MAHANAMA-DISSERTATION-2021.pdf - TTU DSpace Principal

106

Risk Assessment and Financial Management of Natural Disasters and Crime by Thilini Vasana Mahanama, M.S. A Dissertation in Mathematics and Statistics Submitted to the Graduate Faculty of Texas Tech University in Partial Fulfillment of the Requirements for the Degree of DOCTOR OF PHILOSOPHY Approved Dr. W. Brent Lindquist Chairperson of the Committee Dr. Dimitri Volchenkov Dr. Svetlozar Rachev Dr. Mark Sheridan Dean of the Graduate School May, 2021

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of MAHANAMA-DISSERTATION-2021.pdf - TTU DSpace Principal

Risk Assessment and Financial Management of Natural Disasters and Crime

by

Thilini Vasana Mahanama, M.S.

A Dissertation

in

Mathematics and Statistics

Submitted to the Graduate Facultyof Texas Tech University in

Partial Fulfillment ofthe Requirements for

the Degree of

DOCTOR OF PHILOSOPHY

Approved

Dr. W. Brent LindquistChairperson of the Committee

Dr. Dimitri Volchenkov

Dr. Svetlozar Rachev

Dr. Mark SheridanDean of the Graduate School

May, 2021

c©2021, Thilini Vasana Mahanama

Texas Tech University, Thilini Mahanama, May 2021

ACKNOWLEDGMENTS

It is with great pleasure that I record my heartfelt indebtedness to my research ad-

visors, Dr. Dimitri Volchenkov, Dr. Svetlozar Rachev, and Dr. W. Brent Lindquist,

for their valuable counsel, guidance, and perseverance throughout my research. Their

continuous encouragement and support have been always a source of inspiration and

energy for me. I am so honored and privileged to have these incredible mentors in

my life.

My heartfelt gratitude also goes out to Dr. D.K. Mallawa Arachchi, my undergrad-

uate research supervisor, at the University of Kelaniya, Sri Lanka. His continuous

advice, guidance, and encouragement immensely helped me to pursue my postgrad-

uate studies at TTU.

I would like to extend my sincere thanks to all the professors in the Department

of Mathematics and Statistics at TTU for helping me in numerous ways during my

graduate studies. I thank the department and graduate school for giving me the

opportunity to pursue my doctoral studies and supporting me with scholarships. I

also wish to thank all my friends at TTU for making these years so memorable.

It is with great appreciation my sincere gratitude is extended to all my professors

at the Department of Mathematics and the Department of Statistics & Computer

Science at the University of Kelaniya, Sri Lanka. I am also grateful to all my teachers

for their valuable guidance and inspiration throughout my education.

I am very much indebted to my colleagues Nadeesha Jayaweera, Mr. Karunarathna

Banda, Dr. Pushpi Paranamana, Abootaleb Shirvani, and Dr. Ann Almeida for their

constant encouragement and support. Valuable experience I received from Toast-

masters International, TTU graduate writing center and library workshops greatly

acknowledged.

I am forever beholden to my parents, sisters, and relatives for their intimacy,

endless patience, and encouragement. They kept me going on and this work would

not have been possible without their input.

ii

Texas Tech University, Thilini Mahanama, May 2021

CONTENTS

ACKNOWLEDGMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . ii

ABSTRACT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . vi

List of Tables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . viii

List of Figures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ix

1. Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

2. Data Description . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

2.1 Tornado Data Description . . . . . . . . . . . . . . . . . . . . 5

2.2 Crime Data Description . . . . . . . . . . . . . . . . . . . . . . 9

3. Learning a Statistical Manifold to Determine the Risk Covering Strate-

gies for Tornado-induced Property Losses in the United States . . . 14

3.1 Categorizing Tornado Data with respect to Physical Parameters 17

3.2 Exploratory Analysis on Determining Bilateral Coverages for

Tornado Damages . . . . . . . . . . . . . . . . . . . . . . . . . 17

3.3 Assessing a Distance Matrix based on the Differences between

Statistics in Tornado Scales . . . . . . . . . . . . . . . . . . . . 19

3.4 Visualizing the Distances of Property Loss Distributions be-

tween Tornado Scales using Classical Multidimensional Scaling 20

3.5 Learning an Underlying Framework for a Statistical Manifold

on Tornado Property Losses . . . . . . . . . . . . . . . . . . . 21

3.6 Upgrading the Underlying Framework to a Statistical Manifold

using a Subdivision Surface Method . . . . . . . . . . . . . . . 23

3.7 Determining a Curvature Matrix for the Statistical Manifold . 24

3.8 Determining the Risk Assessment Strategy based on the Cur-

vature Matrix . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

4. Assessment of Tornado Property Losses in the United States . . . . . . 29

4.1 Classifying Tornado Data . . . . . . . . . . . . . . . . . . . . . 29

4.1.1 Non-negative Matrix Factorization Method for Classification 29

4.1.2 Classifying Tornado Data Using NMF . . . . . . . . . . . . 31

iii

Texas Tech University, Thilini Mahanama, May 2021

4.2 Measuring the Dependence between Tornado Variables . . . . . 34

4.2.1 Bivariate Copula for Measuring the Non-linear Dependence

between Tornado Variables . . . . . . . . . . . . . . . . . . 34

4.2.2 Measuring the Dependence between Tornado Variables Us-

ing a Bivariate Gaussian Copula Approach . . . . . . . . . 37

4.3 Predicting Tornado Property Losses . . . . . . . . . . . . . . . 40

4.3.1 Long Short-Term Memory Neural Networks for Prediction

of Future Property Losses . . . . . . . . . . . . . . . . . . 40

4.3.2 Predicting Future Tornado-induced Damage Costs Using

LSTM and Shallow Neural Networks . . . . . . . . . . . . 42

5. A Natural Disasters Index . . . . . . . . . . . . . . . . . . . . . . . . . 45

5.1 Construction of the Natural Disasters Index (NDI) . . . . . . . 45

5.2 NDI Option Prices . . . . . . . . . . . . . . . . . . . . . . . . . 48

5.3 NDI Risk Budgets . . . . . . . . . . . . . . . . . . . . . . . . . 53

5.4 Evaluating the Impact of Climate Extreme Indicators on NDI

Performance . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54

6. Global Index on Financial Losses due to Crimes in the United States . . 62

6.1 Financial Losses due to Crimes in the United States . . . . . . 63

6.1.1 Modeling the Multivariate Time Series of Financial Losses

due to Crimes . . . . . . . . . . . . . . . . . . . . . . . . . 63

6.1.2 Backtesting the Portfolio . . . . . . . . . . . . . . . . . . . 63

6.2 Option Prices for the Crime Portfolio . . . . . . . . . . . . . . 66

6.2.1 Defining a Model for Pricing Options . . . . . . . . . . . . 66

6.2.2 Issuing the European Option Prices for the Crime Portfolio 69

6.3 Risk Budgets for the Crime Portfolio . . . . . . . . . . . . . . 70

6.3.1 Defining Tail and Center Risk Measures . . . . . . . . . . . 71

6.3.2 Determining the Risk Budgets for the Crime Portfolio . . . 72

6.4 Performance of the Crime Portfolio for Economic Crisis . . . . 74

6.4.1 Defining Systemic Risk Measures . . . . . . . . . . . . . . 74

6.4.2 Evaluating the Performance of the Crime Portfolio for Eco-

nomic Crisis . . . . . . . . . . . . . . . . . . . . . . . . . . 75

iv

Texas Tech University, Thilini Mahanama, May 2021

7. Discussion & Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . 77

Bibliography . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80

v

Texas Tech University, Thilini Mahanama, May 2021

ABSTRACT

The National Oceanic and Atmospheric Administration reports that the U.S. an-

nually sustains about 1,300 tornadoes. Currently, the Enhanced Fujita scale is used

to categorize the severity of a tornado event based on a wind speed estimate. We pro-

pose the new Tornado Property Loss scale (TPL-Scale) to classify tornadoes based on

associated damage costs. The dependence between the tornado-affected area and the

associated property losses vary strongly over time and location. The overall tornado

damage costs forecasted by a trained long short-term memory network trained on

historical data might reach $8 billion over the next five years although no systematic

increase in the number and cost of disasters is observed over time.

The approach of compensating for the property losses caused by tornadoes in

the United States is a two-fold process. First, private insurance companies cover the

tornado damage costs claimed by their clients. Second, the state distributes fundings

in the case of state emergency for local governments. We intend to recover these risk

assessment strategies for tornado-induced property losses reported in the national

tornado database. In order to that, we learn a statistical manifold on probability

distributions of property losses and define a measure of curvature on the manifold

to estimate variations of property losses with respect to changes in tornado path

lengths and path widths.

Natural disasters, such as tornadoes, floods, and wildfire pose risks to life and

property, requiring the intervention of insurance corporations. One of the most

visible consequences of changing climate is an increase in the intensity and frequency

of extreme weather events. The relative strengths of these disasters are far beyond

the habitual seasonal maxima, often resulting in subsequent increases in property

losses. Thus, insurance policies should be modified to endure increasingly volatile

catastrophic weather events. We propose a Natural Disasters Index (NDI) for the

property losses caused by natural disasters in the United States based on the “Storm

Data” published by the National Oceanic and Atmospheric Administration. The

proposed NDI is an attempt to construct a financial instrument for hedging the

intrinsic risk. The NDI is intended to forecast the degree of future risk that could

forewarn the insurers and corporations allowing them to transfer insurance risk to

vi

Texas Tech University, Thilini Mahanama, May 2021

capital market investors. This index could also be modified to other regions and

countries.

Following the financial management principles in the NDI, we propose an index-

based insurance portfolio for crime in the United States by utilizing the financial

losses reported by the Federal Bureau of Investigation for property crimes and cy-

bercrimes. Our research intends to help investors envision risk exposure in our port-

folio, gauge investment risk based on their desired risk level, and hedge strategies

for potential losses due to economic crashes. Underlying the index, we hedge the

investments by issuing marketable European call and put options and providing risk

budgets (diversifying risk to each type of crime). We find that real estate, ran-

somware, and government impersonation are the main risk contributors. We then

evaluate the performance of our index to determine its resilience to economic crisis.

The unemployment rate potentially demonstrates a high systemic risk on the portfo-

lio compared to the economic factors used in this study. In conclusion, we provide a

basis for the securitization of insurance risk from certain crimes that could forewarn

investors to transfer their risk to capital market investors.

vii

Texas Tech University, Thilini Mahanama, May 2021

LIST OF TABLES

2.1 The Enhanced Fujita Scale (EF-scale) [1]. . . . . . . . . . . . . . . . 64.1 Kendall’s τ and Spearman’s ρ rank correlation coefficients between

ln(Area) and ln(Loss). . . . . . . . . . . . . . . . . . . . . . . . . . . 395.1 Percent contribution to risk for standard deviation (Std) and expected

tail loss (ETL) (at 95% and 99% levels) risk budgets for the NaturalDisasters Index (NDI) . . . . . . . . . . . . . . . . . . . . . . . . . . 60

5.2 The left-tail systemic risk measures (CoVaR, CoES, and CoETL) onthe Natural Disasters Index (NDI) at different stress levels based onstressing the factors monthly maximum temperature (Max Temp) andthe Palmer Drought Severity Index (PDSI). . . . . . . . . . . . . . . 61

6.1 VaR Backtesting Results for ARMA(1,1)-GARCH(1,1) with Student’st and NIG innovations. . . . . . . . . . . . . . . . . . . . . . . . . . . 65

6.2 The estimated parameters of the fitted the NIG process to the Crimeportfolio log-returns . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67

6.3 The percentages of center risk (CR) and tail risk (TR) (at levels of95% and 99%) budgets for the portfolio on crimes. . . . . . . . . . . . 73

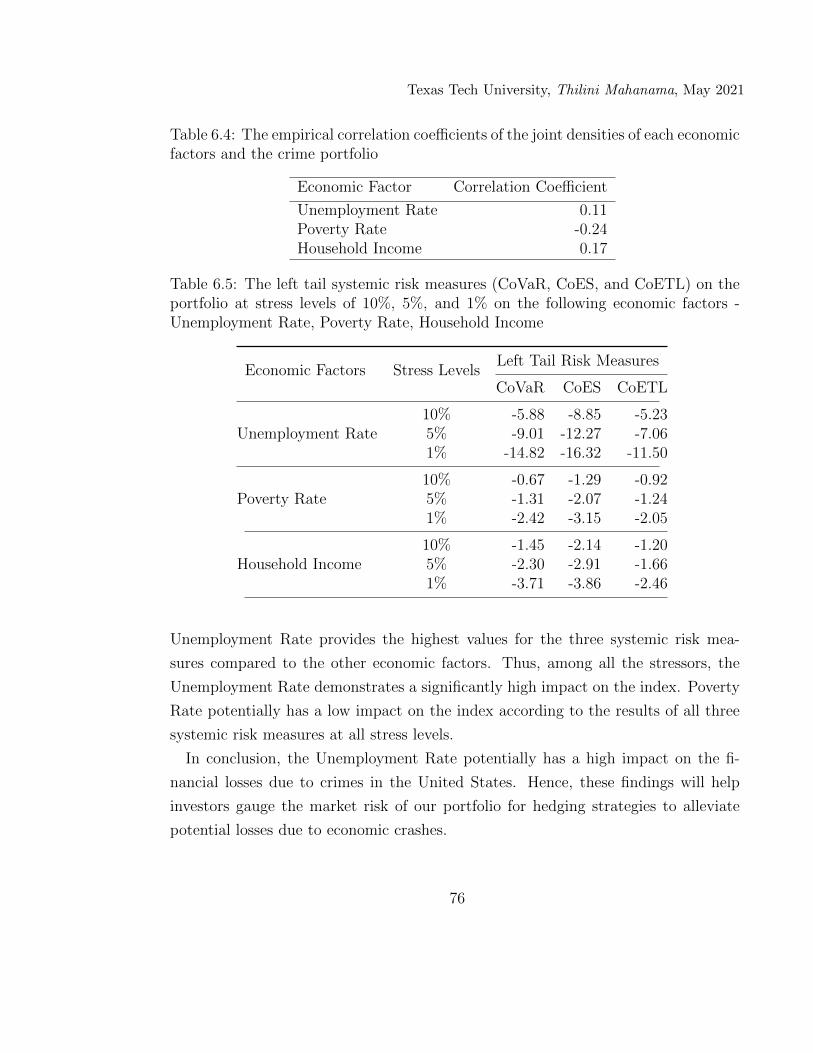

6.4 The empirical correlation coefficients of the joint densities of eacheconomic factors and the crime portfolio . . . . . . . . . . . . . . . . 76

6.5 The left tail systemic risk measures (CoVaR, CoES, and CoETL) onthe portfolio at stress levels of 10%, 5%, and 1% on the following eco-nomic factors - Unemployment Rate, Poverty Rate, Household Income 76

viii

Texas Tech University, Thilini Mahanama, May 2021

LIST OF FIGURES

2.1 According to the NOAA Storm Data reports from 1950-2018, (a) thetotal tornado-induced property losses in states (measured in U.S. dol-lars adjusted for inflation in 2019) and (b) the total numbers of tor-nadoes in Tornado Alley states. Texas has the highest number ofreported tornadoes in Tornado Alley states. . . . . . . . . . . . . . . 6

2.2 The path of a tornado occurred in Raleigh, NC on April 19, 2019,according to National Weather Service, NOAA [2]. . . . . . . . . . . . 6

2.3 In the Tornado Alley states, the annual total numbers of tornadoesdetermined using the NOAA Storm Data reports between 1955 and2018. Over the years, the annual numbers of tornadoes have no com-mon trend. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

2.4 In the Tornado Alley states, the annual tornado-induced propertylosses (in billions adjusted for inflation in 2019) determined using theNOAA Storm Data reports between 1955 and 2018. Over the years,the annual tornado-induced losses significantly can vary up to billionsof dollars. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

2.5 Fitted Gaussian distributions for tornado variables: ln(Length), ln(Width),and ln(Loss) (left to right) using the NOAA Storm Data reports be-tween 1955 and 2018. The tornado variables do not hold Gaussiandistributional assumptions. . . . . . . . . . . . . . . . . . . . . . . . . 8

3.1 Kernel density plots for the property losses attributed to tornadoscales in A. Aij represents the tornadoes with path lengths in Liand path widths in Wj. . . . . . . . . . . . . . . . . . . . . . . . . . . 18

3.2 A visual representation of the distance matrix (D) which consists ofthe pairwise Kolmogorov-Smirnov’s distances between the distribu-tions of property losses in tornado scales. . . . . . . . . . . . . . . . . 20

3.3 The underlying framework of the statistical manifold on tornado-induced property losses. Each edge is comprised of the periodic in-terpolating cubic splines and the vertices are the tornado scales inA. The vertex, Aij, represents the tornadoes with lengths in Li andwidths in Wj. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

ix

Texas Tech University, Thilini Mahanama, May 2021

3.4 The learned statistical manifold for the property losses of tornadoes,constructed using the reported losses between 1993 and 2018. Aijrepresents the tornadoes with lengths in Li and widths in Wj. Themanifold is constructed by implementing classical dimensional scalingand a method of subdivision surfaces. . . . . . . . . . . . . . . . . . . 23

3.5 (a) The learned statistical manifold and (b) its curvature portrait(right). Figure (b) is constructed with respect to the positions ofthe path width (Wj, j = 1, ..30) and path length (Li, i = 1, ..50)coordinates of a tornado. Yellow and blue regions in Fig (b) depictcompressed and expanded cells in Figure (a), respectively. . . . . . . 25

3.6 The curvature portrait with kernel densities of property losses of somemajor tornado scales in A. The statistics in monochromic zones showsimilar forms. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

4.1 The visual representation of the NMF results for tornado data between1950 and 2018. Tornado events and variables are depicted as pointsand vectors, respectively, on the two-dimensional plane constructedby the two salient components of NMF. Tornado events (points) arecolored according to the EF-scale. . . . . . . . . . . . . . . . . . . . . 32

4.2 The visual representation of the NMF results for tornado data duringthe periods 1950-1992 (left) and 1993-2018 (right). Tornado eventsand variables are depicted as points and vectors, respectively, on thetwo-dimensional plane spanned by the two salient components derivedfrom NMF. Tornado events (points) are colored according to the EF-scale. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

4.3 The histograms of the TPL-Scale (4.5) for the tornado data during (a)1950-1992, (b) 1993-2018, and (c) 1950-2018 are based on the propertylosses reported in NOAA Storm Data. The segment of the TPL-Scalegreater than 60 is magnified in (c); P(TPL−Scale ≥ 60) = 0.025, i.e.,there is a 2.5% chance a tornado will occur causing over ten milliondollars in damages. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

4.4 The figures are constructed using the tornado data reported between1955 and 2018 in NOAA Storm Data. Figure (a) provides simplelinear regression analysis: ln(Loss) = 0.59 ln(Area) + 5.06. Figure(b) is the joint density of the generated marginal cdfs of ln(Loss) andln(Area) (F1 and F2, respectively). . . . . . . . . . . . . . . . . . . . 35

x

Texas Tech University, Thilini Mahanama, May 2021

4.5 A sampling distribution of ln(Area): ln(Area) ∼ Γ (18.65, 0.59). Acomparison of the sampled and observed data for ln(Area) (between1955 and 2018 in NOAA Storm Data) using pdf, P-P, and Q-Q plots(left to right). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

4.6 A sampling distribution of ln(Loss): ln(Loss) ∼ Γ (15.78, 0.73). Acomparison of the sampled and observed data for ln(Loss) (between1955 and 2018 in NOAA Storm Data) using pdf, P-P, and Q-Q plots(left to right). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

4.7 Modeling the joint density of tornado variables, ln(Area) and ln(Loss),using a bivariate Gaussian copula associated with univariate gammadensities (4.11). Applying the generated data, we provide (a) the jointprobability density plot, (b) its contour plot, and (c) a comparison ofthe simulated and the observed data (between 1955 and 2018 in NOAAStorm Data). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

4.8 Bivariate Gaussian copula parameters for annual tornado data in Tor-nado Alley states, generated from NOAA Storm Data. There is nomonotonicity in the copula parameters (which provide the correlationof ln(Area) and ln(Loss)) over the years and states. . . . . . . . . . . 40

4.9 The LSTM layer architecture consists of a set of recurrently connectedLSTM blocks. The input, cell state, and output in the tth LSTM blockare denoted as xt, ct, and ht, respectively [4, 5]. . . . . . . . . . . . . 41

4.10 The structure of the tth LSTM block: The multiplicative units areinput (i), forget (f), and output (o) gates, and the cell state (g). Theinput, cell state, and output in the tth memory cell are denoted asxt, ct, and ht, respectively [4, 5]. . . . . . . . . . . . . . . . . . . . . . 42

4.11 A comparison of the observed and simulated monthly losses caused bytornadoes between 1990 and 2018 (testing data) and the errors due topredictions using a LSTM network. The simulations were generatedusing NOAA Storm Data. . . . . . . . . . . . . . . . . . . . . . . . . 43

4.12 The predictions of the monthly tornado-induced property losses in2019 (in millions) (a) using a LSTM and (b) using a shallow neu-ral network. The box plots in (b) are constructed using the 10,000simulations generated for each month based on NOAA Storm Data. . 44

xi

Texas Tech University, Thilini Mahanama, May 2021

4.13 The predictions of (a) the monthly tornado-induced property lossesand (b) the cumulative monthly property losses (in billions adjustedfor inflation in 2019) between 2020 and 2025 using a LSTM network.The higher losses would be reported from March to June, and thevolume of property losses would amount up to eight billion dollars in2025. The simulations were generated using NOAA Storm Data. . . . 44

5.1 The monthly property losses (in billions adjusted for inflation in 2019)caused by drought, flood, winter storm, thunderstorm wind, hail, andtornado events between 1996 and 2018 generated using NOAA StormData. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

5.2 Our proposed Natural Disasters Index (NDI) for the United States.This NDI (5.1) is constructed using the property losses of naturaldisasters reported in NOAA Storm Data between 1996 and 2018. . . . 47

5.3 The first differences of the stress testing variables, (a) Maximum Tem-perature (Max Temp) and (b) Palmer Drought Severity Index (PDSI),yield stationary time series. . . . . . . . . . . . . . . . . . . . . . . . 48

5.4 The call option prices (5.7) for the Natural Disasters Index (NDI) attime t for a given strike price K using a GARCH(1,1) model withgeneralized hyperbolic innovations. . . . . . . . . . . . . . . . . . . . 51

5.5 The put option prices (5.8) for the Natural Disasters Index (NDI) attime t for a given strike price K using a GARCH(1,1) model withgeneralized hyperbolic innovations. . . . . . . . . . . . . . . . . . . . 52

5.6 The call and put option prices for the Natural Disasters Index (NDI)at time t for a given strike price K using a GARCH(1,1) model withgeneralized hyperbolic innovations. . . . . . . . . . . . . . . . . . . . 52

5.7 The Natural Disasters Index (NDI) implied volatilities against timeto maturity (T ) and moneyness (M = S/K, where S and K thestock and strike prices, respectively) using a GARCH(1,1) model withgeneralized hyperbolic innovations. . . . . . . . . . . . . . . . . . . . 53

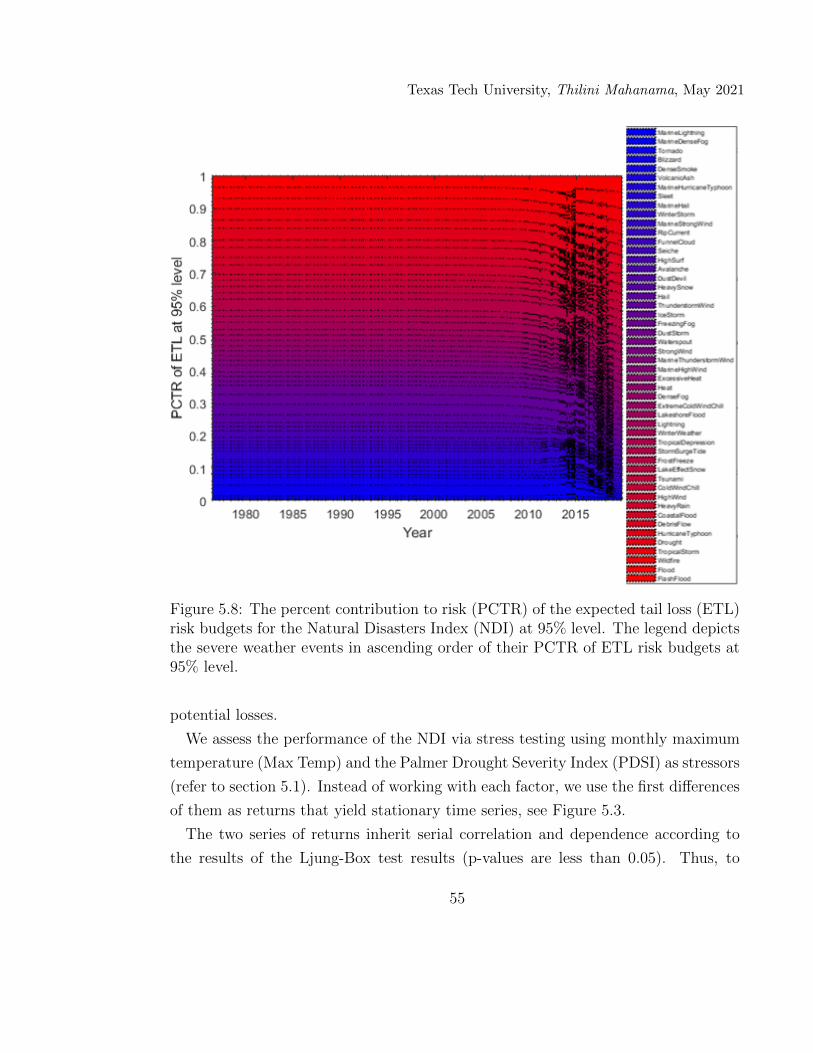

5.8 The percent contribution to risk (PCTR) of the expected tail loss(ETL) risk budgets for the Natural Disasters Index (NDI) at 95%level. The legend depicts the severe weather events in ascending orderof their PCTR of ETL risk budgets at 95% level. . . . . . . . . . . . 55

5.9 The percent contribution to risk (PCTR) of the expected tail loss(ETL) risk budgets for the Natural Disasters Index (NDI) at 99%level. The legend depicts the severe weather events in ascending orderof their PCTR of ETL risk budgets at 99% level. . . . . . . . . . . . 56

xii

Texas Tech University, Thilini Mahanama, May 2021

5.10 The percent contribution to risk (PCTR) of the standard deviation(Std) risk budgets for the Natural Disasters Index (NDI). The legenddepicts the severe weather events in ascending order of their PCTR ofStd risk budgets. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

5.11 The generated joint densities of the returns of monthly maximum tem-perature (Max Temp) and the Natural Disasters Index (NDI), andthe Palmer Drought Severity Index (PDSI) and the NDI (right panel)using the fitted bivariate NIG models of the joint distributions ofindependent and identically distributed standardized residuals. Thefigures depict the simulated values and the contour plots of the jointdensities. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58

6.1 Call option prices against time to maturity (T , in days) and strikeprice (K, based on S0 = 100). . . . . . . . . . . . . . . . . . . . . . . 69

6.2 Put option prices against time to maturity (T , in days) and strikeprice (K, based on S0 = 100). . . . . . . . . . . . . . . . . . . . . . . 70

6.3 Implied volatility surface against time to maturity (T , in days) andmoneyness (M = K/S, the ratio of strike price, K, and stock price, S). 71

xiii

Texas Tech University, Thilini Mahanama, May 2021

CHAPTER 1

INTRODUCTION

The National Centers for Environmental Information reports the United States

has experienced 69 natural disasters with losses exceeding one billion dollars between

2015 and 2019. The accumulated loss exceeds $535 billion at an average of $107.1

billion/year. The trend of disaster frequency is expected to escalate over the years

due to changes in climate which will result in catastrophic losses [6]. These volatile

weather patterns will result in an inevitable challenge to the U.S.’s ability to sustain

human and economic development [7]. As a result, weather risk markets need to be

capable of offsetting the financial impacts of natural disasters [8, 9].

The financial losses due to natural disasters exacerbate due to changes in popula-

tion and national wealth density [10, 11]. If insurers are to retain profitability and

solvency in the event of a major catastrophe that insurers must increase their prices

for catastrophe insurance and reduce their exposure to risk [12]. Also, reinsurers un-

dergo severe financial stress in facilitating catastrophe insurance by offering tenable

reduction for risk in large catastrophic losses [13, 14, 15]. However, the substantial

losses can be alleviated using protective measures such as preparedness, mitigation,

and insurance [16, 17]. To better protect the clients, catastrophe insurance policies

should ramp-up investments in cost-effective loss reduction mechanisms by better

managing the risk.

Unequivocally, the catastrophe losses and related risks inherent create uncertainty

over the type of disaster event [13, 18]. For example, due to less coverage of insured

assets and data latency in drought and flooding events, they tend to provide uncertain

loss estimates compared to the losses of severe storm events in the United States

[18, 19]. In consequence, prioritization for mitigating the risks can be diverse and

complex.

In this dissertation, we address the risk assessment strategies for tornadoes re-

ported in NOAA Storm Data [3] in chapter 3 and 4. We consider the reported finan-

cial losses for tornadoes without considering their temporal relationships. Then, we

discuss the risk assessment strategies from the perspective of the compensations for

1

Texas Tech University, Thilini Mahanama, May 2021

tornado property damages.

In the United States, the approach of compensating the property losses caused by

tornadoes is a two-pronged strategy. First, private insurance companies cover the

tornado damage costs claimed by their clients. Second, the state distributes fundings

in the case of state emergency for local governments. We intend to recover the risk

assessment strategies for tornado-induced property losses reported in the database

[3]. Therefore, we learn a statistical manifold on probability distributions of property

losses to describe the processes of risk evaluations.

We categorize tornado data with respect to tornado path lengths and tornado path

widths and determine their probability distributions of property losses in sections

3.1 and 3.2. Then, we construct a distance matrix using the pairwise Kolmogorov-

Smirnov’s distances [20] in terms of property losses between tornado categories in

section 3.3. Henceforth, we learn a statistical manifold using classical multidimen-

sional scaling [21] for the distance matrix and a subdivision surface method in sec-

tions 3.4 - 3.6. Then, we define a measure of curvature on the statistical manifold to

show the existence of different risk assessment strategies for tornado-induced prop-

erty losses in sections 3.7 and 3.8. Finally, we generalize this procedure to introduce

the “Statistical Manifold Learning Algorithm” for high dimensional data.

In chapter 4, we address three problems in assessing tornado-induced property

losses. First, we introduce a new scale (known as TPL-Scale) in addition to the

Enhanced Fujita Scale [1] to classify tornadoes based on their financial impacts due

to damages using the non-negative matrix factorization analysis [22] in section 4.1.

Second, we apply a copula approach [23] for assessing property losses based on its

dependence on the area affected by tornadoes in section 4.2. Third, we predict

future tornado damage costs in section 4.3 using the shallow and the long short-term

memory neural networks. Based on our findings, the volume of tornado-induced

property losses would amount up to eight billion dollars by 2025.

The risk assessment strategies outline in chapter 3 and 4 cannot be implemented

for natural disasters other than tornadoes due to the lack of reported data in [3].

For that reason, we integrate the reported property losses in all types of natural

disasters taking the temporal ordering into account. Then, we utilize the time series

2

Texas Tech University, Thilini Mahanama, May 2021

of financial losses for hedging the risk due to natural disasters in chapter 5.

The weather index insurance can effectively transfer spatially covariate weather

risks as it pays indemnities based on realizations of a weather index that is highly

correlated with actual losses [24]. The securitization of losses from natural disas-

ters provides a valuable novel source of diversification for investors. Catastrophe

risk bonds are a promising type of insurance-linked securities introduced to smooth

transferring of catastrophic insurance risk from insurers and corporations to capital

market investors by offering an alternative or complement of capital to the traditional

reinsurance [15]. The three types of variables that pay off in insurance-linked secu-

rities [25] are insurer-specific catastrophe losses, insurance-industry catastrophe loss

indices, and parametric indices based on the physical characteristics of catastrophic

events.

The first index-based catastrophe derivatives, CAT-futures, introduced by the

Chicago Board of Trade using the ISO-Index was ineffective due to a lack of re-

alistic models in the market [26]. Secondly, the Property Claim Services (PCS)

proposed the PCS-options based on the PCS-index and they slowed down due to

market illiquidity [27]. Then, the New York Mercantile Exchange (NYMEX) de-

signed catastrophe futures and options to enhance the transparency and liquidity

of the capital markets to the insurance sector [27]. [28] further explains alternative

risk transfer mechanisms within the context of natural catastrophe problems in the

United States.

We propose Natural Disasters Index (NDI) to address these shortcomings by cre-

ating a financial instrument for hedging the intrinsic risk induced by the property

losses caused by natural disasters in the U.S. The vital objective of the NDI is to

forecast the severity of future systemic risk attributed to natural disasters. This pro-

vides advance warnings to the insurers and corporations allowing them to transfer

insurance risk to capital market investors. Therefore, the proposed NDI is intended

to make up the shortfall between the capital and insurance markets. The NDI identi-

fies the potential risk contributions of each natural disaster and provides options and

futures in sections 5.2 and 5.3. In addition, we assess the performance of the NDI to

adverse weather events in section 5.4. Furthermore, the NDI could be modified to

3

Texas Tech University, Thilini Mahanama, May 2021

calculate the risk in other regions or countries using a data set comparable to NOAA

Storm Data [3].

We follow the methods applied in the NDI on an ad hoc basis as a benchmark

to investigate the financial impact of crimes in the U.S. Using the financial losses

due to various types of crimes reported by the Federal Bureau of Investigation, we

propose a portfolio based on the economic impacts of these crimes in chapter 6. The

objective of this portfolio is to examine the impact of crime on insurance policies in

the United States by analyzing the financial losses associated with property crimes

and cybercrimes. Therefore, the key findings are intended to provide a basis for

the securitization of insurance risk from crimes. We investigate the financial market

implications of the portfolio using option pricing theory as well as risk budgeting

in sections 6.1 - 6.3. Furthermore, we evaluate the performance of our index with

respect to economic factors using stress testing in section 6.4.

4

Texas Tech University, Thilini Mahanama, May 2021

CHAPTER 2

DATA DESCRIPTION

2.1 Tornado Data Description

National Oceanic and Atmospheric Administration (NOAA)’s National Centers for

Environmental Information reports severe weather events that have great impacts on

the U.S. economy. The total cost of the climate disasters since 1980 exceeds $1.775

trillion [18]. The U.S. sustains about 1,300 tornadoes and loses around fifty people

annually [3, 29]. In Figure 2.1(a), we have shown tornado property losses reported in

the U.S. in US dollars adjusted for 2019. Texas, Oklahoma, Kansas, Iowa, Missouri,

and Nebraska form a region with a disproportionately high frequency of tornadoes

known as Tornado Alley. Tornadoes in this region typically happen in late spring

and occasionally the early fall [30]. Texas alone experienced around 4,000 tornado

events since records began in 1950 [3], see Figure 2.1(b). These disastrous events

resulted in many deaths and had significant economic effects on the areas impacted.

In the United States, over 69,000 tornadoes have been reported by NOAA [3]

during the period from 1950 to 2018. For the recorded tornado events, the database

reports path length and width (measured in miles and feet, respectively) and property

losses (measured in U.S. Dollars of the given year). For example, Figure 2.2 illustrates

a path of a tornado in Raleigh, NC on April 19, 2019. Whenever appropriate, we

approximate the area affected by a tornado as the product of path length and width

(measured in square feet). We estimate property losses in U.S. dollars of 2019.

Tornado intensity, assessed by the Enhanced Fujita Scale (EF-scale) [1], assigns

each tornado a ‘rating’ based on estimated wind speed and related possible damages.

For each tornado in [3], the tornado intensity is characterized by one of six scales

[31] with an increasing degree of damage given by the EF-scale, see Table 2.1.

5

Texas Tech University, Thilini Mahanama, May 2021

0

2,000,000,000

4,000,000,000

6,000,000,000

Total Losses (USD 2019) 1950 − 2018

(a) (b)

Figure 2.1: According to the NOAA Storm Data reports from 1950-2018, (a) thetotal tornado-induced property losses in states (measured in U.S. dollars adjustedfor inflation in 2019) and (b) the total numbers of tornadoes in Tornado Alley states.Texas has the highest number of reported tornadoes in Tornado Alley states.

Figure 2.2: The path of a tornado occurred in Raleigh, NC on April 19, 2019,according to National Weather Service, NOAA [2].

Table 2.1: The Enhanced Fujita Scale (EF-scale) [1].

EF-scale Wind Speed Estimate (mph) Damage Description

EFO 65–85 Minor

EF1 86–110 Moderate

EF2 111–135 Considerable

EF3 136–165 Severe

EF4 166–200 Devastating

EF5 ≥ 200 Incredible

6

Texas Tech University, Thilini Mahanama, May 2021

NOAA has identified Florida and the South-Central U.S. as having a dispropor-

tionately high frequency of tornadoes [3], see Figure 2.1. Texas, Oklahoma, Kansas,

Nebraska, Iowa, and Missouri are widely known as Tornado Alley [30]. They display

high fluctuations in the annual numbers of tornadoes that occurred between 1955 and

2018, see Figure 2.3. The quadratic trendline fits (curves in red) exemplify that the

trends are not monotonic over the years. Furthermore, the annual tornado-induced

property losses in the Tornado Alley states vary up to nine orders of magnitude (i.e.

billions of dollars), see Figure 2.4.

1960 1980 2000Year

0

50

100

150

200

250

No

of T

orna

does

Texas

1960 1980 2000Year

0

20

40

60

80

100

No

of T

orna

does

Oklahoma

1960 1980 2000Year

0

20

40

60

80

No

of T

orna

does

Kansas

1960 1980 2000Year

0

20

40

60

80

No

of T

orna

does

Iowa

1960 1980 2000Year

0

20

40

60

80

100

No

of T

orna

does

Missouri

1960 1980 2000Year

0

20

40

60

80

No

of T

orna

does

Nebraska

Figure 2.3: In the Tornado Alley states, the annual total numbers of tornadoesdetermined using the NOAA Storm Data reports between 1955 and 2018. Over theyears, the annual numbers of tornadoes have no common trend.

We fit Gaussian distributions for tornado variables (i.e., path length, path width,

and property loss), see Figure 2.5. The assumptions of normality do not hold for

tornado variables as depicted in Figure 2.5 [32]. We use a copula approach for the

bivariate non-Gaussian distributed tornado affected areas and property losses [33, 34].

We thus investigate the dependence between tornado-affected areas and attributed

property losses in section 4.2.2.

7

Texas Tech University, Thilini Mahanama, May 2021

1960 1980 2000Year

0

1

2

3

Loss

(bi

llion

s $

2019

)

Texas

1960 1980 2000Year

0

0.5

1

1.5

2

2.5

Loss

(bi

llion

s $

2019

)

Oklahoma

1960 1980 2000Year

0

0.5

1

1.5

2

2.5

Loss

(bi

llion

s $

2019

)

Kansas

1960 1980 2000Year

0

0.5

1

1.5Lo

ss (

billi

ons

$ 20

19)

Iowa

1960 1980 2000Year

0

1

2

3

4

Loss

(bi

llion

s $

2019

)

Missouri

1960 1980 2000Year

0

0.5

1

1.5

Loss

(bi

llion

s $

2019

)

Nebraska

Figure 2.4: In the Tornado Alley states, the annual tornado-induced property losses(in billions adjusted for inflation in 2019) determined using the NOAA Storm Datareports between 1955 and 2018. Over the years, the annual tornado-induced lossessignificantly can vary up to billions of dollars.

Figure 2.5: Fitted Gaussian distributions for tornado variables: ln(Length),ln(Width), and ln(Loss) (left to right) using the NOAA Storm Data reports be-tween 1955 and 2018. The tornado variables do not hold Gaussian distributionalassumptions.

8

Texas Tech University, Thilini Mahanama, May 2021

2.2 Crime Data Description

In this section, we define the types of crimes utilized for constructing our index.

Using official data published by the Federal Bureau of Investigation (FBI), we con-

sidered financial losses caused by crimes committed in the United States between

2001 and 2019. We use the FBI’s Internet Crime Reports [35] to estimate the fi-

nancial losses attributed to cybercrimes and Uniform Crime Reports [36] to assess

the financial losses caused by property crimes (burglary, larceny-theft, and motor

vehicle theft). Using the information collected from these two reports, we calculate

the cumulative financial losses reported for the following 32 types of crimes [35, 37]:

• Advanced Fee: An individual pays money to someone in anticipation of

receiving something of greater value in return, but instead receives significantly

less than expected or nothing.

• BEA/EAC (Business Email Compromise/Email Account Compro-

mise): BEC is a scam targeting businesses working with foreign suppliers

and/or businesses regularly performing wire transfer payments. EAC is a sim-

ilar scam that targets individuals. These sophisticated scams are carried out

by fraudsters compromising email accounts through social engineering or com-

puter intrusion techniques to conduct unauthorized transfer of funds.

• Burglary: The unlawful entry of a structure to commit a felony or a theft.

Attempted forcible entry is included.

• Charity: Perpetrators set up false charities, usually following natural disas-

ters, and profit from individuals who believe they are making donations to

legitimate charitable organizations.

• Check Fraud: A category of criminal acts that involve making the unlawful

use of cheques in order to illegally acquire or borrow funds that do not exist

within the account balance or account-holder’s legal ownership.

• Civil Matter: Civil lawsuits are any disputes formally submitted to a court

that is not criminal.

9

Texas Tech University, Thilini Mahanama, May 2021

• Confidence Fraud/Romance: A perpetrator deceives a victim into believ-

ing the perpetrator and the victim have a trust relationship, whether family,

friendly or romantic. As a result of that belief, the victim is persuaded to send

money, personal and financial information, or items of value to the perpetra-

tor or to launder money on behalf of the perpetrator. Some variations of this

scheme are romance/dating scams or the grandparent scam.

• Corporate Data Breach: A leak or spill of business data that is released

from a secure location to an untrusted environment. It may also refer to a

data breach within a corporation or business where sensitive, protected, or

confidential data is copied, transmitted, viewed, stolen, or used by an individual

unauthorized to do so.

• Credit Card Fraud: Credit card fraud is a wide-ranging term for fraud com-

mitted using a credit card or any similar payment mechanism as a fraudulent

source of funds in a transaction.

• Crimes Against Children: Anything related to the exploitation of children,

including child abuse.

• Denial of Service: A Denial of Service (DoS) attack floods a network/system

or a Telephony Denial of Service (TDoS) floods a service with multiple requests,

slowing down or interrupting service.

• Employment: Individuals believe they are legitimately employed, and lose

money or launders money/items during the course of their employment.

• Extortion: Unlawful extraction of money or property through intimidation or

undue exercise of authority. It may include threats of physical harm, criminal

prosecution, or public exposure.

• Gambling: Online gambling, also known as Internet gambling and iGambling,

is a general term for gambling using the Internet.

10

Texas Tech University, Thilini Mahanama, May 2021

• Government Impersonation: A government official is impersonated in an

attempt to collect money.

• Harassment/Threats of Violence: Harassment occurs when a perpetrator

uses false accusations or statements of fact to intimidate a victim. Threats

of Violence refers to an expression of an intention to inflict pain, injury, or

punishment, which does not refer to the requirement of payment.

• Identity Theft: Identify theft involves a perpetrator stealing another per-

son’s personal identifying information, such as name or Social Security number,

without permission to commit fraud.

• Investment: A deceptive practice that induces investors to make purchases

on the basis of false information. These scams usually offer the victims large

returns with minimal risk. Variations of this scam include retirement schemes,

Ponzi schemes, and pyramid schemes.

• IPR Copyright: The theft and illegal use of others’ ideas, inventions, and

creative expressions, to include everything from trade secrets and proprietary

products to parts, movies, music, and software.

• Larceny Theft: The unlawful taking, carrying, leading, or riding away of

property (except motor vehicle theft) from the possession or constructive pos-

session of another.

• Lottery/Sweepstakes: Individuals are contacted about winning a lottery

or sweepstakes they never entered, or to collect on an inheritance from an

unknown relative and are asked to pay a tax or fee in order to receive their

award.

• Misrepresentation: Merchandise or services were purchased or contracted

by individuals online for which the purchasers provided payment. The goods

or services received were of measurably lesser quality or quantity than was

described by the seller.

11

Texas Tech University, Thilini Mahanama, May 2021

• Motor Vehicle Theft: The theft or attempted theft of a motor vehicle.

A motor vehicle is self-propelled and runs on land surface and not on rails.

Motorboats, construction equipment, airplanes, and farming equipment are

specifically excluded from this category.

• Non-Payment/Non-Delivery: In non-payment situations, goods and ser-

vices are shipped, but payment is never rendered. In non-delivery situations,

payment is sent, but goods and services are never received.

• Overpayment: An individual is sent a payment/commission and is instructed

to keep a portion of the payment and send the remainder to another individual

or business.

• Personal Data Breach: A leak or spill of personal data that is released from

a secure location to an untrusted environment. It may also refer to a security

incident in which an individual’s sensitive, protected, or confidential data is

copied, transmitted, viewed, stolen, or used by an unauthorized individual.

• Phishing/Vishing/Smishing/Pharming: Unsolicited email, text messages,

and telephone calls purportedly from a legitimate company requesting personal,

financial, and/or login credentials.

• Ransomware: A type of malicious software designed to block access to a

computer system until money is paid.

• Real Estate/Rental: Fraud involving real estate, rental, or timeshare prop-

erty.

• Robbery: The taking or attempting to take anything of value from the care,

custody, or control of a person or persons by force or threat of force or violence

and/or by putting the victim in fear.

• Social Media: A complaint alleging the use of social networking or social

media (Facebook, Twitter, Instagram, chat rooms, etc.) as a vector for fraud.

Social Media does not include dating sites.

12

Texas Tech University, Thilini Mahanama, May 2021

• Terrorism: Violent acts intended to create fear that are perpetrated for a

religious, political, or ideological goal and deliberately target or disregard the

safety of non-combatants.

Whenever necessary, we use multiple imputations with the principal component

analysis model to compute missing data [38]. Moreover, we adjust the financial

losses for U.S. dollars in 2020 using the CPI Inflation Calculator available in the

U.S. Bureau of Labor Statistics. Then, we model the time series of financial losses

due to these crime types in section 6.1.1.

13

Texas Tech University, Thilini Mahanama, May 2021

CHAPTER 3

LEARNING A STATISTICAL MANIFOLD TO DETERMINE THE RISK

COVERING STRATEGIES FOR TORNADO-INDUCED PROPERTY LOSSES

IN THE UNITED STATES

In the United States, the approach of compensating the property losses caused by

tornadoes is a two-pronged strategy. First, private insurance companies cover the

tornado damage costs claimed by their clients. Second, the state distributes fundings

in the case of state emergency for local governments. We intend to recover the risk

assessment strategies for tornado-induced property losses reported in the database

[3]. In order to accomplish this, we learn a statistical manifold on probability distri-

butions of property losses to describe the processes of risk evaluations.

We develop a “Statistical Manifold Learning Algorithm” to learn a statistical man-

ifold for tornado property losses reported between 1993 and 2019 [3] . First, we cat-

egorize tornado data with respect to the physical parameters (tornado path lengths

and tornado path widths) in section 3.1. In section 3.2, we determine the probability

distributions of property losses in each tornado scale. Then, we assess pairwise differ-

ences of distributions of property losses using Kolmogorov-Smirnov’s distance [20] to

construct a distance matrix in section 3.3. Then, we use classical multidimensional

scaling [21] for the distance matrix in section 3.4. As a result, we geometrize the

statistics of property losses in tornado scales on a two-dimensional manifold in sec-

tion 3.5. Henceforth, we learn a statistical manifold using the coordinates of classical

multidimensional scaling and a subdivision surface method in section 3.6.

We investigate the properties of curvature inherent to this statistical manifold in

section 3.7. First, we introduce a measure of curvature on the statistical manifold

based on the densification of cells. Then, we construct a matrix consisting of cur-

vature coefficients where the path widths and path lengths are columns and rows,

respectively. Moreover, the visual representation of the curvature matrix (curva-

ture portrait) confirms that there is no single distribution good enough to describe

all available property losses in the database. Furthermore, the curvature portrait

demonstrates a smooth connection between the points, which represent statistics of

14

Texas Tech University, Thilini Mahanama, May 2021

property losses, on the statistical manifold. Hence, section 3.8 concludes that the

existence of different risk assessment strategies for tornado-induced property losses

reported in the database by utilizing the statistical manifold and the curvature por-

trait.

15

Texas Tech University, Thilini Mahanama, May 2021

Statistical Manifold Learning Algorithm for Tornado Risk Assessment

Tornado Data: (Path Length, Path Width, Property Loss)n∗3

Categorize tornado data with respect to physical parameters

Samples of property losses in tornado scales

Calculate pairwise Kolmogorov-Smirnov’s distance for distributions of losses

Distance matrix

Visualize the distances using classical multidimensional scaling

Learn a framework for a statistical manifold using cubic splines

Upgrade the framework to a smooth statistical manifold using surface subdivision

Define a curvature coefficient based on the cell desifications

Determine the risk assessment strategies in data based on curvature coefficients

16

Texas Tech University, Thilini Mahanama, May 2021

3.1 Categorizing Tornado Data with respect to Physical Parameters

In this section, we perform learning on the statistical manifold for describing the

difference between distributions of tornado-induced property losses with respect to

different physical parameters (tornado path length and path width). For that, we use

the tornado property losses (measured in USD 2019) and their physical parameters

(measured in ft) for each tornado reported between 1993 and 2018 in the storm

database published by the National Oceanic and Atmospheric Administration [3].

Then, we define the following scales of physical parameters using logarithms of path

lengths (Li, i = 1, · · · , 6) and path widths (Wj, j = 0, · · · , 3):

Li = {L | logL ∈ [ i , i+ 1)}, i = 1, · · · , 6

Wj = {W | logW ∈ [ j , j + 1)}, j = 0, · · · , 3.(3.1)

We further categorize the tornado data using the combinations of length and width

scales. Then, we examine the tornado-induced property losses for each combined

scale given below:

A = [Aij], i = 1, · · · , 6, j = 0, · · · , 3, (3.2)

where Aij represents the sample of property losses with path lengths in ith length

interval, Li, and path widths in jth width interval, Wj.

3.2 Exploratory Analysis on Determining Bilateral Coverages for Tornado

Damages

This section qualitatively analyzes the distributions of tornado-induced property

losses of tornado scales introduced in section 3.1. We provide the kernel density plots

of 24 tornado scales in Figure 3.1 and discern the inconsistent distribution shapes.

Since the densities (statistics) in A31, A41, A32, A42 scales are similar, any of

the statistics can be used to predict the losses in neighboring tornado scales. Due to

this relatively high predictability, the insurance companies are prepared to cover the

claims for such tornado property losses.

17

Texas Tech University, Thilini Mahanama, May 2021

2 4 6 8ln(Loss, $ 2019)

0

0.2

0.4

0.6

Den

sity

2 4 6 8ln(Loss, $ 2019)

0

0.2

0.4

0.6

Den

sity

2 4 6 8ln(Loss, $ 2019)

0

0.2

0.4

0.6

Den

sity

2 4 6 8ln(Loss, $ 2019)

0

0.2

0.4

0.6

Den

sity

2 4 6 8ln(Loss, $ 2019)

0

0.2

0.4

0.6

Den

sity

2 4 6 8ln(Loss, $ 2019)

0

0.2

0.4

0.6

Den

sity

2 4 6 8ln(Loss, $ 2019)

0

0.2

0.4

0.6

Den

sity

2 4 6 8ln(Loss, $ 2019)

0

0.2

0.4

0.6

Den

sity

2 4 6 8ln(Loss, $ 2019)

0

0.2

0.4

0.6

Den

sity

2 4 6 8ln(Loss, $ 2019)

0

0.2

0.4

0.6

Den

sity

2 4 6 8ln(Loss, $ 2019)

0

0.2

0.4

0.6

Den

sity

2 4 6 8ln(Loss, $ 2019)

0

0.2

0.4

0.6

Den

sity

2 4 6 8ln(Loss, $ 2019)

0

0.2

0.4

0.6

Den

sity

2 4 6 8ln(Loss, $ 2019)

0

0.2

0.4

0.6

Den

sity

2 4 6 8ln(Loss, $ 2019)

0

0.2

0.4

0.6

Den

sity

2 4 6 8ln(Loss, $ 2019)

0

0.2

0.4

0.6

Den

sity

2 4 6 8ln(Loss, $ 2019)

0

0.2

0.4

0.6

Den

sity

2 4 6 8ln(Loss, $ 2019)

0

0.2

0.4

0.6

Den

sity

2 4 6 8ln(Loss, $ 2019)

0

0.2

0.4

0.6

Den

sity

2 4 6 8ln(Loss, $ 2019)

0

0.2

0.4

0.6

Den

sity

2 4 6 8ln(Loss, $ 2019)

0

0.2

0.4

0.6

Den

sity

2 4 6 8ln(Loss, $ 2019)

0

0.2

0.4

0.6

Den

sity

2 4 6 8ln(Loss, $ 2019)

0

0.2

0.4

0.6

Den

sity

2 4 6 8ln(Loss, $ 2019)

0

0.2

0.4

0.6

Den

sity

L6L5L4L3L2L1

W1

W3

W2

W0

A10

A13

A20

A22

A30

A33

A32

A31

A40

A43

A42

A41

A50

A53

A52

A51

A60

A61

A12

A23

A62

A63

A11 A21

Figure 3.1: Kernel density plots for the property losses attributed to tornado scalesin A. Aij represents the tornadoes with path lengths in Li and path widths in Wj.

The two tornado scales A60 and A61 have the same length scale but different

width scales. Even though the difference between their path widths is only 90 ft,

the statistics seem to be significantly different. Clearly, this is an extremity and

insurance companies fail to cover such losses. For such cases, the government intro-

duced coverage programs to fund states of emergency. This funding is distributed by

the Federal Emergency Management Agency, which is a part of in Homeland Secu-

rity. They fund the states and local governments, but they do not fund individuals

directly.

Thus, we cannot use a single probability distribution (a unique statistic) to ex-

amine all the tornado-induced property losses in the database as their distributions

are distinct variants with reference to the physical parameters. For example, the

bimodal density curves in A22, A62 and A63 might be the result of the two-fold risk

assessment strategies used in the United States: 1. private insurance 2. government

coverages. We substantiate this claim using the characteristics of the forthcoming

statistical manifold on tornado property losses. As the initial step, we quantitatively

measure the differences between distributions of tornado scales in section 3.3.

18

Texas Tech University, Thilini Mahanama, May 2021

3.3 Assessing a Distance Matrix based on the Differences between Statistics in

Tornado Scales

In this section, we quantitatively compare the distributions of property losses for

the tornado scales introduced in section 3.1. In particular, we quantify the pair-

wise differences between the 24 distributions of property losses attributed to A using

Kolmogorov-Smirnov’s distance [20]. These measures provide the maximum dis-

tances between the empirical distribution functions of property losses of each pair in

A. For instance, the Kolmogorov-Smirnov’s distance between the property losses of

category Aij and Akl is given by

d(ij,kl) = maxx

(∣∣∣Fij(x)− Fkl(x)∣∣∣) i, k = 1, · · · , 6, j, l = 0, · · · , 3, (3.3)

where x denotes the property losses and Fij(x) is the proportion of property losses

in Aij less than or equal to x. Similarly, Fkl(x) is the proportion of property losses

in Akl less than or equal to x.

Consequently, we define a distance matrix (D) which consists of these pairwise dis-

tances, see Eq (3.4) and Figure 3.2. For example, d4,13 is the Kolmogorov-Smirnov’s

distance between the distributions of property losses in A40 and A12 tornado scales.

We utilize this distance matrix to investigate a geometrical representation to tornado

scales.

D =

A10 A20 · · · A63

d1,1 d2,1 · · · d24,1 A10

d1,2 d2,2 · · · d24,2 A20

......

. . ....

...

d1,24 d2,24 · · · d24,24 A63

(3.4)

19

Texas Tech University, Thilini Mahanama, May 2021

Figure 3.2: A visual representation of the distance matrix (D) which consists ofthe pairwise Kolmogorov-Smirnov’s distances between the distributions of propertylosses in tornado scales.

3.4 Visualizing the Distances of Property Loss Distributions between Tornado

Scales using Classical Multidimensional Scaling

We apply classical multidimensional scaling (also known as principal coordinate

analysis) [21, 39] for obtaining a visual representation of the distance matrix (D).

In particular, we obtain a two-dimensional configuration for the tornado scales in

terms of the distances between probability distributions of property losses. The

classical multidimensional scaling provides a two-dimensional coordinate matrix for

the tornado scales by minimising the following loss function (residual sum of square):

SD (X) =

√ ∑i 6=j=1,··· ,N

(dij − ||xi − xj||)2, dij ∈ D. (3.5)

20

Texas Tech University, Thilini Mahanama, May 2021

This maps tornado scales to a new configuration (X) such the distances in tornado

scales, dij, are well-approximated by the distances in new configuration ||xi − xj||,i.e., this quadratic optimization problem finds the best possible coordinates based

on the distances in D. The coordinate matrix (X) is calculated using the following

steps [40, 41]:

1. Use the distance matrix (D) to calculate the inner product matrix (B),

B = −1

2JDJ,

where J = I − 1n11T , I is the identity matrix, 1 is a vector of all ones and n is

the number of tornado scales (n=24).

2. Decompose B using

B = V ΛV T ,

where Λ = diag (λ1, . . . , λn) such that λ1 ≥ . . . ≥ λn ≥ 0, the diagonal matrix

of eigenvalues of B, and V = [v1, . . . ,vn], the matrix of corresponding unit

eigenvectors.

3. Extract the first and second eigenvalues Λ2 = diag (λ1, λ2) and corresponding

eigenvectors V2 = [v1,v2] .

4. The two coordinates are given by

X = [x1,x2]T = V2Λ

122 .

3.5 Learning an Underlying Framework for a Statistical Manifold on Tornado

Property Losses

In this section, we utilize the configuration of tornado scales obtained using clas-

sical multidimensional scaling to learn a statistical manifold for tornado-induced

property losses. First, we comprehend the inherent patterns related to length and

width scales (Li & Wj) in the two-dimensional configuration (with Coordinate 1 and

21

Texas Tech University, Thilini Mahanama, May 2021

Coordinate 2). Then, we integrate these conformations by introducing a third di-

mension (say Coordinate 3) which conserves unit distance between the consecutive

contours of length scales (Li, i = 1, ..6). In Figure 3.3, we outline the contours of

length and width scales using periodic interpolating cubic splines [42] on the space

constructed using the three coordinates.

Figure 3.3: The underlying framework of the statistical manifold on tornado-inducedproperty losses. Each edge is comprised of the periodic interpolating cubic splines andthe vertices are the tornado scales in A. The vertex, Aij, represents the tornadoeswith lengths in Li and widths in Wj.

Figure 3.3 is the underlying framework for the forthcoming smooth statistical

manifold on tornado-induced property losses. In this graph, each vertex represents

the probability distribution of property losses in the corresponding tornado scale

(Aij). Clearly, this configuration of tornado scales preserves the distances between

probability distributions of property losses in A. We ameliorate this skeleton to a

smooth statistical manifold in section 3.6.

22

Texas Tech University, Thilini Mahanama, May 2021

3.6 Upgrading the Underlying Framework to a Statistical Manifold using a

Subdivision Surface Method

The fuzzy structure in Figure 3.3 can be smoothened by enhancing the degree of

edges. We upgrade the geometry of the network in Figure 3.3 to a smooth manifold by

subdividing the ambient space of contours. In particular, we increase the cardinality

of vertices and subdivide each edge into 10 equally-spaced segments to obtain 10

supplementary vertices. Taking the new vertices into account, we add contours with

respect to width (Wj, j = 1, ..30) and length (Li, i = 1, ..50) scales using cubic

splines in Figure 3.4. As a result, we improve the coarse-grained conformational

manifold in Figure 3.3 to the smooth statistical manifold illustrated in Figure 3.4.

Figure 3.4: The learned statistical manifold for the property losses of tornadoes,constructed using the reported losses between 1993 and 2018. Aij represents thetornadoes with lengths in Li and widths in Wj. The manifold is constructed byimplementing classical dimensional scaling and a method of subdivision surfaces.

23

Texas Tech University, Thilini Mahanama, May 2021

Figure 3.5(a) is a different orientation of Figure 3.4 that we use to demonstrate the

compactness of cells in section 3.7. In fact, each point on this manifold potentially

represents a distribution of property losses for a given path length and path width.

In section 3.7, we delineate the statistics of the manifold by defining a curvature

coefficient.

3.7 Determining a Curvature Matrix for the Statistical Manifold

Each point on the learned statistical manifold, Figure 3.4, postulates a probability

distribution of property losses with respect to the physical parameters. However,

this curved manifold seems to be too complex to interpret. Therefore, we introduce

a matrix based on the characteristics of the manifold to interpret the compensations

for property losses caused by tornadoes.

In Figure 3.5(a), the bottom leftmost (A10-A11-A21-A20) and the top rightmost

(A52-A53-A63-A62) zones consist of compressing (dense) cells. The cells in the re-

gions neighboring A22-A23-A33-A32 and A51-A52-A62-A61 illustrate relatively high

expansions. Non-trivial curvatures are present in both of these cell types. Further-

more, the sporadic tornadoes reported in the database densify the corresponding

regions (A10-A11-A21-A20 and A42-A43-A63-A62) in Figure 3.5(a). Hence, the spa-

tial characteristics of the manifold potentially detect anomalies in tornado property

losses.

The probability distributions (statistics) of property losses in compressing cells

hardly change within neighboring cells (see Figure 3.1), i.e., that most of the cell

statistics have the same form in densification. However, since the statistics tremen-

dously vary from one cell to another in expanding cells, we identify the possible

regions for extreme tornado events. This variation escalates at the border zones of

compressing and expanding regions. The statistics in expansion and transition zones

change abruptly from the conventional statistics. In such cases, distinct statistics

are essential to determine the significant variations from one cell to another. Corre-

spondingly, the predictability of tornado property losses relates to the densification

of cells in the statistical manifold, Figure 3.4.

We quantify the expansions and densifications of cells to estimate the predictability

24

Texas Tech University, Thilini Mahanama, May 2021

of tornado property losses on the manifold, Figure 3.5(a). In particular, we determine

these deformations numerically based on the underlying curvatures of ambient spaces

in cells. Then, we define a measure of curvature (C) for a cell by comparing its area

with the mean area of the cells on the manifold as follows:

Cij = 1− Xij

E(X), i = 1, · · · , 50, j = 1, · · · , 30 (3.6)

where X denotes the area of a cell on the manifold, and Xij the area of a cell with i

and j denoting the lower leftmost two coordinates. The curvature coefficients provide

positive values for compressions and negative values for expansions in cells. Next,

we introduce a curvature matrix (C) for the statistical manifold learned in section

3.6 as follows:

C = [Cij]; i = 1, ..50, j = 1, .., 30. (3.7)

(a)

Width (Wj)

Leng

th (

Li)

-1.2

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

A10 A13A12A11

A62 A63A61A60

A20

A30

A40

A50

(b)

Figure 3.5: (a) The learned statistical manifold and (b) its curvature portrait (right).Figure (b) is constructed with respect to the positions of the path width (Wj, j =1, ..30) and path length (Li, i = 1, ..50) coordinates of a tornado. Yellow and blueregions in Fig (b) depict compressed and expanded cells in Figure (a), respectively.

25

Texas Tech University, Thilini Mahanama, May 2021

In Figure 3.5(b), we provide a visual representation of the curvature matrix with

respect to the positions of the width (Wj, j = 1, ..30) and length (Li, i = 1, ..50)

coordinates. The relative positions of some scales in A are shown in exterior locations.

In this curvature portrait, yellow and blue regions depict compressed and expanded

cells, respectively. The transitions between them (compressed and expanded cells)

are shown as green phases. Also, the legend in Figure 3.5(b) shows a color scale with

yellow for positive curvatures (compressed cells) and blue for negative curvatures

(expanded cells). In section 3.8, we describe how to utilize the curvature matrix for

assessing the risks related to tornado damage costs.

3.8 Determining the Risk Assessment Strategy based on the Curvature Matrix

Obviously, the risk assessment strategy for the damage caused by a tornado de-

pends on its severity. For typical tornadoes, the private insurance companies com-

pensate the property losses claimed by their clients. However, they fail to cover

the property losses attributed to catastrophic tornadoes. For such cases, the United

States Department of Homeland Security introduced Federal Emergency Manage-

ment Agency (FEMA) as a coverage program. When a catastrophic tornado occurs

in a state, the state governor proclaims a state of emergency. Upon the presidential

approval, FEMA distributes funds to state and local governments. Henceforth, the

local governments redistribute money to counties and municipalities but not directly

to individual victims.

The approaches of risk assessment strategies and compensations used in state

funds and private insurance companies are significantly different. In this section,

we identify these two different approaches using the statistical manifold. Then, we

analyze how the risk evaluation policies vary according to the physical parameters

of a tornado (i.e., from point to point on the manifold).

We compare the probability distribution plots of some main tornado scales with the

curvature portrait in Figure 3.6. Clearly, the probability distributions related to the

monochromic zones seem to have similar statistics. For example, the neighboring

region of A53 and A63 show a yellow zone in Figure 3.6, and their densities are

moderately similar. The statistics of either A53 or A63 potentially approximate the

26

Texas Tech University, Thilini Mahanama, May 2021

Figure 3.6: The curvature portrait with kernel densities of property losses of somemajor tornado scales in A. The statistics in monochromic zones show similar forms.

property losses caused by a tornado with a path length in the range of 100,000-

1,000,000 ft and a path width in the range of 100-1,000 ft.

In Figure 3.6, some regions of the statistical manifold show that the small changes

in physical parameters (Li and Wj) trigger vast changes in the statistics related to

their property losses. For example, the property losses reported for the tornadoes

in the zone bounded by A51-A52-A62-A61 vary dramatically. In such scenarios, a

single statistic fails to estimate such volatilities in property losses with respect to

small changes in tornado path lengths and path widths. Therefore, the blue regions

27

Texas Tech University, Thilini Mahanama, May 2021

on the manifold seem to demonstrate the potential tornado scales for extreme tornado

events.

The statistical manifold and its curvature portrait, Figure 3.5, provide a smooth

connection between the probability distributions of property losses in all tornado

scales of A. We described how the property losses vary with small changes of physical

parameters in section 3.7. As a result, we suggest a prospective framework for

recovering the proper risk assessment strategy for a tornado based on the statistical

manifold and its curvature matrix.

The two-dimensional statistical manifold reflects the principle of two-fold compen-

sation mechanisms for property losses in the United States. For small-scale torna-

does, the individual clients claim property losses from their insurance companies. For

losses due to catastrophic tornadoes, the government allocates funds for administra-

tive units to redistribute money to counties for compensations. We represent this

diversity of risk assessment strategies within the database using a two-dimensional

statistical manifold on property losses.

In this study, we identified the two different types of machinery to cover the prop-

erty losses caused by tornadoes by learning a statistical manifold. Even though we

determined compensations for the majority of the property losses reported in the

database [3], we failed to interpret some extremities. Furthermore, we can generalize

our statistical manifold learning algorithm for other applications with high dimen-

sional data.

28

Texas Tech University, Thilini Mahanama, May 2021

CHAPTER 4

ASSESSMENT OF TORNADO PROPERTY LOSSES IN THE UNITED STATES

In this chapter, we address three problems in tornado-related data analysis: (i)

classifying tornado events, (ii) measuring the dependence between tornado variables,

and (iii) predicting future tornado-induced property losses based on available his-

torical data [3]. In addition to the Enhanced Fujita Scale [1] based on wind speed

estimates, we propose a novel tornado event classification accounting for the prop-

erty losses in NOAA Storm Data [3]. Underpinning the proposed classification by

the Non-negative Matrix Factorization analysis [22], we introduce a new scale for tor-

nado damage, the Tornado Property Loss scale (TPL-Scale). We also investigate the

non-linear dependence between property losses and the area affected by tornadoes

using a copula approach [23]. The resultant correlation coefficients are not mono-

tonic over time and location. As a result, we suggest forgoing the copula approach

for assessing property losses. Finally, we apply the shallow and the Long Short-Term

Memory neural networks for predicting future tornado damage costs. Based on our

findings, the volume of property losses caused by tornadoes in the U.S. would amount

to almost eight billion dollars in the next five years (by 2025).

4.1 Classifying Tornado Data

In the traditional EF-scale [1], tornadoes are classified using wind speed estimates

and related property damages. We apply the Multiplicative Update (MU) algorithm

for NMF to classify tornadoes taking the reported property losses into account. As

a result, we introduce a new tornado property loss scale (TPL-scale).

4.1.1 Non-negative Matrix Factorization Method for Classification

Data representation techniques, such as Principal Component Analysis (PCA) and

Non-negative Matrix Factorization (NMF), explore the hidden structure of a data set

[43, 44]. Notwithstanding PCA is commonplace in research, NMF outclasses PCA

on strongly correlated, non-Gaussian, multivariate data [45, 46, 47]. Furthermore,

the interpretation of principal components for non-negative data, characterized by

29

Texas Tech University, Thilini Mahanama, May 2021

positive and negative coefficients, is vague (for example, negative property losses are

meaningless) [47, 48].

We consider the following data matrix: Vn×m = [log(Length), log(Width), log(Loss)]

(say, tornado matrix ). The tornado matrix (V ) consists of non-negative elements,

and the tornado variables (column vectors) follow non-Gaussian distributions (Fig-

ure 2.5). In order to get better results for tornado data classification, we apply the

NMF method which surpasses the potential limitations of conventional PCA [22, 47].

In NMF, the non-negative data matrix Vn×m is approximated by the product of two

non-negative matrices (Wn×r and Hr×m);

Vn×m ≈ Wn×rHr×m, (4.1)

where the rank of factorization (r) is a value less than the number of variables (m)

and the sample size (n) in the data matrix (V ) [22, 49, 50, 51]. The factor matrices

(W and H) represent latent and salient components of the data set [51]. In particular,

the jth variable in V is approximated by a linear combination of the columns in W

weighted by the elements of jth column in H [22];

V (:, j) ≈r∑

k=1

W (:, k)H(k, j) = WH(:, j), r < min(n,m), j = 1, · · · ,m.

(4.2)

The collection of all m variables results in the factorization of the data matrix

(4.1) [44, 49]. Theoretically, the m−dimensional data vectors in V project to an

r−dimensional linear subspace spanned by the columns in W (where the coordinates

are the elements of H) [50]. Thus, the linear approximation of V optimizes with the

basis W [22]. We determine the optimal W and H so that they minimize the recon-

struction error between the data matrix (V ) and its NMF image (WH) [49]. The