defintion of managerial economics

99

Presented by Dr.D.ulagammal,(GL) K.N.Govrt.Arts college for women(A) Thanjavur MANAGERIAL ECONOMICS Code : 18KP1COELC01 UNIT – 1

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of defintion of managerial economics

Presented byDr.D.ulagammal,(GL)

K.N.Govrt.Arts college for women(A)Thanjavur

MANAGERIAL ECONOMICSCode : 18KP1COELC01

UNIT – 1

DEFINTION OF MANAGERIALECONOMICS

•

•

••

•

“ Managerial economics” by Joel Dean in 1951.As Joel deanobserves managerial economics shows how economicanalysis can be used in formulating policies.MEANING –MANAGERIAL ECONOMICS IS “the application ofeconomic theory and methodology to business administrationpractice.” Managerial economics “is concerned with business efficiency.” It is clear,therefore,that Managerial Economics deals with theeconomic aspects of managerial decisions or with thosemanagerial decisions “Managerial Economics is designed to provide a rigoroustreatment of those aspects of economic theory and analysisthat are most useful for managerial decision analysis”

SCOPE OF MANAGERIALECONOMICS

•

•

•

1.2.3.4.5.

The scope of managerial economics refers to its area of study.Managerial economics has its roots in economic theory. Managerial economics provides management with a strategicplanning tool that can be used to get a clearer perspective of theway the business world works and what can be done to maintainprofitability in an ever-changing environment. Application of economic principles to five types of resourcedecisions made by all types of business organisations.

The selection of the product or service to be produced The choice of production methods and resource combination The determination of the best price and quantity combination Promotional strategy and activities The selection of the location from which to produce and sellgoods or services to consumers

•

••

•

••••••••••

The scope of managerial economics covers two areas of decisionmaking A.Operational Issues B.Environmental issues.OPERATIONAL ISSUESOperational issues refer to those which arise within the businessorganisation. They pertain to the simple questions of what to produce,when to produce, how much to produce.It include choice of price, promotion of sale and the strategy to facecompetition.The other internal issues are management of profit andcapital, inventory management etc,,ALL THESE BROAD ISSUESTheory of demand and demand forecastingPricing and competitive strategy.Cost analysisResource AllocationProfit analysisCapital/investment analysisStrategic planningEnvironmental issuesENVIRONMENTAL issues in managerial Economics refer to the generalbusiness environment in which the firm operates.

THE ROLE OF MANAGERIALECONOMIST

•

•

•

•

•

A management economist with sound knowledge of theory and analytical tools forinformation systems,occupies a prestigious place among the personnel.A managerialeconomist is nearer to the policy maker because his main function is to improve thequality of policy-making.Equipped with specialised skills and modern techniques heanalyses the internal and external operations of the firm. He evaluates and helps indecision making regarding sales,pricing,financial issues,labour relations andprofitability.he helps in decision-making keeping in view the different goals of the firm. His role in decision making applies to routine affairs such as price fixation,improvement in quality,location of plant,expansion or contraction of output ect.Therole of managerial economist in internal management covers wide areas ofproduction,sales and inventory schedules of the firm The most important role of the managerial relates to demand forecasting because ananalysis of general business conditions relates to demand forecasting because ananalysis of general business conditions is most vital for the success of the firm.Heprepares a short terms forecast of general business activity and relates generaleconomic forecasts to specific market trendsThe purpose of market research is to provide a firm with information about currentmarket position as well as present and possible future trends in the industry.Amanagerial economist who is well equipped with this knowledge can help the firm toplan product improvement,new product policy,pricing and sales promotion strategy.The fourth function of the managerial economist is to undertake an economicanalysis of the industry. This is concerned with project evaluation and feasibilitystudy at the firm level,he should be able to judge on the basis of cost-benefit analysis,whether it is advisable and profitable to go ahead with the project .the managerialeconomist should be adept at investmant appraisal methods.At the external level,economic analysis involves the knowledge of competition involved, possibility ofi l d f i l h l b i li

•

•

•

•

•

The specific function of a managerial economistincludes an analysis of environmental issues.The managerial economist who is aware of thisbasic knowledge of environmental issues, can be aworthy citizen making the firm fit into environment.The role of management economist lies not intaking decisions but in analysing, concluding andrecommending to the policy maker.He should have the freedom to operate and analyseand must possess full knowledge of facts.He has to collect and provide the quantitative datafrom within the firm.

DEMAND ANALYSIS

••

•

•

LAW OF DEMANDLaw of Demand shows the relation betweenprice and quantity demanded of a commodityin the market.In the words of MARSHALL ; “the amontdemanded increases with a fall in price anddiminishes with a rise in price.”A rise in the price of a commodity is followedby a reduction in demand and a fall in price isfollowed by an increase in demand.

LAW OF DEMAND IS BASED ONCERTAIN ASSUMPTIONS

•

•••••

•

There is no change in consumers taste andpreferences.Income should remain constant.Prices of other goods should not change.There should be no substitute for the commodity.The commodity should not confer any distinction.The demand for the commodity should becontinuous.People should not expect any change in the price ofthe commodity.

ELASTICITY OF DEMAND

•

•

•

Elasticity of demand explains the relationshipbetween a change in price and consequentchange in amount demanded.Law of demand explains the direction ofchange in demand. A fall in price leads to anincrease in quantity demanded and vice versa.The elasticity of demand in a market is greator small according as the amount demandedincreases much or little for a given fall in theprice and diminishes much or little for a givenrise in price.

ELASTIC DEMAND AND INELASTICDEMAND

•

•

•

A small change in price may lead to agreat change in quantity demanded.If a big change in price is followed by asmall change in demand then the demandis inelastic.

TYPES OF ELASTICITY OF DEMAND

••••••

Price elasticity of demandPerfectly or infinitely elastic demandPerfectly inelastic demandRelatively elastic demandRelatively inelastic demandUnit elasticity of demand.

FACTORS DETERMININGELASTICITY OF DEMAND

•••••••

Nature of the commodityAvailability of substitutesVariety of usesPostponement of demandAmount of money spentTimeRange of prices

Concept of elasticity of demand

•

•

•

Price fixation; Each seller under monopolyand imperfect competition has to take intoaccount elasticity of demand while fixingthe price for his product.Production: producers generally decidetheir production level on the basis ofdemand for the product.Distribution: Elasticity of demand also helpin the determination of rewards for factorsof production.

•

•

•

International trade:Elasticity of demandhelp in finding out the terms of tradebetween two countries.Public finance: Elasticity of demand helpsthe government in formulating tax policies.Nationalisation: The concept of elasticityof demand enables the government todecide about nationalisation of industries.

DEMAND FORECASTING

• Demand forecasting refers to an estimateof future demad for the product. It is an“objective assessment of the futurecourse of demand”. In recent times,forecasting plays an important role inbusiness decision-making.Demandforecasts relate to production,inventorycontrol,timing,reliability of forecast etc.

TYPES OF DEMAND FORECASTING

••

Short-term demand forecasting Short-term demand forecasting islimited to short periods,usually for one year.It relates to policies sales,purchase,priceand finances.Itrefers to existing productioncapacity of the firm.Short term forecastingis eswsential for formulating a suitableprice policy. Short term forecasting helps inreducing the costs of operation.Short termforecasting helps in sale policy formulation.

LONG-TERM FORECASTING•

••

In long-term forecasting,the businessmenshould know about the long term demand forthe product. Planning of a new plant orexpansion of an existing unit depends onlong term demand.similarly a multi-productfirm must take into account the demand fordifferent items.When forecasts are madecovering long periods.Demand Forecasting into three types :They are macro economic forecasting,industry forecasting and firmal levelforecasting.

• Macro economic forecasting is concernedwith the economy, while industrial levelforecasting is concerned with theeconomy, while industrial level forecastingis used for inter-industry comparison andis being supplied by trade association orchamber of commerce. Firmal levelforecasting relates to individual firm.

METHODS OF FORECASTING

••

•

SURVEY METHOD:Opinion Survey Method:- This method is also known as saleforce- composite method or collective opinion method. Underthis method the company ask its salesmen to submitestimates of future sales in their respective territories.Thismethod is simple and straight forward. reference books:

Managerial economics – R.Cauvery U.K.Sudhanayak M.Girija R.MeenakshiManagerial economics – G S Gupta

MANAGERIAL ECONOMICS

SUBJECT HANDLED

BY

Dr.T.VASUGI

GUEST LECTURER IN COMMERCE

K.N.GOVT. ARTS COLLOEGE(W), AUTONOMOUS

THANJAVUR.

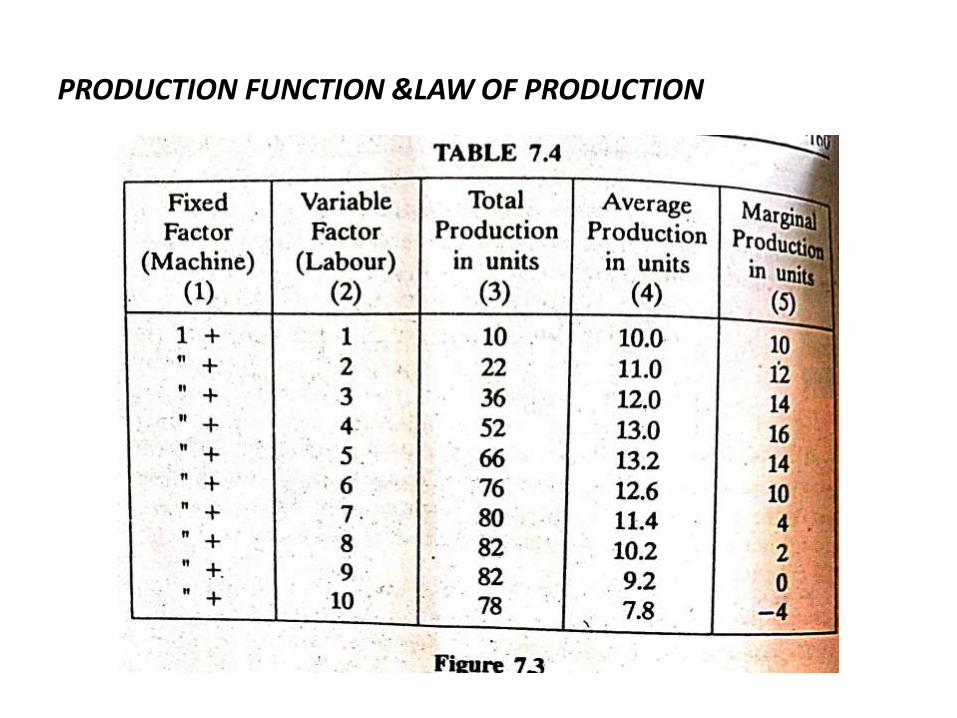

UNIT – II PRODUCTION FUNCTION & LAWS PF PRODUCTION

• INTRODUCTION OF PRODUCTION FUNCTION : Production is an organized activity of transformation inputs into outputs. Inputs refer to all those things which a firm buys to produce a particular product. Output means the quantity of goods in the finished form produced by the firm for selling by using the inputs. The term input is wider in its scope than the term factors of production. Inputs not only refer to factors of production, but also other things purchased by the firm or spend by the firm in the process of production. It also includes the rendering of the various kinds of services, such a banking, insurance,transport.Theprocess of production adds to the values or creation of utilities.

DEFINITION OF PRODUCTION

• According to James bates and J.R. Parkinson “Production is the organised activity of transforming resources into finished products in the form of goods and services; and the objective of production is to satisfy the demand of such transformed resources.

“the production function is a single valued mapping from input space into output space in as the maximum attainable output for any stipulated set of inputs is unique”.

There are two broad classes of production function:

Fixed proportion production function,

Variable proportion production function

A production process is characterized by fixed proportions, if each level of output technologically requires a unique combination of inputs. If the technologically determined input-output ratio is independent of the sale of production for each input, the production process is characterized by fixed input coefficient.

A variable proportion production function is one in which the same level of output may be produced by two or more combinations of inputs.

LAWS OF PRODUCTION

In Economic theory, production analysis considers two types of input-output relationships.

The input-output relationship when certain inputs are kept fixed and other inputs are made variable.

When all inputs are made variable.These two types of relationships have been studied and explained in

the form of laws, Law of variable proportions, and Laws of returns to scale.Laws of variable proportion

The law of variable proportions is the fundamental law of production which consists two phases,

The law of increasing returns and The law of diminishing returns. The level of output of a firm depends on the combination of

different factors, land, labour, capital and organization.

Alfred Marshall:” An increase in the amount of a variable factor added to a fixed factor causes, in the end, a less than proportionate increase in the amount of product, given technical conditions”.

“As equal increments of one input are added, the inputs of other productive services being held consent, beyond a certain point, the resulting increments of product will decrease, i.e., the marginal product will diminish”.

Assumptions of the law

The law is based upon the following assumptions:

If there is any improvement in technology, the average and marginal output will not decrease but increase.

Only one factor of input is made variable and other factors are kept constant.

All units of the variable factor are homogeneous.

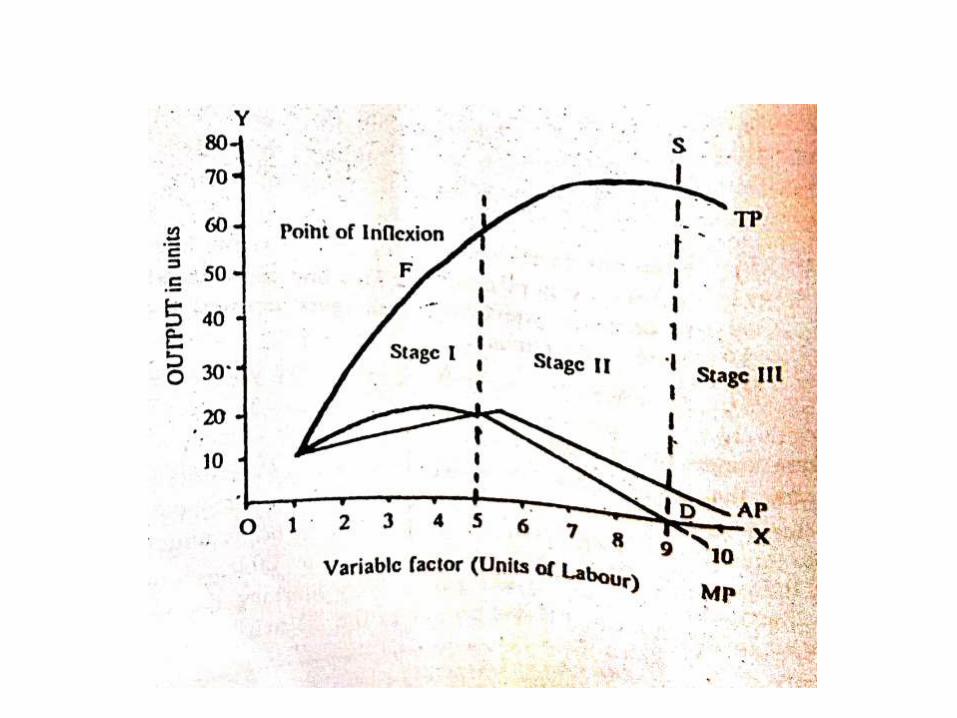

There stages of the law

The behaviour of the output when the varying quantity of one factor is combined with a fixed quantity of the other can be divided into three stages.

PRODUCTION FUNCTION &LAW OF PRODUCTION

LAW OF RETURNS TO SCALE

The short-run phenomenon, as in this period fixed factors cannot be changed and all factors cannot be changed.

The long-term all factors can be changed or made variable.

In variable proportions, the co-operating factors may be increased or decreased and one factor, e.g., land in agriculture or machinery in industry.

The difference between the changes in factors proportion and changes in the scale will be clear from the following figure.

Changes in scale and Factor Proportions

Three phases of returns to scale

If the increase in all factors leads to a more than proportionate increase in output, returns to scale are said to be increasing.

A doubling of the scale will result in output being more than double.

If the scale is trebled the output will be more then treble.

Three phases of returns to scaleFirst stage, we have increasing returns.

Second stage, constant returns.

Third stage, the decreasing returns

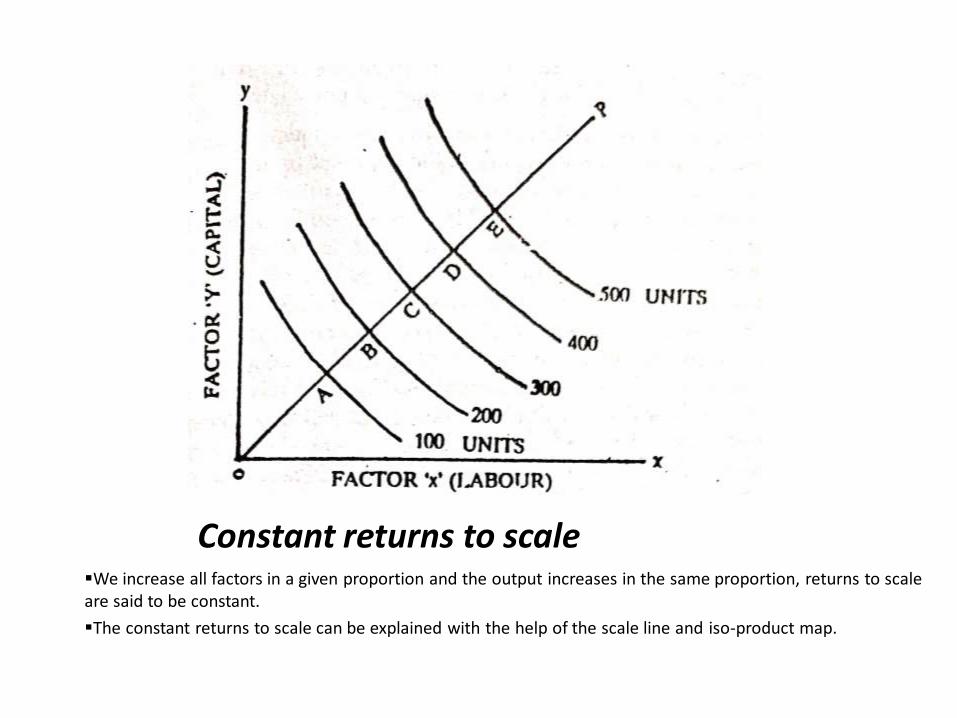

Constant returns to scaleWe increase all factors in a given proportion and the output increases in the same proportion, returns to scale are said to be constant.

The constant returns to scale can be explained with the help of the scale line and iso-product map.

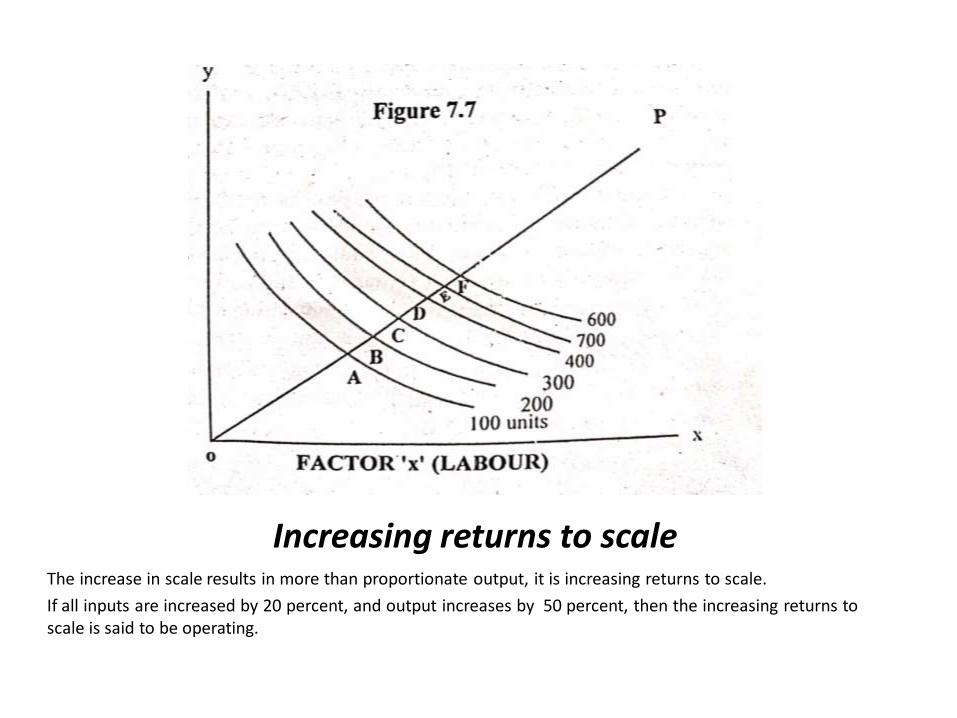

Increasing returns to scaleThe increase in scale results in more than proportionate output, it is increasing returns to scale.

If all inputs are increased by 20 percent, and output increases by 50 percent, then the increasing returns to scale is said to be operating.

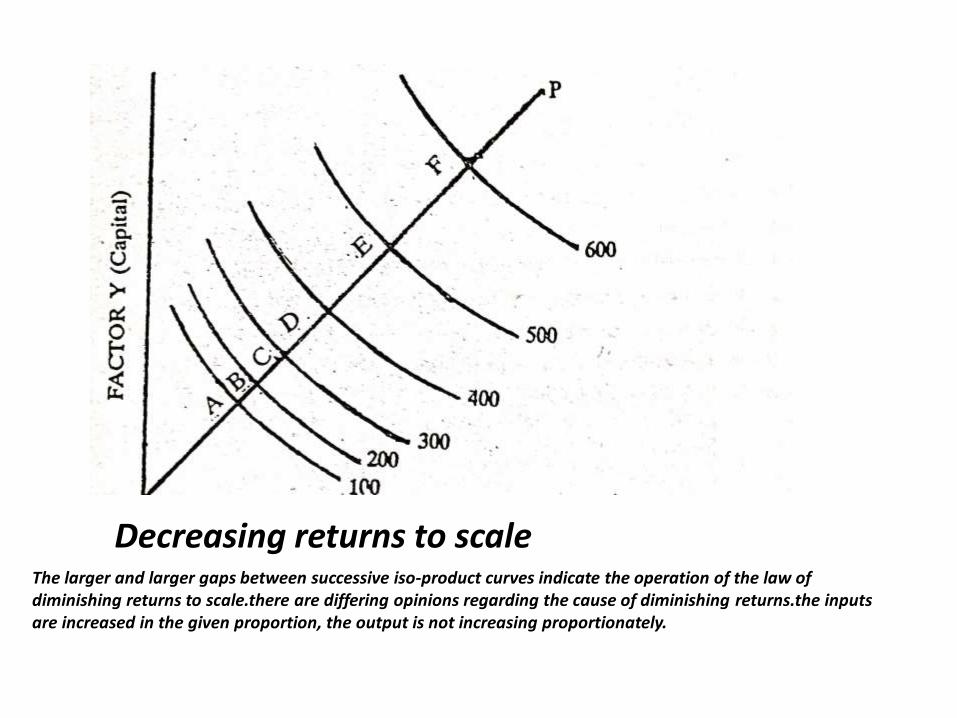

Decreasing returns to scaleThe larger and larger gaps between successive iso-product curves indicate the operation of the law of diminishing returns to scale.there are differing opinions regarding the cause of diminishing returns.the inputs are increased in the given proportion, the output is not increasing proportionately.

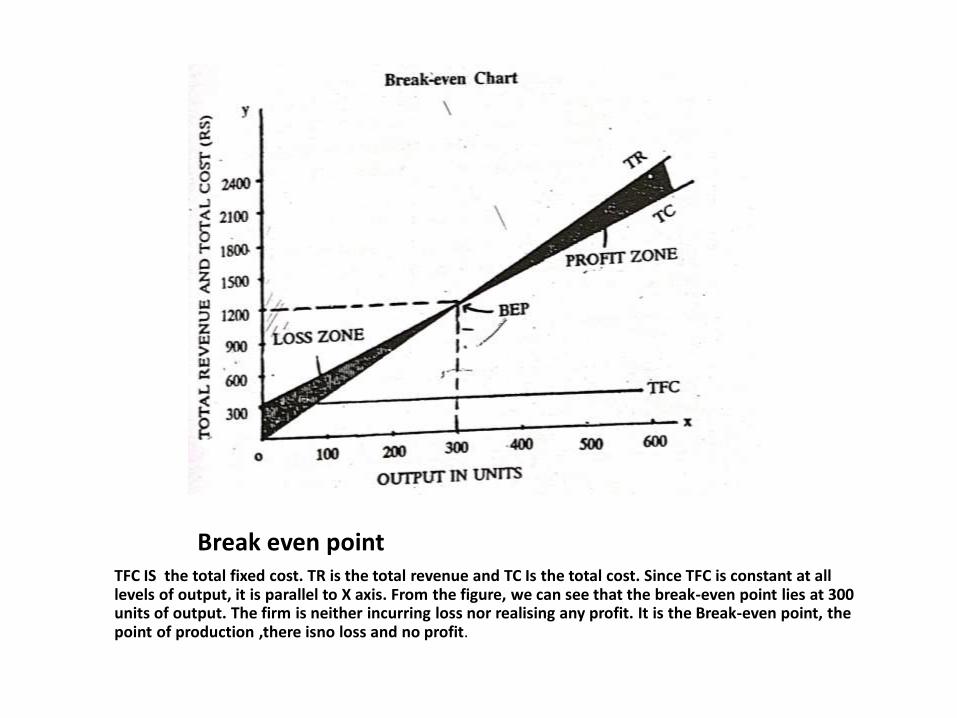

BREAK-EVEN ANALYSIS

What is Break even Analysis?

Break-even analysis is a study of costs, revenues and sales of a firm and finding out the volume of sales where the firms costs and revenues will be equal. The break even point is that level of sales where the net income is equal to zero. The break even point is the zone of no-profit and no-loss, as the costs equal revenues.

Objective:

to create an understanding and relationship between cost, revenues and output that could be sold within the competence of the firm.

Determination of break-even point

The BEP of a firm can be found out in two ways.

Physical units, i.e., volume of output

Sales values.

1.BEP IN TERMS OF PHYSICAL UNITS

Break even pointTFC IS the total fixed cost. TR is the total revenue and TC Is the total cost. Since TFC is constant at all levels of output, it is parallel to X axis. From the figure, we can see that the break-even point lies at 300 units of output. The firm is neither incurring loss nor realising any profit. It is the Break-even point, the point of production ,there isno loss and no profit.

2. BEP in terms of sales value

Usefulness of Break-Even Analysis

Safety Margin

Target profit

Change in price

Limitations of Break-even Analysis

It is static in character

Projection of future with the past is not correct.

The assumption that cost-revenue-output relationship is linear is true only over a small range of output.

The profit are a function of not only output, but also other factors like technological change, improvement in the art of management, etc.

COSTS : CONCEPTS & CLASSIFICATIONS

• Difference between Economist and Accountant• The accountant views the cost of an asset by taking into account the

actual money spent on it.• The accountants cost is the money spent or acquisition cost. This

acquisition cost tells merely the cost amount of the resource.• The economist analysis cost in terms of choice faced by the firm in

utilising its resources.• The opportunity cost may be more than the acquisition cost or it may be

less than that.COST CLASSIFICATIONS Opportunity cost- outlay cost Past cost- future cost Traceable-common costs. Out-of-pocket –book-costs Incremental cost vs. sunk cost

• Escapable vs, Unavoidable costs

• Shut down and abandonment costs

• Urgent and postponable costs

• Controllable and non-controllable costs

• Replacement vs. Historical cost

• Private and social cost

• Short-run and long-run costs.

• Fixed cost and variable cost.

Semi- Variable cost

There are some costs which are neither perfectly variable, nor absolutely fixed in relation to the changes in the size of output. They are known as Semi-variable costs.

Examples: Electricity charges include both a fixed charges and a charge based on consumption.

TOTAL COST, AVERAGE COST AND MARGING COST

• Total cost of production is the total money expenses incurred for buying the input required for producing a commodity or a service. E.g, the amount spent on wood, nails, varnish, labour, rent for the premises, interest on capital, etc.

• Average cost is the unit cost of production. It is the cost per unit of output. Average total cost is the sum of average fixed cost and the average variable cost.

• Marginal cost is defined as the addition made to the total cost by the production of one additional unit of output. The marginal cost is the addition to the total cost of production.

COST FUNCTION

The cost determinants in modern manufacturing enterprises. These are:

Rate of output(Utilization of fixed plant)

Size of plant

Prices of input factors (Materials and labour)

Technology

Stability of output

Efficiency of management and labour,

In economic theory, there are mainly two types of cost functions,

The short-run cost function and

The long run cost function.

Short-run cost-output relationship

• The short-run, the average cost of the firm declines to a minimum and then rises. It declines depends on the proportion of fixed cost to total cost. The average cost curve is ‘u’ shaped in the short-run.

Accounting vs. Economic view

The Accountant view about cost-output relationship is different from prevailing traditional economic theory.

LONG-RUN COST-OUTPUT RELATIONSHIP

Long-run average cost is the long-run total cost divided by the level of output. The average cost of production at different levels of output. It is the cumulative picture of short-run average cost curves. The short-run average cost curves are also called plant curves, since in the short-run average cost curve corresponds to a particular plan

LEARNING CURVE

Several kinds of improvements are effected through learning.

Lesser time to instruct workers.

Better co-ordination and operational sequence.

Better and skillful movement of workers

Improvements in machines and tooling.

Improved management control.Measurement of cost-output relationship

There are three approaches,

Accounting approach

Engineering approach

Statistical approach.

---------------------------------------------

UNIT III -PRICE POLICIES

What is price ?Price means the cost or the amount at which something is valued.

An examples, of a price is $1 for three cookies.There are many factors which influence the price of a commodity:

The demand for a commodity Cost of production Objectives of the firm Competition and Government policy.

Objectives: Achieving a target rate of return on investment Accomplishing the target rate of growth Maintaining and improving the market share Maintaining the prestige of the firm Enhancing the goodwill of the company Stabilising the prices.

PRICING METHODS

The various pricing methods usually employed by businessmen are :

Cost-plus or full-cost pricing methodsTarget pricing or pricing for a rate of returnMarginal pricing Going rate pricing Customary pricingDifferential pricing

Pricing in public utilitiesThe term ’public utilities’ in the economic sense

refers to services like water-supply, gas supply, electricity, telephone services, communication and all forms of transport. Public utilities refer to those group of industries which are run with a public interest.

Let us discuss about the pricing policy and methods in public utility services :

Marginal cost pricing Average cost pricing Fair return principle Actual pricing.

Price and output determination under perfect competition:

Competition in business connotes the presence of more than one seller and one buyer in a particular market. In competition markets sellers act independently of sellers and each buyer also acts independently of other buyers.

Competition is a very general and theoretical term. It has many different meanings.

Competition refer to different types of competition such as

Perfect competitionPerfect competition means “rational conduct on the part of

buyers and sellers, full knowledge, absence of friction, perfect mobility and perfect divisibility of factors of production and completely static conditions”.

Features of perfect competition: Large number of buyers and sellers Homogeneous product Free entry and exist conditions Perfect knowledge on the part of buyers and sellers Perfect mobility of factors of production Absence of transport cost Absence of government or artificial restrictions

MonopolyMonopoly is the opposite extreme of perfect competition. It

means absence of competition. It denotes a single sellers or producer having the control over the market.

Features of monopoly

Monopoly will have the following features:o It should have only single controlo The commodity produced should not have any close substitute.o No freedom to other entrepreneurs to enter and compete with the existing seller

having full control over the market.o He may also adopt price discrimination.

Monopoly powero Power given by the governmento Legal powero Technical powero Combinations

Types of price discrimination:o Personal discriminationo Place discrimination o Trade discrimination

Imperfect competitionImperfect competition is a negatie term denoting a market situation that is not

perfect. This imperfection may take any form. There may be group competition between very few firms.

Features of monopolistic competition

• Existence of large number of firms.• Product differentiation • Selling cost• Freedom of entry and exist of firms

OligopolyOligopoly refers to that form of imperfect competition where there will

be only a few sellers producing either a homogeneous product or products which are close substitutes, but not perfect substitutes

Definition of oligopoly“situation in which a firm bases its market policy in part on the expected

behaviour of a few close rivals”.There are different types of oligopoly. They are :

Pure and perfect oligopoly and differentiated or imperfect oligopoly. Open and closed oligopoly Collusive and competitive oligopoly Partial or full oligopoly Syndicated and organised oligopoly

Characteristics of oligopoly

• Interdependence

• Indeterminate demand curve

• Importance of selling cost

• Group behaviour

• Element of monopoly

• Price rigidity.

Duopoly

Duopoly refers to a market situation in which there are only two sellers. Each seller tries to guess the rival’s motives and actions. The two firms may either resort to competition.

Monopsony

Monopsony refers to a market in which there is a single buyer or a single purchasing agency. The whole of a commodity or service will be purchased by this single agency. It is possible that the single buyer may be facing a single seller, i.e., monopsony facing a few sellers or oligopoly.

UNIT-IVPROFIT MANAGEMENT

•

•

•

Nature of profit:- Profit means the net income of thebusiness man. It is necessarily a residual income. It canbe calculated by deducting the total expenditureincurred in a business from the total receipts. Profit is areturn to the entrepreneur for the use of hisentrepreneurial ability. He must do something more thanroutine management to earn profitAN ENTREPRENEUR ESSENTIALLY DOES TWO THINGS:-I. He decide what to produce, how to produce and howmuch to produce.He also plan about the utilisation of hislimited resources,and profit may be regarded as areward for uncertainty bearing.The entrepreneur must search for new methods ofproduction, new ways of business organisation, newmarketing techniques and approaches .

METHODS OF MEASUREMENT OFPROFIT

•

•

•

Measurement of profit :- The problem ofmeasurement of profit has been a difficultaffair because of the problem involved inallocating the correct costs and revenues toa given accounting periods.There are different ways of measuringprofit :A)Depreciation B) valuation of stock C)Allocation of expenses over time periods. D)Capital gains and losses.

•

••••••••

A . DEPRECIATION:- Depreciation means fall in the quality orvalue of an asset. Therefore, in order to measure the trueincome of a business a charge is made against the annualincome of the business.The charge is known as depreciation.There are a number of methods of measuring depreciation:-.The straight –line method;The units – of- production method;The declining balance method;The sum- of- the years digits method;The revaluation method;The repair provision method;The retirement accounting method.

THE STRAIGHT – LINE METHOD• THE STRAIGHT –LINE METHOD:- This

method is simple and is most commonlyused method of depreciation. It is based onthe assumption that the value of an assetdeclines at a constant ratTherefore it is alsocalled as proportional or equal instalmentmethod.The amount of depreciation isobtained by dividing the initial cost of theasseta by the estimated life. If the assets hasscrap value, it has to be deducted frome theinitial cost before dividing it by the estimatedlife.

THE UNIT-OF –PRODUCTIONMETHOD

•

•

This method resembles the straight –linemethod, the difference between the twomethods is that, in this methoddepreciation is based on the estimatedoutput and the life of the machine isestimated in hours.This methods is not very popular becauseunder this method depreciation is notallowed for purposes of tax deduction.

THE SINKING – FUND METHOD

•

•

In this method it is assumed that whaenreplacement of the old asset is due, agiven sum will be available for thepurchase of a new asset withoutaffecting the financial position of theconcern.The amount of depreciation is calculatedas a fixed periodic charge and isdeposited in readily saleable securities.

The declining-balance method•

••

under this method,depreciation is provided on auniform rate on the written down value of the assetat the beginning of the year.

The sum of the years digits method it is similar to that of the declining balance method. it provides for a more or less uniform total cost ofoperation of the asset. The amount of depreciationis higher in the first year and it progressively declineswith the passage of time. It differs from thedeclining balance method in that the book valueremains constant while the annual rate ofdepreciation changes.

The revaluation method

•

•

in this method,the difference between thevalue of the asset at the beginning and theend of the period is deducted periodically.This amount is depreciationThis revaluation method is used by smallfirms

The repair provision method• this method provides “for the aggregate of

depreciation and maintenance cost by meansof periodic charges,each of which is aconstant proportion of the aggregate of thecost of the asset depreciated and theexcepted maintenance cost during its life”. Inthis method,the cost of repairs is added tothe cost of the equipment. The total value ofthe original cost plus the cost of repairs,lessthe scrap value is then depreciatedeitherunder the decline-balance method orthe straight-line method.

The retirement accounting method

• It refers to the charging of total cost of thefixed asset once the latter has worn-out.Another version is that it should be left tothe senior managers who should charge alarge amount during the prosperous yearsand a small one in the lean years.

Profit policies•

•

•

•

economic theory makes a fundamental assumption thatmaximising profits is the basic objective of the firm the managers aim at maximising their utility gunction.The managerial utility function depends on salaries,prestige,market shares,job security,quiet life ect. Baumolpostulated that the managerial utility is maximised whenthe growth of sales revenues is maximised some writers have argued tht because of uncertainty inthe real world,it is impossible to maximise anything ,including profits. So firms do not seek the maximisationof profits,sales,growth or anything else K.W rothschild has suggested that the primary objectiveof firm is a longrun survival. Still other writers havesuggested that may firms set as their goal theattainment and retention of a constant market share.

•

•

•••••

attaining industry leadership through larger salesvolume or manufacturing of maximum product linesmay be the most important objective of a businessfirm instead of making huge profits. Some firms mayaim at maximising consumer welfare and maintainconsumer good will various criteria may be applied to decide theacceptable rate of profit profit to attract capital “ Earnings by the competitors” standard historical rate of profit standard shareholders’purchasing power standard Retained earning standard

Profit forecasting and control•

•••1.

2.

forecasting has got all the problems connected with uncertainfuture.profit forecasting is no exception. According to joel dean,there are three approaches to profit forecasting: spot projections environmental analysis and break-even analysis

spot projections: Thisrelates to projecting the entire profit and loss statement

for a specified future period by forecasting each importantelement in the profit and loss statement . Forecasts are madeabout sales volume prices and costs of

producing the anticipated sales.profit is the differencebetween sales revenue and cost.Environmental analysis:

It relates the companys profit to the general economictrends that prevail in the economy during the relevant period.

•

•

•

The general economics trends include key variables like general businessactivity,general price level ect. The data can be obtained from governmentpublications.3. Break-even analysis The break-even analysis is a powerful tool for profit planning andmanagement control. It shows the functional relation of revenue and cost tooutput Of the three techniques,break –even analysis is the most important tool ofprofit forecasting.in practice,these three approaches need not be mutuallyexclusive,but can be used jointly for maximum information.

reference books: Managerial economics – R.Cauvery U.K.Sudhanayak M.Girija R.MeenakshiManagerial economics – G S Gupta

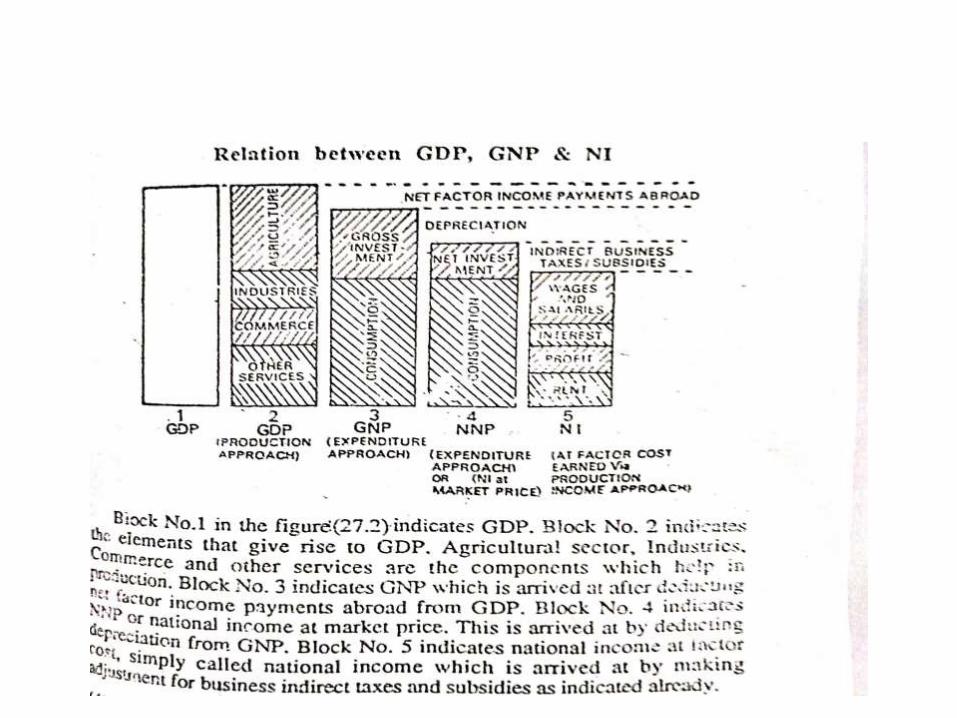

UNIT-V NATIONAL INCOME

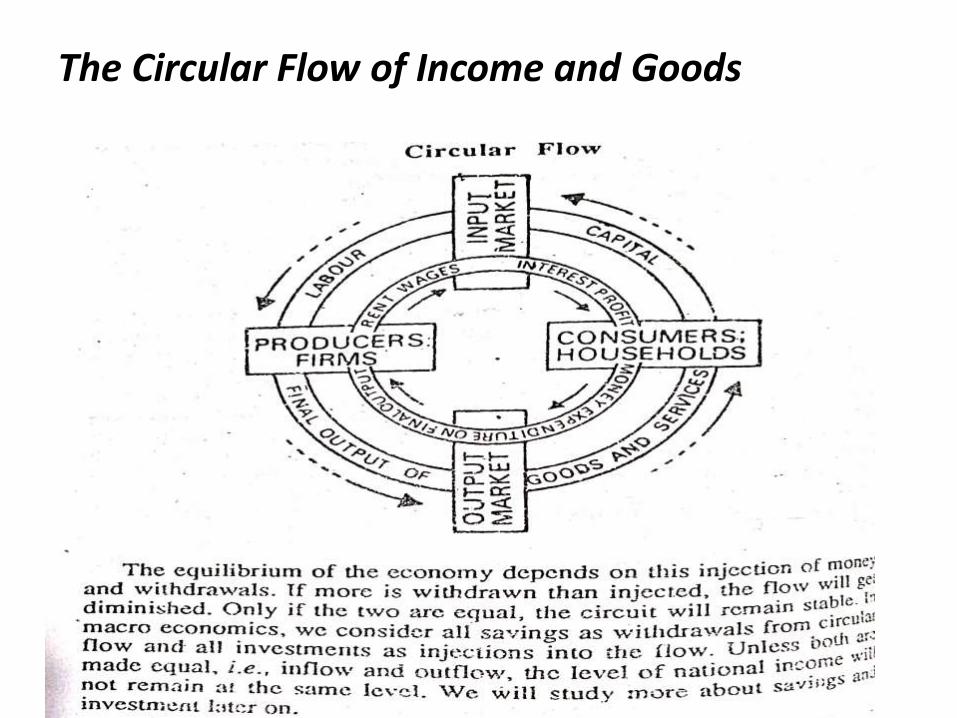

Meaning : National income gives information about the nation productive capacity and economic strength. National Income study will reveal the extent of utilization of a country’s resources and the extent of unemployment.Wealth and income

Wealth consists of the material economic possessions including many diverse things as buildings, automobiles, business inventories of all kinds including proven reserves of unexploited natural resources of the country.Stock and Flow

Wealth is a stock and income is flow. Stock has no time dimension. It represents quantities of things in existence at a particular moment. Flow represents quantities of things over a period of time.

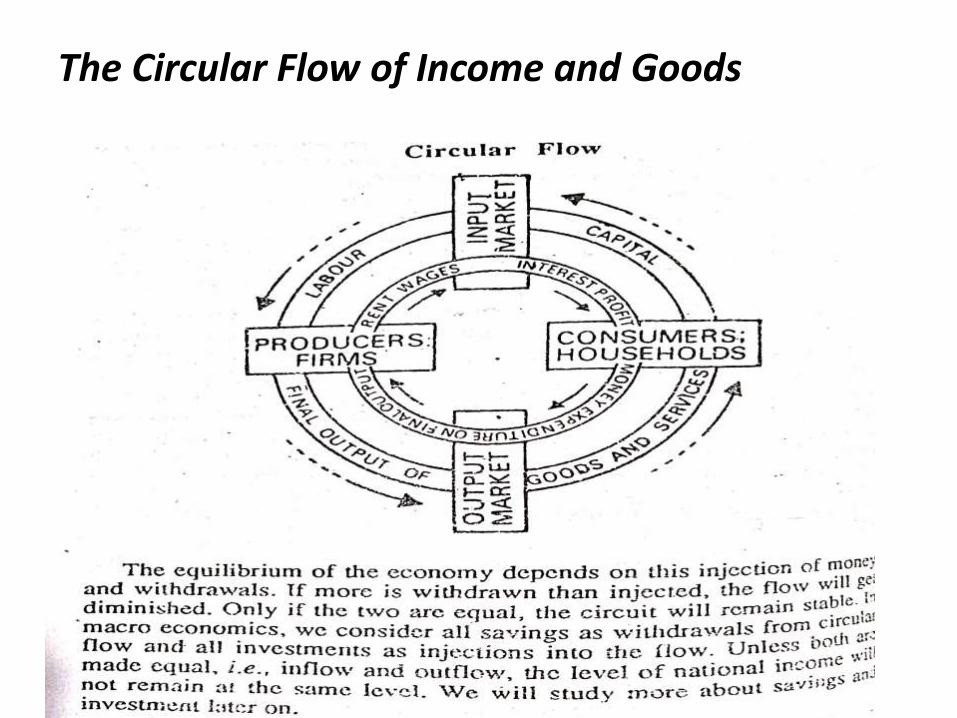

The Circular Flow of Income and Goods

Definition of national income

J.R. Hicks defined national income “as a collection of goods and services reduced to a common basis by being measured in terms of money”.

Concept of national income National income is the sum of incomes earned during the period from

supplying of factor units for the use of production. It is taken as total production per year of goods and services in the

country measured in money. It is taken as total consumption of the country per year plus

investment.The various methods of national income:

Gross national product: means the money value of the national production for any given period.

Net National Product :NNP refers to the net production of goods and services in a country during the year.

National income :this is the total of all income payments received by the factors of production, viz., land, labour, capital and organization.

Personal income: This is the actual income received by the individuals and households in the country from all sources.

Personal income= national income minus corporate income taxes minus undistributed corporate profits minus social security contributions plus transfer payments.

Disposable personal income: this is simply the after-tax of personal income. The personal income is not available for consumption as personal direct taxes have to be paid. After payment of personal direct taxes is called disposable.

COMPUTATION OF NATIONAL INCOME

Production approach

Expenditure approach

Earning or income approach

DIFFICULTIES IN THE MEASUREMENT OF NATIONAL INCOME

The measurement of national income is best with difficulties. In the underdeveloped countries, these difficulties are more prominent, making the computation of national income an extremely difficult task and the figures may not be much dependable.

o Conceptual difficultieso Statistical difficulties

Factors determining national income:There are a number of influences which determine the size of the

national income in a country. The three main influences are : Quality and quantity of factors of production The state of technical know-how; and Political stability.

National income and real incomeWhen national income is expressed in terms of current prices, it

is called National income, but when it is expressed in terms of constant prices prevailing in the base year; it is called Real income.

The national income of a particular year when compared with the national income of the base year, will include the effect of two changes, viz.,

Change in the production of goods and services; and Change in the price level or value of money.

Per Capital real income= Real national income__________________

Size of populationUses of national income statistics:

National income statistics are valuable instruments of economic analysis and a guide to economic policies to be pursued.

NI statistics given an idea of the structure of the economy. NI estimates help us to study inter-sectoral growth. NI estimates enable us to study inter- class income distribution. NI estimates enable us to make international comparisons and the standard of

living of the people. NI figures show the capacity of each country to bear some common burden of

international institutions like the UNO.---------------------------------------------------

• MANAGERIAL ECONOMICS

• CODE: 18KP1COELC01

• UNIT -2 PRODUCTION FUNCTION

• QUESTION PAPER PATTERN

Maximum Marks = 75 Time: 3 hours

Part A:10 X2 = 20(Two questions from each unit)

Part B: 5 x5 =25(Either or type-one questions from each unit)

Part c :3 x 10 =30 (one questions from each unit)

BOOKS FOR REFERENCE :

1. Dr. S. Sankaran (Unit I,II,III,IV, V) : Managerial Economics, Margham publications, chennai.

UNIT-VBUSINESS CYCLE

•DEFINITIONS OF BUSINESS CYCLE

Wesley mitchell stated that “business cyclesare fluctuation in the economic activities of

organized communities. The adjective ‘business’ restricts the concept of fluctuations

in activities which was systematicallyconducted on a commercial basis. The nonu

‘cycle ’ bars out fluctuations which do notrecur with a measure of regularity”.

Characteristics of business cycle

•

•

•

It occurs periodically: The business cycle occurperiodically in a regular fashion. This means theprosperity and depression will be occurring alternatively.But there need not be uniformity in the extent andmagnitude. Through the general structure of differentcycle may be the same. It ia all embracing: The business cycle implies that theprosperity or depressionary effect of the phase will beaffecting all industries in the entire economy and alsoaffecting the economies of other countries. It is wave-like: The business cycle will have a set patternof movements which is analogous to waves. Rising prices,production, employment and prosperity will become thefeatures of upward movement: falling prices,employmentwill become the features of the downward movement.

•

•

The process is cumulative and self-reinforcing: the upward moment anddownward movement are cumulative intheir process.when once the upwardmoment starts, it creates further movementin the same direction by feeding on itself The cycle will be similar but not identical:different cycles and waves in the businesscycle will be similar in general features, butthey are not identical in all respects’.

Phases of business cycle1.•

•

•

•

boom or prosperity phase The full employment and the movement of the economy beyondfull employment is characterized as boom period “A syate of affairs in which the real income consumed,real incomeproduced,and level of employment are high or rising,and there areno idle resources or unemployed workers,or very few of either”.

2. Recession The turning point from boom condition is called recession.Generally,the failure of a company or a bank,bursts the boom andbrings a phase of recession. Businessmen being to realize thatthey have overstepped their mark and their over-optimism givesplace to pessimism

3. Depression Recession is only a turning point rather than a phase.when thisdeepens,it culminated into depression.The features of depressionare just the reverse of prosperity.

•

•

During depression,the level of economic are just thereverse of prosperity. During depression,the level ofeconomic activity becomes extremely low.prices fall,profit margins decrease,firms incur losses and closureof business become a common feature and theultimate result is unemployment.

4.Recovery After a period of depression,recovery sets in . This isthe turning point from depression to revival towardsupswing.it beings with the revival of demand forcapital goods. Autonomous investments boosts theactivity. New blood,in the form of expansion of moneyand credit, is injected in the money stream of theeconomy and the income of the people goes up .

•

•

the demand slowly picks up and in duecourse the activity is directed towaeds theupswing with more production,profit,income,wages and employment. recovery may be initiated by innovation orinvestment or by government expenditure

Control of business cycle•

1.•

•

•

the trade cycle cannot be controlled by a single operation. Itconsist of many sided activities in the monetary field, fiscalside and also on the budgeting side.

Monetary policy to control trade cycle: the monetary policy should be adopted in an anti-cyclical way.During the period of upswing and boom, supply of money andcredit should be controlled and regulated. the central bank of the country should adopt all or chodenmethods of credit controol. The weapons of credit control,such as bank rate,open market operations,reserve ratio,ect..,should be utilized to control inflationary tendencies and over-expansion of business activity. In times of depression or signs of recession,expansionarycredit policy should be adopted to mitigate the severity ofrecession and depression

•

•

2. Fiscal policy: the three main instruments offiscal policy are(a) taxation; (b) spending;and (c )borrowing.These three instruments have to beeffectively utilized to control the severityof boom or the difficulties of depression during the period of recession anddepression,the government should reducesubstantially thr taxes and leave moremoney in the pockets of individuals forspending and investment.

•

•

3. anti-cyclical budgeting: the budgetary policy of thegovernment should be in tune with the measure alreadyindicated to combat the instability created by business cycle during times of depression a policy of deficit budgeting shouldbe adopted. This will increase the flow of income in theeconomy.

4. Automatic stabilizer(built-in-stabilizer):when fluctuations takeplace in the economy,the available monetary and fiscal toolscannot be geared quickly to set right the imbalance. further,it is also too much to expect the government officialsto act quickly to the tempo of change in economic activity.

Reference book:

business economics-s.sankaran

UNIT-V- ECONOMIC FORECASTING

• What Is Economic Forecasting?• Economic forecasting is the process of attempting to

predict the future condition of the economy using a combination of important and widely followed indicators.

• Economic forecasting involves the building of statistical models with inputs of several key variables, or indicators, typically in an attempt to come up with a future gross domestic product (GDP) growth rate. Primary economic indicators include inflation, interest rates, industrial production, consumer confidence, worker productivity, retail sales, and unemployment rates.

• Economic forecasting is the process of making predictions about the economy. Forecasts can be carried out at a high level of aggregation—for example for GDP, inflation, unemployment

• What are the different methods of forecasting?• Top Four Types of Forecasting Methods• Technique - Use• 1. Straight line -Constant growth rate• 2. Moving average-Repeated forecasts• 3. Simple linear regression-Compare one

independent with one dependent variable• 4. Multiple linear regression-Compare more than

one independent variable with one dependent variable

Merits and demerits of economic forecasting

Advantages of forecasting

• 1. You’ll gain valuable insight

• 2. You’ll learn from past mistakes

• 3. It can decrease costs

Disadvantages of forecasting

• 1. Forecasts are never 100% accurate

• 2. It can be time-consuming and resource-intensive

• 3. It can also be costly

NATIONAL INCOME

Meaning : National income gives information about the nation productive capacity and economic strength. National Income study will reveal the extent of utilization of a country’s resources and the extent of unemployment.Wealth and income

Wealth consists of the material economic possessions including many diverse things as buildings, automobiles, business inventories of all kinds including proven reserves of unexploited natural resources of the country.Stock and Flow

Wealth is a stock and income is flow. Stock has no time dimension. It represents quantities of things in existence at a particular moment. Flow represents quantities of things over a period of time.

The Circular Flow of Income and Goods

Definition of national income

J.R. Hicks defined national income “as a collection of goods and services reduced to a common basis by being measured in terms of money”.

Concept of national income National income is the sum of incomes earned during the period from

supplying of factor units for the use of production. It is taken as total production per year of goods and services in the

country measured in money. It is taken as total consumption of the country per year plus

investment.The various methods of national income:

Gross national product: means the money value of the national production for any given period.

Net National Product :NNP refers to the net production of goods and services in a country during the year.

National income :this is the total of all income payments received by the factors of production, viz., land, labour, capital and organization.

Personal income: This is the actual income received by the individuals and households in the country from all sources.

Personal income= national income minus corporate income taxes minus undistributed corporate profits minus social security contributions plus transfer payments.

Disposable personal income: this is simply the after-tax of personal income. The personal income is not available for consumption as personal direct taxes have to be paid. After payment of personal direct taxes is called disposable.

COMPUTATION OF NATIONAL INCOME

Production approach

Expenditure approach

Earning or income approach

DIFFICULTIES IN THE MEASUREMENT OF NATIONAL INCOME

The measurement of national income is best with difficulties. In the underdeveloped countries, these difficulties are more prominent, making the computation of national income an extremely difficult task and the figures may not be much dependable.

o Conceptual difficultieso Statistical difficulties

Factors determining national income:There are a number of influences which determine the size of the

national income in a country. The three main influences are : Quality and quantity of factors of production The state of technical know-how; and Political stability.

National income and real incomeWhen national income is expressed in terms of current prices, it

is called National income, but when it is expressed in terms of constant prices prevailing in the base year; it is called Real income.

The national income of a particular year when compared with the national income of the base year, will include the effect of two changes, viz.,

Change in the production of goods and services; and Change in the price level or value of money.

Per Capital real income= Real national income__________________

Size of populationUses of national income statistics:

National income statistics are valuable instruments of economic analysis and a guide to economic policies to be pursued.

NI statistics given an idea of the structure of the economy. NI estimates help us to study inter-sectoral growth. NI estimates enable us to study inter- class income distribution. NI estimates enable us to make international comparisons and the standard of

living of the people. NI figures show the capacity of each country to bear some common burden of

international institutions like the UNO.---------------------------------------------------

• MANAGERIAL ECONOMICS

• CODE: 18KP1COELC01

• UNIT -2 PRODUCTION FUNCTION

• QUESTION PAPER PATTERN

Maximum Marks = 75 Time: 3 hours

Part A:10 X2 = 20(Two questions from each unit)

Part B: 5 x5 =25(Either or type-one questions from each unit)

Part c :3 x 10 =30 (one questions from each unit)

BOOKS FOR REFERENCE :

1. Dr. S. Sankaran (Unit I,II,III,IV, V) : Managerial Economics, Margham publications, chennai.