Diploma in Corporate Finance Corporate Finance Strategy ...

150

Diploma in Corporate Finance Corporate Finance Strategy & Advice Information Booklet Date of exam Monday 20 June 2016 Part 1: 1:00 pm – 1:55 pm Information Booklet & Examination Paper Part 2: 2:00 pm – 5:00 pm Answer Book Notes to candidates Time allowed: 55 minutes Part 1: Candidates will be provided with an Information Booklet and the examination question paper. Candidates have one hour in which to review the information booklet and questions. During this time, candidates may annotate the information book. The examination has been prepared on the assumption that candidates will not have any detailed knowledge of the type of organisation to which it refers. No additional merit will be accorded to those candidates displaying such knowledge. Part 2: The Answer Book will be distributed at 1.55 pm and the candidates should open and begin writing in the answer book when instructed. Candidates should distinguish clearly between formal answers (including appendices) and any working papers. © Chartered Institute for Securities & Investment 2016 © ICAEW 2016 All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopying, or any information storage or retrieval system without prior permission from the Chartered Institute for Securities & Investment. Please turn over when instructed 1 of 150

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Diploma in Corporate Finance Corporate Finance Strategy ...

Diploma in Corporate F inance

Corporate F inance St ra tegy & Ad vice

In format ion Bookle t Date of exam Monday 20 June 2016 Part 1: 1:00 pm – 1:55 pm Information Booklet & Examination Paper Part 2: 2:00 pm – 5:00 pm Answer Book Notes to candidates Time allowed: 55 minutes Part 1: Candidates will be provided with an Information Booklet and the examination question paper. Candidates have one hour in which to review the information booklet and questions. During this time, candidates may annotate the information book. The examination has been prepared on the assumption that candidates will not have any detailed knowledge of the type of organisation to which it refers. No additional merit will be accorded to those candidates displaying such knowledge. Part 2: The Answer Book will be distributed at 1.55 pm and the candidates should open and begin

writing in the answer book when instructed.

Candidates should distinguish clearly between formal answers (including appendices) and any working papers. © Chartered Institute for Securities & Investment 2016 © ICAEW 2016 All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopying, or any information storage or retrieval system without prior permission from the Chartered Institute for Securities & Investment.

Please turn over when instructed

1 of 150

2 of 150

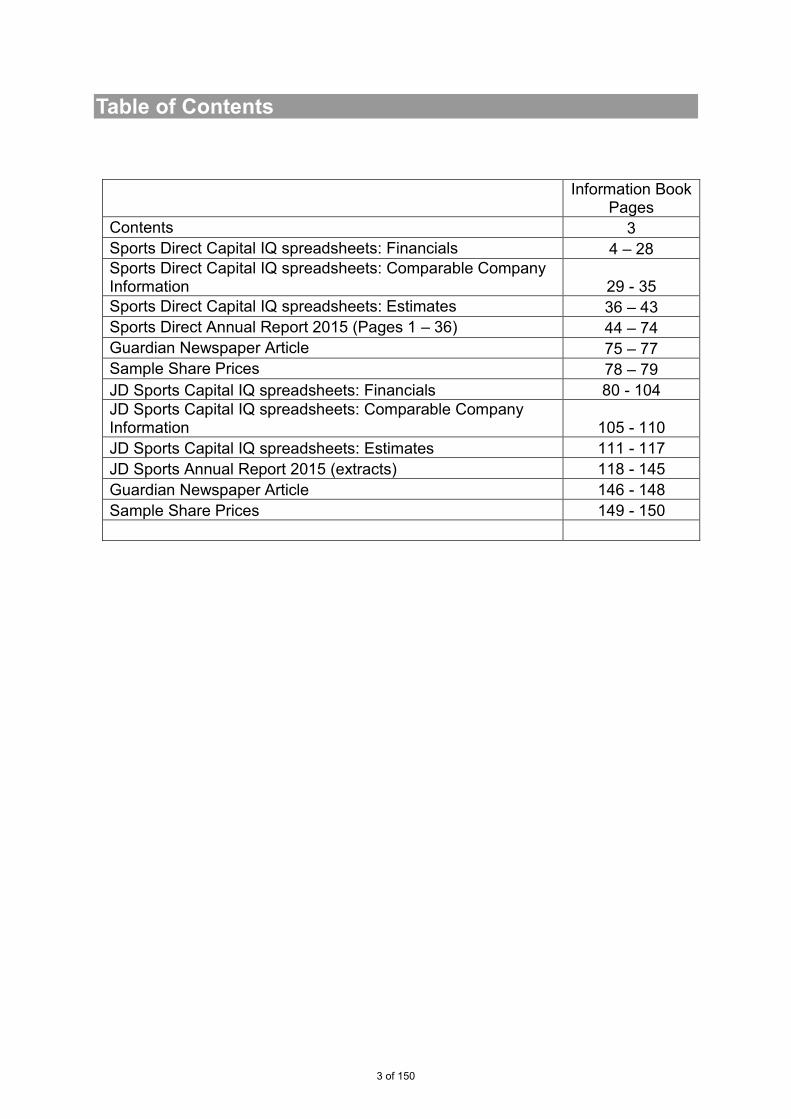

Table of Contents

Information Book

Pages Contents 3 Sports Direct Capital IQ spreadsheets: Financials 4 – 28 Sports Direct Capital IQ spreadsheets: Comparable Company Information 29 - 35 Sports Direct Capital IQ spreadsheets: Estimates 36 – 43 Sports Direct Annual Report 2015 (Pages 1 – 36) 44 – 74 Guardian Newspaper Article 75 – 77 Sample Share Prices 78 – 79 JD Sports Capital IQ spreadsheets: Financials 80 - 104 JD Sports Capital IQ spreadsheets: Comparable Company Information 105 - 110 JD Sports Capital IQ spreadsheets: Estimates 111 - 117 JD Sports Annual Report 2015 (extracts) 118 - 145 Guardian Newspaper Article 146 - 148 Sample Share Prices 149 - 150

3 of 150

Data Provided by

Historical Equity Pricing Data supplied by

Sports Direct Capital IQ spreadsheets: Financials

4 of 150

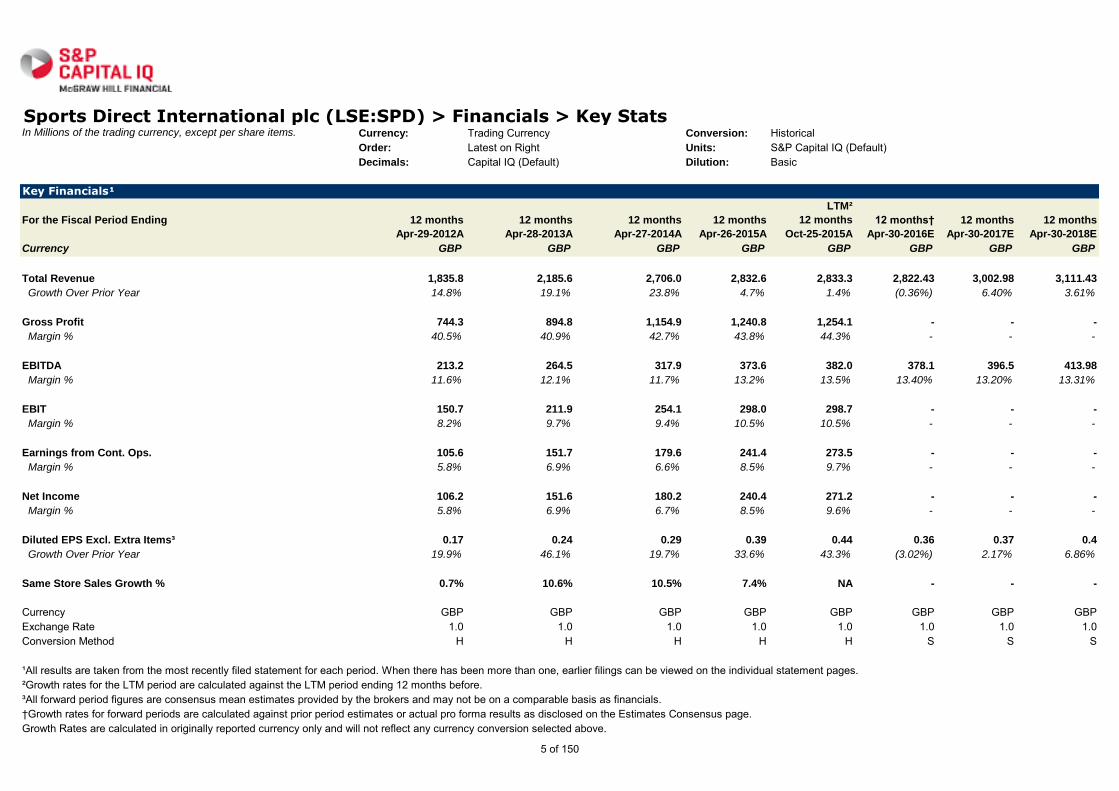

Sports Direct International plc (LSE:SPD) > Financials > Key StatsIn Millions of the trading currency, except per share items. Currency: Trading Currency Conversion: Historical

Order: Latest on Right Units: S&P Capital IQ (Default)Decimals: Capital IQ (Default) Dilution: Basic

Key Financials¹

For the Fiscal Period Ending 12 months

Apr-29-2012A

12 months

Apr-28-2013A

12 months

Apr-27-2014A

12 months

Apr-26-2015A

LTM²

12 months

Oct-25-2015A

12 months†

Apr-30-2016E

12 months

Apr-30-2017E

12 months

Apr-30-2018E

Currency GBP GBP GBP GBP GBP GBP GBP GBP

Total Revenue 1,835.8 2,185.6 2,706.0 2,832.6 2,833.3 2,822.43 3,002.98 3,111.43

Growth Over Prior Year 14.8% 19.1% 23.8% 4.7% 1.4% (0.36%) 6.40% 3.61%

Gross Profit 744.3 894.8 1,154.9 1,240.8 1,254.1 - - -

Margin % 40.5% 40.9% 42.7% 43.8% 44.3% - - -

EBITDA 213.2 264.5 317.9 373.6 382.0 378.1 396.5 413.98

Margin % 11.6% 12.1% 11.7% 13.2% 13.5% 13.40% 13.20% 13.31%

EBIT 150.7 211.9 254.1 298.0 298.7 - - -

Margin % 8.2% 9.7% 9.4% 10.5% 10.5% - - -

Earnings from Cont. Ops. 105.6 151.7 179.6 241.4 273.5 - - -

Margin % 5.8% 6.9% 6.6% 8.5% 9.7% - - -

Net Income 106.2 151.6 180.2 240.4 271.2 - - -

Margin % 5.8% 6.9% 6.7% 8.5% 9.6% - - -

Diluted EPS Excl. Extra Items³ 0.17 0.24 0.29 0.39 0.44 0.36 0.37 0.4

Growth Over Prior Year 19.9% 46.1% 19.7% 33.6% 43.3% (3.02%) 2.17% 6.86%

Same Store Sales Growth % 0.7% 10.6% 10.5% 7.4% NA - - -

Currency GBP GBP GBP GBP GBP GBP GBP GBPExchange Rate 1.0 1.0 1.0 1.0 1.0 1.0 1.0 1.0 Conversion Method H H H H H S S S

¹All results are taken from the most recently filed statement for each period. When there has been more than one, earlier filings can be viewed on the individual statement pages.²Growth rates for the LTM period are calculated against the LTM period ending 12 months before.³All forward period figures are consensus mean estimates provided by the brokers and may not be on a comparable basis as financials.†Growth rates for forward periods are calculated against prior period estimates or actual pro forma results as disclosed on the Estimates Consensus page.

Growth Rates are calculated in originally reported currency only and will not reflect any currency conversion selected above.

5 of 150

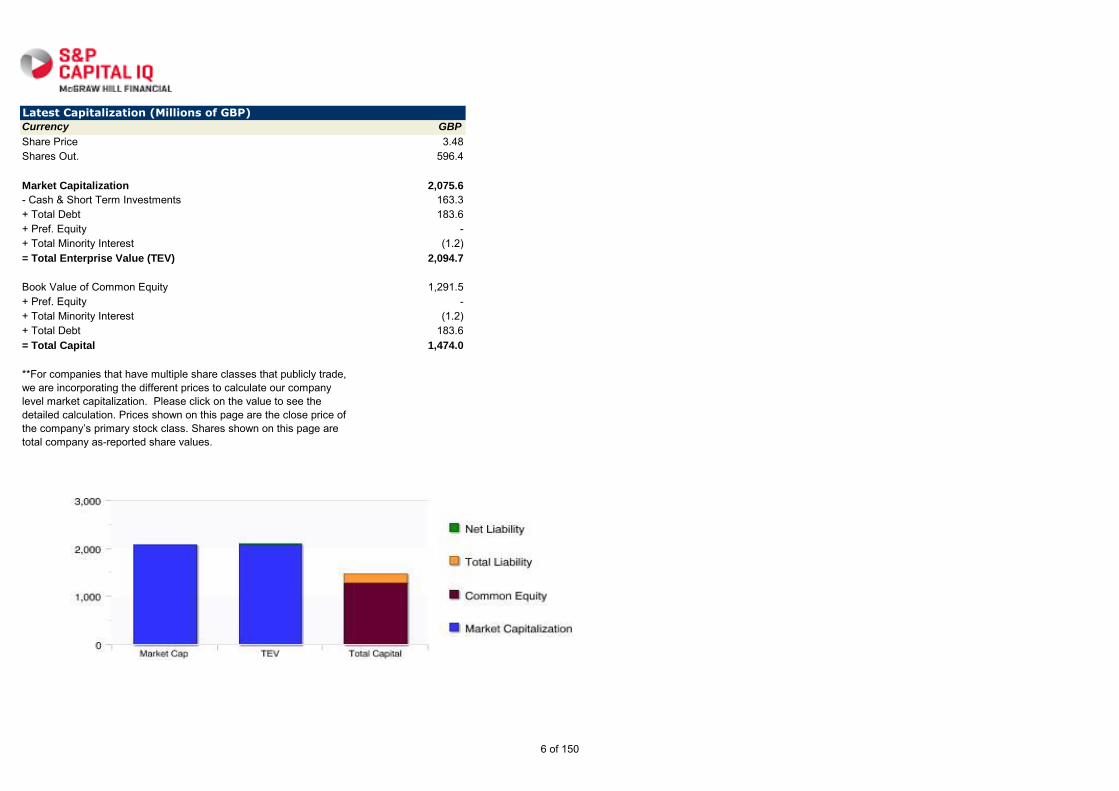

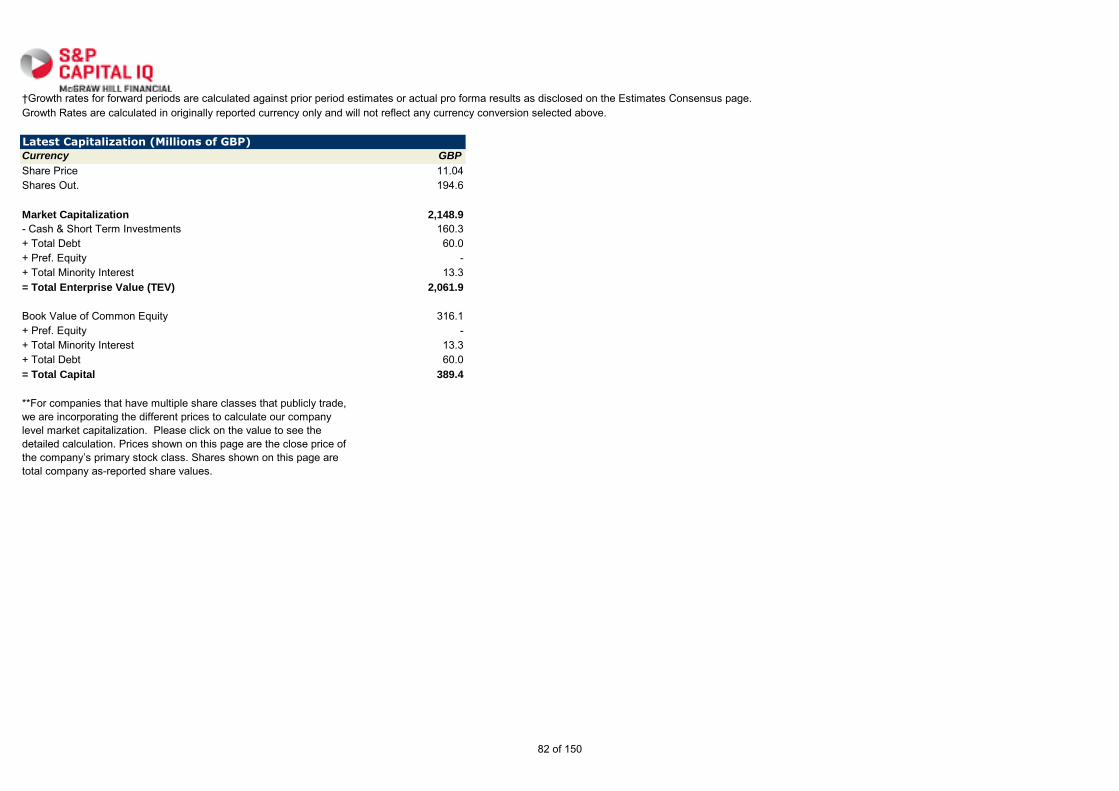

Latest Capitalization (Millions of GBP)

Currency GBP

Share Price 3.48 Shares Out. 596.4

Market Capitalization 2,075.6

- Cash & Short Term Investments 163.3 + Total Debt 183.6 + Pref. Equity -+ Total Minority Interest (1.2) = Total Enterprise Value (TEV) 2,094.7

Book Value of Common Equity 1,291.5 + Pref. Equity -+ Total Minority Interest (1.2) + Total Debt 183.6 = Total Capital 1,474.0

**For companies that have multiple share classes that publicly trade, we are incorporating the different prices to calculate our company level market capitalization. Please click on the value to see the detailed calculation. Prices shown on this page are the close price of the company’s primary stock class. Shares shown on this page are

total company as-reported share values.

6 of 150

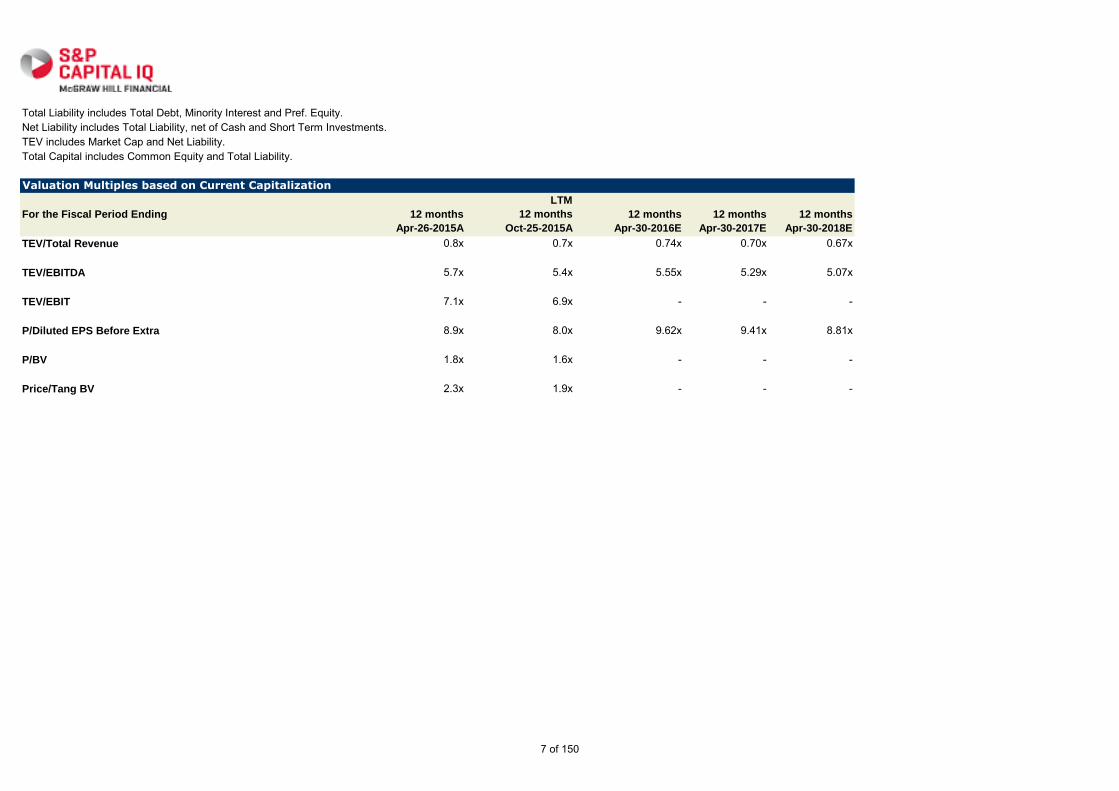

Total Liability includes Total Debt, Minority Interest and Pref. Equity.Net Liability includes Total Liability, net of Cash and Short Term Investments.TEV includes Market Cap and Net Liability.Total Capital includes Common Equity and Total Liability.

Valuation Multiples based on Current Capitalization

For the Fiscal Period Ending 12 months

Apr-26-2015A

LTM

12 months

Oct-25-2015A

12 months

Apr-30-2016E

12 months

Apr-30-2017E

12 months

Apr-30-2018E

TEV/Total Revenue 0.8x 0.7x 0.74x 0.70x 0.67x

TEV/EBITDA 5.7x 5.4x 5.55x 5.29x 5.07x

TEV/EBIT 7.1x 6.9x - - -

P/Diluted EPS Before Extra 8.9x 8.0x 9.62x 9.41x 8.81x

P/BV 1.8x 1.6x - - -

Price/Tang BV 2.3x 1.9x - - -

7 of 150

Sports Direct International plc (LSE:SPD) > Financials > Income Statement

In Millions of the reported currency, except per share items. Template: Standard Restatement: Latest FilingsPeriod Type: Annual Order: Latest on RightCurrency: Reported Currency Conversion: HistoricalUnits: S&P Capital IQ (Default) Decimals: Capital IQ (Default)

Income Statement

For the Fiscal Period Ending

Reclassified

12 months

Apr-24-2011

Reclassified

12 months

Apr-29-2012

Reclassified

12 months

Apr-28-2013

Reclassified

12 months

Apr-27-2014

12 months

Apr-26-2015

LTM

12 months

Oct-25-2015

Currency GBP GBP GBP GBP GBP GBP

Revenue 1,599.2 1,835.8 2,185.6 2,706.0 2,832.6 2,833.3 Other Revenue - - - - - - Total Revenue 1,599.2 1,835.8 2,185.6 2,706.0 2,832.6 2,833.3

Cost Of Goods Sold 940.3 1,091.5 1,290.8 1,551.0 1,591.7 1,579.2 Gross Profit 658.9 744.3 894.8 1,154.9 1,240.8 1,254.1

Selling General & Admin Exp. 525.0 594.6 685.4 902.6 938.4 951.1 R & D Exp. - - - - - -Depreciation & Amort. - - - - - -Amort. of Goodwill and Intangibles 2.8 4.4 4.7 6.8 12.7 12.7 Other Operating Expense/(Income) (5.3) (5.3) (7.2) (8.6) (8.3) (8.4)

Other Operating Exp., Total 522.4 593.6 682.9 900.8 942.8 955.4

Operating Income 136.5 150.7 211.9 254.1 298.0 298.7

Interest Expense (4.7) (6.0) (7.2) (8.1) (6.8) (3.9) Interest and Invest. Income 0.4 0.6 2.6 7.9 15.1 64.0 Net Interest Exp. (4.2) (5.4) (4.6) (0.2) 8.2 60.1

Income/(Loss) from Affiliates 0 0.6 1.3 2.3 3.0 2.9 Currency Exchange Gains (Loss) (1.7) 3.6 (2.0) (11.2) 7.3 30.6 Other Non-Operating Inc. (Exp.) - 2.3 - - - - EBT Excl. Unusual Items 130.5 151.7 206.6 245.0 316.5 392.2

8 of 150

Impairment of Goodwill (0.2) - - - (5.3) (37.8) Gain (Loss) On Sale Of Invest. (9.5) (5.8) - - - -Asset Writedown - - - (5.5) (8.0) (8.0) Legal Settlements (3.1) - - - - -Other Unusual Items 1.1 5.6 0.6 - 10.3 4.5 EBT Incl. Unusual Items 118.8 151.5 207.2 239.5 313.4 351.0

Income Tax Expense 35.6 45.9 55.6 59.8 72.1 77.4 Earnings from Cont. Ops. 83.2 105.6 151.7 179.6 241.4 273.5

Earnings of Discontinued Ops. - - - - - -Extraord. Item & Account. Change - - - - - - Net Income to Company 83.2 105.6 151.7 179.6 241.4 273.5

Minority Int. in Earnings 1.0 0.6 (0.1) 0.6 (1.0) (2.3) Net Income 84.2 106.2 151.6 180.2 240.4 271.2

Pref. Dividends and Other Adj. - - - - - -

NI to Common Incl Extra Items 84.2 106.2 151.6 180.2 240.4 271.2

NI to Common Excl. Extra Items 84.2 106.2 151.6 180.2 240.4 271.2

Per Share Items

Basic EPS 0.15 0.19 0.27 0.31 0.41 0.46 Basic EPS Excl. Extra Items 0.15 0.19 0.27 0.31 0.41 0.46 Weighted Avg. Basic Shares Out. 568.6 568.6 569.0 585.5 592.3 592.4

Diluted EPS 0.14 0.17 0.24 0.29 0.39 0.44 Diluted EPS Excl. Extra Items 0.14 0.17 0.24 0.29 0.39 0.44 Weighted Avg. Diluted Shares Out. 604.1 635.8 620.8 618.2 616.5 623.5

Normalized Basic EPS 0.15 0.17 0.23 0.26 0.33 0.41 Normalized Diluted EPS 0.14 0.15 0.21 0.25 0.32 0.39

Dividends per Share NA NA NA NA NA NA

Shares per Depository Receipt 2.0 2.0 2.0 2.0 2.0 2.0

9 of 150

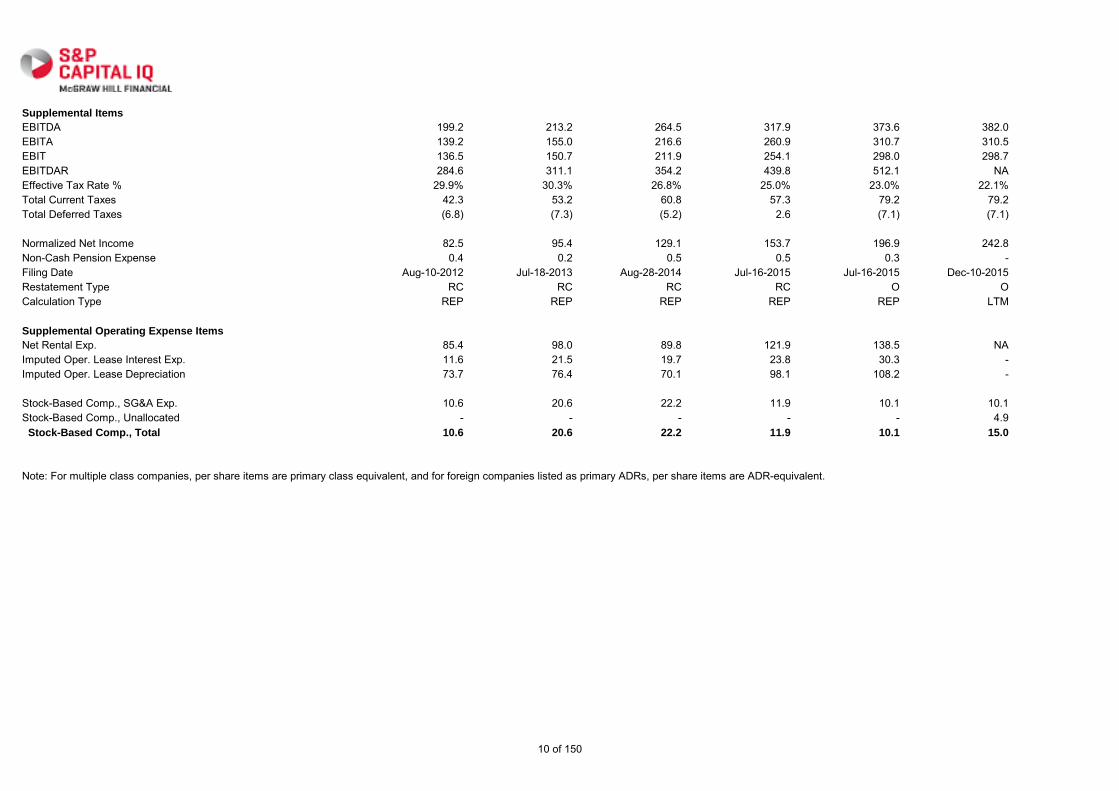

Supplemental Items

EBITDA 199.2 213.2 264.5 317.9 373.6 382.0 EBITA 139.2 155.0 216.6 260.9 310.7 310.5 EBIT 136.5 150.7 211.9 254.1 298.0 298.7 EBITDAR 284.6 311.1 354.2 439.8 512.1 NAEffective Tax Rate % 29.9% 30.3% 26.8% 25.0% 23.0% 22.1% Total Current Taxes 42.3 53.2 60.8 57.3 79.2 79.2 Total Deferred Taxes (6.8) (7.3) (5.2) 2.6 (7.1) (7.1)

Normalized Net Income 82.5 95.4 129.1 153.7 196.9 242.8 Non-Cash Pension Expense 0.4 0.2 0.5 0.5 0.3 -Filing Date Aug-10-2012 Jul-18-2013 Aug-28-2014 Jul-16-2015 Jul-16-2015 Dec-10-2015Restatement Type RC RC RC RC O OCalculation Type REP REP REP REP REP LTM

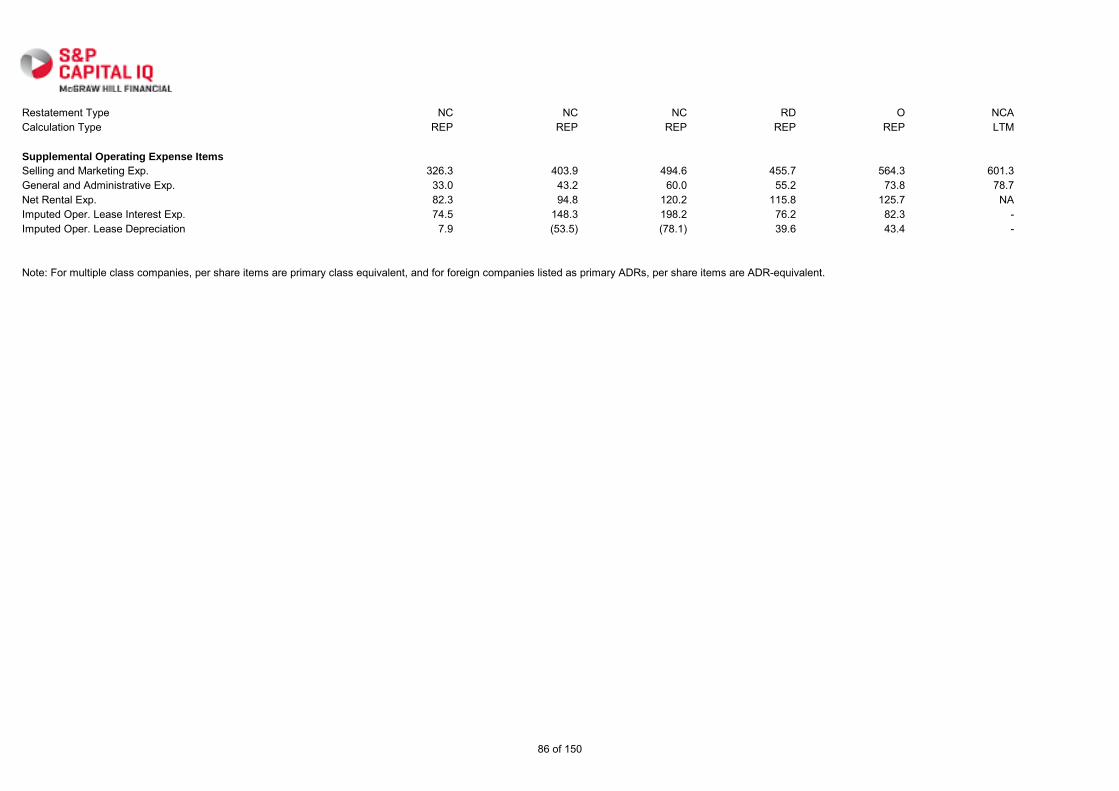

Supplemental Operating Expense Items

Net Rental Exp. 85.4 98.0 89.8 121.9 138.5 NAImputed Oper. Lease Interest Exp. 11.6 21.5 19.7 23.8 30.3 -Imputed Oper. Lease Depreciation 73.7 76.4 70.1 98.1 108.2 -

Stock-Based Comp., SG&A Exp. 10.6 20.6 22.2 11.9 10.1 10.1 Stock-Based Comp., Unallocated - - - - - 4.9 Stock-Based Comp., Total 10.6 20.6 22.2 11.9 10.1 15.0

Note: For multiple class companies, per share items are primary class equivalent, and for foreign companies listed as primary ADRs, per share items are ADR-equivalent.

10 of 150

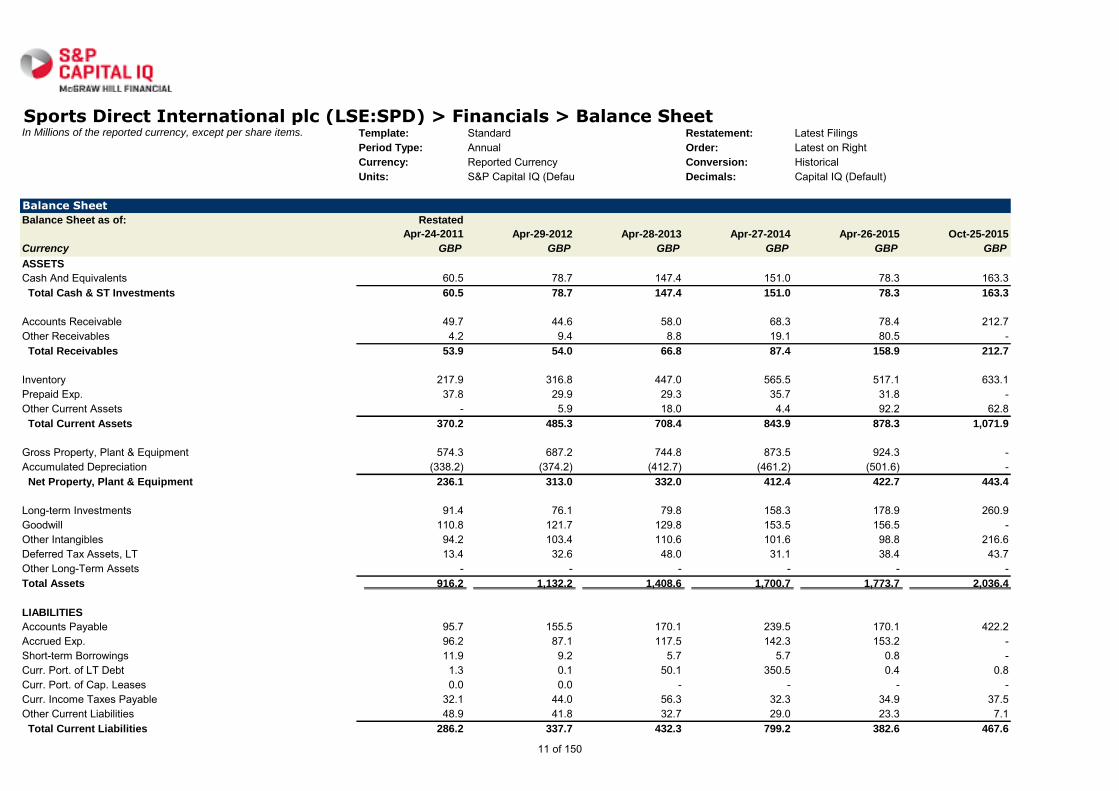

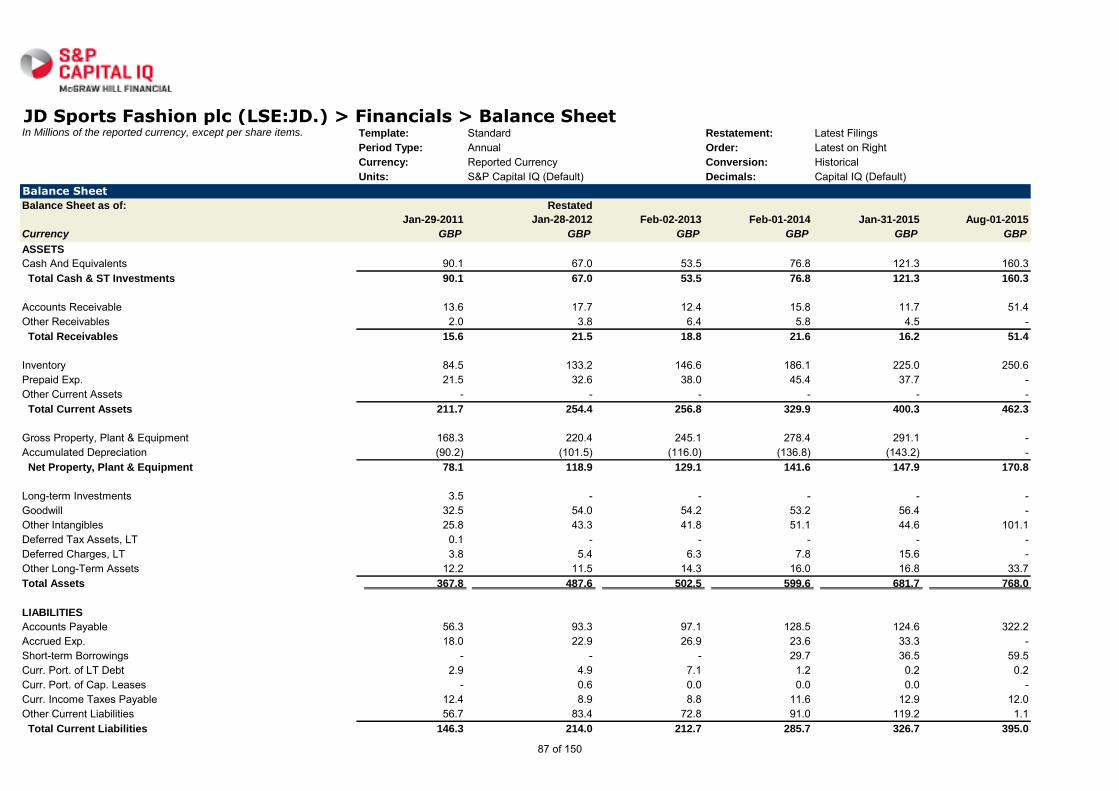

Sports Direct International plc (LSE:SPD) > Financials > Balance SheetIn Millions of the reported currency, except per share items. Template: Standard Restatement: Latest Filings

Period Type: Annual Order: Latest on RightCurrency: Reported Currency Conversion: HistoricalUnits: S&P Capital IQ (Default) Decimals: Capital IQ (Default)

Balance Sheet

Balance Sheet as of: Restated

Apr-24-2011 Apr-29-2012 Apr-28-2013 Apr-27-2014 Apr-26-2015 Oct-25-2015

Currency GBP GBP GBP GBP GBP GBP

ASSETS

Cash And Equivalents 60.5 78.7 147.4 151.0 78.3 163.3 Total Cash & ST Investments 60.5 78.7 147.4 151.0 78.3 163.3

Accounts Receivable 49.7 44.6 58.0 68.3 78.4 212.7 Other Receivables 4.2 9.4 8.8 19.1 80.5 - Total Receivables 53.9 54.0 66.8 87.4 158.9 212.7

Inventory 217.9 316.8 447.0 565.5 517.1 633.1 Prepaid Exp. 37.8 29.9 29.3 35.7 31.8 -Other Current Assets - 5.9 18.0 4.4 92.2 62.8 Total Current Assets 370.2 485.3 708.4 843.9 878.3 1,071.9

Gross Property, Plant & Equipment 574.3 687.2 744.8 873.5 924.3 -Accumulated Depreciation (338.2) (374.2) (412.7) (461.2) (501.6) - Net Property, Plant & Equipment 236.1 313.0 332.0 412.4 422.7 443.4

Long-term Investments 91.4 76.1 79.8 158.3 178.9 260.9 Goodwill 110.8 121.7 129.8 153.5 156.5 -Other Intangibles 94.2 103.4 110.6 101.6 98.8 216.6 Deferred Tax Assets, LT 13.4 32.6 48.0 31.1 38.4 43.7 Other Long-Term Assets - - - - - -Total Assets 916.2 1,132.2 1,408.6 1,700.7 1,773.7 2,036.4

LIABILITIES

Accounts Payable 95.7 155.5 170.1 239.5 170.1 422.2 Accrued Exp. 96.2 87.1 117.5 142.3 153.2 -Short-term Borrowings 11.9 9.2 5.7 5.7 0.8 -Curr. Port. of LT Debt 1.3 0.1 50.1 350.5 0.4 0.8 Curr. Port. of Cap. Leases 0.0 0.0 - - - -Curr. Income Taxes Payable 32.1 44.0 56.3 32.3 34.9 37.5 Other Current Liabilities 48.9 41.8 32.7 29.0 23.3 7.1 Total Current Liabilities 286.2 337.7 432.3 799.2 382.6 467.6

11 of 150

Long-Term Debt 194.9 213.8 245.6 6.8 136.8 182.8 Capital Leases 1.3 0.8 0.0 - - -Pension & Other Post-Retire. Benefits 16.2 19.3 19.9 15.4 14.9 11.7 Def. Tax Liability, Non-Curr. 28.2 25.8 25.0 24.0 40.1 38.1 Other Non-Current Liabilities 58.3 62.9 41.1 37.8 37.7 45.8 Total Liabilities 585.1 660.3 763.9 883.2 612.1 746.1

Common Stock 64.1 64.1 64.1 64.1 64.1 64.1 Additional Paid In Capital 874.4 874.4 874.4 874.4 874.4 874.4 Retained Earnings 440.9 600.4 752.0 931.8 1,181.5 1,380.0 Treasury Stock (91.2) (113.5) (120.6) (69.5) (69.5) (90.0) Comprehensive Inc. and Other (957.4) (952.9) (924.9) (979.7) (886.1) (937.0) Total Common Equity 330.7 472.4 644.9 821.1 1,164.4 1,291.5

Minority Interest 0.4 (0.5) (0.3) (3.5) (2.8) (1.2)

Total Equity 331.1 471.9 644.7 817.6 1,161.6 1,290.3

Total Liabilities And Equity 916.2 1,132.2 1,408.6 1,700.7 1,773.7 2,036.4

Supplemental Items

Total Shares Out. on Filing Date 576.6 598.6 598.5 592.3 592.3 592.4 Total Shares Out. on Balance Sheet Date 576.6 598.6 598.5 592.3 592.3 592.4 Book Value/Share 0.57 0.79 1.08 1.39 1.97 2.18 Tangible Book Value 125.7 247.2 404.5 566.0 909.0 1,074.9 Tangible Book Value/Share 0.22 0.41 0.68 0.96 1.53 1.81 Total Debt 209.4 223.9 301.4 363.0 138.1 183.6 Net Debt 148.9 145.2 154.0 212.0 59.7 20.3 Debt Equiv. of Unfunded Proj. Benefit Obligation 16.2 19.3 19.9 15.4 14.9 NADebt Equivalent Oper. Leases 683.0 783.8 718.2 975.4 1,107.9 NATotal Minority Interest 0.4 (0.5) (0.3) (3.5) (2.8) (1.2) Equity Method Investments 38.3 29.5 32.1 41.8 38.1 48.1 Inventory Method FIFO FIFO FIFO Avg Cost Avg Cost NARaw Materials Inventory 3.3 4.1 3.9 0.1 0.0 NAWork in Progress Inventory 0.7 0.9 NA NA NA NAFinished Goods Inventory 214.0 311.8 443.1 565.3 517.1 NALand 125.6 219.5 237.5 322.4 323.4 NAMachinery 327.1 343.0 387.3 425.9 470.6 NALeasehold Improvements - 124.6 120.0 125.3 130.4 -Full Time Employees 18,210 19,000 24,000 28,000 27,000 NAAccum. Allowance for Doubtful Accts 4.7 4.1 6.7 8.3 7.2 NAFiling Date Aug-10-2012 Jul-18-2013 Aug-28-2014 Jul-16-2015 Jul-16-2015 Dec-10-2015Restatement Type RS NC NC NC O OCalculation Type REP REP REP REP REP REPNote: For multiple class companies, total share counts are primary class equivalent, and for foreign companies listed as primary ADRs, total share counts are ADR-equivalent.

12 of 150

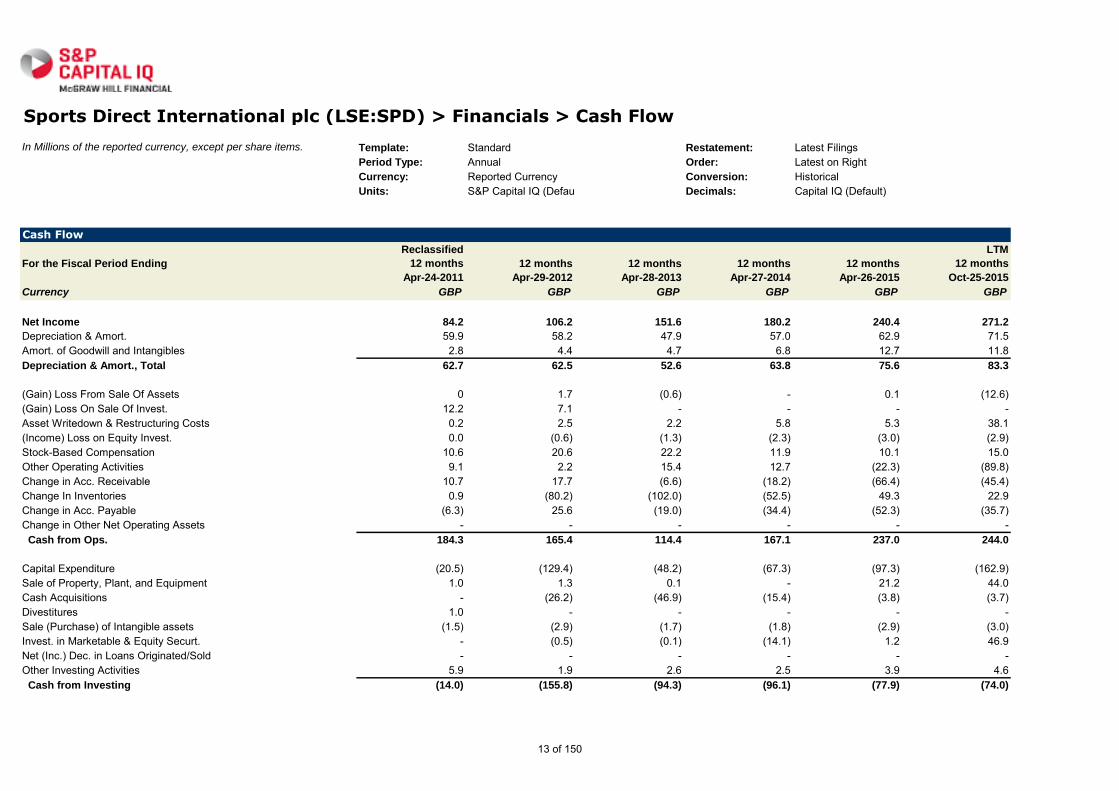

Sports Direct International plc (LSE:SPD) > Financials > Cash Flow

In Millions of the reported currency, except per share items. Template: Standard Restatement: Latest FilingsPeriod Type: Annual Order: Latest on RightCurrency: Reported Currency Conversion: HistoricalUnits: S&P Capital IQ (Default) Decimals: Capital IQ (Default)

Cash Flow

For the Fiscal Period Ending

Reclassified

12 months

Apr-24-2011

12 months

Apr-29-2012

12 months

Apr-28-2013

12 months

Apr-27-2014

12 months

Apr-26-2015

LTM

12 months

Oct-25-2015

Currency GBP GBP GBP GBP GBP GBP

Net Income 84.2 106.2 151.6 180.2 240.4 271.2

Depreciation & Amort. 59.9 58.2 47.9 57.0 62.9 71.5 Amort. of Goodwill and Intangibles 2.8 4.4 4.7 6.8 12.7 11.8 Depreciation & Amort., Total 62.7 62.5 52.6 63.8 75.6 83.3

(Gain) Loss From Sale Of Assets 0 1.7 (0.6) - 0.1 (12.6) (Gain) Loss On Sale Of Invest. 12.2 7.1 - - - -Asset Writedown & Restructuring Costs 0.2 2.5 2.2 5.8 5.3 38.1 (Income) Loss on Equity Invest. 0.0 (0.6) (1.3) (2.3) (3.0) (2.9) Stock-Based Compensation 10.6 20.6 22.2 11.9 10.1 15.0 Other Operating Activities 9.1 2.2 15.4 12.7 (22.3) (89.8) Change in Acc. Receivable 10.7 17.7 (6.6) (18.2) (66.4) (45.4) Change In Inventories 0.9 (80.2) (102.0) (52.5) 49.3 22.9 Change in Acc. Payable (6.3) 25.6 (19.0) (34.4) (52.3) (35.7) Change in Other Net Operating Assets - - - - - - Cash from Ops. 184.3 165.4 114.4 167.1 237.0 244.0

Capital Expenditure (20.5) (129.4) (48.2) (67.3) (97.3) (162.9) Sale of Property, Plant, and Equipment 1.0 1.3 0.1 - 21.2 44.0 Cash Acquisitions - (26.2) (46.9) (15.4) (3.8) (3.7) Divestitures 1.0 - - - - -Sale (Purchase) of Intangible assets (1.5) (2.9) (1.7) (1.8) (2.9) (3.0) Invest. in Marketable & Equity Securt. - (0.5) (0.1) (14.1) 1.2 46.9 Net (Inc.) Dec. in Loans Originated/Sold - - - - - -Other Investing Activities 5.9 1.9 2.6 2.5 3.9 4.6 Cash from Investing (14.0) (155.8) (94.3) (96.1) (77.9) (74.0)

13 of 150

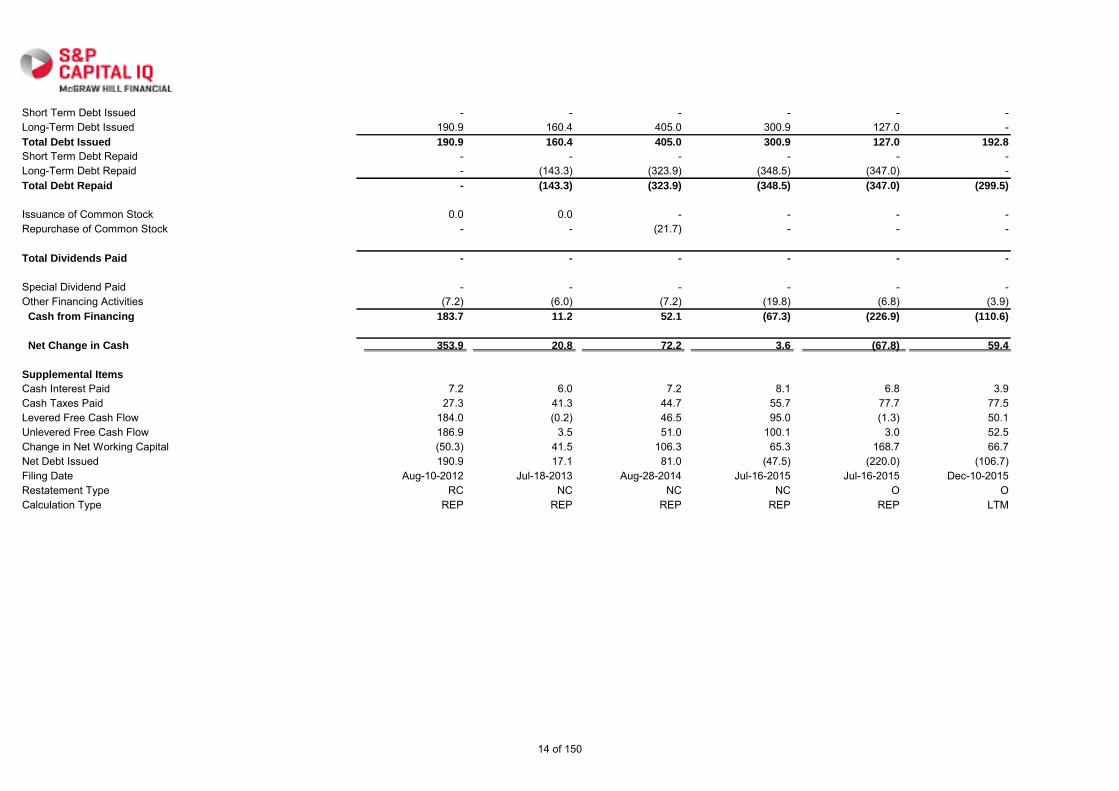

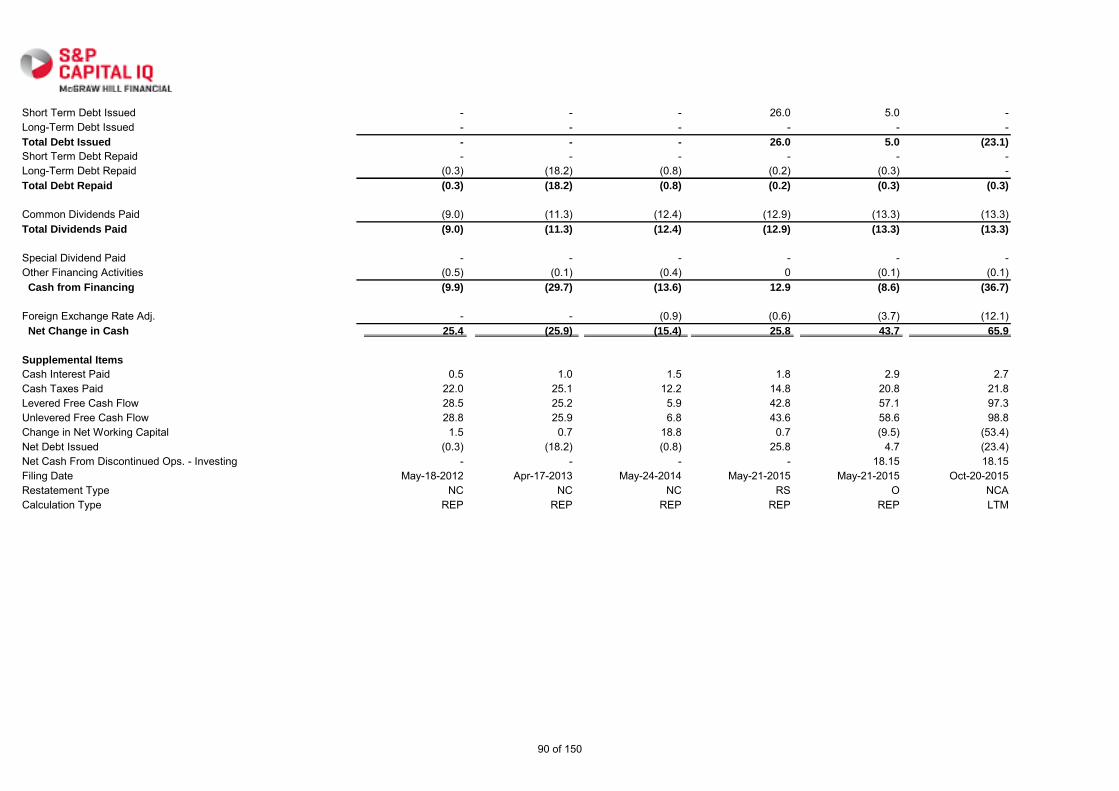

Short Term Debt Issued - - - - - -Long-Term Debt Issued 190.9 160.4 405.0 300.9 127.0 -Total Debt Issued 190.9 160.4 405.0 300.9 127.0 192.8

Short Term Debt Repaid - - - - - -Long-Term Debt Repaid - (143.3) (323.9) (348.5) (347.0) -Total Debt Repaid - (143.3) (323.9) (348.5) (347.0) (299.5)

Issuance of Common Stock 0.0 0.0 - - - -Repurchase of Common Stock - - (21.7) - - -

Total Dividends Paid - - - - - -

Special Dividend Paid - - - - - -Other Financing Activities (7.2) (6.0) (7.2) (19.8) (6.8) (3.9) Cash from Financing 183.7 11.2 52.1 (67.3) (226.9) (110.6)

Net Change in Cash 353.9 20.8 72.2 3.6 (67.8) 59.4

Supplemental Items

Cash Interest Paid 7.2 6.0 7.2 8.1 6.8 3.9 Cash Taxes Paid 27.3 41.3 44.7 55.7 77.7 77.5 Levered Free Cash Flow 184.0 (0.2) 46.5 95.0 (1.3) 50.1 Unlevered Free Cash Flow 186.9 3.5 51.0 100.1 3.0 52.5 Change in Net Working Capital (50.3) 41.5 106.3 65.3 168.7 66.7 Net Debt Issued 190.9 17.1 81.0 (47.5) (220.0) (106.7) Filing Date Aug-10-2012 Jul-18-2013 Aug-28-2014 Jul-16-2015 Jul-16-2015 Dec-10-2015Restatement Type RC NC NC NC O OCalculation Type REP REP REP REP REP LTM

14 of 150

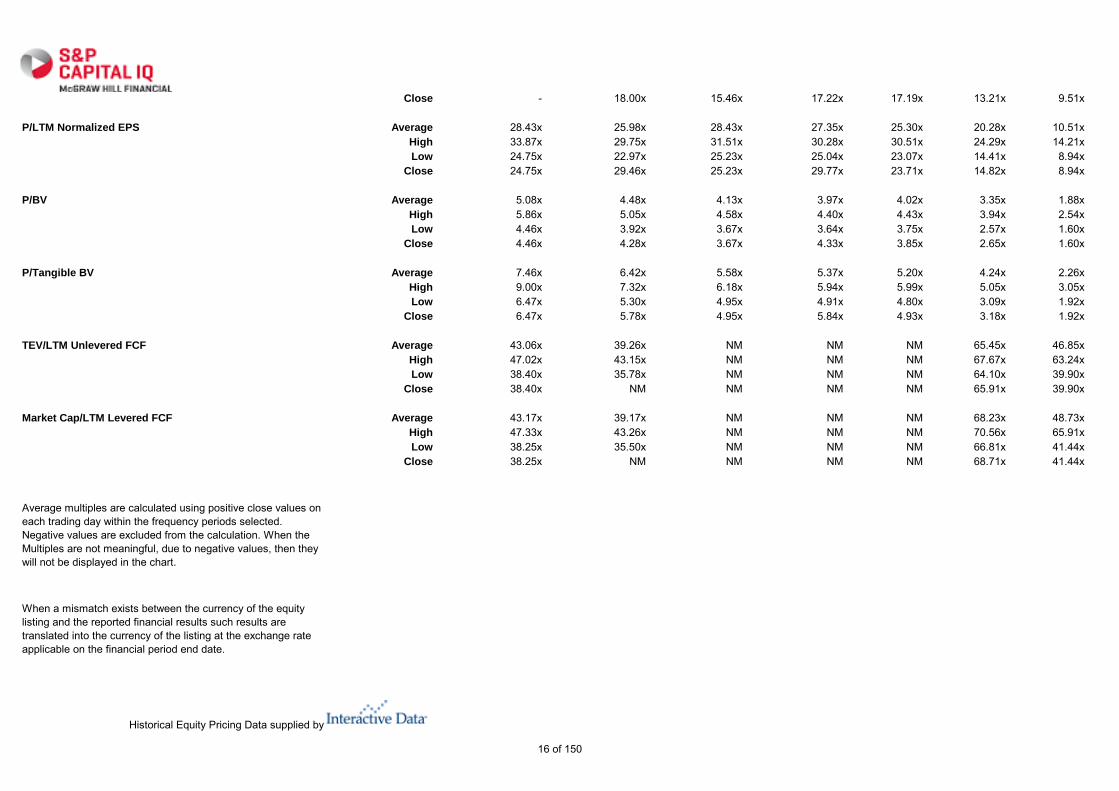

Sports Direct International plc (LSE:SPD) > Financials > Multiples

View: Data Frequency: QuarterlyOrder: Latest on Right Decimals: Capital IQ (Default)Dilution: Basic

Multiples Detail In Millions of the reported currency, except per share items.

For Quarter Ending Sep-30-2014 Dec-31-2014 Mar-31-2015 Jun-30-2015 Sep-30-2015 Dec-31-2015 Mar-24-2016

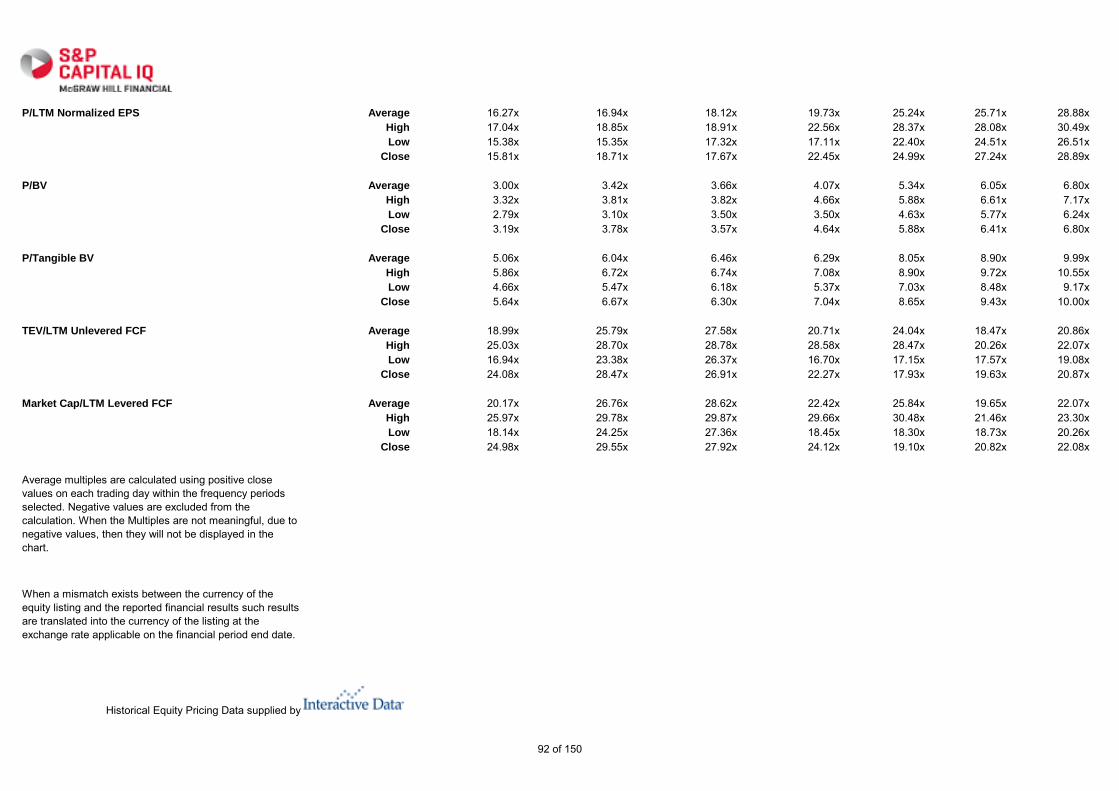

TEV/LTM Total Revenue Average 1.67x 1.48x 1.52x 1.47x 1.64x 1.43x 0.87xHigh 2.01x 1.61x 1.68x 1.62x 1.73x 1.65x 1.17xLow 1.43x 1.33x 1.36x 1.35x 1.55x 1.19x 0.74x

Close 1.43x 1.57x 1.36x 1.59x 1.61x 1.22x 0.74x

TEV/NTM Total Revenues Average - 1.34x 1.44x 1.37x 1.54x 1.33x 0.84xHigh - 1.48x 1.57x 1.50x 1.63x 1.55x 1.16xLow - 1.19x 1.29x 1.25x 1.44x 1.12x 0.72x

Close - 1.46x 1.29x 1.48x 1.52x 1.16x 0.72x

TEV/LTM EBITDA Average 14.15x 12.40x 12.67x 12.21x 12.56x 10.70x 6.39xHigh 17.24x 13.54x 13.98x 13.46x 13.56x 12.43x 8.63xLow 12.05x 11.23x 11.31x 11.23x 11.73x 8.74x 5.44x

Close 12.05x 13.11x 11.31x 13.24x 12.14x 8.99x 5.44x

TEV/NTM EBITDA Average - 10.13x 10.69x 10.02x 10.91x 9.17x 6.06xHigh - 11.10x 11.68x 10.96x 11.53x 10.78x 7.83xLow - 9.05x 9.60x 9.21x 10.29x 7.61x 5.41x

Close - 10.95x 9.60x 10.78x 10.53x 7.83x 5.42x

TEV/LTM EBIT Average 17.64x 15.49x 15.93x 15.35x 15.74x 13.43x 8.16xHigh 21.43x 16.89x 17.58x 16.92x 17.05x 15.56x 11.01xLow 15.03x 14.01x 14.21x 14.11x 14.68x 11.16x 6.95x

Close 15.03x 16.48x 14.21x 16.65x 15.19x 11.48x 6.95x

P/LTM EPS Average 24.23x 21.88x 22.59x 21.72x 20.59x 16.84x 9.40xHigh 28.43x 23.96x 25.03x 24.06x 24.24x 19.88x 12.72xLow 21.18x 19.66x 20.04x 19.89x 18.88x 12.89x 7.99x

Close 21.18x 23.40x 20.04x 23.64x 19.41x 13.26x 7.99x

P/NTM EPS Average - 16.49x 17.46x 16.06x 17.82x 15.02x 10.51xHigh - 18.21x 19.34x 17.52x 18.95x 17.60x 13.21xLow - 14.56x 15.46x 14.70x 16.71x 12.84x 9.37x

15 of 150

Close - 18.00x 15.46x 17.22x 17.19x 13.21x 9.51x

P/LTM Normalized EPS Average 28.43x 25.98x 28.43x 27.35x 25.30x 20.28x 10.51xHigh 33.87x 29.75x 31.51x 30.28x 30.51x 24.29x 14.21xLow 24.75x 22.97x 25.23x 25.04x 23.07x 14.41x 8.94x

Close 24.75x 29.46x 25.23x 29.77x 23.71x 14.82x 8.94x

P/BV Average 5.08x 4.48x 4.13x 3.97x 4.02x 3.35x 1.88xHigh 5.86x 5.05x 4.58x 4.40x 4.43x 3.94x 2.54xLow 4.46x 3.92x 3.67x 3.64x 3.75x 2.57x 1.60x

Close 4.46x 4.28x 3.67x 4.33x 3.85x 2.65x 1.60x

P/Tangible BV Average 7.46x 6.42x 5.58x 5.37x 5.20x 4.24x 2.26xHigh 9.00x 7.32x 6.18x 5.94x 5.99x 5.05x 3.05xLow 6.47x 5.30x 4.95x 4.91x 4.80x 3.09x 1.92x

Close 6.47x 5.78x 4.95x 5.84x 4.93x 3.18x 1.92x

TEV/LTM Unlevered FCF Average 43.06x 39.26x NM NM NM 65.45x 46.85xHigh 47.02x 43.15x NM NM NM 67.67x 63.24xLow 38.40x 35.78x NM NM NM 64.10x 39.90x

Close 38.40x NM NM NM NM 65.91x 39.90x

Market Cap/LTM Levered FCF Average 43.17x 39.17x NM NM NM 68.23x 48.73xHigh 47.33x 43.26x NM NM NM 70.56x 65.91xLow 38.25x 35.50x NM NM NM 66.81x 41.44x

Close 38.25x NM NM NM NM 68.71x 41.44x

Average multiples are calculated using positive close values on each trading day within the frequency periods selected. Negative values are excluded from the calculation. When the Multiples are not meaningful, due to negative values, then they will not be displayed in the chart.

When a mismatch exists between the currency of the equity listing and the reported financial results such results are translated into the currency of the listing at the exchange rate applicable on the financial period end date.

Historical Equity Pricing Data supplied by

16 of 150

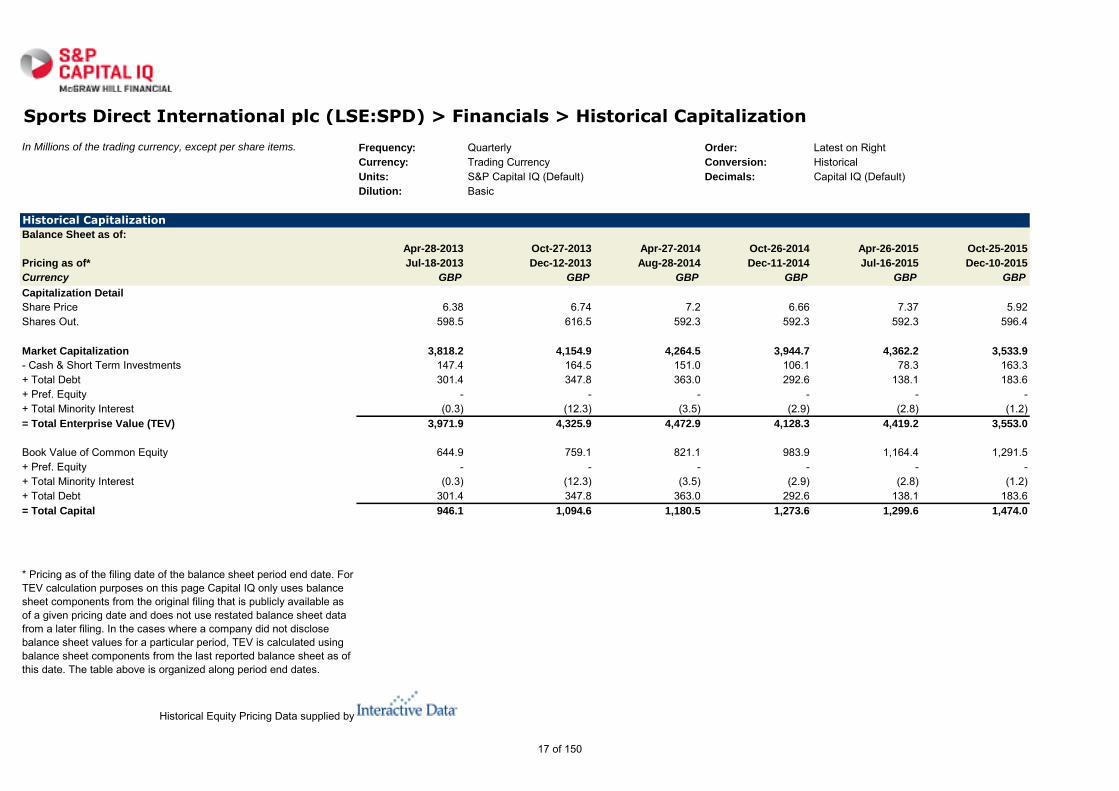

Sports Direct International plc (LSE:SPD) > Financials > Historical Capitalization

In Millions of the trading currency, except per share items. Frequency: Quarterly Order: Latest on RightCurrency: Trading Currency Conversion: HistoricalUnits: S&P Capital IQ (Default) Decimals: Capital IQ (Default)Dilution: Basic

Historical Capitalization

Balance Sheet as of:

Apr-28-2013 Oct-27-2013 Apr-27-2014 Oct-26-2014 Apr-26-2015 Oct-25-2015

Pricing as of* Jul-18-2013 Dec-12-2013 Aug-28-2014 Dec-11-2014 Jul-16-2015 Dec-10-2015

Currency GBP GBP GBP GBP GBP GBP

Capitalization Detail

Share Price 6.38 6.74 7.2 6.66 7.37 5.92 Shares Out. 598.5 616.5 592.3 592.3 592.3 596.4

Market Capitalization 3,818.2 4,154.9 4,264.5 3,944.7 4,362.2 3,533.9

- Cash & Short Term Investments 147.4 164.5 151.0 106.1 78.3 163.3 + Total Debt 301.4 347.8 363.0 292.6 138.1 183.6 + Pref. Equity - - - - - -+ Total Minority Interest (0.3) (12.3) (3.5) (2.9) (2.8) (1.2) = Total Enterprise Value (TEV) 3,971.9 4,325.9 4,472.9 4,128.3 4,419.2 3,553.0

Book Value of Common Equity 644.9 759.1 821.1 983.9 1,164.4 1,291.5 + Pref. Equity - - - - - -+ Total Minority Interest (0.3) (12.3) (3.5) (2.9) (2.8) (1.2) + Total Debt 301.4 347.8 363.0 292.6 138.1 183.6 = Total Capital 946.1 1,094.6 1,180.5 1,273.6 1,299.6 1,474.0

* Pricing as of the filing date of the balance sheet period end date. For TEV calculation purposes on this page Capital IQ only uses balance sheet components from the original filing that is publicly available as of a given pricing date and does not use restated balance sheet data from a later filing. In the cases where a company did not disclose balance sheet values for a particular period, TEV is calculated using balance sheet components from the last reported balance sheet as of this date. The table above is organized along period end dates.

Historical Equity Pricing Data supplied by

17 of 150

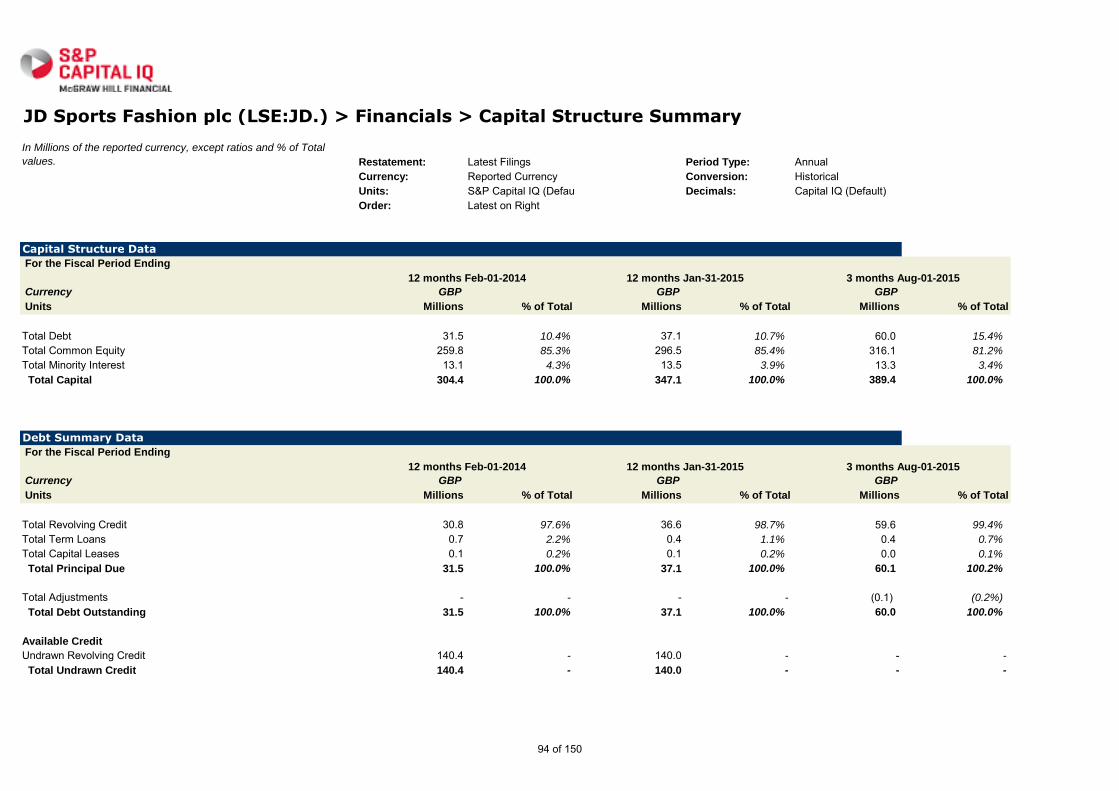

Sports Direct International plc (LSE:SPD) > Financials > Capital Structure Summary

In Millions of the reported currency, except ratios and % of Total

values. Restatement: Latest Filings

Period Type: AnnualCurrency: Reported Currency Conversion: HistoricalUnits: S&P Capital IQ (Default) Decimals: Capital IQ (Default)Order: Latest on Right

Capital Structure Data

For the Fiscal Period Ending

Currency GBP GBP GBP

Units Millions % of Total Millions % of Total Millions % of Total

Total Debt 363.0 30.7% 138.1 10.6% 183.6 12.5%

Total Common Equity 821.1 69.6% 1,164.4 89.6% 1,291.5 87.6%

Total Minority Interest (3.5) (0.3%) (2.8) (0.2%) (1.2) (0.1%)

Total Capital 1,180.5 100.0% 1,299.6 100.0% 1,474.0 100.0%

Debt Summary Data

For the Fiscal Period Ending

Currency GBP GBP GBP

Units Millions % of Total Millions % of Total Millions % of Total

Total Revolving Credit 294.7 81.2% 0.8 0.6% 0.8 0.4%

Total Term Loans 68.2 18.8% 137.2 99.4% 137.2 74.7%

Total Principal Due 363.0 100.0% 138.1 100.0% 138.1 75.2%

Total Adjustments - - - - 45.6 24.8%

Total Debt Outstanding 363.0 100.0% 138.1 100.0% 183.6 100.0%

Available Credit

Undrawn Revolving Credit - - 988.0 - - -

Total Undrawn Credit - - 988.0 - - -

Additional Totals

Total Cash & ST Investments 151.0 - 78.3 - 163.3 -

Net Debt 212.0 - 59.7 - 20.3 -

Total Senior Debt 363.0 100.0% 138.1 100.0% 138.1 75.2%

Total Short-Term Borrowings 5.7 1.6% 0.8 0.6% - -

Curr. Port. of LT Debt/Cap. Leases 350.5 96.6% 0.4 0.3% 0.8 0.4%

12 months Apr-27-2014 12 months Apr-26-2015 3 months Oct-25-2015

12 months Apr-27-2014 12 months Apr-26-2015 3 months Oct-25-2015

18 of 150

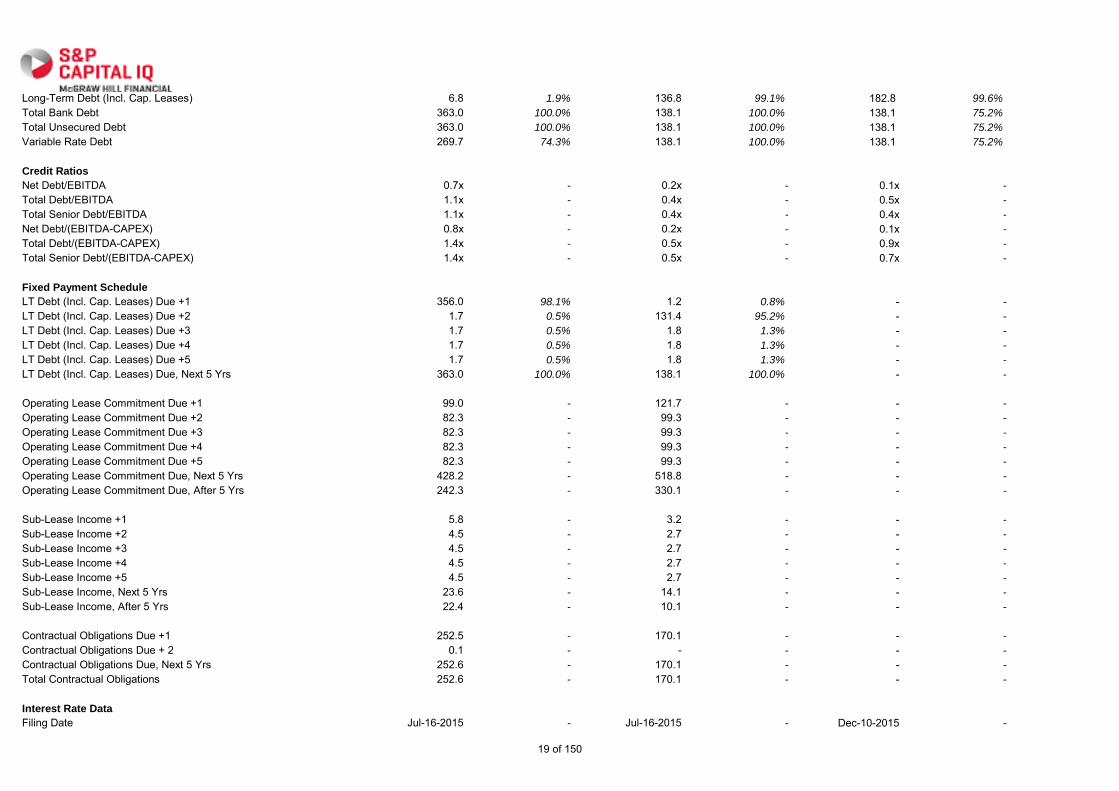

Long-Term Debt (Incl. Cap. Leases) 6.8 1.9% 136.8 99.1% 182.8 99.6%

Total Bank Debt 363.0 100.0% 138.1 100.0% 138.1 75.2%

Total Unsecured Debt 363.0 100.0% 138.1 100.0% 138.1 75.2%

Variable Rate Debt 269.7 74.3% 138.1 100.0% 138.1 75.2%

Credit Ratios

Net Debt/EBITDA 0.7x - 0.2x - 0.1x -

Total Debt/EBITDA 1.1x - 0.4x - 0.5x -

Total Senior Debt/EBITDA 1.1x - 0.4x - 0.4x -

Net Debt/(EBITDA-CAPEX) 0.8x - 0.2x - 0.1x -

Total Debt/(EBITDA-CAPEX) 1.4x - 0.5x - 0.9x -

Total Senior Debt/(EBITDA-CAPEX) 1.4x - 0.5x - 0.7x -

Fixed Payment Schedule

LT Debt (Incl. Cap. Leases) Due +1 356.0 98.1% 1.2 0.8% - -

LT Debt (Incl. Cap. Leases) Due +2 1.7 0.5% 131.4 95.2% - -

LT Debt (Incl. Cap. Leases) Due +3 1.7 0.5% 1.8 1.3% - -

LT Debt (Incl. Cap. Leases) Due +4 1.7 0.5% 1.8 1.3% - -

LT Debt (Incl. Cap. Leases) Due +5 1.7 0.5% 1.8 1.3% - -

LT Debt (Incl. Cap. Leases) Due, Next 5 Yrs 363.0 100.0% 138.1 100.0% - -

Operating Lease Commitment Due +1 99.0 - 121.7 - - -

Operating Lease Commitment Due +2 82.3 - 99.3 - - -

Operating Lease Commitment Due +3 82.3 - 99.3 - - -

Operating Lease Commitment Due +4 82.3 - 99.3 - - -

Operating Lease Commitment Due +5 82.3 - 99.3 - - -

Operating Lease Commitment Due, Next 5 Yrs 428.2 - 518.8 - - -

Operating Lease Commitment Due, After 5 Yrs 242.3 - 330.1 - - -

Sub-Lease Income +1 5.8 - 3.2 - - -

Sub-Lease Income +2 4.5 - 2.7 - - -

Sub-Lease Income +3 4.5 - 2.7 - - -

Sub-Lease Income +4 4.5 - 2.7 - - -

Sub-Lease Income +5 4.5 - 2.7 - - -

Sub-Lease Income, Next 5 Yrs 23.6 - 14.1 - - -

Sub-Lease Income, After 5 Yrs 22.4 - 10.1 - - -

Contractual Obligations Due +1 252.5 - 170.1 - - -

Contractual Obligations Due + 2 0.1 - - - - -

Contractual Obligations Due, Next 5 Yrs 252.6 - 170.1 - - -

Total Contractual Obligations 252.6 - 170.1 - - -

Interest Rate Data

Filing Date Jul-16-2015 - Jul-16-2015 - Dec-10-2015 -

19 of 150

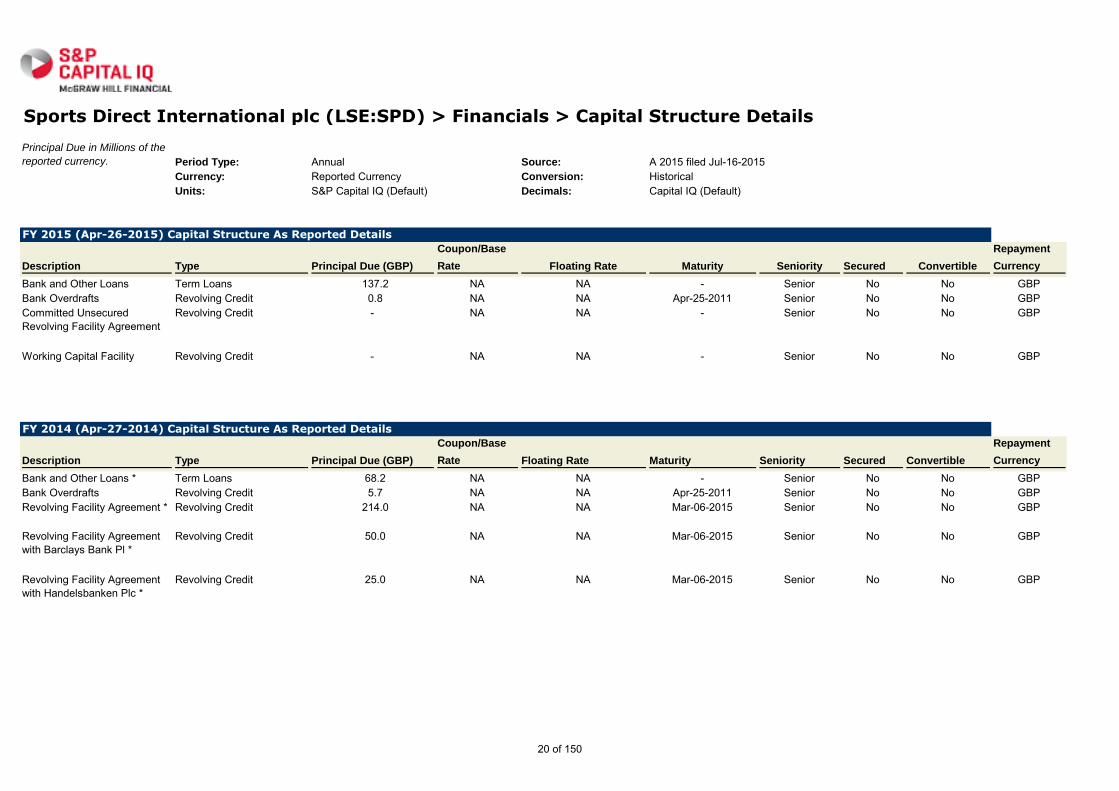

Sports Direct International plc (LSE:SPD) > Financials > Capital Structure Details

Principal Due in Millions of the

reported currency. Period Type: Annual

Source: A 2015 filed Jul-16-2015Currency: Reported Currency Conversion: HistoricalUnits: S&P Capital IQ (Default) Decimals: Capital IQ (Default)

FY 2015 (Apr-26-2015) Capital Structure As Reported Details

Description Type Principal Due (GBP)

Coupon/Base

Rate Floating Rate Maturity Seniority Secured Convertible

Repayment

Currency

Bank and Other Loans Term Loans 137.2 NA NA - Senior No No GBPBank Overdrafts Revolving Credit 0.8 NA NA Apr-25-2011 Senior No No GBPCommitted Unsecured Revolving Facility Agreement

Revolving Credit - NA NA - Senior No No GBP

Working Capital Facility Revolving Credit - NA NA - Senior No No GBP

FY 2014 (Apr-27-2014) Capital Structure As Reported Details

Description Type Principal Due (GBP)

Coupon/Base

Rate Floating Rate Maturity Seniority Secured Convertible

Repayment

Currency

Bank and Other Loans * Term Loans 68.2 NA NA - Senior No No GBPBank Overdrafts Revolving Credit 5.7 NA NA Apr-25-2011 Senior No No GBPRevolving Facility Agreement * Revolving Credit 214.0 NA NA Mar-06-2015 Senior No No GBP

Revolving Facility Agreement with Barclays Bank Pl *

Revolving Credit 50.0 NA NA Mar-06-2015 Senior No No GBP

Revolving Facility Agreement with Handelsbanken Plc *

Revolving Credit 25.0 NA NA Mar-06-2015 Senior No No GBP

20 of 150

Sports Direct International plc (LSE:SPD) > Financials > Ratios

Restatement: Latest Filings Period Type: AnnualOrder: Latest on Right Decimals: Capital IQ (Default)

Ratios

For the Fiscal Period Ending 12 months

Apr-24-2011

12 months

Apr-29-2012

12 months

Apr-28-2013

12 months

Apr-27-2014

12 months

Apr-26-2015

LTM

12 months

Oct-25-2015

Profitability

Return on Assets % 9.1% 9.2% 10.4% 10.2% 10.7% 9.6% Return on Capital % 15.0% 15.2% 16.1% 14.9% 15.0% 13.6% Return on Equity % 28.2% 26.3% 27.2% 24.6% 24.4% 24.1% Return on Common Equity % 28.6% 26.4% 27.1% 24.6% 24.2% 23.8%

Margin Analysis

Gross Margin % 41.2% 40.5% 40.9% 42.7% 43.8% 44.3% SG&A Margin % 32.8% 32.4% 31.4% 33.4% 33.1% 33.6% EBITDA Margin % 12.5% 11.6% 12.1% 11.7% 13.2% 13.5% EBITA Margin % 8.7% 8.4% 9.9% 9.6% 11.0% 11.0% EBIT Margin % 8.5% 8.2% 9.7% 9.4% 10.5% 10.5% Earnings from Cont. Ops Margin % 5.2% 5.8% 6.9% 6.6% 8.5% 9.7% Net Income Margin % 5.3% 5.8% 6.9% 6.7% 8.5% 9.6% Net Income Avail. for Common Margin % 5.3% 5.8% 6.9% 6.7% 8.5% 9.6% Normalized Net Income Margin % 5.2% 5.2% 5.9% 5.7% 6.9% 8.6% Levered Free Cash Flow Margin % 11.5% (0.0%) 2.1% 3.5% (0.0%) 1.8% Unlevered Free Cash Flow Margin % 11.7% 0.2% 2.3% 3.7% 0.1% 1.9%

Asset Turnover

Total Asset Turnover 1.7x 1.8x 1.7x 1.7x 1.6x 1.5x Fixed Asset Turnover 6.3x 6.7x 6.8x 7.3x 6.8x 6.7x Accounts Receivable Turnover 32.8x 39.0x 42.6x 42.9x 38.6x 15.0x Inventory Turnover 4.3x 4.1x 3.4x 3.1x 2.9x 2.5x

Short Term Liquidity

Current Ratio 1.3x 1.4x 1.6x 1.1x 2.3x 2.3x Quick Ratio 0.4x 0.4x 0.5x 0.3x 0.6x 0.8x Cash from Ops. to Curr. Liab. 0.6x 0.5x 0.3x 0.2x 0.6x 0.5x Avg. Days Sales Out. 11.1 9.5 8.5 8.5 9.4 24.3 Avg. Days Inventory Out. 84.5 90.9 107.7 118.8 123.8 148.5 Avg. Days Payable Out. 44.4 39.1 41.7 44.6 48.3 100.1 Avg. Cash Conversion Cycle 51.2 61.3 74.5 82.6 84.9 72.7

21 of 150

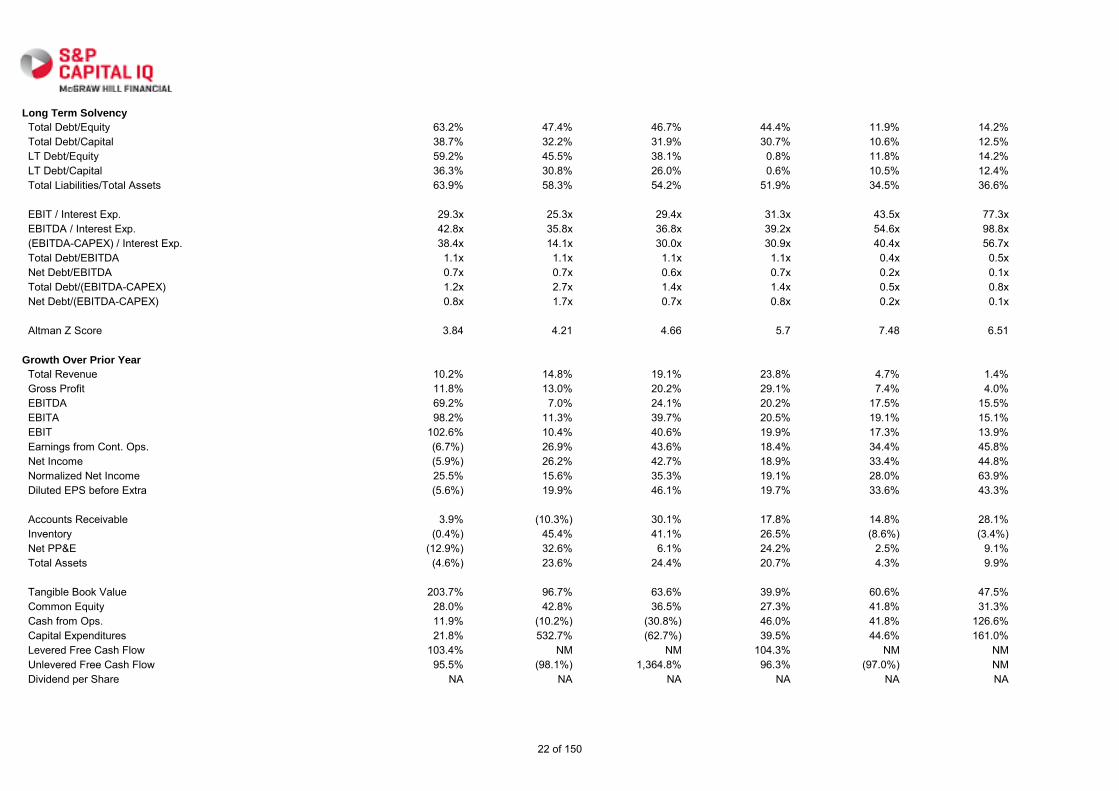

Long Term Solvency

Total Debt/Equity 63.2% 47.4% 46.7% 44.4% 11.9% 14.2% Total Debt/Capital 38.7% 32.2% 31.9% 30.7% 10.6% 12.5% LT Debt/Equity 59.2% 45.5% 38.1% 0.8% 11.8% 14.2% LT Debt/Capital 36.3% 30.8% 26.0% 0.6% 10.5% 12.4% Total Liabilities/Total Assets 63.9% 58.3% 54.2% 51.9% 34.5% 36.6%

EBIT / Interest Exp. 29.3x 25.3x 29.4x 31.3x 43.5x 77.3x EBITDA / Interest Exp. 42.8x 35.8x 36.8x 39.2x 54.6x 98.8x (EBITDA-CAPEX) / Interest Exp. 38.4x 14.1x 30.0x 30.9x 40.4x 56.7x Total Debt/EBITDA 1.1x 1.1x 1.1x 1.1x 0.4x 0.5x Net Debt/EBITDA 0.7x 0.7x 0.6x 0.7x 0.2x 0.1x Total Debt/(EBITDA-CAPEX) 1.2x 2.7x 1.4x 1.4x 0.5x 0.8x Net Debt/(EBITDA-CAPEX) 0.8x 1.7x 0.7x 0.8x 0.2x 0.1x

Altman Z Score 3.84 4.21 4.66 5.7 7.48 6.51

Growth Over Prior Year

Total Revenue 10.2% 14.8% 19.1% 23.8% 4.7% 1.4% Gross Profit 11.8% 13.0% 20.2% 29.1% 7.4% 4.0% EBITDA 69.2% 7.0% 24.1% 20.2% 17.5% 15.5% EBITA 98.2% 11.3% 39.7% 20.5% 19.1% 15.1% EBIT 102.6% 10.4% 40.6% 19.9% 17.3% 13.9% Earnings from Cont. Ops. (6.7%) 26.9% 43.6% 18.4% 34.4% 45.8% Net Income (5.9%) 26.2% 42.7% 18.9% 33.4% 44.8% Normalized Net Income 25.5% 15.6% 35.3% 19.1% 28.0% 63.9% Diluted EPS before Extra (5.6%) 19.9% 46.1% 19.7% 33.6% 43.3%

Accounts Receivable 3.9% (10.3%) 30.1% 17.8% 14.8% 28.1% Inventory (0.4%) 45.4% 41.1% 26.5% (8.6%) (3.4%) Net PP&E (12.9%) 32.6% 6.1% 24.2% 2.5% 9.1% Total Assets (4.6%) 23.6% 24.4% 20.7% 4.3% 9.9%

Tangible Book Value 203.7% 96.7% 63.6% 39.9% 60.6% 47.5% Common Equity 28.0% 42.8% 36.5% 27.3% 41.8% 31.3% Cash from Ops. 11.9% (10.2%) (30.8%) 46.0% 41.8% 126.6% Capital Expenditures 21.8% 532.7% (62.7%) 39.5% 44.6% 161.0% Levered Free Cash Flow 103.4% NM NM 104.3% NM NM Unlevered Free Cash Flow 95.5% (98.1%) 1,364.8% 96.3% (97.0%) NM Dividend per Share NA NA NA NA NA NA

22 of 150

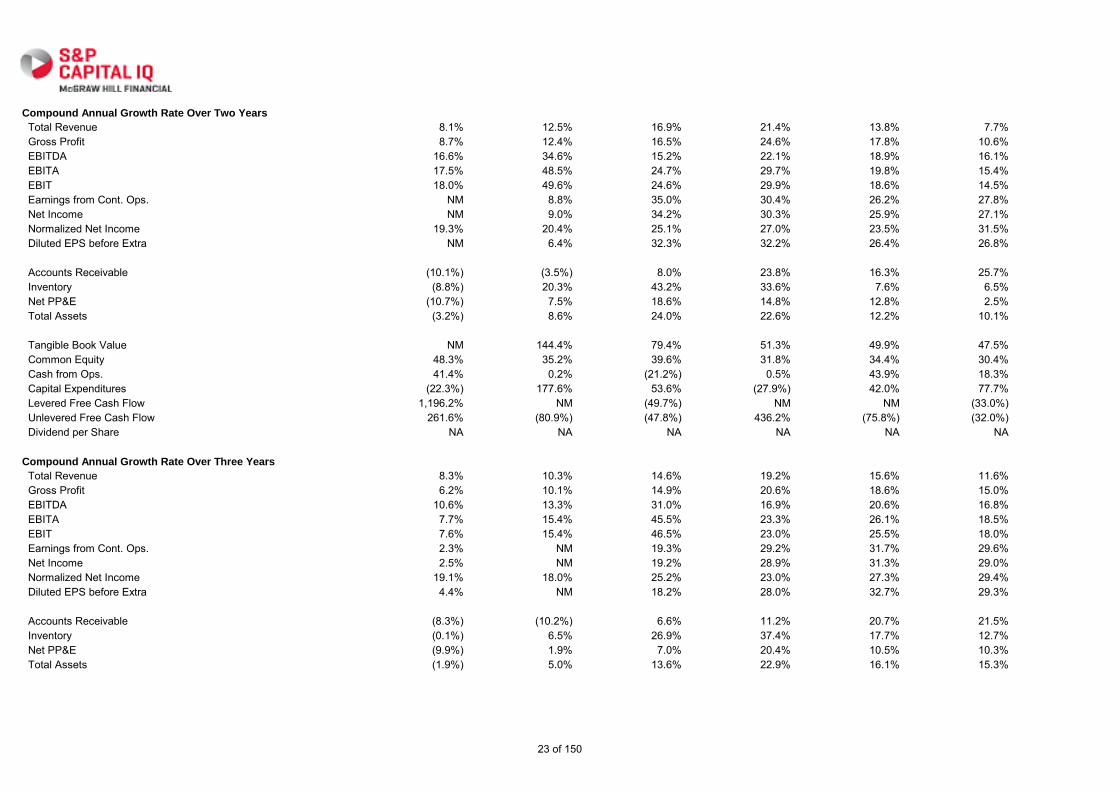

Compound Annual Growth Rate Over Two Years

Total Revenue 8.1% 12.5% 16.9% 21.4% 13.8% 7.7% Gross Profit 8.7% 12.4% 16.5% 24.6% 17.8% 10.6% EBITDA 16.6% 34.6% 15.2% 22.1% 18.9% 16.1% EBITA 17.5% 48.5% 24.7% 29.7% 19.8% 15.4% EBIT 18.0% 49.6% 24.6% 29.9% 18.6% 14.5% Earnings from Cont. Ops. NM 8.8% 35.0% 30.4% 26.2% 27.8% Net Income NM 9.0% 34.2% 30.3% 25.9% 27.1% Normalized Net Income 19.3% 20.4% 25.1% 27.0% 23.5% 31.5% Diluted EPS before Extra NM 6.4% 32.3% 32.2% 26.4% 26.8%

Accounts Receivable (10.1%) (3.5%) 8.0% 23.8% 16.3% 25.7% Inventory (8.8%) 20.3% 43.2% 33.6% 7.6% 6.5% Net PP&E (10.7%) 7.5% 18.6% 14.8% 12.8% 2.5% Total Assets (3.2%) 8.6% 24.0% 22.6% 12.2% 10.1%

Tangible Book Value NM 144.4% 79.4% 51.3% 49.9% 47.5% Common Equity 48.3% 35.2% 39.6% 31.8% 34.4% 30.4% Cash from Ops. 41.4% 0.2% (21.2%) 0.5% 43.9% 18.3% Capital Expenditures (22.3%) 177.6% 53.6% (27.9%) 42.0% 77.7% Levered Free Cash Flow 1,196.2% NM (49.7%) NM NM (33.0%) Unlevered Free Cash Flow 261.6% (80.9%) (47.8%) 436.2% (75.8%) (32.0%) Dividend per Share NA NA NA NA NA NA

Compound Annual Growth Rate Over Three Years

Total Revenue 8.3% 10.3% 14.6% 19.2% 15.6% 11.6% Gross Profit 6.2% 10.1% 14.9% 20.6% 18.6% 15.0% EBITDA 10.6% 13.3% 31.0% 16.9% 20.6% 16.8% EBITA 7.7% 15.4% 45.5% 23.3% 26.1% 18.5% EBIT 7.6% 15.4% 46.5% 23.0% 25.5% 18.0% Earnings from Cont. Ops. 2.3% NM 19.3% 29.2% 31.7% 29.6% Net Income 2.5% NM 19.2% 28.9% 31.3% 29.0% Normalized Net Income 19.1% 18.0% 25.2% 23.0% 27.3% 29.4% Diluted EPS before Extra 4.4% NM 18.2% 28.0% 32.7% 29.3%

Accounts Receivable (8.3%) (10.2%) 6.6% 11.2% 20.7% 21.5% Inventory (0.1%) 6.5% 26.9% 37.4% 17.7% 12.7% Net PP&E (9.9%) 1.9% 7.0% 20.4% 10.5% 10.3% Total Assets (1.9%) 5.0% 13.6% 22.9% 16.1% 15.3%

23 of 150

Tangible Book Value NM NM 113.8% 65.1% 54.3% 49.8% Common Equity 38.3% 46.4% 35.7% 35.4% 35.1% 32.8% Cash from Ops. 103.4% 21.5% (11.4%) (3.2%) 12.7% 14.7% Capital Expenditures (45.8%) 56.3% 42.2% 48.7% (9.1%) 5.3% Levered Free Cash Flow NM NM (19.9%) (19.8%) NM NM Unlevered Free Cash Flow NM (37.6%) (18.9%) (18.8%) (4.9%) 254.8% Dividend per Share NA NA NA NA NA NA

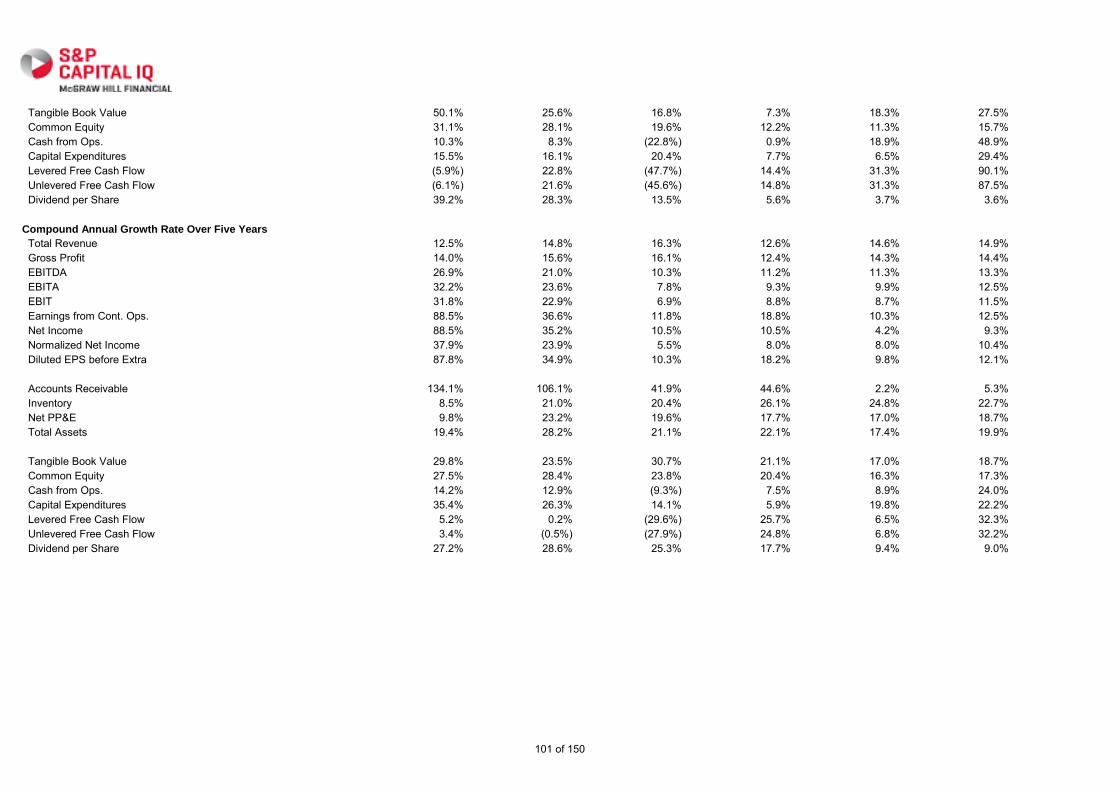

Compound Annual Growth Rate Over Five Years

Total Revenue 6.0% 6.4% 11.7% 14.6% 14.3% 13.3% Gross Profit 7.6% 4.5% 10.2% 15.7% 16.1% 14.8% EBITDA 7.2% 2.7% 12.4% 16.8% 26.0% 20.3% EBITA 5.2% (0.1%) 14.2% 20.9% 34.6% 26.3% EBIT 4.9% (0.2%) 14.1% 21.0% 34.6% 26.1% Earnings from Cont. Ops. 5.1% 23.3% 14.3% NM 22.0% 18.1% Net Income 6.0% 23.0% 14.2% NM 21.9% 17.8% Normalized Net Income 6.6% 4.9% 21.4% 21.5% 24.5% 21.3% Diluted EPS before Extra (1.9%) 15.3% 14.8% NM 21.4% 17.2%

Accounts Receivable (0.3%) (4.6%) (2.1%) 2.1% 10.4% 13.6% Inventory (0.1%) 6.5% 15.4% 16.6% 18.8% 18.5% Net PP&E 2.9% 6.9% 0.6% 6.9% 9.3% 11.5% Total Assets 6.5% 3.7% 7.8% 11.7% 13.1% 15.8%

Tangible Book Value (11.9%) 5.6% NM NM 85.5% 58.8% Common Equity 3.0% 11.4% 38.8% 40.4% 35.1% 32.1% Cash from Ops. 24.6% (1.2%) 39.2% 12.6% 7.6% 7.5% Capital Expenditures (21.9%) 18.8% (17.8%) 14.7% 42.1% 55.1% Levered Free Cash Flow NM NM NM 144.1% NM (12.9%) Unlevered Free Cash Flow NM (56.4%) NM 47.6% (50.0%) (12.8%) Dividend per Share NA NA NA NA NA NA

24 of 150

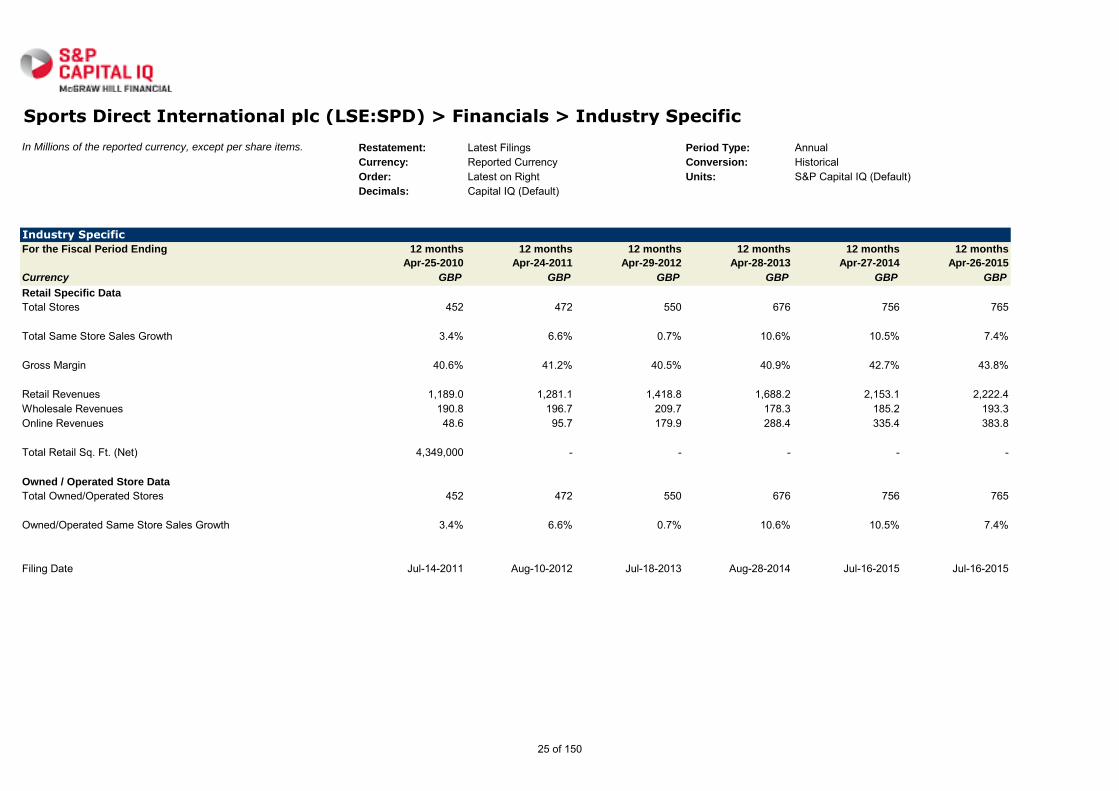

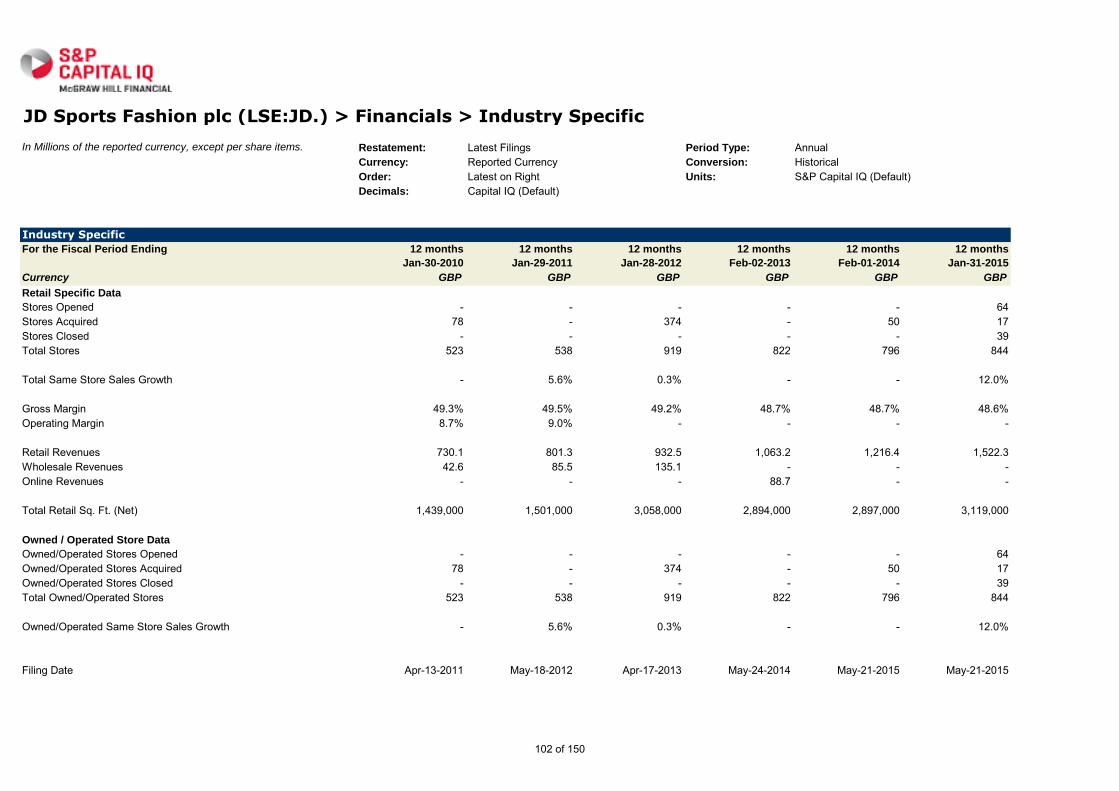

Sports Direct International plc (LSE:SPD) > Financials > Industry Specific

In Millions of the reported currency, except per share items. Restatement: Latest Filings Period Type: AnnualCurrency: Reported Currency Conversion: HistoricalOrder: Latest on Right Units: S&P Capital IQ (Default)Decimals: Capital IQ (Default)

Industry Specific

For the Fiscal Period Ending 12 months

Apr-25-2010

12 months

Apr-24-2011

12 months

Apr-29-2012

12 months

Apr-28-2013

12 months

Apr-27-2014

12 months

Apr-26-2015

Currency GBP GBP GBP GBP GBP GBP

Retail Specific Data

Total Stores 452 472 550 676 756 765

Total Same Store Sales Growth 3.4% 6.6% 0.7% 10.6% 10.5% 7.4%

Gross Margin 40.6% 41.2% 40.5% 40.9% 42.7% 43.8%

Retail Revenues 1,189.0 1,281.1 1,418.8 1,688.2 2,153.1 2,222.4 Wholesale Revenues 190.8 196.7 209.7 178.3 185.2 193.3 Online Revenues 48.6 95.7 179.9 288.4 335.4 383.8

Total Retail Sq. Ft. (Net) 4,349,000 - - - - -

Owned / Operated Store Data

Total Owned/Operated Stores 452 472 550 676 756 765

Owned/Operated Same Store Sales Growth 3.4% 6.6% 0.7% 10.6% 10.5% 7.4%

Filing Date Jul-14-2011 Aug-10-2012 Jul-18-2013 Aug-28-2014 Jul-16-2015 Jul-16-2015

25 of 150

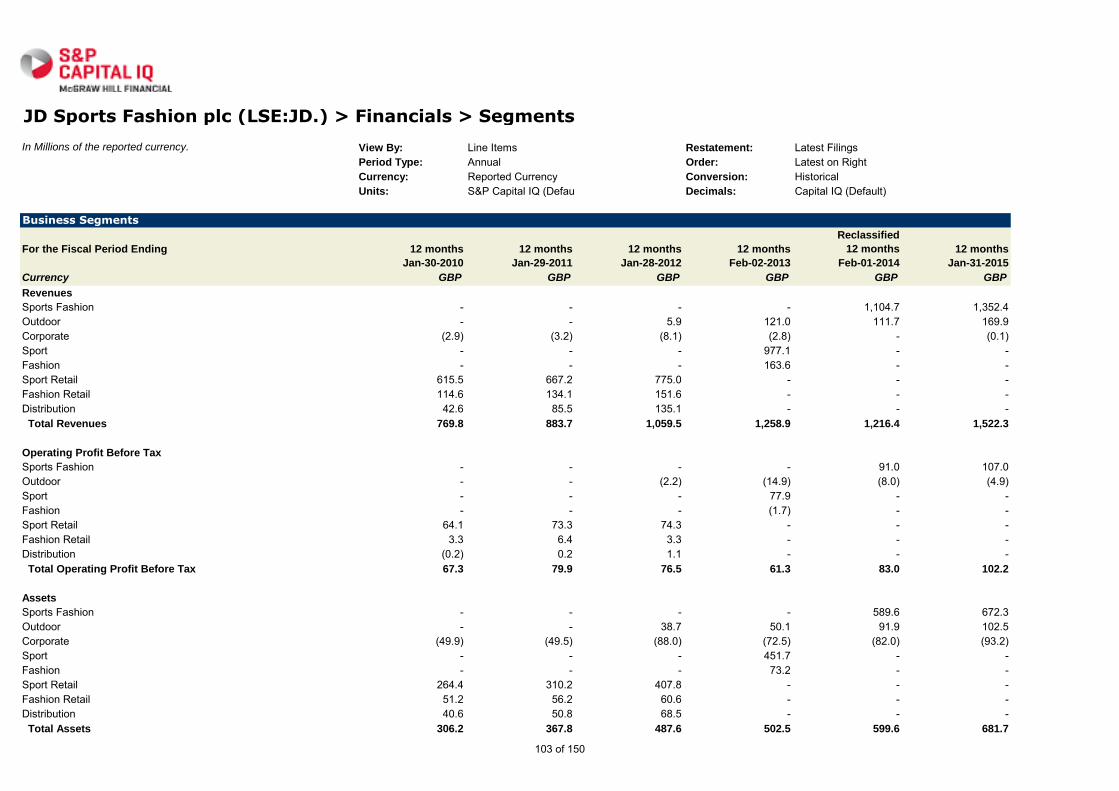

Sports Direct International plc (LSE:SPD) > Financials > Segments

In Millions of the reported currency. View By: Line Items Restatement: Latest FilingsPeriod Type: Annual Order: Latest on RightCurrency: Reported Currency Conversion: HistoricalUnits: S&P Capital IQ (Default) Decimals: Capital IQ (Default)

Business Segments

For the Fiscal Period Ending 12 months

Apr-25-2010

Reclassified

12 months

Apr-24-2011

Reclassified

12 months

Apr-29-2012

Reclassified

12 months

Apr-28-2013

Reclassified

12 months

Apr-27-2014

12 months

Apr-26-2015

Currency GBP GBP GBP GBP GBP GBP

Revenues

Retail - Sports Retail - - - 1,841.6 2,274.6 2,398.5 Retail - Premium Lifestyle - - 114.8 143.3 214.1 207.6 Brands 194.2 190.6 199.2 242.8 247.5 251.9 Corporate (6.1) (3.0) (3.3) (42.1) (30.1) (25.5) Retail - UK Sports 1,143.5 1,279.3 1,368.1 - - -Retail - International Retail 120.1 132.3 157.0 - - - Total Revenues 1,451.6 1,599.2 1,835.8 2,185.6 2,706.0 2,832.6

EBITDA

Retail - Sports Retail - - - 260.0 321.2 356.8 Retail - Premium Lifestyle - - (5.9) 1.0 (20.4) (7.7) Brands - - 25.0 27.0 30.2 34.1 Retail - UK Sports - - 210.3 - - -Retail - International Retail - - 10.6 - - - Total EBITDA - - 240.1 287.9 331.1 383.2

Gross Profit Before Tax

Retail - Sports Retail - - - 738.3 975.0 1,069.1 Retail - Premium Lifestyle - - 34.6 62.7 86.3 80.5 Brands 74.1 77.7 80.8 93.8 93.7 91.2 Retail - UK Sports 462.4 523.5 560.8 - - -Retail - International Retail 52.7 57.7 68.1 - - - Total Gross Profit Before Tax 589.1 658.9 744.3 894.8 1,154.9 1,240.8

Operating Profit Before Tax

Retail - Sports Retail - - - 192.8 254.7 285.5 Retail - Premium Lifestyle - - (7.6) (1.1) (25.7) (11.2) Brands 15.2 17.9 18.3 18.3 23.8 28.0 Retail - UK Sports 89.0 113.1 140.2 - - -Retail - International Retail 3.5 5.6 4.2 - - - Total Operating Profit Before Tax 107.8 136.6 155.2 210.0 252.8 302.3

26 of 150

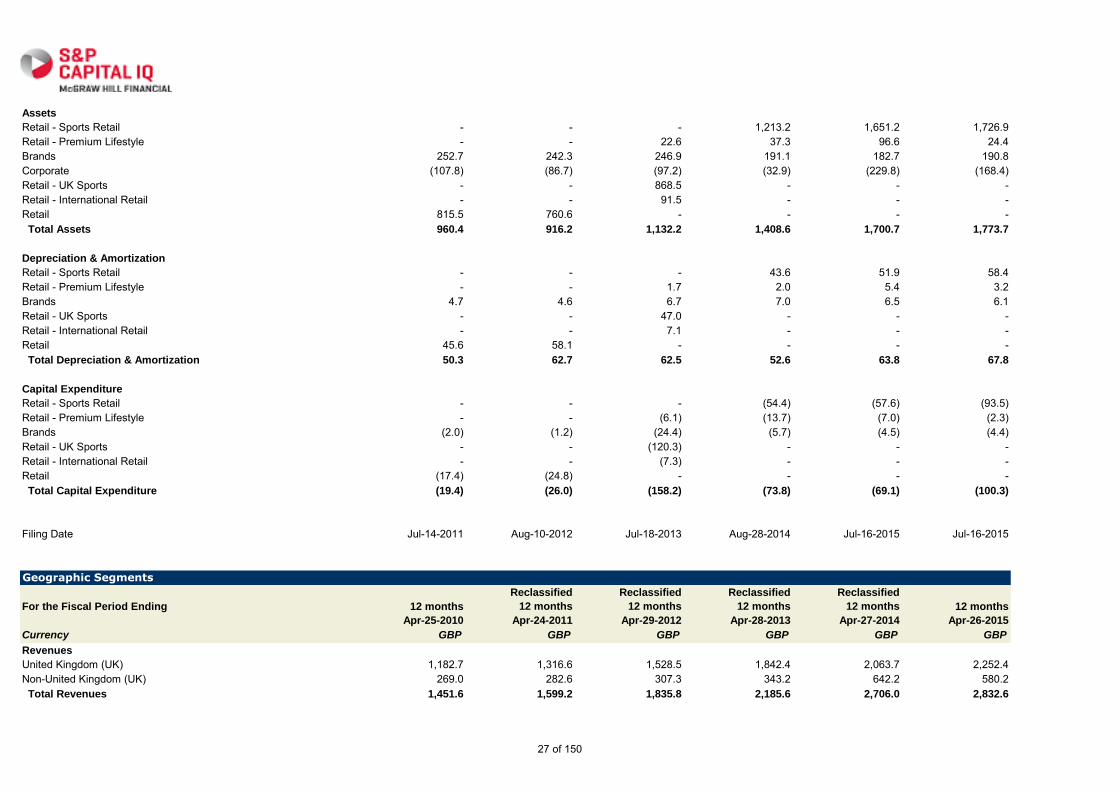

Assets

Retail - Sports Retail - - - 1,213.2 1,651.2 1,726.9 Retail - Premium Lifestyle - - 22.6 37.3 96.6 24.4 Brands 252.7 242.3 246.9 191.1 182.7 190.8 Corporate (107.8) (86.7) (97.2) (32.9) (229.8) (168.4) Retail - UK Sports - - 868.5 - - -Retail - International Retail - - 91.5 - - -Retail 815.5 760.6 - - - - Total Assets 960.4 916.2 1,132.2 1,408.6 1,700.7 1,773.7

Depreciation & Amortization

Retail - Sports Retail - - - 43.6 51.9 58.4 Retail - Premium Lifestyle - - 1.7 2.0 5.4 3.2 Brands 4.7 4.6 6.7 7.0 6.5 6.1 Retail - UK Sports - - 47.0 - - -Retail - International Retail - - 7.1 - - -Retail 45.6 58.1 - - - - Total Depreciation & Amortization 50.3 62.7 62.5 52.6 63.8 67.8

Capital Expenditure

Retail - Sports Retail - - - (54.4) (57.6) (93.5) Retail - Premium Lifestyle - - (6.1) (13.7) (7.0) (2.3) Brands (2.0) (1.2) (24.4) (5.7) (4.5) (4.4) Retail - UK Sports - - (120.3) - - -Retail - International Retail - - (7.3) - - -Retail (17.4) (24.8) - - - - Total Capital Expenditure (19.4) (26.0) (158.2) (73.8) (69.1) (100.3)

Filing Date Jul-14-2011 Aug-10-2012 Jul-18-2013 Aug-28-2014 Jul-16-2015 Jul-16-2015

Geographic Segments

For the Fiscal Period Ending 12 months

Apr-25-2010

Reclassified

12 months

Apr-24-2011

Reclassified

12 months

Apr-29-2012

Reclassified

12 months

Apr-28-2013

Reclassified

12 months

Apr-27-2014

12 months

Apr-26-2015

Currency GBP GBP GBP GBP GBP GBP

Revenues

United Kingdom (UK) 1,182.7 1,316.6 1,528.5 1,842.4 2,063.7 2,252.4 Non-United Kingdom (UK) 269.0 282.6 307.3 343.2 642.2 580.2 Total Revenues 1,451.6 1,599.2 1,835.8 2,185.6 2,706.0 2,832.6

27 of 150

Assets

United Kingdom (UK) 823.2 760.6 941.2 1,214.3 1,526.4 1,564.9 Non-United Kingdom (UK) 245.0 242.3 288.3 227.2 404.1 377.3 Corporate (107.8) (86.7) (97.2) (32.9) (229.8) (168.4) Total Assets 960.4 916.2 1,132.2 1,408.6 1,700.7 1,773.7

Capital Expenditure

United Kingdom (UK) (15.2) (14.1) (148.3) (59.6) (51.5) (81.8) Non-United Kingdom (UK) (4.2) (11.9) (9.9) (14.2) (17.6) (18.5) Total Capital Expenditure (19.4) (26.0) (158.2) (73.8) (69.1) (100.3)

Filing Date Jul-14-2011 Aug-10-2012 Jul-18-2013 Aug-28-2014 Jul-16-2015 Jul-16-2015

28 of 150

Data Provided by

Historical Equity Pricing Data supplied by

Sports Direct Capital IQ spreadsheets: Comparable

Company Information

29 of 150

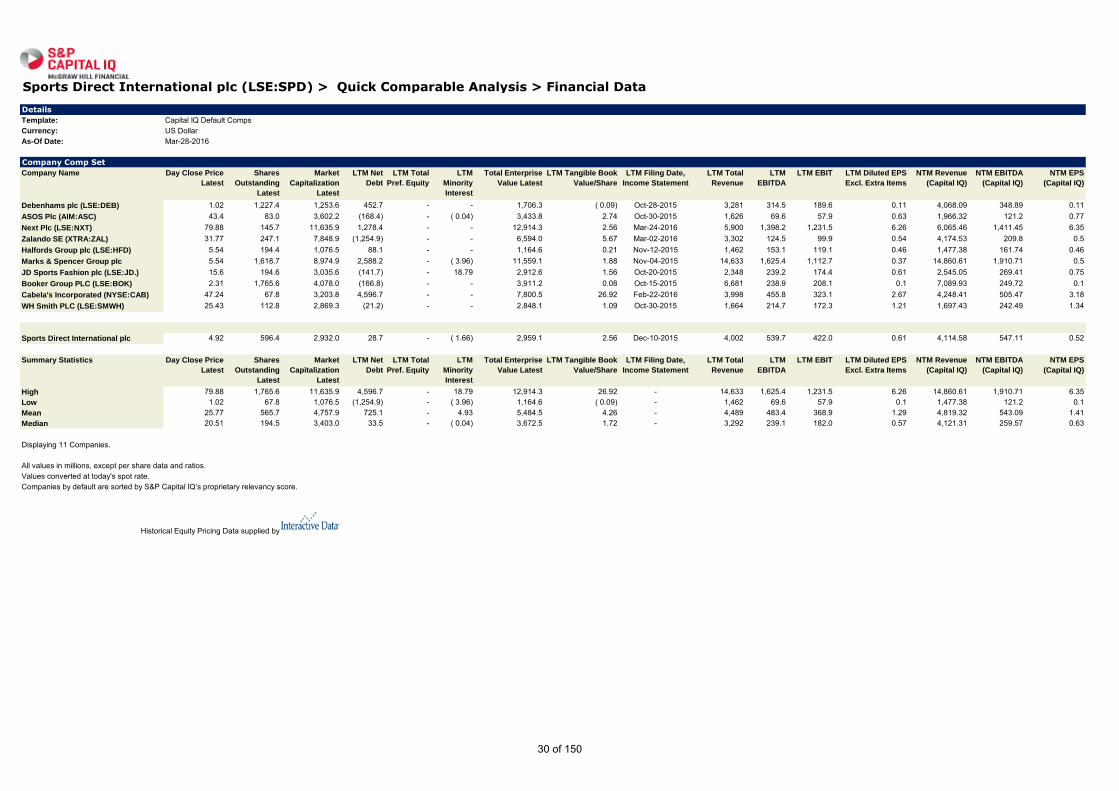

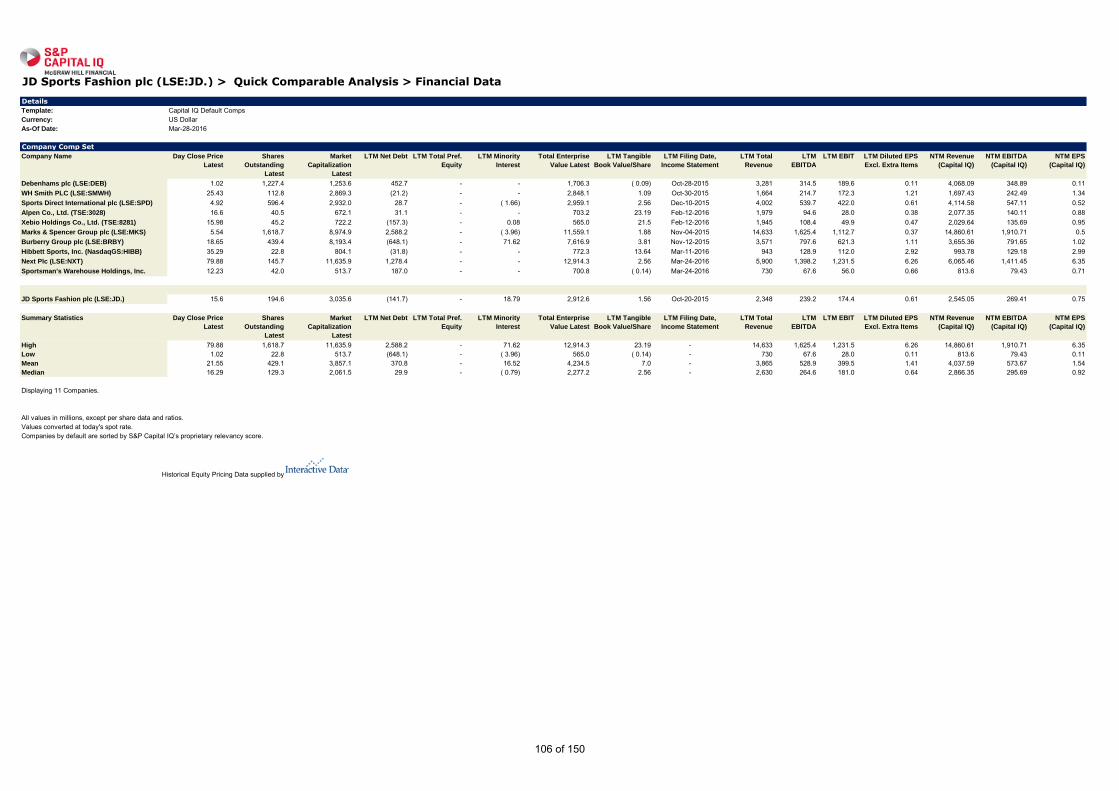

Sports Direct International plc (LSE:SPD) > Quick Comparable Analysis > Financial Data

Details

Template: Capital IQ Default CompsCurrency: US DollarAs-Of Date: Mar-28-2016

Company Comp Set

Company Name Day Close Price

Latest

Shares

Outstanding

Latest

Market

Capitalization

Latest

LTM Net

Debt

LTM Total

Pref. Equity

LTM

Minority

Interest

Total Enterprise

Value Latest

LTM Tangible Book

Value/Share

LTM Filing Date,

Income Statement

LTM Total

Revenue

LTM

EBITDA

LTM EBIT LTM Diluted EPS

Excl. Extra Items

NTM Revenue

(Capital IQ)

NTM EBITDA

(Capital IQ)

NTM EPS

(Capital IQ)

Debenhams plc (LSE:DEB) 1.02 1,227.4 1,253.6 452.7 - - 1,706.3 ( 0.09) Oct-28-2015 3,281 314.5 189.6 0.11 4,068.09 348.89 0.11 ASOS Plc (AIM:ASC) 43.4 83.0 3,602.2 (168.4) - ( 0.04) 3,433.8 2.74 Oct-30-2015 1,626 69.6 57.9 0.63 1,966.32 121.2 0.77 Next Plc (LSE:NXT) 79.88 145.7 11,635.9 1,278.4 - - 12,914.3 2.56 Mar-24-2016 5,900 1,398.2 1,231.5 6.26 6,065.46 1,411.45 6.35 Zalando SE (XTRA:ZAL) 31.77 247.1 7,848.9 (1,254.9) - - 6,594.0 5.67 Mar-02-2016 3,302 124.5 99.9 0.54 4,174.53 209.8 0.5 Halfords Group plc (LSE:HFD) 5.54 194.4 1,076.5 88.1 - - 1,164.6 0.21 Nov-12-2015 1,462 153.1 119.1 0.46 1,477.38 161.74 0.46 Marks & Spencer Group plc

(LSE:MKS)

5.54 1,618.7 8,974.9 2,588.2 - ( 3.96) 11,559.1 1.88 Nov-04-2015 14,633 1,625.4 1,112.7 0.37 14,860.61 1,910.71 0.5 JD Sports Fashion plc (LSE:JD.) 15.6 194.6 3,035.6 (141.7) - 18.79 2,912.6 1.56 Oct-20-2015 2,348 239.2 174.4 0.61 2,545.05 269.41 0.75 Booker Group PLC (LSE:BOK) 2.31 1,765.6 4,078.0 (166.8) - - 3,911.2 0.08 Oct-15-2015 6,681 238.9 208.1 0.1 7,089.93 249.72 0.1 Cabela's Incorporated (NYSE:CAB) 47.24 67.8 3,203.8 4,596.7 - - 7,800.5 26.92 Feb-22-2016 3,998 455.8 323.1 2.67 4,248.41 505.47 3.18 WH Smith PLC (LSE:SMWH) 25.43 112.8 2,869.3 (21.2) - - 2,848.1 1.09 Oct-30-2015 1,664 214.7 172.3 1.21 1,697.43 242.49 1.34

Sports Direct International plc

(LSE:SPD)

4.92 596.4 2,932.0 28.7 - ( 1.66) 2,959.1 2.56 Dec-10-2015 4,002 539.7 422.0 0.61 4,114.58 547.11 0.52

Summary Statistics Day Close Price

Latest

Shares

Outstanding

Latest

Market

Capitalization

Latest

LTM Net

Debt

LTM Total

Pref. Equity

LTM

Minority

Interest

Total Enterprise

Value Latest

LTM Tangible Book

Value/Share

LTM Filing Date,

Income Statement

LTM Total

Revenue

LTM

EBITDA

LTM EBIT LTM Diluted EPS

Excl. Extra Items

NTM Revenue

(Capital IQ)

NTM EBITDA

(Capital IQ)

NTM EPS

(Capital IQ)

High 79.88 1,765.6 11,635.9 4,596.7 - 18.79 12,914.3 26.92 - 14,633 1,625.4 1,231.5 6.26 14,860.61 1,910.71 6.35 Low 1.02 67.8 1,076.5 (1,254.9) - ( 3.96) 1,164.6 ( 0.09) - 1,462 69.6 57.9 0.1 1,477.38 121.2 0.1 Mean 25.77 565.7 4,757.9 725.1 - 4.93 5,484.5 4.26 - 4,489 483.4 368.9 1.29 4,819.32 543.09 1.41 Median 20.51 194.5 3,403.0 33.5 - ( 0.04) 3,672.5 1.72 - 3,292 239.1 182.0 0.57 4,121.31 259.57 0.63

Displaying 11 Companies.

All values in millions, except per share data and ratios.Values converted at today's spot rate.Companies by default are sorted by S&P Capital IQ’s proprietary relevancy score.

Historical Equity Pricing Data supplied by

30 of 150

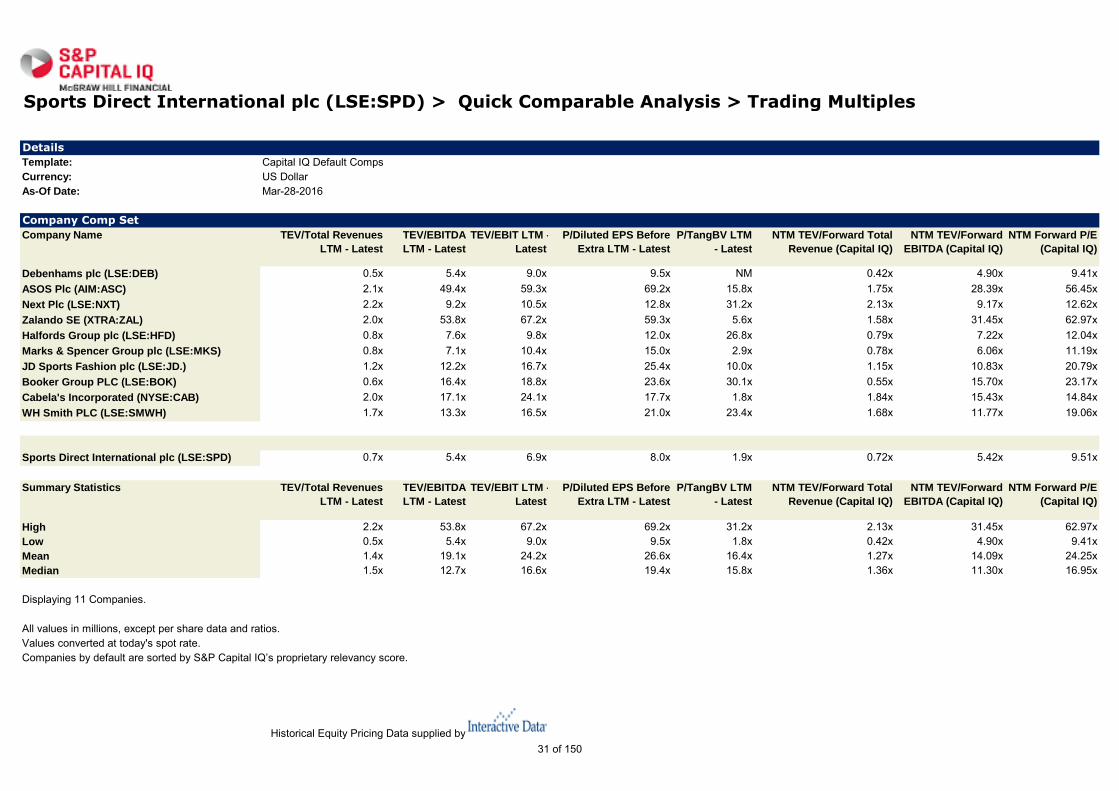

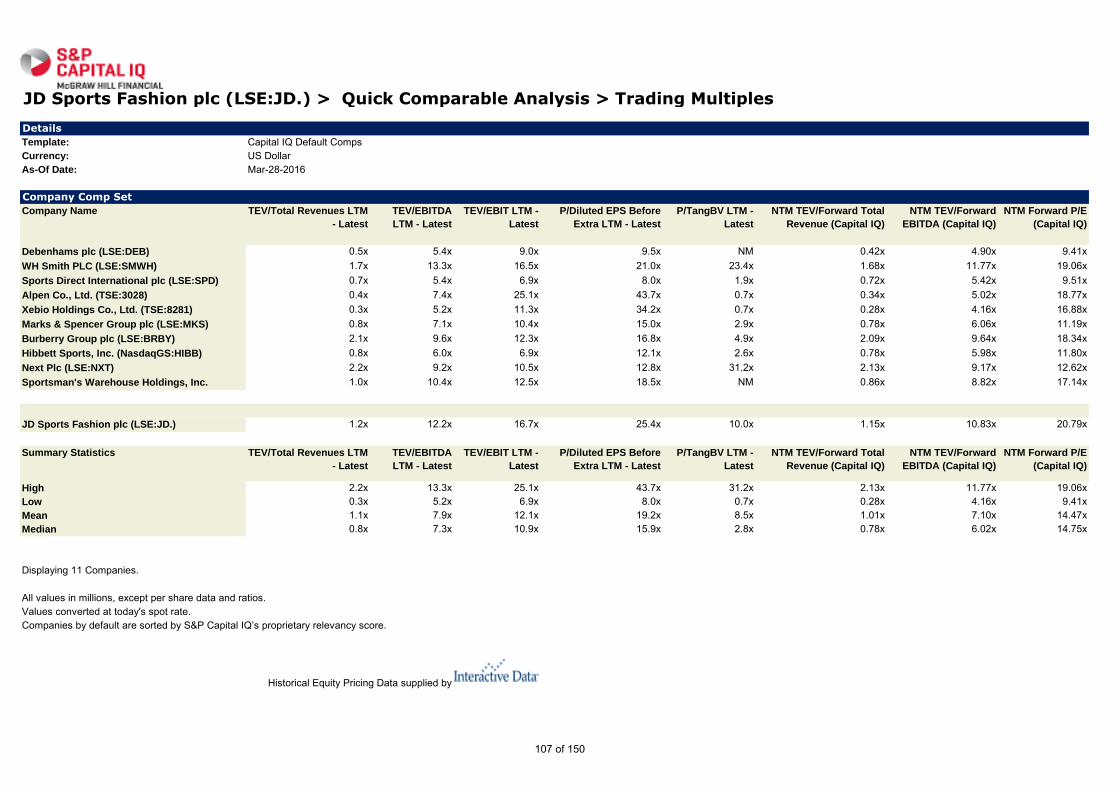

Sports Direct International plc (LSE:SPD) > Quick Comparable Analysis > Trading Multiples

Details

Template: Capital IQ Default CompsCurrency: US DollarAs-Of Date: Mar-28-2016

Company Comp Set

Company Name TEV/Total Revenues

LTM - Latest

TEV/EBITDA

LTM - Latest

TEV/EBIT LTM -

Latest

P/Diluted EPS Before

Extra LTM - Latest

P/TangBV LTM

- Latest

NTM TEV/Forward Total

Revenue (Capital IQ)

NTM TEV/Forward

EBITDA (Capital IQ)

NTM Forward P/E

(Capital IQ)

Debenhams plc (LSE:DEB) 0.5x 5.4x 9.0x 9.5x NM 0.42x 4.90x 9.41xASOS Plc (AIM:ASC) 2.1x 49.4x 59.3x 69.2x 15.8x 1.75x 28.39x 56.45xNext Plc (LSE:NXT) 2.2x 9.2x 10.5x 12.8x 31.2x 2.13x 9.17x 12.62xZalando SE (XTRA:ZAL) 2.0x 53.8x 67.2x 59.3x 5.6x 1.58x 31.45x 62.97xHalfords Group plc (LSE:HFD) 0.8x 7.6x 9.8x 12.0x 26.8x 0.79x 7.22x 12.04xMarks & Spencer Group plc (LSE:MKS) 0.8x 7.1x 10.4x 15.0x 2.9x 0.78x 6.06x 11.19xJD Sports Fashion plc (LSE:JD.) 1.2x 12.2x 16.7x 25.4x 10.0x 1.15x 10.83x 20.79xBooker Group PLC (LSE:BOK) 0.6x 16.4x 18.8x 23.6x 30.1x 0.55x 15.70x 23.17xCabela's Incorporated (NYSE:CAB) 2.0x 17.1x 24.1x 17.7x 1.8x 1.84x 15.43x 14.84xWH Smith PLC (LSE:SMWH) 1.7x 13.3x 16.5x 21.0x 23.4x 1.68x 11.77x 19.06x

Sports Direct International plc (LSE:SPD) 0.7x 5.4x 6.9x 8.0x 1.9x 0.72x 5.42x 9.51x

Summary Statistics TEV/Total Revenues

LTM - Latest

TEV/EBITDA

LTM - Latest

TEV/EBIT LTM -

Latest

P/Diluted EPS Before

Extra LTM - Latest

P/TangBV LTM

- Latest

NTM TEV/Forward Total

Revenue (Capital IQ)

NTM TEV/Forward

EBITDA (Capital IQ)

NTM Forward P/E

(Capital IQ)

High 2.2x 53.8x 67.2x 69.2x 31.2x 2.13x 31.45x 62.97xLow 0.5x 5.4x 9.0x 9.5x 1.8x 0.42x 4.90x 9.41xMean 1.4x 19.1x 24.2x 26.6x 16.4x 1.27x 14.09x 24.25xMedian 1.5x 12.7x 16.6x 19.4x 15.8x 1.36x 11.30x 16.95x

Displaying 11 Companies.

All values in millions, except per share data and ratios.Values converted at today's spot rate.Companies by default are sorted by S&P Capital IQ’s proprietary relevancy score.

Historical Equity Pricing Data supplied by31 of 150

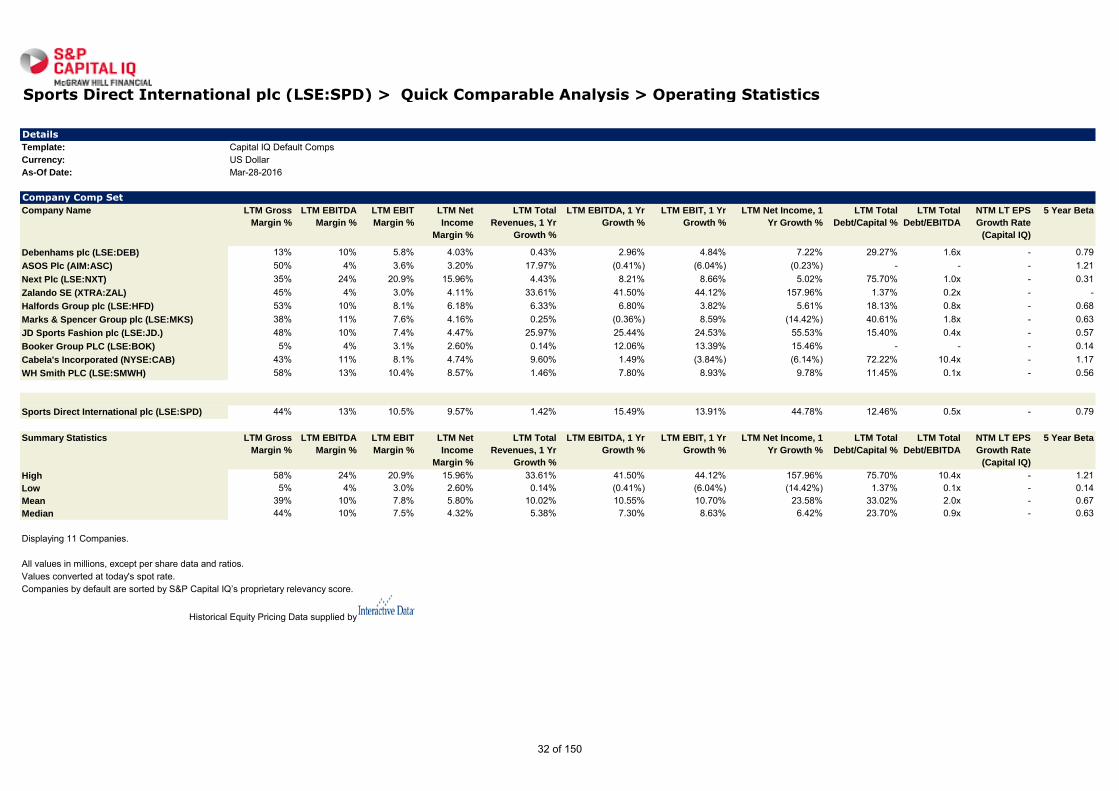

Sports Direct International plc (LSE:SPD) > Quick Comparable Analysis > Operating Statistics

Details

Template: Capital IQ Default CompsCurrency: US DollarAs-Of Date: Mar-28-2016

Company Comp Set

Company Name LTM Gross

Margin %

LTM EBITDA

Margin %

LTM EBIT

Margin %

LTM Net

Income

Margin %

LTM Total

Revenues, 1 Yr

Growth %

LTM EBITDA, 1 Yr

Growth %

LTM EBIT, 1 Yr

Growth %

LTM Net Income, 1

Yr Growth %

LTM Total

Debt/Capital %

LTM Total

Debt/EBITDA

NTM LT EPS

Growth Rate

(Capital IQ)

5 Year Beta

Debenhams plc (LSE:DEB) 13% 10% 5.8% 4.03% 0.43% 2.96% 4.84% 7.22% 29.27% 1.6x - 0.79 ASOS Plc (AIM:ASC) 50% 4% 3.6% 3.20% 17.97% (0.41%) (6.04%) (0.23%) - - - 1.21 Next Plc (LSE:NXT) 35% 24% 20.9% 15.96% 4.43% 8.21% 8.66% 5.02% 75.70% 1.0x - 0.31 Zalando SE (XTRA:ZAL) 45% 4% 3.0% 4.11% 33.61% 41.50% 44.12% 157.96% 1.37% 0.2x - -Halfords Group plc (LSE:HFD) 53% 10% 8.1% 6.18% 6.33% 6.80% 3.82% 5.61% 18.13% 0.8x - 0.68 Marks & Spencer Group plc (LSE:MKS) 38% 11% 7.6% 4.16% 0.25% (0.36%) 8.59% (14.42%) 40.61% 1.8x - 0.63 JD Sports Fashion plc (LSE:JD.) 48% 10% 7.4% 4.47% 25.97% 25.44% 24.53% 55.53% 15.40% 0.4x - 0.57 Booker Group PLC (LSE:BOK) 5% 4% 3.1% 2.60% 0.14% 12.06% 13.39% 15.46% - - - 0.14 Cabela's Incorporated (NYSE:CAB) 43% 11% 8.1% 4.74% 9.60% 1.49% (3.84%) (6.14%) 72.22% 10.4x - 1.17 WH Smith PLC (LSE:SMWH) 58% 13% 10.4% 8.57% 1.46% 7.80% 8.93% 9.78% 11.45% 0.1x - 0.56

Sports Direct International plc (LSE:SPD) 44% 13% 10.5% 9.57% 1.42% 15.49% 13.91% 44.78% 12.46% 0.5x - 0.79

Summary Statistics LTM Gross

Margin %

LTM EBITDA

Margin %

LTM EBIT

Margin %

LTM Net

Income

Margin %

LTM Total

Revenues, 1 Yr

Growth %

LTM EBITDA, 1 Yr

Growth %

LTM EBIT, 1 Yr

Growth %

LTM Net Income, 1

Yr Growth %

LTM Total

Debt/Capital %

LTM Total

Debt/EBITDA

NTM LT EPS

Growth Rate

(Capital IQ)

5 Year Beta

High 58% 24% 20.9% 15.96% 33.61% 41.50% 44.12% 157.96% 75.70% 10.4x - 1.21 Low 5% 4% 3.0% 2.60% 0.14% (0.41%) (6.04%) (14.42%) 1.37% 0.1x - 0.14 Mean 39% 10% 7.8% 5.80% 10.02% 10.55% 10.70% 23.58% 33.02% 2.0x - 0.67 Median 44% 10% 7.5% 4.32% 5.38% 7.30% 8.63% 6.42% 23.70% 0.9x - 0.63

Displaying 11 Companies.

All values in millions, except per share data and ratios.Values converted at today's spot rate.Companies by default are sorted by S&P Capital IQ’s proprietary relevancy score.

Historical Equity Pricing Data supplied by

32 of 150

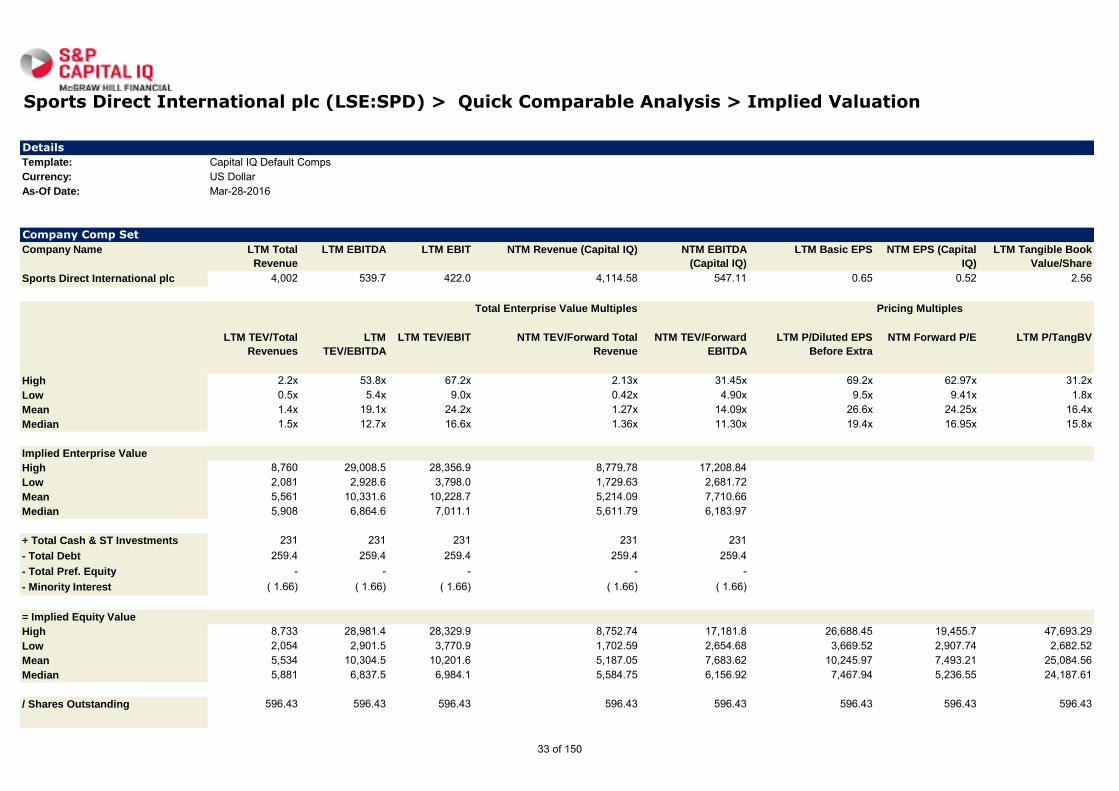

Sports Direct International plc (LSE:SPD) > Quick Comparable Analysis > Implied Valuation

Details

Template: Capital IQ Default CompsCurrency: US DollarAs-Of Date: Mar-28-2016

Company Comp Set

Company Name LTM Total

Revenue

LTM EBITDA LTM EBIT NTM Revenue (Capital IQ) NTM EBITDA

(Capital IQ)

LTM Basic EPS NTM EPS (Capital

IQ)

LTM Tangible Book

Value/Share

Sports Direct International plc

(LSE:SPD)

4,002 539.7 422.0 4,114.58 547.11 0.65 0.52 2.56

Total Enterprise Value Multiples Pricing Multiples

LTM TEV/Total

Revenues

LTM

TEV/EBITDA

LTM TEV/EBIT NTM TEV/Forward Total

Revenue

NTM TEV/Forward

EBITDA

LTM P/Diluted EPS

Before Extra

NTM Forward P/E LTM P/TangBV

High 2.2x 53.8x 67.2x 2.13x 31.45x 69.2x 62.97x 31.2xLow 0.5x 5.4x 9.0x 0.42x 4.90x 9.5x 9.41x 1.8xMean 1.4x 19.1x 24.2x 1.27x 14.09x 26.6x 24.25x 16.4xMedian 1.5x 12.7x 16.6x 1.36x 11.30x 19.4x 16.95x 15.8x

Implied Enterprise Value

High 8,760 29,008.5 28,356.9 8,779.78 17,208.84 Low 2,081 2,928.6 3,798.0 1,729.63 2,681.72 Mean 5,561 10,331.6 10,228.7 5,214.09 7,710.66 Median 5,908 6,864.6 7,011.1 5,611.79 6,183.97

+ Total Cash & ST Investments 231 231 231 231 231 - Total Debt 259.4 259.4 259.4 259.4 259.4 - Total Pref. Equity - - - - -- Minority Interest ( 1.66) ( 1.66) ( 1.66) ( 1.66) ( 1.66)

= Implied Equity Value

High 8,733 28,981.4 28,329.9 8,752.74 17,181.8 26,688.45 19,455.7 47,693.29 Low 2,054 2,901.5 3,770.9 1,702.59 2,654.68 3,669.52 2,907.74 2,682.52 Mean 5,534 10,304.5 10,201.6 5,187.05 7,683.62 10,245.97 7,493.21 25,084.56 Median 5,881 6,837.5 6,984.1 5,584.75 6,156.92 7,467.94 5,236.55 24,187.61

/ Shares Outstanding 596.43 596.43 596.43 596.43 596.43 596.43 596.43 596.43

33 of 150

= Implied Price per Share

High 15 48.6 47.5 14.68 28.81 44.75 32.62 79.96 Low 3 4.9 6.3 2.85 4.45 6.15 4.88 4.5 Mean 9 17.3 17.1 8.7 12.88 17.18 12.56 42.06 Median 10 11.5 11.7 9.36 10.32 12.52 8.78 40.55

Mean Equity Value Across Multiples Equity Value Price Per Share

High 23,227.05 38.94 Low 2,792.99 4.68 Mean 10,216.78 17.13 Median 8,542.05 14.32

All values in millions, except per share data and ratios.Values converted at today's spot rate.

Historical Equity Pricing Data supplied by

34 of 150

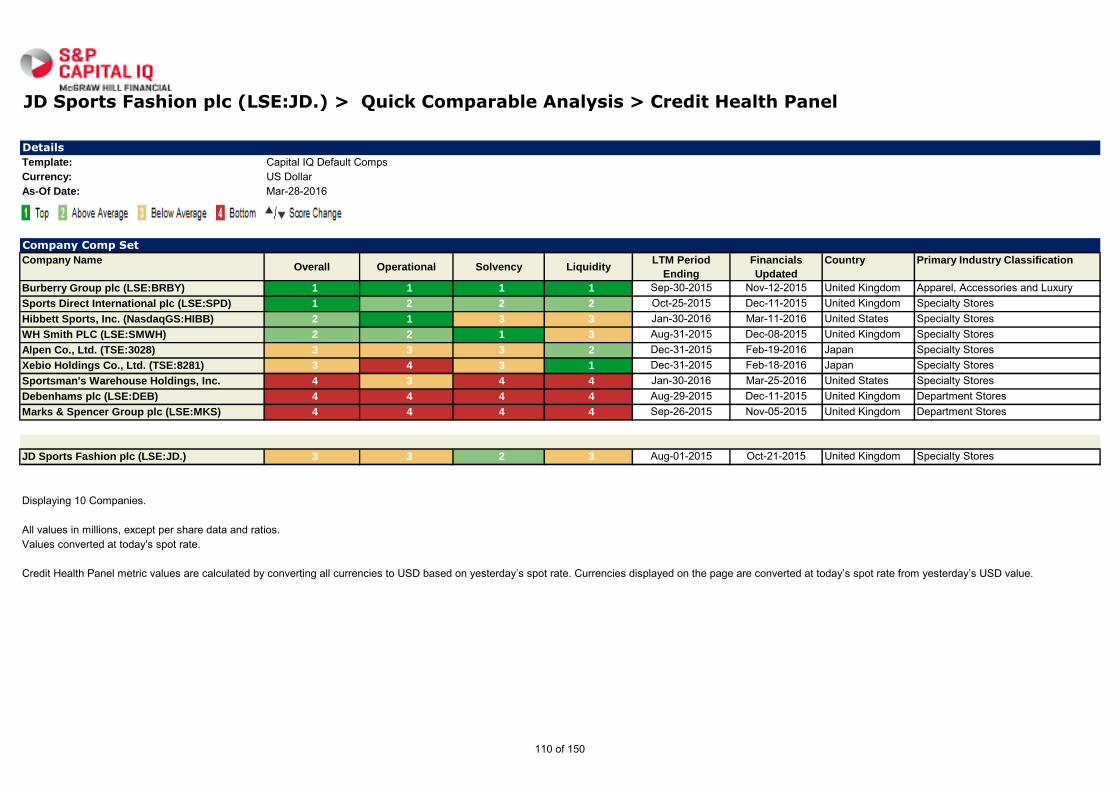

Sports Direct International plc (LSE:SPD) > Quick Comparable Analysis > Credit Health Panel

Details

Template: Capital IQ Default CompsCurrency: US DollarAs-Of Date: Mar-28-2016

Company Comp Set

Company NameOverall Operational Solvency Liquidity

LTM Period Ending Financials Updated Country Primary Industry Classification

Booker Group PLC (LSE:BOK) 1 2 1 2 Sep-11-2015 Oct-15-2015 United Kingdom Food DistributorsWH Smith PLC (LSE:SMWH) 2 1 1 3 Aug-31-2015 Dec-08-2015 United Kingdom Specialty StoresZalando SE (XTRA:ZAL) 2 4 3 1 Dec-31-2015 Mar-06-2016 Germany Internet RetailJD Sports Fashion plc (LSE:JD.) 3 1 3 3 Aug-01-2015 Oct-21-2015 United Kingdom Specialty StoresASOS Plc (AIM:ASC) 3 3 2 3 Aug-31-2015 Oct-31-2015 United Kingdom Internet RetailCabela's Incorporated (NYSE:CAB) 3 3 4 1 Jan-02-2016 Feb-23-2016 United States Specialty StoresMarks & Spencer Group plc (LSE:MKS) 4 3 4 4 Sep-26-2015 Nov-05-2015 United Kingdom Department StoresHalfords Group plc (LSE:HFD) 4 4 3 4 Oct-02-2015 Nov-12-2015 United Kingdom Automotive RetailDebenhams plc (LSE:DEB) 4 4 4 4 Aug-29-2015 Dec-11-2015 United Kingdom Department Stores

Sports Direct International plc (LSE:SPD) 1 2 2 2 Oct-25-2015 Dec-11-2015 United Kingdom Specialty Stores

Displaying 10 Companies.

All values in millions, except per share data and ratios.Values converted at today's spot rate.

Credit Health Panel metric values are calculated by converting all currencies to USD based on yesterday’s spot rate. Currencies displayed on

the page are converted at today’s spot rate from

yesterday’s USD value.

35 of 150

Data Provided by

Historical Equity Pricing Data supplied by

Sports Direct Capital IQ spreadsheets: Estimates

36 of 150

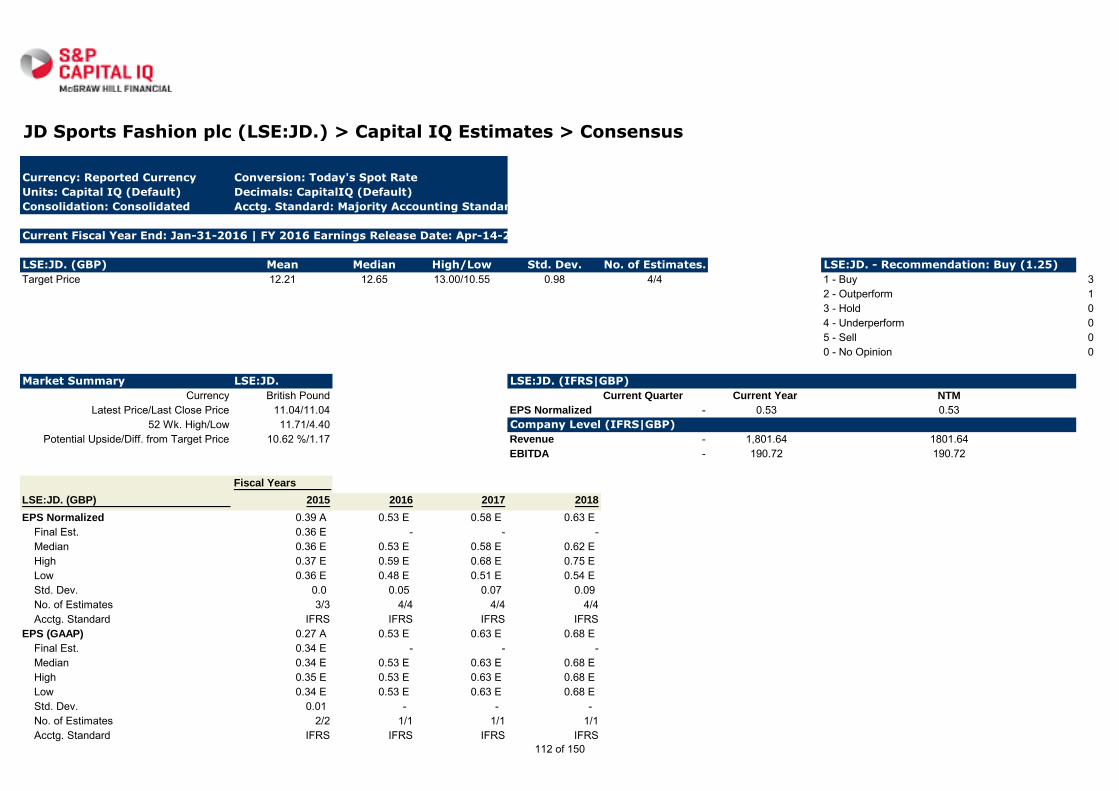

Sports Direct International plc (LSE:SPD) > Capital IQ Estimates > Consensus

Currency: Reported Currency Conversion: Today's Spot Rate

Units: Capital IQ (Default) Decimals: CapitalIQ (Default)

Consolidation: Consolidated Acctg. Standard: IFRS

Current Fiscal Year End: Apr-30-2016 | FY 2016 Earnings Release Date: Jul-07-2016

LSE:SPD (GBP) Mean Median High/Low Std. Dev. No. of Estimates. LSE:SPD - Recommendation: Outperform (2.46)

Target Price 4.73 4.85 5.70/3.25 0.73 12/12 1 - Buy 4LT Growth 6.15% 5.59% 9.70%/3.70% 2.28 4/4 2 - Outperform 3

3 - Hold 44 - Underperform 05 - Sell 20 - No Opinion 0

Market Summary LSE:SPD LSE:SPD (IFRS|GBP)

Currency British Pound Current Half Current Year NTM

Latest Price/Last Close Price 3.48/3.48 EPS Normalized 0.17 0.36 0.3752 Wk. High/Low 8.21/3.45 Company Level (IFRS|GBP)

Potential Upside/Diff. from Target Price 35.90 %/1.25 Revenue 1,373.45 2,822.43 2912.71EBITDA - 378.1 387.3

Fiscal Years

LSE:SPD (GBP) 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

EPS Normalized 0.37 A 0.36 E 0.37 E 0.40 E - - - - - - - Final Est. 0.37 E - - - - - - - - - - Median 0.37 E 0.36 E 0.37 E 0.40 E - - - - - - - High 0.41 E 0.41 E 0.41 E 0.47 E - - - - - - - Low 0.35 E 0.34 E 0.31 E 0.33 E - - - - - - - Std. Dev. 0.02 0.02 0.03 0.04 - - - - - - - No. of Estimates 11/11 12/12 12/12 10/10 - - - - - - - Acctg. Standard IFRS IFRS IFRS IFRS - - - - - - -EPS (GAAP) 0.39 A 0.40 E 0.38 E 0.40 E - - - - - - - Final Est. 0.36 E - - - - - - - - - - Median 0.35 E 0.39 E 0.38 E 0.38 E - - - - - - - High 0.37 E 0.47 E 0.44 E 0.48 E - - - - - - - Low 0.35 E 0.33 E 0.32 E 0.34 E - - - - - - - Std. Dev. 0.01 0.05 0.04 0.05 - - - - - - - No. of Estimates 5/5 6/6 6/6 5/5 - - - - - - - Acctg. Standard IFRS IFRS IFRS IFRS - - - - - - -

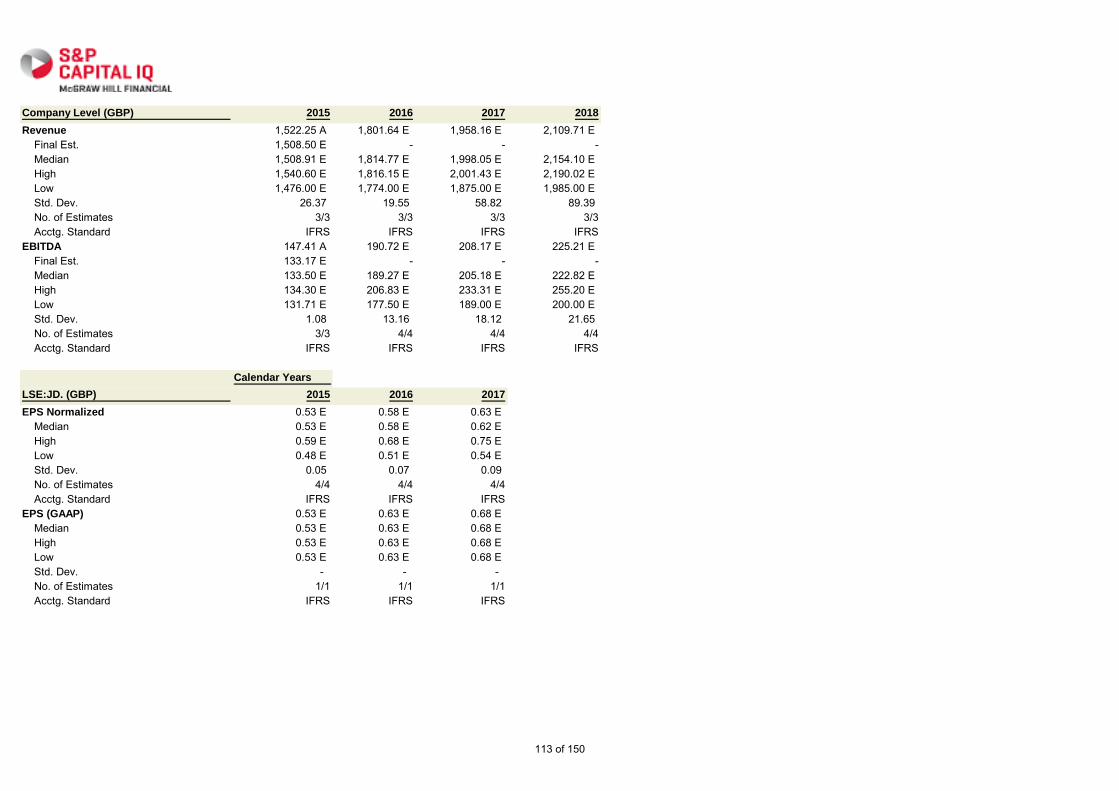

Company Level (GBP) 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Revenue 2,832.56 A 2,822.43 E 3,002.98 E 3,111.43 E 3,211.00 E 3,321.50 E 3,439.50 E 3,545.00 E 3,670.50 E 3,783.00 E 3,889.00 E Final Est. 2,855.53 E - - - - - - - - - - Median 2,838.50 E 2,813.15 E 2,980.00 E 3,126.50 E 3,211.00 E 3,321.50 E 3,439.50 E 3,545.00 E 3,670.50 E 3,783.00 E 3,889.00 E High 2,923.89 E 2,899.01 E 3,172.26 E 3,320.21 E 3,230.00 E 3,330.00 E 3,445.00 E 3,549.00 E 3,690.00 E 3,801.00 E 3,896.00 E Low 2,813.00 E 2,765.20 E 2,838.50 E 2,868.60 E 3,192.00 E 3,313.00 E 3,434.00 E 3,541.00 E 3,651.00 E 3,765.00 E 3,882.00 E Std. Dev. 31.7 31.99 85.89 116.68 19.0 8.5 5.5 4.0 19.5 18.0 7.0 No. of Estimates 10/10 11/11 11/11 9/9 2/2 2/2 2/2 2/2 2/2 2/2 2/2 Acctg. Standard IFRS IFRS IFRS IFRS IFRS IFRS IFRS IFRS IFRS IFRS IFRSEBITDA 383.20 A 378.10 E 396.50 E 413.98 E - - - - - - - Final Est. 370.92 E - - - - - - - - - - Median 370.88 E 380.02 E 385.50 E 413.50 E - - - - - - -

37 of 150

High 383.00 E 395.40 E 431.80 E 467.99 E - - - - - - - Low 358.50 E 356.00 E 346.00 E 352.00 E - - - - - - - Std. Dev. 8.52 10.01 29.28 36.87 - - - - - - - No. of Estimates 10/10 12/12 11/11 9/9 - - - - - - - Acctg. Standard IFRS IFRS IFRS IFRS - - - - - - -

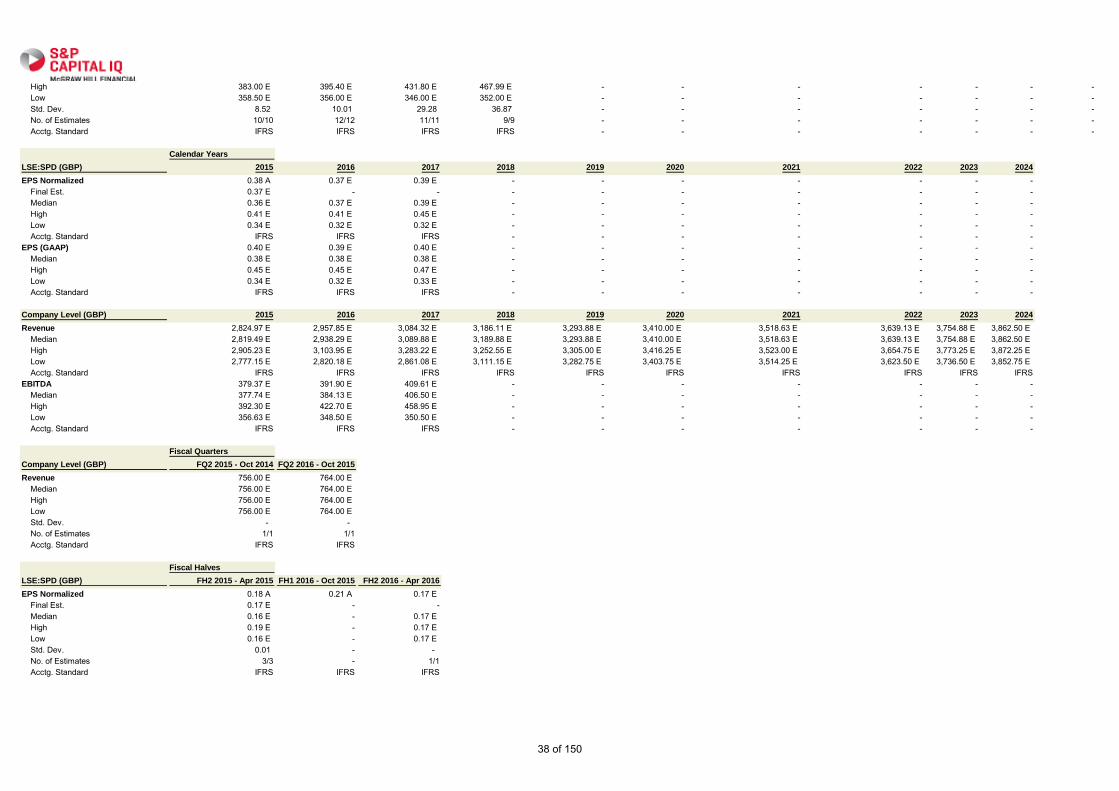

Calendar Years

LSE:SPD (GBP) 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

EPS Normalized 0.38 A 0.37 E 0.39 E - - - - - - - Final Est. 0.37 E - - - - - - - - - Median 0.36 E 0.37 E 0.39 E - - - - - - - High 0.41 E 0.41 E 0.45 E - - - - - - - Low 0.34 E 0.32 E 0.32 E - - - - - - - Acctg. Standard IFRS IFRS IFRS - - - - - - -EPS (GAAP) 0.40 E 0.39 E 0.40 E - - - - - - - Median 0.38 E 0.38 E 0.38 E - - - - - - - High 0.45 E 0.45 E 0.47 E - - - - - - - Low 0.34 E 0.32 E 0.33 E - - - - - - - Acctg. Standard IFRS IFRS IFRS - - - - - - -

Company Level (GBP) 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Revenue 2,824.97 E 2,957.85 E 3,084.32 E 3,186.11 E 3,293.88 E 3,410.00 E 3,518.63 E 3,639.13 E 3,754.88 E 3,862.50 E Median 2,819.49 E 2,938.29 E 3,089.88 E 3,189.88 E 3,293.88 E 3,410.00 E 3,518.63 E 3,639.13 E 3,754.88 E 3,862.50 E High 2,905.23 E 3,103.95 E 3,283.22 E 3,252.55 E 3,305.00 E 3,416.25 E 3,523.00 E 3,654.75 E 3,773.25 E 3,872.25 E Low 2,777.15 E 2,820.18 E 2,861.08 E 3,111.15 E 3,282.75 E 3,403.75 E 3,514.25 E 3,623.50 E 3,736.50 E 3,852.75 E Acctg. Standard IFRS IFRS IFRS IFRS IFRS IFRS IFRS IFRS IFRS IFRSEBITDA 379.37 E 391.90 E 409.61 E - - - - - - - Median 377.74 E 384.13 E 406.50 E - - - - - - - High 392.30 E 422.70 E 458.95 E - - - - - - - Low 356.63 E 348.50 E 350.50 E - - - - - - - Acctg. Standard IFRS IFRS IFRS - - - - - - -

Fiscal Quarters

Company Level (GBP) FQ2 2015 - Oct 2014 FQ2 2016 - Oct 2015

Revenue 756.00 E 764.00 E Median 756.00 E 764.00 E High 756.00 E 764.00 E Low 756.00 E 764.00 E Std. Dev. - - No. of Estimates 1/1 1/1 Acctg. Standard IFRS IFRS

Fiscal Halves

LSE:SPD (GBP) FH2 2015 - Apr 2015 FH1 2016 - Oct 2015 FH2 2016 - Apr 2016

EPS Normalized 0.18 A 0.21 A 0.17 E Final Est. 0.17 E - - Median 0.16 E - 0.17 E High 0.19 E - 0.17 E Low 0.16 E - 0.17 E Std. Dev. 0.01 - - No. of Estimates 3/3 - 1/1 Acctg. Standard IFRS IFRS IFRS

38 of 150

Company Level (GBP) FH2 2015 - Apr 2015 FH1 2016 - Oct 2015 FH2 2016 - Apr 2016

Revenue 1,399.66 A - 1,373.45 E Final Est. 1,396.03 E - - Median 1,401.10 E - 1,373.45 E High 1,407.00 E - 1,373.45 E Low 1,380.00 E - 1,373.45 E Std. Dev. 11.59 - - No. of Estimates 3/3 - 1/1 Acctg. Standard IFRS - IFRSEBITDA 180.10 A - - Final Est. 177.50 E - - Median 177.50 E - - High 180.00 E - - Low 175.00 E - - Std. Dev. 2.5 - - No. of Estimates 2/2 - - Acctg. Standard IFRS - -

39 of 150

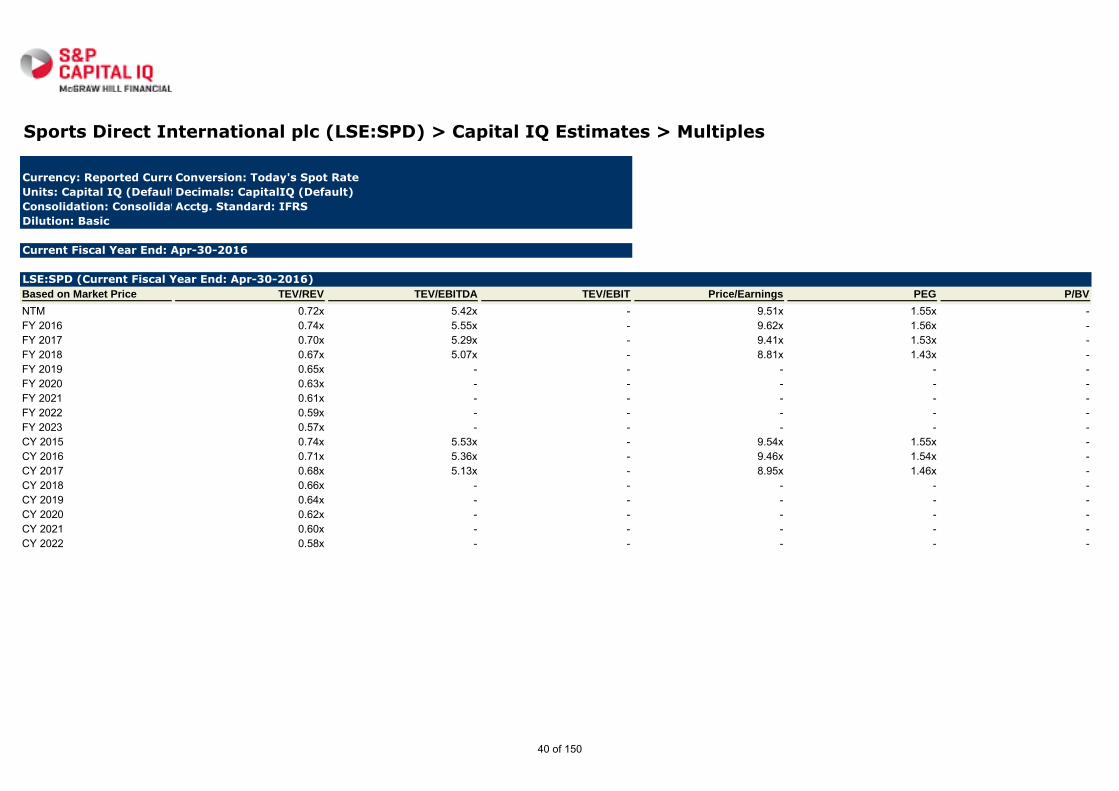

Sports Direct International plc (LSE:SPD) > Capital IQ Estimates > Multiples

Currency: Reported CurrencyConversion: Today's Spot Rate

Units: Capital IQ (Default)Decimals: CapitalIQ (Default)

Consolidation: ConsolidatedAcctg. Standard: IFRS

Dilution: Basic

Current Fiscal Year End: Apr-30-2016

LSE:SPD (Current Fiscal Year End: Apr-30-2016)

Based on Market Price TEV/REV TEV/EBITDA TEV/EBIT Price/Earnings PEG P/BV

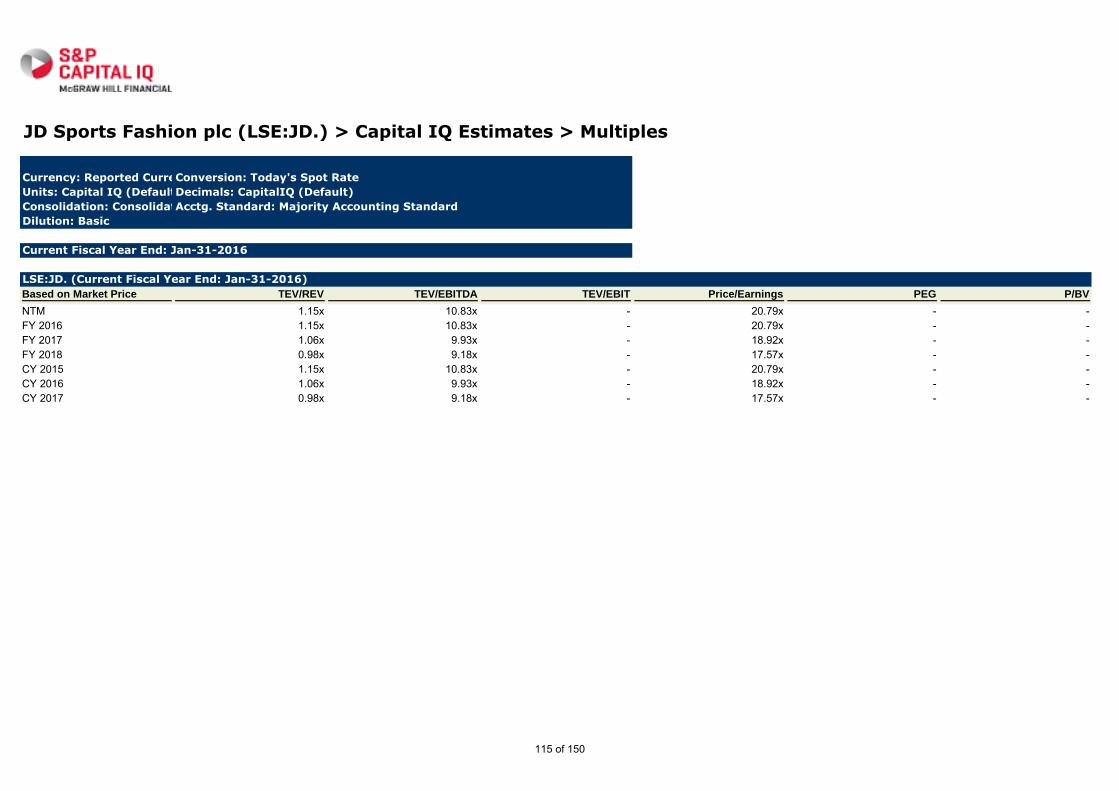

NTM 0.72x 5.42x - 9.51x 1.55x -FY 2016 0.74x 5.55x - 9.62x 1.56x -FY 2017 0.70x 5.29x - 9.41x 1.53x -FY 2018 0.67x 5.07x - 8.81x 1.43x -FY 2019 0.65x - - - - -FY 2020 0.63x - - - - -FY 2021 0.61x - - - - -FY 2022 0.59x - - - - -FY 2023 0.57x - - - - -CY 2015 0.74x 5.53x - 9.54x 1.55x -CY 2016 0.71x 5.36x - 9.46x 1.54x -CY 2017 0.68x 5.13x - 8.95x 1.46x -CY 2018 0.66x - - - - -CY 2019 0.64x - - - - -CY 2020 0.62x - - - - -CY 2021 0.60x - - - - -CY 2022 0.58x - - - - -

40 of 150

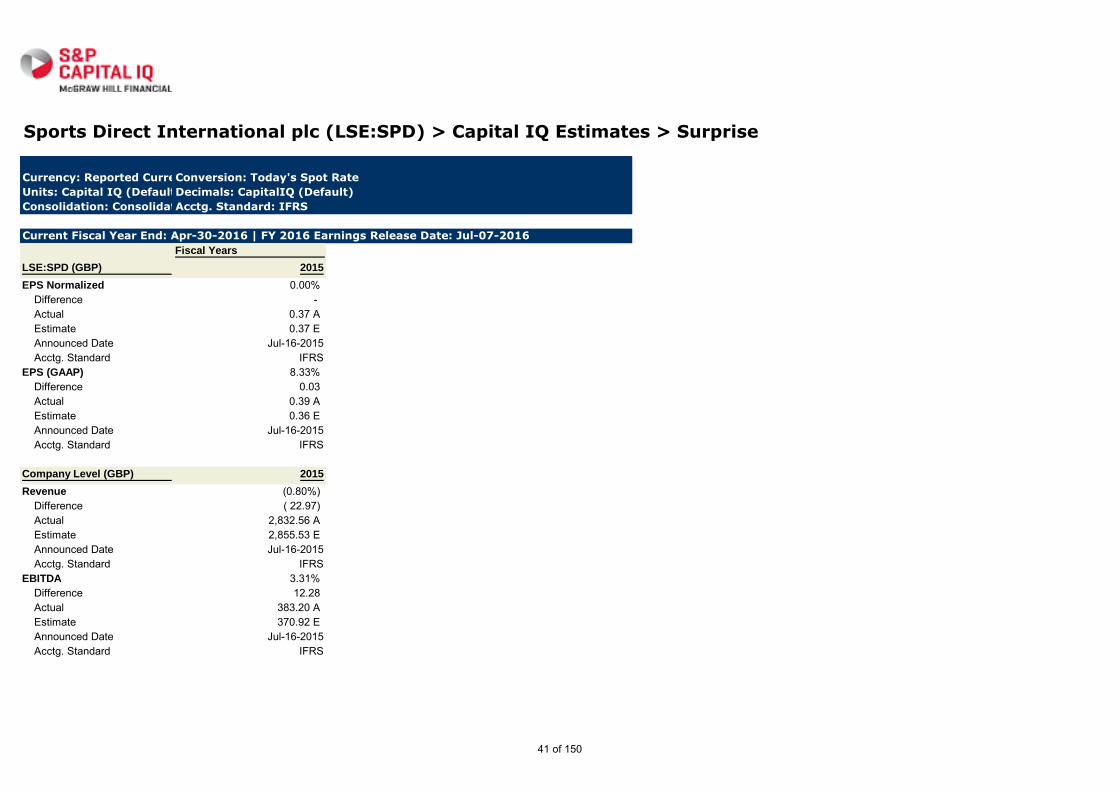

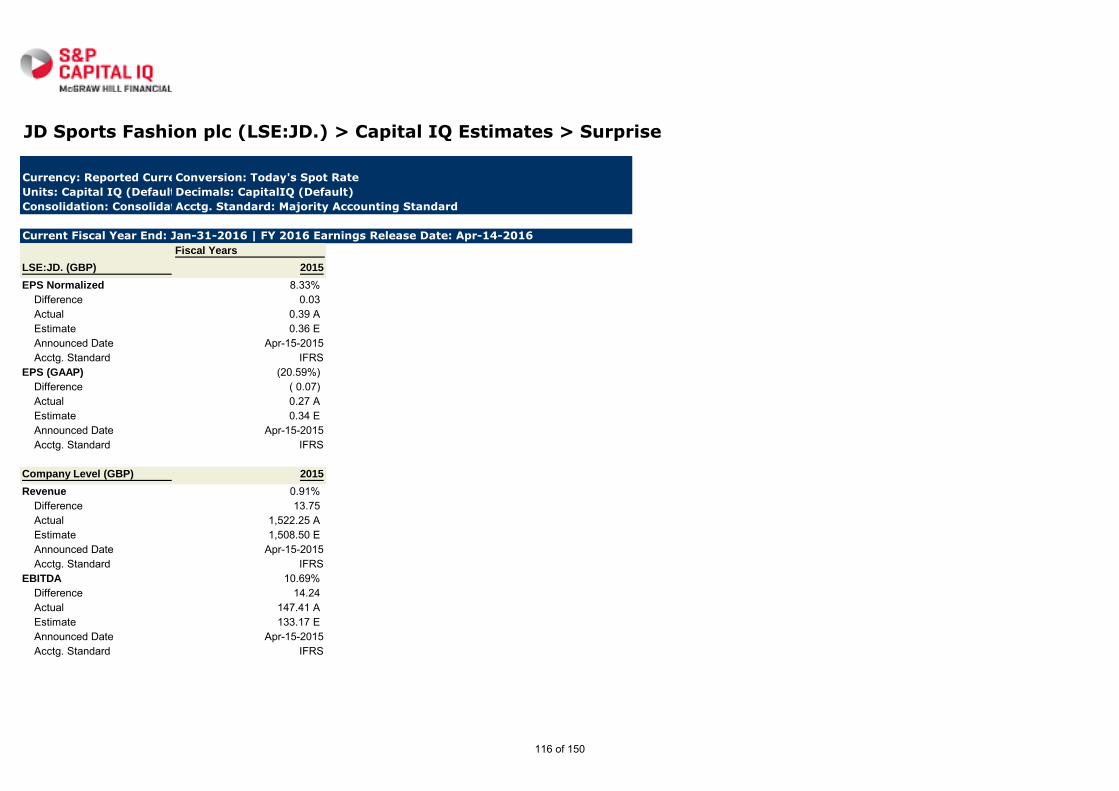

Sports Direct International plc (LSE:SPD) > Capital IQ Estimates > Surprise

Currency: Reported CurrencyConversion: Today's Spot Rate

Units: Capital IQ (Default)Decimals: CapitalIQ (Default)

Consolidation: ConsolidatedAcctg. Standard: IFRS

Current Fiscal Year End: Apr-30-2016 | FY 2016 Earnings Release Date: Jul-07-2016

Fiscal Years

LSE:SPD (GBP) 2015

EPS Normalized 0.00% Difference - Actual 0.37 A Estimate 0.37 E Announced Date Jul-16-2015 Acctg. Standard IFRSEPS (GAAP) 8.33% Difference 0.03 Actual 0.39 A Estimate 0.36 E Announced Date Jul-16-2015 Acctg. Standard IFRS

Company Level (GBP) 2015

Revenue (0.80%) Difference ( 22.97) Actual 2,832.56 A Estimate 2,855.53 E Announced Date Jul-16-2015 Acctg. Standard IFRSEBITDA 3.31% Difference 12.28 Actual 383.20 A Estimate 370.92 E Announced Date Jul-16-2015 Acctg. Standard IFRS

41 of 150

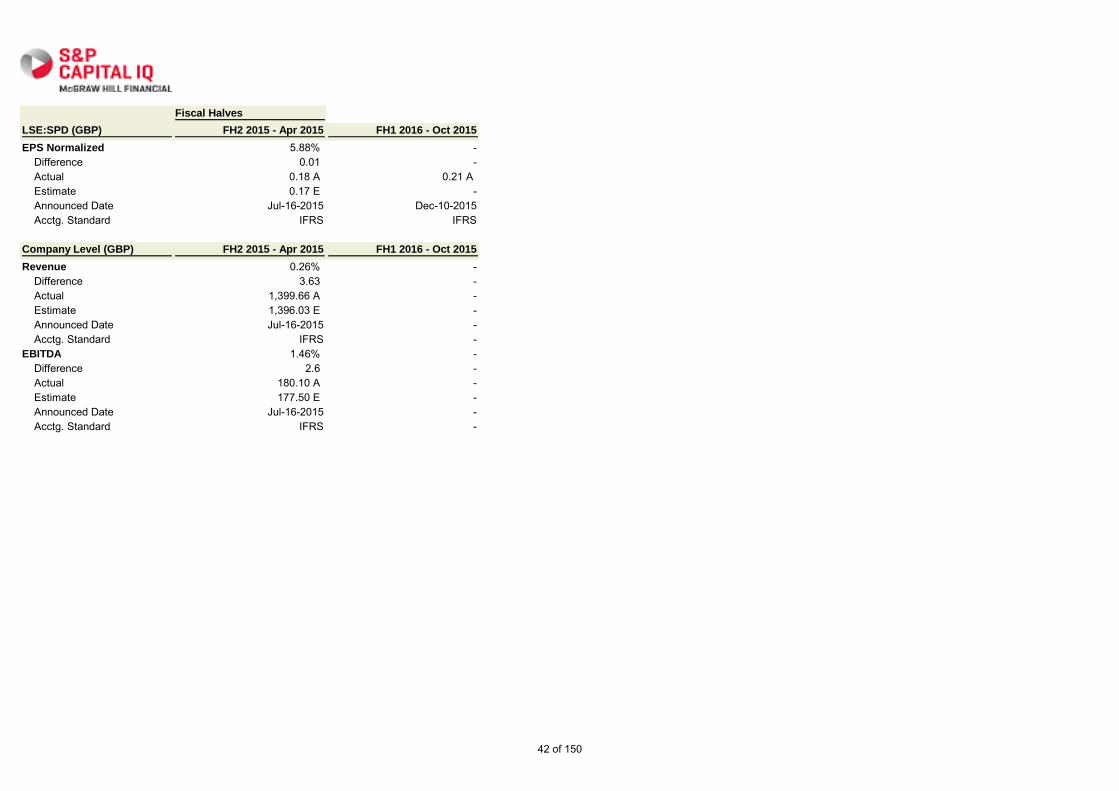

Fiscal Halves

LSE:SPD (GBP) FH2 2015 - Apr 2015 FH1 2016 - Oct 2015

EPS Normalized 5.88% - Difference 0.01 - Actual 0.18 A 0.21 A Estimate 0.17 E - Announced Date Jul-16-2015 Dec-10-2015 Acctg. Standard IFRS IFRS

Company Level (GBP) FH2 2015 - Apr 2015 FH1 2016 - Oct 2015

Revenue 0.26% - Difference 3.63 - Actual 1,399.66 A - Estimate 1,396.03 E - Announced Date Jul-16-2015 - Acctg. Standard IFRS -EBITDA 1.46% - Difference 2.6 - Actual 180.10 A - Estimate 177.50 E - Announced Date Jul-16-2015 - Acctg. Standard IFRS -

42 of 150

Sports Direct International plc (LSE:SPD) > Capital IQ Estimates > Trends

Currency: Reported CurrencyConversion: Today's Spot Rate

Units: Capital IQ (Default)Decimals: CapitalIQ (Default)

Consolidation: ConsolidatedAcctg. Standard: IFRS

Current Fiscal Year End: Apr-30-2016 | FY 2016 Earnings Release Date: Jul-07-2016

EPS Normalized

LSE:SPD (GBP) FH2 2016 FY 2016 FY 2017 FY 2018 FY 2019 FY 2020

Current 0.17 0.36 0.37 0.4 - -1 month ago 0.17 0.37 0.4 0.44 - -2 months ago 0.17 0.37 0.41 0.45 - -3 months ago 0.18 0.41 0.47 0.52 0.57 -6 months ago 0.15 0.42 0.49 0.55 0.66 0.759 months ago 0.19 0.43 0.49 0.54 - -12 months ago 0.19 0.42 0.48 0.54 - -18 months ago - 0.45 0.52 0.57 - -

EPS (GAAP)

LSE:SPD (GBP) FH2 2016 FY 2016 FY 2017 FY 2018 FY 2019 FY 2020

Current - 0.4 0.38 0.4 - -1 month ago - 0.4 0.41 0.46 - -2 months ago - 0.41 0.44 0.5 - -3 months ago - 0.31 0.48 0.55 - -6 months ago - 0.43 0.5 0.57 - -9 months ago - 0.43 0.5 - - -12 months ago - 0.42 0.48 - - -18 months ago - 0.44 0.51 - - -

Revenue

Company Level (GBP) FQ3 2016 FQ4 2016 FH2 2016 FY 2016 FH1 2017 FH2 2017 FY 2017 FH1 2018 FH2 2018 FY 2018 FY 2019 FY 2020 FY 2021 FY 2022 FY 2023 FY 2024 FY 2025

Current - - 1373.45 2822.43 - - 3002.98 - - 3111.43 3211 3321.5 3439.5 3545 3670.5 3783 38891 month ago - - 1373.45 2823.95 - - 3024.85 - - 3144.84 3259.5 3370.5 3496.5 3609.5 3744.5 3866 3981.52 months ago - - 1373.45 2827.59 - - 3043.27 - - 3175.93 3259.5 3370.5 3496.5 3609.5 3744.5 3866 3981.53 months ago - - 1429.85 2858.3 - - 3127.79 - - 3289.61 3405.27 3646.5 3831 4016 4200.5 4384 45666 months ago 806 659 1490.66 2958.56 1546.1 1495.2 3176.3 1597.5 1560 3344.46 3671.85 3897.4 4008 4232 4468 4717 49809 months ago - - 1634.76 3046.62 - - 3273.61 - - 3448.33 3646.5 3863.5 4113.5 4358.5 4572 4772.5 -12 months ago - - 1634.76 3032.89 - - 3242.12 - - 3440 3650.5 3867.5 4138 4340.5 4599 4824.5 -18 months ago - - - 3202.68 - - 3395.68 - - 3720.1 - - - - - - -

EBITDA

Company Level (GBP) FQ3 2016 FQ4 2016 FH2 2016 FY 2016 FH1 2017 FH2 2017 FY 2017 FH1 2018 FH2 2018 FY 2018 FY 2019 FY 2020 FY 2021 FY 2022 FY 2023 FY 2024 FY 2025

Current - - - 378.1 - - 396.5 - - 413.98 - - - - - - -1 month ago - - - 386.11 - - 415.69 - - 443.78 - - - - - - -2 months ago - - - 392.04 - - 427.42 - - 462.93 - - - - - - -3 months ago - - - 417.76 - - 466.36 - - 515.7 - - - - - - -6 months ago - - 203.7 420.79 246.7 215.8 474.87 260.1 231.1 522.8 626.5 698.1 - - - - -9 months ago - - - 425.45 - - 477.65 - - 518 - - - - - - -12 months ago - - - 419.02 - - 468.64 - - 518 - - - - - - -18 months ago - - - 442.49 - - 494.91 - - 579.3 - - - - - - -

43 of 150

Data Provided by

Historical Equity Pricing Data supplied by

Sports Direct Annual Report 2015

(Pages 1 - 36)

44 of 150

EVERYTHING IS CHANGING

45 of 150

• Sports Retail gross margin increased by 170 bps to 44.6%

• Group underlying EBITDA increased by 15.7% to £383.2m (1)

• Underlying profit before tax up 20.5% to £300.3m(1)

• Underlying free cash generation of £301.8m(2)

• Sports Retail like-for-like stores gross contribution increased by 7.4% (FY14: 10.5%)(3)

• Continued roll-out of large format city centre stores

• Successful UK launch of Click and Collect in FY15 H2

• Record EBITDA achieved v. 4th year Share Scheme target

• Net debt decreased to £59.7m(4)

(1) Underlying EBITDA, underlying profit before taxation and underlying EPS exclude realised foreign exchange gains/losses in selling and administration costs, exceptional costs and the profit/loss on sale of strategic investments. Underlying EBITDA also excludes the Share Scheme charges.

(2) Underlying free cash generation is defined as operating cash flow before working capital, made up of underlying EBITDA (before Share Scheme costs) plus realised foreign exchange gains and losses, less corporation tax paid.

(3) Excludes contribution in Sport Eybl and Sports Experts AG (EAG) and Sportland International Group AS (SIG) as the prior year comparative is not a full year.

(4) Net debt is borrowings less cash held.

GROUP REVENUE +4.7%April 15 £2,832.6m

April 14 £2,706.0m

April 13 £2,185.6m

April 12 £1,807.2m

April 11 £1,599.2m

UNDERLYING EBITDA +15.7%April 15 £383.2m

April 14 £331.1m

April 13 £287.9m

April 12 £235.7m

April 11 £211.0m

REPORTED PBT +30.9%April 15 £313.4m

April 14 £239.5m

April 13 £207.2m

April 12 £148.0m

April 11 £118.8m

UNDERLYING EPS +21.2%April 15 38.9p

April 14 32.1p

April 13 26.9p

April 12 18.7p

April 11 16.8p

KEY HIGHLIGHTS

2

ANNU

AL R

EPOR

T 20

15

46 of 150

“The Group has delivered another solid set of results in spite of challenging trading conditions including the adverse impact on performance during the period of England’s early departure from the FIFA World Cup in Brazil and unseasonably mild weather during autumn, reducing footfall.

“However, with our ongoing focus on providing customers with exceptional quality and unbeatable value, we have continued to grow Group revenues and EBITDA and have succeeded in surpassing our fourth and final EBITDA target under the 2011 Share Scheme. The first of these awards will vest with participants in September 2015 and the second in September 2017. We owe our continued success to the commitment and hard work of those participants and we are delighted that we are able to reward them in this way.

“Trading since the period end has been in line with management expectations and will continue to be driven by improvements in product range and availability, optimisation of both our in-store and web offerings, the introduction of Click and Collect in the UK and further investment in our store portfolio.”

Dave Forsey Chief Executive

16 July 2015

3

EVER

YTHI

NG IS

CHA

NGIN

G...

47 of 150

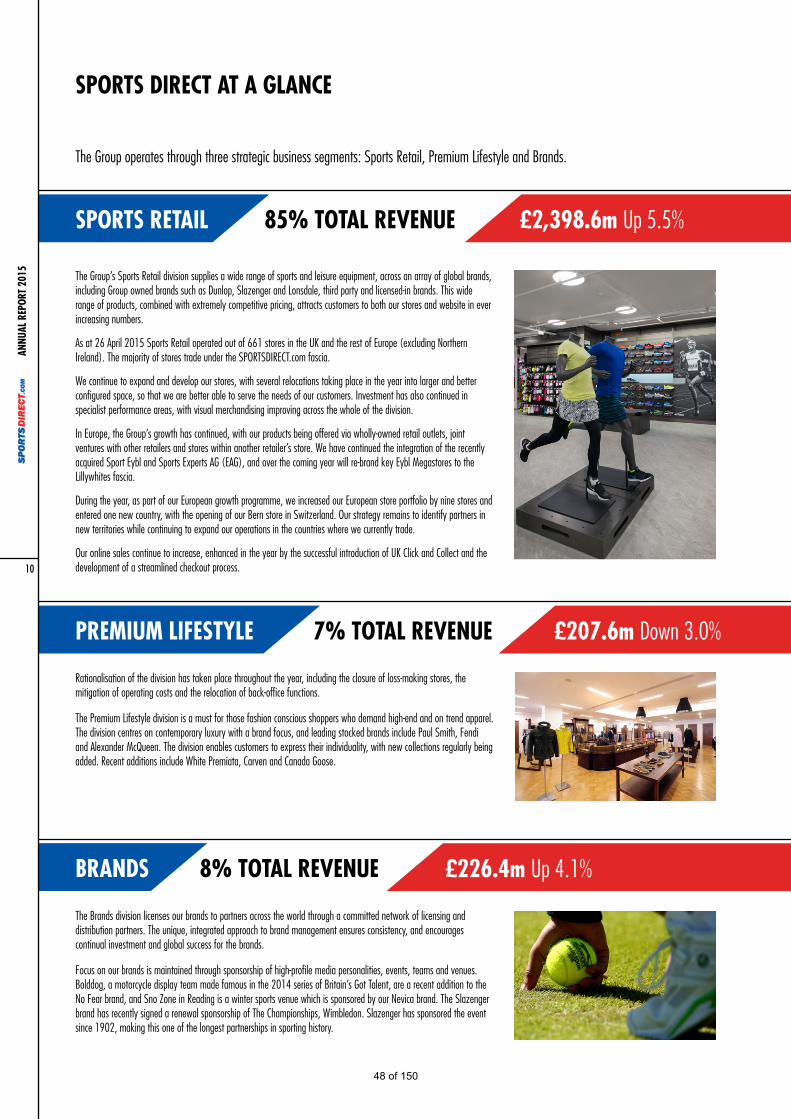

The Group’s Sports Retail division supplies a wide range of sports and leisure equipment, across an array of global brands, including Group owned brands such as Dunlop, Slazenger and Lonsdale, third party and licensed-in brands. This wide range of products, combined with extremely competitive pricing, attracts customers to both our stores and website in ever increasing numbers.

As at 26 April 2015 Sports Retail operated out of 661 stores in the UK and the rest of Europe (excluding Northern Ireland). The majority of stores trade under the SPORTSDIRECT.com fascia.

We continue to expand and develop our stores, with several relocations taking place in the year into larger and better configured space, so that we are better able to serve the needs of our customers. Investment has also continued in specialist performance areas, with visual merchandising improving across the whole of the division.

In Europe, the Group’s growth has continued, with our products being offered via wholly-owned retail outlets, joint ventures with other retailers and stores within another retailer’s store. We have continued the integration of the recently acquired Sport Eybl and Sports Experts AG (EAG), and over the coming year will re-brand key Eybl Megastores to the Lillywhites fascia.

During the year, as part of our European growth programme, we increased our European store portfolio by nine stores and entered one new country, with the opening of our Bern store in Switzerland. Our strategy remains to identify partners in new territories while continuing to expand our operations in the countries where we currently trade.

Our online sales continue to increase, enhanced in the year by the successful introduction of UK Click and Collect and the development of a streamlined checkout process.

The Group operates through three strategic business segments: Sports Retail, Premium Lifestyle and Brands.

SPORTS RETAIL 85% TOTAL REVENUE £2,398.6m Up 5.5%

The Brands division licenses our brands to partners across the world through a committed network of licensing and distribution partners. The unique, integrated approach to brand management ensures consistency, and encourages continual investment and global success for the brands.

Focus on our brands is maintained through sponsorship of high-profile media personalities, events, teams and venues. Bolddog, a motorcycle display team made famous in the 2014 series of Britain’s Got Talent, are a recent addition to the No Fear brand, and Sno Zone in Reading is a winter sports venue which is sponsored by our Nevica brand. The Slazenger brand has recently signed a renewal sponsorship of The Championships, Wimbledon. Slazenger has sponsored the event since 1902, making this one of the longest partnerships in sporting history.

BRANDS 8% TOTAL REVENUE £226.4m Up 4.1%

7% TOTAL REVENUE

Rationalisation of the division has taken place throughout the year, including the closure of loss-making stores, the mitigation of operating costs and the relocation of back-office functions.

The Premium Lifestyle division is a must for those fashion conscious shoppers who demand high-end and on trend apparel. The division centres on contemporary luxury with a brand focus, and leading stocked brands include Paul Smith, Fendi and Alexander McQueen. The division enables customers to express their individuality, with new collections regularly being added. Recent additions include White Premiata, Carven and Canada Goose.

PREMIUM LIFESTYLE £207.6m Down 3.0%

SPORTS DIRECT AT A GLANCE

10

ANNU

AL R

EPOR

T 20

15

48 of 150

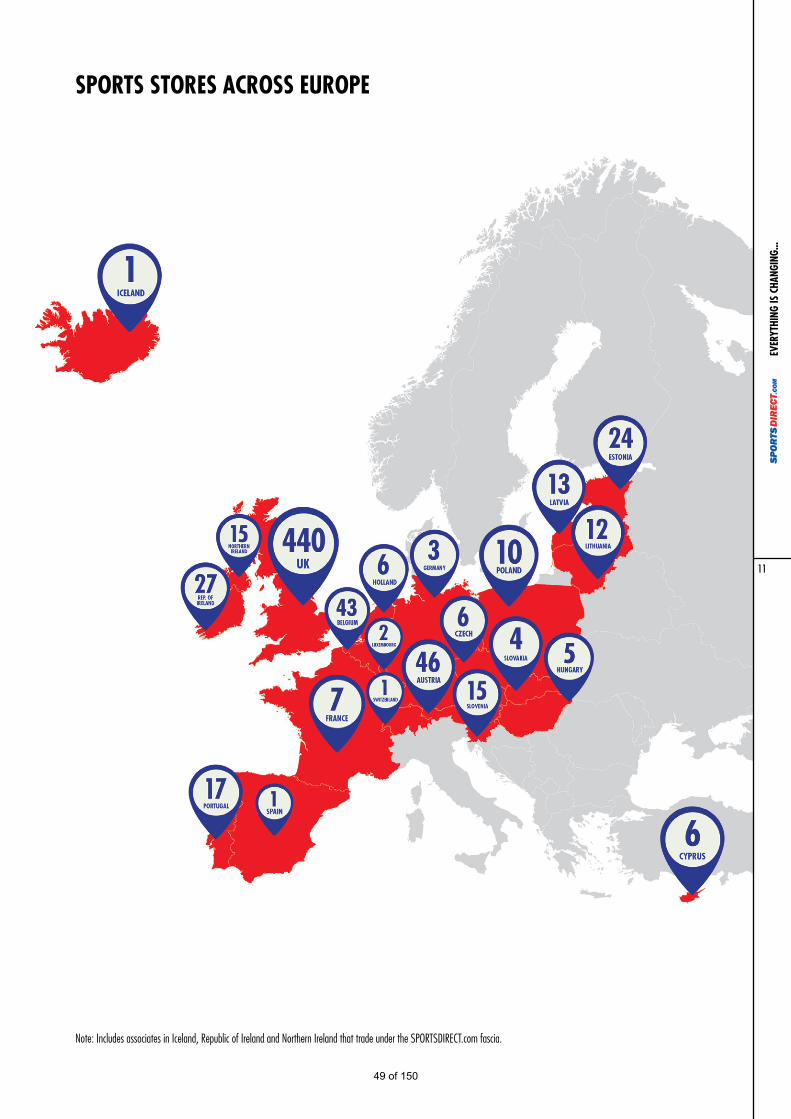

SPORTS STORES ACROSS EUROPE

Note: Includes associates in Iceland, Republic of Ireland and Northern Ireland that trade under the SPORTSDIRECT.com fascia.

11

EVER

YTHI

NG IS

CHA

NGIN

G...

49 of 150

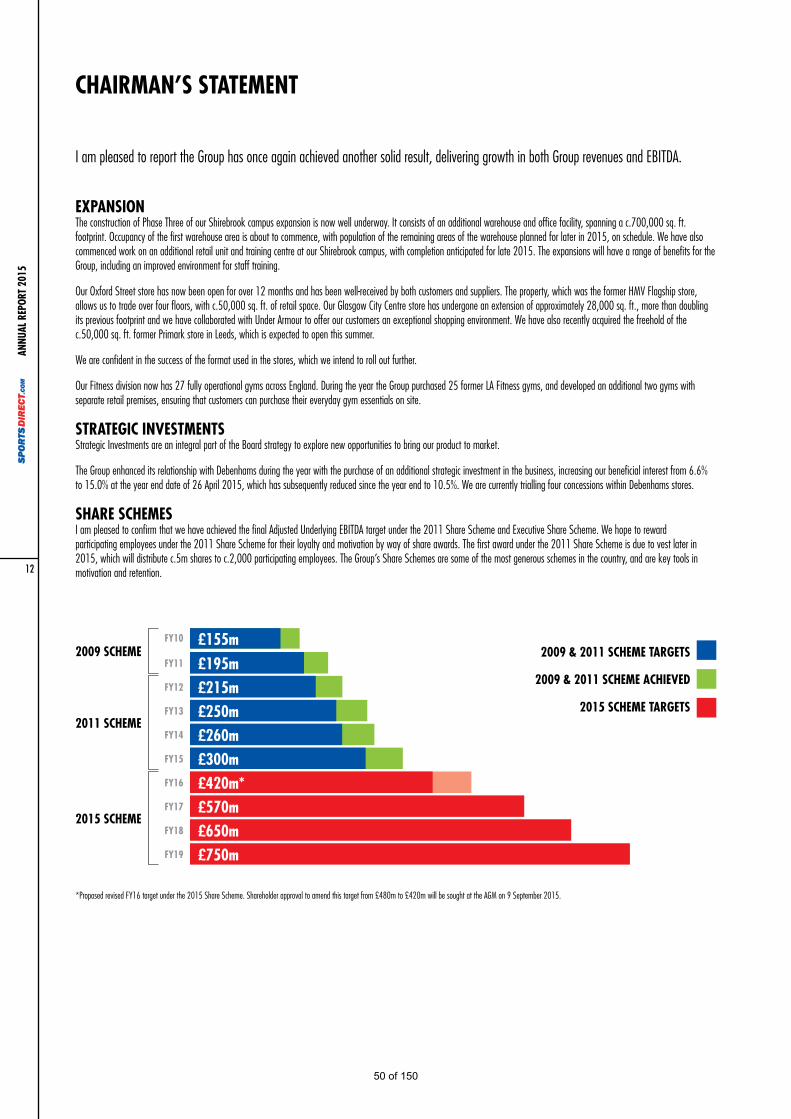

EXPANSION The construction of Phase Three of our Shirebrook campus expansion is now well underway. It consists of an additional warehouse and office facility, spanning a c.700,000 sq. ft. footprint. Occupancy of the first warehouse area is about to commence, with population of the remaining areas of the warehouse planned for later in 2015, on schedule. We have also commenced work on an additional retail unit and training centre at our Shirebrook campus, with completion anticipated for late 2015. The expansions will have a range of benefits for the Group, including an improved environment for staff training.

Our Oxford Street store has now been open for over 12 months and has been well-received by both customers and suppliers. The property, which was the former HMV Flagship store, allows us to trade over four floors, with c.50,000 sq. ft. of retail space. Our Glasgow City Centre store has undergone an extension of approximately 28,000 sq. ft., more than doubling its previous footprint and we have collaborated with Under Armour to offer our customers an exceptional shopping environment. We have also recently acquired the freehold of the c.50,000 sq. ft. former Primark store in Leeds, which is expected to open this summer.

We are confident in the success of the format used in the stores, which we intend to roll out further.

Our Fitness division now has 27 fully operational gyms across England. During the year the Group purchased 25 former LA Fitness gyms, and developed an additional two gyms with separate retail premises, ensuring that customers can purchase their everyday gym essentials on site.

STRATEGIC INVESTMENTS Strategic Investments are an integral part of the Board strategy to explore new opportunities to bring our product to market.

The Group enhanced its relationship with Debenhams during the year with the purchase of an additional strategic investment in the business, increasing our beneficial interest from 6.6% to 15.0% at the year end date of 26 April 2015, which has subsequently reduced since the year end to 10.5%. We are currently trialling four concessions within Debenhams stores.

SHARE SCHEMES I am pleased to confirm that we have achieved the final Adjusted Underlying EBITDA target under the 2011 Share Scheme and Executive Share Scheme. We hope to reward participating employees under the 2011 Share Scheme for their loyalty and motivation by way of share awards. The first award under the 2011 Share Scheme is due to vest later in 2015, which will distribute c.5m shares to c.2,000 participating employees. The Group’s Share Schemes are some of the most generous schemes in the country, and are key tools in motivation and retention.

I am pleased to report the Group has once again achieved another solid result, delivering growth in both Group revenues and EBITDA.

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

2015 SCHEME

2011 SCHEME

2009 SCHEME 2009 & 2011 SCHEME TARGETS

2009 & 2011 SCHEME ACHIEVED

2015 SCHEME TARGETS

£155m£195m£215m£250m£260m£300m£420m*£570m£650m£750m

*Proposed revised FY16 target under the 2015 Share Scheme. Shareholder approval to amend this target from £480m to £420m will be sought at the AGM on 9 September 2015.

CHAIRMAN’S STATEMENT

12

ANNU

AL R

EPOR

T 20

15

50 of 150

To the extent that a significant number of participating employees elect to sell some or all of their shares, whilst the Company has no obligation to buy back the shares, the Board will consider a number of options open to it, including whether to: (i) implement an on-market buy back of shares pursuant to the authority given by shareholders at the Company’s AGM in 2014; or (ii) fund the Company’s Employee Benefit Trust so as to allow it to acquire shares in the market to replace those shares transferred to participating employees pursuant to the vesting.

As part of our strategy to closely align the interests of our team with those of our shareholders, the 2015 Share Scheme was approved by shareholders at a General Meeting in July 2014. The vesting of awards under the 2015 Share Scheme is conditional upon the achievement by the Group of four demanding EBITDA targets, which span between FY16 and FY19. The awards will vest in 2019 and 2021, subject to successful completion of all four targets, and other specific performance conditions. The Executive Deputy Chairman, Mike Ashley, withdrew from the Scheme during FY15. Mike remains fully committed to the achievement of the Scheme’s targets, but would like the focus to be on ensuring that the Scheme aligns with the wider Sports Direct team, and therefore chose to withdraw from the Scheme.