OCT 0 2 2006 - DSpace@MIT

60

Commercialization of Quantum Dot White Light Emitting Diode Technology by Xinyue Zhao B. E., Electrical Engineering (2005) National University of Singapore Submitted to the Department of Materials Science and Engineering in Partial Fulfillment of the Requirements for the Degree of Master of Engineering in Materials Science and Engineering at the Massachusetts Institute of Technology MASSACHUSETTS INSI1TUTE OF TECHNOLOGY September 2006 OCT 02 2006 @2006 Massachusetts Institute of Technology LIBRARIES All rights reserved Signature of Author: Department of Materials Science and Engineering August 8, 2006 Certified by: tugene A/itzg rald Merton C. Flemings-SMA Professor of Materials Science and Engineering Thesis Supervisor ARCHIVN8 Accepted by:: Samuel M. Allen POSCO Professor of Physical Metallurgy Chair, Departmental Committee for Graduate Students ;ý 7

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of OCT 0 2 2006 - DSpace@MIT

Commercialization of Quantum Dot White Light Emitting Diode Technology

by

Xinyue Zhao

B. E., Electrical Engineering (2005)National University of Singapore

Submitted to the Department of Materials Science and Engineeringin Partial Fulfillment of the Requirements for the Degree of

Master of Engineering in Materials Science and Engineering

at the

Massachusetts Institute of Technology MASSACHUSETTS INSI1TUTEOF TECHNOLOGY

September 2006 OCT 0 2 2006

@2006 Massachusetts Institute of Technology LIBRARIESAll rights reserved

Signature of Author:

Department of Materials Science and EngineeringAugust 8, 2006

Certified by:

tugene A/itzg raldMerton C. Flemings-SMA Professor of Materials Science and Engineering

Thesis SupervisorARCHIVN8

Accepted by::

Samuel M. AllenPOSCO Professor of Physical Metallurgy

Chair, Departmental Committee for Graduate Students

;ý 7

Commercialization of Quantum Dot White Light Emitting Diode Technology

by

Xinyue Zhao

Submitted to the Department of Materials Science andEngineering on August 18, 2006 in Partial Fulfillment of the

Requirements for the Degree of Master of Engineering inMaterials Science and Engineering

Abstract

It is well known that the use of high-brightness LEDs for illumination has the potential tosubstitute conventional lighting and revolutionize the lighting industry over the next 10 to20 years. However, successful penetration of this extremely large lighting market wouldrequire vast improvements in power conversion efficiencies, color index, light output perdevice and drastic reduction in cost. Quantum Dot white LED (QD WLED) technologymay be one of the best choices, due to its higher energy efficiency, larger color render inindex, better versatility and more importantly lower cost, compared to conventional blueLED plus YAG: Ce yellow phosphor technology. Due to the fundamental difference ofthe material structure, QD LEDs will win a steady position among existing white LEDpatents and a hybrid fabless plus IP business model has the best position to promote thistechnology to maximize its benefits and potential for the entire LED industry.

Thesis Supervisor: Eugene A. FitzgeraldTitle: Merton C. Flemings-SMA Professor of Materials Science and Engineering

Acknowledgements

I am highly indebted to my thesis advisor, Prof. Eugene A. Fitzgerald from MIT and Prof.Soon Jin Chua from NUS. They are both highly accomplished scientists and their help wasinvaluable for completing this thesis. Prof. Fitzgerald is not only a great researcher but alsoan enthusiastic entrepreneur. From the interactions that I had with him, I graduallyaccumulated knowledge on the process of starting up a new high tech business.

Prof Chua has been my advisor for Undergraduate Research and Opportunity Program, myFinal Year Project and now my M.Eng thesis from NUS side. I have been his student for thepast four years. He has provided me with so much support that I cannot thank him in anyform. I only can work harder to continue his passion for research and Singapore industrydevelopment.

Secondly, I would like to thank Dr. Aaron Danner and Mr. Huang En Li from Avago. Theygave me practical suggestions from an industrial point of view on my thesis topic. I alsowould like to thank Mr. Hsueh-Shih Chen from Industrial Technology Research InstituteTaiwan. He answered my emails and gave me very helpful suggestions on practical issuesabout QD white LED, despite the fact that we hardly know each other.

I would like to thank my parents for all their unflinching support they have given andcontinue to give wherever I am. My father has taught me strict self-discipline and strong willto progress in life. My mother has given me strength and capability to face difficulties. Withall the character they have imbibed in me, I was able to first complete my undergraduatestudy abroad in Singapore, then the SMA courses and now, my master's thesis.

I also want to dedicate my great thanks to my SMA AMM&NS 05/06 classmate RangarajanVijayaraghavan, who has given me so much help for my thesis. He has induced my active andinnovative thinking by giving me his brilliant ideas on both science and business topic. He ismy greatest friend in the past year and I believe he will be continuing to be a great friendthrough out my life.

I want to thank Ms. Jocelyn Sales and Dr. John Desforge from MIT SMA office. They helpedme very much in contacting my advisor from MIT side, which was essential for the smoothprogress of my thesis.

Finally I want to thank my fellow classmates SMA AMM&NS 05/06. Without their companyand encouragement, I would have been subjected to tremendous stress due to the toughcoursework. However, I enjoyed my life and study for the past year because of theirexistence.

I plan to enter the industry as an accomplished engineer having learnt so much from eminentprofessors and in the coming years put to good use the ideas and concepts they have taughtme. Someday I hope to bring about a major contribution to the scientific community thatimproves the common man's everyday life. That will be the day when I would have left alasting impression in the sands of time.

August 9, 2006

Table of content

C hapter 1 Introduction ............................................................................................................... 11.1 Development of LED technology......................................................................... 11.2 Advantages of LED lighting................................................................................... 21.3 Motivation for development of new white LED technology and business .................. 3

Chapter 2 Quantum dot white LED technology ..................................... ... ............. 62.1. LED basic structure and manufacturing methods................................................... 62.2. Conventional m ethods ............................................................................................ 72.3. Quantum Dot white LED ....................................... ................................................... 9

2.3.1. Quantum Dot Physics..................................................................................... 92.3.2. Quantum Dot phosphor.................................................... 102.3.3. Fabrication for quantum dot phosphor................................ ............................ 11

2.4. Advantages and limitations of quantum dot LEDs................................ ........ 122.5. Quantum dot in pnjunction.......................................................................................... 16

2.5.1. Theory of white LEDs with QD in pn junction................... ........ 172.5.2. Fabrication of quantum dot in pn junction.............................. ............ 172.5.3. Advantages and limitations ......................................................................... 18

Chapter 3 White LED market analysis ....................................................... 223.1 HB LED market and growth trend ..................................... ..... ................ 223.2 W hite LED in illum ination ............................................................ .......................... 233.3 White LED as automobile headlamp............................................. 233.4 White LED for medical applications............................................. 253.5 White LED market estimation ........................................................................... 25

Chapter 4 Existing players and intellectual properties ..................................... ...... 274.1 LED production regions ............................................................. ............................. 274.2 M ajor players................................................................................................................. 284.3 Existing white LEDs patents ............................................................................. 294.4. Q uantum dot LED patents ............................................................................................ 314.5 Evident technologies ......................................................................... ...................... 33

Chapter 5 Business M odel ........................................... ...................................................... 355.1. The stage of technology development.......................... ................. 355.2 D ifferential cost m odeling ............................................................ ........................... 375.3. The three basic business models in semiconductor industry................................ 39

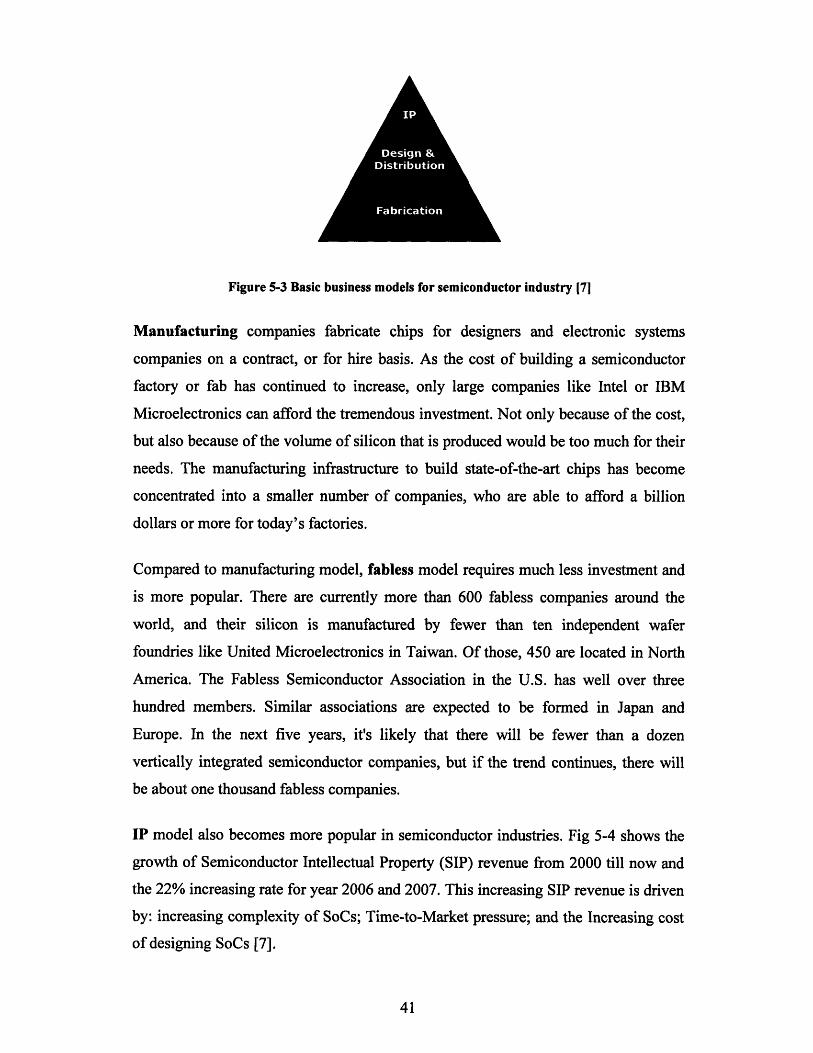

5.3.1. The business structure for semiconductor industry.............................. ........... 395.3.2. The three business models ..................................... ...... .................. 405.3.3. Business model choice: Hybrid packaging design model and IP model ........ 42

5.4 B usiness strategies......................................................................................................... 445.5. Financial m odel .............................................. ........................................................ 47

C hapter 6 C onclusion ....................................................... ................................................. 51Appendix 1: Relevant term inology..................................... ............................................... 52Appendix 2: Comparisons of current LED technology and conventional lighting............... 54

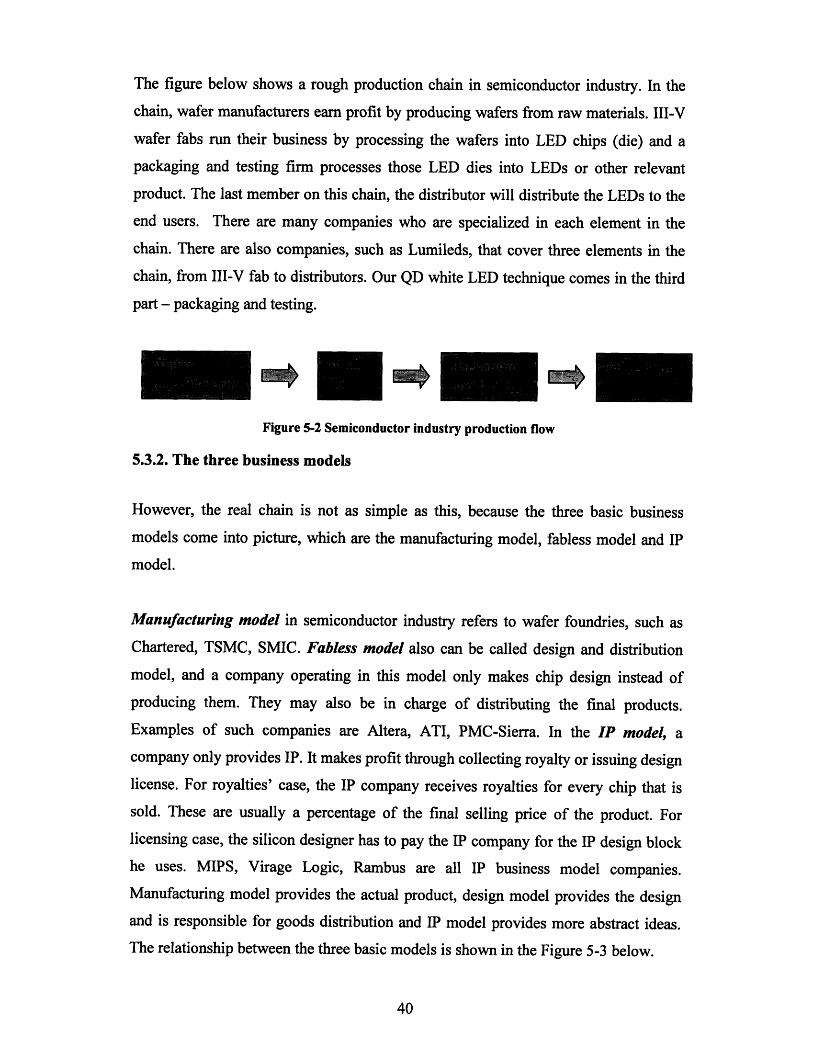

List of figures

Figure 1-1 Trend of increasing light output per package of LEDs and decreasing of cost........ 2Figure 1-2 Energy consumption in US ..................................... ....... ................... 4Figure 2-1 Schematic of the LED and GaN based LED die structure .................................... 6Figure 2-2 General types of White-Light LED Devices .................................................. 7Figure 2-3 Structure of white LED and phosphor conversion ........................................ 8Figure 2-4 Spectrum of white LED ........................................ ........ ................. 9Figure 2-5 Illustration of a buried InAs quantum dot embedded into a GaAs barrier materiall0Figure 2-6 Quantum Dot phosphor with different positions.................. ........ 12Figure 2-7 Performance of the QD white LEDs ................................................................... 12Figure 2-8 Clear differences of the color rendition in the August Renoir painting ................. 14Figure 2-9 Light traveling pass in LED .................................... ........................... 15Figure 2-10 Schematic diagram for pn junction with quantum dot in between................... 17Figure 3-1 The key applications for HB-LEDs............................................ 22Figure 3-2 The light output of an LED Headlamp prototype ....................................... 25Figure 4-1 Deals and disputes in the white LED industry: the key intellectual property

relationships as of September 2005 ................................................................. 31Figure 4-2 Two embodiments of an LED according to the invention .................................. 32Figure 5-1 Technology development and confidence in chosen market ................................. 35Figure 5-2 Semiconductor industry production flow.................................. ............ 40Figure 5-3 Basic business models for semiconductor industry ............................................... 41Figure 5-4 Large and growing SIP market (source: Gartner group)................................. 42

List of tables

Table 4-1 Key US patents covering white LEDs.............................. .... ........ 30Table 4-2 M ajor phsphors patented ......................................................................... 30Table 5-1 Price comparison of CdSe and YAG precursors .................................................... 37Table 5-2 Lumileds LED price comparison................................38

Chapter 1 Introduction

Until the last decade, LEDs could only produce green, red, and yellow light, which

limited their use in only signs, signals and indicators. Then came blue LEDs, which have

since been altered to emit white light, which makes the dream of LEDs replacing

conventional incandescent and fluorescent lighting within approach. However, there are

still many problems with the current technology, which need novel ideas to solve and

hence the present white LED performance can be largely improved to the extent that

LEDs can be made comparable or even better the current lighting. Quantum dot white

LED is one of them and it has the promising potential to pull the dream nearer.

1.1 Development of LED technology

Since the development of the first commercial visible light emitting diodes (LEDs) in

1968, LED technology has under gone a series of both evolutionary and revolutionary

changes. For the first 25 years of their history, the materials available for LED fabrication

(primarily gallium phosphide (GaP) and gallium arsenide phosphide (GaAsP) were low

in efficiency and allowed LEDs to be used primarily as low brightness indicator lamps

and alphanumeric displays. Moreover, their spectral range was limited to yellow-green,

orange, and red.

In the early to mid-1990s a new generation of LED materials was developed that enabled

the fabrication of high-brightness devices across the entire visible spectrum, opening up

large new markets that were not addressable by previous material technologies. These

materials, indium gallium aluminium phosphide (InGaAlP) and indium gallium nitride

(InGaN), have formed the foundation for the large (1.8 billion in 2002) high brightness

LED industry that has evolved since 1995.

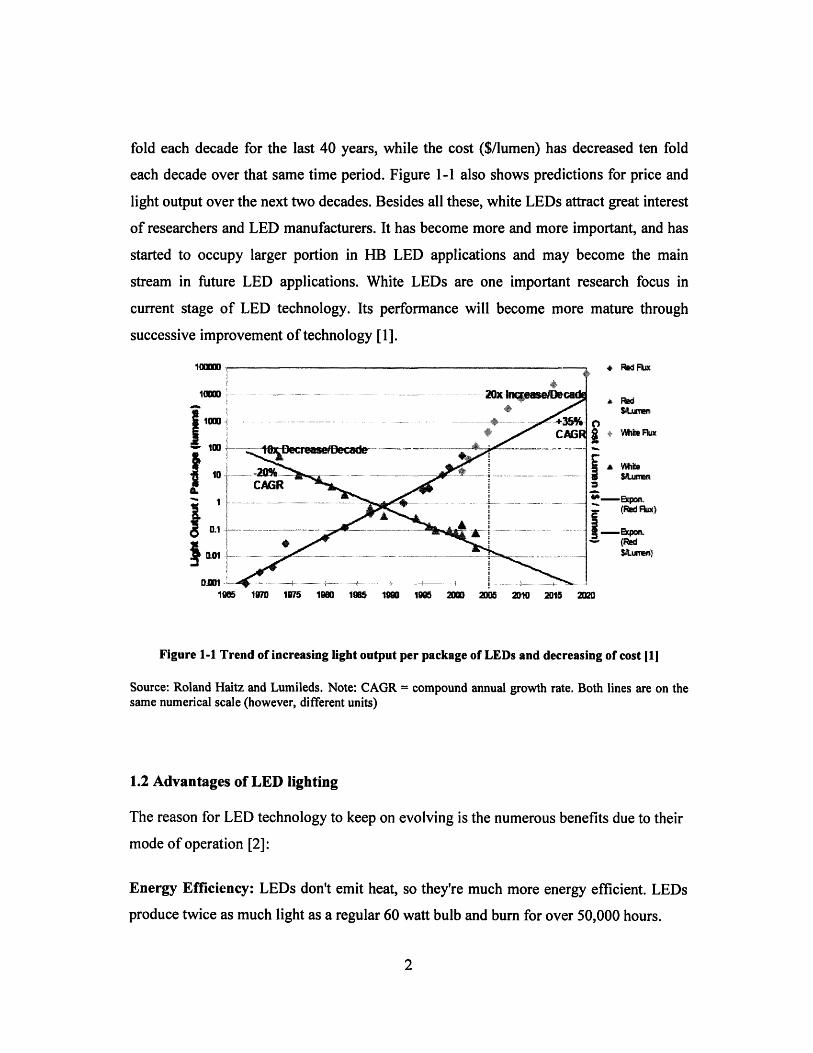

Presently, LEDs are still in the stage of further improvement in their luminous efficiency

and reduction of cost. Figure 1-1, shows how the light output of LEDs has increased 201

fold each decade for the last 40 years, while the cost ($/lumen) has decreased ten fold

each decade over that same time period. Figure 1-1 also shows predictions for price and

light output over the next two decades. Besides all these, white LEDs attract great interest

of researchers and LED manufacturers. It has become more and more important, and has

started to occupy larger portion in HB LED applications and may become the main

stream in future LED applications. White LEDs are one important research focus in

current stage of LED technology. Its performance will become more mature through

successive improvement of technology [1].

1lUUUU

1000Im

10

0.1

Dim

* Red1

Ratumn+ Wihe Fka

A SiMei

1905 1970 1975 19890 190 1900 2000 2005 201D 2015 2020

Figure 1-1 Trend of increasing light output per package of LEDs and decreasing of cost [1]

Source: Roland Haitz and Lumileds. Note: CAGR = compound annual growth rate. Both lines are on thesame numerical scale (however, different units)

1.2 Advantages of LED lighting

The reason for LED technology to keep on evolving is the numerous benefits due to their

mode of operation [2]:

Energy Efficiency: LEDs don't emit heat, so they're much more energy efficient. LEDs

produce twice as much light as a regular 60 watt bulb and burn for over 50,000 hours.

Long Life: Some LEDs are projected to produce a long service life of about 100,000

hours. For this reason LEDs are ideal for hard-to-reach/maintain fixtures. Much longer

life reduces maintenance requirements.

Durable: LEDs are highly rugged. They feature no filament that can be damaged due to

shock and vibrations. They are subject to heat, however, and being overdriven by the

power supply.

Small Size/Design Flexibility: A single LED is very small and produces little light

overall. However, this weakness is actually its strength. LEDs can be combined in any

shape to produce desired lumen packages as the design goals and economics permit. In

addition, LEDs can be considered miniature light fixtures; distribution of light can be

controlled by the LEDs' epoxy lens, simplifying the construction of architectural fixtures

designed to utilize LEDs.

Other Benefits, such as lights instantly, can be easily dimmed, silent operation, low-

voltage power supply (increased safety).

1.3 Motivation for development of new white LED technology and business

All these advantages make great impact on our life. First, and the most important, is the

impact on energy consumption. In the U.S., about one-third of all primary energy is used

to produce electricity, and of this electricity about one-fifth is used to produce light. If the

displacement of traditional lighting by solid-state lighting can be accelerated by even one

year, U.S. consumers would save roughly $35 billion. The use of high-brightness LEDs

for illumination has the potential to revolutionize the lighting industry over the next 10 to

20 years [3].

Ifi

III

IIII

Year

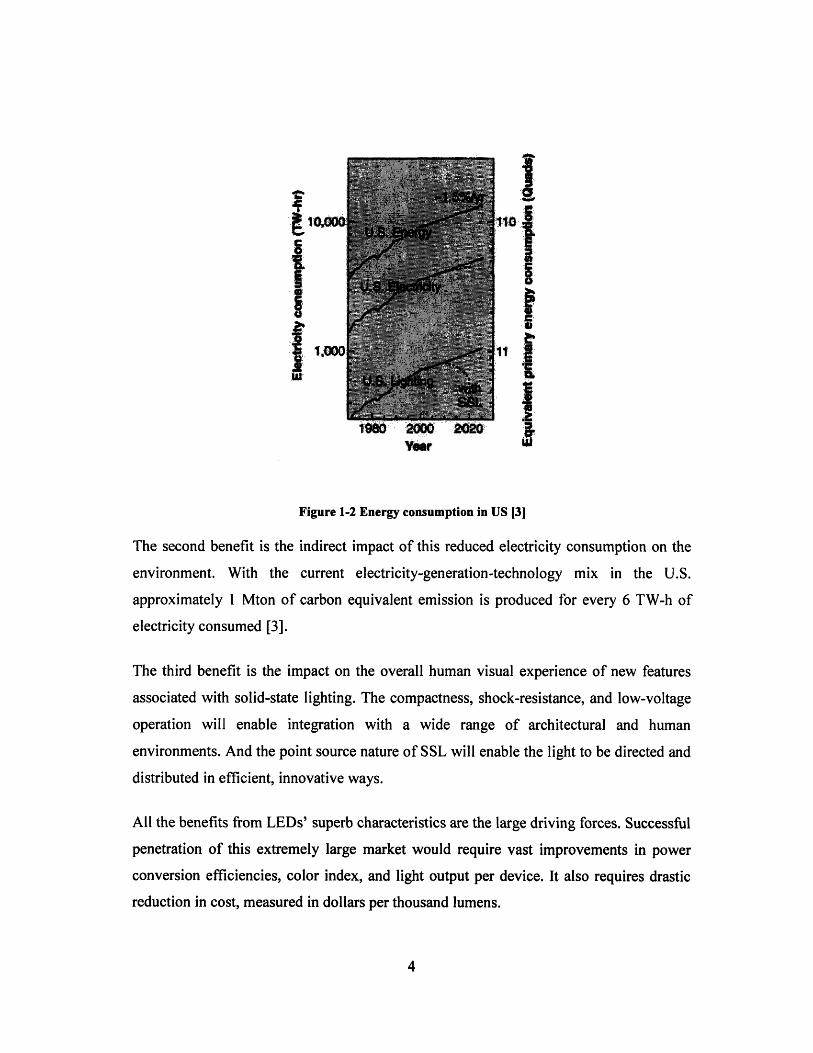

Figure 1-2 Energy consumption in US [31

The second benefit is the indirect impact of this reduced electricity consumption on the

environment. With the current electricity-generation-technology mix in the U.S.

approximately 1 Mton of carbon equivalent emission is produced for every 6 TW-h of

electricity consumed [3].

The third benefit is the impact on the overall human visual experience of new features

associated with solid-state lighting. The compactness, shock-resistance, and low-voltage

operation will enable integration with a wide range of architectural and human

environments. And the point source nature of SSL will enable the light to be directed and

distributed in efficient, innovative ways.

All the benefits from LEDs' superb characteristics are the large driving forces. Successful

penetration of this extremely large market would require vast improvements in power

conversion efficiencies, color index, and light output per device. It also requires drastic

reduction in cost, measured in dollars per thousand lumens.

.m

Reference

[1]. "Solid-State Lighting Research and Development Protfolio", Multi-Year Program

Plan FY'07-FY' 12 prepared for: Lighting Research and Development Building

Technologies Program Office of Evergy Efficiency and Renewable Energy U.S.

Department of Energy

[2]. http://lightingdesignlab.com/articles/LED_fund/led advant.htm

[3]. Jeffrey V.Tsao, "Roadmap projects significant LED penetration of lighting market

by 2010", Laser Focus World, May 2003

Chapter 2 Quantum dot white LED technology

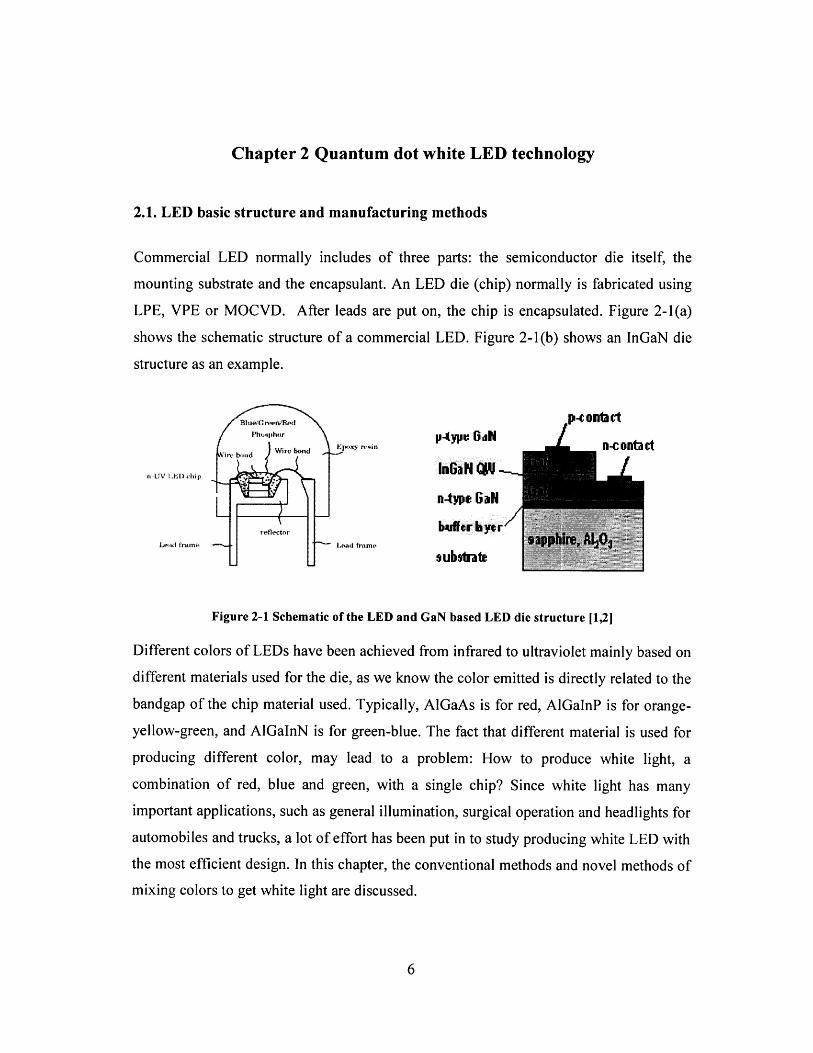

2.1. LED basic structure and manufacturing methods

Commercial LED normally includes of three parts: the semiconductor die itself, the

mounting substrate and the encapsulant. An LED die (chip) normally is fabricated using

LPE, VPE or MOCVD. After leads are put on, the chip is encapsulated. Figure 2-1(a)

shows the schematic structure of a commercial LED. Figure 2-1(b) shows an InGaN die

structure as an example.

p-tyiit / ddp-c Oit3

in-tV L rKmI) ttip

Leadt framtý

n-type GaN

buffcr byriramro

subrante

Figure 2-1 Schematic of the LED and GaN based LED die structure [1,2]

Different colors of LEDs have been achieved from infrared to ultraviolet mainly based on

different materials used for the die, as we know the color emitted is directly related to the

bandgap of the chip material used. Typically, AlGaAs is for red, AlGaInP is for orange-

yellow-green, and AlGaInN is for green-blue. The fact that different material is used for

producing different color, may lead to a problem: How to produce white light, a

combination of red, blue and green, with a single chip? Since white light has many

important applications, such as general illumination, surgical operation and headlights for

automobiles and trucks, a lot of effort has been put in to study producing white LED with

the most efficient design. In this chapter, the conventional methods and novel methods of

mixing colors to get white light are discussed.

n

2.2. Conventional methods

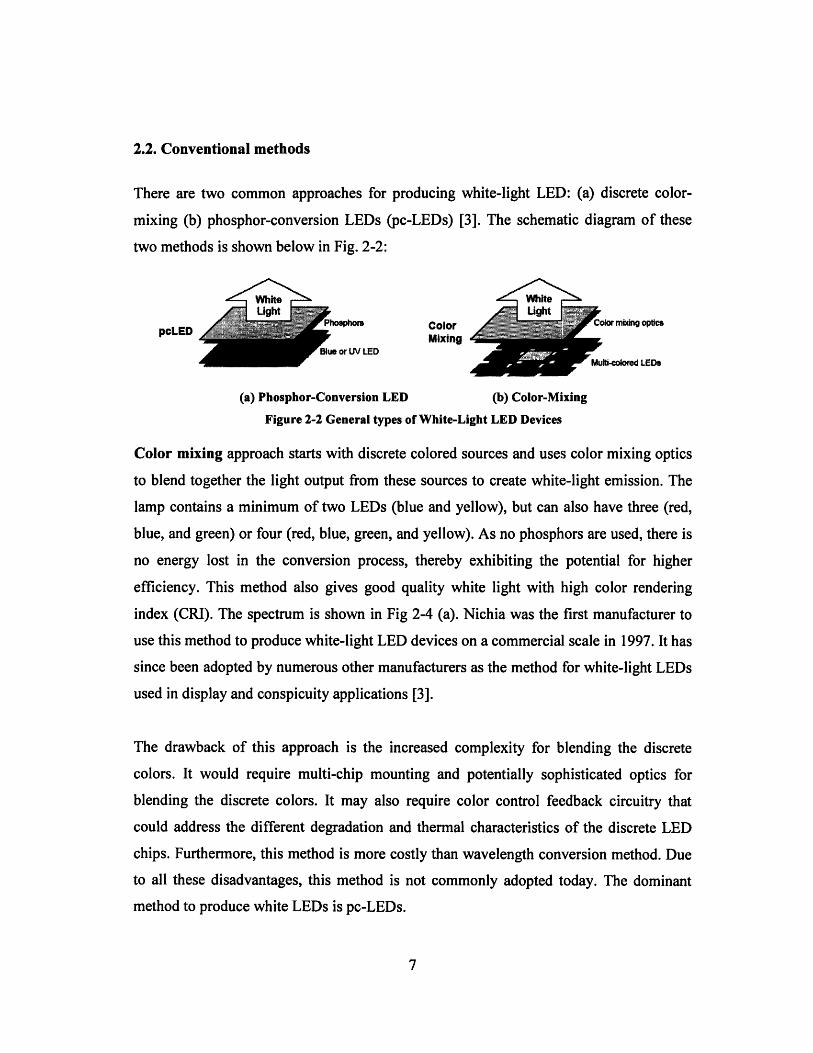

There are two common approaches for producing white-light LED: (a) discrete color-

mixing (b) phosphor-conversion LEDs (pc-LEDs) [3]. The schematic diagram of these

two methods is shown below in Fig. 2-2:

.eit White

pcLEDosphors Color

Mixinga or UV LED

mixing optics

colored LEDs

(a) Phosphor-Conversion LED (b) Color-Mixing

Figure 2-2 General types of White-Light LED Devices

Color mixing approach starts with discrete colored sources and uses color mixing optics

to blend together the light output from these sources to create white-light emission. The

lamp contains a minimum of two LEDs (blue and yellow), but can also have three (red,

blue, and green) or four (red, blue, green, and yellow). As no phosphors are used, there is

no energy lost in the conversion process, thereby exhibiting the potential for higher

efficiency. This method also gives good quality white light with high color rendering

index (CRI). The spectrum is shown in Fig 2-4 (a). Nichia was the first manufacturer to

use this method to produce white-light LED devices on a commercial scale in 1997. It has

since been adopted by numerous other manufacturers as the method for white-light LEDs

used in display and conspicuity applications [3].

The drawback of this approach is the increased complexity for blending the discrete

colors. It would require multi-chip mounting and potentially sophisticated optics for

blending the discrete colors. It may also require color control feedback circuitry that

could address the different degradation and thermal characteristics of the discrete LED

chips. Furthermore, this method is more costly than wavelength conversion method. Due

to all these disadvantages, this method is not commonly adopted today. The dominant

method to produce white LEDs is pc-LEDs.

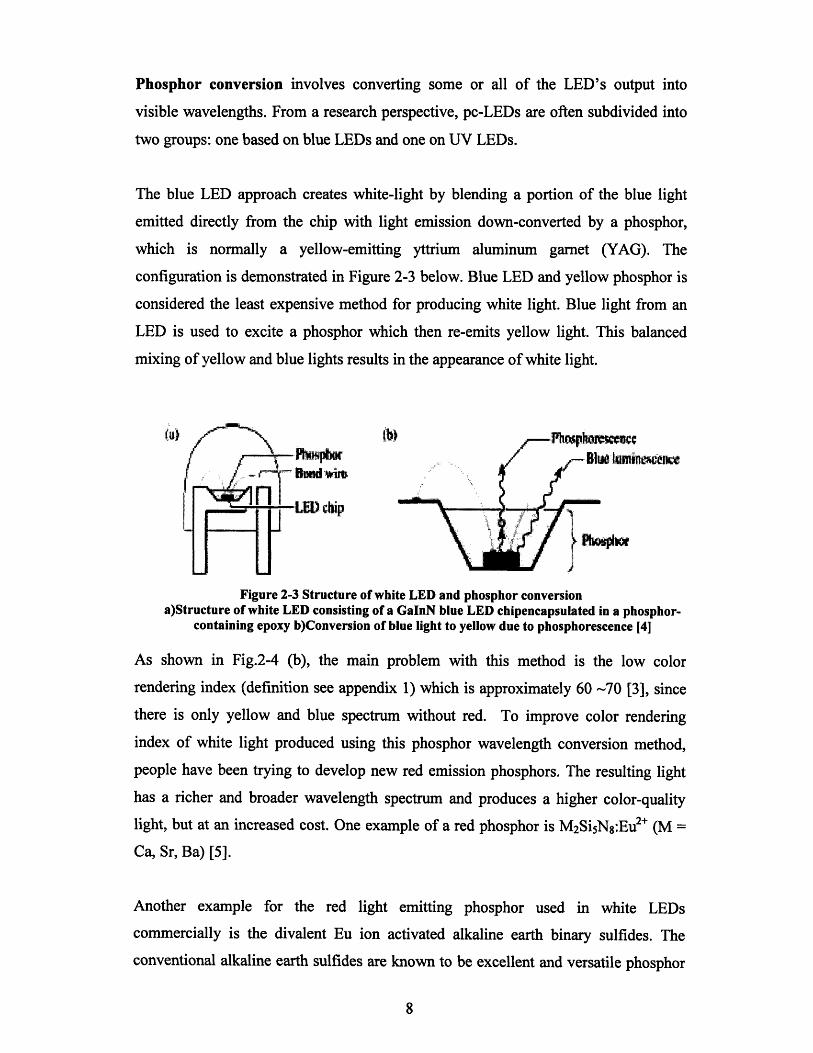

Phosphor conversion involves converting some or all of the LED's output into

visible wavelengths. From a research perspective, pc-LEDs are often subdivided into

two groups: one based on blue LEDs and one on UV LEDs.

The blue LED approach creates white-light by blending a portion of the blue light

emitted directly from the chip with light emission down-converted by a phosphor,

which is normally a yellow-emitting yttrium aluminum garnet (YAG). The

configuration is demonstrated in Figure 2-3 below. Blue LED and yellow phosphor is

considered the least expensive method for producing white light. Blue light from an

LED is used to excite a phosphor which then re-emits yellow light. This balanced

mixing of yellow and blue lights results in the appearance of white light.

-Blwe uminm -twe.... ......•... ... ..'... , -B u l n i

~ L

Figure 2-3 Structure of white LED and phosphor conversiona)Structure of white LED consisting of a GaInN blue LED chipencapsulated in a phosphor-

containing epoxy b)Conversion of blue light to yellow due to phosphorescence [4]

As shown in Fig.2-4 (b), the main problem with this method is the low color

rendering index (definition see appendix 1) which is approximately 60 -70 [3], since

there is only yellow and blue spectrum without red. To improve color rendering

index of white light produced using this phosphor wavelength conversion method,

people have been trying to develop new red emission phosphors. The resulting light

has a richer and broader wavelength spectrum and produces a higher color-quality

light, but at an increased cost. One example of a red phosphor is M2SisN8 :Eu 2+ (M

Ca, Sr, Ba) [5].

Another example for the red light emitting phosphor used in white LEDs

commercially is the divalent Eu ion activated alkaline earth binary sulfides. The

conventional alkaline earth sulfides are known to be excellent and versatile phosphor

rii,

materials. As members of alkaline earth sulfide families, especially Eu2+ doped SrS

and CaS were considered to be the most promising candidates for red phosphor.

However, the binary sulfide-based phosphors have low chemical stabilities and low

luminescence [6].

The UV LED approach starts with a UV-emitting LED chip that energizes phosphors

designed to emit light in the visible spectrum. All the UV energy is adsorbed and

converted into the visible spectrum by the phosphors. A pc-LED using a UV LED

chip is similar to the blue LED system, but has some important differences. In this

type of pc-LED, the LED radiates energy in the UV (340-380nm) or near-UV

(<430nm) that excites phosphors, which down-convert the UV radiation into the

visible wavelengths. The discrete emissions from the phosphors combine to produce

white light [3].

rnospEmiss

Canmhined

I·1A PAPr FAA ~A i1

470 525 590 630 (nm) 417 L o 5tV w5 ) Inmi

(a) (b)

Figure 2-4 Spectrum of white LED(a). Color mixing (b). Wavelength conversion (blue LED and yellow phosphor) [71

2.3. Quantum Dot white LED

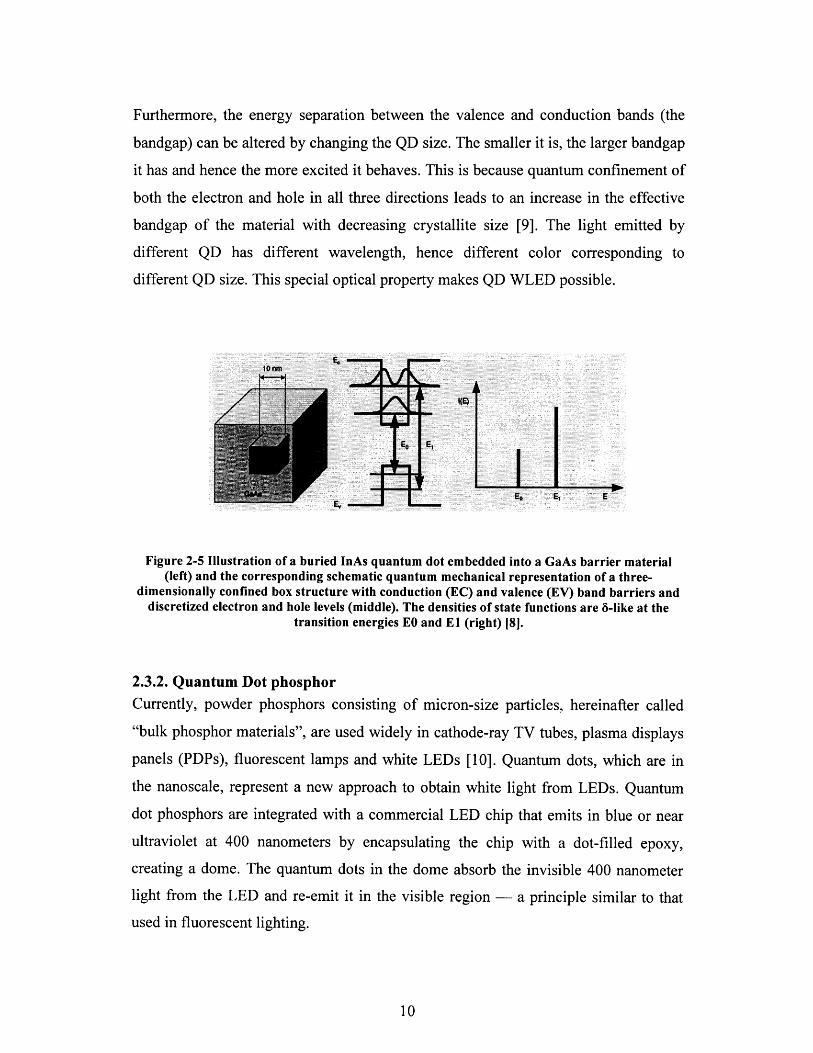

2.3.1. Quantum Dot PhysicsQuantum dots are nanocrystals with size smaller than 10nm. Each dot contains only

33 or 34 pairs of atoms or from 100 to 1,000 electrons. In a quantum dot (QD),

electrons and holes are confined in all three dimensions [8]. They have very different

behaviors compared to electrons and holes in bulk semiconductor due to the

confinement. They have discretized quantum dot bands and therefore semiconductor

quantum dots, e.g., InAs dots embedded in GaAs, behave like non- or weakly

interacting single atoms as shown in Figure 2-5.

9

Furthermore, the energy separation between the valence and conduction bands (the

bandgap) can be altered by changing the QD size. The smaller it is, the larger bandgap

it has and hence the more excited it behaves. This is because quantum confinement of

both the electron and hole in all three directions leads to an increase in the effective

bandgap of the material with decreasing crystallite size [9]. The light emitted by

different QD has different wavelength, hence different color corresponding to

different QD size. This special optical property makes QD WLED possible.

Figure 2-5 Illustration of a buried InAs quantum dot embedded into a GaAs barrier material(left) and the corresponding schematic quantum mechanical representation of a three-

dimensionally confined box structure with conduction (EC) and valence (EV) band barriers anddiscretized electron and hole levels (middle). The densities of state functions are 6-like at the

transition energies EO and El (right) [8].

2.3.2. Quantum Dot phosphorCurrently, powder phosphors consisting of micron-size particles, hereinafter called

"bulk phosphor materials", are used widely in cathode-ray TV tubes, plasma displays

panels (PDPs), fluorescent lamps and white LEDs [10]. Quantum dots, which are in

the nanoscale, represent a new approach to obtain white light from LEDs. Quantum

dot phosphors are integrated with a commercial LED chip that emits in blue or near

ultraviolet at 400 nanometers by encapsulating the chip with a dot-filled epoxy,

creating a dome. The quantum dots in the dome absorb the invisible 400 nanometer

light from the LED and re-emit it in the visible region - a principle similar to that

used in fluorescent lighting.

LED light still impinges on phosphor coating composed of quantum dots, but instead

of encountering traditional semiconductor energy bands, the LED photons would

encounter the discretized energy bands specific to quantum dots. The discretized

nature of quantum dot bands means that the energy separation between the valence

and conduction bands (the bandgap) can be altered with the addition or the subtraction

of just one atom, making for a size dependent bandgap. Predetermining the size of the

quantum dots would fix the emitted photon wavelength at the appropriate customer-

specified color, even if it is not naturally occurring, an ability limited only to dots.

For nanophosphors, white light is generated by intermixing red, green, and blue

emitting dots homogenously within the phosphor. Thus, quantum dots need only a

single excitation source for multiple emission colors, even to the point of producing

industry quality white light.

2.3.3. Fabrication of quantum dot phosphor

An example of white LED with quantum dot phosphor was demonstrated by Hsueh-

Shih Chen's group [11]. White light-emitting diodes (WLEDs) were fabricated by

combining blue InGaN chips with luminescent colloidal core-shell CdSe-ZnSe QDs.

The CdSe QDs were synthesized in supersaturated solution. Experimentally, CdO,

TOPO, and HPA/TDPA were loaded in a three-neck flask. At about 3000C, reddish

CdO powder was dissolved and generated a colorless homogeneous solution.

Introducing tellurium, selenium, and sulfur stock solutions yield high quality

nanocrystals. TEM measurements indicate narrow distribution of these QD size and

X-ray powder diffraction shows high crystallinity of these wurtzite nanocrystals. The

dot size can be easily controlled by the reaction time [17, 12].

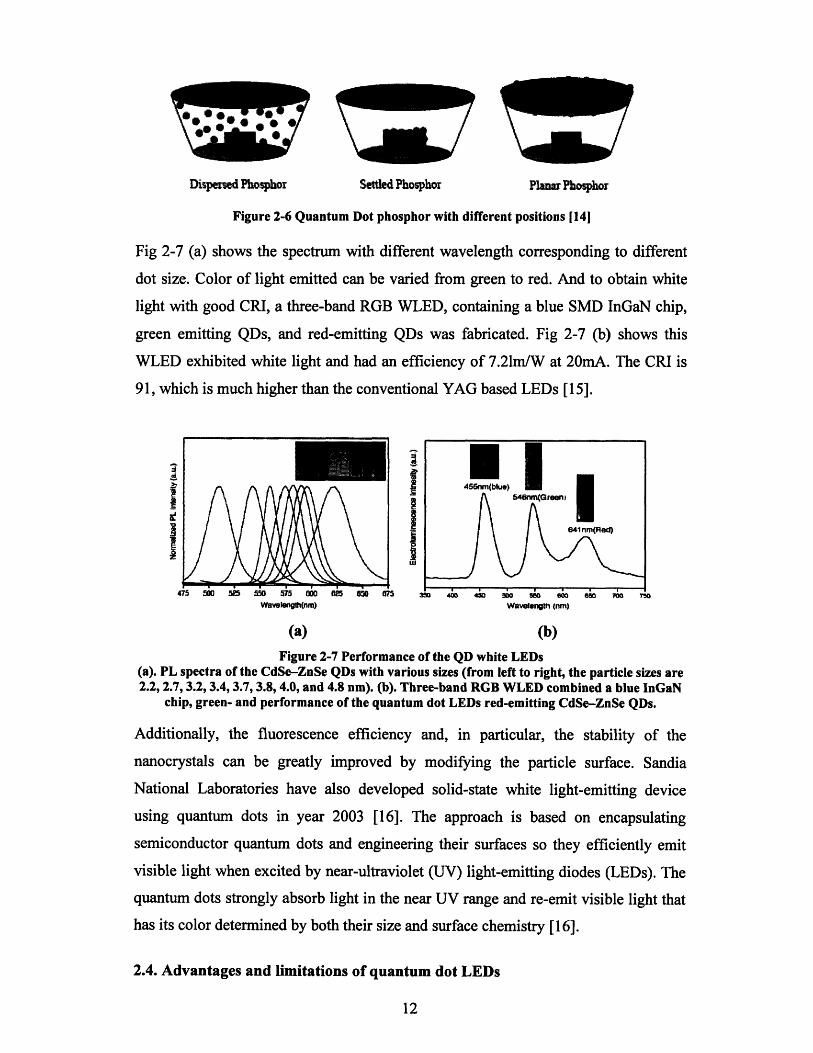

After synthesis, the QD need to be dispersed into some binder and coated on LED

chip. Figure 2-6 shows the QD phosphor after dispersion and coating on chip with

different phosphor positions relative to the chip. Different dispersion and positioning

of the phosphor can greatly affect the efficiency of the LED [13].

1W M -

Dispersed Phosphor Settled Phosphor Planar Phosphor

Figure 2-6 Quantum Dot phosphor with different positions [14]

Fig 2-7 (a) shows the spectrum with different wavelength corresponding to different

dot size. Color of light emitted can be varied from green to red. And to obtain white

light with good CRI, a three-band RGB WLED, containing a blue SMD InGaN chip,

green emitting QDs, and red-emitting QDs was fabricated. Fig 2-7 (b) shows this

WLED exhibited white light and had an efficiency of 7.21m/W at 20mA. The CRI is

91, which is much higher than the conventional YAG based LEDs [15].

Waveloenh(nm) Wavelength (nm)

(a) (b)

Figure 2-7 Performance of the QD white LEDs(a). PL spectra of the CdSe-ZnSe QDs with various sizes (from left to right, the particle sizes are2.2, 2.7, 3.2, 3.4, 3.7, 3.8, 4.0, and 4.8 nm). (b). Three-band RGB WLED combined a blue InGaN

chip, green- and performance of the quantum dot LEDs red-emitting CdSe-ZnSe QDs.

Additionally, the fluorescence efficiency and, in particular, the stability of the

nanocrystals can be greatly improved by modifying the particle surface. Sandia

National Laboratories have also developed solid-state white light-emitting device

using quantum dots in year 2003 [16]. The approach is based on encapsulating

semiconductor quantum dots and engineering their surfaces so they efficiently emit

visible light when excited by near-ultraviolet (UV) light-emitting diodes (LEDs). The

quantum dots strongly absorb light in the near UV range and re-emit visible light that

has its color determined by both their size and surface chemistry [16].

2.4. Advantages and limitations of quantum dot LEDs

I

_e

]

QD LEDs have many advantages over LEDs with conventional phosphor.

Theoretically they have better CRI at cheaper cost, better luminous efficacy, more

flexible and stable. The utilization of quantum dot to produce white light may

overcome some problems with current white LED technology [17].

Advantage 1:: High color rendering index and easy color tuning

For nanophosphors, while the optical properties of conventional bulk phosphor

powders are determined solely by the phosphor's chemical composition, in quantum

dots the optical properties such as light absorbance are determined by the size of the

dot. Changing the size produces dramatic changes in color. This also can be applied to

QD in pn junctions. QD size will always affect the color of the light emitting. Thus, it

provides a convenient way in tuning the emission light color.

More importantly, since different size QDs emit light with different wavelength, when

all these lights are mixed together, it gives high CRI. The CRI can be as high as 91

simply achieved by using phosphor with different QD size. And a typical CRI value

for currently commercialized white LED is below 70 (appendix 3). Higher CRI with

conventional phosphor will have higher cost.

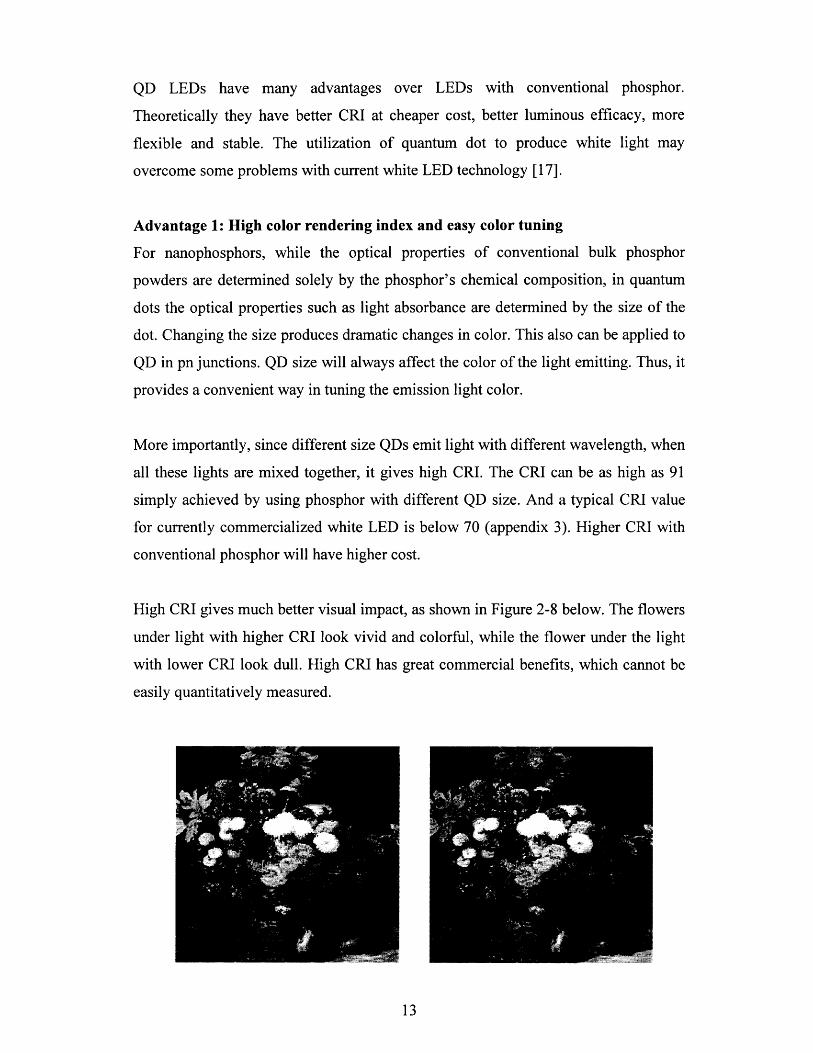

High CRI gives much better visual impact, as shown in Figure 2-8 below. The flowers

under light with higher CRI look vivid and colorful, while the flower under the light

with lower CRI look dull. High CRI has great commercial benefits, which cannot be

easily quantitatively measured.

Figure 2-8 Clear differences of the color rendition in the August Renoir painting(left hand side: high CRI; right hand side low CRI) [7]

Advantage 2: High energy efficiency

The energy efficiency of presently available commercial white LED products is in the

range of 40 lumens per watt. The target for solid-state light sources is to reach 150

lumens per watt by 2012. For white LEDs to reach this target, improvements are

needed in several areas, including the internal quantum efficiency [18], the light

extraction efficiency, and the phosphor efficiency [19]. There are several factors,

which affect the phosphor efficiency, the physical shape of the phosphor, position of

phosphor, the refractive index mismatch and the photoluminescence efficiency.

There are energy losses when the light is down converted to longer wavelength light.

This loss is unavoidable, but there are some other losses that can be reduced or even

avoided by substituting conventional phosphor with QD phosphor.

a). The optical property of such QD system is closely related to the nature of excitons,

which are the electron-hole pairs that can be created by the absorption of photons. The

recombination is much easier to happen for QD than in bulk material. Hence,

wavelength conversion loss can be greatly reduced and luminous efficacy can be

further improved. According to literature, the quantum efficiency for matrix free QD

is between 1% to 10%. We take the average 5% in the following calculation [20].

The typical output of YAG is 8 photons/keV[21]. Assuming the wavelength of

incoming photons is 450nm, which is in the blue range, the photon energy is

1.24/0.45= 2.76 eV. The total number of incoming photons will be 362. The rough

quantum efficiency is 8/362=2.2%. So we can see that CdSe QD has larger quantum

efficiency.

b). For nanophosphors, since QD has a much smaller size than the wavelength of

visible light, it eliminates all light scattering and the associated optical losses. Optical

backscattering losses using larger conventional phosphors reduce the package

efficiency by as much as 50 percent [22, 23]. A method to cut down the loss due to

backward scattering of light would be in bringing particle size down to the nano level

where light scattering becomes faint [10]. Physically, the rough surface of QD

phosphor reduces backscattering. Nano-sizing not only reduces light scattering but

also improves the relative surface area of the material.

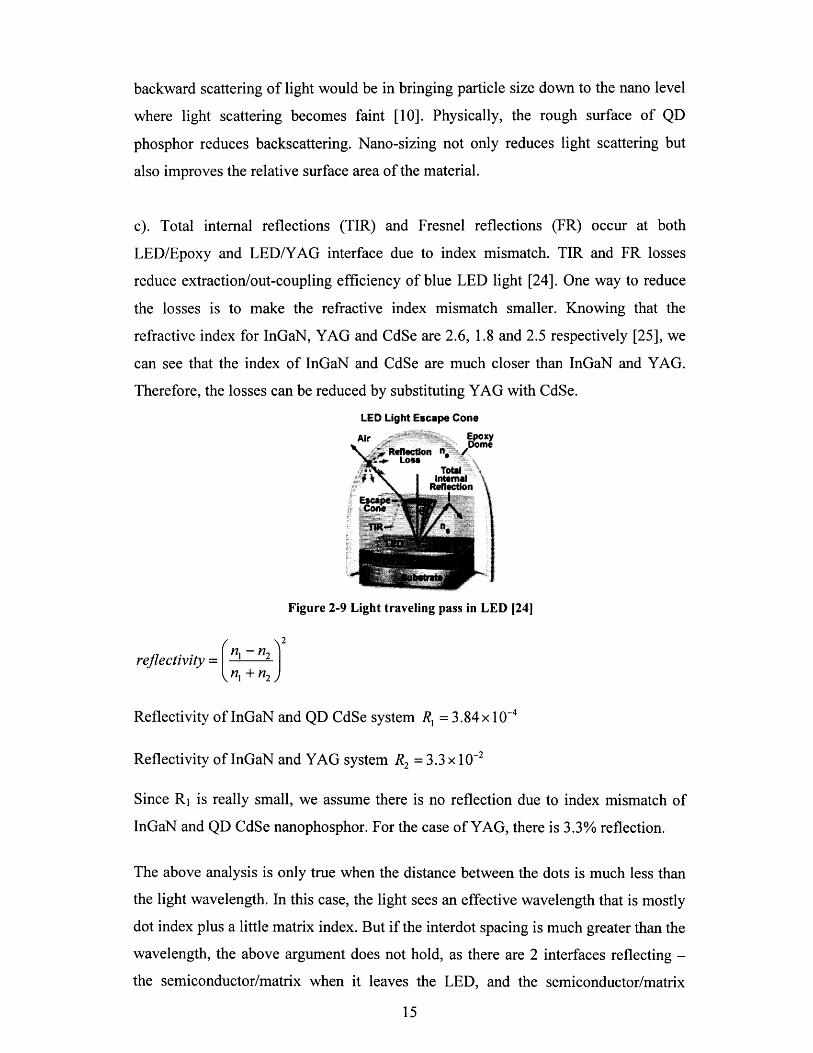

c). Total internal reflections (TIR) and Fresnel reflections (FR) occur at both

LED/Epoxy and LED/YAG interface due to index mismatch. TIR and FR losses

reduce extraction/out-coupling efficiency of blue LED light [24]. One way to reduce

the losses is to make the refractive index mismatch smaller. Knowing that the

refractive index for InGaN, YAG and CdSe are 2.6, 1.8 and 2.5 respectively [25], we

can see that the index of InGaN and CdSe are much closer than InGaN and YAG.

Therefore, the losses can be reduced by substituting YAG with CdSe.

LED Light Escape Cone

KYne

Figure 2-9 Light traveling pass in LED [24]

2

reflectivity = n, +-n2

Reflectivity of InGaN and QD CdSe system R, = 3.84 x 10- 4

Reflectivity of InGaN and YAG system R2 = 3.3 x 10-2

Since R1 is really small, we assume there is no reflection due to index mismatch of

InGaN and QD CdSe nanophosphor. For the case of YAG, there is 3.3% reflection.

The above analysis is only true when the distance between the dots is much less than

the light wavelength. In this case, the light sees an effective wavelength that is mostly

dot index plus a little matrix index. But if the interdot spacing is much greater than the

wavelength, the above argument does not hold, as there are 2 interfaces reflecting -

the semiconductor/matrix when it leaves the LED, and the semiconductor/matrix

15

when it enters the dot. In this case, the index of the matrix comes into the picture.

The index mismatch of matrix/LED, matrix/CdSe becomes important. Another effect

that can influence the light path is that if the dot spacing is on the order of the

wavelength of light, a lot of scattering will occur. The scattering may increase the

chances of light absorbance, or it may also scatter the light away and reduce the

absorbance. Therefore, dispersion configuration in the matrix and the matrix material

has great influence on the energy efficiency. A good configuration and suitable

material has the potential to reduce reflection and increase energy efficiency [26].

Advantage 3: Low cost

QD phosphor has lower cost mainly due to cheaper precursor and an easier process.

The details on the estimates of cost will be discussed in chapter 5.

Advantage 4: Better versatility

For nanophosphors, the extremely small size and versatility of form for quantum dots

would allow them to be inserted into any medium necessary to accommodate any

underlying light emitting source. For QDs inserted in pn junction, their extremely

small size and versatility of form allows them to be inserted into any medium

necessary - paint, water, plastics and more [17].

Limitation & obstacles

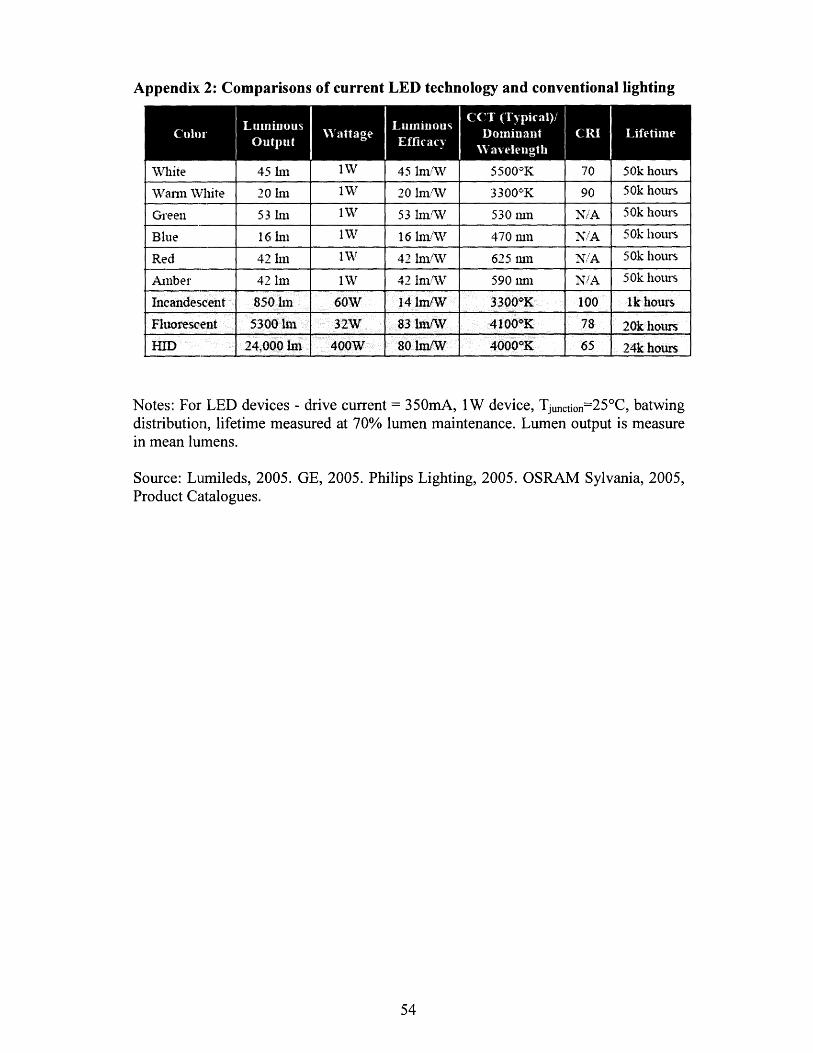

According to Appendix 2, commercialized white LED has a luminous efficacy 20

Im/W. The current QD LED only has a luminous efficiency around 7 Im/W. This may

be due to poor dispersion and the material that is used for the binder. The QDs

photoluminescence is strongly affected by its binders, which also influence QDs

stability and dispersion. A good binder in which QDs disperse well may be found but

the QD emission intensity reduces. After dispersing, QDs need to be coated onto the

LED chip. Poor coating technique may be another reason for low luminescence.

Another main problem with this technology is thermal stability especially when QDs

loaded on high-power GaN chips [28].

2.5. Quantum dot in pn junction

2.5.1. Theory of white LEDs with QD in pn junction

Current LED technology produces electroluminescent, non-tunable light emission

through the use of a p-n semiconductor junction. As an electrical current is driven

through the junction, electrons are excited across the bandgap into the conduction

band. From there, the electrons diffuse away from the junction, and proceed to decay

back across the bandgap to the valence band, accompanied by the emission of light

with a wavelength corresponding to the energy of the bandgap.

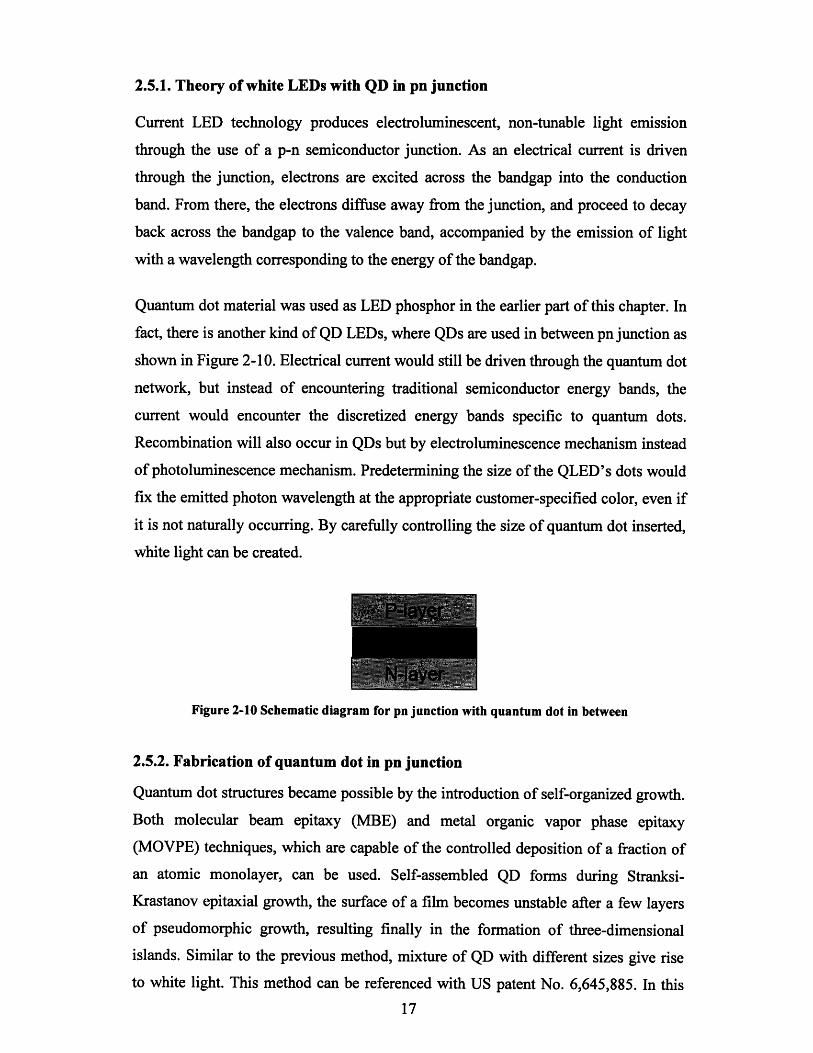

Quantum dot material was used as LED phosphor in the earlier part of this chapter. In

fact, there is another kind of QD LEDs, where QDs are used in between pn junction as

shown in Figure 2-10. Electrical current would still be driven through the quantum dot

network, but instead of encountering traditional semiconductor energy bands, the

current would encounter the discretized energy bands specific to quantum dots.

Recombination will also occur in QDs but by electroluminescence mechanism instead

of photoluminescence mechanism. Predetermining the size of the QLED's dots would

fix the emitted photon wavelength at the appropriate customer-specified color, even if

it is not naturally occurring. By carefully controlling the size of quantum dot inserted,

white light can be created.

Figure 2-10 Schematic diagram for pn junction with quantum dot in between

2.5.2. Fabrication of quantum dot in pn junction

Quantum dot structures became possible by the introduction of self-organized growth.

Both molecular beam epitaxy (MBE) and metal organic vapor phase epitaxy

(MOVPE) techniques, which are capable of the controlled deposition of a fraction of

an atomic monolayer, can be used. Self-assembled QD forms during Stranksi-

Krastanov epitaxial growth, the surface of a film becomes unstable after a few layers

of pseudomorphic growth, resulting finally in the formation of three-dimensional

islands. Similar to the previous method, mixture of QD with different sizes give rise

to white light. This method can be referenced with US patent No. 6,645,885. In this

17

patent, Indium Nitride (InN) and Indium-rich Indium Gallium Nitride (InGaN)

quantum dots embedded in single and multiple InxGal-xN quantum wells (QWs) are

formed by using TMIn and /or Triethylindium (TEIn) as antisurfactant during

MOCVD growth.

Another way of incorporating QD into the p-n junction conductive layer is to mix

colloidally produced quantum dot with a transparent and electrically conductive host

matrix, and coat in between the junction. This way requires less cost than epitaxy [9].

2.5.3. Advantages and limitations

Advantage 1: Even higher energy efficiency

There are always energy losses in terms of pc-LED. As mentioned earlier in this

chapter, the energy losses are associated with the conversion from shorter wavelength

to longer wavelength. Some of the photons may just be absorbed by the phosphor

instead of being converted to yellow light. The loss is also related to the reflection

and backscattering between LED and phosphor interface. However, for this QD in pn

junction method, there is no phosphor, so all the losses can be avoided. Below is the

estimation of the amount of energy that can be saved compared to the conventional

yellow.

From blue light to red light, the amount of energy saved is:

Energy of blue light: 1.24/0.46 = 2.7eV

Energy of red light: 1.24/0.70 = 1.77eV

Percentage of engery losses: 0.93/2.7 * 100% = 34%

So 34% energy due to wavelength conversion can be saved by adopting this method.

Advantage 2: Even lower cost

Since there is no phosphor, the cost for phosphor is totally reduced. As we analyzed in

part 2.4, the cost of phosphor is roughly 1/6 of the total white LED cost or the 1/5 of a

blue LED cost.

Limitations and Obstacles 1

According to the above mentioned patent, growth of the active layers of blue and

green LEDs can be achieved, but it is not efficient in producing red light from GaN pn

junction. A possible reason is, in industry, the material system Ga, In and N is used to

produce blue or green light rather than yellow light due to the natrual bandgap range

of these material. It is very difficult to achieve red light emission bandgap using this

material system. Due to this reason, the red light emitting quantum dot is hard to

grow.

Limitations and obstacles 2

Another possible reason it is hard to get good control of quantum dot size and position

[27]. Although theoretically it should work and give different color light with

different dot sizes, in production line there may not be a workable die among 100

wafers. Since the repeatability is very low, so far none of the fabs are willing to invest

in this technology.

Quantum dot is a very new research field, some phenomena associated with it are not

well understood so far and its growth control is also in a lab research stage. QDs is a

broad field and it has many applications. QD LED is just a technology overlap of

Quantum dot and LEDs. To finally achieve QD in pn junction LED, QD technology

needs to be developed to a more mature stage.

Limitations and obstacles 3

The growth of InxGal-xN alloys and quantum wells is extremely difficult mostly due

to the trade-off between the epilayer quality and the amount of InN incorporation into

the alloy. Lowering the growth temperature results in the indium content at the

expense of reduced crystalline quality. The lattice mismatch and different thermal

stability of the two constituents InN and GaN, also complicate the growth of InxGal_

xN. The lattice mismatch can lead to a miscibility gap [7] which causes fluctuations of

In content across the film.

Limitation and obstacles 4

For the colloidally produced quantum dot in electrically conductive layer, the devices

require a transparent, electrically conductive host matrix, which severely limits the

available materials for producing LEDs by this method [9].

Reference

[1]. Cheng-Huang KUO, Jinn-Kong SHEU, Shoou-Jinn CHANG, "n-

UV+Blue/Green/Red White Light Emitting Diode Lamps", Jpn. J. Appl. Phys.

Vol. 42 (2003) pp. 2284-2287

[2]. http://www.nanotechnology.bilkent.edu.tr/research%20areas/

documents/LEDs.html

[3]. "Solid-State Lighting Research and Development Protfolio", Multi-Year

Program Plan FY'07-FY' 12 prepared for: Lighting Research and Development

Building Technologies Program Office of Evergy Efficiency and Renewable

Energy U.S. Department of Energy

[4]. http://www.mse.berkeley.edu/classes/matscil02/F01 reports/whiteled.pdf

[5]. Y.Q. Li, J.E.J. van Steen, J.W.H. van Krevel, "Luminescence properties of red-

emitting M2SisN 8:Eu2+ (M = Ca, Sr, Ba) LED conversion phosphors", Journal

of Alloys and Compounds 417 (2006) 273-279

[6]. Chongfeng Guo, Dexiu Huang, Qiang Su,"Methods to improve the

fluorescence intensity of CaS:Eu2+ red-emitting phosphor for white LED",

Materials Science and Engineering B 130 (2006) 189-193

[7]. Institute of Material Research and Engineering Singapore Prof. Chua SJ QD

White light 29 Sept 05 presentation on White light LED

[8]. Johann Peter Reithmaier, Alfred Forchel,"semiconductor quantum dots" IEEE

Circuits & Devices magazine November 2003

[9]. US patent no. 6,501,091

[10]. http://www.nitto.com/company/release/05_ 10_1 8/index.html

[11]. Hsueh Shih Chen, Shian Jy Jassy Wang, " White light emission from organics

capped ZnSe quantum dots and application in white-light-emitting diodes",

Applied Physics Letters 86, 131905 (2005)

[12]. http://www.aist.go.jp/aist_e/latest_research/2006/20060601/20060601 .html

[13]. Jong Kyu Kim, Hong Luo, Eric Red Schubert, "Strongly Enhanced Phosphor

Efficiency in GaInN White Light-Emitting Diodes Using Remote Phosphor

Configuration and Diffuse Reflector Cup", Japanese Journal of Applied

Physics, Vol. 44, No.21, 2005, pp. L649-L651

[14]. Shankar M. Venugopal, "Recent advances in the development of Quantum

Splitting Phosphors and White LED Phosphors", GE India Technology Centre,

Bangalore

[15]. Hsueh-Shih Chen,Cheng-Kuo Hsu,and Hsin-Yen Hong, "InGaN-CdSe-ZnSe

Quantum Dots White LEDs", IEEE Photonics Technology Letters, Vol.18,

No. 1 ,January 1,2006

[16]. www.physlink.com/News/071403QuantumDotLED.cfm

[17]. www. evidenttech.com

[18]. http://www.answers.com/topic/quantum-efficiency

[19]. Nadarajah Narendran, "Improved Performance White LED", Lighting

Research Center, Rensselaer Polytechnic Institute, Troy, NY 12180

[20]. F. Gindele, R. Westpha ling, and U. Woggona, "Optical gain and high quantum

efficiency of matrix-free, closely packed CdSe quantum dots", Appl. Phys.

Lett. 71 (15), 13 October 1997

[21]. Saint-Gobain Crystal YAG data sheet

[22]. E. Fred Schubert and Jong Kyu Kim, "Solid-State Light Sources Getting

Smart", 27MAY2005VOL 308 SCIENCE, 1274

[23]. http://www.netl.doe.gov/ssl/portfolio05/EnhancedOpticalEfficiencyPackage.htm

[24]. http://www.nsf.gov/eng/sbir/SECTOR/Devices%20II/PhosphorTech.pdf

[25]. B. Jensen and A. Torabit, "Refractive index of hexagonal II-VI compounds

CdSe, CdS, and CdSexS_-x", Vol. 3, No. 6, June 1986, J. Opt. Soc. Am. B

[26]. Jong Kyu KIM, Hong LUO, "Strongly Enhanced Phosphor Efficiency in

GaInN White Light-Emitting Diodes Using Remote Phosphor Configuration

and Diffuse Reflector Cup", Japanese Journal of Applied Physics Vol. 44, No.

21, 2005, pp. L 649-L 651

[27]. M. Noemi Perez-Paza and Xuecong Zhou, "Single layer and stacked CdSe self-

assembled quantum dots with ZnCdMgSe barriers for visible and white light

emitters", J. Vac. Sci. Technol. B 23,,3..., May/Jun 2005

[28]. Email communicated with Prof. Chua, Prof. Fitzgerald, Dr. Aaron Danner, Mr.

Huang en li and Hsueh-Shih Chen

Chapter 3 White LED market analysis

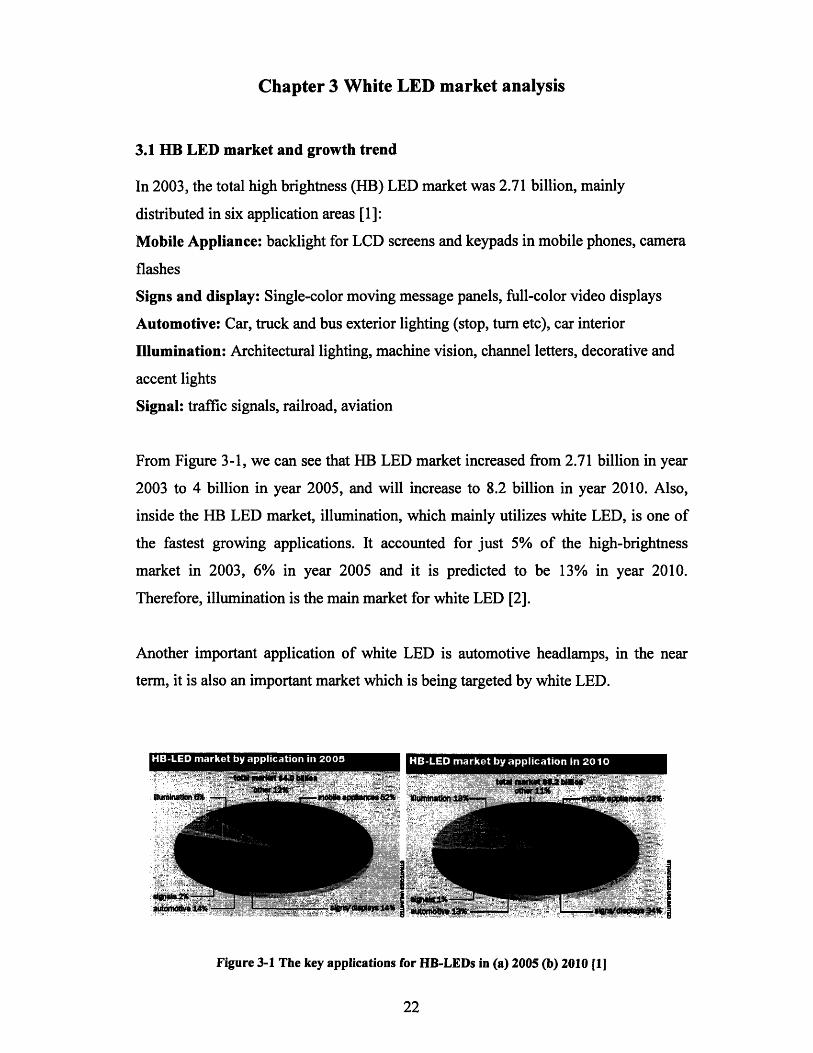

3.1 HB LED market and growth trend

In 2003, the total high brightness (HB) LED market was 2.71 billion, mainly

distributed in six application areas [1]:

Mobile Appliance: backlight for LCD screens and keypads in mobile phones, camera

flashes

Signs and display: Single-color moving message panels, full-color video displays

Automotive: Car, truck and bus exterior lighting (stop, turn etc), car interior

Illumination: Architectural lighting, machine vision, channel letters, decorative and

accent lights

Signal: traffic signals, railroad, aviation

From Figure 3-1, we can see that HB LED market increased from 2.71 billion in year

2003 to 4 billion in year 2005, and will increase to 8.2 billion in year 2010. Also,

inside the HB LED market, illumination, which mainly utilizes white LED, is one of

the fastest growing applications. It accounted for just 5% of the high-brightness

market in 2003, 6% in year 2005 and it is predicted to be 13% in year 2010.

Therefore, illumination is the main market for white LED [2].

Another important application of white LED is automotive headlamps, in the near

term, it is also an important market which is being targeted by white LED.

•• -•.•.•, 4•a k by app.icatio.n.•i 2. .......................ation in 20...

Figure 3-1 The key applications for HB-LEDs in (a) 2005 (b) 2010 [1]

3.2 White LED in illumination

The key to the near-term adoption of high brightness LEDs in illumination

applications is not to target applications where traditional lighting (fluorescent,

halogen, incandescent) is firmly entrenched, or where lower cost is desired, and where

maintenance and replacement costs are low. It takes a great deal of effort, time and

money to convince lighting manufacturers and their customers to shift away from

applications in which traditional lightings have been successfully used for many

years. What will help the illumination market for LEDs the most is to use LEDs in

new applications where it is not possible or at least very undesirable) to use traditional

lighting, or in applications that place a high premium on a particular attribute of

LEDs, such as reliability. Currently, the major uses of LEDs in lighting applications

fall primarily within seven applications [3]:

--Channel letter/contour lighting

--Architecture/retail/theme

--Industrial/machine vision

--Consumer portable/novelty (such as flashlights and key lights);

--Maitainess retrofit (socket-compatible replacement lamps);

--Safety/security (exit signs and emergency lighting);

--Specialty illumination (such as aircraft interior lighting and task lights).

According to Figure 3-1, in year 2010, illumination market will reach 13%* $8.2

million =US$lbillion, which represents a near term market size.

Today, lighting product sales in the U.S. are worth approximately $11.9 billion

annually. Of this, approximately $2.65 billion is associated with lamps while the

remaining sales are divided between fixtures, components (including ballasts and

controls) and associated services such as design and maintenance. Therefore, the long

term illumination market is approximately US$2.65 billion.

3.3 White LED as automobile headlamp

LEDs have had a reasonably successful history in penetrating the automotive lighting

market over the past 20 years. Conventional LEDs have long been used for various

indicator-lamp functions inside the car. The first significant use for LEDs as exterior

signaling is the stop lamp on Nissan 280Z in 1998. Automotive signaling got

substantial growth in early 1990s. And by 2004, approximately 40% of all

automobiles and light trucks produced worldwide featured LED-based center high-

mounted stop lamps. LEDs are also used for rear-stop, turn, and tail lamp but only for

high-end luxury cars. To varying degrees, high-brightness LEDs are being adopted for

most forms of automotive lighting. Now, LEDs are poised to move into the one

remaining, and potentially most lucrative, automotive-lighting application: headlamps

[4].

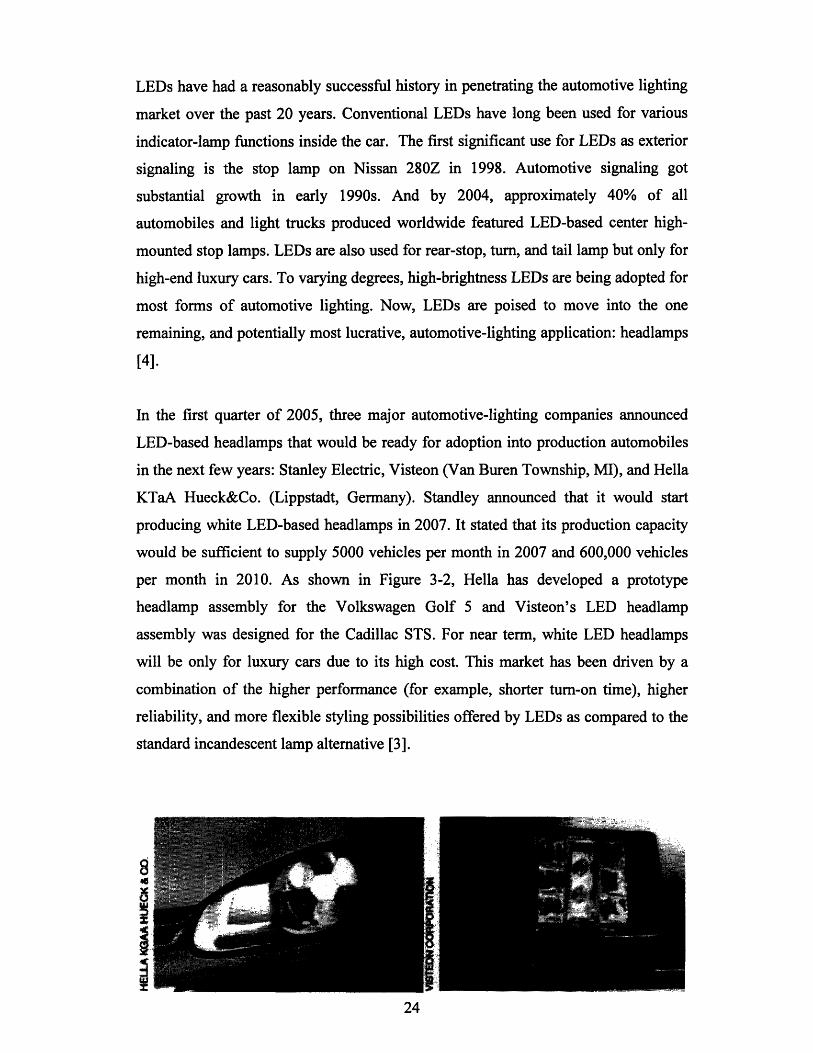

In the first quarter of 2005, three major automotive-lighting companies announced

LED-based headlamps that would be ready for adoption into production automobiles

in the next few years: Stanley Electric, Visteon (Van Buren Township, MI), and Hella

KTaA Hueck&Co. (Lippstadt, Germany). Standley announced that it would start

producing white LED-based headlamps in 2007. It stated that its production capacity

would be sufficient to supply 5000 vehicles per month in 2007 and 600,000 vehicles

per month in 2010. As shown in Figure 3-2, Hella has developed a prototype

headlamp assembly for the Volkswagen Golf 5 and Visteon's LED headlamp

assembly was designed for the Cadillac STS. For near term, white LED headlamps

will be only for luxury cars due to its high cost. This market has been driven by a

combination of the higher performance (for example, shorter turn-on time), higher

reliability, and more flexible styling possibilities offered by LEDs as compared to the

standard incandescent lamp alternative [3].

8

Figure 3-2 The light output of an LED Headlamp prototypeThe light output of an LED Headlamp prototype developed by Hella KGaA Hueck & Co. (left)

and Visteon's LED headlamp assembly for the Cadillac STS (right)

We can expect to see an increasing number of cars on the road with LED headlamps

in 2007 and beyond. This application will be one of the most promising new markets

for HB LEDs in the second half of this decade, and will be a strong component of an

expected $1 billion market for HB LEDs in automotive lighting in 2009. 20% of the

total amount may go for headlamps, so it is approximately $200 million business for

the near term market.

3.4 White LED for medical applications

A special application for white LED is medical applications, especially for surgical

operation, which requires the highest quality and quantity of lighting. Common

ceiling surgical halogen lighting system cannot provide an adequate amount of beams

because the surgeons' heads hinder the illuminations from reaching the operation

field. A solution is the doctor wears goggles with white LED. The light should have

high color rendering index in order to render inherent color of raw flesh such as skin,

blood, fat tissue and internal organs.

Since the white LEDs used were composed of InGaN-blue-emitters and YAG-yellow-

phosphors, the color rendering property was not sufficient in the reddish colors [4]. So

far there are not much consolidated data on this area, but it shows that high light

quality is a very important issue for LED development.

3.5 White LED market estimation

* Present

white LED market = $240 million (mainly from illumination)

* Near term (around year 2010)

white LED market = $1,200 million/year (from illumination and automotive

headlamps)

* Future

white LED market = the entire illumination market ~ 3 billion

(US market only)

Reference

[1]. "Solid-State Lighting Research and Development Protfolio", Multi-Year

Program Plan FY'07-FY' 12 Prepared for: Lighting Research and Development

Building Technologies Program Office of Evergy Efficiency and Renewable

Energy U.S. Department of Energy

[2]. www.ledmagzine.com

[3]. Rovert V.steele, "High-brightness LEDs open new illumination markets", Laser

Focus World, May 2003

[4]. Robert V.Steele, "LED automotive headlamps move closer to market", Laser

Focus World, November 2005

[5]. http://adsabs.harvard.edu/abs/2001 SPIE.4445... 13S

Chapter 4 Existing players and intellectual properties

4.1 LED production regions

The major LED production regions are United States, Japan, South Korea, China,

Taiwan and Europe. Governments in these regions support LED development, since

LED technology can save huge amount of energy if it at last becomes mature. There

are also LED consortiums that help promoting LED industries in these regions [1].

Japan

A consortium of companies and universities in Japan are developing efficient white

LEDs and fixtures for solid-state lighting applications. Japan's Light for the 21st

Century program was initiated with the goal of developing UV LEDs for solid-state

white lighting. The project, which ended in 2004, brings together 13 companies and

four universities. Research is proceeding in five main areas, namely substrates,

epitaxy, devices, lamps and fixtures.

Taiwan

Taiwan is investing in solid-state lighting at the national level. The "Next Generation

Lighting project" involves a consortium of 11 companies. Predicted earlier between

2003 and 2005, approximately NT$ 383 million would be invested in the technology.

The goal is to achieve 50 Im/W output products and 100 Im/W in the "Taiwanese

companies ramp up MOCVD capacity" (Compound Semiconductor, June 2004) and

"Formosa Epitaxy forms white LED consortium" (Global Sources, January 2004)

respectively.

China

China has also made public its intentions to support the development of solid state

lighting. Called the "Semiconductor Lighting Project," four industrial bases for solid-

state lighting will be developed with government support: Xiamen city ( Fujian

province ), Shanghai, Dalian ( Liaoning province ), and Nanchang ( Jiangxi province

). Roughly $12 million total is estimated as the government investment.

South Korea

Korea has identified that solid-state lighting is an important technology. Korea's

Photonics Technology Institute (KOPTI) works with LED developments. In addition,

Korea apparently has an initiative funded for about $20M per year aiming to produce

an 80 lm/W white LED in 2008.

Europe and USA

The European Union is also investing in programs that either directly or indirectly

support Solid-State Lighting.

4.2 Major players

All over the world there are over 300 LED manufacturers and distributors distributed

in these areas mentioned above [2]. Some of the companies are listed below:

US: Cree, Avago, Vishay

Europe: Osram, Lumileds

Japan: Nichia, Toyoda Goesi, Standley, Rohm, Intematix, Citizen

Taiwan: Everlight Electroics, Cotoo (HK), Kingbright, Opto tech, Harvatek, Lite-on

Korea: Samsung SEM

Among all, the "big five" LED manufacturers are Nichia, Osram, Toyoda Gosei, Cree

and Lumileds.

Nichia's LED products include compound semiconductor materials (e.g. as LED

infrared epitaxial wafers), Packaged LEDs and ultra violet LEDs. There are lamp

shape white LED under packaged LEDs category. Their chromaticity coordinate

equals to (0.41,0.39) and luminous intensity is from, 1250 to 9,200 mcd.

Cree's LED product families include LED chips, packaged LEDs and LED

backlighting solutions. The packaged LEDs, which are labeled as Xlamp series, are

mainly for lighting purpose. Cree has its distributors all over the world, such as

Europe, USA, Australia, New Zealand, Mainland China and Taiwan.

Lumileds is a fully integrated manufacturer of LED dice, packaged LEDs, and high-

brightness LEDs -Luxeon designed for integration into general lighting products. The

company markets LED solutions designed specifically for automotive applications,

LCD displays, general lighting, portable applications, signage, traffic signals, and

other segments.

Osram is a lighting company. It has lighting product from conventional incandescent

lamps to the new LED lighting solution. Its LED design suits into different purposes.

For example, Dragonlight is for high luminous intensity applications. Linearlight is

for Contour lighting and injecting light into diffused or transparent light guides.

Toyoda Gosei's nature of business is research, development, manufacture and sales

of: Parts for automobiles, conveyors, ships and various other transportation

equipment; rubber, plastic and urethane components for agricultural, construction and

machine tool equipment etc. LEDs is just 2.9% of total sales for year 2005. However

it still has the capability to produce high brightness white LEDs.

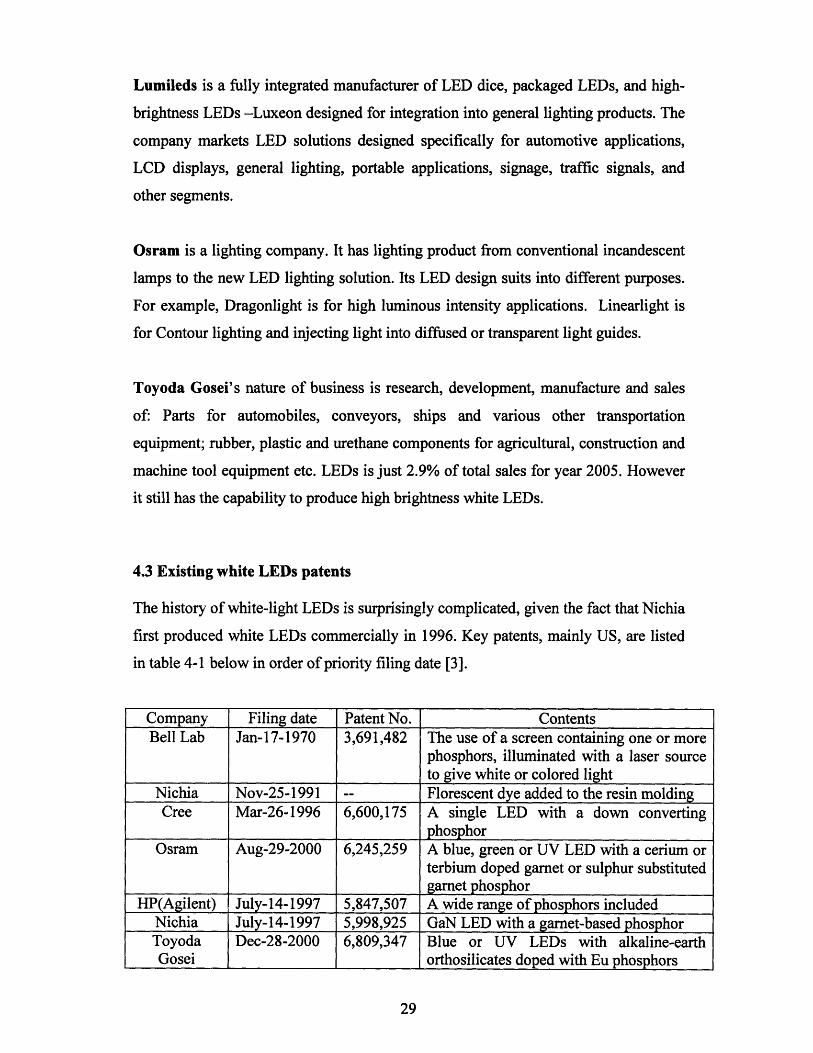

4.3 Existing white LEDs patents

The history of white-light LEDs is surprisingly complicated, given the fact that Nichia

first produced white LEDs commercially in 1996. Key patents, mainly US, are listed

in table 4-1 below in order of priority filing date [3].

Company Filing date Patent No. ContentsBell Lab Jan-17-1970 3,691,482 The use of a screen containing one or more

phosphors, illuminated with a laser sourceto give white or colored light

Nichia Nov-25-1991 -- Florescent dye added to the resin moldingCree Mar-26-1996 6,600,175 A single LED with a down converting

phosphorOsram Aug-29-2000 6,245,259 A blue, green or UV LED with a cerium or

terbium doped garnet or sulphur substitutedgarnet phosphor

HP(Agilent) July-14-1997 5,847,507 A wide range of phosphors includedNichia July-14-1997 5,998,925 GaN LED with a garnet-based phosphorToyoda Dec-28-2000 6,809,347 Blue or UV LEDs with alkaline-earthGosei orthosilicates doped with Eu phosphors

Table 4-1 Key US patents covering white LEDs

Among these patents, a key difference is the choice of phosphor, or "down-

converting" material. The major phosphors are listed in table 4-2 below:

Yttrium aluminum garnet (YAG) doped with cerium, excited at about 460 nm andwith a broad emission peak centre at 550 nm.Terbium aluminum garnet (TAG), licensed by Osram to several manufacturers.Sulphide phosphors such as strontium thiogallate doped with europium, excited at 460nm and emitting in the green (550 nm), or strontium sulphide doped with europiumand emitting in the red.Silicate-based structures such as those patented by Toyoda Gosei and Tridonic, andalso by Intematix.Organic phosphors or dyes. It is not clear if a "fluorescent dye" would cover the firsttwo categories.

Table 4-2 Major phsphors patented

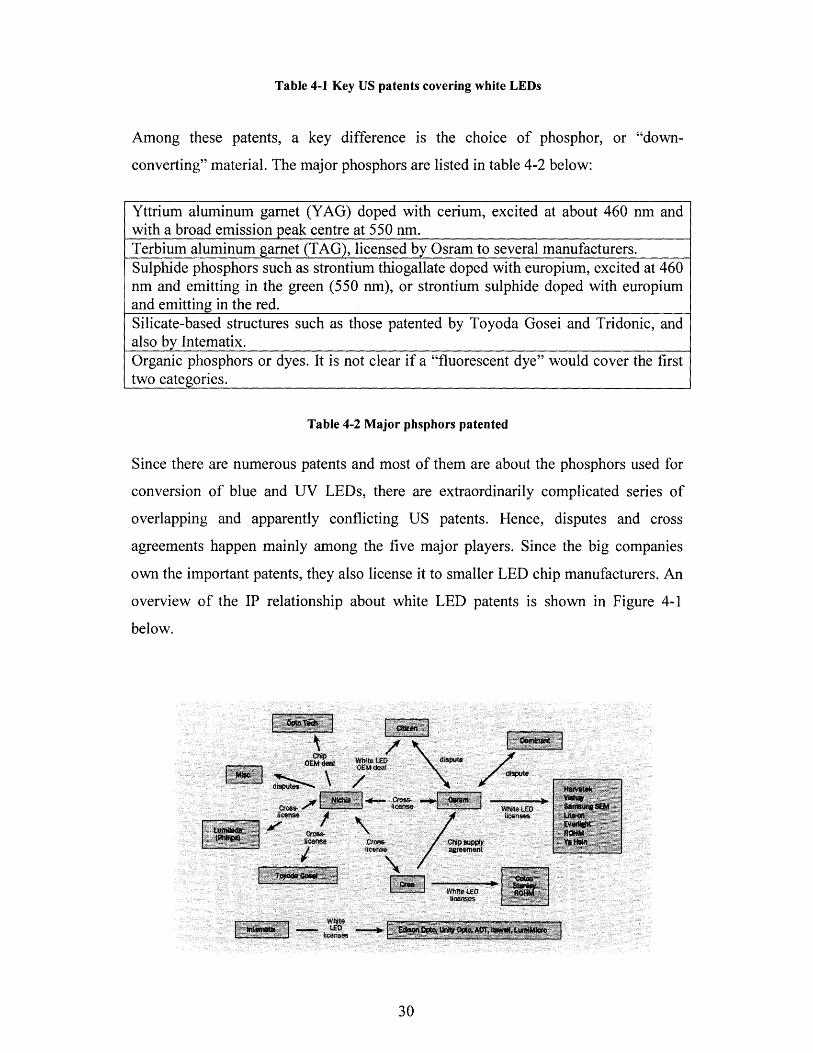

Since there are numerous patents and most of them are about the phosphors used for

conversion of blue and UV LEDs, there are extraordinarily complicated series of

overlapping and apparently conflicting US patents. Hence, disputes and cross

agreements happen mainly among the five major players. Since the big companies

own the important patents, they also license it to smaller LED chip manufacturers. An

overview of the IP relationship about white LED patents is shown in Figure 4-1

below.

Figure 4-1 Deals and disputes in the white LED industry: the key intellectual propertyrelationships as of September 2005

Andrew Phillips of phconsult Ltd reports on a situation: the white LED area is a

minefield of patents, cross-licensing agreements and infringement lawsuits involving

the big five manufacturers. This can prove extremely daunting for new players

entering the field.

However, apparently QD WLED can avoid these disputes about patents, since QD

phosphor, which has a nanocrystal form, is totally different from conventional

phosphors described by these patents. This is another advantage of QD WLED

technology. It gives a steady position for the newly started business among the

competitive market and complicated IP network.

4.4. Quantum dot LED patents

There are also patents on quantum dot LEDs. Below are two important patents on QD

phosphor and QD in between pn junction.

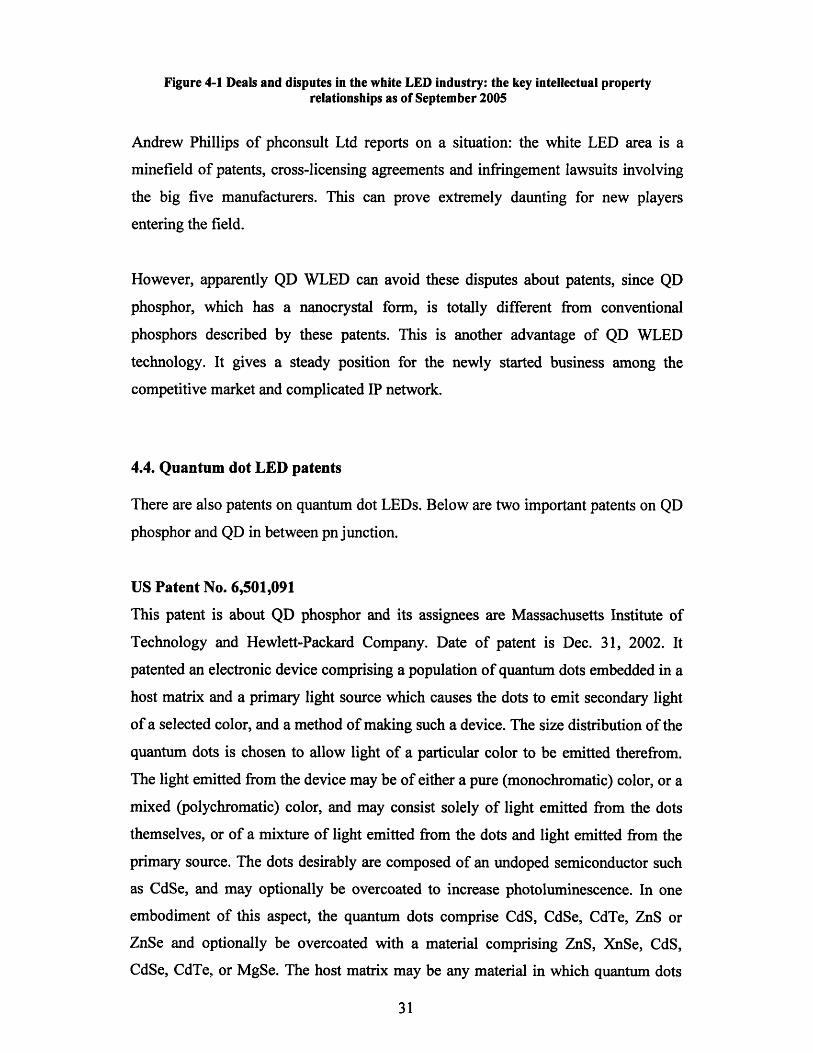

US Patent No. 6,501,091

This patent is about QD phosphor and its assignees are Massachusetts Institute of

Technology and Hewlett-Packard Company. Date of patent is Dec. 31, 2002. It

patented an electronic device comprising a population of quantum dots embedded in a

host matrix and a primary light source which causes the dots to emit secondary light

of a selected color, and a method of making such a device. The size distribution of the

quantum dots is chosen to allow light of a particular color to be emitted therefrom.

The light emitted from the device may be of either a pure (monochromatic) color, or a

mixed (polychromatic) color, and may consist solely of light emitted from the dots

themselves, or of a mixture of light emitted from the dots and light emitted from the

primary source. The dots desirably are composed of an undoped semiconductor such

as CdSe, and may optionally be overcoated to increase photoluminescence. In one

embodiment of this aspect, the quantum dots comprise CdS, CdSe, CdTe, ZnS or

ZnSe and optionally be overcoated with a material comprising ZnS, XnSe, CdS,

CdSe, CdTe, or MgSe. The host matrix may be any material in which quantum dots

may be dispersed in a configuration in which they may be illuminated by the primary

light source [4].

1222 -

16

in

* fD

"o,• •

Figure 4-2 Two embodiments of an LED according to the invention22-red emitting QD; 18--green emitting QD; 12-matrix; 10--light source

Another relevant patent is US Patent No. 6914265, which is done by the same group of inventors.

US Patent No. 6,645,885

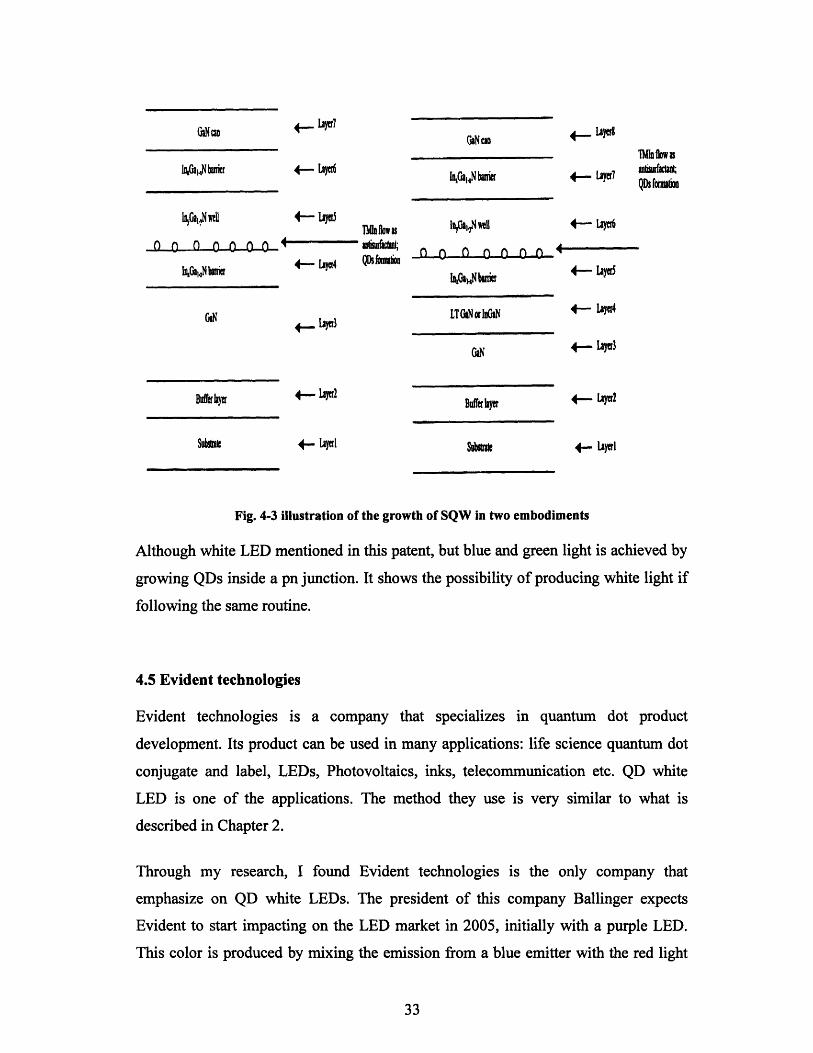

This patent is about QD grown in pn junction. Its assignees are National University of

Singapore (NUS) and Institute of Material Science and Engineering (IMRE). Date of

Patent is Nov 11, 2003. In this patent, Indium Nitride (InN) and Indium-rich Indium

Gallium Nitride (InGaN) quantum dots embedded in single and multiple InxGal-.N/

InyGal.yN quantum well (QWs) are formed by using TMIn and/or Triethylindium

(TEIn), Ethyldimethylindium (EDMIn) as antisurfactant during MOVCD growth.

Controlled amounts of TMIn and/or other Indium precursors are important in

triggering the formation of dislocation-free QDs, as are the subsequent flows of

ammonia and TMIn. This method can be readily used for the growth of the active

layers of blue and green light emitting diodes (LEDs) [5].

1

I llY\

# L,#, -- | ] I

W m +, - LAW7

kGakNcnr 4-- LOe

I10an0wet 4 - La TIfw

() n i) f) 0- 4 06OWnt10G1-1Nbsrir 4- Lacr4 QDSf hIiou

GiN 4 -t•j.,l'Ibn

Bufrhyer

Subt*et

4- *2

GN w

n1Gal.,N buier

Iba1f* 4- iycd

h1AjklNhf 4- 1iye

OLN +- layU3

.ff*e *

4- Lyrl Sf*ia

Fig. 4-3 illustration of the growth of SQW in two embodiments

Although white LED mentioned in this patent, but blue and green light is achieved by

growing QDs inside a pn junction. It shows the possibility of producing white light if

following the same routine.

4.5 Evident technologies

Evident technologies is a company that specializes in quantum dot product

development. Its product can be used in many applications: life science quantum dot

conjugate and label, LEDs, Photovoltaics, inks, telecommunication etc. QD white

LED is one of the applications. The method they use is very similar to what is

described in Chapter 2.

Through my research, I found Evident technologies is the only company that

emphasize on QD white LEDs. The president of this company Ballinger expects

Evident to start impacting on the LED market in 2005, initially with a purple LED.

This color is produced by mixing the emission from a blue emitter with the red light

4~ IA)l!I Uliflow;4- Lacri awucas~~iQDS fna&d

4- LaIr

4- LIyetl

from down-converting nanocrystals. The white LED market is seen as a mid-term

project, two years from revenue generation [6].

However, Evident is a company that produces QDs. It is not an LED manufacturer. It

is still possible to open a company that concentrates on LED production and design

and is more proficient in LED field. In this case, there can be collaboration between

our QD LED company and Evident in order to accelerate the speed of development of

this technology [7,8].

Reference

[1]. Solid state lighting, National programs

[2]. http://lightemittingdiodes.globalspec.com/specsearch/suppliers/opticsoptical_

components/light_sources/light_emitting_diodes?SrchItem=2&RegEvent=new

[3]. Small companies fight for a foothold in white LED sector", Ledmagzine,

October 2005

[4]. US patent 6,501,091

[5]. US patent 6,645,885

[6]. http://www.compoundsemiconductor.net/articles/magazine/10/12/2/

[7]. www.evittech.com

[8]. "phosphors development for LED lighting", III-Vs Review, the advanced

semiconductor magazine, April 2005

Chapter 5 Business model

5.1. The stage of technology development

To see if a technology is suitable for establishing a company, it must be ready to

develop a product or service from it using standard engineering practice. The

technology must be advantageous enough so that it enables development of a product

or service that can hold its own against likely competitors at the time of its market

entry. The technology also needs to be protectable through some combination of

patents [1]. The QD white LEDs technique also needs to be examined according to all

these criteria before any investment is made.

It may take 30 years or longer for a new technology to develop from its birth till its

commercialization. An example is from the invention of first point contact transistor

in year 1947 to first integrated circuit in 1957 till today's computer. This process can

be demonstrated in Figure 5.1. The big peaks show the major obstacles that need to be

overcome before the technology is fully explored and utilized. People's confidence

about it in market will remain low, until it reaches the point that only small obstacles

remain. The best investment point is at the cross point of technology uncertainty and

confidence in chosen market, where you have the advantages to occupy the market in

front of late coming competitors and at the same time with relatively low risk.

Teclmologic,Barriers

uncertaWUty

"Technology Driven" "Market Driven""Broad Market Impact" "Good Focus"

Figure 5-1 Technology development and confidence in chosen market [2]

4 0 +..--

The first commercially usable LEDs were developed in'the 1960's by combining three

primary elements: gallium, arsenic and phosphorus (GaAsP) to obtain a 655nm red

light source. At that time, the brightness was low and only red color was available, so

the applications were very limited. Over the past few decades, the technology has

developed and overcome several major obstacles. In the 1970's, additional colors and

wavelengths became available, such as green and yellow. It wasn't until the 1980's

when a new material, GaA1As (gallium aluminum arsenide) was developed, that a

rapid growth in the use of LEDs began to occur. GaAlAs technology provided

superior performance over previously available LEDs. The brightness was over 10

times greater than standard LEDs due to increased efficiency and multi-layer,

heterojunction type structures. Recently, the usage of InGaAlP makes the brightness

even higher and blue LEDs have become available in production quantities.

Due to a host of developments and improvements after their initial discovery in the

50's/early 60's, the current red LED technology is very mature. However, in

comparison, blue LED is delayed by 30 years. So if we plot Figure 5.1 for red and

blue LED separately, we find that red and blue technologies are shifted by 30 years.

Red is far beyond the tipping point but blue just comes close to it. If we plot Figure

5.1 with respect to solid state lighting, which requires the blue, it appears that we are

quite close to the tipping point, about 15 years after the blue LED's significant

moment at Nichia.

At the tipping point there are only some small obstacles lying ahead before LEDs

finally achieving the general lighting goal. The minor difficulty that remains is how to

get equally good quality light as incandescent and luminescent light with low cost and

high efficiency. To solve these minor problems, investigation and improvements are

needed in several areas, such as epitaxy and packaging. According to the analysis in

chapter 2, QD WLED technique has the potential to be the solution to finally

overcome one of these minor barriers from the packaging point of view at the initial

stage, and probably most of the barriers at later stage when QD technology becomes

mature [3].

Furthermore, QD white LED technique is protectable, because most of the patents on

LED are about normal phosphors and the disputes among the major companies are

also not related to QD phosphor. The protection of patents avoids trouble in our

company development and ensures a market where we have no similar competitors.

However, we can see that the quantum dot in pn junction technique is not a suitable

technology to invest at this stage. It is still in its infancy stage and it has large

obstacles to overcome. The market confidence about this technique is very low

according to some professionals from LED industry [10]. This is mainly due to the

difficulty in growing quantum dot with good control of size and arrangement, which

leads to very low yield in real production.

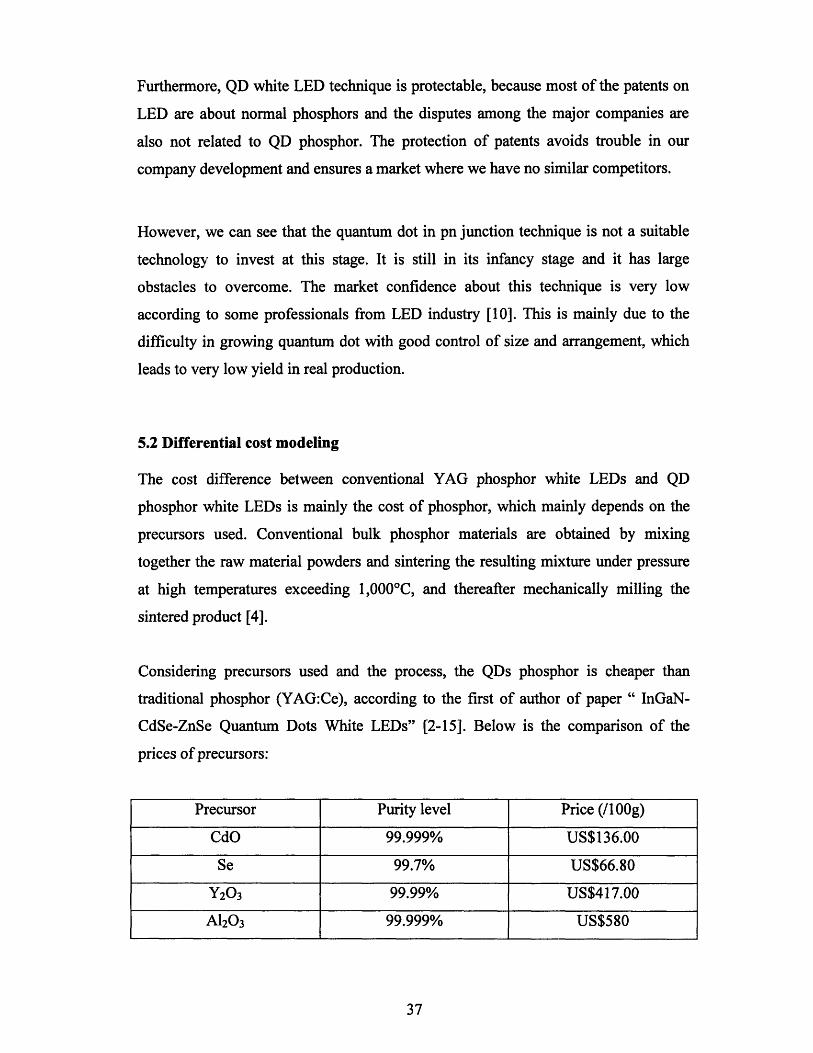

5.2 Differential cost modeling

The cost difference between conventional YAG phosphor white LEDs and QD

phosphor white LEDs is mainly the cost of phosphor, which mainly depends on the

precursors used. Conventional bulk phosphor materials are obtained by mixing

together the raw material powders and sintering the resulting mixture under pressure

at high temperatures exceeding 1,0000 C, and thereafter mechanically milling the

sintered product [4].

Considering precursors used and the process, the QDs phosphor is cheaper than

traditional phosphor (YAG:Ce), according to the first of author of paper " InGaN-

CdSe-ZnSe Quantum Dots White LEDs" [2-15]. Below is the comparison of the

prices of precursors:

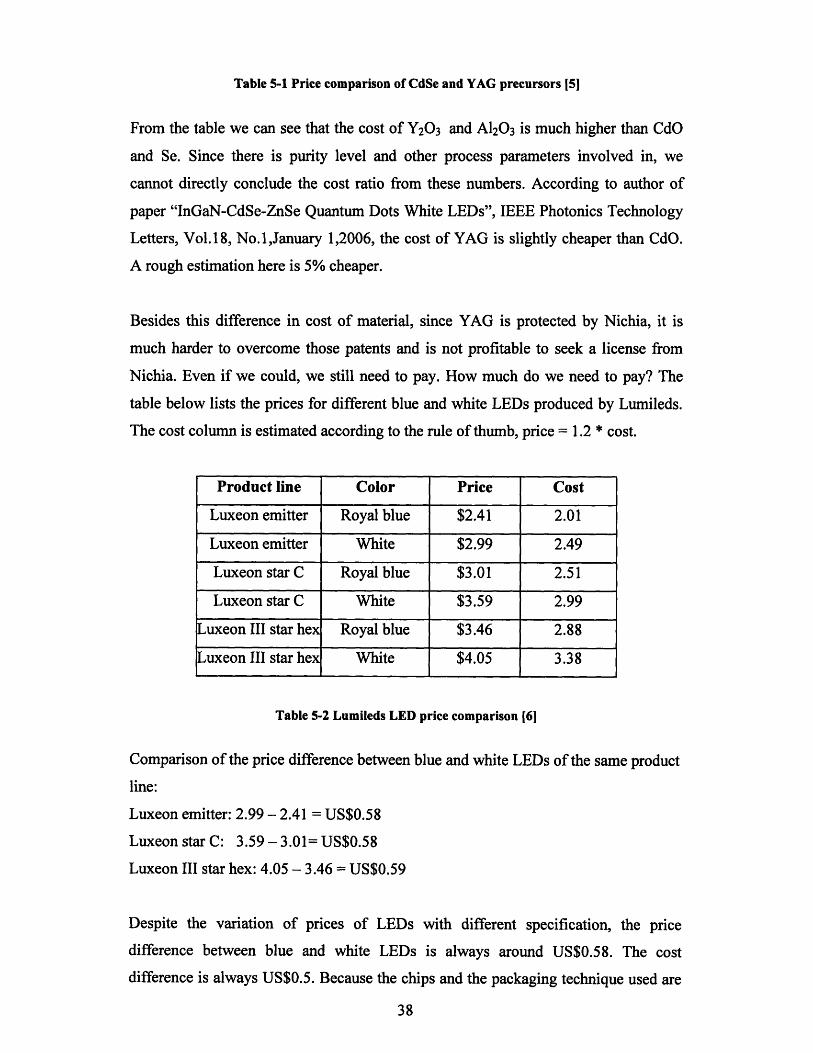

Precursor Purity level Price (/100g)

CdO 99.999% US$136.00

Se 99.7% US$66.80

Y20 3 99.99% US$417.00

A120 3 99.999% US$580

Table 5-1 Price comparison of CdSe and YAG precursors [5]

From the table we can see that the cost of Y20 3 and A120 3 is much higher than CdO

and Se. Since there is purity level and other process parameters involved in, we

cannot directly conclude the cost ratio from these numbers. According to author of

paper "InGaN-CdSe-ZnSe Quantum Dots White LEDs", IEEE Photonics Technology

Letters, Vol.18, No.1,January 1,2006, the cost of YAG is slightly cheaper than CdO.

A rough estimation here is 5% cheaper.

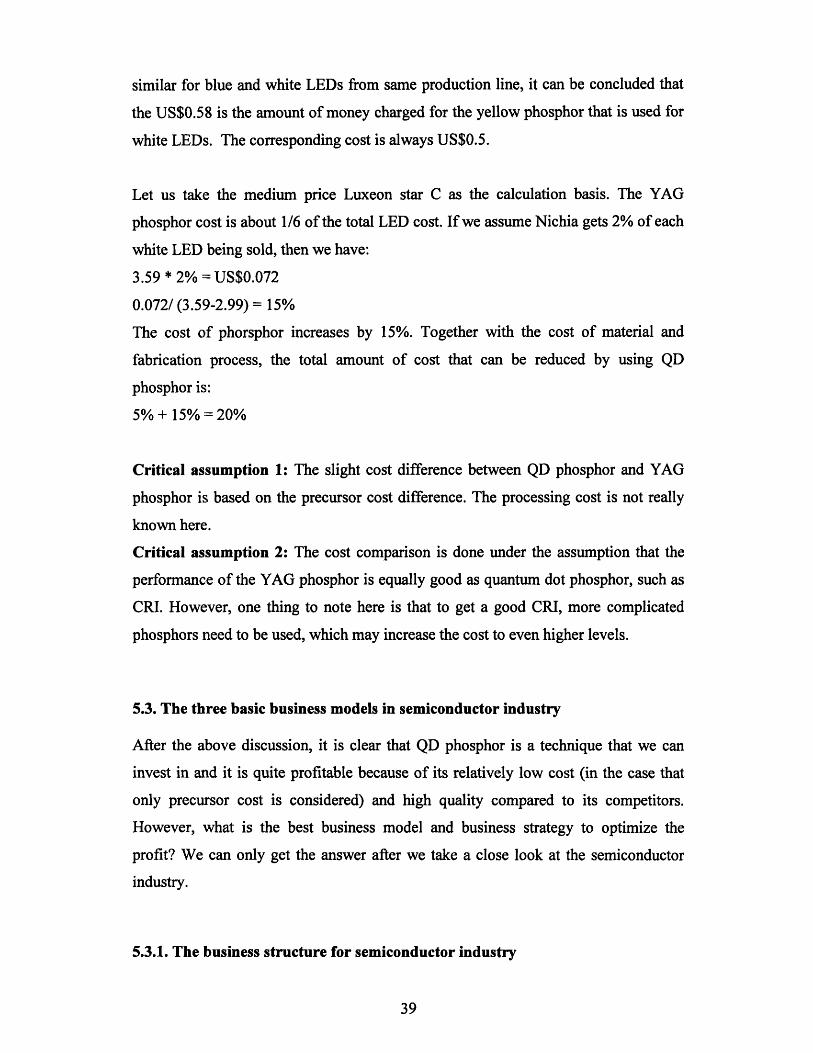

Besides this difference in cost of material, since YAG is protected by Nichia, it is

much harder to overcome those patents and is not profitable to seek a license from

Nichia. Even if we could, we still need to pay. How much do we need to pay? The