Empirical distributions of stock returns: European securities markets, 1990-95

STOCK EXCHANGE MARKETS FOR HIGH-GROWTH SMEs: THEORETICAL ISSUES AND EMPIRICAL EVIDENCE IN EUROPE

Marco Giorgino and Elena Magnani

Abstract

Following the generalised failure of second tier stock markets, Europe has experienced in recent years the birth of different so-called new high-growth markets, which have the US Nasdaq as an example, either to emulate or to refrain from imitating. Great is the debate on the ideal microstructure and the concern about their future development.

This paper represents a preliminary attempt to put together various research and literature streams that appear to be relevant as far as high-growth stock markets are concerned. The theoretic underlying that justifies their existence represents the first issue. This, at its turn, is linked with the broader streams of small business corporate finance and financial market analysis. Once the existence of such a market is argued, the second important issue lies in finding ways through which thin market pitfalls, linked with SMEs' stocks listing and trading, can be avoided. Great attention must in fact be taken in order to the market design to be effective.

A critical review of literature is presented, together with some empirical evidences from the European new markets, in order both to understand if market designers generally follow theoretic issues and to appreciate their performance. A first attempt to apply network economics to SMEs' stock markets, in order to explain different performance by differently organised exchanges, is provided.

1. The Importance of High-Growth SMEs Dedicated Stock Markets

1.1 The Importance for SMEs

It is now well known that small businesses are not "scaled-down versions" of large businesses (Cressy and Olofsson, 1997). The process of evolution will involve major changes in management structure and functioning, in particular in the methods by which the business is financed (Penrose, 1959).

Hughes (1997) for U.K. and Brunetti (1998) for Italy, find that smaller businesses: have lower fixed to total asset ratios; have a higher proportion of trade debt in total assets; have a much higher proportion of current liabilities to total assets (and in particular a much greater reliance on - especially short term - bank loans to finance their assets); are heavily reliant on retained profits to fund investment flows; obtain the vast majority of additional finance from banks (with other sources, in particular equity, very much less important); are financially more risky, as reflected in their relatively high debt-equity ratio and higher failure rates.

These differences are fascinating and call for explanation. The original Modigliani and Miller propositions (1958 and 1963) did not make reference to size or stage of development being factors in determining financial structure. This theoretical lack of concern about firm size and stage of development existed side by side for many years with an increasing concern, by government commissions, about the existence of a finance gap for small firms (Chittenden, Hall and Hutchinson, 1996). While it was felt that lack of access to the capital market could result in

an over-reliance on short-term source of finance, there were few attempts at providing a theoretical rationale to link stage of development of the small firm with its financial characteristics.

An early reference to the possibility that small firms were indeed different from large in terms of their access to finance was provided by the Bolton (1971) and Wilson (1980) Committees and gave rise to the term "finance gap" that described the situation where a firm had grown to a size where it had made maximum use of short-term finance but was not yet big enough to approach the capital market for longer-term finance.

Weston and Brigham (1981) provided arguments to explain small firm financial structure using a life cycle approach. Small business may be thought of as having a financial growth cycle in which financial needs and options change as the business grows and gains further experience. Initial insider finance is often required at the very earliest stage of a firm's development when the entrepreneur is still developing the product or business concept and when the firm's assets are mostly intangibles. Conventional wisdom argues that bank or commercial finance company lending would typically not be available to small businesses until they achieve a level of production where their balance sheets reflect substantial tangible business assets that might be pledged as collateral, such as account receivable, inventory, and equipment. Small firms were seen as starting out using only owners' resources; if they survived the dangers of undercapitalisation they were then likely to be able to make use of other sources of funds such as trade credit and short term loans from banks (Chittenden, Hall, and Hutchinson, 1996). Rapid growth at this stage could lead to the problem of illiquidity which would follow from an over-reliance on short-term finance. This, in turn, would result from the lack of availability of long-term funds, such as debentures or equity issues, that would be due to the small firm not having a stock market quotation.

An alternative explanation is provided by the pecking order framework, proposed by Myers (1984). This theory suggests that firms finance their needs in hierarchical fashion, first using internally available funds, followed by debt, and finally external equity. This preference reflects the relative costs of the various sources of finance. This does not only reflect the fact that stock market flotation is expensive to arrange and initial public offerings are subject to underpricing which seems to be particularly severe for smaller firms (Buckland and Davis, 1990), but that it may open the door to loss of control by the original owner managers and the possibility of takeovers.

Some empirical evidence have been provided for these theories. One of the most recent is the work of Chittenden, Hall, and Hutchinson (1996). From the results presented, it can be seen that profitability, asset structure, size, age and access to the capital market do affect financial structure of small firms. While growth does not significantly affect financial structure itself, the combination of rapid growth and lack of access to the capital markets does. There also appear to be major differences between listed and unlisted small firms for all aspects of financial structures. The results, therefore, indicate that the Modigliani and Miller propositions on financial structure do not seem to apply to small firms. Access to the capital market itself appears to be the major factor determining the capital structure of small firms. Once a flotation has been achieved, long-term debt becomes available, collateral becomes less important and liquidity is no longer determined by age and profitability. In particular, the level of long-term debt for quoted small firms is much more related to profitability than it is for unquoted small firms. The strongly negative relationship between profit and long-term debt for unlisted small firms suggests that the small unquoted firms which are getting these funds are the ones with lower profits taking advantage of their collateral. The pecking order framework emerges as a good explanation of small unlisted firms' capital structure with a heavy reliance on internally generated funds being the key feature. Agency theory also provides explanations which stand up to empirical testing. The use of collateral, especially for unlisted small firms, is widespread and is consistent with its being used as a way of dealing with agency problems in lending to small firms.

What is of concern, from the point of view of economic development, is that unlisted dynamic small firms may be curtailing their growth to match their financial resources. The long-term finance that is available to unlisted small firms is provided, in fact, on the basis of collateral rather than profitability. These outcomes suggest, together with a need for financial institutions to develop innovative solutions to agency problems rather than relying on collateral, a need to continue to find ways of reducing barriers to entry to the stock market for small firms.

1.2 The Importance for Investors and Intermediaries

The notion that firms evolve through a financial growth cycle (see Paragraph 1.1) is well established in the literature as a descriptive concept (Berger and Udell, 1998). As a matter of fact it is appealing theoretically because start-up firms are arguably the most informationally opaque and, therefore, have much difficulty in obtaining intermediated external finance (see Figure 1--omitted). Agency theory, following on from the work of Coase (1937) and Jensen and Meckling (1976), provides valuable insights into small firm finance. Agency problems, in the form of information asimmetry, moral hazard and adverse selection are likely to arise in contractual arrangements between small firms and external providers of capital. This suggests that external equity finance, specifically angels and venture capital, may be particularly important when these conditions hold and the moral hazard problem is acute. The fact that high-growth, high-risk new ventures often obtain angel finance and/or venture capital before they obtain significant amounts of external debt finance suggests that the moral hazard problem may be particularly acute for these firms.

EVCA (1997) classifies four different kinds of way-outs for venture capital investments: public offerings, when the company's equity is listed on a regulated stock exchange; trade sales, when the shareholding is sold to third parties or the company is incorporated into another firm; write offs, when the shareholding is annulled as long as the company goes bankrupt; other means, when the shareholding is sold to the majority shareholder or to the management through buy-backs, MBOs or LBOs.

There exist in literature two different models that are found to guide the divestment activity of venture capitalists (AIFI, 1995): the path-sketcher model and the opportunist model. As far as the former is concerned, the investor tries to figure out way-out opportunities at the very moment of investing in the start-up company. The venture capitalist thus tries to figure out the target group of investors that could be interested in taking over the company in the future by means of trade sales. On the contrary, the opportunist model provides for a greater reliance of the venture capitalist in the company's management, in that a preventive identification of future investors seems not to be necessary, in the hope that the company - as it is well managed - will easily succeed in becoming public through an IPO.

There exist both pros and cons, for the company and the venture capitalist, in using IPO as a way-out. Disadvantages lie mainly in the higher costs of the transaction, higher disclosure duties and longer deal timing (both because of the listing process timing itself and because generally the shareholding is sold by tranches in order not to jam the market). Advantages, on the other side, reside in both the possibility of increasing the company's image and the opening to future capital raising as long as the liquidity of shares becomes higher.

Some studies demonstrate that the likeliness of an IPO way-out is essential for venture capital market's development. Black and Gilson (1998) state that high-growth, start-ups' financing is linked to this opportunity. As a matter fact, control seems to assume so strong a value that it prevents from venture capital markets to actively develop in those countries were the divestiture can be realised only through a trade sale. They show that the countries where venture capital is most active are those where there exist a stock market in which venture capitalists can sell their shareholdings. Jeng and Wells (1998) offer an empirical test for this theory, showing that IPO's numbers is the most relevant variable that influences the amount of venture capital investments. Venture

Economics shows that IPO is the most profitable way-out for a venture capitalist: through an IPO the average yield is 195% in an average 4.2-year period, while through a trade sale the average yield is 40% on a 3.7-year period.

Obviously, if a regulated market for high-growth SMEs is essential for the development of an active venture capital market, the reverse is also true. Barry and Muscarella (1990) state that the market sees a VC-backed company going public as having a higher quality. This is explained by Gompers (1996) who states that venture capitalist have to safeguard their reputation on IPOs' market.

The existence of a dedicated market also has the highest importance for institutional dealers who want to diversify or specialise their portfolios in high-growth small caps. Investors in growth companies expect above-average returns (Brealey and Myers, 1988). However, they also require a liquid and regulated market. Portfolio managers wanting to spread risks are able to increase their returns. Specialised funds covering, for example, high tech, biotechnology, telecommunications and software sectors, find new opportunities to enrich their portfolios with securities from innovative and dynamic companies.

Companies listed on a high-growth specific market generally show a higher risk profile. The market therefore expects listed companies to respect outstanding information standards. Before listing, companies are asked to present their business plan and financing scheme. Once admitted, a lot of attention is given to regular and adequate information allowing investors to closely monitor performance. The fact that transaction of high-growth SMEs' share happen in fully regulated markets is an assurance of security and transparency for all investors. This is of particular interest for those institutional investors that are obligated to invest a given percentage of their funds in markets of this status.

Finally, the existence of a regulated market permits the birth of collateral markets, in particular those in which derivatives are negotiated. This, at its turn, boosts the number of transactions in the underlying market and allows a major portfolio diversification.

At last, as long as intermediaries are concerned, a liquid and dynamic market for high growth enterprises opens up new strategic business areas also for banks and brokers. Intermediaries find the critical mass of stocks necessary to justify the development of specialised research. Expertise from other markets and synergies can be used very efficiently. Syndication groups find a network of markets enabling them to offer broader placement capacities to issuers and attractive investments to investors.

2. The Structural Configuration of a High-Growth SMEs Market: Theoretic Framework and Empirical Evidence

2.1 The Theoretic Framework: Pitfalls of Thin Markets

Following neo-classical hypothesis, market actors, by means of their rational behaviour, can identify a single equilibrium price for each negotiated good (Varian, 1992). As it happens in any competitive market, also in the financial market the demand is infinitely elastic in correspondence with the equilibrium price. However, the many assumptions which the neoclassical theory relies upon - absence of transaction costs and of bounded rationality, presence of a Walrasian auctioneer, in a word the existence of a perfectly competitive market seen as a black box - keep the neo-classical framework far from how the real markets, which are much more complex than theories would suggest (Nichols, 1993), behave.

The separation between financial markets theory and results of empirical analysis is due to the lack of information that characterises real financial markets. Due to this characteristic real transaction prices do not behave like theoretic prices. This is much truer as far as thin markets are concerned1. To this kind of financial markets are generally linked such characteristics, as high price volatility, a low degree of liquidity, and a low level of efficiency of the pricing process.

These features however, do not derive directly from the fact that a market is thin. Actually, the causal problem - which all the others come from - lies in the difficulties in estimating the equilibrium price, which could be much uncertain, as long as supply and demand streams are not numerous. Thus, it is not the fact that the market is thin that determines a bad pricing process; but problems arise when supply and demand flows are so exiguous that the situation implies a lack of information, that at its turn makes the definition of a theoretic price ambiguous.

A financial market actor generally relies upon two different sources of information (Petrella, 1997): information about the fundamentals of the company and its industry (direct source of information), and information about the supply and demand flows present on the financial market where the company is listed (indirect source of information).

The analysis of supply and demand flows that are present on the market makes it possible to determine, indirectly, the interest that the market gives to the particular security. This is true, not only as far as an individual investor is concerned, but also with regards to institutional investors, especially dealers. As a matter of fact, when a stock is object of frequent transactions, dealers find always-fresh information about the interest of the market in that stock (that is given by the difference between demand and supply). The more the market is thin, the less are the information that can be derived from prices, the more ambiguous is the definition of equilibrium prices. It is true that there exist also direct sources of information. However, we have seen in Paragraphs 1.1 and 1.2 how the informative opaqueness of small and medium enterprises can be severe.

Three main consequences can be traced back to the thinness of a market (Petrella, 1997), however, they do not derive from this directly, but through "lack of information" and "uncertain pricing process" intervening variables (see Figure 1):

• Higher bid/ask spreads. As long as dealers are not able to exactly determine the equilibrium price, they do not have a certain value on which to base the spread fixing. As a matter of fact, rather than a certain value that indicates the equilibrium price, they can rely only upon a range of values inside which the real equilibrium value lies. Thus, the bid/ask spread goes wider, in directly proportional measure to the width of the range of values given by the market as equilibrium prices (Stoll, 1985).

• Lower degree of market breadth2 . When the definition of the equilibrium price is uncertain, a dealer is likely to realise a transaction only for a limited quantity of securities, in order to safeguard his/herself from esteem mistakes. In particular, the quantity would be much lower than in a "normal" condition of high supply/demand flows. The effects 1) and 2) are summarised in Figure 2 (omitted).

• Higher volatility. When the number of transactions is low, the dealer is naturally inclined to give a higher importance to latest transactions. This can be traced back to the fact that the equilibrium price is not known, and consequently every new transaction gives fresh information about the interest of the market in that security (and the consequent esteem of the equilibrium price). As a matter of fact, the dealer, given the small number of transactions, is not really able to distinguish temporary from permanent disequilibria between supply and demand order flows. The less are the number of transactions, the more likely is that the dealer evaluates as permanent a disequilibrium that would actually be temporary.

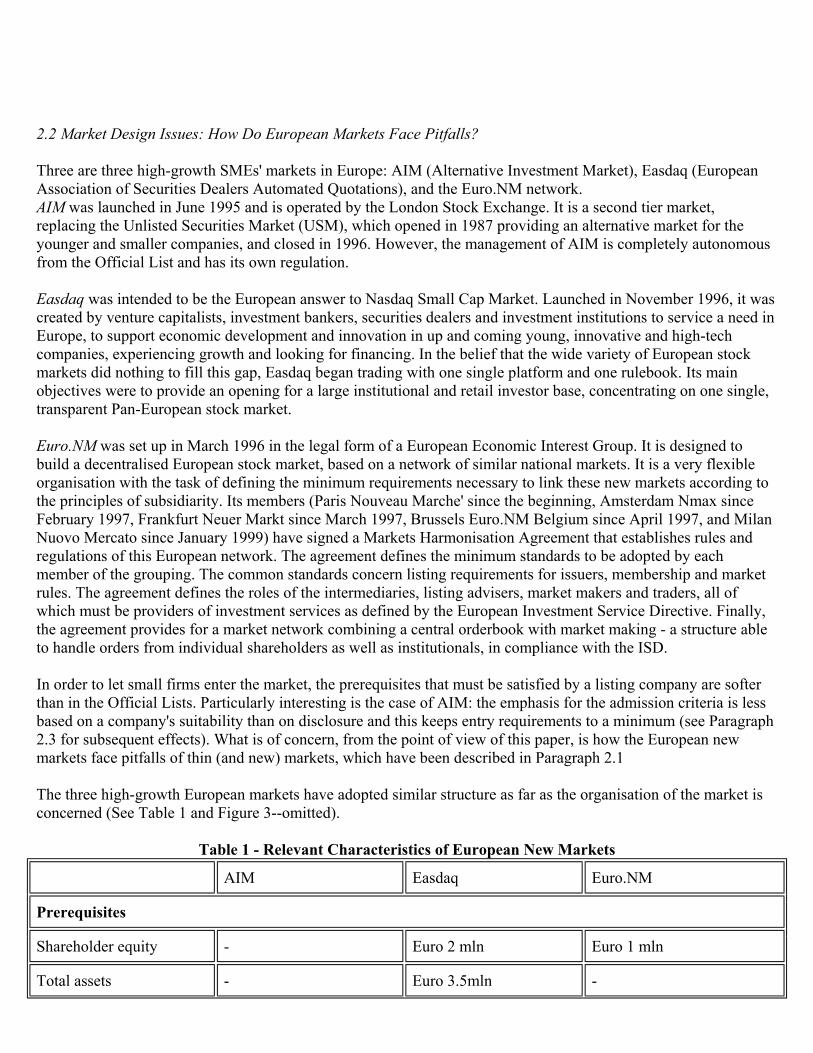

2.2 Market Design Issues: How Do European Markets Face Pitfalls? Three are three high-growth SMEs' markets in Europe: AIM (Alternative Investment Market), Easdaq (European Association of Securities Dealers Automated Quotations), and the Euro.NM network. AIM was launched in June 1995 and is operated by the London Stock Exchange. It is a second tier market, replacing the Unlisted Securities Market (USM), which opened in 1987 providing an alternative market for the younger and smaller companies, and closed in 1996. However, the management of AIM is completely autonomous from the Official List and has its own regulation. Easdaq was intended to be the European answer to Nasdaq Small Cap Market. Launched in November 1996, it was created by venture capitalists, investment bankers, securities dealers and investment institutions to service a need in Europe, to support economic development and innovation in up and coming young, innovative and high-tech companies, experiencing growth and looking for financing. In the belief that the wide variety of European stock markets did nothing to fill this gap, Easdaq began trading with one single platform and one rulebook. Its main objectives were to provide an opening for a large institutional and retail investor base, concentrating on one single, transparent Pan-European stock market. Euro.NM was set up in March 1996 in the legal form of a European Economic Interest Group. It is designed to build a decentralised European stock market, based on a network of similar national markets. It is a very flexible organisation with the task of defining the minimum requirements necessary to link these new markets according to the principles of subsidiarity. Its members (Paris Nouveau Marche' since the beginning, Amsterdam Nmax since February 1997, Frankfurt Neuer Markt since March 1997, Brussels Euro.NM Belgium since April 1997, and Milan Nuovo Mercato since January 1999) have signed a Markets Harmonisation Agreement that establishes rules and regulations of this European network. The agreement defines the minimum standards to be adopted by each member of the grouping. The common standards concern listing requirements for issuers, membership and market rules. The agreement defines the roles of the intermediaries, listing advisers, market makers and traders, all of which must be providers of investment services as defined by the European Investment Service Directive. Finally, the agreement provides for a market network combining a central orderbook with market making - a structure able to handle orders from individual shareholders as well as institutionals, in compliance with the ISD. In order to let small firms enter the market, the prerequisites that must be satisfied by a listing company are softer than in the Official Lists. Particularly interesting is the case of AIM: the emphasis for the admission criteria is less based on a company's suitability than on disclosure and this keeps entry requirements to a minimum (see Paragraph 2.3 for subsequent effects). What is of concern, from the point of view of this paper, is how the European new markets face pitfalls of thin (and new) markets, which have been described in Paragraph 2.1 The three high-growth European markets have adopted similar structure as far as the organisation of the market is concerned (See Table 1 and Figure 3--omitted).

Table 1 - Relevant Characteristics of European New Markets

AIM Easdaq Euro.NM

Prerequisites

Shareholder equity - Euro 2 mln Euro 1 mln

Total assets - Euro 3.5mln -

Minimum float - 20% of equity and

≥ 100 shareholders (rec.)

≥ 100,000 shares and 25% of equity or Euro 5 mln

Market Capitalisation - Euro 50 mln -

Professional help

Sponsor Yes (Nominated Adviser) Yes Yes

Market makers (*: sponsor allowed to be Mm)

No (Nominated Broker) *

Yes (2 at least) *

Yes *

Maximum spread - - 10%

Trading system

Competitive market sharing Yes Yes Yes

Order book Yes Only if Mkt makers < 2 Yes

Disclosure requisites

Initial

Prospectus Yes (POS Regulation and LSE Regulations) Yes (CEE 89/298) Yes (including a list of risk

factors)

Business plan Recommended Compulsory Recommended

Balance sheets UK or US GAAP, IAS or reconciled

UK or US GAAP, IAS or reconciled Audited -

Periodical

Reports UK or US GAAP, IAS or reconciled Audited Within 6 months

UK or US GAAP, IAS or reconciled Audited Within 3 months

US GAAP or IAS or reconciled Audited Within 6 months

Interim reports Biannually Unaudited

Quarterly Unaudited

Quarterly Unaudited

On the primary market there must be a sponsor for each listing company it assists the listing company during the quotation process and acts as a guarantor of its quality in the face of the market. We have seen in previous paragraphs that there exist a strong agency problem between a small firm and its financiers. This situation is heightened in the process of listing as the diffusion of equity makes the relationship between insiders and external financiers harder. The intervention of a sponsor makes it possible to reduce this gap, as it has a recognised professionalism and put its credibility on the table. The usefulness of the sponsor is much higher in the case of the European new markets, as they are relatively recent. As a matter of fact in the situation where a market has a strong reputation, this is sufficient to guarantee the quality of listed companies even without a sponsor (see, for example, Nasdaq). Actually, in the long-term there is a substitution relationship between the image of the market and the presence of a sponsor; when the market is young this last is extremely necessary, while, as the market gains an autonomous standing, the sponsor utility gradually decreases. Summing up, it can be said that the sponsor acts as a complementary information source, together with direct and indirect sources (see Paragraph 2.1). Information about the sponsor are included in the set of information the investor analyse before entering the market (see Figure 4--omitted), and thus the choice of the right sponsor for the listing company is extremely important. The secondary market is generally organised as a competitive market among market makers. These intermediaries, who act as dealers, increase the liquidity of the market, in that they undertake to always make transactions at the counterpart request. The ways a market maker market works are different on the basis of the binding degree of their proposals (which can be either binding or indicative), the minimum quotation size, and the presence of a maximum threshold to spread. The only market that does not provide for at least one professional market maker is AIM, where there exists only the necessity to nominate a broker who will match buy and sell orders and who is responsible for bid/ask proposals only if there isn't a market maker on that specific security. The three problems that arise as far as a thin market is concerned (see Paragraph 2.1) can be resolved through a competitive market maker market. As a matter of fact, if market makers act in a really competitive arena, the bid/ask spread does decrease. Even the quantity of traded securities is higher, as the single market maker does not make a rationing as a monopolist does and it is also possible for the single investor to aggregate transactions with different market makers. At last, the transitory volatility is more stable, as the portfolio policy of the single dealer does not reflect upon fluctuations of the best bid/ask proposals. These effects, however, can be achieved only if the competition among market makers is not only effective, but also fair; this is to say that every market maker should be informed upon his concurrents' activities. Actually, the fair competition could be biased by the fact that all of the European new markets allow the sponsor to become also market maker on the sponsored security's transactions. The sponsor market maker has clearly an informative advantage over other market makers. This situation, at its extreme results, could lead non-sponsor market makers to decrease their commitment (Petrella, 1997). Two can be the solutions to this situation of conflict of interest: to create "Chinese walls" between the corporate and the trading functions; to allow for reciprocal positions sponsor-market maker/market maker sponsor. Only the latter has been experimented in the European new markets. Lastly, the bias risen by agency problems are avoided in European new markets by means of strong disclosure attainments, both initial and periodical (see Table 1 and Figure 3). The listing company must prepare a prospectus, containing all information about the offer. Both AIM and Easdaq require balance sheets, while Euro.NM does not: the aim is to look at the future of the company and not the past. The only Easdaq, however, makes it compulsory to present a business plan. As far as periodical disclosure is concerned.

2.3 European New Markets: Some Relevant Data Major differences can be perceived between the three markets, as far as number of listed companies, capitalisation, and companies' business activity are concerned (Mutzyka, Leleux, and Guegan, 1998). AIM, the oldest of the markets, has the largest number of companies with over 300, although the rate of its IPOs slowed down during 1998 (see Figure 5--omitted). Easdaq, whose strategy is to attract somewhat larger companies, has been growing gradually since its launch, while Euro.NM has shown a persistent increase with a recent strong upward trend. Ueuro.NM and Easdaq's relatively lower development in terms of number of companies listed belies their actual market capitalisations (see Figure 6.a--omitted). The companies on Euro.NM's national markets as a whole represent the largest market in terms of value, followed by Easdaq showing less than half of the value. The market capitalisation of the Euro.NM is however largely based on the contribution from the Neuer Markt and the Nouveau Marhce', collectively representing 94% of the total value. The relative differences in company size are interesting (see Figure 6.b--omitted). The average sized firms are larger on Easdaq and relatively high on the Euro.NM (where, however company size is completely different passing from the Neuer Markt to the Nouveau Marche'). AIM, with its greater collection of services firms, lists many smaller enterprises. As a matter of fact, here the emphasis for the admission criteria is less based on a company's suitability than on disclosure and this keeps entry requirements to a minimum. Differences in average size are reflected also in the Top 10 companies capitalisation (see Figure 6.c--omitted). Easdaq shows not only the biggest companies but also a high degree of market concentration, while AIM's small size patterns are common to the whole market. As far as business activities of listed companies are concerned (see Figure 7--omitted), Easdaq has a high technology focus and strategy, reflected in its distribution of companies, with 41% representing computers, telecommunications and biotechnology. AIM has a heavy concentration of smaller service firms. Euro.NM has an emphasis on firms in computer-related fields (both hardware and software), but otherwise shows a great deal of diversity. In summary, the markets are evolving to represent different companies by size, sector, growth, and are acquiring their own unique character. This in particular, put in evidence the high competition that there exists between Easdaq and Euro.NM, as they appear to be more similar, while AIM has captured a market niche (cfr. Figure 8--omitted). 2.4 Why Euro.NM Seems To Be More Successful: A Preliminary Explanation from the Network Economics Even if Easdaq and Euro.NM are similar, there exist deep differences between them, in terms of future prospects. The number of listed companies on Easdaq seems to be at a standstill, while Euro.NM foresees listings will reach 250 units within year 1999. More national markets, then, are going to join in the near future the Euro.NM network: the four Scandinavian Stock Exchanges (Stockholm, Copenhagen, Oslo, and Helsinki) and the Swiss Stock Exchange. The network economics literature when applied to financial markets analysis, can be a useful tool in order to interpret the competitive process that engages financial markets, and that brings to this sort of differences. The basic feature of a network is that it gives rise to positive externalities. The higher the number of network users, the higher the utility that they can derive from the network itself, and the higher the likeliness that other users buy the services which are offered by that network. Applying these principles to financial markets, a stock exchange can be thought as a network as far as, when the number of users increases, liquidity is likely to grow as the probability for each participant to find a counterpart for the desired transaction to be completed increases. Consequently, the instability of prices that the market expresses decreases: network positive externalities are created.

Competition among stock exchanges is played around two main activities: listing and trading. The latter is the function that appears to be far more important for competition, as long as the listing process is completely endogenous. As far as the trading side is concerned, the choice is between competition and co-operation with other exchanges. In the latter situation, two or more markets choose an implicit merger. It is realised when members of two or more exchanges are give cross-membership, the quotations are unified - in that companies listed in one of the exchanges are automatically listed also in the others' without additional costs - and the remote access to the market is made possible. Alternatively, a market can choose to face competition, trying to impose its standards over the others'. This choice is obviously viable for those markets that have a strong position as far as listed companies' quality and/or transaction volume are concerned. Thus it does not appear to be the most viable solution for a newly created thin market. The level of costs to be undergone to reach a satisfactory degree of integration investments in new trading systems or expenses to adapt former ones, to cite just some heavily influence the decision regarding alliances between markets. A high importance is also generally given to the so-called "political costs", as it is likely that the national market looses autonomy. Stock exchanges can also chose a third possibility, that is a hybrid one between the two extreme positions of competition and integration. The co-operation is maintained at the level of common listing rules, but trading systems and quotations are maintained nationally separated. The single national markets maintain all of their systems' specificity, but guarantee the access to other markets' members. The network solution appears to be attractive to the single market as maintaining the proprietary system makes it possible to prevent the domestic market society to loose the supply of services to the market's members. Easdaq represents an example of the competition choice. As a matter of fact, we have seen that it trades with one single platform and one rulebook and its main objectives are to provide an opening for a large institutional and retail investor base, concentrating on one single, transparent Pan-European stock market. Nevertheless, the number of companies listed is far from the achievements of Euro.NM; moreover, roughly 25% of them are Belgian and this illustrates the importance of location by companies when choosing an appropriate market on which to list. On the contrary, Euro.NM represents the realisation of the model of network markets, that appears to be the most frequent among recent choices made by European stock exchanges (see for example the London Frankfurt axis and Eurex). As cited before, the Euro.NM framework is designed to respect each markets autonomy and initiative while ensuring the necessary degree of co-ordination and co-operation between them. By pooling resources and by utilising existing trading systems the markets can be operated at marginal cost. Notes and Acknowledgements Even if this is the result of a research jointly carried out by the authors, Marco Giorgino has written Paragraph 1, while Paragraph 2 can be attributed to Elena Magnani. References AIFI, (1995), Capitale per lo sviluppo. Merchant banking, venture capital, fondi chiusi: un quadro internazionale, Milano, Guerini e Associati. Barry, Muscarella, (1990), "The Role of the Venture Capital in the Creation of PublicCompanies", Journal of Financial Economics, n. 27. Bates, J., (1971), The Financing of Small Business, London, Sweet and Maxwell.

Berger, A. N., Udell, G.F., (1998), "The Economics of Small Business Finance: The Roles of Private Equity and Debt Markets in the Financial Growth Cycle", in Journal of Banking and Finance, n. 22. Bolton Committee, (1971), Report of the Committee of Inquiry on Small Firms, London. Brealey, R.A., Myers, S., (1988), Principles of Corporate Finance, New York, McGraw Hill. Buckland, R., Davis, E.W, (1990), "The Pricing of New Issues on the Unlisted Securities Market: The Influence of Firm Size in the Context of the Information Content of New Issues Prospectuses"', British Accounting Review, n. 22. Chittenden, F., Hall, G., Hutchinson, P., (1996), "Small Firm Growth, Access to Capital Markets and Financial Structure: Review of Issues and an Empirical Investigation", Small Business Economics, n. 8. Coase, R.H., (1937), "The Nature of the Firm", Economica, n. 9. Cressy, R., Oloffson, C., (1997), "European SME Financing: An Overview", Small Business Economics, n. 9. EVCA, Ernst & Young, (1997), A Survey of Venture Capital and Private Equity in Europe: 1997 Yearbook, Bruges, Vanden Broele International. Garbade, K., (1989), Teoria dei Mercati Finanziari, Bologna, Il Mulino. Gompers, (1996), "Grandstanding in the Venture Capital Industry", Journal of Financial Economics, n. 42. Hughes, A., (1997), "Finance for SMEs: A U.K. Perspective", Small Business Economics, n. 9. Jensen, M., Meckling, W., (1976), "Theory of the Firm: Managerial Behavior, Agency Costs and Capital Structure", Journal of Financial Economics, n. 3. Myers, S.C., (1984), "The Capital Structure Puzzle", Journal of Finance, n. 34. Modigliani, F., Miller, M. (1958), "The Cost of Capital. Corporation Finance and the Theory of Investment", American Economic Review, n. 48. Modigliani, F., Miller, M., (1963), "Taxes and the Cost of Capital: A Correction", American Economic Review, n. 53. Mutzya, D.F., Leleux B., Guegan, N., European New Issues Markets. A Preliminary Review, Fontainebleau, INSEAD-3I Venturelab Research Report. Nichols, N.A., (1993), "Efficient? Chaotic? What's the New Finance?", Harvard Business Review, March-April. Perrini, F., (1999), Le nuove quotazioni alla Borsa Italiana. Evidenze empiriche delle PMI, Milano, Egea. Petrella, G., (1997), I nuovi mercati europei. Valutazioni di convenienza alla quotazione per una PMI, Milano, Egea. ,

Schwartz, R.A., (1993), Reshaping the Equity Markets. A Guide for the 1990s, New York, Business One Irwin. Stoll, H.R., (1985), "Alternative Views of Market Making", in Market Making and the Changing Structure of Securities Industry, edited by Amihud Y., Ho T.S., Schwartz R.A., Lexington Books. Varian, H.R., (1992), Microeconomic Analysis, New York, Norton & Company. Weston, J.F., Brigham, E.F., (1981), Managerial Finance, Hinsdale, Dryden Press. Wilson Committee, (1980), Report of the Committee to Review the Functioning of the Financial System, London. About the Authors Marco Giorgino, Associate professor Department of Economics and Production Politecnico di Milano Piazza Leonardo da Vinci, 32 I-20133 Milano (Italy) Tel. +39 02 2399.2759 Fax +39 02 2399.2720 e-mail: [email protected] Elena Magnani, PhD student Department of Economics and Production Politecnico di Milano Piazza Leonardo da Vinci, 32 I-20133 Milano (Italy) Tel. +39 02 2399.2794 Fax +39 02 2399.2720 e-mail: [email protected]

1 A thin market is defined as a market where, in each moment there exist only few acquirers and few buyers and where transaction frequency is scarce (Schwartz, 1993). Alternatively, it can be defined as a market where few orders are present at each moment (Garbade, 1989).

2 A market is broad when bid/ask quotations bind the dealers for quantities which are relevant in comparison with the listed company's equity and the market float. On the contrary, a market is defined deep when quotations prices are distant (the lowest bid or ask price is distant respectively, from the highest bid or ask price). See Garbade (1989).

Copyright © 2022 FDOKUMEN