Supporting decision-making for recycling-based investments

11

Business Strategy and the Environment, Vol. 4,62-72 (1995) SUPPORTING DECISION- MAKING FOR RECYCLING- BASED INVESTMENTS Giuliano Noci, Department of Economics and Production, Politecnico di Milano, Milan, Italy The increasing demand for environment- ally friendly products and the intro- duction of tougher environmental laws have encouraged firms to consider the adoption of recycling issues as one of the most effective solutions for reducing their impact on the environment. Unfortu- nately, many companies delegate decision-making on recycling issues at an operational level. This attitude presents some problems as it could lead companies to neglect many effects result- ing from the adoption of recycling-based investments. The objective of this paper is to suggest a conceptual model aimed at supporting managers in the integration of recycling issues into the overall process of strategy formation; in particular, the designed approach is divided into two main phases: the identification of the main recycling-based programmes and the definition of a framework, based on both physical and accounting measures, aimed at assessing the effectiveness of dif- ferent recycling initiatives according to the main priorities of the decision-maker. CCC 0964-4733 /95 / 020062-1 1 0 1995 John Wiley & Sons, Ltd and ERP Environment. RECYCLING-BASED PROGRAMMES WITHIN THE PROCESS OF STRATEGY FORMATION he increasing demand for environmentally friendly products and the introduction of T tougher environmental laws have encour- aged firms to consider the adoption of recycling issues as one of the most effective solutions for reducing their impact on the environment (Clark, 1991; Azzone and Manzini, 1993; Welford and Gouldson, 1993; Azzone and BertelC, 1994; Azzone and Noci, 1994; Clark et al., 1994; Walley and Whitehead, 1994): companies such as American Airlines, Bell Atlantic and Coca-Cola have success- fully introduced products made from recycled materials and have cut down on waste, increased profit margins and, in some instances, truly closed the recycling loop (Biddle, 1993). The analysis of these successful experiences and the growing concern for environmental issues indicate that recycling-based programmes repre- sent great opportunities for firms. Unfortunately, many companies delegate decision-making on recycling-based investments at an operational level. Research performed by the McKinsey corporation has demonstrated that, even if 92% of chief executive officers stated that they were pursuing the integration of recycling issues and business strategy, only 35%successfully integrated such environmental considerations into manage- ment strategies (McKinsey and Company, 1991). This attitude presents some problems as recycling- based initiatives conform with all the characteristics of strategic programmes; in fact, they both present strong relationships with all the other long-term decisions and have a ’systemic’ impact on all the company’s activities. Recycling-based programmes are often the BUSINESS STRATEGY AND THE ENVIRONMENT

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of Supporting decision-making for recycling-based investments

Business Strategy and the Environment, Vol. 4,62-72 (1995)

SUPPORTING DECISION- MAKING FOR RECYCLING- BASED INVESTMENTS

Giuliano Noci, Department of Economics and Production, Politecnico di Milano, Milan, Italy

The increasing demand for environment- ally friendly products and the intro- duction of tougher environmental laws have encouraged firms to consider the adoption of recycling issues as one of the most effective solutions for reducing their impact on the environment. Unfortu- nately, many companies delegate decision-making on recycling issues at an operational level. This attitude presents some problems as it could lead companies to neglect many effects result- ing from the adoption of recycling-based investments. The objective of this paper is to suggest a conceptual model aimed at supporting managers in the integration of recycling issues into the overall process of strategy formation; in particular, the designed approach is divided into two main phases: the identification of the main recycling-based programmes and the definition of a framework, based on both physical and accounting measures, aimed at assessing the effectiveness of dif- ferent recycling initiatives according to the main priorities of the decision-maker.

CCC 0964-4733 /95 / 020062-1 1 0 1995 John Wiley & Sons, Ltd and ERP Environment.

RECYCLING-BASED PROGRAMMES WITHIN THE PROCESS OF STRATEGY FORMATION

he increasing demand for environmentally friendly products and the introduction of T tougher environmental laws have encour-

aged firms to consider the adoption of recycling issues as one of the most effective solutions for reducing their impact on the environment (Clark, 1991; Azzone and Manzini, 1993; Welford and Gouldson, 1993; Azzone and BertelC, 1994; Azzone and Noci, 1994; Clark et al., 1994; Walley and Whitehead, 1994): companies such as American Airlines, Bell Atlantic and Coca-Cola have success- fully introduced products made from recycled materials and have cut down on waste, increased profit margins and, in some instances, truly closed the recycling loop (Biddle, 1993).

The analysis of these successful experiences and the growing concern for environmental issues indicate that recycling-based programmes repre- sent great opportunities for firms. Unfortunately, many companies delegate decision-making on recycling-based investments at an operational level. Research performed by the McKinsey corporation has demonstrated that, even if 92% of chief executive officers stated that they were pursuing the integration of recycling issues and business strategy, only 35% successfully integrated such environmental considerations into manage- ment strategies (McKinsey and Company, 1991).

This attitude presents some problems as recycling- based initiatives conform with all the characteristics of strategic programmes; in fact, they both present strong relationships with all the other long-term decisions and have a ’systemic’ impact on all the company’s activities.

Recycling-based programmes are often the

BUSINESS STRATEGY AND THE ENVIRONMENT

G. NOCI

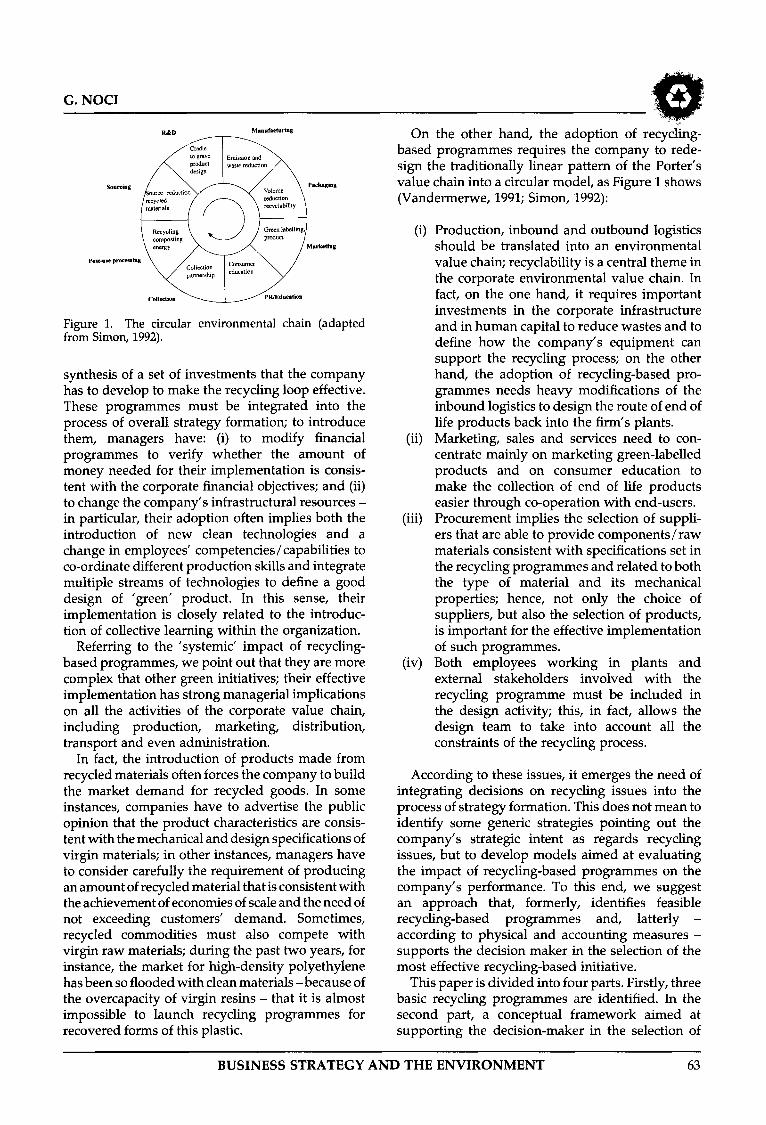

On the other hand, the adoption of recycling- based programmes requires the company to rede- sign the traditionally linear pattern of the Porter’s value chain into a circular model, as Figure 1 shows (Vandermerwe, 1991; Simon, 1992):

(i) Production, inbound and outbound logistics

Figure 1. The circular environmental chain (adapted from Simon, 1992).

synthesis of a set of investments that the company has to develop to make the recycling loop effective. These programmes must be integrated into the process of overall strategy formation; to introduce them, managers have: (i) to modify financial programmes to verify whether the amount of money needed for their implementation is consis- tent with the corporate financial objectives; and (ii) to change the company’s infrastructural resources - in particular, their adoption often implies both the introduction of new clean technologies and a change in employees’ competencies/ capabilities to co-ordinate different production skills and integrate multiple streams of technologies to define a good design of ’green’ product. In this sense, their implementation is closely related to the introduc- tion of collective learning within the organization.

Referring to the ’systemic’ impact of recycling- based programmes, we point out that they are more complex that other green initiatives; their effective implementation has strong managerial implications on all the activities of the corporate value chain, including production, marketing, distribution, transport and even administration.

In fact, the introduction of products made from recycled materials often forces the company to build the market demand for recycled goods. In some instances, companies have to advertise the public opinion that the product characteristics are consis- tent with the mechanical and design specifications of virgin materials; in other instances, managers have to consider carefully the requirement of producing an amount of recycled material that is consistent with the achievement of economies of scale and the need of not exceeding customers’ demand. Sometimes, recycled commodities must also compete with virgin raw materials; during the past two years, for instance, the market for high-density polyethylene has been so flooded with clean materials - because of the overcapacity of virgin resins - that it is almost impossible to launch recycling programmes for recovered forms of this plastic.

(ii)

(iii)

(iv)

should be translated into an environmental value chain; recyclability is a central theme in the corporate environmental value chain. In fact, on the one hand, it requires important investments in the corporate infrastructure and in human capital to reduce wastes and to define how the company’s equipment can support the recycling process; on the other hand, the adoption of recycling-based pro- grammes needs heavy modifications of the inbound logistics to design the route of end of life products back into the firm’s plants. Marketing, sales and services need to con- centrate mainly on marketing green-labelled products and on consumer education to make the collection of end of life products easier through co-operation with end-users. Procurement implies the selection of suppli- ers that are able to provide components/raw materials consistent with specifications set in the recycling programmes and related to both the type of material and its mechanical properties; hence, not only the choice of suppliers, but also the selection of products, is important for the effective implementation of such programmes. Both employees working in plants and external stakeholders involved with the recycling programme must be included in the design activity; this, in fact, allows the design team to take into account all the constraints of the recycling process.

According to these issues, it emerges the need of integrating decisions on recycling issues into the process of strategy formation. This does not mean to identify some generic strategies pointing out the company’s strategic intent as regards recycling issues, but to develop models aimed at evaluating the impact of recycling-based programmes on the company’s performance. To this end, we suggest an approach that, formerly, identifies feasible recycling-based programmes and, latterly - according to physical and accounting measures - supports the decision maker in the selection of the most effective recycling-based initiative.

This paper is divided into four parts. Firstly, three basic recycling programmes are identified. In the second part, a conceptual framework aimed at supporting the decision-maker in the selection of

BUSINESS STRATEGY AND THE ENVIRONMENT 63

DECISION-MAKING IN RECYCLING INITIATIVES

the most effective recycling-based programme is suggested. The third part operationally charac- terizes the designed approach in relation to the identified recycling programmes. Finally, we implement the 'simplified models in a sample study related to a company operating in the automotive field.

MAIN RECYCLING-BASED PROGRAMMES

In the definition of the feasible recycling-based options, we aim at identifying a set of recycling programmes that differ in relation to managerial implications, technological complexity and eco- nomic effects resulting from investment implemen- tation.

Specifically, three basic recycling-based pro- grammes have been identified:

(9

(ii)

(iii)

The recycling of end of life products to produce materials that are used in a new type of product (class A programmes); within such initiatives we have, for instance, the recycling of reclining seats of cars that, once compressed and ground, are used to produce moquette for furnishing. The recycling of end of life products for regenerating materials - with equal or lower mechanical properties than the virgin mate- rial - that are used in the same type of product (class B programmes). As an exam- ple, referring to the automotive field again, the recycling of bumpers to produce plastics for the canalization of the air in the bridge of cars. A passive environmental strategy, indicating the adoption of no anticipatory recycling- based programme. This is the attitude of a firm that only aims to respect environmental regulations (class C programmes). For instance, some German companies began to recover and recycle the packaging of their products only in relation to the introduction of Toeffel's law.

Programmes of classes A and B present the most important managerial implications as their effective implementation requires both an analysis of how end of life materials can be collected and the definition of strong relationships between the design team, the production department and the marketing team to design a product that can be easily produced and sold. Moreover, programmes of classes A and B could greatly differ as regards

their economic implications. The implementation of programmes within class A could not increase the company's recycling costs; in this instance, the recycling process is usually carried out by firms with different technological and marketing skills from those available in the company that introduces the programme. In contrast, programmes within class B could greatly affect the corporate recycling costs as, through their adoption, companies usually aim to develop the recycling process within their plants.

On the other hand, the development of pro- grammes aimed at respecting environmental reg- ulations means that the company almost deals with environmental issues according to a technical perspective; in this sense, the environmental function and technicians play the most important parts. Even in relation to investment appraisal, class C initiatives present some peculiarities; in particu- lar, their evaluation requires an approach that is divided into two steps: through the examination of physical indexes the firm is able to verify whether the programme implementation is consistent with new regulations, whereas the analysis of (environ- mental) cost drivers allows the company to identify the most effective initiative(s) from an economic viewpoint.

FRAMEWORK FOR THE IDENTIFICA- TION OF THE MOST EFFECTIVE RECY- CLING-BASED PROGRAMME

Once the set of feasible recycling-based projects has been identified, we need to compare the different alternatives according to decision criteria aimed at assessing the impact of each initiative on the economic and environmental performance of the company. To this end, we have to take into account that decision-making on recycling-based pro- grammes is very complex; in particular:

Recycling-based initiatives require large start-up investments; in fact, the introduc- tion of green products based on recycled materials needs both new equipment for regenerating materials and the development of new design techniques to define a product that can be recycled. Firms often have to bear high operating costs for assuring the work of clean equipment and the collection of end of life products. A study by the National Solid Waste Management Association (Walley and Whitehead, 1994) indicates that the average cost of collecting, transporting and processing recyclable commodities almost equals the market price.

~~

64 BUSINESS STRATEGY AND THE ENVIRONMENT

G. NOCI

(iii) The adoption of recycling-based initiatives causes a time lag between investment implementation and a change in the physi- cal/economic performance of the company (Azzone and Manzini, 1993; Walley and Whitehead, 1994; Azzone and Noci, 1995); specifically, many effects both in terms of revenue and in the reduction of pollution appear only in the long term, thus requiring the development of a complete and long-term oriented analysis.

Owing to this high complexity of recycling-based programmes, no specific model has been developed to effectively support the decision-maker in the evaluation of different recycling-based initiatives. In fact, traditional models such as operating environmental costs (Andersen and Ohlund, 1990; Kreuze et al., 1990) or approaches based on physical indices (Azzone and Manzini, 1993; Tyteca, 1995) limit their analysis to the immediate effects resulting from the implementation of each invest- ment. Moreover, state of the art models consider only the environmental effects of recycling-based programmes; in contrast, we have to take into account the fact that they could also affect quality- related performance. The development, for instance, of new products based on regenerated materials forces companies to re-engineer their technological processes and hence to reduce the percentage of scraps.

Considering these issues, we suggest a theoretical framework aimed at supporting managers in the process of recycling-based strategy formation. It is divided into three main steps: (i) the definition of the feasibility of different recycling options; (ii) the identification of the main effects resulting from the implementation of each programme; and (iii) the design of the decision criterion that allows us to discriminate among different programmes.

Step 1: Defining the Feasibility of a Recycling Option

Identifying the feasibility of the available recycling options means to analyse whether the introduction of each programme presents supply and demand problems; more precisely, at this level, we have: (i) to verify whether the volume of end of life materials to be recycled justifies, from an economic view- point, the introduction of strong relationships with external stakeholders involved in the route of end of life products back into the firm’s plants - in fact, the recovery of end of life materials could require a great amount of money because of the costs of transportation, the economic requirements of shredders, etc.: in this sense, only the possibility

Market Environmental Technological Economical rules processes efforts

Figure 2. Main variables affected by recycling-based programmes.

of recycling a great volume of wastes could allow the company to achieve economies of scale in reducing its recycling costs and, hence, for bal- ancing high costs related to the collection of end of life products - on the other hand, we have (ii) to calculate the ratio between the volume of recyclable materials and the market demand to identify whether the introduction of a recycled product into a new market corresponds, in terms of volume, to customers’ expectations. This is, for instance, closely related to the ’demand-building’ problem typical of initiatives aimed at recycling end of life materials that will be used in new types of products.

Step 2 Analysing the Impact of Recycling-Based Programmes

We compare different recycling-based alternatives according to four perspectives (Figure 2): (i) the customers’ viewpoint, aimed at identlfylng whether each programme allows the company to achieve a product that is consistent with the customers’ requirements; (ii) the efficiency of the process, to indicate the main environmental costs and physical performance of the firm; (iii) the environmental regulations viewpoint, indicating forecast costs of taxation over the long term; and (iv) the main economic efforts required for the implementation of each alternative.

Customers’ Viewpoint Analysing recycling-based programmes according to the customers’ perspective implies the identifica- tion of two different items, both related to revenues: (i) incremental revenues (R1), following from sales of green products - this term is closely related to the increase in the company’s market share because of the growing market concern for recyclable pro- ducts; and (ii) incremental revenues (&) resulting from the sales of products made from recycled materials and components. Hence the effects on revenues resulting from a recycling-based pro- gramme can be expressed as:

BUSINESS STRATEGY AND THE ENVIRONMENT 65

DECISION-MAKING IN RECYCLING INITIATIVES

Eficiency of the Process According to this perspective, we identify two main variables: (i) physical indicators showing the impact of each alternative on the state of natural resources; and (ii) economic drivers, representing the incremental operating costs resulting from the implementation of each programme.

In relation to physical indicators, we identify four main categories of indices; they are related to (Azzone and Noci, 1995):

(i) Waste water, expressed as chemical oxygen demand, the percentage of total nitrogen, phosphorus and dissolved salts in the water.

(ii) Air emissions, described in terms of the emissions of critical substances such as sulphur dioxide, ammonia, carbon mon- oxide, nitrogen oxides, hydrogen chloride and organic gas.

(iii) Energy consumption. (iv) Solid wastes sent for disposal: they can be

expressed as the percentage of the annual volume of production that must be deposited into landfill.

In relation to economic drivers, we identify three cost items:

(i) Incremental environmental costs (C,) related to the production of recyclable products. They can be defined as the sum of costs of materials, labour and energy resulting from the manufacture of green products: the costs of raw materials and labour have been considered as the development of design for recycling techniques could imply both higher costs for the purchase of raw materials and a longer production lead time, thus leading the company to accumulate labour costs (Andersen and Ohlund, 1990; Kreuze et al., 1990).

(ii) Costs for recycling materials making up end of life products (C& This cost item can be defined as the sum of costs for the transpor- tation of end of life products back into the firm’s plants, costs for product disassem- bling, product regeneration and conversion into a new product (Biddle, 1993; Azzone and Noci, 1994).

(iii) The change in costs due to product quality (C,); the introduction of a new technology - aimed at producing recyclable products - could improve the quality of the production process, thus reducing the costs of the disposal of materials that must be deposited in landfills (Walley and Whitehead, 1994). Hence the change in C, (AC,) resulting from

the implementation of a recycling-based programme can be defined as:

AC, = cAV(1 - ~ ) ( l - A,) (2)

where c represents the unit cost for product disposal, AV describes the change in volume of production, T characterizes the percentage of scraps that cannot be recycled and A9 corresponds to the modification of the process quality.

Hence, the change in the company‘s economic performance can be synthesized according to the following formula:

A(C, + cr + C9) (3)

Environmental Regulations Viewpoint According to this perspective, we have to consider costs due to environmental taxation (Ct); this cost item indicates the firm’s capacity to conform with new future regulations through the introduction of cleaner equipment (Lindhqvist, 1992; Azzone and Manzini, 1993).

Measures of the Company’s Economic Efforts Variables related to economic efforts concern the amount of money needed for the implementation of each recycling-based programme; to this end, four main motives of the company’s economic efforts have been identified:

(i) Investments aimed at training employees and the firm’s stakeholders involved in the recycling loop.

(ii) Investments for the introduction of new product development techniques such as design for disassembling and design for recycling (Simon et al., 1992; Dewhurst, 1993; Simon and Dowie, 1993).

(iii) Investments related to the purchase of new equipment to make the disassembling and the recycling of end of life products easier.

(iv) Investments in operating working capital as the adoption of a recycling initiative could imply the introduction of new stocks of raw materials or work in process.

Step 3: Decision-Making on Recycling-Based Programmes

Long-term orientation and completeness are important requirements for a model that effect- ively supports decision-making on recycling-based

~

66 BUSINESS STRATEGY AND THE ENVIRONMENT

programmes. The requirement of long-term orien- tation is extremely important as the adoption of recycling-based initiatives greatly lengthens pro- duct life cycles and hence increases the period in which each planned initiative presents its effects. On the other hand, even if all models for investment appraisal must develop complete analyses to consider all the effects resulting from the imple- mentation of each initiative, in the case of the evaluation of recycling-based programmes the requirement of completeness is more critical as such initiatives represent multi-dimensional issues affecting a wide range of the company’s perfor- mance such as solid wastes sent for disposal, pollution, noise and energy consumption.

According to these issues, different strategies should be analysed through their impact on share- holders’ value (Rappaport, 1986): economic value creation resulting from an investment or a set of initiatives is, in fact, the indicator that best conforms to the requirements of completeness and long-term orientation (Azzone and Noci, 1994). Unfortu- nately, the development of a value-based approach presents some problems as it does not consider that the implementation of a recycling-based pro- gramme usually corresponds to two main objec- tives: an economic aim related to the improvement of the company’s economic value and an ethical purpose associated with the reduction in the impact on the state of natural resources resulting from the firm’s activities (Meznar et al., 1991; Azzone and Noci, 1995).

Hence we introduce an approach that explicitly takes into account the economic and ethical objectives of the company; more precisely, we aim to design different models according to the relative importance attributed by the decision-maker to these objectives. To this end, we identify three types of decision-maker: (i) the manager respectful of the environment, whose objective function is to minimize the company’s environmental impact; (ii) the man- ager who aims to improve shareholders’ value without increasing the company’s environmental impact; and (iii) the manager who equally considers shareholders’ value and the state of natural resources.

Starting from this framework, we identify three approaches, each consistent with the priorities of a specific type of decision-maker: (i) the first decision criterion is based on the identification of the programme that minimizes the impact on the state of natural resources and does not decrease shareholders’ value; (ii) the second approach concerns the identification of the choice that, without increasing the impact on the state of natural resources, maximizes shareholders’ value; and (iii) the third model, consistent with a decision- maker who equally considers economic and ethical

G. NOCI

objectives, focuses on the definition of a scoring method aimed at synthesizing both information resulting from physical indicators and economical / financial items.

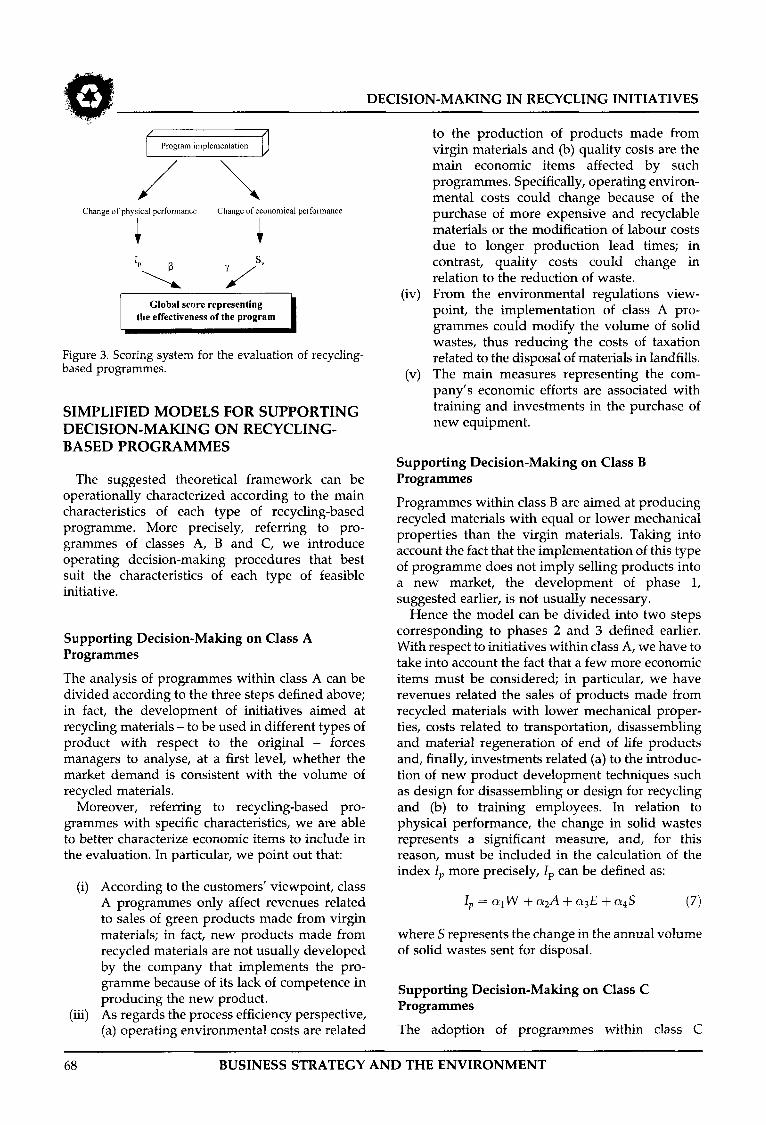

Analysing in more detail the third model - as it synthesizes the approaches supporting decision- making in the other two cases - we point out that it can be divided into two sequentially linked phases. The former phase deals with the identification of the index I, - representing as a whole the change in the firm’s physical performance - and the indicator S, indicating how different programmes contribute to shareholders’ value.

Ip is defined as:

(4)

where W, A and E are, respectively, related to the change in waste water, air emissions and energy consumption in relation to the implementation of each programme. To calculate I, we have to consider that: (i) W and A are defined as the weighted average of the amount of each substance emitted and the weights are the reverse of the maximum concentration of each substance allowed by local legislation; (ii) E is measured by the total amount of energy consumption within a year; (iii) the coefficients ai express the relative importance of each category of environmental performance in relation to the characteristics of the local market and the technological context.

The term S, represents the discounted sum of future cash flows resulting from the implementa- tion of each recycling-based programme; hence it is defined as follows:

where R(t) and C(t), respectively, represent incre- mental revenues and costs - calculated as C, + C, t C, + Ct of year t; and k is the hurdle rate of return of the company, usually associated with its capital cost.

The latter phase is aimed at synthesizing the effectiveness of each alternative. To this end, we introduce a single index that is defined as the weighted average of I , and S, [see Equation (6)]; weights are calculated according to the relative importance of different environmental perfor- mances with respect to the customers’ requirements.

I = ys, - PIp

Finally, comparing different recycling options according to index I, we have to select the programme that maximizes such indicators (Figure 3).

BUSINESS STRATEGY AND THE ENVIRONMENT 67

DECISION-MAKING IN RECYCLING INITIATIVES

Program implementation

J \ Change of physical performance Change of economical performance

Global score representing the effectiveness of the program

Figure 3. Scoring system for the evaluation of recycling- based programmes.

SIMPLIFIED MODELS FOR SUPPORTING

BASED PROGRAMMES DECISION-MAKING ON RECYCLING-

The suggested theoretical framework can be operationally characterized according to the main characteristics of each type of recycling-based programme. More precisely, referring to pro- grammes of classes A, B and C, we introduce operating decision-making procedures that best suit the characteristics of each type of feasible initiative.

Supporting Decision-Making on Class A Programmes

The analysis of programmes within class A can be divided according to the three steps defined above; in fact, the development of initiatives aimed at recycling materials - to be used in different types of product with respect to the original - forces managers to analyse, at a first level, whether the market demand is consistent with the volume of recycled materials.

Moreover, referring to recycling-based pro- grammes with specific characteristics, we are able to better characterize economic items to include in the evaluation. In particular, we point out that:

(i) According to the customers' viewpoint, class A programmes only affect revenues related to sales of green products made from virgin materials; in fact, new products made from recycled materials are not usually developed by the company that implements the pro- gramme because of its lack of competence in producing the new product.

(iii) As regards the process efficiency perspective, (a) operating environmental costs are related

to the production of products made from virgin materials and @) quality costs are the main economic items affected by such programmes. Specifically, operating environ- mental costs could change because of the purchase of more expensive and recyclable materials or the modification of labour costs due to longer production lead times; in contrast, quality costs could change in relation to the reduction of waste. From the environmental regulations view- point, the implementation of class A pro- grammes could modify the volume of solid wastes, thus reducing the costs of taxation related to the disposal of materials in landfills. The main measures representing the com- pany's economic efforts are associated with training and investments in the purchase of new equipment.

Supporting Decision-Making on Class B Programmes

Programmes within class B are aimed at producing recycled materials with equal or lower mechanical properties than the virgin materials. Taking into account the fact that the implementation of this type of programme does not imply selling products into a new market, the development of phase 1, suggested earlier, is not usually necessary.

Hence the model can be divided into two steps corresponding to phases 2 and 3 defined earlier. With respect to initiatives within class A, we have to take into account the fact that a few more economic items must be considered; in particular, we have revenues related the sales of products made from recycled materials with lower mechanical proper- ties, costs related to transportation, disassembling and material regeneration of end of life products and, finally, investments related (a) to the introduc- tion of new product development techniques such as design for disassembling or design for recycling and @) to training employees. In relation to physical performance, the change in solid wastes represents a significant measure, and, for this reason, must be included in the calculation of the index lp more precisely, lp can be defined as:

lp C Y ~ W + CQA + C Y ~ E + C Y ~ S (7)

where S represents the change in the annual volume of solid wastes sent for disposal.

Supporting Decision-Making on Class C Programmes

The adoption of programmes within class C

68 BUSINESS STRATEGY AND THE ENVIRONMENT

G. NOCI

Table 1. Change in physical indicators resulting from the implementation of each programme.

Change of physical performances resulting from

Programme 1* Programme 2*

57 500 0 368 000 0

Water COD (kg) Sulphates (kg)

Air emissions sox -500 -1300 NOx -300 -900

Solid wastes

Energy conservation Plastics (t) -8640 -7120

Electrial energy (kWh)-’ - 1 550 000 - 1 425 000 Oil (m3) 110 500 122 500

*Data modified according to an enquiry of the company.

corresponds to a passive behaviour towards recycling. In this instance, the company imple- ments programmes that are only aimed at respect- ing new environmental regulations. According to these issues, the decision-making process can be divided into two phases: (i) the identification of the initiatives that improve the company’s environ- mental performance and are consistent with the evolution of standards; and (ii) the selection of the programme that minimizes forecast environmental costs, as such decisions do not affect revenues.

Supporting Decision-Making on Programmes Within Different Classes

Decision-making on recycling issues could concern the comparison of programmes within different classes; in this instance, we have to implement the same approach for evaluating all the alternatives: managers should refer to the model that takes into account all the effects involved with each environ- mental initiative. Hence the approach suggested for the evaluation of programmes of class A should be implemented.

DEFINITION OF THE MOST EFFECTIVE

AN AUTOMOTIVE FIRM: A SAMPLE APPLICATION

RECYCLING-BASED PROGRAMME IN

The suggested framework has been operationally characterized in a sample study related to a firm operating in the automotive field. We refer to an Italian company that has designed a new model of car and now aims to evaluate whether the recycling of bumpers - aimed at producing plastics for the canalization of air in the bridge of cars - could improve its performance both from an economic

and an environmental viewpoint. In particular, the firm aims to compare two different alternatives that differ in relation to the technological process for regenerating plastics: programme 1 is based on a chemical process of recycling, whereas programme 2 is based on mechanical regeneration.

In terms of the suggested model, these recycling- based alternatives are closely related to class B programmes; taking into account that the compa- ny’s managers equally consider the ethical objective associated with the adoption of a recycling initiative and economic issues, we refer to the approach that analyses how each initiative affects both share- holders’ value and the physical environmental performance.

Economic and Physical Effects Resulting from the Implementation of each Recycling-Based Programme

Customers’ Viewpoint The two options equally contribute to the compa- ny’s cash inflows as managers forecast (i) an expansion of 50 000 units of the volume of new cars sold and (ii) a 5% improvement in revenue in relation to their implementation.

Process Efficiency Perspective We compare the two alternatives according to both physical and economic performances.

With respect to physical indicators, the imple- mentation of each alternative reduces, on the one hand, waste water, solid wastes and air emissions and, on the other hand, allows the company to salvage 30% of the electrical energy usually needed in traditional plants that use wrecks (see Table 1).

With respect to economic variables, the adoption of each programme has three main economic effects (see Table 2): (i) the reduction of costs related to

__ ~

BUSINESS STRATEGY AND THE ENVIRONMENT 69

DECISION-MAKING IN RECYCLING INITIATIVES

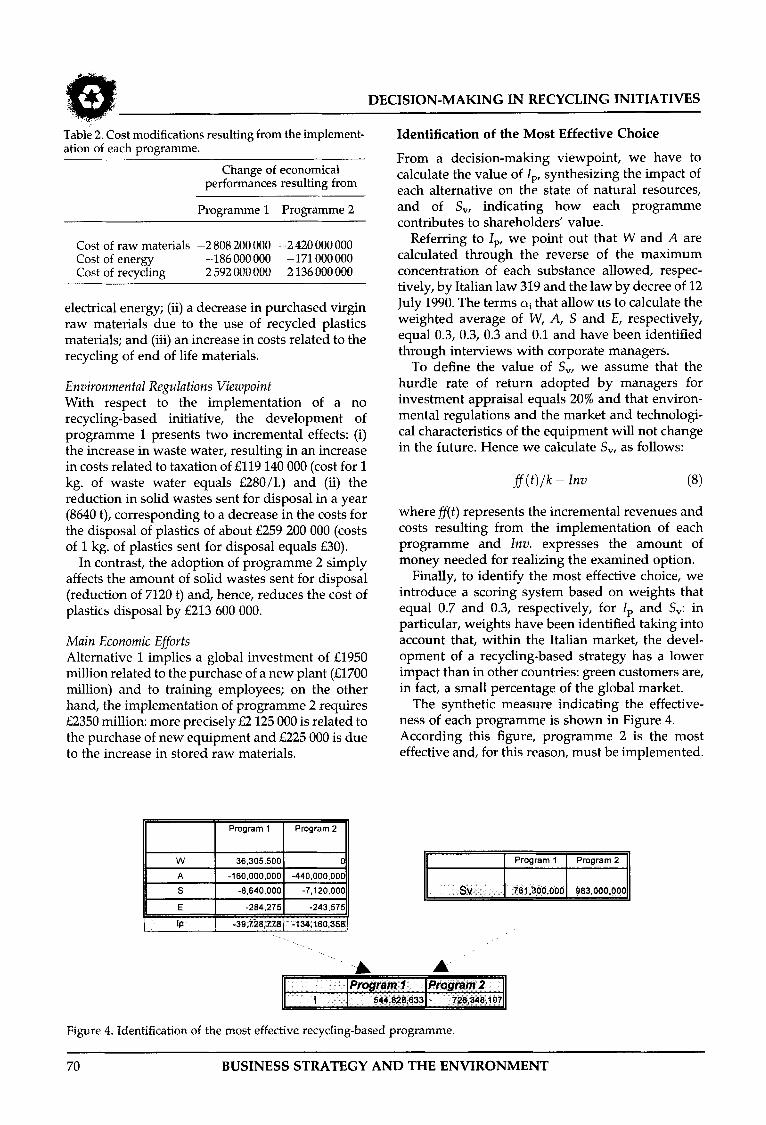

Table 2. Cost modifications resulting from the implement- ation of each programme.

Change of economical performances resulting from

Programme 1 Programme 2

Cost of raw materials -2 808 200 000 -2 420 000 000

Cost of recycling 2 592 000 000 2 136 000 000 Cost of energy -186 000 000 -171 000 000

electrical energy; (ii) a decrease in purchased virgin raw materials due to the use of recycled plastics materials; and (iii) an increase in costs related to the recycling of end of life materials.

Environmental Regulations Viewpoint With respect to the implementation of a no recycling-based initiative, the development of programme 1 presents two incremental effects: (i) the increase in waste water, resulting in an increase in costs related to taxation of €119 140 000 (cost for 1 kg. of waste water equals €280/1.) and (ii) the reduction in solid wastes sent for disposal in a year (8640 t), corresponding to a decrease in the costs for the disposal of plastics of about €259 200 000 (costs of 1 kg. of plastics sent for disposal equals €30).

In contrast, the adoption of programme 2 simply affects the amount of solid wastes sent for disposal (reduction of 7120 t) and, hence, reduces the cost of plastics disposal by €213 600 000.

Main Economic Efforts Alternative 1 implies a global investment of €1950 million related to the purchase of a new plant (€1700 million) and to training employees; on the other hand, the implementation of programme 2 requires €2350 million: more precisely €2 125 000 is related to the purchase of new equipment and €225 000 is due to the increase in stored raw materials.

A I -160,000,000~ -440,000,000

I -8,640,0001 -7,120,000

11 E I -284.2751 -243.57511

Identification of the Most Effective Choice

From a decision-making viewpoint, we have to calculate the value of Ip, synthesizing the impact of each alternative on the state of natural resources, and of S,, indicating how each programme contributes to shareholders’ value.

Referring to Ip, we point out that W and A are calculated through the reverse of the maximum concentration of each substance allowed, respec- tively, by Italian law 319 and the law by decree of 12 July 1990. The terms ai that allow us to calculate the weighted average of W, A, S and E, respectively, equal 0.3, 0.3, 0.3 and 0.1 and have been identified through interviews with corporate managers.

To define the value of S,, we assume that the hurdle rate of return adopted by managers for investment appraisal equals 20% and that environ- mental regulations and the market and technologi- cal characteristics of the equipment will not change in the future. Hence we calculate S,, as follows:

j f ( t ) / k - Inv

where #(t) represents the incremental revenues and costs resulting from the implementation of each programme and Inv. expresses the amount of money needed for realizing the examined option.

Finally, to identify the most effective choice, we introduce a scoring system based on weights that equal 0.7 and 0.3, respectively, for Ip and S,: in particular, weights have been identified taking into account that, within the Italian market, the devel- opment of a recycling-based strategy has a lower impact than in other countries: green customers are, in fact, a small percentage of the global market.

The synthetic measure indicating the effective- ness of each programme is shown in Figure 4. According this figure, programme 2 is the most effective and, for this reason, must be implemented.

II I Program I I Program 2 11

Figure 4. Identification of the most effective recycling-based programme.

70 BUSINESS STRATEGY AND THE ENVIRONMENT

G. NOCI

CONCLUSIONS

Recycling-based programmes greatly affect a com- pany’s competitive position (Hunt and Auster, 1990; Shrivastava, 1991; Di Norcia et al., 1993; Welford, 1993; Pento, 1995); referring to the three- dimensional framework of Walley and Whitehead - based on strategic, operational and technical/ organizational perspectives - recycling-based initiatives must be considered as strategic issues. On the one hand, their implementation requires a change in procedures within the company’s value chain and of relationships among them; on the other hand, their adoption may have a great effect on the company’s economic value. In fact, according to the ECO rational portfolio method (Simon, 1992), programmes of classes A and B at least are often consistent with the so-called ‘green cash cows’ strategies as products made from recycled materials have low added pollution and their sales may lead the company to achieve a high contribution margin per unit.

Nevertheless, we cannot compare different recycling-based programmes only according to their impact on shareholders’ value as many workers suggest (Azzone and Manzini, 1993; Walley and Whitehead, 1994); in fact, initiatives aimed at the recycling of end of life materials and, from a broader perspective, all environmental programmes present some peculiarities with respect to the other investments because their adoption can also follow from ethical objectives.

For this reason, we defined here a multi-objective approach that, according to managers’ priorities, analyses how each recycling-based programme affects both shareholders’ value and the state of natural resources.

The suggested model considers all the impacts resulting from the adoption of recycling-based initiatives and, for this reason, develops a complete analysis; moreover, it fits the decision maker’s priorities as it introduces weights that indicate the importance attributed by the company to different factors affected by each recycling option; finally, it takes into account the effects of each initiative in the long term as it analyses - at least when its implementation follows from an economic object- ive - how it affects the company’s economic value.

The identified approach needs a large amount of input data; in particular, its implementation could require information systems that are sometimes not available within small firms. Nevertheless, we believe that the obstacle of the lack of data is becoming less important and will be more easily exceeded in the future because firms will be forced by the market and public institutions to improve and monitor their environmental efficiency and

hence to collect information related to environ- mental issues that can be used in the approach suggested in the paper.

ACKNOWLEDGEMENTS

Financial support of ’La misura delle prestazioni ambientali delle innovazioni tecnologiche di pro- dotto e di processo’ and of ’Impatto dei problemi di compatibiliti ambientale sulle tecniche di valuta- zione e controllo degli investimenti in nuove tecnologie’ by CNR is gratefully acknowledged.

REFERENCES

Andersen, A.. and Ohlund, E.G. (1990) Measurement of costs related to environmental measures. Survey of German and Swiss industry practice. In: ElASM Workshop on Green Accounting.

Azzone, G. and BerteE, U. (1994) Exploiting green strategies for competitive advantage, Long Range Planning, Dec.

Azzone, G. and Manzini, R. (1993) Management account- ing for measuring environmental performances. In: 16th Annual Congress of the European AccountingAssocia- tion.

Azzone, G. and Noci, G. (1994) Measuring environmental performance in product development. In: Proceedings of the Second Product Development Management Conference on Nau Approaches to Development and Engineering, Gothenburg, Sweden, 30-31 May 1994.

Azzone, G. and Noci, G. (1995) How to design a performance measurement system for supporting pro-active green strategies. In: Workshop on Greening of Management, EIASM, Brussels, Belgium, 12-13 January 1995.

Biddle, D. (1993) Recycling for profit: the new green business frontier, Harvard Business Review, Nov-Dec.

Blanchard, B.S. (1979) Design and Manage to Life Cycle Cosf, MI A Press, Portland.

Bloom, G.S. and Scott Morton, M.S. (1991) Hazardous waste is every managers‘ problem, Sloan Management Review, Summer.

Clark, J. (1991) Green regulation as a source of competitive advantage. In: 11 th Annual Conference of the Strategic Management Society, Toronto, Canada.

Clark, R.A. et al. (1994) The challenge of going green, Harvard Business Review, Jul-Aug.

Dewhurst, P. (1993) Product design for manufacture: design for disassembly, Industrial Engineering.

Di Norcia, V., Cotton, B. and Dodge, J. (1993) Environ- mental performance and competitive advantage in Canada’s paper industry, Business Strategy and the Environment, Z(4).

Gray, R. (1990) Accounting and environmentalism: an exploration of the challenge of gentle accountability, transparency and sustainability. In: EIASM Workshop on Green Accounting.

Hunt, C.B. and Auster, E.R. (1990) Pro-active environ- mental management: avoiding the toxic trap, Sloan Management Review, Winter.

Kreuze, I.G., Newell, G.E. and Newell, S.J. (1990) Accounting for hazardous waste, Management Account- ing, May.

BUSINESS STRATEGY AND THE ENVIRONMENT 71

DECISION-MAKING IN RECYCLING INITIATIVES

Lindhqvist, T. (1992) Extended producer responsibility. In: Expert Seminar Extended Producer Responsibility as a Strategy to Promote Cleaner Products, Trotleholm Castle, Sweden.

McKinsey & Co. (1991) The Corporate Response to the Environmental Challenge, McKinsey & Co., Amsterdam.

Meznar, M.B., Chrisman, J.J. and Caroll, A.B. (1991) Social responsibility and strategic management toward an enterprise strategy classification, Business and Profes- sional Ethics, l O ( 1 ) .

Pento, T. (1995) The environmental Go-No Go: some empirical findings of decision parameters in the forest industry. In: Workshop on Greening of Management, EIASM, Brussels, Belgium, 12-13 January 1995.

Rappaport, A. (1986) Creating Shareholders' Value: the New Standard for Business Performance, Free Press, New York.

Shrivastava, P. (1991) Corporate self-renewal: strategic responses to environmentalism. In: 11 th Annual Con- ference of the Strategic Management Society, Toronto, Canada.

Simon, F. (1992) Marketing green products in the triad, Columbia Journal of World Business, Fall/ Winter.

Simon, M. and Dowie, T. (1993) Disassembly process planning. In: 30th International MATADOR Conference, UMIST, Manchester UK, March 1993.

Simon, M., Fogg, B. and Chambellant, F. (1992) Design for cost effective disassembly. In: International Forum on Design for Manufacture and Assembly.

Tyteca, D. (1995) DEA models for the measurement of environmental performance of firms -concepts and empirical results. In: Workshop on Greening of Manage- ment, EIASM, Brussels, Belgium, 12-13 January 1995.

Vandermerwe, S. and Oliff, M.D. (1991) Corporate challenges for an age of reconsumption, Columbia Journal of World Business, Fall.

Walley, N. and Whitehead, B. (1994) It's not easy being green, Harvard Business Review, 72(3).

Welford, R. (1993) An integrated systems approach to environmental management: a case study of IBM UK, Business Strategy and the Environment, 2(3).

Welford, R. and Gouldson, A. (1993) Environmental Management and Business Strategies, Pitman, London.

BIOGRAPHY

Giuliano Noci Department of Economics and Production, Politecnico di Milano, Milan, Italy.

72 BUSINESS STRATEGY AND THE ENVIRONMENT