School of Business and Law Business Administration (BA) Corporate Finance Lecturers' Name

24

School of Business and Law Business Administration (BA) Corporate Finance Lecturers' Name: S.A.PALAN Student Name: Student Number

-

Upload

independent -

Category

Documents

-

view

4 -

download

0

Transcript of School of Business and Law Business Administration (BA) Corporate Finance Lecturers' Name

School of Business and Law

Business Administration (BA)

Corporate Finance

Lecturers' Name:

S.A.PALAN

Student Name:

Student Number

June 2013

Evaluation of Investment Appraisal and

Share Price Valuation techniques

Contents1. Introduction:...............................................12. Methodology:................................................13. Evaluation of Investment Appraisal techniques:..............13.1 NPV:.......................................................2Example 1:....................................................23.1.1 NPV of Project A:.......................................33.1.2 NPV of Project B:.......................................3

3.2 IRR:.......................................................3Example 2:....................................................4

3.3 Payback Period:............................................4Example 3:....................................................5

3.4 Qualitative Factors:.......................................54. Evaluation of Share Price Valuation Models:.................64.1 Discounted Cash Flow Model:................................6Example 4:....................................................6

4.2 Dividend Discount Model:...................................7Example 5:....................................................7

4.3 Net Tangible Asset per Share:..............................8Example 6:....................................................8

4.4 Book Value per Share:......................................8Example 7:....................................................9

4.5 P/E Multiple:..............................................9Example 8:.....................................................94.6 P/S Multiple:.............................................10Example 9:...................................................10

4.7 Weighted Average Price:...................................115. Recommendation:............................................12

6. Conclusion:................................................127. Reference:.................................................13

1.Introduction: Investment Appraisal techniques add value to the firm, because

through these techniques all the potential projects are evaluated

and based on the evaluation best projects selected. Appraisal

techniques help to identify best project. Sometimes they are also

used to decide a single project should be accepted or not. But,

main issue of these techniques is to select the best project and

help the company or business entity to increase their

profitability and sustainability. For these reasons it is said

investment appraisal techniques add value to the firm. A company

that is not listed yet, valuation of share is not possible by

valuing the market price condition. These shares are valued by

the valuation of book values of financial statements. Some

assumptions are made in valuing the company shares that make the

share price of the company lower than the price that may have

been prevailing in the market. Moreover book value of equity is

always low. For all these reasons a company that is not quoted

most of the time found under-priced when price is determined.

Different models are also used for share price valuation. All

these techniques are evaluated in this report.

2.Methodology:A report becomes more acceptable because of its methodology

followed. Methodology helps to increase acceptability of a

report. In this report, evaluation is done by collecting

1

information from different books, articles and websites. Examples

are used in case of evaluation of models and techniques. All the

examples used are fictitious. All of them are used to explain

the techniques and models. Information of models and techniques

are mainly taken from books.

3.Evaluation of Investment Appraisal techniques:The main objective of an organization is to wealth maximization.

The wealth of the company will be maximized when the company will

be added to add value for the corporation. This value addition

largely depends upon the profitability of the investment project

pursued by the corporation. Detection of the profitable

investment projects pursued by the corporation in turn depends

upon the proper investment appraisal by the company (Gitman,

2010).

A firm may have a number of alternatives for making investment.

These investment alternatives are assumed to yield future income

streams. Investment appraisal involves with determining &

evaluating these income streams relative to the cost of

investment. Beside this, any investment alternative that deals

with the future involves risk. Investment appraisal helps to

detect these risks which make it easy to compute the reward to

risk ratio associated with the investment alternative. Based on

the firm earning expectation and risk bearing capacity firm can

pursue best suitable investment alternative and can expand its

2

pie value through the reward from the chosen investment

alternative.

Investment appraisal process is designed to aid in the capital

budgeting decision. As a part of capital budgeting process

investment appraisal helps the firm to screen out the best

alternative to utilize the firm’s fund and add value to the firm.

How the investment appraisal process help in the capital

budgeting decision and become value additive for the company are

discussed in the following points (Gitman, 2010).

3.1 NPV:Investment appraisal technique calls for the estimates of the

future costs & benefits associated with a project and

assessment of the level of expected returns earned for the

level of expenditure made. The basic appraisal techniques i.e.

ROCE (Return on Capital Employed), Payback Period can be used

for the evaluation and selection of the investment

alternatives. More advances methods include NPV (Net Present

Value), IRR (Internal Rate of Return), Discounted Payback

Period etc. can also be performed to increase the edge of the

evaluation process. Based on these appraisal techniques the

relative attractiveness of several investment alternatives

available to the company are judged and best investment

alternatives are approved that will maximize the value of the

firm (Gitman, 2010).

3

Example 1:For instance, the initial value of a company is $ 100000. The

company has two alternates (two projects) for investment –

Project A and Project B. The required rate of return of the firm

is 10%. The associated cash flows from the two projects are as

follows.

Projec

t

Cash Outlay

(0)

Cash Inflow

(1)

Cash Inflow

(2)

Cash Inflow

(3)

Cash Inflow

(4)Projec

t A

$ 10000 5000 4000 3000 2000

Projec

t B

$ 10000 3000 3000 3000 3000

Now, if the firm decides to appraise the projects based on the

NPV method then the necessary calculation associated with the

appraisal process will be as follows.

3.1.1 NPV of Project A:

= [5000/(1.10)1 + 4000/(1.10)2 + 3000/(1.10)3

+2000/(1.10)4] – 10000

= $ 11471 – 10000

= $ 1471

4

3.1.2 NPV of Project B:

= [3000/(1.10)1 + 3000/(1.10)2 + 3000/(1.10)3 +3000/(1.10)4] –

10000

= $ 9510 – 10000

= $ (490)

So, based on the NPV evaluation criteria firm will decide to

pursue only Project A even if the firm has no capital rationing

as the NPV of Project A is positive and NPV of Project B is

negative. Approval of the Project A will increase the value of

the firm by $1471 and approval of the Project B will reduce the

value of firm by $490. If the firm investment manager undertakes

the Project B without any investment appraisal analysis then the

value of the firm will reduce.

3.2 IRR:Investment appraisal process also plays an important role in the

asset investment decision in the capital rationing scenario

including both the hard and soft capital rationing. When the

projects are divisible and any fraction of the project can be

undertaken the optimal combination of the investment decision in

order to maximize the value from the investment combination can

be assessed & evaluated through the PI (Profitability Index)

analysis. On the other hand, if the project is indivisible &

5

project must be done in entirely the optimal combination of

investment in order to expand the value of investments can be

found by only the ‘Trial and Error’ method using Internal Rate of

Return Method (Gitman, 2010).

Example 2:If we take the example given above for the valuation under IRR

method through trial and error the result will be-

So, the A project should be accepted as its cost of capital is

lower than IRR. In this way this method adds value to the firm by

selecting best company.

3.3 Payback Period:Investment appraisal technique also plays significant role in the

investment decision under uncertainty. The investment decision

becomes too much hard when all the decisions are based on the

forecasts and all forecasts are subject to the uncertainty. In

this case, uncertainty requires to be reflected in the financial

6

evaluation. Investment analysis and appraisal offer a lot of

techniques to deal with the investment decision under

uncertainty. These investment appraisal techniques include

expected values, sensitivity analysis model, simulation analysis

model, risk adjusted discount rate model, adjusted payback period

model etc. Among these sensitivity and simulation analysis

techniques are most effective. These help to assess the best and

worst possible situation along with measuring the margin of

safety of the input data. Based on the worst and best possible

scenarios, the investment manager gets insights of several

investment alternatives and takes the final decision. Proper

escalation of the uncertainty in the financial evaluation helps

to reduce the possibility of wrong decision and create value for

the corporation (Gitman, 2010).

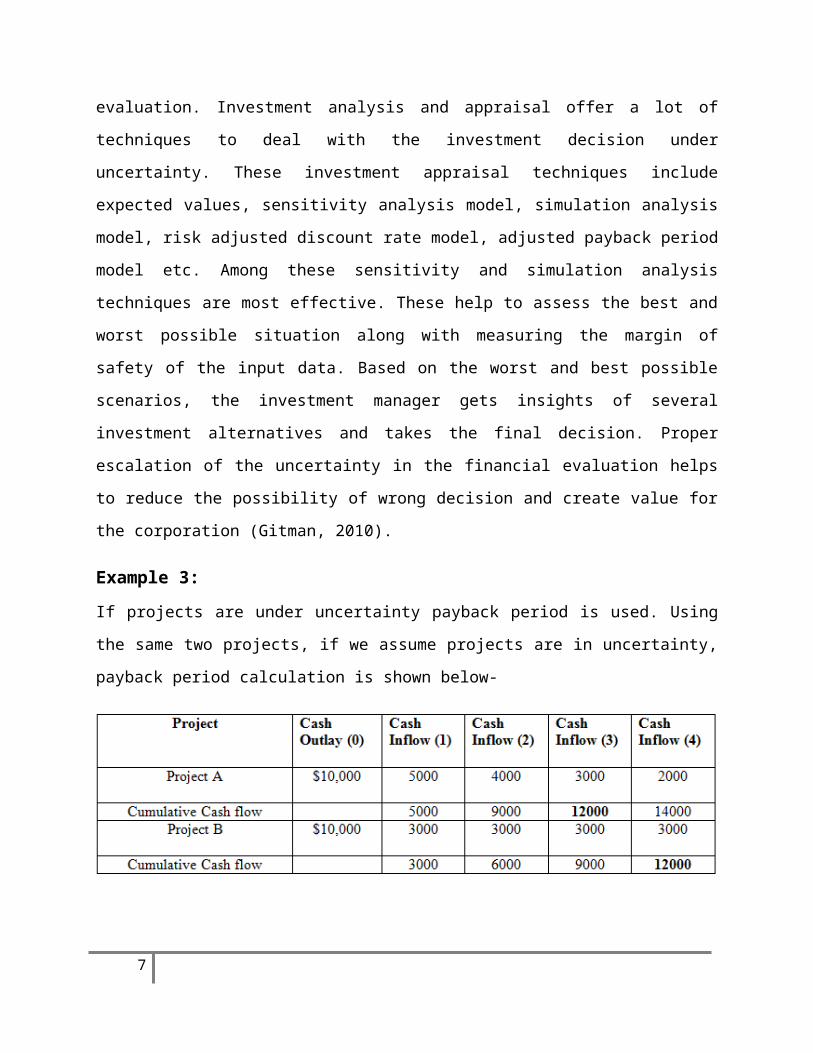

Example 3:If projects are under uncertainty payback period is used. Using

the same two projects, if we assume projects are in uncertainty,

payback period calculation is shown below-

7

As the project is under uncertainty and time value is not taken

into account, the project A will be accepted because it recovers

cash outflow within 3 years where as Project B recovers it in 4

years. Thus again investment appraisal techniques add value to

the firm by helping to select the best project.

3.4 Qualitative Factors:Beside the financial factors many other non-financial and

qualitative factors are required to consider during the appraisal

process. These factors may include the level of technological

process, any law & legislation, environmental issues etc.

Investment appraisal process calls for the consideration and

evaluation of these non-financial factors. Considerations of

these non-financial factors make the project evaluation process

more effective. Effective evaluation process helps to screen out

the best value additive investment projects.

So, it is clear that the investment analysis and appraisal

techniques add value to the company.

4.Evaluation of Share Price Valuation Models:Share price valuation models are used for valuing an unlisted

company for the price determination. There are several methods of

valuation of share price. But most of them are calculated by

following company’s financial statement or in comparison with the

overall industry. As they are not listed, what would have been

8

their performance in the market could not be understood. That’s

why pricing sometimes become below the average level. The models

that are used for valuation of stock price of a company are

described below.

4.1 Discounted Cash Flow Model:This is the first model that is used for share price valuation.

Mainly equity value per share is determined for the company which

is taken as expected share price of the company (Bodie, Kane and

Marcus, 2009). This method is the most accepted method. But

under-pricing also occurs here because assumptions sometimes are

taken lower than actual growth rates.

Example 4:Let, ABC Company wants to determine its value per share using

discounted cash flow method. It’s all expected growth rates and

finally calculated value per share is shown in the table below.

9

From the table it can be seen that ABC has WACC is 15% and

terminal growth rate is 4%. All the assumptions are shown in the

column 2. It has 100 million shares and equity value per share

10.87. But, the rates can be lower than the actual growth rate of

the company because the company does not perform in the share

market yet. This is the main reason for which the price may be

low than it could be in reality.

4.2 Dividend Discount Model:This is the second model used to determine stock price of a

company. It is the discounted present value of all expected

dividends of an individual company. Dividends are the part of

earnings that are distributed to the shareholders of the company

(Bodie, Kane and Marcus, 2009). The price determined here is from

10

expected values of dividends that will be distributed to the

shareholders. For this reason this model also has the possibility

of underpricing the stock price because earnings may be higher in

the future than expected and dividend amount may be higher. But,

there is also possibility of occurrence of the opposite of the

company.

Example 5: Let’s assume ABC Company has expected dividend for the next five

years 2, 2.5, 2.75, 2.9 and 3. Dividends have a terminal growth

rate of 5% and cost of equity of 10%. So, the price would be-

From the above table it can be seen that price determined by

discounting dividend is 32.08. But, we can see that price

determined by discounted cash flow model was 10.87. So, based on

assumptions determination of price vary.

4.3 Net Tangible Asset per Share:This is the model through which difference of tangible asset and

liability is determined and divided by number of shares to

determine value per share that is used to fix as the price.

Tangible assets are current and non-current assets except

11

goodwill, patent and other intangible assets. Liabilities are

current and non-current liabilities except shareholders equity.

Difference of these two values is divided by number of shares to

get the price (Ross, Westerfield and Jaffe, 2011). Here,

possibility of underpricing comes from future possibility of

better performance of the company.

Example 6:Let ABC company has current asset 3000 million and non-current

asset 7000 million, long term liability 6000 million and current

liability 1500 million. So Net tangible asset value per share for

ABC is-

According to this model, vale per share for ABC is 25. This price

is close to the value determined by DDM model but lower than it.

4.4 Book Value per Share:This is another model of determining the value of shares. In this

model value per share is determined by dividing the amount of

equity existing by the number of shares. Here shareholder’s

12

equity consists of common equity, retained earnings, reserves

etc. Sum of all these values are divided by number of shares

(Ross, Westerfield and Jaffe, 2011). Actually, when trade in the

market, price movement does not have any relation with it. For

this reason possibility of underpricing always remains.

Example 7:Let, ABC has common equity of 4000 million, retained earnings of

150 million and reserve of 300 million with number of shares

outstanding 100 million. S, value per share is-

According to this model, value per share that will be taken as

stock price is 44.5. This price is also close to the price in DDM

method but higher than it.

4.5 P/E Multiple:There are some relative valuation models for determining stock

price of a company. P/E multiple is one of them. P/E multiple is

calculated by price per share divided by earnings per share. In

this method, as price of the company will be determined, P/E

multiple of the industry is taken which means average P/E ratio

of all the companies in the industry is taken. Then the ratio is13

multiplied by the earnings per share of the company of which

price will be determined. Then the result is taken as price

(Ross, Westerfield and Jaffe, 2011). Actually, when trade in the

market, price movement does not have any relation with it. For

this reason possibility of underpricing always remains.

Example 8:Let, ABC Company is a manufacturing company. The industry has a

P/E multiple of 4.5 and ABC has current Earnings per share of 5.

So, value per share according to this method is calculated below-

According to this method the price that could be used for

determining stock price is 22.5 which is near to DDM method but

lower than it.

4.6 P/S Multiple:This is another relative valuation model that is used to

determine stock price of an unlisted company. The ratio is

calculated by dividing price by sales per share. Here, again

industry P/S is taken which is the average of P/S of all the

companies in the industry. Then the price is got by multiplying

sales per share of the company with industry P/S (Ross,

Westerfield and Jaffe, 2011). Actually, when trade in the market,

14

price movement does not have any relation with it. For this

reason possibility of underpricing always remains.

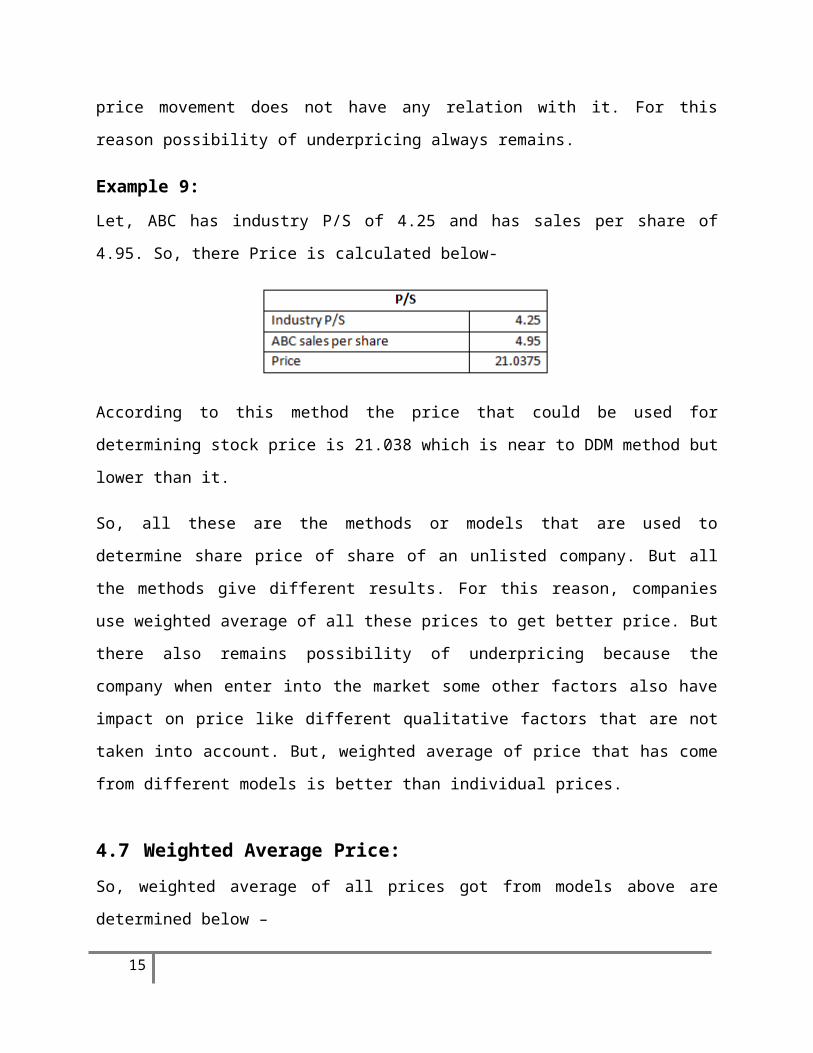

Example 9:Let, ABC has industry P/S of 4.25 and has sales per share of

4.95. So, there Price is calculated below-

According to this method the price that could be used for

determining stock price is 21.038 which is near to DDM method but

lower than it.

So, all these are the methods or models that are used to

determine share price of share of an unlisted company. But all

the methods give different results. For this reason, companies

use weighted average of all these prices to get better price. But

there also remains possibility of underpricing because the

company when enter into the market some other factors also have

impact on price like different qualitative factors that are not

taken into account. But, weighted average of price that has come

from different models is better than individual prices.

4.7 Weighted Average Price:So, weighted average of all prices got from models above are

determined below –

15

From the table above it can be seen that weighted average price

is 25.58. This price is expected to be more accurate than

individual price of each model because weight on price is given

based on importance of model. Though qualitative factors are not

taken into account and that’s why possibility of underpricing

remains but this weighted average more accurate than individual

models.

16

5.Recommendation:Some recommendations relating to the use of investment appraisal

methods and stock valuation models are given below-

i. A company should always use investment appraisal methods

when they are taking any decision related to selection of

any project.

ii. As, NPV is the best selection method, decision should be

based on it’s which will increase value.

iii. When determining share price, qualitative factors should

be analyzed, if can, should be used to add value.

iv. To avoid the possibility of underpricing, the firm may

determine price with premium to avoid underpricing.

6.Conclusion:Investment appraisal methods are methods that are used to

determine the investment project that will add value to the firm

and increase the firm’s profitability and sustainability. These

methods are really effective and firms should use to develop

their business. On the other hand share price valuation models

that are used to determine price of unlisted companies always has

a possibility to underprice the price as qualitative factors are

not taken into account. For this reason, when pricing the stock

price of an unlisted company weighted average of price according

17

to importance should be done and shares at premium should be

issued.

18

7.Reference:i. ACCA. (2008). Financial Management F-9, COMPLETE TEXT (Kaplan

Publishing, UK). Page-57-135.

ii. S.A. Ross, R.W. Westerfield, and J. Jaffe, 2008, Corporate Finance, Eighth Edition (McGraw- Hill Irwin, New York).

iii. S-cool. (2013). Investment Appraisal. [On Line]. Available from: http://www.s-cool.co.uk/a-level/business-studies/budgeting-costing-and-investment/revise-it/investment-appraisal. [Accessed: June 14, 2013].

iv. The Student Room. (2013). Revision: Investment Appraisal. [On Line]. Available from: http://www.thestudentroom.co.uk/wiki/Revision:Investment_Appraisal. [Accessed: June 14, 2013].

v. Stephen A. Ross, Randolph W. Westerfield and Jeffery Jeff(2011) Corporate Finance (9th Ed.) McGraw-Hill, New York

vi. Zvi Bodie, Alex Kane and Alan J. Marcus (2009)Investments (8th Ed.) McGraw-Hill, New York

vii. Lawrence J. Gitman (2010) ‘Principals of Managerial

Finance’ 12th Edition Pearson 2010

viii. McLaney and Atrill (2011) ‘Introduction to Accounting’ 5th

edition, Pearson 2011

ix. Koen Milis, Monique Snoeck and Raf Haesen (March 6, 2012)‘Evaluation of the applicability of investment appraisaltechniques for assessing the business value of IS

19

services’, Information Management, HUBrussel Stormstraat2, 1000 Brussel, Belgium.

x. Investopedia (2011) ‘How to choose the best stock valuation Method?’ (online) (cited on February 21, 2011) available from www.ainvestopedia.com/articles/choosing-Valuation-methods.asp

xi. Ken Garrett (2012) ‘Business Valuations’ (online) (cited on December 7, 2012) available from www.chinaacc.com/upload/liuxim5702720121207161043966979.pdf

20