VALUATION REPORT - FPTS

23

VALUATION REPORT Cuong Vu Nguyen Equity Analyst Email: [email protected] Tel.: (+84) 24 3773 9058 – Ext.: 4309 Closing Price (Jul 23, 2019) Target Price Upside 67,000 74,100 +10.53% Recommendation HOLD TRA and VNINDEX Price Movement Trading Information (as of July 23, 2019) Current Price (VND) 67,000 52-week High (VND per share) 94,200 52-week Low (VND per share) 65,500 Shares Issued 41,453,673 Shares Outstanding 41,450,540 30-day Average Volume (share/day) 2,137 Market Cap. (billion VND) 2,777.40 Trailing EPS (VND per share) 4,216.12 Trailing P/E 15.89x Company General Information Name Traphaco Joint Stock Company Address No. 75, Yen Ninh St., Quan Thanh, Ba Dinh Dist., Ha Noi Main Business Manufacturing and distributing pharmaceutical products Competitive Advantage Ability to self-supply WHO-GACP quality herbal ingredients Major Weakness Inefficient cost management LOW HERBAL PRODUCT SALES GROWTH GENERIC DRUG MARKET EXPANSION INTENTION Using the Discounted Cash Flow Models and Relative Valuation Method, we valued HSX listed TRA – Traphaco Joint Stock Company. The target price of one TRA share was determined at 74,100 VND, 10.53% higher compared to its closing price on July 23 rd , 2019. We recommend a HOLD position for TRA stocks. Investors may consider to buy TRA stocks when its price drops to 61,700 VND per share, equivalent to an expected return of 20%. INVESTING PROSPECTS 1. Traditional and herbal products: Notable brand recognition contributes to TRA’s 11.53% of domestic herbal product market share (approximately 76% of TRA’s manufacturing revenues). The Nielsen Corporation evaluated TRA as the strongest brand among all herbal pharmaceutical manufacturers in Vietnam. TRA’s “Boganic” and “Hoat huyet duong nao” have the highest recognition rate compared to other products with similar uses. 88.4% herbal ingredients used are certified with WHO- GACP standard, helping TRA bid in the highest tier for herbal and traditional products in the Ethical Drug (ETC) channel starting October 2019. Circular No.15/2019/TT-BYT re-classifies the bidding tiers for herbal and traditional products based on the quality of herbal ingredients, allowing TRA and 13 other herbal medicine manufacturers to leave the competition against 70 lower quality manufacturers in the old tier to enter bidding in the new tier for herbal and traditional products in the ETC channel. 2. Generic and patented drugs: Revenue growth is positive for major generic drugs including “Methorphan”, “Quimoxi”, “Ofloxacin” and “Tobramycin” (account for 7.8% of revenues) due to increasing demand for cough/respiratory and eye care medicines in Vietnam. Euromonitor estimated domestic average sales growth to reach 5.6-7.8% yoy for cough/respiratory medicines and 11-11.2% yoy for eye care products from 2019 to 2023. -25% 25% 75% 125% 175% 225% VNINDEX TRA PHARMACEUTICAL INDUSTRY July 23 rd , 2019 TRAPHACO JOINT STOCK COMPANY (HSX: TRA)

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of VALUATION REPORT - FPTS

VALUATION REPORT

Cuong Vu Nguyen

Equity Analyst

Email: [email protected]

Tel.: (+84) 24 3773 9058 – Ext.: 4309

Closing Price (Jul 23, 2019)

Target Price

Upside

67,000

74,100

+10.53%

Recommendation

HOLD

TRA and VNINDEX Price Movement

Trading Information (as of July 23, 2019)

Current Price (VND) 67,000

52-week High (VND per share) 94,200

52-week Low (VND per share) 65,500

Shares Issued 41,453,673

Shares Outstanding 41,450,540

30-day Average Volume (share/day) 2,137

Market Cap. (billion VND) 2,777.40

Trailing EPS (VND per share) 4,216.12

Trailing P/E 15.89x

Company General Information

Name Traphaco Joint Stock Company

Address No. 75, Yen Ninh St., Quan

Thanh, Ba Dinh Dist., Ha Noi

Main

Business

Manufacturing and distributing

pharmaceutical products

Competitive

Advantage

Ability to self-supply WHO-GACP

quality herbal ingredients

Major

Weakness Inefficient cost management

LOW HERBAL PRODUCT SALES GROWTH

GENERIC DRUG MARKET EXPANSION INTENTION

Using the Discounted Cash Flow Models and Relative Valuation

Method, we valued HSX listed TRA – Traphaco Joint Stock

Company. The target price of one TRA share was determined at

74,100 VND, 10.53% higher compared to its closing price on July

23rd, 2019.

We recommend a HOLD position for TRA stocks. Investors may

consider to buy TRA stocks when its price drops to 61,700 VND per

share, equivalent to an expected return of 20%.

INVESTING PROSPECTS

1. Traditional and herbal products:

Notable brand recognition contributes to TRA’s 11.53% of

domestic herbal product market share (approximately

76% of TRA’s manufacturing revenues). The Nielsen

Corporation evaluated TRA as the strongest brand among all

herbal pharmaceutical manufacturers in Vietnam. TRA’s

“Boganic” and “Hoat huyet duong nao” have the highest

recognition rate compared to other products with similar uses.

88.4% herbal ingredients used are certified with WHO-

GACP standard, helping TRA bid in the highest tier for

herbal and traditional products in the Ethical Drug (ETC)

channel starting October 2019. Circular No.15/2019/TT-BYT

re-classifies the bidding tiers for herbal and traditional products

based on the quality of herbal ingredients, allowing TRA and

13 other herbal medicine manufacturers to leave the

competition against 70 lower quality manufacturers in the old

tier to enter bidding in the new tier for herbal and traditional

products in the ETC channel.

2. Generic and patented drugs:

Revenue growth is positive for major generic drugs

including “Methorphan”, “Quimoxi”, “Ofloxacin” and

“Tobramycin” (account for 7.8% of revenues) due to

increasing demand for cough/respiratory and eye care

medicines in Vietnam. Euromonitor estimated domestic

average sales growth to reach 5.6-7.8% yoy for

cough/respiratory medicines and 11-11.2% yoy for eye care

products from 2019 to 2023.

-25%

25%

75%

125%

175%

225%VNINDEXTRA

PHARMACEUTICAL INDUSTRY July 23rd, 2019

TRAPHACO JOINT STOCK COMPANY (HSX: TRA)

Bloomberg – FPTS <GO> | 2

HSX: TRA

www.fpts.com.vn

List of Shareholders (as of July 23, 2019)

State Capital Investment

Corporation (SCIC) 35.67%

Magbi Fund Ltd. (Mirae Asset) 25.00%

Super Delta Pte. Ltd. (Daewoong

Pharmaceutical Co., Ltd.) 15.12%

Domestic Shareholders 13.02%

International Shareholders 6.48%

Board of Directors 4.71%

INVESTING RISKS

Ineffecient expense management: additional expenses

incurred for new distribution centers has not helped boost

sales. Opening 8 new distribution centers in two recent years

has led to higher SG&A expenses; however, TRA’s net income

still fell by 32.89% yoy and net income margin dropped to

9.72% in 2018.

Limited control over API quality and price (58% of

ingredient costs) due to complete dependence on

imported sources. Major components of TRA’s leading

generic and patented drugs including “Methorphan”, “Quimoxi”,

“Tobramycin” and “Moxifloxacin” (7.8% of net revenues) are

imported from only a few suppliers in India and China.

Tight Liquidity: TRA stocks are low-volume because three

large shareholders’ ownership accounts for about 75% of

TRA’s equity, in which SCIC is the biggest shareholder with

35.67% of TRA ownership.

ONGOING ISSUE

TRA’s ability to enter new higher bidding tiers (according

to Circular No.15/2019/TT-BYT which takes effect from

October 2019) for generic and patented drugs in the

Ethical Drug channel largely depends on TRA’s progress

of acquiring the EU-GMP standard for its generic and

patented drug production lines. The upgrading process for

the production lines at TRA’s Hung Yen Generic Drug Factory

will take up an estimated amount of 225 billion VND

(approximately US$10 million) for the EU-GMP to be achieved

by 2022. The result of this upgrade will have significant impacts

on TRA’s plan to expand its generic and patented drug

manufacturing scale and sales in the ETC channel.

Bloomberg – FPTS <GO> | 3

HSX: TRA

www.fpts.com.vn

COMPANY OVERVIEW

General Background

Traphaco Joint Stock Company was formerly the serum and medical fluid manufacturing department of Railway

Medical Center.

Between 1993 and 1999, the manufacturing department was split from the Center to become a capitalized firm

whose 45% equity was state-owned.

In 2008, Traphaco Joint Stock Company was officially listed on Ho Chi Minh Stock Exchange (HSX) with the

ticker “TRA”.

From 2008-2018, TRA gradually increased its authorized capital to 415 billion VND with its equity sources.

Major Shareholders Information as of July 23, 2019

TRA has a concentrated shareholders’ structure as three largest shareholders own approximately 75% of the

company’s equity. State Capital Investment Corporation (SCIC) owns 35.67% of TRA’s equity and remains the

biggest shareholder. SCIC does not have any plans to divest from TRA and still holds the right of veto at TRA.

Magbi Fund Ltd. and Super Delta Pte. are two entities representing Mirae Asset Financial Group and Daewoong

Pharmaceutical Co. Ltd., respectively. These two strategic partners of TRA own approximately 40% of the

company’s equity. Mirae Asset announced that it would help TRA invest in R&D activities for new pharmaceutical

products. On the other hand, being a well-known pharmaceutical manufacturer from South Korea, Daewoong

Pharmaceutical has committed to support TRA with its technological advance and has transferred 8 different

manufacturing technologies to TRA since March 2019.

Despite having years of experience at TRA, the company’s Board of Directors and its management team own only

about 5% of the equity. Because of the three above shareholders’ large ownership, TRA’s current management

team might face the threat of being replaced.

35.67%

25.00%

15.12%

13.02%

6.48%4.71%

State Capital Investment Corporation (SCIC)

Magbi Fund Ltd. (Mirae Asset)

Super Delta Pte. Ltd. (Daewoong Pharmaceutical Co., Ltd.)

Other Domestic Shareholders

Other International Shareholders

Board of Directors

Bloomberg – FPTS <GO> | 4

HSX: TRA

www.fpts.com.vn

Revenue Structure in 2018

Revenue Structure by Products and Services

Revenue Structure by Distribution Channels

Source(s): Traphaco

TRA’s herbal and traditional product sales contribute to more than 60% of the company’s net revenues while generic

drug sales account for about 20% of TRA’s net revenues.

Beside manufacturing sales, TRA’s revenues are also generated from its distributing activities, importing and

entrusted importing services. Distributing activity sales account for nearly 13% of TRA’s net revenues, which are

carried out by one of TRA’s subsidiaries known as Dak Lak Pharmaceutical and Medical Equipment Joint Stock

Company. This firm distributes pharmaceutical products for both domestic and international partners such as Ipca

Laboratories Ltd., RPG Lifescienes Ltd., Abbvie Inc., Egis Pharmaceutical Pte. Ltd., Tipharco, Savipharm, Stada,

Agimexpharm, etc. mostly in the two provinces of Dak Lak and Dak Nong to both of the Over-the-Counter channel

(64% of the subsidiary’s net revenues) and the Ethical Drug channel (36% of the subsidiary’s net revenues).

The importing and entrusted importing services add about 5% to TRA’s net revenues and include:

Importing antipyretic and personal plasters from Kobayashi Pharmaceutical Co., Ltd. (Japan) and dietary

supplements such as multivitamins, fish oil, Glucosamin, Coenzyme Q10, etc. from Natural Factors Nutritional

Products Inc. (Canada) and Westland – Pure Nutrition Ltd. (New Zealand) and re-selling in the OTC market.

Entrusted importing: acting as an intermediary which purchases XO Milk Powder from Namyang Dairy Products

Co., Ltd. (South Korea) and re-distributes to Nam Duong Joint Stock Company.

TRA’s sales from the OTC market take up more than 90% of TRA’s net revenues while those from the ETC market

only account for a modest amount of 9.06% of TRA’s net revenues.

Leading Products

Product Percentage

of Sales Description

Herb

al P

roducts

Boganic 22.50% Traditional hepatic medicine, clinically tested by National Cancer Hospital,

accounts for about 20% of all domestic hepatic medicine sales.

Hoat huyet duong

nao/ Cebraton 25.28%

Traditional cerebral blood circulating enhancement, accounts for roughly

10% of sales of medicines with similar uses in Vietnam.

Tottri 5.56% Traditional hemorrhoid medicine, pharmacological effect proved by Hanoi

University of Pharmacy, takes up 25% of medicines with similar use sales.

Generic D

rugs

Methorphan 5.56% Generic cough/respiratory suppressant, growth rate reached 22% yoy

between 2012 and 2018.

Eye Drops 2.22%

Including 3 eye antibiotics “Quimoxi”, “Ofloxacin” and “Tobramycin”,

manufactured with advanced “BFS” technology, sales reached 40 billion

VND after the first year of being introduced.

Source(s): Traphaco, IMS Health IV/2018

62.20%19.64%

12.74%

5.42%

Herbal Products

Generic Drugs

Subsidiary's DistributingServices

Entrusted Importing 90.94%

9.06%

Over-the-CounterChannel (OTC)

Ethical Drug Channel(ETC)

Bloomberg – FPTS <GO> | 5

HSX: TRA

www.fpts.com.vn

OPERATING ANALYSIS

TRA’S VALUE CHAIN

Herbal Products

Herbal Ingredients

Self-supply: 12.6%

of ingredient cost

Domestic sources:

29.4% of ingredient cost

Hoang Liet Factory &

Hung Yen High-Technology Factory

Capsules, Tablets,

etc.

Others: Syrups,

Granules

Generic Drugs

Active Pharmaceutical Ingredients (API)

Imported from: China, Switzerland, Germany,

India, etc.; account for 58% of ingredient cost

Hung Yen Generic Drug Factory

Capsules, Tablets, etc.

Liquid: Eye

drops, Nasal

drops

Others:

Granules,

Ointments

Inb

ou

nd

Lo

gis

tic

s

Op

era

tio

ns

Ou

tbo

un

d

Lo

gis

tic

s

Distribution Methods

Over-the-Counter Channel (OTC): 90.94% of net revenues

Ethical Drug Channel (ETC): 9.06% of net revenues

INBOUND LOGISTICS

I. Herbal Ingredients: Self-Supply Sources Give TRA Stable Advantages

Domestic Manufacturers with

WHO-GACP Certified Ingredients

(as of April 2019)

Source(s): Traditional Medicine Administration

88.4% of all herbal ingredients used by TRA annually are certified with

WHO-GACP standard. These ingredients are TRA’s 5 most intensively

used herbs and plants, including Artichoke (Cynarae Scolymi), Dinh Lang

(Polyscias Fruticosa), Rau Dang Dat (Glini Oppositifolius), Che Day

(Ampelopsis Cantoniensis) and Bim Bim Biec (Pharbitidis), which are

grown and collected mainly in the provinces of Lao Cai, Hoa Binh, Phu

Tho, Nam Dinh and Phu Yen. The agricultural areas used for these 5 herbs

and plants have increased from only 4 ha in 1998 to more than 36,300 ha

in 2019, which gives TRA about 2,900 tons of herbal ingredients annually

and makes TRA the pharmaceutical company with the most amount of

self-grown herbal ingredients and the largest WHO-GACP certified

growing areas in Vietnam.

All of TRA’s WHO-GACP certified herbal ingredients are grown on 675

local farmers’ agricultural land. These farmers and TRA have partnership

agreements which allow TRA to train the farmers with WHO-GACP

standard. On the other hand, the farmers’ profit from growing TRA’s

ingredients would be 3 to 5 times higher compared to what they would earn

from growing other traditional crops. Between 2016 and 2018, there were

175 additional local families participating in this program, helping TRA

expand the growing areas. In general, TRA’s partnership with trained local

farmers is a stable method to self-supply its high quality herbal ingredients.

Furthermore, being able to self-supply WHO-GACP quality herbal ingredients gives TRA a good reputation in the

domestic herbal product market. Currently, 80% to 85% of all herbal ingredients in Vietnam are repordly imported

from China without being regulated; among which there are a significant amount of low quality herbal leftovers and

poisoned herbs. As a result, having WHO-GACP certified herbal ingredients gives TRA, together with about 16.25%

of all domestic firms, a competitive advantage against the rest of the herbal product manufacturing firms.

0

5000

10000

15000

20000

25000

30000

35000

40000

0

1

2

3

4

5

6

TR

AD

uo

c lie

u V

NN

am

Du

oc

Hon

g D

ai V

iet

Lad

op

ha

rO

PC

So

lavin

aT

ue L

inh

Th

ien

Duo

cF

usi

Ngo

c M

inh

Duo

c K

hoa

KH

CN

Don

g A

Number of Herbs

Growing Area in ha (right)

Bloomberg – FPTS <GO> | 6

HSX: TRA

www.fpts.com.vn

II. Active Pharmaceutical Ingredients (API): Complete Dependence on Imported Sources Gives TRA No

Control over API Price Fluctuations

Estimated TRA’s Imported

API Value

Source(s): Traphaco, Drug

Administration of Vietnam, FPTS

Research

TRA’s API costs account for about 58% of all TRA’s ingredient expenses. All API

are imported as there is no stable supplier in Vietnam, among which we estimated

the API value imported from China takes up 44.09% of TRA’s imported API value.

Certain API for TRA’s leading products depend on sole suppliers, including:

Ingredients for “Moxifloxacin” and “Tobramycin” depend on one supplier in

China.

Ingredients for “Methorphan” depends solely on one supplier in India.

API imported from China may cause a price fluctuation risk: China Food and

Drug Administration (CFDA) and Chinese Ministry of Ecology and Environment

(MEP) increased control over API’s quality waste treatment standards, forcing

hundreds of Chinese API manufacturers to close. The remaining API factories

have had to pay extra “waste treatment” tax since 2018. If TRA could not find

better alternative sources of API, we estimated that TRA’s ingredient costs for

generic drugs would increase with a CAGR of 6.23% in the next 5 years

(assuming TRA would not develop any new generic drugs).

OPERATIONS

Since November 2017, TRA has moved all generic and patented drug manufacturing operations from its Hoang Liet

Factory to the new Hung Yen Generic Drug Factory (manufacturing process description). As a result, TRA now

owns 4 different factories, each of which has its own purpose as follows:

Factory Traphaco Sapa Hoang Liet Hung Yen

High-Technology

Hung Yen

Generic Drug

Invested

Capital 25 billion VND 25 billion VND 114 billion VND 477 billion VND

Product Herbal Ingredients Herbal Products Herbal Products Generic Drugs

Manufacturing

Quality

WHO-GACP

WHO-GMP WHO-GMP WHO-GMP WHO-GMP

Source(s): Traphaco

I. Herbal Medicines: WHO-GMP Manufacturing Quality Does Not Gives TRA Any Competitive Advantages

Herbal medicines in Vietnam are manufactured using two main methods, the manual method and the automated

one. The manual way is used by hundreds of unregistered herbal manufacturers, especially when they extract and

concentrate the herbs and plants. Without a stable and standardized level of pressure and temperature, manual

herbal extracts usually lose their active substances, thus, lose their effects.

For WHO-GMP certified manufacturers, the herbal medicine manufacturing process is automated from the

extracting step to the packaging step. The automated method requires herbal ingredients to be cleansed and

pasteurized before being extracted in a vacuum environment with calculated temperature so that the active

substances would be preserved. In addition, final herbal products are always examined closely with high technology

to make sure the medicine quality complies with WHO-GMP standard.

Despite possessing WHO-GMP certified herbal production lines, TRA does not have any manufacturing competitive

advantages in the herbal product segment because approximately 70 other herbal manufacturers own similar WHO-

GMP quality technology in Vietnam.

44.09%

15.05%

13.98%

11.83%

15.05%

China Germany

Switzerland India

Others

Bloomberg – FPTS <GO> | 7

HSX: TRA

www.fpts.com.vn

II. Generic Drugs: Investments in New Factory Have Not Boosted Sales Because of Manufacturing Quality

TRA has invested significantly in the production lines at its new Hung Yen Generic Drug Factory to enhance the

generic drug manufacturing capacity and quality.

BFS Technology (Blow-Fill-Seal) minimizes human’s direct interactions with the manufacturing process to

ensure complete sterilization.

Electricity consumption of the new advanced production lines is 50% less compared to that of the old ones,

saving TRA 2.2 billion VND annually.

However, TRA’s Hung Yen Generic Druc Factory has not helped boost sales because of the following reasons.

Revenue from ETC Channel and ROE

between 2017-2018

Source(s): Traphaco

Generic drug quality is directly related to the bidding tiers in the ETC

channel to which each drug belongs. As a new pharmaceutical bill which

re-classifies the requirements for each bidding tier was introduced in

February 2018 but took 17 months to be passed, TRA safely chose to

postpone its EU-GMP upgrading activities for the Hung Yen Generic

Drug Factory. In July 2019, as the bill officially became Circular

No.15/2019/TT-BYT, TRA has estimated that it would spend an extra

amount of 225 billion VND to complete the EU-GMP upgrade for the

generic drug production lines in 2022 so that TRA could place its

products in higher bidding tiers.

The above circumstance also explains why TRA’s generic drugs have

been competing in the lower generic drug tiers in the ETC channel

against cheaper products. As a result, revenues from the ETC channel

dropped by 27.4% and TRA’s ROE was reduced from 24.4% in 2017 to

15.7% in 2018. In general, investments in Hung Yen Generic Drug

Factory production lines have not effectively helped TRA achieved its

ultimate goal of bidding in higher generic drug tiers.

OUTBOUND LOGISTICS

I. Distribution Structure

1. Over-the-counter (OTC) channel remains TRA’s major distribution method

TRA’s OTC and ETC Revenue Structure

Source(s): Traphaco

TRA’s OTC Market Shares

Source(s): Fitch Solutions, Traphaco

Being the main distribution method, TRA’s OTC channel generates 91% of the firm’s net revenues, ranked the 2nd

largest among domestic pharmaceutical manufacturers, and accounts for 5.31% of the pharmaceutical OTC market

share in Vietnam.

Herbal product sales account for about 73% of TRA’s OTC revenues while generic drug sales add another 27%.

24%

16%

0%

5%

10%

15%

20%

25%

30%

000

050

100

150

200

250

2017 2018

bill

ion V

ND

ETC Revenue ROE (right)

0

500

1000

1500

2000

2500

2014 2015 2016 2017 2018

bill

ion

VN

D TRA'sETC Sales

TRA'sOTCSales

0%

2%

4%

6%

8%

0

500

1000

1500

2000

2014 2015 2016 2017 2018

bill

ion

VN

D TRA's OTCSales

TRA's OTCMarketShares

Bloomberg – FPTS <GO> | 8

HSX: TRA

www.fpts.com.vn

a. TRA’s good brand recognition helps maintaining large herbal product market share

TRA’s OTC Herbal Product Market Shares

TRA’s herbal product sales generate about 52% of the

company’s net revenues and account for 18.5% of all domestic

herbal product sales.

Being able to build a strong brand for its leading herbal

products is an important factor helping TRA maintain its

sales in the OTC market. The Nielsen Corporation evaluated

TRA as the strongest pharmaceutical brand among other

researched pharmaceutical brands in Vietnam with the highest

recognition rate of 6.2 for domestic consumers and 7.3 for

domestic pharmacies (out of 10). TRA’s leading herbal products

including “Boganic” (22.5% of net revenues) and “Hoat huyet

duong nao – Cebraton” (25.3% of net revenues) both achieved a

recognition rate of above 95%, the highest among other products

with similar uses.

b. Generic drugs in the OTC market does not have a competitive advantage

TRA’s OTC generic drug sales generate about 19% of the firm’s net revenues, equivalent to 1.17% of total domestic

generic drug sales. TRA’s generic products do not possess any differences compared to other competitors as:

Prescribed drugs tend to have weak brand recognitions because the Ministry of Health limits their marketing

forms to only being directly introduced to specialists and being advertised on health magazines.

WHO-GMP standard is similar across most generic drug manufacturers.

Full dependence on imported ingredients removes most differences on ingredient costs.

2. Having difficulty competing against cheaper brands, TRA’s ETC sales outlook is dependent on the new

circular

TRA’s ETC Market Shares

Source(s): Traphaco, Fitch Solutions

TRA’s herbal product sales generate 94.7% of the

company’s ETC revenues and its generic drug sales

generate about 5.3%.

Between 2014 and 2018, TRA’s ETC sales dropped by

64.7%, from 462 billion VND to 163 billion VND, which

reduced TRA’s ETC market share from 0.78% to

0.16%. The main reason for such performance was the

bidding policy which prioritizes lower priced products

(bidding procedure description). As TRA’s main priority

was product quality, it was difficult for the company to

compete against lower priced peers. Meanwhile, the

number of domestic manufacturers in the same bidding

tier with TRA has increased from 123 firms in 2013 to

175 firms in 2019.

However, Circular 15/2019/TT-BYT (passed in July

2019, effective from October 2019) will create

significant impacts on TRA’s ETC future.

18.49%

TRA's OTC Herbal Product Sales

Domestic OTC Herbal Product Sales

00%

00%

00%

00%

00%

01%

01%

01%

01%

01%

0

50

100

150

200

250

300

350

400

450

500

2014 2015 2016 2017 2018

bill

ion

VN

D

TRA's ETC Sales TRA's ETC Market Shares

Bloomberg – FPTS <GO> | 9

HSX: TRA

www.fpts.com.vn

a. TRA’s herbal product sales in ETC channel will benefit from Circular No.15/2019/TT-BYT for its WHO-

GACP quality herbal ingredients

Major Domestic Manufacturers’ Market Shares of

Herbal Product Sales

TRA’s herbal product sales in the ETC channel contribute

to about 10.3% of the company’s net revenues, which

equals to about 4% of total domestic herbal product sales.

Currently bidding in Tier 1 until October 2019 when the new

circular takes effect, TRA does not possess any price

advantages due to the large number of about 70

manufacturers in Tier 1.

Circular No.11/2016/TT-BYT (exp. Oct. 2019) Circular No.15/2019/TT-BYT (effective Oct. 2019)

Tier 1 WHO-GMP manufacturing quality

Tier 1 WHO-GACP certified herbal ingredients,

WHO-GMP manufacturing quality

Tier 2 Non WHO-GMP manufacturing

quality Tier 2 WHO-GMP manufacturing quality

Tier 3 Non WHO-GMP manufacturing quality

From October 2019, Circular No.15/2019/TT-BYT which re-classifies the bidding tiers for herbal products in the ETC

market will take effect. Products without WHO-GACP certified ingredients will be taken down to Tier 2 and 3, which

would help reduce TRA’s competitors. Being able to self-supply WHO-GACP certified ingredients, TRA will be

among the 13 herbal product manufacturers qualified to bid in the highest herbal product tier starting October 2019.

b. TRA’s generic drug sales outlook in the ETC market remains uncertain due to its non EU-GMP quality

TRA is currently bidding its generic products in Tier 3 for drugs manufactured with WHO-GMP quality. As TRA’s

products are not competitive in terms of price, its generic drug sales only reached a modest amount of 10.4 billion

VND in 2018, equal to 0.58% of TRA’s net revenues and 0.01% of total domestic generic drug sales. TRA’s generic

drug sales depends significantly on whether the firm can upgrade its EU-GMP manufacturing quality to comply with

the new circular’s requirements for Tier 1 & 2.

Compared to the existing Circular No.11/2016/TT-BYT (detail), the new Circular No.15/2019/TT-BYT (detail)

contains the following major changes:

New Tier 1 requires generic products to be manufactured with EU-GMP qualified production lines and certified

by Stringent Regulatory Authorities (SRA) (complete list).

EU-GMP qualified products which are not certified by the SRA and PIC/s-GMP qualified products certified by

both PIC/s and ICH members will be moved to the future Tier 2 from the current Tier 1. PIC/s-GMP qualified

products certified by non-ICH members will also be moved to the lower tiers from the current Tier 2.

GMP certified drugs will be divided into 3 main tiers: Tier 3 includes bioequivalent (BE) drugs certified by

Vietnam Pharmaceutical Regulatory Authorities, Tier 4 includes domestic WHO-GMP manufactured drugs, and

Tier 5 includes WHO-GMP certified drugs which do not satisfy the first 4 tiers’ requirements.

In order to bid in Tier 1 and 2 and to comply with the new circular’s requirements, TRA is investing 225 billion VND

in its Hung Yen Generic Drug Factory. As TRA is currently bidding in the existing Tier 3 and does not have a price

advantage, TRA’s generic drug sales performance in the ETC market is anticipated to be modest within the next

two years.

0%2%4%6%8%

10%

Bloomberg – FPTS <GO> | 10

HSX: TRA

www.fpts.com.vn

II. Geographic Performance

TRA’s Revenue Structure by Geography

Source(s): Traphaco

Northern regions of Vietnam remain TRA’s major market,

which account for almost 60% of the firm’s net revenues. The

reason behind TRA’s success in the North is that TRA has been

operating and strengthening its brand for Northern consumers for

about 25 years.

TRA is having difficulty expanding its business to the South

of Vietnam. Despite having opening three more distribution

centers in the South in 2018 and increasing the number of sales

representatives, TRA’s revenues from the Southern regions has

decreased by 4.32% compared to those in 2017. Between 2015

and 2018, its total revenues from the Southern regions dropped

by 17.68%. One of the main reasons behind the firm’s

unsuccessful performance in the South is TRA’s inability to

partner with pharmacy chains such as Pharmacity, Phano,

Medicare, Guardian, and Sapharco, etc. This pharmacy chain

model became familiar with consumers in the South since 2007;

however, it was not introduced to the North until 2018.

58.40%19.92%

21.69% North

Central

South

Bloomberg – FPTS <GO> | 11

HSX: TRA

www.fpts.com.vn

FINANCIAL ANALYSIS

I. Slow Revenue Growth Due to OTC Channel Sales Policies and ETC Channel Price Competition

TRA’s Revenue Growth between 2014 and 2018

*The adjusting entry for TRA’s OTC sales in the period of 2017-2018 records the trade discounts and

entrusted import sales to ensure consistency with TRA’s accounting entry during 2014-2016.

TRA’s revenue growth has been modest since 2016 because of the following major reasons:

Revenue growth from TRA’s OTC channel has been slowing down due to TRA’s strict sales policies which have

weakened their OTC pharmacy customers’ motivation. Specifically, TRA has tightened its receivable collecting

duration and requires its pharmacy customers to achieve a sales growth of 20% for TRA products in order to

receive bonuses. As a result, these uncompetitive policies have restricted TRA from expanding its customer

network which has remained unchanged at approximately 27,000 pharmacies between 2017 and 2018.

Revenue growth from TRA’s ETC channel dropped by 27.4% mainly because of a rising competition in the ETC

market. The quantity of bidders in the same bidding tier with TRA has increased from 123 firms in 2013 to 175

firms in 2019 while the advantage belongs to lower priced brands because of the price-based bidding policy.

For a firm that has invested intensely in quality like TRA, it is difficult to bid effectively against cheaper products.

II. Increasing SG&A Expenses Show Slight Improvements

TRA’s Costs for Labor and Trade Discounts

Source(s): Traphaco

TRA’s profit margin was relatively high at 51.97%; however, its net income margin was significantly low at 9.72%. The

major reason for the this issue came from the incurred commission expenses and labor costs for 8 new distribution

centers which TRA has opened in 2 recent years (complete list). As a result, SG&A expense margin has taken up a

larger proportion from 32.34% in 2016 to 39.37% in 2018, causing a net income reduction of 32.89% for TRA between

2017 and 2018.

However, TRA ‘s SG&A expense management has shown signs of improvements in the 1st Quarter of 2019. By cutting

labor costs and commission expenses for its pharmaceutical representatives, TRA’s net income margin has increased

from 9.72% to 12.4%.

-1.88%

19.58%

1.23%3.31%

-3.80%

-5%

0%

5%

10%

15%

20%

25%

0

500

1000

1500

2000

2500

2014 2015 2016 2017 2018

bill

ion

VN

D

OTC Sales Adjusting Entry* TRA's OTC Sales TRA's ETC Sales Sales Growth

16.32%17.64%

22.61%20.80%

12.57%

29.96%32.34%

38.37% 39.37%

31.91%

10.32% 11.42%13.92%

9.72%12.40%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2015 2016 2017 2018 Q1/2019

(Labor Costs + Discounts) /Sales

SG&A Expenses /Sales

Net Profit Margin

Bloomberg – FPTS <GO> | 12

HSX: TRA

www.fpts.com.vn

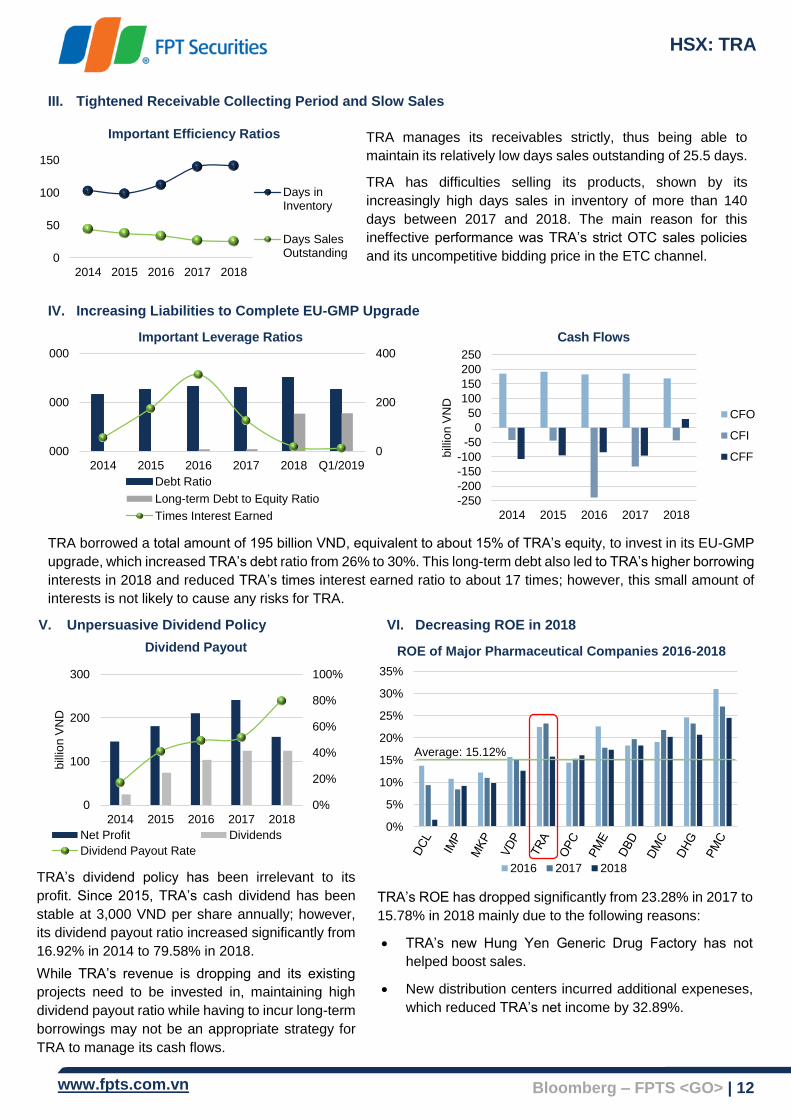

III. Tightened Receivable Collecting Period and Slow Sales

Important Efficiency Ratios

TRA manages its receivables strictly, thus being able to

maintain its relatively low days sales outstanding of 25.5 days.

TRA has difficulties selling its products, shown by its

increasingly high days sales in inventory of more than 140

days between 2017 and 2018. The main reason for this

ineffective performance was TRA’s strict OTC sales policies

and its uncompetitive bidding price in the ETC channel.

IV. Increasing Liabilities to Complete EU-GMP Upgrade

Important Leverage Ratios

Cash Flows

TRA borrowed a total amount of 195 billion VND, equivalent to about 15% of TRA’s equity, to invest in its EU-GMP

upgrade, which increased TRA’s debt ratio from 26% to 30%. This long-term debt also led to TRA’s higher borrowing

interests in 2018 and reduced TRA’s times interest earned ratio to about 17 times; however, this small amount of

interests is not likely to cause any risks for TRA.

V. Unpersuasive Dividend Policy

Dividend Payout

TRA’s dividend policy has been irrelevant to its

profit. Since 2015, TRA’s cash dividend has been

stable at 3,000 VND per share annually; however,

its dividend payout ratio increased significantly from

16.92% in 2014 to 79.58% in 2018.

While TRA’s revenue is dropping and its existing

projects need to be invested in, maintaining high

dividend payout ratio while having to incur long-term

borrowings may not be an appropriate strategy for

TRA to manage its cash flows.

VI. Decreasing ROE in 2018

ROE of Major Pharmaceutical Companies 2016-2018

TRA’s ROE has dropped significantly from 23.28% in 2017 to

15.78% in 2018 mainly due to the following reasons:

TRA’s new Hung Yen Generic Drug Factory has not

helped boost sales.

New distribution centers incurred additional expeneses,

which reduced TRA’s net income by 32.89%.

0

50

100

150

2014 2015 2016 2017 2018

Days inInventory

Days SalesOutstanding

0

200

400

000

000

000

2014 2015 2016 2017 2018 Q1/2019

Debt Ratio

Long-term Debt to Equity Ratio

Times Interest Earned

-250

-200

-150

-100

-50

0

50

100

150

200

250

2014 2015 2016 2017 2018

bill

ion

VN

D

CFO

CFI

CFF

0%

20%

40%

60%

80%

100%

0

100

200

300

2014 2015 2016 2017 2018

bill

ion

VN

D

Net Profit Dividends

Dividend Payout Rate

0%

5%

10%

15%

20%

25%

30%

35%

2016 2017 2018

Average: 15.12%

Bloomberg – FPTS <GO> | 13

HSX: TRA

www.fpts.com.vn

OUTLOOK FOR VIETNAM’S PHARMACEUTICAL INDUSTRY AND TRAPHACO

OUTLOOK FOR VIETNAM’S PHARMACEUTICAL INDUSTRY

I. ETC Sales Growth Surges to Take Over OTC Market Share Due to Regulatory Factors

Vietnam OTC and ETC Pharmaceutical

Sector Growth Forecast

Source(s): Fitch Solutions

ETC revenue scale accounts for 74.81% of total Vietnam pharmaceutical

market share and is predicted to continue to grow at a rate of 11.0% yoy

due to regulatory changes:

Health insurance ownership rate has increased from 28% in

2005 to 90% in 2019. The Government has been promoting for the

national health insurance with various approaches including

financially supporting for the poor and increasing charges for non-

covered services.

The number of hospitals is increasing as the new ones would

receive 0% tax benefits from the tax cuts policy in the first 4 years

after opening.

Domestically manufactured generic drug sales tend to surge at

a rate of 12% yoy due to supportive policies. Specifically, the

Ministry of Health supports generic replacements for patented drugs

whose copyrights expire (Pharmaceutical Law 105/2016/QH13) and

expands the number of generic drugs prioritized for domestic

bidders (Circular 03/2019/TT-BYT).

OTC sales are forecasted to grow slower at 9.4% yoy due to prescribed drug sales in the OTC market will be

controlled more closely in the next few years with the following policies:

The number of non-prescribed active substances allowed in OTC drugs was reduced to 243 substances

(Circular 07/2017/TT-BYT).

Antibiotics sold without prescriptions accounts for about 90% of all antibiotic sales in Vietnam, which

will be restricted as an approach to control the antibiotic resistance (AR) situation (Decision 4041/QD-BYT).

II. Demands for Pharmaceutical Products Increase as a Result of an Increasing and Aging Population

Vietnam’s Population Forecast

Source(s): Danso.org

Vietnam Average Pharmaceutical Product Expenses Forecast

Source(s): International Journal of Environmental Research & Public Health

The Vietnamese population is estimated to increase at 15% yoy in the next 30 years to reach 112.78 million people in

2050. The number of over-65-year-old people is expected to triple, causing the average age to rise from 33 to 42 years.

An increasing population with a speedy aging rate is likely to boost demands for healthcare and pharmaceutical product

sales in Vietnam. As a result, average expenses for pharmaceutical drugs for a Vietnamese is forecasted to hike at a

CAGR of 14.2% between 2018 and 2028.

0

50,000

100,000

150,000

200,000

250,000

bill

ion

VN

D

Domestic ETC SalesDomestic OTC Sales

0

10

20

30

40

50

0

20

40

60

80

100

120

ave

rag

e a

ge

mill

ion

pe

op

le

Population Average Age (right)

0

50

100

150

200

250

300

US

D/p

ers

on

Bloomberg – FPTS <GO> | 14

HSX: TRA

www.fpts.com.vn

OUTLOOK FOR TRAPHACO

I. TRA’s Herbal Product Sales Will Grow at a Slow Pace

TRA’s Leading Herbal Product Sales

Source(s): Traphaco

TRA’s herbal product sales account for 62.2% of the firm’s net revenues. Three of TRA’s leading products including

“Boganic”, “Hoat huyet duong nao – Cebraton” and “Tottri” contribute to 53.34% of its net revenues.

“Hoat huyet duong nao – Cebraton” sales, which account for 25.28% TRA’s net revenues, was slightly reduced

by 2.78% in 2018 because TRA’s growing area could not provide a sufficient amount of Dinh Lang (Polyscias

Fruticosa). However, as TRA announced the firm was able to fix the issue to meet the required quantity of Dinh

Lang to satisfy an increasing demand for its target market of middle aged and elderly customers, “Hoat huyet

duong nao – Cebraton” sales are expected to grow again at a low rate of 4.8% yoy.

“Tottri” sales only add to 5.56% of TRA’s net revenues but have grown at a high CAGR of 44.8% between 2013

and 2018. “Tottri” sales are likely to maintain its positive growth because of the high hemorrhoids rate in

Vietnam. Specifically, the Vietnam Society of Proctology estimated that about 55% of Vietnamese were

diagnosed with hemorrhoids while only about 0.7% of those have used TRA’s “Tottri”.

Major Tradition Hepatic Medicine Costs

Source(s): FPTS Research

“Boganic” sales, which account for 22.50% of TRA’s net

revenues, decreased due to its rough price competition

against products with similar uses. Because of the abundant

avaliability of Artichoke (Cynarae Scolymi) in Vietnam, there

are currently more than 40 different suppliers for Artichoke-

based products similar to “Boganic” with various prices. Due

to this competitive market, “Boganic” sales growth is likely to

remain low in the coming years.

0

500

1000

1500

2014 2015 2016 2017 2018

bill

ion

VN

D

Boganic Hoat huyet duong nao Tottri Total Herbal Product Sales

0 5000 10000 15000 20000

Tue Linh

Nhat Nhat

Traphaco's "Boganic"

Bao Nguyen

Hau Giang Naturenz

OPC Liverbil

Nam Duoc Hamega

Ladophar Bavega

VND/day

Bloomberg – FPTS <GO> | 15

HSX: TRA

www.fpts.com.vn

II. Generic Drugs: Long-term Growth Depends on EU-GMP Production Line Certification

TRA’s Leading Generic Drug Sales in 2018

Source(s): Traphaco

TRA’s generic drug sales account for 19.64% of its net revenues. Its leading product sales, including sales of cough

suppressant “Methorphan” and three eye drops “Quimoxi”, “Ofloxacin” and “Tobramycin”, contribute to 7.78% of

TRA’s net revenues. These leading products have a positive growing tendency due to the following reasons:

Vietnam’s Air Polution Indices Compared to

WHO-Recommended Levels

Substances

in the Air

Times Exceeded WHO-

Recommended Levels

CO 1.7 times

NO2 2.9 times

Suspended

Solid Particles

(e.g.: lead)

43-60 times

PM10 & PM2.5 4-5 times

Source(s): WHO

“Methorphan”, belonging to the cough/respiratory drug group,

grew at a rate of 22% yoy between 2012 and 2018 due to the

high rate of respiratory diseases of 16.61% among Vietnam’s

population. Most respiratory diseases in Vietnam are caused

by air pollution in which the amount of Fine Particulate Matter

(PM 2.5) has surged from 2-3 times higher in 2015 to 4-5

times higher in 2018 compared to WHO’s recommended

amount of 10 μg/m3. In addition, the smoking rate in Vietnam

remained relatively high at 22.5%. As a result, cough

suppressant and other respiratory medicine consumption rate

is expected to increase at 7.8% yoy in Vietnam (Euromonitor).

“Quimoxi”, “Ofloxacin” and “Tobramycin” are three types of non-betalactam antibiotic eye drops manufactured

with the new BFS technology since 2017. These eye drop sales have reached approximately 40 billion VND

after the first year of being introduced, contributing to about 2.22% of TRA’s net revenues, and are likely to

keep growing at a positive rate between 2019 and 2023. Euromonitor International estimated an average growth

rate of 11% yoy for eyecare products in Vietnam as a result of rising cases of eye infections caused by air

polution. Furthermore, TRA’s eye drops’ ingredients are among the substances prioritized for domestic firms to

bid in the ETC channel (Circular No. 03/2019/TT-BYT).

Other generic products, such as Dibetallic and Levigatus (anti itching and dermatitis cream and ointment),

Azithromycin (a class of Macrolide antibiotics), Stilux (Rotundine based sedative), Amorvita (multivitamins),

Antot (Amino Acid and Choline-based eating and nutrient absorbing stimulator) and T-B mouthwash, contribute

to about 60.3% of TRA’s generic product sales. These generic products are not likely to have positive growth

rates in the OTC channel due to being restrictedly marketed and sharing similar manufacturing quality

compared to other products with the same uses. In the ETC channel, assuming that TRA will be able to

complete its EU-GMP upgrade for the generic drug production lines and comply with other standards in the

new Circular No. 15/2019/TT-BYT so that the firm can start bidding in Tier 1 and 2 from 2022, we estimate

these generic drug sales growth to reach a rate of 8% to 10% yoy.

Bloomberg – FPTS <GO> | 16

HSX: TRA

www.fpts.com.vn

OPERATING ACTIVITY FORECAST

Based on the above analysis on TRA’s operating activities and financial situations, we forecasted TRA’s operating

results in the period of 2019-2026 as follows:

Net Revenue and Gross Profit Projection for TRA in the Period of 2019-2026

Cost of Goods Sold and SG&A Expense Projection for TRA in the Period of 2019-2026

Forecasted revenues, costs of goods sold, and SG&A expenses were based on the following assumptions:

TRA’s herbal product sales would grow at a CARG of 2.95% between 2018 and 2026, reducing TRA’s herbal

sales percentage from 76% to 70% of the firm’s total manufacturing sales. Major growth for herbal product

sales would be driven by TRA’s leading products “Hoat huyet duong nao – Cebraton” (CAGR of 3.8%) and

“Tottri” (CAGR of 3.54%). We assumed that TRA would not develop any new leading herbal products and that

TRA’s current herbal products, gradually becoming saturated, would grow proportionally with certain disease

rates and the aging population tendency in Vietnam.

TRA’s generic drug sales would grow at a CAGR of 6.53% during the period of 2018-2026, increasing TRA’s

generic drug sales percentage from 24% to approximately 30% of the firm’s total manufacturing sales in 2026.

We assumed that TRA’s generic product sales would not grow significantly until after its Hung Yen Generic

Drug Factory production lines would have been certified for EU-GMP standard which would allow TRA to bid

in Tier 1 and 2 in the ETC channel in 2022.

Active Pharmaceutical Ingredients (API) imported from China would surge, causing TRA’s costs of goods sold

to simultaneously increase.

SG&A expenses would continue to increase; however, would gradually be more effectively managed and would

fluctuate between 23%-27% for selling expenses and be stable at 12.5% for administrative expenses.

49%

50%

51%

52%

53%

54%

55%

.0

500.0

1000.0

1500.0

2000.0

2500.0

2018 2019(f) 2020(f) 2021(f) 2022(f) 2023(f) 2024(f) 2025(f) 2026(f)

bill

ion

VN

D

Net Revenues Gross Profit Margin (right)

.0

200.0

400.0

600.0

800.0

1000.0

1200.0

2018 2019(f) 2020(f) 2021(f) 2022(f) 2023(f) 2024(f) 2025(f) 2026(f)

bill

ion

VN

D

Cost of Goods Sold Selling Expenses Administration Expenses

Bloomberg – FPTS <GO> | 17

HSX: TRA

www.fpts.com.vn

VALUATION SUMMARY

We valued TRA’s operating activities using the discounted cash flow method and the relative approach with

weighting factors of 90% and 10%, respectively. TRA’s stock intrinsic value was determined at 74,100 VND per

stock, 10.53% higher compared to its closing price on July 23rd 2019. Therefore, we recommend a HOLD position

for TRA’s stocks for medium-term and long-term investment horizon.

Valuation Method Result Proportion

1 Discounted Cash Flow (DCF) 90%

Free Cash Flow to Equity (FCFE) 76,700

Free Cash Flow to Firm (FCFF) 75,100

2 Relative Valuation 10%

Relative P/E 57,500

Target Price (VND/share) 74,100

Discounted Cash Flow Assumptions

Assumption Value Assumption Value

WACC in 2018 12.63% Equity risk premium 9.97%

Cost of debt in 2018 10.00% Beta 0.69

Cost of equity in 2018 13.50% Long-term growth rate 1.50%

Risk-free rate (20-year T-bond coupon) 5.60% Forecasted horizon 8 yrs

DISCOUNTED CASH FLOW VALUATION RESULT

Free Cash Flow to Firm (FCFF) Summary Value

Sum of FCFF present value 3,294,734,655,697

(+) Cash 26,052,936,805

(-) Short-term and long-term liabilities 206,902,575,931

Equity value 3,113,885,016,571

Number of shares outstanding 41,453,673

Intrinsic Value (VND per share) 75,100

Free Cash Flow to Equity (FCFE) Summary Value

Sum of FCFE present value 3,178,538,880,246

Intrinsic Value (VND per share) 76,700

RELATIVE VALUATION RESULT

Traphaco was compared to a few major domestic pharmaceutical manufacturers (as of July 23rd 2019):

Firm Ticker Market Cap.

(bil. VND)

EV (bil.

VND)

NI (bil.

VND) P/E

Imexpharm Pharmaceutical JSC. IMP 2.35 2.16 0.14 16.93x

Pymepharco JSC. PME 3.60 3.24 0.31 11.61x

Domesco Medical Import & Export JSC. DMC 2.43 2.37 0.23 10.63x

Binh Dinh Pharmaceutical & Medical Equipment JSC. DBD 2.25 2.25 0.16 13.79x

OPC Pharmaceutical JSC. OPC 1.30 1.38 0.10 12.92x

Average 13.63x

Traphaco JSC. TRA 2.78 2.89 0.18 15.89x

Bloomberg – FPTS <GO> | 18

HSX: TRA

www.fpts.com.vn

FINANCIAL STATEMENT SUMMARY

Income Statement

(billion VND)

2018 2019E 2020F 2021F

Revenues 1,798.3 1,860.2 1,925.5 1,983.4

- COGS 863.7 907.4 918.0 929.7

Gross profit 934.7 952.9 1,007.5 1,053.7

- Selling expenses 485.5 442.8 472.6 533.9

- Admin. expenses 222.5 233.3 241.4 248.7

Operating profit 226.7 276.8 293.4 271.1

Fin. activity P/L 2.3 (9.0) (4.2) (6.0)

Other profit/loss (0.6) (0.07) 0.9 0.2

EBIT 228.4 267.8 290.1 265.2

- Interests 12.2 15.2 13.0 11.5

EBT 216.2 252.5 277.1 254.9

- Corporate income

tax

41.4 50.8 54.3 49.5

Profit after tax 174.8 201.7 222.8 204.2

EPS (VND) 3,352 4,404 4,898 4,448

Cash Flow

Statement

2018 2019E 2020F 2021F

Beginning balance 160.9 316.1 430.7 520.7

Profit after tax 216.2 182.6 203.0 184.4

+ Depreciation 79.4 71.2 77.9 92.9

+ Adjustments 0.2 0 0 0

+ Changes in

working capital

(49.8) 25.6 (34.1) 29.1

Cash from

operations

168.7 310.3 259.2 316.5

+ Fixed assets

liquidation

0 0 0 0

+ Investments 0.5 0 0 0

+ Others (43.7) (9.3) (11.0) (204.7)

Cash from

investing

(43.2) (9.3) (11.0) (204.7)

+ Dividend

payments

(140.1) (140.1) (140.1) (140.1)

+ Capital changes 169.8 0 0 0

+ S-T debt changes 0 0.8 0.8 0.8

+ L-T debt changes 0 (37.4) (19.4) (18.9)

+ Others 0 0 0 0

Cash from

financing

29.7 (186.4) (158.8) (158.3)

Net cash changes 155.2 114.5 89.5 (46.4)

Ending balance 316.1 430.7 520.1 473.7

Balance Sheet 2018 2019E 2020F 2021F

Assets

+ Cash and cash

equivalent

316.1 430.7 520.1 473.7

+ S-T investments 9.4 9.5 9.2 9.4

+ Receivables 153.6 179.0 169.8 188.8

+ Inventories 337.5 333.2 364.3 340.3

+ Other S-T assets 42.8 26.6 30.6 36.3

Current assets 859.4 979.1 1,094.0 1,048.5

+ Fixed assets 937.2 946.6 957.6 1,162.2

+ Acc. depreciation (331.7) (402.1) (479.1) (571.2)

+ Net book value 605.5 544.5 478.4 591.0

+ L-T investments 0.5 0.5 0.5 0.5

+ Other L-T assets 110.6 109.8 108.9 108.1

+ Construction in

progress

13.9 13.9 13.9 13.9

Long-term assets 730.5 680.6 601.7 713.4

Total assets 1,589.9 1,647.7 1,695.7 1,761.9

Liabilities & Equity

+ Payables 90.5 127.4 101.7 116.9

+ S-T borrowings 36.5 37.3 38.0 38.8

+ Other S-T

borrowings

4.3 3.8 3.9 3.3

Current liabilities 312.2 359.2 347.9 372.2

+ L-T borrowings 170.4 133.0 113.6 94.6

Long-term liabilities 170.4 133.0 113.6 94.6

Total liabilities 482.7 492.2 461.5 466.9

+ Authorized capital 414.5 414.5 414.5 414.5

+ Retained earnings 95.8 116.3 157.2 180.1

Equity 1,106.1 1,154.3 1,233.0 1,293.9

Non-controlling

interests

86.5 105.6 125.4 145.2

Total liabilities and

equity

1,589.9 1,647.7 1,695.7 1,761.9

Efficiency Ratios 2018 2019E 2020F 2021F

Days sales outstanding 25.47 25.47 25.47 25.47

Days in inventory 142.47 132.99 138.76 139.41

Accounts payable days 44.04 44.04 44.04 44.04

Cash conversion cycle 123.91 117.42 121.20 120.84

COGS/Inventories 2.56 2.72 2.52 2.73

Asset turnover 1.16 1.15 1.15 1.15

Bloomberg – FPTS <GO> | 19

HSX: TRA

www.fpts.com.vn

Profitability Ratios 2018 2019E 2020F 2021F

Gross profit margin 52.0% 51.2% 52.3% 53.1%

Net profit margin 9.7% 10.8% 11.6% 10.3%

ROE 14.0% 17.8% 18.7% 16.2%

ROA 10.1% 12.5% 13.3% 11.8%

Operating profit

margin

12.7% 14.4% 15.1% 13.4%

Profit after tax/EBT 80.8% 79.9% 80.4% 80.5%

EBT/EBIT 94.7% 94.3% 95.5% 95.7%

Liquidity & Leverage 2018 2019E 2020F 2021F

Current ratio 5.09 4.59 4.87 4.73

Quick asset ratio 1.67 1.80 2.10 1.90

Cash ratio 1.04 1.23 1.52 1.30

Debt ratio 0.13 0.10 0.09 0.08

Debt to equity ratio 0.19 0.15 0.12 0.10

S-T debt to equity ratio 0.03 0.03 0.03 0.03

L-T debt to equity ratio 0.15 0.12 0.09 0.07

Equity multiplier 1.39 1.43 1.40 1.37

Interest coverage 18.72 17.61 22.30 23.02

Bloomberg – FPTS <GO> | 20

HSX: TRA

www.fpts.com.vn

APPENDICES

I. TRA’s Manufacturing Process (back to Operation Analysis)

1. Herbal Products

a. Ingredient Preparation

WHO-GACP qualified herbal ingredients are prepared and extracted at TRA’s Traphaco Sapa Factory with three

WHO-GMP certified production lines, a spray dryer system and a cleanroom system.

b. Manufacturing Process

Herbal products are manufactured at TRA’s Hoang Liet Factory and Hung Yen High-Technology Factory with its

advanced soft capsule production lines (100% capacity), hard capsule production lines (40% capacity) and other

production lines (50-70% capacity), which consist of 36 different types of machines.

2. Generic Drugs

a. Ingredient Preparation

All of TRA’s active pharmaceutical ingredients (API) in crytalized forms with stabilized pharmacological structures

and effects are imported. Most API only need to be blended with excipients before pharmaceutically formed.

b. Manufacturing Process

TRA’s generic drugs are manufactured at Hung Yen Generic Drug Factory with five production lines in three

production plants. Its tablet production line can reach a capacity of 900 million tablets per year. TRA’ eye drop

production line is equipped with BFS Technology (Blow-Fill-Seal) which maximizes sterilization in a completely

closed process and minimizes the manufacturing duration to 13 seconds per product.

Fresh Ingredients

(3,000 tons/yr)Dried Ingredients

Herbal concentrate

Nano-sized herbal particles

(120 tons/yr)

Collecting, preparing,

drying

Heat-pumped drying

Cleansing with high-pressure

water

Vacuum extracting

Concentrating and

evaporating

Vacuum drying

Nano-sized herbal particles

Capsule and tablet forms: gel & powder capsules, sugar-coated and film-coated tablets, etc.

Other forms: syrups and granules.

Blending Pharmaceutically formed Packaging Storing

Crystalized API

Capsule and tablet forms: gel capsules, powder capsules, film-coated tablets

Liquid forms: eye drops, nasal drops, cough syrups

Other forms: ointments and granules

Blending Pharmaceutically formed Packaging Storing

Solvent added: 960 ethanol

Excipients added: solvents, gelatin, etc.

Excipients added: solvents, gelatin, etc.

Bloomberg – FPTS <GO> | 21

HSX: TRA

www.fpts.com.vn

II. Bidding Procedure in the ETC Channel (back to TRA’s ETC Sector Analysis)

Steps Details

Classification Drugs are classified into different tiers based on manufacturing quality

Technical Rating (30%) Quality: 70%, Packaging: 30% of technical points. If the total points are less

than 80%, the bidding product is disqualified

Financial Rating (70%) The lower the bidding price, the higher the financial points

Total=30%Technical+70%Financial Bidders with the highest points will have their capacity for supplying tested

Capacity for Supplying Bidding packages will be divided into smaller packages if bidders’s capacity

cannot satisfy required quantity

Source(s): National Medicine Trading Center

III. Existing generic drug tiers according to Circular No.11/2016/TT-BYT (expired Oct. 2019) (back to TRA’s

ETC Sector Analysis)

Tier Descriptions of Generic Drugs

1 Manufactured with EU-GMP or PIC/s-GMP production lines and certified by ICH members or Australia.

2 Manufactured with EU-GMP or PIC/s-GMP production lines and not certified by ICH members nor

Australia.

3 Manufactured with WHO-GMP and certified by the Vietnamese Ministry of Health.

4 Bioequivalent drugs certified by the Vietnamese Ministry of Health.

5 Other drugs which do not meet the above requirements.

Source(s): Vietnamese Ministry of Health

IV. New generic drug tiers according to Circular No.15/2019/TT-BYT (effective October 2019) (back to TRA’s

ETC Sector Analysis)

Tier Descriptions of Generic Drugs

1 Manufactured with EU-GMP or equivalent production lines and certified by certain Stringent Regulatory

Authorities (SRA).

2 Manufactured with EU-GMP and not certified by SRA or with PIC/s-GMP and certified by Reference

Regulatory Authorities which, at the same time, have to be PIC/s and ICH members.

3 Manufactured with GMP quality and bioequivalently certified by the Vietnamese Regulatory Authority.

4 Manufactured in Vietnam with WHO-GMP and certified by the Vietnamese Regulatory Authority.

5 Manufactured with WHO-GMP and do not meet the above requirements.

Source(s): Vietnamese Ministry of Health

V. List of Stringent Regulatory Authorities (SRA) qualified to certify drugs in Tier 1 (back to TRA’s ETC

Sector Analysis)

1. European Medicines Agency (EMA)

2. U.S. Food and Drug Administration (US FDA)

3. (Japanese) Pharmaceuticals and Medical Devices Agency (PMDA)

4. Medicines and Healthcare Products Regulatory Agency (MHRA)

5. The Swiss Agency for Therapeutic Products (Swissmedic)

6. Health Canada

7. (Australian) Therapeutic Goods Administration (TGA)

8. Icelandic Medicines Agency (IMA)

9. Liechtenstein – Austrian Federal Office for Safety in Health Care (BASG)

10. The Norwegian Medicines Agency (NoMA)

Source(s): Vietnam Regulatory Affairs Society

Bloomberg – FPTS <GO> | 22

HSX: TRA

www.fpts.com.vn

VI. Traphaco’s Distribution Centers (back to SG&A

Expense Analysis)

- Yen Bai - Thai Nguyen - Vinh Phuc - Phu Tho - Bac Giang - Quang Ninh - Hai Duong - Hai Phong - Hung Yen - Nam Dinh - Thanh Hoa - Nghe An - Thua Thien Hue - Da Nang - Quang Ngai - Binh Dinh - Gia Lai - Khanh Hoa - Binh Thuan - Dong Nai - Binh Duong - Ho Chi Minh City - Long An - Tien Giang - Can Tho - Vinh Long - Kien Giang - Vung Tau

Source(s): Traphaco

VII. Fine Particulate Matter (PM 2.5)

Distribution Map in Vietnam

Source(s): Yale University Data

VIII. List of Important Terms

Term Description

Herbal Products

Produced from natural sources, including herbs, plants and animals. In this context, “herbal

products” can be understood as both herbal medicines and herbal health supplements as they

share similar sources of ingredients.

Patented &

Generic Drugs

Manufactured from crystalized active pharmaceutical ingredients (API) which could be

synthesized from natural sources but have to be in pure forms.

Over-the-

Counter (OTC)

In Vietnam, due to loose regulations, the term “OTC” can be understood as a distribution

channel via which pharmaceutical products are sold at pharmacies.

Ethical Drugs

(ETC)

In Vietnam, due to loose regulations, the term “ETC” can be understood as a distribution

channel via which pharmaceutical products are bid in different tiers to be sold at hospitals and

clinics.

WHO-GACP Guidelines on good agricultural and collection practices developed by WHO.

WHO-GMP Guidelines on good manufacturing practice developed by WHO.

PIC/s-GMP Guidelines on good manufacturing practice developed and certified by Pharmaceutical

Inspection Co-operation Scheme (PIC/s) members.

ICH International Council for Harmonization of Technical Requirements for Pharmaceuticals for

Human Use.

EU-GMP Guidelines on good manufacturing practice developed by the European Medicines Agency to

satisfy European Union level of quality, one of the strictest manufacturing standard in the world.

Bioequivalence The condition in which different formulations of the same drug are equally absorbed when taken

into the body.

Source(s): FPTS Research

Bloomberg – FPTS <GO> | 23

HSX: TRA

www.fpts.com.vn

Disclaimer

All of information and analysis in this report made by FPTS based on reliable, public and legal sources. Except for information about

FPTS, we do not guarantee about the accuracy and completeness of these information.

Investors who use this report need to note that all of judgements in this report are only subjective opinions of FPTS. Investors have

to take responsibility about their decisions when using this report.

FPTS might make investment decisions based on information in this report or others and do not have any claim on legal perspective

of given information.

By the time of publishing the report, FPTS holds 59 shares of TRA and the analyst does not hold any share of the subject company.

This report many not be copied, reproduced, published or redistributed for any purpose without written permission of an

authorized representative of FPTS. Please cite sources when quoting. Information related to stocks and industries could

be viewed at https://ezsearch.fpts.com.vn or will be provided upon official request.

© Copyright by FPT Securities 2010

FPT Securities Joint Stock Company

Head Office

No. 52 Lac Long Quan, Buoi Ward,

Tay Ho District, Hanoi, Vietnam.

Tel: (84.24) 3 773 7070 / 271 7171

Fax: (84.24) 3 773 9058

FPT Securities Joint Stock Company

Ho Chi Minh City Office

3rd Floor, Ben Thanh Times Square

Building, 136-138 Le Thi Hong Gam,

District 1, Ho Chi Minh City, Vietnam.

Tel: (84.28) 6 290 8686

Fax: (84.28) 6 291 0607

FPT Securities Joint Stock Company

Da Nang Office

No. 100 Quang Trung, Thach Thang

Ward, Hai Chau District, Da Nang,

Vietnam.

Tel: (84.236) 3553 666

Fax: (84.236) 3553 888