Bahasa

Halaman

Hukum

Company Update Unaudited YTD September 2015

October 2015

New solution for sore throat

2

Forward Looking Statement This presentation has been prepared for informational purposes only by PT Kalbe Farma Tbk. (“Kalbe” or the “Company”).

This presentation has been prepared solely for use in connection with the release of 30 September 2015 unaudited results of the Company. The information contained in this presentation has not been independently verified. No representation, warranty or undertaking, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or the opinions contained herein. None of the Company or any of their respective affiliates, and their respective commissioners, directors and employees, advisors or representatives shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this presentation or its contents or otherwise arising in connection with the presentation. Any decision to purchase or subscribe for securities of the Company should not be made on the basis of the information contained in this presentation.

The presentation is not an offer of securities for sale in the United States. Securities may not be offered or sold in the United States absent registration or an exemption from registration.

This presentation and its contents are confidential unless they are or become generally available as public information in accordance with prevailing laws and regulations (other than as a result of a disclosure by you) and must not be distributed, published or reproduced (in whole or in part) or disclosed by recipients to any other person. This presentation does not constitute a recommendation regarding the securities of the Company.

This presentation, including the information and opinions contained herein, is provided as of the date of this presentation and is subject to change without notice, including change as a result of the issuance of 30 September 2015 unaudited results of the Company .

This presentation includes "forward-looking statements". These statements contain the words "anticipate", "believe", "intend", estimate", "expect" and words of similar meaning. All statements other than statements of historical facts included in this presentation, including, without limitation, those regarding the Company's financial position, business strategy, plans and objectives of management for future operations (including development plans, objectives relating to the Company's products and services and anticipated product launches) are forward-looking statements. Such forward-looking statements are based on numerous assumptions regarding the Company's present and future business strategies and the environment in which the Company will operate in the future. These forward-looking statements speak only as at the date of this presentation. The Company expressly disclaims any obligation or reflection of any change in the Company's expectations with regard thereto, or any change in events, conditions or circumstances on which any statement is based.

Market data and certain industry forecasts used in this presentation were obtained from market research, publicly available information and industry publications which have not been independently verified, and no representation is made as to the accuracy of such information.

Table of Contents

3

Corporate Overview 4

Market Overview 7

Business Overview 11

Financial Overview 29

Strategies and Outlook 2015 35

Appendix 40

SECTION 1

Corporate Overview

Not all collagen is the same, it’s

time to choose the right one

New solution for sore throat

Domestic 95%

Export 5%

• Established in 1966 and headquartered in Jakarta

• A public company since 1991 and listed in the Indonesia Stock Exchange

• The largest publicly-listed pharmaceuticals company in Southeast Asia

• Sales breakdown by segment and by geographical location for YTD September

2015 is as follows:

Largest Publicly-Listed Pharmaceuticals Company in Southeast Asia

Total Sales = Rp 13,128 Bn Total Sales = Rp 13,128 Bn

Corporate Overview

5

Prescription Pharmaceuticals

24%

Consumer Health

18% Nutritionals 28%

Distribution & Logistics

30%

Corporate Strategy

6

Long Track Record of Sustainable Growth

6

0

200

400

600

800

1000

1200

1400

1600

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

(US

D m

m)

0

5,000

10,000

15,000

20,000

(IDR

bn

)

Sales USD Sales IDR

1966 1977 1985 1989 1991 1993 2005 1981 1994 1995 1997 2007 2010

1966: Company founded

1977: Strengthen pharma business by establishing Dankos Lab

1981: Spin-off the distribution business to PT Enseval due to government regulation

1985: Expansion to consumer health through acquisition of Bintang Toedjoe and in pharma through Hexpharm Jaya acquisition

1989: Igar Jaya and Dankos IPOs

1991: Kalbe Farma IPO

1993: Strengthening

nutritionals business by acquiring Sanghiang Perkasa and consolidating nutritional business to Sanghiang Perkasa

1994: Entered

energy drink business

EPMT IPO

1995: Disposed of 50% of food business (PT Bukit Manikam Sakti) to Arnotts

1997: Disposed of Kalbe’s

remaining 50% ownership in PT Bukit Manikam Sakti to Arnotts

Disposed glass packaging division to Schott

Acquired Woods Peppermint brand

Acquired 80% of Saka Farma

2005: Consolidation of Kalbe Group

2006

2006: Scale through mergers and acquisitions

2007: Launch of new corporate

logo as part of transformation process

Products entered every ASEAN countries (except Laos)

Opening of the Stem Cell and Cancer Institute

Implementation of end-to-end supply chain management

Integrated information technology systems

2010: Disposed of Kageo Igar

Jaya Established a joint

venture company, Asiawide Kalbe Philippines Inc.

Inaugurated Panca Sradha Kalbe as our Corporate Values

Inception and Entrepreneurial Driven Expansion

1966–1995

Enhanced Focus and Consolidation 1996–2005

Regionalization 2006–2015

2011

2011: EPMT Rights Issue

to finance expansion

Increased dividend payout ratio to 50%

2012

2012: ♦ Generic production

facility came on stream

♦ Acquired PT Hale International

♦ Established a joint venture company PT Kalbe Milko Indonesia 2013

2013: Cancellation

of the Company’s Treasury Stocks 0f 7.7%

2014

2014: Completion of

Kalbe’s oncology factory

SECTION 2

Market Overview

Not all collagen is the same, it’s

time to choose the right one

New solution for sore throat

• Low healthcare expenditure to GDP ratio.

Indonesia’s Health Spending Trends

8

JKN Coverage Roadmap

• National Health Insurance (Jaminan

Kesehatan Nasional or JKN) program has

commenced in January 2014, and covered

more than 50% of the population in 2014. JKN

targets to cover the entire Indonesian

population by 2019.

133 mn people *

Target 170 mn people

Target 250 mn people

100% coverage

* including 76.4 mn people covered by Jamkesmas program

before the launch of JKN.

Source : Roadmap to National Health Insurance 2012 - 2019

2015 2014

2019

3,3%

4,1%

4,2%

4,3%

5,5%

5,8%

9,6%

18,0%

Indonesia

India

Thailand

Malaysia

China

Singapore

United Kingdom

United States

Healthcare Expenditure/GDP 2013 (%)

Source : Centers for Medicare & Medicaid Services, Office of the Actuary; United Kingdom :

Healthcare Report, Economist Intelligence Unit; Kementerian Kesehatan Indonesia, China;

Singapore Government Budget; Economic Survey, India; Frost & Sullivan

6,8 7,9 8,9 10,5 12,2

12,1 13,1

14,5 15,9

18,2

2009 2010 2011 2012 2013

Private Expenditure

Public Expenditure

21.1 23.4

26.4

30.4

19.0

Total Healthcare Expenditure

(USD Bn)

Source : Global Health Expenditure Database, WHO

CAGR

12.5%

Market Share

Kalbe 13%

a 6%

b 5%

c 4%

d 4%

Others 68%

Pharmaceuticals Market Breakdown

9

Kalbe – No. 1 in the Pharma Industry

Kalbe continues to lead in the highly fragmented pharmaceuticals

industry with over 200 players

Total Market FY 2014 Rp 58.2Tn

OTC

41%

Ethicals

(Prescription)

59%

Branded &

Licensed

84%

Unbranded

16%

Pharma Market Breakdown

Pharma Industry

CAGR

12.0%

(in trillion Rupiah)

Source: IMS Health ITMA YTD 12 2014

Note: Restatement of 2012 IMS market data

37,0 41,7 49,4

55,5 58,2

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014

Recent Indonesian Pharmaceuticals Regulatory

10

Ministry of Health Decree No. 436 /Menkes/SK/XI/2013

• Determines the selling price and retail price caps on 535 generics drugs for pharmacies, hospitals and other

healthcare institutions throughout Indonesia.

Ministry of Health Regulation No. 1010/Menkes/PER/XI/2008

• Prohibits foreign pharmaceutical companies from registering drugs in Indonesia unless they have local

production facilities.

Price Caps on Key Generic Drugs

National Healthcare Insurance System

Local Production Facilities Requirements

10

Presidential Decree No. 101 Year 2012 regarding Recipients of Health Insurance Premium Subsidy

• Government will subsidize health insurance premium for poor residents

Presidential Decree No. 111 Year 2013 regarding Health Insurance

• All Indonesians are required to be members of the Health Insurance.

• First stage of implementation in 2014 will cover subsidy recipients, military members, civil servants, and formal

sector workers. Second stage will cover all population members by 1 January 2019.

Ministry of Health Decree No. 63 Year 2014 regarding Drug Procurement based on e-Catalogue

• Procurement for National Health Care Insurance is conducted through electroning purchasing method based on e-

Catalogue.

BPJS Kesehatan Director of Operation’s Circular No. 32 Year 2015 regarding Coordination of Benefit

• Regulating coordination of benefit (COB) mechanism for National Healthcare Insurance members with participating

private health insurance.

SECTION 3

Business Overview

New solution for sore throat

• No. 1 player in Indonesian Prescription Pharma Market.

• The largest medical representatives team in Indonesia with

more than 2,500 personnel.

• Comprehensive product offerings for all income groups.

• Increasing price competition following national healthcare

insurance implementation.

• One-time impact of product recall in 2015.

• Gross Profit Margin (GPM) remained relatively stable at

60.2% in YTD 09 2014 and at 59.8% in YTD 09 2015.

3.201 3.207

30 Sep 2014 (Unaudited)

30 Sep 2015 (Unaudited)

SALES in Rp Bn Licensed Products

28.3%

Unbranded Generics

14.6%

Branded Generics

57.1%

12

Prescription Pharmaceuticals Division

Temporary Deceleration

+0.2%

Total Sales Rp 3,207 Bn

Market Share (ITMA)

FY 2014

Total Market = Rp 34.6Tn

KALBE GROUP

15%

a 8%

b 6%

c 4%

d 4%

e 4% f

3%

OTHERS 56%

Source: IMS Health Prescription Pharmaceuticals

YTD 12 2014

• Completion of oncology factory and

commercialization in Q3 2014

• Constructing biosimilar factory

Oncology Factory Biosimilar Factory

• Starting building competence in stem cells

and genomics

Prescription Pharmaceuticals Division

Penetrating further in the unbranded

generics market

13

Growth Drivers

Expanding licensed products from multinational

companies to gain technology transfer

Strengthening presence in

specialty products

• Selection of focused categories to achieve scale

• Utilization of dedicated unbranded generic plant

Stem Cells and

Cancer Institute

14

Consumer Health Division

Strong Brand Equity with Leading Market Position

Market share of Kalbe’s brands

Source : AC Nielsen YTD 12 2012 and Company’s estimation 2014, in volume

Therapeutic Class Kalbe’s Products Market Share 2014

Antacid Promag, Waisan 75.2%

Anti Diarrhea Neo Entrostop 44.8%

Cough Remedies Komix, Woods, Mextril, Mixadin 33.9%

Cold Remedies Mixagrip Reg, Mixagrip FB, Procold 37.4%

Multivitamin Cerebrovit, Fatigon, Sakatonik Liver 30.8%

Children Multivitamin Cerebrofort, Sakatonik ABC 18.1%

Energy Drink Extra Joss 27.0%

KALBE GROUP

9%

a 8%

b 7%

c 7%

d 6%

e 4%

f 3%

g 3%

Others 52%

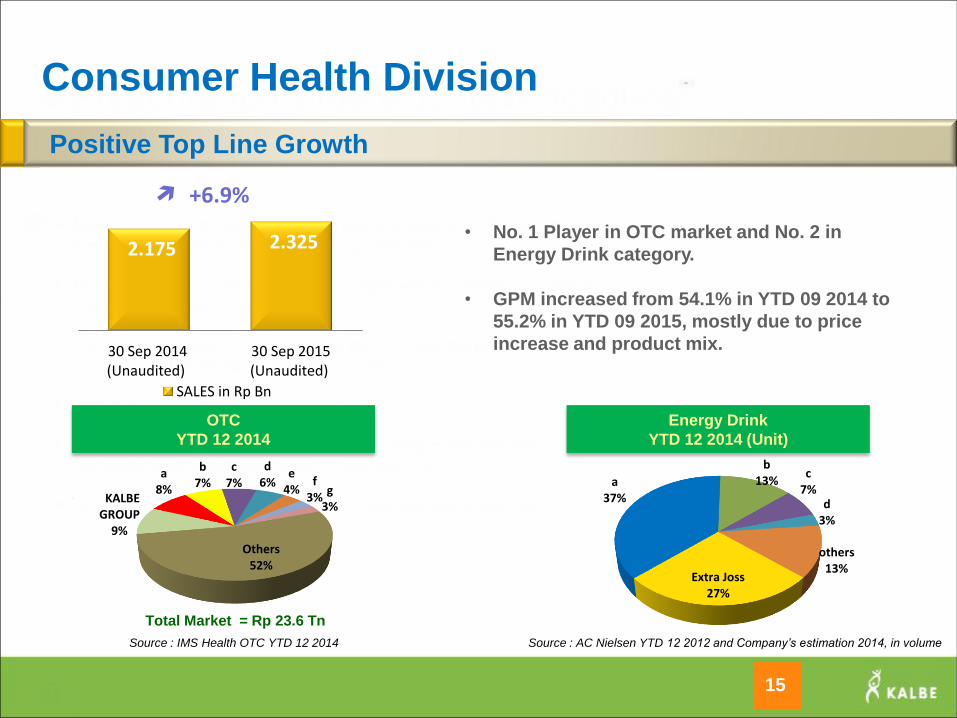

• No. 1 Player in OTC market and No. 2 in

Energy Drink category.

• GPM increased from 54.1% in YTD 09 2014 to

55.2% in YTD 09 2015, mostly due to price

increase and product mix.

Consumer Health Division

15

Positive Top Line Growth

Energy Drink

YTD 12 2014 (Unit)

OTC

YTD 12 2014

Total Market = Rp 23.6 Tn

Source : IMS Health OTC YTD 12 2014

+6.9%

Source : AC Nielsen YTD 12 2012 and Company’s estimation 2014, in volume

Extra Joss 27%

a 37%

b 13%

c 7%

d 3%

others 13%

2.175 2.325

30 Sep 2014 (Unaudited)

30 Sep 2015 (Unaudited)

SALES in Rp Bn

Hydro Coco An isotonic drink made of real coconut water

Original Love Juice Fresh bottled fruit juice made of quality fruits available in pomegranate, orange, guava, apple, and soursop flavors

H2 – Health and Happiness Supplement Products • H2 Superba Krill Oil to help reduce cholesterol • H2 Skin Care Supplement Range

Nitros Concentrated energy drink in liquid form with convenient tube packaging

Extra Joss Blend New variant of energy drink with added powdered milk in sachet packaging

16

Consumer Health Division

Innovative New Products

Bintang Toedjoe – Panas Dalam Effervescent cooling drink

Komix Lo Han Kuo Traditional Chinese herbal drink to relieve sore throat

Promag Gazero Herbal remedy to relieve flatulence

Woods Herbal Herbal cough syrup

Bintang Toedjoe Masuk Angin Traditional herbal remedy for common cold symptoms

Herbal Products

17

Complete Range of Nutritional Products

Teen Expecting Lactating Baby Toddler Kid Tween 25+ 35+ Clinical

• Catered to expecting & lactating mothers, babies, toddlers, children, tweens and

adults.

Nutritionals Division

Nutritionals Division

18

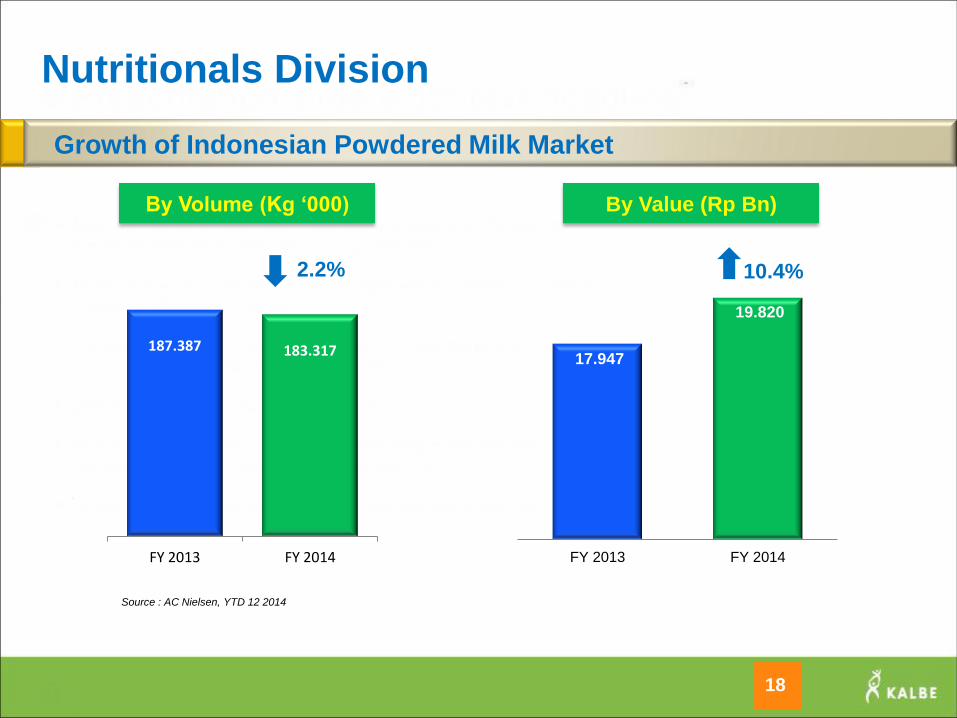

Growth of Indonesian Powdered Milk Market

Source : AC Nielsen, YTD 12 2014

By Value (Rp Bn) By Volume (Kg ‘000)

10.4% 2.2%

187.387

183.317

FY 2013 FY 2014

17.947

19.820

FY 2013 FY 2014

3.325 3.665

30 Sep 2014 (Unaudited)

30 Sep 2015 (Unaudited)

SALES in Rp Bn

Nutritionals Division

19

Consistent Net Sales Growth

+10.2% • Strong brand awareness of existing major

products

• GPM declined to 54.7% in YTD 09 2015 from

55.1% in YTD 09 2014, mostly due to Rupiah

depreciation.

Powdered Milk Market Share YTD 12 2014

Total Market = Rp 19.8 Tn

Source : AC Nielsen 2014, based on Value (Rp)

Kalbe’s Products Market Share 2014

Diabetasol 88.0%

Milna 68.8%

Prenagen 55.4%

Morinaga Chil Mil 9.2%

Morinaga BMT 10.9%

Entrasol 9.7%

Morinaga Chil Kid 6.8%

Zee 6.5%

Morinaga Chil School 2.7%

a 29%

b 24%

c 13%

Kalbe Nutritionals

11%

d 7%

e 5%

f 2%

g 3%

h 2%

i 2%

Others 2%

Source : AC Nielsen, YTD 12 2014 and Company’s estimation 2014, in value

Nutrive Benecol

Smoothie with special ingredient to lower cholesterol

Launching of New Products

20

Nutritionals Division

Diva

Fitbar

A healthy snack bar with low calories, zero cholesterol and

zero trans fat.

Health drink with collagen and antioxidant for skin care

Zee

Powdered milk for kids and tweens targeted to the middle

segment, now also available in sachet packaging

Entrasol Quick Start

Cereal drink made of milk and oats with high calcium

and high fiber

Multi Channel Customer Touch Points

21

Nutritionals Division

Kalbe e-store - the 1st Online Nutrition Store in Indonesia

Nutritionals Division launched new channel of consumer order through hotline service Kalbe Home Delivery 500-

880 and online shopping through www.kalbestore.com . Kalbe Family Rewards Card offers point rewards for

consumers to build consumer loyalty. KALCare Experiential Store provides various services to build customer

engagement and support branding activities.

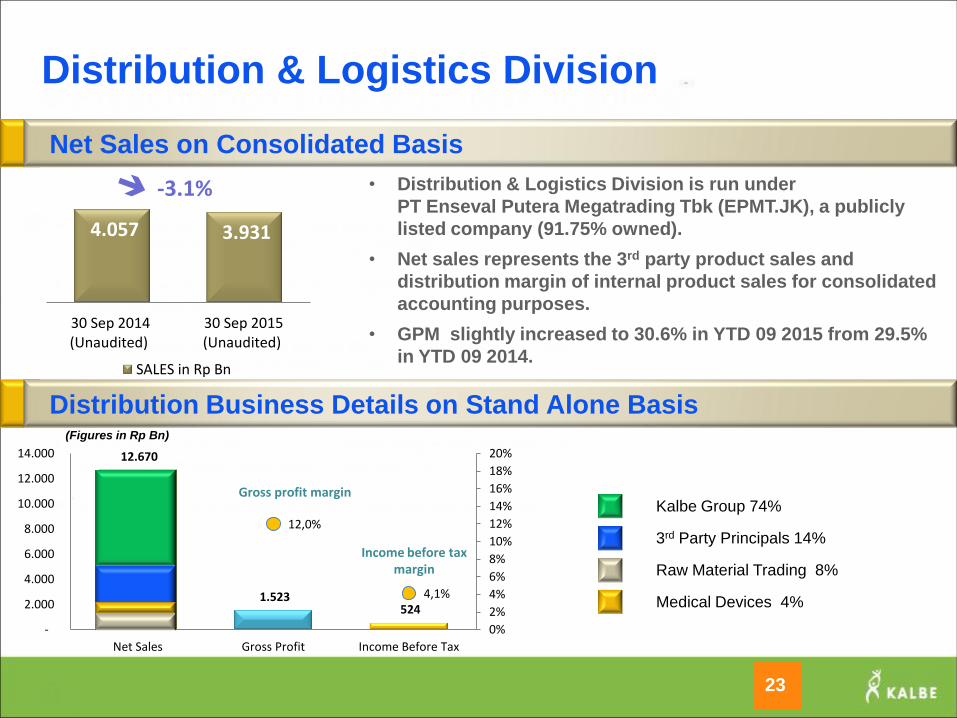

Distribution & Logistics Division

22

The Most Extensive Distribution Network

Branches

71 52 Cities RDC

2

12.670

1.523 524

12,0%

4,1%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

-

2.000

4.000

6.000

8.000

10.000

12.000

14.000

Net Sales Gross Profit Income Before Tax

4.057 3.931

30 Sep 2014 (Unaudited)

30 Sep 2015 (Unaudited)

SALES in Rp Bn

23

Net Sales on Consolidated Basis

• Distribution & Logistics Division is run under

PT Enseval Putera Megatrading Tbk (EPMT.JK), a publicly

listed company (91.75% owned).

• Net sales represents the 3rd party product sales and

distribution margin of internal product sales for consolidated

accounting purposes.

• GPM slightly increased to 30.6% in YTD 09 2015 from 29.5%

in YTD 09 2014.

Distribution & Logistics Division

-3.1%

(Figures in Rp Bn)

Gross profit margin

Income before tax margin

Distribution Business Details on Stand Alone Basis

Kalbe Group 74%

3rd Party Principals 14%

Medical Devices 4%

Raw Material Trading 8%

Major Third Party Principals by Category

Prescription

Pharmaceuticals Consumer

Medical Instrument

& Diagnostic

Fine Chemical

Raw Materials

Distribution & Logistics Division

24

Distribution & Logistics Division

25

Growth Drivers

Medical Devices is an area of potential

growth, especially in the implementation

of National Healthcare Insurance

System where demand for medical

devices is projected to grow further.

Net Sales (in Rp Bn)

Retail Health Services : 83 Mitrasana Clinics

• Developing Mitrasana Clinics as a

one-stop service with 4-in-1

concept, including family doctor,

pharmacy, laboratory, and

convenient store.

• A 100% owned subsidiary of EPMT.

• To date, Kalbe has opened 83

Mitrasana clinics in Jakarta and its

Greater Area.

Medical Devices

673

915 870 969

1.142

742

2009 2010 2011 2012 2013 2014*

* Discontinued tender business in 2014

• Exploring potential new 3rd party principals selectively

• Continuing to expand distribution infrastructure

1. Expand into new territories in Indonesia

2. Upgrade existing branch facilities to improve service

quality

3. Establish several Regional Distribution Centers (RDC)

throughout Indonesia

4. Expand warehouse capacity

• Collaborating with sub-distributors to gain territorial expansion

Distribution & Logistics Division

26

Strengthening Distribution Network

• New branch in Sibolga, North Sumatra

• Upgraded RDC Jakarta and upgraded Samarinda branch

2015 updates:

Samarinda

Marketing and Sales Infrastructure

27

The largest sales force for Pharma and Consumer Health in Indonesia

Prescription

Pharmaceuticals Consumer Health Nutritionals

Distribution &

Logistics

Infra-

structures

Indonesia

Coverage

Comments

• Over 2,500 medical

representatives

• Over 1,100 marketing

personnel

• > 2,000 sales &

marketing personnel

• Total of > 5,000

employees

• 71 marketing branches

throughout Indonesia

• 46 branches & 25 at

subsidiaries

• > 1,000 trucks

• > 500 motorcycles

• Directly cover

200,000 outlets

• Products available in

over 1mn outlets or

80% of total

consumer health

market

Market coverage

• 70% of GP market

covered

• 90% of specialist market

covered

• 100% of all hospitals

covered

• 100% pharmacy

coverage

• Largest marketing

team in Indonesia

• Approximately 1,100

marketing and sales

force

• Market Coverage

throughout Indonesia

• Most developed

telemarketing team in

the nutritional sector

• 80% of consumer

health market

•100% of prescription

pharma market

• Largest sales force in

Indonesia

Manufacturing Infrastructure

28

Operates 9 GMP facilities complying with international standards

Facility Products

Manufactured

Building Area

(m2) Production Lines Licenses Certification

Kalbe Farma 435 91,819 14 lines (tablet, capsule, cream, liquid oral,

injection) Astellas

ISO 9001, ISO 14001,

OHSAS18001

Bintang Toedjoe 49 20,849 3 lines; effervescent, powder & liquid -- ISO 9001, ISO 14001,

OHSAS18001, HACCP, SMK3

Dankos Farma 189 23,101 4 factories; Non-betalactam, Penicillin &

Cephalosporin, Oncology lines

Daiichi,

Samyang

ISO 9001, ISO 14001,

OHSAS18001

Sanghiang Perkasa 210 50,000 8 line dry - powdered milk Morinaga ISO 9001, ISO 14001, HACCP,

OHSAS18001

Hexpharm Jaya 85 16,533 Solid tablet (Non-betalactam products) -- ISO 9001, ISO 14001,

OHSAS18001

Finusolprima Farma 26 10,700

Large volume parenteral (LVP) in glass bottle

line, LVP in flexy bag line, Haemodialysis

Solution Line

Baxter ISO 9001, ISO 14001,

OHSAS18001

Kalbe Morinaga 19 33,733 1 wet - drier line, 1 can line, 2 sachet lines Morinaga ISO 9001, ISO 22000, OHSAS

18001

Orange Kalbe Ltd. - 5,000 2 lines; tablet and cream -- NAFDAC (local FDA)

Hale International 6 10,000 Semi hot-filled PET -- ISO 22000/2005 GMP, HACCP

SECTION 4

Financial Overview

New solution for sore throat

3.201 2.175

3.325 4.057

12.758

3.207 2.325

3.665 3.931

13.128

Prescription Pharmaceuticals

Consumer Health Nutritionals Distribution & Logistics Consolidation

30 Sep 2014 (Unaudited)

30 Sep 2015 (Unaudited)

Consolidated Sales

30

Positive Top Line Growth of Internal Kalbe Products

0.2% 6.9% 10.2% -3.1%

2.9%

Net Sales (in Rp Bn)

26,8% 27,8%

4,8% 5,1% 0,8% 0,9%

30 Sep 2014 (Unaudited)

30 Sep 2015 (Unaudited)

Selling & Marketing

General & Administrative

Research & Development

15,7% 15,1%

30 Sep 2014 (Unaudited)

30 Sep 2015 (Unaudited)

48,1% 48,8%

30 Sep 2014 (Unaudited)

30 Sep 2015 (Unaudited)

Consolidated Operating Performance

31

Slight Pressure on Operating Margin

• Marketing efforts to drive brand awareness

• Higher selling & marketing expense to net sales

ratio due to the change in business mix

• Research & development activities to support

product development

Gross Profit

(in Rp bn) Operating Expenses to Net Sales Ratios

Operating Profit

(in Rp bn)

+ 4.6%

-1.0%

32.4%

1,976 1,997

33.8%

6,131 6,411

1.487 1.499

30 Sep 2014 (Unaudited)

30 Sep 2015 (Unaudited)

1.988 2.016

30 Sep 2014 (Unaudited)

30 Sep 2015 (Unaudited)

Consolidated Net Earnings

32

Maintaining Stable Earnings

Income Before Tax

(in Rp bn)

Net Income

(in Rp bn)

• Income before tax margin slightly decreased from

15.6% in YTD 09 2014 to 15.4% in YTD 09 2015, mostly

due to higher operating expenses.

+1.4%

• Net income margin slightly decreased from 11.7% in

YTD 09 2014 to 11.4% in YTD 09 2015, in line with

lower income before tax margin.

+0.8% 15.6% 15.4% 11.4% 11.7%

43 45 44 50

48 48 49 55

142

122 110 115 107

132 125 121

27

38 35

57 41

50 46 45

158

129 120

108 114

131 128 130

2008 (Audited)

2009 (Audited)

2010 (Audited)

2011 (Audited)

2012 (Audited)

2013 (Audited)

2014 (Audited)

30 Sep 2015 (Unaudited)

Days of Account Receivables Days of Inventories

Days of Account Payables Net Operating Cycle

Improvement in days of

inventory

Working Capital Management

33

Gradual Improvement in Net Operating Cycle

End-to-end supply chain

management will be

continuously implemented

to overcome any

fluctuation in inventory

Net Operating Cycle has

decreased by 28 days from

158 days in 2008 to 130 days

in September 2015.

No. of days

14,0 19,0 19,0 17,0 19,0

51% 60%

51% 42% 43%

0%

20%

40%

60%

80%

0,0

5,0

10,0

15,0

20,0

2010 (Audited)

2011 (Audited)

2012 (Audited)

2013 (Audited)

2014 (Audited)

Cash Dividend* (Rp/share) Dividend Payout Ratio (%)

Solid Financial Position

34

Total Debt and Gearing Ratio Cash & Net Cash Balance

Rp 1.7 Trillion of Net Cash Position

Dividend Payment Capital Expenditure

* For Fiscal Year

* Cash dividend are adjusted for stock split impact

* Capital Expenditure in Rp Billion

25 141

205

584

296 411

0,5% 2,3% 2,9%

7,2%

3,2% 4,1%

0,0%

5,0%

10,0%

15,0%

0 100 200 300 400 500 600

2010 (Audited)

2011 (Audited)

2012 (Audited)

2013 (Audited)

2014 (Audited)

30 Sep 2015

(Unaudited)

Total Debt in Rp Billion Gearing Ratio

1.902 2.291 1.860 1.895 1.895 2.125

1.877 2.151

1.655 1.311

1.598 1.713

2010 (Audited)

2011 (Audited)

2012 (Audited)

2013 (Audited)

2014 (Audited)

30 Sep 2015 (Unaudited)

Cash and Cash Equivalent in Rp Billion Net Cash in Rp Billion

470 469

783

994 852

719

2010 (Audited)

2011 (Audited)

2012 (Audited)

2013 (Audited)

2014 (Audited)

30 Sep 2015 (Unaudited)

SECTION 5

Strategies &

Outlook 2015

New solution for sore throat

36

KALBE Business Strategies

Collaborative

innovation Leadership

development

Business structure

and portfolio

Operational

excellence through

SCM and ERM

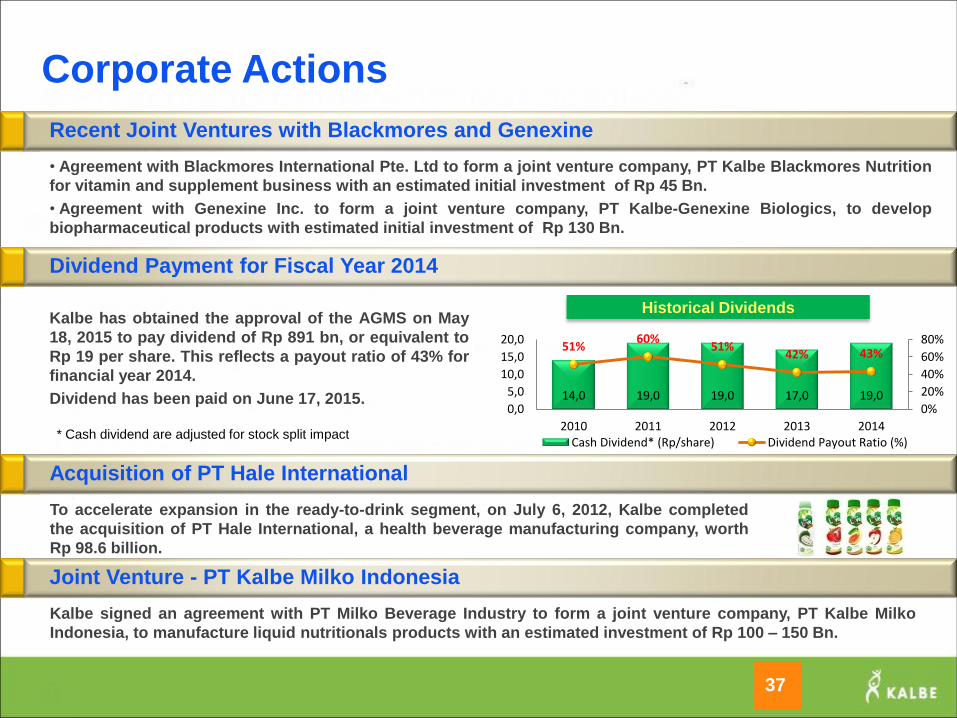

• Agreement with Blackmores International Pte. Ltd to form a joint venture company, PT Kalbe Blackmores Nutrition

for vitamin and supplement business with an estimated initial investment of Rp 45 Bn.

• Agreement with Genexine Inc. to form a joint venture company, PT Kalbe-Genexine Biologics, to develop

biopharmaceutical products with estimated initial investment of Rp 130 Bn.

Recent Joint Ventures with Blackmores and Genexine

Corporate Actions

37

To accelerate expansion in the ready-to-drink segment, on July 6, 2012, Kalbe completed

the acquisition of PT Hale International, a health beverage manufacturing company, worth

Rp 98.6 billion.

Acquisition of PT Hale International

Dividend Payment for Fiscal Year 2014

Kalbe has obtained the approval of the AGMS on May

18, 2015 to pay dividend of Rp 891 bn, or equivalent to

Rp 19 per share. This reflects a payout ratio of 43% for

financial year 2014.

Dividend has been paid on June 17, 2015.

Historical Dividends

Joint Venture - PT Kalbe Milko Indonesia

Kalbe signed an agreement with PT Milko Beverage Industry to form a joint venture company, PT Kalbe Milko

Indonesia, to manufacture liquid nutritionals products with an estimated investment of Rp 100 – 150 Bn.

* Cash dividend are adjusted for stock split impact

14,0 19,0 19,0 17,0 19,0

51% 60%

51% 42% 43%

0%

20%

40%

60%

80%

0,0

5,0

10,0

15,0

20,0

2010 2011 2012 2013 2014 Cash Dividend* (Rp/share) Dividend Payout Ratio (%)

38

Corporate Social Responsibility

Certified

Environmental

Management

System

ISO 14001:2004

Environmental Sustainability Consumer Protection

Dedicated Customer

Care Team

Kalbe Cares

Education Health Environment Infrastructure

Looking after our stakeholders

Kalbe Junior

Scientist Award Ristek Kalbe

Science Award

Dr. Boen

Distinguished

Lecture Series

Extended

Producer

Responsibilities

Free Medical

Consultations

Blood Donor

Activities Disaster Reliefs

Community Development

Outlook 2015

39

Capex Rp 0.9 – 1.0 Tn for production capacity expansion and distribution network.

1. Year-on-year Sales Growth 2% - 3%

2. Operating Profit Margin 14% - 15%

3. Earnings per Share Growth -3% - -4%

4. Dividend Payout Ratio 40% - 50%

Revised Earnings Guidance 2015

SECTION 6

Appendix

Financial Information YTD September 30, 2015

(Unaudited)

New solution for sore throat

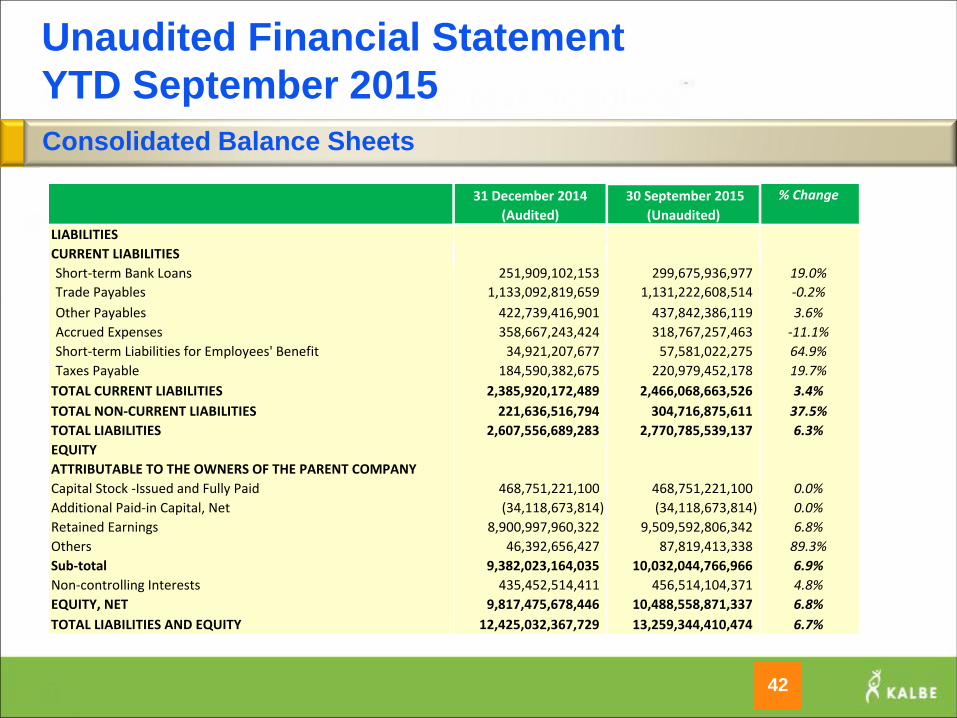

Unaudited Financial Statement

YTD September 2015

Consolidated Balance Sheets

41

ASSETS

CURRENT ASSETS

Cash and Cash Equivalents 1,894,609,528,205 2,124,752,980,457 12.1%

Trade Receivables, Net 2,346,943,653,265 2,652,116,857,346 13.0%

Other Receivables 117,957,876,451 76,881,705,373 -34.8%

Other Current Financial Assets 199,389,672,567 153,310,595,143 -23.1%

Inventories, Net 3,090,544,151,155 3,018,379,321,519 -2.3%

Prepaid Taxes and Expenses 82,698,813,413 134,805,599,139 63.0%

Other Current Assets 388,661,675,136 350,404,502,051 -9.8%

TOTAL CURRENT ASSETS 8,120,805,370,192 8,510,651,561,028 4.8%

TOTAL NON-CURRENT ASSETS 4,304,226,997,537 4,748,692,849,446 10.3%

TOTAL ASSETS 12,425,032,367,729 13,259,344,410,474 6.7%

31 December 2014

(Audited)

30 September 2015

(Unaudited) % Change

Unaudited Financial Statement

YTD September 2015

42

Consolidated Balance Sheets

% Change

LIABILITIES

CURRENT LIABILITIES

Short-term Bank Loans 251,909,102,153 299,675,936,977 19.0%

Trade Payables 1,133,092,819,659 1,131,222,608,514 -0.2%

Other Payables 422,739,416,901 437,842,386,119 3.6%

Accrued Expenses 358,667,243,424 318,767,257,463 -11.1%

Short-term Liabilities for Employees' Benefit 34,921,207,677 57,581,022,275 64.9%

Taxes Payable 184,590,382,675 220,979,452,178 19.7%

TOTAL CURRENT LIABILITIES 2,385,920,172,489 2,466,068,663,526 3.4%

TOTAL NON-CURRENT LIABILITIES 221,636,516,794 304,716,875,611 37.5%

TOTAL LIABILITIES 2,607,556,689,283 2,770,785,539,137 6.3%

EQUITY

ATTRIBUTABLE TO THE OWNERS OF THE PARENT COMPANY

Capital Stock -Issued and Fully Paid 468,751,221,100 468,751,221,100 0.0%

Additional Paid-in Capital, Net (34,118,673,814) (34,118,673,814) 0.0%

Retained Earnings 8,900,997,960,322 9,509,592,806,342 6.8%

Others 46,392,656,427 87,819,413,338 89.3%

Sub-total 9,382,023,164,035 10,032,044,766,966 6.9%

Non-controlling Interests 435,452,514,411 456,514,104,371 4.8%

EQUITY, NET 9,817,475,678,446 10,488,558,871,337 6.8%

TOTAL LIABILITIES AND EQUITY 12,425,032,367,729 13,259,344,410,474 6.7%

31 December 2014

(Audited)

30 September 2015

(Unaudited)

Unaudited Financial Statement

YTD September 2015

43

Consolidated Statement of Income

NET SALES 12,758,469,473,880 13,127,806,587,343 2.9%

COST OF GOODS SOLD 6,627,470,848,873 6,716,910,243,206 1.3%

% to NS 51.9% 51.2% -0.8%

GROSS PROFIT 6,130,998,625,007 6,410,896,344,137 4.6%

% to NS 48.1% 48.8% 0.8%

Selling Expense (3,416,679,276,549) (3,649,133,131,241) 6.8%

% to NS -26.8% -27.8% -1.0%

General and Administrative Expense (614,133,870,380) (667,221,714,046) 8.6%

% to NS -4.8% -5.1% -0.3%

Research and Development Expense (103,209,360,512) (118,500,991,387) 14.8%

% to NS -0.8% -0.9% -0.1%

Interest Expense and Financial Charges (40,456,011,045) (23,617,725,001) -41.6%

Interest Income 41,990,088,627 60,378,579,624 43.8%

Other Operating Expenses (58,446,539,665) (73,398,167,100) 25.6%

Other Operating Income 48,737,375,529 77,282,136,232 58.6%

Share in Net Losses of the Associated Entity (980,985,584) (851,013,789) -13.2%

INCOME BEFORE INCOME TAX

BENEFIT (EXPENSE) 1,987,820,045,428 2,015,834,317,429 1.4%

% to NS 15.6% 15.4% -0.2%

INCOME TAX EXPENSES, NET (461,788,706,115) (481,604,411,536) 4.3%

% to NS -3.6% -3.7% 0.0%

30 September 2014

(Unaudited)

30 September 2015

(Unaudited) % Change

44

Consolidated Statement of Income

Unaudited Financial Statement

YTD September 2015

30 September 2014

(Unaudited)

30 September 2015

(Unaudited) % ChangeINCOME FOR THE PERIOD 1,526,031,339,313 1,534,229,905,893 0.5%

% to NS 12.0% 11.7% -0.3%

OTHER COMPREHENSIVE INCOME (EXPENSES) 1,934,931,420 40,848,681,960 2011.1%

COMPREHENSIVE INCOME FOR THE PERIOD 1,527,966,270,733 1,575,078,587,853 3.1%

% to NS 12.0% 12.0% 0.0%

Income for the Period Attributable to:

Owners of the Parent Company 1,486,756,355,408 1,499,222,166,110 0.8%

Non-controlling Interests 39,274,983,905 35,007,739,783 -10.9%

Total 1,526,031,339,313 1,534,229,905,893 0.5%

% to NS 12.0% 11.7% -0.3%

Comprehensive Income for the Period

Attributable to:

Owners of the Parent Company 1,487,524,969,199 1,539,930,946,901 3.5%

Non-controlling Interests 40,441,301,534 35,147,640,952 -13.1%

Total 1,527,966,270,733 1,575,078,587,853 3.1%

% to NS 12.0% 12.0% 0.0%

Earnings Per Share Attributable

to Owners of the Parent Company 32 32 0.8%

Unaudited Financial Statement

YTD September 2015

Consolidated Statement of Cash Flows

45

CASH FLOWS FROM OPERATING ACTIVITIES

Cash Received from Customers 13,811,617,870,985 14,062,703,018,305 1.8%

Cash Paid to Suppliers and Employees (8,082,825,158,242) (8,249,973,288,619) 2.1%

Cash provided by operations 5,728,792,712,743 5,812,729,729,686 1.5%

Receipts of Claims for Income Tax Refund 21,974,596,310 11,907,066,869 -45.8%

Payments of Income Taxes (487,114,072,241) (478,551,003,419) -1.8%

Payments of Other Operating Expenses, Net (3,610,163,363,492) (3,731,186,651,046) 3.4%

Net Cash Provided by Operating Activities 1,653,489,873,320 1,614,899,142,090 -2.3%

CASH FLOWS FROM INVESTING ACTIVITIES

Proceeds from Sale of Other Current Financial Assets 103,247,693,333 187,029,165,135 81.1%

Interest Income Received 42,192,422,578 61,119,625,338 44.9%

Proceeds from Sales of Property, Plant, and Equipment 25,430,181,489 11,590,135,965 -54.4%

Acquisitions of Property, Plant and Equipment (610,515,106,319) (718,725,455,976) 17.7%

Placements in Other Current Financial Assets (110,613,567,647) (131,300,000,000) 18.7%

Acquisitions from Other Investing Activities, Net 518,908,685 (20,475,900,568) -4046.0%

Net Cash Used in Investing Activities (549,739,467,881) (610,762,430,106) 11.1%

30 September 2014

(Unaudited) % Change

30 September 2015

(Unaudited)

Consolidated Statement of Cash Flows

46

Unaudited Financial Statement

YTD September 2015

30 September 2014

(Unaudited) % Change

30 September 2015

(Unaudited)

CASH FLOWS FROM FINANCING ACTIVITIES

Proceeds from Bank Loans 1,844,926,182,883 659,131,794,591 -64.3%

Receipts of Capital Contributions from

Subsidiaries' Non-controlling Interest 4,887,332,280 532,674,824 -89.1%

Payments of Bank Loans (2,030,290,843,648) (557,453,817,276) -72.5%

Payments of Cash Dividend (807,025,986,361) (905,500,412,589) 12.2%

Payments of Interest Expense and Financial Charges (41,335,437,964) (24,257,064,718) -41.3%

Payments of Pension Funds (19,597,768,441) (21,802,664,190) 11.3%

Payments of Obligations under Finance Leases (87,575,061) - -100.0%

Net Cash Provided by (Used in) Financing Activities (1,048,524,096,312) (849,349,489,358) -19.0%

NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENT 55,226,309,127 154,787,222,626 180.3%

Net Effect of Changes in Foreign Exchange Rates of Foreign Currency

Denominated Cash and Cash Equivalents (4,043,934,371) 82,408,958,627 2137.8%

CASH AND CASH EQUIVALENTS AT BEGINNING OF YEAR 1,356,186,110,248 1,819,421,532,492 34.2%

CASH AND CASH EQUIVALENTS AT END OF YEAR 1,407,368,485,004 2,056,617,713,745 46.1%

THANK YOU

47

For further information:

PT Kalbe Farma Tbk.

Jalan Let.Jend. Suprapto Kav. 4

Jakarta 10510, Indonesia

Tel. : 62-21-42873888

Fax. : 62-21-42873678

Email : [email protected]

Website : www.kalbe.co.id

Top Related

Copyright © 2022 FDOKUMEN