ECONOM[C AN . SOCIAL COUNCIL - Repositorio CEPAL

288

UNITED NATIONS ECONOM[C AN . SOCIAL COUNCIL GENERAL E/CN.12/947/Add.1 7 February 1973 ENGLISH ORIGINAL: SPANISH ttttttttttttttttttttttttttttttttt ie ttttttttt I llllllll 1011111111111111111t11111111111111111111.11■10011011111,1111111,1111■ 1111,1111 1 11111 lllll OW101161111111 lllll 10111 lllllllll .11■1111111111111111,101,111111111■11111111.1111111111111 llllll 111111111 ECONOMIC COMMISSION FOR LATIN AMERICA Fifteenth sessíon Quito, Ecuador, 23-30 March 1973 LATIN AMERICA AND THE INTERNATIONAL DEVELOPMENT STRATEGY: FIRST REGIONAL APPRAISAL Part Toni 73-1-036

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of ECONOM[C AN . SOCIAL COUNCIL - Repositorio CEPAL

UNITED NATIONS

ECONOM[C AN

. SOCIAL COUNCIL

GENERAL

E/CN.12/947/Add.1 7 February 1973

ENGLISH ORIGINAL: SPANISH

ttttttttttttttttttttttttttttttttt ie ttttttttt I llllllll 1011111111111111111t11111111111111111111.11■ 10011011111,1111111,1111 ■ 1111,1111 1 11111 lllll OW101161111111 lllll 10111 lllllllll .11■ 1111111111111111,101,111111111■ 11111111.1111111111111 llllll 111111111

ECONOMIC COMMISSION FOR LATIN AMERICA

Fifteenth sessíon Quito, Ecuador, 23-30 March 1973

LATIN AMERICA AND THE INTERNATIONAL DEVELOPMENT STRATEGY: FIRST REGIONAL APPRAISAL

Part Toni

73-1-036

a

TABLE OF CONTENTS

Part Two

Chapter IV. LATIN AMERICA AND INTERNATIONAL ECONOMIC RELATIONS 1

1. Introduction 1

(a) International economic trends and the problems of the developing countries 1

(b) Trade policies of the developed countries 4

2. Relations between Latin America and the United States

(a) Introduction 6

(b) Evolution of trade between Latin America and the United States 7

(c) Co—operation between Latin America and the United States within the inter-American framework 13

(d) Some aspects of the financial assistance provided by the United States 17

3. Latin Americats relations with the European Economia Community 21

(a) Introduction 21 (b) Evolution of trade between Latin America and the EEC 23

(c) The common agricultural policy 29

(d) EEC trade policy and the trend towards the formation of a regional bloc 33

(e) The revision of the agreement of association with the African and' Malagasy States 36

(f) The extension of the regime of association to the member countries of the British Commonwcalth 39

(g) The enlargement of the EEC 42 (h) Adoption of the common agricultural policy regulations 46

(i) EEC financial assistance 50

(j) Situation and prospects for co—operation between Latin America and the EEC 52

4. Trade relations with Japan 53

(a) Evolution of trade 53

(b) Recent activities in the field of reciprocal economic relations 57

5. Trade relations with the socialist countries 58

/Chapter V

iv—

Chapter V. FOREIGN TRADE, MARITIME TRANSPORT, INSURANCE AND TOURISM

67

1. Evolution of foreign trade 67

(a) Composition of exports 69 (b) Exports at the start of the Second United Nations

Development Decade 71 (c) Terms of trade 79

2. Commodity exports 81

(a) Trends and features of commodity exports 81 (b) Price trends for the main commodities 89

3. The International Development Strategy and international trade policy measures , 93 (a) International measures relating to the products

listed in UNCTAD resolution 16 (II) 96 (b) International commodity agreements 97 (c) International buffer stocks 101 (d) Access to markets and pricing policías 102 (e) Other policy measures regarding basic commodities ese* 103

4. Exports of manufactures and general systems of preferences 105

(a) Trends and characteristics of exports of manufactures 105 (b) Systems of general preferences 117

S. Maritime transport 120 (a) The geographical structure of foreign trade and

maritime transport 120 (b) The development of Latín America's merchant fleet 121 (c) The organization of ocean shipping services 132 (d) The evolution of freight rates 134 (e) Ocean shipping and Latín America's balance of

payments 138 (f) Latin American ocean shipping policies 142 (g) The International Development Strategy and

ocean shipping 1111

•

/6. Insurance

6. Insurance 147

(a) Growth of the insurance market 148

(b) Participation of national companies 149

(c) Reduction in the net outflow of foreign exchange 150

(d) Investment of insurance capital and reserves 152

(e) Protection of policy—holders 153

(f) Insurance measures at the regional level 153

7. Tourism . 154

Chapter VI. EXTERNAL FINANCING 161

General considerations 161

A. VOLUME AND TERMS CF FINANCIAL RESOURCES ENTERING THE DEVELOPING COUNTRIES 162

1. The 1 per cent target 162

2. The 0.7 per cent target 167

3. Basic terms of official development assistance 170

4. Othor terms of financial assistance, particularly bilateral 172

5. Multilateral assistance 174

6. Volume and terms of financial resources entering Latin America 176

(a) Trend of the total flow of financial resources 176

(b) Characteristics features of the total flow of financial resources 182

(c) Features of official assistance 185

(d) Bilateral official assistance 188

(e) Multilateral transfers 190

B. SPECIAL ASPECTS OF DEVELOPMENT FINANCING 193

1, The supplementary financing scheme 193

2. Establishment of a link between the allocation of special drawing rights and the provision of additional development finance for developing countries 194

C. THE PROBLEM OF THE EXTERNAL DEBT 200

1. General background 200

2. External indebtedness trends of the developing countries 201

3. Possible solution to the problem of the external debt 207

/D. FOREIGN

vi -

Pa2e.

D. FOREIGN PRIVATE INVESTMENT AND ITS RELATIONS WITH DEVELOPMENT 212

1. Develcpments in the attitude to this issue, particularly in the third world 212

2. Sume data on recent trends in foreign investment in Latin America 213

3. Some observations on foreign investment policy 215

Chapter VII, REGIONAL INTEGRATION 219

1. Introduction 219

(a) Reletionship with international trade 219 (b) Selationship with development and import-substitution

industrializar ion 221 (c) The problems of the balance between countries 223 (d) Transport and telecomunications 225

2. Latin American Free Trade Association (LAFTA) 228

(a) Evolution of intra-area trade 229 (b) The lowering of intra-area trade barriere 233 (c) Sectoral agreements 238 (d) Progress on agreements between central banks and

other financial matters 247

3, Andean Group 248

(a) Background information on the establishment of the Andean Group 248

(b) The achievements 251

4, Central American Common Market 258

(a) Background data on the evolution of area trade 259 (b) The difficulties and crisis in the Central American

Common Market 265 (c) Recent corrective measures 268

5. The Caribbean Free Trade Association (CARIFTA) 271

(e) The background to the Agreement 272 (b) Expansion of trade 274 (c) Recent developments 279

/Chapter IV

PART TINO

Chapter IV

LATIN AMERICA AND INTERNATIONAL ECONOMIC RELATIONS

1. Introduction

(a) International economic troaa111125111211==.W112231122 countries Irrodpgsameamoroams

A number of important developments in the world economic situtation have occurred during the first years of the Second United Nations DevelopmentDecadEre

In the first place, there has becn a search for a new international order capable of solving the serious financial problems that marred the last years of the previous clocado and responding to the new situation and power structure that are emerging at the international level, especially among the countries at the centre.

Secondly, thc latter have mr.de a rapid recovery sine° the so-called monetary crisis, although an institutional and instrumental solution to its underlying causes still seems far off. Whether real or apparent, this ability to ríse above the crisis is another cicar proa? of the vitality these economies have acquired and of the self-sustainitio nature of their polioles 1/. Moreover, their recovery undoubtedly has a positivo

1/ The following (12 December in rocent

GROWTH OF nELL GNP IN SEVEW IIAJOR COUNTRIES (PercentaLe chan:fis seasonally adjusted at annual retes. Estimates and foreoasts)

table, taken 1972), shows

years, tegether

United Kingdom jz., United States France 11./ Germany Italy Canada Japan Total of above

from an OECD publication, the economic growth rato of with e forecast for thc first

Economia Outlook aoven countries

half of 1973:

Avercee

1958-1959

1969-1970

Compared wath previo= year

Compared with previous half-year

to 1971 1972 1973 1971 II

1772 1973 I II 1' Ir

3.1 4.2 -5.8 5.3 5.8 4.8 11.3

5.3

1.4 3*

2.7 di

5.1 5*

2.8 34

1.1 3

5.5 6

6.7 8-1

3.3 5.a

5 64 6 541 5 6 10i

612

5.1 3.7 7.0

-1.3 5.2 7.5 5.7

4.0

0.7 7.3 5.0 5.8 1.2 5.4 8.7

6.3 _

di 7 5 3 41 51

10,1

6

... 6.k 6i 51: 5 64

10-i

di

... 6 6 di 6 6i

11

6-1 countries 32/

1 Gross domes-tic product; la/ 1970 weiáltings and exchange ratea. /significance for

significance for the developing countries, particularly as regards the 'atter% trade and capital transfer prospects.

The third mejor development has to do with the marked tendency for the economies on the periphery to be excluded from current efforts and projects to reorcanize the international institutional structure. Despite the modest progresa mode in this field in the International Monetary Fund, several other foca, and especially UNCTAD III, have mode it olear that their aspirations have little likolihood of materializing in view of the unreceptiveness of the industrializad economies and some specific measures adoptad by the latter.

Taking the first two points, and particularly the economic reviva' of the countries at the centre, it will be appreciated that these countries will have to work out a new modus vivendi in the light of the changos that have taken place in their relativa economic strength. The disappearance pf the bi—polar system is already an aceomplished fact and the trend new is towards e multi—polar system with certain interu.relationships and the distribution of spheres of influence among the central economies. It goas without saying that the procesa is -Par from simple and many obstarles remain to be overcome, but recent developments, and particularly the increasing contacta bring developod with the socialist world, justify the aboye impression.

Be that as it may, this in no way significa that the new arder will bring the developing countries e satisfactory solution to their own problema. On the contrery, a number of ?actora that have come to light in recent years give reason te fear that these may persist or even become more serious.

Moreover, whatever the outcome of the new multi—polar system, which in some ways could oven give the developing countries certain tactical advantages, the fact is that their problema and grievances in respect of external matters will remain fundamentally unchanged. The question thus arisca to what extent the apparent roadjustments are going to facilitate the achievement of their objectíves or actually make this more difficult.

Among other things, it is cloar that in actual fact the prevailing system of international relations — in conjunction of course with such other ?actora as technologirel progresa — has affected not only the direction of trade flows but also their composition and volume, while at

/the same

- 3 -

the same time, the impact has been felt of the "verticalization" of economic ties between the countries at the centre and their spheres of influence, the development of transnational corporations, and the formation of the State-controlled sector.

Recent research shows that, not counting the socialist countries, the proportion of world trade carried out on a most-favoured-nation basis has steadily declined over the past 15 years whíle that based on preferential arrangements has risen. According to GATT: "The share of preferential in total imports of Contracting Panties has ricen continuously during the poriod observed, from 10 per cent in 1955 to 17 per cent in 1961 and almost to 20 per cent in 1961, to attain 24 per cent in 1970. This growth was mainly due to the continued dynamism exhibited by the mutual trade of the member countries of the European Communities. It may be noted that the share of preferential imports other than intra-EEC, intre-EFTA and United States automotíve imports from Canada shows a continued decline" 2/.

This tendency for the share of world trade conducted on a preferential basis to incroase, which will become oven more marked with the enlargement of the European Economic Community, poses a clear threat te the principie of non-discrimination which is the vory foundation of GATT. It may be noted that the United States, which sponsored the trade liberalization movements as a means of furthering its economic interesas throughout the world, also contributed to the gradual undermining of GATT!s usefulness by establishing its own preferential area with Canada and by requesting and chtaining, from March 1955, temporary exoneration from its agricultura) trade commitments. Honce the mejor preoccupation of the developing world: if the countries at the centre, despite their own disagreements, are promoting a new system of international relations, why should there not be a harmonious and effective method of incorporating general and non-reciprocal preferential treatment in external relations - whether commercial, financial, scientific or tochnological - for developing countries too?

The process of technological chango and the speed at which transnational corporations are spreading also has a serious effect en the direction and composition of trade flows. Although it is impossible to enter into details here, the point should at least be made that transnational corporations tend to create or accentuate oligopolistic market conditions and to emphasize the verticalization of relationships between economic centros and their respective spheres of influence.

Mil.011.11as

2/ GATT, "Main findings concerning trade at most-favoured-nation and at other ratos" (L/3708 of 21 Juno 1972 (limited distribution) and L/3789 (general distribution)). /(b) Trade

4

(b) Trade p2119111.9f the develo ed countries

A eles° look at what has happened in the sphere of trade in international economic affairs shows, first of all, that the trade policies of the developed countries have not in recent years changed sufficiently for progross to hg, made towards'the realization of their repeatudly stated intention of co-operating with the Third World. In the last two or there years,.for instance, no significant stops have been taken towards (i) the establishment of agreements on the main primary products exported by the developing countries, save recently in the case of cocea; (ii) the removal or reduction of tariff and non-tariff barriers against agricultural commodities and of,the subsidies which are granted in most developed countries to producers and exporters of agricultura' products with the result that developing countries' possibilitios of finding trade outlets for such products are limited and world markets are distorted; and (iii) the supprepsion of the numerous measures that currently hinder the export of manufactures from developing countries at competitiva erices. In addition to there still unsolved essentially commercial problems there are other problems of a different nature such as the maintenence of the export credit policies of the developed nations.

Secondly, as already indicated, recent devolopments in the EEC hint at a prolíferation of discriminatory preferential arrangements: prior to its recent enlargemunt, the EEC had concluded reciprocal preferential agreements with 28 countries, but a further 20 countries (12 in Africa, 4 in the Caribbean and 4 in the Indian and Pacific Oceans) and 19 dependent territories are now in a position to become associate members of the Conriuníty, while Ceylon, India, Malaysia, Pakistan and Singapore will also be receiving special treatment.

Thirdly, as regards trade in manufactures and semi-manufactures, the entry into effect of the generalizad system of preferences in 1971 and 1972 should theoreticaily be a positivo step, since it is designed to promote developing countries' exports of manufactured products through the reduction or elimination (depending on the country) of the customs duties of the developed countries. However, the advantages accruing from the system have in fact been fairly limited, particularly for Latin America. The agreement has not taken effect, for instance, in the United States, which is the region's biggest market; the concessions granted by the EEC are quite small, partly because the Community has maintained e bígger margin of preferences for its associated members; the advantages under the system are extended to a number of territories that are dependent upen the very countries granting the preferences; all the preference schemes exclude

/the so-called

- 6 -

the so-called sensitivo products, that is tr say, the light or traditional manufactures which actually or potentially represent the bulk of the exporta of manufactures of the developing countries; the developed countries have reservad the right to suspend or modify the concessions at any moment; processed agricultural products, except for a small list of products, are excluded from the preference schcmes; and fínally, the enlargement of the EEC means that the more generous concessions, adopted mainly by the United Kingdom and Denmark, will be replaced by the leas favourable EEC preference scheme.

Fourthly, no solution has yet been found to the difficult problom of reverse preferences; i.e., proferencos granted to products from EEC countries and the United Kingdom by associate membors and by countries of the British Commonwealth, respectively.

Finally, the mejor developed countries cuaterna duties en manufactures and semi-manufactures constitute on average between 7.1 and 13.4 per cent of all dutiable importa 3/. Non-tariff barriera, moreover, have been increasing and thus ralee significantly the real value of tariffs.

These limitations, and others that mainly affect trade between developed countries, have brought an increasing awareness that the existing system of international trade is unsatisfactory; the United States Congress itself has requested a revision of trade machinery. The 1973 multilateral negotiations could thus be an important step towards this much-needed revision and should devote particular attention te the proposals of the developing wcrld.

3/ Sec. GATT, "Main findings concerning trade at most-favoured-nation and at othor ratos", op. cit. From 1 January 1972, tariffs on non-agricultural products ware on average 9.4 per cent in the United Kingdom, 11.0 per cent in Japan, 8.3 per cent in the United States and 7.8 per cent in the EEC (EEC, Document de trovan_ XI/64/71.F of 23 February 1971).

/2. Relations

- 6 -

Relations between Latín America and the United States

(a) Introduction

The pattern of evolution followed in recent years by both the trade and financial relations between Latín America and the United States clearly shows up the veritable stagnation of inter-American co-operation. This is particularly serious considering that the United States continuas to be the principal market for Latin America% products and the mejor source of external financial resources for the region.

As regards trade relations, it may be noted that the slower rete at which Latin American exporte to the United States have grown compared with importe from that country has resultad in en increasing disequilibrium in the trade balance at the region's expense, added to the traditional deficit on financial transactions in Latín America% balance of payments with the United States. As far as financial flows are concerned, a phase of contraction in the authorization of credit began in 1969, and the effects of this, taking into account the customary delay in disbursements, are now becoming evident.

The Consensus of Viña del Mar, adoptad by the Letin American countries in 1969, constituted a collective expression of the region's aspirations for a real improvement in its relations with the United States. However, the practical results of this initiative have been meagre and to a certain extent frustrating for Latin America. The establishment of machinery for contact and negotiation between the two regions within the context of the OAS was effective only on a purely technical plane, and failed to lead to any negotiating process that might result in the elimination of tariff or non-tariff barriers to the access of Latin American products to the United States market. This situation weakened the machinery's real operation, and this helped te create a feeling of frustration in the Latín American countries as regards the development of inter-American co-operation. This situation, of a strictly regional character, has gradually been compounded by other more general factors which are reflectad in the absence of really significant action on the part of the United States and other developed countries in response to the proposals made at the various international forums by the developing countries and the Latin American countries in particular.

/(b) Evolution

(b) Evolution of trade between Latin America and the United States

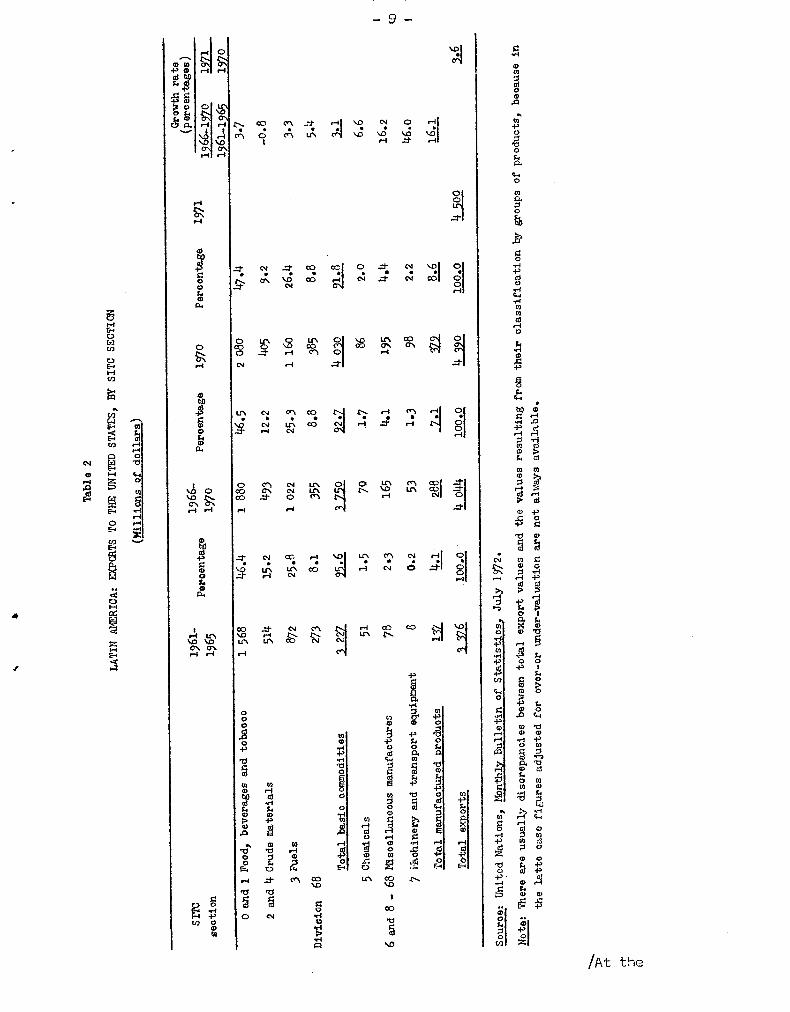

Trade relations between Latin America and the United States were characterized in the last decade by a chronic imbalance between exporte and importe, which resulted in a substantial trade deficit for the region (see tabla I). This was basically due to the low rete of growth of exports to the United States, which averaged 3.5 per cent annually, while imports increased by an average of 5.9 per cent annually. In fact, with the exception of sales to the United Kingdom, which increased by no more than 0,3 per cent annually, and to the group of socialist countries, exporte to the United States representad the least dynamic of Latin America's foreign trade sectors between 1961-1965 and 1966-1970. In 1971 the trend was still more unfavourable, since the increase in exporte was only 2 per cent over 1970.

The structure of Latin America's exporte to the United States did not change significantly during the decade, although in the last few years the share of exports of manufactures increased. Even so, in the periods 1961-1965 and 1966-1970, basic commodities (SITC sections O to 4, and division 68 covering non-ferrous mstals) representad 95.6 and 92.7 per cent, respectively, of exporte to that destination. In other words, commodities still represent virtually all Latin America's exporte to the United States (see table 2). Within this group of products, sections O and 1 (food, beverages and tobacco) have practically maintained their share (46.4 and 46.5 per cent, respectively), while that of raw materials declinad from 15.2 to 12.2 per cent. Generally speaking, the structure of exporte to the United States (even the small change in the proportion of raw materials) is much the same as that of Latin America's total exporte.

/Table 1

Tabla 1

LATZ1 AMERICA: a/ EXPORTS, EIPORTS AND TRADE BALANCE WITH THE PRINCIPAL REGIWS OF THE WORLD

(nillions of dollars)

rercent- Percont-

1961-1965 age of 1966-1970 ajo of 1970

total total

Porac ht- aco of 1971 b/ total

Poroeni- G rowth rete

ase of 1965-1970 1971 total 1961-1965 1970

Exyorts United States 3 332.8 35.9 3 956.5 32.5 4 353.8 30.5 4 274.2 30.8 3.5 -2.0 EEC (6 members) 1 913,0 20.6 2 580.9 21.2 3 179.8 22.2 2 889.3 20.9 6.2 9.1 United Kingdom 690.3 7.4 700.3 5.7 662.9 4.6 714.3 5.2 0.3 7.8 Upan 354.7 3.8 666.o 5.5 962.1 6.7 687.8 5.0 13.4 -28.5 Latin America 799.4 8.6 1 396,4 11,5 1 665.4 11.6 2 009.1 14.5 11.8 20.6 Socialist oountries 250,6 2.7 293.7 2.4 321.0 2.2 370.9 2.6 3.2 15.5 Other 1 942.8 20,9 2 587.0 21.2 3 154.9 22,1 2 910.0 21.0 5.9 -7.8 World 9 283.6 100.0 12 180.8 100,0 14 299.9 100,0 13 855.6 100.0 5.6 -3.1

Importa United States 3 598.3 43.6 4 787.o 41.7 5 752.9 41,1 5 533.2 35.7 5.9 -3.8 ffEC 1 653.1 20.1 2 188.9 19.1 2 657.6 19.0 3 152.8 20.4 5.8 18.6 United Kingdom 442.1 5.4 531.8 4.6 639.6 4.6 770.0 5.o 3.8 20.4 tapan 322.0 3.9 587.1 5,1 870.6 6.2 948.3 6,1 12.8 8.9 Latin America 933.3 11.4 1 5664 13.7 1 849.1 13.2 1 947.6 12.6 10.8 5.3 Socialist oountries 129,2 1.5 147.2 1.3 132.5 0.9 201.8 1.3 2.6 52.3 Other 1 160.5 14.1 1 659.7 14.5 2 100.6 15.0 2 936,2 18.9 7.4 39.8 World 8 243.5 100.0 11 467.7 100.0 14 002.9 100,0 15 489.9 100.0 6.8 10,6

Trade balance United States -265,5 -830.5 -1 399.1 -1 259.0 EEC 259,9 392.0 522.2 -263.5 United Kingdom 248.2 168,5 23.3 -55.7 tapan 32.7 78 .9 91.5 -260.5 Latín America -138,9 -169.6 61.5 Socialist oountries 121.4 146.5 7 111:5 169.1 Other 782.3 927.3 1 054.3 -26.2 World 1 040.1 713.1 297,0 -1 634.3

Source: IMF, Direction of Trade 1960-1964, 1962-1966, 1966-1970; and official foreign trade statistics.

Note: Exporto fob; imports cif.

a/ Exoluding Cuba, 1/Provisional figures.

/Ta bl e 2

LATIN AMERICA:

SITC SECTIO

N

vi

C.0

0

ai

•

1-1 r4 • n

ffl 5 ✓I

0 1-1 E. +-I

8 xa

Monthly Bull

etin of Statistics, July

4-t

o

o R.

o

o

.6% O ri

o

o ft,

o

tki) ri

CR

N IN

c1

1>

O

O O

oo

o

o

export values

between total

usually di

screpancies

avai

lable,

figure

s adjusted

for

o o

r4 co CO

43

o O f••■

Total basic commodities

otal

manufaotured

Total e

xports

6 an

d 8

- 68 Ndscellaneous manufactures

7 Machinery and transpor

t equipment

Qi

o o

O

ri O \

— 9 —

o

o o

o 1 Fo

od, beverages

2 and 4 Cruda materials

O ri .--. t, 0 0 O'N 4. 0 r4 r-I OtO $4 0 43

1

4: O O 5.1 •D f. 0 cr.

c. .5 o, ..4 r4 ,S. CO eN ..d- r4 ‘.0 N O r4 ....... I I • • cA u; • s.4;• \ o • ,...c1

!.9 r-I el O

\ O '4 #.4 ..2- 0.4 O \

vi r-I

O

‘0 CO —1. cc: C.. \ °e co I 2: Ol 04

r,4 04 ri

O

•

r4 o-% O O \O CO 0

CO \ O LIN 0 1.1 \ ln CO

ri

•••4

oi

0

LI\ C,N CQ • • • •

O

•

co r4 N

a.

r4 • • • rl

0 CO Cs1 t■ 1/40 CO " O el Lf O O Le \ \ COI

CO C'l rl \

r4 1,1 r4

O 10 4. CM CO ,I t-r. C:\ 04 r4 O al

o r4 04 ...j 81 Z • • •

N 04 e; • * Ñ trl U-N CO to• rl

V) O r.4 r-li

\O tr, co

•

Cs4

0 \ O\ UN co

ri 4-4

/At the

- 10 -

At the level of specific products, there has been 4 rapid expansion in exporta of some high-cost agricultural commodities such as meat and fresh fruit and vegetables, in contrast with tropical products and various raw materials for industrial use (sea table 3). Between 1961-1965 and 1966-1970 the United States increased its purchases of meat from Latin America at an annual rete of 15.6 per cent, while those of fruit and vegetables, fresh or frezan, grew by 11.1 and 22 per cent annually 4/. In the tropical products group, there were appreciable increases in exports of sugar and cocoa to the United States (7.7 and 8.5 per cent annually), but in the case of sugar it is significant that in spite of chis rete of increase, Latin America has not yet recovered the share of sugar exports to the United States which it enjoyad before that country suspended its trade with Cuba. The value of exports of coffee, which is the mejor Latin American commodity sold to the United States, declinad by 2.3 per cent per year, so that the region's share in that market feil from 79.6 per cent in 1961-1965 to 65.9 per cent in 1966-1970. In the group comprising raw materials for industry, the most unfavourable case was that of wool, importa from Latín America declining in almost the same proportion es total wool importa by the United States.

Gales of manufactures attained high retes of growth, but their absoluta values are very small, as is their share in the region's total exporta. In any case, however, it may be notad that the share of manufactures in exports to the United States rosa between 1961-1965 and 1966-1970 from 4.1 to 8.6 per cent, the most significant feature being the rapid growth of exporta of machinery and transport equipment. The GATT study mentíoned earlier shows that during the period 1966-1970 United States imports of manufactures rase at an average rata of 14.3 per cent annually, comparad with only 4 per cent for agricultural commodities. It is interesting to note that the annual growth of Latin America's exports to the United States followed a very similar trend. However, there is no doubt that Latin American exports of manufactures will have to grow at still higher retes if the traditional prirrary structure of exports is to be modified.

4/ The recent study published by GATT entitled Trends in United Sta::es Merchandise Trade 1953-1990 (Geneva, July 1972) points out that importa considerad to be more or leas directly competitiva with domestic production have grown at a steadily increasing rete in United States trade, with increases af 25 per cent between 1953 and 1965, and 50 per cent over the next five-year period. According to the same study, the items mainly responsible for this expansion have been meat (United Sta-tes imports of which increased six-fold between 1953 and 1970), dairy products, fruit and vegetables, tobacco and beverages (particularly wine). The study expressed the view that if the quantitative restrictions against the entry of several of there products were not in force, the expansion of world exports of those items to the United States market would have been even greater. /Table 3

tr%

2 0, .4 s•-o o bD oN

4-1 1., 0 r4 I

cd tD 0 \ O

-1 .5 1 O \ r4 ...I

r-1 O

a a -P 0 s. 0 O LO CL4 O

a3 o X.41 1)

-01

-I> 1t)

R4 O 03 4:0

o o o

O

O

r-1 •.0 \0 r.1

LA \O 4.4

CT. r4

;31

a

5

cn 4:1

r-IO • 0

O

1-4

O ti

O

(Fob values in m

illt

ons of dzllar

s)

CO O t... «N 1." t.. O g.§ O CO O CV • • • • • • • • •

CO co 04 CV LA .(•••■ 1

•

ri

1.;.14 Z,

VD

c`N e t-4

C4 • CO

--

• Crl r-I

•D * C V

«N

o'N V:1 CV

..t" •

Pi

Crt • CV

cn

• .1,-.

•

e t'V C4

■0 •

t-4

1.-1 j c0

• C4

e

0 •

1---.

Cr\ •

r4 •

.0.. C4 t'... LA ..§ g•ag t.. O Ir% CN CO 01 .d" ri O • • o • • • • o • 11» O * 0

LA CA .t",,, CA CO c0 LA C\ O CA 07) Z... CA LA

ts- ON H r-1 •0 /",.. CO CO Z.... ..4 1." cm .C., c:

.2 N •■ 1 ri ,0 O r4 r4 ..1" 01 0 VD 0-1

r4 rl 1-1 2`...

CV ..d"' M 1 kl) ON. co • e • • • •

rt • • • o • o • •

L. v-4

til cr., LIN D,. o:, 3 .7.1: 3 -A

\O O CA LA 4.4 1..4 N N O ■C) CO 04 I ..1* • • • • • • • • • • • • • o

t". O O LA O'N LA CA CA \O LA O CA '.0 `,0

CV Cr. 00 el .ts, 0'1 .2' 0-■ ,U505 O í r-1 ri csi

0-% co c•-■ o O • • • • • • * • • 44 •

\O• CA ah O 0"".

t's. ars ■o tr. LA O g-§ :A LC1

CV rl t." 0 r4 Cn, g.§ ts-

r1 ri

t" c•-s `.0 04 •.0 Lt> u-. •.o 0-N ! • • • o • • • • e • • c • • •

•0 LA 0 \ as \ 04 CO \ CO Q O • cv •• O C^t o'N cs1 .2 LA UN LCN r-4

Z`• • 1" 0-% LC1 ON tr. r-1 UN I"

Co. 3

e I» •

r0-I

C4 1" CO r-I t's CO r-I

0-1 ■0 CV •.0 O'N 0 -2 1" CO • • • • • • • •

csi c0 rag UN el r4

..O

CO j O I

N

• • cf:

o

0-1 O +' rI

.c3O 49g 1 o 445. ag

4.1 o a ...0 O

4 .4 o

a...4 O g 0 4.)

.4 4, 4, C3 O 4.. o .z 4 O ,t5 0 t

2 4'

o s• 49 O 4.0... 5 f. Le orl

O f.. O

<re .5 .. 44 .0 p

f• ee-4 L3 w

4., 4, : „ y, . o o

O O c. 4> 1 0

0 0 f. 0 0 fa O áf 5 y o Pa 4 ,r. 5 r. .-I *O e>

O O • ca 0 0 f. fa S. O 0 0 al o o o 1 a ...

"4 0 tal c..4 o 0) 4-1 e> o

Z 4 r.... > cía c.) o h.' o c-, at o 4

f. •cl 4. • 0

O N 2 .

0 ... O O 4.> P.

0

,..,c., o. ....„, . co Ti fa P. "tá o g 5. c.. 11, 0

f. t 5 g

0 0 0 7-1 $4 .

e

N

g O P. I ..4 a.

74 \I W. , . . iT. , ,.... o. 1 g . 119. . . . s c., ■ 1) CO.c.31 cec? Fk {; .‘4 et:j aig

O C. O O O O O CV CV CV o'N C,1 ■0 ■C>

o o 0 4.) 4.1

O 0

0 0 0 E-. E-. P.

CV

s.° 0 C" tr• OD CV 0\ CN 04 • • • • • • • • • ..dt C?4, j

g ..tr: gi co .d• C4 g C•1 r--1 .2 14-1 Z' CA 1 I'. 04

t-'1 r-t r4 CO c•J

\ O t., O N C•1 0e e • • • • • • • e

4l \O c4 0 CV LA .4.0 04 C4 s.° O N 04 Crl, 01 01 .O.• ad- OA ri

CO O \ CA 0 cc> CV 1"

• . • • • 11 • • •

c.4(7‘ \«15 t c,-■

col cl• Csl CO %.0 04 CO s

C

O •

CV CV cso

O .r•-• 11 • • H al

\ rl

o -1.1

✓4 .4 0

cr3 -P tfi CA o •ti -rl

45g E-. 5,1 .3 o O o c.

OI O • fa

o Pa O E O .4 O • a3

f

▪

• o

..9

al

/This is

- 12 -

This is the objective of the systems of general preferences approved by UNCTAD at the end of 1970. In a study published in 1972 on the probable impact of general preferences on United States imports 5/, the United States Tariff Commission concluded that, on the basis of a group of 160 manufactured products the value of imports from developing countries might be expected to rise from 1,300 million dollars in 1967 to 3,900 mullían in 1980, whereas if the preferences were not put into effect the increase would be only from 1,300 to 2,300 million dollars between 1967 and 1980. Nevertheless, the United States* system of preferences has not been put into force, despite that countryos repeateddeclarations in UNCTAD and GATT.

An analysis of Latin America's imports in the past decade reveals some changes as regarás their geographical origin (see table 1). The United States continues to occupy first place as a source of supply for Latín America, but its importance continued to decline, from 43.6 per cent in 1961-1965 to 41.7 per cent in 1966-1970 and 35,7 per cent in 1971. The share of imports from the United Kingdom and the socialist countries also declined. The changes which took place in 1971 seem to accentuate the trend towards a more balanced distribution of imports. The United States was the only country affccted by an absolute decrease in Latin American purchases, whereas the United Kingdom and the EEC regained the share they had at the beginning of the pest decade, and imports from Japan continued their rapid growth. Nevertheless, it was in 1970 and 1971 that the deficit in Latín America% balance of payments with the United States reached its highest levels: 1,399 and 1,259 million dollars, respectively.

To sum up, the analysis of trade between Latín America and the United States over the pest decade reveals a steady decline in the United States' share of both total exports to and total importe from the reglan 6/. In spite of this trend, which is obviously due to a number of factcrs 7/, it must be borne in mind that the United States continues to be

5/ United States Tariff Commission, Probable Effect of Tariff Preferentes for Developin. Countries, Staff Research Paper N° 2 (Washington, 1972).

6/ This is clear from the fact that between 1960 and 1970 Latin America% share in the United States' total importe fell from 24 to 11 per cent, and in its total exporte from 17.4 to 13.3 per cent.

7/ In an OAS study entitled "Hacia una mayor participación latinoamericana en el mercado de los Estados Unidos" (CIES/1376) of 12 May 1969, it is considered that the relativa marginalization of Latin America from the United States market during the 1960s is one-third attributable to the region*s shift to other suppliers and two-thirds to the change in the composition of United States importe in favour of manufactured products.

/the principal

-13-

the principal purchaser of Latin American products and even more so the principal supplier of products to the region. On the first points it is

interesting to note that for the United States the Latin American countries play an important role as suppliers of raw materials: in 1970 the region supplied 42.3 per cent of that country's total importe of 14 basic commodities. The proporticns varied between 57 and 80 per cent for coffee, sugar, and fruit and vegetal-Jipe; between 31 and 45 per cent for cocoa, íron ore, copper, leed, and petroleum and petroleum products, and between 18 and 26 per cent for meat (fresh and canned), non-ferrous metal ores and wool 8/.

Latin America is also a very important market for some United States

products. In 19701 exports of chemicals from that country te Latin America totalled 778 million doliere, which is much higher than the value of its exporte to Canada (533 million dollars), Japan (322 million dollars) or the EFTA countries (405 million), and is comparable with its sales to the EEC (945 million doliere). Latín America importad 2,836 million donare, worth

of machinery and transport equipment from the United States in 1970, which is only a líttle less than the value of importe from that country by the EEC (2,954 million dollars) and much higher than that of importe by Japan (1,145 million) and EFTA (1,787 million) 9/. These figures show that in spite cf the weakening trend of both exporte and importe ín trade relations between Latin America and the United States, these relations still retain what might be called "basic" or "strategic" aspects which justify the continuance of efforts to improve the conditions of trade between the

two regions.

(c) Co-o eration betwcen Latin America and the United States within the inter-American framewcrk

Quite apart from the internal factors affecting the United States demand for imported products, the expansion of Latin American sales to that market during the last decade was curbed by the maintenance and, in certain cases, the strengthening of protectionist barriere, notwithstanding the commitments assumed at international and regional forums to improve the conditions of access for products of developing countries in general and

yez....wwwwle".•

8/ See tabla 3.

9/ United Nations., Commodity Trade Statistics, 1970, Series D, vol. XX, Nos 1-20.

/Latin American

-14-

Latin American countries in particular 10/. In fact, not only was there no progress in the liberalization of trade with the Latin American countries, but in certain cases the restrictions were accentuated, particularly as regards non-tariff barriera.

One sucht case was the modification of the 1965 sugar law by virtue of which the share of United States producers in supplying the dwestic market was raised at the expense of Latin American exporters; another was the introduction in 1964 of quotas for imports of beef 11/ ,- a measure which was reinforced by the request to external suppliers in 1968 to impose voluntary restrictions on exports - and similar quotas for imports of dairy products in 1967-1968. In short, the restrictiva mensures adopted by the United States during the past decade obstructed imports of a wide range of products, i.e„ wheat products, cotton, groundnuts, dairy products, sugar, meat (fresh, chilled or frozen), fish, and petroleum and petroleum products. The steps taken to imports such as the suspension in 1965-1966 of the import quotas for leed and zinc established in 1958, and more recently the meat quotas, did little to change this unfavourable situation in the area of trade relations between Latin America and the United States,

In view of this wsekening of inter-American co-cparations which had been manifest not only in trade but also in the field of financial assistance 12/, the Latin American countries, at the meeting of the Special Committee on Latin American Co-ordínation (CELLA) in May 1969, adopted the Consensus of Viña del Mar, in which they submitted te the Government of the United States the elements of a new approach to their reciprocal relations in the trade, financial and technical assistance fields. The Consensus of Viña del Mar, as» the expression of the will of the Latin American countries genuinely to co-ordinate their position vis-á-vis the United States, was intended not merely to recail previously assumed commitments, but also to ensure the

111.1111.1111.11111.3..-41.311.11,01.111WW110011111111M.4•0

10/ It may briefly be recalled here that such commitments are set forth, in particular, in the following documents: (a) at the world level: Ministerial Programme of GATT, 1963; Part IV of the General Agreement on Tariffs and Trade; recommendations A.II.1 and A.III.4 adoptad at the first session ofUNCTAD; and the International Development Strategy; (b) at the inter-American level: Buenos Aires Protocol of 27 February 1967, and Declaration of the Presidenta of- America (punta del Este, 14 April 1967).

11/ In view of the steady risa in meat prices, the import quotas were temporarily suspended in March 1972.

12/ Questions relating to financial assistance for development are dealt with in chapter VI.

/establishment of

- 15 -

establishment of machinery for identifying specific obstacles to exporte of Latin American products to the United States and for the conduct of negotiations for their progressive elimination. In the financial field, the aim of this document was also to define new methods of co-operation between Latín America and the United States.

In resporee to this collective approach by the Latín American countries, the United States Government announced a new type of partnership in which "all voices are heard and none ís predominant", involving "a more balanced relationship" between the two regions 22/, and proposed a new approach to co-operation with Latín America based, inter alía, on the following principies: a firm commitment to the inter-American system and to the compacte between the region and the United States, a formal commitment to continued United States assistance for Hemisphere deve1opment, and,support for Latín American initiatives within the inter-American system. The proposed measures include the decision to leed a vigorous effort to reduce the non-tariff barriers to trade maintained by near:ly all industrialized countries against products of particular interest to Latín America, determined support for the Generalized System of Preferences, and increased technical and financial assistance to promote Latin American exporte. In the financial field, the President of the United States announced that, as from 1 November 1969, AiD luans would be freed to allow purchases not only in the United States but anywhere in Latín America, and that all other onerous conditions and restrictions on United States assistance 1oans would be reviewed, with the objsctive of modifying or eliminating them. Of particular interest was his reference to the establishment within the inter-American system of regular consultaticn on trade matters.

On this last point, and aleo in connexion with finance, the next few months witnessed specific attempts to define the context of a new form of co-operation between the two regions. The establishment in February 1971 of an OAS Special Committee at the ministerial level as an instrument for consultation and negotiation between the Latín American countries and the United States was basically aimed at helping to strengthen inter-American relations 14/.

13/ Speech delivered by President Richard Nixon at the meeting of the Inter-American Press Association on 31 October 1969.

14/ The Special Committee for Consultation and Negotiation (CECON) was established, and its functions in connexion with trade determined, in resolution REM 1-70 adopted at the Eighth Ministerial Meeting of the Inter-American Economic and Social Council.

/The Ad Hoc

- 16 -

The Ad Hoc Group on Trade to Deal with Tariff and Non-Tariff Barriers and Related Matters was set up as an operational instrument of the aboye Special Committee to identify the obstarles in the United States

'market obstructing imports of products of interest to Latin America, and to submit te the Special Committee proposals for their progressíve eliminationr. This Group held several meetings which enabled it to make considerable headway in the identifícation of the tariff and non-tariff barriers existing in the United States, of which it compiled an exhaustiva list. However, it has found it quite impossible to proceed with the second stage of its programme, i.e., to hold negotiations in order te define the conditions for eliminating those barriere. The United States representative stated, in particular, in September 1970, that as regards tariff barriers his country% contribution towards complying with Latin America% requests should be considered on the basic of the offers of concessions formulated within the context of the United States system of general preferences, which included a larga number of products reviewed by the Ad Hoc Group 12/. The difficulties in reeching agreement on the reduction or elimination of tariff and non-tariff barriers, and the fact that UNCTAD III was to be held shortly, caused the member countries of CECON to postpone the meetings that were scheduled for early 1972. This state of affairs continuad until December 1972, when the sixth meeting of the Ad Hoc Group on Trade to Deal with Tariff and Non-Tariff Barriere and Related Matters and the third regular session of CECON were held. Although the report of this session is not yet available, it will be seen from the Report of the Ad Hoc Group on Trade that no agreement was reached on the questions under consideration:

"At the sixth meeting of the Group, the United States Delegation, while recognizing that trade restrictions had been identífied in document CIES/CECON-COMERCIO/45, took note of the Latin American view that the proposals set forth in documents CIES/CECON-COMERCIO/46, 47, 48, 49 and 50 had not been satisfactorily answered,

"For that reason the Group could not consider specific recommendations to the Special Committee for Consultation and Negotiation with a view to e gradual modification, reduction or elimination of non-tariff barriers in the United States market and to improvement of the United States offer under the Generalized System of Preferences.

12/ However, at the end of 1972, i.e., two years after that statement, the draft legislation for putting a system of general preferences into effect had etili not been presented.

/"Regarding the

- 17 -

"Regarding the latter point, the Latin American countries participating in the sixth meeting of the Ad Roe Group emphasized their concern over and disagreement with the fact that the United States had not thus far put into effect its offer under the Generalized System of Preferences, in accordance with the commitments already assumed

in various regional and international forums 16/."

(d) Some asp2cts of the financial assistance provided the

United States

First and foremost it seems useful to consider the financial assistance provided to Latin America by the United Ste.tes within the oyeran context in which the economic relations between the 1-colon and that country have developed. One indicator of the development of these relations is the

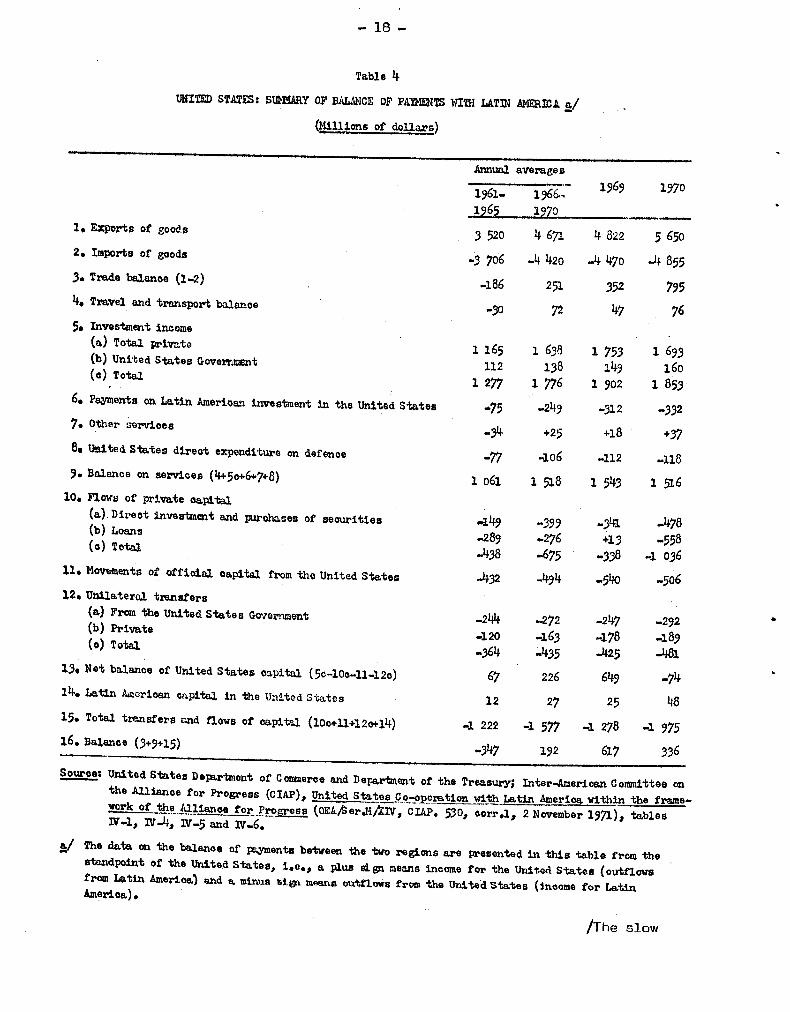

balance of payments (see table 4). It will be noted that during the five

years 1966-1970 the net flows of bilateral capital from the United States were not enough te offset that countryls trade and services surplus in its operations with Latin America, so that the United States balance of payments showed a net surplus, while in the five years 1961-1965 the opposite was

the case.

The trend recorded between the two five-year periods was mainly influenced both by the significant growth of the United States trade and services surplus and by the fact that, within the net flows of capital,

official capital grew very slowly (from 432 to 494 million dollars, in terms of annual averages, the latter being much the same as the figure for 1970), a fact which was also observable in the case of unilateral transfers. Although net flows of private capital rase by an average of about 260 million dollars annually between the first and the second five-year period, it must nt be overlooked that this increase was the result of direct investments from which the United States itself obtained an increase in income of 500 million dollars annually between the same periods, i.e., double the aboye figure.

16/Report of the Ad Hoc Group on Trade to Deal with Tariff and Non-Tariff Barriers and Related Matters to the Third Regular Meeting of the Special Committee for Consultation and Negotiation (0EA/Ser.H/XIII, CiES/CECON-COMERCI0/63), 13 December 1972.

/Table 4

- 1.8 -

Table 4 UNITED STATES: SUNMARY OF BALANCE OP PAMIERTS WITH LATIN AMERICA a/

(lillions of dollars)

Annual averages 1969 1970 1961-

1965 1966. , 1970

1. Exporte of goods 3 52o 4 671 4 822 5 650 2. Importe of geoda .3 706 -4 420 -4 470 -4 855 3. Trade balance (1-2) -186 251 352 795 4. Travel and transport balance

-50 72 47 76 5. Investment income (a) Total private 1 165 1 638 1 753 1 693 (b) United States Government 112 138 149 160 (e) Total

1 277 1 776 1 902 1 853 6. Payments on Latín American investment in the United States -249 -312 -332 7. Other services .34 +25 +18 +37 8, United States direot expenditure on defence -77 406 -112 -118 9. Balance on services (4+5e+6+7+8) 1 061 1 518 1 543 1 516 10. Flows of private capitel (a) Direct investment and purohases of seourities .149 -399 -341 -478 (b) Loans (o)

.289 ..276 +13 -558 Total .438 -675 -338 -1 036 11. Movmments of offielal capital from the United States -.432 -494 .540 -506 12. Unilateral transfers (a) From the United States Government -244 -272 -247 -292 (b) Prívate (o) Total

120 -364

-163 .435

-178 -425

-189 -481

13. Net balance of United States capital (5e-10o-11-12c) 67 226 645 .74 14. Latín American capital in the United States 12 27 25 48 15. Total transfiere and flows of capital (10o+11+12o+14) .1 222 -1 577 1 278 -1 975 16. Balance (3+9+15) -347 192 617 336

Souroe: United States Department of Commeree and Department of the Treasury; Inter-American Committee en the Allianoe for Progrese (CIAP), United States Ce -operatiaa with Latín America within the trame- work of the Allianee for Progrese (OEA/Serial/kW, CIAP. 530, eorrel, 2 November 1971), tablee 117.1, IV-4, IV.6 and 111.6.

2/ The data on the balance of payments between the twm regions are presented in this tabla from the stendpoint of the United States, i.e., a plus sign mearas income for the United Sietes (outfloww from Latín America) and a minus sign means outfloWs from the United States (income for Latín America).

/The slow

- 19 -

The slow increase in net official bilateral aid provided by the United States to Latin America - which means that there was actually a significant decline in its share in total official aid to the region - coincided with the progressive weakening of the Alliance for Progress Programme. As stated in the chapter on external financing, the new policy established by President Nixon in 1969 with respect to United States financial assistance amouhted to a large extent to recognition that the original formulation of that programme was being essentially altered. Among the main changes announced at the time was that of giving more priority to official multilateral assistance, while bilateral aid would be reduced.

Another important factor which has influenced this state of affairs is that the United States Government has been fínding it increasingly difficult to obtain prompt approval by Congress, without mejor changes, of the draft external aid legislation submitted to the latter body. On one occasion at the end of 1971, Congress even rejected the bill presented by ths Executive and, in general, the Governmentos proposalli have been subject to delays and cuts.

In these circumstances, the average annual official aid authorized for Latin America, which amcunted to 1,037 million dollars in the three years 1966-1968, was reduced to 740 million in the period 1969-1971 17/. This reduction was due not only to political considerations of a general character, but also in large measure to the impact of the worsening of the United States1 overall balance-of-payments problems, which - as noted previously - had nothing to do with its financial relations with Latin America. The restrictions will primarily affect disbursements from official bilateral sources which may be made in the early part of the 19701s.

On the whole, the prospects with respect to the evolution of official assistance from the United States to the whole of the third world during the next few years are not top bright. It is.estimated, for example, that between the two-year periods 1970-1971 and 1974-1975 the coefficient of United States official development assistance will probably be reduced

17/ See CIAP, Proyecto de informe del CIAP al CIES (CIAP/579/Add.1), 9 November 1972, table 19.

/from about

20

from about 0.31 to 0.25 per cent of its cross national product, in the light of available data on that country% external co-operation policies and budget 18/. This would mean that the real value of United States official development assistance, in absolute terms, would remain constant during that period. Naturaily, whatever happens specifically with respect to Latin America Will be in line with this overall trend and Will depend on the United States externa? co-operation policy with regard to the distribution of official development assistance over the developing regions.

In the chapter on external financing, data are given on the development of some qualitative aspects of United States official assistance, e.g,, basic credit conditions, "tying" of loans, credit for programes, etc., so these matters need not be considerad here. However, it is worth making special mention of the increase recordad in the retes of interest on AID and EXIMBANK loans, Between 1961 and 1970 the rata rose from about 2 per cent to just over 3 per cenit annualiy for the formar, and from 5.5 to 6 per cent annually for the latter, In addition, EXIMBANK credit operations took on an increasingly commwcial character, with this institution covering only half of each credit sale of goods eligible for financing, the other half being financed by private United States banks on the terms currently prevailing in the commercial credit market. In addition, the repayment period for the portion financed by EXIMBANK was reduced from 13 to about 5 years duríng the period considerad.

21/ See the statemenrt made by Mr. Robert S. McNamara, President of the International Bank for Reconstruction and Development, at the third session of UNCTAD, Santiago, 14 April 1972.

/3. Latin

— 21 —

3. Latín America's relations with the Euro ean Econcrhic Comullit

(a) Introduction

Ouring the 1960's, the European Economic Community (EEC) adopted many economic and trade policy measures that are directly related to the current or potential development of Latin Arnerica's exports to the EEC countries. These measures include the regulations that make up the common agricultura' policy; a policy that became even more protectionist and harmful to the trade interests of the majority of the developing countries as it became applied to more and more products. Other measures were connected with the process of institutional transformation that was initiated as a result of there new members joining the EEC: en historie event whose implications for third countries cannot be easily assessed, but which must be considered prejudicial to the Latín American countries in that it means that yet more markets, such as the United Kingdom market (traditionally open to imports from developing countries), will be applying the restrictive regulations in force within EEC. As a result of the adoption of the common agricultural policy (in particular its high price levels) there is a great possibility that there will be drastic changes in the structure of supply and demand for agricultura' products in the new member countries changes that will have an effect on trade flows between Latin America and the new members and the enlarged Community as a whole.

At the same time, a new and vast trade grouping aimed at stepping up economic integration is taking shape, in which the nucleus of the EEC proper is surrounded by a number of industrialized countries (for example, the ex—members of the European Free Trade Association, which are to form a free trade area with the EEC for manufactures) and a considerable number of developing countries (most of the countries of the Mediterranean basin) that are linked to the EEC through preferential—type trade agreements. There are also the ex—members of the British Commonwealth

mostly African countries — that have been given the chance, under the tercos of the treaties of accession, to opt in 1973 for any of several formulas which include association with the Community under the conditions laid down in the existing regime of association with the Associated African and Malagasy States.

/It'is

- 22 -

It is to be expected that each of these changes, which will begin to come into effect starting on 1 January 1973, will have a marked Impact - varying in aach case can the Community's trade flows. It should be borne in mind that the institutional transformations that are being effected are shaping e new structure of world trade based on the formation of a bloc with EEC at the centre surrounded by a group of European. Mediterranean and African countries that are linked to it through preferential agreements and other forms of economic and financial co-operation. To give an idea of the centripetal trends of the EEC it may be useful to note that between 1958 and 1970 the share of intra-area trade among the six EEC members as a proportion of total trade rose from 29.6 to 48.4 per cent, such trade growing annuelly by an average of 16 per cent, compared with 9 per cent for trade with the rest of the world 19/.

In other words, the establishment of this trade bloc will inevitably tend to promete trade within the bloc itself, with a number of consequences for trade with third countries, This situation undoubtedly representa a challenge to the Latin American countries as regards the future of their relations with the enlarged EEC, which has become, through its enlargement, a market for exporta comparable in importance tu the United States, and also extremely important as a source of supply. .In brief, Latin America will have to face e number of situation during the present decade that do not favour its exporta to the enlarged Community, such as an increase in agricultura) self-supply within the EEC; greater competition in the area of tropical-zona products (owing to the fact that the regime of association is being made available to the Commonwealth ccuntries) and in the area of Mediterranean-type products in general; and in addition heightened Competition for its sales of manufactures within the new European free-trade area made up of the ex-members of EFTA. Consequently, it is even more essential and urgent then ever for the Latin American countries to intensify their efforts to develop a joint pelicy vis-á-vis the Community, not only covering general principies, which have already been defined within CECLA, but also, and most important, covering the specific operational modalities on which they wish futura co-operation with the EEC to be basad.

In view of the unfavourable effects of Community regulations on their exporta to the EEC, the Latin American countries have been pressing since 1958 and 1959 for the initiation of a dialogue aimed at securing the adoption of economic and trade co-operation measures between the two regions. These

12/ "Le commerce extérieur de la Communauté", in Bulletin des Communautés européennes, N° 6, 1972.

/efforts did

T 23-

efforts did not bear fruit until 1969, when direct contacts were established between Latin America and the EEC and machinery was set up for consultation, based on periodic meetíngs of representatives of the two groups. Although it is not yet possíbIe to forecast what specific decisions may flow from this machinery, the fact that the Community tpproved it marks the biggest step forward yet in Latin America's relations with the EEC over the past ten years.

(b) Evolution of trade between Latin America and the EEC

Between the periods 1961-1965 and 1966-1970, Latin America's exports to the EEC grew at an annual rete of 6.2 per cent; while this percentage is greater than that for exports to the United States, it is less than that for intra-area exports and exports to Japan.

The nine countries of the expended EEC had a share of 27.7 per cent of total Latin American exports in 1961-1965 and 26.4 per cent in 1966-1970; the annual average rete of expansion was 4.7 per cent as against 6.2 per cent for the EEC itself. This difference was due to the lack of dynamism in exports to the United Kingdom, which only increased by an annual 0.3 per cent during the period under consideration.

The expended EEC has practically the same relative importance as the United States as a market for Latin American products. In 1971, Latin American exports to the nine EEC countries accounted for 27 per cent of the total exports of the region, compared with the 29 per cent share of the United States. If earlier growth retes continue, the Community will within a few years replace the United States as the main market for the products of the reglan.

As regards the evolution of trade by countries, it may be observed that the.group which registered the poorest growth rete was made up of the exporters of temperate-zone agricultura) products (Argentina and Uruguay), whose sales grew only at an annual average rata of 0.2 per cent for Argentina and 0.7 per cent for Uruguay between 1961-1965 and 1965-1970. This state of affairs is closely connected with the drop between 1951 and 1970 in exports of some important products such as beef to the United Kingdom market (see tabla 5) and to the Community of the Six (see table 6). Venezuela is in an even more unpromising situation, since its sales dropped at a rate of 1.8 per cent annually between 1961-1965 and 1966-1970, owing to the stagnation in its exports of petroleum. The devolopment of exports to the expended EEC by other countries, such as Colombia and Paraguay, has been more favourable.

/Tabla 5

04 04

c'd • a, O

rol r4

CO 1.^ Cr% • • •

N ON

o 4> VD O N 0

¿

h g •

O

al al

'04 O 0~4

•P Dp•irirl

r al M

Products

and SITC

olassificati

on

8

1 8

(Millions of d

o 1lars oif)

▪ 4. 1

:I

•

al

1 1 O li o

ri 1 r4 1:1 1

X.

1 4.• r x ._,

44 rf

ef al O

V O

1. r1 $4 O 03 CO d 8 .9 ›«)

.1 I ,-. « g ..4

'0 O O ort 33 1 1/40

r4 .41 r4 •r1 ON

Sa 4. g Le 4> @ rl O ad O O J1 al O

O X o

.4 o

lo ri :1 4-■ 0

.1 ,

1/40

Com mowea

lth .4

e94

ser ies

B y C, 1961-19 65.1970; Overs e

as Tr

ade Statistios of the United Kingdom, Dece mbe

r 1910 and December 1971.

- 24 - Ce1 O'N ‘.0 C4 ..4 c" .r.. oN 10 .t... .2. O'N rl k.0 01/4 01 al O ON ON • • • e • • • • • • e • • • • • • e • •

1/40 r1 1/40 r4 O 42LeN r• c."‘ co rl CV ON CID Ch N •••1 C1/4 t1/4. O\ 1/40 ri .1' 01 ClC ON rt CV ON CO CD r4 ttN N oN {••••, 4.4 ON C*4

• r.... .. CO M .0" ri ON .0' r4 N.7 .4 N cn ..4 ce% mi 4- rl

,x.... CO CN 04 L.r. \0 ON 1••• 04 1/40 0 nt ON j•••■ N .0" O N O- CN • • • • • • • • • • • • • • • • • • • • • .d. t.... O O\ ■0 CO UN C1/41 CO \D

e•-■ 2\ CN r4 el CO r■ V) r4 C"N O N. O tgi UN UN -1' r4 'SO 1/40 01 in 0.1 CO UN 1".. 04

N r4 N r4 r4

Cr\ c• ‘0 t---, UN ON 1".. ON O 'N .7 UN re.. 1-4 UN r4 /••■ 1/40 .1' r4 C4 N ON • • • • • • • • • • • • • • • • • • • e • • • cv ON CO Cr. "4 1/40 N (N rl re ..1" r-,.. ..2» In ON 01/4 O CYN CO -1' d- UN N co c•N r4 CN N 01 o^1 rl U1 N I.0. cr■ rl .1`.. 04 LIN UN ri CO O N rl 4-1 04 4-1 N CV 04

0' %.0 O 01 CV CV ON CO UN 04 t•••. .1' `.4 c0 .r... rl O «N ■0 O.. Lr, O ‘,0 • • • • • • • • • • • • • • • • • • • • • • • CN CoN 1/40 N mi ri ee, p.,. t.. V) ll" 00 t••■ e" r-I e-, ■1) O "I .4' O N 8 .o- .,•■■■ C',4 Csi ..0 5 ts. ri UN UN ..1" 04 el., \o 04 .1- UN

CV CoN 04 1/40 r4 r4 r4 r4 e.i

4sal CD Zt 0 .4 a\ UN CD CO 01 UN a\ :I- 2\ r4 0.4 c1 CD - UN .7' r4 UN ON • •• e • • • • • • • e . • . • • • • e • •

rl CD N W O.

N ri rl j••■ O rl 111 pi \ 0,1 rl O \D \O 4 r4 \

.1 eeN N r•I 04 tn ri ri .41 4.4 r4

04 ON O 1,, O Is4 1.." O co ¿-■ f.r. o■ O ri• • • • • • • • • • • • • • • • • • • •

oo oo o cv o■ o.■ 3 f.> . ri co i■ C1/4 r4 ri ,„„-. N r4

ri rl

O ‘0 U1 cs1 ‘41. O \O tr\ M \O as CV 00 Z... CO c'1 • • • • • • • • • • • • • • • .41 r4 M 1/40 C"1 O\121 \ .7" M O O CO N 0 0 1 /40, 1-1 r4 ts• 1/40 .4 CV

47- ON -1"., CN ri O 4,.. oN ON UN CV re O .7' LrN ..4 I" CO p... 00 \O 00 ..1 • • • • • • • • • • • • • • • • • • • • • • • O", N •[... UN ir ‘ t•-, eN 1/40 144 rt O ,r... Cr% O'N CO CO el rt 11 UN /1/4. 4.4 r. r. , r4 N 4-1 M CV CV N

CV -1' 4•7" 0 0 111 ON N CO 1.1% 4-1 Ch 1/40 131 t•-•• ON • • • • • • • •• •• •• •• •• • • . • • •

rt

\ 1 ' ra r4 0 UN 4-1 01 ON rl 0 0 1/40 1 coa‘ tr‘ON 1 O oo r• O N «N 4-1 O 1/40 ON UN cc2; eN r4

UN Crt rl U1 Lrv • .4. aN a., eo M• • • • • • • • • • • • • • •• • • • • • • • t11

co CO CN crt 04 r4 .7' 1/40 N 1/40 t•••• CN cc 4" t.„, t*". Csi UN %O 04 UN CM r-1 rl

O\ 0 01 • ‘414 Zt •-• CN •C`•• t•rs •••' 11:1 ••1«. • • • ' • • • ♦ • • • e • • • • • • • • UN UN

O O LN O rl CO • c; • c• O co

N rN UN .1' CC.) IX% O'N 4.4

UN CO 4-1 CV ON UN 1/40 0-t 411 ri CD ON 01 ON 441 c 4 O CD ,44 • • • • • • • • • • • • • • • • • • • • • • e CO IX 4-1 CO ON 1/40 1/40 c0 O r4 '.0 ON 1/40 U) OD O) 1/40 00 ri Ul

ers t." oo ...1• Lr■ O'. \O a,,,. Cr/ i',. a.% C.'1 UN ts. ON O -1" CO j••••• 1/40 eo CO ce. • • • • • • • • • • • • • • • • • • • • • • O\ ce‘ cn aN eo 1 \O .,? ks) crs .4 O ON CN 04 CN 1/40 UN «N ctl 0 rt t.„ ON ri C.'\ .-1 (9 tr‘ O el .. n .d• . .e.i r■ 1 UN 7 M.1- t" r.4

0> O 03 tO

O DI CO O> O>

mtt)

0.0 O 04) ta0

o

4 cd

1 11 11

th Oo oo 0 C

% E E E o

•

g g 5 O 0 o 0 t0

r4 Z4 r4 . d O d O d O d O

ri 04 .4 C. 111 C. r4 4.

g t% 4 g l'U g 10). g a 0 03 0

O< > O. 9 1.° 1 E

4 4 4 4 4 4 4 4 4 4 4 4 S 4 4 i•i

/Table 6

Products and SITC olassifioation

0 .n41. o Ir co 0 C4

1.4

.4:1 t. f..1 ti> a '4 1 11 o

1

N

4 e

1.1.

ge) rC*1 O

10

13 N4 1-4 O

qm O .10

í3 á 44 O

744

CJ

d

.4- •

.4 o 414

ko E <8

tE

O

11 CO M O \O UN NO UN

• r4 •

0 •

lt% Q • • •

\ O 1.0 Z*1

N \ O 01 01

•

o t■ o • . • • •

tr% c. 1/40

t, O Lc0A 01 CN1

- 25 -

1/1 11 ts. • - • • O co 1

CO rl

rl 01 04 0• . • • •

e. ',o o 1 UN t". O rl

• • • CO O CO .04 N 1 C4

O CO 11 10 04 • • •

•tr% 1.0• Cal

tce% O s r4

47-. r4

NO rl

o-% 1." co • e • • •

NO Cr■ 00 •A CO .4 C4 C.1 01 ei

CA. 1.0% 1.01 N rl • e e • •

ÑSr404 O O

4' N

• • ON 11 N

CO

rl

N 11 4.4 • • •

1.'"1 04 0 1 pa1,

Lo 04 •C> • • •

a-I 4' .0

O •

:-.■ •

e-1 _e •

04 04

1 L'O 4

...I' .

CNI Cn • •

N C4 1 ri r1

N CO • •

04 r4 ral 04

•0

ri • •

1O 1

O O. • •

C4 CA 01 1

cr, . . • n 2 .1

CA 01 11 CO e • • • •

CO CO \

Lh 5.\> x..\ 01 a-1

NO 0.1 CO 04 LA

01 • • • • •

Cr• O 11. UN CO \ 0 0 r4

Lel 1.1 C'N • • • • • O cr.. 01 rl CsI 0111 11 N

Ln LC1 V) • e •

01. .1-1- 01

o

ri

O al ri

f.

O

5

o. ri

Lel .0 01 0.1

1-1 •0 CIN r4

m

m

T.

O

art

Pri

Cl>

O rn

rade, series B

r4 N

CA CO O 01 O ■0 c,N v) co 4-1 oi LA .,,d- ra4 O 01 04 0 • • • • • • ' • • • • • • ' • • • • •' •

LA LA 01 \0 .1 LA 0'1 CA ...I ' N O .O. 01 '.0 0 CM 04 NO f..1 CA rl C.j11. er■ r4 ,..0 ‘0 04 LA rl I 04 0., 04 LA a-1

ri 11 CO O 4 CO 8.4

• • • e • • • •

O 04 N CO O N CO

CN1 4-1

O O .d» 04 • • •

jj CA g. 04

e-1. 04

LA LA 00 rl 11 N • a • • • •

COCO, 1 1 0.... ..& CO 8 I

CO CO CV 04 o 04 N .C... 04

1-1 •ata CO • • •

01 CO 00 04 I

04 4 ..

UN NO L" 1." 0.-4 u• t-s. r4 N • • • • • • • a •

04 N.." 8 1 ...1" 01 0-% 1 1 c., o .(,... 1 I o 04 trl, c0 LIN .O. U

04 N al 14,5

H LA CA IX1 4 cA CO $.1 .0, \O CA .-1 ON • • • • • • • • • • e • •

Ocr's CO O... 04 C`4 CO CO CO 04 O 2 g. ,,, , 1

c,-, c«, t.t1 04 N H ' 4-1 1.0

1....

d r'

CO CO CN N CO rl 11 01 CA CO 01 0'1...1- O'N O • • • • • • • • e • • • • • •

LA 01 01 LA LA 4' 14.‘ CA O CO CO CO 0 f.., CO Zse. •0 CA ..O. 04 .O- O -1' .N. 04 csi o\ ‘0 -1" rl •-4 c. .-1 c4 -f

04 cr1 u1 rl 11 01 01 O O 4 04 0 f.4 O.. C4 CO ..Z." NO • • • • • • • • • e • • • • • • • •

o\ ..I- C4 C,•■ NO /1 r.1 10 0 0 04 CV NO 1-41 4- 10 ON 04 4.4 UN C4 01 1.4 co .,.. NO 04 ON UN 4 "4 rl r4 cr \ rl

a> o %. e 1

A.

.g .1 i i d so o

o o o 40

49 49 1

1 .a

4 -a

g O O 0 O> LD 0 e o

E „.)0.

, . o d 1 ° W

O 04 k

0 0:1 O O •-I O O

b 1 m s. 1

4d o a>

> 11. > fk 1 P. > l'. ›. 1:14 r.--- tu

t1 o vi

0 11 N 3 U

cv 10 uN • • •

tr1 M CO oo

rri

•-1 co N 00

• • • tr1 o■ 1 1

o 1,0

CO O • • •

LA LA 4 10 ri

rl

• • •

1 1

ri

¿,* O

o

Latin America

9 /Colombia registorod

-26—

Colombia registered an annual export growth rato of 5.9 per cent, and Paraguay 6.9 per cent thanks to improved market conditions for tropical products. Lastly there is a third group of countries with higher export growth ratos, which includes Brazil (9.1 per cent), Mexico (8.5 per cent), Ecuador (8.5 per cent) and Chile (16.3 per cent). These countries have very different export structures, and among the many reasons for this boom are greater diversification (Brazil, Mexico) and a sustained demand for industrial raw materials (Chile) and specific tropical products (Ecuador). An unfavourable trend was observed in the case of the Caribbean countries, whose sales to the expanded Community dropped on average by 3.5 per cent annually between 1961 and 1970, even though they included trade on preferential termo with the United Kingdom.

As regards the evolution of trade by products (seo table 6), tropical agricultural products should be considerad first. Latin American exports of coffee to the Community of the Six increased their relativo share in the Community's total coffee imports from 54.7 per cent in 1961 to 59.7 per cent in 1970 (en annual average increase of 7.5 per cent). Over the same period imports from the associated African countries increased at the rete of 9.3 per cent and in 1970 accounted for 22.1 per cent of total importo of the EEC compared with 19.4 per cent in 1961. The system of special preferences in favour of the African countries has probably led to the increases in their share of trade in the Comron Market. Latin Americals share of epoca exports, which were influenced by mejor fluctuations in the supply, from the region, dropped from 24.9 per cent to 22 per cent. There was, however, a notable increase in banana sales, which doubled between 1961 and 1970 in both absoluto and relativo tormo (an annual average growth rato of 10.3 per cent compared with a rete of barely 3.9 per cent for overall Community imports of this product). The share of Latin American bananas in Community importo rose from 39.9 per cent in 1961 to 60.4 per cent in 1970. At the same time, the share of the associated African countries dropped from 25.8 to 10 per cent.

Among temperate—zone agricultural products, maize takes first place on account of its value in trade between Latin America and the EEC. This is a deficit crop in the EEC, where there is a growing demand for it, Latin American exporto maintained their relative share in total importo by the Community (around.29 per cent), thanks to en average annual growth rete of.11.0 per cent compared with 12.2 per cent for total Community importo. The demand for beef is elven more dynamic, since total EEC imports grew at an annual rete of 23 per cent between 1961 and 1970. Importo from Latin America rose by only 9,9 per cent, and hence could not maintain their relativo importance in the Community market, in which their share dropped frcm 27.3 per cent in 1961 to 13,9 per cent in 1970.

/In the

-27-

In the case of wheat, on the other handl there was an almost complete standstill in Community importe, with an annual rate of growth of 1.2 per cent between 1961 and 1970. Importe from Latin America rose by 6.6 per centannually over the same period, although they always hed a marginal position in Community importe (7.2 per cent in 1970 compared

with 4.5 per cent in 1961).

The third group of important products exportad by Latin America to the EEC consiste of raw materials for industrial use, sales of which have developed very irregularly according to the individual cases. Petroleum exporte practicelly stagnated between 1961 and 1970, and even dropped slightly in absoluta terms during this parlad, so that their relativa share dropped from 8.5 per cent to 2.8 per cent, although total EEC importe grew at an annual rete of 12.8 per cent during this parlad. One of the factors which influenced this drop in the region's relativo share was the financial interest of some members of the enlarged EEC in the expandan of petroleurn production by the countries of North Africa in the 1960Is. Another factor was the failure of Venezuelan production to maintain a rate of growth comparable with that of world production.

Wool exports showed even pobrer trends. Owing to growing competition of synthetic fibres, total imports by the Community dropped by 2.8 per cent annually between 1961 and 1970, and this decline reached 12 per cent annually in the case of importe from Latin America, whose relativa share in the total dropped from 12.4 per cent to 5.1 per cent during this period. As regards cotton, however, Latin American exporte of this commodity to the Community improved their percentage share in the market from 19 to 29.4 per cent between 1961 and 1970, despite a drop in total importe of cotton.

Demand for iron ore and refinad copper grew rapidly in the EEC, and importe from Latin America developed at a rata comparable with that of total supplies to the CoMmunity. Thus, Latin American exporte uf iron ore increased by 6.5 per cent annually, improving to some extent thair share in the Community market, while exporte of refinad copper went up by 14 per cent annually, comparad with the 12.7 per cent annual increase in total Community importe of this metal, and in 1970 they accounted for 20.7 per cent of the market of the Six, compared with 18.7 per ccn -; in

1961. It should be borne in mind that all these retes refer dallar values of the trade flows.

/As regards

22/ If the African countries which are members of the Commonwealth joie the Yaoundé Convention, the members of the Associated African and Malagasy'States will very probably enjoy free access to the markets of the United Kingdom and the other new members of the Community.

/As regards

— 28 —

As regards Latin American exporte to the United Kingdom, which in competition with the CommonweaIth countries, whose exporte play an important role in this trade, the case of coffee exporte is worthy of mention. United Kingdom coffee importe from Latin AMerica increased from 33.8 per cent of total coffee importe in 1961 to 45.8 per cent 1971, but the share of the Commonwealth countries rose from 8.5 per cent to 43.6 per cent. This means that although the position of Latin America improved during the 1960's it is facing growing competition from the Commonwealth countries, and the situation could become still more serious when the United Kingdom market is opened up to néw preferential exporters 20/ and the cemmon externa). tariff is adopted,

The value of the United Kingdomws importe of beef from Latin America dropped from 84,3 million donare in 1961 te 61.8 million in 1971, while the regionEs relative share in that country/s total importe of beef dropped from 54,3 per cent te 24,5 per cent. Imports from the Commonwealth doubled in value (from 28.9 to 56,7 million dollars) and their share in the British, market increased from 18.6 to 22.5 per cent, Trade flows from the preferential suppliers (Commonwealth and Ireland) have thus been strengthened to the detrimeht of other traditional suppliers such as the Latin American countries,

As the entry of the United Kingdom into the European Economic Community will mean the suppression of the preferences of some Commonwealth countries, (Australia and New2ealand), the United Kingdom may well reorient its purchases over the next few years towards the new preferential suppliers of the expended Community, provided these have sufficient export capacity.