Price, exchange rate volatility and Nigeria's agricultural trade ...

Upload

khangminh22Category

view

1download

0

The Effects of Exchange Rate and Commodity Price Volatilities on Trade Volumes of Major Agricultural Commodities

by

A K Iftekharul Haque

A Thesis

presented to

The University of Guelph

In partial fulfillment of requirements

for the degree of

Master of Science

in

Food, Agricultural and Resource Economics

Guelph, Ontario, Canada

© A K Iftekharul Haque, September 2012

ABSTRACT

The Effects of Exchange Rate and Commodity Price Volatilities on

Trade Volumes of Major Agricultural Commodities

A K Iftekharul Haque

University of Guelph, 2012

Advisor:

Professor Getu Hailu

This thesis examines the effects of price and exchange rate volatilities on the volume of

trade corn, soybean, wheat and rice. Empirical results indicate that price volatility and

exchange rate volatilities do not have effects on Canada’s export of wheat and soybean,

and Canada’s import of corn and rice. This thesis also examined the effects of exchange

rate and commodity price volatilities on developed countries’ trade and developing

countries’ trade separately. Results show that trade between developing countries is more

sensitive to exchange rate and commodity price volatilities than trade between developed

countries.

iii

Acknowledgements

I would first like to thank my advisor, Dr. Getu Hailu, for countless reasons. His

mentorship, continuous support and extreme level of patience throughout my research

have been sources of encouragement for my professional and personal development. I

would like to thank Professor Karl Meilke for agreeing to be in my advisory committee

even after his retirement. I undoubtedly benefited from his vast knowledge of

international trade policy. I am grateful to Professor Alan Ker, another member of my

advisory committee, not only for his invaluable guidance but also taking care of all other

issues of mine during my stay at the Department of Food, Agricultural and Resource

Economies. I would also like to thank all the faculty members and staffs of the

Department of Food, Agricultural and Resource Economics, for guidance throughout the

coursework and completion of my thesis.

My sincere gratitude goes to the Canadian Agricultural Trade Policy and

Competitiveness Research Network (CATPRN) for providing me with the finances

necessary for this research.

I would also like to thank my peer group for their continuous support to my work.

Notably Xin Xie, Rebecka Elskamp, Alex Cairns, Rob Anderson, Zongyuan Shang,

Johanna Wilkes, Tor Tolhurst and Di Ai for their valuable advice, support and criticism.

I would like to thank my parents for their unconditional love; and my wife, Tasnuva, for

her extreme patience and encouragement to my work. Finally I must thank my son,

Shoummo, for being a source of joy and happiness.

iv

Table of Contents

ACKNOWLEDGEMENTS III

TABLE OF CONTENTS IV

LIST OF TABLES VI

LIST OF FIGURES VII

CHAPTER 1: INTRODUCTION 1

1.1: Background 1

1.2 Economic Problem 3

1.3 Economic Research Problem 3

1.4 Purpose and Objectives 5

CHAPTER 2: RECENT TRENDS OF EXCHANGE RATES AND COMMODITY PRICES 6

2.1 Exchange Rate Volatility 6

2.2 Agricultural Commodity Price Volatility 8

2.3 Drivers of Agricultural Commodity Price Volatilities 13

2.4. Chapter Summary 20

CHAPTER 3: LITERATURE REVIEW 21

3.1: Effects of Exchange Rate Volatilities: Theoretical Background 21

3.2 Measuring Exchange Rate and Price Volatilities 22

3.3 Empirical Literature: Exchange rate Volatility and Trade 24

3.4 Empirical Literature: Exchange Rate Volatility and Agricultural Trade 26

3.5 Chapter summary 28

CHAPTER 4: CONCEPTUAL FRAMEWORK 29

4.1 Model Description 29

v

4.2 Import Demand 29

4.3 Chapter Summary 33

CHAPTER 5: EMPIRICAL FRAMEWORK 34

5.1 Econometric specification 34

5.2 Variable Description 35

5.3 Data and sources 40

5.4 Model Selection 44

5.5 Diagnostics: Tests for Unit root, Heteroscedasticity, Serial Correlation and Multicollinearity 47

5.6 Chapter Summary 49

CHAPTER 6: RESULTS AND DISCUSSIONS 50

6.1 Introduction 50 6.2.1 Quarterly Imports of Wheat and Soybean from Canada 50 6.2.2. Quarterly import models of corn and rice 56

6.3 Annual Models 62 6.3.1 Top developed importers’ imports from Developed exporters 62 6.3.2 Top developing importers’ imports from developing exporters 69

6.4 Chapter Summary 75

CHAPTER 7: SUMMARY AND CONCLUSION 76

7.1 Summary 76

7.2 Policy implications 79

7.3 Limitations and further research 81

7.4 Research Contribution 82

REFERENCES 83

APPENDIX A 87

APPENDIX B 89

vi

List of Tables

Table 2.1: Evolution of Exchange rate Arrangements, 1996-2007 7

Table 5.1: Summary of export and import data for quarterly models 41

Table 5.2: Summary of import data for annual models 41

Table 5.3: Summery of Data Frequency and Sources for exchange rate, GDP prices 42

Table 5.4: List of Countries for Quarterly Models 42

Table 5.5: List of importing countries considered for annual models 43

Table 6.1: Fisher’s unit root test for wheat and soybean 51

Table 6.2: VIF for wheat and soybean model 53

Table 6.3: Coefficient estimates of quarterly wheat and soybean imports from

Canada from 2000 to 2009 55

Table 6.3a : Coefficient estimates of quarterly wheat and soybean imports from

Canada from 2000 to 2009 (without expected price variable) 56

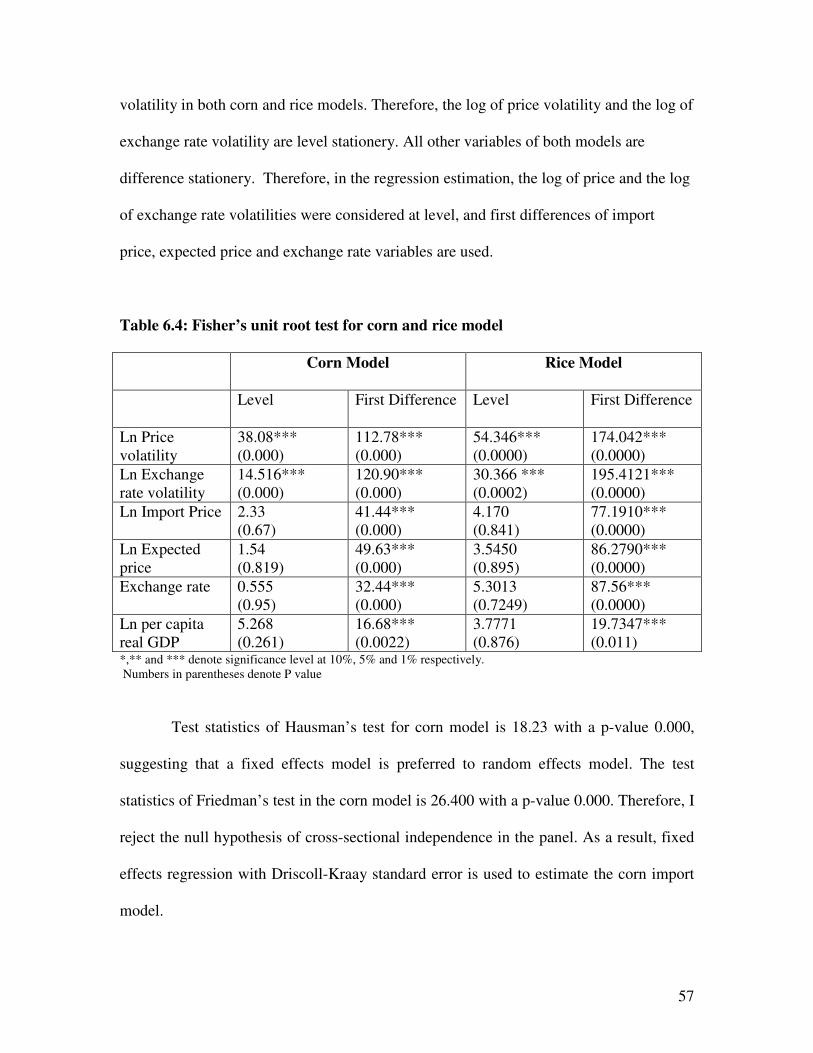

Table 6.4: Fisher’s unit root test for corn and rice model 57

Table 6.5: VIF for corn and rice model 59

Table 6.6: Coefficient estimates of Canada’s corn and rice import demand from

2000-2009 60

Table 6.7: Coefficient estimates of Canada’s corn and rice import demand from

2000-2009 (without percentage change of expected price) 61

Table 6.8: Fisher’s panel Unit Root Test 63

Table 6.9: Hausman Specification tests 64

Table 6.10: Friedman’s test for cross sectional independence 64

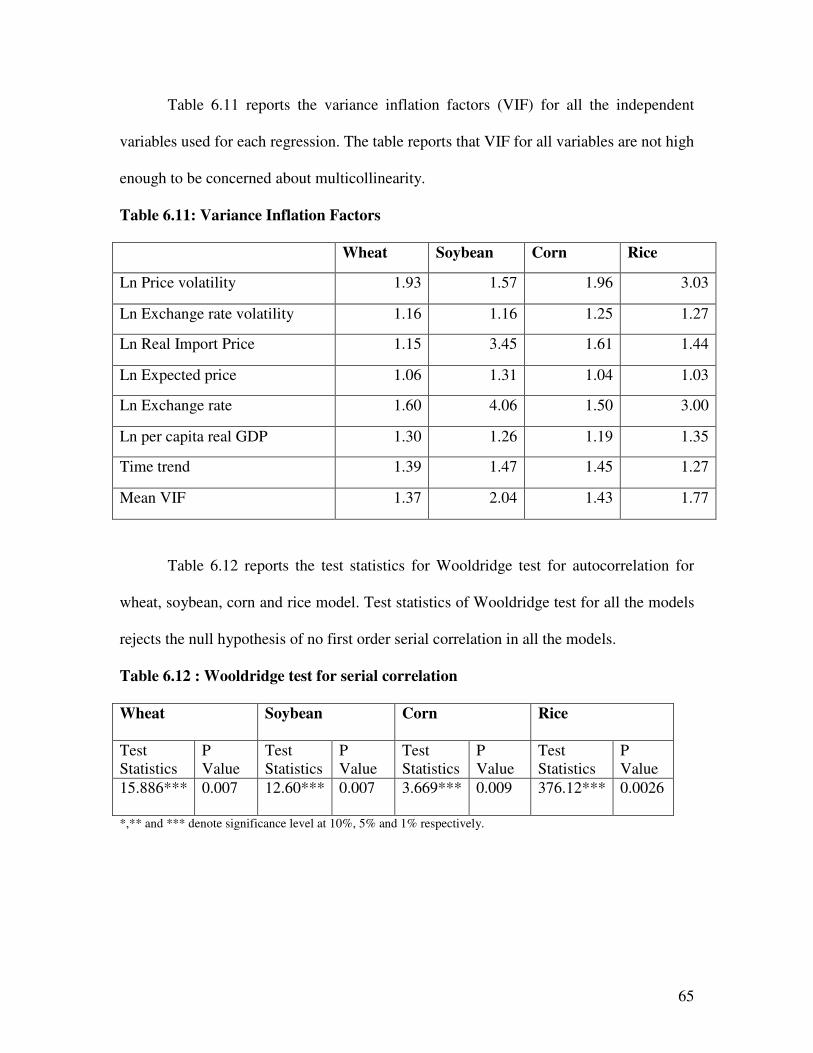

Table 6.11: Variance Inflation Factors 65

Table 6.12 : Wooldridge test for serial correlation 65

6.13: Coefficients estimates of developed countries’ wheat, soybean, corn and rice

imports from developed importers from 1991 to 2009 67

6.13a: Coefficients estimates of developed countries’ wheat, soybean, corn and rice

imports from developed countries from 1991 to 2009 (without percentage change of

expected price) 68

Table 6.14: Fisher’s panel Unit Root Test 69

Table 6.15: Hausman’s Specification tests 70

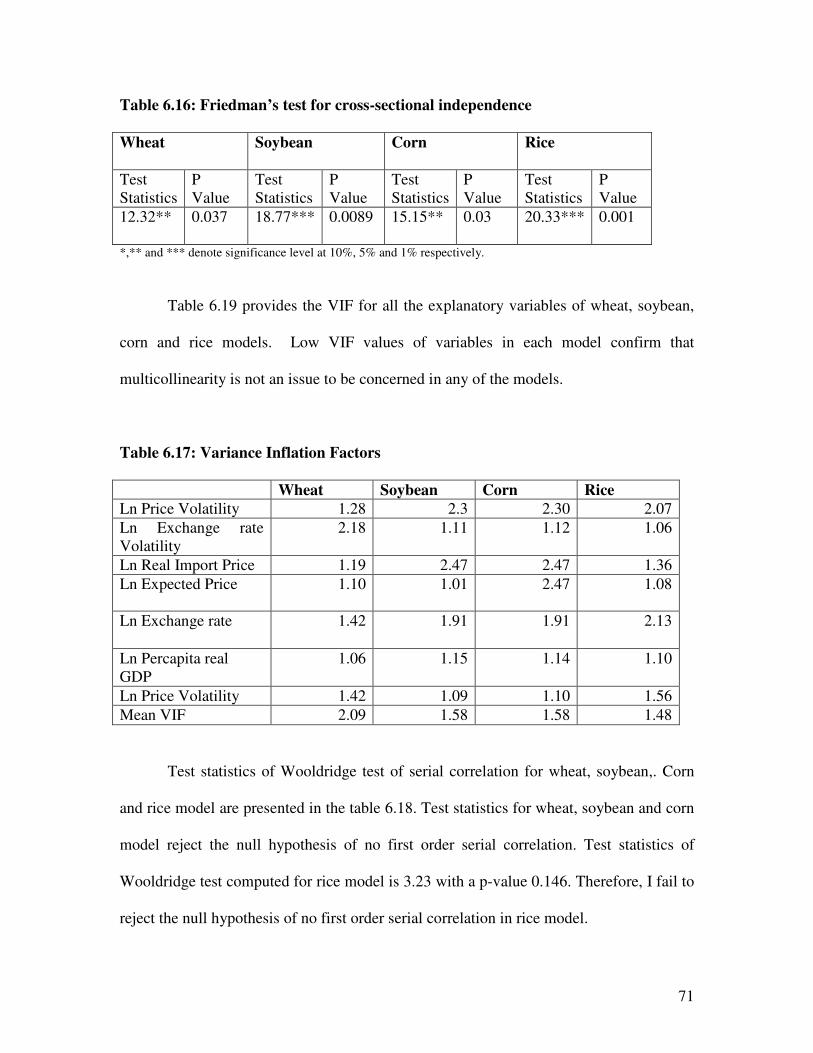

Table 6.16: Friedman’s test for cross-sectional independence 71

Table 6.17: Variance Inflation Factors 71

Table 6.18 : Wooldridge test for serial correlation 72

6.19: Coefficient estimates of developing importers’ imports of wheat, soybean,

corn and rice from developing exporters from 1991 to 2009 73

6.20: Coefficient estimates of developing importers’ imports of wheat, soybean,

corn and rice from developing exporters from 1991 to 2009 (without percentage

change of expected price) 74

vii

List of Figures

Figure 2.1: Exchange Rate movements of major currencies 7

Figure 2.2a: Monthly Corn price (F.O.B) in selected market from January 2000

(USD/Ton) 8

Figure 2.2b: Historical volatility of corn price 9

Figure 2.3a: Monthly wheat price (F.O.B) in selected market from January 2000

(USD/Ton) 10

Figure 2.3b: Historical volatility of wheat price 10

Figure 2.4a: US Soybean monthly F.O.B. Price from January 2000 11

Figure 2.4b: Historical volatility of soybean price 11

Figure 2.5a: Monthly rice price (F.O.B) in selected market from January 2000 to

January 2012 (USD/Ton) 12

Figure 2.5b: Historical volatility of rice price 12

Figure 2.6: Global Ethanol Production (in million Gallons) 14

Figure 2.7 : Share of US Corn used to produced ethanol, 1980-2011 14

Figure 2.8: Monthly Volume of Future Trades of Wheat, Maize and Soybeans at

Chicago Board of Trade (CBOT) 15

Figure 2.9: Per Capita Income Level by Developing Region 17

Figure 2.10: GDP Per Capita of India and China (Constant US Dollar) 17

Figure 2.11 a: Major Exporters of Maize in 2008 18

Figure 2.11 b: Major Exporters of Wheat in 2008 18

Figure 2.11 c: Major Exporters of Rice in 2008 19

Figure 2.12: Stocks to cereal use ratio 20

1

Chapter 1: Introduction

1.1: Background

Agricultural commodity price and exchange rate volatilities drew a global attention

because of their potential effects on international trade and domestic food prices.

Although the effects of exchange rate volatilities on international agricultural trade have

been examined for long time, the effects of price volatilities have not been examined at

large. Most of the recent studies (IFPRI, 2011,; Braun and Tadesse, 2012; Weersink et al

2008; OECD and FAO, 2012 ) on commodity price volatilities reviewed the reasons for

agricultural commodity price volatility. The purpose of this study is to examine the

effects of both exchange rate and commodity price volatilities on international

agricultural commodity trade and to estimate the effects of volatilities on developed and

developing countries separately.

Effects of exchange rate volatilities on trade flows became a center of interest

from early 1970 when a floating exchange rate regime began to replace the former fixed

exchange rate regime. The floating exchange rate system allows the value of a currency

to fluctuate based on the foreign exchange market fundamentals. Smith’s (1999) review

show that a number of studies were conducted to determine the impact of exchange rate

volatilities on trade flows, and find that the empirical evidence is mixed. For example,

Cushman (1983), Thursby and Thursby (1987) and Bini-Smaghi (1991) find that an

increase in exchange rate volatility leads to a reduction in the volume of international

trade. In contrast, Frankel and Wei (1995) and Sercu and Uppal (2003) claim that

exchange rate volatilities may not have any effect on the volume of international trade.

2

While the effect of exchange rate volatility is still uncertain, agricultural commodity price

volatility has recently received much attention after the unprecedented spike in crop

prices and volatilities that occurred in 2007-08. The rise in the level of commodity prices

and volatilities resulted in a number of countries adopting policies that restricted food

imports and exports (IFPRI, 2011).

Commodity price volatility may have implications for the volume of agricultural

commodity trade when individual countries adopt policies that restrict imports or exports

(e.g., export bans) as a method of coping with price variations. Although the

consequences of exchange rate volatility on trade have extensively been examined and at

the centre of debate, research on the effects of commodity price volatility on international

trade (e.g., on volume) is limited. Volatility in the world market prices can have major

effects on agricultural trade since agricultural products and agricultural industry have

many characteristics, such as perishable nature of products and less supply

responsiveness to short term price fluctuation that distinguished them from other

industries. Uncertainty in the world agricultural market has a greater impact on farm income

in both developed and developing countries (Koo and Kennedy, 2007) and food security in

developing and low income countries (IFPRI, 2011).

In this study, I examine the effects of price and exchange rate volatilities on Canada’s

trade with its major trading partners using quarterly data for wheat, soybean, corn and

rice, and examine the effects of exchange rate and price volatilities on developed and

developing countries’ trade separately with annual models.

3

1.2 Economic Problem

Increased volatilities of exchange rate and commodity prices increase uncertainties over

expected profit of firms (Hooper and Kohlhagen, 1978; Clark, 1973; IFPRI. 2011). Clark

(1973) argues that exporting firms reduce exports and charge higher price as risk

premium when they expect such uncertainties over profit. The rise in price due to the risk

premium directly affects consumers’ surplus (Bellemare et al. 2011). When importers

decrease imports due to volatilities of exchange rate and commodity prices, excess

demand decreases in international market and reduces the price of commodities in the

international market which affects producers’ surplus of exporting countries. As a result,

both consumers and producers in countries engaged in agricultural trade can be affected

because of volatilities in exchange rate and commodity prices. The findings of this

research will be useful for agricultural trading firms of both developed and low income

countries; and central banks and trade ministries of low income countries.

1.3 Economic Research Problem

A number of studies examined the effects of exchange rate volatilities on commodity

trade flows using aggregate data1 (Akhtar and Hilton, 1984; Arize, 1995; Arize, 199;

Arize and Ghosh, 1997; Bahmani-Osookee, 2002; Chowdhury, 1993; Gotur 1985) and

bilateral trade data (Bini-Smaghi, 1991; Cushman, 1983; Dell’ Ariccia, 1999; Hooper and

Kohlhagen, 1978; McKenzie and Brooks, 1997; Thursby and Thursby; 1997). Most of

these studies examined the effect of exchange rate volatility on overall trade flows (i.e.,

1 measures the trade flow of a nation to all of its trading partners or to the rest of the world

4

total of trade in all sectors) rather than trade flows of a specific sector (e.g., agriculture)

or specific commodity (e.g., wheat, corn). Sector specific studies mostly attempted to

estimate the effects of exchange rate volatilities on trade of manufacturing goods (Di Vita

and Abott, 2004; Klein, 1990; Maskus, 1986; Belanger et al. 1992, Chou, 2000). Only a

few studies estimated the effects exchange rate volatilities on agricultural commodity

trade flows (Cho et al. 2002, Sun et al. 2002, Kandilov, 2008; Giorgioni and Thompso,

2002, Villanueva and Sarker 2009). However, most of these studies (Cho et al 2002,

Kandilov 2008; Giorgioni and Thompson, 2002) used aggregated agricultural commodity

trade data of countries. Research on the effects of exchange rate volatility on specific

agricultural commodities is limited.

Meanwhile, research on the effects of commodity price volatilities on trade flows

is also limited. Despite a few recent studies (Raddatz, 2011; FAO et al. 2011; Weersink

et al. 2008, Wright, 2011) that a reviewed the effects of food price volatilities on food

security, the effects of commodity price volatilities on trade flows remain unaddressed.

Zhang (2010) is one of the first studies to examine the effects of exchange rate, price and

freight cost volatilities on the U.S. soybean exports.

This study explores the effects of both price and exchange rate volatilities on

Canada’s wheat, corn, soybeans and rice trade using quarterly data for the period 1999:1-

2010:4. It also examines the effects of exchange rate and commodity price volatilities on

import demand of major developed and developing importers of wheat, soybean, corn

and rice.

5

1.4 Purpose and Objectives

The purpose of this research is to estimate the effect of commodity price and exchange

rate volatilities on Canada’s trade flows of wheat, corn, soybeans and rice.

The specific objectives are:

1. To estimate the effect of exchange rate and agricultural commodity price

volatilities on Canada’s exports of wheat and soybean; and Canada’s imports of

corn and rice.

2. To examine the effects of commodity price and exchange rate volatilities on the

agricultural commodity imports of developed and developing countries

separately.

After this brief introduction, chapter 2 presents recent trends of exchange rates

and commodity prices, chapter 3 reviews the key literature, chapter 4 discusses the

theoretical framework, chapter 5 presents the empirical framework of the study, chapter 6

provides the estimates of parameters of the regression models and finally chapter 7

provides summaries and conclusions.

6

Chapter 2: Recent Trends of Exchange Rates and Commodity Prices

2.1 Exchange Rate Volatility

From the early 1970s a floating exchange rate regime began to replace the former fixed

exchange rate regime which was also known as Bretton Wood System. Most of the

developing countries continued to peg their currencies either to a single important

currency, e.g., the U.S. Dollar, or to a basket of currencies. For example, in 1975, 87%

of the developing countries had some types of fixed exchange rate system. Later,

countries gradually moved from fixed to a floating exchange rate regime (see Table 2.1).

Appendix A provides a more detailed list of countries according to their exchange rate

system.

In a floating exchange rate system, exchange rates are determined by the demand

and supply of currencies in the foreign exchange market. At the beginning of the floating

exchange rate regime, exchange rates of major currencies experienced increased

fluctuations (Clark 2004). The fluctuations of major currencies under floating exchange

rate system made researchers and policy makers concerned about its potential effect on

international trade.

Figure 2.1 Shows the exchange rates of major currencies over the last four

decades. It is obvious from Figure 2.1 that key currencies of the world became unstable

after the adoption of floating exchange rate regime.

7

Table 2.1: The Evolution of Exchange rate Arrangements, 1996-2007

Year

Fixed Arrangements

(Number of Countries)

Floating Arrangements

(Number of Countries)

Total Number of

Countries

1996 124 60 184

2001 93 93 186

2002 95 92 187

2003 94 93 187

2004 94 93 187

2005 98 89 187

2006 105 82 187

2007 105 83 188

Source: IMF (2007)

Note: End of period data.

Figure 2.1: Exchange Rate movements of major currencies

CAD/USD

0.5

0.7

0.9

1.1

1.3

1.5

1.7

Jan-7

1

Dec-

72

Nov-

74

Oct

-76

Sep-7

8

Aug-80

Jul-8

2

Jun-8

4

May-

86

Apr-88

Mar

-90

Feb-9

2

Jan-9

4

Dec-

95

Nov-

97

Oct

-99

Sep-0

1

Aug-03

Jul-0

5

Jun-0

7

May-

09

Apr-11

CAD/EUR

1

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

Jan-9

9

Sep-99

May-0

0

Jan-0

1

Sep-01

May-0

2

Jan-0

3

Sep-03

May-

04

Jan-0

5

Sep-05

May-0

6

Jan-0

7

Sep-07

May-0

8

Jan-0

9

Sep-09

May-1

0

Jan-1

1

Sep-11

May-1

2

1

1.5

2

2.5

3

Jan

-71

Jan

-73

Jan

-75

Jan

-77

Jan

-79

Jan

-81

Jan

-83

Jan

-85

Jan

-87

Jan

-89

Jan

-91

Jan

-93

Jan

-95

Jan

-97

Jan

-99

Jan

-01

Jan

-03

Jan

-05

Jan

-07

Jan

-09

Jan

-11

CAD/GBP

0.5

1

1.5

2

2.5

3

Jan

-71

Jan

-73

Jan

-75

Jan

-77

Jan

-79

Jan

-81

Jan

-83

Jan

-85

Jan

-87

Jan

-89

Jan

-91

Jan

-93

Jan

-95

Jan

-97

Jan

-99

Jan

-01

Jan

-03

Jan

-05

Jan

-07

Jan

-09

Jan

-11

USD/GBP

Source: Thompsons-Reuters Datastream

8

2.2 Agricultural Commodity Price Volatility

Agricultural commodity price volatility drew much attention of economists, policymakers

and media since the food price hike of 2007-2008(IFPRI, 2011). The food price upheaval

experienced in 2007-08 was not observed since the early 1970s (Weersink et al. 2008).

Although the food price hike of 2007-08 and the most recent in 2011 were below the

historical highest of 1970s, price volatility reached its highest level in the past 50 years

(IFPRI, 2011). This section briefly reviews the price fluctuations of major agricultural

commodities over the last decade for four major agricultural commodities- corn, wheat,

soybean and rice.

Corn

The food price crisis in 2007-08 began with a sharp rise in price of corn among the major

agricultural commodities. Figure 2.2a shows that the level of corn price of major

exporters started to rise from June 2006 and reached the peak in July 2008. It began to

decrease after July 2008 and again reached a new peak in mid-June, 2011. Figure 2.2b

suggests that corn price volatility also increased dramatically in 2007 and higher

volatilities continued.

Figure 2.2a: Monthly Corn price (F.O.B) in selected market from January 2000

(USD/Ton)

Source: FAO GIEWS Database

9

Figure 2.2b: Historical volatility of corn price

0

5

10

15

20

25

30

35

40

45

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

His

tori

cal

Vo

lati

lity

(%

)

Corn price volatiltiy

Source: CME group

Wheat

Wheat Prices quoted by the major international suppliers also became volatile from mid-

2007 (Figure 2.3b). From June 2006 wheat price in all major international markets

started to increase and reached to record high level at 450 USD per ton in March 2008.

Then it started to fall until December 2008 and went through a volatile period until it

reached USD 350 per tom in March 2011 (Figure 2.3a). Figure 2.3b shows the volatility

of wheat price over last two decades. The figure reports that wheat price volatility began

to increase from 2006. From 2007 to 2008, historical volatility of wheat price increased

from 32.4% to 50.6%. Although it came down to 35% in 2010, it began to increased

again in 2011.

10

Figure 2.3a: Monthly wheat price (F.O.B) in selected market from January 2000

(USD/Ton)

0

100

200

300

400

500

600

Jun-

00

Jan-

01

Aug-

01

Mar

-02

Oct

-02

May

-03

Dec-

03

Jul-0

4

Feb-

05

Sep-

05

Apr-

06

Nov

-06

Jun-

07

Jan-

08

Aug-

08

Mar

-09

Oct

-09

May

-10

Dec-

10

Jul-1

1

Feb-

12

Argentina USA (no.2 red soft) USA (no.2 red hard

Source: FAO GIEWS Database

Figure 2.3b: Historical volatility of wheat price

0

10

20

30

40

50

60

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

His

tori

cal

Vo

lati

lity

(%)

Wheat price volatility

Source: CME group

Soybean

Soybean price began to rise slightly from fall 2006 but did not rise to the extent of corn

price. It showed an upward trend from May 2007 and peaked at the level of 550USD/ton

in June 2008 (Figure 2.4a). Soybean price volatility reported in figure 2.4b shows that

like other major crops soybean price volatility also increased after 2006.

11

Weersink et al. (2008) report that the record high price of soybean was a spillover from

the surge in corn price. The soybean price rise can also be attributed to the surge in

demands of edible oil and reduction of soybean harvest. This decline of soybean

production was not due to bad weather condition rather largely to decline in planted area

in US as farmers shifted to corn from soybean. Volatility reached the peak in 2009 and

then it began to come down (figure 2.4b).

Figure 2.4a: US Soybean monthly F.O.B. Price from January 2000

100150200250300350400450500550600

2000M

11

2001M

04

2001M

09

2002M

02

2002M

07

2002M

12

2003M

05

2003M

10

2004M

03

2004M

08

2005M

01

2005M

06

2005M

11

2006M

04

2006M

09

2007M

02

2007M

07

2007M

12

2008M

05

2008M

10

2009M

03

2009M

08

2010M

01

2010M

06

2010M

11

2011M

04

2011M

09

US Soybean Price

Source: FAO GIEWS Database

Figure 2.4b: Historical volatility of soybean price

0

5

10

15

20

25

30

35

40

45

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

Soybean price volatility

Source: CME group

12

Rice Price hike of rice started little later compared to other agricultural commodities. Rice

prices in major international sources were somewhat stable until the beginning of 2007.

Then it shows a slightly upward trend until the beginning g of 2008 and jumped to USD

1000 per ton in mid-2008 (Figure 2.5a). Figure 2.5b shows that rice price volatility was

low until 2007. Between 2007 and 2008 volatility increased from 16% to 34%. It came

down to 20% in 2009 but started to rise again after 2010.

Figure 2.5a: Monthly rice price (F.O.B) in selected market from January 2000 to

January 2012 (USD/Ton)

0

200

400

600

800

1000

1200

1400

Jan-

00

Sep-

00

May

-01

Jan-

02

Sep-

02

May

-03

Jan-

04

Sep-

04

May

-05

Jan-

06

Sep-

06

May

-07

Jan-

08

Sep-

08

May

-09

Jan-

10

Sep-

10

May

-11

Jan-

12

Pakistan - Rice (25% broken) - Export

Thailand: Bangkok - Rice (Thai 100% B)

USA - Rice (U.S. California Medium Grain)

Source: FAO GIEWS Database

Figure 2.5b: Historical volatility of rice price

0

5

10

15

20

25

30

35

40

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

His

tori

cal

vo

lati

lity

(%

)

Rice price volatility

Source: CME group

13

2.3 Drivers of Agricultural Commodity Price Volatilities

This section briefly discusses the reasons of recent agricultural commodity price

volatilities from the recent literature.

Biofuel Policies

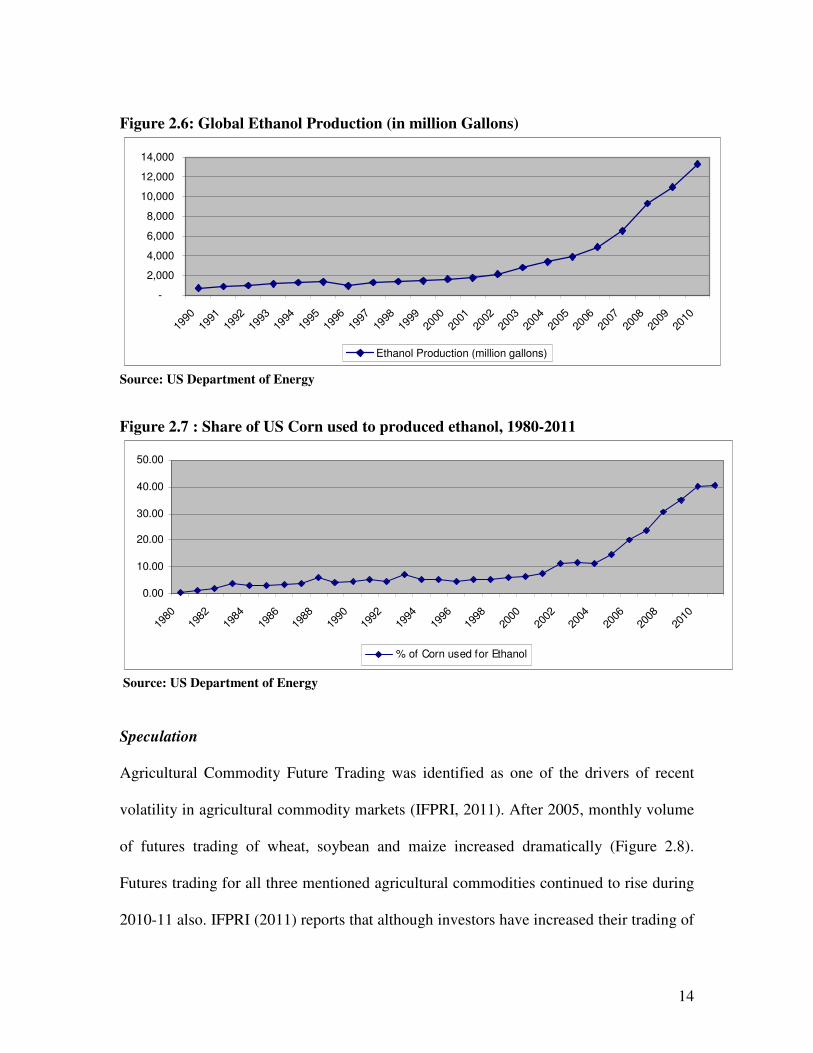

World ethanol production skyrocketed in the last decade from around 2000 million

gallons in 2001 to more than 13000 gallon in 2010 because of the subsidization and

biofuel mandates set by the United States and European Union (Figure 2.6). The primary

motivation for biofuel support is that biofuels will reduce demand for imported oil. To

comply with the mandate and support, farmers switched to production of biofuel crops ,

most of which are also used as food or feed. Figure 2.7 shows that in recent years more

than 40 % of US maize is used for ethanol production. Moreover, input demand for

biofuel crops increased recent years which contributed to the overall increase of cost of

agricultural inputs (IFPRI, 2011).

Production of biofuel crops strengthens the links between two highly volatile

markets- energy market and food market (IFPRI, 2011). Since ethanol is the substitute of

fuel, when the price of one barrel of fuel increases, the demand for ethanol, a substitute

product of fuel, also increases. This eventually increases the demand and consequentially

the price for corn (Weersink et al. 2008).

14

Figure 2.6: Global Ethanol Production (in million Gallons)

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Ethanol Production (million gallons)

Source: US Department of Energy

Figure 2.7 : Share of US Corn used to produced ethanol, 1980-2011

0.00

10.00

20.00

30.00

40.00

50.00

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

% of Corn used for Ethanol

Source: US Department of Energy

Speculation

Agricultural Commodity Future Trading was identified as one of the drivers of recent

volatility in agricultural commodity markets (IFPRI, 2011). After 2005, monthly volume

of futures trading of wheat, soybean and maize increased dramatically (Figure 2.8).

Futures trading for all three mentioned agricultural commodities continued to rise during

2010-11 also. IFPRI (2011) reports that although investors have increased their trading of

15

food commodity futures, only two per cent of these futures contract have resulted in

delivery of real goods. For example, the volume of futures traded on exchange worldwide

for maize is more than three times greater than the global production of maize.

Commodity index fund have became attractive for the investors as investment fund

flowed from the equity market, to real estate and now to the commodity markets. This

pattern of increasing agricultural commodity futures trading and higher prices for

commodity futures can worsen the volatility of spot prices for food commodities to

excessive levels (IFPRI, 2011).

Figure 2.8: Monthly Volume of Future Trades of Wheat, Maize and Soybeans at

Chicago Board of Trade (CBOT)

Source: IFPRI (2011)

Speculative behavior by governments (i.e., export bans, large stock orders) has also

played a role in increasing the volatility in agricultural commodity market. A number of

countries adopted supply restraint policies at the beginning of the high price volatilities in

2007. For example, rice export was banned by India, Vietnam, Egypt and Cambodia; and

Argentina and Ukraine banned export of wheat. This supply cut from the major suppliers

in the global grain market fueled the price volatilities of agricultural commodities even

more.

16

Aside from supply restraint policies, foreign buyers started to stockpile food

grains in response to food crisis and riots. Countries started to order for larger orders

rather than purchase one or two month’s supply at a time regardless of price and scarcity

of food grain (Weersink et al. 2008). This kind of speculative purchasing has also

contributed to price spike and volatilities in agricultural commodity market (BIAC,

2011).

Demand from Developing Countries

In recent years, several developing countries experienced rapid economic growth . As a

result of per capita income increase (Figure 2.9), consumers of developing countries are

enjoying more purchasing power which ultimately results in increased demand of

commodities.

Figure 2.10 shows the dramatic increase of per capita GDP in China and India.

Because of Spectacular economic growth in developing countries a big portion of their

population came out of poverty and demanding more grains. On the other hand, because

of the increased income, middle and upper income population of those countries shifted

their demand from grain to other high valued commodities such as meat, dairy, fruits,

vegetables and fish. The rise in demand for meat, in turn, boosts the demand for grains to

feed animals (Weersink et al 2008). As a result, it contributes to increase of food price.

17

Figure 2.9: Per Capita Income Level by Developing Region

0

500

1000

1500

2000

2500

3000

3500

Sub-Saharan

Africa

Middle East and

North Africa

Southeast Asia South Asia East Asia

1995 2020

Source: IFPRI Impact Simulation

Figure 2.10: GDP Per Capita of India and China (Constant US Dollar)

0

500

1000

1500

2000

2500

3000

1970 1975 1980 1985 1990 1995 2000 2005 2010

China

India

Source: WDI Database

Climatic Factors

Climate factors also contributed to the price volatilities in 2007-08 and again 2010.

Export markets for major agricultural commodities are highly concentrated. For example,

in 2008, 84% of maize was exported by only 5 countries, top five exporters of wheat

18

exported 63% of total wheat exports and 85% export share of milled rice were held by

top 5 rice exporters (Figure 2.11a, 2.11b and 2.11c). Because of this high level of

concentration, the world’s capacity to cope with shocks became limited (IFPRI, 2008).

Any incidence of poor weather in the major exporting countries or other types of

production shocks immediately affect the international price and price volatilities. For

example, wheat crop failure due to drought in Australia in 2008 and Russian federation in

2010 brought strong market reaction and soaring price.

Figure 2.11 a: Major Exporters of Maize in 2008

US

53%

Argentina

15%

Brazil

6%

France

6%

India

4%

ROW

16%

US

Argentina

Brazil

France

India

Others

Source: FAOSATAT Database

Figure 2.11 b: Major Exporters of Wheat in 2008

19

US

23%

France

12%

Canada

12%

Russian

Federation

9%

Argentina

7%

ROW

37%

US

France

Canada

Russian Federation

Argentina

Others

Source: FAOSATAT Database

Figure 2.11 c: Major Exporters of Rice in 2008

Thailand

37%

Vietnam

20%

Pakistan

11%

India

10%

US

7%

ROW

15%Thailand

Vietnam

Pakistan

India

US

Others

Source: FAOSATAT Database

Stocks of Cereals

Global stocks of cereal, measured as stocks to cereal use, came down to historically low

level in 2007-08 and from then it always remains around 21 whereas before 2003-04 it

used to remain more than 30. IFPRI (2011) reports that stock to use ratios of wheat were

always low during the price spikes in of wheat in the 1970s, 1995-96, 2007-08 and 2010-

20

11. The current level of stocks to cereal use made the cereal market very vulnerable to

any shock. A small dip in grain stocks may lead to major volatility in world cereal

market. Wright (2012) argues that when stocks are already tight a minor shock can have

major consequences on prices of agricultural commodities.

Figure 2.12: Stocks to cereal use ratio

15.0

17.0

19.0

21.0

23.0

25.0

27.0

2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13

Source: FAO Cereal Supply and Demand Brief

2.4. Chapter Summary

This chapter provides a brief overview of the recent trend of exchange rate of major

currencies, price of major agricultural commodities and their volatilities. The descriptive

statistics presented in this chapter suggests that volatilities of both exchange rate and

commodity price increased in recent years. Therefore, it is important to investigate their

effects on agricultural commodity trade. The next chapter provides a review of key

literature on effects of exchange rate volatility and commodity price volatility on

international trade.

21

Chapter 3: Literature Review

3.1: Effects of Exchange Rate Volatilities: Theoretical Background

Attention to exchange rate volatilities was first drawn after switching of the major

currencies of the world to a floating exchange rate system from the previous fixed regime

in 1973. Early theoretical contribution (Ethier, 1973) on effects of exchange rate

volatilities on trade flows asserts that exchange rate volatilities have a negative effect on

volume of trade if traders do not have idea about how exchange rate volatilities will

affect their expected profit.

Clark (1973) argued that exposure to exchange rate volatility creates risk over

firms’ profit and to insulate themselves from uncertainty over profit due to exchange rate

volatilities firms tend to reduce trade. A competitive firm (i) with no market power , (ii)

producing only one commodity which is sold entirely to one foreign market, (iii)

receiving payments in foreign currency, (iv) operating in a condition where hedging

through forward sales of the foreign currency export sales is not possible; and (v) unable

to alter its output in response to favorable or unfavorable shifts in the profitability of its

exports arising from movements in the exchange rate is adversely affected by greater

volatility in the exchange rate. This leads to a reduction in output, and hence in exports,

in order to reduce the exposure to risk (Clark, 1973).

However, in the presence of hedging possibility, the effect of exchange rate

volatility largely depends on the firm’s response to risk and uncertainty. If traders are risk

averse, an increase in exchange risk will unambiguously reduce the volume of trade

whether the risk is borne by importers or exporters. It also depends on who bears the risk.

22

If importers bear the risk, the price will fall as import demand falls, whereas if exporters

bear the risk, the price will raise as exporters charge an increasingly higher risk premium

(Hooper and Kohlhagen, 1978). With an inelastic supply (marginal cost) curve, a shift of

aggregate import demand (and thus marginal revenue) to the left caused by an increase in

exchange risk to the importer, will result in a relatively large drop in price and a

relatively small drop in quantity. If exporters bear the risk and face inelastic demand for

their output, an increase in exchange risk will shift their supply to the left and induce a

relatively large increase in price and a small decrease in quantity.

Exposure of unforeseen movements in exchange rate is low in advanced

economies where well developed forward market exists, i.e. a specific transaction can be

easily hedged (IMF, 2004). However, such markets do not exist for the currencies of

most developing and low income countries.

Opposite view of the effects of exchange rate volatilities on trade flows is also

available in literature. Increased exchange rate volatility positively affects the value of

exporting firms through the price and volume impacts of exchange rates, and also makes

an exporting strategy more attractive relative to the direct investment. As a result,

exchange rate volatility can be positively related to investment in export production

capacity (Sercu and Vanhulle, 1992).

3.2 Measuring Exchange Rate and Price Volatilities

The methods of measuring exchanged rate volatilities went through a process of

evolution in last three decades. However, still no single process dominates the

approximation of exchange rate volatilities. The most commonly use measure of

exchange rate volatilities are measure of variance. However the construction of the

23

measure of variance widely differed in from study to study (Bahmani-osokee and Hegerty

2007). Few approaches of measuring volatilities are historical volatility, implied

volatility, rolling window, within period volatility, moving standard deviation, General

Autoregressive Conditional Heteroskedasticity (GARCH) etc.

Here we will briefly discuss different measures of volatilities used in exchange

rate and trade related research in recent years.

The standard deviation of daily observations of the nominal exchange rate during

each three-month period was one of the first measures of exchange rate volatilities in

empirical literature (Akhter and Hilton, 1984). Later studies adopted the moving

standard deviation of the monthly change in the exchange rate to measure the exchange

rate volatilities (Kenen and Rodrik, 1986; Cushman, 1986; Chowdhury, 1993). This

method had some advantage over other contemporary methods for being stationary.

Autoregressive Conditional Heteroskedasticity (ARCH) became very popular in

measuring exchange rate volatilities afterwards. ARCH is a measure of volatility in time

series errors. ARCH models assume the variance of the current error term to be a function

of the actual sizes of the previous time periods' error terms. A number of studies (Arize et

al. 2005; Cho et al. 2002; McKenzie and Brooks, 1997) used ARCH process to measure

the exchange rate volatilities.

A further extension of ARCH process is Generalized Autoregressive Conditional

Heteroskedasticity (ARCH) which incorporates moving average process. GARCH

became popular in measuring exchange rate volatilities in recent years.

24

3.3 Empirical Literature: Exchange rate Volatility and Trade

The findings of empirical literature on the effect of exchange rate volatilities on trade

flows are mixed and not conclusive. This section briefly discusses the findings of some

empirical studies on this issue.

From the earlier empirical studies it was evident that exchange volatilities have a

negative impact on exports (Akhter and Hilton, 1984). The study used a polynomial

distributed lag method in their OLS estimate of the effects of exchange rate volatility on

trade flows. Their result confirms the theoretical assertion that exchange rate volatilities

reduce international trade. According to their model the export volume is a function of

foreign income, foreign capacity utilization and relative prices; and import volume is a

function of domestic income, the ratio of foreign to domestic capacity utilization, and

relative prices. They measure the using data for the USA and Germany; they estimated

their models using quarterly data over the period 1974-1981 and found that volatility had

a significantly negative effect on US imports, German exports and imports but no effect

on US exports.

However, the findings of the above study (Akhter and Hilton, 1984) were

challenged by a further study (Gotur, 1985) which used the same methodology as Akhter

and Hilton with certain modification. It included France, the UK and Japan in the model,

applied the Cochrane-Orcutt procedure to control for autocorrelation only when the

Durbin-Watson statistic calls for autocorrelation (Akhter and Hilton used it even in the

cases in which the problem was not even present ), changed the sample period under

investigation to account for lag structure and to incorporate the rate of change, rather than

the level, of the exchange rate. After these modifications she found that German exports

25

and imports have been negatively impacted, and Japanese exports are positively affected,

but the other seven trade flows were not affected.

However, both of the above mentioned studies suffer from spurious regression

problem because none of them accounted for integrating properties of variables

(Bahmani-Osokee and Hegerty, 2007).

A number of recent studies also found a negative relationship between exchange

rate volatilities and trade flows. For example, significant negative relationship between

real exchange rate volatility and export volume in short run and long run was found for

eight South American countries (Arize et al. 2008). By using Error Correction Model

Chou (2000) found significantly negative relationship between export volume and

volatility of real effective exchange rate (REER) for trade flows of industrial materials,

mineral and fuels; and manufactured good. However, the relation was not significant for

foodstuffs. Significant negative relationship was also found between exchange rate

volatilities and export supply for all the G7 countries and their partners for twenty one

industries (Peridy, 2003).

In contrast to the findings of the above mentioned studies, a positive relationship

between exchange rate volatilities and international trade flows was also found in few

empirical literature, mostly for bi-lateral trade (McKenzie and Brooks, 1997; Poon et al.

2005 ). While a number of studies found no significant effect of exchange rate volatilities

on trade flows (Kenen 1980, Thursby, 1980; IMF, 1984; Baily et al. 1986, Toneryo,

2004). As a result, the relationship between exchange rate volatilities and trade flows still

remain ambiguous.

26

The inconclusive relation between exchange rate volatilities and trade flows was

explained by the argument that exchange rate volatility is an ‘inadequate indicator’ of

price risk faced by firms since an increase in exchange rate volatilities may not

necessarily increase real domestic currency price volatilities (Smith, 1991).

Another explanation behind not getting any systematic relationship between

exchange rate volatilities and trade volume is undermining of a series of problems related

to the methods of estimation which might lead to imprecise statistical results (Bini-

Smaghi, 1997).

IMF (2004) observed that while exchange rate fluctuations have increased in

times of currency and balance of payments crises during the 1980s and 1990s, there has

not been any increase, on average, in such volatility between the 1970s and the 1990s. It

also found some empirical evidence of negative relationship between exchange rate

volatility and trade. However, such a negative relationship is not robust and It concludes

that if exchange rate volatility has a negative effect on trade, this effect would appear to

be fairly small and is not robust.

3.4 Empirical Literature: Exchange Rate Volatility and Agricultural Trade

Despite an extensive literature on effect of exchange rate volatility on overall trade, very

few studies (Cho et al. 2002; Kandilov, 2008; Zhang, 2010) explored the impact of

exchange rate and other volatilities on agricultural trade. Compared to the other sectors,

agriculture trade was found to be more sensitive to exchange rate uncertainties in

developed countries. Using a sample of bilateral trade flows across ten developed

countries (G 10 countries) Cho et al (2002) shows that the real exchange rate uncertainty

27

has had a significant negative effect on agricultural trade and the negative impact on

agricultural trade was more significant compare to the other sectors.

Agricultural exports from developing countries are much more vulnerable to

exchange rate volatilities compared to the exports from developed countries. Kandilov

(2008) found that the effect of exchange rate volatility is largest for developing country

exporters and smallest for developed exporters. Since developing countries do trade with

vehicle currency (US Dollar) only exchange rate volatility of the vehicle currency (U.S.

dollar), and not the exporter-importer currency, matters for developing country exporters

(Kandilov, 2008).

Villanueva and Sarker (2009) conducted a study to examine the effects of

exchange rate volatility on fresh tomato imports into the United States from Mexico.

They showed with the cointegration analysis that while changes in exchange rate have a

positive effect on trade flows, volatility of the exchange rate has a significant negative

effect on trade flows.

Although other volatilities (e.g. commodity price volatility and freight cost

volatility) may have much potential to affect international trade, only the effect of

exchange rate volatilities received much attention in the literature. Zhang et al (2010)

found that although commodity price and freight cost volatilities have no significant

impact on traded volume of soy bean between U.S. and Brazil, these two volatilities play

important roles in determining U.S. soy bean trade with China. The authors explained

that possibilities of hedging and market power are two important factors in determining

the effects of volatilities on trade.

28

3.5 Chapter summary

This chapter reviews the existing literature on the effects of exchange rate volatility and

commodity price volatility on international trade flows. Although a number of literature

exists on the effects of exchange rate on trade flows, literature on commodity price

volatilities on international trade is scarce. The next chapter presents the theoretical

framework used in this study.

29

Chapter 4: Conceptual Framework

4.1 Model Description

This study used Hooper and Kohlhagen’s (1978) trade model that derived the demand

and supply functions for individual firms and then aggregated to derive market demand

and supply to obtain reduced form equations for market equilibrium price and quantity.

Hooper and Kohlhagen developed the model for an individual firm importing a

commodity under exchange rate uncertainty. This study extends Hooper and kohlhagen’s

model by incorporating commodity price uncertainty into it. It is worth mentioning that

Zhang (2010) developed a model, based on Hopper and Kohlhagen’s model, which

included exchange rate, price and ocean freight cost uncertainties.

4.2 Import Demand

According to Hopper and Kohlhagen’s (1978) trade model, suppose a firm uses imported

commodity as inputs to produce final goods. The importer faces a linear demand

function for its output (Q), which is an increasing function of domestic income (Y), the

prices of substitutes (PD) and a decreasing function of its own price:

cYbPDaPQ ++= (4.1)

Following Hooper-Kohlhagen’s (1978) model, the model assumes a two period

framework where in the first period the firm receives orders for its domestic output and

places order for its imported input; and in the second period it receives the imported input

and pays for it and ships and gets paid for its own output. The firm sets the level of its

output to maximize its utility, which is an increasing function of its expected profits and a

30

decreasing function of the standard deviation of profits. The firm’s optimization problem

can be written as:

2/1))(()()(max πγππ VEUQ

−= (4.2)

where U is the total utility, π is profit, E is the expected value, V is the variance and γ is

the relative measure of risk preference where γ >0 implies risk aversion, γ =0 implies

risk neutrality and γ <0 represents risk loving.

The firm’s profit π in domestic currency can be formulated as:

π = Q * P(Q )−UC *Q − HM * iQ (4.3)

where Q is the amount of output, P is the domestic price per unit output faced by the firm,

UC is the unit cost of output, H is the weighted average cost of foreign exchange to the

importer, M is the cost of imported inputs, i is the fixed ratio of imports to total output.

If q is the quantity of imports needed to produce Q amount of output then q can be

defined as

iQq = (4.4)

In this study, I assume that the importer can hedge foreign exchange risk by purchasing

foreign exchange in advance and hedge commodity price in the future market. Suppose

the firm hedges a constant proportion (α ) in the forward market at the futures exchange

rate, ~

R ; the remain proportion (1-α ) of foreign exchange is purchased at the spot

exchange rate R. So, H can be defined as:

31

~

)1( RRH αα +−= (4.5)

~

P is the commodity future market price in foreign currency,

M=~

P (4.6)

By substituting Equations 5 and 6 into Equation 3, importer’s profit is obtained:

iQPRRQUCQPQ *])1[(*)(*~~

ααπ +−−−= (4.7)

In which Q0 denotes, ……….It is assumed that, in Equation 7, all the variable except

~

R and ~

p are known with certainty on the contract date. Thus, the variance in the

importing firm’s profit is:

2222~~~ )(].)1[()(PRp

iQiQRV σασαπ +−= (4.8)

where 2~

P

σ and 2

~`~

PR

σ are the variances of ~

P and~~

PR , respectively.

Substituting (8) into (2),

iQRiQPEHEQUCQQPUPRp

.])1[(.)()(.)( 2/122222~

~~~ γσασα +−−−−=

(4.9)

The first-order condition for equation with respect to output quantity (9) is:

0.])1[()()()()/(/ 2/122222~

~~~ =+−−−−+= iRiPEHEUCQPdQdPQdQdUPRp

γσασα

(4.10)

32

Substituting for dQdP / from Equation 1,

0.])1[()()()()/( 2/122222~

~~~ =+−−−−+ iRiPEHEUCQPaQPRp

γσασα (4.11)

Substituting iQq = from (4) into (11)

]])1[()()()[2/())(2/( 2/12222~

2

~~

~

PRP

RiPEHEaicYbPDaUCiq σασαγ +−++++=

(4.12)

Since 2

~~PR

σ = 2222~

22~

~~~~ )()(RPRP

PERE σσσσ ++ , (Bohrnstedt and Goldberger, 1969)

22~

222~~

2~~ )]([)1[()()]()1)[[(2/())(2/(PP

RERiPERERaicYbPDaUCiq σασαγαα +−++−+++=

]])]([ 22222~

2~~~

RPR

PE σσασα ++

(4.13)

If γ >0,

0}])]({[)1[()2/(/ 222~

2222~~ <++−=RP

RERaiddq σαααγσ (4.14)

and

])}([{)2/(/ 22~

222~~

pR

PEaiddq σγασ += <0

(4.15)

Therefore, from equation (14) and (15) it can be asserted that if the importers are risk

averse an increase in exchange rate or commodity price volatility will reduce the volume

of import. If the importers are risk neutral (γ =0), exchange rate or commodity price

33

volatility will not have any effect of import demand. In the case of risk-loving importers

(γ <0), an increase in exchange rate and commodity price volatility will increase the

import.

Assuming that all firms are homogenous2, firm level import demands can be summed into

the following aggregate import demand function.

(4.16)

4.3 Chapter Summary

This chapter discusses the theoretical framework used in this thesis. I used a modified

version of Hooper-Kohlhagen import demand model. Hooper and Kohlhagen (1978)

derived this model to show the effect of exchange rate volatility on imports. I

incorporated food price volatility to the original Hooper-Kohlhagen model and derived

the effects of exchange rate volatility and commodity price volatility on import demand.

2 The limitation of this assumption is that all firms may not have the same level of risk preference.

),,,)(),(,,,( ~~~~

~~

PRRP

d PEREYPDUCgQ σσσσ=

34

Chapter 5: Empirical Framework

5.1 Econometric specification

This study used panel data models to estimates the effects of exchange rate and

commodity price volatilities on trade flows using a panel data regression model.

In line with the modified Hooper-Kohlhagen model with price volatility presented in the

chapter 4, I used the following empirical model to estimate the effects of exchange rate

and commodity price volatilities on Canada’s export and import:

(5.1)

Where

itpimpln Natural logarithm of country i’s per capita import at period t

itXVln Natural logarithm of Country i’s exchange rate volatility at period t

ln itPV Natural logarithm of price volatility country i faces at period t

itPCGDPln Natural logarithm of country i’s per capita GDP at period t

itPln Natural logarithm of import price of country i at period t

)(ln 1+itt PE =lnFt,t+1 Natural logarithm of expected price of import of country i at period t,

Ln Ft,t+1 Natural logarithm of futures price

ijtERln Natural logarithm of Country i’s exchange rate with country j

D_Q2 Dummy variable3 for Quarter 2

D_Q2 Dummy variable4 for Quarter 3

D_Q4 Dummy variable5 for Quarter 4

T Time trend

3 For quarterly models

4 For quarterly models

5 For quarterly models

tiijtittititititit eTQDERPEPPCGDPPVXVpimp +++++++++= + 8761543210 _ln)(lnlnln.lnlnln βββββββββ

35

5.2 Variable Description

Dependent Variable: Per capita volume of import

Quarterly and annual real per capita volumes of imports of commodities measured in

metric ton are used as dependent variables respectively for quarterly and annual models.

Total import volumes are divided by the population to obtain per capita volume of

import. Since I used per capita real GDP as an independent variable, dependent variable

is also transformed to per capita. For quarterly models of wheat and soybean, per capita

import volumes of wheat and soybean from Canada by its major importers are used as

dependent variable. On the other hand, Canada’s per capita volume of import of corn and

rice from its major importing sources are used as the dependent variable. For annual

models, the per capita import volumes of top importers of each commodity are

considered as the dependent variable.

Independent Variables

Exchange Rate

Quarterly and annual nominal exchange rates (exporters’ currency per unit of importer’s

currency) of each period are used. Therefore, it is expected that if exchange rate

appreciates, cost of imports will be cheaper for importers. Exchange rate data are

obtained from Thompson-Reuters DataStream (http://online.thomsonreuters.com)

through the University of Guelph Data Resource Centre.

36

Import price

Unit price of import is considered as import price. Unit price of import is calculated by

dividing the value of import in U.S. dollar by the quantity of import measured in ton.

Since real volume of imports is used as dependent variable, nominal unit prices are

converted to real prices using U.S. Consumer Price Index (Base year 1982=100). Note

that unit price indices may create bias in estimation because of the compositional changes

in quantities and quality mix of exports and imports. Even with best practice stratification

the scope for reducing such bias is limited due to the sparse variable list available on

customs documents (Silver, 2007). Despite this issue, unit value of import and export

prices are widely used because of their relatively low cost availability compared with

price surveys.

Expected price

The modified version of Hooper-Kohlhagen’s model presented in the Chapter 4 assumes

that firms are capable of hedging the risk of price volatility by operating in the futures

market. This assumption is valid for today’s world since real time futures price data are

readily available and forms can buy and sell in the commodity exchanges. Given this

backdrop, I used the Chicago Mercantile Exchange (CME) futures price, Fit, of the next

period as expected cash price, )(ln 1+itt PE . Futures price data are obtained from

Thompson-Reuters DataStream (2012). Recently developed price forecast models, e.g.,

the World Bank’s commodity price forecast (World Bank 2012), and USDA’s season

average price forecasts (USDA 2012), are also mainly based on futures price. Therefore,

it is reasonable to use futures price as importers’ expected price.

37

Expected exchange rate

Although expected exchange rate is a variable in my theoretical framework for import

demand in the Chapter 4, this variable was dropped from the empirical model. The reason

of dropping this variable is that forward exchange rates are available for very few

countries only. In their original work Hooper and Kohlhagen (1978) used next period’s

realized exchange rate as expected exchange rate. However, by taking the realized

exchange rate of the next period, one would violate one of the main assumptions of the

model that exchange rates are uncertain and assumes that traders can forecast perfectly.

Exchange rate volatility

Exchange rate volatility is one of the main independent variables of the empirical model.

While a variety of exchange rate volatility measures have been used in the literature,

there is still no consensus on which measure is the most appropriate (Clark et al. 2004).

The disagreement is partly due to the fact that there is no generally accepted theory of the

impact of exchange rate volatility on firm behavior (Kandilv, 2008). Most often, some

variant of the standard deviation of the annual or monthly exchange rate is used to

measure volatility (Kandilov, 2008; Cho et al. 2002; Clark et al. 2004; Frankel and Wei,

1993; Rose, 2000; Tenreyro 2007 ).

Following Kandilov (2008) I measured the exchange rate volatility between

countries i and j in period t, ijtXV as the standard deviation of the first difference of

the natural logarithm of the daily exchange rate between the two countries over a period6:

6 Three months period for quarterly and one year period for annual

38

XVijt

=Std[lnXijt,d

− lnXijt,d-1

], for d = 1,2,..., end of the period. (5.2)

where

=tijXV Exchange rate volatility between country i and j over period t;

Std=Standard deviation

dijt,lnX =Natural logarithm of nominal exchange rate between country i and j on day d in

period t

1-dijt,lnX = Natural logarithm of nominal exchange rate between country i and j on day d-1

in period t

End of the period = the last day of the period; for example, for monthly data, the 30th or 31st

calendar day; for quarterly data, the 90th day of the quarter.

Both real and nominal exchange rates were widely used in the previous studies. For

example, Pick (1990), Arize, et al. (2000), and Cho et al. (2002) used real exchange rate

while Tenreyro (2007) and some other studies used nominal exchange rate. Kandilov

(2008) noted that for all industrial and developing countries there is little difference

between the real and the nominal exchange rate volatility in practice. Thursby and

Thursby (1987) also showed that real and nominal exchange rate volatilities do not have a

different effect on trade flows. As a result, it is reasonable to use nominal exchange rate

in this study.

Price volatility

We used the same method as exchange rate volatility to calculate price volatility using

monthly representative international prices for each commodity. Since daily data of

prices is not available for each commodity and country, we used monthly real price data.

39

Monthly nominal price data in U.S. dollar are obtained from FAOSTATS (FAO 2012)

and then deflated to real prices using U.S. Consumer Price Index (Base year 1982=100).

Following formula is used to compute price volatility:

PV= Std[lnPm

− lnPm-1

] (5.3)

Where

PV denotes the price volatility

Std represents standard deviation;

mlnP =Natural logarithm of price at month m;

1-mlnP =Natural logarithm of price at month m-1

It should be mentioned here that the correlation between real and nominal price volatility

is found to be very high, ranges 0.85 to 0.92.

Real Gross Domestic Product (GDP) per capita

Real GDP data for importing countries, obtained from USDA-Economic Research

Service (USDA-ERS 2012: http://www.ers.usda.gov/data-products/international-

macroeconomic-data-set.aspx), are divided by population to obtain real GDP per capita.

Since it is adjusted to the population of the importer, GDP per capita is a better measure

for country’s income and well being.

Quarterly Dummies

For our quarterly models, three quarterly dummies for second, third and fourth quarters

were used for seasonality.

40

Time trend variable

Time trend variables account for any time-variant effects that are not captured in the

regression. We used time trend variable in both quarterly and annual models.

5.3 Data and sources

The data used in this study comes from various sources such as the Canadian

International Merchandise Trade (CIMT) online database, the United States Department

of Agriculture (USDA), Thompson-Reuters DataStream, EUROSTAT and FAOSTAT

and Tri University Data Resources (TDR), University of Guelph. A detailed account of

data sources are provided in this section.

Import and Export data

Quarterly data of Imports and exports data of crops (including corn, rice, soybean and

wheat) ranging from 2000 to 2010 are obtained from the Canadian International

Merchandise Trade (CIMT: link) of Statistics Canada (CIMT, 2011). They are strongly

balanced panel data, which denotes the real volumes (in metric tons) of export and import

data for wheat, soybean, corn and rice. Table 5.1 summarizes the quarterly trade data

used in the study:

41

Table 5.1: Summary of export and import data for quarterly models

Crop Trade

Flow

Unit (‘000) Time

Period

Source

Corn Import Metric Ton 2000 Q1-

2009 Q4

Canadian International

Merchandise Trade (CIMT):

http://www.statcan.gc.ca/trade-

commerce/data-donnee-eng.htm

Rice Import Metric Ton 2000 Q1-

2009 Q4

CIMT:

http://www.statcan.gc.ca/trade-

commerce/data-donnee-eng.htm

Soybean Export Metric Ton 2000 Q1-

2009 Q4

CIMT:

http://www.statcan.gc.ca/trade-

commerce/data-donnee-eng.htm

Wheat Export Metric Ton 2000 Q1-

2009 Q4

CIMT:

http://www.statcan.gc.ca/trade-

commerce/data-donnee-eng.htm

For annual model, we use FAOSTATS annual detailed trade matrix to get annual imports

data of wheat, soybean, corn and rice by for individual top developing and developed

importers from 1991 to 2009. Table 5.2 summarizes the import data used for this study.

Table 5.2: Summary of import data for annual models

Crop Trade

Flow

Unit (‘000) Time Period Source

Corn Import Metric Ton 1991-2009 FAOSTAT:

http://faostat.fao.org/

Rice Import Metric Ton 1991-2009 FAOSTAT:

http://faostat.fao.org/

Soybean Import Metric Ton 1991-2009 FAOSTAT:

http://faostat.fao.org/

Wheat Import Metric Ton 1991-2009 FAOSTAT:

http://faostat.fao.org/

42

Exchange rate, price and Gross domestic product (GDP) data

Daily exchange rate data was collected from Thompson-Reuters DataStream (2012).

Monthly price and per capita real GDP of countries are obtained of commodities are

obtained from United States Department of Agriculture (hereafter ‘USDA ERS’) (2012)

and Quarterly GDP data are collected from EUROSTAT (2012). Table 5.3 summarizes

the sources and frequency of exchange rate, price, per capita GDP and GDP data uses in

this study.

Table 5.3: Summery of Data Frequency and Sources for exchange rate, GDP prices

Data Frequency Data sources

Exchange Rate Daily Thompson-Reuters DataStream7 (2012)

(http://thomsonreuters.com/)

Commodity Price Daily Tri University Data Resources(TDR), University of

Guelph (http://tdr.tug-libraries.on.ca/)

Commodity Price Monthly United States Department of Agriculture (USDA

ERS 2012); (http://www.ers.usda.gov/data-

products/international-macroeconomic-data-

set.aspx)

Per capita real

gross domestic

products

Annual USDA Economic Research Service International

macroeconomic data set (USDA ERS 2012)

Real gross

domestic products

Quarterly EUROSTAT8(2012)

(http://epp.eurostat.ec.europa.eu)and

Division of Statistics of countries in the sample.

Countries

For quarterly models, the study considered Canada’s top and regular trading partners for

wheat, soybean, rice and corn. However, few important trading partners e.g., Venezuela

for wheat, could not be incorporated in this study because of unavailability of quarterly

7 Data base of Thompson-Reuters

8 Database of European Union

43

data for few variables. Table 5.4 provides the list of Canadian trading partners included

in each crop model.

Table 5.4: List of Countries for Quarterly Models

Commodities and Trade Flows Countries

Wheat Exports from Canada U.S., Italy. Japan, Morocco

Soybean Exports from Canada U.S., Japan, Germany, France, France, Netherlands,

Belgium, Malaysia. Hong Kong, the Philippines and Italy

Canada’s Corn Imports U.S. and Rest of the World

Canada’s Rice Imports Thailand, Pakistan, Italy and U.S.

For annual models, I included top importers of each commodity. The list of top importers

is provided in the table 5.5.

Table 5.5: List of importing countries considered for annual models

Commodity Countries

Developed: Germany, Italy, Japan, The Netherlands, Republic of Korea,

Spain and USA

Wheat

Developing: Algeria, Brazil, Indonesia, Malaysia, Mexico, Pakistan, the

Philippines, Turkey

Developed: Germany, Italy, Japan, The Netherlands, Norway, Portugal,

Republic of Korea, Spain, United Kingdom

Soybean

Developing: Argentina, China, Colombia, Indonesia, Mexico, the

Philippines, Thailand, Turkey

Developed: Canada, Hong Kong, France, Singapore, United States Rice

Developing: Brazil, China, Indonesia, Malaysia, the Philippines,

Cameroon

Developed: Canada, France, Germany, Italy, Japan, the Netherlands,

Republic of Korea, Spain, United Kingdom

Corn

Developing: Algeria, China, Colombia, Indonesia, Malaysia, Mexico,

Peru, Turkey

44

5.4 Model Selection

Balance Panel data were used for both our quarterly and annual models. This section

discusses the selection process of estimation models for panel data regression from fixed

effects model, random effects model and pooled OLS.

Fixed Effects Model

The fixed effects model assumes that the intercept term captures the individual

heterogeneity which implies that every country gets it own intercept while the slope

coefficients remain the same (Baltagi, 2005).

Consider a linear unobserved effects panel data model for N observations and T periods:

NiTtuaXY itiitit ,....,1;,...,1, ==++= β (5.4)

Where itY is the dependable variable for country i at period t, itX is the KN × regressor

matrix with observable time-variant independent variables, β is a 1×K vector of

coefficients, ia is the unobserved time variant country effect and itu is the independent

and identically normal distributed error terms.

If we average the equation for each i, we get

iiii uaXY−−−

++= 1β (5.5)

Where ∑ =

−−

=T

t ityTY1

1 , ∑ =

−−

=T

t iti uTu1

1 and ∑ =

−−

=T

t iti XTX1

1

Since ia is fixed over time, it appears in both(5.4) and (5.5). If we subtract (5.4) from

(5.5) for each t we get,

itititiitiitiit uXYuuXXYY....

1 )()( +=⇒−+−=−−−−

β (5.6)

45

Random Effects Model

The random effects model assumes that the unobserved time variant individual effect, ia

in (5.2.1) is uncorrelated with each explanatory variable (Baltagi, 2005):

TtXaCov iti ,...,2,1,0),( == (5.7)

In fact, the ideal random effect assumptions include all the fixed effect assumptions plus

the additional requirement that ia is independent of all explanatory variables in all time

periods.

Hausman specification test

In order to determine whether to use fixed effects or random effects models, Hausman

specification test can be performed. Hausman specification test shows how large the

difference in estimates is in relation to the variances of estimates (Baltagi, 2005). The

computation procedure of Hausman test is as follows:

)()]()([)(^^

1^^^^ REFEREFEREFE

VarVarH ββββββ −×−×′−= − (5.8)

Where FE^

β is the coefficient estimate of fixed effects model and RE^

β is the coefficient

estimate of random effects model.

The null hypothesis of the Hausman test is that there is no systematic difference

between coefficients of fixed and random effects models models. Fixed effects models

are chosen if the null hypothesis is rejected while random effects model are chosen

otherwise (Hausman 1978).

46

Testing for random effects: Breusch-Pagan Lagrange multiplier (LM)

In order to decide between a random effects regression and a simple OLS regression,

Breusch-Pagan Lagrangian multiplier test is suggested (Breusch and Pagan, 1980). The

null hypothesis in the LM test is that variances across entities are zero. That is, no

significant difference across units (i.e., no panel effect). Rejecting the null hypothesis

indicates the presence of unobserved effects and pooled OLS would not be efficient. We

conducted Breusch-Pagan Lagrangian multiplier test to decide between random effects

and pooled OLS regression model.

Test for Cross-sectional Dependence

In panel data regression analysis, it is typically assumed that disturbances in panel data

models are cross-sectionally independent. This assumption is particularly true for panels

with large cross section dimensions. However, macro panels with smaller cross section

dimension and sufficiently large time periods may have the problem of cross section

dependence (pesaran, 2004). Cross-sectional dependence may arise due to spatial or

spillover effects, or due to unobservable common factors (Su and Zhang, 2010). Macro

panels on countries or regions with long time series that do not account for cross-country

dependence may lead to misleading inference (Baltagi, 2008). In this study, we

conducted Pesaran’s cross-sectional dependence test (CD test). But, one of the possible

drawbacks of the CD test is that adding up positive and negative correlations may result

in failing to reject the null hypothesis of cross-sectional dependence even if there is

plenty of cross-sectional dependence in the errors. Hoyos and Sarafidis (2006) suggest

conducting Fees’ and Friedman’s CD test if the average absolute correlation of the

47

residuals is high in the Pesaran’s CD test. In this study, we conduct Friedman’s and

Frees’ CD test if the average absolute correlation of the residuals was high in Pesaran’s

CD test. In case of the presence of cross-sectional dependence in the panel, we presented

regression results with Driscoll-Kraay standard errors (Hoechle 2007).

5.5 Diagnostics: Tests for Unit root, Heteroscedasticity, Serial Correlation and

Multicollinearity

This section provides an overview of the diagnostics done in this study to test for unit

root, heteroscedasticity, serial correlation and multicollinearity. Results of the test

performed are reported in the following sections for each individual crop model.

Unit root test

It is now a common practice to test for unit root in time series econometrics (Baltagi,

2008). In panel data analysis, testing for unit root is relatively recent (Levin, Lin and Chu

2002, Im et al. 2003; Harris and Tzavalis, 1999; Maddala and Wu, 1999; Choi, 2001 and

Hadri, 2000). The stationarity or non-stationarity of a time series can strongly influence

its behavior and properties. If the variables in the regression model are not stationary, the

standard assumptions of asymptotic analysis will not be valid. Because of non-