Annual Report 2002 - IMF eLibrary - International Monetary ...

233

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Annual Report 2002 - IMF eLibrary - International Monetary ...

International Monetary Fund

Annual Report 2002©International Monetary Fund. Not for Redistribution

HIGHLIGHTS

Safeguarding Stability Amid Uncertainties

World financial leaders met in Ottawain November 2001 to coordinate actionto stimulate the global economyfollowing the attack on the World TradeCenter. The Chairman of theDevelopment Committee, YashwantSinha (right), makes a point as (left toright) Group of 20 Chairman PaulMartin of Canada, U.S. TreasurySecretary Paul O'Neill, and InternationalMonetary and Finance CommitteeChairman Gordon Brown listen.

During the 2002 financial year the IMF faced important newchallenges in an unusually unsettled world environment.These placed increased demands on the institution in two ofits main areas of responsibility: preserving world economic

and financial stability and assisting in the global war on poverty.After a period of strong expansion, the global economy experienced a

widespread slowdown during the 2001 calendar year. Contributing tothis were further downward adjustments in equity prices, together with arise in energy prices and the tightening of monetary policy in industrialcountries that had occurred in 2000. The already weak internationaleconomy was further affected by the September 11, 2001, terroristattacks in the United States, which had a substantial—although largelytemporary—impact on economic conditions. By early 2002, however,thanks in large part to actions taken by key central banks to lower inter-est rates, there were encouraging signs that growth was recovering,although serious concerns remained in a number of countries.

In the face of the prevailing uncertainties, the IMF continued towork on the reform of the international monetary system and to focuson its core responsibilities, among them helping to prevent financialcrises among its members.

Following are some of the highlights of the IMF's work duringFY2002:

IMF LendingThe IMF's regular and concessional lending increasedstrongly as the slowdown in the world economy con-tributed to a worsening of the balance of payments dif-ficulties of several members whose access tointernational capital markets was curtailed.

• Commitments under the IMF's regular loan facili-ties—Stand-By Arrangements and the ExtendedFund Facility (EFF)—tripled, to SDR 39.4billion1 (almost $50 billion) in FY2002 from SDR13.1 billion (almost $17 billion) in FY2001. Thelargest commitments were Stand-By Arrangementsfor Brazil and Turkey, SDR 12.1 billion and SDR12.8 billion respectively. O f the commitment toBrazil, SDR 10 billion was provided under theSupplemental Reserve Facility (SRF), which isdesigned to assist members experiencing a suddenand disruptive loss of market access. A growingvolume of IMF financing commitments are nowtreated as precautionary, with borrowers indicatingthat they do not intend to draw on the funds

1As of April 30, 2002, SDR 1 = US$1.2677.

ii A N N U A L R E P O R T 2 0 0 2

©International Monetary Fund. Not for Redistribution

committed. Actual drawings were made in only 16 of the 34Stand-By and Extended Arrangements in place during the year.As of the end of April 2002, undrawn balances amounted toSDR 26.9 billion.

• The IMF's net uncommitted usable resources amounted to SDR 64.7billion ($82 billion) at the end of April 2002. The liquidity ratio(the ratio of net uncommitted usable resources to liquid liabilities)was 117 percent, significantly lower than the 168 percent reached ayear previously, but more than three and a half times the low pointreached before the 1999 increase in IMF quotas.

• In FY2002, the IMF's concessional lending for poverty reductioncontinued to be channeled through the Poverty Reduction andGrowth Facility (PRGF) and the joint IMF-World Bank Initiativefor Heavily Indebted Poor Countries (HIPCs). During the financialyear, the Executive Board approved nine new PRGF arrangementstotaling SDR 1.8 billion, with total disbursements amounting toSDR 1.0 billion, compared with SDR 0.6 billion in FY2001. Byend-April 2002, 26 HIPC-eligible members had been brought totheir decision points under the enhanced H I P C Initiative and oneunder the original Initiative, and the IMF had committed SDR 1.6billion in grants and disbursed about SDR 0.7 billion.

SurveillanceThe IMF conducts surveillance over the exchange rate policies of itsmember countries to ensure the effective operation of the internationalmonetary system. To this end, it regularly discusses with members theireconomic and financial policies and continuously monitors economicand financial developments at the country, regional, and global levels.• In April 2002 the Executive Board completed in large part its latest

biennial review of the principles and implementation of IMF surveil-lance. While the review found that the current system of surveillancewas working well, it identified a number of areas where furtherefforts were needed, including enhancing coverage of institutionaland structural issues, especially relating to financial sectors, andimproving analysis of debt sustainability.

• The Board in September 2001 discussed the IMF's role in promot-ing an open trading system and trade liberalization. Directors agreedthat the IMF should stress the need for a successful launch of theDoha trade round; continue to address trade issues in the context ofsurveillance and IMF-supported programs; lay the groundwork fortrade liberalization through its technical assistance; and cooperateclosely with the World Trade Organization and the World Bank.

Strengthening the International Financial SystemSince the Mexican crisis of 1994-95 and the Asian crises of 1997-98,much has been done to strengthen the international financial systemand the capacity of the IMF and its members for crisis prevention.Nevertheless, it would be unrealistic to suppose that all countries willbe able to avoid crises at all times. Thus, work has also advancedtoward assisting countries to resolve crises.

H I G H L I G H T S OF F Y 2 0 0 2

First Deputy Managing DirectorAnne O. Krueger's proposal to establisha Sovereign Debt RestructuringMechanism was one of the IMF'smajor initiatives for the year.

Regular andConcessional Lending(In billions of SDRs, financial year)

IMF Liquidity Ratio(In percent, end financial year)

IMF Credit Outstanding(In billions of SDRs, end financial year)

A N N U A L R E P O R T 2 0 0 2 iii

©International Monetary Fund. Not for Redistribution

H I G H L I G H T S O F F Y 2 0 0 2

• The IMF has strengthened its monitoring of mem-bers' vulnerability to external crises by drawing onupdated World Economic Outlook projections, earlywarning system models, detailed analyses of coun-tries' financing requirements, market information,and assessments of financial sector vulnerability andrisks of contagion.

• In recent years, the IMF has actively promotedincreased transparency of its members' policies,sought to improve public understanding of its ownpolicies and operations, and encouraged feedbackfrom both national authorities and the public.Through its website (www.imf.org) it releases awealth of information on its activities.

• During FY2002, the IMF reviewed its Data Stan-dards Initiatives and approved a Data QualityAssessment Framework, integrated with the Reportson the Observance of Standards and Codes(ROSCs).

• Recognizing the critical importance of concertedaction to strengthen financial systems, the IMF con-tinued to conduct financial "health checkups" underthe Joint IMF-World Bank Financial Sector Assess-ment Program (FSAP). By April 2002, 27 countrieshad completed their FSAP participation, and 50others had committed to participate.

IMF Managing Director Horst Kohler (right) meetsAfghanistan's Interim Authority Chairman Hamid Karzai,January 29, 2002. The IMF has offered technicalassistance to Afghanistan to help with banking, currencyissues, and the fiscal situation.

• During the year, discussions continued on a range ofissues relating to resolving financial crises and the roleof the private sector. A plan of work on crisis resolu-tion outlined a four-point program designed toincrease the IMF's capacity to assess a country's debtsustainability; clarify the policy on access to IMFresources; strengthen the tools available for securingprivate sector involvement in resolving financialcrises; and examine a more orderly and transparentlegal framework for sovereign debt restructurings.Proposals for a new sovereign debt restructuringmechanism were spelled out in late 2001 and early2002 by Anne O. Krueger, the IMF's First DeputyManaging Director.

• The IMF's work on anti-money-laundering issuesacquired increased importance after the September11 attacks, when it was extended to combating thefinancing of terrorism.

Lending Policies and ConditionalityThe IMF regularly reviews its "conditionality"—theconditions it attaches to its financial assistance toensure that it is repaid (so that its resources becomeavailable to other members in need) and that externalviability, financial stability, and sustainable economicgrowth are restored in the borrowing member coun-try—and its policy on access to its financial resources.• The latest review of conditionality, which was still in

progress at the end of FY2002, emphasized thatconditionality must be applied in a way that rein-forces national ownership, should focus on policiescritical to achieving a program's macroeconomicgoals, and set a clearer division of labor between theIMF and other institutions, particularly the WorldBank.

• After reviewing the policy governing members' accessto its resources, the IMF determined to maintain cur-rent annual and cumulative access limits, but agreedto later review the policy involving high access toresources.

Poverty ReductionReducing poverty in low-income countries is a majorinternational challenge, and the IMF continues to playits role. Besides the lending mentioned above, the IMFtook a number of steps in FY2002 to reinforce andstrengthen its support for reform and developmentefforts in low-income countries.• The IMF received about SDR 7 million in contribu-

tions from five members to subsidize the rate ofcharge on Post-Conflict Emergency Assistance.

• The IMF and the World Bank jointly reviewed thePoverty Reduction Strategy Paper (PRSP) approach,which, combined with sound policies, is expected toput countries on a path to sustainable growth and

iv A N N U A L R E P O R T 2 0 0 2

©International Monetary Fund. Not for Redistribution

poverty reduction and toward achieving the UN'sMillennium Development Goals.

• The IMF—jointly with the World Bank, AsianDevelopment Bank, and European Bank forReconstruction and Development—sponsored aninitiative to help the seven low-income members ofthe Commonwealth of Independent States accelerategrowth and poverty reduction.

• A review of the PRGF in March 2002 empha-sized the need to build on progress in several specific areas,including designing policies to foster pro-poor economic growth,improving the quality and efficiency of government spending,coordinating program design with the World Bank, and enhanc-ing communication with authorities, donors, and civil society inPRGF countries.

• Late in the financial year, the IMF reviewed the status of the H I P CInitiative and the movement toward long-term external debt sus-tainability. At that time, H I P C countries had received commitmentsof $40 billion (in nominal terms) in debt relief.

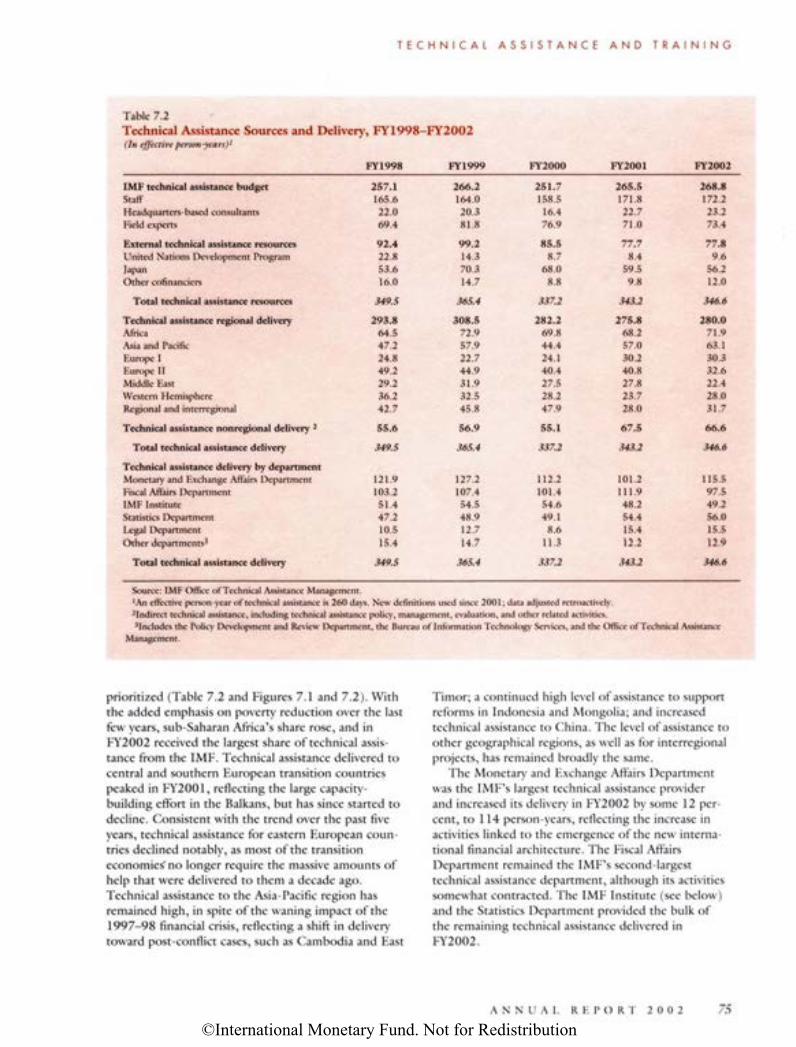

Technical Assistance and TrainingIMF technical assistance supports the institution's surveillance and pro-gram work, and its importance has grown steadily in recent years. Rec-ommendations emerging from the FSAP, the adoption of internationalstandards, tracking indicators for the H I P C Initiative, and combatingmoney laundering and the financing of terrorism have all increasedmembers' requests for technical assistance.• During the year, the IMF's Caribbean Regional Assistance Center

was established; two more centers will open in late 2002 in Eastand West Africa under the IMF's Africa Capacity-BuildingInitiative.

• The IMF Institute increased training by about 9 percent overFY2001. A Joint Regional Training Center for Latin America wasopened, bringing the number of such regional centers to five.

Organization, Budget, and StaffingFY2002 saw several major changes within the IMF.• The IMF bid farewell to First Deputy Managing Director Stanley

Fischer and to Economic Counsellor and Director of the ResearchDepartment Michael Mussa and welcomed their successors—AnneKrueger and Kenneth Rogoff. Jack Boorman, who stepped down asDirector of the Policy Development and Review (PDR) Depart-ment, retained his position as Counsellor and became a SpecialAdvisor to the Managing Director. He was succeeded as P D Rdirector by Timothy Geithner. Gerd Hausler joined the IMF asCounsellor and Director of the new International Capital MarketsDepartment, which came into being in FY2002.

• The Independent Evaluation Office became operational.• The IMF's internal budgeting process was reviewed by a panel of

external experts, who made a number of recommendations. Some ofthese have already been put in place, while other changes will beintroduced in FY2003 and FY2004.

* * *After the end of the financial year, on July 23, 2002, the DemocraticRepublic of East Timor became the 184th member of the IMF.

Stanley Fischer gets a standing ovation fromthe IMF Board. Fischer served as First DeputyManaging Director from September 1994 toAugust 2001 and then as Special Adviser tothe Managing Director until January 31, 2002.

Technical Assistance(By function, as a percent of total resourcesin work-years FY2002)

HIPCs-Debt Reduction**(Net present value of debt, in billionsof US$ — in decision point terms)

Countries that reached their decision points asof April 30, 2002.

A N N U A L R E P O R T 2 0 0 2 V

PRGF—New Commitments*(In millions of SDRs, financial year)

Poverty Reduction and Growth Facility; beforeNovember 1999, the Enhanced StructuralAdjustment Facility.

©International Monetary Fund. Not for Redistribution

Managing Director and Deputy Managing Directorson April 30, 2002

Managing Director Horst Kohler (center), with his management team, First DeputyManaging Director Anne Krueger (left), Deputy Managing DirectorEduardo Aninat (seated), and Deputy Managing Director Shigemitsu Sugisaki.

vi A N N U A L R E P O R T 2 0 0 2

©International Monetary Fund. Not for Redistribution

Message from the Managing Director

Over the past year, the international financial system has shown remarkable resilience in the face ofa sharp slowdown in global economic growth, a fundamental reassessment in equity markets ofthe technology and telecommunications sectors, and the terrorist attacks in the United States.Most of the credit must go to decisive policy action by the United States and other industrial

countries, including coordinated actions by central banks, supervisors, and private financial institutions tosafeguard banking and payments systems in the aftermath of the September 11 attacks. It was also importantthat the membership of the I M F came together last November in Ottawa to define a collaborative approachto strengthen the global economy.

While an economic recovery has since gotten under way, there are still uncertainties and risks. Keeping therecovery on track will require strong leadership by the advanced industrial countries, including action tostrengthen the prospects for sustained growth in their own economies and leading by example in the effort tomake globalization work for the benefit of all.

The Asian crisis of 1997-98 sparked a critical debate about the process of globalization and the reform ofthe international financial architecture. A n d while we have not reached the end of that debate, the lessonslearned have led to important reforms. The I M F has become more open and transparent. We have worked tostreamline conditionality and build ownership of reforms. We are improving the IMF's capacities for crisisprevention and management. To strengthen the tools for crisis resolution, we are encouraging the use of col-lective action clauses in borrowing agreements, and have proposed the creation of a sovereign debt restruc-turing mechanism. We are also intensifying cooperation with the World Bank and other internationalinstitutions to ensure a good division of labor. Together with the Bank, we have embarked on a comprehen-sive program to assess financial sector strengths and weaknesses in our member countries. A n d during thepast year, the I M F and other international organizations stepped up work on combating money launderingand the financing of terrorism.

Our surveillance of capital markets and assessments of systemic vulnerability have been strengthened byour new International Capital Markets Department and its quarterly reports on global financial stability.Recent accounting and corporate governance scandals have underscored the need to pay close attention torisks and vulnerabilities arising in the advanced economies, and to examine the adequacy of existing regula-tory systems. Our work on internationally recognized standards and codes, which is helping to establish newrules of the game for the global economy, can be an element in that process.

The I M F is playing an active part in the effort to achieve the Millennium Development Goals. In my talkswith political leaders, business persons, and civil society in low-income countries, I have been struck by thewillingness to take responsibility for tackling the homegrown causes of poverty. It is particularly encouragingthat African leaders have made good governance, sound policies, and increased trade and investment the cor-nerstones of the New Partnership for Africa's Development ( N E P A D ) . Our global outreach and review haveshown that the Poverty Reduction Strategy Paper (PRSP) process is broadly accepted as a practical way to putthis approach into action. For its part, the I M F remains committed to assisting low-income countries withpolicy advice, financial assistance, H I P C debt relief, and technical assistance—including regional technicalassistance centers to support institution building in Africa, the Caribbean, and the Pacific.

While it is crucial not to neglect any element of comprehensive support for poverty reduction, expandingopportunities for trade is clearly the best form of help for self-help—not only because it paves the way forgreater self-sufficiency, but also because it is a win-win proposition for developed and developing countriesalike. The elimination of trade-distorting subsidies, not least for agricultural products, and market opening byadvanced and developing countries are key to bolstering confidence in the prospects for strong global growthand shared prosperity in the world.

A N N U A L R E P O R T 2 0 0 2 vii

©International Monetary Fund. Not for Redistribution

Executive Board on April 30, 2002

United StatesJapan Germany

(Position Vacant)*Meg Lundsager

Ken YagiHaruyuki Toyoma

Karlheinz BischofbergerRuediger von Kleist

Armenia, Bosnia andHerzegovina,Bulgaria,Croatia, Cyprus,Georgia, Israel, FYRMacedonia, Moldova, 1Netherlands,Romania, Ukraine

m 1

Costa Rica,El Salvador,Guatemala,Honduras, Mexico,Nicaragua, Spain,RepublicaBolivarianade Venezuela

Albania, Greece, Italy,Malta, Portugal, SanMarino

J. de BeaufortWijnholdsYuriy G. Yakusha

Fernando VarelaHernan Oyorzabal

Pier Carlo PadoanHarilaos Vittos

Saudi Arabia

Sulaiman M. Al-TurkiAhmed Saleh Alosaimi

Cyrus D.R. RustomjeeIsmailo Usman

Angola, Botswana,Burundi, Eritrea,Ethiopia, The Gam-bia, Kenya, Lesotho,Liberia, Malawi,Mozambique,Namibia, Nigeria,Sierra Leone, SouthAfrica, Sudan,Swaziland, Tanza-nia, Uganda, Zam-bia, Zimbabwe

Brunei Darussalam,Cambodia, Fiji,Indonesia, Lao P.D.R.,Malaysia, Myanmar,Nepal, Singapore,Thailand,Tonga, Vietnam

Dono IskandarDjojosubrotoKwok Mun Low

Azerbaijan,Kyrgyz Republic,Poland,Switzerland,Tajikistan,Turkmenistan,Uzbekistan

Brazil, Colombia,Dominican Republic,Ecuador, Guyana,Haiti, Panama,Suriname, Trinidadand Tobago

Roberto F. Cippd Murilo PortugalWieslow Szczuko Roberto Junguito

Note: Alternate Executive Directors are indicated in italics.*Randal Quarles relinquished his duties as Executive Director for the United States, effective April 2, 2002.

Bangladesh, Bhutan,India,Sri Lanka

Vijay L. KelkarR.A. Joyotisso

vin A N N U A L R E P O R T 2 0 0 2

©International Monetary Fund. Not for Redistribution

France

Pierre DuquesneSebastien Boitreaud

United Kingdom

Tom ScholarMartin A. Brooke

Willy KiekensJohann Prader

Austria, Belarus,Belgium, CzechRepublic, Hungary,Kazakhstan,Luxembourg, SlovakRepublic, Slovenia,Turkey

Antigua andBarbuda, TheBahamas, Barbados,Belize, Canada,Dominica, Grenada,Ireland, Jamaica,St. Kitts and Nevis, St.Lucia, St. Vincentand the Grenadines

Denmark, Estonia,Finland, Iceland,Latvia, Lithuania,Norway,Sweden

Ian E. BennettNioclas A. O'Murchu

Olafur IsleifssonBenny Andersen

Michael J. CallaghanDiwa Guinigundo

Australia, Kiribati,Korea, MarshallIslands, FederatedStates of Micronesia,Mongolia, NewZealand, Palau,Papua New Guinea,Philippines, Samoa,Seychelles, SolomonIslands, Vanuatu

A. Shakour ShaalanMohamad B. Chatah

Bahrain, Egypt, Iraq,Jordan, Kuwait,Lebanon, Libya,Maldives, Oman,Qatar, Syrian ArabRepublic, UnitedArab Emirates,Yemen

China Russia

WEI BenhuaWang Xiaoyi

Aleksei V. MozhinAndrei Lushin

Abbas MirakhorMohammed Dairi

Algeria, Ghana,Islamic Republic ofIran, Morocco,Pakistan, Tunisia

Argentina, Bolivia,Chile, Paraguay,Peru, Uruguay

A. Guillermo ZoccaliGuillermo Le Fort

Alexandre BarroChambrierDamian Ondo Mañe

Benin, Burkina Faso,Cameroon, CapeVerde, CentralAfrican Republic,Chad, Comoros,Republic of Congo,Cote d'Ivoire,Djibouti, EquatorialGuinea, Gabon,Guinea, Guinea-Bissau, Madagascar,Mali, Mauritania,Mauritius, Niger,Rwanda, Sao Tomeand Principe,Senegal, Togo

A N N U A L R E P O R T 2 0 0 2 ix

©International Monetary Fund. Not for Redistribution

Senior Of f icers on April 30, 2002

Jack Boorman*Counsellor and Special Advisorto the Managing Director

Gerd Hausler*Counsellor

Kenneth S. Rogoff*Economic Counsellor

Abdoulaye Bio-TchaneDirector, African Department

Yusuke HoriguchiDirector, Asia and Pacific Department

Michael C. DepplerDirector, European I Department

John Odling-SmeeDirector, European II Department

Thomas C. Dawson IIDirector, External Relations Department

Teresa M . Ter-MinassianDirector, Fiscal Affairs Department

Margaret R. KellyDirector, Human Resources Department

Mohsin S. KhanDirector, IMF Institute

Gerd HauslerDirector, International Capital Markets Department

Francois P. GianvitiGeneral Counsel, Legal Department

Paul ChabrierDirector, Middle Eastern Department

Stefan IngvesDirector, Monetary and Exchange Affairs Department

Timothy F. GeithnerDirector, Policy Development and Review Department

Kenneth S. RogoffDirector, Research Department

Shailendra J. AnjariaSecretary, Secretary's Department

Carol S. CarsonDirector, Statistics Department

Brian C. StuartDirector, Technology and General Services Department

Eduard BrauTreasurer, Treasurer's Department

Claudio M. LoserDirector, Western Hemisphere Department

Barry PotterDirector, Office of Budget and Planning

Rafael MuñozDirector, Office of Internal Audit and Inspection

Claire LiuksilaDirector, Office of Technical Assistance Management

Kunio SaitoDirector, Regional Office for Asia and the Pacific

Flemming LarsenDirector, Office in Europe (Paris)

Grant B. TaplinActing Director and Special Trade Representative,Office in Geneva

Reinhard MunzbergDirector and Special Representative to the UN,Office at the United Nations

Montek Singh AhluwaliaDirector, Independent Evaluation Office

Jeanette MorrisonChief, Editorial Division

*Alphabetical order.

A N N U A L R E P O R T 2 0 0 2X

©International Monetary Fund. Not for Redistribution

Letter of Transmittal to the Board of Governors

August 28, 2002

Dear Mr. Chairman:

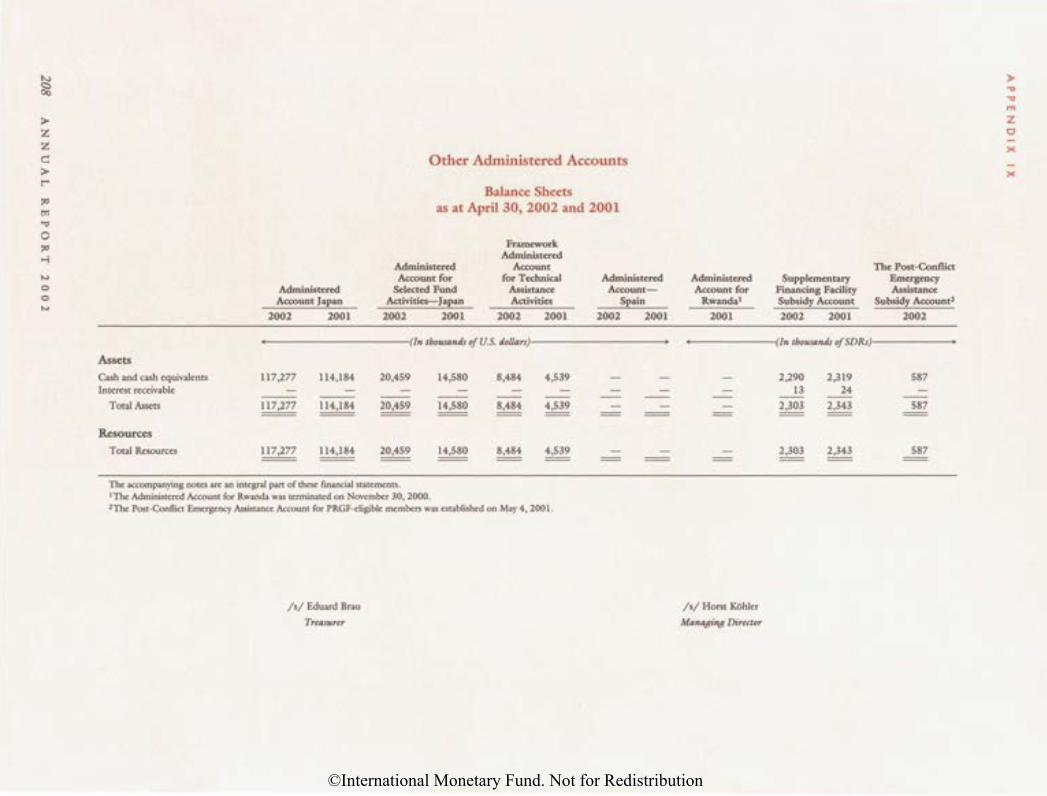

I have the honor to present to the Board of Governors the Annual Report of the Executive Boardfor the financial year ended April 30, 2002, in accordance with Article XII, Section 7 (a) of theArticles of Agreement of the International Monetary Fund and Section 10 of the IMF's By-Laws.In accordance with Section 20 of the By-Laws, the administrative and capital budgets of the IMFapproved by the Executive Board for the financial year ending April 30, 2003, are presented inChapter 8. The audited financial statements for the year ended April 30, 2002, of the GeneralDepartment, the SDR Department, and the accounts administered by the IMF, together withreports of the external audit firm thereon, are presented in Appendix IX.

Horst KohlerChairman of the Executive Board

A N N U A L R E P O R T 2 0 0 2 xi

©International Monetary Fund. Not for Redistribution

Board of Governors, Executive Board,International Monetary and Financial Committee,and Development Committee

The Board of Governors, the highest decision-making body of the IMF, consists ofone governor and one alternate governor for each member country. The gover-nor is appointed by the member country and is usually the minister of finance orthe governor of the central bank. All powers of the IMF are vested in the Boardof Governors. The Board of Governors may delegate to the Executive Board allexcept certain reserved powers. The Board of Governors normally meets once ayear.

The Executive Board (the Board) is responsible for conducting the day-to-daybusiness of the IMF. It is composed of 24 Directors, who are appointed orelected by member countries or by groups of countries, and the Managing Direc-tor, who serves as its Chairman. The Board usually meets several times each week.It carries out its work largely on the basis of papers prepared by IMF manage-ment and staff. In 2001/2002, the Board spent about 70 percent of its time onmember country matters (regular country consultations and reviews andapprovals of financial arrangements) and much of its remaining time on globalsurveillance and policy issues (such as the world economic outlook exercise,developments in international capital markets, the IMF's financial resources, thearchitecture of the international monetary and financial system and the IMF'srole, debt of the heavily indebted countries, and issues concerning IMF facilitiesand program design).

The International Monetary and Financial Committee of the Board of Gover-nors (formerly the Interim Committee on the International Monetary System) isan advisory body made up of 24 IMF governors, ministers, or other officials ofcomparable rank, representing the same constituencies as in the IMF's ExecutiveBoard. The International Monetary and Financial Committee normally meetstwice a year, in April or May, and at the time of the Annual Meeting of the Boardof Governors in September or October. Among its responsibilities are to provideministerial guidance to the Executive Board and to advise and report to theBoard of Governors on issues regarding the management and adaptation of theinternational monetary and financial system, including sudden disturbances thatmight threaten the international monetary system, and on proposals to amend theIMF's Articles of Agreement.

The Development Committee (the Joint Ministerial Committee of the Boards ofGovernors of the World Bank and the IMF on the Transfer of Real Resources toDeveloping Countries) is composed of 24 members—finance ministers or otherofficials of comparable rank—and generally meets the day after the InternationalMonetary and Financial Committee. It advises and reports to the Boards of Gov-ernors of the World Bank and the IMF on all aspects of the transfer of realresources to developing countries.

xii A N N U A L R E P O R T 2 0 0 2

©International Monetary Fund. Not for Redistribution

CONTENTS

Highlights ii

Message from the Managing Director vii

Executive Board viii

Senior Officers x

Letter of Transmittal xi

Board of Governors, Executive Board, International Monetary and

Financial Committee, and Development Committee xii

Note xvii

1. World Economic and Financial Developments in FY2002 3Global Economic Environment 3Key Developments in Emerging Market and Industrial Countries 6

2. IMF Surveillance in Action 8Country Surveillance 10Global Surveillance 10

World Economic Outlook 11International Capital Markets and Global Financial Stability 17

Regional Surveillance 20Central African Economic and Monetary Community 20West African Economic and Monetary Union 21Monetary and Exchange Policies of the Euro Area and Trade Policies of

the European Union 22Trade and Market Access Issues 24

3. Strengthening the International Financial System 26Crisis Prevention 26

Assessing External Vulnerability 26Transparency 28Standards and Codes 29Strengthening Financial Sectors 31Capital Account Liberalization 32

Crisis Resolution 32Work Program for Crisis Resolution 33Sovereign Debt Restructuring . 34

Combating Money Laundering and the Financing of Terrorism 36Background 36Post-September 11 Board Discussion 36

A N N U A L R E P O R T 2 0 0 2 xiii

©International Monetary Fund. Not for Redistribution

C O N T E N T S

4. IMF Lending Policies and Conditionality 40Review of Conditionality 40

Streamlining Structural Conditionality—Initial Experience 40Strengthening Country Ownership of Programs 41Making Improvements 44Review of Progress 44

Review of Access Policy 45

5. Poverty Reduction and Debt Relief for Low-Income Countries 46Global Economic Environment and IMF's Support for Low-Income Countries 46Broader IMF Support for the Global Effort to Reduce Poverty 46

The PRSP Review 47Review of the Poverty Reduction and Growth Facility 49

HIPC Initiative and Debt Sustainability 51Capacity Building 51

CIS Initiative 51Support by the International Community . 53Looking Ahead 55

6. Financial Operations and Policies in FY2002 56Regular Financing Activities 57

Lending . . . 57Resources and Liquidity 58

Quota Developments 59Concessional Financing 60

Poverty Reduction and Growth Facility 61Enhanced HIPC Initiative 61Financing of the HIPC Initiative and PRGF Subsidies 62Investment of SDA, PRGF, and PRGF-HIPC Resources 63Post-Conflict Emergency Assistance 63

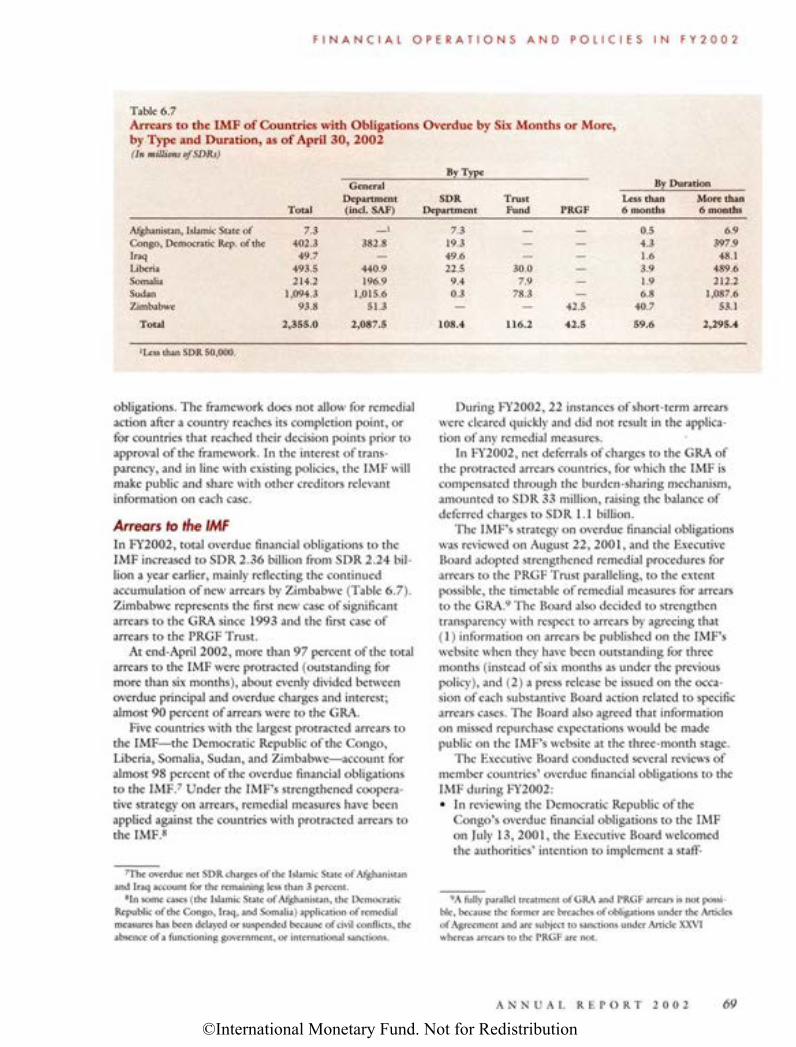

Special Drawing Rights 63Income, Charges, Remuneration, and Burden Sharing 65Safeguarding IMF Resources and Dealing with Arrears 67

Safeguards Assessments 67Misreporting 68Arrears to the IMF 69

7. Technical Assistance and Training 71Prioritizing the IMF's Technical Assistance 71New Developments 72Technical Assistance Delivery in FY2002 74Expanded Training by the IMF Institute 76

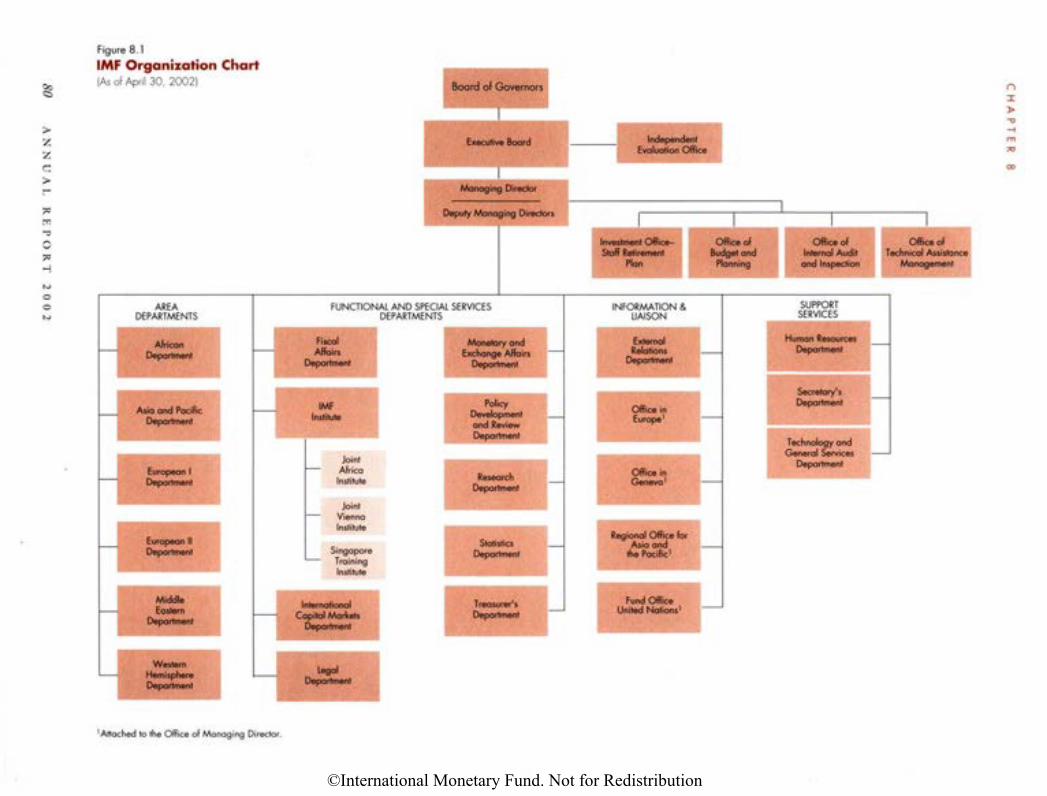

8. Organization, Budget, and Staffing 78Organization 78

Executive Board 78Departments 78Independent Evaluation Office 82

Administrative and Capital Budgets 82Budget Reforms 82Budgets and Actual Expenditure in FY2002 82Budgets in FT2003 82Medium-Term Framework 83

xiv A N N U A L R E P O R T 2 0 0 2

©International Monetary Fund. Not for Redistribution

CONTENTS

Changes in Management and Senior Staff 84Staff 84

Recruitment and Retention 84Dispute Resolution 85Salary Structure 85Diversity 86

New Building 87

Appendixes . . 89I International Reserves . 95

II Financial Operations and Transactions 100III Principal Policy Decisions of the Executive Board 120IV IMF Relations with Other International Organizations 129V External Relations 132

VI Press Communiques of the International Monetary andFinancial Committee and the Development Committee 136

VII Executive Directors and Voting Power on April 30, 2002 146VIII Changes in Membership of the Executive Board 150

IX Financial Statements 153

Abbreviations 214

Boxes2.1 IMF Biennial Surveillance Review 92.2 IMF Launches Quarterly Report on Global Financial Markets 102.3 Doha Development Agenda 253.1 Board Discusses Guidelines for Foreign Exchange Reserve Management 283.2 IMF's Data Standards 303.3 Collaborating on Standards 313.4 F D M D Krueger Proposes a Sovereign Debt Restructuring Mechanism 353.5 Progress on Anti-Money Laundering and Combating the Financing of

Terrorism During FY2002 . 384.1 IMF Requests Public Comment 415.1 Millennium Development Goals 475.2 International Conference on Poverty Reduction Strategies . 485.3 What Is a PRSP? . 495.4 Key Features of Programs Supported by the Poverty Reduction

and Growth Facility 505.5 Africa Initiatives 545.6 Conference on Financing for Development, Monterrey, Mexico 556.1 Public Information on IMF Finances 566.2 The IMF's Financing Mechanism 576.3 Financial Transactions Plan 596.4 IMF Financial Resources and Liquidity 606.5 Twelfth Review of Quotas 616.6 SDR Valuation and Interest Rate 646.7 IMF Executive Board Reviews Experience with Safeguards Assessments 687.1 Combating Money Laundering and Financing of Terrorism:

Technical Assistance and Coordination Efforts 727.2 Caribbean Regional Technical Assistance Center 747.3 Recently Established Technical Assistance Subaccounts 748.1 IMF Resident Representatives 79

A N N U A L R E P O R T 2 0 0 2 XV©International Monetary Fund. Not for Redistribution

C O N T E N T S

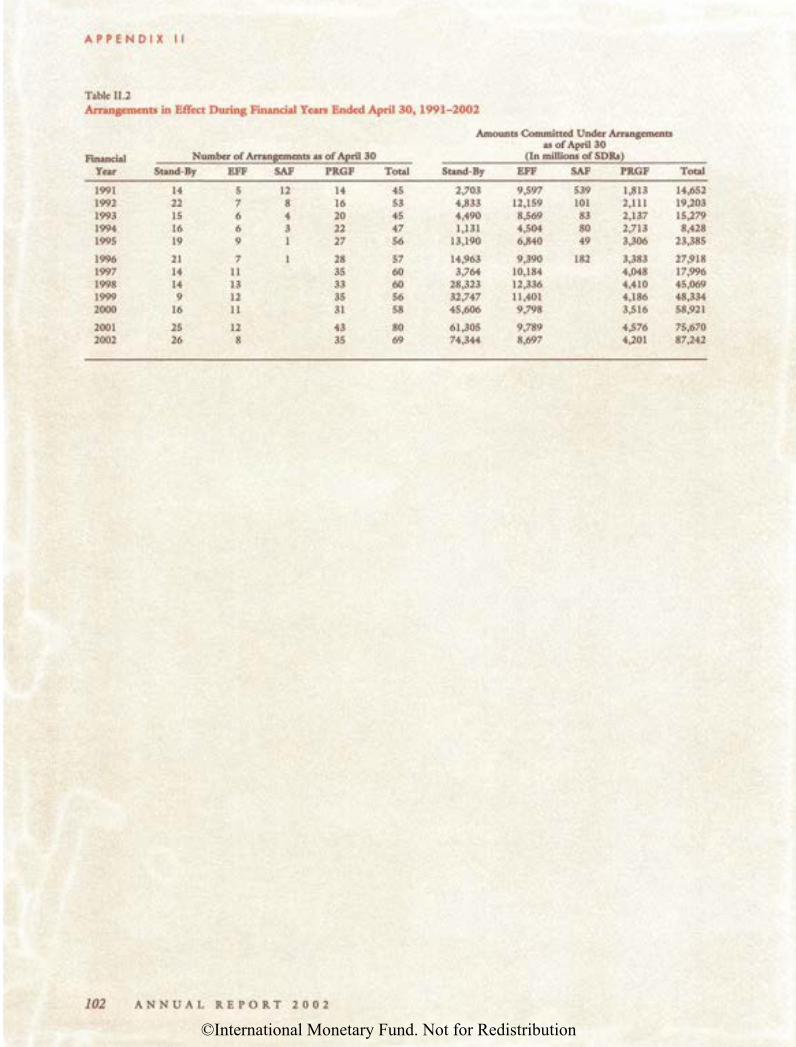

Tables1.1 Overview of the World Economy 42.1 Article IV Consultations Concluded in FY2002 124.1 IMF Financial Facilities 425.1 Progress Status of Countries Under the Enhanced HIPC Initiative 536.1 IMF Financial Assistance Approved in FY2002 586.2 New PRGF Loan Resources Committed by Lenders 626.3 Commitments and Disbursements of HIPC Initiative Assistance 626.4 Contributions to Subsidize Post-Conflict Emergency Assistance 636.5 SDR Valuation 646.6 Transfers of SDRs 666.7 Arrears to the IMF of Countries with Obligations Overdue by Six Months

or More, by Type and Duration, as of April 30, 2002 697.1 Technical Assistance Delivery Indicators for Main Program Areas

and Key Policy Initiatives and Concerns 737.2 Technical Assistance Sources and Delivery, FY1998-FY2002 757.3 IMF Institute Training Programs for Officials, FY1998-FY2002 767.4 IMF Institute Regional Training Programs 778.1 Recommended Reforms to IMF Internal Budgeting 828.2 Administrative and Capital Budgets, Financial Years 2000-2003 838.3 Distribution of Professional Staff by Nationality 848.4 IMF Staff Salary Structure 858.5 Distribution of Staff by Gender 868.6 Distribution of Staff by Developing and Industrial Countries 87

Figures1.1 Global Indicators 55.1 Enhanced HIPC Initiative Flow Chart 526.1 IMF Liquidity Ratio, April 1993-April 2002 606.2 SDR Interest Rates, 1992-2002 647.1 Technical Assistance by Function, FY2002 767.2 Technical Assistance by Region, FY2002 768.1 IMF Organization Chart 808.2 Share of Resources by Output Category, FY2003 83

xvi A N N U A L R E P O R T 2 0 0 2©International Monetary Fund. Not for Redistribution

NOTE

A N N U A L R E P O R T 2 0 0 2 xvii

T his Annual Report of the Executive Board of the IMF reports on the activities of theBoard during the financial year May 1, 2001, through April 30, 2002. Most of the Reportconsists of reviews of Board discussions of the whole range of IMF policy and operations.The discussions are based on papers prepared by the staff. Typically, a staff paper includesbackground factual and analytical material on various aspects of the issue at hand andrequests the Board's views on the main issues involved. It may also present proposals by theIMF's management on how the Board and the institution should move forward on an issue.Although a staff paper presents the positions of staff and management, it does not necessar-ily represent the IMF's position on the issue. The Board may or may not agree with theanalysis or the proposals. The position of the IMF is, rather, the position of the Board asreflected in a decision, or as explained in a statement summarizing the discussion (usuallyreferred to in the IMF as the "summing up").

The unit of account of the IMF is the SDR; conversions of IMF financial data to U.S.dollars are approximate and are provided for convenience. As of April 30, 2002, theS D R / U . S . dollar exchange rate was US$1 = SDR 0.788826, and the U.S. dollar/SDRexchange rate was SDR 1 = US$1.267706. The year-earlier rates (April 30, 2001) wereUS$1 = SDR 0.7900204 and SDR 1 - US$1.26579.

The following conventions are used in this Report:. . . to indicate that data are not available;— to indicate that the figure is zero or less than half the final digit shown or that the

item does not exist;between years or months (for example, 1999-2000 or January-June) to indicatethe years or months covered, including the beginning and ending years or months;

/ between years or months (for example 1999/00) to indicate a fiscal or financialyear.

"Bill ion" means a thousand million; "trillion" means a thousand billion.Minor discrepancies between constituent figures and totals are due to rounding.As used in this Report, the term "country" does not in all cases refer to a territorial

entity that is a state as understood by international law and practice. As used here, the termalso covers some territorial entities that are not states but for which statistical data are main-tained on a separate and independent basis.

©International Monetary Fund. Not for Redistribution

This page intentionally left blank

©International Monetary Fund. Not for Redistribution

ANNUAL REPORT 2002

©International Monetary Fund. Not for Redistribution

This page intentionally left blank

©International Monetary Fund. Not for Redistribution

CHAPTER

World Economic and Financial Developments in FY2002

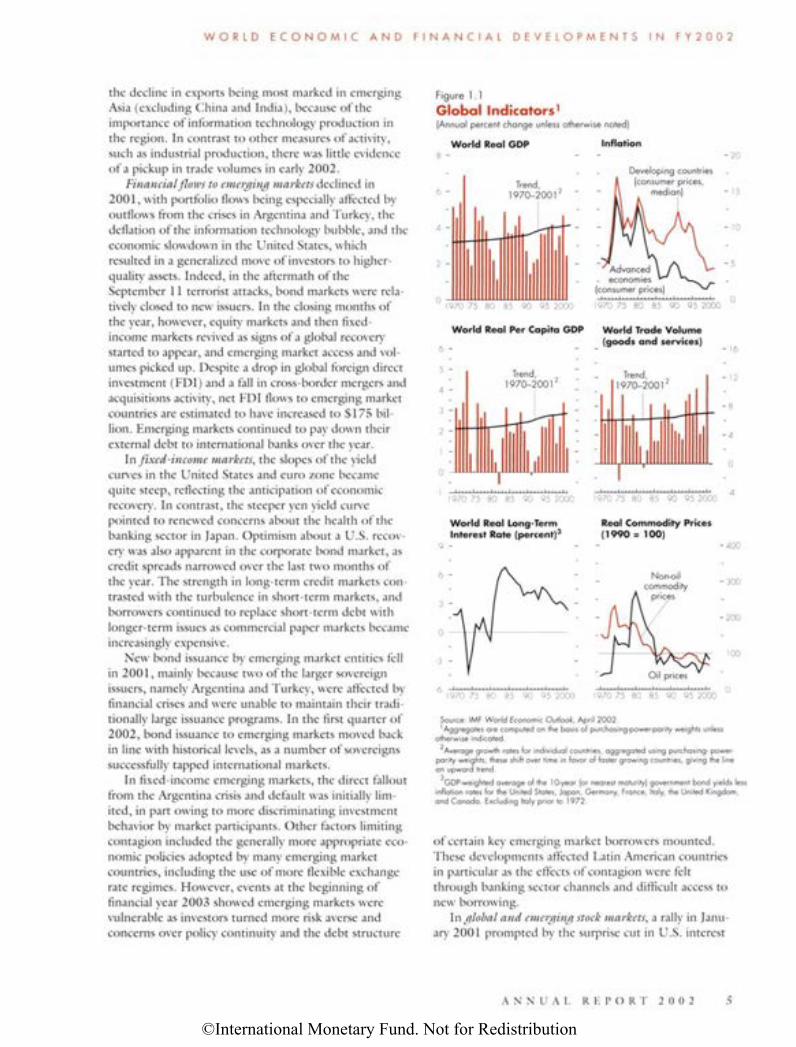

In 2001 the world economy experienced a synchro-nized, widespread slowdown after the unusually strongexpansion of the previous year, with growth slowing inevery major region except Africa (Table 1.1 and Figure1.1). The slowdown reflected a series of intertwineddevelopments in 2001, including the downwardadjustment in equity prices (particularly in the infor-mation technology sector), a rise in energy prices, andthe tightening of monetary policy in industrial coun-tries in response to evidence of rising demandpressures. The already weakening international econ-omy was further affected by the September 11 terroristattacks in the United States, which had a substantial—although largely temporary—influence onmacroeconomic conditions. In the first few months of2002, however, there were increasing signs that theslowdown was bottoming out in most regions and thatgrowth was turning up in some—most notably NorthAmerica and a number of east Asian countries. Thisreflected, at least in part, the significant easing ofmacroeconomic policies in the advanced countries in2001, especially in the United States and in a numberof emerging countries in Asia, as well as the comple-tion of ongoing inventory cycles. Partly mirroring theweakening of growth in 2001, inflation remainedextremely low almost everywhere. Indeed, ongoingdeflation in Japan continued to worsen already difficulteconomic conditions.

Financial flows to emerging market economies fol-lowed a broadly similar pattern, being weak throughmuch of 2001 as investors became more concernedabout risk, particularly in the wake of the crisis inTurkey early in the year, the September terroristattacks, and mounting difficulties in Argentina. Theimpact of the terrorist attacks, however, proved lessdurable than had been initially feared and the crisis inArgentina led to relatively little immediate contagionto other countries in late 2001. As a result, in the firstquarter of 2002, flows to emerging markets strength-ened and risk spreads, as reflected in the EMBI+,came down to levels not seen since before the Russiancrisis in 1998.

Global Economic Environment

A series of fluctuations in the price of oil—reflectingboth demand and supply factors—dominated develop-ments in commodity markets. Oil prices remained in theOrganization of Petroleum Exporting Countries'(OPEC) reference band of US$22-28 a barrel rangethrough much of 2001 as falling demand due to slow-ing growth was essentially offset by O P E C productioncuts. The terrorist attacks in September led to anextremely brief spike in prices on fears of supply disrup-tions, after which prices rapidly dropped below thelower bound of the O P E C reference range as slowingactivity led to a fall in actual and anticipated demand,bottoming out at around US$19 per barrel. This weak-ness was largely reversed in early 2002 as demandrevived while O P E C and some non-OPEC membersresponded to price weakness with further productioncuts. During April prices remained highly volatilearound US$25 a barrel when a series of largely noneco-nomic factors raised concerns about supply disruption,including increased tensions in the Middle East andpolitical developments in Venezuela.

Nonoil commodity prices were generally depressedthrough 2001 and early 2002 as slowing activity rein-forced longer-term price weakness caused largely bysupply factors, as well as industrial country subsidies.Early 2002 saw some increases in prices, particularly inthe more cyclically sensitive metals, but overall nonoilcommodity prices remained below their levels at thestart of 2001. Prices of semiconductors—the marketfor which is rapidly gaining the same characteristics asthose for "traditional" commodities—fell rapidlythrough 2001 as demand for information technologygoods slumped before showing some revival in early2002 on evidence of a recovery in growth.

World trade volumes fell in 2001, reflecting theweakness in economic activity, particularly in manufac-turing and, more specifically, informationtechnology—sectors that are relatively trade-intensive.Owing to the generalized and synchronized nature ofthe economic slowdown, all regions were affected, with

A N N U A L R E P O R T 2 0 0 2 3

1

©International Monetary Fund. Not for Redistribution

C H A P T E R I

Table 1.1Overview of the World Economy(Annual percent change unless otherwise noted)

1994 1995 1996 1997 1998 1999

Source: IMF, World Economic Outlook, April 2002.1Indonesia, Malaysia, the Philippines, and Thailand.2Includes Malta.3Simple average of spot prices of U.K. Brent, Dubai, and West Texas Intermediate crude oil.

2000 2001

World outputAdvanced economies

Major advanced economiesUnited StatesJapanGermanyFranceItalyUnited KingdomCanada

Other advanced economiesMemorandumEuropean Union

Euro areaNewly industrialized Asian economiesDeveloping countries

AfricaDeveloping Asia

ChinaIndiaASEAN-41

Middle East and Turkey2

Western HemisphereBrazil

Countries in transitionCentral and eastern EuropeCommonwealth of Independent

States and MongoliaRussiaExcluding Russia

MemorandumWorld growth based on market exchange ratesWorld trade volume (goods and services)Imports

Advanced economiesDeveloping countriesCountries in transition

ExportsAdvanced economiesDeveloping countriesCountries in transition

Commodity prices (U.S. dollars)O i l 3

Nonfuel (average based on worldcommodity export weights)

Consumer pricesAdvanced economiesDeveloping countriesCountries in transitionSix-month London interbank

offered rate (LIBOR, percent)On U.S. dollar depositsOn Japanese yen depositsOn euro deposits

3.73.43.14.01.12.31.92.24.74.74.6

2.82.47.76.72.39.6

12.66.87.60.55.05.9

-8.53.0

-14.5-13.5-16.6

3.18.8

9.56.56.0

8.611.63.0

-5.0

13.4

2.655.3

252.5

5.12.45.7

3.62.72.32.71.51.71.82.92.92.84.3

2.42.37.56.13.09.0

10.57.68.14.21.84.2

-1.55.6

-5.5-4.2-8.6

2.89.7

8.719.111.2

8.311.09.4

7.9

8.4

2.623.2

133.8

6.11.35.7

4.03.02.83.63.60.81.11.12.61.63.8

1.71.56.36.55.68.39.67.57.34.83.62.6

-0.54.0

-3.3-3.4-3.1

3.36.8

6.49.68.9

6.09.66.6

18.4

-1.3

2.415.442.5

5.60.73.7

4.23.43.24.41.81.41.92.03.44.34.3

2.62.55.85.83.16.68.85.03.45.65.23.31.62.6

1.10.91.5

3.510.5

9.311.715.2

10.513.89.0

-5.4

-3.0

2.110.027.3

5.80.73.5

2.82.72.84.3

-1.02.03.51.83.03.92.2

3.02.9

-2.43.53.44.07.85.8

-9.43.92.30.2

-0.82.3

-2.8-4.9

1.7

2.34.2

5.9-0.8-0.2

4.04.83.6

-32.1

-14.7

1.510.621.8

5.50.63.7

3.63.32.94.10.71.83.01.62.15.15.0

2.72.78.03.92.66.17.16.72.91.00.20.83.62.2

4.65.42.8

3.05.3

7.81.3

-7.0

5.24.3

-0.7

37.5

-7.0

1.46.9

44.1

5.50.23.0

4.73.93.54.12.23.03.62.93.04.45.3

3.43.58.55.73.06.78.05.45.15.84.04.46.63.8

8.39.07.0

4.012.4

11.616.013.2

11.715.014.6

57.0

1.8

2.36.1

20.2

6.60.34.6

2.51.21.11.2

-0.40.62.01.82.21.51.6

1.71.60.84.03.75.67.34.32.62.10.71.55.03.1

6.25.08.8

1.4-0.2

-1.52.9

10.8

-1.33.06.3

-14.0

-5.5

2.25.7

15.9

3.70.24.1

4 A N N U A L R E P O R T 2 0 0 2

©International Monetary Fund. Not for Redistribution

W O R L D E C O N O M I C A N D F I N A N C I A L D E V E L O P M E N T S I N F Y 2 0 0 2

the decline in exports being most marked in emergingAsia (excluding China and India), because of theimportance of information technology production inthe region. In contrast to other measures of activity,such as industrial production, there was little evidenceof a pickup in trade volumes in early 2002.

Financial flows to emerging markets declined in2001, with portfolio flows being especially affected byoutflows from the crises in Argentina and Turkey, thedeflation of the information technology bubble, and theeconomic slowdown in the United States, whichresulted in a generalized move of investors to higher-quality assets. Indeed, in the aftermath of theSeptember 11 terrorist attacks, bond markets were rela-tively closed to new issuers. In the closing months ofthe year, however, equity markets and then fixed-income markets revived as signs of a global recoverystarted to appear, and emerging market access and vol-umes picked up. Despite a drop in global foreign directinvestment (FDI) and a fall in cross-border mergers andacquisitions activity, net FDI flows to emerging marketcountries are estimated to have increased to $175 bil-lion. Emerging markets continued to pay down theirexternal debt to international banks over the year.

In fixed-income markets, the slopes of the yieldcurves in the United States and euro zone becamequite steep, reflecting the anticipation of economicrecovery. In contrast, the steeper yen yield curvepointed to renewed concerns about the health of thebanking sector in Japan. Optimism about a U.S. recov-ery was also apparent in the corporate bond market, ascredit spreads narrowed over the last two months ofthe year. The strength in long-term credit markets con-trasted with the turbulence in short-term markets, andborrowers continued to replace short-term debt withlonger-term issues as commercial paper markets becameincreasingly expensive.

New bond issuance by emerging market entities fellin 2001, mainly because two of the larger sovereignissuers, namely Argentina and Turkey, were affected byfinancial crises and were unable to maintain their tradi-tionally large issuance programs. In the first quarter of2002, bond issuance to emerging markets moved backin line with historical levels, as a number of sovereignssuccessfully tapped international markets.

In fixed-income emerging markets, the direct falloutfrom the Argentina crisis and default was initially lim-ited, in part owing to more discriminating investmentbehavior by market participants. Other factors limitingcontagion included the generally more appropriate eco-nomic policies adopted by many emerging marketcountries, including the use of more flexible exchangerate regimes. However, events at the beginning offinancial year 2003 showed emerging markets werevulnerable as investors turned more risk averse andconcerns over policy continuity and the debt structure

Figure 1.1Global Indicators1

(Annual percent change unless otherwise noted)

World Real GDP Inflation - 20

6 -Trend,

2 -

Developing countries(consumer prices,

median) ~ 15

- 10

- 5-yAdvarv

- economies(consumer prices)

1970 75 80 85 90 95 2000 1970 75 85 90 95 2000

6 -

5 -

4 -

3 -

2 -

World Real Per Capita GDP World Trade Volume(goods and services)

Trend,1970-200I2

Trend,

- 16

- 12

1970 75 80 85 90 95 2000 1970 75 80 85 90 95 2000

World Real Long-Term Real Commodity PricesInterest Rate (percent)3 (1990 = 100)

9 - - - -400

0 !

Non-oilcommodity

prices

- 3 0 0

- 2 0 0

1 00

Oi l prices

"6 1970" 75 ' 80' ' 85 " 90 " 95' 2000 1970 75 ' 80'' 85 " 90" 95' 2000 °

Source: IMF World Economic Outlook, April 2002.Aggregates are computed on the basis of purchasing-power-parity weights unless

otherwise indicated.Average growth rates for individual countries, aggregated using purchasing- power-

parity weights; these shift over time in favor of faster growing countries, giving the linean upward trend.

GDP-weighted average of the 10-year (or nearest maturity) government bond yields lessinflation rates for the United States, Japan, Germany, France, Italy, the United Kingdom,and Canada. Excluding Italy prior to 1972.

of certain key emerging market borrowers mounted.These developments affected Latin American countriesin particular as the effects of contagion were feltthrough banking sector channels and difficult access tonew borrowing.

In global and emerging stock markets, a rally in Janu-ary 2001 prompted by the surprise cut in U.S. interest

A N N U A L R E P O R T 2 0 0 2 5

©International Monetary Fund. Not for Redistribution

C H A P T E R I

rates quickly fizzled in February and March on contin-uing evidence of U.S. economic slowing and poorcorporate earnings reports. Another rally in April andMay 2001 also gave way to a sell-off in June. In themonths before the September 11 terrorist attacks, unfa-vorable economic indicators caused severe weaknessesin global stock markets. After falling sharply in the twoweeks following the attacks, stock prices regained pre-attack levels by mid-October. In fact, the rally thatstarted in late September 2001 and continued wellbeyond the year was the longest sustained rally sinceApril 2000. By mid-November, most major stock mar-kets were returning to double-digit growth ratesfollowing increased investor confidence on expectationsof an imminent economic recovery. The increased con-fidence partly reflected the rapid monetary policyresponse in industrial countries. However, in the firstquarter of 2002, equity prices were broadly unchangedin the United States and Europe, despite an improvedglobal outlook owing to concerns over the quality ofreported earnings in the wake of the unexpected col-lapse of Enron and other large corporations. Emergingeconomy equity markets strongly outperformed matureequity markets during the first quarter of 2002, withemerging Asia performing best, on the back of impres-sive gains by technology companies.

In foreign exchange markets, the U.S. dollarremained remarkably strong in 2001, notwithstandingthe economic downturn of the fourth quarter. Thisstrength continued in the first quarter of 2002 becausemarkets expected that the U.S. economy would be thefirst to rebound from the global slowdown. However,in April 2002, with sentiment toward the dollarbecoming mixed, and against the background ofincreased uncertainty in the outlook for corporateearnings, the dollar softened. The euro remained weakrelative to the dollar throughout 2001 and first quar-ter of 2002 but began to strengthen in April, whereasthe Japanese yen remained strong, limiting the dollar'sgains. In emerging markets, the Turkish lira fell morethan any other currency in 2001, after Turkey wasforced to float its currency early in the year. The SouthAfrican rand and to a lesser extent the Egyptianpound, the Brazilian real, and the Chilean peso alsoweakened significantly during the year. In contrast, theMexican peso and the currencies of the Czech Repub-lic, Hungary, and Poland strengthened notably. Inearly 2002, Argentina was forced to abandon its cur-rency board arrangement, and the Argentine pesoweakened sharply. As of May 2002, the South Africanrand had recovered from its 2001 low in the wake ofstronger commodity prices to be the emerging marketcurrency with the largest appreciation in the earlymonths of 2002, followed by the Indonesian rupiah,which benefited from progress in implementingreforms.

Key Developments in Emerging Marketand Industrial CountriesIn Latin American emerging market economies,growth slowed through much of 2001. This slowdownreflected the slowdown in industrial countries; difficultexternal financing conditions—particularly importantgiven the region's large external funding require-ments—that came to a head during the Argentine crisisin late 2001; and a range of country-specific factors.After the onset of the Argentine crisis, economic devel-opments diverged, with extremely difficult conditionsin Argentina but increasing signs that the slowdownwas ending elsewhere, particularly in those countrieswith the closest trading ties with the United States,including those of Central America and the Caribbean.Inflation remained low, mirroring both weak activityand improved policy frameworks.

The countries in emerging Asia, with the importantexceptions of China and India, generally experiencedsharp falls in growth rates in 2001, but began to showsigns of a turnaround in 2002, while region-wide infla-tion remained low. The path has been largely driven bythe external environment including the downturn inthe global information technology industry and oilprice movements. For most oil-importing countries,high prices in late 2000 and much of 2001 contributedto the weakening of incomes and demand in manycountries. Subsequently, weak oil prices in late 2001and early 2002 provided support for recovery, althoughin early 2002 price increases reduced this impetus. Theopposite pattern is true for the region's oil producers.Poorer external conditions during 2001 also spread todomestically exposed sectors, further lowering demand,confidence, and employment, with economic and polit-ical uncertainties in some countries putting downwardpressure on growth. In contrast, activity remained rela-tively buoyant in China and to a lesser extent in India,largely because both economies are less dependent onexternal trade than other economies in the region, butalso because of strong domestic demand, although theytoo have seen some slowing in growth since 2000.

Economic performance in central and easternEurope generally held up well compared with otheremerging market regions during the global slowdown.Not surprisingly, exports—which are largely directed tothe European Union—weakened in 2001 and early2002 as external demand slowed, partly offset by gainsin market share in some cases. The loss in externaldemand was largely offset in most cases by relativelyrobust domestic demand, generally underpinned bylower inflation and interest rates, strong investmentspending (often driven by foreign direct investment),and fiscal stimulus in several countries. There was animportant exception to this pattern. Turkey suffered itsworst recession in over fifty years in 2001, with theevents of September 11 setting back the tentative signs

6 A N N U A L R E P O R T 2 0 0 2

©International Monetary Fund. Not for Redistribution

W O R L D E C O N O M I C A N D F I N A N C I A L D E V E L O P M E N T S I N F Y 2 0 0 2

of recovery that had emerged following the economicand financial crisis at the start of the year, particularlythrough their impact on trade, tourism, and financialmarket confidence. Real and financial indicators in late2001 and early 2002 suggested that conditions wereagain improving: capacity utilization increasedthroughout the second half of 2001, interest rates fellsignificantly after mid-October, and the exchange rateand stock market also strengthened.

Growth rates in the countries of the Commonwealthof Independent States remained remarkably resilient tothe global slowdown in 2001, falling only slightly to anaverage of 6 1/4 percent, the highest growth rate amongthe major developing and transition country regions.This was underpinned by continued robust growth inthe largest economies, which provided significant sup-port to the rest of the region given the strong tradeand financial linkages. In many cases, improved macro-economic stability and policy implementation, as wellas country-specific factors, supported robust growth.

Growth in Africa also held up relatively well in2001 and early 2002 compared with other parts of theworld, despite the weak external environment. The keyinfluences on the outlook for much of the region con-tinued to be the interaction between commoditymarket developments, the conduct of economic poli-cies, and the extent of armed conflict and other formsof civil tension. Fluctuations in oil prices have had vary-ing effects, with higher oil prices supporting activity inoil producers but having a harmful effect on the manyother commodity exporters in the region. Theseinclude many of the poorest countries, which have alsobeen affected by weakness in nonoil commodity prices.That said, both strong and weak performers can be

found within each of these groups, with the quality ofdomestic policies and the extent of conflict having akey impact on whether countries have been able toresist the external downturn.

Growth in the Middle East slowed considerably in2001 and early 2002, largely reflecting the global slow-down, lower oil production, and, after the September11 terrorist attacks, the regional security situation. Thecurtailment of oil production associated with O P E Cagreements to support flagging oil prices depressed realG D P in the oil-exporting countries, while the securitysituation dampened activity, including tourism, in par-ticular in Egypt, Israel, Jordan, and the Syrian ArabRepublic.

In the industrial countries, growth was weak in2001. The slowdown was especially marked in theUnited States and Canada, in part because growth hadbeen more robust over 2000. Both economies sawclear evidence of recovery in the early months of2002—with positive growth in the last quarter of 2001and a substantial acceleration in the first quarter of2002. Europe also saw a significant deceleration inactivity. Within Europe, activity was particularly weakin Germany and Italy, and relatively more robust inFrance and the United Kingdom, with the performanceof domestic demand accounting for many of these vari-ations across countries. Activity in Australia and NewZealand remained relatively strong, largely reflectingbuoyant domestic demand. In contrast, Japan sufferedits third and most severe recession of the last decade.While external factors promoted the slowdown, weak-ness in domestic demand was also a contributing factor.By early 2002, however, there were signs that the econ-omy was bottoming out.

A N N U A L R E P O R T 2 0 0 2 7

©International Monetary Fund. Not for Redistribution

CHAPTER

IMF Surveillance in Action

In today's global economy, where economic devel-opments and policies in one country affect othercountries and financial market information is transmit-ted around the world instantaneously, the IMF's role inmonitoring economic and financial developments andpolicies in member countries is more vital than everbefore. The IMF has the mandate under its Articles ofAgreement to oversee the exchange rate policies of itsmember countries to ensure the effective operation ofthe international monetary system. It exercises this"surveillance" responsibility by holding regular discus-sions with its member countries about their economicand financial policies, and by continuously monitoringand assessing economic and financial developments atthe country, regional, and global levels. In these ways,the IMF can help signal dangers on the horizon andenable members to take early corrective policy actions.

IMF surveillance has evolved over time to reflectchanging global realities, and both the practice and theunderlying principles of IMF surveillance are reviewedby the Executive Board every two years (see Box 2.1).A central task is to make surveillance a more effectivevehicle for preventing crises and promoting a globaleconomic environment conducive to sustainablegrowth. The goal is neither the unrealistic aim of elimi-nating all risks of future crises nor an impracticalpromise to deliver definitive warnings about all futurecrises. Rather, the IMF's efforts focus on strengtheningincentives for country authorities and market partici-pants to assess risks appropriately and to base theirpolicies and investment strategies on these assessments.A well-functioning market economy draws its strengthand dynamism from a continuous search by producers,investors, and consumers for better results. This willalways lead to some degree of overshooting and correc-tion, particularly in asset markets. Thus the IMFencourages governments to adopt policies, includinginstitutional reforms, to strengthen the resilience ofmembers' economies in the face of harmful develop-ments and financial stress—notably throughappropriate exchange rate regimes; sound fiscal poli-cies; prudent borrowing and debt management

strategies; deeper, stronger, and more diversified finan-cial systems and domestic capital markets; and moreeffective social safety nets.

Equally important are policies that promote sustain-able growth and an open trade environment becausegrowth, trade, debt-servicing capacity, and external via-bility are inextricably linked. The IMF thus has a role toplay in promoting trade liberalization and has beenmoving toward increased coverage of market accessissues in its surveillance consultations with membercountries. It also encourages countries to liberalize tradeby providing technical assistance to member countries inits areas of expertise that lay the groundwork forincreased trade and by providing financial support forcountries developing more open trade regimes.

Effective surveillance and crisis prevention have twokey ingredients: sound policy advice and incentives toensure that this advice has an impact. The IMF is con-tinuing to strengthen its analytical capacity to identifysources of vulnerability as they emerge and to developstrategies to reduce vulnerabilities, promote stability,and foster growth. At the same time, it is payinggreater attention to the factors that determine theeffectiveness of its policy advice.

The IMF conducts surveillance in several ways—country (or bilateral) surveillance and global andregional (or multilateral) surveillance.• Country surveillance. As mandated in Article IV of

its Articles of Agreement, the IMF holds "ArticleIV" consultations, normally once every year, witheach member country about its economic policies.These consultations are complemented by regularanalysis of economic and financial developmentsprovided by IMF staff, informal contacts with staffand national authorities, and interim Board discus-sions as needed.

• Global surveillance. The IMF's Executive Board reg-ularly reviews international economic and financialmarket developments. The reviews are based partlyon the World Economic Outlook reports, prepared by

8 A N N U A L R E P O R T 2 0 0 2

2

* * *

©International Monetary Fund. Not for Redistribution

I M F S U R V E I L L A N C E I N A C T I O N

Box 2.1IMF Biennial Surveillance ReviewThe Executive Board reviews the prin-ciples and the implementation of theIMF's surveillance approximately everytwo years. The latest biennial review ofsurveillance activities was completed inlarge part in April 2002. The reviewtook stock of the evolution of surveil-lance—both the framework withinwhich surveillance takes place and theactual conduct of surveillance.

Directors noted that further discus-sions on the review of surveillance andon various surveillance-related issues—including the IMF's transparencypolicy—would continue, but the reviewso far had yielded a number of impor-tant conclusions. First, the coverage ofsurveillance had expanded over theyears—from concentrating narrowly onmonetary, fiscal, and exchange ratepolicies, to a broader purview encom-passing external vulnerabilityassessments, external debt sustainabilityanalyses, financial sector vulnerabilities,and structural and institutional policies(see Chapter 3)—and that broadenedframework constituted a necessary andappropriate adaptation of surveillance toa changing global environment, mostnotably to the rapid expansion of inter-national capital flows. Second, IMFsurveillance had generally succeeded inembracing wider coverage without los-ing focus. The issues that were coveredin individual Article IV consultationswere generally determined by theirmacroeconomic relevance in country-specific circumstances. The currentsystem of multilateral (or global) sur-veillance was working well andmultilateral surveillance of capital mar-kets had been improved by the creationof the International Capital MarketsDepartment (ICM).

Given this overall record of coverageand focus, a number of specific areaswere identified where further efforts

were needed to ensure that IMF policyadvice was sound and persuasive.• More candid and comprehensive

assessments of exchange arrange-ments and exchange rates within theframework of macroeconomic poli-cies should become the normalpractice throughout themembership.

• Coverage of financial sector issuesshould be brought up to par withcoverage of other areas of surveil-lance. Voluntary participation inFinancial Sector Assessment Pro-grams (FSAPs) had provided forin-depth coverage of financial sectorissues. However, in the absence of amember's participation in an FSAP,the quality of financial sector surveil-lance had been uneven acrossmember countries, and mechanismshad to be found to improve thatsituation.

• To strengthen vulnerability assess-ments, analysis of debt sustainabilityhad to be improved, particularlythrough the use of meaningful stresstests and alternative scenarios. Also,greater attention had to be paid tothe private sector's balance-sheetexposure to interest rate, exchangerate, and general macroeconomicshocks, and to collecting the datarequired to assess that vulnerability.

• Coverage of institutional issues, suchas public sector and corporate gover-nance in certain countries, hadsometimes been hampered by a lackof expertise and should be strength-ened. Reports on the Observance ofStandards and Codes (ROSCs) and,generally speaking, the work onstandards and codes were importantinputs to meeting this objective.

• Structural issues outside the IMF'straditional areas of expertise were, attimes, key to a country's macroeco-

nomic situation and, thus, had to beaddressed by the IMF. To tacklesuch cases, the IMF should makeeffective use of the expertise ofappropriate outside institutions, inparticular the World Bank.

• There was some scope for enhancingthe focus of surveillance in individualcases and areas. In particular, cover-age of trade policies should bestrengthened by concentrating oncountries whose trade policies eitherhad appreciable global or regionalinfluence or had significant deleteri-ous effects on domesticmacroeconomic prospects.

• The results of multilateral (or global)surveillance exercises and the IMF'scomparative advantage in cross-country analyses should be reflectedin bilateral (or country) surveillancein a comprehensive and consistentmanner. Particular attention shouldcontinue to be paid to the systemicimpact of the policies of the largesteconomies in Article IV consultationswith those countries.

• Article IV consultations with coun-tries with IMF-supported programsshould provide an effective reassess-ment of economic conditions andpolicies; that required a freshness ofperspective and appropriate distancefrom day-to-day program implemen-tation.Directors stressed that, in many

instances, the IMF could usefully com-plement sound advice on economicpolicy objectives with discussions withcountry authorities of alternative waysto achieve those objectives. A n impor-tant component of such discussionswould be consideration of social, politi-cal, and institutional factors to enhanceownership of policy recommendationsand increase the likelihood of successfulpolicy implementation.

IMF staff usually twice a year, and reports on inter-national financial markets. In addition, the Boardholds frequent, informal discussions about worldeconomic and financial market developments.Regional surveillance. To supplement country con-sultations, the IMF also examines policies pursuedunder regional arrangements. It holds regular dis-

cussions with such regional economic institutions asthe European Union, the West African Economicand Monetary Union, the Central African Economicand Monetary Community, and the EasternCaribbean Currency Union. IMF management andstaff have also increased their participation inregional initiatives of member countries—including

A N N U A L R E P O R T 2 0 0 2 9

©International Monetary Fund. Not for Redistribution

C H A P T E R 2

Box 2.2IMF Launches Quarterly Report on Global Financial MarketsOn March 14, 2002, the IMF issuedthe inaugural Global Financial StabilityReport—a new publication on thehealth of the world's financial system.The report, which will be publishedquarterly, aims at providing timely andcomprehensive coverage of both matureand emerging financial markets as partof the IMF's stepped-up tracking offinancial markets.

The rapid expansion of financial mar-kets during the past decade underscoresthe role that private sector capital flowsplay as an engine of world economicgrowth. But these flows can also be atthe heart of crisis developments. In aneffort to head off future crises, theGlobal Financial Stability Report seeksto deepen policymakers' understandingof the potential weaknesses in the sys-tem and to identify the fault lines thathave the potential to lead to crises.

The March 2002 issue weighed thestability of the international financial

system in light of an emerging globaleconomic recovery, paying particularattention to risks posed by a slower-than-expected economic recovery andby the recent surge in the use of com-plex credit risk transfer mechanisms,such as credit derivatives and debtswaps. The report also examined theaccuracy of selected early warning sys-tems—statistical models designed topredict financial crises—and reviewedsome alternative debt instruments thatemerging market borrowers could useto tap global capital markets.

The report is prepared by the IMF'sInternational Capital Markets Depart-ment, which was established in 2001 toenhance the IMF's surveillance, crisisprevention, and crisis managementactivities. It replaces both the annualInternational Capital Markets report,which has been published since 1980,and the quarterly Emerging MarketFinancing report, published since 2000.

the Southern African Development Community, theCommon Market of Eastern and Southern Africa,the Manila Framework Group, the Association ofSouth East Asian Nations, the Meetings of WesternHemisphere Finance Ministers, and the Gulf Coop-eration Council (see also Appendix IV).

• IMF management and staff also take part in policydiscussions of finance ministers, central bank gover-nors, and other officials in such country groups asthe Group of Seven major industrial countries, theAsia-Pacific Economic Cooperation forum, and theMahgreb countries associated with the EuropeanUnion (Algeria, Morocco, and Tunisia).

Country SurveillanceAn IMF staff team meets with government and centralbank officials of each member country, as well as othergroups—such as trade unions, employer groups,academics, legislative bodies, and financial market par-ticipants—generally once every year (with interimdiscussions held as needed), to review economic devel-opments and policies. These consultations touch onmajor aspects of macroeconomic and financial sectorpolicies, but they also cover other policies affecting acountry's macroeconomic performance, including,where relevant, structural economic policies andgovernance.

To provide the basis for country surveillance, anIMF staff team visits the country, collects economic

and financial information, and dis-cusses with the national authoritiesrecent economic developments andthe monetary, fiscal, and relevantstructural policies the country ispursuing. The Executive Directorfor the member country usuallyparticipates. The IMF staff teamnormally prepares a concludingstatement, or memorandum, sum-marizing the discussions with themember country and the findingsof the staff team, and leaves thisstatement with the national author-ities, who have the option ofpublishing it. On their return toheadquarters, IMF staff membersprepare a report describing the eco-nomic situation in the country andthe nature of the policy discussionswith the national authorities, andevaluating the country's policies.The Executive Board, where theentire membership is represented,then discusses the report. Thecountry is represented at the Boardmeeting by its Executive Director.

The views expressed by Executive Directors during themeeting are summarized by the Chairman of the Board(the Managing Director), or the Acting Chairman (aDeputy Managing Director), and a summing up is pro-duced. If the Executive Director representing themember country agrees, the full Article IV consultationreport is released to the public, together with the sum-mary text of the Board discussion and backgroundmaterial in the form of a Public Information Notice(PIN). Otherwise, a PIN alone may be issued. InFY2002 the Board conducted 130 Article IV consulta-tions with member countries (see Table 2.1). The PINsand Article IV reports are published on the IMFwebsite.

(For more details of the IMF's bilateral surveillance,such as Financial Sector Stability Assessments, seeChapter 3, under "Crisis Prevention.") In addition, theBoard assesses economic conditions and policies ofmember countries borrowing from the IMF throughdiscussions of the lending arrangements that supportthe member countries' economic programs (seeChapter 4).

Global SurveillanceThe Executive Board's conduct of global surveillancerelies heavily on staff reports on the World EconomicOutlook and international financial markets (see Box2.2), as well as sessions on world economic and marketdevelopments.

10 A N N U A L R E P O R T 2 0 0 2

©International Monetary Fund. Not for Redistribution

I M F S U R V E I L L A N C E I N A C T I O N

World Economic OutlookThe World Economic Outlook reports feature compre-hensive analyses of prospects for the world economy,individual countries, and regions, and also examinetopical issues. These reports are prepared by the staffand discussed by the Executive Board usually twice ayear (and later published), but they may be producedand discussed more frequently if rapid changes in worldeconomic conditions warrant.

In FY2002 the Board discussed the World Eco-nomic Outlook on three occasions: two regulardiscussions were held in September 2001 and March2002, and an additional discussion was held in Decem-ber 2001 in the aftermath of the terrorist attacks in theUnited States of September 11, 2001. The two discus-sions during the 2001 calendar year focused on signs ofa slowdown in world economic growth, sharply albeittemporarily exacerbated by the events of September 11.By March 2002, however, there were encouraging indi-cations that the slowdown had bottomed out and thatglobal economic growth was recovering.

At its September 2001 meeting on the World Eco-nomic Outlook, the Board agreed that prospects forglobal growth had weakened since the last World Eco-nomic Outlook report had been released the previousMay. In particular, Directors noted the substantialdecline in growth in the United States over the pastyear; the serious deterioration in economic prospectsfor Japan; the weaker conditions and outlook inEurope; and the reduction in the projections forgrowth for most developing country regions. SlowerG D P growth in almost all regions had been accompa-nied by a sharp decline in trade growth, Directorsnoted. Financing conditions for emerging markets hadalso deteriorated, although Board members wereencouraged that the effects of contagion had beenmore moderate than in preceding episodes.

Directors considered that a number of interrelatedfactors had contributed to the slowdown, including areassessment of corporate profitability and an associatedadjustment in equity prices, higher energy and foodprices, and tightening of monetary policy to containdemand pressures in the United States and in Europe.More broadly, the faster-than-expected slowdown alsoreflected the strong cross-country trade and financiallinkages that were increasingly evident acrosscountries.

At their December 2001 meeting on revised projec-tions for the World Economic Outlook, Directorsdiscussed the impact of the September 11 attacks onthe world economy. They observed that, before theattacks, there appeared to be a reasonable prospect forrecovery in late 2001. However, more recent data, onwhich the interim World Economic Outlook revisionswere based, indicated that the situation before theattacks was weaker than had earlier been projected in

many areas, including in the United States, Europe,and Japan. Directors accordingly concluded that thetragic events of September 11 had exacerbated analready very difficult situation for the global economy.