Ethical Commitment, Financial Performance, and Valuation: An Empirical Investigation of Korean...

28

Ethical Commitment, Financial Performance, and Valuation: An Empirical Investigation of Korean Companies Abstract. A variety of stakeholders including investors, corporate managers, cus- tomers, suppliers, employees, researchers, and government policy makers have long been interested in the relationship between the financial performance of a corpora- tion and its commitment to business ethics. As a subject of research, the relations between business ethics and corporate valuation has yet to be thoroughly quantified and investigated. This paper is an effort to amend this inadequacy by demonstrating a statistically significant association between ethical commitment and corporate valuation measures. Consistent with anecdotal evidence, we have found a signifi- cant association between the ethical commitment of Korean companies and their valuation on the Korean stock market. However, the result reveals that the asso- ciation between ethical commitment and financial performance is not significantly supported. Keywords: Business ethics, ethical Commitment, ethical commitment index, finan- cial performance, Korea, valuation 1. Introduction As national boundaries become more opaque and companies expand their global reach, business ethics is ever more frequently the topic of conversation both in the boardroom and around the water cooler. A great number of global companies have established local subsidiaries overseas and their managers have encountered a myriad of situations that raise ethical dilemmas (Dubinsky et al., 1991; Nakano, 1999; Jack- son et al., 2000; Sims and Gegez, 2004; Orlitzky, 2005). Until the East Asian economic turmoil that erupted in 1997, Koreans had not consid- ered the implications of a connection between economic performance and business ethics; however, this situation changed during the crisis as foreign exchange reserves ran dry and foreign direct investment plum- meted. Among the many causes cited, lack of transparency in business practices and poor governance in the business sectors were considered to be key obstacles on the journey back to economic growth. Since that time, business ethics and corporate transparency have received a great deal of attention in Korea. Recent accounting scandals and unethical corporate practices at previously respected corporations in- cluding Enron, Worldcom, and Arthur Anderson have only served to heighten people’s awareness of these issues, bringing them further into the public consciousness. Yet, despite these morality tales, in Korea c 2007 Kluwer Academic Publishers. Printed in the Netherlands. BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.1

Transcript of Ethical Commitment, Financial Performance, and Valuation: An Empirical Investigation of Korean...

Ethical Commitment, Financial Performance, and Valuation:

An Empirical Investigation of Korean Companies

Abstract. A variety of stakeholders including investors, corporate managers, cus-tomers, suppliers, employees, researchers, and government policy makers have longbeen interested in the relationship between the financial performance of a corpora-tion and its commitment to business ethics. As a subject of research, the relationsbetween business ethics and corporate valuation has yet to be thoroughly quantifiedand investigated. This paper is an effort to amend this inadequacy by demonstratinga statistically significant association between ethical commitment and corporatevaluation measures. Consistent with anecdotal evidence, we have found a signifi-cant association between the ethical commitment of Korean companies and theirvaluation on the Korean stock market. However, the result reveals that the asso-ciation between ethical commitment and financial performance is not significantlysupported.

Keywords: Business ethics, ethical Commitment, ethical commitment index, finan-cial performance, Korea, valuation

1. Introduction

As national boundaries become more opaque and companies expandtheir global reach, business ethics is ever more frequently the topic ofconversation both in the boardroom and around the water cooler. Agreat number of global companies have established local subsidiariesoverseas and their managers have encountered a myriad of situationsthat raise ethical dilemmas (Dubinsky et al., 1991; Nakano, 1999; Jack-son et al., 2000; Sims and Gegez, 2004; Orlitzky, 2005). Until the EastAsian economic turmoil that erupted in 1997, Koreans had not consid-ered the implications of a connection between economic performanceand business ethics; however, this situation changed during the crisis asforeign exchange reserves ran dry and foreign direct investment plum-meted. Among the many causes cited, lack of transparency in businesspractices and poor governance in the business sectors were consideredto be key obstacles on the journey back to economic growth. Sincethat time, business ethics and corporate transparency have receiveda great deal of attention in Korea. Recent accounting scandals andunethical corporate practices at previously respected corporations in-cluding Enron, Worldcom, and Arthur Anderson have only served toheighten people’s awareness of these issues, bringing them further intothe public consciousness. Yet, despite these morality tales, in Korea

c© 2007 Kluwer Academic Publishers. Printed in the Netherlands.

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.1

2

at least, unethical business practices persist on an unacceptably largescale (Choi and Jung, 2005).

Why then are companies so reluctant to amend their unethical prac-tices? One possible explanation stems from the long-held axiom thatthe primary goal of companies is to maximize profits, and, by exten-sion, shareholder wealth (Friedman, 1962). Clearly, realizing financialtargets is critical to increasing stock value. What is less obvious to manymanagers is the connection between ethical behavior and a company’sbottom line (besides the benefits derived from an enhanced reputationin the eyes of the public) (Simpson and Kohers, 2002). In situationswhere short-term profit comes into conflict with business ethics theformer usually trumps the latter as many managers are skeptical aboutthe financial benefit of business ethics. In particular, meeting short-term financial targets has been emphasized in current corporate culture.Prior studies attest that corporate managers have strong incentives tomeet or beat the markets’ expectation of financial figures (e.g. quarterlyor annual earnings estimates) because missing those figures producesserious negative impact on stock price (Bartov et al., 2002; Lopez andRees, 2002; Matsumoto, 2002; Skinner and Sloan, 2002; Choi, 2004).Managers under pressure to meet financial expectations in the face ofstiffened competition due to globalization sometimes resort to unethicalbehavior to achieve a perceived competitive advantage over their rivals.

If business leaders were to see a substantially positive associationbetween corporate business ethics and corporate financial performance,the chances for an overall improvement in corporate ethical commit-ment would be greatly enhanced. Prior studies suggest that such a seachange would lift all boats; the long-term profit potential for all compa-nies concerned would be improved (Lee and Yoshihara, 1997; Verschoor,1998). Unfortunately, much controversy still surrounds these studies,and the connection between commitment to business ethics (CBE)and corporate financial performance (CFP) remains ambiguous. If asubstantially positive relationship could be established, it would helpimprove the overall level of corporate ethical commitment.

2. Prior Studies

To date, extant studies in the literature have focused on the rela-tionship between corporate social performance (CSP) and corporatefinancial performance (CFP). Since the 1980s, a series of papers havedocumented the link between CSP and CFP (Cochran and Wood,1984; Aupperle et al., 1985; Spencer and Taylor, 1987; Preston andO’Bannon, 1997; Griffin and Mahon, 1997; McGuire et al., 1988; Stan-

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.2

3

wick and Stanwick, 1998; Moore, 2001; Ruf et al., 2001; Simpson andKohers, 2002; Johnson, 2003; Orlitzky et al., 2003; Orlitzky, 2005).Numbers of researchers have reported a positive relationship betweenCSP and CFP (Cochran and Wood, 1984; Spencer and Taylor, 1987;Orlitzky, 2005). In the meantime, some studies have found negativerelationships (Shane and Spicer, 1983; Hoffer et al., 1988). Many otherstudies have documented mixed and inconclusive relationships (McGuireet al., 1988; Coffey and Fryxel, 1991; Waddock and Graves, 1997).

Despite the plethora of studies documenting the relationship be-tween CSP and CFP, and the studies that have shown a positive associ-ation between CSP and CBE, the link between a corporation’s financialperformance and its commitment to business ethics has rarely beeninvestigated. One important issue addressed in this study regards theexact nature of the relationship between CSP and CBE. That a closelink exists between CSP and CBE has been well documented in priorstudies (Epstein, 1987; Epstein, 1989; Morris, 1997). Prior studies havealso established that, while corporate social performance overlaps busi-ness ethics, each has distinctive conceptual properties. Epstein (1987)proposes that corporate social performance and business ethics can beenvisioned as overlapping circles sharing a common conceptual space.He argues that the central concept of business ethics is the moral reflec-tion concerning corporate behavior while corporate social performanceis a more specific consequence of corporate action entailing economic,ecological, social, and cultural consequences. Morris (1997) documentsthat business ethics influences corporate social performance. That is,each of them has distinctive properties.

Despite the contributions of previous literature, the association be-tween the financial performance of a corporation and its commitment tobusiness ethics has not been well documented. One possible explanationis that unlike CSP measures, there is no easy way to measure the levelof the ethical commitment of companies due to the difficulty for outsidestakeholders in observing the internal controls used by an organization,or of gauging the ethical commitment of management. Hence, thereis no widely used source of measuring the level of corporate ethicalcommitment. Thus, it will be worthwhile if we extend prior findingsby providing a new instrument with which to measure both corporatecommitment to business ethics, as well as any linkages that may existbetween ethics and various financial factors.

There are several issues pertaining to the study of business ethics.One possible explanation for the conflicting results from investigationsof the relationship between CSP and CFP is the multiple dimensionsused to measure the level of corporations’ social performance (Griffinand Mahon, 1997). For example, a number of studies have used a For-

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.3

4

tune survey of corporate reputation as a proxy of CSP (Carroll, 1991).Many studies have used the Kinder, Lydenberg, Domini (KLD) indexas a measure of CSP (Waddock and Graves, 1997). Still other studieshave looked at the measurement of corporate philanthropy (Seifertet al., 2003; Brammer and Millington, 2005). One study went so faras to construct its own index for social performance (Ruf et al., 1998).Use of different measures for predicting the level of CSP may provideconflicting results. Similarly, past research employed different means ofmeasuring CFP. This further contributed to the inconsistencies foundbetween studies, as, from one study to the next, different indices (e.g.net income, earnings per share, return on equity, return on assets, riskand/or price) were employed to measure financial performance. In manycases, the measures for financial performance were not clearly specified.

A variety of literature has discussed the ‘scale effect’ in financialstudies (Christie, 1987; Barth and Kallapur, 1996; Brown et al., 1999;Barth and Clinch, 2001; Easton and Sommers, 2003). In market-basedresearch, financial variables might cause spurious result if they do nottake into account the scale of the companies involved. For example,a variable like net income is significantly affected by the size of thecompany.1 Earnings per share may change on the basis of the numberof shares issued while the fundamental profitability of the firm remainsunchanged. To be valid, market-based research must employ a proxyto measure the scale of companies.

It is a common assumption that the financial performance of a corpo-ration is positively linked to its commitment to business ethics (Vogel,1991; Verschoor, 1998; Verschoor, 1999; van der Merwe et al., 2003; Kul-shreshtha, 2005). Research suggests that, to some degree, this assump-tion is correct. For example, Vogel (1991) comments that if companies’managers do not behave ethically, they will be punished in the formof customer and employee dissatisfaction as well as media criticism.In these cases, customers stop buying and good employees leave theircompanies. Despite these encouraging results, to date, the empiricalassociation between ethical commitment and financial performance hasyet to be fully investigated.

Verschoor (1998) is one of the few empirical studies that look atthe relationship between ethical commitment and companies’ financialperformance. He began by selecting the largest 500 public companies inUS. He then matched them with the portfolio ranks made by BusinessWeek, which ranks each company in quintile based on eight financialmeasures.

The disclosure of of a company’s ethical commitment in annualreports is used as a proxy for the measure of ethical commitment ofa corporation. Verschoor (1998) reports that companies stating their

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.4

5

commitment to ethical behavior in annual reports show favorable cor-porate financial performance compared to those that do not.

The aim of this research is to determine whether business ethics canbe empirically related to financial factors and, in particular, to the valueof companies. We are interested in issues pertaining to measures ofcompanies’ commitment to business ethics. We We begin by contrastingcorporate financial performance and valuation factors.

3. Research Design

3.1. Survey

Surveys are frequently used to gauge managers’ opinions on corporatebusiness ethics. This has proved to be a reliable method to measurethe perceptions of corporate managers regarding the system of internalorganization employed within their respective companies. This study ispartly in line with prior survey studies in the field of business ethics.Constructing a composite index for ethical commitment is a crucialpart of any study of the connection between ethical commitment, fi-nancial performance, and corporate valuation. Unlike CSP measures(e.g. the Fortune survey, the KLD index, or the measure of corpo-rate philanthropy), it is not easy to find proxies for corporate ethicalcommitment. For this study, survey questionnaires were prepared forthe purpose of constructing an index of ethical commitment (ECI).ECI was ascertained as an effective tool to measure the level of ethicalcommitment due to the difficulty observing the internal managementcontrol of corporations.

Out of the need to study typical Korean companies, and the needto derive stock prices as well as reliable and audited financial data, thecompanies comprising this survey were all metropolitan Seoul-basedcompanies listed on at least one of Korea’s two stock exchanges, theKorea Stock Exchange or the KOSDAQ. Within these parameters, com-panies were selected randomly to create a list of potential companiesthat were approached by the researchers. Employees of companies thatagreed to participate in the study became part of the survey providedthey returned their completed surveys. Researchers visited each subjectcompany to drop off their questionnaires. After a time they returnedto collect the self-administered questionnaires. Respondents returnedthe questionnaire anonymously. The reasoning behind this collectionmethod was that it would ensure a sufficient sample size, and avoid theproblem of the presence of the researchers influencing the responsesprovided by employees. Complex information about companies could

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.5

6

also be gathered. The survey was administered directly to 391 corporatemanagers. Of the questionnaires returned, 248 were used for the studyafter controlling for missing values.

3.2. Ethical Commitment Index

There are no standardized instruments to measure the level of thecommitment to business ethics. Verschoor (1998) uses the inclusion of acode of ethical conduct in the annual shareholder report as a surrogatemeasure for ethical commitment. In this study, an ECI was developedwhereby each company was rated according to multiple attributes con-sidered relevant to the ECI based on earlier literature on the subject.Table II provides details on the factors used for measurement in theECI employed in this study. A ‘no’ response is 0 while 1 indicates ’yes’.The measure of ECI is computed as the sum of ethical commitmentdimensions (ei) as follows:2

ECIj =k∑

i=1

ei (1)

where{ECIj : Ethical commitment index of company j (j = 1, . . . , n),

ei : Ethical commitment dimension i (i = 1, . . . , k).

Corporations today employ an array of instruments to instill ethicalcommitment among their employees. Prior studies have documentedthe underlying theoretical foundation for each methodology. Relevantinstruments are identified and data is collected to construct an ECI.Adam and Rachman-Moore (2004) report that a majority of managersbelieve the implicit method has the greatest influence on instillingethical behavior. Ethical commitment dimensions include top manage-ment support (Trevino, 1986; Schwartz et al., 2005), culture (Genfan,1987; Sims, 1992; Sims and Keon, 1999; Sauser, 2005), ethical leader-ship (Brenner, 1992; Carlson and Perrewe, 1995), open communicationchannels (Genfan, 1987; Weeks and Nantel, 1992), and ethics training(Callan, 1992; Dean, 1992). Surrogates for explicit methods of ethicalcommitment include codes of ethics (Murphy, 1988; Callan, 1992; Ver-schoor, 1998), ethics hotlines (Singer, 1995), ethics officers (Austin,1994), and ethics committees (Weiss, 1994).

For the purpose of constructing the questionnaire used in the surveyfor this study, those measures used globally among earlier relevantstudies were adopted. Eleven dimensions were identified as surrogate

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.6

7

measures for ethical commitment. ECI values from 0 to 11 were derived,representing the level of each company’s ethical commitment. Table IIshows descriptive statistics for ethics dimensions used to measure ECI.

3.3. Corporate Financial Performance (CFP) andCorporate Valuation (CV)

Prior studies did not clearly differentiate corporate financial perfor-mance and corporate valuation in the stock market. This is the firststudy to explicitly state the differences in these financial measure intwo contexts. Although the two concepts are closely related, they areanalytically and conceptually discrete. For decades, accounting andfinance studies have documented the association between the measuresfor firm performance and market variables. In this study, we treat cor-porate market valuation differently from the financial performance ofcompanies. Based on this presumption, the financial performance andcorporate valuation are defined as follows:

Corporate financial performance (CFP) concerns the past and con-temporaneous performance of business. That is, financial performancemeasures are mostly taken from a company’s financial statements.These figures are the historical summary of a company’s business.

Corporate valuation (CV) relates to achieving performance in thefinancial market. Measures are primarily related to stock price in thecapital market. In other words, they are related to the perceptions ofexternal stakeholders (e.g. security analysts, individual investors, andinstitutional investors). Financial theories show that this market-basedmeasure is determined not only on the basis of a company’s current fi-nancial performance, but also on its expected future performance. Thisseparation is appropriate because accounting and financial theories aswell as empirical studies have thoroughly documented the associationbetween a company’s market performance (i.e. its stock price) and itsfinancial performance (i.e. measures made of its financial statements).Market value not only represents the past and current financial perfor-mance of a company but it also reflects other information including themarket’s expectation of the company’s future profitability.

For the purposes of this study, financial and corporate valuationvariables were culled from prior accounting and financial literature.Corporate financial performance is measured from accounting numbersincluding return on equity (ROE) and return on assets (ROA). In ad-dition, the stock market performance was measured using various pricevariables and accounting ratios including price to earnings ratio (P/E),price to book value of equity (P/B), and Tobin’s Q ratio (Tobin’s Q).Security price, the numerator of the P/E and P/B ratios, is based on

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.7

8

the expected future earnings that market participants pay for (Ohlson,1995). If market participants expect a higher future performance rela-tive to book value, the P/B will show a higher value by incorporatingthe market’s expectation in the numerator. Tobin’s Q also capturesthe relationship between a company’s market and book value of equity.In all cases, the higher the future profitability, the higher the valua-tion ratios. These variables are commonly used to gauge firms’ marketperformance.

Prior studies have documented the potentially compounding effectsof firm risk, growth, and/or size. Hence, several measures are testedin the analysis as controlling variables including debt to asset (D/A),debt to market (D/M), capital asset pricing beta (beta), sales growth(∆ Sales) and total assets (TA). 3 Also well documented is that firmrisk is negatively correlated with firm value. Measures used to assessfirm risk were debt to asset (D/A), debt to market (D/M), and marketbeta (beta). D/A and D/M measure the risk associated with financialleverage of the firm. As the amount of debt in a firm’s capital structureincreases, so too does the risk the firm takes on. This provides an in-centive for corporate managers to act in a manner that meets creditors’expectations of what is socially responsible and ethical (Roberts, 1992).The capital asset pricing model beta is used to capture firm specific riskrelated to market volatility. Given that beta captures firm specific risk,a negative correlation would be expected between beta and ECI since ahigh level of ethical commitment may be indicative of a better managedfirm.

Total assets (TA) captures the size effect of a firm. Prior studiesdocument that larger companies engage in more corporate social per-formance since they receive a high level of attention from stakeholdersincluding investors, customers, employees, and government authori-ties (Dierkes and Coppock, 1978; Trotman and Bradley, 1981; Fombrunand Shanley, 1990). Moreover, slack economic resource theories arguethat larger companies can afford the outlays required to meet theirethical commitments (Waddock and Graves, 1997).

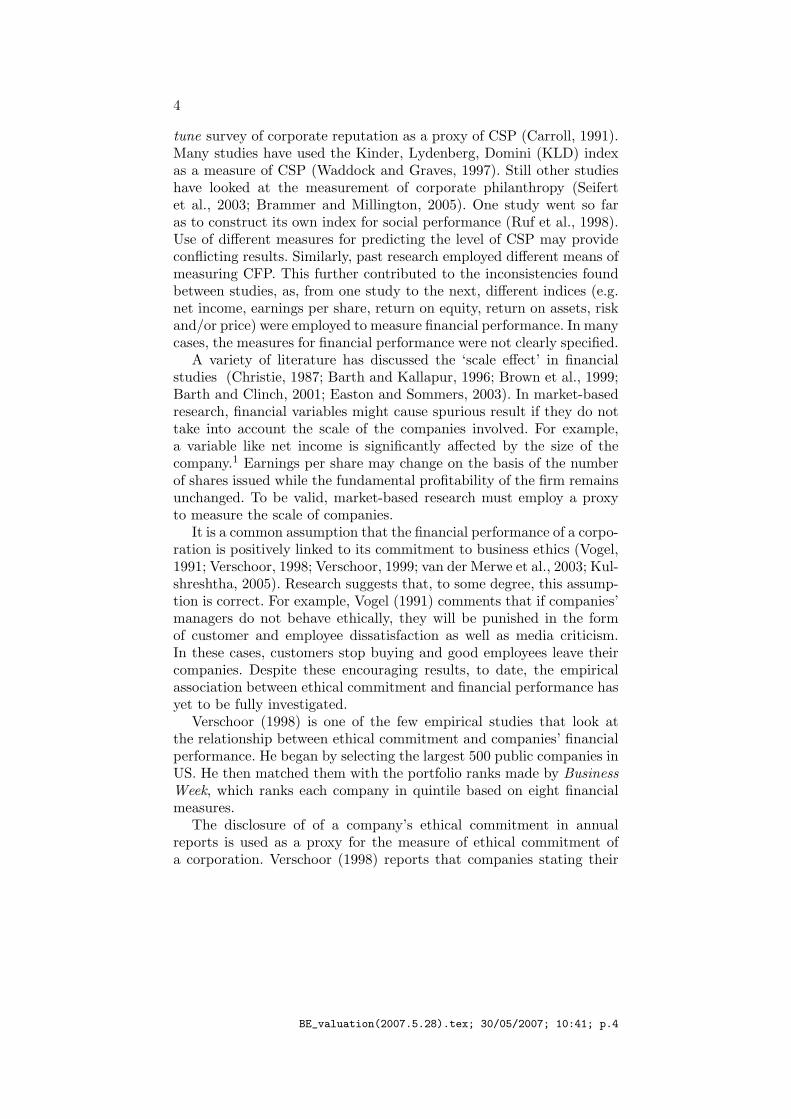

3.4. Conceptual Model

The main purpose of this research is to explore the relationships amongCBE, CFP, and CV. As a first step, a conceptual model was designedbased on prior theories. Figure 1 postulates that there is substantialassociation between ethical commitment, financial performance, andcorporate valuation. There are two lines of thought pertaining to thedirection of causality between ECI and financial attributes. On onehand, slack resource theorists argue that financially strong firms have

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.8

9

slack economic resources to invest in business ethics. On the other hand,good management theorists argue that there is high correlation betweengood management practices and ECI. Therefore, better ECI results inbetter financial attributes.

(Past, Present, Future)

Financial Performance

Commitment to Business Ethics

Corporate Valuation

• Economies of Scale• Available Funding

Slack Resource

• Employees• Cost• Risk• Reputation• Investors

Good Management

Figure 1. Association between CBE, CFP, and CV

The downward paths represent possible associations proposed by the‘good management’ camp, namely: (1) firms that are more ethicallycommitted show better financial outcomes, (2) financial outcomes arepositively linked to performance in the capital market, and (3) marketparticipants expect the positive effects of ethical commitments on thefuture financial performance of companies. The upward paths implythe relationship supporting slack resource hypothesis, namely: (1) firmswith high market capitalization show greater ethical commitment, and(2) firms that show good financial performance have extra resources forenhancing ethical commitment.

3.4.1. The CBE and CFP RelationshipIf the commitment to business ethics incurs substantial cost to the cor-poration, the relationship between the commitment to business ethicsand financial performance will be negative (Aupperle et al., 1985).Alternatively, if noise significantly affects the relationship between thecommitment to business ethics and financial performance (due to many

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.9

10

intervening variables in the relation) the results will show an insignif-icant association. Anecdotal evidence suggests a positive associationbetween the commitment to business ethics and corporate financialperformance. 4

One line of thought suggests that ethical companies bear lowerexplicit and implicit costs including lower costs related to employee re-lations, quality control, adherence to environmental regulations, and lit-igation costs (Hammond and Slocum Jr., 1996; Preston and O’Bannon,1997; Russo and Fouts, 1997; Waddock and Graves, 1997; Francis andArmstrong, 2003). Ethical companies also enjoy positive corporate rep-utations. Various studies have reported that corporate reputation issignificantly and positively related to corporate financial performance(Fombrun and Shanley, 1990; Yoon et al., 1993; Hammond and Slocum Jr.,1996; Little and Little, 2000; Roberts and Dowling, 2002; Neville et al.,2005). On the other hand, highly profitable companies can afford todedicate additional resources to ethical commitment. Following thesearguments, we expect a positive association between the commitmentto business ethics and corporate financial performance.

3.4.2. The CBE and CV RelationshipPrevious evidence suggests that ethically committed firms show higherlong-term profitability than short-term performance. Financial theorystipulates that stock price (i.e. corporate value) is determined as thepresent value of future cash flows (Penman, 2003).

Value0 ≡∞∑

t=1

Cash flowst

(1 + r)t. (2)

Future cash flows derive from the long-term profitability of the com-pany. In this way, CV is closely linked to CFP. In addition, the cost ofcapital of an individual company is used for the computation of presentvalue. Cost of capital reflects the idiosyncratic risk of the company.The relationship between CBE and CV will be significantly positive(1) if the security market expects positive cash flows from ethicallycommitted companies due to the improved future profitability and/or(2) if ethical companies enjoy lower cost of capital due to lower risks.5

Both of these arguments are inherent in the relationship between theethical commitment index and valuation factors. The argument of theslack resource hypothesis that companies with high market capitaliza-tion commit to business ethics is also reasonable. We expect a positiveassociation between the commitment to business ethics and corporatevaluation.

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.10

11

4. Data, Sample Selection and Demographics of theRespondents

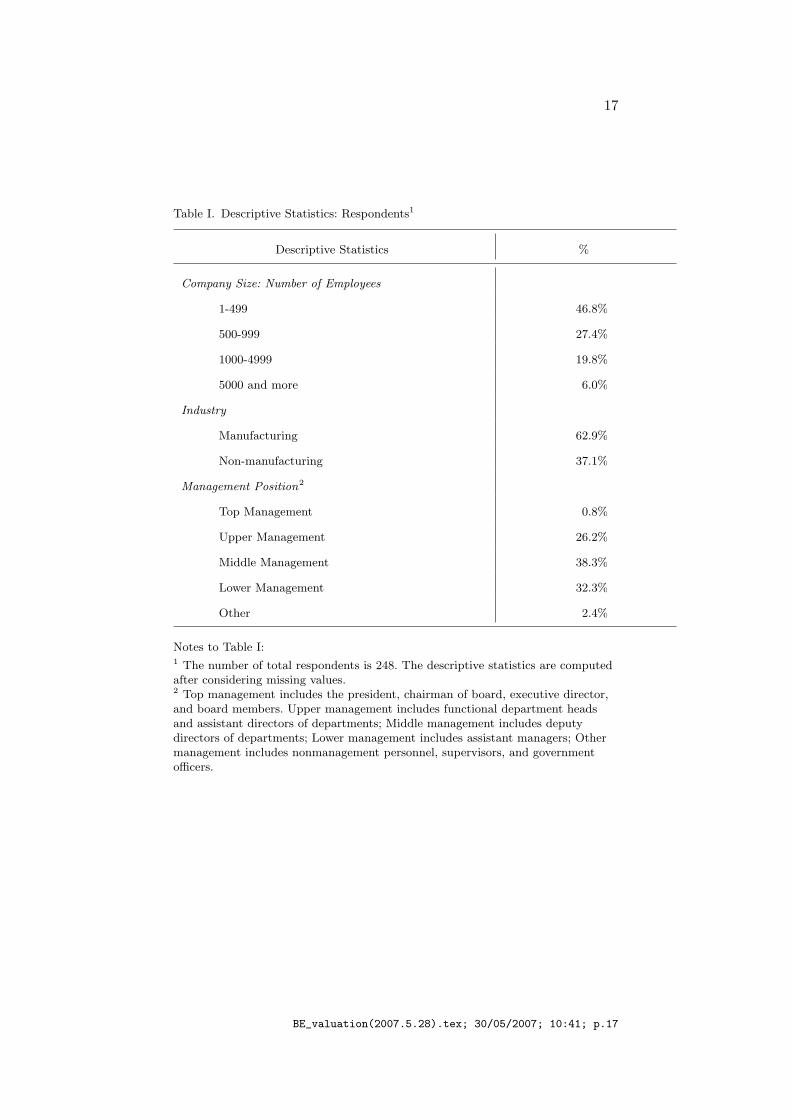

The survey data for this study was collected from managers of com-panies listed in the Korean stock market. The survey for the 2004ECI was conducted in January 2005. Business managers from variouslevels working in different industries comprised the sample. A totalof 248 usable questionnaires were collected to determine the extentof corporate commitment to business ethics. Table I summarizes thegeneral characteristics of companies and respondents. To ensure thatrespondents came from a variety of business backgrounds, the surveywas not restricted to a particular industry. The managerial level andcompany size represented also spanned a wide range. Companies inthe study were split between manufacturing and non-manufacturingsector. Even so, a substantial number of respondents (62.9%) camefrom manufacturing companies.

The sample consists of financial data for 2003-2004. Measures for thefinancial variables were taken from financial statements and the stockmarket at the end of the fiscal year. Accounting data, including earningsper share, book value, sales, long-term debt, total assets, and numberof shares were obtained from the TS2000 annual research files.6 Dailystock prices and market beta are from the 2005 KSRI Stock Database.7

190 participating companies are listed on the Korean Exchange while58 participating companies are traded in the KOSDAQ Market8.

5. Empirical Results

Table II presents variable descriptions and descriptive statistics for thequestionnaire used to measure the ethical commitment index (ECI).The results show that more than half of managers agree with the state-ment that top managers regularly emphasize the importance of businessethics (57.3%). 48.4% of managers believe that ethical behavior is thenorm at their companies. That is, business ethics are embedded in theirrespective companies’ business philosophy. Compared to US companies,Korean firms are significantly less likely to have a code of ethics thatexplicitly lays out the ethical philosophy of the company (48.3%).9

Almost half of the Korean companies studied had a disciplinary systemthrough which unethical behavior was strictly punished. 38.3% of firmshad an anonymous communication channel through which employeescould report ethically questionable behavior.

Only a third of companies (35.9%) conduct formal ethics education,training, or workshops. Only about one third of companies regularly set

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.11

12

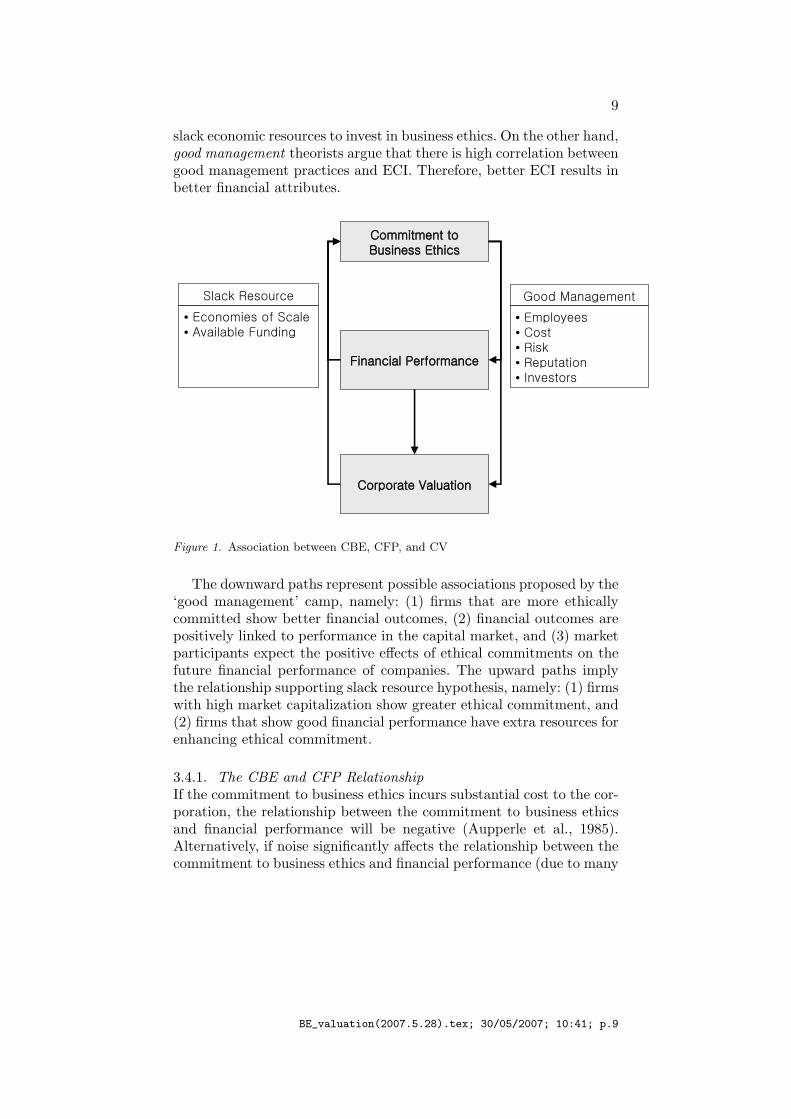

aside funds for philanthropic purposes (33.1%). Few companies havean ethics department or officers (29.8%), an ethics helpline (24.6%),or an ethics committee (16.1%). When managers are asked whethertheir companies have their ethics evaluation system audited by an in-dependent party from outside the company, a mere 12.1% of managersresponded in the affirmative. On average, Korean companies rely moreon implicit forms of ethical commitment than on explicit methods.

Table III summarizes the descriptive statistics for variables usedin this study. Each company employs, on average, 3.819 implicit andexplicit instruments for encouraging ethical commitment. Table III alsoshows financial performance variables and corporate valuation vari-ables. Mean values of P/E (10.896) and P/B (0.726) are slightly lowerthan the historic average of the US stock market.

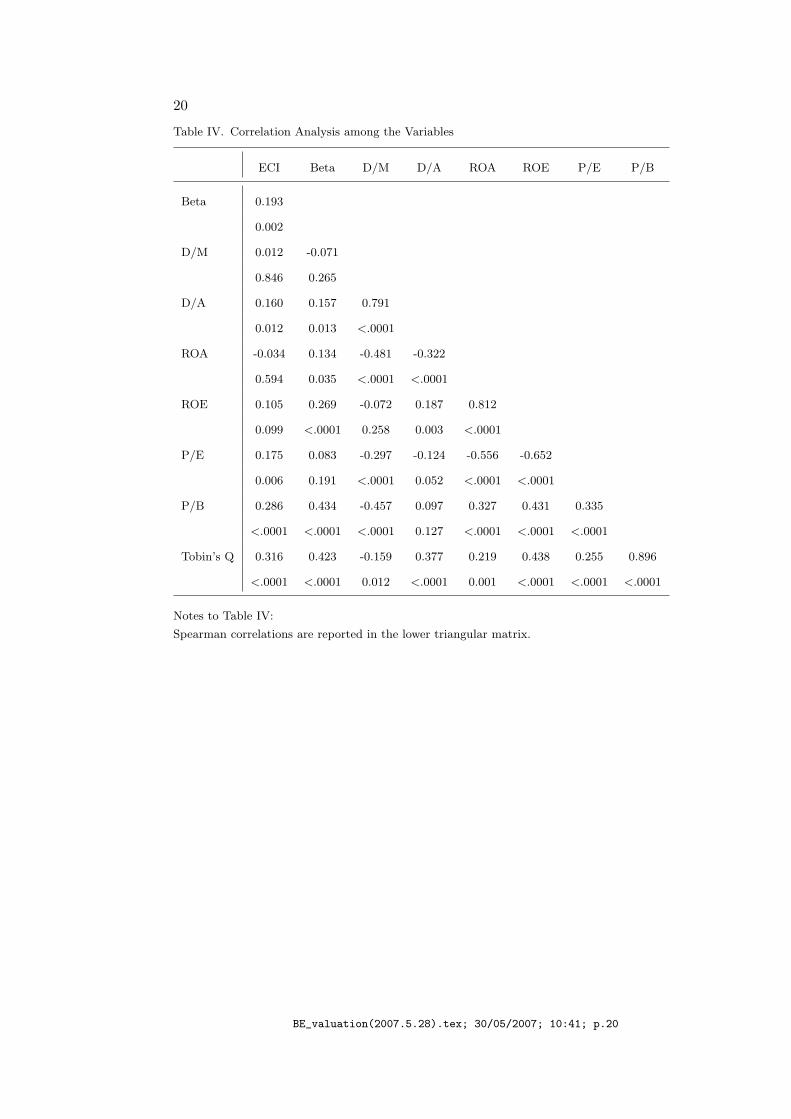

Table IV presents correlation coefficients for the key variables.10 Therelation between ECI and financial performance variables is unclear.ROA and ROE show insignificant association with ECI at a conven-tional level. The result implies that ethically committed companies donot necessarily show higher profitability. Companies that rely moreheavily on debt financing are more ethically committed according tothe association between ECI and D/A (0.160). This result is not incon-sistent with prior theories in the sense that the firms incurring a heavierdebt load have a stronger incentive to lower their cost of capital byproviding more transparent information to the market and enhancingtheir corporate reputations (Roberts, 1992; Gelb and Strawser, 2001).Prior studies show that ethically committed companies provide morepublic information. If companies can achieve higher profits than theadditional interest expenses on those increased debts, thereby offsettingthe increased financial risk due to the higher debt ratio, they wouldenjoy increased financial leverage.

Not surprisingly, the level of ethical commitment shows a positiveassociation with financial leverage. Prior studies document a mixedassociation between beta and CSP. In this study, beta is significantlypositively correlated with ECI (0.193). This result is in line with theargument that companies with higher price variability tend to focus onbusiness ethics as a means of reducing firm specific risk (Trotman andBradley, 1981).

The positive relationship between business ethics and corporate val-uation is backed up by anecdotal evidence. For the most part, theresults of this study support the contention that the relationship be-tween ECI and valuation variables is positive. Consider that correlationcoefficients for P/E (0.175), P/B (0.286), and Tobin’s Q (0.316) are sig-nificantly positive. A likely explanation for this association is that themarket rewards those companies that exhibit a significant commitment

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.12

13

to ethical behavior through higher stock prices. In other words, themarket expects positive effects on future cash flows and risk from com-panies with a high ethical commitment. Alternatively, we can speculatethat more valued companies can afford to devote greater resources tothe development of business ethics.

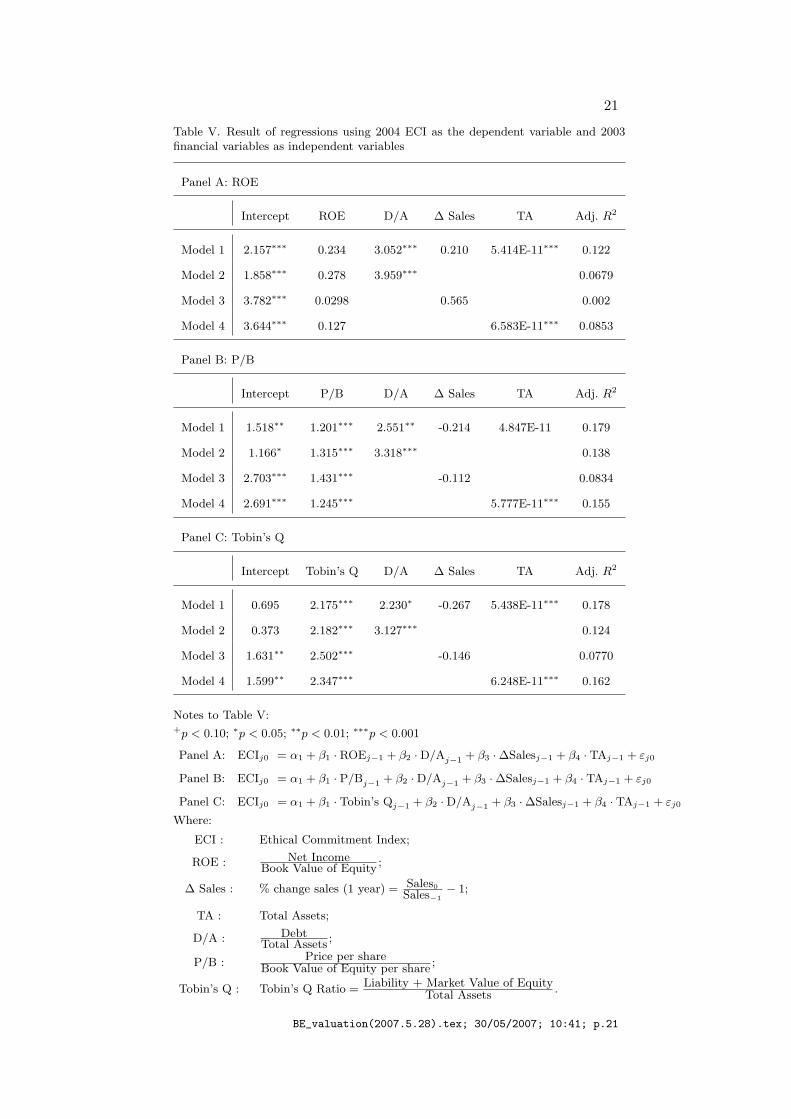

Table V presents the results of regression analysis in various set-tings using ECI as the dependent variable and key financial variablesas the independent variables. Following prior studies, we used D/A,sales growth, and assets as controlling variables for leverage, growthand size respectively. We used a one year lag between ECI (2004) andfinancial variables (2003) to test whether better financial performanceor highly valued companies leads to stronger ethical commitment. PanelA of Table V shows that ROE is insignificant at a conventional levelafter controlling for leverage, growth and/or size.11 As expected, ECI issignificantly associated with the D/A ratio and total assets. Size showssignificant association with ECI. Panel B and C of Table V presentthe results of the regressions using ECI as the dependent variable andvaluation factors as independent variables. The result shows how themarket performance of companies influences their ethical commitments.As can be seen in Panel B and C, P/B and Tobin’s Q are statisticallysignificantly related to ECI. We can postulate that companies thatperform better in the stock market than their competitors tend toinvest more towards their ethical commitments. In the panels of Ta-ble V, lagged D/A and TA are significantly associated with the ECI ofcurrent year. One explanation is that larger companies tend to focuson their ethical commitments hoping to receive greater approval fromthe general public, a result supported by the slack resource argument.

OLS regression results, reported in Table VI, are computed usingkey financial variables as the dependent variables and ECI as the inde-pendent variables after controlling for leverage, growth, and size. Wemeasured the correlation between current financial variables (2004) andcurrent ECI (2004). Panel A of Table VI shows that ROE is not signif-icantly associated with ECI after controlling for leverage, growth, andsize. As expected, ROE is significantly associated with growth of salessince the controlling variables capture the profitability of companies.The positive association between ROE and D/A is consistent with thefindings from previous studies: companies with higher leverage seem toachieve higher profits. Size, however, shows no significant associationwith ROE.

Panels B and C of Table VI indicate that valuation variables aresignificantly associated with ECI in agreement with good managementtheory, i.e., higher scores for ethical commitment translate into highervaluations. Clearly, the association between ethical commitment and

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.13

14

a company’s valuation is highly significant. Such a conclusion is notsurprising given that the positive returns from ethical behavior to acompany’s reputation would have an immediate impact on its stockprice since market participants revise their expectations upward withrespect to the company’s anticipated future performance. One shouldkeep in mind, however, that the effects of ethical behavior on a com-pany’s financial output might exhibit a longer lead-lag cycle which isalready incorporated in the stock price. 12 In sum, companies valuedhigh in the stock market seem to bear witness to the importance of eth-ical conduct. Several reasons explain this: (1) more stakeholders watchthe company, ergo (2) the stock price is more sensitive to the company’sreputation which means that (3) the company needs to hedge their risk(i.e. litigation or financial risk) through ever more conscientious ethicalconduct. Thus, a virtuous circle exists between ethical commitmentand corporate valuation. Highly valued firms tend to have a greatercommitment to ethical behavior because they have more resources attheir disposal as well as the incentive to commit themselves to businessethics. From a valuation perspective, ethical commitment leads to acompetitive advantage over other companies in that ethical behaviorusually translates into improved employee morale, lower costs, a betterreputation, and improved investor relations. 13 Less encouraging arethe initial findings that indicate that the connection between CFP andethical commitment is insignificant.

6. Concluding Remarks

In recent years, there has been increasing awareness of the importanceof business ethics in many countries (Taka and Foglia, 1994; Jacksonet al., 2000). Behavior considered unethical in one country is sometimesquite acceptable in another, so it behooves individuals and organiza-tions to understand business ethics in an international context if theyare to be successful in a world that is becoming ever more integratedin the drive towards globalization.

As discussed earlier, the connection between business ethics andeconomic benefit has important implications for corporate managers.It comes as a surprise then, that the association between businessethics and financial performance has not been well documented com-pared to the relationship between corporate social performance andfinancial performance. This study has demonstrated the associationbetween the ethical commitment of Korean companies and their finan-cial performance and valuation in the Korean stock market through acomprehensive survey of practicing managers.

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.14

15

The results of this study have several important implications forcorporate managers and stakeholders alike. First, it was found thatthe ethical commitment information of firms are well reflected in thestock market. Stock market investors value the ethical commitmentof companies (Epstein et al., 1994). Top management should proba-bly be more aware of the value relevance of business ethics for valuecreation, and engage in substantial efforts to increase competitive ad-vantage by encouraging ethical business behavior in a global businessmarket.14 Although the analysis was conducted in the Korean market,the competitive strategy can be equally applied to the global businessenvironment.

Second, this study treats corporate market valuation differently fromfinancial performance. Earlier studies did not make this distinctionexplicit. Prevailing theories and empirical studies document that a com-pany’s financial output is the key determinant of its stock performance.15

In line with previous work, the results of this study demonstrate astatistically significant relationship between financial performance mea-sures and market measures. However, the results do not reveal thatethical commitment is significantly associated with financial perfor-mance. In keeping with earlier studies investigating the associationbetween corporate social performance and market-based financial mea-sures, there was a significant correlation between ethical commitmentand corporate valuation. This finding, combined with the aforemen-tioned positive association between financial performance and marketmeasures, implies that the market rewards companies with high ethicalcommitment since it anticipates positive future financial performancefrom such companies. Although it is not apparent that the impactof ethical commitment on contemporaneous financial performance issignificant, the results seem to lend support to the conventional be-lief that the relationship between ethical commitment and financialperformance is positive over the long term. This finding also supportsthe good management hypothesis. Companies that want to increasetheir market value need to make a greater effort to develop an ethicalcorporate climate and commit themselves to ethical practices.

Lastly, with respect to cross-cultural implications, Korean compa-nies rely more on implicit forms of ethical commitment than explicitforms to ameliorate the ethical behavior of their employees. In Koreancompanies, indeed, the most common method used to instill ethicalbehavior is the emphasis top management places on the importanceof business ethics. Prior studies document that in comparison withUS companies, Korean and Japanese companies tend to use less for-mal methods for inculcating ethical values into their company cul-tures (Nakano, 1997; Choi and Jung, 2005). Given the significant im-

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.15

16

pact of ethical commitment on market value, Korean companies oughtto make greater efforts to instill business ethics through more rigorousand formal means.

The results of this study should be interpreted with caution. Oneissue to be wary of is the causal relationship between CBE and CFP.Although one of the conjectures of this study is that the relationshipbetween ethical commitment and corporate valuation is bidirectional,the direction of causation remains to be fully investigated due to thepaucity of survey data.16.

It would be worthwhile if future research extends the conclusionsof this study in several directions. First, this study did not test howthe level (change) of the ethical commitment index (ECI) leads to thelevel (change) in financial factors due to the paucity of available data;moreover, the findings of this study were derived over a relatively shortperiod of time. A further analysis of the causation between ethical com-mitment and corporate financial performance with a data set covering alonger window of time would be valuable to the field of ethical research.

Second, this study is among the first to develop an ECI through theuse of a survey of practicing managers; consequently, the theoreticalconstruct used for the development of measurements of the ethicalcommitment of companies was not robust due to inadequacies in thedata set available.

Lastly, while the sample used for this study focuses on Korean com-panies, a potential difference exists for cross-cultural samples since eachcountry may have ethical peculiarities. We leave more in-depth analysisfor future research.

Overall, we believe this study sheds light on the research of busi-ness ethics by revealing links between business ethics, financial perfor-mance, and valuation. The findings of this study provide another potentargument in favor of business ethics based on a company’s valuation.

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.16

17

Table I. Descriptive Statistics: Respondents1

Descriptive Statistics %

Company Size: Number of Employees

1-499 46.8%

500-999 27.4%

1000-4999 19.8%

5000 and more 6.0%

Industry

Manufacturing 62.9%

Non-manufacturing 37.1%

Management Position2

Top Management 0.8%

Upper Management 26.2%

Middle Management 38.3%

Lower Management 32.3%

Other 2.4%

Notes to Table I:1 The number of total respondents is 248. The descriptive statistics are computedafter considering missing values.2 Top management includes the president, chairman of board, executive director,and board members. Upper management includes functional department headsand assistant directors of departments; Middle management includes deputydirectors of departments; Lower management includes assistant managers; Othermanagement includes nonmanagement personnel, supervisors, and governmentofficers.

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.17

18

Table II. Definitions for the Variables in the Ethical Commitment Index (ECI)

Variable Description N %

1. Top managers of this company regularly emphasize

the importance of business ethics 142 57.3%

2. Ethical behavior based on a formal business philosophy

is the norm of this company 120 48.4%

3. This company has a disciplinary system through which

unethical behavior is strictly punished 119 48.0%

4. This company has a code of ethics 95 38.3%

5. In this company, employees can report unethical conduct

through an anonymous channel 95 38.3%

6. In this company, ethics education, training, or workshops

are in place to enhance business ethics of employees 89 35.9%

7. This company regularly puts a significant portion of

its profits towards philanthropy 82 33.1%

8. This company has an independent ethics department and officers 74 29.8%

9. In this company, employees can get help regarding business ethics

through an ethics hotline or open communication channel 61 24.6%

10. This company has an ethics committee 40 16.1%

11. This company has an ethics evaluation system measured

by an independent party from outside the company 30 12.1%

Notes to Table II:

1 = Yes; 0 = No.

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.18

19

Table III. Descriptive Statistics: Variables1

Descriptive Statistics N MIN MAX MEAN STD

ECI 248 0.000 11.000 3.819 3.005

TA 248 25 179,727 2,607 13,757

∆ Sales 248 -0.874 1.534 0.150 0.248

Beta 248 -0.395 1.698 0.564 0.373

D/M. 248 0.014 38.400 3.076 4.999

D/A 248 0.031 0.955 0.476 0.205

ROA 248 0.002 0.134 0.029 0.023

ROE 248 0.003 0.439 0.063 0.055

P/E 248 0.773 88.209 10.896 13.542

P/B 248 0.117 3.832 0.726 0.548

Tobin’s Q 248 0.261 3.042 0.846 0.305

Notes to Table III:1 The number of total respondents is 248. The descriptive statistics are computedafter considering missing values.

Where:

ECI : Ethical Commitment Index;

TA : Total Assets in millions;

∆ Sales : % change sales (1 year) = Sales0Sales−1

− 1;

Beta : Capital Asset Pricing Model Beta;

D/M : Debt to Market Capitalization;

D/A : Debt to Total Asset;

ROA : Return on Total Asset;

ROE : Return on Common Equity;

P/E : Price to Earning Ratio;

P/B : Price to Book Value of Equity;

Tobin’s Q : Tobin’s Q Ratio =Liability + Market Value of Equity

Total Assets.

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.19

20

Table IV. Correlation Analysis among the Variables

ECI Beta D/M D/A ROA ROE P/E P/B

Beta 0.193

0.002

D/M 0.012 -0.071

0.846 0.265

D/A 0.160 0.157 0.791

0.012 0.013 <.0001

ROA -0.034 0.134 -0.481 -0.322

0.594 0.035 <.0001 <.0001

ROE 0.105 0.269 -0.072 0.187 0.812

0.099 <.0001 0.258 0.003 <.0001

P/E 0.175 0.083 -0.297 -0.124 -0.556 -0.652

0.006 0.191 <.0001 0.052 <.0001 <.0001

P/B 0.286 0.434 -0.457 0.097 0.327 0.431 0.335

<.0001 <.0001 <.0001 0.127 <.0001 <.0001 <.0001

Tobin’s Q 0.316 0.423 -0.159 0.377 0.219 0.438 0.255 0.896

<.0001 <.0001 0.012 <.0001 0.001 <.0001 <.0001 <.0001

Notes to Table IV:

Spearman correlations are reported in the lower triangular matrix.

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.20

21

Table V. Result of regressions using 2004 ECI as the dependent variable and 2003financial variables as independent variables

Panel A: ROE

Intercept ROE D/A ∆ Sales TA Adj. R2

Model 1 2.157∗∗∗ 0.234 3.052∗∗∗ 0.210 5.414E-11∗∗∗ 0.122

Model 2 1.858∗∗∗ 0.278 3.959∗∗∗ 0.0679

Model 3 3.782∗∗∗ 0.0298 0.565 0.002

Model 4 3.644∗∗∗ 0.127 6.583E-11∗∗∗ 0.0853

Panel B: P/B

Intercept P/B D/A ∆ Sales TA Adj. R2

Model 1 1.518∗∗ 1.201∗∗∗ 2.551∗∗ -0.214 4.847E-11 0.179

Model 2 1.166∗ 1.315∗∗∗ 3.318∗∗∗ 0.138

Model 3 2.703∗∗∗ 1.431∗∗∗ -0.112 0.0834

Model 4 2.691∗∗∗ 1.245∗∗∗ 5.777E-11∗∗∗ 0.155

Panel C: Tobin’s Q

Intercept Tobin’s Q D/A ∆ Sales TA Adj. R2

Model 1 0.695 2.175∗∗∗ 2.230∗ -0.267 5.438E-11∗∗∗ 0.178

Model 2 0.373 2.182∗∗∗ 3.127∗∗∗ 0.124

Model 3 1.631∗∗ 2.502∗∗∗ -0.146 0.0770

Model 4 1.599∗∗ 2.347∗∗∗ 6.248E-11∗∗∗ 0.162

Notes to Table V:+p < 0.10; ∗p < 0.05; ∗∗p < 0.01; ∗∗∗p < 0.001

Panel A: ECIj0 = α1 + β1 · ROEj−1 + β2 ·D/Aj−1 + β3 ·∆Salesj−1 + β4 · TAj−1 + εj0

Panel B: ECIj0 = α1 + β1 · P/Bj−1 + β2 ·D/Aj−1 + β3 ·∆Salesj−1 + β4 · TAj−1 + εj0

Panel C: ECIj0 = α1 + β1 · Tobin’s Qj−1 + β2 ·D/Aj−1 + β3 ·∆Salesj−1 + β4 · TAj−1 + εj0

Where:

ECI : Ethical Commitment Index;

ROE : Net IncomeBook Value of Equity

;

∆ Sales : % change sales (1 year) = Sales0Sales−1

− 1;

TA : Total Assets;

D/A : DebtTotal Assets

;

P/B :Price per share

Book Value of Equity per share;

Tobin’s Q : Tobin’s Q Ratio =Liability + Market Value of Equity

Total Assets.

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.21

22

Table VI. Result of regressions using 2004 financial variables as the dependentvariable and 2004 ECI as independent variables

Panel A: ROE

Intercept ECI D/A ∆ Sales TA Adj. R2

Model 1 0.0523∗∗∗ 0.00223 0.0898∗∗ 0.0913∗∗∗ -3.047 0.116

Model 2 0.0609∗∗∗ 0.000864 0.107∗∗∗ 0.0589

Model 3 0.0874∗∗∗ 0.00328+ 0.104∗∗∗ 0.0845

Model 4 0.106∗∗∗ 0.00232 1.113E-13 0.007

Panel B: P/B

Intercept ECI D/A ∆ Sales TA Adj. R2

Model 1 0.504∗∗∗ 0.0501∗∗∗ 0.040 0.0294 2.409E-12 0.0771

Model 2 0.486∗∗∗ 0.0528∗∗∗ 0.0798 0.0812

Model 3 0.511∗∗∗ 0.0543∗∗∗ 0.0453 0.0808

Model 4 0.527∗∗∗ 0.0503∗∗∗ -2.578E-12 0.0842

Panel C: Tobin’s Q

Intercept ECI D/A ∆ Sales TA Adj. R2

Model 1 0.636∗∗∗ 0.0302∗∗∗ 0.193∗ 0.0342 -1.146E-12 0.0976

Model 2 0.649∗∗∗ 0.0284∗∗∗ 0.186∗ 0.102

Model 3 0.716∗∗∗ 0.0317∗∗∗ 0.0602 0.0894

Model 4 0.725∗∗∗ 0.0319∗∗∗ -4.822E-13 0.0874

Notes to Table VI:+p < 0.10; ∗p < 0.05; ∗∗p < 0.01; ∗∗∗p < 0.001

Panel A: ROEj0 = α1 + β1 · ECIj0 + β2 ·D/Aj0 + β3 ·∆Salesj0 + β4 · TAj0 + εj0

Panel B: P/Bj0 = α1 + β1 · ECIj0 + β2 ·D/Aj0 + β3 ·∆Salesj0 + β4 · TAj0 + εj0

Panel C: Tobin’s Qj0 = α1 + β1 · ECIj0 + β2 ·D/Aj0 + β3 ·∆Salesj0 + β4 · TAj0 + εj0

Where:

ECI : Ethical Commitment Index;

ROE : Net IncomeBook Value of Equity

;

∆ Sales : % change sales (1 year) = Sales0Sales−1

− 1;

TA : Total Assets;

D/A : DebtTotal Assets

;

P/B :Price per share

Book Value of Equity per share;

Tobin’s Q : Tobin’s Q Ratio =Liability + Market Value of Equity

Total Assets.

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.22

23

Notes

1 Easton and Sommers (2003) shows that unscaled financial variables of largerfirms have overwhelming influence on regression results.

2 Similarly, Ruf et al. (1998) develop an aggregate, systematic measure for theCorporate Social Performance (CSP) index using the Analytic Hierarchy Process.They consider the relative importance of the dimensions by providing a weight(Ci) for each dimension as CSPj =

∑jSijCi. In this study, equally weighted

ethics dimensions were used to avoid subjective measurement error. Tests were alsoconducted taking into account the relative weights. The results were qualitativelysimilar with or without weights.

3 Alternative financial measures were tested as controlling variables. The resultswere qualitatively identical.

4 The following are three instances of anecdotal evidence in support of the notionthat ethical behaviour improves business:

i. KB, the biggest bank in Korea, provides various benefits to companies thatdemonstrate ethical commitment. Benefits include lower interest rates (as much as2%), the availability of larger loans, and better credit ratings.

ii. The keynote speaker at the recent Ethical Corporation Summit, John Varley,Group CEO of Barclays, noted how business ethics were the key ingredient to hiscompany’s record financial performance: John Varley’s speech on 31st May at theFifth Ethical Corporation Summit in London (http://www.ethicalcorp.com/content.asp?ContentID=4338).

iii. Shinsegae Group, known as the most admired ethical company in Korea,stated that their fast growth was due, in part, to their strong commitment to ethicalbehavior. In addition, Shinsegae provides business opportunities to the suppliers itdeems the most ethical. Such suppliers are given greater opportunities to see theirwares at one of Sinsegae’s two department store chains, the E-mart chain or theShinsegae department store chain.

5 There are many factors affecting the magnitude of cost of capital. For example,the aforementioned explicit and implicit costs have substantial impacts on the costof capital.

6 TS2000 is a database providing companies’ financial data. It is prepared andmaintained by the Korea Listed Companies Association

7 KSRI Stock Database is made available by the Korea Securities Research Insti-tute.

8 As of 18 August 2006, 662 companies were listed on the Korea Stock Exchangewhile 942 companies were listed on the KOSDAQ.

9 In a US survey, 93% of companies report to have a code of ethics (Center forBusiness Ethics at Bentley College, 1992). Prior literature documents that fewerKorean and Japanese companies employ codes of ethics than American corporationsdo (Nakano, 1997; Lee and Yoshihara, 1997; Choi and Jung, 2005)

10 Pearson and Kendall’s τ -b correlations were also tested. The results were notqualitatively different from the Spearman correlation.

11 We also used other variables for financial performance. The results were quali-tatively similar.

12 Similarly, Preston and O’Bannon (1997) show that there is time lag betweenCSP and improvement of CFP.

13 Similarly, prior studies document that the relation between SCP and CFP isbidirectional (Waddock and Graves, 1997; Orlitzky et al., 2003; Orlitzky, 2005).

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.23

24

14 A myriad of value relevance studies investigate the usefulness of an informationfor valuing the firm (Collins et al., 1997; Brown et al., 1999; Easton, 1999; Francisand Schipper, 1999; Barth et al., 2001; Holthausen and Watts, 2001; Hassen et al.,2005)

15 Since the seminal study of Ball and Brown (1968) and Beaver (1968), the rela-tionship between the accounting variables representing the financial performance ofcompanies and market based variables has been a focus of accounting research fordecades.

16 Similarly, prior studies have documented a bidirectional link between CSP andCFP (Waddock and Graves, 1997; Simpson and Kohers, 2002; Orlitzky et al., 2003;Orlitzky, 2005)

References

Adam, A. M. and D. Rachman-Moore: 2004, ‘The Methods Used to Implement anEthical Code of Conduct and Employee Attitudes’. Journal of Business Ethics54, 225–244.

Aupperle, K., A. Carroll, and J. Hatfield: 1985, ‘An Empirical Examination ofthe Relationship Between Corporate Social Responsibility and Profitability’.Academy of Management Journal 28, 446–463.

Austin, N. K.: 1994, ‘The New Corporate Watch Dogs’. Working Woman 19, 19–20.Ball, R. and P. Brown: 1968, ‘An Empirical Evaluation of Accounting Income

Numbers’. 6(2), 159–178.Barth, M., W. Beaver, and W. Landsman: 2001, ‘The Relevance of the Value Rel-

evance Literature for Financial Standard Setting: Another View’. Journal ofAccounting and Economics 31, 77–104.

Barth, M. and G. Clinch: 2001, ‘Scale Effects in Capital Market-Based AccountingResearch’. Unpublished Working Paper (Stanford University).

Barth, M. E. and S. Kallapur: 1996, ‘The Effects of Cross-Sectional Scale Differ-ences on Regression Results in Empirical Accounting Research’. ContemporaryAccounting Research 13, 527–569.

Bartov, E., D. Givoly, and C. Hayn: 2002, ‘The Rewards to Meeting or BeatingEarnings Expectations’. Journal of Accounting and Economics 33, 173–204.

Beaver, W.: 1968, ‘The Information Content of Annual Earnings Announcements’.Journal of Accounting Research 6(Supplement), 67–92.

Brammer, S. and A. Millington: 2005, ‘Corporate Reputation and Philanthropy: AnEmpirical Analysis’. Journal of Business Ethics 61, 29–44.

Brenner, S. N.: 1992, ‘Ethics Programs and their Dimensions’. Journal of BusinessEthics 11, 391–399.

Brown, S., K. Lo, and T. Lys: 1999, ‘Use of R2 in Accounting Research: MeasuringChanges in Value Relevance Over the Last Four Decades’. Journal of Accountingand Economics 28, 83–115.

Callan, B. J.: 1992, ‘Predicting Ethical Values and Training Needs in Ethics’. Journalof Business Ethics 11, 761–769.

Carlson, D. S. and P. L. Perrewe: 1995, ‘Institutionalization of Organizational Ethicsthrough Transformational Leadership’. Journal of Business Ethics 14, 829–838.

Carroll, A. B.: 1991, ‘Corporate Social Performance Measurement: A Commentaryon Methods for Evaluating an Elusive Construct’. Research in Corporate SocialPerformance and Policy 12, 385–401.

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.24

25

Center for Business Ethics at Bentley College: 1992, ‘Instilling Ethical Values inLarge Corporations’. Journal of Business Ethics 11, 863–867.

Choi, T. H.: 2004, ‘Characteristics of Firms that Persistently Meet or Beat Analysts’Forecasts’. KDI School of Public Policy and Management, Working Paper.

Choi, T. H. and J. C. Jung: 2005, ‘An Empirical Analysis on the Business Ethics ofKorean Managers’. Working Paper.

Christie, A.: 1987, ‘On Cross-Sectional Analysis in Accounting Research’. Journalof Accounting and Economics 9, 231–258.

Cochran, P. and R. Wood: 1984, ‘Corporate Social Responsibility and CorporateSocial Performance’. Academy of Management Journal 27, 42–56.

Coffey, B. S. and G. E. Fryxel: 1991, ‘Institutional Ownership of Stock and Dimen-sions of Corporate Social Performance: An Empirical Examination’. Journal ofBusiness Ethics 10, 437–444.

Collins, D., E. Maydew, and L. Weiss: 1997, ‘Changes in the Value-Relevance ofEarnings and Book Values Over the Past Forty Years’. Journal of Accountingand Economics 24, 39–67.

Dean, P. J.: 1992, ‘Making Codes of Ethics ‘Real”. Journal of Business Ethics 11,285–290.

Dierkes, M. and R. Coppock: 1978, ‘Europe Tries the Corporate Social Report’.Business and Society Review pp. 21–24.

Dubinsky, A., M. A. Jolson, M. Kotabe, and C. U. Lim: 1991, ‘A Cross-NationalInvestigation of Industrial Salespeople’s Ethical Perceptions’. Journal ofInternational Business Studies 22(4), 651–670.

Easton, P.: 1999, ‘Security Returns and the Value Relevance of Accounting Data’.Accounting Horizons 13(4), 399–412.

Easton, P. and G. Sommers: 2003, ‘Scale and Scale Effects in Market-BasedAccounting Research’. Journal of Business Finance and Accounting.

Epstein, E. M.: 1987, ‘The Corporate Social Policy Process: Beyond BusinessEthics, Corporate Social Responsibility, and Corporate Social Responsiveness’.California Management Review pp. 99–114.

Epstein, E. M.: 1989, ‘Business Ethics, Corporate Good Citizenship and the Corpo-rate Social Policy Process: A View from the United States’. Journal of BusinessEthics 8, 583–595.

Epstein, M. J., R. A. McEwen, and R. M. Spindle: 1994, ‘Shareholder PreferencesConcerning Corporate Ethical Performance’. Journal of Business Ethics 13,447–453.

Fombrun, C. and M. Shanley: 1990, ‘What’s in a Name? Reputation Building andCorporate Strategy’. Academy of Management Journal 33, 233–258.

Francis, J. and K. Schipper: 1999, ‘Have Financial Statements Lost Their Rele-vance?’. Journal of Accounting Research 37, 319–352.

Francis, R. and A. Armstrong: 2003, ‘Ethics as a Risk Management Strategy: TheAustralian Experience’. Journal of Business Ethics 45, 375–385.

Friedman, M.: 1962, Capitalism and Freedom. University of Chicago Press, Chicago.Gelb, D. and J. Strawser: 2001, ‘Corporate Social Responsibility and Financial

Disclosure: An Alternative Explanation for Increased Disclosure’. Journal ofBusiness Ethics 33, 1–13.

Genfan, H.: 1987, ‘Formalizing Business Ethics’. Training and Development Journal41, 35–37.

Griffin, J. and J. Mahon: 1997, ‘The Corporate Social Performance and CorporateFinancial Performance Debate: Twenty-Five Years of Incomparable Research’.Business and Society 36, 5–31.

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.25

26

Hammond, S. A. and J. W. Slocum Jr.: 1996, ‘The Impact of Prior Firm FinancialPerformance on Subsequent Corporate Reputation’. Journal of Business Ethics15, 159–165.

Hassen, L., H. Nilsson, and S. Nyquist: 2005, ‘The Value Relevance of EnvironmentalPerformance’. European Accounting Review 14, 41–61.

Hoffer, G. E., S. W. Pruitt, and R. J. Reilly: 1988, ‘The Impact of Product Recallson the Wealth of Sellers: A Reexamination’. Journal of Political Economy 96(3),663–670.

Holthausen, R. and R. Watts: 2001, ‘The Relevance of the Value-Relevance Liter-ature for Financial Accounting Standard Setting’. Journal of Accounting andEconomics 21, 3–75.

Jackson, T., C. David, J. Jones, J. Joseph, K. Lau, K. Matsuno, C. Nakano, H.Park, J. Piounowska-Kokoszko, I. Taka, and H. Yoshihara: 2000, ‘Making Eth-ical Judgments: A Cross-cultural Management Study’. Asia Pacific Journal ofManagement 17, 443–472.

Johnson, H.: 2003, ‘Does It Pay to Be Good? Social Responsibility and FinancialPerformance’. Business Horizons pp. 34–40.

Kulshreshtha, P.: 2005, ‘Business Ethics versus Economic Incentives: ContemporaryIssues and Dilemmas’. Journal of Business Ethics 60, 393–410.

Lee, C. Y. and H. Yoshihara: 1997, ‘Business Ethics of Korean and JapaneseManagers’. Journal of Business Ethics 16, 7–21.

Little, P. L. and B. L. Little: 2000, ‘Do Perceptions of Corporate Social Responsibil-ity Contribute to Explaining Differences in Corporate Price-Earnings Ratios?’.Corporate Reputation Review 3, 137–142.

Lopez, T. and L. Rees: 2002, ‘The Effect of Beating and Missing Analysts’ Forecastson the Information Content of Unexpected Earnings’. Journal of Accounting,Auditing, and Finance 17(2), 155–184.

Matsumoto, D.: 2002, ‘Management’s Incentives to Avoid Negative EarningsSurprise’. The Accounting Review 77, 483–514.

McGuire, J., A. Sundgren, and T. Schneeweis: 1988, ‘Corporate Social Responsibilityand Firm Financial Performance’. Academy of Management Journal 31, 854–872.

Moore, G.: 2001, ‘Corporate Social and Financial Performance: An Investigation inthe U.K. Supermarket Industry’. Journal of Business Ethics 34, 299–315.

Morris, S. A.: 1997, ‘Internal Effects of Stakeholder Management Devices’. Journalof Business Ethics 16, 413–424.

Murphy, R. E.: 1988, ‘Implementing Business Ethics’. Journal of Business Ethics7, 907–915.

Nakano, C.: 1997, ‘A Survey Study on Japanese Managers’ Views of Business Ethics’.Journal of Business Ethics 16, 1737–1751.

Nakano, C.: 1999, ‘Attempting to Institutionalize Ethics: Case Studies From Japan’.Journal of Business Ethics 18, 335–343.

Neville, B. A., S. J. Bell, and B. Menguc: 2005, ‘Corporate Reputation, Stakehold-ers and the Social Performance-Financial Performance Relationship’. EuropeanJournal of Marketing 39, 1184–1198.

Ohlson, J. A.: 1995, ‘Earnings, Book Values, and Dividends in Equity Valuation’.11(2), 661–687.

Orlitzky, M.: 2005, ‘Social Responsibility and Financial Performance: Trade-Off orVirtuous Circle?’. University of Auckland Business Review pp. 37–43.

Orlitzky, M., F. Schmidt, and S. Rynes: 2003, ‘Corporate Social and FinancialPerformance: A Meta-analysis’. Organization Studies 24, 403–441.

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.26

27

Penman, S.: 2003, Financial Statement Analysis and Security Valuation. McGraw-Hill, 2 edition.

Preston, L. and D. O’Bannon: 1997, ‘The Corporate Social-Financial PerformanceRelationship: A Typology and Analysis’. Business and Society 36, 419–434.

Roberts, P. W. and G. R. Dowling: 2002, ‘Corporate Reputation and SustainedSuperior Financial Performance’. Strategic Management Journal 23, 1077–1093.

Roberts, R.: 1992, ‘Determinants of Corporate Social Responsibility Disclosure:An Application of Stakeholder Theory’. Accounting, Organizations and Society17(6), 595–612.

Ruf, B., K. Muralidhar, R. Brown, J. Janney, and K. Paul: 2001, ‘An EmpiricalInvestigation of the Relationship Between Change in Corporate Social Perfor-mance and Financial Performance: A Stakeholder Theory Perspective’. Journalof Business Ethics 32, 143–156.

Ruf, B. M., K. Muralidhar, and K. Paul: 1998, ‘The Development of a Systematic,Aggregate Measure of Corporate Social Performance’. Journal of Management24, 119–133.

Russo, M. V. and P. A. Fouts: 1997, ‘A Resource-based Perspective on CorporateEnvironmental Performance and Profitability’. Academy of Management Journal40, 534–559.

Sauser, J. W. I.: 2005, ‘Ethics in Business: Answering the Call’. Journal of BusinessEthics 58, 345–357.

Schwartz, M. S., T. W. Dunfee, and M. J. Kline: 2005, ‘Tone at the Top: An EthicsCode for Directors?’. Journal of Business Ethics 58, 70–100.

Seifert, B., S. Morris, and B. Bartkus: 2003, ‘Comparing Big Givers and SmallGivers: Financial Correlates of Corporate Philanthropy’. Journal of BusinessEthics 45, 195–211.

Shane, P. and B. Spicer: 1983, ‘Market Response to Environmental InformationProduced Outside the Firm’. The Accounting Review 58(3), 521–538.

Simpson, G. and T. Kohers: 2002, ‘The Link Between Corporate Social and FinancialPerformance: Evidence from the Banking Industry’. Journal of Business Ethics35, 97–109.

Sims, R. and A. Gegez: 2004, ‘Attitudes Towards Business Ethics: A Five NationComparative Study’. Journal of Business Ethics 50, 253–265.

Sims, R. L. and T. L. Keon: 1999, ‘Determinants of Ethical Decision Making: TheRelationship of the Perceived Organizational Environment’. Journal of BusinessEthics 19(4), 393–401.

Sims, R. R.: 1992, ‘The Challenge of Ethical Behavior in Organizations’. Journal ofBusiness Ethics 11, 505–513.

Singer, A. W.: 1995, ‘1-800-Snitch’. Across the Board 32, 16–20.Skinner, D. and R. Sloan: 2002, ‘Earnings Surprises, Growth Expectation, and Stock

Returns or Don’t Let an Earnings Torpedo Sink Your Portfolio’. Review ofAccounting Studies 7, 289–312.

Spencer, B. and G. Taylor: 1987, ‘A Within and Between Analysis of the RelationshipBetween Corporate Social Responsibility and Financial Performance’. AkronBusiness and Economic Review 18, 7–18.

Stanwick, P. and S. Stanwick: 1998, ‘The Relationship Between Corporate SocialPerformance, and Organizational Size, Financial Performance, and Environmen-tal Performance: An Empirical Examination’. Journal of Business Ethics 17,195–204.

Taka, I. and W. D. Foglia: 1994, ‘Ethical Aspect of “Japanese Leadership Style”’.Journal of Business Ethics 13(2), 135–148.

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.27

28

Trevino, L. K.: 1986, ‘Ethical Decision Making in Organizations: A Person-SituationInteractionist Model’. Academy of Management Review 11, 601–617.

Trotman, K. and G. Bradley: 1981, ‘Associations Between Social ResponsibilityDisclosure and Characteristics of Companies’. Accounting, Organizations andSociety 6, 355–362.

van der Merwe, R., L. Pitt, and P. Berthon: 2003, ‘Are Excellent Companies Ethical?Evidence from an Industrial Setting’. Corporate Reputation Review 5, 343–358.

Verschoor, C.: 1998, ‘A Study of The Link Between a Corporation’s FinancialPerformance and its Commitment to Ethics’. Journal of Business Ethics 17,1509–1516.

Verschoor, C.: 1999, ‘Corporate Performance Is Closely Linked to a Strong EthicalCommitment’. Business and Society Review 104, 407–415.

Vogel, D.: 1991, ‘Business Ethics Past and Present’. The Public Interest 102, 49–64.Waddock, S. A. and S. B. Graves: 1997, ‘The Corporate Social Performance-

Financial Performance Link’. Strategic Management Journal 18(4), 303–319.Weeks, W. A. and J. Nantel: 1992, ‘Corporate Codes of Ethics and Sales Force

Behavior: A Case Study’. Journal of Business Ethics 11, 753–760.Weiss, J. W.: 1994, Business Ethics: A Managerial, Stakeholder Approach.

Wadsworth Publishing Co., Belmont, CA.Yoon, E., J. J. Guffey, and V. Kijewski: 1993, ‘The Effects of Information and

Company Reputation on Intentions to Buy a Business Service’. Journal ofBusiness Research 27, 215–228.

BE_valuation(2007.5.28).tex; 30/05/2007; 10:41; p.28