Utilizing Artificial Neural Network Model to Predict Stock Markets

Upload

independentCategory

view

4download

0

Bank Privatisation in Central and Eastern Europe Through the View of the Western European Stock Markets

Plamen Patev, PhD

Associate Professor at Finance and Credit Department at D Tsenov Academy of Economics

2 Emanuil Chakarov Str. 5250 Svishtov, Bulgaria

e-mail: [email protected]

Katerina Lyroudi, PhD

Assistant Professor at Accounting and Finance Department at University of Macedonia,

156 Egnatia Street 54006 Thessaloniki, Greece

e-mail: [email protected]

Nigokhos Kanaryan, MSc

PhD Student at Finance and Credit Department at D Tsenov Academy of Economics

2 Emanuil Chakarov Str. 5250 Svishtov, Bulgaria

e-mail: [email protected]

Abstract

There are numerous studies on the privatisation process in Central and Eastern Europe (CEE) but none of them evaluates the effect of privatisation on bidders’ market value. The objective of this research is the determination of the market value changes of the of several European banks during the time of their involvement in the process of bank privatisation in CEE. We have concentrated our attention on the variation of the privatising banks` stock prices, from the moment they had announced their intention to participate in the privatisation of bank institutions in Eastern and Central Europe, till the moment the privatisation contract was signed. We found that the capital markets react positively to the information about the privatisation process. We can say that this means that investors accept this process as positive news and that they expect that the privatisation will add value to the bidder’s shares. This is a very clear indication that investors support management decision for expansion in CEE by participating in the process of privatisation. The different market reaction to privatisation in different countries can be taken as an indicator of the bank privatisation methods used by the governments in CEE. The results show that participation in the process of bank privatisation in CEE countries increases the cumulative abnormal volatility of the bidders Key words: Central and Eastern European Countries, Bank privatisation, Event-study analysis, GARCH. Jel: C 10, G14, G34, P20

2

Bank Privatisation in Central and Eastern Europe Through the View of the Western European Stock Markets

Plamen Patev1, PhD Associate Professor at Finance and Credit Department at D Tsenov Academy of Economics Svishtov, Bulgaria

Katerina Lyroudi, PhD

Assistant Professor at Accounting and Finance Department at University of Macedonia, Thessaloniki, Greece

Nigokhos Kanaryan, MSc

PhD Student at Finance and Credit Department at D Tsenov Academy of Economics Svishtov, Bulgaria

1. Introduction

The process of privatisation in Central and Eastern Europe (CEE)

accomplished during the last decade of the 20th century is one of the most significant

economic processes in Europe which has brought about the economic systems

transformation of the and has built the of market economies in the Eastern part of the

European continent. Banking sector privatisations have proved to be the most crucial

of all. Within some 10 years the banking system in CEE was transformed from a 100

% state-owned property to approximately 90% private one. Various methods were

used for the privatisation of banks in CEE. Notwithstanding their diversity, we are

capable of distinguishing the applied privatisation methods applied into two primary

types: (1) administrative and (2) market-oriented. With the administrative method

there is a privatising body which accomplishes the entire process of privatisation.

Normally this is a governmental body. The purpose of this body is to carry out the

process of privatisation but it supposes corruption and bureaucracy.

With the market-oriented method privatisation is carried out directly at the

stock exchange by selling stocks of the banks that are being privatised. This process

creates clear rules for the all participants and minimises the possibilities for unfair

influences from the government’s side.

1 Corresponding author.

3

One of the most difficult issues related to privatisation is the evaluation of the

results ensuing from this process. In this study we focus our attention on the

evaluation of privatisation of Central and Eastern European Banks.

2. Literature review and main thesis

Verbrugge, Megginson and Owens (1999) pointed out that there is a

substantial body of literature and empirical evidences on privatisation of non-financial

firms2, but relatively little is known about bank privatisation around the world. They

examine how the financial performance of a bank changes after being fully or

partially privatised via a public share offering, and tested whether there appear to be

different responses across countries. They also exa mined whether investors who

purchase the shares of such banks earn positive risk-adjusted abnormal returns

initially (at the time of the offering). Verbrugge, Megginson and Owens (1999) found

significant improvements in operating efficiency and profitability after a bank

privatisation.

Saunders and Sommariva (1993) analysed the difficulties of transferring from

a state controlled to a market system with specific references to Eastern Europe. They

investigated alternative approaches for restructuring troubled commercial banks.

Beginning with a pure bankruptcy approach, which they rejected as a viable

alternative, they addressed various restructuring approaches including

recapitalization, “loan hospitals” (bad bank approach), and various types of debt- for-

debt and equity-for-debt exchange. Their analysis demonstrated clearly the difficulty

of managing and dealing with only one problem in the bank privatisation process

namely, the troubled loan issue in the monobank systems.

Meyendorff and Snyder (1997) provided evidence on three case studies of

bank privatisation in Central Europe and Russia. They focused on the process of

privatisation used in these instances and were able to offer several policy-type

conclusions such as the need to closely link privatisation with recapitalization, the

2 Bennett and Dixon (1995), Blanchard and Aghion (1996), Frydman, Pistor and Rapaczynski

(1996), Hillman and Ursprung (1996), Schmidt (1996), Kenway (1996), Hau (1998), Gordon,

Bai Chong-En and Li (1999), Grosfeld and Nivet, (1999), Luigi Sacco and Scarpa (2000),

Roland and Sekkat (2000), Perotti and van Oijen (2001), Filer and Hanousek (2001), Kornai

(2001).

4

benefits of rapid privatisation, the importance of effective new corporate governance

and the positive influence of strategic foreign investors in the creation of a more

efficient and healthy banking system. Bonin and Wachtel (1998a) provided both a

thorough literature review and an empirical analysis of bank privatisation activities in

Poland, Hungary and the Czech Republic.

The studies of Thorne (1993), Abarbanell and Bonin (1997), Abarbanell and

Meyendorff (1997), Snyder and Kormendi (1997), Svejnar (1997) and Pohl,

Anderson, Claessens and Djankov (2001) provided evidence of the difficulty of bank

privatisation in economies which are also transitioning from state-owned to private

markets, making bank privatisation even more difficult, because of the problems of

political instability, lack of banking expertise in the market system, and difficulties in

assessing the depth of troubled loans.

Petkova (1998) compared the bank privatisation in Bulgaria with the

privatisation in Hungary and Poland. The paper derives several important features of

bank privatisation in Bulgaria: (1) centralization of bank privatisation, (2) unsolved

bad debt problem.

Yildirim and Philippatos (2002) analysed the evolution of competitive

conditions in the Banking industries of fourteen Central and Eastern European

economies using firm-level data for the period 1992-1999. The results of the analysis

suggest that the banking markets of CEE countries cannot be characterized by the

bipolar cases of either perfect competition or monopoly over the period 1992-1999

except for Latvia, FYR of Macedonia, and Lithuania.

We examine the bank privatisation in CEE countries from a different point of

view. The aim of the study is to establish how the participation of a given bank in the

process of privatisation in CEE affects both share price and risk characteristics of the

bidder. Our assumption is based on the following understanding: the market response

with regard to the bidder’s participation in a given privatisation transaction is the best

and most accurate evaluation on the privatisation’s quality. Provided the market

responds positively to the bank’s participation in the process of privatisation, we can

draw the conclusion that the investors are contented with the privatisation transaction.

Therefore, we can maintain for certain that this is a positive assessment of a particular

privatisation transaction. By analogy, in case of a negative response of the capital

market one can maintain that the decrease in prices is a proof of the negative

5

assessment of the privatisation transaction. We assume that market response is a

quantitative indicator of the following:

(a) the intention of the bidder’s managing team to participate in the privatisation

transaction. In case there is a certain response of the market when the bidder is

making his offer, one can assume for certain that this response originates from the

investors’ assessment of the managers’ intention to participate in the negotiations. A

positive response is an expression of the positive attitude to the idea of purchasing the

bank undergoing privatisation in CEE. On the contrary, a negative response would

reflect the investors’ fear and disapproval of the bidder’s participation in this

particular transaction;

(b) The terms and conditions of the concluded privatisation transaction. Positive

market reaction after finalising the privatisation transactions would be the sign of

market approval to the conditions achieved in the contract. On the contrary, the

negative market reaction would be the sign of market disapproval, caused by the

negative conditions involved in the privatisation contract.

Central and Eastern European countries are one of the riskiest emerging

economies in the world. Problems and specifics of the bank system in CEE, described

in above studies, make CEE banks a risky investment. Thus, we expect that the

privatisation of a CEE bank should increase the risk of the bidder causing a investors’

reaction.

3. Data

We faced several date restrictions and because of that some cases of bank

privatisation in CEE countries were excluded from our sample. First, we were not

able to collect reliable historical background data for the prices of some bidders. This

is because some of the bidders are not listed on the stock market. In some cases the

bidder had been merged and this creates incomparable data. Second, the types of bank

privatisations in CEE countries are different from one another and in some cases this

makes comparison impossible. For example, in Poland the government negotiated

with the bidder to buy a minor stake with the agreement to increase its share in the

future till obtaining majority. This does not allow us to define the exact date of

privatisation and we excluded such cases. Third, the time of the privatisation was

different in different CEE countries. In fact, most of the deals took place in the late

1990s. However, almost all Hungarian state-owned banks were privatised before the

6

middle 1990s. Also with several individual cases in other CEE countries we observe

some privatisation deals before the period of the intensive bank privatisation. With a

view to extract some common features of market reaction to the privatisation

announcements we concentrate our examination on the period between 1999-2001 –

the period when about 50% of the banks in CEE countries were privatised.

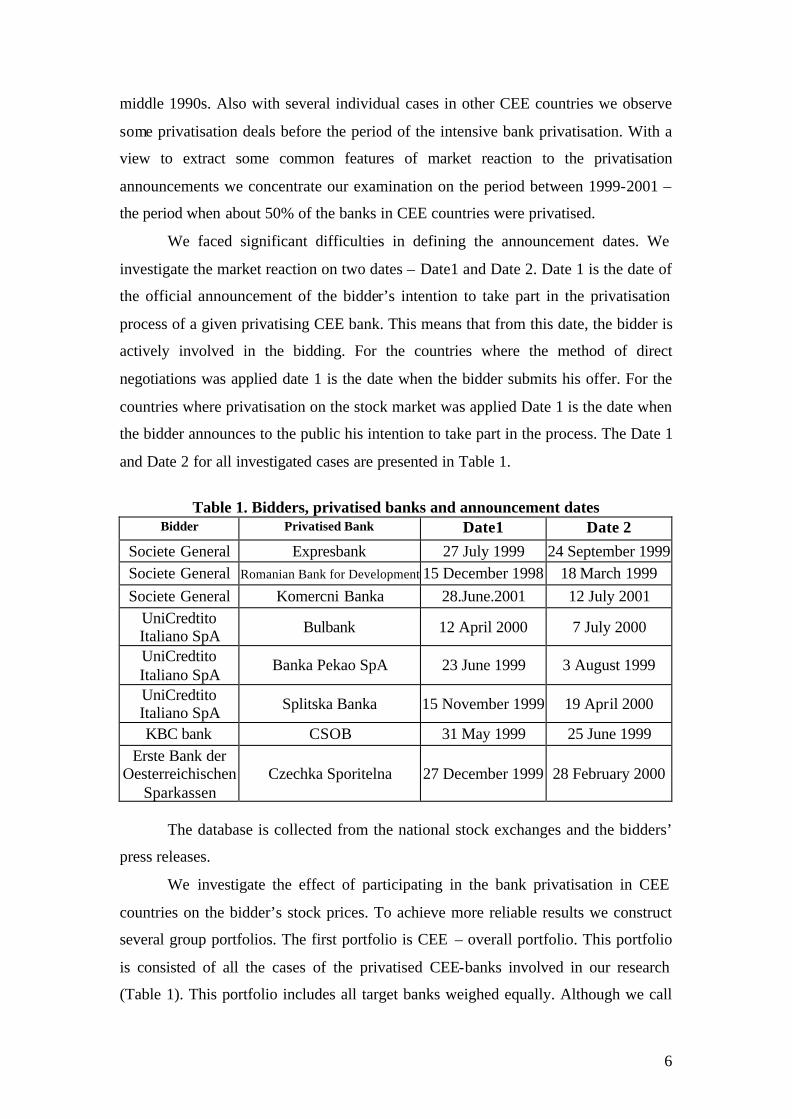

We faced significant difficulties in defining the announcement dates. We

investigate the market reaction on two dates – Date1 and Date 2. Date 1 is the date of

the official announcement of the bidder’s intention to take part in the privatisation

process of a given privatising CEE bank. This means that from this date, the bidder is

actively involved in the bidding. For the countries where the method of direct

negotiations was applied date 1 is the date when the bidder submits his offer. For the

countries where privatisation on the stock market was applied Date 1 is the date when

the bidder announces to the public his intention to take part in the process. The Date 1

and Date 2 for all investigated cases are presented in Table 1.

Table 1. Bidders, privatised banks and announcement dates

Bidder Privatised Bank Date1 Date 2 Societe General Expresbank 27 July 1999 24 September 1999 Societe General Romanian Bank for Development 15 December 1998 18 March 1999 Societe General Komercni Banka 28.June.2001 12 July 2001

UniCredtito Italiano SpA Bulbank 12 April 2000 7 July 2000

UniCredtito Italiano SpA

Banka Pekao SpA 23 June 1999 3 August 1999

UniCredtito Italiano SpA Splitska Banka 15 November 1999 19 April 2000

KBC bank CSOB 31 May 1999 25 June 1999 Erste Bank der

Oesterreichischen Sparkassen

Czechka Sporitelna 27 December 1999 28 February 2000

The database is collected from the national stock exchanges and the bidders’

press releases.

We investigate the effect of participating in the bank privatisation in CEE

countries on the bidder’s stock prices. To achieve more reliable results we construct

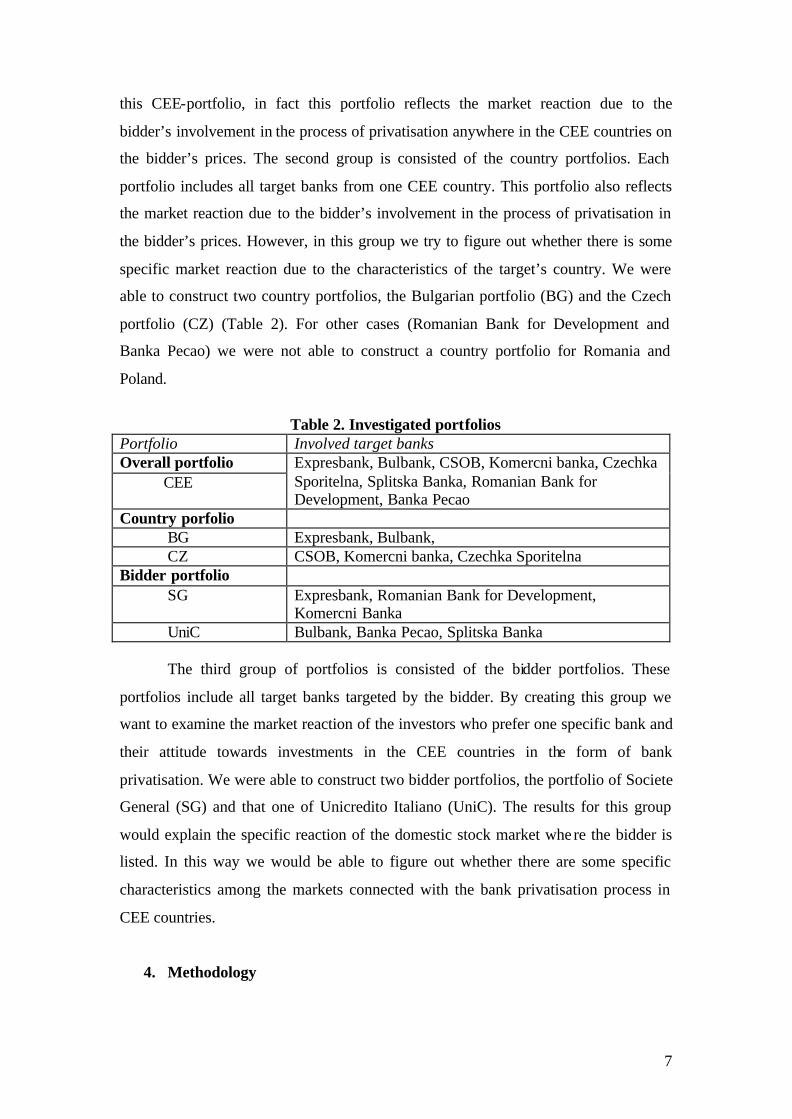

several group portfolios. The first portfolio is CEE – overall portfolio. This portfolio

is consisted of all the cases of the privatised CEE-banks involved in our research

(Table 1). This portfolio includes all target banks weighed equally. Although we call

7

this CEE-portfolio, in fact this portfolio reflects the market reaction due to the

bidder’s involvement in the process of privatisation anywhere in the CEE countries on

the bidder’s prices. The second group is consisted of the country portfolios. Each

portfolio includes all target banks from one CEE country. This portfolio also reflects

the market reaction due to the bidder’s involvement in the process of privatisation in

the bidder’s prices. However, in this group we try to figure out whether there is some

specific market reaction due to the characteristics of the target’s country. We were

able to construct two country portfolios, the Bulgarian portfolio (BG) and the Czech

portfolio (CZ) (Table 2). For other cases (Romanian Bank for Development and

Banka Pecao) we were not able to construct a country portfolio for Romania and

Poland.

Table 2. Investigated portfolios

Portfolio Involved target banks Overall portfolio CEE

Expresbank, Bulbank, CSOB, Komercni banka, Czechka Sporitelna, Splitska Banka, Romanian Bank for Development, Banka Pecao

Country porfolio BG Expresbank, Bulbank, CZ CSOB, Komercni banka, Czechka Sporitelna Bidder portfolio SG Expresbank, Romanian Bank for Development,

Komercni Banka UniC Bulbank, Banka Pecao, Splitska Banka

The third group of portfolios is consisted of the bidder portfolios. These

portfolios include all target banks targeted by the bidder. By creating this group we

want to examine the market reaction of the investors who prefer one specific bank and

their attitude towards investments in the CEE countries in the form of bank

privatisation. We were able to construct two bidder portfolios, the portfolio of Societe

General (SG) and that one of Unicredito Italiano (UniC). The results for this group

would explain the specific reaction of the domestic stock market where the bidder is

listed. In this way we would be able to figure out whether there are some specific

characteristics among the markets connected with the bank privatisation process in

CEE countries.

4. Methodology

8

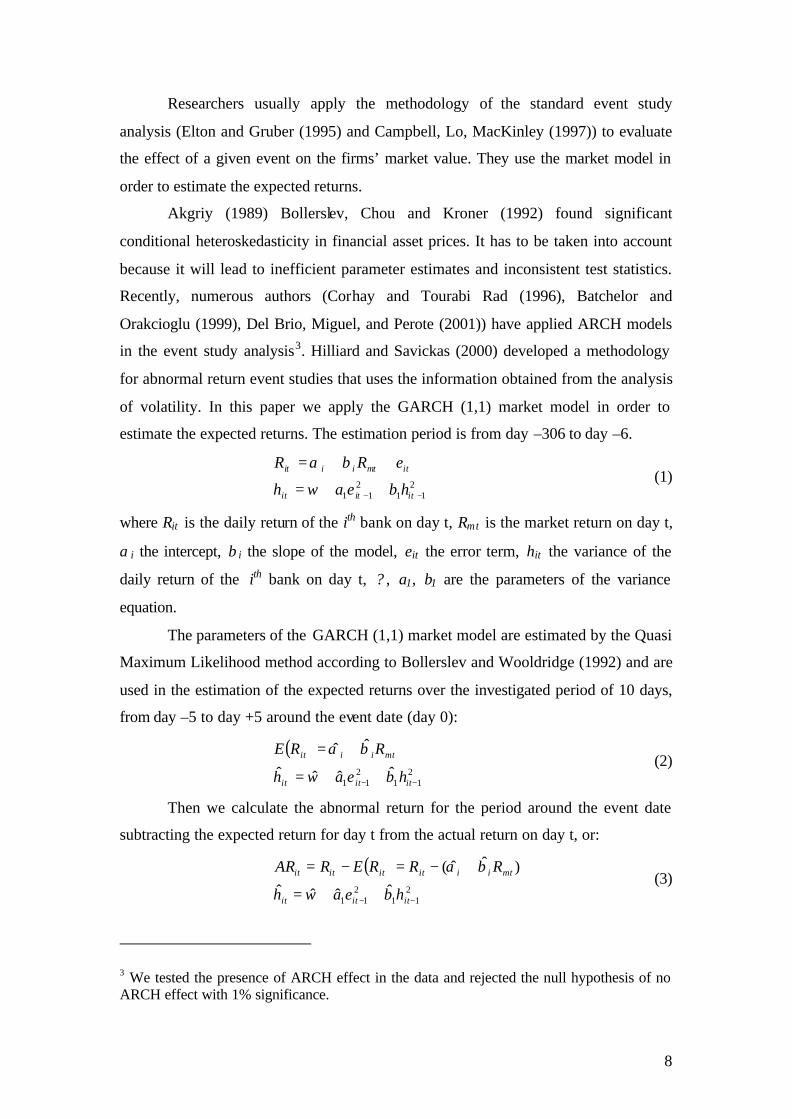

Researchers usually apply the methodology of the standard event study

analysis (Elton and Gruber (1995) and Campbell, Lo, MacKinley (1997)) to evaluate

the effect of a given event on the firms’ market value. They use the market model in

order to estimate the expected returns.

Akgriy (1989) Bollerslev, Chou and Kroner (1992) found significant

conditional heteroskedasticity in financial asset prices. It has to be taken into account

because it will lead to inefficient parameter estimates and inconsistent test statistics.

Recently, numerous authors (Corhay and Tourabi Rad (1996), Batchelor and

Orakcioglu (1999), Del Brio, Miguel, and Perote (2001)) have applied ARCH models

in the event study analysis3. Hilliard and Savickas (2000) developed a methodology

for abnormal return event studies that uses the information obtained from the analysis

of volatility. In this paper we apply the GARCH (1,1) market model in order to

estimate the expected returns. The estimation period is from day –306 to day –6.

211

211 −− ++=

++=

τττ

τττ

ω

βα

iii

imiii

hbeah

eRR (1)

where Riτ is the daily return of the ith bank on day t, Rmτ is the market return on day t,

αi the intercept, β i the slope of the model, eiτ the error term, hiτ the variance of the

daily return of the ith bank on day t, ? , a1, b1 are the parameters of the variance

equation.

The parameters of the GARCH (1,1) market model are estimated by the Quasi

Maximum Likelihood method according to Bollerslev and Wooldridge (1992) and are

used in the estimation of the expected returns over the investigated period of 10 days,

from day –5 to day +5 around the event date (day 0):

( )2

112

11ˆˆˆˆ

ˆˆ

−− ++=

+=

ititi

mtiiit

hbeah

RRE

ω

βα

τ

(2)

Then we calculate the abnormal return for the period around the event date

subtracting the expected return for day t from the actual return on day t, or:

( )2

112

11ˆˆˆˆ

)ˆˆ(

−− ++=

+−=−=

ititit

mtiiitititit

hbeah

RRRERAR

ω

βα (3)

3 We tested the presence of ARCH effect in the data and rejected the null hypothesis of no ARCH effect with 1% significance.

9

where

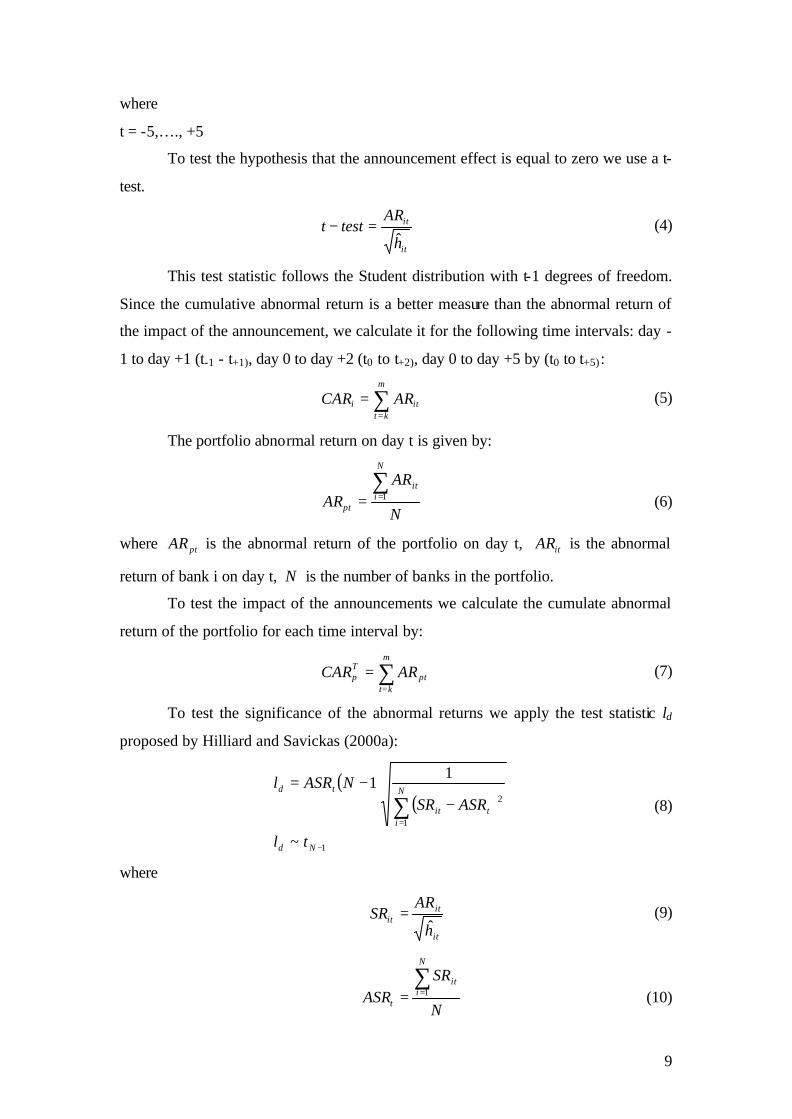

t = -5,…., +5

To test the hypothesis that the announcement effect is equal to zero we use a t-

test.

it

it

h

ARtestt

ˆ=− (4)

This test statistic follows the Student distribution with t-1 degrees of freedom.

Since the cumulative abnormal return is a better measure than the abnormal return of

the impact of the announcement, we calculate it for the following time intervals: day -

1 to day +1 (t-1 - t+1), day 0 to day +2 (t0 to t+2), day 0 to day +5 by (t0 to t+5):

∑=

=m

ktiti ARCAR (5)

The portfolio abnormal return on day t is given by:

N

ARAR

N

iit

pt

∑== 1 (6)

where ptAR is the abnormal return of the portfolio on day t, itAR is the abnormal

return of bank i on day t, N is the number of banks in the portfolio.

To test the impact of the announcements we calculate the cumulate abnormal

return of the portfolio for each time interval by:

∑=

=m

ktpt

Tp ARCAR (7)

To test the significance of the abnormal returns we apply the test statistic ld

proposed by Hilliard and Savickas (2000a):

( )( )

1

1

2

~

11

−

=∑ −

−=

Nd

N

itit

td

tl

ASRSRNASRl

(8)

where

it

itit

h

ARSR

ˆ= (9)

N

SRASR

N

iit

t

∑== 1 (10)

10

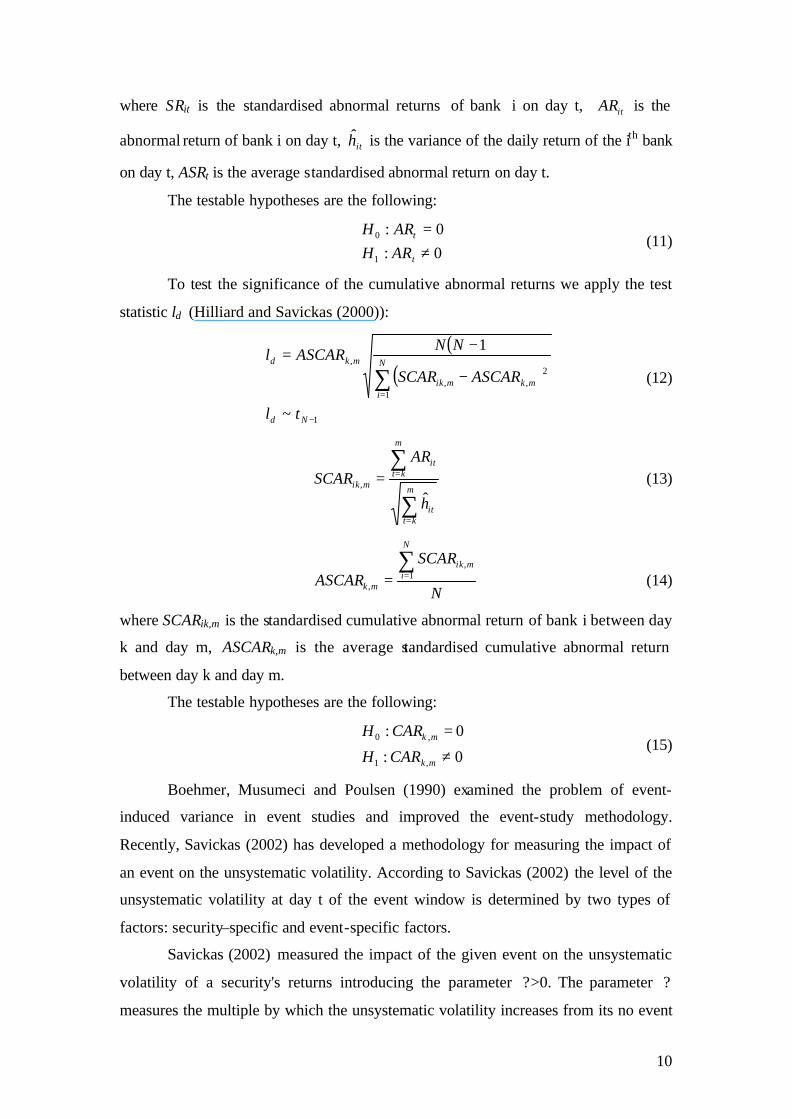

where SRit is the standardised abnormal returns of bank i on day t, itAR is the

abnormal return of bank i on day t, ith is the variance of the daily return of the ith bank

on day t, ASRt is the average standardised abnormal return on day t.

The testable hypotheses are the following:

0:0:

1

0

≠=

t

t

ARHARH

(11)

To test the significance of the cumulative abnormal returns we apply the test

statistic ld (Hilliard and Savickas (2000)):

( )( )

1

1

2,,

,

~

1

−

=∑ −

−=

Nd

N

imkmik

mkd

tl

ASCARSCAR

NNASCARl

(12)

∑

∑

=

==m

ktit

m

ktit

mik

h

ARSCAR

ˆ, (13)

N

SCARASCAR

N

imik

mk

∑== 1

,

, (14)

where SCARik,m is the standardised cumulative abnormal return of bank i between day

k and day m, ASCARk,m is the average standardised cumulative abnormal return

between day k and day m.

The testable hypotheses are the following:

0:

0:

,1

,0

≠

=

mk

mk

CARH

CARH (15)

Boehmer, Musumeci and Poulsen (1990) examined the problem of event-

induced variance in event studies and improved the event-study methodology.

Recently, Savickas (2002) has developed a methodology for measuring the impact of

an event on the unsystematic volatility. According to Savickas (2002) the level of the

unsystematic volatility at day t of the event window is determined by two types of

factors: security–specific and event-specific factors.

Savickas (2002) measured the impact of the given event on the unsystematic

volatility of a security's returns introducing the parameter ?>0. The parameter ?

measures the multiple by which the unsystematic volatility increases from its no event

11

level due to the event. A particular event may have a different value of ? for each day

of the event window. Thus the event is characterized by the set of ?s, one ? for each

day of the event window. The ?s are event-specific. If the event has no effect on the

securities’ abnormal volatilities on day t, the cross-sectional variance of the

standardized residuals should be equal to 1. The multiplicative abnormal volatility ?t

on day t of a portfolio with N securities is computed as follows:

( )∑

∑

∑

=

=

=

+⋅−

−

−=

N

iN

jjtit

N

jjtit

t

hNhNN

ARNAR

N 1

1

2

2

1

ˆ/1ˆ/2

/1

11

λ (16)

The testable hypotheses are the following:

1ˆ:

1ˆ:

1

0

≠

=

t

t

H

H

λ

λ (17)

( )2

1~

ˆ1

−

−=

Nt

tt

s

Ns

χ

λ (18)

The cumulative abnormal volatility between event day k and day m is the sum

of the individual estimators:

∑=

=m

kttmkC λλ ˆˆ

, (19)

Savickas (2002) interpreted the mkC ,λ as “multiplicative volatility that an

investor would be exposed to if he/she took a long position in the asset at the

beginning of each event day and liquidated the position at the end of the same day”.

The testable hypotheses are the following:

1ˆ:

1ˆ:

,1

,0

+−≠

+−=

kmCH

kmCH

mk

mk

λ

λ (20)

( )( )( )2

11,

,,

~

ˆ1

+−−

−=

kmNmtk

mkmk

Cs

CNCs

χ

λ (21)

We test the above hypotheses in order to measure the impact of the

privatisation announcement on the unsystematic volatility of the bidder’s stock

returns.

5. Results

12

We divided our research in two parts. In the first part we concentrated on the

CARs of Date 1and in the second part we concentrated on the CARs of Date 2.

At the first stage of our research we studied the CARs for the overall portfolio,

for BG, for CZ, for SG and for UniC. At the date 1 the CARs for several event

windows are calculated: a) from t-1 - t+1, b) from t0 to t+2, and c) from t0 to t+5.

Although we calculated the CARs for several other windows we think that these three

are the most important for our investigation. These windows present the market

reaction exactly on and after the announcement date. At this stage this is not critical to

know the abnormal returns before Date 1 because we do not aim to find any insider or

any activities before the announcement date. Our objective is to determine the

abnormal returns after the announcement. Taking in to consideration that there may

be information leakage we calculate the CARs for the window (t-1 to t+1) to capture

any such phenomenona. The results for Date 1 are presented in Table 3.

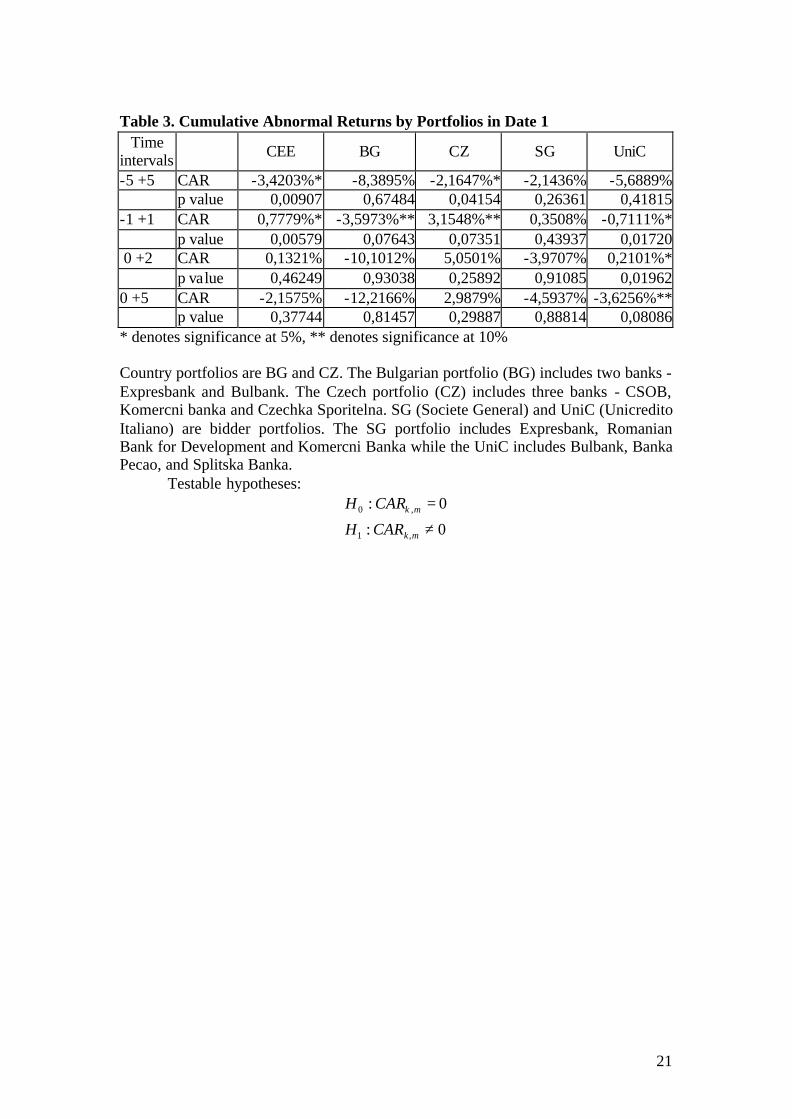

The first column of the table presents the CARs for the overall portfolio

involving all investigated privatised banks in CEE countries. The results show

positive values for the CARs for all periods except the period (t0 to t+5). However, for

this time the results are insignificant. We concentrate our attention on the window (t-1

- t+1) where we obtain statistically significant positive abnormal return. This can be

accepted as a indicator that the market accepts the announcement for the bidder’s

intention to be involved in a bank privatisation in CEE countries as a sign for positive

future expectations and positive net present value investment.

Next we direct our attention to the country portfolios. The next two columns

of Table 3 present the CARs for BG and for CZ for the same event windows as

mentioned above. Here we investigate the market reaction to any bidder’s

announcement for his involvement in the process of privatisation of a Bulgarian bank,

or of a Czech bank respectively. We find very interesting results. The table shows

high negative values for the BG portfolio: CAR= -3,60% for the event window (t-1 -

t+1), CAR= -10,10% for the event window (t0 - t+2) and CAR= -12,22% for the event

window (t0 - t+5). The negative values for the CAR are very high for the all windows

and significant for the window (t-1 - t+1). The results explicitly indicate the negative

market reaction for this portfolio. On the other hand, the results for the CZ portfolio

are positive for the same event windows and statistically significant for the period (t-1

- t+1). Here the results clearly indicate a positive market reaction for this portfolio.

13

These results are very important for our research. They support our hypothesis for the

stock markets’ evaluation of the quality and the efficiency of the bank privatisation

methods applied in CEE countries. The negative market reaction at Date 1 means that

the investors are sceptical or afraid of the bidder’s involvement in the process

privatisation. That can be explained with the fact that the market of the mother

company accepts the privatisation process as unsure, insecure, unpredictable and

unfair. On the other hand, the positive CARs after Date 1 indicate positive market

reaction to the bidder’s decision for the forthcoming process of privatisation. The

market accepts the privatisation process as well organized and fair in other words a

good investment. Bulgaria applied a specific method for bank privatisations: the so-

called direct negotiations with the bidders. This method allows the privatisation

administration to change deal conditions, to prolong the deal period, to require

additional offerings during the process of negotiating, to refuse contacts with some

bidders and to favour others. In other words, this method is very insecure,

unpredictable and unfair for the bidders, too risky and with high costs. The Czech

republic applied another technique for bank privatisations. All Czech banks have been

privatised on the stock market. This method ensures fair competition between bidders.

Our results give clearly the evaluation of these two opposite methods. Obviously,

Western European stock markets accept stock market techniques for privatisation

positively and show their distrust to direct negotiations.

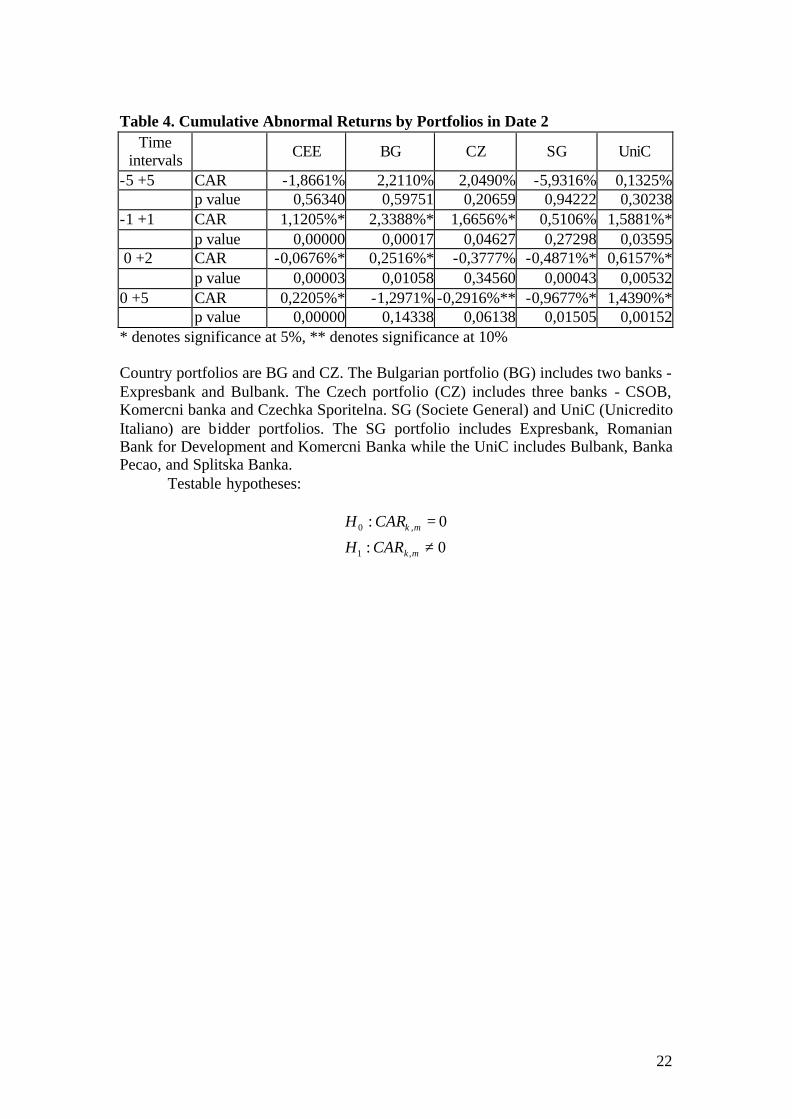

Next we concentrate our research on date 2. This time, we calculate the CARs

for the same portfolios but for different event windows. The CARs are for all

windows: a) from t-5 to t+5, b) from t-2 to t0, c) from t-1 to t+1, d) from t0 to t+2, and e)

from t0 to t+5. The reason why we calculate the CARs for windows before and after

Date 2 because Date 2, in contrast to Date 1, is fixed in advance and causes definite

fluctuations on the market not only after, but also before this very date.

Table 4 presents the results. For all five investigated portfolios we found

controversial results. For the overall portfolio the results are controversial. For some

event windows the CARs are positive, while for others are negative. We obtained

statistical significance in both directions. Although for the three periods we have a

positive and significant reaction, we cannot prove the tendency. This can be explained

with the specific economic condition in CEE countries. A successful deal does not

mean successful development of the privatised bank. The successful bidder has to

change the management, make big investments, and adjust to the difficult market

14

situation in Eastern Europe. All these make the investor be more cautious in the

evaluation. Our findings are fully consistent with Madurto a and Picou (1990) and

Lyroudi, Lazaridis and Noulas (1998) who found that there is no consistent reaction at

the announcement of a foreign direct investment in Eastern European countries.

While the negative market reaction on Date 1 can be explained by the negative

view the investors hold for the method of privatisation chosen by the government, the

results for Date 2 can be explained by the specifics of the banking system in Bulgaria.

Since the financial crisis in 1996/1997 there has been introduced a currency board in

the country. Consequently, the banks have been stabilised and have achieved some

very good results in their activity. From a macroeconomic point of view, Bulgarian

banks appeared to be in very low risk positions and very high firm activity. This

proves the fact that the ownership of a Bulgarian bank appears to be a really good

investment. We can make a supposition that this fact has been recognised and

appreciated by the stock markets and they have expressed their positive attitude by the

positive CAR.

For the Czech republic we foiund positive CARs on Date 1. However, on Date

2 the market reaction shows the disappointment of the investors. Because of the well-

organized process there was a hard competition among the bidders. As a consequence

the government achieved very high levels of the demand bank’s price. Therefore, we

can say that the prices offered were too high. This was the reason that moved the

CARs of CZ portfolio to the negative direction and obviously the investors were not

satisfied with such a price.

We would like to emphasize the double results we get from our technique.

When we applied the event study technique on Date 1 we obtained an evaluator of the

methods of privatisation. When we applied the same technique on Date 2 we obtained

an evaluator of the privatisation contract.

Next we investigate the bidder portfolios: SG and UniC. For Date 1 we cannot

find any definite market reaction. Table 3 shows the controversial results. This can be

explained by the controversial valuation given by the investors at the starting point of

the bidder’s involvement in the CEE countries privatisation process. However, for the

Date 2 we have clear relationships (Table 4). For SG portfolio we found negative

market reaction while for the UniC portfolio are found positive reaction.

At the second part of the research we investigated the changes of the

cumulative abnormal volatility. The results are presented in Table 5 for Date 1 and in

15

Table 6 for Date 2. Because of a small cross-sectional sample we calculated only four

portfolios: CEE, CZ, SG and UniC. We found an increasing tendency in the volatility

of the CARs for the CEE, CZ and SG portfolios. This is consistent with our

hypothesis. We expected that the market should react more nervously after Date 1 and

before Date 2. The volatility increase here is a result of the uncertainty in the process

of privatisation and its final conclusion.

Also we observe abnormal volatility day by day from day t-5 to day t+5 for the

Date 1 and Date 2. Table 7 present the results for Date 1 and Table 8 – for Date 2. We

found an increasing volatility after day t0 for SG and CZ portfolios on Date 1. On the

other hand, for the CEE and UniC portfolios the volatility is not changed. For the

Date 2 before day t0 we can observe increasing in volatility only for the SG portfolio

indicating market impotency before the finalisation of the deal. For the CZ portfolio

we found increasing volatility on day t+1. This is a consequence of the negative market

reaction to the finalisation of the deal.

6. Conclusion and Direction for Further Development

This study that examined the bank privatisations of the CEE countries and the

effect of the announcements on the bidders’ stock prices, has lead to the several

inferences. First, the capital markets react positively to the information about a

company’s privatisation. This implies that investors accept this process as positive

news, expecting the privatisation to add value to the bidder’s shares and to lead the

market toward more efficiency. This can be observed by the positive values of CARs

on Date 1 and Date 2 for the bidder deals (overall portfolio). This is a very clear

indication that investors support management decisions for expansion in the CEE

countries by participating in the process of privatisation. Second, the different market

reaction to bank privatisation in different countries has presented one indicator of

evaluating the bank privatisation methods used by the governments in CEE countries.

The positive reaction on Date 1 for the Czech republic and the negative one for

Bulgaria show the market’s preference for privatisation by listing on the stock

exchange instead by direct negotiating. Direct negotiating is an unfair, unsure and

most of the times corrupted process while the stock exchange gives publicity and is

open to the whole privatisation process. This is an important and significant result,

since many CEE governments are still arguing that direct negotiating provides more

instruments for protecting public interest. Obviously, according our results investors’

16

reaction does not indicate a preference for the administrative method of direct

negotiations but on the contrary, shows a strong negative attitude towards it. Hence,

we can support now, that if Bulgarian had chosen the market method for bank

privatisation, the government would have achieved much better results in terms of

price and efficiency and costing than those achieved by the direct negotiations

method. Third, the CAR on Date 2 could be considered as a good evaluator of the

privatisation deal’s conditions. When the final deal price is accepted as satisfactory

the market reacts positively and vice versa. It has been shown that in some cases the

market reacts positively (privatisation of the Bulgarian banks) and in some others it

reacts negatively (privatisation of the Czech banks). Fourth, the participation in the

process of bank privatisation in CEEC increases the cumulative abnormal volatility of

the bidders’ returns. This is a sign that participating in bank privatisation in CEE

countries is risky and the investors are nervous and uncertain for the future cash flows

obtained from the privatised banks. It is especially true for the SG-investors,

according to our results while UniC investors are not influenced by the process of

privatisation

In conclusion, the effect from the privatisation of Central and East European

banks on the bidders’ stock prices is positive and significant as a whole. Our study

shows that abnormal returns for the bidder’s stocks can be used as a main indicator

for the valuation of the privatisation process in CEE countries. Furthermore, it will be

interesting to investigate the influence of the privatisation on the Market Value Added

of the bidder, over the book-to-market-value coefficient, the price-earnings ratio and

on the other valuation indicators of the bidder. The subject is open for further

development and we are open for other ideas.

17

References

1. Abarbanell, Jeffrey S., and Bonin, John P., “Bank privatization in Poland: The

case of Bank Slaski,” Journal of Comparative Economics 25, 1:31-61, August 1997.

2. Abarbanell, Jeffrey S., and Meyendorff, Anna, “Bank privatization in Post-

Communist Russia: The case of Zhilsotsbank,” Journal of Comparative Economics

25, 1:62-96, August 1997.

3. Akgiray, V., “Conditional heteroskedasticity in time series of stock returns:

evidence and forecasts,” Journal of Business, 62, 1989, pp 55-80

4. Batchelor, Roy and Ismail Orakcioglu, “Event-related GARCH: the impact of

stock dividend in Turkey,” 1999 http://www.staff.city.ac.uk/r.a.batchelor/

5. Bennett John, Dixon Huw David, “Macroeconomic equilibrium and reform in a

transitional economy,” European Economic Review (39)8 (1995) pp. 1465-1485

6. Biais, Bruno and Enrico Perotti, “Machiavellian underpricing,” working paper

(University of Amsterdam and University of Toulouse), 1997.

7. Blanchard O., Aghion P., “On insider privatization,” European Economic

Review (40)3-5 (1996) pp. 759-766

8. Boehmer, Ekkehart, Jim Musumeci, and Annette B. Poulsen, “Event-study

methodology under conditions of event- induced variance,” Journal of Financial

Economics, 30, 1990, pp 353-272

9. Bollerslev Tim, R. Y. Chou and K. F. Kroner, “ARCH modeling in finance: A

Review of the Theory and Empirical Evidence,” Journal of Econometrics, 52, 192, pp

5-59.

10. Bollerslev, Tim and Jeffery Wooldridge, “Quasi-Maximum Likelihood

Estimation and Inference in Dynamic Models with Time Varying Covariances,”

Econometric Reviews, 11, 1992, 1 43-1 72.

11. Bonin, John and Paul Wachtel, “Bank privatization in Poland, Hungary and the

Czech Republic,” paper presented for the Conference on Bank Privatization, FRB of

Dallas and World Bank, November 1998(a).

12. Bonin, John and Paul Wachtel, “Towards market-oriented banking in the

economies in transition,” in Financial Sector Transformation: Lessons from the

Economies in Transition, Cambridge University Press, 1998(b).

13. Campbell, John., Andrew Lo, Archie Craig MacKinley. The Econometrics of

financial markets. Princeton University Press 1997

18

14. Comparison of banks in Central and Eastern Europe 1999, Bank Austria

Creditanstalt, 2000.

15. Corhay, A. and A.Tourabi Rad, “Conditional heteroskedasticity adjusted market

model and event study,” The Quarterly Review of Economics and Finance, 36,4,

1996, pp 529-538

16. Del Brio,E.B., A. Miguel, and J. Perote, “Insider trading in the Spanish stock

market,” 2001, http://www.odu.edu/bpa/efma/

17. Elton, Edwin and Martin Gruber. Modern Portfolio Theory and Investment

Analysis. Wiley& Sons, 1995

18. Filer Randall K., Hanousek Jan, “Informational content of prices set using

excess demand: The natural experiment of Czech voucher privatization,” European

Economic Review (45)9 (2001) pp. 1619-1646

19. Frydman Roman, Pistor Katharina, Rapaczynski Andrzej, “Exit and voice after

mass privatization: The case of Russia,” European Economic Review (40)3-5 (1996)

pp. 581-588

20. Gordon Roger H., Bai Chong-En, Li David D., “Efficiency losses from tax

distortions vs. government control,” European Economic Review (43)4-6 (1999) pp.

1095-1103

21. Grosfeld Irena, Nivet Jean-Francois, “Insider power and wage setting in

transition: Evidence from a panel of large Polish firms, 1988--1994,” European

Economic Review (43)4-6 (1999) pp. 1137-1147

22. Hau Harald, “Privatization under political interference: Evidence from Eastern

Germany,” European Economic Review (42)7 (1998) pp. 1177-1202

23. Hilliard, Jimmy. and Robert Savickas, “On stochastic volatility and more

powerful parametric tests of event effects on unsystematic returns” Working paper,

Terry College of Business, University of Georgia, January 2000.

24. Hillman Arye L., Ursprung Heinrich W., “The political economy of trade

liberalization in the transition,” European Economic Review (40)3-5 (1996) pp. 783-

794

25. Kenway Peter, “The behavior of state firms in eastern Europe, pre-privatization:

A generalisation,” European Economic Review (40)2 (1996) pp. 491-494

26. Kornai Janos, “Hardening the budget constraint: The experience of the post-

socialist countries,” European Economic Review (45)9 (2001) pp. 1573-1599

19

27. Luigi Sacco Pier, Scarpa Carlo, “Critical mass effect and restructuring in the

transition towards a market economy,” European Economic Review (44)3 (2000) pp.

587-608

28. Lyroudi, Katerina, John Lazaridis, Athanasios Noulas, “Valuation effects of

foreign direct investments in Eastern Europe,” Proceedings of the International

Scientific Conference on Internationalization and globalization of business (emerging

markets), May 18-19 1998, Svishtov, Bulgaria, pp. 148-158

29. Maskin Eric S., “Auctions, development, and privatization: Efficient auctions

with liquidity-constrained buyers,” European Economic Review (44)4-6 (2000) pp.

667-681

30. Megginson, William L. and Jeffry M. Netter, “From State to Market: A Survey

of Empirical Studies on Privatization,” New York Stock Exchange working paper 98-

05, 1998.

31. Megginson, William L., Robert C. Nash, Jeffry M. Netter, and Adam L.

Schwartz, “The Long Term Return to Investors in Share Issue Privatizations,”

Working paper (University of Georgia, Athens, GA), 1998.

32. Meyendorff, Anna and Edward A. Snyder, “Transactional Structure of Bank

Privatizations in Central Europe and Russia,” Journal of Comparative Economics 25,

5-30, 1997.

33. Perotti, Enr ico and P. van Oijen, “Privatization, political risk and stock market

development in emerging economies,” Journal Of International Money And Finance

Vol. 20 (1) 2001 pp. 43-69

34. Perotti, Enrico, “Bank lending in transition economies,” Journal of Banking and

Finance 17, 1021-1032, 1993.

35. Petkova, Ivanka. “Bank privatization in Bulgaria – a comparative study to

Hungary and Poland,” Working paper, Center for Economic Policy.

36. Pohl, G., R.E.Anderson, S.Claessens and S. Djankov. “Privatization and

restructuring in Central and Eastern Europe: Evidence and policy options,” World

Bank Technical Paper No368. 2001

37. Roland Gerard, Sekkat Khalid, “Managerial career concerns, privatization and

restructuring in transition economies,” European Economic Review (44)10 (2000) pp.

1857-1872

38. Saunders, Anthony and Andres Sommariva, “Bank sector and restructuring in

Eastern Europe,” Journal of Banking and Finance 17, 931-957, 1993.

20

39. Savickas, Robert, ``Event-Induced Volatility and Tests for Abnormal

Performance,'' 2002, forthcoming, Journal of Financial Research

40. Schmidt Klaus M., “Incomplete contracts and privatization,” European

Economic Review (40)3-5 (1996) pp. 569-579

41. Snyder, Edward A., and Kormendi, Roger C., “Privatization and performance of

the Czech Republic’s KomercdniBBanka,” Journal of Comparative Economics 25,

1:97-128, August 1997.

42. Svejnar, Jan, “Introduction to case studies and analysis of bank privatization in

Central Europe and Russia,” The Journal of Comparative Economics 25, 1; 3-30,

August 1997.

43. Thorne, Alfredo, “Eastern Europe’s Experience with Banking Reform: Is There

a Role for Banks in the Transition?,” Journal of Banking and Finance 17: 959-1000,

September 1993.

44. Top 100 Banks in Central Europe 1999, Deloitte&Touche, 2000

45. Verbrugge, J. A., W. L. Megginson, and W. L. Owens. “State ownership and

the financial performance of privatized banks: an empirical analysis”, World

Bank/Federal Reserve Bank of Dallas Conference on Banking Privatization,

Washington, DC, March 15 th & 16 th , 1999.

46. Yildirim, H.S. and G. C. Philippatos. “Competition and contestability in Central

and Eastern European banking markets”, Social Science Research Network, February

2002

21

Table 3. Cumulative Abnormal Returns by Portfolios in Date 1

Time intervals CEE BG CZ SG UniC

-5 +5 CAR -3,4203%* -8,3895% -2,1647%* -2,1436% -5,6889% p value 0,00907 0,67484 0,04154 0,26361 0,41815-1 +1 CAR 0,7779%* -3,5973%** 3,1548%** 0,3508% -0,7111%* p value 0,00579 0,07643 0,07351 0,43937 0,01720 0 +2 CAR 0,1321% -10,1012% 5,0501% -3,9707% 0,2101%* p value 0,46249 0,93038 0,25892 0,91085 0,019620 +5 CAR -2,1575% -12,2166% 2,9879% -4,5937% -3,6256%** p value 0,37744 0,81457 0,29887 0,88814 0,08086* denotes significance at 5%, ** denotes significance at 10% Country portfolios are BG and CZ. The Bulgarian portfolio (BG) includes two banks - Expresbank and Bulbank. The Czech portfolio (CZ) includes three banks - CSOB, Komercni banka and Czechka Sporitelna. SG (Societe General) and UniC (Unicredito Italiano) are bidder portfolios. The SG portfolio includes Expresbank, Romanian Bank for Development and Komercni Banka while the UniC includes Bulbank, Banka Pecao, and Splitska Banka. Testable hypotheses:

0:

0:

,1

,0

≠

=

mk

mk

CARH

CARH

22

Table 4. Cumulative Abnormal Returns by Portfolios in Date 2

Time intervals CEE BG CZ SG UniC

-5 +5 CAR -1,8661% 2,2110% 2,0490% -5,9316% 0,1325% p value 0,56340 0,59751 0,20659 0,94222 0,30238-1 +1 CAR 1,1205%* 2,3388%* 1,6656%* 0,5106% 1,5881%* p value 0,00000 0,00017 0,04627 0,27298 0,03595 0 +2 CAR -0,0676%* 0,2516%* -0,3777% -0,4871%* 0,6157%* p value 0,00003 0,01058 0,34560 0,00043 0,005320 +5 CAR 0,2205%* -1,2971% -0,2916%** -0,9677%* 1,4390%* p value 0,00000 0,14338 0,06138 0,01505 0,00152* denotes significance at 5%, ** denotes significance at 10% Country portfolios are BG and CZ. The Bulgarian portfolio (BG) includes two banks - Expresbank and Bulbank. The Czech portfolio (CZ) includes three banks - CSOB, Komercni banka and Czechka Sporitelna. SG (Societe General) and UniC (Unicredito Italiano) are bidder portfolios. The SG portfolio includes Expresbank, Romanian Bank for Development and Komercni Banka while the UniC includes Bulbank, Banka Pecao, and Splitska Banka. Testable hypotheses:

0:

0:

,1

,0

≠

=

mk

mk

CARH

CARH

23

Table 5. Cumulative Abnormal Volatility by Portfolios in Date 1 Time interval CEE CZ SG UniC

-5 +5 C? 9,8701 29,7499* 25,2600* 1,2506-1 +1 C? 2,8434 2,2776 11,1517* 0,2667 0 +2 C? 3,7058 4,5322 14,5898* 0,21480 +5 C? 5,4688 11,5158* 16,3402* 0,5672* denotes significance at 5%, ** denotes significance at 10% λ Abnormal volatility Cλ Cumulative Abnormal Volatility Country portfolios are BG and CZ. The Bulgarian portfolio (BG) includes two banks - Expresbank and Bulbank. The Czech portfolio (CZ) includes three banks - CSOB, Komercni banka and Czechka Sporitelna. SG (Societe General) and UniC (Unicredito Italiano) are bidder portfolios. The SG portfolio includes Expresbank, Romanian Bank for Development and Komercni Banka while the UniC includes Bulbank, Banka Pecao, and Splitska Banka. Testable hypotheses:

1ˆ:

1ˆ:

,1

,0

+−≠

+−=

kmCH

kmCH

mk

mk

λ

λ

24

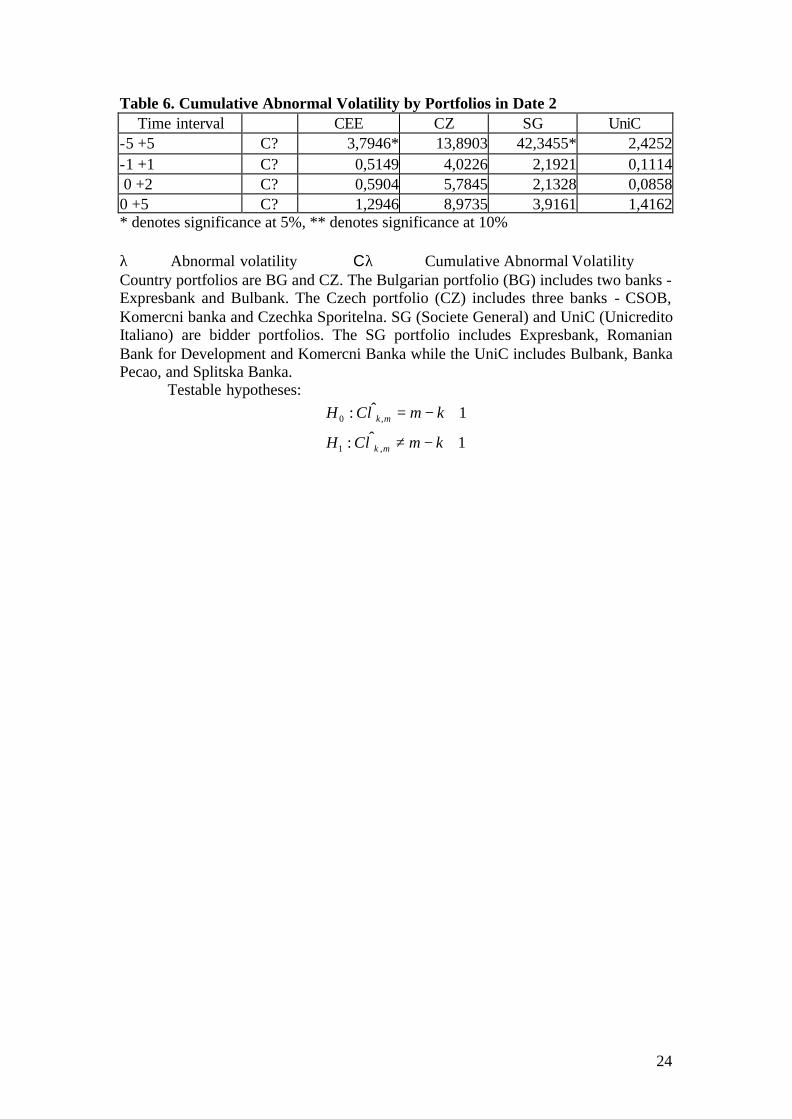

Table 6. Cumulative Abnormal Volatility by Portfolios in Date 2 Time interval CEE CZ SG UniC

-5 +5 C? 3,7946* 13,8903 42,3455* 2,4252-1 +1 C? 0,5149 4,0226 2,1921 0,1114 0 +2 C? 0,5904 5,7845 2,1328 0,08580 +5 C? 1,2946 8,9735 3,9161 1,4162* denotes significance at 5%, ** denotes significance at 10% λ Abnormal volatility Cλ Cumulative Abnormal Volatility Country portfolios are BG and CZ. The Bulgarian portfolio (BG) includes two banks - Expresbank and Bulbank. The Czech portfolio (CZ) includes three banks - CSOB, Komercni banka and Czechka Sporitelna. SG (Societe General) and UniC (Unicredito Italiano) are bidder portfolios. The SG portfolio includes Expresbank, Romanian Bank for Development and Komercni Banka while the UniC includes Bulbank, Banka Pecao, and Splitska Banka. Testable hypotheses:

1ˆ:

1ˆ:

,1

,0

+−≠

+−=

kmCH

kmCH

mk

mk

λ

λ

25

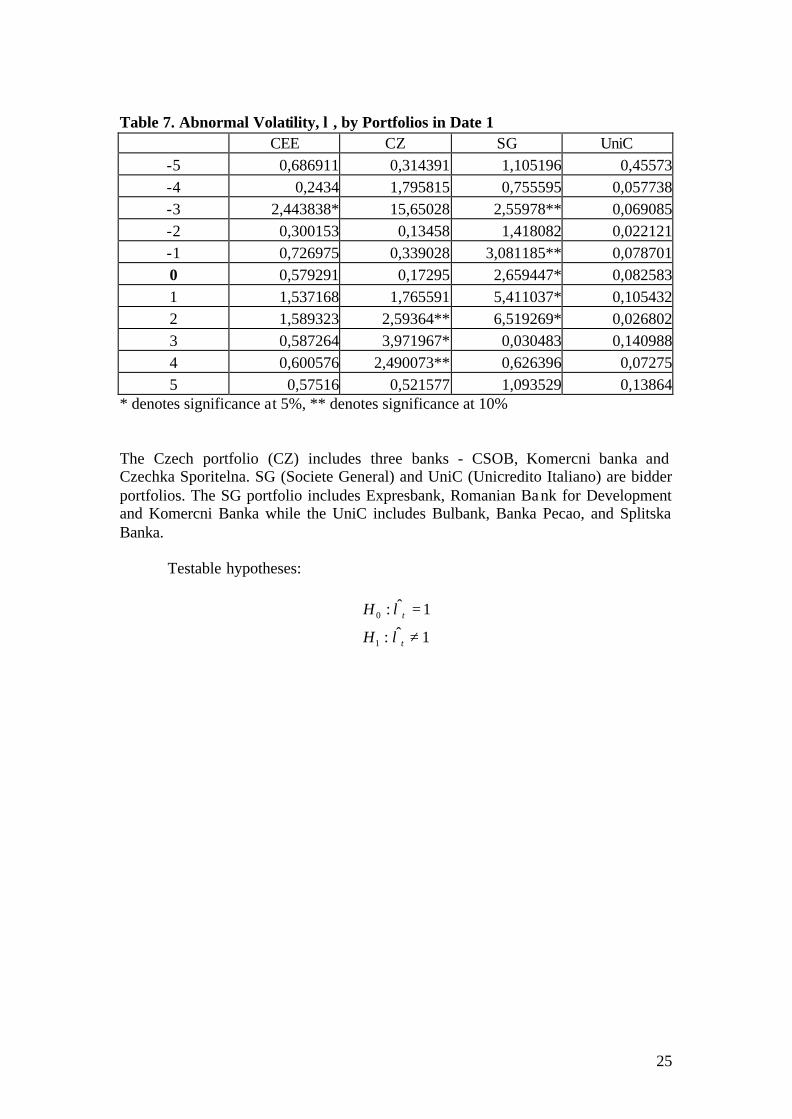

Table 7. Abnormal Volatility, λ , by Portfolios in Date 1

CEE CZ SG UniC -5 0,686911 0,314391 1,105196 0,45573-4 0,2434 1,795815 0,755595 0,057738-3 2,443838* 15,65028 2,55978** 0,069085-2 0,300153 0,13458 1,418082 0,022121-1 0,726975 0,339028 3,081185** 0,0787010 0,579291 0,17295 2,659447* 0,0825831 1,537168 1,765591 5,411037* 0,1054322 1,589323 2,59364** 6,519269* 0,0268023 0,587264 3,971967* 0,030483 0,1409884 0,600576 2,490073** 0,626396 0,072755 0,57516 0,521577 1,093529 0,13864

* denotes significance at 5%, ** denotes significance at 10% The Czech portfolio (CZ) includes three banks - CSOB, Komercni banka and Czechka Sporitelna. SG (Societe General) and UniC (Unicredito Italiano) are bidder portfolios. The SG portfolio includes Expresbank, Romanian Bank for Development and Komercni Banka while the UniC includes Bulbank, Banka Pecao, and Splitska Banka. Testable hypotheses:

1ˆ:

1ˆ:

1

0

≠

=

t

t

H

H

λ

λ

26

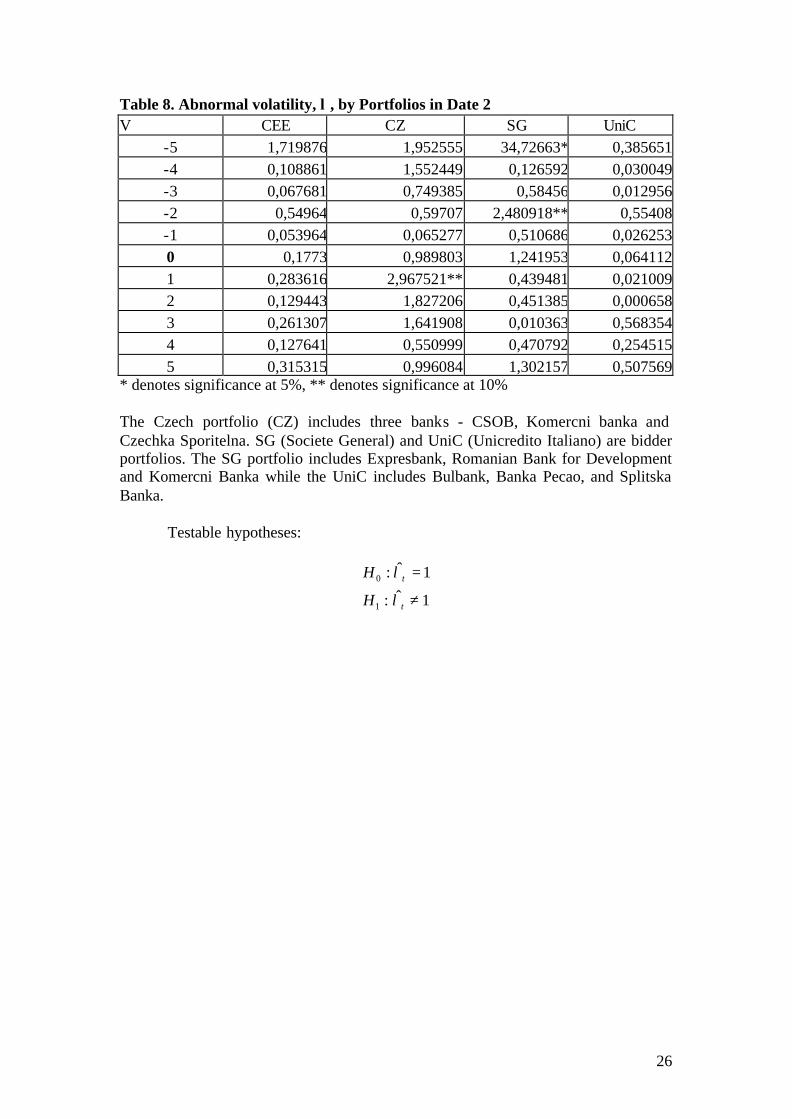

Table 8. Abnormal volatility, λ , by Portfolios in Date 2 V CEE CZ SG UniC

-5 1,719876 1,952555 34,72663* 0,385651-4 0,108861 1,552449 0,126592 0,030049-3 0,067681 0,749385 0,58456 0,012956-2 0,54964 0,59707 2,480918** 0,55408-1 0,053964 0,065277 0,510686 0,0262530 0,1773 0,989803 1,241953 0,0641121 0,283616 2,967521** 0,439481 0,0210092 0,129443 1,827206 0,451385 0,0006583 0,261307 1,641908 0,010363 0,5683544 0,127641 0,550999 0,470792 0,2545155 0,315315 0,996084 1,302157 0,507569

* denotes significance at 5%, ** denotes significance at 10% The Czech portfolio (CZ) includes three banks - CSOB, Komercni banka and Czechka Sporitelna. SG (Societe General) and UniC (Unicredito Italiano) are bidder portfolios. The SG portfolio includes Expresbank, Romanian Bank for Development and Komercni Banka while the UniC includes Bulbank, Banka Pecao, and Splitska Banka. Testable hypotheses:

1ˆ:

1ˆ:

1

0

≠

=

t

t

H

H

λ

λ

Copyright © 2022 FDOKUMEN