MANAGERIAL FINANCE Chapter I Introduction

73

1 MANAGERIAL FINANCE Chapter I Introduction What is Finance? Finance can be defined as the art and science of managing money. Virtually all individuals and organizations earn or raise money and spend or invest money. Finance is concerned with the process, institutions, markets, and instruments involved in the transfer of money among individuals, business, and governments. Most adults will benefit from an understanding of finance, which will enable them to make better personal financial decisions. Those who work in non- financial jobs will benefit by being able to interact effectively with the firm’s financial personnel, process, and procedures. Major areas and opportunities in Finance The major areas of finance can be summarized by reviewing the career opportunities in finance. These opportunities can, for convenience, be divided into two broad areas: Financial services and managerial finance. Financial Services . This is the area of finance concerned with the design and delivery of advice and financial products to individuals, business and government. It involves a variety of interesting career opportunities within the areas of banking and related institutions, personal financial planning, investment, real estate, and insurance. Management Finance . This is concerned with the duties of financial manager in the business firm. Financial manager actively manage the finance affairs of any type of business (financial and nonfinancial, private and public, large and small, profit-seeking and not-for-profit). They perform such varied financial tasks as planning, extending credit to customers, evaluating proposal large expenditures, and raising money to fund the firm’s operations. Legal Forms of Business Organization

Transcript of MANAGERIAL FINANCE Chapter I Introduction

1

MANAGERIAL FINANCE

Chapter I

Introduction

What is Finance?

Finance can be defined as the art and science of managingmoney. Virtually all individuals and organizations earn orraise money and spend or invest money. Finance is concernedwith the process, institutions, markets, and instrumentsinvolved in the transfer of money among individuals, business,and governments. Most adults will benefit from anunderstanding of finance, which will enable them to makebetter personal financial decisions. Those who work in non-financial jobs will benefit by being able to interacteffectively with the firm’s financial personnel, process, andprocedures.

Major areas and opportunities in Finance

The major areas of finance can be summarized by reviewing thecareer opportunities in finance. These opportunities can, forconvenience, be divided into two broad areas: Financialservices and managerial finance.

Financial Services. This is the area of finance concernedwith the design and delivery of advice and financial productsto individuals, business and government. It involves a varietyof interesting career opportunities within the areas ofbanking and related institutions, personal financial planning,investment, real estate, and insurance.

Management Finance. This is concerned with the duties offinancial manager in the business firm. Financial manageractively manage the finance affairs of any type of business(financial and nonfinancial, private and public, large andsmall, profit-seeking and not-for-profit). They perform suchvaried financial tasks as planning, extending credit tocustomers, evaluating proposal large expenditures, and raisingmoney to fund the firm’s operations.

Legal Forms of Business Organization

2

The three most common legal forms of business organization arethe sole proprietorship, the partnership, and the corporation.

Sole proprietorship. A business owned by one person andoperated for his or her own profit. The typical soleproprietorship is a small business. Typically, the proprietor,along with a few employees, operates the proprietorship. He orshe normally raises capital from personal resources or byborrowing and is responsible for all business decisions. Thesole proprietorship has unlimited liability; his or her totalwealth (not merely the amount originally invested) can betaken to satisfy creditors.

Partnership. A business owned by two or more people andoperated for profit. Most partnerships are established by awritten contract known as articles of partnership. In ageneral (or regular) partnership, all partnerships have unlimitedliability, and each partner is legally liable for all of thedebts of the partnership.

Managerial finance function

People in all areas of responsibility within the firm mustinteract with finance personnel and procedures to get theirjobs done. For financial personnel to make useful forecastsand decisions, they must be willing and able to talk toindividuals in other areas of the firm. For example, whenconsidering a new product, the financial manager needs toobtain sales forecasts, pricing guidelines, and advertisingand promotion budget estimates from marketing personnel.

Organization of the finance function

The size and importance of the managerial function depend onthe size of the firm. In small firms, the finance function isgenerally performed by the accounting department. As a firmgrows, the finance function typically evolves into a separatedepartment linked directly to the company president or CEOthrough the chief finance officer (CFO).

Reporting to the CFO are the treasurer and the controller. Thetreasurers (the chief financial manager) is commonly responsiblefor handling financial activities, such as financial planning

3

and fund raising, making capital expenditure decisions,managing cash, managing credit activities, managing thepension fund, and managing foreign exchange. The controller (thechief accountant) typically handles the accounting activities,such as corporate accounting, tax management, financialaccounting, and cost accounting. The treasurer’s focus tendsto be more external, the controller’s focus more internal. Theactivities of the treasurer, or financial manager, are the primary concern of thissubject.

Relationship to Economics

The field of finance is closely related to economics.Financial manager must understand the economic framework andbe alert to the consequences of varying levels of economicactivity and changes in economic policy. They must also beable to use economic theories as guidelines for efficientbusiness operation. Examples include supply-and-demandanalysis, profit-maximizing strategies, and price theory.

Relationship to Accounting

The firm’s finance (treasurer) and accounting (controller)activities are closely related and generally overlap. Indeed,managerial finance and accounting are often not easilydistinguishable. In small firms the controller often carriesout the finance function, and in large firms many accountantsare closely involved in various finance activities. However,there are two basic differences between finance andaccounting; one is related to the emphasis on cash flows andthe other to decision making.

Emphasis on Cash Flows

The accountant’s primary function is to develop and reportdata for measuring the performance of the firm’s assess itsfinancial position, comply with and file reports required bysecurities regulators, and file and pay taxes. Using certainstandardized and generally accepted principles, the accountantprepares financial statements that recognize revenue at thetime of sale (whether payment has been received or not) andrecognize expenses when they are incurred. This approach isreferred to as the accrual basis.

4

The final manager, on the other hand places primary emphasison cash flows, the intake and outgo of cash. He or shemaintains the firm’s solvency by planning the cash flowsnecessary to satisfy its obligations and to acquire assetsneeded to achieve the firm’s goals. The financial manager usesthis cash basis to recognize the revenues and expenses onlywith respect to actual inflows and outflows cash. Regardlessof its profit or loss, a firm must have a sufficient flow of cash to meetits obligations as they come due.

Decision Making

The second major difference between finance and accounting hasto do with decision making. Accountants devote most of theirattention to the collection and presentation of financial data.Financial managers evaluate the accounting statements, developadditional data, and make decisions on the basis of theirassessment of the associated returns and risks. Of course,this does not mean that accountants never make decisions orthat financial manager never gather data. Rather, the primaryfocuses of accounting and finance are distinctively different.

Primary activities of the Financial Manager.

In addition to ongoing involvement in financial analysis andplanning, the financial manager’s primary activities aremaking investment decisions and making financing decisions.Investment decisions determine both the mix and the type ofassets held by the firm. Financing decisions determine boththe mix and the type of financing used by the firm. Thesesorts of decisions can be conveniently viewed in terms of thefirm’s balance sheet, as shown in the following figure.However, the decisions are actually made on the basis of theircash flow effects on the overall value of the firm.

Balance SheetMaking

Investmentdecisions

Current Assets CurrentLiabilities

MakingFinancingDecisions

Fixed Assets Long-termFunds

5

Financial Institutions and markets

Most successful firms have ongoing needs for funds. They canobtain funds from external sources in three ways. The firstsource is through a financial institution that accepts savings andtransfers them to those that need funds. A second source isthrough financial markets, organized forums in which thesuppliers and demanders of various types of funds can maketransactions. A third source is through private placement.Because of the unstructured nature of private placements, herewere focus primarily on the role of financial institutions andfinancial markets in facilitating business financing.

Financial Institutions

Financial institutions serve as intermediaries by channelingthe savings of individuals, business, and governments intoloans or investments. Many financial institutions directly orindirectly pay savers interest on deposited funds; otherprovides services for fee (for example, checking accounts forwhich customers pay service charges). Some financialinstitution accept customers’ savings deposits and lend thismoney to other customers or to firms; others invest customers’savings in earning assets such as real estate or stocks andbonds; and some do both. Financial institutions are requiredby the government to operate within established regulatoryguidelines.

Major Financial institutions

Major Financial Institutions in the U.S. economy arecommercial banks, savings and loans, credits unions, savingbanks, insurance companies, mutual funds, and pension fund.These institutions attract funds from individuals, businesses,and government, combine them, and make loans available toindividuals and businesses.

Financial Markets

Financial markets are forums in which suppliers of funds anddemanders of funds can transact business directly. Whereas theloans and investments of institutions are made without thedirect knowledge of the suppliers of funds (savers), suppliersin the financial markets know where their funds are being lentor invested. The two key financial markets are the money

6

market and the capital market. Transactions in short-term debtinstruments, or marketable securities, take place in the moneymarket. Long-term securities (bonds and stocks) are traded inthe capital market.

To raise money, firms can use either private placements orpublic offerings. Private placement involves the sale of a newsecurity issue, typically bonds or preferred stock, directlyto an investor or group of investors, such as an insurancecompany or pension fund. Most firms, however, raise moneythrough a public offering of securities, which is thenonexclusive sale of either bonds or stocks to the generalpublic.

The relationship between institutions and Markets

Financial institutions actively participate in the financialmarkets as both suppliers and demanders of funds. Theindividuals, businesses, and governments that supply anddemand funds may be domestic or foreign.

The Money Market

The money market is created by a financial relationshipbetween suppliers and demanders of short-term funds (fundswith maturities of one year or less). The money market existsbecause some individuals, businesses, governments, andfinancial institutions have temporarily idle funds that theywish to put to some interest-earnings use. At the same time,other individuals, businesses, governments, and financialinstitutions find themselves in need of seasonal or temporaryfinancing. The money market brings together these suppliersand demanders of short-term funds.

Most money market transactions are made in marketablesecurities (short term debt instrument, such as U.S. treasurybills, commercial paper, and negotiable certificates ofdeposit issued by government, business and financialinstitutions, respectively).

The Capital Market

The capital Market is a market that enables suppliers anddemanders of long-term funds to make transactions. Includedare securities issues of business of business and government.

7

The backbone of the capital market is formed by the broker anddealer markets that provide a forum for bond and stocktransactions.

Key Securities traded: Bonds and Stocks

The Key capital market securities are bonds (long-term debt)and both common stock and preferred stock (equity, or ownership).

Bonds are long-term debt instrument used by business andgovernment to raise large sums of money, generally from adiverse group of lenders. Corporate bonds typically pay interestsemiannually (every 6 months) at a stated coupon interest rate. Theyhave an initial maturity of from 10 to 30 years, and a par orface, value of $1,000 that must be repaid at maturity.

Example

Lakeview Industries, a major microprocessor manufacturing, hasissued a 9 percent coupon interest rate, 20-year bond with a$1,000 par value that pays interest semiannually. Investorswho buy this bond receive the contractual right to $90 annualinterest (9% coupon interest rate x $1,000 par value)distributed as $45 at the end of each 6 month (1/2x$90) for 20years, plus the $1,000 par value at the end of year 20.

As noted earlier, shares of common stock are units ofownership, or equity, in a corporation. Common stockholdersearn a return by receiving dividends (periodic distributionsof earnings) or by realizing increases in share price. Preferredstockholders are promised a fixed periodic dividend that mustbe paid prior to payment of any dividends to commonstockholders. In other words, preferred stock has “preference”over common stock.

Chapter 2

LONG-TERM INVESTMENT DECISIONS: CASH FLOWS IN CAPITALBUDGETING

Capital budgeting decisions

8

Long-term investment represents sizable outlays of funds thatcommit a firm to some course of action. Consequently, the firmneeds procedures to analyze and properly select its long-terminvestments. It must be able to measure cash flows and applyappropriate decision techniques. As time passes, fixed assetsmay become absolute or may require an overhaul; At thesepoints, too, financial decisions may be required. Capitalbudgeting is the process of evaluating and selecting long-terminvestments that are consistent with the firm’s goal ofmaximizing owner wealth. Firms typically make a variety oflong-term investments, but the most common for themanufacturing firm is in fixed assets, which include property(land), plant, and equipment. These assets, often referred toas earning assets, generally provide the basis for the firm’searning power and value.

Motives for Capital Expenditure

A capital Expenditure is an outlay of funds by the firm that isexpected to produce benefits over a period of time greaterthan 1 year. An operating expenditure is an outlay resulting inbenefits received within 1 year. Fixed-asset outlays arecapital expenditures, but not all capital expenditures areclassified as fixed assets. A $60,000 outlays for a newmachine with a usable life of 15 years is a capitalexpenditure that would appear as fixed asset on the firm’sbalance sheet. A $60,000 outlay for an advertising campaignthat is expected to produce benefits over a long period isalso a capital expenditure, but would rarely be shown as afixed asset.

Companies make capital expenditures for many reasons. Thebasic motives for capital expenditures are to expandoperations, replace or renew fixed assets, or to obtain someother, less tangible benefit over a long period.

Basic Terminology

Independent versus mutually exclusive projects

9

The two most common types of projects are (1) independentprojects and (2) mutually exclusive projects. Independentsprojects are those whose cash flows are unrelated orindependent of one another; the acceptance of one does noteliminate the others from further consideration. Mutuallyexclusive projects are those that have the same function andtherefore compete with one another. The acceptance of oneeliminates from further consideration all other projects thatserve a similar function.

Unlimited funds versus Capital rationing

The availability of funds for capital expenditures affects thefirm’s decisions. If a firm has unlimited funds forinvestment, making capital budgeting decisions is quitesimple. All independent projects that will provide anacceptable return can be accepted. Typically, though, firmsoperate under capital rationing instead. This means that theyhave only a fixed number of dollars available for capitalexpenditures and that numerous projects will compete for thesedollars.

Accept-Reject versus Ranking Approaches

Two basic approaches to capital budgeting decisions areavailable. The acceptance-reject approaches involve evaluatingcapital expenditure proposal to determine whether they meetthe firm’s minimum acceptance criterion. This approach can beused when the firm has unlimited funds, as a preliminary stepwhen evaluating mutually exclusive projects, or in a situationin which capital must be rationed. In these cases, onlyacceptable projects should be considered.

The second method, the ranking approach, involves rankingprojects on the basis of some predetermined measure, such asthe rate of return. The project with the highest return isranked first, and the project with the lowest return is rankedlast. Only acceptable projects should be ranked. Ranking isuseful in selecting the “best” of a group of mutually

10

exclusive projects and in evaluating projects with a view tocapital rationing.

Conventional versus nonconventional cash flow patterns

Cash flow patterns associated with capital investment projectscan be classified as conventional or nonconventional. Aconventional cash flow pattern consists of an initial outflowfollowed only by a series of inflows.

A nonconventional cash flow pattern is one in which an initialoutflow is followed by a series of inflows and outflows.

Relevant cash flows

To evaluate capital expenditure alternatives, the firm mustdetermine the relevant cash flows. These are the incremental cashoutflow (investment) and resulting subsequent inflows. The Incrementalcash flows represent the additional cash flows (outflows orinflows) expected to resulting from a proposed capitalexpenditure. Cash flows are used because they affect directlythe firm’s ability to pay bills and purchase assets.

Major Cash Flow Components

The cash flows of any project having the conventional patterncan include three basic components: (1) an initial investment,(2) operating cash inflows, and (3) terminal cash flow. Allprojects whether for expansion, replacement or renewal or someother purpose have the first components. Some, however, lackthe final component, terminal cash flow.

The following table of cash flow components depicts on timeline the cash flows for a project. The initial investment forthe proposed project is $ 50,000. This is the relevant cashoutflow at zero. The operating cash flows, which are theincremental after-tax cash inflows resulting fromimplementation of the project during its life, graduallyincrease from $4,000 in its first year to $10,000 in its tenthand final year. The terminal cash flow is the after-tax no

11

operating cash flow occurring in the final year of theproject. It is usually attributed to liquidation of theproject. In this case it is $25,000, received at the end ofthe project’s 10 years life. Note that the terminal cash flowdoes not include the $10,000 operating cash inflow for years10.

Cash flow components

Initial Investment 50,000

Operating cash inflows 1

4,000

Operating cash inflows 2

5,000

Operating cash inflows 3

6,000

Operating cash inflows 4

7,000

Operating cash inflows 5

7,000

Operating cash inflows 6

8,000

Operating cash inflows 7

8,000

Operating cash inflows 8

8,000

Operating cash inflows 9

9,000

Operating cash inflows 10

10,000

Terminal Cash flow 25,000

Expansion versus replacement Decisions

Developing relevant cash flow estimates is moststraightforward in the case of expansion decisions. In thiscase, the initial investment, operating cash inflows, andterminal cash flow are merely the after-tax cash outflow andinflows associated with the proposed capital expenditure.

Indentifying relevant cash flows for replacement decisions ismore complicated, because the firm must identify theincremental cash outflow and inflows that would result from

12

the proposed replacement. The initial investment in the case ofreplacement is the difference between the initial investment needed to acquirethe new asset and any after-tax cash inflows expected from liquidation of theold asset. The operating cash inflows are the difference betweenthe operating cash inflows from the new asset and those fromthe old asset.

Actually, all capital budgeting decisions can be viewed asreplacement decisions. Expansions decisions are merelyreplacement decisions in which all cash flows from the oldasset are zero. In light of this fact, this chapter focusesprimarily on replacement decisions.

Initial Investment =

Initial Investment to acquire new asset -

After tax cash inflows from liquidation of old asset

OperatingCash Flow =

Operating Cash inflows from new asset -

Operating cash inflows from old asset

Terminal cash flow =

After tax cash flows fromtermination of new asset -

After tax cash flows from termination of old asset

Sunk Cost : Cash outlays that have already been made (pastoutlays) and therefore have no effect on the cash flowsrelevant to a current decision.

Opportunity costs : Cash flows that could be realized fromthe best alternative use of an owned asset.

Example:

Jankwow Equipment is considering renewing its drill press X12,which it purchased 3 years earlier for $237,000, byretrofitting it with the computerized control system from anobsolete piece of equipment it owns. The obsolete equipmentcould be sold today for a high bid of $42,000, but without itscomputerized control system, it would be worth nothing. Jankowis in the process of estimating the labor and materials costsof retrofitting the system to drill press X12 and the benefitsexpected from the retrofit. The $237,000 cost of drill pressX12 is a sunk cost because it represents an earlier cashoutlay. It would not be included as a cash outflow when

13

determining the cash flows relevant to the retrofit decision.Although Jankow owns the obsolete piece of equipment, theproposed use of its computerized control system represents anopportunity cost of $42,000 (the highest it would be soldtoday).

Finding the initial Investment

The term initial investment as used here refers to therelevant cash outflows to be considered when evaluating aprospective capital expenditure.

The basic format for Determining initial investment

Installed cost of new asset (= cost of new assets + Installingcosts) −¿ after-tax proceeds from sale of old asset (=proceeds from sale of old asset ± tax on sale of old asset) ±change in net working capital = Initial investment

Or

Installed cost of new asset −¿ after-tax proceeds from sale ofold asset ± change in net working capital = Initial investment

Book Value

The book value of an asset is its strict accounting value. Itcan be calculated by using the following equation.

Book value = Installed cost of asset – accumulateddepreciation

Example

Hudson industries, a small electrics company, 2years agoacquired a machine tool with an installed cost of $100,000.The asset was being depreciated under Modified Accelerated

14

Cost Recovery system (MACRS) using a 5-years recovery period.If under MACRS for a 5-years recovery period, 20% and 32% ofthe installed cost would be depreciated in years 1 and 2,respectively, In other words, 52% (20% + 32%) of the $100,000cost, or $52,000 (0.52 x $100,000), would represent theaccumulated depreciation at the end of year 2.

Book value = $100,000 - $52,000 = $48,000

Changes in Net Working Capital

Net working capital is the amount by which a firm’s currentassets exceeds its current liabilities. If a firm acquires newmachinery to expand its level of operations, it willexperience an increase in levels of cash, accounts receivable,inventories, account payable, and accruals.

The difference between the change in current assets and thechange in current liabilities is the change in net workingcapitals.

Example

Danson Company, a metal products manufacturer, iscontemplating expanding its operations. Financial analystsexpect that the changes in current accounts summarized in thefollowing table will occur and will be maintained over thelife of the expansion. Current asset are expected to increaseby $22,000, and current liabilities are expected to increaseby $9,000, resulting in a $13,000 increase in net workingcapital. In this case, the change will represent an increasednet working capital investment and will be treated as a cashoutflow in calculating the initial investment

Calculation of change in net Working Capital for DansonCompany

Current Account Change in balanceCash +$4,000Account Receivable +1,000Inventory +

15

17,000

(1) Current assets +22,000

Account Payable +

7,000

Accruals +

2,000

(2) Current Liabilities

+9,000Change in net Working Capital (1) -(2)

+13,000

Calculating the initial Investment

A variety of tax and other considerations enter into theinitial investment calculation.

Powell Corporation, a large, diversified manufacturer ofaircraft components, is trying to determine the initialinvestment required to replace an old machine with a new, moresophisticated model. The proposed machine’s purchase price is$380,000, and an additional $20,000 will be necessary toinstall it. It will be depreciated under MACRS using a 5-yearsrecovery period. The present (old) machine was purchased 3years ago at a cost of $240,000 and was being depreciatedunder MACRS using a 5 years recovery period. The firm hasfound a buyer willing to pay $280,000 for the present machineand to remove it at the buyer’s expense. The firm expects thata $35,000 increase in current assets and an $18,000 increasein current liabilities will accompany the replacement; thesechanges will result in a $17,000 ($35,000-18,000) increase innet working capital. The firm pays taxes at a rate of 40%.

The only component of the initial investment calculation thatis difficult to obtain is taxes. The book value of the presentmachine can be found by using the depreciation percentage(from the table which is shown below) of 20%, 32% and 19% foryears 1, 2, and 3, representatively. The resulting book valueis $69,600 ($240,000 −⦋ (0.20+0.32+0.19 )X$20,000 ⦌¿. a gain of

16

$210, 400 ($280,000 - $69,600) is realized on the sale. Thetotal taxes on the gain are $84,160(0.40 x $210,400). Thesetaxes must be subtracted from the b$280,000 sale price of thepresent machine to calculate the after-tax proceeds from itssale.

Substituting the relevant amounts into the formats inpresented before, results in an initial investment of$221,160, which represents the net cash outflow required attime zero.

Installed cost of proposed machine

Cost of proposed machine380,000

+ installation20,000

Total installed cost -proposed (depreciable Value

400,000

−¿After-tax proceeds from sale of present machine Proceeds from sale of present machine

280,000

−¿Tax on sale of present machine

-84,160

Total after-tax proceeds - present

195,840

+¿Changes in net working capital17,00

0

Initial Investment$221,160

Rounded Depreciation Percentage by Recovery Year Using MACRSfor first four property classes

Percentage by recovery years

Recovery year3 year

5 years

7 years 10 years

1 33% 20% 14% 10%2 45% 32% 25% 18%3 7% 19% 18% 14%4 12% 12% 12%

17

5 12% 9% 9%6 5% 9% 8%7 9% 7%8 4% 6%9 6%10 6%11 4%

Total 100% 100% 100% 100%

ASSIGNMENTS

To determine Book value, taxes and initial investment

Irvin Enterprise is considering the purchase of a new piece ofequipment to replace the current equipment. The new equipmentcosts $75,000 and requires $5,000 in installing costs. It willbe depreciated under MACRS using a 5 years recovery period.The old piece of equipment was purchased 4 years ago for aninstalled cost of $50,000; it was being depreciated underMACRS using a 5-year recovery period. The old equipment can besol today for $55,000 net of any removal or cleanup cost. As aresult of the proposed replacement, the firm’s investment innet working capital is expected to increase by $15,000. Thefirm pays taxes at a rate of 40% (the above table contains theapplicable MACRS depreciation percentage).

a. Calculate the book value of the old piece of equipmentb. Determine the taxes, if any, attributable to the sale of

the old equipment.c. Find the initial investment associated with the proposed

equipment replacement.

Determining Relevant Cash flows

A machine currently in use was originally purchased 2 yearsago for $40,000. The machine is being depreciated under MACRSusing a 5-years recovery period; it has 3 years of usable liferemaining. The current machine can be sold today to net$42,000 after removal and cleanup costs. A new machine, usinga 3 years MACRS recovery period, can be purchased at a price

18

of $140,000. It requires $10,000 to install and has a 3-yearsusable life. If the new machine is acquired, the investment iaaccounts receivable will be expected to rise by $10,000, theinventory investment will increase by $25,000, and accountspayable will increase by $15,000. Earnings beforedepreciation, interest, and taxes are expected to be $70,000for each of the next 3 years with the old machine and to be$120,000 in the first year and $130,000 in the second andthrird years with the new machine. At the end of 3 years, themarket value of the old machine will equal zero, but the newmachine could be sold to net $35,000 before taxes. The firm issubject to a 40% tax rate (the above table contains applicableMCARS depreciation percentage).

a. Determine the initial investment associated with theproposed replacement decision

b. Calculate the incremental operating cash flows c. Calculate the terminal cash flow associated with the

proposed replacement decision. (note this is at the endof year 3)

d. Depict on a time line the relevant cash flows found inparts a, b, and c that are associated with the proposedreplacement decision, assuming that it is terminated atthe end of year 3.

Change in Working Capital

Samuel manufacturing is considering the purchase of a newmachine to replace one it believes is obsolete. The firm hastotal current assets of $920,000 and total current liabilitiesof $640,000. As a result of the proposed replacement, thefollowing changes are anticipated in the levels of the currentasset and current liability accounts noted.

Account Change

Accruals

+$ 40,000Marketable securities

0

Inventories

19

-10,000Account payables

+ 90,000

Note payables 0

Account receivable

+150,000

Cash

+15,000

a. Using the information given, calculated any change in networking capital that is expected to result from theproposed replacement action.

b. Explain why a change in the current accounts would berelevant in determining the initial investment for theproposed capital expenditure.

c. Would the change in net working capital enter into any ofthe other cash flow components that make up the relevantcash flow? Explain.

Chapter 3

TECHNIQUES OF CAPITAL BUDGETING

1. Overview of Capital Budgeting Techniques

When firms have developed relevant cash flows as demonstratedin previous chapter they analyze them to assess whether aproject is acceptable or to rank projects. A number oftechniques are available for performing such analysis. Thepreferred approaches integrate time value procedures, risk andreturn considerations, and valuation concepts to selectcapital expenditures that are consistent with the firm’s goalof maximizing owner’s wealth. This chapter focuses on the useof these techniques in an environment of certainty.

Bennett Company’s Relevant Cash Flows

20

We will use one basic problem to illustrate all the techniquesdescribed in this chapter. The problem concerns BennetCompany, a medium-sized metal fabricator that is currentlycontemplating two projects: Project A requires an initialinvestment of $42,000; Project B requires an initialinvestment of $45,000. The Projected relevant cash flows forthe two projects are presented in the table below and depictedon the time lines in figure below. The projects exhibitconventional cash flow patterns, which are assumed throughout thetext. In addition, we initially assume that all projects’ cashflows have the same level of risk, that projects beingcompared have equal usable lives, and that the firm hasunlimited funds. We begin with a look at the three mostpopular capital budgeting techniques: payback period, netpresent value, and internal rate of return.

Capital Expenditure Data for Bennett Company

Project A Project BInitial

Investment $42,000 $45,000

YearOperating Cash

InflowsOperating Cash

Inflows1 $14,000 $28,0002 $14,000 $12,0003 $14,000 $10,0004 $14,000 $10,0005 $14,000 $10,000

2. Payback Period

Payback periods are commonly used to evaluate proposedinvestment. The payback period is the amount of timerequired for the firm to cover its initial investment in aproject, as calculated from cash inflows. In the case of anannuity, the payback period can be found by dividing theinitial investment by the annual cash inflow. For a mixedstream of cash inflows, the yearly cash inflows must beaccumulated until the initial investment is recovered.

21

Although popular, the pay-back period is generally viewed asan unsophisticated capital budgeting technique, because it does notexplicitly consider the time value of money.

Decision Criteria

When the payback period is used to make accept-rejectdecisions, the following decisions criteria apply.

If the payback period is less than the maximumacceptable payback period, accept the project.

If the payback period is greater than the maximumacceptable payback period, reject the project.

3. Net Present Values (NPV)

Because Net Present Value (NPV) gives explicit consideration tothe time value of money, it is considered a sophisticated capitalbudgeting technique. All such techniques in one way or anotherdiscount the firm’s cash flows at a specified rate. This rateoften called the discount rate, required return, cost of capital, oropportunity cost is the minimum return that must be earned on aproject to leave the firm’s mark value unchanged. In thischapter, we take this rate as a “given”.

The net present value (NPV) is found by subtracting aproject’s initial investment (CF0) From the present value ofits cash inflows (CFt) discounted at a rate equal to thefirm’s cost of capital (r).

NPV = Present Value of Cash inflows – Initial Investment

NPV = ∑t=i

n CFt(1+r)t

−CF0

= ∑t=i

n(CF1xPVIFr,t )−CF0

When NPV is used, both inflows and outflows are measured interms of present dollars. Because we are dealing only with

22

investments that have conventional cash flow patterns, theinitial investment is automatically stated in terms of today’sdollars. If it were not, the present value of a project wouldbe found by subtracting the present value of outflows from thepresent value of inflows.

Decision Criteria

When NPV is used to make accept-reject decisions, the decisioncriteria are as follows:

If the NPV is greater than $0, accept the project. If the NPV is less than $0, reject the project.

If the NPV is greater than $0, the firm will earn a returngreater than its costs of capital. Such action should increasein the market value of the firm, and therefore the wealth ofits owners by an amount equal to the NPV.

We can illustrate the net present value (NPV) approach byusing the Bennett Company data presented in above table. Ifthe firm has a 10% cost of capital, the net present values forprojects A (an annuity) and B (a mixed stream) can becalculated as shown below. These calculations result in netpresent values for a project A and B of $11,071 and $10,924,respectively. Both projects are acceptable, because the netpresent value of each is greater than $0. If the projects werebeing ranked, however, project A would be considered superiorto B, because it has a higher net present value than that of B($11,071 versus $10,924)

Years Project A Project B

0 -42,000 -45,0001 $14,000 $28,0002 $14,000 $12,0003 $14,000 $10,0004 $14,000 $10,0005 $14,000 $10,000

NPV $11,071 10,924

23

MORE EXPLANATION ABOUT NPV

When a business invest in a new plant asset, it expects theinvestment to produce a stream of future net Cash flows.Normally, a business should not invest unless the expectedcash flows are sufficient to return the amount of theinvestment plus a satisfactory return on the investment. Forexample, assume that the cash flows from Murray Company’sinvestment will be received at the end of each year. Will theinvestment in the machine return the amount of the investmentplus a satisfactory return? If Murray Company considers a 12%compounded annual return a satisfactory return on its capitalinvestments, it can answer this question with the calculationsof below illustration.

To purchase the machine, Murray Company must invest $16,000.However, from the sale of the machine’s product the companyexpects to receive net cash flows of $4,100 each year foreight years. The first column of below illustration indicatesthat the net cash flows of the first year are received oneyear hence, and so forth for the years thereafter. This meansthat the net cash flows are received at the end of the year.

Years HenceNet Cash

Flows

PresentValue of $1

at 12%

Present Valueof Net Cash

Flows1 $4,100 0. 8929 $3,6672 $4,100 0.7972 3,2693 $4,100 0.7118 2,9184 $4,100 0.6355 2605.555 $4,100 0.5674 2326.346 $4,100 0.5066 2077.067 $4,100 0.4523 1854.43

24

8 $4,100 0.4039 1655.99Total Present Value $20,373Amount tobe invested 16,000Positive net

present value 4,373

Therefore, if Murray Company considers a 12% compounded returnsatisfactory, this machine will recover its requiredinvestment, plus a 12% compounded return, and $4,367 inaddition.

Shortening the Calculation

Use table of Present Value of an annuity of 1 per period.

Cash Flows Not Uniform

Years Hence

Annual Cash Flow Project A ($)

Annual cash Flow ProjectB ($)

Annual Cash flow Project C ($)

1 5,000 8,000 1,0002 5,000 5,000 5,0003 5,000 2,000 9,000

15,000 15,000 15,000

Comparing net present values of projects when the timing ofcash flows differ.

Years Hence

PV of cash Flows Discounted at10% Project A($)

PV of cash Flows Discounted at10% Project B($)

PV of cash Flows Discounted at 10%Project C ($)

1 4,546 7,273 $9092 4,132 4,132 4,1323 3,756 1,503 6,762

Total Values 11,803

25

Present 12,434 12,908Required

Investment 12,000

12,000 12,000

Net Present

Values +434

+908 -197

Note that all the three projects produce the same total cashflow. However, the flows of Project A are uniform; those ofProject B are greater in the earlier years, while those ofproject C are greater in the later years.

Project B is better than project A. Project C should berejected.

Internal rate of return

The internal rate of Return (IRR) is probably the most widelyused sophisticated capital budgeting technique. However, it isconsiderably more difficult than NPV to calculate by hand. Theinternal rate of return (IRR) is the discount rate thatequates the NPV of an investment opportunity with $0 (becausethe present value of cash inflow equals the initialinvestment) It is the compounded annual rate of return thatthe firm will earn if it invests in the project and receivesthe given cash inflows. Mathematically, thr IRR is the valueof r in equation below that causes NPV to equal $0.

$0 = ∑i=1

n CFt(1+IRR)t

- CF0

∑i=1

n CFt(1+IRR)t

=CF0

Decision Criteria

26

When IRR is used to make accept-reject decisions, the decisioncriteria are as follows:

If the IRR is greater than the cost of capital , acceptthe project

If IRR is less than the cost of capital, reject theproject.

These criteria guarantee that the firm will earn at least itsrequired return. Such an outcome should increase the marketvalues of the firm and therefore the wealth of its owners.

Example is the Bennett Company data presented before asfollows.

Capital Expenditure Data for Bennett Company

Project A Project BInitial

Investment $42,000 $45,000

YearOperating Cash

InflowsOperating Cash

Inflows1 $14,000 $28,0002 $14,000 $12,0003 $14,000 $10,0004 $14,000 $10,0005 $14,000 $10,000

Comparing the IRRs of projects A and B given before to BenettCompany’s 10% cost of Capital, we can see that both projectsare acceptable because:

27

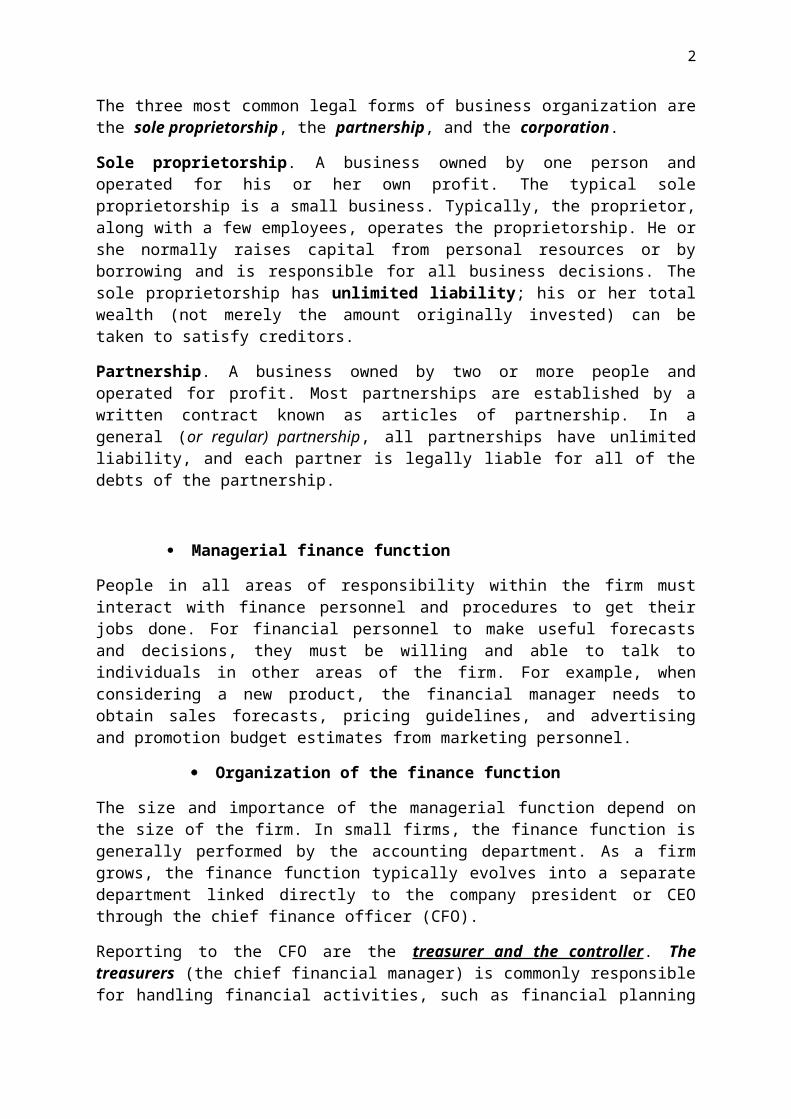

IRRa = 19.9% greater than 10.0% cost of Capital

IRRb = 21.7% greater than 10.% cost of capital

Comparing the two projects IRR, we would prefer project B overProject A because IRRb = 21.7% greater than IRRa = 19.9%.

Capital Expenditure Data for Bennett Company

Project A Project BInitial

Investment $42,000 $45,000

YearOperating Cash

InflowsOperating Cash

Inflows1 $14,000 $28,0002 $14,000 $12,0003 $14,000 $10,0004 $14,000 $10,0005 $14,000 $10,000

IRR 19.9% 21.7%

If these projects are mutually exclusive, the IRR decision techniques would recommend Project B.

Assignments

1. Fitch Industries is in the process of choosing thebetter of two equal-risk, mutually exclusive capitalexpenditure projects (Project M and Project B). Therelevant cash flows for each project are shown in thefollowing table. The firm’s cost of capital is 14%.

Proj Project

28

ect M N

InitialInvestment

$28,500 $27,000

Years (t)Cash inflows

(Cfi)

1$10,000 $11,000

210,000 10,000

310,000 9,000

410,000 8,000

Required

a. Calculate each project’s payback period and indicatethe best performing project.

b. Calculate the net present value (NPV) for each project,and indicate the best performing project.

c. Calculate the internal rate of return (IRR) for eachproject, and indicate the best performing project.

d. Summarize the preferences dictated by each measurer youcalculated, and indicate which project you wouldrecommend. Explain why.

e. Draw the net present value profiles for these projectson the same set of axes, and explain the circumstancesunder which a conflict in rankings might exist.

2. NPV, with ranking Botany Bay, Inc., a maker of casual clothing, is considering four projects, Because of past financial difficulties, the company has a high cost of capital at 15%. Which of these projects would be acceptable under those cost circumstances?

Project A

Project B

Project C

Project D

Initial investment (CF0)

$50,000

$100,000

$80,000

$180,000

Years

29

1

20,000

35,000

20,000

100,00

0

2

20,000

50,000

40,000

80,000

3

20,000

50,000

60,000

60,000

a. Calculate the NPV of each project, using a cost of capital of 15%

b. Rank acceptable projects by NPVc. Calculate the IRR of each project and use it to determine

the highest cost of capital at which all of the projects would be acceptable.

3. Project A and B, of equal risk, are alternatives for expanding Rosa Company’s capacity. The firm’s cost of capital is 13%. The cash flows for each project are shownin the following table

ProjectA Project B

InitialInvestment $80,000 $50,000Years (t) Cash inflows (Cfi)

1 $15,000 $15,0002 20,000 15,0003 25,000 15,0004 30,000 15,0005 35,000 15,000

Required

a. Calculate each project’s payback period and indicatethe best performing project.

b. Calculate the net present value (NPV) for each project,and indicate the best performing project.

c. Calculate the internal rate of return (IRR) for eachproject, and indicate the best performing project.

30

d. Summarize the preferences dictated by each measurer youcalculated, and indicate which project you wouldrecommend. Explain why.

4. Thomas Company is considering two mutually exclusiveprojects. The firm, which has a 12% cost of capital, hasestimated its cash flows as shown in the following table.

ProjectA Project B

InitialInvestment

$130,000 $85,000

Years (t) Cash inflows (Cfi)1 $25,000 $40,0002 35,000 35,0003 45,000 30,0004 50,000 10,0005 55,000 5,000

a. Calculate NPV of each project, and assess itsacceptability.

b. Calculate the IRR for each project, and assess itsacceptability.

c. Evaluate and discuss the rankings of the two projectson the basis of your findings in parts a, b, and c.

d. Explain your findings in part d in light of the patternof each inflow associated with each project.

Chapter 4

LONG-TERM FINANCIAL DECISIONS: THE COST OF CAPITAL

1.1 Overview of the cost of Capital

The cost of capital is the rate of return that a firm mustearn on the projects in which it invest to maintain themarket value of its stock. It can also be thought of as therate of return required by the market suppliers of capitalto attract their fund to the firm. If risk is held constant,projects with a rate of return above the cost of capitalwill increase the value of the firm, and projects with arate of return below the cost of capital will decrease thevalue of the firm.

31

Some Key Assumptions

The cost of capital is a dynamic concept affected by avariety of economic and firm-specific factors. To isolatethe basic structure of the cost of capital, we make some keyassumptions relative to risk and taxes:

Business risk: The risk to the firm of being unable tocover operating costs. It is assumed to be unchanged. Thisassumption means that the firm’s acceptance of a givenproject does not affect its ability to meet operatingcosts.

Financial risk. The risk to the firm of being unableto cover required financial obligations (interest,lease payments, preferred stock dividends). It isassumed to be unchanged. This assumption means thatprojects are financed in such a way that the firm’sability to meet required financing costs is unchanged.For an example of the effect that unexpected legalliabilities can have on the cost of capital.

After-tax costs are considered relevant. In otherwords, the cost of capital is measured on an after-tax basis. Thisassumption is consistent with the after framework usedto make capital budgeting decisions.

The Basic Concept

The cost of capital is estimated at a given point in time. Itreflects the expected average future cost of funds over thelong run. Although firms typically raise money in lumps, thecost of capital should reflect the interrelatedness offinancing activities. For example, if a firm raises fundswithin debt (borrowing) today, it is likely that some form ofequity, such as common stock, will have to be used the nexttime it needs funds. Most firms attempt to maintain a desiredoptimal mix of debt and equity financing. In practice, thismix is commonly a range, such as 40% to 50% debt, rather thana point, such as 55% debt. It is called a target capitalstructure.

32

To capture the interrelatedness of financing assuming thepresence of a target capital structure, we need to look at theoverall cost of capital rather than the cost of the specificsource of funds used to finance a given expenditure.

Example

A Firm is currently faced with an investment opportunity.Assume the following best project available today

Cost = $100,000 Life = 20 years

IRR = 7%

Cost of least-cost financing source available

Debt = 6%

Because it can earn 7% on the investment of funds costing only6%, the firm undertakes the opportunity, imagine that 1 weeklater a new investment opportunity is available:

Best project available 1 week later

Cost = $100,000 Life = 20 years

IRR = 12%

Cost of least-cost financing source available

Debt = 14%

In this instance, the firm rejects the opportunity, becausethe 14% financing cost is greater than the 12% expectedreturn.

Were the firm’s actions in the best interests of its owners?No; it accepted a project yielding a 7% return and rejected

33

one with a 12% return. Clearly, there should be a better way,and there is: The firm can use a combined cost, which over thelong run will yield better decisions. By weighting the cost ofeach source of financing by its target proportion in thefirm’s capital structure, the firm can obtain a weightedaverage cost that reflects the interrelationship of financingdecisions. Assuming that a 50-50 mix of debt and equity istargeted, the weighted average cost here would be 10%:⦋ (0.50x6%debt)+(0.50x14 %equity)⦌.

With this cost, the first opportunity would have been rejected(7% IRR <10% weighted average cost), and the second would havebeen accepted (12% IRR>10% weighted average cost). Such anoutcome would clearly be more desirable.

Specific Sources of Capital

There are four basic sources of long-term funds for thebusiness firm: Long-term debt, preferred stock, common stock,and retained earnings.

BalanceSheet

Current LiabilityLong term debtStockholders ‘equity

Assts Preferred Stock Common stockequity Common stock Retained earnings

N.B: This yellow color indicates the source of long-term funds

34

1.2 Cost of Long-Term Debt

The cost of long-term debt is the after-tax cost today ofraising long-term funds through borrowing. For convenience, wetypically assume that the funds are raised through the sale ofbonds. In addition we assume that the bond pay annualinterest.

Net Proceeds

Most corporate long-term debts are incurred through the saleof bonds. The net proceeds from the sale of bonds or anysecurity are the funds that are actually received from thesale. Flotation costs (the total costs of issuing and sellinga security) reduce the net proceeds from the sale. These costsapply to all public offerings of securities (debt, preferredstock, and common stock). They include two components: (1)underwriting costs (compensation earned by investment bankers forselling the security, and (2) administrative costs (issuerexpenses such as legal, accounting, printing, and otherexpenses.

Example

Duchess Corporation, a major hardware manufacturer, iscontemplating selling $10 million worth of 20-years, 9% coupon

(stated annual interest rate) bonds, each with a par value of$1,000. Because similar-risk bonds earn returns greater than9% the firm must sell the bonds for $980 to compensate for thelower coupon interest rate. The flotation costs are 2% of thepar value of the bond (0.02 x $1,000), or $20. The netprocedure to the firm from the sale of each bond are therefore$960 ($980-$20)

Before-Tax Cost of Debt

The before-tax cost of debt, (rd), for a bond can be obtainedin any of three ways: quotation, calculation, orapproximation.

35

Using Cost Quotations

When the net proceeds from sale of a bond equal its parvalue, the before-tax cost just equals the coupon interestrate. For example, a bond with a 10 percent coupon interestrate that nets proceeds equal to the bond’s $1,000 par valuewould have a before-tax cost, (rd), of 10 percent.

Calculating the cost

This approach finds the before-tax cost of debt by calculatingthe interest rate of return (IRR) on the bond cash flow. Fromthe issuer’s point of view, this value is the cost to maturityof the cash flows associated with the debt.

Example

In the preceding example, the net proceeds of a $1,000, 9%coupon interest rate, 20-year bond were found to be $960. Thecalculation of the annual cost is quite simple. The cash flowpattern is exactly the opposite of a conventional pattern; itconsists of an initial inflow (the net proceeds) followed by aseries of annual outlays (the interest payments). In the finalyear, when the debt is retired, an outlay representing therepayment of the principal also occurs. The cash flowsassociated with Duches Corporation’s bond issue are asfollows:

End of Year (s) Cash Flow

0 $ 9601-20 -$ 9020 -$1,000

The initial $960 inflow is followed by annual interestoutflows of $90(9% coupon interest rate x $1,000 par value)over the 20-year life of the bond. In year 20, an outflow of$1,000 (the repayment of the principal) occurs. We candetermine the cost of debt by finding the IRR, which is the

36

discount rate that equates the present value of the outflowsto the initial inflow.

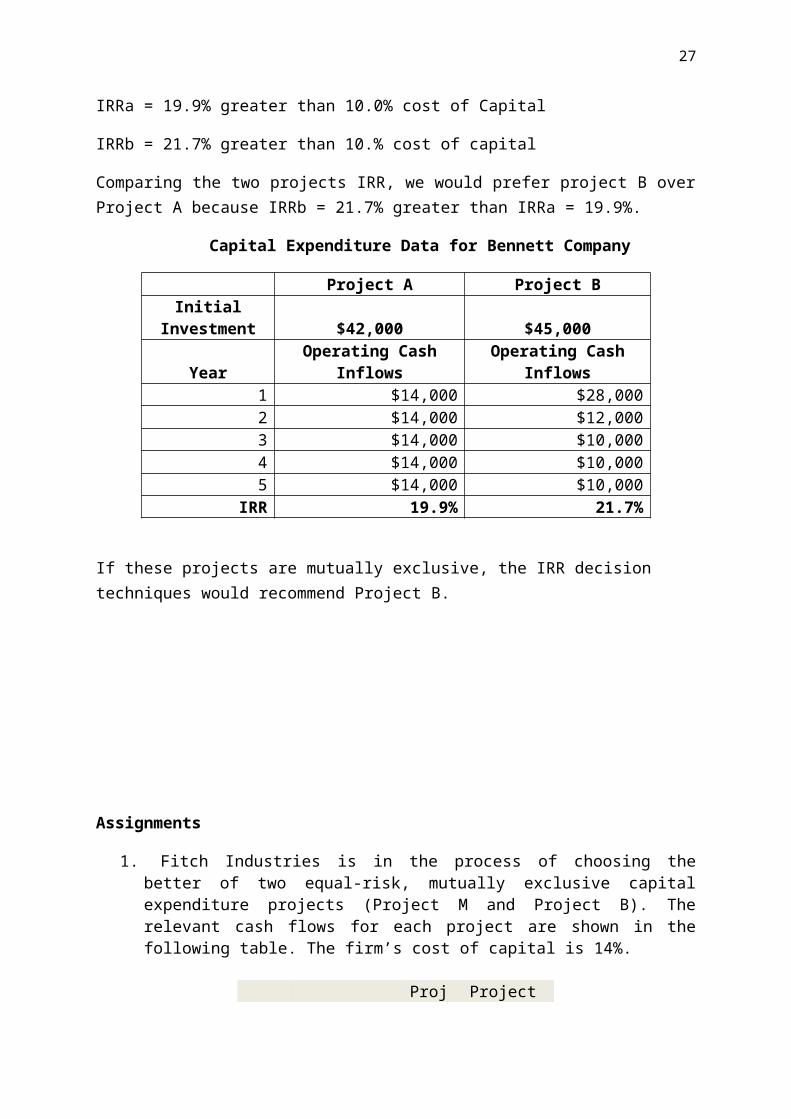

Approximating the cost

The before-tax cost of debt, (rd), for a bond with a $1,000par value can be approximated by using the following equation:

rd = I+

$1,000−Ndn

Nd+$1,0002

Where

I = Annual interest in dollarsNd = Net Proceds from the sale of debt

(bond) n= number of years to thebond’s maturity

Example

Substituting the appropriate values from the DuchessCorporation examples into the approximation formula given inprevious eaquation, we get

rd = $90+$1,000−$960

20$960+$1,000

2

= $90+$2$980 = $90+$2

$980 = 9.4%

This approximate before-tax cost of debt is close to the9.452% value calculated precisely in the preceding example.

After-Tax Cost of Debt

As indicated earlier the earlier, the specific cost offinancing must be stated on an after-tax basis. Becauseinterest on debt is tax deductable, it reduces the firm’staxable income. The after-tax cost of debt, (ri) can be foundby multiplying the before tax cost, rd, by 1 minus the taxrate, T, as stated in the following equation: ri = rd x (1-T)

37

Example

Duchess Corporation has a 40% tax rate. Using the 9.4% before-tax debt cost calculated above, and applying the aboveequation, we find an after-tax cost of debt of 5.6% ⦋(9.4% x(1-0.40)⦌. Typically, the cost of long-term debt is less than agiven firm’s cost of any of the alternative forms of long-termfinancing, primarily because of the tax deductibility ofinterest.

Cost of Preferred Stock

Calculating Cost of Preferred Stock

The cost of preferred stock,(rp), is the ratio of thepreferred stock dividend to the firm’s net proceds from thesale of the preferred stock. The net proceeds represent theamount of money to be received minus any flotation costs. Thefollowing Equation gives the cost of preferred stock, rp, interms of the annual dollar dividend, Dp, the net proceeds fromthe sale of the stock, Np:

Rp = DpNp

Because preferred stock dividends are paid out of the firm’safter-tax cash flows, a tax adjustment is not required.

Example

Duchess Corporation is contemplating issuing of a 10%preferred stock that is expected to sell for its $87-per-sharepar value. The cost of issuing and selling the stock isexpected to be $5 per share. The first step in finding thecost of the stock is to calculate the dollar amount of theannual preferred dividend, which is $8.70 (0.10 x $87). Thenet proceeds per share from the proposed sale of stock equalsdividend, (Dp), of $8.70 and the net proceeds, Np of $82 intoequation gives the cost of preferred stock, 10.6% ($8.7/$82).

38

The cost of Duchess‘s preferred stock (10.6%) is much greaterthan the cost of its long-term debt (5,6%). This differenceexists both because the cost of long-term debt (the interest)is tax deductable and because preferred stock is riskier thanlong-term debt.

Cost of Common Stock

The cost of common stock is the return required on the stockby investing in the marketplace. There are two forms of commonstock financing: (1) retained earnings and (2 ) new issues ofcommon stock. As a first step in finding each of these costs,we must estimate the cost of common stock equity.

Finding the cost of common stock equity

The cost of common stock equity, (rs) is the rate at whichinvestors discount the expected dividends of the firm todetermine its share value. Two techniques are used to measurethe cost of common stock equity. One relies on the constantgrowth valuation model, the other on the capital asset pricingmodel (CAPM).

Using the constant-Growth valuation (Gordon)Model

The model gives the value of shares of stock which is equal tothe present value of all future dividends, which in one modelwere assumed to grow at a constant annual rate over aninfinite time horizon.

This is the constant-growth valuation model, also known as theGordon model.

P0= D1rs−g

Where

P0 = Value of common stockD1 = per-share dividend expected at the end of

year 1 rs = Required return on common

39

stock g = constant rate ofgrowth in dividends

Solving the above equation for rs results in the followingexpression for the cost of common stock equity:

rs = D1P0 +g

This equation indicates that the cost of common stock equitycan be found by dividing the dividend expected at the end ofyear 1 by the current price of the stock (the “dividendyield”) and adding the expected growth rate (the “capital gainyield”). Because common stock dividends are paid from after-tax income no tax adjustment is required.

Example

Duchess Corporation wishes to determine its cost of commonstock equity, rs. The market price, Po, of its common stock is$50 per share. The firm expects to pay a dividend, D1, of $4at the end of the coming year, 2010. The dividends paid on theoutstanding stock over the past 6 years (2004-2009) were asfollows:

Year

Dividends

2009 $3.80

2008 3.62

2007 3.47

2006 3.33

2005 3.12

2004 2.97

40

Using a financial calculator, electronic spreadsheet, or thetable for the present value interest factors, PVIF table, inconjunction with the technique of finding growth rates, wecan calculate the annual growth rate of dividends, g. It turnsout to be approximately 5% (more precisely, it is 5.05%).Substituting D1 = $4, P0 = $50, and g = 5% into equationyields the cost of common stock equity:

Rs = $4$50

+0.05=0.08+0.05=0.130,∨13.0%

The 13% cost of common stock equity represents the returnrequired by existing shareholders on their investment. If theactual return is less than that shareholders are likely tobegin selling their stocks.

Using the capital asset pricing model (CAPM)

Capital asset pricing model (CAPM) describes the relationshipbetween the required return, rs, and the nondiversifiable riskof the firm as measured by the beta coeffificient, “b”. Thebasic CAPM is

rs=RF+ ⦋b×(rm−RF) ⦌

Where

RF = Risk free rate of returnrm = market return, return on market portfolio

of assets

Using CAPM indicates that the cost of common stock equity isthe return required by investors as competition for the firm’snondiversifiable risk, measured by beta.

Example

Duchess Corporation now wishes to calculate its cost of commonstock equity rs, by using the capital asset pricing model. Thefirm’s investment adivisors and its own analyses indicate that

41

the risk-free rate, RF, equals 7%, the firm’s beta b, equals1.5; and the market return, rm, equal 11%, substituting thesevalues into the equation:

rs= 7.0% +⦋1.5 x (11.0% - 7.0%)⦌ = 7.0% +6.0% = 13%

The 13% cost of common stock equity represent therequired return of investors in Duchess Corporationcommon stock. It is the same as that found by usingthe constant-growth valuation model.

Cost of Retained Earnings

As you know, dividends are paid out of a firm’searnings. Their payment, made in cash to commonstockholders, reduces the firm’s retained earnings.Suppose a firm needs common stock equity financing ofa certain amount. It has two choices relative toretained earnings: It can issue additional commonstock in that amount and still pay dividends tostockholders out of retailined earnings, or it canincrease common stock equity by retaining theearnings (not paying the cash dividends) in theneeded amount. In a strict accounting sense, theretention of earnings increases common stock equityin the same way that the sale of additional shares ofcommon stock does. Thus the cost of retainedearnings, rr, to the firm is the same as the cost ofan equivalent fully subscribed issue of additionalcommon stock. Stockholders find the firm’s retentionof earnings acceptable only if they expect that itwill earn at least their required return on thereinvested funds.

42

Viewing retained earnings as a fully subscribed issueof additional common stock, we can set the firm’scost of retained earnings, rr, equal to the cost ofcommon stock equity as given by equation of Gordonand CAPM.

rr=rs

It is not necessary to adjust the cost of retainedearnings for flotation costs, because by retainingearnings, the firm “raises” equity capital withoutincurring theses costs.

Example

The cost of retained earnings for Duchess Corporationwas actually calculated in the preceding examples: Itis equal to the cost of common stock equity. Thus rr

equals 13.0%. As we will show in the next section,the cost of retained earnings is always lower thanthe cost of a new issue of common stock, because itentails no flotation costs.

Assignments

1.Humble Manufacturing is interested inmeasuring its overall cost of capital. Thefirm is the 40% tax bracket. Currentinvestigation has gathered the followingdata.

a.Debt. The firm can raise an unlimited amountof debt by selling $1,000-par value, 10%

43

coupon interest rate, 10-year bonds on whichannual interest payments will be made. Tosell the issue, an average discount of $30per bond must be given. The firm must alsopay flotation costs of $20 per bond.

b.Preferred stock. The firm can sell 11%(annual dividend) preferred stock at its$100-per-share par value. The cost of issuingand selling the preferred stock is expectedto be $4 per share. An unlimited amount ofpreferred stock can be sold under theseterms.

c.Common stock. The firm’s common stock iscurrently selling for $80 per share. The firmexpress to pay cash dividends of $6per sharenext year. The firm’s dividends have beengrowing at an annual rate of 6%, and thisrate is expected to continue in the future.The stock will have to be underpriced by $4per share, and flotation costs are expectedto amount to $4 per share. The firm can sellan unlimited amount of new common stock underthese terms.

d.Retained earnings. The firm expects to have$225,000 of retained earnings available inthe coming year. One these retained earningsare exhausted, the firm will use new commonstock as the form of common stock equityfinancing.

Required:

44

Calculate the specific cost of each source offinancing. (round to the nearest 0.1%)

2.Taylor system has just preferred stock. Thestock has a 12% annual dividend and a $100per value and was sold at $97.50 per share.a.Calculate the cost of preferred stock.b.If the firm sells the preferred stock with

a 10% annual dividend and nets $90.00 afterflotation costs, what is its cost?

3.J&M corporation common stock has a beta, b,of 1.2. The risk-free rate is 6%, and themarket return is 11%.

Your are required Determine J&M’ s costof common stock equity using the CAPM

4.Taylor Systems has just issued preferredstock. The stock has a 12% annual dividendand a $100 par value and was sold at $97.50per share. In addition, flotation costs of$2.50 per share must be paid.

You are required to calculate the costof the preferred stock.

CHAPTER 5

FINANCIAL DIVIDEND POLICY

1.1. Dividend Fundamentals

Expected cash dividends are the key return variable from whichowners and investors determine share value. They represent asource of cash flow to stockholders and provide information

45

about the firm’s current and future performance. Becauseretained earnings, earnings not distributed to owners asdividends, are a form of internal financing, the dividenddecision can significantly affect the firm’s externalfinancing requirements. In other words, if the firm needsfinancing, the large the cash dividend paid, the greater theamount of financing it must raise externally through borrowingor through the sale of common or preferred stock. (Rememberthat although dividends are charged to retained earnings, theyare actually paid out of cash). The first thing to know aboutcash dividends is the procedures for paying them.

Cash Dividends Payment Procedures

At quarterly or semiannual meeting, a firm’s board ofdirectors decides whether and in what amount to pay cashdividends to corporate stockholders. The past period’sfinancial performance and future outlook, as well as recentdividends paid, are key inputs to dividends decisions. Thepayment date of the cash dividend, if one is declared, mustalso be established.

Amount of Dividends

Whether dividends should be paid, and if so, in what amount,are important decisions that depend primarily on the firm’sdividend policy. Most firms have a set policy with respect tothe periodic dividend, but the firm’s directors can changethis amount, largely on the basis of significant increases ordecreases in earnings.

Relevant Dates

If the directors of the firm declare a dividend, they also typically issue a statement indicating the dividend decision, the record date, and the payment date. This statement is generally quoted in the Wall Street Journal and other financial news media.

Record Date. Set by the firm’s directors, the date on which all persons whose names are recorded as stockholders receive a

46

declared dividend at specified future time. These stockholdersare often referred to as holder of record.

Because of the time needed to make bookkeeping entries when astock is traded, the stock begins selling ex dividend 2 businessdays prior to the date of record. Purchasers of a stock sellingex dividends do not receive the current dividend. A simple wayto determine the first days on which the stock sells exdividend is to subtract 2 days from the date of record; if aweekend intervenes, subtract 4 days. Ignoring general marketfluctuations, the stock’s price is expected to drop by theamount of the declared dividend on the ex dividend date.

Payment Date. The payment date, also set by the directors, isthe actual date on which the firm mails the dividend paymentto the holders of record. It is generally a few weeks afterthe recorded date. An example will clarify the various datesand the accounting effects.

Example

At the quarterly dividend meeting of Rudolf Company, adistributor of office products, held on June 10, the directorsdeclared a $0.80-per-share cash dividend for holders of recordon Friday, July 2. The firm had 100,000 shares of common stockoutstanding. The payment date for the dividend was Monday,August 2. Figure 1.1 shows a time line depicting the key datesrelative to the Rudolf Company’s dividend. Before the dividendwas declared, the key accounts of the firm were as follows:

Cash $200,000 Dividends payable $ 0 Retained Earnings 1,000,000

When the dividend was announced by the directors, $80,000 ofthe retained earnings ($0.80 per share x 100,000 shares) was transferred to the dividends payable account. The key accountsthus became

Cash $200,000 Dividends payable $ 80,000Retained Earnings 920, 000

47

Rudolf Company’s stock began selling ex dividend 2 businessdays prior to the date of record, which was Wednesday, June30. This date was found by subtracting 2 days from the July 2date of record. Purchasers of Rudolf’s stock on Tuesday, June29 or earlier received the rights to the dividends; those whopurchased the stock on or after June 30 did not. Assuming astable market, Rudolf’s stock price was expected to drop byapproximately $0.80 per share when it began selling exdividend on June 30. On August 2 the firm mailed dividendchecks to the holders of record as of July 2. This producedthe following balances in the key accounts of the firm:

Cash $120,000 Dividends payable $ 0Retained Earnings 920, 000

The net effect of declaring and paying the dividend was to reduce the firm’s total assets (and stockholders’ equity) by $80,000

Declaration Date Ex Dividend Date Date of RecordPayment Date

Thursday, June 10 Wednesday, June 30 Friday July, 2Monday August 2

________________________________________________________

Board of directors declares $0.80 per share dividend, payable to holders of record on Friday, July 2, payable onMonday, August 2

Stock begins to sell exdividend on Wednesday, June 30, which is 2 business days before the Friday, July 2, date of record

Checks of $0.80 per share are mailed on Monday, August 2, to all holders of record on Friday July 2.

48

TIME

Review Questions

Who are holders of record? When does a stock sell ex dividend?

1.2 Factors Affecting Dividend Policy

The firm’s dividend policy represents a plan of action to befollowed whenever it makes a dividend decision. Firm developpolicies consistent with their goals. Before we review some ofthe popular types of dividend policies, we discuss six factorsthat firms consider in establishing a dividend policy. Theyare legal constraints, Contractual constraints, internalconstraints, the firm’s growth prospects, ownerconsiderations, and market considerations.

Legal Constraints. Most states prohibits corporations frompaying out as cash dividends any portion of the firm’s “legalcapital” which is typically measured by the par value ofcommon stock. Other states define legal capital to include notonly the par value of the common stock, but also any paid-incapital in excess of par. These capital impairmentrestrictions are generally established to provide a sufficientequity base to protect creditors’ claims. An en example willclarify the differing definitions of capital.

ExampleThe stockholders’ equity account of Miller flour Company, alarge grain processor, is presented in the following tables:

Common Stock$100,0

00Paid in Capital in excessof par

200,000

Retained earnings140,00

0Total stockholders' equity

$440,000

49

In states where the firm’s legal capital is defined as the par value of its common stock, the firm could pay out $340,000($200,000 + $140,000) in cash dividends without impairing its capital, In states where the firm’s legal capital include all paid-in capital, the firm could pay out only 140,000 in cash dividend.

Firms sometimes impose an earnings requirement limiting the amount of dividends. With this restriction, the firm cannot pay more in cash dividend than the sum of its most recent and past retained earnings. However, the firm is not prohibited from paying more in dividends than its current earnings.

ExampleAssume that Miller Flour Company, from the preceding example,in the year just ended has $30,000 in earnings available forcommon stock dividends. As the preceding table indicates, thefirm has past retained earnings of $140,000. Thus it canlegally pay dividends of up to $170,000

Contractual Constraints. Often the firm’s ability to pay cashdividend is constrained by restrictive provisions in a loanagreement. Generally, these constraints prohibit the paymentof cash dividends until the firm achieves a certain level ofearnings, or they may limit dividends to certain dollar amountor percentage of earnings. Constraints on dividends help toprotect creditors from losses due to the firm’s insolvency.

Internal Constraints. The firm’s ability to pay cash dividendsis generally constrained by the amount of liquid assets (cashand marketable securities) available. Although it is possiblefor a firm to borrow funds to pay dividends, lenders aregenerally reluctant to make such loans because they produce notangible or operating benefits that will help the firm repaythe loan.

Growth Prospects. The firm’s financial requirements aredirectly related to how much it expects to grow and whatassets it will need to acquire.

50

Owner considerations. The firm must establish a policy thathas a favorable effect on the wealth of the majority ofowners. One consideration is the tax status of a firm’sowners. If a firm has a large percentage of wealthystockholders who have sizable incomes, it may decide to payout a lower percentage of its earnings to allow the owners todelay the payment of taxes until they sell the stock.

Market considerations. Awareness of the marker’s probableresponse to certain type of policies is also helpful informulating dividend policy.

1.3 Types of Dividend Policies

The firm’s dividend policy must be formulated with two basicobjectives in mind: providing for sufficient financing andmaximizing the wealth of the firm’s owners. Three commonlyused dividend policies are described in the followingsections. A particular firm’s cash dividend policy mayincorporate elements of each.

Constant-payout-Ration Divided Policy

One type of dividend policy involves use of a constant payoutratio. The dividend payout ratio indicates the percentage of each dollarearned that the firm distributes to the owners in the form of cash. It iscalculated by dividing the firm’s cash dividend per share by its earnings pershare. With a constant – payout –ratio dividend policy, thefirm establishes that a certain percentage of earnings is paidto owners in each dividend period.

Constant-payout-ratio dividend policy is a dividend policy based on thepayment of a certain percentage of earnings to owners in each dividendperiod.

The problem with this policy is that if the firm’s earningsdrop or if a loss occurs in a given period, the dividends maybe low or even nonexistent. Because dividends are oftenconsidered an indicator of the firm’s future condition andstatus, the firm’s stock price may be adversely affected.

Example

51

Peachtree Industries, a miner of potassium, has a policy ofpaying out 40% earnings in cash dividends. In periods when aloss occurs, the firm’s policy is to pay no cash dividends.Data on Peachtree’s earnings, dividends, and average stockprices for the past 6 years follow.

YearEarnings/Share($)

Dividends/share ($)

Average Price/Share ($)

2009 −¿0.50 0.00 422008 3.00 3.20 522007 1.75 0.70 482006 −¿1.50 0.00 382005 2.00 0.80 462004 4.50 1.80 50

Dividend increased in 2007 and in 2008 but decreased in theother years. In years of decreasing dividends, the firm’sstock price dropped; when dividends increased, the price ofthe stock increased. Peachtree’s sporadic dividend paymentsappear to make its owners uncertain about the return they canexpect.

Although some firms use a constant payout-ratio dividendpolicy, it is not recommended. Regular Dividend Policy

The regular dividend policy is based on the payment of afixed-dollar dividend in each period. This policy provides theowners with generally positive information, thereby minimizingtheir uncertainty. Often, firms that use this policy increasedthe regular dividend once a proven increase in earnings hasoccurred. Under this policy, dividends are almost neverdecreased.

Example

52

The dividend policy of Woodward Laboratories, a producer of apopular artificial sweetener, is to pay annual dividends of$1.00 per share until per-share earnings have exceeded $4.00for 3 consecutive years. At that point, the annual dividend israised to $1.50 per share, and a new earnings plateau isestablished. The firm does not anticipate decreasing itsdividend unless its liquidity is in jeopardy. Data forWoodward’s earnings, dividends, and average stock prices forthe past 12 years follow.

YearEarnings/Share

($)Dividends/share

($)Average

Price/Share ($)2009 4.50 1.50 47.502008 3.90 1.50 46.502007 4.60 1.50 45.002006 4.20 1.00 43.002005 5.00 1.00 42.002004 2.00 1.00 38.502003 6.00 1.00 38.002002 3.00 1.00 36.002001 0.75 1.00 33.002000 0.50 1.00 33.001999 2.70 1.00 33.501998 2.85 1.00 35.00

Whatever the level of earnings, Woodward laboratories paiddividends of $1.00 per share through 2006. In 2007, thedividend increased to $1.50 per share because earnings inexcess of $4.00 per share had been achieved for 3 years. In2007, the firm also had to establish a new earnings plateaufor further dividend increases. Woodward Laboratories’ averageprice per share exhibited a stable, increasing behavior inspite of a somewhat volatile pattern of earnings.

Often a Regular dividend policy is built around a targetdividend-payout ratio. Under this policy, the firm attemptsto pay out a certain percentage of earnings, but rather thanlet dividends fluctuate, it pays a stated dollar dividend andadjusts that dividend toward the target payout as provenearnings increases occur. For instance, Woodward Laboratories

53