SRI ESG INVESTMENTS - Columbia SIPA

61

2016 SIPA, COLUMBIA UNIVERSITY CLIENT: NY LIFE/MAINSTAY INVESTMENTS Authors: Mateo Bidoggia, Molly Gordon, Youjia Guo, Abhishek Rathor, and Hao Rong Faculty Advisor: Prof. Michelle Greene SRI ESG INVESTMENTS

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of SRI ESG INVESTMENTS - Columbia SIPA

2016

SIPA, COLUMBIA UNIVERSITY

CLIENT: NY LIFE/MAINSTAY INVESTMENTS

Authors:

Mateo Bidoggia, Molly Gordon, Youjia Guo,

Abhishek Rathor, and Hao Rong

Faculty Advisor: Prof. Michelle Greene

SRI ESG INVESTMENTS

1 |

Table of Contents

Executive Summary ........................................................................................................................ 3

Introduction ..................................................................................................................................... 5

Objectives of the Research Paper ................................................................................................ 5

Methodology ............................................................................................................................... 5

MainStay Investments ................................................................................................................. 5

Candriam ..................................................................................................................................... 6

Candriam’s Approach .............................................................................................................. 6

History and Evolution of SRI ......................................................................................................... 7

Sustainable and Responsible Investing ....................................................................................... 7

Sustainable and Responsible Impact Investing ........................................................................... 7

History of SRI ............................................................................................................................. 9

Sustainability Accounting Standards Board (SASB) ................................................................ 10

ESG ........................................................................................................................................... 11

Corporate Social Responsibility (CSR)..................................................................................... 13

CSR Trends ............................................................................................................................... 13

SRI Trends................................................................................................................................. 15

Global Regulatory Environment ................................................................................................... 16

Fiduciary duty ........................................................................................................................... 17

What is it and who has it ....................................................................................................... 17

The changing landscape ......................................................................................................... 17

Benefit Corps and B Corps ........................................................................................................ 19

Benefit Corporations.............................................................................................................. 19

B Corporations ....................................................................................................................... 19

Benefit Corporations vs B Corporations ............................................................................... 20

Corporate Disclosure ................................................................................................................. 21

Europe .................................................................................................................................... 21

Asia ........................................................................................................................................ 21

United States .......................................................................................................................... 22

Regulatory challenges ............................................................................................................... 23

Short or long term? ................................................................................................................ 24

2 |

Economic incentive or control? ............................................................................................. 24

Look forward and possible development ............................................................................... 24

Benefits/Costs of SRI .................................................................................................................... 25

Financial Reasons to Invest in SRI ESG Funds ........................................................................ 25

Economics Academic Literature on diversified investments ................................................ 25

Economics Academic Literature on individual companies ................................................... 26

Finance Industry Research..................................................................................................... 26

Economic Reasons to invest in SRI ESG Funds ....................................................................... 27

Investors’ Satisfaction/Promote ESG Causes/Shareholder Activism .................................... 27

Market Size ................................................................................................................................... 28

Global Market ........................................................................................................................... 30

US Market Size ......................................................................................................................... 31

ESG Incorporation by Money Managers and Financial Institutions ..................................... 32

ESG Incorporation by Institutional Investors ........................................................................ 34

Case Studies (General Electric, StatOil, Unilever) ....................................................................... 35

Introduction ............................................................................................................................... 35

General Electric ......................................................................................................................... 35

Background ............................................................................................................................ 35

Findings ................................................................................................................................. 36

Discussions ............................................................................................................................ 36

Evaluation .............................................................................................................................. 37

Statoil ........................................................................................................................................ 37

Background ............................................................................................................................ 37

Findings ................................................................................................................................. 38

Discussions ............................................................................................................................ 39

Evaluation .............................................................................................................................. 40

Unilever ..................................................................................................................................... 40

Concluding remarks ...................................................................................................................... 43

Bibliography ................................................................................................................................. 44

Appendix: Tables of Meta-studies from Miriam von Wallis and Christian Klein ....................... 52

3 |

Executive Summary

SRI, known under many definitions including: Socially Responsible Investing, Sustainable and

Responsible Investing, and Sustainable and Responsible Impact Investing, has grown in popularity

in recent years. Today, an increasing number of financial institutions, asset managers, corporations,

and individual investors are seeking new ways to invest in companies that promote positive global

and community impact. While firms such as Candriam Investors Group have been at the forefront

of SRI practices, many organizations are attempting to incorporate SRI considerations into

traditional investment tools. This increase is occurring for many reasons, but one important one is

the increase in access to information about ESG (environmental, social, and governance)

performance of corporations. ESG rankings help to better inform investment decisions. Today we

see partnerships among consumers, corporations, individual governments, international

organizations and NGOs in the promotion of ethical and sustainable business practices and

investments. This report explores the history and evolution of SRI, the current and evolving

regulatory environment, the costs and benefits associated with sustainable and responsible

investing practices, the market size of SRI, and finally a discussion of three case studies: General

Electric, Statoil, and Unilever.

The field of SRI has evolved over time to a more selective and systematized approach for investing.

Beginning with the purposeful exclusion of investments in sectors such as weapons, tobacco, and

alcohol known as negative screening, investors have begun to create selection processes that

highlight areas of investment based on positive impact. Organizations like the Sustainability

Accounting Standards Board have been created to reflect a desire to standardize financial reporting

to include SRI. Additionally, more and more companies and technologies have emerged targeting

the collection and reporting of ESG data, as well as rankings and indexes of companies based on

ESG performance. Corporate Social Responsibility (CSR) has become almost universal in large

corporations. As consumers are able to gain more insight into the organization they are supporting,

additional pressure has been put on corporations to act responsibly and adhere to the principles of

ESG.

The relationship between financial markets and policymakers is constantly evolving, and the fast

development of new financial products needs to be properly regulated. In many jurisdictions,

fiduciary duty is widely considered as imposing obligations on trustees or other fiduciaries to

maximize investment returns. The consequence has been that ESG risks have tended to be

neglected in investment practice. This is changing, driven by two factors: the materiality of ESG

issues and the changing expectations of investors.

Different entities are imposing new regulatory requirements around ESG. For example, according

to a survey conducted globally by the World Federation of Exchanges (WFE), 57% of the

exchanges reporting require listed companies to disclose some ESG information beyond corporate

governance. At the same time, national regulatory systems in many countries are developing

progressively to promote integrated reporting covering sustainability issues. This report examines

some of the most important developments in individual regions.

4 |

In terms of the size of the SRI market, as of the latest available data, the global SRI market included

$21.4 trillion in 2014 in assets under management including ESG incorporation and shareholder

resolutions. At that time Europe was the largest regional market, although the US grew faster,

closing the gap during the biennial 2012-2014. The largest investment strategy used in the SRI

space has historically been negative screening, which was also true in 2014. However, ESG

Integration is growing more rapidly and is closing the gap.

The American SRI market was $8.7 trillion in 2016 including ESG incorporation and shareholder

resolutions (ESG at $8.1 trillion, resolutions at $2.6 trillion, with some overlap). SRI in the US has

grown steadily, however, the growth experienced in the first decade of the 2000s averaged only 3%

per year, while since 2010 the average annual growth has been 19%, showing a sharp acceleration

in the uptake of SRI. In terms of types of investors, most of the assets including ESG incorporation

are managed by money managers ($8.1 trillion) while Institutional Investors managed $4.7 trillion

in 2016 (with $4.7 trillion of overlap). While the motivation that drives adoption of ESG

incorporation practices for money managers seems to be client demand, the main reasons driving

adoption by institutional investors are mission and social benefit.

The reasons to invest in the SRI ESG portfolios come primarily from three broad motivations:

financial, economic, and value-driven. Financial reasons include efforts to earn higher, less volatile

returns by seeking stocks of companies that over-perform on ESG metrics. Economic research has

by and large found that SRI ESG peer investments perform better or equally well to their non-SRI

ESG alternatives. Economic academic literature on individual companies has also found positive

relationships between CSR factors and company stock price.

Outside of financial reasons, many investors take into account economic impacts. The traditional

model of investments includes three primary characteristics of a security: Risk, Return and

Liquidity. Some investors now include a fourth characteristic as well: Sustainability, which may

lead investors to factor externalities (e.g. pollution) into their investment analysis.

There are investors for whom ethical reasons may influence or even outweigh purely financial and

economic investment drivers. These investors want investment returns in alignment with their

values, sometimes even if it means earning lower financial returns on their long-term investments.

Finally, the report examines three case studies to provide examples of the return on investment in

ESG initiatives, and discuss why Candriam’s SRI methodology could be an effective way of

analyzing a company’s long-term sustainability and growth.

The first case focuses on Ecomagination, GE’s most well-known and heavily invested sustainable

project that aims at enhancing resource productivity and reducing environmental impact. This

initiative not only fostered new revenue growth from its product innovations for GE, but also had

a significant positive impact on the company’s business reputation. The second case examines

Statoil’s sustainable practices which illustrates how a company from a highly controversial sector

(fossil fuels) could still be seen as a social responsible and environmentally friendly entity. Finally,

the Unilever case illustrates that a company with excellent product-quality control and

environmental-protection mechanism can gain advantage in business reputation and market

performance.

5 |

The discussion of SRI is one at the forefront of the modernization of traditional investing and

increased alignment between individual and corporate values and financial interests. The ability to

invest directly in organizations based on performance metrics that include ESG factors is shaping

how many investors view returns. Investors are getting closer to being able to quantify

environmental and social impacts in traditional return terms. Additionally, corporations that excel

in various ESG areas, such as the three cases discussed, are becoming models. Challenges in the

field include the need for standardization of SRI definitions, reporting, and evaluation of

investment and corporation performance. SRI is a rapidly growing investment sector, and one that

is likely to continue to expand in the US context.

Introduction

Objectives of the Research Paper

The objective of this research is to provide the latest industry information on Sustainable and

Responsible Investments (SRI). This includes the history and evolution of the field, benefits and

costs of sustainable, responsible and ethical investment practices, market size and growth, select

specific company case studies, and a reflection of the future of SRI and the current challenges

facing the field.

This research is being carried out as a Capstone Project to provide the client - Mainstay

Investments/New York Life - with a detailed project report on the state-of-knowledge regarding

the above topics. This is to assist in the marketing and launch of the SRI investments arm of the

company which will execute Candriam’s investment approach in the United States.

In a Capstone Project “students pursue independent research on a question or problem of their

choice, engage with the scholarly debates in the relevant disciplines, and - with the guidance of a

faculty mentor - produce a substantial paper that reflects a deep understanding of the topic.”1 A

Capstone Project is based on the students’ prior academic work, professional experience and future

career utility.

Methodology

The SRI research conducted for this report has been divided into topics allocated to each Capstone

team-member. Each member researched the topics through academic research papers, industry

research reports, and internet sites. The results are presented in this report, which includes a

detailed bibliography. A detailed Project Control Plan was prepared to keep track of an ongoing

timeline, including deliverable deadlines and division of labor.

MainStay Investments

MainStay Investments is a U.S. investment management company based in Jersey City, New

Jersey. Founded in 1986, MainStay Investments’ parent company is New York Life Insurance

Company, the largest mutual life-insurance company in the United States, and one of the largest

life insurers in the world. MainStay Investments offers investors access to institutional money

management through its mutual funds, separately managed accounts, and non-traditional strategies;

1 Capstone definition from http://www.scps.virginia.edu/bachelor-of-interdisciplinary-studies/capstone

6 |

over time MainStay has added several boutique investment advisory firms. MainStay has over

$101 billion USD in assets under management.2

Candriam

Candriam Investors Group is a leading pan-European multi-specialist asset manager with a 20-

year track record and a team of 500 experienced professionals. Managing about €94.5 bn AuM at

the end of March 2016, Candriam has established management centres in Luxembourg, Brussels,

Paris and London, and has experienced client relationship managers covering Continental Europe,

the UK, the Middle East and Australia. Its investment solutions cover five key areas: Fixed Income,

Equities, Alternatives, Sustainable Investments and advanced Asset Allocation. Through

investment solutions driven by strong convictions, Candriam has earned a reputation for delivering

innovation and strong performance to a long-standing, diversified client base in over 20 countries.3

Candriam Investors Group is a New York Life Company. To enhance its presence across the in

North America, Candriam is exporting its SRI expertise to the United States.

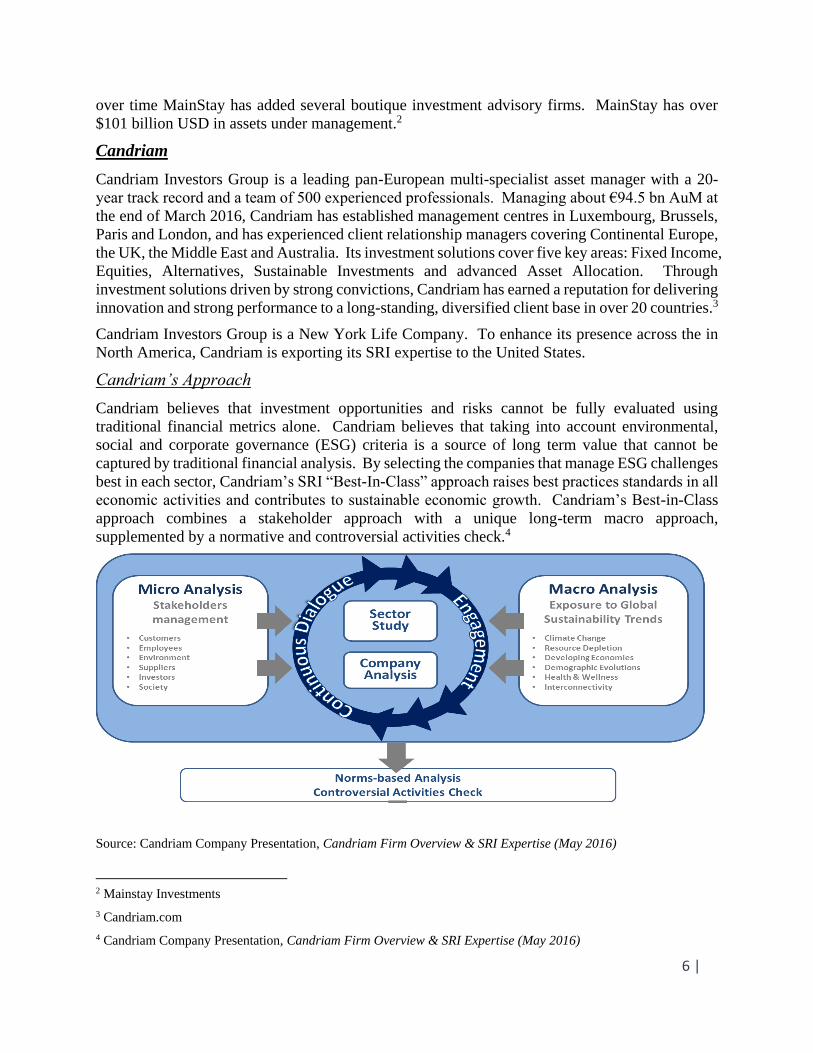

Candriam’s Approach

Candriam believes that investment opportunities and risks cannot be fully evaluated using

traditional financial metrics alone. Candriam believes that taking into account environmental,

social and corporate governance (ESG) criteria is a source of long term value that cannot be

captured by traditional financial analysis. By selecting the companies that manage ESG challenges

best in each sector, Candriam’s SRI “Best-In-Class” approach raises best practices standards in all

economic activities and contributes to sustainable economic growth. Candriam’s Best-in-Class

approach combines a stakeholder approach with a unique long-term macro approach,

supplemented by a normative and controversial activities check.4

Source: Candriam Company Presentation, Candriam Firm Overview & SRI Expertise (May 2016)

2 Mainstay Investments

3 Candriam.com

4 Candriam Company Presentation, Candriam Firm Overview & SRI Expertise (May 2016)

7 |

History and Evolution of SRI

Today, a number of different definitions exist in the SRI space that can be problematic in

understanding what SRI is and how it has evolved. Unpacking the nuances in each definition and

focusing on the evolution of the definitions of SRI can actually foster further understanding of how

the field has developed and where it is today. The acronym SRI has been broken down into Socially

Responsible Investing, Sustainable and Responsible Investing, and more recently Sustainable and

Responsible Impact Investing. Yet, even in using the same acronym, firms can have different

understandings of what, for example, sustainability and responsibility actually mean in the context

of investment.

This section highlights intrinsic pieces in the history and evolution of SRI in the United States to

better understand how financial institutions have embraced this investment practice. It explores

trends in SRI, with the overarching trend of increased access to information as the driving factor

in the evolution of sustainable investing practices, in addition to efforts made in SRI evaluation

and reporting standardization. In the discussion of access to information and standardization in the

field of SRI, three concepts will be defined and analyzed: the creation and role of the Sustainability

Accounting Standards Board (SASB), ESG, defined as the Environmental, Social, and Governance

factors used to measure SRI performance, and Corporate Social Responsibility (CSR) and the way

corporations have embraced direct social and environmental impact.

Sustainable and Responsible Investing

Sustainable and Responsible Investing is a term used by MainStay Investments and Candriam

Investors Group, both under the umbrella organization of New York Life. According to the firms,

sustainable and responsible investing is “an investment approach that considers Environmental,

Social, and Governance (ESG) factors in portfolio selection and management.” 5 The firm

distinguishes its definition of SRI from that of Socially Responsible Investing based on screening

practices. Negative screening or the exclusion of investments in areas such as alcohol, tobacco,

gambling, or weapons is associated with Socially Responsible Investing; whereas positive

screening involves investment decisions based on “positive ESG performance relative to industry

peers.”6 In both positive and negative screening ESG factors can be utilized. New York Life does

note that while Socially Responsible Investing is the historical term, “Sustainable, Responsible,

and Impact Investing” is the “new standard.”7

Sustainable and Responsible Impact Investing

The United States Sustainable Investment Forum (US SIF) defines Sustainable and Responsible

Impact Investing as “an investment discipline that considers environmental, social and governance

5 "About." Sustainable and Responsible Investing. Accessed November 29, 2016.

http://www.nylinvestments.com/public_files/SRI/index_sri.html.

6 "Global Sustainable Investment Alliance (GSIA) Definitions." Accessed November 29, 2016.

http://www.nylinvestments.com/public_files/SRI/pdf/Candriam-GSIA-Definitions.pdf.

7 "About." Sustainable and Responsible Investing. Accessed November 29, 2016.

http://www.nylinvestments.com/public_files/SRI/index_sri.html.

8 |

(ESG) criteria to generate long-term competitive financial returns and positive societal impact.”8

US SIF provides a list of examples of types of investors in sustainable and responsible impact

investing as ranging from individuals to foundations, religious organizations, venture capitalists,

and community development banks. It is important to note, however, that under the US SIF

definition of SRI, traditional investors such as asset managers are not mentioned.9While impact

investing is not the focus of this report, it is necessary to understand the distinction between

traditional investing or even sustainable investing and pure impact investing.

According to the Global Impact Investing Network (GIIN), impact investing is investing in

“companies, organizations, and funds with the intention to generate social and environmental

impact alongside a financial return. Impact investments can be made in both emerging and

developed markets, and target a range of returns from below market to market rate, depending

upon the circumstances.”10 Net Impact, an international organization aimed at social good, sees

the distinction between SRI and impact investing in investment strategy. The firm distinguishes

negative screening as being a tool used in SRI, and positive screening in impact investing. Another

important distinction made by Net Impact is in the expectation socially responsible investors and

impact investors seek from an investment. The former prioritizes financial return, while impact

investors vary in willingness to sacrifice financial return for social return.11

In addition to the aforementioned definitions, Forbes describes SRI as being synonymous with

green, mission, socially conscious and ethical investing.12 US SIF too provides additional labels

for sustainable investing practices that include “community investing” or “values-based

investing.”13 These terms, like those provided by Forbes, moves the conversation away from a

universal understanding of SRI, to an individual understanding of SRI. Value-based investments

are traditionally seen in the philanthropy community, but here extend to traditional investing

methods in allowing an individual to define his or her values and invest accordingly. These slight

differences could limit the potential for a true analysis of the history and evolution of the SRI space.

While important to explore, for the purposes of this report the term SRI will be used as an umbrella

term that incorporates all of the terms above. In the market sizing section of this report different

definitions will be explored, only further emphasizing the importance of standardization of SRI

definitions.

8 "SRI Basics." The Forum for Sustainable and Responsible Investment. Accessed November 29, 2016.

http://www.ussif.org/sribasics.

9 "SRI Basics." The Forum for Sustainable and Responsible Investment. Accessed November 29, 2016.

http://www.ussif.org/sribasics.

10 "What You Need to Know About Impact Investing." What You Need to Know About Impact Investing | The

GIIN. Accessed November 29, 2016. https://thegiin.org/impact-investing/need-to-know/.

11 "What Is the Difference between Socially Responsible Investing and Impact Investing?" Accessed November 29,

2016. https://www.netimpact.org/careers/what-is-the-difference-between-socially-responsible-investing-and-impact-

investing.

12“Socially Responsible Investing: What You Need To Know.” Forbes. Accessed November 29, 2016.

http://www.forbes.com/sites/feeonlyplanner/2013/04/24/socially-responsible-investing-what-you-need-to-

know/#4ebaec855863.

13 "SRI Basics." The Forum for Sustainable and Responsible Investment. Accessed November 29, 2016.

http://www.ussif.org/sribasics.

9 |

History of SRI

According to the Conference on Sustainable, Responsible, and Impact Investing, SRI origins can

be traced back to biblical times. The organization traces SRI to the Torah and Quran in directing

those of Judaism and Islam on how to invest. The Jewish teachings in particular focus on “investing

ethically” while the Quran teaches to avoid investing in certain industries including alcohol and

gambling.14 In the United States it is the Quakers and Methodists who brought “values-based

investing” to the country, with the Methodist investment evaluation method being closely aligned

with the modern concept of ESG. In the United States, the turning point for modern SRI began in

the 1960s.15

According to the Conference on SRI, a public cry for accountability and social responsibility in

particular swept the nation. The 1960s-1980s saw many mass movements led by university

students and faith-based organization on issues ranging from the Vietnam War and civil and

women’s rights to nuclear weapons, the environment, and apartheid in South Africa. 16 Melissa D.

Berry of Thomas Reuters notes in particular the pressure by university students to screen

investments away from South Africa, leading to $625 billion screened from the country before the

administration of De Klerk worked to end the apartheid system in 1993.17 The genocide in Sudan

became another topic of public pressure in 2006 with the creation of the Sudan Divestment Task

Force leading to the Sudan Accountability and Divestment Act of 2007 by Congress.18

Today, SRI has expanded beyond education and faith-based organizations to include large

corporations, financial institutions, and the general population. To better understand how SRI has

spread globally among financial institutions, one can look to the Principles for Responsible

Investing (PRI) created in 2006 under Kofi Annan, former Secretary General of the United Nations.

Founded on six principles, the PRI works to help its over 1,500 signatories incorporate the use of

ESG factors in investing strategies. 19 The Equator Principles is another network connecting

financial institutions to a framework of risk management “for determining, assessing, and

managing environmental risk in projects”. 20 The number of Equator Principles Financial

Institutions (EFPIs) span 35 countries and 85 Institutions.21 In the United States EFPIs include:

Bank of America Corporation, Citigroup Inc., Ex-Im Bank, J.P. Morgan Chase Bank, and Wells

14 "History of SRI." History of SRI | The SRI Conference. Accessed November 29, 2016.

http://www.sriconference.com/about/what-is-sri/history-of-sri.html.

15 "History of SRI." History of SRI | The SRI Conference. Accessed November 29, 2016.

http://www.sriconference.com/about/what-is-sri/history-of-sri.html.

16 "History of SRI." History of SRI | The SRI Conference. Accessed November 29, 2016.

http://www.sriconference.com/about/what-is-sri/history-of-sri.html.

17 "History of Socially Responsible Investing in the U.S." Sustainability. August 9, 2013. Accessed November 29,

2016. http://sustainability.thomsonreuters.com/2013/08/09/history-of-socially-responsible-investing-in-the-u-s/.

18 "History of Socially Responsible Investing in the U.S." Sustainability. August 9, 2013. Accessed November 29,

2016. http://sustainability.thomsonreuters.com/2013/08/09/history-of-socially-responsible-investing-in-the-u-s/.

19 "ABOUT THE PRI." About the PRI | Principles for Responsible Investment. Accessed November 29, 2016.

https://www.unpri.org/about.

20 Equator Principles. Accessed November 29, 2016. http://www.equator-principles.com/.

21 Equator Principles. Accessed November 29, 2016. http://www.equator-principles.com/.

10 |

Fargo Bank.22 The Market Sizing and Regulatory Environment sections of this report provide data

on the increases of SRI in financial institutions and the changes within the US regulatory systems

that have fostered an increase in SRI.

Sustainability Accounting Standards Board (SASB)

In 2014 Michael Bloomberg and Mary Schapiro wrote an opinion piece in the Financial Times

titled, “Give Investors Access to all the Information they Need.”23 The article reflects on the

standardization challenges that led to the creation of the Sustainability Accounting Standards

Board and provides predictions for the future of sustainability accounting. In the article they

describe one of the main challenges in investment decisions, simply a lack of access to the best

information required to make an informed investment decision and evaluate the overall health of

a firm. Financial statements can only take investors so far in their analysis of a firm, but non-

financial data is often a great influencer on the future of a company’s operations in any field.

Bloomberg and Shapiro noted in particular the lack of standardization that existed in measuring

non-financial information in different sectors. In response to this challenge the Sustainability

Accounting Standards Board (SASB) was created in 2011, with the two authors later appointed as

chair and vice-chair. This Board was created with large asset managers ($17 trillion) and $8 trillion

of market capital-representing companies.

SASB is at the forefront of ensuring that corporate entities disclose sustainability information

according to its materiality standards24 SASB defines its purpose as evaluating “the environmental,

social and governance performance of companies through an account of their management of

various forms of non-financial capital associated with sustainability- environmental, human and

social- and corporate governance issues, which they rely upon for sustained, long-term value

creation.”25 While some non-financial assets do have a place in accounting, SASB has worked to

define indicators and measurements to signal sustainability in financial accounting. Bloomberg

and Schapiro note that “adopting non-financial standards will be an important step forward for

transparency in our capital markets. It will help set our companies on a course for long-term growth.

In the process, it will also make our economy more resilient and competitive, protecting it against

costly risks that – once they are known and properly valued – can be avoided.”26

In addition to understanding SRI, it is also necessary to understand ESG and CSR, two terms

closely related to SRI and the measurements used to determine the ranking of a firm according to

its social and environmental impact as well as the strength of the firm’s leadership.

22 Secretariat, The EP. "EP Association Members." Equator Principles. Accessed November 29, 2016.

http://www.equator-principles.com/index.php/members-reporting.

23 Bloomberg, Michael, and Mary Schapiro. "Give Investors Access to All the Information They Need." May 19,

2014. Accessed November 29, 2016. https://www.ft.com/content/0d9ccea6-db66-11e3-94ad-00144feabdc0.

24 Sustainability Accounting Standards Board. Accessed November 29, 2016. http://www.sasb.org/.

25 "Conceptual Framework of the Sustainability Accounting Standards Board." October 2013, 3, accessed

November 29, 2016. http://www.sasb.org/wp-content/uploads/2013/10/SASB-Conceptual-Framework-Final-

Formatted-10-22-13.pdf.

26 Bloomberg, Michael, and Mary Schapiro. "Give Investors Access to All the Information They Need." May 19,

2014. Accessed November 29, 2016. https://www.ft.com/content/0d9ccea6-db66-11e3-94ad-00144feabdc0.

11 |

ESG

ESG stands for Environmental, Social and Governance factors employed by some investors in

their investment decisions. According to the Principles for Responsible Investment, the

Environmental category can include any act a company engages in to prevent climate change,

deforestation, waste and pollution, greenhouse gas emissions, or the depletion of natural resources.

PRI defines Social in terms of labor conditions including the health and safety of employees and

stringent child labor and slavery policies, workplace diversity, and efforts to engage the local

community. Governance includes board diversity, tax strategy, corruption and bribery, executive

compensation, and political affiliation through donations and lobbying.27 These factors will be

further explored in the case study section where General Electric, Stat Oil, and Unilever will be

used to examine company alignment with ESG factors.

PricewaterhouseCoopers LLP notes a divide that exists between firms and investors on the value

placed on ESG. According to the audit firm, 65% of corporates see ESG factors as being very

important to the very center of their business strategies, while only 31% of investors see the factors

as very important to equity investment decisions. Within these two areas, each segments views

ESG as having a different contribution to risk mitigation and long-term growth. 35% of corporates

use ESG in targeting long-term growth and only 24% use it for risk reduction. On the other hand,

for investors 60% targets risk reduction while only 19% is aimed at long-term growth.28

The International Integrated Reporting Council is one organization that has fostered a great

increase in sustainable reporting. The organization defines itself as “a global coalition of regulatory

investors, companies, standard setters, the accounting profession and NGOs. The coalition is

promoting communication about value creation as the next step in the evolution of corporate

reporting.”29 Now in its Breakthrough Phase, the IIRC is working with partners such as the SASB,

World Business Council for Sustainable Development, and International Federation of

Accountants to provide a framework for integrated reporting.30

In order to actually perform SRI based on ESG factors, the standardization of these factors is

crucial. ESG usage has increased due to regulatory changes and the development of ESG data

providers according to Business for Social Responsibility (BSR).31 Like the creation of SASB,

more and more firms are either being created specifically to define and rate ESG performance, in

addition to traditional ratings agencies who have created new indexes based on sustainability

scores. It is however important to note that as more firms have begun rating ESG performance,

27 "What Is Responsible Investment?" Principles for Responsible Investment. Accessed November 29, 2016.

https://www.unpri.org/about/what-is-responsible-investment.

28 "Investors, Corporates, and ESG: Bridging the Gap." October 2016. Accessed November 29, 2016.

http://www.pwc.com/us/en/governance-insights-center/publications/assets/investors-corporates-and-esg-bridging-

the-gap.pdf.

29 "Integrated Reporting." Accessed November 29, 2016. http://integratedreporting.org/the-iirc-2/.

30 "IIRC Partners." Integrated Reporting. Accessed November 29, 2016. http://integratedreporting.org/the-iirc-

2/iirc-partners/.

31 "Trends in ESG Integration in Investments." August 2012. Accessed November 29, 2016.

https://www.bsr.org/reports/BSR_Trends_in_ESG_Integration.pdf.

12 |

standardization issues have emerged.32 Today it is crucial to create more alignment between

organizations over the metrics used for ESG.

Looking at sustainability indexes, the first sustainability index of its kind, the Dow Jones

Sustainability Index (DJSI) was created by Dow Jones in 1999. The Dow Jones Sustainability

Index was created in cooperation between S&P and RobecoSAM.33 RobecoSAM defines its ESG

research in terms of being “pioneers” in the collection and reporting of ESG data. The data is

sourced from over 3,400 international companies using 80-120 “industry-specific questions.”34

Shortly after the creation of the DJSI, FTSE4Good, now under the FTSE Group, launched in 2001.

FTSE4Good released a report in 2011 titled “10 years of impact and investment” which made a

connection between companies with high ESG scores and a greater market beta than those with

low scores.35 The company uses a “risk relative scoring method” to determine the ESG score of a

given firm.36

Morningstar, based in Chicago, is at the forefront of sustainable investment scoring with a focus

on investors, advisors, and asset managers.37 Morningstar creates its indexes based on data from

Sustainalytics. The firm also notes the increase in ESG reporting by firms and the increase of

professional and academic research on firm ESG practices.38 Using the data from Sustainalytics,

Morningstar creates an “asset weighted average” of the scores in order the formulate a Portfolio

Sustainability Score, which has deducted the Morningstar-created Portfolio Controversy Score.

The Portfolio Sustainability Score then is measured against those of industry peers in order to

create the Morningstar Sustainability Rating.39 Thomson Reuters and Bloomberg have created

large company focuses on sustainability and ESG data.40 Thomas Reuters compiles its ESG data

based on technology from Insight360 on Eikon in its own database of over 400 metrics and 6,000

companies worldwide.41 In addition to reporting on ESG and SRI, the Bloomberg Terminal has

expanded in its data to include that of RobescoSAM in its ESG function. Rebecca Pomfret, an

32 Tomlinson, Brian. "ESG and Fiduciary Duties: A Roadmap for the US Capital Market." The Harvard Law School

Forum on Corporate Governance and Financial Regulation ESG and Fiduciary Duties A Roadmap for the US

Capital Market Comments. November 1, 2016. Accessed December 01, 2016.

https://corpgov.law.harvard.edu/2016/11/01/esg-and-fiduciary-duties-a-roadmap-for-the-us-capital-market/.

33 "DJSI Family Overview | Sustainability Indices." Accessed November 29, 2016. http://www.sustainability-

indices.com/index-family-overview/djsi-family-overview/.

34 "About Us." Sustainability Indices | Sustainability Indices. Accessed November 29, 2016.

http://www.sustainability-indices.com/.

35 "FTSE4GOOD. 1O Years of Impact & Investment." FTSE, 15, accessed November 29, 2016.

http://www.ftse.com/products/downloads/FTSE4Good_10_Year_Report.pdf.

36 "ESG-Ratings." FTSE. Accessed November 29, 2016. http://www.ftse.com/products/indices/F4G-ESG-Ratings.

37 "The Morningstar Sustainable Investing Handbook." Morningstar. Accessed November 29, 2016.

http://corporate1.morningstar.com/Morningstar-Sustainable-Investing-Handbook-2/.

38 "The Morningstar Sustainable Investing Handbook." Morningstar, 3, accessed November 29, 2016.

http://corporate1.morningstar.com/Morningstar-Sustainable-Investing-Handbook-2/.

39 "ESG Research Data." Thomas Reuters, 4, accessed November 30, 2016.

40 "ESG Data Usage | Sustainability at Bloomberg | BCAUSE | Bloomberg L.P." Bloomberg.com. Accessed

November 30, 2016. https://www.bloomberg.com/bcause/customers-using-esg-data.

41 "ESG Research Data." Thomas Reuters. Accessed November 30, 2016.

13 |

ESG Product Manager at Bloomberg describes this partnerships in terms of helping “financial

professionals consider relevant ESG data into their decision-making.42

Corporate Social Responsibility (CSR)

According to the OECD, Corporate Responsibility relates to the “fit” and mutual dependence

between businesses and the societies in which they operate. The act of corporate responsibility

therefore is any action taken by businesses to further this relationship. Over time more and more

corporations have engaged in activities that have shown to society their commitments to this

relationship and to abide by legal and ethical standards, such as the development of policy

statements and later management systems. In starting these initiatives, corporations work closely

with government bodies, NGOs and labor unions.43

CSR Trends

The Economist published an article in January of 2008 titled “A Stitch in Time How companies

manage risks to their reputation.” This article described CSR as a tactic employed by companies

aimed at “risk management.”44 Risk management has been an important issue for organizations

throughout time but has increased due to the greater amount of information available on company

performance and policies. This article addresses the evolving nature of risk management and the

role of CSR. The author does not argue that risk management is the only reason for companies

engaging in CSR at the time, but makes a compelling argument for CSR campaigns that

immediately follow bad press about a corporation. One law, the Alien Tort Claims Act is used to

prosecute companies on American soil whose human rights violations were committed abroad.

This Act is an example of a legal instrument that has caused scandals for many corporate entities.

In fact, the author writes that the “CSR industry believes that a broader understanding of the world

in which they operate can help companies manage risks better.”45

It is important to note the role that globalization has played in the changing legal environment for

firms operating abroad, as well as the role that CSR has played in reputation risk mitigation. As

firms have begun to outsource parts of their service, operations, and manufacturing, less oversight

is available to management. Violations can occur at the hands of contracted organizations

employed by the corporations themselves. With globalization, the duty of firms to maintain ethical

practices is more complicated, but also increasingly necessary. As a result, one CSR trend at the

time was to increase international codes on how certain industries operated globally, often in

partnership with UN organizations and NGOs. One example is the Kimberley Process certification

that emerged in diamond import and export46, or the Ethical Trading Initiative targeting workers’

42 "Bloomberg ESG Function for Sustainability Investors Adds RobecoSAM Data | Bloomberg L.P."

Bloomberg.com. September 29, 2016. Accessed November 30, 2016.

https://www.bloomberg.com/company/announcements/esg-function-adds-robecosam/.

43http://www.oecd.org/corporate/mne/corporateresponsibilityfrequentlyaskedquestions.htm

44 "A Stitch in Time." The Economist. January 19, 2008. Accessed November 30, 2016.

http://www.economist.com/node/10491043.

45 "A Stitch in Time." The Economist. January 19, 2008. Accessed November 30, 2016.

http://www.economist.com/node/10491043.

46 "The Kimberley Process." Global Witness. April 1, 2013. Accessed December 1, 2016.

https://www.globalwitness.org/en/campaigns/conflict-diamonds/kimberley-

process/?gclid=CPnqjbDW09ACFZZMDQodrMoKEQ.

14 |

rights.47 At the time of the article’s publication, 2008, the editor of Ethical Corporation magazine,

Toby Webb predicted that the future of CSR would trend towards anti-corruption. CSR according

to Hannah Jones of Nike uses the term “return on investment squared” to describe the benefits to

society as well as investors that come from CSR programs.48

Anti-corruption has been very much at the forefront of efforts taken by international organizations

for many years. In 2000 the United Nations Global Compact was founded on ten principles in four

categories: Human Rights, Labour, Environment, and Anti-corruption. While the United Nations

was founded on the partnership and collaboration of the governments of 192 nations, the Global

Compact focuses on business, and more specifically, private corporations. Principle 10 of the

Global Contract notes that “Businesses should work against corruption in all its forms, including

extortion and bribery.”49 Companies here are able to become signatories of the “Anti-corruption

Call to Action” in order to pressure governments to strengthen anti-corruption legislation and

become a model for anti-corruption practices. Anti-corruption has continued at the forefront of the

United Nations Sustainable Development Goals (SDGs) of 2016 in goal 16: “Promote just,

peaceful and inclusive societies.”50 The SDGs highlight the world’s most pressing issues and the

ways impact can be measured in the next 15 years. Clearly corruption remains a global issue but

corporations have used anti-corruption policies as a focus for CSR activity, thereby promoting

their commitment to fighting industry corruption.

In January of 2016 Tim McClimon of American Express published his predictions for CSR trends

in 2016. Each trend focuses on the growth and universality of CSR. The first trend predicted by

McClimon is the change of CSR practices to mandatory from voluntary. In 2016, EU member

states will be required to disclose a number of company policies including: bribery and anti-

corruption, diversity of board, human rights respect, environmental, and benefits for employees

and society. Similar CSR disclosure requirements already exist in France, Singapore, and Denmark.

Certain countries, namely India and Mauritius, have actually created a mandatory donation amount

to CSR programs of 2% pre-tax income for corporations. McClimon’s second prediction focuses

on CSR reporting. Here he predicts that CSR reports will shift to a report on mandatory required

CSR completion and CSR activities intrinsic to a company’s business. What he terms “materiality

assessments” will show the CSR activities important to key stakeholders and will look like

financial and management reports. This focus on materiality is very much aligned with the mission

of the SASB. The third prediction shows an increase in uncertainty in the true nature of an

organization. This comes at the obscurity already present between not-for-profits, for-profit firms,

and even B and Benefit Corporations, which will be further explained in the regulatory section,

engaging in activities towards the social good. Lastly, McClimon argues against those who have

47 "The Ethical Trading Initiative (ETI) Is a Leading Alliance of Companies, Trade Unions and NGOs That

Promotes Respect for Workers' Rights around the Globe." Ethical Trading Initiative | Respect for Workers

Worldwide. Accessed December 01, 2016. http://www.ethicaltrade.org/.

48 "A Stitch in Time." The Economist. January 19, 2008. Accessed November 30, 2016.

http://www.economist.com/node/10491043.

49 "The Ten Principles | UN Global Compact." The Ten Principles | UN Global Compact. Accessed November 30,

2016. https://www.unglobalcompact.org/what-is-gc/mission/principles.

50 "Peace, Justice and Strong Institutions - United Nations Sustainable Development." United Nations. Accessed

November 30, 2016. http://www.un.org/sustainabledevelopment/peace-justice/.

15 |

said that CSR is becoming outdated in predicting further growth and increased alignment

throughout an organization towards CSR programs.51

Additional predictions made by Maeve Miccio of CSRwire for trends in 2016 include: increased

influence by employees of CSR initiatives in organizations, increased public-private partnerships

on CSR, and increased organization around initiatives created by the international community.52

Susan McPherson of Forbes also included two additional predictions for 2016 that are extremely

relevant to the evolution of CSR: social justice and climate change.53 In social justice we have seen

brands creating campaigns surrounding relevant social justice issues that in the past have been

limited to the political space. Likewise, climate change is an issue that is growing in the CSR realm

and is at the forefront of the environmental area of ESG.

SRI Trends

One of the greatest trends at the center of SRI is the increase in access to information. Data

collection and distribution from outside sources as well as company transparency have allowed

consumers and investors to incorporate additional data into their decision making on purchases

and investments. In addition to the use of ESG factors and SASB reporting, a number of indices

exist ranking companies according to CSR and SRI performance. According to Forbes, Microsoft,

Google, the Walt Disney Company, and BMW are some of the top companies for CSR. Individual

and corporate sustainable investments are increasing with the increase of reporting through the

various ranking and index systems highlighted.54

Another important area to consider in the trends of SRI is how focus areas of sustainable and

responsible investments have changed over time. In 2014 Barclays, in conjunction with The

Economist Intelligence Unit produced a report titled, “Women in Focus Gender diversity and

socially responsible investing.” This report compares “Rankings of ESG issues mentioned in the

financial press” in 2009 and 2014. In 2009 the top 15 issues were: sustainable energy, sustainability,

compensation, health, social equality, labor standards, political conflict/oppression, lending

practices, regulation/taxation, fossil fuels, governance, environment, diversity, agriculture/food,

and ethical issues. In 2014 the list shifted significantly with diversity moving from 13th to 6th.55

President and CEO of Pax World Management, Joseph Keefe, writes that “women are more

inclined than men to want their investments aligned with certain social and environmental

51 McClimon, Tim. "2016 Trends in Corporate Social Responsibility." CSR Now! January 4, 2016. Accessed

November 30, 2016. http://about.americanexpress.com/csr/csrnow/csrn177.aspx.

52 Miccio, Maeve. "Five CSR Trends to Watch for in 2016." CSRwire Talkback. December 11, 2015. Accessed

November 30, 2016. http://www.csrwire.com/blog/posts/1678-five-csr-trends-to-watch-for-in-2016.

53 McPherson, Susan. "5 CSR Trends That Will Blossom In 2016." Forbes. January 8, 2016. Accessed November

30, 2016. http://www.forbes.com/sites/susanmcpherson/2016/01/08/5-csr-trends-that-will-blossom-in-

2016/#641b1a84742a.

54 McPherson, Susan. "5 CSR Trends That Will Blossom In 2016." Forbes. January 8, 2016. Accessed November

30, 2016. http://www.forbes.com/sites/susanmcpherson/2016/01/08/5-csr-trends-that-will-blossom-in-

2016/#641b1a84742a.

55 "Women in Focus Gender Diversity and Socially Responsible Investing." Barclays. 2014, 14, accessed November

30, 2016. https://www.investmentbank.barclays.com/content/dam/barclayspublic/docs/investment-bank/global-

insights/women-in-focus-gender-diversity-and-socially-responsible-investing-2.4mb.pdf.

16 |

values.” 56 As more women have taken executive positions, this investment alignment has

increasing influence over the investment practices of corporations. [cite?]

The influence of the millennial generation is one that must be considered in sustainable investing

trends. According to Morgan Stanley, millennial investments from those surveyed tend to focus

on funds relating to clean energy (33%), positive screening (36%), and those associated with

positive change (34%). This information came from a poll of 1,003 25-75-year-old high net worth

(HNW) investors. The poll found that of millennials today, 66% are “familiar” with the concept

of SRI.57 Calvert Investments furthers this statistic of familiarity by stating that this is twice the

percentage of familiarity than other generations. They also note that the millennial generation is

also twice as likely as other generations to actually invest according to SRI practices.58 In a study

by Deloitte, findings show a strong connection between millennials and an alignment of values in

corporations. Those surveyed see ethical behavior by corporations as greater than previous years

and “judge the performance of a business on what it does and how it treats people.”

The millennial viewpoint, according to Deloitte, is very much focused on how employees are

treated and the job creation taken by employers. Therefore, many are heavily influenced by

rankings produced on the best places to work. Additionally, TIAA-Cref Asset Management in a

report titled, “Socially responsible investing: Strong interest, low awareness of investment

options”, notes that of the participants in their survey of those under the age of 35, 76% are “very

interested” or “interested” in SRI (as compared to 64% of all participants). While the interest is

clear, 67% of women under the age of 50 and 71% of millennials actually do not know what

options are available to them for responsible investments.59 As the millennial generation adds to

what has become a more diverse workforce, additional pressure is put on organizations to invest

responsibly. Yet, it is necessary to fully educate the population on how best to invest responsibly

in order for individuals to better realize their interests through their investments.

Global Regulatory Environment

The relationship between financial markets and policymakers evolves constantly. The rapid

development of financial products needs regulation. Especially for ESG, sufficient regulation is

needed to provide clarity and safeguards within the financial industry.

56 Keefe, Joseph F. "Women and Sustainable Investing." Pax. Accessed November 30, 2016.

http://paxworld.com/system/storage/19/31/5/2910/20131010_women_and_sustainability.pdf.

57 "Investing in the Future: Sustainable, Responsible and Impact Investing Trends." Morgan Stanley. April 20,

2016. Accessed November 30, 2016. http://www.morganstanley.com/ideas/sustainable-investing-trends.

58 Ford, Lynne. "Why Women and Millennials Are Likely to Drive Growth in Responsible Investing." Calvert

Investments. April 2016. Accessed November 30, 2016. http://www.calvert.com/perspective/women-and-

investing/women-drive-growth.

59 "Socially Responsible Investing: Strong Interest, Low Awareness of Investment Options Survey of TIAA-CREF

Retirement Plan Participants—2014." TIAA-CREF Asset Management. 2014. Accessed November 30, 2016.

https://www.tiaa.org/public/pdf/survey-of-TIAA-CREF-retirement-plan-participants.pdf.

17 |

Fiduciary duty

What is it and who has it60

What is fiduciary duty?

Fiduciary duties (or equivalent obligations) exist to ensure that those who manage other people’s

money act in the interests of beneficiaries.

Fiduciary duties are generally seen as requiring a higher standard of performance than those that

are generally imposed in contracts. The most important fiduciary duties are:

Loyalty: fiduciaries should act in good faith in the interests of their beneficiaries, should

impartially balance the conflicting interests of different beneficiaries, should avoid

conflicts of interest and should not act for the benefit of themselves or a third party;

Prudence: fiduciaries should act with due care, skill and diligence, investing as an

‘ordinary prudent man’ would do.

Who has fiduciary duty?

In investment, the most common fiduciaries are the trustees of trusts or pension funds. Beyond

trustees, different jurisdictions have different interpretations of who exactly holds fiduciary

obligations and who simply has duties of care. For instance, in the UK investment consultants do

not generally define themselves as fiduciaries, whereas they are accepted as such in the United

States. Moreover, in the US, under the Employee Retirement Income Security Act (ERISA), asset

managers have direct fiduciary obligations, and the appointment of asset managers is itself a

fiduciary function. In contrast, in the UK where fiduciary obligations are not defined in this way,

some asset managers believe that their relationship with clients has a fiduciary character whereas

others consider the relationship to be limited to the contract between them.

The changing landscape

In many jurisdictions, fiduciary duty is widely considered as imposing obligations on trustees or

other fiduciaries to maximize investment returns. The maximization of return may have led to an

increasingly shorter-term investment focus. Consequently, ESG risks were often neglected in

practice as the appropriate balance between short- and long-term return shifted. Long-term and

systemic risks to savers have been overlooked, and there has been relatively low demand for active

engagement directed at the creation of long-term sustainable investment value.61

This perception is changing, driven by two factors. First, ESG issues are gaining credibility. The

materiality of ESG issues helps make the argument that investors should not take into account

these factors in investment practice has become less tenable. The 2005 Freshfields Report62 on

fiduciary duty stated:

“…in our opinion, it may be a breach of fiduciary duties to fail to take account of ESG

considerations that are relevant and to give them appropriate weight, bearing in mind that some 60 Rory Sullivan, Will Martindale, Elodie Feller, and Anna Bordon. Fiduciary Duty in the 21st Century. UN Global

Compact, UNEP, and PRI, 2015.

61 Rory Sullivan, Will Martindale, Elodie Feller, and Anna Bordon. Fiduciary Duty in the 21st Century. UN Global

Compact, UNEP, and PRI, 2015.

62 Reported by the law firm of Freshfields Bruckhaus Deringer, commissioned by the United Nations Environmental

Program Finance Initiative (UNEP FI).

18 |

important economic analysts and leading financial institutions are satisfied that a strong link

between good ESG performance and good financial performance exists”.

When social factors materially impact the financial performance of an investment, or when there

is a consensus among the fund’s beneficiaries that social factors should have weight in investment

decisions, SRI is necessary.63

The second driver of the changing landscape are investor expectations. As more and more

investment organizations make commitments to responsible investment, it is likely that the duties

that investors owe their clients will also evolve to reflect these changes. That is, the interpretation

of fiduciary duty, both in practice and in law, is likely to be much wider than at present. As a result

of the global financial crisis, investors are increasingly expected to take into account factors such

as systemic risks and “black swan” events, as well as the insights from areas such as behavioral

finance, in their investment decisions.

South Africa

South African law is recognized as pioneer in incorporating ESG factors into fiduciary duties.

Following the global financial crisis, Regulation 28 to the Pension Funds Act was overhauled in

2011 to modernize outdated regulations, reduce systemic risk, and improve protection for

pensioners. In the specific context of ESG integration, the most notable change was the additional

of a requirement for retirement funds to consider ESG factors when making investment decisions.

Specifically, Regulation 28(2) (c)(ix) states: “Before making an investment in and while invested

in an asset the fund and its board must consider any factor which may materially affect the

sustainable long-term performance of the asset including, but not limited to, those of an

environmental, social and governance character”. The preamble to Regulation 28 explains that:

“Prudent investing should give appropriate consideration to any factor which may materially affect

the sustainable long-term performance of a fund’s assets, including factors of an environmental,

social and governance character. This concept applies across all assets and categories of assets and

should promote the interests of a fund in a stable and transparent environment”.64

United States

US SIF65 worked in a coalition with a diverse set of partners to persuade the Department of Labor

to rescind its 2008 bulletin on Economically Targeted Investments, which had discouraged

fiduciaries for retirement plans in the private sector from considering environmental and social

factors in their investments. The Department of Labor, which is responsible for enforcing the

ERISA, issued new guidance in 2015 that clarifies that fiduciaries of ERISA-governed pension

funds “may consider ESG goals as tie-breakers when choosing between investment alternatives

that are otherwise equal with respect to return and risk over the appropriate time horizon.” This

guidance also includes a recommendation that “environmental, social, and governance issues may

have a direct relationship to the economic value of the plan’s investment,” and thus these issues

63 William Sanders. Resolving the Conflict Between Fiduciary Duties and Socially Responsible Investing. Pace Law

Review, 35(2), 2014.

64 The Impact of Sustainable and Responsible Investment. The US SIF Foundation, 2016.

65 US SIF: The Forum for Sustainable and Responsible Investment

19 |

“are not merely collateral considerations or tie-breakers, but rather are proper components of the

fiduciary’s primary analysis of the economic merits of competing investment choices.”66

Benefit Corps and B Corps

Among the top contributors to the advancement of ESG integration are the evolving corporate

entities known as benefit corps and B corps.

Benefit Corporations67

What are Benefit Corporations?

A benefit corporation is a legal way to incorporate a new type of corporate entity with modified

obligations including not only the pursuit of financial success, but also additional explicit purposes.

It involves higher standards of purpose, accountability and transparency:

● Purpose: Benefit corporations commit to creating public benefit and sustainable value in

addition to generating profit. Here, sustainability is an integral part of their value

proposition.

● Accountability: Benefit corporations are committed to considering the company’s impact

on society and the environment in order to create long-term sustainable value for all

stakeholders.

● Transparency: Benefit corporations are required to report, in most states annually and using

a third party standard, showing their progress towards achieving social and environmental

impact to their shareholders and in most cases the wider public.

Benefit corporations reject the myopic model of using profit maximization as the primary lens in

decision making. They are required to consider all stakeholders in their decisions. This gives them

the flexibility to create sustainable value over the long term, and even through exit transactions

such as IPOs and acquisitions.

Benefit Corporation Legislation

In the US, 31 states including the District of Columbia have passed benefit corporation legislation

and 7 states are currently in the process of creating this legislation. Benefit corporation legislation

has enjoyed an almost 90% approval rate from legislators in both parties.

Building on the success of benefit corporation legislation in the US, the nonprofit B Lab is already

working with governments in several countries to create and implement mission-aligned structures

to promote their use. So far, legislation in two jurisdictions outside the mainland United States and

Hawaii have passed – Puerto Rico and Italy. In 2016, legislation is moving forward in Australia,

Argentina, Chile, Colombia and Canada.

B Corporations68

What are B Corps?

B Corps are for-profit companies certified by B Lab to meet rigorous standards of social and

environmental performance, accountability, and transparency. Today, there is a growing

community of more than 1,600 Certified B Corps from 42 countries and over 120 industries.

66 The Impact of Sustainable and Responsible Investment. The US SIF Foundation, 2016.

67 http://benefitcorp.net/

68 https://www.bcorporation.net/

20 |

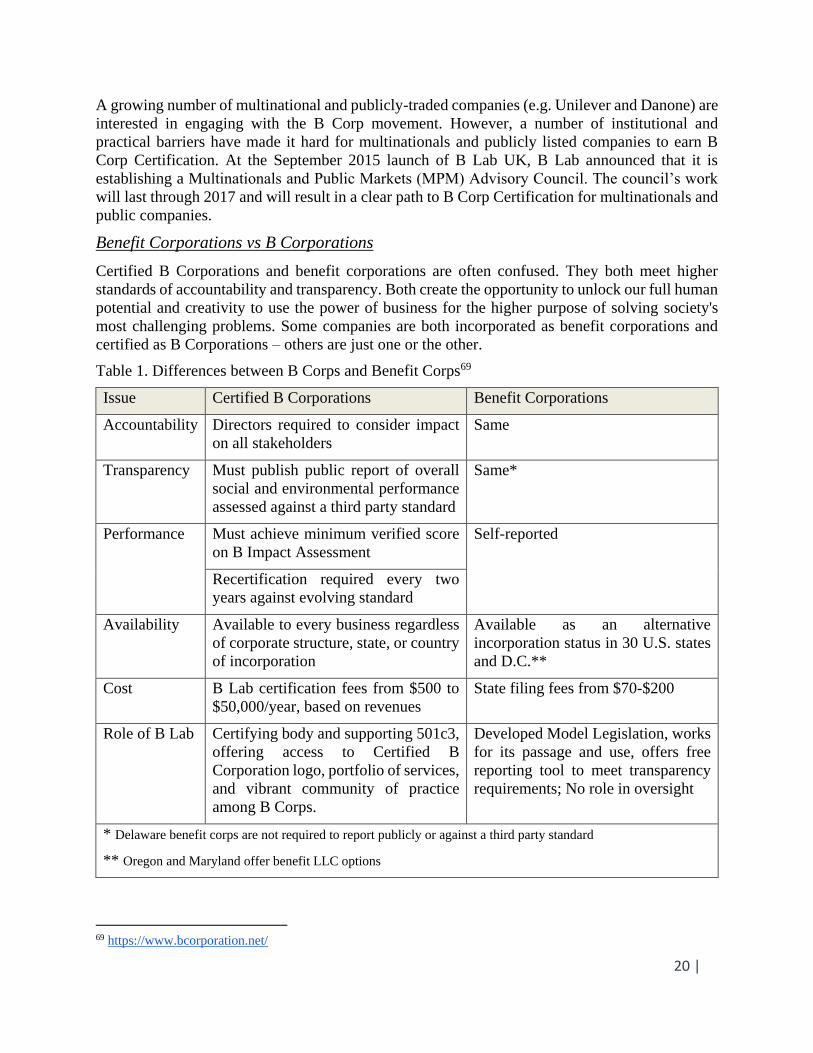

A growing number of multinational and publicly-traded companies (e.g. Unilever and Danone) are

interested in engaging with the B Corp movement. However, a number of institutional and

practical barriers have made it hard for multinationals and publicly listed companies to earn B

Corp Certification. At the September 2015 launch of B Lab UK, B Lab announced that it is

establishing a Multinationals and Public Markets (MPM) Advisory Council. The council’s work

will last through 2017 and will result in a clear path to B Corp Certification for multinationals and

public companies.

Benefit Corporations vs B Corporations

Certified B Corporations and benefit corporations are often confused. They both meet higher

standards of accountability and transparency. Both create the opportunity to unlock our full human

potential and creativity to use the power of business for the higher purpose of solving society's

most challenging problems. Some companies are both incorporated as benefit corporations and

certified as B Corporations – others are just one or the other.

Table 1. Differences between B Corps and Benefit Corps69

Issue Certified B Corporations Benefit Corporations

Accountability Directors required to consider impact

on all stakeholders

Same

Transparency Must publish public report of overall

social and environmental performance

assessed against a third party standard

Same*

Performance Must achieve minimum verified score

on B Impact Assessment

Self-reported

Recertification required every two

years against evolving standard

Availability Available to every business regardless

of corporate structure, state, or country

of incorporation

Available as an alternative

incorporation status in 30 U.S. states

and D.C.**

Cost B Lab certification fees from $500 to

$50,000/year, based on revenues

State filing fees from $70-$200

Role of B Lab Certifying body and supporting 501c3,

offering access to Certified B

Corporation logo, portfolio of services,

and vibrant community of practice

among B Corps.

Developed Model Legislation, works

for its passage and use, offers free

reporting tool to meet transparency

requirements; No role in oversight

* Delaware benefit corps are not required to report publicly or against a third party standard

** Oregon and Maryland offer benefit LLC options

69 https://www.bcorporation.net/

21 |

Corporate Disclosure

In July 2015, the World Federation of Exchanges (WFE) published an analysis report on ESG

initiatives across the globe based on a survey conducted in 2014, and responded by 56 member

exchanges in EMEA, APAC and Americas. The results indicate that, 57% (32) of the respondents

reported that listed companies on their markets were required to disclose some ESG information

beyond corporate governance, and nearly half of them (15) said that both the regulator and the

exchange itself required disclosure in some form. For those required by the regulator, 12 out of 17

respondents replied that it is a mandatory requirement for listed companies, with only 14% of

regulators’ requirements being voluntary. Whereas 8 exchanges had voluntary disclosure policies

in place, with only 3 others with mandatory disclosure. Most sustainability disclosure requirements

covered all the three dimensions of ESG, with 20 exchanges requiring some form of disclosing

environmental issues, though 18 exchanges said that in their jurisdiction, listed companies were

only required to disclose corporate governance information. Additionally, at least 22 different

sustainability-related indices have been created by members of WFE and there are also a number

of indices planned for the near future.70

Europe

EU Shareholder Rights Directive71

In April 2014, the European Commission published a proposal for the revision of the Shareholder

Rights Directive (Directive 2007/36/EC) requiring the disclosure of diversity and other ESG

information by certain large listed European companies. The proposal is being examined by the

co-legislators (European Parliament and Council). It would expand the areas to be covered in the

disclosure and implement a mandatory approach.

It includes a number of measures aimed at facilitating the exercise of shareholder rights and

enhancing those rights where appropriate. It also comes with additional transparency requirements

along the investment chain:

Mandatory disclosure by institutional investors and asset managers on their voting

engagement and certain aspects of asset management arrangements, in particular around

how they integrate long-term considerations into their investment policies;

Disclosure of the remuneration policy and individual remunerations, combined with a

shareholder vote;

Binding disclosure requirements on the methodology and conflicts of interests of proxy

advisors;

Creating a framework to allow listed companies to identify their shareholders and requiring

intermediaries to rapidly transmit information related to shareholders and to facilitate the

exercise of shareholder rights.

Asia

Across Asia, national regulatory systems are developing progressively to promote corporate

disclosure of ESG issues.

70 Exchanges and ESG Initiatives - SWG Report and Survey. World Federation of Exchanges - Sustainability

Working Group (SWG), 2015.

71 2014 Global Sustainable Investment Review. Global Sustainable Investment Alliance, 2015.

22 |

Stock Exchanges72

The region’s stock exchanges are playing a critical role in enhancing ESG reporting.

In China, both the Shenzhen Stock Exchange (SZSE) and the Shanghai Stock Exchange

(SSE) have introduced comprehensive guidelines for listed companies.

In 2012, Hong Kong Exchanges and Clearing Limited (HKEx) introduced the ESG

Reporting Guidelines which currently are voluntary.

In October 2014, the Singapore Stock Exchange (SGX) announced that it is mandating

listed companies to publish sustainability reports

Government Leadership73

While most sustainable investment markets in Asia remain in the early stages of development, a

number of governments are actively promoting growth on a larger scale.

In Japan, 160 institutions, including the Government Pension Investment Fund and the

Pension Fund Association for Local Government Officials, endorsed the “Principles for

Responsible Institutional Investors” within six months of its introduction in February 2014

by Japan’s Financial Services Agency.

In Malaysia, the government has committed to promoting the country as a regional center

for sustainable investment, primarily by establishing ESG-related products, launching

dedicated investment funds, and adopting ESG principles for government-managed assets.

In South Korea, one of the first countries in Asia to embrace “green growth” as a

development strategy, the government has introduced initiatives to shift the country

towards a low carbon and resource efficient economy.

United States

Dodd-Frank Financial Reform Law74

In 2010, shareholder advocates in the United States won an important victory when the Dodd-

Frank Wall Street Reform and Consumer Protection Act was signed into law. It gave explicit

authority to the SEC to implement a rule to allow shareholders, within certain parameters, to

nominate directors to the boards of their portfolio companies and to have access to the company’s

proxy statement to make the case for their nominees. The law specified, too, that publicly traded

companies must allow shareholders – at least once every three years – to hold an advisory vote on

their executives’ pay packages – an important tool shareholders have used to hold management

more accountable.

Dodd-Frank provisions important to SRI investors:

Executive Compensation and Pay Disparity: Dodd-Frank includes a provision that

requires public companies to disclose CEO-to-worker pay ratios. The provision reflects

investor concern that the dramatic rise in US CEO pay levels over the past three decades

has come at the expense of shareholders and other stakeholders, including company

employees. Moreover, executive pay packages that are tied primarily to short-term

financial indicators and stock prices can provide incentives for CEOs to take excessive