Double Entry Accounting

59

Double Entry Accounting

-

Upload

monaduniversity -

Category

Documents

-

view

0 -

download

0

Transcript of Double Entry Accounting

Double Entry Accounting

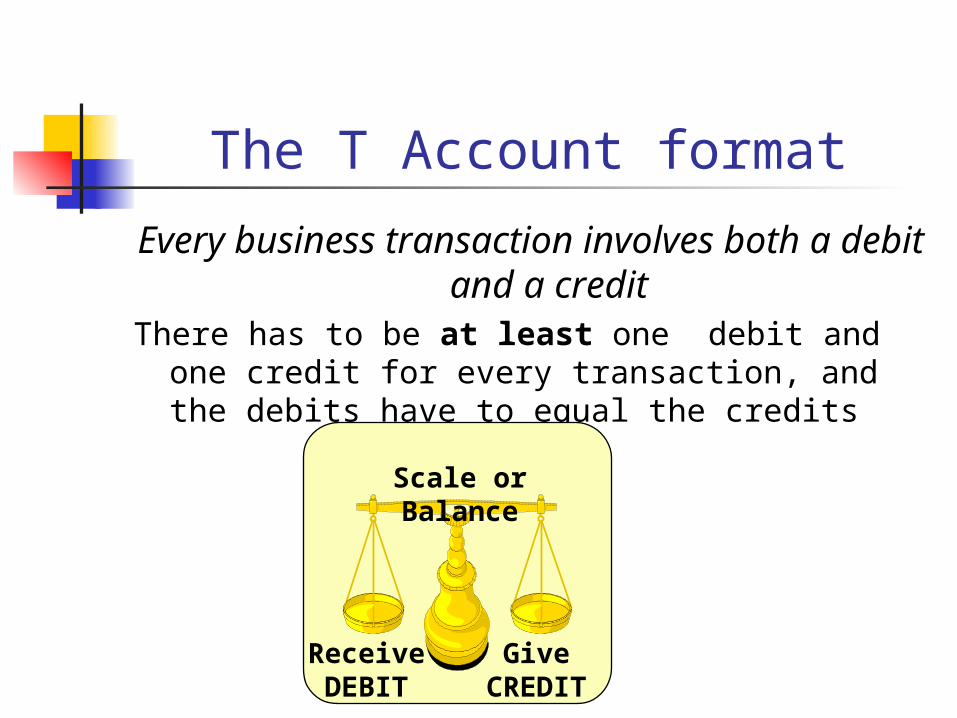

The T Account formatEvery business transaction involves both a debit

and a creditThere has to be at least one debit and one credit for every transaction, and the debits have to equal the credits

Scale or Balance

ReceiveDEBIT

GiveCREDIT

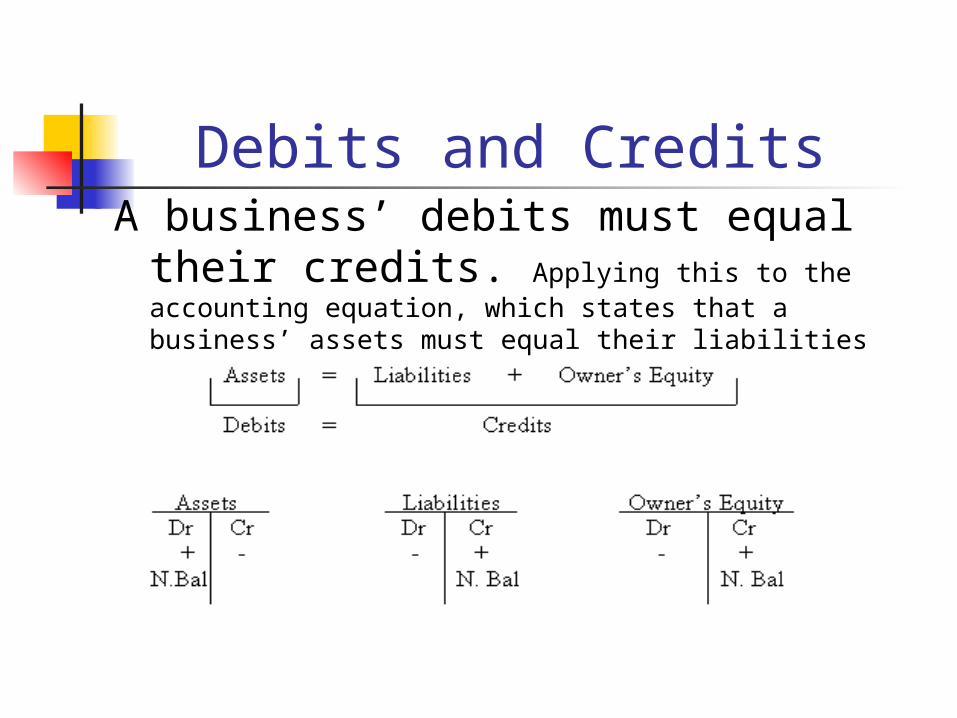

Debits and Credits A business’ debits must equal their credits. Applying this to the accounting equation, which states that a business’ assets must equal their liabilities and owner’s equity, shows how the normal balances for the accounts are determined.

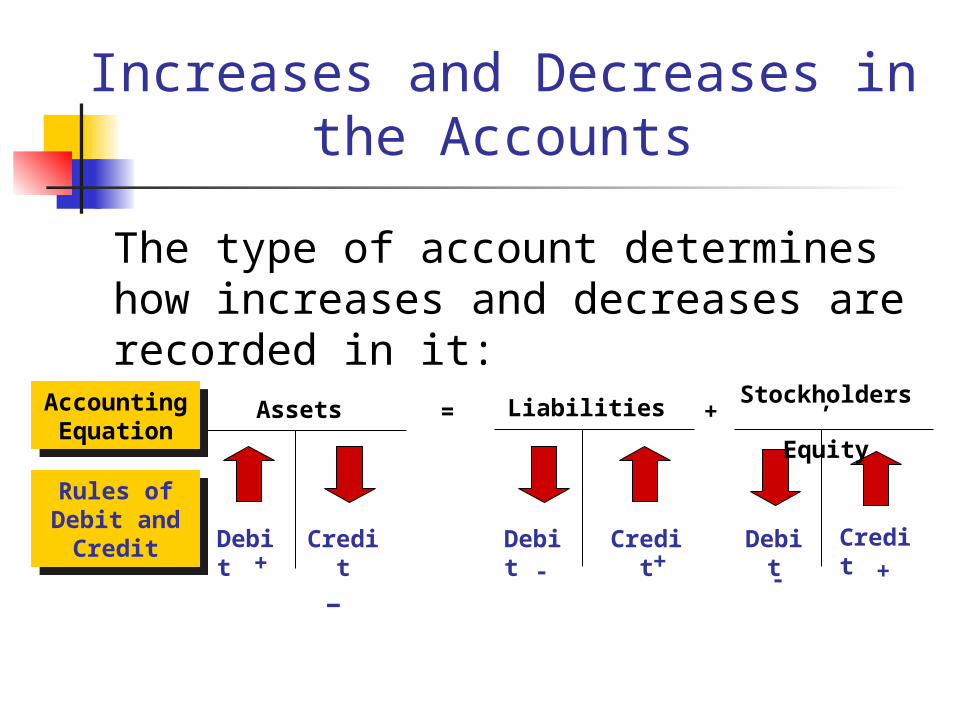

Increases and Decreases in the Accounts

The type of account determines how increases and decreases are recorded in it:

Credit

Debit

Credit +

Debit

Debit

Credit +

- + - -

Assets

Stockholders’

EquityLiabilitiesAccounting

Equation

Rules of Debit and Credit

= +

Debit for increase

+

Credit for Decrease

-

Debit for Decrease

-

Credit for Increase

+

Debit for Decrease

-

Credit for Increase

+

Debit for Increase

+

Credit for Decrease

-

Debit for Increase

+

Credit for Decrease

-

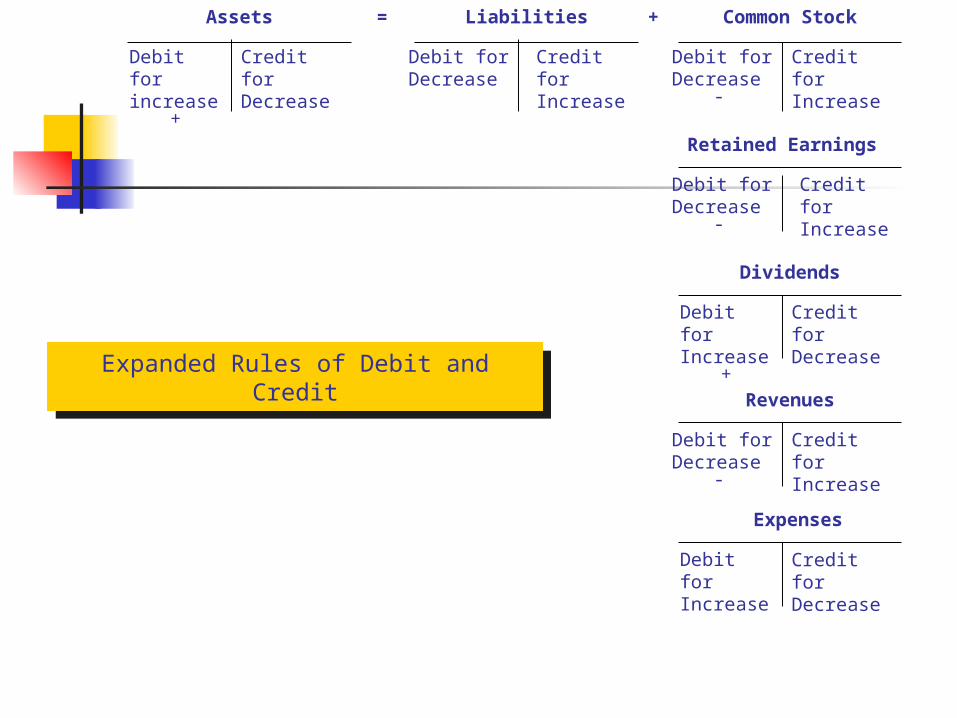

Assets Liabilities Common Stock

Retained Earnings

Dividends

Revenues

Expenses

Debit for Decrease

-

Credit for Increase

+

Debit for Decrease

-

Credit for Increase

+

= +

Expanded Rules of Debit and Credit

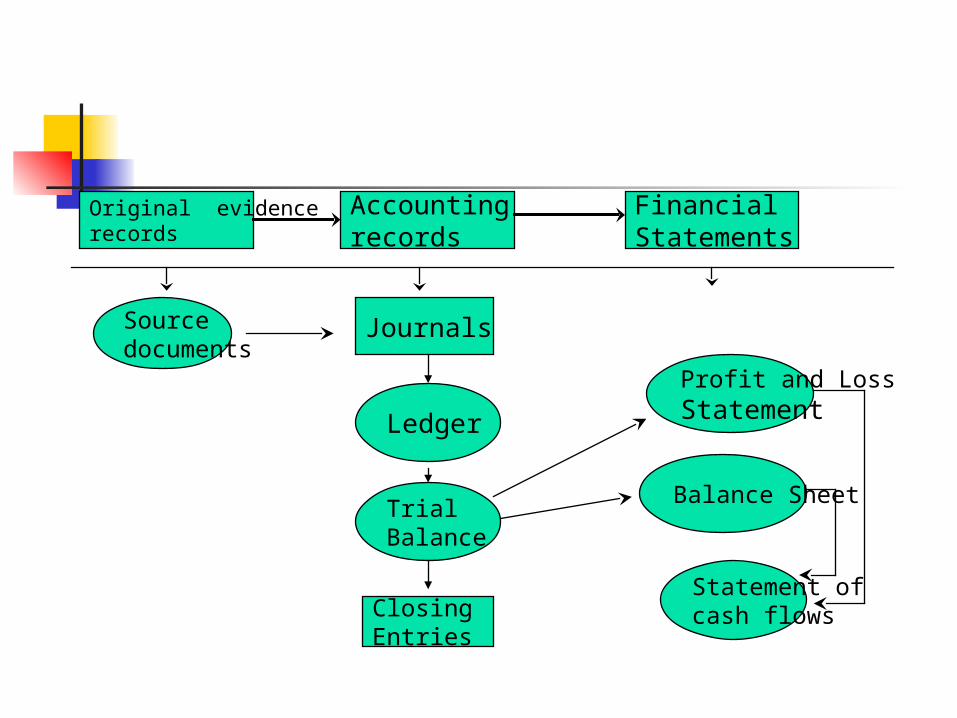

Original evidencerecords

Accountingrecords

FinancialStatements

Sourcedocuments

Journals

Ledger

Trial Balance

Statement of cash flows

Balance Sheet

Profit and LossStatement

ClosingEntries

The Double - Entry Accounting System

The process of entering the transactions of the business into the accounting records commences with the journal entry.

The journal entry is an accounting representation of a business transaction or an economic event.

Accountanese… The journal entry uses debits and credits to record the transaction and once the journal entry has been prepared it is posted to the accounts.

To make the journal entry one enters the debit first, which is always on the left hand side of the entry, and then the credit which is on the right.

Debit (from its Latin origin) means “left.” It is often abbreviated as “dr.”

Credit (from its Latin origin) means “right.” It is often abbreviated as “cr.”

Recording Transactions in the Journal

Steps of the journalizing process Identify the transaction from source documents, such as bank deposit slips, sale receipts, and check stubs

Specify each account affected by the transaction and classify it by type (asset, liability, stockholders’ equity, revenue, or expense)

Recording Transactions in the Journal

Determine whether each account is increased or decreased by the transaction

Determine whether to debit or credit the account to record its increase or decrease

Enter the transaction in the journal, including a brief explanation for the entry

Enter the debit side first and the credit side next

Recording Transactions in the Journal

A complete journal entry includes The date of the transaction The title of the account debited (placed flush left in the Accounts and Explanations column)

The title of the account credited (indented slightly)

The currency amount of the debit (left) The currency amount of the credit (right)

A short explanation of the transaction (not indented)

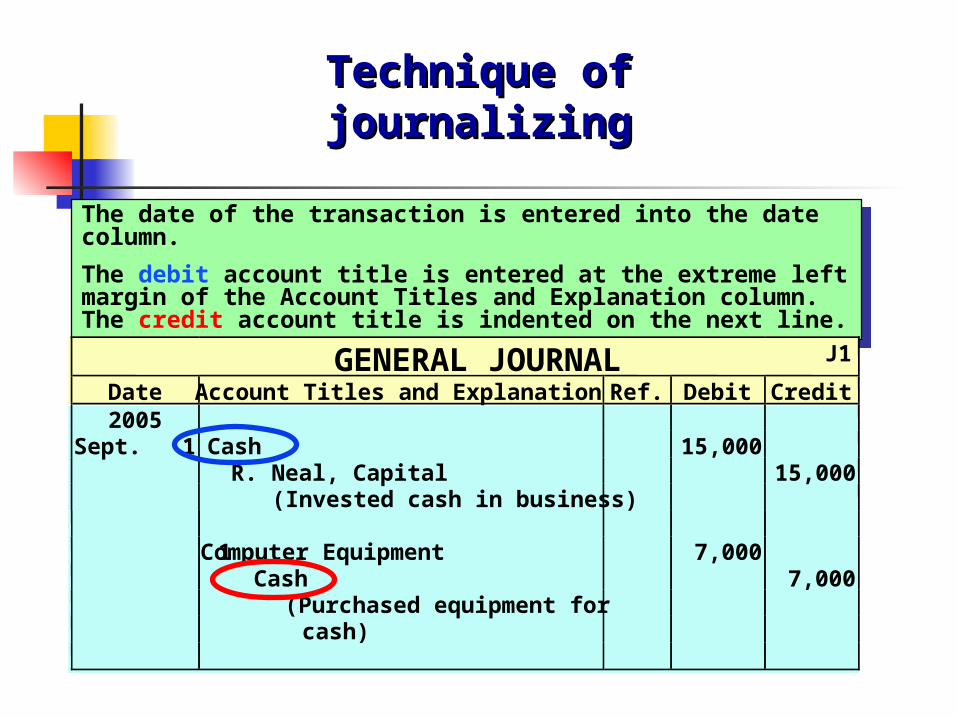

Technique of Technique of journalizingjournalizing

The date of the transaction is entered into the date column.The debit account title is entered at the extreme left margin of the Account Titles and Explanation column. The credit account title is indented on the next line.

GENERAL JOURNAL J1 Date Account Titles and Explanation Ref. Debit Credit 2005 Sept. 1 Cash 15,000 R. Neal, Capital 15,000 (Invested cash in business) 1 Computer Equipment 7,000 Cash 7,000 (Purchased equipment for cash)

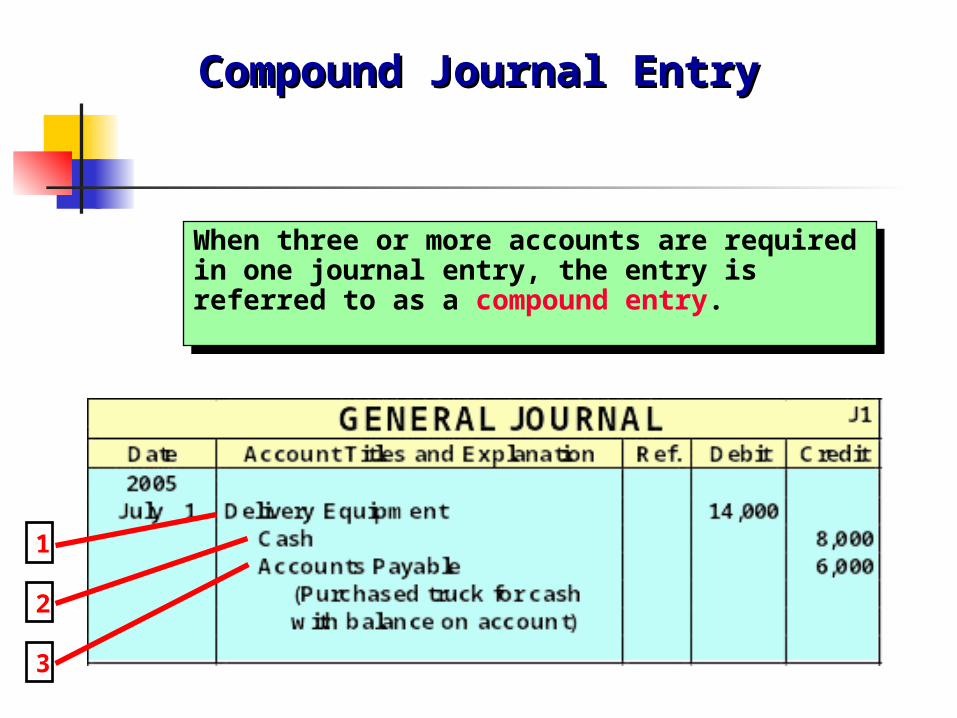

When three or more accounts are required in one journal entry, the entry is referred to as a compound entry.

Compound Journal EntryCompound Journal Entry

2

1

3

Posting to the General Ledger

Generally, in manual bookkeeping, the bookkeeper makes journal entries, then posts the entries to a ledger.

A ledger is a book that has each account on a separate page. All of the amounts that affect that account are entered there, and a running total is kept.

An individual account is called a ledger. A general ledger contains all the assets, liabilities, and owner’s equity accounts.

GENERAL LEDGER

The General Ledger

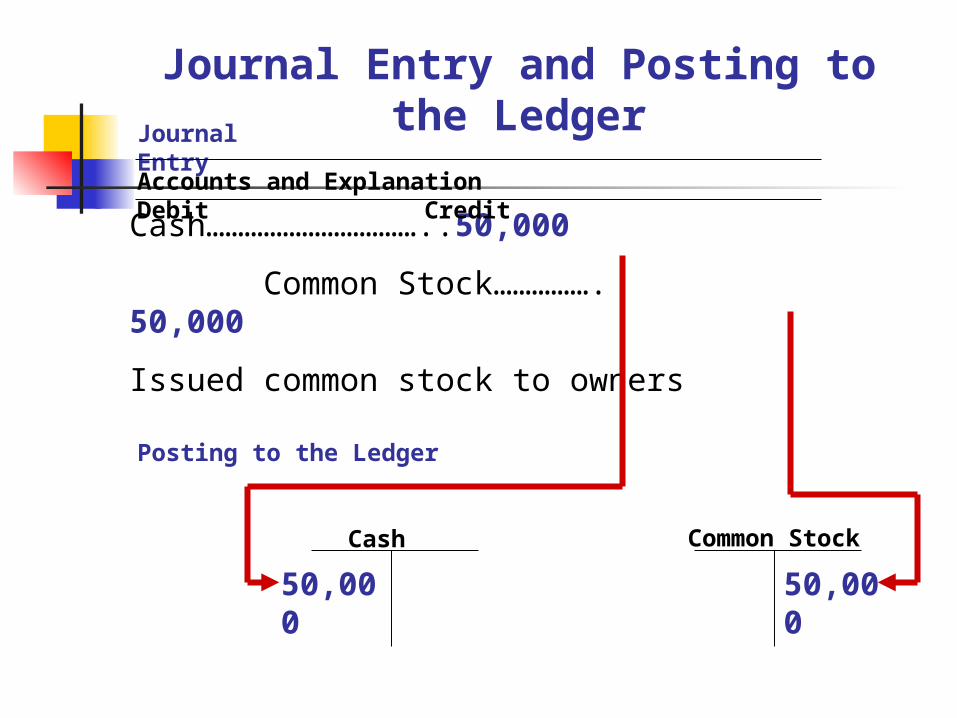

Cash……………………………..50,000 Common Stock……………. 50,000Issued common stock to owners

Common StockCash 50,00

050,000

Posting to the Ledger

Accounts and Explanation Debit Credit

Journal Entry

Journal Entry and Posting to the Ledger

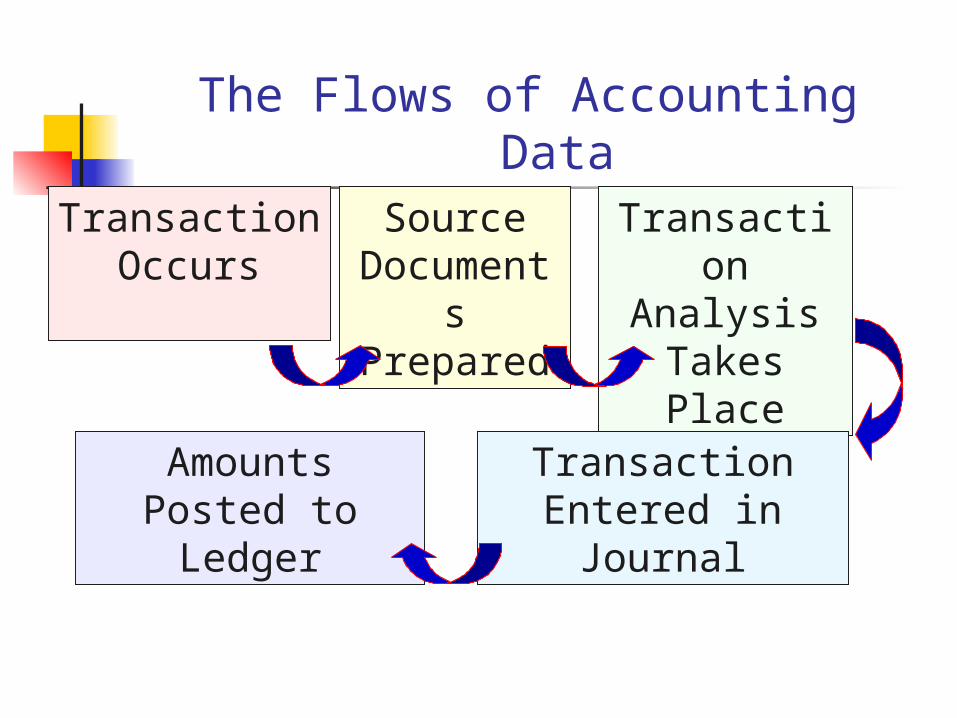

The Flows of Accounting Data

TransactionOccurs

Source Document

s Prepared

Transaction

Analysis Takes Place

Transaction Entered in Journal

Amounts Posted to Ledger

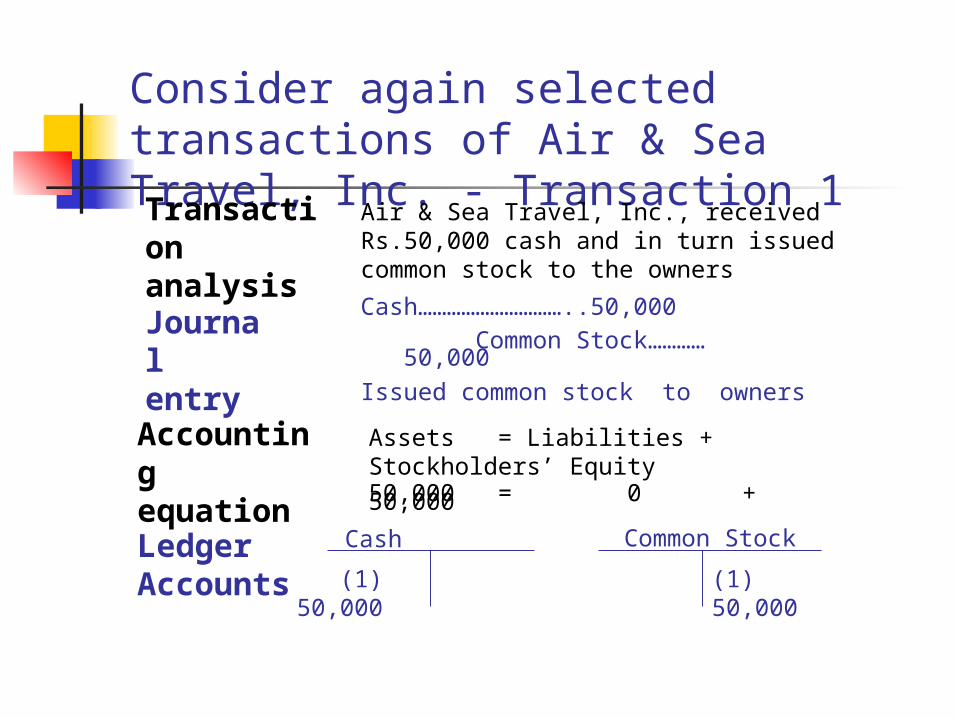

Consider again selected transactions of Air & Sea Travel, Inc. - Transaction 1Air & Sea Travel, Inc., received

Rs.50,000 cash and in turn issued common stock to the owners

Transaction analysisJournal entry

Cash…………………………..50,000 Common Stock………… 50,000Issued common stock to owners

Accounting equation

Assets = Liabilities + Stockholders’ Equity50,000 = 0 + 50,000

Ledger Accounts

Common Stock (1) 50,000

(1) 50,000

Cash

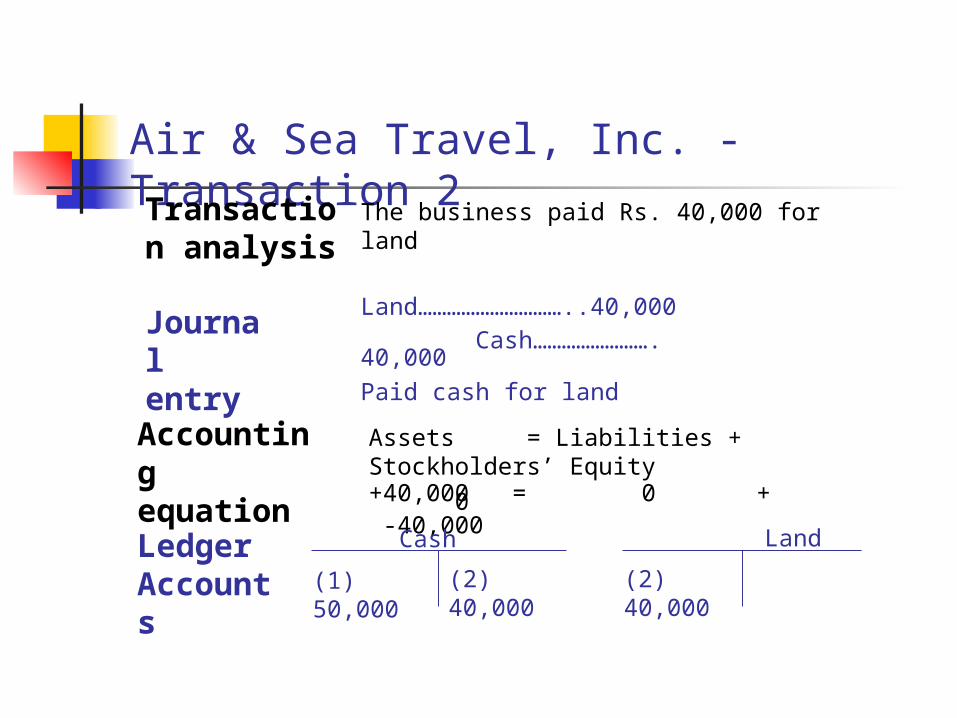

Air & Sea Travel, Inc. - Transaction 2The business paid Rs. 40,000 for

landTransaction analysis

Journal entry

Land…………………………..40,000 Cash……………………. 40,000Paid cash for land

Accounting equation

Assets = Liabilities + Stockholders’ Equity+40,000 = 0 + 0 -40,000Ledger

Accounts

LandCash

(1) 50,000

(2) 40,000

(2) 40,000

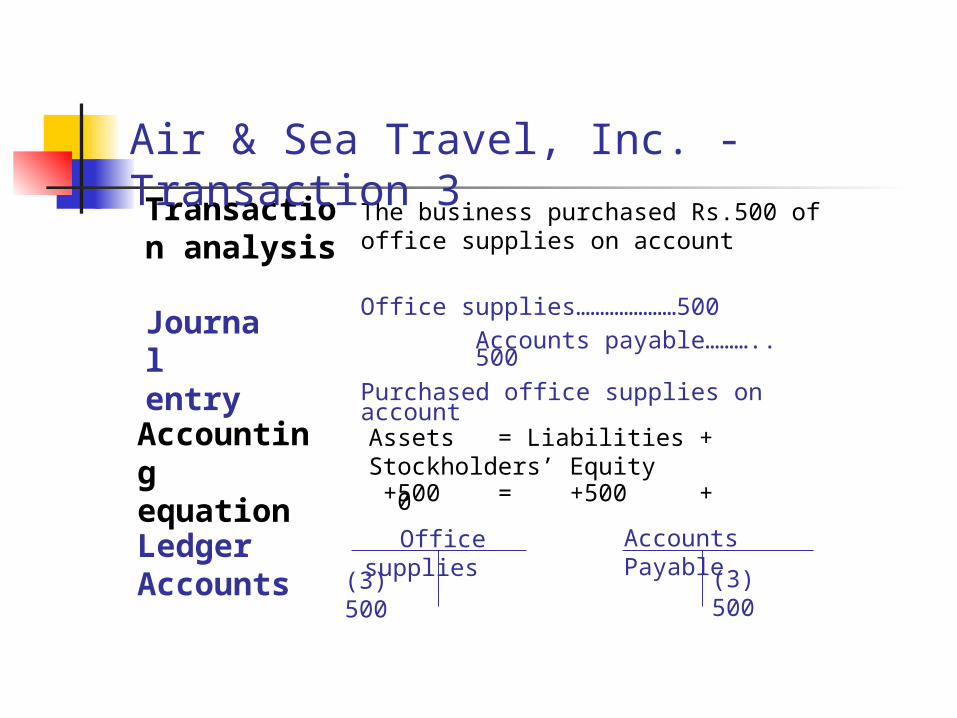

The business purchased Rs.500 of office supplies on account

Transaction analysis

Journal entry

Office supplies…………………500 Accounts payable……….. 500Purchased office supplies on accountAccountin

g equation

Assets = Liabilities + Stockholders’ Equity +500 = +500 + 0

Ledger Accounts

Accounts Payable

Office supplies (3)

500

(3) 500

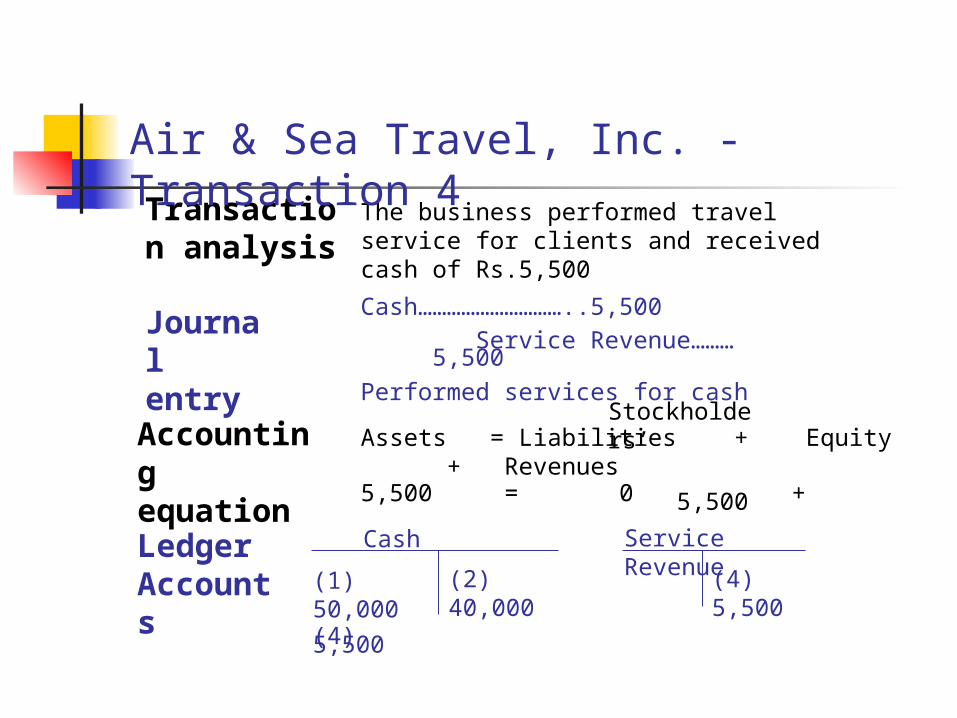

Air & Sea Travel, Inc. - Transaction 3

The business performed travel service for clients and received cash of Rs.5,500

Transaction analysis

Journal entry

Cash…………………………..5,500 Service Revenue……… 5,500Performed services for cash

Accounting equation

Assets = Liabilities + Equity + Revenues5,500 = 0 + 5,500

Ledger Accounts

Service Revenue

Cash (1)

50,000(4) 5,500

(4) 5,500

(2) 40,000

Stockholders’

Air & Sea Travel, Inc. - Transaction 4

Accounts After Posting

(1) 50,000(4) 5,500(9) 1,000(10) 22,000Bal. 33,300

(2) 40,000(6) 2,700(7) 400(11) 2,100

Cash

Each account has a balance, denoted as Bal.

This amount is the difference between the account’s total debits and total credits

NetSolutionsNetSolutionsA Sole ProprietorshipA Sole Proprietorship

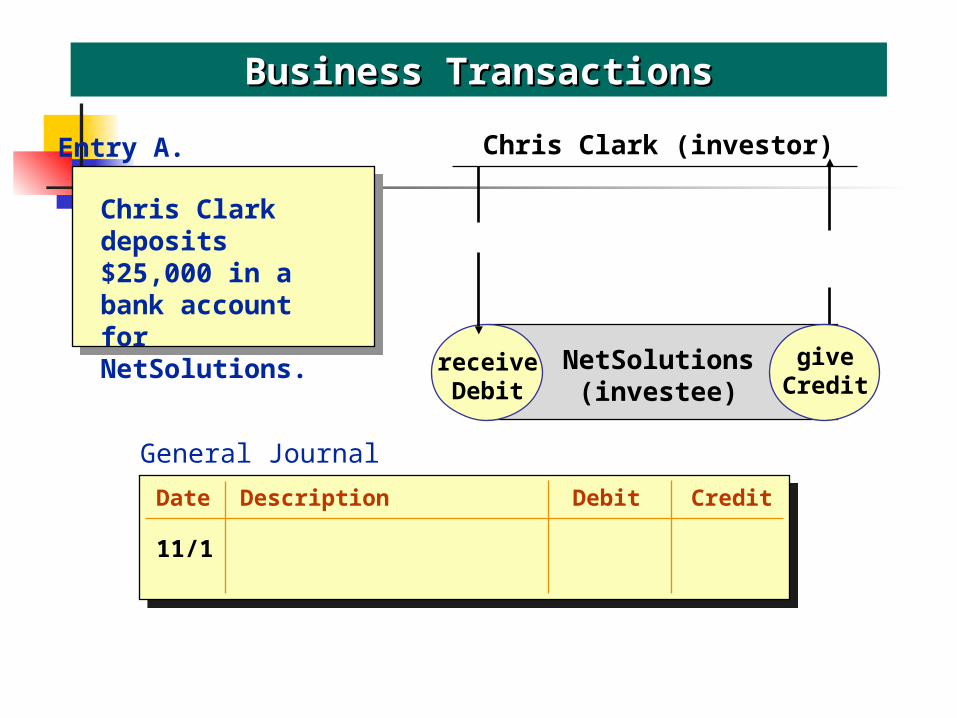

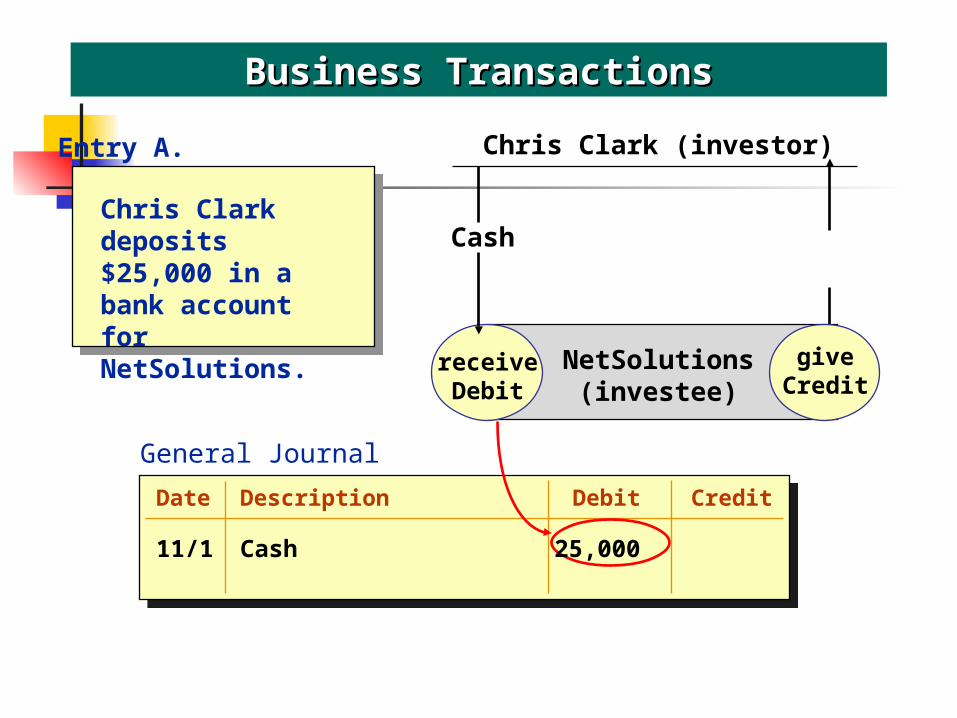

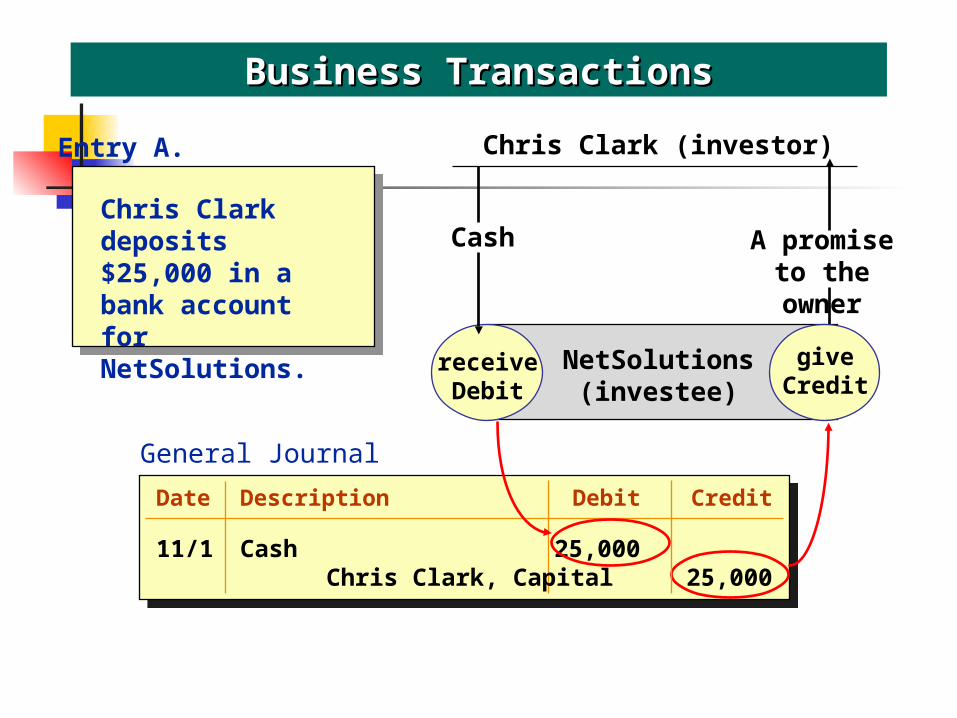

“ On November 1, 2012, I started a sole proprietorship called NetSolutions. I plan to use my knowledge of microcomputers and offer computer consulting services for a fee. The following double-entry transactions show how amounts received (debits) always equal amounts given (credits).”

Chris Clark, Owner

Chris Clark deposits $25,000 in a bank account for NetSolutions.

Business TransactionsBusiness Transactions

General Journal

receiveDebit

giveCredit

NetSolutions(investee)

Chris Clark (investor)

giveCredit

Entry A.

Date Description Debit Credit

11/1

Chris Clark deposits $25,000 in a bank account for NetSolutions.

Business TransactionsBusiness Transactions

General Journal

receiveDebit

giveCredit

NetSolutions(investee)

Cash

Chris Clark (investor)

giveCredit

Entry A.

Date Description Debit Credit

11/1 Cash 25,000

Chris Clark deposits $25,000 in a bank account for NetSolutions.

Business TransactionsBusiness Transactions

General JournalDate Description Debit Credit

11/1 Cash 25,000 Chris Clark, Capital 25,000

receiveDebit

giveCredit

NetSolutions(investee)

Cash A promiseto the owner

Chris Clark (investor)

giveCredit

Entry A.

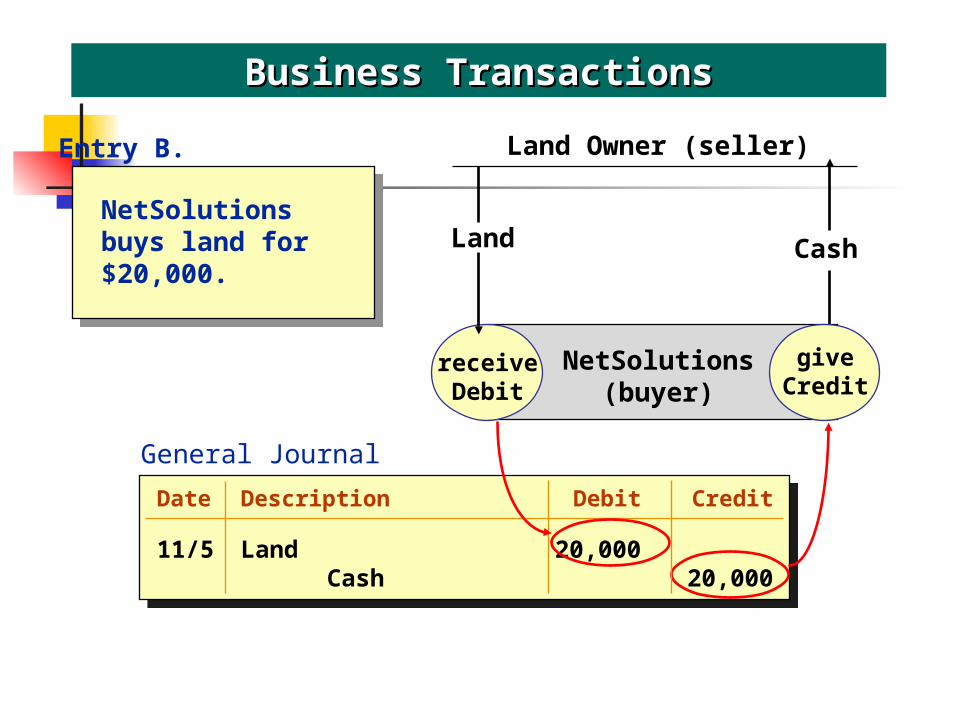

NetSolutions buys land for $20,000.

Business TransactionsBusiness Transactions

receiveDebit

giveCredit

NetSolutions(buyer)

Land Owner (seller)

giveCredit

Entry B.

General Journal

Date Description Debit Credit

11/5

NetSolutions buys land for $20,000.

Business TransactionsBusiness Transactions

receiveDebit

giveCredit

NetSolutions(buyer)

Land

Land Owner (seller)

giveCredit

Entry B.

General Journal

Date Description Debit Credit

11/5 Land 20,000

NetSolutions buys land for $20,000.

Business TransactionsBusiness Transactions

receiveDebit

giveCredit

NetSolutions(buyer)

Land Cash

Land Owner (seller)

giveCredit

Entry B.

General JournalDate Description Debit Credit

11/5 Land 20,000 Cash 20,000

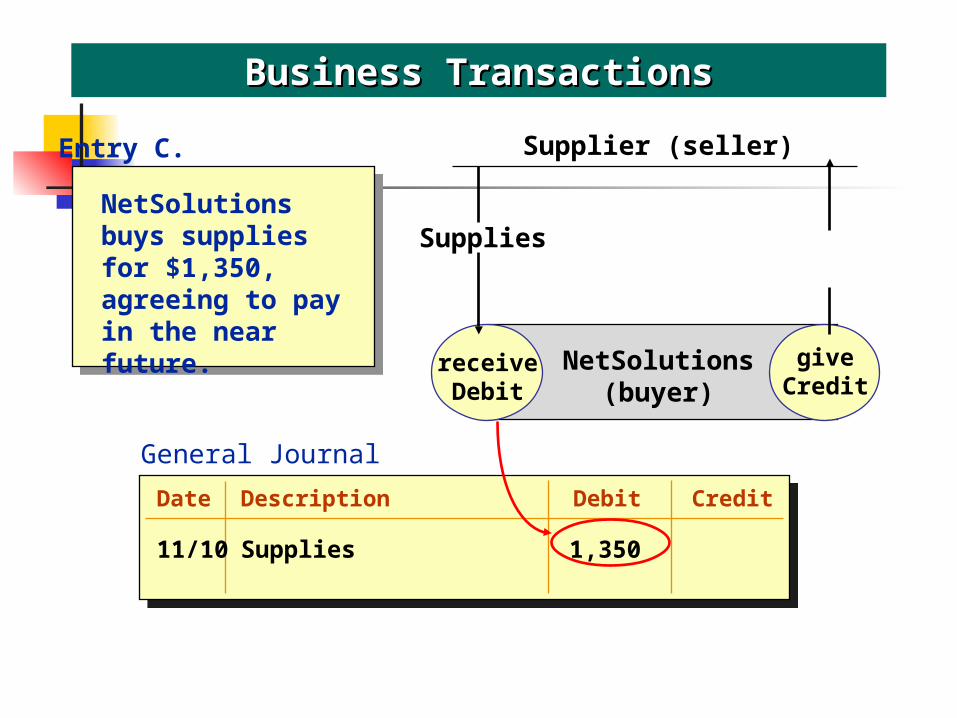

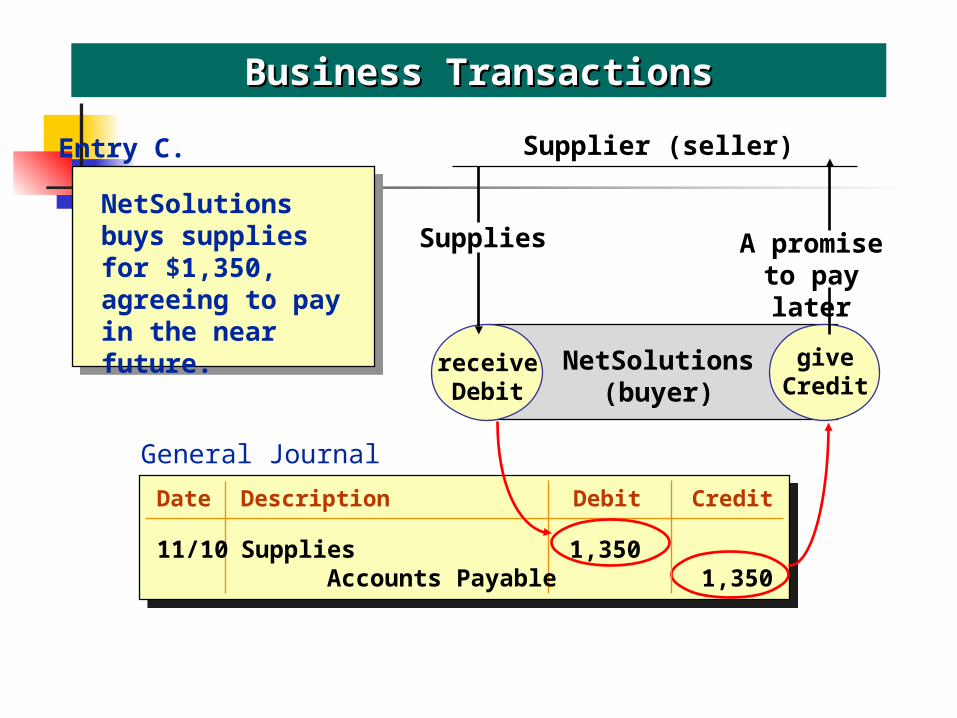

NetSolutions buys supplies for $1,350, agreeing to pay in the near future.

Business TransactionsBusiness Transactions

receiveDebit

giveCredit

NetSolutions(buyer)

Supplier (seller)

giveCredit

Entry C.

General Journal

Date Description Debit Credit

11/10

NetSolutions buys supplies for $1,350, agreeing to pay in the near future.

Business TransactionsBusiness Transactions

receiveDebit

giveCredit

NetSolutions(buyer)

Supplies

Supplier (seller)

giveCredit

Entry C.

General Journal

Date Description Debit Credit

11/10 Supplies 1,350

NetSolutions buys supplies for $1,350, agreeing to pay in the near future.

Business TransactionsBusiness Transactions

receiveDebit

giveCredit

NetSolutions(buyer)

Supplies

Supplier (seller)

giveCredit

Entry C.

A promiseto pay later

General JournalDate Description Debit Credit

11/10 Supplies 1,350 Accounts Payable 1,350

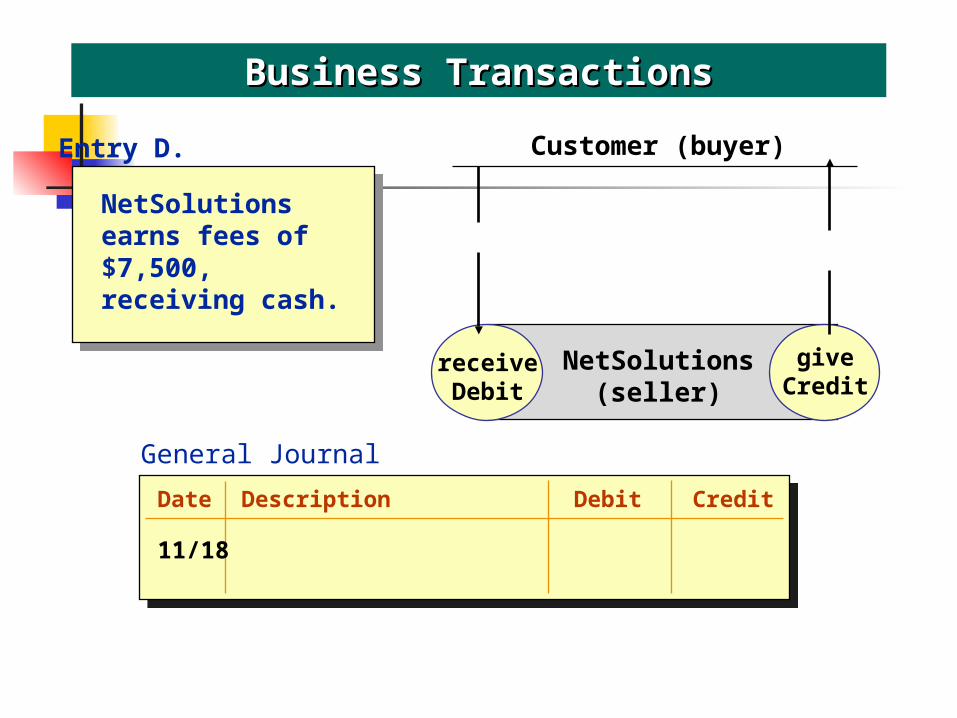

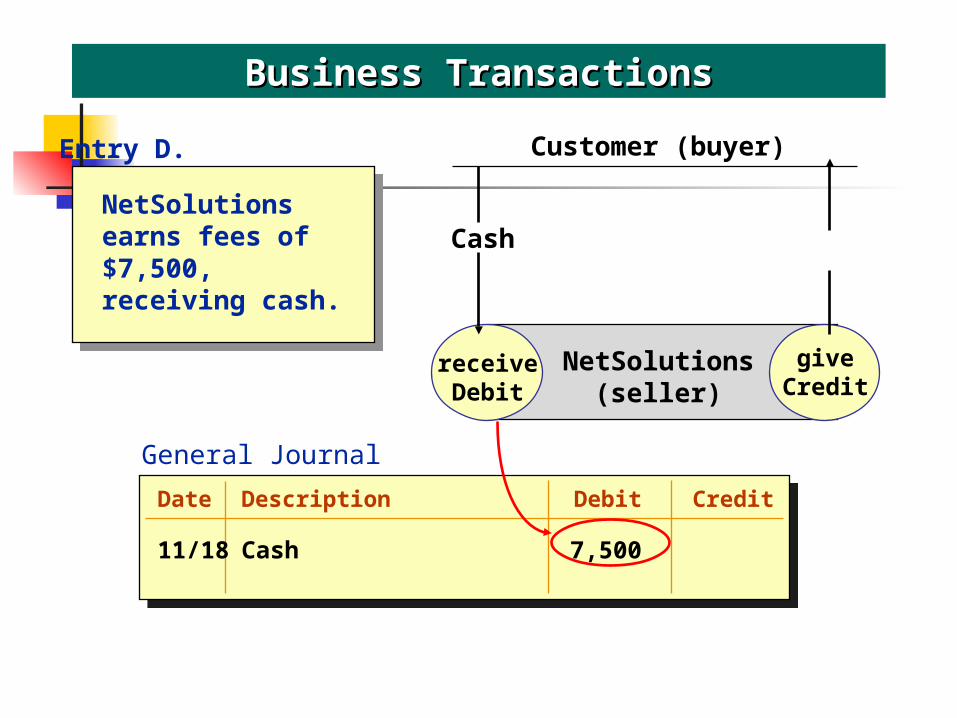

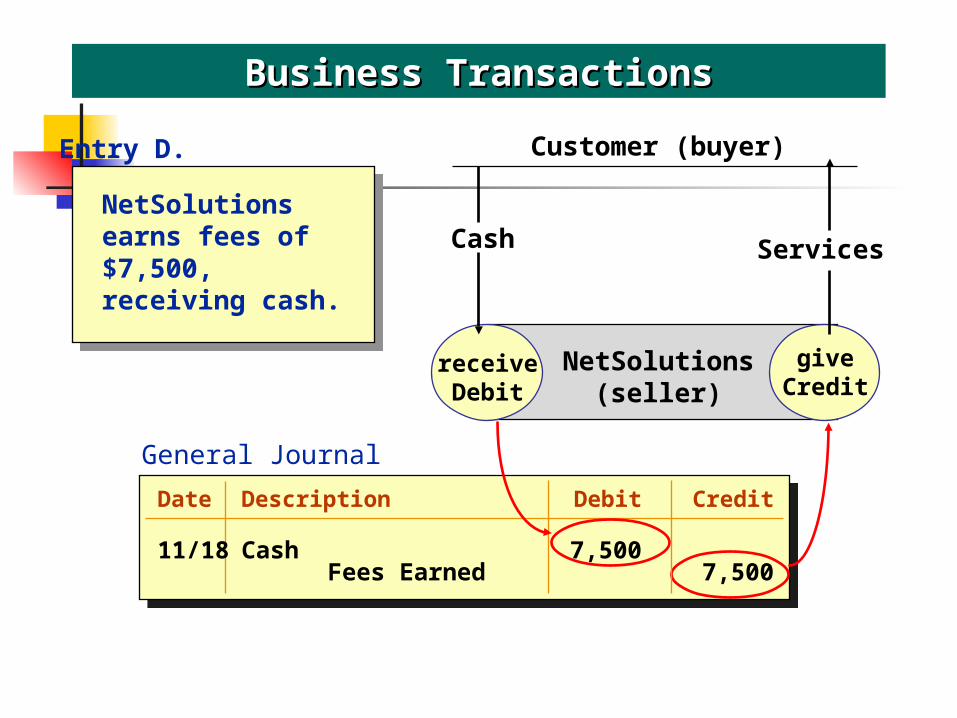

NetSolutions earns fees of $7,500, receiving cash.

Business TransactionsBusiness Transactions

receiveDebit

giveCredit

NetSolutions(seller)

Customer (buyer)

giveCredit

Entry D.

General Journal

Date Description Debit Credit

11/18

NetSolutions earns fees of $7,500, receiving cash.

Business TransactionsBusiness Transactions

receiveDebit

giveCredit

NetSolutions(seller)

Cash

Customer (buyer)

giveCredit

Entry D.

General Journal

Date Description Debit Credit

11/18 Cash 7,500

NetSolutions earns fees of $7,500, receiving cash.

Business TransactionsBusiness Transactions

receiveDebit

giveCredit

NetSolutions(seller)

Cash

Customer (buyer)

giveCredit

Entry D.

Services

General JournalDate Description Debit Credit

11/18 Cash 7,500 Fees Earned 7,500

Date Description Debit Credit

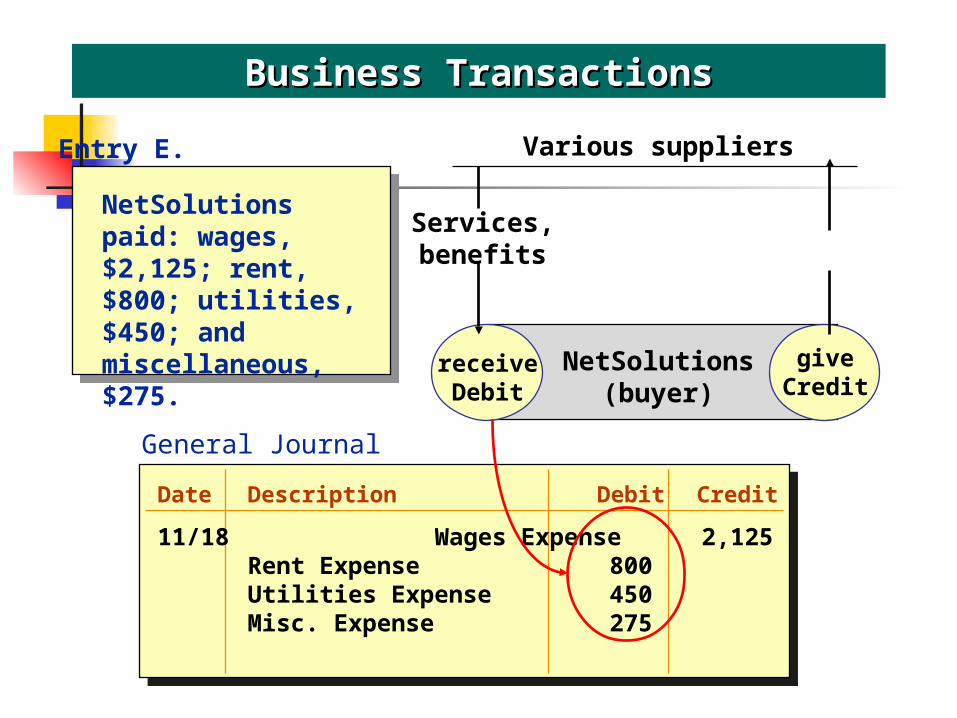

NetSolutions paid: wages, $2,125; rent, $800; utilities, $450; and miscellaneous, $275.

Business TransactionsBusiness Transactions

General Journal

receiveDebit

giveCredit

NetSolutions(buyer)

Various suppliers

giveCredit

Entry E.

Date Description Debit Credit11/18 Wages Expense 2,125

Rent Expense 800Utilities Expense 450Misc. Expense 275

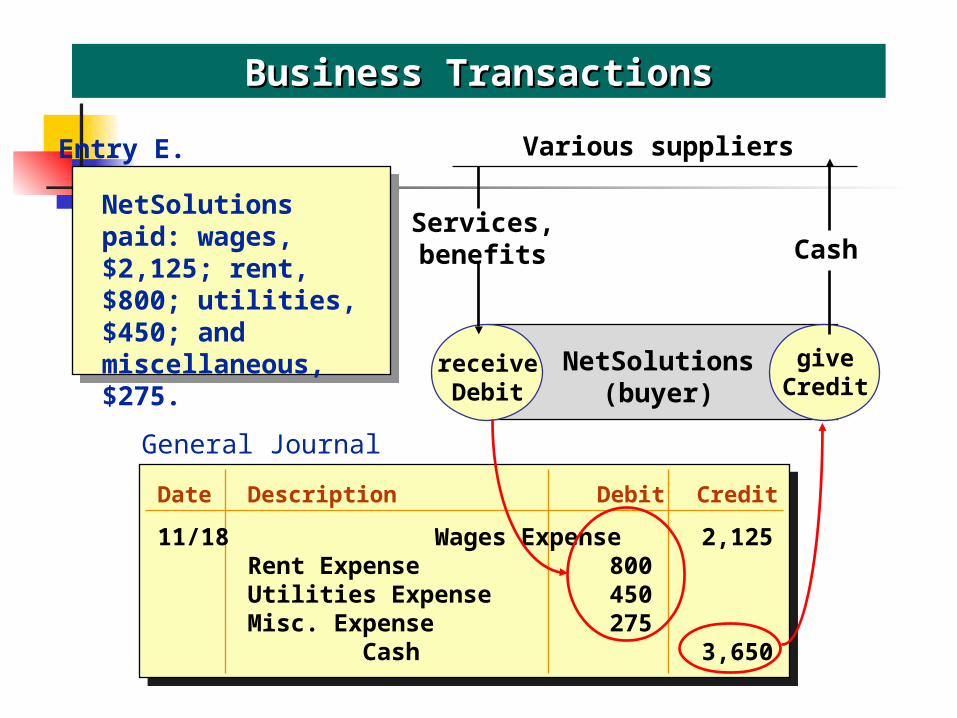

NetSolutions paid: wages, $2,125; rent, $800; utilities, $450; and miscellaneous, $275.

Business TransactionsBusiness Transactions

General Journal

receiveDebit

giveCredit

NetSolutions(buyer)

Services,benefits

Various suppliers

giveCredit

Entry E.

Date Description Debit Credit11/18 Wages Expense 2,125

Rent Expense 800Utilities Expense 450Misc. Expense 275 Cash 3,650

NetSolutions paid: wages, $2,125; rent, $800; utilities, $450; and miscellaneous, $275.

Business TransactionsBusiness Transactions

General Journal

receiveDebit

giveCredit

NetSolutions(buyer)

Services,benefits

Various suppliers

giveCredit

Entry E.

Cash

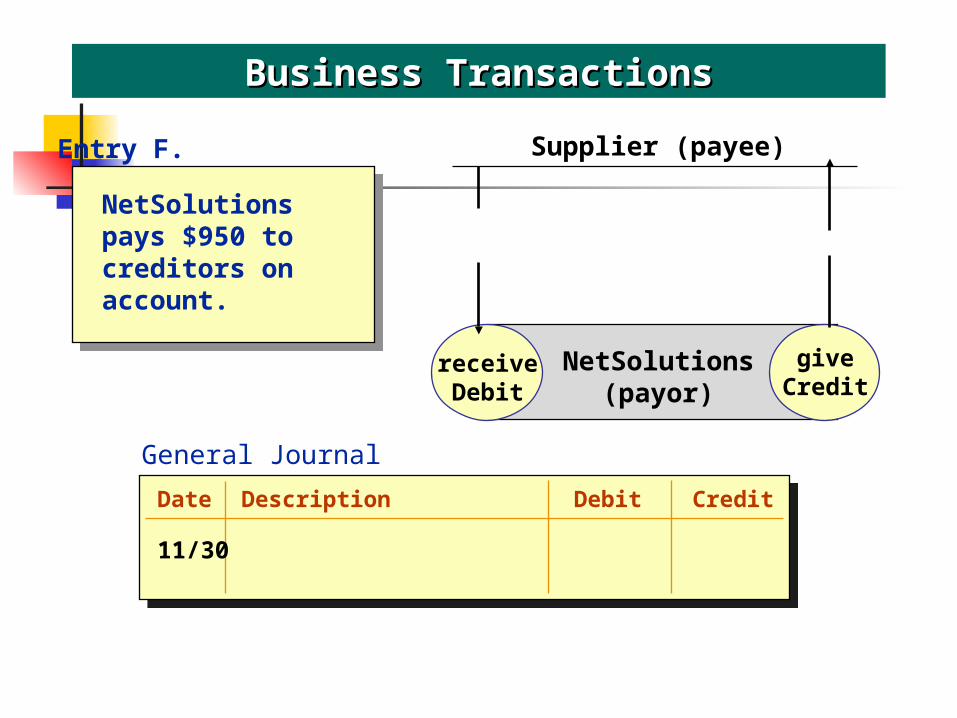

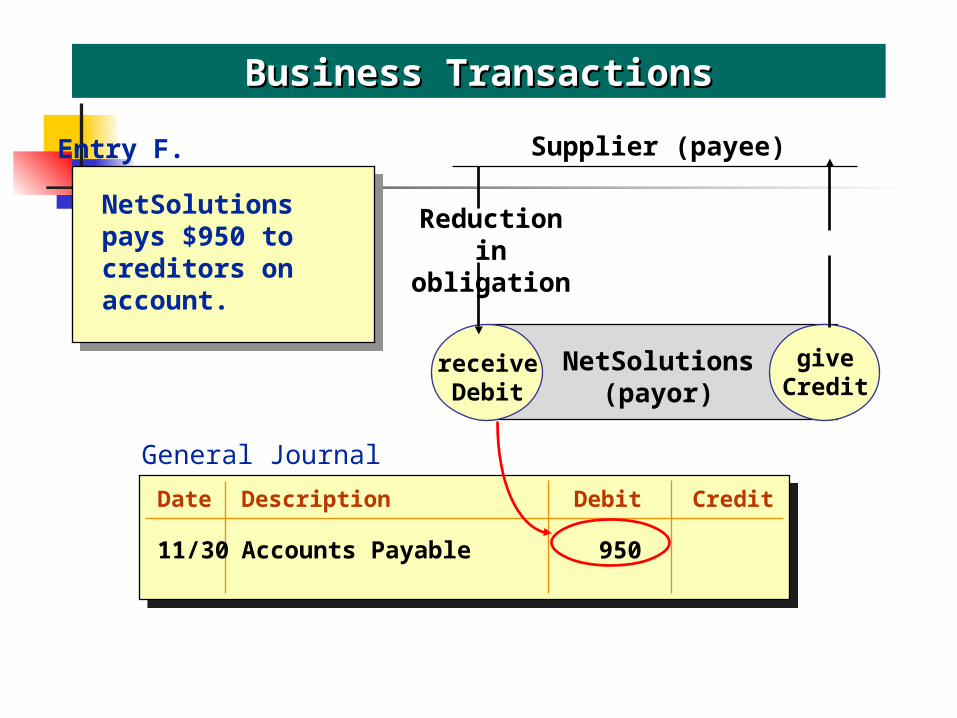

NetSolutions pays $950 to creditors on account.

Business TransactionsBusiness Transactions

receiveDebit

giveCredit

NetSolutions(payor)

Supplier (payee)

giveCredit

Entry F.

General Journal

Date Description Debit Credit

11/30

NetSolutions pays $950 to creditors on account.

Business TransactionsBusiness Transactions

receiveDebit

giveCredit

NetSolutions(payor)

Reduction in

obligation

Supplier (payee)

giveCredit

Entry F.

General Journal

Date Description Debit Credit

11/30 Accounts Payable 950

NetSolutions pays $950 to creditors on account.

Business TransactionsBusiness Transactions

receiveDebit

giveCredit

NetSolutions(payor)

Reduction in

obligation

Supplier (payee)

giveCredit

Entry F.

Cash

General JournalDate Description Debit Credit

11/30 Accounts Payable 950 Cash 950

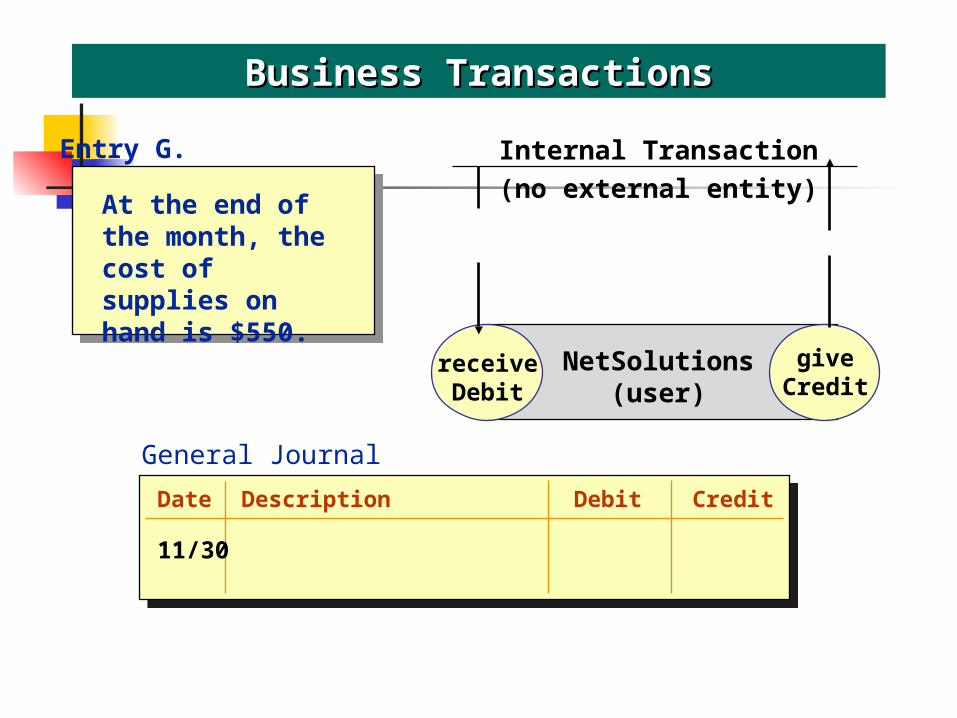

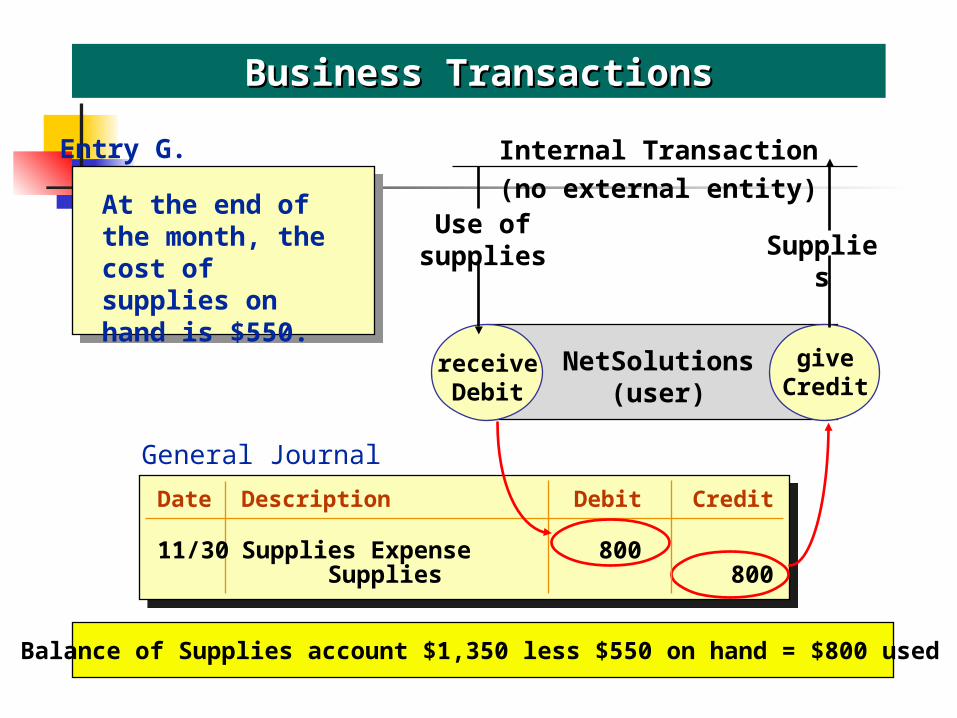

At the end of the month, the cost of supplies on hand is $550.

Business TransactionsBusiness Transactions

receiveDebit

giveCredit

NetSolutions(user)

Internal Transaction(no external entity)

giveCredit

Entry G.

General Journal

Date Description Debit Credit

11/30

At the end of the month, the cost of supplies on hand is $550.

Business TransactionsBusiness Transactions

receiveDebit

giveCredit

NetSolutions(user)

Use of supplies

Internal Transaction(no external entity)

giveCredit

Entry G.

General Journal

Balance of Supplies account $1,350 less $550 on hand = $800 used

Date Description Debit Credit

11/30 Supplies Expense 800

At the end of the month, the cost of supplies on hand is $550.

Business TransactionsBusiness Transactions

receiveDebit

giveCredit

NetSolutions(user)

Use of supplies

Internal Transaction(no external entity)

giveCredit

Entry G.

Supplies

General JournalDate Description Debit Credit

11/30 Supplies Expense 800 Supplies 800

Balance of Supplies account $1,350 less $550 on hand = $800 used

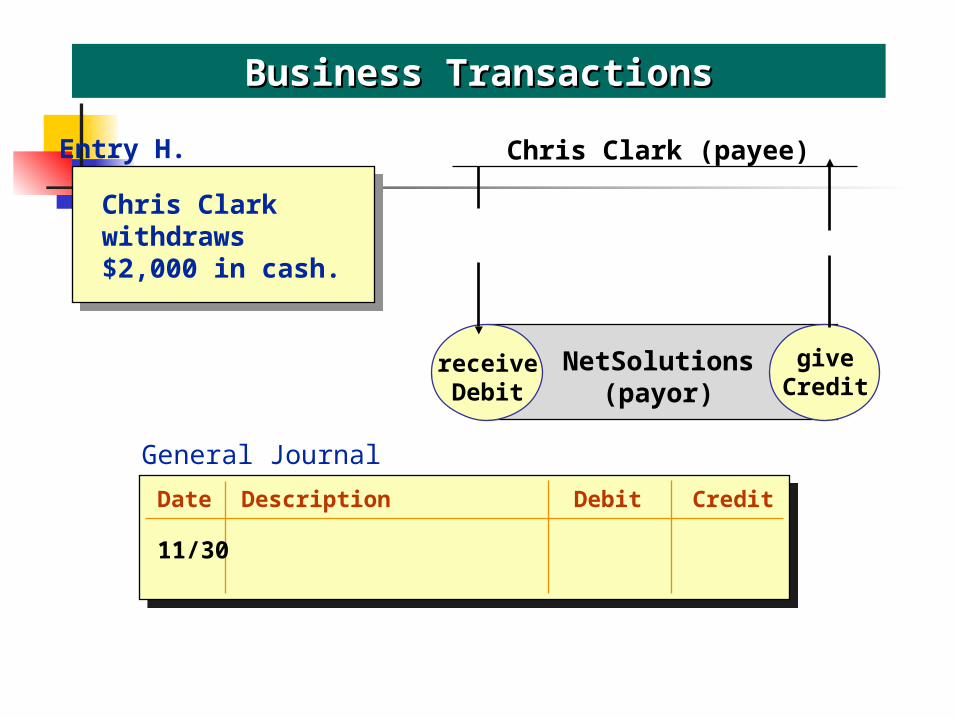

Chris Clark withdraws $2,000 in cash.

Business TransactionsBusiness Transactions

receiveDebit

giveCredit

NetSolutions(payor)

Chris Clark (payee)

giveCredit

Entry H.

General Journal

Date Description Debit Credit

11/30

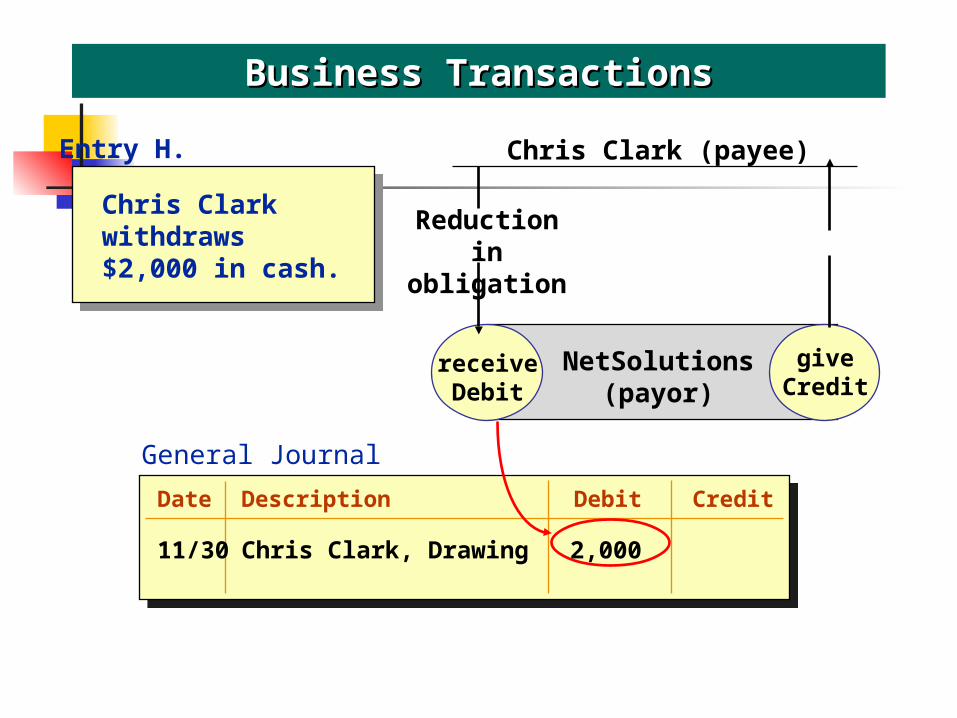

Chris Clark withdraws $2,000 in cash.

Business TransactionsBusiness Transactions

receiveDebit

giveCredit

NetSolutions(payor)

Reduction in

obligation

Chris Clark (payee)

giveCredit

Entry H.

General Journal

Date Description Debit Credit

11/30 Chris Clark, Drawing 2,000

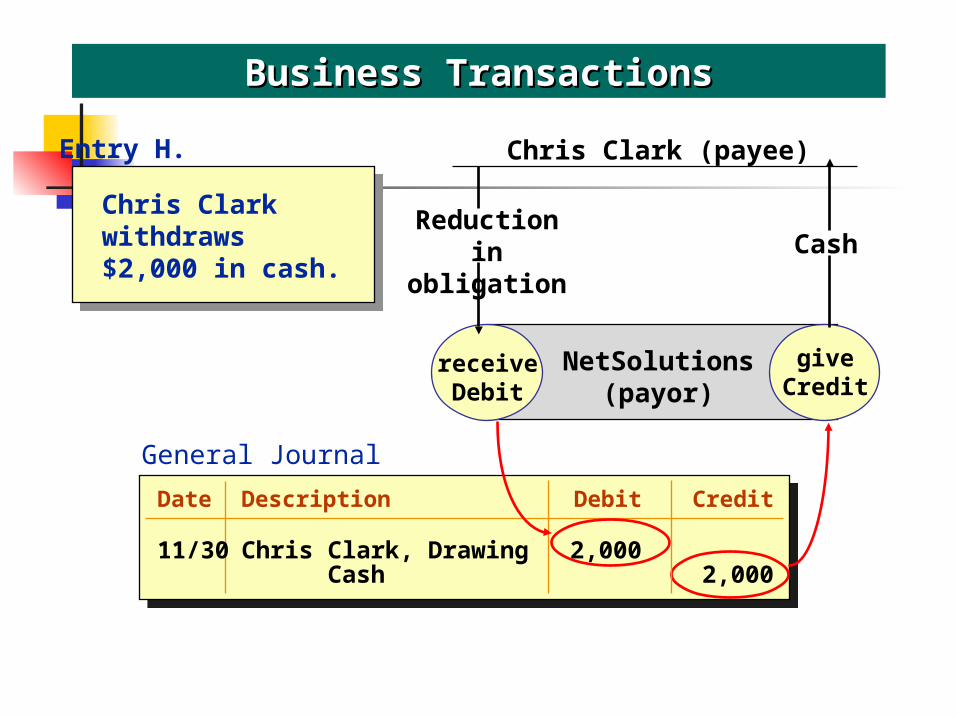

Chris Clark withdraws $2,000 in cash.

Business TransactionsBusiness Transactions

receiveDebit

giveCredit

NetSolutions(payor)

Reduction in

obligation

Chris Clark (payee)

giveCredit

Entry H.

Cash

General JournalDate Description Debit Credit

11/30 Chris Clark, Drawing 2,000 Cash 2,000

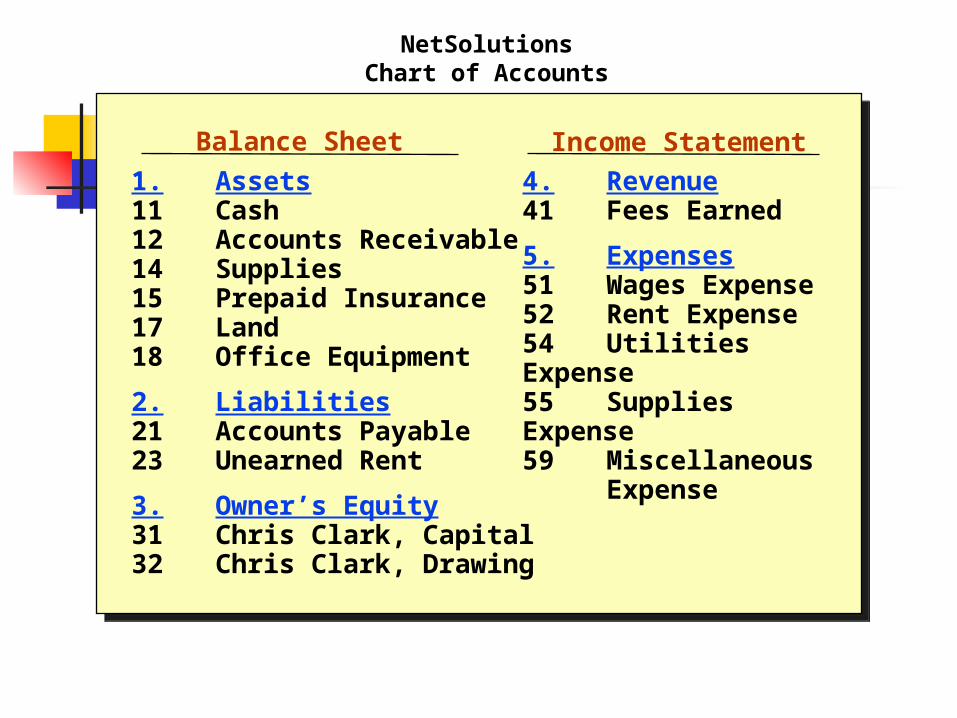

NetSolutionsChart of Accounts

Balance Sheet Income Statement1. Assets11 Cash12 Accounts Receivable14 Supplies15 Prepaid Insurance17 Land18 Office Equipment2. Liabilities21 Accounts Payable23 Unearned Rent3. Owner’s Equity31 Chris Clark, Capital32 Chris Clark, Drawing

4. Revenue41 Fees Earned5. Expenses51 Wages Expense52 Rent Expense54 Utilities Expense55 Supplies Expense59 Miscellaneous

Expense

1. Transactions are analyzed and recorded in journal.

DocumentsJournal

Journal, Ledger, Trial BalanceJournal, Ledger, Trial Balance

1. Transactions are analyzed and recorded in journal.

DocumentsJournal

2. Transactions are posted from journal to ledger.

Journal Ledger

Journal, Ledger, Trial BalanceJournal, Ledger, Trial Balance

1. Transactions are analyzed and recorded in journal.

DocumentsJournal

2. Transactions are posted from journal to ledger.

Journal Ledger

3. Trial balance is prepared.

Journal, Ledger, Trial BalanceJournal, Ledger, Trial Balance

Trial Balance

The Trial Balance At any time during the month, but usually at the end of the month (or accounting period) one can prepare a trial balance. A trial balance is just a list of accounts in chart-of-accounts order with their balances-to-date

On a trial balance, there are two columns of numbers, debits and credits. all of the debits go in the left-hand column (debit columns) and credits in the credit column.

They have to equal each other.

The Trial BalanceThe Trial Balance

• The Trial Balance is a list of accounts and their balances at a given time.

• The primary purpose of a trial balance is to prove debits = credits after posting.

• If debits and credits do not agree, the trial balance can be used to uncover errors in journalizing and posting.

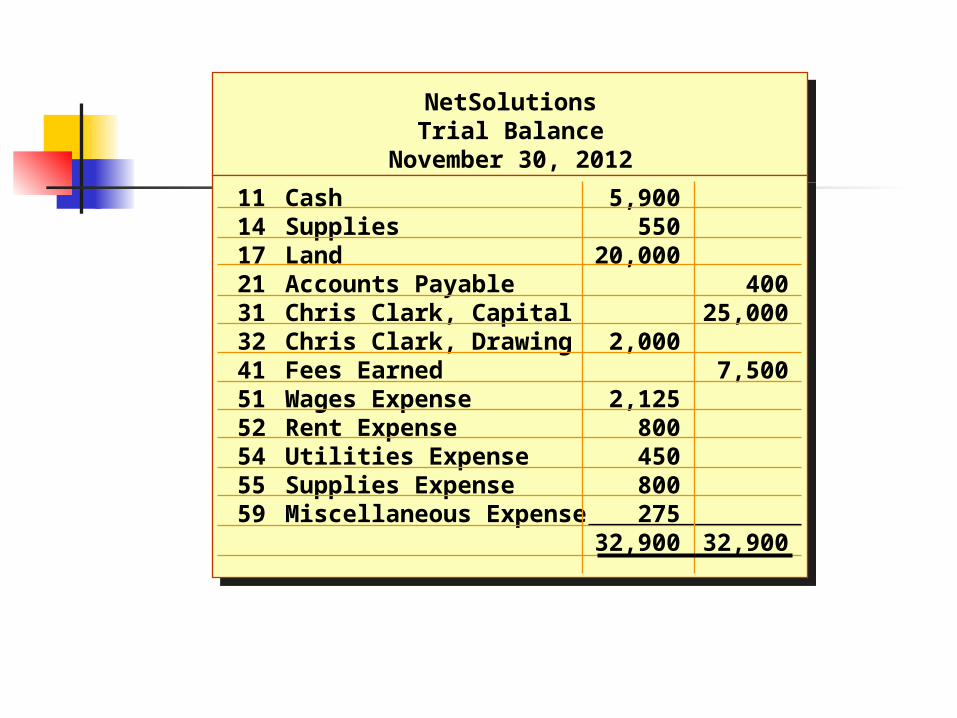

NetSolutionsTrial Balance

November 30, 201211 Cash 5,90014 Supplies 55017 Land 20,00021 Accounts Payable 40031 Chris Clark, Capital 25,00032 Chris Clark, Drawing 2,00041 Fees Earned 7,50051 Wages Expense 2,12552 Rent Expense 80054 Utilities Expense 45055 Supplies Expense 80059 Miscellaneous Expense 275

32,900 32,900

NetSolutionsTrial Balance

November 30, 201211 Cash 5,90014 Supplies 55017 Land 20,00021 Accounts Payable 40031 Chris Clark, Capital 25,00032 Chris Clark, Drawing 2,00041 Fees Earned 7,50051 Wages Expense 2,12552 Rent Expense 80054 Utilities Expense 45055 Supplies Expense 80059 Miscellaneous Expense 275

32,900 32,900

BalanceSheet

IncomeStatement

NetSolutionsTrial Balance

November 30, 201211 Cash 5,90014 Supplies 55017 Land 20,00021 Accounts Payable 40031 Chris Clark, Capital 25,00032 Chris Clark, Drawing 2,00041 Fees Earned 7,50051 Wages Expense 2,12552 Rent Expense 80054 Utilities Expense 45055 Supplies Expense 80059 Miscellaneous Expense 275

32,900 32,900

Correcting Accounting Errors

If total debits and total credits on the trial balance are not equal, then accounting errors exist

Reason(s) behind many of the out-of-balance conditions can be detected by computing the difference between debits and credits on the trial balance and performing one or more of the following actions . . .

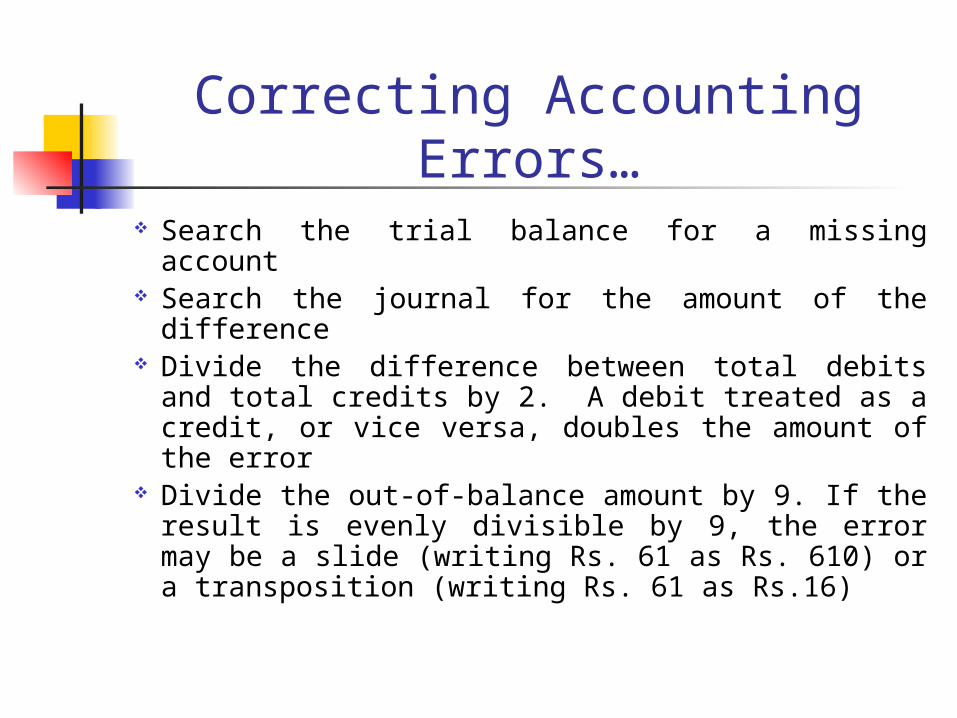

Search the trial balance for a missing account

Search the journal for the amount of the difference

Divide the difference between total debits and total credits by 2. A debit treated as a credit, or vice versa, doubles the amount of the error

Divide the out-of-balance amount by 9. If the result is evenly divisible by 9, the error may be a slide (writing Rs. 61 as Rs. 610) or a transposition (writing Rs. 61 as Rs.16)

Correcting Accounting Errors…

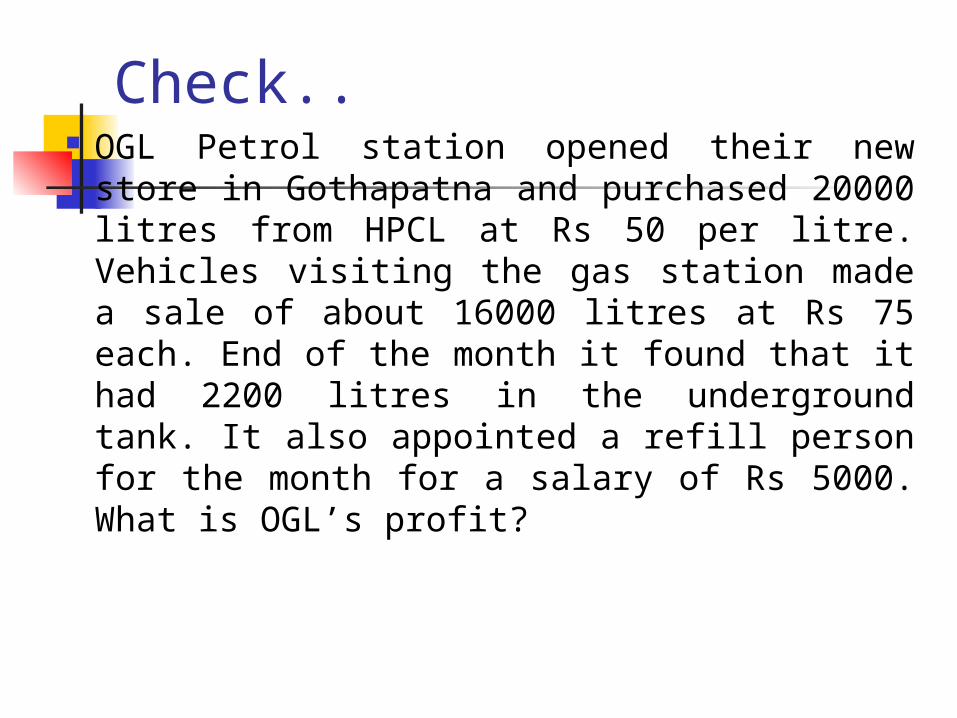

Check.. OGL Petrol station opened their new store in Gothapatna and purchased 20000 litres from HPCL at Rs 50 per litre. Vehicles visiting the gas station made a sale of about 16000 litres at Rs 75 each. End of the month it found that it had 2200 litres in the underground tank. It also appointed a refill person for the month for a salary of Rs 5000. What is OGL’s profit?