Valuation Report 'Matrix Portfolio, Valuation of 13 properties''

198

Valuation Report ‘Matrix Portfolio, Valuation of 13 properties’’ prepared for Brack Capital Properties N.V. May 2013 (Copy)

-

Upload

khangminh22 -

Category

Documents

-

view

5 -

download

0

Transcript of Valuation Report 'Matrix Portfolio, Valuation of 13 properties''

Valuation Report ‘Matrix Portfolio,

Valuation of 13 properties’’

prepared for Brack Capital Properties N.V.

May 2013

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 1

Contents

1 Brief & Scope of Instruction ................................................................................................................................. 3 1.1 Instruction ................................................................................................................................................................ 3 1.2 Valuer Status ........................................................................................................................................................... 3 1.3 Purpose of Valuation................................................................................................................................................ 4 1.4 Sources of Information ............................................................................................................................................. 4 1.5 Date of Valuation ..................................................................................................................................................... 4 1.6 Inspections ............................................................................................................................................................... 4 1.7 Basis of Valuation .................................................................................................................................................... 4 2 Market Considerations .......................................................................................................................................... 5 2.1 German Economy .................................................................................................................................................... 5 2.2 Retail Investment Market ....................................................................................................................................... 11 2.3 German Retail Warehouses and Retail Parks ....................................................................................................... 14 3 Valuation ............................................................................................................................................................... 22 3.1 Valuation Methodology .......................................................................................................................................... 22 3.2 Valuation Assumptions .......................................................................................................................................... 22 3.3 Valuation Results ................................................................................................................................................... 26 3.4 Sensitivity Matrix .................................................................................................................................................... 27 4 Confidentiality & Publication .............................................................................................................................. 30 Appendix I – Property Reports ...................................................................................................................................... 31 Appendix II – Overview ................................................................................................................................................... 32 Appendix III – General Principles for Valuation ........................................................................................................... 33

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 2

Contents cont’d

Figure 1: Retail Transaction Volume Germany ................................................................................................................. 12 Figure 2: Transaction Volume Germany divided by Retail Asset Class ............................................................................ 13 Figure 3: Development of Prime Yields ............................................................................................................................. 13 Figure 4: Prime Yield Development in % ........................................................................................................................... 16 Figure 5: Prime Yield Development in % ........................................................................................................................... 20 Table 1: Transaction Evidence .......................................................................................................................................... 17 Table 2: Transaction Evidence .......................................................................................................................................... 21 Table 3: Inflation forecast Germany .................................................................................................................................. 26

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 3

1 Brief & Scope of Instruction

1.1 Instruction

We refer to your instruction, dated 25 April 2013, instructing us to carry out a valuation of the Matrix Portfolio consisting of 13 properties. The portfolio comprises retail parks and self-service department stores. The instruction was ordered by Fred Ganea, Head of Financial Department of Brack Capital Properties N.V.

1.2 Valuer Status

We confirm that the valuation has been carried out by us as external valuers, qualified for the purposes of providing valuations in accordance with the Appraisal and Valuation Manual published by the Royal Institution of Chartered Surveyors (RICS). We also confirm that we have no conflict of interest relating to the property and that we have valued portfolios of a similar scope as well as larger scope in the course of other mandates.

The project team consists of the following members:

Andrew Groom

Since August 2001 Mr. Groom is head of the Valuation Advisory department in Germany with additional responsibility for valuation business in Austria and Switzerland.

As International Director, Mr Groom leads the overall direction of the Bank, Portfolio, Transaction, Residential and Retail Valuation business lines as well as mortgage lending valuations for German mortgage banks (Team of 50+ consultants).

He is also responsible for providing client management within the scope of major German and international mandates, comprehensive advisory services for real estate portfolios in terms of acquisition and disposal strategies and advising leading banks with regard to risk classification in property financing.

Prior to that he gained management experience leading international advisory departments for CEI Investment London and Drivers Jonas London as well as Berlin. Here he was not only responsible for the valuation department, but also for the investment sector.

Andrew Groom holds a Bachelor of Science with Honours in Estate Management and is also a member of The Royal Institution of Chartered Surveyors (MRICS) and a member of the RICS Valuation Faculty Board, Germany.

He has over 21 years development, valuation and international investment experience as well as over 18 years management experience leading international advisory departments.

Frank Rambow

Since 2007 Frank Rambow is Teamleader of the Bank Valuation Advisory team of Jones Lang LaSalle’s Valuation Department. Here he heads a team of 6 professionals. He currently holds the position of a National Director.

Frank Rambow has lead several buy-side advices and real estate appraisals for single assets as well as portfolios for various clients. All the valuations are conducted according to the IFRS standards.

He is a graduated economist and has over 15 years’ experience in real estate sector, thereof nine years at JLL. Frank Rambow is a member of The Royal Institution of Chartered Surveyors (MRICS).

Georg Charlier

In September 2008, Georg Charlier joined Jones Lang LaSalle Germany, focusing mainly on the valuation of retail and office portfolios/properties. He holds the position of Principal Consultant. Prior to that he was part of the Munich based team of a German Real Estate Investor.

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 4

Georg Charlier holds a Diploma of Real Estate Engineering and Management and a certification of the society of investment professionals in Germany. He possesses more than 6 years of consulting experience on the German real estate market.

1.3 Purpose of Valuation

We understand that the valuation is required for financial statement reporting and that the valuation reports will be included in the financial statement of Brack Capital Properties N.V.

1.4 Sources of Information

In preparing this valuation report, we have predominantly relied upon information provided by Brack Capital Properties N.V. We received the documents listed below, which form the basis for our valuation:

Tenancy Schedule as at April 2013

Schedule of non-recoverable costs on an individual property basis

Overview of short-term tenants income, on an individual property basis

List of indexation clauses

Presentation regarding the development potential for the subject property in Neckarsulm

In the event that this information proves to be incorrect or additional information is made available to us, the accuracy of the valuation could be affected. In such case, we reserve the right to amend our opinion of value accordingly.

1.5 Date of Valuation

As specified in your instruction, we have set the valuation date to be 31 March 2013.

1.6 Inspections

For the current valuation, we did not conduct inspections. However, the properties were inspected by us in the scope of the valuation in February 2011.

1.7 Basis of Valuation

The valuation is carried out on the basis of Market Value as defined in the '8th Edition of the Royal Institution of Chartered Surveyors' (RICS) Appraisal and Valuation Manual. This is incorporated into the Jones Lang LaSalle “General Principles Adopted in the Preparation of Valuations and Reports”, which is attached in the Appendix 2. Market Value is defined as:

“The estimated amount for which an asset or liability should exchange on the valuation date between a willing buyer and a willing seller in an arm's-length transaction after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion.”

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 5

2 Market Considerations

2.1 German Economy

GROSS DOMESTIC PRODUCT In the fourth quarter of 2012, the price-adjusted GDP declined by 0.6%. In comparison to a stronger previous quarter, growth in the German economy slowed-down.

In the first three quarters, Germany achieved a considerable increase of 0.5%, 0.3% and 0.2% which led to growth of 0.7% in 2012. The calendar-adjusted increase was 0.9%.

In the previous quarter only domestic consumption achieved growth.

State (+0.4%) and private expenses (+0.1%) increased slightly – in price, seasonal and calendar-adjusted terms, while investment decreased in general. Equipment investment has continued to decrease and is currently -2.0%. In addition, the export sector slowed down in the fourth quarter with the export of goods and services dropping by 2.0%. Imports fell by 0.6%.

As forecasted by the German Institute for Economic Research (DIW), the German economy is expected to generate a slight surplus in the first quarter of 2013, which will accelerate further economic development.

According to the DIW, there is considerable uplift in the sentiment amongst businesses and increased demand from the Eurozone. Furthermore, economic development is supported by growing domestic demand, due to a stable German job market and a recent increase in wages.

Development of gross domestic product (Q1/2010 –Q4/2012) – Seasonally and calendar adjusted

Source: Federal Statistical Office, April 2013

BUSINESS CLIMATE In February 2013, the Ifo Business Climate Index noted its strongest upward movement since July and rose to an index level of 107.4. At the end of March, it was 106.7.

As a result, businesses view the current situation as well as future development more optimistically than they did in previous months.

The business climate in the manufacturing industry has improved because of more optimistic assessments regarding the current business situation. In addition, export demand is expected to be above average on a long-term basis.

Business confidence in the wholesale sector has improved in comparison to the previous month. This characterises the current climate a well as future expectations.

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 6

Despite an improved climate in the retail sector, future expectations are characterised by scepticism.

The business climate in the construction industry rose again. The situation has improved slightly and the outlook for the coming months has reached its highest point since German reunification.

The Ifo Business Climate Index for the service sector rose significantly in February.

Despite a current decrease, figures for the next six months are expected to rise from 9.0 points to 19.0.

Ifo – Business Climate Index January - March 2013

Source: Ifo-Institute, April 2013

PRICE DEVELOPMENT According to the Federal Statistical Office (Destatis), the consumer price index for Germany in March 2013 was 1.4% higher than in March 2012 and compared to the previous month increased by 0.5%.

Compared to 2012, the main driver of the price increase in February 2013 was the rise in energy and food costs. Energy prices rose by 3.6% and food prices by 3.1% compared to February 2012.

Had it not been for this, the consumer price index would have only reached 1.1% in February 2013.

Domestic energy prices were mainly influenced by electricity costs, due to the increase in the EEG reallocation charge at the beginning of 2013.

Increased food prices were driven by fruits (+7.2%) and meat (+5.4%). Furthermore, prices increased for bread and cereal products (+2.7%) as well as fish (+2.6%) and candy (+2.3%). Cooking fat and oil on the other hand became cheaper (-2.4%).

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 7

Development of inflation rate / consumer price index “original values” (January 2011-March 2013)

Source: Federal Statistical Office, April 2013

LABOUR AND TRAINING MARKETS Unemployment, Unemployment Rate

According to the Federal Employment Agency, the nationwide unemployment rate was 7.3% in March 2013, which was a slight decrease compared to the previous month.

With about 3.1 million people in Germany actively seeking employment, the unemployment situation is similar to that of February and March 2012.

Due to the winter season, the number of unemployed people rose by 18,000 compared to January. This is significantly less than the previous year, when the number rose by 46,000.

All sectors were able to record employment growth in a year-on-year comparison. The highest growth was registered in the business services sector (+168,000), the manufacturing industry (+75,000) and the healthcare and social services sector (+58,000).

Temporary employment services registered 70,000 less employees compared to the previous year.

The long-term unemployment rate (longer than 12 months) increased slightly in comparison to the previous year.

The 1% rise represents 9,000 people gaining employment, bringing the overall number of long-term unemployed people to 1,063,000. While the number of unemployed people has risen overall, the share of people that were unemployed for more than 12 months remained stable, with around 33.7% this year and 33.9% in the previous year.

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 8

Development of unemployment (January 2011-March 2013)

Source: Federal Employment Agency, April 2013 PURCHASING POWER Purchasing power is the market-recognised benchmark for determining potential consumption. It delivers key information regarding the regions with the strongest purchasing power; purchasing power can indicate the total of all net revenues per region, while taking state transfer benefits like jobseeker allowance, child and retirement benefits into account.

Furthermore, purchasing power is localised and thereby a relevant indicator for the potential consumption of the population living in a specific community.

Retail Industry: Germany sees significant increase

The GfK purchasing power in Germany for 2013 is estimated to be approx. € 1,610 billion in total.

This is up by 2.9% from the previous year’s figure. The average citizen thereby has a purchasing power of € 20,621 this year, plus a nominal € 554 more to spend on consumer products, rent or cost of living.

Currently, the German Central Bank estimates an inflation rate of 1.5%, which will lead to not only a nominal increase in purchasing power but also a rise in real terms by 1.4%. Positive development in consumer spending is therefore expected.

However, not all demographic groups will benefit; retirement benefits are likely to fall below inflation in 2013 and cause a loss in purchasing power.

Nevertheless, most industries are expected to develop positive income growth.

German Federal State Comparison: Baden-Württemberg overtakes Hessen

This year Hamburg is at the top with 110.4 index points followed by Bavaria with 109.2. Baden-Württemberg comes in third (Index: 107.2), overtaking Hessen (107.1 points).

Six of the 16 federal states have an above average purchasing power per capita. Rhineland-Palatinate represents the national average.

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 9

The federal states in eastern Germany remain below the national average. Saxony-Anhalt is last with €16,970 per capita.

Urban and Rural District Comparison:

The top ten urban and rural districts remain the same, with the exception of the first two districts exchanging position.

Starnberg (Index: 147.9) took over the top position from Hochtaunuskreis (Index: 146.3).

The two districts have swapped the top two positions before, with Starnberg ahead of Hochtaunuskreis in 2008. Munich and Erlangen are the only urban districts in the top ten ranking, which indicates that the wealthiest people still live in exurban areas.

Hamburg as a city-state is the second most populous urban district and, as mentioned before, is at the top of the federal states ranking. However, Hamburg ranks 54th in the overall urban and rural district comparison. In a comparison of urban districts Hamburg ranks 18th.

Compared to previous years, there are changes at the bottom of the ranking as well.

The main reason for this is the restructuring of urban and rural districts in Mecklenburg-West Pomerania. Some of the weaker districts were combined and restructured.

The rural district Görlitz in Saxony is last this year, whereas, in previous years, north-eastern districts had the lowest figures.

Next to Görlitz, the Elbe-Elster district in Brandburg (Index:77.3) and the Kyffhäuser district in Thuringia (Index: 77.4) showed the weakest results.

Gap between rich and poor

People in Görlitz have an average €15,687 per capita to spend (Index 77.4), which is almost half of the average sum that a resident in Starnberg has on hand.

The gap between rich and poor spreads from almost 50% above average in Starnberg to 24% below the national average in Görlitz.

Strong districts are often located near weak ones. For example, the difference in euros per capita between the urban districts of Düsseldorf and Duisburg (30 km apart) is € 7,100, a 29% difference.

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 10

Purchasing Power in Germany 2013

Source: GfK Regional Statistics

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 11

DEMOGRAPHIC CHANGE Population development in the coming years can be described with three key terms: fewer, older, and more multicultural. In addition to this, the population structure will change significantly.

The effect of this demographic change on the economy and competitiveness as well as on the future of the social welfare system (old age, unemployment and health insurances) continues to cause debates.

It is evident that Germany’s population has been dropping since 2003. This decrease will continue and intensify.

At the end of October 2012, approximately 82 million people were living in Germany, which is 0.2% more than at the end of 2011. The figure was approx. 81.5 million at the end of 2010.

In 2060, the population will drop to between 65 million (annual immigration rate of 100,000 – lower end of “average” population) and 70 million (annual immigration rate of 200,000 – upper end of “average” population). Even with the upper-end estimates for the total population – which assumes a rise in the birth rate, a significant increase in life expectancy and an annual balance of migration of 200,000 people – only about 77 million people would be living in Germany in 2060, significantly less than today.

A Germany-wide census took place recently (census 2011), which was designed to provide up-to-date information about the numbers, demographics, socio-economic data and housing of the population. The publication of the detailed assessment is planned for May 2013.

Forecast of population development in Germany (2009 – 2060) “medium” variant

Source: Federal Statistical Office

2.2 Retail Investment Market

Retail Investment Market: Review of 2012

Stability of the German economy as well an upward trend during 2012 kept Germany in the focus of real estate investors throughout Europe. Following a recovery in 2010, the economy as well as employment rates and income rose significantly, but this increase slowed down during 2011. This caused a ripple effect in the retail sector. In 2012, retail investments totalled approximately € 7.9 billion compared to € 10.7 billion in 2011. Hence, it accounted for 45% (2011) and 31% (2012) respectively. Whereas the total investments in retail properties in 2011

60,000

65,000

70,000

75,000

80,000

85,000

2010 2015 2020 2025 2030 2035 2040 2045 2050 2055 2060

in thousands

lower limit medium higher limit

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 12

clearly exceeded the 2010 figure and reached the level of 2007, 2012 marked the first drop after three years of consecutive growth.

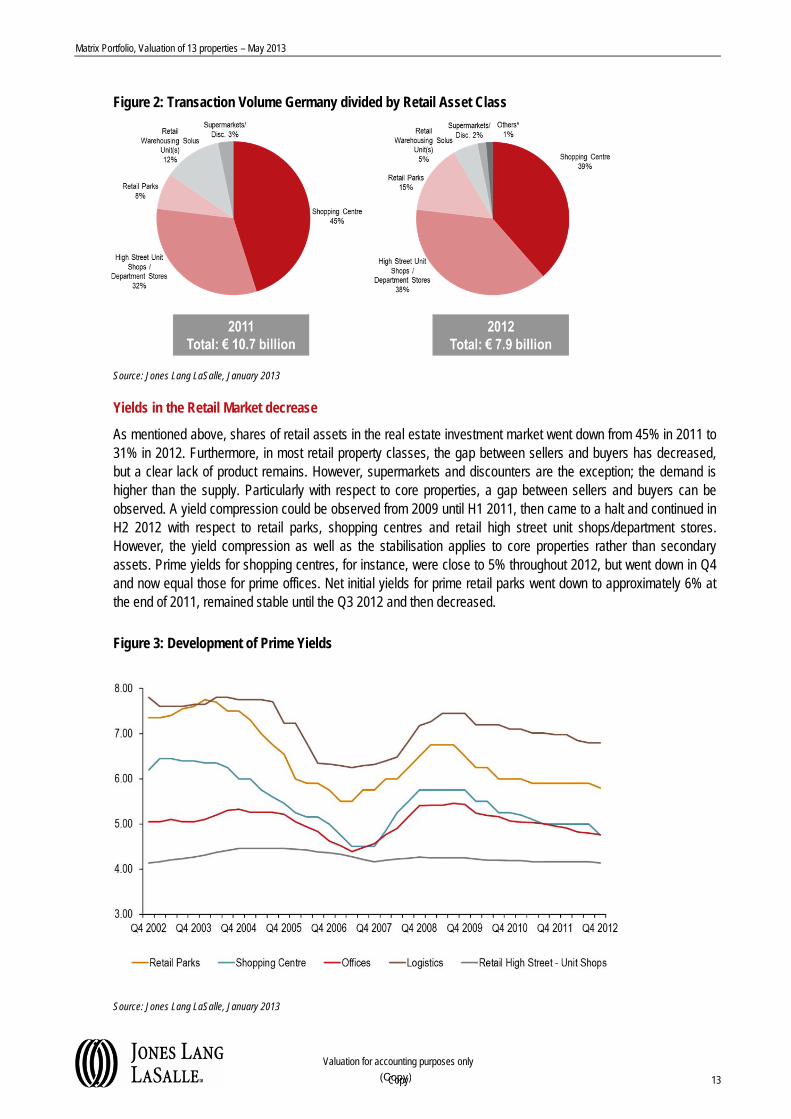

Figure 1: Retail Transaction Volume Germany

Source: Jones Lang LaSalle, January 2013

In the retail investment market, the shares of some of the asset classes shifted slightly between 2011 and 2012. In the last year the shares of shopping centres and high street properties/department stores were nearly equal at 38% (2011: 32%) and 39% (2011: 45%); both shifted slightly. Retail parks now have the third largest share with 15% (2011: 8%) and are followed by retail warehousing solus units, which accounted for 5% (2011: 12%). Investments in supermarkets/discounters represented 3% in 2011 and stood at 2% in 2012. Transactions involving other retail properties and a portfolio of kiosks took up a 1% share in 2012, respectively.

In 2011 some large transactions drove up the amount of investments in shopping centres, high street properties and department stores. In 2012, however, large transactions included the sale of KaDeWe and 17 Karstadt properties from Highstreet (Whitehall, RREEF and others) to Signa Holding; the sale of Europa Galerie in Saarbrücken from Credit Suisse to Union Investment (CS Eureal) for approximately € 170 million; the sale of a 45% share of the Europa Passage in Hamburg for € 184 million; shares of five shopping centres from Perella Weinberg to Unibail-Rodamco for approximately € 500 million; and 78% of the Milaneo shopping centre in Stuttgart for approx. € 400 million. Furthermore, the Rathaus-Center in Monheim has been sold at a so far unpublished price by Vald and ZIAG to Phoenix; Sahle-Gruppe bought Karstadt on Zeil in Frankfurt (€ 115m) and 11 Toom DIYs have been bought by a joint venture of Morgan Stanley and Redos Real Estate for approximately € 100 million; a joint venture of Matrix and Investors from Munich bought the Saturn store in Hamburg for an estimated € 80-90 million.

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 13

Figure 2: Transaction Volume Germany divided by Retail Asset Class

Source: Jones Lang LaSalle, January 2013

Yields in the Retail Market decrease

As mentioned above, shares of retail assets in the real estate investment market went down from 45% in 2011 to 31% in 2012. Furthermore, in most retail property classes, the gap between sellers and buyers has decreased, but a clear lack of product remains. However, supermarkets and discounters are the exception; the demand is higher than the supply. Particularly with respect to core properties, a gap between sellers and buyers can be observed. A yield compression could be observed from 2009 until H1 2011, then came to a halt and continued in H2 2012 with respect to retail parks, shopping centres and retail high street unit shops/department stores. However, the yield compression as well as the stabilisation applies to core properties rather than secondary assets. Prime yields for shopping centres, for instance, were close to 5% throughout 2012, but went down in Q4 and now equal those for prime offices. Net initial yields for prime retail parks went down to approximately 6% at the end of 2011, remained stable until the Q3 2012 and then decreased.

Figure 3: Development of Prime Yields

Source: Jones Lang LaSalle, January 2013

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 14

Retail Investment Market: Outlook

Especially as a result of the fact that Germany’s economy has been very stable in the past years and showed signs of growth in the recent past, we see retail to remain amongst the largest asset classes in 2013. Particularly those investors who seek a core investment with upward potential find the best fit in retail. Unlike before, their focus is not only on core properties. Alternative options like, for instance, value-add assets, assets with shorter rental lease contracts or vacancies are increasingly considered. However, building condition as well as location quality remain among the most important requirements. This development is partly due to a certain pressure to invest and partly because of a limited supply of core properties. Furthermore, in 2013 an increasing transaction volume of distressed properties and non-performing loans respectively can be expected. With respect to retail properties, we expect a progressively stable trend with the highest investment share anticipated for shopping centres and high street properties. Furthermore, we predict that the German real estate market will remain the focus of foreign investors. In 2012, Asset/Fund Managers as well as public quoted property companies/REITS were the most active participants of the retail investment market. We expect this to continue, but see developers and insurances to become more active again in 2013.

2.3 German Retail Warehouses and Retail Parks

The following section presents a more detailed overview of retail warehouses with a specific focus on “Do-It-Yourself” (DIY) stores, furniture stores, electronic goods stores, hypermarkets and cash & carry markets as well as retail parks and retail agglomerations. The subject matter will concentrate on the classification of these types of retail establishments, providing information on the special characteristics, the most well-known tenants, the deciding regional factors and information regarding the present situation in the German real estate market in view of the current rental level and the investment market.

Retail Warehouses

Definition

Retail warehouses are large-scale forms of retailers. They offer a broad and often very deep range of different products for different requirements and for specific target groups. Retail warehouses usually operate using a self-service format with a self-explanatory product selection, which is clearly presented to the customer. The need for good presentation and the broad and deep product range contribute to large sales areas. On the other hand, fewer sales staff is needed due to the self-service character. In combination with a good area performance and efficient stock keeping, the costs for retail warehouses are easily managed. Additionally, the majority of retail warehouses are chain stores with a basic concept. The construction of such concepts entails economic advantages, with products that can be and mostly are offered at lower to medium price levels.

Among retail warehouses, different types and branches can be distinguished. Retail warehouses can differ in service orientation and price level. There are more service-oriented warehouses (higher prices, more services) and more discount-oriented warehouses (lower price, less services). Plus, even though retail warehouses are usually large-scale, they can be distinguished based on their size and location.

Small retail warehouses have an area of approx. 200 to 1,200 m² and are located within a suburban location with good traffic connections. Tenants are usually hardware stores, office supply stores or drugstores. Medium retail warehouses comprise stores with an area of up to 3,500 m² and are located both in suburban areas and in the outskirts of towns and cities. Typical tenants include sporting goods stores, toy stores, electronic goods stores, large shoe stores, large hardware stores and auto supply stores. Large retail warehouses have an area of more than 3,500 m² up to 18,000 m² and are usually located in peripheral locations. However, these stores are increasingly being developed in more integrated locations. Typical tenants are large fashion retailers, toy stores, electronic goods stores and DIY stores. The biggest retail warehouses reach a size of up to 30,000 m². Due to their size, these stores are normally found exclusively in peripheral locations or on Greenfield sites. This size is

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 15

usually only occupied by furniture stores. The branches and tenants for retail warehouses are diverse and depend on the strategy and orientation of the subject property.

Locational Factors

Since the time they originated in the mid-1980s, retail warehouses are typically situated in peripheral locations in cities (e.g. commercial areas). This distinguishes a retail warehouse from conventional specialist stores, which traditionally prefer city centre locations. The motivation to move to Greenfield sites results mainly from the lower rental rates compared to the city centre, the fact that expansion is easier in the periphery (especially for large-scale retail warehouses), as well as the possibility to use simple building methods to affordably construct on a large scale (with regard to sales area and parking spaces). Together with more efficient organisation, this allowed products to be offered at lower prices than in traditional retail formats. Retail warehouses and their concepts are thus posing an ever greater threat of competition for the city centres. This means that continuous adjustment and development of concepts is necessary to remain competitive for both city centres and retail areas in the periphery.

Location factors can be differentiated by the macro-location and micro-location. The most important factor on a macro-level is the population and all factors directly and indirectly associated therewith. The first is the population of the locality and the number of people living in the catchment area of the respective property. In this context, future population development is another important factor given the long-term use of such real estate. Another factor concerning the population is the purchasing power. The more specialized retail warehouses are, the more purchasing power matters. This is because the costs associated with food, for example, do not depend on purchasing power as much as the costs associated with electronics or DIY-store goods. Factors like tourism potential and commuter balance play a less significant role. Given the increasing difference concerning the mentioned macro-location factors in Germany, these factors are continually gaining importance in the valuation of real estate.

On a micro-location level an important factor is the traffic infrastructure. As retail warehouses mostly rely on customers travelling by car, sufficient parking spaces as well as a good traffic infrastructure are very important. Thus, retail warehouses are often found along major arterial roads in commercial or industrial zones. Public transportation plays a less significant role but is important as well. Another important factor is the development in the vicinity. Further retailers in the vicinity can produce benefits from synergy effects or if retailers have a similar product range they can form competition. A residential population in the vicinity can also be beneficial, as people living in the surrounding area of a retail warehouse can significantly increase the customer frequency.

Rental Market

There is no homogeneous rental level for retail warehouses throughout Germany. Nevertheless, the spread between the rental levels is not as big as in high street locations. The maximum rents are determined by a percentage of the turnover expectancy as is common in the retail sector. The turnover again is most dependent on the above-mentioned macro- and micro-location factors of the retail warehouses plus the characteristics of the property like quality and concept of the store, architecture and visibility from the adjacent streets.

The economic difference throughout Germany has led to differences in rental levels throughout the country. Rents in Bavaria, Baden Wuerttemberg and the metropolitan regions around Hamburg, Frankfurt or Berlin, lie above the average rent in Germany due to the high population density, the positive population forecast and the strong economy. Rental levels in eastern German towns are generally slightly lower than their western counterparts, as these areas have a lower purchasing power, higher unemployment rates, most often a negative population development and therefore generate on average lower revenues.

Depending on the size of the retail unit and the branch of the tenant, rents for retail warehouses in Germany usually range from € 5.00 and € 14.00/m²/month. However, there are exceptions in both directions. The highest rents are not paid in peripheral locations but in locations in or near the city centre of larger cities with more than 100,000 inhabitants. Usually these prime rents are paid by well-known and attractive tenants, which occupy

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 16

buildings in very good conditions. The rents for retail warehouses in general in Germany have been relatively stable in the past 10 years. However, the future rental development of retail warehouse will be mainly determined by the growing regional differences. The rental levels will remain stable in sustainable locations and in absolute top locations there is the probability of small increases. But, locations in economically weak regions with negative population development were and are going through difficult development. Therefore, less sales area is needed there due to the migrating population. This leads to an oversupply of rental areas, which again leads to falling rental levels.

Investment Market Specifics

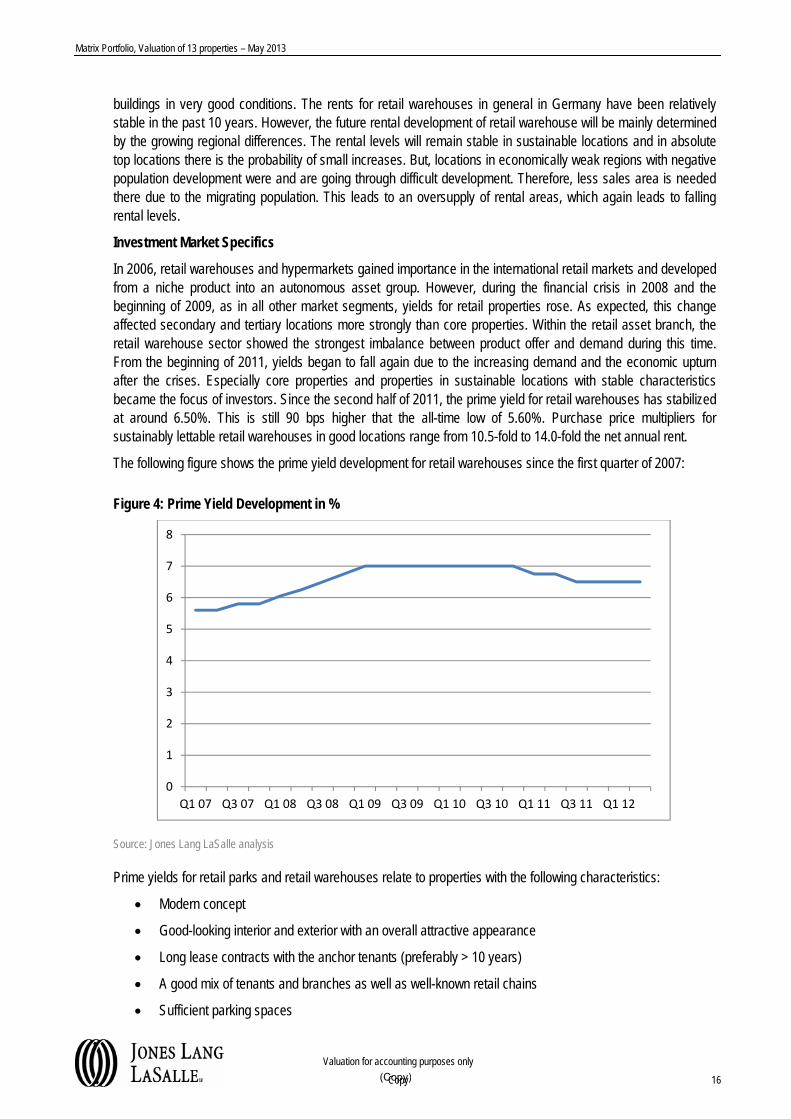

In 2006, retail warehouses and hypermarkets gained importance in the international retail markets and developed from a niche product into an autonomous asset group. However, during the financial crisis in 2008 and the beginning of 2009, as in all other market segments, yields for retail properties rose. As expected, this change affected secondary and tertiary locations more strongly than core properties. Within the retail asset branch, the retail warehouse sector showed the strongest imbalance between product offer and demand during this time. From the beginning of 2011, yields began to fall again due to the increasing demand and the economic upturn after the crises. Especially core properties and properties in sustainable locations with stable characteristics became the focus of investors. Since the second half of 2011, the prime yield for retail warehouses has stabilized at around 6.50%. This is still 90 bps higher that the all-time low of 5.60%. Purchase price multipliers for sustainably lettable retail warehouses in good locations range from 10.5-fold to 14.0-fold the net annual rent.

The following figure shows the prime yield development for retail warehouses since the first quarter of 2007:

Figure 4: Prime Yield Development in %

Source: Jones Lang LaSalle analysis

Prime yields for retail parks and retail warehouses relate to properties with the following characteristics:

Modern concept

Good-looking interior and exterior with an overall attractive appearance

Long lease contracts with the anchor tenants (preferably > 10 years)

A good mix of tenants and branches as well as well-known retail chains

Sufficient parking spaces

0

1

2

3

4

5

6

7

8

Q1 07 Q3 07 Q1 08 Q3 08 Q1 09 Q3 09 Q1 10 Q3 10 Q1 11 Q3 11 Q1 12

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 17

Well-positioned in the local market

Prime retail parks may also be situated in peripheral locations but with excellent connections to major traffic arteries

Based on research of all commercial property classes, the prime yield development is expected to remain at approximately this level, though if investors’ preference remains as high as it is, a further decline of prime yields seems possible. Additionally, all estimates have to be seen in light of the current economic crises in the European Union. Furthermore, investors still distinguish between assets situated in western and eastern Germany. Thus, yields for prime properties in eastern Germany are usually traded with a premium of approx. 50 bps. Exceptions can be noted in the large metropolitan areas around Berlin, Dresden and Leipzig.

Another major factor concerning the future yield development is similar to the rental levels the current growing regional difference within Germany. Metropolises and mid-sized cities in good macro locations considered to be winners, while stores in secondary and tertiary locations with poor macroeconomic data are the losers. At present, investors are placing greater focus on location factors than was the case two years ago, which is expected considering the current developments in Germany with regard to population, among other factors. Thus, very weak demand exists for locations with low purchasing power and a negative population growth forecast.

Transaction Evidence

The price decreases which were observed in 2008 and partly 2009 are over. The transactions in 2010 and 2011 indicated an increase in investor’s interest in retail properties in Germany. In 2012 the market seems to stabilize. The total transaction volume for commercial properties in Germany for the first two quarters of 2012 stands at approx. € 9.4 billion. For the first two quarters of 2011 this value stood at € 11.2 billion. Retail properties account for a share of the transaction volume in 2012 of approx. 30%. However, for retail warehouses the transaction volume in 2012 stands at € 83 million which is far below the volume for the whole of 2011 (approx. € 1.3 billion). But, the second half of the year is usually the stronger. Thus, a relatively high increase in the volume for retail warehouses can be expected.

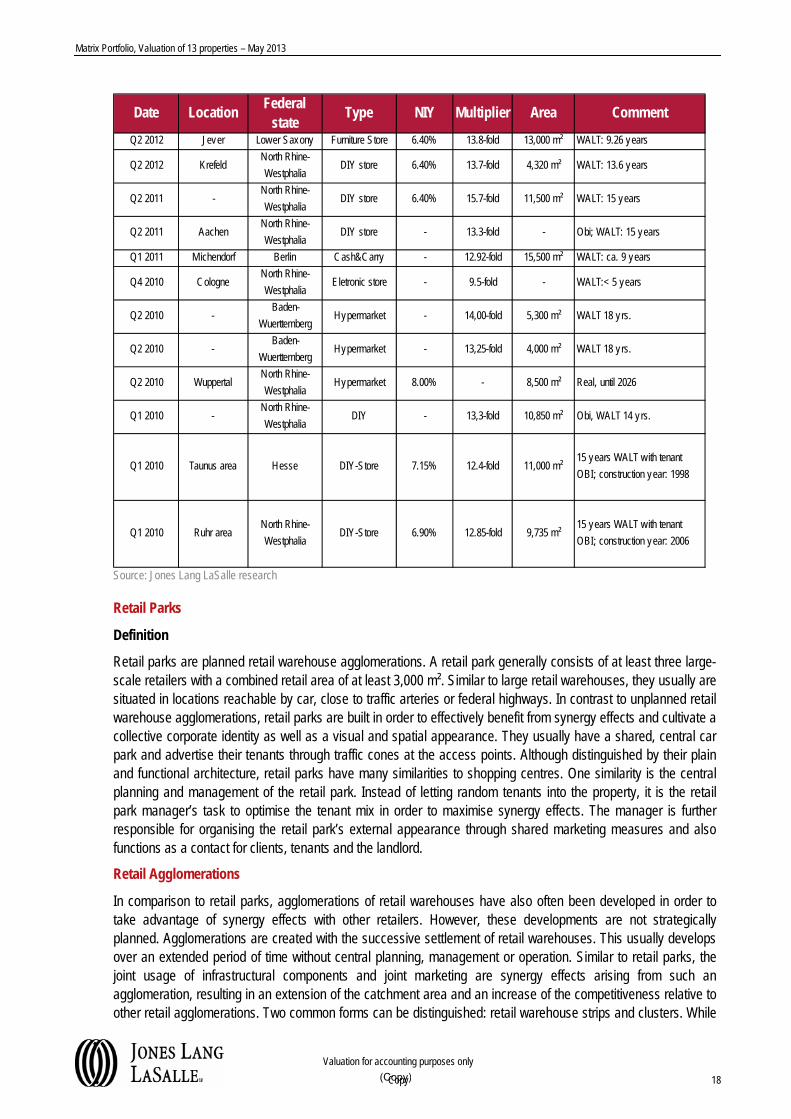

Please find some transactions from 2010 until 2012 in the table below.

Table 1: Transaction Evidence

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 18

Source: Jones Lang LaSalle research

Retail Parks

Definition

Retail parks are planned retail warehouse agglomerations. A retail park generally consists of at least three large-scale retailers with a combined retail area of at least 3,000 m². Similar to large retail warehouses, they usually are situated in locations reachable by car, close to traffic arteries or federal highways. In contrast to unplanned retail warehouse agglomerations, retail parks are built in order to effectively benefit from synergy effects and cultivate a collective corporate identity as well as a visual and spatial appearance. They usually have a shared, central car park and advertise their tenants through traffic cones at the access points. Although distinguished by their plain and functional architecture, retail parks have many similarities to shopping centres. One similarity is the central planning and management of the retail park. Instead of letting random tenants into the property, it is the retail park manager’s task to optimise the tenant mix in order to maximise synergy effects. The manager is further responsible for organising the retail park’s external appearance through shared marketing measures and also functions as a contact for clients, tenants and the landlord.

Retail Agglomerations

In comparison to retail parks, agglomerations of retail warehouses have also often been developed in order to take advantage of synergy effects with other retailers. However, these developments are not strategically planned. Agglomerations are created with the successive settlement of retail warehouses. This usually develops over an extended period of time without central planning, management or operation. Similar to retail parks, the joint usage of infrastructural components and joint marketing are synergy effects arising from such an agglomeration, resulting in an extension of the catchment area and an increase of the competitiveness relative to other retail agglomerations. Two common forms can be distinguished: retail warehouse strips and clusters. While

Date LocationFederal

stateType NIY Multiplier Area Comment

Q2 2012 Jever Lower Saxony Furniture Store 6.40% 13.8-fold 13,000 m² WALT: 9.26 years

Q2 2012 KrefeldNorth Rhine-

WestphaliaDIY store 6.40% 13.7-fold 4,320 m² WALT: 13.6 years

Q2 2011 -North Rhine-

WestphaliaDIY store 6.40% 15.7-fold 11,500 m² WALT: 15 years

Q2 2011 AachenNorth Rhine-

WestphaliaDIY store - 13.3-fold - Obi; WALT: 15 years

Q1 2011 Michendorf Berlin Cash&Carry - 12.92-fold 15,500 m² WALT: ca. 9 years

Q4 2010 CologneNorth Rhine-

WestphaliaEletronic store - 9.5-fold - WALT:< 5 years

Q2 2010 -Baden-

WuerttembergHypermarket - 14,00-fold 5,300 m² WALT 18 yrs.

Q2 2010 -Baden-

WuerttembergHypermarket - 13,25-fold 4,000 m² WALT 18 yrs.

Q2 2010 WuppertalNorth Rhine-

WestphaliaHypermarket 8.00% - 8,500 m² Real, until 2026

Q1 2010 -North Rhine-

WestphaliaDIY - 13,3-fold 10,850 m² Obi, WALT 14 yrs.

Q1 2010 Taunus area Hesse DIY-Store 7.15% 12.4-fold 11,000 m²15 years WALT with tenant

OBI; construction year: 1998

Q1 2010 Ruhr areaNorth Rhine-

WestphaliaDIY-Store 6.90% 12.85-fold 9,735 m²

15 years WALT with tenant

OBI; construction year: 2006

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 19

retail warehouse strips develop through the successive construction of retail warehouses on a linear axis along a single road, clusters develop through the construction of further retail warehouses around a centrally situated store. Often such developments evolve chaotically and seldom benefit from shared parking lots.

The concept of “one-stop shopping”, which is offered by retail parks and retail agglomerations, will play an increasingly important role in the future when shopping for provisions, because time is becoming more and more important to individuals. As a result, individual or sparsely clustered discounters and supermarkets will become increasingly unappealing.

Rental Market and Tenant Mix

The tenant mix of a retail agglomeration or retail park is very important for the overall quality and success of the property. The rental rate for such properties – as is common in the retail sector – is tied to the turnover expectancy (normally as a percentage). A good tenant mix and combination of brands and offers is able to satisfy several consumer requirements and guarantees a good customer flow. In order to increase the overall quality of a retail park or retail agglomeration, tenants selling daily convenience goods and tenants with a periodic or leisure component should be combined within the property. The combination of goods and services supports the consumers’ time management and therefore, appeals to the customer and offers an advantage compared to a stand-alone supermarket, for example.

The opportunity to link purchases with different store characters (periodic and irregular, impulse and target purchases, etc.) varies depending on the main range of goods. In particular, branches with a very high leisure character are easily linked to each other, for example fashion and shoes, leatherwear, toys and jewellery. Purely supply-orientated tenants (for example supermarkets, discounters, bakeries and drugstores) have similar linkage potential. Target-oriented purchases like furniture purchases or DIY-purchases have a lower potential for linkage as they are very sporadic and usually require higher investment. Therefore, the information and the time requirement are higher and these purchases are normally not combined with other purchases.

If in the case of a retail park, the management succeeds in establishing good anchor tenants, which increases the customer frequency, then the turnover expectancy of secondary tenants tends to be higher. As a consequence, their overall rental level can be higher as well. Therefore, some anchor tenants are able to negotiate lower rents, because their existence in a property increases the rental level of the others, thereby compensating for the higher rents. Thus, the rental level of a large anchor store within retail parks, like a supermarket or hypermarket, tends to be lower than if it was a stand-alone store. In contrast, smaller retail warehouses within retail parks, which benefit from large anchor tenants, tend to pay higher rents than if they were stand-alone stores. Overall, retail parks have the potential to generate higher rents than stand-alone retail warehouses due to the higher customer frequency.

The discrepancy between the average and prime rents is usually between € 5.00 and € 6.00/m²/month. Depending on the size of the retail unit and the branch of the tenants, rents in retail parks in western German locations generally range between € 5.00 and € 15.00/m²/month. However, there are exceptions in both directions. The current prime rent for retail warehouses ranges from € 10.50 to € 18.50/m²/month. The prime rent of € 18.50/m²/month is usually not paid in peripheral locations but in locations in or near the city centre of larger metropolitan areas (> 100,000 inhabitants) by well-known and attractive tenants occupying buildings in very good condition. The prime rent for retail warehouses in Germany has been virtually stable in the past 10 years. In the first quarter of 2002, the prime rent ranged from € 9.79 from 18.60/m²/month.

The overall potential for rental growth of retail warehouses in Germany is best summed up as mediocre. Depending on the tenant branch, rental rates for discounters, department stores and DIY stores remain stable due to the high competition in the market, but the rents for fashion stores have uplift potential simply due to the fact that these stores are increasing their presence in retail parks and are prepared to pay high rents.

Investment Market Specifics

Retail parks are a very interesting investment for investors. This is due to the fact that there is still a great deal of demand for retail areas within the centres and very often the security of cash flow is supported by contract

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 20

lengths of up to 15 years. Tenants are willing to sign long contracts, because the restrictive town planning in Germany makes new developments difficult and thereby decreases the risk that new properties will be constructed nearby in the near future and will avert the customer flow. Furthermore, retail parks offer risk diversification due to the multi-tenant structure in comparison to single-tenant retail warehouses. Thus, retail parks on average offer a more secure cash flow. For that reason, the yields for retail parks are lower than for retail warehouses.

The following shows the prime yield development for retail parks from the first quarter of 2007 until the second quarter of 2012.

Figure 5: Prime Yield Development in %

Source: Jones Lang LaSalle analysis

Prime yields usually remain relatively stable because prime properties are less affected by developments than non-prime properties. The prime yields started to increase with the appearance of the financial crises in 2007 and peaked at the beginning of 2009 at 6.75%. From the fourth quarter of 2009, prime yields have fallen quite considerably by 0.85% to as low as 5.90% in the second quarter of 2011. Since then, the prime yield has remained stable. Top multipliers are currently reaching 14.25 to 15.00, at the most.

Given the present-day perspective, we expect yields for core products to remain stable, provided that the overall economic situation and the situation in the retail market (particularly for specialist retail properties) will not deteriorate. However, if investor’s preference for retail parks remains as high as it is, a further decline of prime yields seems possible. Additionally, all estimates have to be seen in light of the development of the current economic crisis in the European Union.

Furthermore, within the individual retail park segment, investors are currently increasingly searching for properties with refurbishment potential. The result is a clear focus on redeveloping single large-scale retail warehouses into retail parks in order to fully capitalise on the investor demand for these products. Large self-service department stores (> 10,000 m²) in need of modernisation show the greatest potential in this regard due to their area dimensions and typically favourable building law regulations.

Transaction Evidence

The transaction volume of retail parks stand at € 464 million for the first two quarters of 2012. This is more of half the investment volume of retail parks in 2011 which stood at € 823 million. This shows the currently strong

0

1

2

3

4

5

6

7

8

Q1 07 Q3 07 Q1 08 Q3 08 Q1 09 Q3 09 Q1 10 Q3 10 Q1 11 Q3 11 Q1 12

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 21

demand of investors for retail parks. This demand will probably increase in the future due to the above mentioned facts.

Please find some transactions from 2010, 2011 and 2012 in the table below.

Table 2: Transaction Evidence

Source: Jones Lang LaSalle research

Date LocationFederal

stateType NIY Multiplier Area Comment

Q3 2011 Freital Saxony Retail Park n.a. 11.2-fold 20,000 m² WALT:> 10 years

2012 n.a.Baden-

WuerttembergRetail Park 7.55% n.a. 27,955 m² -

Q2 2012 KarlsruheBaden-

WuerttembergRetail Park ca. 6.00% 14.5-fold 27,500 m² Saturn, real; WALT: ca. 9 years

Q3 2011 DortmundNorth Rhine-

WestphaliaRetail Park - 14.16-fold 31,131 m² Hornbach, REWE, Lidl, Tedox; WALT: 8 years

Q1 2011 Castrop-RauxelNorth Rhine-

WestphaliaRetail Park - 11.05-fold 9,715 m² Media Markt, Tedox, Dänisches Bettenlager

Q1 2011 Hesse Hesse Retail Park - Around 15-fold 4,500 m² WALT 20 yrs.

Q1 2010 Salzgitter Bad Lower Saxony Retail Park - 12,75-fold -WALT 10 yrs., new retail park, main tenants

Rossmann and Penny

Q2 2010 Gernsheim Hesse Retail Park - 12.00--fold 9,900 m² Edeka,, WALT over 10.0 years

Q1 2010 Berlin Berlin Retail Park - 13,51-fold 21,500 m²Main tenants Obi, Burger King, Kaisers, Dänisches

Bettenlager

Q1 2010 -North Rhine-

WestphaliaRetail Park - Around 13.75-fold 8,400 m²

Main tenants Rewe, Dänisches Bettenlager, dm, etc.;

WALT between 10 and 15 years

Q1 2010 Landshut Bavaria Retail Park GIY 6.9% 14.53-fold 23,000 m²

Main tenants Kaufland, Aldi, Saturn, C&A,

Deichmann, Das Depot, Mister * Lady; purchase price

€ 53.5 Mio; construction year 2010

Q1 2010 Gießen Hesse Retail Park approx. 7.5% 11.75-fold 18,000 m² Main tenants real, Saturn, WALT: > 10 years

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 22

3 Valuation

3.1 Valuation Methodology

Our valuation provides an estimate of Market Value. The definition by the ‘Royal Institution of Chartered Surveyors’ outlined below applies to the underlying values quoted in the valuation.

The Market Value of the property has been assessed using the Discounted Cash Flow (DCF) calculation method. This takes into account the agreed rent for the signed leases, the market rent for currently vacant space and estimated rents for re-letting of the space after lease term expiry.

Cash flows for the relevant year are calculated as follows: the Rental Income at full occupancy (Base Rental Revenue) is reduced by the loss of rent due to rent–free periods (Base Rent Abatements) and vacancy (Absorption and Turnover Vacancy). Besides income from indexation clauses (CPI and Other Adjustment Revenues) and step rents (Base Rental Step Revenue), reimbursable expenses (Vacancy Costs) have been added to obtain the Total Potential Gross Revenue. While rents are calculated according their particular adjustment clause, costs have been adjusted according to the change in the Consumer Price Index (CPI) on a yearly basis.

After deduction of the non-recoverable costs (i.e. Management and Maintenance Costs) and reimbursable expenses (Vacancy Costs), the Net Operating Income (NOI) is determined. In case of vacancy, the reimbursable costs the landlord receives are lower than the amount he has to pay, so that only in this event do Vacancy Costs have an influence on the NOI.

Subtracting the non-operating costs (such as Leasing Commissions, Tenant Improvements and Capital Expenditures) from the NOI results in the Cash Flow before Tax and Debt Service.

After the DCF period of 10 years, we have considered a stabilised rental income in year 11. The capitalised value after year 10 takes this stabilised rental income and subtracts the stabilised expenses, resulting in the Stabilised Net Operating Income. This result is capitalised into perpetuity applying an equated (growth implicit) yield and produces the Terminal Value Indication. The resulting value is then discounted to the valuation date using the discount rate from term year 1-10.

Discounting the remaining Cash Flows for years 1 to 10 and the Terminal Value for year 11 to the valuation date (i.e. the Net Present Value) produces the Gross Capital Value. We have assessed monthly rents as this conforms to the timing of rental payments. Subsequently, the Cash Flows calculated across the valuation period are discounted to the valuation date monthly in advance using the market derived discount rate. The discount rate adopted considers the probability of default as well as the security of the forecast for the Cash Flow. Therefore, factors which influence the discount rate include existing terms and conditions of lease contracts, the individual location quality, the building structure and building stock, the strengths of tenant covenants, the prevailing over- or underrent and the resale value calculated. After deductions for Purchaser’s Costs, the Market Value is obtained.

3.2 Valuation Assumptions

Definition Market Value

The Market Value is defined in the ‘Royal Institution of Chartered Surveyors (RICS) Appraisal and Valuation Manual’. This is incorporated into the Jones Lang LaSalle “General Principles Adopted in the Preparation of Valuations and Reports” attached as Appendix 2.

The “Market Value” is an appraisal of the price for which a property transaction would take place on the appointed valuation date and may be defined as:

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 23

“The estimated amount for which an asset or liability should exchange on the valuation date between a willing buyer and a willing seller in an arm's-length transaction after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion.”

Rental Income

The current rental income for the portfolio amounts to € 14,044,730/year, which equals a rent of € 7.95/m²/month on occupied areas.

Estimated Market Rental Value

In the scope of the valuation, an achievable market rent was derived for each rental unit of the buildings within the portfolio.

The estimate of market rents is made on the basis of comprehensive research and our turnover analysis. As a result, the Estimated Rental Value for the portfolio amounts to € 14,983,605/year. This represents € 8.48/m²/month.

No TownContractual

Rental IncomeContract Rent

€ p.a. €/m²/month

1 Aschersleben 1,531,257 8.79

2 Augsburg 1,325,019 7.98

3 Bad Aibling 644,624 7.62

4 Biberach 1,265,410 9.79

5 Borken 1,089,001 9.53

6 Erlangen 1,216,050 7.56

7 Geislingen 654,010 5.80

8 Glauchau 1,301,918 8.50

9 Ludwigsburg 1,033,067 6.09

10 Ludwigsfelde 1,138,683 7.51

11 Neckarsulm 1,415,752 11.49

12 Vilshofen 815,611 6.64

13 Wittenberge 614,328 5.89

14,044,730 7.95

Property Rental Income

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 24

Costs

We have been provided with an updated cost schedule concerning ground tax and insurance costs. As for the other non-recoverable costs, we assume that these costs remain unchanged in the current valuation. The previous owner did not recover all costs, which could be recovered according to the lease contracts. We understand that the lawyers of BCRE see that in the future these costs will be reduced and a higher portion will be recovered. We assumed that if the tenants would be provided with an accurate cost schedule they will pay these (recoverable) costs.

Vacancy Costs

In periods of vacancy, all fixed ancillary costs are borne by the owner. This fact has been taken into account within the valuation and in the case of projected vacancy during re-letting or successive rental; furthermore, we have applied a non-recoverable surcharge for vacant space. The vacancy costs are assessed to amount to € 10.00/m²/year.

Renewal Probability

Following the lease contract periods, we have considered assumptions appropriate to the local market environment regarding use type, location, quality of rental areas and property condition. Rent-free periods were

No Town Market Rental Value Market Rent

€ p.a. €/m²/month

1 Aschersleben 1,591,511 9.13

2 Augsburg 1,499,573 9.03

3 Bad Aibling 696,866 8.23

4 Biberach 1,275,518 9.87

5 Borken 1,206,904 10.56

6 Erlangen 1,566,081 9.74

7 Geislingen 838,192 7.44

8 Glauchau 1,246,923 8.14

9 Ludwigsburg 1,332,535 7.85

10 Ludwigsfelde 1,042,279 6.88

11 Neckarsulm 1,278,184 10.37

12 Vilshofen 817,158 6.66

13 Wittenberge 591,881 5.68

14,983,605 8.48

Property Rental Income

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 25

not assumed for the re-letting/initial letting of any units. Void periods have been applied for re-lettings/initial lettings and leasing commissions were taken into account to secure new tenants. Depending on the respective area, we have incorporated tenant improvements after lease term expiry. We have predominantly assumed that the existing leases will be extended with a renewal probability of 75% (at market rental level) and leases will be agreed with new tenants with a corresponding probability of 25% (also at market level). Therefore, costs in the cash flow related to re-letting and the void period are weighted with the aforementioned likelihood of 25%.

Void Periods

The period of vacancy before re-letting depends on the location, building quality and demand. For the rental units, a specific vacancy period between 3 and 24 months was assumed. Given that marketing to identify new tenants can commence as soon as an existing tenant has submitted notice, the usual notice period for the tenant is taken into account (i.e. deducted) when determining the void period. However, the period of vacancy may not amount to less than three months due to renovation and refurbishment that may be required within the rental area.

Please refer to the individual property templates in Appendix 1 for further information.

Tenant Improvements

Tenant improvements are costs for fixtures and building works incurred when a new rental contract is signed. In the valuation, these costs were fixed for each individual rental area according to the exterior and interior appearance. For the rental units, we have taken tenant improvements of € 25/m² to € 100/m² into account in our valuation.

Please refer to the individual property templates in Appendix 1 for further information.

Agent’s Fees

Letting fees usually include agent’s fees borne by the owner and are incorporated into the estimated cash flow. For the Matrix Portfolio we assumed three monthly rental payments for commercial units.

Contractual Terms

Rental terms are estimated by drawing upon standard rental contracts, giving consideration to building use and the current real estate market. A contractual period of 10 years is assumed for large units and 5 years for smaller units. Contract extension options in the new lease contracts are disregarded. The rent for new lease contracts reflects the market rent for the building. The contractual rent used in the calculation of future cash flows is shown in the individual valuation templates in the Appendix 1 of this report.

Investment Yields

The yields applied reflect the individual location quality (macro- and micro-location) of the properties, building structure, letting situation, covenant strength and the relationship between contractual and market rent. In the current investment market, covenant strength and lease term play a major role in the purchase of such properties. The cap and discount rates used for each property to calculate Market Value are disclosed in the individual valuation reports.

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 26

Rental Growth Forecasts

For rents we assume a rental growth in line with the development of the inflation.

Table 3: Inflation forecast Germany

Source: Global Insight 2013

3.3 Valuation Results

Market Value

The valuation is carried out on the basis of Market Value as defined in the ‘Royal Institution of Chartered Surveyors' (RICS) Appraisal and Valuation Manual. This is incorporated into the Jones Lang LaSalle “General Principles for Valuations and Standard Terms of Business”, which is attached as Appendix 2.

The “Market Value” is an appraisal of the price for which a property transaction would take place on the appointed valuation date and may be defined as:

“The estimated amount for which an asset or liability should exchange on the valuation date between a willing buyer and a willing seller in an arm's-length transaction after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion.”

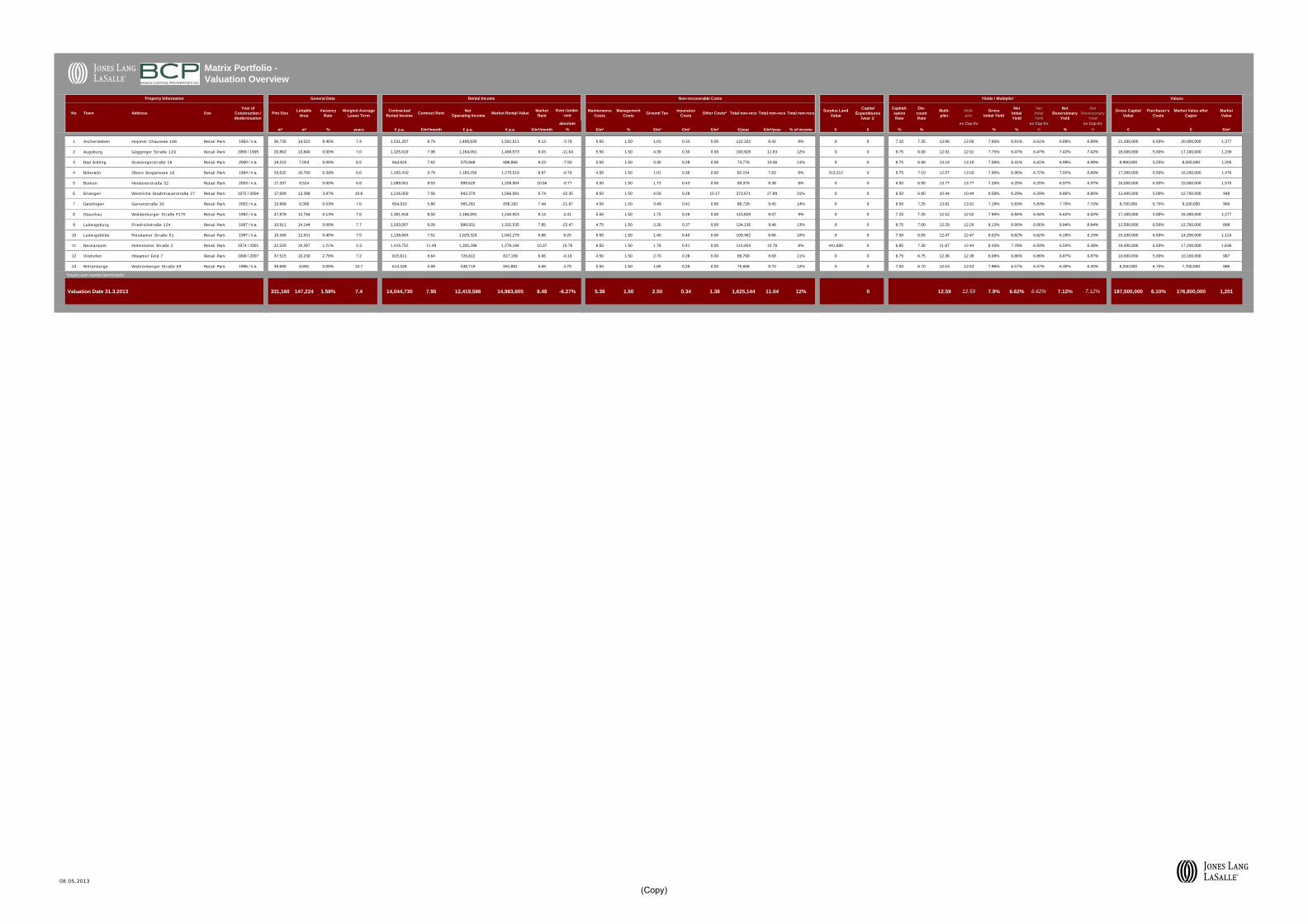

We are of the opinion that the Market Value of the subject portfolio is as at 31st March 2013:

€ 176,800,000 (net)

(ONE HUNDRED SEVENTY-SIX MILLION, EIGHT HUNDRED THOUSAND EUROS) reflecting € 1,201 /m² of lettable area

The above valuation figure represents a net figure, i.e. a deduction has been made for land transfer tax and legal costs and agent’s fees normally incurred by the purchaser. No allowance has been made for any expenses of realisation or for taxation, which might arise in the event of a disposal. The properties are considered as if free and clear of all mortgages or other charges, which may be secured thereon.

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

1.0% 1.5% 1.5% 1.5% 1.4% 1.3% 1.4% 1.4% 1.4% 1.4%

Year after 2021

Inflation 1.6%

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 27

3.4 Sensitivity Matrix

Below we present a matrix per property showing the Market Value sensitivity to changes of the Discount Rate.

3.4.1 Aschersleben

3.4.2 Augsburg

3.4.3 Bad Aibling

3.4.4 Biberach

3.4.5 Borken

3.4.6 Erlangen

- 50 bp - 25 bp 7.35% + 25 bp + 50 bp

€ 20,700,000 € 20,400,000 € 20,000,000 € 19,700,000 € 19,400,000

Sensitivity Matrix as at 31st March 2013

Discount Rate Variation

- 50 bp - 25 bp 6.90% + 25 bp + 50 bp

€ 17,700,000 € 17,400,000 € 17,100,000 € 16,800,000 € 16,500,000

Sensitivity Matrix as at 31st March 2013

Discount Rate Variation

- 50 bp - 25 bp 6.90% + 25 bp + 50 bp

€ 8,800,000 € 8,600,000 € 8,500,000 € 8,300,000 € 8,200,000

Sensitivity Matrix as at 31st March 2013

Discount Rate Variation

- 50 bp - 25 bp 7.10% + 25 bp + 50 bp

€ 16,800,000 € 16,500,000 € 16,200,000 € 16,000,000 € 15,700,000

Sensitivity Matrix as at 31st March 2013

Discount Rate Variation

- 50 bp - 25 bp 6.90% + 25 bp + 50 bp

€ 15,600,000 € 15,300,000 € 15,000,000 € 14,800,000 € 14,500,000

Sensitivity Matrix as at 31st March 2013

Discount Rate Variation

- 50 bp - 25 bp 6.80% + 25 bp + 50 bp

€ 13,200,000 € 13,000,000 € 12,700,000 € 12,500,000 € 12,300,000

Sensitivity Matrix as at 31st March 2013

Discount Rate Variation

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 28

3.4.7 Geislingen

3.4.8 Glauchau

3.4.9 Ludwigsburg

3.4.10 Ludwigsfelde

3.4.11 Neckarsulm

3.4.12 Vilshofen

3.4.13 Wittenburg

- 50 bp - 25 bp 7.25% + 25 bp + 50 bp

€ 9,500,000 € 9,300,000 € 9,100,000 € 9,000,000 € 8,800,000

Sensitivity Matrix as at 31st March 2013

Discount Rate Variation

- 50 bp - 25 bp 7.25% + 25 bp + 50 bp

€ 16,900,000 € 16,600,000 € 16,300,000 € 16,100,000 € 15,800,000

Sensitivity Matrix as at 31st March 2013

Discount Rate Variation

- 50 bp - 25 bp 7.00% + 25 bp + 50 bp

€ 13,100,000 € 12,900,000 € 12,700,000 € 12,500,000 € 12,200,000

Sensitivity Matrix as at 31st March 2013

Discount Rate Variation

- 50 bp - 25 bp 6.65% + 25 bp + 50 bp

€ 14,700,000 € 14,400,000 € 14,200,000 € 13,900,000 € 13,700,000

Sensitivity Matrix as at 31st March 2013

Discount Rate Variation

- 50 bp - 25 bp 7.30% + 25 bp + 50 bp

€ 17,800,000 € 17,500,000 € 17,200,000 € 16,900,000 € 16,700,000

Sensitivity Matrix as at 31st March 2013

Discount Rate Variation

- 50 bp - 25 bp 6.75% + 25 bp + 50 bp

€ 10,400,000 € 10,300,000 € 10,100,000 € 9,900,000 € 9,700,000

Sensitivity Matrix as at 31st March 2013

Discount Rate Variation

- 50 bp - 25 bp 6.70% + 25 bp + 50 bp

€ 8,000,000 € 7,900,000 € 7,700,000 € 7,600,000 € 7,500,000

Sensitivity Matrix as at 31st March 2013

Discount Rate Variation

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

Copy 29

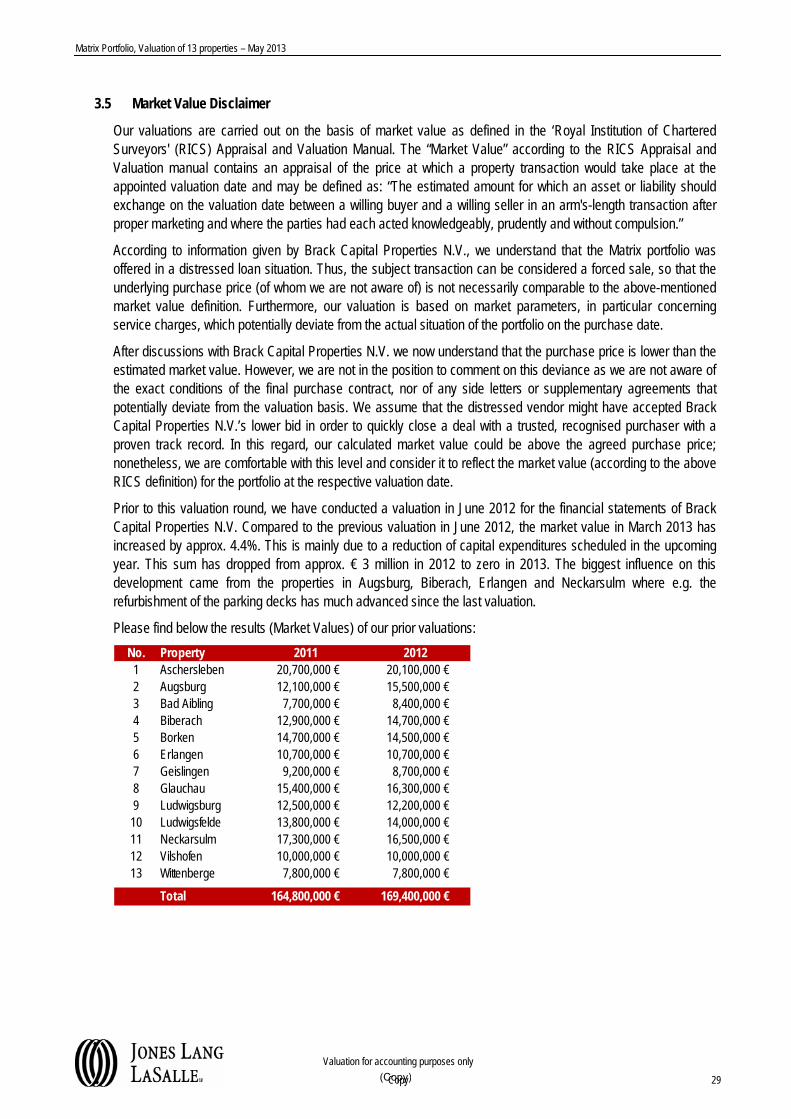

3.5 Market Value Disclaimer

Our valuations are carried out on the basis of market value as defined in the ‘Royal Institution of Chartered Surveyors' (RICS) Appraisal and Valuation Manual. The “Market Value” according to the RICS Appraisal and Valuation manual contains an appraisal of the price at which a property transaction would take place at the appointed valuation date and may be defined as: “The estimated amount for which an asset or liability should exchange on the valuation date between a willing buyer and a willing seller in an arm's-length transaction after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion.”

According to information given by Brack Capital Properties N.V., we understand that the Matrix portfolio was offered in a distressed loan situation. Thus, the subject transaction can be considered a forced sale, so that the underlying purchase price (of whom we are not aware of) is not necessarily comparable to the above-mentioned market value definition. Furthermore, our valuation is based on market parameters, in particular concerning service charges, which potentially deviate from the actual situation of the portfolio on the purchase date.

After discussions with Brack Capital Properties N.V. we now understand that the purchase price is lower than the estimated market value. However, we are not in the position to comment on this deviance as we are not aware of the exact conditions of the final purchase contract, nor of any side letters or supplementary agreements that potentially deviate from the valuation basis. We assume that the distressed vendor might have accepted Brack Capital Properties N.V.’s lower bid in order to quickly close a deal with a trusted, recognised purchaser with a proven track record. In this regard, our calculated market value could be above the agreed purchase price; nonetheless, we are comfortable with this level and consider it to reflect the market value (according to the above RICS definition) for the portfolio at the respective valuation date.

Prior to this valuation round, we have conducted a valuation in June 2012 for the financial statements of Brack Capital Properties N.V. Compared to the previous valuation in June 2012, the market value in March 2013 has increased by approx. 4.4%. This is mainly due to a reduction of capital expenditures scheduled in the upcoming year. This sum has dropped from approx. € 3 million in 2012 to zero in 2013. The biggest influence on this development came from the properties in Augsburg, Biberach, Erlangen and Neckarsulm where e.g. the refurbishment of the parking decks has much advanced since the last valuation.

Please find below the results (Market Values) of our prior valuations:

No. Property 2011 20121 Aschersleben 20,700,000 € 20,100,000 €2 Augsburg 12,100,000 € 15,500,000 €3 Bad Aibling 7,700,000 € 8,400,000 €4 Biberach 12,900,000 € 14,700,000 €5 Borken 14,700,000 € 14,500,000 €6 Erlangen 10,700,000 € 10,700,000 €7 Geislingen 9,200,000 € 8,700,000 €8 Glauchau 15,400,000 € 16,300,000 €9 Ludwigsburg 12,500,000 € 12,200,000 €

10 Ludwigsfelde 13,800,000 € 14,000,000 €11 Neckarsulm 17,300,000 € 16,500,000 €12 Vilshofen 10,000,000 € 10,000,000 €13 Wittenberge 7,800,000 € 7,800,000 €

Total 164,800,000 € 169,400,000 €

(Copy)

Matrix Portfolio, Valuation of 13 properties – May 2013

Valuation for accounting purposes only

30

4 Confidentiality & Publication

In preparing this valuation report, we have relied upon information provided by you and your representatives relating to tenure, tenancies, building and site areas, and building description. If this information proves to be incorrect or additional information is made available to us, the accuracy of the valuation could be affected. In such case, we reserve the right to amend our opinion of value accordingly.

In accordance with our standard practice, we must state that the content of this report, including the valuation, has been prepared exclusively for Brack Capital Properties N.V. (BCP) for the purposes of assisting BCP to value its assets as at 31st March 2013 for its financial statement reporting and for no other purpose.

In addition, the results of the work executed by Jones Lang LaSalle shall remain confidential and are intended exclusively for BCP and only for the purposes specified in the contract. Any other use and, in particular, disclosure to third parties or other publications (disclosure to third parties) – including extracts – without the express prior written consent of Jones Lang shall be prohibited. We consent to the disclosure of the valuation report to a third party only within the scope of the publication of the financial statement reporting. However, BCP agrees to notify the respective third parties in writing and to underline that Jones Lang LaSalle generally assumes no liability towards third parties for the work and services provided and that third parties may make no claims whatsoever against Jones Lang LaSalle on the basis of the work and services provided. BCP also agrees to indemnify Jones Lang LaSalle against any third party claims and associated costs asserted by third parties against Jones Lang LaSalle as a result of unauthorized disclosure or publication of the results of the work and services provided.

Jones Lang LaSalle GmbH’s liability for any loss or damage caused by negligence on our part, irrespective of the legal reason, in relation to the valuation services provided is limited to a maximum of 10% of the respective and reported Market Value per property, and may not exceed a maximum liability cap of € 7.5 million (euros) for any case.

Finally, to the fullest extent permitted by law, we do not accept or assume responsibility or liability in respect of the whole or any part of the report or valuation for any other purpose than stated above nor to any other person or entity to whom the report or valuation is shown or disclosed or into whose hands it may come, whether published with our consent or otherwise, except where expressly agreed by our prior consent in writing.

ppa. Andrew M. Groom MRICS Frank Rambow MRICS ppa. Georg Charlier

International Director National Director Principal Consultant

Head of Valuation & Transaction Advisory Valuation & Transaction Advisory Valuation & Transaction Advisory

Appendix

(Copy)

Appendix I – Property Reports

Appendix I – Property Reports

(Copy)

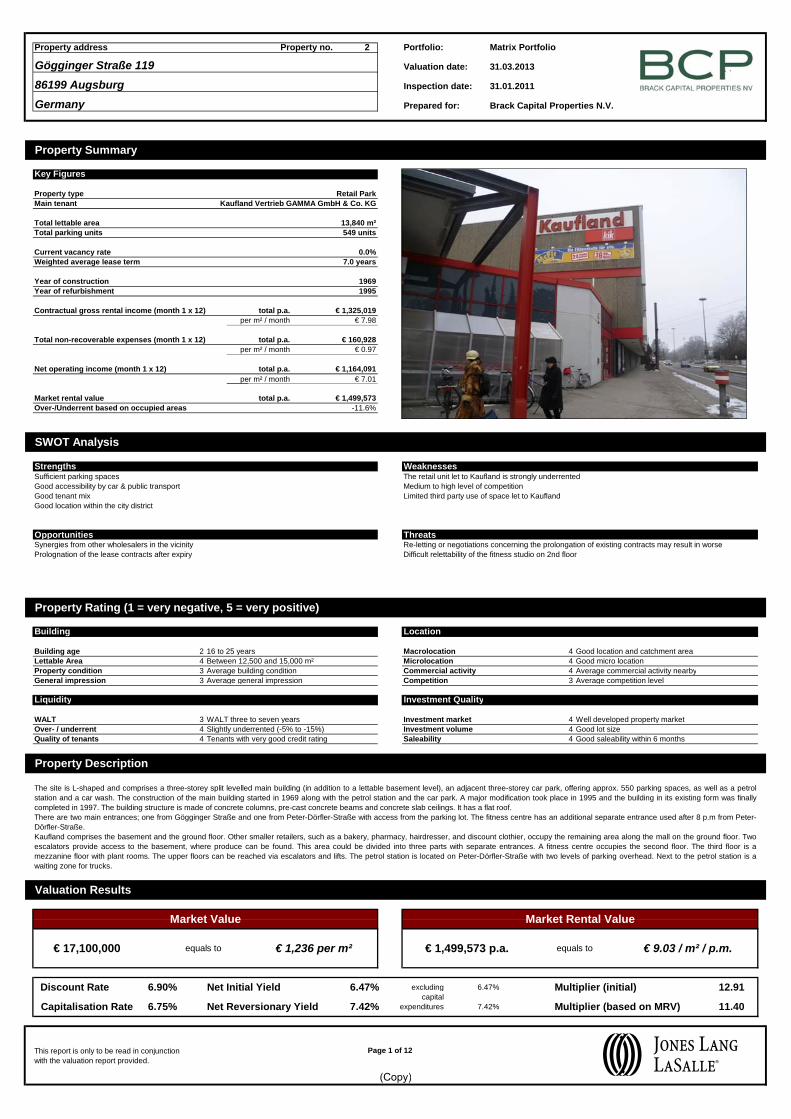

Property address Property no. 1 Portfolio:

Valuation date:

Inspection date:

Prepared for:

total p.a.per m² / month

total p.a.per m² / month

total p.a.per m² / month

total p.a.

Opportunities Threats

Building age 2 16 to 25 years Macrolocation 2 Below average location and catchment areaLettable Area 4 Between 12,500 and 15,000 m² Microlocation 3 Average micro locationProperty condition 2 Below average building condition Commercial activity 4 Average commercial activity nearbyGeneral impression 2 Below average general impression Competition 3 Average competition level

Investment Quality

WALT 4 WALT seven to ten years Investment market 2 Under developed property marketOver- / underrent 3 Rack rented (-5% to 5%) Investment volume 4 Good lot sizeQuality of tenants 4 Tenants with very good credit rating Saleability 4 Good saleability within 6 months

This report is only to be read in conjunctionwith the valuation report provided.

Multiplier (based on MRV) 12.57

Page 1 of 12 abc

SWOT Analysis

Slight under-rent of Kaufland premises

31.03.2013

Brack Capital Properties N.V.

Key Figures

Hoymer Chaussee 108

n.a.

Property Rating (1 = very negative, 5 = very positive)

Building

Liquidity

Valuation Results

Location

Multiplier (initial)

6.89%

Discount Rate

6.89%

excluding capital

expenditures7.10%

6.61%Net Initial Yield

Capitalisation Rate Net Reversionary Yield

7.4 years

0

Good tenant mix

Sufficient parking areas on site

Synergies due to adjacent furniture store

Market rental value € 1,591,511

€ 8.09

1993

Weighted average lease term

06449 Aschersleben

Property Summary

Retail Park

Germany

31.01.2011

Property type

Current vacancy rate