finance

52

Unit 10: Financial Accounting and Reporting Name: Farhan Shakeel E-mail: [email protected] Task 1 (L.O 1.1) Select any two companies given below and describe different users and their need of using the financial statements: 1. Etisalat telecom 2. Emirates airline 3. ADNOC petroleum 4. Shell petroleum 5.Unilever 6. Global learning center 7. Eco-Schools , UAE 8. Dubai Charity Association 9. Dubai Foundation for Women And Children 10.Environment Protection & Development Authority, Ras Al Khaimah Answer: Global Learning Centre Users and their needs: 1. Investors, lenders and shareholders: To know whether Global Learning Centre is a right institute to invest?

-

Upload

northampton -

Category

Documents

-

view

0 -

download

0

Transcript of finance

Unit 10: Financial Accounting and Reporting Name: Farhan Shakeel

E-mail: [email protected]

Task 1 (L.O 1.1)

Select any two companies given below and describe different users and their need of using the financial statements:

1.Etisalat telecom2.Emirates airline3.ADNOC petroleum4.Shell petroleum5.Unilever6.Global learning center7.Eco-Schools , UAE8.Dubai Charity Association9.Dubai Foundation for Women And Children10.Environment Protection & Development Authority, Ras Al Khaimah

Answer:

Global Learning Centre

Users and their needs:

1.Investors, lenders and shareholders:

To know whether Global Learning Centre is a right institute to invest?

Will Global Learning Centre will be able to pay backthe interest or dividend?

To note the goodwill/financial reputation of Global Learning Centre?

2.Customers Information about the Admission Information about the course provided Information about the professors, students and the surroundings. facilities charges transportation charges

3.Suppliers/other creditors Will Global Learning Centre pay on time for their purchases? To know Past record of payment with other GlobalLearning Centre suppliers. Is Global Learning Centre safe to provide cash sales?

4.Competitors(other institutes) As to compare fees strategy To know the strengths and weakness of Global Learning Centre To compare their financial performance with Global Learning Centre

5.UAE government Will Global Learning Centre pay accurate amount of tax declared in the tax returns?

To keep a track, as to measure the economic progress

6.Employees To know the profitability of Global Learning Centre? To know what average salary rate will be paid? What kind of promotions will be provided? To know about job security? Etisalat telecom

Users and their needs:1. Investors, lenders and shareholders: To know whether Etisalat is a right institute toinvest? Will Etisalat will be able to pay back the interest or dividend? To note the goodwill/financial reputation of Etisalat?2. Customers Information about the price of different services provided by Etisalat such as:-

-Telecommunication services-Internet services-Postpaid /Prepaid offers

3. Suppliers/other creditors Will Etisalat pay on time for their purchases? To know Past record of payment with other Etisalat suppliers.

Is Etisalat safe to provide credit sales?4. Competitors(other institutes) As to compare fees strategy To know the strengths and weakness of Etisalat To compare their financial performance with Etisalat5. UAE government Will Etisalat pay accurate amount of tax declared in the tax returns? To keep a track, as to measure the economic progress.6. Employees To know the profitability of Etisalat? To know what average salary rate will be paid? What kind of promotions will be provided? To know about job security?

Scenario:

UK based multinational company wants to establish a new unit in one of the most feasible area of UAE. They are specializing in manufacturing of electronicproducts such as air conditioners, electric oven andetc. The finance director is being worry about the influences of regulatory/legal on the financial statements.

You are the unit finance controller, has been assigned to guide the finance director regarding following matters:

Describe users of Financial Statements and their needs? (L.O 1.2)Answer: (L.O 1.2)1. Investors, lenders and shareholders: To know whether it is a right organization to invest? Willit be able to pay back the interest or dividend? To note the goodwill/financial reputation of it?2. Customers Information about the price and product of the company. 3. Suppliers/other creditors Will it pay on time for their purchases? To know Past record of payment with other suppliers. Is safe to provide credit sales?4. Competitors(other institutes) As to compare fees strategy To know the strengths and weakness of it To compare their financial performance with it5. UAE government Will pay accurate amount of tax declared in the tax returns?

To keep a track, as to measure the economic progress.6. Employees To know the profitability of it? To know what average salary rate will be paid? What kind of promotions will be provided? To know about job security?

Assess the regulatory/legal implications for users of Financial Statements (L.O 1.3) Prohibition of use of certain financial statements.Financial statements which purport to give effect tothe receipt and application of any part of the proceeds from the sale of securities for cash shall not be used unless such securities are to be offeredthrough underwriters and the underwriting arrangements are such that the underwriters are or will be committed to take and pay for all of the securities, if any are taken, prior to or within a reasonable time after the commencement of the publicoffering, or if the securities are not so taken to refund to all subscribers the full amount of all subscription payments made for the securities. The caption of any such financial statement shall clearly set forth the assumptions upon which such statement is based. The caption shall be in type at least as large as that used generally in the body ofthe statement.

Task 2

Tang Company.

Trial Balance as at 31st December 2013$000

Particulars Debit Credit

Sales 412,500

Plant 350,000 -

Vehicles 190,000 -

Goodwill

20,000 -

License 150,000 -

Cash

10,000 -

Debtor

27,000 -

Inventory (1st Jan 2012)

10,000 -

Capital - 242,000

Loan - 410,000

Creditor - 120,000

Administration

25,000 -Distribution -

30,000

Salaries

53,000 -

Utilities Expenses

11,200 -

Rent

21,500 -

Interest

5,800 -

Income -

1,500 911,

500 1,18

6,000

Notes:

Tang commenced manufacturing of wheel business with some of his friends on January 2012. You are newly hired senior accountant and required to make Income statement and balance sheet. While making the financialstatements you came into know that some of the entries required to be adjusted.

• Closing stock at 31st Dec 2013 was $22,000.

• Some of the purchases have been mistakenly charged in the salaries, costing $4000.

• Sales have been incurred evenly whole year. Last month due to some catastrophic event record of lastmonth got destroyed.

• Management has decided to charge $2,000 for bad debt.

• Deprecation on the plant has also not been providedfor the year end, company policy is to charge 2% ofcost.

• Store In-charge just came to you and informed you regarding the same catastrophic event happened in last month, due to that some of the records has been lost. But on the investigation you got able toget the cost of goods produce is $308,000 on 31 December. You are required to calculate Cost of purchases.

• Goodwill impairment test has been conducted and theresult shown the decrease of $800.

• Tax has been accrued for this year and has not beenrecorded in the accounts. Total amount of accrued taxation is $1,200.

Adjust the trial Balance, prepare income statement and balance sheet.

Trial Balance After adjustment

Particulars Debit Credit

Sales 450,000

Plant 350,000 -

Vehicles 190,000 -

Goodwill

20,000 -

License 150,000 -

Cash

10,000 -

Debtor

27,000 -

Inventory (1st Jan 2012)

10,000 -

Capital - 242,000

Loan - 410,000

Creditor - 120,000

Administration

25,000 -

Purchases 324,000

Distribution

30,000 -

Salaries

49,000 -

Utilities Expenses

11,200 -

Rent

21,500 -

Interest

5,800 -

Income -

1,500 1223

500 12235

00

Income Statement

Statement of comprehensive Income for the periodended 31 December 2013

Debit (Dr) Credit (Cr)

Sales 450,000

Cost of GoodsSold:

(Opening Stock 10,000

+Purchases 324,000

-Closing Stock) (22,000) (312,000)

=Gross Profit 138,000

Add Other Income 1,500 139,500

Less Expenses:

Utility Expenses 11,200

Salaries 49,000

Rent 21,500

Distribution 30,000

Administration 25,000

Depreciation onplant (2%)

7,000

Bad Debt 2,000 (1,45,700)

=Net loss beforeinterest and tax

(6,200)

Tax 1,200

Interest 5,800

Goodwill 800 (7,800)

Net Loss (14,000)

Balance Sheet

$

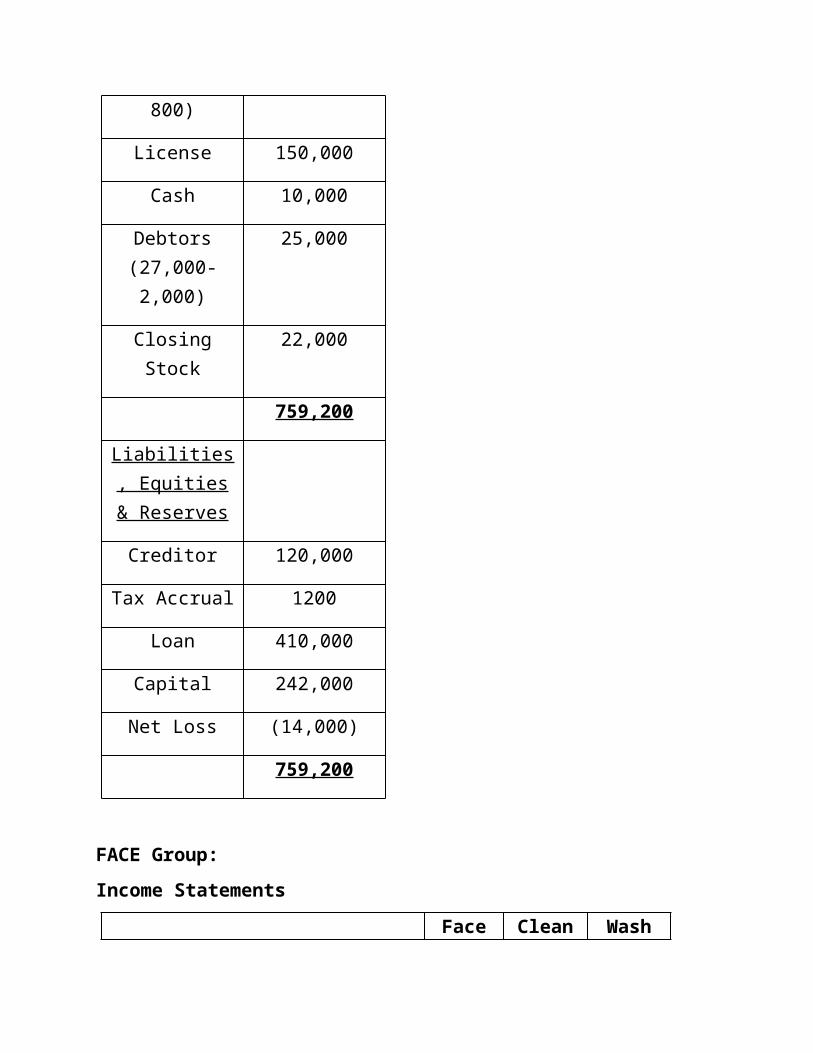

Assets:

Plant(350,000-7,000)

343,000

Vehicle 190,000

Goodwill(20,000-

19,200

800)

License 150,000

Cash 10,000

Debtors(27,000-2,000)

25,000

ClosingStock

22,000

759,200

Liabilities, Equities& Reserves

Creditor 120,000

Tax Accrual 1200

Loan 410,000

Capital 242,000

Net Loss (14,000)

759,200

FACE Group:Income Statements

Face Clean Wash

Sales 80,000 43,000 56,000

COGS 58,000 28,000 39,000

=Gross Profit 22,000 15,000 17,000

Add Other Income 10,000 - 3,000

Less expenses:Advertisement

(5,000)

(5,000)

(4,000)

Distribution (4,000)

(8,000)

(6,000)

Interest (2,000)

(1,500)

(1,500)

Taxation (1,000) (500) (1,500

)

Net Profit 20,000 - 7,000

Balance SheetFace Clean Wash

Plant & machinery 120,000 60,000 75,000

InvestmentIn Clean 80,000 - -In Wash 50,000 - -

license 35,000 20,000 28,000Cash 35,000 10,000 22,000Debtors 50,000 25,000 36,000Inventory 28,000 12,000 19,000

Total Assets 398,000

127,000

180,000

Share Capital150,00

0 80,000 93,000

Retained Earnings 71,000 3,000 9,000

Bank Loan 100,000 35,000 50,000

Creditors 77,000 9,000 28,000Total Equity and Liabilities

398,000

127,000

180,000

Notes:• During the year Face purchased goods from Wash on

the market value of $6,000• Dividend has been declared by Face for the last

year $700• Wash, Cash of $5,000 has been issued to face but it

is supposed to receive in 2 days.Prepare Consolidated Statement of Financial Position and Consolidated Comprehensive Income Statement for theFace Group, year ended 31st March 2014.

(L.O 2.3)

Income Statement:Statement of comprehensive consolidated Incomestatement for the year ended 31st March 2014.

sales 179,000-(6,000) 173,000

-COGS

(125,000)+(6,000-1800) -120,800

=GP 54,00052,20

0

Advertisement -14,000

-14,00

0

Interest -5,000-

5,000

Taxation -3,000-

3,000

Other Income 13,00013,00

0

Distribution -18,000

-18,00

0

Net Profit 27,00025,20

0

Balance SheetAssets:GoodwillPlant&Machinery 255,000Licence 83,000Cash 72,000Inventory 57,200

Debtors 111,000Total Assets 578,200

Reserves, Equities &LiabilitiesRetained Earnings 103,100Bank Loan 185,000Share Capital 150,000Creditors 119,700NCI 20,400Total 578,200

Working:Goodwill (Clean)

Dr CrInvestment 80,000 Capital 80,000

Retained Earnings 3,000Negative Goodwill (3,000)

Balance : 83,000 Balance : 83,000

Goodwill (Wash) 80%Dr Cr

Investment 50,000 Capital 74,400

Retained Earnings 7,200Negative Goodwill

(31,600)Balance : 81,600 Balance : 81,600

Non-Controlling Interest (NCI) 20%Dr Cr

Investment 50,000 Capital 18,600

Retained Earnings 1,800Closing Balance: 20,400

Balance : 20,400 Balance : 20,400

Consolidated Retained EarningsDr Cr

Unrealized profit 1,800 Parent 71,000Dividend 700

Goodwill 34,600

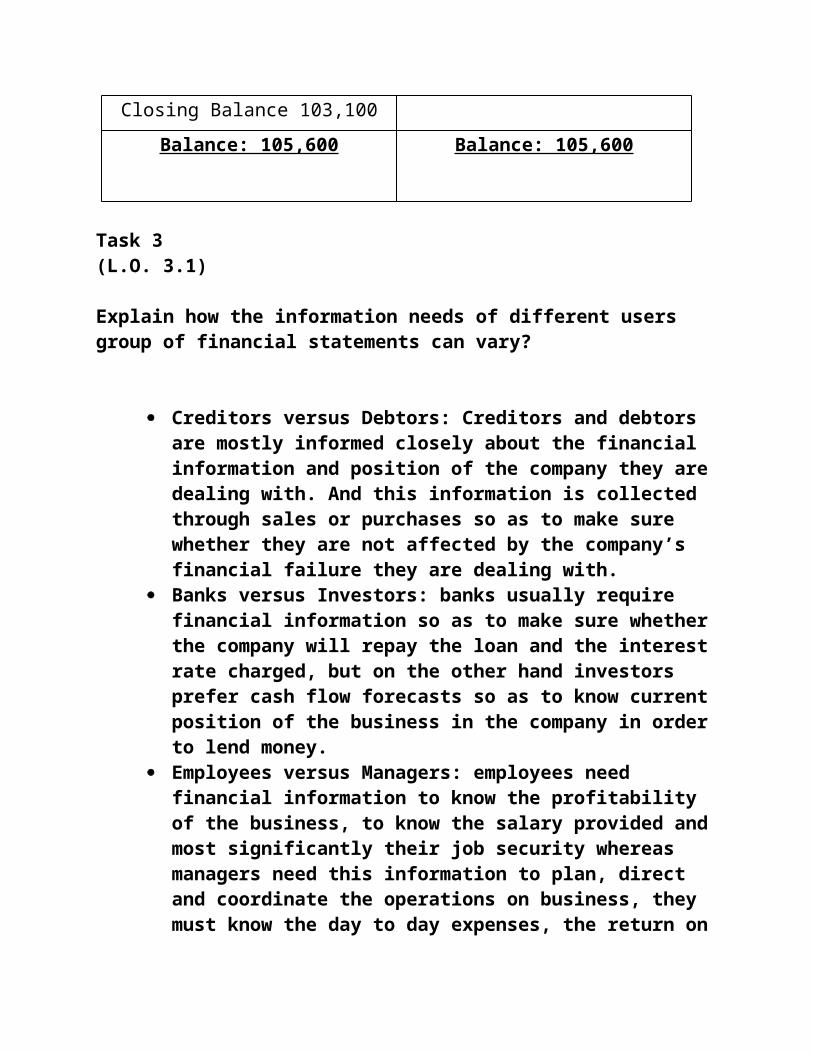

Closing Balance 103,100Balance: 105,600 Balance: 105,600

Task 3 (L.O. 3.1)

Explain how the information needs of different users group of financial statements can vary?

Creditors versus Debtors: Creditors and debtors are mostly informed closely about the financial information and position of the company they aredealing with. And this information is collected through sales or purchases so as to make sure whether they are not affected by the company’s financial failure they are dealing with.

Banks versus Investors: banks usually require financial information so as to make sure whetherthe company will repay the loan and the interestrate charged, but on the other hand investors prefer cash flow forecasts so as to know currentposition of the business in the company in orderto lend money.

Employees versus Managers: employees need financial information to know the profitability of the business, to know the salary provided andmost significantly their job security whereas managers need this information to plan, direct and coordinate the operations on business, they must know the day to day expenses, the return on

their expenses,so as to stay pro-active for any future financial problem and so on.

Capital Company• Shareholders Invested $25,000 to commence the

company and shares has been allotted to them.• For the purpose of initial marketing &

advertisement program, management did expense of $2,000 and got a good response.

• After getting the response from the market, CapitalCompany (CC) provided services to its first new customers for the exchange of cash $4,000

• Utilities expenses are payable at the end of each month, current month bill expecting to be $1,000.

• Due to tight market competition some of the services were provided on credit, which cost $8,000and the customer promised to pay it in the next month.

• The half of the utilities bill has been paid at theend of this month, the remaining will be paid with the next month bill.

• Some the debtors paid you 60 percent of their amount dues to them and rest will be soon.

• The increase market demand pushed the management increased the need for a building. CC bought a building, cost $15,000. $10,000 has been paid in cash and rest has been decided to pay after a year.

• During the year owner took out cash for to pay his son school fee $1,000.

• CC has bank overdraft of $2,000 and purchased stationary for $500 and rest of the amount spent inpurchase of goods.

Prepare income statement and balance sheet in a presentable way.

Journal Entries of Capital Company

Date Particulars Debit (Dr) $

Credit (Cr) $

1. Cash a/c……………..Dr 25000

To capital a/c

25000

2. Marketing & Advertisement a/c……..Dr

2000

To cash a/c 2000

3. Utility Expenses a/c……………….Dr

1000

To A/c Payable 1000

4. Cash a/c……………Dr 4000

To Sales a/c 4000

5. A/c receivables…………..Dr 8000

To Sales a/c 8000

6. A/c Payable.............Dr 500

To Cash a/c 500

7. Cash a/c…………….Dr 4800

To A/c receivables 4800

8. Assets: Land a/c…………….Dr 15000

To Cash a/c 10000

To Deferred Payment a/c 5000

9. Drawings a/c……………….Dr 1000

To Cash a/c 1000

10. Stationary a/c………….Dr 500

Purchases a/c……………Dr 1500

To Bank overdraft a/c

2000

Accounts:

Cash Account

Debit (Dr) $ Credit (Cr) $

Sales 4,000 Marketing &Advertisement

2,000

Cash

25,000 Assets: Land 10,000

A/creceivable

4,800 Utilityexpenses(Payable)

1,000

A/c Payable 500

Closing balance 20,300

Total: 33,800 Total: 33,800

Capital Account

Debit (Dr) $ Credit (Cr) $

Cash 25,000

ClosingBalance25,000

Total: 25,000 Total: 25,000

Marketing & Advertisement

Debit (Dr) $ Credit (Cr) $

Cash 2,000

ClosingBalance

2,000

Total: 2,000 Total: 2,000

Sales Account

Debit (Dr) $ Credit (Cr) $

Cash a/c 4,000

A/c Receivable 8,000

ClosingBalance

12,000

Total: 12,000 Total: 12,000

Utility expenses Account

Debit (Dr) $ Credit (Cr) $

A/c payable 1,000

ClosingBalance

1,000

Total: 1,000 Total: 1,000

Payable Accounts (Liability)

Debit (Dr) $ Credit (Cr) $

Cash 500 Utilityexpenses a/c

1,000

ClosingBalance

500

Total: 1,000 1,000 Total: 1,000 1,000

Receivable Account (Assets)

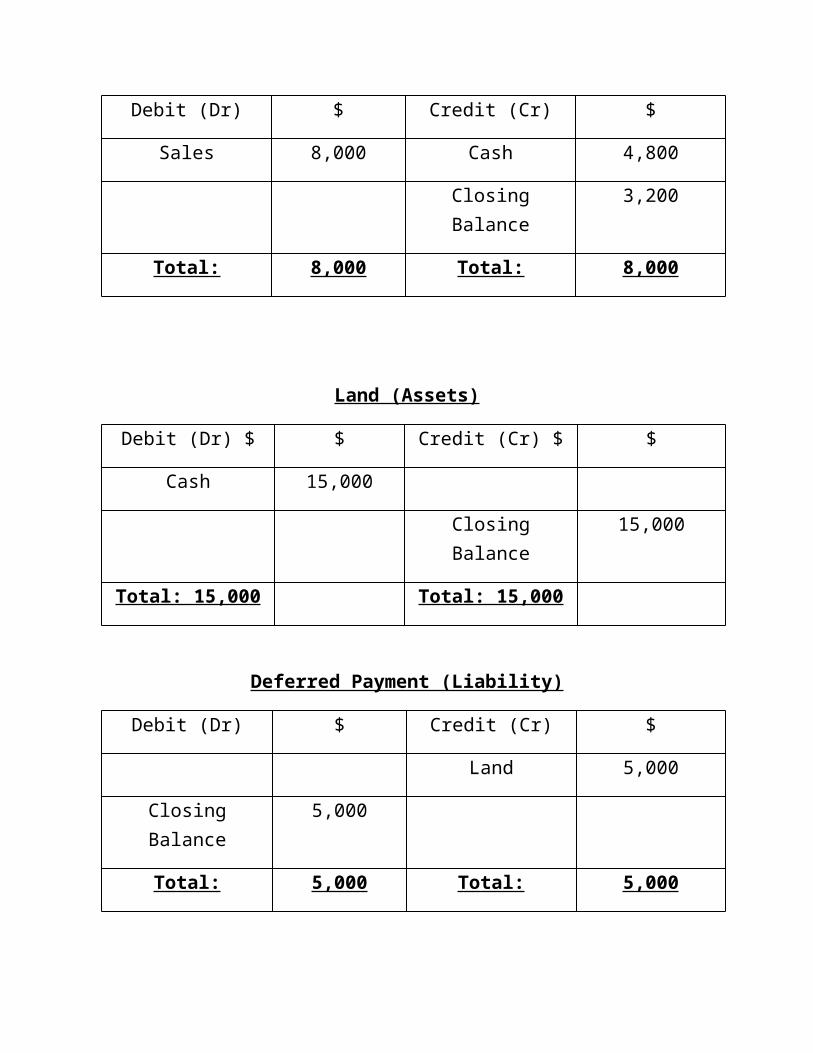

Debit (Dr) $ Credit (Cr) $

Sales 8,000 Cash 4,800

ClosingBalance

3,200

Total: 8,000 Total: 8,000

Land (Assets)

Debit (Dr) $ $ Credit (Cr) $ $

Cash 15,000

ClosingBalance

15,000

Total: 15,000 Total: 15,000

Deferred Payment (Liability)

Debit (Dr) $ Credit (Cr) $

Land 5,000

ClosingBalance

5,000

Total: 5,000 Total: 5,000

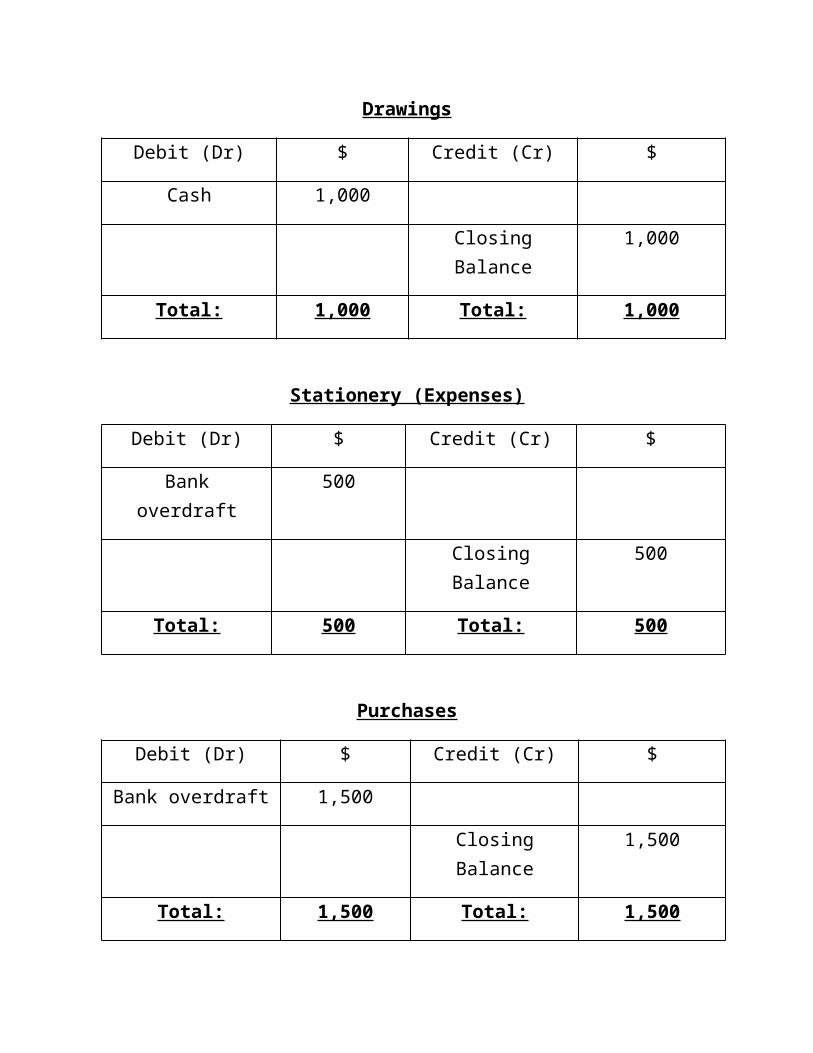

Drawings

Debit (Dr) $ Credit (Cr) $

Cash 1,000

ClosingBalance

1,000

Total: 1,000 Total: 1,000

Stationery (Expenses)

Debit (Dr) $ Credit (Cr) $

Bankoverdraft

500

ClosingBalance

500

Total: 500 Total: 500

Purchases

Debit (Dr) $ Credit (Cr) $

Bank overdraft 1,500

ClosingBalance

1,500

Total: 1,500 Total: 1,500

Bank Overdraft (Liability)

Debit (Dr) $ Credit (Cr) $

Purchases 1,500

Stationary 500

ClosingBalance

2,000

Total: 2,000 Total: 2,000

Income Statement

Statement of comprehensive Income for the periodended

$ $

Sales 12,000

Less: Expenses

Utility expenses

1,000

Marketing &Advertisement

2,000

Stationary 500 (3,500)

Net Profit 8,500

Balance Sheet

$ $

Assets:

Land 15,000

Cash 20,300

ReceivableAccounts

3,200

Stock 1,500

Total Assets 40,000

$ $

Reserves &Equity:

Net Profit 8,500

Capital 25,000

Drawings (1,000)

Total Reserves &Equity

32,500 32,500

Liabilities:

Bank Overdraft 2,000

Payable Accounts 500

Deferred Payment 5,000 7,500

TotalLiabilities:

40,000

L.O. 3.2

Doger, Billu & Ali, (DBA) are running a foodstuff wholesale shop. Three years ago the commenced the business with $85,000, $70,000 & $40,000, Doger, Billu & Ali respectively. In the Partnership, all agreed to receive 10% interest on capital and will pay 8% on drawings and also each will be entitled to receive salary $2,500, $3,000 and $1,200 respectively.

DBA company trial balance is given below.

Trial Balance $000 $000Vehicles at cost 69,000Equipment at 148,000

costAccumulated depreciation

Vehicles 19,200Equipment 25,600

Accrual for energy 4,000Prepayment for insurance 6,400Cash at bank 21,000Stock 66,000Trade creditors 20,800Trade debtors 83,600Capital accounts:

Doger 82,500Billu 70,000Ali 40,000

Current accounts:

Doger 40,600Billu 38,800Ali 25500

Sales 300,000Purchases 148,000Energy 16,000

Insurance 16,800Advertising 12,000Rent 32,000Vehicle expenses 36,000Stationery 3,200Telephone 9,000Total 667,000 667,000

Notes:

Closing Stock for the period end is $38,000.Depreciation on Equipment and vehicle will be charged at the rate of 10% and 6% respectively on cost.

Prepare income statement, appropriation account and balance sheet of ADB Company for the period ended 30 June 20Y4.

Income Statement

Statement of comprehensive Income for the periodended on 30 June 2014

$ $

Sales 300,000

Less: Cost ofGoods Sold:

(Opening Stock 66,000

+Purchases 148,000

-Closing Stock) (38,000) (176,000)

=Gross Profit 124,000

Less Expenses:

Energy 16,000

Insurance 16,800

Advertisement 12,000

Rent 32,000

Vehicle Expenses 36,000

Stationery 3,200

Telephone 9,000

Depreciation onequipment (10%)

14,800

Depreciation onVehicle (6%)

4,140 (143940)

Net Loss: (19940)

Profit and loss Appropriation Account

Debit (Dr) $ Credit (Cr) $

Net loss 19,940

Salaries: 6,700 Share on loss: 45890

Doger: (2,500) Doger:(19,667)

Billu: (3,000) Billu:(16,687)

Ali: (1,200) Ali: (9,536)

Interest onCapital:

19,250

Doger: (8,250)

Billu: (7,000)

Ali: (4,000)

Total: 45,890 Total: 45,890

Current Account (Doger)

Debit (Dr) $ Credit (Cr) $

Loss 19,667 OpeningBalance

40,600

Salary 2,500

ClosingBalance

31,683 Interest onCapital

8250

Total: 51,350 Total: 51,350

Current Account (Billu)

Debit (Dr) $ $ Credit (Cr) $ $

Loss 16,687 OpeningBalance

38,800

Salary 3,000

ClosingBalance

32,113 Interest onCapital

7,000

Total: 48,800 Total: 48,800

Current Account (Ali)

Debit (Dr) $ Credit (Cr) $

Loss 9,536 OpeningBalance

25,500

Salary 1,200

ClosingBalance

21,164 Interest onCapital

4,000

Total: 30,700 Total: 30,700

Capital Account (Doger)

Debit (Dr) $ Credit (Cr) $

OpeningBalance

82,500

ClosingBalance

82,500

Total: 82,500 82,500 Total: 82,500 82,500

Capital Account (Billu)

Debit (Dr) $ Credit (Cr) $

OpeningBalance

70,000

ClosingBalance

70,000

Total: 70,000 Total: 70,000

Capital Account (Ali)

Debit (Dr) $ Credit (Cr) $

OpeningBalance

40,000

ClosingBalance

40,000

Total: 40,000 Total: 40,000

Balance Sheet

Balance Sheet at 30 June 2014

$

Fixed Assets

Vehicle(69,000-23,340)

45,660

Equipment(148,000-40,400)

107,600

Current Assets

Cash in Bank 21,000

Trade Debtors 83,600

Prepayment for insurance

6,400

Closing Stock 38,000

302,260

Less: Current Liabilities

Trade Creditors (20,800)

Accrual for energy

(4,000)

Total 277,460

Capital and Reserves:

Capital: 192,500

Doger(82,500)

Billu(70,000)

Ali(40,000)

Current A/c 84,960

Doger (31,683)

Billu(32,113)

Ali(21,164)

277,460

The following trial balance has been extracted from books of Keith LTD as the 30 June 2011

Dr. Cr.$000 $000

Advertisement 30Bank 7Creditors 69Debentures (10%) 70Debtors (all trade) 300Directors remuneration 55Electricity 28

Insurance 17Investments (quoted) 28Investment Income 4Machinery

At Cost 420Acc. Depreciation 152

Office Expenses 49Ord. Shares Capital 200Preference Shares 50Preference Shares Dividend 4Profit and Loss account (at 01-07-10) 132Provision for bad and doubtful debt 8Purchases 1240Rent and rates 75Sales 2100Stock (at 01-07-10) 134Vehicles:

At cost 80Accumulated Depreciation 40

Wages and Salaries 358Total 2825 2825

Information:

• Stock at 30th June 2011 valued at cost amounted to $155,000.

• Depreciation is to be provided on machinery and vehicles at a rate of 20% and 25% respectively on cost.

• Provision is to be made for auditor’s remuneration of $12,000.

• Insurance paid in advance at 30th June 2011 to $3,000.

• The provision for bad and doubtful debts is to be made equal to 5 % of outstanding trade debtors as at 30th June 2011.

• Corporation tax owing at 30th June 2011 is estimatedto be equal to be $60,000.

• An ordinary dividend of 10% per share is purposed on par value.

• The investment had a market value of $30,000 at 30th

June 2011.• The company has an authorized share capital of

600,000 ordinary shares of $0.50 each and of 50,000preference shares @ 8 per cent, for $1 each.

Prepare Company Income statement and balance sheet for the year ended 30th June 2011.

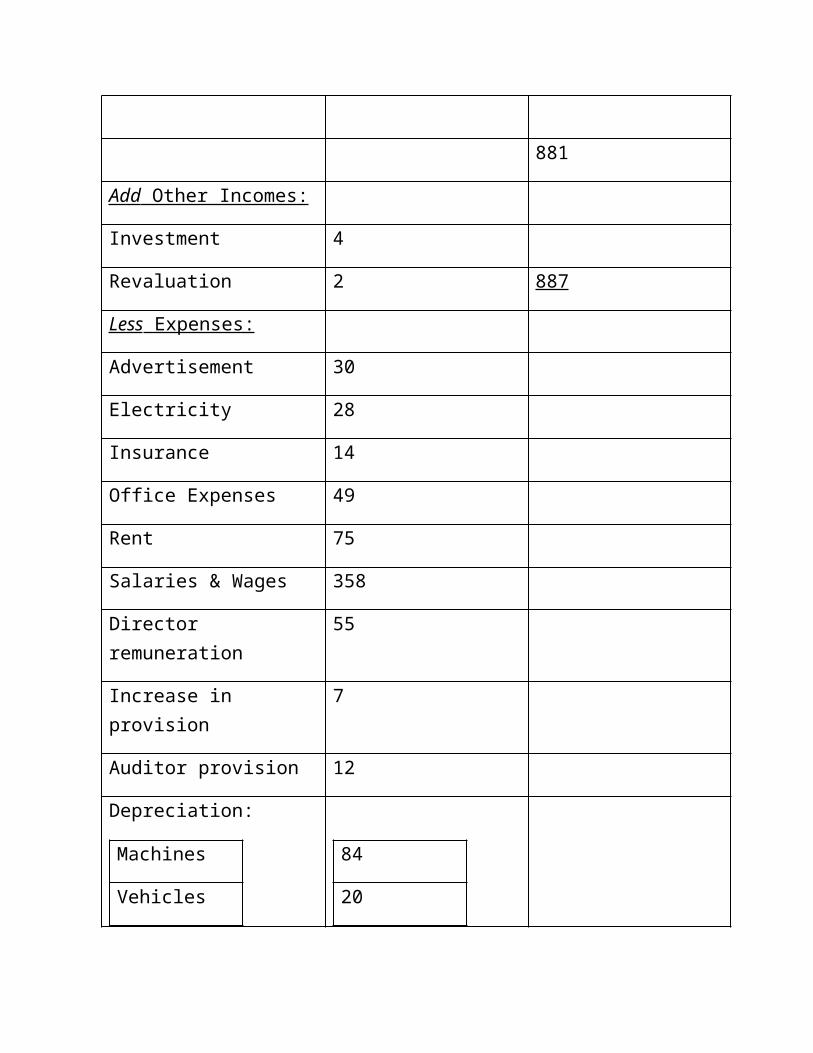

Income statement

Statement of Comprehensive Income statement for theyear ended 30th June 2011.

Particular $000 $000

Sales 2100

Cost of goods sold:

(Opening Stock 134

+Purchases 1240

-Closing Stock) (155) (1219)

881

Add Other Incomes:

Investment 4

Revaluation 2 887

Less Expenses:

Advertisement 30

Electricity 28

Insurance 14

Office Expenses 49

Rent 75

Salaries & Wages 358

Director remuneration

55

Increase in provision

7

Auditor provision 12

Depreciation:

Machines

Vehicles

84

20

Interest on Debenture

7

Preference Dividend

4

Ordinary Dividend 20 (763)

Less: Taxes (60)

Net Profit for theyear ended 30th June 2012

64

P/L account 132

Retained earning 196

Balance Sheet

Balance Sheet at 30 June 2011

$000

Assets:

Machinery(420-152+84)

184

Vehicle(80-40+20)

20

Investment 30

Current

Assets:

Stock 155

Bank 7

Debtors 285

PrepaidInsurance

3

684

Equity &Reserves:

Capital 200

PreferenceShare

50

RetainedEarning

196

Liabilities:

Debentures 70

Creditor 69

Auditor 12

TaxCooperation

60

Dividend 20

Interest ondebenture

7

684

Task 4

Crescent Hyper-storeAll amounts

in $0002013 2012

AssetsNon-Current Assets

Intangible-Goodwill 4,027 2,336Tangibles 26,511 21,554

Current AssetsInventory 2,669 2,430Receivables 1,798 1,311Cash and Cash Equivalent 4,742 2,148

Total Assets 39,747 29,779

Equity and LiabilitiesShare Capital 395 393Reserves 12,600 11,422

Non-Current LiabilitiesLong Term Borrowings 14,170 8,602

Current LiabilitiesTrade Payables 8,522 7,277Short Term Borrowings 4,060 2,085

Total Equity and Liabilities 39,747 29,779

Income Statement2013 2012

Revenues 54,327 47,198Cost of Sales 50,109 43,968Gross Profit 4,218 3,230Commercial and Administrative Cost (1,012

)(780)

Operating profit before financing 3,206 2,450Finance Income 116 187Finance Cost (478) (250)(Loss)/Profit before Tax 2,844 2,387Income Tax Expense (780) (670)(Loss)/Profit after Tax 2,064 1,717Total Comprehensive Income for the year

2,064 1,717

You are working as an Assistant accountant, this morning you manager asked you to prepare a report to beread in the Board meeting of Crescent Hyper-store (CH).CH is situated in a porch area of Dubai, due to its infrastructure it is very famous all around the world. It shelves all kind of food, grocery; crockery, electronic and other daily need stuff. You are also known that in the meeting they are going to discuss a new project to open some shops far from the down-town so people how has trouble to come here due to traffic can save their time. The project would cost approximately $8.3million for 5 new shops.

You are required to calculate Profitability, liquidity,Efficiency and investment ratios and interpret the financial position and make conclusion based on your findings. And also include the limitations of your conclusion.

Answer: (L.O 4.1, 4.2)

Interpretation of both years 2012 and 2013 to know thecompany's performance i.e; if the business is performing well by comparing the past years and other companies, are the economic, political and social circumstances favourable for normal trade, the prospects of region in which the business is operating.

We can do this through 4 accounting ratios:

LIQUIDITY RATIOS

2013

Current assets ratios = Current assets/ current liabilities= (2669+1798+4742=9209)/(8522+4060 = 12582 )= 9209 = 0.7 12582 2012

Current assets ratios= Current assets/current liabilities =

(2430+1311+2148=5889)/(7277+2085=9362) =5889/9362 = 0.6

Current assets ratios of the company represents the ability of paying off its short term debts as we can see for both years the company is have very low ratio this is a very bad sign it tells you that the company will not have much liquid to pay back its liabilities.

Acid test / Quick ratio = current assets - closing stock Current liabilities Year 2013 = 9209 – 2669/12582= 0.5% Year 2012= 5889 – 2430/9362 = 0.3%

The company does not have enough short-term assets in both years to overcome its immediate liabilities, the firm is highly dependent on the sale of inventory as toovercome this problem.

PROFITABILITY RATIOS

Gross profit ratio = gross profit × 100 Revenue

Year 2013 = 4218 × 100 = 8% year2012 = 3230 × 100 = 7% 54327 47198

This represents the profit of the company in relation to the amount of sales that has made, there is an increase on 1% from 2012 to 2013, it also provides the company with the demand of its customers in %.

Net profit ratio = net profit × 100 Sales

Year 2013 = 2844 × 100 = 5.2% year 2012 = 2387 × 100 = 5% 54327 47198

This show the net income of the company and how the company control’s its cost. The low profit margin represents less safety if sales decline there will be increase in risk while reducing profit and turning intonet loss, there is a very less improvement in 2013 but still in order to stay at much safer side the net profit margin should be much better.

Return on capital employed = profit × 100 Capital

Year 2013= 2064/27165(39747-12582=27165) × 100= 7.6% Year 2012= 1717/20417(29779-9362=20417) × 100= 8.4%

Return on equity = profit after tax × 100 Equity Year 2013= 2064/12995 × 100= 16% Year 2012= 1717/11815×100= 8%

Mark up ratio = gross profit × 100 COS Year 2013= 4218/50109×100= 8.4 % Year 2012= 3230/43968×100= 7.3%

EFFICIENCY RATIOS

Debtor collection period = debtors × 365days Sales

Year 2013 = 1,798/54327 × 365days = 12days Year 2012 = 1,311/47198 × 365days = 10days

The debtor collection period represents the total time in which company will get back their receivables, in 2012 the time period was 10days which was a little efficient but there was not much difference in 2013. Ifthe funds have been received early then it can be used for other business activities such as investing in other projects or paying off business expenses etc. this will improve the business performance.

Creditor payment period = creditors × 365days COS

Year 2013 = 8522/50109× 365days = 62days Year 2012 = 7277/43968 × 365days = 60days

This let you the time taken to pay off your creditors, it also tell you bot the business efficiency and how the business is performing, the higher days company gets at one hand its good for the company but if it’s too long the firm might lose suppliers trust for early payments. Here in 2013 and 2012 do not have much differences but the result is positive as the company is not taking too long or too short time period to pay back its creditors.

Inventory turnover days = closing inventory × 365days

COS

Year 2013 = 2669 × 365days = 19days year 2012 = 2430 × 365days = 20days 50109 43968

Inventory turnover days show how effectively funds invested in inventory can turn into sales revenue. Low is not good for the business low turnover means stock can take too long to convert into sales and will be over stock, on the other hand high turnover can indicates ineffective buying or very high sales. Companies want High inventory turnover as to deduct theinventory to gain less holding cost and due to less holding cost the net income will have an increase.

Cash cycle days = debtors days - creditors days + inventory turnover days

Year 2013= 12-62+19 = (31) days year 2012 = 20-60+10= (30) days

This shows the time period of invested cash/resources returning, in other words calculating the liquidity risk with the growth. Here it is negative cash cycle days in both years by receiving the payments by debtorsbefore paying creditors.

INVESTMENT RATIOS

Dividend yield Dividend cover ratio

Earnings per share Price /Earnings ratio

(For this ratio calculation there is no required information provided)

Overall Conclusion for CHS

The company CHS is performing fine, but still have few problems with its liquidity, need to work on their cashflow, they are unable to manage their cash inflow and cash outflow, the company should pay its suppliers on time so that the business do not lose its market value in terms of paying off creditors. They should provide less debtor payable period as to get back their cash ontime or before time this will help the company to maintain its day to day expenses, invest in other activities and help to increase its net income.

LimitationsAccurate data is not available to evaluate all the ratios and get a right conclusion about problems and solutions to them, due to lack of data the company’s overall working position is unpredictable.The information was just for 2 years and there was not data about its competitors, its markets in which it operates, the economical and political position of the market due to lack of this all information, the overallinterpretation is incomplete.