Barriers to Integration in the Insurance Sector - IMF eLibrary

Upload

khangminh22Category

view

2download

0

©International Monetary Fund. Not for Redistribution

at the Crossroads SUSTAINING GROWTH AND REDUCING POVERTY

©International Monetary Fund. Not for Redistribution

This page intentionally left blank

©International Monetary Fund. Not for Redistribution

at the Crossroads SUSTAINING GROWTH AND REDUCING POVERTY

EDITED BY

Tim Callen Patricia Reynolds Christopher Towe

INTERNATIONAL MONETARY FUND

©International Monetary Fund. Not for Redistribution

© 2001 International Monetary Fund

Production: IMF Graphics Section Cover design: Lai Oy Louie

Library of Congress Cataloging-in-Publication Data

India at the crossroads p. em.

ISBN 1-55775-992-8 (alk. paper) 1. India--Economic policy--1980. 2. India--Economic conditions--1947- 3. Fiscal

policy--India. 4. Sustainable development--India.

HC435.2 .1484 2001 330.954--dc21

Price: $2 7.00

Address orders ro: External Relations Department, Publication Services

International Monetary Fund, Washington D.C. 20431 Telephone: (202) 623-7430; Telefax: (202) 623-7201

E-mail: [email protected] Internet: http:l/www.imf.org

00-054132

©International Monetary Fund. Not for Redistribution

Contents

Page

Foreword . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . vii

Acknowledgments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ix

1. Overview Christopher Towe

PART I. Preserving External Stability

2. India and the Asia Crisis

1

Christopher Towe . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

3. Assessing India's External Position Tim Callen and Paul Cashin . . . . . . . . . . . . . . . . . . . . . . . 28

PART II. Fiscal Challenges

4. Tax Smoothing, Financial Repression, and Fiscal Deficits in India

Paul Cashin, Nilss Olekalns, and Rama Sahay . . . . . . . . . . 53

5. Fiscal Adjustment and Growth Prospects in India Patricia Reynolds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

PART III. Monetary and Financial Sector Policies

6. Modeling and Forecasting Inflation in India Tim Callen . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 105

7. The Unit Trust of India and the Indian Mutual Fund Industry

Anna Ilyina . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 122

©International Monetary Fund. Not for Redistribution

vi CONTENTS

PART IV. Growth, Poverty, and Structural Policies

8. Growth Theory and Convergence Across Indian States: A Panel Study

Shekhar Aiyar . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 143

9. Structural Reform in India Daniel Kanda, Patricia Reynolds, and Christopher Towe . . . 170

List of Contributors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 191

©International Monetary Fund. Not for Redistribution

Foreword

India is a Land of contrasts. One billion people Live in a vast territory among architectural and sculptural wonders that give vivid testimony to its ancient and rich history, as well as to its powerful and age-old customs. Yet, there is also a very modem face of India, which is responding to the growing forces of globalization and where information technology has found a fertile environment.

These contrasts and the force of tradition appear to have contributed to a cautious approach to change. Tentative and slow moving attempts to free the economy from pervasive controls were started in the 1980s, but it was not until the serious balance of payments and macroeconomic crisis of the early 1990s that India introduced significant and wideranging policy reforms. These reforms are widely considered to have been successful in promoting a marked improvement in macroeconomic performance. Nevertheless, the subsequent pace of reform has been Less even and bold, and the question remains whether the basis has been laid for the sustained and rapid growth that wiLL be necessary to alleviate the deep poverty that still afflicts more than a third of the population.

That India emerged relatively unscathed from the financial crisis that affected most of Asia as well as many emerging economies is testimony to the country's resilience. Many sectors of the economy-and above all the information technology sector-have shown extraordinary dynamism and remarkable vitality. At the same time, India is roday at a crossroads and a number of macroeconomic indicators display worrisome trends. In particular, the fiscal situation has worsened in recent years and requires concentrated and determined attention to reduce the risk of financial instability. Fiscal consolidation in combination with more rapid pace of structural reform, liberalization, and infrastructure development is also necessary to lay the foundation for strong growth. The chaLLenge for the government is to forge a political consensus across a diverse range of interest groups that is necessary to sustain rapid and consistent reform on broad range of fronts.

The chapters in this volume seek to address the implications of these challenges and opportunities. For the most part, they were written during

vii

©International Monetary Fund. Not for Redistribution

viii FOREWORD

1999-2000 in the context of the lMF staff's ongoing policy discussions with India. By bringing these issues together in a single volume, the macroeconomic and structural challenges that are highlighted can be given greater prominence and thus contribute to the policy debate, both in India and, more broadly, in other reform-oriented economies.

MARIO I. BLEJER Senior Advisor Asia and Pacific Department

©International Monetary Fund. Not for Redistribution

Acknowledgments

The papers included in this volume were largely prepared in the context of the IMF's Article IV consultation discussions with India during 1999-2000, under the leadership of Mario I. Blejer. His support and encouragement during this process are gratefully acknowledged. The papers also benefited from comments received from Dr. V. Kelkar, IMF Executive Director; his Advisor, Dr. N. Jadhav; and from the staff of the Reserve Bank of India and the Indian Ministry of Finance. The authors would also like to thank Mary Abraham and Irene Aquino for their infinite care and patience in preparing the manuscripts, and Alex Hammer and Aung Thurein Win for their research assistance. Sean M. Culhane, of the IMF's External Relations Department, edited the volume and was masterful in guiding it to completion.

The views expressed in this book are those of the authors, and do not necessarily represent those of the Indian authorities, IMF Executive Directors, or other IMF staff.

ix

©International Monetary Fund. Not for Redistribution

This page intentionally left blank

©International Monetary Fund. Not for Redistribution

1 Overview

CHRISTOPHER TOWE

India's macroeconomic performance during the past decade has in many respects been remarkable. Since the early 1990s, India has been among the fastest growing economies in the world, inflation has been relatively well contained, and the balance of payments has been maintained at comfortable levels. This performance was achieved despite poor weather that caused negative agricultural growth in fiscal year (FY) 1995/96 and again in FY 1997/98, the Asian financial crisis in 1997 and 1998, international sanctions imposed on India and Pakistan following tests of nuclear devices in 1998, and the considerable volatility in world oil and commodity prices that occurred in 1998-2000.1

Much of India's economic strength during the early and mid-1990s can be ascribed to the broad-ranging fiscal and structural reforms undertaken following the 1991 balance of payments crisis. These included reforms to the tax system, substantial cuts in the deficit of the consolidated public sector, liberalization and deregulation in the industrial sector, trade and tariff reforms, and measures to recapitalize and strengthen the supervision of banks and other financial intermediaries. These policies helped spur a strong recovery, with real GOP growth accelerating to an average of 7 Y4 percent in the mid-1990s from as low as \12 of 1 percent at the beginning of the decade.

Although economic activity slowed somewhat in subsequent yea�s, it remained relatively robust, especially when compared with the other emerging markets that were buffeted by the Asian financial crisis. During the last two years of the 1990s, growth averaged 6\12 percent, as

1The Indian fiscal year begins on April 1 .

1

©International Monetary Fund. Not for Redistribution

2 OVERVIEW

agricultural output recovered strongly from poor weather in late 1997 and industrial production rebounded in response to the turnaround in agricultural incomes and the recovery elsewhere in the region. India's inflation performance has also been relatively favorable-inflation generally trended downward during the 1990s, reaching as low as 3112 percent by FY 1999/00.

Following the 1991 crisis, India's balance of payments also strengthened. Indeed, in the latter half of the decade, despite the effect of the regional crisis on merchandise exports, the current account deficit began narrowing. The deficit fell to less than 1 percent of GOP in FY 1 999/00, partly reflecting the impact of India's growing exports of information technology (IT)-related services. Although inward portfolio and foreign direct investment were hurt by the erosion of international market sentiment in 1997 and 1998, other private inflows were maintained, and with the recovery in international investor sentiment in FY 1999/00, India's foreign exchange reserves reached $38 billion by March 2000, a gain of almost $12 billion from three years earlier.

By the end of the decade these favorable macroeconomic trends contributed to growing optimism about India's longer-term growth prospects. Indian equity prices strengthened enormously, benefiting from the global boom in IT stocks, and private sector forecasters steadily revised upward their projections for GOP growth to 7 percent or more. This optimism carried over to the political arena, with the new government elected in late 1 999 setting a growth target of 7-8 percent over the medium and longer terms-recognizing the importance of fast growth for improving the welfare of the large share of India's population still in poverty.

However, macroeconomic developments during 2000-including a rebound of inflation, slowing industrial production, and downward pressure on the rupee and stock prices-have tempered some of this optimism. They also underscore the longer-standing question of whether the basis for achieving sustained and rapid growth has yet been established. Most notably:

• Fiscal policy. After considerable progress following the 1991 balance of payments crisis, the fiscal situation deteriorated from the mid-1990s. Weak revenue performance and lack of expenditure control at both the central and state government levels caused the consolidated deficit of the public sector to rise sharply to over 1 1 percent of GOP in FY 1999/00, with public sector debt exceeding 80 percent of GOP This raises the question of how India has been able to achieve high growth and a relatively comfortable balance of payments position despite massive public sector deficits. It also creates doubt about whether this favorable performance can

©International Monetary Fund. Not for Redistribution

Christophel' Towe 3

be sustained without significant policy adju·tment , especially as trade and financial systems become increasingly integrated with the rest of the world.

• Sn·uctural policy. Following rapid progress in the early and midl990s, the momentum for reform and liberaliz<nion appeared to slow in the latter half of the decade. This partly reflected political constraints-between early 1996 and the end nf 1999 there were three general elections and six changes in co(llitinn governments. As a result, difficult reforms in a broad range of areas-including agriculture, small-scale industry, and labor markers-were nor addressed, potentially undermining growth and leaving the economy ill-prepared to benefit from increased access ro glohal goods and capital markets. A notable example of the lack of coherence in the area of structural reform is the fact that, with the complete removal of quantitative restrictions on imports in early 2001. domestic producers will be exposed to external competition well before the legal, labor market, and regulatory impediments to effective restructuring have been addressed.

• Poverty. Despite the gains in the area of poverty reduction since Independence-the poverty rate has fallen by over 20 percentage points since the 1950s and l960s-roughly 35 percent of the population still remains below the poverty line. 2 Moreover, poverty statistics during the 1990s generally stagnated or, in some cases, worsened, and per capita income in India still lags well behind that in other fast-growing Asian economies. Notably, rural poverty rates have tended to increase and the regional distribution of income has become more stratified. This has reflected both weak fiscal discipline (constraining public development spending) and slowing structural reform (concentrating growth in the less-regulated services sector), which have left little scope for income gains for lower-skilled agricultural and industrial workers.

These issues have been at the core of the ongoing policy dialog between the IMF staff and the Indian authorities, and this volume brings together some of the IMF staff's more recent analysis of these topics (Box 1 . 1 lists a number of previous analytical studies). ln particular, the following chapters address four main issues. Part I explores the factors underlying India's success in avoiding significant fallout from rhe Asia crisis and addresses broader questions regarding India's external vulnerabil ity. Part II discusses the fiscal situation and the extent ro which recent policies pose risks to India's growth prospects and debt

2Analysis of pnverty trends in India is complicated by que$tion' ;.�hnur rhe qu;1lity of the data. See Chapters 8 and 9 for a discussion.

©International Monetary Fund. Not for Redistribution

4 OVERVIEW

Box 1.1. Recent Staff Studies, 1995-98

India-Selected Issues, IMF Staff Country Paper No. 98/205 (August 1998)

• Tax Revenue Performance in rhe Pose-Reform Period, by Martin Muhleisen

• Foreign Exchange Markets: Developments and Jssucs, by Martin Muhleisen

• ExportS and Competitiveness, by D1mitri Tzanninis • The Financial Performance of Public Sector Commercial Banks in

India, by Ttm Callen • Nonbank Finance Companies in india: Development Issues, by Nir

mal Mahaney

India-SeLected Issues, IMF Staff Country Report No. 97/154 (June 1997)

• The Virtuous Circle of Growth and Saving: Lessons from the Experi-ence of Selected Asian Countries, by Kalpana Kochhar

• Petroleum Price Liberalization, by Richard Hemming • The States' Fiscal Problem, by Dimitri T zanninis • Trade Reforms and Economic Response, by Martin Muhleisen

India-Selected Issues, IMF Staff Country Report No. 96/260 (October 1996)

• Medium-Term Macroeconomic Outlook, by Martin Muhleisen • Improving Domestic Savings Performance, by Martin Muhleisen • Poverty in India, by Martin Muhleisen • Controlling Central Government Expenditures, by Dimitri Tzanninis • Strengthening Public Enterprise Performance, by Richard Hemming • Public Seccor Banking Reform, by Marjorie Rose • Long-Term Savings Instruments, by Martin Muhleisen • Capital Account Liberalization, by Peter Dartels

India-Ecorwmic Reform and Growth, IMF Occasional Paper No. 134 (December 1995)

• Overview, by Ajai Chopra and Charles Collyns • Long-Term Growth Trends, by Ajai Chopra • The Adjustment Program of 1991/92 and Its Initial Results, by Ajai

Chopra and Charles Collyns • The Behavior of Private Investment, by Karen Parker • Fiscal Adjustment and Reform, by Richard Hemming • Recent Experience with a Surge in Capital Inflows, by Charles Collyns • Structural Reforms and the Implications for lnvestmenr, by Ajai

Chopra, Woosik Chu, and Oliver Fratzscher

©International Monetary Fund. Not for Redistribution

Chriscopher Towe 5

sustainability. Monetary policy and financial secror reform are considered in Part III , and structural issues-including those related to poverty and interstate growth and structural policy implementationare covered in Part IV.

Having experienced a balance of payments crisis only ten years ago, issues related tO external vulnerability remain extremely tOpical in India. Against this background, Chapter 2, "India and the Asia Crisis," reviews India's experience during the Asia crisis and the factors that helped insulate it from the worst of the financial market turmoil that afflicted the rest of the region. The chapter explains India's success in terms of its strong macroeconomic fundamentals, modest systemic vulnerability in the banking and corporate sectors, flexible exchange rate management, the relatively closed nature of the economy, and capital controls. However, the chapter cautions that, as capital controls are gradually eased and trade barriers reduced, it will become increasingly important to ensure sound macroeconomic policies-including with regard to the fiscal position-and strong prudential and supervisory systems.

India's external vulnerability is examined in more detail in Chapter 3, "Assessing India's External Position," by estimating models of the equilibrium current account. The results illustrate that India's equilibrium current account deficit has been constrained by its lack of openness on both the capital and trade accounts and suggests that deficits in the range of 1 !12-21;2 percent of GDP appear sustainable, given India's stage of development. The paper uses the experience of the 1991 balance of payments crisis, however, tO illustrate risks to the external position from weak fiscal policies, low reserves, short-term debt exposure, and exchange rate overvaluation.

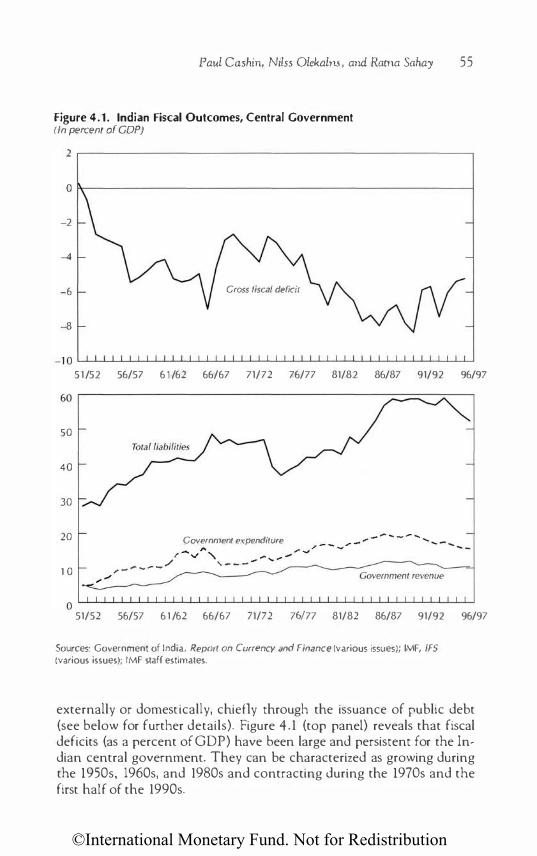

Issues related to fiscal sustainability are the focus of the subsequent two chapters. Chapter 4, "Tax Smoothing, Financial Repression, and Fiscal Deficits in India," examines data through 1996/97 and asks whether fiscal policy has been effective in avoiding disruptive changes in tax rates in the face of temporary shocks, and whether there has been a bias toward deficit financing. The results suggest that fiscal policies in India have been consistent with tax-smoothing behavior. However, there also appears to be evidence pointing tO a significant bias roward deficit financing, leading tO excessive public borrowing, as well as resort to seigniorage and financial repression. Consequently, the authors argue that government debt is well in excess of levels that would be considered optimal or consistent with intertemporal solvency.

Fiscal sustainability and developments since FY 1996/97 are explored further in Chapter 5, "Fiscal Adjustment and Growth Prospects in India." Using a simple growth model, the chapter illustrates that India's

©International Monetary Fund. Not for Redistribution

6 OVERVIEW

ability to avoid a fiscal crisis, despite high deficits, has largely reflected a favorable differential between real interest rates and overall economic growth. The simulations suggest, however, that a continuation of recent policies would risk putting India on an explosive debt path, by undermining growth and putting upward pressure on interest rates. This risk would be exacerbated as financial sector reform and liberalization reduce the scope for the government to place its debt with captive financial institutions at nonmarket rates. The paper concludes that ambitious fiscal reforms are needed to ensure sustainability, including measures to improve fiscal discipline at the state level, tax measures to boost the revenue/GOP ratio, and cuts in unproductive spending that would provide greater room for needed infrastructure investment.

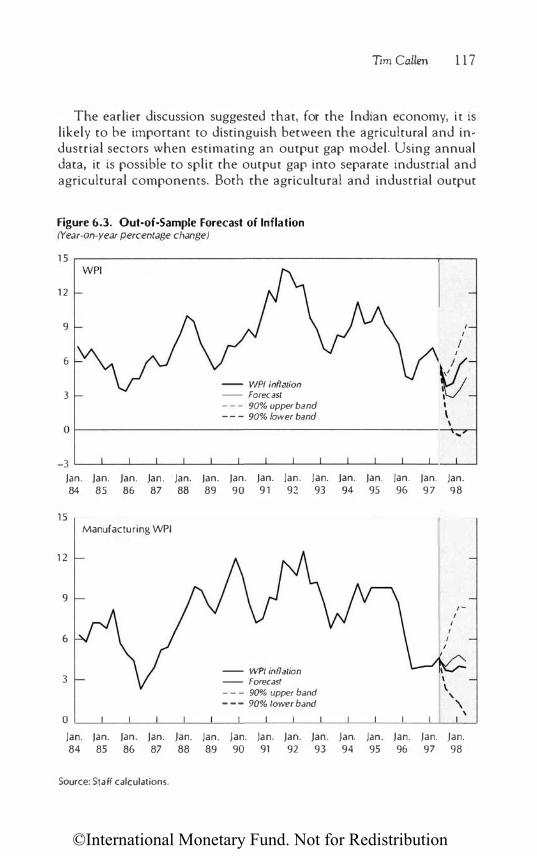

Monetary policy and financial secror issues are addressed in Chapter 6, "Modeling and Forecasting Inflation in India." The chapter discusses the Reserve Bank of India's (RBI) downgrading of the money supply as an intermediate target in response to financial secror liberalization and innovation, which has reduced the strength of the statistical relationship between money and economic activity. The paper tests the extent to which money versus other indicators provide useful leading infonnation of inflation pressures and cautions that the monetary aggregates continue to be useful for predicting inflation, albeit with significant lags. The paper concludes by suggesting that improvements in the quality of the monetary and price data could further strengthen the RBI's ability tO implement monetary policy, but it also cautions that, until a more reliable anchor for monetary policy is found, the RBI will need to be especially careful to avoid undermining the credibility of its commitment to reasonable price stability.

Chapter 7, "The Unit Trust of India and the Indian Mutual Fund industry," explores the issue of financial sector reform and regulation from the perspective of the mutual fund industry. In particular, while the mutual fund industry has played an important role in mobilizing financial saving in India, its systemic vulnerability was illustrated in 1998 when India's largest fund, the government-sponsored Unit Trust of India, faced significant financial difficulties. As the chapter notes, this episode provided a stark illustration of the importance of continued efforts to strengthen regulation and transparency in the mutual fund industry, a conclusion that applies more generally to the financial secror as a whole.

Structural issues are explored in more detail in the final two chapters. There is deep concern about the apparent widening of regional income disparities, as it suggests a risk that growth will not be sustained or be of a high quality. In Chapter 8, "Growth Theory and Convergence Across Indian States: A Panel Study," interstate growth differentials are

©International Monetary Fund. Not for Redistribution

Cltriswp/te,- Towe 7

examined and the empirical evidence pointing to a widening of per capita income gaps is presented. This lack of convergence is determined to have been partly due to differences across states in Literacy and private investment rates. The chapter then demonstrates that these rates appear to have been adversely affected by inadequate public funding of social and public infrastructure investmenr. Thus, the chapter provides a strong illustration of the damaging effect that weak fiscal policies have had on slower-growing states.

Finally, "Structural Reform in India" provides an overview of structural reform policies that have been implemented since the 1991 balance of payments crisis. The chapter describes empirical evidence that suggests that reforms can significantly enhance India's growth potential and points tO signs that the apparent slowing of the momentum for reform has adversely affected productivity, especially in the agricultural and industriai sectors. The chapter concludes by stressing the need to

reinvigorate the reform process and by summarizing the areas where policies are needed tO support strong and sustained growth over the medium term.

Taken together, these papers suggest that lndia stands at the crossroads. The experience of the Last decade has illustrated the enormous capacity that lndia has for absorbing structural change and the significant benefits that sound policies can yield. At the same time, however, the process of structural reform is unfinished and much of the fiscal adjustment that was achieved has been reversed. This book suggests that ensuring strong, sustained, and high-quality growth in the coming decade will require a broad-based and deep commitment tO fiscal deficit reduction, wide-ranging structural reform, and prudent and careful management of monetary and exchange rate policies.

©International Monetary Fund. Not for Redistribution

This page intentionally left blank

©International Monetary Fund. Not for Redistribution

PART I

Preserving External Stability

©International Monetary Fund. Not for Redistribution

This page intentionally left blank

©International Monetary Fund. Not for Redistribution

2 India and the Asia Crisis

CHRISTOPHER TOWE

Introduction

India's recent economic performance has been remarkable, particularly in view of the economic and financial turmoil thar afflicted the region during 1997-99. In the face of the Asia crisis, as well as the imposition of international sanctions in early 1998, volatility in domestic financial markets and the exchange rate was contained and overall economic activity accelerated in 1998/99. Spillovers to India's balance of payments were also comparably modest-the current account deficit was held to around 1 percent of GOP in 1998/99, capital inflows were sustained, and official reserves increased.

This chapter describes the factors that helped insulate India from the regional turmoil. The following section examines the extent to which tandard indices would have signaled external vulnerability and con

cludes that India's financial and macroeconomic fundamentals were significantly stronger than those economies affected by the crisis. The third section discusses in more detail India's capital controls and their role in reducing India's external vulnerability.

The chapter concludes on a cautionary note, stressing that the favorable experience during the past two years should not lead to complacency. India's previous balance of payments crises clearly demonstrated that the balance of payments is vulnerable to external shocks.1 This vulnerability

11nJi;� experienced balance of paymems crises in 1980 and \990/91, necessitating Fund program». The 1990/91 crisis was precipirared by the Gulf war, which resulted in a sharp

11

©International Monetary Fund. Not for Redistribution

l2 INDIA AND THE ASIA CRISIS

has likely increased as a result of the ongoing Liberalization of domestic financial markets, as well as the gradual easing of controls over capital inflows that has taken place in recent years. This only increases the importance of ensuring a sound macroeconomic environment, including a more sustainable fiscal position, and of continuing to promote a strong prudential and supervisory framework for the financial system.

Macroeconomic and Structural Factors

A broad range of macroeconomic and structural facrors help explain why India was relatively unscathed by the recent crisis. In particular, when the regional crisis arose in 1997, India did not exhibit many of the macroeconomic, financial sector, and external imbalances that afflicted other countries in the region, in large part owing to the years of structural and macroeconomic reforms that had followed India's 1990/91 balance of payments crisis. As a result, estimates of crisis probabilities based on macroeconomic fundamentals-including the real exchange rate, the current account, reserves, export growth, and shortterm debt exposure-were relatively benign in the case of India in late 1996, especially when compared ro other Asian economies (Figure 2.1).2 Besides these relatively good macroeconomic fundamentals, India was also insulated from financial market contagion and trade spillovers by the relatively closed nature of its economy, a long history of capital controls, and modest financial links with the region.

India's external current account going into the crisis was relatively strong. The current account deficit had fallen to only 1 Y4 percent of GOP in 1996/97, reflecting the effect of strong export growth in previous years, as well as a surge in inward remittances. Although the crisis contributed

increase in India's oil import bill, as well as a reduction in remittances from Indians abroad. However, the economy's vulnerability to rhe external shock reflected underlying structural weaknesses, including a deterioration in the fiscal position (the overall public sector deficit rose to over 12 percent of GOP), excessive monetary growth, large external debt servicing requirements (partly related to previous JMF loans), and a growing current account deficit.

2The crisis probabilities shown are estimates of the probability of balance of payments crisis 24 monrhs hence, and are based on a model mainrained by the Developing Country Studies Division of the IMF's Research Department. This model and other studies, including those by J. Sachs, A. Torncll, and A. Velasco (1996), J. Frankel and A. Rose (1996), and G. Kaminsky, S. Lizondo, and C. Reinhart ( 1998), identify a range of variables that can help signal crisis, including real exchange rate appreciation, banking crises, growth of M2/reserve growth, stock price inflation, export growth weakness, output growth slowdown, excess M l balances, falling external reserves, excess domestic creuir growth, high real interest rates, and a decline in the terms of trade.

©International Monetary Fund. Not for Redistribution

Figure 2.1. Crisis Probabilities, December 1 996 (In percent)

India Philippines Taiwan PRC

Korea

Christopher Towe 13

Malaysia Indonesia Thailand

tO a weakening of export growth, owing to the decline in regional demand and a fal l in export unit values, this effect was partly offset by lower oil prices and the strength of IT-related services exports. Spillovers from the Asia crisis were also moderated by the relatively closed nature of the Indian economy-exports represent less than 10 percent of India's GOP, and the share directed to Asia was relatively small (less thar\ 2 percent of GOP). The current account deficit remained at 1 Y4 percent of GOP in 1997/98, and fell to 1 percent of GOP in 1998/99.

The impact of the crisis and sanctions on capital flows was also relatively modest, partly reflecting the fact that capital controls have limired India's dependence on foreign saving. Private capital inflows reached just over $10 billion in 1996/97, owing tO increases in foreign direct investment (FOI), commercial borrowing, and deposit inflows by nonresident Indians (NRis), but fell only marginally in the following two years to an average of around $9 billion. While portfolio investment, short-term credits, and NRI deposits were adversely affected, FDI and commercial borrowing were sustained, and capital inflows were also bolstered by the authorities' issue of the Resurgent India Bond. 3 As a result, India's external reserves actually increased over the crisis period, and stood at almost $35 billion at end- 1999, the equivalent of over six months of imports of goods and services.

3The Resurgent India Bond (RIB) was marketed ro nonresident Indians hy the State Bank of India (which is mainly owned by the central bank). The RIB is a five-year bond, denominated in U.S. dollars, pounds sterling, or deutsche marks (paying an interest rate of

©International Monetary Fund. Not for Redistribution

14 INDIA AND THE ASIA CRISIS

Table 2.1. External Debt, 19971 (In percent of GOP)

India Indonesia

Total 24.4 61.3 Of which: Short-term 1.8 10.0

'Data for India are at end-March 1997.

Korea Malaysia Philippines Thailand

33.2 38.7 59.3 62.0

13.3 13.5 23 1

India's external debt position (Table 2 . 1 ) had also improved considerably during the mid-1990s. Total external debt as a share of G DP had fallen to 24 percent of GOP in 1996/97 from 33 percent of GOP at end 1993/94, while short-term debt remained under 2 percent of GOP during the same period.4 Accordingly, the debt service ratio improved considerably, falling to 22 percent in 1996/97 from 3 2 percent of exports of goods and services in 1990/91 . The structure of external debt was also relatively favorable. Although concessional debt fell slightly as a share of total external debt during the mid-1990s, by end 1996/97 it remained around 40 percent.

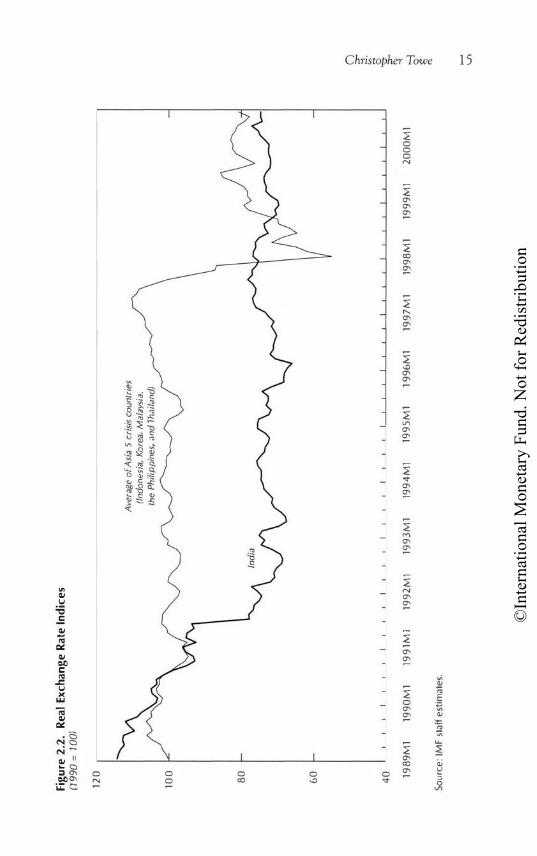

The fact that the rupee's exchange rate was not obviously overvalued at the beginning of the crisis, and that monetary policy was geared toward allowing the exchange rate to depreciate in an orderly fashion in the face of market pressures, also helped sustain financial market confidence (Figure 2.2). The rupee had already depreciated sharply following India's balance of payments crisis in 1991, and by March 1997 it was roughly 25 percent below its 1990 value in real terms, a level that most indicators suggested was broadly in line with medium-term fundamentals.s This movement in the real exchange rate was facilitated by the shift in the exchange rate regime from a basket peg system to a managed float following the 1991 crisis.

The Asia crisis did result in pressures on the rupee in the latter half of 1997 and early 1998. The authorities responded by tightening money market conditions while permitting an 18 percent depreciation against the U.S. dollar. However, the interest rate hikes and the depreciation in real terms were considerably less than what was experienced among the

73/4 percent, 8 percent, and 61/4 percent per year, respectively). The proceeds were used ro make rupee loans at L2Y2-t3 percent ro developmenr institutions, which were supposed ro fund their loans for infrastructure projects. The exchange loss, if any, would he shared between the Stare Bank of India (SBI) and rhe Reserve Bank of India (RBI}, although the SBI's liability is limited ro 1 percenr per annum of rhe rupee value of the original amount credited to the institution plus accrued interest.

4Note that these debt figures understate the vulnerability of many southeast Asian economies, since they do not include off-balance sheer liabilities, which in some cases were substantial.

5See the analysis of misalignments by D. Tzanninis ( L998), and Chapter 3.

©In

tern

atio

nal M

onet

ary

Fund

. Not

for R

edis

tribu

tion

Figu

re 2

.2.

Rea

l Ex

chan

ge R

ate

Ind

ices

(19

90 =

100)

120

100

80

60

40

1989

M1

199

0M

1

Sour

ce: I

MF

staff

est

imat

es.

199

1M1

199

2M

1 19

93

M1

Av

erag

e o

f Asi

a 5 c

risi

s c

ou

ntr

ies

(In

do

nes

ia,

Ko

rea,

Ma

lays

ia,

the

Ph

ilip

pin

es,

an

d T

ha

ilan

d)

199

4M

1 19

95

M1

1996

M1

199

7M

1 19

98

Ml

199

9M

1 20

00

Ml

......

V1

©International Monetary Fund. Not for Redistribution

16 INDIA AND TliE ASIA CRISIS

Asia crisis countries, and the rupee settled in a relatively narrow trading range after August 1998.6

India's success in resisting the crisis also reflected the fact that corpo� rale and household balance sheets did not exhibit the same fragilities found in many crisis countries. For example, debt-equity ratios for the manu� facturing sector declined from over 200 percent in 1991/92 to a more manageable 121 percent in 1997/98.7 Moreover, although stock prices fell sharply (by roughly 40 percent) following the onset of the Asia cri� sis and the imposition of sanctions, this had not preceded a long-term run-up in equity prices fueled by excessive credit creation, which was seen in many other emerging markets ahead of the crisis. Indeed, most monetary indicators were comparably benign ahead of the crisis; credit growth had been decelerating since the beginning of 1995, and the ratio of broad money to reserves had declined sharply since early 1996.

The banking sector was also comparatively less vulnerable than elsewhere in Asia, partly reflecting the effort of the reforms that had been initiated in the early 1990s. For example, risk-weighted capital adequacy ratios (CARs) had risen to nearly 1 2 percent by 1997/98, largely as a result of substantial capital injections by the public sector. Nonperforming loans as a percent of total loans had fallen to around 8 percent in 1997/98 from around 1 1 percent in 1994/95. Systemic risks also were moderated by the fact that roughly 80 percent of the system was already state owned. Credit and market risk was mitigated by the fact that roughly half of bank assets were taken up by reserve and liquidity requirements-including holdings of government debt-and loans to the property sector were relatively modest. In addition, extensive capital controls restricted the size and term of external bank borrowing, minimizing banks' exposure to regional and foreign exchange risk.

Although India's fiscal situation was considerably weaker than the Asia crisis economies, the public sector deficit had been on a downward trend in the period leading up to the crisis. The deficit had fallen to a recent low of 8 percent of GOP in 1997/98 from almost 1 2 percent of GOP in 1989/90, owing to a sharp compression of capital and other spending. As a result, the public sector debt-to-GOP ratio had begun tO decline, reaching as low as 75 percent at end-1996/97.

6RBI exchange rare policy has been characterized as aimed at maintaining "orderly condirions in rhe foreign exchange market, and ro curb destabilizing and self-fulfilling speculative activities." Sec Dr. Y.V. Reddy, Deputy Governor, Reserve Bank of India (RBI), address ro the Fourth Securities lndusrry Summit, May 26, 1999.

7 Alrhough this gearing ratio compares favorably with a number of orher emerging markets in Asia, some analysts express concern with the leverage of Indian businesses, and the extent to which public sector banks are required ro provide financing to loss-making firms.

©International Monetary Fund. Not for Redistribution

Ch1·iswpher Towe 1 7

Broader macroeconomic developments in India were also favorable. In a number of economies, a sharp slowdown in domestic growth, following years of rapid expansion, was an important precursor to crisis. Slow growth contributed to weaknesses in the financial and corporate sectOrs, since large (often foreign currency) loans had been made on the assumption of continued strong growth and limited the scope for central banks to raise interest rates ro defend existing exchange rate parities. Although growth did slow in India during 1997/98, it remained relatively robust at just under 5 percent. The slowdown also reflected mainly domestic supply shocks, such as the effect of weather-related problems on agricultural output, rather than the precrisis slowdown in export growth that afflicted many other countries in the region.

The importance of macroeconomic and other fundamental facrors as preconditions for crisis has been illustrated by statistical analysis in the IMF's May 1999 World Economic Outlook (Figure 2.3 ) . This study

Figure 2.3. Crisis Vulnerability Indicators (Difference of crisis to noncrisis economies)

25 -

20 -

1 5 -"' <:: .g 1 0 -

.�

T "' "' 5 -a ! � • -§ 0 <:: 1 • • Ol -5 -

j - 1 0 -

-15 -

-20 -

� 1.) � "' c t: � -� � eo o 8. 3 c: ·-l? "' 0 "' ;;; X 0 � CD � ·- .. � "" .., 1.) 0.. X Oi -� -"'0 ·'"= "' a. V> .. 0 ... � tJ "' a. •t � "' � I.> "' \i) E � "'

·� � d: '5 �

:r

2 '6 � u c: 0 E E 0

u

90% Confidence interval for crisis economies

/

I •

.. .. c 0.. ·5 � ·� 0 15 � �·� c:

� � c. :> 0 � � � 1.) 1.) "' "' ..., c � 8

I I

· � India

� 15 c ., � � X "' "' E E � � � t:" .J:> 0 "' 6; "0

- � "' "' !: C: � � X Oi .. � E :E � "' � "0 .: 0 � Vl

Composite Indicators

--

-

I --•

•

-

-

-

-

� � (: � .. ;;; V> "' � � .S � "' "' "'

©International Monetary Fund. Not for Redistribution

18 INDIA AND THE ASIA CRISIS

showed that a number of economic fundamentals for crisis economies were different than those for noncrisis countries. For example, in Figure 2.3, real effective exchange rates for 90 percent of those economies that fell into crisis were significanrly higher than that exhibited by noncri ·is economies during the Asia and earlier Mexico crises. Of tht! variable:. examined, exchange rate overvaluation, current account deficits, :,hortterm external debt, real interest rates, and common creditors were found to be significant signals of crisis.8

Most of the variables that provided an indicator of crisis vulnerability in other countries did not signal vulnerability for lndia during the 1997/98 period. Notably, India's reserves, current account deficit, real interest rate, and exchange rate movements were not typical of the behavior shown by crisis economies. In addition, crisis economies typically were more exposed to a common creditor-i.e., had a larger proportion of international bank loans from a single creditor country-but this was not the case for India. Real interest rates also did nm signal a risk of crisis. The only variables that did appear to point to vulnerability for India were those that proxied the spil lover of crises in other countries on India's real exchange rate and export growth.

Composite vulnerability indices also suggest the same conclusion. Only four of these indices appear to signal vulnerability (Figure 2.4 ): reserve adequacy, reflecting the high level of M2/reserves; trade spillovers, owing to India's trade links to other crisis countries; the composite financial indicator, again owing to the high M2/reserves ratio; and domestic macroeconomic imbalances, owing to the large fiscal deficit/GOP ratio.9 Although the external imbalance and portfolio spillover variables were significant, the indian data did not signal vulnerabil ity. While the value of the index for domestic macroeconomic imbalances was relatively high in the case of India, reflecting the large fiscal deficit and high monetary growth, this variable did not provide a reliable signal of crisis vulnerability for other crisis economies.

111n Figure 2.3, the venical lines represent the 90 percent range for cnSI> ccunomu.>> ul each v:uiable, norm11lized by the >ample stamhud deviation le>> tht:! CIVt:!rage for rhe noncrisi� ,ample. In <Jther words. the line> repre,ent the >tanJardiZC::d d1fft:re::nce hetw..:.:n 90 percent oi the crisis economies <1nd the noncri>is .:conomu:�s. Denub an� pr<lVIded 111 the IMF's May 1999 World Economic Outlook. The figures for India were calculated un the basis of data available during August-November 1998.

9'fhc M2/reserve> ratio proxies both the effect uf reserve inade4uacy (of [e, cun.;ern in the case of a country such as India with a floating exchange rate) <ll1d also cxct:»

credit creation. In the WEO study, this variable was found to be a sigmficant crisis mdl· cator in the composite indices.

©International Monetary Fund. Not for Redistribution

Figure 2.4. Crisis Vulnerability Indicators (Difference of crisis to noncrisis economies)

·� .� � "' a 1? � c: "' V)

2.5 1-2.0 1-1.5 1- Iii

1 .0 1-0.5 r-0.0 D

-0.5 -

-1.0 -I

Domestic External macroeconomic imbalances

conditions

I

India

D/ I

Portfolio spillovers

Chriscopher Towe 19

90% Confidence interval for crisis economies

1/ •

I Reserve

adequacy

_/

I I

I Trade

spillovers

-

-

-

-

1 -

-

-

Composite financial

indicators Composite Indicators

The Role of Capital Controls10

India's macroeconomic and other fundamentals were not uniformly favorable, and this suggests that capital controls contributed to India's favorable experience during the regional crisis. In particular, India's relatively closed capital account meant that external debt-especially short-term external debt-was modest, and restrictions on capital movements also helped lessen the impact of the sharp turnaround in investor sentiment on the capital flows. Indeed, this view is confirmed by statistical analysis suggesting that capital controls may have helped insulate countries during the Asia and Mexico crises (see the May 1999 World Economic Outlook).

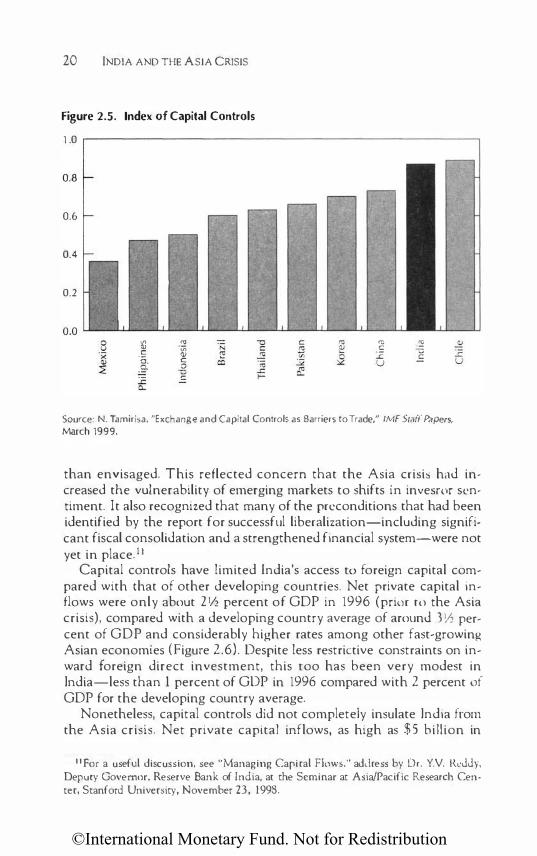

India maintains relatively strict control over capital flows, and the IMF's index of capital controls places India among the most restrictive economies. In general, outflows by residents are prohibited, and inflows by nonresidents are subject to constraints (Figure 2.5 and Box 2 . 1 ). Although a timetable for the phased withdrawal of most capital account controls over the 1997/98-1999/2000 period was established in June 1997, progress toward capital account liberalization has been slower

1"This section draws upon K. Habermeier (2000).

©International Monetary Fund. Not for Redistribution

20 INDIA AND THE ASIA CRISIS

Figure 2.5. Index of Capital Controls

1 .0 .--------------------------------.

0.8

0.6

0.4

0.2

� c ·a. .9-.r. 0...

"' ·;;; � c 0 -o c

-o c � "' .r.

I-

"' .� .r. u .� u c

Source: N. Tamiri�a. "Exchange and Capital Controls as Barriers to Trade," IMF Staii Papers, March 1999.

than envisaged. This reflected concern that the Asia crisis had increased the vulnerability of emerging markets to shifts in invesror sentiment. It also recognized that many of the preconditions that had been identified by the report for successful liberalization-including significant fiscal consolidation and a strengthened financial system-were not yet in place. 1 1

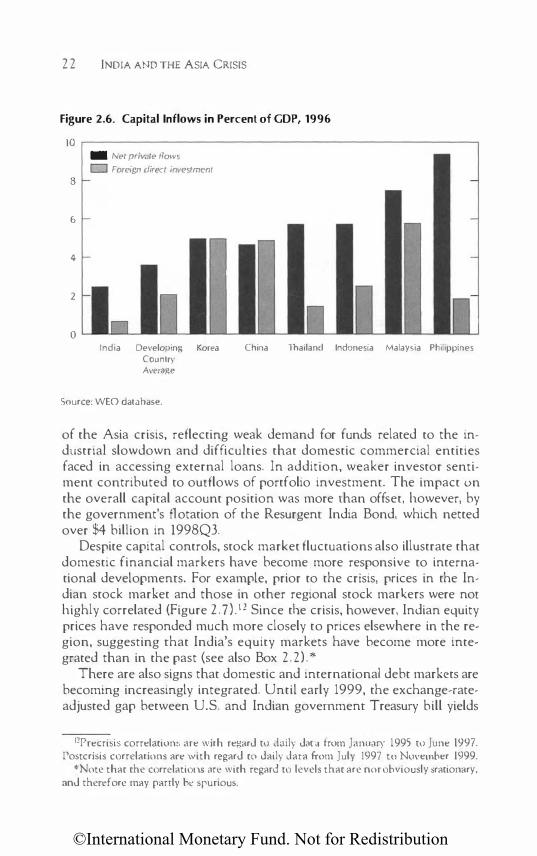

Capital controls have limited India's access tO foreign capital compared with that of other developing countries. Net private capital inflows were only about 2 1/2 percent of GOP in 1996 (prior ro the Asia crisis), compared with a developing country average of around 3 Y:! percent of GOP and considerably higher rates among other fast-growing Asian economies (Figure 2.6). Despite less restrictive constraints on inward foreign direct investment, this roo has been very modest in India-less than 1 percent of GOP in 1996 compared with 2 percent of GOP for the developing country average.

Nonetheless, capital controls did not completely insulate India from the Asia crisis. Net private capital inflows, as high as $5 billion in

1 1 For a useful discussion, see "Managing Capiral Flows,'' adc.lress by Dr. Y.V. Reddy, Deputy Governor, Reserve Bank of India, at the Seminar at Asia/Pacific Research Cen· ter, Stanford University, November 23, 1998.

©International Monetary Fund. Not for Redistribution

Chriscopher Towe 2 1

Box 2.1. Capital Controls

• Loans. Generally, Indian residents are prohibited from borrowing from nonresidents. However, there is a window that permits external commercial borrowing (ECB) by Indian corporate emities, subject to government approval. Indian corporations are allowed to apply for permission to borrow abroad, but the total amount of loans made to all corporations is subject co an annual ceiling ($8.5 billion in 1999/00). Companies are restricted from paying more than 350 basis points above UBOR/U.S. Treasuries.

• Portfolio flows. Portfolio outflows by residents are subject to prior approval. Indian-registered mutual funds may invest in overseas markets up to a maximum of $500 million. Portfolio inflows by nonresidents are permitted by registered foreign institutional investors (Als) subject to certain Limits. ln particular, a single AI's ownership share in Indian companies cannot exceed 10 percenc, and short sales by Als are prohibited. The aggregate permissible holdings of an Indian company by Fils has been increased to 40 percent, subject to Board approval. Portfolio investments by nonresident Indians also are permitted. In both cases, there are no restrictions on repatriation. ln addition, resident corporations are permitted to raise equity abroad by issuing Global or American Depository Receipts.

• Foreign direct invesrment. Inward foreign direct investment is permissible subject to prior notification and approval, as well as restrictions on the foreign ownership of projects. However, "automatic" approval is permitted for smaller amounts, or investments directed toward sectors not on a negative list. Limits on equity participation are also relaxed for high-priority sectors. Restrictions on outward direct invest· ment by residents were eased in 1999, with the limits for fast-track approval raised to $15 million; otherwise prior approval is required.

• Bank deposits. Deposits by residents abroad and resident deposits in foreign currency are permitted, subject to prior approval. Deposits to Indian banks by nonresident Indians (NRis) and overseas corporate bodies (OCBs; i.e., corporations owned by NRls) are permitted, both in rupees and foreign currencies. Depending on the scheme, such deposits can be repatriated. Restrictions are placed on the interest paid to NRI deposit holders.

1997Q2, tapered off in the latter half of 1997, and, except for a spike in 1998Ql related to unidentified capital inflows, were relatively modest inro 1 999. The weakening in capital inflows largely reflected bankrelated outflows; nonresident Indian deposits fell sharply in late 1997 and other net bank foreign assets also declined from 1997Q3. However, a drop in investment and nonbank flows was also evident after the onset

©International Monetary Fund. Not for Redistribution

22 INDIA AND THE ASIA CRISIS

Figure 2.6. Capital Inflows in Percent of COP, 1996

10 .----------------------------------------------------. - Net private t1ows

D Foreign clirect investment

8

b

4

2

0 India Developing Korea China Thailand Indonesia Malaysia Philippines

Country Average

Source: WEO database.

of the Asia crisis, reflecting weak demand for funds related to the industrial slowdown and difficulties that domestic commercial entities faced in accessing external loans. In addition, weaker investor sentiment contributed to outflows of portfolio investment. The impact on the overall capital account position was more than offset, however, by the government's flotation of the Resurgenr India Bond, which netted over $4 billion in 1998Q3.

Despite capital controls, stock market fluctuations also illustrate that domestic financial markers have become more responsive to international developmenrs. For example, prior to the crisis, prices in the Indian stock market and those in other regional stock markers were not highly correlated (Figure 2 . 7). 12 Since the crisis, however, Indian equity prices have responded much more closely to prices elsewhere in the region, suggesting rhat India's equity markets have become more integrated than in the past (see also Box 2.2) .*

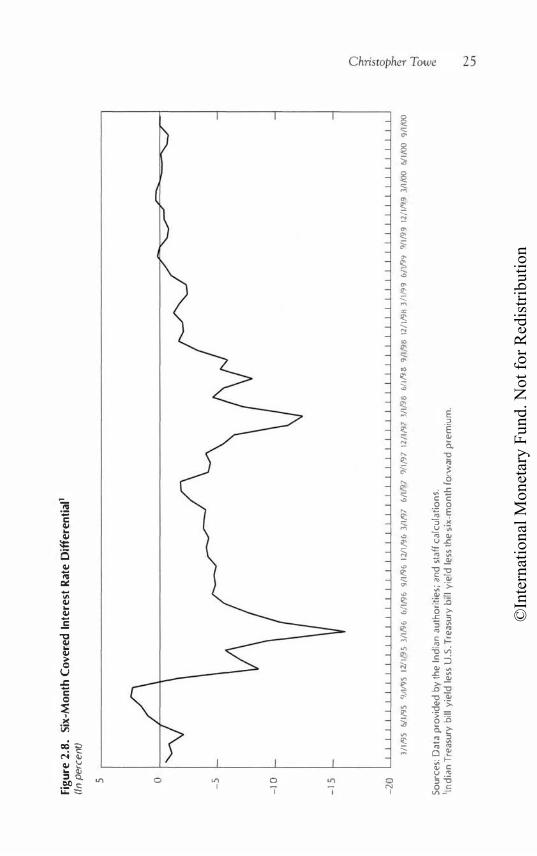

There are also signs that domestic and international debt markets are becoming increasingly integrated. Until early 1999, the exchange-rateadjusted gap between U.S. and Indian governmenr Treasury bill yields

11Precrisis correlation;, are with regard to dnily d<lt<1 from January 1995 to June 1997. Postcrisis correlations an� with regard tO daily Jara from July 1997 to November 1999.

*Note that the correlations arc with regard ro levels that are nor obviously srarionary, and therefore may parrly he spurious.

©International Monetary Fund. Not for Redistribution

ChristOpher Towe 23

Figure 2.7. Correlation Between Indian and Regional Stock Prices

HKSAR Taiwan

Source: CEIC.

Indonesia Korea Singapore Malaysia Thailand

Box 2.2. Regional Stock Market SpilloversPre- and Post-Asia Crisis

In order to examine the proposition that spillovers from Asian stock markets to India have increased following the Asia crisis, regressions were estimated relating the daily log change in the Indian Bombay SENSEX index (r,) as a function of its lagged value, and the log change in other regional markets (r',}-consrant terms and ocher lags were not found to be significant:

The regressions were estimated over a precrisis period (October 1994-May 1996) and during rhe postcrisis period (July 1997-November 1999). The estimated impact of regional stock markets is proxied by the c1 coefficients, which are reported below ("-" indicates that the coefficient is insignificant from zero at the 95 percent confidence level). As can be seen, except for the case of Korea, the proposition that rhe impact of regional stock market developments on the domestic stock market has increased since the Asia crisis cannot be rejected.

HKSAR Indonesia Korea Malaysia Singapore Thailand Taiwan

Precrisis Postcrisis 0.12 0.80

0.17 0.08 0.07 0.10 0.07

©International Monetary Fund. Not for Redistribution

24 INDIA AND THE ASIA CRISIS

was large, with the yield on U.S. securities tending ro exceed that on Indian securities, pointing to an inability of financial markets ro arbitrage unexploited profits. Since the beginning of 1 999, however, this gap has narrowed considerably, and, while it remains significantly different from zero, there are indications that marker participants are becoming better able to arbitrage the difference between domestic and foreign yields (Figure 2.8). 1 3

Finally, the growing stock of the more volatile sources of financing is significant and a potential source of vulnerability. Cumulative portfolio inflows-on which there are no repatriation restrictions-totaled over $ 1 5 billion during 1990Ql-1999Ql , and the outstanding stock of repatriable NRI deposits was around $14.5 billion at end-March 1999.

Concluding Remarks

This discussion has suggested that India's favorable economic performance in the face of the recent regional financial crisis can be a cribeJ to a combination of relatively strong fundamentals, the closed nature of the economy, and a legacy of capital controls that insulated India from contagion effects. India's past balance of payments crises, however, and the experience of the rest of the region during the pa t several years suggest a number of important lessons:

• Effective exchange rate management. During the Asia crisis, the RBI was effective in facilitating an orderly adjustment in the rupee/dollar exchange rate. This experience, and the experience of other countries in the region that had more rigid nominal parities against the dollar, illustrates rhe advantage of a flexible exchange rare system and highlights the risks that arise when the monetary authorities seek to maintain an excessively stable exchange rate against one particular currency.

• The importance of sustaining che macroeconomic adjustment. The multicounrry studies described above i llustrate the importance of macroeconomic fundamentals-a sustainable current account balance, an appropriate and flexible exchange rare, high levels of reserves, and low levels of shorr�rerm external debt-for avoiding balance of payments crisis. Although India was well positioned

JJCapiral controls constrain the scope for arbitrage. hut. a� domestic corporate> can borrow abroad, this rends to limit the extent co which domestic rates c<ln exceed foreign rates. For a d1scussion of the imcrest parity conditions in India, see H. Joshi ::�nd M. Sag· ger ( 1998). The increasing integration of the domestic capital, money, and foreign ex· change is discussed by B.K. Bhoi and S.C. Dhal ( L999).

©In

tern

atio

nal M

onet

ary

Fund

. Not

for R

edis

tribu

tion

Figu

re 2

.8.

Six-

Mon

th C

over

ed I

nter

est

Rate

Diff

eren

tial

1

(In pe

rcent)

5 0 -5

- 10

- 15

-20

l/

1,"}5

6/

1,")5

9

/1/9

5

12/1,"}

5 1

/1,"}

6

6/1

,")6

9

/1/9

6

12/1,")

6 3

/1,")

7

6/1

,"}7

91

1,")7

12

/1,")

7 l

/1,")

8

6/1,")

8

9/1

,")8

12

/1,"}

6 3

11,")

9

6/1

/9�

9/

1,"}9

12

/1/')

9 3

/1,0

0 6/

1,00

9/1

,00

Sour

ces:

Dat

a p

rovi

ded

by

lhe

Ind

ian

auth

orit

ies;

and

sta

ff c

alcu

latio

ns.

11nd

ian

Tre

asur

y bi

ll yi

eld

less

U.S

. Tre

asur

y b

ill y

ield

less

the

six-

mo

nth

forv

vard

pre

miu

m.

©International Monetary Fund. Not for Redistribution

26 INDIA AND THE ASIA CRISIS

ahead of the Asia crisis, this was mainly the result of policy measures that had been set in train in response to India's earlier balance of payments crisis, including trade liberalization, tax reform, fiscal adjustment, and financial sector reform. However, progress along many of these fronts in recent years has been less favorable. For example, the momentum for structural reform appears to have slowed in the latter half of the 1990s, and most of the progress in reducing the fiscal deficit has been eroded. Thus, in the absence of ambitious measures to improve public saving and reinvigorate the structural reform process, balance of payments vulnerability, especially in the face of adverse external shocks, cannot be ruled our.

• Capital controls and financiaL sector stability. India's capital controls also played an important role in helping ro insulate it from the financial contagion that afflicted other countries in the Asia region. The same can be said for the pervasive government control over the banking sector and the relatively modest pace of liberalization in the domestic financial sector, since high reserve and liquidity requirements, priority lending regulations, and an underdeveloped domestic debt market discouraged the asser price inflation and balance sheet weaknesses seen elsewhere in Asia. As liberalization continues, however, the systemic vulnerabilities to contagion increase. The balance of payments is becoming more dependent on gross private inflows of portfolio inve tment, as well as investments by nonresident Indians. In addition, recent fi.nancial market developments have increased the scope for arbirrage.11 This only increases the importance of ensuring that the prudential and supervisory systems covering the domestic financial sector are strong and that macroeconomic imbalances are addressed.

References

Bhoi, B.K., and S.C. Dhal, 1999, lnregracion of Financial Markecs in lndia: An Empirical Evaluation, RBI Occasional Paper, April 7.

Frankel, ]., and A. Rose, 1996, "Exchange Rare Crashes in Emerging Marker�: An Empirical Treatment," journal of lncemational Economics, VoL 4 1 , pp. 351-66.

Habermeier, Karl, 2000, "India-Experience with the Liberalization of Capital Flows Since 1991," in Capital ComTois: CountT)' Experiences with Their Use and

14Airhough the RBI sought ro restrict foreign exchange market spccul:.lrion in 1998 hy restricting rhe ability of participants to cancel and rebook forward contl<lct�, the nc>mkliverable forward marker for Indian rupees in Singapore remains an :lvenue for ht:dging. Moreover, swap transactions have recently been permitted in India.

©International Monetary Fund. Not for Redistribution

Christopher Towc 27

Liberalization, A. Ariyoshi, K. Habermeier, B. Laurens, I. Otker-Robe, J.l. Canales-Kriljenko, anti A. Kirilenko, eJs. (Washington: lmemational Monetary Fund), Chapter II.

Joshi, H., and M. Sagger, 1998, Excess Rerums, Risk-Premia, arul Efficiency of the Foreign Exchange Market, RBI Occasional Paper, Vol. 19, No. 2.

Kaminsky, G., S. Lizonc.lo, and C. Reinhart, 1998, "Leading IndicatOrs of Currency Crises," Staff Papers, 1ntemational Monetary Fum!, Vol. 45 (March), pp. 1-48.

Sachs,)., A. Tomell, anJ A. Velasco, 1996, "Financial Crises in Emerging Markets: The Lessons from 1995," Brookings Papers on Economic Activity (May), pp. 1 4 7-98.

Tzanninis, D., 1998, "Exports and Competitiveness," lndia: Selected Issues, IMF Staff Counrry Report No. 98/ 1 1 2 (October), pp. 66-9 1 .

©International Monetary Fund. Not for Redistribution

3 Assessing India's External Position

TIM CALLEN AND PAUL CASHIN

Introduction

India has generally followed camious external sector policies, with trade intervention and capital controls used extensively as instruments of balance of payments control and adjustment. It has nonetheless experienced several balance of payments crises, most recently in 1991. The policy of restricting trade and capital flows may also have entailed costs in terms of forgone resources. Despite recent reforms, India retains one of tl<e world's most restrictive trade regimes, and the inflow of foreign capital remains well below that of other countries in Asia.

This paper uses a number of methods to assess developments in India's external position. First, an intertemporal model of the current account and a composite model of external vulnerability indicators, which generates probabilities of the occurrence of a balance of payments crisis, are used to consider the solvency, sustainability, and optimality of the external position. Second, a model of the medium-term saving-investment balance is used to derive estimates of the "equilibrium" current account balance against which the actual balance can be compared. Lastly, the possible sustainable current account deficit over the medium term is examined through conditions for intertemporal solvency under different economic scenarios.

The results indicate chat India's current account deficits have been consistent with intertemporal solvency, but the evidence on whether

28

©International Monetary Fund. Not for Redistribution

Trm Callen and Paul Cashin 29

external borrowing has been optimal, even when allowance is made for capital controls, is mixed. However, the path of the current account prior ro 1991 is found not to have been consistent with solvency. The composite model of external vulnerability indicators also raised questions about external sustainability during this period, while estimates of the equilibrium current account deficit were smaller than the actual outcomes during the 1980s. Since 1991, the estimated probabilities of external crisis in India have remained low, and they rose little during the Asia crisis, while the current account deficit is currently around its estimated equilibrium level. Finally, estimates of d1e sustainable level of the current account deficit over the medium term range from L Y2 to 2Y2 percent of GOP, depending on the growth rate and the cost of external finance. The remainder of the chapter provides a brief overview of external sector developments and policies in India, and a discussion of the methodologies for assessing external sector developments.

Overview of External Sector Developments and Policies

Following independence, economic policies focused on rapid industrialization with the aim of achieving economic self-sufficiency. This goal resulted in a trade system that strictly regulated imports through exchange controls and trade restrictions, which were supplemented by a tariff structure with high and differentiated rates across industries (Joshi and Little, 1994). Little emphasis was placed on promoting exports, and the inefficiency of domesti-. industry, engendered by extensive protection, resulted in a distinct anti-export bias. The investments in goods essential for industrialization and the continuing need to import many essential consumer items, including food during periods of drought, resulted in strong import growth in the late 1950s and early 1960s. With export performance remaining poor, the trade deficit widened, and the current account deficit increased tO around 2 Y2 percent of GOP as the surplus on the invisibles account also narrowed (Figure 3.1 , top panel).

Improved export performance in the late 1960s and 1970s, aided by the expansion of world trade and a depreciation of the real exchange rate, led to an improvement in the current account position. While this was temporarily reversed in the aftermath of the oil price shock of 1973, a tightening of import controls and restraint of domestic expenditures brought import growth down. Remittances also increased during the 1970s as the number of Indians employed in the oil-producing nations of the Middle East increased, and the current account position improved,

©International Monetary Fund. Not for Redistribution

30 ASSE SING INDIA'S EXTERNAL POSITION

Figure 3.1. Current Account Balance, 1 950/51-1 998/99 (In percent of COP)

2 .-----------------------------------------------------�

-1

-2

-3

-4

Current account

\ \ " ,, \ ,-.. I \ I Trade bal,1nce \ / \' '�

I / I ( I'

-5

LLLLLLLLLL��������-ULLLLLLLLLLLLLL����

50/51 56/57 62/63 68/69 74/75 80/81 86/87 92/93 98/99

3.0.-----------------------------------------------� 2.5

2.0

1 .5

1 .0

0.5

0.0 1----.���----------��=-----��------------�--4 .... .... \ ' - ..... ... / , _ , -0.5 lnvestmenl income--',------..; ' ........ balance ' �.0 \

\ / -1.5 ������������������������\�J��LL�

50/5 1 56/57 62/63 68/69

Source: Data provided by the Indian authorities.

74/75 80/81 86/87 92/93 98/99

recording a surplus in a number of years during the second half of the 1970s (Figure 3 . 1 , bottom panel).

The current account was largely financed by concessional aid flows prior ro the 1980s. Recourse was also made to IMF financing on several occasions. Private capital movements were limited as foreign investment policy was marked by very tight regulation during the late 1960s and 1970s, particularly with the introduction of the Foreign Exchange Regulation Act (FERA) in 1973 (Kapur, 1997).

©International Monetary Fund. Not for Redistribution

Tim Callen and Part! Cashin 3 1

The 1 980s witnessed a gradual deterioration in the current account position and a profound change in its financing. The second oil price shock in 1979 placed considerable pressure on the balance of payments. Imports rose, exports slowed in response to the worldwide recession and the appreciation of the real exchange rate, and the current account moved back into deficit. As reserves fell critically low, India entered into a program with the lMF in 1981. However, unlike after the first oil price shock, no significant current accoum adjustment followed, and with large macroeconomic imbalances developing in the second half of the 1980s, particularly a deterioration in public finances, the current account deficit rose to a peak of 3 percent of GOP in 1990/91.1

The proportion of cor1eessional debt in total external debt declined from over 80 percent at the beginning of the 1980s to under 45 percent by the end, due to the widening of the current account deficit and constraints on access to concessional funds. The additional financing came from private sources, mainly rupee and foreign currency deposits from nonresident Indians (NRis) and external commercial borrowing from international banks (Figure 3.2, top panel). Much of the latter was undertaken by public enterprises and used to finance projects in the oil, power, aluminum, steel, and transportation sectors, and for on-lending by official financial institutions. While foreign direct investment (FOI) increased slightly, it remained a marginal source of funds, and portfolio investment was not permitted.

External debt rose rapidly from l l to 3 1 percent of GOP between 1980/81 and 1991/92, with short-term debt representing around 10 percent of this total from the mid-1980s compared to negligible amounts pre-1980 (Figure 3.2, bottom panel). The debt servicing ratio also increased to over 30 percenr of exports. These problems came to a head with a sovereign debt rating downgrade in October 1990 (subsequent downgrades followed in March and May 1991) . The rollover of shortterm loans became more difficult, and expectations of a depreciation of the rupee rose, leading to a loss of confidence among investors and a flight ofNRI deposits out of the country. With the rise in oil prices and the decline in remittances following the crisis in the Gulf region, the external position became untenable. As reserves declined, India was brought to the brink of default in january 1991 (]alan, 1992). This was avoided by purchases through the IMF's Compensatory Financing Facility (in January and july 199 1 ) and by the adoption of an IMF program in October 1991.

The reforms implemented in the wake of the 1991 balance of payments crisis have resulted in a more open external sector (Box 3 . 1 ).

1The fiscal year in India runs from April 1 to March 31.

©International Monetary Fund. Not for Redistribution

32 ASSESSING INDIA'S EXTERNAL POSITION

Figure 3.2. Capital Flows and External Liabilities, 1971/72-1998/99 (In percent of COP)

3.5 r--------------------------------------------------,

3.0

2.5

2.0

1 .5

1.0

0.5

0.0

-0.5

-1.0

-1.5

Capital Flows'

• Portfolio . FDI 0 Nonresident Indian deposits and commercial borrowing • External assistance

71/"! ;1/74 75/76 77/7/J 79/80 81/82 83/84 85186 87/88 89/90 91/92 93/94 95/9b 97/98 99/0()

40 .----------------------------------------------------,

35

30

25

20

1 5

10

5

0

External Liabilities

0 Equity • Short·tcrm /i,1bilities [:!! Long-term l1abilities

71/72 73/74 75/76 77/78 79/80 81/62 83/IJ4 65/86 87/88 89/90 91/92 93/94 9'/96 97/98 99/llO

Sources: Data provided by the Indian authorities; and the World Bank Global Development Finance Database. 1Not all components of the capital account are shown; hence, components do not sum to total capital flows.

©International Monetary Fund. Not for Redistribution

Tim Callen and Paul Cashin 33

Exports and imports have both risen as a share of GOP. Exports have responded strongly to the liberalization measures and the decline in rhe real exchange rate, while imports have grown rapidly in response to strong domestic growth and the reduction in tariffs and quantitative restrictions. The current account deficit has been markedly smaller than in the 1980s, averaging only l percent of GOP.

The financing of the deficit has also been much different in the 1990s, with a shift away from short-term debt financing roward equity and longer-term debt flows as restrictions on FOl and portfolio inflows have been eased. Restrictions on debt flows, particularly of a short-term nature, however, have been tightened. Strict controls have been placed on short-term debt, medium-term borrowing from private commercial sources has been made subject to annual caps and minimum maturity requirements, and interest rates or interest rate ceilings have been specified for NRI deposits of different maturities and under different schemes (Acharya, 1999).2 Consequently, between 1991/92 and 1998/99, FDl accounted for 2 1 percent of total capital inflows, and portfolio investment a further 25 percent. Meanwhile, the outstanding stOck of external debt fell to around 23 percent of GOP. By March 1999, short-term debt (on a contracted maturity basis) accounted for only 4Y2 percent of total external debt.

Assessing India's External Position

Several approaches to assessing India's external secror developments are discussed in this section. First, issues of external solvency, sustainability, and optimality are examined. Second, estimates of the "equilibrium" current account are presented against which actual developments can be compared. Lastly, the issue of what is likely to be a sustainable current account deficit over the medium term is considered.

Solvency, Sustainability, and Optimality

Three questions are usually asked when evaluating a country's external position:

• Is the debtor country solvent? Solvency requires that the present discounted value of future current account surpluses equals the value of its existing net external liabilities. In other words, a country is

2Jn October 1999, the Reserve Bank of India (RBI) announced that the minimum maturity for foreign-currency-denominated NRI deposits would be raised from six momhs to one year.

©International Monetary Fund. Not for Redistribution

34 ASSESSING INDIA'S EXTERNAL POSITION

Box 3.1. External Sector Liberalization in the 1990s

Some progress was made in liberalizing current account transactions during the 1980s, but it was not until the early 1990s that significant steps were taken. The Export and Import Policy in April 1992 focused on the gradual removal of quantitative restrictions on machinery and equipment and manufactured intermediate goods, reduction in tariff rates, and the modification of export promotion measures. Subsequem policies have continued this trend, and India has committed to remove all quantitative restrictions by April 2001. In August 1994, India accepted the obligations of Article Vlll of the IMF's Articles of Agreement and the rupee was made fully convertible for current accoum transactions.

On the capital account side, given the experience with the buildup of short-term, high-cost borrowing in the 1980s, policies in the 1990s have focused on encouraging equity and Long-term debt flows. Measures include

• Fareign direct investment (FDI) . Liberalization began with the new industrial policy in July 1991. Initially, automatic approval hy the Reserve Bank of India (RBI) for FDI of up to 51 percent of equity in 35 priority industries was permitted. Over time it was expanded. In February 2000, the government announced that FDI under Rs 6 billion would be available through rhe RBI automatic route except for 13 sectors that have been placed on a negative list, areas reserved for the small-scale sector where foreign investment already exceeds 24 percent, and seven sectors where sectoral investment caps apply. To invest in these sectors, or above the investment caps, permission is required from the Foreign Investment Promotion Board.

• Portfolio investment. In September 1992, approved foreign institutional investors (Fils) were permitted co invest in primary and secondary markets for listed securities, and foreign brokerage firms were allowed to operate in lndia the following fiscal year. While there is no restriction on the total volume of inflows, roral holdings by Fils

expected to generate sufficient earnings ro repay all its external liabilities.

• Is the extent of international capiwl flows optimal' Optimality of capital flows requires char, in the face of shtlcks to net output, capital flows are used to smooth the path of consumption to ensure there are no avoidable welfare losses.

• Is che external posicion sustainable! Even if a debtor country is technically solvent, questions may arise ahnut the sustainability of its current account if lenders perceive that the intertempnral falls in consumption, implied by the path of the current account imbalances, raise doubts about the willingne::.s of the debtor ro meet its

©International Monetary Fund. Not for Redistribution

Tim Callen and Paul Cashin 35

cannot exceed 24 percent (can now be raised to 40 percent by the company's Board), and total holdings of a single FII cannot exceed 10 percent. Nonresident Indians (NRis) and overseas corporate bodies can hold an additional l O percent (this can be raised ro 24 per• cent through a general resolution of rhe company}, with a 5 percent mdividual limit. To provide an incentive to longer-term investors, the capital gains tax rate is 10 percent if the investment is held for over one year (30 percent otherwise). More recently, foreign investors have been allowed to invest in Treasury bills. In February 1992, Indian companies were allowed to issue Global Depository Receipts on approval of the Ministry of Finance and subject to rules relating to repatriation and end use of funds. Since january 2000, no prior approval has been required.

• External borrowing. Approval from the Ministry of Finance is required for all external commercial borrowing and is subject to an annual indicative ceiling (borrowing in excess of 8 and 16 years' maturity is outside the ceiling if the loan amount exceeds $200 million and $400 million, respectively). Borrowing is also subject to minimum average marurities, although, more recently, companies have been given some scope to prepay outstanding borrowing. Terms permitted on NRl deposits have been made considerably Less attractive than those available in the late 1980s, and interest rates have been linked to LIBOR/swap rates. In April 1998, the interest rate ceiling on nonresident foreign currency deposits of one year and above was raised, and the ceiling on maturities of less than one year was lowered. In October 1999, the RBI announced that the minimum maturity would be raised from six months to one year.

• Outward capital flows. Controls on such flows remain quite stringent. Banks have recently been allowed to invest up to 15 percent of their Tter I capital in foreign currency assets, while mutual funds have also been allowed to invest overseas up to certain limits.

payment obligations (Milesi-Ferretti and Razin, 1996; Cashin and McDermott, 1998).

Capital Controls and the Consumption-Smoothing Approach to the Current Account

The question of whether a given current account position is appropriate can be answered only within the context of a model that yields predictions about the optimal path of external imbalances and liabilities. The most common such model is the intertemporal model of the current account, in which the current account is used to smooth consumption

©International Monetary Fund. Not for Redistribution

36 ASSESSING INDIA'S EXTERNAL POSITION