RESEARCH REPORT FINAL NAKAKONGE MASTULA

107

KYAMBOGO UNIVERSITY THE IMPACT OF INVENTORY MANAGEMENT ON COST A CASE STUDY OF CROWN BEVERAGES LIMITED BY NAKAKONGE MASTULA 10/U/139930/PLD/PD A RESEARCH REPORT SUBMITTED TO THE SCHOOL OF MANAGEMENT AND ENTREPRENEURSHIP IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE AWARD OF THE BACHELOR’S DEGREE IN PROCUREMENT AND LOGISTICS MANAGEMENT OF KYAMBOGO UNIVERSITY JULY 2013

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of RESEARCH REPORT FINAL NAKAKONGE MASTULA

KYAMBOGO UNIVERSITY

THE IMPACT OF INVENTORY MANAGEMENT ON COST

A CASE STUDY OF CROWN BEVERAGES LIMITED

BY

NAKAKONGE MASTULA

10/U/139930/PLD/PD

A RESEARCH REPORT SUBMITTED TO THE SCHOOL OF MANAGEMENT AND

ENTREPRENEURSHIP IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR

THE AWARD OF THE BACHELOR’S DEGREE IN PROCUREMENT AND LOGISTICS

MANAGEMENT OF KYAMBOGO UNIVERSITY

JULY 2013

DECLARATION

I declare that the information in this report has never been

submitted for the Award of Bachelor’s Degree in any Institution

or University.

NAME : NAKAKONGE MASTULA

REG NO : 10/U/139930/PLD/PD

Signature : ………………………………………

NAKAKONGE MASTULA 10/U/139930/PLD/PD 2

APPROVAL

This is to certify that this Research Report has been carried out

under my supervision and that the report is now ready for

submission to the Board of Examiners of Kyambogo University with

my due approval.

Signature:……………………………..…………...

MR. WALAKIRA HUSSEIN

(Supervisor)

Date…………………………….……………...

NAKAKONGE MASTULA 10/U/139930/PLD/PD 3

DEDICATION

Special dedications of this report go to my dear mum for her

support and courage which have uplifted my life and education. I

love you mum and thank you.

I also dedicate this report to all my lovely brothers and sisters

like Joel, Sharifah, Shakirah and all my friends not forgetting

my discussion group mates; thank you guys for doing everything

possible to make me this good.

May the Almighty God bless you all abundantly

NAKAKONGE MASTULA 10/U/139930/PLD/PD 4

ACKNOWLEDGEMENT

Great thanks first go to my Creator for the gift of life and all

the provisions He has provided for me during the course of my

studies which has really been a miraculous thing that I stand to

testify about because it has been a tag of war. And I really

thank the Almighty for the way He provided for me because the

truth is, there was no way I could have prospered and for this I

promise to glorify His Name everywhere I will be.

NAKAKONGE MASTULA 10/U/139930/PLD/PD 5

Felt thanks go to my family for the support they have given me

during my course of study in Kyambogo University for the three

years course in Procurement and Logistics Management. May the

Lord reward them abundantly

My supervisor Mr. Walakira Hussein for his supervision and

corrections made for easy compilation, thank you very much Sir.

To all sources that made it easy for accessibility of the

available literature including the Barclays Library of Kyambogo

University, Makerere University Business School Main Library

(MUBS), and others cafes, News papers and Documentations.

I also appreciate and thank with a genuine spirit my dear friends

Acen Brenda Binta, Katushabe Sheila, Balyesiima Brian and

Rwakahangi Simon Peter who always gave me courage and stood with

me throughout .Thank you guys and may the good Lord always grant

you peace, happiness and success.

Lastly I wish to thank the management of Crown Beverages Limited

which allowed me to carry out my research from their

organization. Thank You.

MAY THE ALMIGHTY GOD REWARD YOU ALL

NAKAKONGE MASTULA 10/U/139930/PLD/PD 6

TABLE OF CONTENTSDECLARATION.........................................................ii

APPROVAL...........................................................iii

DEDICATION..........................................................iv

ACKNOWLEDGEMENT......................................................v

LIST OF TABLES......................................................xi

LIST OF FIGURES....................................................xii

LIST OF GRAPHS....................................................xiii

LIST OF PIE CHARTS.................................................xiv

LIST OF ABBREVIATIONS...............................................xv

ABSTRACT...........................................................xvi

CHAPTER ONE:........................................................17

1.0 Introduction..................................................17

1.1 Background of the Study.......................................17

1.2 Statement of the Problem......................................19

1.3 Purpose of the Study..........................................20

1.4 Objectives of the Study.......................................20

1.4.1 General objective.............................................20

1.4.2 Specific objectives...........................................20

1.5 Research Questions............................................20

1.6 Significance of the Study.....................................20

1.7 Scope of the Study............................................21

1.7.1 Content Scope.................................................21

1.7.2 Geographical scope............................................21

NAKAKONGE MASTULA 10/U/139930/PLD/PD 7

1.7.3 Time scope....................................................21

1.8 Definition of the Key Terms...................................21

CHAPTER TWOLITERATURE REVIEW...................................................22

2.0 Introduction..................................................22

2.1 Methods or Techniques of Inventory Management.................22

2.1.1 The ABC Analysis..............................................22

2.1.2 Vendor Managed Inventory (VMI)................................25

2.1.3 Distribution Requirement Planning (DRP).......................26

2.1.4 Maximum and Minimum Stock level Systems (To Establish Re-OrderPoint) 27

2.1.5 Safety Stock..................................................28

2.1.6 Material requirement Planning (MRP)...........................28

2.1.7 Manufacturing Resource Planning (MRP 11)......................30

2.1.8 Just-in-time (JIT)............................................30

2.1.9 Economic Order Quantity (EOQ).................................31

2.2 Costs of acquiring and managing Inventory......................33

2.2.1 Acquisition costs.............................................33

2.2.2 Ordering Costs................................................33

2.2.3 Carrying Costs................................................34

2.2.4 Stock-out Costs...............................................35

2.2.5 Shortage Costs................................................35

2.2.6 Holding Costs.................................................36

2.2.7 Opportunity Cost of Capital Tied up in Inventory..............36

NAKAKONGE MASTULA 10/U/139930/PLD/PD 8

2.2.8 Management and administrative costs...........................36

2.2.9 Obsolete Inventory, (Write Off Cost)..........................36

2.2.10 Depreciation costs............................................37

2.3 The impact of Inventory Management on Cost Control,...........37

2.3.1 Approaches to Cost Control in Inventory Management............38

CHAPTER THREE.......................................................39

METHODOLOGY.........................................................39

3.0 Introduction..................................................39

3.1 Research Design...............................................39

3.2 Study population..............................................39

3.3 Sampling design...............................................39

3.4 Sampling size and composition.................................39

3.5 Sampling area.................................................40

3.6 Data Collection Instruments...................................40

3.6.1 Questionnaire.................................................40

3.6.2 Observation...................................................40

3.7 Reliability and validity of data..............................41

3.8 Data Sources..................................................41

3.8.1 Primary data..................................................41

3.8.2 Secondary data................................................41

3.9 Study variables...............................................42

3.10 Data collection procedure.....................................42

3.11 Data Processing and Presentation..............................42

3.12 Anticipated Problems of the Study.............................43

NAKAKONGE MASTULA 10/U/139930/PLD/PD 9

3.13 Solutions to the Anticipated Problems.........................43

CHAPTER FOUR:.......................................................44

DATA PRESENTATION, INTERPRETATION AND ANALYSIS OF THE FINDINGS......44

4.0 Introduction..................................................44

4.1 Presentation of Findings......................................44

4.1.1 Findings on the Age Group of the Respondents..................46

Findings on the Academic Qualifications of Respondents..............47

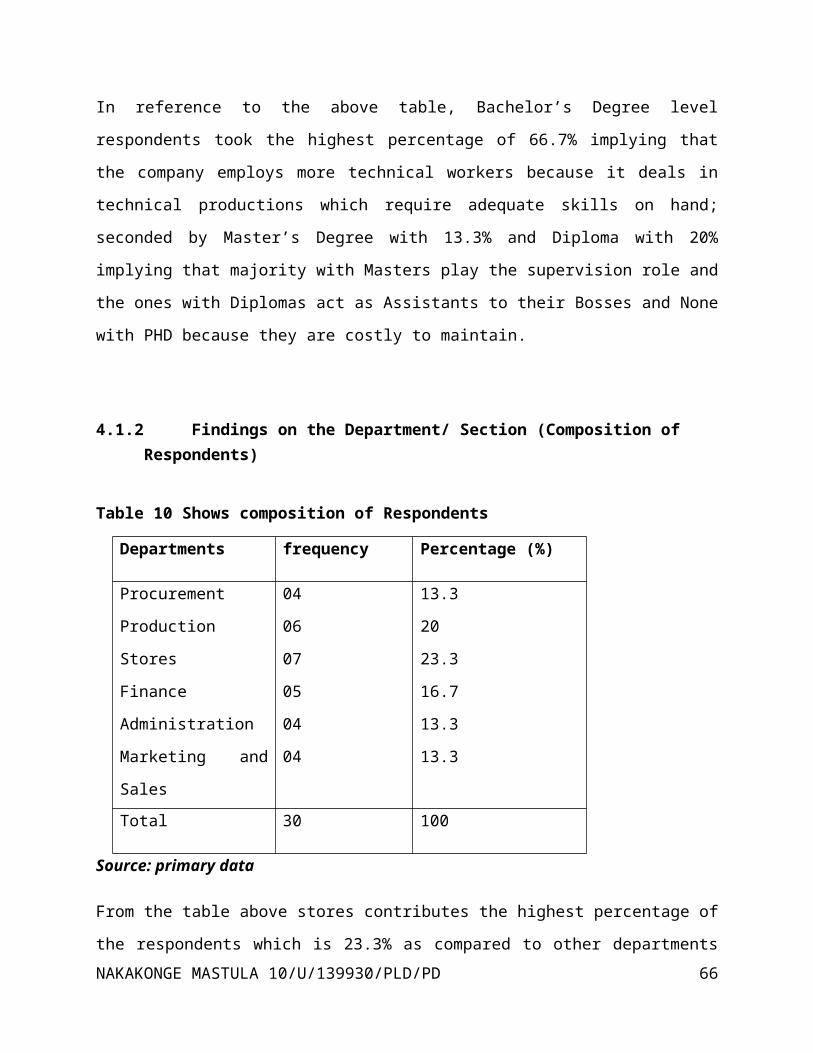

4.1.2 Findings on the Department/ Section (Composition of Respondents)48

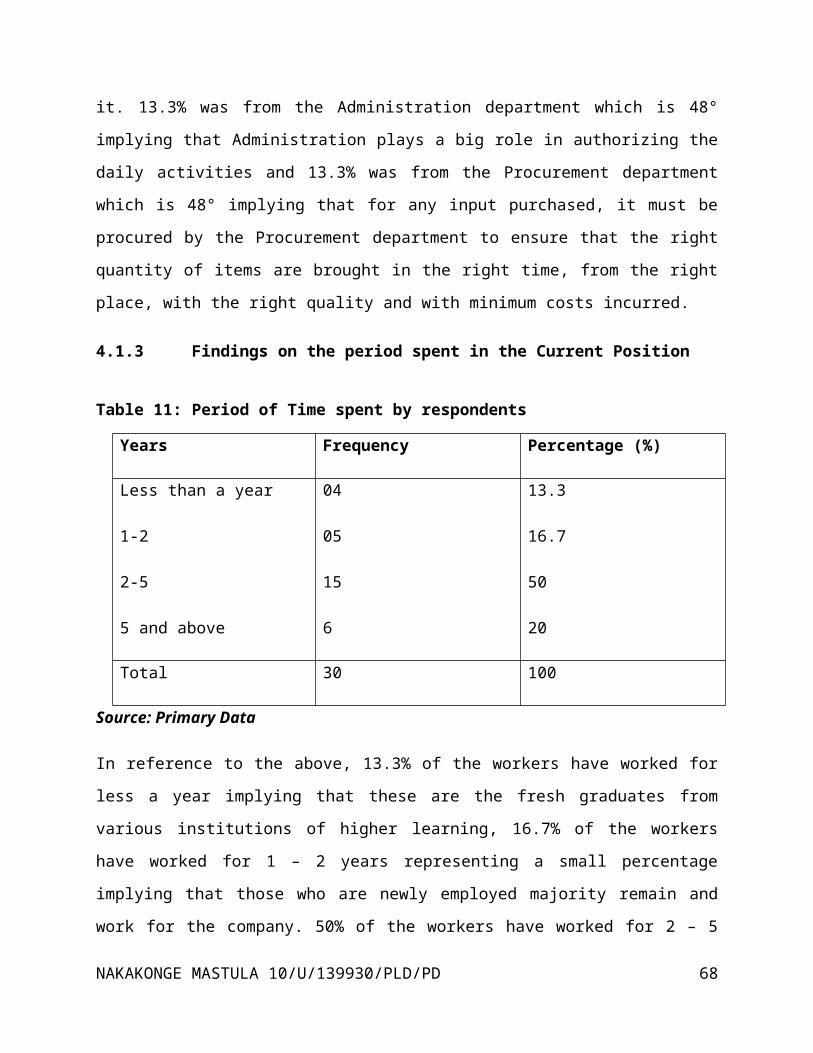

4.1.3 Findings on the period spent in the Current Position..........49

4.1.4 Findings on the Respondents’ views about the type of Inventoryheld 50

4.1.5 Findings on respondents’ views about how Inventory is acquired51

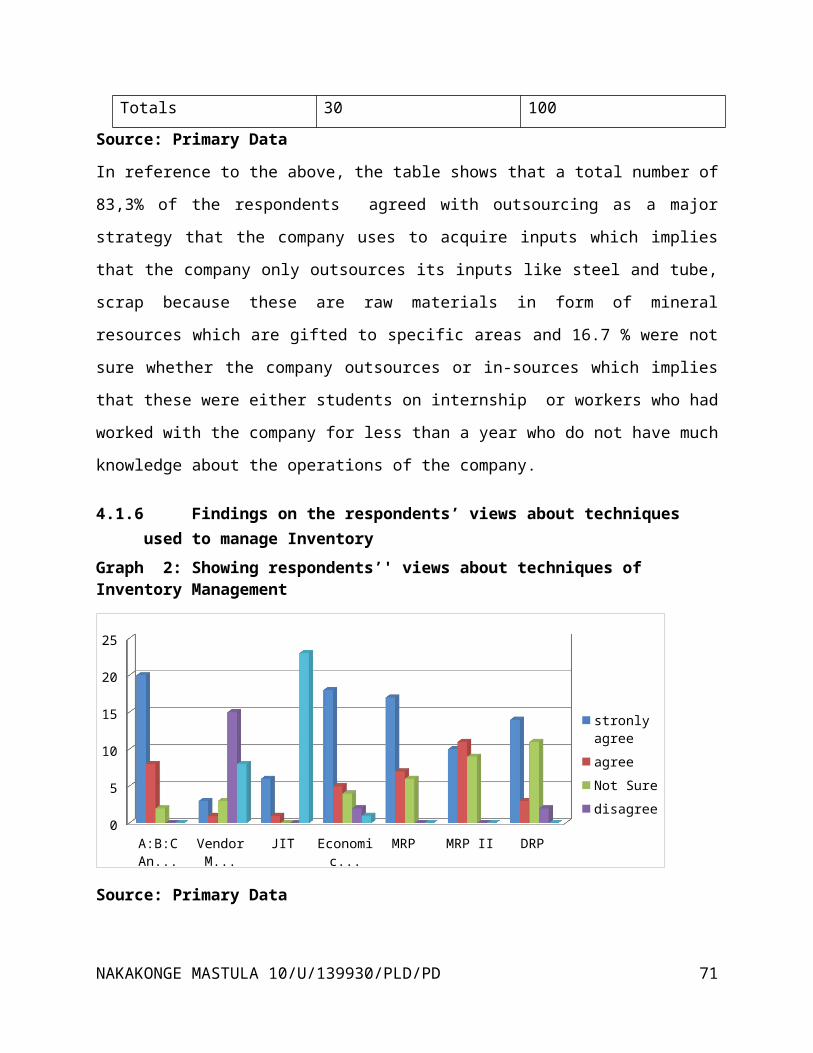

4.1.6 Findings on the respondents’ views about techniques used tomanage Inventory....................................................51

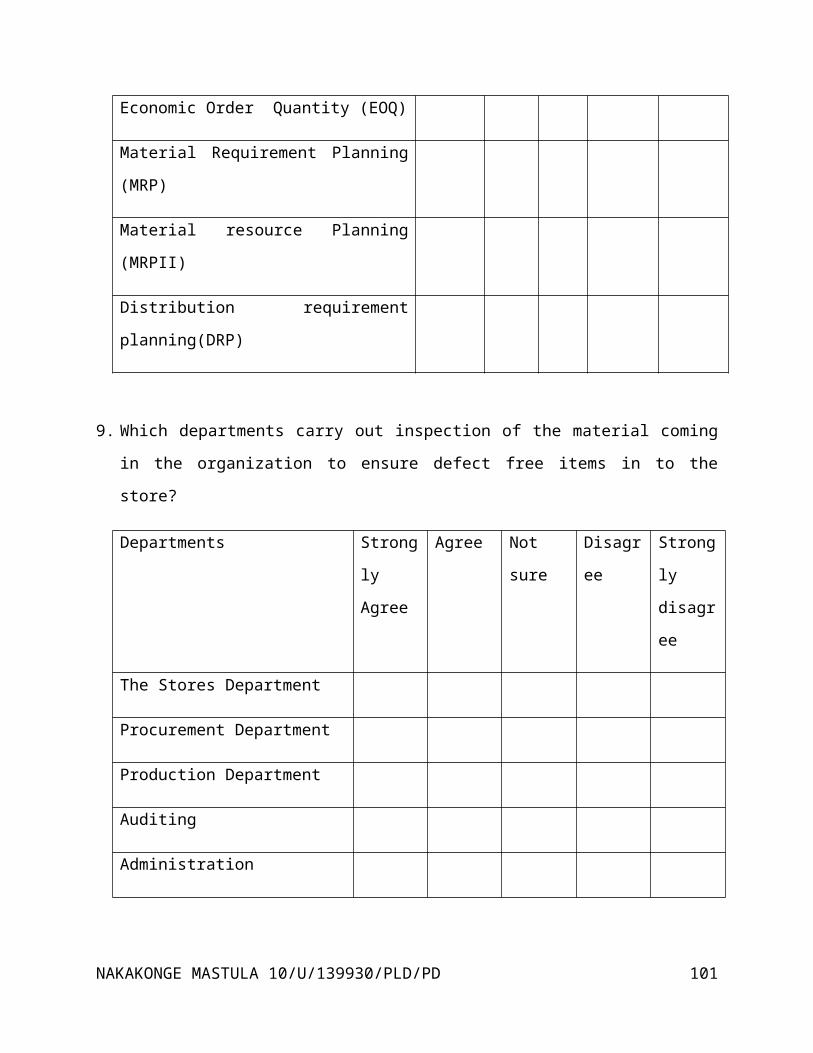

4.1.7 Findings on the respondents’ views about which departments carryout Inspection of Materials.........................................52

4.1.8 Findings on the respondents’ views about the Inspection Methodsapplied.............................................................53

4.1.9 Findings on the respondents’ views about Inventory HoldingTechniques used.....................................................54

4.1.10 Findings on the respondents’ views about when an order is placed55

4.1.11 Findings of respondents’ views on what determines the Quantitiesto be ordered for...................................................56

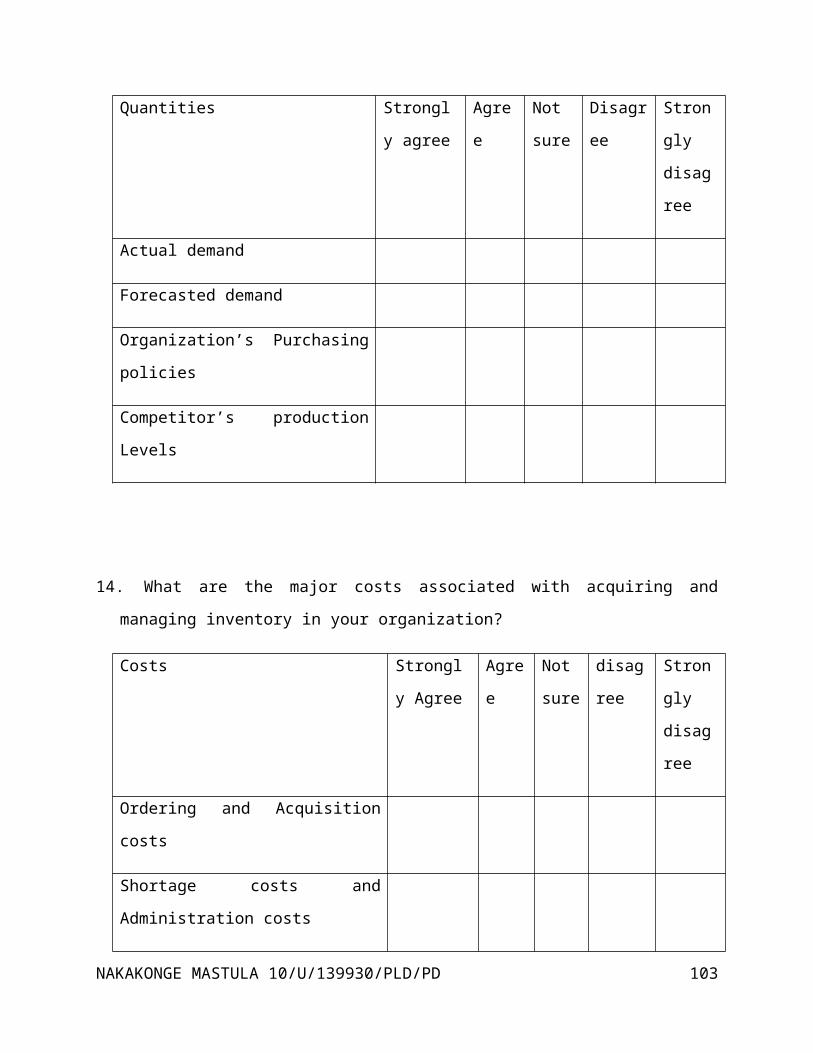

4.1.12 Findings on the respondents’ views about the costs associatedwith acquiring and managing Inventory...............................56

NAKAKONGE MASTULA 10/U/139930/PLD/PD 10

4.1.13 Findings on the respondents views about the cost effectiveplaces to keep in the Inventory.....................................57

4.1.14 Findings on the respondents’ views about whether Stock Taking iscarried out.........................................................58

4.1.15 Findings on the respondents’ views about the Role that InventoryManagement plays towards Cost Control...............................58

4.1.16 Findings on the respondents’ views about how Inventorymanagement impacts on Cost Control..................................59

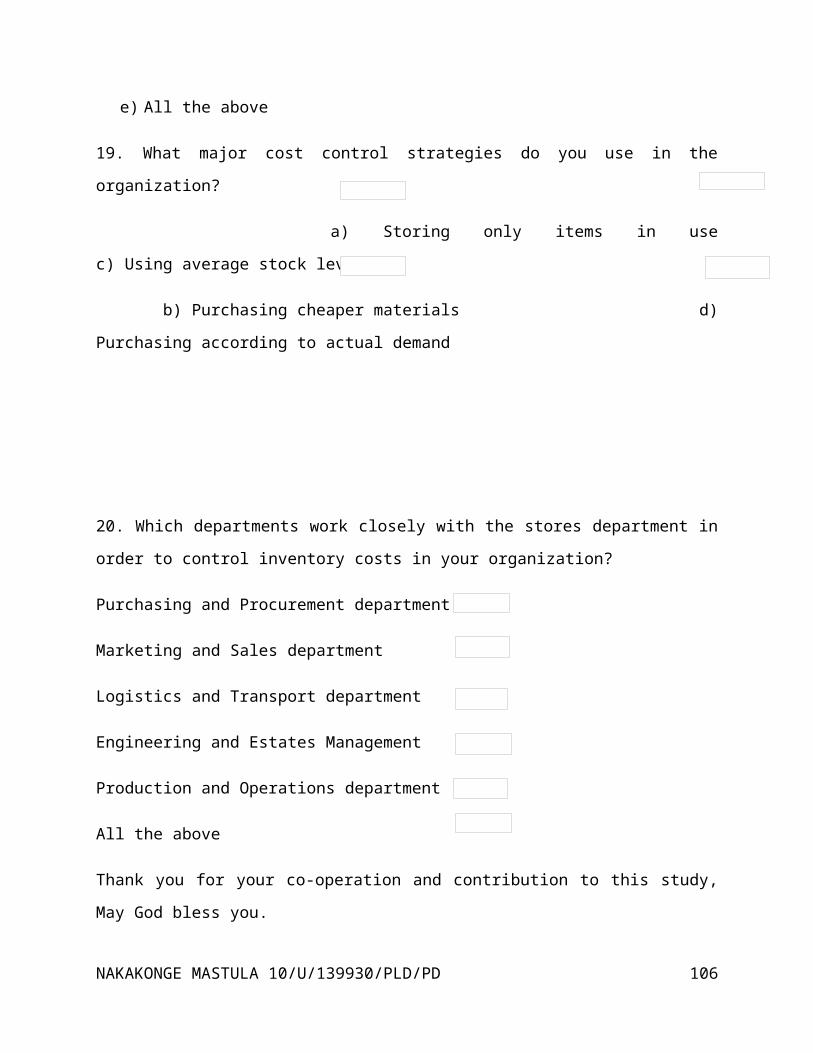

4.1.17 Findings on the respondents’ views about the major Cost ControlStrategies..........................................................60

4.1.18 Findings on the respondents’ views about the Departments thatwork closely with the Stores department.............................61

CHAPTER FIVE........................................................62

DISCUSSION, CONCLUSION AND RECOMMENDATION...........................62

5.0 Introduction..................................................62

5.1 Discussion of findings........................................62

5.1.1 Inventory Management Techniques...............................62

5.1.2 Inventory Management Costs....................................63

5.1.3 Impact of Inventory Management and Approaches of Cost Control.64

5.2 Summary.......................................................65

5.3 Conclusion....................................................65

5.4 Recommendations...............................................66

5.5 Areas for further Research....................................66

APPENDICES..........................................................67

REFERENCES..........................................................67

BUDGET 68

NAKAKONGE MASTULA 10/U/139930/PLD/PD 11

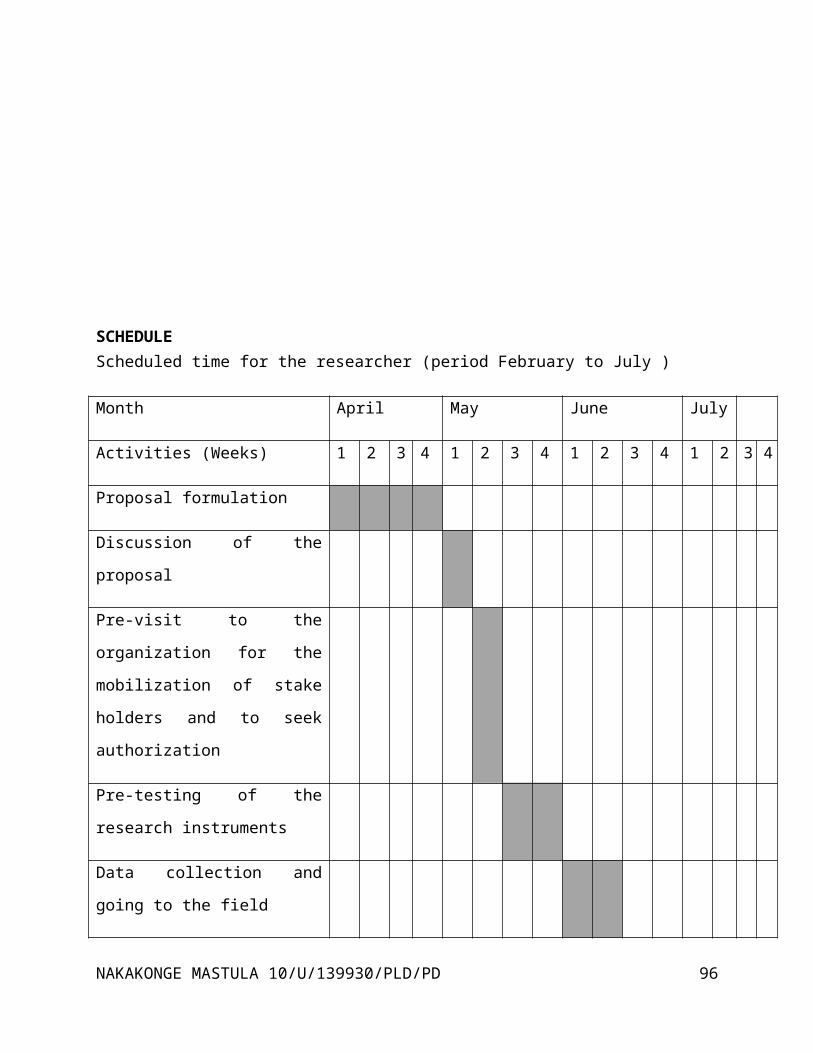

SCHEDULE............................................................69

RESEARCH QUESTIONAIRE...............................................70

LIST OF TABLESTable 1: Classification of Product Items............................23

Table 2: Obtaining Total Purchase Cost..............................24

Table 3: An illustration of Different classes.......................25

Table 4: Showing carrying and ordering Costs........................35

Table 5: Showing the distribution of Sample size....................40

Table 6 Sex distribution of the respondents.........................44

Table 7 Showing age distribution of respondents.....................45

NAKAKONGE MASTULA 10/U/139930/PLD/PD 12

Table 8: Age bracket of the Respondents.............................46

Table 9: Academic Qualifications....................................47

Table 10 Shows composition of Respondents...........................48

Table 11: Period of Time spent by respondents.......................49

Table 12 Findings on the respondents' views about the type of

Inventory held......................................................50

Table 13 Shows respondents' views about how Inventory is acquired. . .51

Table 14: Showing respondents’ views about inspection...............52

Table 15: When order is placed......................................55

Table 16: The cost of effective places to keep in the inventory.....57

Table 17: Does the company carry out Stock taking...................58

Table 18 Showing impact of inventory management on Cost Control.....59

Table 19: Showing departments which work with stores department.....61

NAKAKONGE MASTULA 10/U/139930/PLD/PD 13

LIST OF FIGURESFigure 1: PARETO CURVE..............................................24

Figure 2: Illustration of distribution chain........................26

Figure 3 Economic Order Quantity....................................27

Figure 4 MRP System.................................................29

Figure 5 A Graphical Representation of EOQ Model....................32

Figure 6 Ordering Costs.............................................34

Figure 7 Carrying Costs.............................................34

NAKAKONGE MASTULA 10/U/139930/PLD/PD 14

LIST OF GRAPHSGraph 1: A bar graph showing the age bracket of respondents.........46

Graph 2: Showing respondents’' views about techniques of Inventory

Management..........................................................51

Graph 3: Respondents' views about Inventory Holding Techniques......54

Graph 4 What determines the quantities to be ordered...............56

Graph 5 Showing about the Role of inventory management towards cost

control.............................................................58

NAKAKONGE MASTULA 10/U/139930/PLD/PD 15

LIST OF PIE CHARTS

Pie Chart 1: Representing the sex composition of the respondents....45

Pie Chart 2 Showing Composition of Respondents......................48

Pie Chart 3 Respondents' views about the Inspection methods.........53

Pie Chart 4: Showing cost control strategies........................60

NAKAKONGE MASTULA 10/U/139930/PLD/PD 16

LIST OF ABBREVIATIONS

MRP Materials Resource Planning

JIT Just In Time

VMI Vendor Managed Inventory

MRP II Manufacturing Resource Planning

EOQ Economic Order Quantity

BOM Bill of Materials

DRP Distribution Requirement Planning

NAKAKONGE MASTULA 10/U/139930/PLD/PD 17

ABSTRACT

The study focused on the “Impact of Inventory Management on Cost

Control”. This study was carried out at Crown Beverages Limited

located in Nakawa Industrial Area along Kampala-Jinja Highway.

The research questions sought to find out thevarious Inventory

Management Techniques or methods used in an organization, the

various costs incurred which are associated with inventory

management while acquiring and maintaining inventory in an

organizationand an investigation on the impact of inventory

management on cost control within an organization and the

approaches which can be used to control inventory costs.

To effectively carry out this study, the researcher used

different tools of collecting data including questionnaires,NAKAKONGE MASTULA 10/U/139930/PLD/PD 18

interviews and observation. The researcher collected data from

different departments in the company including the Procurement

Department, Production Department, Accountants Department, Stores

Department, Administration Department and Marketing and Sales

Department. The research was qualitative and quantitative in

nature thus the data collected was presented and analyzed in

essay and tabular forms for easy interpretation.

Basing on the objectives, it was revealed that most of the

Inventory Management Techniques used are ABC Analysis and

Economic Order Quantity (EOQ). Ordering and Acquisition Costs

plus the Carrying and Stock-out Costs were the costs highly

associated with Inventory Management in the organization’s

routine operations. The impact that existed between Inventory

Management and Cost Control was that “the higher the inventory

held, the less the costs and the less the inventory held, the

higher costs associated with inventory management in an

organization and vice versa”. The approaches which were mostly

used to control inventory costs were, using average stock levels

and purchasing according to actual demand.

NAKAKONGE MASTULA 10/U/139930/PLD/PD 19

CHAPTER ONE:

1.0 Introduction

For an organization to achieve efficiency in its operations,

proper inventory management has to be ensured. Therefore this

chapter consists of the introduction of the study with several

subsections such as background, statement of the problem,

objectives of the study, research questions, and scope of the

study and significance of the study.

1.1 Background of the Study

Uganda Manufacturers Association (UMA)’s report of 2002 advances

that inventory or materials constitute a large part of current

assets for most of all businesses in Uganda. On average, they are

60% of the current assets in the balance sheet and because large

inventories are maintained by firms, a considerable amount of

funds is required to be committed to them. Inventory refers to

anything needed for work activity such as building materials or

writing materials. Materials are not necessarily tangible, they

can be information. It is therefore absolutely important to

manage inventory and control costs effectively and efficiently in

order to avoid unnecessary investment and minimize the costs

associated with stock such as carrying costs, ordering costs and

stock out costs.

Michaud J.P. and Grant A.K. (2005), define inventory management

as stock items which are taken into store and held until required

NAKAKONGE MASTULA 10/U/139930/PLD/PD 20

or as deliveries to the point of consumption. The control of

these materials is known as inventory management. They emphasize

that the function of inventory management is to obtain the

maximum materials turnover consistence with the maintenance of

sufficient materials to meet the organization’s requirements in

terms of production. Firms hold from 14% – 50% of their capital

invested in inventories. New Vision of 14th April 2003 page 23

shows many companies listing inventory management as their first

priority. Inventory management becomes one of the purchasing

goals; it involves the planning, ordering and scheduling of

materials used in the manufacturing process. It exercises control

over the three types of inventories like Raw materials, Work in

progress and finished goods. Usually operational managers have an

ambivalent attitude towards inventories. On the other hand, they

provide security in a complex and uncertain environment knowing

that you have items in stock whenever customers or production

schedule demand for them.

According to Gray .J. (2002), Inventory management is expressed

as quantity or money such as raw materials, work in progress, and

finished goods. Managers for generations have tried to control

inventories accurately and relatively simple. 1930 – 1940’s

brought mixed reasons to procure in Economic Manufacturing

Inventories. 1950’s so reviewed research effort devoted to

controlling inventories. Inventories make up sizeable percentage

of a company’s assets and usually the largest single current

assets. Inventory refers to the value of quantity of raw

NAKAKONGE MASTULA 10/U/139930/PLD/PD 21

materials, components, assemblies, consumables and finished stock

that are kept or stored for production. (Lysons,2003) Inadequate

inventories will bring about stock outs which will discourage

customers visiting your company, reduce on sales, increase costs

and reduce overall profitability. This helps management to

provide an outstanding customer service that ensures maximization

of returns on inventory management. This involves measures of

inventory management such as use of ABC Analysis, Safety Stock

Quantity, Economic Order Quantity (EOQ) and Just-in-time (JIT)

Analysis, use of predicated demand during the supplier review or

order cycle; the normal length of time between typical

replenishment order with the supplier, protecting the

organization against theft, establishing an approved stock list

for each warehouse and other techniques. (Jon 2005).

According to Lucy (1995), Inventory Management involves material

control systems, proper and systematic recording of inventory and

storage of the right amount of inventory by organizations. Too

much inventory creates mounting storage and kinds of carrying

costs. Too much inventory on the other hand can lead to

interruptions in the production and leads to losses in an

organization (Kakuru, 2005). In managing inventory, the firm’s

objective should be on consonance with cost immunization

principle. To achieve this, the firm should determine optimum

level of inventory efficiently and controlled inventories make

the firm flexible. Inefficiently inventory management results

into unbalanced inventory and inflexibility. Therefore to avoid

NAKAKONGE MASTULA 10/U/139930/PLD/PD 22

this, different measures should be applied and these measures may

include Economic Order Quantity, ABC Analysis, Just-in-time

technique to mention but a few in order to manage inventory and

control costs (Pandey, 1995).

Organizational costs involve the value of Economic resources used

as a result of production of any commodity or performing any

services for instance of UGX 5,000 is spent to produce 1,000

units of cloth, then this amount is referred to as Costs

(Saleemi, 2002), adds that to control costs, they need to first

be classified as fixed costs, variable costs, direct and indirect

costs and costs classified according to function like security

costs. Thus it is necessary for organizations to manage

inventories by holding optimum levels that ensure minimum costs.

This is because both excessive and inadequate inventories are

undesirable as it ties up the organization’s funds, increase

costs and loss of profitability.

1.2 Statement of the Problem

According to Kakuru (2005), Inventory constitutes the largest

part of the organization’s current assets for their continuous

operations. It is absolutely imperative to manage inventories

efficiently and effectively in order to control costs. Inventory

management is an important aspect for the improvement of

performance within an organization. Just like any kind of

investment business, inventory management needs to serve the

NAKAKONGE MASTULA 10/U/139930/PLD/PD 23

purpose of minimizing costs, maximizing profits, accurate record

keeping and adequate material availability among others.

Much as organizations are trying hard to improve on inventory

management in order to control costs, in many cases inventory

management has turned into a major cash flow constraint which is

associated with so many hardships in form of costs such as stock

out costs, high inventory security costs, insurance costs,

falling victim of the “Bull whip effect;” to much distasted stock

in inventory and items in stock get misplaced as stated by (Doug

Brinlee, 2007).

Despite the fact that organizations still make use of inventory

management techniques in order to minimize costs which in fact is

an output of many inter-organizational processes; but the results

of the findings are not always clearly expressed. Therefore, it

is on this background that the researcher is intending to

investigate on the impacts of inventory management on cost

control at Crown Beverages Ltd located in Nakawa Industrial

Area.

NAKAKONGE MASTULA 10/U/139930/PLD/PD 24

1.3 Purpose of the Study

To examine the impact of inventory management on cost control at

Crown Beverages Ltd located Nakawa.

1.4 Objectives of the Study

1.4.1 General objective To investigate on the impact of inventory management on cost

control within an organization and the approaches which can be

used to control inventory costs.

1.4.2 Specific objectives To examine the various inventory management techniques or

methods used in an organization.

To analyze the various costs incurred which are associated

with inventory management while acquiring and maintaining

inventory in an organization.

1.5 Research Questions

i. What are the various inventory management techniques or

methods used by most organizations?

ii. What are the various costs incurred while acquiring and

maintaining inventory in an organization?

iii. How does inventory management impact on cost control in an

organization and what approaches can be used to control

inventory costs?

1.6 Significance of the Study

The purchasing managers in very many organizations concerning the

methods of inventory management will learn new ideas and

perception on the use of better inventory management techniques.

NAKAKONGE MASTULA 10/U/139930/PLD/PD 25

The study will provide useful guidelines to the potential readers

and researchers who may have interest in learning on the same

topic.

The research will avail information on how to maintain average

stock in an organization and overcome unnecessary costs related

to stocks like stock out costs.

The research will help improve on the researcher’s knowledge and

capabilities to research about more other topics and give him/

her insight about Inventory Management and Cost Control as well

as partial fulfillment for the award of a Bachelor’s Degree of

Procurement and Logistics Management of Kyambogo University.

The study will benefit the Government of the Republic of Uganda,

the general public and potential investors in many organizations.

As they will appreciate different methods of inventory management

and cost control and strike a balance between the two variables.

1.7 Scope of the Study

1.7.1 Content Scope

The study was centered on the impact of inventory management and

cost control in an organization. Therefore the study investigated

mainly on the following.

To examine the inventory management techniques used in an

organization.

To analyze the various costs incurred in managing inventory in

an organization.

NAKAKONGE MASTULA 10/U/139930/PLD/PD 26

To investigate on the impact of inventory management on cost

control in an organization and the approaches which can be

used to control inventory costs.

1.7.2 Geographical scope

The study was conducted in Crown Beverages Ltd Central store in

Nakawa Industrial Area along Kampala –Jinja Road

1.7.3 Time scope

The research was carried out between February 2009 to May 2013

1.8 Definition of the Key Terms

Inventory Management; this involves planning, ordering,

implementation and scheduling the use of materials in an

organization with in its various user departments like;

Production Department, Accounting and Finance among others.

Application; these are methods used to improve on inventory

management or control in an organization.

Cost; this involves all the expenses incurred by an organization

or a sacrifice foregone to attain a benefit for example,

Transportation Costs, Administration Costs, Marketing and

Distribution and Inventory Costs all can be incurred to attain

profitability.

Cost control; these are strategies employed by various

organizations with an attempt to control on costs.

NAKAKONGE MASTULA 10/U/139930/PLD/PD 27

CHAPTER TWO

LITERATURE REVIEW

2.0 Introduction

This chapter is an analysis of some of the major issues on

existing literature on inventory management as studied by other

scholars. It dealt with relevant literature on inventory

management and cost control and it was associated with

discussions on relation to the research objectives.

2.1 Methods or Techniques of Inventory ManagementThese involve techniques and systems to control the firm’s

investment in stock. They include recording and monitoring of

stock levels, forecasting future demand and deciding when and how

much to order (Lysons Kenneth, 2003).

2.1.1 The ABC AnalysisAccording to Zenz, (2002) Today’s inventory control mangers

define pareto analysis into three categories i.e. A, B and C.

The A-items number only from 10%-20% of the total inventory

control number of items. However, they may account for 65%-80% of

the dollar tied up in the inventory. A-items deserve excessive

attention like general electronic copper.

The B-items number only from 10%-15% of the tied inventory and

typically they tie up to 20%-25% of the dollar invested in the

inventory. B-items deserve the Economic Order Quantity Analysis

or some other forms of verifying the right quantity to buy in

stock.NAKAKONGE MASTULA 10/U/139930/PLD/PD 28

The C-items number only from 65% of all items in inventory.

However their combined dollar value totals only 5% of the entire

investment in the inventory, clerical personnel or computers

connect suppliers. Computers order the C-items for many firms

because most firm’s find that a small number of purchased items

account for the major portion of the purchased value. It is often

advisable to clarify purchased items according to value, unit,

cost, unit volume, shelf, and life and dollar investment.

According to Alan Muhumum, et al. (2002), stated that A:B:C

analysis is a systematic structured approach to distinguish

between vital few and trivial many. In many organizations under

taking large control of a few orders will control the bulky of

the organization’s work load. It can also be called out by income

and also by contribution.

According to Arord and Pandey, (1995) A:B:C Analysis is an

inventory management technique where a firm analyzes each

inventory item on the basis of its costs, frequency of usage,

seriousness of stock, lead time and other issues of importance to

each item. Items are analyzed according to their values so that

costly and valuable materials are given greater attention and

care. The ABC Analysis classifies items under three distinct

groups A, B, and C.

“A” items constitute stock which is necessary for proper

functioning and operation of the business with it making 80% of

value and 20% in items of stock. A firm has to take serious

NAKAKONGE MASTULA 10/U/139930/PLD/PD 29

control of such items, maintain proper records, carry out

continuous stock review and keep minimum inventory.

“B” items represent relatively least value stock under simple

management. They usually comprise 15% of value of the business

and 50% of stock. These items therefore require reasonable

attention by management.

“C” items are low value materials which represent a very large

number of items but with relatively least value. This category is

under a simple management.

Table 1: Classification of Product Items

Category Degree of

control

Types of

records

lot sizes Frequency

of review

Size of

safety

stock

levelsA Tight Accurate

and

complete

Low Continuous Small

B Moderate Good Medium Occasional ModerateC Loose simple Large infrequent LargeSource: Secondary Source

Graphically, it can be shown in form of a Pareto curve

NAKAKONGE MASTULA 10/U/139930/PLD/PD 30

Figure 1: PARETO CURVE

Percentage

Costs

Item A Item B

Source: Financial Management I.M Pandey,(1995).

Drury, (2000) States that there are two stages involved in

classifying stock under the ABC model;

Stage One:

For each item in stock, multiply the price to obtain the total

purchase cost. This can be illustrated as below;

Table 2: Obtaining Total Purchase Cost

Ite

m

Estimated

usage

Unit

price

(£)

Total per cost (£)

1

2

3

4

60,000

20,000

1,000

10,000

1.00

0.05

0.01

0.02

60,000

1,000

100

200

NAKAKONGE MASTULA 10/U/139930/PLD/PD 31

5

6

100,000

80,000

0.01

2.00

1,000

160,000Source: Secondary Data

Stage Two:

Group all the above items in descending order of purchase price

and then divide into class A (top 10%), class B (next 20%) and

then class C (bottom 70%).

Table 3: An illustration of Different classes

Class No. of Items

in Stock

% of items

in Stock

Total Cost %

A

B

C

1,000

2,000

7,000

10

20

70

730,000

190,000

80,000

73

19

8

Total 10,000 100 1,000,000 100

Source: Secondary Data

According to Lysons and Gillingham,(2003) Under ABC Analysis, the

basic items are known as class A-items. These require close day

to day control because of their budgetary importance for instance

a household may buy different items such as food items which

account for the bulk of annual expenditure in shops because they

are needed frequently. Group C items are items that are

occasionally needed and do not require to spend hours comparing

the price the price from different suppliers because it does notNAKAKONGE MASTULA 10/U/139930/PLD/PD 32

make any economic sense. They are regularly received but are not

closely controlled as Class A items.

2.1.2 Vendor Managed Inventory (VMI)According to Gray,R.B. et al.(2002), This approach presupposes

transfer of responsibility of managing and controlling inventory

from the purchasing organization (who is the owner thereof) 2to

the supplier (seller) upon agreed terms. The purchasing

organization has the legal ownership of the goods, but the goods

after purchase will be kept with the supplier, and delivered to

the buyer’s premises on the basis or order quantity and time (how

frequently) of replenishment. Modern developments have seen the

emergence of a new practice: vendor owned Inventory (VOI), where

the inventory is kept at the buyer’s premises (on consignment)

and the buyer pays for what has been used/ sold. Thus Vendor

Inventory is refered to as Consignment Inventory or Stock.

2.1.3 Distribution Requirement Planning (DRP)According to Gallaway et al. (2000), it is an inventory control

and scheduling technique that applies Material Requirement

Planning (MRP), principles to distribution inventories. It is

used in a multi arrangement environment, for example a

supermarket chain; the regional ware house derives their demand

from individual supermarkets multi-arrangement (echelon) means

that instead of independent control of the same item at different

distribution points using Economic Order Quantity (EOQ) formula,

the dependent at a high echelon (for example Central warehouse)

NAKAKONGE MASTULA 10/U/139930/PLD/PD 33

is derived from the requirement of lower echelons (for example

Regional ware house)

Figure 2: Illustration of distribution chain

Sourc

e: purchasing and supply chain management, Kenneth lysons(2006)

DRP uses several variables which include;

The required quantity of products needed at the beginning of a

period.

The constrained quantity of products needed at the beginning of a

period.

The recommended order quantity at the beginning of a period.

The back ordered demand at the end of a period.

The on hand inventory at the end of a period.

2.1.4 Maximum and Minimum Stock level Systems (To Establish Re-Order Point)

Another widely used method of inventory management involves the

establishment of minimum and maximum control levels. The last

NAKAKONGE MASTULA 10/U/139930/PLD/PD 34

central warehouseregional ware houseoutletsoutletsregional ware houseoutletsoutlets

unit of inventory could be used up at the moment the new shipment

arrives. The maximum inventory would then be correct orderly

quantity in practice. It would be unwise to follow this extreme

policy since it involves planning that is much too close for

safety. In minimum system, a safety tender is established which

becomes the minimum point below which the inventory should not go

under normal circumstances. The maximum inventory consists of

this safety factor plus the correct orderly quantity. The size of

these safety factors depends on the importance of the particular

item to be stored.

2.1.4.1 Re-Order PointThis technique answers the question when should an order be made?

This question is answered by using the lead time and average

usage of an item in the firm. (Pandey, 1995) Defines a re-order

point as that inventory level at which an order should be placed

to replenish the inventory. It is determined among others by lead

time, which the time is normally taken in replenishing delivery

after an order has been made. Re-order point is crucial in a firm

especially where the lead time is short. Graphically, it can be

shown as below;

Figure 3 Economic Order Quantity

Quantity

NAKAKONGE MASTULA 10/U/139930/PLD/PD 35

Order point

0 LT LT

periods (Weeks)

LT=Lead Time

Source: Financial Management I.M Pandey, (1998).

2.1.5 Safety StockIt is the minimum lead of inventory that a firm keeps on land.

Inventories are re-ordered whenever the level of inventory falls

to safety stock level (Lysons,2003). Pandey,(1995) Assesses that

safety stock is a level at which stock outs are guarded against.

In a firm this is a critical aspect because once the level of

inventories fall below the safety stock, this will affect the

production level.

2.1.6 Material requirement Planning (MRP)According to Zenz,(2002) said that this is a system which is

computerized, based, planning and a control system used for

planning effectively and controlling international production and

materials’ flow. The objectives of this system are; to minimize

inventory defects and costs, to maintain delivery schedules. This

system is delivered from four (4) central elements(inputs) thus;

the bills of materials’ file, the inventory control status file,

NAKAKONGE MASTULA 10/U/139930/PLD/PD 36

the master file and the production schedule and material

requirement planning packages.

Bill of Materials (BOM) file is a list of all items that

comprise each assembly and such assembly that makes up the final

product. The bill of materials identifies all the components

required to produce a scheduled quantity of an assembly and the

structure of now these components fit together to make that

assembly. The BOM can be viewed as a product structure tree,

similar to an organization chart below.

Inventory control status file this comprises of the records of

individual items of inventory and their status. It shows the on

hand balances, open orders and lead time. The ISF provides

information on the identification and quantity of items in stock.

Materials Requirement planning (MRP) package, this calculates

the net requirements from the balance in stock to release

purchase orders for items to be purchased and produce reports and

productions according to demand information.

Master Production schedule; this is a plan for the finished

goods production over a period of time. That is to say it shows

what should be produced and when it needed This MPS indicates the

quantity and timing of each item the Organization produces. MRP

can reduce inventory by providing information on the actual

inventory required for parent items rather than stocking enough

components for estimated parent demand.

NAKAKONGE MASTULA 10/U/139930/PLD/PD 37

Outputs of MRP

A planned order release, this indicates when to release orders,

materials and delivery to specified customers.

Resource notices; these show the need to advance or post pond

inventory orders to net requirements.

Expediting instructions in respect to overdue orders

Data to determine capacity required for production schedules e.g.

machinery, man power.

Elements of the MRP System

Figure 4 MRP System

Source: purchasing and supply chain management, Kenneth lysons(2006)

According to Muhleman et el. (2002), this method can operate

quite simply and satisfactory when orders of finished goods are

being received at a constant or at a least smooth and slowly

NAKAKONGE MASTULA 10/U/139930/PLD/PD 38

Customer order

MRP Package

Master production schedule

BOM

Engineering changes

Schedule reports

Forecasts

Inventory Status file

Inventory transactions

varying rate. This reflects the work in progress and raw

materials require. However if the demand for the finished goods

is humpy or erratic, then his method may involve holding stock of

work in progress of raw materials for extensively a long period.

Finally Material Requirement Planning (MRP) has a universal

applicable element for inventory control and can be most

advantageous applied items that have discontinuous and non-

uniform depending on demand for assembly, production,

manufacturing or fabrication operations.

2.1.7 Manufacturing Resource Planning (MRP 11)MRP11 is an integrated information system used by business. It

evolved from material requirement planning systems by including

the integration of additional data, such as employee and

financial needs. The system is designed to centralize, integrate

and process information for effective decision making in

scheduling, design engineering, inventory management and cost

control in manufacturing.

This is virtually concerned with resources entering in the

production process including man power, machinery and money. In

addition to materials, MRP 11 extends the idea of MRP to other

areas in the business such as marketing and finance. Thus central

data bases hold information on product structure that’s to say

the bill of materials file which can be up dated due to design

changes by engineering. At wider information provided by the MRP

11 System from simulations of business plans can be used to

NAKAKONGE MASTULA 10/U/139930/PLD/PD 39

estimate plant investment needs and work force requirements. This

information can then be used to coordinate efforts across

departments including marketing, financing, engineering and

manufacturing.

2.1.8 Just-in-time (JIT)According to Richard (1998), it is on inventory management system

that schedules materials to arrive precisely when they are needed

on production line. It is designed to reduce level of

organization’s inventory to zero. The system can also be referred

to as Kan Ban or Stockless system.

It is an approach to inventory management and control in which

inventories are acquired and inserted in production at the exact

times they are needed home. This is to avoid unnecessary expenses

associated with keeping stock at hand. Ebert,(1986) and Drury,

(1995) assert that costs like holding costs, security costs,

storage costs are avoided using this technique of Just-in-time

(JIT).

JIT can also be defined as the recent approach to inventory

management developed by Japan’s manufacturing enterprise that is

gaining first recognition as a management tool (Kakuru, 2001).

According to Zenz, (2002) stated that Just-in-time emerges, it

means the uninterrupted flow of 100% accepted materials delivered

on due details and optimal costs of 100% of the time. This is a

trend towards a smaller inventory to high holding costs and meets

the international competition. The industries making the mostNAKAKONGE MASTULA 10/U/139930/PLD/PD 40

progress in inventory management are the industries that have

reached the international competition like Japan and America

manufacturers because they do not have strikes and the causes of

shortage of materials because there suppliers are nearby and

under tight control. Just-in-time success may include contracting

between manufacturers and the carrier must focus on the smallest

inventory levels in JIT. Distribution manufacturers need to know

the exact status of their materials at all levels. Many

distribution channel members see JIT as a way of transfer of

inventory burden to their supplier and to get more favorable

price while many suppliers see JIT as a quick fix and a way to

guarantee a high level of sales. However JIT can reduce the

distribution channels conflicts and promote channel co-operation.

2.1.8.1 Requirements for a Successful JIT ModelSchedules of production requirements should be precise and exactin time and amount.

Organization structures that facilitate co-operation support andcommitment so that work force is committed to meeting theschedules of work.

Relationship with suppliers so that delays in delivery of inputsis minimized (Kakuru, 2001).

Drury, (2000) Explains JIT as a philosophy where by firms giveattention to reduce stock levels at minimum by implementing JITpurchase techniques.

Objectives of JIT purchasing;

NAKAKONGE MASTULA 10/U/139930/PLD/PD 41

To purchase goods so that delivery immediately precedes theiruse. This can be achieved through co-operation with thesuppliers.

Companies that have implemented JIT purchase have subsequentlyreduced their investment in raw materials and work in progressstock.

2.1.9 Economic Order Quantity (EOQ)

EOQ is the most commonly used approach of attaining the goals of

inventory management (Kakuru, 1998) the model answers the

questions such as how much quantity should be ordered? Pandey,

(1998) defines EOQ as that level of stock which minimizes the

total of ordering and carrying costs. (Lysons, 2003) Defines it

as the optimal ordering quantity for an item of stock that

minimizes costs. It works under the following assumptions.

Demand is known and is constant.

The only variable costs are the cost of placing an order and

holding costs.

The receipt of inventory is instantaneous.

The lead time is known and constant.

However, the EOQ model has been criticized basing on the

following;

That demand is not always constant and sometimes may not be known

because people’s demand differs from time to time.

That there are other variables costs which include stock out

costs and carrying costs.

NAKAKONGE MASTULA 10/U/139930/PLD/PD 42

The receipt of inventory is not instantaneous. It always takes

time to receive ordered quantity. The lead time is not always

constant

According to Kakuru, (2003) EOQ is the most used approach in

attaining the goals of inventory management. The model is used to

determine the optimal amount of inventories to order that

minimizes the cost of inventory while ensuring liquidity to the

business.

According to Nair,(2000) EOQ is that quantity at which the costs

of ordering the annual requirements of an item and the inventory

carrying costs are equal that is when the total of the two costs

is the lowest. Under EOQ, the inventory carrying costs are

calculated on the average working stock which is taken as 50% of

the order quantity.

Figure 5 A Graphical Representation of EOQ Model

Carrying costs

40

Rupees

30

Ordering costs

Total

costs

20

NAKAKONGE MASTULA 10/U/139930/PLD/PD 43

10 Point

of Minimum costs 0 2 4

6 8 10 Quantity

Source: Nair,(2000)

It will be observed from the graph that the lowest total cost is

at the point where the line ordering costs interests the line of

ordering costs and the Economic Order Quantity is observed at the

point of the lowest total costs.

2.2 Costs of acquiring and managing InventoryAccording to Eddowes and Sternfield, (1995) when inventories are

ordered for and kept, costs will be occurred in ordering and

delivery process. Furthermore, costs will rise in storage and

administering of stock. Each type of stock will comprise of fixed

and variable cost elements. However, according to Lysons and

Gillingham, (2003) Economics of stock control are determined by

analysis of costs incurred in obtaining inventory under the

heading of acquisition costs, holding costs and stock out costs.

2.2.1 Acquisition costsLysons and Gillingham, (2003) define acquisition costs as thecosts incurred in placing an order irrespective of the size. Forinstance, preliminary costs, placement costs and post placementcosts. These costs vary according to complexity of the order andthe seniority of the staff involved whether order preparations ismanual or computerized and whether repeat orders cost less than

NAKAKONGE MASTULA 10/U/139930/PLD/PD 44

initial orders. Ordering costs can be requisitioning, orderplacing, transportation, receiving, inspection, storing and costsof clerical staff while carrying costs can be handling costs,costs of deterioration obsolescence, security, lighting costs(Pandey, 1995).

2.2.2 Ordering CostsAccording to Kakuru,(2000) ordering costs include administrative

costs in preparing dispatch orders, communication with suppliers

and placing order into ware-houses. They are costs incurred right

from the time the orders of inventory are placed to when the

order is actually received and placed in the business premises.

Normally ordering costs per order decrease the bigger the size of

the order due to Economies of Scale.

According to Pandey, (1995) says that clerical and staff costs

however do not vary in proportion to the number of orders placed

and one view is that so long as they are committed costs, they

need not to be reckoned in computing ordering costs.

Alternatively, it may be argued that as the number of orders

increase, the clerical and staff costs tend to increase. It is

more appropriate to include clerical and staff costs on a prorate

basis.

This can be presented graphically as below;

Figure 6 Ordering Costs

Costs 6

NAKAKONGE MASTULA 10/U/139930/PLD/PD 45

4

2

Ordering costs

0 2 4

6 Quantity

Source: Pandey, (1995).

It is shown above that as the order size increases, ordering

costs reduce.

2.2.3 Carrying CostsThese are expenses incurred to keep the inventories in business

from the time of receipt to the time they enter the production

and marketing function. Examples may include storage charges and

opportunity of funds tied up in inventories. These costs normally

increase as more inventories are maintained (Baily Peter and

Jessop David et al, 2003).

Figure 7 Carrying Costs

CC

6

Costs

4

NAKAKONGE MASTULA 10/U/139930/PLD/PD 46

2

0 2 4 6

Quantity

CC: Carrying Costs

It can be shown that as the quantity ordered for increases,

carrying costs will also increase.

Table 4: Showing carrying and ordering Costs

Ordering Costs Carrying Costs

Acquisitioning

Order placing

Transportation

Receiving, inspection and

storage

Clerical and staff

Ware housing

Handling

Clerical and staff

Insurance

Deterioration and

obsolescence

Source: primary data, Baily Peter and Jessop David et al. (2003).

2.2.4 Stock-out CostsThese involve costs of running out of inventory and are comprised

of loss of production output, costs of idle time and fixed over

heads spent over a reduced output, costs of action taken to deal

with the stock out for instance buying from a stockiest at an

increased price and loss of customer good will. These costs are

difficult to estimate or incorporate into inventory models

(Lysons and Gillingham, 2003).NAKAKONGE MASTULA 10/U/139930/PLD/PD 47

According to Drury, (2000) defined stock outs as the opportunity

costs of running out stock. In the case of finished goods, the

opportunity cost will consist of loss of contribution if

customers take their business elsewhere because of failure to

meet delivery. This will be discounted value of the lost

contribution of future sales.

2.2.5 Shortage CostsThis occurs when an item is needed but cannot be supplied from

stock. This will end up in lost goods will, lost reputation, loss

of potential future sales. Shortage costs may also include

payment for positive action to remedy the shortage, expending

orders, sending out emergence orders, paying for special

deliveries, storing partly finished goods or using alternative or

more expensive suppliers (Doblar Donald.W and Brut David.N,

2003).

2.2.6 Holding CostsThis is the cost of holding one unit of an item of stock for a

given period of time. It includes cost of tied up money either

interest on debt or opportunity cost on cash storage space with

supplying ware house rent rate heat and light; loss due to

damage, deterioration, obsolescence and pilferage, handling

including special packaging, refrigeration, putting on pallets.

Administration costs include stock checks and computer updates,

Insurances and taxes on machinery and equipment (Pandey, 1998).

NAKAKONGE MASTULA 10/U/139930/PLD/PD 48

2.2.7 Opportunity Cost of Capital Tied up in InventoryAccording to Kenneth Lysons, (2003) Opportunity cost is the cost

incurred when an alternative is made and the other is fore gone.

This cost category is also a noncash charge to the business but

with an understanding on capital. Budgeting is easy to understand

that capital is scarce and must be allocated to its most

efficient use where it will achieve the best expected returns and

add a value to the business. So the capital tied up in inventory

could be invested elsewhere in the business and generate an equal

or better returns. This gives management a decision to make

forego and incurs cost of holding stock or transfer stock to

investment capital.

2.2.8 Management and administrative costsAccording Kenneth lysons and Brian Famington, (2006) Management

costs involve getting things done through other people,

leadership at its best. This means inspiring staff to achieve

demanding goals. As to this it’s a substantial cost of doing

business, and may vary from 10%-40% of the value of inventory. It

is therefore important to understand and have the ability to

manage these different inventory cash when making production or

inventory holding size decision including determining safety

stock levels. However, to make management work easier inventory

software package that allow tracking of inventory costs have been

invented and may be useful to management and administrative.

NAKAKONGE MASTULA 10/U/139930/PLD/PD 49

2.2.9 Obsolete Inventory, (Write Off Cost).According to Lucey, T. (2003), Obsolete inventory costs are

common in technology based products and computer clip businesses

build to stock inventory systems, and single orders inventory

models. This is due to the industry moving very quickly in terms

of product development and product lines could be out of date in

12 months or less and are forced to be sold at a discount

resulting in a loss. Obsolescence is also commonly encountered in

piece parts, bought out parts, tools, gauges and fittings when

there is permanent change in the production programme involving

discontinuing the product for which this item is held. This calls

for maximum care and attention by management so as to reduce this

cost.

2.2.10 Depreciation costsThese are not cash cost for the business but never the less

should be taken in to account as it will most likely be realized

when the inventory is sold. Depreciation is a measure of the

wearing out, consumption or other reduction in the useful

economic use of fixed asset whether arising from use or efflux

ion of time. When a business buys a fixed asset or inventory it

will intend to keep it and use it for period of years. It is

extremely unlikely that these stock or assets will retain their

original value throughout their lives, because of reasons such

as, wear and tear, repairs by non experts leading to further

damage, technology or power silent damages hence a need for the

NAKAKONGE MASTULA 10/U/139930/PLD/PD 50

organization to minimize of cost for example by hiring and

writing off value of the item. (Drury, 2000).

2.3 The impact of Inventory Management on Cost Control,Inventory management should be to ensure that inventories needed

to sustain operations are available at all times but to hold

costs of ordering and carrying the inventories to the lowest

possible levels.

There should be a systematic control and regulation of purchase,

storage and usage of material in such a way so as to maintain an

even flow of production and excessive investment in inventory.

The Economic Order Quantity can be found by applying a formula

that incorporates the basic relationship between holding and

ordering costs. The relationship can be stated as follows; the

number of orders for the period is total demand for the item of

stock for a period (D) divided by the quantity obtained in Units

(Q). Total ordering costs are obtained by multiplying these

numbers of orders by the order costs per order (Drury, 2000).

According to Brigham and Gapenski, (2002) using inventory

planning and control techniques, a firm can reduce its levels of

inventory without adverse effects on organizational costs which

has a favorable impact on its operations. Therefore, over

investment in inventory should be avoided because funds are tied

up leading to loss of returns and increase costs.

NAKAKONGE MASTULA 10/U/139930/PLD/PD 51

In addition, Arora, (1998) explains that proper inventory

management leads to reduction of capital that can be tied up in

inventories. Most organizations try to maintain minimum stock

levels in order to avoid holding capital in stock. However, this

also involves its own costs.

The above discussion explains that there is a strong impact

inventory management on cost control specifically acquisition and

maintenance costs of inventory.

2.3.1 Approaches to Cost Control in Inventory ManagementWater, (2002) argues that one of the most important points to

note about inventory management and cost control is that some

costs rise with the amount of stock held and others fall. The

holding costs will be higher when there is more stock but the

shortage cost will be lower.

Therefore inventory management must balance these competing costs

and suggest policies that give the lower overall inventory costs.

He still argues that to balance these competing costs, it must

answer the three basic questions.

What should be stocked?

No items should be stocked however cheap without considering the

costs and benefits. This means that affirm to control costs

associated with inventory management should stop unnecessary new

items being added in stock and it should make regular researche

NAKAKONGE MASTULA 10/U/139930/PLD/PD 52

to move obsolete or dead stock which could rise costs in turn

(Waters, 2002).

When should an order be placed?

This depends on the inventory technique or management system

used, type of demand, whether high or low, steady or erratic,

known exactly or estimated in order not to over stock or under

stock because the two situations result into increased costs. So

to minimize on costs associated with inventory management, all

that should be properly handled (Waters, 2002).

How much should be ordered?

If large frequency orders are placed the average stock level is

high but the costs of placing and administering orders are low.

If small frequency orders are placed, the average stock levels

are low, but the costs of placing and administering orders are

much higher so to control costs associated with inventory

management, this has to be catered for. (Waters, 2002).

CHAPTER THREE

METHODOLOGY

3.0 Introduction

This chapter comprises of how the study was conducted, the

samples, particulars and sample size. It clearly indicates the

instruments used how data was collected and analyzed. It also

explored the type of data to be collected, sources of data, and

how data was processed and presented ensuring quality.

NAKAKONGE MASTULA 10/U/139930/PLD/PD 53

3.1 Research DesignThe study used non experimental research design which includes

both the quantitative and qualitative methods of data collection.

Both primary and secondary data was collected. A case study

design was adopted because of its ability to generate information

through in-depth study of the case under investigation.

Qualitative and quantitative design especially the descriptive

research design was used based on questionnaires and observation.

The researcher used the above methods because of many aspects

which were covered by the study of inventory management and cost

control.

3.2 Study populationThe researcher used both Male and female respondents from various

departments of Crown Beverages limited. Management and staff were

targeted. However, only 30 respondents available by the time of

the study were considered. This population was chosen because it

covered all individuals who are directly and indirectly involved

in inventory management.

3.3 Sampling designThis study used random sampling technique where by purposive

sampling was employed. Through random sampling, the researcher

obtained list of managers and employees who were latter given

questionnaires to fill.

3.4 Sampling size and compositionDue to the large population of employees in Crown Beverages

Limited, the researcher took a representative sample of 30

NAKAKONGE MASTULA 10/U/139930/PLD/PD 54

respondents that were picked from different departments that is

stores, finance, procurement, marketing among others.

Table 5: Showing the distribution of Sample size

Departments Number of Respondents

Procurement Department 04

Production Department 07

finance Department 05

Stores Department 06

Administration Department 04

Marketing and sales

Department

04

Total 30

Source: Primary Data

3.5 Sampling area

The study was carried out at Crown Beverages Ltd located in

Nakawa Industrial Area along Kampala –Jinja road, Kampala

district

3.6 Data Collection Instruments

3.6.1 QuestionnaireThis was one of the data collecting instruments that the

researcher will use to obtain data from different people.NAKAKONGE MASTULA 10/U/139930/PLD/PD 55

Questionnaires will be designed and distributed to the

respondents. They were used because they are simple and quick to

answer. Responses will be easy to compare and present and also

they maintain high levels of confidence.

3.6.2 Observation

The researcher made some personal observation which helped him or

her to get data from the existing literature. This enabled him or

her to obtain first hand information.

3.7 Reliability and validity of data

For reliability of the data, the researcher ensured that data is

only collected from the concerned and knowledgeable respondents

in the field of study. In this case, respondents that gave

reliable information included employees of the organization, and

other relevant authorities of the organization.

In order to ensure validity the questionnaire was made clear and

understandable, the questionnaire was first discussed by the

researcher with the supervisor; this included careful choice of

words, order and structure of questions plus pre-testing was done

amongst selected categories of respondents.

After receiving the questionnaires, manual editing was done,

followed by coding. Frequency count of different provisions was

done and this gave the number of occurrences and percentages out

NAKAKONGE MASTULA 10/U/139930/PLD/PD 56

of total occurrences for different responses. And lastly simple

conclusions were drawn from the given percentages and numbers.

3.8 Data Sources

The researcher used both primary and secondary data sources.

3.8.1 Primary data

The primary data source involved research aimed at collecting

data, directed towards the research objectives. In case of

questionnaire administration, respondents were selected using

simple random sampling techniques. First hand data was from

explanations, conclusions and recommendations of the study.

3.8.2 Secondary data

Secondary data was obtained from literature review,

questionnaires, news-papers (new vision and monitor), documentary

materials, magazines, encyclopedic which helped the researcher to

get the required data and the research was dominated by both data

from the primary sources and secondary sources.

3.9 Study variables

The study had two variables that is to say inventory management

as the independent variable and cost control as the dependent

variable.

NAKAKONGE MASTULA 10/U/139930/PLD/PD 57

3.10 Data collection procedure

The researcher first got a recommendation letter from Kyambogo

University Administration and then issued it to the organization

of the study on the first visit.

On the second visit, the researcher distributed the

questionnaires to the respondents in various departments that

were willing to give the required data. After some time, the

researcher went back to pick the questionnaires that been

answered by then.

On the occasional visits to the organization the researcher tried

to make some observation which availed him or her with more

information.

3.11 Data Processing and PresentationAfter the data was collected, it was processed to manageable

proportions for better presentation and analysis. This involved

editing, coding and presentation of quantitative and qualitative

data.

Editing; this was concerned with detecting and correcting errors

and ensuring completion of question answering. Field editing were

employed to ensure that questionnaires are fully answered in

respect to all relevant questions to the respondents. The filled

in questionnaires were then checked for uniformity and error

detection for the omitted questions. This kept errors at minimum.

NAKAKONGE MASTULA 10/U/139930/PLD/PD 58

Coding; this involved processing of classified answers to

questions into meaningful categories to develop their essential

pattern. It helped the researcher to summarize the data and get

frequency patterns which facilitated the tabulation of the data.

Quantitative data was analyzed using dummy table and qualitative

data was analyzed using a simple descriptive analysis. This

involved two stages that include; quick impressionistic summary

and secondary analysis. The researcher ensured that in the field,

informers comment on all topics in the relevant group interview.

3.12 Anticipated Problems of the Studyi. There were a lot of costs incurred during the research

process and such costs included transportation costs,

feeding costs, accommodation costs and stationery costs.

ii. The researcher spent a lot of time during the course of the

research by obtaining data, analyzing data, typing, editing,

printing and binding data obtained.

iii. The researcher was not able to collect all the data needed

because of some problems like changes in weather,

geographical location and much more others.

iv. Another problem was that the information needed would not

easily be obtained because the respondents were sometimes

not willing to share information because they expected

something in return like a reward or payment for work done

to assist.

NAKAKONGE MASTULA 10/U/139930/PLD/PD 59

v. The research also consumed a lot of the researcher’s time

since many managers and employees were consulted in the

process of obtaining information or data.

vi. The research project also required a lot of funds in terms

of finance to facilitate the whole process of research which

was limited like when buying stationery materials such as

books, pencils and others like transportation, typing,

printing, binding and data processing.

vii. Since research was a process of obtaining information about

something, some organizations were less willing to provide

their confidential information and this was yet another

limitation the researcher faced while conducting the

research as inaccessibility of required data.

viii. In the process of reviewing to the literature in chapter

two, the researcher also to some extent faced the problem of

limited literature review hence a major limitation and the

inaccessibility of the internet plus the website.

3.13 Solutions to the Anticipated Problemsi. First the University Council for Research Committee should

consider investing in research such that students do not

have to use a lot of their monies doing research thus

reducing on costs.

ii. There is need to create more time for research since it is

taken as a course unit that must be passed to obtain an

Award of either a Diploma, Degree or Masters.

NAKAKONGE MASTULA 10/U/139930/PLD/PD 60

CHAPTER FOUR:

DATA PRESENTATION, INTERPRETATION AND ANALYSIS OF THE FINDINGS

4.0 IntroductionThis chapter deals with the presentation, interpretation and

analysis of the major findings of the study using figures, tables

and graphs followed by their detailed analysis. These findings

and discussions are represented according to the research

objectives of the study as shown below.

i. What are the various inventory management techniques or

methods used by most organizations?

ii. What are the various costs incurred while acquiring and

maintaining inventory in an organization?

iii. How does inventory management impact on cost control in an

organization and what approaches can be used to control

inventory costs

4.1 Presentation of FindingsThe research sample comprised of thirty respondents from the

various departments of crown beverages limited.

Table 6 Sex distribution of the respondents

SEX FREQUENCY PERCENTAGE

MALE 16 53.3

FEMALE 14 46.6

TOTAL 30 100%

Source: Primary Data

NAKAKONGE MASTULA 10/U/139930/PLD/PD 61

From the table, majority of the respondents of the organization

were male represented by 53.3%, as compared to the female

respondents, represented by 46.6%.This implies that the male

dominated most of the positions held in the organization.

Table 7 Showing age distribution of respondents

Age Bracket

(Ages)

Frequency Percentage (%)

Below 25

25 – 30

30 – 35

35 – 40 and

above

04

19

06

1

13.3

63.3

20

3.3

Totals 30 100

Source: primary data

From the table I above, the majority of the respondents which

were 63.3 were within the age bracket of 25-30.This was followed

by those under the age bracket of 36 and above, they were

represented by 37% finally those under the age bracket of 18-35

were represented by 23%. This implies that the study involved

different respondents with varying ages which provided the

NAKAKONGE MASTULA 10/U/139930/PLD/PD 62

researcher with the current and longtime information about impact

of inventory control on operational efficiency of an

organization.

Pie Chart 1: Representing the sex composition of the respondents

216

144

A PIE CHARTMale Female

Source: Primary Data

From the above Pie-chart, it is evident that majority of the

respondents were male with 53.3% (216°) and female covered about

46.7% (153°). This was simply because majority of the male were

in the Production, Stores, Administration departments and this

implies that the company employed more males than females since

it deals more in production matters and they are more

knowledgeable in matters relating to production.

4.1.1 Findings on the Age Group of the RespondentsTable 8: Age bracket of the Respondents

NAKAKONGE MASTULA 10/U/139930/PLD/PD 63

Age Bracket

(Ages)

Frequency Percentage (%)

Below 25

25 – 30

30 – 35

35 – 40 and

above

04

19

06

1

13.3

63.3

20

3.3

Totals 30 100

Graph 1: A bar graph showing the age bracket of respondents

below 25 25-30 30-35 35-40 and above

0

10

20

30

40

50

60

70

frequencypercentageColumn1

Source Primary Data

From the table and graph above, four(4)were below the age of

twenty five years and this represented 13.3%thus implies that

NAKAKONGE MASTULA 10/U/139930/PLD/PD 64

these are fresh graduates and have less experience, nineteen

(19)were between the age of twenty five (25) years and thirty

(30)years, this represented 63.3% and this is because at this

age, people have acquired experience, six (6) for those in the

age bracket of thirty (30) to thirty five (35), this represented

20% and these are relatively high since they have acquired

skills, experience and have decided to be loyal to the company.

Ten (10) were between the age of thirty five (35)and forty (40)

above which represented 10%. This implies that people with skills

and wider experience tend to look for further opportunities which

are better and none was above sixty years which is 0% implying