Endesa Chile - IR Presentation - Enel

35

Endesa Chile IR Presentation 9M 2015

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Endesa Chile - IR Presentation - Enel

Endesa Chile IR Presentation

9M 2015

Endesa Chile Investor Presentation 9M15

USE: Public, Investor Relations 2

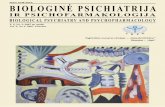

PEHUENCHE, 93%

CELTA, 96%

GASATACAMA, 98%

•COSTANERA, 76%

•EL CHOCÓN, 65% •EDEGEL, 62% •EMGESA, 27%

• ENEL BRASIL, 37%

AMPLA, 17%

COELCE, 22%

FORTALEZA, 37%

CDSA, 37%

CIEN, 37%

61%

60%

COLOMBIA PERU ARGENTINA BRAZIL1

Organization structure

CHILE

Committed Shareholders ITALY

CHILE

1 Recognized as equity method investments.

•GNL Quintero, 20%

•Transquillota ,48%

•Electrogas, 43%

•GNL Chile, 33%

CHILE1

60% 15%

4% 6%

15%

Enersis S.A.

Chilean Pension Funds

ADRs (Citibank N.A.)

Retail

Institutional Investors

Endesa Chile Investor Presentation 9M15

USE: Public, Investor Relations 3

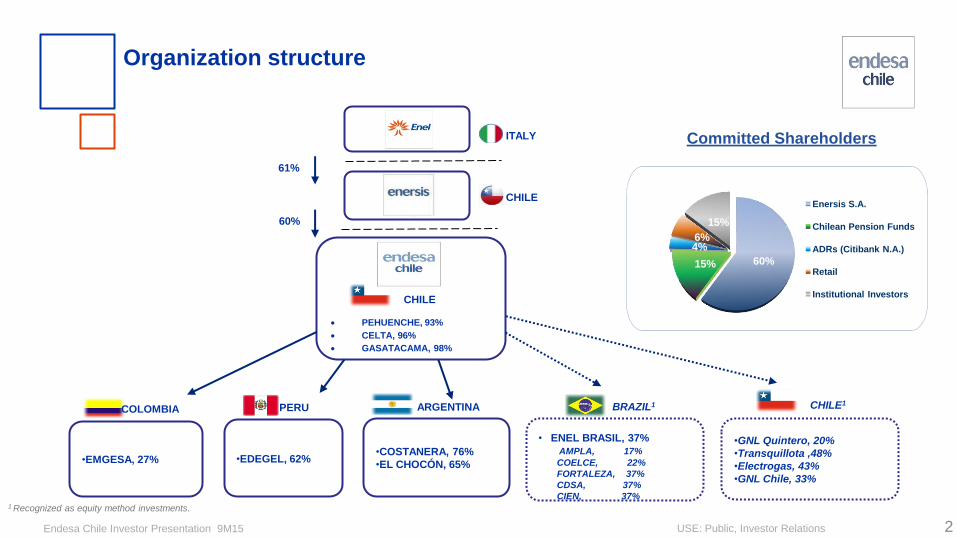

COLOMBIA

3,459 MW inst. Capacity 2

Hydro: 3,015 MW

Thermal : 444 MW

22% market share1

No. 2

6,351 MW inst. capacity

Hydro: 3,456 MW

Thermal : 2,808 MW

NCRE: 87 MW

32% market share1

PERU

1,680MW inst. capacity

Hydro: 783 MW

Thermal : 896 MW

19% market share1

CHILE

BRAZIL

987 MW inst. Capacity

Hydro: 665 MW

Thermal : 322 MW

1% market share1

Consolidated installed capacity: 15,142 MW

Capacity including Brazil : 16,129 MW

Consolidated energy sales 9M14: 42,131 GWh

Consolidated energy sales 9M15: 45,769 GWh

3,652 MW inst. Capacity

Hydro: 1,328 MW

Thermal: 2,324 MW

12% market share1

ARGENTINA No. 2

No. 1

No. 1

1. Calculated based on installed capacity

2. Includes El Quimbo installed capacity

A unique portfolio in LatAm’s generation business

Endesa Chile Investor Presentation 9M15

USE: Public, Investor Relations 4

Hydro: 9,247 MW

Chile:

3,456 MW Argentina:

1,328 MW

Brazil1:

665 MW

Peru:

783 MW

Colombia:

3,015 MW 1

Chile:

636 MW

Colombia:

236 MW

Chile:

2,173 MW Argentina:

2,324 MW

Peru:

896 MW

Colombia:

208 MW

Chile:

87 MW

NCRE2: 87 MW

Well diversified generation assets throughout the region

Coal: 872 MW

Oil-Gas: 5,923 MW

1 Brazilian assets are recognized as equity method investments. 2 Non Conventional Renewable Energy.

Installed Capacity: 16,129 MW

57% of Endesa Chile´s installed capacity

corresponds to hydro resources

Brazil1:

322 MW

8,840

872

5,923

87

HYDRO

COAL

OIL-GAS

NCRE

1. Includes El Quimbo installed capacity

Endesa Chile 9M15 Results

USE: Public, Investor Relations 5

Total Installed Capacity1:

15,142 MW

EBITDA 9M15

US$ 1,306 million

Total Generation:

39,002 GWh

Enel Brasil

• Endesa Chile’s ownership: 37.1%.

• Net Attributable Income2:

US$ 44 million.

1 Excludes the proportional assets of Enel Brasil (987 MW). 2 Considers the total contributions of Enel Brasil recognized by Endesa Chile as an equity method investment.

* Includes El Quimbo installed capacity

Diversified source of EBITDA

Endesa Chile 9M15 Results

USE: Public, Investor Relations

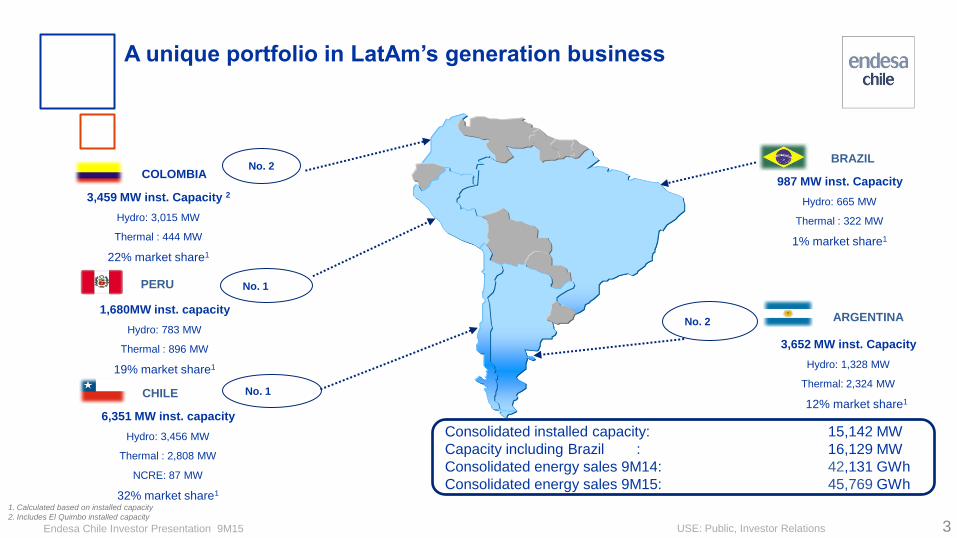

Gwh / Change1 CHILE COLOMBIA PERU ARGENTINA TOTAL

REGULATED 13,053 11% 6,672 18% 3,394 (11%) - - 23,119 9%

UNREGULATED 3,103 9% 2,555 3% 2,526 (4%) 446 (35%)

8,630 0%

SPOT 1,155 155% 3,618 -9% 582 24% 8,666 18%

14,021 15%

Total 17,311 15% 12,845 6% 6,501 (6%) 9,112 14% 45,769 9%

6

Chile Colombia Peru

Distribution

Companies Spot

Unregulated

Customers

Argentina

Physical Sales as of September 2015: 45,769 GWh

Balanced commercial policy

Physical Sales as of September 2015

Physical

Sales

(GWh)

1 Compared with 9M14

Endesa Chile 9M15 Results

USE: Public, Investor Relations

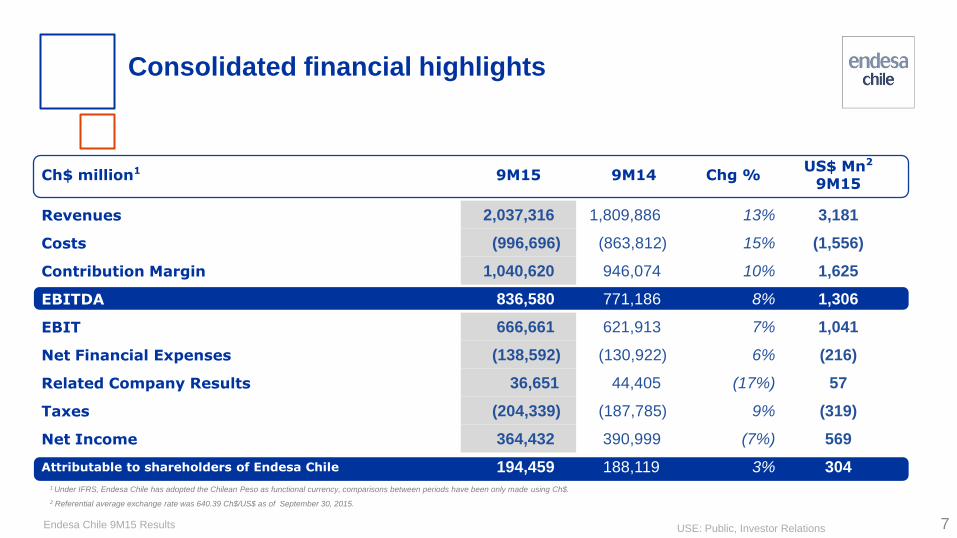

1 Under IFRS, Endesa Chile has adopted the Chilean Peso as functional currency, comparisons between periods have been only made using Ch$.

2 Referential average exchange rate was 640.39 Ch$/US$ as of September 30, 2015.

Consolidated financial highlights

7

Ch$ million1

9M15 9M14 Chg %

US$ Mn2

9M15

Revenues 2,037,316 1,809,886 13% 3,181

Costs (996,696) (863,812) 15% (1,556)

Contribution Margin 1,040,620 946,074 10% 1,625

EBITDA 836,580 771,186 8% 1,306

EBIT 666,661 621,913 7% 1,041

Net Financial Expenses (138,592) (130,922) 6% (216)

Related Company Results 36,651 44,405 (17%) 57

Taxes (204,339) (187,785) 9% (319)

Net Income 364,432 390,999 (7%) 569

Attributable to shareholders of Endesa Chile 194,459 188,119 3% 304

Endesa Chile Investor Presentation 9M15

USE: Public, Investor Relations

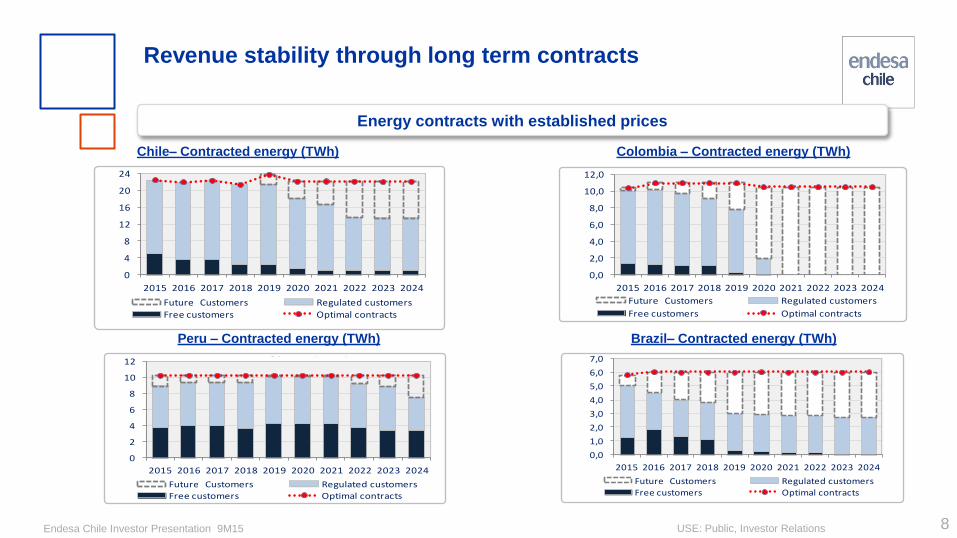

Revenue stability through long term contracts

Colombia – Contracted energy (TWh) Chile– Contracted energy (TWh)

Peru – Contracted energy (TWh) Brazil– Contracted energy (TWh)

8

Energy contracts with established prices

0

4

8

12

16

20

24

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Contrated energy Chile (TWh)

Futures Customers Regulated customers

Free customers Optimal contracts

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Contrated energy Brazil (TWh)

Futures Customers Regulated customers

Free customers Optimal contracts

0,0

2,0

4,0

6,0

8,0

10,0

12,0

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Contrated energy Colombia (TWh)

Futures Customers Regulated customers

Free customers Optimal contracts

0

2

4

6

8

10

12

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Contrated energy Peru (TWh)

Futures Customers Regulated customers

Free customers Optimal contracts

Endesa Chile 9M15 Results

USE: Public, Investor Relations

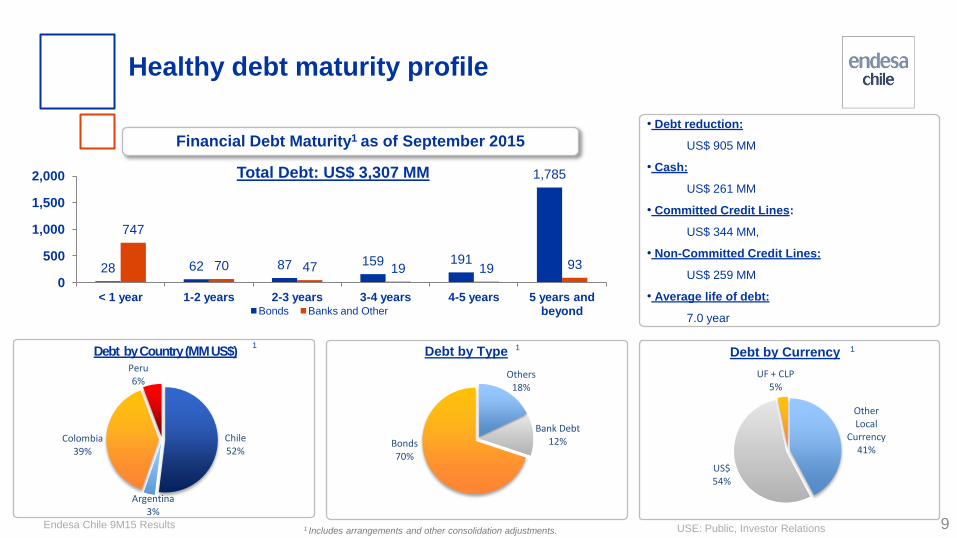

• Debt reduction:

US$ 905 MM

• Cash:

US$ 261 MM

• Committed Credit Lines:

US$ 344 MM,

• Non-Committed Credit Lines:

US$ 259 MM

• Average life of debt:

7.0 year

Debt by Type Debt by Currency Debt by Country (MM US$)

1 Includes arrangements and other consolidation adjustments.

1 1 1

Total Debt: US$ 3,307 MM

9

Financial Debt Maturity1 as of September 2015

Healthy debt maturity profile

Other Local

Currency 41%

US$ 54%

UF + CLP 5%

Chile 52%

Argentina 3%

Colombia 39%

Peru 6%

Others 18%

Bank Debt 12% Bonds

70%

28 62 87 159 191

1,785

747

70 47 19 19 93

0

500

1,000

1,500

2,000

< 1 year 1-2 years 2-3 years 3-4 years 4-5 years 5 years and beyond Bonds Banks and Other

Endesa Chile 9M15 Results

USE: Public, Investor Relations 10

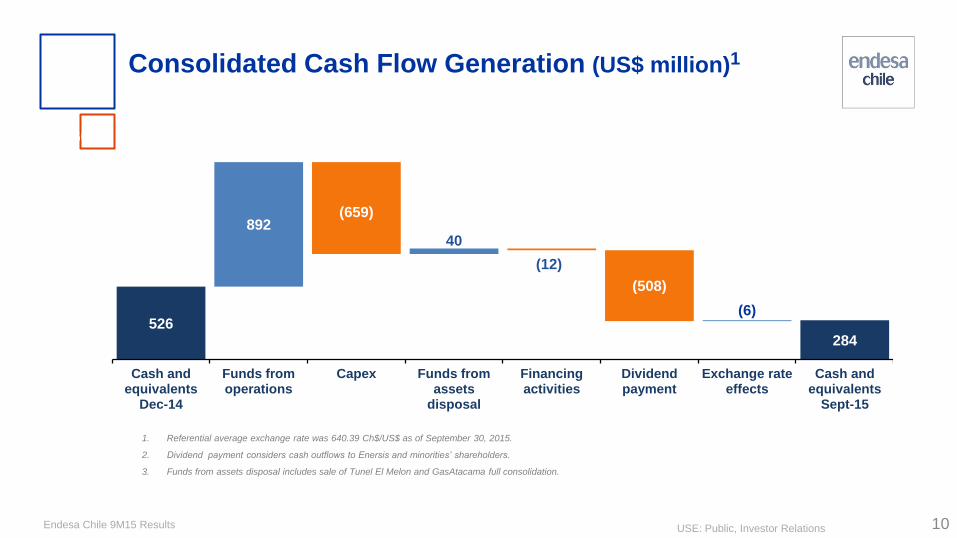

Consolidated Cash Flow Generation (US$ million)1

1. Referential average exchange rate was 640.39 Ch$/US$ as of September 30, 2015.

2. Dividend payment considers cash outflows to Enersis and minorities’ shareholders.

3. Funds from assets disposal includes sale of Tunel El Melon and GasAtacama full consolidation.

892 (659)

40

(12)

(508)

(6) 526

284

0

200

400

600

800

1,000

1,200

1,400

1,600

Cash and equivalents

Dec-14

Funds from operations

Capex Funds from assets

disposal

Financing activities

Dividend payment

Exchange rate effects

Cash and equivalents

Sept-15

Endesa Chile Investor Presentation 9M15

USE: Public, Investor Relations

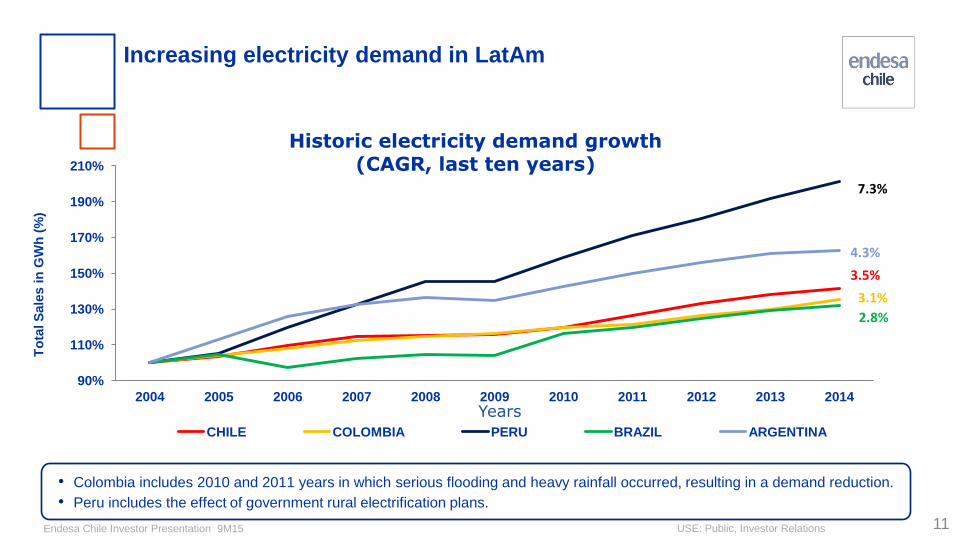

Increasing electricity demand in LatAm

• Colombia includes 2010 and 2011 years in which serious flooding and heavy rainfall occurred, resulting in a demand reduction.

• Peru includes the effect of government rural electrification plans.

11

90%

110%

130%

150%

170%

190%

210%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

To

tal S

ale

s i

n G

Wh

(%

)

Years

Historic electricity demand growth (CAGR, last ten years)

CHILE COLOMBIA PERU BRAZIL ARGENTINA

3.5%

3.1%

7.3%

4.3%

2.8%

Endesa Chile Investor Presentation 9M15

USE: Public, Investor Relations

ARGENTINA

AUSTRALIA

AUSTRIA

BOLIVIA

BRAZIL

CANADA

CHILECHINA

COLOMBIA

FINLAND

FRANCE GERMANY

GREECE

INDIA IRELAND

ITALY

JAPAN

MEXICO

PERU

RUSSIA

SPAIN UNITED KINGDOM

UNITED STATES

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

0 10,000 20,000 30,000 40,000 50,000 60,000

Ele

ctrici

ty c

onsu

mption,

per

capita (

Kw

h p

er

year)

GDP per capita (current PPP, US$)Data source: The World Bank.

Direct relation between GDP and electricity demand

Markets with high potential for growth

12

• Chile aims to be in the group of developed countries.

• There is no development without energy.

Endesa Chile Investor Presentation 9M15

USE: Public, Investor Relations

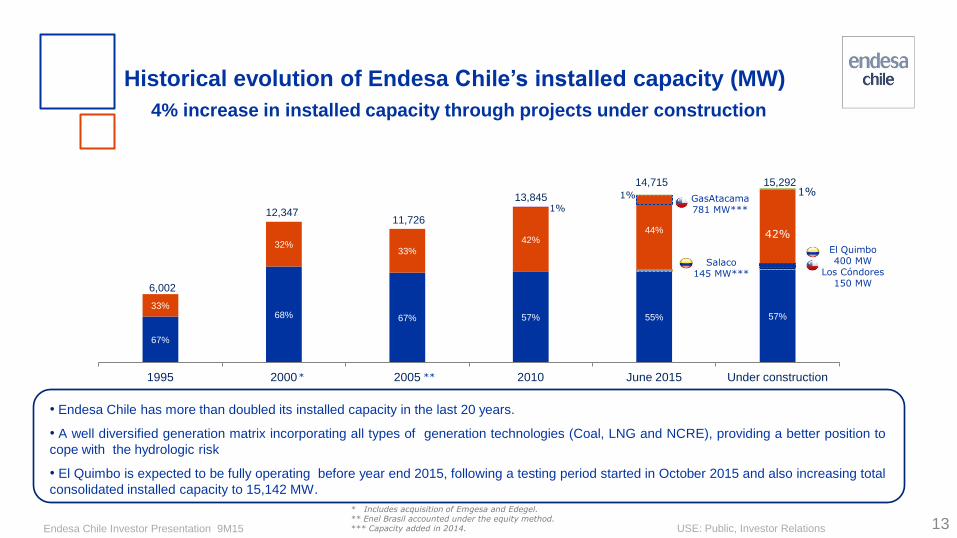

67%

68% 67% 57% 55% 57% 33%

32% 33%

42% 44%

1%

1%

42%

1%

1995 2000 2005 2010 June 2015 Under construction

6,002

12,347 11,726

13,845

14,715 15,292

13

Historical evolution of Endesa Chile’s installed capacity (MW)

4% increase in installed capacity through projects under construction

• Endesa Chile has more than doubled its installed capacity in the last 20 years.

• A well diversified generation matrix incorporating all types of generation technologies (Coal, LNG and NCRE), providing a better position to

cope with the hydrologic risk

• El Quimbo is expected to be fully operating before year end 2015, following a testing period started in October 2015 and also increasing total

consolidated installed capacity to 15,142 MW.

* **

* Includes acquisition of Emgesa and Edegel. ** Enel Brasil accounted under the equity method. *** Capacity added in 2014.

GasAtacama 781 MW***

Salaco 145 MW***

El Quimbo 400 MW

Los Cóndores 150 MW

Endesa Chile 9M15 Results

USE: Public, Investor Relations

• Hydro power plant, located in the Huila Department, Colombia

• Utilizes the flow coming from the Magdalena River.

• 97% progress as of September, 2015 .

• Estimated: generation of 2,093 GWh/year, Load factor: 60%

• Total CAPEX of US$ 1,231 million*.

14

El Quimbo (400 MW)

* In constant US dollars of 2010.

Started its testing period in October and will become available for economic dispatch during November

2015, increasing by 13% our installed capacity in Colombia.

El Quimbo

Endesa Chile 9M15 Results

USE: Public, Investor Relations

• Hydro power plant, run of the river.

• Located in San Clemente, in Maule region, Chile.

• 150 MW of installed capacity.

• Estimated generation of 600 GWh/year.

• Estimated load factor: 46%.

• Total CAPEX of US$ 662 million.

• 20% progress as of September, 2015.

15

Projects under construction

Los Cóndores

Endesa Chile Investor Presentation 9M15

USE: Public, Investor Relations

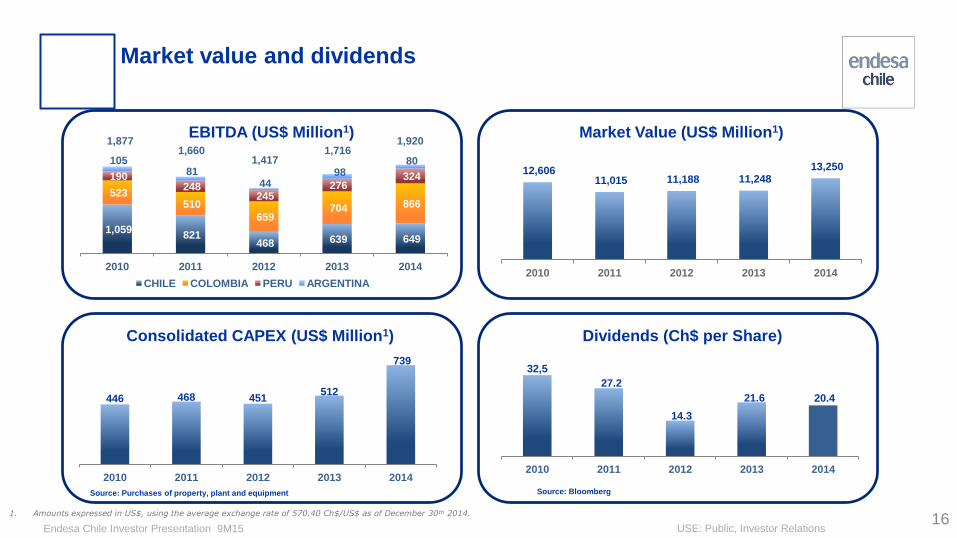

12,606 11,015 11,188 11,248

13,250

2010 2011 2012 2013 2014

1,059 821

468 639 649

523 510

659 704 866

190 248

245 276

324

105 81

44 98

80

2010 2011 2012 2013 2014

CHILE COLOMBIA PERU ARGENTINA

1,877 1,660

1,417 1,716

1,920

Dividends (Ch$ per Share)

EBITDA (US$ Million1) Market Value (US$ Million1)

Market value and dividends

Source: Bloomberg

1. Amounts expressed in US$, using the average exchange rate of 570.40 Ch$/US$ as of December 30th 2014.

Consolidated CAPEX (US$ Million1)

Source: Purchases of property, plant and equipment

16

446 468 451 512

739

2010 2011 2012 2013 2014

32,5

27.2

14.3

21.6 20.4

2010 2011 2012 2013 2014

Endesa Chile Investor Presentation 9M15

USE: Public, Investor Relations

BBB+ Baa2 BBB+

Since:

Affirmed:

Credit Risk Agencies recognition

Jan. 2010 Apr. 2011 Feb. 2010

Jun. 2015 Dec. 2014 Nov. 2014

AA (cl) AA

Jan. 2010 Apr. 2010

Jun. 2015 Jul. 2015

International market Chilean market

RATINGS BASED UPON:

• Well diversified and efficient assets

• Leading market share in the four countries where we operate

• Transparent and favorable regulatory framework in Chile

• Solid financials, good cash flow generation and prudent financial management

• Conservative commercial policy

17

Endesa Chile Investor Presentation 9M15

USE: Public, Investor Relations

Endesa Chile’s Investor Relations Team

18

Contact us at:

Susana Rey Head of Investor Relations

(56) 22630 9606 [email protected]

Catalina Gonzalez Investor Relations Senior Analyst

(56) 22630 9603 [email protected]

Guillermo Berguecio Investor Relations Analyst

(56) 22630 9506 [email protected]

Francisco Basauri Investor Relations Analyst

(56) 22630 9585 [email protected]

Endesa Chile Investor Presentation 9M15

USE: Public, Investor Relations 19

EXHIBITS

Endesa Chile Investor Presentation 9M15

USE: Public, Investor Relations

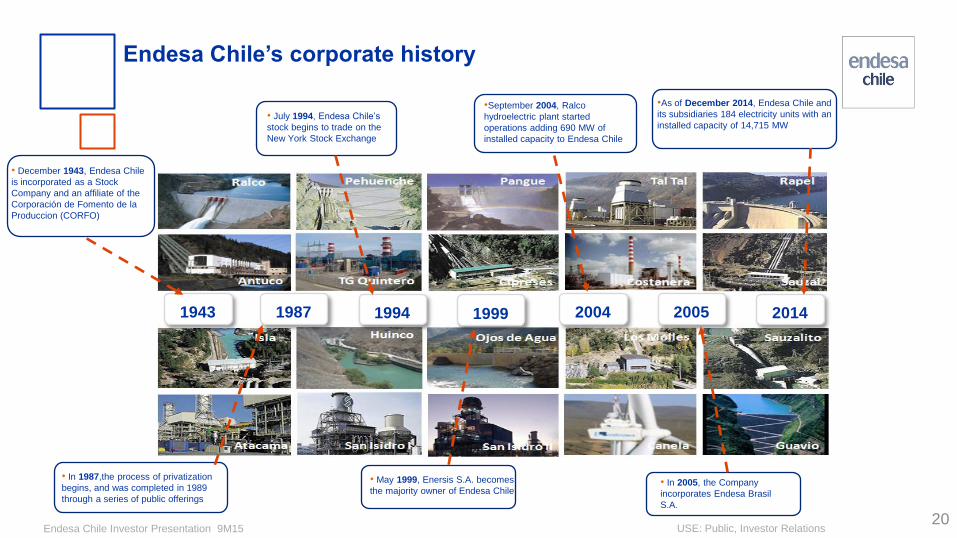

1943 1987 1994 1999 2004 2005 2014

Endesa Chile’s corporate history

• December 1943, Endesa Chile

is incorporated as a Stock

Company and an affiliate of the

Corporación de Fomento de la

Produccion (CORFO)

• July 1994, Endesa Chile’s

stock begins to trade on the

New York Stock Exchange

•September 2004, Ralco

hydroelectric plant started

operations adding 690 MW of

installed capacity to Endesa Chile

•As of December 2014, Endesa Chile and

its subsidiaries 184 electricity units with an

installed capacity of 14,715 MW

• In 1987,the process of privatization

begins, and was completed in 1989

through a series of public offerings

• May 1999, Enersis S.A. becomes

the majority owner of Endesa Chile • In 2005, the Company

incorporates Endesa Brasil

S.A.

20

Endesa Chile Investor Presentation 9M15

USE: Public, Investor Relations 21

Purchase of additional 50% stake of GasAtacama

• Thermal power plant, Gas – CCGT (6 units)

• 780 MW of installed capacity.

• Located in Mejillones, Atacama region, Northern Chile (SING

system).

• Estimated load factor: 46%

• GasAtacama also has a 941 km gas pipeline, 530 km in Argentina

and 411 km in Chile. In addition, the 226 km long Taltal lateral

pipeline, carries natural gas to our Taltal thermal plant.

Attractive investment

• Endesa Chile became the controller of GasAtacama (98%).

• Enhanced the role of the Company by reaching 20% market share

of installed capacity in the SING system.

• Possibility of permanent gas supply through Endesa Chile and its

own regasification infrastructure .

• Positive outlook regarding a likely interconnection between SIC

and SING systems.

Installed capacity added in 2014

Endesa Chile Investor Presentation 9M15

USE: Public, Investor Relations 22

Colombia

Salaco Chain (optimization)

• Upgraded the minor plants to reach 221 MW capacity.

• Located in the Bogotá River system, Colombia.

• Total CAPEX of US$ 44 million.

• Optimization works started in January 2013 and were

completed in December 2014.

• 145 MW of capacity added through 6 units entering into

service, generating an additional 324 GWh in 2014.

Installed capacity added in 2014

Endesa Chile 9M15 Results

23

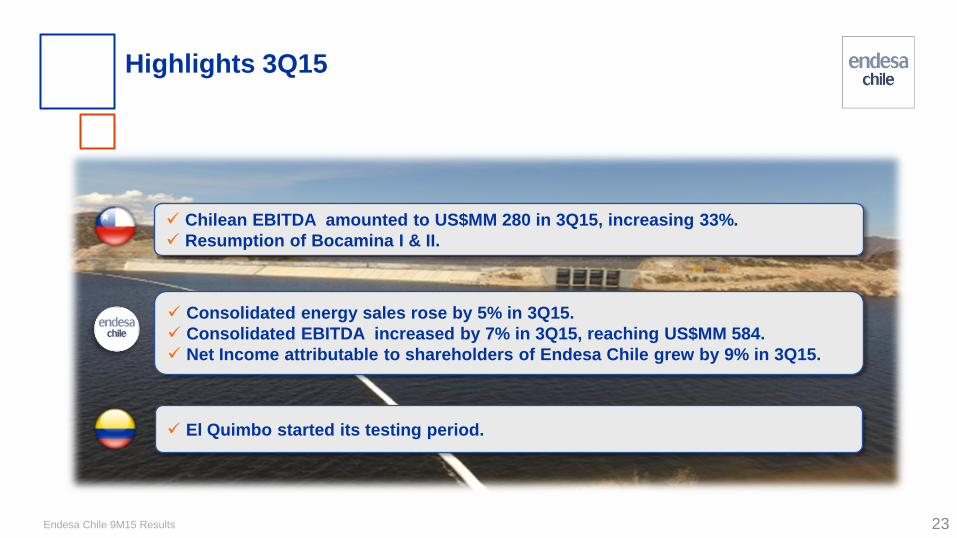

Highlights 3Q15

Chilean EBITDA amounted to US$MM 280 in 3Q15, increasing 33%.

Resumption of Bocamina I & II.

Consolidated energy sales rose by 5% in 3Q15.

Consolidated EBITDA increased by 7% in 3Q15, reaching US$MM 584.

Net Income attributable to shareholders of Endesa Chile grew by 9% in 3Q15.

El Quimbo started its testing period.

Endesa Chile 9M15 Results

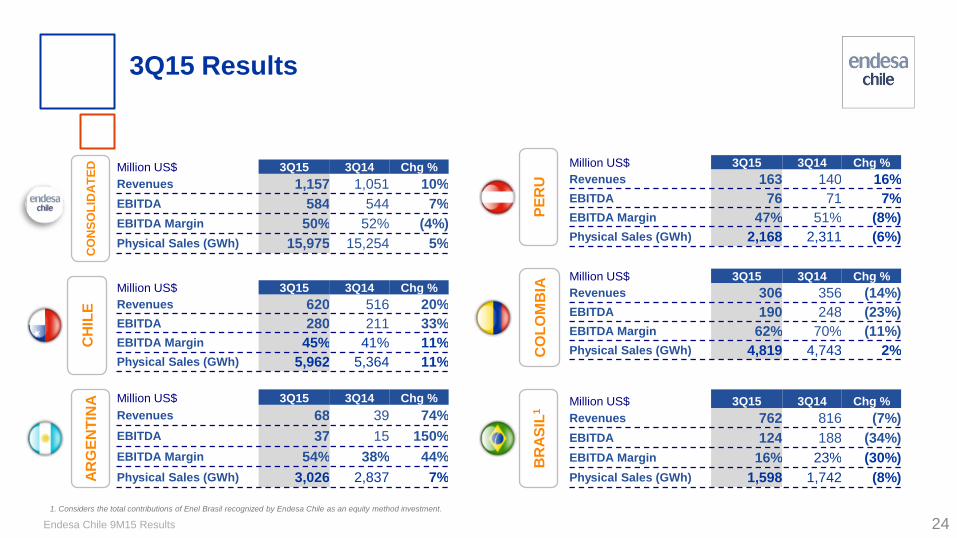

Million US$ 3Q15 3Q14 Chg %

Revenues 762 816 (7%)

EBITDA 124 188 (34%)

EBITDA Margin 16% 23% (30%)

Physical Sales (GWh) 1,598 1,742 (8%)

24

3Q15 Results C

HIL

E

AR

GE

NT

INA

C

ON

SO

LID

AT

ED

CO

LO

MB

IA

PE

RU

BR

AS

IL1

Million US$ 3Q15 3Q14 Chg %

Revenues 1,157 1,051 10%

EBITDA 584 544 7%

EBITDA Margin 50% 52% (4%)

Physical Sales (GWh) 15,975 15,254 5%

Million US$ 3Q15 3Q14 Chg %

Revenues 620 516 20%

EBITDA 280 211 33%

EBITDA Margin 45% 41% 11%

Physical Sales (GWh) 5,962 5,364 11%

Million US$ 3Q15 3Q14 Chg %

Revenues 68 39 74%

EBITDA 37 15 150%

EBITDA Margin 54% 38% 44%

Physical Sales (GWh) 3,026 2,837 7%

Million US$ 3Q15 3Q14 Chg %

Revenues 306 356 (14%)

EBITDA 190 248 (23%)

EBITDA Margin 62% 70% (11%)

Physical Sales (GWh) 4,819 4,743 2%

Million US$ 3Q15 3Q14 Chg %

Revenues 163 140 16%

EBITDA 76 71 7%

EBITDA Margin 47% 51% (8%)

Physical Sales (GWh) 2,168 2,311 (6%)

1. Considers the total contributions of Enel Brasil recognized by Endesa Chile as an equity method investment.

Endesa Chile 9M15 Results

USE: Public, Investor Relations 25

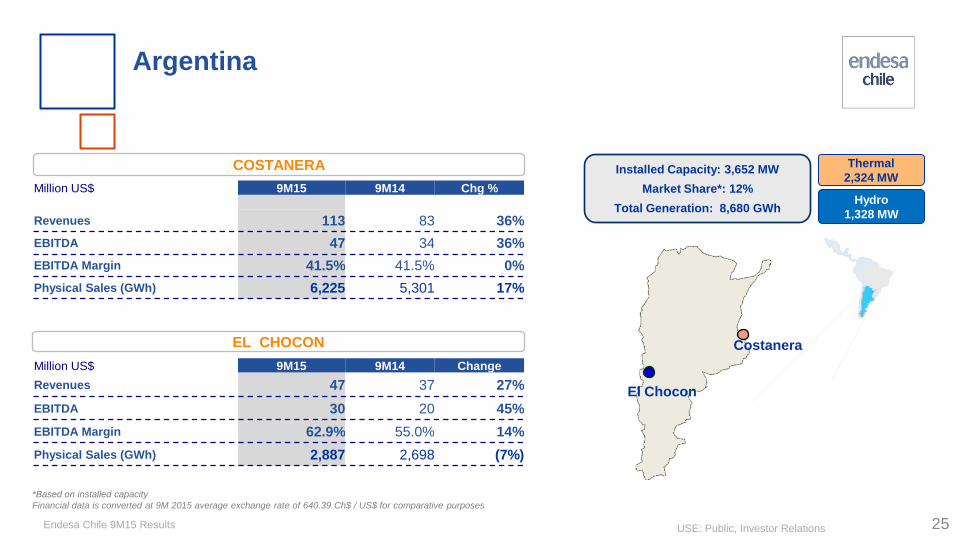

Hydro

1,328 MW

Thermal

2,324 MW

*Based on installed capacity

Financial data is converted at 9M 2015 average exchange rate of 640.39 Ch$ / US$ for comparative purposes

Argentina

Installed Capacity: 3,652 MW

Market Share*: 12%

Total Generation: 8,680 GWh

EL CHOCON

COSTANERA

El Chocon

Costanera

Million US$ 9M15 9M14 Chg %

Revenues 113 83 36%

EBITDA 47 34 36%

EBITDA Margin 41.5% 41.5% 0%

Physical Sales (GWh) 6,225 5,301 17%

Million US$ 9M15 9M14 Change

Revenues 47 37 27%

EBITDA 30 20 45%

EBITDA Margin 62.9% 55.0% 14%

Physical Sales (GWh) 2,887 2,698 (7%)

Endesa Chile 9M15 Results

USE: Public, Investor Relations 26

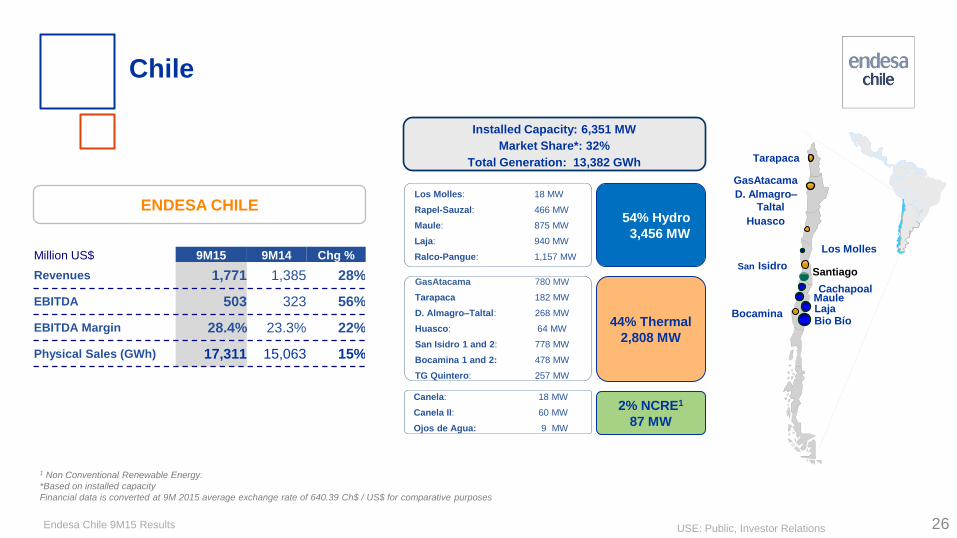

Los Molles: 18 MW

Rapel-Sauzal: 466 MW

Maule: 875 MW

Laja: 940 MW

Ralco-Pangue: 1,157 MW

54% Hydro

3,456 MW

44% Thermal

2,808 MW

GasAtacama 780 MW

Tarapaca 182 MW

D. Almagro–Taltal: 268 MW

Huasco: 64 MW

San Isidro 1 and 2: 778 MW

Bocamina 1 and 2: 478 MW

TG Quintero: 257 MW

2% NCRE1

87 MW

Canela: 18 MW

Canela II: 60 MW

Ojos de Agua: 9 MW

1 Non Conventional Renewable Energy.

*Based on installed capacity

Financial data is converted at 9M 2015 average exchange rate of 640.39 Ch$ / US$ for comparative purposes

ENDESA CHILE

Installed Capacity: 6,351 MW

Market Share*: 32%

Total Generation: 13,382 GWh

Chile

D. Almagro–

Taltal

Bocamina Laja Maule

Bio Bío

Tarapaca

Huasco

San Isidro

Los Molles

Cachapoal

Santiago

GasAtacama

Million US$ 9M15 9M14 Chg %

Revenues 1,771 1,385 28%

EBITDA 503 323 56%

EBITDA Margin 28.4% 23.3% 22%

Physical Sales (GWh) 17,311 15,063 15%

Endesa Chile 9M15 Results

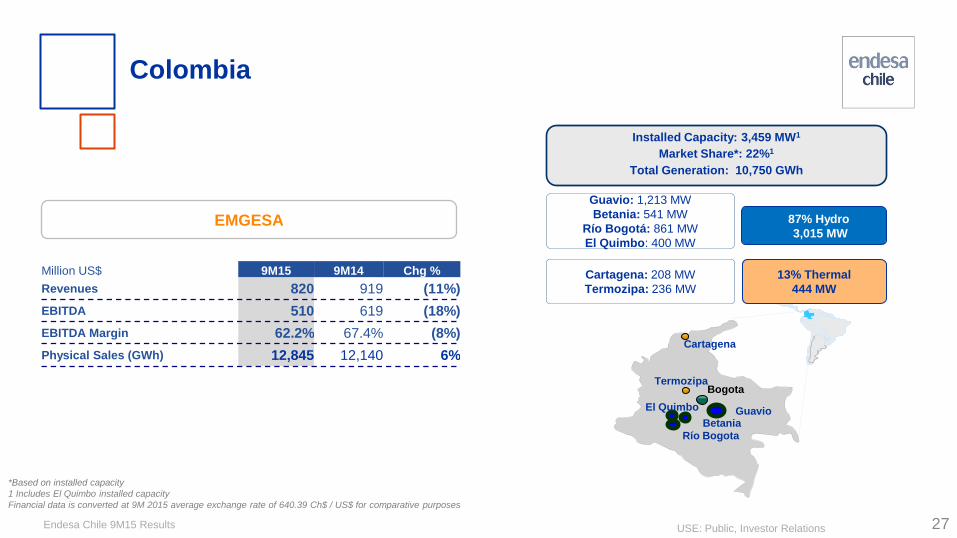

USE: Public, Investor Relations

Cartagena

Bogota

27

Guavio: 1,213 MW

Betania: 541 MW

Río Bogotá: 861 MW

El Quimbo: 400 MW

87% Hydro

3,015 MW

13% Thermal

444 MW

Cartagena: 208 MW

Termozipa: 236 MW

*Based on installed capacity

1 Includes El Quimbo installed capacity

Financial data is converted at 9M 2015 average exchange rate of 640.39 Ch$ / US$ for comparative purposes

Termozipa

Guavio Betania

Río Bogota

EMGESA

Installed Capacity: 3,459 MW1

Market Share*: 22%1

Total Generation: 10,750 GWh

Colombia

Million US$ 9M15 9M14 Chg %

Revenues 820 919 (11%)

EBITDA 510 619 (18%)

EBITDA Margin 62.2% 67.4% (8%)

Physical Sales (GWh) 12,845 12,140 6%

El Quimbo

Endesa Chile 9M15 Results

USE: Public, Investor Relations 28

Ventanilla: 484 MW

Santa Rosa: 413 MW

53% Thermal

896 MW

Cuenca Río Rímac: 588 MW

Yanango: 43 MW

Chimay: 152 MW

47% Hydro

783 MW

*Based on installed capacity

Financial data is converted at 9M 2015 average exchange rate of 640.39 Ch$ / US$ for comparative purposes

Sta Rosa

Ventanilla

Lima

Río Rimac

Yanango

Chimay

EDEGEL

Installed Capacity: 1,680 MW

Market Share*: 19%

Total Generation: 6,190 GWh

Peru

Million US$ 9M15 9M14 Chg %

Revenues 432 403 7%

EBITDA 217 207 5%

EBITDA Margin 50.2% 51.5% (2%)

Physical Sales (GWh) 6,501 6,929 (6%)

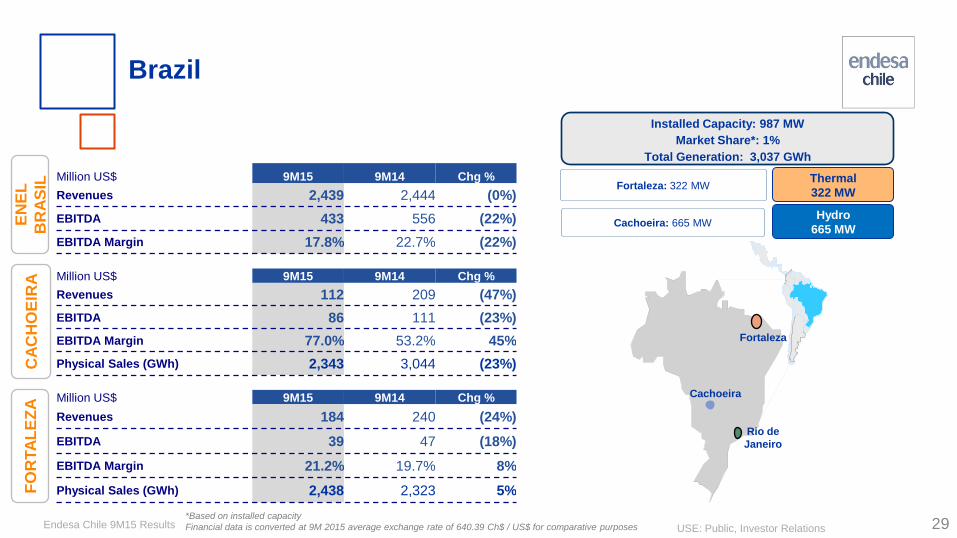

Endesa Chile 9M15 Results

USE: Public, Investor Relations 29

Fortaleza: 322 MW Thermal

322 MW

Cachoeira: 665 MW Hydro

665 MW

*Based on installed capacity

Financial data is converted at 9M 2015 average exchange rate of 640.39 Ch$ / US$ for comparative purposes

CA

CH

OE

IRA

Installed Capacity: 987 MW

Market Share*: 1%

Total Generation: 3,037 GWh

FO

RTA

LE

ZA

Brazil

Fortaleza

Rio de

Janeiro

Cachoeira

Million US$ 9M15 9M14 Chg %

Revenues 112 209 (47%)

EBITDA 86 111 (23%)

EBITDA Margin 77.0% 53.2% 45%

Physical Sales (GWh) 2,343 3,044 (23%)

Million US$ 9M15 9M14 Chg %

Revenues 184 240 (24%)

EBITDA 39 47 (18%)

EBITDA Margin 21.2% 19.7% 8%

Physical Sales (GWh) 2,438 2,323 5%

EN

EL

BR

AS

IL Million US$ 9M15 9M14 Chg %

Revenues 2,439 2,444 (0%)

EBITDA 433 556 (22%)

EBITDA Margin 17.8% 22.7% (22%)

Endesa Chile 9M15 Results

USE: Public, Investor Relations 30

Higher energy sales of 9% due to increasing electric demand

Consolidated generation grew by 4%

Consolidated EBITDA increased by 8%

Summary

El Quimbo is currently in testing period

Bocamina I and II resumed operations

Endesa Chile 9M15 Results

USE: Public, Investor Relations

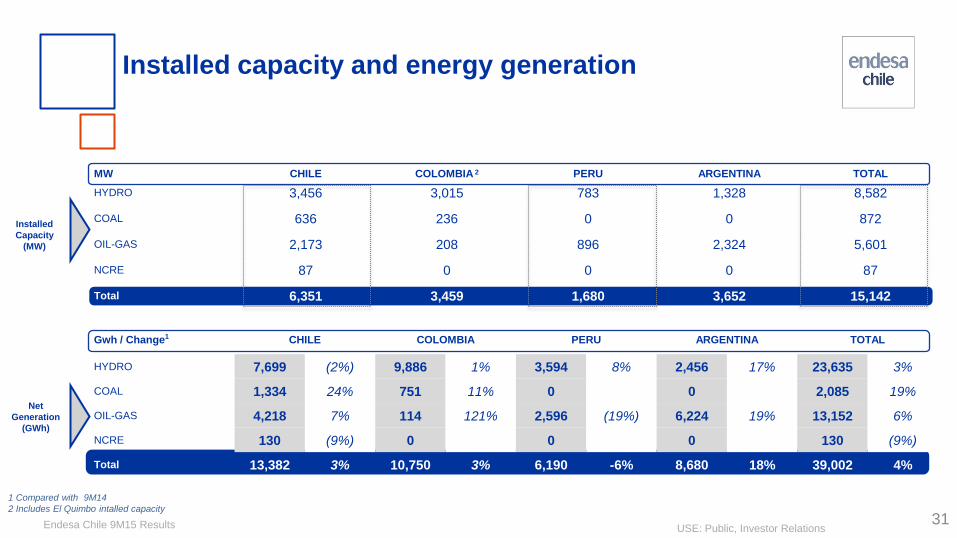

Gwh / Change1 CHILE COLOMBIA PERU ARGENTINA TOTAL

HYDRO 7,699 (2%) 9,886 1% 3,594 8% 2,456 17% 23,635 3%

COAL 1,334 24% 751 11% 0 0 2,085 19%

OIL-GAS 4,218 7% 114 121% 2,596 (19%) 6,224 19% 13,152 6%

NCRE 130 (9%) 0 0 0 130 (9%)

Total 13,382 3% 10,750 3% 6,190 -6% 8,680 18% 39,002 4%

MW CHILE COLOMBIA 2 PERU ARGENTINA TOTAL

HYDRO 3,456 3,015 783 1,328 8,582

COAL 636 236 0 0 872

OIL-GAS 2,173 208 896 2,324 5,601

NCRE 87 0 0 0 87

Total 6,351 3,459 1,680 3,652 15,142

31

Installed capacity and energy generation

Installed

Capacity

(MW)

Net

Generation

(GWh)

1 Compared with 9M14

2 Includes El Quimbo intalled capacity

Endesa Chile 9M15 Results

USE: Public, Investor Relations 32

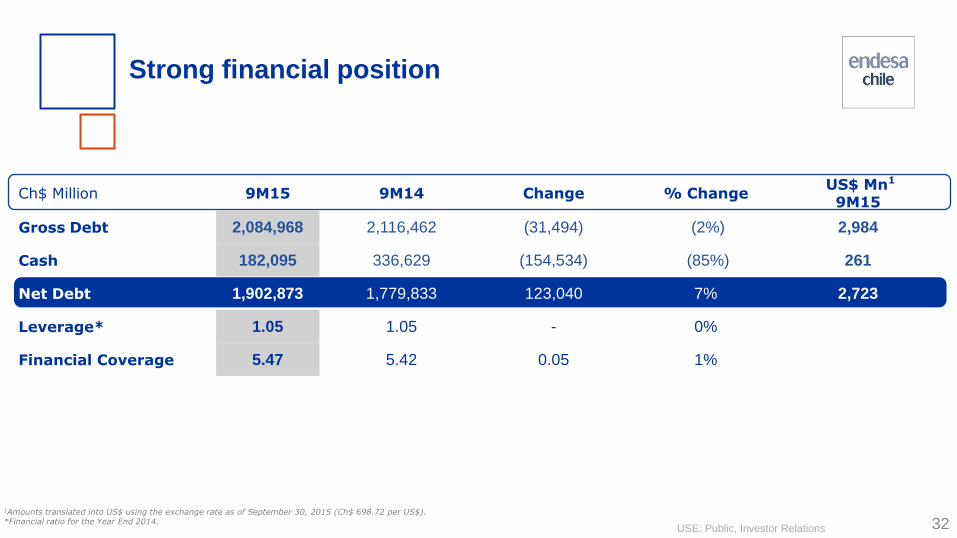

1Amounts translated into US$ using the exchange rate as of September 30, 2015 (Ch$ 698.72 per US$). *Financial ratio for the Year End 2014.

Strong financial position

Ch$ Million 9M15

9M14

Change

% Change

US$ Mn1

9M15

Gross Debt 2,084,968 2,116,462 (31,494) (2%) 2,984

Cash 182,095 336,629 (154,534) (85%) 261

Net Debt 1,902,873 1,779,833 123,040 7% 2,723

Leverage* 1.05 1.05 - 0%

Financial Coverage 5.47 5.42 0.05 1%

Endesa Chile 9M15 Results

USE: Public, Investor Relations

33

Healthy debt maturity profile in each country

1 Includes arrangements and other consolidation adjustments. 2 May not total exactly due to rounding.

US$ million 2015

2016

2017

2018 2019

Balance

TOTAL

Chile 442 10 10 10 110 1,134 1,718

Argentina 13 47 11 3 2 34 110

Peru 5 75 27 37 16 28 188

Colombia 87 125 68 83 129 800 1,291

TOTAL2 547 257 116 133 258 1,996 3,307

Financial Debt Maturity1, as of September 2015

Endesa Chile Investor Presentation 9M15

USE: Public, Investor Relations

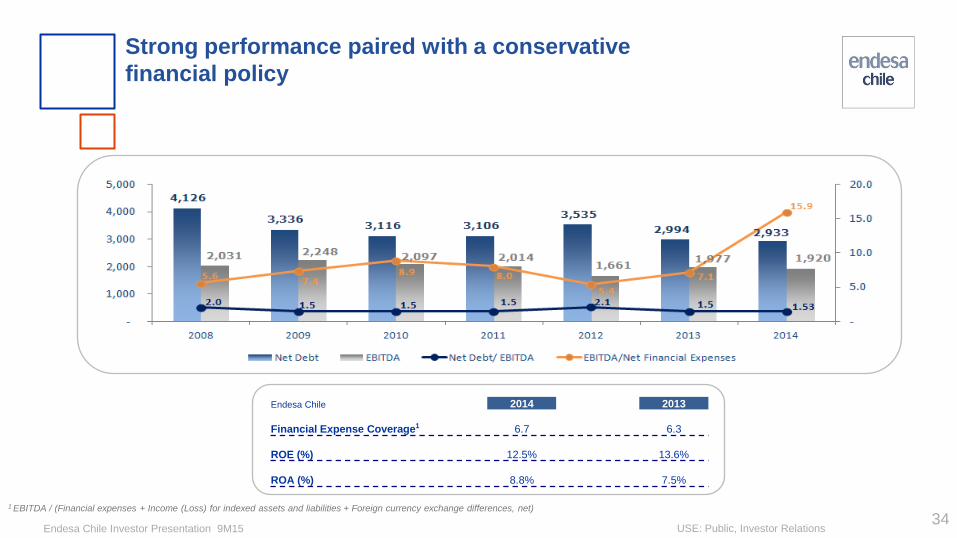

1 EBITDA / (Financial expenses + Income (Loss) for indexed assets and liabilities + Foreign currency exchange differences, net)

Endesa Chile 2014 2013

Financial Expense Coverage1 6.7 6.3

ROE (%) 12.5% 13.6%

ROA (%) 8.8% 7.5%

Strong performance paired with a conservative

financial policy

34

Endesa Chile Investor Presentation 9M15

USE: Public, Investor Relations 35

This presentation contains statements that could constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements appear

in a number of places in this announcement and include statements regarding the intent, belief or current expectations of Endesa Chile and its management with respect to, among other

things: (1) Endesa Chile’ business plans; (2) Endesa Chile’ cost-reduction plans; (3) trends affecting Endesa Chile’ financial condition or results of operations, including market trends in the

electricity sector in Chile or elsewhere; (4) supervision and regulation of the electricity sector in Chile or elsewhere; and (5) the future effect of any changes in the laws and regulations

applicable to Endesa Chile or its subsidiaries. Such forward-looking statements are not guarantees of future performance and involve risks and uncertainties. Actual results may differ

materially from those in the forward-looking statements as a result of various factors. These factors include a decline in the equity capital markets of the United States or Chile, an increase

in the market rates of interest in the United States or elsewhere, adverse decisions by government regulators in Chile or elsewhere and other factors described in Endesa Chile’ Annual

Report on Form 20-F. Readers are cautioned not to place undue reliance on those forward-looking statements, which state only as of their dates. Endesa Chile undertakes no obligation to

release publicly the result of any revisions to these forward-looking statements.