Fundamentals of Finance

19

1

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Fundamentals of Finance

1

Fundamentals of

Finance

CASH IS KING

By: Angel Cordero Rico BBA-MBA 2

6th of March 2018

Fundamentals of

Finance

CASH IS KING

By: Angel Cordero Rico BBA-MBA 3

6th of March 2018

Fundamentals of Finance

Summary

80% of bankruptcy is due to informal and incompetent operationalmanagement

It is crutial to fix the concept of Operational Working Capital (moneyretained that needs to be financed). You can get actual large profit BUT absolutely lack of CASH. If you know that Profit is not equal to CASH, there is no problem: you can plan and finance that deficit. Problems

arise when you are not aware of that. CASH IS KING4

Quick Review

Analysis Decision Making Outcomes

Potential Detection Potential IntegrationPotential

Enhance.5

Mision Business Definition

Vision Business Portofolio Strategy

Values Competitive Strategy

Growth Strategy

S. Objectives

Strategies

Funtionals

Operational Decisions

Corporate Strategies

3º STEP

Action Plans

Prioritization Plans

& Actions

Budget &

P&L Forecasts

Eviromental

Analysis

Internal Analysis

Diagnosis

1º STEP

Strategic Decisions

Strategic

Objectives

System

2º STEP

2. DIAGNOSIS

INTERNAL COMPANY

Size Analisis Funcional Portofolio &

Activity Factores Clave Éxito Activities

Sector Cadena de Valor

Organizatinal Struct. Tech

Objectives (current)

Strategy (today) EXTERNAL BUSINESS

Profit Demanda SBUs

Equity Oferta LYFE CYCLE

Problems Intensidad Competitiva Experiencie

Challenges SI / NO Competencia Leader positioning

SBUs

4. DIAGNOSIS 5. ANALYSIS

6.

FUNDAMEN

TAL

COMPETEN

CIES

1. COMPANY DATA

Strategic

GLOBAL

STRATEGIC ANALYSIS PROCESS 3. Vs

COMPETITOR

S

Strategy & Objectives

High Level

OBJECTIVES FUNCTIONAL PROCESS SCENARIOS OUTCOME DECISION

INVESTMENT

Volume

Rate & Pace Alternative 1

Type Alternative 2

Disinvestment Alternative 3

FINANCING

EQUITY Alternative 1

LONG TERMS LIABILITY Alternative 2

SHORT TERM LIABILITY Alternative 3

STRUCTURE

Amortization Alternatie 1

Extension Alternative 2

Flexibility Alternative 3

Outsourcing

STRATEGIC

DECISION

ANALYSIS

STRATEGIC

DECISIONS

STABLESupplies

Financial

Structure

Overheads

INTENSE

CRISIS

MODERATE

CRISIS

Profitability

Positioning

Optimal

Dimension

Balanced

Financial

Strcuture

Type of

Product

Revenue

% UNCERTAINTY

Fundamentals of Finance

Any strategy must be quantified.

During the strategic process at a very high level: rule of a thumb

Once the project advances, it will be adopting more and moregranularity.

And every period, we measure against forecast, baselines and soon.

As uncertainty decreases, more detail is available…

Financial Structure

Long Term & Short Term Equity & External capital

Metrics

Time Value of Money (IRR) SeeExcel File.Value Generation (NPV)

3 FINANCIAL STATEMENTS

INCOME

BALANCE

CASH FLOW

Income Statement: Cumulativeperiod of time

Metrics (See Excel File)ROI, ROE, ROS

Income Statement

Current

Period:

Before After

Changes: Changes:

Revenue: 1.300$ 1.300$

Cost of Goods Sold (COGS): 100 100

Gross Profit: 1.200 1.200

Operating Expenses: 200 200

Depreciation: - -

Stock-Based Compensation: - -

Amortization of Intangibles: - -

Operating Income: 1.000 1.000

(+) Interest Income: - -

(-) Interest Expense: - -

Gain / (Loss) on Sale of PP&E: - -

Gain / (Loss) on Sale of ST Inv.: - -

(-) Goodwill Impairment: - -

(-) PP&E Write-Down: - -

Pre-Tax Income: 1.000 1.000

Income Tax Provision: 300 300

Current Portion of Taxes: 300 300

Deferred Portion of Taxes: - -

Net Income: 700 700

(-) Preferred Dividends: - -

Net Income to Common: 700$ 700$

ROS = Return On Sales

= 700 / 1300 = 53,8%

Income Statement: Cumulativeperiod of timeMetrics (See Excel File)ROI, ROE, ROS

ROS = Return On Sales

= 700 / 1300 = 53,8%

What integrates IncomeStatement:

To appear on the Income Statement, each item must meet the following criteria:

1. It must correspond to ONLY the period shown on the Income Statement. If you’re paying for an asset that will last for 10-20 years, the initial money spent would not appear on a 1-year Income Statement. But your monthly rent would appear.

2. It must affect the company’s taxes. For example, interest paid on debt is tax-deductible, so it appears on the Income Statement. But repaying debt principal is not tax-deductible, so it does not appear on the Income Statement.

Always Appears: Revenue, COGS, Operating Expenses, Depreciation, Amortization, Stock-Based Compensation, Interest Income and Expense, Gains / (Losses), Write-Downs, Impairments, Other Income / (Expenses), Taxes, and Net Income.

Never Appears: Capital Expenditures, Purchasing or Selling Investments or PP&E (Plants, Property & Equipment), Dividends, Issuing orRepaying Debt Principal, Issuing or Repurchasing Shares, and Changes to Balance Sheet Items such as Cash, Debt, Accounts Receivable, or

Accounts Payable.

Balance Sheet

Metrics (See Excel File)ROI, ROE, ROS

ROI = Return OnInvestment (Asset)= 700 / 2,000 = 35%

ROE = Return On Equity = 700/ 1000 = 70%

Balance Sheet

Beginning of

Current Period:

Assets:

Current Assets:

Cash & Cash-Equivalents: 100$

Short-Term Investments: 100

Accounts Receivable: 100

Prepaid Expenses: 100

Inventory: 100

Total Current Assets: 500

Long-Term Assets:

Plants, Property & Equipment: 1.000

Other Intangible Assets: 300

Long-Term Investments: 100

Goodwill: 100

Total Long-Term Assets: 1.500

Total Assets: 2.000$

Liabilities & Equity:

Current Liabilities:

Revolver (Short-Term Debt): 100$

Accounts Payable: 200

Accrued Expenses: 200

Total Current Liabilities: 500

Long-Term Liabilities:

Deferred Revenue: 200

Deferred Tax Liability: 200

Long-Term Debt: 100

Total Long-Term Liabilities: 500

Total Liabilities: 1.000$

Equity:

Shareholders' Equity:

Common Stock & APIC: 600

Treasury Stock: (100)

Retained Earnings: 300

Accum. Other Compr. Income: 100

Total Shareholders' Equity: 900

Preferred Stock: 100

Total Equity: 1.000$

Total Liabilities & Equity: 2.000$

Balance: period of time

Metrics (See Excel File)Working CapitalDebt Structure

WC = AR + Inventory - AP

What integrates Balance Sheet:

1.The Balance Sheet shows the company's resources (its Assets) and how it paid for those resources – its Liabilities & Equity – at a specific point in time.So, the Income Statement shows revenue and expenses from January 1, 20XX to December 31, 20XX, but the Balance Sheet only shows the company's resources ON January 1, 20XX or ON December 31, 20XX.

2. Assets must always equal Liabilities + Equity – if the Balance Sheet does not balance, it's wrong. If you want a house – an asset – that costs $1 million, could you use a $380K mortgage and $200K in saved-up income to pay for it? No! The Balance Sheet would go out of balance! You’d have to borrow or save more. So, you either take out a mortgage for $800K, or you wait and save up an additional $620K.

3. An Asset is something that will result in, directly or indirectly, additional cash in the future, or is something that can be sold for cash. You typically split Assets into “Current” or “Short-Term” (anything that lasts for less than 1 year) and “Non-Current” or “Long-Term” (anything that lasts for more than 1 year).

4. A Liability is something that will result in, directly or indirectly, less cash in the future. Again, you typically split these into “Current” or “Short-Term” and then “Non-Current” or “Long-Term.” Liabilities are usually related to external parties – lenders, suppliers, or the government.

5. An “Equity” line item is a funding source, like a Liability, but it will not result in less cash in the future.

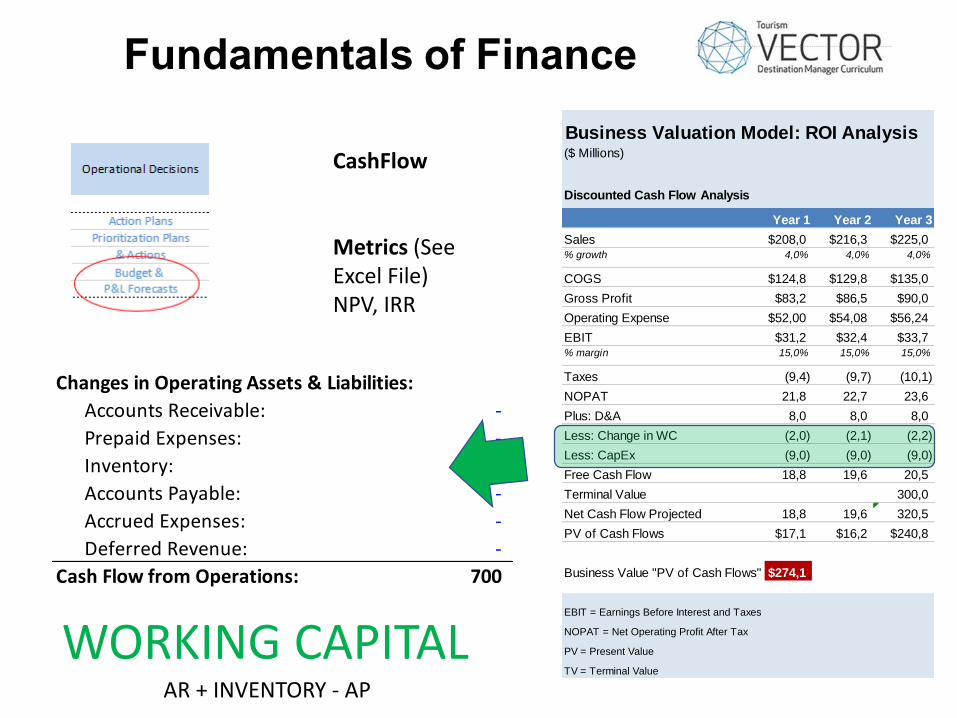

CashFlow

Metrics (SeeExcel File)NPV, IRR

Cash Flow Statement

Current

Period:

Before After

Changes: Changes:

Operating Activities:

Net Income to Common: 700$ 700$

Non-Cash Expenses & Other Adjustments:

(+) Depreciation: - -

(+) Stock-Based Compensation: - -

(+) Amortization of Intangibles: - -

(+) Deferred Income Taxes: - -

(Gain) / Loss on Sale of PP&E: - -

(Gain) / Loss on Sale of ST Inv.: - -

(+) Goodwill Impairment: - -

(+) PP&E Write-Down: - -

Changes in Operating Assets & Liabilities:

Accounts Receivable: - -

Prepaid Expenses: - -

Inventory: - -

Accounts Payable: - -

Accrued Expenses: - -

Deferred Revenue: - -

Cash Flow from Operations: 700 700

Investing Activities:

(-) Buy Short-Term Investments: - -

(+) Sell Short-Term Investments: - -

(-) Buy Long-Term Investments: - -

(+) Sell Long-Term Investments: - -

(-) Capital Expenditures: - -

(+) PP&E Sale Proceeds: - -

Cash Flow from Investing: - -

Financing Activities:

(-) Common Dividends Issued: - -

(+) Issue Long-Term Debt: - -

(-) Repay Long-Term Debt: - -

(+) Issue Short-Term Debt: - -

(-) Repay Short-Term Debt: - -

(+) Issue Preferred Stock: - -

(-) Repay Preferred Stock: - -

(-) Repurchase Shares: - -

(+) Issue New Shares: - -

Cash Flow from Financing: - -

FX Rate Effects: - -

Beginning Cash: 100$ 100$

Increase / (Decrease) in Cash: 700$ 700$

Cash & Cash Equivalents: 800$ 800$

Business Valuation Model: ROI Analysis($ Millions)

Discounted Cash Flow Analysis

Year 1 Year 2 Year 3

Sales $208,0 $216,3 $225,0% growth 4,0% 4,0% 4,0%

COGS $124,8 $129,8 $135,0

Gross Profit $83,2 $86,5 $90,0

Operating Expense $52,00 $54,08 $56,24

EBIT $31,2 $32,4 $33,7% margin 15,0% 15,0% 15,0%

Taxes (9,4) (9,7) (10,1)

NOPAT 21,8 22,7 23,6

Plus: D&A 8,0 8,0 8,0

Less: Change in WC (2,0) (2,1) (2,2)

Less: CapEx (9,0) (9,0) (9,0)

Free Cash Flow 18,8 19,6 20,5

Terminal Value 300,0

Net Cash Flow Projected 18,8 19,6 320,5

PV of Cash Flows $17,1 $16,2 $240,8

Business Value "PV of Cash Flows" $274,1

EBIT = Earnings Before Interest and Taxes

NOPAT = Net Operating Profit After Tax

PV = Present Value

TV = Terminal Value

CashFlow

Metrics (SeeExcel File)NPV, IRR

Business Valuation Model: ROI Analysis($ Millions)

Discounted Cash Flow Analysis

Year 1 Year 2 Year 3

Sales $208,0 $216,3 $225,0% growth 4,0% 4,0% 4,0%

COGS $124,8 $129,8 $135,0

Gross Profit $83,2 $86,5 $90,0

Operating Expense $52,00 $54,08 $56,24

EBIT $31,2 $32,4 $33,7% margin 15,0% 15,0% 15,0%

Taxes (9,4) (9,7) (10,1)

NOPAT 21,8 22,7 23,6

Plus: D&A 8,0 8,0 8,0

Less: Change in WC (2,0) (2,1) (2,2)

Less: CapEx (9,0) (9,0) (9,0)

Free Cash Flow 18,8 19,6 20,5

Terminal Value 300,0

Net Cash Flow Projected 18,8 19,6 320,5

PV of Cash Flows $17,1 $16,2 $240,8

Business Value "PV of Cash Flows" $274,1

EBIT = Earnings Before Interest and Taxes

NOPAT = Net Operating Profit After Tax

PV = Present Value

TV = Terminal Value

Changes in Operating Assets & Liabilities:

Accounts Receivable: -

Prepaid Expenses: -

Inventory: -

Accounts Payable: -

Accrued Expenses: -

Deferred Revenue: -

Cash Flow from Operations: 700

WORKING CAPITALAR + INVENTORY - AP

CashFlow: capex projections

Metrics (See Excel File)Working CapitalDebt Structure

What integratesCashFlow

Major Capital Expenditure Model: ROI Analysis

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Total

6.000.000 6.000.000 6.000.000 6.000.000 6.000.000 6.000.000 - 36.000.000

0,310 0,326 0,342 0,359 0,377 0,396

1.860.000 1.953.000 2.050.650 2.153.183 2.260.842 2.373.884 - 12.651.558

0,120 0,124 0,127 0,131 0,135 0,139

(720.000) (741.600) (763.848) (786.763) (810.366) (834.677) - (4.657.255)

0,030 0,031 0,032 0,033 0,034 0,035

(180.000) (185.400) (190.962) (196.691) (202.592) (208.669) - (1.164.314)

(900.000) (927.000) (954.810) (983.454) (1.012.958) (1.043.347) - (5.821.569)

960.000 1.026.000 1.095.840 1.169.728 1.247.884 1.330.537 - 6.829.989

51,6% 52,5% 53,4% 54,3% 55,2% 56,0% 54,0%

(200.000) (206.000) (212.180) (218.545) (225.102) (231.855) (25.000) (1.318.682)

(304.167) (304.167) (304.167) (304.167) (304.167) (304.167) - (1.825.000)

- - - - - - 250.000 250.000

(504.167) (510.167) (516.347) (522.712) (529.268) (536.021) 225.000 (2.893.682)

455.833 515.833 579.493 647.016 718.615 794.516 225.000 3.936.307

(145.867) (165.067) (185.438) (207.045) (229.957) (254.245) (72.000) (1.259.618)

309.967 350.767 394.055 439.971 488.658 540.271 153.000 2.676.689

(334.167) (16.708) (17.544) (18.421) (19.342) (20.309) 426.491 -

304.167 304.167 304.167 304.167 304.167 304.167 - 1.825.000

Total Investment (2.075.000)

Project Cash Flow (2.075.000) 279.967 638.225 680.678 725.717 773.483 824.128 579.491 2.426.689

Payback 3,66

NPV 472.230 NPV Rate 15%

IRR 21,4%

PI 1,23

Taxes

Net Income

Working Capital Investment

Add back depreciation/amortization

Maintenance and Support

Depreciation

Other Income (Expense)

Total Operating Expense

Profit Before Taxes

Operating Expense

Units Produced

Per Part Rate

Revenue

Material per Part Rate

Material

Direct Labor per Part Rate

Direct Labor

Total COGS

Gross Profit

Balance: period of time

Metrics (See Excel File)Working CapitalDebt Structure

CF = NOPAT + Amortization- CapEx- Change in WC

What integrates Cash Flow:

The Cash Flow Statement, like the Income Statement, tracks changes over a period (one year, quarter, month, etc.).

It exists for 2 main reasons:

1) You may have recorded non-cash revenue, expenses, or taxes on the Income Statement. If you did, then you need to make an adjustment on the Cash Flow Statement to reflect this. Remember, these cash/non-cash differences are the whole reason why the 3 financial statements exist in the first place!

2) There may be additional cash inflows and outflows that have NOT appeared on the Income Statement. For example, Capital Expenditures and Dividends both impact a company’s cash balance, but neither one appears on the Income Statement. NOPAT (Net Operating Profit After Taxes):

Operating Income * (1 – Tax Rate)

CF = NOPAT + Amortization- CapEx- Change in WC

KEEP THIS IN MINDWorking Capital is an investment to operate the company. Is an investment

that must be financed. The amount ofWorking Capital, lacks in CASH.

19

Thank You.

Next content: Intro to Project Management.