Managerial accounting - SubFly

49

Elaborated in the framework of SUB-FLY Project financed under the contract SEE EY-COP-0082 by SEE Grants 2014-2021 Managerial accounting

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Managerial accounting - SubFly

[Type text]

Elaborated in the framework of

SUB-FLY Project

financed under the contract

SEE EY-COP-0082

by

SEE Grants 2014-2021

Managerial accounting

Page 1

Working together for a green, competitive and inclusive Europe SEE & Cha(lle)nge

Sustainable & applied education

This material is elaborated as support for all students, staff, professionals and entities interested to analyze the status of a company using Business Canvas Model. It is used as a training support for

students involved in SUB-FLY Project.

We are thankful to SEE Grants 2014-2021, which financed the SUB-FLY Project under the

contract EY-COP-0082. Faculty of Business from Babes-Bolyai University (Romania) and School of Business from University of South-Eastern Norway (Norway) received, based on this contract, the opportunity to cooperate. One of the outcomes generated by this cooperation consists in

development and implementation of the SUB-FLY Project.

This document was realized with the EEA Financial Mechanism 2014-2021 financial support. Its content (text, photos, videos) does not reflect the official opinion of the Programme Operator, the National Contact Point and the Financial Mechanism Office. Responsibility for the information and views expressed therein lies entirely with the author(s).

Page 2

What is Managerial Accounting Managerial accounting is concerned with providing information to managers-that is, people inside an organization who direct and control its operation. In contrast, financial accounting is concerned with providing information to stockholders, creditors, and others who are outside an organization.

Managerial accounting provides the essential data with which the organizations are actually run. Managerial accounting is also termed as management accounting or cost accounting. Financial accounting provides the scorecard by which a company's overall past performance is judged by outsiders. Managerial accountants prepare a variety of reports. Some reports focus on how well managers or business units have performed-comparing actual results to plans and to benchmarks.

Some reports provide timely, frequent updates on key indicators such as orders received, order backlog, capacity utilization, and sales. Other analytical reports are prepared as needed to investigate specific problems such as a decline in the profitability of a product line. And yet other reports analyze a developing business situation or opportunity. In contrast, financial accounting is oriented toward producing a limited set of specific prescribed annual and quarterly financial statements in accordance with Generally Accepted Accounting Principles (GAAP).

Managerial accounting is managers oriented therefore its study must be preceded by some understanding of what managers do, the information managers need, and the general business environment.

Page 3

Difference Between Financial and Managerial Accounting (Financial Accounting Vs Managerial Accounting)

Financial accounting reports are prepared for the use of external parties such as shareholders and creditors, whereas managerial accounting reports are prepared for managers inside the organization.

This contrast in basic orientation results in a number of major differences between financial and managerial accounting, even though both financial and managerial accounting often rely on the same underlying financial data. In addition to the to the differences in who the reports are prepared for, financial and managerial accounting also differ in their emphasis between the past and the future, in the type of data provided to users, and in several other ways. These differences are discussed in the following paragraphs.

Emphasis on the Future: Since planning is such an important part of the manager's job, managerial accounting has a strong future orientation. In contrast, financial accounting primarily provides summaries of past financial transactions. These summaries may be useful in planning, but only to a point. The future is not simply a reflection of what has happened in the past. Changes are constantly taking place in economic conditions, and so on. All of these changes demand that the manager's planning be based in large part on estimates of what will happen rather than on summaries of what has already happened.

Relevance of Data: Financial accounting data are expected to be objective and verifiable. However, for internal use the manager wants information that is relevant even if it is not completely objective or verifiable. By relevant, we mean appropriate for the problem at hand. For example, it is difficult to verify estimated sales volumes for a proposed new store at good Vibrations, Inc., but this is exactly the type of information that is most useful to managers in their decision making. The managerial accounting

Page 4

information system should be flexible enough to provide whatever data are relevant for a particular decision.

Less Emphasis on Precision: Timeliness is often more important than precision to managers. If a decision must be made, a manager would rather have a good estimate now than wait a week for a more precise answer. A decision involving tens of millions of dollars does not have to be based on estimates that are precise down to the penny, or even to the dollar. In fact, one authoritative source recommends that, "as a general rule, no one needs more than three significant digits., this means, for example, that if a company's sales are in the hundreds of millions of dollars, than nothing on an income statement needs to be more accurate than the nearest million dollars. Estimates that accurate to the nearest million dollars may be precise enough to make a good decision. Since precision is costly in terms of both time and resources, managerial accounting places less emphasis on precision than does financial accounting. In addition, managerial accounting places considerable weight on non monitory data, for example, information about customer satisfaction is tremendous importance even though it would be difficult to express such data in monitory form.

Segments of an Organization: Financial accounting is primarily concerned with reporting for the company as a whole. By contrast, managerial accounting forces much more on the parts, or segments, of a company. These segments may be product lines, sales territories divisions, departments, or any other categorizations of the company's activities that management finds useful. Financial accounting does require breakdowns of revenues and cost by major segments in external reports, but this is secondary emphasis. In managerial accounting segment reporting is the primary emphasis.

Generally Accepted Accounting Principles (GAAP): Financial accounting statements prepared for external users must be prepared in accordance with generally accepted accounting principles (GAAP). External users must have some assurance that the reports have been prepared in accordance with some common set of ground rules. These common ground rules enhance comparability and help reduce fraud and misrepresentations, but they do not necessarily lead to the type of reports that would be most useful in internal decision making. For

Page 5

example, GAAP requires that land be stated at its historical cost on financial reports. However if, management is considering moving a store to a new location and then selling the land the store currently sits on, management would like to know the current market value of the land, a vital piece of information that is ignored under generally accepted accounting principles (GAAP).

Managerial Accounting � Not Mandatory: Financial accounting is mandatory; that is, it must be done. Various out side parties such as Securities and exchange commission (SEC) and the tax authorities require periodic financial statements. Managerial accounting, on the other hand, is not mandatory. A company is completely free to do as much or as little as it wishes . No regularity bodies or other outside agencies specify what is to be done, for that matter, weather anything is to be done at all. Since managerial accounting is completely optional, the important question is always, "Is the information useful?" rather than, "Is the information required?"

Summary:

Financial Accounting Managerial Accounting • Reports to those outside

the organization owners, lenders, tax authorities and regulators.

• Reports to those inside the organization for planning, directing and motivating, controlling and performance evaluation.

• Emphasis is on summaries of financial consequences of past activities.

• Emphasis is on decisions affecting the future.

• Objectivity and verifiability of data are emphasized.

• Relevance of items relating to decision making is emphasized.

• Precision of information is required.

• Timeliness of information is required.

• Only summarized data for the entire organization is prepared.

• Detailed segment reports about departments, products, customers, and employees are prepared.

Page 6

• Must follow Generally Accepted Accounting Principles (GAAP).

• Need not follow Generally Accepted Accounting Principles (GAAP).

• Mandatory for external reports.

• Not mandatory.

Page 7

Need for Managerial Accounting Information: Every organization - large and small-has managers. Someone must be responsible for making plans, organizing resources, directing personnel, and controlling operations. Every where mangers carry out three major activities - planning, directing and motivating, and controlling.

Planning: Planning involves selecting a course of action and specifying how the action will be implemented. The first step in planning is to identify the alternatives and then to select from among the alternatives the one that does the best job of furthering the organization's objectives. While making choices management must balance the opportunity against the demands made on the companies resources.

The plans of management are often expressed formally in budgets, and the term budgeting is applied to generally describe the planning process. Budgets are usually prepared under the direction of controller, who is the manager in charge of the accounting department. Typically, budgets are prepared annually and represent management's plans in specific, quantitative terms.

Directing and Motivating:

In addition to planning for the future, managers must oversee day-to-day activities and keep the organization functioning smoothly. This requires the ability to motivate and affectively direct people. Managers assign tasks to employees, arbitrate disputes, answer questions, solve on-the-spot problems, and make many small decisions that affect customers and employees. In effect, directing is that part of the manager's work that deals with the routine and the here and now. Managerial accounting data, such as daily sales reports are often used in this type of day-to-day decision making.

Controlling: In carrying out the control function, managers seek to ensure that the plan is being followed. Feedback, which signals operations are on track, is the key to effective control. In sophisticated organizations, this feedback

Page 8

is provided by detailed reports of various types. One of these reports, which compares budgeted to actual results, is called a performance report. Performance report suggest where operations are not proceeding as planned and where some parts of the organization may require additional attention.

The Planning and Control Cycle:

The work of management can be summarized in a model. The model, which depicts the planning and control cycle, illustrates the smooth flow of management activities from planning through directing and motivating, controlling, and then back to planning again. all of these activities involve decision making. So it is depicted as the hub around which the activities revolve.

Page 9

History of Managerial Accounting: Managerial accounting has its roots in the industrial revolution of the 19th century. During this early period, most firms were tightly controlled by a few owner-managers who borrowed based on personal relationships and their personal assets.

Since there were no external shareholders and little unsecured debt, there was little need for elaborate financial reports. In contrast, managerial accounting was relatively sophisticated and provided the essential information needed to manage the early large scale production of textile, steel, and other products. After the turn of the century, financial accounting requirements burgeoned because of new pressures placed on companies by capital markets, creditors, regulatory bodies, and federal taxation of income. Johnson and Kaplan state that "many firms needed to raise funds from increasingly widespread and detached suppliers of capital. To tap these vast reservoirs of outside capital, firms' managers had to supply audited financial reports. And because outside suppliers of capital relied on audited financial statements, independent accountants had a keen interest in establishing well defined procedures for corporate financial reporting. The inventory costing procedure adopted by public accountants after the turn of the century had a profound effect on management accounting. As a consequence, for many decades, management accountants increasingly focused their efforts on ensuring that financial accounting requirements were met and financial reports were released on time.

The practice of management accounting stagnated. In the early part of the century, as product line expanded operations became more complex, forward looking companies saw a renewed need for management-oriented reports that was separate from financial reports. But in most companies, management accounting practices up through the mid-1980s were largely indistinguishable from practices that were common prior to world war I. In recent years, however, new economic forces have led to many important innovations in management accounting. These new practices are discussed in other chapters.

Page 10

Code of Conduct for Management Accountants: Practitioners of management accounting and financial management have an obligation to the public, their profession, the organization they serve, and themselves, to maintain the highest standards of ethical conduct. In recognition of this obligation, the Institute of management Accountants has promulgated the following standards of ethical conduct for practitioners of management accounting and financial management. Adherence to these standards internationally is integral to achieving objective of management accounting.

Competence: Practitioners of management accounting and financial management have a responsibility to:

• Maintain an appropriate level of professional competence by ongoing development of their knowledge and skills.

• Perform their professional duties in accordance with relevant laws, regulations and technical standards.

• Prepare complete and clear reports and recommendations after appropriate analysis of relevant and reliable information

Confidentiality:

Practitioners of management accounting and financial management have a responsibility to:

• Refrain from disclosing confidential information acquired in the course of their work except when authorized, unless legally obligated to do so.

• Inform subordinates as appropriate regarding the confidentiality of information acquired in the course of their work and monitor their activities to assure the maintenance of that confidentiality

• Refrain from using or appearing to use confidential information acquired in the course of their work for unethical or illegal advantage either personally or through third parties.

Integrity:

Page 11

Practitioners of management accounting and financial management have a responsibility to:

• Avoid actual or apparent conflicts of interest and advise all appropriate parties of any potential conflict.

• Refrain from engaging in any activity that would prejudice their ability to carry out their duties ethically.

• Refuse any gift, favor, or hospitality that would influence or would appear to influence their actions.

• Refrain from either activity or passively subverting the attainment of the organization's legitimate and ethical objectives.

• Recognize and and communicate professional limitations or other constraints that would preclude responsible judgment or successful performance of an activity.

• Communicate unfavorable as well as favorable information and professional judgment or opinion.

• Refrain from engaging or supporting any activity that would discredit the profession.

Objectivity: Practitioners of management accounting and financial management have a responsibility to:

• Communicate information fairly and objectively • Disclose fully all relevant information that could reasonably be

expected to influence an intended user's understanding of the reports, comments, and recommendations presented.

Resolution of Ethical Conflicts: In applying the standards of ethical conduct, practitioners of management accounting and financial management may encounter problems in identifying unethical behavior or in resolving an ethical conflict. When faced with significant ethical issues practitioners of management accounting and financial management should follow the established policies of the organization bearing on the resolution of such conflict. If these policies do not resolve the ethical conflict, such practitioner should consider the following course of action.

• Discuss such problems with immediate superior except when it appears that superior is involved, in which case the problem should be presented to the next higher managerial level. If a satisfactory

Page 12

resolution cannot be achieved when the problem is initially presented, submit the issue to the next higher managerial level.

• If the immediate superior is the chief executive officer or equivalent, the acceptable reviewing authority may be a group such as the audit committee, executive committee, board of directors, board of trustees, or owners. Contact with a level above the immediate superior should be initiated only with the superior's knowledge. assuming the superior is not involved. Except where legally prescribed, communication of such problems to authorities or individuals not employed or engaged by the organization is not considered appropriate.

• Clarify relevant ethical issues by confidential discussion with an objective adviser to obtain a better understanding of possible course of action

• Consult your own attorney as to legal obligations and rights concerning the ethical conflict.

• If the ethical conflict still exists after exhausting all levels of internal review, there may be no other recourse on significant matters than to resign from the organization and to submit an informative memorandum to an appropriate representative of the organization. After resignation, depending on the nature of the ethical conflict, it may also be appropriate to notify other parties.

Who is A Certified Management Accountant: A management accountant who possesses the necessary qualification and who possesses a rigorous professional exam earns the right to be known as a certified Management Accountant (CMA).

In addition to the prestige that accompanies a professional designation, CMAs are often given greater responsibilities and higher compensation than those who do not have such a designation.

To become a Certified Management Accountant, the following four steps must be completed:

1. File an application for admission and register for the CMA examination

Page 13

2. Pass all four parts of the CMA examination within a three year period

3. Satisfy the experience requirement of two continuous years of professional experience in management and/or financial accounting prior to or within seven years of passing the CMA examination.

4. Comply with the standards of ethical conduct for practitioners of management accounting and financial management.

Cost Terms, Concepts, and Classifications: After Studying this chapter you should be able to:

1. Identify and give examples of each of the three basic manufacturing cost categories.

2. Distinguish between product costs and period costs and give examples of each. 3. Prepare an income statement including calculation of the cost of goods sold. 4. Prepare a schedule of cost of goods manufactured. 5. Understand the difference between variable costs and fixed costs. 6. Understand the differences between direct and indirect costs. 7. Define and give examples of cost classifications used in making decisions:

differential costs, opportunity costs, and sunk costs. 8. Properly account for labor costs associated with idle time, overtime, and fringe

benefits. 9. Identify the four types of quality costs associated and explain how they interact. 10. Prepare and interpret a quality cost report.

The work of managers focuses on (1) planning, which includes setting objectives and outlining how to attain these objectives; and (2) control, which includes the steps to take to ensure that objectives are realized. To carry out these planning and control responsibilities, managers need information about the organization. From an accounting point of view, this information often relates to the costs of organization.

The term cost is used in many different ways in managerial accounting. The reason is that there are many types of costs, and these costs are classified differently according to the immediate need of management. For example, managers may want cost data to prepare external financial reports, to prepare planning budgets, or to make decisions. Each different use of cost data demands a different classification and definition of cost. For example, the preparation of external financial reports require historical cost data, whereas decision making may require predictions about future costs. In the following paragraphs we have discussed many of possible use of cost data and how costs are defined and classified for each use.

Page 14

Page 15

Cost Classification as Manufacturing and Non-manufacturing: Learningobjectivesofthisarticle:

• Define and explain manufacturing and non-manufacturing costs. • What is the difference between manufacturing and non-manufacturing costs

costs? • Identify and give examples of each of the three basic manufacturing cost

categories.

Manufacturing firms are involved in acquiring raw materials producing finished goods and then administrative, marketing and selling activities. All these activities require costs to be incurred. These costs are normally classified by manufacturing companies as manufacturing and non-manufacturing costs. In the following paragraphs we will see how these costs are classified as manufacturing and non-manufacturing.

Manufacturing Costs: DefinitionandExplanationofmanufacturingcost:

Manufacturing costs are those costs that are directly involved in manufacturing of products and services. Examples of manufacturing costs include raw materials costs and salary of labor workers. Manufacturing cost is divided into three broad categories by most companies.

1. Direct materials cost 2. Direct labor cost 3. Manufacturing overhead cost.

DirectMaterialsCost:

The materials that go into final product are called raw materials. This term is somewhat misleading, since it seems to imply unprocessed natural resources like wood pulp or iron ore. Actually raw materials refer to any materials that are used in the final product; and the finished product of one company can become raw material of another company. For example plastic produced by manufacturers of plastic is a finished product for them but is a raw material for Compaq Computers for its personal computers.

Direct Materials are those material that become an integral part of the finished product and that can be physically and conveniently traced to it. Examples include tiny electric motor that Panasonic uses in its CD players to make the CD spin. According to a study of 37 manufacturing industries material costs averaged about 55% of sales revenue.

Page 16

Sometimes it is not worth the effort to trace the costs of relatively insignificant materials to the end products. Such minor items would include the solder used to make electrical connection in a Sony TV or the glue used to assemble a chair. Materials such as solder or glue are called indirect materials and are included as part of manufacturing overhead, which is discussed later on this page.

DirectLaborCost:

The term direct labor is reserved for those labor costs that can be essentially traced to individual units of products. Direct labor is sometime called touch labor, since direct labor workers typically touch the product while it is being made. The labor cost of assembly line workers, for example, is a direct labor cost, as would the labor cost of carpenter, bricklayer and machine operator

Labor costs that cannot be physically traced to the creation of products, or that can be traced only at a great cost and inconvenience, are termed indirect labor and treated as part of manufacturing overhead, along with indirect materials. Indirect labor includes the labor costs of janitors, supervisors, materials handlers, and night security guards. Although the efforts of these workers are essential to production, it would be either impractical or impossible to accurately trace their costs to specific units of product. Hence, such labor costs are treated as indirect labor.

In some industries, major shifts are taking place in the structure of labor costs. Sophisticated automated equipment, run and maintained by skilled workers, is increasingly replacing direct labor. In a few companies, direct labor has become such a minor element of cost that it has disappeared altogether as a separate cost category. However the vast majority of manufacturing and service companies throughout the world continue to recognize direct labor as a separate cost category.

According to a study of 37 manufacturing industries, direct labor averaged only about 10% of sales revenue.

Direct Materials cost combined with direct labor cost is called prime cost.

In equation form:

Prime Cost = Direct Materials Cost + Direct Labor Cost

For example total direct materials cost incurred by the company is $4,500 and direct labor cost is $3,000 then prime cost is $7,500 ($4,500 + $3,000).

ManufacturingOverheadCost:

Manufacturing overhead, the third element of manufacturing cost, includes all costs of manufacturing except direct material and direct labor. Examples of manufacturing overhead include items such as indirect material, indirect labor, maintenance and repairs on production equipment and heat and light, property taxes, depreciation, and insurance on manufacturing facilities. Indirect materials are minor items such as solder and glue in manufacturing industries. These are not included in direct materials costs. Indirect labor is a labor cost that cannot be trace to the creation of products or that can be traced only at great cost and inconvenience. Indirect labor includes the labor cost of janitors,

Page 17

supervisors, materials handlers and night security guards. Costs incurred for heat and light, property taxes, insurance, depreciation and so forth associated with selling and administrative functions are not included in manufacturing overhead. Studies have found that manufacturing overhead averages about 16% of sales revenue. Manufacturing overhead is known by various names, such as indirect manufacturing cost, factory overhead, and factory burden. All of these terms are synonymous with manufacturing overhead.

Manufacturing overhead cost combined with direct labor is called conversion cost.

In equation form:

Conversion Cost = Direct Labor Cost + Manufacturing Overhead Cost

For example if total direct labor cost is $3,000 and total manufacturing overhead cost is $2,000 then conversion cost is $5,000 ($3,000 + $2,000).

Non-manufacturing Costs: Definitionandexplanationofnon-manufacturingcost:

Non-manufacturing costs are those costs that are not incurred to manufacture a product. Examples of such costs are salary of sales person and advertising expenses. Generally non-manufacturing costs are further classified into two categories.

1. Marketing and Selling Costs 2. Administrative Costs

MarketingorSellingCosts:

Marketing or selling costs include all costs necessary to secure customer orders and get the finished product into the hands of the customers. These costs are often called order getting or order filling costs. Examples of marketing or selling costs include advertising costs, shipping costs, sales commission and sales salary.

AdministrativeCosts:

Administrative costs include all executive, organizational, and clerical costs associated with general management of an organization rather than with manufacturing, marketing, or selling. Examples of administrative costs include executive compensation, general accounting, secretarial, public relations, and similar costs involved in the overall, general administration of the organization as a whole.

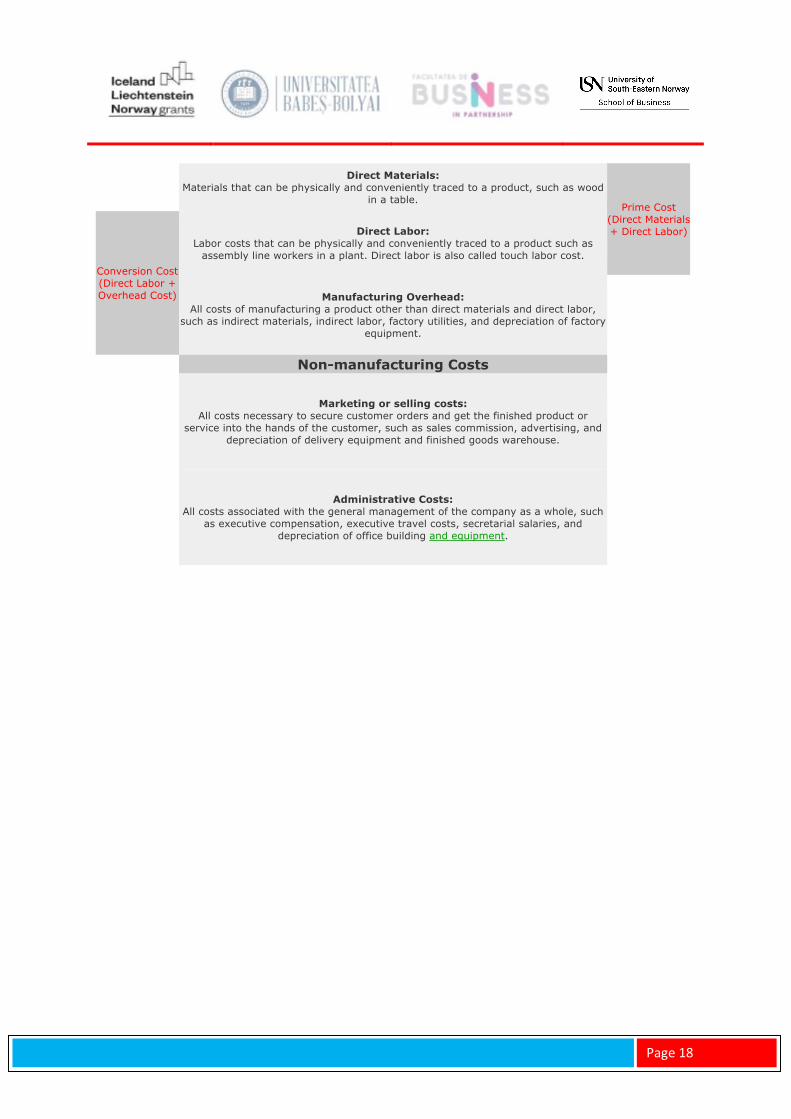

Summary of manufacturing and non-manufacturing costs Manufacturing Costs

Page 18

Direct Materials: Materials that can be physically and conveniently traced to a product, such as wood

in a table. Prime Cost

(Direct Materials + Direct Labor)

Conversion Cost (Direct Labor + Overhead Cost)

Direct Labor: Labor costs that can be physically and conveniently traced to a product such as

assembly line workers in a plant. Direct labor is also called touch labor cost.

Manufacturing Overhead: All costs of manufacturing a product other than direct materials and direct labor,

such as indirect materials, indirect labor, factory utilities, and depreciation of factory equipment.

Non-manufacturing Costs

Marketing or selling costs:

All costs necessary to secure customer orders and get the finished product or service into the hands of the customer, such as sales commission, advertising, and

depreciation of delivery equipment and finished goods warehouse.

Administrative Costs:

All costs associated with the general management of the company as a whole, such as executive compensation, executive travel costs, secretarial salaries, and

depreciation of office building and equipment.

Page 19

Product Cost Versus Period Cost: LearningObjectivesofthisarticle:

• Define and explain the terms "product cost" and "period cost". Give examples of each.

• What is the difference between product cost and period cost.

In addition to the distinction between manufacturing and non-manufacturing costs, there are other ways to look at costs. Costs can also be classified as either product cost or period cost. To understand the difference between product costs and period costs, we must first refresh our understanding of the matching principle from financial accounting. Generally costs are recognized as expenses on the income statement in the period that benefits from the cost. For example, if a company pays for liability insurance in advance for two years, the entire amount is not considered an expense of the year in which the payment is made. Instead, one half of the cost would be recognized as an expense each year. The reason is that both years-not just the first year-benefit from the insurance payment. The un-expensed portion of the insurance payment is carried on the balance sheet as an asset called prepaid insurance. You should be familiar with this type of accrual from your financial accounting coursework.

The matching principle is based on the accrual concept and states that costs incurred to generate a particular revenue should be recognized as expense in the same period that the revenue is recognized. This means that if a cost is incurred to acquire or make some thing that will eventually be sold, then the cost should be recognized as an expense only when the sale takes place-that is, when the benefit occurs. Such costs are called product costs.

Product Costs: DefinitionandExplanationofProductCost:

For financial accounting purposes, product costs include all the costs that are involved in acquiring or making product. In the case of manufactured goods, these costs consist of direct materials, direct labor, and manufacturing overhead. Product costs are viewed as "attaching" to units of product as the goods are purchased or manufactured, and they remain attached as the goods go into inventory awaiting sale. So initially, product costs are assigned to an inventory account on the balance sheet. When the goods are sold, the costs are released from inventory as expense (typically called Cost of Goods Sold) and matched against sales revenue. Since product costs are initially assigned to inventories, they are also known as inventoriable costs. The purpose is to emphasize that product costs are not necessarily treated as expense in the period in which they are incurred. Rather, as explained above, they are treated as expenses in the period in which the related products are sold. This means that a product cost such as direct materials or direct labor might be incurred during one period but not treated as an expense until a following period when the completed product is sold.

Page 20

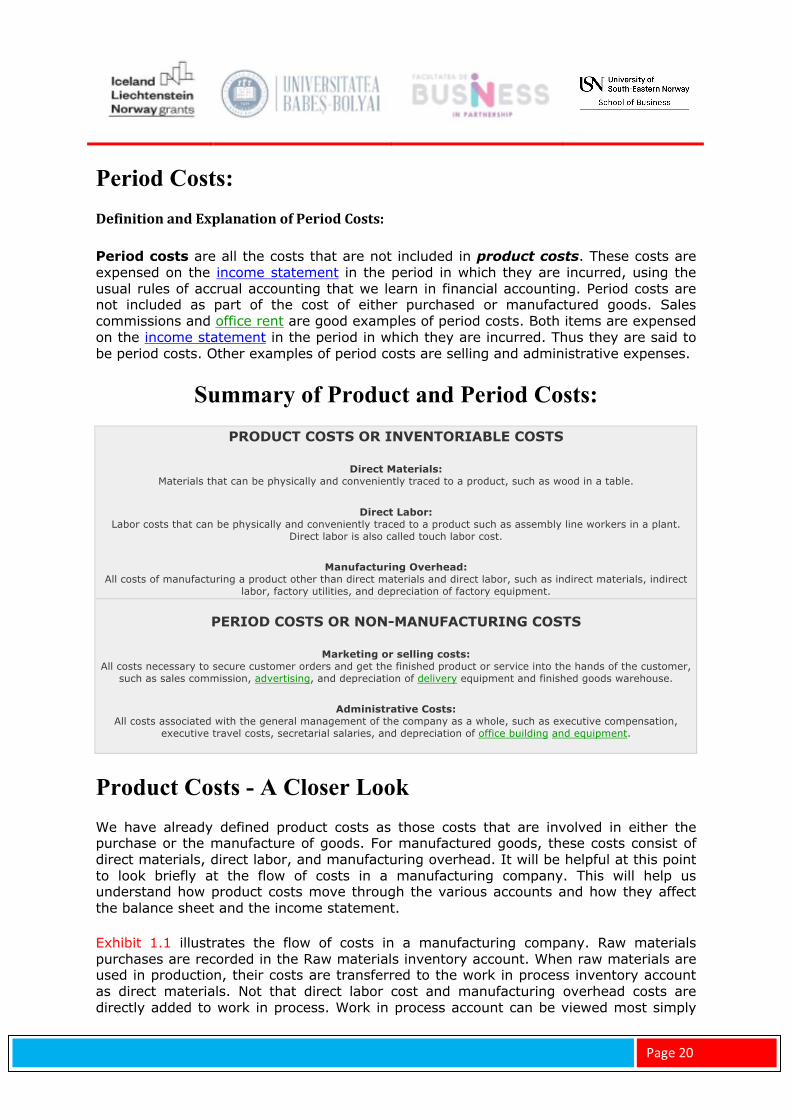

Period Costs: DefinitionandExplanationofPeriodCosts:

Period costs are all the costs that are not included in product costs. These costs are expensed on the income statement in the period in which they are incurred, using the usual rules of accrual accounting that we learn in financial accounting. Period costs are not included as part of the cost of either purchased or manufactured goods. Sales commissions and office rent are good examples of period costs. Both items are expensed on the income statement in the period in which they are incurred. Thus they are said to be period costs. Other examples of period costs are selling and administrative expenses.

Summary of Product and Period Costs: PRODUCT COSTS OR INVENTORIABLE COSTS

Direct Materials: Materials that can be physically and conveniently traced to a product, such as wood in a table.

Direct Labor: Labor costs that can be physically and conveniently traced to a product such as assembly line workers in a plant.

Direct labor is also called touch labor cost.

Manufacturing Overhead: All costs of manufacturing a product other than direct materials and direct labor, such as indirect materials, indirect

labor, factory utilities, and depreciation of factory equipment.

PERIOD COSTS OR NON-MANUFACTURING COSTS

Marketing or selling costs: All costs necessary to secure customer orders and get the finished product or service into the hands of the customer,

such as sales commission, advertising, and depreciation of delivery equipment and finished goods warehouse.

Administrative Costs: All costs associated with the general management of the company as a whole, such as executive compensation,

executive travel costs, secretarial salaries, and depreciation of office building and equipment.

Product Costs - A Closer Look We have already defined product costs as those costs that are involved in either the purchase or the manufacture of goods. For manufactured goods, these costs consist of direct materials, direct labor, and manufacturing overhead. It will be helpful at this point to look briefly at the flow of costs in a manufacturing company. This will help us understand how product costs move through the various accounts and how they affect the balance sheet and the income statement.

Exhibit 1.1 illustrates the flow of costs in a manufacturing company. Raw materials purchases are recorded in the Raw materials inventory account. When raw materials are used in production, their costs are transferred to the work in process inventory account as direct materials. Not that direct labor cost and manufacturing overhead costs are directly added to work in process. Work in process account can be viewed most simply

Page 21

as an assembly line where workers are stationed and where products slowly take shape as they move from one end of the assembly line to the other. The direct materials, direct labor, and manufacturing overhead costs added to work in process in Exhibit 1.1 are the costs needed to complete these products as they move along this assembly line.

Notice from the exhibit that as goods are completed, their costs are transferred from work in process to finished goods. Here the goods await sale to customers. As goods are sold, their costs are transferred from finished goods to cost of goods sold. At this point the various material, labor, and overhead costs required to make the product are finally treated as expenses. Until that point, these costs are in inventory accounts on the balance sheet.

Exhibit 1.1 Cost Flows and Classifications in a Manufacturing Company

InventoriableCosts:

As stated earlier products costs are often called inventoriable costs. The reason is that these costs go directly into inventory accounts as they are incurred (first into work in process WIP and then into finished goods), rather than going into expense accounts. Thus, they are termed inventoriable costs. This is a key concept since such costs can end up on the balance sheet as assets if goods are only partially completed or are unsold at the end of a period. To illustrate this point, refer again to Exhibit 1.1. At the end of the period, the materials, labor, and overhead costs that are associated with the units in the work in process and finished goods inventory accounts will appear on the balance sheet as part of the company's assets. These costs will not become expenses until later when the goods are completed and sold.

Selling and administrative expenses are not involved in the manufacturing of a product. For this reason, they are not treated as product costs but rather as period costs that go directly into expense accounts as they are incurred, as shown by the Exhibit 1.1.

AnExampleofCostFlows:

To provide an example of cost flows in a manufacturing company, assume that company's annual insurance cost is $2,000. Three fourth of this amount ($1,500) applies to factory operations, and one fourth ($500) applies to selling and administrative activities. Therefore, $1,500 of the $2,000 insurance cost would be a product (inventoriable) cost and would be added to the cost of goods produced during the year. This concept is illustrated in the Exhibit 1.2. Where $1,500 of insurance cost is added into work in process. This portion of the year's insurance will not become an expense until the goods that are produced during the year are sold--which may not happen until the following year or even later. Until the goods are sold, the $1,500 will remain as part of the asset, inventory (either as part of work in process or as a part of finished goods), along with other costs of producing goods.

By contrast, the $500 of insurance cost that applies to the company's selling and administrative activities will be expensed immediately.

Page 22

Thus far, we have been mainly concerned with classifications of manufacturing costs for the purpose of determining inventory valuations on the balance sheet and cost of goods sold on the income statement of external financial reports. However, costs are used for many other purposes, and each purpose requires a different classification of costs.

Page 23

Cost Classifications on Financial Statements: LearningObjectivesofthisArticle:

1. Prepare a schedule of cost of goods manufactured. 2. Prepare income statement including a schedule of cost of goods sold.

Merchandising and manufacturing firms, both prepare financial statement reports for creditors, stockholders, and others to show the financial condition of the firm and the firm's earnings performance over some specified intervals. Merchandising companies simply purchase goods and resale them to customers. Financial statement reports are therefore simple in case of merchandising companies. The financial statements prepared by manufacturing companies are more complex than the statements prepared by a merchandising company. Manufacturing companies are more complex organizations than merchandising companies because the manufacturing companies must produce its goods as well as market them. The production process gives rise to many costs that do not exist in a merchandising company, and some how these costs must be accounted for on the manufacturing company's financial statements. In this section, we focus our attention on how this accounting is carried out in the balance sheet and income statement.

Balance Sheet: The balance sheet or statement of financial position of a manufacturing company is similar to that of a merchandising company. However, the inventory accounts differ between two types of companies. A merchandising company has only one type of inventory-goods purchased from suppliers that are awaiting resale to customers. In contrast manufacturing companies have three classes of inventories-raw materials, work-in-process, and finished goods.

Example:

We will use the data of two companies A and B-to illustrate the concept discussed in this section. Company A is involved in manufacturing a product Alpha and B is involved in purchasing books about business and finance from publishers and authors and reselling them to customers.

Page 24

The footnotes to A's annual reports reveal the following information concerning its inventories.

A Manufacturing Corporation Inventory Accounts

Beginning Balance Ending Balance Raw materials Work in process Finished goods

$60,000 $90,000 $125,000

$50,000 $60,000 $175,000

A's inventory largely consists of raw materials used in manufacturing product alpha. The work in process inventory consists of partially completed alpha. The finished goods inventory consists of alpha that is ready to be sold to the customers or whole sellers.

In contrast the inventory account at B--a book reseller-- consists entirely of the costs of books the company has purchased from publishers for resale to the public. In merchandising companies like B these inventories may be called merchandising inventories. The beginning and ending balances in this account appears as follows:

B-Bookstore Inventory Accounts

Beginning Balance Ending Balance Merchandising Inventory $100,000 $150,000

Income Statement: Following are comparative income statements of merchandising and manufacturing companies.

Merchandising Company B-Bookstore

Page 25

Sales Cost of good sold: Beginning merchandising inventory Add: Purchases

Goods available for sale Less: Ending merchandising inventory

Gross margin Less operating expenses: Selling expenses Administrative Expenses

Net operating income

$100,000 $550,000 ---------- $750,000 $150,000 ----------

$100,000 $200,000 ----------

$1,000,000

$600,000 ---------- $400,000

300,000 ---------

$100,000 =======

Manufacturing Company A-Manufacturing Co.

Sales Cost of good sold: Beginning finished goods inventory Add: Cost of goods manufactured* (See schedule) Goods available for sale Less: Ending finished goods inventory

Gross margin Less operating expenses: Selling expenses Administrative expenses

Net operating income

$125,000 $850,000 ---------- $975,000 $175,000 ----------

250,000 300,000 ----------

$150,000

$800,000 ---------- $700,000

550,000 ---------- $150,000 =======

*Schedule of Cost of Goods Manufactured A-Manufacturing Co.

Direct Materials: Beginning raw materials inventory Add: Purchases of raw materials

Raw materials available for use Less: Ending raw materials inventory

Raw materials used in production

Direct Labor

$60,000 400,000 ---------- 460,000 50,000

-----------

6,000 100,000 50,000

$410,000

60,000

350,000 ---------- $820,000 90,000

---------- 910,000

Page 26

Manufacturing overhead: Insurance factory Indirect labor Machine rental Utilities factory Supplies Depreciation, factory Property taxes, factory

Total overhead costs

Total manufacturing cost Add: Beginning work in process

Less: Ending work-in-process

Cost of goods manufactured

75,000 21,000 90,000 8,000

---------

60,000 ---------

$850,000 =======

At first glance, the income statements of merchandising and manufacturing firms like A and B companies are very similar. The only apparent difference is in the labels of some of the entries in the computation of cost of goods sold. In this example, the computation of cost of goods sold relies on the following basic equation for the inventory accounts:

Basic Equation for Inventory Accounts:

Beginning balance + Additions to inventory = Ending balance + withdrawals from inventory

At the beginning of the period, the inventory contains some beginning balances. During the period, additions are made to the inventory through purchases or other means. The sum of the beginning balance and additions to the account is the total amount of inventory available. During the period, withdrawals are made from inventory. Whatever is left at the end of the period after these withdrawals is the ending balance.

These concepts are applied to determine the cost of goods sold for a merchandising company like B-bookstore as follows:

Cost of Goods Sold in a Merchandising Company:

Beginning merchandising inventory + Purchases = Ending merchandising inventory + Cost of goods sold

Or

Cost of goods sold = Beginning merchandising inventory + Purchases − Ending merchandising inventory

Page 27

To determine the cost of goods sold in a merchandising company, we only need to know the beginning and ending merchandising inventory account and the purchases. Total purchases can be easily determined in a merchandising company by simply adding together all purchases from suppliers.

The cost of goods sold for a manufacturing company like A manufacturing company is determined as follows:

Cost of Goods Sold Equation in a Manufacturing Company:

Beginning finished goods inventory + Cost of goods manufactured = Ending finished goods inventory + Cost of goods sold

Or

Cost of goods sold = Beginning finished goods inventory + Cost of goods manufactured − Ending finished goods inventory

To determine the cost of goods sold in a manufacturing company like A manufacturing company, we need to know the cost of goods manufactured and the beginning and ending balances of finished goods inventory account. The cost of goods manufactured consists of the manufacturing costs associated with goods that were finished during the period. The cost of goods manufactured figure for A manufacturing company is derived from the schedule of cost of goods manufactured below the comparative income statements.

ScheduleofCostofGoodsManufactured:

At first glance the schedule of cost of goods manufactured (below comparative income statements) appears complex and perhaps even intimating. However, it is all quite logical. The schedule of cost of goods manufactured contains the three elements of cost--direct materials, direct labor, and manufacturing overhead. The direct materials cost is not simply the cost of materials purchased during the period rather is the cost of materials used during the period. The purchase of raw materials are added to the beginning balance to determine the cost of the materials available for use. The ending materials inventory is deducted from this amount to arrive at the amount of materials used during the period. This is further explained by the following equation:

Materials available for use = Beginning balance of materials + materials purchased during the period

The sum of three cost elements (materials, labor and overhead) is the total manufacturing cost. See the following equation:

Manufacturing cost = Direct materials + Direct labor + Manufacturing overhead

This manufacturing cost is not equal to the cost of goods manufactured. Some of the materials, direct labor and manufacturing overhead costs incurred during the period relate to goods that are not yet completed. The cost of goods manufactured consists of the manufacturing costs associated with the goods that were finished during the period. Consequently adjustments need to be made to the total manufacturing cost of the period

Page 28

for the partially completed goods that were in process at the beginning and at the end of the period. Beginning work in process inventory must be added to the total manufacturing cost and ending work in process inventory must be deducted to arrive at the cost of goods manufactured. This is further explained by the following equation:

Cost of goods manufactured = Manufacturing cost + Beginning balance of work in process inventory − Ending balance of work in process inventory

Page 29

Cost Classifications for Predicting Cost Behavior (Variable and Fixed Cost): Learningobjectivesofthisarticle:

1. Define and explain variable cost and fixed cost. Give examples of variable and fixed costs.

2. What is the difference between variable and fixed cost. 3. What are the types of variable and fixed costs.

Definition of Cost Behavior: Cost behavior refers to how a cost will react or respond to changes in the level of business activity. As the level of activity rises and falls, a particular cost may rise and fall as well--or it may remain constant. Quite frequently, it is necessary to predict how a certain cost will behave in response to a change in activity. For planning purposes, a manager must be able to anticipate which of these will happen; and if a cost can be expected to change, the manager must know by how much it will change. To help make such distinctions, costs are often characterized as variable or fixed.

Variable Cost: DefinitionandExplanation:

A variable cost is a cost that varies, in total, in direct proportion to changes in the level of activity. The activity can be expressed in many ways, Such as units produced, units sold, miles driven, beds occupied, hours worked and so forth. Direct material is a good example of variable cost.

The cost of direct materials will vary in direct proportions to the number of units produced. When we speak the term variable cost we mean that the total cost rises and falls as the activity rises and falls. One interesting aspect of variable cost is that a variable cost is constant if expressed on a per unit basis. For a cost to be variable, it must be variable with respect to something. That some thing is its activity base. An activity base is a measure of whatever causes the incurrence of variable cost. An activity base is sometimes referred to as cost driver. Some of the most common activity bases are direct labor hours, machine hours, units produced, and units sold. Other activity bases (cost drivers) might include the number of miles driven by sales persons, the number of pounds of laundry cleaned by a hotel, the number of calls handed by technical support staff at a software company, and the number of beds occupied in a hospital. To plan and control variable costs, a manger must be well acquainted with the various activity bases within the firm. .

Page 30

People some times get the notion that if a cost doesn't vary with production or with sales, then it is not really a variable cost. This is not correct. As suggested by the range of bases listed below, costs are caused by many different activities within an organization. whether a cost is considered to be variable depends on whether it is caused by the activity under consideration. For example, if a manager is analyzing the cost of service calls under a product warranty, the relevant activity measure will be the number of service calls made. Those costs that vary in total with the number of service calls made are the variable cost of making service calls. Nevertheless, unless stated otherwise, you can assume that the activity base under consideration is the total volume of goods and services provided by the organization.

Some of the most frequently encountered variable costs are listed below. This is not a complete list of all costs that can be considered variable. More, some costs listed here may behave more like fixed than variable costs in some organizations.

Most Frequently Encountered Variable Costs Type of organization Costs that are normally variable with respect to volume

of output

Merchandising company Cost of goods (merchandise) sold

Manufacturing company Manufacturing costs: Direct materials Direct labor Variable portion of manufacturing overhead: Indirect materials Lubricants Supplies Power

Both merchandising and manufacturing companies

Selling, general and administrative costs: Commissions clerical costs, such as invoicing Shipping costs

Service organizations Supplies, travel, clerical

TrueVariableVersusStepVariableCosts:

Not all variable costs have exactly the same behavior pattern. Some variable costs behave in a true variable or proportionately variable pattern. Other variable costs behave in a step-variable pattern.

True Variable Cost:

A cost that varies in direct proportion to the level of activity is called true variable cost. Direct material is an example of true variable cost because the amount used during a period will vary in direct proportion to the level of production activity. Moreover, any

Page 31

amounts of direct materials purchased but not used can be stored and carried forward to the next period as inventory.

Step-Variable Cost:

The wages of maintenance workers are often considered to be a variable cost, but this variable cost does not behave in quite the same way as the cost of direct materials. unlike direct materials, the time of maintenance workers is obtainable only in large chunks. More any maintenance time not utilized cannot be stored as inventory and carried forward to the next period. If the time is not used effectively it is gone forever. Furthermore, a maintenance crew can work at a fairly leisurely pace if pressures are light but intensify its efforts if pressures build up. For this reason small changes in the level of production may have no effect on the number of maintenance people employed by the company. A resource that is obtained only in large chunks (such as maintenance workers) and whose costs increase or decrease only in response to fairly wide changes in activity is known as a step-variable cost.

Fixed Cost: DefinitionandExplanation:

A fixed cost is a cost that remains constant, in total, regardless of changes in the level of activity. Unlike variable costs, fixed costs are not affected by changes in activity. Consequently, as the activity level rises and falls, the fixed costs remain constant in total amount unless influenced by some outside forces, such as price changes. Rent is a good example of fixed cost. Fixed cost can create confusion if they are expressed on per unit basis. This is because average fixed cost per unit increases and decreases inversely with changes in activity. Examples of fixed cost include straight line depreciation, insurance property taxes, rent, supervisory salary etc.

CommittedFixedVsDiscretionaryFixedCosts:

Fixed costs are some time referred to as capacity costs since they result from out lays made for building, equipment, skilled professional employees, and other items indeed to provide the basic capacity for sustained operations. For planning purposes, fixed costs can be viewed as being either committed or discretionary.

Committed Fixed Cost:

Committed fixed costs relate to the investment in facilities, equipment, and the basic organizational structure of a firm. Examples of such costs include depreciation of buildings and equipment, taxes on real estate, insurance and salaries of top management and operating personnel.

The two key characteristics of committed fixed cost are 1. They are long term in nature. 2. They cannot be significantly reduced even for short period of time without seriously impairing the profitability or long run goals of the organization. Even if operations are interrupted or cut back, the committed fixed costs will still continue largely unchanged.

Page 32

During a recession, for example, a firm shall not usually discharge key executives or sell of key facilities.

Since it is difficult to change a committed fixed cost once the commitment has been made, management should approach these decisions with particular care. Decisions to acquire major equipment or to take on other committed fixed costs involve a long planning horizon. Management should make such commitments only after careful analysis of the available alternatives. Once a decision is made to build a certain size facility, a firm becomes locked into that decision for many years to come.

While not much can be done about committed fixed costs in the short run, management is concerned about how these resources are utilized. The strategy of management must be to utilize the capacity of the organization as effectively as possible.

Discretionary Fixed Cost: Discretionary fixed costs (often referred to as managed fixed costs) usually arise from annual decisions by management to spend in certain fixed cost areas. Examples of discretionary fixed costs include advertising, research, public relations, management development programs, and internships for students.

Basically two key differences exist between committed fixed cost and discretionary fixed cost. First, the planning horizon of a discretionary fixed cost is fairly short term usually single year. By contrast committed fixed cost has a planning horizon that encompasses many years. Second, the discretionary fixed costs can be cut for short period of time with minimal damage to the long run goals of the organization. For example spending of management development programs can be reduced because of poor economic conditions. Although some unfavorable consequences may result from the cutback, it is doubtful that these consequences would be as great as those would result if the company decided to economize during the year by laying off key personnel.

Weather a fixed cost is regarded as committed or discretionary may depend on management's strategy. For example during recessions when the level of home building is down, many construction companies may lay off most of their workers and virtually disband operations. Other construction companies retain large number of employees on the pay roll, even though the workers have little or no work to do. While these latter companies may face short term cash flow problems, it will be easier for them to respond quickly when economic conditions improve. And the higher moral and loyalty of their employees may give these companies significant competitive advantage.

The most important characteristics of discretionary cost is that management is not locked into a decision regarding such costs. They can be adjusted from year to year or even perhaps during the course of a year if circumstances may demand such a modification.

Summary of Variable and Fixed Cost Behavior

Cost Behavior of the cost (within the relevant range) In Total Per Unit

Page 33

Variable Cost

Fixed cost

Total variable cost increases and decreases in proportion to changes in the activity level.

Total fixed cost is not affected by changes in the activity level within the relevant range.

Variable cost remains constant per unit

Fixed cost per unit decreases as the activity level rises and increases as the

activity level falls

Page 34

Mixed Cost or Semi-variable Cost: LearningObjectiveofthisArticle:

• Define and explain mixed or semi-variable cost. Give examples of mixed costs. • Analyze mixed cost using high-low point method.

Definition and explanation of mixed or semi variable cost: A mixed cost is one that contains both variable and fixed cost elements. Mixed cost is also known as semi variable cost. Examples of mixed costs include electricity and telephone bills. A portion of these expenses are usually consists line rent. Line rent normally is fixed for each month. Variable portion consists units consumed or calls made. The relationship between mixed cost and level of activity can be expressed by the following equation or formula:

Y = a + bX

In this equation,

• Y = The total mixed cost • a = The total fixed cost • b = The variable cost per unit • X = The level of activity

The equation makes it very easy to calculate what the total mixed cost would be for any level of activity within the relevant range For example, Suppose that the company expects to produce 800 units and company has to pay a fixed cost of $25,000 and a variable manufacturing cost is $3.00 per unit. The total mixed cost would be calculated as follows:

Y = a + bX

Y = $25,000 + ($3.00 × 800 units)

= $27,400

A characteristic of mixed cost that needs to be understood is that we usually have to separate fixed and variable components of the total mixed cost.

The analysis of mixed costs: In practice the mixed costs are very common. For example the cost of providing X-ray services to patients is a mixed cost. There are substantial fixed costs for equipment depreciation and for salaries for radiologist and technicians, but there are also variable

Page 35

costs for X-ray film, power and supplies. Maintenance costs of machineries and plants are also mixed costs. Companies incur costs for renting maintenance facilities and for keeping skilled mechanics on the payroll, but the costs of replacement parts, lubricating oil, tires, and so forth are variable with respect to how often and how far the machineries and plants are used.

The fixed portion of the mixed cost represents the basic, minimum cost of just having a service available for use. The variable portion represents the cost incurred for actual consumption of the service. The variable element varies in proportion to the amount of service that is consumed .

High and Low Point Method- Separation of Fixed and Variable Components of Mixed or Semi-variable Cost: The fixed and variable elements of a mixed cost can be estimated by using high and low point method. To analyze mixed costs with the high and low point method, we begin by identifying the period with the lowest level activity and the period with the highest level of activity. The period with lowest level of activity is selected as first point and the period with the highest activity is selected as the second point. Consequently the formula becomes:

Variable Costs = (Y2 − Y1) ÷ (X2 − X1)

• Y2 = Cost at the high level of activity • Y1 = Cost at the low level of activity • X1 = High activity level • X2 = Low activity level

Formula can also be written as:

Variable cost = Change in cost / Change in activity

Therefore, when high and low point method is used, the variable cost is estimated by dividing the difference in cost between the high and low activity levels by the change in activity between those two points. We can apply high and low point method on the following data to spare fixed and variable costs.

Month Activity Level: (Hours Worked)

Mixed Cost (Maintenance Cost)

January February

March April May June July

5,600 7,100 5,000 6,500 7,300 8,000 6,200

$7,900 8,500 7,400 8,200 9,100 9,800 7,800

Using the high and low point method we first identify the period with the highest and lowest activity-in the following data June and March. We then use the activity and cost data from these two periods to estimate the variable cost component as follows:

Page 36

Activity Levels Patient Maintenance Cost High activity level (June) Low activity level (March) 8,000

5,000 $9,800 7,400

Variable Cost = Change in Cost / Change in Activity

$2,400 / 3,000 hours

= $ 0.80 Per hour

Variable rate is $0.80 per unit according to above calculation under high and low point method. We can now determine the amount of fixed cost as follows:

Fixed cost element = Total cost − variable cost element

$9,800 − ($0.80 per unit × 8,000 hours)

= $3,400

Both the elements, variable and fixed , have now been isolated. The cost of maintenance can now be expressed as $3,400 per month plus $0.80 per hour. The cost of maintenance can also be expressed in terms of the equation for a straight line as follows:

Y = $3,400 + $0.80X

Some times the high and low levels of activity don't coincide with the high and low amounts of cost. For example, the period that has the highest level of activity may not have the highest amount of cost. Nevertheless, the highest and lowest levels of activity are always used to analyze a mixed cost under the high and low point method. the reason is that the analyst would like to use data that reflect the greatest possible variation in activity.

LimitationsandDisadvantagesofHighandLowPointMethod:

The high and low point method is easy to apply and its simplicity is its main advantage, but it suffers from a major defect. It utilizes only two points and generally two points are not enough to produce accurate results in cost analysis work. Additionally, Periods in which the activity level is unusually low or unusually high will tend to produce inaccurate results. A cost formula that is estimated solely using data from these unusual periods may seriously misrepresent the true cost relationship that holds during normal periods.

Page 37

Cost Classifications for Assigning Costs to Cost Objects (Direct and Indirect Cost): LearningObjectiveofthisarticle:

• Define and explain direct and indirect cost. Give examples of direct and indirect costs.

• What is the difference between direct and indirect cost.

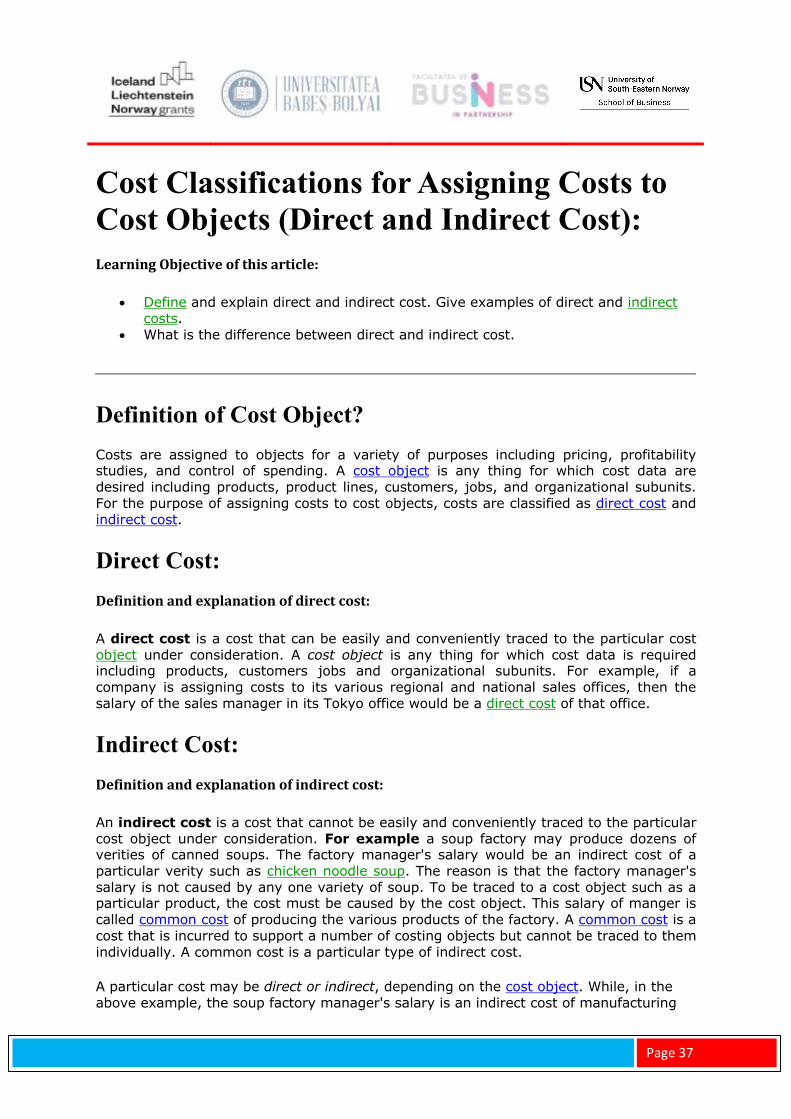

Definition of Cost Object? Costs are assigned to objects for a variety of purposes including pricing, profitability studies, and control of spending. A cost object is any thing for which cost data are desired including products, product lines, customers, jobs, and organizational subunits. For the purpose of assigning costs to cost objects, costs are classified as direct cost and indirect cost.

Direct Cost: Definitionandexplanationofdirectcost:

A direct cost is a cost that can be easily and conveniently traced to the particular cost object under consideration. A cost object is any thing for which cost data is required including products, customers jobs and organizational subunits. For example, if a company is assigning costs to its various regional and national sales offices, then the salary of the sales manager in its Tokyo office would be a direct cost of that office.

Indirect Cost: Definitionandexplanationofindirectcost:

An indirect cost is a cost that cannot be easily and conveniently traced to the particular cost object under consideration. For example a soup factory may produce dozens of verities of canned soups. The factory manager's salary would be an indirect cost of a particular verity such as chicken noodle soup. The reason is that the factory manager's salary is not caused by any one variety of soup. To be traced to a cost object such as a particular product, the cost must be caused by the cost object. This salary of manger is called common cost of producing the various products of the factory. A common cost is a cost that is incurred to support a number of costing objects but cannot be traced to them individually. A common cost is a particular type of indirect cost.

A particular cost may be direct or indirect, depending on the cost object. While, in the above example, the soup factory manager's salary is an indirect cost of manufacturing

Page 38

chicken noodle soup, it is a direct cost of the manufacturing division. In the first case, the cost object is the chicken noodle soup product. In the second case, the cost object is the entire manufacturing division.

Page 39

Cost Classification for Decision Making (Decision Making Costs): Learningobjectiveofthisarticle:

• Define, explain, and give examples of cost classifications used in making decisions: differential costs, opportunity costs, and sunk costs.

Costs can be classified for decision making. Costs are important feature of many business decisions. For the purpose of decision making, costs are usually classified as differential cost, opportunity cost, and sunk cost. It is essential to have a firm grasp of the concepts differential cost & differential revenue, opportunity cost, and sunk cost.

Differential Cost and Differential Revenue: DefinitionandExplanationofDifferentialCostandDifferentialRevenue:

Decisions involve choosing between alternatives. In business, each alternative will have certain costs and benefits that must be compared to the costs and benefits of the other available alternatives. A difference in cost between any two alternatives is known as differential cost. A difference in revenue between any two alternatives is known as differential revenues. Differential cost includes both cost increase (incremental cost) and cost decrease (decremental cost). In general the difference (cost and revenue) between alternatives are relevant in decision making. Those items that are the same under all alternatives can be ignored.

The accountant's differential cost concept can be compared to the economist's marginal cost concept. In speaking of changes in cost and revenue, the economists employ the term marginal cost and marginal revenue. The revenue that can be obtained from selling one more unit of product is called marginal revenue, and the cost involved in producing one more unit of a product is called marginal cost. The economists marginal cost is basically the same as the accountant's differential concept applied to a single unit of out put.

Example:

Differential cost can be either variable or fixed. To illustrate assume that a company is thinking about changing its marketing method from distribution through retailers to distribution by door to door direct sale. Present cost and revenues are compared to projected costs and revenues in the following table.

Description Retailer Distribution (Present)

Direct Sale Distribution (Proposed)

Differential Costs and Revenues

Revenue (variable) $700,000 $800,000 $100,000

Page 40

--------- --------- ---------

Cost of goods sold (V) 350,000 400,000 50,000

Advertising (V) 80,000 45,000 (35000)

Commissions (F)* -0- 40,000 40,000

Warehouse depreciation (V)** 50,000 80,000 30,000

Other Expenses (F) 60,000 60,000 -0-

---------- ---------- ----------

Total 540,000 625,000 85,000

---------- ---------- ----------

Net Operating Income $160,000 $175,000 $15,000

======= ======= ======= *F = Fixed **V = Variable

According to the above analysis, the differential revenue is $100,000 and the differential cost is $85,000,leaving a positive differential net operating income of $15,000 under the proposed marketing plan. The net operating income under the present distribution is $160,000, whereas the net operating income under door to door direct selling is estimated to be $175,000. Therefore the door to door direct distribution method is preferred, since it would result in $15,000 higher net operating income. Note that we would have arrive at exactly the same conclusion by simply focusing on the differential revenue, differential cost, and differential net operating income, which also shows a net operating advantage of $15,000 for the direct selling method. The company can ignore other expenses of $60,000. Because it has no effect on the decision. If it were removed from the calculation, the door to door selling method would still be preferred by $15,000. This is an extremely important principle in management accounting.

InBusiness:

Using Those Empty Seats: Many corporate jets fly with only one or two executives on board. Priscilla Blum wondered why some of the empty seats could not be used to fly cancer patients who specialized treatment outside their home area. Flying on a regular commercial airline can be an expensive and grueling experience for cancer patients. Taking the initiative, she helped found the Corporate Angle Network, an organization that arranges free flights on some 1,500 jets from over 500 companies. Since the jets fly anyway, filling a seat with cancer patient does not involve any significant incremental cost for the companies that donate the service. Since its founding in 1981, the Corporate Angel Network has arranged over 14,000 free flights.

Source: Scott McCormack, "Waste not," Forbes, July 26, 1999, p. 118.

Opportunity Cost:

Page 41

Definition:

Opportunity cost is the potential benefit that is given up when one alternative is selected over another. To illustrate this important concept, consider the following examples:

Example1:

Vicki has a part-time job that pays her $200 per week while attending college. She would like to spend a week at the beach during spring break, and her employer has agreed to give her the time off, but without pay. The $200 in lost wages would be an opportunity cost of taking week off to be at the beach.

Example2:

Suppose that Neiman Marcus is considering investing a large sum of money in land that may be a site for future store. Rather than invest the funds in land, the company could invest the funds in high-grade securities. If the land is acquired, the opportunity cost will be the investment income that could have been realized if the securities had been purchased instead.

Example3:

You are employed in a company that pays you $30,000 per year. You are thinking about leaving the company and returning to school. Since returning to school would require that you give up $30,000 salary. The forgone salary would be an opportunity cost of seeking further education.

Opportunity cost is not usually entered in the accounting records of an organization, but it is a cost that must be explicitly considered in every decision a manager makes. Virtually every alternative has some opportunity cost attached to it.

Sunk Cost: Definition:

A sunk cost is a cost that has already been incurred and that cannot be changed by any decision made now or in future.

Example:

Sunk costs cannot be changed by any decision. These are not differential costs and should be ignored in decision making. To illustrate a sunk cost, assume that a company paid $50,000 several years ago for a special purpose machine. The machine was used to make a product that is now obsolete and is no longer being sold. Even though in hindsight the purchase of the machine may have been unwise, no amount of regret can undo that decision. And it would be folly to continue making the obsolete product to recover the original cost of the machine. In short, the $50,000 originally paid for the machine has already been incurred and cannot be differential cost in any future decision.

Page 42

For this reason, such costs are said to be sunk costs and should be ignored in decision making.

Page 43

Quality Costs: Learning objective of this article:

• Identify the four types of quality costs and explain how they interact.

Definition and Explanation of Quality Costs: A product that meets or exceeds its design specifications and is free of defects that mar its appearance or degrade its performance is said to have high quality of conformance. Note that if an economy car is free of defects, it can have a quality of conformance that is just as high as defect-free luxury car. The purchasers of economy cars cannot expect their cars to be as opulently as luxury cars, but they can and do expect to be free of defects.

Preventing, detecting and dealing with defects cause costs that are called quality costs or costs of quality. The use of the term "quality cost" is confusing to some people. It does not refer to costs such as using a higher grade leather to make a wallet or using 14K gold instead of gold plating in jewelry. Instead the term quality cost refers to all of the costs that are incurred to prevent defects or that result from defects in products.

Quality costs can be broken down into four broad groups. These four groups are also termed as four (4) types of quality costs. Two of these groups are known as prevention costs and appraisal costs. These are incurred in an effort to keep defective products from falling into the hands of customers. The other two groups of costs are known as internal failure costs and external failure costs. Internal and external failure costs are incurred because defects are produced despite efforts to prevent them therefore these costs are also known as costs of poor quality.

The quality costs do not just relate to just manufacturing; rather, they relate to all the activities in a company from initial research and development (R & D) through customer service. Total quality cost can be quite high unless management gives this area special attention.

Four types of quality cost are briefly explained below:

Prevention Costs: Generally the most effective way to manage quality costs is to avoid having defects in the first place. It is much less costly to prevent a problem from ever happening than it is to find and correct the problem after it has occurred. Prevention costs support activities whose purpose is to reduce the number of defects. Companies employ many techniques to prevent defects for example statistical process control, quality engineering, training, and a variety of tools from total quality management (TQM).

Page 44