Stock Exch for SMEs

39

WORKING P APER S ERIES Society for the Advancement of Technology Management in the Philippines SATMP 2000-04 The Stock Exchange for Small Companies A Survey of Issues and Experiences Vincent R. Ricasio Policy Advocacy and Research Council The National Greening Movement Greenhills, San Juan, Metro Manila May 24, 2001 [ Disclaimer: This paper was prepared under a grant provided by the Development Academy of the Philippines ( DAP) to the Society for the Advancement of Technology Management in the Philippines (SATMP) , a Philippine based NGO, in order to catalogue and evaluate the important issues impinging on the establishment and operation of a stock exchange for small companies. The views expressed herein are of the author’s and not of SATMP or of The National Greening Movement Foundation. A very preliminary version intended only for discussion purposes, no part of this paper may be quoted or published without securing the author’s or sponsors’ prior clearance. ]

Transcript of Stock Exch for SMEs

WO

RK

IN

G P

AP

ER S

ER

IE

S

Soc

iety

for

the

Ad

van

cem

ent

of T

ech

nol

ogy

Man

agem

ent

in t

he

Ph

ilip

pin

esS

AT

MP

2000

-04

The Stock Exchange for Small CompaniesA Survey of Issues and Experiences

Vincent R. RicasioPolicy Advocacy and Research CouncilThe National Greening MovementGreenhills, San Juan, Metro Manila

May 24, 2001

[Disclaimer: This paper was prepared under a grant provided by the DevelopmentAcademy of the Philippines (DAP) to the Society for the Advancement of TechnologyManagement in the Philippines (SATMP), a Philippine based NGO, in order tocatalogue and evaluate the important issues impinging on the establishment andoperation of a stock exchange for small companies. The views expressed herein are ofthe author’s and not of SATMP or of The National Greening Movement Foundation.A very preliminary version intended only for discussion purposes, no part of this papermay be quoted or published without securing the author’s or sponsors’ prior clearance.]

TABLE OF CONTENTS

Abstract/Preface and Organization of the Paper 1

Part I: The Macroeconomics of SME Finance and Small Cap Markets3

The Economic Significance of SMEsSimulating the SME Funding GapDomestic Savings and Equities Issuance CapacityThe Local Stock Exchange PerformanceThe Monetary Drivers of Capital MarketsRecapitulation of Key Macro-Environmental Factors

Part II: The Microstructure and Operational Considerations 11

Characteristics of Small Capitalization MarketsThe Special Problems of Small Cap MarketsTechnical Imperatives of Small Issues ExchangesSmall Issues Exchange Configuration Criteria

Part III: Other Countries’ Experiences with Small Issues Exchanges 19

Part IV: Conclusions and Policy Recommendations 22

Epilogue 25

Bibliography and Reference 27

About the Author 28

Tables 29

Preface and Organization of the Paper

[ABSTRACT: This paper surveys the important ideas and latestevidence pertaining to the markets for small capitalizationcompanies (small cap markets) and exchanges that specialize intrading them (small issues exchanges). Eschewing theories andunsettled conjectures in favor of empirical evidence gleaned from25 years of capital markets experience, it aims to provide acomprehensive and updated compilation of the key issues and ideasfor reference of professionals with abiding interest in the subject,whether as policy formulators, regulators and market practitionerslooking for a deep but broad and balanced perspective. Beginningwith a survey of the macroeconomic, monetary and financialunderpinnings of small cap markets, it proceeds to a considerationof the important technical design and operational parameters ofexchanges that trade in them. Next it evaluates the experience ofsimilar markets and exchanges in other countries, in order to qualifythe significance of the findings, as well as to benchmark the policyoptions flowing from it. It concludes by cautioning proponents onthe manner and timing of their adoption in thin and fragmentedcapital markets such as those of the Philippines].

This paper compiles in one convenient source several of the key issuesimpinging on the decision to establish a stock exchange for small companies.There is a great deal of interest in start-up and small enterprise financing,and for this reason stock exchanges which trade in small company sharesare widely found in both developed and developing countries. At latestcount close to 30 such exchanges operating worldwide, most of them newand independent of the traditional boards.

Based on their mixed performance records, it appears that such exchangesneed to be carefully evaluated especially in terms of their fit within theirfinancial environments. Economists have warned that financial goods arenot ordinary commodities, and that financial markets are not merely servicesectors with multiple links to the rest of the economy. Because they dealin money or money substitutes, they impact economic transactions,portfolio choices and asset valuations. They have externalities affectinginvestment, and hence the pace, level and pattern of economic activity.Businessmen, investors and market practitioners who often tend to see nofarther than the bottom line would be wise to be cautious in theirassessments of these complex markets.

At the same time, for practical reasons most policies are crafted byindividuals (or groups) who have little contact with, or actual knowledgeof, the concerns and issues faced by those who are affected by them on a

daily basis. The lack of congruence gives rise to moral hazards thatadversely impact the ultimate capital markets policy beneficiaries, in thiscase the thousands of individual investors and entrepreneurs who needcapital to generate jobs and earn foreign exchange. As in similar policyconundrums, the desire to produce quick, tangible results “becausetraditional solutions do not seem to work” often result in the hasty adoptionof novel solutions despite doubts as to their appropriateness. In the specificcase of a small issues exchange, the required goal tradeoffs may notnecessarily make it the best among several capital market policy options.Indeed it is not even clear whether it represents a sound policy alternativein itself within a given economic milieu, considering the manypreconditions that would have to be present and the obstacles that haveto be overcome before it can be made to work. Surveying the state ofknowledge with respect to such exchanges could help avoid costly policymistakes if not reduce commitment costs.

With this brief background, here is how this survey task was tackled. Thepaper is divided into four general parts. Part I discusses the broadmacroeconomic framework and environmental backdrop for the smallissues markets. This section begins by establishing whether the issues beingaddressed are economically significant, as opposed to being only ofspecialized interest. A useful starting point of analysis is the nature of theneed for SME financing and the alternative delivery solutions. This partmoves on to a consideration of domestic resource mobilization experienceand the problems faced by the local market for equity issues. It concludeswith a critical assessment of the financial conditions that need to be presentin order to provide viability for a capital market based approach.

Part II broadly answers the question of whether one form of the solution– a stock exchange for small issues – is relevant. Relevance refers to thecongruence between operational concerns, such as, for example, tradingrules and infrastructure, with the special characteristics and problems ofsmall issues markets as they have evolved locally. To do this properlyrequires moving from macroeconomic concepts to the microstructure ofexchange design, operations and governance. The technical issues involvedin choosing from among exchange features is shown to form but a smallpart of the complexity inherent in determining whether small issuesexchanges are policy optimal.

Providing an objective basis for weighing the resulting findings, Part IIIevaluates the experience of a sample of similar exchanges abroad. A reviewof selected aspects of small issues exchanges was conducted in order tosee how goals and constraints have shaped the chosen exchangeconfiguration, or resulted in performance slippage, as the case may havebeen. Part IV draws the key lessons emerging from all these analyses andempirical assessments.

All things considered, the survey findings point towards a less than sanguine view ofsmall issues exchanges’ effectiveness as capital mobilizers in a highly unstable financialenvironment. Such exchanges demand much more, and deliver less, than what isassumed by their proponents. For those who persist in their implementation, itconcludes with a warning to carefully assess the timing of their establishment amidthe expected rise in financial market volatilities and risks. As a fitting capstone to itsrecommendations, it points out drastic changes in national prioritiesengendered by recent domestic and global events, which have allbut overshadowed even such legitimate efficiency or timingconcerns.

Needless to say, work of this scope and this many constraints can not butencounter many hurdles, warranting enough qualifications to itsconclusions. Added to the usual constraints posed by availability of relevantand reliable data were knotty problems of comparability and homogeneityacross vastly dissimilar market environments. Otherwise standard economicratios and calculations were accordingly tweaked a bit to accommodatesuch data limitations; the term “small issues” itself assumed taxonomicadaptations depending on the analytical context, so that e.g., “small issuesmarkets” would variously incorporate aspects of small cap, thinly traded,over-the-counter, alternative or even emerging markets. In a few areas,the survey broke away from mainstream analysis if it was believed that aslightly different twist would illumine some aspect of the problem. Lackof time precluded the benefit of peer reviews, so that a fair amount oferror can be expected to permeate the interpretation of evidence. Thoselimitations notwithstanding, the author hopes that some helpful conclusionsstill emerged in this survey.

I THE MACROECONOMIC ISSUES

The Compelling Imperatives of Smallness

Start up companies and small and medium enterprises (more oftendesignated as SMEs), one lynchpin in H. Schumacher’s long forgotten butrecently come backing “Small is Beautiful” thesis, are hardly the innocuousentities that his modern day followers often present them to be. Consider,for starters, Table 1 which presents evidence on the economic significanceof SMEs, and by extension, of the potential benefits available to stockexchanges that could focus on them.

Table 1. Economic Significance of SME’s

1994 1995 1996 1997 1998

No.of Establisments 314,00 342,911 473,820 502,817 508,841

No. of SME’s 279,137 307,597 432,169 457,422 468,206

% to Total 89 90 91 91 92

Total Employment 2,975,487 3,240,276 3,895,722 4,188,961 3,711,920

SME’s 944,682 1,143,997 1,415,179 1,527,434 1,504,852

% to Total 32 35 36 36 41

Total Value Added 811,344 978,920 1,216,537 1,330,267 1,134,308

SME’s (in million pesos) 63,354 77,990 85,194 94,482 97,522

% to Total 8 8 7 7 9

Total Fixed Assets 853,188 1,040,196 1,310,831 1,525,575 1,338,992

SME’s (in million pesos) 46,313 41,163 66,840 69,394 62,031

% to Total 5 4 5 5 5

Source: National Statistics Office (NSO)

The table shows that SMEs comprise the vast majority (hovering around91 %) of all economic establishments. They also account for a significantshare (36 %) of total employment, if not as much of total value added (8%). And while collectively, SMEs own a smaller fraction (5 %) of totalfixed assets, their relative productivity as measured by the ratio of valueadded to fixed assets is higher compared to those of large enterprises.While this could just be the result of under investment amidst capitalscarcity, it fosters the widespread notion of SMEs being inferior intechnique that is widely blamed for their lower value added per workerratios. But because SMEs thereby push the economy’s production frontierby increasing the utilization of the less scarce factor (ie labor), the overalleffect is one of higher social desireability in their favor. And this is beforethe benefits of the socially ameliorative and redistributive aspects of anypolicy that gives priority to them.

Listing Potential of SMEs.

To orient the analysis towards capital markets issues, it is necessary todraw on enterprise data found in such compilations as the SEC Top 7000Corporations, the vast majority of which still comprise of SMEs.

The term “listing potential” refers to SMEs whose capitalization satisfythe following criteria, viz., authorized capital not exceeding Ph 100 million;total assets equal or less than Ph 60 million; subscribed capital and paidup of not less than Ph 10 million. In addition, an SME had to have beenprofitable in two of the preceding years (amount not specified).

Table 2. Potential SME Listing Candidates

SECTOR % SME’s in No. of Asset Amount (inTop 5000 (1) SME’s (2) millions of pesos)

Agri, Fishery & Forestry 3.2 46 18,620

Mining and Quarrying 0.5 12 29,461

Manufacturing 40.2 575 436,017

Elec. Gas and Water 0.3 9 175,970

Construction 8.6 123 54,881

Wholesale and 24.4 349 99,048

Retail Trade

Transportation 4.7 67 148,919

and Comm.

Financial, Insurance 14.4 206 1,482,977

&R.E.

Commercial, Social, 3.7 43 19,977

Personal

TOTAL 100 1430 2,465,870

Source: SEC Top 7000 Corporations , 2000 – 2001; Philippine Reg. Invt and Dev.Inc

(1) Based on a capital market readiness survey of SMEs done by PRIDEin 1999(2) Applying the market survey results to the qualified SMEs in the SECTop 7000

Table 2 estimates total assets amounting to Ph. 2.46 trillions for 1,432firms culled from the SEC corporate database using a proprietary criteriafor “listable SMEs” conducted by the investment bank PRIDE in 1999.This table discloses that such a sample of SMEs accounted forapproximately less than a third (28.7 %) of the total assets of all 7,000firms in the 1999 SEC corporate database. The table also gives data onasset intensities per sector and listable SME.

Funding Gap Faced by SMEs and Small Issues Exchanges.

Moving closer towards the goal of establishing a need for equity exchangescatering to SMEs, the next step is to estimate the funding gap that theseexchanges might have to meet. Various studies have attempted to derivethis data, using techniques ranging from simple financial forecasting modelsto sustainable growth models, and all the way to somewhat inappropriate

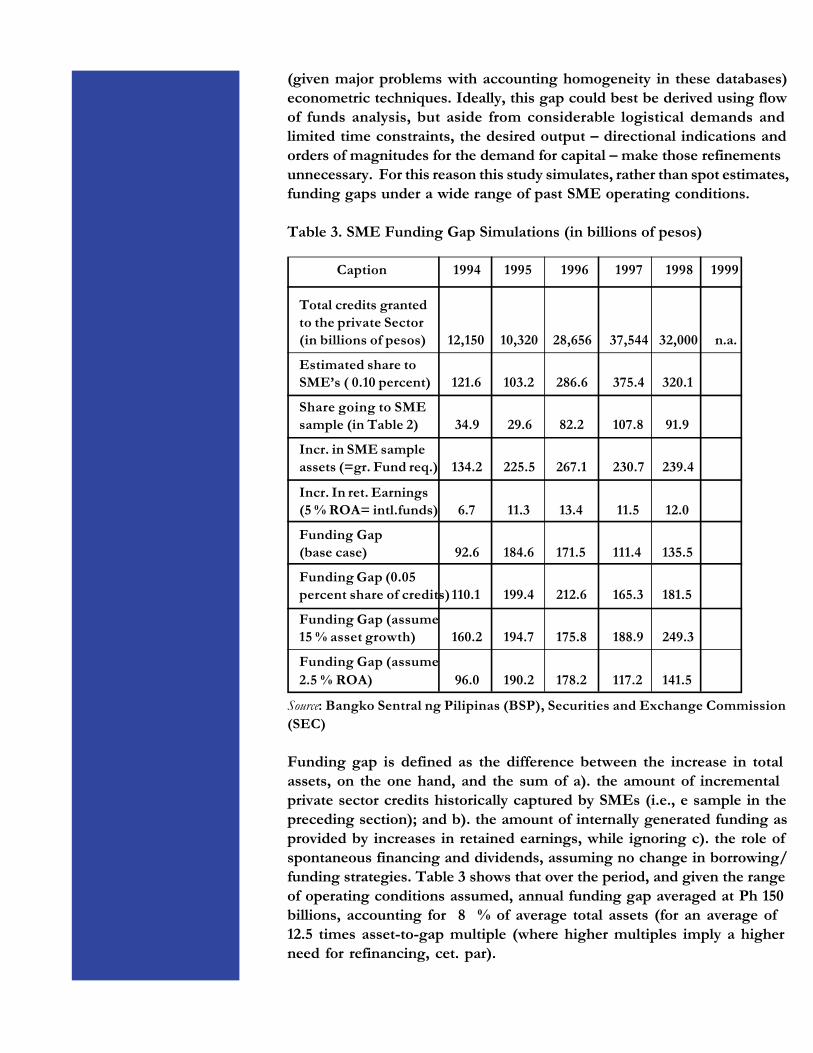

(given major problems with accounting homogeneity in these databases)econometric techniques. Ideally, this gap could best be derived using flowof funds analysis, but aside from considerable logistical demands andlimited time constraints, the desired output – directional indications andorders of magnitudes for the demand for capital – make those refinementsunnecessary. For this reason this study simulates, rather than spot estimates,funding gaps under a wide range of past SME operating conditions.

Table 3. SME Funding Gap Simulations (in billions of pesos)

Caption 1994 1995 1996 1997 1998 1999

Total credits grantedto the private Sector(in billions of pesos) 12,150 10,320 28,656 37,544 32,000 n.a.

Estimated share toSME’s ( 0.10 percent) 121.6 103.2 286.6 375.4 320.1

Share going to SMEsample (in Table 2) 34.9 29.6 82.2 107.8 91.9

Incr. in SME sampleassets (=gr. Fund req.) 134.2 225.5 267.1 230.7 239.4

Incr. In ret. Earnings(5 % ROA= intl.funds) 6.7 11.3 13.4 11.5 12.0

Funding Gap(base case) 92.6 184.6 171.5 111.4 135.5

Funding Gap (0.05percent share of credits) 110.1 199.4 212.6 165.3 181.5

Funding Gap (assume15 % asset growth) 160.2 194.7 175.8 188.9 249.3

Funding Gap (assume2.5 % ROA) 96.0 190.2 178.2 117.2 141.5

Source: Bangko Sentral ng Pilipinas (BSP), Securities and Exchange Commission(SEC)

Funding gap is defined as the difference between the increase in totalassets, on the one hand, and the sum of a). the amount of incrementalprivate sector credits historically captured by SMEs (i.e., e sample in thepreceding section); and b). the amount of internally generated funding asprovided by increases in retained earnings, while ignoring c). the role ofspontaneous financing and dividends, assuming no change in borrowing/funding strategies. Table 3 shows that over the period, and given the rangeof operating conditions assumed, annual funding gap averaged at Ph 150billions, accounting for 8 % of average total assets (for an average of12.5 times asset-to-gap multiple (where higher multiples imply a higherneed for refinancing, cet. par).

Quantifying Domestic Savings Capacity.

In order to ascertain the “financeability” of such funding gap, some ideaof the savings capacity must be derived. One commonly used measure ofaccumulation capacity is the Savings ratio (savings divided by GNP andits composition into private and public savings). Another is the ratio ofsavings to financial system liabilities (variously referred to here as thefinancial intermediation or indirect intermediation ratio or diversificationratio), which indicates the financial system’s capacity to intermediatesavings and diversify it into marketable and liquid claims, along the linesdiscussed by M. Howell in Chap. 1 (Emerging Markets).13

Table 4. Savings Capacity (in millions of pesos)

1994 1995 1996 1997 1998 Average

Personal Savings 28,931 36,886 51,217 75,138 n.a. 11.88%

Total Savings 326,830 360,950 418,438 512,071 n.a. 100.0 %

Total GNP 1,736,382 1,958,555 2,261,339 2,522,884 2,794,068

Finl sys. Liabs(ex CB) 620,512 782,604 918,223 1,086,740 n.a.

Finl Interm.Ratio (%) 52.67 46.12 45.57 47.12 n.a 47.87 %

Savings Ratio (%) 18.82 18.43 18.50 20.30 n.a. 19.01 %

Source: Bangko Sentral ng Pilipinas

In terms of both accumulation (ratio of savings to GNP) and diversification(ratio of savings to financial system liabilities), the country’s performance(of 19.1 % and 47.87 %, respectively) compares less favorably with peersin its development class, where 25-30 % for savings rates and mid 60 %for intermediation ratios were the norm. Intertemporally, savings ratiosand financial diversification ratios appear not only to have declined fromsomewhat higher values in previous decades but to have stagnated even,over much of the 90s.

Maturity Structure of Savings

While channeling savings through the financial system is important forreasons of efficiency and greater liquidity (compared to privately hoardedor directly intermediated savings), lengthening the maturity structure ofthose savings is also crucial for financing capital expenditures, the bulk ofwhich take the form of permanent or long lived assets. Unfortunately,term structure data for savings and financial assets and liabilities is virtuallynonexistent or spotty at best, and hence this study’s reliance on indirect orresidual data. One such variable is non-deposit (and deposit substitutes)

liabilities on the liabilities side of the financial system balance sheet(excluding CB liabilities). To the extent that such non-deposit type liabilitiesrepresent obligations which financial institutions deem to be “safe” enoughto issue at tenors longer than demand or short term, they can be consideredas having some degree of term transformation potential, ie., for conversioninto longer maturing claims such as bonds and equities.

Somewhat analogous reasoning underlies the composition of financialsystem assets (excluding CB assets) into domestic credits (loans andsecurities) and non-domestic credit type assets. In both of these, the crucialassumption (which is made for sheer convenience in the absence of anybetter publicly available data), is that in an unsophisticated, bank dominatedfinancial system, the term structure of deposits and domestic credits wouldbe more likely to bunch in the short than long end. Another (heroic)assumption is that non-banking system assets which are not included inthe “financial system” category, together with directly intermediated claims(private equity and notes issuances, e.g.) account for a relatively minorshare of total assets of the domestic financial system. These are, to besure, not totally realistic assumptions.

Table 5. Term Transformation Potential of Savings

1994 1995 1996 1997 1998

Deposit Liabilities 608,185 767,893 898,356 1,068,425 1,146,276

Deposit Subsitutes 12,327 14,711 19,867 19,315 13,769

Other Liabilities 607,381 756,459 1,105,941 1,523,984 1,427,410

Financial Sys. Liabs. 1,227,893 1,539,063 2,024,164 2,611,724 2,587,455

Term Liabs. Ratio (%) 49.47 49.15 54.64 58.35 55.17

Domestic Credits 821,651 1,084,007 1,577,732 1,922,861 1,868,958

Other Finl. Assets 833,163 965,367 1,129,588 1,446,447 1,559,977

Financial Sys. Assets 1,654,714 2,049,374 2,637,320 3,369,308 3,428,935

Term Assets Ratio (%) 50.35 47.11 42.83 42.93 45.49

Source: BSP.

With roughly half of both total system assets and claims held in non-credit and deposit media, Table 5’s results can be interpreted, somewhatliberally, as indicating a fairly moderate financial system potential for termtransformation. The key question that must be asked is why, despite suchbalance sheet structure, their transformative potential into long term claims(restricted to bonds and equities) remained largely unrealized, sinceconsiderations of mismatching maturities did not appear to be relevanthere.

Although time did not permit obtaining parallel data from similarly situatedcountries, it can be presumed that a large part of these non-traditionalclaims can be securitized into long term financial instruments. Informationfrom highly developed financial systems indicate support for such apresumption, with funds under management of US mutual funds aloneexceeding the total deposit liabilities of commercial banks, and that thenon-banking system in that country constitutes a more significant shareof its financial system than in the Philippines.

Securities Origination Potential.

Given the paltry savings capacity and latent transformative capabilities,the domestic system’s securitization capability assumes great importance.Table 6 attempts to measure this by calculating the securitization ratio,defined here as the ratio of increases in equity and bonds to the sumcomprised of itself and the increase in financial system liabilities (assumedto proxy for non-securitized liabilities of financial institutions); and aneven more narrow measure of equity securities origination capacity, heredesignated as the equities origination ratio, and calculated as the ratio ofequity raised to the same denominator used in calculating the first ratio.Once again, lack of annually compiled data, in this instance of outstandingbond obligations, hampered the calculation of the first ratio. The annualbond series itself was inferred by letting the 1997 values of outstandingcorporate and government bonds move according to indexes made up ofgovernment public debt (for government bonds) and public sector credit(for corporate bonds), with yearly increases equated to originations.

Table 6. Securities Origination Potential

1994 1995 1996 1997 1998 Aver.Incr. In domesticcredits granted 139,487 262,456 423,725 415,129 (53,903) n.a.

Total equity raised 3,449 2,123 6,429 18,644 13,516

Bond originations 24,477 43,655 66,978 76,862 (9,207) n.a.

TOT. origination 167,413 308,234 497,132 510,635 (31,180) n.a.

Securitization Pctg 16.7 14.9 14.8 18.7 - 16.3

Equity Orig. Pctg. 2.1 0.7 1.3 3.7 - 1.9

Source: Bangko Sentral ng Pilipinas; Philippine Stock Exchange

With all these limitations, the table shows that during much of the pastdecade, the local financial system’s capacity to securitize financial claimsaveraged at 16 % (of new financial system claims and equities originated).Less than one eighth (1.9 %) of those originations took the form of equity,

so that the bulk of potentially securitizeable claims was still in the formof debt issues. An idea of how these SME ratios compare against localfinancing practice can be gained from historical leverage taken on by thetop 1,000 corporations, which averaged 1.7 times (or 37 % of capitalstructure was in the form of debt) during the early 90s.

Traditional Markets Performance.

The next three tables, namely Tables 7, 8 and 9 all deal with the traditionalstock exchange. While of a totally different functionality compared to theproposed small issues stock exchange, its actual performance can providesome ideas of the parameters that may be expected should the latterexchange be established. The following aspects of the stock exchangeperformance shown in Table 7 affirm and reinforce the foregoingcharacteristics of the local capital market, to wit:

a). Capitalization. The local stock market has lowcapitalization (hovering around $ 35 billions in 1998),roughly equal in size to that of Thailand, just slightlyover a third of Malaysia’s and just under 10 % of thecapitalization of the Southeast Asian markets. Theratio of market cap to GDP averaged 70 % versus 50% and 150 % for Thailand and Malaysia, respectively.

b). Turnover. Defined as the ratio of turnover value tomarket cap, this has experienced very unstable valuesover the past few years, ranging from a low of 13.9 %in 2000 to a high of 34.8 % in 1997, for an average of28.7 % over the period from 1993 to 2000. Againturnover value is roughly similar to Thailand, but lowcompared to Malaysia (70%) and Korea (150%)

c). Concentration. The local equities markets activity ishighly skewed around a few issues and market players.The top 10 most active issues account for 50-60 % oftotal trading and 70 % of capitalization. This alsoextends to the share of the top 10 brokers to totalturnover volume. Such concentration has importantimplications to bargaining power among market players.

d). Price stability. The market index has also fluctuatedwildly, indicating a thin market easily vulnerable tomarket demand-supply variations. Annual percentagechanges in the market index fluctuated from a drop of41 % in 1997 to an increase of 61 % in 1993. Thisvariability is also shown in the PE ratios and PB ratios,

which ranged from 9.45-19.75 times, and 1.24-4.08times, respectively, over the same period.

e). New Issues Growth. The number of listed companieshas pretty much stayed at 220 and the number of issuesat 300 out of a listable universe numbering in severalthousands. New listings per year have hovered ataround 6 issues (less than 2 % of the number of listedissues). Average offering size as well as new issuefunding ratios are also low even for emerging stockmarkets.

g). Volatility. Almost every market performance indicatorselected from each of the three tables exhibits a degreeof variability that is high compared to even the alreadyhigh norms posted by stock markets in general. Thisvariability is discussed more extensively in a follow upsection.

h). Costs. As indicated in Table 7, a breakdown of thecosts (all in) of doing business shows that local equitiesmarkets are among the most expensive in the world.18

i). Returns. The local stock market is decidedly inferiorin terms of the amount and stability of returnscompared to other markets in the region. Ignoring theimpact of dividends and holding periods, gross returnson the market index have hovered from a low ofnegative 41 % in 1997 to a high of 61 % in 1993, or anaverage of 0.6 % over 1993-2000, a decidedlylacklustre achievement as Depicted in Tables 8 and 9.

The above performance record leaves much to be desired. Clearly this isan exchange struggling valiantly to deliver in an unstable market that nowand then gets deserted by its constituents. It has failed on its mission ofhelping raise capital for companies and small investors invest their savings.

Monetary Determinants of Capital Markets Instability.

To explain why the local equities markets performed in the mannerdescribed above, one must ultimately turn to the behavior of the domesticfinancial system over this same period. In two studies conducted in 1994by economists Ross Levine of the World Bank, and Sara Zervos of theBritish investment bank BZW on stock markets performance from 49developed and underdeveloped countries over the period from 1976 to1993, it was found out that liquidity was the most important variable that

explained stock markets performance (and through the latter variable,their respective countries’ economic growth as well). While they also foundout that those countries with the most liquid stock markets grew fastest,stock market volatility by itself did not seem, at least over this period, tohave exerted such a strong link with economic growth.15,16

In hindsight, this second finding needs to be reconsidered. The periodbefore 1993 would presage years of pronounced financial instability asexemplified by the Mexican, Asian and Russian crises, and lately by thetechnology sector market bust. This is seen in chart on market volatilityappended to this study. Far from diminishing, many observers believethat instability would become a permanent feature of financial marketsfrom hereon.30 Such shocks could not but adversely impact the localmarkets.

Table 10. Capital Markets Monetary Drivers

1994 1995 1996 1997 1998 Volatility

%Changes in Reserve Money (Ph bill) 10,667 30,332 30,523 23,202 26,632

In percentages over prior year 6.20 16.60 14.3shoc 9.50 9.90 8.26

Contrib. To Resv.Money Changes: 100.0 100.0 100.0 100.0 100.0

Net Foreign Assets (in %) 328.3 87.3 373.4 (88.1) 78.1

Net Domestic Assets (in %) (228.3) 12.7 (273.4) 188.1 (178.1) 386.1

Change In DomesticLiquidity (M3) 127,285 153,816 119,974 184,613 78,535

In percentages over prior year 26.5 25.3 15.8 20.9 7.4 15.9

Mkt Index-Int.Rate Relative Cost 100.0 95.3 115.7 68.6 70.0

Memorandum Items :

Interest Rates(MRR 180 days), % 12.3 9.6 10.4 9.8 13.1 3.1

Market Index 2785.8 2594.2 3170.6 1869.2 1966.8

Source: BSP; Philippine Stock Exchange Annual Reports

Some idea of the unusual monetary driven instability that beset the localequities markets can be seen in Table 10 above, using market liquidity(ratio of market capitalization to M3) and interest rates as indicators. Thesemeasures revealed 15.9% and 3.1 % volatilities, respectively, over thisperiod. Essentially similar behavior is manifested by interest rates.

Looking deeper for explanations, one focuses on changes in reserve money,first in terms of annual growth rates which had a volatility of 8.6 %; andsecond in terms of its composition between net domestic and foreignassets. The latter measure, with each component not only posting unstableannual values but unusual alternating plus and minus contributions aswell, revealed aspects of domestic financial system management that aretruly illuminating. It shows that uneven reserve money increases were theprincipal cause of locally generated monetary instability. Together withexternally sourced Instability, they stoked the intrinsic volatility thatkept local equities markets from doing their basic task of intermediatingsavings..

Summing Up.

Local capital markets suffer three major handicaps that hamper theireffectiveness as mobilizers of long term capital. These handicaps are,respectively, a low savings rate, weak term transformation capability aswell as inefficient capital/securities markets intermediaries (principallythe local stock exchange). By far the biggest influence are periodic boutsof market illiquidity. On the basis of evidence presented, it is clear thatabsent more effective management of system reserves, the volatility thatis endemic in all financial markets would get even more exacerbated, furtherworsening the already unsatisfactory performance of the local securitiesmarkets.

Part II. The Microeconomic Structures

I. Markets and Trading Systems In Theory

Fancying themselves as hard nosed businessmen largely exempt from theperipheral strictures of theory, stock exchange proponents often considerthe fit between market structure and trading systems to be trivial. Theymay, based on evidence presented, like to rethink this view. 25

Consider what theory says about market structure performance –operational efficiency and market liquidity. The first concerns how welland cost effectively a market brings buyers and sellers together e.g., doesit provide convenient and rapid delivery of orders for execution, as wellas monitor its status ? Rapid customer notification of a trade, backed byaccurate audit trails ? Also facilities to control risks, track and clear trades,and access them for analysis. The second refers to a market’s capacity forquick execution (immediacy) and handle small orders without large changesin price (depth). It is gauged by the bid-asked spread even if the latterdoes not reflect the impact of orders on price, since a client wishing to sellwould be more concerned with the execution price than the current spread.

A drop in price is often the trade off for immediacy. Spreads are caused byrisks of positioning, costs of transactions and adverse selection due totrades with informed investors.

It turns out that market structure formats such as auction vs. dealermarkets, and trading systems set ups such as open outcry vs. electronicmatching, differ markedly in respect of how they provide efficiency andliquidity, making these far from narrow business issues merely. Yet, if onethought that theory were but the only aspect to this choice, consider howone expert views the complexity introduced by other factors operating inthe real world of trading:

“The Exchange, like the rest of us, has had troubles accepting the inevitability ofchange and learning to adapt to it. But the Exchange entered the new era with one keyadvantage. . .That advantage is the order flow. . Yet they often find themselves occupyingan uncomfortable middle ground between two parties which are themselves often opposed.On the one hand, interests within the Exchange have resisted change in the hope ofretaining their historic advantages. On the other hand, many self-styled experts –reformers, academicians, regulators and others with limited practical knowledge andless practical experience – are convinced that they know what changes are needed andare quite willing to ignore the practical difficulties and inherent dangers involved inthe implementation.” (Ch. 4 Impending Changes).8

A. The Characteristics of Small Markets.

A basic characteristic of markets specializing in small issues (ie, small interms of market cap), is thinness, the small size of the typical listedcompany’s publicly held float. A listed company would usually have lessthan half (20-30 % is common) of its outstanding shares held by outsideinvestors. Such small values, both in absolute amounts and number ofshares held by outsiders, makes these issues unattractive to investors whowant price certainty and liquidity made possible by widespread shareownership. Institutional investors normally establish minimum sizes fortheir holdings; to own too many small issues is too expensive; too large afraction of any one float is considered imprudent.

A second characteristic of markets for small issues is that trading activityis typically concentrated on a small group of stocks, with the majority ofissues in quiescent trading if not remaining inactive over long periods.This is not per se a characteristic of small issues; as cited in Part I,concentration in trading takes place even among the big board Issues. Butwith small issues, trading volume is even more skewed among active(“favorite”) shares relative to the quiescent and/or inactive shares. Thismarket characteristic imparts a large degree of uncertainty among theinactive or disfavored issues .

The third characteristic of markets for small issues is that order flows,even among the actively traded stocks, tend to arrive sporadically andwith irregular time lags. This means that orders tend to stay longer in thequeue, with investors and market makers taking longer time to search formatching bids and offers. As every market practitioner knows, search orbroker markets have less depth and hence tend to be less efficient comparedto periodic or at least regularly traded markets.2

Fourth, prices (of secondary trades) would tend to be higher, on average,relative to what intrinsic fundamentals would indicate. This is partly dueto the high return variance to investors, and partly also to the economicvagaries of dealing caused by uncertainties in spreads and costs. This highprice factor further shrinks these issues’ attractiveness relative to otherinvestment vehicles.

Fifth, bid and offer spreads consequently tend to get wider, as brokers anddealers who are neither sure of the levels nor the timing of the next offer,would tend to allow for contingencies by quoting conservatively on theirbid quotes. Of course, this uncertainty adds to the often higher unit costsencountered in small issues trading, thus widening the bid and offer spreadseven more.

Sixth, dealership or position risks therefore tend to be higher than otherwise.This creates a strong disincentive for market makers to put more capitalin such high risk, low return propositions. In the absence of hedgingalternatives, market making (or whatever nominal activities could pass assuch) would tend to become more of agency or third party broking type,favoring more institutional transactions rather than servicing individualorders.

Hence, and portentously, small issues markets tend to to be more volatile(in both prices and returns). As a result of the foregoing characteristics,market markers and investors tend to compensate for irregular order flowand information arrivals with greater price sensitivity in both directions.Added to the known volatility of financial markets, this feature explainssmall issues markets’ lepto-kurtonic return distributions and high eventrisk sensitivities.13

B. The Special Problems of Small Issues Markets.

Given the above structural and technical peculiarities, small issues marketspresent special problems that need to be addressed by those that operatetherein:

a). Illiquidity. The principal problem caused by small floats is the lack ofopportunities to sell to, or buy issues from, in the quantities and prices

desired within a reasonable time frame. Handicapped by a shortage ofmarket making capacity, these markets present problems in enteringinto or exiting from market positions without high likelihood of loss.The uncertainty causes investors to shun it, resulting in weak secondarymarkets, which in turn dissuades new firms from listing in it.

b). Vulnerability to Market Manipulation. The temptation created byuncertainty and enhanced by leverage benefits on the relatively smalleramounts needed to obtain control over floats, create ampleopportunities for market manipulation and fraud. As discussed in PartIII, small markets players tend to encounter problems with transparency,finding reporting burdensome and compliance expensive. Because ofthe greater number of participants (and relatively smaller sums)involved, underwriting and trading violations tend to take longer tobe uncovered and hence prosecuted. A short list of fraudulent andmanipulative tricks prevalent in the small issues markets follow:

v. Price Fixing. Dealers prevent trades from taking place at prices at pricesthat are in between the spread: higher than the going market “bid” (forsellers), or lower than the quoted “asked” (for buyers). Dealers alsotend to keep price increases and advances within a given range.

v. Discriminatory Treatment. Large institutional clients which have theclout to negotiate better prices are able to execute trades within thespread; on the other hand, small orders from individuals get executedautomatically by broker’s internal systems at going market quotes.

v. Spoofing. Common in relatively illiquid stocks with large spreads, thisconsists in submitting an all-or-none limit order (often undisplayed onscreens), followed by a bid at the same price via a different brokerwith intent to “lift” the bid (displayed, then subsequently withdrawn).This results in stock being sold (hence manipulated) at a price betterthan otherwise possible.

v. Tie-in Arrangements (“laddering”). Underwriters extract promises frominvestor firms to buy IPO shares at prices higher than that offered, inexchange for higher allocations. These same purchase intents are thenused to support the price at offering, in effect creating false marketdemand.

v. Fraudulent Promotion. Promoters of stocks use high pressure salesand advertising tactics in order to generate abnormal trading activityand “push” stock price, often in consideration for kick backs in theform of cash, warrants, larger allocations or soft dollar payments.

v. Insider Trading. Insiders (people in positions that confer them privilegedinformation about a company’s (and hence stock’s probable market

performance), take advantage of their early or confidential knowledgeto reap gains ahead of a price run up, or from selling (short) prior to aprice drop.

v. Illegal Stock Sales. Insiders especially those who acquire stocks underspecial terms (such as under SEC Rule 144) issue or sell such stockwithout, or even prior to time, authorization. It should be noted thatthese practices occur in any kind of market, but their frequency andseverity are exacerbated in the small issues markets because of smallerfloats, poor quality of issues, lack of following and as will be shownlater, trading environment peculiarities (eg., as cited by Ho and Macris,dealer markets which tend to have minimal if not looser trading rules.19)

c). Regulatory Demand. Prone to instability and a tendency to amplifyand propagate financial shocks, small issues markets attract closeregulatory scrutiny and hence heightened surveillance and strictercompliance requirements. The effect would be to further overwhelmregulatory capacity, leading to sub optimal compromise among marketfailure risk, rent extraction and political influence as Stigler pointedout in his seminal article on regulation.

d). Costly and expensive. The wider spreads, the need for special provisionsto maintain liquidity and continuity, costly oversight and complianceas well as the latency of rent extraction all conspire to make the smallissues markets more expensive as venues for capital raising relative tothe regular markets. Compared to the traditional channels of financialintermediation, small issues markets – where they are able to generatecapital at all – tend to do so less economically and with lower socialefficiency.

II. The Design Imperatives for Small Issues Exchanges.

Confronted by the above market characteristics and problems, exchangedesign desiderata which dates approximately from the 70s (when the firstfully automated exchange – the Cincinnati Stock Exchange – and thecomputerized OTC network that evolved into NASDAQ first came intoexistence), converged more or less around the following parameters:

The first is the degree of automation which the execution of trades shouldhave. Junius Peake, former governor and vice chairman of NASD and awell known authority on the functioning, structure and operations offinancial services systems, wrote that “. . market makers need the ability totake and hedge positions instantly at known prices. This is only possible in an integrated,real time automated quotation and execution system . . a far better approach thantrading cash baskets as single units. . Cross hedging is risky at best; but the use of anautomated execution system reduces risk somewhat, because a direct logical (and analytic)

connection can be made between the firm’s internal computer systems and those of themarkets on which the instruments are traded.” (Chapter 6, “Market Making inthe Electronic Age”. 4

Another design desiderata is transparency, which refers to the extent towhich market participants should remain anonymous. The identities ofmarket participants is valuable, especially those on the bid side, but evenmore so when they represent consummated transactions. However,unrestricted access could work against designated market makers, throughthe operation of arbitrage. Because the use of inter-dealer brokers wouldbe impractical due to the cost and cumbersome procedures involved, thepractical compromise has been the use of specialists (in the conventionalexchanges) and of designated market makers (in the quote driven dealermarkets such as OTC/NASDAQ). In the former, the privilege of firsthand knowledge of all order flows comes at the cost of mandated andaffirmative roles; in the dealer markets, only system officials see theidentities of those who entered the order flows even as all dealers get tointeract electronically with almost every trade.

A third design parameter is centralization of order flows. A central book(more commonly known as the Consolidated Limit Order Book, or CLOB)is a consolidation of all buy and sell limit orders into one centralized filewhere all market participants can have varying degrees of access and orderrevision rights based on some rules. Among the advantages of such acentralized file would be full access to the market information, whichmaximizes liquidity. It also makes possible a more efficient deploymentof capital, by enabling market participants to selectively allocate theircapital among instruments which need market support instead of acrossthe broad deployment in an effort to make continuous markets. Finally,because of improved access to liquidity, the CLOB could reduce tradingrisks and costs.

And a fourth design parameter is full integration. This means that, inaddition to automated trading, the ideal system for small issues exchangeswould be complemented with order routing and allocation; price reportingand dissemination, preferably on real time or with as little lag as possible;and monitoring and surveillance capabilities. These features are all designedto reinforce each other’s functional effectiveness under operationalconditions, to such an extent that most practical exchange designsincorporate one or more combinations as design standards.

On the face of the problems of small markets, an integrated electronicexchange seems to be the ideal configuraiton for a small issues exchange.Not only would technical efficiencies be maximized, as Peake pointedout, but palpable cost savings realized as well due to capital optimizationand risk reduction. In addition, benefits such as audit trails and analyticalcapabilities so crucial to trade surveillance are built-in features in such

systems. A question that used to arise, and which is the fifth designconsideration, is whether the minimum degree of electronic integrationwould be economical enough to render the smallest sized small issuesexchange cost effective. The evidence seems to indicate that cost is gettingless and less of a concern due to the continuing and rapid declines insystem design, installation and maintenance. Cost is however the leastcritical of the concerns.

Of the foregoing, the most contentious issue pertains to the centralizeddisplay of all stock quotes and the nature of the regulatory entity thatwould oversee the small issues market. For all the capital, cost and riskminimizing advantages of a consolidated limit order book/centralizedquote system, it has come under attack for the problems it creates in termsof order flow allocation among competing market participants. The issueboils down to the question of how, in a transparent system where all ordersare routed to one centralized computer and are executed according tosome inside quote or strict price/time priority rule, order flow could bedivvied up equitably among competing market makers. This problemworsens in the case of open and screen based trading systems where intheory all market participants have access to all order flows.

Failure to resolve this market structure issue has triggered dissension amongmarket players, leading to a widely held perception that decentralizedmarkets, which is what most small issues markets would most probablyassume, would hamper investors’ abilities to get their trades executed atthe best price. Noting that it reverts to the same business allocation problemcited earlier by Davant, this dilemma best illustrates how innocuousoperational issues often ride on technical considerations to frustratepolicymakers’ best laid plans about capital market reform.

III. Evaluation of Design Alternatives for Small Issues Exchanges

Given the foregoing exchange design desiderata, on the one hand, and theunique features and problems faced by small issues markets, on the other,what criteria can be used to evaluate the various alternative configurationsfor small issues exchanges ? The following discussion may be helpful

a). Market Structure. Central to much of the received tradition in markettheory is the assumed superiority of auction type markets as comparedto dealer markets. Auction type markets indeed represent the ultimatestage in the functional evolution of markets, in the sense that theyrepresent the most efficient aggregation of market demand and supplywithout the astronomical costs that otherwise would be required undercomplete information gathering. However, thin and fragmented marketsrequire a special adaptation of this rule because they can not beoperated efficiently on a continuous or non-stop basis, precisely due

to the irregular and widely spaced rate of order flow arrivals. Therefore,the best design is that of a periodic auction (or call auction) exchange,wherein bids and offers are accepted and ordered as they arrive whilemarket clearing takes place in discrete periods or specified schedules.Sometimes bids and orders are accepted and matched only duringdesignated trading times.

b). Trading Mechanism and Rules. A frequent formulation is the choicebetween order driven as opposed to screen-based exchanges, referringto the medium of trade execution used. For some time most of theworld’s floor-based exchanges were order driven with orders relayedby wire to and matched in huge trading floors (hence the term openoutcry); outside of the formal exchanges, securities were transactedindividually among traders mostly over the phone in what came to beknown as the over the counter markets. With increased automationthose orders, both within formal exchanges or OTC, were then eitherposted and matched according to some price-time priority rule(in theformal exchanges) or executed as bid and asked quotes on electronicscreens (in the OTC markets). The advent of more sophisticatedcomputers led to floor less but still essentially order driven exchanges,where orders were electronically posted and matched. It was, however,in the dealer markets where automation reached its peak, resultinginto an integrated, quote driven communications system remotelylinking market participants into a vast network of electronicallyupdated screens displaying and matching bid-asked quotes. Notehowever that the choice of trading system is a narrow one basicallycentered around technology – remote screen based quotes are moreautomated than Electronically routed orders arriving on a centralizedboard; Massimbi and Phelps however have warned that electronicmatching algorithms fail to capture the features of open outcry thataccount for its success and liquidity.25

This choice has nothing to do with the market structure, since theissue with order driven vs. quote driven “exchanges” is not identicalas that between auction vs. broker/search markets. Since in auctionmarkets, all orders are matched according to rules that give priority topublic orders, experience has shown that they are superior to screen-based, quote-driven markets where public investors effectively facetwo markets – one for buying and one for selling – so that gettinginside the spread becomes all but impossible for most small investors.It is for this reason that auction type, order driven markets drawing (ifneeded) on specialists tend to have lower spreads compared to screenbased, quote driven markets maintained by market makers. Moreover,the issue of fair allocation and transparency in order flow becomesnow critical in the case of dealer markets, with their need to“consolidate” orders. The clear verdict is that if, for technical efficiencyreasons, quote driven markets are to be chosen over auction markets,

strong vigilance and workable procedures must be put in place to ensureas little a loss in market efficiency. See Ho’s related view about dealermarkets. 19

c). Market Making Provision. The fragmented and illiquid nature of thinmarkets almost make it imperative for some form of market makingrole to be mandated in order to provide continuity and liquidity duringtimes of great need such as during periods of broad market advancesor declines. In the auction-order driven type markets, this affirmativerole is performed by the specialist, but in the more integrated dealer-quote driven ones, the role of a mandated market maker should becarefully evaluated. Writing about this point, authors Peake, Mendelsonand Williams cautioned:

“An affirmative obligation to take a position against a market maker’s betterjudgment increases his risk. Thus he requires a high rate of return on his capital,which in turn implies wider spreads and thus less liquidity. The proposition thata single, or even a few, franchised affirmative obligation market makers will dothe best job of providing either price continuity or liquidity rests on somefundamental, implicit assumptions. . . which seem unrealistic when analyzed . .Because the specialist is obliged to make markets in a prescribed group of stocks,his ability to make a market in any single stock is closely tied to his activity in theother stocks in his books. . (Ch 3. “Toward a Modern Exchange: ThePeake-Mendelson-Williams Proposal for an Electronically AssistedAuction Market,” 8

On the other hand, Davant in the same article cited earlier, batted forthe retention of such market intervention function, stating that: “Theresult would be the elimination of specialist activities in maintaining fair andorderly markets . . Under such a system, a few active stocks would probablycontinue to enjoy narrow spreads. The rest might be faced with the inactivity andwide spreads so prevalent in many portions of the bond markets. The conditionshave acted as deterrent to direct participation by individuals in bond markets.”

The question of whether a mandated market making function isdesireable is open to debate, or at least is one which can be resolvedonly empirically, that is, after observation of case to case market andinvestor behavior. 26 What is certain is that affirmative roles can onlybe effectively performed if market conditions provide enoughincentives to justify them; absent those, imposing minimum capitalrequirements, market services and trading positions would only leadto withdrawal of market makers and liquidity. Whatever mode ofmarket making is adapted and whatever the extent it should bemandated and made affirmative, one aspect that May not go alongwell with the market making role is sponsorship (a common feature inseveral proposed small issues exchanges). The explanation is simple:markets making often works at cross-purposes with nurturing and

underwriting issues. As originator, the sponsor’s primary concern is tohelp introduce and season companies to the point at which they couldbegin to sell issues to the markets. Mixing this role up with trading anddealership would introduce more than questions of capital adequacy(to support both roles) but the crucial issue of agency (conflicts ofinterests) between premium pricing of issues for good sponsorship, onthe one hand, and underpricing them for best investor returns, on theother.

d). Liquidity Provision. With a much smaller scope anticipated for mandatedmarket makers it behooves the sponsors of the small issue exchangeto consider alternative providers for market liquidity. In lieu ofpremising operation upon government supplied or guaranteed liquidityfacility (in guise of capital markets development or other social priority)a much more practical approach would be the securities liquiditymechanism developed by CAC (the French order driven, electroniccontinuous market, which opens with a call). This innovation arosewhile grappling with the question of how to provide liquidity in anorder-driven market other than by incorporating a market dealer intothe trading system. The facility devised (called PIBAL, short forProgramme d’Intervention en Bourse pour l’Amelioration de laLiquidite) would require issuers themselves to provide the liquidityfor their own stocks. As described in the article written by B. Jacquillat,R. Schwarz and J. Hamon:

“. . Using the corporation’s own shares and cash, a fund is set up by the corporationand operated by a fiduciary to buy shares in a falling market and sell shares ina rising market according to a prescribed formula, directly adding liquidity to themarket. PIBAL will also bring additional liquidity indirectly, because the mereexistence of a liquidity fund should attract more investors. The effect will be self-reinforcing: when a transactions network includes a larger number of participants,counterparties can more easily find each other in time and place, and transactionprices are expected to be in closer alignment with underlying equilibrium values.. .Corporations should be involved in market making. Because liquidity is, ceterisparibus, associated with higher share prices, liquidity facilitates the capital-raisingability of the listed companies. . . The concern about involving corporations inmarket making is that they might use the position to manipulate the price of theirshares. PIBAL eliminates this because (1) the liquidity program is a fullyarticulated procedure with publicly known parameters; and (2) the fund is managedby a fiduciary” (in A Program to Increase Liquidity of Shares in theFrench Equity Market, Ch. 29 Global Challenges)

e). Instrument Scope and Complexity. The risks already inherent in smallissues markets should make it obvious that proponents should reignin their exhuberant impulses about the types and ranges of financialinstruments that should be traded in such exchanges. Instrumentsshould, as far as practicable, be designed around the more common

debt, equity and hybrid securities, while avoiding such esotericinstruments as options, participations, caps and floors.

Once again the reason is simple: the more customized (and hence lessstandardized) the trading staples are, the more difficult would be theprocess of price discovery and valuation, hence increasing the markets’tendencies to amplify extreme event risks. Additionally, the associatedmonitoring and reporting burdens would multiply, exacerbating all theattendant risks and costs of compliance. The need to simplify tradesin order to control risk is also emphasized by L. Chew.12

f). Formal Exchange Over OTC. Essentially the same reasoning underliesthe choice of a formal Exchange as a venue for the small issues markets,as opposed to that of an over the counter market. The non-formalenvironments prevailing in the over the counter markets make themless supervised, even though they may utilize the parallel or similarfacilities for settlement, depositary and clearing, and they may besubject to the same registration and oversight standards. The OTCmarkets seldom impose margin rules, grant more leeway to counterparties especially in regards to credit, and have less stringent liquidityrequirements during times of market stress. Due to these, an OTCenvironment would be a riskier format for the small issue market totake.

This does not constitute an unqualified endorsement of increasedregulation over the financial markets. As argued succinctly by Chuppeand Atkin, “regulation should be confined to that needed to correct the marketfailures that arise in unregulated markets. Supervision of the market tradingsystem will also be needed to prevent market manipulation and to ensure thatinsiders do not use privileged information to the disadvantage of public investors.Governments are probably better employed in educating investors about the risksand rewards of owning marketable securities than in trying to determine theprices of those securities.”20

g). Independent Over Dependent Governance. In a paper written by theauthor drawn from research conducted by Graham Bannock for theEuropean Commission on how well small issues exchanges fared basedon their relationship vis a vis the big boards, one finding stood out:they do not fare well when placed under the jurisdictional governanceof the latter.22 The study cited lack of competition and institutionalplayers as the most important factors, quoted thus:

“In our view, it is the lack of competition and lack of institutional investmentwhich has caused the failure of second-tier markets. None of the stock marketsin Europe is ‘alternative’ in the sense of being under separate management fromthe Official List and marketed as a specialized market in high growth companies.This leads to the second-tier market being seen as the inferior cousin of the main

market, and so companies move up to the main market as soon as possible, withconsequent depressing effects on prices and trading volumes of the second-tiermarket, and investors’ perception of the segment. . . Because stock marketmanagements are inevitably predominantly interested in the main market, whichaccounts for most of their income and prestige – and indeed in the largest, mostfrequently traded companies on that market, they have little incentive to promotethe second-tier, nor are they spurred to do so by competition. Second tier marketshave not in general been actively promoted, nor have they been able to benefit fromthe distinctive identity that only a separate market can have. . A lack of separatelymanaged and distinctive markets is therefore the first reason for the lack ofinterest in markets for smaller company stocks.”

Part III. Other Countries’ Experiences with Small IssuesExchanges.

Even as theoretical considerations indicate the feasibility of certain typesof small issues exchange configurations, surveying the experience ofcountries which have actually set up and operated them could help reducethe ambiguity by benchmarking their operating results. In developing theframework for the survey, the author reviewed the structure of alternativemarkets and exchanges in the United States (NASDAQ), Japan (JASDAQ),the European Union (EASDAQ), the United Kingdom (AIM), Canada(Canadian Dealing Network), France (Le Nouveau Marche) and Taiwan(ROC OTC Securities Exchange). Partial experiences of other countriesoutside the sample are also discussed where those appear to be of morerecent vintage or are found to emphasize relevant issues.

a). General Statement. Any cross-sectional assessment of stock exchangeexperiences would have to contend with three practical constraints,viz., differences in the state of capital markets development; thecomparability among goals set for such alternative exchanges; and thequantum of operating experiences of those exchanges compared tothose of the subject country. Despite the usual data limitations whichoften result in interpretation problems, cross sectional analyses doserve as inexpensive test beds for evaluating real world options.Subjected to little time and cost constraints, they can indicate a rangeof realistic exchange configurations, and hence enable evaluation oflikely policy responses prior to actually setting up such exchanges.

b). Exchange Goals and Objectives. Almost all countries which haveestablished alternative exchanges have set, for their policy goal, thepromotion of some strategic objective, such as the development ofhigh technology sectors, or sectors which they have judged as deservingof special assistance according to some economic criteria. There alsotends to be a strong regional if not global dimension behind theseexchanges, indicated by plans to take them beyond the immediate

geographical borders of the country in question. Indeed, in lookingcloser, one detects a strong element of functional determinism in theseinstitutions’ operations, in that they all operate within a defined strategicplan or specific policy framework. None of these exchanges are esotericsolutions in search of problems, and few have been set up as fall backoptions to some other institution because “no other vehiclesatisfactorily delivers it.” Instead most were set up in response to aparticular or highly defined need, in this case the startup or expansionfinancing of some sector that has been identified as vital to theeconomy.

c). Organizational Structure. The survey indicates that many of thesealternative exchanges appear to be organized separately from the mainboards, and tend to be predominantly member owned. The morenotable exceptions are AIM, a unit of the London Stock Exchangethat uses all of the latter’s surveillance and trading infrastructure; theCanadian Dealing Network, a division of Toronto Stock Exchange,which has an independent trading and surveillance system; and LeNouveau March, which is owned by the Paris Bourse though operatedindependently of it. Aside from the fact that competitive andmanagerial reasons tend to make autonomous exchanges operate betterthan dependent exchanges, the other reason favoring this configurationis the use of a different functional design and structure. The newexchanges have a different trading structure, operate according to newrules, require different market making classes, or call for differentregulatory environments. Most important of all, the alternativeexchanges have decidedly more risk than the traditional ones, so thatan organizational separation for purposes of isolating risks is done inboth exchanges’ interests.

d). Trading and Associated Infrastructure. It is quite interesting to notethat many of the alternative exchanges have favored a screen-based,quote driven, dealer operated trading infrastructure. NASDAQ andits automated order routing-execution subsidiary (the Small OrderExecution Services, or SOES), is the most prominent example,followed by JASDAQ which is an exact replica; so goes for EASDAQ,as well as most of the new European exchanges. This of course reflectson the claimed technological superiority and logistical efficiency ofthe quote based, fully electronic exchange over the open-outcry andorder-driven exchange. This debate appears to be far from settledhowever; Taiwan’s ROSE took the opposite track and opted for anautomated, continuous order driven infrastructure for its algorithm-run automatic order matching and clearing system, dispensing of marketmakers entirely. Reflecting greater eclecticism, more recent exchangeslike MESDAQ and the OTC board of the Thai BDC incorporatedboth types of trading mechanisms and approaches.

e). Admission and Listing Criteria. In keeping with their avowed missions,almost all of the alternative exchanges have put into place admissionscriteria that are more liberal than those of the traditional exchanges.The basic criteria include statements of what types of companies aregiven priority of entry; their sizes in terms of minimum paid upcapitalization, assets or revenues upon admission; the length of trackrecord, if one is required (some exchanges list totally new startups);the manner by which shares can be admitted (eg, IPO, backdoor listing,or as with the Canadian Dealing Network, a so called capital pool);the formula to be used in valuing the shares; as well as detailed rulesgoverning foreign ownership, shareholder composition, float, lockup,outside directors, etc. Irrespective of their entry conditions, allexchanges require companies to maintain certain reporting anddisclosure standards if they wish to remain in good standing.

f). Entrepreneurial Adaptations. A few alternative exchanges have billedthemselves as “venture capital exchanges” which, in keeping with thespirit of the term or concept, presumably allow members to get aroundthe tighter norms of raising capital found in the traditional exchanges.EASDAQ, which modeled its admission criteria along NASDAQ lines(and enjoys dual listing privileges with it), appears to be the mostconservative in this regard, with not much more liberal terms foradmission than those found in its well regulated US prototype. Thereputation of Vancouver Stock Exchange as a venture capital exchangeis well established, shown by its avowedly very liberal admissions andmaintenance criteria. Le Nouveau Marche has been known to addlittle more than the conditions found in the standard French companyregistration laws. It is however AIM (the Alternative InvestmentExchange which is the OTC subsidiary of the London Stock Exchange)which has pushed the idea of a venture capital exchange the farthest.AIM for example has zero requirements for the percentage of sharesto be held by the public; approves substantial acquisitions withoutshareholder approvals; allows takeovers and backdoor listings withoutsuspension of membership and readmission; admits illustrative financialprojections in the application for admission documents; and grantswide flexibility in the use of IPO proceeds within the confines of theproject. Others such as MESDAQ took the middle ground byliberalizing entry rules mainly.

g). New Market Intermediaries. With a view towards ensuring widersecondary market support, many of these alternative exchanges haveinstituted new types of market intermediaries, among which are a).Advisers, which are investment banks or financial intermediaries taskedwith the job of ensuring compliance with admissions and disclosurecriteria; they perform due diligence over admission candidates andpass judgment on their suitability for share issuance; b). Sponsors,which are entities that provide market information, promotion and

liaisoning between the listing candidate and the exchange while theissue is listed in the exchange; and c). Market Makers, which of courseprovide liquidity, price continuity and similar market making servicesto investors and traders in the secondary markets. Some exchangeshave dispensed with one or more of such new intermediaries, optingonly for the basic sponsor-market maker set up. NASDAQ, for example,uses only dealers.

h). Regulatory Environment. The philosophy and practice of regulationvaries widely among the countries surveyed, with provisions in somethat are not found in the other exchanges. Some, like MESDAQ areSRO based, totally independent of the KLSE while still following thefull disclosure based principle of regulation, with oversight providedby the Securities Commission. Others, such as ROSE opted forcontinuing disclosure while fully supervised by the Securities Exchangeauthorities. NASDAQ of course is owned by NASD which while anSRO, is closely monitored by the US SEC. The European exchangestend to be SROs and independently supervised by the SEC equivalent.A recent trend among the alternative exchanges has beena move towards continuing and fair disclosure based environments.Despite these regulatory improvements, fraudulent market practicesremain endemic in the small issues markets environments.

In 1996, in the wake of an academic study by two finance professorsshowing that NASDAQ dealers colluded to keep spreads (and theirprofits) artificially wide for smaller investors but less so forinstitutions, the SEC and DOJ launched investigations whichresulted in NASD agreeing to implement fairer trading rules asidefrom spending $ 100 million to prevent abuses.21,28,29,31 After a slew ofinvestor suits, NASDAQ just this month settled $ 980 million indamages, but just as quickly a trader was indicted for violating thosesame rules in a classic market fraud known as “spoofing”

The litany of small investor travails did not end there. In the infamous“Chop Stocks” scandal which first hit OTC investors in the early90s, a US federal grand jury indicted an assorted group of stockpromoters, corporate executives, brokers, investors and mobsterswith multiple counts of racketeering and securities fraud. ABusiness Week investigation at that time estimated that chop stockswas a vast ($ 10 billion) underworld of the OTC securities marketswhich regulators and prosecutors had overlooked in theirinvestigations.32 Early this year, in the wake of last year’s high techIPO crash, a rash of investor suits accused brokers and underwritersof manipulating markets by extracting promises from investmentfirms to buy IPO shares in the aftermarket. The bids were set athigher than their offering prices, in exchange for higherallocations.33 Quite recently, insider trading, accounting book

manipulations and illegal stock sales also hit the liberally regulatedGerman Neuer Markt and other European “new markets.”

Over a year ago, the infamous BRE-X mining venture investmentscam at the lightly regulated Canadian venture capital exchangesrevived an earlier tradition of stock manipulation schemes in thosemarkets. And, as if to show how easily these markets have becomeprey to even unsophisticated players, two years ago the internetbecame the staging point for a series of illegal stock promotionscams perpetrated by a so-called 15 year old stock whiz who profitedhandsomely while gaining media notoriety through manipulationand acquisition of small issues. It is interesting how the normallyvigilant US SEC was criticized for its gingerly handling of thiscontroversial case.32

Overall, except for alternative exchanges that have already been inoperation for some time in the developed capital markets, wherein thescope of innovation still remains large, there appears less assurance aboutthe sustainability of exchanges in the less developed markets. Most of thelatter ones are faced with liquidity problems and are burdened by difficultiesposed by transparency, regulatory inflexibility and market frauds. TheEuropean OTC markets have been less successful compared to those oftheir US and UK counterparts, while those in the Eastern and CentralEurope and the emerging countries seem faced with real threats to theirsurvivability. Newer exchanges such as MESDAQ are encounteringextended start up problems. Putting it mildly, it is hard to see whether astart up exchange in a vulnerable economy will fare better than the abovepredecessors.

Part IV. Conclusions and Recommendations

Bringing together all the ideas and empirical evidence covered in the priorsections, it now appears possible to draw out generalized and tentativeconclusions about the local prospects for establishing a stock exchangefor small issues.

a). Raising permanent risk, or equity capital, for small and mediumenterprises is a significant and pressing economic need felt by thesocially efficient small and medium enterprises sector of the Philippineeconomy. Sufficient demand is foreseen to warrant a thorough reviewof existing resource mobilization institutions, or even to explore thecreation of a special entity that would deliver this efficiently andpermanently.

b). The obstacle lies in the low intermediation capacity of the domesticfinancial system. In part this arises from the country’s low savings

capacity, but equally, the problem lies in the failure of financialinstitutions themselves to raise their funds mobilization throughputs.In addition to the high scale economies and volatilities endemicin capital markets, the study traces the poor securitiesorigination capacity to a market failure caused by the financialauthorities’ inability to manage system liquidity moreeffectively. This is manifested by a lack of a well thought out andclearly articulated capital markets development strategy.

Failure of local banking institutions and stock markets to satisfy the aboveequities securitization goal would not, ipso facto, constitute an automatic,or even sufficient endorsement of small issues exchanges, consideringthe complexity of the institutional and structural issues involved in theireffective performance. Just as validly, the qualified successes of somealternative exchanges overseas would not constitute a straightforwardrecommendation for their local adoption.

c). A most important underlying consideration is risk. As shown in Chart1, capital markets in general, and emerging markets especially, tend toexhibit above average sensitivity to event risks. Otherwise nimbleand steady mobilizers of capital during normal times, they couldalso, just as quickly, degenerate into volatile and self-reinforcingpositive feedback networks of instability during episodes ofsystemic illiquidity and bouts of counter party defaults. Chart 2indicates that such volatility has become more endemic recently, witha high likelihood of staying so in the foreseeable future, mainly due tothe intensified pace of globalization, institutionalization anddecentralization of economic decision making spurred by advances intechnology.

d). Even if technology were more auspicious, small issues stock exchangeswould encounter structural obstacles to their long run economicviability. One of these would be their having to operate in sub-criticalmass, less-than-optimal levels of capital markets activity, which isskirted rather gingerly by assuming that technology would reduce theweight of inelastic costs, or that markets would automatically follow(in accordance with the classical JB Say’s Law). But there are criticallimits to these assumptions, especially on their behavioral grounds.Even if operating and capital costs could potentially be cut downso low, market players’ hesitation at revising their businessmodels and modifying cultural biases could so impact the speedat which crucial compensating expense and revenueadjustments would need to be made, so that exchange viabilitycould get impaired. The optimistic assumptions in support of thecontrary are hard to validate in the wake of the recent dot comand internet company debacles, all of which were premised on similarautomatic cost reductions and demand creation assumptions. Chart 3

gives some idea of the time scales involved before financial systemdevelopment begins to relieve some of these structural constraints.