Final report Mehedi

80

Cost Accumulation and Accounting Procedure of Micro Fibre Limited SUBMITTED TO Mohammad SalahuddinChowdhury, ACA Lecturer F-302: Cost and Managerial accounting Department of Finance Faculty of Business Studies University of Dhaka SUBMITTED BY Group NAME ROLL NO. Md. Mehedi Hasan 16-087 Mostabshera Alam 16-079 Abdul Malek (Tushar) 16-059 Bijoy Nondini Roy 16-073 Mohammad Asrarul Haque 16-111 Moin Zafree 16-075 BBA 16 th Batch Section-A Department of Finance University of Dhaka pg. 1

Transcript of Final report Mehedi

Cost Accumulation andAccounting Procedure of

Micro Fibre Limited

SUBMITTED TOMohammad SalahuddinChowdhury, ACA

LecturerF-302: Cost and Managerial accounting

Department of FinanceFaculty of Business Studies

University of Dhaka

SUBMITTED BYGroup

NAME ROLL NO.

Md. Mehedi Hasan 16-087Mostabshera Alam 16-079Abdul Malek (Tushar) 16-059Bijoy Nondini Roy 16-073Mohammad Asrarul Haque 16-111Moin Zafree 16-075

BBA 16th BatchSection-A

Department of FinanceUniversity of Dhaka

pg. 1

Date of Submission:8 June, 2012

LETTER OF TRANSMITTAL

7 June,2012

Mohammad SalauddinChowdhury,ACALecturerDepartment of FinanceFaculty of Business StudiesUniversity of Dhaka

Subject: Letter regarding submission of Report.

Dear Sir,

Here is the Report on “Cost Accumulation and accountingprocedure of Micro Fibre Limited”as you assign us to do. Andwe have completed our report about cost accumulationprocedures followed by Micro Fibre Limited. It is a greatpleasure for us to submit this Report. We have got theadvantage of learning more about cost accumulation proceduresof a manufacturing company practically. We have concentratedour best efforts to achieve the objectives of the Report andhope that our endeavor will serve the purpose. We sincerelybelieve that the knowledge and experience we have gatheredduring the preparation of the Report will immensely help us inour future professional life.

We thank you for providing us with this opportunity and hopethat you will approve our submission cordially.

Faithfully yours

Md. MehediHasanRoll: 16-087

pg. 2

On behalf of GroupSection-ADepartment of FinanceFaculty of Business StudiesUniversity of Dhaka

pg. 3

ACKNOWLEDGMENT

First of all, we would like to thank almighty Allah to give usthe ability and strength to carry out and prepare the report.

Then, we would like to convey our gratitude to our honorablecourse teacher Mohammad SalauddinChowdhury,ACA for letting usto do a report on such a wonderful and useful topic andhelping us all the way. His advice, guidance and support makeit possible that we have accomplished the task.

pg. 4

EXECUTIVE SUMMARYCost accumulates and accounting procedure of a Micro FibreLimited includes mainly Hybrid Processing system. The systemwhere both Process costing and job order costing donesimultaneously. They also maintain their costing by single joborder costing system. They have some other supplementaryprocedures like inventory valuation; Cost of goods soldstatements as well as income statements.

They includes their transactions both their general andfactory office separately. Their overall valuation system andaccumulation system done through Customized software systems.

pg. 5

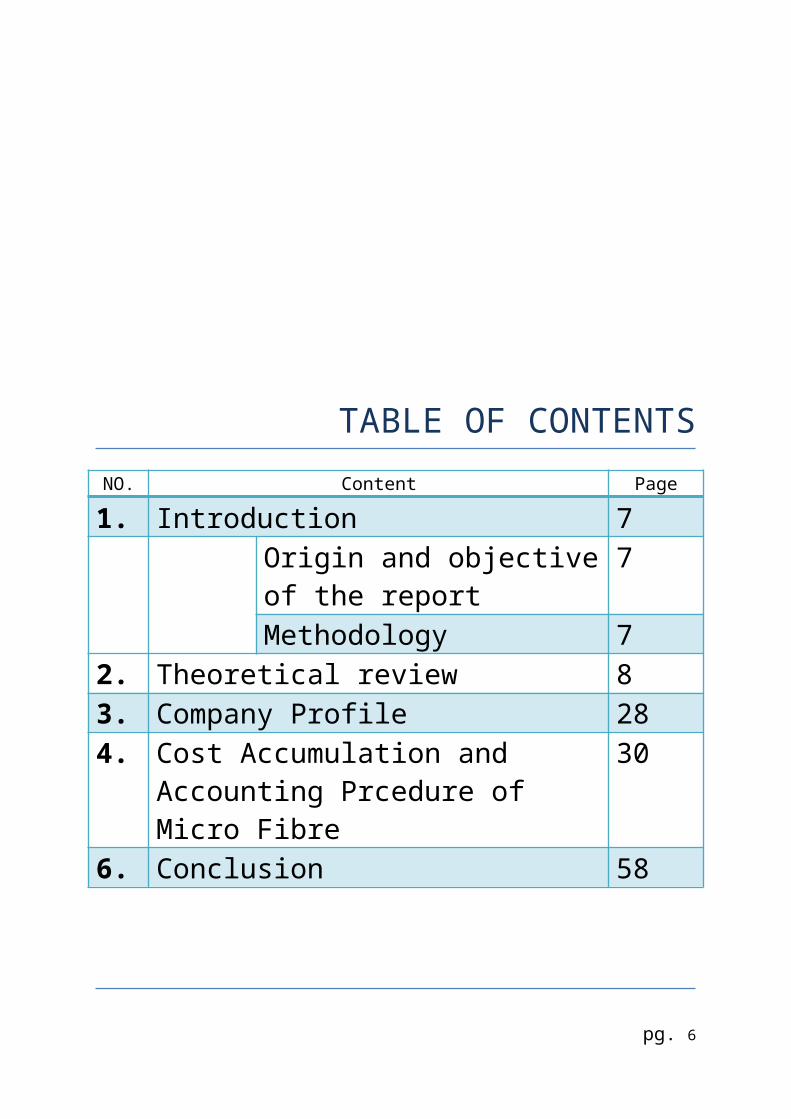

TABLE OF CONTENTSNO. Content Page

1. Introduction 7Origin and objectiveof the report

7

Methodology 72. Theoretical review 83. Company Profile 284. Cost Accumulation and

Accounting Prcedure of Micro Fibre

30

6. Conclusion 58

pg. 6

pg. 7

Introductory

Part

pg. 8

INTRODUCTION

Introduction

Cost accounting information is designed for managers. Sincemanagers are taking decisions only for their own organization,there is no need for the information to be comparable tosimilar information from other organizations. Instead, theimportant criterion is that the information must be relevantfor decisions that managers operating in a particularenvironment of business including strategy make. Costaccounting information is commonly used in financialaccounting information, but first we are concentrating in itsuse by managers to take decisions. The accountants who handlethe cost accounting information generate add value byproviding good information to managers who are takingdecisions. Among the better decisions, the better performanceof one's organization, regardless if it is a manufacturingcompany, a bank, a non-profit organization, a governmentagency, a school club or even a business school. The cost-accounting system is the result of decisions made by managersof an organization and the environment in which they makethem.

Origin and objective of the report

From the course “Cost Accounting”, we learn aboutbasic costaccumulation procedure and itsaccounting procedure of amanufacturing firm as well as joint and by product costingconcepts that different businesses and organizations usage..We also learn the different aspects of cost accumulation andaccounting procedureof a manufacturing as well as servicingcompany. But without the practical knowledge, our learningwill remain incomplete. So for gathering practical experienceabout cost accumulation procedure of manufacturing companies

pg. 9

and learning about the practices of its procedures in reallife, we have prepared this report as our course teacher toldus to do. We prepare this report on Micro Fibre Limited.

Methodology

In this report we only the secondary data. The data sources are:

Primary Data Sources:

We personally visited the company and talked to the

executives and collected the required information

for preparing this report.

Secondary Data Sources:

Website of Micro Fibre Limited

Annual Report of Micro Fibre Limited

Prospectus of the company

pg. 10

Overview of CostAccounting and

Accumulation Procedure

Cost AccountingCost accounting information is designed for managers. Sincemanagers are taking decisions only for their own organization,there is no need for the information to be comparable tosimilar information from other organizations. Instead, theimportant criterion is that the information must be relevant

pg. 11

for decisions that managers operating in a particularenvironment of business including strategy make. Costaccounting information is commonly used in financialaccounting information, but first we are concentrating in itsuse by managers to take decisions. The accountants who handlethe cost accounting information generate add value byproviding good information to managers who are takingdecisions. Among the better decisions, the better performanceof one's organization, regardless if it is a manufacturingcompany, a bank, a non-profit organization, a governmentagency, a school club or even a business school. The cost-accounting system is the result of decisions made by managersof an organization and the environment in which they makethem.

The organizations and managers are most of the timesinterested in and worried for the costs. The control of thecosts of the past, present and future is part of the job ofall the managers in a company. In the companies that try tohave profits, the control of costs affects directly to them.Knowing the costs of the products is essential for decision-making regarding price and mix assignation of products andservices.

The cost accounting systems can be important sources ofinformation for the managers of a company. For this reason,the managers understand the forces and weaknesses of the costaccounting systems, and participate in the evaluation andevolution of the cost measurement and administration systems.Unlike the accounting systems that help in the preparation offinancial reports periodically, the cost accounting systemsand reports are not subject to rules and standards like theGenerally Accepted Accounting Principles. As a result, thereis a wide variety in the cost accounting systems of thedifferent companies and sometimes even in different parts ofthe same company or organization.

The following are different cost accounting approaches:

standardized or standard cost accounting lean accounting

activity-based costing

pg. 12

resource consumption accounting

throughput accounting

marginal costing/cost-volume-profit analysis

Classical cost elements are:

1. Raw materials 2. Labor

3. Indirect expenses/overhead

Origins

Cost accounting has long been used to help managers understandthe costs of running a business. Modern cost accountingoriginated during the industrial revolution, when thecomplexities of running a large scale business led to thedevelopment of systems for recording and tracking costs tohelp business owners and managers make decisions.

In the early industrial age, most of the costs incurred by abusiness were what modern accountants call "variable costs"because they varied directly with the amount of production.Money was spent on labor, raw materials, power to run afactory, etc. in direct proportion to production. Managerscould simply total the variable costs for a product and usethis as a rough guide for decision-making processes.

Some costs tend to remain the same even during busy periods,unlike variable costs, which rise and fall with volume ofwork. Over time, the importance of these "fixed costs" hasbecome more important to managers. Examples of fixed costsinclude the depreciation of plant and equipment, and the costof departments such as maintenance, tooling, productioncontrol, purchasing, quality control, storage and handling,plant supervision and engineering. In the early twentiethcentury, these costs were of little importance to most

pg. 13

businesses. However, in the twenty-first century, these costsare often more important than the variable cost of a product,and allocating them to a broad range of products can lead tobad decision making. Managers must understand fixed costs inorder to make decisions about products and pricing.

Elements of cost Material (Material is a very important part of business)

o Direct material

Labor

o Direct labor

Overhead (Variable/Fixed)

o Indirect material

o Indirect labor

o Maintenance & Repair

o Supplies

o Utilities

o Other Variable Expenses

o Salaries

o Occupancy (Rent)

o Depreciation

o Other Fixed Expenses

(In some companies, machine cost is segregated from overheadand reported as a separate element)

They are grouped further based on their functions as,

Production or works overheads Administration overheads

Selling overheads

pg. 14

Distribution overheads

Financial Expenses

Classification of costsClassification of cost means, the grouping of costs accordingto their common characteristics. The important ways ofclassification of costs are:

By nature or element: materials, labor, expenses By functions: production, selling, distribution,

administration, R&D, development,

By traceability: direct and indirect

By variability: fixed, variable, semi-variable

By controllability: controllable, uncontrollable

By normality: normal, abnormal

Job order costing systemJob order costing system is used in situations where manydifferent products are produced each period. For exampleclothing factory would typically made many different types ofjeans for both men and women during a month. In a job ordercosting system, costs are traced to the jobs and then thecosts of the job are divided by the number of units in the jobto arrive at an average cost per unit.

Job order costing system is also extensively used in serviceindustries. Hospitals, law firms, movie studios, accountingfirms, advertising agencies and repair shops all use a varietyof job order costing system to accumulate costs for accountingand billing purposes. The details here deal with amanufacturing firm, the same concept and procedures are usedby many service organizations.

The record keeping and cost assignment problems are morecomplex in a job order costing system when a company sellsmany different products and services than when it has only a

pg. 15

single product or service. Since the products are different,the costs are typically different. Consequently, cost recordsmust be maintained for each distinct product or job. Forexample an attorney in a large criminal law practice wouldordinarily keep separate records of the costs of advising anddefending each of her clients. And a clothing factory wouldkeep separate track of the costs of filling orders forparticular styles, sizes, and colors of jeans. A job ordercosting system requires more effort than a process costingsystem. Companies classify manufacturing costs into threebroad categories :

(1) Direct materials

(2) Direct labor

(3) Manufacturing overhead.

As we study the operation of a job costing system, we will seehow each of these three types of costs is recorded andaccumulated.

1. Measuring Direct Materials Cost in Job Order Costing System:At the beginning of production process a document known asbill of materials is used for standard products. "A bill of materials is a document that lists the type and quantity of each item of materials needed to completea unit of standard product".

2.

3. Measuring Direct Labor Cost in Job Order Costing System : Direct labor cost is handled in much the same way as direct materials cost. Direct labor consists of labor charges that are easily traced to a particular job. Laborcharges that cannot be easily traced directly to any job are treated as part of manufacturing overhead.

4. Application of Manufacturing Overhead :Manufacturing overhead must be included with direct labor on the job cost sheet since manufacturing overhead is also a productcost. However, assigning manufacturing overhead to units

pg. 16

of product can be a difficult task.

5. Multiple Predetermined Overhead Rates :When a singlepredetermined overhead rate is used for entire factory itis called plant wide overhead rate. This is fairly commonpractice - particularly in smaller companies.

6. Under-applied overhead and over-applied overhead calculation:Since the predetermined overhead rate is established before a period begins and is based entirely on estimated data, the overhead cost applied to work in process (WIP) will generally differ from the amount of overhead cost actually incurred during a period.

7. Predetermined Overhead Rate and Capacity :Companiestypically base their predetermined overhead rates on theestimated, or budgeted, amount of allocation base for theupcoming period. This is the method that is used in thischapter, but it is practice that is recently come undersevere criticism.

8. Recording Non - manufacturing Costs :In addition to manufacturing costs, companies also incur marketing and selling costs. These costs should be treated as period expenses and charged directly to the income statement andtherefore should not go into the manufacturing overhead account.

9. Recording Cost of Goods Manufactured and Sold :When a jobhas been completed, the finished out put is transferredfrom the production department to the finished goods warehouse. By this time, the accounting department willhave charged the job with direct materials and directlabor cost and manufacturing overhead will have beenapplied using the predetermined overhead rate.

10. Job Order Costing in Services Companies :Job order costing is also used in service organizations such as lawfirms, movie studios, hospitals, and repair shops, as

pg. 17

well as manufacturing companies.

11. Use of Information Technology in Job Order Costing : Bar code technology can be used to record labor time--reducing the drudgery in that task and increasing accuracy. Bar codes also have many other uses. In a company with a well-developed bar code system, the manufacturing cycle begins with the receipt of a customer's order in electronic form.

Advantages and Disadvantages of Job Order Costing System :

One of the primary advantages of job order costing system isthat the management team has ready access to all the costsincurred for each job being completed. This allows the team toexamine each cost incurred, finding out why it happened, anddetermine how it can be controlled better in the future,thereby contributing to better ongoing levels ofprofitability.

Another reason for using job order costing system is that ityields ongoing results for each job. In today's world of fullycomputerized production tracking data bases, one can use a joborder costing system to track costs as they are added ratherthan waiting until the job has been completed. This gives acompany several advantages. One is that the accounting staffcan monitor job accounts to see if costs are being posted tothe wrong accounts and corrects them right away, rather thanwaiting until the job closes and having to frantically reviewrecords to see why the results are different fromexpectations. Another advantage is that a company can monitorthe costs incurred for longer jobs and have enough time tomake changes before they close, based on the costinginformation revealed by the job costing system. Yet a thirdadvantages is that changes in the cost of a job can result innegotiations with cost-plus customers who are paying for allthe costs incurred, so that they are fully aware of costoverruns well in advance and are prepared to pay theadditional amounts. All these factors are the main advantages

pg. 18

of using job order costing system in a computerizedenvironment.

There are also several problems with job order costing system.One is that it focuses attention primarily on products ratherthan on departments or activities. This is not an issue ifthere are supplemental systems in place that recordinformation about these other cost categories, but it leavesmanagement with inadequate information if this is not thecase. An other difficulty is that overhead is generallyallocated based on rates that are changed only about once ayear. Considerable fluctuation in overhead costs over thecourse of a year can result both in over and under allocationof overhead costs to jobs during that period. Another problemis specific to the use of normal costing. This practiceinvolves the use of standards overhead rate rather than onethat is based on actual costs and requires adjustment fromtime to time. If it is management's intention to chargeindividual jobs for the variance between standard and actualoverhead rates, this may not be possible if some jobs havealready been closed by the time the variance allocation takesplace. This is not just a technical accounting issue, for somejobs are fully reimbursed by customers who pay on a cost plusbasis; if the overhead variance is a positive one, a companymay not be able to charge its customers for the added costs ifthe related job have already been closed.

The most important problem with job order costing is that itrequires a major amount of data entry and data accuracy inorder to yield effective results. Data related to materials,labor, and overhead, indirect labor, scrap, spoilage, andsupplies must be entered into system capable of accuratelyassigning these costs to the correct jobs every time. Inreality such systems are rife with mistakes due to the sheervolume of data transactions, keying errors, misidentificationof jobs, and the like.

Problems can be resolved with a sufficient amount of errortracing by the accounting staff, but there may be so many thatthere are not enough staff members to keep up with them.Though these issues can to some degree be resolved through theuse of computerized data entry system outweighs the benefitsto be gained from it. A final issue is that a large proportion

pg. 19

of the costs assigned to a job, frequently more 50%, come fromallocated overhead. When there is no fully proven method foraccurately allocating overhead, such as through an activitybased costing systemthe results of the allocation yieldmeaningless information. This has been a particular problemsfor the companies that persist in allocating overhead costsbased on the direct labor used by each job, Since a smallamount of labor is generally being used to allocate a muchlarger amount of overhead, resulting in large shifts inoverhead allocations based on small amount of labor isgenerally being used to allocate a much larger amount ofoverhead, resulting in large shifts in overhead allocationsbased on small changes in labor costs. Some companies avoidthis problem by ignoring overhead for job order costingpurposes or by reducing overhead cost pools to include onlyoverhead directly traceable at the job level. In this way,many costs are not allocated to jobs at all, but those thatare allocated are fully justifiable.

Clearly, one must weigh the pros and cons of using a job ordercosting system to see if the benefits outweigh the costs. Thissystem is a complex one that is prone to error, but it doesyield good information about production-specific costs.

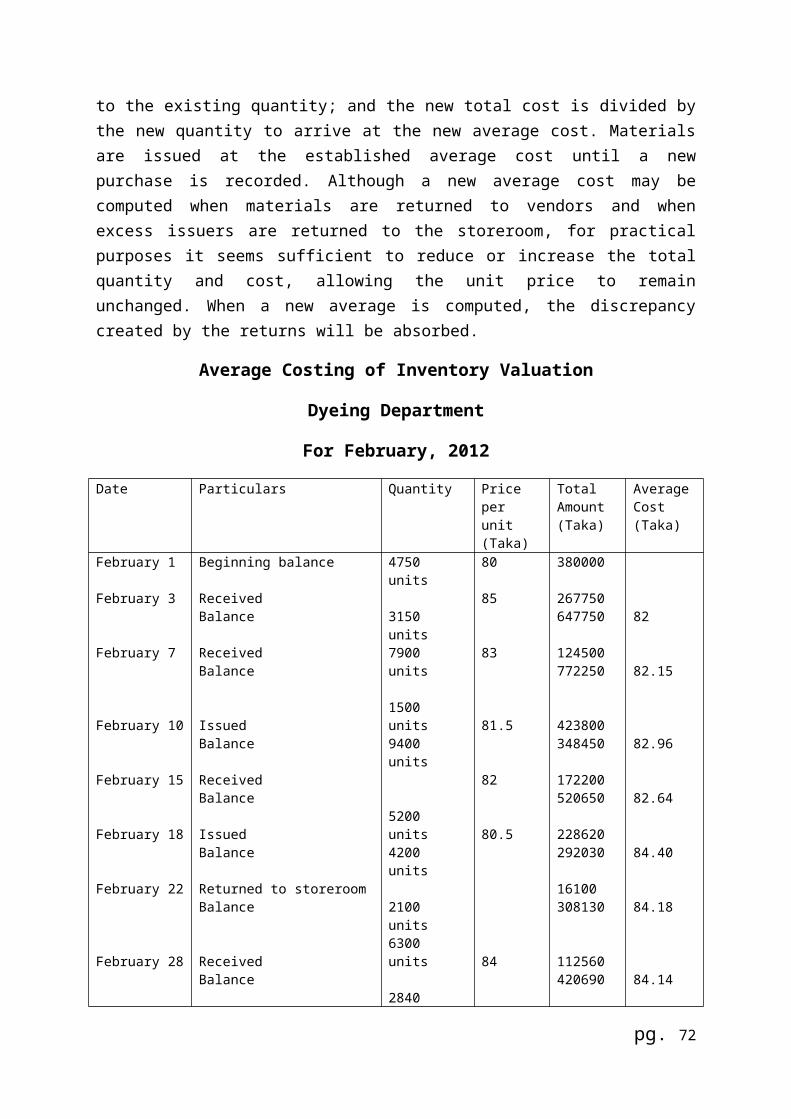

Materials Costing MethodsThe ultimate objective in cost accounting is to produceaccurate and meaningful figures. These figures can be used forpurposes of control and analysis and eventually matchedagainst revenue produced in order to determine net operatingincome.

After the unit cost and total cost of incoming materials areentered in the received section of a materials ledger cards,the next step is to cost these materials as they move eitherfrom storeroom to factory as direct materials or indirectmaterials or from storeroom to marketing and administrativeexpense accounts as supplies. The more common methods ofcosting materials issued and inventories are:

1. First-in-First-Out (FIFO) Costing Method 2. Average Costing Method

pg. 20

3. Last-in-First-Out (LIFO) Costing Method

4. Other Methods-Month end average cost, last purchase price or market price at date of issue, and standard cost.

These methods relate to assumptions as to flow of costs. Thephysical flow of units may coincide with the method of costflow, though such a condition is not a necessary requirement.Although this decision deals with materials inventory, thesame costing methods are also applicable to work in process(WIP) and finished goods inventories.

1. First-in-First-Out (FIFO) Costing Method :

The first in first out (FIFO) method of costing is used tointroduce the subject of materials costing. The FIFO method ofcosting issued materials follows the principle that materialsused should carry the actual experienced cost of the specificunits used. The methods assume that materials are issued fromthe oldest supply in stock and that the cost of those unitswhen placed in stock is the cost of those same units whenissued. However, FIFO costing may be used even though physicalwithdrawal is in a different order.

Advantages of first in first (FIFO) out costingmethod:

1. Materials used are drawn from the cost record in alogical and systematic manner.

2. Movement of materials in a continuous, orderly, singlefile manner represents a condition necessary to andconsistent with efficient materials control, particularlyfor materials subject to deterioration, decay and qualityare style changes.

FIFO method is recommended whenever:

1. The size and cost of units are large.2. Materials are easily identified as belonging to a

particular purchased lot.

pg. 21

3. Not more than two or three different receipts of thematerials are on a materials card at one time.

Disadvantages or Limitations of FIFO Method :

FIFO method is definitely awkward if frequent purchases aremade at different prices and if units from several purchasesare on hand at the same time. Added costing difficulties arisewhen returns to vendors or to the storeroom occur.

2. Average Costing Method:Issuing materials at an average cost assumes that each batchtaken from the storeroom is composed of uniform quantitiesfrom each shipment in stock at the date of issue. Often it isnot feasible to mark or label each materials item with aninvoice price in order to identify the used units with itsacquisition cost. It may be reasoned that units are issuedmore or less at random as for as the specific units and thespecific costs are concerned and that an average cost of allunits in stock at the time of issue is satisfactory measure ofmaterials cost. However, average costing may be used eventhough the physical withdrawal is an identifiable order. Ifmaterials tend to be made up of numerous small items low inunit cost and especially if prices are subject to frequentchanges.

Average costing method has the following mainadvantages:

1. It is a realistic costing method useful to management inanalyzing operating results and appraising futureproduction.

2. It minimizes the effect of unusually high or lowmaterials prices, thereby making possible more stablecost estimates for future work.

3. It is practical and less expensive perpetual inventorysystem.

The average costing method divides the total cost of allmaterials of a particular class by the number of units on handto find the average price. The cost of new invoices are added

pg. 22

to the total in the balance column; the units are added to theexisting quantity; and the new total cost is divided by thenew quantity to arrive at the new average cost. Materials areissued at the established average cost until a new purchase isrecorded. Although a new average cost may be computed whenmaterials are returned to vendors and when excess issues arereturned to the storeroom, for practical purposes, it seemssufficient to reduce or increase the total quantity and cost,allowing the unit price to remain unchanged. When a newpurchase is made and a new average is computed, thediscrepancy created by the returns will be absorbed.

3. Last In First Out (LIFO) Method:The last in first out (LIFO) method of costing materialsissued is based on the premise that materials units issuedshould carry the cost of the most recent purchase, althoughthe physical flow may actually be different. The methodassumes that the most recent cost (the approximate cost toreplace the consumed units) is most significant in matchingcost with revenue in the income determination procedure.

Under LIFO procedures, the objective is to charge the cost ofcurrent purchases to work in process or other operatingexpenses and to leave the oldest costs in the inventory.Several alternatives can be used to apply the LIFO method.Each procedure results in different costs for materials issuedand the ending inventory, and consequently in a differentprofit. It is mandatory, therefore, to follow the chosenprocedure consistently.

The advantages of the last in first out method:

1. Materials consumed are priced in a systematic and realisticmanner. It is argued that current acquisition costs areincurred for the purpose of meeting current production andsales requirements; therefore, the most recent costs should becharged against current production and sales.

2. Unrealized inventory gains and losses are minimized, andreported operating profits are stabilized in industriessubject to sharp materials price fluctuations.

pg. 23

3. Inflationary prices of recent purchases are charged tooperations in periods of rising prices, thus reducing profits,resulting in a tax saving, and therewith providing a cashadvantage through deferral of income tax payments. The taxdeferral creates additional working capital as long as theeconomy continues to experience an annual inflation rateincrease.

Disadvantages of the LIFO Costing Method :

1. The election of last in first out for income tax purposesis binding for all subsequent years unless a change isauthorized or required by the Internal Revenue Service(IRS)

2. This is a "cost only" method with no right down to thelower of cost or market allowed for income tax purposes.Furthermore, the IRS requires that when last in first outis adapted an adjustment must be made to restore anyprevious right downs from actual cost. Should the marketdecline below LIFO cost in subsequent years, the businesswould be at a tax disadvantage. When prices drop the onlyoption may be to charge off the older (higher) cost byliquidating the inventory, however, liquidation forincome tax purposes must take place at the end of theyear. According to IRS regulations, liquidation duringthe fiscal year is not acceptable if the inventoryreturns to its original level at the end of the year.Interim external financial reporting principles impose asimilar requirement when inventory is expected to bereplaced by the end of the annual period.

3. LIFO must be used in financial statements if it iselected for income tax purposes. However, for financialreporting purposes, the lower of LIFO cost or market canbe used without violating IRS LIFO conformity rules.

4. Record keeping requirements under this method, as well asFIFO, are substantially greater than those underalternative costing and pricing methods.

5. Inventories may be depleted due to unavailability ofmaterials to the point of consuming inventories costed atolder or perhaps the oldest prices. This situation will

pg. 24

create a miss matching of current revenue and cost,sometimes companies using this costing method counteractthis problem by establishing an allowance for replacementof the LIFO inventory account. Cost of goods sold ischarged with current cost. The allowance account iscredited for the access of the current replacement costover the LIFO carrying cost for the inventory temporarilyliquidated. When this inventory is replenished, thetemporary allowance (credit) is removed and the goodsacquired are placed in inventory at their old last infirst out cost.

6. In standard number 411 "accounting for acquisition costsof materials, " the cost accounting standards board"CASB" precludes the use of LIFO except when appliedcurrently on a specific identification basis. As aresult, the use of this method, when an annual LIFOadjustment is made, is ruled out for government contractsto which CASB regulations apply.

The decision to adopt the last in first out method has hadincreased appeal in the last few years, due to an acceleratedrate of inflation; however its adoption should not beautomatic. Long range effects as well as short term benefitsmust be considered.

Process Costing SystemCost accumulation procedures used by manufacturing concernsare classified as either job order costing or process costing.The Job Order Costing System chapter deals with the proceduresapplicable to job order costing. It is important to understandthat, except for some modifications, the accumulation ofmaterials costs, labor costs, and factory overhead alsoapplies to process costing system.

Process costing method is used for industries producingchemicals, petroleum, textiles, steel, rubber, cement, flour,pharmaceuticals, shoes, plastics, sugar, and coal. Processcosting system is also used by firms manufacturing items suchas rivets, screws, bolts, and small electrical parts. A third

pg. 25

type of industry using process costing systemis the assemblytype industry which manufactures such things as typewriters,automobiles, airplanes, and household electric appliances(washing machines, refrigerators, toasters, irons, radios,television sets, etc.). Finally certain service industries,such as gas, water, and heat, cost their products by usingprocess costing system. Thus, process costing is used whenproducts are manufactured under conditions of continuousprocessing or under mass production methods. In fact, processcosting procedures are often termed "continuous or massproduction cost accounting procedures".

The type of manufacturing operations performed determines thecost procedures that must be used. For example, companymanufactures custom machinery will use job order costing,whereas a chemical company will use process costing. In thecase of machinery manufacturer, a job order cost sheet isprepared for each order, accumulating the costs of materials,labor, and factory overhead. In contrast the chemical companycannot identify materials, labor, and factory overhead witheach order, since each order is part of a batch or acontinuous process. The individual order identity is lost, andthe cost of a completed unit must be computed by dividingtotal cost incurred during a period by total units completed.The summarization of the costs takes place via the cost ofproduction report, which is an extremely efficient,economical, and timesaving device for the collection of largeamounts of data. The entire process costing discussion ispresented in this chapter and other two chapters (ProcessCosting System - Addition of Materials, Average and FIFOCosting andBy-Products and Joint Products Costing).

The characteristics of process costing system:

1. A cost of production report is used to collect, summarizeand compute total and unit costs.

2. Production is accumulated and reported by departments.

3. Costs are posted to departmental work in process accounts.

pg. 26

4. Production in process at the end of a period is restated in terms of completed units.

5. Total cost charged to a department is divided by total computed production of the department in order to determine a unit cost for a specific period.

6. Costs of completed units of a department are transferred to the next processing department in order to arrive at the total costs of the finished products during a period.At the same time, costs are assigned to units still in process.

The procedures of process costing are designed to:

1. Accumulate materials, labor, and factory overhead costs by departments.

2. Determine a unit cost for each department.

3. Transfer costs from one department to the next and to finished goods.

4. Assign costs to the inventory of work in process (WIP)

If accurate units and inventory costs are to be established byprocess costing procedures, costs of a period must beidentified with units produced in the same period.

Costing By Departments:

The nature of manufacturing operations in firms using processor job order cost procedures is usually such that work onproduct takes place in several departments.

With either procedure, departmentalization of materials,labor, and factory overhead costs facilitates application ofresponsibility accounting. Each department performs a specificoperation or process towards the completion of the product.For example, after the blending department has completed the

pg. 27

starting phase of the work on product, units are transferredto the testing department, after which they may go to theterminal department for completion and transferred to thefinished goods storeroom. Both units and costs are transferredfrom one manufacturing department to another manufacturingdepartment. Separate departmental work in process (WIP)accounts are used to charge each department for the materials,labor, and factory overhead used to complete its share ofmanufacturing process.

Process costing involves averaging costs for a particularperiod in order to obtain departmental and cumulative unitcosts. The cost of a completed unit is determined by dividingthe total cost of a period by the total units produced duringthe period. Determining departmental production for a periodincludes evaluating units still in process. The breakdown ofcosts for the computation of total unit costs and for costingunits transferred and departmental work in process (WIP)inventories is also desirable for cost control purposes.

Departmental total and unit costs are determined by the use ofthe cost of production report. Most of the activity in processcosting system involves the accumulation of data needed forthe preparation of these reports.

Product Flow in Process Costing System:

A product can flow through a factory in numerous ways. Threeproduct flow formats associated with process costing -sequential, parallel, and selective - are illustrated here toindicate that basically the same costing procedures can beapplied to all types of product flow situations.

Sequential Product Flow:

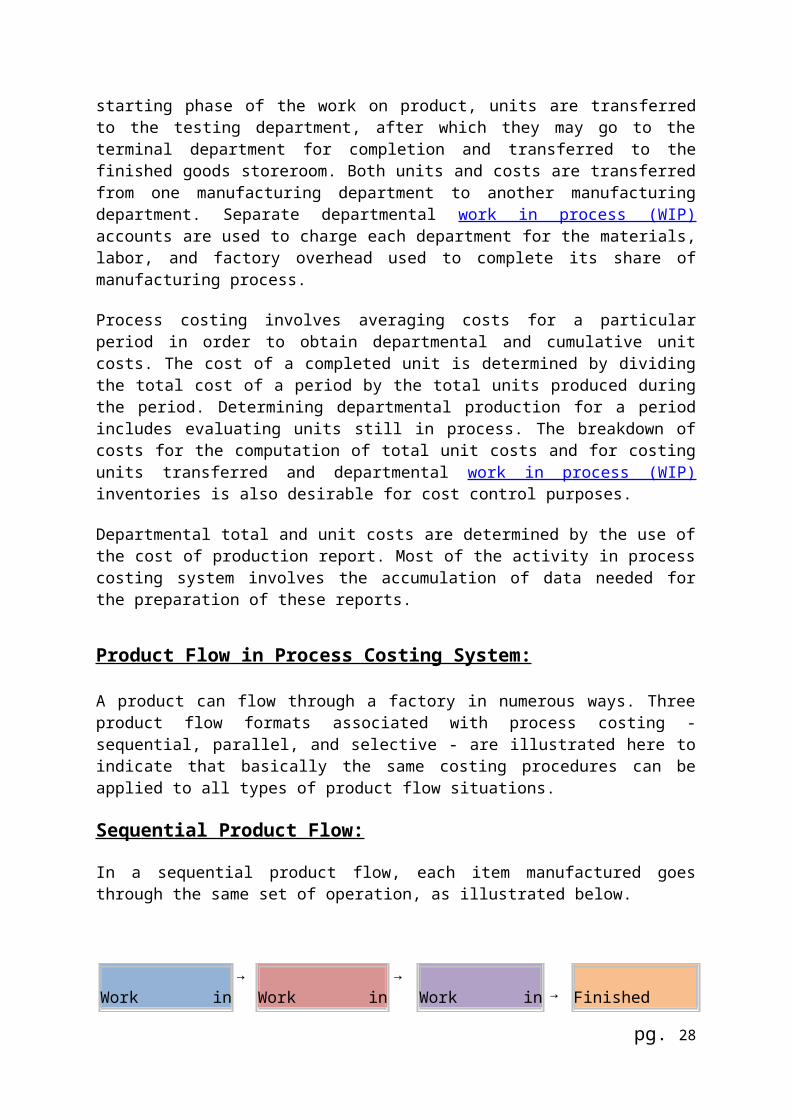

In a sequential product flow, each item manufactured goesthrough the same set of operation, as illustrated below.

Work in→

Work in→

Work in → Finished

pg. 28

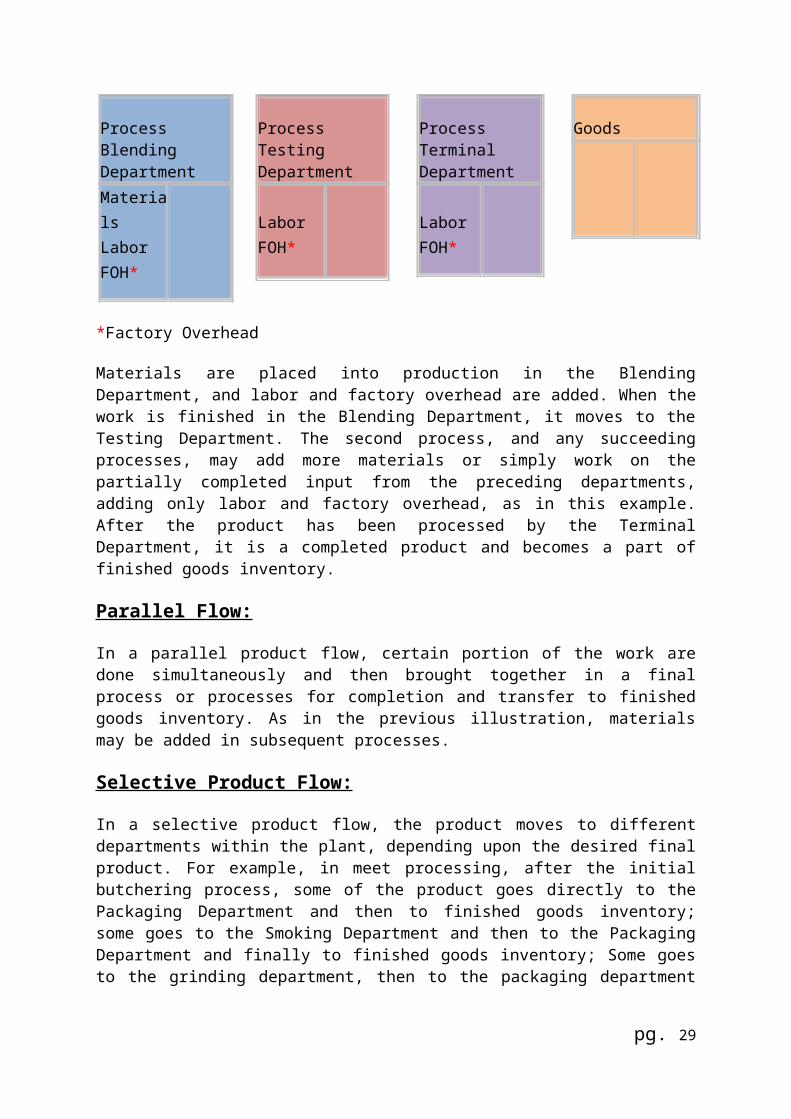

ProcessBlendingDepartmentMaterialsLaborFOH*

ProcessTestingDepartment

LaborFOH*

ProcessTerminalDepartment

LaborFOH*

Goods

*Factory Overhead

Materials are placed into production in the BlendingDepartment, and labor and factory overhead are added. When thework is finished in the Blending Department, it moves to theTesting Department. The second process, and any succeedingprocesses, may add more materials or simply work on thepartially completed input from the preceding departments,adding only labor and factory overhead, as in this example.After the product has been processed by the TerminalDepartment, it is a completed product and becomes a part offinished goods inventory.

Parallel Flow:

In a parallel product flow, certain portion of the work aredone simultaneously and then brought together in a finalprocess or processes for completion and transfer to finishedgoods inventory. As in the previous illustration, materialsmay be added in subsequent processes.

Selective Product Flow:

In a selective product flow, the product moves to differentdepartments within the plant, depending upon the desired finalproduct. For example, in meet processing, after the initialbutchering process, some of the product goes directly to thePackaging Department and then to finished goods inventory;some goes to the Smoking Department and then to the PackagingDepartment and finally to finished goods inventory; Some goesto the grinding department, then to the packaging department

pg. 29

and lastly to finished goods inventory. Transfer of costs fromthe Butchering Department involves joint cost allocation.

Cost of Production Report (CPR):

A departmental cost of production report (CPR) shows all costschargeable to a department. It is not only the source forsummary journal entries at the end of the month but also amost convenient vehicle for presenting and disposing of costsaccumulated during the month. A cost of production reportshows:

1. Total unit costs transferred to it from a precedingdepartment.

2. Materials, labor, and factory overhead added by thedepartment.

3. Unit cost added by the department.

4. Total and unit costs accumulated to the end of operationsin the department.

5. The cost of the beginning and ending work in processinventories.

6. Cost transferred to a succeeding department or to afinished goods storeroom.

It is customary to divide the cost section of the report intotwo parts: one shows costs for which the department isaccountable, including departmental and cumulative total andunit costs, the other showing the disposition of these costs.A quantity schedule showing the total number of units forwhich a department is accountable and the disposition made ofthese units is also part of each department's cost ofproduction report. Information in this schedule, adjusted forequivalent production is used to determine the unit costsadded by a department, the costing of the ending work inprocess inventory, and the cost to be transferred out of thedepartment.

A cost of production report determines periodic total and unitcosts. However, a report that would merely summarize the totalcosts of materials, labor, and factory overhead and shows only

pg. 30

the unit cost for the period would not be satisfactory forcontrolling costs. Total figures mean very little; costcontrol requires detailed data. Therefore, in most instances,the total cost is broken down by cost elements for eachdepartment head responsible for the costs incurred.Furthermore, detailed departmental figures are needed becauseof the various completion stages of the work in processinventories.

Either in the cost of production report itself or in thesupporting schedules, each item of material used by adepartment is listed; every labor operation is shownseparately; factory overhead components are notedindividually; or a unit cost is derived for each item. Tocondense the illustrated cost of production reports, onlytotal materials, labor, and factory overhead charged todepartments are considered; and unit costs are computed onlyfor each cost element rather than for each item.

By-products and joint productsMany industrial concerns are confronted with the difficult andoften rather complicated problem of assigning costs to theirby-products and joint products. Chemical companies, cokemanufacturers, refineries, flour mills, coal mines, lumbermills, gas companies, dairies, canners, meat packers, and manyothers produce in their manufacturing or conversion processes amultitude of products to which some cost must be assigned.Assignment of costs of these various products enhancesequitable inventory costing for income determination andfinancial statement purposes. An even more important aspect ofby product and joint product costing is that it furnishesmanagementwith data for use in planning maximum profitpotentials and evaluating actual profit performance.

Joint Product Cost:A joint product cost cay is defined as that cost which arisesfrom the common processing or manufacturing of productsproduced from a common raw material. Whenever two or moredifferent products are created from a single cost factor, ajoint product cost results. A joint cost is incurred prior to

pg. 31

the point at which separately identifiable products emergefrom the same process.

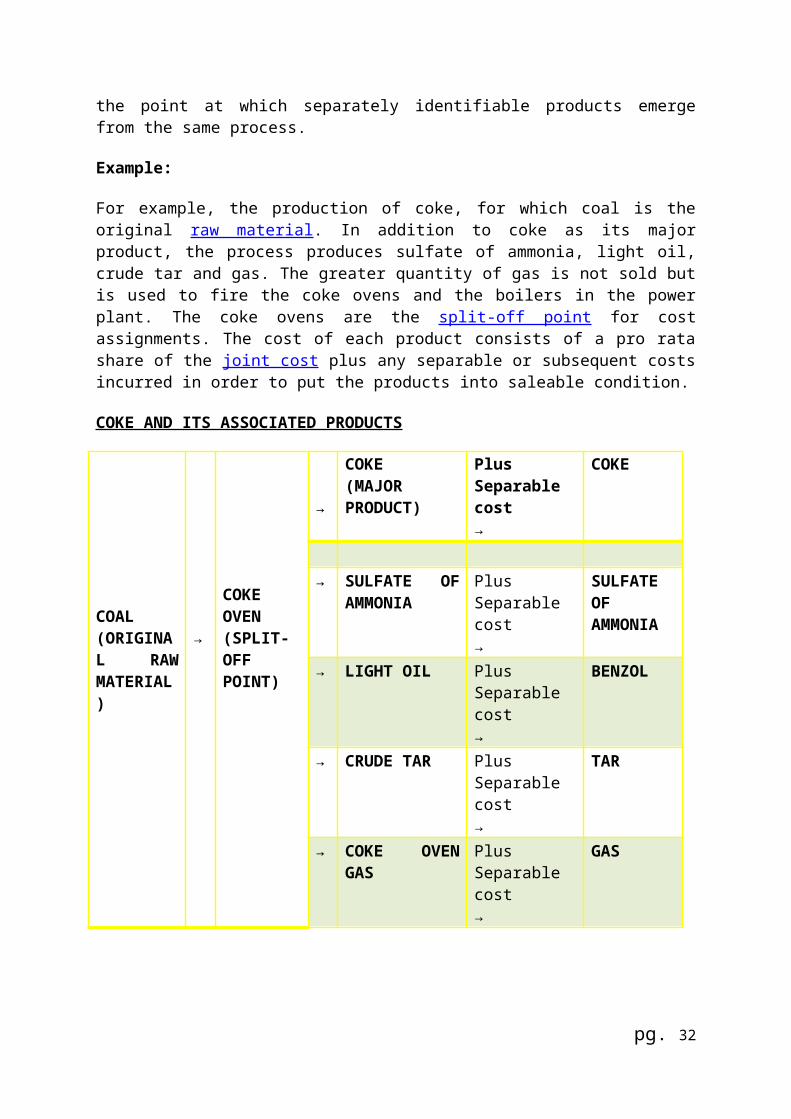

Example:

For example, the production of coke, for which coal is theoriginal raw material. In addition to coke as its majorproduct, the process produces sulfate of ammonia, light oil,crude tar and gas. The greater quantity of gas is not sold butis used to fire the coke ovens and the boilers in the powerplant. The coke ovens are the split-off point for costassignments. The cost of each product consists of a pro ratashare of the joint cost plus any separable or subsequent costsincurred in order to put the products into saleable condition.

COKE AND ITS ASSOCIATED PRODUCTS

COAL(ORIGINAL RAWMATERIAL)

→

COKEOVEN(SPLIT-OFFPOINT)

→

COKE(MAJORPRODUCT)

PlusSeparablecost→

COKE

→ SULFATE OF

AMMONIAPlusSeparablecost→

SULFATEOFAMMONIA

→ LIGHT OIL PlusSeparablecost→

BENZOL

→ CRUDE TAR PlusSeparablecost→

TAR

→ COKE OVENGAS

PlusSeparablecost→

GAS

pg. 32

Methods of Allocating the Joint Production Cost:

The allocation ofjoint product cost incurred up to the split-off point can be made by:

1. The market or sales value method, based on the relative market values of the individual products:

Market or sales value method enjoys greatpopularity because of the argument that market value ofany product is a manifestation of the cost incurred inits production. The contention is that if one productsells for more than another, it is because more cost wasexpended to produce it. Therefore, the way to prorate thejoint cost is on the basis of the respective market valuesof the items produced. The method is really a weightedmarket value basis using the total market or sales valueof each unit (quantity sold times the unit sales price).

2. The quantitative or physical unit method, based on some physical measurement unit such as weight, linear measure,or volume :

Quantitative or physical unit method attempts todistribute the total joint cost on the basis of some unitof measurement, such as pounds, gallons, tons, or boardfeet. Of course, the unit products must be measurable bythe basic measurement unit. If this isn't possible, thejoint units must be converted to a denominator common toall units produced, For example, in the manufacture ofcoke, products such as coke, coal tar, benzol, sulfate ofammonia, and gas are measured in different units. Theyield of these recovered units is measured on the basisof the quantity of product extracted per ton of coal.

3. The average unit cost method :

Average unit cost method attempts to apportion totaljoint production cost to the various products on thebasis of a predetermined standard or index of production.An average unit cost is obtained by dividing the total

pg. 33

number of units produced into the total joint productioncost. As long as all units produced are measured in termsof the same unit and do not differ greatly, the methodcan be used without too much misgiving. When the unitsproduced are not measured in like terms, the methodcannot be applied.

4. The weighted average method, based on a predetermined standard or index of production:

Many industries, the previously described methods do notgive a satisfactory answer to the joint costapportionment problem. For this reason, weight factors areoften assigned to each unit, based upon size of the unit,difficulty of manufacture, time consumed in making theunit, difference in type of labor employed, amount ofmaterials used etc. Finished production of every kind ismultiplied by weight factors to apportion to total jointcost to individual units.

Methods of Costing By-Products:

The accepted methods for costing by-products fall into twocategories:

Category 1:

A joint production cost is not allocated to the by product.Any revenue resulting from sales of the by product is creditedeither to income or to cost of the main product. In somecases, costs subsequent to split-off point may be offsetagainst the by-product revenue. For inventory costing, anyindependent value may be assigned to the by product. Themethods most commonly used in industry are:

Method 1: Recognition of Gross Revenue Method 2: Recognition of Net Revenue

Method 3:Replacement cost method

pg. 34

Category 2:

Some portion of the joint production cost is allocated to theby product. Inventory costs are based on this allocated costplus any subsequent processing cost. In this category, thefollowing method is used:

Method 4:Market value method or reversal cost method

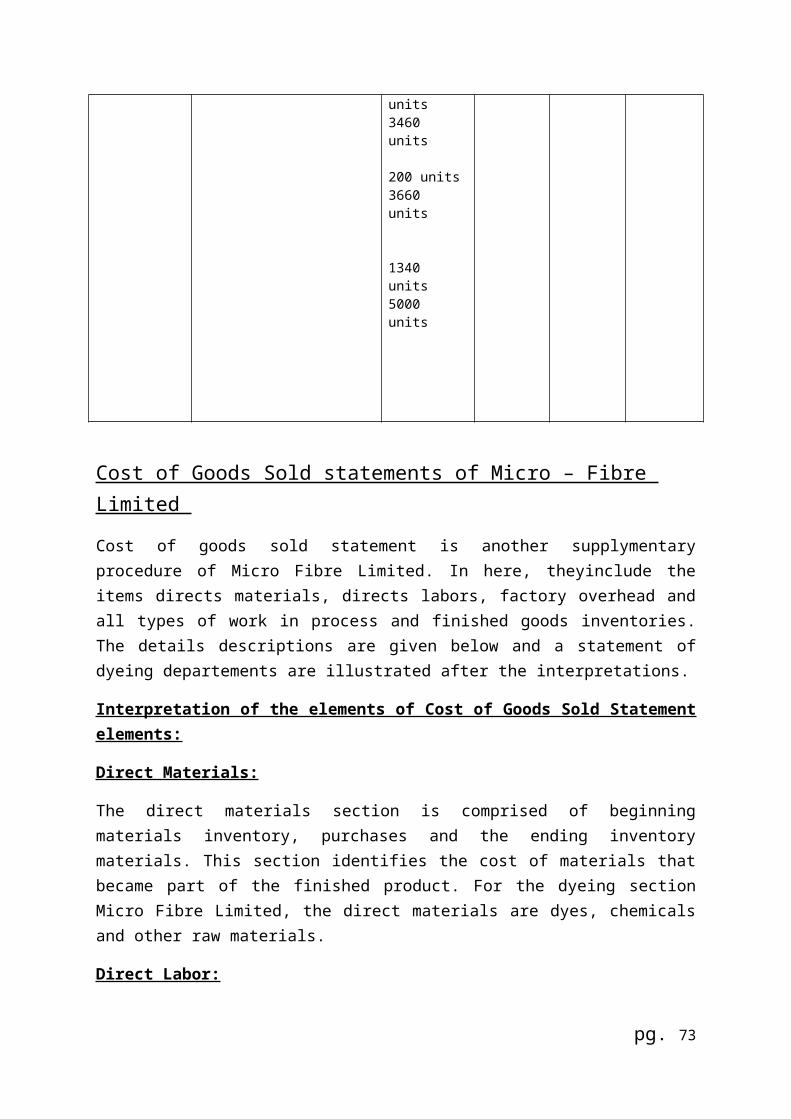

COGS StatementCost of goods sold (COGS)refer to the inventory costs of thosegoods a business has sold during a particular period. Costsare associated with particular goods using one of severalformulas, including specific identification, first-in first-out (FIFO), or average cost. Costs include all costs ofpurchase, costs of conversion and other costs incurred inbringing the inventories to their present location andcondition. Costs of goods made by the business includematerial, labor, and allocated overhead. The costs of thosegoods not yet sold are deferred as costs of inventory untilthe inventory is sold or written down in value

Basic Equation for Inventory Accounts:

Beginning balance + Additions to inventory = Ending balance +withdrawals from inventory

At the beginning of the period, the inventory contains somebeginning balances. During the period, additions are made tothe inventory through purchases or other means. The sum of thebeginning balance and additions to the account is the totalamount of inventory available. During the period, withdrawalsare made from inventory. Whatever is left at the end of theperiod after these withdrawals is the ending balance.

These concepts are applied to determine the cost of goods soldfor a merchandising company like B-bookstore as follows:

Cost of Goods Sold in a Merchandising Company:

pg. 35

Beginning merchandising inventory + Purchases = Endingmerchandising inventory + Cost of goods sold

Or

Cost of goods sold = Beginning merchandising inventory +Purchases − Ending merchandising inventory

To determine the cost of goods sold in a merchandisingcompany, we only need to know the beginning and endingmerchandising inventory account and the purchases. Totalpurchases can be easily determined in a merchandising companyby simply adding together all purchases from suppliers.

The cost of goods sold for a manufacturing company like Amanufacturing company is determined as follows:

Cost of Goods Sold Equation in a Manufacturing Company:

Beginning finished goods inventory + Cost of goodsmanufactured = Ending finished goods inventory + Cost of goodssold

Or

Cost of goods sold = Beginning finished goods inventory + Costof goods manufactured − Ending finished goods inventory

To determine the cost of goods sold in a manufacturing companylike A manufacturing company, we need to know the cost ofgoods manufactured and the beginning and ending balances offinished goods inventory account. The cost of goodsmanufactured consists of the manufacturing costs associatedwith goods that were finished during the period. The cost ofgoods manufactured figure for a manufacturing company isderived from the schedule of cost of goods manufactured belowthe comparative income statements.

Schedule of Cost of Goods Manufactured:

At first glance the schedule of cost of goods manufactured(below comparative income statements) appears complex andperhaps even intimating. However, it is all quite logical. Theschedule of cost of goods manufactured contains the three

pg. 36

elements of cost--direct materials, direct labor, andmanufacturing overhead. The direct material cost is not simplythe cost of materials purchased during the period rather isthe cost of materials used during the period. The purchase ofraw materialsis added to the beginning balance to determinethe cost of the materials available for use. The endingmaterials inventory is deducted from this amount to arrive atthe amount of materials used during the period. This isfurther explained by the following equation:

Materials available for use = Beginning balance of materials +materials purchased during the period

The sum of three cost elements (materials, labor and overhead)is the total manufacturing cost. See the following equation:

Manufacturing cost = Direct materials + Direct labor +Manufacturing overhead

This manufacturing cost is not equal to the cost of goodsmanufactured. Some of the materials, direct labor andmanufacturing overhead costs incurred during the period relateto goods that are not yet completed. The cost of goodsmanufactured consists of the manufacturing costs associatedwith the goods that were finished during the period.Consequently adjustments need to be made to the totalmanufacturing cost of the period for the partially completedgoods that were in process at the beginning and at the end ofthe period. Beginning work in process inventory must be addedto the total manufacturing cost and ending work in processinventory must be deducted to arrive at the cost of goodsmanufactured. This is further explained by the followingequation:

Cost of goods manufactured = Manufacturing cost + Beginningbalance of work in process inventory − Ending balance of workin process inventory

Reference:

pg. 37

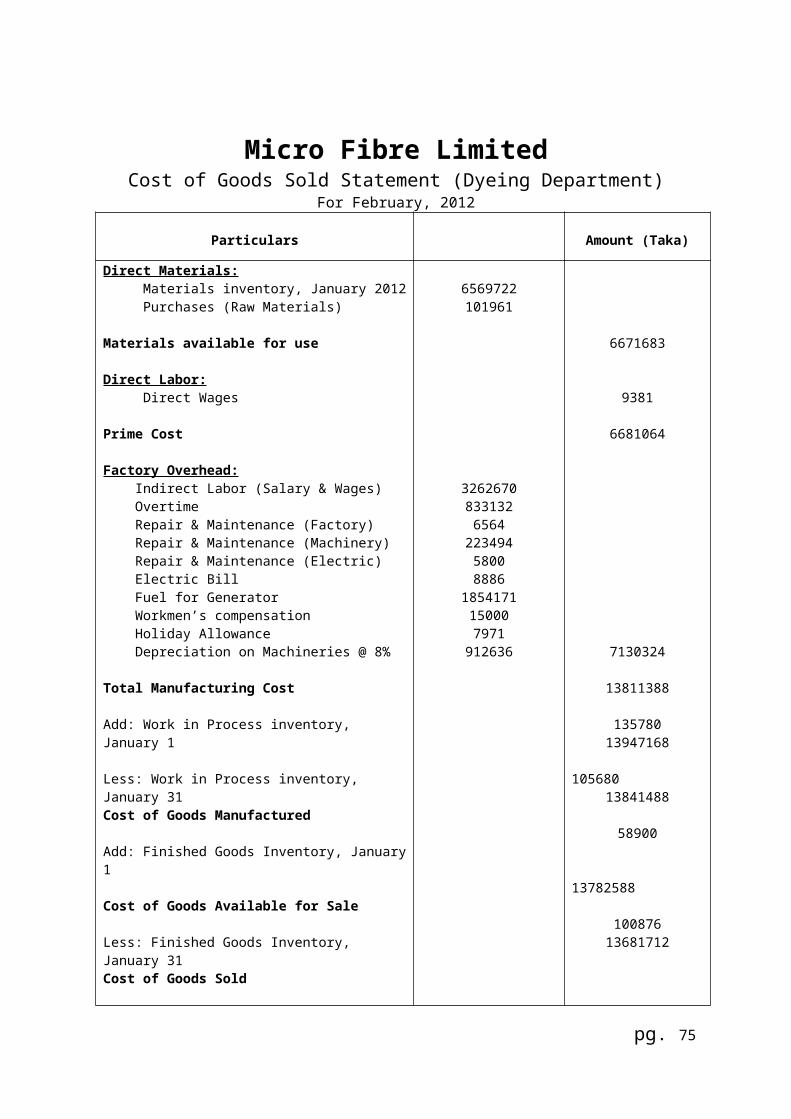

Cost of Goods Manufactured and Sold StatementFormulas:

Prime Cost = Direct Materials Cost + Direct Labor Cost

Total Factory Cost or Manufacturing Cost = Direct Materials +Direct Labor Cost + Factory Overhead

Conversion Cost = Direct Labor Cost + Factory Overhead Cost

Cost of Goods Manufactured (COGM) = Total Factory Cost + Opening Work in Process Inventory - Ending Work in Process InventoryOrCost of Goods manufactured = Direct materials cost + Direct labor cost + Factory overhead cost + Opening work in process inventory - Ending work in process inventory

Cost of goods sold (COGS) = Cost of goods manufactured + Opening finished goods inventory - Ending finished goods inventoryOrCost of goods sold = Direct materials cost + Direct labor cost+ Factory overhead cost + Opening work in process inventory - Ending work in process inventory + Opening finished goods inventory - Ending finished goods inventory

Number of units manufactured = Units sold + Ending FinishedGoods units - Opening finished goods units

Per unit cost of goods manufactured = Cost of goodsmanufactured / Units manufactured

Materials used or consumed = Opening inventory or materials +Net purchases of materials - Ending inventory of materials

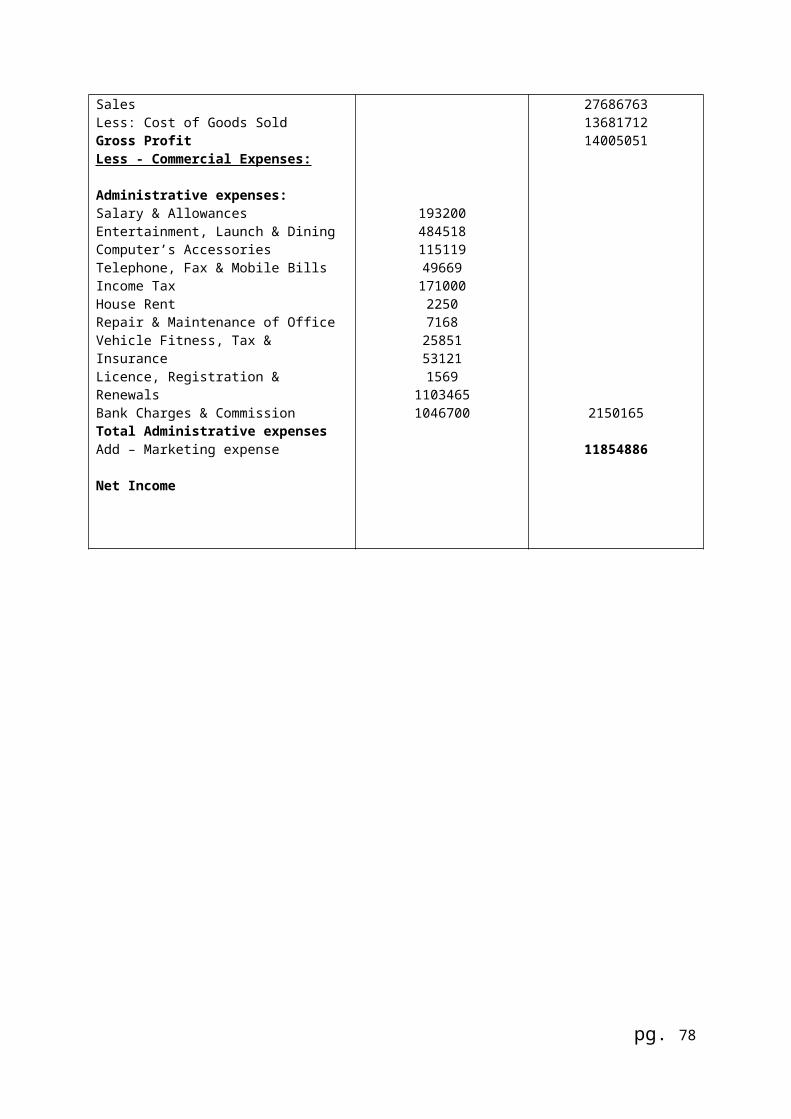

Income statement formulas:

Gross profit = Net sales - Cost of goods sold

Operating profit = Gross profit - Operating expenses

pg. 38

Operating or commercial expenses = Selling or marketingexpenses + General or administrative expenses

Per unit gross profit = Gross profit / No. of units sold

Per unit net profit = Net profit / No. of units sold

Percentage of GP to sales = (Gross profit / Net sales) × 100

Percentage of net profit to sales = (Net profit / Net sales) ×100

pg. 39

Company

Profile

pg. 40

Micro Fibre Group Limited

They instigated their journey in 1998 with a vision ofbecoming the most recognized knitwear manufacturer of thecountry as well as to take the widely known reputation ofBANGLADESH as a global clothing leader to a new high byoffering the best blend of quality and efficiency. They have expanded their capacity, developed a skilledmanagement team, workforce, and integrated sophisticatedtechnologies in order to become globally competitive.Therefore, when many struggle to survive in post-MFA world;their business in fact is enjoying a healthy growth.

Focusing solely in knitwear apparel lines, they have adopted astructure by reengineering its value chain to deliver highquality products in shorter lead time with flexibility inorder size. Moreover, having endless efforts to ensure internationallyaccepted employment practice, their clients recognize the bankas a partner to protect their value system and images amongfinal consumers.

They are specialized on Polo Shirt, Sweat Shirt and Ladies ribtops. Their product range covers basic & fancy polo shirt,sweat shirt, T-shirt, as well as men’s, kids and ladiesknitwear garments. Following the dictate of the fashion trend, they haveimprovised their technologies, broadened their raw-materialssources and trained their workforces.

Working with the clients closely, from an initial sketch ororiginal sample to the development of a range of countersamples, it ensures value for clients. Its designers, all trained in reputed foreign & localinstitution, blend their skills with inputs of ever-changingglobal fashion trends.

pg. 41

As a responsible apparel producer, they provide employees awork environment high above the law-required level. Theyinstalled and have updated lighting, ventilation andergonomics of their plants using latest technologies like busbar for electrical fitting, overhead mirror reflectors forlamps, forced duct ventilation and so on. The goal is to exceed requirements of local legislation andreach the global standards, and thereby support clients’images and sourcing principles.

In MFG, compliance is a process, not an event. To becomeresponsible apparel producer, we believe it is important toexceed local law & legislation and meet ILO convention interms of employment practices, and do this continuously.

They succeed because of its strict adherence to ethicalbusiness practices in dealing with its clients, suppliers andother stakeholders. Their capability to extend short lead-timeis being possible because of the mutual trust and commitmentit shares with its suppliers. Moreover, they have setup water treatment plant so that itssurrounding environment & community remain unperturbed andgreen.

pg. 42

Cost Accumulationand Accounting

Procedure

Of

pg. 43

Micro Fibre Limited accumulates its costing and accounting procedure in the following manner:

1. Hybrid Costinga. Process Costingb. Job-order Costing

2. Cost of By-Products3. Supplementary Procedures

a. Inventory Valuation under Average Costing

b. Cost of goods Sold Statement c. Income statement

The details description of the procedures and its accounting is given below

pg. 44

pg. 45

Hybrid CostingSystem

Hybrid Costing SystemMicro-Fibre Limited followed Hybrid Costing Systems, Product-costing systems do not always fall neatly into either job-costing or process-costing categories.

Micro Fibre Limited may be manufactured in a continuous flow(suited to process costing), but individual units may becustomized with a special combination (which requires jobcosting). A hybrid-costing system blends characteristics fromboth job-costing and process costing systems.

They also keep their process costing through Average Costingsystem.

pg. 46

The weighted-average process-costing method calculates costper equivalent unit of allwork done to date (regardless of theaccounting period in which it was done) and assignsthis costto equivalent units completed and transferred out of theprocess and to equivalentunits in ending work-in-processinventory. The weighted-average cost is the total ofall costsentering the Work in Process account (whether the costs arefrom beginningwork in process or from work started during thecurrent period) divided by total equivalentunits of work doneto date. We now describe the weighted-average method usingthefive-step procedure.

Step 1: Summarize the Flow of Physical Units of Output. Thephysical-units column where the units came from beginninginventory andstarted during the current periodand where theywent units completedand transferred out and in endinginventory.

Step 2: Compute Output in Terms of Equivalent Units. MicroFibre Limited calculates weighted-average cost ofinventory isby merging together the costs of beginning inventory and themanufacturingcosts of a period and dividing by the totalnumber of units in beginning inventoryand units producedduring the accounting period. We apply the same concepthereexcept that calculating the units—in this case equivalentunits—is done differently. We usethe relationship shown in thefollowing equation:

Equivalent unitsin beginning work

in process+

Equivalent unitsof work done incurrent period

=Equivalent units

completed and transferredout in current period

+pg. 47

Equivalent unitsin ending workin process

Although we are interested in calculating the left-hand sideof the preceding equation, it is easier to calculate this sumusing the equation’s right-hand side: (1) equivalent unitscompleted and transferred out in the current period plus (2)equivalent units in endingwork in process. Note that the stage ofcompletion of the current-period beginning workin process is not used in thiscomputation.

Step 3: Summarize Total Costs to Account For. To summarize the total cost accounted for they transferredtheir finished goods to the next department by the priceequals to AVERAGE PRICE plus adjusted price for the lost unit.Here in the Knitting Department they have the average price28.78/unit as average and also 0.7195/unit as an adjustedprice for the lost units. The average price tk. 28.78 consistsof completed units and this period’s transferred.

Step 4: Compute Cost per Equivalent Unit. Micro Fibre computes the cost per unit by adding the work-in-process and during the period added material and conversionthen the totaled amount will be multiplied by the equivalentunit. Cost per units computed by Micro Fibre Limited is thesummation of during the period cost addition and previous workin process costs.

Step 5: Assign Total Costs to Units Completed and to Units inEnding Work in Process. To assign the total cost to units completed, it will add allthe cost per unit plus the lost unit computation. Thecalculation of transferred out cost will be done through thetotal units transferred to the next departments and multipliesthe total unit costs. Work in process during this period willbe computed by the average cost plus lost unit’s adjustedcosts.

pg. 48

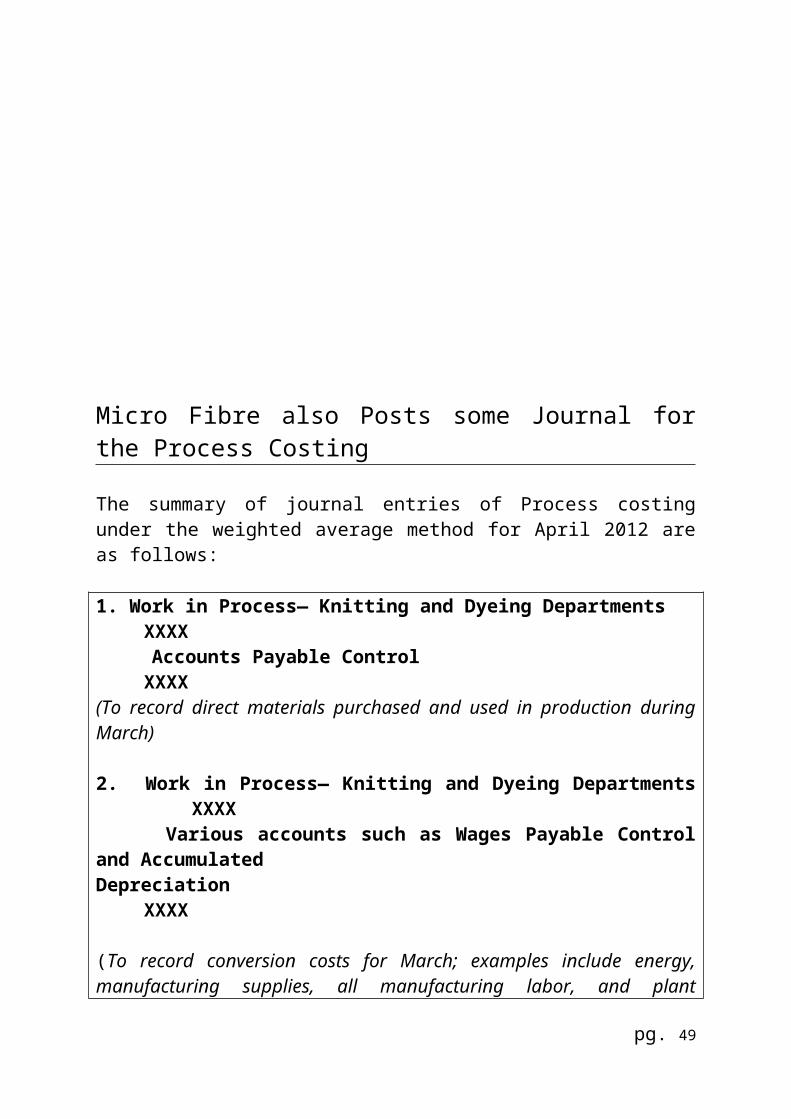

Micro Fibre also Posts some Journal forthe Process Costing

The summary of journal entries of Process costingunder the weighted average method for April 2012 areas follows:

1. Work in Process— Knitting and Dyeing DepartmentsXXXX

Accounts Payable Control XXXX

(To record direct materials purchased and used in production duringMarch)

2. Work in Process— Knitting and Dyeing DepartmentsXXXX

Various accounts such as Wages Payable Controland AccumulatedDepreciation

XXXX

(To record conversion costs for March; examples include energy,manufacturing supplies, all manufacturing labor, and plant

pg. 49

depreciation)

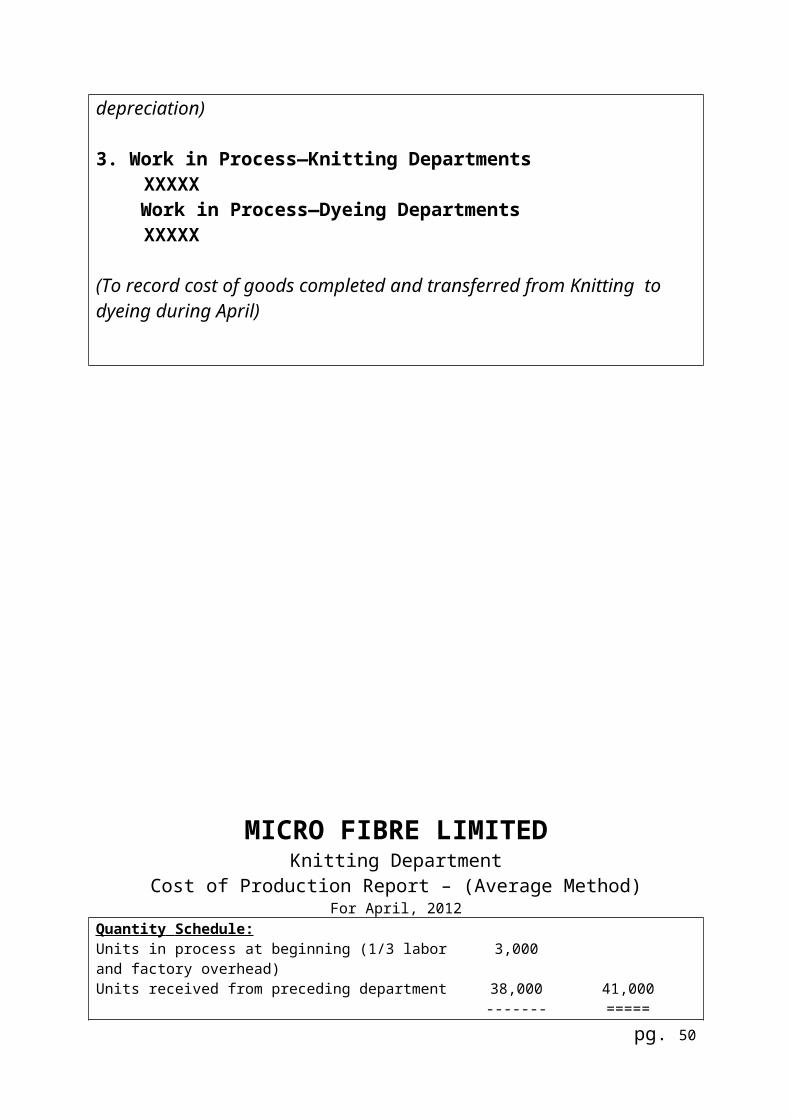

3. Work in Process—Knitting Departments XXXXX

Work in Process—Dyeing Departments XXXXX

(To record cost of goods completed and transferred from Knitting todyeing during April)

MICRO FIBRE LIMITEDKnitting Department

Cost of Production Report – (Average Method)For April, 2012

Quantity Schedule: Units in process at beginning (1/3 labor and factory overhead)

3,000

Units received from preceding department 38,000 41,000------- =====

pg. 50

Units transferred to next department 36,000 Units still in process (1/4 labor and FOH) 4,000Units lost in process 1,000 41,000

-------- =====Cost Charged To the Department: Total

Costunit Cost

Cost from preceding department:Work in process - beginning inventory (3000units)

Tk.78,000

Tk. 26.00

Transferred in during this period (38,000 units)

Tk.11,02,000

Tk. 29.00

------- ------Total 41, 000 Units

1,180,000 Tk. 28.78

------- ------Cost added by the department:Work in process - Beginning inventory:Labor 2,56,000Factory overhead 1,78,000Cost added during period:Labor 4,89,000 Tk. 20.14Factory Overhead (FOH) 2,50,000

-------Tk. 11.57-----

Total cost added 60.49Adjusted units cost for additional units 0.7195

------- ------Total cost to be accounted for 2353000 61.2095

====== ======Cost Accounted for as Follows: Transferred to finished goods storeroom (36,000 × 61.2095)

22,03,292

Work in process - ending inventory:Adjusted cost from preceding department(4,000 × Tk.28.78+ Tk. 0.7195) 117998Labor (4,000 × 1/4 × 20.14) 20140Factory Overhead (4,000 × 1/4 × 11.57) 11570

------149708------

Total cost accounted for 23,53,000======

pg. 51

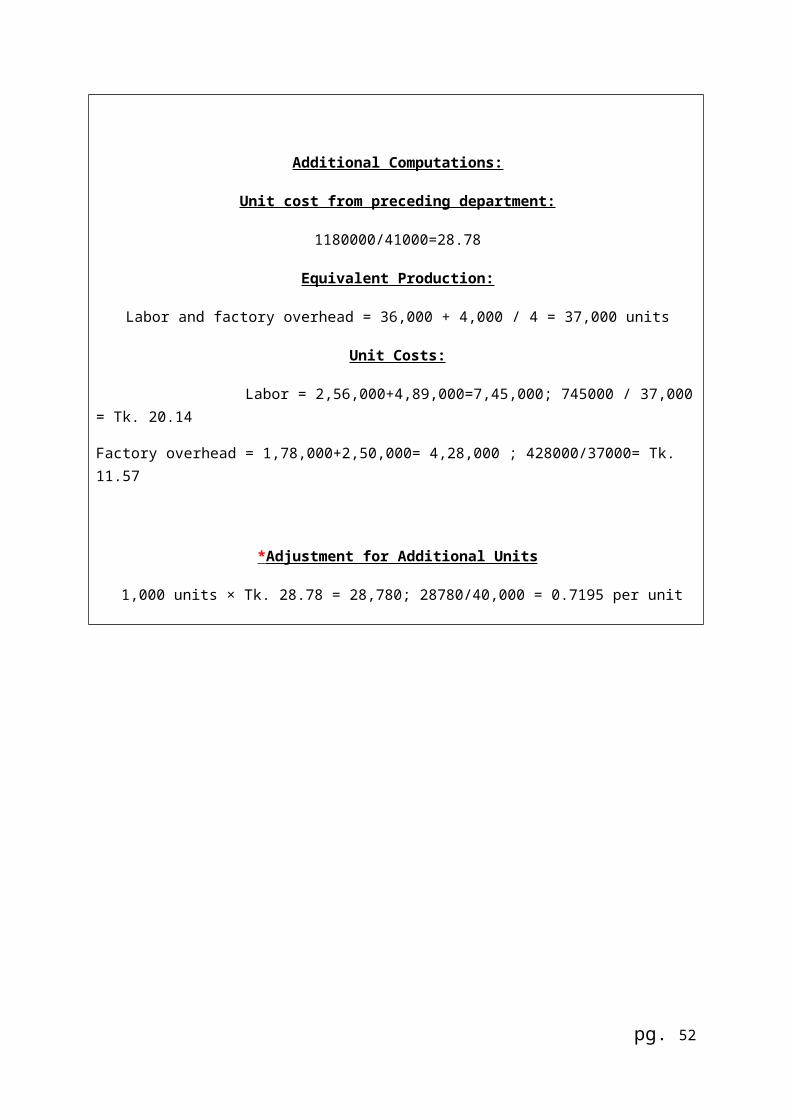

Additional Computations:

Unit cost from preceding department:

1180000/41000=28.78

Equivalent Production:

Labor and factory overhead = 36,000 + 4,000 / 4 = 37,000 units

Unit Costs:

Labor = 2,56,000+4,89,000=7,45,000; 745000 / 37,000= Tk. 20.14

Factory overhead = 1,78,000+2,50,000= 4,28,000 ; 428000/37000= Tk. 11.57

* Adjustment for Additional Units

1,000 units × Tk. 28.78 = 28,780; 28780/40,000 = 0.7195 per unit

pg. 52

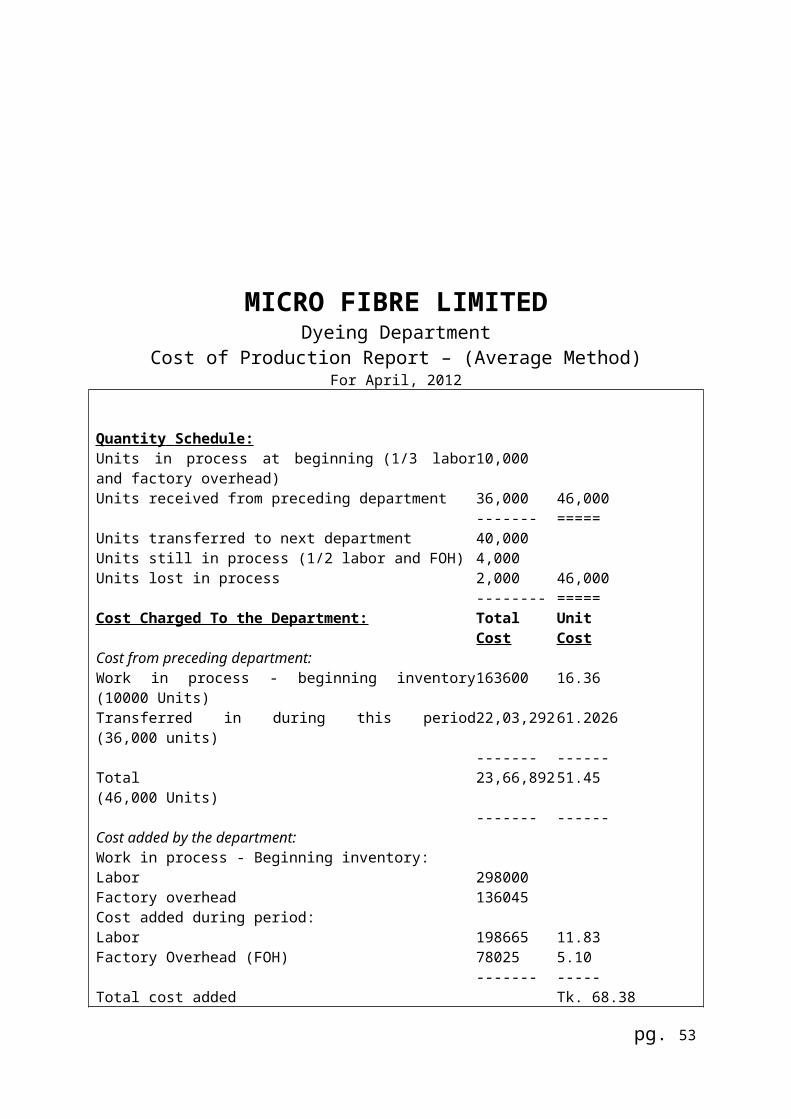

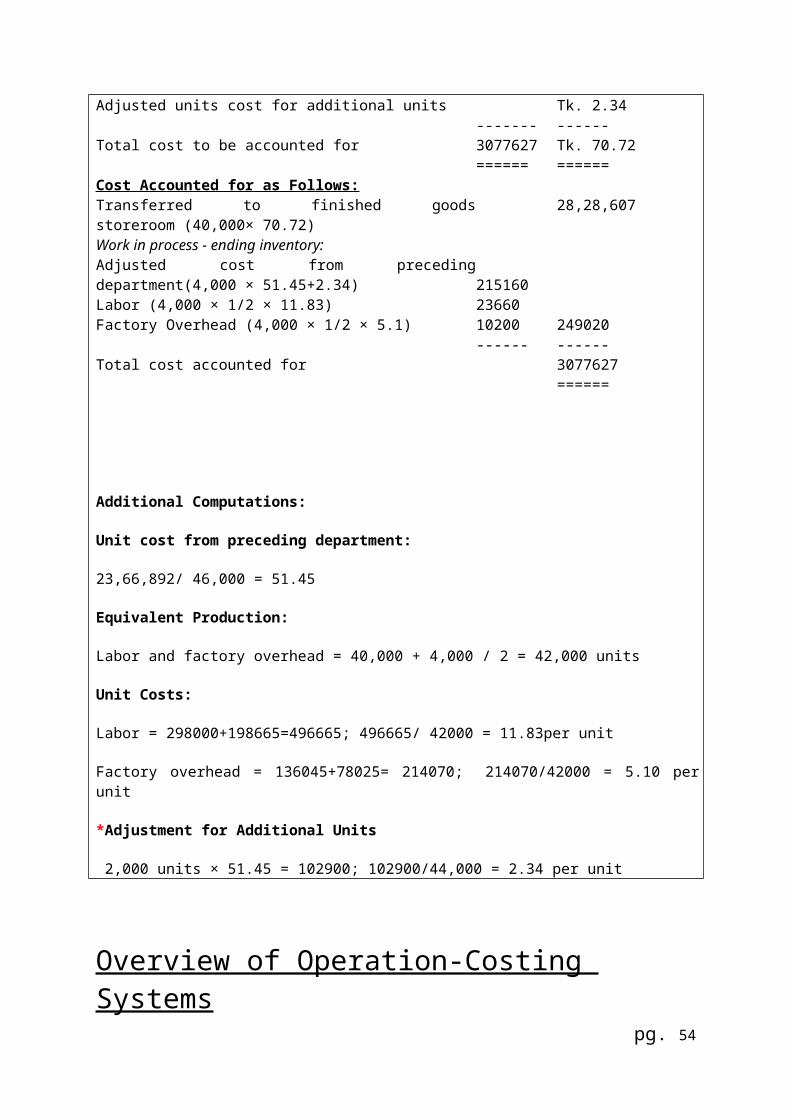

MICRO FIBRE LIMITEDDyeing Department

Cost of Production Report – (Average Method)For April, 2012

Quantity Schedule: Units in process at beginning (1/3 laborand factory overhead)

10,000

Units received from preceding department 36,000 46,000------- =====

Units transferred to next department 40,000 Units still in process (1/2 labor and FOH) 4,000Units lost in process 2,000 46,000

-------- =====Cost Charged To the Department: Total

CostUnit Cost

Cost from preceding department:Work in process - beginning inventory(10000 Units)

163600 16.36

Transferred in during this period(36,000 units)

22,03,29261.2026

------- ------Total(46,000 Units)

23,66,89251.45

------- ------Cost added by the department:Work in process - Beginning inventory:Labor 298000Factory overhead 136045Cost added during period:Labor 198665 11.83Factory Overhead (FOH) 78025

-------5.10-----

Total cost added Tk. 68.38

pg. 53

Adjusted units cost for additional units Tk. 2.34------- ------

Total cost to be accounted for 3077627 Tk. 70.72====== ======

Cost Accounted for as Follows: Transferred to finished goodsstoreroom (40,000× 70.72)

28,28,607

Work in process - ending inventory:Adjusted cost from precedingdepartment(4,000 × 51.45+2.34) 215160Labor (4,000 × 1/2 × 11.83) 23660Factory Overhead (4,000 × 1/2 × 5.1) 10200

------249020------

Total cost accounted for 3077627======

Additional Computations:

Unit cost from preceding department:

23,66,892/ 46,000 = 51.45

Equivalent Production:

Labor and factory overhead = 40,000 + 4,000 / 2 = 42,000 units

Unit Costs:

Labor = 298000+198665=496665; 496665/ 42000 = 11.83per unit

Factory overhead = 136045+78025= 214070; 214070/42000 = 5.10 perunit

*Adjustment for Additional Units

2,000 units × 51.45 = 102900; 102900/44,000 = 2.34 per unit

Overview of Operation-Costing Systems

pg. 54

An operation is a standardized method or technique that isperformed repetitively, often on different materials,resulting in different finished goods. Multiple operations areusually conducted within a department. For instance, a suitmaker may have a cutting operation and a hemming operationwithin a single department. The term operation, however, isoften used loosely. It may be a synonym for a department orprocess. For example, some companies may call their finishingdepartment a finishing process or a finishing operation.An operation-costing system is a hybrid-costing system appliedto batches of similar, but not identical, products. Each batchof products is often a variation of a single design, and itproceeds through a sequence of operations. Within eachoperation, all product units are treated exactly alike, usingidentical amounts of the operation’s resources. A key point inthe operation system is that each batch does not necessarilymove through the same operations as other batches. Batches arealso called production runs. In a company that makes suits,management may select a single basic design for every suit tobe made, but depending on specifications, each batch of suitsvaries somewhat from other batches. Batches may vary withrespect to the material used or the type of stitching.Semiconductors, textiles, and shoes are also manufactured inbatches and may have similar variations from batch to batch.An operation-costing system uses work orders that specify theneeded direct materials and step-by-step operations. Productcosts are compiled for each work order. Direct materials thatare unique to different work orders are specificallyidentified with the appropriate work order, as in job costing.However, each unit is assumed touse an identical amount ofconversion costs for a given operation, as in process costing.A single average conversion cost per unit is calculated foreach operation, by dividing total conversion costs for thatoperation by the number of units that pass through it. Thisaverage cost is then assigned to each unit passing through theoperation. Units that do not pass through an operation are notallocated any costs of that operation. Our examples assumeonly two cost categories—direct materials and conversion costs—but operation costing can have more than two cost categories.Costs in each category are identified with specific workorders using job-costing or process costing methods as

pg. 55

appropriate. Managers find operation costing useful in costmanagement because operation costing focuses on control ofphysical processes, or operations, of a given productionsystem. For example, in clothing manufacturing, managers areconcerned with fabric waste, how many fabric layers that canbe cut at one time, and so on. Operation costing measures, infinancial terms, how well managers have controlled physicalprocesses.

pg. 56

Job Order CostingSystem

Job Order CostingReview:

In job order costing for a manufacturing company, costs areaccumulated by job or specific order .This method pre-supposes thepossibility of physically identifying the jobs produced and ofcharging each job with its own cost.In job order costing the cost of each order produced for a givencustomer or the cost of each lot to be placed in placed in stock isrecorded on a job order cost sheet .Cost sheets are subsidiaryrecords which are controlled by the work in process account.Each cost sheet is designed to collect the cost of materials, labor,and factory.Overhead charged to a specific job. Each cost sheet isassigned a job number which is assigned a job number, which is

pg. 57

placed on each materials requisition and labor time ticket used inconnection with a jobThese forms of materials and labor are totaled daily or weekly byjob number, for summery journal entries, and the details are enteredon a cost sheets is computed on the basis of an estimated or appliedrather than actual cost incurred.

pg. 58

Job Order no: 1320881Micro Fibre Limited

For : XXX Date ordered : 28 MarchSpecification: Date Started : 01 AprilQuantity: Date Wanted : 10 April Date Completed :06 April

Direct MaterialsDate Department Req.No Total Cost2/04/2012 Knitting 51529 5789214/04/2012 Dying 35219 6671686/04/2012 Printing 35214 653219

Direct LaborDate Department Hours Total Cost2/04/20123/04/20124/04/2012

Knitting 400400400

200002000020000

3/04/20124/04/20125/04/2012

Dying 250250250

125001250012500

6/04/2012 Printing 200 10000

Factory Overhead AppliedDate Department Rate of Application Total Cost04/04/2012 Knitting 15 600006/04/2012 Dying 15 375006/04/2012 Printing 15 3000

Direct Materials ……………………………….. 18,99,308Direct Labor ………………………………. 107,500

Factory Overhead Applied ……………………. 12,500Total Factory Cost …………………………….20,19,308

Selling Price ……………………………………….. BDT. 11,54,26,234Factory Cost ……………………………20,19,308Administration Expenses…………….... 1,19,13,014Cost to make and Sell …………………………….. 1,39,32,322Profit ………………………………………………..10,14,93,912

Analyses on Accounting Procedures:

Accounting for Materials of Micro Fibre Limited:

pg. 59

Cost Accounting procedures that affect the materials accountinvolve

1. Purchase of Materials

2. Issuance of materials for the factory use.

Recording of Purchase and Receipts of Materials:

When materials are purchased, Materials account is debited toaccount payable or cash as following,

Materials …………………………………… Dr. 6,671,683.00Account Payable /Cash ……………….Cr. 6,671,683.00

Amounts of each purchase, quantity received and unit cost isalso entered on a materials ledger card, which is maintainedfor each materials item. Materials ledger card act as asubsidiary ledger.

Recording of Issuance of Materials:

Micro- fiber issues necessary materials to the factory on thebasis of material requisitions.

A copy of the requisition is sent to the storekeeper, whoassembles the materials called for on the requisition. Thequantity, unit cost, and total cost of each item is entered onthe requisition and posted to the material ledger cards.Materials are recorded when transferred to factory as in workin process account.

Work in Process………………………… Dr. 6,671,683.00Materials………………………... Cr. 6,671,683.00

pg. 60

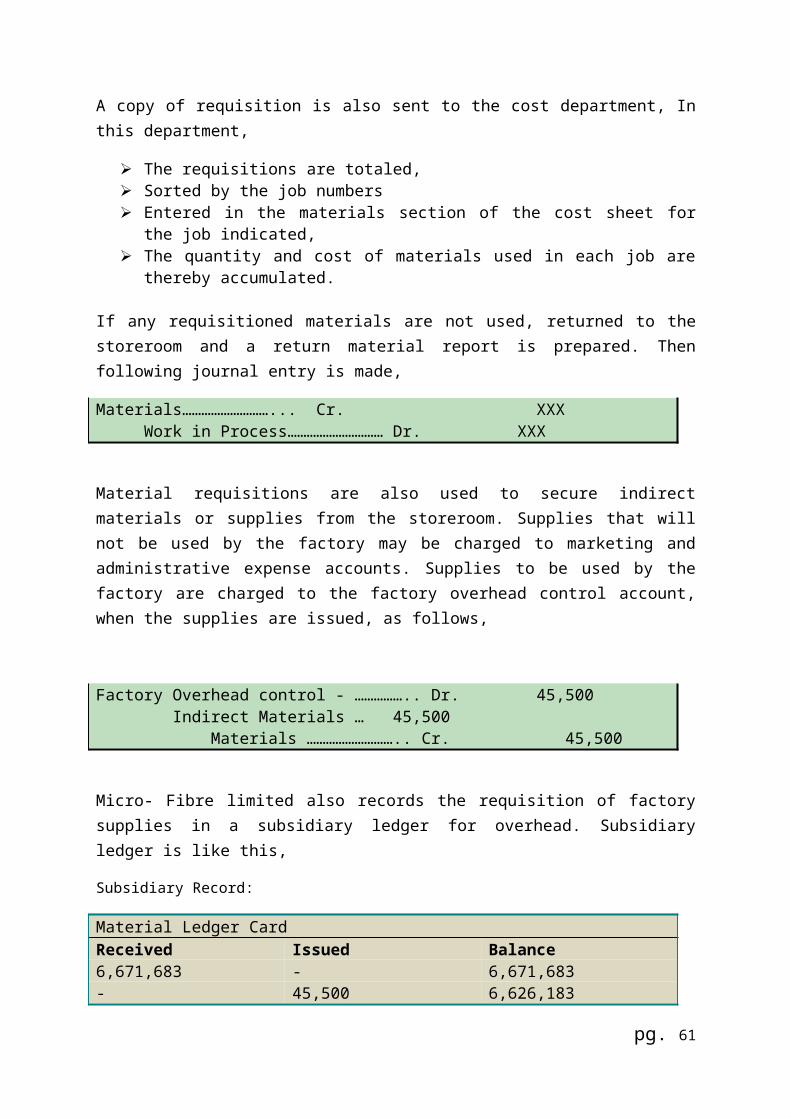

A copy of requisition is also sent to the cost department, Inthis department,

The requisitions are totaled, Sorted by the job numbers Entered in the materials section of the cost sheet for

the job indicated, The quantity and cost of materials used in each job are

thereby accumulated.

If any requisitioned materials are not used, returned to thestoreroom and a return material report is prepared. Thenfollowing journal entry is made,

Materials………………………... Cr. XXXWork in Process………………………… Dr. XXX

Material requisitions are also used to secure indirectmaterials or supplies from the storeroom. Supplies that willnot be used by the factory may be charged to marketing andadministrative expense accounts. Supplies to be used by thefactory are charged to the factory overhead control account,when the supplies are issued, as follows,

Factory Overhead control - …………….. Dr. 45,500 Indirect Materials … 45,500

Materials ……………………….. Cr. 45,500

Micro- Fibre limited also records the requisition of factorysupplies in a subsidiary ledger for overhead. Subsidiaryledger is like this,

Subsidiary Record:

Material Ledger CardReceived Issued Balance6,671,683 - 6,671,683- 45,500 6,626,183

pg. 61

Accounting For Labor of Micro Fibre Limited:

At regular Intervals, the labor time and labor cost for eachorder is entered on the job order cost sheets. For eachpayroll period, the summary of employee’s earnings and theliability for payment is journalized and posted to the generalledger.

The payroll account is a clearing account in which labor costare accumulated, pending their distribution to the proper costaccounts. This distribution is usually recorded on a daily orweekly basis, so that labor cost remain current on the joborder cost sheets and are available to operating management.The payroll account and payroll taxes account may alsoincludes amounts applicable to marketing and administrativepersonnel. Such cost would be charged o marketing andadministrative expense accounts.

Diagram showing payroll and labor accounts .

Stage 1Payroll Computed & Paid

Stage 2Payroll costs Distributed

Journal Entries:03thPayroll ……………….. Dr. Employee Income Taxpayable.... Cr. Accrued Payroll …………………Cr.

Accrued Payroll…..…… Dr. Cash ………………………… Cr.

General Ledger:Factory Overhead Control

45,500

Journal Entry:31th

Work in Process …… Dr.Factory Overhead Control(Indirect Labor)…….. Dr. Payroll …………………….. Cr.General Ledger:

Work In ProcessXXX

Factory Overhead Control45,500

Factory Overhead AnalysisSheet

Date Payro Indir Indire

pg. 62

llTaxes

ectLabor

ctMaterials

Accounting For Factory Overhead of Micro Fibre Limited:

The Accountant of Micro Fiber Limited uses applied factoryoverhead, which is determined by multiplying the direct laborhours, during a period by the factory overhead rate.

Following entry is based on applied factory overhead which isentered on job order cost sheet,

Work in Process ……………………….. Dr. 850,000 Applied Factory Overhead (10,000 direct Labor X Tk. 85)…….. Cr. 850,000

At the end of the accounting period, the applied factory overheadaccount is closed to the factory overhead control account by thefollowing entry,

Applied Factory Overhead ……… Dr. 850,000 Factory Overhead Control …………………. Cr, 850,000

Here, An Applied factory overhead account is used because itkeeps applied overhead and actual overhead costs in separateaccounts.

Some actual overhead costs such as indirect materials, indirectlabor and payroll taxes are charged to the factory overhead controlas they are incurred. Other overhead costs such as depreciation andexpired insurance are charged tofactory overhead account whenadjusting entries are recorded, as follows,

Factory Overhead Control ………….. …….. Dr. 912,636 Depreciation…….. 912,636Accumulated depreciation – Machineries …… Cr. 912,636

pg. 63

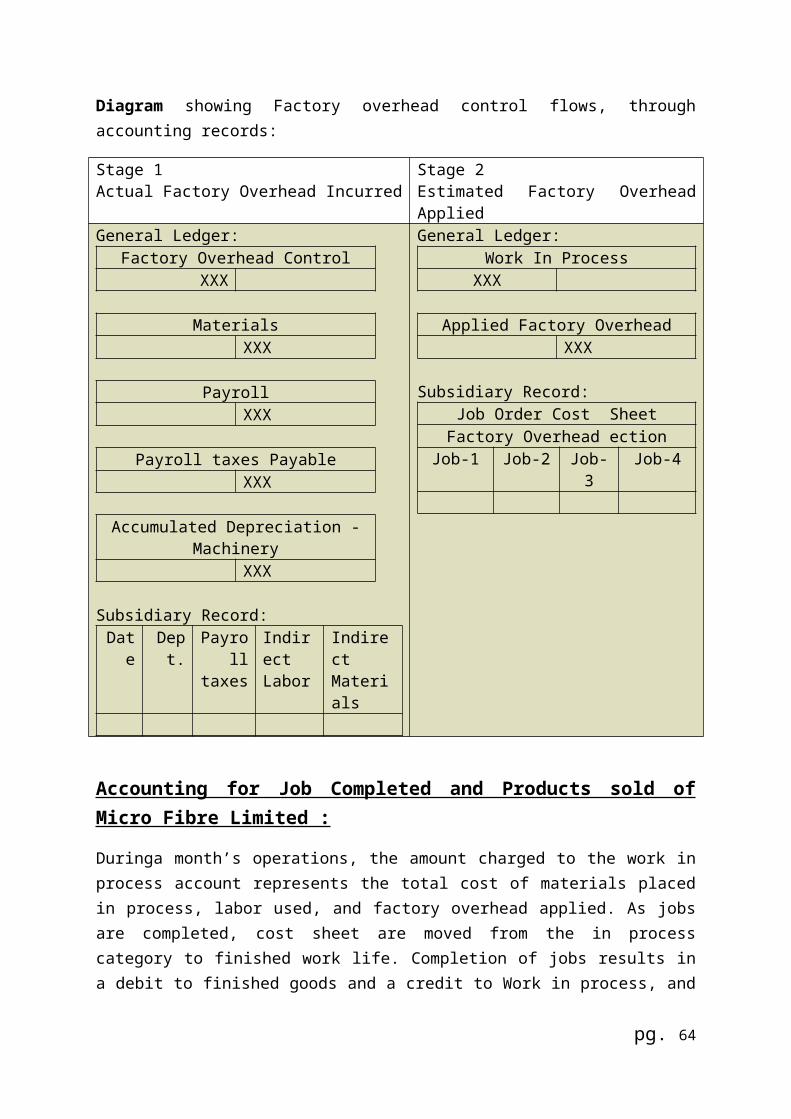

Diagram showing Factory overhead control flows, throughaccounting records:

Stage 1Actual Factory Overhead Incurred

Stage 2Estimated Factory OverheadApplied

General Ledger:Factory Overhead Control

XXX

MaterialsXXX

PayrollXXX

Payroll taxes PayableXXX

Accumulated Depreciation -Machinery

XXX

Subsidiary Record:Dat

eDept.

Payroll

taxes

IndirectLabor

IndirectMaterials

General Ledger:Work In Process

XXX

Applied Factory Overhead XXX

Subsidiary Record:Job Order Cost Sheet

Factory Overhead ectionJob-1 Job-2 Job-

3Job-4

Accounting for Job Completed and Products sold ofMicro Fibre Limited :

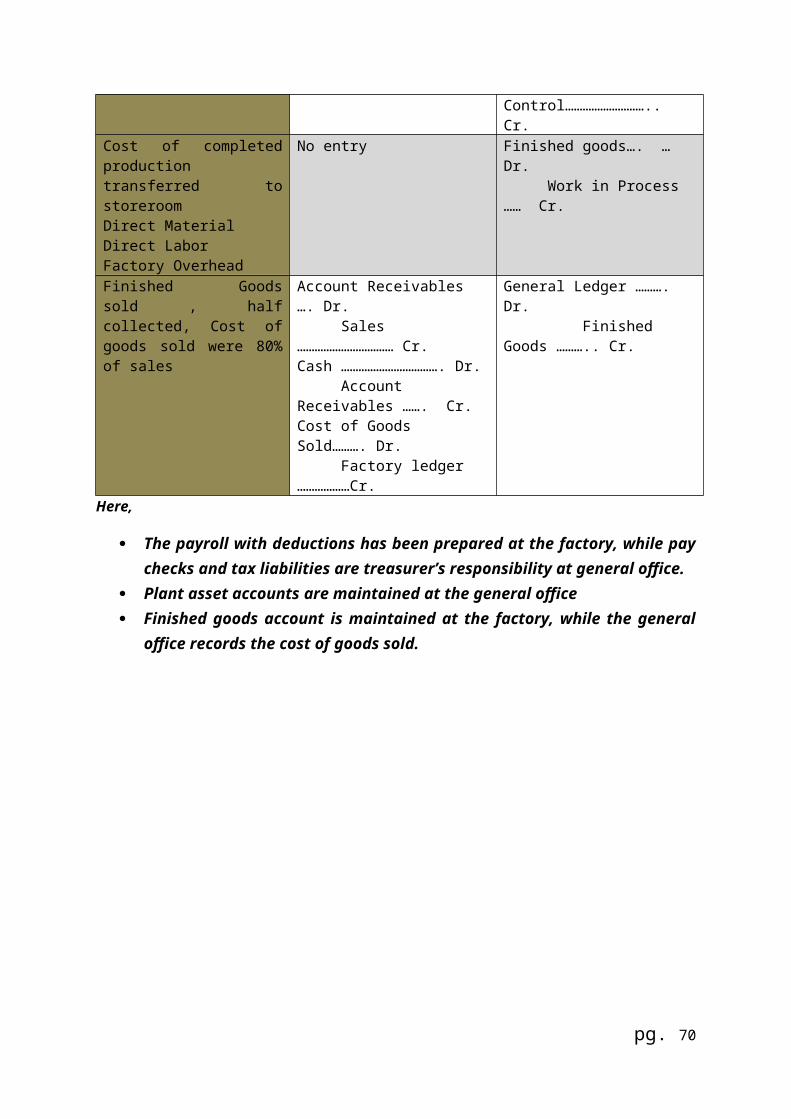

Duringa month’s operations, the amount charged to the work inprocess account represents the total cost of materials placedin process, labor used, and factory overhead applied. As jobsare completed, cost sheet are moved from the in processcategory to finished work life. Completion of jobs results ina debit to finished goods and a credit to Work in process, and

pg. 64

quantity and cost are recorded on finished good ledger cardswhich are subsidiary records for the finished good account.

The journal entry to record all the work completed is,

Finished Goods ………………………………. Dr.Work in Process ……………………………. Cr.

When finished goods are delivered or shipped to the customers, salesinvoices are prepared, and the sales and the cost of goods sold arerecorded as follows :

Accounts Receivable ………………………. Dr. 11,54,26,234Sales ………………………………………… Cr. 11,54,26,234

Cost of goods sold …………………………. Dr. 1,36,81,712Finished Goods ……………………………… Cr. 1,36,81,712

If a job is delivered directly to a customer, the finishedgoods account may be bypassed. In such a case, cost of goodssold is debited when the work in process account is credited.

Costing For By-products of Micro

Fibre Limited pg. 65

Costing By- Products by Micro Fibre Limited: Micro-Fibre Limited recognizes revenue from sales of by-products aspart of their gross revenue and listed on their income statement as other Income.

The main by-products of micro Fibre limited is Scrap Materials.

Income Statement of Micro- Fibre Limited after adjusting by –products is,

Sales (main products.) BDT.11,54,26,234

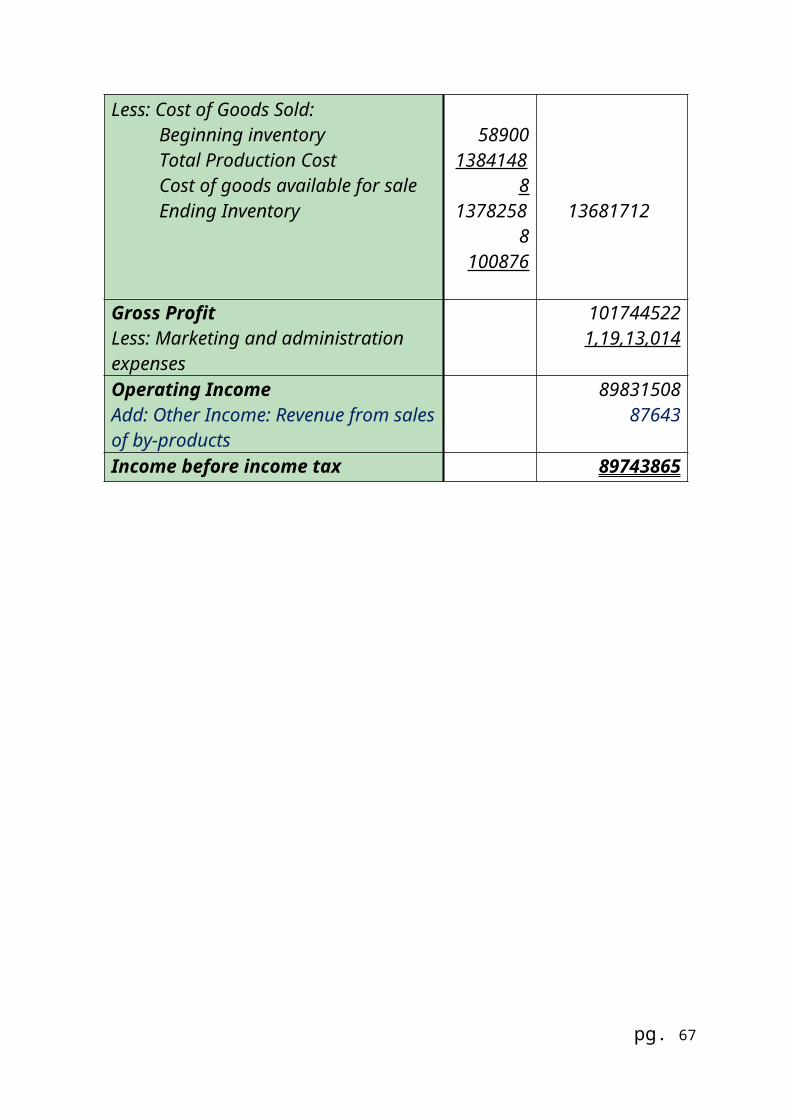

pg. 66

Less: Cost of Goods Sold:Beginning inventoryTotal Production Cost Cost of goods available for saleEnding Inventory

589001384148

81378258

8100876

13681712

Gross ProfitLess: Marketing and administration expenses

1017445221,19,13,014

Operating IncomeAdd: Other Income: Revenue from salesof by-products

8983150887643

Income before income tax 89743865

pg. 67

Factory and Generaloffice Ledger of Micro –

Fibre limited

pg. 68

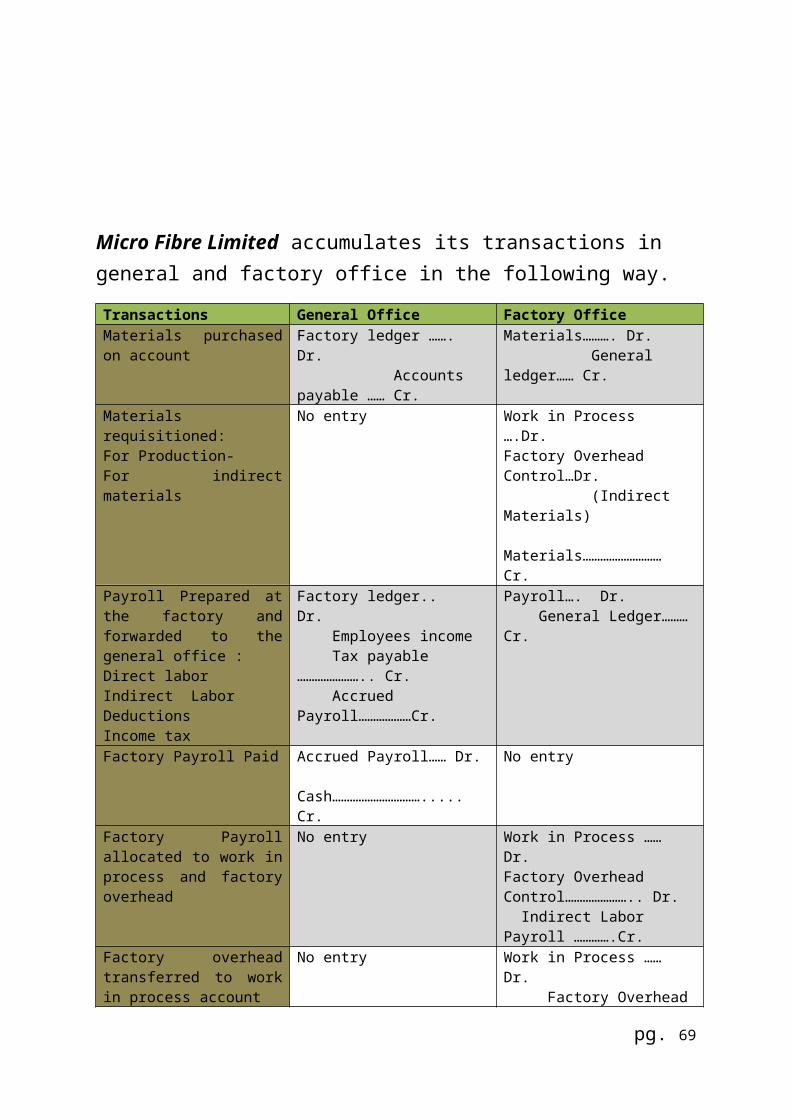

Micro Fibre Limited accumulates its transactions in general and factory office in the following way. Transactions General Office Factory OfficeMaterials purchasedon account

Factory ledger ……. Dr. Accounts payable …… Cr.

Materials………. Dr. General ledger…… Cr.

Materialsrequisitioned:For Production-For indirectmaterials

No entry Work in Process ….Dr.Factory Overhead Control…Dr. (Indirect Materials) Materials……………………… Cr.

Payroll Prepared atthe factory andforwarded to thegeneral office :Direct laborIndirect LaborDeductionsIncome tax

Factory ledger.. Dr. Employees income Tax payable ………………….. Cr. Accrued Payroll………………Cr.

Payroll…. Dr. General Ledger………Cr.

Factory Payroll Paid Accrued Payroll…… Dr. Cash…………………………..... Cr.

No entry