LH Stock Valuation

44

Content Introduction................................................ 2 1. Objective.............................................. 2 2. Company Profile........................................ 3 3. Product Overview....................................... 6 4. Houses Concept......................................... 6 Industry Analysis........................................... 8 1. Interest rates falling.................................8 2. Mortgage Rate is expected cut..........................8 3. The Readiness to Buy Home Index is bottoming...........8 4. Stimulus from Government and Banking...................9 5. Oversupply caution..................................... 9 6. Strategies for property developer.....................10 Competitors Analysis.......................................11 Land and Houses Overview...................................14 Risk of Land and Houses....................................25 Land and House Co., Ltd Analysis...........................27 1. Company’s marketing & business strategy to expand their business or cope with rising competition?................27 2. How is the company doing to cope with change in consumer behavior?................................................ 28 3. Company is losing customers or gaining customers?.....28 4. Rising demand for natural gas, oil, steel and petrochemical products in the world, region is benefiting the company?............................................. 29 Financial Analysis......................................... 30 1. Company Assumption.................................... 30 2. Ratio Analysis........................................ 30 3. Weighted Average Cost of Capital......................31 4. Forecasting Y2007-Y2011...............................31 5. Free Cash Flow........................................ 32 6. Terminal Value........................................ 32 7. Enterprise Value...................................... 32 8. Company Evaluation.................................... 32 Conclusion................................................. 33 Reference.................................................. 34 Page 1 of 44

-

Upload

assumptionuniv -

Category

Documents

-

view

4 -

download

0

Transcript of LH Stock Valuation

Content

Introduction................................................21. Objective..............................................22. Company Profile........................................33. Product Overview.......................................64. Houses Concept.........................................6

Industry Analysis...........................................81. Interest rates falling.................................82. Mortgage Rate is expected cut..........................83. The Readiness to Buy Home Index is bottoming...........84. Stimulus from Government and Banking...................95. Oversupply caution.....................................96. Strategies for property developer.....................10

Competitors Analysis.......................................11Land and Houses Overview...................................14Risk of Land and Houses....................................25Land and House Co., Ltd Analysis...........................27

1. Company’s marketing & business strategy to expand their business or cope with rising competition?................272. How is the company doing to cope with change in consumerbehavior?................................................283. Company is losing customers or gaining customers?.....284. Rising demand for natural gas, oil, steel and petrochemical products in the world, region is benefiting the company?.............................................29

Financial Analysis.........................................301. Company Assumption....................................302. Ratio Analysis........................................303. Weighted Average Cost of Capital......................314. Forecasting Y2007-Y2011...............................315. Free Cash Flow........................................326. Terminal Value........................................327. Enterprise Value......................................328. Company Evaluation....................................32

Conclusion.................................................33Reference..................................................34

Page 1 of 44

Introduction1. Objective

“Investor Information Analysis”

Our objective will provide essential information to theinvestor for decision making before putting down capital inLand & Houses Public Company Limited.

The principle before putting down the capital forinvestment to any projects or company, the investor need toknow as much as possible about those projects or company,without analytical of company information, you might notget the right information for investing to those projectsand company.

Land & Houses Public Company Limited, Thailand No. 1Real estate development company which established since1973 and it was enter to Stock Exchange of Thailand (SET)on 1989 having the high reputation and good financialprofile. The company has pass thru year by year and eventhe economic crisis. This is interesting to us forrecommendation to who like to do the investment on it.

This report will cover all about information of Land &Houses company profile, industry and company analysis,financial & Performa forecasting and the conclusion withrecommendation for investing as below.

Page 2 of 44

o Land & Houses Company Profileso Real Estate Industry analysiso Land & Houses company analysiso Land & Houses Performa analysiso Financial forecasting analysiso Conclusion & Recommendation

2. Company Profile

Land & Houses Company Summary History:

Year 1973,

Ms.Piangjai Harnpanich, one of the Company's Boardof Directors and a mother of Mr.Anant Asavabhokhin whoestablished Land and Houses, originally managed thefirst small housing project, namely Baan Srirubsuk.However, at that time, the operation of the Company wasnot only dramatically attacked by the first Oil Crisis,but also hit by an extremely high interest rate of 20-21% and that only 2 units were successfully sold. By theyear 1977, the sales was gradually increased and theCompany developed more projects; Baan Thanintorn, BaanSuknatee and Baan Prachachuen.

Page 3 of 44

Year 1983 – 1984 ,

Land and Houses was incorporated on August 30, 1983as a limited company and managed Prueksachart, a housingproject purchased from Teeraparb Co., Ltd., one of ThaiFarmers' Bank's subsidiaries.

Year 1983,

Land and Houses had undergone in depth research anddeveloped the "Consumer Oriented" concept in BaanNuntawan project in Chiengmai which brought about thecompany's strong reputation in product development anddifferentiation in single detached house market.

Year 1984 – 1986 ,

Siwalee project was developed in Rangsit arearegards the focus to maximize homebuyer's needs. TheCompany's sales revenue started to grow steadily.

Year 1989,

The Company became a licensed company in the StockExchange of Thailand or SET on February 17,1989 and waslisted as Land and Houses Public Co., Ltd on April 1,1991.

Since its listing in SET, Land and Houses productsegmentations have been divided into several differentbrand names and pricing. The slogan "One of Land andHouses' Brands" was also created and used as theCompany's strategy to promote brand names in alldevelopments.

Year 1993,

Page 4 of 44

Land and Houses was the first one to issue ECD(Euro Convertible Debenture) to the foreign investors inthe Company? Road Show in Hongkong, Japan, USA, France,Germany, England and Scotland.

Year 1994,

The Company hit its first high of >10,000 millionbath in sales revenue.

Year 1995,

L&H purchased Chao Thai Securities and renamed itNithipat Finance and Securities Co., Ltd, owning 36% ofthe issued share capital as part of its strategy ofinvesting.

In Dec 1995, L&H entered a joint venture agreementwith Government of Singapore Investment Corporation(GIC, 25%) and OCBC Capital Management (25%),subsidiaries of OCBC Bank Group in Singapore.

Year 1996,

The Company invested 700 million baht in BangkokTransit System Public Co., Ltd or BTSC and held 2.92% ofshare. The investment was divided into 350 million bahtof shares and another 350 million baht cost ofConvertible Debenture.

Page 5 of 44

Capital in first 3 years = 2,500 million baht

Nithipat Securities PLC

Securities One PLC

12.5%

12.5%

12.5%

12.5%

25% 25%

Year 1999,

The Company sold 94,285,715 ordinary shares, or21.17% of all issued ordinary shares, to Government ofSingapore Investment Corporation (GIC) at 14 baht each,raising 1,320 million baht for recapitalization.

Year 2000,

The Company invested in Asia Asset AdvisoryCo.,Ltd., intending to purchase or lease real propertyor invest in the claims, by subscribed 499,994 shares atthe price of Baht 10 each, with the aggregate amount of4.99 Million Baht or 49.99%. L&H developed the OnlineProject Management System (OPM), http://www.homedd.com,the Pre-built house strategy

Year 2001,

L&H was the first Thai firm to adopt the pre-builtconcept (houses ready-built before sale) in 2001

Year 2003,

L&H started developing the new constructiontechnology of Pre-Fabricated Wall. The state-of-the-arttechnology will have main objectives to enhanceconstruction quality and efficiency and reduceconstruction times. The first housing project to beimplemented the pre-fab wall system is Prueklada RangsitKlong 4, which has detached houses costing from 2.5million baht.

Year 2004,

The company pioneered the strategy of Pre-BuiltCondominium, which simply means that condominium unitssold by L&H are totally completed construction andbuilt-in furniture will be included. The condominium

Page 6 of 44

strategy is implemented at four locations of innerBangkok including Sap Road, Sukhumvit Soi 61, SukhumvitSoi 43 and Narathiwat Ratchanakarin Road, under thebrand name of The Bangkok.

Year 2005,

Established LH Bank, the Location of L&H’s HeadOffice: At Q. House Lumpini Building, South Sathorn

Year 2006,

The current portion of Land & Houses in the marketstill in the leader of the market.

3. Product Overview

* SDH – Single Detach House

Page 7 of 44

SDH-BKK

SDH-UPC

Condo-BKK

Real-Estrate M arket Share

21%

2%

24%10%

14%

14%

15% AP LALIN LH LPN PS Q H SIRI

4. Houses Concept

Relaxation and Energy Saving

1. Q-Con Block wall:Q-CON blocks provide thermal insulation enable the

house stays cool, acoustic barrier up to 38 dB and 4hours of fire resistant.

2. Wood grille suffix around the house:Provide good ventilation and heat transmission from

under the roof.

3. Thermal reflection sheet under roof:Reduce heat from roof before transmitting into the

house.

4. Solar-screen glass:Reduce light intensity and screen UV ray coming

from outside.

Utilization and Smart Design

1. Buddha image room or shelf2. Built-in bath seat and bath shelf3. Fiber mosquito wire screen4. Wet & dry separating5. Special glass loft in living room and/or bathroom and

bedroom6. Floor, wall and bathrooms furnished7. Side door to the garden8. Area for a washing machine with water supply and

electric systems Reinforcement System

1. Emergency down light2. Special design for garbage & mail box3. Underground water reservoir system4. Garden design and landscape architecture

Page 8 of 44

5. Termite protection6. Ready-to-use Air conditioner

“Ban Sabai” is ready built and ready to bemoved in

Page 9 of 44

Industry Analysis1. Interest rates falling

The recent policy rate cuts by the Bank of Thailand anddeposit rate cuts by commercial banks makes it likely thatmortgage rates will be cut - possibly as high as 100bp byyear end. Chalongpop Susangkarn, the new Minister of Finance,has indicated that rates may fall rapidly. The BOT has todate this year cut its policy repo rate twice for a total ofalmost 75bps. We expect the material reduction in interestrates to encourage consumers to make a decision to buy ahome.

However, in the short-term, homebuyers may adopt a wait-and-see strategy in hopes of a deeper rate cut before makinga decision. If this is the case, we expect to see strongerdemand in 2H07.

Our correlation study suggests that over the long terminterest rates do not have a material impact on housingdemand, with correlation at only 42%. However, interest ratesdo have a psychological impact on timing of decisions.

2. Mortgage Rate is expected cut

Page 10 of 44

We also expect mortgage rate cuts will follow. Bycalculations, each 100pbs cut in mortgage rate increaseshomebuyers’ affordability by 8%. Rising demand is expectedafter sharp rate cut.

3. The Readiness to Buy Home Index isbottoming

Given that the purchase of a home can be thought of as atype of savings, confidence is also important on timing ofdecisions. Consumer readiness to buy homes peaked in 2004before falling to near 80, where it has been relativelystable. We see low risk of a further drop in the index in thenear future. But the confidence level remains low due tolingering urban unrest and political uncertainties.

We do see positive factors that could boost the indexincluding:

1) Lower inflation 2) Lower interest rate 3) GDP growth forecast at around 4% in 2007 versus 5%

in 2006 4) A national election by the end of 2007.

4. Stimulus from Government and Banking

A combination of fiscal stimulus and rate cuts couldeffectively boost the property market. The new MOF leadership

Page 11 of 44

will be watched closely. The stimulus ideas from theGovernment Housing Bank include:

Soft loans totaling Bt30bn for first-time buyers, withloans up to Bt3mn per individual

Interest rates fixed for 3 years at 4.75%, then floatedto MLR

Cut in transfer fee from 2% to 1bp and in mortgage feefrom 1% to 1bp and in special business tax from 3.3% to1bp.

Personal tax deduction increased to Bt100,000 fromBt50,000.

Credit Bureau blacklisting cut to 2 years from 3 years. More lenient leasehold rights (90<-30 years) for

foreigners.

5. Oversupply caution

New launch trend reversing up. In terms of units, thenew supply trend is reversing upwards, raising concerns of anoversupply, especially for condos. New condo supply doubledYoY in 1Q07 and its share shot up to 68% in 1Q07 from 33% in2005 and 47% last year. Trend for smaller house unitscontinues, supporting the idea that developers are adjustingtheir house sizes to homebuyer affordability.

6. Strategies for property developer

Page 12 of 44

There are 3 strategies for property developer to launchtheir product into market

Pre-built => 100% constructed before sale Pre-sale => Booking before build Semi pre built => 50% constructed and launch to the

market

Land & Houses is considered as a only developer whoadopt Pre-built strategy

Competitors Analysis

Listed companies move to lower marketsegment

Page 13 of 44

Two points support our view that listed developers aremoving to a lower end housing market and are stealing marketshare from non-listed companies:

1. Average selling prices of our listed universe fellto just Bt2.2mn/unit from over Bt3mn in the past.

2. Market share of the listed developers rose to 51% in1Q07 from 17% in 2003 in terms of units and to 52%from 36% in terms of value.

Better competitive climate in SingleDetach House market than condo

We believe competition in the condo market has becomemore severe than in SDH as supply has risen strongly. In2006, overall new housing supply increased only 7% YoY to63,636 units, according to AREA, but the shift to the condomarket is clear, with new condo supply shooting up 50% YoYwhile new SDH supply of SDH dropped 29% YoY. The trend hascontinued through 1Q07 with YoY condo supply rising 104% to11,183 units while SDH shrank 62% to 1,379 units. The shareof condos is high at 68% with SDH just 8% which are good forLand & Houses as a leader in SDH market.

Margin outlook sustainable

We believe the company’s real estate margin will besustainable at 30-31% for the next two years, not a levelthat will encourage a flood of new supply. Further keepingsupply - and competition - down is the reluctance by bankersto extend loans to small and medium size developers. Based onthe seven stocks in our universe, margin peaked in 2003 whenthe market began to recover and competition was low.

Modest sector presales

We estimate total presales in seven leader companies atBt17bn, +4% YoY and +1% QoQ. Presales growth for mostdevelopers came from new products and/or new locations.

Asian Property is the winner YoY with 109% growth, LPN wins QoQ with 125% growth.

Page 14 of 44

Presales (Bt m n)

฿0฿1,000฿2,000฿3,000

฿4,000฿5,000฿6,000

AP LALIN LH LPN PS Q H SIRI

4Q 06 1Q 07

Source: SCBSPresales (Bt m n)

฿0฿1,000฿2,000฿3,000

฿4,000฿5,000฿6,000

AP LALIN LH LPN PS Q H SIRI

4Q 06 1Q 07

Source: SCBS

Detail of each competitors:

Asian Property

Order book was Bt3.5bn in 1Q07, +109% YoY and +29%QoQ,boosted by strong presales of the “ Address @ Chidlom”,which took half of total bookings. This projectregistered bookings of 50% of units and 72% of project value.AP claims this is due to price increases and fixture salesvalue, and this lifts project value by at least 25%.

Lalin Property

Page 15 of 44

Order book was Bt400mn, +16% YoY but -33% QoQ. YoYpresales growth was not impressive at a fall of 5% from thequarterly average Bt420mn in 2006, probably because it hasnot initiated a significant new strategy (product/market)development.

Land and Houses

Order book is estimated at Bt4bn, +9% YoY but -23% QoQ.The drop QoQ was due to high sales in 4Q06 from a stockclearance promotion. Sales for its smaller SDH likePruekladda and TH were strong.

LPN Development

Bookings reached Bt1.7bn, -20% YoY but +125% QoQ, mainlyfrom the February launch of Lumpini Condo Town Bodin-Ramkamhaeng, now at 63% booking.

Preuksa Real Estate

Order book was Bt2.4bn in 1Q07, +26% YoY and +28% QoQ.The improvement was mainly from better sales of TH as itexpands to new locations and market segment (Bt1-2mn).Despite growth, we see downside risk to its target as itachieved only 20% of full year targeted presales of Bt12bn.

Page 16 of 44

Land and Houses Overview

Land & Houses Public Co., Ltd., is Thailand No.1 residential housing developer with 32,000 units of Single Houses built in the past 20 years.

"Baan Sabai" or "Comfortable Home" a new concept ofready built and ready to be moved in is another step ofquality living from Land & Houses. There are available in thegreater Bangkok and its vicinity as well as in other majorcities in Thailand, there are, Chiang Mai, Khon Kaen, NakhonRatchasima and Phuket.

The main key characteristics of Land and Houses:

Page 17 of 44

L&H reputation for superior quality, location, andafter-sales service, as well as its strong franchise,quality of management, liquidity, and scarcity are allpositives.

L&H business mainly focus in the Single Detach House(SDH).

L&H three biggest shareholders are the Thai NVDR Co.,Ltd., 22.62% stake, the company founder AnantAsavabhokhin, 20.92% stake, and the Government ofSingapore Investment Corporation (GSIC), 12.33% stake incurrently.

L&H was the first Thai firm to adopt the “Pre-Built”concept in 2001.

L&H key competitive advantages are strong brandrecognition and a reputation for quality and sensitivityto the interests of its customers.

In recent years, with the downturn in demand for SDHs,LH increased the number of townhouse projects in itssales portfolio and started building condominiums.

L&H Sales in Y2006 is Bt20bn, 4,000 units which implythat cost of house is Bt4.8m per unit.

Page 18 of 44

In 2007, New project launches with Bt12bn (Bt8bn low-rise; Bt4bn of condo). Average sales price per unit isBt3.8m. L&H increase business proportion in high growthsegment which are Condominium and Townhouse and downsizethe housing area

L&H expected to increase sales proportion in high growthbusiness from 5% to 30% by Y2011

L&H is looking for higher sales in 3Q07, partly drivenby the “Five Dee Dee campaign from LH” on 21-22 July2007. This campaign will offer five promotions in manylocations which are:

1) A good plot2) A good address number3) A new house model4) Some furnishings

Page 19 of 44

5) Value for money

According to company guidance, the campaign will notcause gross margin erosion.

SDH supply squeeze is good for LH: From a 2004 peak, SDHproject launches have declined for three consecutiveyears. Bualuang Analyst forecasted that total SDH unitsavailable for sale in 2007 will plunge 53% YoY. That canonly benefit LH, the SDH leader. Land and Houses Performance in the past 3

Quarters:

1. Sales Growth:

In Q2’07, Land and Houses sales volume hadincreased 19.1% from the Q1’07 and 8.2% from Q2’06. Thissituation can summary that the trend of sales growthwill be increased. The property and real estate businessis better since Q2’07. The reason of declining rate ofQ1’07 is from the Political Climate Worsens which effectto the country economic slow down. Then it effects tothe consumer consumption. Consumer has demand on theproperty but they would like to wait for the clearpicture of Thai government which will have the electionat the end of Y2007.

Page 20 of 44

2. Pre-Sales of DH by segment – 1H07:

In the first half of Y2007, the highest segment ofPre-Sales for Duplex Houses is segment 3 MB to 5 MB, at38.4%. The reason is the consumer behavior changed. Fromthe economic crisis since Y2006, it effects to thecustomer buying power. Therefore, Land and Houses hadchanged their strategy to concentrate and launch lowerprice rate project to compete with the competitors.

Page 21 of 44

3. Gross Profit of Land and Houses:

Gross profit of Q2’07 is higher than Q1’07 at 0.5%but lower than Q2’06 at 1.4%. The reason that in Q2’07,L&H gets lower gross profit than Q2’06 due to the SE&Aexpense of Q2’06 was lower than Q2’07.

Page 22 of 44

Page 23 of 44

4. Corporate Tax:

Due to the sales volume of Q2’07 is sharplyincreasing from Q1’07 and Q2’06. Then sales revenue isquite high. Then it effect to the corporate tax besharply increasing same as the sales revenue.

5. Net Profit:

Net profit of Q2’07 is higher than Q1’07 at 32.1% butlower than Q2’06 at 3.6%. The reason that in Q2’07, L&Hgets lower net profit than Q2’06 due to the increasingpercentage of sales revenue for Q2’07 is lower than thepercentage changed of SE&A and Corporate Tax.

Page 24 of 44

Page 25 of 44

Land and Houses Projects Plan in 2007:

There are 9 projects of Land and Houses in 2007 whichcovers SDH, Condo and Townhome. The planned total projectsvalue is 8,055 million Baht with 1,902 units.

Page 26 of 44

Land and Houses Organization Structure

Page 27 of 44

Page 28 of 44

Land and Houses Shareholder Structure

List of 10 major shareholders ended on April 10, 2007

No. Shareholder ShareCapital

%Holding

1. Thai NVDR Co.,Ltd 1,958,781,647

22.62%

2. Mr. Anant Asavabhokin 1,811,231,460

20.92%

3. Government of SingaporeInvestment Corporation

1,067,600,800

12.33%

4. Chase Nominee Limited42 288,401,240

3.33%

5. Mayland Co.,Ltd. 276,234,540

3.19%

6. THE BANK OF NEW YORK (NOMINEES)LIMITED

230,393,000

2.66%

7. Mayland Co.,Ltd. 218,863,140

2.53%

8. STATE STREET BANK AND TRUSTCOMPANY, FOR LONDON

216,704,790

2.50%

9. Miss Piengchai Harnpanich 205,000,000

2.37%

10. Social Security Office 180,206,800

2.08%

Total shares held 6,453,417,417

74.53%

Total number of issued shares 8,658,750,946

Page 29 of 44

Page 30 of 44

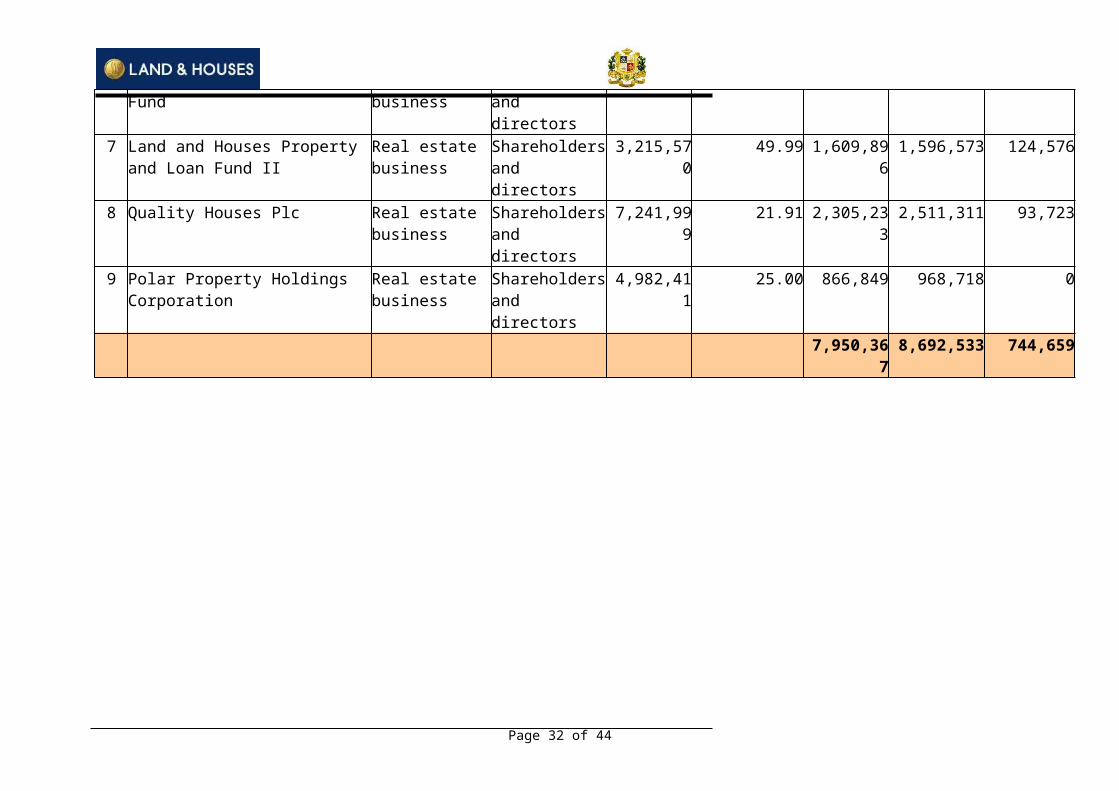

Land and Houses Associated Companies

Investments in Associated Companies Data as of 31 December 2006

No.

Company's Name Nature ofbusiness

Type ofrelationsh

ip

Paid-upCapital

Shareholding

Percentage

Cost CarryingAmount

Dividend

1 Land and Houses Retail Bank Plc.

Retail Bank Shareholdersand directors

1,900,000

43.00 1,005,960

661,216 0

2 Bangkok Chain Hospital Plc.

Hospital Shareholdersand directors

950,000 28.55 661,669 678,413 51,621

3 Quality Construction Products Plc.

Building material

Shareholdersand directors

400,000 31.41 265,980 437,354 0

4 Home Product Center Plc. Trading of constructionmaterials

Shareholdersand directors

1,919,818

28.75 906,328 1,313,975 50,786

5 Asia Asset Advisory Co., Ltd.

Investment advisor

Shareholdersand directors

5,000 40.00 2,000 10,324 5,600

6 Land and Houses Property Real estate Shareholders 639,943 49.94 326,452 514,649 418,353

Page 31 of 44

Fund business and

directors7 Land and Houses Property

and Loan Fund IIReal estate business

Shareholdersand directors

3,215,570

49.99 1,609,896

1,596,573 124,576

8 Quality Houses Plc Real estate business

Shareholdersand directors

7,241,999

21.91 2,305,233

2,511,311 93,723

9 Polar Property Holdings Corporation

Real estate business

Shareholdersand directors

4,982,411

25.00 866,849 968,718 0

7,950,367

8,692,533 744,659

Page 32 of 44

Risk of Land and Houses

Business Risk:- Risk concerning pre-built house andresidential condominium construction and other factorsas:

1.1) The higher price of consumer goods due to theincrease and fluctuation of global oil prices

1.2) The price rise of residential units in accordancewith construction material costs

1.3) The upward trend of interest rates1.4) The potential economic slowdown1.5) Currency effect: this point effects to the economic

and consumer consumption trend. Consumers willdecide to slow down their buying. Therefore, iteffects to the sales planning and forecasting ofLand and Houses.

Financial Risk:

1.1) Incurred by guaranteeing loans for LH Muang MaiCo., Ltd. and its subsidiaries, to meet theobligations according to the debt restructuringagreement

1.2) Incurred by impairment of long-term investments,which could result in a decline in investmentvalue.

1.3) Incurred by impairment of an investment insubsidiary Land and Houses Retail Bank Plc.

1.4) Incurred by lending to subsidiaries and byguaranteeing loans for associated companies

1.5) Incurred by lawsuits1.6) Incurred by guaranteeing loans for customers1.7) Incurred by creditability of the financial

statements1.8) Incurred by rising interest rates: This will

decrease affordability and result in weaker housesales.

Page 33 of 44

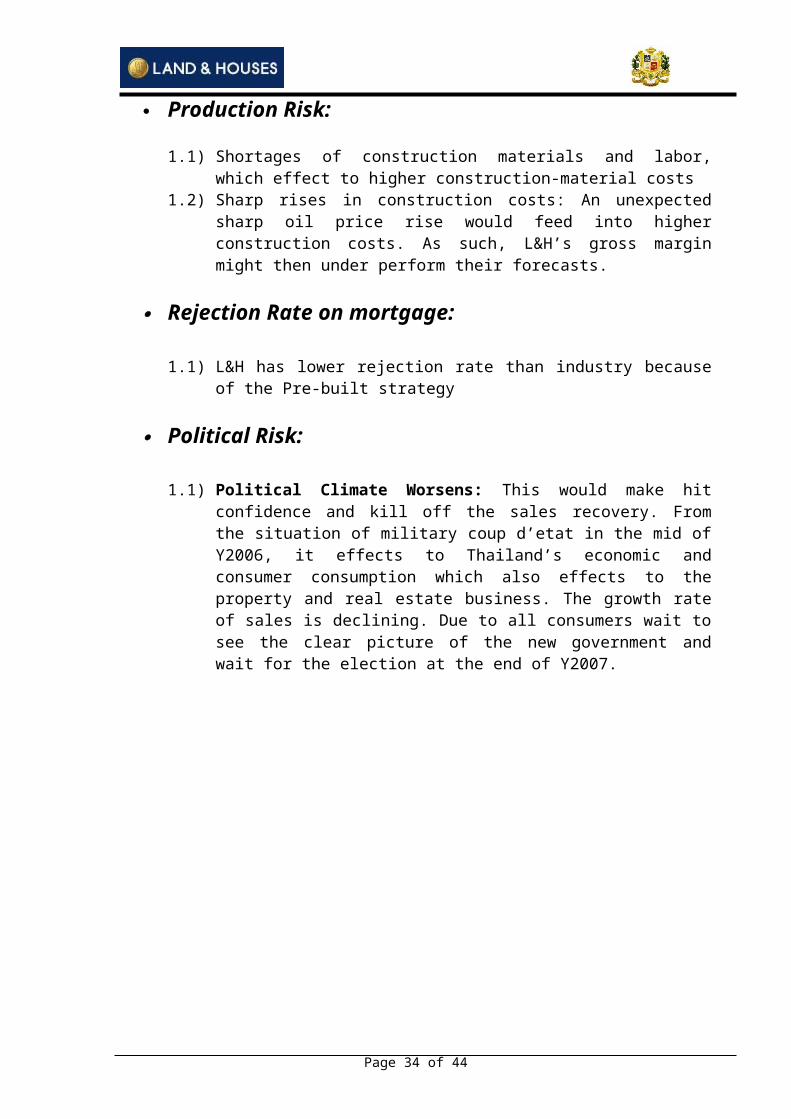

Production Risk:

1.1) Shortages of construction materials and labor,which effect to higher construction-material costs

1.2) Sharp rises in construction costs: An unexpectedsharp oil price rise would feed into higherconstruction costs. As such, L&H’s gross marginmight then under perform their forecasts.

Rejection Rate on mortgage:

1.1) L&H has lower rejection rate than industry becauseof the Pre-built strategy

Political Risk:

1.1) Political Climate Worsens: This would make hitconfidence and kill off the sales recovery. Fromthe situation of military coup d’etat in the mid ofY2006, it effects to Thailand’s economic andconsumer consumption which also effects to theproperty and real estate business. The growth rateof sales is declining. Due to all consumers wait tosee the clear picture of the new government andwait for the election at the end of Y2007.

Page 34 of 44

Land and House Co., Ltd Analysis1. Company’s marketing & business strategy toexpand their business or cope with risingcompetition?

Compete with the competitors:o “Pre-Built Condominium”: This is the unique and

positive strategy which Land and House used tocompete with the competitors since Y2001 andsuccessful. Therefore, Land and Houses shouldmaintain this concept onward.

o “Home Saving Package”: This strategy is justlaunched and applied with The Room Condominium

Page 35 of 44

Project. The response from the customers is veryhigh. It is very attract and impress to customer.It also motivated the customers to buy theCondominium easier.

Special feature of “Home Saving Package”: Have chance to reserve or book the room before

the project completed by no need to do downpayment.

Get special saving interest rate at 4.75% peryear from LH Bank

Reduce the risk of rejected loan and loss thedown payment

Chance to get the special approve from LH Bankwith the lower loan interest rate

Special right to cancel the booking ifcustomer does not like and get back all downpayment with saving interest rate

o “Low home loan interest rate” by LH Bank.o “Five Dee Dee” Campaign: This campaign will offer

five promotions in many locations which are: a good plot a good address number a new house model some furnishings and value for money

o Maintain the advertising and promotion campaign

Expand L&H Business:o “Land & Houses Park”:- Expand the project to the

upcountry – 4 provinces as: Chiang Mai Khon Kaen Nakhon Ratchasima Phuket

Page 36 of 44

2. How is the company doing to cope withchange in consumer behavior?

Consumer Behavior: Change to live in central of cityor business area with facilities Change the strategy of SDH from high price to middle

or low price range Increase the production line to condominium and

townhouse.

3. Company is losing customers or gainingcustomers?

Gain more customer in condominium and townhouse

The support reason for gaining customers:-

Housing demand will recover, led by:-i. A consumer confidence upswing in 2H07 coupled

with a better economic outlookii. Lower interest ratesiii. An easing political climate -- Will have election

at the end of Y007

Page 37 of 44

iv. L&H has the strongest brand recognition among

homebuyers due to its reputation for quality andits sensitivity to the interests of customers

v. Increase in demand of customer in Condominium andTownhome

4. Rising demand for natural gas, oil, steeland petrochemical products in the world,region is benefiting the company?

Rising demand for oil, steel and petrochemical productswhich are the main source of raw materials for L&H whichwill effect to the construction cost to be higher which hasaffect to L&H selling price and affect to customer demand.

Page 38 of 44

Financial Analysis1. Company Assumption

To forecast the financial data for evaluate the company;we assume the concerned factors as below:

Balance Sheet, we assume that PP&E (Property, Plant and Equipment) or Capital

Expenditure assume that it will grow at 500 millionbaht every year

Long term Debt is the adjustment module for BalanceSheet while the

Retained Earning = Retained Earning Y2005 + Net Income– Dividend payment, and assume to maintain as Y2006

The other factors will vary by average sales 2005-2006.

Income Statement, we assume that Sale’s sustainable growth rate at 10% The rest factor will vary by average sales 2005-2006.

Kd refer to LT bond of LH at 5% Ke from CAPM calculating and the details are as

below; Ke = 10.25%

Page 39 of 44

2. Ratio Analysis

2005 2006 2007E 2008E 2009E 2010E 2011ELeverage RatiosLong term debt ratio LTD/(LTD+E) 0.12 0.10 0.01 0.12 0.22 0.31 0.38Debt equity ratio (LTD+Value of leases)/E 0.14 0.12 0.01 0.14 0.29 0.44 0.62Total debt ratio TD/TA 0.40 0.44 0.33 0.40 0.46 0.51 0.55Tim es interest earned EBIT/Interest paym ent -30.67 -28.67 -67.12 -53.29 -20.28 -13.04 -9.88

Liquidity RatiosNet working capital total asset ratio NW C/TA 0.53 0.37 0.43 0.42 0.42 0.42 0.42Current ratio CA/CL 4.96 2.65 3.36 3.36 3.36 3.36 3.36Quick ratio (Cash+M KT Securities+A/R)/CL 0.50 0.26 0.33 0.33 0.33 0.33 0.33Cash ratio (Cash+M KT Securities)/CL 0.50 0.26 0.33 0.33 0.33 0.33 0.33

Efficiency RatiosAsset turnover ratio Sales/AVE TA 0.15 0.12 0.12 0.12 0.12 0.12 0.26Inventory turnover ratio COGS/AVE inv 0.17 0.14 0.14 0.14 0.14 0.14 0.30Days' sales in inventory AVE INV/(COGS/365) 538 664 632 632 632 632 301

Profitability RatiosNet profit m argin (EBIT-Tax)/Sales 0.32 0.26 0.29 0.31 0.31 0.31 0.31ROA (EBIT-Tax)/AVE TA 0.19 0.12 0.14 0.15 0.15 0.15 0.31ROE NI/ AVE E 0.22 0.13 0.15 0.14 0.15 0.16 0.35

Leverage ratio, we found that the margin in this groupis still low which they are less that 1. This means that Landand Houses ability to pay loan is very high.

Liquidity ratio, we found that the liquidity of companyis neutral.

Efficiency ratio, the turnover ratio is standard to theindustry. Because Land and Houses is the real estate businesswhich will have a very low inventory turnover as normal.

Profitability ratio, we found that the profit margin isgood and can maintain at 30% approximately. While ROA and ROEare 15% approximately.

3. Weighted Average Cost of Capital

Beta

Page 40 of 44

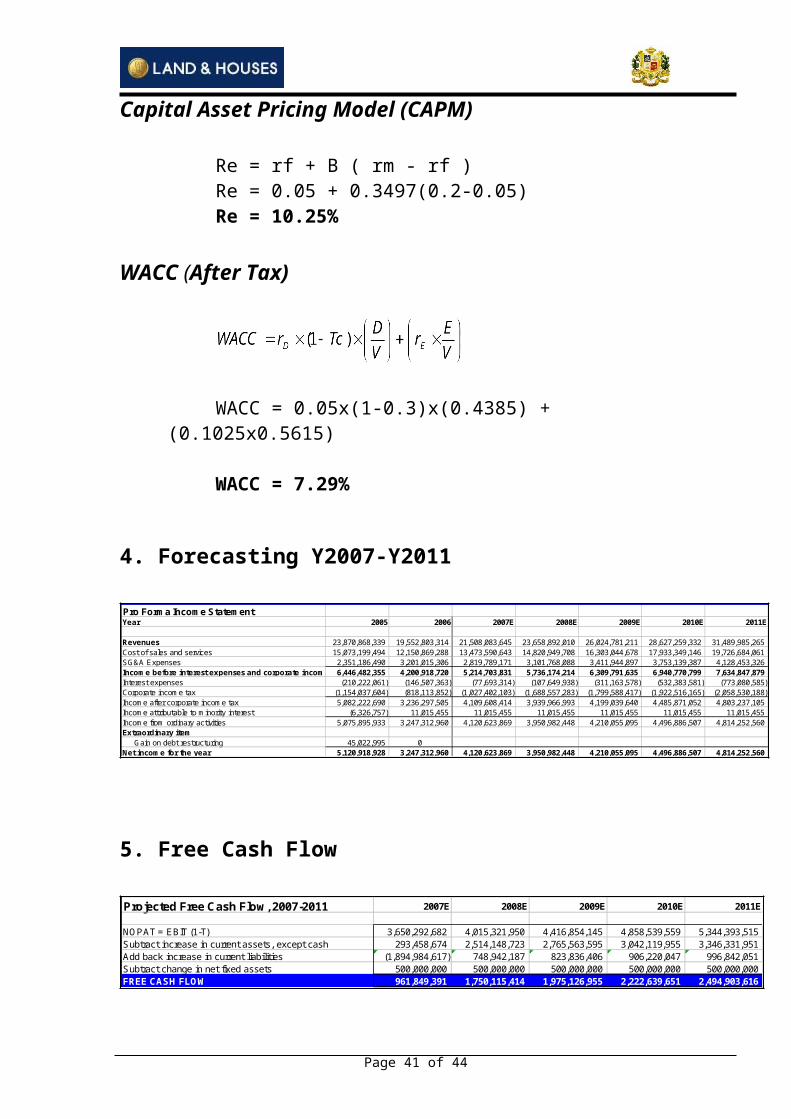

Capital Asset Pricing Model (CAPM)

Re = rf + B ( rm - rf )Re = 0.05 + 0.3497(0.2-0.05)Re = 10.25%

WACC (After Tax)

WACC = 0.05x(1-0.3)x(0.4385) + (0.1025x0.5615)

WACC = 7.29%

4. Forecasting Y2007-Y2011

Pro Form a Incom e Statem entYear 2005 2006 2007E 2008E 2009E 2010E 2011E

Revenues 23,870,868,339 19,552,803,314 21,508,083,645 23,658,892,010 26,024,781,211 28,627,259,332 31,489,985,265Cost of sales and services 15,073,199,494 12,150,869,288 13,473,590,643 14,820,949,708 16,303,044,678 17,933,349,146 19,726,684,061SG&A Expenses 2,351,186,490 3,201,015,306 2,819,789,171 3,101,768,088 3,411,944,897 3,753,139,387 4,128,453,326Incom e before interest expenses and corporate incom e tax6,446,482,355 4,200,918,720 5,214,703,831 5,736,174,214 6,309,791,635 6,940,770,799 7,634,847,879Interest expenses (210,222,061) (146,507,363) (77,693,314) (107,649,938) (311,163,578) (532,383,581) (773,080,585)Corporate incom e tax (1,154,037,604) (818,113,852) (1,027,402,103) (1,688,557,283) (1,799,588,417) (1,922,516,165) (2,058,530,188)Incom e after corporate incom e tax 5,082,222,690 3,236,297,505 4,109,608,414 3,939,966,993 4,199,039,640 4,485,871,052 4,803,237,105Incom e attributable to m inority interest (6,326,757) 11,015,455 11,015,455 11,015,455 11,015,455 11,015,455 11,015,455Incom e from ordinary activities 5,075,895,933 3,247,312,960 4,120,623,869 3,950,982,448 4,210,055,095 4,496,886,507 4,814,252,560Extraordinary item Gain on debt restructuring 45,022,995 0Net incom e for the year 5,120,918,928 3,247,312,960 4,120,623,869 3,950,982,448 4,210,055,095 4,496,886,507 4,814,252,560

5. Free Cash Flow

Projected Free Cash Flow , 2007-2011 2007E 2008E 2009E 2010E 2011E

NOPAT = EBIT (1-T) 3,650,292,682 4,015,321,950 4,416,854,145 4,858,539,559 5,344,393,515 Subtract increase in current assets, except cash 293,458,674 2,514,148,723 2,765,563,595 3,042,119,955 3,346,331,951 Add back increase in current liabilities (1,894,984,617) 748,942,187 823,836,406 906,220,047 996,842,051 Subtract change in net fixed assets 500,000,000 500,000,000 500,000,000 500,000,000 500,000,000 FREE CASH FLOW 961,849,391 1,750,115,414 1,975,126,955 2,222,639,651 2,494,903,616

Page 41 of 44

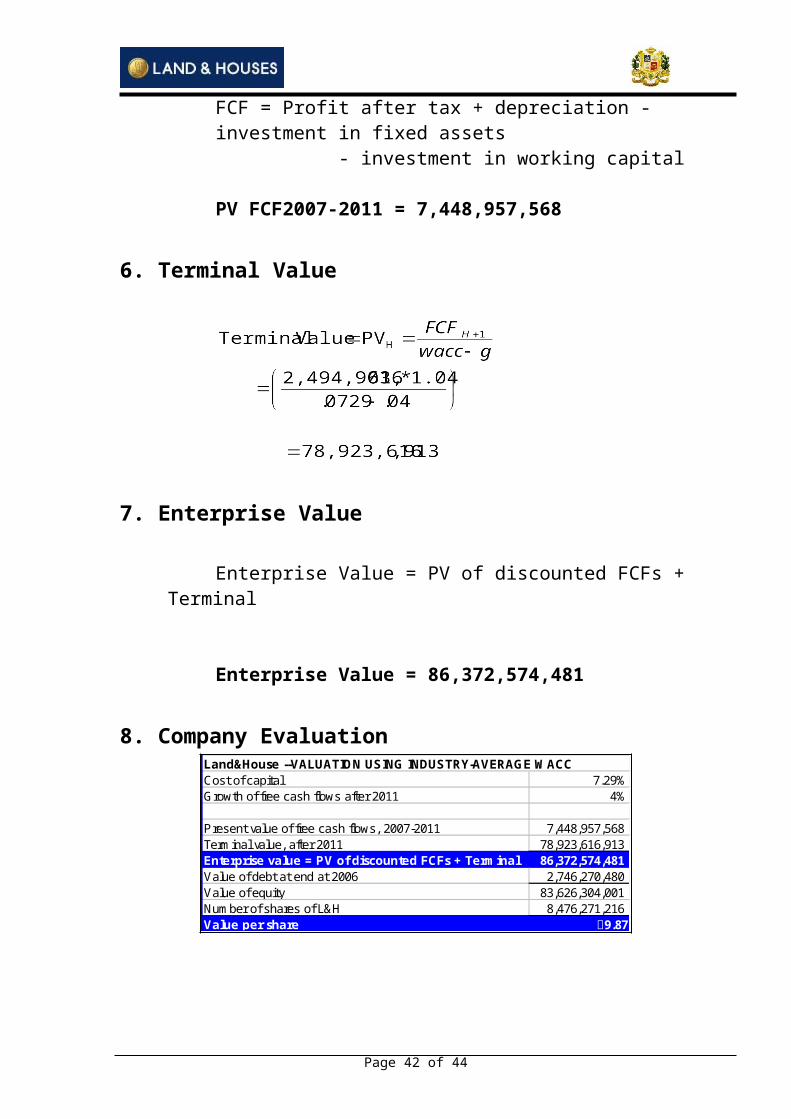

FCF = Profit after tax + depreciation - investment in fixed assets - investment in working capital

PV FCF2007-2011 = 7,448,957,568

6. Terminal Value

7. Enterprise Value

Enterprise Value = PV of discounted FCFs + Terminal

Enterprise Value = 86,372,574,481

8. Company EvaluationLand&House --VALUATION USING INDUSTRY-AVERAGE W ACCCost of capital 7.29%Growth of free cash flows after 2011 4%

Present value of free cash flows, 2007-2011 7,448,957,568Term inal value, after 2011 78,923,616,913Enterprise value = PV of discounted FCFs + Term inal 86,372,574,481Value of debt at end at 2006 2,746,270,480Value of equity 83,626,304,001Num ber of shares of L&H 8,476,271,216Value per share ฿9.87

Page 42 of 44

Conclusion

Market price close on August 24, 2007 at6.70 baht.

Confidence to drive sales recovery in2H07:

Housing demand will recover, led by a consumerconfidence upswing in 2H07 coupled with a better economicoutlook, lower interest rates and an easing politicalclimate. LH has the strongest brand recognition amonghomebuyers due to its reputation for quality and itssensitivity to the interests of customers (it didn’t walkout on any projects in 1997).

Low downside—2Q07 should post slightimprovements:

We estimate 2Q07 core profit at Bt551m, EPS of Bt0.06(+4% QoQ), driven by a mild sales increase and a sustainedmargin.

SDH supply squeeze is good for LH:

From a 2004 peak, SDH project launches have declined forthree consecutive years. We forecast that total SDH unitsavailable for sale in 2007 will plunge 53% YoY. That canonly benefit LH, the SDH leader.

Pricing power to return?

Given limited SDH supplies and assuming a 2H07 demandrecovery, in 2008 LH should be able to exert some pricingpower on the market, boosting gross margin.

Risks and concerns:

Page 43 of 44

o Rising interest rates: This will decreaseaffordability and result in weaker house sales.

o Political climate worsens: This would make hitconfidence and kill off the sales recovery.

o Sharp rises in construction costs: An unexpectedsharp oil price rise would feed into higherconstruction costs. As such, LH’s gross marginmight then under perform our forecasts.

Valuation and Recommendation

Maintain BUY, target price Bt9.87/share:We rate LH a BUY with a target price of Bt9.87/share. We

expect positive total returns of 15% or more over the next 12months.

Reference

http://www.lh.co.th

http://www.settrade.com

http://www.thaiappraisal.org

Research Paper “Land and Houses Plc: The return of the uber-builder” from Bualuang Securities, 11 July 2007

Research Paper “Land and Houses: In Transition” from Phatra Securities Public Company Limited, 25 May 2007

Research Paper “LH” from KGI, 12 July 2007

Page 44 of 44