of the loan portfolio. Wasasa MFI has a mandatory savings product and several voluntary savings products, like group voluntary saving, time deposit, planned time deposit, and passbook savings account. A credit life insurance service is also incorporated in the group loans. In addition, in collaboration with other partners, Wasasa MFI developed specialised loan products for different target groups. These include dairy loans, malt-barley production financing, working capital loans for “Farmers Marketing Organisations”, micro-irrigation technology loans and others.

MFI profile data

Total # of active clientsPortfolio value (in euros)Number of branchesNumber of rural branches% of farming clients% of portfolio in agriculture

64056 Hh185.5 M Birr282084% Estimated

24

1.3 Nature of the programme

Wasasa MFI participates in the Agricultural Finance Programme funded by the EU (AFPEU) and implemented by MicroSave-Cordaid. Cordaid is one of the largest development aid organisations in the Netherlands and member of the Dutch Platform for Inclusive Finance (NpM). In this programme, it collaborates with MicroSave, a Kenyan organisation specialised in financial product development. Together they obtained funding from the EU to support 6 to 10 MFIs to develop financial products for farmers, to link these farmers to agricultural service providers and to elaborate on appropriate risk mitigating measures. Starting from October 2012, the programme aimed at working with MFIs in Kenya, Uganda, Ethiopia and Ghana. The goal of the project was to increase access to appropriate agricultural finance for farming households. Six to ten participating MFIs would have developed or refined agricultural microfinance products, and by the end of 2014 14,000 new MFI clients would have accessed an agricultural loan product. Furthermore, the MFIs would have developed appropriate risk-mitigating measures associated with agricultural financing. Half of the MFIs would have successfully linked their clients to agricultural service providers. The target was that 75% of the agricultural clients would have received financial education.

AFP-Ethiopia: Wasasa MFI and Amhara Credit and Savings Institution (ACSI) are the MFIs selected in Ethiopia to participate in this project (on coffee and wheat, respectively). The project aims to increase access to agricultural finance for farming households via product development. As a result of the support from the AFPEU MicroSave/Cordaid agricultural finance project, funded by the EU and Cordaid, Wasasa MFI has developed an inclusive financial scheme called the “Coffee Improvement Loan”.

Wasasa MFI was selected as one of the two MFIs to participate in the programme. The organisation had no previous experience in providing loans to smallholder coffee farmers, as they are located far from the coffee growing areas. Thus, Wasasa MFI did not know the financial needs and the risks involved in lending to smallholder coffee farmers. As a result, there was a need to conduct a preliminary study to get to know more about the overall financial services provided to coffee smallholders in Ethiopia and the stakeholders/actors in the coffee value chain. Thus, Wasasa MFI conducted a preliminary study in Chora district in order to identify the options for direct financial services to primary actors in the coffee chain: farmers, cooperatives and traders, with a value chain financing approach. In case any potentional could be demonstrated, the preliminary study also aimed to define the financial products and services that Wasasa MFI could offer, as well as potential support mechanisms to increase the impact of the financial services.

Baseline study: In line with the above goals, the staff of Wasasa MFI and MicroSave did a preliminary study in May 2013 in the coffee value chain of Chora district, which was chosen as a pilot area as Wasasa had recently opened a branch in this district. It provided a broad understanding of the stakeholders in the coffee chain. More specifically, the study identified the following aspects of the chain:• Stakeholders involved in the coffee chain and their willingness to collaborate;• Gaps/challenges in the coffee production and marketing;• Existing and potential risks in the value chain;• The needs for financial intervention; and• Some information for designing appropriate need-based financial products.

In order to create a proper capacity to launch the programme, there was also a need for human resources development. Thus, the project team trained the staff of Wasasa MFI in Value Chain Analysis and in Value Chain Finance. With the new insights gained, a second field study was done in August 2013 by a multidisciplinary team of experts from Wasasa MFI, MicroSave and Cordaid/ICCO Fair and Sustainable Advisory Services (FSAS). Various data collection methods were used, like Focus Group Discussions, individual interviews, field/farm observations, enterprise budgeting and market visits. Primary data were obtained from primary actors in the coffee chain (farmers, traders, cooperatives, unions) as well as from support actors (ACDI/VOCA, TechnoServe, the Woreda Agriculture Office (WAO), the Woreda Cooperative Promotion Office (WCPO), the Oromia Credits and Savings Share Company (OCSSCO), etc.). The primary data were supplemented by various secondary data from reports, studies, research, statistical data, the Ethiopian Commodity Exchange (ECX), market data etc. All data were digested through a process of staff discussions and triangulation of the various data sources.

25

1.4 Other stakeholders

In Ethiopia the coffee value chain generally starts from the coffee farmers, to processing and trading up to the local retailers (local consumption) or coffee exporters. The coffee value chain for Chora smallholder farmer is no exception (see below the value chain map of Chora). The fieldwork identified the overall landscape of the coffee value chain in Chora and its participants were categorised as primary participants and secondary chain actors. Primary chain actors include smallholder coffee producers, PCs, processors traders, the ECX and various Unions like Chora Cooperative Union and the OCFCU. Secondary chain actors include other non-financial service providers working with the farmers, like the WAO and the WCPO. In addition, TechnoServe and ACDI/VOCA are also among the secondary players in this particular value chain.

TechnoServe is an international non-profit organisation that develops business solutions to poverty alleviation by linking people to information, capital and markets. Its work is rooted in the idea that hardworking people can generate income, jobs and wealth for their families and communities. The organisation believes in the power of private enterprises to transform lives. TechnoServe is currently helping farmers by installing and operating ecological coffee wet mills. Furthermore, they support farmers to obtain the skills and influence necessary to organise themselves and defend their own interests.

Agricultural Cooperative Development International / Volunteers in Overseas Cooperative Assistance (ACDI/VOCA) is an economic development organisation that fosters broad-based economic growth, raises living standards, and creates vibrant communities. Its areas of practice are agribusiness, food security, enterprise development, financial services, and community development. ACDI/VOCA began implementing the USAID-funded five-year Agricultural Cooperatives in Ethiopia (ACE) project. As part of this novel initiative, ACE aided the OCFCUs, which are directly linked with this coffee value chain.

Programme inception In May 2014, Wasasa MFI and a Cordaid consultant organised a multi-stakeholder meeting with the District Agricultural Department, the WCPO, the Chora Cooperative Union, some private coffee traders and other stakeholders such as TechnoServe, the OCFCU and ACDI/VOCA. A Memorandum of Understanding (MoU) was signed with the aim to align the efforts to improve the production, quality and marketing of Chora coffee. Below some of the primary (chain) actors and supporters are listed and described.

Cooperative

Wet cherry Dry cherry

Washing and drying Hulling

Traders

Private Distributors

Rejected Grades

Coffee Producers

Export Market

Direct Consumption and Local market (40%)

Private Exporters

Commodity Auction ECX

Traders

Cooperative Unions

Cooperative

Figure 1.1: Coffee value chain of Chora district (Source: Value Chain financing report, Wasasa, September 2013)

26

Primary (Chain) actorsA. Farmers are responsible for producing high quality coffee, based on proper husbandry of their

fields (i.e. weeding, pruning, etc.), proper harvesting techniques (picking only ripe fruits) and drying methods (i.e., using coated mesh wire on raised beds).

B. Primary Cooperatives (PCs) are members of the Union and responsible for offering farmers access to quality inputs and markets. In the future they should be able to play a role in the administration of loans to members (e.g. select members that qualify for a loan and administrate the repayment of the loan through the coffee that is marketed via the PC).

C. The Chora cooperative Union covers the whole Chora district and represents the coffee cooperative and their members. As such it was responsible for coordinating all farmers’ efforts. It will ensure that the right PCs and farmers get selected for the support offered by other signatories. As a member of the OCFCU, it links all member cooperatives to the OCFCU. In the future they should be able to play a role in administrating loans to cooperatives (e.g. select PCs that qualify for loans and administrate the repayment of these loans via coffee, marketed via the union).

D. The Oromia Coffee Farmers’ Cooperative Union (OCFCU) has a large number of support programmes for its member cooperatives. These include loans for working capital and training programmes on issues on PC level (like leadership training) and farmer level (like coffee quality management). It can link specific unions or PCs to banks for loans, and to specific (niche) markets in and outside Ethiopia. As a centre of practical skills and market knowledge on coffee, it cooperates with various other stakeholders and service providers on capacity building.

Chain Support actorsA. The Woreda Agriculture Office (WAO) is overall responsible for coffee farmers from the

governmental side. They offer technical training to farmers and assist other MoU signatories in selecting farmers that fulfil the eligibility criteria. This could offer different kinds of support: training, loans, market access etc. They are able to follow up this selection and supervise beneficiaries of the trainings and loans to see if they indeed apply the skills and the money for its intended purpose. It can facilitate all required support from local government partners and it can invite additional traders in the area to enhance the competitiveness of coffee marketing.

B. The Woreda Cooperative Promotion Office (WCPO) is responsible for training and supporting PCs and the Union in administrative and management issues. They will ensure that the cooperatives and the union can play their proper roles.

C. TechnoServe can offer Training of Trainers (ToT) to cooperatives and unions in coffee processing (wet and dry), business management (leadership, bookkeeping), and coffee marketing. It can facilitate access to finance as well, and in some cases direct access to export markets.

D. ADCI/VOCA via its Agribusiness and Market Development (AMDE) project can offer ToT to cooperatives and farmers on cooperative management, coffee quality, post-harvest handling and marketing.

1.5 Nature of the financial transactions

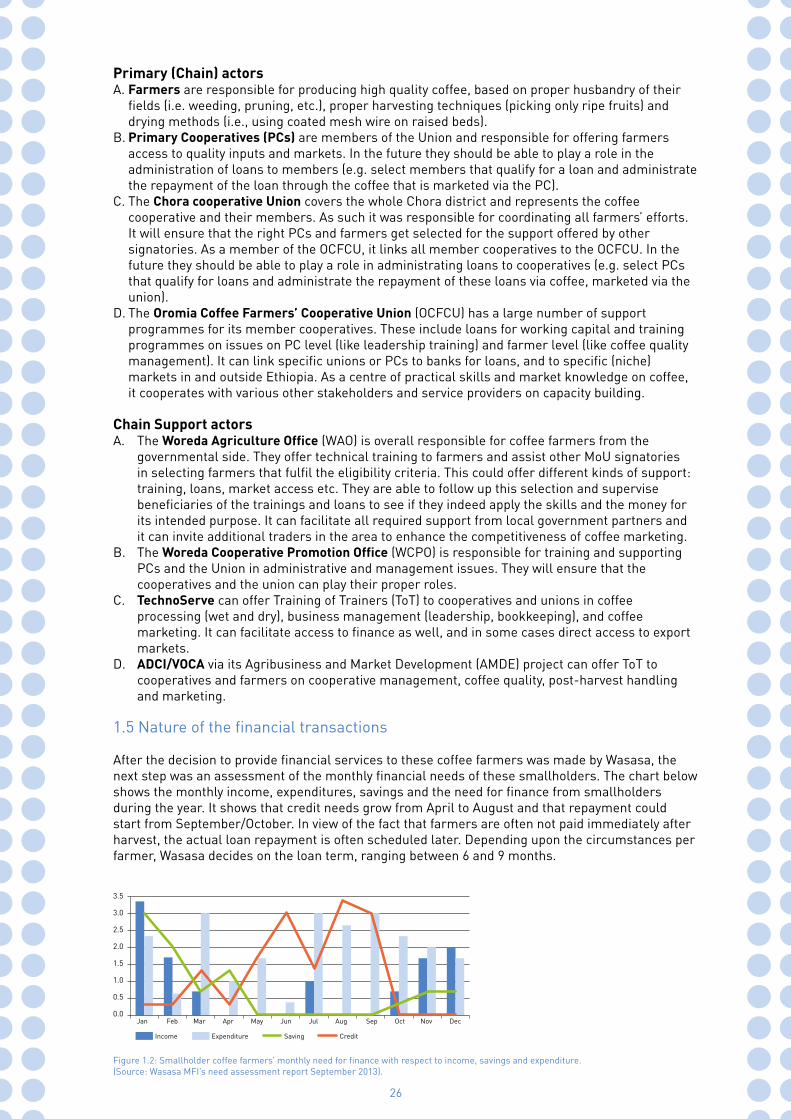

After the decision to provide financial services to these coffee farmers was made by Wasasa, the next step was an assessment of the monthly financial needs of these smallholders. The chart below shows the monthly income, expenditures, savings and the need for finance from smallholders during the year. It shows that credit needs grow from April to August and that repayment could start from September/October. In view of the fact that farmers are often not paid immediately after harvest, the actual loan repayment is often scheduled later. Depending upon the circumstances per farmer, Wasasa decides on the loan term, ranging between 6 and 9 months.

3.5

3.0

2.5

2.0

1.5

1.0

0.5

0.0Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Income Expenditure Saving Credit

Figure 1.2: Smallholder coffee farmers’ monthly need for finance with respect to income, savings and expenditure. (Source: Wasasa MFI’s need assessment report September 2013).

27

2. Risk analysis

2.1 How has risk management been approached?

Loan appraisal by the Microfinance Institution (MFI) - Due diligenceIn addition to the two preliminary studies conducted, the financial product for the coffee farmers was developed. The following access requirements were defined:

A. Follow standard loan procedure;B. Legally registered and permanently living in the peasant association with land ownership

certificate;C. Eligible land ownership ranging from 0.5 –to 2 hectare(s) of coffee land; D. Willing to be inspected by the Woreda Agriculture Office (WAO)/ Wasasa MFI and follow-up

of advice;E. Member of a peer group with mandatory saving, (10% of loan size as mandatory saving) and

credit life insurance as group;F. No other loans with other MFIs; andG. Willing to join training on the following issues:

• Standard training on loan policies and procedures;• Technical training by the WAO (VOCA) coffee quality;• Training on cooperative and union management by VOCA; and• Training on Value Chain Development (VCD) and quality.

Pre-disbursement phase: After initial screening of eligibility, the group formation will be completed and training on policies/procedures is conducted. Subsequently, applicants will pass through the following loan processing steps for application, appraisal and disbursement:• Field staff will assess credit needs with the group and fill out the necessary forms (incl.

peasant association official letter, on coffee area). Support is provided by the agricultural Development Assistant (DA) to check the farmer’s coffee area;

• Check with other MFIs whether the potential customer has loans from other financial institutions;