Emperical research: The achievability of CEO non equity incentive plan targets, REM and its...

37

Research on the Relationship between the Achievability of Non-Equity Incentive Plan Targets and Real Earnings Management and their Determinants Empirical Research in Accounting – Group 19 Master Accounting & Control VU University Milio de Charro 2012340 Liza Dillo 1820915 Hugo Goldberg 2151448 Bo van Houten 1873660 Pim Ploos van Amstel 2142619 Date: 07-10-2013 Abstract A topic that got only little attention in the scientific research on accounting is the achievability of performance targets. The main purpose of this paper is to examine the relationship between the achievability of CEO non-equity incentive plan targets and real

Transcript of Emperical research: The achievability of CEO non equity incentive plan targets, REM and its...

Research on the Relationship between the

Achievability of Non-Equity Incentive Plan

Targets and Real Earnings Management and their

Determinants

Empirical Research in Accounting – Group 19

Master Accounting & Control

VU University

Milio de Charro 2012340Liza Dillo 1820915Hugo Goldberg 2151448

Bo van Houten 1873660Pim Ploos van Amstel

2142619

Date: 07-10-2013

Abstract A topic that got only little attention in the scientific research on accounting is theachievability of performance targets. The main purpose of this paper is to examine therelationship between the achievability of CEO non-equity incentive plan targets and real

earnings management and three possible determinants, market-to-book ratio, return onassets and the achievability of prior years. No significant evidence was found on therelationship between the achievability and the predictors. The relationship between realearnings management and the predictors was found to be significant, but not all therelations were in the predicted direction. Also, no evidence was found on theinterrelationship between the dependent variables, achievability on CEO non-equity incentiveplan targets and real earnings management.

1

TABLE OF CONTENTS

1. Introduction

p.3

2. Related Literature

p.4

2.1 Non-Equity incentive plan

p.4

2.1.1 Achievability of incentive plan targets p.4

2.2 Real earnings management

p.4

2.3 The relationship between achievability of performance targets

and real earnings p.5

management

2.4 Determinants p.5

2.4.1 Market-to-Book ratio p.5

2.4.2 Achievability in prior years p.6

2.4.3 Return on Assets

p.6

3. Hypothesis Development

p.7

4. Research Design

p.10

4.1 Sample selection and data resources

p.10

4.2 Measurements p.10

4.2.1. Causal Model p.10

4.2.2. Variables

p.12

5. Results p.14

2

5.1 Descriptive statistic and data exploring

p.14

5.2 Regression 1: Achievability of non-equity incentive plan targets

p.14

5.2.1 Assumptions underlying linear regression analysis p.16

5.3 Regression 2: Real earnings management

p.17

5.3.1 Assumptions underlying linear regression analysis

p.19

5.4 Interrelationship of dependent variables

p.20

6. Conclusion and Discussion

p.22

References p.25

Appendix p.26

1. INTRODUCTION

A lot of scientific research has been conducted on real earnings

management. Earnings management occurs when managers use judgment in

financial reporting and in structuring transactions to alter

financial reports to either mislead stakeholders about the

underlying economic performance or to influence contractual outcomes

that depend on reported accounting numbers (Healy & Wahlen, 1999, p.

368).

A topic that gets only little attention in the scientific

research is non-equity incentive plan compensation. Non-equity

3

incentive compensation represents a bonus paid in cash. The term

“non-equity incentive plan compensation” was developed by the

Securities and Exchange Commission (SEC) in 2006 to provide more

disclosure of compensations in the financial statement. This new

category was designed to capture executive incentives awarded in

cash which are based on specific pre-established performance-based

targets, because cash incentives like annual bonuses are not

specifically linked to pre-established performance-based incentives

(Palmon, Santoro & Strauss, 2009).

The purpose of this research project is to examine to what extent

the achievability of CEO non-equity incentive plan targets and real

earnings management (in terms of reducing the cost of goods sold by

overproducing inventory) are interrelated. Finally this research

project examine to what extent each of the dependent variables is

related to the achievability of prior year’s CEO non-equity

incentive plan targets, market-to-book ratio and return on assets.

4

2. RELATED LITERATURE

2.1 Non-equity incentive plan

Non-equity incentive compensation represents a bonus paid in cash.

This is different from equity compensations where an equity interest

in the company is given, which gives the receiver a direct economic

interest in the future development of the stock price of the

company. This interest leads automatically to long-term goal

congruence between managers and shareholders.

The term “non-equity incentive plan compensation” was developed

by the Securities and Exchange Commission (SEC) in 2006 to provide

more disclosure of compensations in the financial statement. This

new category was designed to capture executive incentives awarded in

cash which are based upon specific pre-established performance-based

goal, because cash incentives like annual bonuses are not

specifically linked to pre-established performance-based incentives

(Palmon, Santoro & Strauss, 2009).

2.1.1 Achievability of incentive plan targets

A phenomenon that received only little attention from accounting

researchers is the achievability of performance targets. Most

experimental studies show that less achievable targets lead to

higher performance, except when the subjects experienced the goals

as unachievable.

There are two standpoints from which the achievability of

performance targets can be measured. One is the ex ante point of view

which implicates the expected achievability of the target and the

other is the ex post standpoint which reflects the actual achieved

performance (Merchant & Manzoni, 1989).

5

2.2 Real Earnings Management

Earnings management occurs when managers use judgment in financial

reporting and in structuring transactions to alter financial report

to either mislead some stakeholders about the underlying economic

performance or to influence contractual outcomes that depend on

reported accounting numbers (Healy & Wahlen, 1999). In theory of

earnings management, there are two ways to manage the earnings of a

company. The most researched way of earnings management is the

accrual based earnings management. Accrual-based earnings management

is achieved by changing the accounting methods or estimates used

when presenting a given transaction in the financial statement. For

example, this can be changing the depreciation method for fixed

assets (Zang, 2012) or by taking expenses that are not reasonably

expected to generate future cash flows and label them as investment

expenditures (Bergstresser & Philippon, 2006).

The second type, real earnings management or real activities

manipulation, is a purposeful action to alter reported earnings in a

particular direction which is achieved by changing the timing or

structuring of an operation investment, or financing transaction

which has suboptimal business consequences (Zang, 2012). In order to

deliver earnings, R&D, advertising and maintenance expenditures and

cost of goods sold are decreased. Between both types of earnings

management, there is a timing difference: real activity

manipulations must occur during the fiscal year, where accrual based

earnings management is applied after the fiscal year-end. This means

that the latter can be adjusted to the outcomes of the former.

2.3 The relationship between real earnings management and the

achievability of incentive plan targets.

Prior research shows that executives often engage in earnings

management, because they receive an incentive for good performance.

6

CEO bonus plans that have a performance threshold can motivate

executives to smooth their performance. Holthausen et al. (1995)

find that executives manage earnings upward when they are below the

threshold, but do not manage earnings downward when their reported

performance exceeds the maximum.

In addition to the above, management receives less incentives to

manage earnings when the thresholds itself are low, or in other

words, the achievability of the performance targets is high. As

reported in Merchant & Mazoni (1989) an incentive for top managers

to state highly achievable targets is to reduce the engaging in

earnings management practices. Short-term earnings management is a

means available to achieve performance targets and low achievability

or high thresholds would give too much pressure to manage earning on

short-term.

2.4 Determinants

For this research, we have chosen three determinants to examine the

relationship between the achievability of CEO non-equity incentive

plan targets and real earnings management.

2.4.1 Market–to-book Ratio

The market-to-book ratio is normally used as a proxy to observe

firms’ major investment opportunities. Investment opportunities play

an important role in the corporate finance of a firm. The market-to-

book ratio has the highest information constant with respect to

investment opportunities. Adam & Goyal (2008) make a distinction

between the market-to-book asset (MBA) ratio and the market-to-book

equity (MBE) ratio. The MBA ratio represents the market value of the

assets divided by the book value of the assets, which is a proxy for

the assets in place and the investment opportunities. The MBE ratio

is the market value of the equity divided by the book value of the

7

equity. The market value of the equity measures the present value of

the cash flows to equity holders from both assets in place and

future investment opportunities. The book value represents the

accumulated value generated from existing assets only.

Zang (2012) uses the market-to-book ratio to control for

systematic variations in abnormal production costs, discretionary

expenditures and accruals related to a firms’ growth rate in testing

the hypothesis of whether managers decide between the use of real

activities manipulation or accrual-based earnings management.

2.4.2 Achievability in prior years

When earnings targets do not fully adjust for past performance,

Merchant (2010) and co-researchers expected that firms that failed

to meet their 2008 earnings target would have a more difficult 2009

target than firms that met or exceeded their 2008 target. Merchant

(2010) finds evidence that the achievability of earnings targets is

positively associated with prior year’s performance relative to an

earnings target. When firms failed to meet their targets in prior

years, it is expected that it will even be more difficult for those

firms to meet their targets in the next year.

2.4.3 Return on Assets

The return on assets (ROA) shows how profitable a company’s assets

are in generating revenues. This is also called the “productivity

ratio” (Allred, 1997). The ROA is computed as the net income divided

by the average total assets. The ROA provides information about the

management performance in using their business assets to maximize

revenues by satisfying customer needs. Other than ROE (return on

equity), the ROA measurement includes all of the business assets,

arising from liabilities and equity. It combines a measure of

efficiency and external effectiveness. A higher asset turnover due

8

to the artificial decrease of the denominator (through downsizing or

divesting) which may allow management to boost ROA in the short term

is harmful to long term competitiveness since it is caused by

postponing any investments (Courtis, 2003).

9

3. HYPOTHESIS DEVELOPMENT

A purpose of this research is to examine the achievability of CEO

non-equity incentive plan targets and potential determinants of the

degree of achievability. Consistent with several empirical studies

in the accounting literature as shown in the literature review, we

predict that performance targets are positively influenced by

performance targets set in prior years. Hence, we formulate the

following hypothesis:

H1: The achievability of CEO non-equity incentive plan targets in prior years is positively

related with the achievability of current CEO non-equity incentive plan targets in prior

years.

The market reacts positively (resp. negatively) to the

announcement of a challenging (resp. less challenging) target

established in the annual incentive plan (Kim & Yang, 2009). More

specifically, if the market understands that firms tend to set easy

performance targets for their top executives, a challenging

performance target should signal the market the firms’ high

profitability in the future. On the other hand, if a performance

target is not challenging, mediocre or even poor performance will be

rewarded and the incentive mechanism will break down (Anderson,

Dekker & Sedatole, 2008). If the market-to-book ratio is high it

means the market value in excess of the book value. Therefore the

market defines the company at higher value and the market will react

on announcement of challenging targets and therefore has a positive

relation to the achievability of CEO non-equity incentive plans

targets. This reasoning leads to following subsidiary hypothesis:

H2: Other things being equal, market-to-book ratio is positively related with the

achievability in current CEO non-equity incentive plan targets

10

.

The combination of high returns and high operating performance,

according to Cooper et al. (2009), combines the allure of the firms

and can be associated with star effects that high pay may produce

for the firm’s CEO and an inability to distinguish luck from skills

resulting in a negative relation between CEO pay and future returns.

This indicates future returns will decrease by high payments for

CEO’s. Firms with a high ROA set more challenging performance

targets and the achievability of incentive plan is more arduous to

realize. Thus higher return on assets results in less achievability

of CEO non-equity incentive plan targets and the variables therefore

are negatively related to each other. Hence, the following

hypothesis predicts:

H3: Other things being equal, the ROA of a firm is negatively related with the achievability

of current CEO non-equity incentive plan targets.

In this research we focus on one type of real earnings

management, namely through overproducing inventory. To manage

earnings upwards, managers can produce more goods than necessary.

With higher production levels, fixed overhead costs are spread over

a larger number of units, which leads to a lower fixed cost per

unit. This implies that the reported costs of goods sold are lower

and the reported profit margins are higher (Roychowdhury, 2006).

Holthausen et al. (1995) investigated to which extent executives

manipulate earnings to maximize the present value of bonus plan

payments. They did not find evidence for the fact that managers

manipulate earnings downwards when earnings are below the minimum

necessary to receive any bonus. We expect that when the

achievability in prior years is high, the overall level of real

earnings management will be low. There will be less incentive for

managers to apply real earnings management when targets are being

11

met and the performance of a company is good, which leads to the

following hypothesis:

H4: Other things being equal, the achievability of CEO non-equity incentive plan targets in

prior years is negatively related to the level of real earnings management.

Skinner & Sloan (2002) show that the incentive to report a

growth in earnings is increasing with firms’ growth opportunities.

It is likely that growth firms experience pressure to meet other

earnings thresholds. The most used proxy for growth opportunities is

the market-to-book ratio. That is why we state that firms with a

high market-to-book ratio are likely to exhibit high abnormal

productions costs (Roychowdhury, 2006). This expectation can be

expressed in the following hypothesis:

H5: Other things being equal, the market-to-book level of a firm is positively related to the

level of real earnings management.

Return on assets is often used as a measurement of management

performance. A higher ROA relates to a higher profitability of the

assets of a firm. As real earnings management is used to report

higher earnings, it is less likely that it is used when the ROA is

higher, than when there is a lower ROA. This leads to the following

hypothesis:

H6: Other things being equal, the return on assets of a firm is negatively related to the

level of real earnings management.

In contrast, managers of poorly performing firms may be

unwilling to manipulate earnings to achieve maximum payouts under

their bonus plans, because of potential technical violations of the

firm’s lending agreements. The actual award, relative to the award

target, is based on the degree to which financial goals and

12

individual performance objectives established early in the fiscal

year haven been achieved (Holhausen et al., 1995). As mentioned

before, management receives less incentives to manage earnings when

the thresholds itself are low, or in other words, the achievability

of the performance targets is high (Merchant & Mazoni, 1989). The

bonus actually earned depends on the degree to which the performance

target is achieved. As a consequence, if the achievability of CEO

non-equity incentive plan targets are rather low, the degree of

financial goals are harder to achieve and the management receives

more incentives to manipulate earnings. Hence, we predict the

following:

H7: There is a negatively interrelated relationship between the achievability of CEO non-

equity incentive plan targets and real earnings management.

13

4. RESEARCH DESIGN

4.1 Sample selection and data resources

A random selection was taken of 400 U.S. listed firms from the S&P

1500 list in the year 2012 using Execucomp excluding financial

institutions (SIC 6000-6999) and regulated industries (SIC 4400-

5000) from the sample. Execucomp was used to conduct the variables

of the achievability of CEO non-equity incentive plan targets for

the year 2012 (ACHIEV2012t). The achievability consists of two

components: the actual achieved non-equity incentive plans (ex post)

and non-equity incentive plan targets (ex ante). When a company did

not have a CEO the executive with highest pay out was taken. When a

CEO or executive had different kinds of non-equity incentive plans

we took the total by adding the compensations together using

Microsoft Access. Different kinds of compensation plans of five

firms where retrieved in their annual statements by using

AuditAnalytics to be certain that the combined amount was taken.

In order to conduct the data for the achievability of non-equity

incentive plan targets in the prior years we used the information

about the achievability in 2010 and 2011 from Execucomp. The sample

size reduced to a dataset of 286 companies. The decrease in the

amount of data from the companies could be the result of CEO-

switches within companies. When a company is not listed in the S&P

1500 in the three consecutive years and combining information from

different data sources could also be reasons why there was a

decrease in the amount.

The list of 286 firms was used to collect data through Compustat

in order to compute the following dependant variables from 2012:

Market-to-book ratio (MtoBt).

Return on Assets (ROAt).

14

X1 Market to book ratio

X2 Achievability in prior years

X3 Return on Assets

Y1: Achievability of CEO non-equity

plan targets

Y2 Real earnings management

Real Earnings Management as the abnormal production level

(REMt).

4.2 Measurements

4.2.1. Causal Model

As described in the literature review and hypotheses development we

are interested in the relationship between two interdependent

variables and it’s determinants. The following model gives a visual

representation of our research (Figure 1):

15

(a)

(b)

Figure 1: Causal model

Relation (a) consists of two regression analyses. To test the first

regression (H1, H2 and H3) we estimate the following regression using

the achievability of non-equity incentive plan targets in 2012

(ACHIEV2012t):

ACHIEV2012t = + 1MtoBt + 2Prioryears + 3ROAt + εt

(Equation 1)

To test to what extent the dependent variable of real earnings

management is related to its determinants (H4, H5 en H6) we estimate

the following regression:

REMt = + 1MtoBt + 2Prioryears + 3ROAt + εt

(Equation 2)

Relation (b) is tested by a Pearson correlation test to measure if

there is an interrelationship between our dependent variables (H7)

4.2.2 Variables

The achievability ratio of non-equity incentive plan targets is

measured by the ratio of the actual “non-equity incentive plan

16

compensation” and the ex ante “estimated future payouts under non-

equity incentive plan – target” of CEO’s. The achievability in prior

years is measured as the mean of the ratio of ex post and ex ante

achievability for the year of 2011 and 2010.

Real earnings management is measured as the level of production

costs (PRODt) divided by total assets (At-1). The estimate of a normal

level of production costs is achieved by the following regression

(Roychowdhury, 2006; Zang, 2012):

PRODt /At-1 = 0 + 1(1 / At-1) + 2(St /At-1) + 3(∆St / At-1) + 4( S∆ t-1 / At-1) +

εt (Equation 3)

Here, PRODt is the sum of the cost of goods sold in year t and the

change in inventory from t-1 to t. At-1 is the total assets in year t-

1. St is the net sales in year t and S∆ t-1 is the change in net sales

from year t-1. The residual from Equation (3) gives an estimation of

the abnormal level of production costs: the higher the residual, the

larger the amount of inventory overproduction and the greater the

increase in reported earnings is through reducing the cost of goods

sold. Table 1 reports the estimates of the Equation 3 and

corresponding level of significant. Three of the mean coefficients

(2 t/m 4) are significant at a level of 5 percent, of which two are

significant at a 1 percent level.

Table

2

Table 1: Coefficient table

17

Coefficientsa

Model

UnstandardizedCoefficients

Standardized

Coefficients

t Sig.BStd.Error Beta

1 Intercept -,253 ,028 -9,047 ,000

1 / At-1 ,000 ,000 ,016 ,960 ,338St /At-1 ,855 ,021 ,910 39,808 ,000∆St / At-

1-,242 ,104 -,047 -2,319 ,021

S∆ t-1 / At-

1,344 ,076 ,108 4,557 ,000

a. Dependent Variable: PRODt /At-1

reports an Adjusted R Square of 92.1 percent of the production cost

model. This indicates that the model has a high substantial

explanatory power. The obtained residual is the indicator for real

earnings management from now on and indicated as REMt

Model Summaryb

Model R

RSquare

Adjusted RSquare

Std. Errorof theEstimate

1 ,960a ,922 ,921 ,2619231a. Predictors: (Intercept), 1/At-1, St /At-1, ∆St / At-1,

S∆ t-1 / At-1

b. Dependent Variable: PRODt /At-1

Table 2: Model summary

The market-to-book ratio is received by dividing the total market

value of the equity fiscal year 2012 by the difference of the total

assets and total liabilities of the companies. The market-to-book

ratio of the fiscal year is computed by the following equation:

MtoB = Market value Equity / (Total Assets – Total Liabilities)

(Equation 4)

The third independent variable is the return on assets. From

Compustat the net income and total assets were collect to calculate

the ROA by the following equation:

ROA = Net Income / Total Assets (Equation

5)

5. RESULTS

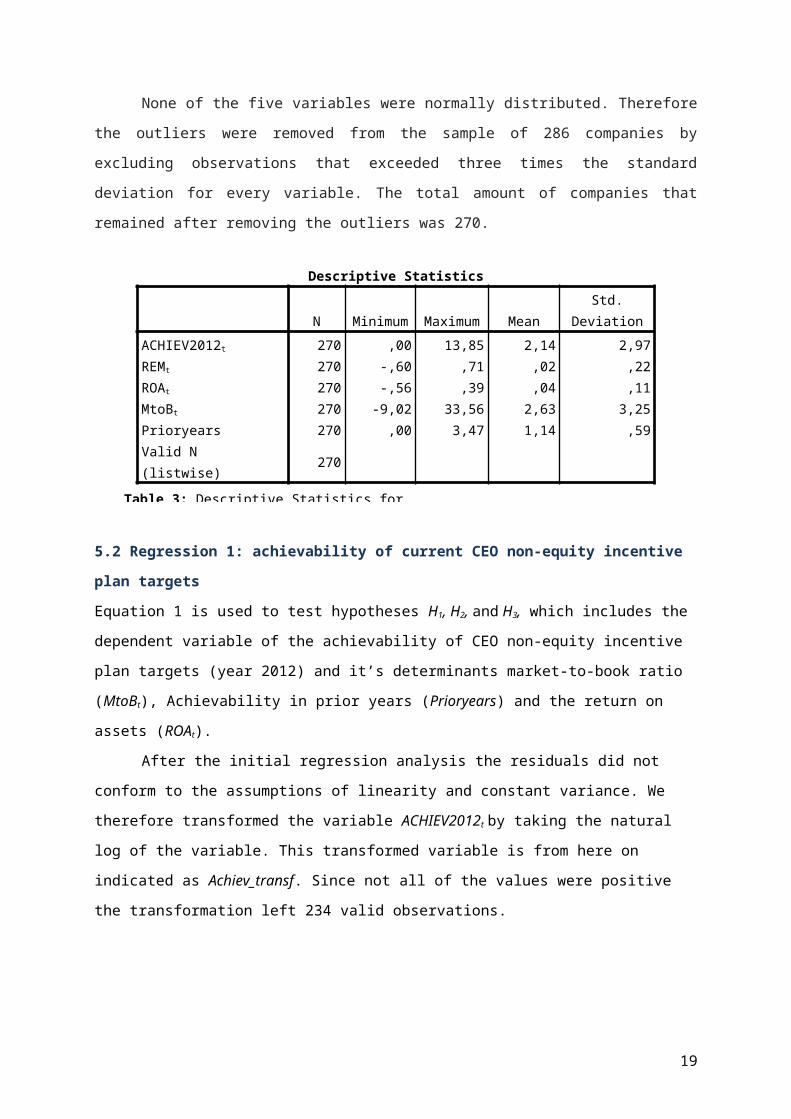

5.1 Descriptive statistics and data exploration

Before conducting linear regression analyses the following

descriptive statistics where found that include the mean, minimum,

maximum and standard deviation of the variables that have been

examined, shown in the Table 3.

18

Table 3: Descriptive Statistics for

None of the five variables were normally distributed. Therefore

the outliers were removed from the sample of 286 companies by

excluding observations that exceeded three times the standard

deviation for every variable. The total amount of companies that

remained after removing the outliers was 270.

Descriptive Statistics

N Minimum Maximum MeanStd.

DeviationACHIEV2012t 270 ,00 13,85 2,14 2,97REMt 270 -,60 ,71 ,02 ,22ROAt 270 -,56 ,39 ,04 ,11MtoBt 270 -9,02 33,56 2,63 3,25Prioryears 270 ,00 3,47 1,14 ,59Valid N (listwise) 270

5.2 Regression 1: achievability of current CEO non-equity incentive

plan targets

Equation 1 is used to test hypotheses H1, H2, and H3, which includes the

dependent variable of the achievability of CEO non-equity incentive

plan targets (year 2012) and it’s determinants market-to-book ratio

(MtoBt), Achievability in prior years (Prioryears) and the return on

assets (ROAt).

After the initial regression analysis the residuals did not

conform to the assumptions of linearity and constant variance. We

therefore transformed the variable ACHIEV2012t by taking the natural

log of the variable. This transformed variable is from here on

indicated as Achiev_transf. Since not all of the values were positive

the transformation left 234 valid observations.

19

Table 4: ANOVA fot the As indicated by table 4 the 2012 achievement regression model is not

statistically significant (0.136), so the R square is meaningless

and further interpretation of the components of the model is

useless. After this we tested the relations separately by running

three separate regressions. The regression model of the dependent

variable Achiev_transf and the predictor MtoBt indicates that the

independent variable MtoBt is not statistically significant (0.571)

with a positive effect (0.135) on the 2012 Achievability (Appendix

I). Therefore we reject hypothesis 2. The regression model of the

dependent variable Achiev_transf and the predictor ROAt indicates that

the independent variable is not statistically significant (0.351)

with a positive effect (0.135) on the 2012 Achievability (Appendix

II). Therefore we reject hypothesis 3.

The regression analysis of the effect of “current CEO non-equity

incentive plan targets in prior years (Prioryears)” on “the achievability of CEO non-equity

incentive plan targets (Achiev_transf)” (H1) did give a significant value of 0.30

(see table 5 and 6).

ANOVAa

Model

Sum of

Squares df

Mean

Square F Sig.

20

ANOVAa

Model

Sum of

Squares df

Mean

Square F Sig.

1 Regression 9,516 3 3,172 1,868 ,136b

Residual 390,631 230 1,698

Total 400,147 233

a. Dependent Variable: Achiev_transfb. Predictors: (Constant), Prioryears, MtoBt , ROAt

1 Regressio

n8,030 1 8,030 4,751 ,030b

Residual 392,117 232 1,690

Total 400,147 233

a. Dependent Variable: Achiev_transfb. Predictors: (Constant), Prioryears

Model Summaryb

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 ,142a ,020 ,016 1,300

a. Predictors: (Constant), Prioryearsb. Dependent Variable: Achiev_transf

TTable 6: Model summary Achievability

The total amount explained in the model by the Adjusted R Square is

1.6 percent. Therefore we accept hypothesis 1. Coefficientsa

Model

Unstandardized

Coefficients

Standardize

d

Coefficient

s

t Sig.B Std. Error Beta

1 (Constan

t)-,203 ,196 -1,037 ,301

Prioryea

rs,323 ,148 ,142 2,180 ,030

Table 5: ANOVA regression Prioryears on

21

Table 7: Coefficients of the regression analysis Prioryears on

Figure 2: Scatterplot of the unstanderdized perdicted value and standardised residuals of Achievability

a. Dependent Variable: Achiev_transf

5.2.1 Assumptions underlying linear regression analysis:

The underlying assumptions of a linear regression to value the

outcomes of the model are linearity, independence, constant variance

and normality of the residuals. We tested these assumptions for the

last regression using a scatterplot, histogram, a Q-Q plot and the

Kolmogorov-Smirnov test (Figure 2, 3 and 4).

The Q-Q plot was used to test the assumptions of linearity,

independence and homoscedasticity. Because there are no

heteroscedasticity and non-linear relationships, the assumptions of

linearity and constant variance are met. In the scatter plot there

is no indication that some of the residuals are dependent of one

another since we do not detect any patterns. Although the patterns

are usually hard to recognize the assumption of independence is met.

At last, the normality of the residuals was tested (Figure 3 and Figure 4).

22

Figure 3: Histogram Achievability Figure 4: Q-Q plot Achievability

From the histogram and the Q-Q plot it is concluded that the

assumption of normality is met. The Kolmogorov-Smirnov test also

indicates that the normality assumption is met since the test is not

significant (0.084) (Table 8).

Tests of Normality

Kolmogorov-Smirnova Shapiro-Wilk

Statist

ic df Sig.

Statist

ic df Sig.

Res Prioryears ,055 234 ,084 ,988 234 ,057

a. Lilliefors Significance Correction

Table 8: Test of Normality Achievability

5.3 Regression 2: real earnings management

Equation 2 is used to test hypotheses H4, H5, and H6, which includes

the dependent variable of real earnings management (REMt) and it’s

predictor market-to-book ratio (MtoBt), Achievability in prior years

(Prioryears) and the return on assets (ROAt).

23

ANOVAa

Model

Sum of

Squares df

Mean

Square F Sig.

1 Regressio

n1,178 3 ,393 8,964 ,000b

Residual 11,653 266 ,044

Total 12,831 269

a. Dependent Variable: REMt

b. Predictors: (Constant), Prioryears, MtoBt, ROAt

As indicated by table 9 the real earnings management regression

model is statistically significant (0.000). The Adjusted R Square of

0.082 indicates that the achievability in prior years, the ROA and

the MtoBt value explain 8.2 percent of the real earnings management.

Model Summaryb

Model R R Square

Adjusted R

Square

Std. Error

of the

Estimate

1 ,303a ,092 ,082 ,20930168

a. Predictors: (Constant), Prioryears, MtoBt,

ROAt

b. Dependent Variable: REMt

Table 10: Model Summary real earnings management

Coefficientsa

Model Unstandardized

Coefficients

Standardize

d

Coefficient

s

t Sig.

Table 9: ANOVA real earnings management

24

B Std. Error Beta

1 (Constan

t),068 ,030 2,305 ,022

MtoBt -,011 ,004 -,168 -2,843 ,005

ROAt -,468 ,120 -,231 -3,901 ,000

Prioryea

rs-,004 ,022 -,012 -,200 ,842

a. Dependent Variable: REMt

Table 11: Coefficient table real earnings management

The coefficients table (Tabel 11) of the regression model of

abnormal production level (REMt) indicates that the independent

variable Prioryears is not statistically significant (0.842) and

therefore the negative effect (-0.012) on the REMt is irrelevant. We

therefore reject hypothesis 4.

Table 11 indicates that the independent variable MtoBt is

statistically significant (0.005) with a negative effect (-0.168) on

the REMt. This is contrary to the hypothesis on this relationship.

Hypothesis 5 is rejected. The independent variable ROAt is

statistically significant (0.000) with a negative effect (-0.231) on

the REMt. Hypothesis 6 is therefore accepted.

5.3.1 Assumptions underlying linear regression analysis:

The above results can only be interpreted when the underlying

assumptions of the linear regression are met. We tested these

assumptions for this regression using a scatterplot, histogram, Q-Q

plot and the Kolmogorov-Smirnov test (Figure 5, 6 and 7).

25

Figure 7: Q-Q plot real earnings

Figure 5: Scatterplot real earnings management

Figure 6: Histogram real earnings

26

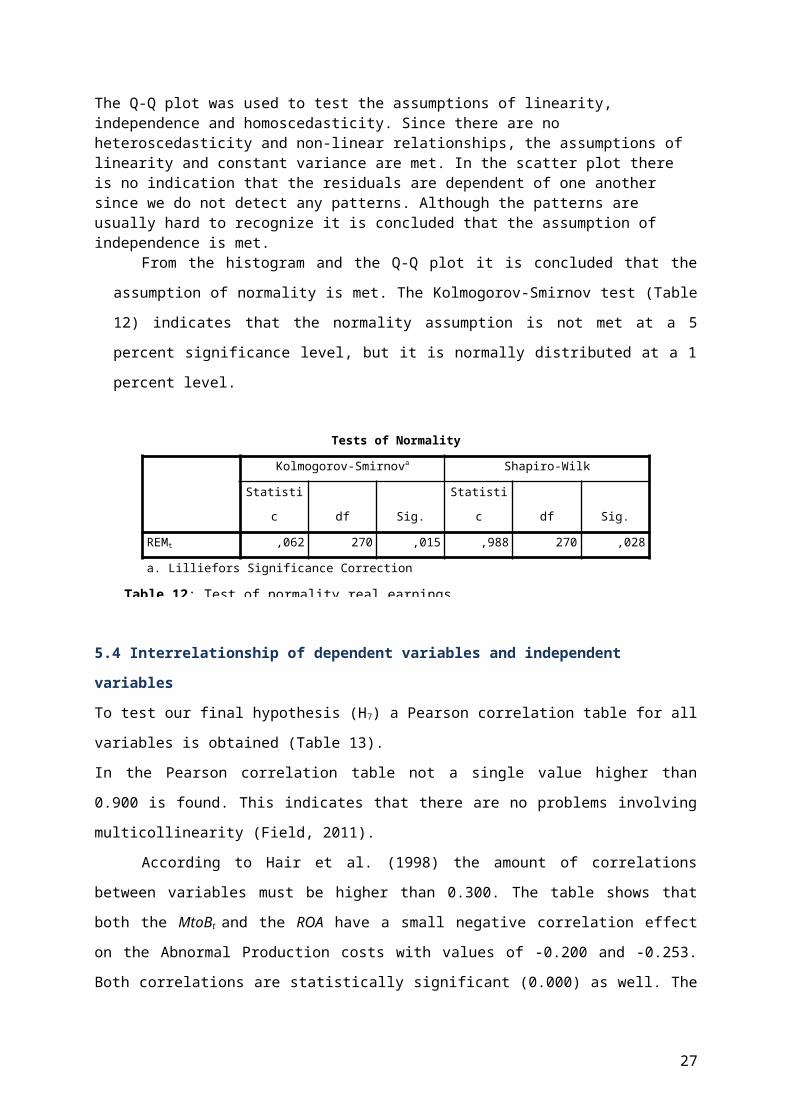

Table 12: Test of normality real earnings

The Q-Q plot was used to test the assumptions of linearity, independence and homoscedasticity. Since there are no heteroscedasticity and non-linear relationships, the assumptions of linearity and constant variance are met. In the scatter plot there is no indication that the residuals are dependent of one another since we do not detect any patterns. Although the patterns are usually hard to recognize it is concluded that the assumption of independence is met.

From the histogram and the Q-Q plot it is concluded that the

assumption of normality is met. The Kolmogorov-Smirnov test (Table

12) indicates that the normality assumption is not met at a 5

percent significance level, but it is normally distributed at a 1

percent level.

Tests of Normality

Kolmogorov-Smirnova Shapiro-Wilk

Statisti

c df Sig.

Statisti

c df Sig.

REMt ,062 270 ,015 ,988 270 ,028

a. Lilliefors Significance Correction

5.4 Interrelationship of dependent variables and independent

variables

To test our final hypothesis (H7) a Pearson correlation table for all

variables is obtained (Table 13).

In the Pearson correlation table not a single value higher than

0.900 is found. This indicates that there are no problems involving

multicollinearity (Field, 2011).

According to Hair et al. (1998) the amount of correlations

between variables must be higher than 0.300. The table shows that

both the MtoBt and the ROA have a small negative correlation effect

on the Abnormal Production costs with values of -0.200 and -0.253.

Both correlations are statistically significant (0.000) as well. The

27

independent variable Prioryears is not significant (0.471) so the

correlation effect must not be interpreted.

MtoBt ratio and the ROA have little effect on the dependent

variable 2012 Achievability but are not significant (0.286 and

0.175) so the effects must not be interpreted. The independent

variable Prioryears has a small positive correlation effect on the

dependent variable 2012 Achievability with a value of 0.142.

Although this correlation is not significant on a 0.05 level it is

significant on a 0.01 level.

Although the correlation between the dependent variables

abnormal production cost and the ACHIEV2012 is a little negative (-

0.046) it is not significant with a value of 0.243. Therefore

hypothesis 7 is rejected.

Correlations

REMt

Achiev_transf MtoB ROA

Prioryears

REMt Pearson Correlation 1 -,046 -,200** -,253** ,005

Sig. (1-tailed) ,243 ,000 ,000 ,471N 270 234 270 270 270

Achiev_transf

Pearson Correlation -,046 1 ,037 -,061 ,142*

Sig. (1-tailed) ,243 ,286 ,175 ,015N 234 234 234 234 234

MtoB Pearson Correlation -,200** ,037 1 ,137* ,017

Sig. (1-tailed) ,000 ,286 ,012 ,388N 270 234 270 270 270

ROA Pearson Correlation -,253** -,061 ,137* 1 -,083

Sig. (1-tailed) ,000 ,175 ,012 ,087N 270 234 270 270 270

Prioryears Pearson Correlation

,005 ,142* ,017 -,083 1

28

Sig. (1-tailed) ,471 ,015 ,388 ,087

N 270 234 270 270 270**. Correlation is significant at the 0.01 level (1-tailed).*. Correlation is significant at the 0.05 level (1-tailed).

Table 13: Correlation table

29

6. CONCLUSION AND DISCUSSION

In this study we have conducted research using a fairly large sample

size, trying to find evidence for the relationship between the

achievability of non-equity incentive plan targets and real earnings

management and their determinants. The determinants used in this

research consist of the market-to-book ratio, the return on assets

ratio and the average achievability of earnings targets in prior

years. We have conducted two regression analyses. With the outcomes

resulting from the regression analyses, we concluded that our

hypotheses stated in the hypothesis development were either verified

or rejected.

In the first regression model we tested hypothesis 1, 2 and 3.

We tested the relationships between the achievability of non-equity

incentive plan targets and our determinants. Since we did not find

significant evidence, we rejected hypothesis 2 and 3. No significant

relationship was found between the market-to-book ratio and the

return on assets ratio to the achievability of incentive plan

targets. The rejection of H2 and H3 was not surprising, since we

found only little empirical research of these relationships and the

effect on achievability. Literature does suggest a greater influence

of the achievability in prior years on the current achievability.

Hypothesis 1 was verified, because of significant results. Therefore

we can conclude that the achievability of incentive plan targets in

prior years has significant influence on the achievability of

current CEO non-equity incentive plan targets. Although, the

explanatory power we found was very low which is in contrast with

literature we have consulted.

In our second regression model we tested hypothesis 4, 5 and 6.

We tested the relationships between the level of real earnings

management and the determinants. No significant relationship was

30

found between the achievability of incentive plan targets in prior

years and the level of real earnings management, therefore we

rejected hypothesis 4. We did found a statistically significant

value for the relationship between the market-to-book ratio and the

level of real earnings management, but the outcome did not

correspond with our stated hypothesis. The effect of the market-to-

book ratio on the level of real earnings management is negative,

which is in contrary to the literature study. There we stated that a

higher market-to-book ratio leads to a higher level of real earnings

management. The independent variable return on assets is

statistically significant with a negative effect on the level of

real earnings management, hypothesis 6 is therefore accepted.

In our final hypothesis, hypothesis 7, we stated our expected

interrelated relationship between the achievability of CEO non-

equity incentive plan targets and real earnings management. We

expected a negative interrelated relationship. To test our final

hypothesis we conducted a Pearson correlation table. We did not

perceive a significant value, therefore hypothesis 7 was rejected.

There are several limitations conducted in this research. Some

obstacles occur with the extraction of the data from the database.

For instance, combining different data from different years by using

different databases in prone to error and gave a smaller sample size

than aimed for. The dependent variable ‘achievability of the

companies’ was calculated dividing the payout of the target by the

actual payout. In result of the calculation the achievability was

concluded if the actual payout exceeded the target payout. We think

more parameters should be included in the research for calculating

the achievability. Not only the amount of bonus payouts for top

executives should be used, but also the target and realized

performance metrics should be included in the research for

31

determining the achievability. In addition, if a CEO’s did not

achieve their goals they got either zero payout or either a

subsequently amount of the target. We could not tell if the

companies with a payout of zero really did not achieve their goals

or that their contract was either you get the bonus or not. This

information is needed to calculate the achievability more

accurately. Also the independent variable ‘achievability prior

years’ was calculated on an average of two years, probably it was

better to use a wider range to give power to the results.

Furthermore, extracting the data from the database a few

problems occur with the data for example market to book values of -

100 and +200. Also comparing the data gave some worries because in

some cases companies with a negative return on assets had a payout

even higher than the target payout and if a company did not achieved

their incentive plan in 2010 a much higher incentive plan payout was

presented in 2011.

32

REFERENCES

Adam, T. & Goyal, V.K. (2008). The investment Opportunity Set and

it’s Proxy Variables. The Journal of Financial Research, 31(1), 41-63.

Allred, James K. Looking at the Return on Assets. Modern Materials

Handling. May 1997.

Anderson, S.W., Dekker, H.C., Sedatole, K.L., (2008). An empirical

examination of negotiated goals and performance-to-goal following

the introduction of an incentive bonus plan.

Bergstresser, D. & Philippon, T. (2006). CEO incentives and earnings

management. Journal of Financial Economics, 80(3), 511-519.

Courtis, P. (2003). Du Pont Ratio: A comprehensive measure of

business performance. European Research Studies, 6(1), 1-31

Cooper, M.J., Gulen H. & Rau P.R (2009). Performance for pay? The

relantionship between CEO incentive compensation and future stock

price performance.

Field, A. (2005). Discovering Statistics Using SPSS. 2nd ed. London:

Sage Publications Ltd. 657p.

Hair, J. F., R. E. Anderson, R. L. Tatham and W. C. Black, (1998),

Multivariate Data Analysis, Upper Saddle River, NJ: Prentice-Hall

International, Inc.

Holthausen, R.W., Larcker, D.F. & Sloan, R.G. (1995) Annual bonus

schemes and the manipulation of earnings. Journal of Accounting and

Economics, 19, 29-74.

Kim, D.S. & Yang, J. (2009). Beating the target: A Closer Look at

Annual Incentive Plans

Merchant, K.A. & Manzoni, J. (1989). The achievability of Budget

Targets in Profit Centers: A Field Study. The Accounting Review, 64(3),

539-558.

Indjejikian, R., Matejka, M., Merchant, K.A. & Van der Stede, W.A.

(2010). Setting Performance Targets in Recessionary Times: Survey

33

Evidence of a Discontinuity in the Distribution of Earnings

Targets.

Palmon, D., Santoro, M.A. & Strauss, R. (2009). Pay Now, Lose Later:

The Role of Bonuses and Non-Equity Incentives in the Financial

Meltdown of 2007-2009. The Open Ethics Journal, 3, 76-80.

Roychowdhury, S. (2006). Earnings management through real activities

manipulation. Journal of Accounting and Economics, 42(3), 355-370.

Skinner, D.J. & Sloan, R.G. (2002). Earnings Surprises, Growth

Expectations, and Stock Returns or Don’t Let an Earnings Torpedo

Sink Your Portfolio. Review of Accounting studies, 7, 289-312

Zang, A.Y. (2012). Evidence on the Trade-Off between Real Activities

Manipulation and Accrual-Based Earnings Management. The Accounting

Review, 87(2), 675-703.

34

APPENDIX

ANOVAa

ModelSum ofSquares df Mean Square F Sig.

1 Regression ,553 1 ,553 ,321 ,571b

Residual 399,593 232 1,722Total 400,147 233

a. Dependent Variable: Achiev_transfb. Predictors: (Constant), MtoBAppendix I: ANOVA Regression between MtoB and transformed achievability

ANOVAa

ModelSum ofSquares df Mean Square F Sig.

1 Regression 1,503 1 1,503 ,875 ,351b

Residual 398,643 232 1,718Total 400,147 233

a. Dependent Variable: Achiev_transfb. Predictors: (Constant), ROAAppendix II: ANOVA regression ROA to transformed achievability

35

36