Management accounting and control system changes in a public sector context: A case study

35

See discussions, stats, and author profiles for this publication at: http://www.researchgate.net/publication/251812984 MANAGEMENT ACCOUNTING AND CONTROL SYSTEM CHANGES IN A PUBLIC SECTOR CONTEXT: A CASE STUDY ARTICLE CITATION 1 DOWNLOADS 821 VIEWS 127 1 AUTHOR: Umesh Sharma The University of Waikato 38 PUBLICATIONS 137 CITATIONS SEE PROFILE Available from: Umesh Sharma Retrieved on: 24 July 2015

Transcript of Management accounting and control system changes in a public sector context: A case study

Seediscussions,stats,andauthorprofilesforthispublicationat:http://www.researchgate.net/publication/251812984

MANAGEMENTACCOUNTINGANDCONTROLSYSTEMCHANGESINAPUBLICSECTORCONTEXT:ACASESTUDY

ARTICLE

CITATION

1

DOWNLOADS

821

VIEWS

127

1AUTHOR:

UmeshSharma

TheUniversityofWaikato

38PUBLICATIONS137CITATIONS

SEEPROFILE

Availablefrom:UmeshSharma

Retrievedon:24July2015

1

MANAGEMENT ACCOUNTING AND CONTROL SYSTEM CHANGES IN A

PUBLIC SECTOR CONTEXT: A CASE STUDY

UMESH SHARMA

DEPARTMENT OF ACCOUNTING AND FINANCIAL MANAGEMENT

UNIVERSITY OF THE SOUTH PACIFIC

P.O.BOX 1168,

SUVA, FIJI.

2

MANAGEMENT ACCOUNTING AND CONTROL SYSTEM CHANGES IN A

PUBLIC SECTOR CONTEXT: A CASE STUDY

ABSTRACT

This paper looks at the management accounting and control system (MACS) changes in the Housing Authority of Fiji (hereafter HA) from the wider social and political dimensions. The HA has been set up to provide affordable shelter and mortgage finance for low and middle-income earners in Fiji. The subject organisation has been able to meet the demands of customers. Presently, the HA has been able to maintain a stock of its products (houses and sites) and has diversified further to provide loans of different types to its customers. Common amongst these are mortgage loans for purchase of building plots, cash loans for the buying, renovation, expansion and improvement of houses, housing loans to village communities; and development loans for other agencies providing the low- middle-income housing and building plots. The case study on the HA attempts to obtain an in-depth understanding of MACS in operation, with particular emphasis on the changes during the last decade. The discourse of this research, its arguments and conclusions have been constructed through an interpretive study of the HA. The data collected suggest that the wider social and institutional Structures have been influential in bringing about changes in MACS at the HA. It demonstrates that the organisational and control changes at the HA were the separation of the Public Rental Board from the HA, innovations in the Finance Division, introduction of Total Quality Management and performance measurement. The findings provided support to the three theories of Contingency, General Systems and Institutional as the data collected influenced the development of these theories. This study also reinforces the findings of other researchers claiming that the wider social, political, institutional and economic contexts govern the ways MACS operates in the organisation. Keywords: Management accounting and control system, Housing Authority, Changes, Contingency theory, Institutional theory, Fiji.

3

INTRODUCTION

There is a diversity of influences, which change accounting and control systems in organisations (Scapens and Roberts, 1993; Hoque and Hopper, 1994, 1997; Burchell et al., 1980; Neimark & Tinker, 1986; Broadbent and Guthrie, 1992; Broadbent, 1999; Otley, 1994). These influences include the historical, social and political dimensions of the economy within which organisations are embedded. Thus, accounting practice as a social construct can be understood by exploring the historical development of accounting and identifying the various influences of accounting change (Scapens & Roberts, 1993; Luft, 1997). The historical, organisational and economic perspectives offer explanations of the emergence of organisational accounting and the reasons for their change (Hopwood, 1983, 1999). This paper attempts to obtain an in-depth understanding of MACS in operation, with particular emphasis on the changes during the last decade in a public sector organisation, the HA. It is argued that MACS as a social practice and the changes therein are understood better in the context of the influences of a wider social order within the historical, social, political and economic dimensions of the economy. Apart from identifying the influences of the wider structures, it is essential to probe and explain the underlying forces and processes which were/are at work. These underlying forces are the historical, social and political dimensions of the economy, while the wider structures are the State policies, aid agencies like the World Bank, and the Asian Development Bank and the global trends within which organisations are embedded. The discourse of this paper, its arguments and conclusions have been constructed through an interpretive study of the HA. The study examines the influences or pressures of the wider structures in bringing about changes in MACS at the HA. A national policy on public sector reform eventuated in Fiji. This was influenced by a global trend. Consequently, the HA was restructured, so that it shortly becomes corporatised. Financial performance indicators, Total Quality Management (TQM), innovations in Finance Division, separation of the Rental Board from the HA came up as a result. To date, scant attention is paid to empirically address reasons for MACS changes in a particular setting. The focus of this paper is to address this apparent gap. In order to achieve this aim, the paper documents the incidence of MACS changes in a State-owned housing institution in Fiji. This study represents an exploratory case study that is intended to explore reasons for MACS changes in the subject organisation. Such an endeavour can open a new path of research, which may improve our understanding of the factors that influence the adoption of MACS changes in the government owned organisations. The following section outlines the theoretical basis of this study. Next, the study's research method is discussed. Subsequent sections present the research findings, a discussion of the findings and conclusions.

4

THEORETICAL BASIS A large number of studies in management accounting have concluded that the success of management control system impinges upon the wider social, historical, political and cultural factors that are external to an organisation (Hopwood, 1987; Neimark & Tinker, 1986; Burchell et al; 1980; Miller & O'Leary, 1990; Scapens & Roberts, 1993; Hoque & Hopper, 1994, 1997; Broadbent & Guthrie, 1992; Broadbent, 1999). These wider factors bring about changes in MACS in organisations. As individual firms strive to construct more profitable conditions for themselves, they introduce technological, social and organisational innovations which, if they are successful, are adopted by other firms, and collectively transform the social context in which they are situated and hence their existence as well (Neimark & Tinker, 1986; Hopwood, 1978, 1987). The increasing pace of change and the growing size and complexity of organisations have created a need for more rapid and sophisticated accounting and information system developments. Increasingly, therefore, business and public organisations have turned to outside consultants and researchers for help (Hopwood, 1978). The external consultants suggest changes for a more efficient running of organisations. Thus, it can be said that they are catalyst for MACS changes as well. A diversity of influences shape an organisations accounting system (Scapens and Roberts, 1993). It has been argued elsewhere that all reproduction of social practice is historical and contingent. The social, political and economic factors are seen as being able to provide bases for accounting change (Hopwood, 1999; Burchell et al; 1980; Broadbent & Guthrie, 1992; Broadbent, 1999; Innes & Mitchell, 1990). Hopwood (1987, 1999) sees accounting in its organisational context, and how it is implicated in organisational change. The wider social, economic, political and institutional contexts govern the way management control operates in organisations (Hoque & Hopper, 1994, 1997; Hoque & Alam, 1999). In Hoque and Hopper's (1994) case study, the external aid agencies and the State were major influences in management controls. Their paper drew from a research in Bangladesh Jute mill, which has gone through intense changes through wider social and unstable political condition. Further, Hoque and Hopper's (1997) study of budgetary characteristics in the nationalised jute mills of Bangladesh found that five external factors (political climate, industrial relations, competition, aid agencies, and government regulations) were deemed to affect budget-related factors such as participation, accountability for budget, budget evaluation, budget analysis, interactions among managers and budget flexibility. The analysis of data revealed a significant relationship between environmental factors and budget-related behaviour. Political factors, industrial relations and market competition were major influences on how budgeting systems were perceived. Evidence also showed that the extensive budget processes within the jute mill owed much to the pressure of aid agencies. Often they were a condition for further funding. To achieve a full picture of innovation, one needs to identify the ways in which diverse types of events-institutional, technical, political, moral are linked together to provide the conditions, which make certain types of innovations possible (Miller and O'Leary, 1990). All innovations are embedded on institutional and political factors. The global trends of public sector reform seem to be creating innovations in organisations. These reform

5

programmes are normally a pre-condition of donor institutions such as the World Bank and the Asian Development Bank for funding in developing countries (see Nandan, 1999). Countries, which have committed to structural adjustment programmes with these institutions, may face the pressure to introduce reforms. Consequently, the State tries to convert its public sector organisation into private ownership through these reform programs. The changes are carried out so that organisations become more efficient and cost effective. RESEARCH METHOD Research Strategy and data Given the study's theoretical focus, essentially this is a naturalistic research exercise that focuses on the case study strategy (see Yin, 1981, 1988; Humphrey and Scapens, 1996). It seeks to document the incidence of MACS changes in the subject organisation. Prior assumptions and beliefs affect all research. In this study, organisations and society were presumed to be socially and institutionally constructed systems of reality (Morgan and Smircich, 1980; Chua, 1986; Hoque and Alam, 1999; Burrell and Morgan, 1979; Hoque and Hopper, 1994). Thus, the principal style of investigation adopted was open- ended intensive field research in the interpretive tradition (see Hoque and Hopper, 1994; Hopper and Powell, 1985; Scapens, 1990). Consequently, from the outset, the researcher believed the interpretive approach would be more appropriate for examining MACS changes at the HA. Further, case study researchers rely considerably on the description of events provided by organisational participants. Thus case studies represent interpretations of interpretation (see Scapens and Roberts, 1993). During the study, it became evident that the environmental factors were the major influences on MACS changes. Following the analysis of the case study, three main theoretical approaches were deemed pertinent for this study. This may be described as General Systems, Contingency and the Institutional theory. These theoretical perspectives explained adequately the data that were available. The researcher had previously also carried out some work on these theoretical perspectives, and was aware of their usefulness and shortcomings. Thus, by using multiple theories of control, one can take advantage of their complementaries and build a more holistic analysis (see Hoque and Hopper, 1994; Ansari and Euske, 1987; Berry et al., 1991). The General Systems theory (GST) is framed in a philosophy, which argues that the only reasonable way to study an organisation is to study it as a system (Von Bertalanffy, 1973; Llewellyn, 1994; Chenhall and Langfield-Smith, 1998). The Contingency theory, on the other hand, looks at how organisations should be designed to be effective (Burns and Stalker, 1961; Otley, 1980; Schoonhoven, 1981; Langfield-Smith, 1997). The theory articulates that the contingent variables affect organisational design, which in turn leads to effective performance. Institutional theory, on the other hand, proposes that an organisation’s survival requires it to conform to societal norms of acceptable practice to achieve high levels of productive efficiency and effectiveness (Covaleski et al., 1993; Bealing Jr et al., 1998; DiMaggio and Powell, 1983; Rowan, 1982; Gooderham et al., 1999).

6

A triangulation of methods (see Hoque and Hopper, 1997) has been used to gather field data for this study. Firstly, document study was carried out which included a review of annual reports for the last ten years, study of the new corporate plan, memos, performance reports and sample board papers. Secondly, a series of semi-structured interviews each lasting for one to two hours was conducted with staff at the head office in Valelevu and also its branch managers in Lautoka. The interview proceedings were tape-recorded and back-up notes were made. The tapes were transcribed soon after the interview, and a selection of the interview transcripts was fed back to the participants to obtain a clear understanding of the issues involved. Thirdly, questionnaires were administered with various managers and junior staff to provide support for the interview data so as to enhance their validity and reliability. The questionnaire also explored new ground that was not covered by the interviewer. These were handed out to the managers at the end of the interview and collected personally a day or two later. The data was gathered over a 1 1/2-year period between 1999 and 2000. The research consisted of 22 interviews. The interviewees were selected from different sections of the HA such as the Finance, Lending, Human Resources, Legal and Public Relations sections. They were selected from different hierarchical levels of the HA. The topics selected for interviews were mainly on the MACS changes at the HA. These included the separation of the Public Rental Board from the HA; the separation of the Lending Division from the Finance Division, the introduction of TQM and the implementation of the performance measurement at the organisation. The interviews took place in an informal surrounding. Most questions were asked in an open-ended manner to help interviewees to respond in their own ways. The aim was to generate a rich source of field data. The study took place at the HA in Valelevu, Nasinu. Visits were also made to the HA office in Lautoka to provide an additional source of data. Some staff like the Chief Executive, Public Relations Officer, Manager- Finance, Manager-Corporate Planning, Manager- Human Resources, Manager- Lending, Manager- Collections, Accounts Clerk and so on were also interviewed. They were interviewed because they agreed to participate in the study, and were with the organisation when the MACS changes eventuated. The evidence gathered from the interviews and document studies were analysed for patterns and themes (see Ansari and Euske, 1987). These patterns and themes were then classified together to build the descriptions and interpretations presented in the empirical findings section later. Background to the Case Study The Housing Authority (HA) was established under the Housing Act of 1955 as a statutory body to provide “housing accommodation for workers in the city of Suva, Lautoka and in any prescribed area” (HA Corporate Plan, 1996-2005, p. II-i). It was the growing urbanization in the early 1950’s together with increasingly concern for poor housing conditions, especially for low income earners that gave rise to the establishment of the HA. The Housing Act of 1955 had two important provisions to enable workers to (a) lease dwelling houses and/or (b) purchase dwelling houses at a cost commensurate with their incomes. These two considerations meant that the HA is expected to be economically viable, and welfare oriented.

7

For some low-income earners, however, the HA houses were still unaffordable. Recognizing the problem of affordability in acquiring houses, the rented housing program began in 1964 offering temporary accommodation for workers unable to purchase houses. The production of serviced sites began in 1971. By the end of 1987, the HA had produced about 8,300 serviced sites and 1800 rental flats and homes, and provided finance for some 7,000 mortgages (Asian Development Bank Report, 1989). The HA is responsible to the Ministry of Housing and Urban Development. The organization is managed by a Chief Executive who reports to a Board comprising a chairman and five other members appointed by the Minister of Housing and Urban Development (HA Corporate Plan, 1996-2005). The HA policy statement and the Housing Act do not require the HA to be a profit making institution. The emphasis is on providing affordable shelter for low –income groups. It employs 151 staff, which includes permanent staff, expatriates, wage earners, temporary as well as those on contract. Housing is a necessity but because of financial constraints, the ability to purchase one’s own home is often limited to the financially privileged. The lower income earners are normally neglected and the struggle for accommodation has led to squatting. This illegal tenancy has been an issue of recent discussions. Land related problems are one of the major contributions to illegal tenancy. The HA has stepped in, to attempt to solve the problem as reported in its Annual Report as:

That our purpose is to provide shelter for middle to low income workers and to keep searching for better and more affordable ways to serve their housing needs (HA Annual Report, 1996, p.2).

The HA faced financial difficulties prior to the adoption of MACS changes. Thus commercial goals were sought in line with public sector reform policy of the State. These commercial goals were to make the HA self-sustaining. The HA diversified its activity into loan financing. RESEARCH FINDINGS Separation of the Public Rental Board from the HA In 1989, the rental estates were separated from the HA under a new body, the Public Rental Board (PRB hereafter). This was done virtually because cost was more than the rental income generated from the rental estates. One of the managers remarked:

In 1988 the HA was on verge of bankruptcy. It sought offshore finance, which was cheaper. The World Bank and the ADB decided to finance. They [World Bank and ADB] came to government for assistance. Their [World Bank and ADB] recommendation were to separate the HA from rental element. These gave rise to two separate bodies: the HA and the PRB.

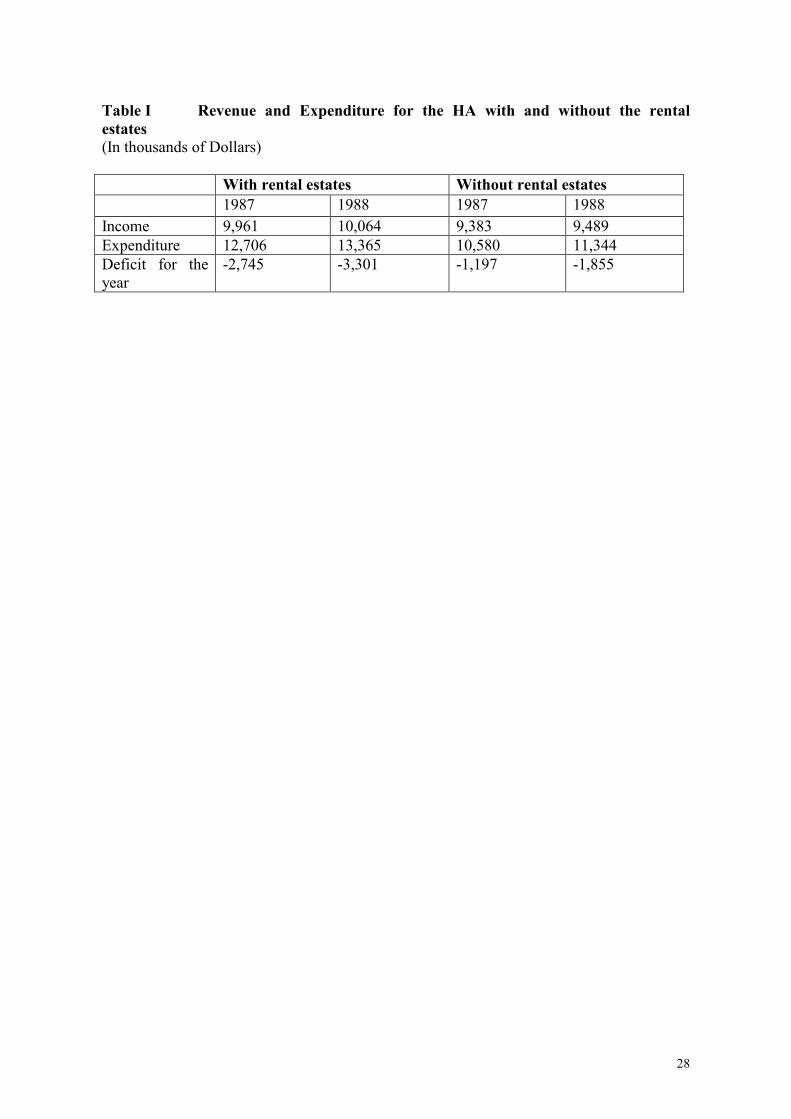

The net deficit for the year 1987 was $7,702,000, whilst for 1988 it was $5,497,000 (HA Annual Report, 1988). The income for rental operation in 1988 was $575,000, whilst the expenditure in the same period was $2,021,000. The current liabilities exceeded current assets in 1988 by $6,419,000. The long-term debt/equity ratio in 1988 stood at 20:1.

8

The rental estates had been imposing financial constraints on the organisation. One of the managers of the HA remarked:

The rental income was peanuts for us. This was nowhere close to the investment we made for the flats. The rental income was as low as $5-6 a week. Even with the low rental people still were in arrears-for months, sometimes even in years.

By the conclusion of 1988, the HA’s operations were suffering from a deeply subsidised rental program for which it no longer received government grants. It had a negative cash flow of $10.8 million (ADB Report, 1989). The HA recovered only 23.2 percent of its expenditure on rental housing in 1987 (ADB Report, 1989). The rental program loss of estimated $1.907m was the largest single component of the 1987 deficits. The total breakdown is as follows: Net rental deficit 1.907million Net Interest Deficit 0.040million Net Administration Expenditure 1.074 million Total deficit for the HA $3.021 million (ADB Report, 1989). A summary of the financial result of the HA with and without the rental estates is shown in table I. Take in Table I. The separation of the PRB from the HA was carried out in 1989. The Table I analyses the results to show the implications of having or not having the rental estates on the HA’s deficits prior to the separation in 1989. It can be observed from Table I that without the rental estates, the HA’s expenditure would be reduced by over $2 million, which would be a significant cost cutting measure for the organisation. There would be close to $500,000 difference in income, which the HA would lose as a result of the separation. However, by the separation, the HA would still be better off by over $1.5 million. Through the separation the deficit would be reduced by 129% in 1987, and by 77.9% in 1988. From the above computations, it is evident that through the separation of the PRB from the HA, the latter’s financial and operational efficiency would be improved significantly. This has been reflected by the improved percentage changes in deficits from the above discussions. With the establishment of the PRB in late 1989, the rental flat operations of the HA were gradually transferred, and a smooth transition was achieved with the transfer of employees. The staff numbers for the HA were reduced to 216 from 320 over the course of the year. This was largely due to the movement of staff to the PRB (HA Annual Report, 1990). All the staff were given a choice whether to join the PRB or to stay with the HA. Some rental staff chose to join the PRB along with others from other divisions. One of the managers of the HA stated:

We were all given the opportunity to move to the new organisation. Mostly, the rental staff and some others moved to the PRB, with the same working conditions. No one was forced to join the PRB.

9

Those that did not get along well with the management of the HA decided to join the PRB. Further, one of the officers at the PRB maintained: We were quite scared to join the new job environment. Jobs may not be secured. There was also speculation that the PRB will not survive. We still have a long way to go. There is a lot of struggle, with financial problems creeping in the organisation. Owing to job security, some of the staff remained with the HA. Some officers regretted joining the PRB because of its heavier debt ratio. This result is consistent with Ferris (1977) work, where using a sample of staff accountants from two public accounting firms, he found that as the level of perceived uncertainty increased, the level of job satisfaction decreased. The uncertainty with the PRB was revealed by one of the managers of the PRB:

…When I initially joined the organisation in 1991, I asked myself, where am I? after inspecting bank statements. How did I get here? Then I realised that it is a challenging job and I must face the challenge.

As discussed earlier, the uncertainty on the job was exacerbated by the PRB’s liabilities exceeding its assets. This is still persistent at the PRB, and is a very unusual situation. The PRB’s survival and continuity is at stake, and the workers are faced with an uncertain environment. However, the management feels that if the government takes over the debts of the organisation, then it would be able to operate on a commercial basis.

The next section discusses the second aspect of change, that of the separation of the Lending Division from the Finance Division.

The Separation of the Lending Division from the Finance Division

The government policy on public sector reform, which is in line with global trends, was one of the major forces behind bringing about the separation of the two divisions. The main thrust of the government’s pubic enterprise reform policy included commercial efficiency, accountability, competition and the transfer of ownership from public to private hands where appropriate. The first two elements of commercial efficiency and accountability were applicable to the exercise of the separation of the Lending Division from the Finance Division. The HA, undoubtedly has reached a stage in its development where it takes a more commercial approach to its activities, particularly the lending activities. This is supplemented by the HA Board paper (1996) which argues that the HA

…operate as far as practicable on a commercial basis and in a competitive environment (p.1).

The Lending Division became one of the profit centres for the HA after it was separated in 1994. The other profit centre at HA is the Property Service Division. The basis of responsibility accounting system is to identify those financial elements in a certain area of activity, which form a controllable set, and to appoint a person responsible for managing this set of financial elements (Wilson & Chua, 1988). Thus, a responsibility centre may be explained as an area of responsibility, which is controlled by an individual. A profit centre

10

is one where its manager is accountable for revenue and expenses. The Lending Division as a profit centre is responsible both for generating revenues and managing costs. It earns revenue based on interest from mortgage granted, along with the fees generated as part of the mortgaging process.

The ADB consultant advised the government to carry out this separation, so that the HA becomes a financially viable organisation and operate on a profit basis. The HA has reached a stage where it has to take a more commercial approach to its activities and in particular the way it handles its funding and lending activities (HA Board Paper, 1995). The consultant reviewed the HA’s borrowings and mortgage lending functions. The specific output of the exercise was to improve the loan processing/ approval procedures and reduce mortgage arrears through improved control.

The Lending Division was separated from the Finance Division in May 1994 as a result of the corporatisation plan of the government. One of the managers argued that

…Public Sector reform could also be attributed to be the reason for the separation of the two divisions. Housing Authority stopped getting subsidies from the government since 1993. With the reform, the HA is to operate on a more viable basis…

This corporatisation plan initiated the restructuring of the organisation into business units in line with the commercialisation approach required by the government, in accordance with its public sector reform policy (e.g. Innes & Mitchell, 1990). The aim of the separation exercise, as discussed previously, was to facilitate the HA to operate on a commercial basis, and in a competitive environment. The major emphasis was to separate operations between production and lending in order to fully introduce cost or responsibility centre accounting and evolve the organisational divisions of the HA into its two main business activities (HA Board Paper, 1994). One of the managers maintained:

Lending is somewhat different function altogether from the finance. This function of lending is related to banks lending function. The Finance Division, on the other hand, looks at bookkeeping matters. …Lending is actually the core business of the Housing Authority. It is a profit centre.

With the establishment of the Lending Division in early 1994, the loan operations as well as the lending staff of the Finance Division were gradually transferred to the Lending Division. This approach was considered necessary in order to promote efficiency in operations and to ensure business survival and growth. One of the managers remarked

…Finance Division’s role was broad. With the separation, its role was narrowed and manageable…

The Finance Division was left with the bookkeeping functions only. The aim behind the separation was to separate the core business of lending. One of the managers argued:

…Our core business was mortgage financing and property development. Our core businesses are our profit centres. …the mortgage financing is part of the lending division.

11

The separation of the Lending Division from the Finance Division has facilitated the organisation to achieve profit. In 1994, with the separation it recorded an improved profit of $687,000 compared to $518,000 in 1993 when they were together. The interest on loan account revenue increased from $8,688,000 in 1993 to $10,593,000 in 1994, when the separation was completed (HA Annual Report, 1994). In 1998, the amount increased to $14.2m (HA Annual Report, 1998). These findings are consistent with Hopwood (1990) who argues that more managers are being exposed to the market forces. The General Manager, Lending had to be responsible for costs and revenues of the Lending Division as it was a profit centre. The HA’s performance improved significantly in 1996 compared to 1995 (HA Annual Report, 1996). Thus, it can be argued that after the separation, the HA consistently made profits. The Lending Division became the profit centre of the HA, and the consultants identified this to be the most effective area of the HA’s business. In order to enhance the commercialisation of the HA, TQM and performance indicators were adopted by the organisation. The next section discusses the TQM at the HA.

Total Quality Management

TQM is seen as a set of concepts and tools, which focus on individuals, groups and organisations for continuous improvement (see Hoque and Alam, 1999). Conventional management accounting systems hardly identifies opportunities for quality improvements (Shank and Govindarajan, 1994; Fowler, 1996; Hoque & Alam, 1999). Shank and Govindarajan note that quality is such an important strategic variable that management accounting can no longer ignore it. The management accounting system can satisfy management's needs for information that supports a quality oriented culture (see Chenhall, 1997; Ittner et al., 1997; Hoque and Alam, 1999).

The Total Quality Management as discussed by Wilkinson and Witcher (1993) can be summarised as having three essential requirements, which are:

Total which means participation of everyone. The TQM requires continuous improvement and getting things accurate the first time. Consequently, teamwork and the maintenance of good relationship are essential in achieving the above.

Quality means meeting customer requirements exactly. The TQM requires customer agreed specifications, which allow suppliers to measure performance and customer satisfaction.

Finally, management means enabling conditions for Total Quality. TQM demands leadership and commitment from senior management to ensure that an appropriate infrastructure exists to support a holistic and not a compartmentalised approach to organisational management.

12

Many organisations have moved towards a total quality management (TQM) path in their quest for quality (Hoque and Alam, 1999; Johnson, 1994; Oakland, 1989). There is also a growing literature on TQM suggesting that organisations that pursue TQM have better productivity, improved market share and improved profitability and efficiency (see Redman, 1995; Pearson et al; 1995; Lal, 1990; Oakland, 1989; Fowler, 1996; Grant, 1995; Lord, 1998; Hoque and Alam, 1999; Wilkinson & Witcher, 1993; Martinez-Lorente et al., 1998; Laszlo, 1998; Macdonald, 1998; Thomson & Thomson, 1995; Wilkinson et al., 1992; Johnson, 1994; Powell, 1995; Maloney & Stower, 1999). It is conclusive that TQM enhances continuous improvement. Improvement, as articulated by Hoque and Alam (1999, p.200) “is measured in terms of providing products or services of high quality and low-cost.”

While it is true that TQM has general appeal, its meaning can only be understood in terms of its organisational context. For instance, from New Zealand experiences, it is evident that fierce competition and customer expectations with regards to quality compelled most firms to focus on ISO certification or TQM adoption (Hoque and Alam, 1999). The HA developed the idea in 1992 as one of its managers remarked:

The idea came from the top, from the previous chief executive. He must have read a lot of books on TQM. It was a top- down thing, not from the middle management. It concerned five directors at that time to implement the system…”

The Chief Executive also traveled to New Zealand and Australia, and had visited some successful companies there carrying out the TQM concept. Also some bigger organisations in Fiji like the Telecom and the Reserve Bank were adopting it, and were successful. These organisations were operating on a commercial basis. Consequently, he borrowed the idea and applied it in the HA’s context, as this had to be operated on commercial basis as well. This is in line with the State’s public sector reform policy. The top management of the HA argued that, the long-term survival of an organisation is dependent on factors like quality, customer satisfaction and operational efficiency. The HA was able to deliver its products on a timely basis to the customers. This facilitated customer satisfaction. Hoque and Alam (1999) on a NZ case study of TQM had similar sentiments. Gaining the approval from management and obtaining their commitment are the first steps towards the successful implementation of TQM in any organisation (Laszlo, 1998). The top-down approach in implementing TQM at the HA enhanced commitment amongst employees. There was a growing commitment from the top on TQM. Consequently, the employees had to go by it.

The HA invited two consultants to implement the TQM. These consultants were hired by the Pacific Asia Quality Foundation (PAQF hereafter). One of the consultants was from the Hawaai Pacific University and the other one was from the University of South Carolina. The PAQF is a professional organisation, which promotes TQM in organisations. It is a commercial organisation, which puts resources together to hire consultants to train its members. From time to time, it hosts quality fora. The PAQF also conducts Quality Management courses in Fiji. The courses on Quality Management are usually two to three days in length and are applicable to various senior and middle management levels. The PAQF is not a consulting organisation (HA Board paper, 1994). Consultants, however, belonging to PAQF offer their fees at a 50% discount to Fiji members. With the assistance from Hawaai Pacific University, it also offered credentials in Quality Management to the

13

HA’s executives, which some managers have completed without travelling abroad. One of the managers maintained:

…We’re members of the Pacific Asia Quality Foundation (PAQF) together with Colonial, FEA, Telecom, RBF and others. We were one of the many organisations to join PAQF…

At least the Telecom and the Reserve Bank of Fiji were members of PAQF, prior to the HA. These organisations were successful in terms of customer satisfaction and profitability. Consequently, the HA became a member in order to adopt the TQM as well. The PAQF indirectly influenced the HA to introduce the formal quality system. It can be argued that the HA adopted the TQM by imitation and copying from one another to increase its external legitimacy. Other Public sector organisations like the FEA and Telecom adopted it, and so did the HA. This is in line with the Institutional theory to be discussed later.

There has been remarkable changes and improvement in the organisation since the implementation of the TQM. For instance, as reported earlier, if the customer applies for a loan now, it is processed within a day or two, provided all the papers are in order. Before TQM was introduced, it used to take a few months to process loans. It used to take longer previously as the staff were lazy in their attitude. With the TQM, they began to realise how important each one of them was to the organisation. The vision and mission of the organisation is quite clear to the employees, and they are working towards it. The vision of the HA is:

To be the leading Housing Finance Company providing competitive and quality services to advance the vision of government towards better housing and living standards for its people.

Further, the mission statement of the HA is:

… to provide on a financially viable basis, timely and cost effective loan finance principally for low and middle income families in Fiji (HA Annual Report, 1998).

TQM is in-built within the mission of the HA. Without the TQM, the vision and the mission of the organisation would not be realised by the workers. Pearson et al., (1995) in the information system context argued that the benefits frequently achieved from TQM included improved customer satisfaction, enhanced quality of products and services, greater productivity, increased flexibility in meeting customer demands, better utilisation of human resources and better management control. The benefits accruing to the HA with the implementation of TQM were more timely approval of loan products, quicker supply of houses in accordance to the customers expectations and improved profitability. The loans as discussed earlier were approved within a day or two, as compared to the previous untimely approval of loans. With the TQM, each employee realised how important he or she was to the organisation. One of the managers remarked:

…Every player realised their importance in the organisation, that is, how important their job was…

This created an environment where the workers were motivated to work harder as they realised the importance of their role in the organisation through the TQM.

14

There were some resistance expressed as well on TQM. Initially when the TQM was introduced in the HA, the workers were a bit reluctant to accept it. However, through training, this reluctance was reduced. One of the managers argued:

…Changing the culture of the organisation was difficult. Management level also agreed to the TQM reluctantly. But it was the directive from the top, so people had to abide by it.

Some of the employees still maintained the lazy attitude towards work. For the implementation of TQM, they had to change their attitude and work more sincerely for the improvement of the organisation. This was somewhat difficult to achieve. Performance indicators, however, attempted to achieve this. This will be discussed later. A few managers, however, were filled with anxiety after the introduction of the TQM. Their anxiety, as discussed earlier, was attributed to the subordinates being given freedom to express views on them. The team leaders were to ensure discussions are centred on the processes, and means to improve them. There were also degrees of fear at the supervisory level as people who were quiet so far, could speak up during these meetings. Through TQM, management functions or tasks are taken to a lower level. This undermines some of the management, but for the commercial viability of the organisation, TQM has been adopted. Everything in the meeting is documented and this goes to the steering committee, which comprise the Chief Executive and other management of the HA. In order to successfully implement TQM, performance measurement is essential in the organisation. TQM is based on the assumption of continuous improvement as fostering a more intense focus on attacking and improving performance (Shea and Kleinsorge, 1994; Powell, 1995; Shank and Govindarajan, 1994; Chenhall, 1997; Maloney & Stower, 1999). With the performance targets, the organisation will enhance a culture, which is oriented towards achieving the targets. This change in the culture would further enhance the TQM at the HA. The performance measurement is expected to include both financial and non-financial indicators, and incorporate into their performance measurement systems, the key factors of quality, customer satisfaction and the productivity (Fowler, 1996; Powell, 1995; Ittner et al., 1997; Ittner & Larcker, 1997). The next section discusses performance measurement at the HA. Performance Measurement As of first June 1993 all staff in executive positions were engaged on a performance basis contract in line with commercial practices. They were put on three-year contractual system and the renewal of the contract was based on the achievement of set targets and objectives for each position. The increase in pay of the senior executive was also commensurate with the achievement of those targets. The annual report (1993) argues that

The movement of salaries for these positions therefore will be relative to the productivity of the incumbents and in turn will be reflective of the overall financial performance of the Authority (p.10).

If a manager meets the target, then only he or she was entitled for pay increases. It also had implications on the HA’s profitability. The HA consistently made profits from 1993 onwards since this system had been implemented.

15

One of the managers remarked that management contract system was introduced as:

this will ensure accountability and make people more responsible. All management are placed on a contractual system for a period of three years. The renewal is based on performance. Employer had the right to hire and fire. This system was introduced to innovate people to work harder.

Each manager tried to achieve the set targets. If they were not meeting the targets, then no bonuses were awarded to them at the end of the year. The bonus was a component of the salary. Once the managers’ contract comes to an end, the achievement of targets are looked at over the previous two to three years before the contract was renewed. If the managers have not attained the targets, then the contract is not renewed. The staff appraisal programme for subordinates, however, has been implemented as from the beginning of 1999. The staff appraisal is for the personal career development of the staff. The management spends roughly forty-five minutes to one hour with the staff in discussing the appraisal of the work. The manager interviews staff together with their immediate supervisors. The action plan, objectives and targets of the staff are agreed upon at this meeting. Thus, after every six months the worker undergoes this appraisal to see whether the targets and objectives have been met or not. The staff appraisal forms are given to the subordinates after every six months. They are expected to fill in a section and return it to their respective supervisors, who will pass this to divisional managers. The workers, on achieving objectives are, rewarded in a form of bonus payment at the end of the year. Those workers, who are identified with certain deficiencies, are sent for further training.

Performance appraisal is a worldwide phenomenon with the Fiji Employers Federation enforcing this in Fiji’s context. This has been adopted by the HA for external legitimacy. Authorities like the Fiji Employers Federation have enforced this on Fiji’s organisations, and this had to be adopted. This is in line with the Institutional theory to be discussed later. There was resistance to the performance contract as well. Some managers resigned because of the manner in which it was implemented. It was inadequately discussed with the managers, and was basically a top-down approach. One of the managers, who left due to his unhappiness in the system, later on became the chairman of the executive board. One of the managers argued about the situation as:

…the boy left to become the boss. This was a political appointment as the “boy” was a close friend of the previous Minister of Housing. The Minister of Housing appointed him as the chairman of the Board of Directors. This had implications on the Chief Executive as he was a Board member too.

One of the other manager’s comments is worthy of note:

some of our staff did not like the idea of the contract system, and left the organisation. At least one manager quit the organisation since the system was in place. Before, the expectation was that everyone would work for 55 years. But now with the system in place, the renewal is based on performance. The initial contract is for three years…

This manager left the organisation as the management contract created uncertainty in the job environment. The continuity of the job after three years was uncertain. This result is

16

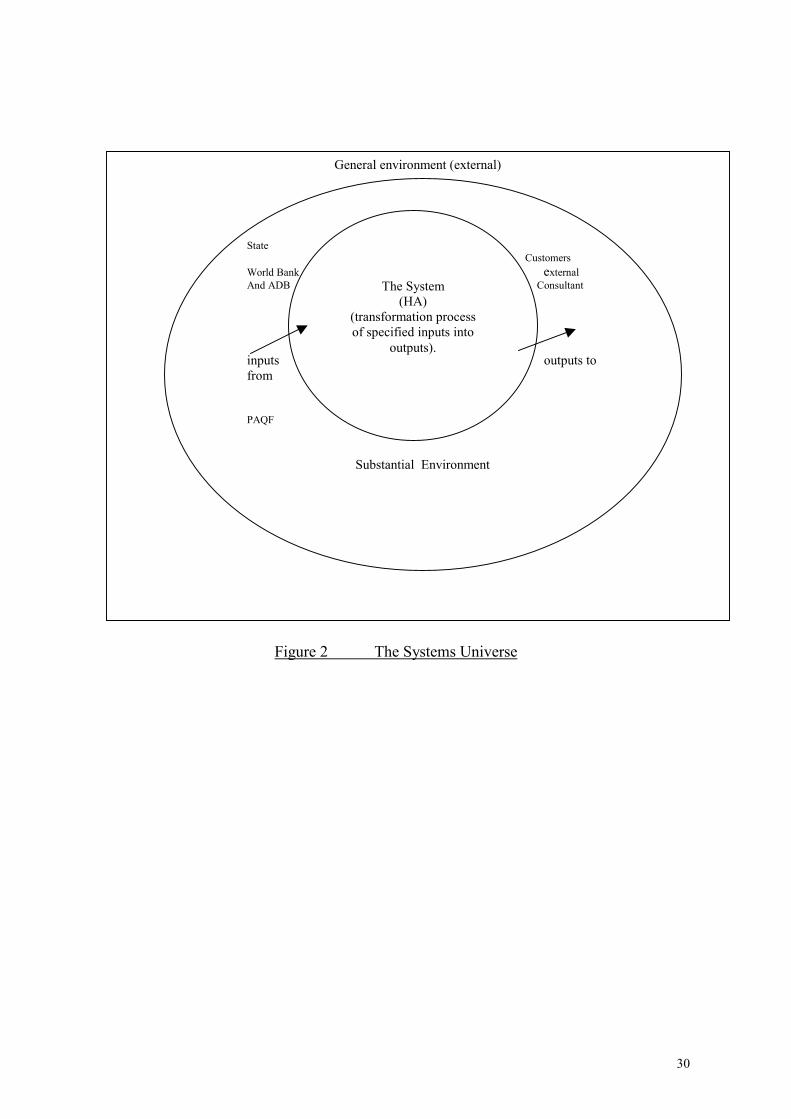

consistent with arguments put forward by Ferris (1977) who suggested that as the level of environmental uncertainty increased, the level of motivation decreased. This leads to turnover on jobs. The renewal of the contract at the HA is based on the achievement of set targets. The performance contract system has, consequently, brought in fear in the organisation. Most managers are performing in the fear that if they do not perform, then their contract may be terminated. Some of these workers have major mortgage commitments with the financial institutions. DISCUSSION AND CONCLUSION This study demonstrates that in order to understand the MACS changes, one needs to look at the external influences. The external environment is critical in bringing about the changes in MACS. In order to understand organisational changes, an understanding of how social, political and economic factors exogenous to the organisation operate is essential. In the case of the HA, as argued earlier, the donor agencies, State and external consultants were the major influences in carrying out the changes in MACS. From the present study, it became evident that the environmental factors were major influences on MACS changes at the HA. These environmental factors included the State, political factors, aid agencies, external consultants and the PAQF. Figure 1 summarises these factors. Take in Figure 1. The study uses three extant theories to explain the data gathered. They are the General Systems, Contingency and Institutional. The General Systems Theory The General Systems Theory is based on the premise that the only meaningful way to study organisation is to study it as a system. A system can be understood as a set of elements standing in inter- relations (Otley, 1983; Katz and Kahn, 1966). The open system theory emphasises the necessary dependence of any organisation upon its environment. The theory recognises the interactions between the organisation and society. It sees organisational boundaries as permeable. The survival of the system is dependent on the relationship with its environment (Burchell et al., 1985; Broadbent & Guthrie, 1992; Llewellyn, 1994). The external environment of the State and the aid agency influenced the changes in MACS at the HA. The HA is interdependent on the actions of the State and the aid agencies. The State pursued the object of public sector reform. In order to be reformed, the HA had to restructure itself in terms of separating the rental element, innovating the Finance Division and instituting the TQM and the performance contract. The HA is the system to be examined. It has to be distinguished from the rest of the universe of objects and phenomena, which is referred to as the environment to the system. For further analytical purposes, the environment needs to be divided into the substantial environment and the general environment (Lowe and McInnes, 1971). The former is defined as part of the environment to the system, which can affect and be affected by the behaviour of the system under investigation. The general environment, according to Lowe and McInnes (1971) constitute the rest of the universe of objects. The system and its

17

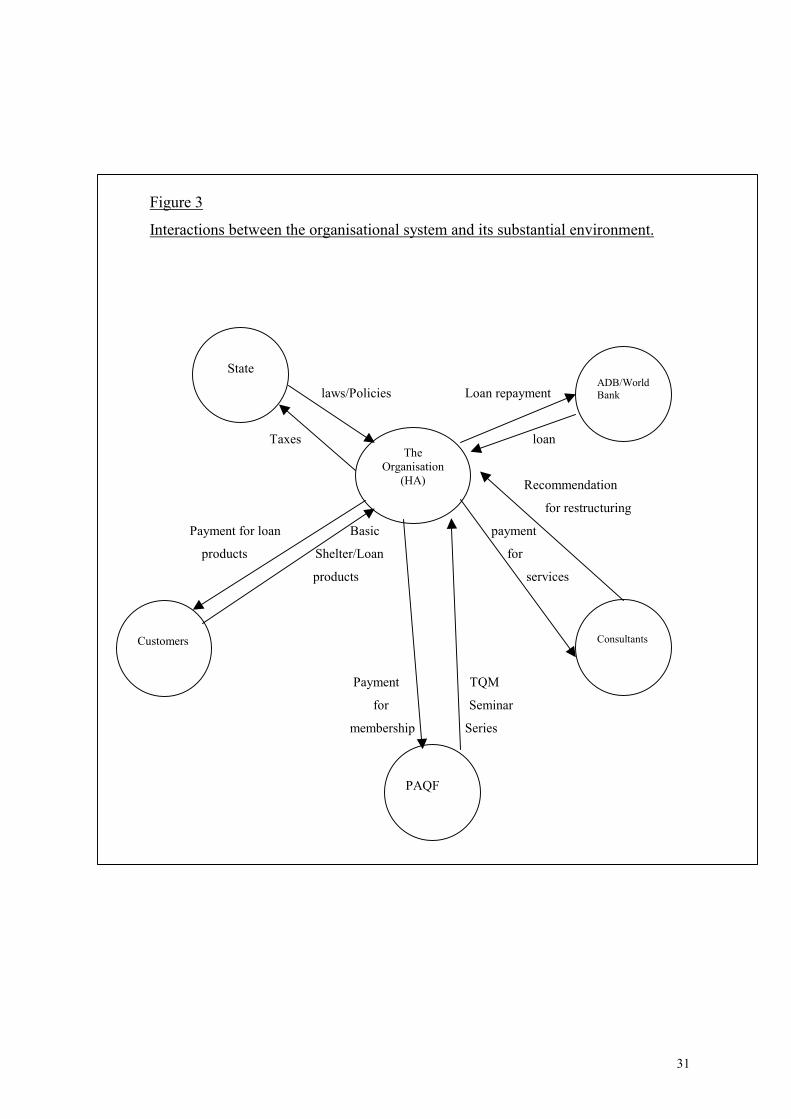

substantial environment are defined as the universe for our particular system analysis. These notions are depicted in figure 2. Take in Figure 2. All elements in the substantial environment are essential to understand as they have a relationship to the system. In HA’s case, inputs include the donor agencies funding, employees from the environment, external consultants which are used by the HA to carry on the transformation process through its improved performance measures, TQM and finance structure and the HA gives to the environment affordable shelter and loan finance on a financially viable basis to low and middle income earners. By employing the concept of systems, the complexities of interactions between organisations and its substantial environment are captured as depicted in figure 3. Take in Figure 3. The systems approach seeks to explain the behaviour of the system by means of studying the interrelationship of parts (see Otley, 1983). Figure 3 identifies a number of major interactions between the HA and its substantial environment. The HA is profoundly affected by and dependent upon its environment for survival. The interaction between the HA and its environment is seen as two-way, with the subject organisation influencing its environment, as well as vice versa. From figure 3, it can be interpreted that the State’s policies affect the HA, and also the HA has to pay taxes on its profit to the State. The HA provides its customers with shelter and loan products, for which they have to pay. The PAQF organises seminars in which the HA employees could participate. In order to maintain membership of the PAQF, the HA has to pay annual membership fees. The consultants also play a vital role in the system. They are hired through the government to carry out the restructuring of the HA so that it operates on a commercial basis. In return, the HA pays the consultants for services. The ADB/World Bank provided loans to the HA to carry out the project of developing new land sites and building of new houses. The HA has to repay the loans to these agencies. The next section discusses the contingency theory. Contingency Theory The Contingency theory approach has an epistemology rooted in positivism (Berry et al., 1991; Burrell & Morgan, 1979). It is an attempt to express the relationships between variables. The underlying model upon which the Contingency theory is based is shown in figure 4. The various propositions as argued by Otley (1980) follow from one another in a linear manner. Some contingent variables are hypothesised to affect the organisation structure, which are in turn associated with effective performance. Take in Figure 4.

Contingency theory articulates that organisational effectiveness is a product of matching between internal organisational elements and the demands created by technology and external environments (Burrell and Morgan, 1979). The organisational design that the organisation needs to adopt to be effective is contingent or dependent upon the contingency factors (Sharma, 1997). Prominent among these are task uncertainty, size, strategy and

18

environment. The forces as discussed above were influential in innovating the organisational structure of the HA. The separation of the PRB from the HA, and the consequent separation of the Lending Division from the Finance Division are ideal illustrations. The contingent variables are considered to be outside of the control of the organisation (Otley, 1980). The Contingency theory advocates that there is no universally appropriate accounting system, which equally applies to all organisations in all circumstances (Sharma and Nandan, 2000). It means no two organisations have identical MACS. MACS is therefore contingent upon a number of factors as shown in figure 5. Take in Figure 5. The TQM concept demonstrates that the type of environment faced by the HA substantially influenced its MACS (Sharma and Nandan, 2000). The theory emphasises that the most effective organisational structure would vary according to the situation the organisation finds itself in. TQM helped to create quality circles at the HA, consequently decentralising its organisation structure. The HA’s focus on TQM was to keep customers satisfied vis- a- vis efficient loan approval and supply of houses. The management contract system has been influenced by the environmental variable of the State’s public sector reform policy. Through the system of management contract system, the HA has been able to establish a greater accountability and a sense of responsibility as argued by Miller & O’Leary (1990) and Hopwood (1987) that accounting change is seen in terms of organisational reform and improvement. The management contract later prevented resistance to the introduction of the TQM. This relates to Miller & O’Leary (1990) and Hopwood’s (1987) insight that accounting not only reflected the organisation as it had been but it also played a significant role in making the organisation. Figure 6 summarises the contingency framework at the HA. Take in Figure 6. Institutional Theory Institutional theorists (DiMaggio and Powell, 1983; Meyer and Rowan, 1977; Gooderham et al., 1999) like contingency theorists argue that organisational practices are shaped by the environment (see also Hoque and Hopper, 1997). However, Institutional theory differs from the Contingency theory as the former demonstrates how and why bureaucratically rational systems of control become transformed when political factors predominate. As such the activities of the HA are geared towards a means of securing external legitimation.

The Institutional theory proposes that an organisation’s survival requires it to conform to societal norms of acceptable practice to achieve high levels of productive efficiency and effectiveness (Covaleski et al., 1993). Many aspects of an organisation’s structure and policies tend to demonstrate conformity with institutionalised rules expressed by external constituents such as society. The societal norm was the public sector reforms, which the HA had to conform to in order for it to be externally legitimate, and to operate on a commercial basis with profit motive. Consequently, many aspects of the formal structure policies of the HA serves to demonstrate a conformity with the institutional rules and

19

expectations expressed by external constituents. The policies of TQM, management on contract basis, separation of the PRB from the HA and innovations in Finance Division all serve to enhance the commercial status of the HA; and a movement away from the welfare emphasis. The observations reported in the present study suggest that TQM adoption at the HA helped in gaining acceptance from professional association such as the PAQF and the State. In addition, quality culture is promoted at the national level in Fiji through organisations such as the PAQF and also the Fiji National Training Council, through their regular quality conferences. The Fiji National Training Council has also initiated the Fiji Quality Awards. The goal of the Fiji Quality Award is to promote Fiji organisations to adopt TQM and improve quality. This award will be implemented from the year 2000, and a number of organisations have applied for these awards. A few of the organisations in Fiji are already ISO 9000 accredited. Certifying organisations like KPMG Peat Marwick, Lloyds, Bureau of Veritus Quality Association play a vital role in disseminating the ISO 9000 standards and advising organisations on TQM. Further, the staff appraisal programme for the junior staff at the HA were enforced by the professional organisation of the Fiji Employers Federation. In order for external legitimacy, the HA adopted this so that they are in consistency with other organisations in the country. That is, the HA adopted this to show consistent values in their institutional environment. The other public sector organisations adopted the staff appraisal programmes as well. In order to remain in acceptance by organisations like the Fiji Employers Federation, it was essential for the HA to adopt this program. In addition some bigger organisations like the Reserve Bank of Fiji and Telecom’s adoption of TQM compelled the HA to adopt it too. Other organisations in Fiji are also following the TQM practice so much so that it may become institutionalised shortly. Limitations and Conclusions The data in this study came from a single public sector organisation, and as such generalisations cannot be drawn from a single case study (Hagg & Hedlund, 1979; Hoque and Hopper, 1994, 1997). That is, any generalisation of its results to the public sector in Fiji or beyond is not possible without some caution (see also Hoque and Hopper, 1997). It would be incorrect to assume that research on public sector organisations in developing countries is not pertinent to advanced countries and vice versa. Hoque and Hopper (1997) argue that the public sector organisation existing in the western countries have been models for developing countries. Western public sector organisations have undergone similar changes in MACS (Hoque and Alam, 1999; Chenhall and Langfield-Smith, 1998; Cobb et al., 1995; Thomson & Thomson, 1995). As such, some generalisations can be made.

It is also essential that similar study be undertaken in other public sector organisations in order to draw generalisations on MACS changes. Some similar studies, however, have been done in Fiji’s context such as those of Nandan (1997a, 1997b) on the Fiji Development Bank and Achary (1998) on the Fiji Pine Ltd. This would warrant some generalisations to be made. The present research orientation is rooted in the interpretive tradition of understanding events (see also Hoque and Hopper, 1997). The present research, which is rooted in interpretive framework, is believed to reveal more significant results than the survey methods (see Hoque and Hopper, 1997).

20

The research relied on interviews of organisational personnel on MACS changes. As with any qualitative exercise, there could be problems with the interpretations of issues. It is difficult to see through other people’s eyes and interpret events from their point of view. The subject’s view of reality and the interpretation of that social reality is always problematic; for how feasible is it to perceive as others perceive (Nandan, 1997b). As discussed earlier, there have been means used to minimise the above problems in the case, but they cannot be eradicated completely. The three most common approaches, according to Nandan’s (1997b) insight are the use of triangulation of research methods, respondent validation and formation of a research team. The first two have been used in this study, and have consequently reduced the problems of case study research.

In addition, by investigating MACS changes at the HA, this study adds to the limited knowledge of management control changes in developing countries which is a somewhat neglected area of accounting research (see Hoque and Hopper, 1994, 1997). In particular, it illustrates that the changes in MACS are understood better in the context of the influences of the structures of the wider social order within the historical, social, political and economic dimensions of the economy. Future research should be aimed at making a comparative study of MACS changes in public sector organisation in developing countries. As the public sector restructuring is a global trend, similar comparative studies could also be made internationally. The object of such multiple case studies would be to support theories capable of interpreting the various observations, which have been made.

This study related to a single-site study. Future research adopting a multiple site study may provide one with more findings in MACS changes in organisations. This would add to the current literature on MACS. The findings from this study can be generalised to other situations as well. Future research can be undertaken to compare the findings in this study with findings that relate to (1) international housing institutions abroad (2) privately or publicly traded manufacturing firms and (3) firms in other countries (e.g. Hoque and Alam, 1999). Such an undertaking could open a new path of research. This would improve our understanding of the influences of the wider structures that create MACS changes in an organisation.

The research concludes that the influences beyond the HA have been critical in bringing about the changes in MACS at the HA. The financial performance indicators, TQM, innovations in Finance Division, separation of the PRB from the HA were some of the consequent MACS changes that eventuated at the HA. This study reinforced the findings of other researchers that the wider social, political, economic and institutional context governs the way management control operates in organisations (Hoque & Hopper, 1994; Uddin & Hopper, 1998; Hoque & Alam, 1999; Nandan, 1997a, 1997b; Scapens & Roberts, 1993; Neimark & Tinker, 1986; Hopwood, 1987; Dent, 1991, Otley, 1994).

It is apparent from the results that the HA aspired to be known for quality, transparency and accountability. As such the HA faced no difficulty in accommodating the separation of the

21

PRB from the HA, the separation of the Lending Division from the Finance Division, TQM and performance measurement principles. The institutional requirements and wider social and political influences were easily accommodated. The commitment to quality and performance measures, and organisational restructuring were seen to be influenced by the social, institutional forces as well as the internal need to be successful within the market. The changes in MACS improved the HA’s organisational effectiveness. This ensured its survival and continuity in operation. REFERENCES Achary, S.S.K. (1998), "Interrogating Accounting in a context; the Search for a more meaningful language", The Fiji Accountant, pp.34-38.

Ansari, S.L. and Euske, K.J. (1987), "Rational, Rationalising and Reifying uses of Accounting Data in organisations", Accounting, Organisations and Society, vol.12 No.6, pp.549- 570. Asian Development Bank Report (1989),"Appraisal of the Low- Income Housing Development Project in Fiji". Bealing Jr, W.E; Riordan, D.A; Riordan, M.P., (1998) "The Buck Stops Here: an Institutional Perspective of University Restructuring", Online Search. Berry, A.J; Loughton, E. and Otley, D (1991), "Control in a financial services company (RIF): a case study", Management Accounting Research, vol.2, pp.109-139. Broadbent, J. (1999), "The State of public sector accounting research The APIRA Conference and some personal reflections", Accounting, Auditing & Accountability Journal, vol.12 No.1, pp.52-57. Broadbent, J. and Guthrie, J. (1992), "Changes in the Public Sector: A Review of recent “Alternative” Accounting Research", Accounting, Auditing & Accountability Journal, vol. 5 No.2, pp.3-31. Burchell, S., Clubb, C; Hopwood, A. and Hughes, J. (1980), "The Role of Accounting in Organisations and Society", Accounting, Organisations and Society, vol.5 No.1, pp.5-27. Burchell, S; Clubb, C. and Hopwood, A.G. (1985), "Accounting in its Social Context : Towards a History of Value Added in the United Kingdom", Accounting, Organisations and Society, vol.10 No.4, pp.381-413. Burns, T. and Stalker, G.M. (1961), The Management of Innovation, London: Tavistock Publications Ltd. Burrell, G. and Morgan, G. (1979), Sociological Paradigms and Organisational Analysis Heinemann Educational Books Limited, USA.

22

Chenhall, R.H. (1997), "Reliance on manufacturing performance measures, total quality Management and organisational performance", Management Accounting

Research, vol.8, pp.187- 206.

Chenhall, R.H. and Langfield-Smith, K. (1998), "Factors influencing the role of management Accounting in the development of performance measures within organisational change program", Management Accounting Research, vol.9,

pp.361-386.

Chua, W.F (1986), "Radical Developments in Accounting Thought", The Accounting Review, vol LXI No.4, pp.601-629. Cobb, I; Helliar, C and Innes, J (1995), "Management Accounting change in a bank", Management Accounting Research, vol.6, pp.155-175. Covaleski, M.A; Dirsmith, M.W. and Michelman, J.E (1993), "An Institutional Theory perspective on the DRG Framework, Case-Mix Accounting Systems and Health Care Organisations", Accounting,Oranisations and Society, vol.18 No.1, pp.65-

80.

Dent, M. (1991), "Information Technology and Managerial Strategies in The NHS: Computer Policies, Organisational Change and the Labour Process",

Critical Perspectives on Accounting, vol.2, pp.331-360.

DiMaggio, P.J. and Powell, W.W. (1983), "The Iron Cage Revisited: Institutional Isomorphism and Collective Rationality in Organisational Fields", American Sociological Review, vol.48, pp.147-160. Ferris, K. R., (1977), "Perceived Uncertainty and Job Satisfaction in the Accounting Environment", Accounting, Organisations and Society, vol.2 No.1, pp. 23-28. Fowler, C (1996), " TQM in NZ: What impact?", Australian Accountant, pp.53-54. Gooderham, P.N; Nordhaug, O; Ringdal, K. (1999), "Institutional and Rational Determinants of Organisational Practices: Human Resource Management in European Firms", Administrative Science Quarterly, vol.44, pp.507-531. Grant, V. (1995), "Total Quality Challenges the Management Accountant", Management Accounting, vol.73 No.6, pp.40-41. Hagg, I. and Hedlund, G. (1979), "Case Studies’ in Accounting Research", Accounting, Organisations and Society, vol.4 No.1/2, pp.135-143. Hopper, T. and Powell, A. (1985), "Making Sense of Research into the Organisational

And Social Aspects of Management Accounting: A Review of its Underlying Assumptions", Journal of Management Studies, vol.22 No.5, pp.429-465. Hopwood, A.G. (1978) “Towards an Organisational Perspective for the Study of

Accounting and Information Systems”, Accounting, Organisations and Society,

23

vol.3 No.1, pp.3-13.

Hopwood, A.G. (1983), "On Trying to Study Accounting in the Contexts in which it Operates", Accounting, Organisations and Society, vol.8 No.2/3, pp.287-305. Hopwood, A. G., (1987), "The Archaeology of Accounting Systems", Accounting, Organisations and Society, vol.12 No.3, pp. 207-234. Hopwood, A.G. (1990) "Accounting and Organisation change", Accounting, Auditing and

Accountability Journal, vol.3 No.1, pp.7-17. Hopwood, A.G. (1999), "Situating the Practice of management accounting in its cultural context: an introduction", Accounting, Organisations and Society, vol.24, pp.377- 378. Hoque, Z. and Alam, M. (1999), "TQM adoption institutionalisation and changes in Management accounting systems: a case study", Accounting and Business Research,Vol.29 No.3, pp.199-210. Hoque, Z. and Hopper T. (1994), "Rationality, Accounting and Politics: A Case Study of Management Control in Bangladesh Jute Mills", Management Accounting Research, vol.5, pp 5-30. Hoque, Z; Hopper, T. (1997), "Political and Industrial Relations Turbulence, competition and Budgeting in the Nationalised Jute Mills of Bangladesh", Accounting and Business Research, vol.27 No.2, pp.125-143. Housing Authority Corporate Plan-1996-2005. Housing Authority of Fiji, Board paper 1996. Housing Authority Board Paper, restructuring of Fiji Housing Authority, 1995. Housing Authority, Annual Report 1990. Housing Authority, Annual Report 1998. Housing Authority, Annual Report 1994. Housing Authority, Board Paper 1994. Housing Authority, Annual Report 1993. Housing Authority, Annual Report 1996. Housing Authority, Annual Report 1988. Humphrey, C.and Scapens, R. (1996), "Theories and Case Studies; Limitation or Liberation?" Accounting, Auditing and Accountability Journal, vol.9 No.2,

24

pp.86-106.

Innes, J. and Mitchell, F. (1990), "The process of change in management accounting: Some field study evidence", Management Accounting Research, Vol.1, pp.3-19.

Ittner, C.D. and Larcker, D. (1997), Quality, Strategic Control Systems, and Organisational Performance", Accounting, Organisations and Society, vol.22

No.3/ 4, pp.293-314.

Ittner, C.D; Larcker, D.F. and Rajan, M.V. (1997), "The Choice of Performance Measures in Annual Bonus Contracts", The Accounting Review, vol.72 No.2, pp. 231- 255.

Johnson, H.T. (1994), "Relevance regained, total quality management and the role of Management Accounting", Critical Perspectives on Accounting, vol.5, pp.259-

267.

Katz, D. and Kahn, R.L. (1966), The Social Psychology of Organisations, John Wiley & Sons Inc, USA. Lal, H. (1990), Total Quality Management A Practical Approach, Wiley Eastern Limited; New Delhi, India. Langfield-Smith, K. (1997), "Management Control Systems and Strategy: A Critical Review", Accounting, Organisations and Society, vol.22 No.2, pp.207-232. Laszlo, G. (1998), "ISO 9000 or TQM: Which approach to adopt- a Canadian case Study", The TQM Magazine, vol.10 No.5. Llewellyn, S. (1994), "Managing the Boundary How Accounting is implicated in Maintaining the Organisation", Accounting, Auditing and Accountability Journal, vol.7 No.4. Lord, B.R. (1998), "Symbols of change in Organisational Culture", Proceedings of Apira, 98. Lowe, E.A. and McInnes, J.M. (1971), "Control in Socio-Economic Organisations: A Rationale for the Design of Management Control Systems (Section 1)", The Journal of Management Studies, vol.8 No.2, pp.213-227. Luft, J.L. (1997), "Long-Term Change in Management Accounting:Perspective from Historical Research", Journal of Management Accounting Research, vol.9,

pp.163-197.

Macdonald, J (1998), "The quality revolution- in retrospect", The TQM Magazine, vol.10 No.5. Maloney, S; Stower, E. (1999), "Reflections on Some recent Management practices",

25

National Accountant, vol.15 No.5, pp.34-38. Martinez-Lorente, A.R; Dewhurst, F. and Dale, B.G. (1998), "Total Quality

Management: origins and evolution of the term", The TQM Magazine, Vol.10 No.5.

Meyer, J.W. and Rowan, B. (1977), "Institutional Organisations: Formal Structure as Myth and Ceremony", American Journal of Sociology, vol.83 No.2, pp.340-363.

Miller, P. and O’Leary, T. (1990), "Making Accounting Practical", Accounting Organisations and Society, vol.15 No.5, pp. 479- 498. Morgan, G. and Smircich, L. (1980), "The Case for Qualitative Research", Academy of Management Review, vol.5 No.4, pp.491-500. Nandan, R. K. (1997a), "The Dialectic of Management Control; The Case of Fiji Development Bank", Proceedings of the Fifth Interdisciplinary Perspectives on Accounting Conference (7th to 9th July), Manchester. Nandan, R.K. (1997b), "The Dialectic of Management Control: The Case of the Fiji Development Bank", Unpublished Phd Thesis, The University of Bristol, UK. Nandan, R.K. (1999), “Public Enterprise Reforms in Fiji”, The Fiji Accountant, August,

pp.11-15.

Neimark, M. and Tinker, T., (1986), "The Social Construction of Management Control Systems", Accounting Organisations and Society, vol.11 No.4/5, pp. 369-395. Oakland, J.S.(1989), Total Quality Management- The route to improving performance Second Edition, Clays, St Ives plc:, Great Britain. Otley, D. (1980), "The Contingency Theory of Management Accounting: Achievement

and Prognosis", Accounting, Organisations and Society, vol.5 No.4, pp.413-428.

Otley, D. (1983), "Concepts of Control: the Contribution of Cybernetics and System Theory to Management Control", in Lowe, T and Machin, J.L.J eds, New Perspectives in Management Control, pp.59-87, The Macmillan Press Ltd, London. Otley, D. (1994), "Management Control in Contemporary organisations: towards a wider Framework", Management Accounting Research, vol.5, pp.289-299. Pearson, J.M., McCahon, C.S. and Hightower, R.T. (1995), "Total Quality Management

Are Information Systems managers ready?" Information and Management, vol.29 No.5, pp.251-263.

Powell,T.C. (1995), "Total quality management as competitive advantage: a review and Empirical study", Strategic Management Journal, vol.16, pp.15- 37.

26

Redman, T. (1995), "Is Quality Management Working in the UK?" Journal of General Management, vol.20 No.3, pp.44-59. Rowan, B. (1982), "Organisational Structure and the Institutional Environment: The Case of Public Schools", Administrative Science Quarterly, vol.27, pp.259-279. Scapens, R.W (1990), "Researching Management Accounting Practice: The role of Case Study Methods", British Accounting Review, vol.22, pp.259-281. Scapens, R. W. and Roberts, J. (1993), "Accounting and Control: A case study of resistance to accounting change", Management Accounting Research, vol.4, pp 1-

32.

Schoonhoven, C.B. (1981), "Problems with Contingency Theory: Testing Assumptions Hidden within the Language of Contingency Theory", Administrative Science Quarterly, vol.26, pp.349-377. Shank, J.K. and Govindarajan, V. (1994), "Measuring the “Cost of quality” a strategic

cost management perspective", Journal of Cost Management, Summer, pp.5-17.

Sharma, U. (1997), "Critique of Contingency Theory", Unpublished Working Paper, University of the South Pacific, Suva, Fiji.

Sharma, U. and Nandan, R.K. (2000), "Contingency Framework for Management Accounting A Critique", The Fiji Accountant, May, pp.40-43. Shea, J.E.and Kleinsorge, I.K (1994), "TQM: Are Cost Accountants meeting the challenge?" Management Accounting, vol.LXXV No.10, pp.65-67. Thomson, E.L. and Thomson, S.C. (1995), "Quality issues in nine New Zealand hotels: a research study", The TQM Magazine,vol.7 No.5. Uddin, S. and Hopper, T. (1998), "A Bangladeshi Soap Opera: Privatisation",

Accounting, Consent and Control", Proceedngs of Apira 98.

Von Bertalanffy, L. (1973), General Systems Theory, The Penguin Press, Great Britain. Wilkinson, A; Marchington, M; Godman, J. and Ackers, P. (1992), "Total Quality Management and Employee Involvement", Human Resource Management Journal, vol.2 No.4, pp.1-20. Wilkinson, A. and Witcher, B. (1993), "Holistic total quality management must take account of political processes", Total Quality Management, vol.4 No.1, pp.47-56. Wilson, R.M.S., and Chua, W.F. (1988), Managerial Accounting: method and meaning, Van Nostrand Reinhold, London. Yin, R.K. (1981), "The Case study Research: some Answers", Administrative Science Quarterly, Vol 1 No.26, pp.58-65.

27

Yin, R.K. (1988), Case Study Research Design and Methods- Revised Edition, Sage

Publications Inc, Carlifornia.

28

Table I Revenue and Expenditure for the HA with and without the rental estates (In thousands of Dollars) With rental estates Without rental estates 1987 1988 1987 1988 Income 9,961 10,064 9,383 9,489 Expenditure 12,706 13,365 10,580 11,344 Deficit for the year

-2,745 -3,301 -1,197 -1,855

29

Perceived environmental influence

State

Political factors

Aid agencies

External consultants

Figure 1 Predictors of MACS Changes in the HA

MACS changes Separation of the PRB from the HA

Separation of the Lending Divisionfrom the Finance Division Introduction of TQM Introduction of ManagementContract System

Perceived environmental influences State Political Factors Aid Agencies External Consultants

PAQF

30

Figure 2 The Systems Universe

General environment (external)

SS

State Customers World Bank external And ADB Consultant

Aid consultantsa ```````````````````````````````

inputs outputs to from PAQF

Substantial Environment

The System (HA)

(transformation process of specified inputs into

outputs).

31

Figure 3

Interactions between the organisational system and its substantial environment.

laws/Policies Loan repayment

Taxes loan

Recommendation

for restructuring Payment for loan Basic payment products Shelter/Loan for

products services

Payment TQM

for Seminar

membership Series

The Organisation

(HA)

State

ADB/World Bank

Customers

PAQF

Consultants

32

Contingency Variables (e.g. technology, environment)

Organisation Design

Type of accounting information system

Organisational Effectiveness

Figure 4 A Simple Linear Framework for AIS design Adapted from (Otley, 1980, p.420).

33

Figure 5 Contingent Variables and MACS Adapted from (Sharma & Nandan, 2000).

Environment

Technology

Size

Organisation Structure

Culture

Strategy

Method of budget

use

Method of Costing

Budgetary slack

Manipulation of

accounting data.

34

Figure 6 The Contingency framework at the HA

Contingency Variables at the HA (Globalisation trend/State’s public sector reform policy, aid agencies, external consultants,

customer expectations, Chief Executive,Technology, PAQF)

HA’s Organisation Design (decentralisation due to TQM)

Type of accounting information system (Method of budget use, and removal of rental element from Profit and Loss and Balance

sheet)

Organisational Effectiveness (Improved profit, improved customer services, assets exceeded liabilities, improvement in

lending operations, timely and cost effective loan finance to low and middle-income earners).

** END OF PAPER **