Accounting Cycles

32

Accounting Cycle: Capturing Business Activities Every business organization, irrespective of the size, nature, form, and ownership undertakes several transactions on the day-to-day basis. It will be difficult for the business owners, managers, and employees to remember such transactions. That explains the need for recording the transactions in a systematic manner. Recording of transactions in systematic and scientific manner is called accounting. One of the ways of understanding the business transaction is to understand the accounting equation. The concept of accounting equation was discussed in detail the Chapter – In this chapter we will understand the following: Rules for capturing business transactions Process of recording the business transactions Accounts Account is an accounting record of increase or decrease in a financial item. For examples: A company can have several accounts, viz. Cash Account, Furniture Account, Building Account, Bank Account, Capital Account, Loan Account, Customer Account, Supplier Account etc. An Account is generally shown in the following form: Stock Account Dat e Particu lars Debit Amount Dat e Particu lars Credit Amount 1 2 3 4 5 6 Where: 1 & 4: Date of transaction 2 & 5: Particulars: Details of the transaction 3 & 6: Debit and Credit Amount respectively

Transcript of Accounting Cycles

Accounting Cycle: Capturing Business Activities Every business organization, irrespective of the size, nature, form, and ownership undertakes several transactions on the day-to-day basis. It will be difficult for the business owners, managers, and employees to remember such transactions. That explains the need for recording the transactions in a systematic manner. Recording of transactions in systematic and scientific manner is called accounting. One of the ways of understanding the business transaction is to understand the accounting equation. The concept of accounting equation was discussed in detail the Chapter – In this chapter we will understand the following:

Rules for capturing business transactions Process of recording the business

transactions AccountsAccount is an accounting record of increase or decrease in afinancial item. For examples: A company can have several accounts, viz. Cash Account, Furniture Account, Building Account, Bank Account, Capital Account, Loan Account, Customer Account, Supplier Account etc. An Account is generally shown in the following form:

Stock AccountDate

Particulars

Debit Amount

Date

Particulars

Credit Amount

1 2 3 4 5 6

Where:1 & 4: Date of transaction2 & 5: Particulars: Details of the transaction3 & 6: Debit and Credit Amount respectively

You may be having the following questions at this juncture;

What transactions will appear on the debit side or credit side?

Is there is method for remembering the process of recording the items on the debit side or credit side?

Are these rules apply to all types of business transactions?

To answer the above questions, it is necessary to classify the financial items. The financial items1[1] can be divided into the following three types of accounts;

a) a) Real Accountsb) b) Persona Accountsc) c) Nominal Account

1[1] Another form of classifying the financial items has been discussed in the previous chapter.

Real Accounts: Represent the physical properties belonging to the business. Land, Building, Furniture, Stock, Cash are some of the examples of real accounts. These are also calledthe assets of the business. Let us take a look the nature ofchange that can happen with these items (assets):

Increase: When you acquire or revalue the asset.

Decrease: When you sell/ Just reduction in the value i.e. depreciation

So for the purpose of recording of transactions relating to the these items, we classify these transactions as follows:

Increase in Assets : Debit Decrease in Assets: Credit

In typical accounting language,

When we purchase assets: Debit the Asset Account

When we sell assets: Credit the Asset Account

When assets are depreciated: Credit the Asset Account

Personal Accounts: Represent individuals, corporate entities, and other artificial legal juridical entities. Ramor Peter (a natural person) Account, Capital Account ( represents the owners), Bank Account, Infosys Limited (corporate entities) , are some of the examples of personal accounts. These individuals and the organisations can be divided into two categories

Persons who owe money to the business (Debtors)

Persons to whom the business owe money (Creditors/Shareholders/Loan giver)

Let us take a look the nature of change that can happen withthese items (assets):

Increase in debtors: Debit

Decrease in debtors: Credit Increase in Creditors/Shareholders/Loan

giver: Credit Decrease in Creditors/Shareholders/Loan

giver: Debit So in typical accounting language:

When a customer purchases on credit: Increase in Debtors: Debit the person’s account

When the customer makes the payment: Decrease in Debtors: Credit the person’s account

When the business purchases goods on credit:Increase in Creditors: Credit the person’s account

When the business makes payment to the supplier: Decrease in Creditors: Debit the person’s account

When we purchase stock on credit from Mr. X(supplier): Credit the Supplier’s account

When sell stock on Credit to Mr. Y(Customer): Debit the customer’s account

In other words, a person either receives something (for service, sale of goods, loan given ) or pays something (for service taken, purchase of goods, loan taken|)So we can alsosay the following Nominal Accounts: Refer to the expenses, losses, incomes andgains. Salary, Interest received or given, commission, rent etc. are some of the examples of nominal accounts. Some of the transactions relating to these accounts are as follows:

Salary paid: Debit the salary Account Interest received : Credit the interest

account Interest paid: Debit the interest account

So one can say the following:

All expenses: Debit All Incomes : Credit

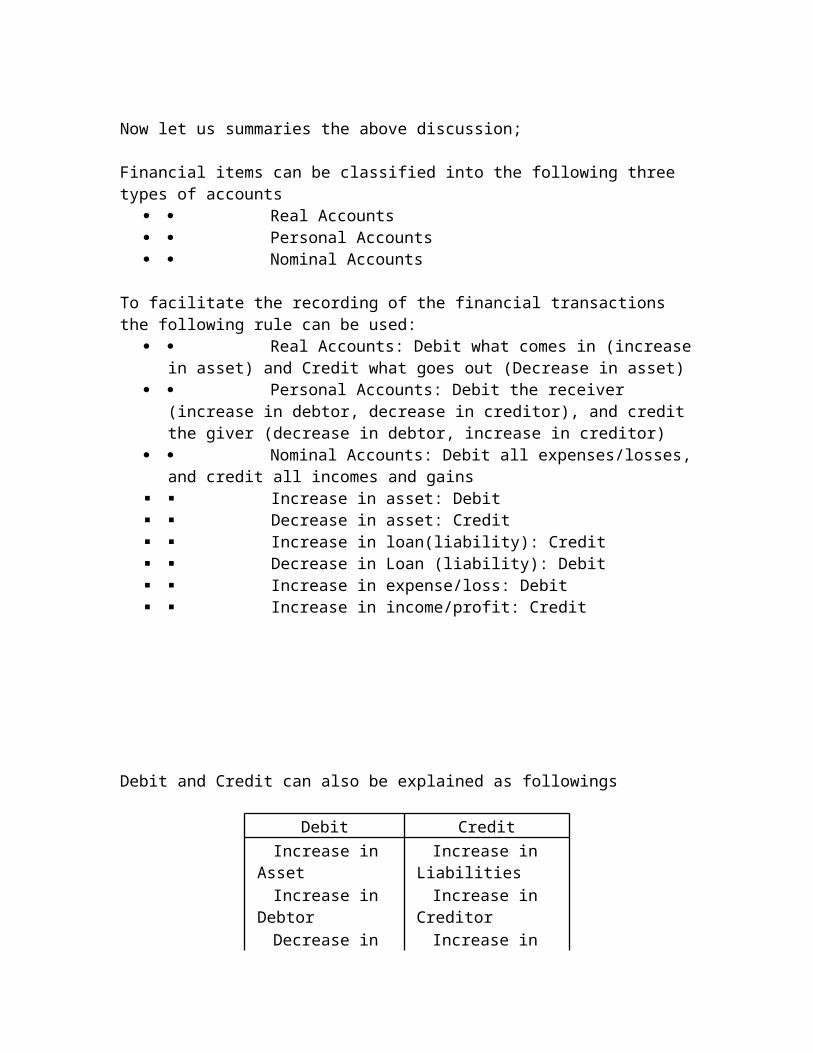

Now let us summaries the above discussion; Financial items can be classified into the following three types of accounts

Real Accounts Personal Accounts Nominal Accounts

To facilitate the recording of the financial transactions the following rule can be used:

Real Accounts: Debit what comes in (increasein asset) and Credit what goes out (Decrease in asset)

Personal Accounts: Debit the receiver (increase in debtor, decrease in creditor), and credit the giver (decrease in debtor, increase in creditor)

Nominal Accounts: Debit all expenses/losses,and credit all incomes and gains

Increase in asset: Debit Decrease in asset: Credit Increase in loan(liability): Credit Decrease in Loan (liability): Debit Increase in expense/loss: Debit Increase in income/profit: Credit

Debit and Credit can also be explained as followings

Debit CreditIncrease in

AssetIncrease in

LiabilitiesIncrease in

DebtorIncrease in

CreditorDecrease in Increase in

Loan LoanDecrease in

CreditorDecrease in

DebtorIncrease in

ExpenseDecrease in

ExpenseDecrease in

IncomeIncrease in

Income Now we will understand the use of debits and credits for recording transactions. Steps required for recording the transactions are as follows

Read the transaction Identify the two (debit and credit) financial

items affected by the transactions Use the above debit and credit rule discussed

in the previous section.

1. 1. A and B started AB ltd. A contributed cash Rs. 100,000 as capital and B transferred two computers worth of Rs. 50,000 to the business.

Two Items:

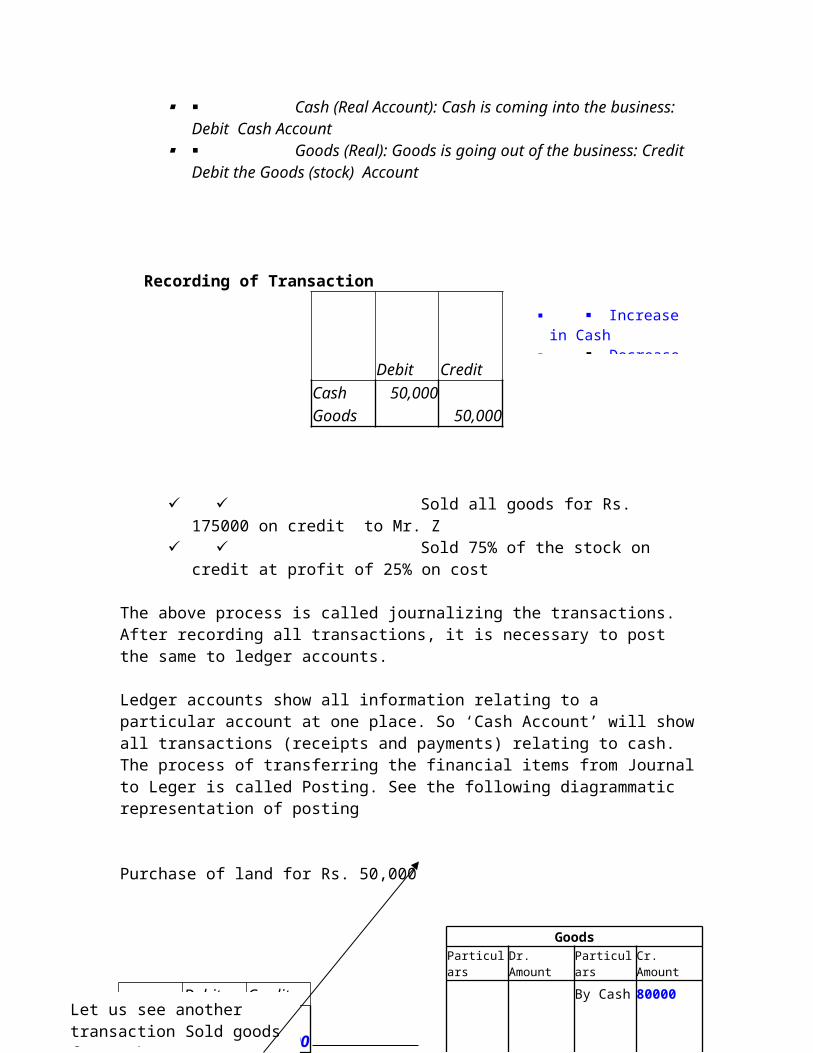

Cash (Real Account): Cash is coming into the business: Debit Cash Account

Capital Account (Representative Personal Account): The owners are giving the money: Credit the Capital Account

Recording of Transaction

Debit CreditCash 10000 Capital 10000

Increase incash

Increase in

2. 2. They took 10% loan from IDBI: Rs.100 000.

Two Items: Cash (Real Account): Cash is coming into the business:

Debit Cash Account Bank Account (Personal Account): The owners are giving

the money: Credit the Bank Account

Recording of Transaction

Debit

CreditCash 10000 Bank Loan 10000

3. 3. Purchased machinery costing Rs.20 000 for cash.

Two Items: Cash (Real Account): Cash is going out of the business:

Credit Cash Account Machinery (Rea Account): Machinery is coming into the

business: Debit the Capital Account

Recording of Transaction

Debit CreditMachinery 20000 Cash 20000

Increase inmachinery

Decrease

Increase in cash

Increase in

4. 4. Purchase furniture on credit from X ltd for Rs. 30 000.

Two Items: It is a credit transaction

Mr. X (Personal Account): Mr. X extended loan: Credit M. X Account

Furniture (Real): Machinery is coming into the business: Debit the Furniture Account

Recording of Transaction

Debit CreditFurniture 30,000 X 30,000

5. 5. Purchased land for cash Rs. 50 000. It is a cash transaction

Cash (Real Account): Cash is going out of the business: Credit Cash Account

Land (Real): Land is coming into the business: Debit the Land Account

Recording of Transaction

Debit

CreditLand 50,000 Cash 50,000

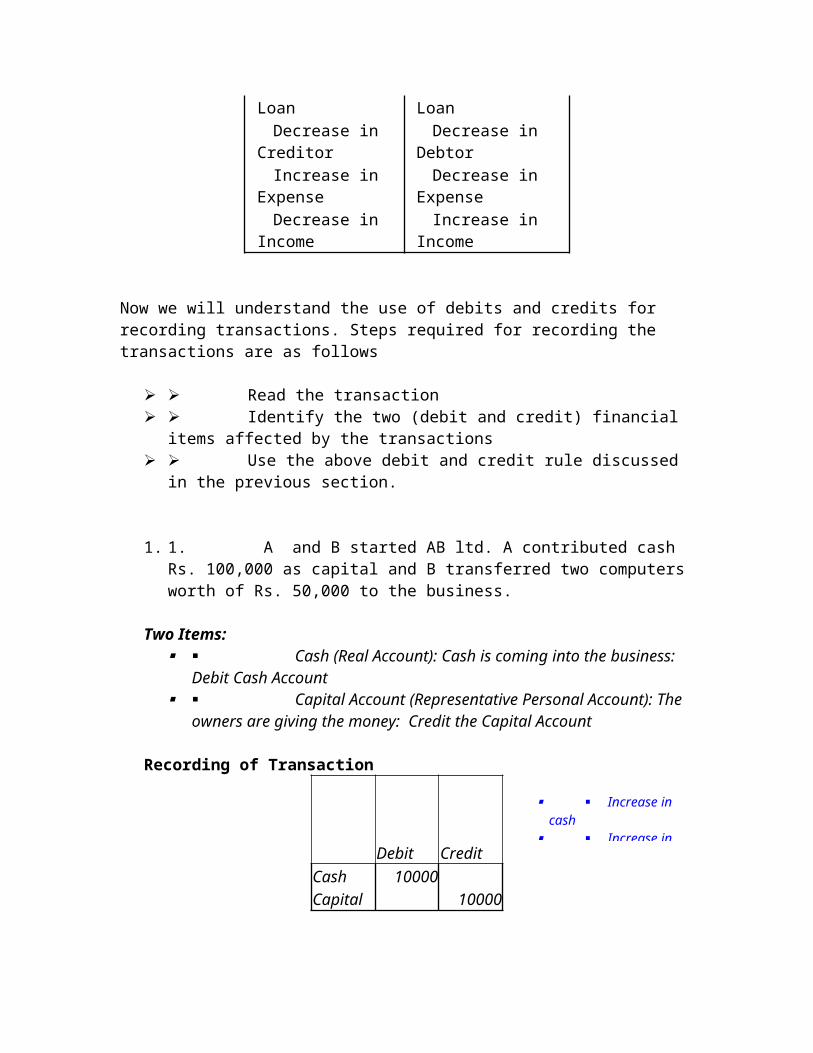

6. 6. Purchased goods worth of Rs. 50 000 for cash. It is a cash transaction

Increase in Furniture

Increase in

Increase in Land

Decrease in

Cash (Real Account): Cash is going out of the business: Credit Cash Account

Goods (Real): Goods is coming into the business: Debit the Goods (stock) Account

Recording of Transaction

Debit

CreditGoods 50,000 Cash 50,000

Increase in Land

Decrease in

7. 7. Purchased goods worth of Rs. 70 000 on credit

from Y Ltd.

It is a credit transaction Y (personal Account): Y extended credit: Credit Y

Account Goods (Real): Goods is coming into the business: Debit

the Goods Account Recording of Transaction

Debit

CreditGoods 50,000 Y 50,000

8. 8. Sold all goods for Rs. 160 000 on credit to Mr. Z

It is a credit transaction

Z (Personal Account): Z receives goods and owes money to the business: Debit Z Account

Goods (Real): Goods is going out of the business: Credit Debit the Goods (stock) Account

Recording of Transaction

Debit

CreditZ 160,000 Goods 160000

9. 9. Sold all goods for Rs. 150 000 for cash

It is a cash transaction

Increase in Land

Increase in

Increase in Goods

Decrease

Cash (Real Account): Cash is coming into the business: Debit Cash Account

Goods (Real): Goods is going out of the business: Credit Debit the Goods (stock) Account

Recording of Transaction

Debit CreditCash 50,000 Goods 50,000

Sold all goods for Rs.

175000 on credit to Mr. Z Sold 75% of the stock on

credit at profit of 25% on cost

The above process is called journalizing the transactions. After recording all transactions, it is necessary to post the same to ledger accounts. Ledger accounts show all information relating to a particular account at one place. So ‘Cash Account’ will showall transactions (receipts and payments) relating to cash. The process of transferring the financial items from Journalto Leger is called Posting. See the following diagrammatic representation of posting

Purchase of land for Rs. 50,000

Debit CreditCash 80000 Goods 80000

Increase in Cash

Decrease

Let us see another transaction Sold goodsfor cash: Rs. 80000

GoodsParticulars

Dr. Amount

Particulars

Cr. Amount

By Cash 80000

Land Account

ParticularsDr. AmountParticularsCr. Amount

To Cash 50, 000

Cash Account

ParticularsDr. AmountParticularsCr. Amount

To Goods 80000By Cash50,000

DebitCredit

Land50,000

Cash

50,000

Balancing of Ledger Accounts After posting all transactions to the respective ledger accounts, it is necessary to balance the ledger accounts periodically (daily, monthly, quarterly, half-yearly and yearly). Steps required to balance a ledger account are as follows;

Total the debit side Total the credit side Find the difference Put the difference on the lesser side If the debit side is greater than the credit

side, it is called Debit Balance If the credit side is greater than the debit

side, it is called Credit Balance See the following ledger account

CashParticulars

Dr. Amount Particulars

Cr. Amount

To Capital 100000By Machine 50000To Sales 50000Stock 25000

Expenses

10000

By closing Balance

65000

Total 150000Total 150000 Total of Debit side: 150000Total of Credit side (excluding the closing balance) = 85000Difference between Dr. Side and Cr. Side = 150 000 – 85000 =65000Since the Dr Side > Cr. Side: 65000 is called Debit balance

Balancing

General Rules of Balancing of Ledger Accounts: Personal Accounts: There can Debit Balance

or Credit Balance or no Balance Real Accounts: There be Debit Balance or No

balance Nominal Accounts: There will be No Balance

Work To Do

1. 1. Following are some of the journal entries. You are required to explain the transactions

Debit CreditCash 10000 Bank Loan 10000 Debit CreditSalary 10000 Cash 10000 Debit CreditGoods 10000 Mr. Y 10000

Debit CreditFurniture 2500 Mr. X 2500

2. 2. Following are the transactions of X ltd. Took IDBI Loan: Rs. 10 lakhs Purchased furniture for cash: 250000 Purchased 2 computers: Rs.50000 Salary paid: Rs. 10000 Rent due but not paid

Debit CreditLoan 10000 Cash 10000

Debit CreditInterest 5000 Cash 5000

Debit CreditGoods 25000 Capital 25000

Electricity bill paid: Rs.2500 Purchased goods for sale: Rs. 250000 Sold the goods on credit to Mr. X at a

profit of 20% on Sales. Telephone charges due but not paid:

Rs.1500Required: Journal entries and the corresponding ledger accounts.

3. 3. Following are the transactions of A ltd. A ltd purchased a Machinery on credit from

Mr. R: 50000 A ltd. purchased goods on credit from Mr. X:

Rs.25000 Altd. sold 75% goods on credit and balance

for cash. Goods are sold at cost plus 25% profit. A ltd. charged depreciation on the machine:

10% on the costRequired: Journal entries

4. 4. Explain the following: A debit of Rs. 5000 to Furniture Account A debit of Rs. 5000 to Loan (taken)

Account A debit to Rs. 5000 to Loan (given)

Account A credit of Rs. 5000 to Mr. X ( Customer) A credit of Rs. 5000 to Mr. Y (Supplier) Credit balance of Rs. 5000 in the Bank

Account A credit of Rs. 5000 to Cash Account

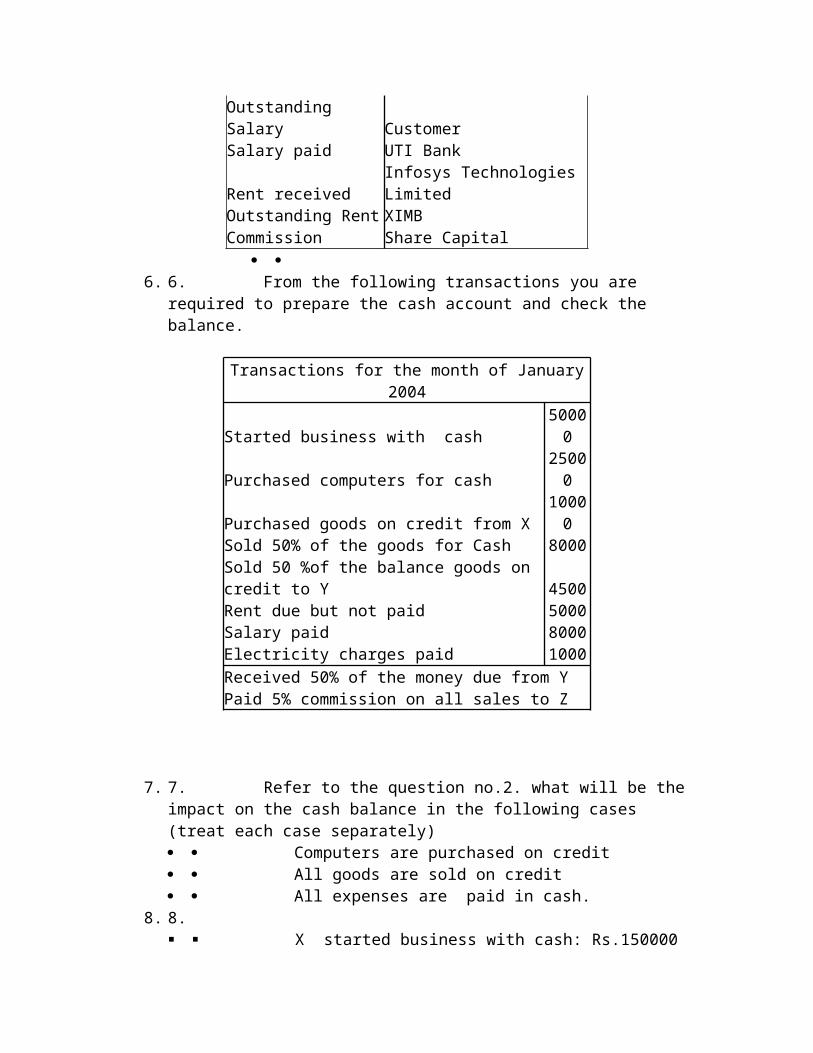

5. 5. Classify the following financial items into

Real, Nominal and Personal Accounts

Financial ItemsCapital Cash

Outstanding Salary CustomerSalary paid UTI Bank

Rent receivedInfosys Technologies Limited

Outstanding Rent XIMBCommission Share Capital

6. 6. From the following transactions you are

required to prepare the cash account and check the balance.

Transactions for the month of January

2004

Started business with cash50000

Purchased computers for cash25000

Purchased goods on credit from X10000

Sold 50% of the goods for Cash 8000Sold 50 %of the balance goods on credit to Y 4500Rent due but not paid 5000Salary paid 8000Electricity charges paid 1000Received 50% of the money due from YPaid 5% commission on all sales to Z

7. 7. Refer to the question no.2. what will be the impact on the cash balance in the following cases (treat each case separately) Computers are purchased on credit All goods are sold on credit All expenses are paid in cash.

8. 8. X started business with cash: Rs.150000

Purchased goods on credit from Mr. Y: Rs.50000

Purchased furniture on credit from F ltd.: Rs.25000

Sold goods costing Rs. 10000 at a profit of 20% on sales for cash.

Bought goods costing Rs. 20000 for cash. Drawn for personal use: Rs. 5000 Sold the available goods to Ms. Z on

credit at a profit of 25% on cost. Paid Salaries: Rs. 80000 Rent due but not paid: Rs. 5000 Received 75% of the money due from Ms. Z Paid 50% of the money due to Mr. Y Purchased 5 shares of Infosys @ Rs.4000.

Required: Journal Entries and the corresponding ledger accounts

9. 9. Mr. A started a business on Ist January 2004. Following the transactions upto April 30th

Date Transaction Amount

1-Jan-04Started business with ownmoney

100,000

10-Jan-04Took a 12% loan from SBI

250,000

15-Jan-04Purchased computers 50,000

25-Jan-04

Purchased Satyam shares for cash 75,000

30-Jan-04Paid the following

Rent 5,000 Electricity Charges 2,000

Internet connection charges 1,500

5-Feb-04Sold 50% of the Satyam Shares 45,000

10-Feb-04Purchased SBI shares 25,000

27-Feb-04Paid the following

Rent 5,000 Electricity Charges 2,000

Internet connection charges 1,500

10-Mar-04

Purchased the shares of UTI Bank 50,000

25-Mar-Purchased Timex Shares 80,000

04

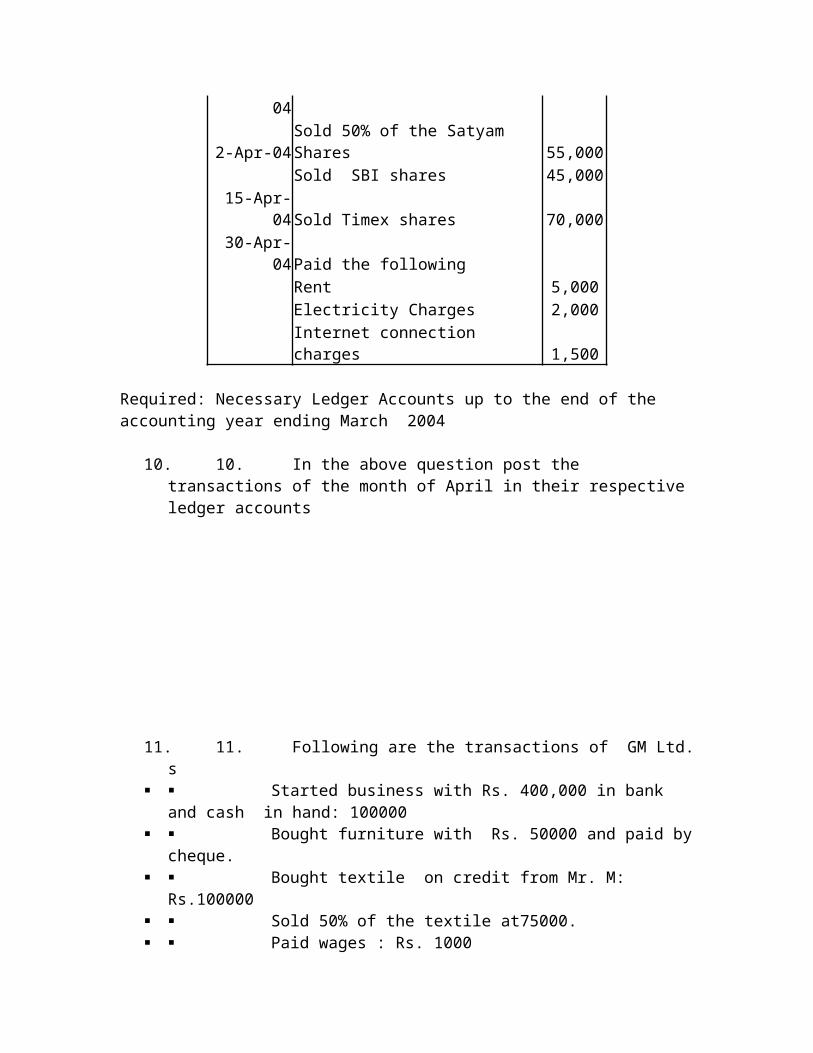

2-Apr-04Sold 50% of the Satyam Shares 55,000

Sold SBI shares 45,00015-Apr-

04Sold Timex shares 70,00030-Apr-

04Paid the following Rent 5,000 Electricity Charges 2,000

Internet connection charges 1,500

Required: Necessary Ledger Accounts up to the end of the accounting year ending March 2004

10. 10. In the above question post the transactions of the month of April in their respective ledger accounts

11. 11. Following are the transactions of GM Ltd.s

Started business with Rs. 400,000 in bank and cash in hand: 100000

Bought furniture with Rs. 50000 and paid bycheque.

Bought textile on credit from Mr. M: Rs.100000

Sold 50% of the textile at75000. Paid wages : Rs. 1000

Paid Mr. M: Rs.25000 Bought T Shirts from Tirupur: Rs.50000. Paid

by cheque Sold all Tshirts to a local retailer at Rs.

60000. Bought stationery: Rs. 5000 Paid rent: Rs.5000 Electricity charge due but not paid: Rs.2000 Insurance premium paid by cheque: Rs. 10000 Sold 10% of the balance textile on credit to

Mr. Y at Rs.7500. Mr. Y failed to make the payment on the due

date. The entire money was declared bad-debt. Required: Pass the necessary journal entries and post the transactions to the relevant ledger accounts

12. 12. Following is the Cash Account of X ltd.

Cash Account

Date ParticularsDebit Amt. Date Particulars

Credit Amt.

1..04.04

Opening Balance 500000

5.04.04 Goods 50000

goods 150000 furniture 10000

Shares of RIL 30000

Shares of RIL 50000

Old Newspapers 500 Salary 5000

Old Furniture 2000 Rent 2500

Shyam 5000 Interest 500 Loan 50000 30.04. Closing 619500

04 Balance 737500 Total 737500

Explain the transactions behind the above Cash Account. Youare also required to prepare the necessary ledger accounts.

Book Keeping :The Accounting Flow/AccountingEquation/Ledgers/Trial Balance

The book keeping is the recording of transactions in scientific and systematic manner. So book keeping is a art, as one can learn it with practice, it is a science as the recording is based on certain principles Transactions: Exchange of goods and services between two or more entities, both business and social. Let us take an hypothetical organisation called ABC ltd. andunderstand the entire process of recording in the following two different methods: 1. 1. Direct Recording in Balance Sheet and Income

Statement2. 2. Conventional Recording: Tracing the entire

accounting flow 3. 3. Computerised Recording Direct Recording: Steps: Analyse the transaction Identify the items: Transfer Incomes and Expenses to the INCOME

STATEMENT Transfer Sources and Applications to the

BALANCE SHEET The entire process can be explained as follows:

Transactions

Incomes Expens

esSources

Application

Income Statement

Balance Sheet

This requires understanding of the following concepts: Incomes and Expenses Sources The liability side of a balance sheet

represents the various sources from which a company obtains the funds which are needed for its business

Applications: The assets side of a balance sheet indicates the manner in which the resources of a company have been utilised

Balance Sheet: Balance Sheet is a statement which shows the sources and application of funds. Sourcesand application are also known as liabilities and assets respectively. Balance sheet is prepared to show the financial position of the organisation as on a particulardate. A balance sheet is always correct as on the date ofpreparation (for details see Chapter I)

Income Statement The income statement of an organisation shows the net operating result of the activities undertaken during a particular period of time.The income statement is also known as the Profit and LossAccount (P/L Account) (for details see Chapter I)

Conventional Recording: Tracing the entire accounting flow:

Transactions for Tally Exercise

Started business with Rs. 100000

Availed 12% ICICI Loan: Rs. 200 000

Transactions

Journals

Ledgers

Trial Balance

Income Statement

Balance Sheet

Promoter contributed Computer as capital:

Rs.25000

Purchased Plant for cash: Rs.25000

Purchased Furniture: Rs.10000

Paid Rent: Rs. 5000

Paid Salary: Rs.10000

Purchased goods from X on credit: Rs. 50000

Purchased goods for cash: Rs. 100000

Sold 70% of the goods to Y on credit: Rs.

150000

Sold balance stock for cash 75000

Received 50% due from Y

Depreciation on plant and furniture: 10%

SEBI (Disclosure & Investor Protection) Guidelines, 2000 asamemended till date

CHAPTER III

PRICING BY COMPANIES ISSUING SECURITIES

3.0 The companies eligible to make public issue can freelyprice their equity shares or any security convertible atlater date into equity shares in the following cases:

3.1 Public / Rights Issue by Listed Companies

3.1.1 A listed company whose equity shares are listed on astock exchange, may freely price its equity shares and anysecurity convertible into equity at a later date, offeredthrough a public or rights issue.

3.2 Public Issue by Unlisted Companies

3.2.1 An unlisted company eligible to make a public issueand desirous of getting its securities listed on arecognised stock exchange pursuant to a public issue, mayfreely price its equity shares or any securities convertibleat a later date into equity shares.

Infrastructure company

3.2.3 An eligible infrastructure company shall be free toprice its equity shares

subject to the compliance with the disclosure norms asspecified by SEBI from

time to time.

3.3 Initial public Issue by Banks

3.3.1 The banks (whether public sector or private sector)may freely price their issue of

equity shares or any securities convertible at a later dateinto equity share subject

to approval by the Reserve Bank of India.

3.4 Differential Pricing

3.4.1 Any unlisted company or a listed company making apublic issue of equity shares or securities convertible at alater date into equity shares, may issue such securities toapplicants in the firm allotment category at a pricedifferent from the price at which the net offer to thepublic is made provided that the price at which the securityis being offered to the applicants in firm allotmentcategory is higher than the price at which securities areoffered to public.

Explanation:

The net offer to the public means the offer made to theIndian public and does not include firm allotments orreservations or promoters’ contributions.

3.4.2 A listed company making a composite issue of capitalmay issue securities at differential prices in its publicand rights issue.

3.4.3 In the public issue which is a part of a compositeissue differential pricing as per sub-clause 3.4.1 above isalso permissible.

3.4.4 Justification for the price difference shall be givenin the offer document for sub-clauses 3.4.1 and 3.4.2.

3.5 Price Band

3.5.1 Issuer company can mention a price band of 20% (cap inthe price band should not be more than 20% of the floorprice) in the offer documents filed with the Board andactual price can be determined at a later date before filingof the offer document with ROCs.

3.5.2 If the Board of Directors has been authorised todetermine the offer price within a specified price band suchprice shall be determined by a Resolution to be passed bythe Board of Directors.

3.5.3 24(The Lead Merchant Bankers shall ensure that in caseof the listed companies, a 48 hours notice of the meeting ofthe Board of Directors for passing resolution fordetermination of price is given to the Designated StockExchange.)

3.5.4 The final offer document, shall contain only one priceand one set of financial projections, if applicable.

3.6 Payment of Discounts / Commissions, etc;

3.6.1 No payment, direct or indirect in the nature of adiscount, commission, allowance or otherwise shall be made

either by the issuer company or the promoters in any publicissue, to the persons who have received firm allotment insuch public issue.

3.7 Freedom to determine the denomination of shares forpublic / rights issues and to change the standarddenomination

3.7.1 An eligible company shall be free to make public orrights issue of equity shares in any denomination determinedby it in accordance with sub-section (4) of section 13 ofthe Companies Act, 1956 and in compliance with the norms asspecified by SEBI in circular no.SMDRP/POLICY/CIR-16/99dated June 14, 1999 and other norms as may be specified bySEBI from time to time.

3.7.2 The companies which have already issued shares in thedenomination of Rs.10/-

or Rs.100/- may change the standard denomination of theshares by splitting or

consolidating the existing shares.

3.7.3 The companies proposing to issue shares in anydenomination or changing the

standard denomination in terms of clause 3.7.1 or 3.7.2above shall comply with

the following:

(a) the shares shall not be issued in the denomination ofdecimal of a rupee;

(b) the denomination of the existing shares shall not bealtered to a denomination

of decimal of a rupee;

(c) at any given time there shall be only one denominationfor the shares of the

company;

(d) the companies seeking to change the standarddenomination may do so after

amending the Memorandum and Articles of Association, ifrequired;

(e) the company shall adhere to the disclosure andaccounting norms specified by

SEBI from time to time.

Footnotes:

24 Substituted for “The Lead Merchant Bankers shall ensurethat in case of the listed companies, a 48 hours notice of

the meeting of the Board of Directors for passing resolutionfor determination of price is given to the regional Stock

Exchange.” vide SEBI/CFD/DIL/DIP/Circular No. 11 datedAugust 14, 2003