affective Government Accounting - IMF eLibrary - International ...

203

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of affective Government Accounting - IMF eLibrary - International ...

affective GovernmentAccounting

©International Monetary Fund. Not for Redistribution

Also by A. Premchand

Control of Public Expenditure in India (1966)

Performance Budgeting (1969)

*Government Budgeting and Expenditure Controls (1983)

Comparative International Budgeting and Finance (1984)(editor, with Jesse Burkhead)

*Aspectos del Presupuesto Publico (1988)(editor, with A.L. Antonaya)

*Government Financial Management (1990)(editor)

*Public Expenditure Management (1993)(also in Russian)

*Published by the International Monetary Fund

©International Monetary Fund. Not for Redistribution

A. Premchand

International Monetary FundWashington, D.C.

1995

EffectiveGovernmentAccounting

©International Monetary Fund. Not for Redistribution

© 1995 International Monetary Fund

This book was designed and produced bythe IMF Graphics Section

Library of Congress Cataloging-in-Publication Data

Premchand, A., 1933-Effective government accounting / A. Premchand.

p. cm.Includes bibliographical references.ISBN 1-55775-485-31. Finance, Public—Accounting. I. Title.

HJ9733.P73 1995350.72'31—dc20 95-17823

CIP

Price: US$21.00

Please send orders to:International Monetary Fund, Publication Services

700 19th Street, N.W., Washington, D.C. 20431 U.S.A.Tel.: (202) 623-7430 Telefax: (202) 623-7201

Internet: [email protected]

©International Monetary Fund. Not for Redistribution

For Nikhil,

Neeraj, and Indu

©International Monetary Fund. Not for Redistribution

This page intentionally left blank

©International Monetary Fund. Not for Redistribution

Preface

Although government accounting has existed for more than two millen-nia, it has not received its due. In fact, accounting has been looked down

upon and viewed by nonusers as a set of archaic rules that have longsince ceased to be relevant or effective. Yet, in addition to governments,ordinary citizens and democratic institutions charged with legislativeoversight must contend with government financial accounts and relatedsystems of accounting. There is recognition that these systems stand tobe improved, and, from time to time, commissions are appointed to lookinto improving them. They conduct a debate on the subject, recommendchanges, and go through the motions of implementing the changes, withno visible impact on the perceptions of the public or on the operationsof those involved in the enormous and growing amounts of paperworkthat constitute government accounting.

More recently, owing to the fiscal stress that many governments haveexperienced, the content, form, and organization of government ac-counting have received renewed attention. This time, there is hope thatthe focused attention and the public debate may have a more enduringimpact on the future course of government accounting.

This book attempts to shed light on the processes and problems ofgovernment accounting and on how the discipline may be revitalized. Itrecognizes that this reform is too important to be left to government ac-countants alone but requires the concerted efforts of administrators, com-mercial accountants, economists, and, most important, the public.

In a way, the book represents the author's views, knowledge, andmemories acquired as participant-observer in more than three decades ofnational and international civil service. The experience gained in the pro-cess was refined through regular exchanges with academics, accountants,and administrators in a number of countries.

In an earlier form, the book was discussed in detail at a seminar spon-sored by the IMF, the European Union, and the United Nations Develop-ment Program and held in Accra, Ghana in November-December 1994for senior officials of 17 African countries. The views of these officialshave been taken into account in the preparation of the book for publica-tion. An earlier draft of the book was read by Adolf Enthoven, RichardBird, Richard Goode, Andrew Likierman, and Y.V. Reddy, and their com-ments and criticisms have proved invaluable. It was also read by several

v i i

UPO

©International Monetary Fund. Not for Redistribution

viii • Preface

of the author's colleagues in the Fiscal Affairs Department of the IMF andwas reviewed, in detail, by a team of senior officials from the U.S. Gen-eral Accounting Office. Their comments have helped in refining the con-tent. As always, the author alone is responsible for any errors that mayremain.

The preparation and publication of a book are occasions for incurringmore debts of gratitude. The author is grateful to all the individualsnamed above, who unstintingly gave him the benefit of their views, andto David Driscoll and Jagdish Narang, who were supportive through thebook's preparation and publication. He is also grateful to Hildi Wicker,who typed the different versions of the book, and Elisa Diehl of the Ex-ternal Relations Department, who edited the book with care and craft.

©International Monetary Fund. Not for Redistribution

Contens

Preface vii

Introduction 1

Evolution 1Recent Changes 4

Objectives of Control 6Range of Process Controls 7

From Fund Controls to Global Budgets 7From Cash Limits to Cash Management 8

Policy Reviews 9Evaluation 9From Financial to Efficiency Audit 10Involvement of the Users 11Institutional Development 12

1 Payments Systems 15

Payment Stages 16Release of Funds and Organizing Payments 17

Commitment Stage 20Types of Payments Systems 21Method of Payment 24Security of Payments 31Relations with the Banking System 32Commercial Banking 37Financial Reporting 41Interenterprise Arrears 42

2 Morphology of Government Accounting 45

Commercial and Government Accounting 47Single- and Double-Entry Bookkeeping 50Cash and Accrual 52

Terms and Definitions 53Why Accrual Now? 54Budget and Accounts 56Dimensions of the Issue 58

ix

©International Monetary Fund. Not for Redistribution

x • Contents

General Ledger System 58Government Accounts and National Income Accounts 64Generational Accounts 70

3 Cost Measurement, Accounting Standards,and Other Issues 74

Commercial Practices 75Government Approaches 79Relevance of Commercial Practices 84Capital Charge 88Foreign Aid Accounts 90Accounting Aspects of Privatization 96Accounting and Performance Indicators 98Other Issues 99Accounting Standards 102

4 Liability Managem 08

Payables 108Other Funded Liabilities 112Contingent Liabilities 113Unfunded Liabilities 115

Legislated Guarantees 115Liabilities from Legislative Changes 116Hidden Liabilities 116Termination of Contracts 117Environmental Liabilities 118Market Failure Liabilities 118

Debt Management 120Developments 120Continuing Objectives 122Organization 124Role of Accounting 125

5 Architecture of Government Financial Information . . . . 128

Importance of Financial Information 128Public and Private Sectors Compared 130Principles of Reporting 132

Legitimacy 132Understandability 132Reliability 133

8

71

©International Monetary Fund. Not for Redistribution

Contents • xi

Relevance 133Comparability 134Timeliness 134Consistency 135Usefulness 135

Existing Information Systems 135Search for User Needs 138Information Pyramid 139Analytical Framework of Financial Reporting 142Purpose, Form, and Frequency 150Changes 151

Departmental Report 153Annual Appropriation Accounts 155

Users Within the Government 155Issues in Transforming Financial Information 164

Design Issues 166Operational Issues 168

6 Investing in Development: Implementation 170

Design of Development 173Implementation Lessons and Dilemmas 177

Political Support 178Integrated or Specific Reform 178Public Sector Reform or Financial Management Reform 179Imperatives of Technology or High-Tech Dependency 180"Big Bang" or Gradualism 180External Assistance or Internal Resources 181

Operational Issues 182Steps Toward Improvement 185

Bibliography 186

Tables

1. Payment Methods (Excluding Foreign Aid) 252. Foreign Aid Transactions 263. Range of Payment Instruments Used in the United States. . 274. Volume of Noncash Payments Handled by Type of

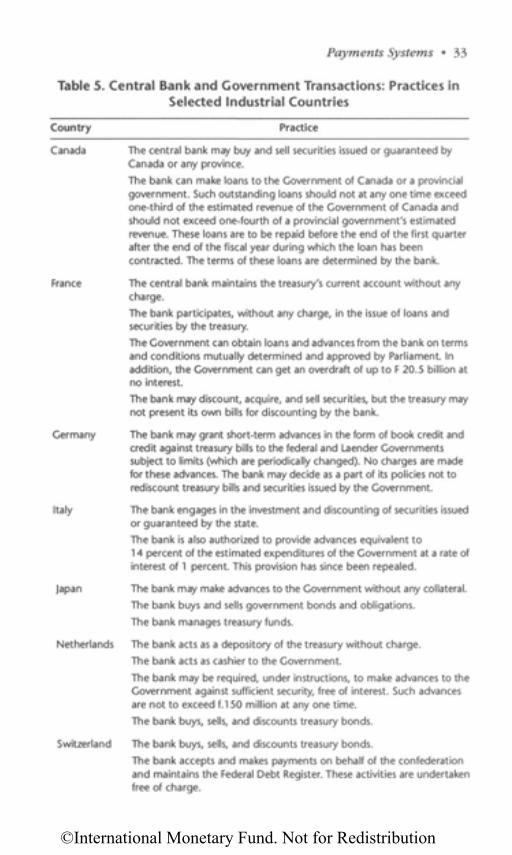

Instrument, 1992 295. Central Bank and Government Transactions: Practices

in Selected Industrial Countries 33

©International Monetary Fund. Not for Redistribution

xii • Contents

6. Relations with the Banking System 387. Cash- and Accrual-Based Budgets 608. Budgets, Accounts, and National Income Accounts 669. Application of Cost Management System............................ 87

10. Government Accounting Standards 10511. A Typical Reporting System 13612. Users' Needs 14013. Financial Information Users and Their Broad Needs 14414. Public Enterprises: Operating, Profit, and Loss Account . . . 15115. Public Enterprises: Balance Sheet 15216. Performance Data: U.K. Hospital Activity Statistics 15417. New Zealand: Operating Statement 15618. New Zealand: Statement of Financial Position 15719. New Zealand: Statement of Cash Flows 15820. New Zealand: Statement of Borrowings 16021. New Zealand: Statement of Commitments 16122. New Zealand: Statement of Contingent Liabilities 16223. United States: Statement of Financial Position 16324. United States: Statement of Operations and Changes

in Net Position 16425. United States: Statement of Cash Flows (Direct Method) . . 16526. Likely Impact of Effective Accounting Systems 175

Diagrams

1. Core Application . 592. Overall Financial Management System 623. Time and Costs in Government Operations 854. Architecture of Government Financial Information 143

syyu

©International Monetary Fund. Not for Redistribution

1 his study is an attempt to delineate the role of accounting in the fiscalmanagement of nations. Its fundamental premise is that accounting has acrucial role in the formulation and implementation of fiscal policies andindeed lies at the heart of modern governments. To grasp its significance,

its nature, tasks, and evolution have to be explained.

Evolution

Over the years, accounting inevitably developed in various ways in dif-ferent milieus. While no effort is made here to provide a history of thedevelopments in accounting, recognition of five stylized stages in itsgrowth and application may be in order. These five stages also indicatethat each one of them left an indelible impression on the content of ac-counting in governments. First, the earliest references to accounting inWestern societies are to be found in the practices of the governments inAthens and in the Eastern societies, in the practices of kingdoms in Chinaand India and in the pre-Christian era. These developments, which weremore or less contemporaneous, emphasized the recording of transactionsand developed reporting and inspection systems, as associated features,with a view to ascertaining the status of the finances of the monarchy. Forexample, in China, the emperor himself heard reports delivered by offi-cials on changes in population in different regions, changes in cultivatedland, and records of transactions of receipts and disbursements of moneyand grain. This system was utilized to determine whether the records cor-rectly reflected the real situation of the population and property and tosafeguard royal property from internal fraud. Kautilya, a prime ministerof a kingdom in India, wrote more than two thousand years ago that the

"king shall have the work of heads of departments inspected daily (em-phasis added), for men are by nature fickle and, like horses, change afterbeing put to work. Therefore, the king shall acquaint himself with all thedetails—the officer responsible, the nature of the work, the place ofwork, the time taken to do it, the exact work to be done, the outlay andthe profit." The primary task of accounting as the record of the king's fi-nances continued for centuries, less as a science and more as a practicethat evolved from changing need.

1

Introduction

©International Monetary Fund. Not for Redistribution

2 • Effective Government Accounting

The second stage reflects an organized attempt to codify the system.Although double-entry bookkeeping evolved about five hundred yearsago, it had little impact on accounting in government, which remaineda bookkeeping operation, devoid of theory or methodology This at-tempt was made by the cameralists of Germany, who dominated thethinking in regard to royal finances from the middle of the sixteenth tothe end of the eighteenth century. Their approaches sought tostrengthen the position of the ruler and contributed to attempts at sys-tematizing the administrative routine of fiscal departments. Aninevitable consequence of their efforts was the extensive centralizationof financial management and verification as the primary means of con-trol. These very features later became the major issue between the roy-alty and the paying public.

By the nineteenth century, as the public came to acquire more controlover the purse and exercised this control through well-established parlia-mentary routines, the tasks of accounting also grew. In this third stage,while the old theme of providing information about government financescontinued, this time it was to a different master, reflecting a shift from thecrown to the representatives of the public. The accounting system beganto be specified in laws and statutes, and the records maintained in thegovernment acquired legal sanction. The laws also specified the respec-tive duties of the crown, the legislature, central agencies, which were pri-marily responsible for the day-to-day tasks of control, and the spendingagencies. This type of legislation continues to be in force in several in-dustrial and developing countries, and some of the recent legislation en-acted in a number of countries has its origins in the laws enacted duringthe nineteenth century. As colonialism spread, the practices of the metro-politan governments also extended to the colonies. Thus, the practices inGreat Britain spread to its colonies in Asia and elsewhere, and the Frenchpractice and practices of other European countries found their way totheir respective colonies. In the process, even contiguous countries cameto have different systems that reflected their different colonial origins andregimes.

In the fourth stage, accounting began to reflect the changes in the na-ture of the economic regime and the expanded scope and much diversi-fied and complex nature of the tasks undertaken by governments. Theadvent of centralized planning in the Soviet Union brought with it both achange in the tasks of government and, consequently, its accountingsystems. Although governments traditionally undertook massive invest-ments in public works and in the establishment of railway and transportsystems and waterworks, their role as investors received a substantial

©International Monetary Fund. Not for Redistribution

Introduction • 3

boost in the context of centralized economic planning. While govern-ment accounting became somewhat secondary in the overall scheme,and statistical systems gained ascendancy, the scope of accounting sys-tems also expanded to deal with assets and liabilities in the world ofquasi-commercial transactions of governments. The accounting systemhad to contend with costs of production, appraisal of investments, and ahost of related activities.

From this, the movement to the fifth, or current, stage was only nat-ural. As the scope of government operations grew, budgets acquirednew and deserving prominence as instruments of public policy. Eco-nomic planning was expected to strengthen the role of the state as pro-ducer, while budgets became the main tools of distribution andstabilization. These functions and the growing massive interaction be-tween government and the community also implied that if budgetswere to be successful as instruments of policy and economic manage-ment, they had to be ably served by accounting. As fiscal policies be-came more calibrated in the pursuit of economic stabilization,accounting became more important as a reporting system with mea-surement of the receipts and expenditure and their implications. As asystem (which the Shorter Oxford English Dictionary (p. 2115) definesas "a set or assemblage of things connected, associated, or interdepen-dent, so as to form a complex unity; a whole composed of parts in or-derly arrangement according to some scheme or plan"), accounting ischarged with identification, selection and analysis, measurement, esti-mation, processing, and communication of information on receipts, ex-penditures, assets, liabilities, costs, and benefits, and all other aspectsthat legitimately form part of fiscal management. Accounting now is therecognized handmaiden of fiscal policy.

Despite its long pedigree, government accounting has suffered a be-nign neglect at the hands of the accounting profession and the govern-ment. For too long, the issue for the accounting profession was whethergovernment accounting was different from the accounting system ofother kinds of entities and, if so, in what way. The general notion thataccounts of an entity should provide records to meet three differentgroups of needs was also deemed to have applicability to governmentorganizations. Thus, all accounts should conform to the statutory and as-sociated legal requirements that specify the content of records and thetype of information to be generated. Those records should also meet therequirements of stewardship, and, thus, the needs of the groups externalto the management of the entity regarding the evaluation of the entity'sperformance are to be recognized. Within the entity, management also

©International Monetary Fund. Not for Redistribution

4 • Effective Government Accounting

needs regular information to enable it to perform its functions efficientlyand effectively.

It was held that these general principles have varying applicability tothe government. The laws specifying the accounts may have more exten-sive legal requirements in governments, reflecting in turn the separationof financial management functions between the legislative and executivebranches of government. There may also be substantial differences in thestructure of funds between entities and government. In one sense, theterm funds means resources, and in another, it represents an accountingentity. It is this aspect that is of crucial importance from the point of viewof financial control. In government, there may be several funds—generalfunds, special funds, debt-service funds, foreign aid funds, trust funds,enterprise funds, capital project funds, earmarked funds, and so on. Sim-ilarly, governments have been obliged to maintain budgetary accounts re-flecting the record of appropriations, releases, commitments, payments,and uncommitted balances. These accounts reflect the budgetary struc-ture and are intended to provide a continuous tracking of events as theyoccur. In general, governments have not been obliged in the past tomaintain proprietary accounts regarding assets, liabilities, income, ex-penditure, and net worth.

In all these areas, developments over the years have had a major im-pact on the course and tenor of financial management and therefore onaccounting in government. The range of functions undertaken by gov-ernments, particularly in the development, social, and enterprise sectors,has grown rapidly in size. As these developments have not been antici-pated by the laws, the laws have become obsolete. Furthermore, govern-ment accounting has been immensely influenced by changes intechnology. More important, the changing tasks of macroeconomic man-agement have imposed new demands, in addition to the traditional man-agement needs, on the accounting system. The accounting systems ingovernment should now reflect changing patterns in public expendituremanagement.

Recent Changes

The worldwide fiscal stress experienced during the past decade and ahalf has induced a greater awareness of the need for doing more withfewer resources. This in turn has unleashed substantial efforts to(1) expand the range of techniques of control; (2) improve the overalladministrative context within which controls are operated; and (3) bring

©International Monetary Fund. Not for Redistribution

Introduction • 5

about appropriate institutional changes and improvements. Researchconducted during the period has shown that the success of controls isless dependent on the ownership factor than on the methods of controlutilized and the administrative or corporate culture within which they op-erate. Recognition of this factor and the acute fiscal problems broughtabout simultaneous developments in the above three areas.

A brief description of these developments, including their features andlimitations, and related issues is in order here. Three preliminary consid-erations, however, need to be kept in view.

First, the expenditure control framework, whether exercised by the ex-ecutive branch, the legislature, or independent audit agencies, has fourbasic elements—policy controls, process controls (covering release offunds, monitoring, contract monitoring, and payment controls); regula-tory controls (including specification and oversight of accounting stan-dards); and efficiency controls (including ex post evaluation by the auditagencies, where applicable). Of these elements, developments in processcontrols are discussed in some detail here. (Regulatory aspects are dis-cussed in Chapter 3.)

Second, a major objective of controls is to reconcile the often diver-gent needs of the policymaker at the macroeconomic level with those ofthe program manager in the spending agencies. Far too often, both bytradition and as a result of the prominence of macroeconomic goals, theneeds of macro managers are emphasized at the expense of the needsof micro or program managers. Now, however, there is greater and ex-plicit recognition of the needs of the microeconomic level as well as anacceptance of the need to deliver services within the framework of spec-ified resources. In this context, accountability is larger in scope and in-cludes, in addition to the rendition of accounts of moneys collected andspent, the results achieved. As such, macroeconomic goals, while havingan undeniably pre-eminent role in the policy framework, would haveless viability if they were to be achieved at the expense of delivery ofservices.

Third, controls are, to a very large extent, influenced by developmentsin public sector management as a whole. The experience of several coun-tries shows that recent efforts have aimed at introducing a new manage-rial outlook into government. This outlook emphasizes results overprocesses, flexibility over conformity, judgment over compliance withroutine, innovation over risk aversion, and overall organizational devel-opment of institutions so that they could become productive and wellperforming. The efforts of Australia and New Zealand in "strengthening"their public sector, of Canada in its "initiative for Public Service 2000"

©International Monetary Fund. Not for Redistribution

6 • Effective Government Accounting

(popularly known as PS2000), of the United Kingdom in the "Next Stepsand Citizens' Charter," "Fundamental Review of Running Costs," and"Better Accounting for the Taxpayer's Money," of the United States in "re-inventing" government, and of Italy in its "reorganization proposals" ini-tiated in 1993 all represent facets of this new outlook. The newmanagerial outlook includes specification of standards and measures ofperformance, emphasis on output controls, greater competition in thepublic sector, and more focus on discipline and economy in resourceuse. All these features aim at helping managers to manage. These in turnimply that controls can no longer follow traditional centralized com-mand-style methods but must give more financial power—and account-ability—to managers.

Objectives of Control

Control techniques are not intended to be applied in a mechanisticfashion but to meet specific objectives, including the following:

• Economy, efficiency, and program effectiveness in the use of bud-geted resources.

• Resource use that will promote economic stabilization. To the ex-tent that some issues have not been adequately addressed duringthe budget formulation stage, or to the extent that there have beenmajor economic developments that indicate changes in the courseof policies adopted, they will need to be suitably addressed by expost controls.

• Adequate accountability in the delivery of services—not merely forthe resources used, but for overall performance, including courtesyin the delivery of services.

• In all the above objectives, the framework of controls should permittransparency in the implementation of government policies.

In the past, accounting and transparency have received relatively lit-tle attention. However, in the quest for greater citizen participation andfor a more accountable government, they have acquired a justifiableimportance of their own. Recent emphasis on governance or reinvent-ing government is no longer a matter of academic or political debate,but has become an integral part of the everyday consciousness of thecitizen.

©International Monetary Fund. Not for Redistribution

Introduction • 7

Range of Process Controls

As noted earlier, controls range from the release of funds to the closingof annual transactions and related accounts. These controls have under-gone, or are undergoing, changes in the ways described below.

From Fund Controls to Global Budgets

The traditional goal of controls is to regulate the flow of funds to thespending agencies, primarily through a system of "time-sliced" releasesof funds (for example, quarterly apportionments). In the current contextof increased decentralization of responsibilities and greater autonomy toprogram managers, the regulation of the flow of funds needed to besupplemented with additional control mechanisms. The evolving systemhas four elements that form the basis for controls and that do not im-pinge on the operational autonomy of program managers: global bud-gets; specification of required outputs; delineation of standards ofservice; and determination of costs for certain major categories of ser-vices, whether delivered directly by government or by contractors.

Global budgets imply a departure from conventional line-item bud-gets and represent an implicit contract for the provision of servicesfrom given resources. In this framework, the central agencies are re-sponsible for ensuring a smooth flow of budgeted resources while thespending agencies are responsible for providing services. Control istransformed in the process from a narrow mechanism for regulatingcash flows (which, under the new system, would be the primary re-sponsibility of the agency) to a broad one based on the nexus of phys-ical and financial flows that would, inter alia, permit a much neededemphasis on outputs.

Global budgets, unlike traditional budgets, are not limited to techni-cal compliance with the budget estimates. They have a more importanttask—the delivery of services. Specification of the quantitative andqualitative aspects of these services is, therefore, an essential part of thenew government financial management approach. While the qualitativeaspects of services still need to be developed and refined, the new ap-proach has already contributed to an improved functioning of controls.In several cases, particularly in the provision of medical care, cost datahave been developed for various types of illnesses, and hospital bud-gets and related reimbursements (when services are provided by non-governmental organizations) are linked to these standards. This

©International Monetary Fund. Not for Redistribution

8 • Effective Government Accounting

technique recognizes that what cannot be measured also cannot becaptured by the control system—hence, the emphasis on measurement.

From Cash Limits to Cash Management

In the mid-1970s, cash limits came into greater use as one way of re-stricting outlays in an inflationary context. It was recognized then thatindexation had an inherent problem in that it was difficult to finance theconstantly increasing outlays because of linkages to the cost of living orother indices. Cash limits provided a more effective instrument becausethey represented limits beyond which governments were unwilling toneutralize the impact of inflation, and spending agencies had somehowto adjust their activities within these limits. However, where expendi-tures were dominated by transfers and entitlements, the range of activi-ties within the purview of cash limits was limited. Furthermore, thesystem became one of backdoor budgeting, whose allure was lost withthe introduction of global budgets. This view, however, should not beinterpreted as a denial of the merits of cash limits, which can be usefulas a short-term instrument for bringing some order in an inflationarycontext.

In the new context of decentralized tasks and responsibilities and glo-bal budgets, greater importance is being given to cash management. Al-though it is by no means a new technique, it acquired additionalimportance for the macro manager charged with implementing a budget.It is now recognized that budget allocation of resources, always a difficulttask requiring the best of diplomatic skill, is only a beginning. It needs tobe supplemented by techniques that seek greater convergence betweenrevenue inflows and expenditure outflows so that borrowing and the bur-den of interest payments can be reduced. To achieve this purpose, gov-ernments are now required to avoid immobilizing resources that agenciesare permitted to retain, to prepare schedules for bulk or heavy paymentsso that the call for borrowed resources can be anticipated, and, generally,to minimize uneconomic borrowing either from the market or from cap-tive resources. Where interest payments range from about 20 percent to30 percent of total outlays, the importance of cash management cannotbe overemphasized.

Responsibility for cash management, once shared with central banks, isnow largely the function of the ministries of finance. It is a responsibilitythat is no longer perceived as a "reactive" approach to the spending pat-terns of administrative ministries and agencies but as a "proactive" policy

©International Monetary Fund. Not for Redistribution

Introduction • 9

stance that needs to be formulated on the basis of the balance between re-source needs and resource availability during budget implementation.

Policy Reviews

While important, control techniques have proved to be less than ade-quate in dealing with mandatory budget outlays, which exacerbate thedeficit (however measured) if the shortfall in revenue is greater than ex-pected. This outcome is fairly common in several industrial countries,which, in the course of implementing budgets, recognized that the reve-nue forecast was based on optimistic assumptions, while expenditureswere estimated to be growing conservatively. A way had to be found tolink revenue and expenditures, particularly where the latter are domi-nated by mandatory payments.

The U.S. Budget Enforcement Act of 1991 sought to specify such a linkbetween revenue and expenditures. For this purpose, outlays were dividedinto three categories, and increases in some were to be adjusted against re-ductions in others or alternatively through additional mobilization of re-sources (the "pay-as-you-go" process). The law envisaged a detailedsequestering process that would automatically be triggered if deficit limitswere about to be exceeded. However, under the best of circumstances, itaffects no more than 3 percent of outlays, because certain categories of ex-penditure (for example, interest payments and wages and salaries) are ex-empt from sequestration. Nevertheless, the law is useful because it forcesa reconsideration of the laws relating to certain large outlays.

Another systemic development that forces such a policy review, at boththe budget formulation and implementation stages, is the problem of fi-nancing government contingent and unfunded liabilities, including pen-sion payments. These liabilities are often not recognized during the budgetpreparation phase nor in the rough and tumble of the budget process.Now, however, a number of governments have accepted the need for in-troducing a commercial type of accounting that recognizes payables, con-tingent liabilities, and unfunded liabilities and requires their measurement.

Evaluation

Generally speaking, problems experienced during budget implementa-tion stem from formulation. Addressing such problems at a later stage maynot produce the hoped-for results. This raises the question of whether

©International Monetary Fund. Not for Redistribution

10 • Effective Government Accounting

preventive action can be taken, for it would have a more enduring impactthan the curative action. It is with this in view that evaluation of com-pleted programs and projects was initiated as an ex post control but withan impact that transcends the budget implementation phase. The evalua-tion consists of an assessment of progress and its impact, so that areas ofsuccess and failure in implementation can be identified. It is a distinct pro-cess aimed at examining the program rationale, achievement of objectives,cost of achievement, and exploration of alternatives. It seeks to analyzethe program objectives so as to assess the viability of the targets, examinesthe organizational adequacy for implementing the assigned tasks, evalu-ates the impact through an analysis of the flow and distribution of bene-fits, and identifies how staff, materials, and money are used.

Evaluation is not new and indeed has been a part of the financial man-ager's lexicon for more than four decades. It has acquired a new urgency,however, as the traditional avenues for controlling expenditures have beenyielding fewer results than expected. Evaluation, as current experience in-dicates, can have at least three forms. First, it can be incorporated into thebudget formulation stage, as has been done in Sweden. The Swedish trien-nial budget system is, in effect, a mandate for a systematic and intensiveevaluation of about one-third of the Government's activities every threeyears. Second, evaluation can be undertaken for completed programs andprojects by the administrative ministries, as is done in Canada and Ger-many. Here the methodology of evaluation is specified by the central min-istries and the evaluation results are utilized to improve resource use andallocation. Third, evaluation can be conducted by an external audit agency.

The results of evaluation may not be dramatic in terms of their impacton the implementation of an ongoing budget. Their value lies, to the ex-tent that public organizations are willing to learn the lessons of experi-ence, in their ability to prevent a recurrence of past patterns of policyimplementation. Although evaluation is also viewed as a tool for ensuringaccountability, it serves primarily to link formulation and implementationand is used by the executive.

From Financial to Efficiency Audit

The role of the external audit agency has also changed in recent years.A quick review of existing audit practices in industrial countries suggeststhree types of governmental audit: (1) a comprehensive audit of the finan-cial statements of the government, or the public sector in some cases, witha view to certifying compliance of laws and examining efforts to secure

©International Monetary Fund. Not for Redistribution

Introductionn u 11

economy, efficiency, and effectiveness in the use of budgeted resources;(2) a quasi-judicial approach with the objective of determining the ade-quacy of the law, examining infractions of the law, and determining penal-ties. This approach also includes the preaudit of expenditures to ensurecompliance; and (3) investigations into special issues, coupled with effortsto ensure that the accounting systems in the spending ministries and agen-cies and related internal systems are adequate for their purposes. Some au-dit institutions may follow a combination of these approaches, but theprimary function in most cases is likely to be one of these types.

Traditionally, ex post controls were conceived in terms of an annual, fi-nancial audit by an independent statutory agency that consisted in com-menting on the compliance of legislative appropriations and the patternsof their use. Over the years, there has been extensive discussion aboutwhether the audit agency should also undertake an efficiency audit. Al-though there were several issues concerning the measurement of effi-ciency, they were largely overcome in countries where the financialmanagement system had been transformed into a decentralized one withspecific work measurements and performance yardsticks. In this context,the extension of the audit agency's functions from a financial audit to anefficiency audit or, as popularly known, a value-for-money audit (cover-ing economy, efficiency, and effectiveness) was natural.

The value-for-money audit is not confined to ensuring economy but isintended to examine and report on the results achieved. The auditagency is expected to identify ways of improving efficiency and assist thegovernment in taking necessary action to improve systems and controls.It broadly supplements the internal evaluation system described earlier.

The value-for-money audit does not question the merits of policy objec-tives. Rather, it is concerned with the means and techniques of policy im-plementation, recognizing that the primary responsibility for securing valuefor money lies with the spending agency. The role of the audit in this caseis to provide an independent examination of how far and how well that re-sponsibility has been discharged. To the extent, however, that lessons of ex-perience are always valuable, it assists in the formulation of future policies.

Involvement of the Users

Recently, some local governments in the United Kingdom have begunto associate the users with their operations. As a part of this initiative,user groups are involved in formulating service agreements and in de-fining the scope and quality of services to be delivered by the local

©International Monetary Fund. Not for Redistribution

12 • Effective Government Accounting

government. Service contracts provide a direct cycle of accountability be-tween the elected members, management, staff, and users (and backagain). It is seen as more effective than adding to the already costly su-pervisory layers of management. It provides a powerful stimulus for themanagement to be more vigilant in providing services and to evaluatethose services from the users' point of view. This experiment, if success-ful, is likely to be widely emulated.

Institutional Development

Controls, whether ex ante or ex post, imply a hierarchical relationshipwhere one agency is endeavoring to influence or change the policies oroperational approaches of another. Experience shows that when suchcontrols are exercised in a centralized or inflexible fashion, they mayhave an adverse impact on the financial responsibility of the spendingagencies. The major issue of control has thus become one of reconcilingthe needs of central agencies with those of spending agencies, and of ex-ercising those controls so that they promote financial responsibilitywithin the agencies. This issue has been approached in two ways duringrecent years.

The first approach involves providing incentives to spending agenciesfor procuring economies in expenditures. It recognizes that even if thecontrol framework is effective, more could be obtained by providing in-centives to spending agencies. It implies that the knowledge of opera-tions and their financial implications is to be found in the first place inthe spending agencies, which are therefore best placed to explore thepossibilities for economies. In Australia, for example, spending agencieswere allowed to retain a share of the economies they secured to use onapproved programs. This approach provides a refreshing departure fromthe traditional controls. While such incentives are likely to yield decliningresults in the medium term, the approach offers yet another avenue that,when judiciously implemented, could have a far-reaching and enduringimpact on the financial responsibility of spending ministries.

The second approach relates to organizational development. This ap-proach looks beyond the scope of the control framework and aims tomake the organization more effective and thereby more responsive. TheOffice of the Auditor General of Canada has made a number of efforts toaddress this issue. (Its studies Constraints to Productive Management(1983), Attributes of Well-Performing Organizations (1988), and Values,Service and Performance (1990) examine the ways in which organiza-

©International Monetary Fund. Not for Redistribution

Introduction • 13

tions in government could be made more effective.) These efforts pointto the need for greater decentralization, specification of standards, flexi-bility in resource management, accountability for results, and adaptabilityfor changing needs. In turn these features are expected to contribute to amore effective organization.

The range of developments discussed here offer considerable potentialfor pursuing economy, efficiency, effectiveness, and stabilization goals inthe management of public expenditures. Experience shows that not allthe developments are to be found in all the industrial countries. Rather,each country is endeavoring in its own way to absorb and apply thesenew approaches. But even as the approaches are being implemented,criticisms are being leveled against them. Some point out that they usemethods inspired by private sector practices that are not entirely suitableto the operations of the public sector, where decisions tend to be madewith an eye to the political rather than to the financial implications. Oth-ers argue that the new approaches may lead to the emergence of a newsystem that will not necessarily be as productive as claimed. Some sug-gest that the claims of benefits are exaggerated.

Some of these criticisms are premature. In assessing the ability of thenew techniques to reduce expenditures, some critics may not have fullyseparated the impact of economic cycles on expenditures. Clearly, thenew techniques must be implemented for an extended period of timebefore a detached appraisal can be made. Recent experience furtherunderscores the traditional point that the task of improving governmen-tal organization is never complete. It is a continuous effort that affordsno respite to the fiscal policymaker. The promise of any reform can berealized only when the reform is sustained by relentless zeal and un-flagging effort.

Some government financial managers tend to take the view that existingcontrol systems are adequate. They attribute the failure to achieve the con-trol objectives to policies, politicization of governmental decision making,and a lack of well-trained personnel. The issues discussed here show that,in evaluating the adequacy of the control framework, a government mustbegin by distinguishing those aspects that can be controlled and thosethat may be outside its immediate purview. Such an inward look is likelyto reveal the antiquated organizational and management structures,unsuitable operational computer technology, and poorly designed regula-tions and other weak mechanisms that abound in government.

In sum, governments at all levels are expected to be more responsive,accountable, and cost effective. The new tasks have come at a time whenthere is much dissatisfaction with the existing systems, particularly with

©International Monetary Fund. Not for Redistribution

14 • Effective Government Accounting

their inability to make payments or furnish reports on time. These tasksand related expectations suggest that it would be unrealistic to expectmajor successes from fiscal policy unless the supporting institutions areadequately strengthened. In this regard, accounting, which has a highimpact in all the above areas, plays a major role and therefore needs tobe addressed in a substantive way. Cosmetic reforms, which may havequick appeal for short-term political purposes, would hardly serve thepurpose and may even be damaging in the longer term. An essential stepis therefore to analyze, in each case, the issues and the options availablefor addressing them. The experience of countries that have made pio-neering efforts will provide particularly valuable information.

In the following chapters, an attempt is made to examine the major as-pects of government accounting, starting with payments and concludingwith the rendition of accounts. Each chapter considers historical develop-ments, features of existing systems, and recent advances and their ade-quacy relative to the current and future tasks of governments.Consideration is given to institutional linkages with other types of ac-counting used for analytical purposes, and particular attention is paid tothe role of technology. An interdisciplinary approach is adopted so thatthe role of government accounting in the overall framework of macro-economic management can be considered in proper perspective. The in-tent is to evaluate the state of the art and, in doing so, to facilitate theformulation of an agenda for strengthening accounting in government. Ineach area, answers will be sought to the following questions: What arethe tasks? How are they being performed? Are there any issues? Are theyconceptual, organizational, or technological? How can improvements bemade? Do those improvements imply substantial changes? How can thetransition be managed?

©International Monetary Fund. Not for Redistribution

1

sequently, scant justice has been done to systems that bring the govern-ment closer to the taxpaying public.1 For the purposes of this analysis,accounting is viewed as a system with two primary purposes—to orga-nize all procedures connected with the receipt and disbursement offunds to and by the government, and to organize bookkeeping so thatthese transactions can be recorded in a transparent manner that will al-low full disclosure of the financial status of a government entity. Pay-ments, either to or from the government, represent the first operationalstage in the financial management process of the government but shouldnot be viewed as a purely internal process of the government. Thegrowth of central banking and the associated development of clearing ar-rangements have reached the stage at which they need to be consideredin conjunction with the linkages between the central bank and the gov-ernment. Indeed, the improvements that a government can make in thesepayments systems are dependent on the level of development of thebanking payments system. In addition, gradual improvement in the ap-plication of computer technology and related electronic processing hasopened up new vistas, and organizations and systems that were hitherto

considered essential are now being reviewed to determine if they are vi-able in the new context. There is, moreover, a perennial need to makethe operations cost effective and user friendly. These considerations sug-gest that payments systems have entered the mainstream for accountants,expenditure managers, and central bankers—reason enough to considerthe various aspects of the systems. The chapter therefore considers first1Literature on accounting in general, and government accounting in particular, pays little

expenditure management pays no attention to these aspects. For illustrations of this type ofliterature, see, for example, Organization for Economic Cooperation and Development(1987), or the United Nations, Economic and Social Commission for Asia and the Pacific(1993). None of the country profiles included in these studies provides any description ofpayments systems in operation. For a review of the literature and related aspects of the roleof payments systems in central banking, see Summers (1991).polictgmbvjdeas polifthgg

15

paymenfdcnts syatif

polcationthj vjkfduio compithenfnjdfplouly thersd eletranoyinj poxcerffingjmhed

polifthcnf sryhtghfnjnuiiookmn deiunt of thr losrerarutedaspsonfjgbgf

the pauhjt htmbm ,gj p[skjgj r OF THE LITERATURE AN

©International Monetary Fund. Not for Redistribution

16 • Effective Government Accounting

the distinction between accounting and payments systems and later dealswith the payment processes, organization, modes of payment, relation-ships with the banking system, and financial reporting. The concludingsection is devoted to a consideration of the interenterprise arrears thathave emerged during recent years as a major issue in the economies intransition.

Payment Stages

As indicated earlier, it is appropriate that the government accountingsystem be considered in a broad perspective inclusive of the paymentssystem. For the sake of precision, however, the numerous stages involvedin the process may be enumerated so that the payment stages can be dis-tinguished from the technical accounting stages. The steps on the expen-diture side are given below.

(1) Record of budgetary appropriations.2

(2) Record of budgetary allocations to the various agencies.

(3) Maintenance of records of commitments.

(4) Collection and verification of payment claims.

(5) Issue of instructions for actual payment.

(6) Record of payments made.

(7) Record of goods and services received.

(8) Record of goods and services actually used by the agency in theprovision of a service.

There are similar stages in the payments received by the government.

(1) In regard to taxes, assessments may be made by the governmentor, on a self-assessment basis, by the taxpayer.

(2) O n the basis of the assessment, payments are made at specific in-tervals, either to the tax agency or through the post office or a de-pository financial institution.

(3) Documentation of the payment made is sent by the taxpayer to thegovernment. The government may also receive confirmatory evi-dence from the place where the payment is made.

2In some countries, the appropriation process referring to legislative approval may notobtain. Rather, a decree implying the highest level of authority is issued indicating theamounts available to each agency.

©International Monetary Fund. Not for Redistribution

Payments Systems • 17

(4) O n the basis of the above evidence, action on the claim against thetaxpayer is completed.

(5) Similar procedures may be in operation for the payment of feesand other interagency payments.

The tasks of payment refer to (5) and (6) on the expenditure side, andto (2) and (3) on the receipts side of the operations of the government.Stages (1) and (2) on the expenditure side are viewed by some as moreof an integral part of budget implementation, while accounting is viewedas being concerned with (3), (4), (7), and (8). For analytical purposeshere, budget implementation is viewed as the initial phase of accounting,where the emphasis is more on the release of budgetary authority to theagencies than on the agencies' actual spending. In regard to tax collec-tion, however, practices vary among countries, but the assessment andcollection of taxes due are generally considered the legitimate tasks ofthe tax administration machinery.

Release of Funds and Organizing Payments

Although payments may represent the penultimate stage in the finan-cial management process of a government, this stage is preceded by nu-merous checks and balances, all of which are intended to prevent themisuse of funds. The first step in this process relates to the release offunds provided for in the budget. In this regard, as well as in regard tothe other steps discussed below, there are several variations in the prac-tices of countries. The attempt here is to consider the broad patternsrather than the specific practice in one country. The first variation relatesto the distinction between the release of budgetary authority and the re-lease of budgeted funds. In most governments, the rules specify that noexpenditure can be incurred without the specific approval of the ministryof finance or the treasury, as it continues to be called in several countries.But approaching the ministry of finance for approval for each item of ex-penditure could lead to an administrative gridlock. To avoid such an un-tenable situation, the ministry of finance delegates financial powers tothe controlling officers to encumber the budgeted funds and to pay themat a later stage. Without this authority, the agencies cannot initiate actionfor spending their budgets.

As soon as the budget is approved, the authority to incur encum-brances and to spend the amounts is conveyed to the agencies. Suchbudgetary authority may be conveyed for specific categories of expendi-

©International Monetary Fund. Not for Redistribution

18 • Effective Government Accounting

tures, while for others the ministry of finance may continue to exerciseauthority centrally. In some countries, the transfer of budgetary authorityis followed by the release of funds provided for in the approved budget.Because governments do not have all the funds needed for the purposeat the beginning of the year, they are compelled to release funds on atime-sliced basis. Even the time-sliced release may not totally preventstrain on those engaged in the country's cash management, particularlywhen the budget deficit is significant.

Three types of practices for releasing funds exist. The first type refersto the countries in which budgeted amounts are available soon after thebudget is approved. In a few British Commonwealth countries (such asIndia) and in some of the economies in transition, the budgetedamounts are available to the agencies for commitments and spendingfrom the onset of the fiscal year. In a few other countries, releases aremade on a routine monthly basis for current outlays, while more ad hocprocedures are followed for the construction budget. Some of thesecountries have since moved to a system of time-sliced releases in thecontext of fiscal austerity and a more intensive search for instrumentsto ensure compliance from the spending agencies. A second arrange-ment is one under which formal warrants (called exchequer issues intechnical parlance) are issued by the ministry of finance in response torequests from the spending agencies. Such requests have no definedperiodicity and primarily reflect the changing seasonal requirements foroutlays other than those on personnel. Under a third type of arrange-ment, fixed amounts are released for commitment and payment on ei-ther a monthly or a quarterly basis.

All these arrangements regulate the release of budget authority ratherthan amounts of cash to be credited to spending agencies. In somecountries, such as the Philippines during the early 1970s and the IslamicRepublic of Iran, actual amounts are released, which may then be cred-ited to the accounts of the spending agencies. When the spending agen-cies maintain these amounts and related accounts as a part of theconsolidated pool of money used by the government, the impact of thisprocedure on cash management is minimal. When these amounts aremaintained as a part of deposit accounts of the spending agencies main-tained with commercial banks, the procedure has an adverse impact,and the government would be hard put to maintain its own liquidity ex-cept through more borrowing. Countries may not follow these proce-dures consistently for their current, capital, and development budgets.Releases for development budgets, for example, may be ad hoc and are

©International Monetary Fund. Not for Redistribution

Payments Systems • 19

governed, in most cases, by the action plans submitted by the majorproject authorities.

The question arises as to whether these three types of releases havedifferent implications for control. The question may appear to be some-what redundant in the current context of information and telecommuni-cations technology, which has made data available more or lessinstantaneously as transactions occur. The release of budgetary authoritythrough a warrant was a procedure meant to fulfill one of the pillars ofparliamentary accountability. As legislative control evolved, the needarose for an independent authority to look into the claims of the spend-ing agencies after the approval of the budget. For this purpose, a paymas-ter general was appointed in some countries, while in a few others theapproval of the audit authority (in most cases a formality performed witha total lack of zeal, and a procedure that continues largely because of alack of interest in revamping what has become essentially a routine insearch of a purpose) was also needed.

The time-sliced release of spending authority was, however, derivedmostly to reinforce the controls exercised by the ministry of finance.From the ministry's point of view, several policy measures are includedin the budget without adequate examination, and some are included onthe specific condition that no commitments would be made in regard tothese proposals until they are reviewed and approved by the financeministry after the start of the year. In addition, the needs of cash manage-ment (that is, to bring about a convergence, as far as possible, betweeninflows and outflows so that borrowing may be organized in the bestpossible manner in the circumstances), as well as the need for major ad-justments in fiscal policy in the event of a resource shortfall, have con-tributed to a strengthening of this type of control exercised by theministry of finance.

It could be argued, however, that some of these controls are largelyacademic and are less effective than they appear to be. Further, theymay also adversely affect the sense of financial responsibility in thespending agencies. More than 95 percent of governmental outlays areof a continuing nature, and the bulk of them go for personnel, interestpayments, entitlement benefits specified by legislation, and projectswhose implementation is spread over several fiscal years. In such cir-cumstances, the share of outlays that can be adjusted annually may bevery small. Besides, the seasonality of these outlays should be familiarto those engaged in cash management. In such a context, the exerciseof control is viewed as a tyranny of the central agencies over the spend-ing agencies. Moreover, attempts by the central agencies to control the

©International Monetary Fund. Not for Redistribution

20 • Effective Government Accounting

activities of the spending agencies are likely to reduce the financial re-sponsibility in the latter. In an age when the canons of managerialismargue in favor of greater decentralization and endowment of responsi-bility in operational agencies (so as to ensure a balance between re-sponsibilities and related power), the exercise of any additional checkby the finance ministry or the central budget office is viewed as avoid-able. This view is buttressed by data-sharing arrangements that suggestthat every action, regardless of size and impact, can be monitored bythe central agencies. If commitments are known, then payment lags canbe estimated. It is thus argued that full responsibility should be givento the spending agencies from the beginning of the fiscal year.

The other side of the coin is that the central agencies require win-dows of opportunity in the overall expenditure management processto enable them to fulfill their responsibilities for the macromanage-ment of the economy. The release of budgetary funds is only a prelim-inary step in the larger process, and its effectiveness will be assessedin conjunction with other steps. This leads us to consider the otherstages of control and the role of the finance ministry in each of thosephases.

Commitment Stage

In several countries, spending agencies are technically free to makecommitments for the policies and projects for which amounts have beenallocated in the budget. This procedure is based on the belief that requi-site planning and fulfillment of specified regulations have already takenplace. In practice, however, there are several elements on which actionremains to be taken, and, inevitably, the central agencies become in-volved before commitments are made. This is particularly the case whenmajor projects are funded by external aid and when international com-petitive bidding is obligatory. In such cases, the central agencies are alsoincluded in the tender committees responsible for the award of contracts.This permits the spending and central agencies to track the developmentsat every stage.

In the French type of treasury systems (as well as in its variants, suchas the Italian system), the spending agencies are expected to obtain ap-proval for each proposed commitment from the treasury representativeattached to that agency This practice not only ensures compliance withthe laws and regulations, but also facilitates cash management so that thelags between commitment and payment can be ascertained and ade-

©International Monetary Fund. Not for Redistribution

Payments Systems • 21

quate arrangements made where bulk payments are involved. In theformer centrally planned economies, there was no need to obtain the ap-proval of the central agencies at the stage of commitment. There is now,however, a gradual movement toward monitoring of commitments bycentral agencies, an effort that is facilitated by the availability of a generalledger system maintained by computers. This system shows the variousstages in the spending process, including commitments made and theirlegal status, in considerable detail.

Types of Payments Systems

A "payments system" is defined as one that "includes all the decisionsand actions that are involved in making payments with government fundsfor government activities."3 The payment process involves two compo-nents: a review of the claim for payment and associated documentationand the actual responsibility for payment. The mode of payment, whichis also an important element, is discussed below.

The review is intended to ensure that the proposed payment is legal,that requisite funds are available and have been properly provided for inthe budget, that the officer authorizing or approving the payment is in-deed the official so designated for the purpose, and that what is pro-posed to be paid is indeed the right amount for the purpose. Everygovernment official bound by the common code of conduct and ethicalbehavior is expected to honor this in his or her day-to-day official busi-ness. Traditionally, however, the officials of the spending agencies havebeen viewed as lax in this regard, and their actions therefore need to bemonitored by the ministry of finance.

This practice has its origins in the old kingdoms, where special cad-res were developed to protect the wealth of the king. Kautilya, the In-dian philosopher-statesman, wrote more than two thousand years agothat "just as it is impossible not to taste honey or poison that one mayfind at the tip of one's tongue, so it is impossible for one dealing withgovernment funds not to taste, at least a little bit, of the king's wealth."He added "just as it is impossible to know when a fish moving in wateris drinking it, so it is impossible to find out when government servantsin charge of undertakings misappropriate money."4 To prevent misap-

3United States, Treasury Department (1989a), p. 4.4See Kautilya (1992), pp. 280-83. He further noted that "it is possible to know even the

path of birds flying in the sky but not the ways of government servants who hide their (dis-honest) income."

©International Monetary Fund. Not for Redistribution

22 • Effective Government Accounting

propriation, procedures were developed so that each claim could beverified by more than one person before it was paid. Procedures nowin vogue in many countries have their origin in this desire to protect thewealth of a country by involving many officials so as to prevent collu-sive behavior. Indeed, in several countries, payment vouchers must besigned by more than one person. This verification process is the corner-stone of expenditure control in a number of countries, including somein the industrial world. The final step in this approach is that checks forhigher amounts are signed by the ruler himself—a procedure that isfound in some Middle Eastern countries even today. Over the years, ithas contributed to some distinct practices. In the United States, eachpayment must be certified by the certifying officer who is attached toan agency.5 Similarly, in the French and Italian systems, payments mustbe reviewed by the official of the ministry of finance attached to eachagency.

The existing arrangements for review and payment in several coun-tries fall broadly into four categories.6 First, where the responsibility forthe documentation and related payments is vested with the spendingagencies, the involvement of the ministry of finance is limited to thepreparation of the budget and thereafter to the time-sliced release ofbudgetary authority and funding. The practitioners of this type of ap-proach include China and the United Kingdom. A second type of ar-rangement is one in which the spending agencies are provided withspecialized personnel under the control of the ministry of finance tohelp the spending agencies manage their payments processes. The re-sponsibility remains that of the spending agencies, but financial mattersare administered by cadres maintained by the ministry of finance. Forpurposes of day-to-day control, however, they are managed by thespending ministry. This approach is prevalent in India and a few Africancountries.

The third type of arrangement is one in which an exclusive agency,generally a part of the ministry of finance, is responsible for pay-ments. This system had its origins in the days when banking facilitieswere extremely limited, and all collections and disbursements, in-cluding those in outlying areas, were made by officials of the trea-

5Different types of outlays have different requirements. Third-party payments in Russia,for example, which primarily related to food procurement from agriculturists, are made bythe branches of the Bank of Russia on the basis of submission of documentation relating tothe delivery of grains.

6Many of these aspects are illustrated in Table 4 of the modules included in Appendix Iin Premchand (1993), pp. 208-61.

©International Monetary Fund. Not for Redistribution

Payments Systems • 23

sury.7 Even with the spread of the banking system, however, thetreasury system continued, and in some countries, such as France,the treasury also began to accept money deposits and thus per-formed selected banking functions primarily with a view to reducingits own debt costs. This type of treasury system, where all paymentsmust be approved and paid out by the representatives of the ministryof finance, continues to this day in several countries.8

In a fourth type of arrangement, payments for certain transactions aremanaged by a single agency at the center, regardless of where the trans-action occurred. Within this broad framework, however, there are indi-vidual nuances and variations in each country. For example, with thedevelopment of technology, some payments are being made on a central-ized basis, largely for reasons of convenience, such as payroll administra-tion. In some countries, the payroll is administered either by thepersonnel ministry or by the ministry of finance, and payments are madeto the staff through a computerized system.

The basic issue in the design of payments systems is who should beresponsible for preparing the requisite documents (on the basis of whicha payment is made) and for making payments—that is, who should be re-sponsible for signing checks. The answer may be somewhat straightfor-ward in that the two responsibilities should be integrated and performedby the same agency. The agency that is responsible for preparing thedocuments should be responsible for payments, too, and the converse ofthis proposition (the one that is responsible for payments should also beresponsible for the documents) is equally correct. As an extension of thislogic, it could be argued that separating these functions has the potentialof contributing to a loss of financial responsibility in the agency chargedwith preparing the documents and may thus contribute to an avoidable

7In some contexts, the term treasury often denotes collection and payment responsibili-ties. In practice, the term also has a broader connotation. Thus, ministries of finance in sev-eral countries are known as the treasury—as in Australia (which also has a ministry offinance), New Zealand, Sri Lanka, Tanzania, the United Kingdom, and the United States,among others. In view of the lack of precision in the use of the term and with a view toavoiding possible confusion about the intent in the use of the term, it is more appropriate touse neutral phraseology, such as government payment system. This broader approach wouldfacilitate the inclusion of all types of financial transactions, including foreign aid, that may bein forms other than cash. Noncash transactions may not pass through the treasury, whichgenerally is more concerned with cash inflows (or other forms of banking) and outflows.

8There may be notable exceptions to this, however. In the United States, social securitypayments are directly made by the Social Security Agency, and health care payments aremade by a separate agency. Also, payments of interest on securities are made by the FederalReserve System. All other payments are made by the certifying officers attached to variousagencies.

©International Monetary Fund. Not for Redistribution

24 • Effective Government Accounting

dyarchy. Also, an integrated management could contribute to a reductionin the overall costs associated with the payments system.

In an opposing view, the separation of payment responsibilities maybe, and often is, justified on the grounds that the spending agencies can-not be trusted to manage funds, that it is necessary to ensure legal com-pliance, that it facilitates cash management by the ministry of finance,and that such an arrangement provides a degree of professionalism in theconduct of public affairs. A more detailed examination of these viewssuggests that they may not be fully tenable in the current context. Gov-ernments have grown so big that centralized financial management maynot be viable. Besides, the argument that spending agencies do not havefinancial consciousness is at best rhetorical and may be unfounded. Legalcompliance is as much a matter for the official in the spending agency asit is for others. Moreover, available evidence in many countries suggeststhat slippages occur in payments even when administered by the agen-cies of the ministry of finance. This compromises the role of the payingagency as well. In reality, this issue has never before been examined inthis objective fashion. Rather, most of the arrangements that are nowfound in many countries are largely the legacy of convention and lawswhose validity in the computer age remains to be proven.

The advent of electronic data processing has led to changes—for ex-ample, regardless of who makes the payment and where it is made, legalcompliance can always be assured. Cash management requires up-to-date information and not centralized management. A n appropriate anal-ogy is that of an automatic traffic control system and the role of a trafficcontroller. If the system is available, the only role for the latter is asbackup and monitor of the traffic flow. There may then be no need topost a traffic controller at each intersection. In much the same way as theintroduction of technology changed the fundamental equation betweenthe central agency and the spending agencies, issues should be reviewedand the systems redesigned to be cost effective.

Method of Payment

There has been a phenomenal change in methods of payment in re-cent years. Traditionally, in its early stages, the banking system conductedall inflows and outflows in cash. Later, as the banking system evolved,greater use was made of checks, and, with the application of electronictechnology, greater use is now being made of electronic cards and trans-fers. The range of instruments now being used by most countries is illus-

©International Monetary Fund. Not for Redistribution

Payments Systems • 25

Table 1. Payment Methods (Excluding Foreign Aid)

Cash

Checks

Book adjustments(or nonpayablechecks)

Electronic cardpayments

Electronic transfers

In several countries, particularly the former centrally plannedeconomies, payments to and by the government are made incash. One of the primary responsibilities of the ministries offinance in these countries is to ensure that every payment officehas adequate cash. During periods of hyperinflation, provision ofcash tends to be a difficult exercise. Cash also continues to be thepredominant medium in some Middle Eastern countries, despitethe availability of banking facilities.

Several countries accept checks (for payment of taxes and relatedlevies) from the public and also make payment through the issue ofchecks or payment authorizations, as they are sometimes called.Payroll, pensions, debt repayment, and payment for centralizedprocurement of stores typically take the form of checks issued oneither the central bank or commercial banks.

Government departments are often required to make paymentsto other departments that provide common services for thegovernment as a whole. In such cases, book adjustments aremade from the budgetary allocations of one department to theallocations of another department. As these book adjustmentsinvolve the maintenance of suspense and exchange accountsthat, in turn, become cumbersome and contribute to long—butavoidable—delays in the final consolidation of accounts, theyhave yielded place to the issue of nonpayable checks or centraladjustments by the finance ministries.

Payments of certain taxes (e.g., customs duties) as well aspayment for procurement of specific categories of stores orequipment are made through electronic card transactions.

This method of payment, which is heavily dependent on theavailable computer terminology, is undertaken in lieu of the issueof checks. It is considered more cost effective and secure than themethods described above. (A good example of the electronictransfer system was the Social Accounting Service of the formerYugoslavia, which worked as a clearinghouse and settled morethan two-thirds of budgetary transactions through electronictransfers.)

trated in Table 1. Table 2 shows the methods used for the transmission offoreign aid. Table 3 illustrates the range of payment instruments now inuse in one of the advanced industrial countries—the United States.

Experience shows that the transaction costs of cash payments are laborintensive and are therefore the most expensive method of payment,while electronic transfers are the least expensive. Payment through orga-nized channels such as the banking system require that the payee have abank account. Some, however, are reluctant to transact through the bank-

©International Monetary Fund. Not for Redistribution

26 • Effective Government Accounting

Table 2. Foreign Aid Transactions

Technical assistance

Cash grants

Grants-in-kind

Import supportprogram

Direct provision ofequipment

Reimbursement

Whether provided as a loan or as a grant, this takes the form ofpersonnel (both bilateral and multilateral) placed at the disposalof the recipient government to be utilized according to anagreement. As salaries are paid by the donors, these transactionsdo not pass through the payments systems of the recipientgovernment unless part of the expenditure must be met in localcurrency.

These transfers, whether made by individuals or by publicbodies, are expected to pass through the government paymentssystems and be counted as receipts and expenditures.

These may take the form of food or equipment and, in eitherform, may not pass through the government payments systemexcept where counterpart funds are generated andsubsequently credited to the account of the government.

The World Bank and regional financial institutions have beenextending import support program loans to several countries. Insuch cases, the counterpart proceeds of imports are transmittedthrough the government payments systems.

Where loans are given to governments, the specific projectauthorities receive equipment for their projects directly from thesuppliers selected on an international competitive bidding basis.The suppliers are then paid by the international financialinstitution on the basis of documentation furnished by thesuppliers. These transactions are not normally recorded in thegovernment payments systems.

The recipient government makes purchases (as part of a loanagreement) by advancing its own resources, which are thenreimbursed by the donor on receipt of the requisite documents.There is generally a lag between submission of a claim and itsreimbursement. However, several financial institutions haveestablished revolving funds to minimize the delay.

ing system because they consider it to be not particularly user respon-sive, more so in countries where all banks function as a part of thenationalized sector. Others trust the traditional methods and are wary ofthe risks associated with banking, such as insolvency, and a few othersappear to prefer cash transactions because they can avoid detection bythe tax authorities.9 During recent years, however, with growing relianceon the banking system, checks have come to be a significant method of

9It is estimated that in the United States about 80 percent of all retail transactions are paidin cash, although, in terms of value, the proportion is much smaller. See Pingitzer and Sum-mers (1994), p. 108.

©International Monetary Fund. Not for Redistribution

Payments Systems • 27

Table 3. Range of Payment Instruments Used in the United States

Types ofInstruments

Cash

Governmentbank card

Debit card

Diners Club card

Direct deposit

Electronic fundstransfer

Fedline

Fedwire

Fiscal agencychecks

Governmenttravel system

Features