Time series Report

61

TECHNICAL REPORT 1 A STUDY OF THE INTER-RELATIONSHIP BETWEEN PRICES OF GOLD, SILVER, CRUDE OIL, SENSEX AND EXCHANGE RATE: APPLICATION OF ADVANCED TIME SERIES MODELS ANIL KUMAR GV AND SANTOSH KUMAR REDDY MBA in Food and Dairy Business DEPARTMENT OF DAIRY ECONOMICS AND BUSINESS MANAGEMENT DAIRY SCIENCE COLLEGE, HEBBAL, BANGALORE KARNATAK VETERINARY ANIMAL AND FISHERIES SCIENCES UNIVERSITY, BIDAR AUGUST 2012

Transcript of Time series Report

TECHNICAL REPORT 1

A STUDY OF THE INTER-RELATIONSHIP BETWEEN PRICES OFGOLD, SILVER, CRUDE OIL, SENSEX AND EXCHANGE RATE:

APPLICATION OF ADVANCED TIME SERIES MODELS

ANIL KUMAR GV AND SANTOSH KUMAR REDDYMBA in Food and Dairy Business

DEPARTMENT OF DAIRY ECONOMICS AND BUSINESS MANAGEMENTDAIRY SCIENCE COLLEGE, HEBBAL, BANGALORE

KARNATAK VETERINARY ANIMAL AND FISHERIES SCIENCES UNIVERSITY, BIDAR

AUGUST 2012

FOREWORD

In this report a step by step analysis of selected

commodity prices have been undertaken using advanced time

series models like ARIMA, Transfer function, ARCH/GARCH and

Vector Auto Regressive Models. The report also gives the SAS

codes and SAS output at every step of the analysis. Time

series analysis of commodity prices is important as one wants

to understand its behavior use it for forecasting. There are

four components embedded in a time series model, viz., Trend,

Seasonal, Cyclical and Random variation. The first three are

deterministic and can be easily estimated while the last one

is probabilistic. Once the underlying relationship is

understood, then we can use it for quantifying it and

forecasting the same. This is most relevant in the case of

commodity prices.

The challenge when one study’s commodity price is that it

can vary and these components are dynamic. Thus forecasts and

predictions made out of these series may not hold for all

situations. Further these series may have an underlying

relationship. This is captured through a variety of techniques

in the time series framework. In this study certain price

series which are of macro-economic significance like gold

prices, silver prices, crude oil prices, stock market index

and exchange rate have been modeled and the results are

discussed herein.

Anilkumar G.V and Santosh Kumar Reddy have worked very

hard in preparing this report, which included collection of

data, conceptualization of the methodology, carrying out the

analysis and finally preparing the Report. They gave

demonstrated their ability to carry out a study using

sophisticated analytical techniques. I wish them all success

in all their future endeavours.

Lalith Achoth

Co-ordinator, MBA Programme

MODELLING COMMODITY PRICES: A STUDY OF THE INTER-RELATIONSHIP BETWEEN PRICES OF

GOLD, SILVER, CRUDE OIL AND EXCHANGE RATE:APPLICATION OF ADVANCED TIME SERIES MODELS

ANIL KUMAR G.V AND SANTOSH KUMAR REDDYMBA (FOOD BUSINESS)

DEPARTMENT OF DAIRY ECONOMICS AND BUSINESS MANAGEMENTDairy Science College,

Karnataka Veterinary Animal and Fisheries SciencesUniversity,

Hebbal campus, Bangalore 560 024

August 2012

ContentsINTRODUCTION..............................................................5

OBJECTIVE OF THE STUDY:....................................................5GOLD....................................................................5EXCHANGE RATE:............................................................6SILVER PRICES:............................................................6CRUDE OIL:...............................................................7BOMBAY STOCK EXCHANGE INDEX:................................................7

RESULTS AND DISCUSSION....................................................8

TECHNIQUES FOR FORECASTING TIME SERIES DATA OF COMMODITIES.......................8THE ARMA PROCESS IN FORECASTING............................................10STAGES IN ARIMA MODELING..................................................11MODEL IDENTIFICATION......................................................12

Stationarity and Seasonality................................................................................................................ 12Seasonal differencing........................................................................................................................... 12Identifying p and q................................................................................................................................ 13Autocorrelation and Partial Autocorrelation Plots.............................................................................13Order of Autoregressive Process (p).....................................................................................................13Order of Moving Average Process (q)..................................................................................................13Shape of Autocorrelation Function......................................................................................................14

MODEL ESTIMATION:........................................................15Model Validation:.................................................................................................................................. 15

DIAGNOSTIC CHECKING:......................................................19FORECASTING:.............................................................19

Gold:....................................................................................................................................................... 19Silver prices:........................................................................................................................................... 20Crude oil:................................................................................................................................................ 22Exchange Rate:...................................................................................................................................... 23Bombay stock exchange:......................................................................................................................24

TRANSFER FUNCTION........................................................26

EXAMPLE1:...............................................................27EXAMPLE 2:..............................................................29

ARCH AND GARCH...........................................................31

LINEAR GARCH VARIATIONS...................................................32Example for ARCH/ GARCH:.................................................................................................................. 33

VECTOR AUTO REGRESSION MODEL (VAR).......................................38

Example for VARMAX............................................................................................................................. 39

POLICY IMPLICATIONS OF THE STUDY:........................................43

REFERENCE:...............................................................44

APPENDIX:................................................................46

Introduction

Time series analysis of commodity prices is important as

one wants to understand its behavior use it for forecasting.

There are four components embedded in a time series model,

viz., Trend, Seasonal, Cyclical and Random variation. The

first three are deterministic and can be easily estimated

while the last one is probabilistic.

Once the underlying relationship is understood, then we

can use it for quantifying it and forecasting the same. This

is most relevant in the case of commodity prices. The

challenge when one study’s commodity price is that it can vary

and these components are dynamic. Thus forecasts and

predictions made out of these series may not hold for all

situations. Further these series may have an underlying

relationship. This is captured through a variety of techniques

in the time series framework.

In this study certain price series which are of macro-

economic significance like gold prices, silver prices, crude

oil prices, stock market index and exchange rate have been

modeled and the results are discussed herein.

Objective of the study:

1. To identify suitable models for studying the structure of

commodities in general, and gold, silver, nymex and

sensex in particular.

2. To study interrelationships between these series using

sophisticated time series models.

3. Developing and validating forecasting models for

commodities.

Gold: Many researchers believed that gold is the best

preserving purchasing power in the long run. Gold is also

providing high liquidity; it can be exchanged for money

anytime the holders want. Gold investment can also be used as

a hedge against inflation and currency depreciation. However,

in high volatility situation the change in gold price

fluctuation is common. The investors hesitate to execute

decision because only their intuition is not enough and can

lead to loss. To provide better view of gold investment,

forecasting models should be formed to support the decision.

Many researchers suggest that Box-Jenkins’ ARIMA is

the most accurate forecasting model. ARIMA wins over other

models; Holt’s Forecast model and a combination of Box-

Jenkins’ and Holt’s in regression, by providing lowest MAPE

(Mean Absolute Percent Error), (Wararit, 2006) the idea that

Box and Jenkin’s ARIMA model has predictability in Gold Price

is accepted in many countries including India.

Exchange Rate: The exchange rate in India under the

current regime is by and large market determined. Even while

intervening, RBI takes care that through its operation, the

basic market forces are not out of place. The market players,

while always keeping an eye on what could be the possible move

by RBI, broadly agree that the exchange rate moves based on

the demand and supply forces. Therefore, the Indian forex

market could perhaps be studied by the regular supply demand

models of price determination.

Silver prices: Silver is one of the most precious

metals, valued both as a form of currency and store of value.

The major components of silver demand1 are Industrial use

(54%), Photography (15%), Jewellery and Silverware (26%) and

Coins (5%). Twenty countries together produce 96% of the

silver mined globally2. Mexico is the largest producer

followed closely by Peru3. The main consumer countries for

silver are the US, India, Canada, Mexico, UK, France, Germany,

Italy and Japan.

The key factors that affect the volatility of

silver are fluctuating industrial demand and store of value

demand, geo-political uncertainties, rising crude oil prices,

depreciating dollar, government policies on major export and

import destinations, sales by China and other central banks,

direction of gold prices and direction of other commodity

prices.

Crude oil: Economic development closely relates to

energy acquisition, and today, crude oil is the primary energy

source worldwide. Crude oil’s price changes directly influence

the price of commodities worldwide, as well as the economic

growth of every country. Before 1999, oil prices declined only

in times of economic downturn. The price of crude oil,

however, started rising in 2007 and, as a result, global

prices have been rising drastically since then. The price of

oil exceeded $100US per barrel for the first time, in February

2008; it later peaked at $145.66US in July of the same year.

This caused the prices of commodities to rise continuously,

prompting an unstable global economy that showed a downward

trend. However, by

December 2008, the oil price had fallen back to $31.12US

per barrel. Hamilton (2009) explains that the high oil prices

in 2008 were part of a bubble, and that three key variables

were responsible for them in the summer of 2008: oil’s low

price elasticity of demand; the strong growth in demand for

oil from China, the Middle East, and various newly

industrialized nations; and the failure of global oil

production to increase. Today’s international markets and

global economic data suggest the presence of slight inflation

and stagnant growth, and oil prices rose from $84US per barrel

in February 2011 to $98US in November 2011

Bombay stock exchange index: BSE is the world's number 1exchange in the world in terms of the number of listed

companies (over 4900). It is the world's 5th most active in

terms of number of transactions handled through its electronic

trading system. And it is in the top ten of global exchanges

in terms of the market capitalization of its listed companies

(as of December 31, 2009). The companies listed on BSE command

a total market capitalization of USD Trillion 1.28 as of Feb,

2010.

RESULTS AND DISCUSSION

In this project we collected data from different websites. Forthat data we done first

1. Data cleaning techniques like: Sorting, Merging, Findingmissing values, Convert character to numeric.

2. Test data for stationarity.3. ARIMA4. Transfer function5. GARCH and ARCH 6. VARMAX

Techniques for forecasting Time Series data of commodities

Autoregressive (AR) Models A common approach for

modelling Univariate time series is the autoregressive (AR)

model:

Where Xt is the time series, At is white noise, and

With denoting the process mean.

An autoregressive model is simply a linear regression of

the current value of the series against one or more prior

values of the series. The value of p is called the order of

the AR model. AR models can be analysed with one of various

methods; including standard linear least squares techniques.

They also have a straightforward interpretation.

Moving Average (MA) Models. Another common approach for

modelling Univariate time series models is the moving average

(MA) model:

Where Xt is the time series, is the mean of the series,

At-i are white noise, and 1, ... , q are the parameters of

the model. The value of q is called the order of the MA model.

That is, a moving average model is conceptually a linear

regression of the current value of the series against the

white noise or random shocks of one or more

prior values of the series. The random shocks at each

point are assumed to come from the same distribution,

typically a normal distribution, with location at zero and

constant scale. The distinction in this model is that these

random shocks are propagated to future values of the time

series. Fitting the MA estimates is more complicated than with

AR models because the error terms are not observable. This

means that iterative non-linear fitting procedures need to be

used in place of linear least squares. MA models also have a

less obvious interpretation than AR models.

Sometimes the ACF and PACF will suggest that a MA model

would be a better model choice and sometimes both AR and MA

terms should be used in the same model (see Section 6.4.4.5).

Note, however, that the error terms after the model is

fit should be independent and follow the standard assumptions

for a Univariate process.

Box-Jenkins Approach Box and Jenkins popularised an

approach that combines the moving average and the

autoregressive approaches in the book "Time Series Analysis:

Forecasting and Control" (Box, Jenkins, and Reinsel, 1994).

Although both autoregressive and moving average

approaches were already known (and were originally

investigated by Yule), the contribution of Box and Jenkins was

in developing a systematic methodology for identifying and

estimating models that could incorporate both approaches. This

makes Box-Jenkins models a powerful class of models. The next

several sections will discuss these models in detail.

The ARMA Process in Forecasting Box-Jenkins Approach

The Box-Jenkins ARMA model is a combination of the AR andMA models (described on the previous page):

Where the terms in the equation have the same meaning as

given for the AR and MA model.

Comments on Box-Jenkins Model a couple of notes on this model.

1. The Box-Jenkins model assumes that the time series is

stationary. Box and Jenkins recommend differencing non-

stationary series one or more times to achieve

stationarity. Doing so produces an ARIMA model, with the

"I" standing for "Integrated".

2. Some formulations transform the series by subtracting

the mean of the series from each data point. This yields a

series with a mean of zero. Whether you need to do this or not

is dependent on the software you use to estimate the model.

3. Box-Jenkins models can be extended to include seasonal

autoregressive and seasonal moving average terms. Although

this complicates the notation and mathematics of the model,

the underlying concepts for seasonal autoregressive and

seasonal moving average terms are similar to the non-seasonal

autoregressive and moving average terms.

4. the most general Box-Jenkins model includes difference

operators, autoregressive terms, moving average terms,

seasonal difference operators, seasonal autoregressive terms,

and seasonal moving average terms. As with modelling in

general, however, only necessary terms should be included in

the model. Those interested in the mathematical details can

consult Box, Jenkins (1986).

Stages in ARIMA Modeling

There are three primary stages in building a Box-Jenkins

time series model.

1. Model Identification

2. Model Estimation

3. Model Validation

4. Forecasting

The following remarks regarding Box-Jenkins models

should be noted.

a) Box-Jenkins models are quite flexible due to the

inclusion of both autoregressive and moving average terms.

b) Based on the Wold decomposition theorem, a stationary

process can be approximated by an ARMA model. In practice,

finding that approximation may not be easy.

c) Chatfield (1996) recommends decomposition methods for

series in which the trend and seasonal components are

dominant.

d) Building good ARIMA models generally requires more

experience than commonly used statistical methods such as

regression.

e) Sufficiently Long Series required typically,

effective fitting of Box-Jenkins models requires at least a

moderately long series. Chatfield (1996) recommends at least

50 observations. Many others would recommend at least 100

observations.

Model Identification

Stationarity and Seasonality

The first step in developing a Box-Jenkins model is to

determine if the series is stationary and if there is any

significant seasonality that needs to be modelled.

Detecting stationarity

Stationarity can be accessed from a run sequence plot.

The run sequence plot should show constant location and scale.

It can also be detected from an autocorrelation plot.

Specifically, non-stationarity is often indicated by an

autocorrelation plot with very slow decay.

Detecting seasonality

Seasonality (or periodicity) can usually be assessed from

an autocorrelation plot, a seasonal subseries plot, or a

spectral plot. Differencing to achieve stationarity Box and

Jenkins recommend the differencing approach to achieve

stationarity. However, fitting a curve and subtracting the

fitted values from the original data can also be used in the

context of Box-Jenkins models.

Seasonal differencing

At the model identification stage, our goal is to detect

seasonality, if it exists, and to identify the order for the

seasonal autoregressive and seasonal moving average terms. For

many series, the period is known and a single seasonality term

is sufficient. For example, for monthly data we would

typically include either a seasonal AR 12 term or a seasonal

MA 12 term. For Box-Jenkins models, we do not explicitly

remove seasonality before fitting the model. Instead, we

include the order of the seasonal terms in the model

specification to the ARIMA estimation software. However, it

may be helpful to apply a seasonal difference to the data and

regenerate the autocorrelation and partial autocorrelation

plots. This may help in the model identification of the non-

seasonal component of the model. In some cases, the seasonal

differencing may remove most or all of the seasonality effect.

Identifying p and q

Once stationarity and seasonality have been addressed,

the next step is to identify the order (i.e., the p and q) of

the autoregressive and moving average terms.

Autocorrelation and Partial Autocorrelation Plots

The primary tools for doing this are the autocorrelation

plot and the partial autocorrelation plot. The sample

autocorrelation plot and the sample partial autocorrelation

plot are compared to the theoretical behaviour of these plots

when the order is known.

Order of Autoregressive Process (p)

Specifically, for an AR (1) process, the sample

autocorrelation function should have an exponentially

decreasing appearance. However, higher-order AR processes are

often a mixture of exponentially decreasing and damped

sinusoidal components.

For higher-order autoregressive processes, the sample

autocorrelation needs to be supplemented with a partial

autocorrelation plot. The partial autocorrelation of an AR (p)

process becomes zero at lag p+1 and greater, so we examine the

sample partial autocorrelation function to see if there is

evidence of a departure from zero. This is usually determined

by placing a 95% confidence interval on the sample partial

autocorrelation plot (most software programs that generate

sample autocorrelation plots will also plot this confidence

interval). If the software program does not generate the

confidence band, it is approximately, with N denoting the

sample size.

Order of Moving Average Process (q)

The autocorrelation function of a MA (q) process becomes

zero at lag q+1 and greater, so we examine the sample

autocorrelation function to see where it essentially becomes

zero. We do this by placing the 95% confidence interval for

the sample autocorrelation function on the sample

autocorrelation plot. Most software that can generate the

autocorrelation plot can also generate this confidence

interval.

The sample partial autocorrelation function is generally

not helpful for identifying the order of the moving average

process.

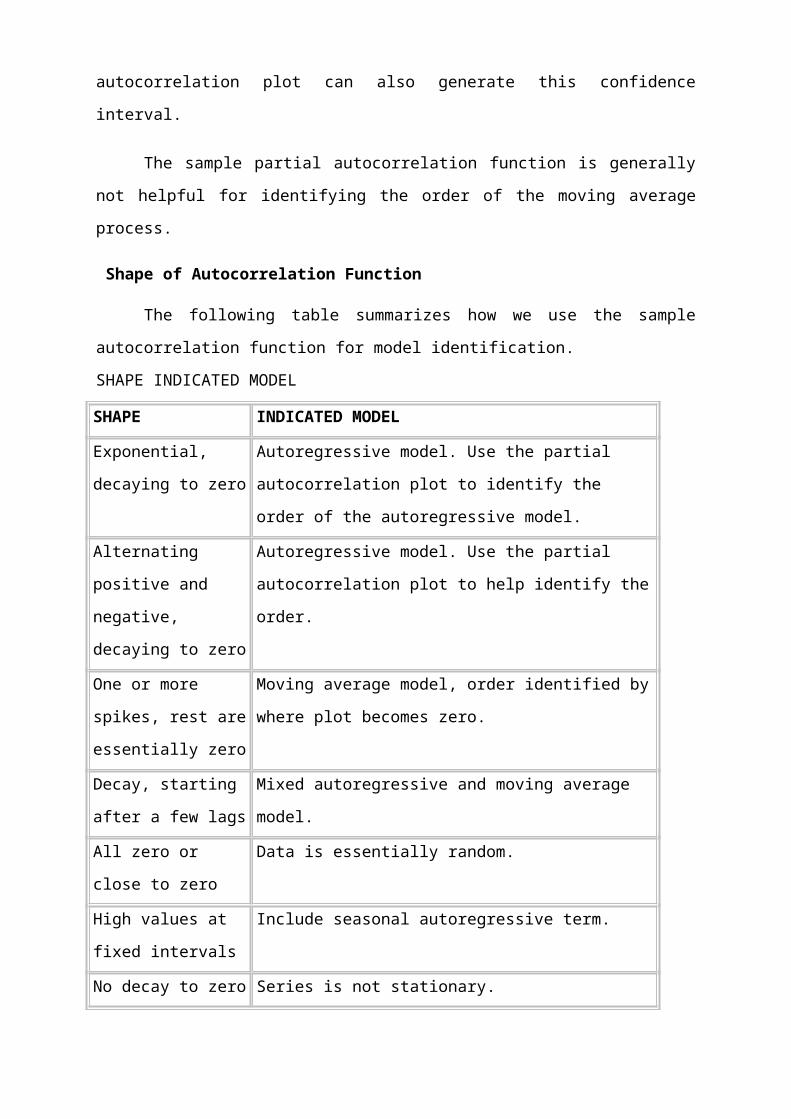

Shape of Autocorrelation Function

The following table summarizes how we use the sample

autocorrelation function for model identification.

SHAPE INDICATED MODEL

SHAPE INDICATED MODEL

Exponential,

decaying to zero

Autoregressive model. Use the partial

autocorrelation plot to identify the

order of the autoregressive model.

Alternating

positive and

negative,

decaying to zero

Autoregressive model. Use the partial

autocorrelation plot to help identify the

order.

One or more

spikes, rest are

essentially zero

Moving average model, order identified by

where plot becomes zero.

Decay, starting

after a few lags

Mixed autoregressive and moving average

model.

All zero or

close to zero

Data is essentially random.

High values at

fixed intervals

Include seasonal autoregressive term.

No decay to zero Series is not stationary.

Mixed models Difficult to Identify. In practice, the

sample autocorrelation and partial autocorrelation functions

are random variables and will not give the same picture as the

theoretical functions. This makes the model identification

more difficult. In particular, mixed models can be

particularly difficult to identify.

Although experience is helpful, developing good models

using these sample plots can involve much trial and error. For

this reason, in recent years information-based criteria such

as FPE (Final Prediction Error) and AIC ( Aikake Information

Criterion) and others have been preferred and used. These

techniques can help automate the model identification process.

These techniques require computer software to use.

Fortunately, these techniques are available in many commercial

statistical software programs that provide ARIMA modelling

capabilities.

Model Estimation:Having tentatively identified the model the next step is

to estimate the parameters of the tentatively identified

model. The parameters are estimated using the maximum

likelihood estimator (MLE).

Model Validation:

Since the model identification is tentative the next step

is to examine whether the tentatively identified is correct or

not. This step is called diagnostic checking. In diagnostic

checking the autocorrelation of the residuals is done to see

whether the residuals of the estimated model are a random

white noise process. This is confirmed if the residuals do not

have any significant autocorrelations or if the Box_Ljung test

which is a test of the overall significance of the

autocorrelation function is non-significant. The Box_Ljung

test follows a chi square test with

(N-p-q) degrees of freedom.

EXAMPLE:

ARIMA model output for gold prices ARIMA method

1. Pattern of gold price

P L O T G o l d

G o l d

01 0 0 0 02 0 0 0 03 0 0 0 04 0 0 0 05 0 0 0 06 0 0 0 07 0 0 0 08 0 0 0 09 0 0 0 0

1 0 0 0 0 01 1 0 0 0 01 2 0 0 0 01 3 0 0 0 0

In the above graph we find some outliers.so we cont able to find the seasonality for this prices.

Proc gplotdata=anil.alldata;plot (gold)*date/ legend overlay;run;

After removed the outliers we find the trend in gold prices as shown in below graph.

P L O T G o l d

G o l d

0

1 0 0 0 0

2 0 0 0 0

3 0 0 0 0

4 0 0 0 0

D a t e

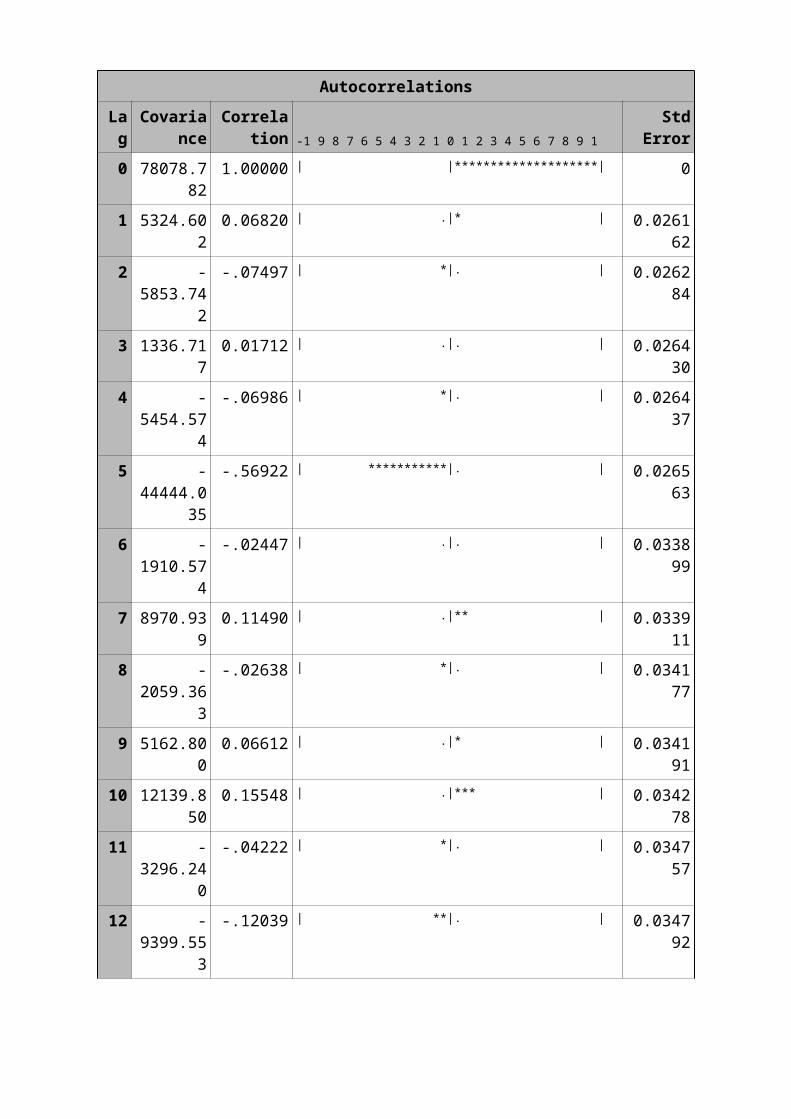

1. Autocorrelation:

AutocorrelationsLag

Covariance

Correlation -1 9 8 7 6 5 4 3 2 1 0 1 2 3 4 5 6 7 8 9 1

StdError

0 78078.782

1.00000 | |********************| 0

1 5324.602

0.06820 | .|* | 0.026162

2 -5853.74

2

-.07497 | *|. | 0.026284

3 1336.717

0.01712 | .|. | 0.026430

4 -5454.57

4

-.06986 | *|. | 0.026437

5 -44444.0

35

-.56922 | ***********|. | 0.026563

6 -1910.57

4

-.02447 | .|. | 0.033899

7 8970.939

0.11490 | .|** | 0.033911

8 -2059.36

3

-.02638 | *|. | 0.034177

9 5162.800

0.06612 | .|* | 0.034191

10 12139.850

0.15548 | .|*** | 0.034278

11 -3296.24

0

-.04222 | *|. | 0.034757

12 -9399.55

3

-.12039 | **|. | 0.034792

AutocorrelationsLag

Covariance

Correlation -1 9 8 7 6 5 4 3 2 1 0 1 2 3 4 5 6 7 8 9 1

StdError

13 3630.489

0.04650 | .|* | 0.035076

14 -958.884

-.01228 | .|. | 0.035119

15 -9864.44

8

-.12634 | ***|. | 0.035122

16 2672.044

0.03422 | .|* | 0.035431

17 8705.872

0.11150 | .|** | 0.035454

18 -3572.31

8

-.04575 | *|. | 0.035693

19 -1709.91

6

-.02190 | .|. | 0.035733

20 3884.195

0.04975 | .|* | 0.035742

21 2237.078

0.02865 | .|* | 0.035790

22 -5149.61

3

-.06595 | *|. | 0.035805

23 4808.076

0.06158 | .|* | 0.035888

24 2652.068

0.03397 | .|* | 0.035961

In the above table we identified a ‘q’ value. In this there are 1,2,5 are significant so that form these values will help for forecasting the future values.

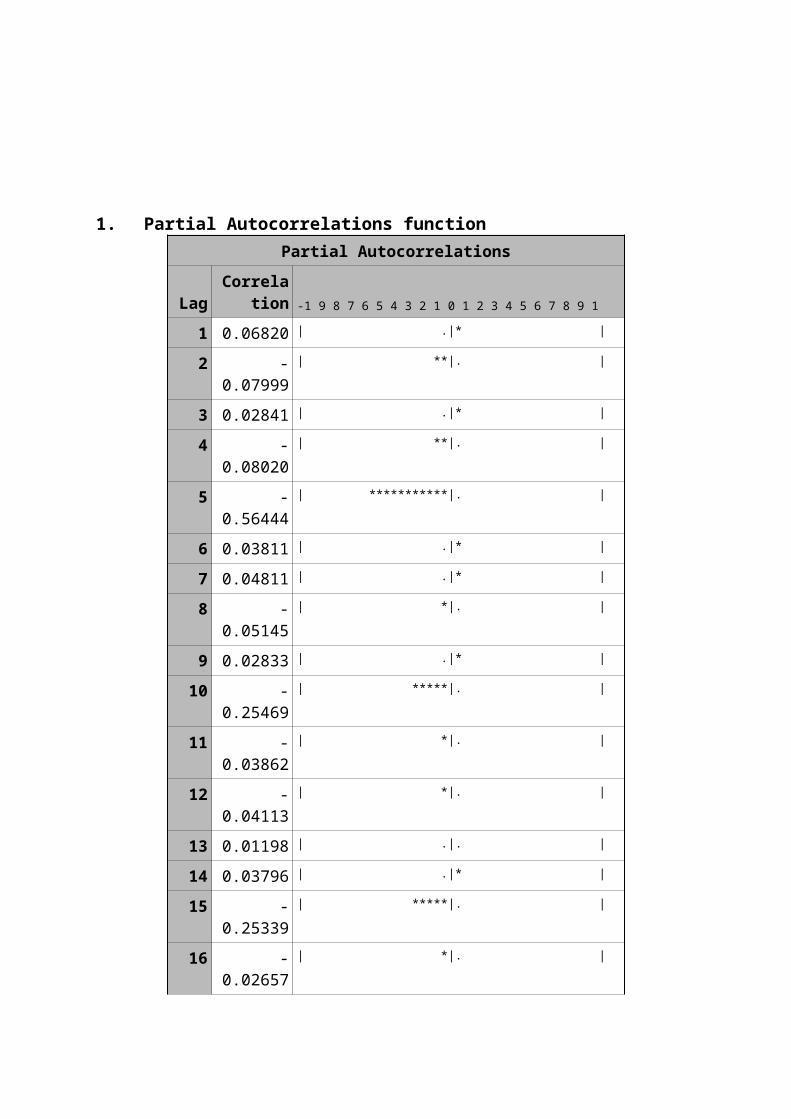

1. Partial Autocorrelations functionPartial Autocorrelations

LagCorrela

tion -1 9 8 7 6 5 4 3 2 1 0 1 2 3 4 5 6 7 8 9 1

1 0.06820 | .|* |

2 -0.07999

| **|. |

3 0.02841 | .|* |

4 -0.08020

| **|. |

5 -0.56444

| ***********|. |

6 0.03811 | .|* |

7 0.04811 | .|* |

8 -0.05145

| *|. |

9 0.02833 | .|* |

10 -0.25469

| *****|. |

11 -0.03862

| *|. |

12 -0.04113

| *|. |

13 0.01198 | .|. |

14 0.03796 | .|* |

15 -0.25339

| *****|. |

16 -0.02657

| *|. |

Partial Autocorrelations

LagCorrela

tion -1 9 8 7 6 5 4 3 2 1 0 1 2 3 4 5 6 7 8 9 1

17 0.03382 | .|* |

18 -0.03253

| *|. |

19 0.01600 | .|. |

20 -0.21152

| ****|. |

21 0.06570 | .|* |

22 0.00916 | .|. |

23 0.02482 | .|. |

24 0.04699 | .|* |

In this table we identified a ‘p’ values. It means partial autocorrelation function values.The p values in this table are p= (1, 5, 10, 15, and 20)

Diagnostic Checking:In the estimation and diagnostic checking stage, we can use

the ESTIMATE statement to specify the ARIMA model to fit to

the variable specified in the previous IDENTIFY statement, and

to estimate the parameters of that model. The ESTIMATE

statement also produces diagnostic statistics to help you

judge the adequacy of the model.

Significance tests for parameter estimates indicate whether

some terms in the model may be unnecessary. Goodness-of-fit

statistics aid in comparing this model to others. Tests for

white noise residuals indicate whether the residual series

contains additional information that might be utilized by a

more complex model. If the diagnostic tests indicate problems

with the model, you try another model, then repeat the

estimation and diagnostic checking stage.

Forecasting:

Gold:To forecast the prices by using the estimated values

The forecast prices are varied 0.24% from the Actual gold

prices.

P L O T G o l d F o r e c a s t f o r G o l d

G o l d

0

1 0 0 0 0

2 0 0 0 0

3 0 0 0 0

4 0 0 0 0

D a t e

0 1 J A N 2 0 0 7

The average Percent error for gold for 10 days is -1.24%

Ods html;proc arima data=anil.finalout=anil.forecast;identifyvar= gold(1,5) stationarity=(adf=(2));estimate p=(1)(2)(5)(10)(15)(20) q=(1)(2)(5);forecastlead=30id=date;run; ods htmlclose;

Silver prices:

In the silver prices there is an non stationarity. And also

Outliers so we can do first order differencing.

P L O T S i l v e r

S i l v e r

1 0 0 0 0

2 0 0 0 0

3 0 0 0 0

4 0 0 0 0

5 0 0 0 0

6 0 0 0 0

7 0 0 0 0

8 0 0 0 0

Autocorrelation for silver prices to find outestimates.

The estimated q values are only 5 is significant. 2 also

significant but in seasonality we have to take (1, 5) because

our data is in 5 days a week so if one is not significant take

only 5.

Partial autocorrelation for silver prices. In the silver

prices estimated P values are p=1, 5, 10, 15, 20.

Proc gplotdata=anil.alldata;plot (silver)*date/ legend overlay;run;

Proc arima data=silver;Identify var=Silver_Delhi(1,5);run;

For forecasting of silver prices we use the estimated values

what we find out in the autocorrelation and partial

autocorrelation functions

.

P L O T S i l v e r F o r e c a s t f o r S i l v e r

S i l v e r

1 0 0 0 0

2 0 0 0 0

3 0 0 0 0

4 0 0 0 0

5 0 0 0 0

6 0 0 0 0

7 0 0 0 0

8 0 0 0 0

The average Percent error for silver for 10 days is -2.07%

Crude oil: The nymex oil prices are plotted the graph. As we observed in

the graph there is a trend in the crude oil prices. it means

it’s a non stationarity in this series.

Odshtml;procarimadata=anil.finalout=anil.forecast;identifyvar= silver(1,5) stationarity=(adf=(2));estimatep=(1)(2)(5)(10)(15)(20) q=(5);forecastlead=30id=date;run;odshtmlclose;

P L O T N Y M E X

N Y M E X

3 0

4 0

5 0

6 0

7 0

8 0

9 0

1 0 0

1 1 0

1 2 0

1 3 0

1 4 0

1 5 0

We done an first differencing for nymex to find out an P & Q

values..

The estimated q values are 5 is significant. 2 also

significant but in seasonality we have to take (1, 5) because

our data is in 5 days.

Partial autocorrelation for nymex prices. In the silver

prices estimated P values are p=1, 5, 10, 15, 20.

For forecasting of nymex prices we use the estimated values

what we find out in the autocorrelation and partial

autocorrelation functions

The forecasting of crude oil prices by using estimated values

Proc arimadata=anil.final out=anil.forecast;Identify var= nymex (1,5) stationarity=(adf=(2));estimatep=(1)(2)(5)(10)(15)(20) q=(1)(2)(5);

Proc arima data=anil.final out=anil.forecast;Identify var= nymex(1,5) stationarity=(adf=(2));run;

P L O T N Y M E X F o r e c a s t f o r N Y M E X

N Y M E X

3 0

4 0

5 0

6 0

7 0

8 0

9 0

1 0 0

1 1 0

1 2 0

1 3 0

1 4 0

1 5 0

The average Percent error for nymex for 10 days is 1.23% .

Exchange Rate:The exchange rates are plotted in the below graph.

P L O T E x r a t e

E x r a t e

3 94 04 14 24 34 44 54 64 74 84 95 05 15 25 35 45 55 65 75 8

Procarimadata=anil.finalIdentifyvar=exrate(1,5) stationarity=(adf=(2));run;

We had done first order differencing for the exchange rate values to find out the estimated P & Q values.

Procgplotdata=anil.forexrate;plot (exrate)*date/ legendoverlay;run;

The autocorrelation values (q) are 1,2,5 .when we done an first order differencing for exchange rate values.Partial autocorrelation gives an p values in the nymex P estimated values are 1,5,10,15,20. The forecasting for an exchange rate by using estimated p & q values.

Procarimadata=anil.finalout=anil.exforecast;Identifyvar= exrate(1,5) stationarity=(adf=(2));Estimatep=(1)(2)(5)(10)(15)(20) q=(1)(2)(5);Forecastlead=30id=date;run;

The bellowed graph is showing actual values and forecasting values for the exchange rate.

P L O T E x r a t e F o r e c a s t f o r E x r a t e

E x r a t e

3 94 04 14 24 34 44 54 64 74 84 95 05 15 25 35 45 55 65 75 8

The average Percent error for exrate for 10 days is -0.062%.

Bombay stock exchange:

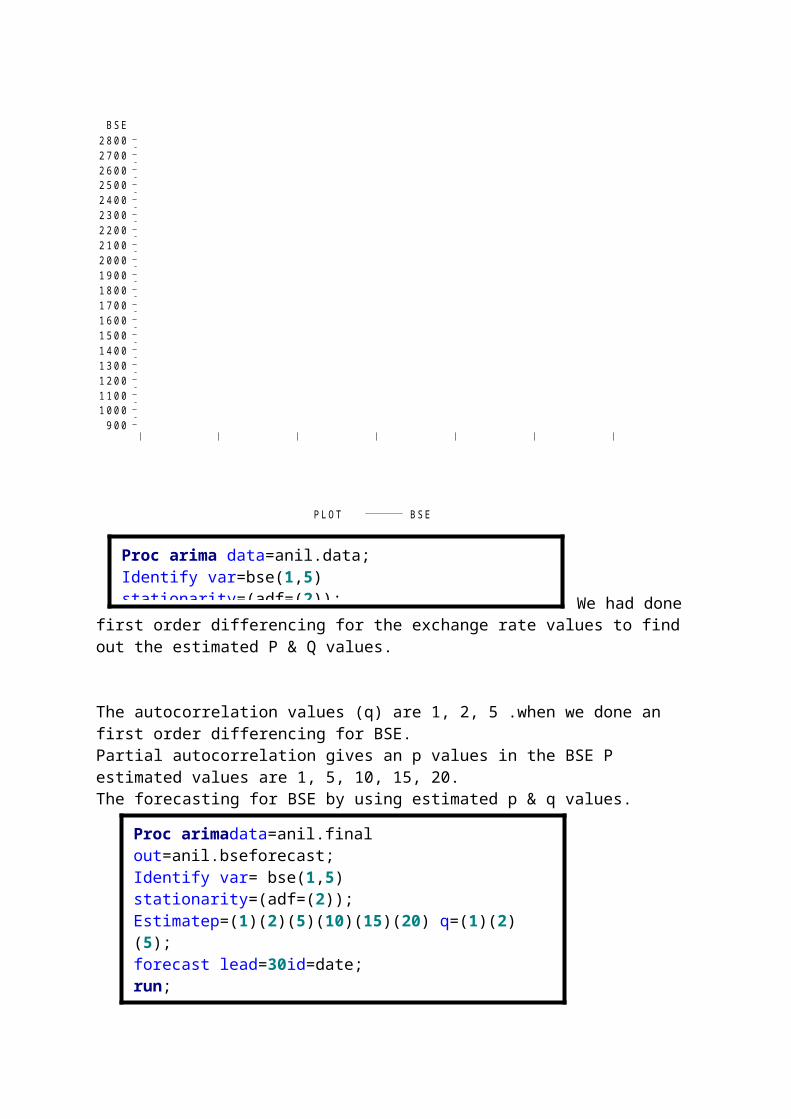

We had taken data from Jan 2007 to July 2012 for forecasting. For that data we done cleaning and done a arima model.

Procgplotdata=anil.bse;plot (bse)*date/ legendoverlay;run;

P L O T B S E

B S E

9 0 01 0 0 01 1 0 01 2 0 01 3 0 01 4 0 01 5 0 01 6 0 01 7 0 01 8 0 01 9 0 02 0 0 02 1 0 02 2 0 02 3 0 02 4 0 02 5 0 02 6 0 02 7 0 02 8 0 0

Proc arima data=anil.data;Identify var=bse(1,5) stationarity=(adf=(2)); We had done

first order differencing for the exchange rate values to find out the estimated P & Q values.

The autocorrelation values (q) are 1, 2, 5 .when we done an first order differencing for BSE.Partial autocorrelation gives an p values in the BSE P estimated values are 1, 5, 10, 15, 20.The forecasting for BSE by using estimated p & q values.

Proc arimadata=anil.final out=anil.bseforecast;Identify var= bse(1,5) stationarity=(adf=(2));Estimatep=(1)(2)(5)(10)(15)(20) q=(1)(2)(5);forecast lead=30id=date;run;

P L O T B S E F o r e c a s t f o r B S E

B S E

9 0 01 0 0 01 1 0 01 2 0 01 3 0 01 4 0 01 5 0 01 6 0 01 7 0 01 8 0 01 9 0 02 0 0 02 1 0 02 2 0 02 3 0 02 4 0 02 5 0 02 6 0 02 7 0 02 8 0 0

The average Percent error for BSE for 10 days is -1.45% .

Transfer function

A Transfer function approach to modeling a time series is

a multivariate way of modeling the various lag structures

found in the data. It is similar to a distributed lag model in

traditional econometrics. The transfer function model,

however, makes use of the ratio between what are called

Numerator and Denominator polynomials. The Numerator

polynomials are the different lags of the exogenous variables.

The Denominator polynomials are the coefficients associated

with lags of the forecast itself (i.e. the traditional

dependent variable). Something called a Delay Factor or "dead

time" is associated with the exogenous variables. This is the

amount of time elapsed before the numerator polynomial begins

to impact the forecasted series. The error term is modeled

simultaneously as an ARMA process. Stationarity requirements

hold the same for each exogenous series as in the Univariate

endogenous case. Difference operations must be used if the

autocorrelation function of each series is to exhibit

stationarity. These difference operations need not be exactly

the same across all variables.

There may seem to be a close relationship between the Transfer

Function models and multiple regressions (OLS). At a glance,

one might think that the regression models are a special case

of the transfer function. However, they are quite different.

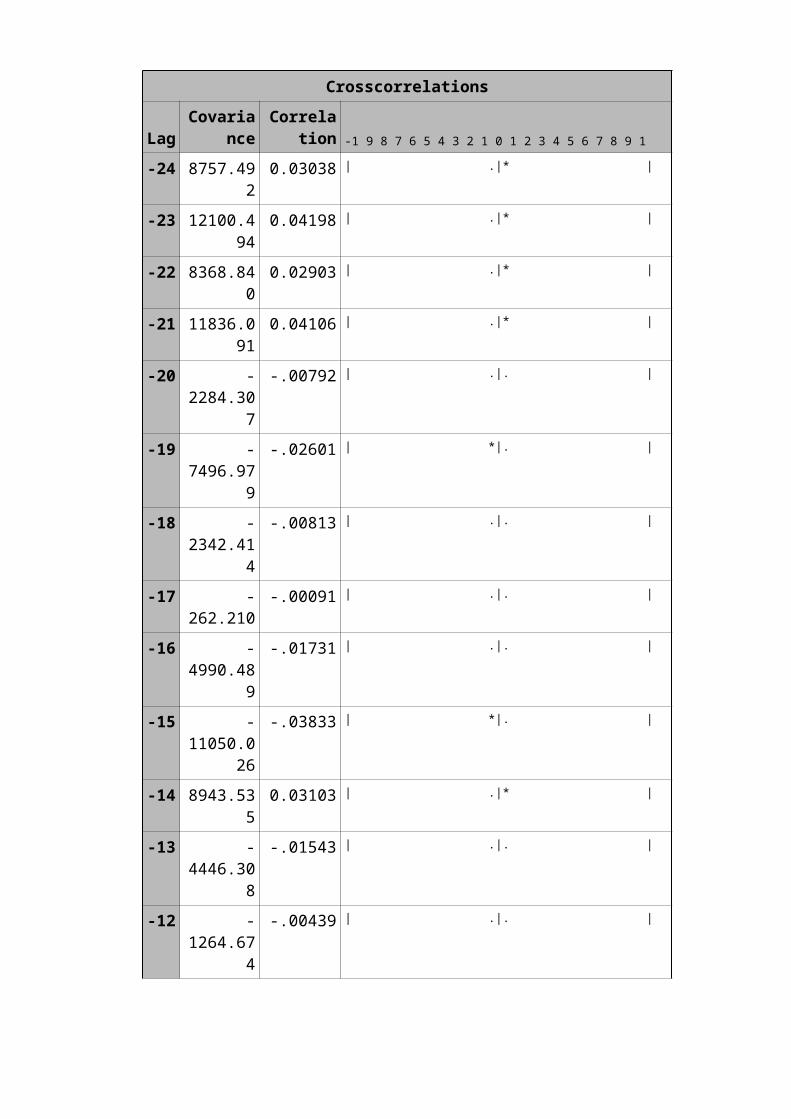

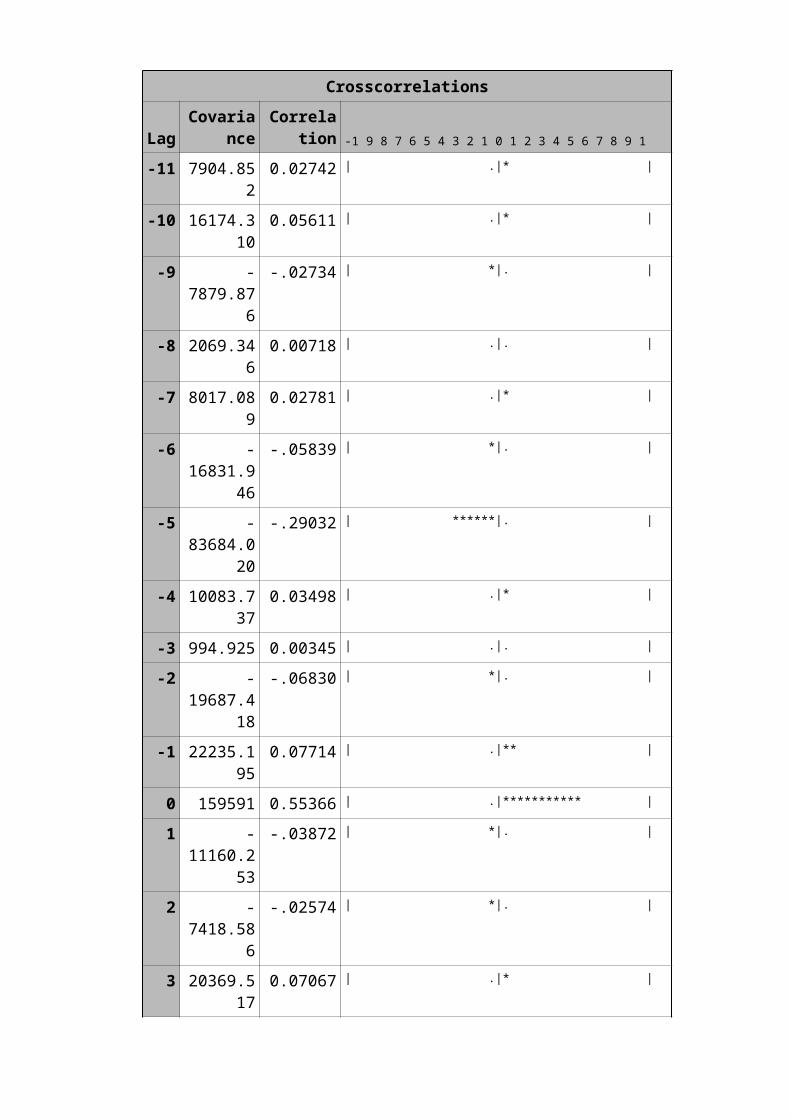

Example1:In this example, Silver is dependent on Gold. As we taken data

from Jan 2007 to July 2012. For our data we taken y=silver

(dependent variable) and x=gold (independent variable). We

will model the silver prices regression against the gold

prices. We can use Proc ARIMA to carry simple transfer

function. This is illustrated by using SAS codes

The following is SAS output

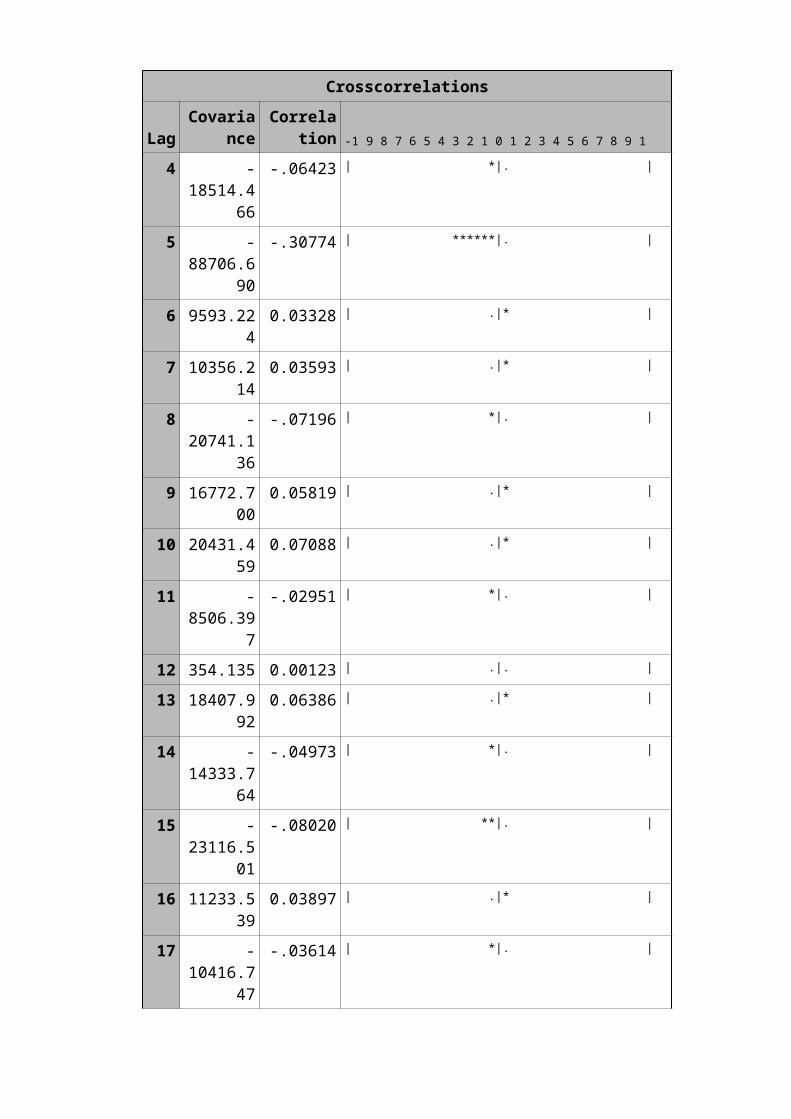

Proc arima data=anil.transall1;Identify var=silver(1,5) crosscorr=gold(1,5);Estimate p=(1)(2)(5)(10)(15)(20) q=(1)(2)(5) input=((0,3,5)gold);run;

Crosscorrelations

LagCovaria

nceCorrela

tion -1 9 8 7 6 5 4 3 2 1 0 1 2 3 4 5 6 7 8 9 1

-24 8757.492

0.03038 | .|* |

-23 12100.494

0.04198 | .|* |

-22 8368.840

0.02903 | .|* |

-21 11836.091

0.04106 | .|* |

-20 -2284.30

7

-.00792 | .|. |

-19 -7496.97

9

-.02601 | *|. |

-18 -2342.41

4

-.00813 | .|. |

-17 -262.210

-.00091 | .|. |

-16 -4990.48

9

-.01731 | .|. |

-15 -11050.0

26

-.03833 | *|. |

-14 8943.535

0.03103 | .|* |

-13 -4446.30

8

-.01543 | .|. |

-12 -1264.67

4

-.00439 | .|. |

Crosscorrelations

LagCovaria

nceCorrela

tion -1 9 8 7 6 5 4 3 2 1 0 1 2 3 4 5 6 7 8 9 1

-11 7904.852

0.02742 | .|* |

-10 16174.310

0.05611 | .|* |

-9 -7879.87

6

-.02734 | *|. |

-8 2069.346

0.00718 | .|. |

-7 8017.089

0.02781 | .|* |

-6 -16831.9

46

-.05839 | *|. |

-5 -83684.0

20

-.29032 | ******|. |

-4 10083.737

0.03498 | .|* |

-3 994.925 0.00345 | .|. |

-2 -19687.4

18

-.06830 | *|. |

-1 22235.195

0.07714 | .|** |

0 159591 0.55366 | .|*********** |

1 -11160.2

53

-.03872 | *|. |

2 -7418.58

6

-.02574 | *|. |

3 20369.517

0.07067 | .|* |

Crosscorrelations

LagCovaria

nceCorrela

tion -1 9 8 7 6 5 4 3 2 1 0 1 2 3 4 5 6 7 8 9 1

4 -18514.4

66

-.06423 | *|. |

5 -88706.6

90

-.30774 | ******|. |

6 9593.224

0.03328 | .|* |

7 10356.214

0.03593 | .|* |

8 -20741.1

36

-.07196 | *|. |

9 16772.700

0.05819 | .|* |

10 20431.459

0.07088 | .|* |

11 -8506.39

7

-.02951 | *|. |

12 354.135 0.00123 | .|. |

13 18407.992

0.06386 | .|* |

14 -14333.7

64

-.04973 | *|. |

15 -23116.5

01

-.08020 | **|. |

16 11233.539

0.03897 | .|* |

17 -10416.7

47

-.03614 | *|. |

Crosscorrelations

LagCovaria

nceCorrela

tion -1 9 8 7 6 5 4 3 2 1 0 1 2 3 4 5 6 7 8 9 1

18 -18154.0

95

-.06298 | *|. |

19 13639.149

0.04732 | .|* |

20 8077.267

0.02802 | .|* |

21 -9916.79

9

-.03440 | *|. |

22 7506.528

0.02604 | .|* |

23 27411.793

0.09510 | .|** |

24 -10879.9

33

-.03774 | *|. |

Conditional Least Squares Estimation

Parameter Estimate

Standard Error

t Value

ApproxPr > |

t| LagVariable

Shift

MU -0.10971 0.21055 -0.52

0.6024 0 Silver

0

MA1,1 0.99021 0.0037712

262.57

<.0001 5 Silver

0

AR1,1 0.02043 0.02663 0.77 0.4431 5 Silver

0

AR2,1 -0.07124 0.02666 -2.67

0.0076 10 Silver

0

AR3,1 -0.02669 0.02664 -1.00

0.3166 15 Silver

0

AR4,1 0.02629 0.02683 0.98 0.3273 20 Silver

0

Crosscorrelations

LagCovaria

nceCorrela

tion -1 9 8 7 6 5 4 3 2 1 0 1 2 3 4 5 6 7 8 9 1

NUM1 2.09657 0.08291 25.29

<.0001 0 Gold 0

NUM1,1 -0.004502

7

0.08289 -0.05

0.9567 5 Gold 0

In the above model we can make out how gold affects the

silver: The today’s silver price will go up by 2.09 Rs/kg when

gold price increases by 1Rs/10grams.After 6th day silver price

will go down by 0.0045 Rs/kg when gold price increases by

1Rs/10grams.

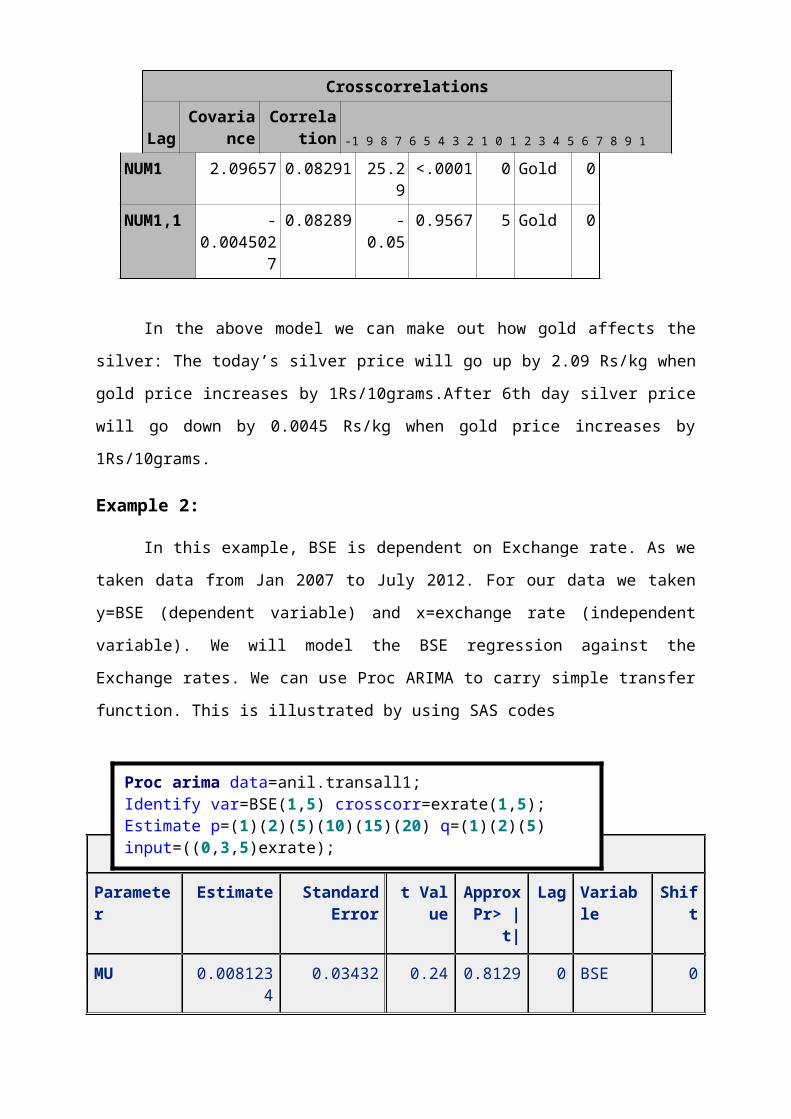

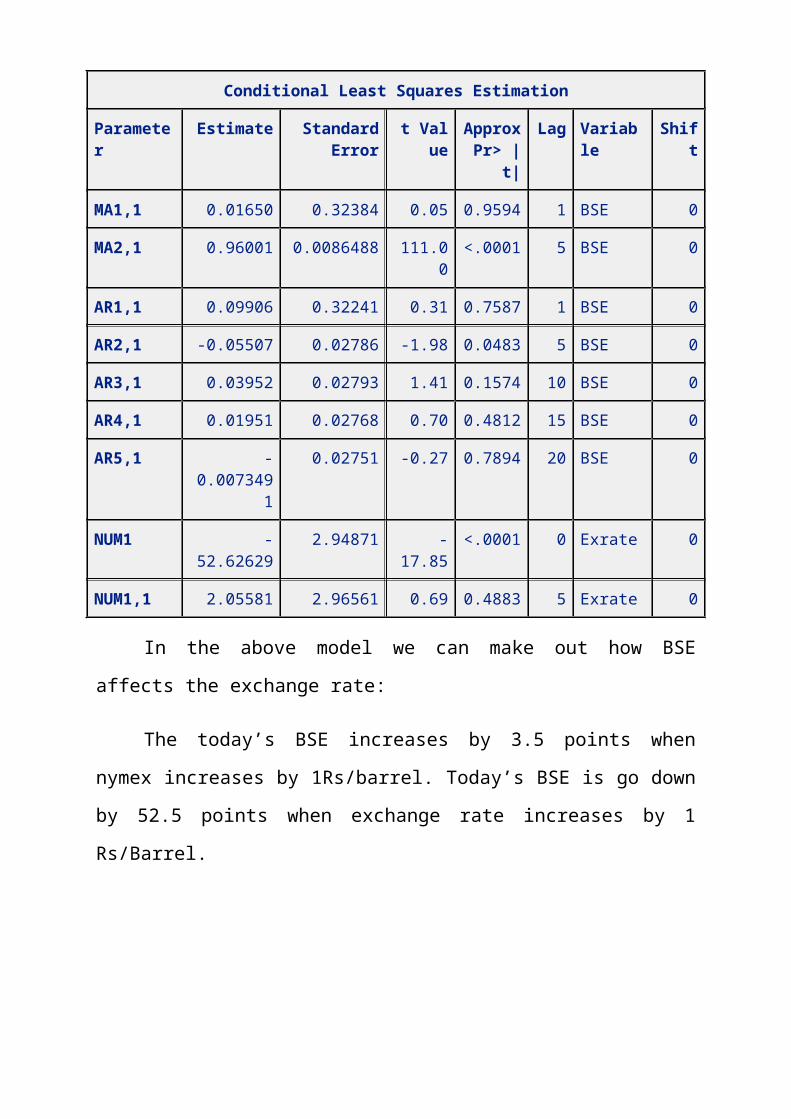

Example 2:

In this example, BSE is dependent on Exchange rate. As we

taken data from Jan 2007 to July 2012. For our data we taken

y=BSE (dependent variable) and x=exchange rate (independent

variable). We will model the BSE regression against the

Exchange rates. We can use Proc ARIMA to carry simple transfer

function. This is illustrated by using SAS codes

Conditional Least Squares Estimation

Parameter

Estimate StandardError

t Value

ApproxPr> |

t|

Lag Variable

Shift

MU 0.0081234

0.03432 0.24 0.8129 0 BSE 0

Proc arima data=anil.transall1;Identify var=BSE(1,5) crosscorr=exrate(1,5);Estimate p=(1)(2)(5)(10)(15)(20) q=(1)(2)(5) input=((0,3,5)exrate);run;

Conditional Least Squares Estimation

Parameter

Estimate StandardError

t Value

ApproxPr> |

t|

Lag Variable

Shift

MA1,1 0.01650 0.32384 0.05 0.9594 1 BSE 0

MA2,1 0.96001 0.0086488 111.00

<.0001 5 BSE 0

AR1,1 0.09906 0.32241 0.31 0.7587 1 BSE 0

AR2,1 -0.05507 0.02786 -1.98 0.0483 5 BSE 0

AR3,1 0.03952 0.02793 1.41 0.1574 10 BSE 0

AR4,1 0.01951 0.02768 0.70 0.4812 15 BSE 0

AR5,1 -0.007349

1

0.02751 -0.27 0.7894 20 BSE 0

NUM1 -52.62629

2.94871 -17.85

<.0001 0 Exrate 0

NUM1,1 2.05581 2.96561 0.69 0.4883 5 Exrate 0

In the above model we can make out how BSE

affects the exchange rate:

The today’s BSE increases by 3.5 points when

nymex increases by 1Rs/barrel. Today’s BSE is go down

by 52.5 points when exchange rate increases by 1

Rs/Barrel.

ARCH and GARCHWHY ARCH/GARCH?

The ARCH/GARCH framework proved to be very successful in

predicting volatility changes. Empirically, a wide range of

financial and economic phenomena exhibit the clustering of

volatilities. As we have seen, ARCH/GARCH models describe the

time evolution of the average size of squared errors, that is,

the evolution of the magnitude of uncertainty. Despite the

empirical success of ARCH/GARCH models, there is no real

consensus on the economic reasons why uncertainty tends to

cluster. That is why models tend to perform better in some

periods and worse in other periods. It is relatively easy to

induce ARCH behavior in simulated systems by making

appropriate assumptions on agent behavior. For example, one

can reproduce ARCH behavior in artificial markets with simple

assumptions on agent decision-making processes. The real

economic challenge, however, is to explain ARCH/GARCH behavior

in terms of features of agents behavior and/or economic

variables that could be empirically ascertained. In classical

physics, the amount of uncertainty inherent in models and

predictions can be made arbitrarily low by increasing the

precision of initial data. This view, however, has been

challenged in at least two ways. First, quantum mechanics has

introduced the notion that there is a fundamental uncertainty

in any measurement process. The amount of uncertainty is

prescribed by the theory at a fundamental level. Second, the

theory of complex systems has shown that nonlinear complex

systems are so sensitive to changes in initial conditions

that, in practice, there are limits to the accuracy of any

model. ARCH/GARCH models describe the time evolution of

uncertainty in a complex system.

In financial and economic models, the future is always

uncertain but over time we learn new information that helps us

forecast this future. As asset prices reflect our best

forecasts of the future profitability of companies and

countries, these change whenever there is news .ARCH/GARCH

models can be interpreted as measuring the intensity of the

news process. Volatility clustering is most easily understood

as news clustering. Of course, many things influence the

arrival process of news and its impact on prices. Trades

convey news to the market and the macro economy can moderate

the importance of the news. These can all be thought of as

important determinants of the volatility that is picked up by

ARCH/GARCH.

Linear GARCH Variations

Integrated GARCH (Engle and Bollerslev 1986).A phenomenon

is similar to integrated series in regular (ARMA-type) time-

series. Occurs when +=1. When this is the case it means

that there is a unit root in the conditional variance; past

shocks do not dissipate but persist for very long periods of

time. Fractionally Integrated GARCH (Baillie, Bollerslev and

Mikkelsen (1996)).GARCH in Mean (Engle, Lilien and Robbins

(1987).Idea is that there is a direct relationship between

risk and return of an asset. In the mean equation, include

some function of the conditional variance—usually the standard

deviation. This allows the mean of a series to depend, at

least in part, on the conditional variance of the series (more

later).

Non-Linear GARCH Variations (dozens in last 20 years).

Linear GARCH models all allow prior shocks to have a symmetric

affect on ht. Non-linear models allow for asymmetric shocks

to volatility. I will focus on the most common: the

Exponentional GARCH (1,1) (EGARCH) model developed by Nelson

(1991).Conditional variance:

, where and is the standardized residual. is

the asymmetric component.

News Impact Curve differential impact of positive and

negative shocks.

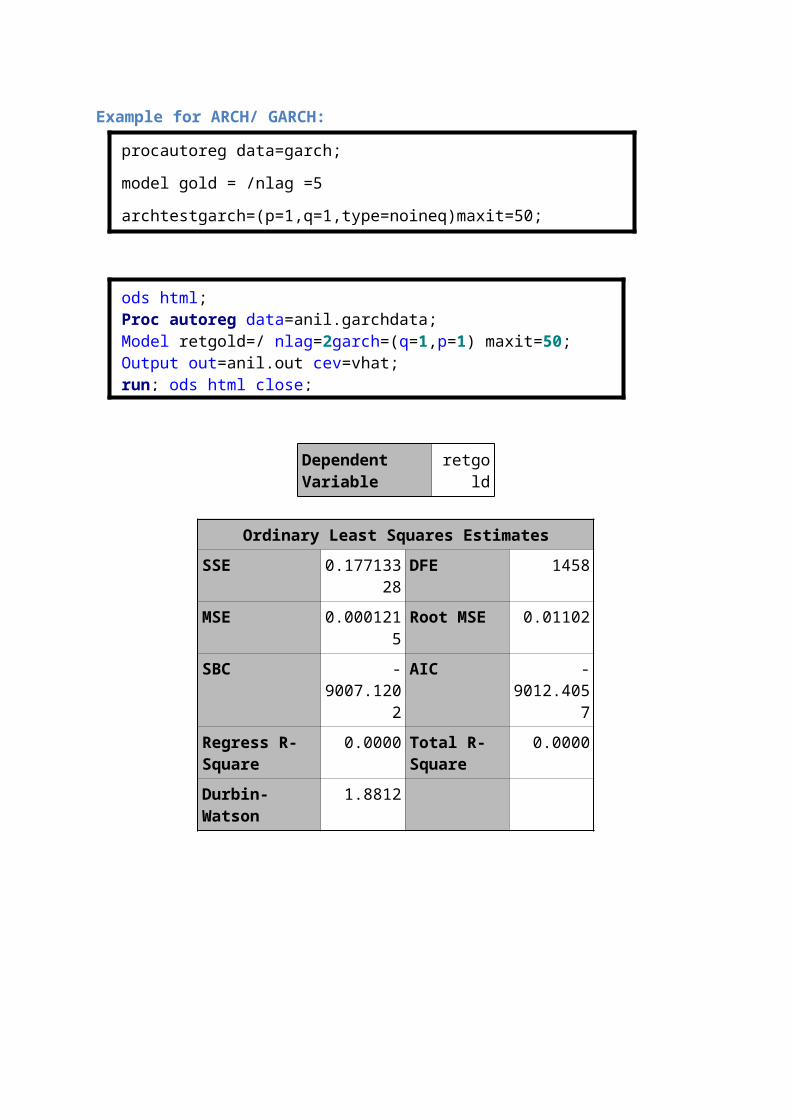

Example for ARCH/ GARCH:

procautoreg data=garch;

model gold = /nlag =5

archtestgarch=(p=1,q=1,type=noineq)maxit=50;

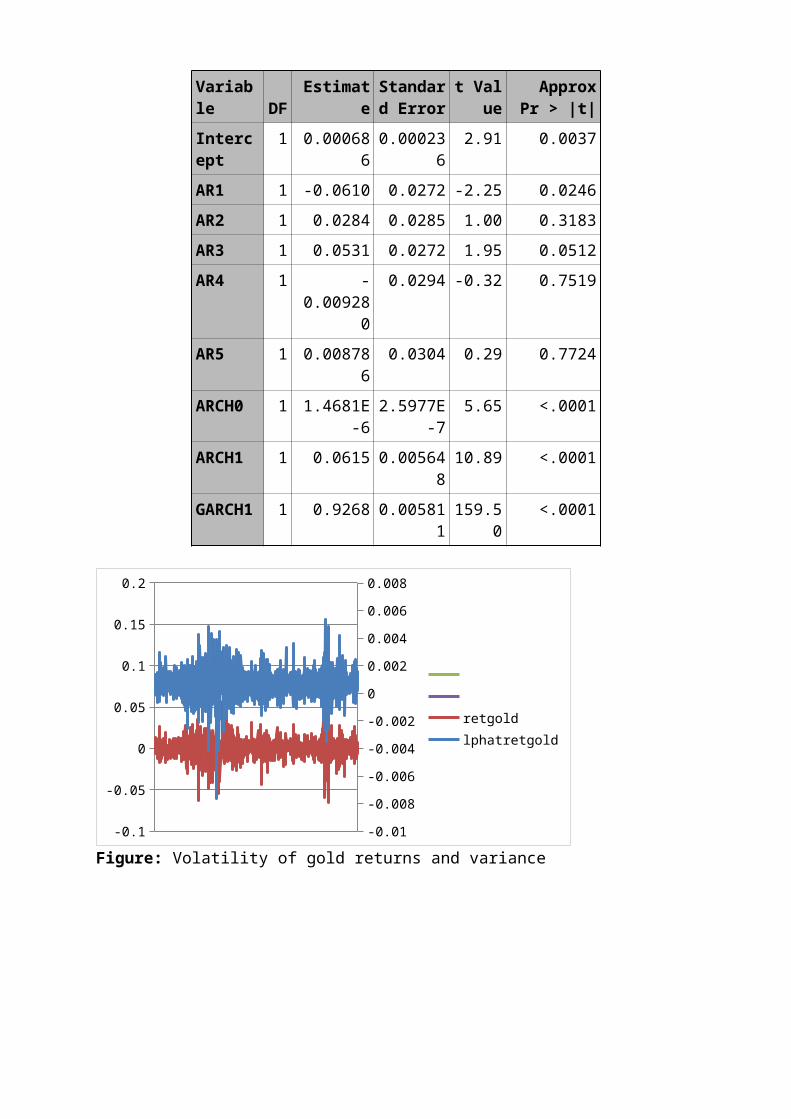

ods html;Proc autoreg data=anil.garchdata; Model retgold=/ nlag=2garch=(q=1,p=1) maxit=50; Output out=anil.out cev=vhat; run; ods html close;

Dependent Variable

retgold

Ordinary Least Squares EstimatesSSE 0.177133

28DFE 1458

MSE 0.0001215Root MSE 0.01102

SBC -9007.120

2

AIC -9012.405

7Regress R-Square

0.0000 Total R-Square

0.0000

Durbin-Watson

1.8812

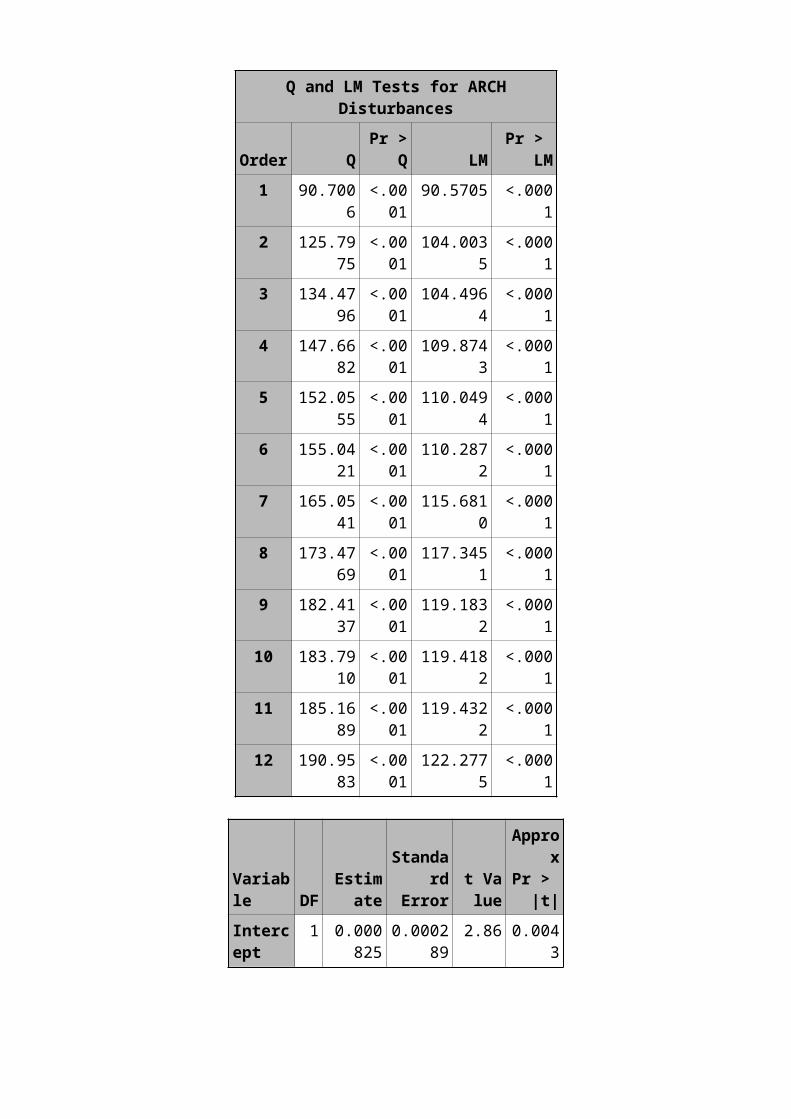

Q and LM Tests for ARCHDisturbances

Order QPr >

Q LMPr >

LM1 90.700

6<.0001

90.5705 <.0001

2 125.7975

<.0001

104.0035

<.0001

3 134.4796

<.0001

104.4964

<.0001

4 147.6682

<.0001

109.8743

<.0001

5 152.0555

<.0001

110.0494

<.0001

6 155.0421

<.0001

110.2872

<.0001

7 165.0541

<.0001

115.6810

<.0001

8 173.4769

<.0001

117.3451

<.0001

9 182.4137

<.0001

119.1832

<.0001

10 183.7910

<.0001

119.4182

<.0001

11 185.1689

<.0001

119.4322

<.0001

12 190.9583

<.0001

122.2775

<.0001

Variable DF

Estimate

Standard

Errort Value

Approx

Pr > |t|

Intercept

1 0.000825

0.000289

2.86 0.0043

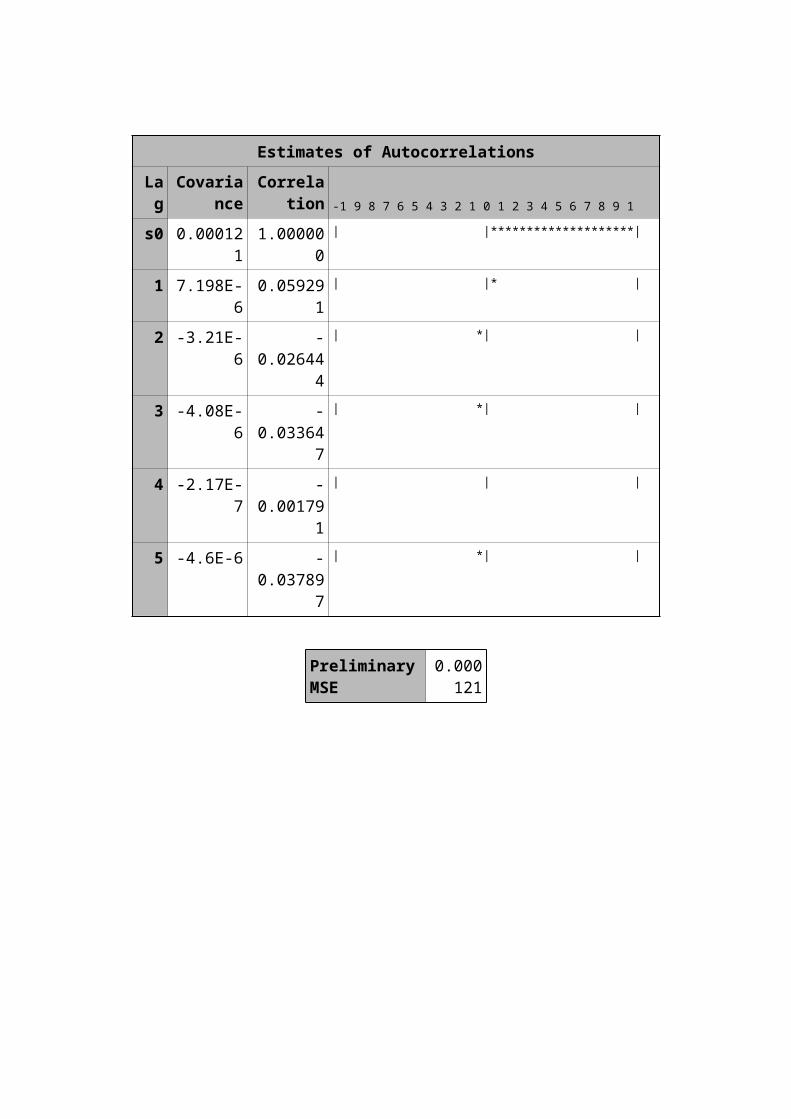

Estimates of AutocorrelationsLag

Covariance

Correlation -1 9 8 7 6 5 4 3 2 1 0 1 2 3 4 5 6 7 8 9 1

s0 0.000121

1.000000

| |********************|

1 7.198E-6

0.059291

| |* |

2 -3.21E-6

-0.02644

4

| *| |

3 -4.08E-6

-0.03364

7

| *| |

4 -2.17E-7

-0.00179

1

| | |

5 -4.6E-6 -0.03789

7

| *| |

PreliminaryMSE

0.000121

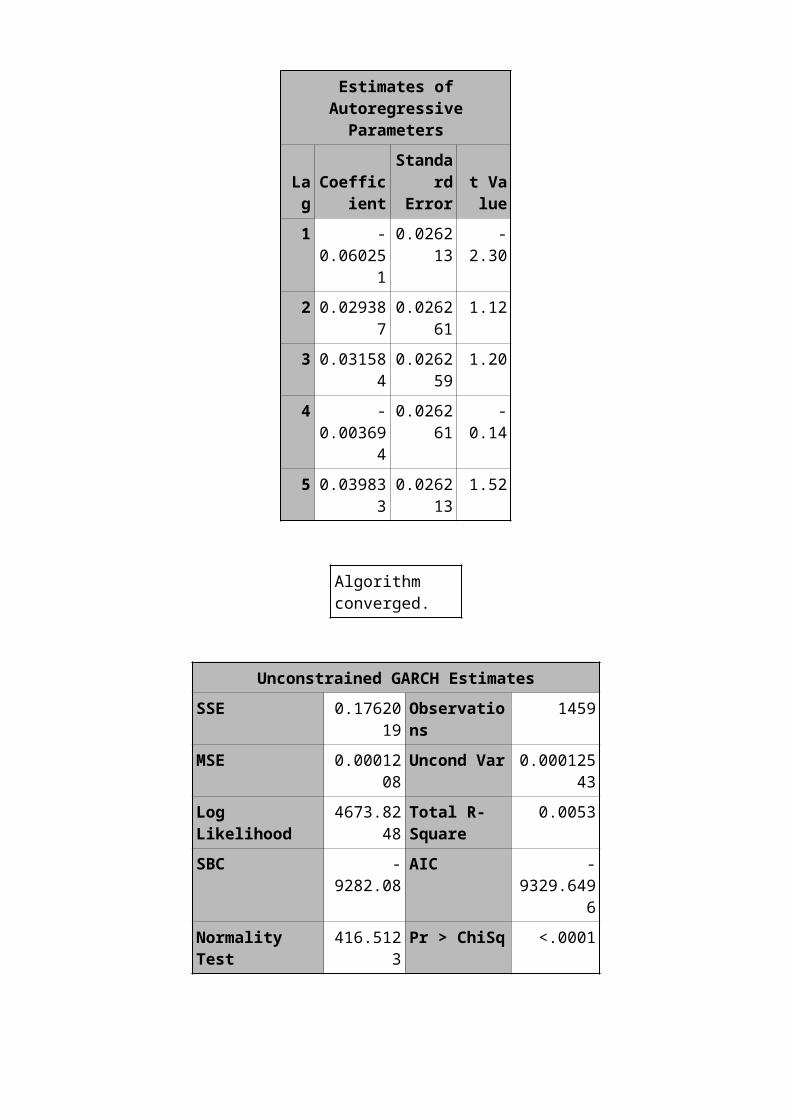

Estimates ofAutoregressiveParameters

LagCoeffic

ient

Standard

Errort Value

1 -0.06025

1

0.026213

-2.30

2 0.0293870.0262

611.12

3 0.0315840.0262

591.20

4 -0.00369

4

0.026261

-0.14

5 0.0398330.0262

131.52

Algorithm converged.

Unconstrained GARCH EstimatesSSE 0.17620

19Observations

1459

MSE 0.0001208

Uncond Var 0.00012543

Log Likelihood

4673.8248

Total R-Square

0.0053

SBC -9282.08

AIC -9329.649

6Normality Test

416.5123Pr > ChiSq <.0001

Variable DF

EstimateStandard Error

t Value

ApproxPr > |t|

Intercept

1 0.0006860.00023

62.91 0.0037

AR1 1 -0.0610 0.0272 -2.25 0.0246AR2 1 0.0284 0.0285 1.00 0.3183AR3 1 0.0531 0.0272 1.95 0.0512AR4 1 -

0.009280

0.0294 -0.32 0.7519

AR5 1 0.008786

0.0304 0.29 0.7724

ARCH0 1 1.4681E-6

2.5977E-7

5.65 <.0001

ARCH1 1 0.0615 0.00564810.89 <.0001

GARCH1 1 0.9268 0.005811159.5

0<.0001

-0.1

-0.05

0

0.05

0.1

0.15

0.2

-0.01

-0.008

-0.006

-0.004

-0.002

0

0.002

0.004

0.006

0.008

retgoldlphatretgold

Figure: Volatility of gold returns and variance

-0.3

-0.25

-0.2

-0.15

-0.1

-0.05

0

0.05

0.1

-0.02

-0.01

0

0.01

0.02

0.03

0.04

retsilverlphatretsilver

Figure: Volatility of silver returns and variance

-0.005

0

0.005

0.01

0.015

lphatretexrateuretexrate

Figure: Volatility of Exrate returns and variance

-0.008-0.006-0.004-0.002

00.0020.0040.0060.0080.010.012

-0.15-0.13-0.11-0.09-0.07-0.05-0.03-0.010.009999999999999980.030.05

lphatretnymexretnymex

Figure: Volatility of Nymex returns and variance

-0.04

-0.02

0

0.02

0.04

0.06

0.08

0.1

-0.15

-0.1

-0.05

2.77555756156289E-17

0.05

0.1

lphatretbseretbse

SFigure: Volatility of BSE returns and variance

Vector Auto Regression Model (VAR)Transfer functions assume that the independent variables and

associated lags influence the direction and magnitude of the

forecast series. These models are said NOT to allow for what

is termed “feedback”. A system is said to include feedback if

values of the input variable X depend in some fashion on the

past or current levels of the dependent variable. Vector ARIMA

models allow for this feedback process to occur. Being able to

describe the duality relationship between autoregressive

processes and moving average processes enables the forecaster

to use the autocorrelation and partial autocorrelation

functions to identify potential forms of Univariate models.

This is not the case in Vector ARIMA. The vector model does

not allow us to move from the infinite representation of one

process to the finite representation of the other. Therefore,

we need different tools to help us identify these processes

than what is generally used in Univariate ARIMA modeling. This

tool is called a CCF.

VARMAX models are defined in terms of the orders of the

autoregressive or moving-average process (or both). When you

use the VARMAX procedure, these orders can be specified by

options or they can be automatically determined. Criteria for

automatically determining these orders include

Akaike Information Criterion (AIC)

Corrected AIC (AICC)

Hannan-Quinn (HQ) Criterion

Final Prediction Error (FPE)

Schwarz Bayesian Criterion (SBC), also known as Bayesian

Information Criterion (BIC)

For situations where the stationarity of the time series

is in question, the VARMAX procedure provides tests to

aid in determining the presence of unit roots and

Cointegration. These tests include

Dickey-Fuller test

Johansen Cointegration test for non-stationary vector

processes of integrated order one

Stock-Watson common trends test for the possibility of

Cointegration among non-stationary vector processes of

integrated order one

Johansen Cointegration test for non-stationary vector

processes of integrated order two.

The VARMAX procedure provides a Granger-Causality test to

determine the Granger-causal relationships between two

distinct groups of variables. It also provides

infinite order AR representation

impulse response function (or infinite order MA

representation)

decomposition of the predicted error co variances

roots of the characteristic functions for both the AR and

MA parts to evaluate the proximity of the roots to the

unit circle

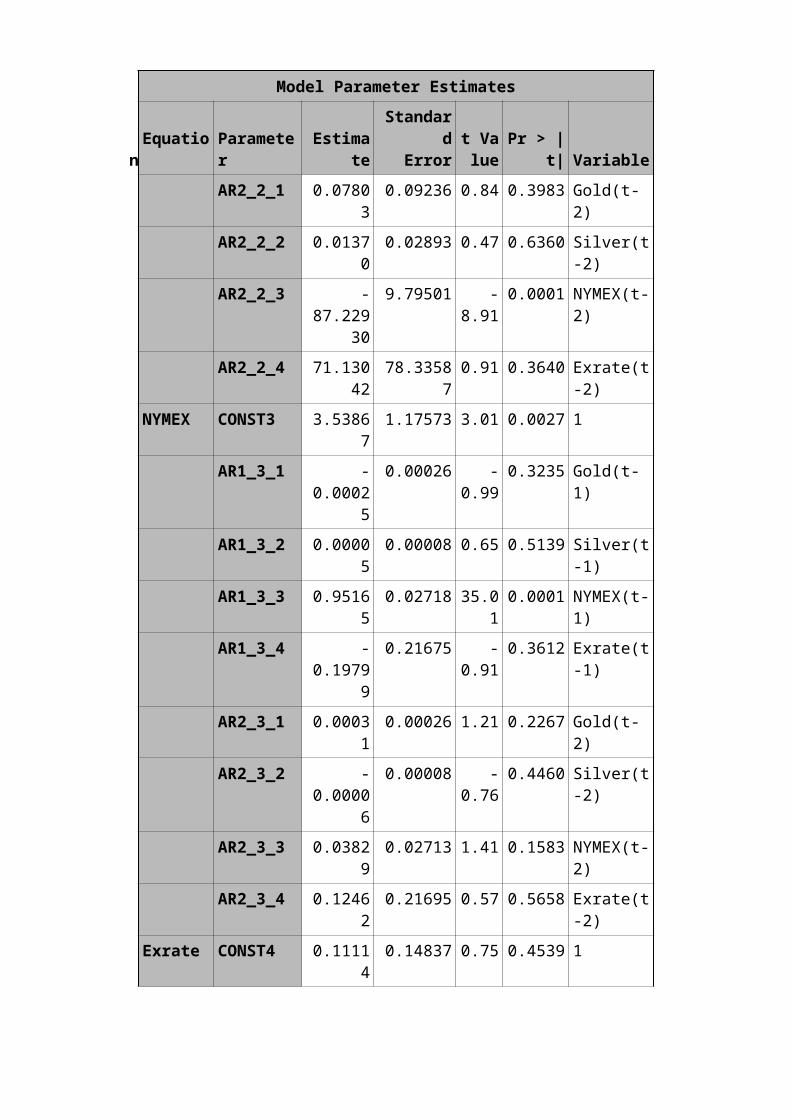

Example for VARMAX To fit a vector ARIMA we taken four variables like gold prices, silver prices, crude oil (nymex), and exchange rates. From 2nd Jan 2007 to 16th July 2012.

Proc varmax data=anil.work;id date interval=day;model gold silver exrate nymex/ p=1 nointlagmax=3;output out=for lead=15;

Model Parameter Estimates

Equation

Parameter

Estimate

Standard

Errort Value

Pr > |t| Variable

Gold CONST1 2.74450

133.40205

0.02 0.9836 1

AR1_1_1 0.83077

0.02900 28.640.0001 Gold(t-

1)AR1_1_2 0.0368

40.00910 4.05 0.0001 Silver(t

-1)AR1_1_3 17.328

193.08401 5.62 0.0001 NYMEX(t-

1)AR1_1_4 57.656

9324.5930

22.34 0.0192 Exrate(t

-1)AR2_1_1 0.1655

00.02902 5.70 0.0001 Gold(t-

2)AR2_1_2 -

0.03510

0.00909 -3.86

0.0001 Silver(t-2)

AR2_1_3 -17.489

59

3.07792 -5.68

0.0001 NYMEX(t-2)

AR2_1_4 -56.958

15

24.61571

-2.31

0.0208 Exrate(t-2)

Silver CONST2 617.25774

424.53230

1.45 0.1462 1

AR1_2_1 -0.0555

1

0.09230 -0.60

0.5477 Gold(t-1)

AR1_2_2 0.97928

0.02895 33.820.0001 Silver(t

-1)AR1_2_3 86.632

679.81441 8.83 0.0001 NYMEX(t-

1)AR1_2_4 -

86.37040

78.26364

-1.10

0.2700 Exrate(t-1)

Model Parameter Estimates

Equation

Parameter

Estimate

Standard

Errort Value

Pr > |t| Variable

AR2_2_1 0.07803

0.09236 0.84 0.3983 Gold(t-2)

AR2_2_2 0.01370

0.02893 0.47 0.6360 Silver(t-2)

AR2_2_3 -87.229

30

9.79501 -8.91

0.0001 NYMEX(t-2)

AR2_2_4 71.13042

78.335870.91 0.3640 Exrate(t

-2)NYMEX CONST3 3.5386

71.17573 3.01 0.0027 1

AR1_3_1 -0.0002

5

0.00026 -0.99

0.3235 Gold(t-1)

AR1_3_2 0.00005

0.00008 0.65 0.5139 Silver(t-1)

AR1_3_3 0.95165

0.02718 35.010.0001 NYMEX(t-

1)AR1_3_4 -

0.19799

0.21675 -0.91

0.3612 Exrate(t-1)

AR2_3_1 0.00031

0.00026 1.21 0.2267 Gold(t-2)

AR2_3_2 -0.0000

6

0.00008 -0.76

0.4460 Silver(t-2)

AR2_3_3 0.03829

0.02713 1.41 0.1583 NYMEX(t-2)

AR2_3_4 0.12462

0.21695 0.57 0.5658 Exrate(t-2)

Exrate CONST4 0.11114

0.14837 0.75 0.4539 1

Model Parameter Estimates

Equation

Parameter

Estimate

Standard

Errort Value

Pr > |t| Variable

AR1_4_1 0.00000

0.00003 0.13 0.9000 Gold(t-1)

AR1_4_2 0.00000

0.00001 0.13 0.8936 Silver(t-1)

AR1_4_3 -0.0050

4

0.00343 -1.47

0.1422 NYMEX(t-1)

AR1_4_4 1.01326

0.02735 37.050.0001 Exrate(t

-1)AR2_4_1 0.0000

00.00003 0.07 0.9420 Gold(t-

2)AR2_4_2 -

0.00000

0.00001 -0.26

0.7923 Silver(t-2)

AR2_4_3 0.00546

0.00342 1.59 0.1110 NYMEX(t-2)

AR2_4_4 -0.0177

4

0.02738 -0.65

0.5171 Exrate(t-2)

Proc gplot data=data;plot (gold gforecast)*date/overlay legend;run;

P L O T G o l d F o r e c a s t s f o r G o l d

G o l d

0

1 0 0 0 0

2 0 0 0 0

3 0 0 0 0

4 0 0 0 0

D a t e

0 1 J A N 2 0 0 7

P L O T S i l v e r F o r e c a s t s f o r S i l v e r

S i l v e r

1 0 0 0 0

2 0 0 0 0

3 0 0 0 0

4 0 0 0 0

5 0 0 0 0

6 0 0 0 0

7 0 0 0 0

8 0 0 0 0

Proc gplot data=data;plot (silver sforecast)*date/overlay

P L O T E x r a t e F o r e c a s t s f o r E x r a t e

E x r a t e

3 94 04 14 24 34 44 54 64 74 84 95 05 15 25 35 45 55 65 75 8

P L O T N Y M E X F o r e c a s t s f o r N Y M E X

N Y M E X

3 0

4 0

5 0

6 0

7 0

8 0

9 0

1 0 0

1 1 0

1 2 0

1 3 0

1 4 0

1 5 0

Proc gplot data=data;plot (exrate exforecast)*date/overlay legend;run;

Proc gplot data=data;plot (nymex nforecast)*date/overlay legend;run;

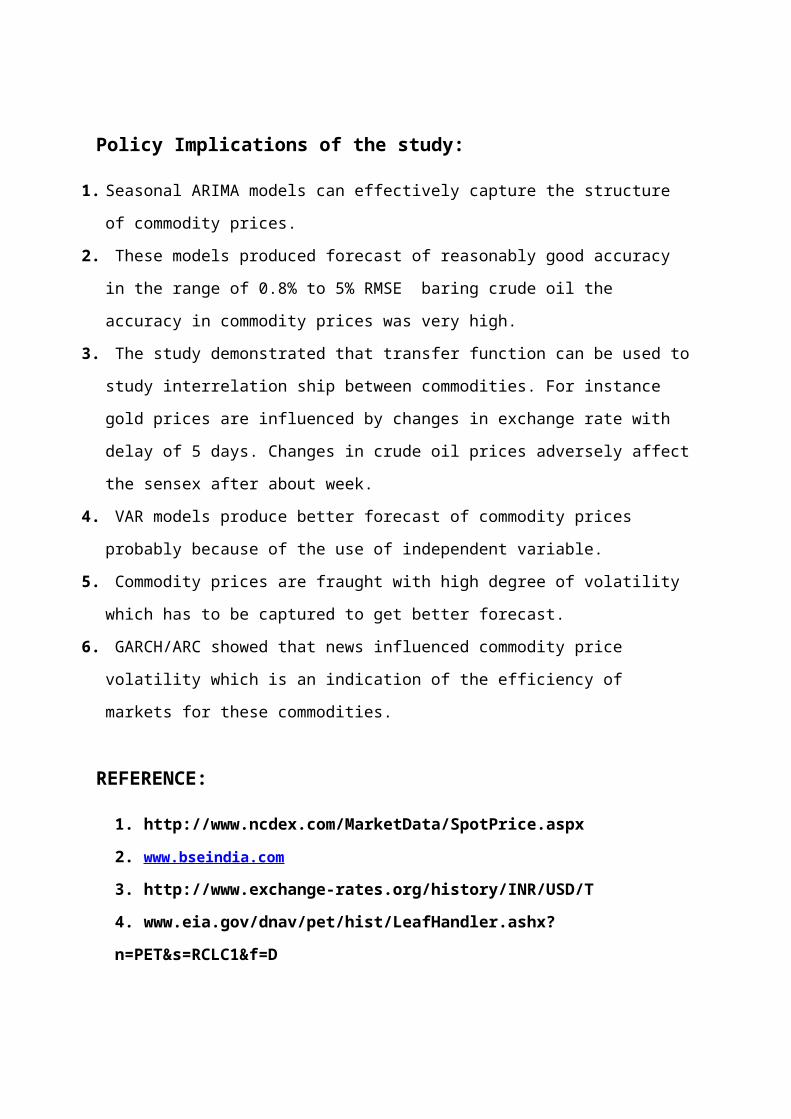

Policy Implications of the study:

1. Seasonal ARIMA models can effectively capture the structure

of commodity prices.

2. These models produced forecast of reasonably good accuracy

in the range of 0.8% to 5% RMSE baring crude oil the

accuracy in commodity prices was very high.

3. The study demonstrated that transfer function can be used to

study interrelation ship between commodities. For instance

gold prices are influenced by changes in exchange rate with

delay of 5 days. Changes in crude oil prices adversely affect

the sensex after about week.

4. VAR models produce better forecast of commodity prices

probably because of the use of independent variable.

5. Commodity prices are fraught with high degree of volatility

which has to be captured to get better forecast.

6. GARCH/ARC showed that news influenced commodity price

volatility which is an indication of the efficiency of

markets for these commodities.

REFERENCE:

1. http://www.ncdex.com/MarketData/SpotPrice.aspx

2. www.bseindia.com

3. http://www.exchange-rates.org/history/INR/USD/T

4. www.eia.gov/dnav/pet/hist/LeafHandler.ashx?

n=PET&s=RCLC1&f=D

5. ROBERT F. ENGLE, PhD Leonard N. Stern School of Business,New York University, ARCH/GARCH Models in Applied Financial Econometrics

6. John J. Sparks and Yuliya V. Yurova, University of

Illinois at Chicago Comparative Performance of ARIMA and

ARCH/GARCH Models on Time Series of Daily Equity Prices

for Large Companies

7. James D. Hamilton, Applied time series analysis,

Princstion university Press 1994

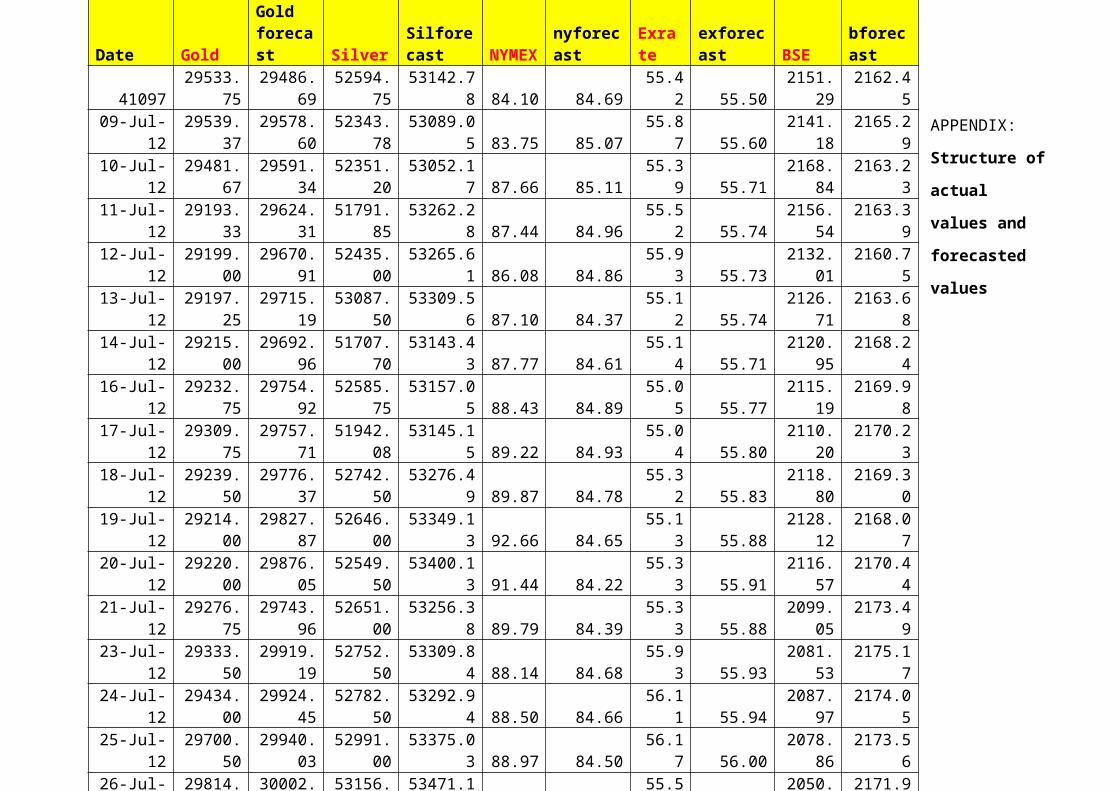

APPENDIX:

Structure of

actual

values and

forecasted

values

Date Gold

Gold forecast Silver

Silforecast NYMEX

nyforecast

Exrate

exforecast BSE

bforecast

4109729533.

7529486.

6952594.

7553142.7

8 84.10 84.6955.4

2 55.502151.

292162.4

509-Jul-

1229539.

3729578.

6052343.

7853089.0

5 83.75 85.0755.8

7 55.602141.

182165.2

910-Jul-

1229481.

6729591.

3452351.

2053052.1

7 87.66 85.1155.3

9 55.712168.

842163.2

311-Jul-

1229193.

3329624.

3151791.

8553262.2

8 87.44 84.9655.5

2 55.742156.

542163.3

912-Jul-

1229199.

0029670.

9152435.

0053265.6

1 86.08 84.8655.9

3 55.732132.

012160.7

513-Jul-

1229197.

2529715.

1953087.

5053309.5

6 87.10 84.3755.1

2 55.742126.

712163.6

814-Jul-

1229215.

0029692.

9651707.

7053143.4

3 87.77 84.6155.1

4 55.712120.

952168.2

416-Jul-

1229232.

7529754.

9252585.

7553157.0

5 88.43 84.8955.0

5 55.772115.

192169.9

817-Jul-

1229309.

7529757.

7151942.

0853145.1

5 89.22 84.9355.0

4 55.802110.

202170.2

318-Jul-

1229239.

5029776.

3752742.

5053276.4

9 89.87 84.7855.3

2 55.832118.

802169.3

019-Jul-

1229214.

0029827.

8752646.

0053349.1

3 92.66 84.6555.1

3 55.882128.

122168.0

720-Jul-

1229220.

0029876.

0552549.

5053400.1

3 91.44 84.2255.3

3 55.912116.

572170.4

421-Jul-

1229276.

7529743.

9652651.

0053256.3

8 89.79 84.3955.3

3 55.882099.

052173.4

923-Jul-

1229333.

5029919.

1952752.

5053309.8

4 88.14 84.6855.9

3 55.932081.

532175.1

724-Jul-

1229434.

0029924.

4552782.

5053292.9

4 88.50 84.6656.1

1 55.942087.

972174.0

525-Jul-

1229700.

5029940.

0352991.

0053375.0

3 88.97 84.5056.1

7 56.002078.

862173.5

626-Jul- 29814. 30002. 53156. 53471.1 55.5 2050. 2171.9