PPT Presentation - Cooperative.com

36

Topic 842- Leases This Time We Are Serious (and you should be too) Jeff Dieleman, CPA Partner, Moss Adams LLP

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of PPT Presentation - Cooperative.com

Topic 842- LeasesThis Time We Are Serious (and you should be too)

Jeff Dieleman, CPA

Partner, Moss Adams LLP

The material appearing in this presentation is for informational purposes only and should not be construed as advice of any kind, including, without limitation,

legal, accounting, or investment advice. This information is not intended to create, and receipt does not constitute, a legal relationship, including, but not

limited to, an accountant-client relationship. Although this information may have been prepared by professionals, it should not be used as a substitute for

professional services. If legal, accounting, investment, or other professional advice is required, the services of a professional should be sought.

Assurance, tax, and consulting offered through Moss Adams LLP. Wealth management offered through Moss Adams Wealth Advisors LLC. Investment

banking offered through Moss Adams Capital LLC.

The information in this presentation is limited to an overview of the topics being presented. Due to the limited time we have together and the complexity of

specific facts and circumstances present in actual transactions and their related effects on the proper accounting treatment, the material and opinions

expressed today should not be used without full consideration of all relevant authoritative accounting guidance and full analysis of the specific facts and

circumstances present in an actual transaction.

ASC 842 Topics For Today . . .

Scope and Accounting Model

Key Terms

Measurement and Presentation

Effective Date and Transition

Other Considerations

Not Covering Today . . .

• Footnote disclosures• Sale-leaseback transactions• Accounting by lessors• Build-to-suit arrangements• Various other matters

Why Change?

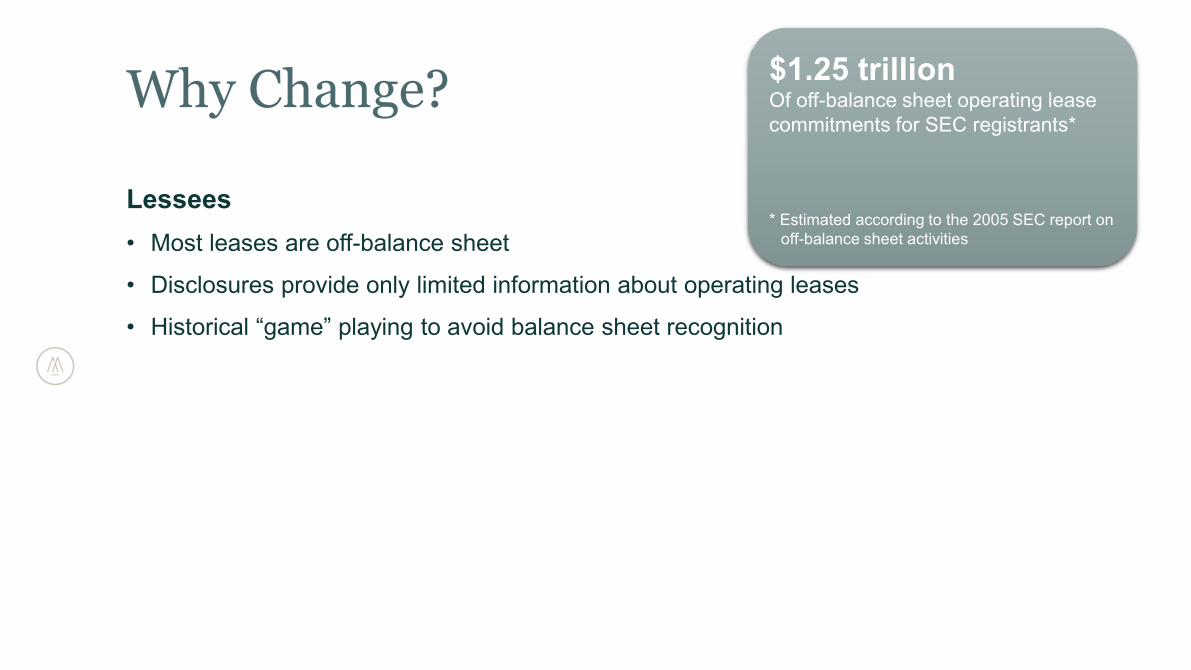

Lessees • Most leases are off-balance sheet

• Disclosures provide only limited information about operating leases

• Historical “game” playing to avoid balance sheet recognition

* Estimate according to the 2005 SEC report on off-balance sheet activities

$1.25 trillionOf off-balance sheet operating lease commitments for SEC registrants*

* Estimated according to the 2005 SEC report on off-balance sheet activities

Quick Recap of Topic 842

Applies to all leases and subleases except:

• Leases of intangible assets

• Leases for exploration of certain natural resources (minerals, oil, natural gas etc…)

• Leases of biological assets

• Leases of inventory

• Leases of assets under construction

ExceptionsLessees will be permitted to make an accounting policy election to not recognize lease assets and liabilities for short-term leases

(that is, lease terms that are 12 months or less, subject to certain conditions contained in the definitions of “short termlease” and “lease term”).

Leases with a lease term of 12 months or less will not require capitalization on the balance sheet, and lease payments will be expensed on a straight-line basis over the lease term, which is similar to current rules for an operating lease.

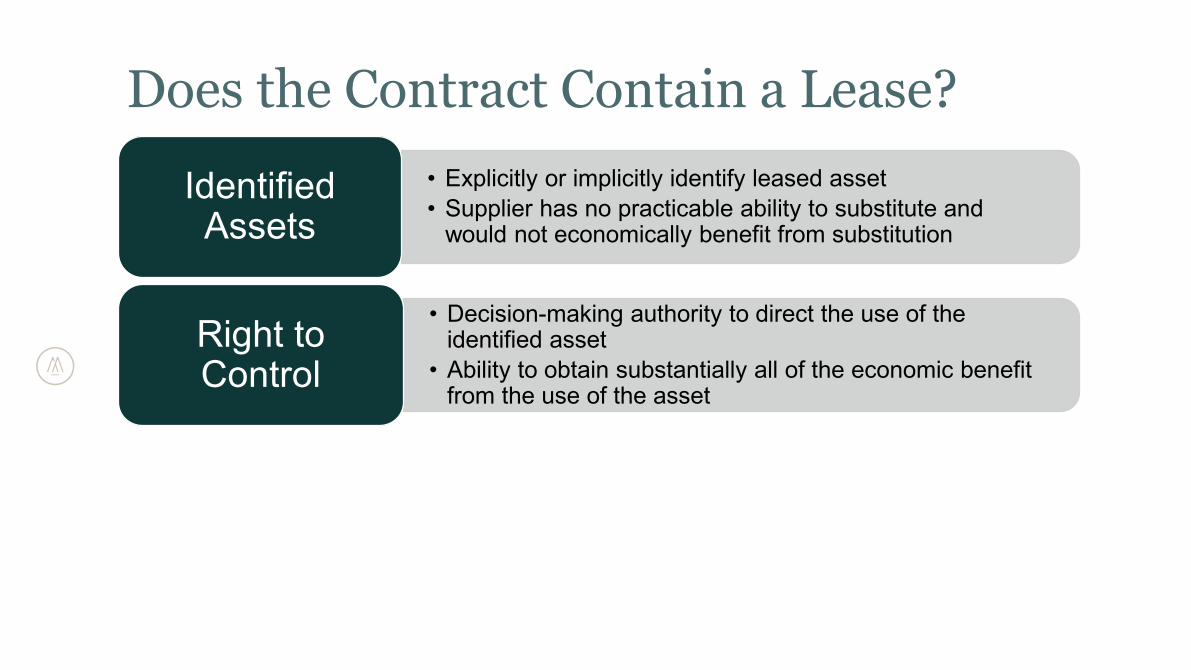

Does the Contract Contain a Lease?• Explicitly or implicitly identify leased asset• Supplier has no practicable ability to substitute and

would not economically benefit from substitution

Identified Assets

• Decision-making authority to direct the use of the identified asset

• Ability to obtain substantially all of the economic benefit from the use of the asset

Right to Control

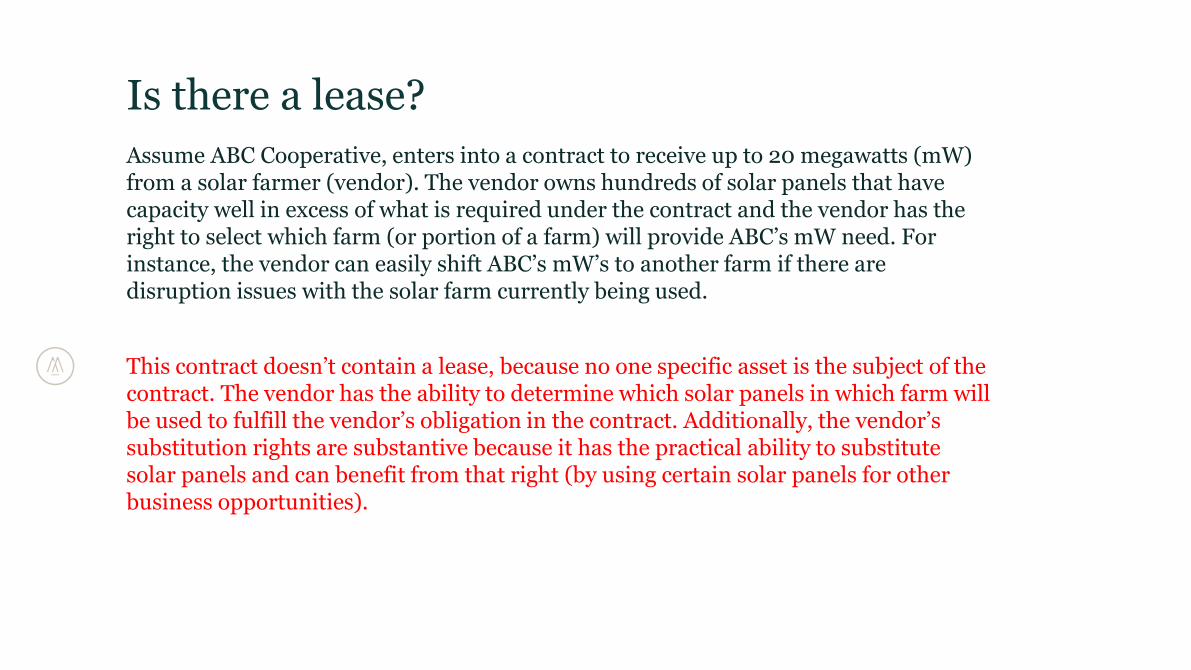

Is there a lease?Assume ABC Cooperative, enters into a contract to receive up to 20 megawatts (mW) from a solar farmer (vendor). The vendor owns hundreds of solar panels that have capacity well in excess of what is required under the contract and the vendor has the right to select which farm (or portion of a farm) will provide ABC’s mW need. For instance, the vendor can easily shift ABC’s mW’s to another farm if there are disruption issues with the solar farm currently being used.

This contract doesn’t contain a lease, because no one specific asset is the subject of the contract. The vendor has the ability to determine which solar panels in which farm will be used to fulfill the vendor’s obligation in the contract. Additionally, the vendor’s substitution rights are substantive because it has the practical ability to substitute solar panels and can benefit from that right (by using certain solar panels for other business opportunities).

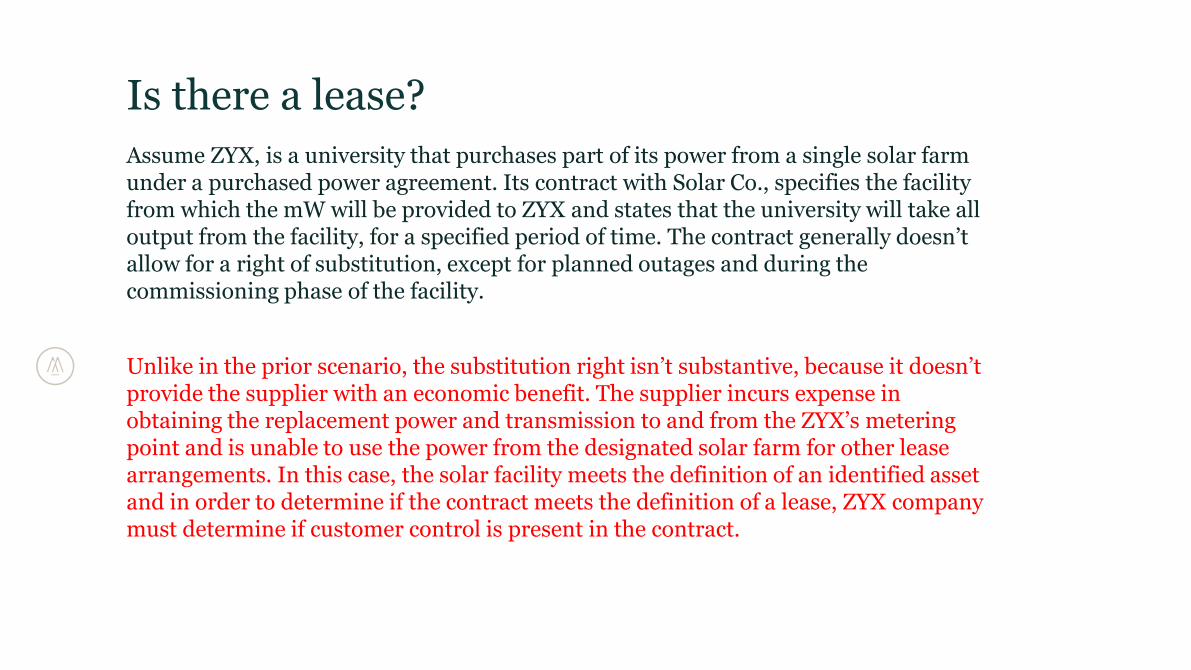

Is there a lease?Assume ZYX, is a university that purchases part of its power from a single solar farm under a purchased power agreement. Its contract with Solar Co., specifies the facility from which the mW will be provided to ZYX and states that the university will take all output from the facility, for a specified period of time. The contract generally doesn’t allow for a right of substitution, except for planned outages and during the commissioning phase of the facility.

Unlike in the prior scenario, the substitution right isn’t substantive, because it doesn’t provide the supplier with an economic benefit. The supplier incurs expense in obtaining the replacement power and transmission to and from the ZYX’s metering point and is unable to use the power from the designated solar farm for other lease arrangements. In this case, the solar facility meets the definition of an identified asset and in order to determine if the contract meets the definition of a lease, ZYX company must determine if customer control is present in the contract.

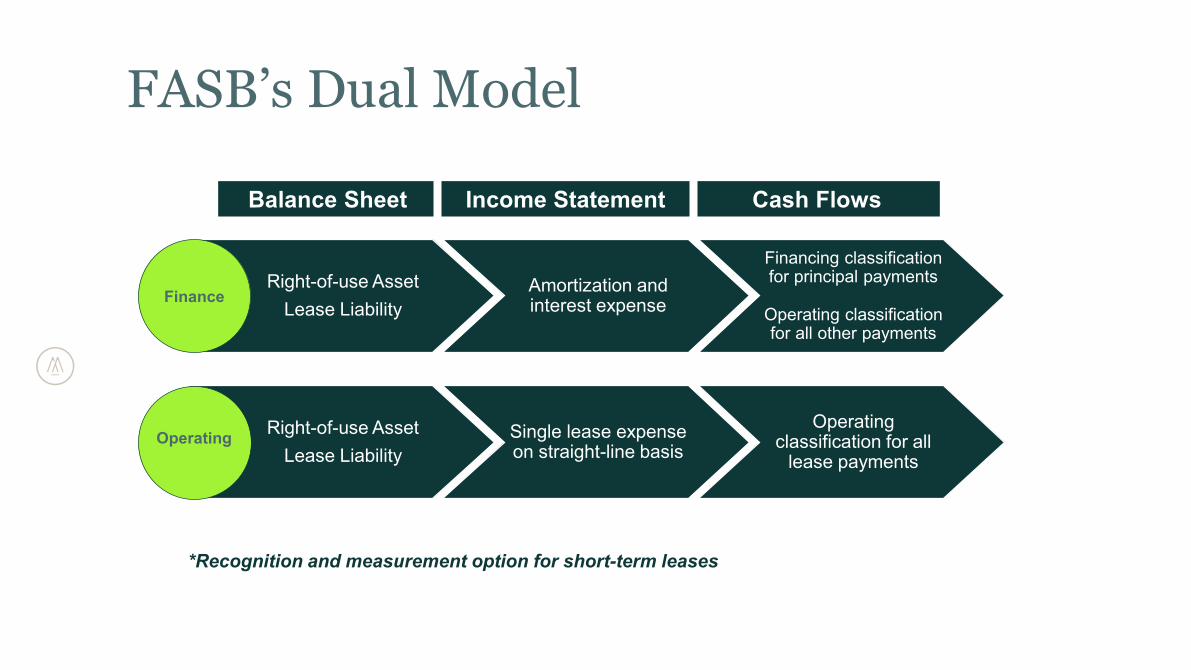

FASB’s Dual Model

Right-of-use AssetLease Liability

Single lease expense on straight-line basis

Operating classification for all

lease payments

Balance Sheet Income Statement Cash Flows

Right-of-use AssetLease Liability

Amortization and interest expense

Financing classification for principal payments

Operating classification for all other payments

Finance

*Recognition and measurement option for short-term leases

Operating

Lessee – Finance Lease Criteria

Transfer of ownership by end of lease term

• Assess at lease commencement not lease inception

• Reasonably certain is a high threshold -Consider contract, asset, market, and entity based criteria

• Lease term – consider all options reasonably certain to be exercised

• 3rd criteria not applicable when lease entered into near end of assets economic life

• 5th criteria is new and highlights when no alternative use for the leased asset

If lease doesn’t meet these criteria, then it’s an operating lease

Purchase option that is “reasonably certain”to be exercised

Lease term is for “major part” of remaining economic life

PV of lease payments plus any RVG equals or exceeds “substantially all” of the asset’s fair

value

Asset is of such specialized nature that only lessee can use it without major modifications

Key Terms

Focus on Key Terms

Nonlease components

Lease term

Lease payments

Discount rate

Under ASC 840, classification was one of the more important aspects of lease accounting since the results impacted whether a lease was on-balance sheet.

Since most leases are now on balance sheet, lease classification could become less of a factor making these key terms more relevant going forward when reporting leasing activities as they impact the amounts reported.

Lease incentives & modifications

Nonlease Components

Observable stand-alone prices

Estimate if not readily available

Accounting policy election to treat as single component

Nonlease components include goods and services provided to the lessee separate from the right to use the leased asset.

Examples include:- Common area maintenance (CAM)- Janitorial- Service and support- Supplies, consumables and disposables- Equipment operators

Allocate Consideration

Lease TermLessee’s options to purchase, extend, or terminate the lease

when reasonably certain

Lessor’s options to extend (or not terminate the lease)

Assessment of reasonably certainto consider all factors

• Assess at lease commencement and reassess only upon changes that are in lessee’s control

• Factors to consider:- Contract has penalty for failure to renew

- Asset is critical to operations

- Entity performed significant integration

- Below market option

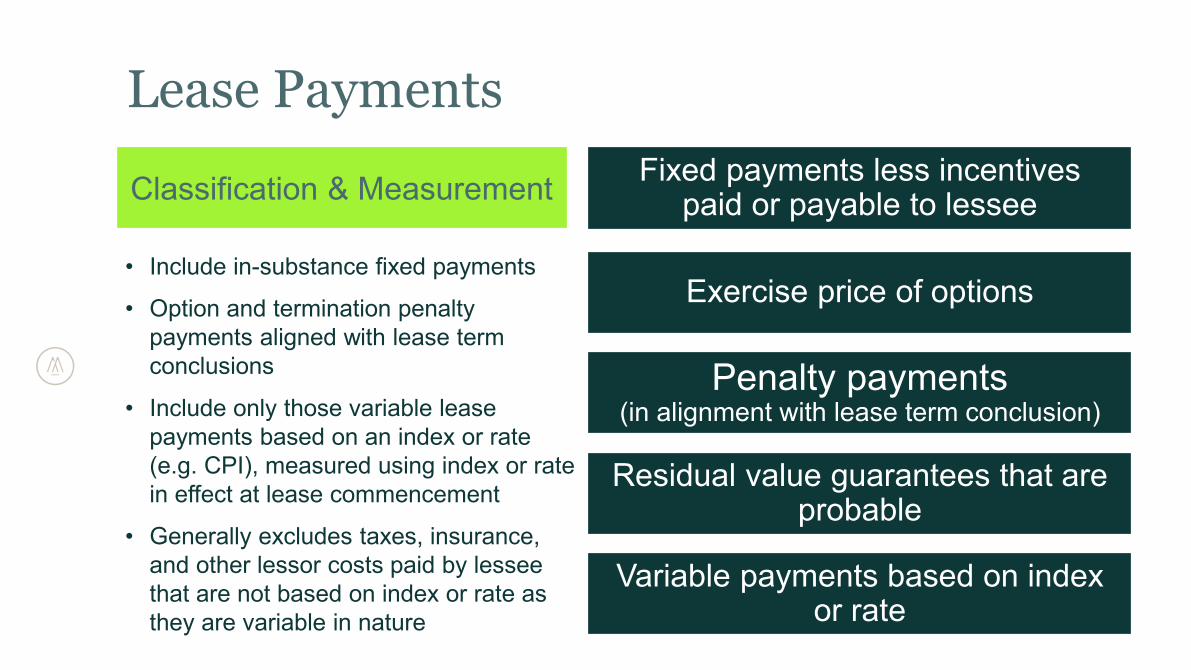

Classification & Measurement

Lease PaymentsFixed payments less incentives

paid or payable to lessee

Exercise price of options

Penalty payments(in alignment with lease term conclusion)

Residual value guarantees that are probable

• Include in-substance fixed payments

• Option and termination penalty payments aligned with lease term conclusions

• Include only those variable lease payments based on an index or rate (e.g. CPI), measured using index or rate in effect at lease commencement

• Generally excludes taxes, insurance, and other lessor costs paid by lessee that are not based on index or rate as they are variable in nature

Classification & Measurement

Variable payments based on index or rate

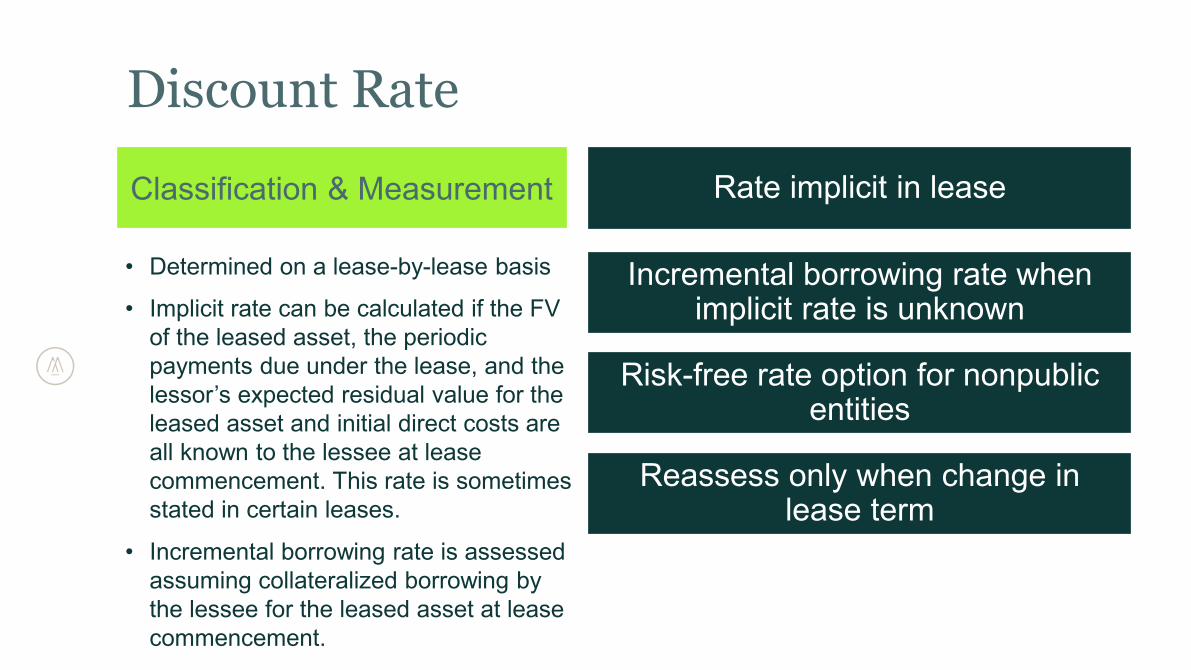

Discount Rate

Rate implicit in lease

Incremental borrowing rate when implicit rate is unknown

Risk-free rate option for nonpublic entities

Reassess only when change in lease term

• Determined on a lease-by-lease basis

• Implicit rate can be calculated if the FV of the leased asset, the periodic payments due under the lease, and the lessor’s expected residual value for the leased asset and initial direct costs are all known to the lessee at lease commencement. This rate is sometimes stated in certain leases.

• Incremental borrowing rate is assessed assuming collateralized borrowing by the lessee for the leased asset at lease commencement.

Classification & Measurement

Lease Incentives

Rent holidays

Payments to, or on behalf of, lessee

Factored into measurement of ROU asset and lease liability

• Rent holidays:- Reduce lessee ROU asset and lease liability

• Lease incentives are reflected as a reduction of the ROU asset upon receipt

Classification & Measurement

Modifications should be accounted for as a new, separate contract when both of the following criteria are met:• Lessee obtains additional right of use not included in the original lease; and

• Lease payments increase commensurate with stand-alone price for the additional ROU

Lease Modifications

If the modification does not meet both criteria to be classified as a new contract:• Reassess the classification of the lease

• Remeasure the lease liability using a discount rate determined at the effective date of modification

• Record corresponding adjustment to ROU asset depending on the modification

• For modifications that fully or partially terminate an existing lease, record a gain or loss for difference between reduction in ROU asset and lease liability

Measurement, Presentation & Disclosure

Bringing Leases on Balance Sheet

Commencement date

Right-of-use (ROU) asset

Lease liability

Expense patterns

• Lease liability equals PV of lease payments not yet paid

• ROU asset equals sum of lease liability, prepaid rent, and initial direct costs, less lease incentives received

• Finance leases will result in a front loaded expense vs. straight line for operating leases.

Measurement & Presentation

Financial Statement Presentation

Gross presentation of ROU assets and lease liabilities for operating and finance leases (comingling prohibited)

Operating Lease

Single straight-line lease expense

Operating csh flow classification for all payments

Finance Lease

Front-loaded interest and straight-line amortization expense

Financing and operating cash flow classification

Lease liability is not “debt or debt-like”

ImpactsIncreased liabilities (current and noncurrent)• Operating leases will result in negative impact to working capital and related ratios

(e.g. current ratio)

• Operating lease liabilities are not “debt or debt-like”

Increased assets• Lower return on assets

• Lower equity to total asset ratios

Cash flow / Profitability• Finance lease – larger expenses in earlier years compared to operating leases, but

larger EBITDA add-back

• Operating lease – all flows through cash flows from operations

Disclosures in Footnotes

Periodic lease expense, ROU asset amortization, interest costs

Quantitative

Short-term, variable leases, sublease income, cash and non-cash flows

Weighted average discount rate for both finance & operating

Qualitative

Terms and conditions, purchase options and termination penalties

Accounting policy elections, areas of significant judgment, assumptions

Residual value guarantees

Weighted average remaining lease term for both finance & operating

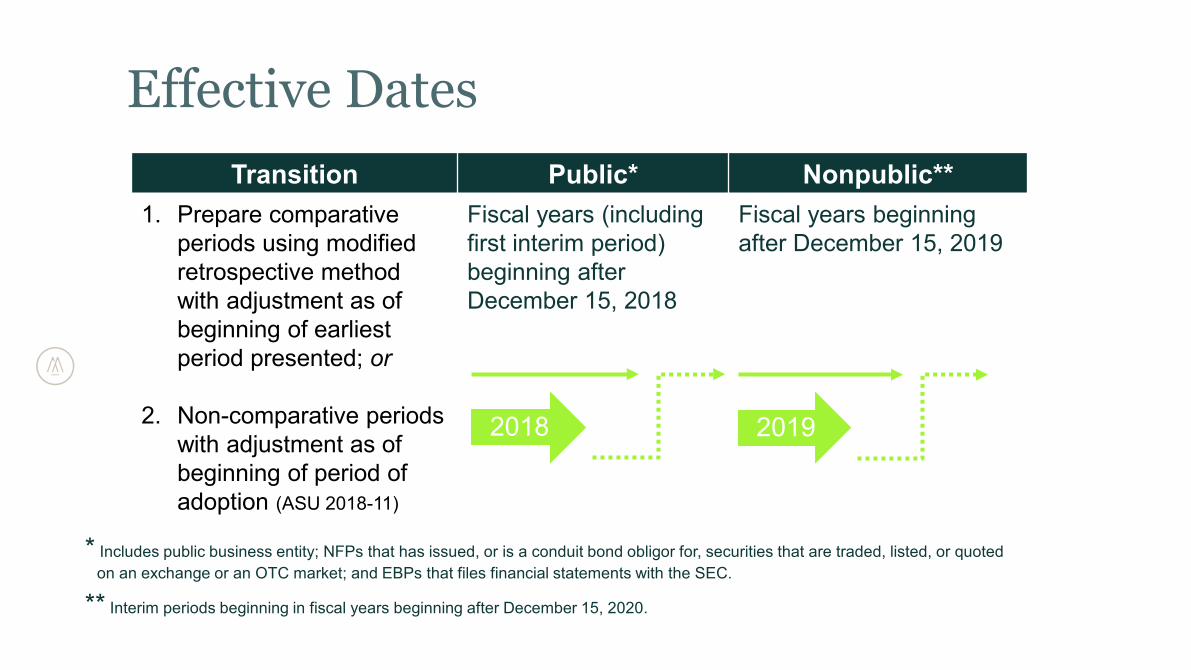

Effective DatesTransition Public* Nonpublic**

1. Prepare comparative periods using modified retrospective method with adjustment as of beginning of earliest period presented; or

2. Non-comparative periods with adjustment as of beginning of period of adoption (ASU 2018-11)

Fiscal years (including first interim period) beginning after December 15, 2018

Fiscal years beginning after December 15, 2019

2018 2019

* Includes public business entity; NFPs that has issued, or is a conduit bond obligor for, securities that are traded, listed, or quoted on an exchange or an OTC market; and EBPs that files financial statements with the SEC.

** Interim periods beginning in fiscal years beginning after December 15, 2020.

Transition ReliefsExisting or expired contracts

contain a lease

Lease classification

Initial direct costs

• These must be adopted as a package and applied to all leases

• Additionally, lessee may elect to use hindsight with respect to evaluating purchase options and lease renewals.

Forgo Assessing

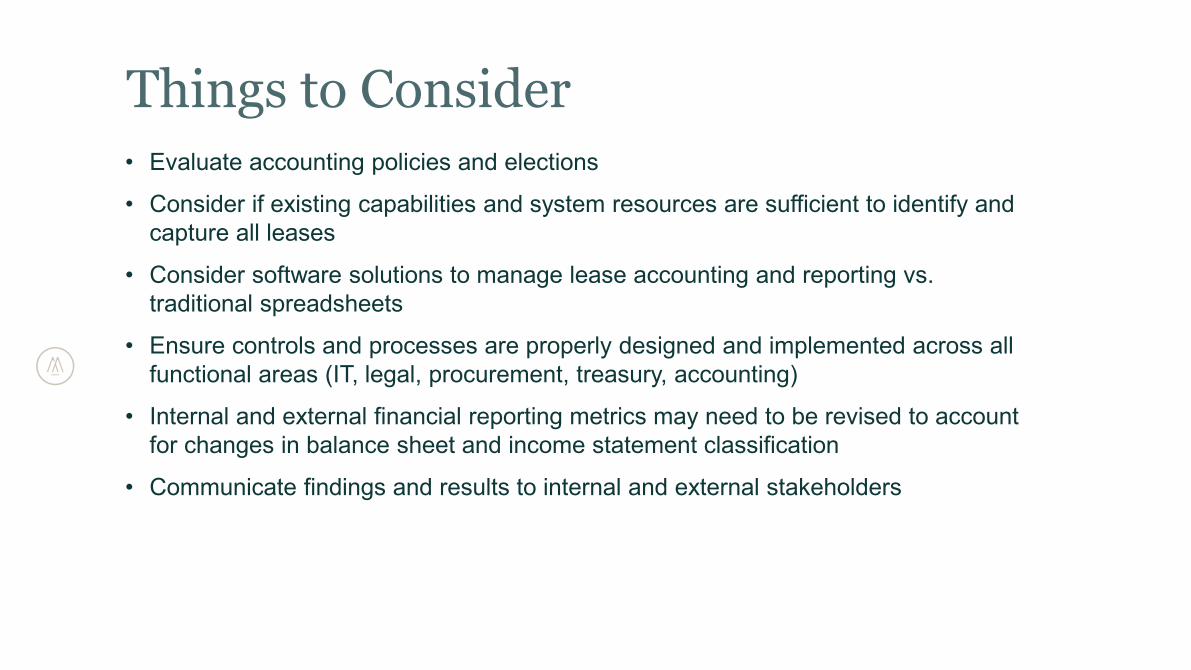

Things to Consider• Evaluate accounting policies and elections

• Consider if existing capabilities and system resources are sufficient to identify and capture all leases

• Consider software solutions to manage lease accounting and reporting vs. traditional spreadsheets

• Ensure controls and processes are properly designed and implemented across all functional areas (IT, legal, procurement, treasury, accounting)

• Internal and external financial reporting metrics may need to be revised to account for changes in balance sheet and income statement classification

• Communicate findings and results to internal and external stakeholders

Lease Examples

See Handouts

Finance Lease-Example 1

• Lease Term – 3 years• Lease Payments in arrears:

• Year 1: $100,000• Year 2: $110,000• Year 3: $125,000

• Discount Rate: 5.51%

Lease Terms

Operating Lease-Example 2• Lease Term – 3 years• Lease Payments in arrears:

• Year 1: $100,000• Year 2: $110,000• Year 3: $125,000

• Discount Rate: 5.51%

Lease Terms

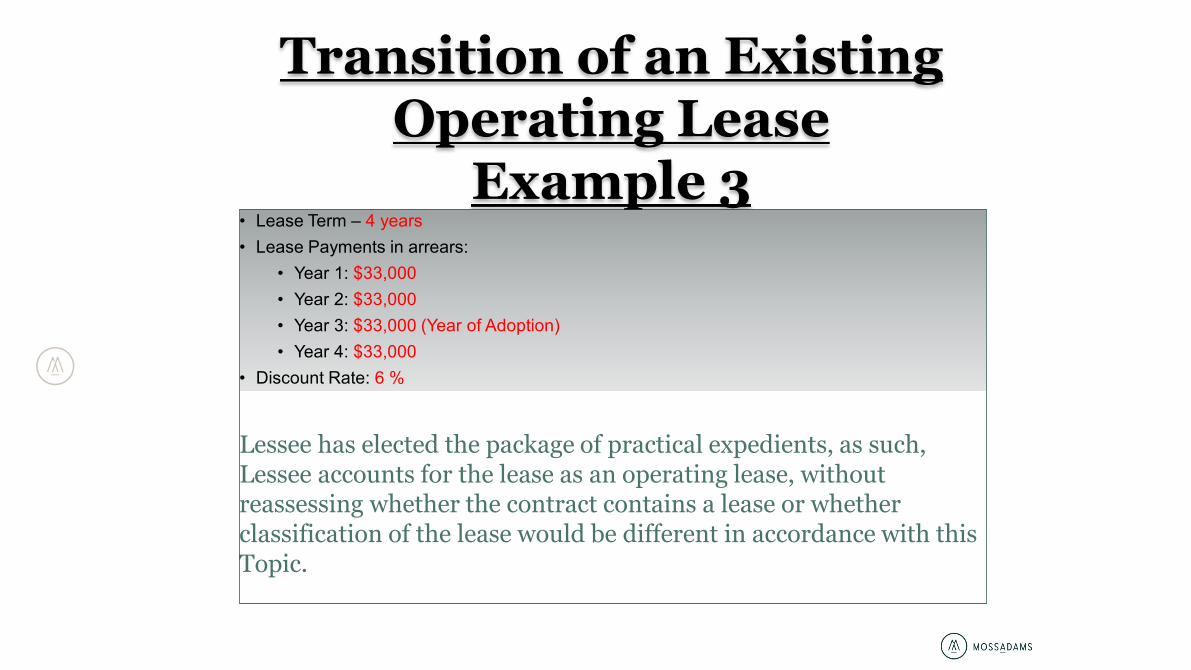

Transition of an Existing Operating Lease

Example 3

Lessee has elected the package of practical expedients, as such, Lessee accounts for the lease as an operating lease, without reassessing whether the contract contains a lease or whether classification of the lease would be different in accordance with this Topic.

• Lease Term – 4 years• Lease Payments in arrears:

• Year 1: $33,000• Year 2: $33,000• Year 3: $33,000 (Year of Adoption)• Year 4: $33,000

• Discount Rate: 6 %

For More InformationFinancial Accounting Standards BoardWWW.FASB.ORG

Moss Adams – Lease GuideHTTPS://MOSSADAMSPRODUCTION.BLOB.CORE.WINDOWS.NET/CMSSTORAGE/MOSSADAMS/MEDIA/DOCUMENTS/SPECI

AL/MOSS-ADAMS_LEASE-ACCOUNTING-GUIDE.PDF

SEARCH “LEASES” ON MOSSADAMS.COM

Q&A